UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-08416

Touchstone Variable Series Trust

(Exact name of registrant as specified in charter)

303 Broadway, Suite 1100

Cincinnati, Ohio 45202-4203

(Address of principal executive offices) (Zip code)

Jill T. McGruder

303 Broadway, Suite 1100

Cincinnati, Ohio 45202-4203

(Name and address of agent for service)

Registrant's telephone number, including area code: 800-638-8194

Date of fiscal year end: December 31

Date of reporting period: December 31, 2012

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget ("OMB") control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 100 F Street, NE, Washington, DC 20549. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

Item 1. Reports to Stockholders.

The Report to Shareholders is attached herewith.

December 31, 2012

Annual Report

Touchstone Variable Series Trust

Touchstone Baron Small Cap Growth Fund

Touchstone Core Bond Fund

Touchstone High Yield Fund

Touchstone Large Cap Core Equity Fund

Touchstone Mid Cap Growth Fund

Touchstone Money Market Fund

Touchstone Third Avenue Value Fund

Touchstone Aggressive ETF Fund

Touchstone Conservative ETF Fund

Touchstone Enhanced ETF Fund

Touchstone Moderate ETF Fund

Table of Contents

| | Page |

| Letter from the President | 3 |

| Management's Discussion of Fund Performance (Unaudited) | 4 - 30 |

| Tabular Presentation of Portfolios of Investments (Unaudited) | 31 - 32 |

| Portfolio of Investments: | |

| Touchstone Baron Small Cap Growth Fund | 33 |

| Touchstone Core Bond Fund | 35 |

| Touchstone High Yield Fund | 42 |

| Touchstone Large Cap Core Equity Fund | 46 |

| Touchstone Mid Cap Growth Fund | 48 |

| Touchstone Money Market Fund | 50 |

| Touchstone Third Avenue Value Fund | 53 |

| Touchstone Aggressive ETF Fund | 55 |

| Touchstone Conservative ETF Fund | 56 |

| Touchstone Enhanced ETF Fund | 57 |

| Touchstone Moderate ETF Fund | 58 |

| Statements of Assets and Liabilities | 60 - 61 |

| Statements of Operations | 62 - 63 |

| Statements of Changes in Net Assets | 64 - 67 |

| Financial Highlights | 68 - 73 |

| Notes to Financial Statements | 74 - 85 |

| Report of Independent Registered Public Accounting Firm | 86 |

| Other Items (Unaudited) | 87 - 95 |

| Management of the Trust (Unaudited) | 96 - 98 |

| Privacy Protection Policy | 99 |

Letter from the President

Dear Shareholder:

We are pleased to provide you with the Touchstone Variable Series Trust Annual Report. Inside you will find key financial information, as well as manager commentaries for the Funds, for the twelve months ended December 31, 2012.

The year 2012 was a remarkable one for stock markets around the globe with substantial liquidity driving above average returns in the U.S., developed non-U.S. and select developing markets. Although volatility and fluctuating economic conditions, as well as consumer confidence, persisted throughout the year, financial markets managed to exceed investors’ low expectations. The advance came despite the “Fiscal Cliff ” in the U.S., the damage from Hurricane Sandy in October, an economic deceleration in China and continued weakness out of Europe. Additional monetary easing and an increased investor appetite for risk also helped to drive the rally. In the U.S., housing slowly improved throughout the year, with home values reportedly increasing year-over-year for the first time since 2006 and inventories remained below historical levels, suggesting that prices would continue to rise.

From a market capitalization and style perspective, mid cap stocks outperformed both large- and small-capitalizations, while value outpaced growth, and emerging markets’ performance surpassed non-U.S. developed markets. Within fixed income markets, high yield bonds and corporate bonds significantly outperformed U.S. Treasuries. Interest rates remained low and the Federal Reserve announced that it would keep rates low, at least until unemployment drops to 6.5 percent and inflation projections are no more than 2.5 percent. This replaced the Fed’s earlier view that rates would stay near zero at least through the middle of 2015.

We continue to believe that diversification is essential to balancing risk and return. We recommend that you continue to work with your financial professional to employ a sound asset allocation strategy that invests in a combination of stock, bond and money market mutual funds to help keep your financial strategy on course. It is critical to maintain a long-term approach to gain the full potential benefits of investing.

Touchstone is committed to helping investors achieve their financial goals by providing access to a distinctive selection of institutional asset managers who are known and respected for proficiency in their specific areas of expertise. We hope that you will find the enclosed commentaries helpful.

We greatly appreciate your continued support. Thank you for including Touchstone as part of your investment plan.

Sincerely,

Jill T. McGruder

President

Touchstone Variable Series Trust

Management's Discussion of Fund Performance (Unaudited)

Touchstone Baron Small Cap Growth Fund

Sub-Advised by BAMCO, Inc.

Investment Philosophy

The Touchstone Baron Small Cap Growth Fund primarily invests in common stocks of small-sized growth companies. The Fund’s sub-advisor, BAMCO, Inc. (“BAMCO”), seeks securities that it believes have (1) favorable price to value characteristics, are well managed, have significant long-term growth prospects and have significant barriers to competition; and (2) the potential to increase in value at least 100 percent over the next four or five years. Securities are selected for their capital appreciation potential and investment income is not a consideration in BAMCO’s stock selection process.

Fund Performance

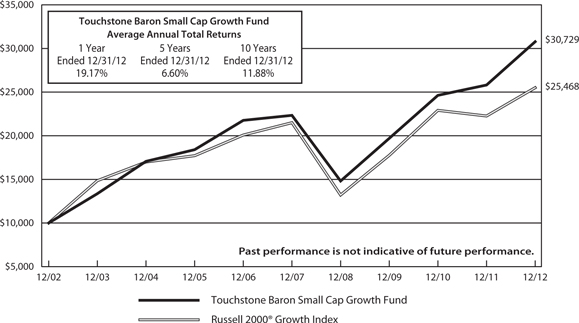

The Touchstone Baron Small Cap Growth Fund outperformed its benchmark, the Russell 2000® Growth Index, for the 12-month period ended December 31, 2012. The Fund’s total return was 19.17 percent while the return of the benchmark was 14.59 percent for the 12-month period ended December 31, 2012.

Market Environment

In 2012, economic conditions remained uncertain and markets were volatile, yet the economy did show positive signs of recovery. The year started on an encouraging note, with uncertainty from Europe and Asia following in the second quarter, along with seesawing consumer confidence. In the third quarter, markets rebounded, as we saw a drop in unemployment and an increase in consumer confidence and housing starts. During the fourth quarter, equities sold off sharply following President Obama’s re-election; they later recovered on optimism that a bipartisan deal could be reached to avert the fiscal cliff, promising economic reports and positive signs on financial stabilization in Europe.

Portfolio Review

The Fund’s investment process hones in on secular growth themes or trends capable of driving strong multi-year growth, seeking companies that are believed to be well run by visionary management teams, with a differentiated long-term strategy, significant competitive advantages, and dominant positions with the opportunity for market share gains. These companies possess what we believe to be strong balance sheets with the ability to reinvest in their businesses to earn high returns.

During the year, the Fund’s favorable stock selection effect and, to a lesser extent, its sector allocations, contributed to relative performance. The Health Care, Industrials, and Consumer Discretionary sectors were the largest contributors to relative and absolute performance for the year.

A combination of strong stock selection and an overweight within the Consumer Discretionary sector made it the top contributing sector. Shares of Lumber Liquidators Holdings, Inc., the leading specialty retailer of hardwood flooring, surged during 2012, after reporting exceptional momentum in its business. This strong move coincided with significant strengthening in the U.S. housing and remodeling markets, as well as the positive traction from merchandizing, sourcing, and advertising initiatives. Another contributor was Dick’s Sporting Goods, Inc., the country’s largest sporting goods retailer, with its shares increasing for the year. The company has grown sales consistently through strong new store productivity, positive same store sales, and improved e-commerce business. Margins have also expanded as a result of additional focus on premium suppliers and additional private label and private branded merchandise. Other notable contributors to relative results in the sector were distributor LKQ Corp. and casino operator Ameristar Casinos, Inc. The largest stock detractor in the sector in 2012 was DeVry, Inc. The company is a provider of diversified post-secondary education emphasizing business, technology, and healthcare. DeVry is experiencing enrollment declines as students, discouraged by

Management's Discussion of Fund Performance (Unaudited) (Continued)

prolonged high unemployment, defer their decision to enroll in college. The lower student count and continued investment spending in growth areas is driving negative operating leverage. Longer term, we are positive on DeVry given its focus on areas which we believe should experience long-term job growth and its solid history of graduate placement.

