UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-08416

Touchstone Variable Series Trust

(Exact name of registrant as specified in charter)

303 Broadway, Suite 1100

Cincinnati, Ohio 45202-4203

(Address of principal executive offices) (Zip code)

Jill T. McGruder

303 Broadway, Suite 1100

Cincinnati, Ohio 45202-4203

(Name and address of agent for service)

Registrant's telephone number, including area code: 800-638-8194

Date of fiscal year end: December 31

Date of reporting period: December 31, 2017

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget ("OMB") control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

Item 1. Reports to Stockholders.

The Report to Shareholders is attached herewith.

December 31, 2017

Annual Report

Touchstone Variable Series Trust

Touchstone Active Bond Fund

Touchstone Balanced Fund

Touchstone Bond Fund

Touchstone Common Stock Fund

Touchstone Focused Fund

Touchstone Large Cap Core Equity Fund

Touchstone Small Company Fund

Touchstone Aggressive ETF Fund

Touchstone Conservative ETF Fund

Touchstone Moderate ETF Fund

Table of Contents

This report identifies the Funds' investments on December 31, 2017. These holdings are subject to change. Not all investments in each Fund performed the same, nor is there any guarantee that these investments will perform as well in the future. Market forecasts provided in this report may not occur.

2

Dear Shareholder:

We are pleased to provide you with the Touchstone Variable Series Trust Annual Report. Inside you will find key financial information, as well as manager commentaries, for the Funds for the 12-months ended December 31, 2017.

Nearly ten years after the 2008 Credit Crisis, the economic recovery finally seemed to have taken hold in calendar year 2017. Economists and market strategists trumpeted the start of a “synchronized global expansion” as economic growth in the U.S., Japan, Europe and China aligned to provide a powerful impetus for a broader acceleration in global growth. While economic strength was synchronized across the world, monetary policies experienced further divergence. The Bank of Japan and the European Central Bank maintained accommodative stances, providing ample stimulus in an effort to sustain recent positive growth trends in gross domestic product after years of economic fragility. Meanwhile, with solid growth entrenched in the U.S., the U.S. Federal Reserve Board (Fed) continued moving toward its goal of monetary policy normalization by raising rates in March, June, and December and announcing plans to reduce the size of its balance sheet.

Global equities posted strong double-digit returns across most broad U.S. and non-U.S. equity indexes. Growth-oriented stocks led U.S. equity markets and outperformed their value-oriented counterparts, while large-capitalization stocks outperformed small- and mid-capitalization stocks. Outside the U.S., emerging market equities generated very strong returns followed closely by developed market equities.

While the Fed’s three rate hikes during the year pushed short-term rates higher, longer-term rates remained mostly range bound. This stable interest rate environment for intermediate to long-term interest rates allowed investment grade corporate bonds to generate solid returns. Non-investment grade bonds benefitted from the low default environment and stronger economic growth to lead the fixed income market.

The new year provides a natural point to assess the recent past and to look toward the future. From a financial perspective, it has been yet another period of strong returns across many asset classes. This makes it a particularly timely juncture to assess your current financial situation and, with the help of your financial advisor, re-assess your plans for the year – and years ahead.

We greatly appreciate your continued support. Thank you for including Touchstone as part of your investment plan.

| Sincerely, | |

| |

| Jill T. McGruder | |

| President | |

| Touchstone Variable Series Trust |

3

Management's Discussion of Fund Performance (Unaudited)

Touchstone Active Bond Fund

Sub-Advised by Fort Washington Investment Advisors, Inc.

Investment Philosophy

The Touchstone Active Bond Fund seeks to provide as high a level of current income as is consistent with the preservation of capital. Capital appreciation is a secondary goal. In deciding what securities to buy and sell for the Fund, the overall investment opportunities and risks in different sectors of the debt securities market are analyzed by focusing on maximizing total return and reducing volatility of the Fund’s portfolio. A disciplined sector allocation process is followed to build a broadly diversified portfolio of investments.

Fund Performance

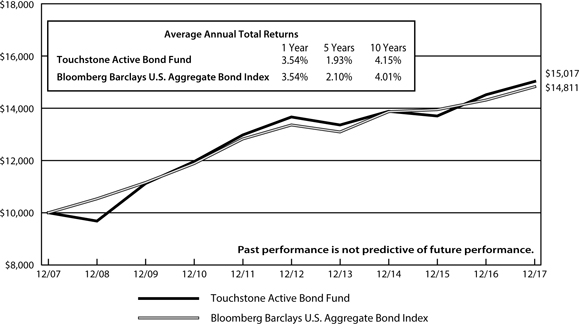

The Touchstone Active Bond Fund performed in-line with its benchmark, the Bloomberg Barclays U.S. Aggregate Bond Index, for the 12-month period ended December 31, 2017. The Fund’s total return was 3.54 percent, while the benchmark’s total return was 3.54 percent.

Market Environment

Risk assets performed well in 2017 and did so at extremely low levels of volatility. Performance was driven by a steady increase in optimism surrounding the prospects for both domestic and global economic growth, which has been substantiated with solid underlying fundamentals. Credit spreads tightened over the course of the year, leading to the outperformance of Corporate Bonds over U.S. Treasuries. High Yield issues produced the strongest performance of any fixed income sector, and investment grade corporates also posted solid returns for the year.

The yield curve flattened in 2017 with rates on the front end of the curve rising, and the long end falling. U.S. 10-year Treasury yields essentially started and ended the year with the same yield. This does not mean, however, that yields were stable during the course of the fiscal year, as they moved considerably. The long end of the curve fell considerably and bottomed in September before rebounding as inflation expectations increased amid solid economic growth and improvement in underlying fundamentals. These same factors prompted the U.S. Federal Reserve Board (Fed) to raise its target overnight rate three times during 2017. We believe markets have priced in between two and three additional hikes in 2018, expectations that seem reasonable given the strong underlying fundamentals currently present in the economy. The appointment of Jerome Powell to lead the Fed is unlikely to materially alter the Fed’s path to raise rates. However, the appointment of five new members of the Fed warrants close attention as they have the potential to shift the path put in place by previous members.

Financial conditions continued to be supportive of risk assets and continued economic growth in 2017, ending the year at the easiest levels since 2014. Credit spreads for both investment grade and high yield bonds contracted significantly and are now at multi-year lows. Global central bank policy has remained generally accommodative, but will directionally move less so in developed countries.

Portfolio Review

Overall, the Fund matched the performance of the benchmark during the fiscal year due to its overweight of non-Treasury sectors and security selection. The Fund’s allocation to High Yield over the year contributed to performance as that sector benefited from tightening credit spreads and a low default rate environment. The Fund’s allocation to High Yield was a strong contributor in the first three quarters of the fiscal year. We believed that the sector offered adequate compensation for credit and liquidity risk, though we reduced the position throughout the year as tightening credit spreads reduced the return potential for High Yield issues. By the end of the third quarter, however, credit spreads had contracted to cycle lows, causing us to eliminate the Fund’s

4

Management's Discussion of Fund Performance (Unaudited) (Continued)

exposure to High Yield, as the risk/reward profile was no longer attractive relative to other non-Treasury sectors. Capital was reallocated to the securitized sector, which we believed offered a more attractive risk/reward profile, particularly within the Asset-Backed and Non-Agency Mortgage-Backed sectors. These are closely related to the health of the consumer, which we believe to be strong given the low unemployment rate and reasonable consumer debt levels. The reduction in High Yield exposure is indicative of a broader de-risking in the portfolio, as rich valuations in the fixed income markets have pushed us to reduce our risk target to the low-end of its range. The Fund remains slightly overweight risk assets relative to the benchmark given our positive economic outlook and anticipation of a benign default environment.

Other drivers of relative performance included security selection within investment grade corporate bonds, as well as interest rate risk and yield curve positioning. The Fund was mostly neutral duration relative to the benchmark for the year, however tactical short term shifts had a positive impact on Fund performance. We have opportunistically invested in Treasury Inflation Protected Securities (TIPS) over the past year, which also contributed to returns as inflation expectations increased in the second half of the year.

Outlook

Financial conditions remain stable, economic fundamentals are solid, and recession risk is increasingly low, notwithstanding the age of the credit cycle. Given this backdrop, the Fund continues to be moderately overweight risk assets relative to the benchmark. However, this overweight has declined somewhat in recent quarters as asset prices have increased to reflect the market’s optimistic view of the economy. While we think the potential for significant further tightening is remote, we believe a sustained widening seems unlikely, barring an external shock as the fundamental and technical outlooks remain strong. As such, we remain comfortable with the Fund’s modest overweight to risk given the positive economic outlook and low rate of expected defaults. Global factors will be watched closely for any broader impact which might influence the economic outlook and affect the Fund’s allocation to risk assets.

