UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number | 811-08510 |

|

Matthews International Funds |

(Exact name of registrant as specified in charter) |

|

Four Embarcadero Center, Suite 550

San Francisco, CA 94111 |

(Address of principal executive offices) (Zip code) |

|

William J. Hackett, President

Four Embarcadero Center, Suite 550

San Francisco, CA 94111 |

(Name and address of agent for service) |

|

Registrant’s telephone number, including area code: | 415-788-6036 | |

|

Date of fiscal year end: | December 31 | |

|

Date of reporting period: | December 31, 2010 | |

| | | | | | |

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget ("OMB") control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 100 F Street, NE, Washington, DC 20549. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

Item 1. Reports to Stockholders.

The Report to Shareholders is attached herewith.

Matthews Asia Funds | Annual Report

December 31, 2010 | matthewsasia.com

Performance and Expenses

Through December 31, 2010

Institutional Class Shares were first offered on October 29, 2010. For performance since that date, please see each Fund's performance table in the report. Performance for the Institutional Class Shares prior to its inception is based on the performance of the Investor Class. Performance differences between the Institutional Class and Investor Class may arise due to differences in fees charged to each class.

| | | | |

Average Annual Total Return | | 2010 Gross

Annual | | 2009 Gross

Annual | |

| | | Inception

Date | | 1 year | | 5 years | | 10 years | | Since

Inception | | Operating

Expenses1 | | Operating

Expenses | |

| Matthews Asian Growth and Income Fund | |

| Investor Class (MACSX) | | 9/12/94 | | | 19.18 | % | | | 11.42 | % | | | 15.35 | % | | | 11.65 | % | | | 1.13 | % | | | 1.18 | % | |

| Institutional Class (MICSX) | | 10/29/10 | | | 19.23 | % | | | 11.43 | % | | | 15.35 | % | | | 11.65 | % | | | 0.93 | % | | | n.a. | | |

| Matthews Asia Dividend Fund | |

| Investor Class (MAPIX) | | 10/31/06 | | | 22.83 | % | | | n.a. | | | | n.a. | | | | 13.73 | % | | | 1.14 | % | | | 1.28 | % | |

| After Fee Waiver, Reimbursement and Recoupment | | | | | | | | | | 1.15%2 | | 1.30%2 | |

| Institutional Class (MIPIX) | | 10/29/10 | | | 22.88 | % | | | n.a. | | | | n.a. | | | | 13.74 | % | | | 1.02 | % | | | n.a. | | |

| Matthews China Dividend Fund | |

| Investor Class (MCDFX) | | 11/30/09 | | | 22.53 | % | | | n.a. | | | | n.a. | | | | 22.60 | % | | | 1.95 | % | | | 10.05 | % | |

| After Fee Waiver, Reimbursement and Recoupment | | | | | | | | | | 1.50%3 | | 1.50%3 | |

| Institutional Class (MICDX) | | 10/29/10 | | | 22.58 | % | | | n.a. | | | | n.a. | | | | 22.64 | % | | | 1.24 | % | | | n.a. | | |

| Matthews Asia Pacific Fund | |

| Investor Class (MPACX) | | 10/31/03 | | | 26.85 | % | | | 8.59 | % | | | n.a. | | | | 12.09 | % | | | 1.19 | % | | | 1.28 | % | |

| Institutional Class (MIAPX) | | 10/29/10 | | | 26.92 | % | | | 8.60 | % | | | n.a. | | | | 12.09 | % | | | 0.99 | % | | | n.a. | | |

| Matthews Pacific Tiger Fund | |

| Investor Class (MAPTX) | | 9/12/94 | | | 22.30 | % | | | 14.47 | % | | | 16.98 | % | | | 9.90 | % | | | 1.09 | % | | | 1.13 | % | |

| Institutional Class (MIPTX) | | 10/29/10 | | | 22.35 | % | | | 14.48 | % | | | 16.99 | % | | | 9.90 | % | | | 0.95 | % | | | n.a. | | |

| Matthews China Fund | |

| Investor Class (MCHFX) | | 2/19/98 | | | 15.77 | % | | | 24.20 | % | | | 19.73 | % | | | 13.70 | % | | | 1.15 | % | | | 1.21 | % | |

| Institutional Class (MICFX) | | 10/29/10 | | | 15.82 | % | | | 24.21 | % | | | 19.74 | % | | | 13.71 | % | | | 0.97 | % | | | n.a. | | |

| Matthews India Fund | |

| Investor Class (MINDX) | | 10/31/05 | | | 32.53 | % | | | 17.15 | % | | | n.a. | | | | 19.38 | % | | | 1.18 | % | | | 1.27 | % | |

| Institutional Class (MIDNX) | | 10/29/10 | | | 32.52 | % | | | 17.15 | % | | | n.a. | | | | 19.38 | % | | | 0.99 | % | | | n.a. | | |

| Matthews Japan Fund | |

| Investor Class (MJFOX) | | 12/31/98 | | | 19.58 | % | | | -4.72 | % | | | 0.75 | % | | | 4.39 | % | | | 1.30 | % | | | 1.31 | % | |

| Institutional Class (MIJFX) | | 10/29/10 | | | 19.58 | % | | | -4.72 | % | | | 0.75 | % | | | 4.39 | % | | | 1.08 | % | | | n.a. | | |

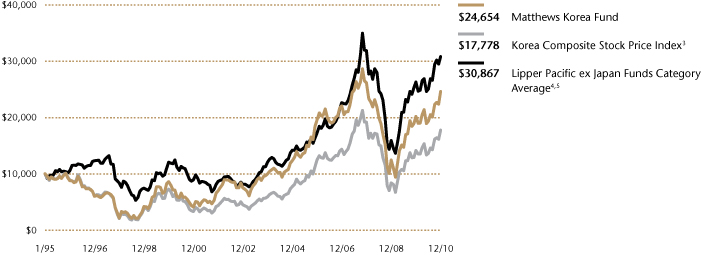

| Matthews Korea Fund | |

| Investor Class (MAKOX) | | 1/3/95 | | | 21.86 | % | | | 4.77 | % | | | 19.83 | % | | | 5.80 | % | | | 1.21 | % | | | 1.30 | % | |

| Institutional Class (MIKOX) | | 10/29/10 | | | 21.86 | % | | | 4.77 | % | | | 19.83 | % | | | 5.80 | % | | | 0.91 | % | | | n.a. | | |

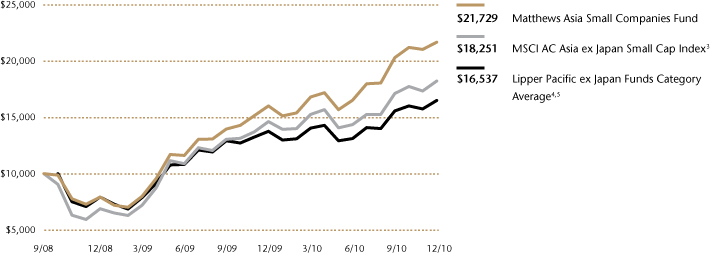

| Matthews Asia Small Companies Fund | |

| Investor Class (MSMLX) | | 9/15/08 | | | 35.54 | % | | | n.a. | | | | n.a. | | | | 40.27 | % | | | 1.59 | % | | | 2.09 | % | |

| After Fee Waiver, Reimbursement and Recoupment | | | | | | | | | | | | | | | | | | | | | 1.63 | %4 | | | 2.00 | %4 | |

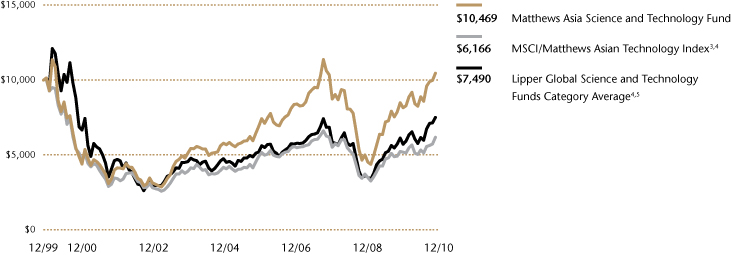

| Matthews Asia Science and Technology Fund | |

| Investor Class (MATFX) | | 12/27/99 | | | 23.58 | % | | | 8.70 | % | | | 9.16 | % | | | 0.42 | % | | | 1.26 | % | | | 1.40 | % | |

1 Gross annual operating expenses for Institutional Class Shares are annualized.

2 The Advisor has contractually agreed to waive Matthews Asia Dividend Fund's fees and reimburse expenses until at least April 30, 2012 to the extent needed to limit total annual operating expenses to 1.50%.

3 The Advisor has contractually agreed to waive Matthews China Dividend Fund's fees and reimburse expenses until at least November 30, 2012 to the extent needed to limit total annual operating expenses to 1.50%.

4 The Advisor has contractually agreed to waive Matthews Asia Small Companies Fund's fees and reimburse expenses until at least April 30, 2012 to the extent needed to limit total annual operating expenses to 2.00%.

Investor Disclosure

Past Performance: All performance quoted in this report is past performance and is no guarantee of future results. Investment return and principal value will fluctuate with changing market conditions so that when redeemed, shares may be worth more or less than their original cost. Current performance may be lower or higher than the returns quoted. If certain of the Funds' fees and expenses had not been waived, returns would have been lower. For the Funds' most recent month-end performance, please call 800.789.ASIA (2742) or visit matthewsasia.com.

Investment Risk: Mutual fund shares are not deposits or obligations of, or guaranteed by, any depositary institution. Shares are not insured by the FDIC, Federal Reserve Board or any government agency and are subject to investment risks, including possible loss of principal amount invested. Investing in international markets may involve additional risks, such as social and political instability, market illiquidity, exchange-rate fluctuations, a high level of volatility and limited regulation. In addition, single-country and sector funds may be subject to a higher degree of market risk than diversified funds because of concentration in a specific industry, sector or geographic location. Investing in small and mid-size companies is more risky than investing in large companies as they may be more volatile and less liquid than larger companies. Please see the Funds' prospectus and Statement of Additional Information for more risk disclosure.

