UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-08200

Bridgeway Funds, Inc.

(Exact name of registrant as specified in charter)

20 Greenway Plaza, Suite 450

Houston, Texas 77046

(Address of principal executive offices) (Zip code)

Michael D. Mulcahy, President

Bridgeway Funds, Inc.

20 Greenway Plaza, Suite 450

Houston, Texas 77046

(Name and address of agent for service)

Registrant’s telephone number, including area code: (713) 661-3500

Date of fiscal year end: June 30

Date of reporting period: July 1, 2011 through December 31, 2011

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 100 F Street, NE, Washington, DC 20549. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

| Item 1. | Reports to Stockholders. |

The Report to Shareholders is attached herewith.

A no-load mutual fund family of domestic funds

Semi-Annual Report

December 31, 2011 (Unaudited)

AGGRESSIVE INVESTORS 1

BRAGX

AGGRESSIVE INVESTORS 2

BRAIX

ULTRA-SMALL COMPANY

BRUSX

(Open to Existing Investors — Direct Only)

ULTRA-SMALL COMPANY MARKET

BRSIX

MICRO-CAP LIMITED

BRMCX

SMALL-CAP MOMENTUM

BRSMX

SMALL-CAP GROWTH

BRSGX

SMALL-CAP VALUE

BRSVX

LARGE-CAP GROWTH

BRLGX

LARGE-CAP VALUE

BRLVX

BLUE CHIP 35 INDEX

BRLIX

MANAGED VOLATILITY

BRBPX

www.bridgeway.com

| TABLE OF CONTENTS |  |

| 1 | ||||

AGGRESSIVE INVESTORS 1 FUND | 16 | |||

| 12 | ||||

| 18 | ||||

AGGRESSIVE INVESTORS 2 FUND | ||||

| 21 | ||||

| 27 | ||||

ULTRA-SMALL COMPANY FUND | ||||

| 30 | ||||

| 36 | ||||

ULTRA-SMALL COMPANY MARKET FUND | ||||

| 41 | ||||

| 47 | ||||

MICRO-CAP LIMITED FUND | ||||

| 58 | ||||

| 63 | ||||

SMALL-CAP MOMENTUM FUND | ||||

| 67 | ||||

| 72 | ||||

SMALL-CAP GROWTH FUND | ||||

| 80 | ||||

| 85 | ||||

SMALL-CAP VALUE FUND | ||||

| 88 | ||||

| 93 | ||||

LARGE-CAP GROWTH FUND | ||||

| 96 | ||||

| 101 | ||||

LARGE-CAP VALUE FUND | ||||

| 104 | ||||

| 109 | ||||

BLUE CHIP 35 INDEX FUND | ||||

| 112 | ||||

| 117 | ||||

MANAGED VOLATILITY FUND | ||||

| 119 | ||||

| 123 | ||||

| 127 | ||||

| 131 | ||||

| 133 | ||||

| 135 | ||||

| 139 | ||||

| 145 | ||||

| 161 | ||||

| 162 | ||||

|

Bridgeway Funds Standardized Returns as of December 31, 2011*

| Annualized | ||||||||||||||||||||||||||||||||

| Fund | Quarter 10/1/11 to 12/31/11 | Six Months to 12/31/11 | 1 Year | 5 Years | 10 Years | Inception to Date | Inception Date | Gross Expense | ||||||||||||||||||||||||

Aggressive Investors 1 | 13.48% | -16.77% | -10.31% | -6.29% | 2.34% | 12.03% | 8/5/1994 | 1.25%3 | ||||||||||||||||||||||||

Aggressive Investors 2 | 10.64% | -18.26% | -11.59% | -5.23% | 2.62% | 2.98% | 10/31/2001 | 0.70% | ||||||||||||||||||||||||

Ultra-Small Company | 14.47% | -16.34% | -14.64% | -3.87% | 9.53% | 14.38% | 8/5/1994 | 1.18% | ||||||||||||||||||||||||

Ultra-Small Co Market | 14.94% | -11.28% | -7.86% | -3.67% | 8.09% | 9.06% | 7/31/1997 | 0.80%1 | ||||||||||||||||||||||||

Micro-Cap Limited | 19.10% | -13.58% | -9.48% | -5.31% | 3.34% | 8.70% | 6/30/1998 | 1.58%3 | ||||||||||||||||||||||||

Small-Cap Momentum | 18.80% | -8.15% | -0.92% | NA | NA | 10.84% | 5/28/2010 | 5.43%1 | ||||||||||||||||||||||||

Small-Cap Growth | 19.95% | -11.83% | -0.63% | -5.05% | NA | 1.19% | 10/31/2003 | 0.98%1 | ||||||||||||||||||||||||

Small-Cap Value | 16.69% | -8.70% | 1.05% | -2.74% | NA | 4.27% | 10/31/2003 | 0.87% | ||||||||||||||||||||||||

Large-Cap Growth | 12.41% | -7.84% | -0.71% | -0.02% | NA | 2.93% | 10/31/2003 | 0.86%1 | ||||||||||||||||||||||||

Large-Cap Value | 12.64% | -5.23% | 2.33% | -0.69% | NA | 5.77% | 10/31/2003 | 1.17%1 | ||||||||||||||||||||||||

Blue Chip 35 Index | 11.84% | -0.23% | 3.17% | 0.44% | 2.71% | 4.27% | 7/31/1997 | 0.27%1 | ||||||||||||||||||||||||

Managed Volatility | 8.98% | -0.43% | 1.94% | 0.74% | 3.77% | 3.36% | 6/30/2001 | 1.22%1 | ||||||||||||||||||||||||

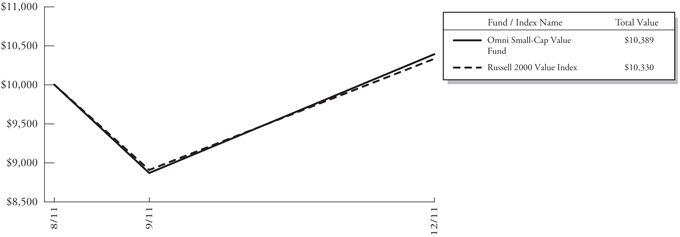

Omni Small-Cap Value4 | 17.13% | NA | NA | NA | NA | 3.89% | 8/31/2011 | 1.00%1 | ||||||||||||||||||||||||

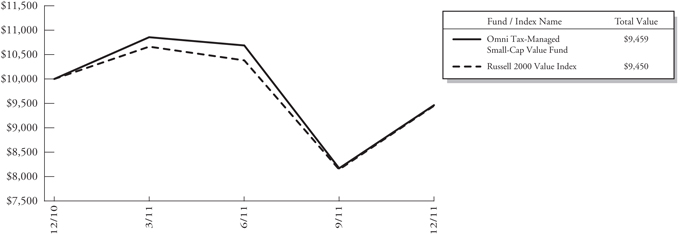

Omni Tax-Managed Small-Cap Value4 | 15.78% | -11.43% | -5.41% | NA | NA | -5.41% | 12/31/2010 | 1.56%1 | ||||||||||||||||||||||||

Bridgeway Funds Returns for Calendar Years 1998 through 2011*

| 1998 | 1999 | 2000 | 2001 | 2002 | 2003 | 2004 | 2005 | 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | |||||||||||||||||||||||||||||||||||||||||||

Aggressive Investors 1 | 19.28% | 120.62% | 13.58% | -11.20% | -18.01% | 53.97% | 12.21% | 14.93% | 7.11% | 25.80% | -56.16% | 23.98% | 17.82% | -10.31% | ||||||||||||||||||||||||||||||||||||||||||

Aggressive Investors 2 | -19.02% | 44.01% | 16.23% | 18.59% | 5.43% | 32.19% | -55.07% | 29.84% | 12.10% | -11.59% | ||||||||||||||||||||||||||||||||||||||||||||||

Ultra-Small Company | -13.11% | 40.41% | 4.75% | 34.00% | 3.98% | 88.57% | 23.33% | 2.99% | 21.55% | -2.77% | -46.24% | 48.93% | 23.55% | -14.64% | ||||||||||||||||||||||||||||||||||||||||||

Ultra-Small Co Market | -1.81% | 31.49% | 0.67% | 23.98% | 4.90% | 79.43% | 20.12% | 4.08% | 11.48% | -5.40% | -39.49% | 25.95% | 24.86% | -7.86% | ||||||||||||||||||||||||||||||||||||||||||

Micro-Cap Limited | 49.55% | 6.02% | 30.20% | -16.61% | 66.97% | 9.46% | 22.55% | -2.34% | -4.97% | -41.74% | 17.65% | 29.11% | -9.48% | |||||||||||||||||||||||||||||||||||||||||||

Small-Cap Momentum | -0.92% | |||||||||||||||||||||||||||||||||||||||||||||||||||||||

Small-Cap Growth | 11.59% | 18.24% | 5.31% | 6.87% | -43.48% | 15.04% | 11.77% | -0.63% | ||||||||||||||||||||||||||||||||||||||||||||||||

Small-Cap Value | 17.33% | 18.92% | 12.77% | 6.93% | -45.57% | 26.98% | 16.55% | 1.05% | ||||||||||||||||||||||||||||||||||||||||||||||||

