UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act file number 811-08416

Touchstone Variable Series Trust

(Exact name of registrant as specified in charter)

303 Broadway, Suite 1100

Cincinnati, Ohio 45202-4203

(Address of principal executive offices) (Zip code)

Jill T. McGruder

303 Broadway, Suite 1100

Cincinnati, Ohio 45202-4203

(Name and address of agent for service)

Registrant's telephone number, including area code:800-638-8194

Date of fiscal year end:December 31

Date of reporting period:December 31, 2018

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget ("OMB") control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

Item 1. Reports to Stockholders.

The Report to Shareholders is attached herewith.

December 31, 2018

Annual Report

Touchstone Variable Series Trust

Touchstone Active Bond Fund

Touchstone Balanced Fund

Touchstone Bond Fund

Touchstone Common Stock Fund

Touchstone Focused Fund

Touchstone Large Cap Core Equity Fund

Touchstone Small Company Fund

Touchstone Aggressive ETF Fund

Touchstone Conservative ETF Fund

Touchstone Moderate ETF Fund

IMPORTANT NOTE: Effective January 1, 2021, as permitted by regulations adopted by the Securities and Exchange Commission, you may not be receiving paper copies of a Fund’s annual or semi-annual shareholder reports by mail, unless you specifically request paper copies of the reports from the insurance company that offers your variable annuity or variable life insurance contract or from your financial intermediary. Instead of delivering paper copies of the report, the insurance company may choose to make the reports available on a website, and the insurance company will notify you by mail each time a shareholder report is posted and provide you with a website link to access the report. Instructions for requesting paper copies will be provided by your insurance company.

If you already elected to receive shareholder reports electronically, you will not be affected by this change and you need not take any action. You may elect to receive shareholder reports and other communications from the insurance company electronically by following the instructions provided by the insurance company.

You may elect to receive all future Fund shareholder reports in paper free of charge from the insurance company. You can inform the insurance company that you wish to continue receiving paper copies of your shareholder reports by following the instructions provided by the insurance company. Your election to receive reports in paper will apply to all portfolio companies available under your contract with the insurance company.

Table of Contents

| | Page | |

| Letter from the President | 3 | |

| Management's Discussion of Fund Performance (Unaudited) | 4 - 29 | |

| Tabular Presentation of Portfolios of Investments (Unaudited) | 30 - 32 | |

| Portfolio of Investments: | | |

| Touchstone Active Bond Fund | 33 | |

| Touchstone Balanced Fund | 39 | |

| Touchstone Bond Fund | 43 | |

| Touchstone Common Stock Fund | 48 | |

| Touchstone Focused Fund | 50 | |

| Touchstone Large Cap Core Equity Fund | 52 | |

| Touchstone Small Company Fund | 53 | |

| Touchstone Aggressive ETF Fund | 55 | |

| Touchstone Conservative ETF Fund | 56 | |

| Touchstone Moderate ETF Fund | 57 | |

| Statements of Assets and Liabilities | 58 - 59 | |

| Statements of Operations | 60 - 61 | |

| Statements of Changes in Net Assets | 62 - 65 | |

| Financial Highlights | 66 - 70 | |

| Notes to Financial Statements | 71 - 85 | |

| Report of Independent Registered Public Accounting Firm | 86 - 87 | |

| Other Items (Unaudited) | 88 - 96 | |

| Management of the Trust (Unaudited) | 97 - 99 | |

| Privacy Protection Policy | 103 | |

This report identifies the Funds' investments on December 31, 2018. These holdings are subject to change. Not all investments in each Fund performed the same, nor is there any guarantee that these investments will perform as well in the future. Market forecasts provided in this report may not occur.

Letter from the President

Dear Shareholder:

We are pleased to provide you with the Touchstone Variable Series Trust Annual Report. Inside you will find key financial information, as well as manager commentaries for the Funds, for the 12 months ended December 31, 2018.

The “synchronized global expansion” that characterized 2017 decoupled in 2018 amid the imposition of tariffs by the U.S. and China, followed by threats of yet more. U.S. economic data was generally strong. Toward year-end, however, some indicators – including home and auto sales and consumer confidence – suggested a slowdown was emerging. Decelerating growth in major economies outside the U.S. became more evident, though none entered recessionary territory. Healthy domestic economic conditions encouraged the U.S. Federal Reserve Board (Fed) to continue normalizing monetary policy with four interest rate increases, yet it also signaled a more patient approach going forward in light of declining inflation expectations. Rising U.S. interest rates, a strong labor market and relatively robust economic conditions attracted global investors to U.S. stocks and bonds and strengthened the U.S. dollar. The Bank of Japan and European Central Bank (ECB) maintained accommodative monetary policies. Hopes of normalizing their respective monetary policies in order to restock their recession-fighting tool-kits faded after mid-year amid weaker growth. The ECB did however fulfill its promise to end its quantitative easing program.

Global macroeconomic concerns led to declines across all broad U.S. and non-U.S. equity indexes. In the U.S., growth-oriented stocks led U.S. equity markets over their value-oriented counterparts, while large capitalization stocks outperformed small- and mid-capitalization stocks. Outside the U.S., emerging market and developed market equities posted double-digit declines. Those declines were compounded for domestic investors in non-U.S. equities due to the U.S. dollar’s strengthening versus most major foreign currencies.

Rising interest rates and widening credit spreads buffeted the fixed income market. The Fed’s rate hikes pushed short-term rates higher over the year, outpacing rising rates on longer maturities. The result was a significantly flatter yield curve, reaching its flattest level since 2007. This gave rise to fears throughout the year of a yield curve inversion1, which historically has been a leading indicator of recessions. While the U.S. Treasury yield curve did not invert, it did finish the year above where it started, creating a headwind for longer maturity bonds. Economic concerns also led to credit spread widening during the year, resulting in negative returns for both investment grade and high yield bonds.

The new year provides a natural point to assess the recent past and consider the future. From a financial perspective, it has been yet another period of challenged returns across many asset classes. This presents a particularly timely juncture to assess your current financial situation and, with the help of your financial advisor, weigh your plans for the year — as well as for the years ahead.

We greatly value your continued support. Thank you for including Touchstone as part of your investment plan.

Sincerely.

Jill T. McGruder

President

Touchstone Variable Series Trust

1A yield curve inversion is defined as when the yield on a 2-year Treasury Bill exceeds the yield on a 10-year Treasury Bond.

Management's Discussion of Fund Performance(Unaudited)

Touchstone Active Bond Fund

Sub-Advised by Fort Washington Investment Advisors, Inc.

Investment Philosophy

The Touchstone Active Bond Fund seeks to provide as high a level of current income as is consistent with the preservation of capital. Capital appreciation is a secondary goal. In deciding what securities to buy and sell for the Fund, the overall investment opportunities and risks in different sectors of the debt securities market are analyzed by focusing on maximizing total return and reducing volatility of the Fund’s portfolio. A disciplined sector allocation process is followed in order to build a broadly diversified portfolio of bonds.

Fund Performance

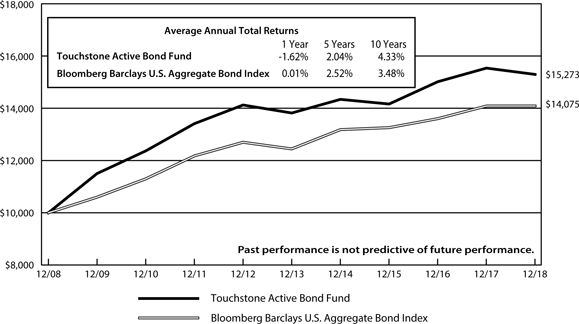

The Touchstone Active Bond Fund underperformed its benchmark, the Bloomberg Barclays U.S. Aggregate Bond Index, for the 12-month period ended December 31, 2018. The Fund’s total return was -1.62 percent, while the total return of the benchmark was 0.01 percent.

Market Environment

Risk assets continued their brisk pace higher to start 2018 following a strong 2017. However, volatility returned which reflected concerns about inflation and rising interest rates, as well as uncertainty about global trade.

During the year, the U.S. Federal Reserve Board (Fed) increased the federal funds rate a total of four times. Interest rates were driven by concerns about future growth in the U.S., slowing growth outside of the U.S. and continued uncertainty related to trade policies. The effects of the Fed’s rate increases, combined with the sharp decline in long-term rates, led to further flattening of the yield curve and an inversion in certain parts of the curve, mainly in short-term maturities.

Market expectations of additional Fed rate hikes decreased during the fourth quarter, as broad financial conditions reached their tightest levels of the year. Driving these financial conditions were the increased federal funds rate, a stronger U.S. dollar, widening credit spreads and the sharp retreat in equities. Global central bank policies were also less accommodative.

