UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT

OF

REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-07239

Name of Registrant: Vanguard Horizon Funds

Address of Registrant: | P.O. Box 2600 |

| Valley Forge, PA 19482 |

| |

Name and address of agent for service: | Heidi Stam, Esquire |

| P.O. Box 876 |

| Valley Forge, PA 19482 |

| |

Registrant’s telephone number, including area code: (610) 669-1000

Date of fiscal year end: September 30

Date of reporting period: October 1, 2008– March 31, 2009

Item 1: Reports to Shareholders |

> | Vanguard Strategic Equity Fund returned about –37% for the six months ended March 31, 2009. The fund’s return trailed that of its benchmark index and its peer-group average. |

> | The broad U.S. stock market returned about –31% for the period. Shares of small and mid-sized companies fared worse than those of large companies. |

> | Like the broad market, the fund experienced declines across all sectors. |

Contents | |

| |

Your Fund’s Total Returns | 1 |

President’s Letter | 2 |

Advisor’s Report | 6 |

Fund Profile | 8 |

Performance Summary | 9 |

Financial Statements | 10 |

About Your Fund’s Expenses | 26 |

Trustees Approve Advisory Arrangement | 28 |

Glossary | 29 |

Please note: The opinions expressed in this report are just that—informed opinions. They should not be considered promises or advice. Also, please keep in mind that the information and opinions cover the period through the date on the front of this report. Of course, the risks of investing in your fund are spelled out in the prospectus.

Your Fund’s Total Returns

Six Months Ended March 31, 2009 | | |

| Ticker | Total |

| Symbol | Returns |

Vanguard Strategic Equity Fund | VSEQX | –36.66% |

MSCI US Small + Mid Cap 2200 Index | | –33.95 |

Average Mid-Cap Core Fund1 | | –31.41 |

Your Fund’s Performance at a Glance | | | |

September 30, 2008–March 31, 2009 | | | |

| | | Distributions Per Share |

| Starting | Ending | Income | Capital |

| Share Price | Share Price | Dividends | Gains |

Vanguard Strategic Equity Fund | $16.42 | $10.18 | $0.241 | $0.000 |

1 Derived from data provided by Lipper Inc.

1

President’s Letter

Dear Shareholder,

Vanguard Strategic Equity Fund returned about –37% for the six-month period ended March 31, 2009, which ranks among the worst half-year spans for the fund since its inception in 1995. The fund trailed its benchmark and its peers for the period, as all ten of its industry sectors recorded negative double-digit returns. Returns for mid- and small-capitalization stocks—the fund’s primary areas of investment—trailed those of large-caps.

Extreme distress dappled with glimmers of hope

The six months ended March 31 witnessed extreme distress in global stock markets, with both U.S. and international stocks returning about –31%. The embattled financial sector continued to struggle, prompting regulators in the United States and abroad to take evermore-aggressive actions to help the big banks fortify their fragile balance sheets.

Even as the gloom intensified, a few signs of recovery appeared on the horizon. Toward the end of the period, the swift contraction in manufacturing activity seemed to lessen. And throughout the six months, news from the housing sector seemed to improve. From their lows in early March through the end of the period, global stock markets generated a double-digit return.

2

Credit-market turmoil provoked dramatic response

Developments in the fixed income market were, if anything, even more unusual. In the months after the September collapse of Lehman Brothers, a major presence in the bond market, the trading of corporate bonds came to a near standstill as investors stampeded into U.S. Treasury bonds—considered the safest, most liquid credits—driving prices higher and yields lower. The difference between the yields of Treasuries and corporate bonds surged to levels not seen since the 1930s.

The Federal Reserve Board responded to the credit-market and economic crises with a dramatic easing of monetary policy, reducing its target for short-term interest rates to an all-time low of 0% to 0.25%.

The Fed also created new programs designed to bring borrowers and lenders back to the market. For the six-month period, the Barclays Capital U.S. Aggregate Bond Index returned 4.70% on the strength of Treasuries and other government-backed bonds. The broad municipal bond market returned 5.00%.

Fund’s declines were steep and broad-based

The Strategic Equity Fund, managed by Vanguard Quantitative Equity Group, seeks to mirror the sector allocations of its benchmark while overweighting or underweighting individual stocks. As with other funds that use quantitative models, the fund’s strategy is based on the idea that many “small wins” achieved through

Market Barometer | |

| Total Returns |

| Periods Ended March 31, 2009 |

| Six Months | One Year | Five Years1 |

Stocks | | | |

Russell 1000 Index (Large-caps) | –30.59% | –38.27% | –4.54% |

Russell 2000 Index (Small-caps) | –37.17 | –37.50 | –5.24 |

Dow Jones Wilshire 5000 Index (Entire market) | –30.72 | –37.69 | –4.24 |

MSCI All Country World Index ex USA (International) | –30.54 | –46.18 | –0.24 |

| | | |

Bonds | | | |

Barclays Capital U.S. Aggregate Bond Index (Broad taxable market) | 4.70% | 3.13% | 4.13% |

Barclays Capital Municipal Bond Index | 5.00 | 2.27 | 3.21 |

Citigroup 3-Month Treasury Bill Index | 0.30 | 1.13 | 3.06 |

| | | |

CPI | | | |

Consumer Price Index | –2.78% | –0.38% | 2.57% |

1 Annualized.

3

its stock selection will enable the fund to outperform the benchmark over time, while maintaining a similar risk profile.

Amid the steep market declines of the past six months (and the fund’s return of about –37%), “keeping score” versus the benchmark seems quite secondary. Returns were negative across the spectrum, and ranged from –13% for telecommunications services to –54% for energy.

Not surprisingly, the fund’s largest areas of investment, on average, during the period—financials and industrials—were also the largest detractors from the fund’s overall performance. Financial stocks, which represented about 18% of the fund’s assets, on average, during the period, returned –40%. Real estate investment trusts (REITs) and insurance firms were areas of significant decline. Industrial stocks, which returned –47%, experienced weakness in areas ranging from office services to farm machinery.

Still, the fund made some key missteps relative to its benchmark, the MSCI US Small + Mid Cap 2200 Index. The industrial, energy, and health care sectors were among the fund’s worst performers on a relative basis.

The Strategic Equity Fund’s few bright spots involved a smattering of stocks that notched positive returns during the period. Several were within the consumer

Expense Ratios1 | | |

Your Fund Compared With Its Peer Group | | |

| | Average |

| | Mid-Cap |

| Fund | Core Fund |

Strategic Equity Fund | 0.32% | 1.30% |

1 The fund expense ratio shown is from the prospectus dated January 28, 2009, and represents estimated costs for the current fiscal year based on the fund’s current net assets. For the six months ended March 31, 2009, the annualized expense ratio was 0.31%. The peer-group expense ratio is derived from data provided by Lipper Inc. and captures information through year-end 2008.

4

discretionary sector, and included restaurants, auto parts stores, and dollar stores.

Respect for risk is crucial in bad times and good

Difficult times often yield valuable lessons. It’s been said that people who lived through the Great Depression developed a lifelong appreciation for thrift. The current economic environment certainly does not approach the widespread hardship experienced during the Depression, but if there’s a silver lining to the recent upheaval in the financial markets, perhaps it’s that today’s investors will gain a lifelong appreciation for market risk.

That means respecting the power of the markets to move up and down—and maintaining an investment strategy (and a long-term outlook) that can help you weather the swings. A portfolio that is balanced across stock, bond, and short-term funds can dampen volatility. We believe the Strategic Equity Fund, with its measured exposure to the economy’s mid-sized companies, can be a key component in a balanced investment strategy.

When the clouds clear from the current financial storm, and it looks like “smooth sailing” ahead, keep in mind that sticking with a balanced portfolio is not just a foul-weather tactic. As we witnessed in the autumn of 2008, the financial markets can move quickly and violently. Maintaining a balanced portfolio can help you capture the “ups” while also bracing for the unexpected “downs.”

Thank you for your continued confidence in Vanguard.

Sincerely,

F. William McNabb III

President and Chief Executive Officer

April 17, 2009

5

Advisor’s Report

For the six months ended March 31, 2009, Vanguard Strategic Equity Fund returned about –37%, while the fund’s benchmark, the MSCI US Small + Mid Cap 2200 Index, returned about –34%. For the most recent 18 months, the fund posted a cumulative return of about –53%; the benchmark returned about –48% for the same period. The overall market, as measured by the MSCI US Broad Market Index, notched a return of about –31% for the half-year and a cumulative return of about –46% for the 18-month period.

The attractively valued, high-quality stocks we prefer underperformed the market over the last six months. This is partly because financial firms, which have been at the center of the market storm, are usually value stocks, and they have pulled down the overall averages. But after adjusting for that effect, value stocks in all industries suffered relative to the fund’s benchmark. Since value stocks have lagged for so long, why do we persist in our preference? We base our view both on judgment and on empirical evidence. In our judgment, although the market is relatively effective in assigning prices to stocks, investors as a group can still overreact to new information.

This overreaction can cause prices to diverge a bit from “true” or “fair” value, providing opportunities to profit from these discrepancies. We identify potentially attractive stocks by looking at multiple signals. Market participants send some signals, such as measures of relative performance or changes in analysts’ opinions. Other signals are provided by company management, such as changes in capital spending or dividends. Finally, there are valuation signals, such as price-to-earnings ratios and yields. Over time, our signals have been an indication of future outperformance, although there are periods, sometimes measured in years, when the combination of these various signals is not effective.

Nonetheless, it seems that consistent exposure to these signals is rewarded over time. In recent months, many investors decided that they do not want any stock market exposure at all. In such an environment, we believe that our portfolio, with its P/E ratio of 10.4x and a return on equity (ROE) of 16.8%, is more attractive than our benchmark, with its P/E ratio of 19.7x and an ROE of 15.1%. These valuation metrics can be lost amid investors’ aversion to stock market risk at any level. Given our opinion that it is better to own attractive stocks at low multiples, we feel that our portfolio is well-positioned for the eventual market rebound.

Over the last six months, our best performance came in the retailing and banking industries. AutoZone and Dollar Tree were our most successful stocks in retail, while Ocwen Financial and Flushing Financial were leaders in banking. Energy and commercial services (a component of the industrials sector) were our worst performing industries. In energy,

6

PetroQuest Energy and Swift Energy were among the worst performers. American Reprographics and Interface were our worst stocks in commercial services.

Although we are dissatisfied with both the performance of the market overall and with our relative performance, we are confident that the stock market will post worthwhile returns for long-term investors in the future and that our investment strategy—based on valuation, market sentiment, and quality—will be successful. We thank you for your investment and look forward to the future.

