UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-08200

BRIDGEWAY FUNDS, INC.

(Exact name of registrant as specified in charter)

| | |

5615 Kirby Drive, Suite 518 | | |

Houston, Texas | | 77005-2448 |

| | |

(Address of principal executive offices) | | (Zip code) |

Michael D. Mulcahy, President

Bridgeway Funds, Inc.

5615 Kirby Drive, Suite 518

Houston, Texas 77005-2448

(Name and address of agent for service)

Registrant’s telephone number, including area code: (713) 661-3500

Date of fiscal year end: June 30

Date of reporting period: July 1, 2008 and December 31, 2008

Item 1. Reports to Stockholders.

| | |

| | A no-load mutual fund family of domestic funds |

| | |

| |

| | Semi-Annual Report December 31, 2008 (Unaudited) |

| | | | |

| | |

| | AGGRESSIVE INVESTORS 1 | | BRAGX |

| | (Closed to New Investors) | | |

| | |

| | AGGRESSIVE INVESTORS 2 | | BRAIX |

| | |

| | ULTRA-SMALL COMPANY | | BRUSX |

| | (Open to Existing Investors—Direct Only) | | |

| | |

| | ULTRA-SMALL COMPANY MARKET | | BRSIX |

| | |

| | MICRO-CAP LIMITED | | BRMCX |

| | |

| | SMALL-CAP GROWTH | | BRSGX |

| | |

| | SMALL-CAP VALUE | | BRSVX |

| | |

| | LARGE-CAP GROWTH | | BRLGX |

| | |

| | LARGE-CAP VALUE | | BRLVX |

| | |

| | BLUE CHIP 35 INDEX | | BRLIX |

| | |

| | BALANCED | | BRBPX |

TABLE OF CONTENTS

Bridgeway Funds Standardized Returns as of December 31, 2008*

| | | | | | | | | | | | | | | |

| | | | | Annualized | | | | | |

| Fund | | Dec. Qtr.

10/1/08

to 12/31/08 | | 1 Year | | 5 Years | | 10 Years | | Inception

to Date | | Inception

Date | | Gross

Expense

Ratio | |

Aggressive Investors 1 | | -32.80% | | -56.16% | | -5.30% | | 7.90% | | 12.59% | | 8/5/1994 | | 1.78% | |

Aggressive Investors 2 | | -32.58% | | -55.07% | | -2.90% | | NA | | 0.65% | | 10/31/2001 | | 1.17% | |

Ultra-Small Company | | -27.19% | | -46.24% | | -4.19% | | 12.05% | | 13.99% | | 8/5/1994 | | 1.07% | |

Ultra-Small Co Market | | -27.93% | | -39.49% | | -4.42% | | 9.44% | | 8.01% | | 7/31/97 | | 0.66% | |

Micro-Cap Limited | | -26.74% | | -41.74% | | -6.22% | | 7.62% | | 8.00% | | 6/30/1998 | | 0.75% | |

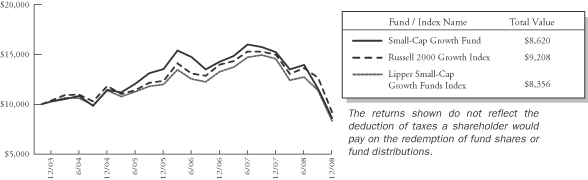

Small-Cap Growth | | -25.43% | | -43.48% | | -3.44% | | NA | | -2.83% | | 10/31/2003 | | 0.87% | |

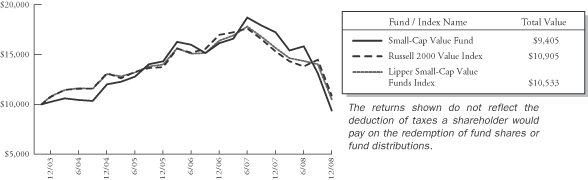

Small-Cap Value | | -28.58% | | -45.57% | | -1.74% | | NA | | -1.18% | | 10/31/2003 | | 0.83% | |

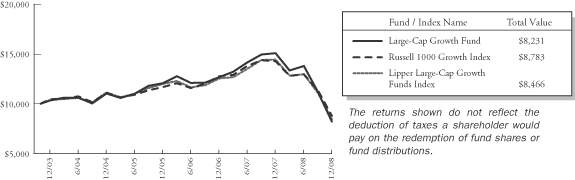

Large-Cap Growth | | -26.49% | | -45.42% | | -4.46% | | NA | | -3.70% | | 10/31/2003 | | 0.71% | |

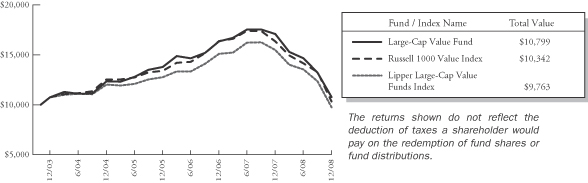

Large-Cap Value | | -18.26% | | -36.83% | | 0.11% | | NA | | 1.50% | | 10/31/2003 | | 0.80% | |

Blue Chip 35 Index | | -19.01% | | -33.30% | | -3.06% | | -0.94% | | 2.09% | | 7/31/97 | | 0.22% | 1 |

Balanced | | -9.19% | | -19.38% | | 1.07% | | NA | | 2.13% | | 6/30/2001 | | 0.88% | |

1 Some of the Fund’s fees were waived or expenses reimbursed otherwise returns would have been lower. The Adviser has contractually agreed to waive fees and/or reimburse expenses such that the total operating expenses of the Fund do not exceed 0.15%. Any material change to this Fund policy would require a vote by shareholders.

Bridgeway Funds Returns for Calendar Years 1995 through 2008*

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | 1995 | | 1996 | | 1997 | | 1998 | | 1999 | | 2000 | | 2001 | | 2002 | | 2003 | | 2004 | | 2005 | | 2006 | | 2007 | | 2008 |

Aggressive Investors 1 | | 27.10% | | 32.20% | | 18.27% | | 19.28% | | 120.62% | | 13.58% | | -11.20% | | -18.01% | | 53.97% | | 12.21% | | 14.93% | | 7.11% | | 25.80% | | -56.16% |

Aggressive Investors 2 | | | | | | | | | | | | | | | | -19.02% | | 44.01% | | 16.23% | | 18.59% | | 5.43% | | 32.19% | | -55.07% |

Ultra-Small Company | | 39.84% | | 29.74% | | 37.99% | | -13.11% | | 40.41% | | 4.75% | | 34.00% | | 3.98% | | 88.57% | | 23.33% | | 2.99% | | 21.55% | | -2.77% | | -46.24% |

Ultra-Small Co Market | | | | | | | | -1.81% | | 31.49% | | 0.67% | | 23.98% | | 4.90% | | 79.43% | | 20.12% | | 4.08% | | 11.48% | | -5.40% | | -39.49% |

Micro-Cap Limited | | | | | | | | | | 49.55% | | 6.02% | | 30.20% | | -16.61% | | 66.97% | | 9.46% | | 22.55% | | -2.34% | | -4.97% | | -41.74% |

Small-Cap Growth | | | | | | | | | | | | | | | | | | | | 11.59% | | 18.24% | | 5.31% | | 6.87% | | -43.48% |

Small-Cap Value | | | | | | | | | | | | | | | | | | | | 17.33% | | 18.92% | | 12.77% | | 6.93% | | -45.57% |

Large-Cap Growth | | | | | | | | | | | | | | | | | | | | 6.77% | | 9.33% | | 4.99% | | 19.01% | | -45.42% |

Large-Cap Value | | | | | | | | | | | | | | | | | | | | 15.15% | | 11.62% | | 18.52% | | 4.49% | | -36.83% |

Blue Chip 35 Index | | | | | | | | 39.11% | | 30.34% | | -15.12% | | -9.06% | | -18.02% | | 28.87% | | 4.79% | | 0.05% | | 15.42% | | 6.07% | | -33.30% |

Balanced | | | | | | | | | | | | | | | | -3.51% | | 17.82% | | 7.61% | | 6.96% | | 6.65% | | 6.58% | | -19.38% |

Performance figures quoted represent past performance and are no guarantee of future results. Current performance may be lower or higher than the performance data quoted. Investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than original cost. To obtain performance current to the most recent month-end, please visit our website at www.bridgeway.com or call 1-800-661-3550. Total return figures include the reimbursement of dividends and capital gains.

This report is submitted for the general information of the shareholders of each Fund. It is not authorized for distribution to prospective investors unless preceded or accompanied by an effective prospectus, which includes information regarding a Fund’s risks, objectives, fees and expenses, experience of its management, and other information. Investors should read the prospectus carefully before investing in a Fund. For questions or other Fund information, call 1-800-661-3550 or visit the Funds’ website www.bridgeway.com. Funds are available for purchase by residents of the United States, Puerto Rico, U.S. Virgin Islands and Guam only. Foreside Fund Services, LLC, Distributor.

The views expressed here are exclusively those of Fund management. These views including those relating to the market, sectors or individual stocks are not meant as investment advice and should be not considered predictive in nature.

* Numbers with green highlight indicate periods when the Fund outperformed its primary benchmark.

