UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-08416

Touchstone Variable Series Trust

(Exact name of registrant as specified in charter)

303 Broadway, Suite 1100

Cincinnati, Ohio 45202-4203

(Address of principal executive offices) (Zip code)

Jill T. McGruder

303 Broadway, Suite 1100

Cincinnati, Ohio 45202-4203

(Name and address of agent for service)

Registrant's telephone number, including area code: 800-638-8194

Date of fiscal year end: December 31

Date of reporting period: December 31, 2016

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget ("OMB") control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

Item 1. Reports to Stockholders.

The Report to Shareholders is attached herewith.

December 31, 2016

Annual Report

Touchstone Variable Series Trust

Touchstone Active Bond Fund

Touchstone Focused Fund

Touchstone Large Cap Core Equity Fund

Touchstone Aggressive ETF Fund

Touchstone Conservative ETF Fund

Touchstone Moderate ETF Fund

Table of Contents

This report identifies the Funds' investments on December 31, 2016. These holdings are subject to change. Not all investments in each Fund performed the same, nor is there any guarantee that these investments will perform as well in the future. Market forecasts provided in this report may not occur.

Letter from the President

Dear Fellow Shareholder:

We are pleased to provide you with the Touchstone Variable Series Trust Annual Report. Inside you will find key financial information, as well as manager commentaries, for the 12 months ended December 31, 2016.

The fiscal year was eventful, featuring volatility in energy and commodity prices, the United Kingdom’s historic vote to leave the European Union and Donald Trump’s unexpected victory in the U.S. presidential election. The U.S. economy maintained steady but moderate growth. While overall growth in gross domestic product was restrained by continued weakness in business investment, strong gains in the labor market buoyed consumer confidence and spending. With the U.S. economy already on solid ground, expectations for growth have shifted higher as a result of the incoming administration’s proposed agenda of reduced regulations, tax cuts and fiscal stimulus. Outside of the U.S., however, the economic landscape was less positive. Growth in Europe and Japan remained anemic despite monetary policy intervention from central banks. Concern over a slowdown in China’s economy led to declines in commodity prices, weakness for emerging markets and increased volatility in capital markets during early 2016.

From their mid-February bottom to the end of the year, equity markets enjoyed broad gains. The surprise outcome of the U.S. presidential election fueled a late rally in equities and other risk assets, as investors priced in higher growth driven by the new administration’s plans to lower taxes and increase fiscal spending. Small capitalization stocks in particular benefited from renewed optimism, notching significant gains and outperforming their large capitalization peers.

After the U.S. Federal Reserve Board (Fed) raised interest rates in December 2015, it went on to make dovish statements in early 2016 surrounding the pace of future rate hikes. Given weak growth and continued quantitative easing in Europe and Japan, interest rates fell throughout the first half of 2016, eventually bottoming at historic lows in early July. Forecasts for a late year rate hike and improved economic data provided the impetus for a rebound in rates in the second half of 2016. Following the presidential election, the rise in bond yields accelerated in the fourth quarter amid expectations for higher economic growth and inflation. Consistent with the risk-on environment in 2016, corporate bonds outperformed Treasuries, with High Yield bonds generating especially strong gains during the period.

After a year of strong returns across many asset classes, we believe that now is a good time to evaluate your financial situation. While determining an appropriate risk/return profile and portfolio allocation is always difficult, the advice of a financial advisor can help illuminate the path to addressing your long-term investment goals.

We appreciate the opportunity you have given us and hope to remain part of your investment plan in the years to come.

Sincerely,

Jill T. McGruder

President

Touchstone Variable Series Trust

Management's Discussion of Fund Performance (Unaudited)

Touchstone Active Bond Fund

Sub-Advised by Fort Washington Investment Advisors, Inc.

Investment Philosophy

The Touchstone Active Bond Fund seeks to provide as high a level of current income as is consistent with the preservation of capital. Capital appreciation is a secondary goal. In deciding what securities to buy and sell for the Fund, the overall investment opportunities and risks in different sectors of the debt securities market are analyzed by focusing on maximizing total return and reducing volatility of the Fund’s portfolio. A disciplined sector allocation process is followed to build a broadly diversified portfolio of investments.

Fund Performance

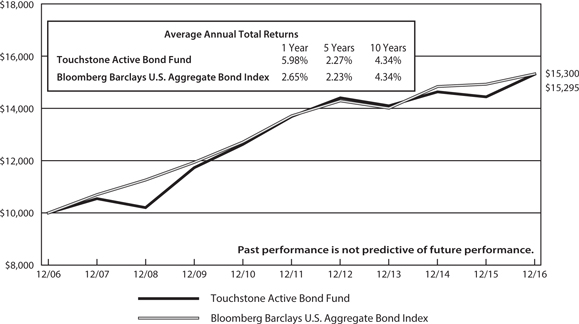

The Touchstone Active Bond Fund outperformed its benchmark the Bloomberg Barclays U.S. Aggregate Bond Index for the 12-month period ended December 31, 2016. The Fund’s total return was 5.98 percent, while the benchmark’s total return was 2.65 percent.

Market Environment

Risk markets performed well over the course of the 12-month period ended December 31, 2016, but the ride was not always a smooth one. Influential market events rattled markets throughout the year, but the resulting volatility proved temporary in each case. Risk assets started the period with weak returns, as the markets faced the possibility of a hard landing for the Chinese economy and a steep decline in oil prices during the first quarter. After oil prices bottomed and economic data allayed investor fears, credit spreads began to tighten and largely continued to do so through Britain’s vote to leave the European Union (Brexit) in June. Then came the unexpected results of the U.S. presidential election in November and the U.S. Federal Reserve Board’s (Fed) decision to raise interest rates in December. The election sparked a late rally in investor sentiment and risk assets, as the markets ended 2016 in a wave of optimism for the prospect of increased domestic growth in 2017.

The yield curve shifted higher during the year with all maturities along the curve rising, though year-over-year comparisons obscure two distinct market regimes during the course of 2016. Yields on the U.S. 10-year Treasury started the year above 2 percent, and then declined for the first half of the period in response to slower economic growth in China and concerns about the potential effects of Brexit. After bottoming at 1.36 percent in early July, interest rates reversed their course and trended higher through December, ending the year higher than they began due to steady underlying economic fundamentals and resilient consumer spending. Rates were also buoyed by renewed optimism surrounding the incoming administration’s stated agenda for tax reform, fiscal expansion and deregulation and its implications for higher economic growth.

Against this backdrop, bond markets were positive across all underlying sectors within the benchmark. Investment Grade and High Yield Bonds along with securitized assets (Mortgage-Backed Securities, Asset-Backed Securities and Commercial Mortgage-Backed Securities), outperformed U.S. Treasuries during the period.

Portfolio Review

The Fund outperformed during the 12-month period due to broad contributions from many areas of the Fund. The Fund’s allocation to High Yield Bonds and other non-U.S. Treasury sectors, positive security selection in Investment Grade Corporate Bonds and securitized assets, and active management of interest rate exposures all contributed positively to performance. The Fund maintained an overweight to the High Yield Bond sector, as the sub-advisor believed that sector offered appropriate compensation for its credit and liquidity risk. While the High Yield exposure was a significant contributor, the Fund’s positions in other non-Treasury sectors also benefited performance as risk premiums across the bond market contracted significantly during the period.

Management's Discussion of Fund Performance (Unaudited) (Continued)

As credit spreads widened significantly in late January and early February 2016, the sub-advisor added to the Fund’s credit risk exposure to reflect the increasingly attractive valuations being offered. In the sub-advisor’s view, there was a dislocation between valuations and their macroeconomic outlook, prompting the increase in exposure to risk assets. This positioning proved beneficial as spreads peaked in mid-February then began to contract for the remainder of 2016. While the Fund maintained a moderate risk position throughout the year given the sub-advisor’s positive macro outlook on U.S. economic growth and accommodative financial conditions, they did reduce the Fund’s overall risk as valuations gradually became richer in the second half of the year. This was accomplished primarily through a reduced exposure to High Yield Bonds.

In terms of interest rate risk and yield curve positioning, the Fund predominantly maintained a neutral duration relative to the benchmark for the period. However short-term tactical shifts, such as opportunistic investments in U.S. Treasury Inflation Protected Securities (TIPS), had a positive impact on Fund performance. As the risk for higher rates became increasingly more likely due to market optimism over improved economic growth, the portfolio adopted a slightly short bias versus the benchmark while making tactical moves to adjust the overall duration of the portfolio in response to short-term dislocations.

Outlook

The sub-advisor believes the greatest opportunities for the Fund come from continued outperformance of risk assets, which will likely be driven by U.S. economic growth, accommodative financial conditions and follow-through on the fiscal policy expectations built into asset prices. The attractiveness to credit exposure is now more a function of carry than the expectation that spreads will tighten further. Given financial conditions that remain relatively easy and with recession risk increasingly low, the sub-advisor continues to be comfortable having an overweight to credit risk. That said, valuations have generally adjusted to a more positive outlook, particularly within High Yield Bonds. As such, the sub-advisor has recently reduced spread risk in the Fund by decreasing exposure to the sector.

Execution risks related to the incoming administration’s agenda for fiscal expansion pose a risk as markets have, in general, already priced in the benefits of such policies. Going forward, the sub-advisor believes global central banks will need to maintain accommodative policies to support nascent recoveries abroad, particularly in Europe. Additionally, rate hikes by the Fed, of which the market has priced in at least two, will further tighten financial conditions as the year progresses.

The Fund’s positioning reflects the sub-advisor’s outlook that the balance of risk is to higher growth and interest rates, though near-term fundamentals need to remain solid and there needs to be tangible progress on fiscal policy to support a sustained upward shift in growth. Thus far, this expectation appears to be reasonable. Global factors will be watched closely for any broader impact which might influence the economic outlook. The sub-advisor expects higher volatility in the coming year, and will tactically adjust positioning in risk assets and rates in response to take advantage of short-term opportunities.

Management's Discussion of Fund Performance (Unaudited) (Continued)

Comparison of the Change in Value of a $10,000 Investment in the

Touchstone Active Bond Fund and the Bloomberg Barclays U.S. Aggregate Bond Index

Performance information does not reflect fees that are paid by the separate accounts through which shares of the Fund are sold. Inclusion of those fees would reduce figures for all periods.

The inception date of the Fund was January 1, 1999.

