UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-08200

Bridgeway Funds, Inc.

(Exact name of registrant as specified in charter)

20 Greenway Plaza, Suite 450

Houston, Texas 77046

(Address of principal executive offices) (Zip code)

Tammira Philippe, President

Bridgeway Funds, Inc.

20 Greenway Plaza, Suite 450

Houston, Texas 77046

(Name and address of agent for service)

Registrant’s telephone number, including area code: (713) 661-3500

Date of fiscal year end: June 30

Date of reporting period: June 30, 2016

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 100 F Street, NE, Washington, DC 20549. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

Item 1. Reports to Stockholders.

The Report to Shareholders is attached herewith.

A no-load mutual fund family of domestic funds

| | | | |

| | |

| | Annual Report | | |

| | |

| | June 30, 2016 | | |

| | |

| | | | |

| | |

| |

| AGGRESSIVE INVESTORS 1 | | BRAGX |

| |

| ULTRA-SMALL COMPANY | | BRUSX |

| (Open to Existing Investors — Direct Only) | | |

| |

| ULTRA-SMALL COMPANY MARKET | | BRSIX |

| |

| SMALL-CAP MOMENTUM | | BRSMX |

| |

| SMALL-CAP GROWTH | | BRSGX |

| |

| SMALL-CAP VALUE | | BRSVX |

| |

| BLUE CHIP 35 INDEX | | BRLIX |

| |

| MANAGED VOLATILITY | | BRBPX |

| | |

| TABLE OF CONTENTS | |  |

| | |

| | |

Bridgeway Funds Standardized Returns as of June 30, 2016* (Unaudited)

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | Annualized | | | | | | |

| Fund | | Quarter | | Six Months | | 1 Year | | 5 Years | | 10 Years | | Inception

to Date | | Inception

Date | | Gross

Expense

Ratio2 | | Net

Expense

Ratio2 |

Aggressive Investors 1 | | | | 2.68% | | | | | 2.28% | | | | | -7.40% | | | | | 8.82% | | | | | 2.59% | | | | | 12.52% | | | | | 8/5/1994 | | | | | 1.32% | | | | | 1.32% | |

Ultra-Small Company | | | | 0.35% | | | | | -1.29% | | | | | -13.53% | | | | | 5.96% | | | | | 3.05% | | | | | 13.67% | | | | | 8/5/1994 | | | | | 1.15% | | | | | 1.15% | |

Ultra-Small Co Market | | | | 2.90% | | | | | -1.01% | | | | | -10.83% | | | | | 8.79% | | | | | 4.17% | | | | | 9.93% | | | | | 7/31/1997 | | | | | 0.78% | | | | | 0.78% | |

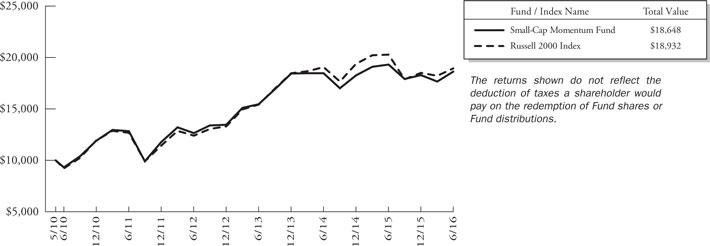

Small-Cap Momentum | | | | 5.60% | | | | | 1.95% | | | | | -3.48% | | | | | 7.77% | | | | | NA | | | | | 10.77% | | | | | 5/28/2010 | | | | | 3.36% | 1 | | | | 0.90% | 1 |

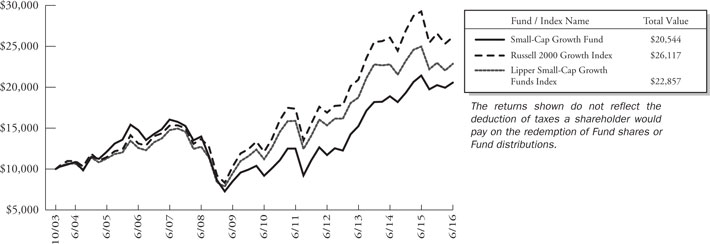

Small-Cap Growth | | | | 3.04% | | | | | 1.55% | | | | | -3.97% | | | | | 10.46% | | | | | 3.37% | | | | | 5.85% | | | | | 10/31/2003 | | | | | 1.08% | 1 | | | | 0.94% | 1 |

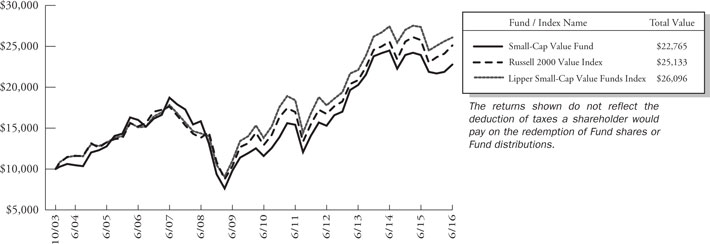

Small-Cap Value | | | | 3.94% | | | | | 4.87% | | | | | -5.02% | | | | | 8.12% | | | | | 3.58% | | | | | 6.71% | | | | | 10/31/2003 | | | | | 0.98% | 1 | | | | 0.94% | 1 |

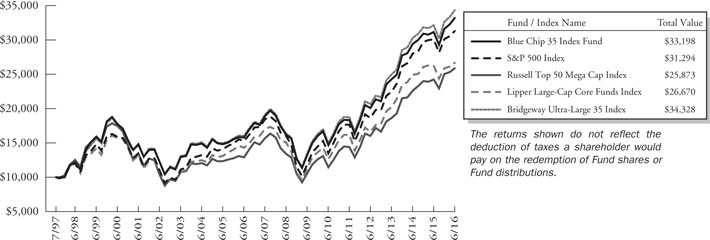

Blue Chip 35 Index | | | | 2.85% | | | | | 5.05% | | | | | 6.60% | | | | | 12.61% | | | | | 7.72% | | | | | 6.55% | | | | | 7/31/1997 | | | | | 0.23% | 1 | | | | 0.15% | 1 |

Managed Volatility | | | | 0.57% | | | | | 1.21% | | | | | 1.10% | | | | | 4.46% | | | | | 2.89% | | | | | 3.87% | | | | | 6/30/2001 | | | | | 1.05% | 1 | | | | 0.95% | 1 |

Bridgeway Funds Returns for Calendar Years 2002 through 2015* (Unaudited)

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | 2002 | | | 2003 | | | 2004 | | | 2005 | | | 2006 | | | 2007 | | | 2008 | | | 2009 | | | 2010 | | | 2011 | | | 2012 | | | 2013 | | | 2014 | | | 2015 | |

Aggressive Investors 1 | | | -18.01% | | | | 53.97% | | | | 12.21% | | | | 14.93% | | | | 7.11% | | | | 25.80% | | | | -56.16% | | | | 23.98% | | | | 17.82% | | | | -10.31% | | | | 21.58% | | | | 42.21% | | | | 14.99% | | | | -9.83% | |

Ultra-Small Company | | | 3.98% | | | | 88.57% | | | | 23.33% | | | | 2.99% | | | | 21.55% | | | | -2.77% | | | | -46.24% | | | | 48.93% | | | | 23.55% | | | | -14.64% | | | | 24.49% | | | | 55.77% | | | | -0.56% | | | | -16.12% | |

Ultra-Small Co Market | | | 4.90% | | | | 79.43% | | | | 20.12% | | | | 4.08% | | | | 11.48% | | | | -5.40% | | | | -39.49% | | | | 25.95% | | | | 24.86% | | | | -7.86% | | | | 19.83% | | | | 50.91% | | | | 4.61% | | | | -8.28% | |

Small-Cap Momentum | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | -0.92% | | | | 14.18% | | | | 37.07% | | | | -0.94% | | | | 0.14% | |

Small-Cap Growth | | | | | | | | | | | 11.59% | | | | 18.24% | | | | 5.31% | | | | 6.87% | | | | -43.48% | | | | 15.04% | | | | 11.77% | | | | -0.63% | | | | 11.05% | | | | 48.52% | | | | 6.13% | | | | 4.93% | |

Small-Cap Value | | | | | | | | | | | 17.33% | | | | 18.92% | | | | 12.77% | | | | 6.93% | | | | -45.57% | | | | 26.98% | | | | 16.55% | | | | 1.05% | | | | 20.99% | | | | 39.72% | | | | 0.79% | | | | -9.43% | |

Blue Chip 35 Index | | | -18.02% | | | | 28.87% | | | | 4.79% | | | | 0.05% | | | | 15.42% | | | | 6.07% | | | | -33.30% | | | | 26.61% | | | | 10.60% | | | | 3.17% | | | | 15.20% | | | | 31.67% | | | | 11.51% | | | | 2.17% | |

Managed Volatility | | | -3.51% | | | | 17.82% | | | | 7.61% | | | | 6.96% | | | | 6.65% | | | | 6.58% | | | | -19.38% | | | | 12.39% | | | | 5.41% | | | | 1.94% | | | | 6.46% | | | | 9.25% | | | | 5.95% | | | | 0.17% | |

Performance figures quoted represent past performance and are no guarantee of future results. Current performance may be lower or higher than the performance data quoted. Investment return and principal value will fluctuate, so that an investor’s shares, when redeemed, may be worth more or less than original cost. To obtain performance current to the most recent month-end, please visit www.bridgeway.com or call 1-800-661-3550. Total return figures include the reinvestment of dividends and capital gains.

| | 1 | Some of the Fund’s fees were waived or expenses reimbursed; otherwise, returns would have been lower. The Adviser has contractually agreed to waive fees and/or reimburse expenses. Any material change to this Fund policy would require a vote by shareholders. |

| | 2 | Expense ratios are as stated in the current prospectus. Please see financial highlights for expense ratios as of June 30, 2016. |

* Numbers highlighted indicate periods when the Fund outperformed its primary benchmark.

This report is submitted for the general information of the shareholders of each Fund. It is not authorized for distribution to prospective investors unless preceded or accompanied by an effective prospectus, which includes information regarding a Fund’s risks, objectives, fees and expenses, experience of its management, and other information. Investors should read the prospectus carefully before investing in a Fund. For questions or other Fund information, call 1-800-661-3550 or visit the Funds’ website at www.bridgeway.com. Funds are available for purchase by residents of the United States, Puerto Rico, U.S. Virgin Islands and Guam only. Foreside Fund Services, LLC, Distributor.