LETTER FROM THE INVESTMENT MANAGEMENT TEAM

December 31, 2008

Dear Fellow Shareholders,

In the midst of the worst quarterly stock market decline since 1987, as well as what has now become the worst overall bear market since the 1930’s, each of our Funds also set new “worst quarter” performance records. On a relative basis, six of eleven funds provided some cushion against the decline of their primary market benchmarks. Our full-year performance was worse, with only four of eleven Funds outperforming their primary market benchmarks. With the exception of one fund (Ultra-Small Company Fund) in 1998, 2008 is the only year in Bridgeway’s 15+ year history that we have underperformed a primary market benchmark in a down year. 2008 was thus a very poor overall record of relative performance by Bridgeway standards. Disappointed is not a strong enough word. Our most aggressive Funds, Aggressive Investors 1 and 2 Funds, lagged their benchmarks the most in the quarter. At the other end of the spectrum, Large-Cap Value, Small-Cap Growth, Blue Chip 35 Index, Ultra-Small Company and Micro-Cap Limited Funds provided some cushion against the fall of their market and peer benchmarks, while Balanced Fund beat its peer benchmark.

An overview of market factors that negatively impacted our returns is described in the “Market Review” section on page 3. Beyond the overall steep market decline, these factors contributed to our poorer-than-benchmark returns:

| | • | | A number of Funds were positioned toward the growth stock spectrum, i.e. companies that have experienced faster rates of growth. Across all size stocks, growth-stocks performed more poorly in the quarter (and year), despite what we measured as strong relative valuations in this market segment. For example, the style box “home” of Aggressive Investors, mid-cap growth stocks (down 43.9%), significantly underperformed small-cap value stocks (down “only” 32.4%) according to data from Morningstar. |

| | • | | Unlike the bear market of 2000-2002, some of the hardest hit stocks had solid balance sheets, strong earnings, and historically favorable valuations. Simiarly, one of our normally diversifying models picked up some “deep-value” stocks, including a financial stock, which were hit late in the downturn. |

| | • | | A number of our models had identified strong picks among chemical and energy stocks. While these stocks significantly helped our strong performance of the June quarter, the models didn’t know that commodity prices, and thus the revenues of these companies, would be falling precipitously, as crude oil prices declined from a peak of $146/barrel in July to a December low of less than $31/barrel. |

| | • | | One of Bridgeway’s risk management “safety nets” is intended to guard against too high an overconcentration in one sector or industry. While this part of our risk process did “kick in,” reducing the amount of chemical and energy stock we would have held otherwise, it didn’t recommend trimming stocks at a rate that would have been as helpful as it did for technology stocks in 1999/2000. More details appear on pages 6 to 7. |

We had such a strong response from our October paper, “How to Survive and Succeed Through a Bear Market,” that we updated it with more current numbers and put it on our website. One of our major conclusions is to focus on “time to return to the previous peak.” You can get our “take” on when the market might recover on pages 3 to 4.

Discussing 2008 and our Funds’ performance feels quite a bit like “Monday morning quarterbacking.” We dissect the results of our worst performers on pages 5 to 6 in a section by the same name. We’re glad to be leaving 2008 behind. And looking forward to climbing back up the performance ladder—though we can’t guarantee and don’t want to guess exactly how long that will take. We do provide two data points of how our Funds have performed during some short-term “bounce back” periods on pages 7 to 8.

After a year like 2008, it’s fair to question the appropriateness of quantitative investing. Our position is presented on page 7. Finally, each calendar year we have a friendly competition against Morningstar’s “Fund picks.” After a pretty good year for Bridgeway in 2007, 2008 goes to Morningstar. The “score” was Bridgeway 3, Morningstar 8.

LETTER FROM THE INVESTMENT MANAGEMENT TEAM (continued)

As always, we appreciate your feedback. We take your comments very seriously and regularly discuss them internally to help in managing our Funds and this company. Please keep your ideas coming—both favorable and critical. They provide us with a vital tool helping us serve you better.

Sincerely,

Your Investment Team

| | |

| 2 | | Semi-Annual Report | December 31, 2008 (Unaudited) |

LETTER FROM THE INVESTMENT MANAGEMENT TEAM (continued)

Market Review

The Short Version: Any way you slice it or dice it, it was a very very ugly year.

The depth of the 2008 bear market trumps every other year since 1931. The sub-prime lending fiasco early in the year spread to the broader credit market, hurting companies dependent on debt for their operating cycle (e.g. funding purchases for inventory) and fixed asset needs (e.g. major equipment). As some people lost their jobs (unemployment rose from under 5% at the beginning of the year to over 7% by the end of the year) and as housing values declined and foreclosures climbed, consumer and corporations alike “pulled in their reins” in the uncertain environment. By the end of the September quarter, declining forecasts and plummeting stock prices had affected the vast majority of businesses. These in turn also fed a “fear mentality,” reinforcing the recession’s progress. Official numbers became available that a recession began in December 2007. Most of this negative news accelerated in the December 2008 quarter, even as the Federal Reserve and Congress struggled to stabilize the economy with rock bottom Federal Funds rates and bailout packages. Assuming it lasts until May 2009, which we think is quite possible, this will become the longest recession since the 1930’s.

How did all of these factors affect the stocks of various industries and sectors? No sector of the economy was left unscathed. Among the components of the S&P 500 Index, financial companies (banks, insurance companies, and real estate companies) led the decline at 55%. Typically, non-cylical companies (food and healthcare) and utilities are the ones that hold up best in a recession since people continue to eat and to heat and cool their homes. However, even these stock prices were hard hit as non-cyclicals declined 20% for the year and utilities declined 29%.

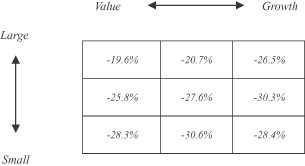

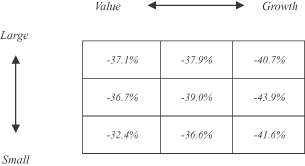

Looking at the market from a “style box” perspective below, no corner of the market, large or small, value or growth, held up either. Nevertheless, there were some dramatic differences between corners of the style box. Mid-cap growth stocks really took it on the chin in both the quarter and the year, especially negatively impacting our Aggressive Investors Funds. The “style box” stock market data below is from Morningstar:

| | |

Dec 2008 Quarter | | Calendar 2008 |

| |  |

How Long Will This Bear Market Last?

The Short Version: (Very) generally speaking, the deeper the recession, the farther the market decline and the longer it takes to recover to a previous stock market peak. The stock market has already declined farther than any time since the 1930’s, and we think it’s likely that unemployment could reach double digits. However, we don’t expect a depression (e.g., 25% unemployment at the peak in the 1930’s). Based on modern history, a normal length of time to recover from these levels would be from a few months to four or five years. Since it’s impossible to know and can be very risky to try to time the market, our own strategy is to “sit tight” (remain invested) with money one doesn’t plan to actually spend in the next few years.

Since our September quarter letter, the broader market averages have broken through to new lows, setting new records. As measured by the percentage decline of the S&P 500 Index from the peak on October 9, 2007, to the low on November 20, 2008, this is now the worst bear market since the Great Depression. The total market capitalization (the value of all shares of all companies’ stock) declined by just more than half between the all time high and the recent low of the current bear market. As mentioned in the cover letter, last October on our website, we presented an analysis of bear markets and actions you can take (and not take) seeking to “survive and succeed” through a bear market. We have now updated that analysis, which is available online at: www.bridgeway.com/assets/pdf/Surviving a Bear Market 2009.02.pdf.

LETTER FROM THE INVESTMENT MANAGEMENT TEAM (continued)

One question frequently asked by shareholders is, “How long will this bear market last?” Bridgeway is not a proponent of macroeconomic analysis to provide insights to stock market movements. However, our investment management team does believe that history can provide good insights into risks. Along these lines, we believe the updated data in the table below gives some relevant insights, which were outlined in the bear market piece referenced above. The conclusion we’d like to highlight is that while most people focus on the magnitude of decline, we think a better place to focus—assuming that it really is long-term money you are investing in the stock market—is length of time to recovery. Thus, the relevance of the question, “How long will this bear market last?”

The data below which includes the Great Depression (first line), shows some correlation between the magnitude of a recession, the magnitude of a stock market decline, and the time it takes for the stock market to recover. One way to look at this is that the stock market, as a leading indicator, is currently “signaling” that this recession will be one of the deeper and longer ones since the 1930’s. We feel it is more likely that the unemployment rate will continue to climb in early 2009. The big questions are, “Has the recent market decline already incorporated the severity of this recession?” and “How long will the recovery take?” If you believe as we do, that the eventual peak of unemployment is on the order of magnitude of 10%, rather than the 25% of the Great Depression, it is reasonable to believe that the time to recovery will look more like recent history, rather than the longer timeframe of the Great Depression. If this is true, a “longer” time to recovery might be four or five more years. But keep in mind that it can also be very quick. In the bear market of 1980-1982, the unemployment rate hit the worst level since the Great Depression, over 10%. However the time to recovery from the trough was a remarkably fast 2 months. Our conclusion is three-fold: a) a reasonable timeframe to recovery is probably two months to four or five years, b) this likely range is quite variable (we translate: impossible to predict with accuracy), and c) it is thus a very bad idea to try to time it. From this we conclude again our philosophy that we have held since Bridgeway’s founding: don’t time the market and don’t put money in the market that you might need in the near term.

