Annual

Report

Needham Funds

Seeking to build wealth for long-term investors.

December 31, 2018

Needham Growth Fund

Needham Aggressive Growth Fund

Needham Small Cap Growth Fund

www.needhamfunds.com

Beginning on January 1, 2021, as permitted by regulations adopted by the Securities and Exchange Commission, paper copies of the Funds’ shareholder reports will no longer be sent by mail, unless you specifically request paper copies of the reports from the Funds or from your financial intermediary, such as a broker-dealer or bank. Instead, the reports will be made available on a website, and you will be notified by mail each time a report is posted and provided with a website link to access the report.

If you already elected to receive shareholder reports electronically, you will not be affected by this change and you need not take any action. You may elect to receive shareholder reports and other communications electronically from the Funds by calling 1-800-625-7071 or by contacting your financial intermediary (such as a broker-dealer or bank).

You may elect to receive all future reports in paper free of charge. You can request to continue receiving paper copies of your shareholder reports by contacting your financial intermediary or, if you invest directly with a Fund, calling 1-800-625-7071 to let the Fund know of your request. Your election to receive in paper will apply to all funds held in your account.

250 Park Avenue, 10th Floor

New York, New York 10177

1-800-625-7071

www.needhamfunds.com

Annual Report

December 31, 2018

Contents

| Letter from the Adviser | 1 |

| Portfolio Characteristics | |

| Needham Growth Fund | 12 |

| Needham Aggressive Growth Fund | 14 |

| Needham Small Cap Growth Fund | 16 |

| Disclosure of Fund Expenses | 18 |

| Schedules of Investments | |

| Needham Growth Fund | 20 |

| Needham Aggressive Growth Fund | 25 |

| Needham Small Cap Growth Fund | 30 |

| Schedules of Securities Sold Short | |

| Needham Growth Fund | 24 |

| Needham Aggressive Growth Fund | 29 |

| Statements of Assets and Liabilities | 34 |

| Statements of Operations | 36 |

| Statements of Changes in Net Assets | 37 |

| Financial Highlights | |

| Needham Growth Fund | 40 |

| Needham Aggressive Growth Fund | 42 |

| Needham Small Cap Growth Fund | 44 |

| Notes to Financial Statements | 46 |

| Report of Independent Registered Public Accounting Firm | 55 |

| Information about Directors and Officers | 56 |

| Supplementary Information and Privacy Policy | 58 |

This report is authorized for distribution to prospective investors only when preceded or accompanied by a current prospectus. The prospectus contains more complete information, including investment objectives, risks, expenses and charges and should be read carefully before investing or sending any money. To obtain a prospectus or summary prospectus, please call 1-800-625-7071.

Portfolios of The Needham Funds, Inc., like all mutual funds:

• Are NOT FDIC insured

• Have no bank guarantee

• May lose value

The Needham Funds, Inc. are distributed by Needham & Company, LLC.

| 250 Park Avenue, 10th Floor |

| New York, NY 10177 |

| (800) 625-7071 |

| www.needhamfunds.com |

February 2019

Dear Shareholders, Friends of Needham and Prospective Shareholders,

We are reporting results for the quarter and year ended December 31, 2018 for the Needham Growth Fund, Needham Aggressive Growth Fund, and Needham Small Cap Growth Fund. Our mission is to create wealth for long-term investors, but the fourth quarter was a step backward. January 2019 was a step forward as the Funds earned back most of the fourth quarter 2018 losses.

Needham Funds’ Fourth Quarter and Year-End 2018 Results

In the fourth quarter, the Needham Growth Fund Institutional and Retail classes returned -14.11% and -14.22%, respectively; the Needham Aggressive Growth Fund Institutional and Retail classes returned -18.41% and -18.49%, respectively; and the Needham Small Cap Growth Fund Institutional and Retail classes returned -16.07% and -16.24% respectively. The Russell 2000 Total Return Index returned -20.20%, and the S&P 500 Total Return Index returned -13.52%. December 2018 was the worst December for the Dow Jones Industrials and the S&P 500 since 1931. January 2019 was a good step forward as the Funds earned back most of the fourth quarter 2018 losses.

In 2018, the Needham Growth Fund Institutional and Retail classes returned -9.83% and -10.26% respectively; the Needham Aggressive Growth Institutional and Retail classes returned -15.36% and -15.80% respectively, and the Needham Small Cap Growth Fund Institutional and Retail classes returned -4.32% and -5.07% respectively. The Russell 2000 Total Return Index returned -11.01%, and the S&P 500 Total Return Index was down -4.38%. It was a horrible quarter, which made for a negative year. It was the worst year for stocks since 2008.

2018

It’s hard to remember, but 2018 began as a continuation of the dream market of the last three years. The market and the Needham Funds responded positively to the Tax Cuts and Jobs Act of 2017. The beginning of February brought a different story. The markets took a sharp downturn as the Federal Reserve raised interest rates and $1.5 trillion in “risk parity” trades began to unravel. The markets and the Needham Funds retraced their January gains.

At the start of the second quarter, rising interest rates and geopolitical risk and trade wars with Russia, China, North Korea and Iran dominated the market’s laundry list of worries. However, May delivered a strong market and outperformance by the Needham Funds. Despite more talk of trade wars, the economy and inflation seemed not too hot and not too cold, and earnings were better than expected.

In June, a strong jobs report was followed by the Federal Open Market Committee’s raise of its target interest rates for the second time in 2018. President Trump had a summit with North Korea’s Kim Jong-un and reached broad outlines of a peace agreement—a shift from

the fears of nuclear war that made headlines earlier in the year. By the end of June, global growth appeared to be robust, assuaging concerns of earlier in the year. The Funds and the markets were positive during the second quarter.

In late July, the U.S. Department of Commerce reported 4.1% annualized GDP growth for the second quarter and unemployment remained low at 4.0%. Some of the Funds’ industrial and semiconductor manufacturing equipment holdings were affected by disappointing guidance relating to their European and Asian businesses. The MSCI EAFE (Europe, Australasia and Far East) Index was down for the year as of July 31, while the Needham Funds and the U.S. markets were all positive. In July, the U.S. announced 10% tariffs on $200 billion of Chinese goods and China responded by imposing duties on over $100 billion of U.S. manufactured goods. These tariffs were effective September 24.

August brought an even better month for the markets and the Needham Funds. By the end of August, the U.S. and Canada had yet to reach a trade agreement. The weakness in international markets persisted and the trade rhetoric between the U.S. and China escalated.

September brought the third Federal Reserve interest rate hike for the year. At of the end of the third quarter, all three Needham Funds and the U.S. markets had positive returns for the year. However, international markets had turned negative; at September 30, China had returned -14.7% year-to-date, Germany -5.2%, Canada -0.8%, and Italy -5.2%.

Then came October with continued international weakness, trade war rhetoric, additional tariffs on U.S./China trade, and the prospect of a Federal Reserve December rate increase. The FAANG stocks were de-fanged in October, as Facebook, Inc. Class A (FB), Amazon.com, Inc. (AMZN), Apple Inc. (AAPL), Netflix, Inc. (NFLX), Alphabet Inc. Class A (GOOGL) and also NVIDIA (NVDA) fell an average of 16.4%; these stocks fell an average of another 11.1% in the first 19 days of November. Other high-growth companies that the market had previously rewarded with high multiples also fell.

October 2018 was one of the worst months for the markets and the Needham Funds in the last decade. The Russell 2000 was down -10.86% and the S&P 500 was down -6.84%. I recall the summer of 2011—it was the peak of the European sovereign debt crisis and included the Standard & Poor’s downgrade of U.S. debt. The Federal Reserve and European monetary authorities responded in force with liquidity measures. The markets rebounded quickly in October and the fourth quarter of 2011 was positive. Ultimately, we suspect the current monetary authorities will respond in similar fashion.

November brought a reprieve, as the markets and Funds were positive or nearly even. During midterm elections, Republicans increased their majority in the Senate and Democrats won control of the House. An increase in the Producer Price Index led to concerns that the Fed would stay on a tightening course. Toward the end of November, Fed Chairman Powell appeared to change his stance, stating that he viewed interest rates as just below a neutral level. Previously, he said rates were a long way from neutral. Foretelling things to come: Apple (AAPL) was down 18.4% in the month.

Then came December—it was worse than October. In fact, it was the worst December since 1931. The Russell 2000 was down -11.88%, the S&P 500 was down -9.03%, and the Needham Funds were also down. To highlight the market’s volatility, the S&P 500 was up or

down more than 1% on 9 of 21 days, compared to 8 times in all of 2017. Trade fears, along with rising interest rates and a slowing global economy, weighed on the market.

On December 2, President Trump and Chinese President Xi Jinping agreed to halt new trade tariffs for 90 days to give time for detailed negotiations. The U.S. agreed not to increase tariffs on another $250 billion of Chinese goods to 25% from 10% on January 1. The market traded up or down based on talk of a trade deal with China.

On December 19, the Fed raised its target range for federal funds to 2.25-2.50%—this was the fourth increase in 2018 and the ninth since the Fed began raising rates in December 2015. The Fed appeared to be on course for two increases in 2019.

John’s Commentary

Outlook for 2019

2019 began with the same market strength we saw in January 2018. However, 2018 started against a backdrop of euphoria, while 2019 began with despair and lower valuations. Through January 31, the Needham Growth Fund Institutional and Retail classes returned 9.57% and 9.47%, respectively; the Needham Aggressive Growth Fund Institutional and Retail classes returned 11.77% and 11.68%, respectively; and the Needham Small Cap Growth Fund Institutional and Retail classes returned 15.35% and 15.32% respectively. The Russell 2000 Total Return Index returned -11.25%, and the S&P 500 Total Return Index returned 8.01%.

The market started its move higher when the Fed indicated a cautious stance on rate increases and highlighted the risks of a slowing economy. While a Federal Reserve pause is good for the equity markets, we also recognize that 2.25-2.50% is still a historically low range for interest rates.