James D. Troyer, CFA,

Principal and Portfolio Manager

Joel M. Dickson,

Principal

Vanguard Quantitative Equity Group

April 13, 2009

7

Strategic Equity Fund

Fund Profile

As of March 31, 2009

Portfolio Characteristics | | |

| | Comparative | Broad |

| Fund | Index1 | Index2 |

Number of Stocks | 733 | 2,178 | 4,489 |

Median Market Cap | $2.0B | $2.2B | $22.3B |

Price/Earnings Ratio | 10.4x | 19.7x | 15.0x |

Price/Book Ratio | 1.4x | 1.4x | 1.7x |

Yield3 | 2.0% | 2.2% | 2.7% |

Return on Equity | 16.8% | 15.1% | 20.2% |

Earnings Growth Rate | 18.6% | 15.2% | 15.0% |

Foreign Holdings | 0.0% | 0.0% | 0.0% |

Turnover Rate4 | 70% | — | — |

Expense Ratio5 | 0.32% | — | — |

Short-Term Reserves | 0.2% | — | — |

Sector Diversification (% of equity exposure) |

| | Comparative | Broad |

| Fund | Index1 | Index2 |

Consumer Discretionary | 15.6% | 14.3% | 9.4% |

Consumer Staples | 4.1 | 4.8 | 11.2 |

Energy | 6.9 | 7.3 | 12.3 |

Financials | 17.6 | 16.8 | 13.1 |

Health Care | 11.7 | 11.7 | 14.6 |

Industrials | 14.8 | 14.8 | 10.0 |

Information Technology | 16.2 | 16.6 | 17.7 |

Materials | 5.0 | 5.2 | 3.7 |

Telecommunication | | | |

Services | 2.3 | 2.1 | 3.6 |

Utilities | 5.8 | 6.4 | 4.4 |

Volatility Measures6 | |

| Fund Versus | Fund Versus |

| Comparative Index1 | Broad Index2 |

R-Squared | 0.98 | 0.93 |

Beta | 1.01 | 1.15 |

Ten Largest Holdings7 (% of total net assets) |

| | |

AutoZone Inc. | automotive retail | 1.1% |

Embarq Corp. | integrated | |

| telecommunication | |

| services | 1.1 |

Parker Hannifin Corp. | industrial machinery | 1.0 |

Dollar Tree, Inc. | general | |

| merchandise stores | 1.0 |

Cooper Industries, Inc. | electrical components | |

Class A | and equipment | 1.0 |

AmerisourceBergen Corp. | health care | |

| distributors | 1.0 |

Western Digital Corp. | computer storage | |

| and peripherals | 1.0 |

H & R Block, Inc. | specialized | |

| consumer services | 0.9 |

SCANA Corp. | multi-utilities | 0.9 |

Cephalon, Inc. | biotechnology | 0.9 |

Top Ten | | 9.9% |

Investment Focus

1 MSCI US Small + Mid Cap 2200 Index.

2 Dow Jones Wilshire 5000 Index.

3 30-day SEC yield for the fund; annualized dividend yield for the indexes. See the Glossary.

4 Annualized.

5 The expense ratio shown is from the prospectus dated January 28, 2009, and represents estimated costs for the current fiscal year based on the fund’s current net assets. For the six months ended March 31, 2009, the annualized expense ratio was 0.31%.

6 For an explanation of R-squared, beta, and other terms used here, see the Glossary.

7 The holdings listed exclude any temporary cash investments and equity index products.

8

Strategic Equity Fund

Performance Summary

All of the returns in this report represent past performance, which is not a guarantee of future results that may be achieved by the fund. (Current performance may be lower or higher than the performance data cited. For performance data current to the most recent month-end, visit our website at www.vanguard.com/performance.) Note, too, that both investment returns and principal value can fluctuate widely, so an investor’s shares, when sold, could be worth more or less than their original cost. The returns shown do not reflect taxes that a shareholder would pay on fund distributions or on the sale of fund shares.

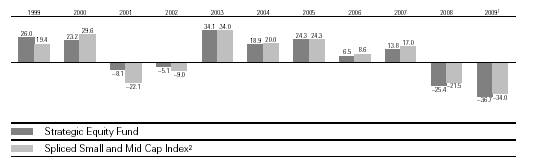

Fiscal-Year Total Returns (%): September 30, 1998–March 31, 2009

Average Annual Total Returns: Periods Ended March 31, 2009 |

| | | | |

| Inception Date | One Year | Five Years | Ten Years |

Strategic Equity Fund3 | 8/14/1995 | –43.57% | –6.68% | 2.66% |

1 Six months ended March 31, 2009.

2 The Spliced Small and Mid Cap Index reflects the return of the Russell 2800 Index through May 31, 2003, and the MSCI US Small + Mid Cap 2200 Index thereafter.

3 Total returns do not include the account service fee that may be applicable to certain accounts with balances below $10,000.

Note: See Financial Highlights table for dividend and capital gains information.

9

Strategic Equity Fund

Financial Statements (unaudited)

Statement of Net Assets

As of March 31, 2009

The fund provides a complete list of its holdings four times in each fiscal year, at the quarter-ends. For the second and fourth fiscal quarters, the lists appear in the fund’s semiannual and annual reports to shareholders. For the first and third fiscal quarters, the fund files the lists with the Securities and Exchange Commission on Form N-Q. Shareholders can look up the fund’s Forms N-Q on the SEC’s website at www.sec.gov. Forms N-Q may also be reviewed and copied at the SEC’s Public Reference Room (see the back cover of this report for further information).