Large-Cap Growth | 6.77% | 9.33% | 4.99% | 19.01% | -45.42% | 36.66% | 13.34% | -0.71% | ||||||||||||||||||||||||||||||||||||||||||||||||

Large-Cap Value | 15.15% | 11.62% | 18.52% | 4.49% | -36.83% | 24.92% | 14.51% | 2.33% | ||||||||||||||||||||||||||||||||||||||||||||||||

Blue Chip 35 Index | 39.11% | 30.34% | -15.12% | -9.06% | -18.02% | 28.87% | 4.79% | 0.05% | 15.42% | 6.07% | -33.30% | 26.61% | 10.60% | 3.17% | ||||||||||||||||||||||||||||||||||||||||||

Managed Volatility | -3.51% | 17.82% | 7.61% | 6.96% | 6.65% | 6.58% | -19.38% | 12.39% | 5.41% | 1.94% | ||||||||||||||||||||||||||||||||||||||||||||||

Omni Small-Cap Value4,5 | NA | |||||||||||||||||||||||||||||||||||||||||||||||||||||||

Omni Tax-Managed | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Small-Cap Value4 | -5.41% | |||||||||||||||||||||||||||||||||||||||||||||||||||||||

Performance figures quoted represent past performance and are no guarantee of future results. Current performance may be lower or higher than the performance data quoted. Investment return and principal value will fluctuate, so that an investor’s shares, when redeemed, may be worth more or less than original cost. To obtain performance current to the most recent month-end, please visit our website at www.bridgeway.com or call 1-800-661-3550. Total return figures include the reinvestment of dividends and capital gains.

1 Some of the Funds’ fees were waived or expenses reimbursed; otherwise, returns would have been lower. The Adviser has contractually agreed to waive fees and/or reimburse expenses. Any material change to this Fund policy would require a vote by shareholders.

2 Expense ratios are as stated in the current prospectus. Please see financial highlights for expense ratios as of December 31, 2011.

3 The management fee included in the gross expense ratio for the Aggressive Investors 1 and Micro-Cap Limited Funds has been restated to reflect only the base management fee payable under each Fund’s performance-based management fee structure. The total actual management fee for the fiscal year ended June 30, 2011 was -0.76% and -0.36%, respectively. The actual total management fee for the prior fiscal year was negative due to the negative performance adjustment of the investment management fee under each Fund’s performance-based management fee structure.

| i | www.bridgeway.com | |

| (continued) | |

4These funds are offered in a separate prospectus and their semi-annual reports are also in a separate book.

5Commenced operations on 8/31/11, therefore the Fund has no 1 year return as of 12/31/11.

* Numbers highlighted in green indicate periods when the Fund outperformed its primary benchmark.

This report is submitted for the general information of the shareholders of each Fund. It is not authorized for distribution to prospective investors unless preceded or accompanied by an effective prospectus, which includes information regarding a Fund’s risks, objectives, fees and expenses, experience of its management, and other information. Investors should read the prospectus carefully before investing in a Fund. For questions or other Fund information, call 1-800-661-3550 or visit the Funds’ website at www.bridgeway.com. Funds are available for purchase by residents of the United States, Puerto Rico, U.S. Virgin Islands and Guam only. Foreside Fund Services, LLC, Distributor.

The views expressed here are exclusively those of Fund management. These views, including those relating to the market, sectors or individual stocks are not meant as investment advice and should not be considered predictive in nature.

| ii | www.bridgeway.com | |

| LETTER FROM THE INVESTMENT MANAGEMENT TEAM | |

December 31, 2011

Dear Fellow Shareholders,

Ten of thirteen Bridgeway Funds beat their primary market benchmarks in the December quarter. The fourteenth, Managed Volatility, met its long-term target (more than 40% of the S&P 500 Index on the upside). On the heels of last quarter, which was characterized by the most macro-driven market on record — an environment particularly unfavorable to our Select Funds (see page 10 for a description of our Select Funds) and more growth leaning Funds — seven of twelve Funds with a full year of operation beat their primary market benchmarks for the full calendar year, with Managed Volatility also meeting its target return. Overall, it was a strong quarter, but mixed calendar year.

A review of the December quarter market environment appears on page 2. Following the steep decline of the September quarter, this was a “bounceback” market, with larger companies making a strong enough comeback at year end to eke out a small positive return for the calendar year. Meanwhile, smaller stocks ended the year with red ink and the smallest ones with quite a bit of red ink. Growth stocks (those growing sales and earnings at a faster clip) trumped value stocks (those that are cheap based on some economic metrics) for the third calendar year in a row, according to Russell Index metrics.

Page 3 presents more details of the characteristics of a macro-driven market, a topic we introduced last quarter. A Q&A follows on this topic, including the possibilities we see going forward. While we do not believe it is possible to predict whether or not the recent macro-dominated market will continue, the adviser has made incremental improvements to its models within the context of an unchanged investment process that it believes will help the relative performance of its Select Funds (defined on page 10) in either climate.

Bridgeway continues to believe that one of the most serious risks facing investors in the next three to five years is inflation risk. Page 7 presents some details as to what investors might expect when and if inflation kicks in, with a focus on stocks, fixed income, gold, real estate securities, and inflation-protected securities.

Each calendar year we have a friendly competition with Morningstar’s “Fund picks.” Indeed, this year Morningstar’s picks did prove to be a higher hurdle than our primary market benchmarks. In the macro-driven 2011 market that we consider unfavorable to a number of our stock picking models, Morningstar beat Bridgeway 8 to 5. See details on page 8.

The Aggressive Investors Funds continue to be a favorite of our founder and chief investment officer, John Montgomery. In spite of a recent track record of underperformance in three of the last four years, see why John still favors these Funds in his personal asset allocation (page 9).

Every Fund we manage at Bridgeway falls under the “statistically driven, evidence based investing” moniker. However, to help investors understand more of how we think of them, we have divided our Funds into two categories: “Select” and “Omni.” See page 10 for this delineation and where your Fund(s) fit in.

You may know that Bridgeway is committed to giving half of its own company profits to charitable and non-profit organizations — part of something we call transformative change. On page 11, our partner, Rebecca Hove, discusses what this means and gives some examples.

As always, we appreciate your feedback. We take your comments very seriously and regularly discuss them internally to help in managing our Funds and this company. Please keep your ideas coming — both favorable and critical. They provide us with a vital tool, helping us serve you better.

Sincerely,

Your Investment Management Team | ||||

|  | |||

| John Montgomery | Christine Liang | |||

|  | |||

| Michael Whipple | Elena Khoziaeva | |||

|  ] ] | |||

| Dick Cancelmo | Rasool Shaik | |||

| 1 | Semi-Annual Report | December 31, 2011 (Unaudited) | |

LETTER FROM THE INVESTMENT MANAGEMENT TEAM (continued) | |

Market Review

The Short Version: Roaring back from an awful quarter ended September 30, 2011, stocks rallied enough to put many market segments slightly into the black for calendar year 2011.

Having endured some of the wildest volatility in years, investors were rewarded with a positive fourth quarter as optimism about the U.S. economy and corporate landscape reigned. Consumer confidence rose. Manufacturing appeared to be on the mend: the Institute for Supply Management Index depicted continued expansion, though flooding in Thailand raised new concerns. Housing starts and home sales rebounded late in the year, though any real sector recovery may be slow in coming. Labor showed signs of improvements as the unemployment rate fell to 8.3% in December. Inflation is not an issue for now, though investors cannot disregard future pressures with oil topping $100 per barrel amid new supply/demand worries. The Fed Funds rate is expected to remain at or near zero percent throughout 2012, and Chairman Bernanke and the Federal Reserve Board are focusing on an improved communications strategy to keep investors informed about plans for the future and the thought processes behind them.

Global geopolitical events continue to impact the U.S. stock market. Just when Europe has seemed to be taking positive steps to move past crisis mode, along come Spain, Italy, and Hungary to remind investors that the road to recovery will be paved with many bumps. Optimism returned at the end of the period, however, following an agreement among major central banks to act together to mitigate Europe’s debt crisis.

Among the various U.S. equity sectors, energy, real estate, consumer staples, and industrials were particularly strong with solid double-digit gains. Other strong performers included consumer discretionary, health care, financials, and materials.

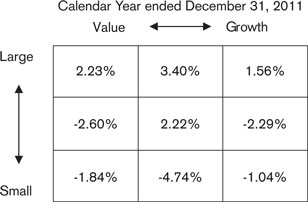

Looking at the market from a “style box” perspective (see below), returns for the quarter were strong across all styles and market capitalizations. According to Morningstar, small-cap value stocks were the strongest market segment in the December quarter, up 17.08% while mid-cap growth stocks were the weakest at 8.60%.

With significant gyrations of the overall market and various market segments, large-cap stocks made a strong enough comeback to achieve positive calendar year returns. Generally speaking, growth stocks beat value stocks — for the third year in a row — but this trend was not uniform. Small stocks lagged significantly (the Russell 2000 Index of small stocks was down 4.18%), and the smallest of the small, ultra-small stocks (as represented by the CRSP 10 Index), were down a whopping 13.98%.

