SECURITIES AND EXCHANGE COMMISSION

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT

OF

REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-07537

Name of Registrant: Royce Capital Fund

Address of Registrant: 745 Fifth Avenue

New York, NY 10151

| Name and address of agent for service: | John E. Denneen, Esquire | |

| 745 Fifth Avenue | ||

| New York, NY 10151 | ||

Registrant’s telephone number, including area code: (212) 508-4500

Date of fiscal year end: December 31

Date of reporting period: January 1, 2009 – June 30, 2009

Item 1. Reports to Shareholders.

| |||||

| Royce Capital Fund— Micro-Cap Portfolio Royce Capital Fund— Small-Cap Portfolio | SEMIANNUAL REVIEW AND REPORT TO SHAREHOLDERS | ||||

www.roycefunds.com |  | ||||

| Performance and Expenses | Through June 30, 2009 |

| Average Annual Total Returns | |||||||||||||||||||||

| Since | Annual Operating | ||||||||||||||||||||

Fund | YTD | 1-Year | 5-Year | 10-Year | Inception | Expenses | |||||||||||||||

| Royce Capital Fund—Micro-Cap Portfolio | 21.56 | % | -25.81 | % | 0.82 | % | 9.82 | % | 10.71 | % | (12/27/96) | 1.49 | % | ||||||||

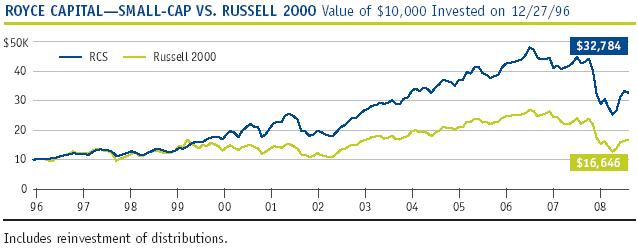

| Royce Capital Fund—Small-Cap Portfolio | 7.32 | % | -23.31 | 1.66 | 9.23 | 9.96 | (12/27/96) | 1.09 | |||||||||||||

| Russell 2000 | 2.64 | % | -25.01 | -1.71 | 2.38 | 4.16 | * | n.a. | |||||||||||||

| * Since Royce Capital Fund’s inception on 12/27/96. | |||||||||||||||||||||

Important Performance, Expense and Risk Information

All performance information in this Review and Report reflects past performance, is presented on a total return basis and reflects the reinvestment of distributions. Past performance is no guarantee of future results. Investment return and principal value of an investment will fluctuate, so that shares may be worth more or less than their original cost when redeemed. Current performance may be higher or lower than performance quoted. Current month-end performance may be obtained at www.roycefunds.com. The performance information in the table above, and in the graphs and tables appearing on pages 10-13 does not reflect any deduction for charges or expenses of the variable contracts or retirement plans investing in the Fund. All performance and expense information reflects results for each Fund’s Investment Class Shares. Service Class Shares bear an annual distribution expense that is not borne by the Investment Class. Operating expenses reflect the Fund’s total annual operating expenses for the Investment Class, as of the Fund’s most current prospectus, and include management fees, other expenses and, in the case of Royce Capital Fund—Micro-Cap Portfolio, acquired fund fees and expenses. Acquired fund fees and expenses are those incurred indirectly as a result of investment in one or more acquired funds, including mutual funds, hedge funds, private equity funds and other pooled investment vehicles.

Royce Capital Fund invests primarily in securities of small- and/or micro-cap companies, which may involve considerably more risk than investments in securities of larger-cap companies (see “Primary Risks for Fund Investors” in the Prospectus). Please read the Prospectus carefully before investing or sending money. The Russell 2000 is an unmanaged, capitalization-weighted index of domestic small-cap stocks. It measures the performance of the 2,000 smallest publicly traded U.S. companies in the Russell 3000 index.

| This page is not part of the 2009 Semiannual Report to Shareholders |

| Table of Contents | |

| Semiannual Review | |

| Performance and Expenses | Inside Cover |

| Letter to Our Shareholders | 2 |

| Semiannual Report to Shareholders | 8 |

| This page is not part of the 2009 Semiannual Report to Shareholders | 1 |

What do people do when they buy stocks? What are their motives and expectations? These may seem like odd, or at least very simple, questions, but we think that they are worth asking in pursuit of a larger, more important point. After all, myriad factors can lead a company’s stock price to higher levels— increased demand for the company’s existing products and/or services, a rapidly expanding business, a higher public profile, an innovative new product, etc. But none of these events ensures that the share-price gains will last. To us, the critical question is, what kind of companies are most likely to experience a sustainable increase in their business value, and thus an increase in share price? As long-term investors with a disciplined value approach, we are therefore less concerned with what may or may not make a stock price climb, particularly in the short run. Short-term gains for our portfolio holdings are always welcome, but our focus is on identifying companies Continued on page 4... | Letter to Our Shareholders  Simple Twist of Fate It was one year ago that, taking a cue from a Bob Dylan song, we wrote that something significant was happening in the markets, but the nature and degree of the event had not yet become clear. The intervening 12 months have certainly clarified things, in about as painful and destructive a fashion as possible from an investment standpoint. Back in March 2008, the fall of Bear Stearns was initially hoped to be, with fingers crossed in one hand and the other knocking on wood, an isolated, anomalous event. It took a few months, but the ongoing implosion of the subprime mortgage market sent shock waves throughout the global financial system. A significant correction in housing prices probably would have created some thorny economic problems in and of itself, but as fate would have it, many of these ill-awarded mortgages were securitized, packaged, ‘tranched’ and traded in a dizzying array of complicated arrangements that may never be completely understood. And once September rolled around, the once-slow pace of decline picked up so quickly that matters barely had time to escalate from bad to disastrous. | ||

| 2 | This page is not part of the 2009 Semiannual Report to Shareholders |

| Lacking the fatalism that has characterized many observers’ forecasts for the economy and the stock market, we believe in the cyclicality of markets and the resourcefulness of our economy, both of which should be factors in the next year as we make our way by fits and starts to better days. | |

Modern Times | ||

As for those days most recently passed, they were definitely better, as the market spent much of the period from March through June rallying from the worrisome depths it had tested in the fall and winter months. The better days began after the most recent market trough on March 9 and continued mostly unimpeded through the end of June, though there were notable sell-offs, particularly late in June and early in July. However, even the most fatalistic observer was likely cheered by the year-to-date results for the major equity indices: The small-cap Russell 2000 was up 2.6% through June 30, 2009, while the large-cap S&P 500 gained 3.2% and the more tech-laden Nasdaq Composite shot up 16.4%. | In such a volatile environment, the question of where market leadership will next reside remains an open one, as does the question of how long any such leadership period is likely to last. |

| This page is not part of the 2009 Semiannual Report to Shareholders | 3 |

capable of long-term success as both businesses and stocks. There are several methods that we use to try to determine this. The first critical step entails a close examination of a company’s financial profile and history. We search for evidence of our definition of quality—a strong balance sheet, a history of solid earnings, the ability to generate positive cash flow and high returns on invested capital. While it’s true that a company possessing each of these qualities is hardly guaranteed positive stock performance (as returns for our Funds in 2008 made painfully clear), we think that businesses with these characteristics are most likely to be solid, if not strong, performers over long-term time horizons. Another route is of particular significance to us, though it may at first seem counterintuitive: A company can achieve an attractive long-term record by losing less during economic or market downturns. Our years of research bear out that those attributes that we value so highly can help a firm to weather these storms— profitable companies with low debt and plentiful cash have historically been stalwarts in poor markets and/or economies (the recent bear market notwithstanding). In other words, we are seeking great companies, not just great stocks. Continued on page 6... | |||

Letter to Our Shareholders all within a compact six months. During the first quarter, the Russell 2000 was down 15.0%, the S&P 500 fell 11.0% and the Nasdaq Composite slipped “only” 3.1%. It should be remembered that these results included the beginning of the recent rally, more than three weeks’ worth of mostly rising stock prices that closed out the quarter and saw each index posting positive double-digit returns from March 9 through March 31, 2009. That the rally then took up almost the entire second quarter was thus a more than welcome development, especially as results for the four indices referenced above represented the largest respective quarterly advances since the second quarter of 2003. Yet we are still a long way from celebration. For the periods ended June 30, 2009, one-year, three-year and five-year average annual returns for all three indices remained negative. Market leadership remains unclear. Consider the following: The Russell 2000 trailed the S&P 500 in the first quarter, outperformed in the second quarter, but remained behind its large-cap counterpart for the year-to-date period ended June 30, 2009. The small-cap index led its large-cap sibling for the one-year period through the end of June, trailed in the three-year period, and led in the five- and 10-year periods. Small-cap stocks also significantly outperformed large-caps for the decade-to-date period, with the Russell 2000 gaining 14.0% versus the S&P 500’s decline of 25.9% from December 31, 1999 through June 30, 2009. With dramatic and well-defined bear and bull periods over the last two years, none of us needs a reminder that market volatility has been very much the norm. However, we think that another important example of its omnipresence can be seen in the near-regular rotation of small- and large-cap leadership over recent shorter-term calendar-based periods. In such an environment, the question of where market leadership will next reside remains an open one, as does the question of how long any such leadership period is likely to last. | ||

It Takes Growth to Laugh, It Takes Value to Cry Within the small-cap universe, the current leadership issue is more than settled. Small-cap growth, as measured by the Russell 2000 Growth index, remained in the top spot over small-cap value, as measured by the Russell 2000 Value index. For the year-to-date period ended June 30, 2009, the Russell 2000 Growth index gained 11.4%, while the Russell 2000 Value index fell 5.2%. Both small-cap indices enjoyed robust results in the second quarter, but the Russell 2000 Value index’s 18.0% gain trailed its growth counterpart’s 23.4% return, so the turn in the tide of stock prices did little to help the small-cap value index to narrow the performance gap. Small-cap growth first gained its advantage in 2009 by outperforming in the bearish first quarter, down 9.7% compared to a decline of 19.6% for small-cap value, which marked the third consecutive quarter | ||

| 4 | This page is not part of the 2009 Semiannual Report to Shareholders |

| Quality is likely to be a lingering presence—a constant in a solid bull market that should otherwise see regular rotations in leadership. | ||

