UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number | 811-08764 |

|

PACE® Select Advisors Trust |

(Exact name of registrant as specified in charter) |

|

1285 Avenue of the Americas, New York, New York | | 10019-6028 |

(Address of principal executive offices) | | (Zip code) |

|

Mark F. Kemper, Esq. UBS Global Asset Management 1285 Avenue of the Americas New York, NY 10019-6028 |

(Name and address of agent for service) |

|

Copy to: |

Jack W. Murphy, Esq. Dechert LLP 1775 I Street, N.W. Washington, DC 20006-2401 |

|

Registrant’s telephone number, including area code: | 212-821 3000 | |

|

Date of fiscal year end: | July 31 | |

|

Date of reporting period: | July 31, 2011 | |

| | | | | | | | |

Item 1. Reports to Stockholders.

PACE Select

Annual Report

PACE® Select Advisors Trust

Annual Report

July 31, 2011

PACE® Select Advisors Trust

| Table of contents | |

|

| Introduction | | | 2 | | |

|

| Portfolio Advisor's and Sub-Advisors' commentaries and schedules of investments | |

|

| PACE® Money Market Investments | | | 5 | | |

|

| PACE® Government Securities Fixed Income Investments | | | 13 | | |

|

| PACE® Intermediate Fixed Income Investments | | | 25 | | |

|

| PACE® Strategic Fixed Income Investments | | | 40 | | |

|

| PACE® Municipal Fixed Income Investments | | | 60 | | |

|

| PACE® International Fixed Income Investments (formerly UBS PACE® Global Fixed Income Investments) | | | 72 | | |

|

| PACE® High Yield Investments | | | 84 | | |

|

| PACE® Large Co Value Equity Investments | | | 99 | | |

|

| PACE® Large Co Growth Equity Investments | | | 108 | | |

|

| PACE® Small/Medium Co Value Equity Investments | | | 120 | | |

|

| PACE® Small/Medium Co Growth Equity Investments | | | 130 | | |

|

| PACE® International Equity Investments | | | 141 | | |

|

| PACE® International Emerging Markets Equity Investments | | | 155 | | |

|

| PACE® Global Real Estate Securities Investments | | | 168 | | |

|

| PACE® Alternative Strategies Investments | | | 177 | | |

|

| Understanding your Portfolio's expenses | | | 228 | | |

|

| Statement of assets and liabilities | | | 234 | | |

|

| Statement of operations | | | 242 | | |

|

| Statement of changes in net assets | | | 246 | | |

|

| Financial highlights | | | 253 | | |

|

| Notes to financial statements | | | 306 | | |

|

| Report of independent registered public accounting firm | | | 347 | | |

|

| Tax information | | | 348 | | |

|

| General information | | | 349 | | |

|

| Board approvals of sub-advisory agreements | | | 350 | | |

|

| Trustees and officers | | | 366 | | |

|

PACE Select Advisors Trust offers multiple share classes representing interests in 15 separate Portfolios. (PACE Money Market Investments offers only one share class.) Different classes of shares and/or Portfolios are offered by separate prospectuses.

For more information on a portfolio or class of shares, contact your financial advisor. He or she can send you a current prospectus relating to a portfolio or class of shares. Investors should carefully read and consider a mutual fund's investment objectives, risks, charges, and expenses before investing. The prospectus contains this and other information about a mutual fund. For a current prospectus, contact UBS Global Asset Management (Americas) Inc. at 888-793 8637, or visit us on the Web at www.ubs.com/globalam-us.

Derivatives vary in complexity, involve risks which are different from, and may be greater than, the risks associated with investing in securities or other instruments. Please see the funds' prospectuses for more complete discussion of the risks associated with investing in derivatives.

1

PACE Select Advisors Trust

Introduction

September 16, 2011

Dear PACE Shareholder,

We are pleased to provide you with the annual report for the PACE portfolios (the "Portfolios"), comprising the PACE Select Advisors Trust. This report includes summaries of the performance of each Portfolio, as well as commentaries from the investment advisor and sub-advisors regarding the events that affected Portfolio performance during the 12 months ended July 31, 2011. Please note that the opinions of the sub-advisors do not necessarily represent those of UBS Global Asset Management (Americas) Inc.

Decelerating Growth in Developed Countries

The US and many developed countries abroad experienced decelerating economic growth during the reporting period. Oil and food prices moved higher during this time, which had a negative impact on consumer spending. In addition, supply disruptions following the devastating earthquake and tsunami in Japan in March led to moderating growth in the manufacturing sector. In the US, gross domestic product ("GDP") growth was 2.5% and 2.3% during the third and fourth quarters of 2010, followed by first and second quarter 2011 GDP growth of 0.4% and 1.0%, respectively.

In contrast to their developed country counterparts, growth in most emerging market economies, such as China and India, remained robust. Against a backdrop of higher inflation, several emerging market central banks raised their interest rates and took other actions in an effort to cool growth and stem rising prices. By the end of the period, commodity prices had declined from their peaks and inflationary pressures appeared to have eased.

Global equities produce strong returns

While the global equity markets gave back a portion of their earlier gains late in the reporting period, overall they generated strong results. Expectations for strengthening growth, corporate profits that were often better than expected and robust demand supported the US stock market during the first nine months of the period. However, risk appetite was later replaced with increased risk aversion as a result of the European sovereign debt crisis, fears that the US may default on its debt obligations and overall disappointing economic data. Despite weakening stock prices during the last three months of the period, the US stock market, as measured by the S&P 500 Index,1 returned 19.65% during the 12-months ended July 31, 2011.

International developed equities (as measured by the MSCI EAFE Index (net)2) proved resilient as well, gaining 17.17% during the reporting period. However, they experienced heightened volatility, at times, in light of fears that the European debt crisis may escalate. Emerging markets equities (as measured by the MSCI Emerging Markets Index3) also posted strong returns, gaining 17.79% over the period. Continued robust growth in developing countries and higher commodity prices supported emerging markets equities.

1 The S&P 500 Index is an unmanaged, weighted index composed of 500 widely held common stocks varying in composition, and is not available for direct investment. Investors should note that indices do not reflect the deduction of fees and expenses.

2 The MSCI EAFE Index (net) is an index of stocks from 22 countries designed to measure the investment returns of developed economies outside of North America. Dividends are reinvested after the deduction of withholding tax, using tax rates applicable to Luxembourg holding companies, as Luxembourg applies the highest rates. The Index is constructed and managed with a view to being fully investable from the perspective of international institutional investors. Investors should note that indices do not reflect the deduction of fees and expenses.

3 The MSCI Emerging Markets Index is a market capitalization-weighted index composed of companies representative of the market structure of 21 emerging market countries in Europe, Latin America, and the Pacific Basin. The Index is constructed and managed with a view to being fully investable from the perspective of international institutional investors. Investors should note that indices do not reflect the deduction of fees and expenses.

2

PACE Select Advisors Trust

Riskier fixed income securities outperform

There was also a meaningful shift in investor sentiment in the fixed income market during the reporting period. This, in turn, impacted the performance of the spread sectors (non-Treasuries). During much of the period, there were hopes for improving economic conditions, coupled with sharply rising oil and commodity prices. Despite hostilities in the Middle East and Northern Africa, the natural disaster in Japan and the European sovereign debt crisis, most spread sectors outperformed Treasuries and yields moved higher. Nonetheless, it was a different story during the last three months of the period. High oil prices hurt consumer spending, and economic data pointed to a soft patch in many developed countries. Against this backdrop, Treasury yields declined and nearly every spread sector lagged Treasuries. All told, during the 12 months ended July 31, 2011, the spread sectors typically outperformed Treasuries and the overall US bond market, as measured by the Barclays Capital US Aggregate Index,4 returned 4.44%.

Despite increased volatility and periodic flights to quality, riskier fixed income asset classes generated solid gains during the reporting period, as the BofA Merrill Lynch US High Yield Cash Pay Constrained Index5 returned 12.74% and the J.P. Morgan Emerging Markets Bond Index Global (EMBI Global)6 rose 9.41%.

Sincerely,

Mark E. Carver

President, PACE Select Advisors Trust

Managing Director, UBS Global Asset Management (Americas) Inc.

4 The Barclays Capital US Aggregate Index is an unmanaged broad based index designed to measure the US- dollar-denominated, investment-grade, fixed rate taxable bond market. The index includes bonds from the Treasury, government-related, corporate, mortgage-backed, asset-backed and commercial mortgage-backed sectors. US agency hybrid adjustable rate mortgage (ARM) securities were added to the Index on April 1, 2007. Investors should note that indices do not reflect the deduction of fees and expenses.

5 The BofA Merrill Lynch US High Yield Cash Pay Constrained Index is an unmanaged index of publicly placed non-convertible, coupon-bearing US-dollar-denominated below investment grade corporate debt with a term to maturity of at least one year. The index is market weighted, so that larger bond issuers have a greater effect on the index's return. However, the representation of any single bond issue is restricted to a maximum of 2% of the total index. Investors should note that indices do not reflect the deduction of fees and expenses.

6 The J.P. Morgan Emerging Markets Bond Index Global (EMBI Global) is an unmanaged index which is designed to track total returns for US-dollar-denominated debt instruments issued by emerging market sovereign and quasi-sovereign entities: Brady bonds, loans and Eurobonds. Investors should note that indices do not reflect the deduction of fees and expenses.

3

PACE Select Advisors Trust

This report is intended to assist investors in understanding how the Portfolios performed during the 12-month period ended July 31, 2011. The views expressed in the Advisor's and Sub-Advisors' Comments sections are as of the end of the reporting period, reflect performance results gross of fees and expenses, and are those of the investment advisor (with respect to PACE Money Market Investments only) and sub-advisors. Sub-advisors' comments on Portfolios that have more than one sub-advisor are reflective of their portion of the Portfolio only. The views and opinions in this report were current as of September 16, 2011. They are not guarantees of performance or investment results and should not be taken as investment advice. Investment decisions reflect a variety of factors, and the investment advisor and sub-advisors reserve the right to change their views about individual securities, sectors and markets at any time. As a result, the views expressed should not be relied upon as a forecast of a Portfolio's future investment intent.

4

PACE Select Advisors Trust

PACE Money Market Investments

Performance

For the 12 months ended July 31, 2011, the Portfolio returned 0.01%, before the deduction of the maximum PACE program fee. (The Portfolio declined 1.97%, after the deduction of the maximum PACE program fee, for the same 12-month period.) Please remember that the PACE program fee is assessed outside the Portfolio at the PACE program account level. The program fee does not impact the determination of the Portfolio's net asset value per share. For comparison purposes, the median return of the Lipper Money Market Funds category was 0.01%. (Returns over various time periods are shown in the "Performance at a glance" table on page 7. Please note that the returns shown do not reflect the deduction of taxes that a shareholder would pay on Portfolio distributions.) For a detailed commentary on the market environment in general during the reporting period, please refer to page 2.