The views expressed here are exclusively those of Fund management. These views, including those relating to the market, sectors, or individual stocks, are not meant as investment advice and should not be considered predictive in nature.

| | |

LETTER FROM THE INVESTMENT MANAGEMENT TEAM | | |

June 30, 2016

Dear Fellow Shareholders,

Performance across the domestic equity markets was positive for the June quarter, and most segments of the market also posted gains for the 12 months ended June 30, 2016. Only small-cap stocks and mid-cap growth stocks recorded losses for the fiscal year. Market highlights appear on page 2. In this environment, the Bridgeway Funds performed within design expectations, guided by our statistically driven, evidence-based investment approach. Please see the enclosed letters for a detailed explanation of each Fund’s performance during the quarter and fiscal year. We hope you find the letters helpful.

The start of the June quarter marked an important milestone for Bridgeway: Tammira Philippe stepped into her new role as President of Bridgeway Capital Management. On page 2, she reflects on her first 90 days as President, and shares her vision for Bridgeway’s future.

The June quarter also saw a turnaround for small-cap value stocks, although the gains were not enough to offset the asset class’s poor performance from earlier in the fiscal year. In fact, small-cap value stocks have lagged the market for several years, which might be causing some investors to wonder whether these stocks still offer a long-term premium. Yet our research indicates that the small-cap value premium isn’t dead, and we explain our reasons for optimism on page 3.

The end of the fiscal year is also the time when we look back on what went well for Bridgeway during the past 12 months, and what didn’t. This year, we’re highlighting the poor performance of our Aggressive Investors 1 Fund as the “worst thing” of the past fiscal year. You can read our breakdown of what went wrong on page 4.

Finally, on page 5, we share one Partner’s very personal approach to creating transformative change in our communities. Tami Groce describes her work supporting two groups of people going through life changes that she’s experienced first hand.

As always, we appreciate your feedback. We take your comments very seriously and regularly discuss them to help us manage our Funds and this company. Please keep your ideas coming — both favorable and critical. They provide us with a vital tool to serve you better.

Sincerely,

Your Investment Management Team

| | |

LETTER FROM THE INVESTMENT MANAGEMENT TEAM (continued) | | |

Market Review

Domestic equity markets rose during the June quarter, despite late-period volatility sparked by the U.K. referendum vote to leave the European Union. Although global stock markets plunged immediately following the June 23 vote, they quickly rebounded in subsequent days. The S&P 500 returned 2.46% for the quarter, and the Dow Jones Industrial Average rose 2.07%. For the fiscal year, the S&P 500 and the DJIA were up 3.99% and 4.50%, respectively, with most of those gains coming during the second half of the 12-month period.

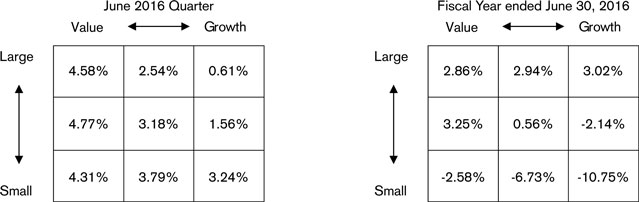

U.S. equity styles, as defined by Russell Indices, recorded positive returns for the quarter. Value stocks outperformed growth stocks, with the largest difference among large-cap stocks. Small-cap stocks generally outperformed larger stocks, with the exception of the value category. As a result, mid-cap value stocks delivered the best performance (4.77%), while large growth stocks produced the lowest return (0.61%).

Six of the 10 S&P 500 sectors posted positive returns for the quarter. The Energy sector led the gains, up 11.6%, followed by Telecommunications (7.1%), Utilities (6.8%) and Health Care (6.3%). Information Technology was the worst performer, returning -2.8%, while the Consumer Discretionary sector recorded the only other quarterly loss (-0.9%).

Below are the stock market style box returns for the quarter and the fiscal year.

Message from the President: Reflections on my First 90 Days

by Tammira Philippe, CFA

Although I have worked at Bridgeway for 11 years, I started my day on March 30 determined to look at our firm from a new perspective.

It was my first day as President of Bridgeway Capital Management — a position I was thrilled to accept after being chosen from among several finalists during a nationwide search — and I was eager to begin leading our firm. I knew that we had a talented team and enjoyed strong momentum thanks to our evidence-based investing philosophy and unique culture. I also knew that my top priority as President would be to build on this foundation and help create an organization that has an even larger positive impact on investors and the world at large.

Before I could take any steps toward accomplishing that goal, though, I needed to be sure my colleagues shared my vision for Bridgeway.

So beginning March 30, I began talking with my colleagues to articulate my ideas to help Bridgeway’s success continue long into the future. I emphasized the importance of our firm’s values, starting with putting our investors’ interests first at all times. I described how our team-based approach is helping to build a stronger, more adaptable company, one in which Partners can learn new skills that help them take on new responsibilities — much as my Bridgeway career gave me experience in strategy, operations and client relationships.

| | |

| 2 | | Annual Report | June 30, 2016 |

| | |

LETTER FROM THE INVESTMENT MANAGEMENT TEAM (continued) | | |

To my great excitement, I found even more alignment among my Partners than I expected. Everyone at Bridgeway knows that we have created something special in the financial world, and they are just as committed as I am to seeing the firm thrive beyond their own careers.

In addition, I listened to advisers, institutional clients and shareholders we serve. I knew from past conversations that some wondered whether the values and approach established by our founder, John Montgomery, would continue to drive Bridgeway in the future. I wanted to assure them, as I assure you today, that John’s values have been thoroughly absorbed into Bridgeway’s DNA, and by all of us. You can see them in our commitment to maintaining a disciplined investment strategy and relentless focus on controlling costs that can help investors achieve their long-term goals — and in our pledge to use our own success to help make the world a better place.

I hope that my appointment as President is a compelling example of how Bridgeway’s culture and values are bigger than any one person. We know there will be challenges along the way. We face increasing competition, shifting regulations and evolving investor needs that will require us to change and adapt. But what will not change is our commitment to our investors and our values. In fact, I believe that the forces changing our industry have made Bridgeway’s culture an even greater asset as we strive to build an enduring firm. I am honored to be the person with the responsibility to protect that legacy and to guide our Partners toward our shared vision for the future.

Is Small-Cap Value Dead?

by Christine Wang, CFA, CPA, Portfolio Manager

Value investors have had a tough few years. At the end of 2015, value stocks had again lagged growth stocks. Even worse, value also underperformed growth during the most recent 3-year, 5-year and 10-year periods.

Results also have been bad for small-cap investors, with large-cap stocks outperforming small-cap growth stocks on a 1-year, 3-year and 5-year basis through the end of 2015. Considering that small-cap value stocks historically have provided a return premium, these trends might leave some investors scratching their heads, wondering if small-cap value still has a place in their portfolios.

While we share the frustration with recent results, our research into historical market data offers reason for optimism. In fact, we believe that small-cap value remains an important part of a diversified investment portfolio, and that abandoning the asset class now could diminish the potential positive impact of the small-cap value premium on your long-term results.

Since 1926, small-cap value stocks have outperformed small-cap growth stocks by 6.07% annually. However, the short-term relative performance of small-cap value stocks often is not for the faint of heart — as we’ve recently experienced. Small-cap value underperformed the market for 21 consecutive months spanning May, 2014 to February, 2016.

But how unusual is that down trend? Looking at market data going back to 1926, we found that the duration of the recent 21-month slump is above average, but not unprecedented. When small-cap value underperformed, the average length of its consecutive monthly underperformance was 11 months, while the longest stretch was 3.5 years, occurring between 1929 and 1932. More recently, small-cap value underperformed for 26 consecutive months between July 1989 and August 1991.

What’s more, although small-cap value stocks frequently underperform the market from year to year, the odds of underperformance greatly decline over longer holding periods: Between 1926 and 2015, there has not been a single 20-year period during which small-cap value lagged the market.

While 21 months can feel like an eternity, it is a relatively short period within an investor’s lifetime and any reasonable equity investment time horizon. And based on our examination of long-term market returns, it’s unlikely that small-cap value stocks will continue to lag the market for a period of more than a decade.

Another important insight from our research: Small-cap value typically rebounds strongly from prolonged slumps, which supports the argument for not giving up now. For example, after small-cap value stocks underperformed the market for 42 consecutive months starting in 1929, they went on to outperform the market by an astonishing 231% during the 42 months after they recovered. After the 26-month period of underperformance starting in 1989, small-cap value posted a 44% cumulative outperformance over the 26 months following its recovery. In these and other periods, the eventual rebound in small-cap value more than wiped out the early losses — rewarding those investors who stuck to their strategy.

| | |

LETTER FROM THE INVESTMENT MANAGEMENT TEAM (continued) | | |

There’s no doubt that recent performance has been difficult for small-cap value investors, but we may already have seen a potential change in that trend: Small-cap value stocks outperformed broad-market Russell 3000 index by 2.17 percentage points during the most recent quarter. Of course, one quarter does not make a trend, but we will continue to monitor small-cap value’s performance for signs of a turnaround.

In the meantime, our analysis shows that the recent stretch of underperformance is within the historic norm for the small-cap value premium. To abandon the asset class based on the past few years of performance alone would just be another version of chasing hot returns by buying high and selling low — the exact opposite of a recipe for success. Instead, recent volatility in small-cap value stocks is a perfect opportunity to rebalance portfolios and remain committed to a well-diversified asset allocation that takes advantage of the historical premiums the market offers.

The Worst Thing of the Fiscal Year

by John Montgomery, Founder and Chief Investment Officer

While we like to celebrate our successes as much as anyone, we also believe that getting the hard stuff on the table is a key ingredient to learning and growing — as individuals and as a corporation.

Additionally, Bridgeway is committed to transparency with you, our shareholders, who are the owners of the Fund. That’s why we have set aside a portion of each annual report to discuss the worst thing that happened during the fiscal year.

This year, we’ve chosen the results for Aggressive Investors 1 — our poorest performing Fund. Although the Fund achieved relatively impressive return rankings for calendar years 2014, 2013 and 2012, and leads its primary market benchmark by more than 3% per year since inception, this year’s -7.40% return and low peer ranking is very disappointing.

Why did it happen? Thanks to a confluence of trends, none of the Fund’s major categories of factors helped performance, and several hurt it significantly.

For example, by design the Fund invests in some small- and mid-cap stocks, deeper value stocks, and certain riskier (high-beta) stocks that our models project are statistically likely to outperform their peers on an economic basis. All of those types of stocks underperformed the market during the past fiscal year. Or stated a different way, our specific approach to diversification in the Fund’s portfolio did not help during this period.

Normally, our company financial health models would have helped offset losses from deeper value’s underperformance. However, stocks in the company financial health category tend not to perform well when markets experience a correlation spike — periods in which stocks of all sizes and styles move in tandem, largely due to macro-trends and not company- or asset-specific factors. We had a high correlation spike in the September 2015 quarter, which meant we got little help from this diversifying category.