The economic environment and the outlook for further action from the Fed points to higher rates. However, we believe sustained inflation is needed to support a broader selloff in U.S. Treasuries. In the near term, we have positioned the Fund with a bias toward shorter key rate durations, favoring a steeper yield curve.

5

Management's Discussion of Fund Performance (Unaudited) (Continued)

Comparison of the Change in Value of a $10,000 Investment in the

Touchstone Active Bond Fund and the Bloomberg Barclays U.S. Aggregate Bond Index

Performance information does not reflect fees that are paid by the separate accounts through which shares of the Fund are sold. Inclusion of those fees would reduce figures for all periods.

The inception date of the Fund was January 1, 1999.

Note to Chart

The Bloomberg Barclays U.S. Aggregate Bond Index is an unmanaged index comprised of U.S. investment grade, fixed rate bond market securities, including government, government agency, corporate and mortgage-backed securities between one and ten years.

6

Management's Discussion of Fund Performance (Unaudited)

Touchstone Balanced Fund

Sub-Advised by Fort Washington Investment Advisors, Inc.

Effective October 28, 2017, the Sentinel Variable Products Balanced Fund was reorganized into the Touchstone Balanced Fund. At that time, Touchstone Advisors, Inc. and Fort Washington Investment Advisors, Inc. were respectively appointed as advisor and sub-advisor to the Fund.

Investment Philosophy

The Fund seeks to achieve its investment goal of providing investors with capital appreciation and current income by generally investing in a diversified portfolio comprising 60% equity securities and 40% fixed-income securities. With respect to equities, the Fund invests primarily in issuers having a market capitalization, at the time of purchase, above $5 billion. Equity securities include common stock and preferred stock. With respect to fixed-income, the Fund will invest primarily in bonds, including mortgage-related securities, asset-backed securities, government securities (both U.S. government securities and foreign sovereign debt), and corporate debt securities.

Fund Performance

The Touchstone Balanced Fund underperformed its first benchmark, the S&P 500® Index, and outperformed its second benchmark, the Bloomberg Barclays U.S. Aggregate Bond Index, for the 12-month period ended December 31, 2017. The Fund’s total return was 14.06 percent while the total return of the S&P 500® Index was 21.83 percent and the total return of the Bloomberg Barclays U.S. Aggregate Bond Index was 3.54 percent.

Market Environment

For the trailing twelve month period ended December 31, 2017, U.S. equities continued the bull market that began in 2009 as the market ended the period near all-time highs. Solid financial conditions and strong profit growth were the key drivers of the market. Consumer and business confidence remained high despite stalled healthcare legislation in the first half of the year. Markets benefited from an added boost in the later stages of 2017 on reports that the White House and Congressional Republican leaders were coalescing around a plan to cut the corporate tax rate. Leading the S&P 500® Index higher was Information Technology, while Health Care, Consumer Discretionary, Materials and Financials sectors also outperformed the broader index over the period. Sectors underperforming the index the most were Energy and Telecommunication Services. Consumer Staples, Utilities, Industrials and Real Estate also lagged.

Within fixed income, U.S. investment grade corporates outperformed U.S. Treasuries and securitized assets. The yield curve flattened over the twelve-month period with short-term rates rising as intermediate- and long-term rates fell. This was driven by the combination of the Fed continuing to gradually raise short-term rates and lower-than-expected inflation subduing the long-end of the yield curve.

Portfolio Review

Among equity sectors, the Fund benefited from stock selection in most sectors with notable success in the Real Estate, Materials and Industrials sectors. The Fund’s stock selection in the Energy and Health Care sectors detracted.

The low interest rate environment and steady economic growth created demand for yield which provided a tailwind to spread sectors. The Fund’s allocations to U.S. Agency bonds were positive contributors to performance, while its underweight to U.S. Corporate Credit detracted. Given the positive move in the market overall, the Fund’s holdings in cash detracted from performance over the period.

7

Management's Discussion of Fund Performance (Unaudited) (Continued)

Outlook

In our view, the equity market is priced at fair value. Three events typically stop a bull market: a credit cycle, higher inflation or an asset bubble. On the credit side, households, corporations, the public sector, and emerging markets are all doing reasonably well at this point. With regard to higher inflation, the balance of power between capital and labor is key. It is labor costs, which comprise approximately 70% of corporate expenses and dominate income statements causing the bulk of profit erosion in the late stages of the business cycle. To address asset bubbles,many investors point to the stocks of Facebook Inc. (Information Technology sector), Apple Inc. (Information Technology sector), Amazon.com Inc. (Consumer Discretionary sector), Netflix Inc. (Consumer Discretionary sector) and Alphabet Inc. (Information Technology sector), the “FAANGs”, as an issue. In our view the FAANGs are undervalued to fairly valued depending on which one you are talking about, plus the makeup of these companies is a far cry from the negative earnings, price-per-click valuation based stocks of the late 1990s. The sectors where below-average discount rates must be used to justify current valuation levels are Consumer Staples, Utilities and part of the Real Estate sector, which are areas where investors typically put their money as a bond substitute. Lastly, the breadth of the market is doing well at this juncture which is a sign of a healthy market. Within fixed income, credit spreads and interest rates are at historically low levels, likely limiting total return potential to income, with little room for price appreciation. Risky assets, such as high yield corporate credit, appear overvalued while “safe haven” assets, such as U.S. Treasuries, provide little return potential with much greater downside risk.

8

Management's Discussion of Fund Performance (Unaudited) (Continued)

Comparison of the Change in Value of a $10,000 Investment in the

Touchstone Balanced Fund, the Bloomberg Barclays U.S. Aggregate Bond Index and the

S&P 500® Index

Performance information does not reflect fees that are paid by the separate accounts through which shares of the Fund are sold. Inclusion of those fees would reduce figures for all periods.

The inception date of the Fund was August 1, 2003.

Notes to Chart

The Bloomberg Barclays U.S. Aggregate Bond Index is an unmanaged index comprised of U.S. investment grade, fixed rate bond market securities, including government, government agency, corporate and mortgage-backed securities between one and ten years.

The S&P 500® Index is a group of 500 widely held stocks and is commonly regarded to be representative of the large capitalization stock universe.

9

Management's Discussion of Fund Performance (Unaudited)

Touchstone Bond Fund

Sub-Advised by Fort Washington Investment Advisors, Inc.

Effective October 28, 2017, the Sentinel Variable Products Bond Fund was reorganized into the Touchstone Bond Fund. At that time,Touchstone Advisors, Inc. and Fort Washington Investment Advisors, Inc. were respectively appointed as advisor and sub-advisor to the Fund.

Investment Philosophy

The Fund seeks to provide as high a level of current income as is consistent with the preservation of capital. Capital appreciation is a secondary goal. Under normal circumstances, the Fund invests at least 80% of its assets in bonds. Bonds include mortgage-related securities, asset-backed securities, government securities and corporate debt securities. The Fund primarily invests in investment-grade debt securities, but may invest up to 30% of the Fund’s total assets in non-investment-grade debt securities.

Fund Performance

The Touchstone Bond Fund outperformed its benchmark, the Bloomberg Barclays U.S. Aggregate Bond Index, for the 12-month period ended December 31, 2017. The Fund’s total return was 3.67 percent, while the benchmark’s total return was 3.54 percent.

Market Environment

The yield curve flattened in 2017 with rates on the front end of the curve rising and on the long end falling. U.S. 10-year Treasury yields started the period at 2.35 percent and essentially ended the year at the same yield, settling at 2.40 percent. This does not mean, however, that yields were stable during the course of the fiscal year, as they moved considerably. The long end of the curve fell considerably and bottomed near 2.00 percent in September 2017 before rebounding as inflation expectations increased amid solid economic growth and improvement in underlying fundamentals. These same factors prompted the Fed to raise its target overnight rate three times during 2017. Markets have priced in between two and three additional hikes in 2018, expectations that seem reasonable given the strong underlying fundamentals currently present in the economy. The appointment of Jerome Powell to lead the Fed is unlikely to materially alter the Fed’s anticipated path to raise rates. However, the appointment of five new members of the Fed warrants close attention, as they have the potential to shift the path put in place by previous members.