Advisor's comments

The economic recovery continued during the reporting period, although growth moderated as the period progressed. Elevated unemployment, housing market weakness, higher oil prices and supply disruptions following the devastating earthquake in Japan caused economic growth to decelerate. Against this backdrop, the Federal Reserve Board (the "Fed") maintained the federal funds rate at a historically low range between 0% and 0.25% during the reporting period. (The federal funds rate, or "fed funds" rate, is the rate that banks charge one another for funds they borrow on an overnight basis.) As a result, the yields of the securities in which the Portfolio invests remained extremely low, which impacted the Portfolio's yield.

We tactically adjusted the Portfolio's weighted average maturity (WAM)—which is the average duration of the securities in the Portfolio—but generally kept it in a fairly narrow range. When the reporting period began, the Portfolio had a WAM of 46 days. As of July 31, 2011, the Fund's WAM was 47 days.

At the issuer level, we maintained a greater-than-usual level of diversification over the 12-month period by investing in smaller positions, with the goal of reducing risk and keeping the Portfolio highly liquid. As the economic recovery continued over the period, we slightly increased the size of our positions in single issuers, typically purchasing up to 3% in single nongovernment issuers by the end of the reporting period. (The Portfolio is generally able to hold up to 5% in any one issuer, subject to certain exceptions.)

In terms of securities, over the 12-month period we increased the Portfolio's exposure to repurchase agreements and, to lesser extents, its allocation to commercial paper and a US bank note. In contrast, we decreased the Portfolio's exposure to US government and agency obligations, CDs and short-term corporate obligations. (Repurchase agreements are transactions in which the seller of a security agrees to buy it back at a predetermined time and price, or upon demand.)

PACE Select Advisors Trust – PACE Money Market Investments

Investment Advisor:

UBS Global Asset Management (Americas) Inc.

Portfolio Manager:

Robert Sabatino

Objective:

Current income consistent with preservation of capital and liquidity

Investment process:

The Portfolio is a money market mutual fund and seeks to maintain a stable price of $1.00 per share, although it may be possible to lose money by investing in this Portfolio. The Portfolio invests in a diversified portfolio of high-quality money market instruments of governmental and private issuers. Security selection is based on the assessment of relative values and changes in market and economic conditions.

5

PACE Select Advisors Trust

PACE Money Market Investments

Advisor's comments – concluded

One final note, in response to revisions to the US Securities and Exchange Commission's ("SEC") rules governing money market funds, beginning on October 7, 2010, the Portfolio began disclosing, on a monthly basis: (a) a complete schedule of its portfolio holdings; and (b) information regarding its weighted average maturity and weighted average life. Also, beginning in February 2011, the Portfolio began including a link on UBS's Web site to more detailed Portfolio information appearing in filings with the SEC on Form N-MFP. This information is available on UBS's Web site at the following Internet address: www.ubs.com/usmoneymarketfundsholdings. This information will be updated monthly.

6

PACE Select Advisors Trust

PACE Money Market Investments

Performance at a glance (unaudited)

| Average annual total returns for periods ended 07/31/11 | | 1 year | | 5 years | | 10 years | |

| PACE Money Market Investments before deducting maximum PACE program fee1 | | | 0.01 | % | | | 1.80 | % | | | 1.82 | % | |

| PACE Money Market Investments after deducting maximum PACE program fee1 | | | (1.97 | )% | | | (0.22 | )% | | | (0.20 | )% | |

| Lipper Money Market Funds median | | | 0.01 | % | | | 1.79 | % | | | 1.74 | % | |

For PACE Money Market Investments, average annual total returns for periods ended June 30, 2011, after deduction of the maximum PACE program fee, were as follows: 1-year period, (1.97)%; 5-year period, (0.14)%; 10-year period, (0.16)%.

For PACE Money Market Investments, the 7-day current yield for the period ended July 31, 2011 was 0.01% (without maximum PACE program fee and after fee waivers and/or expense reimbursements; the yield was (0.96)% before fee waivers and/or expense reimbursements). With the maximum PACE program fee, the 7-day current yield was (1.99)% after fee waivers and/or expense reimbursements; the yield was (2.96)% before fee waivers and/or expense reimbursements. The Portfolio's yield quotation more closely reflects the current earnings of the Portfolio than the total return quotation. Yields will fluctuate and reflect fee waivers and/or expense reimbursements.

1 The maximum annual PACE program fee is 2% of the value of PACE assets. Prior to June 14, 2010, the maximum annual PACE program fee was 1.5% of the value of PACE assets; however, the current maximum annual PACE program fee of 2% is reflected in the performance returns throughout all periods in the average annual total returns shown above.

Past performance does not predict future performance and the performance information provided does not reflect the deduction of taxes that a shareholder would pay on Portfolio distributions. The return of an investment will fluctuate. Performance results assume reinvestment of all dividends and capital gain distributions at net asset value on the payable dates. Current performance may be higher or lower than the performance data quoted.

Lipper peer group data calculated by Lipper Inc.; used with permission. The Lipper median is the return of the fund that places in the middle of a Lipper peer group.

An investment in PACE Money Market Investments is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency. Although the Portfolio seeks to preserve the value of your investment at $1.00 per share, it is possible to lose money by investing in the Portfolio.

Not FDIC Insured. May lose value. No Bank guarantee.

7

PACE Select Advisors Trust

PACE Money Market Investments

Portfolio statistics (unaudited)

| Characteristics | | 07/31/11 | |

| Net assets (mm) | | $ | 365.8 | | |

| Number of holdings | | | 91 | | |

| Weighted average maturity | | | 47 days | | |

| Portfolio composition1 | | 07/31/11 | |

| Commercial paper | | | 41.2 | % | |

| Repurchase agreements | | | 21.3 | | |

| US government and agency obligations | | | 19.7 | | |

| Certificates of deposit | | | 12.4 | | |

| Short-term corporate obligations | | | 1.5 | | |

| Bank note | | | 0.8 | | |

| Other assets less liabilities | | | 3.1 | | |

| Total | | | 100.0 | % | |

| Top 10 holdings1 | | 07/31/11 | |

| Repurchase agreement with Deutsche Bank Securities, 0.180% due 08/01/11 | | | 15.8 | % | |

| Repurchase agreement with Barclays Bank PLC, 0.140% due 08/01/11 | | | 5.5 | | |

| US Treasury Notes, 0.750% due 05/31/12 | | | 2.5 | | |

| General Electric Co., 0.100% due 08/05/11 | | | 1.9 | | |

| Market Street Funding LLC, 0.150% due 08/01/11 | | | 1.6 | | |

| Atlantic Asset Securitization LLC, 0.160% due 08/05/11 | | | 1.6 | | |

| Bank of Nova Scotia, 0.180% due 10/03/11 | | | 1.4 | | |

| Amsterdam Funding Corp., 0.180% due 08/01/11 | | | 1.4 | | |

| Barclays US Funding Corp., 0.130% due 08/01/11 | | | 1.4 | | |

| Deutsche Bank Financial LLC, 0.100% due 08/01/11 | | | 1.4 | | |

| Total | | | 34.5 | % | |

1 Weightings represent percentages of the Portfolio's net assets as of July 31, 2011. The Portfolio is actively managed and its composition will vary over time.

8

PACE Select Advisors Trust

PACE Money Market Investments

Portfolio of investments—July 31, 2011

| | | Face

amount | | Value | |

US government and agency

obligations—19.71% | |

Federal Farm Credit Bank

0.230%, due 11/08/111 | | $ | 3,000,000 | | | $ | 2,998,102 | | |

Federal Home Loan Bank

0.165%, due 08/01/112 | | | 3,000,000 | | | | 3,000,000 | | |

| 0.280%, due 08/07/112 | | | 3,000,000 | | | | 3,000,000 | | |

| 0.040%, due 08/09/111 | | | 5,000,000 | | | | 4,999,956 | | |

| 0.300%, due 09/15/112 | | | 3,000,000 | | | | 3,000,000 | | |

| 0.270%, due 09/30/112 | | | 4,500,000 | | | | 4,500,000 | | |

| 0.280%, due 10/12/112 | | | 3,500,000 | | | | 3,500,000 | | |

| 0.270%, due 02/17/121 | | | 3,000,000 | | | | 2,995,500 | | |

Federal Home Loan Mortgage Corp.*

0.135%, due 08/06/112 | | | 3,000,000 | | | | 2,997,855 | | |

| 0.230%, due 08/23/111 | | | 5,000,000 | | | | 4,999,297 | | |

Federal National Mortgage

Association*

0.290%, due 08/08/111 | | | 2,000,000 | | | | 1,999,887 | | |

| 0.210%, due 09/01/111 | | | 4,000,000 | | | | 3,999,277 | | |

US Treasury Bills

0.155%, due 09/22/111 | | | 5,000,000 | | | | 4,998,881 | | |

| 0.040%, due 10/27/111 | | | 3,000,000 | | | | 2,999,709 | | |

| 0.250%, due 03/08/121 | | | 2,000,000 | | | | 1,996,944 | | |

US Treasury Notes

1.000%, due 12/31/11 | | | 2,000,000 | | | | 2,006,341 | | |

| 0.875%, due 02/29/12 | | | 3,000,000 | | | | 3,008,922 | | |

| 1.000%, due 04/30/12 | | | 3,000,000 | | | | 3,014,055 | | |

| 0.750%, due 05/31/12 | | | 9,000,000 | | | | 9,039,324 | | |

| 1.875%, due 06/15/12 | | | 3,000,000 | | | | 3,043,317 | | |

Total US government and agency

obligations

(cost—$72,097,367) | | | | | | | 72,097,367 | | |

| Bank note—0.82% | |

| Banking-US—0.82% | |

Bank of America N.A.

0.120%, due 08/24/11

(cost—$3,000,000) | | | 3,000,000 | | | | 3,000,000 | | |

| Certificates of deposit—12.37% | |

| Banking-non-US—12.37% | |

Abbey National Treasury Services PLC

0.700%, due 10/17/112 | | | 3,500,000 | | | | 3,500,000 | | |

| 0.450%, due 10/18/112 | | | 1,500,000 | | | | 1,500,000 | | |

Bank of Nova Scotia

0.190%, due 08/01/112 | | | 1,500,000 | | | | 1,500,000 | | |

| 0.190%, due 08/03/11 | | | 3,000,000 | | | | 3,000,000 | | |

| 0.180%, due 10/03/11 | | | 5,000,000 | | | | 5,000,000 | | |

BNP Paribas SA

0.399%, due 10/17/112 | | | 1,750,000 | | | | 1,750,000 | | |

Dnb NOR ASA

0.240%, due 12/28/11 | | | 2,000,000 | | | | 2,000,000 | | |

Lloyds TSB Bank PLC

0.500%, due 10/19/112 | | | 3,500,000 | | | | 3,500,000 | | |

Mitsubishi UFJ Trust & Banking Corp.

0.220%, due 08/16/11 | | | 3,000,000 | | | | 3,000,000 | | |

| | | Face

amount | | Value | |

| Certificates of deposit—(Concluded) | |

| Banking-non-US—(Concluded) | |

National Australia Bank Ltd.

0.269%, due 10/14/112 | | $ | 1,000,000 | | | $ | 1,000,000 | | |

| 0.270%, due 10/19/112 | | | 750,000 | | | | 749,966 | | |

Natixis

0.366%, due 10/13/112 | | | 1,000,000 | | | | 1,000,000 | | |

Nordea Bank Finland

0.400%, due 06/12/12 | | | 2,500,000 | | | | 2,500,000 | | |

Rabobank Nederland N.V.