Note to Chart

The Bloomberg Barclays U.S. Aggregate Bond Index is an unmanaged index comprised of U.S. investment grade, fixed rate bond market securities, including government, government agency, corporate and mortgage-backed securities between one and ten years.

Management's Discussion of Fund Performance (Unaudited)

Touchstone Focused Fund

Sub-Advised by Fort Washington Investment Advisors, Inc.

Investment Philosophy

The Fund seeks to invest in companies of all capitalizations that are trading below what is believed to be the estimate of their intrinsic value and have a sustainable competitive advantage or a high barrier to entry in place. The barrier(s) to entry can be created through a cost advantage, economies of scale, high customer loyalty or a government barrier (e.g. license or subsidy). The sub-advisor believes that the strongest barrier to entry is the combination of economies of scale and high customer loyalty.

Fund Performance

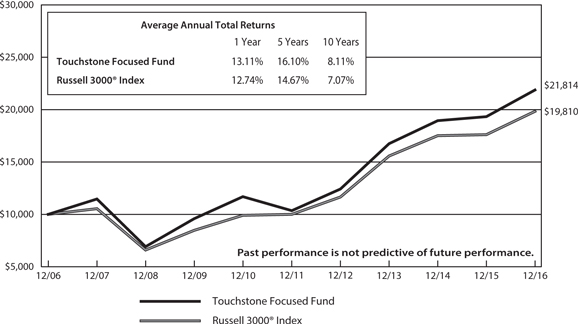

The Touchstone Focused Fund outperformed its benchmark, the Russell 3000® Index, for the 12-month period ended December 31, 2016. The Fund’s total return was 13.11 percent while the benchmark’s total return was 12.74 percent.

Market Environment

During 2016, U.S. equities continued the bull market that began in 2009 as the market finished the year at all-time highs. Investors shrugged off the sting of a positive vote in the UK to exit the European Union earlier in the year and enjoyed the stabilization of commodities throughout 2016. The market ended the year strong as investors cheered President-elect Donald Trump’s pro-growth agenda which also led to rising interest rates as inflationary expectations increased. The top-performing sectors within the Russell 3000® Index were Energy, Telecommunication Services, and Financials. Lagging the index the most were Health Care, Consumer Discretionary and Consumer Staples.

Portfolio Review

Outperformance was primarily attributable to stock selection. LinkedIn Corp. (Information Technology sector), Sysco Corp. (Consumer Staples sector) and Halliburton Co. (Energy sector) were among the top performing stocks during the past 12 months. LinkedIn was one of the top performing names in the Fund in 2016 as the company was acquired by Microsoft Corp. (Information Technology) at a significant premium. Despite numerous headwinds in its core food distribution business, Sysco surprised investors by increasing its outlook driven primarily by rising profit margins. Halliburton rebounded from a difficult 2015 as crude prices stabilized leading to the expectation of increased spending by its customers.

Novartis AG (Health Care sector), Stericycle Inc. (Industrials sector) and Abbott Laboratories (Health Care sector) were among the stocks that detracted from performance. Novartis lowered guidance in 2016 blaming additional investments needed to support its key heart failure drug along with continued weakness in its eye care segment. Shares in Stericycle underperformed after the company reported weaker than expected organic growth in its core industrial waste business. Abbott Labs declined as investors became concerned about the valuation it is paying for rival St. Jude Medical.

During the past 12 months, the Fund increased its weighting in Real Estate, Telecommunication Services, Consumer Discretionary, and Industrials. The Fund decreased its weighting in Materials, Consumer Staples, Health Care, and its cash position. From a market cap perspective the Fund currently has a zero weight in smaller cap stocks (companies with a market cap below $2 billion) and an underweight to mid-cap businesses compared to the benchmark. Throughout the year the Fund continued to increase its weight in larger cap businesses (companies with a market cap above $10 billion) to an overweight position relative to the benchmark.

Management's Discussion of Fund Performance (Unaudited) (Continued)

Outlook

U.S. equities, bond yields and the dollar have all surged since the November presidential election amid expectations that the new administration will pursue a pro-growth strategy. While there are valid reasons for expecting the economy to accelerate in the next year or two, there are also considerable risks that need to be weighed. They include the possibility the economy fails to meet high expectations, the prospect for outsized budget and trade deficits in the next few years, and the increased possibility of a trade war with China and a further weakening of the European Union.

Weighing these considerations, our outlook for the stock market is mixed. Stronger growth would lift corporate profits, which had stagnated until the second half of 2016. However, valuations are somewhat stretched. Rising interest rates and a strong dollar would be impediments. The clearer call, in the sub-advisor’s view, is that rotation away from Utility stocks and other high dividend-paying equities is likely to continue.

The sub-advisor continues to focus on buying and holding high quality businesses with solid returns on capital, strong balance sheets and sustainable barriers to entry.

Management's Discussion of Fund Performance (Unaudited) (Continued)

Comparison of the Change in Value of a $10,000 Investment in the

Touchstone Focused Fund and the Russell 3000® Index

Performance information does not reflect fees that are paid by the separate accounts through which shares of the Fund are sold. Inclusion of those fees would reduce figures for all periods.

The inception date of the Fund was November 21, 1994.

Note to Chart

Russell 3000® Index measures the performance of the 3,000 largest U.S. companies based on total market capitalization, which represents approximately 98% of the investable U.S. equity market.

The Frank Russell Company (FRC) is the source and owner of the Index data contained or reflected in this material and all trademarks and copyrights related thereto. The material may contain confidential information and unauthorized use, disclosure, copying, dissemination or redistribution is strictly prohibited. This is a Touchstone Investments presentation of the data, and FRC is not responsible for the formatting or configuration of this material or for any inaccuracy in the presentation thereof.

Management's Discussion of Fund Performance (Unaudited)

Touchstone Large Cap Core Equity Fund

Sub-Advised by London Company of Virginia, LLC d/b/a The London Company

Investment Philosophy

The Touchstone Large Cap Core Equity Fund seeks to provide investors with long-term capital growth by investing primarily in common stocks of large-cap U.S. listed companies. The sub-advisor, The London Company, uses a bottom-up security selection process that screens potential investments against a proprietary quantitative model for return on capital, earnings to value ratio, free cash flow and return on equity. Fund management seeks to purchase financially stable large-cap companies that it believes are consistently generating high returns of unleveraged operating capital, run by shareholder-oriented management and trading at a discount to the company’s respective private market values.

Fund Performance

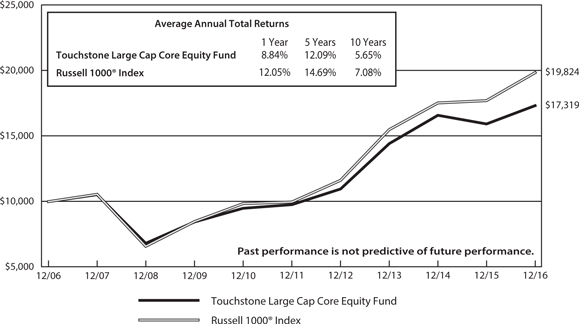

The Touchstone Large Cap Core Equity Fund underperformed its benchmark, the Russell 1000® Index, for the 12-month period ended December 31, 2016. The Fund’s total return was 8.84 percent, while the benchmark’s total return was 12.05 percent.

Market Environment

Market volatility was consistent during the trailing twelve months, with the overall market experiencing a strong rally in the second half of the year. Generally, the market rewarded more cyclical companies, value stocks, and those stocks with higher beta1 and smaller market capitalizations. At the beginning of the year, investors’ overriding concerns about a slowdown in China’s economy and commodity weakness contributed to one of the worst first quarter starts in history. Mid-year, growing apprehension about rising interest rates, Britain’s exit from the European Union (Brexit), and uncertainty related to the U.S. presidential election all led to increased short-term volatility. However, improved economic data and optimism surrounding potential reductions in corporate and individual taxes, greater infrastructure spending, less government oversight and repatriation of foreign earnings helped the market rally toward the end of the year. As expected, the U.S. Federal Reserve Board (Fed) increased interest rates by 0.25 percent in December 2016.

Portfolio Review

The Fund’s sector allocation contributed to performance while stock selection detracted during the period. From a sector perspective, the Fund’s overweight to the Financials sector and underweight to the Health Care sector positively impacted relative performance. This was partially offset by the negative impact of the Fund’s overweight to the Consumer Discretionary sector and an underweight to the Energy sector. Benchmark performance was led by the Energy, Telecommunication Services, and Financials sectors, while the Health Care and Real Estate sectors lagged.

Among the individual stocks that contributed to performance during the period were Deere & Co., General Dynamics Corp., Norfolk Southern Corp. (all from the Industrials sector), Alleghany Corp. (Financials sector) and Altria Group Inc. (Consumer Staples sector). Deere is a manufacturer of agricultural, construction and forestry machinery. The stock increased meaningfully, which was driven by the expectation of greater industrial growth in the economy as well as optimism that the agriculture cycle has neared the bottom. After years of weak demand for global farm equipment, the sub-advisor believes Deere is positioned well going forward. General Dynamics, an aerospace and defense company, outperformed, which reflected solid performance in the defense business and stabilization in the company’s subsidiary, Gulfstream Aerospace Corp. Following the presidential election, the outlook for defense spending improved and thus the sub-advisor believes General Dynamics is expected to be positioned well for growth going forward. The sub-advisor believes the company’s strong balance sheet should also limit significant downside. Transportation company Norfolk Southern rallied

Management's Discussion of Fund Performance (Unaudited) (Continued)

during the year as the macro environment showed signs of improvement and the company was able to effectively manage expenses through soft market conditions. The company has benefited from a solid balance sheet and the sub-advisor believes there is room for additional margin expansion via cost savings. Alleghany, an investment holding company, outperformed as a result of better than expected underwriting, strong investment income and improved profitability. The company also consistently grew its book value during the year, which benefited the stock. Long term, the sub-advisor believes the company should continue to increase its book value, thus driving the stock higher. Altria, a tobacco and cigarette company, posted solid financial results, including share gains and margin improvement. The company’s pricing power was evident in the consolidating tobacco industry and the company continued to return cash to shareholders via dividends and share repurchases.