Following are the stock market “style box” returns from Morningstar for the quarter and year:

|  |

| www.bridgeway.com | 2 | |

LETTER FROM THE INVESTMENT MANAGEMENT TEAM (continued) | |

Follow up to (statistically) the Most Macro-Driven Market in History — August/September 2011

The Short Version: When Wall Street focuses on macro economic events rather than the underlying economic health of individual companies, the growth leaning models of our higher turnover “Select” Funds suffer mightily, typically giving back the strong performance of prior periods. This section examines the dynamics of macro-driven markets and analyzes the returns of one Fund, Aggressive Investors 1, centering on the issues of volatility, bear markets, and macro-driven markets. Within the context of an unchanged investment process, the adviser has made incremental changes to its stock picking models that we believe will help relative performance in future macro-driven markets without any cost to our performance in micro-driven markets, which historically comprise the vast majority of markets.

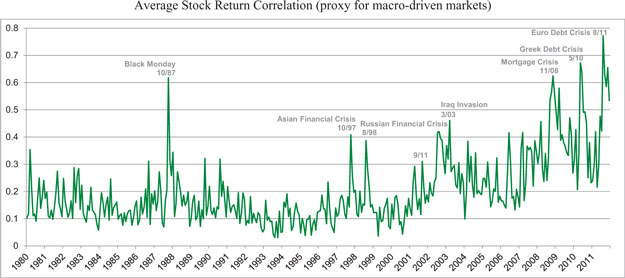

Last quarter, we introduced the concept of macro-driven markets, markets where investors focus on macro events instead of the fundamental economic health of individual companies. Statistically, we can measure macro-driven markets as peaks of stock correlation. Stock correlation is a measurement of the degree to which the returns of individual stocks go up and down in a linear (proportional) relationship to the market overall. When the correlation coefficient spikes up, it is due to some “macro” event — for example, the European banking crisis, recession, fiscal gridlock, or war, just to name a few — and investors tend to focus on this “macro” news. When this happens, investors take their eyes “off the ball” of the economic health of individual companies in favor of moving money into entire segments of the market (in the recent quarter ended September 30, 2011, into the perceived safety of utilities and staples) or into other asset classes altogether (such as U.S. Treasury securities, bonds, or gold).

Over the last eight decades there have been six very macro-driven markets, environments within which investors sell whole groups of stocks as they panic, and stop paying attention to the fundamental economic health of individual companies. These are not the same as bear markets, since, for example, the bear market of 2000-2002 was strongly “micro-driven.” It occurred because investors had become concerned with the exuberance surrounding large technology and internet stocks and began looking seriously at the health and actual earnings capacity of individual companies. That bear market environment was much more favorable to our growthier, higher turnover stock picking models. Our Funds that use stock picking models extensively and selectively (and thus focus on the economic health of individual companies) are at a significant disadvantage during macro-driven markets, such as the quarter ended September 30, 2011. Unfortunately, three of the biggest macro-driven markets in history have occurred in the last three and a half years, badly hurting the relative returns of some of our Funds in this recent period.

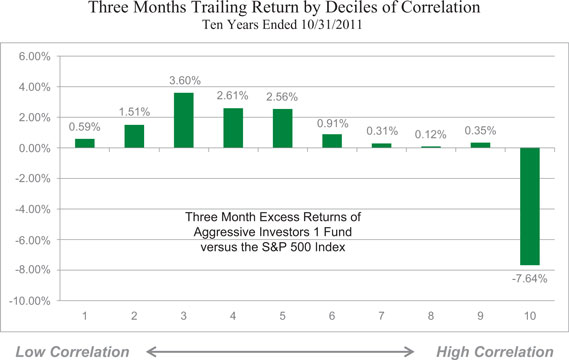

The graph below presents the average correlation coefficients among stock returns of Russell 1000 Index companies. As this graph indicates, nearly all of the biggest spikes (those above 0.5 in correlation) of the last few decades have occurred in the last three and a half year period. In fact, going back to 1926, there have been just six such spikes of volatility, and fully half have been in recent years.

| 3 | Semi-Annual Report | December 31, 2011 (Unaudited) | |

| LETTER FROM THE INVESTMENT MANAGEMENT TEAM (continued) | |

What are the implications of these correlation spikes or “macro-driven” market environments?

Most of Bridgeway’s stock picking models rely on company level data, such as economic data from income statements, balance sheets, and cash flow statements. These models seek to predict the relative attractiveness of one stock versus all the others in our universe of companies. When the stock market correlations spike, relative stock performance generally has little effect on individual stock prices, and our higher turnover growth leaning models tend to do more poorly. This is especially true if a spike follows a period of strong outperformance. Thus, our strong performance in the months and years leading up to June 2008 was followed by a particularly painful July 2008 through March 2009, when the mortage and banking crisis resulted in a macro-driven market. Similarly, a relatively strong fiscal year ending June 2011 was followed by a painful September quarter 2011, when stock correlations spiked up again.

Which Bridgeway Funds are most negatively affected by macro-driven markets?

Poorer returns in macro-driven markets tend to align with four factors: a) our “Select” Funds, those that hold a smaller number of “purer” stock picks, b) those with significant exposure to “growth” rather than “value” stocks, c) mid- and small-size rather than large companies, and d) higher turnover Funds. Thus, Aggressive Investors 1 and 2 Funds, Micro-Cap Limited Fund, Ultra-Small Company Fund, and Small-Cap Growth Fund have been the hardest hit over the last three and a half years. Large-Cap Growth Fund has also been hurt, due to its growth orientation and fewer (less than 100) holdings, although its lower turnover and larger company size have protected it to some degree. Relatively unaffected have been Large-Cap Value Fund, and our “Omni” or asset-class Funds that tend to hold many more stocks, Ultra-Small Company Market, Omni Small-Cap Value, Omni Tax-Managed Small-Cap Value, Blue Chip 35 Index, and Small-Cap Momentum Funds.

In order to demonstrate the effects of a macro-driven market on Fund returns, we will use Aggressive Investors 1 Fund in this Q&A, since it is a fund with an 18 year history and it exhibits all of the characteristics that would make it susceptible to the negative impacts of macro-driven markets.

How often does a macro-driven market occur?

Historically, it has been rare. In the last three and a half years it has been frequent.

To demonstrate how narrowly our Aggressive Investors 1 Fund returns have aligned with macro-driven markets (measured as spikes in the correlation of stock returns) we put the trailing three-month returns relative to the S&P 500 Index into ten equal “buckets” from very low correlation (“micro-driven”) markets to very high correlation (“macro-driven”) markets.

| www.bridgeway.com | 4 | |

| LETTER FROM THE INVESTMENT MANAGEMENT TEAM (continued) | |

As this graph indicates, Aggressive Investors 1 Fund has tended to outperform the market over the full spectrum of correlation, except, very notably, the high correlation peaks. The implications of this graph are significant. High correlation markets in and of themselves are not a big problem to our models: it’s the spikes that are a big problem.

Don’t the last three years represent the “new normal” for the market?

It is noteworthy that from July 2010 through June 2011, stock return correlations dropped back down significantly to the range of 0.2 to 0.4. During that year, Aggressive Investors 1 Fund outperformed its market benchmark by 10%. So we have recently seen one year without a correlation spike, and it was good for our performance generally (though not uniformly). We don’t believe low correlation markets are dead.

More specifically, Bridgeway’s investment team believes that eventually, the market has to focus at the level of individual companies’ health. While stock prices may move in lock step (proportionally) for periods of time, the underlying health of our nation’s companies do not. Eventually, the prices must follow economic health at the individual corporate level.

Negative news and macro events have been present throughout history. Why do stock price movements focus very broadly on these events some of the time, as in the recent macro-driven market, but not most of the time?

One theory is that there are many more investment vehicles today that allow people to invest in broad sectors of the market that were not previously available. These include index funds, program trading (credited with the correlation spike in 1987), complex derivative contracts available to institutions, and exchange traded funds. The latter, in particular, are a relatively new phenomenon and make up a very significant portion of stock market trading today.

However, while these instruments make it easier to trade whole segments of the market, we do not believe that they are in and of themselves responsible for it. In a fascinating (ok, fascinating if you are a statistical economist) paper by Jonathan LeBarge (“The Bane of Investors’ Existence: Why is Correlation High and When Will it Fall?,” BCA Research, January 4, 2012) on the “whys” of high stock correlation, the authors make a compelling argument that the underlying cause is due, paradoxically, to “the previous moderation in economic volatility and the rise in financial leverage that resulted.” Thus, financial leverage (borrowing), in its many forms (individual, national, and especially in the banking system itself) makes the system less stable; that’s

| �� | ||

| 5 | Semi-Annual Report | December 31, 2011 (Unaudited) | |

| LETTER FROM THE INVESTMENT MANAGEMENT TEAM (continued) | |

the nature of leverage. We believe that it will take time to reduce this leverage, and that in the meantime the base level of stock correlation will remain high. However, the spikes in correlation are the real problem for certain of our Funds, rather than an elevated base level. It is much less clear whether we will continue to see the correlation spikes in the next few years.