0.267%, due 08/18/112 | | | 1,000,000 | | | | 1,000,000 | | |

Royal Bank of Canada

0.260%, due 08/01/112 | | | 1,500,000 | | | | 1,500,000 | | |

| 0.275%, due 08/01/112 | | | 1,500,000 | | | | 1,500,000 | | |

| 0.260%, due 01/11/12 | | | 3,000,000 | | | | 3,000,000 | | |

Royal Bank of Scotland PLC

0.553%, due 10/25/112 | | | 3,500,000 | | | | 3,500,000 | | |

Toronto-Dominion Bank

0.105%, due 08/08/11 | | | 3,000,000 | | | | 3,000,000 | | |

Westpac Banking Corp.

0.270%, due 08/01/112 | | | 1,750,000 | | | | 1,750,000 | | |

Total certificates of deposit

(cost—$45,249,966) | | | | | | | 45,249,966 | | |

| Commercial paper1—41.24% | |

| Asset backed-banking—1.91% | |

Atlantis One Funding

0.200%, due 08/01/11 | | | 4,000,000 | | | | 4,000,000 | | |

| 0.160%, due 09/13/11 | | | 3,000,000 | | | | 2,999,427 | | |

| | | | 6,999,427 | | |

| Asset backed-miscellaneous—15.05% | |

Amsterdam Funding Corp.

0.180%, due 08/01/11 | | | 5,000,000 | | | | 5,000,000 | | |

Atlantic Asset Securitization LLC

0.160%, due 08/05/11 | | | 6,000,000 | | | | 5,999,893 | | |

Barton Capital LLC

0.150%, due 08/02/11 | | | 3,000,000 | | | | 2,999,988 | | |

Gotham Funding Corp.

0.160%, due 08/05/11 | | | 2,000,000 | | | | 1,999,964 | | |

| 0.160%, due 08/08/11 | | | 3,000,000 | | | | 2,999,907 | | |

LMA Americas LLC

0.200%, due 08/22/11 | | | 3,000,000 | | | | 2,999,650 | | |

Market Street Funding LLC

0.150%, due 08/01/11 | | | 6,000,000 | | | | 6,000,000 | | |

Regency Markets No. 1 LLC

0.150%, due 08/15/11 | | | 5,000,000 | | | | 4,999,708 | | |

| 0.150%, due 08/16/11 | | | 3,000,000 | | | | 2,999,813 | | |

Salisbury Receivables Co. LLC

0.140%, due 08/25/11 | | | 5,000,000 | | | | 4,999,533 | | |

Thunderbay Funding

0.170%, due 09/13/11 | | | 5,000,000 | | | | 4,998,985 | | |

Windmill Funding Corp.

0.140%, due 08/04/11 | | | 3,000,000 | | | | 2,999,965 | | |

| 0.140%, due 08/09/11 | | | 3,000,000 | | | | 2,999,907 | | |

| 0.140%, due 08/10/11 | | | 3,050,000 | | | | 3,049,893 | | |

| | | | 55,047,206 | | |

9

PACE Select Advisors Trust

PACE Money Market Investments

Portfolio of investments—July 31, 2011

| | | Face

amount | | Value | |

| Commercial paper1—(Continued) | |

| Asset backed-securities—1.09% | |

Argento Variable Funding Co. LLC

0.180%, due 08/23/11 | | $ | 3,000,000 | | | $ | 2,999,670 | | |

Grampian Funding LLC

0.210%, due 09/15/11 | | | 1,000,000 | | | | 999,737 | | |

| | | | 3,999,407 | | |

| Banking-non-US—6.90% | |

Commonwealth Bank of Australia

0.265%, due 08/08/112,3 | | | 1,000,000 | | | | 999,981 | | |

| 0.180%, due 10/11/11 | | | 3,000,000 | | | | 2,998,935 | | |

Credit Suisse

0.190%, due 08/17/11 | | | 3,000,000 | | | | 2,999,747 | | |

| 0.190%, due 10/12/11 | | | 1,000,000 | | | | 999,620 | | |

Dnb NOR ASA

0.130%, due 08/05/11 | | | 5,000,000 | | | | 4,999,928 | | |

Kreditanstalt für Wiederaufbau

0.140%, due 09/08/11 | | | 3,000,000 | | | | 2,999,557 | | |

Sumitomo Mitsui Banking Corp.

0.180%, due 08/08/11 | | | 3,000,000 | | | | 2,999,895 | | |

Svenska Handelsbanken, Inc.

0.250%, due 12/14/11 | | | 5,000,000 | | | | 4,995,312 | | |

Westpac Securities NZ Ltd.

0.284%, due 09/01/112,3 | | | 1,250,000 | | | | 1,250,000 | | |

| | | | 25,242,975 | | |

| Banking-US—10.82% | |

Barclays US Funding Corp.

0.130%, due 08/01/11 | | | 5,000,000 | | | | 5,000,000 | | |

| 0.210%, due 08/17/11 | | | 5,000,000 | | | | 4,999,533 | | |

Deutsche Bank Financial LLC

0.100%, due 08/01/11 | | | 5,000,000 | | | | 5,000,000 | | |

| 0.200%, due 10/03/11 | | | 3,000,000 | | | | 2,998,950 | | |

ING (US) Funding LLC

0.240%, due 08/05/11 | | | 3,000,000 | | | | 2,999,920 | | |

| 0.160%, due 08/09/11 | | | 3,000,000 | | | | 2,999,893 | | |

| 0.360%, due 11/03/11 | | | 3,000,000 | | | | 2,997,180 | | |

JPMorgan Chase & Co.

0.150%, due 09/07/11 | | | 3,000,000 | | | | 2,999,538 | | |

Natixis US Finance Co. LLC

0.250%, due 09/12/11 | | | 3,000,000 | | | | 2,999,125 | | |

Nordea N.A., Inc.

0.230%, due 12/07/11 | | | 2,000,000 | | | | 1,998,364 | | |

Societe Generale N.A., Inc.

0.210%, due 08/01/11 | | | 1,575,000 | | | | 1,575,000 | | |

State Street Bank & Trust Co.

0.150%, due 10/13/11 | | | 3,000,000 | | | | 2,999,088 | | |

| | | | 39,566,591 | | |

| | | Face

amount | | Value | |

| Commercial paper1—(Concluded) | |

| Diversified manufacturing—1.91% | |

General Electric Co.

0.100%, due 08/05/11 | | $ | 7,000,000 | | | $ | 6,999,922 | | |

| Finance-captive automotive—1.37% | |

Toyota Motor Credit Corp.

0.160%, due 08/10/11 | | | 5,000,000 | | | | 4,999,800 | | |

| Insurance-life—2.19% | |

Axa Financial, Inc.

0.160%, due 08/11/11 | | | 3,000,000 | | | | 2,999,867 | | |

MetLife Short Term Funding LLC

0.140%, due 08/01/11 | | | 2,000,000 | | | | 2,000,000 | | |

| 0.150%, due 09/14/11 | | | 3,000,000 | | | | 2,999,450 | | |

| | | | 7,999,317 | | |

Total commercial paper

(cost—$150,854,645) | | | | | | | 150,854,645 | | |

| Short-term corporate obligations—1.50% | |

| Banking-non-US—1.09% | |

Svenska Handelsbanken, Inc.

0.292%, due 09/08/112,3 | | | 2,500,000 | | | | 2,500,000 | | |

Westpac Securities NZ Ltd.

0.355%, due 08/04/112,3 | | | 1,500,000 | | | | 1,500,000 | | |

| | | | 4,000,000 | | |

| Banking-US—0.41% | |

JPMorgan Chase Bank N.A.

0.275%, due 09/09/112 | | | 1,500,000 | | | | 1,500,000 | | |

Total short-term corporate

obligations

(cost—$5,500,000) | | | | | | | 5,500,000 | | |

| Repurchase agreements—21.34% | |

Repurchase agreement dated

07/29/11 with Barclays Bank

PLC, 0.140% due 08/01/11,

collateralized by $8,824,000

Federal Farm Credit Bank

obligations, 1.875% due 12/07/12

and $11,396,000 Federal National

Mortgage Association obligations,

zero coupon due 05/01/12;

(value—$20,400,564);

proceeds: $20,000,233 | | | 20,000,000 | | | | 20,000,000 | | |

Repurchase agreement dated

07/29/11 with Deutsche Bank

Securities, 0.180% due 08/01/11,

collateralized by $59,100,000

Federal Home Loan Bank

obligations, 0.320% due

12/09/11; (value—$59,162,318);

proceeds: $58,000,870 | | | 58,000,000 | | | | 58,000,000 | | |

10

PACE Select Advisors Trust

PACE Money Market Investments

Portfolio of investments—July 31, 2011

| | | Face

amount | | Value | |

| Repurchase agreements—(Concluded) | |

Repurchase agreement dated

07/29/11 with State Street Bank &

Trust Co., 0.010% due 08/01/11,

collateralized by $370 Federal

Home Loan Mortgage Corp.

obligations, 5.125% due 07/15/12

and $81,406 US Treasury Bills,

zero coupon due 08/04/11 to

07/26/12; (value—$81,632);

proceeds: $80,000 | | $ | 80,000 | | | $ | 80,000 | | |

Total repurchase agreements

(cost—$78,080,000) | | | | | | | 78,080,000 | | |

Total investments

(cost—$354,781,978,

which approximates cost

for federal income

tax purposes)—96.98% | | | | | | | 354,781,978 | | |

Other assets in excess

of liabilities—3.02% | | | | | | | 11,061,651 | | |

Net assets (applicable to 365,845,932

shares of beneficial interest

outstanding equivalent to $1.00

per share)—100.00% | | $ | 365,843,629 | | |

For a listing of defined portfolio acronyms and currency abbreviations that are used throughout the Portfolio of investments as well as the tables that follow, please refer to page 227.

* On September 7, 2008, the Federal Housing Finance Agency placed the Federal National Mortgage Association and the Federal Home Loan Mortgage Corporation into conservatorship, and the US Treasury guaranteed the debt issued by those organizations.

1 Rates shown are the discount rates at date of purchase.

2 Variable or floating rate security. The interest rate shown is the current rate as of July 31, 2011 and changes periodically. The maturity date reflects earlier of reset date or stated maturity date.

3 Security exempt from registration pursuant to Rule 144A under the Securities Act of 1933. These securities, which represent 1.71% of net assets as of July 31, 2011, are considered liquid and may be resold in transactions exempt from registration, normally to qualified institutional buyers.

Affiliated issuer activity

The table below details the Portfolio's transaction activity in an affiliated issuer during the year ended July 31, 2011.