While underlying growth of the U.S. economy began to show signs of further deceleration toward the end of the year, it still remained near trend at approximately 2.0 to 2.5 percent. The strength of the economy was buoyed by the resiliency of labor markets and, as effects from fiscal policy and tax legislation began to fade, it was the most important factor for sustaining the current growth rate. During the period, labor markets were consistently strong in terms of jobs added month to month. Wage growth was also strong and began to show signs of acceleration. Core inflation readings were in line with the Fed’s 2 percent target and were expected to hover around 2 percent in the near term as data indicated solid, but not accelerating inflation.

Within the index, Investment Grade Corporate Bonds, Mortgage-Backed Securities (MBS), Asset-Backed Securities (ABS) and Commercial Mortgage-Backed Securities (CMBS) all underperformed U.S. Treasuries during the period. High Yield bonds also underperformed for the year.

Portfolio Review

The main detractors from Fund performance during the 12-month period were an overweight to Investment Grade bonds and interest rate management, specifically duration positioning and an allocation to Treasury Inflation Protected Securities (TIPS). The Fund’s allocation to U.S. dollar-denominated Emerging Markets bonds also detracted over the period, while security selection was strong within Securitized Assets, particularly ABS. This helped offset some of the losses incurred from the Fund’s allocation to Emerging Markets. The Fund

Management's Discussion of Fund Performance(Unaudited) (Continued)

maintained a modest allocation to U.S. dollar-denominated Emerging Markets bonds during the period as the additional yield relative to Investment Grade Corporate and High Yield bonds remained attractive.

Outlook

Looking ahead, we believe risk assets offer the greatest potential to the Fund, driven by U.S. economic growth, steady inflation, amicable resolutions to trade disputes, and accommodative central bank policies both domestically and abroad. Due to tightening financial conditions, increased market volatility and increases in the federal funds rate, we believe current market conditions could become headwinds to the Fund in 2019. Valuations have adjusted to tighter borrowing costs, the slowdown in global growth and the uncertainty around trade issues. As a result, we believe the potential upside for price appreciation is limited. We have taken advantage of opportunities among securitized assets when possible, where we believe attractive risk/reward profiles can be found in the ABS and Non-Agency MBS sectors. We like these sectors’ close connections to consumer spending, which continues to be healthy.

We believe global central banks need to maintain accommodative policies in order to support ongoing expansion abroad. Rate hikes by the Fed will further tighten financial conditions, which may negatively impact the Fund’s overweight position to risk assets. Further escalation of trade disputes, specifically between the U.S. and China, may also adversely impact risk assets.

We believe current interest rates fully reflect the uncertainty surrounding the economic outlook which has seemed to embrace growth deceleration and a less active Federal Open Market Committee. There is little downside for rates at these levels unless actual economic weakness materializes. As a result, in the near term, the Fund is positioned with a neutral duration and curve relative to the benchmark. We also expect the Fund to hold a modest allocation to U.S. dollar-denominated Emerging Markets bonds because of their additional yield relative to Investment Grade and High Yield bonds.

Management's Discussion of Fund Performance(Unaudited) (Continued)

Comparison of the Change in Value of a $10,000 Investment in the

Touchstone Active Bond Fund and the Bloomberg Barclays U.S. Aggregate Bond Index

Performance information does not reflect fees that are paid by the separate accounts through which shares of the Fund are sold. Inclusion of those fees would reduce figures for all periods.

The inception date of the Fund was January 1, 1999.

Note to Chart

The Bloomberg Barclays U.S. Aggregate Bond Index is an unmanaged index comprised of U.S. investment grade, fixed rate bond market securities, including government, government agency, corporate and mortgage-backed securities between one and ten years.

Management's Discussion of Fund Performance(Unaudited)

Touchstone Balanced Fund

Sub-Advised by Fort Washington Investment Advisors, Inc.

Investment Philosophy

The Touchstone Balanced Fund seeks to achieve its investment goal of providing investors with capital appreciation and current income by generally investing in a diversified portfolio comprising 60 percent equity securities and 40 percent fixed-income securities. With respect to equities, the Fund invests primarily in issuers having a market capitalization, at the time of purchase, above $5 billion. Equity securities include common stock and preferred stock. With respect to fixed-income, the Fund invests primarily in bonds, including mortgage-related securities, asset-backed securities, government securities (both U.S. government securities and foreign sovereign debt), and corporate debt securities.

Fund Performance

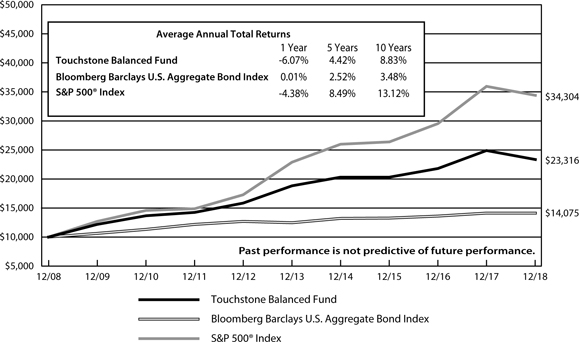

The Touchstone Balanced Fund underperformed both of its benchmarks, the S&P 500® Index and the Bloomberg Barclays U.S. Aggregate Bond Index, for the 12-month period ended December 31, 2018. The Fund’s total return was -6.07 percent while the total return of the S&P 500® Index was -4.38 percent and the total return of the Bloomberg Barclays U.S. Aggregate Bond Index was 0.01 percent.

Market Environment

Risk assets continued their brisk pace higher to start 2018 following a strong 2017. However, volatility returned which reflected concerns about inflation and rising interest rates, as well as uncertainty about global trade.

During the year, the U.S. Federal Reserve Board (Fed) increased the federal funds rate a total of four times. Interest rates were driven by concerns about future growth in the U.S., slowing growth outside of the U.S. and continued uncertainty related to trade policies. The effects of the Fed’s rate increases, combined with the sharp decline in long-term rates led to further flattening of the curve and an inversion in certain parts of the curve, mainly in short-term maturities. Market expectations of additional Fed rate hikes decreased during the fourth quarter, as broad financial conditions reached their tightest levels of the year. Driving these financial conditions were the increased federal funds rate, a stronger U.S. dollar, widening credit spreads and the sharp retreat in equities. Global central bank policies were also less accommodative.

While underlying growth of the U.S. economy began to show signs of further deceleration toward the end of the year, it still remained near trend at approximately 2.0 to 2.5 percent. The strength of the economy was buoyed by the resiliency of labor markets and, as effects from fiscal policy and tax legislation began to fade, it was the most important factor for sustaining the current growth rate. During the period, labor markets were consistently strong in terms of jobs added month to month. Wage growth was also strong and began to show signs of acceleration. Core inflation readings were in line with the Fed’s 2 percent target and were expected to hover around 2 percent in the near term as data indicated solid, but not accelerating inflation.

The major theme surrounding U.S. equities was the return of volatility. For the year, sectors that outperformed the equity benchmark the most included Health Care, Utilities and Information Technology. Energy, Materials and Industrials were the main detractors.

Within fixed income, Investment Grade Corporate bonds, Mortgage-Backed Securities (MBS), Asset-Backed Securities (ABS) and Commercial Mortgage-Backed Securities (CMBS) all underperformed U.S. Treasuries during the period. High Yield bonds also underperformed for the year.

Management's Discussion of Fund Performance(Unaudited) (Continued)

Portfolio Review

Within the equity allocation, stock selection in the Health Care, Industrials and Energy sectors were the largest relative underperformers. Stock selection within the Financials and Information Technology sectors contributed to performance. Sector allocation contributed to relative performance, primarily due to an overweight to the Consumer Discretionary sector and an underweight to the Energy sector.

The primary detractors within the fixed income allocation were an overweight to Investment Grade bonds and interest rate management, specifically duration positioning and an allocation to Treasury Inflation Protected Securities (TIPS). The Fund’s allocation to U.S. dollar-denominated Emerging Markets bonds also detracted over the period, while security selection was strong within Securitized Assets, particularly ABS. This helped offset some of the losses incurred from the Fund’s allocation to Emerging Markets. The Fund’s cash position had a positive impact on performance given the negative moves in the market.

There were no significant changes made to the Fund’s allocation for the year as the Fund maintained a slight overweight to Equities versus Fixed Income. Within Fixed Income, the overall allocation continued to have a modest overweight to risk with the largest overweight position to Investment Grade Credit. The Fund also maintained a modest allocation to U.S. dollar-denominated Emerging Markets debt.