Financial conditions continued to be supportive of risk assets and continued economic growth in 2017, ending the year at the easiest levels since 2014. Credit spreads for both investment grade and High Yield Bonds contracted significantly and are now at multi-year lows. Global central bank policy has remained generally accommodative, but will directionally move less so in developed countries.

Portfolio Review

Outperformance for the period was primarily driven by an overweight to corporate bonds, a sector which performed well during the year. Amid an environment of improving economic growth, default rates remained low and credit spreads for corporate bonds tightened.

While returns on cash equivalents improved throughout the year as short-term interest rates increased, cash and cash equivalents still lagged the broader benchmark. As a result, the Fund’s large cash position detracted from relative returns.

With respect to duration, the Fund maintained a barbell approach with large positions in very short maturity securities (e.g., cash and cash equivalents) and longer maturity securities. In aggregate, the Fund had a slightly

10

Management's Discussion of Fund Performance (Unaudited) (Continued)

longer duration relative to the benchmark. With the 10-year Treasury yield relatively unchanged from the start of the fiscal year to the end, this duration positioning was not a significant driver of relative performance.

Outlook

Financial conditions remain stable, economic fundamentals are solid, and recession risk is increasingly low notwithstanding the age of the credit cycle. Given this backdrop, the Fund continued to be moderately overweight risk assets relative to the benchmark. However, this overweight has declined somewhat in recent quarters as asset prices have increased to reflect the market’s optimistic view of the economy. While we think that the potential for significant further tightening is remote, we also believe a sustained widening seems unlikely, barring an external shock as the fundamental and technical outlooks remain strong. As such, we remain comfortable with a modest overweight to risk given the positive economic outlook and low rate of expected defaults. Global factors will be watched closely for any broader impact which might influence the economic outlook and affect the Fund’s allocation to risk assets.

The economic environment and the outlook for further action from the Fed points to higher rates. However, we believe sustained inflation is needed to support a broader selloff in U.S. Treasuries. In the near term, we have positioned the Fund with a bias toward shorter durations, favoring a steeper yield curve.

11

Management's Discussion of Fund Performance (Unaudited) (Continued)

Comparison of the Change in Value of a $10,000 Investment in the

Touchstone Bond Fund and the Bloomberg Barclays U.S. Aggregate Bond Index

Performance information does not reflect fees that are paid by the separate accounts through which shares of the Fund are sold. Inclusion of those fees would reduce figures for all periods.

The inception date of the Fund was August 1, 2003.

Note to Chart

The Bloomberg Barclays U.S. Aggregate Bond Index is an unmanaged index comprised of U.S. investment grade, fixed rate bond market securities, including government, government agency, corporate and mortgage-backed securities between one and ten years.

12

Management's Discussion of Fund Performance (Unaudited)

Touchstone Common Stock Fund

Sub-Advised by Fort Washington Investment Advisors, Inc.

Effective October 28, 2017, the Sentinel Variable Products Common Stock Fund was reorganized into the Touchstone Common Stock Fund. At that time, Touchstone Advisors, Inc. and Fort Washington Investment Advisors, Inc. were respectively appointed as advisor and sub-advisor to the Fund.

Investment Philosophy

The Fund seeks to invest at least 80 percent of its assets in large capitalization equity securities. The Fund’s sub-advisor, Fort Washington Investment Advisors, Inc., seeks to invest in companies that are trading below what is believed to be the estimate of the companies’ intrinsic value and have a sustainable competitive advantage or a high barrier to entry in place. The barrier(s) to entry can be created through a cost advantage, economies of scale, high customer loyalty or a government barrier (e.g. license or subsidy). Fort Washington believes that the strongest barrier to entry is the combination of economies of scale and high customer loyalty.

Fund Performance

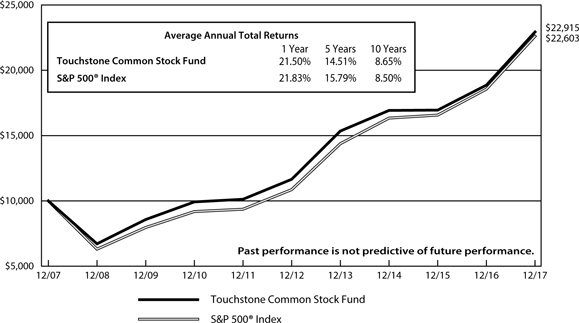

The Touchstone Common Stock Fund underperformed its benchmark, the S&P 500® Index, for the 12-month period ended December 31, 2017. The Fund’s total return was 21.50 percent while the benchmark’s total return was 21.83 percent.

Market Environment

For the year, U.S. equities continued the bull market that began in 2009 as the market ended the period near all-time highs. Solid financial conditions and strong profit growth were the key drivers of the market. Consumer and business confidence remained high despite stalled healthcare legislation in the first half of the year. Markets benefited from an added boost in the later stages of 2017 as the White House and Congressional Republican leaders coalesced around a plan for tax reform. Leading the S&P 500® Index higher were the Information Technology, Health Care, Materials, Consumer Discretionary, and Financials sectors. Weaker sectors were Energy, Telecommunication Services, Consumer Staples, Real Estate, and Utilities, while the Industrials sector performed roughly in-line with the benchmark.

Portfolio Review

Sectors in which the Fund outperformed the benchmark included Real Estate, Materials, Industrials, Consumer Staples,Telecommunication Services, and Financials. Consumer Discretionary and Health Care sector positions underperformed while Energy and Information Technology positions performed roughly in-line with the sector. The Fund did not own any Utilities sector stocks during the year. Given the positive move in the market overall, holdings in cash equivalents detracted from performance over the period. Sector allocation was a slight negative to performance primarily due to the overweight in the Energy sector and the aforementioned cash drag.

The Fund’s top contributors for the year were Boeing Co. (Industrials sector), Estee Lauder Co. (Consumer Staples sector), and Equinix, Inc. (Real Estate sector). Boeing, the manufacturer of commercial aircraft, rose significantly during 2017 due to a better-than-expected increase in airplane production and reported large order pipeline. Estee Lauder, the maker of beauty and skin care products, experienced a strong stock price rise during the second half of the year following better-than-expected financial results from its skin care product line. Equinix, a real estate investment trust (REIT) that owns and operates data centers, saw its price rise significantly in the first half of the year following its acquisition of data center properties from Verizon.

The Fund’s top three performance detractors for the year were Amazon.com Inc. and Omnicom Group Inc. (both from the Consumer Discretionary sector), and Merck & Co. (Health Care sector). Amazon.com, an online retail and web services company, experienced strong stock price performance during the year due to

13

Management's Discussion of Fund Performance (Unaudited) (Continued)

better-than-expected reported profit and cash flow figures. However, the Fund bought Amazon.com late in the year during the manager transition and experienced limited participation in the stock. Omnicom Group, an advertising and marketing company primarily operating in traditional media (e.g. print), experienced a decline in its stock price due to a decline within the traditional media market. Merck & Co., a large pharmaceutical company, withdrew its application with the European Union for a lung cancer drug during the fourth quarter. This unexpected news caused a significant, short-term stock sell off in the fourth quarter.

Outlook

While much of the financial media is focused on the latest moves in Bitcoin, the stock market continues to move ahead. The gains were supported by a favorable macroeconomic backdrop. Global economic growth has accelerated at a solid pace, synchronized across major regions. Corporate earnings have enjoyed a strong upturn from their earlier slump in 2015/early 2016 and have outperformed expectations. Plus, inflation has remained low, thereby keeping the Fed and other major central banks in accommodative mode. Finally, we believe passage of the tax reform package will improve corporate cash flows. All these things have combined to fuel higher equity valuations.

In our view, the equity market is priced at fair value. That said, three events that may typically stop a bull market are a credit cycle, higher inflation or an asset bubble. On the credit side, households, corporations, the public sector, and emerging markets are all doing reasonably well at this point. With regard to higher inflation, the balance between capital and labor is key. It is labor costs, which are approximately 70 percent of corporate costs that dominate income statements and cause the bulk of profit erosion in the late stages of the business cycle. Many investors cite the FAANG stocks to make a case for stock valuations being at an asset bubble level. However, our view is that the FAANGs are undervalued to fairly-valued depending on which stock is being analyzed. Plus, the composition of each of these companies is quite different from the negative earnings, price-per-click valuation stocks of the late 1990s. In some circumstances these are winner-take-all industries where scale and network effects allow just a few companies to dominate. But one could argue that the stocks that are potentially overvalued are within the Consumer Staples, Utilities and portions of the Real Estate sectors. More specifically, these stocks operate in more stable, often slower growth parts of the economy and are more sensitive to interest rate changes. Finally, the breadth of the market is broadly doing well at this juncture which is a sign of a healthy market.