Things Have Changed | |||

The significant question, of course, is what happens next? Late June and early July saw just enough selling for many observers to be convinced that the rally might have breathed its last, at least until more compelling evidence of a growing economy surfaces. Our own take is that the first phase of the bull market is probably complete. The rally that began in March was characterized by dynamic, double-digit returns, and stocks of all sizes in nearly all sectors and industries benefiting greatly. Around the middle of June, the market fell into a corrective period, almost as if it were catching its breath after the wild run-up of stock prices. This period could last for another few months or could be over by the time this Semiannual Review and Report is being read. We would expect |

| This page is not part of the 2009 Semiannual Report to Shareholders | 5 |

At first, this may appear to be a distinction without a difference, but the difference is very real to us because we see ourselves as business buyers. We have always taken very seriously the simple truth that when one buys even one share of stock, one becomes a stakeholder in a business. This is why our approach generally requires developing a deep understanding of what a company does and how it operates. In addition to our discussions with a company’s management, we often speak to suppliers, customers and competitors in order to expand our knowledge of the company. To be sure, we buy stocks to make money, but the means to that sought-after end are very specific. We are looking for the happy marriage of a strong financial profile with a wonderful business that we think we know well. This necessitates a commitment to a disciplined process, one that demands we know as much about these businesses as we possibly can. It involves making an investment in a business as if we were purchasing the entire company, as if we were owners, because, after all, that is what we become when we buy stocks. | Letter to Our Shareholders an overall modest decline in the range of 10%-15%, regardless of the time frame. We also expect the next phase in the current cycle to be different—still bullish, but with returns that will not be as lofty. It seems to us we will see more historically typical performance patterns, frequent sector and industry rotation and greater discrimination on the part of investors for quality companies. We also feel confident that stocks of higher quality companies—those with solid earnings, high returns on invested capital and/or that pay dividends—should take the lead in the next bull phase. Our reasoning is that enough investors should begin to focus on company quality now that the period of momentum-driven results appears to be behind us and a recovering economy in front of us, though no one knows how far ahead it lies. Recent selling has been driven more by fundamentals than liquidity, which is a good sign for the stability of equities as a whole. Without the sense of panic that was so prevalent in the last four months of 2008, investors would be free to think more about factors such as risk, long-term performance and sustainable growth. In such a setting, we think that quality stocks would do well across virtually all asset classes and in all industries where they can be found. So we may see, for example, small-cap leadership for a short time, then a period of large-cap outperformance, etc. However, quality is likely to be a lingering presence—a constant in a solid bull market that should otherwise see regular rotations in leadership. Beyond Here Lies... The economy is the elephant in the room. The recent rally was fueled in large part by investors’ expectations of an economic recovery that, perhaps needless to say, has thus far not materialized. We suspect that some investors may have confused economic stabilization with economic recovery, something that surely helped the prices of certain stocks to run ahead of what their fundamentals might suggest, which in part explains why the rally lost steam in June. From an equity investor’s standpoint, economic recovery is necessary for the market’s bullish moves to be sustained. Rancorous debate about where the economy is and where it is going will continue. There will be plenty of disappointment and cynicism, as well as an ample supply of naysayers braying along the road to economic recovery, which we think will proceed slowly, at times at a pace of two steps forward one step back, to the point that within a year a recovery should be well under way. We do not think that it will be as driven by consumer spending, but instead will be led by revived industrial activity, natural resources and perhaps even financial services. Consumer activity will still play an important role, but we expect consumer spending to account for far less of GDP than it did prior to the recession, which will be a positive development. | ||

| 6 | This page is not part of the 2009 Semiannual Report to Shareholders |

| |||||||

| |||||||

| |||||||

|  |  | |||||

Charles M. Royce | W. Whitney George | Jack E. Fockler, Jr. | |||||

President | Vice President | Vice President | |||||

July 31, 2009 | |||||||

| This page is not part of the 2009 Semiannual Report to Shareholders | 7 |

| Table of Contents | ||||||||||||||||||||

Semiannual Report to Shareholders | ||||||||||||||||||||

| Notes to Performance and Other Important Information | 9 | |||||||||||||||||||

| Managers’ Discussions of Fund Performance | ||||||||||||||||||||

| Royce Capital Fund—Micro-Cap Portfolio | 10 | |||||||||||||||||||

| Royce Capital Fund—Small-Cap Portfolio | 12 | |||||||||||||||||||

| Schedules of Investments and Financial Statements | 14 | |||||||||||||||||||

| Notes to Financial Statements | 24 | |||||||||||||||||||

| Understanding Your Fund’s Expenses | 27 | |||||||||||||||||||

| Board Approval of Investment Advisory Agreements | 28 | |||||||||||||||||||

| 8 | Royce Capital Fund 2009 Semiannual Report to Shareholders |

Notes to Performance and Other Important Information

The thoughts expressed in this report concerning recent market movements and future prospects for small company stocks are solely the opinion of Royce at June 30, 2009, and, of course, historical market trends are not necessarily indicative of future market movements. Statements regarding the future prospects for particular securities held in the Funds’ portfolios and Royce’s investment intentions with respect to those securities reflect Royce’s opinions as of June 30, 2009 and are subject to change at any time without notice. There can be no assurance that securities mentioned in this report will be included in any Royce-managed portfolio in the future. The Russell 2000 is an index of domestic small-cap stocks. It measures the performance of the 2,000 smallest publicly traded U.S. companies in the Russell 3000 index. The Russell 2000 Value and Growth indices consist of the respective value and growth stocks within the Russell 2000 as determined by Russell Investments. The S&P 500 is an index of U.S. large-cap stocks selected by Standard & Poor’s based on market size, liquidity and industry grouping, among other factors. The Nasdaq Composite is an index of the more than 3,000 common equities listed on the Nasdaq stock exchange. Returns for the market indices used in this report were based on information supplied to Royce by Russell Investments. Royce has not independently verified the above described information. The Royce Funds is a service mark of The Royce Funds. Distributor: Royce Fund Services, Inc. Royce Capital Fund—Micro-Cap Portfolio invests primarily in securities of micro-cap companies and Royce Capital Fund—Small-Cap Portfolio invests primarily in securities of small-cap companies that may involve considerably more risk than investments in securities of larger-cap companies (Please see “Primary Risks for Fund Investors” in the prospectus). The Funds may invest up to 25% of their respective |

| assets in foreign securities that may involve political, economic, currency and other risks not encountered in U.S. investments. Please read the prospectus carefully before investing or sending money. | ||

| Forward-Looking Statements | ||

| This material contains forward-looking statements within the meaning of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), that involve risks and uncertainties, including, among others, statements as to: | ||

| • | the Funds’ future operating results, | |

| • | the prospects of the Funds’ portfolio companies, | |

| • | the impact of investments that the Funds have made or may make, | |

| • | the dependence of the Funds’ future success on the general economy and its impact on the companies and industries in which the Funds invest, and | |

| • | the ability of the Funds’ portfolio companies to achieve their objectives. | |

| This review and report use words such as “anticipates,” “believes,” “expects,” “future,” “intends,” and similar expressions to identify forward-looking statements. Actual results may differ materially from those projected in the forward looking statements for any reason. | ||

The Royce Funds have based the forward-looking statements included in this review and report on information available to us on the date of the report, and we assume no obligation to update any such forward-looking statements. Although The Royce Funds undertake no obligation to revise or update any forward-looking statements, whether as a result of new information, future events or otherwise, you are advised to consult any additional disclosures that we may make through future shareholder communications or reports. | ||

| Proxy Voting | ||

A copy of the policies and procedures that The Royce Funds use to determine how to vote proxies relating to portfolio securities and information regarding how each of The Royce Funds voted proxies relating to portfolio securities during the most recent 12-month period ended June 30 is available, without charge, on The Royce Funds’ website at www.roycefunds.com, by calling (800) 221-4268 (toll-free) and on the website of the Securities and Exchange Commission (“SEC”), at www.sec.gov. | ||

| Form N-Q Filing | ||

The Funds file their complete schedules of investments with the SEC for the first and third quarters of each fiscal year on Form N-Q. The Funds’ Forms N-Q are available on The Royce Funds’ website at www.roycefunds.com and on the SEC’s website at www.sec.gov. The Funds’ Forms N-Q may also be reviewed and copied at the SEC’s Public Reference Room in Washington, D.C. To find out more about this public service, call the SEC at (202) 942-8090. The Funds’ complete schedules of investments are updated quarterly, and are available at www.roycefunds.com. | ||