Outlook

Looking ahead, we believe risk assets offer the greatest potential to the Fund, driven by U.S. economic growth, steady inflation, amicable resolutions to trade disputes, and accommodative central bank policies both domestically and abroad. Due to tightening financial conditions, increased market volatility and increases in the federal funds rate, we believe current market conditions could become headwinds to the Fund in 2019. Valuations have adjusted to tighter borrowing costs, the slowdown in global growth and the uncertainty around trade issues. As a result, we believe the potential upside for price appreciation is limited. Within equities, we have taken advantage of opportunities to position the Fund for the later stages of the market cycle. The Fund continues to be skewed toward larger cap, “franchise value” businesses with higher barriers to entry. We also expect to emphasize businesses with lower financial leverage and pricing power to help offset wage inflation. In the Fund’s fixed income holdings, we have taken advantage of opportunities among securitized assets when possible, where we believe attractive risk-reward profiles can be found in the ABS and Non-Agency MBS sectors. We like these sectors’ close connections to consumer spending, which continues to be healthy.

We believe global central banks need to maintain accommodative policies in order to support ongoing expansion abroad. Rate hikes by the Fed will further tighten financial conditions, which may negatively impact the Fund’s overweight position to risk assets. Further escalation of trade disputes, specifically between the U.S. and China, may also adversely impact risk assets.

We believe current rates fully reflect the uncertainty surrounding the economic outlook which has seemed to embrace growth deceleration and a less active Federal Open Market Committee. There is little downside for rates at these levels unless actual economic weakness materializes. As a result, in the near term, the Fund is positioned with a neutral duration and curve relative to the benchmark. We also expect to hold a modest allocation to U.S. dollar-denominated Emerging Markets bonds because of their additional yield relative to Investment Grade and High Yield bonds.

Management's Discussion of Fund Performance(Unaudited) (Continued)

Comparison of the Change in Value of a $10,000 Investment in the

Touchstone Balanced Fund, the Bloomberg Barclays U.S. Aggregate Bond Index and the

S&P 500® Index

Performance information does not reflect fees that are paid by the separate accounts through which shares of the Fund are sold. Inclusion of those fees would reduce figures for all periods.

The inception date of the Fund was August 1, 2003.

Notes to Chart

S&P 500® Index is a group of 500 widely held stocks and is commonly regarded to be representative of the large capitalization stock universe.

The Bloomberg Barclays U.S. Aggregate Bond Index is an unmanaged index comprised of U.S. investment grade, fixed rate bond market securities, including government, government agency, corporate and mortgage-backed securities between one and ten years.

Management's Discussion of Fund Performance(Unaudited)

Touchstone Bond Fund

Sub-Advised by Fort Washington Investment Advisors, Inc.

Investment Philosophy

The Touchstone Bond Fund seeks to provide as high a level of current income as is consistent with the preservation of capital. Capital appreciation is a secondary goal. Under normal circumstances, the Fund invests at least 80 percent of its assets in bonds. Bonds include mortgage-related securities, asset-backed securities, government securities and corporate debt securities. The Fund primarily invests in investment-grade debt securities, but may invest up to 30 percent of the Fund’s total assets in non-investment-grade debt securities.

Fund Performance

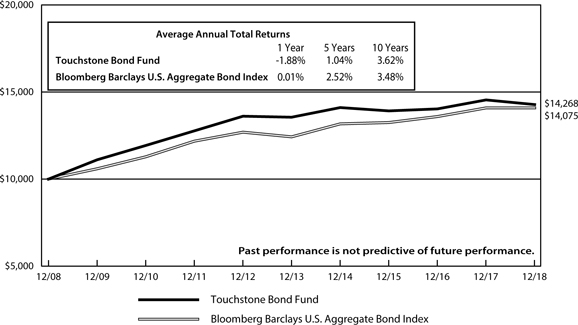

The Touchstone Bond Fund underperformed its benchmark, the Bloomberg Barclays U.S. Aggregate Bond Index, for the 12-month period ended December 31, 2018. The Fund’s total return was -1.88 percent, while the total return of the benchmark was 0.01 percent.

Market Environment

Risk assets continued their brisk pace higher to start 2018 following a strong 2017. However, volatility returned which reflected concerns about inflation and rising interest rates, as well as uncertainty about global trade.

During the year, the U.S. Federal Reserve Board (Fed) increased the federal funds rate a total of four times. Interest rates were driven by concerns about future growth in the U.S., slowing growth outside of the U.S. and continued uncertainty related to trade policies. The effects of the Fed’s rate increases, combined with the sharp decline in long-term rates led to further flattening of the yield curve and an inversion in certain parts of the curve, mainly in short-term maturities.

Market expectations of additional Fed rate hikes decreased during the fourth quarter, as broad financial conditions reached their tightest levels of the year. Driving these financial conditions were the increased federal funds rate, a stronger U.S. dollar, widening credit spreads and the sharp retreat in equities. Global central bank policies were also less accommodative.

While underlying growth of the U.S. economy began to show signs of further deceleration toward the end of the year, it still remained near trend at approximately 2.0 to 2.5 percent. The strength of the economy was buoyed by the resiliency of labor markets and, as effects from fiscal policy and tax legislation began to fade, it was the most important factor for sustaining the current growth rate. During the period, labor markets were consistently strong in terms of jobs added month to month. Wage growth was also strong and began to show signs of acceleration. Core inflation readings were in line with the Fed’s 2 percent target and were expected to hover around 2 percent in the near term as data indicated solid, but not accelerating inflation.

Portfolio Review

The main detractors from Fund performance during the year were an overweight to Investment Grade bonds and interest rate management, specifically duration positioning and an allocation to Treasury Inflation Protected Securities (TIPS). The Fund’s allocation to U.S. dollar-denominated Emerging Markets bonds also detracted over the period, while security selection was strong within Securitized Assets, particularly ABS. This helped offset some of the losses incurred from the Fund’s allocation to Emerging Markets. The Fund maintained a modest allocation to U.S. dollar-denominated Emerging Markets bonds during the period as the additional yield relative to Investment Grade corporate and High Yield bonds remained attractive.

Management's Discussion of Fund Performance (Unaudited) (Continued)

Outlook

Looking ahead, we believe risk assets offer the greatest potential to the Fund, driven by U.S. economic growth, steady inflation, amicable resolutions to trade disputes, and accommodative central bank policies both domestically and abroad. Due to tightening financial conditions, increased market volatility and increases in the federal funds rate, we believe current market conditions could become headwinds to the Fund in 2019. Valuations have adjusted to tighter borrowing costs, the slowdown in global growth and the uncertainty around trade issues. As a result, we believe the potential upside for price appreciation is limited. We have taken advantage of opportunities among securitized assets when possible, where we believe attractive risk/reward profiles can be found in the ABS and Non-Agency MBS sectors. We like these sectors’ close connections to consumer spending, which continues to be healthy.

We believe global central banks need to maintain accommodative policies in order to support ongoing expansion abroad. Rate hikes by the Fed will further tighten financial conditions, which may negatively impact the Fund’s overweight position to risk assets. Further escalation of trade disputes, specifically between the U.S. and China, may also adversely impact risk assets.

We believe current interest rates fully reflect the uncertainty surrounding the economic outlook which has seemed to embrace growth deceleration and a less active Federal Open Market Committee. There is little downside for rates at these levels unless actual economic weakness materializes. As a result, in the near term, the Fund is positioned with a neutral duration and curve relative to the benchmark. We also expect the Fund to hold a modest allocation to U.S. dollar-denominated Emerging Markets bonds because of their additional yield relative to Investment Grade and High Yield bonds.

Management's Discussion of Fund Performance (Unaudited) (Continued)

Comparison of the Change in Value of a $10,000 Investment in the

Touchstone Bond Fund and the Bloomberg Barclays U.S. Aggregate Bond Index

Performance information does not reflect fees that are paid by the separate accounts through which shares of the Fund are sold. Inclusion of those fees would reduce figures for all periods.

The inception date of the Fund was August 1, 2003.

Note to Chart

The Bloomberg Barclays U.S. Aggregate Bond Index is an unmanaged index comprised of U.S. investment grade, fixed rate bond market securities, including government, government agency, corporate and mortgage-backed securities between one and ten years.

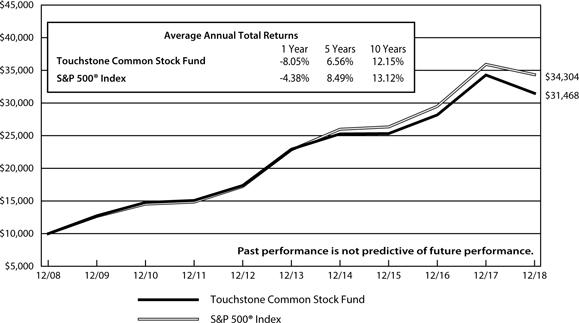

Management's Discussion of Fund Performance (Unaudited)

Touchstone Common Stock Fund

Sub-Advised by Fort Washington Investment Advisors, Inc.

Investment Philosophy

The Fund seeks to invest at least 80 percent of its assets in large capitalization equity securities. The Fund’s sub-advisor, Fort Washington Investment Advisors, Inc., seeks to invest in companies that are trading below what is believed to be the estimate of the companies’ intrinsic value and have a sustainable competitive advantage or a high barrier to entry in place. The barrier(s) to entry can be created through a cost advantage, economies of scale, high customer loyalty or a government barrier (e.g. license or subsidy). Fort Washington believes that the strongest barrier to entry is the combination of economies of scale and high customer loyalty.