The investment manager earns a management fee from UBS Private Money Market Fund LLC.

| Security description | | Value at

07/31/10 | | Purchases

during the

year ended

07/31/11 | | Sales

during the

year ended

07/31/11 | | Value at

07/31/11 | | Net income

earned from

affiliate for the

year ended

07/31/11 | |

| UBS Private Money Market Fund LLC | | $ | — | | | $ | 5,865,000 | | | $ | 5,865,000 | | | $ | — | | | $ | 24 | | |

11

PACE Select Advisors Trust

PACE Money Market Investments

Portfolio of investments—July 31, 2011

The following is a summary of the fair valuations according to the inputs used as of July 31, 2011 in valuing the Portfolio's investments:

| | | Unadjusted

quoted prices in

active markets for

identical investments

(Level 1) | | Other significant

observable inputs

(Level 2) | | Unobservable

inputs

(Level 3) | | Total | |

| US government and agency obligations | | $ | — | | | $ | 72,097,367 | | | $ | — | | | $ | 72,097,367 | | |

| Bank note | | | — | | | | 3,000,000 | | | | — | | | | 3,000,000 | | |

| Certificates of deposit | | | — | | | | 45,249,966 | | | | — | | | | 45,249,966 | | |

| Commercial paper | | | — | | | | 150,854,645 | | | | — | | | | 150,854,645 | | |

| Short-term corporate obligations | | | — | | | | 5,500,000 | | | | — | | | | 5,500,000 | | |

| Repurchase agreements | | | — | | | | 78,080,000 | | | | — | | | | 78,080,000 | | |

| Total | | $ | — | | | $ | 354,781,978 | | | $ | — | | | $ | 354,781,978 | | |

Issuer breakdown by country of origin (unaudited)

| | | Percentage of

total investments | |

| United States | | | 76.8 | % | |

| Canada | | | 5.2 | | |

| United Kingdom | | | 4.2 | | |

| Japan | | | 3.1 | | |

| Australia | | | 2.9 | | |

| Sweden | | | 2.1 | | |

| Norway | | | 2.0 | | |

| Switzerland | | | 1.1 | | |

| Germany | | | 0.8 | | |

| France | | | 0.8 | | |

| Finland | | | 0.7 | | |

| Netherlands | | | 0.3 | | |

| Total | | | 100.0 | % | |

Weighted average maturity—47 days

See accompanying notes to financial statements.

12

PACE Select Advisors Trust

PACE Government Securities Fixed Income Investments

Performance

For the 12 months ended July 31, 2011, the Portfolio's Class P shares returned 4.08%, before the deduction of the maximum PACE Select program fee. (Class P shares returned 2.02%, after the deduction of the maximum PACE Select program fee, for the same 12-month period.) In comparison, the Barclays Capital US Mortgage-Backed Securities Index (the "benchmark") returned 3.85%, and the Lipper US Mortgage Funds category posted a median return of 4.03%. (Returns for all share classes over various time periods are shown in the "Performance at a glance" table on page 16. Please note that the returns shown do not reflect the deduction of taxes that a shareholder would pay on Portfolio distributions or the redemption of Portfolio shares.) For a detailed commentary on the market environment in general during the reporting period, please refer to page 2.

Sub-Advisor's comments1

The Portfolio outperformed its benchmark during the reporting period, helped by an emphasis on attractively priced, high-quality assets. Tactical security selection among agency mortgage backed securities ("MBS") was positive for performance. This included an underweight to higher coupon securities in the first half of the period, as these were the most adversely impacted by refinancing concerns. Detractors from relative performance included a modest underweight to Ginnie Mae MBS in the second half of the period, as these securities outperformed conventional (Fannie Mae and Freddie Mac) MBS due to strong demand from banks and international investors.

Exposure to senior non-agency MBS benefited the Portfolio, as the sector remained resilient amid negative foreclosure headlines, and gained from limited supply in conjunction with strong investor demand for higher yielding assets. However, this benefit was mitigated by the sector's underperformance in the latter stages of the period, amid further signs of slowing economic growth. An allocation to commercial mortgage-backed securities ("CMBS") in the beginning of the reporting period also benefited the Portfolio, as spreads in this sector tightened given continued demand for higher yielding assets. (Spread measures the difference in yield between a fixed income security and a government bond of similar duration.)

1 All Sub-Advisors discuss performance on a gross of fees basis—meaning that no fees or expenses are reflected in their sleeves'/sleeve's performance. Alternately, Fund performance is shown net of fees, which does factor in fees and expenses associated with the Fund.

PACE Select Advisors Trust – PACE Government Securities Fixed Income Investments

Investment Sub-Advisor:

Pacific Investment Management Company LLC ("PIMCO")

Portfolio Manager:

W. Scott Simon

Objective:

Current income

Investment process:

The Portfolio invests primarily in government fixed income securities which include US bonds, including those backed by mortgages, and related repurchase agreements. Mortgage-backed securities include "to be announced" or "TBA" securities which usually are traded on a forward commitment basis with an approximate principal amount and no defined maturity date; issued or guaranteed by US government agencies and instrumentalities. The Portfolio also invests, to a lesser extent, in investment grade bonds of private issuers, including those backed by mortgages or other assets. The Portfolio may invest in bonds of varying maturities, but normally limits its duration to within two years (plus or minus) of the effective duration of the Portfolio's benchmark index. (Duration is a measure of a portfolio's sensitivity to interest rate changes.) The Portfolio may engage in short selling with respect to securities issued by the US Treasury and certain TBA securities coupon trades. PIMCO establishes duration targets based on its expectations for changes in interest rates, and then positions the Portfolio to take advantage of yield curve shifts. PIMCO decides to buy and sell specific bonds based on an analysis of their values relative to other similar securities.

13

PACE Select Advisors Trust

PACE Government Securities Fixed Income Investments

Sub-Advisor's comments – concluded

Duration positioning, including a shorter-than-benchmark duration in the latter half of the period as rates fell, was negative for relative performance. (Duration measures a portfolio's sensitivity to interest rate changes.)

A number of derivative instruments were used during the reporting period. Interest rate swaps were used to adjust interest rate and yield curve exposures, as well as to substitute for physical securities. Credit default swaps were used to manage credit exposure in lieu of the direct buying or selling of securities. Options were primarily used to manage interest rate and volatility exposures, but they were also used to generate income in expected interest rate scenarios. Mortgage derivatives were used to manage portfolio duration or enhance yield, while government futures were used to adjust interest rate exposures and replicate government bond positions. Overall, the use of these derivatives was beneficial during the reporting period.

Special considerations

The Portfolio may be appropriate for long-term investors seeking current income who are able to withstand short-term fluctuations in the fixed income markets in return for potentially higher returns over the long term. The yield and value of the Portfolio change every day and can be affected by changes in interest rates, general market conditions and other political, social and economic developments, as well as specific matters relating to the issuers in which the Portfolio invests. It is important to note that an investment in the Portfolio is only one component of a balanced investment plan.

14

PACE Select Advisors Trust

PACE Government Securities Fixed Income Investments

Illustration of an assumed investment of $10,000 in Class P shares of the Portfolio (unaudited)

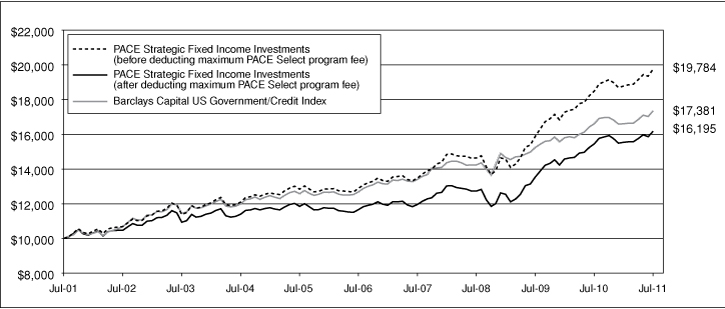

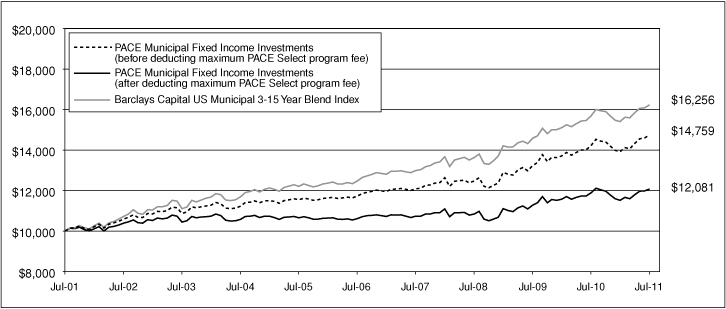

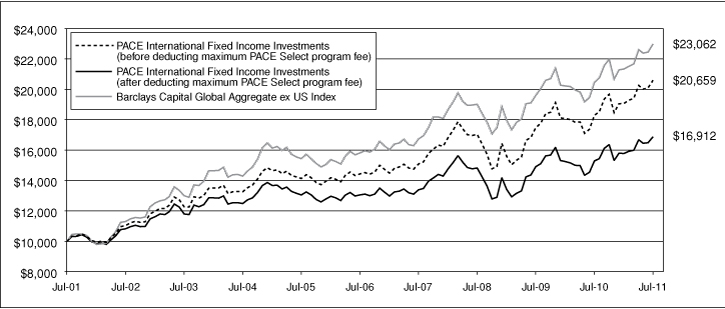

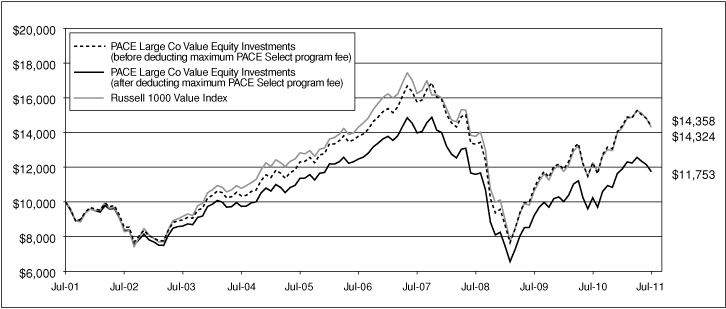

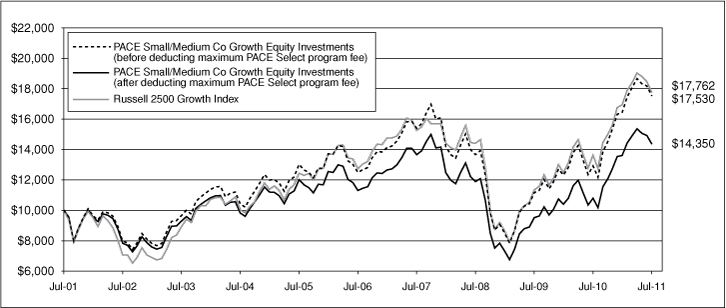

The following graph depicts the performance of PACE Government Securities Fixed Income Investments Class P shares versus the Barclays Capital US Mortgage-Backed Securities Index over the 10 years ended July 31, 2011. The performance of the other classes will vary based upon the different class specific expenses and sales charges. The performance provided does not reflect the deduction of taxes that a shareholder would pay on Portfolio distributions or the redemption of Portfolio shares. Past performance is no guarantee of future results. Share price and returns will vary with market conditions; investors may realize a gain or loss upon redemption. It is important to note that PACE Government Securities Fixed Income Investments is a professionally managed portfolio while the Index is not available for investment and is unmanaged. The comparison is shown for illustration purposes only.