14

Management's Discussion of Fund Performance (Unaudited) (Continued)

Comparison of the Change in Value of a $10,000 Investment in the

Touchstone Common Stock Fund and the S&P 500® Index

Performance information does not reflect fees that are paid by the separate accounts through which shares of the Fund are sold. Inclusion of those fees would reduce figures for all periods.

The inception date of the Fund was November 30, 2000.

Note to Chart

The S&P 500® Index is a group of 500 widely held stocks and is commonly regarded to be representative of the large capitalization stock universe.

15

Management's Discussion of Fund Performance (Unaudited)

Touchstone Focused Fund

Sub-Advised by Fort Washington Investment Advisors, Inc.

Investment Philosophy

The Touchstone Focused Fund seeks to invest in companies of all capitalizations that are trading below what is believed to be the estimate of their intrinsic value and have a sustainable competitive advantage or a high barrier to entry in place. The barrier(s) to entry can be created through a cost advantage, economies of scale, high customer loyalty or a government barrier (e.g. license or subsidy). Fort Washington believes that the strongest barrier to entry is the combination of economies of scale and high customer loyalty.

Fund Performance

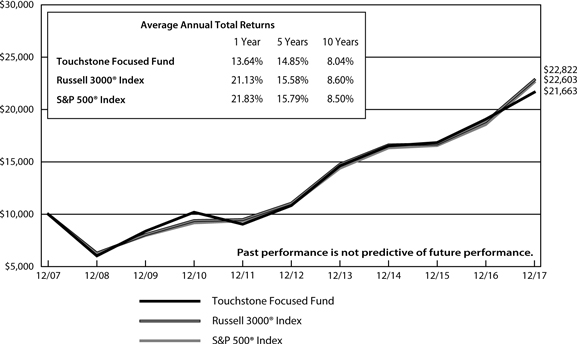

The Touchstone Focused Fund underperformed its benchmarks, the Russell 3000® Index and the S&P 500® Index, for the 12-month period ended December 31, 2017. The Fund’s total return was 13.64 percent while the total return of the Russell 3000® Index was 21.13 percent and the total return of the S&P 500® Index was 21.83 percent.

Market Environment

For the year, U.S. equities continued the bull market that began in 2009 as the market ended the period near all-time highs. Solid financial conditions and strong profit growth were the key drivers of the market. Consumer and business confidence remained high despite stalled healthcare legislation in the first half of the year. Markets benefited from an added boost in the later stages of 2017 as the White House and Congressional Republican leaders coalesced around a plan for tax reform.

Leading the benchmark higher were the Information Technology, Health Care, Materials, Industrials and Consumer Discretionary sectors. The weaker sectors were Energy, Financials and Real Estate.

Portfolio Review

Sectors in which the Fund outperformed the benchmark included Consumer Discretionary and Real Estate. The Industrials, Energy, Consumer Staples, Materials, Telecommunication Services, and Information Technology sectors all underperformed the benchmark. The Financials and Health Care sectors performed approximately in-line with the benchmark over the course of the year. Given the positive move in the market overall, holdings in cash detracted from performance. In sum, sector allocation was slightly positive primarily due to underweights in the Utilities and Consumer Staples sectors.

The Fund’s largest relative contributors were Amazon.com Inc. and Yum China Holdings Inc. (both from the Consumer Discretionary sector), and Jones Lang Lasalle Inc. (Real Estate sector). Amazon.com rose due to acceleration of growth in Prime and Amazon Web Services. Yum China benefited from expansion of its geographic footprint in China and positive results in its existing restaurants. Jones Lang Lasalle rose on higher fee revenue from leasing and property management.

The Fund’s largest detractors to relative performance were General Electric Co. and Vista Outdoor Inc.(both from the Industrials sector), and Avnet Inc. (Information Technology sector). General Electric declined due to weakness in oil, gas, and power end markets combined with the dividend cut and reduced guidance. Vista Outdoor declined due to overcapacity in the ammunition market. Avnet fell as the company had challenges with the implementation of a new Enterprise Resource Planning system that led to customer departures.

From a market cap perspective, the Fund continued to maintain an overweight to larger-cap businesses (companies with a market cap above $10 billion), while maintaining an underweight allocation to both mid-cap (companies with a market cap between $2 billion and $10 billion) and small-cap stocks (companies with a market cap

16

Management's Discussion of Fund Performance (Unaudited) (Continued)

below $2 billion). Collectively, this allocation decision was additive to relative performance as large-cap stocks outperformed mid- and small-cap stocks during the year. Investments made in international companies outperformed the benchmark while domestic holdings lagged.

During the year we increased the weighting to the Information Technology and Consumer Discretionary sectors while we decreased the weight to the Consumer Staples, Energy, Health Care, Industrials sectors and cash holdings. At the end of the year, the Fund had overweight allocations to the Consumer Discretionary and Information Technology sectors and underweight allocations to the Consumer Staples, Materials, and Industrials sectors. The weights to the Energy, Health Care, Financials, Real Estate, and Telecommunication Services sectors were approximately equal to the benchmark. No positions were held in the Utilities sector at the end of the year.

Outlook

While much of the financial media is focused on the latest moves in Bitcoin, the stock market continues to move ahead. The gains were supported by a favorable macroeconomic backdrop. Global economic growth has accelerated at a solid pace, synchronized across major regions. Corporate earnings have enjoyed a strong upturn from their earlier slump in 2015/early 2016 and have outperformed expectations. Plus, inflation has remained low, thereby keeping the Fed and other major central banks in accommodative mode. Finally, we believe passage of the tax reform package will improve corporate cash flows. All these things have combined to fuel higher equity valuations.

In our view, the equity market is priced at fair value. That said, three events that may typically stop a bull market are a credit cycle, higher inflation or an asset bubble. On the credit side, households, corporations, the public sector, and emerging markets are all doing reasonably well at this point. With regard to higher inflation, the balance between capital and labor is key. It is labor costs, which are approximately 70 percent of corporate costs, that dominate income statements and cause the bulk of profit erosion in the late stages of the business cycle. Many investors cite the FAANG stocks to make a case for stock valuations being at an asset bubble level. However, our view is that the FAANGs are undervalued to fairly-valued depending on which stock is being analyzed. Plus, the composition of each of these companies is quite different from the negative earnings, price-per-click valuation stocks of the late 1990s. In some circumstances, we believe these are winner-take-all industries where scale and network effects allow just a few companies to dominate. But one could argue that the stocks that are potentially overvalued are within the Consumer Staples, Utilities and portions of the Real Estate sectors. Specifically, we believe these stocks operate in more stable, often slower growth parts of the economy and are more sensitive to interest rate changes. Finally, the breadth of the market is broadly doing well at this juncture which is a sign of a healthy market.

17

Management's Discussion of Fund Performance (Unaudited) (Continued)

Comparison of the Change in Value of a $10,000 Investment in the

Touchstone Focused Fund, the Russell 3000® Index and the S&P 500® Index

Performance information does not reflect fees that are paid by the separate accounts through which shares of the Fund are sold. Inclusion of those fees would reduce figures for all periods.

The inception date of the Fund was November 21, 1994.

Notes to Chart

The Russell 3000® Index measures the performance of the 3,000 largest U.S. companies based on total market capitalization, which represents approximately 98% of the investable U.S. equity market.

The S&P 500® Index is a group of 500 widely held stocks and is commonly regarded to be representative of the large capitalization stock universe.

The Frank Russell Company (FRC) is the source and owner of the Russell 3000® Index data contained or reflected in this material and all trademarks and copyrights related thereto. The material may contain confidential information and unauthorized use, disclosure, copying, dissemination or redistribution is strictly prohibited. This is a Touchstone Investments presentation of the data, and FRC is not responsible for the formatting or configuration of this material or for any inaccuracy in the presentation thereof.

18

Management's Discussion of Fund Performance (Unaudited)

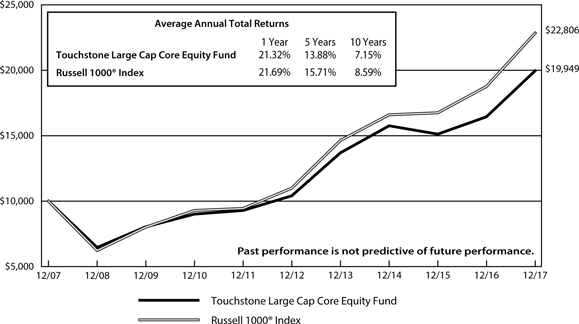

Touchstone Large Cap Core Equity Fund

Sub-Advised by The London Company

Investment Philosophy

The Touchstone Large Cap Core Equity Fund seeks long-term capital growth by investing primarily in common stocks of large-cap U.S. listed companies. The Fund seeks to purchase financially stable large-cap companies that the sub-advisor believes are consistently generating high returns on unleveraged operating capital, run by shareholder-oriented management, and trading at a discount to the company’s respective private market values.