Among the individual stocks that detracted from Fund performance were Eli Lilly and Co., Bristol-Myers Squibb Co. (both from the Health Care sector), Edgewell Personal Care Co. (Consumer Staples sector), Carnival Corp. and Dollar Tree Inc. (both from the Consumer Discretionary sector). Eli Lilly, a pharmaceutical company, moved lower following reports of a slightly weaker than expected fourth quarter and negative data surrounding one of its promising drugs for Alzheimer’s disease. The sub-advisor remains attracted to the company’s strong balance sheet, cash flow generation and favorable history of turning research and development spending into successful drugs. Edgewell Personal Care, a consumer products company, reported results that were better than expected in the fourth quarter but overriding concerns about the competitive industry environment negatively impacted the stock. Foreign exchange rates also detracted. The sub-advisor remains attracted to the company’s strong brands in large markets and its long-term potential for mergers and acquisitions (M&A) activity.

Bristol-Myers, a biopharmaceutical company, traded down during the year as it faced poor trial results in one of its flagship drugs OPDIVO®. Investors were optimistic about OPDIVO®, so the news came as a surprise. Bristol-Myers also faced pressure from negative pharmaceutical headlines throughout the year. However, the sub-advisor remains attracted to the company’s strong portfolio and pipeline. Cruise line operator Carnival was volatile all year. While the company reported solid results with improved bookings and onboard spending, performance was offset by investors’ concerns about weak global gross domestic product (GDP) growth and the potential for excess capacity in some markets. The sub-advisor believes pricing should improve over time as the industry has high barriers to entry. Dollar Tree, a discount variety store chain, was volatile during the year but ended relatively flat. Investors’ concerns surrounding weak same-store sales at the company’s acquired Family Dollar stores pressured the stock. Long term, the sub-advisor believes there is significant room for margin expansion at Family Dollar while the legacy Dollar Tree stores should continue to post industry-leading results.

During the period, the Fund sold its positions in ConocoPhillips (Energy sector), Pfizer Inc. (Health Care sector), EMC Corp., Microsoft Corp. and International Business Machines Corp. (all from Information Technology sector). The Fund trimmed positions in Bristol-Myers Squibb (Health Care sector), Altria Group (Consumer Staples sector), Visa Inc. (Information Technology sector), Lowe’s Companies Inc. (Consumer Discretionary sector), The Mosaic Co. (Materials sector) and Bank of America Corp. (Financials sector).

During the twelve-month period, the Fund initiated positions in General Electric Co. (Industrials sector), Progressive Corp. (Financials sector), NIKE Inc. (Consumer Discretionary sector) and Apple Inc. (Information Technology sector). General Electric is a technology-driven industrial and financial services company that develops and manufactures products for the generation, transmission, distribution, control and utilization of electricity. The sub-advisor believes the company’s plan to create a simple, more valuable business by dramatically reducing the size of its financial services businesses will result in an increase in profitability, accountability and shareholder value. Progressive specializes in insurance products primarily related to motor vehicles. Progressive’s strong brand and conservative underwriting philosophy gave the company a wide moat in the volatile insurance market. Progressive has consistently operated a low-cost structure business, giving the company the ability to generate strong returns in competitive markets. The company has also returned significant amounts of capital back to shareholders through its consistent dividend and share buyback programs. NIKE is a market share leader in

Management's Discussion of Fund Performance (Unaudited) (Continued)

the large and growing markets for sports apparel and shoes. The company’s competitive advantage stems from its leading brand and culture of innovation. This has led to pricing power and improving margins and returns. While the stock is not cheap, the sub-advisor believes downside is limited as a result of the company’s brand strength, business stability and solid balance sheet. Apple is a technology company that designs, develops and sells consumer electronics. Historically, the company has generated very high margins and returns on capital, which has been driven by Apple’s ability to integrate hardware, software and services into differentiated devices such as the iPhone. While the company’s strong track record of innovation is impressive, the key to the sub-advisor’s thesis is the limited downside from current levels.

Outlook

U.S. economic data showed marked improvement late in 2016, which helped drive stocks higher. In addition to a stronger economy, some investors are enthusiastic about a change in presidential leadership and the potential for lower corporate and individual taxes, less regulatory oversight, repatriation of foreign earnings and greater infrastructure spending. While the new administration may lead to an increase in GDP growth, it could detract from the U.S. budget. What president Donald Trump decides to pursue is still uncertain; however, it is clear that the U.S. economy has generated moderate growth with a relatively strong labor market. Further, the sub-advisor believes the U.S. consumer is in good shape, which bodes well for future spending. While interest rates may move higher over the next few months, the sub-advisor believes rates will remain low relative to history for some time, and low rates could be positive for equity market valuations.

Going forward, the sub-advisor believes company-specific fundamentals will drive the market and investors will reward companies that wisely deploy capital, repurchase shares at attractive prices and engage in M&A activity. Further, the sub-advisor believes the Fund’s downside risk can be mitigated by the Fund’s focus on those companies with pricing power, copious cash generation and prudent capital allocation. The sub-advisor seeks companies with strong returns on capital and flexibility to enhance shareholder value using the balance sheet. Low interest rates and relatively high equity risk premiums can also enable companies to increase shareholder value by adjusting the capital structure of the company. Looking ahead, the sub-advisor believes the Fund is positioned well for a slow growth environment that rewards strong capital allocation.

| 1 | Beta is a measure of the volatility of a portfolio relative to its benchmark. |

Management's Discussion of Fund Performance (Unaudited) (Continued)

Comparison of the Change in Value of a $10,000 Investment in the

Touchstone Large Cap Core Equity Fund and the Russell 1000® Index

Performance information does not reflect fees that are paid by the separate accounts through which shares of the Fund are sold. Inclusion of those fees would reduce figures for all periods.

The inception date of the Fund was May 1, 1999.

Note to Chart

Russell 1000® Index measures the performance of the 1,000 largest companies in the Russell 3000® Index.

The Frank Russell Company (FRC) is the source and owner of the Index data contained or reflected in this material and all trademarks and copyrights related thereto. The material may contain confidential information and unauthorized use, disclosure, copying, dissemination or redistribution is strictly prohibited. This is a Touchstone Investments presentation of the data, and FRC is not responsible for the formatting or configuration of this material or for any inaccuracy in the presentation thereof.

Management's Discussion of Fund Performance (Unaudited)

Touchstone ETF Funds

Sub-Advised by Wilshire Associates Incorporated

Touchstone Aggressive ETF Fund

Touchstone Conservative ETF Fund

Touchstone Moderate ETF Fund

Effective April 30, 2016, Wilshire Associates Incorporated (“Wilshire”) was appointed as sub-advisor to the Touchstone Aggressive ETF Fund, the Touchstone Conservative ETF Fund and the Touchstone Moderate ETF Fund. Concurrent with this change, the Funds’ Principal Investment Strategies, Principal Risks and benchmark index have changed to reflect those of Wilshire’s strategy. Todd Asset Management LLC was sub-advisor to the Funds from January 1, 2016 to April 29, 2016.

Investment Philosophy

Three funds which invest in Exchanged Traded Funds (ETFs) are available for investors seeking “lifestyle” products for their annuity holdings. The three strategic options include: the Conservative, Moderate, and Aggressive ETF Funds. These funds allocate their assets among up to ten ETFs. These ten ETF selections generally do not change dramatically over time. The more conservative fund has a higher bond weighting and the more aggressive fund has a lower bond weighting.

Fund Performance

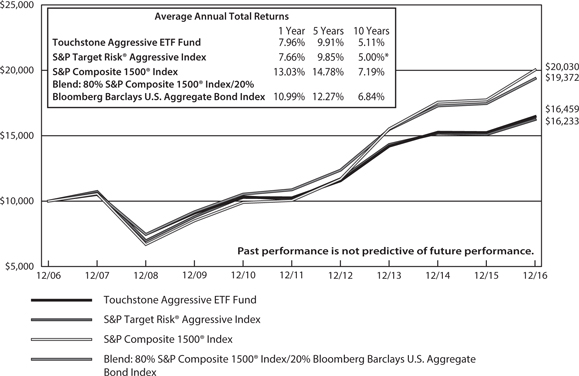

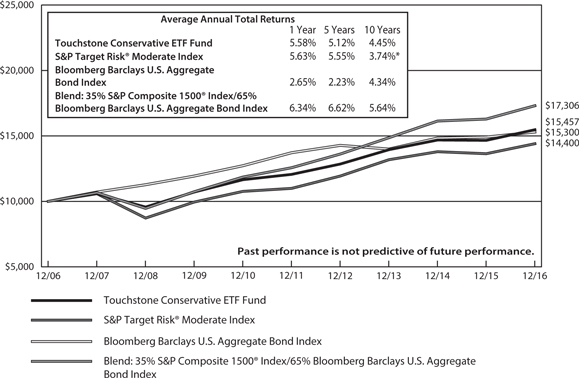

The Touchstone Aggressive ETF Fund outperformed its benchmark, the S&P Target Risk® Aggressive Index, for the 12-month period ended December 31, 2016. The Fund’s total return was 7.96 percent while the total return of the benchmark was 7.66 percent. The Touchstone Conservative ETF Fund underperformed its benchmark, the S&P Target Risk® Moderate Index, for the 12-month period ended December 31, 2016. The Fund’s total return was 5.58 percent while the total return of the benchmark was 5.63 percent. The Touchstone Moderate ETF Fund outperformed its benchmark , the S&P Target Risk® Growth Index, for the 12-month period ended December 31, 2016. The Fund’s total return was 6.85 percent while the total return of the benchmark was 6.67 percent.

Market Environment

The broad U.S. stock market posted strong gains for 2016. Nearly all sectors were positive during the year. The best performing sector was Energy, followed by Telecommunication Services and Financials. The main laggard was the Health Care sector. During the calendar year, large-cap stocks underperformed their small-cap counterparts and growth stocks trailed value stocks in both the large- and small-cap spaces. Outside the U.S., developed and emerging equity markets were in positive territory for 2016. During the fourth quarter, however, foreign markets softened as results of the U.S. election led to investor fears of weakening prospects for global trade and diminishing exports from emerging market countries. Higher U.S. interest rates and a stronger dollar also hurt returns in the fourth quarter.

After falling for much of the first half of 2016, U.S. Treasury yields reversed course and moved higher for the remainder of the year. The bellwether 10-year Treasury yield finished 2015 at 2.27 percent, reached a historic low of 1.37 percent in early July before climbing to end 2016 at 2.45 percent, accelerating its rise after the November election. At its December meeting, the U.S. Federal Reserve Board decided to increase its overnight rate by 0.25 percent, for only the second time since 2008.