| | | Market |

| | | Value• |

| | Shares | ($000) |

Common Stocks (97.7%)1 | | |

Consumer Discretionary (15.3%) | | |

* | AutoZone Inc. | 187,600 | 30,508 |

* | Dollar Tree, Inc. | 632,447 | 28,176 |

| H & R Block, Inc. | 1,449,950 | 26,375 |

| Polo Ralph Lauren Corp. | 563,289 | 23,799 |

* | Priceline.com, Inc. | 236,900 | 18,663 |

* | Marvel Entertainment, Inc. | 634,900 | 16,857 |

| Sherwin-Williams Co. | 321,857 | 16,727 |

| Whirlpool Corp. | 558,500 | 16,526 |

| Darden Restaurants Inc. | 435,032 | 14,904 |

* | Aeropostale, Inc. | 503,650 | 13,377 |

* | ITT Educational | | |

| Services, Inc. | 107,000 | 12,992 |

| Ross Stores, Inc. | 311,462 | 11,175 |

* | Big Lots Inc. | 480,385 | 9,982 |

| VF Corp. | 161,212 | 9,207 |

* | JAKKS Pacific, Inc. | 644,327 | 7,957 |

| Autoliv, Inc. | 387,614 | 7,198 |

| Bob Evans Farms, Inc. | 309,517 | 6,939 |

| DeVry, Inc. | 140,788 | 6,783 |

| The Stanley Works | 228,300 | 6,648 |

* | Interpublic Group of | | |

| Cos., Inc. | 1,589,364 | 6,548 |

| Cablevision Systems | | |

| NY Group Class A | 445,400 | 5,763 |

* | Rent-A-Center, Inc. | 273,198 | 5,292 |

* | Jarden Corp. | 412,528 | 5,227 |

* | Panera Bread Co. | 93,157 | 5,207 |

* | DreamWorks | | |

| Animation SKG, Inc. | 237,200 | 5,133 |

* | CEC Entertainment Inc. | 189,351 | 4,900 |

| Wyndham | | |

| Worldwide Corp. | 1,050,183 | 4,411 |

| Meredith Corp. | 253,620 | 4,220 |

* | Urban Outfitters, Inc. | 242,900 | 3,976 |

| International | | |

| Speedway Corp. | 178,547 | 3,939 |

| Polaris Industries, Inc. | 175,178 | 3,756 |

* | The Warnaco Group, Inc. | 154,659 | 3,712 |

| | | Market |

| | | Value• |

| | Shares | ($000) |

* | True Religion Apparel, Inc. | 310,939 | 3,672 |

* | WMS Industries, Inc. | 173,407 | 3,626 |

* | Helen of Troy Ltd. | 249,900 | 3,436 |

* | Exide Technologies | 1,086,700 | 3,260 |

| RadioShack Corp. | 375,078 | 3,214 |

* | Denny’s Corp. | 1,896,580 | 3,167 |

*,^ | Jos. A. Bank Clothiers, Inc. | 106,600 | 2,965 |

| UniFirst Corp. | 103,603 | 2,884 |

| Columbia Sportswear Co. | 86,258 | 2,581 |

* | The Children’s Place | | |

| Retail Stores, Inc. | 111,867 | 2,449 |

| Interactive Data Corp. | 95,734 | 2,380 |

| Burger King Holdings Inc. | 102,600 | 2,355 |

* | Jo-Ann Stores, Inc. | 144,038 | 2,354 |

| Snap-On Inc. | 82,500 | 2,071 |

* | Steiner Leisure Ltd. | 82,209 | 2,007 |

* | Collective Brands, Inc. | 198,273 | 1,931 |

| Regal Entertainment Group | | |

| Class A | 129,047 | 1,731 |

* | Penn National Gaming, Inc. | 63,708 | 1,539 |

* | Pre-Paid Legal Services, Inc. | 52,462 | 1,523 |

* | Bally Technologies Inc. | 81,090 | 1,494 |

* | Fuel Systems | | |

| Solutions, Inc. | 106,193 | 1,431 |

| CSS Industries, Inc. | 80,400 | 1,367 |

| Black & Decker Corp. | 39,700 | 1,253 |

* | Jack in the Box Inc. | 44,965 | 1,047 |

| KB Home | 78,954 | 1,041 |

* | Carter’s, Inc. | 52,200 | 982 |

* | Ascent Media Corp. | 37,700 | 943 |

* | Career Education Corp. | 39,200 | 939 |

| Sinclair Broadcast | | |

| Group, Inc. | 892,016 | 919 |

* | Timberland Co. | 74,111 | 885 |

| Genesco, Inc. | 46,373 | 873 |

| Tupperware Brands Corp. | 51,183 | 870 |

| Fisher Communications, Inc. | 87,709 | 856 |

| Fred’s, Inc. | 71,700 | 809 |

| WABCO Holdings Inc. | 65,144 | 802 |

* | Mediacom | | |

| Communications Corp. | 192,210 | 775 |

10

Strategic Equity Fund

| | | Market |

| | | Value• |

| | Shares | ($000) |

| The Buckle, Inc. | 23,450 | 749 |

| Regis Corp. | 51,100 | 738 |

* | The Wet Seal, Inc. Class A | 196,600 | 661 |

| Movado Group, Inc. | 80,600 | 608 |

| Cinemark Holdings Inc. | 61,500 | 577 |

| Service Corp. International | 158,307 | 553 |

| Limited Brands, Inc. | 59,200 | 515 |

| Pulte Homes, Inc. | 43,900 | 480 |

* | Isle of Capri Casinos, Inc. | 89,900 | 476 |

| CKE Restaurants Inc. | 55,500 | 466 |

| Weight Watchers | | |

| International, Inc. | 23,422 | 434 |

| Stage Stores, Inc. | 42,500 | 428 |

* | AFC Enterprises, Inc. | 91,626 | 413 |

| Scholastic Corp. | 25,700 | 387 |

| Foot Locker, Inc. | 36,900 | 387 |

* | Overstock.com, Inc. | 39,626 | 363 |

| Dover Downs Gaming | | |

| & Entertainment, Inc. | 117,872 | 362 |

| Cracker Barrel Old | | |

| Country Store Inc. | 12,300 | 352 |

* | Town Sports International | | |

| Holdings, Inc. | 110,000 | 329 |

| Wolverine World Wide, Inc. | 19,700 | 307 |

| Barnes & Noble, Inc. | 14,200 | 304 |

| Ryland Group, Inc. | 17,900 | 298 |

| Leggett & Platt, Inc. | 21,800 | 283 |

*,^ | Blockbuster Inc. Class A | 324,200 | 233 |

* | Cabela’s Inc. | 25,400 | 231 |

| Phillips-Van Heusen Corp. | 10,200 | 231 |

| Callaway Golf Co. | 31,600 | 227 |

| Sonic Automotive, Inc. | 128,429 | 205 |

* | Hot Topic, Inc. | 17,100 | 191 |

* | Papa John’s | | |

| International, Inc. | 7,700 | 176 |

* | Lincoln Educational Services | 9,100 | 167 |

| MDC Holdings, Inc. | 5,200 | 162 |

* | P.F. Chang’s China Bistro, Inc. | 6,600 | 151 |

| Oxford Industries, Inc. | 23,000 | 142 |

| D. R. Horton, Inc. | 13,500 | 131 |

| Advance Auto Parts, Inc. | 3,100 | 127 |

* | Quiksilver, Inc. | 96,100 | 123 |

| Scripps Networks Interactive | 5,300 | 119 |

| Cato Corp. Class A | 5,600 | 102 |

* | HSN, Inc. | 16,207 | 83 |

* | California Pizza Kitchen, Inc. | 5,700 | 75 |

| Family Dollar Stores, Inc. | 2,000 | 67 |

* | Unifi, Inc. | 92,800 | 59 |

| PRIMEDIA Inc. | 22,610 | 56 |

| Lennar Corp. Class A | 7,100 | 53 |

* | Brink’s Home | | |

| Security Holdings, Inc. | 2,200 | 50 |

| Stewart Enterprises, Inc.Class A | 11,900 | 39 |

* | The Gymboree Corp. | 1,800 | 38 |

* | Warner Music Group Corp. | 15,500 | 36 |

| | | Market |

| | | Value• |

| | Shares | ($000) |

| Speedway Motorsports, Inc. | 2,900 | 34 |

* | Lear Corp. | 40,451 | 30 |

| New York Times Co. Class A | 5,300 | 24 |

| Belo Corp. Class A | 34,600 | 21 |

| John Wiley & Sons Class A | 700 | 21 |

* | Zale Corp. | 6,700 | 13 |

* | Cox Radio, Inc. | 2,200 | 9 |

* | Ticketmaster | | |

| Entertainment Inc. | 1,600 | 6 |

| American Greetings Corp. | | |

| Class A | 1,073 | 5 |

* | Lin TV Corp. | 3,600 | 4 |

| Journal Communications, Inc. | 1,030 | 1 |

| | | 427,220 |

Consumer Staples (4.0%) | | |

* | Dr. Pepper | | |

| Snapple Group, Inc. | 1,025,800 | 17,346 |

* | Ralcorp Holdings, Inc. | 192,699 | 10,383 |

| Herbalife Ltd. | 658,952 | 9,871 |

| Molson Coors | | |

| Brewing Co. Class B | 287,025 | 9,839 |

| Cal-Maine Foods, Inc. | 420,197 | 9,408 |

| Nash-Finch Co. | 272,595 | 7,657 |

| Corn Products | | |

| International, Inc. | 274,766 | 5,825 |

| PepsiAmericas, Inc. | 321,305 | 5,542 |

* | Chiquita Brands | | |

| International, Inc. | 718,936 | 4,767 |

| Del Monte Foods Co. | 533,110 | 3,886 |

| SUPERVALU Inc. | 246,895 | 3,526 |

| Universal Corp. (VA) | 115,936 | 3,469 |

| The Pepsi Bottling | | |

| Group, Inc. | 152,840 | 3,384 |

| Lancaster Colony Corp. | 54,115 | 2,245 |

* | Alliance One | | |

| International, Inc. | 542,200 | 2,082 |

* | Energizer Holdings, Inc. | 39,300 | 1,953 |

* | The Pantry, Inc. | 90,863 | 1,600 |

* | Central Garden & Pet Co. | | |

| Class A | 182,100 | 1,369 |

* | Prestige Brands | | |

| Holdings Inc. | 238,903 | 1,238 |

* | Revlon, Inc. | 487,833 | 1,210 |

| Spartan Stores, Inc. | 74,124 | 1,142 |

| Village Super Market Inc. | | |

| Class A | 31,722 | 989 |

* | BJ’s Wholesale Club, Inc. | 23,200 | 742 |

| Bunge Ltd. | 11,500 | 651 |

* | Dean Foods Co. | 35,600 | 644 |

| Coca-Cola Bottling Co. | 6,400 | 333 |

| Alberto-Culver Co. | 14,100 | 319 |

| Vector Group Ltd. | 15,400 | 200 |

* | National Beverage Corp. | 10,330 | 95 |

| Flowers Foods, Inc. | 1,100 | 26 |

| | | 111,741 |

11

Strategic Equity Fund

| | | Market |

| | | Value• |

| | Shares | ($000) |

Energy (6.8%) | | |

| ENSCO International, Inc. | 803,609 | 21,215 |

| Murphy Oil Corp. | 429,200 | 19,215 |

| Helmerich & Payne, Inc. | 792,542 | 18,046 |

* | Plains Exploration & | | |

| Production Co. | 756,400 | 13,033 |

| Tidewater Inc. | 345,400 | 12,825 |

| Noble Corp. | 496,222 | 11,954 |

* | Comstock Resources, Inc. | 363,796 | 10,841 |

| El Paso Corp. | 1,723,154 | 10,770 |

| Massey Energy Co. | 788,712 | 7,982 |

* | Ultra Petroleum Corp. | 156,500 | 5,617 |

* | Mariner Energy Inc. | 708,500 | 5,491 |

* | SEACOR Holdings Inc. | 88,249 | 5,146 |

* | Denbury Resources, Inc. | 337,356 | 5,013 |

* | Superior Energy | | |