What would lead to more correlation spikes?

Additional, very negative news on the financial front would be more likely to lead to another spike in correlation. These could include: further major declines in the U.S. real estate market, continued or accelerated national fiscal gridlock, a reversal of recent declining unemployment, and a true meltdown in Europe. The opposite would likely lead to declining correlation.

Isn’t the performance problem with Bridgeway select growth models just that they perform poorly in big down markets?

No; in fact, it is instructive to study the three major bear markets since inception of Aggressive Investors 1 Fund:

| “Normal Bear” | “Ideal Bear” | “Macro Driven Bear” | ||||||||||||||||||||||||||

| High Correl. | Low Correl. | Low Correl. | Low Correl. | High Correl. | High Correl. | |||||||||||||||||||||||

| Russian Default | Bouncebk. | “Internet Bust” | Bouncebk. | Bear Mkt | Junk Rally | |||||||||||||||||||||||

| (3/98-9/98) | (9/98-9/99) | (3/00-12/02) | (12/02-12/03) | (3/08-3/09) | (3/09-6/10*) | |||||||||||||||||||||||

Aggr. Investors 1 | -25.5 | % | 80.5 | % | -26.6 | % | 54.0 | % | -53.1 | % | 20.3 | % | ||||||||||||||||

S&P 500 Index | -7.0 | % | 27.8 | % | -39.0 | % | 28.7 | % | -38.1 | % | 32.7 | % | ||||||||||||||||

Difference | -18.5 | % | 52.7 | % | 12.4 | % | 25.3 | % | -15.0 | % | -12.4 | % | ||||||||||||||||

* Performance greater than one year is annualized.

During the high correlation bear market of mid-1998, our Fund performed much more poorly than the overall market. Fortunately, it was followed by a low correlation recovery period, within which our Fund performed excellently, more than making up for the prior downfall. This is what our team thinks of as a “normal” bear market. Of course, in reality each market has its own unique characteristics.

The extended and painful bear market of 2000-2002 was low correlation (micro-driven) and favorable to our Fund’s relative performance. You may recall that this was the period of the “internet bust,” during which investors specifically focused on the actual fundamentals of companies, rather than on the hope for future revenues and earnings or on macro-economic events. Thus, it was a “micro-driven” market, favorable to our Fund. We actually provided some nice “cushion” in this downturn. And when the market bounced back, we continued to do well.

The most recent bear market has been most unfavorable to our Fund. It was a precipitous fall driven by macro events that lead to a deep recession. But the recovery period has also been characterized by two more spikes of correlation, most recently as investors focus on the European Banking crisis, Italy and Greece, and the spectre of a “double dip” recession in the U.S.

Isn’t the performance problem with Bridgeway’s “growthier” select models just that they perform poorly in highly volatile market environments?

No. It is true that the recent correlation spikes line up with high volatility. But as the table above indicates, we have seen other high volatility markets during which we performed relatively well.

Overall, our relative performance has related much more to stock market correlation peaks than to the existence of a bull or a bear environment or low or high volatility.

If there is still risk of another correlation spike and it’s so detrimental to some of Bridgeway’s Funds, shouldn’t we just sell before they occur?

We believe that predicting future macro-economic events is a loser’s proposition. The best economists have a mediocre track record at best in this regard. Even if you forecast one or two pieces correctly, the full system is wildly complex. Further, you have to make two excellent calls: when to get out and when to get back in; one good call by itself can still leave you in a worse

| www.bridgeway.com | 6 | |

| LETTER FROM THE INVESTMENT MANAGEMENT TEAM (continued) | |

off situation. Finally, you may make two correct calls on the economy, but be off slightly on the timing of the market itself and still come out behind. Bridgeway’s investment team believes strongly that waiting for the market to come back “before you get back in” is a losing proposition for all of the reasons above, plus the fact that when it does bounce back it can do so very quickly. Overall, timing the economy, like timing the market itself, is a wildly risky business. As difficult as it may feel, we believe sticking with an appropriate long term plan is the best course of action.

If macro-driven markets represent such a problem for Bridgeway’s more growth-oriented select models and Funds, isn’t there anything Bridgeway can do to correct this?

Yes. Bridgeway has made strong ongoing investments in our research staff, data, and systems over the last few years. We have made incremental improvements to our models without changing anything about our investment philosophy or process. We believe these improvements, based on our backtesting and research, will help relative returns even in macro- and micro-driven markets. Improvements include adding more and higher quality data, testing of different data sources, a new proprietary valuation metric, testing of a new and exciting variable, calibrating some models for narrower market niches, better testing the “depth” (how many stocks in a ranking give strong returns) of our models, retiring some poorer performing models, and better modeling our sell rules.

While we believe that backtesting over multiple market and economic cycles is the best way to understand risks and potential return relationships, past performance, whether modeled or of a specific Fund, does not guarantee future returns.

Returns in a High Inflationary Environment — no place to hide?

The Short Version: With inflation at low single digit levels, people aren’t talking about it much. Yet Bridgeway’s investment management team believes this is one of the very significant investment risks on the horizon. In this section we present why we are worried, what investments historically provide the best hedge, and why they may not work so well this time. Taking a long term, disciplined, and diversified view is still probably one of the best antidotes.

Bridgeway studies stock market history going back many decades, primarily with a view toward understanding risks. Looking forward, one of the biggest risks we see in the two to five-year timefame is increasing inflation. Due to fiscal policy decisions, TARP in the context of a major recession, and war, the national debt as a percent of gross national product is near the highest level since the mid-1940’s. Historically, the U.S. has “inflated” its way out of high debt periods and we think that will likely be true this time. Here is our view of various asset classes:

Long-term bonds. With yields at very low levels, the probability for increasing rates appears much higher than normal. Inflation would accelerate this. When interest rates rise, bond prices fall. We think long-term U.S. treasuries are very risky for this reason. We would be less concerned about default risk, which was in the news last year when treasuries lost their AAA rating. Of higher concern to us is inflation risk. The risks of corporate bonds are similar, though somewhat moderated. Investors have been pulling money out of stock market mutual funds in favor of fixed income funds for four straight years now. We worry that this move is timed just wrong with respect to inflation risk.

Short-term treasuries, CD’s, and money market accounts. The advantage of short-term treasuries and money market accounts is that as inflation heats up and rates rise, investors get the benefit of rising rates. A thirty year bond holder is locked into the current low fixed yields for thirty years. Short-term fixed income holders are not. However, even short-term fixed income can be risky. From 1940 to 1950, for example, the purchase power of 90-day treasuries (with interest reinvested) declined a whopping 41% due to inflation.

Treasury inflation protected securities (TIPS). This has been one of Bridgeway’s favorites as a hedge against inflation for a fixed income investor. Unfortunately (looking forward), mid-term TIPS have had double digit returns in three of the last five years. This is unusual and not at all sustainable. Returns have skyrocketed because interest rates have declined and inflationary fears have heated up to some degree. This leave TIPS with a negative real yield. Thus, investors are paying a hefty premium for the inflation “insurance” feature of this instrument. We still like them as a good long term diversifier, but it seems late to get the full benefit of this investment over the next few years.

Gold. Gold is one traditional hedge against inflation. Over very long time periods, however, gold has been a poor investment. That’s what we dislike the most about it. Gold has very little commercial use and doesn’t tend to create value as stocks and

| 7 | Semi-Annual Report | December 31, 2011 (Unaudited) | |

| LETTER FROM THE INVESTMENT MANAGEMENT TEAM (continued) | |

bonds do. It glitters, and it could be useful as an international currency in time of war. With the almost six-fold increase in gold over the last five years, however, we would be very concerned that it may be fundamentally overpriced. Translate: risky.

Real estate. This is another classical hedge against inflation. Actual real estate is highly illiquid, and if purchased with debt, highly risky. REITs are a liquid alternative; that is, you can buy and sell them easily. But they have also had quite a run in the last three years. REITS are within about 10% of their early 2008 levels. Similar to gold and TIPS, it seems late to establish a new position.

Stocks. Stocks typically suffer as inflation heats up, but then recover as companies increase the prices for their goods and services to keep up with inflation. That’s what we like about stocks over the long term with respect to inflation.

Our conclusions? If you have overexposure to fixed income instruments: beware. The best solution is probably the same we recommend in any market environment: get a long term asset allocation plan consistent with your cash needs, investment horizon and risk tolerance. Put it in place and don’t deviate from it, especially when it feels most uncomfortable to stay the course.

Performance Versus Morningstar Analyst Picks

The Short Version: A close race: Bridgeway 5, Morningstar 8. While a majority of the Bridgeway Funds (7 of 13) outperformed their respective market benchmarks in calendar year 2011, Morningstar did slightly better and edged out Bridgeway’s record by three.

Morningstar, the Chicago-based independent research firm publishes a list of “analysts’ picks” every year for each asset class, as determined by its analysts. Each year in January, when the final tallies are in, we compare the performance of each of our Funds to the average returns of Morningstar’s top picks for the comparable asset class. How did we do in 2011?