Real estate securities were up for the year, both in the U.S. and globally. Commodities were up for the year as crude oil rose from $37.87 per barrel to $53.72 per barrel. Natural gas prices were up with a gain of 63 percent,

Management's Discussion of Fund Performance (Unaudited) (Continued)

ending the year at $3.72 per million BTUs. MLP (Master Limited Partnership) returns were positive as the sector benefited from an agreement by oil producers that is aimed at balancing supply and demand. Gold prices rose and fell throughout 2016, but finished with a return of 8.59 percent for the year.

Portfolio Review

The Touchstone Conservative ETF Fund underperformed its benchmark during 2016, while the Touchstone Moderate ETF and Touchstone Aggressive ETF outperformed their benchmarks. The Funds’ investments are determined by an optimization process that considers the long-term historical risk and return profiles of various asset classes. For instance, non-U.S. equities have been included due to the diversification benefits they provided to the Funds as a whole. During the 2016 market environment, when non-U.S. equities underperformed U.S. stocks, the underweight positioning in the ETFs relative to their respective benchmarks contributed to relative performance. Similarly, the overweight of the Touchstone Aggressive ETF and the Touchstone Conservative ETF to mid- and small-cap stocks within their U.S. equity allocations was advantageous to relative returns.

The ETF Funds have slowly migrated towards a more conservative positioning based upon the sub-advisor’s rising concern that equity markets may suffer from investor and economic uncertainty. The sub-advisor believes the changes made increased portfolio diversification, reduced equity market risk and reduced the exposure to foreign equities. Within fixed income, the Funds have moved to increase positioning in investment grade fixed income versus lower quality credit based on rising global risk. Credit, however, continues to offer attractive spreads relative to investment grade fixed income so the sub-advisor does not yet believe it would be prudent to materially underweight credit.

Outlook

The sub-advisor believes there is little concern of a recession in the near term across most of the world’s major economies. Coupled with generally accommodative central banks, the sub-advisor believes this provides comfort that most asset classes are likely to avoid a short-term decline. Although the sub-advisor has modestly reduced risk relative to long-term targets, the sub-advisor is seeking to remain invested in risk assets. The sub-advisor believes the opportunities are more attractive in lower beta1, less economically sensitive equities. The sub-advisor also finds investments with a strong carry to be attractive, since the carry provides income without relying solely on capital appreciation to generate returns.

| 1 | Beta is a measure of the volatility of a portfolio relative to its benchmark. |

Management's Discussion of Fund Performance (Unaudited) (Continued)

Comparison of the Change in Value of a $10,000 Investment in the

Touchstone Aggressive ETF Fund, the S&P Target Risk® Aggressive Index, the S&P Composite

1500® Index and the Blend: 80% S&P Composite 1500® Index/20% Bloomberg Barclays U.S.

Aggregate Bond Index

*The launch date of the S&P Target Risk® Aggressive Index was September 25, 2008. All information for the index prior to its launch date is back-tested, based on the methodology that was in effect on the launch date. Back-tested performance, which is hypothetical and not actual performance, is subject to inherent limitations because it reflects application of an Index methodology and selection of index constituents in hindsight. No theoretical approach can take into account all of the factors in the markets in general and the impact of decisions that might have been made during the actual operation of an index. Actual returns may differ from, and be lower than, back-tested returns.

Performance information does not reflect fees that are paid by the separate accounts through which shares of the Fund are sold. Inclusion of those fees would reduce figures for all periods.

The inception date of the Fund was July 16, 2004.

Notes to Chart

The S&P Target Risk® Aggressive Index is one of four multi-asset class indices that compose the S&P Target Risk Series. The S&P Target Risk® Aggressive Index emphasizes exposure to equities, maximizing opportunities for long-term capital accumulation. It may include small allocations to fixed income to enhance portfolio efficiency.

S&P Composite 1500® Index is an unmanaged, broad market index representing the large-cap, mid-cap, and small-cap segments of the U.S. equity market.

The Bloomberg Barclays U.S. Aggregate Bond Index is an unmanaged index comprised of U.S. investment grade, fixed rate bond market securities, including government, government agency, corporate and mortgage-backed securities between one and ten years.

Management's Discussion of Fund Performance (Unaudited) (Continued)

Comparison of the Change in Value of a $10,000 Investment in the

Touchstone Conservative ETF Fund, the S&P Target Risk® Moderate Index, the Bloomberg

Barclays U.S. Aggregate Bond Index and the Blend: 35% S&P Composite 1500® Index /65%

Bloomberg Barclays U.S. Aggregate Bond Index

*The launch date of the S&P Target Risk® Moderate Index was September 25, 2008. All information for the index prior to its launch date is back-tested, based on the methodology that was in effect on the launch date. Back-tested performance, which is hypothetical and not actual performance, is subject to inherent limitations because it reflects application of an Index methodology and selection of index constituents in hindsight. No theoretical approach can take into account all of the factors in the markets in general and the impact of decisions that might have been made during the actual operation of an index. Actual returns may differ from, and be lower than, back-tested returns.

Performance information does not reflect fees that are paid by the separate accounts through which shares of the Fund are sold. Inclusion of those fees would reduce figures for all periods.

The inception date of the Fund was July 16, 2004.

Notes to Chart

The S&P Target Risk® Moderate Index is one of four multi-asset class indices that compose the S&P Target Risk Series. The S&P Target Risk® Moderate Index offers significant exposure to fixed income, while also increasing opportunities for higher returns through equities.

The Bloomberg Barclays U.S. Aggregate Bond Index is an unmanaged index comprised of U.S. investment grade, fixed rate bond market securities, including government, government agency, corporate and mortgage-backed securities between one and ten years.

S&P Composite 1500® Index is an unmanaged, broad market index representing the large-cap, mid-cap, and small-cap segments of the U.S. equity market.

Management's Discussion of Fund Performance (Unaudited) (Continued)

Comparison of the Change in Value of a $10,000 Investment in the

Touchstone Moderate ETF Fund, the S&P Target Risk® Growth Index, the S&P Composite

1500® Index and the Blend: 60% S&P Composite 1500® Index/40% Bloomberg Barclays U.S.

Aggregate Bond Index

*The launch date of the S&P Target Risk® Growth Index was September 25, 2008. All information for the index prior to its launch date is back-tested, based on the methodology that was in effect on the launch date. Back-tested performance, which is hypothetical and not actual performance, is subject to inherent limitations because it reflects application of an Index methodology and selection of index constituents in hindsight. No theoretical approach can take into account all of the factors in the markets in general and the impact of decisions that might have been made during the actual operation of an index. Actual returns may differ from, and be lower than, back-tested returns.

Performance information does not reflect fees that are paid by the separate accounts through which shares of the Fund are sold. Inclusion of those fees would reduce figures for all periods.

The inception date of the Fund was July 16, 2004.

Notes to Chart

The S&P Target Risk® Growth Index is one of four multi-asset class indices that compose the S&P Target Risk Series. The S&P Target Risk® Growth Index increases exposure to equities, while also providing limited fixed income exposure to diversify risk.

S&P Composite 1500® Index is an unmanaged, broad market index representing the large-cap, mid-cap, and small-cap segments of the U.S. equity market.

The Bloomberg Barclays U.S. Aggregate Bond Index is an unmanaged index comprised of U.S. investment grade, fixed rate bond market securities, including government, government agency, corporate and mortgage-backed securities between one and ten years.

Tabular Presentation of Portfolios of Investments (Unaudited)

December 31, 2016

The illustrations below provide each Fund’s credit quality or sector allocation. We hope it will be useful to shareholders as it summarizes key information about each Fund’s investments.

| Touchstone Active Bond Fund | | | |

| Credit Quality* | | (% of Investment Securities) | |

| AAA/Aaa | | | 43.7 | % |

| AA/Aa | | | 2.1 | |

| A/A | | | 7.5 | |

| BBB/Baa | | | 24.7 | |

| BB/Ba | | | 12.0 | |

| B/B | | | 4.7 | |

| CCC | | | 1.2 | |

| Not Rated | | | 1.8 | |

| Cash Equivalents | | | 2.3 | |

| Total | | | 100.0 | % |

| | | | | |

| Touchstone Focused Fund | | | |

| Sector Allocation** | | | (% of Net Assets) | |

| Information Technology | | | 19.2 | % |

| Financials | | | 15.1 | |

| Health Care | | | 14.2 | |

| Consumer Discretionary | | | 13.7 | |

| Industrials | | | 10.8 | |

| Energy | | | 7.6 | |

| Consumer Staples | | | 7.2 | |

| Real Estate | | | 3.5 | |

| Telecommunication Services | | | 2.6 | |

| Materials | | | 2.4 | |

| Investment Fund | | | 3.9 | |

| Other Assets/Liabilities (Net) | | | (0.2 | ) |

| Total | | | 100.0 | % |

| | | | | |

| Touchstone Large Cap Core Equity Fund | | | |

| Sector Allocation** | | (% of Net Assets) | |

| Financials | | | 24.4 | % |

| Consumer Discretionary | | | 21.9 | |

| Industrials | | | 16.1 | |

| Information Technology | | | 10.5 | |

| Consumer Staples | | | 10.5 | |

| Health Care | | | 6.1 | |

| Materials | | | 4.9 | |

| Energy | | | 2.7 | |

| Telecommunication Services | | | 2.0 | |

| Investment Fund | | | 1.0 | |

| Other Assets/Liabilities (Net) | | | (0.1 | ) |

| Total | | | 100.0 | % |

| | | | | |

| Touchstone Aggressive ETF Fund | | | |

| Sector Allocation | | | (% of Net Assets) | |

| Exchange Traded Funds | | | | |

| Equity Funds | | | 74.9 | % |

| Fixed Income Funds | | | 22.4 | |

| Investment Fund | | | 2.9 | |

| Other Assets/Liabilities (Net) | | | (0.2 | ) |

| Total | | | 100.0 | % |

| | | | | |

| * | Credit quality ratings are from Standard & Poor's (“S&P”) and Moody's Investors Service (“Moody's”). If agency ratings differ, the higher rating will be used. Where no rating has been assigned, it may be for reasons unrelated to the creditworthiness of the issuer. |

| ** | Sector Classifications are based upon the Global Industry Classification Standard (GICS®). |