Fund Performance

The Touchstone Common Stock Fund underperformed its benchmark, the S&P 500® Index, for the 12-month period ended December 31, 2018. The Fund’s total return was -8.05 percent while the benchmark’s total return was -4.38 percent.

Market Environment

In 2018, U.S. equities recorded negative returns for the 12-month period as global growth, trade relations between the U.S. and China, and fiscal tightening by the U.S. Federal Reserve Board (Fed) concerned investors.

The major theme surrounding U.S. equities was the return of volatility. Sectors that outperformed the S&P 500® Index the most during the year included Health Care, Utilities, and Information Technology. Sectors that underperformed the broader index the most included Energy, Materials, and Industrials.

Portfolio Review

Stock selection was the primary cause of relative underperformance. Stock selection within the Materials, Financials, and Information Technology sectors contributed to relative performance. Energy, Health Care, Industrials and Communication Services were among the underperforming sectors.

The Fund’s top contributors to relative performance for the year were Amazon.com, Inc. (Consumer Discretionary sector), Twenty-First Century Fox, Inc. (Communication Services sector), Salesforce.com, Inc. (Information Technology sector), Microsoft Corp. (Information Technology sector), Starbucks Corp. (Consumer Discretionary sector) and Berkshire Hathaway Inc. Class B Shares (Financials sector). Among the stocks that detracted from relative performance were Facebook, Inc. (Communication Services sector), General Electric Co. (Industrials sector), Goldman Sachs Group, Inc. (Financials sector), Stericycle, Inc. (Industrials sector), and JD.com, Inc. (Consumer Discretionary sector).

Outlook and Conclusion

The U.S. stock market recorded a pullback in the fourth quarter that helped produce the first negative year since 2008. Concerns driving the market lower in the fourth quarter included, but were not limited to, lingering trade concerns between the U.S. and China, commentary by the Fed early in the quarter signaling more rate increases and slowing growth in foreign economies. The elevated volatility in the fourth quarter leads to the question of whether this is another transitory market pullback or the end of a bull market. Each of the critical indicators we track signal it is the former. However, there are ongoing items that need to be monitored closely including market and individual company valuations, the state of the global economy, unit labor costs and

Management's Discussion of Fund Performance (Unaudited) (Continued)

market breadth. These are all items we are focused on as the cycle matures. While we do not see signs of a bear market on the immediate horizon, we have taken opportunities to position the Fund for the later stages of the market cycle.

Comparison of the Change in Value of a $10,000 Investment in the

Touchstone Common Stock Fund and the S&P 500® Index

Performance information does not reflect fees that are paid by the separate accounts through which shares of the Fund are sold. Inclusion of those fees would reduce figures for all periods.

The inception date of the Fund was November 30, 2000.

Note to Chart

S&P 500® Index is a group of 500 widely held stocks and is commonly regarded to be representative of the large capitalization stock universe.

Management's Discussion of Fund Performance (Unaudited)

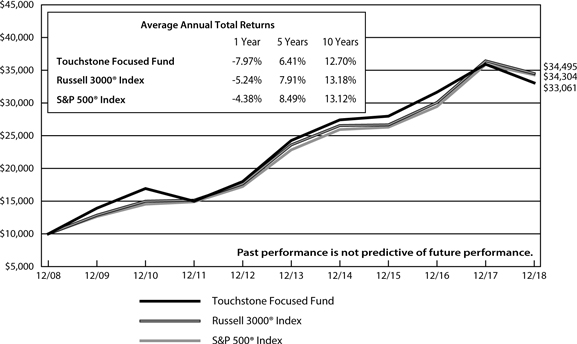

Touchstone Focused Fund

Sub-Advised by Fort Washington Investment Advisors, Inc.

Investment Philosophy

The Touchstone Focused Fund seeks to invest in companies of all capitalizations that are trading below what is believed to be the estimate of their intrinsic value and have a sustainable competitive advantage or a high barrier to entry in place. The barrier(s) to entry can be created through a cost advantage, economies of scale, high customer loyalty or a government barrier (e.g. license or subsidy). Fort Washington believes that the strongest barrier to entry is the combination of economies of scale and high customer loyalty.

Fund Performance

The Touchstone Focused Fund underperformed its primary benchmark, the Russell 3000® Index, and its secondary benchmark, the S&P 500® Index, for the 12-month period ended December 31, 2018. The Fund’s total return was -7.97 percent, while the total return of the Russell 3000® Index was -5.24 percent and the total return of the S&P 500® Index was -4.38 percent.

Market Environment

U.S. equities recorded negative returns for the 12-month period as global growth, trade relations between the U.S. and China, and fiscal tightening by the U.S. Federal Reserve Board (Fed) weighed on investors.

The major theme surrounding U.S. equities was the return of volatility. For the year, the sectors that outperformed the Russell 3000® Index the most included Health Care, Utilities and Information Technology. Energy, Materials and Industrials were the worst performing sectors.

Portfolio Review

The Fund’s stock selection within the Materials, Consumer Discretionary, Information Technology and Financials sectors outperformed relative to the benchmark. Stock selection within Energy, Health Care, Communication Services, and Industrials detracted from relative performance. Sector allocation contributed to relative performance, primarily due to underweights to the Materials, Industrials and Energy sectors. The Fund’s cash position had a positive impact on performance given the negative moves in the market.

Among the individual stocks that contributed to relative performance were Amazon.com,Inc. (Consumer Discretionary sector), Salesforce.com, Inc. (Information Technology sector) and Twenty-First Century Fox, Inc. (Communication Services sector). Amazon.com is an e-commerce retailer and cloud computing software company. The stock rose during the period due to the acceleration of growth in the company’s Amazon Prime subscription service and its Amazon Web Services subsidiary. Salesforce.com, a cloud-based software business, increased primarily due to higher than expected revenue growth and management’s announcement that it raised fiscal year revenue guidance for 2019. Twenty-First Century Fox, a multinational mass media company, moved higher following a proposed acquisition from Walt Disney Co.

Among the individual stocks that detracted from relative performance were Stericycle, Inc. (Industrials sector), JD.com, Inc. (Consumer Discretionary sector) and Goldman Sachs Group Inc. (Financials sector). Stericycle specializes in collecting and disposing of regulated substances - such as medical waste pharmaceuticals - and provides compliance training solutions. The stock underperformed primarily due to weak performance by the company’s core regulated medical waste business as well as softer than expected revenues in its communications solutions business. JD.com, a China-based e-commerce business, moved lower due to concerns about growth and the company’s ongoing investments that have negatively impacted margins. Further, the news cycle surrounding criminal allegations against the company’s CEO also weighed on its stock price.

Management's Discussion of Fund Performance (Unaudited) (Continued)

From a market cap perspective, the Fund maintained underweight positions in small-cap companies - with market caps below $2 billion - and mid-cap companies. The Fund continued to maintain an overweight to large-cap businesses, which includes companies with market caps above $10 billion. The Fund’s market cap allocation contributed to performance as large-cap stocks outperformed the benchmark during the period.

During the period, the Fund initiated positions in Monster Beverage Corp. (Consumer Staples sector), AmerisourceBergen Corp. (Health Care sector), Baidu, Inc. (Communication Services sector), JD.com Inc., Alibaba Group Holding Ltd. (both from the Consumer Discretionary sector), Deere & Co., Inc. and FedEx Corp. (both from the Industrials sector). The Fund exited positions in Mondelez International, Inc. (Consumer Discretionary sector), Bank OZK (Financials sector), Johnson Controls International PLC (Industrials sector), Cisco Systems, Inc. (Information Technology sector) and Nutrien Ltd. (Materials sector).

At the end of the year, the Fund was overweight to the Communication Services, Financials, Consumer Discretionary and Real Estate sectors, and underweight to the Consumer Staples, Energy and Industrials sectors. Allocations to the Health Care and Information Technology sectors were generally matched to that of the benchmark. The Fund did not hold any stocks within the Utilities or Materials sectors at the end of the period.

Outlook

The U.S. stock market recorded a significant pullback in the fourth quarter, which contributed to the first year of negative results since 2008. Events driving the market lower in the fourth quarter included, but were not limited to, concerns surrounding lingering trade concerns between the U.S. and China, commentary by the Fed signaling more rate increases and slowing growth in foreign economies. The elevated volatility in the fourth quarter also led some to question whether this was another transitory market pullback or the end of a bull market. Each of the critical indicators we track signal it was the former. However, we believe there are ongoing items that will need to be monitored closely going forward, including market and individual company valuations, the state of the global economy, unit labor costs and market breadth.