In the face of the macro-driven market described on page 3, 2011 was a mediocre year relative to our market benchmarks —seven of thirteen Bridgeway Funds beat their primary market benchmarks. We fared worse against the “higher hurdle” —and it was a higher hurdle in 2011 — of Morningstar’s “top picks.”

The table below depicts the results by Morningstar category and relevant Bridgeway Fund.

| Bridgeway Funds | Morningstar Analyst “Picks” | |||||||||

| Name | 2011 Return | Morningstar Category | 2011 Return | |||||||

Aggressive Investors 1 | -10.31% | *Mid-cap growth | -4.58% | |||||||

Aggressive Investors 2 | -11.59% | *Mid-cap growth | -4.58% | |||||||

Ultra-Small Company | -14.64% | *Small growth | 0.03% | |||||||

Ultra-Small Company Market | -7.86% | *Small blend | -1.49% | |||||||

Micro-Cap Limited | -9.48% | *Small growth | 0.03% | |||||||

Small-Cap Growth | -0.63% | *Small growth | 0.03% | |||||||

*Small-Cap Value | 1.05% | Small value | -9.69% | |||||||

*Omni Tax-Managed | -5.41% | Small value | -9.69% | |||||||

Small-Cap Momentum | -0.92% | *Small growth | 0.03% | |||||||

*Large-Cap Growth | -0.71% | Large-cap growth | -2.84% | |||||||

*Large-Cap Value | 2.33% | Large-cap value | -7.27% | |||||||

*Blue Chip 35 Index | 3.17% | Large-cap blend | 1.87% | |||||||

Managed Volatility | 1.94% | *Long-Short Equity | 4.67% | |||||||

1This fund is offered in a separate prospectus and its semi-annual report is also in a separate book.

“*” means a “win” on that contest. Past performance is not an indicator of future results. The Bridgeway Funds’ adviser, Bridgeway Capital Management, Inc., does not have any influence on the selection of the funds chosen by Morningstar’s analysts. The number and specific funds used in the comparison are in the control and discretion of Morningstar and their analysts and are subject to change. Morningstar’s criteria for choosing Analyst Picks includes, but is not limited to, factors such as

| www.bridgeway.com | 8 | |

| LETTER FROM THE INVESTMENT MANAGEMENT TEAM (continued) | |

performance, expenses, and quality of fund management. In addition, the comparison of Bridgeway Funds to the Morningstar Analyst Picks is limited to performance only and does not take into consideration other factors that are considered by Morningstar when compiling their list of Analyst Picks.

Each Bridgeway Fund is compared to the average total return of the group of funds selected by Morningstar at the beginning of 2011 for the one-year period ended December 31, 2011. These averages in the table are comprised of between two and seventeen funds from within each category. In an effort to provide a complete and balanced assessment, all of the Bridgeway Funds are used in the comparison table shown above such that no attempt is made to cull out unfavorable results. The purpose of this comparison is to “raise the bar” on performance comparison as this analysis uses an arguably higher benchmark by comparing the Bridgeway Funds to other funds chosen by an independent source that specializes in investment research.

“One Star Fund” a Favorite

The Short Version: One of Bridgeway’s first funds has underperformed in three of the last four calendar years. That’s not a record we’re proud of, but John Montgomery is staying put and has even invested more. [As discussed in our June 2011 annual report; we are not suggesting that you simply copy John’s lead; his investment horizon and risk tolerance could be different from yours.] Here he discusses in Q&A format the reasons a data-driven investor such as himself would do that.

In our last annual report for the period ended June 30, 2011, Bridgeway’s founder and investment team leader, John Montgomery, disclosed his personal asset allocation targets. Fully half of the funds he expects to retire on are in the Aggressive Investors (1 and 2) style. The following is an interview with John about this holding:

Since Aggressive Investors 1 and 2 have been Bridgeway’s two poorest performing Funds over the last four years, but also your largest holding, isn’t it time to jettison them?

My long-term allocation includes a very healthy slice of Aggressive Investors 1 and 2. I “eat my own cooking.” I also take a long-term view, and if you think as I do that the strategy is viable, the worst time to sell it would be when it’s most out of favor. So no, I’m not selling it.

What do you mean by “long term view?”

First of all, although I’m 56, I don’t plan to retire anytime soon, so the long-term investment horizon, at least five years and preferably ten years or more, is appropriate for me. Second, I have a high tolerance for risk. “Aggressive” is in the name of the Fund for a reason. The main way I manage risks is to keep my expenses low relative to my income. That means I can save and invest more and give more away. The Aggressive Investors strategy has done very well for me over the long haul and for eight of the nine years leading up to 2008 — but not in the macro-driven markets that began in mid-2008. Sadly, some of our investors got in after a performance run (“buy high”) and bailed after the downturn (“sell low”). That’s a formula for financial disaster that we see too often.

How do you decide when to buy and sell?

I stay put and look at rebalancing annually or when I have more money to invest. If I were in net withdrawal mode, I’d be harvesting from what has done the best to get me back to my target. It’s a contrarian strategy that forces me to invest more in what has recently done poorly. That means I’ve been adding to Aggressive Investors 1 and 2, Ultra-Small Company, and Micro-Cap Limited Funds.

But when might an investor consider selling an underperforming fund?

The time to reconsider the appropriateness of an investment is when your own circumstances change or when the investment process or management changes. My financial circumstances haven’t changed, and our investment process has not changed, although we continue to update models, and no one has left our investment management team in eleven years. We have increasingly skilled and experienced people working on our performance just as we would whether we were outperforming or not. Also, it gives me comfort that we can explain our periods of under- and outperformance. For example, the worst time to sell a previously strong performing value fund with a solid investment process was in 1999, when growth had just had an amazing run, but was about to reverse.

| 9 | Semi-Annual Report | December 31, 2011 (Unaudited) | |

| LETTER FROM THE INVESTMENT MANAGEMENT TEAM (continued) | |

When will the aggressive investors style be back in favor?

We will never know the exact timing. We do know that macro-driven markets have presented an uphill performance terrain for Aggressive Investors 1 and 2 that relates to the investment process of the Funds. Specifically, the models that are the big engine of the Fund are focused on the economic health of individual companies, while the market has significantly ignored these factors during the correlation spikes. The macro-driven markets may continue into 2012 and 2013, but we don’t think they will continue forever, and it would not surprise me to see no more major spikes for a decade.

Can’t the investment team do anything to improve performance during these correlation spikes, or macro-driven markets?

Yes, we think we have enough data on these environments to reasonably address them — should they continue. But we’re doing this in such a way that it doesn’t change our process, and more importantly, based on our research, would not have hurt our returns in low correlation markets. The last thing we want to do is make changes to the Funds that address the last battle at the cost of most other market environments. The value managers who moved toward a growth process in 1999 didn’t fare too well in the first half of the 2000’s.

Introducing Bridgeway Omni and Bridgeway Select Fund Strategies

We have recently divided our Funds into two distinct styles, Omni and Select. While the two styles are very different, our basic investment philosophy continues to be the same statistically driven, evidence-based philosophy we have always used. We will describe the similarities and differences between the two styles in the following paragraphs.

Our Basic Investment Philosophy

If you have visited our website in the past year, you may have noticed that we have two new Funds with the Omni name attached. While the name is new, the concept within Bridgeway has been around for many years. Our investment philosophy of putting investors first and our passion for logic, data and evidence remain consistent throughout everything we do, as do our mission, values and commitment to transformational change for our company and the communities in which we live and work. Much of our investment process is similar through both investment styles. We use a statistically driven, evidence-based investment style that is grounded in academic theory. We have a rigorous testing process that starts with data quality. Our process is disciplined and seeks to avoid behavioral biases and to make continuous improvements through our investment in ongoing research. Risk management is embedded in the innovative design of each Fund that we manage. Our adherence to fund design and trading efficiencies highlight our execution expertise, regardless of the investment style. We strongly believe in maintaining a long-term investment horizon and sticking to your asset allocation through all types of market volatility.

Bridgeway Omni Style

The Omni style began with the Bridgeway Blue-Chip 35 Index Fund and the Ultra-Small Company Market Fund. Both were designed to give shareholders the ability to capture the returns of a particular asset class of stocks. We have recently added three more Funds to the Omni classification (Small-Cap Momentum, Omni Small-Cap Value and Omni Tax-Managed Small-Cap Value), although only Small-Cap Momentum Fund is available to the general public. Each of these Funds is meant to capture the risk premiums of their specific asset class while capitalizing on the concept of efficient markets. Each Fund has a focus on low tracking error to an unpublished index representing the Fund’s style and, with the exception of Small-Cap Momentum Fund, each is designed for low turnover. Also, with the exception of Blue Chip 35 Index, each Fund normally holds a basket of greater than 300 securities in order to gain exposure to an entire asset class.

