UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-01735

fpa NEW Income, inc.

(Exact name of registrant as specified in charter)

11601 WILSHIRE BLVD., STE. 1200

LOS ANGELES, CALIFORNIA 90025

(Address of principal executive offices)(Zip code)

| (Name and Address of Agent for Service) | Copy to: |

J. RICHARD ATWOOD, PRESIDENT FPA NEW INCOME, INC. 11601 WILSHIRE BLVD., STE. 1200 LOS ANGELES, CALIFORNIA 90025 | MARK D. PERLOW, ESQ. DECHERT LLP ONE BUSH STREET, STE. 1600 SAN FRANCISCO, CA 94104 |

Registrant’s telephone number, including area code: (310) 473-0225

Date of fiscal year end: September 30

Date of reporting period: March 31, 2020

Item 1: Report to Shareholders.

Distributor:

UMB DISTRIBUTION SERVICES, LLC

235 West Galena Street

Milwaukee, Wisconsin 53212

Beginning on January 1, 2021, as permitted by regulations adopted by the Securities and Exchange Commission, we intend to no longer mail paper copies of the Fund's shareholder reports, unless you specifically request paper copies of the reports from the Fund or from your financial intermediary, such as a broker-dealer or bank. Instead, the reports will be made available on the FPA Funds website (fpa.com/funds), and you will be notified by mail each time a report is posted and provided with a website link to access the report. If you already elected to receive shareholder reports electronically, you will not be affected by this change and you need not take any action. If you prefer to receive shareholder reports and other communications electronically, you may update your mailing preferences with your financial intermediary, or enroll in e-delivery at fpa.com (for accounts held directly with the Fund).

You may elect to continue to receive paper copies of all future reports free of charge. If you invest through a financial intermediary, you may contact your financial intermediary to request that you continue to receive paper copies of your shareholder reports. If you invest directly with the Fund, you may inform the Fund that you wish to continue receiving paper copies of your shareholder reports by contacting us at (800) 638-3060. Your election to receive reports in paper will apply to all funds held with the FPA Funds or through your financial intermediary.

FPA NEW INCOME, INC.

LETTER TO SHAREHOLDERS

Dear Fellow Shareholders,

FPA New Income, Inc. (the "Fund") returned -1.38% in the first quarter of 2020.

As of March 31, the portfolio had a yield-to-worst1 of 4.01% and an effective duration of 1.35 years. The spread of the COVID-19 virus around the world led to a historic sell-off in global financial markets as overall worldwide economic growth turned into a severe economic recession of uncertain length. Risk-free rates declined significantly in response to aggressive monetary easing by central banks and the prices of risk assets fell, resulting in higher credit spreads across all segments of the fixed income market. We spent the last several years increasing the overall credit quality of the portfolio, most notably via a reduction in holdings rated below investment grade. Out of concern that fixed income markets were too expensive, we also spent the last several years reducing the portfolio's exposure to rising credit spreads. Despite these actions, the portfolio was not immune to the historic decline in bond prices. However, because of our steps to insulate the portfolio from a decline in bond prices, the Fund's drawdown during the sell-off was relatively muted compared to its peers in the Morningstar Short-Term Bond Category, which returned -2.14% for the quarter. Recently, in response to the decline in risk-free rates, we shortened the portfolio's duration. As prices fell and yields rose for short-duration high-quality bonds (rated single-A or higher), we selectively added to these holdings. Finally, we also deployed a modest amount of capital into credit (defined as investments rated BBB or lower). Given the uncertainty in the economic outlook and the volatility in financial markets, all of our investment activity will be undertaken with the goal of achieving a positive return in 2020 while also maintaining adequate liquidity in the portfolio. Cash and equivalents increased from 7.1% of the portfolio as of Dec. 31, 2019, to 7.7% at March 31, 2020.

Portfolio Attribution2

The following table shows contributors to and detractors from the portfolio's first quarter performance:

| | | Average Weight (%) | | Q1 2020

Total Return (%) | | Contribution

to return (%) | |

ABS | | | 54.81 | | | | -1.67 | | | | -1.04 | | |

Auto | | | 19.99 | | | | -1.26 | | | | -0.31 | | |

Equipment | | | 17.21 | | | | -1.49 | | | | -0.28 | | |

CLO | | | 9.25 | | | | -3.69 | | | | -0.36 | | |

1 Yield to Worst ("YTW") is presented gross of fees and reflects the lowest possible yield on a callable bond without the issuer defaulting. It does not represent the yield an investor should expect to receive. As of March 31, 2020, the Fund's subsidized/unsubsidized 30-day SEC standardized yield ("SEC Yield") was 2.64%/2.57% respectively. The SEC Yield calculation is an annualized measure of the Fund's dividend and interest payments for the last 30 days, less Fund expenses. Subsidized yield reflects fee waivers and/or expense reimbursements during the period. Without waivers and/or reimbursements, yields would be reduced. Unsubsidized yield does not adjust for any fee waivers and/or expense reimbursements in effect. The SEC Yield calculation is based on the price of the Fund at the beginning of the month.

2 See the end of this Commentary for additional information pertaining to attribution for the quarter ending March 31, 2020. Top contributors and detractors to the Fund's performance are based on contribution to return for the periods noted. Contribution is presented gross of investment management fees, transactions costs, and Fund operating expenses, which if included, would reduce the returns presented. This information is not a recommendation for a specific security or sector and these securities/sectors may not be in the Fund at the time you receive this report. The information provided does not reflect all positions purchased, sold or recommended by FPA during the quarter. A copy of the methodology used and a list of every sector's contribution to the overall Fund's performance during the quarter is available by contacting FPA at crm@fpa.com. The portfolio holdings as of the most recent quarter-end may be obtained at www.fpa.com.

Past performance is no guarantee, nor is it indicative, of future results.

1

FPA NEW INCOME, INC.

LETTER TO SHAREHOLDERS

(Continued)

| | | Average Weight (%) | | Q1 2020

Total Return (%) | | Contribution

to return (%) | |

Credit Cards | | | 4.28 | | | | -0.77 | | | | -0.05 | | |

Other | | | 4.08 | | | | -1.13 | | | | -0.05 | | |

CMO | | | 8.43 | | | | -0.19 | | | | 0.01 | | |

Agency | | | 2.29 | | | | 2.22 | | | | 0.05 | | |

Non-Agency | | | 6.14 | | | | -1.11 | | | | -0.04 | | |

CMBS | | | 8.47 | | | | -1.53 | | | | -0.14 | | |

Agency | | | 1.51 | | | | 1.91 | | | | 0.03 | | |

Non-Agency | | | 4.56 | | | | -0.29 | | | | -0.04 | | |

Stripped | | | 2.41 | | | | -5.41 | | | | -0.14 | | |

Mortgage Pass-Through | | | 6.42 | | | | 2.22 | | | | 0.15 | | |

Treasury | | | 7.34 | | | | 3.10 | | | | 0.23 | | |

Agencies | | | 1.16 | | | | 1.05 | | | | 0.01 | | |

Cash and equivalents | | | 7.03 | | | | 0.32 | | | | 0.02 | | |

MBS Stripped | | | 0.01 | | | | -2.52 | | | | 0.00 | | |

Corporate | | | 6.35 | | | | -6.13 | | | | -0.40 | | |

Bank Debt | | | 4.27 | | | | -7.60 | | | | -0.35 | | |

Corporate Bonds | | | 1.74 | | | | -2.81 | | | | -0.04 | | |

Common Stock | | | 0.33 | | | | -2.90 | | | | -0.01 | | |

Total | | | 100.00 | | | | -1.17 | | | | -1.17 | | |

During the first quarter, the largest contributors to performance were Treasuries, which appreciated in price as Treasury yields declined during the quarter. The second- and third-largest contributors to performance were agency mortgage pools and agency collateralized mortgage obligations (CMOs), both of which also appreciated in price due to lower Treasury yields (though the price increases were tempered by wider spreads).

Credit spreads increased during the quarter across all sectors and ratings within fixed income to levels not seen since the 2008-09 financial crisis. The asset-backed securities (ABS) holdings, which are predominantly rated single-A and higher, were the largest detractors from performance during the quarter. The ABS holdings themselves performed relatively well during the quarter, with a total return of approximately -1.7%. But because they averaged about 55% of the portfolio, they were a relatively large detractor from overall performance.

The second-largest detractors from performance were corporate bank debt (i.e., leveraged loans) and bond holdings, which are predominantly rated less than BBB. Approximately two-thirds of the portfolio's corporate holdings are in bank debt, with the rest mostly in high-yield bonds. The leveraged loan and high-yield markets experienced historic price declines during the quarter. As a result, despite representing just 6% of the portfolio on average, the corporate holdings were a relatively large detractor from performance.

The third-largest detractors from performance were GNMA project loan interest-only bonds, which were also subject to significantly wider spreads during the quarter. The GNMA project loan interest-only bonds appear in the table above as stripped commercial mortgage-backed securities (CMBS).

As discussed in more detail below, we view the Fund's negative performance as a temporary mark-to-market impact on the portfolio. Given the overall high-quality nature of the portfolio's holdings, we do not believe the portfolio's capital is permanently impaired. As such, we believe we are well-positioned to recover much of

2

FPA NEW INCOME, INC.