Contents

| Messages to Shareholders | | | 2 | | |

|

| Manager Commentaries, Fund Characteristics and Schedules of Investments: | |

|

| ASIA GROWTH AND INCOME STRATEGIES | |

|

| Matthews Asian Growth and Income Fund | | | 4 | | |

|

| Matthews Asia Dividend Fund | | | 10 | | |

|

| Matthews China Dividend Fund | | | 15 | | |

|

| ASIA GROWTH STRATEGIES | |

|

| Matthews Asia Pacific Fund | | | 20 | | |

|

| Matthews Pacific Tiger Fund | | | 25 | | |

|

| Matthews China Fund | | | 30 | | |

|

| Matthews India Fund | | | 35 | | |

|

| Matthews Japan Fund | | | 40 | | |

|

| Matthews Korea Fund | | | 45 | | |

|

| ASIA SMALL COMPANY STRATEGY | |

|

| Matthews Asia Small Companies Fund | | | 50 | | |

|

| ASIA SPECIALTY STRATEGY | |

|

| Matthews Asia Science and Technology Fund | | | 55 | | |

|

| Disclosures and Index Definitions | | | 59 | | |

|

| Disclosure of Fund Expenses | | | 60 | | |

|

| Statements of Assets and Liabilities | | | 62 | | |

|

| Statements of Operations | | | 64 | | |

|

| Statements of Changes in Net Assets | | | 66 | | |

|

| Financial Highlights | | | 72 | | |

|

| Notes to Financial Statements | | | 83 | | |

|

| Report of Independent Registered Public Accounting Firm | | | 97 | | |

|

| Tax Information | | | 98 | | |

|

| Approval of Investment Advisory Agreement | | | 99 | | |

|

| Trustees and Officers of the Funds | | | 103 | | |

|

Cover Photo: Baha'i Lotus Temple, New Delhi, India

This report has been prepared for Matthews Asia Funds shareholders. It is not authorized for distribution to prospective investors unless accompanied or preceded by a current Matthews Asia Funds prospectus, which contains more complete information about the Funds' investment objectives, risks and expenses. Additional copies of the prospectus may be obtained at matthewsasia.com. Please read the prospectus carefully before you invest or send money.

The views and opinions in this report were current as of December 31, 2010. They are not guarantees of performance or investment results and should not be taken as investment advice. Investment decisions reflect a variety of factors, and the managers reserve the right to change their views about individual stocks, sectors and the markets at any time. As a result, the views expressed should not be relied upon as a forecast of a Fund's future investment intent.

Statements of fact are from sources considered reliable, but neither the Funds nor the Investment Advisor makes any representation or guarantee as to their completeness or accuracy.

Matthews Asia Funds are distributed by:

BNY Mellon Distributors Inc. | 760 Moore Road | King of Prussia, PA 19406

"We set out to invest 'through the cycle.' That means we are looking for profit opportunities that depend on solid financials and sustainable business advantages, rather than being driven by the short-term ebbs and flows of the stream of spending in an economy."

Message to Shareholders

from the Investment Advisor

Dear Fellow Shareholders,

2010 was the year that the global economy steadied itself, but was not revitalized. Growth rates were positive in most large economies. However, growth for the most part was not sufficient enough to lift employment rates. This situation has been described as the "new normal." And yet, it is surely abnormal to have nearly 10% unemployment in the U.S. and Europe as a whole, as well as 20% of people out of work in large economies such as Spain. As one might expect in such an environment, overall prices were subdued, rising 1.6% in both the U.S. and Europe, despite policymakers' attempts to "jump start" their economies through aggressive fiscal expansion, monetary stimulus, or both. Those attempts have, to general consensus, produced lackluster results—although the argument rages as to whether that was because the efforts were too little or whether they were of the kind that would fail even more disastrously if they were tried on a larger scale. The experience in Asia, of course, has been very different. Asian economies were revitalized in 2010, and reached new heights of production and income. Accordingly, policymakers in Asia are stepping on the brakes to try to rein in prices and credit growth for fear that they might be in danger of igniting the same kind of bubbles that have brought the West's economies to a crawl.

How investors will react depends very much on what they want from the markets. If they seek fast profits, then the current environment may seem an exciting one. What is the possibility of an Asian equity bubble? Will the demand for raw materials in Asia push commodity prices to new highs in the very near future? Will the great wall of liquidity—created by the West's policy response to stagnant growth—push asset prices to historic highs? Will it also be further accommodated by Asian government efforts to hold down currencies that should appreciate by increasing the quantity of currency in circulation? However, if an investor's commitment to the markets is longer-term in nature, as ours is at Matthews, then these issues become distinctly less enticing—for what we are witnessing is a distortion in pricing. The degrees of relative price changes are not being determined by the underlying changes to domestic demand, and can be misleading. Put another way, if the price changes that are directing true profit opportunities are being overwhelmed by speculative trading, then the investment waters are being muddied.

This makes it a peculiar and difficult time for Matthews' style of investing. We set out to invest "through the cycle." That means we are looking for profit opportunities that depend on solid financials and sustainable business advantages, rather than being driven by the short-term ebbs and flows of the stream of spending in an economy. We try to train ourselves to set our sights over the kind of time horizon that would take into account a complete business cycle. We, therefore, anticipate seeing temporary fluctuations in industries and in our own performance within that timeframe. Trying to remain true to our essential philosophy and beliefs in investing has therefore been a key test for our investment team over the past year—and one in which, I believe, our portfolio managers performed admirably. Looking ahead in what we expect may be a volatile environment, it will be even more important to stay true to our principles, and to properly manage portfolios for market risks, than to accurately predict each sway and twist of the markets.

2 MATTHEWS ASIA FUNDS

An Eye for New Trends

We have to guard against many errors, but in this context, one is more apparent than any other—that is mistaking the beginning of a new trend for just another cyclical quirk. Industries have in the past morphed from cyclical to secular growth. Being mindful of these opportunities is paramount. One example of the past is the information technology industry. Certainly overhyped in the late 1990s and very dependent on corporate capital expenditure cycles, the IT industry has become more exposed over time to consumer demand and growth. As technologies and research and development have coalesced around a core set of platforms, the industry has moderated its cycles and become more transparent. We believe there are similar opportunities across the Asian markets. In the financials sector, industries such as wealth management have in the past been very cyclical, as they have lacked a deep client base or a diverse enough pool of assets in which to invest. As financial markets deepen and savings behavior changes, these businesses could change as well. The same could be said across many other emergent industries in the services and consumer sectors, such as marketing and advertising. Properly assessing these opportunities is a task for our analysts and portfolio managers.

Foremost in our minds is the energy and materials sector. Talk of commodity supercycles is always quick to surface whenever higher liquidity or a lower U.S. dollar drives prices in these sectors—and yet the key catalyst has remained monetary, despite the underlying demand in Asia's economies. Nevertheless, at some point there will be a structural shift in the way that Asia manages its energy needs, driven partly by costs in traditional raw commodities and partly—perhaps more sustainably—by an ongoing desire to change the quality of life.

Our investment process remains informed ultimately by our confidence in the underlying business investment. But when we do try to pierce the murky future and identify broad themes and attractive industries, we do so with the knowledge that these are driven by forces and demands that are more widespread and enduring than the actions of politicians and central bankers. In so doing, we hope that we are continuing to place emphasis on stock selection, whilst neither ignoring the macroeconomic environment, nor placing too much faith in short-term forecasts of overly broad indicators such as GDP and interest rates.

Finally, Matthews continuously monitors capacity and asset flows on each of its investment strategies. If we believe the pace of inflows and/or a Fund's asset levels could impede the Firm's ability to achieve its investment objectives, Matthews considers strategy closures. Recently, two Funds were closed to most new investors—the Matthews Asia Small Companies and Matthews Asian Growth and Income Funds closed on November 12, 2010 and January 7, 2011, respectively. The Funds' closures apply to both Investor and Institutional Class shares. We believe that limiting access to these Funds is a prudent step toward maintaining the integrity of our investment process.

As always, it is an honor to serve as your investment advisor.

Robert Horrocks, PhD

Chief Investment Officer

Matthews International Capital Management, LLC

matthewsasia.com | 800.789.ASIA 3

ASIA GROWTH AND INCOME STRATEGIES

PORTFOLIO MANAGERS

Andrew Foster

Lead Manager

Robert J. Horrocks, PhD

Co-Manager

FUND FACTS

| | | Investor Class | | Institutional Class | |

| Ticker | | MACSX | | MICSX | |

| CUSIP | | 577130206 | | 577130842 | |

| Inception | | 9/12/94 | | 10/29/10 | |

| NAV | | $18.04 | | $18.04 | |

| Initial Investment | | $2,500 | | $3 million | |

| Gross Expense Ratio1 | | 1.13% | | 0.93% | |

Portfolio Statistics

| Total # of Positions | | 85 | |

| Net Assets | | $4.1 billion | |

| Weighted Average Market Cap | | $22.3 billion | |

| Portfolio Turnover | | 19.84%2 | |

Benchmark

MSCI AC Asia ex Japan Index

Redemption Fee

2% within first 90 calendar days of purchase

OBJECTIVE

Long-term capital appreciation. The Fund also seeks to provide some current income.

STRATEGY

Under normal market conditions, the Fund seeks to achieve its investment objective by investing at least 80% of its total net assets, which include borrowings for investment purposes, in dividend-paying equity securities and the convertible securities, of any duration or quality, of companies located in Asia.

1 Gross expense ratio for Institutional Class is annualized. Matthews Asia Funds does not charge 12b-1 fees.

2 The lesser of fiscal year 2010 long-term purchase costs or sales proceeds divided by the average monthly market value of long-term securities.

Matthews Asian Growth and Income Fund

Portfolio Manager Commentary

For the year ending December 31, 2010, the Matthews Asian Growth and Income Fund returned 19.18% (Investor Class) and 19.23% (Institutional Class), while its benchmark, the MSCI All Country Asia ex Japan Index, rose 19.93%. By way of broader comparison, the U.S. S&P 500 Index rose 15.08% during the year, and the international MSCI EAFE Index climbed 8.21%. During the fourth quarter, the Fund gained 4.70% (Investor Class) and 4.75% (Institutional Class), versus a 6.72% increase in the benchmark. The Fund began 2010 with a share price of $15.77, and shareholders who were invested throughout the year would have received income distributions totaling approximately 47 cents (Investor Class), or 3.0%, of the share price at the start of the year.