| Services, Inc. | 247,347 | 3,188 |

* | Oil States International, Inc. | 234,728 | 3,150 |

| World Fuel Services Corp. | 99,149 | 3,136 |

* | Encore Acquisition Co. | 132,102 | 3,074 |

* | Alpha Natural | | |

| Resources, Inc. | 162,660 | 2,887 |

* | Contango Oil & Gas Co. | 60,905 | 2,387 |

| Overseas Shipholding | | |

| Group Inc. | 91,909 | 2,084 |

* | Matrix Service Co. | 236,915 | 1,947 |

| Noble Energy, Inc. | 34,300 | 1,848 |

| Walter Industries, Inc. | 77,200 | 1,766 |

| Sunoco, Inc. | 64,500 | 1,708 |

* | Clayton Williams Energy, Inc. | 47,524 | 1,390 |

* | Pride International, Inc. | 64,200 | 1,154 |

* | Rosetta Resources, Inc. | 206,500 | 1,022 |

* | Gulfmark Offshore, Inc. | 39,900 | 952 |

| Foundation Coal | | |

| Holdings, Inc. | 64,000 | 918 |

* | Nabors Industries, Inc. | 90,662 | 906 |

| CARBO Ceramics Inc. | 30,800 | 876 |

* | Concho Resources, Inc. | 29,696 | 760 |

| Tesoro Corp. | 55,900 | 753 |

* | Newpark Resources, Inc. | 290,981 | 736 |

| Holly Corp. | 24,500 | 519 |

* | Vaalco Energy, Inc. | 88,146 | 466 |

| General Maritime Corp. | 65,178 | 456 |

* | CVR Energy, Inc. | 81,112 | 449 |

* | Whiting Petroleum Corp. | 16,100 | 416 |

* | Goodrich Petroleum Corp. | 19,750 | 382 |

* | McMoRan Exploration Co. | 68,200 | 321 |

| CONSOL Energy, Inc. | 12,000 | 303 |

| Southern Union Co. | 18,900 | 288 |

* | PHI Inc. Non-Voting Shares | 23,600 | 236 |

* | Veneco Inc. | 53,400 | 175 |

* | Swift Energy Co. | 20,400 | 149 |

* | Dresser Rand Group, Inc. | 5,500 | 122 |

* | James River Coal Co. | 8,300 | 102 |

* | Forest Oil Corp. | 3,200 | 42 |

| | | Market |

| | | Value• |

| | Shares | ($000) |

* | Unit Corp. | 1,900 | 40 |

* | Complete Production | | |

| Services, Inc. | 12,900 | 40 |

| St. Mary Land & | | |

| Exploration Co. | 2,100 | 28 |

* | International Coal Group, Inc. | 7,700 | 12 |

* | Energy Partners, Ltd. | 9,000 | 1 |

| | | 188,337 |

Financials (17.0%) | | |

| Cullen/Frost Bankers, Inc. | 547,053 | 25,679 |

| Unum Group | 1,882,000 | 23,525 |

| Bank of Hawaii Corp. | 677,564 | 22,346 |

* | TD Ameritrade | | |

| Holding Corp. | 1,579,307 | 21,810 |

* | Nasdaq Stock Market Inc. | 1,085,400 | 21,252 |

| Axis Capital Holdings Ltd. | 764,080 | 17,222 |

| FirstMerit Corp. | 866,391 | 15,768 |

* | Arch Capital Group Ltd. | 284,300 | 15,312 |

| Platinum Underwriters | | |

| Holdings, Ltd. | 491,800 | 13,947 |

| Torchmark Corp. | 454,947 | 11,933 |

| Annaly Capital | | |

| Management Inc. REIT | 851,900 | 11,816 |

| Aspen Insurance | | |

| Holdings Ltd. | 420,300 | 9,440 |

| HCP, Inc. REIT | 480,700 | 8,581 |

| Plum Creek Timber Co. Inc. | | |

| REIT | 271,900 | 7,904 |

* | EZCORP, Inc. | 675,417 | 7,815 |

| NBT Bancorp, Inc. | 352,499 | 7,628 |

| UMB Financial Corp. | 163,558 | 6,950 |

| PartnerRe Ltd. | 103,719 | 6,438 |

| IPC Holdings Ltd. | 218,100 | 5,897 |

* | Interactive Brokers | | |

| Group, Inc. | 361,024 | 5,823 |

| Federated Investors, Inc. | 251,530 | 5,599 |

| Nationwide Health | | |

| Properties, Inc. REIT | 249,300 | 5,532 |

* | The St. Joe Co. | 273,600 | 4,580 |

* | Ocwen Financial Corp. | 399,981 | 4,572 |

* | Knight Capital Group, Inc. | | |

| Class A | 307,948 | 4,539 |

| City Holding Co. | 163,555 | 4,463 |

| Highwood Properties, Inc. | | |

| REIT | 207,846 | 4,452 |

| Senior Housing | | |

| Properties Trust REIT | 316,300 | 4,435 |

| Host Hotels & Resorts Inc. | | |

| REIT | 1,117,400 | 4,380 |

| Associated Banc-Corp. | 278,623 | 4,302 |

| Rayonier Inc. REIT | 141,450 | 4,275 |

| Hospitality Properties Trust | | |

| REIT | 353,100 | 4,237 |

| American Financial Group, Inc. | 260,244 | 4,177 |

12

Strategic Equity Fund

| | | Market |

| | | Value• |

| | Shares | ($000) |

| National Retail Properties | | |

| REIT | 259,600 | 4,112 |

| BOK Financial Corp. | 117,527 | 4,061 |

| Mid-America Apartment | | |

| Communities, Inc. REIT | 124,508 | 3,839 |

| Healthcare Realty Trust Inc. | | |

| REIT | 253,954 | 3,807 |

| Home Properties, Inc. REIT | 123,756 | 3,793 |

| Mack-Cali Realty Corp. REIT | 189,900 | 3,762 |

| Washington REIT | 207,116 | 3,583 |

| Odyssey Re Holdings Corp. | 92,871 | 3,523 |

| PS Business Parks, Inc. REIT | 92,532 | 3,410 |

| Provident Financial | | |

| Services Inc. | 298,225 | 3,224 |

| Sun Communities, Inc. | | |

| REIT | 269,868 | 3,193 |

| Reinsurance Group of | | |

| America, Inc. | 96,507 | 3,126 |

| Bank of the Ozarks, Inc. | 133,233 | 3,075 |

| Republic Bancorp, Inc. | | |

| Class A | 163,411 | 3,051 |

| Sovran Self Storage, Inc. | | |

| REIT | 147,224 | 2,956 |

| First Financial | | |

| Bankshares, Inc. | 58,522 | 2,819 |

| Jones Lang LaSalle Inc. | 117,800 | 2,740 |

| American Physicians | | |

| Capital, Inc. | 66,557 | 2,724 |

| Entertainment | | |

| Properties Trust REIT | 170,700 | 2,690 |

| Avalonbay Communities, Inc. | | |

| REIT | 56,414 | 2,655 |

| Douglas Emmett, Inc. REIT | 352,800 | 2,607 |

| Willis Group Holdings Ltd. | 116,100 | 2,554 |

| BancFirst Corp. | 67,922 | 2,472 |

| Kilroy Realty Corp. REIT | 135,947 | 2,337 |

* | Amerisafe Inc. | 150,560 | 2,307 |

| Health Care Inc. REIT | 71,800 | 2,196 |

| Community Bank | | |

| System, Inc. | 129,761 | 2,174 |

| Ventas, Inc. REIT | 95,600 | 2,162 |

| Parkway Properties Inc. | | |

| REIT | 191,075 | 1,968 |

| Tompkins Trustco, Inc. | 42,569 | 1,830 |

* | Nelnet, Inc. | 200,193 | 1,770 |

* | FPIC Insurance Group, Inc. | 47,184 | 1,747 |

* | CNA Surety Corp. | 93,833 | 1,730 |

* | CB Richard Ellis Group, Inc. | 413,600 | 1,667 |

| WSFS Financial Corp. | 71,750 | 1,604 |

| Provident New York Bancorp, Inc. | 187,398 | 1,602 |

| First BanCorp Puerto Rico | 362,862 | 1,546 |

| Lakeland Financial Corp. | 79,936 | 1,534 |

| Employers Holdings, Inc. | 157,982 | 1,507 |

| Potlatch Corp. REIT | 62,100 | 1,440 |

| LTC Properties, Inc. REIT | 73,100 | 1,282 |

| | | Market |

| | | Value• |

| | Shares | ($000) |

| Suffolk Bancorp | 49,193 | 1,279 |

| Arrow Financial Corp. | 51,011 | 1,208 |

| Cash America | | |

| International Inc. | 72,200 | 1,131 |

| TriCo Bancshares | 66,980 | 1,121 |

| Berkshire Hills Bancorp, Inc. | 48,556 | 1,113 |

| Colonial Properties Trust | | |

| REIT | 286,560 | 1,092 |

| Federal Realty | | |

| Investment Trust REIT | 23,300 | 1,072 |

| Oriental Financial Group Inc. | 208,800 | 1,019 |

| Kimco Realty Corp. REIT | 130,773 | 996 |

| Extra Space Storage Inc. | | |

| REIT | 170,800 | 941 |

| First Community | | |

| Bancshares, Inc. | 80,600 | 941 |

^ | Pennsylvania REIT | 264,600 | 939 |

^ | Heartland Financial USA, Inc. | 68,500 | 927 |

| Prospect Energy Corp. | 108,022 | 920 |

| Westamerica Bancorporation | 19,700 | 898 |

| Safety Insurance Group, Inc. | 28,553 | 887 |

* | LaBranche & Co. Inc. | 235,229 | 880 |

| Saul Centers, Inc. REIT | 35,045 | 805 |

| First Commonwealth | | |

| Financial Corp. | 90,020 | 798 |

^ | Life Partners Holdings | 46,000 | 785 |

| Prosperity Bancshares, Inc. | 28,500 | 779 |

| Hudson City Bancorp, Inc. | 66,600 | 779 |

| S & T Bancorp, Inc. | 36,500 | 774 |

| New York Community | | |

| Bancorp, Inc. | 67,700 | 756 |

| CapitalSource Inc. REIT | 615,200 | 751 |

* | Crawford & Co. Class B | 110,600 | 743 |

| First Merchants Corp. | 68,030 | 734 |

| Simmons First | | |

| National Corp. | 29,009 | 731 |

| Financial Federal Corp. | 31,000 | 657 |

| Bank Mutual Corp. | 68,800 | 623 |

* | thinkorswim Group, Inc. | 71,100 | 614 |

^ | iStar Financial Inc. REIT | 201,800 | 567 |

| Anworth Mortgage | | |

| Asset Corp. REIT | 85,700 | 525 |

| First Source Corp. | 29,000 | 523 |

| The Hanover Insurance | | |

| Group Inc. | 17,900 | 516 |

| Clifton Savings Bancorp, Inc. | 51,581 | 516 |

| Winthrop Realty Trust REIT | 73,490 | 508 |

| Southside Bancshares, Inc. | 26,673 | 504 |

| Digital Realty Trust, Inc. REIT | 15,000 | 498 |

| International | | |

| Bancshares Corp. | 63,600 | 496 |

| Commerce Bancshares, Inc. | 12,701 | 461 |

| Omega Healthcare Investors, Inc. REIT | 32,200 | 453 |

| U-Store-It Trust REIT | 214,500 | 433 |

| Harleysville National Corp. | 70,689 | 428 |

13

Strategic Equity Fund

| | | Market |

| | | Value• |

| | Shares | ($000) |

| S.Y. Bancorp, Inc. | 16,900 | 411 |

| MFA Mortgage | | |

| Investments, Inc. REIT | 68,100 | 400 |

| BRE Properties Inc. Class A | | |

| REIT | 19,761 | 388 |