In the Industrials sector, shares of Generac Holdings, Inc., a leading designer and manufacturer of standby and portable generators for the residential, industrial, and commercial markets, increased sharply during the year, contributing to performance. This was due to a rapid rise in sales due to increased awareness and adoption of its temporary power solutions, which was driven by strong storm activity and corresponding power outages. In addition, Generac paid a dividend to shareholders as a result of a leveraged recapitalization. Strength within the sector was also attributable to the Fund’s investments in industrial machinery stocks, led by Colfax Corp., a diversified global industrial manufacturing and engineering company that provides gas and fluid handling technology products, and Valmont Industries, Inc., a diversified industrial company that produces fabricated metal products for infrastructure. Shares of Colfax outperformed in 2012 as the company completed the acquisition of Charter PLC. We believe the acquisition could create significant value due to the substantial potential for operating margin improvement.

In the Health Care sector, the Fund’s largest contributor to performance was AMERIGROUP Corp., a leading Medicaid HMO. AMERIGROUP’s revenue grew from $1.6 billion in 2003, when the Fund first invested in the company, to $6 billion in 2011. In July, WellPoint, Inc. bid for AMERIGROUP, at a 43 percent premium to the prior day’s close. Subsequently, the position was sold. Another contributor to relative results in the sector was Community Health Systems, Inc. ITC Holdings Corp., the Fund’s only holding in the Utilities sector, outperformed for the year; however, the Fund’s larger exposure to the sector, one of the worst performers in the benchmark, was the largest detractor from relative performance.

The Energy sector was another detractor to Fund performance, led by CARBO Ceramics, Inc. and SM Energy Co. CARBO is the leading supplier of ceramic proppant, which is used in hydraulic fracturing. CARBO’s share price suffered through the first three quarters of the year from a series of downward earnings estimate revisions related to declining demand as drilling shifted from gas to oil, an oversupply of proppants from a flood of Chinese imports, and higher than usual logistics expenses. We believe most of these issues are behind the company, and the stock price rebounded in the quarter. SM Energy is an exploration and productions (E&P) company, with operations largely focused on the Eagle Ford shale and Williston Basin in the U.S. SM Energy’s shares declined in 2012 as a result of several factors. Specifically, the company was conservative in its 2011 reserve bookings; infrastructure challenges caused lower than expected production in the second quarter; and natural gas liquids’ prices declined sharply, hurting the perceived value of SM Energy’s assets. These factors have either been rectified or, we believe will be shortly, and SM Energy’s shares remain valued below our net asset value (NAV) estimates.

Booz Allen Hamilton Holdings Corp., a provider of high-end government Information Technolgy services, and Choice Hotels International Inc., the largest franchisor of hotels in the U.S., distributed special cash dividends during the year due to each company generating strong free-cash-flows.

We believe we have been successful because we invest for the long-term and are less focused on short-term macro events. New purchases accounted for about 8 percent of net assets and complete sales accounted for about 22 percent of net assets at year end.

Outlook

We continue to believe that stock market valuations are attractive. U.S. interest rates remain near historically low levels, and the fixed income markets offer limited inflation-adjusted returns. Investors continue to hold substantial sums in cash, which we believe will eventually be deployed into equities. Regulators are increasing

Management's Discussion of Fund Performance (Unaudited) (Continued)

their efforts to make our financial markets function more efficiently and fairly. We believe this will help restore the faith of individual and institutional investors in capital markets.

Although growth in the U.S. during the next few years will probably be slower than in prior decades, we believe that the competitive advantage of our country’s low cost and plentiful shale energy, at about one-third of the cost of the rest of the world, will boost our nation’s growth, as will the cost of electricity in the U.S., which is now about half that of the rest of the world. We believe a recovering housing market, which has only recently begun to improve, will also propel our nation’s economic growth. About 40 percent of our nation’s jobs lost in the Great Recession were in construction. We think the nascent housing recovery and a greater need for healthcare services will last for many years and will make an important contribution to lowering unemployment.

2013 started well as the fiscal cliff was avoided by a last ditch compromise. Although the market rallied, unfortunately, we believe the deal struck is disappointing in that it accomplished much less in deficit reduction than needed ($600 billion over ten years vs. $2.5 trillion sought). In addition, the deal did not include any spending or entitlement cuts, nor did it address the looming debt ceiling. The budget battles will likely intensify as the next deadline draws near, and the drag on the economy it is causing may linger. We believe that as soon as the government’s issues are addressed, business will strengthen and the markets will continue to perform well. We expect the Fund to outperform the market in normal conditions, and underperform in markets with extreme downward movements, such as those greater than 25 percent. The Fund’s investment philosophy seeks well managed businesses with sustainable competitive advantages and the ability to grow significantly over the long-term. The Fund continues to invest in a diversified portfolio of businesses that we believe have significantly better financial characteristics than its benchmark Index.

The Fund’s businesses typically have significantly higher growth rates, operating profit margins, net margins, EBITDA margins (earnings before interest, taxes, depreciation and amortization), return on invested capital, return on equity, and return on assets. In addition, they have substantially lower standard deviations of earnings growth. We believe they are better managed and contribute in an uncorrelated manner, given that their businesses, clients and competitive advantages are dissimilar.

Management's Discussion of Fund Performance (Unaudited) (Continued)

Comparison of the Change in Value of a $10,000 Investment in the

Touchstone Baron Small Cap Growth Fund and the Russell 2000® Growth Index

Performance information does not reflect fees that are paid by the separate accounts through which shares of the Fund are sold. Inclusion of those fees would reduce figures for all periods.

The Fund commenced operations on December 14, 1992.

Note to Chart

The Russell 2000® Growth Index measures the performance of those Russell 2000 companies with higher price-to-book ratios and higher forecasted growth values.

Management's Discussion of Fund Performance (Unaudited)

Touchstone Core Bond Fund

Sub-Advised by Fort Washington Investment Advisors, Inc.

Investment Philosophy

The Touchstone Core Bond Fund seeks to provide as high a level of current income as is consistent with the preservation of capital. Capital appreciation is a secondary goal. In deciding what securities to buy and sell for the Fund, the overall investment opportunities and risks in different sectors of the debt securities market are analyzed by focusing on maximizing total return and reducing the volatility of the Fund’s portfolio. A disciplined sector allocation process is followed in order to build a broadly diversified portfolio of bonds.

Fund Performance

The Touchstone Core Bond Fund outperformed its benchmark, the Barclays U.S. Aggregate Bond Index for the 12-month period ended December 31, 2012. The Fund’s total return was 5.28 percent while the total return of the benchmark was 4.21 percent for the 12-month period ended December 31, 2012.

Market Environment

Over the past year, the markets have been influenced by a sluggish economic environment in the U.S., continued stress in the eurozone, and bold central bank action. Asset returns in fixed income were positively influenced by these factors, with broad strength seen in the non-U.S. Treasury sectors of the bond market. Commercial Mortgage-Backed Securities (CMBS), Corporate Bonds, and High Yield Bonds each outperformed U.S. Treasuries. Intermediate interest rates fell slightly over the period, but long-term interest rates were mostly unchanged. There was significant volatility in interest rates, with ongoing concern in the eurozone, uneven U.S. economic data, and aggressive responses by the European Central Bank (ECB) and U.S.Federal Reserve (Fed). At period end, U.S. Treasury yields were up slightly with very limited volatility, as concern in the eurozone diminished and was overshadowed by the U.S. “fiscal cliff.”

In the eurozone, mounting tensions in the Greek, Spanish, and Italian bond markets, along with broader concern over recession, prompted the ECB to unveil a host of new programs, including, most recently, the unlimited securities purchases of troubled countries. For its part, the Fed instituted and then extended a version of “Operation Twist,” in which it extended the maturity of its portfolio in an effort to reduce interest rates. Recently, faced with “grave concern” over the labor market in the U.S. during third quarter, the Fed embarked on a new round of quantitative easing (QE3), focused on mortgage-backed securities (MBS) and U.S. Treasuries. The Fed also indicated that it was likely to maintain an accommodative policy even as the economic recovery continued through year end.

Portfolio Review

In general, the Fund performed well over the past year due to its overweight, relative to the benchmark, of non-U.S. Treasury sectors. The Fund’s overweight in the CMBS sector contributed to performance. The Fund’s Agency MBS sector was underweight and detracted from performance, and Corporate Bonds had little impact. Risk premiums across the spectrum of non-U.S. Treasury sectors tightened significantly in the latter part of the period.

The Fund’s allocation to High Yield contributed to performance. The High Yield market (as represented by the BofA Merrill Lynch U.S. Cash Pay High Yield Index) outperformed during the period.

In terms of interest rate risk and yield curve positioning, we were mostly neutral duration relative to the benchmark for the year and had little impact on the performance of the Fund. We have opportunistically invested in Treasury-Inflation Protected Securities (TIPS) during the period, but this had minimal impact on performance.