During the latter half of 2010, stock markets around the world performed exceedingly well, casting a rosy tint over perceptions of the year as a whole. However, the year was punctuated by sharp volatility, prompted by concerns over the solvency of several European nations, and by the tepid recovery of the U.S. economy. Though now only an afterthought, six months ago markets were mired in losses. Against this backdrop of falling stocks, the Fund held up better than market averages, and exhibited reduced volatility. As markets rose, the Fund outpaced its benchmark for most of the year, though sustained gains in markets meant the Fund's performance was eclipsed by the index in the final week of 2010. Since its inception, the Fund has sought to participate in the region's long-term growth potential, balanced by a desire to mitigate excess volatility and to offer a degree of downside protection. Amid a rocky year that proved profitable only near its end, the Fund's stability and steady gains meant that it performed as it intended.

The Fund's gains during the year had less-obvious origins: namely, its exposure to industrials, and its holdings in Japan. The Fund has historically sought to minimize exposure to cyclical elements; this has meant that industrials have not always played a large role in the portfolio. However, in recent years, we have determined that a number of industrials—particularly larger issuers in technology, industrial services and specialized manufacturing—have exhibited characteristics associated with maturation. As growth in these areas has moderated, their need for investment and capital expenditure has been tempered, as has the cyclicality associated with their businesses.

Happily, this has meant these issuers have enjoyed higher levels of residual cash profits that can be used to fortify their balance sheets, or to expand dividend payments. With improved prospects for dividend payment, and often-underappreciated growth, such industrials include some of the Fund's largest holdings: Singapore Technologies Engineering, Taiwan Semiconductor Manufacturing and Keppel. All three of these positions paid ample dividends during the year, exhibited relatively steady stock performance during market declines, and most importantly, saw their growth prospects surpass market expectations, leading to large gains for the Fund.

Perhaps even less expected is the contribution of the Fund's Japanese holdings to performance. Though bolstered by substantial strength in the yen during the year, the Japanese holdings nevertheless generated gains that, on average, handily surpassed the Fund's overall return. During the past several years, the Fund has increased its allocation to Japanese equities and real estate investment trusts (REITs), but not because of an overall belief that the Japanese market might rally. Instead, we have discovered select companies that offer stable business models, and which present balance sheets replete with substantial levels of liquid cash, typically accompanied by little or no

(continued)

Closed to most new investors as of January 7, 2011.

4 MATTHEWS ASIA FUNDS

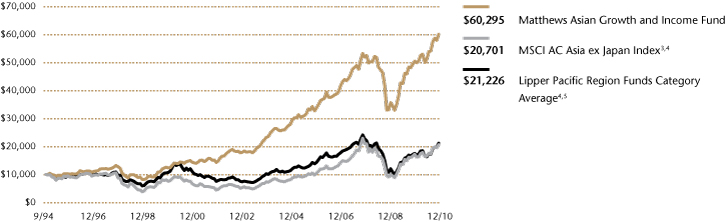

PERFORMANCE AS OF DECEMBER 31, 2010

Institutional Class Shares were first offered on October 29, 2010. Performance since that date was 2.49%. Performance for the Institutional Class shares prior to its inception is based on the performance of the Investor Class. Performance differences between the Institutional Class and Investor Class may arise due to differences in fees charged to each class.

| | | | | | | Average Annual Total Returns | |

| | | Inception Date | | 3 Months | | 1 Year | | 3 Years | | 5 Years | | 10 Years | | Since

Inception | |

| Investor Class (MACSX) | | 9/12/94 | | | 4.70 | % | | | 19.18 | % | | | 4.62 | % | | | 11.42 | % | | | 15.35 | % | | | 11.65 | % | |

| Institutional Class (MICSX) | | 10/29/10 | | | 4.75 | % | | | 19.23 | % | | | 4.63 | % | | | 11.43 | % | | | 15.35 | % | | | 11.65 | % | |

| MSCI AC Asia ex Japan Index3 | | | | | 6.72 | % | | | 19.93 | % | | | -0.38 | % | | | 13.19 | % | | | 13.31 | % | | | 4.56 | %4 | |

| Lipper Pacific Region Funds Category Average5 | | | | | 9.11 | % | | | 16.87 | % | | | -3.10 | % | | | 4.94 | % | | | 8.17 | % | | | 4.32 | %4 | |

Performance assumes reinvestment of all dividends and/or distributions before taxes. All performance quoted represents past performance and is no guarantee of future results. Investment return and principal value will fluctuate with market conditions so that when redeemed, shares may be worth more or less than their original cost. Current performance may be lower or higher than the return figures quoted. Returns would have been lower if certain of the Fund's fees and expenses had not been waived. For the Fund's most recent month-end performance visit matthewsasia.com.

2010 INCOME DISTRIBUTION HISTORY

| | | June | | December | | Total | |

| Investor Class (MACSX) | | $ | 0.19 | | | $ | 0.28 | | | $ | 0.47 | | |

| Institutional Class (MICSX) | | | — | | | $ | 0.29 | | | $ | 0.29 | | |

Note: This table does not include capital gains distributions. Institutional Class Shares were first offered on October 29, 2010. For income distribution history, visit matthewsasia.com.

30-DAY YIELD:

0.93% (Investor Class) 1.18% (Institutional Class)

The 30-Day Yield represents net investment income earned by the Fund over the 30-day period ended 12/31/10, expressed as an annual percentage rate based on the Fund's share price at the end of the 30-day period. The 30-Day Yield should be regarded as an estimate of the Fund's rate of investment income, and it may not equal the Fund's actual income distribution rate.

Source: BNY Mellon Investment Servicing (US) Inc.

DIVIDEND YIELD: 3.75%

The dividend yield (trailing) for the portfolio is the weighted average sum of the dividend paid per share during the last 12 months divided by the current price. The annualized dividend yield for the Fund is for the equity-only portion of the portfolio. Please note that this is based on gross portfolio holdings and does not reflect the actual yield an investor in the Fund would receive. Past yields are no guarantee of future yields.

Source: FactSet Research Systems

GROWTH OF A $10,000 INVESTMENT SINCE INCEPTION—INVESTOR CLASS

Plotted monthly. The performance data and graph do not reflect the deduction of taxes that a shareholder would pay on dividends, capital gain distributions or redemption of Fund shares. Values are in US$.

3 It is not possible to invest directly in an index. Source: Index data from Morgan Stanley Capital International and Bloomberg; total return calculations performed by BNY Mellon Investment Servicing (US) Inc. Please see page 59 for index definitions.

4 Calculated from 8/31/94.

5 The Lipper Category Average does not reflect sales charges and is based on total return, including reinvestment of dividends and capital gains for the stated periods.

TOP TEN HOLDINGS6

| | | Country | | % of Net Assets | |

| Singapore Technologies Engineering, Ltd. | | Singapore | | | 3.5 | % | |

| Taiwan Semiconductor Manufacturing Co., Ltd. | | Taiwan | | | 3.1 | % | |

| Telstra Corp., Ltd. | | Australia | | | 2.8 | % | |

| Keppel Corp., Ltd. | | Singapore | | | 2.7 | % | |

| CLP Holdings, Ltd. | | China/Hong Kong | | | 2.6 | % | |

| Hisamitsu Pharmaceutical Co., Inc. | | Japan | | | 2.6 | % | |

| China Petroleum & Chemical Corp. (Sinopec), Cnv., 0.000%, 04/24/2014 | | China/Hong Kong | | | 2.3 | % | |

| Trend Micro, Inc. | | Japan | | | 2.3 | % | |

| HSBC Holdings PLC | | United Kingdom | | | 2.3 | % | |

| PTT Public Co., Ltd. | | Thailand | | | 2.2 | % | |

| % OF ASSETS IN TOP TEN | | | | | 26.4 | % | |

6 Holdings may combine more than one security from same issuer and related depositary receipts.

matthewsasia.com | 800.789.ASIA 5

COUNTRY ALLOCATION (%)7

| China/Hong Kong | | | 26.0 | | |

| Singapore | | | 15.0 | | |

| Japan | | | 12.2 | | |

| South Korea | | | 8.0 | | |

| India | | | 7.3 | | |

| Taiwan | | | 6.5 | | |

| Malaysia | | | 5.7 | | |

| Thailand | | | 5.1 | | |

| Australia | | | 3.9 | | |

| United Kingdom | | | 2.3 | | |

| Vietnam | | | 2.1 | | |

| Indonesia | | | 1.1 | | |

| Philippines | | | 1.0 | | |

Cash and Other Assets,

Less Liabilities | | | 3.8 | | |

SECTOR ALLOCATION (%)

| Financials | | | 25.9 | | |

| Telecommunication Services | | | 15.4 | | |

| Industrials | | | 14.6 | | |

| Information Technology | | | 13.5 | | |

| Consumer Discretionary | | | 6.2 | | |

| Utilities | | | 5.7 | | |

| Consumer Staples | | | 4.8 | | |

| Energy | | | 4.6 | | |

| Health Care | | | 4.2 | | |

| Non Classified | | | 0.8 | | |

| Materials | | | 0.5 | | |

Cash and Other Assets,

Less Liabilities | | | 3.8 | | |

MARKET CAP EXPOSURE (%)8

| Large Cap (over $5B) | | | 60.2 | | |

| Mid Cap ($1B–$5B) | | | 27.8 | | |

| Small Cap (under $1B) | | | 7.5 | | |

| Non Classified | | | 0.7 | | |

Cash and Other Assets,

Less Liabilities | | | 3.8 | | |

BREAKDOWN BY SECURITY TYPE (%)8,9

| Common Equities | | | 71.4 | | |

| Convertible Bonds | | | 20.2 | | |

| Preferred Equities | | | 2.5 | | |

| Corporate Bonds | | | 1.1 | | |

| Government Bonds | | | 0.7 | | |

| Warrants | | | 0.4 | | |

Cash and Other Assets,

Less Liabilities | | | 3.8 | | |

7 Australia, United Kingdom and Japan are not included in the MSCI All Country Asia ex Japan Index.

8 Source: FactSet Research Systems. Percentage values in data are rounded to the nearest tenth of one percent; the values may not sum to 100% due to rounding.