One other note to highlight from the table: with reference to the last line, based on recent market activity, we are not sure if we have reached the low for the current bear market.

| | | | | | | | | | | | | | | |

| Analysis of Bear Markets Since the Great Depression | |

Date of

Peak | | Date of

Low | | Date Back

to Previous

Peak | | Magnitude

of Decline | | | Peak

Unemployment

Rate | | | # of Months

From Peak

to Low | | # of Months

From Low to

Prev. Peak | |

| Sep 16, 1929 | | Jun 1, 1932 | | Jan 3, 1945 | | -84.7 | % | | 24.9 | % | | 33 | | 151 | * |

| May 31, 1946 | | Oct 9, 1946 | | Oct 11, 1949 | | -25.5 | % | | 7.9 | % | | 5 | | 36 | |

| Dec 12, 1961 | | Jun 26, 1962 | | Apr 24, 1963 | | -26.9 | % | | 6.0 | % | | 6 | | 10 | |

| Feb 9, 1966 | | Oct 7, 1966 | | Mar 23, 1967 | | -20.4 | % | | 3.9 | % | | 8 | | 5 | |

| Nov 29, 1968 | | May 26, 1970 | | Mar 15, 1971 | | -33.1 | % | | 6.1 | % | | 18 | | 10 | |

| Jan 11, 1973 | | Oct 4, 1974 | | July 9, 1976 | | -44.8 | % | | 9.0 | % | | 21 | | 21 | |

| Nov 28, 1980 | | Aug 12, 1982 | | Oct 7, 1982 | | -20.2 | % | | 10.4 | % | | 21 | | 2 | |

| Aug 25, 1987 | | Oct 19, 1987 | | May 17, 1989 | | -32.9 | % | | 6.0 | % | | 2 | | 19 | |

| Sep 1, 2000 | | Oct 9, 2002 | | Oct 23, 2006 | | -47.5 | % | | 6.3 | % | | 25 | | 48 | |

| Oct 9, 2007 | | Nov 20, 2008 | | NA | | -50.7 | % | | 7.2 | % | | 13 | | | |

| Avg. excluding Great Depression & current | | -31.4 | % | | 7.0 | % | | 13 | | 19 | |

Information for the current bear market is through December 31, 2008

| * | While the S&P Composite Index took twelve and a half years to return to the previous peak in the Great Depression, some market benchmarks touched the level of the previous high in seven years, before dipping down again. |

Underperforming in a Down Market Year—A major dent in Bridgeway’s armor

The Short Version: With the exception of one Fund in one year, Bridgeway has never underperformed a primary market benchmark in a down year. Unfortunately, 2008 shattered that record.

Before 2008, Bridgeway had 15 (overlapping) data points about how the active funds we manage performed against market benchmarks in the same style. The down years were 1998 (ultra-small stocks only), 2000 (all stock categories), 2001 (large stocks), 2002 (all stock categories), and 2007 (ultra-small, micro-cap, small-cap value, and large-cap value stocks). In 14 of the 15 cases, we outperformed in these down market years. The only other periods of underperformance were in up market

| | |

| 4 | | Semi-Annual Report | December 31, 2008 (Unaudited) |

LETTER FROM THE INVESTMENT MANAGEMENT TEAM (continued)

years. This was not surprising to us, since our stock picking model design, investment process, and risk process are all designed with an objective of not “adding to the pain” by underperforming in a down market. That record was reasonably shattered in 2008—the worst stock market calendar year since 1931—as seven of nine actively managed Bridgeway Funds underperformed their market benchmarks and only five of all eleven Bridgeway Funds outperformed their peer benchmarks. The following several sections attempt to answer the questions “How were our Funds positioned with respect to the bear market?” and “What contributed to the dismal performance? ”and “Do we think quantitative investing will work again in the future?”

Monday Morning Quarterbacking for 2008

The Short Version: At the beginning of 2008, if you knew this was going to be a bad year led by the financial sector, knew we were positioned light on financial stocks and light on companies with debt, you might think that at least this would be a good year on a relative basis. Not so for a majority of our Funds.

In a calendar year in which only four of our eleven funds beat their market benchmarks and five beat their peer benchmarks, it’s appropriate to look back and reflect, to understand the reasons for lagging returns where they occurred. Each Fund section below will address this by individual Fund, but since some of the reasons are common across a number of Funds, we’d like to address these in summary fashion, concentrating on our actively managed Funds, and specifically our highest octane Funds (Aggressive Investors 1 and 2)—which performed the most poorly.

If all we knew at the beginning of the calendar year was that a) we were entering a recession and the worst bear market of the last 75 years, b) Bridgeway has outperformed our market benchmarks in down years the vast majority of the time, c) this bear market would be led by a financial crisis and financial stocks would fall the farthest of any sector, d) our models were significantly underweighted in financial stocks, e) the stocks we did own had, in aggregate, less debt versus their peers, and were thus more conservatively positioned with respect to the negative effects of financial leverage in a recession, and f) we were significantly overweighted in the stocks that historically have correlated least well with the overall market (i.e., in stocks that provided the most diversification historically), we would conclude that chances were strong that it would be a rough year on an absolute basis, but that we would likely provide some nice “cushion” against the fall, as we have in most previous down market years. Unfortunately, this was not so across most of our Funds, and two, Aggressive Investors 1 and 2, underperformed their market benchmarks by double digit amounts. What happened?

Dissecting the 2008 Underperformance of Aggressive Investors 1 and 2

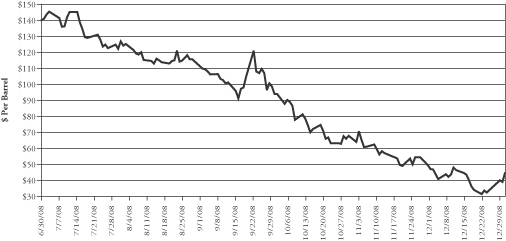

The Short Version: As with the September quarter, the precipitous decline of commodity prices took a strong bite out of some of our Funds.

The primary reasons for our December quarter Aggressive Investors poor performance were very similar to the September quarter, as outlined in the prior quarter shareholder letter. While financial stocks continued to take much of the business news headlines, we were significantly underweighted in these stocks, and the stocks we did own outperformed their category, in total adding more than two percentage points to returns on a relative basis. However, approximately 18% of the Aggressive Investors Funds was invested in stocks of basic materials (mostly chemicals) during the December quarter, while approximately 10% was invested in energy stocks. Energy and other commodity prices continued to plummet during the quarter, pounding oil and gas, coal, iron and steel, and chemical stocks in the process. In spite of the fact that the indicated valuations of these stocks had become amazingly cheap, the adage “cheap stocks can, nevertheless, always become cheaper” was definitely true. And ultimately, if commodity prices remain at the current depressed levels, revenues and earnings of

LETTER FROM THE INVESTMENT MANAGEMENT TEAM (continued)

these companies dry up, along with the stellar cash flows and strong balance sheets. The graph below presents the prices of crude oil, just one example of commodity prices, which nevertheless tells the story.

West Texas Crude Oil June 30, 2008 to December 31, 2008

Cash is King or The Effects of Cash on Relative Performance

The Short Version: The average mutual fund maintains about 5% cash. This provides some cushion in a severe bear market, but is a significant drag on performance over the long haul. Since our strategy is based on long-term performance, we seek “full investment” or close to zero cash.

In a bear market and recession, it’s great to be sitting on a bunch of cash. In fact, coming into the December quarter, the average domestic equity fund held more than 5% of net assets in cash. Two advantages of this are that you can theoretically deploy this cash to invest in stocks that are much cheaper than at the market peak, and mathematically, it shields a Fund from some of the free fall of a bear market. For example, if a Fund held 5% cash from the market peak in October 2007 through the 50% decline in November 2008, the cash would add roughly 2 1/2 percent return relative to the broader market. That’s not chump change. So why did Aggressive Investors 1 and 2 hold almost no cash during this period?

One concept in engineering and economics is “opportunity cost,” or the cost of an opportunity that must be forgone in order to pursue a certain action. The benefit of a fund holding cash is improved relative performance in a downturn, and potentially putting that cash to work at a favorable price. The disadvantage or opportunity cost is “cash drag” in an up market. Thus, if the average interest on cash is about three and a half percent per year and the average return of stocks is ten percent per year (the average over the last eight decades including the Great Depression and current bear market), you will come out ahead owning stocks over the long haul. This begs the question of whether a Fund manager could hold little or no cash on the way up and more on the way down. However, previous studies indicate that the reverse is true; managers tend to move into cash closer to a market bottom than a market top. Since we think trying to time the market is a very bad idea, we think holding cash is a doubly bad idea.

Top-Down Risk Control

The Short Version: Our process in managing the risk of industry and sector concentration did not work as well in 2008 in our Aggressive Investors’ styles as in some previous years.

Part of Bridgeway’s risk management process is to review sector and industry concentrations (how much we own of chemical stocks or technology stocks, for example) to ensure that related stocks don’t all decline at the same time. For example, late in 1999, technology stocks comprised too large a percentage of Aggressive Investors 1 Fund’s net assets and we both put a hold on new buys and looked for early opportunities to trim back on these stocks, even though our stock picking models continued to identify new technology buys. Our trimming helped cushion the stock market decline in 2000, as these stocks were particularly hard hit. Similarly, this risk “hold/trim” process kicked in with respect to internet stocks in Micro-Cap Limited Fund in 2003 as these stocks came roaring back. Energy stocks received the same treatment in Aggressive Investors 1 and 2 in 2005, as energy comprised a concentrated 35% of our Fund in September of that year. A natural question, then, is “Why didn’t this process ‘kick in’ with respect to Aggressive Investors’ concentration in basic materials and energy stocks?

| | |

| 6 | | Semi-Annual Report | December 31, 2008 (Unaudited) |

LETTER FROM THE INVESTMENT MANAGEMENT TEAM (continued)

The short answer is, “they did, just not as early and as dramatically as would have been really helpful.” In fact, by late summer both basic materials and energy stocks were on our “watch list” with respect to risk. We noticed that these two groups had become unusually strongly correlated with each other and we put a “hold” on the sum of these two groups. Thus, we did, in fact, buy fewer of these stocks than we would have otherwise. However, the risk was not appraised to be so dramatic that we aggressively sold these stocks. Thus, we bore significantly more damage from a concentrated part of our Fund than at any time in Bridgeway’s history, or John’s experience before Bridgeway.