Tabular Presentation of Portfolios of Investments (Unaudited) (Continued)

| Touchstone Conservative ETF | | | |

| Sector Allocation | | | (% of Net Assets) | |

| Exchange Traded Funds | | | | |

| Fixed Income Funds | | | 60.9 | % |

| Equity Funds | | | 36.9 | |

| Investment Fund | | | 2.6 | |

| Other Assets/Liabilities (Net) | | | (0.4 | ) |

| Total | | | 100.0 | % |

| | | | | |

| Touchstone Moderate ETF | | | |

| Sector Allocation | | | (% of Net Assets) | |

| Exchange Traded Funds | | | | |

| Equity Funds | | | 55.9 | % |

| Fixed Income Funds | | | 41.4 | |

| Investment Fund | | | 3.0 | |

| Other Assets/Liabilities (Net) | | | (0.3 | ) |

| Total | | | 100.0 | % |

| | | | | |

Portfolio of Investments

Touchstone Active Bond Fund – December 31, 2016

| Principal | | | | | Market | |

| Amount | | | | | Value | |

| | | | | | | |

| | | | | Corporate Bonds — 48.7% | | | | |

| | | | | | | | | |

| | | | | Financials — 10.3% | | | | |

| $ | 22,000 | | | Aircastle Ltd. (Bermuda), | | | | |

| | | | | 5.500%, 2/15/22 | | $ | 23,320 | |

| | 134,000 | | | Ally Financial, Inc., 8.000%, 11/1/31 | | | 155,105 | |

| | 344,000 | | | Bank of America Corp., 6.100%(A)(B) | | | 345,892 | |

| | 245,000 | | | Bank of America Corp. MTN, | | | | |

| | | | | 4.000%, 1/22/25 | | | 245,308 | |

| | 200,000 | | | Barclays PLC (United Kingdom), | | | | |

| | | | | 3.250%, 1/12/21 | | | 200,195 | |

| | 265,000 | | | Capital One NA, 1.650%, 2/5/18 | | | 264,485 | |

| | 164,000 | | | Chubb INA Holdings, Inc., | | | | |

| | | | | 4.350%, 11/3/45 | | | 173,234 | |

| | 98,000 | | | CIT Group, Inc., 5.000%, 8/15/22 | | | 102,165 | |

| | 320,000 | | | Citigroup, Inc., 2.361%, 9/1/23(A) | | | 326,363 | |

| | 125,000 | | | Citigroup, Inc., 3.300%, 4/27/25 | | | 122,465 | |

| | 86,000 | | | Citigroup, Inc., 6.125%(A)(B) | | | 89,010 | |

| | 17,000 | | | Credit Acceptance Corp., | | | | |

| | | | | 6.125%, 2/15/21 | | | 17,170 | |

| | 27,000 | | | Credit Acceptance Corp., | | | | |

| | | | | 7.375%, 3/15/23 | | | 27,742 | |

| | 250,000 | | | Credit Suisse Group Funding Guernsey Ltd. (Guernsey), | | | | |

| | | | | 2.750%, 3/26/20 | | | 247,830 | |

| | 175,000 | | | Fifth Third Bancorp, 2.875%, 7/27/20 | | | 176,925 | |

| | 79,000 | | | FirstCash, Inc., 6.750%, 4/1/21 | | | 81,568 | |

| | 130,000 | | | General Electric Co. MTN, | | | | |

| | | | | 4.650%, 10/17/21 | | | 142,602 | |

| | 223,000 | | | General Motors Financial Co., Inc., | | | | |

| | | | | 3.200%, 7/13/20 | | | 223,671 | |

| | 7,000 | | | General Motors Financial Co., Inc., | | | | |

| | | | | 4.250%, 5/15/23 | | | 7,084 | |

| | 115,000 | | | Goldman Sachs Group, Inc. (The), | | | | |

| | | | | 5.250%, 7/27/21 | | | 126,039 | |

| | 86,000 | | | Goldman Sachs Group, Inc. (The), | | | | |

| | | | | 5.375%(A)(B) | | | 86,860 | |

| | 300,000 | | | Goldman Sachs Group, Inc. (The), | | | | |

| | | | | 5.700%(A)(B) | | | 307,440 | |

| | 200,000 | | | HSBC Holdings PLC (United Kingdom), | | | | |

| | | | | 2.499%, 1/5/22(A) | | | 203,727 | |

| | 250,000 | | | Huntington National Bank (The), | | | | |

| | | | | 2.200%, 11/6/18 | | | 250,708 | |

| | 105,000 | | | International Lease Finance Corp., | | | | |

| | | | | 5.875%, 8/15/22 | | | 113,925 | |

| | 145,000 | | | JPMorgan Chase & Co., | | | | |

| | | | | 3.250%, 9/23/22 | | | 146,637 | |

| | 300,000 | | | JPMorgan Chase & Co., 5.150%(A)(B) | | | 286,920 | |

| | 48,000 | | | JPMorgan Chase & Co., 5.300%(A)(B) | | | 48,987 | |

| | 60,000 | | | MetLife, Inc., 5.250%(A)(B) | | | 60,750 | |

| | 80,000 | | | Morgan Stanley, 3.950%, 4/23/27 | | | 79,193 | |

| | 24,000 | | | Navient Corp., 5.000%, 10/26/20 | | | 24,480 | |

| | 19,000 | | | Navient Corp., 5.875%, 10/25/24 | | | 18,050 | |

| | 79,000 | | | Navient Corp. MTN, 6.125%, 3/25/24 | | | 76,729 | |

| | 44,000 | | | OneMain Financial Holdings LLC, 144a, 7.250%, 12/15/21 | | | 45,870 | |

| | 160,000 | | | PNC Bank NA, 2.700%, 11/1/22 | | | 157,507 | |

| | 165,000 | | | Prudential Financial, Inc., | | | | |

| | | | | 5.625%, 6/15/43(A) | | | 171,394 | |

| 43,000 | | | Quicken Loans, Inc., 144a, | | | | |

| | | | | 5.750%, 5/1/25 | | | 41,818 | |

| | 130,000 | | | Teachers Insurance & Annuity Association of America, 144a, | | | | |

| | | | | 6.850%, 12/16/39 | | | 168,704 | |

| | 275,000 | | | Wells Fargo & Co., 5.900%(A)(B) | | | 276,375 | |

| | | | | | | | 5,664,247 | |

| | | | | | | | | |

| | | | | Consumer Discretionary — 9.0% | | | | |

| | 16,000 | | | ACCO Brands Corp., 144a, | | | | |

| | | | | 5.250%, 12/15/24 | | | 16,110 | |

| | 64,000 | | | Albea Beauty Holdings SA (Luxembourg), 144a, | | | | |

| | | | | 8.375%, 11/1/19 | | | 66,560 | |

| | 36,000 | | | Allegion US Holding Co., Inc., | | | | |

| | | | | 5.750%, 10/1/21 | | | 37,620 | |

| | 10,000 | | | AMC Entertainment Holdings, Inc., | | | | |

| | | | | 5.750%, 6/15/25 | | | 10,225 | |

| | 29,000 | | | AMC Entertainment Holdings, Inc., 144a, 5.875%, 11/15/26 | | | 29,652 | |

| | 13,000 | | | AMC Networks, Inc., 4.750%, 12/15/22 | | | 13,081 | |

| | 9,000 | | | American Builders & Contractors Supply Co., Inc., 144a, | | | | |

| | | | | 5.750%, 12/15/23 | | | 9,270 | |

| | 146,000 | | | Anheuser-Busch InBev Finance, Inc., | | | | |

| | | | | 4.900%, 2/1/46 | | | 157,807 | |

| | 230,000 | | | AutoNation, Inc., 5.500%, 2/1/20 | | | 247,173 | |

| | 36,000 | | | Belo Corp., 7.250%, 9/15/27 | | | 38,070 | |

| | 47,000 | | | Brinker International, Inc., 144a, | | | | |

| | | | | 5.000%, 10/1/24 | | | 46,882 | |

| | 28,000 | | | Brookfield Residential Properties, Inc. / Brookfield Residential US Corp. (Canada), 144a, 6.125%, 7/1/22 | | | 28,140 | |

| | 21,000 | | | Cable One, Inc., 144a, 5.750%, 6/15/22 | | | 21,630 | |

| | 104,000 | | | Cablevision Systems Corp., | | | | |

| | | | | 5.875%, 9/15/22 | | | 101,400 | |

| | 28,000 | | | CalAtlantic Group, Inc., | | | | |

| | | | | 5.375%, 10/1/22 | | | 28,560 | |

| | 5,000 | | | Cardtronics, Inc., 5.125%, 8/1/22 | | | 5,038 | |

| | 215,000 | | | CBS Corp., 4.900%, 8/15/44 | | | 215,214 | |

| | 59,000 | | | CCO Holdings LLC / CCO Holdings Capital Corp., 144a, 5.375%, 5/1/25 | | | 60,770 | |

| | 142,000 | | | CCO Holdings LLC / CCO Holdings Capital Corp., 144a, 5.750%, 2/15/26 | | | 146,970 | |

| | 46,000 | | | Cequel Communications Holdings I LLC / Cequel Capital Corp., 144a, | | | | |

| | | | | 6.375%, 9/15/20 | | | 47,380 | |

| | 52,000 | | | Cogeco Communications, Inc. (Canada), 144a, 4.875%, 5/1/20 | | | 53,495 | |

| | 210,000 | | | Delphi Automotive PLC (Jersey), | | | | |

| | | | | 3.150%, 11/19/20 | | | 213,362 | |

| | 86,000 | | | DISH DBS Corp., 5.875%, 7/15/22 | | | 90,515 | |

| | 35,000 | | | DISH DBS Corp., 7.875%, 9/1/19 | | | 38,850 | |

| | 182,000 | | | Dollar General Corp., 3.250%, 4/15/23 | | | 179,602 | |

| | 24,000 | | | Dollar Tree, Inc., 5.750%, 3/1/23 | | | 25,412 | |

| | 80,000 | | | Ford Motor Co., 4.750%, 1/15/43 | | | 75,953 | |

Touchstone Active Bond Fund (Continued)