9 Bonds are not included in the MSCI All Country Asia ex Japan Index.

Matthews Asian Growth and Income Fund

Portfolio Manager Commentary (continued)

borrowings. Perhaps surprising to some, these same companies are capable of producing admirable growth amid a moribund and deflationary economy. As these companies are located in a market burdened by sustained negative perception, their performance has gone less noticed, and equities have been reasonably priced, with attractive dividends. Though the Fund's allocation is not permanent in any sense, it is likely to maintain a tactical allocation to the Japanese market for some time.

Looking forward, aggregate valuation levels in Asia appear challenging, though not unworkable. Currently forecasted price-to-earnings multiples for stocks are not unreasonable—set at approximately 13 times estimated future earnings. However, this ratio is dependant on corporate profits expanding at a relatively robust pace. This assumption may be at odds with the global economic environment, which may see sluggish growth in developed markets, and more moderate growth in China. Convertible bonds have often proven attractive as an alternative asset class for the Fund; however, such bonds have been subject to aggressive valuations throughout the year, limiting their immediate attraction. Still, issuance in the convertible market has begun to expand dramatically, and with it, the possibility the Fund may find new avenues for investment in that asset class. In the meantime, we are favoring investment in the large-capitalization stocks of business with stable prospects and elevated dividend yields, particularly such as those found in the telecommunications industry.

The year ahead will present several challenges for investors in the Asian region, including burgeoning inflation. Inflationary pressures have escalated to the extent that policy reaction appears unavoidable. Already the region has seen higher interest rates, heightened administrative controls over the commercial banking sector, and restrictions on the free-flow of capital across borders. The unpredictable consequence of these policies will likely create headwinds for stocks, at least in the near-term. Another challenge stems from the threat of military conflict or violence within the region.

The third major challenge stems from the growing misperception over China's long-term growth potential. After several decades of successful and rapid expansion, public consensus has assigned an elevated expectation for China's growth. Forecasts are underpinned by assumptions that the country will sidestep major shocks to its domestic economy. Along the way, forecasters expect that China should grow its economy from US$5.8 trillion today, to well over US$18 trillion a decade later. Yet such forecasts ignore the fact that as China's economy grows, its challenges will also grow exponentially. It is far more straightforward to expand from a small base than it is to compound growth from a much larger one.

To be clear, we remain positive about China's long-term growth prospects. Yet our evidence indicates that the economy is entering a period of structural transition, one in which its growth should moderate, even as the quality and sustainability of that growth may improve. China's economy may not realize the substantial scale that some have predicted unless it promotes growth in its service industries; it must curtail and reverse damage to its natural environment; and it must undertake difficult public and private reforms. This may not happen in a smooth, straight line as has been forecast. Yet we continue to invest in the market on the premise that it will indeed occur, but only over a horizon that will benefit investors who possess patience, persistence and time.

We would also like to note that the Fund closed to most new investors on January 7, 2011 in order to limit the pace of inflows. We believe that limiting access to the Fund at this time is a prudent step toward maintaining the integrity of our investment process. We thank you for your investment in the Fund.

6 MATTHEWS ASIA FUNDS

Matthews Asian Growth and Income Fund December 31, 2010

Schedule of Investments

COMMON EQUITIES: 71.3%

| | | Shares | | Value | |

| CHINA/HONG KONG: 18.4% | |

| CLP Holdings, Ltd. | | | 13,196,700 | | | $ | 107,131,506 | | |

| Hang Seng Bank, Ltd. | | | 5,417,500 | | | | 89,074,272 | | |

China Pacific Insurance Group Co., Ltd.

H Shares | | | 19,906,800 | | | | 82,723,039 | | |

| Hang Lung Properties, Ltd. | | | 14,525,920 | | | | 67,931,401 | | |

Shandong Weigao Group Medical

Polymer Co., Ltd. H Shares | | | 23,340,000 | | | | 66,211,275 | | |

| China Mobile, Ltd. ADR | | | 1,199,400 | | | | 59,514,228 | | |

| Television Broadcasts, Ltd. | | | 9,622,000 | | | | 51,992,075 | | |

China Communications Services

Corp., Ltd. H Shares | | | 84,998,000 | | | | 50,630,499 | | |

| Vitasoy International Holdings, Ltd.† | | | 51,771,000 | | | | 43,160,261 | | |

| VTech Holdings, Ltd. | | | 3,430,300 | | | | 40,358,807 | | |

Citic Telecom International

Holdings, Ltd. | | | 110,763,000 | | | | 35,340,192 | | |

| Inspur International, Ltd.† | | | 299,510,000 | | | | 26,202,501 | | |

| I-CABLE Communications, Ltd.a† | | | 128,079,000 | | | | 15,983,511 | | |

| SinoCom Software Group, Ltd.† | | | 83,028,000 | | | | 9,400,041 | | |

| Total China/Hong Kong | | | | | 745,653,608 | | |

| JAPAN: 12.2% | |

| Hisamitsu Pharmaceutical Co., Inc. | | | 2,513,600 | | | | 105,881,414 | | |

| Trend Micro, Inc. | | | 2,832,700 | | | | 93,539,459 | | |

| Rohm Co., Ltd. | | | 1,249,100 | | | | 81,539,968 | | |

| Japan Real Estate Investment Corp., REIT | | | 7,113 | | | | 73,767,040 | | |

| Nintendo Co., Ltd. | | | 214,300 | | | | 62,898,990 | | |

| Hamamatsu Photonics, K.K. | | | 1,624,700 | | | | 59,392,901 | | |

| Nippon Building Fund, Inc., REIT | | | 1,701 | | | | 17,452,063 | | |

| Total Japan | | | | | 494,471,835 | | |

| SINGAPORE: 11.7% | |

| Singapore Technologies Engineering, Ltd. | | | 52,627,125 | | | | 140,246,050 | | |

| Keppel Corp., Ltd. | | | 12,239,000 | | | | 107,956,115 | | |

| Ascendas REIT | | | 40,920,000 | | | | 66,002,571 | | |

| Hong Leong Finance, Ltd. | | | 14,950,000 | | | | 35,297,074 | | |

| Singapore Post, Ltd. | | | 38,209,000 | | | | 35,131,975 | | |

| ARA Asset Management, Ltd. | | | 25,801,000 | | | | 31,161,842 | | |

| Cerebos Pacific, Ltd. | | | 7,740,000 | | | | 29,733,276 | | |

| Fraser and Neave, Ltd. | | | 5,801,100 | | | | 28,974,988 | | |

| Total Singapore | | | | | 474,503,891 | | |

| TAIWAN: 6.5% | |

Taiwan Semiconductor Manufacturing

Co., Ltd. | | | 29,923,187 | | | | 72,866,986 | | |

| Cathay Financial Holding Co., Ltd. | | | 31,056,902 | | | | 55,069,773 | | |

Taiwan Semiconductor Manufacturing

Co., Ltd. ADR | | | 4,055,624 | | | | 50,857,525 | | |

| Chunghwa Telecom Co., Ltd. ADR | | | 1,596,907 | | | | 40,353,840 | | |

| CyberLink Corp.† | | | 5,990,128 | | | | 22,599,217 | | |

| Taiwan Hon Chuan Enterprise Co., Ltd. | | | 9,282,000 | | | | 21,170,339 | | |

| Total Taiwan | | | | | 262,917,680 | | |

| | | Shares | | Value | |

| THAILAND: 5.1% | |

| PTT Public Co., Ltd. | | | 8,557,300 | | | $ | 90,838,812 | | |

| BEC World Public Co., Ltd. | | | 34,557,800 | | | | 36,397,749 | | |

| Land & Houses Public Co., Ltd. NVDR | | | 164,864,400 | | | | 35,275,349 | | |

| Glow Energy Public Co., Ltd. | | | 21,887,400 | | | | 34,306,839 | | |

| Thai Reinsurance Public Co., Ltd. NVDR | | | 44,014,435 | | | | 9,417,585 | | |

| Thai Reinsurance Public Co., Ltd. | | | 8,066,665 | | | | 1,725,991 | | |

| Home Product Center Public Co., Ltd. | | | 2,241,200 | | | | 654,257 | | |

| Total Thailand | | | | | 208,616,582 | | |

| SOUTH KOREAb: 5.0% | |

| S1 Corp. | | | 973,615 | | | | 48,027,664 | | |

| KT Corp. ADR | | | 2,016,405 | | | | 41,941,224 | | |

| GS Home Shopping, Inc.† | | | 430,049 | | | | 41,327,663 | | |

| SK Telecom Co., Ltd. ADR | | | 1,736,333 | | | | 32,347,884 | | |

| SK Telecom Co., Ltd. | | | 211,862 | | | | 32,319,974 | | |

| Daehan City Gas Co., Ltd. | | | 346,870 | | | | 8,919,566 | | |

| Total South Korea | | | | | 204,883,975 | | |

| AUSTRALIA: 3.9% | |

| Telstra Corp., Ltd. | | | 40,441,233 | | | | 115,403,362 | | |

| AXA Asia Pacific Holdings, Ltd. | | | 6,513,015 | | | | 42,034,057 | | |

| Total Australia | | | | | 157,437,419 | | |

| UNITED KINGDOM: 2.3% | |

| HSBC Holdings PLC ADR | | | 1,795,633 | | | | 91,649,108 | | |

| Total United Kingdom | | | | | 91,649,108 | | |

| MALAYSIA: 1.8% | |

| AMMB Holdings BHD | | | 22,022,100 | | | | 50,207,674 | | |

| YTL Power International BHD | | | 30,167,418 | | | | 23,871,737 | | |

| Total Malaysia | | | | | 74,079,411 | | |

| VIETNAM: 1.3% | |

| Baoviet Holdings | | | 10,449,101 | | | | 32,108,777 | | |

| Vietnam Dairy Products JSC | | | 2,835,060 | | | | 11,615,712 | | |

| Kinh Do Corp. | | | 4,466,000 | | | | 10,957,490 | | |

| Total Vietnam | | | | | 54,681,979 | | |

| INDONESIA: 1.1% | |

| PT Telekomunikasi Indonesia ADR | | | 1,217,800 | | | | 43,414,570 | | |

| Total Indonesia | | | | | 43,414,570 | | |

| INDIA: 1.0% | |

| Oriental Bank of Commerce | | | 4,536,984 | | | | 41,123,552 | | |

| Total India | | | | | 41,123,552 | | |

| PHILIPPINES: 1.0% | |

| Globe Telecom, Inc. | | | 2,125,510 | | | | 38,813,239 | | |

| Total Philippines | | | | | 38,813,239 | | |

| TOTAL COMMON EQUITIES | | | | | 2,892,246,849 | | |

| (Cost $2,360,684,902) | | | | | | | |

matthewsasia.com | 800.789.ASIA 7

Matthews Asian Growth and Income Fund December 31, 2010

Schedule of Investments (continued)