Our portfolio companies’ fourth quarter earnings reports have shown a slowing in China business. While it’s easy to point to trade friction, it’s more likely that China’s infrastructure spending got ahead of real demand and is due for a pause. We believe the U.S. and China could reach a productive trade agreement, which could be positive for the markets.

As I look to invest in North American small-cap companies with unrecognized growth potential, I believe that our small-cap portfolio companies’ destinies are more in their control than perceived, and that they are less likely victims of macro risk. Success with their new products and services may happen, even if the Chinese economy slows or the Federal Reserve increases rates in 2019. We note that as a rule, monetary authorities pursue easy money policies. Paul Volcker is the one exception in the last 40 years. We believe equity markets could benefit in 2019 from those easy monetary policies.

Quantitative Strategies and ETFs versus the Needham Funds

At Needham Funds, we are active, fundamental managers in a world headed toward passive management and quantitative strategies. We evaluate companies and their business prospects. Actually, I am an inactive/active manager. I look to hold a company for a long time, which results in low turnover. I am a long-term investor in a few companies which I believe can outperform over the long term.

In January, The Wall Street Journal ran an article on quantitative strategies and the fourth quarter.1 It quoted Rufus Rankin, Director of Research and Portfolio Manager at Equinox Institutional Management, “A lot of trend-followers ended the year down because it was tricky to catch many trends.” Kathryn Kaminski, Chief Research Strategist at Alpha Simplex said, “But using mathematical models to predict where markets are headed has been difficult as prices have been whipsawed by trade negotiations and mixed economic signals.” To see a more humorous interpretation please see the video titled, “World’s Worst Sheep Dog.”2 A funny guy on Twitter re-titled this, “Quant Traders in the Fourth Quarter.”

As the quants fine-tune their models to capture performance from new factors, they create a self-reinforcing momentum mechanism, which, for the most part, we don’t participate in. While most of our stocks were down in the fourth quarter, our companies continued to make progress on their new projects. In fact, the Needham Funds have rebounded and recovered all of their December losses as of January 31.

In the last decade, “growth at any price” stocks have worked and value has underperformed. While we are a growth-oriented firm, we are sensitive to valuation. We don’t buy blindly value in the form of a low price-to-book or P/E. These companies may have overstated book values or business models broken by new technology competitors. Rather, we are attracted to technology companies with low multiples-to-revenue that invest in new products or distribution. Sometimes these companies take time to see the benefits of their investments and, in the meantime, the stocks underperform. I am hopeful that 2019 will be a year of stock outperformance for some of our top small cap holdings, including PDF Solutions, Inc. (PDFS), Oil-Dri Corporation of America (ODC), KVH Industries, Inc. (KVHI), GSE Systems, Inc. (GVP), DIRTT Environmental Solutions Ltd. (DRT:TSE), and FormFactor, Inc. (FORM).

The Needham Funds Are Very Different from an Index

At Needham, we view our Funds’ investments similar to a venture capital investor. Months, quarters or even years can pass without markets recognizing progress behind the scenes. Consequently, the Needham Funds are not correlated with the averages, as shown by an R-Squared of 79.97 relative to the Russell 20003 for the Needham Aggressive Growth Fund; 69.47 relative to the Russell 20004 for the Needham Small Cap Growth Fund; and 55.06 relative to the S&P 5005 for the Needham Growth Fund. R-Squared measures the percentage of a fund’s returns that can be explained by the returns of the benchmark.

As of December 31, 2018, Needham Aggressive Growth Fund held 58 long positions. The Fund’s top 10 holdings represent 62.52% of net assets. Therefore, the Fund has a very different constitution than the indices, as shown by its high Active Share6 of 106.3% versus the Russell 2000 Total Return Index. The other Needham Funds also have high

____________

1 | https://www.wsj.com/articles/computer-models-to-investors-short-everything-11547038800 |

2 | https://www.youtube.com/watch?v=p-9-3DtUzug |

3 | Since inception of the Fund on 9/4/01. As of 12/31/18. |

4 | Since inception of the Fund on 5/22/02. As of 12/31/18. |

5 | Since inception of the Fund on 1/1/96. As of 12/31/18. |

6 | Active Share represents the proportion of portfolio holdings that differ from those in the benchmark index. As of 12/31/18. |

Active Share—Needham Growth Fund is 105.7% versus the S&P 500 TR Index, and Needham Small Cap Growth Fund is 98.5% versus the Russell 2000. We don’t try to rotate sectors to match or beat an index. We look to invest in companies that might earn an above market, compounding long-term return.

Needham Small Cap Growth Fund (NESGX/NESIX)

The Needham Small Cap Growth Fund Institutional class returned -16.07% and the Retail class returned -16.24% in the quarter ended December 31, 2018. For the year, the Fund’s Institutional class returned -4.32% and the Retail class returned -5.07% while the Russell 2000 Total Return Index returned -20.20% for the quarter and -11.01% for the year.

We were pleased with the Fund’s significant quarterly and annual outperformance of the Russell 2000 Total Return Index. Outperformance was consistent throughout the year with many of our concentrated positions outperforming the broader markets. However, in the last few weeks of December, some of these positions declined owing to an overall market correction. While the fourth quarter turned the Fund’s year from positive to negative, our cautious cash position and trading flexibility allowed us to take advantage of the correction and deploy significant amounts of our cash position into stocks at the end of December. Thankfully, this strategic decision allowed us to capture substantial recovery in the early part of 2019. The market for small cap companies continues to offer good value, and we will evaluate our position sizes and valuation targets.

The Fund continued its lean toward a concentrated portfolio of stocks, with top 10 holdings representing 55.35% of net assets at December 31, 2018. Top holdings at December 31, 2018 included Photronics, Inc. (PLAB), Amber Road, Inc. (AMBR), PDF Solutions, Inc. (PDFS), EMCORE Corp. (EMKR), Aquantia Corp. (AQ), Aspen Aerogels, Inc. (ASPN), Ultra Clean Holdings, Inc. (UCTT), Super Micro Computer, Inc.(SMCI), Hawaiian Holdings, Inc. (HA), and Electronics for Imaging, Inc. (EFII). The Fund’s top fourth quarter contributors included Corium International, Inc., Akoustis Technologies, Inc. (AKTS), FormFactor, Inc. (FORM), Frequency Electronics, Inc. (FEIM), and Zscaler, Inc. (ZS).

The Fund’s largest fourth quarter detractors were Aspen Aerogels, Aquantia, Ultra Clean Holdings, Electronics for Imaging, and Super Micro Computer. With regard to Aspen Aerogels’ poor performance throughout the quarter, we observed that a significant institutional shareholder of the stock had been selling their position along with a general trend of tax-loss selling of small capitalization companies across the market. We do not believe that the fundamental story of the company has changed, and we remain excited about its new product launches and future growth trajectory. The stock has since partially recovered in January off its December lows, and its funding needs were greatly improved with a cash infusion from its product line partner BASF.

While volatility may seem to be a bad word for the overall markets, it is a great chance for active managers to find buying opportunities. It is in these volatile markets when a cash position is truly strategic for small cap fund managers. Many small cap investment opportunities “trade by appointment,” and we like to capitalize on these opportunities when liquidity is available to both buy and sell stock positions. We added to existing positions and also added many new small positions to the Fund, including Akoustis Technologies, TTM Technologies, Inc. (TTMI), Cohu, Inc. (COHU), Five9, Inc. (FIVN), Intevac, Inc. (IVAC),

and Everbridge, Inc. (EVBG). We exited our holding in WageWorks, Inc. (WAGE), FireEye, Inc. (FEYE), and Orbotech, Ltd. (ORBK). The Fund ended the quarter with a cash position of 4.9%. We remain excited about the composition of the portfolio as we enter 2019, and we look forward to learning about new small cap prospects this year.

We continue to believe that a good environment remains for investment in equities. Three themes we are focused on include: 1) continuation of the growth in the semiconductor capital equipment industry; 2) 5G communication infrastructure; and 3) military and defense modernization. These three areas of investment impact much of our portfolio, and we believe that long term, they should create shareholder value.

We expect a continuation of volatility into 2019, as the markets evaluate any economic slowdowns, interest rate curve risks, Federal Reserve actions, government shutdowns, trade policy negotiations, and overall geopolitical risks. The Federal Reserve has indicated at this point in time that they are on hold for the near-term for any short-term interest rate hikes. This position may change if economic data improves throughout the year, but at the moment, the markets are applauding this pause in rate policy. The expectation of pro-growth policies has boosted confidence for both individuals and corporations, and this should translate ultimately into higher economic activity for many of our portfolio companies. The high-yield markets showed signs of weakness at the end of 2018 but has since recovered, which is also supportive of the small cap asset class valuations.

The Fund benefited from the previously discussed sale of Invuity and also saw the sale of its holdings in Corium International and Reis, Inc. We were very happy with the results, as Corium received a nice premium to current price and, similar to Invuity, avoided returning to the capital markets. Reis had announced it was running a strategic review of its business and it ultimately sold to Moody’s Corporation (MCO). We reiterate from our last quarterly letter that mergers and acquisitions continued in the small cap universe, but have slowed since 2016. We believe this trend is a pause, and we expect to see increased M&A activity as well as economic growth to improve and benefit the Needham Small Cap Growth Fund in 2019.

Needham Growth Fund (NEEGX/NEEIX)

The Needham Growth Fund Institutional class was down -14.11% and the Retail class was down -14.22% in the fourth quarter, underperforming the S&P 500, which was down -13.52%. For the year, the Needham Growth Fund Institutional class returned -9.83% and the Retail class was down -10.26%, compared to the S&P 500 which was down -4.38%.

For the fourth quarter, the short position in Medallion Financial Corp. (MFIN) was the Fund’s top contributor as the stock fell 29.5%. Historically, Medallion was a taxi cab medallion lender and is aggressively expanding their business in consumer and small business loans at the low-end of the credit spectrum. In a downturn, these loans could have higher than average default rates. Red Hat, Inc. (RHT) was the second-leading contributor and returned 30.7%. Red Hat agreed to be purchased by International Business Machines Corporation (IBM).