LETTER TO SHAREHOLDERS

(Continued)

this negative performance over time as our high-quality short-maturity holdings mature and/or credit spreads normalize.

Portfolio Activity

The table below shows the portfolio's exposures as of March 31, 2020 compared to Dec. 31, 2019:

Fund3 | | As of

12/31/2019 | | As of

3/31/2020 | |

Yield-to-worst | | | 2.71 | % | | | 4.01 | % | |

Subsidized SEC Yield4 | | | 2.50 | % | | | 2.64 | % | |

Effective Duration (years) | | | 1.57 | | | | 1.35 | | |

Fund | | % Portfolio

12/31/2019 | | % Portfolio

3/31/2020 | |

ABS5 | | | 52.1 | | | | 62.5 | | |

Mortgage Backed (CMO)6 | | | 9.3 | | | | 8.4 | | |

Stripped Mortgage-backed | | | 2.6 | | | | 2.4 | | |

Corporate | | | 6.3 | | | | 6.9 | | |

CMBS6 | | | 6.1 | | | | 7.9 | | |

Mortgage Pass-through | | | 8.4 | | | | 2.9 | | |

U.S. Treasury | | | 6.9 | | | | 0.0 | | |

Agencies | | | 1.2 | | | | 1.3 | | |

Cash and equivalents | | | 7.1 | | | | 7.7 | | |

Total | | | 100.0 | | | | 100.0 | | |

With the goal of a positive 12 month return in mind, our investment activity during the quarter centered around shortening the portfolio's duration while opportunistically adding investments in structured products as markets sold off. Early in the quarter, we sold longer-duration agency mortgage pools, Treasuries, agency mortgage CMOs, agency CMBS and non-agency mortgages as interest rates declined because they no longer offered enough yield to compensate for the duration risk. We purchased high-quality, short-duration auto ABS, equipment ABS, credit card ABS, CMBS and collateralized loan obligations (CLOs). We also selectively added to existing credit positions as the market sold off, and made an investment in a short-term working capital-based corporate bridge loan.

Market Commentary

The spread of COVID-19 around the world led investors and policymakers to reset their expectations for economic growth as social distancing and "stay at home" orders brought much of the world economy to a halt.

3 Source: FactSet. Portfolio composition will change due to ongoing management of the Fund. Totals may not add due to rounding.

4 As of March 31, 2020, FPNIX subsidized/unsubsidized 30-day SEC standardized yield ("SEC Yield") was 2.64%/2.57% respectively.

5 ABS (Asset Backed Securities) are securities backed by a loan, lease or receivables against assets other than real estate.

6 Collateralized mortgage obligations ("CMO") are mortgage-backed securities that separate mortgage pools into different maturity classes. Commercial mortgage-backed securities ("CMBS") are securities backed by commercial mortgages rather than residential mortgages.

3

FPA NEW INCOME, INC.

LETTER TO SHAREHOLDERS

(Continued)

The U.S. economy is likely already in recession owing to a broad collapse in consumer spending that affected travel, leisure, clothing, capital goods, cars, etc. Few areas of the economy have been spared. This decline in consumer spending negatively impacts employment and business investment. From a societal standpoint, the most important question is when will there be a cure and/or treatment? From an economic perspective, substantial containment of the virus directly affects when and at what pace economic activity can resume. That, in turn, will determine the depth and length of the recession and, subsequently, the vigor and speed of the recovery. Ever the weighing machine, financial markets responded to the uncertainty in historic fashion.

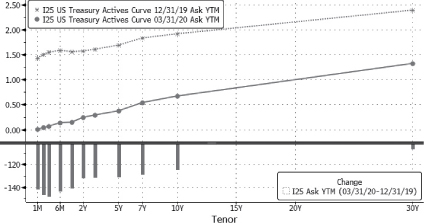

As shown in the following chart, Treasury yields declined to unprecedented levels during the quarter as the Treasury market responded first to the likely arrival of a recession and then to the Federal Reserve's aggressive response. Notably, two- to three-year maturity Treasuries, which fit the duration profile that we have recently targeted for investment, declined in yield by approximately 130 basis points (bps), while longer-maturity bonds declined by over 120 bps.

Treasury Yield Curve

Source: Bloomberg

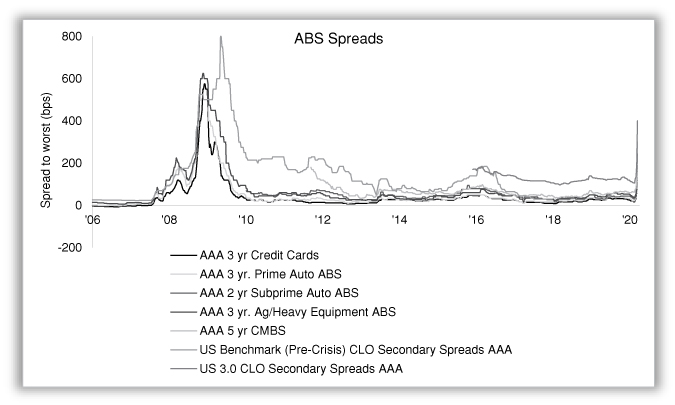

The chart below is most pertinent to our portfolio given our large exposure to investment grade structured products. This chart shows that spreads on AAA-rated ABS bonds and CLOs increased to the second-highest levels on record and are far higher than in recent years.

4

FPA NEW INCOME, INC.

LETTER TO SHAREHOLDERS

(Continued)

Spread to worst (bps) | | 12/26/2019 | | Q1'20 Peak Spread | | 4/9/2020 | |

AAA 3 yr Credit Cards | | | 26 | | | | 200 | | | | 80 | | |

AAA 3 yr. Prime Auto ABS | | | 33 | | | | 200 | | | | 95 | | |

AAA 2 yr Subprime Auto ABS | | | 44 | | | | 300 | | | | 300 | | |

AAA 3 yr. Ag/Heavy Equipment ABS | | | 53 | | | | 300 | | | | 175 | | |

AAA 5 yr CMBS | | | 62 | | | | 300 | | | | 230 | | |

US 3.0 CLO Secondary Spreads AAA | | | 120 | | | | 400 | | | | 260 | | |

Source: J.P. Morgan. Chart data from January 5, 2006 through April 9, 2020.

Selling pressure in the market for high-quality, short-duration assets exacerbated the price declines and spread increases in AAA-rated asset-backed securities. Some fund managers (though not FPA) faced redemptions due to poor performance. In addition, some fund managers (again, not FPA) were forced to sell bonds to raise cash for margin calls on other investments. In times like these, investment managers tend to unload bonds they think they can sell at prices closest to par. That typically ends up being the highest-quality, shortest bonds.

As shown in the table above, following a significant increase, spreads began to decline toward the end of the quarter following a push by the Federal Reserve to improve market liquidity and lower financing costs for borrowers. To do that, the Fed resurrected old programs (e.g. the term asset-backed securities loan facility, or TALF) and announced new programs designed to improve liquidity in the bond market.

5

FPA NEW INCOME, INC.

LETTER TO SHAREHOLDERS

(Continued)

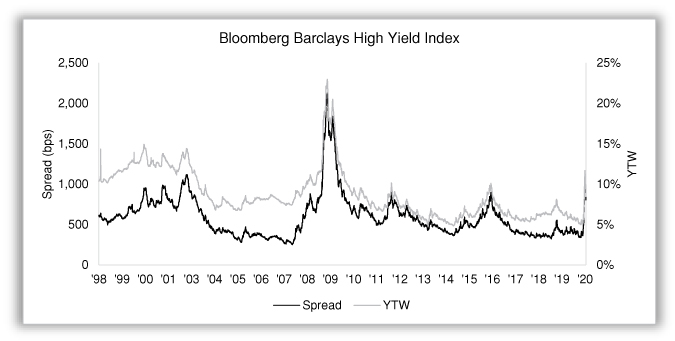

The chart below shows the yield and spread on the Bloomberg Barclays High-Yield Index. It illustrates a similar theme, with yields and spreads reaching levels not seen since 2008-09.

| | | 12/31/2019 | | Q1'20 Peak Spread | | 4/9/2020 | |

Spread (bps) | | | 357 | | | | 1,123 | | | | 804 | | |

YTW | | | 5.19 | % | | | 11.69 | % | | | 8.48 | % | |

Source: Bloomberg Barclays. Chart data is from November 1, 1998 through April 9, 2020.

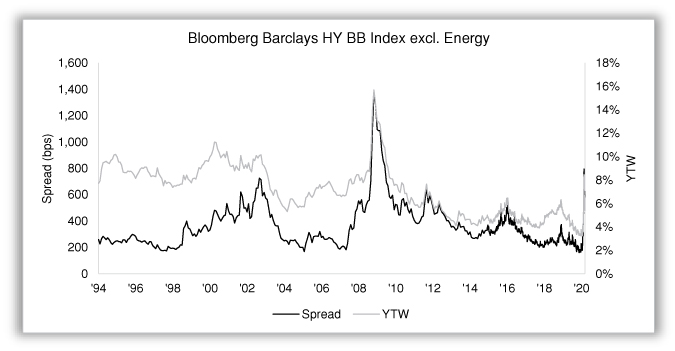

Unfortunately, the pandemic isn't the only thing roiling financial markets. Investors are also digesting the impact of a price war in the oil market, which saw oil prices collapse from over $60 per barrel at the start of the year to $20 per barrel in March. Fluctuations in energy markets have significant repercussions for high-yield energy companies. For this reason, we tend to focus on the non-energy BB component of the high-yield market to get a better sense of how expensive or cheap the core market is (while ignoring the fringes that tend to be more volatile). By that measure as well, the high-yield market reached levels not seen since the 2008-09 financial crisis.