While we do not see signs of a bear market on the immediate horizon, we have taken advantage of opportunities to position the Fund for the later stages of the market cycle. The Fund continues to be skewed toward larger cap, franchise value businesses with higher barriers to entry. We also expect to emphasize businesses with lower financial leverage and pricing power to help offset wage inflation.

Management's Discussion of Fund Performance (Unaudited) (Continued)

Comparison of the Change in Value of a $10,000 Investment in the

Touchstone Focused Fund, the Russell 3000®Index and the S&P 500® Index

Performance information does not reflect fees that are paid by the separate accounts through which shares of the Fund are sold. Inclusion of those fees would reduce figures for all periods.

The inception date of the Fund was November 21, 1994.

Notes to Chart

The Frank Russell Company (FRC) is the source and owner of the Russell 3000® Index data contained or reflected in this material and all trademarks and copyrights related thereto. The material may contain confidential information and unauthorized use, disclosure, copying, dissemination or redistribution is strictly prohibited. This is a Touchstone Investments presentation of the data, and FRC is not responsible for the formatting or configuration of this material or for any inaccuracy in the presentation thereof.

Russell 3000® Index measures the performance of the 3,000 largest U.S. companies based on total market capitalization, which represents approximately 98% of the investable U.S. equity market.

S&P 500® Index is a group of 500 widely held stocks and is commonly regarded to be representative of the large capitalization stock universe.

Management's Discussion of Fund Performance (Unaudited)

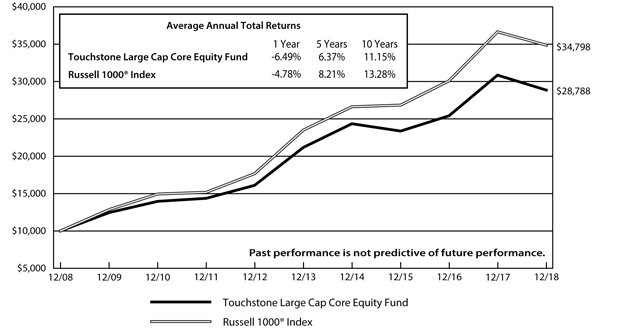

Touchstone Large Cap Core Equity Fund

Sub-Advised by The London Company

Investment Philosophy

The Touchstone Large Cap Core Equity Fund seeks long-term capital growth by investing primarily in common stocks of large-cap U.S. listed companies. The Fund seeks to purchase financially stable large-cap companies that it believes are consistently generating high returns on unleveraged operating capital, run by shareholder-oriented management, and trading at a discount to the company’s respective private market values.

Fund Performance

The Touchstone Large Cap Core Equity Fund underperformed its benchmark, the Russell 1000® Index, for the 12-month period ended December 31, 2018. The Fund’s total return was -6.49 percent, while the benchmark’s total return was -4.78 percent.

Market Environment

U.S. equities ended the year lower, but the ride from start to finish was anything but linear as volatility made an impactful return. After ending 2017 with historically low market volatility, January 2018 posted returns that were among the best on record, while December posted some of the worst.

Economic data was mostly positive for the year, but there were areas of potential concern, including housing and the impact of tariffs. While housing starts and existing home sales were relatively stable, growth was limited. Rhetoric surrounding potential trade wars dominated headlines throughout the year and intensified during the fourth quarter. The main risk, in particular, was between the U.S. and China, where a number of tariffs were either announced or already enacted.

In terms of monetary policy, as expected, the U.S. Federal Reserve Board (Fed) increased the federal funds rate by 25 basis points during December, with a new target of 2.25 to 2.5 percent. This marked the fourth rate hike during the 12-month period and ninth rate hike since the Fed began raising rates in December 2015. The Fed also communicated that any additional rate hikes would be dependent on economic data. Thus, following concerns about recent economic data, expectations for three additional rate hikes in 2019 were changed to only two hikes. Further, the pace of inflation continued to trend in the 2 percent range during the year, which was in line with the Fed’s target.

At the end of the 12-month period, all of the major stock indexes posted declines, with large-cap stocks faring better than small-cap stocks. Growth stocks outperformed value stocks for the year, value stocks outperformed growth stocks during the fourth quarter. Benchmark performance was led by the Health Care and Information Technology sectors, while the Energy, Materials, Industrials and Financials sectors lagged.

Portfolio Review

During the 12-month period, stock selection contributed positively to relative Fund performance but was offset by negative sector allocation. At the sector level, an underweight to the Health Care sector and an overweight to the Financials sector had a negative impact on relative performance. This was offset by the positive impact from an overweight to the Consumer Discretionary sector and an underweight to Energy.

Among the individual stocks that contributed to relative Fund performance during the period were O’Reilly Automotive Inc., Nike Inc. (both from the Consumer Discretionary sector), Visa Inc. (Information Technology sector), Progressive Corp. and Berkshire Hathaway Inc. (both from the Financials sector).

O’Reilly Automotive, an automotive parts retailer, outperformed as the company reported better than expected same-store sales and increased guidance. O’Reilly also continued to gain market share in both mature and new

Management's Discussion of Fund Performance (Unaudited) (Continued)

markets, and it remained the gold standard for service and logistics in its industry. Additionally, the average age of cars on the road has continued to rise, which should be a tailwind for the stock in the mid-term. Nike is a retailer of footwear, apparel, sports equipment and accessories. Nike outperformed during the period in which the Fund owned the stock, following a resumption of growth in its North American segment after several quarters of deceleration. The stock was sold from the Fund early during the fourth quarter due to valuation concerns. Visa, a global payments technology company, traded higher during the year which was driven by consistently strong results. In particular, Visa has produced strong cash flow and redistributed extra cash to shareholders. It also has a firm position in the market for global payments with significant barriers to entry. Looking forward, we believe the economic backdrop for Visa should remain strong, driven by healthy economies around the world, and the shift to credit and electronic commerce. Progressive, an insurance provider, outperformed as the company continued to post strong premium growth along with profitable underwriting results, and its combined expense ratio came in lower than expected. Progressive also posted improved top-line growth in both its auto and home insurance policies, and both of its digital and agency platforms increased market share. Berkshire Hathaway, a multinational conglomerate holding company, moved higher during the year following solid operating results across most of its segments. In July, the board of directors amended its share repurchase program to allow for buybacks at such time a repurchase price is believed to be below intrinsic value, which was a revision from the prior program. Going forward, we believe the company offers downside protection, particularly in light of management’s extensive record of superb capital allocation.

Among the individual stocks that detracted from relative Fund performance during the period were FedEx Corp., Southwest Airlines Co. (both from the Industrials sector), Carnival Corp. (Consumer Discretionary sector), Altria Group Inc. (Consumer Staples sector) and BlackRock Inc. (Financials sector). FedEx, a multinational courier delivery service, was generally flat most of the year but fell sharply during the fourth quarter. In general, economically sensitive transportation stocks were hit hard during the quarter based on concerns of macroeconomic weakening. FedEx, in particular, moved lower after its third-quarter results were impacted unexpectedly by weakness in Europe and troubles with its integration of TNT Express NV that caused management to push cost savings targets out several years. Southwest Airlines, a low-cost airline carrier, lagged early in the year resulting from headwinds to its unit revenues and costs. The stock underperformed sharply in the fourth quarter as commentary surrounding its unit costs for 2019 unnerved investors. We view these issues as largely transitory and feel the market overreacted, as the company still expects to expand margins next year. Going forward, we feel that Southwest Airlines is a best-of-breed business with strong management, a good balance sheet and favorable capital allocation policies. Carnival Corp., a cruise ship operator, underperformed as investors grew concerned about the combination of weakening demand from Europe and increasing capacity. The stock fell sharply during the fourth quarter as the market responded negatively to Carnival’s reports of a solid fiscal quarter but disappointing guidance for 2019. Though investor sentiment was depressed, we believe Carnival’s focus on return on capital and its policy of returning excess cash to shareholders should benefit the company going forward. Altria, the owner of multiple tobacco operating companies, struggled in 2018 as volumes continued to decline. During the fourth quarter, the company came under pressure after announcing investments in both Cronos Group Inc. (a Canadian cannabis company) and Juul (a U.S. vaporizer company). In general, the market has viewed the Juul acquisition negatively. However, we believe Altria has historically been an intelligent capital allocator, and we think people are likely underestimating the potential value that the partnership between Altria and Juul could create. BlackRock, a global investment management company, underperformed along with its peers as concerns about asset flows weighed on sentiment. We maintained the Fund’s position as we believe BlackRock is a well-run company with a conservative balance sheet, attractive cash flow profile and shareholder-friendly mindset. Longer term, we believe BlackRock is positioned to benefit from the trend toward passive investing due to its scale and technological leadership.