Royce Capital Fund 2009 Semiannual Report to Shareholders | 9 |

| AVERAGE ANNUAL TOTAL RETURNS Through 6/30/09 | ||||||||||||

| Jan - June 2009* | 21.56 | % | ||||||||||

| One-Year | -25.81 | |||||||||||

| Three-Year | -7.97 | |||||||||||

| Five-Year | 0.82 | |||||||||||

| 10-Year | 9.82 | |||||||||||

| Since Inception (12/27/96) | 10.71 | |||||||||||

| ANNUAL EXPENSE RATIO | ||||||||||||

| Operating Expenses | 1.49 | % | ||||||||||

| * Not annualized | ||||||||||||

| CALENDAR YEAR TOTAL RETURNS | ||||||||||||

| Year | RCM | Year | RCM | |||||||||

| 2008 | -43.3 | % | 2002 | -12.9 | % | |||||||

| 2007 | 4.0 | 2001 | 29.7 | |||||||||

| 2006 | 21.1 | 2000 | 18.5 | |||||||||

| 2005 | 11.6 | 1999 | 28.1 | |||||||||

| 2004 | 13.8 | 1998 | 4.1 | |||||||||

| 2003 | 49.2 | 1997 | 21.2 | |||||||||

| TOP 10 POSITIONS % of Net Assets | ||||||||||||

| Atlantic Tele-Network | 1.4 | % | ||||||||||

| Olympic Steel | 1.4 | |||||||||||

| Patriot Transportation Holding | 1.1 | |||||||||||

| Allied Nevada Gold | 1.1 | |||||||||||

| Kennedy-Wilson | 1.1 | |||||||||||

| Cavco Industries | 1.0 | |||||||||||

| Fronteer Development Group | 1.0 | |||||||||||

| Anaren | 1.0 | |||||||||||

| Semperit AG Holding | 1.0 | |||||||||||

| Silvercorp Metals | 1.0 | |||||||||||

| PORTFOLIO SECTOR BREAKDOWN % of Net Assets | ||||||||||||

| Natural Resources | 16.5 | % | ||||||||||

| Technology | 15.5 | |||||||||||

| Industrial Services | 13.8 | |||||||||||

| Industrial Products | 11.2 | |||||||||||

| Health | 10.7 | |||||||||||

| Consumer Products | 8.2 | |||||||||||

| Consumer Services | 5.9 | |||||||||||

| Financial Intermediaries | 4.2 | |||||||||||

| Financial Services | 3.4 | |||||||||||

| Miscellaneous | 3.4 | |||||||||||

| Preferred Stock | 0.5 | |||||||||||

| Cash and Cash Equivalents | 6.7 | |||||||||||

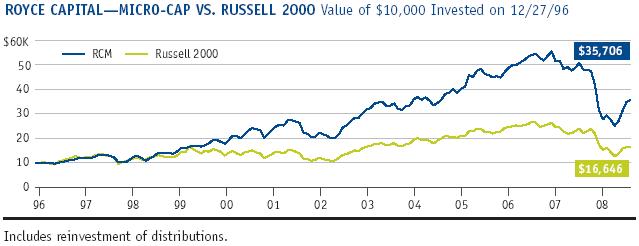

Royce Capital Fund—Micro-Cap Portfolio  Managers’ Discussion Managers’ DiscussionIf not for the stubborn and unfortunate fact that we are still in a bear market, recent performance for Royce Capital Fund—Micro-Cap Portfolio (RCM) would be nothing less than spectacular. As things stand, we will settle for ‘highly encouraging.’ The Fund gained 21.6% for the year-to-date period ended 6/30/09, well ahead of its small-cap benchmark, the Russell 2000, which was up 2.6%, and the Russell Microcap index, which rose 6.0%, for the same period. The Fund’s first-half outperformance was a near-ideal combination of a strong relative showing in the first-quarter downturn and a terrific absolute and relative result in the second-quarter upswing. RCM lost 7.5% in the opening quarter of 2009, compared to respective declines of 15.0% and 15.2% for the Russell 2000 and Russell Microcap indices. When stock prices rose in the second quarter, the Fund was up an impressive 31.4% versus a gain of 20.7% for its small-cap benchmark and 25.0% for the micro-cap index. | |||||||||||||

The Fund also showed much-improved relative returns in the recent market cycle. First, in the rally that began following the small-cap low on 3/9/09 through 6/30/09, RCM was up 56.6% versus gains of 48.9% for the Russell 2000 and 54.6% for the Russell Microcap index. For the market cycle period that began with the most recent small-cap peak on 7/13/07 (and thus marked the beginning of the current bear market) through 6/30/09, RCM fell 35.9%, again outperforming its benchmark, which lost 38.8%, and the micro-cap index, which declined 44.7%. As welcome as the bullish period was, we were even more pleased to see the Fund lose less than its benchmark through the first two-plus months of 2009. Over longer-term periods, the news remained positive. From the previous small-cap market peak on 3/9/00 through 6/30/09, RCM handily outpaced the Russell 2000, up 113.8% versus a loss of 5.2%. (Data for the Russell Microcap index only goes back to 2002.) Similarly, the Fund was ahead of its benchmark during the most recently completed small-cap market cycle, which ran from 3/9/00 through 7/13/07, a period in which RCM rose 233.6%, while the Russell 2000 was up 54.9%. The Fund’s strong market cycle returns were a critical factor in beating its benchmark for the three-, five-, 10-year and since inception (12/27/96) periods ended 6/30/09. RCM’s average annual total return since inception was 10.7%. Technology and Natural Resources, the Fund’s two largest sectors at the end of June, also made the most significant positive contributions to performance in the first half. Within | GOOD IDEAS THAT WORKED Top Contributors To Performance Year-to-Date Through 6/30/09* | ||||||||||||

| Fuqi International | 1.26% | ||||||||||||

| Stein Mart | 0.84 | ||||||||||||

| Buckle (The) | 0.69 | ||||||||||||

| Allied Nevada Gold | 0.66 | ||||||||||||

| Sipef | 0.65 | ||||||||||||

| *Includes Dividends | |||||||||||||

Important Performance and Expense Information All performance information in this Report reflects past performance, is presented on a total return basis and reflects the reinvestment of distributions. Past performance is no guarantee of future results. Investment return and principal value of an investment will fluctuate, so that shares may be worth more or less than their original cost when redeemed. Current performance may be higher or lower than performance quoted. The Fund’s total returns do not reflect any deduction for charges or expenses of the variable contracts of retirement plans investing in the Fund. Returns as of the recent month-end may be obtained at www.roycefunds.com. All performance and risk information for RCM reflects Investment Class results. Shares of RCM’s Service Class bear an annual distribution expense that is not borne by the Investment Class. Operating expenses reflect the Fund’s total annual operating expenses for the Investment Class, as of the date of the Fund’s most current prospectus, and include management fees, other expenses and acquired fund fees and expenses. Acquired fund fees and expenses are those incurred indirectly as a result of investment in one or more acquired funds, including mutual funds, hedge funds, private equity funds and other pooled investment vehicles. | |||||||||||||

10 | Royce Capital Fund 2009 Semiannual Report to Shareholders

Performance and Portfolio Review Natural Resources, precious metals and mining dominated, the result of stable or rising commodity prices and a decline in the costs of mining. There was also greater access to capital, as improved commodity prices seemed to make financing easier to obtain. Each of these factors played a role in the mostly rising share prices of several mining stocks in the portfolio, including Allied Nevada Gold, Fronteer Development Group, U.S. Gold and Silvercorp Metals. We liked the ongoing prospects for the industry and also thought that, first-half gains notwithstanding, several holdings still had ample room for growth. Allied Nevada Gold, Fronteer Development Group and Silvercorp Metals were top-ten positions at the end of June. Net gains in the Technology sector were mostly clustered in three industries—semiconductors and equipment, telecommunications, and components and systems. Few areas of the market held lower expectations heading into 2009 than consumer stocks. Hit hard at each stage of the bear market, they were also subject to grim forecasts about how little consumers across the globe would be spending during the recession. In part because most | ||||

| consumer stocks were (at least in our view) wildly oversold into early 2009 and in part because several businesses reported results in 2009 that, while not quite good, were far from disastrous, many rallied in the first half. Fuqi International designs and sells precious metal jewelry in China. Its recent earnings were actually both positive and better than expected, which drove its share price to lofty heights. We reduced our position substantially in June. We also trimmed our stake in clothing and accessories retailer The Buckle and sold shares in fashion merchandiser Stein Mart as their stock prices climbed. Sipef is a holding company that, among other things, operates rubber and palm oil plantations. Much of its profit comes from its palm oil business, which we think offers terrific growth potential in China, India and elsewhere in Asia. After palm oil prices fell dramatically in the second half of 2008, they rebounded in the first half of 2009, helping Sipef ’s stock price to do the same. It was the Fund’s twelfth largest holding at the end of June. Media company Journal Communications proved a disappointment in a market where we saw what we deemed sounder opportunities elsewhere. We sold our shares in March. Key Technology makes process automation systems that integrate electro-optical inspection, sorting, and product preparation equipment. Its business and share price have been hurt by the recession, but we like its balance sheet and its prospects, especially as it seeks to introduce its products into the pharmaceutical industry. | ||||

GOOD IDEAS AT THE TIME | ||||

| Journal Communications Cl. A | -0.64% | |||

| Key Technology | -0.60 | |||

| LaCrosse Footwear | -0.38 | |||

| United Fire & Casualty | -0.35 | |||

| Dyax Corporation | -0.29 | |||

| *Net of Dividends | ||||

| ||||

| FUND INFORMATION AND PORTFOLIO DIAGNOSTICS | |||||||

| Average Market Capitalization* | $252 million | ||||||

| Weighted Average P/B Ratio | 1.2x | ||||||

| Weighted Average Portfolio Yield | 2.0% | ||||||

| Fund Net Assets | $400 million | ||||||

| Turnover Rate | 20% | ||||||

| U.S. Investments (% of Net Assets) | 68.7% | ||||||

| Non-U.S. Investments (% of Net Assets) | 24.6% | ||||||

| Number of Holdings | 205 | ||||||

| Symbol | |||||||

| Investment Class | RCMCX | ||||||

| Service Class | RCMSX | ||||||

| * Geometrically calculated | |||||||

| |||||||

Royce Capital Fund 2009 Semiannual Report to Shareholders | 11

| ||||||||||||

| AVERAGE ANNUAL TOTAL RETURNS Through 6/30/09 | ||||||||||||

| Jan - June 2009* | -7.32 | % | ||||||||||

| One-Year | -23.31 | |||||||||||

| Three-Year | -5.47 | |||||||||||

| Five-Year | 1.66 | |||||||||||

| 10-Year | 9.23 | |||||||||||

| Since Inception (12/27/96) | 9.96 | |||||||||||

| ANNUAL EXPENSE RATIO | ||||||||||||

| Operating Expenses | 1.09 | % | ||||||||||

| * Not annualized | ||||||||||||

| CALENDAR YEAR TOTAL RETURNS | ||||||||||||

| Year | RCS | Year | RCS | |||||||||

| 2008 | -27.2 | % | 2002 | -13.8 | % | |||||||

| 2007 | -2.1 | 2001 | 21.0 | |||||||||

| 2006 | 15.6 | 2000 | 33.3 | |||||||||

| 2005 | 8.6 | 1999 | 8.2 | |||||||||

| 2004 | 25.0 | 1998 | 8.9 | |||||||||

| 2003 | 41.1 | 1997 | 17.1 | |||||||||

| TOP 10 POSITIONS % of Net Assets | ||||||||||||

| Knight Capital Group Cl. A | 2.3 | % | ||||||||||

| Oil States International | 2.3 | |||||||||||

| NBTY | 2.3 | |||||||||||

| Federated Investors Cl. B | 2.3 | |||||||||||

| Steven Madden | 2.1 | |||||||||||

| Aspen Insurance Holdings | 2.1 | |||||||||||

| Wolverine World Wide | 2.0 | |||||||||||

| Dress Barn (The) | 1.9 | |||||||||||

| Comtech Telecommunications | 1.8 | |||||||||||

| Buckle (The) | 1.8 | |||||||||||

| PORTFOLIO SECTOR BREAKDOWN % of Net Assets | ||||||||||||

| Financial Intermediaries | 15.1 | % | ||||||||||

| Natural Resources | 13.9 | |||||||||||

| Industrial Services | 10.8 | |||||||||||

| Technology | 10.4 | |||||||||||

| Industrial Products | 10.1 | |||||||||||

| Consumer Services | 9.4 | |||||||||||

| Consumer Products | 9.4 | |||||||||||

| Health | 8.2 | |||||||||||

| Financial Services | 2.3 | |||||||||||

| Miscellaneous | 1.8 | |||||||||||

| Cash and Cash Equivalents | 8.6 | |||||||||||

Royce Capital Fund—Small-Cap Portfolio  Manager’s Discussion Manager’s DiscussionThe welcome recovery in stock prices showed much of its favor to lower-quality issues, but that did not prevent a solid performance for the limited portfolio of Royce Capital Fund–Small-Cap Portfolio (RCS), which includes what we believe are small-cap stocks of the highest quality. (We define quality as companies with strong balance sheets, the ability to generate free cash flow and high returns on invested capital.) The Fund rose 7.3% for the year-to-date period ended 6/30/09, ahead of its small-cap benchmark, the Russell 2000, which was up 2.6% for the same period. A more-than-respectable absolute and relative performance was satisfying enough, but we were even more pleased by the way in which the Fund achieved its edge, with solid relative down market results and strong absolute and relative up market performance. In the dreary first quarter, a period in which the Russell 2000 declined 15.0%, RCS lost 12.5%. Stock prices began to recover in March, spurring the second-quarter rally. Between April and June, when the small-cap index was up 20.7%, the Fund gained 22.6%. | |||||||||||||