6

FPA NEW INCOME, INC.

LETTER TO SHAREHOLDERS

(Continued)

| | | 12/31/2019 | | Q1'20 Peak Spread | | 4/9/2020 | |

Spread (bps) | | | 177 | | | | 794 | | | | 495 | | |

YTW | | | 3.41 | % | | | 8.44 | % | | | 5.40 | % | |

Source: Bloomberg Barclays. Chart data is from January 1, 1994 through April 9, 2020.

In the span of one month during the first quarter, the BB component of the high-yield index excluding energy declined in price by over 17% versus its Q1 peak! That represented the second-largest monthly price decline on record.

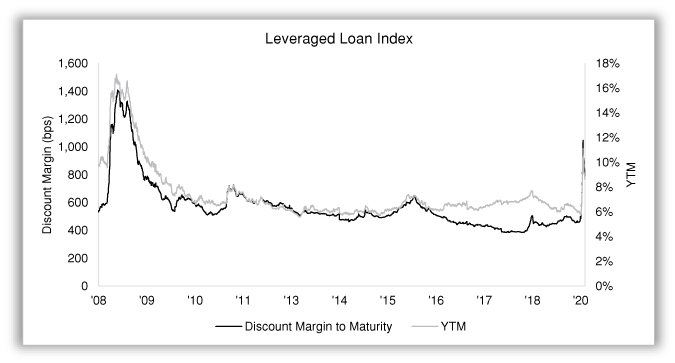

In similar fashion, the leveraged loan index also had its second-largest price decline. The following chart shows the yield and spread on the leveraged loan index.

7

FPA NEW INCOME, INC.

LETTER TO SHAREHOLDERS

(Continued)

| | | 12/31/2019 | | Q1'20 Peak Spread | | 4/9/2020 | |

Discount Margin to Maturity (bps) | | | 471 | | | | 1,047 | | | | 758 | | |

YTM | | | 6.43 | % | | | 11.10 | % | | | 8.26 | % | |

Source: Credit Suisse. Chart data is from June 30, 2008 through April 8, 2020.

While the magnitude and pace of the declines in credit markets were extraordinary, so too were the magnitude and pace of the price recovery. Though still far from achieving their pre-pandemic levels, the high-yield index and leveraged loan markets both gained 7-8% within a week of reaching their respective nadirs, due in no small part to the Federal Reserve's initiatives to support the market.

Several years ago, we began positioning the portfolio to preserve capital. We did not do that because we knew there was going to be a global pandemic. Rather, we felt the market was priced to perfection. Consequently, it did not make sense for us to have a lot of exposure to various forms of risk when there's no room for bad things to happen. Below are the steps we took prior to the virus infecting the markets:

We shortened the portfolio's duration. As we have discussed in the past, we actively manage the portfolio's duration by striving to own bonds that we expect will produce a breakeven or positive total return over 12 months if we assume that yields increase by 100 bps during that time. The purpose of this approach is to own holdings with an attractive risk versus reward profile at all times with respect to interest rate risk rather than owning a specific duration at all times. As interest rates

We shortened the portfolio's duration. As we have discussed in the past, we actively manage the portfolio's duration by striving to own bonds that we expect will produce a breakeven or positive total return over 12 months if we assume that yields increase by 100 bps during that time. The purpose of this approach is to own holdings with an attractive risk versus reward profile at all times with respect to interest rate risk rather than owning a specific duration at all times. As interest rates

8

FPA NEW INCOME, INC.

LETTER TO SHAREHOLDERS

(Continued)

declined at the beginning of the first quarter, prior to the increase in spreads, we took that opportunity to sell some of the portfolio's longer-duration holdings and redeployed the proceeds into shorter-duration bonds. Doing so provides protection against rising interest rates (which may be helpful now, when Treasuries yield less than 50 bps going out to five years). This duration shortening also provides protection against an increase in credit spreads since it reduces the mark-to-market risk of our bonds in the event that spreads increase.

We actively reduced our exposure to higher spreads. For several quarters, we have commented that spreads on high-quality bonds are low relative to historical norms. To account for this, we have been adjusting our usual 100 bps duration test (described above). Specifically, we limited our purchases to bonds we thought could produce a breakeven total return if the yield on the bond increased by more than 100 bps with the amount over 100 bps determined based on the spread increase required to return the bond's spread to what we viewed as a more normal level. We had no expectation that spreads would increase as much as they did this past quarter, but in combination with the reduction in duration described above, this reduction in spread exposure decreased the short-term decline in the portfolio's price once spreads increased.

We actively reduced our exposure to higher spreads. For several quarters, we have commented that spreads on high-quality bonds are low relative to historical norms. To account for this, we have been adjusting our usual 100 bps duration test (described above). Specifically, we limited our purchases to bonds we thought could produce a breakeven total return if the yield on the bond increased by more than 100 bps with the amount over 100 bps determined based on the spread increase required to return the bond's spread to what we viewed as a more normal level. We had no expectation that spreads would increase as much as they did this past quarter, but in combination with the reduction in duration described above, this reduction in spread exposure decreased the short-term decline in the portfolio's price once spreads increased.

We increased the overall quality of our holdings. For years we have commented that credit markets, in general, do not compensate investors for the underlying fundamental credit risk. In line with those comments, we had been reducing the portfolio's credit exposure for the past several years. Further, as spreads in high-quality bonds declined prior to this past quarter, we also did not see value in the lower tiers of the investment grade bond market, particularly BBB bonds. In fact, we published a note describing our concerns with the BBB bond market, "Risk Is Where You're Not Looking" (available on our website at https://fpa.com/news-special-commentaries/special-commentaries/2019/01/02/risk-is-where-you're-not-looking). We also eschewed investing in esoteric and newly created asset classes like marketplace lending because we did not see adequate compensation for the credit risk — even in the investment-grade tranches — especially in light of the limited performance history of those asset classes across economic cycles. Thus, in addition to reducing the portfolio's exposure to bonds rated BBB or lower, we migrated toward widely-held, more liquid bonds rated AAA and AA within the rest of the portfolio. Finally, we took the further step of increasing the portfolio's holdings of Treasury bonds because we determined that the low spread environment sufficiently lowered the opportunity cost of owning Treasuries and that the

We increased the overall quality of our holdings. For years we have commented that credit markets, in general, do not compensate investors for the underlying fundamental credit risk. In line with those comments, we had been reducing the portfolio's credit exposure for the past several years. Further, as spreads in high-quality bonds declined prior to this past quarter, we also did not see value in the lower tiers of the investment grade bond market, particularly BBB bonds. In fact, we published a note describing our concerns with the BBB bond market, "Risk Is Where You're Not Looking" (available on our website at https://fpa.com/news-special-commentaries/special-commentaries/2019/01/02/risk-is-where-you're-not-looking). We also eschewed investing in esoteric and newly created asset classes like marketplace lending because we did not see adequate compensation for the credit risk — even in the investment-grade tranches — especially in light of the limited performance history of those asset classes across economic cycles. Thus, in addition to reducing the portfolio's exposure to bonds rated BBB or lower, we migrated toward widely-held, more liquid bonds rated AAA and AA within the rest of the portfolio. Finally, we took the further step of increasing the portfolio's holdings of Treasury bonds because we determined that the low spread environment sufficiently lowered the opportunity cost of owning Treasuries and that the

9

FPA NEW INCOME, INC.

LETTER TO SHAREHOLDERS

(Continued)

better liquidity of Treasury bonds would be valuable in a market sell-off. The chart below shows the portfolio's exposure over time to Treasuries, AAA-rated bonds and credit-sensitive securities:

We do not use margin or leverage. For decades, the New Income Fund has owned its investments outright, without margin or leverage. That means the Fund sacrificed the higher returns that leverage can create in good times. However, we believe leverage makes investors engage in uneconomic decision making. Leverage may lead investors to overpay for assets because of a focus on the levered return rather than the unlevered return. Leverage also may lead investors to sell at the wrong time, such as when price declines trigger margin calls. We saw that phenomenon over the past few weeks. These sales harm a fund's investors because the fund is selling at unattractive prices. In addition, the margin calls sop up a fund's liquidity right when it should be buying attractively priced investments. Since the Fund operates without leverage, we are never forced to sell and we are always prepared to be an opportunistic buyer. Our prohibition against leverage also helps us maintain enough liquidity to meet our investors' redemption requests on time.

We do not use margin or leverage. For decades, the New Income Fund has owned its investments outright, without margin or leverage. That means the Fund sacrificed the higher returns that leverage can create in good times. However, we believe leverage makes investors engage in uneconomic decision making. Leverage may lead investors to overpay for assets because of a focus on the levered return rather than the unlevered return. Leverage also may lead investors to sell at the wrong time, such as when price declines trigger margin calls. We saw that phenomenon over the past few weeks. These sales harm a fund's investors because the fund is selling at unattractive prices. In addition, the margin calls sop up a fund's liquidity right when it should be buying attractively priced investments. Since the Fund operates without leverage, we are never forced to sell and we are always prepared to be an opportunistic buyer. Our prohibition against leverage also helps us maintain enough liquidity to meet our investors' redemption requests on time.