Management's Discussion of Fund Performance (Unaudited) (Continued)

The most significant changes to the Fund’s positioning were in the Investment Grade Corporate Bond and High Yield credit sectors. The High Yield market performed well into the beginning of the period, and we subsequently reduced the allocation in the first half of 2012. Risk premiums have narrowed significantly over the past 12 months and, while still representing value in the fixed income market, the attractiveness is reduced in light of the significant risks present in the U.S. and Europe.

In contrast, we determined that the risk premium of the Investment Grade Corporate Bond sector no longer offered adequate compensation for additional credit or liquidity risk. Late in the third quarter, we reduced the Fund’s weight to Investment Grade Corporate Bonds and the Fund is now underweight relative to the benchmark. If the economy continues to grow in a sub-par fashion, Corporate Bonds may underperform due to increased concern over credit quality. In an environment where growth increases significantly and investors allocate away from fixed income, the Investment Grade Corporate Bond sector could experience weakness due to lack of liquidity.

For much of the past year, the duration of the Fund had been neutral relative to the benchmark, but we actively managed its duration in an approximate band of +/-10% versus the benchmark. Over the period, the duration positioning of the Fund had little impact on the performance of the Fund. Currently, the Fund is positioned with slightly less interest rate risk in longer maturities than the benchmark.

Outlook

The biggest opportunities over the near term are likely to be short-term in nature given the overall low level of yields and risk premiums. The Fed’s actions should result in lower overall market volatility, which will require the Fund to be nimble and capture short-term opportunities.

From a top-down perspective, there are likely to be imbalances created in the market with the Fed influencing asset prices that may differ significantly from equilibrium levels. The unwinding of these imbalances will create opportunities; however, that may take several months. For example, while we expect Fed policy to keep rates low over the near-term, long-term interest rates may be especially vulnerable (higher rates) to economic improvement and resultant expectations of higher inflation over the next few quarters. The Fund is positioned with slightly less interest rate risk in longer maturities than its benchmark to reflect this view.

On a sector allocation basis, we continue to see opportunity in CMBS due to the high-quality nature of the bonds we hold, along with the yield and relatively limited interest rate risk. In contrast, we believe that the risk premium of the Investment Grade Corporate Bond sector no longer offers adequate compensation for additional credit or liquidity risk. We recently reduced our weighting to the sector and are now underweight relative to the benchmark. Although we believe High Yield remains an attractive opportunity and continue a weighting to this sector, we believe additional risk premium narrowing may lead us to reduce the exposure.

The evolution of the U.S. economy and the impact on monetary policy will be the biggest driver of volatility in 2013. The Fed is pursuing aggressive policies and the market will have to discern the direction of those policies given the outlook. Going forward, we expect interest rates to remain near current levels. However, recent Fed actions have raised the concern that long-term interest rates may be especially vulnerable (higher rates) to economic improvement and resultant expectations of higher inflation.

Management's Discussion of Fund Performance (Unaudited) (Continued)

Over the near-term, however, the markets are most likely to be influenced by the potential resolution of the debt ceiling/sequester issue, which has the potential to generate significant volatility across all markets. Longer-term, the greatest concern relates to the overall low level of interest rates and risk premiums across the entire bond market. The potential return of fixed income in general will be challenged going forward, and the low level of risk premiums will make it difficult to add alpha1 through overweighting/underweighting sectors relative to the benchmark.

1Alpha is the portion of a fund’s total return that is unique to that fund and is independent of movements in the benchmark.

Management's Discussion of Fund Performance (Unaudited) (Continued)

Comparison of the Change in Value of a $10,000 Investment in the

Touchstone Core Bond Fund and the Barclays U.S. Aggregate Bond Index

Performance information does not reflect fees that are paid by the separate accounts through which shares of the Fund are sold. Inclusion of those fees would reduce figures for all periods.

The Fund commenced operations on October 3, 1994.

Note to Chart

The Barclays U.S. Aggregate Bond Index is an unmanaged index comprised of U.S. investment grade, fixed rate bond market securities, including government, government agency, corporate and mortgage-backed securities between one and ten years.

Management's Discussion of Fund Performance (Unaudited)

Touchstone High Yield Fund

Sub-Advised by Fort Washington Investment Advisors, Inc.

Investment Philosophy

The Touchstone High Yield Fund seeks high current income and capital appreciation by primarily investing in non-investment grade securities. The Fund emphasizes the higher-quality segment of the high yield market. It utilizes a research process designed to maximize risk-adjusted returns by avoiding lower-rated securities.

Fund Performance

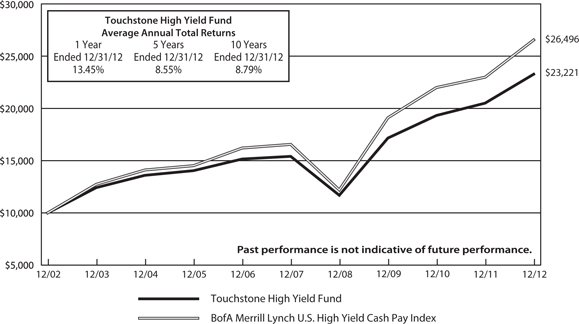

The Touchstone High Yield Fund underperformed its benchmark, the BofA Merrill Lynch High Yield Cash Pay Index for the 12-month period ended December 31, 2012. The Fund’s total return was 13.45 percent while the total return of the benchmark was 15.44 percent for the 12-month period ended December 31, 2012.

Market Environment

Investors had good reason to celebrate considering the performance of financial markets in 2012, with most risky assets posting double-digit returns. After surging in the first part of the year, stocks and other risk assets plummeted in the second quarter before staging a strong second-half rally.

While the U.S. economy continued to improve throughout 2012 and posted 3% growth in the third quarter, it grew at only about half that pace in the final quarter. U.S. businesses were cautious about hiring new workers, and they scaled back on investment spending amid uncertainty about U.S. fiscal policy and the health of the global economy.

The global economy slowed to its weakest pace since the onset of recovery in mid-2009. The main drag came from Europe, where the peripheral countries in the eurozone were mired in recession while growth in the core economies faltered. At the same time, growth of the Chinese economy decelerated and Japan’s economy stagnated.

In the U.S., aggregate Gross Domestic Product (GDP) statistics reflected a gradual improvement in private sector spending, including a revival of auto demand and a turnaround in residential housing – sectors that typically lead economic expansions. Residential construction made a positive contribution to GDP for the first time in six years, while home prices posted solid gains in the second half of the year. The increase in spending on big-ticket discretionary items was accompanied by a rebound in consumer confidence to its highest level since the financial crisis and by a stabilization of the personal saving rate at about 4 percent of disposable income.

At the same time, U.S. businesses undertook significant adjustments to improve their balance sheets and restore overall profitability during the period. Corporate profits as a share of GDP soared to post-war highs, and U.S. businesses are sitting on record amounts of cash. The improvement in profitability and balance sheet positions is mirrored in the strong showing of the U.S. stock and corporate bond markets in the past four years.

High Yield bond spreads tightened by more than 160 basis points, generating significant capital appreciation. Lower quality (CCC-rated) securities outperformed while higher quality (BB-rated securities) lagged. Although there were many opportunities for volatility (elections, Europe, concerns over GDP growth, budget negotiations, etc.), the High Yield market continued to attract capital owing to fair valuations and a lack of compelling alternatives. Somewhat surprisingly, the market shrugged off concerns over the “fiscal cliff” and possible sequestration rallying strongly into the end of the year. While spreads do remain reasonable, yields were at an all-time low and the dollar price was approaching a record high at period end.

Management's Discussion of Fund Performance (Unaudited) (Continued)

Portfolio Review

The Fund’s performance lagged the broader indices primarily due to its lack of lower quality (CCC-rated) securities and negative attribution from sector allocation. Attribution from security selection was essentially flat. With respect to sector allocation, the Fund’s underweight exposure to the Banks & Thrifts sector detracted from performance as did its overweight allocation to the Midstream Energy and Metals/Mining sectors. Conversely, the overweight allocation to the Telecommunications sector and underweight allocation to the Utilities sector both contributed to performance.

With respect to security selection, the Fund experienced outperformance within the Energy and Industrials sectors. Expro Finance (Energy sector), an oilfield services company, benefited from asset sales and reduced leverage, while Plains Exploration (Industrials sector) outperformed after competitor Freeport-McMoRan Copper & Gold Inc. announced its intent to purchase the company. The Fund suffered from poor security selection within the Telecommunications and Technology sectors. Sprint Nextel (Telecommunications sector), a Central American wireless provider, exhibited weakness from slowing economies coupled with a heavy capital expenditure program. Kemet Corporation (Technology sector) lagged as a result of a softening semiconductor market.