Fund Performance

The Touchstone Large Cap Core Equity Fund underperformed its benchmark, the Russell 1000® Index, for the 12-month period ended December 31, 2017. The Fund’s total return was 21.32 percent, while the benchmark’s total return was 21.69 percent.

Market Environment

For the trailing twelve months ended December 31, 2017, the stock market was strong and steady. The S&P 500® Index also exhibited twelve straight months of positive returns. Large-capitalization stocks outperformed both mid- and small-capitalization stocks, though all posted solid gains. Growth stocks significantly outpaced value stocks across the market cap spectrum, and cyclical sectors outperformed defensive sectors with the exception of the mid-capitalization segment. We believe the meaningful near-term outperformance of growth compared to value was due, in part, to the continued dominance of a few Information Technology companies known as FAANG stocks, along with other high-flying technology and cloud-focused companies. The dramatic outperformance of these stocks created challenging comparisons for value benchmarks.

During the period, the benchmark was led by the Information Technology, Materials, Consumer Discretionary and Health Care sectors, while the Energy and Telecommunication Services sectors lagged. The Information Technology sector benefited from the revitalization of the FAANG stocks which provided a significant boost to the outperforming sector. Overall, returns were generally outsized for growth stocks and for Information Technology specifically, but performance was conjoined by an unprecedented absence of volatility. In fact, the Chicago Board Options Exchange (CBOE) Volatility Index (VIX) was near record-low territory on a daily basis during the period.

The year ended with strong investor optimism surrounding tax cuts with the passage of a new tax reform bill. Further, there continued to be speculation about the Fed’s plans to normalize rates which could dictate asset levels going forward.

Portfolio Review

The Fund’s sector allocation and stock selection contributed to relative returns during the period. From a sector perspective, the Fund’s underweight to the Energy and Real Estate sectors had a positive impact on relative performance. This was partially offset by the negative impact of an underweight to the Information Technology and Health Care sectors.

Among the individual stocks that contributed to Fund performance during the period were Deere & Co. (Industrials sector), Visa Inc. (Information Technology sector), Dollar Tree Inc. (Consumer Discretionary sector), Progressive Corp. and BlackRock Inc. (both from the Financials sector). Deere & Co. is a manufacturer of agricultural, construction and forestry machinery. The stock moved notably higher during the period reflecting growth in the global economy and optimism that the agriculture cycle is nearing the bottom. Deere’s recent acquisition of the Wirtgen Group is expected to provide a leadership position in the road construction equipment market

19

Management's Discussion of Fund Performance (Unaudited) (Continued)

in Europe. Visa, a payments technology company, moved steadily higher throughout the year along with the Information Technology sector. The company continued to benefit from a global shift toward spending using credit cards and was rewarded for solid growth in a low-growth environment. Visa also hosted an encouraging investor day that outlined its plans for new opportunities to drive long-term expansion of its platform. Visa has historically generated copious cash flow and benefited from significant barriers to entry, a duopoly with Mastercard Inc. and an attractive long-term growth profile. Dollar Tree, a chain of discount variety stores, rallied as the company showed improvement at its Family Dollar stores that were acquired in 2015. Two consecutive quarters of positive same-store sales and margin improvement at Family Dollar along with consistent results at Dollar Tree stores drove the stock. Progressive, an insurance provider, outperformed as the company continued to take market share in the auto insurance market. The company’s attractive pricing also helped drive share gains while its conservative underwriting kept losses to a minimum. The company has been slowly building its homeowner’s insurance business and can now sell joint policies, which we believe should drive policy growth over time. BlackRock, an investment management corporation, moved higher as the company experienced positive asset flows largely driven by its leadership position in the exchange traded funds market. If the trend toward passive investing continues, we believe BlackRock is positioned well for future growth while maintaining a strong balance sheet.

Among the stocks that detracted from Fund performance were O’Reilly Automotive Inc., CarMax Inc. (both from the Consumer Discretionary sector), Alleghany Corp. (Financials sector), NewMarket Corp. (Materials sector) and Alexion Pharmaceuticals Inc. (Health Care sector). O’Reilly Automotive, an auto parts retailer, declined during the period due to softer than expected earnings which management attributed to a warm winter and delays in consumer tax refunds. While same-store sales trends were weaker than expected, the company experienced solid increases in its average ticket (the average size of individual credit card sales). Additionally, the threat of Amazon.com Inc. taking market share in the do-it-yourself retail business has led to concern among investors. Going forward, however, we believe fundamental industry factors remain healthy and demand should remain positive. CarMax, a used-car retailer, ended the year essentially flat after declining during the fourth quarter due to disappointing same-store sales growth. Investors have grown increasingly concerned about weaker auto sales; however, while reports suggest auto sales were down for 2017 versus 2016, the decline was minimal and total sales remained near all-time highs. Going forward, we believe CarMax has been successful at managing its gross profit per used-car sale and we remain attracted to the company’s differentiated store format and ability to add more stores in the U.S. Alleghany, an insurance holding company, ended the period relatively flat despite a strong year in 2016, primarily due to the massive hurricane losses during the third quarter of 2017. We remain attracted to the stock based on the company’s excellent record of book value growth over time despite the vagaries of the insurance underwriting cycle. NewMarket, a petroleum additives company, underperformed which reflected higher raw material costs and lower pricing. We remain attracted to the company’s solid revenue outlook in the market for fuel additives and lubricants, as well as its pricing power in a consolidated industry and excellent history of capital allocation. Alexion Pharmaceuticals, a biopharmaceutical company focused on therapeutic products, for patients with ultra-rare disorders through the development and commercialization of life-transforming therapeutic products declined during the portion of the year in which the Fund owned the stock. Initial optimism surrounding a corporate restructuring and the potential for higher margins gave way to concerns about a competitor in the European market. We were, however, encouraged by the company’s recent patent extensions in the U.S. and Japan, and a decision in Europe is expected within the year. Further, recent insider purchases and cooperation with an activist investor should benefit the company, along with its monopolistic position in the rare disease space.

During the period, the Fund sold its positions in Mosaic Inc. (Materials sector), General Electric Co. (Industrials sector) and Edgewell Personal Care Inc. (Consumer Staples sector). Mosaic was sold after the company hit the Fund’s soft stop loss. With regard to General Electric and Edgewell, confidence waned in each company’s

20

Management's Discussion of Fund Performance (Unaudited) (Continued)

ability to provide suitable downside protection for the Fund. Further, the transition at General Electric has taken longer than expected and new competition from online razor competitors threatened the long-term viability at Edgewell.

The Fund initiated positions in Southwest Airlines Co. (Industrials sector), Alphabet Inc. Class C Shares (Information Technology sector) and Alexion Pharmaceuticals Inc. (Health Care sector). Southwest Airlines is the largest U.S. carrier offering a point-to-point network, which allows the company to avoid more congested hubs and increase airplane utilization. Return on capital has improved significantly in recent years reflecting consolidation in the industry, network optimization and lower fuel prices. We believe the more consolidated industry is a long-term positive for pricing and should lead to higher returns on capital. The company’s balance sheet is also strong with a net cash position. We believe the stock trades at an attractive discount to its intrinsic value, assuming conservative growth. The purchase of Alphabet, or Google as many people know it, reflects our optimism surrounding the company’s competitive advantages and leading market share in its Search, Maps, Ads, YouTube, Android and Chrome divisions. The company generates attractive returns on capital and maintains a strong balance sheet. The stock is not cheap by traditional valuation metrics, but we believe the company’s competitive advantages will persist while its cash flow generation and balance sheet may limit potential downside. We believe Alexion’s focus on ultra-rare diseases should insulate the company from recent industry concerns over drug pricing. Legislatures generally view the Orphan Drug Act as necessary to promote research and development as well as an investment into rare diseases that would be otherwise overlooked. Given that the drugs are lifesaving, Alexion can also make a strong argument that its drugs meet the value-based pricing criteria. Company management also expects growth to come from volume gains with new indications of its drug Soliris. Recent management additions and significant insider purchases provided further confidence in the stock.