PREFERRED EQUITIES: 2.5%

| | | Shares | | Value | |

| SOUTH KOREAb: 2.5% | |

Samsung Fire & Marine Insurance

Co., Ltd., Pfd. | | | 507,311 | | | $ | 39,123,038 | | |

| Hyundai Motor Co., Ltd., Pfd. | | | 566,280 | | | | 29,397,401 | | |

| LG Household & Health Care, Ltd., Pfd. | | | 210,290 | | | | 17,395,529 | | |

| Hyundai Motor Co., Ltd., 2nd Pfd. | | | 305,760 | | | | 17,071,852 | | |

| Total South Korea | | | | | 102,987,820 | | |

| TOTAL PREFERRED EQUITIES | | | | | 102,987,820 | | |

| (Cost $49,628,944) | | | | | | | |

WARRANTS: 0.4%

| INDIA: 0.4% | |

Housing Development Finance Corp.,

expires 08/23/12 | | | 3,875,750 | | | | 15,554,139 | | |

| Total India | | | | | 15,554,139 | | |

| TOTAL WARRANTS | | | | | 15,554,139 | | |

| (Cost $6,834,750) | | | | | | | |

INTERNATIONAL BONDS: 22.0%

| | | Face Amount | | | |

| CHINA/HONG KONG: 7.6% | |

China Petroleum & Chemical Corp.

(Sinopec), Cnv.

0.000%, 04/24/14 | | HKD | 638,940,000 | | | | 94,326,838 | | |

Hongkong Land CB 2005, Ltd., Cnv.

2.750%, 12/21/12 | | | 41,400,000 | | | | 77,625,000 | | |

China High Speed Transmission

Equipment Group Co., Ltd., Cnv.

0.000%, 05/14/11 | | CNY | 247,700,000 | | | | 40,737,040 | | |

Yue Yuen Industrial Holdings, Ltd., Cnv.

0.000%, 11/17/11 | | HKD | 246,300,000 | | | | 37,549,596 | | |

Power Regal Group, Ltd., Cnv.

2.250%, 06/02/14 | | HKD | 207,640,000 | | | | 33,557,710 | | |

PB Issuer No. 2, Ltd.,Cnv.

1.750%, 04/12/16 | | | 13,200,000 | | | | 13,411,200 | | |

PB Issuer, Ltd., Cnv.

3.300%, 02/01/13 | | | 11,880,000 | | | | 11,897,820 | | |

| Total China/Hong Kong | | | | | 309,105,204 | | |

| | | Face Amount | | Value | |

| INDIA: 5.9% | |

Tata Power Co., Ltd., Cnv.

1.750%, 11/21/14 | | $ | 47,700,000 | | | $ | 55,498,950 | | |

Reliance Communications, Ltd., Cnv.

0.000%, 05/10/11 | | | 35,315,000 | | | | 43,923,031 | | |

Housing Development Finance Corp.

0.000%, 08/24/12 | | INR | 1,800,000,000 | | | | 43,618,249 | | |

Larsen & Toubro, Ltd., Cnv.

3.500%, 10/22/14 | | | 27,000,000 | | | | 33,750,000 | | |

Sintex Industries, Ltd., Cnv.

0.000%, 03/13/13 | | | 28,400,000 | | | | 32,589,000 | | |

Financial Technologies India, Ltd., Cnv.

0.000%, 12/21/11 | | | 20,114,000 | | | | 27,757,320 | | |

| Total India | | | | | 237,136,550 | | |

| MALAYSIA: 3.9% | |

Rafflesia Capital, Ltd., Cnv.

1.250%c, 10/04/11 | | | 48,100,000 | | | | 69,865,250 | | |

Cherating Capital, Ltd., Cnv.

2.000%c, 07/05/12 | | | 50,000,000 | | | | 65,375,000 | | |

Paka Capital, Ltd., Cnv.

0.000%, 03/12/13 | | | 22,300,000 | | | | 22,885,375 | | |

| Total Malaysia | | | | | 158,125,625 | | |

| SINGAPORE: 3.3% | |

CapitaLand, Ltd., Cnv.

3.125%, 03/05/18 | | SGD | 67,000,000 | | | | 53,838,587 | | |

Wilmar International, Ltd., Cnv.

0.000%, 12/18/12 | | | 36,100,000 | | | | 46,298,250 | | |

Olam International, Ltd., Cnv.

6.000%, 10/15/16 | | | 25,300,000 | | | | 35,040,500 | | |

| Total Singapore | | | | | 135,177,337 | | |

| VIETNAM: 0.8% | |

Socialist Republic of Vietnam

6.875%, 01/15/16 | | | 28,611,000 | | | | 29,970,023 | | |

| Total Vietnam | | | | | 29,970,023 | | |

| SOUTH KOREAb: 0.5% | |

LG Uplus Corp., Cnv.

5.000%c, 09/29/12 | | | 20,400,000 | | | | 21,471,000 | | |

| Total South Korea | | | | | 21,471,000 | | |

8 MATTHEWS ASIA FUNDS

Matthews Asian Growth and Income Fund December 31, 2010

Schedule of Investments (continued)

INTERNATIONAL BONDS (continued)

| | | Value | |

TOTAL INTERNATIONAL BONDS

(Cost $796,139,481) | | $ | 890,985,739 | | |

TOTAL INVESTMENTS: 96.2%

(Cost $3,213,288,077d) | | | 3,901,774,547 | | |

CASH AND OTHER ASSETS,

LESS LIABILITIES: 3.8% | | | 152,896,032 | | |

| NET ASSETS: 100.0% | | $ | 4,054,670,579 | | |

a Non–income producing security.

b Certain securities were fair valued under the discretion of the Board of Trustees (Note 2-A).

c Variable rate security. The rate represents the rate in effect at December 31, 2010.

d Cost for federal income tax purposes is $3,243,052,978 and net unrealized appreciation consists of:

| Gross unrealized appreciation | | $ | 737,080,209 | | |

| Gross unrealized depreciation | | | (78,358,640 | ) | |

| Net unrealized appreciation | | $ | 658,721,569 | | |

† Affiliated Issuer, as defined under the Investment Company Act of 1940 (ownership of 5% or more of the outstanding voting securities of this issuer)

ADR American Depositary Receipt

BHD Berhad

CNY Chinese Renminbi (Yuan)

Cnv. Convertible

HKD Hong Kong Dollar

INR Indian Rupee

JSC Joint Stock Co.

NVDR Non-voting Depositary Receipt

Pfd. Preferred

REIT Real Estate Investment Trust

SGD Singapore Dollar

See accompanying notes to financial statements.

matthewsasia.com | 800.789.ASIA 9

ASIA GROWTH AND INCOME STRATEGIES

PORTFOLIO MANAGERS

Jesper O. Madsen, CFA

Lead Manager

Andrew Foster

Co-Manager

FUND FACTS

| | | Investor Class | | Institutional Class | |

| Ticker | | MAPIX | | MIPIX | |

| CUSIP | | 577125107 | | 577130750 | |

| Inception | | 10/31/06 | | 10/29/10 | |

| NAV | | $14.33 | | $14.33 | |

| Initial Investment | | $2,500 | | $3 million | |

| Gross Expense Ratio1 | | 1.14% | | 1.02% | |

After Fee Waiver,

Reimbursement and

Recoupment | | 1.15% | | n.a. | |

Portfolio Statistics

| Total # of Positions | | 74 | |

| Net Assets | | $2.0 billion | |

| Weighted Average Market Cap | | $21.3 billion | |

| Portfolio Turnover | | 10.48%2 | |

Benchmark

MSCI AC Asia Pacific Index

Redemption Fee

2% within first 90 calendar days of purchase

OBJECTIVE

Total return with an emphasis on providing current income.

STRATEGY

Under normal market conditions, the Fund seeks to achieve its investment objective by investing at least 80% of its total net assets, which include borrowings for investment purposes, in income-paying equity securities of companies located in the Asia region.

1 Gross expense ratio for Institutional Class is annualized. The Advisor has contractually agreed to waive certain fees and reimburse certain expenses for Matthews Asia Dividend Fund. Please see page 91 for additional information. Matthews Asia Funds does not charge 12b-1 fees.

2 The lesser of fiscal year 2010 long-term purchase costs or sales proceeds divided by the average monthly market value of long-term securities.

Matthews Asia Dividend Fund

Portfolio Manager Commentary

For the year ending December 31, 2010, the Matthews Asia Dividend Fund gained 22.83% (Investor Class) and 22.88% (Institutional Class), outperforming its benchmark, the MSCI All Country Asia Pacific Index, which rose 17.25%. For the fourth quarter, the Fund rose 4.62% (Investor Class) and 4.66% (Institutional Class), while the benchmark gained 9.30%. The Fund began 2010 with a share price of $12.06, and shareholders who were invested throughout the year would have received income distributions totaling approximately 41 cents (Investor and Institutional Class), or 3.4%, of the share price at the start of the year.