In total, these steps helped insulate the portfolio from the dramatic spread increases seen throughout fixed income markets in the first quarter. But despite our efforts, the portfolio did experience a decline in the value of its holdings, though those declines were less than what befell many of our peers.7 We believe these price declines will have a short-term impact on performance.

There are two determinants of performance: short-term mark-to-market price changes and permanent impairments of capital. We believe that we do not have a permanent impairment of the fund's capital. Thus, as we

7 As represented by the Morningstar Short-Term Bond Category, which had 1Q 2020 performance of -2.14%. Past performance is no guarantee, nor is it indicative, of future results.

10

FPA NEW INCOME, INC.

LETTER TO SHAREHOLDERS

(Continued)

noted earlier, we believe our portfolio experienced a short-term mark-to-market price decline that we believe will be recovered over time as our short maturity holdings mature and we earn the coupon on our holdings.

Because of our underwriting of our investments, we believe the portfolio's price movements are short term and not reflective of a permanent impairment of capital. The table below breaks down the portfolio by sector and rating.

Fund | | Cash | | US govt/

Agency

guaranteed | | AAA | | AA | | A | | BBB | | BB | | B | | CCC | | NR | | Total | |

ABS | | | — | | | | — | | | | 50 | % | | | 9 | % | | | 3 | % | | | 0 | % | | | 0 | % | | | — | | | | — | | | | — | | | | 63 | % | |

Mortgage-backed (CMO) | | | — | | | | 2 | % | | | 5 | % | | | 1 | % | | | — | | | | — | | | | — | | | | — | | | | — | | | | — | | | | 8 | % | |

Stripped Mortgage-backed | | | — | | | | — | | | | — | | | | 2 | % | | | — | | | | — | | | | — | | | | — | | | | — | | | | — | | | | 2 | % | |

Corporate | | | — | | | | — | | | | — | | | | — | | | | 0 | % | | | 0 | % | | | — | | | | 1 | % | | | 3 | % | | | 3 | % | | | 7 | % | |

CMBS | | | — | | | | 2 | % | | | 6 | % | | | 0 | % | | | 0 | % | | | — | | | | 0 | % | | | — | | | | — | | | | — | | | | 8 | % | |

Mortgage Pass-through | | | — | | | | 3 | % | | | — | | | | — | | | | — | | | | — | | | | — | | | | — | | | | — | | | | — | | | | 3 | % | |

U.S. Treasury | | | — | | | | — | | | | — | | | | — | | | | — | | | | — | | | | — | | | | — | | | | — | | | | — | | | | — | | |

Agencies | | | — | | | | 1 | % | | | — | | | | — | | | | — | | | | — | | | | — | | | | — | | | | — | | | | — | | | | 1 | % | |

Cash and equivalents | | | 3 | % | | | 5 | % | | | — | | | | — | | | | — | | | | — | | | | — | | | | — | | | | — | | | | — | | | | 8 | % | |

Total | | | 3 | % | | | 13 | % | | | 61 | % | | | 12 | % | | | 4 | % | | | 0 | % | | | 0 | % | | | 1 | % | | | 3 | % | | | 3 | % | | | 100 | % | |

Source: FPA. Ratings reflect the Barclays Capital Family of Indices ratings rules and use the median if more than two ratings are available from all Nationally Recognized Statistical Ratings Organizations (NRSROs). Lower of the two is used if only two ratings are available from all NRSROs. Portfolio composition will change due to ongoing management of the Fund.

As of the end of the quarter, approximately 16% of the portfolio was in cash and government obligations. Beyond that, over 75% of the portfolio is held in investments rated AAA to A-, mostly in ABS.

The NRSRO ratings are the only available third-party arbiter of credit quality that has worldwide acceptance. However, we have never relied on these ratings to make our investment decisions. While the world has only recently woken up to the possibility of a recession, we have been worrying about a recession for years. For the past 10+ years, we have been buying bonds on the assumption that we would see a repeat of the 2008-09 financial crisis. That approach continues today. Here are a few examples that highlight our underwriting process:

The Fund's prime auto ABS bonds, representing approximately 18% of the portfolio at quarter end, were chosen based on their ability to withstand large losses in the underlying prime auto loans. Based on our analysis, the Fund's bonds can withstand losses that, on average, are 20 times greater than the losses experienced by these same auto lenders during the last financial crisis.

The Fund's prime auto ABS bonds, representing approximately 18% of the portfolio at quarter end, were chosen based on their ability to withstand large losses in the underlying prime auto loans. Based on our analysis, the Fund's bonds can withstand losses that, on average, are 20 times greater than the losses experienced by these same auto lenders during the last financial crisis.

In a similar manner, the Fund's subprime auto ABS bonds, representing approximately 5% of the portfolio at quarter end, can withstand losses that are over three times greater than what the same lenders experienced during the 2008-09 financial crisis. Importantly, we have only invested with issuers that have a history of managing their businesses through a recession.

In a similar manner, the Fund's subprime auto ABS bonds, representing approximately 5% of the portfolio at quarter end, can withstand losses that are over three times greater than what the same lenders experienced during the 2008-09 financial crisis. Importantly, we have only invested with issuers that have a history of managing their businesses through a recession.

The Fund's non-agency mortgage-backed securities represent approximately 6% of the portfolio at quarter end and have an average loan-to-value ratio of less than 40% of the home value at the time we made the investment. Taking into account home price appreciation that has occurred since the time of our investment, the loan-to-value on these bonds is now less than 30%.

The Fund's non-agency mortgage-backed securities represent approximately 6% of the portfolio at quarter end and have an average loan-to-value ratio of less than 40% of the home value at the time we made the investment. Taking into account home price appreciation that has occurred since the time of our investment, the loan-to-value on these bonds is now less than 30%.

11

FPA NEW INCOME, INC.

LETTER TO SHAREHOLDERS

(Continued)

Collateralized loan obligations represent approximately 10% of the portfolio at quarter end. Among that group, 80% of those holdings are rated AAA with an expected weighted average life of two years. We underwrote the AAA bonds on the assumption that losses on the underlying leveraged loans would be three times greater than what occurred during the 2008-09 financial crisis.

Collateralized loan obligations represent approximately 10% of the portfolio at quarter end. Among that group, 80% of those holdings are rated AAA with an expected weighted average life of two years. We underwrote the AAA bonds on the assumption that losses on the underlying leveraged loans would be three times greater than what occurred during the 2008-09 financial crisis.

Though we are now likely in the throes of a sudden and severe recession, we have been preparing for such a situation for a long time. Because of our long-held downside-focused investment approach, we are confident that the portfolio's capital is not permanently impaired.

As we manage the portfolio to our goal of a positive return in 2020, the portfolio should benefit from two sources of return. First, approximately 13% of the portfolio has an expected average life of nine months or less. Based on our underwriting, we expect the majority of those investments to convert to cash by the end of 2020, and anticipate capturing the discount at which those bonds are priced.8 Second, we expect to earn the coupon on the Fund's investments. Thus far, the portfolio has only earned three months of coupon. Receipt of the remaining nine months of this year's coupon should further offset price declines in the portfolio.

Going forward, we will employ the same approach that led us to protect the portfolio in advance of the pandemic and contributed to our relatively small drawdown. That is, our investment process will focus on fundamental value and absolute return, taking into account the impact that this new economic environment could have on asset values and borrowers' cash flow. Consistent discipline is the best tool to navigate the investment landscape. Unfortunately, as of the writing of this letter, the Fed had already announced unprecedented actions to support the financial markets, including purchases of investment grade and high-yield bonds. Those actions have made our jobs more difficult because the intervention pushed bond prices up significantly, divorcing them from economic reality. Because of these new monetary policy measures (some would say price-fixing), bond prices are no longer an accurate measure of a borrower's economic health. Just because a high-yield bond trades as if it won't default does not mean that it won't default. We believe default-adjusted returns are worse now because the probability and severity of default is certainly higher than it was three months ago, and yet yields do not currently reflect that.

Investors should ask themselves how their portfolios would have performed had the Federal Reserve not stepped in to support the markets. We have always managed our portfolio without assuming that we would have a Fed put (the so-called "Fed put" is the market's expectation that the Fed will prop up financial markets) because we cannot predict which companies the Fed and the government will choose to be the winners and losers in a crisis. For the reasons outlined above, we feel confident that we would have protected our investors' capital because we acted prudently. Can others say the same?

Investors now face a choice: Invest prudently or follow the Fed. Prudent investors will avoid taking on uncompensated risk and will have a portfolio that is better positioned to withstand further short-term declines in asset prices and to benefit from better long-term risk-adjusted performance. Those who follow the Fed will no longer be investors. Rather, they will be following the money, hoping that their investments will end up on the list of government-anointed winners. We choose prudence. What do you choose?

8 Investments that have a weighted average life of nine months in many instances have a principal payment schedule that is longer than nine months, but they have an average principal repayment time of nine months.

12

FPA NEW INCOME, INC.