Outlook

Going forward, with little opportunity to differentiate on the upside due to the high-dollar/low- yield environment, there will be significant opportunity to differentiate on the downside. As such, we have attempted to limit downside risk through the reduction of volatile securities that might be susceptible to company-specific weakness and/or general market volatility. We are well positioned to take advantage of such volatility.

Heavy flows into the market coupled with continued lack of liquidity make the Fund’s portfolio construction and management challenging. Such is particularly true in a “risk-on” environment in which we currently operate given our higher quality philosophy.

We think spreads are fair and we continue to advocate allocations to High Yield. However, we think it is ever more important to understand the limited upside in High Yield. As mentioned above, while spreads do remain reasonable, yields are at an all time low and dollar price is approaching a record high resulting in limited opportunity for capital appreciation. It will be nearly impossible to generate returns in 2013 that are similar to those posted in 2012.

Regardless, with confidence in economic fundamentals, we think the prospects for High Yield in 2013 are attractive, particularly when compared to alternatives, and we have positioned the Fund to be modestly higher in quality. While we acknowledge that downside risk may be greater than upside potential, we consider the likelihood of significant principal erosion to be remote. Further, we think any volatility would be temporary and met with increased asset flows based upon the long-term fundamental outlook for the asset class.

Management's Discussion of Fund Performance (Unaudited) (Continued)

Comparison of the Change in Value of a $10,000 Investment in the

Touchstone High Yield Fund and the BofA Merrill Lynch U.S. High Yield Cash Pay Index

Performance information does not reflect fees that are paid by the separate accounts through which shares of the Fund are sold. Inclusion of those fees would reduce figures for all periods.

The Fund commenced operations on May 1, 1999.

Note to Chart

The BofA Merrill Lynch U.S. High Yield Cash Pay Index is an unmanaged index used as a general measure of market performance consisting of fixed-rate, coupon-bearing bonds with an outstanding par which is greater than or equal to $50 million, a maturity range greater than or equal to one year and must be less than BBB/Baa3 rated but not in default.

Management's Discussion of Fund Performance (Unaudited)

Touchstone Large Cap Core Equity Fund

Sub-Advised by Todd-Veredus Asset Management LLC.

Investment Philosophy

TheTouchstone Large Cap Core Equity Fund primarily invests in common stocks of large capitalization companies. The Fund’s sub-advisor, Todd-Veredus Asset Management LLC (“Todd-Veredus”), selects stocks that it believes are attractively valued with active catalysts in place. Todd-Veredus uses a database of 4,000 stocks from which to choose the companies that will be selected for the Fund’s portfolio. As a result, the portfolio generally consists of 40-60 positions. Todd-Veredus’s selection process is expected to cause the Fund’s portfolio to have some of the following characteristics: attractive relative value, unrecognized earnings potential, above-average market capitalization, seasoned management and dominant industry.

Fund Performance

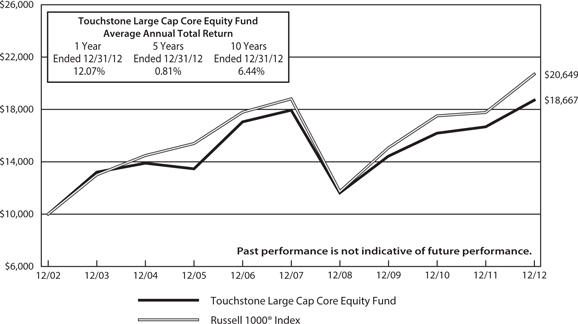

The Touchstone Large Cap Core Equity Fund underperformed its benchmark, the Russell 1000® Index, for the 12-month period ended December 31, 2012. The Fund’s total return was 12.07 percent while the total return of the benchmark was 16.42 percent for the 12-month period ended December 31, 2012.

Market Environment

The equity market moved forward primarily based on the idea that the world was past the point of highest danger from the financial crisis in Europe. While markets were breathing a sigh of relief with the European Crisis abating, the economy still did not feel positive about economic growth in most parts of the world. The U.S. was the steadiest economy last year, while Europe suffered a recession and most Emerging Market countries saw a significant slowing. One of the byproducts of better U.S. economic growth was that companies with less foreign exposure tended to outperform.

Portfolio Review

The Fund’s emphasis on quality multinational companies without financial problems hurt the Fund during the year, as the market staged a low quality beta1 led rally for the second time in three years. It was a frustrating year because our normally trustworthy multi-factor ranking model saw the lowest ranked stocks outperform all other categories for most of the year.

Stock selection drove most of the Fund’s underperformance, specifically relative performance in the Consumer Discretionary, Health Care and Financials sectors. Stock selection in the Energy, Utilities and Consumer Staples sectors contributed to relative performance. Contributors to performance included Marathon Petroleum Corp. (Energy sector) where improved refining margins helped raise profits. Oracle Corp.’s (Information Technology sector) concerns over sluggish software sales evaporated as new products gained. Aflac Inc.’s (Financials sector) easing European concerns reduced worries. Ensco PLC’s (Energy sector) earnings were revised up as higher day-rates improved. Illinois Tool Works’ (Industrials sector) earnings outlook firmed with recovery end markets.

Detractors from performance included GameStop Corp. (Consumer Discretionary sector) who was hurt by earnings uncertainty related to new product introductions. McDonald’s Corp. (Consumer Discretionary sector) was affected by slowing same store sales and tougher comparables. Coach, Inc. (Consumer Discretionary sector) was impacted by concerns about a slowdown in luxury products. NYSE Euronext, Inc.’s (Financials sector) lower trading volumes weakened the outlook. Intel Corp.’s (Information Technology sector) weaker personal computer sales led to decreased earnings expectations.

Management's Discussion of Fund Performance (Unaudited) (Continued)

Additionally, Consumer Discretionary stocks performed very well for the year, led by the levered homebuilders and auto parts manufacturers. Most of these names have significantly higher volatility than the stocks that are in the Fund’s portfolio.

The Fund is underweight in the Consumer Discretionary, Consumer Staples and Utilities sectors versus the Index. The Fund’s allocation to the Financials sector increased as several recovering banks have started instituting significant cost cutting measures. Additionally, the amount of problem assets on the books is decreasing each quarter, putting the banks on sounder footing to participate in the economic recovery. The Fund’s Health Care sector holdings increased during the year, as we believe the market is willing to look through the patent cliffs and anticipate product pipeline success for many of the larger drug companies.

Outlook

The market’s internal characteristics are acting like an early stage bull market recovering from a financial crisis. That is typically when low quality and Beta1 outperform by this margin. Interestingly, the economy is acting like it is in early stage recovery as well, with autos and housing leading. Perhaps this is an extended cycle like we used to get in the Greenspan era, and a more “normal” recovery can begin after a period of consumer deleveraging.

Political wrangling may have damaged consumer sentiment in the U.S. A higher payroll tax will probably dampen consumer demand in the first half of 2013. Also, U.S. capital spending has been restrained and may remain so if companies favor dividend increases over building productive capacity. Additionally, what was one event became a series of events: the Fiscal Cliff turned into the “Fill in the Blank” Cliffs. We passed the first hurdle with an extension to the tax cuts for people making less than $450,000. Now we face the Debt Ceiling debate, and potentially numerous other mini-cliffs regarding spending, entitlement cuts and the like. However, it looks like the economic expansion will continue, and international economies may be past the worst of their challenges.

With some “normalcy” returning to the market and the crisis atmosphere abating, the Fund’s disciplines may return to favor in 2013. We are skeptical that the end of 2012 marks the end of the secular bear market for equities. The market may still experience modest gains in equity indices.

1Beta is a measure of the volatility of a portfolio relative to its benchmark.

Management's Discussion of Fund Performance (Unaudited) (Continued)

Comparison of the Change in Value of a $10,000 Investment in the

Touchstone Large Cap Core Equity Fund and the Russell 1000® Index

Performance information does not reflect fees that are paid by the separate accounts through which shares of the Fund are sold. Inclusion of those fees would reduce figures for all periods.

The Fund commenced operations on May 1, 1999.

Note to Chart

The Russell 1000® Index measures the performance of the 1,000 largest companies in the Russell 3000® Index.

Management's Discussion of Fund Performance (Unaudited)

Touchstone Mid Cap Growth Fund

Sub-Advised by Westfield Capital Management Company, L.P.

Investment Philosophy

The Touchstone Mid Cap Growth Fund invests primarily in stocks of domestic mid-cap companies that are believed to have a demonstrated record of achievement with excellent prospects for earnings growth over a 1 to 3 year period. Fund management believes that companies that exhibit faster earnings growth offer the best opportunity for superior real rates of return and that reasonably priced stocks of companies with high forecasted earnings potential are best identified through in-depth, fundamental research and first-hand knowledge of company operations derived through on-site visits and meetings with management.