15

PACE Select Advisors Trust

PACE Government Securities Fixed Income Investments

Performance at a glance (unaudited)

| Average annual total returns for periods ended 07/31/11 | | 1 year | | 5 years | | 10 years | |

| Before deducting | | Class A1 | | | 3.74 | % | | | 6.53 | % | | | 5.14 | % | |

| maximum sales charge | | Class B2 | | | 3.03 | % | | | 5.73 | % | | | 4.65 | %6 | |

| or PACE Select | | Class C3 | | | 3.22 | % | | | 5.99 | % | | | 4.60 | % | |

| program fee | | Class Y4 | | | 4.00 | % | | | 6.81 | % | | | 5.44 | % | |

| | | Class P5 | | | 4.08 | % | | | 6.80 | % | | | 5.40 | % | |

| After deducting | | Class A1 | | | (0.96 | )% | | | 5.55 | % | | | 4.65 | % | |

| maximum sales charge | | Class B2 | | | (1.83 | )% | | | 5.40 | % | | | 4.65 | %6 | |

| or PACE Select | | Class C3 | | | 2.49 | % | | | 5.99 | % | | | 4.60 | % | |

| program fee | | Class P5 | | | 2.02 | % | | | 4.68 | % | | | 3.31 | % | |

| Barclays Capital US Mortgage-Backed Securities Index7 | | | | | 3.85 | % | | | 6.85 | % | | | 5.71 | % | |

| Lipper US Mortgage Funds median | | | | | 4.03 | % | | | 5.90 | % | | | 4.83 | % | |

Average annual total returns for periods ended June 30, 2011, after deduction of the maximum sales charge or PACE Select program fee, were as follows: Class A—1-year period, (0.69)%; 5-year period, 5.69%; 10-year period, 4.80%; Class B—1-year period, (1.67)%; 5-year period, 5.55%; 10-year period, 4.80%; Class C—1-year period, 2.74%; 5-year period, 6.12%; 10-year period, 4.74%; Class Y—1-year period, 4.24%; 5-year period, 6.95%; 10-year period, 5.59%; Class P—1-year period, 2.18%; 5-year period, 4.82%; 10-year period, 3.44%.

The annualized gross and net expense ratios, respectively, for each class of shares as in the November 28, 2010 prospectuses, were as follows: Class A—1.08% and 1.02%; Class B—1.91% and 1.77%; Class C—1.61% and 1.52%; Class Y—0.89% and 0.77%; and Class P—0.88% and 0.77%. Net expenses reflect fee waivers and/or expense reimbursements, if any, pursuant to an agreement that is in effect to cap the expenses. The Portfolio and UBS Global Asset Management (Americas) Inc. ("UBS Global AM") have entered into a written fee waiver/expense reimbursement agreement pursuant to which UBS Global AM is contractually obligated to (1) waive its management fees through November 28, 2011 to the extent necessary to reflect the lower sub-advisory fee paid by UBS Global AM to Pacific Investment Management Company LLC, the Portfolio's investment advisor; and (2) waive its management fees and/or reimburse expenses so that the Portfolio's ordinary total operating expenses of each class through November 28, 2011 (excluding dividend expense, borrowing costs, and interest expense relating to short sales, and interest, taxes, brokerage commissions and extraordinary expenses) would not exceed Class A—1.02%; Class B—1.77%; Class C—1.52%; Class Y—0.77%; and Class P—0.77%. The Portfolio has agreed to repay UBS Global AM for any waived fees/reimbursed expenses (pursuant to item (2)) to the extent that it can do so over the following three fiscal years without causing the Portfolio's expenses in any of those three years to exceed these expense caps. The fee waiver/expense reimbursement agreement may be terminated by the Portfolio's board at any time and also will terminate automatically upon the expiration or termination of the Portfolio's advisory contract with UBS Global AM. Upon termination of the agreement, however, UBS Global AM's three year recoupment rights will survive.

1 Maximum sales charge for Class A shares is 4.5%. Class A shares bear ongoing 12b-1 service fees.

2 Maximum contingent deferred sales charge for Class B shares is 5% imposed on redemptions and is reduced to 0% after a maximum of six years. Class B shares bear ongoing 12b-1 service and distribution fees.

3 Maximum contingent deferred sales charge for Class C shares is 0.75% imposed on redemptions and is reduced to 0% after one year. Class C shares bear ongoing 12b-1 service and distribution fees. Prior to September 30, 2003, Class C shares were subject to a maximum front-end sales charge of 1.00%; this front-end sales charge is not reflected in the average annual total returns presented for the Class C shares shown above.

4 The Portfolio offers Class Y shares to a limited group of eligible investors, including certain qualifying retirement plans. Class Y shares do not bear initial or contingent deferred sales charges or ongoing 12b-1 service and distribution fees.

5 Class P shares do not bear initial or contingent deferred sales charges or ongoing 12b-1 service and distribution fees, but are subject to a maximum annual PACE Select program fee of 2% of the value of Class P shares. Prior to June 14, 2010, the maximum annual PACE Select program fee was 1.5% of the value of Class P shares; however, the current maximum annual PACE Select program fee of 2% is reflected in the performance returns throughout all periods in the average annual total returns presented for the Class P shares shown above.

6 Assumes the conversion of Class B to Class A shares at the end of the sixth year.

7 The Barclays Capital US Mortgage-Backed Securities Index is an unmanaged index which primarily covers agency mortgage-backed pass-through securities issued by Ginnie Mae (formally known as Government National Mortgage Association or GNMA), Freddie Mac (formally known as Federal Home Loan Mortgage Corporation or FHLMC), and Fannie Mae (formally known as Federal National Mortgage Association or FNMA). Investors should note that indices do not reflect the deduction of fees and expenses.

If an investor sells or exchanges shares less than 90 days after purchase, a redemption fee of 1.00% of the amount sold or exchanged will be deducted at the time of the transaction, except as noted otherwise in the prospectuses.

Past performance does not predict future performance, and the performance information provided does not reflect the deduction of taxes that a shareholder would pay on Portfolio distributions or the redemption of Portfolio shares. The return and principal value of an investment will fluctuate, so that an investor's shares, when redeemed, may be worth more or less than their original cost. Performance results assume reinvestment of all dividends and capital gain distributions at net asset value on the ex-dividend dates. Current performance may be higher or lower than the performance data quoted. For month-end performance figures, please visit http://www.ubs.com.

Lipper peer group data calculated by Lipper Inc.; used with permission. The Lipper median is the return of the fund that places in the middle of a Lipper peer group.

16

PACE Select Advisors Trust

PACE Government Securities Fixed Income Investments

Portfolio statistics (unaudited)

| Characteristics | | 07/31/11 | |

| Weighted average duration | | | 3.0 yrs. | | |

| Weighted average maturity | | | 3.5 yrs. | | |

| Average coupon | | | 3.57 | % | |

| Average quality1 | | | AAA | | |

| Net assets (mm) | | $ | 607.6 | | |

| Number of holdings | | | 390 | | |

| Portfolio composition2 | | 07/31/11 | |

| Bonds | | | 152.1 | % | |

| Investments sold short | | | (43.6 | ) | |

| Cash equivalents and other assets less liabilities | | | (8.5 | ) | |

| Total | | | 100.0 | % | |

| Asset allocation2 | | 07/31/11 | |

| US government agency mortgage pass-through certificates | | | 134.5 | % | |

| Collateralized mortgage obligations | | | 13.8 | | |

| Asset-backed securities | | | 2.7 | | |

| Stripped mortgage-backed securities | | | 1.1 | | |

| Investments sold short | | | (43.6 | ) | |

| Cash equivalents and other assets less liabilities | | | (8.5 | ) | |

| Total | | | 100.0 | % | |

1 Credit quality ratings shown are based on the ratings assigned to portfolio holdings by Standard & Poor's Ratings Group, an independent rating agency.

2 Weightings represent percentages of the Portfolio's net assets as of July 31, 2011. The Portfolio is actively managed and its composition will vary over time.