For the year, the Fund’s largest holding, Thermo Fisher Scientific, Inc. (TMO), was the leading contributor returning 18.2%. The Fund first invested in Thermo Fisher in January 2000 at $13 per share and the investment has compounded at 17.6% per year. Thermo Fisher had a good year across its market segments, including biopharma, industrial, academia, and

diagnostics. Trade Desk, Inc. Class A (TTD) was the second-leading contributor and returned 153.8%. The Trade Desk provides Software-as-a-Service used by ad agencies and brand managers for programmatic, digital ad campaigns. The growth of over-the-top video is a major opportunity for The Trade Desk. 2018 revenue is expected to have grown 48% with 21% GAAP operating income margin. The company has a culture of profitable growth.

The third-leading 2018 contributor was Red Hat, followed by Corium International, Inc. and Invuity, Inc.

The leading detractor for the fourth quarter was KVH Industries, Inc. which returned -21.5%. The company’s third quarter revenue and earnings results were fine and at 1x enterprise value-to-revenues, valuation is moderate. Most likely the stock decline was a result of being a small cap stock caught in a risk-off, tax-selling period.

KVH’s AgilePlans provides connectivity-as-a-service to the maritime industry and bundles a satellite antenna, air time, and news, entertainment and training programming. Customers pay monthly and are not required to sign a long-term contract. Customers save the capex upfront and retain flexibility should their business circumstances change. It has led to a 100% increase in unit bookings year-to-date through September 30, 2018. These strong results could show through in revenue and earnings in 2019.

In 2018, KVH worked to develop a photonic chip, a cost-reduced version of its fiber optic gyroscope (FOG) products. In December, KVH delivered prototypes to leading automotive companies. KVH’s FOGs are used on most self-driving car programs today. FOGs help vehicles maintain positioning when they are out of range of GPS satellites. The cost-reduced version is designed to meet the requirements for mass deployment on autonomous vehicles. Sometime in 2019, KVH could announce a partner for scale manufacturing and automotive expertise. Long term, we believe KVH could be a significantly larger company and earn several dollars per share.

Super Micro Computer, Inc. also detracted from fourth quarter and annual performance—the stock was down 33.0% in the fourth quarter. The company was victim of a bizarre story published by Bloomberg Businessweek about Chinese People’s Liberation Army hackers inserting “microchips the size of a grain of sand” into Super Micro servers, allowing the Chinese to spy on customers, including Apple, Amazon, and the Department of Defense. All of these entities and many others denied the story. Tim Cook of Apple personally called for Bloomberg to retract the story. From my experience in the electronics industry prior to Wall Street, I find the story highly unlikely. The article took Super Micro from $21.50 per share to a low of $8.50 in one day. The stock closed the quarter at $13.80.

The story hit Super Micro at a time of vulnerability, as it has yet to file its 10K for the June 2017 fiscal year. The company has concluded that the restatement is expected to move at most $50 million of revenue and under $10 million of net income between 2015 through 2017. These amounts represent 1-2% of revenue and less than 10% of net income. For all of the effort and expense, these changes seem immaterial. Despite weakness in the market for data center equipment, we believe Super Micro has earnings power of $2-3 per share.

Gilead Sciences, Inc. (GILD), another significant detractor, was down 18.3% in the fourth quarter. Gilead reported positive results for the third quarter and moved lower with the market. We note that with Bristol Myers-Squib Company’s (BMY) proposed acquisition of

Celgene Corporation (CELG), one Wall Street analyst suggested Gilead could be worth $104 per share in a merger. As of December 31, 2018, Gilead is the second-largest holding of the Fund at 6.45% of net assets.

For the year, PDF Solutions, Inc. returned -46.3% and was the Fund’s leading detractor. PDF’s legacy business declined and its largest customer, Global Foundries, announced that it was ending efforts to compete with Taiwan Semiconductor Manufacturing (TSMC). PDF had been working with GlobalFoundries on many leading-edge programs.

Throughout 2018, PDF investors waited for a contract announcement for the new DFI (Design for Inspection) offering. Importantly, the announcement came in mid-January 2019. I believe that PDF’s Exensio Big Data Analytics, cash flow from the legacy business and cash on the balance sheet are worth $11-12 per share, above the December 31st share price of $8.43. Should DFI and Exensio grow over the next few years, I believe PDF could earn several dollars per share and the stock could outperform.

The Fund’s short position in Ubiquiti Networks, Inc. (UBNT) contributed in the fourth quarter, but detracted for the year, as the stock appreciated 40.7%. Last February, the Securities and Exchange Commission issued subpoenas to Ubiquiti and some of its officers requesting information relating to accounting practices, financial information, auditors, international trade practices, and relationships with third parties. The company stated it is in the process of responding to the requests and intends to cooperate fully with the SEC. Through the end of September, Ubiquiti bought back $400 million of stock, and on November 6, 2018, they authorized a new $200 million buyback. Management has done a good job of supporting the stock.

In 2018, the Fund added new positions, including DIRTT Environmental Solutions Ltd., which closed the year at 3.4% of net assets, Cryoport, Inc. (CYRX) at 1.1% of net assets, Taiwan Semiconductor (TSMC), and Zuoro, Inc. Class A (ZUO). DIRTT Environmental is using technology to disrupt the interior construction industry. DIRTT has an incredible 3-D virtual reality CAD (computer-aided design) system that allows peers in different locations to walk through a VR model of their design prior to sign-off. The CAD system then feeds manufacturing, which is done at several factories and assembled on-site. DIRTT competes with drywall and on-site construction. It is green as there is minimal waste at the factories and no waste material on-site. It is predictable and helps contractors stick to schedule.

When we first invested, I was attracted to DIRTT because of its Founder & CEO. Late in 2018, the Board replaced almost all of DIRTT’s senior management team with people that have great experience in growing companies. I was skeptical at first, but have come to believe that the new team is making important changes that can help DIRTT reach its potential at multiples of its current sales level.

Cryoport is at the center of the ecosystem for transporting CAR-T cancer immunotherapies at temperatures as cold as -150C. Cyroport is part of the Gilead/Kite Pharmaceuticals’ Yescarta launch and the Novartis AG’s (NVS) Kymriah launch. CAR-T is a miracle of science, but as investors, we become immune (pun intended) to scientific miracles. By chance, I met a person who put a human face on CAR-T. He was recently treated with Yescarta at the Dana Farber Cancer Center outside Boston. He had gone through many other treatments. Yescarta was his last hope and after about a month, his cancer was gone. I met him at a CrossFit workout about six weeks after he left the hospital. The drug worked a miracle.

With GlobalFoundries’ strategic choice to stop developing leading-edge semiconductor manufacturing processes, Taiwan Semiconductor is the sole supplier for Apple (AAPL), NVIDIA Corporation (NVDA), Advanced Micro Devices, Inc. (AMD), and all others except for Intel Corporation (INTC) and Samsung Electronics Co. Ltd (005930-KRX). While the semiconductor industry is suffering a downturn, we believe Taiwan Semiconductor will emerge as a strong leader.

Zuora went public in 2018. It is a software-as-a-service company that enables accounting and subscription management for the subscription economy. The economy is becoming subscription-centric; even industrial equipment companies are looking for ways of monetizing data and analytics through subscription business models.

The Fund exited its position in ComScore, Inc. (SCOR) as valuation appeared stretched given the outlook for the next few years. Comscore successfully completed filing its delinquent financials in March 2018 with its last previous filing over 2 years before. This was a costly and protracted restatement process. We also exited our long-time holding in WageWorks, as the company announced in March that it was unable to file its financials.

As of December 31, 2018, the top 10 positions were 57.56% of net assets. The Fund had trailing 12-month turnover of just 8% and Active Share of 109.1% vs. the S&P 500.

Needham Aggressive Growth Fund (NEAGX/NEAIX)

Needham Aggressive Growth Fund Institutional class was down -18.41% in the fourth quarter and the Retail class was down -18.49%, compared to a -20.20% return for the Russell 2000. In 2018, the Needham Aggressive Growth Fund Institutional class returned -15.36% and the Retail class returned -15.80% compared to -11.01% for the Russell 2000.

Vicor (VICR) was the Fund’s top contributor in 2018 but one of the largest detractors for the fourth quarter. Vicor returned 80.8% in 2018, as its modular power conversion systems were adopted in leading data centers. Vicor has worked with Alphabet Inc. (GOOGL) on its Open Compute data centers to distribute DC (direct current) power throughout a data center. In most data centers today, power goes through inefficient conversions from DC to AC (alternating current) and back again to DC. In March 2018, NVIDIA announced its newest DGX-2 artificial intelligence system, which uses Vicor power converters. Vicor is uniquely positioned to meet future data center, artificial intelligence and automotive processing needs. The stock may fluctuate based on the quarterly outlook for data center spending, but long term, Vicor addresses big markets, has strong potential margins and return on capital, is founder-run, and has no analyst coverage. That’s my kind of company.

Other top contributors in 2018 were The Trade Desk, Cryoport, and Reis, Inc. In August, Reis agreed to be purchased by Moody’s.

The short positions in Medallion Financial and Health Insurance Innovations, Inc. Class A (HIIQ) were the top contributors in the fourth quarter. FormFactor (FORM) was the third-leading contributor for the quarter, returning 2.5%. FormFactor reported a good quarter with positive results from wafer probe cards used for advanced logic and memory applications and from system sales, which offset weakness at Intel and Samsung.