Does Bridgeway Think Quantitative Investing Will Work in the Future?

The Short Version: Not all of our Funds underperformed in 2008, but our highest octane ones certainly did. The statistical concept of “reversion to the mean” would indicate that the “pendulum” may swing back the other direction toward positive relative performance, but we advise people against trying to time this. Overall, we have faith in our process, and actual history over 14 years gives us both experience and confidence.

Focusing on Aggressive Investors 1 as one of our longest running actively managed funds, our quantitative models have helped us beat our primary market benchmark in nine of fourteen years since inception and by an average of 5.8% per year as presented on page 10. One to two-year periods of underperformance have been followed by periods of outperformance. We can’t make any representations about future performance, but we can state definitively what we think are the advantages of quantitative investing:

| | • | | taking emotion out of the process. Emotions tend to push investors in the direction of selling when stocks are low and buying after a runup. This is a formula for financial disaster, and quantitative models are extremely helpful in keeping us disciplined and unemotional. |

| | • | | lack of dependence on a single person (a four-person team runs the models, and this team is supported by experienced staff in trading, accounting, compliance, information technology, etc.) |

| | • | | a historical framework to assess risk. |

| | • | | an efficient structure which feeds a low cost structure. |

| | • | | the ability to back-test, learn and refine with real, historic data. |

Why Did Bridgeway’s More Actively Managed Funds Perform So Much Better in the Bear Market of 2000-2002?

The Short Version: The 2000-2002 bear market was driven more by company economics and our models did very well on a relative basis. Event driven markets, or ones where there is not a strong relationship between stock prices and company level economic results are not as favorable to our models overall.

Each bear market—and bull market, for the matter—has its own unique characteristics. The bear market of 2000-2002 was driven by fundamental economic factors that were measurable based on company level financial data. Relative valuations also played a big role. Our quantitative models did a good job of picking up on these valuations and trends. For example, Internet stocks, many of which had little in the way of actual revenues, earnings, and cash flows were among those hardest hit. Since, in aggregate (this is not true across the board), our models look for these financial fundamentals and rank their attractiveness, we were “light” on those stocks which were hardest hit. By contrast, the bear market of 2008 was very fast moving and some of the companies hardest hit started out the bear market with very strong valuations based on historical standards. Nevertheless, company fundamentals were eventually affected, either by plummeting commodity prices, as highlighted above, or with deteriorating financial performance as various real aspects of the recession kicked into high gear. Examples of the latter are a decline in capital spending and shrinking inventories, as companies scaled back in anticipation of lean times and as it became very difficult or impossible to plan for future demand for a company’s goods or services. Some of this is fear driven which feeds on itself. Event driven markets, or ones where there is a delinking of company level economic results and stock price movements tend to be a poorer environment for our models.

“Bounce-Back” Data

The Short Version: When the markets do eventually turn around, will our Funds bounce back with them? Only time will tell, but we can look at two smaller data points on this topic. With respect to our higher octane actively managed Funds—those that dropped the most in the downturn—both of these data points are positive.

One of our biggest concerns in a precipitous bear market is that we might do more poorly than the market on the way down, as we have—our first market-lagging returns in a down market year—only to have our models then rotate into more conservative stocks, which do more poorly on the way back up, if the latter also happened precipitously. There are some safeguards in Bridgeway’s process to protect against this, but we’ve been looking for some periods where the market bounces back off a low point to measure our Funds’ reaction. Now we have a couple of confirming data points in the current bear market. On October 13, 2008, for example, the S&P 500 Index popped back up 11.58% after a horrible prior week. Bridgeway Aggressive Investors 1 and 2 popped back up 14.99% and 15.20%, respectively. More importantly—but still just

LETTER FROM THE INVESTMENT MANAGEMENT TEAM (continued)

a data point—we bounced back significantly farther from the current bear market low on November 20 to a recent, or intermediate, high point on January 6, 2009. The table below presents the results for our actively managed Funds. Our more aggressive Funds bounced back very nicely. Also noteworthy is the fact that of the two Funds which didn’t bounce back farther than their respective market benchmarks, neither were among our more aggressive Funds, and one had outperformed it’s benchmark over the full calendar.

| | | | | | | | |

| | | | | “Bounce-back” Performance 11/20/08-1/6/09 |

| Fund | | Market

Benchmark | | Market

Benchmark | | Fund | | Difference |

Aggressive Investors 1 | | S&P 500 Index | | 24.69% | | 35.50% | | 10.81% |

Aggressive Investors 2 | | S&P 500 Index | | 24.69% | | 34.02% | | 9.33% |

Ultra-Small Company | | CRSP 10 (estimated) | | 28.74% | | 33.75% | | 5.01% |

Micro-Cap Limited | | CRSP 9 (estimated) | | 29.23% | | 36.50% | | 7.27% |

Small-Cap Growth | | Russell 2000 Growth | | 33.99% | | 30.03% | | -3.96% |

Small-Cap Value | | Russell 2000 Value | | 33.96% | | 38.40% | | 4.44% |

Large-Cap Growth | | Russell 1000 Growth | | 25.17% | | 26.99% | | 1.82% |

Large-Cap Value | | Russell 1000 Value | | 26.98% | | 24.74% | | -2.24% |

Balanced | | Balanced Benchmark | | 10.21% | | 13.27% | | 3.06% |

Please note that the two data points referenced in this section are very short term in duration and were specifically picked to investigate “bounce-back” potential within the bear market environment. They may not be representative of “bounce-back” potential of a much longer duration or higher magnitude market move. In any case, past performance does not guarantee future returns.

Debt Levels and the Recession

The Short Version: In aggregate, each of our Funds is more conservatively positioned than the broader market with respect to debt.

You may recall that for Bridgeway’s actively managed Funds, those except Blue Chip 35 Index and Ultra-Small Company Market, we consider ourselves to be a “bottom-up stock picking shop.” This means we don’t do “top-down” macroeconomic or sector fundamental analysis, but rather seek to buy one stock at a time by considering company level data. However, three things we do pursue from a “top-down” basis are a) cost efficiency (operating costs, such as the cost to service your account, and transaction costs, the costs associated with buying and selling shares of stock), b) tax efficiency (paying attention to the timing of taxable gains), and c) risk management, themes that run through our shareholder letters. In the last category, we discussed risk management associated with sector and industry concentration risk above. Another risk we began focusing on early last summer was the level of debt our companies held. At a time that credit became very tight, i.e. banks were increasingly unwilling to lend or might look for excuses to discontinue or “call” outstanding loans, we asked the question, “What is the next shoe to fall?” We became worried that even companies that were reasonably conservatively managed with respect to debt might have debt come due at a time no one was willing to lend for a reasonable interest rate. In such an environment, bankruptcies could skyrocket, and we wanted to make sure we didn’t have too much exposure to debt-laden companies. Our analysis across all our Funds indicated that our aggregate debt levels were less than the broader market, and it was unnecessary to consider dramatic action. If the section above (“bounce-back” data) provides some encouragement that we would participate in a market turnaround, the following table might similarly provide some encouragement should the bear market get significantly worse—but even then, only on a relative basis. Here’s the debt data for our Funds:

| | | | | | | | | | | | |

| | | Short-Term Debt/Equity* | | Total Debt/Equity* |

| | | Fund | | Index | | Difference | | Fund | | Index | | Difference |

Aggressive Investors 1 vs. S&P 500 Index | | 7.7% | | 17.9% | | -10.2% | | 45.1% | | 83.5% | | -38.4% |

Aggressive Investors 2 vs. S&P 500 Index | | 7.3% | | 17.9% | | -10.6% | | 54.3% | | 83.5% | | -29.2% |

Ultra-Small Company vs. CRSP 10 Index | | 5.2% | | 18.7% | | -13.5% | | 30.4% | | 306.8% | | -276.4% |

Ultra-Small Company Market vs. CRSP 10 Index | | 3.9% | | 18.7% | | -14.8% | | 174.0% | | 306.8% | | -132.8% |

Micro-Cap Limited vs. Russell 2000 Growth Index | | 3.8% | | 13.9% | | -10.1% | | 35.7% | | 161.4% | | -125.7% |

Small-Cap Growth vs. Russell 2000 Growth Index | | 3.8% | | 13.9% | | -10.1% | | 96.3% | | 161.4% | | -65.1% |

Small-Cap Value vs. Russell 2000 Value Index | | 7.0% | | 5.5% | | 1.5% | | 65.3% | | 65.3% | | 0.0% |

Large-Cap Growth vs. Russell 1000 Growth Index | | 7.7% | | 13.1% | | -5.4% | | 42.9% | | 71.0% | | -28.1% |

Large-Cap Value vs. Russell 1000 Value Index | | 11.9% | | 14.0% | | -2.1% | | 61.1% | | 74.0% | | -12.9% |

Blue Chip 35 Index vs. S&P 500 Index | | 13.5% | | 17.9% | | -4.4% | | 47.8% | | 83.5% | | -35.7% |

| | | | | | | | | | | | | |

| * | All calculations exclude financial stocks since the adviser believes they skew the data unreasonably. The differences are even greater if financial companies are included. |

| | |

| 8 | | Semi-Annual Report | December 31, 2008 (Unaudited) |

LETTER FROM THE INVESTMENT MANAGEMENT TEAM (continued)

Bridgeway 3, Morningstar 8

The Short Version: After a good year for Bridgeway in 2007, Morningstar takes the honors in 2008.