Outlook

The U.S. economy continued to expand at a moderate pace with relatively low inflation. Looking ahead, we remain optimistic about the economy and believe there are a number of positives that should support consumer spending in the future, including a strong labor market, solid housing and lower tax rates beginning in 2018. Furthermore, the core rate of inflation remained below the Fed’s target level of two percent.

With regard to monetary policy, the Fed raised the short-term federal funds rate by 25 basis points in December. The consensus view is that another three additional rate hikes will occur in 2018 as the Fed continues to normalize its balance sheet. While we do not expect a big change in long-term rates from the balance sheet normalization process, over time the reversal of quantitative easing could lead to a steepening of the yield curve.

The combination of solid economic growth, low inflation and relatively low interest rates usually creates a positive environment for stocks. We believe this holds true today, but there are risks. We believe the potential risks include relatively high valuations for stocks using traditional metrics, geopolitical turmoil, excessive government stimulus, rising inflation or the Fed taking a more aggressive stance. We believe the risks and rewards are somewhat balanced as they relate to stocks overall, but we will remain cautious and focused on limiting downside in the Fund’s holdings.

Looking ahead, we remain optimistic despite the current market headwinds. We believe the attractive candidates we are vetting today are a result of what the market is providing, and are consistent with our general outlook. Specifically, we believe the Fund’s downside risk can be mitigated by remaining focused on those companies with pricing power, copious cash generation and prudent capital allocation. We seek companies with strong returns on capital and flexibility to enhance shareholder value using the balance sheet. We believe over time that markets will self-correct and as such the Fund’s process is positioned well for a slow growth environment that rewards strong capital allocation.

21

Management's Discussion of Fund Performance (Unaudited) (Continued)

Comparison of the Change in Value of a $10,000 Investment in the

Touchstone Large Cap Core Equity Fund and the Russell 1000® Index

Performance information does not reflect fees that are paid by the separate accounts through which shares of the Fund are sold. Inclusion of those fees would reduce figures for all periods.

The inception date of the Fund was May 1, 1999.

Notes to Chart

The Russell 1000® Index measures the performance of the 1,000 largest companies in the Russell 3000® Index.

The Frank Russell Company (FRC) is the source and owner of the Russell 1000® Index data contained or reflected in this material and all trademarks and copyrights related thereto. The material may contain confidential information and unauthorized use, disclosure, copying, dissemination or redistribution is strictly prohibited. This is a Touchstone Investments presentation of the data, and FRC is not responsible for the formatting or configuration of this material or for any inaccuracy in the presentation thereof.

22

Management's Discussion of Fund Performance (Unaudited)

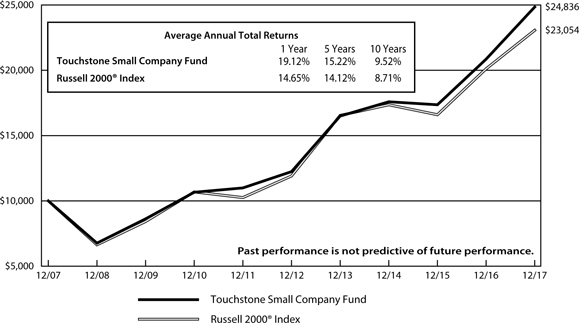

Touchstone Small Company Fund

Sub-Advised by Fort Washington Investment Advisors, Inc.

Effective October 28, 2017, the Sentinel Variable Products Small Company Fund was reorganized into the Touchstone Small Company Fund. At that time, Touchstone Advisors, Inc. and Fort Washington Investment Advisors, Inc. were respectively appointed as advisor and sub-advisor to the Fund.

Investment Philosophy

The Fund seeks to provide investors with growth of capital by investing primarily in common stocks of small companies that the sub-advisor believes are high quality, have superior business models, solid management teams, sustainable growth potential and are attractively valued.

Fund Performance

The Touchstone Small Company Fund outperformed its benchmark, the Russell 2000® Index, for the 12-month period ended December 31, 2017. The Fund’s total return was 19.12 percent while the total return of the benchmark was 14.65 percent.

Market Environment

U.S. small-cap equities posted strong returns for calendar year 2017. The small-cap market traded in a narrow range for the majority of the year until mid-August, then rallied into year-end to close near all-time highs.

The overall market and macroeconomic backdrop were favorable for risk assets, including small-cap equities. However, U.S. small-cap companies are only growing earnings in the low single digits. With this relatively low earnings growth rate, we believe market returns have principally been driven by expansion of the market’s increased valuation multiples. Volatility remained low in 2017.

U.S. small-cap sector performance was balanced. The Health Care, Industrials, Information Technology, Materials, and Consumer Discretionary sectors outperformed the benchmark, while Utilities, Financials, Real Estate, Telecommunication Services, and Consumer Staples underperformed the benchmark. Energy was the only sector that declined over the year.

Portfolio Review

The Consumer Discretionary sector was the top contributor to the Fund’s relative returns versus the benchmark during the fiscal year. While a relatively small exposure within the Fund, positioning in the Media industry was an area of particular strength. Solid performance in the Consumer Durables & Apparel and Consumer Services spaces more than offset the relative underperformance of the Fund’s retailing holdings. The Information Technology sector also contributed to relative performance. Semiconductors and Software & Services led the way. Technology hardware and equipment detracted from absolute performance.

Though an area of strong absolute returns during the year, the Fund’s Health Care positioning underperformed on a relative basis versus the benchmark. The underperformance was primarily driven by a lack of exposure to Pharmaceuticals and Biotechnology companies. The Fund historically has had little to no exposure to the Pharma and Biotech industry group, as we believe these companies typically have no earnings and offer a poor fit with our fundamentally based investment discipline. Ultimately, the Fund’s primary performance drag was not specific stocks, but rather an underexposure to the broad market. The Fund’s cash position was driven up by infusions of cash from liquidating several positions that had either been acquired in mergers and acquisitions (M&A) deals or that no longer met out market capitalization criteria detracted from performance. We were cautious in redeploying capital into a market that in our opinion appeared to be stretched from a valuation perspective.

23

Management's Discussion of Fund Performance (Unaudited) (Continued)

Penn National Gaming Inc. (Consumer Discretionary sector), an owner and operator of regional gaming and racing facilities, contributed to performance. Gaming industry trends improved in 2017, and Penn capitalized on the industry tailwind as the continued ramp up of newer properties and business segments performed ahead of expectations. Additionally, speculation (which was eventually confirmed by the company) for potential industry consolidation favorably impacted the stock price.

Tower Semiconductor Ltd. (Information Technology sector), a global leader in specialty semiconductor foundry services, also posted strong returns. The semiconductor industry experienced a strong up-cycle in 2017, with demand acceleration and industry consolidation benefiting all players. We believe Tower outperformed the industry with its focus on specialized niche markets that drove organic growth, with higher earnings and cash flow growth.

The Fund’s bottom two performing stocks were in the challenged retail industry. Tile Shop Holdings Inc. (Consumer Discretionary sector), an operator of specialty flooring stores, executed poorly on new product introductions at the same time it was experiencing a deceleration in sales trends and margin compression. The stock lost more than half of its value during the period. Meanwhile, specialty nutrition store operator Vitamin Shoppe Inc. (Consumer Discretionary sector) declined significantly after missing earnings expectations multiple times during the year. The Fund exited both stocks.

There were no significant changes to the Fund’s positioning during the 12-month period. Sector weights remained consistent, with the Information Technology and Health Care sectors holding the largest weights compared to the benchmark. The Financials sector remained the Fund’s largest underweight.

Outlook

U.S. small-cap equities have experienced significant appreciation off their February 2016 market bottom, achieving all-time highs. We believe much of the recent appreciation has been driven by corporate tax reform. Meaningful corporate tax reform would be a positive development for U.S. small caps given their larger degree of exposure to domestic activity and earnings. M&A activity has historically been a driver of small-cap and Fund returns. The current environment is conducive to M&A activity and we believe companies may gain additional impetus for deal-making considering the new tax plan.

In this environment, we remained focused and will continue to focus on executing our fundamental stock selection and portfolio construction process. We believe that an attractive risk/reward profile can be generated by investing in quality small-cap companies that are poised to benefit from improvements in their business model, leadership teams, and/or industry positioning. We believe disciplined valuation analysis is needed to identify favorable entry and exit points.