RCS’s strong first half helped to improve its recent market cycle performance. From the small-cap peak on 7/13/07 through the most recent low on 3/9/09, the Fund lost 54.0% while the Russell 2000 declined 58.9%. For the period beginning with that same small-cap peak through 6/30/09, which reflects the rally that kicked off on 3/9/09, RCS was down 32.4% versus a loss of 38.8% for the Russell 2000. The Fund’s showing in the recent upswing was impressive, though it trailed its benchmark. From 3/9/09 through 6/30/09, RCS was up 46.9% versus a gain of 48.9% for the small-cap index. The Fund’s market cycle and other long-term results were also solid. From the previous small-cap peak on 3/9/00 through 6/30/09, the Fund handily trounced the Russell 2000, up 125.3% versus the benchmark’s loss of 5.2%. This strong performance helped RCS to best the small-cap index for the one-, three-, five-, 10-year and since inception (12/27/96) periods ended 6/30/09.The Fund’s average annual total return since inception was 10.0%. After the relative and absolute disappointments of 2008, we were pleased to see reversals in the stock prices of many portfolio holdings. Perhaps none was less expected than the dynamic rebound of companies in the Fund’s two consumer sectors. Seven of RCS’s 20 best-performing holdings in the first half came from either the Consumer Services or Consumer Products sectors. While some of these stocks showed impressive growth through the still-recessionary first half, nearly all had been, in our view, thoroughly oversold by the end of | GOOD IDEAS THAT WORKED Top Contributors To Performance Year-to-Date Through 6/30/09* | ||||||||||||

| NBTY | 1.10% | ||||||||||||

| Buckle (The) | 0.93 | ||||||||||||

| American Eagle Outfitters | 0.75 | ||||||||||||

| Federated Investors Cl. B | 0.72 | ||||||||||||

| Sims Metal Management ADR | 0.69 | ||||||||||||

| *Includes Dividends | |||||||||||||

Important Performance and Expense Information All performance information in this Report reflects past performance, is presented on a total return basis and reflects the reinvestment of distributions. Past performance is no guarantee of future results. Investment return and principal value of an investment will fluctuate, so that shares may be worth more or less than their original cost when redeemed. Current performance may be higher or lower than performance quoted. The Fund’s total returns do not reflect any deduction for charges or expenses of the variable contracts of retirement plans investing in the Fund. Returns as of the recent month-end may be obtained at www.roycefunds.com. All performance and risk information for RCS reflects Investment Class results. Shares of RCS’s Service Class bear an annual distribution expense that is not borne by the Investment Class. Operating expenses reflect the Fund’s total annual operating expenses for the Investment Class, as of the date of the Fund’s most current prospectus, and include management fees and other expenses. | |||||||||||||

12 | Royce Capital Fund 2009 Semiannual Report to Shareholders

Performance and Portfolio Review 2008. Their recovery, then, was surprising but not shocking—some recovery after such a violent sell-off seemed appropriate, if only in hindsight. The Fund’s strongest-performing industry was retail stores, which was dominated by strong results from three companies. The Buckle operates as a retailer of casual apparel, footwear and accessories for younger people. We first bought shares in RCS in 2001 and have held a position continuously since 2004. We began to re-build our stake in October 2008, still confident that, as a well-managed company with ample cash, it was capable of enduring through the recession and thriving in an economic recovery. Its growth has slowed, but recent earnings remained positive as the firm continued to prove that it could offer sought-after merchandise. It was a top-ten position at the end of June. Another large holding that we built during some of the darkest days of the bear market was The Dress Barn, which operates a chain of women’s apparel specialty stores. It too has been an effective survivor of a brutal market for retailers that we think could benefit from an economic | ||||

| turnaround. The price of American Eagle Outfitters hit single digits through most of the period between October and March, and we re-built our position between October and February. Better-than-expected results began to attract investors later in March. We sold some shares during April and May. NBTY makes and distributes nutritional supplements. The company went through an awful latter half of 2008, battling increases in the cost of raw materials needed to make vitamins and sagging sales. In 2009, sales growth resumed, raw materials costs fell and the firm bought a competitor out of bankruptcy, all of which seemed to convince investors of its overall good health. It was RCS’s third-largest holding at the end of June. When mobile-data communications equipment maker Comtech Telecommunications reduced its sales and profit outlook for fiscal 2009 in March, its stock price suffered its worst decline in 29 years. We were thinking more about the company’s strong balance sheet and attractive long-term prospects, especially in the areas of satellite and mobile-tracking equipment that it provides to the U.S. military, both of which made adding to our stake a simple decision. Aircraft and industrial parts maker Woodward Governor saw its stock price plummet, which, along with a 2008 acquisition that caused more dilution to its balance sheet than we would have liked, led us to begin reducing our position in March. | ||||

GOOD IDEAS AT THE TIME | ||||

| Comtech Telecommunications | -1.32% | |||

| Woodward Governor | -0.77 | |||

| Entegris | -0.57 | |||

| Lincoln Electric Holdings | -0.47 | |||

| Montpelier Re Holdings | -0.40 | |||

| *Net of Dividends | ||||

| ||||

| FUND INFORMATION AND PORTFOLIO DIAGNOSTICS | |||||||

| Average Market Capitalization* | $924 million | ||||||

| Weighted Average P/E Ratio** | 11.2x | ||||||

| Weighted Average P/B Ratio | 1.3x | ||||||

| Weighted Average Portfolio Yield | 1.2% | ||||||

| U.S. Investments (% of Net Assets) | 88.9% | ||||||

| Non-U.S. Investments (% of Net Assets) | 2.5% | ||||||

| Fund Net Assets | $347 million | ||||||

| Turnover Rate | 23% | ||||||

| Number of Holdings | 92 | ||||||

| Symbol | |||||||

| Investment Class | RCPFX | ||||||

| Service Class | RCSSX | ||||||

| * Geometrically calculated | |||||||

** The Fund’s P/E calculation excludes companies with zero or negative earnings (21% of portfolio holdings as of 6/30/09). | |||||||