The objective of the Matthews Asia Dividend Fund is total return with an emphasis on providing current income. Since its inception, dividends reinvested have accounted for roughly a third of the Fund's total return, with the remainder derived from capital appreciation. Every company is evaluated based on its ability to deliver a combination of current dividend yield and potential for dividend growth. The Fund's benchmark does not dictate our bottom-up stock selection process or portfolio weights and, therefore, the portfolio will often diverge significantly from the Index. The Fund, for instance, did not make a single investment in India during 2010, even though the country accounted for 5% of the Index as of December 31, 2010. Thai companies on the other hand were given a substantial overweight relative to the Index. The rationale was simple. While India has a host of great growth companies, they tend to pay less of their earnings in dividends and are generally trading on high multiples to earnings, resulting in some of the lowest dividend yields in Asia. Thai companies, on the other hand, began 2010 with some of the highest yields in Asia. By our assessment, these companies could deliver attractive rates of dividend growth on top of the already high dividend yields, making them attractive candidates from a total return perspective. During the year, Thailand continued to grapple with unresolved internal political struggles, culminating in fatal riots on the streets of Bangkok. Not surprisingly, companies have tended to trade at a discount to the region. While India dominates more headlines than Thailand does due to the scale of the country and its longer-term growth potential, in terms of stock market performance, the Stock Exchange of Thailand Index returned 62.79%, compared to 24.36% for Bombay Stock Exchange Sensitive Index during the year, making Thailand a substantial contributor to performance in 2010.

The Fund's Japanese holdings were the main contributors to performance over the year. Not only was this due to the nearly 15% appreciation in the yen, but also due to the performance of the portfolio's individual holdings, which outperformed the Japanese market. Japanese securities continue to play an important role in the Fund, first and foremost because we continue to find companies that offer the potential for dividend growth at attractive valuations. Exposure to Japanese equities and currency also allows for greater diversification.

By sector, the Fund's information technology holdings were the main contributors to performance. This was mainly due to HTC of Taiwan. As a leading maker of smartphones, the company experienced rapid growth as consumers increasingly upgraded to more sophisticated handsets. HTC is also one of the few Asian companies with a growing global brand presence. The combination of exposure to a rapidly expanding market segment, along with a focus on building a longer-lasting brand presence attracted us to the company. Lastly, at a dividend yield of 8% when we initiated our

(continued)

10 MATTHEWS ASIA FUNDS

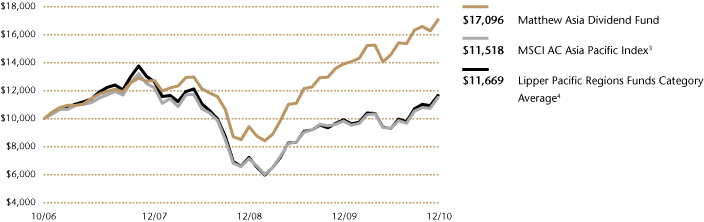

PERFORMANCE AS OF DECEMBER 31, 2010

Institutional Class Shares were first offered on October 29, 2010. Performance since that date was 2.95%. Performance for the Institutional Class shares prior to its inception is based on the performance of the Investor Class. Performance differences between the Institutional Class and Investor Class may arise due to differences in fees charged to each class.

| | | | | | | Average Annual Total Returns | |

| | | Inception Date | | 3 Months | | 1 Year | | 3 Years | | Since

Inception | |

| Investor Class (MAPIX) | | 10/31/06 | | | 4.62 | % | | | 22.83 | % | | | 10.31 | % | | | 13.73 | % | |

| Institutional Class (MIPIX) | | 10/29/10 | | | 4.66 | % | | | 22.88 | % | | | 10.32 | % | | | 13.74 | % | |

| MSCI AC Asia Pacific Index3 | | | | | | | 9.30 | % | | | 17.25 | % | | | -1.91 | % | | | 3.45 | % | |

| Lipper Pacific Region Funds Category Average4 | | | | | | | 9.11 | % | | | 16.87 | % | | | -3.10 | % | | | 3.55 | % | |

Performance assumes reinvestment of all dividends and/or distributions before taxes. All performance quoted represents past performance and is no guarantee of future results. Investment return and principal value will fluctuate with market conditions so that when redeemed, shares may be worth more or less than their original cost. Current performance may be lower or higher than the return figures quoted. Returns would have been lower if certain of the Fund's fees and expenses had not been waived. For the Fund's most recent month-end performance visit matthewsasia.com.

2010 INCOME DISTRIBUTION HISTORY

| | | Q1 | | Q2 | | Q3 | | Q4 | | Total | |

| Investor Class (MAPIX) | | $ | 0.05 | | | $ | 0.08 | | | $ | 0.11 | | | $ | 0.17 | | | $ | 0.41 | | |

| Institutional Class (MIPIX) | | | — | | | | — | | | | — | | | $ | 0.17 | | | $ | 0.17 | | |

Note: This table does not include capital gains distributions. Institutional Class Shares were first offered on October 29, 2010. For income distribution history, visit matthewsasia.com.

30-DAY YIELD:

2.05% (Investor Class) 2.29% (Institutional Class)

The 30-Day Yield represents net investment income earned by the Fund over the 30-day period ended 12/31/10, expressed as an annual percentage rate based on the Fund's share price at the end of the 30-day period. The 30-Day Yield should be regarded as an estimate of the Fund's rate of investment income, and it may not equal the Fund's actual income distribution rate.

Source: BNY Mellon Investment Servicing (US) Inc.

DIVIDEND YIELD: 3.82%

The dividend yield (trailing) for the portfolio is the weighted average sum of the dividend paid per share during the last 12 months divided by the current price. The annualized dividend yield for the Fund is for the equity-only portion of the portfolio. Please note that this is based on gross portfolio holdings and does not reflect the actual yield an investor in the Fund would receive. Past yields are no guarantee of future yields.

Source: FactSet Research Systems.

GROWTH OF A $10,000 INVESTMENT SINCE INCEPTION—INVESTOR CLASS

Plotted monthly. The performance data and graph do not reflect the deduction of taxes that a shareholder would pay on dividends, capital gain distributions or redemption of Fund shares. Values are in US$.

3 It is not possible to invest directly in an index. Source: Index data from Morgan Stanley Capital International and Bloomberg; total return calculations performed by BNY Mellon Investment Servicing (US) Inc. Please see page 59 for index definition.

4 The Lipper Category Average does not reflect sales charges and is based on total return, including reinvestment of dividends and capital gains for the stated periods.

TOP TEN HOLDINGS5

| | | Country | | % of Net Assets | |

| China Mobile, Ltd. | | China/Hong Kong | | | 3.3 | % | |

| HSBC Holdings PLC | | United Kingdom | | | 3.3 | % | |

| Metcash, Ltd | | Australia | | | 3.2 | % | |

| Taiwan Semiconductor Manufacturing Co., Ltd. | | Taiwan | | | 3.2 | % | |

| ITOCHU Corp. | | Japan | | | 3.1 | % | |

| Cheung Kong Infrastructure Holdings, Ltd. | | China/Hong Kong | | | 3.0 | % | |

| PT Perusahaan Gas Negara | | Indonesia | | | 2.8 | % | |

| QBE Insurance Group, Ltd. | | Australia | | | 2.6 | % | |

| PTT Exploration & Production Public Co., Ltd. | | Thailand | | | 2.4 | % | |

| ORIX Corp. | | Japan | | | 2.3 | % | |

| % OF ASSETS IN TOP TEN | | | | | 29.2 | % | |

5 Holdings may combine more than one security from same issuer and related depositary receipts.

matthewsasia.com | 800.789.ASIA 11

COUNTRY ALLOCATION (%)6

| China/Hong Kong | | | 23.3 | | |

| Japan | | | 23.2 | | |

| Taiwan | | | 11.2 | | |

| South Korea | | | 8.9 | | |

| Australia | | | 8.0 | | |

| Thailand | | | 6.5 | | |

| Indonesia | | | 5.0 | | |

| Singapore | | | 4.2 | | |

| United Kingdom | | | 3.3 | | |

| Philippines | | | 1.5 | | |

| Malaysia | | | 0.6 | | |

Cash and Other Assets,

Less Liabilities | | | 4.3 | | |

SECTOR ALLOCATION (%)

| Financials | | | 16.4 | | |

| Consumer Discretionary | | | 15.7 | | |

| Consumer Staples | | | 15.3 | | |

| Telecommunication Services | | | 12.4 | | |

| Information Technology | | | 10.9 | | |

| Health Care | | | 6.7 | | |

| Utilities | | | 6.6 | | |

| Industrials | | | 6.0 | | |

| Energy | | | 3.6 | | |

| Materials | | | 2.1 | | |

Cash and Other Assets,

Less Liabilities | | | 4.3 | | |

MARKET CAP EXPOSURE (%)7

| Large Cap (over $5B) | | | 45.2 | | |

| Mid Cap ($1B–$5B) | | | 28.2 | | |

| Small Cap (under $1B) | | | 22.3 | | |

Cash and Other Assets,

Less Liabilities | | | 4.3 | | |

6 The United Kingdom is not included in the MSCI All Country Asia Pacific Index.

7 Source: FactSet Research Systems. Percentage values in data are rounded to the nearest tenth of one percent; the values may not sum to 100% due to rounding.

Matthews Asia Dividend Fund

Portfolio Manager Commentary (continued)

investment, the valuation was attractive. Our holdings within the financials and health care sectors were also significant contributors to performance. Within financials, the Fund predominantly focused on companies with real estate exposure, such as developers or real estate investment trusts, rather than banks. These real estate-related holdings generally offer higher dividend yields, exposure to hard assets and often greater transparency in terms of the underlying assets.

Some of the Fund's main detractors to performance were its apparel-related holdings. Esprit Holdings of Hong Kong, Billabong International of Australia and Point of Japan all posted negative returns for the year. Esprit, with its reliance on European sales, faced ongoing uncertainty given the macroeconomic climate in Europe. Billabong faced headwinds from a strong Australian dollar that reduced the value of overseas sales once converted into Australian dollars. More fundamentally, the company is exposed to consumers in developed markets. Investors are also not yet convinced that ongoing restructuring efforts as well as the integration of recent acquisitions will be successful. Point operated in a sluggish retail environment in Japan while undertaking restructuring of its procurement and in-house design capabilities to better match its current scale. We continuously monitor operational performance and remain invested with all of the above, given current valuations and longer-term growth potential.