LETTER TO SHAREHOLDERS

(Continued)

Macro Commentary or Rinse, Lather, Repeat

Why the cute title? It's because this is the fourth consecutive time that an economic expansion has been heavily influenced by monetary and regulatory policies designed to stimulate — or 'lather up' — asset prices through leverage. The following is a list of these downturns along with the asset classes that were lathered with excess leverage:

1990 savings and loan crisis and commercial real estate loans

1990 savings and loan crisis and commercial real estate loans

2001 dot-com bubble, Long Term Capital Management bailout and high yield corporate debt

2001 dot-com bubble, Long Term Capital Management bailout and high yield corporate debt

2008 sub-prime mortgage debt and financial institutions

2008 sub-prime mortgage debt and financial institutions

2020 corporate leverage, government leverage.

2020 corporate leverage, government leverage.

Each of the preceding economic expansions had a different catalyst that caused them to end. The catalyst is not the point. The commonality of each expansion is over leverage (easy credit to a segment of the economy) and asset price appreciation that results in a very similar set of events once the economic downturn has started. Another similarity is that the policy response, whether it be fiscal and or monetary, is more expansive each time. The common element in each policy response is the encouragement of leverage as the tool for igniting a recovery. The end result is that over time, the whole economic system is more levered and therefore the next successive downturn is more dramatic than the last.

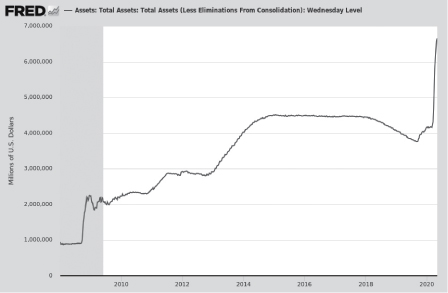

An examination of this current downturn illustrates the problem. To battle the current downturn, the Treasury Department and Federal Reserve resurrected every asset-buying program from the 2008-09 Great Financial Crisis (plus others) to allow the Treasury Department — aided by leverage from the Federal Reserve — to buy a wider variety of investment-grade and some less-than-investment-grade assets. Additionally, the central bank undertook an unlimited buying program of Treasury, agency debt and agency mortgage assets. Many Fed followers predict that by the time those programs are completed, the Fed's balance sheet will reach $9 trillion, or more than double what it was at the beginning of this year. We have no idea if that is correct, but we do know that, longer term, the balance sheet will continue to grow. What we also know is that the Fed's actions will have both intended and unintended consequences. Given what happened in the past, one consequence is that we can expect the Fed's asset purchases to remain on its balance sheet in perpetuity. Graph 1, below, shows the magnitude of the central bank's latest buying spree.

13

FPA NEW INCOME, INC.

LETTER TO SHAREHOLDERS

(Continued)

Source: Board of Governors of the Federal Reserve System (US)

The Federal Open Market Committee (FOMC) also reduced the Fed Funds interest rate to the 0% -.25% range. The Treasury yield curve shown earlier in this commentary reflects the effects of both the Fed's asset purchases and interest rate cut. At this time there appears to be very little upside potential for Treasury bonds unless an investor is confident that Treasury yields will be negative. The Federal Reserve Bank has stated that a negative Fed Funds Rate is not its objective.

Based on this and past reactions, the primary objective of the Fed's actions seems to be to keep the capital markets functioning. The regulatory changes post-2008 worked to prevent the banks/broker-dealers from taking on excessive leverage and limited their exposure to certain market trading activities. However, as we have often noted, the new rules preclude this group of entities from acting as a buffer in times of heavy selling. Their absence leads to increased market volatility and creates pressure on the Treasury department and Federal Reserve Bank to step in and try to create a functioning marketplace. As a data point, from March 11, 2020 to March 31, 2020 exchange-traded bond funds (ETFs) and mutual funds saw a net outflow of $316 billion, the largest outflow ever in such a short period of time.9

14

FPA NEW INCOME, INC.

LETTER TO SHAREHOLDERS

(Continued)

To some degree, the capital markets are now in part a function of government intervention. Hopefully, that will not morph into government control. By law, the Fed's mandate is full employment and stable prices (or avoiding inflation above a 2% target), and neither one is tied to orderly capital markets. However, the concern is that today's Federal Reserve Bank thinks it has three mandates — full employment, stable prices and orderly financial markets, and the last one is of its own making and not rooted in the law.

The federal government acted with unusual speed to help cushion the pandemic's economic effects with a $2.2 trillion relief package to businesses and households. The key question now is, can the government bureaucracy efficiently deliver that aid? Households with previously established direct deposit links with the IRS began to receive one-time relief payments around April 15, while other households may not see checks until later in the summer. Meanwhile, the small business lending program faced start-up delays and quickly ran out of money. Without going into detail, the small business loans are designed to provide the recipients with bridge financing to stave off bankruptcy during the "stay at home" order. Timing is critical for this strategy to work, and delays and insufficient funds could make it less effective, resulting in both a deeper downturn and a slower recovery. The government's programs are not a stimulus package but a relief package meant to partially replace lost revenue and wages. If it's timely, the programs may help minimize the GDP downturn, but it will not boost GDP later. However, there is one thing that is guaranteed to surge: the interest expense from the massive increase in borrowing. Pre-coronavirus forecasts from the Congressional Budget Office estimated the size of the federal government deficit would hover around $1 trillion for several years to come. Those estimates are now understated, with budget deficits potentially growing multiple times larger and lasting much longer. It is difficult to see a scenario where such a dramatic increase in debt has no impact on interest rates and inflation over the long term. It is just that today, that impact is still an unknown risk.

Both the central bank and federal government actions are focused on the near term, while the economy is in "stay at home" mode. The more important investment question, however, is what will the economy be like once this social policy is changed? Is the "stay at home" order just removed or relaxed over time? Will the virus reappear in the fall, or will relaxing "stay at home" orders immediately trigger further spreading of the virus? Will we have adequate testing to prevent that? How quickly will we have effective treatments for the disease caused by the virus, thus reducing deaths? Will we be able to develop a vaccine? All of these are questions that pertain to the rest of 2020. So again, what about longer term? Societal norms could change significantly because of the tremendous shock associated with the virus and our mitigation efforts. Psychologists say it takes 4-6 weeks to change a habit or behavior, and since the current mitigation effort could easily last 6-8 weeks, there are likely to be some permanent changes in behavior and our economy. Below is a list of the household, government and company behavior changes envisioned by Torsten Slok, an economist at Deutsche Bank. There are several other lists that predict similar behavior changes.

Reasons why growth over the coming quarters will be more muted

Household sector

Increase in precautionary savings for households, similar to what we saw after the Great Depression in the 1930s

Increase in precautionary savings for households, similar to what we saw after the Great Depression in the 1930s

More space between seats at restaurants, cinemas, sport events, concerts, conferences, trains, buses, and airplanes

More space between seats at restaurants, cinemas, sport events, concerts, conferences, trains, buses, and airplanes

15

FPA NEW INCOME, INC.

LETTER TO SHAREHOLDERS

(Continued)

Fewer people traveling on vacation and going out until we have a vaccine, all contributing to lower consumer spending

Fewer people traveling on vacation and going out until we have a vaccine, all contributing to lower consumer spending

Older generations staying at home until a vaccine is released, less willingness to put parents in retirement homes

Older generations staying at home until a vaccine is released, less willingness to put parents in retirement homes

Limits on the number of people in supermarkets at the same time, more online shopping, more online doctor visits

Limits on the number of people in supermarkets at the same time, more online shopping, more online doctor visits

Fewer people going to fitness centers, doing group sports

Fewer people going to fitness centers, doing group sports

More people driving their own car to avoid public transportation

More people driving their own car to avoid public transportation

Health insurance premiums going up

Health insurance premiums going up

Corporate sector

Less business travel globally, more video conferencing

Less business travel globally, more video conferencing

Staggered work schedules, more distance between seats in offices, fewer cubicles

Staggered work schedules, more distance between seats in offices, fewer cubicles

More permanent work from home solutions, more disaster planning

More permanent work from home solutions, more disaster planning

Fewer buybacks, lower dividend payouts

Fewer buybacks, lower dividend payouts

Health insurance costs going up, higher insurance premiums

Health insurance costs going up, higher insurance premiums

Increased pressure for paid sick leave, health benefits, labor protection, including for gig workers

Increased pressure for paid sick leave, health benefits, labor protection, including for gig workers

Government sector

Global restrictions on travel to high-risk areas, more fever scanners at airports, borders

Global restrictions on travel to high-risk areas, more fever scanners at airports, borders

More regulation forcing households and corporates to hold, say, three months of cash in emergency savings

More regulation forcing households and corporates to hold, say, three months of cash in emergency savings

More regulation and spending to ensure health care system is better prepared

More regulation and spending to ensure health care system is better prepared

Increased health safety regulations for retirement homes

Increased health safety regulations for retirement homes

Stocking of medical supplies, including ventilators, domestically, a desire to be less dependent on other countries

Stocking of medical supplies, including ventilators, domestically, a desire to be less dependent on other countries

More systematic planning and preparedness, perhaps introduce better automatic stabilizers

More systematic planning and preparedness, perhaps introduce better automatic stabilizers

More supply of government bonds, increasing risk of a debt crisis

More supply of government bonds, increasing risk of a debt crisis

Source: Deutsche Bank Research report dated April 2020.