| |||||||

Royce Capital Fund 2009 Semiannual Report to Shareholders | 13

Schedules of Investments

Royce Capital Fund – Micro-Cap Portfolio |

| SHARES | VALUE | |||||

COMMON STOCKS – 92.8% | ||||||

Consumer Products – 8.2% | ||||||

Apparel, Shoes and Accessories - 2.9% | ||||||

| 64,999 | $ | 1,346,129 | ||||

LaCrosse Footwear | 277,231 | 2,592,110 | ||||

| 135,400 | 3,019,420 | |||||

Van De Velde | 42,950 | 1,569,155 | ||||

| 258,800 | 3,235,000 | |||||

| 11,761,814 | ||||||

Food/Beverage/Tobacco - 2.6% | ||||||

Anglo-Eastern Plantations | 187,700 | 1,105,516 | ||||

Asian Citrus Holdings | 654,000 | 2,233,781 | ||||

HQ Sustainable Maritime Industries b | 167,000 | 1,528,050 | ||||

Sipef | 79,000 | 3,787,711 | ||||

Societe Internationale de Plantations d’Heveas | 50,600 | 1,876,904 | ||||

| 10,531,962 | ||||||

Health, Beauty and Nutrition - 0.4% | ||||||

Nutraceutical International b | 146,500 | 1,522,135 | ||||

Home Furnishing and Appliances - 1.0% | ||||||

AS Creation Tapeten | 90,810 | 2,163,308 | ||||

Ekornes | 72,500 | 965,911 | ||||

| 44,800 | 706,048 | |||||

| 3,835,267 | ||||||

Sports and Recreation - 1.3% | ||||||

Arctic Cat b | 556,360 | 2,247,694 | ||||

Piscines Desjoyaux | 155,181 | 979,195 | ||||

RC2 Corporation b | 157,000 | 2,077,110 | ||||

| 5,303,999 | ||||||

Total (Cost $44,741,397) | 32,955,177 | |||||

Consumer Services – 5.9% | ||||||

Direct Marketing - 0.4% | ||||||

Manutan International | 32,666 | 1,627,284 | ||||

Leisure and Entertainment - 0.6% | ||||||

Multimedia Games b | 500,538 | 2,482,668 | ||||

Online Commerce - 0.6% | ||||||

CryptoLogic | 397,000 | 2,429,640 | ||||

Restaurants and Lodgings - 0.8% | ||||||

| 61,314 | 417,548 | |||||

| 127,930 | 808,518 | |||||

City Lodge Hotels | 222,000 | 1,989,454 | ||||

| 3,215,520 | ||||||

Retail Stores - 3.5% | ||||||

A.C. Moore Arts & Crafts b | 127,300 | 478,648 | ||||

Buckle (The) | 104,025 | 3,304,874 | ||||

Cache b | 438,250 | 1,700,410 | ||||

Cato Corporation (The) Cl. A | 116,400 | 2,030,016 | ||||

| 82,800 | 2,853,288 | |||||

Lewis Group | 231,000 | 1,447,512 | ||||

| SHARES | VALUE | |||||

Consumer Services (continued) | ||||||

Retail Stores (continued) | ||||||

Stein Mart b | 230,343 | $ | 2,040,839 | |||

| 13,855,587 | ||||||

Total (Cost $22,213,584) | 23,610,699 | |||||

Financial Intermediaries – 4.2% | ||||||

Banking - 1.0% | ||||||

Bancorp (The) b | 127,528 | 765,168 | ||||

BCB Holdings b | 743,907 | 1,530,279 | ||||

Canadian Western Bank | 128,600 | 1,872,917 | ||||

| 4,168,364 | ||||||

Insurance - 2.0% | ||||||

American Physicians Service Group | 40,000 | 907,600 | ||||

American Safety Insurance Holdings b | 143,200 | 1,948,952 | ||||

Argo Group International Holdings b | 70,027 | 1,976,162 | ||||

Navigators Group b | 42,500 | 1,888,275 | ||||

United Fire & Casualty | 78,630 | 1,348,505 | ||||

| 8,069,494 | ||||||

Securities Brokers - 1.2% | ||||||

Sanders Morris Harris Group | 529,400 | 2,911,700 | ||||

Thomas Weisel Partners Group b | 281,400 | 1,694,028 | ||||

| 4,605,728 | ||||||

Total (Cost $21,310,190) | 16,843,586 | |||||

Financial Services – 3.4% | ||||||

Investment Management - 3.4% | ||||||

Brait | 744,000 | 1,515,837 | ||||

CapMan Cl. B b | 1,126,855 | 1,586,527 | ||||

Deutsche Beteiligungs | 197,700 | 3,383,639 | ||||

Endeavour Financial a | 722,900 | 870,103 | ||||

† Gluskin Sheff + Associates | 187,900 | 2,600,859 | ||||

Sprott Resource b | 928,100 | 2,457,592 | ||||

U.S. Global Investors Cl. A | 112,300 | 1,039,898 | ||||

Total (Cost $26,692,321) | 13,454,455 | |||||

Health – 10.7% | ||||||

Commercial Services - 0.2% | ||||||

PDI b | 197,700 | 810,570 | ||||

Drugs and Biotech - 3.9% | ||||||

Anika Therapeutics b | 133,252 | 632,947 | ||||

| 160,800 | 1,125,600 | |||||

Dyax Corporation b | 493,516 | 1,056,124 | ||||

Fornix Biosciences | 106,128 | 969,444 | ||||

Genoptix b | 79,624 | 2,547,172 | ||||

Lexicon Pharmaceuticals b | 1,718,686 | 2,131,171 | ||||

Maxygen b | 117,200 | 787,584 | ||||

| 326,400 | 2,738,496 | |||||

Orchid Cellmark b | 884,200 | 1,414,720 | ||||

| 2,077,690 | 332,430 | |||||

Vetoquinol | 70,000 | 1,454,634 | ||||

YM Biosciences b | 737,800 | 413,168 | ||||

| 15,603,490 | ||||||

| 14 | Royce Capital Fund 2009 Semiannual Report to Shareholders | THE ACCOMPANYING NOTES ARE AN INTEGRAL PART OF THESE FINANCIAL STATEMENTS. |

| SHARES | VALUE | |||||

Health (continued) | ||||||

Health Services - 1.7% | ||||||

Bio-Imaging Technologies b | 272,023 | $ | 973,842 | |||

Computer Programs and Systems | 59,300 | 2,271,783 | ||||

CorVel Corporation b | 66,225 | 1,507,943 | ||||

U.S. Physical Therapy b | 141,960 | 2,093,910 | ||||

| 6,847,478 | ||||||

Medical Products and Devices - 4.9% | ||||||

Bruker Corporation b | 178,406 | 1,652,040 | ||||

Cerus Corporation b | 400,000 | 412,000 | ||||

Cynosure Cl. A b | 198,900 | 1,521,585 | ||||

Exactech b | 115,900 | 1,680,550 | ||||

Merit Medical Systems b | 42,000 | 684,600 | ||||

Neogen Corporation b | 119,950 | 3,476,151 | ||||

NMT Medical b | 174,800 | 391,552 | ||||

SenoRx b | 327,833 | 1,098,240 | ||||

Shamir Optical Industry b | 145,700 | 738,699 | ||||

Solta Medical b | 415,761 | 648,587 | ||||

STRATEC Biomedical Systems | 36,000 | 911,481 | ||||

Syneron Medical b | 448,294 | 3,236,683 | ||||

| 30,925 | 279,253 | |||||

Young Innovations | 131,465 | 2,864,622 | ||||

| 19,596,043 | ||||||

Total (Cost $61,218,887) | 42,857,581 | |||||

Industrial Products – 11.2% | ||||||

Automotive - 0.9% | ||||||

Landi Renzo | 797,000 | 3,609,376 | ||||

Building Systems and Components - 1.9% | ||||||

AAON | 126,704 | 2,523,944 | ||||

Drew Industries b | 276,533 | 3,365,407 | ||||

LSI Industries | 308,599 | 1,681,864 | ||||

| 7,571,215 | ||||||

Industrial Components - 0.8% | ||||||

Graham Corporation | 169,900 | 2,259,670 | ||||

| 205,600 | 771,000 | |||||

| 3,030,670 | ||||||

Machinery - 2.2% | ||||||

Burckhardt Compression Holding | 27,000 | 3,498,361 | ||||

Kadant b | 198,531 | 2,241,415 | ||||

Key Technology b | 217,429 | 2,150,373 | ||||

Manitou BF b | 60,802 | 725,606 | ||||

Technotrans b | 46,775 | 253,098 | ||||

| 8,868,853 | ||||||

Metal Fabrication and Distribution - 2.7% | ||||||

Castle (A.M.) & Co. | 181,221 | 2,189,150 | ||||

Foster (L.B.) Company Cl. A b | 90,976 | 2,735,648 | ||||

Olympic Steel | 221,500 | 5,420,105 | ||||

Samuel Manu-Tech | 231,000 | 659,348 | ||||

| 11,004,251 | ||||||

Miscellaneous Manufacturing - 1.0% | ||||||

Semperit AG Holding | 148,713 | 3,976,568 | ||||

Pumps, Valves and Bearings - 0.7% | ||||||

Pfeiffer Vacuum Technology | 38,000 | 2,788,016 | ||||

| SHARES | VALUE | |||||

Industrial Products (continued) | ||||||

Specialty Chemicals and Materials - 1.0% | ||||||

American Vanguard | 164,133 | $ | 1,854,703 | |||

Phoscan Chemical b | 1,681,800 | 578,360 | ||||

Victrex | 160,000 | 1,488,036 | ||||

| 3,921,099 | ||||||

Total (Cost $52,633,806) | 44,770,048 | |||||

Industrial Services – 13.8% | ||||||

Commercial Services - 5.7% | ||||||

ATC Technology b | 157,937 | 2,290,086 | ||||

Barrett Business Services | 84,099 | 883,039 | ||||

Begbies Traynor | 923,700 | 1,573,115 | ||||

Brunel International | 116,346 | 2,663,843 | ||||

CRA International b | 60,106 | 1,668,543 | ||||

Electro Rent | 148,200 | 1,406,418 | ||||

Forrester Research b | 44,200 | 1,085,110 | ||||

GP Strategies b | 535,700 | 3,155,273 | ||||

Healthcare Locums | 410,000 | 1,289,196 | ||||

Heritage-Crystal Clean b | 90,267 | 1,096,744 | ||||

Intersections b | 278,445 | 1,291,985 | ||||

Kforce b | 263,833 | 2,181,899 | ||||

Lincoln Educational Services b | 79,735 | 1,668,853 | ||||

Willdan Group b | 277,700 | 541,515 | ||||

| 22,795,619 | ||||||

Engineering and Construction - 2.7% | ||||||

| 159,804 | 4,047,835 | |||||

Exponent b | 128,988 | 3,161,496 | ||||

Layne Christensen b | 73,200 | 1,496,940 | ||||

Sterling Construction b | 136,700 | 2,086,042 | ||||

| 10,792,313 | ||||||

Food, Tobacco and Agriculture - 0.6% | ||||||

Zapata Corporation b | 344,300 | 2,344,683 | ||||

Industrial Distribution - 0.3% | ||||||

Houston Wire & Cable | 110,400 | 1,314,864 | ||||

Printing - 1.8% | ||||||

Courier Corporation | 159,618 | 2,435,771 | ||||

CSS Industries | 84,300 | 1,718,034 | ||||

Domino Printing Sciences | 349,352 | 1,448,282 | ||||

Ennis | 140,600 | 1,751,876 | ||||

| 7,353,963 | ||||||

Transportation and Logistics - 2.7% | ||||||

Euroseas | 488,628 | 2,335,642 | ||||

Marten Transport b | 80,049 | 1,661,817 | ||||

Patriot Transportation Holding b | 61,281 | 4,469,224 | ||||

Vitran Corporation b | 224,050 | 2,218,095 | ||||

| 10,684,778 | ||||||

Total (Cost $65,740,829) | 55,286,220 | |||||

Natural Resources – 16.5% | ||||||

Energy Services - 5.8% | ||||||

Boots & Coots b | 1,311,500 | 1,822,985 | ||||

Dawson Geophysical b | 104,502 | 3,119,385 | ||||

Gulf Island Fabrication | 106,900 | 1,692,227 | ||||

Lamprell | 1,426,100 | 2,696,533 | ||||

| THE ACCOMPANYING NOTES ARE AN INTEGRAL PART OF THESE FINANCIAL STATEMENTS. | Royce Capital Fund 2009 Semiannual Report to Shareholders | 15 |