| Principal | | | | | Market | |

| Amount | | | | | Value | |

| | | | | | | |

| | | | | Corporate Bonds — 48.7% (Continued) | | | | |

| | | | | | | | | |

| | | | | Consumer Discretionary — (Continued) | | | | |

| $ | 205,000 | | | Forest Laboratories LLC, 144a, | | | | |

| | | | | 5.000%, 12/15/21 | | $ | 221,643 | |

| | 10,000 | | | GLP Capital LP / GLP Financing II, Inc., | | | | |

| | | | | 5.375%, 11/1/23 | | | 10,700 | |

| | 47,000 | | | GLP Capital LP / GLP Financing II, Inc., | | | | |

| | | | | 5.375%, 4/15/26 | | | 49,016 | |

| | 51,000 | | | Goodyear Tire & Rubber Co. (The), | | | | |

| | | | | 8.750%, 8/15/20 | | | 60,818 | |

| | 41,000 | | | Hanesbrands, Inc., 144a, | | | | |

| | | | | 4.625%, 5/15/24 | | | 39,770 | |

| | 150,000 | | | Home Depot, Inc. (The), | | | | |

| | | | | 5.950%, 4/1/41 | | | 190,690 | |

| | 200,000 | | | Imperial Brands Finance PLC (United Kingdom), 144a, 3.500%, 2/11/23 | | | 201,097 | |

| | 34,000 | | | International Game Technology PLC (United Kingdom), 144a, | | | | |

| | | | | 5.625%, 2/15/20 | | | 35,870 | |

| | 18,000 | | | International Game Technology PLC (United Kingdom), 144a, | | | | |

| | | | | 6.250%, 2/15/22 | | | 19,305 | |

| | 24,000 | | | L Brands, Inc., 5.625%, 2/15/22 | | | 25,620 | |

| | 17,000 | | | Lennar Corp., 4.875%, 12/15/23 | | | 16,830 | |

| | 13,000 | | | Live Nation Entertainment, Inc., 144a, | | | | |

| | | | | 4.875%, 11/1/24 | | | 13,032 | |

| | 19,000 | | | LKQ Corp., 4.750%, 5/15/23 | | | 18,905 | |

| | 28,000 | | | LSC Communications, Inc., 144a, | | | | |

| | | | | 8.750%, 10/15/23 | | | 28,140 | |

| | 40,000 | | | M/I Homes, Inc., 6.750%, 1/15/21 | | | 41,702 | |

| | 22,000 | | | Mattamy Group Corp. (Canada), 144a, | | | | |

| | | | | 6.875%, 12/15/23 | | | 22,275 | |

| | 47,000 | | | MDC Partners, Inc. (Canada), 144a, | | | | |

| | | | | 6.500%, 5/1/24 | | | 42,300 | |

| | 24,000 | | | Men's Wearhouse, Inc. (The), | | | | |

| | | | | 7.000%, 7/1/22 | | | 23,520 | |

| | 25,000 | | | Meritage Homes Corp., | | | | |

| | | | | 7.150%, 4/15/20 | | | 27,125 | |

| | 65,000 | | | MGM Resorts International, | | | | |

| | | | | 6.000%, 3/15/23 | | | 70,200 | |

| | 160,000 | | | Mylan NV (Netherlands), 144a, | | | | |

| | | | | 3.000%, 12/15/18 | | | 161,157 | |

| | 52,000 | | | NCL Corp. Ltd. (Bermuda), 144a, | | | | |

| | | | | 4.625%, 11/15/20 | | | 52,910 | |

| | 23,000 | | | NCL Corp. Ltd. (Bermuda), 144a, | | | | |

| | | | | 4.750%, 12/15/21 | | | 22,986 | |

| | 8,000 | | | Netflix, Inc., 5.750%, 3/1/24 | | | 8,560 | |

| | 26,000 | | | Netflix, Inc., 5.875%, 2/15/25 | | | 28,048 | |

| | 154,000 | | | Newell Brands, Inc., 2.875%, 12/1/19 | | | 156,746 | |

| | 103,000 | | | Newell Brands, Inc., 4.200%, 4/1/26 | | | 107,509 | |

| | 44,000 | | | Nexstar Broadcasting, Inc., 144a, | | | | |

| | | | | 6.125%, 2/15/22 | | | 45,540 | |

| | 24,000 | | | PulteGroup, Inc., 5.500%, 3/1/26 | | | 23,820 | |

| | 43,000 | | | Quad/Graphics, Inc., 7.000%, 5/1/22 | | | 41,925 | |

| | 57,000 | | | Quebecor Media, Inc. (Canada), | | | | |

| | | | | 5.750%, 1/15/23 | | | 59,138 | |

| 26,574 | | | Reynolds Group Issuer, Inc. / Reynolds Group Issuer LLC / Reynolds Group Issuer, | | | | |

| | | | | 6.875%, 2/15/21 | | | 27,344 | |

| | 37,000 | | | Royal Caribbean Cruises Ltd. (Liberia), | | | | |

| | | | | 5.250%, 11/15/22 | | | 39,544 | |

| | 20,000 | | | Sabre GLBL, Inc., 144a, | | | | |

| | | | | 5.250%, 11/15/23 | | | 20,537 | |

| | 55,000 | | | Sabre GLBL, Inc., 144a, | | | | |

| | | | | 5.375%, 4/15/23 | | | 56,100 | |

| | 240,000 | | | Scripps Networks Interactive, Inc., | | | | |

| | | | | 2.750%, 11/15/19 | | | 243,404 | |

| | 15,000 | | | Service Corp. International, | | | | |

| | | | | 8.000%, 11/15/21 | | | 17,475 | |

| | 40,000 | | | ServiceMaster Co. LLC (The), 144a, | | | | |

| | | | | 5.125%, 11/15/24 | | | 40,600 | |

| | 204,000 | | | Shire Acquisitions Investments Ireland DAC (Ireland), | | | | |

| | | | | 2.400%, 9/23/21 | | | 197,061 | |

| | 12,000 | | | Sirius XM Radio, Inc., 144a, | | | | |

| | | | | 5.375%, 4/15/25 | | | 11,940 | |

| | 77,000 | | | Sirius XM Radio, Inc., 144a, | | | | |

| | | | | 5.375%, 7/15/26 | | | 75,268 | |

| | 34,000 | | | Sonic Automotive, Inc., | | | | |

| | | | | 7.000%, 7/15/22 | | | 35,615 | |

| | 55,000 | | | Taylor Morrison Communities, Inc. / Monarch Communities, Inc., 144a, | | | | |

| | | | | 5.250%, 4/15/21 | | | 56,375 | |

| | 11,000 | | | TEGNA, Inc., 144a, 4.875%, 9/15/21 | | | 11,192 | |

| | 21,000 | | | Tenneco, Inc., 5.000%, 7/15/26 | | | 20,606 | |

| | 30,000 | | | Toll Brothers Finance Corp., | | | | |

| | | | | 4.875%, 11/15/25 | | | 29,475 | |

| | 34,000 | | | Toll Brothers Finance Corp., | | | | |

| | | | | 5.875%, 2/15/22 | | | 36,890 | |

| | 25,000 | | | TRI Pointe Group, Inc., 4.875%, 7/1/21 | | | 25,500 | |

| | 14,000 | | | United Rentals North America, Inc., | | | | |

| | | | | 4.625%, 7/15/23 | | | 14,280 | |

| | 22,000 | | | United Rentals North America, Inc., | | | | |

| | | | | 5.750%, 11/15/24 | | | 23,100 | |

| | 23,000 | | | Vista Outdoor, Inc., 5.875%, 10/1/23 | | | 24,078 | |

| | 11,000 | | | ZF North America Capital, Inc., 144a, | | | | |

| | | | | 4.500%, 4/29/22 | | | 11,344 | |

| | 44,000 | | | ZF North America Capital, Inc., 144a, | | | | |

| | | | | 4.750%, 4/29/25 | | | 44,770 | |

| | | | | | | | 4,934,136 | |

| | | | | | | | | |

| | | | | Energy — 6.2% | | | | |

| | 37,000 | | | Antero Resources Corp., | | | | |

| | | | | 5.375%, 11/1/21 | | | 37,832 | |

| | 53,000 | | | Archrock Partners LP / Archrock Partners Finance Corp., | | | | |

| | | | | 6.000%, 4/1/21 | | | 51,410 | |

| | 276,000 | | | Boardwalk Pipelines LP, 3.375%, 2/1/23 | | | 262,747 | |

| | 92,000 | | | Buckeye Partners LP, 4.150%, 7/1/23 | | | 93,094 | |

| | 150,000 | | | Cenovus Energy, Inc. (Canada), | | | | |

| | | | | 6.750%, 11/15/39 | | | 167,246 | |

| | 7,000 | | | Continental Resources, Inc., | | | | |

| | | | | 4.500%, 4/15/23 | | | 6,860 | |

Touchstone Active Bond Fund (Continued)

| Principal | | | | | Market | |

| Amount | | | | | Value | |

| | | | | | | |

| | | | | Corporate Bonds — 48.7% (Continued) | | | | |

| | | | | | | | | |

| | | | | Energy — (Continued) | | | | |

| $ | 52,000 | | | Continental Resources, Inc., | | | | |

| | | | | 5.000%, 9/15/22 | | $ | 52,488 | |

| | 37,000 | | | DCP Midstream LLC, 144a, | | | | |

| | | | | 5.350%, 3/15/20 | | | 38,388 | |

| | 104,000 | | | Enterprise Products Operating LLC, | | | | |

| | | | | 7.000%, 6/1/67(A) | | | 88,400 | |

| | 22,000 | | | FTS International, Inc., 144a, | | | | |

| | | | | 8.463%, 6/15/20(A) | | | 22,000 | |

| | 71,000 | | | Genesis Energy LP / Genesis Energy Finance Corp., 5.750%, 2/15/21 | | | 71,710 | |

| | 45,000 | | | Gibson Energy, Inc. (Canada), 144a, | | | | |

| | | | | 6.750%, 7/15/21 | | | 46,688 | |

| | 40,000 | | | Gulfport Energy Corp., 144a, | | | | |

| | | | | 6.375%, 5/15/25 | | | 40,508 | |

| | 24,000 | | | Hilcorp Energy I LP / Hilcorp Finance Co., 144a, 5.000%, 12/1/24 | | | 23,820 | |

| | 8,000 | | | Holly Energy Partners LP / Holly Energy Finance Corp., 144a, | | | | |

| | | | | 6.000%, 8/1/24 | | | 8,340 | |

| | 113,000 | | | HollyFrontier Corp., 5.875%, 4/1/26 | | | 115,476 | |

| | 158,000 | | | Kinder Morgan Energy Partners LP, | | | | |

| | | | | 3.500%, 9/1/23 | | | 155,835 | |

| | 205,000 | | | Marathon Oil Corp., 2.800%, 11/1/22 | | | 196,034 | |

| | 123,000 | | | Midcontinent Express Pipeline LLC, 144a, 6.700%, 9/15/19 | | | 129,150 | |