PDF Solutions was the Fund’s largest detractor in 2018 and the fourth quarter. GSE Systems, Inc. also hurt 2018 performance. Despite good results all year, GSE Systems fell 41.7% in the fourth quarter. I believe this micro-cap stock fell victim to tax-loss-selling in a horrible

market. GSE Systems made progress on its vision of being a leader in training, consulting and technology-enabled engineering solutions to the power and process industries. In May 2018, GSE acquired True North Consulting. True North has complementary skills in in-service inspection for specialty engineering and in-service testing for nuclear engineering programs. GSE currently has a run rate of about $100 million in revenue, with about $10 million of EBITDA, and a market cap of just $60 million.

Other significant detractors for the year were WageWorks, Ubiquiti Networks (short), and IPG Photonics Corp. (IPGP).

In the fourth quarter, long-time holding Apple fell 28.9% and was the Fund’s second-largest detractor. Apple reported weakness in China and with its new high-end phones. Apple was purchased by my predecessor on the Fund in 2006, before the iPhone was introduced. I continue to believe Apple represents a compelling value with long-term growth opportunities, thus it stays in the Fund. Other significant detractors in the fourth quarter were KVH Industries, Super-Micro, and Oil-Dri.

In 2018, we added three positions that remain above 0.4% holdings: Taiwan Semiconductor, Zuora, and Alpha Pro Tech, Ltd (APT). Alpha Pro Tech makes protective apparel for medical, industrial and infection control uses. It also makes covering products used in construction. Alpha Pro Tech is a micro-cap with no research coverage, it is family run, earns a good return on capital, and uses cash generated to shrink the share base.

The Fund exited long-time positions in Gilead Sciences, Comscore, WageWorks, and Reis. We trimmed or reduced positions in many of the largest holdings, including Entegris, Akamai, Apple, Form Factor, MKS Instruments, Vicor, and Nova Measuring Instruments Ltd. (NVMI). At December 31, 2018, the Fund’s top 10 positions were 62.52% of net assets. The Fund had an Active Share of 106.3% versus the Russell 2000 and had trailing 12-month turnover of 8%.

We welcome our new investors and thank all of our investors for their continued support. If you have any questions, thoughts or concerns, please contact us at (800) 625-7071 or at cretzler@needhamco.com or jbarr@needhamco.com. For information about the funds, please visit our website at www.needhamfunds.com.

Sincerely,

|  |

| Chris Retzler | John O. Barr |

| Portfolio Manager | Portfolio Manager |

Fact Sheet Links:

Needham Growth Fund

Needham Aggressive Growth Fund

Needham Small Cap Growth Fund

The information presented in this commentary is not intended as personalized investment advice and does not constitute a recommendation to buy or sell a particular security or other investments. Past performance is no guarantee of future results. The views of the Adviser and the securities described in this report are as of December 31, 2018; these views and portfolio holdings may have changed subsequent to this date. The specific securities discussed may, in aggregate, represent only a small percentage of a Portfolio’s holdings. It should not be assumed that securities identified and discussed were, or will be, profitable, or that the investment decisions made in the future will be profitable, or equal the investment performance of the securities discussed herein. There can be no guarantee as to the accuracy of any outlooks for markets, sectors and securities as discussed herein.

This message is not an offer of the Needham Growth Fund, the Needham Aggressive Growth Fund or the Needham Small Cap Growth Fund. Shares are sold only through the currently effective prospectus. Please read the prospectus carefully and consider the investment objectives, risks, and charges and expenses of the Fund carefully before you invest. The prospectus contains this and other information about the Fund. A copy of the prospectus is available at www.needhamfunds.com or by contacting the Fund’s transfer agent, U.S. Bancorp Fund Services, LLC doing business as U.S. Bank Global Fund Services (“Fund Services”) at 1-800-625-7071.

All three of the Needham Funds have substantial exposure to small and micro capitalized companies. Funds holding smaller capitalized companies are subject to greater price fluctuation than those of larger companies.

Needham & Company, LLC, member FINRA/SIPC, is the distributor of The Needham Funds, Inc.

Portfolio holdings subject to change. Needham Funds’ ownership as a percentage of net assets in the stated securities as of 12/31/18:

| SECURITY | NEEGX | NEAGX | NESGX | SECURITY | NEEGX | NEAGX | NESGX | SECURITY | NEEGX | NEAGX | NESGX |

| PDFS | 5.01% | 7.59% | 6.98% | ZS | 0.00% | 0.00% | 0.08% | TSM | 0.27% | 0.41% | 0.00% |

| ODC | 0.59% | 2.94% | 0.54% | TTMI | 0.00% | 0.00% | 1.58% | UBNT | -5.19% | -4.77% | 0.00% |

| GVP | 0.00% | 5.79% | 0.00% | COHU | 0.00% | 0.00% | 1.96% | CYRX | 0.80% | 1.15% | 0.82% |

| DRT | 0.16% | 3.31% | 0.73% | FIVN | 0.00% | 0.00% | 0.35% | ZUO | 0.72% | 0.45% | 1.43% |

| FORM | 4.88% | 4.65% | 0.79% | IVAC | 0.00% | 0.00% | 0.65% | NVS | 0.00% | 0.00% | 0.00% |

| PLAB | 1.83% | 2.24% | 9.23% | EVBG | 0.65% | 0.63% | 0.46% | AAPL | 0.51% | 7.77% | 0.00% |

| AMBR | 4.39% | 3.32% | 8.68% | WAGE | 0.00% | 0.00% | 0.00% | NVDA | 0.00% | 0.00% | 0.00% |

| EMKR | 0.00% | 0.00% | 5.28% | FEYE | 0.00% | 0.00% | 0.00% | AMD | 0.00% | 0.00% | 0.00% |

| AQ | 0.45% | 0.00% | 4.98% | ORBK | 0.00% | 0.00% | 0.00% | INTC | 0.00% | 0.00% | 0.00% |

| ASPN | 1.11% | 0.87% | 4.28% | MFIN | -1.01% | -2.37% | 0.00% | 005930KRX | 0.00% | 0.00% | 0.00% |

| UCTT | 0.25% | 0.04% | 4.29% | RHT | 0.00% | 0.00% | 0.00% | VICR | 0.88% | 5.23% | 0.00% |

| SMCI | 3.23% | 3.00% | 3.84% | IBM | 0.00% | 0.00% | 0.00% | GOOGL | 0.00% | 0.00% | 0.00% |

| HA | 0.30% | 0.16% | 4.02% | TMO | 9.39% | 0.00% | 0.00% | HIIQ | -0.03% | -0.07% | 0.00% |

| EFII | 1.98% | 0.98% | 3.77% | TTD | 0.97% | 0.71% | 0.00% | IPGP | 0.85% | 1.95% | 0.00% |

| AKTS | 0.00% | 0.00% | 3.23% | GILD | 6.45% | 0.00% | 0.00% | APT | 0.00% | 0.55% | 0.00% |

| FEIM | 0.45% | 0.25% | 3.05% | BMY | 0.00% | 0.00% | 0.00% | NVMI | 1.60% | 3.54% | 0.00% |

The Russell 2000 Index is a broad unmanaged index composed of the smallest 2,000 companies in the Russell 3000 Index. The Russell 3000 Index is a market-capitalization-weighted equity index that provides exposure to the entire U.S. stock market. The Russell 3000 Index tracks the performance of the 3,000 largest U.S.-traded stocks. The Russell 2000 Total Return Index assumes cash distributions, such as dividends, are reinvested back into the index. Please see the disclaimer regarding these indexes under “Supplementary Information—Index Disclaimer” on page [59] of this report.

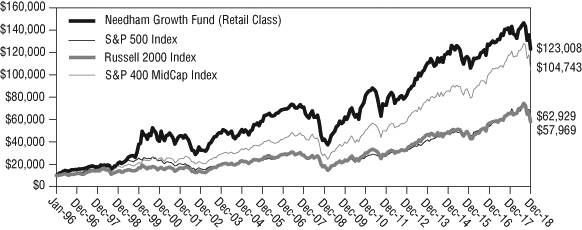

| NEEDHAM GROWTH FUND | Retail Class |

| | Ticker Symbol: NEEGX |

| | Institutional Class |

| | Ticker Symbol: NEEIX |

Comparison of Change in Value of a $10,000 Investment

The chart above assumes an initial gross investment of $10,000 made on January 1, 1996. The Fund’s performance figures are for the year ended December 31, 2018. The Performance data quoted is historical. Past performance is no guarantee of future results. Current performance may be higher or lower than the performance data quoted. The principal value and investment return of an investment will fluctuate so that your shares, when redeemed, may be worth more or less than their original cost. The returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or on the redemptions of Fund shares. In the absence of fee waivers and reimbursements, when they are necessary to keep expenses at the expense cap, total return would be reduced. Performance figures for periods greater than one year are annualized.

The Global Industry Classification Standard (GICS®) was developed by and/or is the exclusive property of MSCI, Inc. and Standard & Poor Financial Services LLC (“S&P”). GICS is a service mark of MSCI and S&P and has been licensed for use by Fund Services.