24

Management's Discussion of Fund Performance (Unaudited) (Continued)

Comparison of the Change in Value of a $10,000 Investment in the

Touchstone Small Company Fund and the Russell 2000® Index

Performance information does not reflect fees that are paid by the separate accounts through which shares of the Fund are sold. Inclusion of those fees would reduce figures for all periods.

The inception date of the Fund was November 30, 2000.

Notes to Chart

The Russell 2000® Index measures the performance of the small-cap segment of the U.S. equity universe.

The Frank Russell Company (FRC) is the source and owner of the Russell 2000® Index data contained or reflected in this material and all trademarks and copyrights related thereto. The material may contain confidential information and unauthorized use, disclosure, copying, dissemination or redistribution is strictly prohibited. This is a Touchstone Investments presentation of the data, and FRC is not responsible for the formatting or configuration of this material or for any inaccuracy in the presentation thereof.

25

Management's Discussion of Fund Performance (Unaudited)

Touchstone ETF Funds

Sub-Advised by Wilshire Associates Incorporated

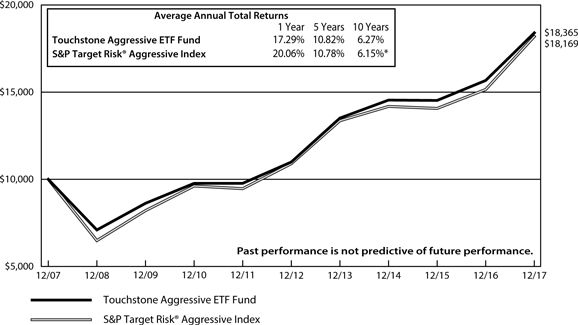

Touchstone Aggressive ETF Fund

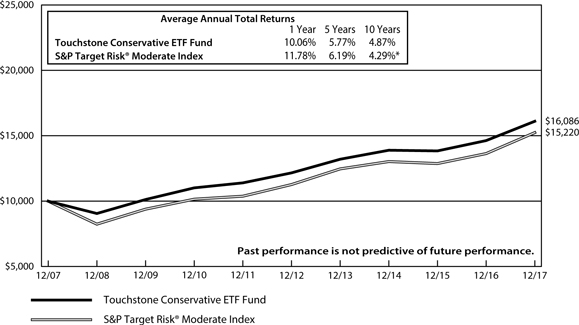

Touchstone Conservative ETF Fund

Touchstone Moderate ETF Fund

Investment Philosophy

Three funds which invest in Exchange-Traded Funds (ETFs) are available for investors seeking “lifestyle” products for their annuity holdings. The three strategic options include: the Conservative, Moderate, and Aggressive ETF Funds. These funds allocate their assets among up to ten ETFs. These ten ETF selections generally do not change dramatically over time. The more conservative fund has a higher bond weighting and the more aggressive fund has a lower bond weighting.

Fund Performance

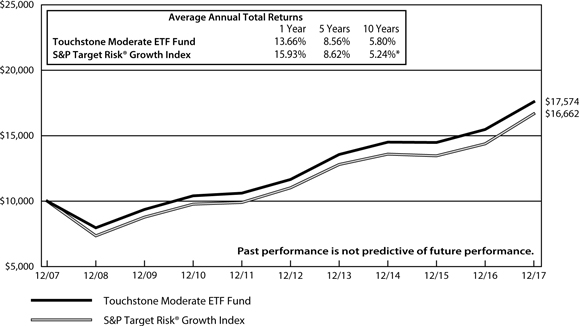

The Touchstone Aggressive ETF Fund underperformed its benchmark, the S&P Target Risk® Aggressive Index, for the 12-month period ended December 31, 2017. The Fund’s total return was 17.29 percent while the total return of the bench mark was 20.06 percent. The Touchstone Conservative ETF Fund underperformed its benchmark, the S&P Target Risk® Moderate Index, for the 12-month period ended December 31, 2017. The Fund’s total return was 10.06 percent while the total return of the benchmark was 11.78 percent. The Touchstone Moderate ETF Fund underperformed its benchmark, the S&P Target Risk® Growth Index, for the 12-month period ended December 31, 2017. The Fund’s total return was 13.66 percent while the total return of the benchmark was 15.93 percent.

Market Environment

The U.S. stock market rose in 2017. Nine of the eleven major sectors produced positive gains, with only Energy and Telecommunications Services ending the year with negative returns. The best performing sectors were Information Technology, Materials and Health Care. Large capitalization stocks outperformed small-caps. Growth stocks led value during the year in both large- and small-capitalization spaces.

Equity markets outside of the U.S. produced strong returns during 2017, in both developed and emerging markets. The U.S. dollar continued to weaken, providing an additional boost for U.S. investors holding foreign currencies. With economic data out of Europe improving, European equities provided strong returns in the second and third quarters of 2017. Japan was one of the strongest developed markets during the fourth quarter due to stimulative policies by both the Bank of Japan and the national government. Japan is now experiencing its strongest economy in more than a decade. Emerging markets led all global equities during 2017 which was the strongest year for broad emerging markets equity since it recovered from the global financial crisis in 2009.

The U.S. Treasury yield curve continued to flatten during the year with short- to intermediate-term rates rising and long-term yields falling. The bellwether 10-year Treasury yield ended the year up slightly from year-end 2016. The Federal Open Market Committee increased its overnight rate three times in 2017, a total increase of 75 basis points and began its balance sheet reduction program. Credit spreads continued to tighten during the year, most noticeably with investment grade credit.

Real estate securities were up in the U.S. during the year with a stronger return globally, due in part to a weakening dollar. Commodities were mixed for the year as crude oil and gold prices rose while natural gas prices and master limited partnership returns were down.

26

Management's Discussion of Fund Performance (Unaudited) (Continued)

Portfolio Review

The Touchstone Conservative ETF Fund, Touchstone Moderate ETF Fund and Touchstone Aggressive ETF Fund underperformed their benchmarks during 2017. The Funds’ investments are determined by an optimization process that considers the long-term historical risk and return profiles of various asset classes. For instance, non-U.S. equities have been included due to the diversification benefits they provided to the Funds as a whole. During the 2017 market environment, when non-U.S. equities outperformed U.S. stocks, the underweight positioning in The Touchstone Funds relative to their respective benchmarks detracted from relative performance. Similarly, the overweight of the Touchstone Funds to Real Estate was a headwind as was their overweight to mid- and small-cap stocks within their U.S. equity allocations.

Several allocation changes occurred since the beginning of 2017. Thematically, those changes were similar across all three Funds. Most notably, the allocation to government fixed income was increased at the expense of investment grade and high yield credit. By adding government fixed income exposure, we added a partial hedge to the equity risk we were adding back to the portfolio. During mid-2017, exposure was initiated to the iShares Floating Rate Bond ETF in order to reduce interest rate risk within the Funds out of concern that a “neutral” duration posture, relative to the Bloomberg Barclays U.S. Aggregate Bond Index was adding materially more interest rate risk than is typical due to the increased duration of the index in recent years.

Exposure to international developed and emerging markets equities was increased substantially during the year due to our increased confidence in the ability of foreign equities to outpace U.S. equities. Every major global economy is growing and the fundamentals have improved rapidly in many regions. Coupled with the potential for U.S. dollar weakening and rapid corporate earnings growth, we believe that foreign equities will continue their recent outperformance versus domestic equities. During the fourth quarter of 2017, exposure to domestic and foreign real estate investment trusts (REITs) was eliminated in exchange for global equity exposure. We believe that REITs are relatively unattractive due to valuation concerns, and eliminating REITs also reduces the Funds’ interest rate sensitivity.

Outlook

Although global equities are not cheap, we believe that there is little risk of a recession in the near term across most of the world’s major economies. We continue to expect a moderating economic growth environment in the foreseeable future, and to believe that the current economic landscape warrants lower interest rates and lower expected returns across asset classes.

Developed markets remain relatively stable in terms of gross domestic product (GDP) growth on a normalized basis, and we are still seeing below average growth in emerging markets, albeit at a faster pace than in developed markets. On a forward looking basis, when we look at the Purchasing Managers Index, which is an indicator of economic health in the manufacturing sector of a country or a region, we continue to witness positive economic momentum in the foreign economies of both the Eurozone and Japan relative to the U.S. On a global basis, measures of inflation are mostly in-line with or slightly below historic averages. Given that global growth and inflation remain moderate, we believe that global central banks will be slower to tighten monetary policy relative to market expectations. Given ultra-low foreign developed market bond yields, we favor domestic fixed income over global fixed income. However, we recognize that further weakness in the U.S. dollar would serve to benefit foreign fixed income.