Another diversifying factor that has been successful in the long term is price momentum. However, the Fund’s exposure to high momentum stocks also hurt because these stocks declined in the fiscal year.

Finally, our models do not weight holdings by company size — giving more weight in the portfolio to the largest companies — as does our primary market benchmark, the S&P 500 Index. As a result, we had lower exposure to larger stocks. These stocks performed well relative to smaller cap stocks during the fiscal year and contributed to our Fund’s 11% underperformance of the S&P 500. By contrast, our fiscal year results were within one percentage point of our secondary market benchmark, the Russell 2000 Index of smaller companies.

In short, it was a perfect storm of diversifying factors not going our way. However, we gave the Fund the factor exposures we intended, based on analysis of long-term market data. We do not consider that anything is “broken,” and we are staying the course. In fact, performance of these factors tends to revert back to their expected long-term returns, which we believe would be beneficial to our Fund in the future.

| | |

| 4 | | Annual Report | June 30, 2016 |

| | |

LETTER FROM THE INVESTMENT MANAGEMENT TEAM (continued) | | |

That said, we continue to conduct research on all of our Funds and models, looking for small, incremental improvements. We will be studying Aggressive Investors 1 in the coming fiscal year, specifically examining model performance in high correlation markets to see if we can further reduce their negative impact.

In summary, it was a poor year for Aggressive Investors 1. We know the reasons why, and we are studying ways to improve the models, but we are not changing our investment process. And as a fellow shareholder, I want to express my personal confidence in the Fund’s research and portfolio management teams. I continue to use Bridgeway-managed portfolios for 100% of my stock market investing needs and Aggressive Investors 1 plays a significant role in that allocation.

Transformative Change: Where I Live

by Tami Groce, Partner, Marketing and Client Service

When we think about transformative change, it is often with an eye toward addressing the needs that seem most significant or universal. Helping the poor and disenfranchised is certainly vital to making the world a better place, and it is a worthwhile endeavor for us all. I find, however, that we often overlook the needs where we live — and by “where we live” I mean both our physical locality and our experiences.

While I am involved in numerous charitable activities, most recently my experience has been informed by two issues that have led me to administer healing to those who often suffer in silence and to those who seek guidance in unchartered waters. The first group consists of couples on the infertility journey, which can be a painful path to parenthood with little spiritual or emotional support. I know the sorrow of infertility firsthand. Though my journey ended with the blessing of two beautiful little boys, I am connected to those still on their own journeys, because that is where I lived for quite a while. As a result, I founded The Waiting Room Infertility Ministry at Wheeler Avenue Baptist Church in Houston. We meet monthly and provide spiritual, educational and financial direction for those who for too long have felt forsaken by others who do not share their experience.

As an ordained, seminary-trained minister, the second group that I have dedicated myself to is seminary students. I lead small groups aimed at equipping seminarians with the tools necessary to their vocation. Additionally, I mentor seminarians at the Fuller Theological Seminary through a structured program that allows for a six-month relationship. Whether they are my mentee or a small group member, each individual will directly intersect with the lives of hundreds (if not thousands) of church members over the course of their ministry. It is important that they understand the lifestyle that comes with that role, and are prepared to handle the responsibilities. For example, burnout is common among ministers, so I urge them to find their own Sabbath day to take time for themselves and recharge, as Sundays are typically busy work days. We also discuss the feelings of isolation and loneliness that many ministers feel as leaders of a church, and I urge them to develop a community of peers with whom they can share their concerns and feel heard.

Beyond that, their personal spiritual care must be a priority. There is a reason that flight attendants ask you to put your oxygen mask on first before assisting others. As ministers, they have to have discernment around their particular calling. I remind them to examine and reconcile the potential hurt and brokenness in their own backgrounds, as well as their limitations, so they are better prepared to help others deal with their issues. I believe I am uniquely equipped to help others understand this process and to move from passion to purpose, because that is also where I live.

| | |

Aggressive Investors 1 Fund MANAGER’S COMMENTARY (Unaudited) | | |

June 30, 2016

Dear Fellow Aggressive Investors 1 Fund Shareholder,

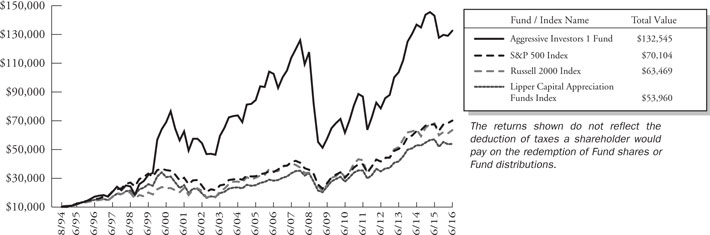

For the quarter ended June 30, 2016, our Fund returned 2.68%, outperforming our primary market benchmark, the S&P 500 Index (2.46%), and our peer benchmark, the Lipper Capital Appreciation Funds Index (0.40%), but underperforming the Russell 2000 Index (3.79%). It was a good quarter.

For the fiscal year, our Fund returned -7.40%, underperforming our primary market benchmark, the S&P 500 Index (3.99%), our peer benchmark, the Lipper Capital Appreciation Funds Index (-5.23%), and the Russell 2000 Index (-6.73%).

The table below presents our June quarter, one-year, five-year, 10-year, 15-year, and inception-to-date financial results. See the next page for a graph of performance since inception.

Standardized Returns as of June 30, 2016

| | | | | | | | | | | | |

| | | | | | | Annualized | | |

| | | | | | |

| | | Quarter | | 1 Year | | 5 Years | | 10 Years | | 15 Years | | Since Inception (8/5/94) |

| | | | | | |

Aggressive Investors 1 Fund | | 2.68% | | -7.40% | | 8.82% | | 2.59% | | 5.15% | | 12.52% |

S&P 500 Index | | 2.46% | | 3.99% | | 12.10% | | 7.42% | | 5.75% | | 9.28% |

Russell 2000 Index | | 3.79% | | -6.73% | | 8.35% | | 6.20% | | 6.96% | | 8.80% |

Lipper Capital Appreciation Funds Index | | 0.40% | | -5.23% | | 8.83% | | 6.66% | | 5.22% | | 7.99% |

Performance figures quoted in the table above represent past performance and are no guarantee of future results. Total return figures in the table above include the reinvestment of dividends and capital gains. The table above does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or on the redemption of Fund shares.

The S&P 500 Index is a broad-based, unmanaged measurement of changes in stock market conditions, based on the average of 500 widely held common stocks with dividends reinvested. The Russell 2000 Index is an unmanaged, market value weighted index that measures performance of the 2,000 companies that are between the 1,000th and 3,000th largest in the market with dividends reinvested. The Lipper Capital Appreciation Funds Index reflects the record of the 30 largest funds in the category of more aggressive domestic growth mutual funds, as reported by Lipper, an independent fund research firm owned by Broadridge Financial Solutions, Inc. It is not possible to invest directly in an index. Periods longer than one year are annualized.

According to data from Lipper as of June 30, 2016, Aggressive Investors 1 Fund ranked 177th of 254 capital appreciation funds for the 12 months ended June 30, 2016, 122nd of 224 over the last five years, 147th of 157 over the last 10 years, and 3rd of 43 since inception in August 1994. Lipper is an independent mutual fund rating service owned by Broadridge Financial Solutions, Inc. that ranks funds in various fund categories by making comparative calculations using total returns.

| | |

| 6 | | Annual Report | June 30, 2016 |

| | |

Aggressive Investors 1 Fund MANAGER’S COMMENTARY (Unaudited) (continued) | | |

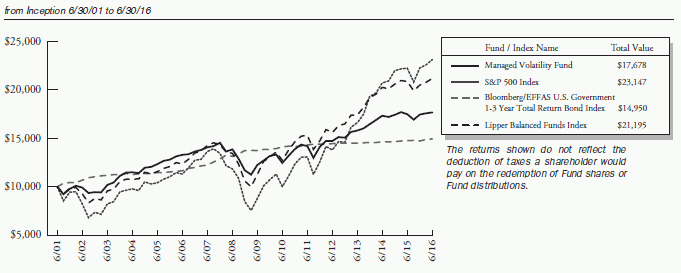

Aggressive Investors 1 Fund vs. S&P 500 Index, Russell 2000 Index & Lipper Capital Appreciation Funds Index

from Inception 8/5/94 to 6/30/16

Detailed Explanation of Quarterly Performance

The Fund’s investment in mid-cap and small-cap stocks boosted relative returns during a quarter in which those shares outpaced large-company stocks. In addition, all our model categories made positive contributions to the Fund’s relative performance.

An underweight position in the lagging Information Technology sector boosted relative performance, as did select holdings within that sector. Holdings in the Materials sector also helped relative results. By contrast, an overweight position and holdings in the lagging Industrials sector detracted from relative performance.

Detailed Explanation of Fiscal Year Performance

The Fund’s bias toward smaller stocks detracted from relative results during the 12-month period, as small company shares significantly underperformed larger stocks in the first half of the fiscal year. Although small-cap stocks rebounded in the second half of the year, it was not enough to overcome previous losses. In addition, all three model categories contributed to the Fund’s fiscal-year underperformance. Our value metrics category was the largest detractor, as these models targeted deeper-value stocks that lagged the Index during the period. The price momentum category also detracted from results, as the stocks selected by this model underperformed. Our company financial health category of stocks underperformed in the market context of a high correlation spike (stocks moving in tandem irrespective of their underlying economic health) in the September quarter. Diversification across these three categories did not help in the market environment of the fiscal year.