Comparative Performance Statistics as of December 31, 2018 (Unaudited)

| | 1 | 5 | 10 | Since |

| | Year | Years | Years | Inception |

Needham Growth Fund Retail Class(1)(2) | -10.26% | 2.14% | 11.25% | 11.53% |

Needham Growth Fund Institutional Class(1)(3) | -9.83% | n/a | n/a | -0.91% |

S&P 500 Index(4)(5) | -4.38% | 8.49% | 13.12% | 8.33%(8) |

S&P 400 MidCap Index(4)(6) | -11.08% | 6.03% | 13.68% | 10.75%(8) |

Russell 2000 Index(4)(7) | -11.01% | 4.41% | 11.97% | 7.94%(8) |

| 1. | Investment results calculated after reinvestment of dividends. |

| 2. | The inception date of the Retail Class was 1/1/96. |

| 3. | The inception date of the Institutional Class was 12/30/16. |

| 4. | It is not possible to invest directly in an index. The performance of the index does not include the deduction of expenses associated with a mutual fund, such as investment management fees. |

| 5. | The S&P 500 Index is a broad unmanaged measure of the U.S. stock market. |

| 6. | The S&P 400 MidCap Index is a broad unmanaged measure of the U.S. stock market. |

| 7. | The Russell 2000 Index is a broad unmanaged index composed of the smallest 2,000 companies in the Russell 3000 Index. |

| 8. | The return shown for the Index is from the Inception date of the Retail Class. |

Top Ten Holdings*

(as a % of total investments,

as of December 31, 2018)

| | | % of Total | |

Security | | Investments | |

| Thermo Fisher Scientific, Inc. | TMO | 9.51% | |

| Gilead Sciences, Inc. | GILD | 6.53% | |

| CarMax, Inc. | KMX | 6.48% | |

| KVH Industries, Inc. | KVHI | 6.08% | |

| Becton Dickinson & Co. | BDX | 5.61% | |

| PDF Solutions, Inc. | PDFS | 5.07% | |

| FormFactor, Inc. | FORM | 4.94% | |

| Entegris, Inc. | ENTG | 4.86% | |

| Comcast Corp., Class A | CMCSA | 4.76% | |

| Amber Road, Inc. | AMBR | 4.45% | |

Top Ten Holdings = 58.29% of Total Investments†

| * | Current portfolio holdings may not be indicative of future portfolio holdings. |

| † | Percentage of total investments less cash. |

Sector Weightings*

(as a % of net investments,

as of December 31, 2018)

Sector | | Long* | | (Short)(1) | | Total(1)(2) | |

| Communication Services | | | 6.0 | % | | — | | | 6.0 | % | |

| Consumer Discretionary | | | 6.9 | % | | — | | | 6.9 | % | |

| Consumer Staples | | | 0.6 | % | | — | �� | | 0.6 | % | |

| Energy | | | 2.2 | % | | — | | | 2.2 | % | |

| Financials | | | 1.0 | % | | (1.1)% | | | (0.1 | )% | |

| Health Care | | | 27.2 | % | | — | | | 27.2 | % | |

| Industrials | | | 3.9 | % | | — | | | 3.9 | % | |

| Information Technology | | | 58.2 | % | | (5.6)% | | | 52.6 | % | |

| Cash | | | 0.7 | % | | — | | | 0.7 | % | |

| * | Current portfolio holdings may not be indicative of future portfolio holdings. |

(1) | Percentage of total investments includes all stocks, plus cash minus all short positions. |

(2) | Total represents the difference between the long exposure and the short exposure, which produces the net exposure. |

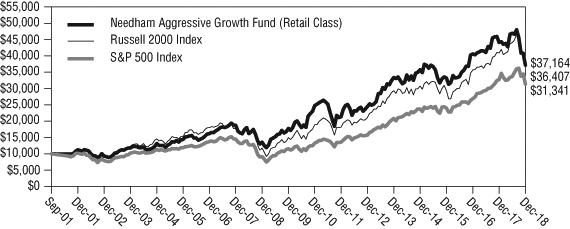

| NEEDHAM AGGRESSIVE GROWTH FUND | Retail Class |

| | Ticker Symbol: NEAGX |

| | Institutional Class |

| | Ticker Symbol: NEAIX |

Comparison of Change in Value of a $10,000 Investment

The chart above assumes an initial gross investment of $10,000 made on September 4, 2001. The Fund’s performance figures are for the year ended December 31, 2018.The Performance data quoted is historical. Past performance is no guarantee of future results. Current performance may be higher or lower than the performance data quoted. The principal value and investment return of an investment will fluctuate so that your shares, when redeemed, may be worth more or less than their original cost. The returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or on the redemptions of Fund shares. In the absence of fee waivers and reimbursements, when they are necessary to keep expenses at the expense cap, total return would be reduced. Performance figures for periods greater than one year are annualized.

Comparative Performance Statistics as of December 31, 2018 (Unaudited)

| | 1 | 5 | 10 | Since |

| | Year | Years | Years | Inception |

Needham Aggressive Growth Fund Retail Class(1)(2) | -15.80% | 2.18% | 10.62% | 7.87% |

Needham Aggressive Growth Fund Institutional Class(1)(3) | -15.36% | n/a | n/a | -3.78% |

S&P 500 Index(4)(5) | -4.38% | 8.49% | 13.12% | 6.82%(7) |

Russell 2000 Index(4)(6) | -11.01% | 4.41% | 11.97% | 7.74%(7) |

| 1. | Investment results calculated after reinvestment of dividends. |

| 2. | The inception date of the Retail Class was 9/4/01. |

| 3. | The inception date of the Institutional Class was 12/30/16. |

| 4. | It is not possible to invest directly in an index. The performance of the index does not include the deduction of expenses associated with a mutual fund, such as investment management fees. |

| 5. | The S&P 500 Index is a broad unmanaged measure of the U.S. stock market. |

| 6. | The Russell 2000 Index is a broad unmanaged index composed of the smallest 2,000 companies in the Russell 3000 Index. |

| 7. | The return shown for the Index is from the Inception date of the Retail Class. |

Top Ten Holdings*

(as a % of total investments,

as of December 31, 2018)

| | | % of Total | |

Security | | Investments | |

| Entegris, Inc. | ENTG | 10.59% | |

| KVH Industries, Inc. | KVHI | 9.19% | |

| Apple, Inc. | AAPL | 7.63% | |

| PDF Solutions, Inc. | PDFS | 7.45% | |

| GSE Systems, Inc. | GVP | 5.69% | |

| Vicor Corp. | VICR | 5.14% | |

| FormFactor, Inc. | FORM | 4.57% | |

| Akamai Technologies, Inc. | AKAM | 4.06% | |

| MKS Instruments, Inc. | MKSI | 3.59% | |

| Nova Measuring | | | |

| Instruments, Ltd. (Israel) | NVMI | 3.47% | |

Top Ten Holdings = 61.38% of Total Investments†

| * | Current portfolio holdings may not be indicative of future portfolio holdings. |

| † | Percentage of total investments less cash. |

Sector Weightings*

(as a % of net investments,

as of December 31, 2018)

Sector | | Long* | | (Short)(1) | | | Total(1)(2) | |

| Communication Services | | | 1.0 | % | | — | | | | 1.0 | % | |

| Consumer Discretionary | | | 3.5 | % | | — | | | | 3.5 | % | |

| Consumer Staples | | | 3.1 | % | | — | | | | 3.1 | % | |

| Energy | | | 0.9 | % | | — | | | | 0.9 | % | |

| Financials | | | 0.5 | % | | (2.6)% | | | | (2.1 | )% | |

| Health Care | | | 5.1 | % | | — | | | | 5.1 | % | |

| Industrials | | | 11.6 | % | | — | | | | 11.6 | % | |

| Information Technology | | | 80.1 | % | | (5.0)% | | | | 75.1 | % | |

| Real Estate | | | 1.8 | % | | — | | | | 1.8 | % | |

| * | Current portfolio holdings may not be indicative of future portfolio holdings. |

(1) | Percentage of total investments includes all stocks, plus cash minus all short positions. |

(2) | Total represents the difference between the long exposure and the short exposure, which produces the net exposure. |

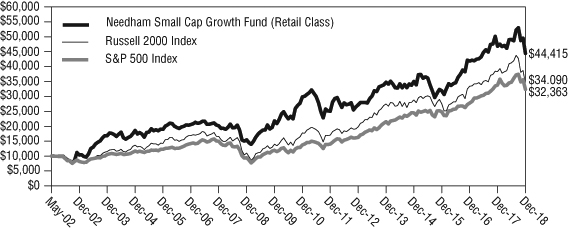

| NEEDHAM SMALL CAP GROWTH FUND | Retail Class |

| | Ticker Symbol: NESGX |

| | Institutional Class |

| | Ticker Symbol: NESIX |

Comparison of Change in Value of a $10,000 Investment

The chart above assumes an initial gross investment of $10,000 made on May 22, 2002. The Fund’s performance figures are for the year ended December 31, 2018.The Performance data quoted is historical. Past performance is no guarantee of future results. Current performance may be higher or lower than the performance data quoted. The principal value and investment return of an investment will fluctuate so that your shares, when redeemed, may be worth more or less than their original cost. The returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or on the redemptions of Fund shares. In the absence of fee waivers and reimbursements, when they are necessary to keep expenses at the expense cap, total return would be reduced. Performance figures for periods greater than one year are annualized.

Comparative Performance Statistics as of December 31, 2018 (Unaudited)

| | 1 | 5 | 10 | Since |

| | Year | Years | Years | Inception |

Needham Small Cap Growth Fund Retail Class(1)(2) | -5.07% | 5.03% | 11.15% | 9.39% |

Needham Small Cap Growth Fund Institutional Class(1)(3) | -4.32% | n/a | n/a | 3.60% |

S&P 500 Index(4)(5) | -4.38% | 8.49% | 13.12% | 7.33%(7) |

Russell 2000 Index(4)(6) | -11.01% | 4.41% | 11.97% | 7.66%(7) |

| 1. | Investment results calculated after reinvestment of dividends. |

| 2. | The inception date of the Retail Class was 5/22/02. |

| 3. | The inception date of the Institutional Class was 12/30/16. |

| 4. | It is not possible to invest directly in an index. The performance of the index does not include the deduction of expenses associated with a mutual fund, such as investment management fees. |

| 5. | The S&P 500 Index is a broad unmanaged measure of the U.S. stock market. |

| 6. | The Russell 2000 Index is a broad unmanaged index composed of the smallest 2,000 companies in the Russell 3000 Index. |

| 7. | The return shown for the Index is from the Inception date of the Retail Class. |