Bridgeway Select Style

Our two original Funds (Aggressive Investors 1 and Ultra-Small Company Funds) were designed for alpha — market beating returns over the long term — through stock selection (rather than through, say, market timing or sector rotation). These two funds as well as Aggressive Investors 2, Micro-Cap Limited, Small-Cap Growth, Small-Cap Value, Large-Cap Growth, Large-Cap Value and Managed Volatility, fall into the classification now known as Select Funds. Each of these seeks to outperform its market benchmark through effective stock selection that is designed for greater upside capture and downside protection. We select stocks for these funds using multiple multi-factor models that are grounded in academic theory and based on extensive backtesting by Bridgeway’s team. We feed quality data into the models to provide what we call an “information premium” that allows for greater upside capture potential. We also add risk premium factors to focus on downside protection.

| www.bridgeway.com | 10 | |

| LETTER FROM THE INVESTMENT MANAGEMENT TEAM (continued) | |

Our numerous growth, value, momentum, growth at a reasonable price (GARP) (shares characteristics of both growth and value) and contrarian models allow a great deal of portfolio flexibility in order to generate alpha.

Omni or Select?

While the Omni style asset class exposure is quite distinct from the Select style alpha generation, both adhere to the basic investment philosophy Bridgeway has used for eighteen years. We haven’t reinvented ourselves, but we have redefined the way we will represent our Funds going forward. There are arguments and advantages for both investment styles, but it is up to individual investors or advisers to decide which style or combination of styles will satisfy their investment needs.

Transformational Change by Rebecca Hove, Bridgeway Partner and Leader in the Area

Each Bridgeway Partner engages in Transformative Change in a self-created way. These engagements are highly variegated, as is the nature of transformation. Though among this constant change, the foundation of our Transformative Change programs has a static, fundamental component: Service. We participate in Service Trips to the developing world and local Service Projects. We serve on these projects with our families, fellow Bridgeway Partners or our business partners, or with personal friends and even strangers who become friends! We serve by giving - of our personal time, our money and other resources, our mental capacities, our labor, and most importantly, our hearts.

You may be thinking, “But Bridgeway is in the financial management business....” Yes, and included in that, we are in the Transformation business. At Bridgeway, we see this as a both/and; not an either/or. Transformation- it’s a current buzz-word, but what does it really mean? More importantly, what does it mean to, and for, you?

Transformation is dynamic. Unbounded variety is intrinsic to the word and work itself; often producing radical results. Perhaps the most profound definition comes from medicine: “The genetic alteration of a cell by introduction of DNA from another cell.” This is indeed the marrow of transformation – to change from the inside and then outside from one ‘being’ into a different ‘being’ as a result of an introduction. You are not WHAT or WHO you used to be, after transformation. You are altered; you have a completely new make-up. That truly is radical... and at Bridgeway we are doing and experiencing it first-hand.

One of our Partners serves on the Board of Navidad en el Barrio, an organization local to Houston that provides disadvantaged kids with the opportunity to experience receiving gifts at Christmas. Due to generous gifts of in-kind and cash donations, volunteers who wrap presents and deliver gifts, as well as put on an event, kids are introduced to a Christmas experience they otherwise would not know. Parents receive grocery bags of fresh fruit, other food items, and a guide to available community resources.

In 2011 we partnered with YES Prep, a charter school in Houston, for a service day with Navidad en el Barrio. About 200 YES Prep middle school and high school students, many of whom could qualify for the Christmas program, served alongside Bridgeway volunteers – giving their time, talent, smiles and heart so others could receive.

The YES Prep students we served with, modeled another aspect of the gift of transformation and how unbounded it is. Regardless of what one does or does not have materially, we all have the ability to serve and give. Transformation can happen anytime, anywhere, and with anybody or anything. It is about giving and receiving - for all involved - two things which are also a constant presence within the variety of transformation.

You see, transformation is in Bridgeway’s DNA. We are transforming internally as individuals as we create and build these interactions. As we serve and give with others, we are changed by them and they are changed by us; together we are changing something external in our local and global community. Like those cells, separate and unique worlds collide, mix, team together, and then build something entirely new. Nothing is left the same as it was upon first introduction – not the people, not the place. For those interested in leverage, THIS is radical, too! We believe so strongly in this philosophy and its results we plan to share Transformative Change stories in every shareholder letter.

So, consider this your own “introduction”. Think about how you plan to invest in transformation personally, because we’re staying in the Transformation business. Its impact is unbeatable!

| 11 | Semi-Annual Report | December 31, 2011 (Unaudited) | |

|

(Unaudited)

December 31, 2011

Dear Fellow Aggressive Investors 1 Fund Shareholder,

The Bridgeway Funds Board of Directors has approved a plan of reorganization providing for the conversion of the Aggressive Investors 2 Fund into shares of the Aggressive Investors 1 Fund. The plan of reorganization providing for the conversion will require the approval of the Aggressive Investors 2 Fund shareholders. If approved, the conversion of shares is expected to take effect in the second quarter of 2012.

For the quarter ended December 31, 2011, Aggressive Investors 1 Fund returned 13.48%, outperforming our primary market benchmark, the S&P 500 Index (+11.82%) and our peer benchmark, the Lipper Capital Appreciation Funds Index (+7.64%). The Fund lagged the smaller-cap Russell 2000 Index (+15.47%) during the three month period. It was a mixed quarter. We would be more pleased, but for the prior quarter’s very poor performance.

For the six-month “semi-annual” period ended December 31, 2011, our Fund couldn’t overcome the “headwind” of the quarter ended September 30, 2011 — the most macro-driven market we have seen (see pages 3 to 7) and an environment not favorable to the Fund. The Fund declined 16.77%, lagging well behind our primary market benchmark, the S&P 500 Index (-3.69%), our peer benchmark, the Lipper Capital Appreciation Funds Index (-9.04%), and the Russell 2000 Index (-9.77%). We are disappointed with these results. We would like to emphasize that we have taken certain actions consistent with our (unchanged) investment philosophy and process to address our underperformance in macro-driven markets such as 2008, 2010, and 2011. See, for example, “If macro-driven markets represent such a problem for Bridgeway’s “growthier” select models and Funds, isn’t there anything Bridgeway can do to correct this?” on page 7 and, “Can’t the investment team do anything to improve performance during these correlation spikes, or macro-driven markets?” on page 10.

Similarly, the very poor September quarter performance overshadowed the positive performance in the first half of calendar year 2011. The Fund dropped 10.31% for the calendar year, underperforming our primary market benchmark, the S&P 500 Index (+2.11%), our peer benchmark, the Lipper Capital Appreciation Funds Index (-5.32%), and the Russell 2000 Index (-4.18%).

The table below presents our quarter, six-month, one-year, five-year, ten-year and life-to-date financial results. See the next page for a graph of performance since inception.

Annualized | ||||||||||||||||||||||||

| Quarter 10/1/11 to 12/31/11 | 6 Months 7/1/11 to 12/31/11 | 1 Year 1/1/11 to 12/31/11 | 5 Years 1/1/07 to 12/31/11 | 10 Years 1/1/02 to 12/31/11 | Life-to-Date to 12/31/11 | |||||||||||||||||||

Aggressive Investors 1 Fund | 13.48% | -16.77% | -10.31% | -6.29% | 2.34% | 12.03% | ||||||||||||||||||

S&P 500 Index (large companies) | 11.82% | -3.69% | 2.11% | -0.25% | 2.92% | 7.98% | ||||||||||||||||||

Lipper Capital Appreciation Funds Index | 7.64% | -9.04% | -5.32% | 1.23% | 3.48% | 6.95% | ||||||||||||||||||

Russell 2000 Index (small companies) | 15.47% | -9.77% | -4.18% | 0.15% | 5.62% | 8.03% | ||||||||||||||||||

Performance figures quoted in the table above and graph below represent past performance and are no guarantee of future results. Total return figures in the table above include the reinvestment of dividends and capital gains. The table above and the graph below do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. The recent growth rate in the stock market has helped to produce short-term returns that are not typical and may not continue in the future.

The S&P 500 Index is a broad-based, unmanaged measurement of changes in stock market conditions, based on the average of 500 widely held common stocks with dividends reinvested. The Russell 2000 Index is an unmanaged, market value weighted index that measures performance of the 2,000 companies that are between the 1,000th and 3,000th largest in the

| www.bridgeway.com | 12 | |

Aggressive Investors 1 Fund MANAGER’S COMMENTARY (continued) | |

(Unaudited)

market with dividends reinvested. The Lipper Capital Appreciation Funds Index reflects the record of the 30 largest funds in the category of more aggressive domestic growth mutual funds, as reported by Lipper, Inc. It is not possible to invest directly in an index.

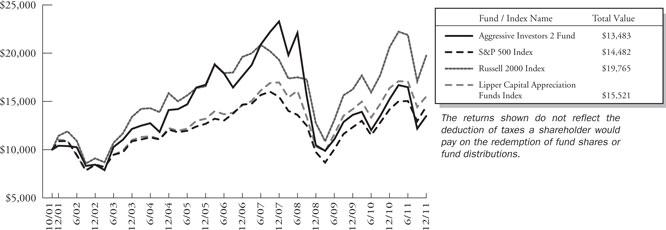

According to data from Lipper, Inc. as of December 31, 2011, Aggressive Investors 1 Fund ranked 257th of 298 capital appreciation funds for the twelve months ending December 31, 2011, 231st of 232 over the last five years, 115th of 163 over the last ten years, and 3rd of 53 since inception in August, 1994. These long-term numbers and the graph below give two snapshots of our long-term success. Lipper, Inc. is an independent mutual fund rating service that ranks funds in various fund categories by making comparative calculations using total returns.