The threat of higher rates of inflation in the region is causing investors much angst as we enter 2011. Over longer periods, inflation can wipe out a significant portion of people's real wealth, which is why a long-term investment should be judged on its ability to generate returns after accounting for inflation. Investing with companies that pay a growing dividend is one way to counter the effects of inflation. During the year, 68% of the Fund's holdings increased their dividend per share, while 16% reduced theirs. For a company to have the ability to sustainably grow dividends at a faster rate than inflation it must have the ability to pass cost increases on to customers. This ability can take many shapes. We focus our investments with companies that exhibit at least one of the following traits: a dominant competitive position within an industry resulting in better pricing power; brand power, which allows for premium pricing disconnected from input costs; operations in a regulated industry, which allows for costs to be passed through as in the case with some utilities; or ownership of assets that will maintain "real value" such as commodities or real estate.

Being invested with companies that have the above traits does not insure against the broader macro risk to equities posed by policy intervention, especially as it pertains to monetary tightening, price controls and/or capital controls. As we enter 2011, Asian central banks are trying to tackle inflationary pressures, but have so far generally been slow to raise interest rates. There is a real risk that central banks will have to become more aggressive in terms of interest rate hikes. However, since Asian central bankers have one eye on their respective currencies, they may resort to other tools such as capital controls to counter potential inflows of "hot money" and currency appreciation. This heightens the risk that equity markets in Asia may increasingly move to the tune of policymakers and central bankers rather than to the performance of the region's companies.

We believe Asia continues to offer attractive opportunities to dividend-focused investors, when compared to fixed-income yields or other regional equity markets globally. For long-term investors, we believe that companies in Asia continue to offer an attractive combination of current yield, dividend growth and diversification opportunities.

12 MATTHEWS ASIA FUNDS

Matthews Asia Dividend Fund December 31, 2010

Schedule of Investments

COMMON EQUITIES: 95.5%

| | | Shares | | Value | |

| CHINA/HONG KONG: 23.3% | |

| China Mobile, Ltd. ADR | | | 1,333,300 | | | $ | 66,158,346 | | |

Cheung Kong Infrastructure

Holdings, Ltd. | | | 12,768,000 | | | | 58,478,386 | | |

| Esprit Holdings, Ltd. | | | 8,510,000 | | | | 40,509,212 | | |

Shenzhou International Group

Holdings, Ltd. | | | 34,891,000 | | | | 40,444,616 | | |

| Television Broadcasts, Ltd. | | | 7,150,000 | | | | 38,634,726 | | |

| Kingboard Laminates Holdings, Ltd. | | | 29,549,000 | | | | 30,032,562 | | |

| China Fishery Group, Ltd. | | | 16,779,000 | | | | 29,286,601 | | |

| The Link REIT | | | 8,990,000 | | | | 27,931,826 | | |

China Communications Services

Corp., Ltd. H Shares | | | 46,740,000 | | | | 27,841,473 | | |

| Jiangsu Expressway Co., Ltd. H Shares | | | 21,474,000 | | | | 24,588,128 | | |

| Sichuan Expressway Co., Ltd. H Shares | | | 34,912,000 | | | | 22,457,801 | | |

| Yip's Chemical Holdings, Ltd. | | | 14,912,000 | | | | 18,321,531 | | |

| Cafe' de Coral Holdings, Ltd. | | | 6,722,000 | | | | 16,621,660 | | |

| Minth Group, Ltd. | | | 4,933,000 | | | | 8,098,122 | | |

| VTech Holdings, Ltd. | | | 557,000 | | | | 6,553,320 | | |

| Guangdong Investment, Ltd. | | | 12,038,000 | | | | 6,194,936 | | |

| Total China/Hong Kong | | | | | 462,153,246 | | |

| JAPAN: 23.0% | |

| ITOCHU Corp. | | | 6,148,000 | | | | 62,244,808 | | |

| ORIX Corp. | | | 468,000 | | | | 46,056,411 | | |

| Point, Inc. | | | 851,080 | | | | 37,370,368 | | |

| Pigeon Corp.† | | | 1,069,300 | | | | 36,350,142 | | |

| Hisamitsu Pharmaceutical Co., Inc. | | | 838,200 | | | | 35,307,846 | | |

| Monex Group, Inc. | | | 109,059 | | | | 32,211,292 | | |

| EPS Co., Ltd.† | | | 12,504 | | | | 30,601,611 | | |

| Lawson, Inc. | | | 527,100 | | | | 26,066,098 | | |

| Hamamatsu Photonics, K.K. | | | 687,700 | | | | 25,139,717 | | |

| Shinko Plantech Co., Ltd.† | | | 2,555,600 | | | | 23,607,587 | | |

| Miraca Holdings, Inc. | | | 535,700 | | | | 21,575,797 | | |

| Hokuto Corp. | | | 922,500 | | | | 21,440,541 | | |

| Nintendo Co., Ltd. | | | 60,400 | | | | 17,727,947 | | |

| Ship Healthcare Holdings, Inc. | | | 1,285,300 | | | | 16,859,767 | | |

| United Urban Investment Corp., REIT | | | 11,100 | | | | 14,191,157 | | |

| FANUC CORP. | | | 61,100 | | | | 9,384,370 | | |

| Total Japan | | | | | 456,135,459 | | |

| TAIWAN: 11.2% | |

Taiwan Semiconductor Manufacturing

Co., Ltd. ADR | | | 4,005,040 | | | | 50,223,202 | | |

| Chunghwa Telecom Co., Ltd. ADR | | | 1,607,127 | | | | 40,612,099 | | |

| TXC Corp.† | | | 15,450,000 | | | | 29,515,374 | | |

| HTC Corp. | | | 764,400 | | | | 23,595,425 | | |

| Taiwan Hon Chuan Enterprise Co., Ltd. | | | 9,881,000 | | | | 22,536,536 | | |

| St. Shine Optical Co., Ltd. | | | 1,611,000 | | | | 21,438,376 | | |

| CyberLink Corp. | | | 4,313,513 | | | | 16,273,779 | | |

Taiwan Semiconductor Manufacturing

Co., Ltd. | | | 5,346,469 | | | | 13,019,371 | | |

| Chunghwa Telecom Co., Ltd. | | | 1,403,705 | | | | 3,567,456 | | |

| Total Taiwan | | | | | 220,781,618 | | |

| | | Shares | | Value | |

| SOUTH KOREAa: 8.9% | |

| KT&G Corp. | | | 803,000 | | | $ | 45,783,524 | | |

| Woongjin Thinkbig Co., Ltd.† | | | 1,475,030 | | | | 28,323,011 | | |

| SK Telecom Co., Ltd. ADR | | | 1,513,250 | | | | 28,191,848 | | |

| Grand Korea Leisure Co., Ltd. | | | 1,533,580 | | | | 27,881,052 | | |

| MegaStudy Co., Ltd. | | | 165,847 | | | | 25,676,007 | | |

| SK Telecom Co., Ltd. | | | 99,414 | | | | 15,165,806 | | |

| Cheil Worldwide, Inc. | | | 441,450 | | | | 5,379,589 | | |

| Total South Korea | | | | | 176,400,837 | | |

| AUSTRALIA: 8.0% | |

| Metcash, Ltd | | | 15,263,162 | | | | 64,161,751 | | |

| QBE Insurance Group, Ltd. | | | 2,745,000 | | | | 50,957,586 | | |

| Coca-Cola Amatil, Ltd. | | | 2,134,730 | | | | 23,711,698 | | |

| Billabong International, Ltd. | | | 2,388,728 | | | | 19,911,968 | | |

| Total Australia | | | | | 158,743,003 | | |

| THAILAND: 6.5% | |

PTT Exploration & Production Public

Co., Ltd. | | | 8,625,000 | | | | 48,067,673 | | |

| Thai Beverage Public Co., Ltd. | | | 177,295,000 | | | | 39,372,794 | | |

| Glow Energy Public Co., Ltd. | | | 7,783,800 | | | | 12,200,516 | | |

| LPN Development Public Co., Ltd. | | | 33,126,300 | | | | 9,780,198 | | |

| Major Cineplex Group Public Co., Ltd. | | | 22,100,900 | | | | 9,530,990 | | |

| Land & Houses Public Co., Ltd. NVDR | | | 38,358,200 | | | | 8,207,344 | | |

| Land & Houses Public Co., Ltd. | | | 10,267,400 | | | | 2,196,873 | | |

| Total Thailand | | | | | 129,356,388 | | |

| INDONESIA: 5.0% | |

| PT Perusahaan Gas Negara | | | 111,585,000 | | | | 54,801,734 | | �� |

| PT Telekomunikasi Indonesia ADR | | | 717,634 | | | | 25,583,652 | | |

| PT Telekomunikasi Indonesia | | | 11,036,500 | | | | 9,738,088 | | |

| PT Ramayana Lestari Sentosa | | | 87,700,000 | | | | 8,273,585 | | |

| Total Indonesia | | | | | 98,397,059 | | |

| SINGAPORE: 4.2% | |

| CapitaRetail China Trust, REIT | | | 30,418,000 | | | | 29,390,517 | | |

| ARA Asset Management, Ltd. | | | 23,096,000 | | | | 27,894,807 | | |

| Super Group, Ltd. | | | 14,868,000 | | | | 16,335,279 | | |

| Parkway Life REIT | | | 4,695,868 | | | | 6,037,466 | | |

| Venture Corp., Ltd. | | | 542,000 | | | | 3,910,796 | | |

| Total Singapore | | | | | 83,568,865 | | |

| UNITED KINGDOM: 3.3% | |

| HSBC Holdings PLC ADR | | | 1,217,791 | | | | 62,156,053 | | |

| HSBC Holdings PLC | | | 256,133 | | | | 2,626,312 | | |

| Total United Kingdom | | | | | 64,782,365 | | |

| PHILIPPINES: 1.5% | |

| Globe Telecom, Inc. | | | 1,598,820 | | | | 29,195,526 | | |

| Total Philippines | | | | | 29,195,526 | | |

matthewsasia.com | 800.789.ASIA 13

Matthews Asia Dividend Fund December 31, 2010

Schedule of Investments (continued)

COMMON EQUITIES (continued)

| | | Shares | | Value | |

| MALAYSIA: 0.6% | |

| Top Glove Corp. BHD | | | 4,891,400 | | | $ | 7,899,845 | | |

| Media Prima BHD | | | 4,931,200 | | | | 4,157,976 | | |

| Total Malaysia | | | | | 12,057,821 | | |

| TOTAL COMMON EQUITIES | | | | | 1,891,572,187 | | |

| (Cost $1,688,611,953) | | | | | | | |

INTERNATIONAL BONDS: 0.2%

| | | Face Amount | | | |

| JAPAN: 0.2% | |

ORIX Corp., Cnv.