Sector allocation did not have a significant impact on performance. Instead, individual stock holdings detracted from results.

| | |

Aggressive Investors 1 Fund MANAGER’S COMMENTARY (Unaudited) (continued) | | |

Top Ten Holdings as of June 30, 2016

| | | | | | | | | |

| Rank Description | | Industry | | |

| % of Net

Assets |

|

| 1 | | AMN Healthcare Services, Inc. | | Health Care Providers & Service | | | | 2.3% | |

| 2 | | Global Payments, Inc. | | Financials | | | | 2.2% | |

| 3 | | John Bean Technologies Corp. | | Machinery | | | | 2.0% | |

| 4 | | Edwards Lifesciences Corp. | | Health Care Equipment & Supplies | | | | 2.0% | |

| 5 | | Windstream Holdings, Inc. | | Diversified Telecommunications Services | | | | 1.8% | |

| 6 | | Aflac, Inc. | | Insurance | | | | 1.5% | |

| 7 | | Equinix, Inc. | | Real Estate Investment Trusts | | | | 1.4% | |

| 8 | | Acuity Brands, Inc. | | Electrical Equipment & Services | | | | 1.4% | |

| 9 | | Ulta Salon Cosmetics & Fragrance, Inc. | | Specialty Retail | | | | 1.4% | |

| 10 | | Antero Resources Corp. | | Oil, Gas & Consumable Fuels | | | | 1.4% | |

| | | |

| | Total | | | | | | 17.4% | |

Industry Sector Representation as of June 30, 2016

| | | | | | | | | | |

| | | % of Net Assets | | | | % of S&P 500

Index | | | | Difference |

Consumer Discretionary | | 15.1% | | | | 12.3% | | | | 2.8% |

Consumer Staples | | 10.5% | | | | 10.6% | | | | -0.1% |

Energy | | 7.7% | | | | 7.4% | | | | 0.3% |

Financials | | 14.7% | | | | 15.7% | | | | -1.0% |

Health Care | | 9.9% | | | | 14.7% | | | | -4.8% |

Industrials | | 17.2% | | | | 10.2% | | | | 7.0% |

Information Technology | | 14.0% | | | | 19.8% | | | | -5.8% |

Materials | | 6.7% | | | | 2.8% | | | | 3.9% |

Telecommunication Services | | 1.8% | | | | 2.9% | | | | -1.1% |

Utilities | | 1.1% | | | | 3.6% | | | | -2.5% |

Cash & Other Assets | | 1.3% | | | | 0.0% | | | | 1.3% |

| | | | | |

Total | | 100.0% | | | | 100.0% | | | | |

Disclaimer

The views expressed here are exclusively those of Fund management. These views, including those related to market sectors or individual stocks, are not meant as investment advice and should not be considered predictive in nature. Any favorable (or unfavorable) description of a holding applies only as of the quarter end, June 30, 2016, unless otherwise stated. Security positions can and do change thereafter. Discussions of historical performance do not guarantee and may not be indicative of future performance.

Market volatility can significantly affect short-term performance. The Fund is not an appropriate investment for short-term investors. Investments in the small companies within this multi-cap fund generally carry greater risk than is customarily associated with larger companies. This additional risk is attributable to a number of factors, including the relatively limited financial resources that are typically available to small companies and the fact that small companies often have comparatively limited product lines. In addition, the stock of small companies tends to be more volatile than the stock of large companies, particularly in the short term and particularly in the early stages of an economic or market downturn. The Fund’s use of options, futures, and leverage can magnify the risk of loss in an unfavorable market, and the Fund’s use of short-sale positions can, in theory, expose shareholders to unlimited loss. Finally, the Fund exposes shareholders to “focus risk,” which may add to Fund volatility through the possibility that a single company could significantly affect total return. Shareholders of the Fund, therefore, are taking on more risk than they would if they invested in the stock market as a whole.

| | |

| 8 | | Annual Report | June 30, 2016 |

| | |

Aggressive Investors 1 Fund MANAGER’S COMMENTARY (Unaudited) (continued) | | |

Conclusion

Thank you for your continued investment in Aggressive Investors 1 Fund. We encourage your feedback; your reactions and concerns are important to us.

Sincerely,

The Investment Management Team

| | |

Aggressive Investors 1 Fund SCHEDULE OF INVESTMENTS | | |

Showing percentage of net assets as of June 30, 2016

| | | | | | | | | | | | |

| Industry Company | | Shares | | | Value | | | | |

| |

COMMON STOCKS - 98.72% | | | | | |

Aerospace & Defense - 0.83% | | | | | |

Spirit Aerosystems Holdings, Inc., Class A* | | | 40,000 | | | | $ 1,720,000 | | | | | |

| |

Airlines - 5.07% | | | | | |

Alaska Air Group, Inc. | | | 40,200 | | | | 2,343,258 | | | | | |

Delta Air Lines, Inc. | | | 46,500 | | | | 1,693,995 | | | | | |

JetBlue Airways Corp.* | | | 95,300 | | | | 1,578,168 | | | | | |

Southwest Airlines Co. | | | 69,800 | | | | 2,736,858 | | | | | |

United Continental Holdings, Inc.* | | | 52,500 | | | | 2,154,600 | | | | | |

| | | | | | | | | | | | |

| | | |

| | | | | | | 10,506,879 | | | | | |

| |

Auto Components - 3.78% | | | | | |

Cooper-Standard Holding, Inc.* | | | 28,300 | | | | 2,235,417 | | | | | |

Drew Industries, Inc. | | | 17,000 | | | | 1,442,280 | | | | | |

Goodyear Tire & Rubber Co. (The) | | | 66,400 | | | | 1,703,824 | | | | | |

Lear Corp. | | | 24,200 | | | | 2,462,592 | | | | | |

| | | | | | | | | | | | |

| | | |

| | | | | | | 7,844,113 | | | | | |

| |

Automobiles - 0.98% | | | | | |

General Motors Co. | | | 71,500 | | | | 2,023,450 | | | | | |

| | | |

Beverages - 1.04% | | | | | | | | | | | | |

Constellation Brands, Inc., Class A | | | 13,000 | | | | 2,150,200 | | | | | |

| |

Biotechnology - 1.05% | | | | | |

Gilead Sciences, Inc. | | | 26,000 | | | | 2,168,920 | | | | | |

| |

Building Products - 2.03% | | | | | |

American Woodmark Corp.* | | | 15,000 | | | | 995,700 | | | | | |

Gibraltar Industries, Inc.* | | | 39,000 | | | | 1,231,230 | | | | | |

U.S. Concrete, Inc.*+ | | | 32,500 | | | | 1,979,575 | | | | | |

| | | | | | | | | | | | |

| | | |

| | | | | | | 4,206,505 | | | | | |

| |

Chemicals - 0.85% | | | | | |

Kraton Performance Polymers, Inc.* | | | 63,000 | | | | 1,759,590 | | | | | |

| |

Commercial Banks - 3.24% | | | | | |

Bank of Nova Scotia (The)+ | | | 43,000 | | | | 2,107,430 | | | | | |

Canadian Imperial Bank of Commerce/Canada+ | | | 27,000 | | | | 2,026,890 | | | | | |

Royal Bank of Canada+ | | | 43,700 | | | | 2,582,233 | | | | | |

| | | | | | | | | | | | |

| | | |

| | | | | | | 6,716,553 | | | | | |

| |

Commercial Services & Supplies - 1.15% | | | | | |

Equifax, Inc. | | | 18,600 | | | | 2,388,240 | | | | | |

| |

Computers & Peripherals - 1.19% | | | | | |

HP, Inc. | | | 196,100 | | | | 2,461,055 | | | | | |

| | | | | | | | | | | | |

| Industry Company | | Shares | | | Value | | | | |

| | | | | |

Construction & Engineering - 1.21% | | | | | |

Comfort Systems USA, Inc. | | | 77,000 | | | | $2,507,890 | | | | | |

|

Consumer Finance - 2.42% | |

Alliance Data Systems Corp.* | | | 10,900 | | | | 2,135,528 | | | | | |

Santander Consumer USA Holdings, Inc.* | | | 101,900 | | | | 1,052,627 | | | | | |