During the 12-month period, we opportunistically took advantage of market weakness and added to the Fund’s position in Alphabet Inc. (Information Technology sector). We believe Alphabet, a multinational conglomerate

Management's Discussion of Fund Performance (Unaudited) (Continued)

that includes Google Inc. and its internet products, is structurally advantaged with long-term tailwinds from cloud computing and data centers. We also added to FedEx Corp. as a result of the strength in the U.S. economy and the company’s strong position in the package delivery market. Finally, we added to Southwest Airlines Co. because of its attractive valuation and signs of improving traffic and higher pricing. We also feel the company is positioned well in a consolidated industry.

We initiated positions in Albemarle Corp. (Materials sector), The Home Depot Inc. (Consumer Discretionary sector), Martin Marietta Materials Inc. (Materials sector) and Nestle SA (Consumer Staples sector). Albemarle is a specialty chemical company with three reporting segments: lithium, bromine specialties and catalysts. A primary use of lithium is in rechargeable batteries, which is expected to see growing demand over the next several years for electric vehicles, portables and rechargeable consumer electronics. Albemarle also maintains a strong balance sheet and has benefited from growth in its operating cash flow. Further, the company generates attractive earnings margins, which reflects its leadership positions in its markets. Home Depot is the world’s largest home improvement specialty retailer, with industry-leading margins and returns on capital. Home Depot has benefited from strong housing-related tailwinds and is expected to do so for some time and has a solid history of capital allocation. Further, the company has produced strong earnings margins and operating cash flow, as well as a solid balance sheet. We initiated the position in Martin Marietta Materials as a result of our positive view of the aggregates industry in particular, its oligopoly with pricing power, strong return on capital and double-digit operating margins. Looking ahead, we believe the company should benefit from volume growth due to a strong U.S. economy and the need for greater infrastructure spending. Nestle is the largest food company in the world with scale and brand advantages. The company is well diversified among geographies with approximately 60 percent of sales occurring in developed markets and 40 percent in emerging markets, where growth and margins are higher. The company is exposed to many large staple categories and also has a valuable stake in L’Oréal Co. Nestle has a strong balance sheet and solid earnings, and also generates an attractive cash flow. Further, we believe the company has balance sheet flexibility to help weather potential downturns in the market.

Outlook

The combination of solid economic growth, low inflation and relatively low interest rates usually create a positive environment for stocks. We believe this holds true today, but we maintain a more balanced view as valuations have improved in recent months; the broader market now trades at a slight discount to its long-term average. We also believe there are potential risks, including rising debt levels, wage inflation, the impact of increasing tariffs, or the Fed taking a more aggressive stance.

Looking ahead, we will continue to seek companies with strong returns on capital and sustainable competitive advantages. We remain attracted to the return-on-capital metric because it speaks to the ability of the company to generate cash, which is ultimately what potentially lowers risk. We also tend to be attracted to businesses that are overcapitalized and under-levered. We believe an under-levered company has more options available to it if the economy falls into a recession, including changing its capital structure to lower its overall cost of capital. We believe the Fund is well-positioned based on the strength of the companies it owns and the overall valuation of its portfolio.

Management's Discussion of Fund Performance (Unaudited) (Continued)

Comparison of the Change in Value of a $10,000 Investment in the

Touchstone Large Cap Core Equity Fund and the Russell 1000® Index

Performance information does not reflect fees that are paid by the separate accounts through which shares of the Fund are sold. Inclusion of those fees would reduce figures for all periods.

The inception date of the Fund was May 1, 1999.

Notes to Chart

Russell 1000® Index measures the performance of the 1,000 largest companies in the Russell 3000® Index.

The Frank Russell Company (FRC) is the source and owner of the Russell 1000® Index data contained or reflected in this material and all trademarks and copyrights related thereto. The material may contain confidential information and unauthorized use, disclosure, copying, dissemination or redistribution is strictly prohibited. This is a Touchstone Investments presentation of the data, and FRC is not responsible for the formatting or configuration of this material or for any inaccuracy in the presentation thereof.

Management's Discussion of Fund Performance (Unaudited)

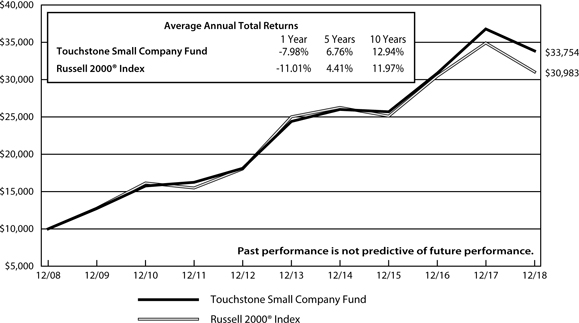

Touchstone Small Company Fund

Sub-Advised by Fort Washington Investment Advisors, Inc.

Investment Philosophy

The Fund seeks to provide investors with growth of capital by investing primarily in common stocks of small companies that the sub-advisor believes are high quality, have superior business models, solid management teams, sustainable growth potential and are attractively valued.

Fund Performance

The Touchstone Small Company Fund outperformed its benchmark, the Russell 2000® Index, for the 12-month period ended December 31, 2018. The Fund’s total return was -7.98 percent while the return of the benchmark was -11.01 percent.

Market Environment

Small-cap equity markets experienced a volatile 2018. The year started slow with the benchmark essentially flat in the first quarter. However, the second and third quarters saw strong gains by the Index, culminating in setting an all-time high in the third quarter. In an abrupt turn of events, the benchmark declined significantly in the fourth quarter and entered bear market territory. We believe that the sell-off was driven by a confluence of factors. One was an expectation of higher than expected interest rates from the U.S. Federal Reserve Board (Fed), and as a result tighter financial conditions. Another factor was intensified global trade dispute concerns, particularly with China. China, as well as emerging and developed economies overseas, experienced a significant deceleration in economic conditions and stock market valuations over 2018. Lastly, there was an increased focus on what stage is the U.S. economy currently operating, and when the next recession may occur.

At the sector level, Consumer Staples, Health Care, Information Technology, Communication Services, Consumer Discretionary, and Utilities outperformed the benchmark. The Financials and Real Estate sectors performed in-line with the benchmark. The Energy, Industrials, and Materials sectors all underperformed.

Portfolio Review

The Fund’s top performing sectors were Information Technology, Industrials, and Health Care. The Fund’s bottom three performing sectors were Financials, Communication Services, and Real Estate. The Fund did not hold any stocks in the Utilities sector which negatively impacted performance as the benchmark sector experienced positive returns for the year.

Mergers and acquisitions activity remained a theme in the Fund’s portfolio and continued to benefit relative performance in 2018. The investment process uncovered stocks of companies that have historically been attractive acquisition targets for strategic and financial buyers. In 2018, long-term holding Esterline Technologies Corp. (Industrials sector), a diversified manufacturer of aerospace and industrials products was acquired by TransDigm Group. A number of Information Technology sector holdings were acquired during the year as well. Finisar Inc., a provider of optical solutions to the data and telecommunications markets, was acquired by II-IV Inc.; Microsemi Corporation, a semiconductor manufacturer, was acquired by strategic buyers. Also, VeriFone Systems, Inc., a leading provider of point-of-sale software and hardware, and Blackhawk Network Holdings, a provider of digital and physical gift cards, were both acquired by private equity firms.

The Fund’s top contributors to relative performance were Haemonetics Corporation and Tactile Systems Technology, Inc. (both Health Care sector), and the aforementioned Esterline Technologies (Industrials sector).

The Fund’s largest detractors to relative performance for the year were Knight-Swift Transportation Holdings Inc. (Industrials sector), MEDNAX, Inc. (Health Care sector), and KB Home (Consumer Discretionary sector).

Management's Discussion of Fund Performance (Unaudited) (Continued)

KB Home and Health Care Services Group were sold from the Fund in 2018, as we believed the challenges that the business models experienced would persist in 2019. The Fund maintained positions in MEDNAX, Inc., Knight-Swift Transportation Holdings Inc., and Tivity Health Inc. at the end of the year for their potential.

At the end of the year, the Fund was overweight to Information Technology, Industrials, and Health Care, roughly in line to Consumer Discretionary, and underweight to Consumer Staples, Real Estate, and Financials. The Fund had no exposure to the Energy, Materials, and Utilities sectors. The overall positioning relative to the small-cap index was consistent through the year.

Outlook

The economic backdrop remains favorable for growth in 2019 with the U.S. offering a relative opportunity compared with non-U.S. equity markets. After the sell-off at year end, the valuations in small-cap companies have become more attractive than where they started the year and are already pricing in a recession. Furthermore, we believe that value has more tailwinds than growth in this environment.

We remain focused on executing our fundamental stock selection and portfolio management process. We believe that stocks experience a four stage investment cycle and our research process is focused on the dynamics that apply to each stage of the investment cycle. We believe that excess returns and lower volatility are driven by the ability to successfully identify a stock’s current stage and the potential for it to transition to a different stage of its investment cycle.