We are not saying that all of these changes will occur, but they represent a framework for how to monitor and analyze the economic impact on households, businesses and governments. One general behavioral change that could sum up the potential post-virus economy is that the focus for companies could shift from efficiency to resiliency, and households could retreat from their free-spending ways to set aside more savings. Government spending should adjust by building stockpiles of critical supplies and building infrastructure to respond to these crises, but that may be wishful thinking. Government actions tend to reflect politicians' desires to meet the immediate wants rather than the long-term needs of their respective populations.

16

FPA NEW INCOME, INC.

LETTER TO SHAREHOLDERS

(Continued)

The aftermath of all the financial market events listed at the beginning of this commentary had various impacts on capital markets, along with abrupt behavior changes from corporations, governments and households. Some were transient and others were more enduring. As an example, the reaction from the Federal Reserve Bank tended to be more intrusive with each succeeding event. With each economic downturn, the Fed's efforts to prop up financial markets were expanded. With each expansion of the so-called central bank put, it becomes harder to measure fixed income risk, whether it be interest rate risk or credit risk. Those risks became more socialized as the central bank stepped in to control them and took on some of the risks that would otherwise be borne by private investors. We expect that this time will not be different.

From our perspective, proper compensation for risk has become a cloudier equation. This does not change our focus on absolute value returns, it merely makes it more difficult to execute. For now, that means every potential investment will be subject to a few additional questions before we commit your capital.

Thank you for your continued trust and support.

Respectfully submitted,

Thomas H. Atteberry

Portfolio Manager

Abhijeet Patwardhan

Portfolio Manager

April 2020

Important Disclosures

This update is for informational and discussion purposes only and does not constitute, and should not be construed as, an offer or solicitation for the purchase or sale of any securities, products or services discussed, and neither does it provide investment advice. Any such offer or solicitation shall only be made pursuant to the Fund's Prospectus, which supersedes the information contained herein in its entirety.

The views expressed herein and any forward-looking statements are as of the date of the publication and are those of the portfolio management team. Future events or results may vary significantly from those expressed and are subject to change at any time in response to changing circumstances and industry developments. This information and data has been prepared from sources believed reliable, but the accuracy and completeness of the information cannot be guaranteed and is not a complete summary or statement of all available data.

17

FPA NEW INCOME, INC.

LETTER TO SHAREHOLDERS

(Continued)

Thomas Atteberry and Abhijeet Patwardhan have been portfolio managers for the Fund since November 2004 and November 2015, respectively, and manage the Fund in a manner that is substantially similar to the prior portfolio manager, Robert Rodriguez. Mr. Rodriguez ceased serving as the Fund's portfolio manager effective December 2009.

Portfolio composition will change due to ongoing management of the Fund. References to individual securities or sectors are for informational purposes only and should not be construed as recommendations by the Fund, the portfolio managers, the Adviser, or the distributor. It should not be assumed that future investments will be profitable or will equal the performance of the security or sector examples discussed. The portfolio holdings as of the most recent quarter-end may be obtained at www.fpa.com.

The statements made herein may be forward-looking and/or based on current expectations, projections, and/or information currently available. Actual results may differ from those anticipated. The portfolio managers and/or FPA cannot assure future results and disclaims any obligation to update or alter any statistical data and/or references thereto, as well as any forward-looking statements, whether as a result of new information, future events, or otherwise. Such statements may or may not be accurate over the long-term.

Investments, including investments in mutual funds, carry risks and investors may lose principal value. Capital markets are volatile and can decline significantly in response to adverse issuer, political, regulatory, market, or economic developments. The Fund may purchase foreign securities, including American Depository Receipts (ADRs) and other depository receipts, which are subject to interest rate, currency exchange rate, economic and political risks; this may be enhanced when investing in emerging markets. Foreign investments, especially those of companies in emerging markets, can be riskier, less liquid, harder to value, and more volatile than investments in the United States. The securities of smaller, less well-known companies can be more volatile than those of larger companies.

The return of principal in a bond fund is not guaranteed. Bond funds have the same issuer, interest rate, inflation and credit risks that are associated with underlying bonds owned by the Fund. Lower rated bonds, convertible securities and other types of debt obligations involve greater risks than higher rated bonds.

Interest rate risk is the risk that when interest rates go up, the value of fixed income securities, such as bonds, typically go down and investors may lose principal value. Credit risk is the risk of loss of principal due to the issuer's failure to repay a loan. Generally, the lower the quality rating of a security, the greater the risk that the issuer will fail to pay interest fully and return principal in a timely manner. If an issuer defaults the security may lose some or all of its value.

Mortgage securities and collateralized mortgage obligations (CMOs) are subject to prepayment risk and the risk of default on the underlying mortgages or other assets; such derivatives may increase volatility. Convertible securities are generally not investment grade and are subject to greater credit risk than higher-rated investments. High yield securities can be volatile and subject to much higher instances of default.

Value style investing presents the risk that the holdings or securities may never reach their full market value because the market fails to recognize what the portfolio management team considers the true business value or because the portfolio management team has misjudged those values. In addition, value style investing may fall out of favor and underperform growth or other styles of investing during given periods.

The ratings agencies that provide ratings are Standard and Poor's, Moody's, and Fitch. Credit ratings range from AAA (highest) to D (lowest). Bonds rated BBB or above are considered investment grade. Credit ratings of BB and below are lower-rated securities (junk bonds). High-yielding, non-investment grade bonds (junk bonds)

18

FPA NEW INCOME, INC.

LETTER TO SHAREHOLDERS

(Continued)

involve higher risks than investment grade bonds. Bonds with credit ratings of CCC or below have high default risk.

The Fund is not authorized for distribution unless preceded or accompanied by a current prospectus. The prospectus can be accessed at: https://fpa.com/request-funds-literature.

Index / Benchmark Definitions

Comparison to any index is for illustrative purposes only and should not be relied upon as a fully accurate measure of comparison. The Fund will be less diversified than the indices noted herein, and may hold non-index securities or securities that are not comparable to those contained in an index. Indices will hold positions that are not within the Fund's investment strategy. Indices are unmanaged, do not reflect any commissions, fees or expenses which would be incurred by an investor purchasing the underlying securities. The Fund does not include outperformance of any index or benchmark in its investment objectives. Investors cannot invest directly in an index.

Bloomberg Barclays US Aggregate Bond Index provides a measure of the performance of the U.S. investment grade bonds market, which includes investment grade U.S. Government bonds, investment grade corporate bonds, mortgage pass-through securities and asset-backed securities that are publicly offered for sale in the United States. The securities in the Index must have at least 1 year remaining in maturity. In addition, the securities must be denominated in U.S. dollars and must be fixed rate, nonconvertible, and taxable.

Bloomberg Barclays US Aggregate 1-3 Year Index provides a measure of the performance of the U.S. investment grade bonds market, which includes investment grade U.S. Government bonds, investment grade corporate bonds, mortgage pass-through securities and asset-backed securities that are publicly offered for sale in the United States. The securities in the Index must have a remaining maturity of 1 to 3 years. In addition, the securities must be denominated in U.S. dollars and must be fixed rate, nonconvertible, and taxable.

Bloomberg Barclays U.S. High Yield Index measures the market of USD-denominated, non-investment grade, fixed-rate, taxable corporate bonds.

Bloomberg Barclays BB U.S. High Yield Index ex. Energy measures the market of USD-denominated, non-investment grade, fixed-rate, taxable corporate bonds rated BB excluding energy sector.

Credit Suisse Leveraged Loan Index is designed to mirror the investable universe of U.S. dollar institutional leveraged loans, including U.S. and international borrowers.

The Consumer Price Index (CPI) is an unmanaged index representing the rate of the inflation of U.S. consumer prices as determined by the U.S. Department of Labor Statistics. The CPI is presented to illustrate the Fund's purchasing power against changes in the prices of goods as opposed to a benchmark, which is used to compare the Fund's performance. There can be no guarantee that the CPI will reflect the exact level of inflation at any given time. This index reflects non-seasonally adjusted returns.

CPI + 100 bps is the measure of the CPI plus an additional 100 basis points.

Basis Point (bps) is equal to one hundredth of one percent, or 0.01%. 100 basis points = 1%.

Corporate holdings include bank debt, corporate bonds and common stock.

A discount margin to maturity is the average expected return of a floating-rate security (typically a bond) that's earned in addition to the index underlying, or reference rate of, the security. The size of the discount margin depends on the price of the floating- or variable-rate security.

19

FPA NEW INCOME, INC.

LETTER TO SHAREHOLDERS

(Continued)

Effective Duration (years) is the duration calculation for bonds with embedded options. Effective duration takes into account that expected cash flows will fluctuate as interest rates change.

Weighted Average Life (years) is the average length of time that each dollar of unpaid principal on a loan, a mortgage or an amortizing bond remains outstanding.

Repo (Repurchase Agreement) is a form of short-term borrowing for dealers in government securities.

Yield to Maturity is the rate of return anticipated on a bond if held until the end of its lifetime. YTM is considered a long-term bond yield expressed as an annual rate. The YTM calculation takes into account the bond's current market price, par value, coupon interest rate and time to maturity. It is also assumed that all coupon payments are reinvested at the same rate as the bond's current yield.