Fund Performance

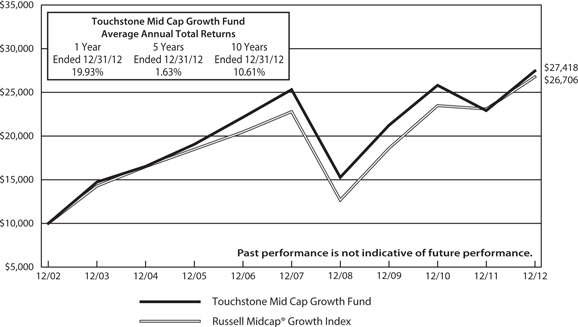

The Touchstone Mid Cap Growth Fund outperformed its benchmark, the Russell Midcap® Growth Index, for the 12-month period ended December 31, 2012. The Fund’s total return was 19.93 percent while the total return of the benchmark was 15.81 percent for the 12-month period ended December 31, 2012.

Market Environment

Against all odds and economic woes, domestic equities delivered double-digit gains in the past twelve months. The advance came despite the unsettled fiscal outlook in the U.S., an economic deceleration in China, and weakness out of Europe. Interestingly, earnings growth, at roughly 6%, represented a relatively small fraction of the move; multiple expansions – perhaps a reflection of monetary easing and an increased investor appetite for risk – was the driving force behind the rally. In September, the Federal Reserve extended their “extremely low rate” guidance through mid-2015. Concerns about declining U.S. corporate profits persist, as do worries about a host of global macroeconomic setbacks. At the same time, our own bottom-up company checks suggest that domestic economic activity has been relatively resilient. U.S. housing and autos, for example, remain strong, and U.S. non-residential construction appears poised to accelerate. We think that North America has become the fastest growing oil and natural gas producing region of the world. According to the International Energy Agency, the shale-oil boom will help the U.S. overtake Saudi Arabia as the world’s largest oil producer by 2020, transforming not just energy supplies but also U.S. politics and diplomacy. We have been very enthusiastic about U.S. housing and non-residential related investments and least attracted to investments with significant European exposure. We also feel that fears about the Chinese economy are overdone, and we are beginning to identify companies that may benefit from improving economic prospects in that country.

Portfolio Review

The Fund’s outperformance was broad-based, as six of the economic sectors in which the Fund was invested contributed to excess returns. Stock selection within the Energy and Information Technology sectors provided the largest incremental benefit to performance results. Investments in the Health Care, Telecommunication Services, and Consumer Discretionary sectors were areas of relative weakness.

The Energy sector contributed to relative results. We continue to believe that refining stocks represent the best opportunities in the sector. West Coast refiner Tesoro Corp. was the Fund’s best absolute and relative performer during the year. The company’s balance sheet has improved dramatically since we bought the stock in 2011 and, given Tesoro’s tapering capital spending and stronger free cash flow, it is our opinion that the company will likely increase its dividend and redeploy cash through strategic acquisitions. We believe Tesoro’s earnings power should benefit significantly from the company’s acquisition of a California-based refining and marketing operation from oil giant BP PLC. The deal was executed at a very attractive price, considering all the assets it included, such as 800 dealer-operated retail sites, an extensive logistics system, and rights to the ARCO retail brand. The Fund’s other refining holding, Valero Energy Corp., also traded higher during the

Management's Discussion of Fund Performance (Unaudited) (Continued)

year. We think Valero has one of the best future earnings growth potentials among its peers given the company’s advantageous locations in the Gulf Coast region and a scheduled decrease in capital expenditures. Ensco PLC, a provider of offshore petroleum drilling services, also augmented relative returns. The company took advantage of offshore rig supply tightness to expand its contract pipeline, adding two years of backlog visibility. Ensco’s healthy balance sheet and ability to generate free cash flow should allow the company to double its quarterly dividend in the next 12-18 months.

Investments in the Information Technology sector outperformed broadly, generating relative gains. Salesforce.com Inc., a provider of enterprise cloud computing applications, rallied dramatically off its January 2012 lows and was one of the Fund’s best relative and absolute performers during the year. We sold the position on strength in late November, after the company reported third quarter earnings and revenues ahead of consensus expectations. NXP Semiconductors N.V., which manufactures high-performance mixed-signal semiconductors, also contributed meaningfully to relative returns. Similarly to Salesforce, the stock was sold from the Fund after advancing on the heels of a better-then-consensus quarterly earnings report. Alliance Data Systems Corp. was another relative performance driver within the sector. The company administers customer loyalty programs for consumer-based businesses, including many well-known brands such as J. Crew, Victoria’s Secret, and the Air Miles reward program in Canada. Alliance Data also provides transaction-based marketing services through its Epsilon segment. We believe the company is well positioned to benefit from a strengthening economy and improving consumer spending, as well as geographical expansion into less-penetrated markets such as Brazil.

The Materials sector contributed to excess returns. Solutia Inc. and Eastman Chemical Co. provided the bulk of the relative performance benefit. In late January, specialty chemicals producer Solutia announced it had entered into a definitive agreement under which it would be acquired by chemical manufacturer Eastman Chemical at a 42% premium to the company’s prevailing market price. The Fund held the Eastman position given the view that the company possesses good relative top line growth driven by product innovation, a secular shift towards greener packaging plastics, and a recovery in construction markets. In addition, cost synergies from the acquired Solutia business should help drive 8-10% profit growth annually from 2013-2015. Ecolab Inc., a provider of water, hygiene and energy technologies, also augmented relative performance. The stock traded sharply higher in mid-October after the company announced its intention to acquire privately-held specialty chemical company Champion Technologies. The position was sold and the proceeds were used to help fund new positions in chemical manufacturers FMC Corp. and Celanese Corp. We like FMC for its positioning in the crop chemicals category, as well as its exposure to growth in the food and beverage ingredients and lithium end markets. Celanese offers a diverse portfolio of businesses with a blend of stable and growth-oriented segments; additionally, we believe the company’s new ethanol opportunity could add to earnings significantly by 2015-2016.

The Financials sector added to relative results, helped by positive stock selection within consumer finance and regional banks. Discover Financial Services, a provider of credit card services, rose over 60% during the period and was sold at the end of the year, when it reached its internal price target. Commercial bank SunTrust Banks Inc., which was another strong relative performer, was also sold earlier in the year, based on concerns over the company’s mortgage servicing business. In addition to these two trades, three new buys were executed in the sector during the year, and the Fund’s Financials sector weight remains essentially in-line with the Index.

Despite a solid return in aggregate, the Fund’s Health Care sector holdings underperformed its Index’s peers. Investments within the health care equipment sub-industry caused much of the relative performance shortfall. Shares of Hologic Inc. plummeted in late April when the company, which manufactures diagnostics and surgical products, announced that it would acquire molecular diagnostic products manufacturer Genprobe.The announcement came at a time when investors were expecting the company to focus on its mammography launch and share repurchases. Despite the negative reaction to the deal, we view Genprobe as an attractive asset given the company’s growth profile, great products, and strong pipeline. After meeting with both the Hologic and Genprobe management

Management's Discussion of Fund Performance (Unaudited) (Continued)

teams, we felt comfortable in the strategic merits and accretion potential of the deal, as well as Hologic’s underlying fundamentals. We are also enthusiastic about Genprobe’s new product, a three-dimensional mammography system, which has shown reduced recall rates and improved detection. As more data are published, and if reimbursement is expanded, adoption should accelerate, improving investor sentiment and likely rerating the stock’s multiple.

The Telecommunication Services sector detracted from relative results, hurt entirely by the Fund’s investments within the wireless telecommunication services sub-industry. NII Holdings Inc., a provider of mobile communications for businesses in Latin America, reported first quarter earnings and revenues below consensus expectations and posted conservative forward guidance for 2012. Given deteriorating fundamental results and a toughening competitive landscape in Brazil, the stock was sold.

The Consumer Discretionary sector was also an area of relative weakness, detracting from excess returns. GNC Holdings Inc., a retailer of health and wellness products, traded off after announcing a secondary offering and comparable same store sales in the most recent fiscal quarter at 9.8%, which was below Wall Street expectations. The Fund continues to hold the shares, as we believe that mid-single digit category growth, new product innovation, and domestic and international store growth should lead to the stock’s price appreciation. Two underperforming positions within the sector, Lear Corp. and Coach Inc., were sold during the year. Lear, an automotive components supplier, was sold given the company’s European exposure and a limited organic growth profile. Coach, Inc., a producer of accessories and personal leather goods, was sold after we determined that increased competition with other designers such as Michael Kors may still be underestimated.