Management's Discussion of Fund Performance (Unaudited) (Continued)

Comparison of the Change in Value of a $10,000 Investment in the

Touchstone Small Company Fund and the Russell 2000® Index

Performance information does not reflect fees that are paid by the separate accounts through which shares of the Fund are sold. Inclusion of those fees would reduce figures for all periods.

The inception date of the Fund was November 30, 2000.

Notes to Chart

Russell 2000® Index measures the performance of the small-cap segment of the U.S. equity universe.

The Frank Russell Company (FRC) is the source and owner of the Russell 2000® Index data contained or reflected in this material and all trademarks and copyrights related thereto. The material may contain confidential information and unauthorized use, disclosure, copying, dissemination or redistribution is strictly prohibited. This is a Touchstone Investments presentation of the data, and FRC is not responsible for the formatting or configuration of this material or for any inaccuracy in the presentation thereof.

Management's Discussion of Fund Performance (Unaudited)

Touchstone ETF Funds

Sub-Advised by Wilshire Associates Incorporated

Touchstone Aggressive ETF Fund

Touchstone Conservative ETF Fund

Touchstone Moderate ETF Fund

Investment Philosophy

Three funds which invest in Exchanged-Traded Funds (ETFs) are available for investors seeking “lifestyle” products for their annuity holdings. The three strategic options include: the Conservative, Moderate, and Aggressive ETF Funds. These funds allocate their assets among up to ten ETFs. These ten ETF selections generally do not change dramatically over time. The more conservative fund has a higher bond weighting and the more aggressive fund has a lower bond weighting.

Fund Performance

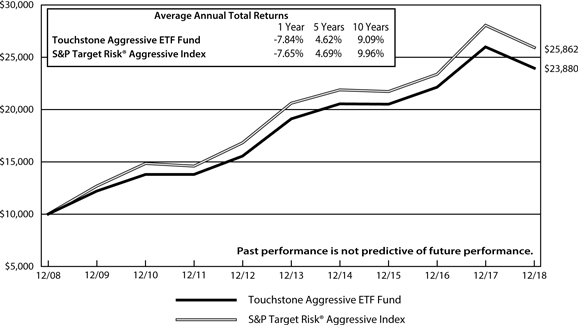

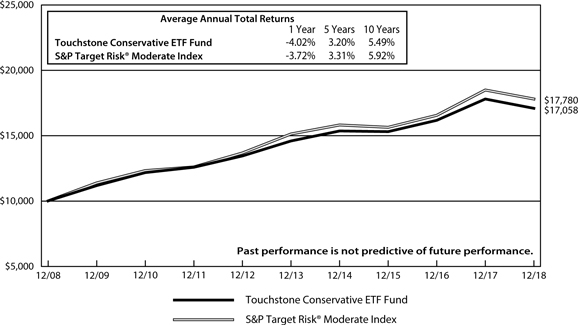

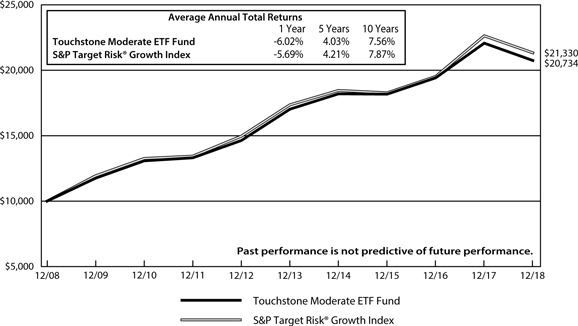

The Touchstone Aggressive ETF Fund underperformed its benchmark, the S&P Target Risk® Aggressive Index, for the 12-month period ended December 31, 2018. The Fund’s total return was -7.84 percent while the total return of the benchmark was -7.65 percent. The Touchstone Conservative ETF Fund underperformed its benchmark, the S&P Target Risk® Moderate Index, for the 12-month period ended December 31, 2018. The Fund’s total return was -4.02 percent while the total return of the benchmark was -3.72 percent. The Touchstone Moderate ETF Fund underperformed its benchmark, the S&P Target Risk® Growth Index, for the 12-month period ended December 31, 2018. The Fund’s total return was -6.02 percent while the total return of the benchmark was -5.69 percent.

Market Environment

The U.S. stock market, represented by the Russell 3000® Index, was down in 2018. Eight of the eleven major sectors declined during 2018, with Health Care, Utilities and Information Technology ending the year with positive returns. The worst performing sectors were Energy and Materials. Large capitalization stocks outperformed small-cap stocks while growth stocks outperformed their value counterparts during the twelve-month period.

Equity markets outside of the U.S. were negative for 2018 in both developed and emerging markets, with double-digit losses across the major indices. Although the European Union began the year in sound economic condition, growth declined steadily throughout the year as gains in unemployment stalled and industrial production reversed course. News out of Japan was grim with a report showing a serious economic contraction during the third quarter that threatened to end Japan’s longest expansion since the 1980s. Emerging Markets underperformed nearly all of the major indices for 2018.

The bellwether 10-year U.S. Treasury yield ended the year at 2.69 percent, up 29 basis points from its 2017 finish of 2.40 percent. The Federal Open Market Committee increased its overnight rate four times in 2018, a total increase of 100 basis points, to a range of 2.25 percent to 2.50 percent. Credit spreads widened during the year within both the investment grade and high yield markets.

Real estate securities declined in the U.S. for the year, but slightly outperformed global real estate. Commodities were down for the one-year period as crude oil fell 25 percent from the close of 2017. Master limited partnership returns remained negative for the year. Finally, gold prices ended 2018 down slightly from last year.

Management's Discussion of Fund Performance (Unaudited) (Continued)

Portfolio Review

The Funds’ investments are determined by an optimization process that considers the long-term historical risk and return profiles of various asset classes. For example, U.S. value equities were boosted relative to growth due to the perceived valuation opportunity and relative attractiveness. During the 2018 market environment, when value underperformed across U.S. stocks, the overweight positioning in the Funds relative to their respective benchmarks detracted from relative performance. Similarly, the overweight of the Funds to credit-sensitive fixed income was a headwind as was the related underweight to investment-grade, foreign fixed income, which outperformed its domestic counterpart.

Thematically, the several changes that occurred during 2018 were similar across all three Funds. Exposure to core and investment grade corporate fixed income was reduced, and a material allocation to short-term fixed income was initiated in order to further reduce portfolio interest rate risk. In addition, an overweight to domestic value equities was initiated, sourced from domestic large-cap blend equities, in order to take advantage of the more attractive valuations for value equities and lower beta1 profile. An overweight to small-cap domestic equities (relative to large-cap) was initiated in order to reduce exposure to the potential negative impacts of a trade war, since small-cap equities generally have had a smaller percentage of their sales attributed to foreign markets. The 2017 tax law changes were also expected to disproportionately benefit profitable small-cap companies, which had less flexibility to declare profits in lower tax foreign markets, rather than in the U.S.

Outlook

After an estimated 25 percent growth in corporate earnings during 2018, earnings are projected to grow less than 10 percent during 2019. Domestic equity markets have priced in reduced growth and on a forward price-earnings (P/E) basis, we believe equities are no longer expensive. Although the Funds remain positioned somewhat conservatively relative to long-term allocation targets, the Funds remain invested in risk assets. We previously pared back credit risk and duration risk, but they are at our target weight for long-only equities. We continue to expect a positive economic growth environment in the near future, and therefore, believe that the current economic landscape warrants low (relative to historical averages) interest rates on the longer end of the curve.

Global economic growth remains positive. While the forward-looking Purchasing Managers’ Index (PMI), which is an indicator of economic health in the manufacturing sector of a country or a region, has fallen in recent quarters, it continues to express positive economic momentum. Although measures of inflation are rising on a global basis, we believe they will remain low by historical standards. Given that global growth and inflation remain moderate, we believe that global central banks will be cautious about tightening monetary policy and will seek to communicate policy changes to the markets well in advance. Given ultra-low foreign developed market bond yields, we favor domestic fixed income over global fixed income; however, we recognize that any weakness in the U.S. dollar could serve to benefit foreign fixed income.

Strong U.S. corporate earnings growth helped propel domestic equity prices upwards early in 2018, but trade concerns weighed on the growth outlook for equities late in the year and led to a sharp sell-off in risk assets. Domestic equities are now mildly cheap in terms of forward P/E ratios. We believe the outlook for continued domestic and foreign gross domestic product (GDP) growth remains positive which reduces the downside risk of a continued equity market sell-off, unless economic growth slows meaningfully and recession fears grow. Rising rates may concern investors who may believe that the increase in interest rates will weigh on corporate earnings going forward. While we acknowledge this risk, we believe that it is important to recognize the potential demand for U.S. Treasury bonds from yield-seeking foreign investors. With respect to credit markets, there is potential that further erosion in the corporate earnings outlook could lead to further spread widening, though credit spreads have already priced in some slowdown and are now trading at what we believe to be more attractive levels.