Morningstar, the Chicago-based independent research firm publishes a list of “best funds” for each asset class as determined by its analysts every year. In January when the final tallies are in, we compare the performance of each of our Funds to the average returns of Morningstar’s top picks for the comparable asset class. We enjoy seeing how we stack up against the “best of the best.”

By a wide 3-8 margin, the Bridgeway Funds lost out to the Morningstar picks in calendar year 2008. Two of the Funds that underperformed (Ultra-Small Company Fund and Ultra-Small Company Market Fund) actually beat their own market benchmarks of much smaller companies. In a period when very small stocks badly lagged the broader market, the headwinds were too strong for these funds compared to the larger company (but still small) peers.

The table below depicts the results by Morningstar category and relevant Bridgeway Fund.

| | | | | | |

| Bridgeway Funds | | Morningstar Analyst “Picks” |

| Name | | 2008 Return | | Morningstar Category | | 2008 Return |

Large-Cap Value | | -36.83% | | Large-cap value | | -40.00% |

Blue Chip 35 Index | | -33.30% | | Large-cap blend | | -39.74% |

Large-Cap Growth | | -45.42% | | Large-cap growth | | -37.21% |

Aggressive Investors 1 | | -56.16% | | Mid-cap growth | | -34.34% |

Aggressive Investors 2 | | -55.07% | | Mid-cap growth | | -34.34% |

Small-Cap Value | | -45.57% | | Small-Value | | -36.07% |

Ultra-Small Co. Market | | -39.49% | | Small Blend | | -37.87% |

Ultra-Small Company | | -46.24% | | Small-Growth | | -42.05% |

Micro-Cap Limited | | -41.74% | | Small-Growth | | -42.05% |

Small-Cap Growth | | -43.48% | | Small-Growth | | -42.05% |

Balanced | | -19.38% | | Conservative Allocation | | -16.17% |

Past performance is not an indicator of future results. The Bridgeway Funds’ adviser, Bridgeway Capital Management, Inc., does not have any influence on the selection of the funds chosen by Morningstar’s analysts. The number and specific funds used in the comparison are in the control and discretion of Morningstar and their analysts and are subject to change. Morningstar’s criteria for choosing Analyst Picks includes, but is not limited to, factors such as performance, expenses, and quality of fund management. In addition, the comparison of Bridgeway Funds to the Morningstar Analyst Picks is limited to performance only and does not take into consideration other factors that are considered by Morningstar when compiling their list of Analyst Picks.

Each Bridgeway Fund is compared to the average total return of the group of funds selected by Morningstar at the beginning of 2008 for the one year period ended December 31, 2008. Although these Analyst Picks changed from the beginning of the year to the final quarter, the same Bridgeway Funds beat the average of the end of year Morningstar picks as well. These averages in the table are comprised of between three and thirteen funds from within each category. In an effort to provide a complete and balanced assessment, all of the Bridgeway Funds are used in the comparison table shown above such that no attempt is made to cull out unfavorable results. The purpose of this comparison is to “raise the bar” on performance comparison as this analysis uses an arguably higher benchmark by comparing the Bridgeway Funds to other funds chosen by an independent source that specializes in investment research.

Aggressive Investors 1 Fund

MANAGER’S COMMENTARY

(Unaudited)

December 31, 2008

Dear Fellow Aggressive Investors 1 Fund Shareholder,

Our Fund’s performance for the December 31, 2008 quarter was the worst quarterly performance for both our Fund and our performance benchmarks during our Fund’s fourteen year history. It was our fifth worst quarter on the basis of returns relative to our primary market benchmark. Aggressive Investors 1 declined 32.80%, compared to declines of 21.94% for the S&P 500 Index (our primary market benchmark), 22.59% for the Lipper Capital Appreciation Funds Index (our peer benchmark), and 26.12% for the Russell 2000 Index of small companies. It was an awful quarter.

For the six-month “semi-annual” period ending December 31, 2008, our Fund declined 53.13%, versus declines of 28.48% for the S&P 500 Index, 35.71% for the Lipper Capital Appreciation Funds Index , and 26.94% for the Russell 2000 Index of small companies. This period was a “perfect storm” of poor positioning: a) a large number of more “growth leaning” companies (those with historical faster growing earnings, for example), b) good, but not strong enough representation among the largest “blue chip” companies that held up best, c) none of our different stock picking models “picked up the slack” in this particular downturn, and d) especially damaging exposure to energy and chemical companies during a period when commodity prices fell off a cliff.

In some other periods of quarterly underperformance, our preceding and/or following quarters were strong enough to make up for the poor quarter. For example, our second worst quarter of underperformance, September 2006, was followed by five market-beating quarters and preceded by two. Our third worst, December 1997, was preceded by two and followed by one. And our fourth worst quarter, September 1998, was followed by the longest running outperformance in our history (eight quarters). With the back to back September and December quarters, however, we have a very significant “hole” from which to work our way back.

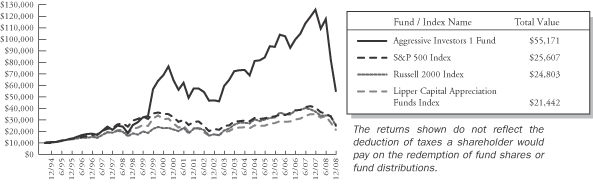

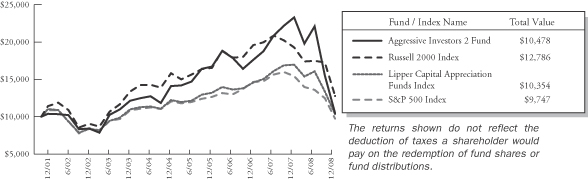

The table below presents our December quarter, six-month, one-year, five-year, ten-year and life-to-date financial results according to the formula required by the SEC. The last two quarters caused even our five year performance to lag our five-year benchmarks for the first time in our history. We still lead all our benchmarks over the last ten years and since inception. See the next page for a graph of performance from inception to December 31, 2008.

| | | | | | | | | | | | |

| | | Dec. Qtr. 10/1/08

to 12/31/08 | | 6 Month

7/1/08

to 12/31/08 | | 1 Year 1/1/08

to 12/31/08 | | 5 Year 1/1/04

to 12/31/08 | | 10 Year 1/1/99

to 12/31/08 | | Life-to-Date 8/5/94 to 12/31/08 |

| | | | | | |

Aggressive Investors 1 Fund | | -32.80% | | -53.13% | | -56.16% | | -5.30% | | 7.90% | | 12.59% |

S&P 500 Index (large companies) | | -21.94% | | -28.48% | | -37.00% | | -2.19% | | -1.38% | | 6.74% |

Lipper Capital Appreciation Funds Index | | -22.59% | | -35.71% | | -39.08% | | -1.19% | | -0.44% | | 5.45% |

Russell 2000 Index (small companies) | | -26.12% | | -26.94% | | -33.79% | | -0.93% | | 3.02% | | 6.51% |

Performance figures quoted in the table above and graph below represent past performance and are no guarantee of future results. The table above and the graph below do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

The S&P 500 Index is a broad-based, unmanaged measurement of changes in stock market conditions based on the average of 500 widely held common stocks with dividends reinvested, while the Russell 2000 Index is an unmanaged, market value weighted index, that measures performance of the 2,000 companies that are between the 1,000th and 3,000th largest in the market with dividends reinvested. The Lipper Capital Appreciation Funds Index reflects the record of the 30 largest funds in this category, comprised of more aggressive domestic growth mutual funds, as reported by Lipper, Inc. It is not possible to invest directly in an index. Periods longer than one year are annualized.

According to data from Lipper, Inc. as of December 31, 2008, Aggressive Investors 1 Fund ranked 208th of 281 capital appreciation funds for the twelve months ending December 31, 2008, 182nd of 212 over the last five years, 5th of 125 over

| | |

| 10 | | Semi-Annual Report | December 31, 2008 (Unaudited) |

Aggressive Investors 1 Fund

MANAGER’S COMMENTARY (continued)

(Unaudited)

the last ten years, and 1st of 54 since inception in August, 1994. These long-term numbers and the graph below give two snapshots of our long- term success. Lipper, Inc. is an independent mutual fund rating service that ranks funds in various fund categories by making comparative calculations using total returns.

Aggressive Investors 1 Fund vs. S&P 500 Index & Lipper Capital Appreciation Funds Index & Russell 2000 Index Inception 8/5/94 to 12/31/08

Why Was our Fund Positioned so Poorly?

Our introductory section on the previous page gives some details on the poor positioning of our Fund for this market environment, while the sections below give details of our performance at the stock level. A fair question to ask is “why the poor positioning?” Answering this question could require a lot of discussion at the level of our individual stock picking models, so we’ll address it more generally in this section.

Growth companies generally fall more in a downturn; why did we hold more than a normal level? Growth companies had been significantly out of favor from 2000-2006. That trend reversed in 2007, and it looked like it might continue into 2008. From a risk perspective, we believed that growth stocks might even provide more “cushion” against a downturn than value stocks, just as small stocks provided more cushion than large stocks in the last bear market of 2000-2002. That strategy turned out not to be the case; growth stocks were much harder hit. In aggregate, our models were picking up on what appeared to be stronger relative valuations among growth stocks, which did not translate into better returns for this period, however.