Synchrony Financial* | | | 72,500 | | | | 1,832,800 | | | | | |

| | | | | | | | | | | | |

| | | |

| | | | | | | 5,020,955 | | | | | |

|

Containers & Packaging - 2.35% | |

Berry Plastics Group, Inc.* | | | 54,000 | | | | 2,097,900 | | | | | |

Crown Holdings, Inc.* | | | 54,800 | | | | 2,776,716 | | | | | |

| | | | | | | | | | | | |

| | | |

| | | | | | | 4,874,616 | | | | | |

|

Diversified Financial Services - 2.35% | |

Berkshire Hathaway, Inc., Class B* | | | 8,700 | | | | 1,259,673 | | | | | |

Citigroup, Inc. | | | 42,000 | | | | 1,780,380 | | | | | |

Voya Financial, Inc. | | | 73,900 | | | | 1,829,764 | | | | | |

| | | | | | | | | | | | |

| | | |

| | | | | | | 4,869,817 | | | | | |

|

Diversified Telecommunication Services - 1.75% | |

Windstream Holdings, Inc.+ | | | 392,100 | | | | 3,634,767 | | | | | |

| |

Electronic Equipment, Instruments &

Components - 4.67% | | | | | |

Acuity Brands, Inc. | | | 12,000 | | | | 2,975,520 | | | | | |

Fabrinet* | | | 29,000 | | | | 1,076,480 | | | | | |

Flextronics International, Ltd.* | | | 207,700 | | | | 2,450,860 | | | | | |

Mettler-Toledo International, Inc.* | | | 5,500 | | | | 2,007,060 | | | | | |

TTM Technologies, Inc.* | | | 155,000 | | | | 1,167,150 | | | | | |

| | | | | | | | | | | | |

| | | |

| | | | | | | 9,677,070 | | | | | |

| |

Energy Equipment & Services - 1.37% | | | | | |

Teekay Corp.+ | | | 110,000 | | | | 784,300 | | | | | |

Tidewater, Inc.+ | | | 115,000 | | | | 507,150 | | | | | |

Unit Corp.* | | | 100,000 | | | | 1,556,000 | | | | | |

| | | | | | | | | | | | |

| | | |

| | | | | | | 2,847,450 | | | | | |

|

Financials - 2.18% | |

Global Payments, Inc. | | | 63,345 | | | | 4,521,566 | | | | | |

|

Food & Staples Retailing - 1.04% | |

Kroger Co. (The) | | | 58,600 | | | | 2,155,894 | | | | | |

| |

Food Products - 7.19% | | | | | |

Campbell Soup Co. | | | 32,500 | | | | 2,162,225 | | | | | |

Dean Foods Co.+ | | | 94,000 | | | | 1,700,460 | | | | | |

Hormel Foods Corp. | | | 55,400 | | | | 2,027,640 | | | | | |

Ingredion, Inc. | | | 20,000 | | | | 2,588,200 | | | | | |

| | |

| 10 | | Annual Report | June 30, 2016 |

| | |

Aggressive Investors 1 Fund SCHEDULE OF INVESTMENTS (continued) | | |

Showing percentage of net assets as of June 30, 2016

| | | | | | | | | | |

| Industry Company | | Shares | | | Value | | | |

| |

Common Stocks (continued) | | | |

Food Products (continued) | | | |

Kellogg Co. | | | 28,000 | | | | $ 2,286,200 | | | |

Pilgrim’s Pride Corp.+ | | | 83,700 | | | | 2,132,676 | | | |

Tyson Foods, Inc., Class A | | | 30,000 | | | | 2,003,700 | | | |

| | | | | | | | | | |

| | | |

| | | | | | | 14,901,101 | | | |

| |

Health Care Equipment & Supplies - 3.00% | | | |

Edwards Lifesciences Corp.* | | | 41,000 | | | | 4,088,930 | | | |

Henry Schein, Inc.* | | | 12,000 | | | | 2,121,600 | | | |

| | | | | | | | | | |

| | | |

| | | | | | | 6,210,530 | | | |

| |

Health Care Providers & Services - 4.91% | | | |

AmerisourceBergen Corp. | | | 28,000 | | | | 2,220,960 | | | |

AMN Healthcare Services, Inc.* | | | 121,500 | | | | 4,856,355 | | | |

Cardinal Health, Inc. | | | 26,600 | | | | 2,075,066 | | | |

Triple-S Management Corp., Class B* | | | 42,000 | | | | 1,026,060 | | | |

| | | | | | | | | | |

| | | |

| | | | | | | 10,178,441 | | | |

| |

Hotels, Restaurants & Leisure - 1.54% | | | |

Boyd Gaming Corp.* | | | 120,000 | | | | 2,208,000 | | | |

Scientific Games Corp., Class A* | | | 106,000 | | | | 974,140 | | | |

| | | | | | | | | | |

| | | |

| | | | | | | 3,182,140 | | | |

| |

Household Products - 1.19% | | | |

Kimberly-Clark Corp. | | | 18,000 | | | | 2,474,640 | | | |

| |

Insurance - 3.04% | | | |

Aflac, Inc. | | | 43,000 | | | | 3,102,880 | | | |

Employers Holdings, Inc. | | | 36,400 | | | | 1,056,328 | | | |

Prudential Financial, Inc. | | | 30,000 | | | | 2,140,200 | | | |

| | | | | | | | | | |

| | | |

| | | | | | | 6,299,408 | | | |

| |

Internet & Catalog Retail - 1.17% | | | |

Amazon.com, Inc.* | | | 3,400 | | | | 2,433,108 | | | |

| |

Internet Software & Services - 1.73% | | | |

EarthLink Holdings Corp. | | | 232,600 | | | | 1,488,640 | | | |

VeriSign, Inc.*+ | | | 24,300 | | | | 2,100,978 | | | |

| | | | | | | | | | |

| | | |

| | | | | | | 3,589,618 | | | |

| |

IT Services - 1.07% | | | |

CSG Systems International, Inc. | | | 55,000 | | | | 2,217,050 | | | |

| |

Leisure Equipment & Products - 0.85% | | | |

Polaris Industries, Inc.+ | | | 21,500 | | | | 1,757,840 | | | |

| |

Machinery - 3.61% | | | |

John Bean Technologies Corp. | | | 68,600 | | | | 4,199,692 | | | |

| | | | | | | | | | |

| Industry Company | | Shares | | | Value | | | |

| | | |

Machinery (continued) |

Wabash National Corp.* | | | 96,000 | | | | $ 1,219,200 | | | |

Xylem, Inc. | | | 46,000 | | | | 2,053,900 | | | |

| | | | | | | | | | |

| | | |

| | | | | | | 7,472,792 | | | |

|

Materials - 1.21% |

Trinseo SA | | | 58,400 | | | | 2,507,112 | | | |

|

Media - 0.95% |

Scripps Networks Interactive, Inc., Class A | | | 31,600 | | | | 1,967,732 | | | |

|

Metals & Mining - 0.96% |

AK Steel Holding Corp.* | | | 426,100 | | | | 1,985,626 | | | |

| |

Oil, Gas & Consumable Fuels - 6.38% | | | |

Antero Resources Corp.* | | | 111,400 | | | | 2,894,172 | | | |

Baytex Energy Corp.+ | | | 302,800 | | | | 1,753,212 | | | |

Encana Corp. | | | 195,000 | | | | 1,519,050 | | | |

McDermott International, Inc.*+ | | | 411,100 | | | | 2,030,834 | | | |

Tesoro Corp. | | | 35,900 | | | | 2,689,628 | | | |

Valero Energy Corp. | | | 45,600 | | | | 2,325,600 | | | |

| | | | | | | | | | |

| | | |

| | | | | | | 13,212,496 | | | |

| |

Paper & Forest Products - 0.41% | | | |

Resolute Forest Products, Inc.*+ | | | 161,199 | | | | 852,743 | | | |

| |

Real Estate Investment Trusts (REITs) - 3.56% | | | |

Digital Realty Trust, Inc.+ | | | 22,300 | | | | 2,430,477 | | | |

Equinix, Inc.+ | | | 7,700 | | | | 2,985,521 | | | |

Public Storage | | | 7,700 | | | | 1,968,043 | | | |

| | | | | | | | | | |

| | | |

| | | | | | | 7,384,041 | | | |

| |

Semiconductors & Semiconductor

Equipment - 3.58% | | | |

Lam Research Corp.+ | | | 30,000 | | | | 2,521,800 | | | |

Micron Technology, Inc.* | | | 197,900 | | | | 2,723,104 | | | |

NVIDIA Corp. | | | 46,100 | | | | 2,167,161 | | | |

| | | | | | | | | | |

| | | |

| | | | | | | 7,412,065 | | | |

| |

Software - 2.06% | | | |

Autodesk, Inc.* | | | 36,000 | | | | 1,949,040 | | | |

MSCI, Inc. | | | 30,000 | | | | 2,313,600 | | | |

| | | | | | | | | | |

| | | |

| | | | | | | 4,262,640 | | | |

| |

Specialty Retail - 4.73% | | | |

Children’s Place, Inc. (The) | | | 28,000 | | | | 2,245,040 | | | |

Home Depot, Inc. (The) | | | 16,400 | | | | 2,094,116 | | | |

Lithia Motors, Inc., Class A | | | 20,800 | | | | 1,478,256 | | | |

Rent-A-Center, Inc. | | | 83,000 | | | | 1,019,240 | | | |

| | |

Aggressive Investors 1 Fund SCHEDULE OF INVESTMENTS (continued) | | |

Showing percentage of net assets as of June 30, 2016

| | | | | | | | | | |

| Industry Company | | | | Shares | | Value | | | |

| |

Common Stocks (continued) | | | |

Specialty Retail (continued) | | | |

Ulta Salon Cosmetics & Fragrance, Inc.* | | 12,200 | | | $ 2,972,408 | | | |

| | | | | | | | | | |

| | | | |

| | | | | | | 9,809,060 | | | |

| |

Trading Companies & Distributors - 3.94% |

AerCap Holdings NV* | | 26,800 | | | 900,212 | | | |

Beacon Roofing Supply, Inc.* | | 50,000 | | | 2,273,500 | | | |

Pool Corp. | | 25,000 | | | 2,350,750 | | | |

United Rentals, Inc.* | | 38,700 | | | 2,596,770 | | | |

Veritiv Corp.* | | 992 | | | 37,279 | | | |

| | | | | | | | | | |

| | | | |

| | | | | | | 8,158,511 | | | |

| |

Water Utilities - 1.09% |

American Water Works Co., Inc. | | | | 26,700 | | | 2,256,417 | | | |

| | | | | | | | | | |

| | |

TOTAL COMMON STOCKS - 98.72% | | | 204,580,641 | | | |

| | | | | | | | | | |

(Cost $191,226,879) | | | | | | |

| |

EXCHANGE TRADED NOTE - 1.13% | | | |

Exchange Traded Note - 1.13% | | | |

VelocityShares Daily Inverse ETN*+ | | 93,200 | | | 2,329,068 | | | |

| | | | | | | | | | |

TOTAL EXCHANGE TRADED

NOTE - 1.13% | | | 2,329,068 | | | |

| | | | | | | | | | |

(Cost $2,206,021) | | | | | | |

| | | | |

| | | Rate^ | | Shares | | Value | | | |

MONEY MARKET FUND - 0.16% | | | |

Dreyfus Cash Management Fund | | 0.30% | | 338,006 | | | 338,006 | | | |

| | | | | | | | | | |

| | |

TOTAL MONEY MARKET

FUND - 0.16% | | | 338,006 | | | |

| | | | | | | | | | |

(Cost $338,006) | | | | | | | | | | |

| |

INVESTMENTS PURCHASED WITH CASH

PROCEEDS FROM SECURITIES

LENDING - 13.34% | | | |

Dreyfus Cash Management Fund** | | 0.30% | | 27,647,275 | | | 27,647,275 | | | |

| | | | | | | | | | |

| | |

TOTAL INVESTMENTS PURCHASED WITH CASH PROCEEDS FROM SECURITIES LENDING - 13.34% | | | 27,647,275 | | | |

| | | | | | | | | | |

(Cost $27,647,275) | | | | | | |

| | | | | | | | |

| | | Value | | | | |

| | |

TOTAL INVESTMENTS - 113.35% | | $ | 234,894,990 | | | | | |

(Cost $221,418,181) | | | | | | | | |

Liabilities in Excess of Other

Assets - (13.35%) | | | (27,665,913 | ) | | | | |

| | | | | | | | |

| | |

NET ASSETS - 100.00% | | $ | 207,229,077 | | | | | |

| | | | | | | | |

| * | Non-income producing security. |

| ** | This security represents the investment of the collateral received in connection with securities out on loan as of June 30, 2016. |

| ^ | Rate disclosed as of June 30, 2016. |

| + | This security or a portion of the security is out on loan as of June 30, 2016. Total loaned securities had a value of $27,172,480 as of June 30, 2016. |

ETN - Exchange Traded Note

Summary of inputs used to value the Fund’s investments as of 06/30/2016 (See Note 2 in Notes to Financial Statements):

| | | | | | | | | | | | | | | | |

| | | Valuation Inputs | |

| | | Investment in Securities (Value) | |

| | | Level 1

Quoted

Prices | | | Level 2

Significant

Observable

Inputs | | | Level 3

Significant Unobservable Inputs | | | Total | |

| | | | |

Common Stocks | | $ | 204,580,641 | | | $ | — | | | $ | — | | | $ | 204,580,641 | |

Exchange Traded Note | | | 2,329,068 | | | | — | | | | — | | | | 2,329,068 | |

Money Market Fund | | | — | | | | 338,006 | | | | — | | | | 338,006 | |

Investments Purchased with Cash Proceeds from Securities Lending | | | — | | | | 27,647,275 | | | | — | | | | 27,647,275 | |

| | | | | | | | | | | | | | | | |

| | | | |

TOTAL | | $ | 206,909,709 | | | $ | 27,985,281 | | | $ | — | | | $ | 234,894,990 | |

| | | | | | | | | | | | | | | | |

See Notes to Financial Statements.

| | |

| 12 | | Annual Report | June 30, 2016 |

| | |

Ultra-Small Company Fund MANAGER’S COMMENTARY (Unaudited) | | |

June 30, 2016

Dear Fellow Ultra-Small Company Fund Shareholder,

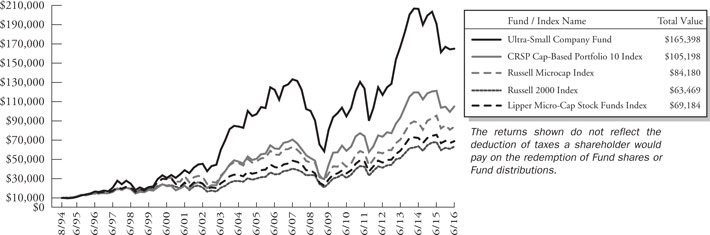

For the quarter ended June 30, 2016, our Fund returned 0.35%, underperforming our primary market benchmark, the CRSP Cap-Based Portfolio 10 Index (5.45%), and our peer benchmark, the Lipper Micro-Cap Stock Funds Index (3.05%). Our Fund also underperformed the Russell 2000 Index (3.79%) and the Russell Microcap Index (3.97%). It was a poor quarter.