Top Ten Holdings*

(as a % of total investments,

as of December 31, 2018)

| | | % of Total | |

Security | | Investments | |

| Photronics, Inc. | PLAB | 9.49% | |

| Amber Road, Inc. | AMBR | 8.93% | |

| PDF Solutions, Inc. | PDFS | 7.18% | |

| EMCORE Corp. | EMKR | 5.43% | |

| Aquantia Corp. | AQ | 5.12% | |

| Ultra Clean Holdings, Inc. | UCTT | 4.42% | |

| Aspen Aerogels, Inc. | ASPN | 4.40% | |

| Hawaiian Holdings, Inc. | HA | 4.13% | |

| Super Micro Computer, Inc. | SMCI | 3.95% | |

| Electronics for Imaging, Inc. | EFII | 3.88% | |

Top Ten Holdings = 56.93% of Total Investments†

| * | Current portfolio holdings may not be indicative of future portfolio holdings. |

| † | Percentage of total investments less cash. |

Sector Weightings*

(as a % of net investments,

as of December 31, 2018)

Sector | Long* | (Short)(1) | Total(1)(2) | |

| Closed-End Funds | 4.4% | — | 4.4% | |

| Consumer Discretionary | 1.7% | — | 1.7% | |

| Consumer Staples | 0.5% | — | 0.5% | |

| Energy | 8.0% | — | 8.0% | |

| Financials | 0.4% | — | 0.4% | |

| Health Care | 4.1% | — | 4.1% | |

| Industrials | 6.4% | — | 6.4% | |

| Information Technology | 69.6% | — | 69.6% | |

| Cash | 4.9% | — | 4.9% | |

| * | Current portfolio holdings may not be indicative of future portfolio holdings. |

(1) | Percentage of total investments includes all stocks, plus cash minus all short positions. |

(2) | Total represents the difference between the long exposure and the short exposure, which produces the net exposure. |

Disclosure of Fund Expenses (Unaudited)

The following expense table is shown so that you can understand the impact of fees on your investment. All mutual funds have operating expenses. As a shareholder of a Portfolio, you incur transactional costs, including redemption fees and ongoing costs, which include costs for portfolio management, administrative services, and shareholder reports, among others. A Portfolio’s expenses are expressed as a percentage of its average net assets. This figure is known as the expense ratio. The following examples are intended to help you understand the ongoing costs (in dollars) of investing in each Portfolio and to compare these costs with those of other mutual funds. The examples are based on an investment of $1,000 made at the beginning of a six-month period and held for the entire period. The expense example table below illustrates your fund’s cost in two ways:

| • | Actual Expenses. This section helps you to estimate the actual expenses after fee waivers that you paid over the period. The “Ending Account Value” shown is derived from the Portfolio’s actual return, and “Expenses Paid During Period” shows the dollar amount that would have been paid by an investor who started with $1,000 in the Portfolio. You may use the information here, together with the amount you invested, to estimate the expenses that you paid over the period. To do so, simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number given for your Portfolio under the heading entitled “Expenses Paid During Period”. |

| | |

| • | Hypothetical Expenses on a 5% Return. This section is intended to help you compare your Portfolio’s costs with those of other mutual funds. It assumes that the Portfolio had a return of 5% before expenses during the period shown, but that the expense ratio is unchanged. In this case, because the return used is not the Portfolio’s actual return, the results do not apply to your investment. The example is useful in making comparisons because the Securities and Exchange Commission requires all mutual funds to calculate expenses based on a 5% return. You can assess your Portfolio’s cost by comparing this hypothetical example with the hypothetical examples that appear in shareholders reports of other funds. |

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as redemption fees or exchange fees. Therefore, the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

For the Period July 1, 2018 to December 31, 2018

Expense Example Table

| | Beginning | Ending | Expenses Paid | Expense Ratio | |

| | Account | Account | During Period* | During Period* | |

| | Value | Value | 7/1/18 – | 7/1/18 – | |

| | 7/1/18 | 12/31/18 | 12/31/18 | 12/31/18 | |

| Needham Growth Fund | | | | | |

| Retail Class Actual Expenses | $1,000.00 | $ 867.10 | $11.95 | 2.54% | |

| Retail Class Hypothetical Example | | | | | |

| for Comparison Purposes | | | | | |

| (5% return before expenses) | $1,000.00 | $1,012.40 | $12.88 | 2.54% | |

| Institutional Class Actual Expenses | $1,000.00 | $ 869.30 | $ 9.38 | 1.99% | |

| Institutional Class Hypothetical | | | | | |

| Example for Comparison Purposes | | | | | |

| (5% return before expenses) | $1,000.00 | $1,015.17 | $10.11 | 1.99% | |

| | | | | | |

| Needham Aggressive Growth Fund | | | | | |

| Retail Class Actual Expenses | $1,000.00 | $ 791.90 | $11.79 | 2.61% | |

| Retail Class Hypothetical Example | | | | | |

| for Comparison Purposes | | | | | |

| (5% return before expenses) | $1,000.00 | $1,012.05 | $13.24 | 2.61% | |

| Institutional Class Actual Expenses | $1,000.00 | $ 793.80 | $9.31 | 2.06% | |

| Institutional Class Hypothetical | | | | | |

| Example for Comparison Purposes | | | | | |

| (5% return before expenses) | $1,000.00 | $1,014.82 | $10.46 | 2.06% | |

| | | | | | |

| Needham Small Cap Growth Fund | | | | | |

| Retail Class Actual Expenses | $1,000.00 | $ 904.80 | $ 9.36 | 1.95% | |

| Retail Class Hypothetical Example | | | | | |

| for Comparison Purposes | | | | | |

| (5% return before expenses) | $1,000.00 | $1,015.38 | $ 9.91 | 1.95% | |

| Institutional Class Actual Expenses | $1,000.00 | $ 907.60 | $ 6.73 | 1.40% | |

| Institutional Class Hypothetical | | | | | |

| Example for Comparison Purposes | | | | | |

| (5% return before expenses) | $1,000.00 | $1,018.15 | $ 7.12 | 1.40% | |

| * | Expenses are equal to the average account value times the Portfolio’s annualized expense ratio multiplied 184/365 (to reflect the one-half-year period). |

Needham Growth Fund

Schedule of Investments

December 31, 2018

| | | Shares | | | Value | |

| (Percentage of Net Assets) | | | | | | |

| | | | | | | |

| Common Stocks (98.8%) | | | | | | |

| | | | | | | |

| Airlines (0.3%) | | | | | | |

| Hawaiian Holdings, Inc. | | | 9,500 | | | $ | 250,895 | |

| | | | | | | | | |

| Biotechnology (6.5%) | | | | | | | | |

| Gilead Sciences, Inc. (c) | | | 86,000 | | | | 5,379,300 | |

| | | | | | | | | |

| Capital Markets (1.0%) | | | | | | | | |

| Oaktree Capital Group LLC, Class A | | | 20,000 | | | | 795,000 | |

| | | | | | | | | |

| Commercial Services & Supplies (0.1%) | | | | | | | | |

| Clean Harbors, Inc. (a) | | | 1,500 | | | | 74,025 | |

| | | | | | | | | |

| Communications Equipment (9.3%) | | | | | | | | |

| KVH Industries, Inc. (a) | | | 486,850 | | | | 5,009,687 | |

| ViaSat, Inc. (a)(c) | | | 47,200 | | | | 2,782,440 | |

| | | | | | | | 7,792,127 | |

| Diversified Manufacturing (0.2%) | | | | | | | | |

| DIRTT Environmental Solutions (Canada) (a) | | | 30,000 | | | | 134,266 | |

| | | | | | | | | |

| Electrical Equipment (0.9%) | | | | | | | | |

| Vicor Corp. (a) | | | 19,500 | | | | 736,905 | |

| | | | | | | | | |

| Electronic Equipment, Instruments & Components (5.5%) | | | | | | | | |

| Corning, Inc. | | | 35,000 | | | | 1,057,350 | |

| FLIR Systems, Inc. | | | 8,500 | | | | 370,090 | |

| Frequency Electronics, Inc. (a) | | | 35,200 | | | | 373,120 | |

| IPG Photonics Corp. (a) | | | 6,250 | | | | 708,063 | |

| National Instruments Corp. | | | 20,000 | | | | 907,600 | |

| nLight, Inc. (a) | | | 3,500 | | | | 62,230 | |

| Vishay Intertechnology, Inc. | | | 60,000 | | | | 1,080,600 | |

| | | | | | | | 4,559,053 | |

| Energy Equipment & Services (1.6%) | | | | | | | | |

| Aspen Aerogels, Inc. (a) | | | 434,050 | | | | 924,526 | |

| Core Laboratories NV (Netherlands) | | | 1,000 | | | | 59,660 | |

| Schlumberger, Ltd. (Curacao) | | | 10,000 | | | | 360,800 | |

| | | | | | | | 1,344,986 | |

See accompanying notes to financial statements.

Needham Growth Fund

Schedule of Investments (Continued)

December 31, 2018

| | | Shares | | | Value | |

| Common Stocks – Continued | | | | | | |

| | | | | | | |

| Entertainment (0.9%) | | | | | | |

| World Wrestling Entertainment, Inc., Class A | | | 9,500 | | | $ | 709,840 | |

| | | | | | | | | |

| Health Care Equipment & Supplies (8.9%) | | | | | | | | |

| Becton Dickinson & Co. | | | 20,500 | | | | 4,619,060 | |

| CryoPort, Inc. (a) | | | 60,150 | | | | 663,454 | |

| GenMark Diagnostics, Inc. (a) | | | 32,000 | | | | 155,520 | |

| Medtronic PLC (Ireland) | | | 22,000 | | | | 2,001,120 | |

| | | | | | | | 7,439,154 | |

| Health Care Providers & Services (0.6%) | | | | | | | | |

| Laboratory Corp. of America Holdings (a) | | | 2,000 | | | | 252,720 | |

| Quest Diagnostics, Inc. | | | 3,000 | | | | 249,810 | |

| | | | | | | | 502,530 | |

| Household Products (0.6%) | | | | | | | | |

| Oil-Dri Corp. of America | | | 18,500 | | | | 490,250 | |

| | | | | | | | | |

| Industrial Conglomerates (0.4%) | | | | | | | | |

| Honeywell International, Inc. | | | 2,500 | | | | 330,300 | |

| | | | | | | | | |

| Interactive Media & Services (0.0%) | | | | | | | | |

| Eventbrite, Inc. (a) | | | 1,000 | | | | 27,810 | |

| | | | | | | | | |

| IT Services (2.7%) | | | | | | | | |

| Akamai Technologies, Inc. (a)(c) | | | 36,500 | | | | 2,229,420 | |

| | | | | | | | | |

| Life Sciences Tools & Services (9.4%) | | | | | | | | |

| Thermo Fisher Scientific, Inc (c) | | | 35,000 | | | | 7,832,650 | |

| | | | | | | | | |

| Media (4.7%) | | | | | | | | |

| Comcast Corp., Class A | | | 115,000 | | | | 3,915,750 | |

| | | | | | | | | |

| Oil, Gas & Consumable Fuels (0.4%) | | | | | | | | |

| Hess Corp. | | | 7,500 | | | | 303,750 | |

| Navigator Holdings, Ltd. (Marshall Islands) (a) | | | 6,000 | | | | 56,400 | |

| | | | | | | | 360,150 | |

| Semiconductors & Semiconductor Equipment (21.7%) | | | | | | | | |

| Applied Materials, Inc. | | | 7,500 | | | | 245,550 | |

| Aquantia Corp. (a) | | | 42,500 | | | | 372,725 | |

| Entegris, Inc. | | | 143,500 | | | | 4,002,932 | |

See accompanying notes to financial statements.