Morningstar Bond Categories

Short-Term Bond Category. Short-term bond portfolios invest primarily in corporate and other investment-grade U.S. fixed-income issues and typically have durations of 1.0 to 3.5 years. These portfolios are attractive to fairly conservative investors, because they are less sensitive to interest rates than portfolios with longer durations. Morningstar calculates monthly breakpoints using the effective duration of the Morningstar Core Bond Index in determining duration assignment. Short-term is defined as 25% to 75% of the three-year average effective duration of the MCBI. Short-Term Bond Category consists of 558 funds.

Morningstar does not adjust total return for sales charges or for redemption fees.

©2020 Morningstar, Inc. All Rights Reserved. The information contained herein: (1) is proprietary to Morningstar and/or its content providers; (2) may not be copied or distributed; and (3) is not warranted by Morningstar to be accurate, complete or timely. Neither Morningstar nor its content providers are responsible for any damages or losses arising from any use of this information. Past performance is no guarantee of future results.

The FPA Funds are distributed by UMB Distribution Services, LLC, 235 W. Galena Street, Milwaukee, WI, 53212.

20

FPA NEW INCOME, INC.

LETTER TO SHAREHOLDERS

(Continued)

The discussions of Fund investments represent the views of the Fund's managers at the time of this report and are subject to change without notice. References to individual securities are for informational purposes only and should not be construed as recommendations to purchase or sell individual securities.

FUND RISKS

Investments in mutual funds carry risks and investors may lose principal value. Stock markets are volatile and can decline significantly in response to adverse issuer, political, regulatory, market, or economic developments. The funds may purchase foreign securities which are subject to interest rate, currency exchange rate, economic and political risks: this may be enhanced when investing in emerging markets. The securities of smaller, less well-known companies can be more volatile than those of larger companies. The return of principal in a bond fund is not guaranteed. Bond funds have the same issuer, interest rate, inflation and credit risks that are associated with underlying bonds owned by the fund. Lower rated bonds, convertible securities and other types of debt obligations involve greater risks than higher rated bonds. Mortgage securities and collateralized mortgage obligations (CMOs) are subject to prepayment risk and the risk of default on the underlying mortgages or other assets; derivatives may increase volatility. High yield securities can be volatile and subject to much higher instances of default.

FORWARD LOOKING STATEMENT DISCLOSURE

As mutual fund managers, one of our responsibilities is to communicate with shareholders in an open and direct manner. Insofar as some of our opinions and comments in our letters to shareholders are based on our current expectations, they are considered "forward-looking statements" which may or may not prove to be accurate over the long term. While we believe we have a reasonable basis for our comments and we have confidence in our opinions, actual results may differ materially from those we anticipate. You can identify forward-looking statements by words such as "believe," "expect," "may," "anticipate," and other similar expressions when discussing prospects for particular portfolio holdings and/or the markets, generally. We cannot, however, assure future results and disclaim any obligation to update or alter any forward-looking statements, whether as a result of new information, future events, or otherwise. Further, information provided in this report should not be construed as a recommendation to purchase or sell any particular security.

21

FPA NEW INCOME, INC.

PORTFOLIO SUMMARY

March 31, 2020 (Unaudited)

Common Stocks | | | | | 0.3 | % | |

Energy | | | 0.3 | % | | | | | |

Industrials | | | 0.0 | % | | | | | |

Bonds & Debentures | | | | | 97.1 | % | |

Asset-Backed Securities | | | 63.0 | % | | | | | |

Residential Mortgage-Backed Securities | | | 12.6 | % | | | | | |

Commercial Mortgage-Backed Securities | | | 9.8 | % | | | | | |

U.S. Treasuries | | | 5.0 | % | | | | | |

Corporate Bank Debt | | | 4.9 | % | | | | | |

Corporate Bonds & Notes | | | 1.8 | % | | | | | |

Short-term Investments | | | | | 1.5 | % | |

Other Assets And Liabilities, Net | | | | | 1.1 | % | |

Net Assets | | | | | 100.0 | % | |

22

FPA NEW INCOME, INC.

PORTFOLIO OF INVESTMENTS

March 31, 2020

(Unaudited)

COMMON STOCKS | | Shares or

Principal

Amount | |

Fair Value | |

ENERGY — 0.3% | |

PHI Group, Inc.(a)(b) | | | 1,203,928 | | | $ | 7,825,532 | | |

PHI Group, Inc., Restricted(a)(b)(c)(e) | | | 2,602,492 | | | | 16,916,198 | | |

| | | $ | 24,741,730 | | |

INDUSTRIALS — 0.0% | |

Boart Longyear Ltd.(a) | | | 874,320 | | | $ | 247,385 | | |

| TOTAL COMMON STOCKS — 0.3% (Cost $31,764,951) | | $ | 24,989,115 | | |

BONDS & DEBENTURES | |

COMMERCIAL MORTGAGE-BACKED SECURITIES — 9.8% | |

AGENCY — 1.6% | |

Federal Home Loan Mortgage Corp. K042 A1 — 2.267% 6/25/2024 | | $ | 14,709,750 | | | $ | 15,007,296 | | |

Federal Home Loan Mortgage Corp. K024 A2 — 2.573% 9/25/2022 | | | 5,758,105 | | | | 5,924,666 | | |

Government National Mortgage Association 2009-119 IO —

0.219% 12/16/2049(d) | | | 7,890,384 | | | | 23,561 | | |

Government National Mortgage Association 2014-175 IO —

0.759% 4/16/2056(d) | | | 178,751,640 | | | | 7,637,807 | | |

Government National Mortgage Association 2014-169 A —

2.600% 11/16/2042 | | | 3,358,578 | | | | 3,397,198 | | |

Government National Mortgage Association 2015-21 A —

2.600% 11/16/2042 | | | 4,961,019 | | | | 5,013,154 | | |

Government National Mortgage Association 2014-148 A —

2.650% 11/16/2043 | | | 10,537,353 | | | | 10,649,859 | | |

Government National Mortgage Association 2019-39 A —

3.100% 5/16/2059 | | | 64,931,729 | | | | 66,699,612 | | |

Government National Mortgage Association 2011-9 C, VRN —

3.485% 9/16/2041(d) | | | 2,190,267 | | | | 2,207,227 | | |

Government National Mortgage Association 2010-148 AC —

7.000% 12/16/2050(d) | | | 21,226 | | | | 21,597 | | |

| | | $ | 116,581,977 | | |

AGENCY STRIPPED — 2.3% | |

Government National Mortgage Association 2004-10 IO —

0.000% 1/16/2044(d) | | $ | 3,762,616 | | | $ | 4 | | |

Government National Mortgage Association 2012-45 IO —

0.000% 4/16/2053(d) | | | 7,716,626 | | | | 31,556 | | |

Government National Mortgage Association 2002-56 IO —

0.043% 6/16/2042(d) | | | 16,288 | | | | 15 | | |

23

FPA NEW INCOME, INC.

PORTFOLIO OF INVESTMENTS (Continued)

March 31, 2020

(Unaudited)

BONDS & DEBENTURES — Continued | | Principal

Amount | | Fair Value | |

Government National Mortgage Association 2009-105 IO —

0.183% 11/16/2049(d) | | $ | 4,867,357 | | | $ | 16,351 | | |

Government National Mortgage Association 2009-86 IO —

0.250% 10/16/2049(d) | | | 11,347,404 | | | | 51,961 | | |

Government National Mortgage Association 2009-71 IO —

0.264% 7/16/2049(d) | | | 3,105,182 | | | | 23,333 | | |

Government National Mortgage Association 2009-49 IO —

0.280% 6/16/2049(d) | | | 5,120,230 | | | | 18,524 | | |

Government National Mortgage Association 2012-125 IO —

0.343% 2/16/2053(d) | | | 68,212,621 | | | | 1,424,607 | | |

Government National Mortgage Association 2008-8 IO —

0.352% 11/16/2047(d) | | | 4,567,508 | | | | 15,585 | | |

Government National Mortgage Association 2009-4 IO —

0.390% 1/16/2049(d) | | | 2,760,714 | | | | 20,010 | | |

Government National Mortgage Association 2012-25 IO —

0.417% 8/16/2052(d) | | | 71,978,589 | | | | 889,591 | | |

Government National Mortgage Association 2010-123 IO —

0.484% 9/16/2050(d) | | | 3,736,148 | | | | 30,648 | | |

Government National Mortgage Association 2009-60 IO —

0.509% 6/16/2049(d) | | | 6,932,501 | | | | 60,794 | | |

Government National Mortgage Association 2014-157 IO —

0.548% 5/16/2055(d) | | | 108,016,963 | | | | 3,129,651 | | |

Government National Mortgage Association 2009-30 IO —

0.570% 3/16/2049(d) | | | 5,071,837 | | | | 135,582 | | |

Government National Mortgage Association 2013-45 IO —

0.572% 12/16/2053(d) | | | 62,570,604 | | | | 1,017,673 | | |

Government National Mortgage Association 2007-77 IO —

0.580% 11/16/2047(d) | | | 20,732,090 | | | | 249,117 | | |

Government National Mortgage Association 2015-41 IO —

0.592% 9/16/2056(d) | | | 31,855,655 | | | | 1,209,257 | | |

Government National Mortgage Association 2008-24 IO —

0.604% 11/16/2047(d) | | | 246,926 | | | | 3 | | |

Government National Mortgage Association 2005-9 IO —

0.627% 1/16/2045(d) | | | 761,955 | | | | 1,878 | | |

Government National Mortgage Association 2013-125 IO —

0.648% 10/16/2054(d) | | | 18,891,984 | | | | 452,253 | | |

Government National Mortgage Association 2012-58 IO —

0.649% 2/16/2053(d) | | | 180,866,177 | | | | 3,747,818 | | |

Government National Mortgage Association 2012-79 IO —

0.655% 3/16/2053(d) | | | 106,867,782 | | | | 2,662,985 | | |

24

FPA NEW INCOME, INC.