For the fiscal year, our Fund returned -13.53%, slightly underperforming the CRSP Cap-Based Portfolio 10 Index (-13.49%). However, our Fund trailed the Russell Microcap Index (-12.06%), the Lipper Micro-Cap Stock Funds Index (-8.93%) and the Russell 2000 Index (-6.73%).

The table below presents our June quarter, one-year, five-year, 10-year, 15-year and inception-to-date financial results. See the next page for a graph of performance since inception.

Standardized Returns as of June 30, 2016

| | | | | | | | | | | | | | | | |

| | | | | | | | Annualized |

| | | Quarter | | | 1 Year | | | | 5 Years | | 10 Years | | 15 Years | | Since Inception (8/5/94) |

| | | | | | | |

Ultra-Small Company Fund | | | 0.35% | | | -13.53% | | | | 5.96% | | 3.05% | | 10.14% | | 13.67% |

CRSP Cap-Based Portfolio 10 Index | | | 5.45% | | | -13.49% | | | | 7.17% | | 5.52% | | 10.74% | | 11.33% |

Russell 2000 Index | | | 3.79% | | | -6.73% | | | | 8.35% | | 6.20% | | 6.96% | | 8.80% |

Russell Microcap Index | | | 3.97% | | | -12.06% | | | | 8.20% | | 4.31% | | 6.46% | | N/A |

Lipper Micro-Cap Stock Funds Index | | | 3.05% | | | -8.93% | | | | 7.50% | | 5.03% | | 6.71% | | N/A |

Performance figures quoted in the table above represent past performance and are no guarantee of future results. Total return figures in the table above include the reinvestment of dividends and capital gains. The table above does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or on the redemption of Fund shares.

The CRSP Cap-Based Portfolio 10 Index is an unmanaged index of 783 of the smallest publicly traded U.S. stocks (with dividends reinvested), as reported by the Center for Research on Security Prices. The Russell Microcap Index is an unmanaged, market value weighted index that measures performance of 1,000 of the smallest securities in the Russell 2000 Index. The Russell 2000 Index is an unmanaged, market value weighted index that measures performance of the 2,000 companies that are between the 1,000th and 3,000th largest in the market (with dividends reinvested). The Lipper Micro-Cap Stock Funds Index is an index of micro-cap funds compiled by Lipper, an independent fund research firm owned by Broadridge Financial Solutions, Inc. It is not possible to invest directly in an index. Periods longer than one year are annualized.

According to data from Lipper as of June 30, 2016, Ultra-Small Company Fund ranked 51st of 71 micro-cap funds for the 12 months ended June 30, 2016, 42nd of 55 over the last five years, 32nd of 39 over the last 10 years, and 1st of 8 since inception in August 1994. Lipper is an independent mutual fund rating service owned by Broadridge Financial Solutions, Inc. that ranks funds in various fund categories by making comparative calculations using total returns.

| | |

Ultra-Small Company Fund MANAGER’S COMMENTARY (Unaudited) (continued) | | |

Ultra-Small Company Fund vs. CRSP Cap-Based Portfolio 10 Index, Russell Microcap Index**, Russell 2000 Index & Lipper Micro-Cap Stock Funds Index* from Inception 8/5/94 to 6/30/16

| * | The Lipper Micro-Cap Stock Funds Index began on 12/31/1995, and the line graph for the Index begins at the same value as the Fund on that date. |

| ** | The Russell Microcap Index began on 6/30/2000, and the line graph for the Index begins at the same value as the Fund on that date. |

Detailed Explanation of Quarterly Performance

All model categories detracted from the Fund’s relative performance during the quarter. Our company financial health models weighed most heavily on relative returns, while our price momentum models detracted the least. Although the Fund held nearly 80% of its assets in CRSP’s 10th decile, which, on average, had positive returns, those holdings still underperformed the primary benchmark. In addition, the Fund’s holdings that were larger than CRSP 10 posted negative returns, on average, for the quarter and detracted from relative performance.

An underweight position and holdings in the Energy sector detracted from relative returns. Holdings in the Financials sector also hurt relative performance. However, an underweight allocation to the Health Care sector boosted relative performance because Health Care was one of the worst-performing sectors in CRSP 10.

The table below presents index performance numbers for stocks in the different deciles during various time periods.

| | | | | | | | | | | | | | | | | | | | |

| CRSP Decile1 | | Quarter | | | 1 Year | | | 5 Years | | | 10 Years | | | 90.5 Years | |

1 (ultra-large) | | | 2.37% | | | | 3.63% | | | | 12.09% | | | | 7.28% | | | | 9.26% | |

2 | | | 4.82% | | | | 1.56% | | | | 12.00% | | | | 8.27% | | | | 10.50% | |

3 | | | 3.60% | | | | -1.78% | | | | 10.11% | | | | 8.09% | | | | 10.97% | |

4 | | | 2.36% | | | | -7.53% | | | | 9.47% | | | | 8.18% | | | | 10.78% | |

5 | | | 2.22% | | | | -9.77% | | | | 7.92% | | | | 8.63% | | | | 11.38% | |

6 | | | 3.48% | | | | -8.86% | | | | 8.87% | | | | 7.41% | | | | 11.25% | |

7 | | | 5.86% | | | | -7.63% | | | | 9.11% | | | | 7.79% | | | | 11.41% | |

8 | | | 4.18% | | | | -11.46% | | | | 8.08% | | | | 7.46% | | | | 11.39% | |

9 | | | 6.02% | | | | -11.64% | | | | 7.40% | | | | 6.40% | | | | 11.31% | |

10 (ultra-small) | | | 5.45% | | | | -13.49% | | | | 7.17% | | | | 5.52% | | | | 13.13% | |

| 1 | Performance figures are as of the period ended June 30, 2016. The CRSP Cap-Based Portfolio Indexes are unmanaged indexes of publicly traded U.S. stocks with dividends reinvested, grouped by market capitalization, as reported by the Center for Research in Security Prices. Past performance is no guarantee of future results. |

| | |

| 14 | | Annual Report | June 30, 2016 |

| | |

Ultra-Small Company Fund MANAGER’S COMMENTARY (Unaudited) (continued) | | |

Detailed Explanation of Fiscal Year Performance

Our value metrics models lagged the benchmark for the fiscal year, detracting from relative results. However, our company financial health and price momentum models added to the Fund’s relative returns and helped offset some of those losses. A higher weighting in larger stocks also detracted from relative results when these stocks underperformed.

Holdings in the Energy, Industrials and Financials sectors weighed most heavily on relative performance. Meanwhile, holdings in the Information Technology sector added to relative performance. The Fund’s lower-than-benchmark exposure to the Health Care sector also helped.

Top Ten Holdings as of June 30, 2016

| | | | | | | | | |

| Rank | | Description | | Industry | | % of Net

Assets |

| 1 | | Olympic Steel, Inc. | | Metals & Mining | | | | 2.8% | |

| 2 | | Supreme Industries, Inc. | | Machinery | | | | 2.4% | |

| 3 | | Ryerson Holding Corp. | | Metals & Mining | | | | 2.2% | |

| 4 | | Oclaro, Inc. | | Communications Equipment | | | | 2.1% | |

| 5 | | Radisys Corp. | | Electronic Equip., Instruments & Components | | | | 2.0% | |

| 6 | | A-Mark Precious Metals, Inc. | | Metals & Mining | | | | 1.8% | |

| 7 | | LSB Industries, Inc. | | Chemicals | | | | 1.8% | |

| 8 | | NV5 Global, Inc. | | Commercial Banks | | | | 1.7% | |

| 9 | | Brightcove, Inc. | | Internet Software & Services | | | | 1.5% | |

| 10 | | Armada Hoffler Properties, Inc. | | Real Estate Investment Trusts | | | | 1.5% | |

| | Total | | | | | | 19.8% | |

Industry Sector Representation as of June 30, 2016

| | | | | | | | | | |

| | | % of Net Assets | | | | % of CRSP 10 Index | | | | Difference |

Consumer Discretionary | | 13.1% | | | | 10.8% | | | | 2.3% |

Consumer Staples | | 3.5% | | | | 2.4% | | | | 1.1% |

Energy | | 8.1% | | | | 11.6% | | | | -3.5% |

Financials | | 23.9% | | | | 22.1% | | | | 1.8% |

Health Care | | 10.0% | | | | 18.6% | | | | -8.6% |

Industrials | | 15.5% | | | | 11.2% | | | | 4.3% |

Information Technology | | 18.0% | | | | 17.0% | | | | 1.0% |

Materials | | 7.5% | | | | 4.6% | | | | 2.9% |

Telecommunication Services | | 0.0% | | | | 0.3% | | | | -0.3% |

Utilities | | 0.6% | | | | 1.4% | | | | -0.8% |

Cash & Other Assets | | -0.2% | | | | 0.0% | | | | -0.2% |

Total | | 100.0% | | | | 100.0% | | | | |

Disclaimer

The views expressed here are exclusively those of Fund management. These views, including those related to market sectors or individual stocks, are not meant as investment advice and should not be considered predictive in nature. Any favorable (or unfavorable) description of a holding applies only as of the quarter end, June 30, 2016, unless otherwise stated. Security positions can and do change thereafter. Discussions of historical performance do not guarantee and may not be indicative of future performance.

| | |

Ultra-Small Company Fund MANAGER’S COMMENTARY (Unaudited) (continued) | | |

The Fund is subject to very high, above market risk (volatility) and is not an appropriate investment for short-term investors. Investments in ultra-small companies generally carry greater risk than is customarily associated with larger companies and even “small companies” for various reasons, such as narrower markets (fewer investors), limited financial resources and greater trading difficulty.

Conclusion

Ultra-Small Company Fund remains closed to new investors. We encourage your feedback; your reactions and concerns are important to us.