| | 44,000 | | | Nabors Industries, Inc., | | | | |

| | | | | 4.625%, 9/15/21 | | | 44,727 | |

| | 46,000 | | | Newfield Exploration Co., | | | | |

| | | | | 5.625%, 7/1/24 | | | 47,955 | |

| | 25,000 | | | NuStar Logistics LP, 4.800%, 9/1/20 | | | 25,062 | |

| | 16,000 | | | NuStar Logistics LP, 6.750%, 2/1/21 | | | 17,280 | |

| | 130,000 | | | Occidental Petroleum Corp., | | | | |

| | | | | 4.100%, 2/15/47 | | | 126,625 | |

| | 23,000 | | | PDC Energy, Inc., 144a, | | | | |

| | | | | 6.125%, 9/15/24 | | | 23,518 | |

| | 135,000 | | | Petroleos Mexicanos (Mexico), | | | | |

| | | | | 4.500%, 1/23/26 | | | 122,985 | |

| | 100,000 | | | Petroleos Mexicanos (Mexico), 144a, | | | | |

| | | | | 5.375%, 3/13/22 | | | 102,398 | |

| | 57,000 | | | Precision Drilling Corp. (Canada), | | | | |

| | | | | 5.250%, 11/15/24 | | | 53,295 | |

| | 3,000 | | | Precision Drilling Corp. (Canada), 144a, | | | | |

| | | | | 7.750%, 12/15/23 | | | 3,165 | |

| | 24,000 | | | QEP Resources, Inc., 5.375%, 10/1/22 | | | 24,060 | |

| | 33,000 | | | QEP Resources, Inc., 6.800%, 3/1/20 | | | 34,320 | |

| | 99,000 | | | Range Resources Corp., 144a, | | | | |

| | | | | 5.000%, 8/15/22 | | | 98,381 | |

| | 20,000 | | | Range Resources Corp., 144a, | | | | |

| | | | | 5.750%, 6/1/21 | | | 20,950 | |

| | 17,000 | | | Rose Rock Midstream LP / Rose Rock Finance Corp., 5.625%, 7/15/22 | | | 16,702 | |

| | 57,000 | | | Rose Rock Midstream LP / Rose Rock Finance Corp., | | | | |

| | | | | 5.625%, 11/15/23 | | | 55,575 | |

| | 21,000 | | | Sabine Pass Liquefaction LLC, | | | | |

| | | | | 5.625%, 2/1/21 | | | 22,470 | |

| | 41,000 | | | Sabine Pass Liquefaction LLC, | | | | |

| | | | | 5.625%, 3/1/25 | | | 43,870 | |

| | 174,000 | | | Sabine Pass Liquefaction LLC, 144a, | | | | |

| | | | | 5.000%, 3/15/27 | | | 175,522 | |

| | 42,000 | | | SemGroup Corp., 7.500%, 6/15/21 | | | 43,260 | |

| | 46,000 | | | SESI LLC, 6.375%, 5/1/19 | | | 46,000 | |

| | 210,000 | | | Shell International Finance BV (Netherlands), 1.875%, 5/10/21 | | | 205,321 | |

| | 11,000 | | | SM Energy Co., 6.750%, 9/15/26 | | | 11,330 | |

| | 48,000 | | | Southwestern Energy Co., | | | | |

| | | | | 4.100%, 3/15/22 | | | 45,350 | |

| | 38,000 | | | Southwestern Energy Co., | | | | |

| | | | | 5.800%, 1/23/20 | | | 39,140 | |

| | 17,000 | | | Summit Midstream Holdings LLC / Summit Midstream Finance Corp., | | | | |

| | | | | 7.500%, 7/1/21 | | | 17,850 | |

| | 6,000 | | | Tesoro Logistics LP / Tesoro Logistics Finance Corp., 5.250%, 1/15/25 | | | 6,128 | |

| | 21,000 | | | Tesoro Logistics LP / Tesoro Logistics Finance Corp., 5.875%, 10/1/20 | | | 21,656 | |

| | 47,000 | | | Transocean Phoenix 2 Ltd. (Cayman Islands), 144a, 7.750%, 10/15/24 | | | 49,585 | |

| | 49,000 | | | Tullow Oil PLC (United Kingdom), 144a, 6.000%, 11/1/20 | | | 46,672 | |

| | 79,000 | | | Unit Corp., 6.625%, 5/15/21 | | | 76,630 | |

| | 25,000 | | | Weatherford International Ltd (Bermuda), 6.500%, 8/1/36 | | | 20,062 | |

| | 112,000 | | | Williams Partners LP, 3.350%, 8/15/22 | | | 110,253 | |

| | | | | | | | 3,406,123 | |

| | | | | | | | | |

| | | | | Telecommunication Services — 4.5% | | | | |

| | 96,000 | | | Altice Financing SA (Luxemburg), 144a, 6.625%, 2/15/23 | | | 98,640 | |

| | 29,000 | | | AMC Networks, Inc., 5.000%, 4/1/24 | | | 29,145 | |

| | 105,000 | | | AT&T, Inc., 3.900%, 3/11/24 | | | 106,170 | |

| | 40,000 | | | AT&T, Inc., 4.350%, 6/15/45 | | | 35,641 | |

| | 125,000 | | | AT&T, Inc., 4.500%, 5/15/35 | | | 120,771 | |

| | 50,000 | | | CenturyLink, Inc., 5.800%, 3/15/22 | | | 51,106 | |

| | 20,000 | | | CenturyLink, Inc., 6.450%, 6/15/21 | | | 21,050 | |

| | 124,000 | | | Charter Communications Operating LLC / Charter Communications Operating Capital, | | | | |

| | | | | 6.484%, 10/23/45 | | | 143,354 | |

| | 190,000 | | | Comcast Corp., 1.625%, 1/15/22 | | | 182,118 | |

| | 52,000 | | | CommScope, Inc., 144a, | | | | |

| | | | | 5.000%, 6/15/21 | | | 53,560 | |

| | 29,000 | | | CSC Holdings LLC, 5.250%, 6/1/24 | | | 28,348 | |

| | 44,000 | | | CSC Holdings LLC, 8.625%, 2/15/19 | | | 48,620 | |

| | 28,000 | | | CSC Holdings LLC, 144a, | | | | |

| | | | | 10.125%, 1/15/23 | | | 32,340 | |

| | 225,000 | | | Discovery Communications LLC, | | | | |

| | | | | 3.450%, 3/15/25 | | | 214,773 | |

| | 13,000 | | | Frontier Communications Corp., | | | | |

| | | | | 6.875%, 1/15/25 | | | 11,018 | |

| | 56,000 | | | Frontier Communications Corp., | | | | |

| | | | | 8.500%, 4/15/20 | | | 58,800 | |

Touchstone Active Bond Fund (Continued)

| Principal | | | | | Market | |

| Amount | | | | | Value | |

| | | | | | | |

| | | | | Corporate Bonds — 48.7% (Continued) | | | | |

| | | | | | | | | |

| | | | | Telecommunication Services — (Continued) | | | | |

| $ | 82,000 | | | Frontier Communications Corp., | | | | |

| | | | | 10.500%, 9/15/22 | | $ | 86,207 | |

| | 38,000 | | | Gray Television, Inc., 144a, | | | | |

| | | | | 5.125%, 10/15/24 | | | 36,765 | |

| | 36,000 | | | Intelsat Jackson Holdings SA (Luxembourg), 5.500%, 8/1/23 | | | 24,257 | |

| | 19,000 | | | Intelsat Jackson Holdings SA (Luxembourg), 7.250%, 4/1/19 | | | 15,960 | |

| | 67,000 | | | Intelsat Jackson Holdings SA (Luxembourg), 7.250%, 10/15/20 | | | 51,925 | |

| | 4,000 | | | LIN Television Corp., 5.875%, 11/15/22 | | | 4,060 | |

| | 5,000 | | | Match Group, Inc., 6.375%, 6/1/24 | | | 5,275 | |

| | 26,000 | | | Nexstar Escrow Corp., 144a, | | | | |

| | | | | 5.625%, 8/1/24 | | | 25,805 | |

| | 170,000 | | | Qwest Corp., 6.750%, 12/1/21 | | | 184,450 | |

| | 60,000 | | | Sprint Communications, Inc., | | | | |

| | | | | 6.000%, 11/15/22 | | | 60,450 | |

| | 5,000 | | | Sprint Communications, Inc., 144a, | | | | |

| | | | | 7.000%, 3/1/20 | | | 5,425 | |

| | 70,000 | | | Sprint Communications, Inc., 144a, | | | | |

| | | | | 9.000%, 11/15/18 | | | 77,175 | |

| | 10,000 | | | Telecom Italia Capital SA (Luxembourg), 7.175%, 6/18/19 | | | 11,075 | |

| | 57,000 | | | T-Mobile USA, Inc., 6.000%, 3/1/23 | | | 60,206 | |

| | 67,000 | | | T-Mobile USA, Inc., 6.000%, 4/15/24 | | | 70,601 | |

| | 21,000 | | | T-Mobile USA, Inc., 6.125%, 1/15/22 | | | 22,155 | |

| | 15,000 | | | T-Mobile USA, Inc., 6.250%, 4/1/21 | | | 15,600 | |

| | 75,000 | | | Univision Communications, Inc., 144a, | | | | |

| | | | | 6.750%, 9/15/22 | | | 78,750 | |

| | 16,000 | | | UPCB Finance IV Ltd. (Cayman Islands), 144a, 5.375%, 1/15/25 | | | 16,120 | |

| | 275,000 | | | Verizon Communications, Inc., | | | | |

| | | | | 6.250%, 4/1/37 | | | 326,040 | |

| | 64,000 | | | ViaSat, Inc., 6.875%, 6/15/20 | | | 65,920 | |

| | | | | | | | 2,479,675 | |

| | | | | | | | | |

| | | | | Health Care — 4.2% | | | | |

| | 198,000 | | | Abbott Laboratories, | | | | |

| | | | | 3.750%, 11/30/26 | | | 196,632 | |

| | 174,000 | | | AbbVie, Inc., 4.450%, 5/14/46 | | | 166,610 | |

| | 55,000 | | | Acadia Healthcare Co., Inc., | | | | |

| | | | | 5.125%, 7/1/22 | | | 54,656 | |

| | 11,000 | | | Acadia Healthcare Co., Inc., | | | | |

| | | | | 5.625%, 2/15/23 | | | 11,000 | |

| | 23,000 | | | Acadia Healthcare Co., Inc., | | | | |

| | | | | 6.500%, 3/1/24 | | | 23,518 | |

| | 90,000 | | | Actavis Funding SCS (Luxembourg), | | | | |

| | | | | 3.800%, 3/15/25 | | | 90,106 | |

| | 185,000 | | | Catholic Health Initiatives, | | | | |

| | | | | 4.200%, 8/1/23 | | | 191,010 | |

| | 30,000 | | | Centene Corp., 4.750%, 1/15/25 | | | 29,288 | |

| | 34,000 | | | Centene Corp., 5.625%, 2/15/21 | | | 35,748 | |

| | 62,000 | | | CHS / Community Health Systems, Inc., 7.125%, 7/15/20 | | | 47,139 | |