Although domestic equities remain fully valued, we believe that the outlook for continued domestic and foreign GDP growth is promising and provides comfort that equities are not poised for an imminent selloff. Given elevated forward price-earnings levels, any disappointment in U.S. corporate earnings growth is likely to be interpreted negatively. Investors have noted concerns that the U.S. Federal Reserve Board’s (Fed) decision to gradually shrink its balance sheet introduces additional risk to U.S. Treasury bonds, as this reduction in demand

27

Management's Discussion of Fund Performance (Unaudited) (Continued)

and increase in supply may introduce the additional risk of a significant rise in yields. While we acknowledge this risk, we believe that it is important to recognize the recent recovery in foreign demand for U.S. Treasury bonds following the net selling activity in 2016. The Fed may be stepping away, but foreign buyers have returned. With respect to credit markets, given the further narrowing of corporate bond yield spreads over Treasuries, we remain less favorable on credit.

28

Management's Discussion of Fund Performance (Unaudited) (Continued)

Comparison of the Change in Value of a $10,000 Investment in the

Touchstone Aggressive ETF Fund and the S&P Target Risk® Aggressive Index

*The launch date of the S&P Target Risk® Aggressive Index was September 25, 2008. All information for the index prior to its launch date is back-tested, based on the methodology that was in effect on the launch date. Back-tested performance, which is hypothetical and not actual performance, is subject to inherent limitations because it reflects application of an Index methodology and selection of index constituents in hindsight. No theoretical approach can take into account all of the factors in the markets in general and the impact of decisions that might have been made during the actual operation of an index. Actual returns may differ from, and be lower than, back-tested returns.

Performance information does not reflect fees that are paid by the separate accounts through which shares of the Fund are sold. Inclusion of those fees would reduce figures for all periods.

The inception date of the Fund was July 16, 2004.

Note to Chart

The S&P Target Risk® Aggressive Index is one of four multi-asset class indices that compose the S&P Target Risk Series. The S&P Target Risk® Aggressive Index emphasizes exposure to equities, maximizing opportunities for long-term capital accumulation. It may include small allocations to fixed income to enhance portfolio efficiency.

29

Management's Discussion of Fund Performance (Unaudited) (Continued)

Comparison of the Change in Value of a $10,000 Investment in the

Touchstone Conservative ETF Fund and the S&P Target Risk® Moderate Index

*The launch date of the S&P Target Risk® Moderate Index was September 25, 2008. All information for the index prior to its launch date is back-tested, based on the methodology that was in effect on the launch date. Back-tested performance, which is hypothetical and not actual performance, is subject to inherent limitations because it reflects application of an Index methodology and selection of index constituents in hindsight. No theoretical approach can take into account all of the factors in the markets in general and the impact of decisions that might have been made during the actual operation of an index. Actual returns may differ from, and be lower than, back-tested returns.

Performance information does not reflect fees that are paid by the separate accounts through which shares of the Fund are sold. Inclusion of those fees would reduce figures for all periods.

The inception date of the Fund was July 16, 2004.

Note to Chart

The S&P Target Risk® Moderate Index is one of four multi-asset class indices that compose the S&P Target Risk Series. The S&P Target Risk® Moderate Index offers significant exposure to fixed income, while also increasing opportunities for higher returns through equities.

30

Management's Discussion of Fund Performance (Unaudited) (Continued)

Comparison of the Change in Value of a $10,000 Investment in the

Touchstone Moderate ETF Fund and the S&P Target Risk® Growth Index

*The launch date of the S&P Target Risk® Growth Index was September 25, 2008. All information for the index prior to its launch date is back-tested, based on the methodology that was in effect on the launch date. Back-tested performance, which is hypothetical and not actual performance, is subject to inherent limitations because it reflects application of an Index methodology and selection of index constituents in hindsight. No theoretical approach can take into account all of the factors in the markets in general and the impact of decisions that might have been made during the actual operation of an index. Actual returns may differ from, and be lower than, back-tested returns.

Performance information does not reflect fees that are paid by the separate accounts through which shares of the Fund are sold. Inclusion of those fees would reduce figures for all periods.

The inception date of the Fund was July 16, 2004.

Note to Chart

The S&P Target Risk® Growth Index is one of four multi-asset class indices that compose the S&P Target Risk Series. The S&P Target Risk® Growth Index increases exposure to equities, while also providing limited fixed income exposure to diversify risk.

31

Tabular Presentation of Portfolios of Investments (Unaudited)

December 31, 2017

The illustrations below provide each Fund’s credit quality and/or sector allocation. We hope it will be useful to shareholders as it summarizes key information about each Fund’s investments.

| Touchstone Active Bond Fund | ||||

| Credit Quality* | (% of Investment Securities) | |||

| AAA/Aaa | 52.4 | % | ||

| AA/Aa | 4.9 | |||

| A/A | 10.0 | |||

| BBB/Baa | 20.8 | |||

| BB/Ba | 0.7 | |||

| CCC | 0.8 | |||

| Not Rated | 5.3 | |||

| Cash Equivalents | 5.1 | |||

| Total | 100.0 | % | ||

| Touchstone Balanced Fund | ||||

| Credit Quality* | (% of Fixed Income Securities) | |||

| AAA/Aaa | 71.9 | % | ||

| AA/Aa | 4.4 | |||

| A/A | 6.8 | |||

| BBB/Baa | 16.2 | |||

| BB/Ba | 0.7 | |||

| 100.0 | % | |||

| Sector Allocation** | (% of Net Assets) | |||

| Common Stocks | ||||

| Information Technology | 17.0 | % | ||

| Consumer Discretionary | 11.5 | |||

| Financials | 10.9 | |||

| Health Care | 7.0 | |||

| Industrials | 6.0 | |||

| Energy | 3.4 | |||

| Real Estate | 2.8 | |||

| Consumer Staples | 2.6 | |||

| Telecommunication Services | 1.4 | |||

| Materials | 1.0 | |||

| U.S. Treasury Obligations | 16.5 | |||

| Corporate Bonds | 9.9 | |||

| U.S. Government Mortgage-Backed Obligations | 8.3 | |||

| Sovereign Bonds | 0.1 | |||

| Short-Term Investment Fund | 0.2 | |||

| Other Assets/Liabilities (Net) | 1.4 | |||

| Total | 100.0 | % | ||

| * | Credit quality ratings are from Standard & Poor's (“S&P”) and Moody's Investors Service (“Moody's”). If agency ratings differ, the higher rating will be used. Where no rating has been assigned, it may be for reasons unrelated to the creditworthiness of the issuer. |

| ** | Sector Classifications are based upon the Global Industry Classification Standard (GICS®). |

32

Tabular Presentation of Portfolios of Investments (Unaudited) (Continued)

| Touchstone Bond Fund | ||||

| Credit Quality* | (% of Investment Securities) | |||

| AAA/Aaa | 62.9 | % | ||

| AA/Aa | 3.5 | |||

| A/A | 15.1 | |||

| BBB/Baa | 10.1 | |||

| BB/Ba | 0.2 | |||

| Not Rated | 2.3 | |||

| Cash Equivalents | 5.9 | |||

| Total | 100.0 | % | ||

| Touchstone Common Stock Fund | ||||

| Sector Allocation** | (% of Net Assets) | |||

| Information Technology | 25.7 | % | ||

| Consumer Discretionary | 17.3 | |||

| Financials | 16.2 | |||

| Health Care | 11.3 | |||

| Industrials | 9.0 | |||

| Energy | 5.2 | |||

| Real Estate | 4.4 | |||

| Consumer Staples | 4.0 | |||

| Telecommunication Services | 2.0 | |||

| Materials | 1.8 | |||

| Short-Term Investment Fund | 3.2 | |||

| Other Assets/Liabilities (Net) | (0.1 | ) | ||

| Total | 100.0 | % | ||

| Touchstone Focused Fund | ||||

| Sector Allocation** | (% of Net Assets) | |||

| Information Technology | 25.8 | % | ||

| Financials | 16.5 | |||

| Consumer Discretionary | 16.1 | |||

| Health Care | 14.3 | |||

| Industrials | 8.7 | |||

| Energy | 5.1 | |||

| Real Estate | 4.4 | |||

| Consumer Staples | 3.5 | |||

| Telecommunication Services | 2.2 | |||

| Materials | 1.7 | |||

| Short-Term Investment Funds | 3.6 | |||

| Other Assets/Liabilities (Net) | (1.9 | ) | ||

| Total | 100.0 | % | ||