Sincerely,

The Investment Management Team

| | |

| 16 | | Annual Report | June 30, 2016 |

| | |

Ultra-Small Company Fund SCHEDULE OF INVESTMENTS | | |

Showing percentage of net assets as of June 30, 2016

| | | | | | | | | | |

| Industry Company | | Shares | | | Value | | | |

| |

COMMON STOCKS - 100.23% | | | |

Aerospace & Defense - 1.02% | | | |

Ducommun, Inc.* | | | 52,300 | | | | $ 1,034,494 | | | |

| |

Air Freight & Logistics - 0.26% | | | |

Air T, Inc.* | | | 12,463 | | | | 267,954 | | | |

| |

Auto Components - 1.22% | | | |

China XD Plastics Co., Ltd.* | | | 69,700 | | | | 224,434 | | | |

Horizon Global Corp.* | | | 89,200 | | | | 1,012,420 | | | |

| | | | | | | | | | |

| | | |

| | | | | | | 1,236,854 | | | |

| |

Beverages - 0.70% | | | |

Primo Water Corp.* | | | 60,000 | | | | 708,600 | | | |

| |

Biotechnology - 3.15% | | | |

Adverum Biotechnologies, Inc.* | | | 132,200 | | | | 417,752 | | | |

CoLucid Pharmaceuticals, Inc.*+ | | | 50,000 | | | | 408,500 | | | |

MacroCure, Ltd.* | | | 200,000 | | | | 284,000 | | | |

MEI Pharma, Inc.* | | | 427,500 | | | | 581,400 | | | |

Nexvet Biopharma PLC* | | | 44,400 | | | | 206,460 | | | |

PharmAthene, Inc.*+ | | | 191,700 | | | | 467,748 | | | |

QLT, Inc.* | | | 172,500 | | | | 244,950 | | | |

Vericel Corp.* | | | 258,000 | | | | 580,500 | | | |

| | | | | | | | | | |

| | | |

| | | | | | | 3,191,310 | | | |

| |

Chemicals - 2.15% | | | |

Gulf Resources, Inc.* | | | 259,000 | | | | 398,860 | | | |

LSB Industries, Inc.*+ | | | 147,700 | | | | 1,784,216 | | | |

| | | | | | | | | | |

| | | |

| | | | | | | 2,183,076 | | | |

| |

Commercial Banks - 11.35% | | | |

American National Bankshares, Inc. | | | 19,000 | | | | 478,420 | | | |

Bankwell Financial Group, Inc.+ | | | 26,200 | | | | 577,972 | | | |

Bar Harbor Bankshares+ | | | 33,000 | | | | 1,158,300 | | | |

C&F Financial Corp.+ | | | 5,200 | | | | 232,752 | | | |

Civista Bancshares, Inc.+ | | | 15,100 | | | | 197,810 | | | |

Coastway Bancorp, Inc.*+ | | | 8,700 | | | | 108,315 | | | |

Codorus Valley Bancorp, Inc.+ | | | 30,500 | | | | 621,285 | | | |

Farmers National Banc Corp.+ | | | 22,400 | | | | 197,120 | | | |

First Business Financial Services, Inc. | | | 28,100 | | | | 659,507 | | | |

First United Corp.* | | | 12,000 | | | | 118,080 | | | |

FS Bancorp, Inc. | | | 5,000 | | | | 126,750 | | | |

Northrim BanCorp, Inc. | | | 16,600 | | | | 436,414 | | | |

NV5 Global, Inc.* | | | 59,600 | | | | 1,695,024 | | | |

Old Line Bancshares, Inc.+ | | | 71,213 | | | | 1,281,834 | | | |

| | | | | | | | | | |

| Industry Company | | Shares | | | Value | | | |

| | | |

| | | | | | | | | | |

Commercial Banks (continued) | | | |

Old Second Bancorp, Inc. | | | 88,400 | | | | $ 603,772 | | | |

Pacific Mercantile Bancorp*+ | | | 72,100 | | | | 511,910 | | | |

Shore Bancshares, Inc. | | | 82,600 | | | | 970,550 | | | |

Southern First Bancshares, Inc.*+ | | | 16,100 | | | | 388,010 | | | |

Westbury Bancorp, Inc.*+ | | | 5,500 | | | | 107,250 | | | |

Your Community Bankshares, Inc.+ | | | 28,100 | | | | 1,044,196 | | | |

| | | | | | | | | | |

| | | |

| | | | | | | 11,515,271 | | | |

| |

Commercial Services & Supplies - 2.36% | | | |

Ascent Capital Group, Inc., Class A* | | | 63,500 | | | | 977,265 | | | |

Cenveo, Inc.* | | | 413,400 | | | | 337,293 | | | |

Civeo Corp.* | | | 350,000 | | | | 630,000 | | | |

Performant Financial Corp.* | | | 191,200 | | | | 309,744 | | | |

Virco Manufacturing Corp.* | | | 32,200 | | | | 140,070 | | | |

| | | | | | | | | | |

| | | |

| | | | | | | 2,394,372 | | | |

| |

Communications Equipment - 2.74% | | | |

Ceragon Networks, Ltd.* | | | 283,900 | | | | 459,918 | | | |

Oclaro, Inc.*+ | | | 440,500 | | | | 2,149,640 | | | |

UTStarcom Holdings Corp.* | | | 90,200 | | | | 172,733 | | | |

| | | | | | | | | | |

| | | |

| | | | | | | 2,782,291 | | | |

| |

Computers & Peripherals - 0.32% | | | |

TransAct Technologies, Inc. | | | 40,200 | | | | 322,404 | | | |

|

Construction & Engineering - 0.10% |

IES Holdings, Inc.*+ | | | 8,200 | | | | 101,844 | | | |

| |

Consumer Finance - 1.02% | | | |

Consumer Portfolio Services, Inc.* | | | 174,300 | | | | 657,111 | | | |

Nicholas Financial, Inc.* | | | 36,800 | | | | 378,304 | | | |

| | | | | | | | | | |

| | | |

| | | | | | | 1,035,415 | | | |

| |

Diversified Consumer Services - 1.82% | | | |

Cambium Learning Group, Inc.* | | | 167,250 | | | | 754,297 | | | |

ITT Educational Services, Inc.*+ | | | 427,300 | | | | 820,416 | | | |

Lincoln Educational Services Corp.* | | | 180,000 | | | | 270,000 | | | |

| | | | | | | | | | |

| | | |

| | | | | | | 1,844,713 | | | |

| |

Diversified Financial Services - 1.14% | | | |

Impac Mortgage Holdings, Inc.*+ | | | 74,000 | | | | 1,160,320 | | | |

| | |

Ultra-Small Company Fund SCHEDULE OF INVESTMENTS (continued) | | |

Showing percentage of net assets as of June 30, 2016

| | | | | | | | | | |

| Industry Company | | Shares | | | Value | | | |

| |

Common Stocks (continued) | | | |

Diversified Telecommunication Services - 0.76% | | | |

HC2 Holdings, Inc.*+ | | | 178,700 | | | | $ 768,410 | | | |

| |

Electrical Equipment - 1.37% | | | |

LSI Industries, Inc. | | | 104,800 | | | | 1,160,136 | | | |

Ultralife Corp.* | | | 46,700 | | | | 233,967 | | | |

| | | | | | | | | | |

| | | |

| | | | | | | 1,394,103 | | | |

| |

Electronic Equipment, Instruments &

Components - 7.05% | | | |

American Superconductor Corp.*+ | | | 128,000 | | | | 1,080,320 | | | |

Electro Scientific Industries, Inc.* | | | 151,600 | | | | 885,344 | | | |

IEC Electronics Corp.* | | | 36,700 | | | | 152,305 | | | |

Kemet Corp.*+ | | | 210,000 | | | | 615,300 | | | |

Key Tronic Corp.*+ | | | 37,100 | | | | 279,363 | | | |

Maxwell Technologies, Inc.*+ | | | 264,500 | | | | 1,396,560 | | | |

NAPCO Security Technologies, Inc.*+ | | | 110,000 | | | | 699,600 | | | |

Radisys Corp.* | | | 456,800 | | | | 2,046,464 | | | |

| | | | | | | | | | |

| | | |

| | | | | | | 7,155,256 | | | |

| |

Energy Equipment & Services - 4.46% | | | |

Basic Energy Services, Inc.*+ | | | 190,300 | | | | 319,704 | | | |

Hercules Offshore, Inc.* | | | 77,900 | | | | 108,281 | | | |

North American Energy Partners, Inc. | | | 58,800 | | | | 165,816 | | | |

North Atlantic Drilling, Ltd.*+ | | | 75,900 | | | | 511,566 | | | |

Ocean Rig UDW, Inc.*+ | | | 451,400 | | | | 1,119,472 | | | |

Parker Drilling Co.* | | | 402,406 | | | | 921,510 | | | |

Willbros Group, Inc.* | | | 545,900 | | | | 1,381,127 | | | |

| | | | | | | | | | |

| | | |

| | | | | | | 4,527,476 | | | |

| |

Food Products - 0.25% | | | |

S&W Seed Co.*+ | | | 57,100 | | | | 248,956 | | | |

| |

Gas Utilities - 0.64% | | | |

Delta Natural Gas Co., Inc.+ | | | 23,900 | | | | 643,866 | | | |

| |

Health Care Equipment & Supplies - 3.28% | | | |

AxoGen, Inc.*+ | | | 180,000 | | | | 1,238,400 | | | |

Digirad Corp. | | | 40,600 | | | | 209,090 | | | |

Electromed, Inc.* | | | 80,000 | | | | 308,800 | | | |

FONAR Corp.* | | | 64,100 | | | | 1,305,076 | | | |

Symmetry Surgical, Inc.* | | | 20,000 | | | | 262,600 | | | |

| | | | | | | | | | |

| | | |

| | | | | | | 3,323,966 | | | |

| |

Health Care Providers & Services - 0.99% | | | |

Chembio Diagnostics, Inc.*+ | | | 107,500 | | | | 880,425 | | | |

InfuSystems Holdings, Inc.* | | | 48,700 | | | | 126,620 | | | |

| | | | | | | | | | |

| | | |

| | | | | | | 1,007,045 | | | |

| | | | | | | | | | |

| Industry Company | | Shares | | | Value | | | |

| | | |

| | | | | | | | | | |

Hotels, Restaurants & Leisure - 3.17% | | | |

Century Casinos, Inc.* | | | 106,400 | | | | $ 662,872 | | | |

Gaming Partners International Corp.* | | | 13,300 | | | | 123,690 | | | |

Golden Entertainment, Inc.+ | | | 35,300 | | | | 412,657 | | | |

Luby’s, Inc.*+ | | | 63,200 | | | | 317,264 | | | |

MCBC Holdings, Inc. | | | 46,100 | | | | 509,405 | | | |

Red Lion Hotels Corp.*+ | | | 82,300 | | | | 597,498 | | | |

Town Sports International Holdings, Inc.* | | | 217,800 | | | | 592,416 | | | |

| | | | | | | | | | |

| | | |

| | | | | | | 3,215,802 | | | |

| |

Household Durables - 0.40% | | | |

Skyline Corp.*+ | | | 20,100 | | | | 188,940 | | | |

UCP, Inc., Class A* | | | 27,200 | | | | 218,144 | | | |

| | | | | | | | | | |

| | | |

| | | | | | | 407,084 | | | |

| |

Insurance - 1.53% | | | |

Blue Capital Reinsurance Holdings, Ltd.+ | | | 23,300 | | | | 431,283 | | | |

eHealth, Inc.* | | | 43,000 | | | | 602,860 | | | |

Health Insurance Innovations, Inc., Class A*+ | | | 132,000 | | | | 518,760 | | | |