PORTFOLIO OF INVESTMENTS (Continued)

March 31, 2020

(Unaudited)

BONDS & DEBENTURES — Continued | | Principal

Amount | | Fair Value | |

Government National Mortgage Association 2012-150 IO —

0.678% 11/16/2052(d) | | $ | 60,673,914 | | | $ | 1,982,453 | | |

Government National Mortgage Association 2014-110 IO —

0.689% 1/16/2057(d) | | | 63,626,631 | | | | 2,674,208 | | |

Government National Mortgage Association 2014-77 IO —

0.713% 12/16/2047(d) | | | 43,820,687 | | | | 1,380,426 | | |

Government National Mortgage Association 2014-138 IO —

0.728% 4/16/2056(d) | | | 25,905,585 | | | | 1,036,524 | | |

Government National Mortgage Association 2015-19 IO —

0.733% 1/16/2057(d) | | | 86,234,989 | | | | 3,885,059 | | |

Government National Mortgage Association 2015-7 IO —

0.735% 1/16/2057(d) | | | 51,856,877 | | | | 2,313,833 | | |

Government National Mortgage Association 2015-86 IO —

0.741% 5/16/2052(d) | | | 61,167,668 | | | | 2,485,768 | | |

Government National Mortgage Association 2004-43 IO —

0.744% 6/16/2044(d) | | | 9,308,195 | | | | 115,655 | | |

Government National Mortgage Association 2014-135 IO —

0.748% 1/16/2056(d) | | | 239,560,159 | | | | 9,036,281 | | |

Government National Mortgage Association 2014-153 IO —

0.752% 4/16/2056(d) | | | 198,451,691 | | | | 8,332,014 | | |

Government National Mortgage Association 2014-187 IO —

0.753% 5/16/2056(d) | | | 123,569,500 | | | | 5,262,479 | | |

Government National Mortgage Association 2012-114 IO —

0.760% 1/16/2053(d) | | | 39,526,983 | | | | 1,621,120 | | |

Government National Mortgage Association 2014-164 IO —

0.775% 1/16/2056(d) | | | 223,472,248 | | | | 8,380,276 | | |

Government National Mortgage Association 2015-47 IO —

0.803% 10/16/2056(d) | | | 148,310,570 | | | | 6,894,588 | | |

Government National Mortgage Association 2015-101 IO —

0.819% 3/16/2052(d) | | | 131,953,500 | | | | 5,993,447 | | |

Government National Mortgage Association 2015-108 IO —

0.835% 10/16/2056(d) | | | 27,835,326 | | | | 1,286,259 | | |

Government National Mortgage Association 2008-45 IO —

0.852% 2/16/2048(d) | | | 2,585,105 | | | | 4,922 | | |

Government National Mortgage Association 2006-55 IO —

0.855% 8/16/2046(d) | | | 6,608,438 | | | | 70,189 | | |

Government National Mortgage Association 2015-114 IO —

0.886% 3/15/2057(d) | | | 134,359,358 | | | | 6,018,171 | | |

Government National Mortgage Association 2015-150 IO —

0.889% 9/16/2057(d) | | | 200,825,263 | | | | 11,142,609 | | |

25

FPA NEW INCOME, INC.

PORTFOLIO OF INVESTMENTS (Continued)

March 31, 2020

(Unaudited)

BONDS & DEBENTURES — Continued | | Principal

Amount | | Fair Value | |

Government National Mortgage Association 2015-160 IO —

0.901% 1/16/2056(d) | | $ | 227,519,179 | | | $ | 11,029,789 | | |

Government National Mortgage Association 2015-169 IO —

0.916% 7/16/2057(d) | | | 215,615,880 | | | | 11,920,734 | | |

Government National Mortgage Association 2015-128 IO —

0.920% 12/16/2056(d) | | | 186,183,942 | | | | 9,110,799 | | |

Government National Mortgage Association 2008-48 IO —

0.968% 4/16/2048(d) | | | 8,705,695 | | | | 124,711 | | |

Government National Mortgage Association 2016-65 IO —

0.982% 1/16/2058(d) | | | 220,696,718 | | | | 13,279,741 | | |

Government National Mortgage Association 2016-125 IO —

0.985% 12/16/2057(d) | | | 118,094,672 | | | | 7,138,162 | | |

Government National Mortgage Association 2016-106 IO —

1.015% 9/16/2058(d) | | | 229,591,261 | | | | 14,956,883 | | |

Government National Mortgage Association 2008-92 IO —

1.206% 10/16/2048(d) | | | 12,176,584 | | | | 110,628 | | |

Government National Mortgage Association 2004-108 IO —

1.919% 12/16/2044(d) | | | 377,780 | | | | 18 | | |

Government National Mortgage Association 2006-30 IO —

2.392% 5/16/2046(d) | | | 842,862 | | | | 9,132 | | |

| | | $ | 162,786,074 | | |

NON-AGENCY — 5.9% | |

Aventura Mall Trust 2013-AVM A — 3.743% 12/5/2032(d)(e) | | $ | 37,824,000 | | | $ | 38,074,671 | | |

Bear Stearns Commercial Mortgage Securities Trust 2005-PWR7 B —

5.117% 2/11/2041(d) | | | 2,048,180 | | | | 2,048,755 | | |

Citigroup Commercial Mortgage Trust 2012-GC8 A4 —

3.024% 9/10/2045 | | | 4,148,778 | | | | 4,149,177 | | |

Citigroup Commercial Mortgage Trust 2017-C4 A2 —

3.190% 10/12/2050 | | | 18,524,000 | | | | 19,003,386 | | |

COMM 2012-CCRE2 Mortgage Trust 2012-CR2 A4 —

3.147% 8/15/2045 | | | 15,226,000 | | | | 15,422,930 | | |

COMM Mortgage Trust 2012-CR5 A3 — 2.540% 12/10/2045 | | | 5,942,220 | | | | 5,955,612 | | |

COMM Mortgage Trust 2013-LC6 A4 — 2.941% 1/10/2046 | | | 8,502,748 | | | | 8,618,304 | | |

COMM Mortgage Trust 2014-FL5 B, 1M LIBOR + 2.150% —

3.045% 10/15/2031(d)(e) | | | 730,827 | | | | 694,937 | | |

COMM Mortgage Trust 2014-FL5 C, 1M LIBOR + 2.150% —

3.045% 10/15/2031(d)(e) | | | 8,340,000 | | | | 7,765,444 | | |

DBUBS Mortgage Trust 2011-LC2A A4 — 4.537% 7/10/2044(e) | | | 44,816,836 | | | | 45,374,908 | | |

GS Mortgage Securities Corp. Trust 2012-ALOH A —

3.551% 4/10/2034(e) | | | 21,003,000 | | | | 20,888,668 | | |

26

FPA NEW INCOME, INC.

PORTFOLIO OF INVESTMENTS (Continued)

March 31, 2020

(Unaudited)

BONDS & DEBENTURES — Continued | | Principal

Amount | | Fair Value | |

J.P. Morgan Chase Commercial Mortgage Securities Trust 2016-WIKI A —

2.798% 10/5/2031(e) | | $ | 7,922,000 | | | $ | 7,561,211 | | |

JP Morgan Chase Commercial Mortgage Securities Trust C 2012-HSBC A —

3.093% 7/5/2032(e) | | | 47,349,537 | | | | 48,271,882 | | |

JPMBB Commercial Mortgage Securities Trust 2015-C30 ASB —

3.559% 7/15/2048 | | | 7,605,000 | | | | 7,775,138 | | |

Latitude Management Real Estate Capita 2016-CRE2 A,

1M LIBOR + 1.700% — 3.329% 11/24/2031(d)(e) | | | 2,122,296 | | | | 2,092,217 | | |

UBS Commercial Mortgage Trust 2012-C1 A3 — 3.400% 5/10/2045 | | | 6,615,816 | | | | 6,672,852 | | |

VNDO E Mortgage Trust 2012-6AVE A — 2.996% 11/15/2030(e) | | | 5,604,681 | | | | 5,674,649 | | |

VNDO E Mortgage Trust 2012-6AVE B — 3.298% 11/15/2030(e) | | | 13,266,000 | | | | 13,198,955 | | |

Wells Fargo Commercial Mortgage Trust 2019-C51 A1 —

2.276% 6/15/2052 | | | 10,384,927 | | | | 10,417,785 | | |

Wells Fargo Commercial Mortgage Trust 2012-LC5 A3 —

2.918% 10/15/2045 | | | 34,087,330 | | | | 34,412,686 | | |

WFRBS Commercial Mortgage Trust 2012-C9 A3 —

2.870% 11/15/2045 | | | 11,229,629 | | | | 11,253,239 | | |

WFRBS Commercial Mortgage Trust 2012-C8 A3 —

3.001% 8/15/2045 | | | 63,956,000 | | | | 64,553,343 | | |