Aggressive Investors 1 Fund vs. S&P 500 Index, Lipper Capital Appreciation Funds Index & Russell 2000 Index

from Inception 8/5/94 to 12/31/11

Detailed Explanation of Quarterly Performance

The Short Version: Media and energy companies helped the most, while information technology stocks held our Fund back. The bounceback of smaller companies also helped.

Energy companies and media firms led the positive charge in the quarter as the cost of oil rose to $100/barrel and helped give a boost to exploration and production companies. The heated election campaign season meant significant advertising dollars for television stations. Three energy companies highlighted the best performers list for the December quarter, and two media holdings combined to contribute over one and one-half percent to the return of the Fund.

These are the Fund’s ten best-contributing stocks for the quarter ended December 31, 2011:

| Rank | Description | Industry | % Contribution to Return | |||

| 1 | Sinclair Broadcast Group, Inc. | Media | 1.1% | |||

| 2 | Amerco, Inc. | Road & Rail | 0.5% | |||

| 3 | W&T Offshore, Inc. | Oil, Gas & Consumable Fuels | 0.5% | |||

| 4 | CBS Corp. | Media | 0.4% | |||

| 5 | Stone Energy Corp. | Oil, Gas & Consumable Fuels | 0.4% | |||

| 6 | RLI Corp. | Insurance | 0.4% | |||

| 7 | Westlake Chemical Corp. | Chemicals | 0.4% | |||

| 8 | Newpark Resources, Inc. | Energy Equipment & Services | 0.4% | |||

| 9 | Credit Acceptance Corp. | Consumer Finance | 0.4% | |||

| 10 | Titan International, Inc. | Machinery | 0.4% |

| 13 | Semi-Annual Report | December 31, 2011 (Unaudited) | |

Aggressive Investors 1 Fund MANAGER’S COMMENTARY (continued) | |

(Unaudited) |

Although viewers complain about all of the negative political ads, they actually pay off quite well for broadcasting companies. One such company, Sinclair Broadcast Group, was the Fund’s top contributor for the quarter. Its stock price soared over 50% during the three-month period as the campaign season heated up and candidates started to air ads in major primary states. Sinclair has been in expansion mode and recently announced the acquisition of media companies with major markets in Florida and New York. In November, the holding posted better-than-expected quarterly results and rewarded shareholders with a cash dividend.

With interest rates at historically low levels, some income investors have sought out returns generated from dividend paying stocks. Amerco, parent of do-it-yourself moving and storage company U-Haul, announced a special dividend in December that translated into a yield in excess of that paid by the five-year treasury (at the time). The company does not currently pay a regular dividend, but with solid cash flow from operations, some analysts expect this move to be a sign of future shareholder rewards. Amerco has experienced favorable increases in profits and revenues from its three key segments (moving/storage, life insurance, property and casualty insurance), and sales have increased over 10% for six straight quarters. The holding contributed one-half of a percent to the Fund’s return for the quarter.

Though the economy has shown signs of rebounding as of late, businesses and consumers still do not appear to be stepping up their purchases of computers and electronics (unless they are manufactured by Apple). Three Information Technology holdings made the list of worst contributors. Combined, they hurt the Fund performance by almost three-fourths of a percent.

These are the Fund’s ten worst-contributing stocks for the quarter ended December 31, 2011:

| Rank | Description | Industry | % Contribution to Return | |||

| 1 | Green Mountain Coffee Roasters, Inc. | Food Products | -0.5% | |||

| 2 | Alcatel-Lucent - Sponsored ADR | Communications Equipment | -0.5% | |||

| 3 | Ultra Petroleum Corp. | Oil, Gas & Consumable Fuels | -0.2% | |||

| 4 | HCA Holdings, Inc. | Health Care Providers & Services | -0.2% | |||

| 5 | Walter Energy, Inc. | Metals & Mining | -0.2% | |||

| 6 | HollyFrontier Corp. | Oil, Gas & Consumable Fuels | -0.1% | |||

| 7 | Best Buy Co., Inc. | Specialty Retail | -0.1% | |||

| 8 | Electronic Arts, Inc. | Software | -0.1% | |||

| 9 | Helix Energy Solutions Group, Inc. | Energy Equipment & Services | -0.1% | |||

| 10 | Dell, Inc. | Computers & Peripherals | -0.1% |

David Einhorn, the hedge fund activist investor, confirmed in October 2011 that he had a significant “short” bet (he expected the stock to fall) on Green Mountain Coffee and he accused management of faulty accounting practices. A month later, Green Mountain posted a sizable earnings shortfall. The holding lost half of its value during the three month period and was the worst contributor to the Fund.

Alcatel-Lucent develops communications software for use in phones, Internet, and mobile devices. During the latter part of the year, fears began to set in that the ongoing economic crisis (domestically and in Europe) would hinder future revenues and margins. In November, the company missed its quarterly revenue expectations, and management offered a very disappointing financial outlook. The stock plunged during the quarter, lost over 40% in value, and was among the weakest holdings in the Fund.

Detailed Explanation of Calendar Year Performance

The Short Version: Unfortunately, our performance in a single quarter (September), the most macro-driven market on record, damaged our calendar year returns. Telecommunications companies and two coffee companies hurt the most.

As the recent holiday season seemed to confirm, consumers are spending more and more time on the Internet and are comfortable shopping and transacting business online. Three Internet-related companies (two retail) comprised the list of top performing holdings for the calendar year. Combined, they contributed over one percent to the Fund’s return.

| www.bridgeway.com | 14 | |

Aggressive Investors 1 Fund MANAGER’S COMMENTARY (continued) | |

| (Unaudited) |

These are the Fund’s ten best-contributing stocks for the calendar year ended December 31, 2011:

| Rank | Description | Industry | % Contribution to Return | |||

| 1 | ARM Holdings | Semiconductors & Semiconductor Equipment | 0.6% | |||

| 2 | RLI Corp. | Insurance | 0.6% | |||

| 3 | Netflix, Inc. | Internet & Catalog Retail | 0.6% | |||

| 4 | Domino’s Pizza, Inc. | Hotels, Restaurants & Leisure | 0.5% | |||

| 5 | Polaris Industries, Inc. | Leisure Equipment & Products | 0.4% | |||

| 6 | CBS Corp. | Media | 0.4% | |||

| 7 | Baidu, Inc. | Internet Software & Services | 0.3% | |||

| 8 | priceline.com, Inc. | Internet & Catalog Retail | 0.3% | |||

| 9 | Credit Acceptance Corp. | Consumer Finance | 0.3% | |||

| 10 | Unisys Corp. | IT Services | 0.3% |

Property and casualty insurer RLI Corp. has made a habit of rewarding shareholders for their confidence through dividends and share repurchases. In this environment of low interest rates, many investors appreciate such a philosophy and are willing to buy into these companies. Over the past five years, RLI has paid investors about $600 million through dividends and share buybacks. Late in the year, the board of directors announced both a special dividend and a regular dividend, due to its continued operational strength. In October, RLI reported earnings that beat analysts’ expectations on strong underwriting income. During the twelve month period, the stock was among the top contributors to the Fund.

Polaris Industries remained in expansion mode throughout the year, manufacturing snowmobiles, off-road vehicles and motorcycles. In June, the company closed on its acquisition of an electric vehicle maker from Chrysler and recently announced the purchase of a minority interest in Brammo—a deal that gives it greater exposure to the electric motorcycle business. Polaris was also awarded new government contracts to provide all-terrain vehicles to security forces in Afghanistan and Iraq. The company posted solid profit numbers in the third quarter, management revised its full-year earnings estimates and now expects sales growth in excess of 30% for the year.

Certain telecommunications companies struggled at various times over the course of the 12-month period, and four such holdings found their way onto the Fund’s worst contributors list for 2011. Combined, they cost the Fund over three percent in performance. Two coffee companies also detracted from the Fund’s return as the commodity’s price plunged to a nine-month low during the most recent quarter.

These are the Fund’s ten worst-contributing stocks for the calendar year ended December 31, 2011:

| Rank | Description | Industry | % Contribution to Return | |||

| 1 | GT Advanced Technologies, Inc. | Semiconductors & Semiconductor Equipment | -1.2% | |||

| 2 | Alcatel-Lucent - Sponsored ADR | Communications Equipment | -1.2% | |||

| 3 | Vonage Holdings Corp. | Diversified Telecommunication Services | -0.9% | |||

| 4 | TRW Automotive Holdings Corp. | Auto Components | -0.7% | |||

| 5 | Silvercorp Metals, Inc. | Metals & Mining | -0.6% | |||

| 6 | Coffee Holding Co., Inc. | Food Products | -0.6% | |||

| 7 | JDS Uniphase Corp. | Communications Equipment | -0.6% | |||

| 8 | Illumina, Inc. | Biotechnology | -0.6% | |||

| 9 | MetroPCS Communications Inc. | Wireless Telecommunication Services | -0.5% | |||

| 10 | Green Mountain Coffee Roasters, Inc. | Food Products | -0.5% |

GT Advanced Technologies provides energy efficient lighting and other equipment and services, primarily for the solar industry. During the year, many related stocks came under pressure as global demand for solar projects slowed and excess capacity prompted severe price cuts throughout the industry. Additionally, the US government began investigating certain Chinese companies within the industry, raising concerns about unfair business practices. GT Advanced Technologies supplies certain machinery and other equipment to China and fears that its operations could be impacted if a trade dispute ensues between the

| 15 | Semi-Annual Report | December 31, 2011 (Unaudited) | |

Aggressive Investors 1 Fund MANAGER’S COMMENTARY (continued) | |

| (Unaudited) |

two countries and causes the stock price to drop. The holding was the worst contributor for the calendar year and cost the Fund over one percent in return.