Outlook

Though we remain in a period of modest global growth, we are excited to have identified clear pockets of strength. U.S. housing and autos remain strong while emerging economies and U.S. non-residential construction appear poised to accelerate. Though we are confident in the outlook for many multi-year investment opportunities, the on-going issues related to the U.S. budget deficit as well as continued sovereign debt issues in Europe suggest that we must remain flexible and opportunistic in our approach. We are focused on building an “all weather” portfolio that is weighted toward the long-term themes that we find most compelling. We believe the Fund is well diversified and is positioned to benefit should the economy accelerate. We also believe many of the Fund’s core holdings, which emphasize solid business models, organic growth and return-of-capital stories, can outperform independent of overall global growth scenarios.

Management's Discussion of Fund Performance (Unaudited) (Continued)

Comparison of the Change in Value of a $10,000 Investment in the

Touchstone Mid Cap Growth Fund and the Russell Midcap® Growth Index

Performance information does not reflect fees that are paid by the separate accounts through which shares of the Fund are sold. Inclusion of those fees would reduce figures for all periods.

The Fund commenced operations on November 21, 1994.

Note to Chart

The Russell Midcap® Growth Index measures the performance of those Russell Midcap companies with higher price-to-book ratios and higher forecasted growth values.

Management's Discussion of Fund Performance (Unaudited)

Touchstone Third Avenue Value Fund

Sub-Advised by Third Avenue Management

Investment Philosophy

The Touchstone Third Avenue Value Fund primarily invests in common stocks of well-financed companies (meaning companies believed to have high quality assets and a relative absence of liabilities) at a discount to what the Fund’s sub-advisor, Third Avenue Management LLC (“TAM”), believes is their intrinsic value. Third Avenue analyzes companies from the bottom up, focusing on business fundamentals such as competent management teams and strong long-term growth prospects.

Fund Performance

The Touchstone Third Avenue Value Fund outperformed its benchmark, the Russell 3000® Value Index, for the 12-month period ended December 31, 2012. The Fund’s total return was 20.71 percent while the total return of the benchmark was 17.55 percent for the 12-month period ended December 31, 2012.

Market Environment

During the year, risk aversion was a priority for some investors, whose concerns over macro events led them to the perceived safety of government bonds and other investments designed to hedge risk. In a continued environment of excess liquidity and ultra-low interest rates, however, investors were rewarded for moving out the risk spectrum into stocks and other higher beta1 assets. Equity markets delivered strong returns worldwide and across market capitalizations even as they climbed a “wall of worry” about continued sovereign debt issues in Europe, a possible slowdown in Hong Kong and China and the “fiscal cliff ” of tax increases and spending cuts that rounded out the year in the United States. The Energy sector was particularly affected by historically low natural gas prices throughout the year, the effects of which have been felt throughout the energy industry, from exploration and production companies to refiners and utilities. Lower energy inputs have also aided manufacturing in America.

Portfolio Review

From the Financials sector, Wheelock & Co. was the Fund’s largest contributor to performance for the year. In June 2012, Wheelock & Company Ltd., announced that its subsidiary, The Wharf Ltd., made a $HK 5.1 billion capital infusion, consisting of common stock and a perpetual security convertible, into Greentown China Holdings Ltd. Founded in 1995, Greentown is a leading China homebuilder with a strong brand name and a 41 million square foot land bank. Through the transaction, Wharf and Greentown will become strategic partners in China, and Wharf will be represented on Greentown’s board. The opportunity was created by the softening of the residential property market over the last year and Greentown’s over-leveraged balance sheet, which we believe serves as a great example of what opportunities can be afforded to the Fund’s companies that maintain strong financial positions.

Another significant performance contributor from the Financials sector for the year was Investor AB, which saw shares climb. Investor AB recently announced the $4 billion sale of Gambro (Information Technology sector), a medical devices company specializing in dialysis machines, to Baxter International Inc. (Health Care sector). We believe the deal is strongly accretive to Investor AB’s net asset value (NAV) and, historically, this has been the type of resource conversion event that has typically driven value creation at the company. In the recent past, we believe Investor AB has benefited not only from improvement in macro events, which has been reflected in the valuations of its listed investments, but also from good performance from its private equity assets. The Fund continues to hold Investor AB as we believe it has ample opportunity for growth, in addition to its dividend income.

Management's Discussion of Fund Performance (Unaudited) (Continued)

The largest detractor to Fund performance for the year from the Energy sector was Pioneer Energy Services Corp. (formerly Pioneer Drilling). Despite the laggard stock performance, Pioneer has reported what we believe are encouraging financial results, including rising revenue from its growing fleet of drilling rigs. During the year, this position was added to the Fund on price weakness.

Throughout the year, appreciating securities were trimmed, such as Henderson Land Development Co., Ltd., Investor AB and Cheung Kong Holdings, Ltd. (all Financials sector). A dozen new positions were added, increasing exposure to the U.S. Financials sector (excluding investment banks) and to the U.S. Energy sector (oil and gas industry). In addition, a dozen securities were sold, some on appreciation, such as Wheelock & Co. Ltd., and others such as Skyline Corp. (Consumer Discretionary sector), and Electronics for Imaging Inc. (Information Technology sector), in order to devote capital to what we believe are better investment ideas.

Outlook

Considerable analytic effort has been spent on the Energy sector as, historically, low natural gas prices have led to mispricings in the industry. We have also paid particular attention to regional banks, such as Comerica Inc., which we believe are available at significant discounts to tangible book value. U.S. high technology companies like Applied Materials Inc., have also been of interest.

We are aware that, should residential housing prices fall in China and Hong Kong, the prices of the Fund’s Hong Kong holdings could be temporarily impacted. We believe that the Fund’s holdings from that region will not be fundamentally affected in the long run as they are well-financed, do not rely on the credit markets in order to function and have diversified revenue streams. Though the fiscal cliff issue in the U.S. was resolved before January 1, 2013, it was not entirely put to rest and we believe there could be another opportunity for policy missteps by the Federal Government in two to three months as the White House and Congress negotiate over a debt ceiling increase. A failure to rationally deal with the debt limit, as seen in the summer of 2011, could result in short-term market disruptions. We believe the Fund’s holdings are in strong financial condition and should ultimately weather such an event and may create buying opportunities for it, made possible given the Fund’s increased cash position.

The Fund maintains a concentrated portfolio of undervalued securities, diversified across regions and industries. We have enhanced our focus on balance sheet strength to help deal with volatility. We believe that, over the long-term, the Fund will generate positive absolute results versus its benchmark.

1Beta is a measure of the volatility of a portfolio relative to its benchmark.

Management's Discussion of Fund Performance (Unaudited) (Continued)

Comparison of the Change in Value of a $10,000 Investment in the

Touchstone Third Avenue Value Fund and the Russell 3000® Value Index

Performance information does not reflect fees that are paid by the separate accounts through which shares of the Fund are sold. Inclusion of those fees would reduce figures for all periods.

The Fund commenced operations on December 14, 1992.

Note to Chart

The Russell 3000® Value Index measures the performance for those Russell 3000® companies with lower price-to book ratios and lower forecasted growth values.

Management's Discussion of Fund Performance (Unaudited)

Touchstone ETF Funds

Sub-Advised by Todd-Veredus Asset Management LLC.

Touchstone Aggressive ETF Fund

Touchstone Conservative ETF Fund

Touchstone Enhanced ETF Fund

Touchstone Moderate ETF Fund

Investment Philosophy

Four Exchanged Traded Funds (ETFs) are available for investors seeking “lifestyle” products for their annuity holdings. The first three strategic options include: the Conservative, Moderate, and Aggressive ETF Funds. These funds allocate their assets among up to nine ETFs. These nine ETF selections, generally do not change dramatically over time, The more conservative funds have higher bond weightings, and the more aggressive funds have lower bond weightings. The fourth option, the Enhanced ETF Fund, employs tactical asset allocation in an effort to generate better returns.