Needham Growth Fund

Schedule of Investments (Continued)

December 31, 2018

| | | Shares | | | Value | |

| Common Stocks – Continued | | | | | | |

| | | | | | | |

| Semiconductors & Semiconductor Equipment – Continued | | | | | | |

| FormFactor, Inc. (a) | | | 288,750 | | | $ | 4,068,488 | |

| Lam Research Corp. | | | 2,500 | | | | 340,425 | |

| MKS Instruments, Inc. | | | 25,000 | | | | 1,615,250 | |

| Nova Measuring Instruments, Ltd. (Israel) (a) | | | 58,500 | | | | 1,332,630 | |

| PDF Solutions, Inc. (a) | | | 495,400 | | | | 4,176,222 | |

| Photronics, Inc. (a) | | | 157,500 | | | | 1,524,600 | |

| Taiwan Semiconductor Manufacturing | | | | | | | | |

| Co., Ltd. (Taiwan) – ADR | | | 6,000 | | | | 221,460 | |

| Ultra Clean Holdings, Inc. (a) | | | 25,000 | | | | 211,750 | |

| | | | | | | | 18,112,032 | |

| Software (9.2%) | | | | | | | | |

| The Trade Desk, Inc., Class A (a) | | | 7,000 | | | | 812,420 | |

| 2U, Inc. (a) | | | 4,000 | | | | 198,880 | |

| Altair Engineering, Inc., Class A (a) | | | 2,996 | | | | 82,630 | |

| Amber Road, Inc. (a) | | | 445,000 | | | | 3,662,350 | |

| Appian Corp., Class A (a) | | | 10,000 | | | | 267,100 | |

| Coupa Software, Inc. (a) | | | 4,800 | | | | 301,728 | |

| Everbridge, Inc. (a) | | | 9,500 | | | | 539,220 | |

| Pluralsight, Inc. (a) | | | 6,000 | | | | 141,300 | |

| Q2 Holdings, Inc. (a) | | | 20,000 | | | | 991,000 | |

| Tenable Holdings, Inc. (a) | | | 5,000 | | | | 110,950 | |

| Zuora, Inc. (a) | | | 33,000 | | | | 598,620 | |

| | | | | | | | 7,706,198 | |

| Specialty Retail (6.4%) | | | | | | | | |

| CarMax, Inc. (a)(c) | | | 85,000 | | | | 5,332,050 | |

| | | | | | | | | |

| Technology Hardware, Storage & Peripherals (5.7%) | | | | | | | | |

| Apple, Inc. | | | 2,700 | | | | 425,898 | |

| Electronics for Imaging, Inc. (a) | | | 66,500 | | | | 1,649,200 | |

| Super Micro Computer, Inc. (a) | | | 195,000 | | | | 2,691,000 | |

| | | | | | | | 4,766,098 | |

| Trading Companies & Distributors (1.8%) | | | | | | | | |

| Air Lease Corp., Class A | | | 50,000 | | | | 1,510,500 | |

| | | | | | | | | |

| Total Common Stocks | | | | | | | | |

| (Cost $42,296,082) | | | | | | $ | 82,331,289 | |

See accompanying notes to financial statements.

Needham Growth Fund

Schedule of Investments (Continued)

December 31, 2018

| | | Shares | | | Value | |

| Short-Term Investments (0.6%) | | | | | | |

| | | | | | | |

| Money Market Fund (0.6%) | | | | | | |

| Dreyfus Treasury Securities Cash Management – | | | | | | |

| Institutional Class 2.20% (b) | | | | | | |

| | | | | | | |

| Total Short Term Investments | | | | | | |

| (Cost $536,118) | | | 536,118 | | | $ | 536,118 | |

| | | | | | | | | |

| Total Investments (99.4%) | | | | | | | | |

| (Cost $42,832,200) | | | | | | | 82,867,407 | |

| Total Securities Sold Short (-6.2%) | | | | | | | (5,195,265 | ) |

| (Proceeds $1,624,399) | | | | | | | | |

| Other Assets in Excess of Liabilities (6.8%) | | | | | | | 5,721,595 | |

| Total Net Assets (100.0%) | | | | | | $ | 83,393,737 | |

Percentages are stated as a percent of net assets.

| (a) | Non-income producing security. |

| (b) | Rate shown is the seven-day yield as of December 31, 2018. |

| (c) | Security position is either entirely or partially held in a segregated account as collateral for securities sold short, aggregating a total market value of $5,665,150. |

See accompanying notes to financial statements.

Needham Growth Fund

Schedule of Securities Sold Short

December 31, 2018

| | | Shares | | | Value | |

| Securities Sold Short (-6.2%) | | | | | | |

| | | | | | | |

| Communications Equipment (-5.2%) | | | | | | |

| Ubiquiti Networks, Inc. | | | 43,500 | | | $ | 4,324,335 | |

| | | | | | | | | |

| Consumer Finance (-1.0%) | | | | | | | | |

| Medallion Financial Corp. (a) | | | 180,000 | | | | 844,200 | |

| | | | | | | | | |

| Insurance (0.0%) | | | | | | | | |

| Health Insurance Innovations, Inc., Class A (a) | | | 1,000 | | | | 26,730 | |

| | | | | | | | | |

| Total Securities Sold Short | | | | | | | | |

| (Proceeds $1,624,399) | | | | | | $ | 5,195,265 | |

| (a) | Non-income producing security. |

See accompanying notes to financial statements.

Needham Aggressive Growth Fund

Schedule of Investments

December 31, 2018

| | | Shares | | | Value | |

| (Percentage of Net Assets) | | | | | | |

| | | | | | | |

| Common Stocks (101.6%) | | | | | | |

| | | | | | | |

| Airlines (0.2%) | | | | | | |

| Hawaiian Holdings, Inc. | | | 2,500 | | | $ | 66,025 | |

| | | | | | | | | |

| Building Products (0.5%) | | | | | | | | |

| Alpha Pro Tech, Ltd. (a) | | | 59,843 | | | | 222,018 | |

| | | | | | | | | |

| Commercial Services & Supplies (1.0%) | | | | | | | | |

| Ecology and Environment, Inc., Class A | | | 34,100 | | | | 386,694 | |

| | | | | | | | | |

| Communications Equipment (9.6%) | | | | | | | | |

| KVH Industries, Inc. (a)(b) | | | 369,400 | | | | 3,801,126 | |

| ViaSat, Inc. (a) | | | 1,800 | | | | 106,110 | |

| | | | | | | | 3,907,236 | |

| Diversified Manufacturing (3.3%) | | | | | | | | |

| DIRTT Environmental Solutions (Canada) (a) | | | 300,000 | | | | 1,342,660 | |

| | | | | | | | | |

| Electrical Equipment (5.2%) | | | | | | | | |

| Vicor Corp. (a) | | | 56,227 | | | | 2,124,818 | |

| | | | | | | | | |

| Electronic Equipment, Instruments & Components (3.8%) | | | | | | | | |

| Frequency Electronics, Inc. (a) | | | 9,500 | | | | 100,700 | |

| II-VI, Inc. (a) | | | 500 | | | | 16,230 | |

| IPG Photonics Corp. (a) | | | 7,000 | | | | 793,030 | |

| National Instruments Corp. | | | 8,000 | | | | 363,040 | |

| nLight, Inc. (a) | | | 1,523 | | | | 27,079 | |

| Vishay Precision Group, Inc. (a) | | | 7,500 | | | | 226,725 | |

| | | | | | | | 1,526,804 | |

| Energy Equipment & Services (0.9%) | | | | | | | | |

| Aspen Aerogels, Inc. (a) | | | 165,450 | | | | 352,409 | |

| | | | | | | | | |

| Entertainment (0.8%) | | | | | | | | |

| World Wrestling Entertainment, Inc., Class A | | | 4,500 | | | | 336,240 | |

| | | | | | | | | |

| Health Care Equipment & Supplies (3.0%) | | | | | | | | |

| Becton Dickinson & Co. | | | 750 | | | | 168,990 | |

| CryoPort, Inc. (a) | | | 42,500 | | | | 468,775 | |

| LeMaitre Vascular, Inc. | | | 25,000 | | | | 591,000 | |

| | | | | | | | 1,228,765 | |

See accompanying notes to financial statements.