17

PACE Select Advisors Trust

PACE Government Securities Fixed Income Investments

Portfolio of investments—July 31, 2011

| | | Face

amount | | Value | |

Government national mortgage association

certificates—30.99% | |

GNMA

3.500%, due 11/15/401 | | $ | 874,410 | | | $ | 869,105 | | |

| 3.500%, due 12/15/401 | | | 41,087,457 | | | | 40,838,187 | | |

| 3.500%, due 01/15/411 | | | 20,311,342 | | | | 20,188,118 | | |

| 3.500%, due 02/15/411 | | | 11,697,665 | | | | 11,626,698 | | |

| 4.500%, due 06/15/391 | | | 914,957 | | | | 979,134 | | |

| 4.500%, due 08/15/391 | | | 1,575,184 | | | | 1,685,056 | | |

| 4.500%, due 09/15/391 | | | 2,786,768 | | | | 2,981,586 | | |

| 4.500%, due 02/15/401 | | | 1,505,281 | | | | 1,606,985 | | |

| 4.500%, due 03/15/401 | | | 691,695 | | | | 738,429 | | |

| 4.500%, due 04/15/401 | | | 1,713,063 | | | | 1,828,805 | | |

| 4.500%, due 05/15/401 | | | 3,533,268 | | | | 3,771,991 | | |

| 5.500%, due 06/15/37 | | | 40,192 | | | | 44,515 | | |

| 5.500%, due 07/15/37 | | | 96,013 | | | | 106,341 | | |

| 5.500%, due 12/15/37 | | | 59,611 | | | | 66,023 | | |

| 5.500%, due 02/15/38 | | | 24,031 | | | | 26,619 | | |

| 5.500%, due 07/15/38 | | | 105,771 | | | | 117,116 | | |

| 5.500%, due 08/15/38 | | | 49,105 | | | | 54,372 | | |

| 5.500%, due 10/15/38 | | | 4,496,246 | | | | 4,979,088 | | |

| 5.500%, due 12/15/38 | | | 84,878 | | | | 93,991 | | |

| 5.500%, due 03/15/39 | | | 821,797 | | | | 909,941 | | |

| 5.500%, due 04/15/39 | | | 32,466 | | | | 35,949 | | |

| 5.500%, due 05/15/39 | | | 716,316 | | | | 793,164 | | |

| 5.500%, due 09/15/39 | | | 3,276,166 | | | | 3,627,730 | | |

| 5.500%, due 12/15/39 | | | 802,262 | | | | 888,311 | | |

| 5.500%, due 01/15/40 | | | 19,627 | | | | 21,732 | | |

| 5.500%, due 02/15/40 | | | 270,422 | | | | 299,427 | | |

| 5.500%, due 03/15/40 | | | 482,485 | | | | 534,235 | | |

| 5.500%, due 04/15/40 | | | 26,998 | | | | 30,003 | | |

| 5.500%, due 05/15/40 | | | 113,207 | | | | 125,350 | | |

| 5.500%, due 06/15/40 | | | 735,123 | | | | 813,971 | | |

| 6.000%, due 10/15/31 | | | 3,483 | | | | 3,913 | | |

| 6.000%, due 03/15/34 | | | 3,734 | | | | 4,190 | | |

| 6.000%, due 08/15/34 | | | 6,303 | | | | 7,073 | | |

| 6.000%, due 07/15/36 | | | 131,775 | | | | 148,499 | | |

| 6.500%, due 02/15/29 | | | 2,375 | | | | 2,725 | | |

| 6.500%, due 11/15/34 | | | 17,847 | | | | 20,204 | | |

| 6.500%, due 01/15/36 | | | 37,325 | | | | 42,253 | | |

| 6.500%, due 03/15/36 | | | 2,087 | | | | 2,359 | | |

| 6.500%, due 09/15/36 | | | 909,864 | | | | 1,028,233 | | |

| 6.500%, due 02/15/37 | | | 43,889 | | | | 49,533 | | |

| 6.500%, due 04/15/37 | | | 26,955 | | | | 30,421 | | |

| 6.500%, due 01/15/38 | | | 18,632 | | | | 21,045 | | |

| 6.500%, due 06/15/38 | | | 170,193 | | | | 192,570 | | |

| 6.500%, due 07/15/38 | | | 76,102 | | | | 85,769 | | |

| 6.500%, due 08/15/38 | | | 4,023 | | | | 4,534 | | |

| 6.500%, due 10/15/38 | | | 384,667 | | | | 433,530 | | |

| 6.500%, due 11/15/38 | | | 38,493 | | | | 43,383 | | |

| 6.500%, due 01/15/39 | | | 12,619 | | | | 14,240 | | |

| 7.500%, due 08/15/21 | | | 5,909 | | | | 6,892 | | |

| 7.500%, due 09/15/23 | | | 941 | | | | 1,099 | | |

| 8.000%, due 02/15/23 | | | 1,386 | | | | 1,634 | | |

| 8.250%, due 04/15/19 | | | 363,561 | | | | 413,073 | | |

| 10.500%, due 02/15/19 | | | 27,392 | | | | 27,699 | | |

| 10.500%, due 06/15/19 | | | 33,452 | | | | 38,468 | | |

| | | Face

amount | | Value | |

Government national mortgage association

certificates—(Continued) | |

| 10.500%, due 07/15/19 | | $ | 68,437 | | | $ | 75,606 | | |

| 10.500%, due 07/15/20 | | | 3,375 | | | | 3,457 | | |

| 10.500%, due 08/15/20 | | | 30,103 | | | | 33,342 | | |

| 10.500%, due 09/15/20 | | | 3,315 | | | | 3,820 | | |

| 11.500%, due 05/15/19 | | | 3,080 | | | | 3,590 | | |

GNMA II

3.500%, due 01/20/411 | | | 8,000,793 | | | | 7,952,254 | | |

| 4.500%, due 08/20/40 | | | 475,387 | | | | 506,541 | | |

| 9.000%, due 04/20/25 | | | 22,568 | | | | 27,168 | | |

| 9.000%, due 12/20/26 | | | 4,167 | | | | 5,019 | | |

| 9.000%, due 01/20/27 | | | 12,590 | | | | 15,177 | | |

| 9.000%, due 06/20/30 | | | 1,517 | | | | 1,611 | | |

| 9.000%, due 09/20/30 | | | 1,290 | | | | 1,376 | | |

| 9.000%, due 10/20/30 | | | 8,384 | | | | 10,201 | | |

| 9.000%, due 11/20/30 | | | 5,799 | | | | 7,056 | | |

GNMA II ARM

2.250%, due 02/20/28 | | | 3,940 | | | | 4,072 | | |

| 2.375%, due 01/20/23 | | | 104,348 | | | | 107,973 | | |

| 2.375%, due 03/20/23 | | | 52,182 | | | | 53,995 | | |

| 2.375%, due 01/20/24 | | | 131,663 | | | | 136,238 | | |

| 2.375%, due 01/20/25 | | | 12,485 | | | | 12,918 | | |

| 2.375%, due 02/20/25 | | | 35,875 | | | | 37,121 | | |

| 2.375%, due 03/20/26 | | | 26,935 | | | | 27,870 | | |

| 2.375%, due 01/20/27 | | | 170,939 | | | | 176,878 | | |

| 2.375%, due 02/20/27 | | | 18,037 | | | | 18,663 | | |

| 2.375%, due 01/20/28 | | | 19,268 | | | | 19,937 | | |

| 2.375%, due 02/20/28 | | | 11,279 | | | | 11,671 | | |

| 2.500%, due 11/20/21 | | | 29,786 | | | | 30,784 | | |

| 2.500%, due 03/20/25 | | | 44,227 | | | | 45,819 | | |

| 2.500%, due 10/20/30 | | | 29,962 | | | | 30,966 | | |

| 2.625%, due 07/20/17 | | | 7,377 | | | | 7,669 | | |

| 2.625%, due 09/20/21 | | | 150,940 | | | | 156,921 | | |

| 2.625%, due 08/20/25 | | | 34,527 | | | | 35,894 | | |

| 2.625%, due 09/20/25 | | | 41,554 | | | | 43,200 | | |

| 2.625%, due 08/20/26 | | | 48,411 | | | | 50,329 | | |

| 2.625%, due 09/20/26 | | | 7,183 | | | | 7,468 | | |

| 2.625%, due 07/20/27 | | | 18,013 | | | | 18,727 | | |

| 2.625%, due 08/20/27 | | | 46,322 | | | | 48,157 | | |

| 2.625%, due 07/20/30 | | | 223,095 | | | | 231,934 | | |

| 2.625%, due 08/20/30 | | | 175,310 | | | | 182,257 | | |

| 3.375%, due 04/20/18 | | | 12,561 | | | | 13,028 | | |

| 3.375%, due 06/20/22 | | | 135,002 | | | | 140,014 | | |

| 3.375%, due 04/20/24 | | | 151,369 | | | | 156,988 | | |

| 3.375%, due 05/20/25 | | | 108,305 | | | | 112,708 | | |

| 3.375%, due 06/20/25 | | | 26,018 | | | | 26,984 | | |

| 3.375%, due 04/20/26 | | | 242,619 | | | | 251,625 | | |

| 3.375%, due 06/20/26 | | | 104,680 | | | | 108,564 | | |

| 3.375%, due 04/20/27 | | | 61,346 | | | | 63,623 | | |

| 3.375%, due 04/20/30 | | | 42,383 | | | | 43,956 | | |

| 3.375%, due 05/20/30 | | | 855,057 | | | | 886,797 | | |

| 3.500%, due 03/20/25 | | | 22,615 | | | | 23,542 | | |

| 4.000%, due 01/20/18 | | | 138,227 | | | | 144,101 | | |

| 4.000%, due 05/20/18 | | | 6,392 | | | | 6,698 | | |

| 4.000%, due 06/20/19 | | | 15,439 | | | | 16,180 | | |

| 4.500%, due 06/20/19 | | | 24,213 | | | | 25,435 | | |

18

PACE Select Advisors Trust

PACE Government Securities Fixed Income Investments

Portfolio of investments—July 31, 2011

| | | Face

amount | | Value | |

Government national mortgage association

certificates—(Concluded) | | | |

GNMA TBA

4.000%, TBA | | $ | 45,925,000 | | | $ | 47,474,969 | | |

| 5.000%, TBA | | | 11,000,000 | | | | 11,984,843 | | |

| 6.000%, TBA | | | 11,000,000 | | | | 12,268,438 | | |

| 6.500%, TBA | | | 1,000,000 | | | | 1,126,250 | | |

Total government national mortgage

association certificates

(cost—$184,429,445) | | | | | | | 188,323,733 | | |

Federal home loan mortgage corporation

certificates*—24.55% | | | |

FHLMC

5.000%, due 10/01/29 | | | 1,851,276 | | | | 1,986,857 | | |

| 5.000%, due 06/01/34 | | | 87,854 | | | | 94,210 | | |

| 5.000%, due 11/01/40 | | | 683,679 | | | | 730,262 | | |

| 5.500%, due 02/01/33 | | | 739,682 | | | | 807,953 | | |

| 5.500%, due 12/01/33 | | | 365,264 | | | | 398,978 | | |

| 5.500%, due 12/01/34 | | | 381,901 | | | | 417,150 | | |

| 5.500%, due 06/01/35 | | | 3,778,544 | | | | 4,127,301 | | |

| 5.500%, due 06/01/36 | | | 3,924,551 | | | | 4,286,784 | | |

| 5.500%, due 03/01/37 | | | 699,221 | | | | 761,355 | | |

| 5.500%, due 04/01/37 | | | 825,321 | | | | 896,339 | | |

| 5.500%, due 10/01/37 | | | 66,975 | | | | 72,739 | | |

| 5.500%, due 11/01/37 | | | 1,898,526 | | | | 2,061,892 | | |

| 5.500%, due 12/01/38 | | | 29,623 | | | | 32,256 | | |

| 6.000%, due 11/01/37 | | | 16,528,242 | | | | 18,239,727 | | |

| 7.000%, due 08/01/25 | | | 1,008 | | | | 1,163 | | |

| 7.500%, due 10/01/17 | | | 1,599 | | | | 1,606 | | |

| 8.000%, due 03/01/13 | | | 10,621 | | | | 10,755 | | |

| 9.000%, due 04/01/25 | | | 37,101 | | | | 45,581 | | |