| Raymond James | | |

| Financial, Inc. | 18,500 | 364 |

* | First Cash Financial | | |

| Services, Inc. | 24,300 | 363 |

| LaSalle Hotel Properties | | |

| REIT | 57,800 | 338 |

| TrustCo Bank NY | 53,400 | 321 |

| Donegal Group Inc. Class A | 20,206 | 311 |

| Presidential Life Corp. | 39,553 | 308 |

| National Western Life | | |

| Insurance Co. Class A | 2,400 | 271 |

| SL Green Realty Corp. | | |

| REIT | 23,526 | 254 |

| Flushing Financial Corp. | 40,837 | 246 |

* | First Acceptance Corp. | 91,187 | 221 |

* | Beneficial Mutual | | |

| Bancorp, Inc. | 21,500 | 212 |

| Acadia Realty Trust REIT | 19,475 | 207 |

| Corporate Office | | |

| Properties Trust, Inc. REIT | 7,720 | 192 |

* | Investment Technology | | |

| Group, Inc. | 7,000 | 179 |

| Everest Re Group, Ltd. | 2,200 | 156 |

| Provident Bankshares Corp. | 20,180 | 142 |

| Park National Corp. | 2,500 | 139 |

| Wilshire Bancorp Inc. | 27,000 | 139 |

| Cincinnati Financial Corp. | 5,100 | 117 |

| Hercules Technology | | |

| Growth Capital, Inc. | 22,529 | 113 |

| The Macerich Co. REIT | 15,000 | 94 |

| Liberty Property Trust REIT | 4,900 | 93 |

| MB Financial, Inc. | 6,400 | 87 |

* | TradeStation Group, Inc. | 12,400 | 82 |

^ | Jer Investor Trust REIT | 118,671 | 77 |

| Regency Centers Corp. | | |

| REIT | 2,100 | 56 |

| Developers Diversified | | |

| Realty Corp. REIT | 21,200 | 45 |

| Univest Corp. | | |

| of Pennsylvania | 2,100 | 37 |

| First Financial Bancorp | 3,500 | 33 |

* | SVB Financial Group | 1,400 | 28 |

| Capitol Federal Financial | 600 | 23 |

| Equity One, Inc. REIT | 1,500 | 18 |

| Allied World | | |

| Assurance Holdings, Ltd. | 400 | 15 |

| BlackRock Kelso Capital Corp. | 1,200 | 5 |

| First Financial Holdings, Inc. | 300 | 2 |

| | | 473,416 |

| | | Market |

| | | Value• |

| | Shares | ($000) |

Health Care (11.4%) | | |

| AmerisourceBergen Corp. | 843,613 | 27,552 |

* | Cephalon, Inc. | 383,300 | 26,103 |

* | Isis Pharmaceuticals, Inc. | 1,457,602 | 21,879 |

* | Lincare Holdings, Inc. | 1,000,471 | 21,810 |

| STERIS Corp. | 790,943 | 18,413 |

* | Express Scripts Inc. | 314,200 | 14,507 |

* | Gen-Probe Inc. | 287,963 | 13,125 |

| Universal Health Services | | |

| Class B | 303,006 | 11,617 |

* | Myriad Genetics, Inc. | 232,600 | 10,576 |

| Omnicare, Inc. | 416,149 | 10,191 |

* | PAREXEL | | |

| International Corp. | 952,700 | 9,270 |

* | Onyx Pharmaceuticals, Inc. | 323,000 | 9,222 |

* | Cubist Pharmaceuticals, Inc. | 390,811 | 6,394 |

* | AMERIGROUP Corp. | 225,827 | 6,219 |

* | Emergent BioSolutions Inc. | 448,008 | 6,053 |

* | Watson | | |

| Pharmaceuticals, Inc. | 182,400 | 5,674 |

* | PharMerica Corp. | 339,573 | 5,650 |

* | Warner Chilcott Ltd. | 520,623 | 5,477 |

| Invacare Corp. | 325,354 | 5,215 |

| Cooper Cos., Inc. | 181,015 | 4,786 |

* | DaVita, Inc. | 98,900 | 4,347 |

* | OSI Pharmaceuticals, Inc. | 101,300 | 3,876 |

* | Emergency Medical | | |

| Services LP Class A | 121,473 | 3,813 |

* | Skilled Healthcare | | |

| Group Inc. | 436,383 | 3,583 |

* | Albany Molecular | | |

| Research, Inc. | 370,346 | 3,492 |

* | Valeant Pharmaceuticals | | |

| International | 175,000 | 3,113 |

* | Gentiva Health | | |

| Services, Inc. | 202,356 | 3,076 |

* | LifePoint Hospitals, Inc. | 144,835 | 3,021 |

| PDL BioPharma Inc. | 398,289 | 2,820 |

* | Questcor | | |

| Pharmaceuticals, Inc. | 534,310 | 2,629 |

* | Psychiatric Solutions, Inc. | 162,000 | 2,548 |

* | Cyberonics, Inc. | 189,784 | 2,518 |

* | Luminex Corp. | 138,000 | 2,501 |

* | Kensey Nash Corp. | 112,575 | 2,394 |

* | Merit Medical Systems, Inc. | 193,000 | 2,357 |

* | ViroPharma Inc. | 438,958 | 2,305 |

| Martek Biosciences Corp. | 119,600 | 2,183 |

* | Centene Corp. | 110,466 | 1,991 |

* | RehabCare Group, Inc. | 113,864 | 1,986 |

* | Bio-Rad Laboratories, Inc. | | |

| Class A | 30,100 | 1,984 |

| Owens & Minor, Inc. | 48,176 | 1,596 |

* | CONMED Corp. | 103,906 | 1,497 |

* | LHC Group Inc. | 62,521 | 1,393 |

* | AmSurg Corp. | 77,520 | 1,229 |

14

Strategic Equity Fund

| | | Market |

| | | Value• |

| | Shares | ($000) |

| Chemed Corp. | 29,800 | 1,159 |

* | American Medical | | |

| Systems Holdings, Inc. | 100,989 | 1,126 |

* | Nabi Biopharmaceuticals | 298,763 | 1,105 |

* | Dionex Corp. | 16,555 | 782 |

* | Kindred Healthcare, Inc. | 50,600 | 756 |

* | Cambrex Corp. | 326,503 | 744 |

* | CV Therapeutics, Inc. | 36,400 | 724 |

| Beckman Coulter, Inc. | 13,300 | 678 |

| Medicis | | |

| Pharmaceutical Corp. | 52,800 | 653 |

* | Henry Schein, Inc. | 14,400 | 576 |

* | Noven Pharmaceuticals, Inc. | 58,776 | 557 |

* | Cynosure Inc. | 79,327 | 483 |

* | eResearch Technology, Inc. | 89,900 | 473 |

* | Mylan Inc. | 33,700 | 452 |

* | Alnylam Pharmaceuticals Inc. | 22,370 | 426 |

* | CorVel Corp. | 19,425 | 393 |

* | King Pharmaceuticals, Inc. | 53,501 | 378 |

* | Endo Pharmaceuticals | | |

| Holdings, Inc. | 20,900 | 370 |

| Quest Diagnostics, Inc. | 7,100 | 337 |

| Ensign Group Inc. | 20,999 | 325 |

* | Cross Country | | |

| Healthcare, Inc. | 44,675 | 293 |

* | Res-Care, Inc. | 17,000 | 248 |

* | Hanger Orthopedic | | |

| Group, Inc. | 17,600 | 233 |

* | Alliance HealthCare | | |

| Services Inc. | 30,100 | 205 |

| Hill-Rom Holdings, Inc. | 17,900 | 177 |

* | Community Health | | |

| Systems, Inc. | 11,400 | 175 |

* | HealthSouth Corp. | 19,000 | 169 |

*,^ | Osiris Therapeutics, Inc. | 10,100 | 139 |

* | Sun Healthcare Group Inc. | 15,700 | 133 |

* | Kendle International Inc. | 6,200 | 130 |

* | Hospira, Inc. | 4,100 | 127 |

| Teleflex Inc. | 2,800 | 109 |

* | K-V Pharmaceutical Co. | | |

| Class A | 40,500 | 67 |

* | PSS World Medical, Inc. | 4,500 | 65 |

* | Alkermes, Inc. | 3,500 | 42 |

* | Healthspring, Inc. | 4,100 | 34 |

* | Facet Biotech Corp. | 2,700 | 26 |

* | Humana Inc. | 900 | 23 |

| Techne Corp. | 400 | 22 |

| | | 316,899 |

Industrials (14.4%) | | |

| Parker Hannifin Corp. | 834,741 | 28,365 |

| Cooper Industries, Inc. Class A | 1,087,500 | 28,123 |

| Goodrich Corp. | 677,976 | 25,689 |

| Ryder System, Inc. | 685,600 | 19,409 |

| Cummins Inc. | 665,572 | 16,939 |

* | AGCO Corp. | 831,300 | 16,293 |

| | | Market |

| | | Value• |

| | Shares | ($000) |

* | EMCOR Group, Inc. | 875,723 | 15,036 |

| Hubbell Inc. Class B | 539,900 | 14,556 |

| Fluor Corp. | 378,727 | 13,085 |

| Trinity Industries, Inc. | 1,342,820 | 12,273 |

* | Gardner Denver Inc. | 546,660 | 11,884 |

| Republic Services, Inc. | | |

| Class A | 623,519 | 10,693 |

*,2 | TBS International Ltd. | 1,412,617 | 10,383 |

| Manpower Inc. | 318,703 | 10,049 |

| GATX Corp. | 487,038 | 9,853 |

* | EnPro Industries, Inc. | 558,000 | 9,542 |

| Pitney Bowes, Inc. | 383,700 | 8,959 |

* | United Stationers, Inc. | 265,761 | 7,463 |

| J.B. Hunt Transport | | |

| Services, Inc. | 288,330 | 6,952 |

| R.R. Donnelley & Sons Co. | 945,045 | 6,927 |

| Flowserve Corp. | 120,694 | 6,773 |

| Comfort Systems USA, Inc. | 614,460 | 6,372 |

* | Sykes Enterprises, Inc. | 351,670 | 5,848 |

| Acuity Brands, Inc. | 188,100 | 4,240 |

| Triumph Group, Inc. | 110,221 | 4,210 |

* | GrafTech International Ltd. | 595,664 | 3,669 |

| Genco Shipping and | | |

| Trading Ltd. | 284,217 | 3,507 |

| Robbins & Myers, Inc. | 222,200 | 3,371 |

| Briggs & Stratton Corp. | 201,083 | 3,318 |

| Joy Global Inc. | 152,717 | 3,253 |

| Knoll, Inc. | 521,238 | 3,195 |

* | TransDigm Group, Inc. | 89,400 | 2,936 |

* | Alliant Techsystems, Inc. | 40,320 | 2,701 |

* | RSC Holdings Inc. | 476,500 | 2,506 |

* | Columbus McKinnon Corp. | 286,137 | 2,495 |

* | Allegiant Travel Co. | 54,000 | 2,455 |

| Werner Enterprises, Inc. | 157,437 | 2,380 |

| Herman Miller, Inc. | 223,000 | 2,377 |

| SPX Corp. | 50,300 | 2,365 |

| The Timken Co. | 167,931 | 2,344 |

| Steelcase Inc. | 460,152 | 2,305 |

* | School Specialty, Inc. | 126,288 | 2,221 |

| Bucyrus International, Inc. | 129,200 | 1,961 |

| Watson Wyatt & | | |

| Co. Holdings | 39,400 | 1,945 |

* | Perini Corp. | 155,800 | 1,916 |

* | ATC Technology Corp. | 169,700 | 1,901 |

* | Marten Transport, Ltd. | 96,657 | 1,806 |

* | Esterline Technologies Corp. | 77,150 | 1,558 |

| Lincoln Electric | | |

| Holdings, Inc. | 48,236 | 1,529 |

| Titan International, Inc. | 299,443 | 1,506 |

| Gibraltar Industries Inc. | 316,323 | 1,493 |

* | Cenveo Inc. | 439,751 | 1,429 |