Needham Aggressive Growth Fund

Schedule of Investments (Continued)

December 31, 2018

| | | Shares | | | Value | |

| Common Stocks – Continued | | | | | | |

| | | | | | | |

| Health Care Providers & Services (0.5%) | | | | | | |

| Laboratory Corp. of America Holdings (a) | | | 500 | | | $ | 63,180 | |

| Quest Diagnostics, Inc. | | | 1,500 | | | | 124,905 | |

| | | | | | | | 188,085 | |

| Health Care Technology (1.4%) | | | | | | | | |

| Omnicell, Inc. (a) | | | 9,000 | | | | 551,160 | |

| | | | | | | | | |

| Household Durables (0.1%) | | | | | | | | |

| iRobot Corp. (a) | | | 500 | | | | 41,870 | |

| | | | | | | | | |

| Household Products (2.9%) | | | | | | | | |

| Oil-Dri Corp. of America | | | 45,000 | | | | 1,192,500 | |

| | | | | | | | | |

| Insurance (0.4%) | | | | | | | | |

| Markel Corp. (a) | | | 175 | | | | 181,659 | |

| | | | | | | | | |

| Interactive Media & Services (0.1%) | | | | | | | | |

| Eventbrite, Inc. (a) | | | 1,500 | | | | 41,715 | |

| | | | | | | | | |

| IT Services (4.1%) | | | | | | | | |

| Akamai Technologies, Inc. (a)(b) | | | 27,500 | | | | 1,679,700 | |

| | | | | | | | | |

| Professional Services (0.5%) | | | | | | | | |

| CRA International, Inc. | | | 5,000 | | | | 212,750 | |

| | | | | | | | | |

| Real Estate Investment Trusts (REITs) (1.7%) | | | | | | | | |

| Equinix, Inc. | | | 2,000 | | | | 705,120 | |

| | | | | | | | | |

| Semiconductors & Semiconductor Equipment (32.9%) (c) | | | | | | | | |

| Entegris, Inc. | | | 157,000 | | | | 4,379,515 | |

| FormFactor, Inc. (a) | | | 134,000 | | | | 1,888,060 | |

| Ichor Holdings, Ltd. (Cayman Islands) (a) | | | 1,000 | | | | 16,300 | |

| MKS Instruments, Inc. | | | 23,000 | | | | 1,486,030 | |

| Nova Measuring Instruments, Ltd. (Israel) (a)(b) | | | 63,000 | | | | 1,435,140 | |

| PDF Solutions, Inc. (a)(b) | | | 365,500 | | | | 3,081,165 | |

| Photronics, Inc. (a) | | | 93,750 | | | | 907,500 | |

| Taiwan Semiconductor Manufacturing | | | | | | | | |

| Co., Ltd. (Taiwan) – ADR | | | 4,500 | | | | 166,095 | |

| Ultra Clean Holdings, Inc. (a) | | | 2,000 | | | | 16,940 | |

| | | | | | | | 13,376,745 | |

See accompanying notes to financial statements.

Needham Aggressive Growth Fund

Schedule of Investments (Continued)

December 31, 2018

| | | Shares | | | Value | |

| Common Stocks – Continued | | | | | | |

| | | | | | | |

| Software (13.6%) | | | | | | |

| The Trade Desk, Inc., Class A (a) | | | 2,500 | | | $ | 290,150 | |

| 2U, Inc. (a) | | | 2,000 | | | | 99,440 | |

| Altair Engineering, Inc., Class A (a) | | | 1,000 | | | | 27,580 | |

| Amber Road, Inc. (a)(b) | | | 163,550 | | | | 1,346,016 | |

| Appian Corp., Class A (a) | | | 5,500 | | | | 146,905 | |

| Carbon Black, Inc. (a) | | | 1,500 | | | | 20,130 | |

| Coupa Software, Inc. (a) | | | 1,200 | | | | 75,432 | |

| Everbridge, Inc. (a) | | | 4,500 | | | | 255,420 | |

| GSE Systems, Inc. (a)(d) | | | 1,120,000 | | | | 2,352,000 | |

| Pluralsight, Inc. (a) | | | 4,000 | | | | 94,200 | |

| Q2 Holdings, Inc. (a) | | | 12,000 | | | | 594,600 | |

| Tenable Holdings, Inc. (a) | | | 2,000 | | | | 44,380 | |

| Zuora, Inc. (a) | | | 10,000 | | | | 181,400 | |

| | | | | | | | 5,527,653 | |

| Specialty Retail (3.2%) | | | | | | | | |

| CarMax, Inc. (a)(b) | | | 20,500 | | | | 1,285,965 | |

| | | | | | | | | |

| Technology Hardware, Storage & Peripherals (11.8%) | | | | | | | | |

| Apple, Inc. (b) | | | 20,000 | | | | 3,154,800 | |

| Electronics for Imaging, Inc. (a) | | | 16,000 | | | | 396,800 | |

| Super Micro Computer, Inc. (a)(b) | | | 88,350 | | | | 1,219,230 | |

| | | | | | | | 4,770,830 | |

See accompanying notes to financial statements.

Needham Aggressive Growth Fund

Schedule of Investments (Continued)

December 31, 2018

| | | Shares | | | Value | |

| Common Stocks – Continued | | | | | | |

| | | | | | | |

| Trading Companies & Distributors (0.2%) | | | | | | |

| Air Lease Corp., Class A | | | 3,000 | | | $ | 90,630 | |

| | | | | | | | | |

| Total Common Stocks | | | | | | | | |

| (Cost $23,318,969) | | | | | | $ | 41,340,051 | |

| | | | | | | | | |

| Total Investments (101.8%) | | | | | | | | |

| (Cost $23,318,969) | | | | | | | 41,340,051 | |

| Total Securities Sold Short (-7.2%) | | | | | | | (2,926,675 | ) |

| (Proceeds $1,142,432) | | | | | | | | |

| Other Assets in Excess of Liabilities (5.4%) | | | | | | | 2,184,037 | |

| Total Net Assets (100.0%) | | | | | | $ | 40,597,413 | |

Percentages are stated as a percent of net assets.

| (a) | Non-income producing security. |

| (b) | Security position is either entirely or partially held in a segregated account as collateral for securities sold short, aggregating a total market value of $4,678,877. |

| (c) | As of December 31, 2018, the Fund had a significant portion of its assets invested in the Semiconductors and Semiconductor Equipment industry. |

| (d) | Affiliated security. Please refer to Note 11 of the Financial Statements. |

| ADR | American Depositary Receipt |

See accompanying notes to financial statements.

Needham Aggressive Growth Fund

Schedule of Securities Sold Short

December 31, 2018

| | | Shares | | | Value | |

| Securities Sold Short (-7.2%) | | | | | | |

| | | | | | | |

| Communications Equipment (-4.8%) | | | | | | |

| Ubiquiti Networks, Inc. | | | 19,500 | | | $ | 1,938,495 | |

| | | | | | | | | |

| Consumer Finance (-2.3%) | | | | | | | | |

| Medallion Financial Corp. (a) | | | 205,000 | | | | 961,450 | |

| | | | | | | | | |

| Insurance (-0.1%) | | | | | | | | |

| Health Insurance Innovations, Inc., Class A (a) | | | 1,000 | | | | 26,730 | |

| | | | | | | | | |

| Total Securities Sold Short | | | | | | | | |

| (Proceeds $1,142,432) | | | | | | $ | 2,926,675 | |

| (a) | Non-income producing security. |

See accompanying notes to financial statements.

Needham Small Cap Growth Fund

Schedule of Investments

December 31, 2018

| | | Shares | | | Value | |

| (Percentage of Net Assets) | | | | | | |

| | | | | | | |

| Common Stocks (92.7%) | | | | | | |

| | | | | | | |

| Airlines (4.0%) | | | | | | |

| Hawaiian Holdings, Inc. | | | 37,500 | | | $ | 990,375 | |

| | | | | | | | | |

| Biotechnology (0.4%) | | | | | | | | |

| Exact Sciences Corp. (a) | | | 1,000 | | | | 63,100 | |

| | | | | | | | | |

| Communications Equipment (8.8%) | | | | | | | | |

| EMCORE Corp. (a) | | | 310,000 | | | | 1,302,000 | |

| KVH Industries, Inc. (a)(b) | | | 37,591 | | | | 386,811 | |

| Quantenna Communications, Inc. (a) | | | 12,500 | | | | 179,375 | |

| ViaSat, Inc. (a) | | | 5,000 | | | | 294,750 | |

| | | | | | | | 2,162,936 | |

| Diversified Manufacturing (0.7%) | | | | | | | | |

| DIRTT Environmental Solutions (Canada) (a) | | | 40,000 | | | | 179,021 | |

| | | | | | | | | |

| Electronic Equipment, Instruments & Components (10.6%) | | | | | | | | |

| Akoustis Technologies, Inc. (a) | | | 160,000 | | | | 795,200 | |

| Coherent, Inc. (a) | | | 1,500 | | | | 158,565 | |

| Frequency Electronics, Inc. (a) | | | 71,000 | | | | 752,600 | |

| II-VI, Inc. (a) | | | 15,000 | | | | 486,900 | |

| TTM Technologies, Inc. (a) | | | 40,000 | | | | 389,200 | |

| Vishay Precision Group, Inc. (a) | | | 1,000 | | | | 30,230 | |

| | | | | | | | 2,612,695 | |

| Energy Equipment & Services (6.1%) | | | | | | | | |

| Aspen Aerogels, Inc. (a) | | | 495,450 | | | | 1,055,308 | |

| Core Laboratories NV (Netherlands) | | | 5,000 | | | | 298,300 | |

| Schlumberger, Ltd. (Curacao) | | | 4,000 | | | | 144,320 | |

| | | | | | | | 1,497,928 | |

| Health Care Equipment & Supplies (3.7%) | | | | | | | | |

| CryoPort, Inc. (a) | | | 18,350 | | | | 202,401 | |

| GenMark Diagnostics, Inc. (a) | | | 148,500 | | | | 721,710 | |

| | | | | | | | 924,111 | |

| Household Durables (1.2%) | | | | | | | | |

| Roku, Inc., Class A (a) | | | 10,000 | | | | 306,400 | |

| | | | | | | | | |