Why did we own so many mid-cap companies that lagged larger ones? Our models pick stocks among all size companies, small, medium, and large ones. However, there are many more mid-cap and small-cap companies to choose from which normally leads to more holdings in this “middle range”. In the current market environment the largest ones fared best, giving an advantage to our large company weighted primary market benchmark. Actually, our models have favored large companies for the last couple of years, but our small and mid-size ones still caused a performance drag of about six percentage points during the quarter relative to the S&P 500 Index.

Bridgeway’s strategy is to use stock picking models of different styles that don’t all go the same direction at the same time. Why didn’t some provide more cushion? As described above, perhaps predictably, strong growth models didn’t do as well in the recent fast moving, very steep decline. On the other end of the spectrum, one of our more value-oriented models that usually does well in a downturn unfortunately picked up some distressed companies, including some financial stocks such as Bank of America. Two more technically focused models did poorly for . . . technical reasons I can’t go into detail with here. One of these was specifically designed to be less volatile than the market, but did not prove to be so this time. In summary, our Fund design includes some models that usually zig while the others zag. Unlike in previous downturns, however, these models all went the same (poor) direction at the same time.

Why did we hold so much of energy and chemicals through the downturn? These companies, as detailed below, caused the most damage to our Fund’s returns. Normally, a turnaround in fundamentals, including inputs such as precipitously falling

Aggressive Investors 1 Fund

MANAGER’S COMMENTARY (continued)

(Unaudited)

commodity prices would result in a sell signal. However, for some models, if the stock price declines at a rate much faster than the fundamentals (e.g. net income) of a company, it may not create a sell signal in anticipation of a “bounce back.” While this has worked in some previous market environments, and contributed to the positive “bounce back” phenomenon on page 7, it added to the pain of the downturn in October and most of November.

Detailed Explanation of Quarterly Performance—Some stocks (slightly) cushioned the blow

The Short Version: With a dramatic December quarter downturn, there were very few stocks that helped cushion the blow. 21 of our 90 stocks had positive returns, with only seven in double digits.

In a quarter where misery found plenty of company, investors had to search long and hard for winners. While every major sector declined double digits amid the credit crisis and broadening economic downturn, non-cyclical consumer stocks held up somewhat better than most. Of the top ten best performers in the Fund, five came from that sector. Combined, they contributed just under one and a half percent to the overall performance of the Fund.

These are the ten best performers for the quarter ended December 31, 2008:

| | | | | | |

| Rank | | Description | | Industry | | % Gain |

| 1 | | Apollo Group Inc | | Commercial Services | | 30.5% |

| 2 | | Thoratec Corp | | Healthcare-Products | | 23.8% |

| 3 | | Broadcom Corp | | Semiconductors | | 15.1% |

| 4 | | Telephone & Data Systems Inc | | Telecommunications | | 14.2% |

| 5 | | Bristol-Myers Squibb Co | | Pharmaceuticals | | 11.5% |

| 6 | | Amgen Inc | | Biotechnology | | 11.3% |

| 7 | | AT&T Inc | | Telecommunications | | 10.0% |

| 8 | | Cerner Corp | | Software | | 9.9% |

| 9 | | Time Warner Inc | | Media | | 9.5% |

| 10 | | Corinthian Colleges Inc | | Commercial Services | | 9.1% |

| | | | | | | |

When the going gets tough, the tough…go back to school. Apollo Group was the best-performing company in the Fund over the past three months and the only one to earn greater than 30% in return. Apollo provides educational programs for high school, college, and graduate levels and operates under such brands as University of Phoenix and College for Financial Planning Institute. During the quarter, enrollment soared by just under 20%, as students realized that additional education (and degrees) could be beneficial amid the struggling job market. The company’s profits doubled in its fiscal 4th quarter, a trend that some analysts expect to continue given the ongoing sluggish economy and dire labor picture.

Detailed Explanation of Quarterly Performance—What Didn’t Work

The Short Version: Basic materials stocks (iron, chemicals) and industrial companies did the most damage in the quarter.

What happened to the commodities boom of a few quarters back? Just six months ago, the top eight performing stocks in the Fund were involved in various commodity-related industries (energy, coal, steel, mining), and each returned over 35% that quarter. When commodity prices turned around, however, the downward trend was relentless, and stock prices followed suit. The global recession is widely recognized as the primary culprit, and demand for such products is expected to decline further in the foreseeable future. Nine of the Fund’s worst-performing holdings were commodity-related (steel, coal, oil, chemicals), and each fell over 50% during the quarter.

| | |

| 12 | | Semi-Annual Report | December 31, 2008 (Unaudited) |

Aggressive Investors 1 Fund

MANAGER’S COMMENTARY (continued)

(Unaudited)

These are the ten stocks that performed the worst in the quarter ended December 31, 2008:

| | | | | | |

| Rank | | Description | | Industry | | % Loss |

| 1 | | Mechel ADR | | Iron/Steel | | -77.7% |

| 2 | | Massey Energy Co | | Coal | | -61.3% |

| 3 | | Bucyrus International Inc | | Machinery-Construction & Mining | | -58.6% |

| 4 | | Energy Conversion Devices Inc | | Electrical Components & Equip | | -57.8% |

| 5 | | Warnaco Group Inc | | Apparel | | -56.7% |

| 6 | | Genco Shipping & Trading Ltd | | Transportation | | -55.5% |

| 7 | | Cliffs Natural Resources Inc | | Iron/Steel | | -54.9% |

| 8 | | Chesapeake Energy Corp | | Oil & Gas | | -54.9% |

| 9 | | United States Steel Corp | | Iron/Steel | | -54.7% |

| 10 | | Dow Chemical Co | | Chemicals | | -52.5% |

| | | | | | | |

Mechel ADR is a coal mining and steel production company based in Russia. Though the company reported strong results for the first nine months of the year, its outlook for 2009 remains extremely weak, while management determines how best to cope with sluggish worldwide demand. The company said it will cut steel production by up to 25% during the year, and analysts do not foresee any imminent rebound in the price of coal, steel, and other commodities over the next few quarters. Management continues to remain optimistic about its long-term prospects and believes the company is in a great position to benefit from a global economic recovery in the future. From early-2007 to mid-2008, the stock had risen five-fold, only to give up all of those gains and more by the end of the year.

Genco Shipping and Trading Ltd. transports drybulk cargos (coal, grains, steel products, etc.) to destinations across the globe. While the bursting of the commodities’ bubble dramatically impacted miners and manufacturers of related products, it also diminished the need for shipping these goods. As such, cargo shipment rates have plunged by up to 90% since summer 2008 in some cases. In November, because of the dwindling demand for its services, Genco cancelled plans to purchase six cargo ships and will be forced to forfeit over $50 million in lost deposits. As a result, the company expects to take a $54 million hit to its bottom line in the fourth quarter. However, some analysts believe that Genco is in a better position to weather the storm than certain competitors, as it maintains longer-term contracts that produce more attractive margins.

Detailed Explanation of Calendar Year Performance—Companies With Positive Returns

The Short Version: Twenty-seven of the 155 stocks we owned during the year had positive returns. Unfortunately, all but two were smaller diversifying positions. In aggregate, these 27 added about a percent and a half to our annual returns.

With all 10 S&P sectors recording sizable market losses in 2008, investors had few places to turn for relief from the equity market carnage. Still, our models found some. Eight of the best-performing stocks returned 10% or more and represented six different sectors, an indication that needles can be found in even the most depressing haystacks. In conjunction with the worst bear market of a lifetime, this is the “leanest” list of top annual performers in our history.

These are the ten best performers for the calendar year ended December 31, 2008:

| | | | | | |

| Rank | | Description | | Industry | | % Gain |

| 1 | | Thoratec Corp | | Healthcare-Products | | 24.9% |

| 2 | | Callaway Golf Co | | Leisure Time | | 16.0% |

| 3 | | Broadcom Corp | | Semiconductors | | 15.1% |

| 4 | | Telephone & Data Systems Inc | | Telecommunications | | 14.2% |

| 5 | | Range Resources Corp | | Oil & Gas | | 12.6% |

| 6 | | Jones Lang LaSalle Inc | | Real Estate | | 12.0% |

| 7 | | Amgen Inc | | Biotechnology | | 11.3% |

| 8 | | AT&T Inc | | Telecommunications | | 10.0% |

| 9 | | Cerner Corp | | Software | | 9.9% |

| 10 | | Time Warner Inc | | Media | | 9.5% |

| | | | | | | |

Aggressive Investors 1 Fund

MANAGER’S COMMENTARY (continued)

(Unaudited)

Thoratec Corp. was the Fund’s best performing company during the year, with much of the returns coming in the fourth quarter (where it was our second top holding). In December, its management reported that a clinical trial for its HeartMate II pump produced better results than its existing products that target similar patients; management believes it could receive its next round of FDA approval more quickly than originally expected. Currently, the HeartMate II is considered a temporary treatment for heart patients in need of transplants, but the strong data could speed up the approval process and make the device available for more candidates. The good news was not limited to the past three months, however. In late July, the company posted outstanding quarterly earnings due to favorable treatment results of its existing medical product line. For the year, Thoratec returned almost 25%.

Detailed Explanation of Calendar Year Performance—What Didn’t Work

The Short Version: As goes the December quarter, so goes the year.

Basic materials and energy, in almost any form, were not a good place to be in 2008; neither coal, iron, steel, oil, nor most chemicals survived the onslaught. As the global recession expanded, the commodities bubble burst, and prices plummeted. Nine of the ten worst-performing companies in the Fund were engaged in some commodities-related operations (mining, drilling, production, transportation, etc.). Of the 155 holdings in the Fund during 2008, 32 declined by at least 50% during the year.