Schedules of Investments

Royce Capital Fund – Micro-Cap Portfolio (continued) |

| SHARES | VALUE | |||||

Natural Resources (continued) | ||||||

Energy Services (continued) | ||||||

OYO Geospace b | 65,308 | $ | 1,675,803 | |||

Pioneer Drilling b | 145,900 | 698,861 | ||||

Superior Well Services b | 131,100 | 780,045 | ||||

T-3 Energy Services b | 225,345 | 2,683,859 | ||||

Tesco Corporation b | 166,980 | 1,325,821 | ||||

TGC Industries b | 645,356 | 3,142,884 | ||||

Total Energy Services | 570,900 | 2,139,986 | ||||

World Energy Solutions b | 230,700 | 1,199,640 | ||||

| 22,978,029 | ||||||

Oil and Gas - 0.9% | ||||||

Approach Resources b | 235,200 | 1,622,880 | ||||

Gran Tierra Energy b | 560,100 | 1,932,345 | ||||

| 163,200 | 0 | |||||

| 3,555,225 | ||||||

Precious Metals and Mining - 8.8% | ||||||

Alamos Gold b | 391,800 | 3,220,228 | ||||

Allied Nevada Gold b | 554,429 | 4,468,698 | ||||

Aquiline Resources b | 1,146,900 | 1,794,573 | ||||

Bear Creek Mining b | 372,200 | 697,585 | ||||

Crosshair Exploration & Mining b | 1,299,500 | 246,905 | ||||

Eldorado Gold b | 183,000 | 1,637,850 | ||||

| 586,300 | 1,008,436 | |||||

Entree Gold b | 988,700 | 988,700 | ||||

Fronteer Development Group b | 1,173,600 | 4,025,448 | ||||

Gammon Gold b | 244,847 | 1,633,130 | ||||

Great Basin Gold b | 1,086,500 | 1,485,221 | ||||

Horsehead Holding b | 335,300 | 2,497,985 | ||||

Lumina Copper b | 1,004,400 | 630,367 | ||||

Quaterra Resources b | 542,500 | 284,508 | ||||

Red Back Mining b | 234,000 | 2,039,943 | ||||

Silvercorp Metals | 1,100,100 | 3,872,352 | ||||

US Gold b | 1,336,796 | 3,529,141 | ||||

Western Copper b | 1,611,200 | 1,038,903 | ||||

| 35,099,973 | ||||||

Real Estate - 0.6% | ||||||

Kennedy-Wilson b | 74,000 | 2,516,000 | ||||

Other Natural Resources - 0.4% | ||||||

| 1,352,300 | 1,743,928 | |||||

Total (Cost $81,292,762) | 65,893,155 | |||||

Technology – 15.5% | ||||||

Aerospace and Defense - 0.5% | ||||||

Ducommun | 115,800 | 2,175,882 | ||||

Components and Systems - 1.9% | ||||||

LaCie | 297,079 | 1,021,302 | ||||

SMART Modular Technologies (WWH) b | 594,340 | 1,349,152 | ||||

Super Micro Computer b | 320,911 | 2,458,178 | ||||

Vaisala Cl. A | 21,730 | 768,279 | ||||

Xyratex b | 417,000 | 2,080,830 | ||||

| 7,677,741 | ||||||

Distribution - 0.7% | ||||||

Diploma | 1,278,000 | 2,798,449 | ||||

| SHARES | VALUE | |||||

Technology (continued) | ||||||

IT Services - 0.6% | ||||||

Neurones | 300,000 | $ | 2,601,480 | |||

Semiconductors and Equipment - 6.2% | ||||||

Advanced Energy Industries b | 160,200 | 1,440,198 | ||||

ATMI b | 183,900 | 2,855,967 | ||||

CEVA b | 379,500 | 3,294,060 | ||||

GSI Technology b | 482,500 | 1,862,450 | ||||

Ikanos Communications b | 309,400 | 495,040 | ||||

| 158,499 | 2,263,366 | |||||

Rudolph Technologies b | 159,500 | 880,440 | ||||

Semitool b | 317,400 | 1,466,388 | ||||

| 66,125 | 1,060,645 | |||||

Smartrac b | 85,000 | 1,528,244 | ||||

Supertex b | 122,300 | 3,070,953 | ||||

TTM Technologies b | 484,800 | 3,859,008 | ||||

Wolfson Microelectronics b | 338,143 | 549,207 | ||||

| 24,625,966 | ||||||

Software - 1.6% | ||||||

Double-Take Software b | 248,850 | 2,152,553 | ||||

Fundtech b | 184,900 | 1,867,490 | ||||

Pervasive Software b | 224,400 | 1,366,596 | ||||

Phoenix Technologies b | 335,088 | 908,088 | ||||

| 6,294,727 | ||||||

Telecommunications - 4.0% | ||||||

Anaren b | 225,158 | 3,980,793 | ||||

Atlantic Tele-Network | 145,450 | 5,714,731 | ||||

Ceragon Networks b | 376,702 | 2,497,534 | ||||

Digi International b | 265,200 | 2,585,700 | ||||

KVH Industries b | 188,400 | 1,286,772 | ||||

| 16,065,530 | ||||||

Total (Cost $69,476,933) | 62,239,775 | |||||

Miscellaneous e – 3.4% | ||||||

Total (Cost $11,829,597) | 13,684,842 | |||||

TOTAL COMMON STOCKS | ||||||

(Cost $457,150,306) | 371,595,538 | |||||

PREFERRED STOCK – 0.5% | ||||||

(Cost $2,408,000) | 2,408 | 1,949,332 | ||||

REPURCHASE AGREEMENT – 6.8% | ||||||

State Street Bank & Trust Company, 0.01% dated 6/30/09, due 7/1/09, maturity value $27,184,008 (collateralized by obligations of various U.S. Government Agencies, 3.75% due 8/18/09-9/1/09, valued at $27,866,331) | ||||||

(Cost $27,184,000) | 27,184,000 | |||||

| 16 | Royce Capital Fund 2009 Semiannual Report to Shareholders | THE ACCOMPANYING NOTES ARE AN INTEGRAL PART OF THESE FINANCIAL STATEMENTS. |

| Royce Capital Fund – Small-Cap Portfolio |

| VALUE | ||||||

COLLATERAL RECEIVED FOR SECURITIES LOANED – 2.1% | ||||||

| Money Market Funds | ||||||

Federated Government Obligations Fund | ||||||

(7 day yield-0.1864%) | ||||||

(Cost $8,211,572) | $ | 8,211,572 | ||||

TOTAL INVESTMENTS – 102.2% | ||||||

(Cost $494,953,878) | 408,940,442 | |||||

LIABILITIES LESS CASH AND OTHER ASSETS – (2.2)% | (8,731,102 | ) | ||||

NET ASSETS – 100.0% | $ | 400,209,340 | ||||

| SHARES | VALUE | |||||

COMMON STOCKS – 91.4% | ||||||

Consumer Products – 9.4% | ||||||

Apparel, Shoes and Accessories - 5.1% | ||||||

Guess? | 134,800 | $ | 3,475,144 | |||

Steven Madden b | 285,928 | 7,276,868 | ||||

Wolverine World Wide | 318,702 | 7,030,566 | ||||

| 17,782,578 | ||||||

Health, Beauty and Nutrition - 4.3% | ||||||

Inter Parfums | 316,296 | 2,321,613 | ||||

NBTY b | 278,800 | 7,839,856 | ||||

Nu Skin Enterprises Cl. A | 117,500 | 1,797,750 | ||||

Nutraceutical International b | 285,104 | 2,962,230 | ||||

| 14,921,449 | ||||||

Total (Cost $31,327,129) | 32,704,027 | |||||

Consumer Services – 9.4% | ||||||

Leisure and Entertainment - 2.3% | ||||||

International Speedway Cl. A | 169,700 | 4,346,017 | ||||

World Wrestling Entertainment Cl. A | 291,159 | 3,656,957 | ||||

| 8,002,974 | ||||||

Restaurants and Lodgings - 0.2% | ||||||

Ark Restaurants b | 65,332 | 816,650 | ||||

Retail Stores - 6.9% | ||||||

Abercrombie & Fitch Cl. A | 114,100 | 2,896,999 | ||||

American Eagle Outfitters | 282,600 | 4,004,442 | ||||

Buckle (The) | 196,100 | 6,230,097 | ||||

Cato Corporation (The) Cl. A | 240,900 | 4,201,296 | ||||

Dress Barn (The) b | 458,400 | 6,555,120 | ||||

| 23,887,954 | ||||||

Total (Cost $32,653,162) | 32,707,578 | |||||

Financial Intermediaries – 15.1% | ||||||

Insurance - 12.8% | ||||||

† Allied World Assurance Company Holdings | 99,100 | 4,046,253 | ||||

| 213,060 | 2,899,747 | |||||

Amerisafe b | 149,200 | 2,321,552 | ||||

Aspen Insurance Holdings | 319,500 | 7,137,630 | ||||

EMC Insurance Group | 67,464 | 1,403,926 | ||||

Harleysville Group | 122,970 | 3,470,213 | ||||

Max Capital Group | 233,303 | 4,306,773 | ||||

Meadowbrook Insurance Group | 526,600 | 3,438,698 | ||||

Montpelier Re Holdings a | 419,377 | 5,573,520 | ||||

Reinsurance Group of America | 150,600 | 5,257,446 | ||||

State Auto Financial | 50,454 | 882,945 | ||||

Validus Holdings a | 172,300 | 3,787,154 | ||||

| 44,525,857 | ||||||

Securities Brokers - 2.3% | ||||||

Knight Capital Group Cl. A b | 472,000 | 8,047,600 | ||||

Total (Cost $55,038,538) | 52,573,457 | |||||

| THE ACCOMPANYING NOTES ARE AN INTEGRAL PART OF THESE FINANCIAL STATEMENTS. | Royce Capital Fund 2009 Semiannual Report to Shareholders | 17 |