| 11.000%, due 09/01/15 | | | 695 | | | | 728 | | |

| 11.000%, due 10/01/15 | | | 271 | | | | 298 | | |

| 11.000%, due 12/01/15 | | | 4,005 | | | | 4,526 | | |

| 11.000%, due 04/01/19 | | | 4,427 | | | | 5,268 | | |

| 11.000%, due 06/01/19 | | | 391 | | | | 393 | | |

| 11.000%, due 08/01/20 | | | 32 | | | | 32 | | |

| 11.000%, due 09/01/20 | | | 1,280 | | | | 1,507 | | |

| 11.500%, due 01/01/16 | | | 2,262 | | | | 2,298 | | |

| 11.500%, due 01/01/18 | | | 7,652 | | | | 8,973 | | |

| 11.500%, due 05/01/19 | | | 2,628 | | | | 2,642 | | |

| 11.500%, due 06/01/19 | | | 18,399 | | | | 22,232 | | |

FHLMC ARM

2.387%, due 01/01/28 | | | 69,376 | | | | 72,487 | | |

| 2.400%, due 11/01/27 | | | 169,306 | | | | 178,008 | | |

| 2.483%, due 04/01/29 | | | 274,145 | | | | 288,030 | | |

| 2.498%, due 07/01/24 | | | 244,477 | | | | 246,129 | | |

| 2.531%, due 10/01/23 | | | 137,410 | | | | 144,222 | | |

| 2.583%, due 12/01/29 | | | 141,433 | | | | 149,116 | | |

| 2.587%, due 11/01/29 | | | 557,769 | | | | 587,601 | | |

| 2.597%, due 06/01/28 | | | 481,423 | | | | 506,946 | | |

| 2.597%, due 07/01/28 | | | 193,141 | | | | 203,167 | | |

| 2.670%, due 11/01/25 | | | 320,836 | | | | 338,936 | | |

| 2.685%, due 01/01/29 | | | 260,508 | | | | 274,801 | | |

| 2.754%, due 10/01/27 | | | 378,846 | | | | 400,416 | | |

| 2.764%, due 10/01/27 | | | 343,838 | | | | 362,791 | | |

| | | Face

amount | | Value | |

Federal home loan mortgage corporation

certificates*—(Concluded) | | | |

| 2.875%, due 01/01/30 | | $ | 36,632 | | | $ | 38,475 | | |

| 5.104%, due 10/01/29 | | | 14,672 | | | | 15,376 | | |

FHLMC TBA

4.000% | | | 22,700,000 | | | | 23,054,687 | | |

| 4.500% | | | 42,000,000 | | | | 43,785,000 | | |

| 5.000% | | | 21,500,000 | | | | 22,914,296 | | |

| 5.500% | | | 19,000,000 | | | | 20,573,437 | | |

Total federal home loan mortgage

corporation certificates

(cost—$147,193,416) | | | | | | | 149,155,726 | | |

Federal housing administration

certificates—0.18% | | | |

FHA GMAC

7.400%, due 02/01/21 | | | 382,416 | | | | 378,591 | | |

FHA Reilly

6.896%, due 07/01/20 | | | 700,224 | | | | 700,224 | | |

Total federal housing administration

certificates

(cost—$1,083,661) | | | | | | | 1,078,815 | | |

Federal national mortgage association

certificates*—78.68% | | | |

FNMA

3.500%, due 11/01/25 | | | 2,500,433 | | | | 2,573,940 | | |

| 3.500%, due 02/01/26 | | | 1,594,884 | | | | 1,642,268 | | |

| 3.500%, due 09/01/391 | | | 295,409 | | | | 289,210 | | |

| 3.500%, due 11/01/391 | | | 492,795 | | | | 482,406 | | |

| 3.500%, due 08/01/401 | | | 808,256 | | | | 792,626 | | |

| 3.500%, due 09/01/401 | | | 55,745 | | | | 54,570 | | |

| 3.500%, due 10/01/401 | | | 255,782 | | | | 250,390 | | |

| 3.500%, due 11/01/401 | | | 2,830,592 | | | | 2,770,915 | | |

| 3.500%, due 12/01/401 | | | 13,022,989 | | | | 12,748,431 | | |

| 3.500%, due 01/01/411 | | | 2,182,543 | | | | 2,136,530 | | |

| 3.500%, due 03/01/411 | | | 9,999,996 | | | | 9,789,170 | | |

| 4.000%, due 05/01/18 | | | 201,720 | | | | 210,930 | | |

| 4.000%, due 03/01/19 | | | 235,888 | | | | 250,821 | | |

| 4.000%, due 06/01/19 | | | 273,857 | | | | 291,194 | | |

| 4.000%, due 04/01/23 | | | 15,750 | | | | 16,582 | | |

| 4.000%, due 03/01/24 | | | 3,048,517 | | | | 3,203,393 | | |

| 4.000%, due 08/01/24 | | | 698,166 | | | | 733,635 | | |

| 4.000%, due 03/01/25 | | | 1,083,209 | | | | 1,137,055 | | |

| 4.000%, due 05/01/25 | | | 1,720,230 | | | | 1,805,742 | | |

| 4.000%, due 05/01/391 | | | 551,627 | | | | 562,579 | | |

| 4.000%, due 09/01/391 | | | 902,191 | | | | 919,681 | | |

| 4.000%, due 09/01/401 | | | 4,102,984 | | | | 4,172,910 | | |

| 4.000%, due 10/01/401 | | | 4,233,803 | | | | 4,305,958 | | |

| 4.000%, due 11/01/401 | | | 9,606,001 | | | | 9,769,710 | | |

| 4.000%, due 12/01/401 | | | 18,920,127 | | | | 19,242,572 | | |

| 4.000%, due 01/01/411 | | | 46,673,728 | | | | 47,469,158 | | |

| 4.000%, due 02/01/411 | | | 42,534,641 | | | | 43,255,431 | | |

| 4.000%, due 03/01/411 | | | 32,435,366 | | | | 32,979,300 | | |

| 4.000%, due 04/01/411 | | | 5,482,407 | | | | 5,574,127 | | |

| 4.000%, due 05/01/411 | | | 22,065,327 | | | | 22,434,479 | | |

| 4.500%, due 03/01/23 | | | 84,386 | | | | 90,287 | | |

19

PACE Select Advisors Trust

PACE Government Securities Fixed Income Investments

Portfolio of investments—July 31, 2011

| | | Face

amount | | Value | |

Federal national mortgage association

certificates*—(Continued) | |

| 4.500%, due 04/01/23 | | $ | 301,088 | | | $ | 320,999 | | |

| 4.500%, due 05/01/24 | | | 2,064,605 | | | | 2,199,813 | | |

| 4.500%, due 11/01/24 | | | 664,820 | | | | 708,138 | | |

| 4.500%, due 01/01/25 | | | 22,950 | | | | 24,445 | | |

| 4.500%, due 02/01/25 | | | 43,787 | | | | 46,612 | | |

| 4.500%, due 03/01/25 | | | 898,117 | | | | 956,073 | | |

| 4.500%, due 04/01/25 | | | 5,977,768 | | | | 6,363,538 | | |

| 4.500%, due 05/01/25 | | | 388,310 | | | | 413,368 | | |

| 4.500%, due 06/01/25 | | | 854,149 | | | | 909,268 | | |

| 4.500%, due 09/01/25 | | | 79,181 | | | | 84,340 | | |

| 4.500%, due 02/01/33 | | | 83,932 | | | | 88,389 | | |

| 4.500%, due 05/01/38 | | | 662,009 | | | | 692,613 | | |

| 4.500%, due 08/01/38 | | | 1,172,835 | | | | 1,227,052 | | |

| 4.500%, due 01/01/39 | | | 53,673 | | | | 56,154 | | |

| 4.500%, due 02/01/39 | | | 589,552 | | | | 616,806 | | |

| 4.500%, due 04/01/39 | | | 1,801,344 | | | | 1,884,616 | | |

| 4.500%, due 07/01/39 | | | 23,633 | | | | 24,777 | | |

| 4.500%, due 09/01/39 | | | 1,193,501 | | | | 1,248,464 | | |

| 4.500%, due 10/01/39 | | | 978,481 | | | | 1,023,255 | | |

| 4.500%, due 01/01/40 | | | 679,381 | | | | 710,469 | | |

| 4.500%, due 07/01/40 | | | 81,107 | | | | 84,882 | | |

| 4.500%, due 04/01/41 | | | 1,033,056 | | | | 1,079,999 | | |

| 4.500%, due 05/01/41 | | | 7,971,131 | | | | 8,332,146 | | |

| 5.000%, due 08/01/18 | | | 46,421 | | | | 49,872 | | |

| 5.000%, due 01/01/23 | | | 1,767,376 | | | | 1,899,578 | | |

| 5.000%, due 02/01/23 | | | 89,490 | | | | 96,142 | | |

| 5.000%, due 03/01/23 | | | 307,099 | | | | 330,103 | | |

| 5.000%, due 04/01/23 | | | 516,158 | | | | 554,524 | | |

| 5.000%, due 05/01/23 | | | 729,882 | | | | 789,837 | | |

| 5.000%, due 06/01/23 | | | 769,713 | | | | 826,925 | | |

| 5.000%, due 07/01/23 | | | 1,405,077 | | | | 1,509,517 | | |

| 5.000%, due 09/01/23 | | | 2,651,389 | | | | 2,883,829 | | |

| 5.000%, due 10/01/23 | | | 122,600 | | | | 131,713 | | |

| 5.000%, due 11/01/23 | | | 120,239 | | | | 129,176 | | |

| 5.000%, due 01/01/24 | | | 687,168 | | | | 738,245 | | |

| 5.000%, due 07/01/24 | | | 3,538,760 | | | | 3,840,147 | | |

| 5.000%, due 12/01/33 | | | 3,817,260 | | | | 4,099,422 | | |

| 5.500%, due 12/01/16 | | | 57,471 | | | | 62,351 | | |

| 5.500%, due 01/01/17 | | | 126,673 | | | | 137,428 | | |

| 5.500%, due 06/01/17 | | | 81,456 | | | | 87,900 | | |

| 5.500%, due 09/01/17 | | | 51,082 | | | | 55,452 | | |

| 5.500%, due 11/01/17 | | | 83,650 | | | | 90,805 | | |

| 5.500%, due 01/01/18 | | | 548,185 | | | | 596,103 | | |

| 5.500%, due 02/01/18 | | | 158,942 | | | | 172,537 | | |

| 5.500%, due 07/01/22 | | | 424,067 | | | | 459,719 | | |

| 5.500%, due 02/01/23 | | | 67,523 | | | | 73,200 | | |

| 5.500%, due 02/01/32 | | | 34,126 | | | | 37,271 | | |

| 5.500%, due 11/01/32 | | | 661,416 | | | | 722,361 | | |

| 5.500%, due 12/01/33 | | | 6,533 | | | | 7,135 | | |

| 5.500%, due 04/01/34 | | | 311,295 | | | | 340,303 | | |

| 5.500%, due 11/01/34 | | | 1,150,859 | | | | 1,256,543 | | |

| 5.500%, due 01/01/35 | | | 240,354 | | | | 262,501 | | |

| 5.500%, due 02/01/35 | | | 29,368 | | | | 32,065 | | |

| 5.500%, due 05/01/37 | | | 1,850,931 | | | | 2,021,481 | | |

| 5.500%, due 07/01/37 | | | 2,966,559 | | | | 3,221,365 | | |

| | | Face

amount | | Value | |

Federal national mortgage association

certificates*—(Continued) | |

| 5.500%, due 01/01/38 | | $ | 10,184,306 | | | $ | 11,059,065 | | |

| 5.500%, due 06/01/39 | | | 9,277,920 | | | | 10,132,815 | | |

| 6.000%, due 11/01/21 | | | 495,834 | | | | 540,072 | | |

| 6.000%, due 06/01/22 | | | 87,801 | | | | 95,470 | | |

| 6.000%, due 01/01/23 | | | 1,001,034 | | | | 1,095,350 | | |

| 6.000%, due 03/01/23 | | | 1,919,577 | | | | 2,090,839 | | |

| 6.000%, due 11/01/26 | | | 200,751 | | | | 221,217 | | |