These are the ten stocks that performed the worst for the calendar year ended December 31, 2008:

| | | | | | |

| Rank | | Description | | Industry | | % Loss |

| 1 | | Mechel ADR | | Iron/Steel | | -92.1% |

| 2 | | Massey Energy Co | | Coal | | -80.5% |

| 3 | | Genco Shipping & Trading Ltd | | Transportation | | -77.5% |

| 4 | | United States Steel Corp | | Iron/Steel | | -75.5% |

| 5 | | Cliffs Natural Resources Inc | | Iron/Steel | | -75.4% |

| 6 | | Arch Coal Inc | | Coal | | -72.4% |

| 7 | | W&T Offshore Inc | | Oil & Gas | | -69.0% |

| 8 | | Chesapeake Energy Corp | | Oil & Gas | | -67.5% |

| 9 | | Sigma Designs Inc | | Semiconductors | | -66.9% |

| 10 | | Terra Industries Inc | | Chemicals | | -66.6% |

| | | | | | | |

Massey Energy produces and markets coal and related products for utilities, steel manufacturers, and industrial companies. The company had benefited dramatically from the surging price of coal early in the year. Emerging markets such as China had been experiencing dramatic growth, and the increased demand for coal was expected to continue with the need to generate electricity in these regions. By mid-year, however, the price of coal peaked and began a freefall that was sustained through the remainder of 2008. A far weaker global economy translates into lower demand for coal and other commodities. Even the largest coal consumer, China, has shown significant signs of a slowdown. This bear market has truly demonstrated how interwoven our world economy has become. As if the news for Massey was not bad enough, late in the year, one of its subsidiaries was fined $4.2 million for safety hazards. The settlement was the largest in the industry’s history. Massey lost over 80% in 2008 and cost the Fund over one and a third percent in return.

Sigma Designs is a chip manufacturer whose processors are used for various video applications. Its stock price plunged early in the year and by mid-March had lost over 60% of its value. At that time, the California-based company offered a lower outlook for the remainder of the year, blaming excess chip inventory at one of its major customers, Motorola, for its misfortunes. Motorola had accounted for over 25% of the sales at Sigma during the prior two quarters. Further, analysts believe that Sigma will face increased competition in chip sales for Internet Protocol TVs and Blu-ray DVDs, two significant markets for the company. Sigma cost the Fund over one and a half percent during the 12-month period.

| | |

| 14 | | Semi-Annual Report | December 31, 2008 (Unaudited) |

Aggressive Investors 1 Fund

MANAGER’S COMMENTARY (continued)

(Unaudited)

Top Ten Holdings as of December 31, 2008

Chemical companies highlighted the Fund’s top ten holdings, as four related stocks comprised the list at year-end. Two of our largest positions were also among the Fund’s top performers of the quarter (Thoratec Corp. and Bristol-Myers). No one holding accounted for greater than five percent of the net assets, indicating that the Fund was well-diversified across many companies in this difficult environment for stocks. The ten largest positions represented just over 25% of the total assets of the Fund.

| | | | | | |

| Rank | | Description | | Industry | | Percent of Net Assets |

| 1 | | Thoratec Corp | | Healthcare-Products | | 4.7% |

| 2 | | Potash Corp of Saskatchewan | | Chemicals | | 3.2% |

| 3 | | Bristol-Myers Squibb Co | | Pharmaceuticals | | 2.9% |

| 4 | | Mosaic Co | | Chemicals | | 2.9% |

| 5 | | Pfizer Inc | | Pharmaceuticals | | 2.9% |

| 6 | | Bucyrus International Inc | | Machinery-Construction & Mining | | 2.5% |

| 7 | | Terra Industries Inc | | Chemicals | | 2.1% |

| 8 | | CF Industries Holdings Inc | | Chemicals | | 2.1% |

| 9 | | Myriad Genetics Inc | | Biotechnology | | 2.0% |

| 10 | | Flir Systems Inc | | Electronics | | 1.9% |

| | | | | | | |

| | | | | | 27.2% |

Industry Sector Representation as of December 31, 2008

No sector of the economy was spared the negative returns of the past three months. Even recession-resistant utilities and consumer non-cyclical stocks were down double digits. For the full year they were each down more than 20%. Our models’ overweighting of basic materials was very costly to the Fund’s performance relative to the benchmarks. We did benefit from our models’ underweighting of financials (with some stronger stock picks), as this sector remained depressed throughout the quarter. At quarter end, the largest sector represented in both the broader market and our Fund was consumer non-cyclicals (e.g. healthcare, food, education).

| | | | | | |

| | | % of Portfolio | | % S&P 500 Index | | Difference |

Basic Materials | | 14.9% | | 3.0% | | 11.9% |

Communications | | 10.0% | | 10.9% | | -0.9% |

Consumer, Cyclical | | 5.9% | | 8.2% | | -2.3% |

Consumer, Non-cyclical | | 29.6% | | 25.2% | | 4.4% |

Energy | | 6.7% | | 13.5% | | -6.8% |

Financial | | 6.6% | | 13.0% | | -6.4% |

Industrial | | 17.0% | | 11.2% | | 5.8% |

Technology | | 7.8% | | 10.9% | | -3.1% |

Utilities | | 0.9% | | 4.1% | | -3.2% |

Diversified | | 0.0% | | 0.0% | | 0.0% |

Cash | | 0.6% | | 0.0% | | 0.6% |

| | | | | | | |

Total | | 100.0% | | 100.0% | | |

Expense Ratio Explanation—What is the Current Expense Ratio?

The Short Version: Our Fund has a “performance based” management fee which goes up and down with our performance relative to our primary market benchmark over a trailing five year period. With our recent poor relative performance, the expense ratio has dropped significantly.

Aggressive Investors 1 Fund

MANAGER’S COMMENTARY (continued)

(Unaudited)

One risk Bridgeway identified and communicated to shareholders in 2004 was that should the fund experience declining assets and underperformance against the benchmark, it might create a situation where the total management fee (base fee +/- performance fee) to the adviser is actually negative. This situation may be approaching us. In our current prospectus, the expense ratio is listed as 1.78%, of which 1.61% is the management fee. Through December 31, 2008, as presented in the financial statements later in this report, the unaudited total management fee for the fund was 0.30%, reflecting both the drop in net assets and our relative performance. However, should the fund not close the gap in performance versus the S&P 500 benchmark, the management fee could drop to 0.0% or even go negative for a period of time. This is the reason our expense ratio has dropped significantly in the recent two quarters.

Disclaimer

The views expressed here are exclusively those of Fund management. These views, including those of market sectors or individual stocks, are not meant as investment advice and should not be considered predictive in nature. Any favorable (or unfavorable) description of a holding applies only as of the quarter end, December 31, 2008, unless otherwise stated. Security positions can and do change thereafter. Discussions of historical performance do not guarantee and may not be indicative of future performance.

Market volatility can significantly affect short-term performance. The Fund is not an appropriate investment for short-term investors. Investments in the small companies within this multi-cap fund generally carry greater risk than is customarily associated with larger companies. This additional risk is attributable to a number of factors, including the relatively limited financial resources that are typically available to small companies, and the fact that small companies often have comparatively limited product lines. In addition, the stock of small companies tends to be more volatile than the stock of large companies, particularly in the short term and particularly in the early stages of an economic or market downturn. The Fund’s use of options, futures, and leverage can magnify the risk of loss in an unfavorable market, and the Fund’s use of short-sale positions can, in theory, expose shareholders to unlimited loss. Finally, the Fund exposes shareholders to “focus risk” which may add to Fund volatility through the possibility that a single company could significantly affect total return. Shareholders of the Fund, therefore, are taking on more risk than they would if they invested in the stock market as a whole.

Conclusion

Thank you for your continued investment in Aggressive Investors 1 Fund. We encourage your feedback; your reactions and concerns are extremely important to us.

Sincerely,

Your Investment Management Team

| | |

| 16 | | Semi-Annual Report | December 31, 2008 (Unaudited) |

THIS PAGE INTENTIONALLY LEFT BLANK

Aggressive Investors 1 Fund

SCHEDULE OF INVESTMENTS

Showing percentage of net assets as of December 31, 2008 (Unaudited)