| | 11,000 | | | CHS/Community Health Systems, Inc., | | | | |

| | | | | 5.125%, 8/15/18† | | | 10,780 | |

| | 21,000 | | | Envision Healthcare Corp., 144a, | | | | |

| | | | | 6.250%, 12/1/24 | | | 22,155 | |

| | 160,000 | | | Express Scripts Holding Co., | | | | |

| | | | | 3.300%, 2/25/21 | | | 163,003 | |

| | 36,000 | | | Grifols Worldwide Operations Ltd. (Ireland), 5.250%, 4/1/22 | | | 37,260 | |

| | 29,000 | | | HCA, Inc., 5.375%, 2/1/25 | | | 29,072 | |

| | 28,000 | | | HCA, Inc., 5.875%, 2/15/26 | | | 28,840 | |

| | 86,000 | | | HCA, Inc., 6.500%, 2/15/20 | | | 94,084 | |

| | 14,000 | | | Kindred Healthcare, Inc., | | | | |

| | | | | 8.000%, 1/15/20 | | | 13,930 | |

| | 10,000 | | | Kindred Healthcare, Inc., | | | | |

| | | | | 8.750%, 1/15/23 | | | 9,350 | |

| | 29,000 | | | LifePoint Health, Inc., 144a, | | | | |

| | | | | 5.375%, 5/1/24 | | | 28,406 | |

| | 44,000 | | | Mallinckrodt International Finance SA (Luxembourg), 4.750%, 4/15/23 | | | 38,280 | |

| | 142,000 | | | Ochsner Clinic Foundation, | | | | |

| | | | | 5.897%, 5/15/45 | | | 164,206 | |

| | 45,000 | | | Select Medical Corp., 6.375%, 6/1/21 | | | 45,000 | |

| | 10,000 | | | Teleflex, Inc., 4.875%, 6/1/26 | | | 9,900 | |

| | 28,000 | | | Tenet Healthcare Corp., | | | | |

| | | | | 4.500%, 4/1/21 | | | 27,720 | |

| | 38,000 | | | Tenet Healthcare Corp., | | | | |

| | | | | 4.750%, 6/1/20 | | | 38,380 | |

| | 55,000 | | | Tenet Healthcare Corp., | | | | |

| | | | | 6.000%, 10/1/20 | | | 57,612 | |

| | 13,000 | | | Tenet Healthcare Corp., 144a, | | | | |

| | | | | 7.500%, 1/1/22 | | | 13,552 | |

| | 88,000 | | | Teva Pharmaceutical Finance Netherlands III BV (Netherlands), | | | | |

| | | | | 2.200%, 7/21/21 | | | 84,188 | |

| | 190,000 | | | Teva Pharmaceutical Finance | | | | |

| | | | | Netherlands III BV (Netherlands), | | | | |

| | | | | 3.150%, 10/1/26 | | | 175,166 | |

| | 25,000 | | | Universal Hospital Services, Inc., | | | | |

| | | | | 7.625%, 8/15/20 | | | 24,750 | |

| | 39,000 | | | Valeant Pharmaceuticals International, | | | | |

| | | | | 144a, 6.375%, 10/15/20 | | | 33,503 | |

| | 40,000 | | | Valeant Pharmaceuticals International, | | | | |

| | | | | 144a, 6.750%, 8/15/21 | | | 33,200 | |

| | 67,000 | | | Valeant Pharmaceuticals International, Inc. (Canada), 144a, 5.500%, 3/1/23 | | | 50,250 | |

| | 20,000 | | | Valeant Pharmaceuticals International, Inc. (Canada), 144a, 6.125%, 4/15/25 | | | 15,025 | |

| | 29,000 | | | Valeant Pharmaceuticals International, Inc. (Canada), 144a, 6.750%, 8/15/18 | | | 27,478 | |

| | 140,000 | | | Zimmer Biomet Holdings, Inc., | | | | |

| | | | | 3.150%, 4/1/22 | | | 139,617 | |

| | 60,000 | | | Zimmer Biomet Holdings, Inc., | | | | |

| | | | | 3.375%, 11/30/21 | | | 60,579 | |

| | | | | | | | 2,320,993 | |

| | | | | | | | | |

| | | | | Information Technology — 4.0% | | | | |

| | 198,000 | | | Activision Blizzard, Inc., 144a, | | | | |

| | | | | 6.125%, 9/15/23 | | | 216,634 | |

| | 148,000 | | | Apple, Inc., 4.650%, 2/23/46 | | | 159,818 | |

Touchstone Active Bond Fund (Continued)

| Principal | | | | | Market | |

| Amount | | | | | Value | |

| | | | | | | |

| | | | | Corporate Bonds — 48.7% (Continued) | | | | |

| | | | | | | | | |

| | | | | Information Technology — (Continued) | | | | |

| $ | 28,000 | | | CDW LLC / CDW Finance Corp., | | | | |

| | | | | 5.000%, 9/1/23 | | $ | 28,035 | |

| | 205,000 | | | Diamond 1 Finance Corp. / Diamond 2 Finance Corp., 144a, | | | | |

| | | | | 4.420%, 6/15/21 | | | 212,123 | |

| | 40,000 | | | Diamond 1 Finance Corp. / Diamond 2 Finance Corp., 144a, | | | | |

| | | | | 5.450%, 6/15/23 | | | 42,430 | |

| | 16,000 | | | Diamond 1 Finance Corp. / Diamond 2 Finance Corp., 144a, | | | | |

| | | | | 5.875%, 6/15/21 | | | 17,023 | |

| | 70,000 | | | Diamond 1 Finance Corp. / Diamond 2 Finance Corp., 144a, | | | | |

| | | | | 7.125%, 6/15/24 | | | 77,712 | |

| | 64,000 | | | Diebold Nixdorf, Inc., 8.500%, 4/15/24 | | | 68,320 | |

| | 206,000 | | | Electronic Arts, Inc., 3.700%, 3/1/21 | | | 212,978 | |

| | 11,000 | | | EMC Corp., 3.375%, 6/1/23† | | | 10,189 | |

| | 230,000 | | | Fidelity National Information Services, Inc., 3.625%, 10/15/20 | | | 238,112 | |

| | 37,000 | | | First Data Corp., 144a, 5.000%, 1/15/24 | | | 37,197 | |

| | 38,000 | | | First Data Corp., 144a, 5.375%, 8/15/23 | | | 39,425 | |

| | 212,000 | | | Hewlett Packard Enterprise Co., 144a, | | | | |

| | | | | 2.450%, 10/5/17 | | | 213,179 | |

| | 22,000 | | | Micron Technology, Inc., 144a, | | | | |

| | | | | 7.500%, 9/15/23 | | | 24,365 | |

| | 85,000 | | | Microsoft Corp., 3.500%, 2/12/35 | | | 81,819 | |

| | 42,000 | | | NCR Corp., 4.625%, 2/15/21 | | | 42,756 | |

| | 41,000 | | | Open Text Corp. (Canada), 144a, | | | | |

| | | | | 5.875%, 6/1/26 | | | 43,255 | |

| | 170,000 | | | Oracle Corp., 2.650%, 7/15/26 | | | 161,366 | |

| | 200,000 | | | QUALCOMM, Inc., 3.450%, 5/20/25 | | | 203,505 | |

| | 27,000 | | | Sensata Technologies BV (Netherlands), 144a, | | | | |

| | | | | 5.000%, 10/1/25 | | | 26,460 | |

| | 37,000 | | | Western Digital Corp., 144a, | | | | |

| | | | | 7.375%, 4/1/23 | | | 40,700 | |

| | 12,000 | | | Western Digital Corp., 144a, | | | | |

| | | | | 10.500%, 4/1/24 | | | 14,190 | |

| | | | | | | | 2,211,591 | |

| | | | | | | | | |

| | | | | Industrials — 3.9% | | | | |

| | 57,000 | | | AECOM Global II LLC / URS Fox US LP, | | | | |

| | | | | 5.000%, 4/1/22 | | | 57,285 | |

| | 200,000 | | | Air Lease Corp., 5.625%, 4/1/17 | | | 201,750 | |

| | 4,000 | | | Allegion PLC (Ireland), | | | | |

| | | | | 5.875%, 9/15/23 | | | 4,240 | |

| | 41,795 | | | American Airlines 2013-2 Class B Pass Through Trust, 144a, | | | | |

| | | | | 5.600%, 7/15/20 | | | 43,362 | |

| | 58,000 | | | Amsted Industries, Inc., 144a, | | | | |

| | | | | 5.000%, 3/15/22 | | | 58,000 | |

| | 17,000 | | | Amsted Industries, Inc., 144a, | | | | |

| | | | | 5.375%, 9/15/24 | | | 16,702 | |

| | 33,000 | | | Anixter, Inc., 5.125%, 10/1/21 | | | 34,320 | |

| | 34,000 | | | Anixter, Inc., 5.500%, 3/1/23 | | | 35,275 | |

| | 265,000 | | | Burlington Northern Santa Fe LLC, | | | | |

| | | | | 5.750%, 5/1/40 | | | 323,407 | |

| | 2,000 | | | Clean Harbors, Inc., 5.125%, 6/1/21 | | | 2,045 | |

| | 42,000 | | | CNH Industrial NV (Netherlands), | | | | |

| | | | | 4.500%, 8/15/23 | | | 41,475 | |

| | 16,000 | | | Eagle Materials, Inc., 4.500%, 8/1/26 | | | 15,960 | |

| | 175,000 | | | FedEx Corp., 5.100%, 1/15/44 | | | 189,881 | |

| | 7,000 | | | Huntington Ingalls Industries, Inc., 144a, 5.000%, 11/15/25 | | | 7,271 | |

| | 24,000 | | | JB Poindexter & Co., Inc., 144a, | | | | |