| 6.000%, due 01/01/32 | | | 41,429 | | | | 46,132 | | |

| 6.000%, due 04/01/32 | | | 52,877 | | | | 58,879 | | |

| 6.000%, due 09/01/32 | | | 38,554 | | | | 42,930 | | |

| 6.000%, due 10/01/32 | | | 66,735 | | | | 74,310 | | |

| 6.000%, due 12/01/32 | | | 108,244 | | | | 120,530 | | |

| 6.000%, due 01/01/33 | | | 238,439 | | | | 265,504 | | |

| 6.000%, due 02/01/33 | | | 129,626 | | | | 144,178 | | |

| 6.000%, due 09/01/34 | | | 901,747 | | | | 1,001,939 | | |

| 6.000%, due 04/01/35 | | | 4,162 | | | | 4,608 | | |

| 6.000%, due 05/01/35 | | | 511,475 | | | | 566,453 | | |

| 6.000%, due 06/01/35 | | | 120,951 | | | | 133,924 | | |

| 6.000%, due 07/01/35 | | | 556,421 | | | | 616,704 | | |

| 6.000%, due 08/01/35 | | | 294,951 | | | | 326,588 | | |

| 6.000%, due 09/01/35 | | | 89,525 | | | | 99,178 | | |

| 6.000%, due 01/01/36 | | | 256,371 | | | | 284,350 | | |

| 6.000%, due 09/01/36 | | | 333,533 | | | | 369,933 | | |

| 6.000%, due 10/01/36 | | | 648,880 | | | | 717,262 | | |

| 6.000%, due 11/01/36 | | | 8,540 | | | | 9,436 | | |

| 6.000%, due 01/01/37 | | | 482,913 | | | | 533,735 | | |

| 6.000%, due 03/01/37 | | | 207,805 | | | | 230,149 | | |

| 6.000%, due 08/01/37 | | | 540,983 | | | | 596,642 | | |

| 6.000%, due 09/01/37 | | | 2,254,178 | | | | 2,486,099 | | |

| 6.000%, due 12/01/37 | | | 388,064 | | | | 427,990 | | |

| 6.000%, due 06/01/38 | | | 70,200 | | | | 77,291 | | |

| 6.000%, due 08/01/38 | | | 74,412 | | | | 81,929 | | |

| 6.000%, due 09/01/38 | | | 2,875,201 | | | | 3,165,625 | | |

| 6.000%, due 10/01/38 | | | 3,790,100 | | | | 4,182,591 | | |

| 6.000%, due 01/01/39 | | | 2,926,040 | | | | 3,226,623 | | |

| 6.000%, due 10/01/39 | | | 75,088 | | | | 82,814 | | |

| 6.500%, due 09/01/12 | | | 1,061 | | | | 1,090 | | |

| 6.500%, due 12/01/12 | | | 2,430 | | | | 2,609 | | |

| 6.500%, due 01/01/13 | | | 613 | | | | 631 | | |

| 6.500%, due 02/01/13 | | | 3,784 | | | | 3,887 | | |

| 6.500%, due 03/01/13 | | | 7,147 | | | | 7,343 | | |

| 6.500%, due 04/01/13 | | | 639 | | | | 657 | | |

| 6.500%, due 06/01/13 | | | 9,984 | | | | 10,420 | | |

| 6.500%, due 07/01/13 | | | 2,768 | | | | 2,883 | | |

| 6.500%, due 08/01/13 | | | 3,120 | | | | 3,260 | | |

| 6.500%, due 09/01/13 | | | 9,764 | | | | 10,201 | | |

| 6.500%, due 10/01/13 | | | 6,807 | | | | 7,105 | | |

| 6.500%, due 11/01/13 | | | 18,801 | | | | 19,643 | | |

| 6.500%, due 07/01/19 | | | 52,606 | | | | 58,448 | | |

| 6.500%, due 10/01/36 | | | 1,557,441 | | | | 1,745,481 | | |

| 7.500%, due 11/01/26 | | | 26,290 | | | | 30,447 | | |

| 8.000%, due 11/01/26 | | | 39,816 | | | | 46,368 | | |

| 9.000%, due 10/01/19 | | | 21,414 | | | | 21,603 | | |

| 9.000%, due 02/01/26 | | | 29,449 | | | | 34,916 | | |

| 10.500%, due 09/01/15 | | | 6,152 | | | | 6,912 | | |

20

PACE Select Advisors Trust

PACE Government Securities Fixed Income Investments

Portfolio of investments—July 31, 2011

| | | Face

amount | | Value | |

Federal national mortgage association

certificates*—(Concluded) | | | |

| 10.500%, due 08/01/20 | | $ | 1,032 | | | $ | 1,087 | | |

| 10.500%, due 04/01/22 | | | 459 | | | | 516 | | |

| 11.000%, due 10/01/15 | | | 1,248 | | | | 1,267 | | |

| 11.000%, due 02/01/16 | | | 1,075 | | | | 1,082 | | |

FNMA ARM

1.478%, due 03/01/44 | | | 622,457 | | | | 635,315 | | |

| 1.724%, due 10/01/26 | | | 740,922 | | | | 764,492 | | |

| 1.750%, due 09/01/15 | | | 39,686 | | | | 39,982 | | |

| 2.329%, due 02/01/26 | | | 50,553 | | | | 53,084 | | |

| 2.352%, due 09/01/26 | | | 34,055 | | | | 35,485 | | |

| 2.520%, due 02/01/30 | | | 45,026 | | | | 47,328 | | |

| 2.645%, due 07/01/30 | | | 26,044 | | | | 27,088 | | |

| 2.782%, due 12/01/27 | | | 43,896 | | | | 46,225 | | |

| 2.907%, due 05/01/30 | | | 118,219 | | | | 124,186 | | |

| 3.139%, due 03/01/25 | | | 225,785 | | | | 237,447 | | |

FNMA TBA

3.500% | | | 8,000,000 | | | | 8,223,750 | | |

| 4.000% | | | 15,000,000 | | | | 15,717,188 | | |

| 4.500% | | | 59,200,000 | | | | 61,966,813 | | |

| 5.000% | | | 7,400,000 | | | | 7,899,688 | | |

| 5.500% | | | 26,500,000 | | | | 28,708,673 | | |

| 6.000% | | | 5,500,000 | | | | 6,034,316 | | |

| 6.500% | | | 10,600,000 | | | | 11,754,406 | | |

Total federal national mortgage

association certificates

(cost—$468,353,367) | | | | | | | 478,110,242 | | |

Collateralized mortgage

obligations—13.81% | | | |

ARM Trust,

Series 2005-8, Class 3A21

5.240%, due 11/25/35 | | | 2,345,679 | | | | 1,709,679 | | |

Bear Stearns Asset Backed

Securities Trust,

Series 2003-AC5, Class A1

5.750%, due 10/25/332 | | | 2,491,001 | | | | 2,510,010 | | |

Series 2004-AC3, Class A2

5.500%, due 06/25/342 | | | 2,689,745 | | | | 2,657,813 | | |

Chevy Chase Funding LLC,

Series 2004-1, Class A1

0.467%, due 01/25/353,4 | | | 256,076 | | | | 189,699 | | |

Chevy Chase Mortgage

Funding Corp.,

Series 2007-2A, Class A1

0.317%, due 05/25/483,4 | | | 1,698,285 | | | | 740,568 | | |

Countrywide Alternative Loan Trust,

Series 2006-0A2, Class A1

0.396%, due 05/20/464 | | | 4,160,987 | | | | 2,219,783 | | |

FHLMC REMIC,*

Series 0023, Class KZ

6.500%, due 11/25/23 | | | 64,957 | | | | 74,270 | | |

Series 0159, Class H

4.500%, due 09/15/21 | | | 16,801 | | | | 17,574 | | |

Series 1003, Class H

0.938%, due 10/15/204 | | | 72,993 | | | | 73,003 | | |

| | | Face

amount | | Value | |

Collateralized mortgage

obligations—(Continued) | |

Series 1349, Class PS

7.500%, due 08/15/22 | | $ | 3,394 | | | $ | 3,903 | | |

Series 1502, Class PX

7.000%, due 04/15/23 | | | 481,765 | | | | 551,530 | | |

Series 1534, Class Z

5.000%, due 06/15/23 | | | 242,400 | | | | 242,353 | | |

Series 1573, Class PZ

7.000%, due 09/15/23 | | | 81,570 | | | | 93,270 | | |

Series 1658, Class GZ

7.000%, due 01/15/24 | | | 40,347 | | | | 46,259 | | |

Series 1694, Class Z

6.500%, due 03/15/24 | | | 345,118 | | | | 376,457 | | |

Series 1775, Class Z

8.500%, due 03/15/25 | | | 8,019 | | | | 9,405 | | |

Series 2411, Class FJ

0.537%, due 12/15/294 | | | 58,218 | | | | 57,857 | | |

Series 3312, Class FN

0.407%, due 07/15/364 | | | 2,923,650 | | | | 2,904,836 | | |

FNMA REMIC,*

Trust 1987-002, Class Z

11.000%, due 11/25/17 | | | 196,842 | | | | 224,902 | | |

Trust 1988-007, Class Z

9.250%, due 04/25/18 | | | 186,205 | | | | 208,391 | | |

Trust 1992-129, Class L

6.000%, due 07/25/22 | | | 11,173 | | | | 12,453 | | |

Trust 1992-158, Class ZZ

7.750%, due 08/25/22 | | | 31,201 | | | | 36,053 | | |

Trust 1993-037, Class PX

7.000%, due 03/25/23 | | | 429,848 | | | | 488,529 | | |

Trust 1993-240, Class Z

6.250%, due 12/25/13 | | | 1,062 | | | | 1,109 | | |

Trust 1993-250, Class Z

7.000%, due 12/25/23 | | | 14,440 | | | | 15,548 | | |

Trust 2004-72, Class F

0.687%, due 09/25/344 | | | 3,188,370 | | | | 3,181,949 | | |

Trust 2005-088, Class A

0.337%, due 10/25/354 | | | 2,840,075 | | | | 2,768,726 | | |

Trust 2007-4, Class DF

0.632%, due 02/25/374 | | | 3,088,177 | | | | 3,067,964 | | |

Trust G92-040, Class ZC

7.000%, due 07/25/22 | | | 46,173 | | | | 51,845 | | |

Trust G94-006, Class PJ

8.000%, due 05/17/24 | | | 57,506 | | | | 66,188 | | |

GNMA REMIC,

Trust 2000-009, Class FH

0.687%, due 02/16/304 | | | 46,909 | | | | 46,995 | | |

Trust 2010-H01, Class FA

1.006%, due 01/20/604,5 | | | 5,860,788 | | | | 5,902,340 | | |

Indymac Index Mortgage Loan Trust,

Series 2005-AR2, Class 2A1A

0.507%, due 02/25/354 | | | 1,120,453 | | | | 742,004 | | |

JPMorgan Alternative Loan Trust,

Series 2008-R4, Class 2A1

0.687%, due 06/27/373,4 | | | 4,051,833 | | | | 3,284,708 | | |

21

PACE Select Advisors Trust

PACE Government Securities Fixed Income Investments

Portfolio of investments—July 31, 2011

| | | Face

amount | | Value | |

Collateralized mortgage

obligations—(Concluded) | |

JPMorgan Chase Commercial

Mortgage Securities Corp.,

Series 2007-FL1A, Class A1

0.562%, due 07/15/193,4 | | $ | 8,012,521 | | | $ | 7,552,512 | | |

LB Commercial Conduit

Mortgage Trust,

Series 2007-C3, Class A4

5.941%, due 07/15/444 | | | 2,500,000 | | | | 2,735,851 | | |

MLCC Mortgage Investors, Inc.,

Series 2004-1, Class 2A2

2.166%, due 12/25/344 | | | 1,058,476 | | | | 1,017,201 | | |

Mortgage Equity Conversion

Asset Trust,

Series 2006-SFG3, Class A

0.690%, due 10/25/413,4,5 | | | 1,455,712 | | | | 1,387,089 | | |

Series 2007-FF1, Class A

0.690%, due 01/25/423,4 | | | 1,647,609 | | | | 1,556,991 | | |