| | | | | | | |

| Industry | | Company | | Shares | | Value |

|

COMMON STOCKS - 99.43% |

Apparel - 1.42% |

| | Warnaco Group, Inc.* | | 101,200 | | $ | 1,986,556 |

|

Banks - 2.76% |

| | BB&T Corp. | | 45,700 | | | 1,254,922 |

| | US Bancorp+ | | 103,800 | | | 2,596,038 |

| | | | | | | |

| | | | | | | 3,850,960 |

|

Biotechnology - 6.69% |

| | Amgen, Inc.* | | 33,200 | | | 1,917,300 |

| | Celgene Corp.* | | 37,600 | | | 2,078,528 |

| | Life Technologies Corp.* | | 107,600 | | | 2,508,156 |

| | Myriad Genetics, Inc.* | | 42,800 | | | 2,835,928 |

| | | | | | | |

| | | | | | | 9,339,912 |

|

Chemicals - 13.29% |

| | CF Industries Holdings, Inc. | | 59,100 | | | 2,905,356 |

| | Dow Chemical Co. | | 82,300 | | | 1,241,907 |

| | Monsanto Co. | | 21,100 | | | 1,484,385 |

| | Mosaic Co.+ | | 116,300 | | | 4,023,980 |

| | Potash Corp. of Saskatchewan, Inc.+# | | 60,900 | | | 4,459,098 |

| | Syngenta AG - ADR+ | | 37,900 | | | 1,483,406 |

| | Terra Industries, Inc. | | 177,570 | | | 2,960,092 |

| | | | | | | |

| | | | | | | 18,558,224 |

|

Coal - 1.56% |

| | Arch Coal, Inc.+ | | 57,100 | | | 930,159 |

| | Massey Energy Co.+ | | 90,600 | | | 1,249,374 |

| | | | | | | |

| | | | | | | 2,179,533 |

|

Commercial Services - 3.96% |

| | Apollo Group, Inc., Class A* | | 22,500 | | | 1,723,950 |

| | Corinthian Colleges, Inc.*+ | | 143,400 | | | 2,347,458 |

| | ITT Educational Services, Inc.*+ | | 15,400 | | | 1,462,692 |

| | | | | | | |

| | | | | | | 5,534,100 |

|

Computers - 1.13% |

| | Diebold, Inc. | | 56,300 | | | 1,581,467 |

|

Distribution/Wholesale - 1.25% |

| | WW Grainger, Inc.+ | | 22,100 | | | 1,742,364 |

|

Electrical Components & Equipment - 0.93% |

| | GrafTech International, Ltd.* | | 156,400 | | | 1,301,248 |

|

Electronics - 2.97% |

| | FLIR Systems, Inc.*+ | | 88,700 | | | 2,721,316 |

| | Woodward Governor Co.+ | | 62,200 | | | 1,431,844 |

| | | | | | | |

| | | | | | | 4,153,160 |

| | | | | | | |

| Industry | | Company | | Shares | | Value |

|

|

Engineering & Construction - 3.96% |

| | ABB, Ltd. - ADR+ | | 143,400 | | $ | 2,152,434 |

| | EMCOR Group, Inc.* | | 78,200 | | | 1,754,026 |

| | Fluor Corp.+ | | 36,300 | | | 1,628,781 |

| | | | | | | |

| | | | | | | 5,535,241 |

|

Environmental Control - 1.08% |

| | Tetra Tech, Inc.* | | 62,300 | | | 1,504,545 |

|

Food - 3.17% |

| | Campbell Soup Co. | | 42,400 | | | 1,272,424 |

| | General Mills, Inc. | | 26,200 | | | 1,591,650 |

| | TreeHouse Foods, Inc.* | | 57,200 | | | 1,558,128 |

| | | | | | | |

| | | | | | | 4,422,202 |

|

Gas - 0.94% |

| | The Laclede Group, Inc. | | 27,900 | | | 1,306,836 |

|

Healthcare - Products - 7.46% |

| | Cyberonics, Inc.* | | 84,100 | | | 1,393,537 |

| | St. Jude Medical, Inc.* | | 76,700 | | | 2,528,032 |

| | Thoratec Corp.*+ | | 199,800 | | | 6,491,502 |

| | | | | | | |

| | | | | | | 10,413,071 |

|

Household Products/Wares - 1.27% |

| | Tupperware Brands Corp. | | 78,200 | | | 1,775,140 |

|

Insurance - 2.80% |

| | AmTrust Financial Services, Inc. | | 209,400 | | | 2,429,040 |

| | Marsh & McLennan Cos., Inc. | | 61,100 | | | 1,482,897 |

| | | | | | | |

| | | | | | | 3,911,937 |

|

Internet - 2.63% |

| | EarthLink, Inc.*+ | | 388,100 | | | 2,623,556 |

| | Symantec Corp.* | | 78,000 | | | 1,054,560 |

| | | | | | | |

| | | | | | | 3,678,116 |

|

Iron/Steel - 0.24% |

| | Mechel - Sponsored ADR+ | | 85,300 | | | 332,670 |

|

Machinery - Construction & Mining - 2.51% |

| | Bucyrus International, Inc., Class A+ | | 189,200 | | | 3,503,984 |

|

Machinery - Diversified - 0.88% |

| | AGCO Corp.*+ | | 52,100 | | | 1,229,039 |

|

Media - 2.17% |

| | Time Warner, Inc.+ | | 164,700 | | | 1,656,882 |

| | |

| 18 | | Semi-Annual Report | December 31, 2008 (Unaudited) |

Aggressive Investors 1 Fund

SCHEDULE OF INVESTMENTS (continued)

Showing percentage of net assets as of December 31, 2008 (Unaudited)

| | | | | | | |

| Industry | | Company | | Shares | | Value |

|

Common Stocks (continued) |

Media - (continued) |

| | Walt Disney Co. | | 60,400 | | $ | 1,370,476 |

| | | | | | | |

| | | | | | | 3,027,358 |

|

Metal Fabrication - Hardware - 1.01% |

| | CIRCOR International, Inc. | | 51,542 | | | 1,417,405 |

|

Miscellaneous Manufacturing - 0.87% |

| | General Electric Co. | | 74,600 | | | 1,208,520 |

|

Oil & Gas - 2.82% |

| | Chesapeake Energy Corp. | | 65,400 | | | 1,057,518 |

| | Petroleo Brasileiro S.A. - ADR | | 68,400 | | | 1,675,116 |

| | W&T Offshore, Inc. | | 84,300 | | | 1,207,176 |

| | | | | | | |

| | | | | | | 3,939,810 |

|

Oil & Gas Services - 2.34% |

| | FMC Technologies, Inc.* | | 51,600 | | | 1,229,628 |

| | National Oilwell Varco, Inc.* | | 83,200 | | | 2,033,408 |

| | | | | | | |

| | | | | | | 3,263,036 |

|

Packaging & Containers - 1.35% |

| | Rock-Tenn Co., Class A | | 55,300 | | | 1,890,154 |

|

Pharmaceuticals - 7.03% |

| | Bristol-Myers Squibb Co. | | 174,300 | | | 4,052,475 |

| | Express Scripts, Inc.* | | 32,300 | | | 1,775,854 |

| | Pfizer, Inc. | | 225,200 | | | 3,988,292 |

| | | | | | | |

| | | | | | | 9,816,621 |

|

Retail - 3.22% |

| | Aeropostale, Inc.*+ | | 91,600 | | | 1,474,760 |

| | Home Depot, Inc. | | 73,800 | | | 1,698,876 |

| | Panera Bread Co., Class A*+ | | 25,400 | | | 1,326,896 |

| | | | | | | |

| | | | | | | 4,500,532 |

|

Savings & Loans - 1.04% |

| | Hudson City Bancorp, Inc. | | 90,600 | | | 1,445,976 |

|

Semiconductors - 4.51% |

| | Altera Corp. | | 146,000 | | | 2,439,660 |

| | Intel Corp. | | 100,100 | | | 1,467,466 |

| | QLogic Corp.* | | 178,300 | | | 2,396,352 |

| | | | | | | |

| | | | | | | 6,303,478 |

|

Software - 2.22% |

| | Cerner Corp.*+ | | 35,600 | | | 1,368,820 |

| | Oracle Corp.* | | 98,000 | | | 1,737,540 |

| | | | | | | |

| | | | | | | 3,106,360 |

| | | | | | | |

| Industry | | Company | | Shares | | Value |

|

|

Telecommunications - 5.17% |

| | AT&T, Inc. | | 53,800 | | $ | 1,533,300 |

| | Comtech Telecommunications Corp.* | | 26,300 | | | 1,205,066 |

| | MasTec, Inc.* | | 174,200 | | | 2,017,236 |

| | NII Holdings, Inc.* | | 27,970 | | | 508,495 |

| | Telephone & Data Systems, Inc. | | 61,700 | | | 1,958,975 |

| | | | | | | |

| | | | | | | 7,223,072 |

|

Transportation - 2.78% |

| | CSX Corp. | | 49,700 | | | 1,613,759 |

| | Genco Shipping & Trading, Ltd.+ | | 47,900 | | | 708,920 |

| | Kirby Corp.* | | 20 | | | 547 |

| | Norfolk Southern Corp. | | 33,000 | | | 1,552,650 |

| | | | | | | |

| | | | | | | 3,875,876 |

| | | | | | | |

| |

TOTAL COMMON STOCKS - 99.43% | | | 138,858,503 |

| | | | | | | |

(Cost $202,393,951) | | | |

| |

TOTAL INVESTMENTS - 99.32% | | $ | 138,858,503 |

(Cost $202,393,951) | | | |

Other Assets in Excess of Liabilities - 0.68% | | | 791,799 |

| | | | | | | |

NET ASSETS - 100.00% | | $ | 139,650,302 |

| | | | | | | |

| * | Non Income Producing Security. |

| + | This security or a portion of the security is out on loan at December 31, 2008. Total loaned securities had a market value of $38,667,815 at December 31, 2008. |

| # | Security subject to call option written by the Fund. |

| ADR | - American Depositary Receipt |

See Notes to Financial Statements.

Aggressive Investors 1 Fund

SCHEDULE OF OPTIONS WRITTEN

Showing percentage of net assets as of December 31, 2008 (Unaudited)

| | | | | | |

| Company | | Number

of Contracts | | Value | |

|

COVERED CALL OPTIONS WRITTEN - (0.11)% | |

Potash Corp. of Saskatchewan, Inc. | | | | | | |

Expiring January, 2009 at $70.00 | | 160 | | $ | (100,800 | ) |

Expiring March, 2009 at $70.00 | | 40 | | | (50,200 | ) |

| | | | | | |

| |

TOTAL COVERED CALL OPTIONS WRITTEN | | $ | (151,000 | ) |

| | | | | | |