* | Kirby Corp. | 53,600 | 1,428 |

* | Genesee & Wyoming Inc. | | |

| Class A | 61,600 | 1,309 |

| AAON, Inc. | 69,993 | 1,268 |

15

Strategic Equity Fund

| | | Market |

| | | Value• |

| | Shares | ($000) |

* | Republic Airways | | |

| Holdings Inc. | 186,200 | 1,207 |

* | Pike Electric Corp. | 124,699 | 1,153 |

| Federal Signal Corp. | 212,702 | 1,121 |

* | First Advantage Corp. | | |

| Class A | 74,600 | 1,028 |

* | Cornell Cos., Inc. | 62,516 | 1,023 |

| Interface, Inc. | 340,600 | 1,018 |

| Kaman Corp. Class A | 81,141 | 1,018 |

| Apogee Enterprises, Inc. | 90,166 | 990 |

| Textainer Group | | |

| Holdings Ltd. | 143,576 | 969 |

| The Standard Register Co. | 208,873 | 957 |

* | Powell Industries, Inc. | 20,272 | 716 |

* | Blount International, Inc. | 148,582 | 686 |

* | Waste Services, Inc. | 157,801 | 675 |

* | CBIZ Inc. | 91,384 | 637 |

* | EnerSys | 50,926 | 617 |

* | Beacon Roofing Supply, Inc. | 45,828 | 614 |

| Encore Wire Corp. | 28,507 | 611 |

| TAL International Group, Inc. | 82,400 | 603 |

| McGrath RentCorp | 37,600 | 593 |

* | Old Dominion | | |

| Freight Line, Inc. | 23,300 | 547 |

* | H&E Equipment | | |

| Services, Inc. | 71,756 | 470 |

| Tredegar Corp. | 27,331 | 446 |

* | American Commercial | | |

| Lines Inc. | 124,293 | 394 |

| CIRCOR International, Inc. | 17,228 | 388 |

* | American | | |

| Reprographics Co. | 103,900 | 368 |

* | Mastec Inc. | 30,300 | 366 |

| The Dun & | | |

| Bradstreet Corp. | 4,600 | 354 |

* | AMR Corp. | 110,327 | 352 |

* | Standard Parking Corp. | 21,068 | 346 |

| A.O. Smith Corp. | 13,700 | 345 |

| Standex International Corp. | 36,600 | 337 |

* | WESCO International, Inc. | 16,200 | 294 |

* | Chart Industries, Inc. | 33,600 | 265 |

| G & K Services, Inc. Class A | 13,600 | 257 |

| Macquarie | | |

| Infrastructure Co. LLC | 140,247 | 194 |

| Ennis, Inc. | 19,200 | 170 |

* | Hawaiian Holdings, Inc. | 43,900 | 164 |

| The Brink’s Co. | 5,800 | 153 |

* | DynCorp International Inc. | | |

| Class A | 11,100 | 148 |

* | Furmanite Corp. | 47,460 | 148 |

| ABM Industries Inc. | 8,900 | 146 |

| Dover Corp. | 4,200 | 111 |

| Granite Construction Co. | 2,900 | 109 |

* | Force Protection, Inc. | 19,500 | 94 |

| Lennox International Inc. | 2,500 | 66 |

| | | Market |

| | | Value• |

| | Shares | ($000) |

* | Energy Conversion | | |

| Devices, Inc. | 3,900 | 52 |

* | US Airways Group Inc. | 15,600 | 39 |

* | M&F Worldwide Corp. | 2,000 | 23 |

| Viad Corp. | 1,600 | 23 |

| | | 401,768 |

Information Technology (15.9%) | |

* | Western Digital Corp. | 1,410,000 | 27,269 |

* | Sybase, Inc. | 828,585 | 25,098 |

* | Hewitt Associates, Inc. | 830,230 | 24,708 |

* | Skyworks Solutions, Inc. | 2,988,916 | 24,091 |

* | Avnet, Inc. | 1,159,500 | 20,303 |

*,^ | Sohu.com Inc. | 483,886 | 19,989 |

* | Marvell Technology | | |

| Group Ltd. | 1,869,000 | 17,120 |

* | Dolby Laboratories Inc. | 488,600 | 16,666 |

* | CSG Systems | | |

| International, Inc. | 1,096,536 | 15,659 |

* | EarthLink, Inc. | 2,330,986 | 15,315 |

* | Metavante Technologies | 753,521 | 15,040 |

| Xilinx, Inc. | 781,816 | 14,980 |

* | Anixter International Inc. | 468,868 | 14,854 |

* | Integrated Device | | |

| Technology Inc. | 2,624,452 | 11,941 |

* | Lexmark International, Inc. | 641,839 | 10,828 |

* | QLogic Corp. | 934,228 | 10,389 |

* | ManTech | | |

| International Corp. | 229,000 | 9,595 |

* | Computer Sciences Corp. | 240,916 | 8,875 |

* | Plexus Corp. | 556,466 | 7,690 |

*,^ | Alliance Data | | |

| Systems Corp. | 189,381 | 6,998 |

| Altera Corp. | 370,567 | 6,503 |

* | Multi-Fineline | | |

| Electronix, Inc. | 329,204 | 5,544 |

* | JDA Software Group, Inc. | 449,575 | 5,193 |

* | Solera Holdings, Inc. | 209,080 | 5,181 |

| National | | |

| Semiconductor Corp. | 463,793 | 4,763 |

* | PMC Sierra Inc. | 745,011 | 4,753 |

* | S1 Corp. | 782,716 | 4,031 |

| United Online, Inc. | 889,720 | 3,968 |

* | NCR Corp. | 497,362 | 3,954 |

* | Silicon Image, Inc. | 1,477,714 | 3,547 |

* | SAIC, Inc. | 186,200 | 3,476 |

| Intersil Corp. | 295,000 | 3,393 |

* | Starent Networks Corp. | 185,992 | 2,941 |

* | Synopsys, Inc. | 140,470 | 2,912 |

| Black Box Corp. | 119,041 | 2,811 |

* | SYNNEX Corp. | 141,200 | 2,777 |

| Diebold, Inc. | 126,061 | 2,691 |

* | TiVo Inc. | 377,507 | 2,658 |

* | Cogent Inc. | 215,974 | 2,570 |

* | MKS Instruments, Inc. | 169,550 | 2,487 |

* | Perot Systems Corp. | 167,623 | 2,159 |

16

Strategic Equity Fund

| | | Market |

| | | Value• |

| | Shares | ($000) |

* | Flextronics | | |

| International Ltd. | 651,400 | 1,883 |

* | Ultratech, Inc. | 149,912 | 1,872 |

* | BigBand Networks Inc. | 266,608 | 1,746 |

* | TIBCO Software Inc. | 293,400 | 1,722 |

| ADTRAN Inc. | 105,200 | 1,705 |

| Acxiom Corp. | 229,496 | 1,698 |

* | j2 Global | | |

| Communications, Inc. | 76,165 | 1,667 |

* | Teradata Corp. | 100,902 | 1,637 |

* | Wind River Systems Inc. | 249,706 | 1,598 |

* | Affiliated Computer | | |

| Services, Inc. Class A | 33,000 | 1,580 |

* | Gartner, Inc. Class A | 137,700 | 1,516 |

* | Avocent Corp. | 116,351 | 1,413 |

* | Netlogic Microsystems Inc. | 43,900 | 1,206 |

| iGATE Corp. | 356,314 | 1,154 |

* | Ciber, Inc. | 422,286 | 1,153 |

* | TNS Inc. | 133,300 | 1,090 |

| Daktronics, Inc. | 156,854 | 1,027 |

| Syntel, Inc. | 48,323 | 995 |

* | Sapient Corp. | 217,300 | 971 |

* | Lawson Software, Inc. | 220,375 | 937 |

* | SPSS, Inc. | 32,716 | 930 |

* | Genpact, Ltd. | 103,484 | 917 |

* | Cirrus Logic, Inc. | 234,700 | 882 |

| Linear Technology Corp. | 36,500 | 839 |

| Broadridge Financial | | |

| Solutions LLC | 41,800 | 778 |

* | NetScout Systems, Inc. | 105,580 | 756 |

* | DTS Inc. | 29,200 | 703 |

| Take-Two Interactive | | |

| Software, Inc. | 83,500 | 697 |

* | Semtech Corp. | 51,113 | 682 |

| CTS Corp. | 183,015 | 661 |

* | 3Com Corp. | 213,100 | 658 |

*,^ | Synaptics Inc. | 23,600 | 632 |

* | NCI, Inc. | 23,500 | 611 |

* | InterDigital, Inc. | 20,700 | 534 |

* | Ariba, Inc. | 58,100 | 507 |

* | Net 1 UEPS | | |

| Technologies, Inc. | 31,900 | 485 |

* | Benchmark Electronics, Inc. | 42,908 | 481 |

* | Harmonic, Inc. | 73,900 | 480 |

* | OSI Systems Inc. | 31,071 | 474 |

* | Compuware Corp. | 62,500 | 412 |

* | ScanSource, Inc. | 22,000 | 409 |

| MAXIMUS, Inc. | 10,200 | 407 |

* | Manhattan Associates, Inc. | 22,400 | 388 |

* | Dice Holdings Inc. | 134,861 | 375 |

| Lender Processing | | |

| Services, Inc. | 12,200 | 373 |

* | Convergys Corp. | 30,700 | 248 |

* | Monotype Imaging | | |

| Holdings Inc. | 59,800 | 224 |

| | | Market |

| | | Value• |

| | Shares | ($000) |

* | Standard | | |

| Microsystem Corp. | 10,662 | 198 |

* | Harris Stratex | | |

| Networks, Inc. Class A | 49,333 | 190 |

* | SuccessFactors Inc. | 23,300 | 178 |

| Micrel, Inc. | 24,800 | 175 |

* | Tekelec | 12,400 | 164 |

* | UTStarcom, Inc. | 198,600 | 155 |

* | TriQuint Semiconductor, Inc. | 56,000 | 138 |

* | CACI International, Inc. | 3,300 | 120 |

* | Mettler-Toledo | | |

| International Inc. | 2,200 | 113 |

* | Ness Technologies Inc. | 37,200 | 110 |

* | Internet Brands Inc. | 16,628 | 98 |

| MTS Systems Corp. | 3,400 | 77 |

| Renaissance Learning, Inc. | 7,049 | 63 |

* | LSI Corp. | 19,000 | 58 |

* | Global Cash Access, Inc. | 11,700 | 45 |

* | EPIQ Systems, Inc. | 2,000 | 36 |

| Marchex, Inc. | 9,803 | 34 |

* | Airvana, Inc. | 5,002 | 29 |

* | Microsemi Corp. | 2,500 | 29 |

* | Veeco Instruments, Inc. | 3,846 | 26 |

* | Sanmina-SCI Corp. | 77,000 | 23 |

* | Atmel Corp. | 6,400 | 23 |

* | Ingram Micro, Inc. Class A | 1,400 | 18 |

| | | 441,933 |

Materials (4.9%) | | |

| Celanese Corp. Series A | 1,192,600 | 15,945 |

| Eastman Chemical Co. | 594,728 | 15,939 |

| Greif Inc. Class A | 449,700 | 14,971 |

* | Owens-Illinois, Inc. | 977,000 | 14,108 |

| Compass Minerals | | |

| International, Inc. | 212,600 | 11,984 |

| FMC Corp. | 242,400 | 10,457 |

| Schnitzer Steel | | |

| Industries, Inc. Class A | 175,900 | 5,522 |

| Cliffs Natural | | |

| Resources Inc. | 299,100 | 5,432 |

| Rock-Tenn Co. | 198,158 | 5,360 |

| Silgan Holdings, Inc. | 96,586 | 5,075 |

| Terra Industries, Inc. | 172,199 | 4,837 |

| Olin Corp. | 318,946 | 4,551 |

| Reliance Steel & | | |

| Aluminum Co. | 171,000 | 4,502 |

| Innophos Holdings Inc. | 260,924 | 2,943 |

| Glatfelter | 456,183 | 2,847 |