While Vonage has been all over the airwaves since it went public in 2006, the mass advertising does not appear to be translating into new customers (or bottom line profits) these days. As the competition picks up for Internet-based telephone communications, Vonage, the largest provider of such services, has been struggling with lower revenue growth and a declining subscriber base. Companies like Skype and Google Voice have made tremendous headways into the market, and Vonage is feeling the pinch. Additionally, some investors worry about the significant stock options and warrants that could potentially dilute its valuation should management not initiate a share buyback strategy at some point in the future. Late in the year, the company introduced a new subscription plan for customers who wish to add a second device (i.e. smart-phone) to their existing plans, hoping to stop the bleeding from customer departures. The holding cost the Fund almost one percent in return over the 12-month period.

Top Ten Holdings as of December 31, 2011

Five of the Fund’s top contributors for the December 2011 quarter were also among the largest holdings at the end of the calendar year: Sinclair, RLI, Credit Acceptance, CBS and Amerco. Two media-related companies made the Fund’s top ten holdings at year-end. Still, the Fund was broadly diversified and no single holding accounted for greater than 2.6% of the net assets. The ten largest positions represented just 20% of the total assets of the Fund.

| Rank | Description | Industry | % of Net Assets | |||

| 1 | Sinclair Broadcast Group, Inc. | Media | 2.6% | |||

| 2 | RPC, Inc. | Energy Equipment & Services | 2.6% | |||

| 3 | NeuStar, Inc. | IT Services | 2.2% | |||

| 4 | Apple, Inc. | Computers & Peripherals | 2.0% | |||

| 5 | Domino’s Pizza, Inc. | Hotels, Restaurants & Leisure | 1.8% | |||

| 6 | RLI Corp. | Insurance | 1.8% | |||

| 7 | Credit Acceptance Corp. | Consumer Finance | 1.8% | |||

| 8 | Dillard’s, Inc. | Multiline Retail | 1.8% | |||

| 9 | CBS Corp. | Media | 1.7% | |||

| 10 | Amerco, Inc. | Road & Rail | 1.7% | |||

| Total | 20.0% |

Industry Sector Representation as of December 31, 2011

The biggest disparity between the Fund and the S&P 500 Index was found in the Consumer Discretionary sector, which also contributed the most to Fund returns for the year. On the other end of the spectrum, we were most underrepresented in the Consumer Staples sector.

| www.bridgeway.com | 16 | |

Aggressive Investors 1 Fund MANAGER’S COMMENTARY (continued) | |

| (Unaudited) |

| % of Net Assets | % of S&P 500 Index | Difference | ||||

Consumer Discretionary | 18.8% | 10.3% | 8.5% | |||

Consumer Staples | 6.9% | 11.6% | -4.7% | |||

Energy | 13.6% | 12.4% | 1.2% | |||

Financials | 17.0% | 13.5% | 3.5% | |||

Health Care | 8.8% | 11.9% | -3.1% | |||

Industrials | 10.2% | 10.8% | -0.6% | |||

Information Technology | 15.1% | 19.2% | -4.1% | |||

Materials | 4.4% | 3.4% | 1.0% | |||

Telecommunication Services | 3.9% | 3.1% | 0.8% | |||

Utilities | 1.1% | 3.8% | -2.7% | |||

Cash & Other Assets | 0.2% | 0.0% | 0.2% | |||

Total | 100.0% | 100.0% |

Disclaimer

The views expressed here are exclusively those of Fund management. These views, including those related to market sectors or individual stocks, are not meant as investment advice and should not be considered predictive in nature. Any favorable (or unfavorable) description of a holding applies only as of December 31, 2011, unless otherwise stated. Security positions can and do change thereafter. Discussions of historical performance do not guarantee and may not be indicative of future performance.

Market volatility can significantly affect short-term performance. The Fund is not an appropriate investment for short-term investors. Investments in the small companies within this multi-cap fund generally carry greater risk than is customarily associated with larger companies. This additional risk is attributable to a number of factors, including the relatively limited financial resources that are typically available to small companies and the fact that small companies often have comparatively limited product lines. In addition, the stock of small companies tends to be more volatile than the stock of large companies, particularly in the short term and particularly in the early stages of an economic or market downturn. The Fund’s use of options, futures, and leverage can magnify the risk of loss in an unfavorable market, and the Fund’s use of short-sale positions can, in theory, expose shareholders to unlimited loss. Finally, the Fund exposes shareholders to “focus risk,” which may add to Fund volatility through the possibility that a single company could significantly affect total return. Shareholders of the Fund, therefore, are taking on more risk than they would if they invested in the stock market as a whole.

Conclusion

Thank you for your continued investment in Aggressive Investors 1 Fund. We encourage your feedback; your reactions and concerns are extremely important to us.

Sincerely,

The Investment Management Team

| 17 | Semi-Annual Report | December 31, 2011 (Unaudited) | |

Bridgeway Aggressive Investors 1 Fund | |

| Showing percentage of net assets as of December 31, 2011 (Unaudited) |

Industry | Company | Shares | Value | |||||||

COMMON STOCKS - 99.89% |

| |||||||||

Aerospace & Defense - 1.15% |

| |||||||||

Triumph Group, Inc. | 16,073 | $ | 939,467 | |||||||

Auto Components - 2.45% |

| |||||||||

Tenneco, Inc.* | 27,900 | 830,862 | ||||||||

TRW Automotive Holdings Corp.* | 36,200 | 1,180,120 | ||||||||

|

| |||||||||

| 2,010,982 | ||||||||||

Beverages - 3.62% |

| |||||||||

Coca-Cola Enterprises, Inc.# | 31,000 | 799,180 | ||||||||

Constellation Brands, Inc., Class A* | 43,300 | 895,011 | ||||||||

Hansen Natural Corp.* | 13,800 | 1,271,532 | ||||||||

|

| |||||||||

| 2,965,723 | ||||||||||

Capital Markets - 2.15% |

| |||||||||

Bank of New York Mellon Corp. (The) | 42,200 | 840,202 | ||||||||

Northern Trust Corp. | 23,300 | 924,078 | ||||||||

|

| |||||||||

| 1,764,280 | ||||||||||

Chemicals - 2.26% |

| |||||||||

CF Industries Holdings, Inc. | 7,400 | 1,072,852 | ||||||||

Westlake Chemical Corp. | 19,400 | 780,656 | ||||||||

|

| |||||||||

| 1,853,508 | ||||||||||

Commercial Services & Supplies - 1.02% |

| |||||||||

Consolidated Graphics, Inc.* | 17,400 | 840,072 | ||||||||

Communications Equipment - 0.56% |

| |||||||||

Alcatel-Lucent - Sponsored ADR* | 296,800 | 463,008 | ||||||||

Computers & Peripherals - 4.02% |

| |||||||||

Apple, Inc.* | 4,100 | 1,660,500 | ||||||||

Dell, Inc.* | 56,700 | 829,521 | ||||||||

Seagate Technology PLC | 49,500 | 811,800 | ||||||||

|

| |||||||||

| 3,301,821 | ||||||||||

Consumer Finance - 4.99% |

| |||||||||

Capital One Financial Corp. | 18,000 | 761,220 | ||||||||

Cash America International, Inc. | 15,900 | 741,417 | ||||||||

Credit Acceptance Corp.* | 17,700 | 1,456,356 | ||||||||

Discover Financial Services | 47,100 | 1,130,400 | ||||||||

|

| |||||||||

| 4,089,393 | ||||||||||

Industry Company | Shares | Value | ||||||||

Containers & Packaging - 1.15% |

| |||||||||

Crown Holdings, Inc.* | 28,200 | $ | 946,956 | |||||||

Diversified Financial Services - 2.45% |

| |||||||||

Interactive Brokers Group, | ||||||||||

Inc., Class A | 60,500 | 903,870 | ||||||||

Moody’s Corp. | 32,800 | 1,104,704 | ||||||||

|

| |||||||||

| 2,008,574 | ||||||||||

Diversified Telecommunication Services - 3.02% |

| |||||||||

Telecom Corp. of New | ||||||||||

Zealand, Ltd.—Sponsored ADR | 165,100 | 1,319,149 | ||||||||

Vonage Holdings Corp.* | 472,600 | 1,157,870 | ||||||||

|

| |||||||||

| 2,477,019 | ||||||||||