| | | | | | | | | | |

| | | |

| | | | | | | 1,552,903 | | | |

| | | |

Internet & Catalog Retail - 1.13% | | | | | | | | | | |

CafePress, Inc.* | | | 64,800 | | | | 200,880 | | | |

Gaiam, Inc., Class A* | | | 58,000 | | | | 448,920 | | | |

US Auto Parts Network, Inc.* | | | 124,800 | | | | 492,960 | | | |

| | | | | | | | | | |

| | | |

| | | | | | | 1,142,760 | | | |

| |

Internet Software & Services - 4.44% | | | |

Autobytel, Inc.* | | | 58,200 | | | | 807,234 | | | |

Brightcove, Inc.* | | | 175,100 | | | | 1,540,880 | | | |

Care.com, Inc.* | | | 91,300 | | | | 1,066,384 | | | |

Demand Media, Inc.* | | | 101,000 | | | | 522,170 | | | |

Marchex, Inc., Class B* | | | 103,200 | | | | 328,176 | | | |

Support.com, Inc.* | | | 285,800 | | | | 240,358 | | | |

| | | | | | | | | | |

| | | |

| | | | | | | 4,505,202 | | | |

| |

IT Services - 2.38% | | | |

BG Staffing, Inc. | | | 18,700 | | | | 353,804 | | | |

Edgewater Technology, Inc.* | | | 27,499 | | | | 237,591 | | | |

Information Services Group, Inc.*+ | | | 60,100 | | | | 225,375 | | | |

NCI, Inc., Class A | | | 87,000 | | | | 1,222,350 | | | |

PRGX Global, Inc.* | | | 71,300 | | | | 372,186 | | | |

| | | | | | | | | | |

| | | |

| | | | | | | 2,411,306 | | | |

| | |

| 18 | | Annual Report | June 30, 2016 |

| | |

Ultra-Small Company Fund SCHEDULE OF INVESTMENTS (continued) | | |

Showing percentage of net assets as of June 30, 2016

| | | | | | | | | | |

| Industry Company | | Shares | | | Value | | | |

| |

Common Stocks (continued) | | | |

Machinery - 3.85% | | | |

Ampco-Pittsburgh Corp. | | | 31,000 | | | | $ 350,610 | | | |

Commercial Vehicle Group, Inc.* | | | 92,900 | | | | 483,080 | | | |

Gencor Industries, Inc.* | | | 36,200 | | | | 561,824 | | | |

Key Technology, Inc.* | | | 11,200 | | | | 103,152 | | | |

Supreme Industries, Inc., Class A | | | 175,400 | | | | 2,402,980 | | | |

| | | | | | | | | | |

| | | |

| | | | | | | 3,901,646 | | | |

| |

Marine - 0.54% | | | |

DryShips, Inc.* | | | 241,600 | | | | 136,021 | | | |

Global Ship Lease, Inc., Class A | | | 321,600 | | | | 408,432 | | | |

| | | | | | | | | | |

| | | |

| | | | | | | 544,453 | | | |

| |

Media - 1.21% | | | |

Global Sources, Ltd.*+ | | | 18,900 | | | | 173,313 | | | |

Lee Enterprises, Inc.*+ | | | 360,200 | | | | 687,982 | | | |

Salem Media Group, Inc. | | | 50,700 | | | | 366,054 | | | |

| | | | | | | | | | |

| | | |

| | | | | | | 1,227,349 | | | |

| |

Metals & Mining - 6.79% | | | |

A-Mark Precious Metals, Inc. | | | 112,700 | | | | 1,823,486 | | | |

Olympic Steel, Inc. | | | 102,800 | | | | 2,807,468 | | | |

Ryerson Holding Corp.* | | | 129,000 | | | | 2,257,500 | | | |

| | | | | | | | | | |

| | | |

| | | | | | | 6,888,454 | | | |

| |

Multiline Retail - 0.41% | | | |

Bon-Ton Stores, Inc. (The) | | | 297,200 | | | | 419,052 | | | |

| |

Oil, Gas & Consumable Fuels - 3.51% | | | |

Adams Resources & Energy, Inc. | | | 4,900 | | | | 188,650 | | | |

Cloud Peak Energy, Inc.*+ | | | 389,900 | | | | 803,194 | | | |

Comstock Resources, Inc.* | | | 429,600 | | | | 360,993 | | | |

Geopark, Ltd.*+ | | | 43,900 | | | | 142,675 | | | |

PrimeEnergy Corp.*+ | | | 4,300 | | | | 259,075 | | | |

W&T Offshore, Inc.*+ | | | 418,700 | | | | 971,384 | | | |

Westmoreland Coal Co.* | | | 87,700 | | | | 834,904 | | | |

| | | | | | | | | | |

| | | |

| | | | | | | 3,560,875 | | | |

| |

Personal Products - 2.53% | | | |

Lifevantage Corp.*+ | | | 80,200 | | | | 1,090,720 | | | |

Mannatech, Inc.*+ | | | 9,500 | | | | 192,280 | | | |

Natural Alternatives International, Inc.* | | | 74,500 | | | | 822,480 | | | |

Nutraceutical International Corp.* | | | 20,000 | | | | 463,000 | | | |

| | | | | | | | | | |

| | | |

| | | | | | | 2,568,480 | | | |

| | | | | | | | | | |

| Industry Company | | Shares | | | Value | | | |

| | | |

| | | | | | | | | | |

Pharmaceuticals - 2.58% | | | |

Aralez Pharmaceuticals, Inc.* | | | 17,486 | | | | $ 57,704 | | | |

Dipexium Pharmaceuticals, Inc.*+ | | | 24,600 | | | | 243,786 | | | |

Juniper Pharmaceuticals, Inc.* | | | 100,900 | | | | 707,309 | | | |

Kindred Biosciences, Inc.* | | | 80,300 | | | | 284,262 | | | |

Tetraphase Pharmaceuticals, Inc.* | | | 126,100 | | | | 542,230 | | | |

Zafgen, Inc.*+ | | | 131,300 | | | | 786,487 | | | |

| | | | | | | | | | |

| | | |

| | | | | | | 2,621,778 | | | |

| |

Real Estate Investment Trusts (REITs) - 1.69% | | | |

Armada Hoffler Properties, Inc. | | | 111,900 | | | | 1,537,506 | | | |

BRT Realty Trust* | | | 24,200 | | | | 173,030 | | | |

| | | | | | | | | | |

| | | |

| | | | | | | 1,710,536 | | | |

| |

Real Estate Management & Development - 0.64% | | | |

Nam Tai Property, Inc.+ | | | 121,100 | | | | 650,307 | | | |

| | | |

Road & Rail - 1.33% | | | | | | | | | | |

USA Truck, Inc.* | | | 77,000 | | | | 1,348,270 | | | |

| |

Semiconductors & Semiconductor Equipment - 0.07% | | | |

Intermolecular, Inc.* | | | 44,900 | | | | 66,452 | | | |

| |

Software - 2.25% | | | |

BSQUARE Corp.*+ | | | 155,700 | | | | 868,806 | | | |

Covisint Corp.* | | | 115,500 | | | | 251,790 | | | |

GlobalSCAPE, Inc. | | | 41,400 | | | | 152,766 | | | |

Planet Payment, Inc.*+ | | | 225,000 | | | | 1,010,250 | | | |

| | | | | | | | | | |

| | | |

| | | | | | | 2,283,612 | | | |

| |

Specialty Retail - 1.46% | | | |

Kingold Jewelry, Inc.* | | | 201,900 | | | | 363,420 | | | |

New York & Co., Inc.* | | | 137,000 | | | | 204,130 | | | |

Sears Hometown & Outlet Stores, Inc.*+ | | | 135,500 | | | | 913,270 | | | |

| | | | | | | | | | |

| | | |

| | | | | | | 1,480,820 | | | |

| |

Textiles, Apparel & Luxury Goods - 1.53% | | | |

Crown Crafts, Inc.+ | | | 26,100 | | | | 246,906 | | | |

Delta Apparel, Inc.* | | | 53,400 | | | | 1,204,170 | | | |

Lakeland Industries, Inc.*+ | | | 12,162 | | | | 105,445 | | | |

| | | | | | | | | | |

| | | |

| | | | | | | 1,556,521 | | | |

| |

Thrifts & Mortgage Finance - 6.40% | | | |

BSB Bancorp, Inc.*+ | | | 14,500 | | | | 328,425 | | | |

Charter Financial Corp. | | | 101,000 | | | | 1,341,280 | | | |

| | |

Ultra-Small Company Fund SCHEDULE OF INVESTMENTS (continued) | | |

Showing percentage of net assets as of June 30, 2016

| | | | | | | | | | | | | | |

| Industry Company | | | | Shares | | Value | | | | | | |

| | |

Common Stocks (continued) | | | | | | | |

Thrifts & Mortgage Finance (continued) | | | | | | | |

Entegra Financial Corp.* | | 12,100 | | | $ 211,629 | | | | | | | |

ESSA Bancorp, Inc. | | 38,100 | | | 510,540 | | | | | | | |

First Financial Northwest, Inc. | | 47,400 | | | 629,472 | | | | | | | |

Fox Chase Bancorp, Inc. | | 7,000 | | | 142,380 | | | | | | | |

Hingham Institution for Savings | | 4,631 | | | 569,242 | | | | | | | |

MMA Capital Management, LLC* | | 20,700 | | | 373,014 | | | | | | | |

Ocean Shore Holding Co.+ | | 19,600 | | | 332,416 | | | | | | | |

Provident Financial Holdings, Inc. | | 47,000 | | | 860,100 | | | | | | | |

Security National Financial Corp., Class A* | | 41,055 | | | 200,759 | | | | | | | |