| Koppers Holdings, Inc. | 171,338 | 2,488 |

| CF Industries Holdings, Inc. | 28,007 | 1,992 |

| Ball Corp. | 39,300 | 1,706 |

| Airgas, Inc. | 40,600 | 1,373 |

| A. Schulman Inc. | 75,709 | 1,026 |

| Schweitzer-Mauduit International, Inc. | 53,339 | 985 |

* | Buckeye Technology, Inc. | 347,858 | 741 |

* | Pactiv Corp. | 38,618 | 563 |

17

Strategic Equity Fund

| | | Market |

| | | Value• |

| | Shares | ($000) |

| Worthington Industries, Inc. | 64,100 | 558 |

| NewMarket Corp. | 5,600 | 248 |

| Stepan Co. | 8,400 | 229 |

| Sensient Technologies Corp. | 6,300 | 148 |

| AK Steel Holding Corp. | 15,354 | 109 |

* | Clearwater Paper Corp. | 12,071 | 97 |

| Scotts Miracle-Gro Co. | 700 | 24 |

| | | 136,760 |

Telecommunication Services (2.3%) | |

| Embarq Corp. | 780,653 | 29,548 |

* | Syniverse Holdings Inc. | 1,152,703 | 18,167 |

* | Cincinnati Bell Inc. | 3,854,600 | 8,865 |

| Windstream Corp. | 306,200 | 2,468 |

| NTELOS Holdings Corp. | 135,973 | 2,466 |

* | Premiere Global | | |

| Services, Inc. | 145,290 | 1,281 |

| Atlantic Tele-Network, Inc. | 64,377 | 1,235 |

| Consolidated | | |

| Communications | | |

| Holdings, Inc. | 50,600 | 519 |

| USA Mobility, Inc. | 15,500 | 143 |

| CenturyTel, Inc. | 1,600 | 45 |

| | | 64,737 |

Utilities (5.7%) | | |

| SCANA Corp. | 845,678 | 26,123 |

| CenterPoint Energy Inc. | 2,185,108 | 22,791 |

| CMS Energy Corp. | 1,687,369 | 19,978 |

| Energen Corp. | 629,272 | 18,331 |

* | Mirant Corp. | 793,452 | 9,045 |

| Wisconsin Energy Corp. | 203,200 | 8,366 |

| Questar Corp. | 274,676 | 8,084 |

| Portland General Electric Co. | 340,700 | 5,993 |

| Atmos Energy Corp. | 238,911 | 5,524 |

| DTE Energy Co. | 179,381 | 4,969 |

| Pepco Holdings, Inc. | 390,834 | 4,878 |

* | NRG Energy, Inc. | 233,500 | 4,110 |

| IDACORP, Inc. | 144,444 | 3,374 |

| Vectren Corp. | 142,323 | 3,002 |

| WGL Holdings Inc. | 82,603 | 2,709 |

| NorthWestern Corp. | 109,597 | 2,354 |

| ONEOK, Inc. | 100,334 | 2,270 |

| Avista Corp. | 151,929 | 2,093 |

| DPL Inc. | 70,900 | 1,598 |

| NiSource, Inc. | 131,300 | 1,287 |

| UGI Corp. Holding Co. | 36,000 | 850 |

| Pinnacle West Capital Corp. | 22,200 | 590 |

| South Jersey Industries, Inc. | 13,890 | 486 |

* | El Paso Electric Co. | 29,100 | 410 |

| UniSource Energy Corp. | 6,800 | 192 |

| ITC Holdings Corp. | 417 | 18 |

| MGE Energy, Inc. | 300 | 9 |

| | | 159,434 |

Total Common Stocks | | |

(Cost $3,956,799) | | 2,722,245 |

| | | Market |

| | | Value• |

| | Shares | ($000) |

Temporary Cash Investments (2.8%)1 | |

Money Market Fund (1.0%) | | |

3,4 | Vanguard Market | | |

| Liquidity Fund, 0.440% | 26,685,444 | 26,685 |

| | | |

| | | |

| | Face | |

| | Amount | |

| | ($000) | |

Commercial Paper (1.3%) | | |

5 | Danske Corp. | | |

| 4.333%, 4/15/09 | 10,750 | 10,748 |

| General Electric Capital Corp. | |

| 3.874%, 4/15/09 | 16,000 | 15,999 |

| Santander Central Hispano | |

| Finance (Delaware), Inc. | | |

| 4.249%, 4/16/09 | 10,750 | 10,748 |

| | | 37,495 |

U.S. Government and Agency Obligations (0.5%) |

6,7 | Federal Home Loan | | |

| Mortgage Corp., | | |

| 1.206%, 4/30/09 | 3,000 | 3,000 |

6,7 | Federal Home Loan | | |

| Mortgage Corp., | | |

| 0.451%, 5/28/09 | 6,000 | 5,999 |

6,7 | Federal Home | | |

| Loan Bank, | | |

| 0.531%, 8/28/09 | 1,000 | 998 |

6,7 | Federal Home Loan | | |

| Mortgage Corp., | | |

| 0.562%, 8/31/09 | 3,000 | 2,996 |

| | | 12,993 |

Total Temporary Cash Investments | |

(Cost $77,109) | | 77,173 |

Total Investments (100.5%) | | |

(Cost $4,033,908) | | 2,799,418 |

Other Assets and Liabilities (–0.5%) | |

Other Assets | | 8,781 |

Liabilities4 | | (22,401) |

| | | (13,620) |

Net Assets (100%) | | |

Applicable to 273,628,330 outstanding | |

$.001 par value shares of beneficial | |

interest (unlimited authorization) | 2,785,798 |

Net Asset Value Per Share | | $10.18 |

18

Strategic Equity Fund

At March 31, 2009, net assets consisted of: | |

| Amount |

| ($000) |

Paid-in Capital | 5,616,815 |

Overdistributed Net Investment Income | (4,763) |

Accumulated Net Realized Losses | (1,594,273) |

Unrealized Appreciation (Depreciation) | |

Investment Securities | (1,234,490) |

Futures Contracts | 2,509 |

Net Assets | 2,785,798 |

• | See Note A in Notes to Financial Statements. |

* | Non-income-producing security. |

^ | Part of security position is on loan to broker-dealers. The total value of securities on loan is $8,843,000. |

1 The fund invests a portion of its cash reserves in equity markets through the use of index futures contracts. After giving effect to futures investments, the fund’s effective common stock and temporary cash investment positions represent 100.0% and 0.5%, respectively, of net assets.

2 Considered an affiliated company of the fund as the fund owns more than 5% of the outstanding voting securities of such company.

3 Affiliated money market fund available only to Vanguard funds and certain trusts and accounts managed by Vanguard. Rate shown is the 7-day yield.

4 Includes $9,266,000 of collateral received for securities on loan.

5 Security exempt from registration under Section 4(2) of the Securities Act of 1933. Such securities may be sold in transactions exempt from registration only to dealers in that program or other “accredited investors.” At March 31, 2009, the value of these securities was $10,748,000, representing 0.4% of net assets.

6 Securities with a value of $12,993,000 have been segregated as initial margin for open futures contracts.

7 The issuer operates under a congressional charter; its securities are not backed by the full faith and credit of the U.S. government.

REIT—Real Estate Investment Trust.

See accompanying Notes, which are an integral part of the Financial Statements.

19

Strategic Equity Fund

Statement of Operations

| Six Months Ended |

| March 31, 2009 |

| ($000) |

Investment Income | |

Income | |

Dividends1 | 23,717 |

Interest1 | 4,663 |

Security Lending | 1,453 |

Total Income | 29,833 |

Expenses | |

The Vanguard Group—Note B | |

Investment Advisory Services | 351 |

Management and Administrative | 3,739 |

Marketing and Distribution | 644 |

Custodian Fees | 46 |

Auditing Fees | 1 |

Shareholders’ Reports | 73 |

Trustees’ Fees and Expenses | 3 |

Total Expenses | 4,857 |

Net Investment Income | 24,976 |

Realized Net Gain (Loss) | |

Investment Securities Sold1 | (1,096,345) |

Futures Contracts | (126,958) |

Realized Net Gain (Loss) | (1,223,303) |

Change in Unrealized Appreciation (Depreciation) | |

Investment Securities | (550,898) |

Futures Contracts | 3,405 |

Change in Unrealized Appreciation (Depreciation) | (547,493) |

Net Increase (Decrease) in Net Assets Resulting from Operations | (1,745,820) |

1 Dividend income, interest income and realized net gain (loss) from affiliated companies of the fund were $0, $584,000, and $0, respectively.

See accompanying Notes, which are an integral part of the Financial Statements.

20

Strategic Equity Fund

Statement of Changes in Net Assets

| Six Months Ended | Year Ended |

| March 31, | September 30, |

| 2009 | 2008 |

| ($000) | ($000) |

Increase (Decrease) in Net Assets | | |

Operations | | |

Net Investment Income | 24,976 | 65,953 |

Realized Net Gain (Loss) | (1,223,303) | (331,389) |

Change in Unrealized Appreciation (Depreciation) | (547,493) | (1,492,805) |

Net Increase (Decrease) in Net Assets Resulting from Operations | (1,745,820) | (1,758,241) |

Distributions | | |

Net Investment Income | (67,840) | (69,137) |

Realized Capital Gain1 | — | (700,017) |

Total Distributions | (67,840) | (769,154) |

Capital Share Transactions | | |

Issued | 276,790 | 774,976 |

Issued in Lieu of Cash Distributions | 63,748 | 726,971 |

Redeemed | (562,742) | (1,851,818) |

Net Increase (Decrease) from Capital Share Transactions | (222,204) | (349,871) |

Total Increase (Decrease) | (2,035,864) | (2,877,266) |

Net Assets | | |

Beginning of Period | 4,821,662 | 7,698,928 |

End of Period2 | 2,785,798 | 4,821,662 |

1 Includes fiscal 2008 short-term gain distributions totaling $83,541,000. Short-term gain distributions are treated as ordinary income dividends for tax purposes.

2 Net Assets—End of Period includes undistributed (overdistributed) net investment income of ($4,763,000) and $38,101,000.

See accompanying Notes, which are an integral part of the Financial Statements.