Fund Performance

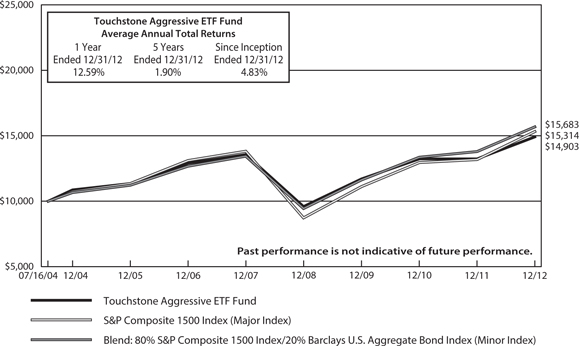

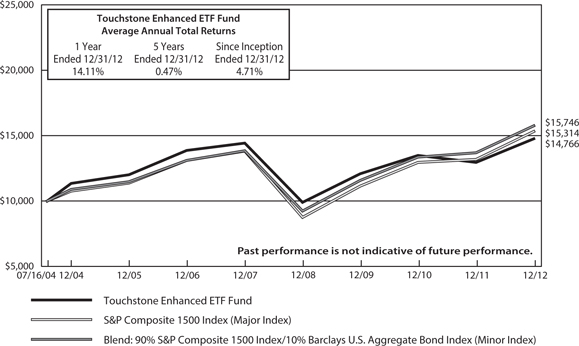

TheTouchstone Conservative ETF Fund’s total return was 6.74 percent for the 12-month period ended December 31, 2012. The Fund outperformed its benchmark. The total return of its benchmark, the Barclays U.S. Aggregate Bond Index, was 4.21 percent for the 12-month period ended December 31, 2012. The Touchstone Moderate ETF Fund’s total return was 9.94 percent for the 12-month period ended December 31, 2012, the Touchstone Aggressive ETF Fund’s total return was 12.59 percent for the 12-month period ended December 31, 2012, and the Touchstone Enhanced Fund’s total return was 14.11 percent for the 12-month period ended December 31, 2012. All three of these Funds underperformed their benchmark. The total return of the S&P Composite 1500 Index was 16.17% for the 12-month period ended December 31, 2012. The specific blended benchmark returns were 8.41 percent for the Conservative ETF Fund, 11.40 percent for the Moderate ETF Fund, 13.79 percent for the Aggressive ETF Fund and 14.98 percent for the Enhanced ETF Fund for the 12-month period ended December 31, 2012.

Market Environment

While markets were breathing a sigh of relief with the European Crisis abating, the market still did not feel positive about economic growth in most parts of the world. The U.S. was the steadiest economy last year, while Europe suffered a recession and most Emerging Markets saw a significant slowing. One of the byproducts of better U.S. economic growth was that companies with less foreign exposure tended to outperform.

Portfolio Review

The funds were rebalanced on May 1, 2012. In the rebalance, the allocation to bonds is always kept very close to the benchmark exposure for the strategic funds. The funds’ exposure to bonds was reduced during the May rebalancing to adjust for the higher exposure to bonds that had developed during the prior year when bonds outperformed other asset classes slightly higher. During this rebalance, the asset allocation model shifted its equity sector to tilt in favor of value stocks slightly more than growth stocks. It also shifted to lower the amount of international exposure the Funds had. The model retained a relative overweighting in the small and mid capitalization indexes. The Touchstone Enhanced ETF Fund moved to overweight the Large and Small Cap Value, International and Bond sectors in November.

Management's Discussion of Fund Performance (Unaudited) (Continued)

Most of the Touchstone ETF Funds are strategic, therefore they only change once per year. Since the Touchstone Enhanced ETF Fund is tactical, it changes twice per year. Its allocation was changed to favor Large and Small Cap Domestic Value, International Stocks and the Barclays Aggregate Bond index.

Outlook

The market’s internal characteristics act like an early stage bull recovering from a financial crisis. That is typically when low quality and beta1 outperform. Interestingly, the market economy is acting like it is in early stage recovery as well, with autos and housing leading. Perhaps this is an extended cycle like we used to get in the Greenspan era, and a more “normal” recovery can begin after a period of consumer deleveraging. We expect with some “normalcy” returning and the crisis atmosphere abating that our disciplines should return to favor this year. We are skeptical that the end of 2012 marks the end of the secular bear market for equities. We may still see some modest new highs in the S&P Index and Russell 1000® Index.

Political wrangling may have damaged consumer sentiment in the U.S. A higher payroll tax will probably dampen consumer demand in the first half of 2013. Also, U.S. capital spending has been restrained and may remain so if companies favor dividend increases over building productive capacity. Additionally, what was one event became a series of events. The Fiscal Cliff turned into the “Fill in the Blank” Cliffs. We passed the first hurdle with an extension to the tax cuts for people making less than $450,000. Now we face the Debt Ceiling debate, and potentially numerous other mini-cliffs regarding spending, entitlement cuts and the like. However, it looks like the economic expansion will continue, and international economies may be past the worst of their challenges.

The Funds with lower bond allocations and higher stock allocations should outperform those with larger bond holdings and lower stock holdings over the long term. Over shorter periods, when bonds outperform, the more conservative Funds will outperform and vice versa.

As noted above, the strategic funds continue to maintain bond weightings in a static stock/bond split in an effort to produce returns that are more predictable.

1Beta is a measure of the volatility of a portfolio relative to its benchmark.

Management's Discussion of Fund Performance (Unaudited) (Continued)

Comparison of the Change in Value of a $10,000 Investment in the

Touchstone Aggressive ETF Fund, the S&P Composite 1500 Index (Major Index)

and the Blend: 80% S&P Composite 1500 Index/20% Barclays U.S. Aggregate Bond Index

(Minor Index)

Performance information does not reflect fees that are paid by the separate accounts through which shares of the Fund are sold. Inclusion of those fees would reduce figures for all periods.

The Fund commenced operations on July 16, 2004.

Notes to Chart

S&P Composite 1500 Index is an unmanaged, broad market index representing the large-cap, mid-cap, and small-cap segments of the U.S. equity market.

The Barclays U.S. Aggregate Bond Index is an unmanaged index comprised of U.S. investment grade, fixed rate bond market securities, including government, government agency, corporate and mortgage-backed securities between one and ten years.

Management's Discussion of Fund Performance (Unaudited) (Continued)

Comparison of the Change in Value of a $10,000 Investment in the

Touchstone Conservative ETF Fund, the Barclays U.S. Aggregate Bond Index (Major Index)

and the Blend: 35% S&P Composite 1500 Index (Minor Index)/65% Barclays U.S. Aggregate

Bond Index

Performance information does not reflect fees that are paid by the separate accounts through which shares of the Fund are sold. Inclusion of those fees would reduce figures for all periods.

The Fund commenced operations on July 16, 2004.

Notes to Chart

The Barclays U.S. Aggregate Bond Index is an unmanaged index comprised of U.S. investment grade, fixed rate bond market securities, including government, government agency, corporate and mortgage-backed securities between one and ten years.

S&P Composite 1500 Index is an unmanaged, broad market index representing the large-cap, mid-cap, and small-cap segments of the U.S. equity market.

Management's Discussion of Fund Performance (Unaudited) (Continued)

Comparison of the Change in Value of a $10,000 Investment in the

Touchstone Enhanced ETF Fund, the S&P Composite 1500 Index (Major Index)

and the Blend: 90% S&P Composite 1500 Index/10% Barclays U.S. Aggregate Bond Index

(Minor Index)

Performance information does not reflect fees that are paid by the separate accounts through which shares of the Fund are sold. Inclusion of those fees would reduce figures for all periods.

The Fund commenced operations on July 16, 2004.

Notes to Chart

S&P Composite 1500 Index is an unmanaged, broad market index representing the large-cap, mid-cap, and small-cap segments of the U.S. equity market.

The Barclays U.S. Aggregate Bond Index is an unmanaged index comprised of U.S. investment grade, fixed rate bond market securities, including government, government agency, corporate and mortgage-backed securities between one and ten years.

Management's Discussion of Fund Performance (Unaudited) (Continued)

Comparison of the Change in Value of a $10,000 Investment in the

Touchstone Moderate ETF Fund, the S&P Composite 1500 Index (Major Index)

and the Blend: 60% S&P Composite 1500 Index/40% Barclays U.S. Aggregate Bond Index

(Minor Index)

Performance information does not reflect fees that are paid by the separate accounts through which shares of the Fund are sold. Inclusion of those fees would reduce figures for all periods.

The Fund commenced operations on July 16, 2004.

Notes to Chart

S&P Composite 1500 Index is an unmanaged, broad market index representing the large-cap, mid-cap, and small-cap segments of the U.S. equity market.

The Barclays U.S. Aggregate Bond Index is an unmanaged index comprised of U.S. investment grade, fixed rate bond market securities, including government, government agency, corporate and mortgage-backed securities between one and ten years.