1Beta is a measure of the volatility of a portfolio relative to its benchmark.

Management's Discussion of Fund Performance (Unaudited) (Continued)

Comparison of the Change in Value of a $10,000 Investment in the

Touchstone Aggressive ETF Fund and the S&P Target Risk® Aggressive Index

Performance information does not reflect fees that are paid by the separate accounts through which shares of the Fund are sold. Inclusion of those fees would reduce figures for all periods.

The inception date of the Fund was July 16, 2004.

Note to Chart

The S&P Target Risk® Aggressive Index is one of four multi-asset class indices that compose the S&P Target Risk Series. The S&P Target Risk® Aggressive Index emphasizes exposure to equities, maximizing opportunities for long-term capital accumulation. It may include small allocations to fixed income to enhance portfolio efficiency.

Management's Discussion of Fund Performance (Unaudited) (Continued)

Comparison of the Change in Value of a $10,000 Investment in the

Touchstone Conservative ETF Fund and the S&P Target Risk® Moderate Index

Performance information does not reflect fees that are paid by the separate accounts through which shares of the Fund are sold. Inclusion of those fees would reduce figures for all periods.

The inception date of the Fund was July 16, 2004.

Note to Chart

The S&P Target Risk® Moderate Index is one of four multi-asset class indices that compose the S&P Target Risk Series. The S&P Target Risk® Moderate Index offers significant exposure to fixed income, while also increasing opportunities for higher returns through equities.

Management's Discussion of Fund Performance (Unaudited) (Continued)

Comparison of the Change in Value of a $10,000 Investment in the

Touchstone Moderate ETF Fund and the S&P Target Risk® Growth Index

Performance information does not reflect fees that are paid by the separate accounts through which shares of the Fund are sold. Inclusion of those fees would reduce figures for all periods.

The inception date of the Fund was July 16, 2004.

Note to Chart

The S&P Target Risk® Growth Index is one of four multi-asset class indices that compose the S&P Target Risk Series. The S&P Target Risk® Growth Index increases exposure to equities, while also providing limited fixed income exposure to diversify risk.

Tabular Presentation of Portfolios of Investments (Unaudited)

December 31, 2018

The illustrations below provide each Fund’s credit quality and/or sector allocation. We hope it will be useful to shareholders as it summarizes key information about each Fund’s investments.

| Touchstone Active Bond Fund | | | |

| Credit Quality* | | (% of Investment Securities) | |

| AAA/Aaa | | | 44.3 | % |

| AA/Aa | | | 5.8 | |

| A/A | | | 11.9 | |

| BBB/Baa | | | 27.2 | |

| BB/Ba | | | 1.0 | |

| CCC | | | 0.5 | |

| Not Rated | | | 7.9 | |

| Cash Equivalents | | | 1.4 | |

| Total | | | 100.0 | % |

| | | | | |

| Touchstone Balanced Fund | | | |

| Credit Quality* | | (% of Fixed Income Securities) | |

| AAA/Aaa | | | 57.0 | % |

| AA/Aa | | | 5.4 | |

| A/A | | | 11.7 | |

| BBB/Baa | | | 25.4 | |

| BB/Ba | | | 0.3 | |

| Not Rated | | | 0.2 | |

| | | | 100.0 | % |

| | | | | |

| Sector Allocation** | | | (% of Net Assets) | |

| Common Stocks | | | | |

| Information Technology | | | 12.6 | % |

| Financials | | | 11.3 | |

| Communication Services | | | 10.6 | |

| Consumer Discretionary | | | 9.0 | |

| Health Care | | | 8.7 | |

| Industrials | | | 4.9 | |

| Real Estate | | | 2.9 | |

| Consumer Staples | | | 2.7 | |

| Energy | | | 2.3 | |

| Corporate Bonds | | | 13.6 | |

| U.S. Treasury Obligations | | | 10.4 | |

| U.S. Government Mortgage-Backed | | | 7.7 | |

| Obligations | | | | |

| Exchange-Traded Fund | | | 1.8 | |

| Sovereign Bonds | | | 0.2 | |

| Preferred Stock | | | 0.1 | |

| Short-Term Investment Fund | | | 1.2 | |

| Other Assets/Liabilities (Net) | | | 0.0 | |

| Total | | | 100.0 | % |

| | | | | |

| * | Credit quality ratings are from Standard & Poor's (“S&P”) and Moody's Investors Service (“Moody's”). If agency ratings differ, the higher rating will be used. Where no rating has been assigned, it may be for reasons unrelated to the creditworthiness of the issuer. |

| ** | Sector Classifications are based upon the Global Industry Classification Standard (GICS®). |

Tabular Presentation of Portfolios of Investments (Unaudited) (Continued)

| Touchstone Bond Fund | | | |

| Credit Quality* | | (% of Investment Securities) | |

| AAA/Aaa | | | 42.7 | % |

| AA/Aa | | | 5.2 | |

| A/A | | | 12.4 | |

| BBB/Baa | | | 27.6 | |

| BB/Ba | | | 1.1 | |

| Not Rated | | | 8.7 | |

| Cash Equivalents | | | 2.3 | |

| Total | | | 100.0 | % |

| | | | | |

| Touchstone Common Stock Fund | | | |

| Sector Allocation** | | (% of Net Assets) | |

| Information Technology | | | 18.7 | % |

| Communication Services | | | 18.3 | |

| Financials | | | 18.0 | |

| Health Care | | | 13.5 | |

| Consumer Discretionary | | | 12.2 | |

| Industrials | | | 6.4 | |

| Real Estate | | | 5.2 | |

| Energy | | | 3.7 | |

| Consumer Staples | | | 3.2 | |

| Short-Term Investment Fund | | | 0.8 | |

| Other Assets/Liabilities (Net) | | | (0.0 | ) |

| Total | | | 100.0 | % |

| | | | | |

| Touchstone Focused Fund | | | |

| Sector Allocation** | | (% of Net Assets) | |

| Information Technology | | | 18.9 | % |

| Financials | | | 16.8 | |

| Health Care | | | 15.8 | |

| Communication Services | | | 15.7 | |

| Consumer Discretionary | | | 12.1 | |

| Industrials | | | 6.4 | |

| Real Estate | | | 5.0 | |

| Energy | | | 3.5 | |

| Consumer Staples | | | 3.3 | |

| Short-Term Investment Fund | | | 2.6 | |

| Other Assets/Liabilities (Net) | | | (0.1 | ) |

| Total | | | 100.0 | % |

| | | | | |

| Touchstone Large Cap Core Equity Fund | | | |

| Sector Allocation** | | (% of Net Assets) | |

| Financials | | | 24.8 | % |

| Consumer Discretionary | | | 20.1 | |

| Information Technology | | | 13.5 | |

| Industrials | | | 13.0 | |

| Materials | | | 8.4 | |

| Consumer Staples | | | 8.0 | |

| Communication Services | | | 7.0 | |

| Energy | | | 2.1 | |

| Health Care | | | 1.9 | |

| Short-Term Investment Fund | | | 1.4 | |

| Other Assets/Liabilities (Net) | | | (0.2 | ) |

| Total | | | 100.0 | % |

| | | | | |

| * | Credit quality ratings are from Standard & Poor's (“S&P”) and Moody's Investors Service (“Moody's”). If agency ratings differ, the higher rating will be used. Where no rating has been assigned, it may be for reasons unrelated to the creditworthiness of the issuer. |

| ** | Sector Classifications are based upon the Global Industry Classification Standard (GICS®). |

Tabular Presentation of Portfolios of Investments (Unaudited) (Continued)

| Touchstone Small Company Fund | | | |

| Sector Allocation* | | (% of Net Assets) | |

| Information Technology | | | 24.1 | % |

| Industrials | | | 22.5 | |

| Health Care | | | 19.8 | |

| Consumer Discretionary | | | 13.8 | |

| Financials | | | 10.1 | |

| Communication Services | | | 2.9 | |

| Consumer Staples | | | 2.1 | |

| Real Estate | | | 1.4 | |

| Short-Term Investment Fund | | | 3.7 | |

| Other Assets/Liabilities (Net) | | | (0.4 | ) |

| Total | | | 100.0 | % |

| | | | | |

| Touchstone Aggressive ETF Fund | | | |

| Sector Allocation | | (% of Net Assets) | |

| Exchange-Traded Funds | | | | |

| Equity Funds | | | 79.8 | % |

| Fixed Income Funds | | | 17.5 | |

| Short-Term Investment Funds | | | 15.9 | |

| Other Assets/Liabilities (Net) | | | (13.2 | ) |

| Total | | | 100.0 | % |

| | | | | |

| Touchstone Conservative ETF Fund | | | |

| Sector Allocation | | (% of Net Assets) | |

| Exchange-Traded Funds | | | | |

| Fixed Income Funds | | | 57.9 | % |

| Equity Funds | | | 39.6 | |