21

Strategic Equity Fund

Financial Highlights

| Six Months | | | | | Nov. 1, | Year |

| Ended | | | | | 2003, to | Ended |

For a Share Outstanding | March 31, | Year Ended September 30, | Sept. 30, | Oct. 31, |

Throughout Each Period | 2009 | 2008 | 2007 | 2006 | 2005 | 20041 | 2003 |

Net Asset Value, | | | | | | | |

Beginning of Period | $16.42 | $24.94 | $23.07 | $23.28 | $19.70 | $17.85 | $13.01 |

Investment Operations | | | | | | | |

Net Investment Income | .091 | .240 | .270 | .270 | .190 | .130 | .130 |

Net Realized and | | | | | | | |

Unrealized Gain (Loss) | | | | | | | |

on Investments | (6.090) | (6.090) | 2.840 | 1.170 | 4.490 | 1.850 | 4.840 |

Total from | | | | | | | |

Investment Operations | (5.999) | (5.850) | 3.110 | 1.440 | 4.680 | 1.980 | 4.970 |

Distributions | | | | | | | |

Dividends from | | | | | | | |

Net Investment Income | (.241) | (.240) | (.260) | (.210) | (.140) | (.130) | (.130) |

Distributions from | | | | | | | |

Realized Capital Gains | — | (2.430) | (.980) | (1.440) | (.960) | — | — |

Total Distributions | (.241) | (2.670) | (1.240) | (1.650) | (1.100) | (.130) | (.130) |

Net Asset Value, | | | | | | | |

End of Period | $10.18 | $16.42 | $24.94 | $23.07 | $23.28 | $19.70 | $17.85 |

| | | | | | | |

Total Return2 | –36.66% | –25.37% | 13.76% | 6.49% | 24.32% | 11.14% | 38.55% |

| | | | | | | |

Ratios/Supplemental Data | | | | | | | |

Net Assets, | | | | | | | |

End of Period (Millions) | $2,786 | $4,822 | $7,699 | $6,755 | $5,183 | $2,953 | $1,714 |

Ratio of Total Expenses to | | | | | | | |

Average Net Assets | 0.31%3 | 0.25% | 0.30% | 0.35% | 0.40% | 0.45%3 | 0.50% |

Ratio of Net Investment | | | | | | | |

Income to Average | | | | | | | |

Net Assets | 1.84%3 | 1.09% | 1.03% | 1.18% | 0.99% | 0.83%3 | 1.04% |

Portfolio Turnover Rate | 70%3 | 79% | 75% | 80% | 75% | 66% | 100% |

1 The fund’s fiscal year-end changed from October 31 to September 30, effective September 30, 2004.

2 Total returns do not include the account service fee that may be applicable to certain accounts with balances below $10,000.

3 Annualized.

See accompanying Notes, which are an integral part of the Financial Statements.

22

Strategic Equity Fund

Notes to Financial Statements

Vanguard Strategic Equity Fund is registered under the Investment Company Act of 1940 as an open-end investment company, or mutual fund.

A. The following significant accounting policies conform to generally accepted accounting principles for U.S. mutual funds. The fund consistently follows such policies in preparing its financial statements.

1. Security Valuation: Securities are valued as of the close of trading on the New York Stock Exchange (generally 4 p.m., Eastern time) on the valuation date. Equity securities are valued at the latest quoted sales prices or official closing prices taken from the primary market in which each security trades; such securities not traded on the valuation date are valued at the mean of the latest quoted bid and asked prices. Securities for which market quotations are not readily available, or whose values have been materially affected by events occurring before the fund’s pricing time but after the close of the securities’ primary markets, are valued by methods deemed by the board of trustees to represent fair value. Investments in Vanguard Market Liquidity Fund are valued at that fund’s net asset value. Temporary cash investments acquired over 60 days to maturity are valued using the latest bid prices or using valuations based on a matrix system (which considers such factors as security prices, yields, maturities, and ratings), both as furnished by independent pricing services. Other temporary cash investments are valued at amortized cost, which approximates market value.

2. Futures Contracts: The fund uses index futures contracts to a limited extent, with the objective of maintaining full exposure to the stock market while maintaining liquidity. The fund may purchase or sell futures contracts to achieve a desired level of investment, whether to accommodate portfolio turnover or cash flows from capital share transactions. The primary risks associated with the use of futures contracts are imperfect correlation between changes in market values of stocks held by the fund and the prices of futures contracts, and the possibility of an illiquid market.

Futures contracts are valued at their quoted daily settlement prices. The aggregate principal amounts of the contracts are not recorded in the Statement of Net Assets. Fluctuations in the value of the contracts are recorded in the Statement of Net Assets as an asset (liability) and in the Statement of Operations as unrealized appreciation (depreciation) until the contracts are closed, when they are recorded as realized futures gains (losses).

3. Federal Income Taxes: The fund intends to continue to qualify as a regulated investment company and distribute all of its taxable income. Management has analyzed the fund’s tax positions taken on federal income tax returns for all open tax years (tax years ended September 30, 2005–2008) and for the period ended March 31, 2009, and has concluded that no provision for federal income tax is required in the fund’s financial statements.

4. Distributions: Distributions to shareholders are recorded on the ex-dividend date.

5. Security Lending: The fund may lend its securities to qualified institutional borrowers to earn additional income. Security loans are required to be secured at all times by collateral at least equal to the market value of securities loaned. The fund invests cash collateral received in Vanguard Market Liquidity Fund, and records a liability for the return of the collateral, during the period the securities are on loan. Security lending income represents the income earned on investing cash collateral, less expenses associated with the loan.

23

Strategic Equity Fund

6. Other: Dividend income is recorded on the ex-dividend date. Interest income includes income distributions received from Vanguard Market Liquidity Fund and is accrued daily. Security transactions are accounted for on the date securities are bought or sold. Costs used to determine realized gains (losses) on the sale of investment securities are those of the specific securities sold.

B. The Vanguard Group furnishes at cost investment advisory, corporate management, administrative, marketing, and distribution services. The costs of such services are allocated to the fund under methods approved by the board of trustees. The fund has committed to provide up to 0.40% of its net assets in capital contributions to Vanguard. At March 31, 2009, the fund had contributed capital of $730,000 to Vanguard (included in Other Assets), representing 0.03% of the fund’s net assets and 0.29% of Vanguard’s capitalization. The fund’s trustees and officers are also directors and officers of Vanguard.

C. Distributions are determined on a tax basis and may differ from net investment income and realized capital gains for financial reporting purposes. Differences may be permanent or temporary. Permanent differences are reclassified among capital accounts in the financial statements to reflect their tax character. Temporary differences arise when certain items of income, expense, gain, or loss are recognized in different periods for financial statement and tax purposes; these differences will reverse at some time in the future. Differences in classification may also result from the treatment of short-term gains as ordinary income for tax purposes.

The fund’s tax-basis capital gains and losses are determined only at the end of each fiscal year. For tax purposes, at September 30, 2008, the fund had available realized losses of $371,403,000 to offset future net capital gains through September 30, 2017. The fund will use these capital losses to offset net taxable capital gains, if any, realized during the year ending September 30, 2009; should the fund realize net capital losses for the year, the losses will be added to the loss carryforward balance above.

At March 31, 2009, the cost of investment securities for tax purposes was $4,033,908,000. Net unrealized depreciation of investment securities for tax purposes was $1,234,490,000, consisting of unrealized gains of $94,263,000 on securities that had risen in value since their purchase and $1,328,753,000 in unrealized losses on securities that had fallen in value since their purchase.

At March 31, 2009, the aggregate settlement value of open futures contracts expiring in June 2009 and the related unrealized appreciation (depreciation) were:

| | | ($000) |

| | Aggregate | Unrealized |

| Number of | Settlement | Appreciation |

Futures Contracts | Long Contracts | Value | (Depreciation) |

E-mini Russell 2000 Index | 954 | 40,191 | 1,607 |

S&P Midcap 400 Index | 84 | 20,492 | 888 |

E-mini S&P Midcap Index | 35 | 1,708 | 14 |

Unrealized appreciation (depreciation) on open futures contracts is required to be treated as realized gain (loss) for tax purposes.

D. During the six months ended March 31, 2009, the fund purchased $1,095,867,000 of investment securities and sold $1,514,739,000 of investment securities, other than temporary cash investments.

24

Strategic Equity Fund

E. Capital shares issued and redeemed were:

| Six Months Ended | Year Ended |

| March 31, 2009 | September 30, 2008 |

| Shares | Shares |

| (000) | (000) |

Issued | 24,695 | 39,124 |

Issued in Lieu of Cash Distributions | 5,712 | 36,367 |

Redeemed | (50,467) | (90,470) |

Net Increase (Decrease) in Shares Outstanding | (20,060) | (14,979) |

F. The fund has invested in a company that is considered to be an affiliated company of the fund because the fund owns more than 5% of the outstanding voting securities of the company. Transactions during the period in securities of this company were as follows:

| | | Current Period Transactions | |

| Sept. 30, 2008 | | Proceeds from | | March 31, 2009 |

| Market | Purchases | Securities | Dividend | Market |

| Value | at Cost | Sold | Income | Value |

| ($000) | ($000) | ($000) | ($000) | ($000) |

TBS International Ltd. | NA1 | 2,487 | 21 | — | 10,383 |

1 At September 30, 2008, the issuer was not an affiliated company of the fund. |

G. In September 2006, the Financial Accounting Standards Board issued Statement of Financial Accounting Standards No. 157 (“FAS 157”), “Fair Value Measurements.” FAS 157 establishes a framework for measuring fair value and expands disclosures about fair value measurements in financial statements.

The various inputs that may be used to determine the value of the fund’s investments are summarized in three broad levels. The inputs or methodologies used for valuing securities are not necessarily an indication of the risk associated with investing in those securities.

Level 1—Quoted prices in active markets for identical securities.

Level 2—Other significant observable inputs (including quoted prices for similar securities, interest rates, prepayment speeds, credit risk, etc.).

Level 3—Significant unobservable inputs (including the fund’s own assumptions used to determine the fair value of investments).

The following table summarizes the fund’s investments as of March 31, 2009, based on the inputs used to value them:

| Investments | Futures |

| in Securities | Contracts |

Valuation Inputs | ($000) | ($000) |

Level 1—Quoted prices | 2,748,930 | 2,509 |

Level 2—Other significant observable inputs | 50,488 | — |

Level 3—Significant unobservable inputs | — | — |

Total | 2,799,418 | 2,509 |

25

About Your Fund’s Expenses

As a shareholder of the fund, you incur ongoing costs, which include costs for portfolio management, administrative services, and shareholder reports (like this one), among others. Operating expenses, which are deducted from a fund’s gross income, directly reduce the investment return of the fund.

A fund’s expenses are expressed as a percentage of its average net assets. This figure is known as the expense ratio. The following examples are intended to help you understand the ongoing costs (in dollars) of investing in your fund and to compare these costs with those of other mutual funds. The examples are based on an investment of $1,000 made at the beginning of the period shown and held for the entire period.

The accompanying table illustrates your fund’s costs in two ways:

• Based on actual fund return. This section helps you to estimate the actual expenses that you paid over the period. The “Ending Account Value” shown is derived from the fund’s actual return, and the third column shows the dollar amount that would have been paid by an investor who started with $1,000 in the fund. You may use the information here, together with the amount you invested, to estimate the expenses that you paid over the period.

To do so, simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number given for your fund under the heading “Expenses Paid During Period.”