Schedules of Investments

Royce Capital Fund – Small-Cap Portfolio (continued) |

| SHARES | VALUE | |||||

Financial Services – 2.3% | ||||||

Investment Management - 2.3% | ||||||

Federated Investors Cl. B | 325,100 | $ | 7,831,659 | |||

Total (Cost $6,915,985) | 7,831,659 | |||||

Health – 8.2% | ||||||

Drugs and Biotech - 2.2% | ||||||

Emergent Biosolutions b | 241,600 | 3,462,128 | ||||

Obagi Medical Products b | 583,424 | 4,253,161 | ||||

| 7,715,289 | ||||||

Health Services - 3.9% | ||||||

| 244,100 | 4,017,886 | |||||

| 133,000 | 5,603,290 | |||||

U.S. Physical Therapy b | 270,600 | 3,991,350 | ||||

| 13,612,526 | ||||||

Medical Products and Devices - 2.1% | ||||||

Home Diagnostics b | 494,755 | 3,037,796 | ||||

| 189,700 | 4,116,490 | |||||

| 7,154,286 | ||||||

Total (Cost $27,366,693) | 28,482,101 | |||||

Industrial Products – 10.1% | ||||||

Automotive - 0.8% | ||||||

Dorman Products b | 208,259 | 2,880,222 | ||||

Building Systems and Components - 1.0% | ||||||

Drew Industries b | 35,300 | 429,601 | ||||

Simpson Manufacturing | 139,485 | 3,015,666 | ||||

| 3,445,267 | ||||||

Industrial Components - 0.2% | ||||||

Bel Fuse Cl. A | 49,762 | 698,658 | ||||

Machinery - 2.0% | ||||||

Lincoln Electric Holdings | 78,300 | 2,821,932 | ||||

Robbins & Myers | 206,300 | 3,971,275 | ||||

| 6,793,207 | ||||||

Metal Fabrication and Distribution - 2.7% | ||||||

Schnitzer Steel Industries Cl. A | 51,100 | 2,701,146 | ||||

Sims Metal Management ADR | 232,470 | 4,793,531 | ||||

Universal Stainless & Alloy Products b | 124,754 | 2,029,748 | ||||

| 9,524,425 | ||||||

Pumps, Valves and Bearings - 3.1% | ||||||

Gardner Denver b | 229,249 | 5,770,197 | ||||

IDEX Corporation | 54,200 | 1,331,694 | ||||

Kaydon Corporation | 106,600 | 3,470,896 | ||||

| 10,572,787 | ||||||

Other Industrial Products - 0.3% | ||||||

MTS Systems | 54,309 | 1,121,481 | ||||

Total (Cost $39,989,299) | 35,036,047 | |||||

Industrial Services – 10.8% | ||||||

Commercial Services - 8.9% | ||||||

ATC Technology b | 327,459 | 4,748,155 | ||||

Barrett Business Services | 206,126 | 2,164,323 | ||||

Heidrick & Struggles International | 146,500 | 2,673,625 | ||||

| SHARES | VALUE | |||||

Industrial Services (continued) | ||||||

Commercial Services (continued) | ||||||

Kforce b | 314,800 | $ | 2,603,396 | |||

Korn/Ferry International b | 354,000 | 3,766,560 | ||||

ManTech International Cl. A b | 130,400 | 5,612,416 | ||||

MAXIMUS | 90,200 | 3,720,750 | ||||

Resources Connection b | 151,700 | 2,604,689 | ||||

TrueBlue b | 366,300 | 3,076,920 | ||||

| 30,970,834 | ||||||

Industrial Distribution - 0.4% | ||||||

Applied Industrial Technologies | 66,000 | 1,300,200 | ||||

Transportation and Logistics - 1.5% | ||||||

Star Bulk Carriers a | 445,053 | 1,633,345 | ||||

Tidewater | 82,100 | 3,519,627 | ||||

| 5,152,972 | ||||||

Total (Cost $49,222,658) | 37,424,006 | |||||

Natural Resources – 13.9% | ||||||

Energy Services - 9.5% | ||||||

Ensign Energy Services | 276,200 | 4,036,797 | ||||

Helmerich & Payne | 100,700 | 3,108,609 | ||||

Major Drilling Group International | 69,900 | 1,097,342 | ||||

Oil States International b | 330,500 | 8,001,405 | ||||

Patterson-UTI Energy | 174,700 | 2,246,642 | ||||

Pioneer Drilling b | 514,464 | 2,464,283 | ||||

Rowan Companies b | 244,200 | 4,717,944 | ||||

Trican Well Service | 151,400 | 1,304,241 | ||||

Unit Corporation b | 223,300 | 6,156,381 | ||||

| 33,133,644 | ||||||

Oil and Gas - 2.3% | ||||||

Cimarex Energy | 157,818 | 4,472,562 | ||||

† Energen Corporation | 88,600 | 3,535,140 | ||||

| 8,007,702 | ||||||

Precious Metals and Mining - 2.1% | ||||||

Agnico-Eagle Mines | 55,500 | 2,912,640 | ||||

Pan American Silver b | 124,900 | 2,289,417 | ||||

Red Back Mining b | 238,000 | 2,074,814 | ||||

| 7,276,871 | ||||||

Total (Cost $52,685,225) | 48,418,217 | |||||

Technology – 10.4% | ||||||

Components and Systems - 1.7% | ||||||

Rimage Corporation b | 244,045 | 4,053,588 | ||||

| 240,291 | 1,840,629 | |||||

| 5,894,217 | ||||||

IT Services - 1.1% | ||||||

Total System Services | 277,200 | 3,711,708 | ||||

Semiconductors and Equipment - 4.5% | ||||||

Advanced Energy Industries b | 305,702 | 2,748,261 | ||||

MKS Instruments b | 243,300 | 3,209,127 | ||||

OmniVision Technologies b | 88,414 | 918,621 | ||||

Rofin-Sinar Technologies b | 148,394 | 2,969,364 | ||||

Varian Semiconductor Equipment Associates b | 122,800 | 2,945,972 | ||||

| 18 | Royce Capital Fund 2009 Semiannual Report to Shareholders | THE ACCOMPANYING NOTES ARE AN INTEGRAL PART OF THESE FINANCIAL STATEMENTS. |

| SHARES | VALUE | |||||

Technology (continued) | ||||||

Semiconductors and Equipment (continued) | ||||||

Verigy b | 224,200 | $ | 2,728,514 | |||

| 15,519,859 | ||||||

Telecommunications - 3.1% | ||||||

Comtech Telecommunications b | 195,866 | 6,244,208 | ||||

NETGEAR b | 327,600 | 4,720,716 | ||||

| 10,964,924 | ||||||

Total (Cost $46,198,053) | 36,090,708 | |||||

Miscellaneous e – 1.8% | ||||||

Total (Cost $5,356,481) | 6,103,455 | |||||

TOTAL COMMON STOCKS | ||||||

(Cost $346,753,223) | 317,371,255 | |||||

REPURCHASE AGREEMENT – 9.0% | ||||||

State Street Bank & Trust Company, 0.01% dated 6/30/09, due 7/1/09, maturity value $31,314,009 (collateralized by obligations of various U.S. Government Agencies, 1.62% due 12/30/09, valued at $32,101,287) | ||||||

(Cost $31,314,000) | 31,314,000 | |||||

COLLATERAL RECEIVED FOR SECURITIES LOANED – 1.6% | ||||||

| Money Market Funds | ||||||

Federated Government Obligations Fund | ||||||

(7 day yield-0.1864%) | ||||||

(Cost $5,723,721) | 5,723,721 | |||||

TOTAL INVESTMENTS – 102.0% | ||||||

(Cost $383,790,944) | 354,408,976 | |||||

LIABILITIES LESS CASH AND OTHER ASSETS – (2.0)% | (7,051,757 | ) | ||||

NET ASSETS – 100.0% | $ | 347,357,219 | ||||

| THE ACCOMPANYING NOTES ARE AN INTEGRAL PART OF THESE FINANCIAL STATEMENTS. | Royce Capital Fund 2009 Semiannual Report to Shareholders | 19 |

| Statements of Assets and Liabilities | June 30, 2009 (unaudited) |

| Micro-Cap | Small-Cap | ||||||

| Portfolio | Portfolio | ||||||

| ASSETS: | |||||||

| Investments at value | |||||||

(including collateral on loaned securities)* | $ | 381,756,442 | $ | 323,094,976 | |||

| Repurchase agreements (at cost and value) | 27,184,000 | 31,314,000 | |||||

| Cash and foreign currency | 14,907 | 34,261 | |||||

| Receivable for investments sold | 1,501,379 | 847,300 | |||||

| Receivable for capital shares sold | 547,895 | 909,752 | |||||

| Receivable for dividends and interest | 246,856 | 190,343 | |||||

| Prepaid expenses and other assets | 3,201 | 2,055 | |||||

Total Assets | 411,254,680 | 356,392,687 | |||||

| LIABILITIES: | |||||||

| Payable for collateral on loaned securities | 8,211,572 | 5,723,721 | |||||

| Payable for investments purchased | 1,920,092 | 747,299 | |||||

| Payable for capital shares redeemed | 407,272 | 2,186,538 | |||||

| Payable for investment advisory fees | 411,399 | 291,277 | |||||

| Accrued expenses | 95,005 | 86,633 | |||||

Total Liabilities | 11,045,340 | 9,035,468 | |||||

Net Assets | $ | 400,209,340 | $ | 347,357,219 | |||

| ANALYSIS OF NET ASSETS: | |||||||

| Paid-in capital | $ | 538,190,838 | $ | 429,302,685 | |||

| Undistributed net investment income (loss) | 397,563 | 234,273 | |||||

| Accumulated net realized gain (loss) on investments and foreign currency | (52,367,813 | ) | (52,797,234 | ) | |||

| Net unrealized appreciation (depreciation) on investments and foreign currency | (86,011,248 | ) | (29,382,505 | ) | |||

Net Assets | $ | 400,209,340 | $ | 347,357,219 | |||

Investment Class | $ | 395,670,716 | $ | 345,458,286 | |||

Service Class | 4,538,624 | 1,898,933 | |||||

| SHARES OUTSTANDING: | |||||||

| (unlimited number of $.001 par value shares authorized for each Fund) | |||||||

Investment Class | 53,949,045 | 50,160,422 | |||||

Service Class | 620,485 | 276,729 | |||||

| NET ASSET VALUES: | |||||||

| (Net Assets ÷ Shares Outstanding) | |||||||

(offering and redemption price per share) | |||||||

Investment Class | $ | 7.33 | $ | 6.89 | |||

Service Class | 7.31 | 6.86 | |||||

| * Investments at identified cost | $ | 467,769,878 | $ | 352,476,944 | |||

| Market value of loaned securities | 7,928,777 | 5,523,747 | |||||

| 20 | Royce Capital Fund 2009 Semiannual Report to Shareholders | THE ACCOMPANYING NOTES ARE AN INTEGRAL PART OF THESE FINANCIAL STATEMENTS. |