Tabular Presentation of Portfolios of Investments (Unaudited)

December 31, 2012

The illustrations below provide each Fund’s credit quality and portfolio allocation. We hope it will be useful to shareholders as it summarizes key information about each Fund’s investments.

| Touchstone Baron Small Cap Growth Fund | | | |

| Sector Allocation* | | (% of Net Assets) | |

| Consumer Discretionary | | | 29.1 | % |

| Financials | | | 19.7 | |

| Industrials | | | 16.5 | |

| Information Technology | | | 12.1 | |

| Consumer Staples | | | 7.0 | |

| Health Care | | | 4.3 | |

| Utilities | | | 4.2 | |

| Energy | | | 4.1 | |

| Telecommunication Services | | | 1.8 | |

| Investment Funds | | | 10.5 | |

| Other Assets/Liabilities (Net) | | | (9.3 | ) |

| Total | | | 100.0 | % |

| Touchstone Core Bond Fund | | | |

| Credit Quality** | | (% of Investment Securities) | |

| AAA/Aaa | | | 66.2 | % |

| AA/Aa | | | 0.7 | |

| A | | | 11.9 | |

| BBB/Baa | | | 8.7 | |

| BB/Ba | | | 3.6 | |

| B | | | 4.6 | |

| CCC | | | 1.0 | |

| CC | | | 0.4 | |

| NR | | | 2.9 | |

| Total | | | 100.0 | % |

| Touchstone High Yield Fund | | | |

| Credit Quality** | | (% of Investment Securities) | |

| BB/Ba | | | 38.9 | % |

| B | | | 57.8 | |

| CCC/Caa | | | 1.0 | |

| NR | | | 2.3 | |

| Total | | | 100.0 | % |

| Touchstone Large Cap Core Equity Fund | | | |

| Sector Allocation* | | (% of Net Assets) | |

| Information Technology | | | 18.7 | % |

| Financials | | | 15.9 | |

| Health Care | | | 15.0 | |

| Industrials | | | 14.1 | |

| Energy | | | 11.5 | |

| Consumer Discretionary | | | 9.3 | |

| Consumer Staples | | | 7.3 | |

| Materials | | | 2.6 | |

| Telecommunication Services | | | 2.3 | |

| Utilities | | | 1.0 | |

| Investment Fund | | | 2.7 | |

| Other Assets/Liabilities (Net) | | | (0.4 | ) |

| Total | | | 100.0 | % |

Tabular Presentation of Portfolios of Investments (Unaudited) (Continued)

| Touchstone Mid Cap Growth Fund | | | |

| Sector Allocation* | | (% of Net Assets) | |

| Consumer Discretionary | | | 20.8 | % |

| Information Technology | | | 17.2 | |

| Health Care | | | 16.8 | |

| Energy | | | 11.7 | |

| Industrials | | | 10.8 | |

| Financials | | | 8.4 | |

| Materials | | | 6.1 | |

| Consumer Staples | | | 6.1 | |

| Telecommunication Services | | | 0.5 | |

| Investment Funds | | | 2.0 | |

| Other Assets/Liabilities (Net) | | | (0.4 | ) |

| Total | | | 100.0 | % |

| Touchstone Money Market Fund | | | |

| Credit Quality | | (% of Investment Securities) | |

| A-1/P-1/F-1 | | | 94.3 | % |

| FW1*** | | | 5.7 | |

| Total | | | 100.0 | % |

| Portfolio Allocation* | | (% of Net Assets) | |

| Variable Rate Demand Notes | | | 42.3 | % |

| Repurchase Agreement | | | 15.8 | |

| U.S. Government Agency Obligations | | | 14.2 | |

| Corporate Bonds | | | 14.1 | |

| Municipal Bonds | | | 11.5 | |

| Certificate of Deposit | | | 1.3 | |

| Other Assets/Liabiliaties (Net) | | | 0.8 | |

| Total | | | 100.0 | % |

| TouchStone Third Avenue Value Fund | | | |

| Sector Allocation* | | (% of Net Assets) | |

| Financials | | | 44.5 | % |

| Energy | | | 15.7 | |

| Consumer Discretionary | | | 8.7 | |

| Information Technology | | | 8.7 | |

| Materials | | | 5.9 | |

| Industrials | | | 3.3 | |

| Health Care | | | 2.0 | |

| Telecommunication Services | | | 1.5 | |

| Investment Funds | | | 12.0 | |

| Other Assets/Liabilities (Net) | | | (2.3 | ) |

| Total | | | 100.0 | % |

| Touchstone Aggressive ETF Fund | | | |

| Sector Allocation* | | (% of Net Assets) | |

| Exchange Traded Funds | | | 98.9 | % |

| Investment Funds | | | 4.3 | |

| Other Assets/Liabilities (Net) | | | (3.2 | ) |

| Total | | | 100.0 | % |

| Touchstone Conservative ETF Fund | | | |

| Sector Allocation* | | (% of Net Assets) | |

| Exchange Traded Funds | | | 98.7 | % |

| Investment Funds | | | 14.8 | |

| Other Assets/Liabilities (Net) | | | (13.5 | ) |

| Total | | | 100.0 | % |

| Touchstone Enhanced ETF Fund | | | |

| Sector Allocation* | | (% of Net Assets) | |

| Exchange Traded Funds | | | 98.4 | % |

| Investment Funds | | | 23.6 | |

| Other Assets/Liabilities (Net) | | | (22.0 | ) |

| Total | | | 100.0 | % |

| Touchstone Moderate ETF | | | |

| Sector Allocation* | | (% of Net Assets) | |

| Exchange Traded Funds | | | 98.7 | % |

| Investment Funds | | | 3.2 | |

| Other Assets/Liabilities (Net) | | | (1.9 | ) |

| Total | | | 100.0 | % |

| * | Sector Classifications are based upon the Global Industry Classification Standard (GICS®). |

| ** | Composite of Standard and Poor's, Moody's and Fitch ratings. |

| *** | Equivalent to Standard & Poor's and Moody's highest short-term ratings of A-1 and P-1, respectively, based upon independent research conducted by First Washington Advisors, Inc. |

NR - Not Rated

Portfolio of Investments

Touchstone Baron Small Cap Growth Fund – December 31, 2012

| | | | | | Market | |

| | | Shares | | | Value | |

| Common Stocks — 98.8% | | | | | | | | |

| | | | | | | | | |

| Consumer Discretionary — 29.1% | | | | | | | | |

| Ameristar Casinos, Inc. | | | 15,000 | | | $ | 393,600 | |

| Choice Hotels International, Inc. | | | 14,500 | | | | 487,490 | |

| DeVry, Inc.† | | | 9,000 | | | | 213,570 | |

| Dick's Sporting Goods, Inc. | | | 13,500 | | | | 614,115 | |

| Interval Leisure Group, Inc. | | | 10,000 | | | | 193,900 | |

| LKQ Corp.* | | | 31,000 | | | | 654,100 | |

| Lumber Liquidators Holdings, Inc.†* | | | 4,900 | | | | 258,867 | |

| Morningstar, Inc. | | | 2,000 | | | | 125,660 | |

| Panera Bread Co. - Class A* | | | 1,880 | | | | 298,600 | |

| Penn National Gaming, Inc.* | | | 9,885 | | | | 485,452 | |

| Ralph Lauren Corp. | | | 3,000 | | | | 449,760 | |

| Under Armour, Inc. - Class A* | | | 10,000 | | | | 485,300 | |

| Vail Resorts, Inc. | | | 11,500 | | | | 622,035 | |

| | | | | | | | 5,282,449 | |

| | | | | | | | | |

| Financials — 19.7% | | | | | | | | |

| Alexander's, Inc. REIT | | | 800 | | | | 264,640 | |

| Alexandria Real Estate Equities, Inc. REIT | | | 2,500 | | | | 173,300 | |

| Arch Capital Group Ltd.* | | | 25,000 | | | | 1,100,500 | |

| Carlyle Group LP (The)† | | | 8,200 | | | | 213,446 | |

| Cohen & Steers, Inc.† | | | 9,500 | | | | 289,465 | |

| Douglas Emmett, Inc. REIT | | | 16,000 | | | | 372,800 | |

| Eaton Vance Corp. | | | 8,000 | | | | 254,800 | |

| Financial Engines, Inc.* | | | 1,490 | | | | 41,348 | |

| LaSalle Hotel Properties REIT | | | 7,500 | | | | 190,425 | |

| Oaktree Capital Group LLC | | | 4,993 | | | | 227,132 | |

| Primerica, Inc. | | | 13,000 | | | | 390,130 | |

| Zillow, Inc. - Class A†* | | | 1,700 | | | | 47,175 | |

| | | | | | | | 3,565,161 | |

| | | | | | | | | |

| Industrials — 16.5% | | | | | | | | |

| Colfax Corp.* | | | 7,700 | | | | 310,695 | |

| Copart, Inc.* | | | 15,000 | | | | 442,500 | |

| Generac Holdings, Inc. | | | 15,000 | | | | 514,650 | |

| Genesee & Wyoming, Inc. - Class A* | | | 12,000 | | | | 912,960 | |

| Middleby Corp.* | | | 3,000 | | | | 384,630 | |

| Rexnord Corp.†* | | | 10,021 | | | | 213,447 | |

| Valmont Industries, Inc. | | | 1,500 | | | | 204,825 | |

| | | | | | | | 2,983,707 | |

| | | | | | | | | |

| Information Technology — 12.1% | | | | | | | | |