1.000%, 03/31/14 | | JPY | 310,000,000 | | | | 4,869,165 | | |

| Total Japan | | | | | 4,869,165 | | |

| TOTAL INTERNATIONAL BONDS | | | | | 4,869,165 | | |

| (Cost $3,377,082) | | | | | | | |

| TOTAL INVESTMENTS: 95.7% | | | | | 1,896,441,352 | | |

| (Cost $1,691,989,035b) | | | | | | | |

CASH AND OTHER ASSETS,

LESS LIABILITIES: 4.3% | | | | | 85,234,955 | | |

| NET ASSETS: 100.0% | | | | $ | 1,981,676,307 | | |

a Certain securities were fair valued under the discretion of the Board of Trustees (Note 2-A).

b Cost for federal income tax purposes is $1,717,394,207 and net unrealized appreciation consists of:

| Gross unrealized appreciation | | $ | 241,710,533 | | |

| Gross unrealized depreciation | | | (62,663,388 | ) | |

| Net unrealized appreciation | | $ | 179,047,145 | | |

† Affiliated Issuer, as defined under the Investment Company Act of 1940 (ownership of 5% or more of the outstanding voting securities of this issuer)

ADR American Depositary Receipt

BHD Berhad

Cnv. Convertible

JPY Japanese Yen

NVDR Non-voting Depositary Receipt

REIT Real Estate Investment Trust

See accompanying notes to financial statements.

14 MATTHEWS ASIA FUNDS

ASIA GROWTH AND INCOME STRATEGIES

PORTFOLIO MANAGERS

Jesper O. Madsen, CFA

Lead Manager

Richard H. Gao

Co-Manager

FUND FACTS

| | | Investor Class | | Institutional Class | |

| Ticker | | MCDFX | | MICDX | |

| CUSIP | | 577125305 | | 577130735 | |

| Inception | | 11/30/09 | | 10/29/10 | |

| NAV | | $12.17 | | $12.17 | |

| Initial Investment | | $2,500 | | $3 million | |

| Gross Expense Ratio1 | | 1.95% | | 1.24% | |

After Fee Waiver,

Reimbursement and

Recoupment | | 1.50% | | n.a. | |

Portfolio Statistics

| Total # of Positions | | 39 | |

| Net Assets | | $45.4 million | |

| Weighted Average Market Cap | | $29.2 billion | |

| Portfolio Turnover | | 6.84%2 | |

Benchmark

MSCI China Index

Redemption Fee

2% within first 90 calendar days of purchase

OBJECTIVE

Total return with an emphasis on providing current income.

STRATEGY

Under normal market conditions, the Fund seeks to achieve its investment objective by investing at least 80% of its total net assets, which include borrowings for investment purposes, in income-paying equity securities of companies located in China and Taiwan. China includes its administrative and other districts, such as Hong Kong.

1 Gross expense ratio for Institutional Class is annualized. The Advisor has contractually agreed to waive certain fees and reimburse certain expenses for Matthews China Dividend Fund. Please see page 91 for additional information. Matthews Asia Funds does not charge 12b-1 fees.

2 The lesser of fiscal year 2010 long-term purchase costs or sales proceeds divided by the average monthly market value of long-term securities.

Matthews China Dividend Fund

Portfolio Manager Commentary

For the year ending December 31, 2010, the Matthews China Dividend Fund gained 22.53% (Investor Class) and 22.58% (Institutional Class), outperforming its benchmark, the MSCI China Index, which rose 4.83%. For the fourth quarter, the Fund rose 5.57% (Investor Class) and 5.60% (Institutional Class), while the benchmark gained 0.70%. The Fund began 2010 with a share price of $10.18 and shareholders who were invested throughout the year would have received income distributions totaling approximately 24 cents (Investor Class), or 2.4%, of the share price at the start of the year.

Now that a little more than a year has passed since the Fund's inception, it seems appropriate to review not just the past year, but also the rationale for the Matthews China Dividend Fund. Similar to the longer-running Matthews Asia Dividend Fund, the Matthews China Dividend Fund has an objective of total return with an emphasis on providing current income. We seek to invest primarily in companies we believe offer attractive current dividend yield and growth in dividends.

We based our decision to launch an additional China-focused fund on our belief that when investing in China, strategy matters. Furthermore, China's equity markets have developed to a point in which it is possible for investors to pursue various strategies within the same geographic region, just as they would in the U.S. The Fund's distinct focus on yield and dividend growth results in a relatively high allocation to conservative business models like those found in the utilities and telecommunication sectors, which exhibit strong balance sheets and stable cash flows. Anchoring the Fund in these larger, more stable dividend-paying companies allows the Fund to maintain a significant allocation of 51% to faster-growing companies with a market capitalization of less than US$5 billion. These companies help raise the overall level of dividend growth for the portfolio. While the track record remains short, the returns of the Fund have been delivered with significantly less volatility than the overall market. This seems to support the notion that it is possible to pursue various investment strategies when investing in China and as one would expect, that the risk and return profile will vary by strategy.

While mostly overlooked, dividends are an essential component of total shareholder return for long-term investors in China. Since 1992, about 68% of the total return for the MSCI China Index has been derived from reinvested dividends. Even though the universe of dividend-paying companies in Asia Pacific, in general, has expanded significantly over the past decade, the growth in Chinese dividend payments stands out. Aggregate dividend payments grew from close to US$8 billion in 1998 to US$81 billion by 2009. Importantly, US$65 billion of the total dividend payment in 2009 was accounted for by companies that became publicly listed after 1998, a reflection of the expanding number of dividend-paying companies.

The health care sector was the main contributor to Fund performance during 2010, predominantly due to the strong performance of Hong Kong's United Laboratories International Holdings, one of the world's largest and lowest-cost manufacturers of antibiotics. St. Shine Optical of Taiwan, the world's largest contract manufacturer of contact lenses mainly for Japanese companies, also greatly contributed to performance. The firm sells its own branded lenses mainly in its home market of Taiwan. The global contact lens industry is broadly speaking two-tiered, with 96% of the market accounted for by the top four branded manufacturers, including

(continued)

matthewsasia.com | 800.789.ASIA 15

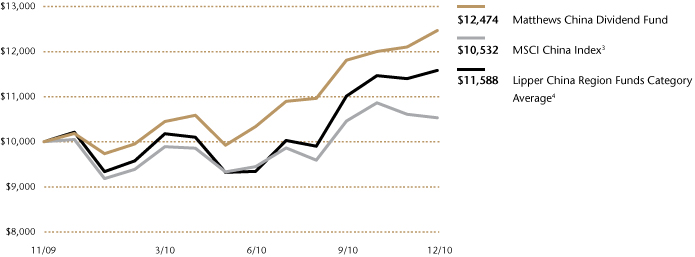

PERFORMANCE AS OF DECEMBER 31, 2010

Institutional Class Shares were first offered on October 29, 2010. Performance since that date was 3.91%. Performance for the Institutional Class shares prior to its inception is based on the performance of the Investor Class. Performance differences between the Institutional Class and Investor Class may arise due to differences in fees charged to each class.

| | | | | | | Average Annual Total Returns | |

| | | Inception Date | | 3 Months | | 1 Year | | Since

Inception | |

| Investor Class (MCDFX) | | 11/30/09 | | | 5.57 | % | | | 22.53 | % | | | 22.60 | % | |

| Institutional Class (MICDX) | | 10/29/10 | | | 5.60 | % | | | 22.58 | % | | | 22.64 | % | |

| MSCI China Index3 | | | | | | | 0.70 | % | | | 4.83 | % | | | 4.89 | % | |

| Lipper China Region Funds Category Average4 | | | | | | | 5.28 | % | | | 13.66 | % | | | 14.56 | % | |

Performance assumes reinvestment of all dividends and/or distributions before taxes. All performance quoted represents past performance and is no guarantee of future results. Investment return and principal value will fluctuate with market conditions so that when redeemed, shares may be worth more or less than their original cost. Current performance may be lower or higher than the return figures quoted. Returns would have been lower if certain of the Fund's fees and expenses had not been waived. For the Fund's most recent month-end performance visit matthewsasia.com.

2010 INCOME DISTRIBUTION HISTORY

| | | June | | December | | Total | |

| Investor Class (MCDFX) | | $ | 0.12 | | | $ | 0.12 | | | $ | 0.24 | | |

| Institutional Class (MICDX) | | | — | | | $ | 0.13 | | | $ | 0.13 | | |

Note: This table does not include capital gains distributions. Institutional Class Shares were first offered on October 29, 2010. For income distribution history, visit matthewsasia.com.

30-DAY YIELD:

1.47% (Investor Class) 1.77% (Institutional Class)

The 30-Day Yield represents net investment income earned by the Fund over the 30-day period ended 12/31/10, expressed as an annual percentage rate based on the Fund's share price at the end of the 30-day period. The 30-Day Yield should be regarded as an estimate of the Fund's rate of investment income, and it may not equal the Fund's actual income distribution rate.

Source: BNY Mellon Investment Servicing (US) Inc.

DIVIDEND YIELD: 3.65%

The dividend yield (trailing) for the portfolio is the weighted average sum of the dividend paid per share during the last 12 months divided by the current price. The annualized dividend yield for the Fund is for the equity-only portion of the portfolio. Please note that this is based on gross portfolio holdings and does not reflect the actual yield an investor in the Fund would receive. Past yields are no guarantee of future yields.

Source: FactSet Research Systems.

GROWTH OF A $10,000 INVESTMENT SINCE INCEPTION—INVESTOR CLASS

Plotted monthly. The performance data does not reflect the deduction of taxes that a shareholder would pay on dividends, capital gain distributions or redemption of Fund shares. Values are in US$.