Statements of Changes in Net Assets

| Micro-Cap Portfolio | Small-Cap Portfolio | |||||||||||||||

| Six months ended | Six months ended | |||||||||||||||

| 6/30/09 | Year ended | 6/30/09 | Year ended | |||||||||||||

| (unaudited) | 12/31/08 | (unaudited) | 12/31/08 | |||||||||||||

| INVESTMENT OPERATIONS: | ||||||||||||||||

| Net investment income (loss) | $ | 467,849 | $ | 5,317,872 | $ | 227,059 | $ | 246,375 | ||||||||

| Net realized gain (loss) on investments and foreign currency | (22,382,891 | ) | (21,207,803 | ) | (42,768,717 | ) | (8,246,378 | ) | ||||||||

| Net change in unrealized appreciation (depreciation) on | ||||||||||||||||

investments and foreign currency | 91,250,716 | (244,986,123 | ) | 66,892,367 | (94,474,073 | ) | ||||||||||

| Net increase (decrease) in net assets from investment operations | 69,335,674 | (260,876,054 | ) | 24,350,709 | (102,474,076 | ) | ||||||||||

| DISTRIBUTIONS: | ||||||||||||||||

| Net investment income | ||||||||||||||||

Investment Class | – | (13,058,155 | ) | – | (2,337,827 | ) | ||||||||||

Service Class | – | (90,960 | ) | – | (6,931 | ) | ||||||||||

| Net realized gain on investments and foreign currency | ||||||||||||||||

Investment Class | – | (54,721,733 | ) | – | (30,054,260 | ) | ||||||||||

Service Class | – | (414,258 | ) | – | (152,571 | ) | ||||||||||

| Total distributions | – | (68,285,106 | ) | – | (32,551,589 | ) | ||||||||||

| CAPITAL SHARE TRANSACTIONS: | ||||||||||||||||

| Value of shares sold | ||||||||||||||||

Investment Class | 42,421,730 | 96,537,277 | 67,464,632 | 105,771,986 | ||||||||||||

Service Class | 332,632 | 3,214,943 | 1,330,686 | 526,046 | ||||||||||||

| Distributions reinvested | ||||||||||||||||

Investment Class | – | 67,779,888 | – | 32,392,087 | ||||||||||||

Service Class | – | 505,218 | – | 159,502 | ||||||||||||

| Value of shares redeemed | ||||||||||||||||

Investment Class | (43,318,809 | ) | (139,333,402 | ) | (38,005,674 | ) | (57,692,282 | ) | ||||||||

Service Class | (346,097 | ) | (1,226,979 | ) | (1,119,187 | ) | (189,298 | ) | ||||||||

Net increase (decrease) in net assets from capital share transactions | (910,544 | ) | 27,476,945 | 29,670,457 | 80,968,041 | |||||||||||

| NET INCREASE (DECREASE) IN NET ASSETS | 68,425,130 | (301,684,215 | ) | 54,021,166 | (54,057,624 | ) | ||||||||||

| NET ASSETS: | ||||||||||||||||

Beginning of period | 331,784,210 | 633,468,425 | 293,336,052 | 347,393,676 | ||||||||||||

End of period | $ | 400,209,340 | $ | 331,784,210 | $ | 347,357,218 | $ | 293,336,052 | ||||||||

| UNDISTRIBUTED NET INVESTMENT | ||||||||||||||||

INCOME (LOSS) AT END OF PERIOD | $ | 397,563 | $ | (70,286 | ) | $ | 234,273 | $ | 7,214 | |||||||

| THE ACCOMPANYING NOTES ARE AN INTEGRAL PART OF THESE FINANCIAL STATEMENTS. | Royce Capital Fund 2009 Semiannual Report to Shareholders | 21 |

| Statements of Operations | Six Months Ended June 30, 2009 (unaudited) |

| Micro-Cap | Small-Cap | |||||||

| Portfolio | Portfolio | |||||||

| INVESTMENT INCOME: | ||||||||

| Income: | ||||||||

Dividends | $ | 2,588,083 | $ | 1,818,952 | ||||

Interest | 12,113 | 11,644 | ||||||

Securities lending | 109,388 | 4,856 | ||||||

| Total income | 2,709,584 | 1,835,452 | ||||||

| Expenses: | ||||||||

Investment advisory fees | 2,074,867 | 1,476,433 | ||||||

Distribution fees | 4,743 | 2,104 | ||||||

Custody | 47,025 | 17,850 | ||||||

Shareholder reports | 32,067 | 34,898 | ||||||

Administrative and office facilities | 26,779 | 22,274 | ||||||

Audit | 17,500 | 17,500 | ||||||

Trustees’ fees | 16,243 | 14,710 | ||||||

Shareholder servicing | 9,875 | 9,693 | ||||||

Legal | 4,655 | 3,693 | ||||||

Registration | 1,083 | 4,763 | ||||||

Other expenses | 11,678 | 8,772 | ||||||

| Total expenses | 2,246,515 | 1,612,690 | ||||||

| Compensating balance credits | – | (31 | ) | |||||

| Expenses reimbursed by investment adviser | (4,780 | ) | (4,266 | ) | ||||

| Net expenses | 2,241,735 | 1,608,393 | ||||||

| Net investment income (loss) | 467,849 | 227,059 | ||||||

| REALIZED AND UNREALIZED GAIN (LOSS) ON INVESTMENTS AND FOREIGN CURRENCY: | ||||||||

| Net realized gain (loss): | ||||||||

Investments | (22,384,585 | ) | (42,768,222 | ) | ||||

Foreign currency transactions | 1,694 | (495 | ) | |||||

| Net change in unrealized appreciation (depreciation): | ||||||||

Investments and foreign currency translations | 91,240,553 | 66,892,369 | ||||||

Other assets and liabilities denominated in foreign currency | 10,163 | (2 | ) | |||||

| Net realized and unrealized gain (loss) on investments and foreign currency | 68,867,825 | 24,123,650 | ||||||

| NET INCREASE (DECREASE) IN NET ASSETS FROM INVESTMENT OPERATIONS | $ | 69,335,674 | $ | 24,350,709 | ||||

| 22 | Royce Capital Fund 2009 Semiannual Report to Shareholders | THE ACCOMPANYING NOTES ARE AN INTEGRAL PART OF THESE FINANCIAL STATEMENTS. |

| This table is presented to show selected data for a share outstanding throughout each period, and to assist shareholders in evaluating a Fund’s performance for the periods presented. Per share amounts have been determined on the basis of the weighted average number of shares outstanding during the period. | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Net Realized and | Distributions from Net | Ratio of Expenses to Average Net Assets | Ratio of Net Investment | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Net Asset Value, Beginning of Period | Net Investment Income (Loss) | Unrealized Gain (Loss) on Investments and Foreign Currency | Total from Investment Operations | Distributions from Net Investment Income | Realized Gain on Investments and Foreign Currency | Total Distributions | Net Asset Value, End of Period | Total Return | Net Assets, End of Period (in thousands) | Prior to Fee Waivers and Balance Credits | Prior to Fee Waivers | Net of Fee Waivers | Income (Loss) to Average Net Assets | Portfolio Turnover Rate | |||||||||||||||||||||||||||||||||||||||||||

| Micro-Cap Portfolio – Investment Class | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| †2009 | $ | 6.03 | $ | 0.01 | $ | 1.29 | $ | 1.30 | $ | – | $ | – | $ | – | $ | 7.33 | 21.56 | %# | $ | 395,671 | 1.35 | %* | 1.35 | %* | 1.35 | %* | 0.28 | %* | 20 | % | |||||||||||||||||||||||||||

| 2008 | 13.47 | 0.13 | (5.99 | ) | (5.86 | ) | (0.30 | ) | (1.28 | ) | (1.58 | ) | 6.03 | (43.27 | ) | 328,059 | 1.32 | 1.32 | 1.32 | 1.05 | 51 | ||||||||||||||||||||||||||||||||||||

| 2007 | 14.40 | 0.03 | 0.53 | 0.56 | (0.22 | ) | (1.27 | ) | (1.49 | ) | 13.47 | 3.98 | 629,953 | 1.31 | 1.31 | 1.31 | 0.19 | 47 | |||||||||||||||||||||||||||||||||||||||

| 2006 | 12.57 | 0.01 | 2.63 | 2.64 | (0.03 | ) | (0.78 | ) | (0.81 | ) | 14.40 | 21.07 | 561,257 | 1.32 | 1.31 | 1.31 | (0.09 | ) | 41 | ||||||||||||||||||||||||||||||||||||||

| 2005 | 11.50 | (0.05 | ) | 1.38 | 1.33 | (0.06 | ) | (0.20 | ) | (0.26 | ) | 12.57 | 11.61 | 384,069 | 1.33 | 1.33 | 1.33 | (0.51 | ) | 38 | |||||||||||||||||||||||||||||||||||||

| 2004 | 10.90 | (0.09 | ) | 1.58 | 1.49 | – | (0.89 | ) | (0.89 | ) | 11.50 | 13.85 | 345,499 | 1.34 | 1.34 | 1.34 | (0.78 | ) | 38 | ||||||||||||||||||||||||||||||||||||||

| Micro-Cap Portfolio – Service Class(a) | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| †2009 | $ | 6.02 | $ | 0.00 | $ | 1.29 | $ | 1.29 | $ | – | $ | – | $ | – | $ | 7.31 | 21.43 | %# | $ | 4,538 | 1.83 | %* | 1.83 | %* | 1.58 | %* | 0.06 | %* | 20 | % | |||||||||||||||||||||||||||

| 2008 | 13.45 | 0.05 | (5.92 | ) | (5.87 | ) | (0.28 | ) | (1.28 | ) | (1.56 | ) | 6.02 | (43.44 | ) | 3,725 | 1.92 | 1.92 | 1.58 | 0.70 | 51 | ||||||||||||||||||||||||||||||||||||

| 2007 | 14.39 | (0.06 | ) | 0.58 | 0.52 | (0.19 | ) | (1.27 | ) | (1.46 | ) | 13.45 | 3.71 | 3,515 | 2.11 | 2.11 | 1.58 | (0.06 | ) | 47 | |||||||||||||||||||||||||||||||||||||

| 2006 | 14.90 | (0.04 | ) | 0.34 | 0.30 | (0.02 | ) | (0.79 | ) | (0.81 | ) | 14.39 | 2.06 | # | 1,262 | 8.67 | * | 8.67 | * | 1.58 | * | 0.16 | * | 41 | |||||||||||||||||||||||||||||||||

| Small-Cap Portfolio – Investment Class | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| †2009 | $ | 6.42 | $ | 0.00 | $ | 0.47 | $ | 0.47 | $ | – | $ | – | $ | – | $ | 6.89 | 7.32 | %# | $ | 345,458 | 1.09 | %* | 1.09 | %* | 1.09 | %* | 0.16 | %* | 23 | % | |||||||||||||||||||||||||||

| 2008 | 9.96 | 0.00 | (2.72 | ) | (2.72 | ) | (0.06 | ) | (0.76 | ) | (0.82 | ) | 6.42 | (27.18 | ) | 291,898 | 1.07 | 1.07 | 1.07 | 0.07 | 45 | ||||||||||||||||||||||||||||||||||||