UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number | 811-07685 |

|

Frontegra Funds, Inc. |

(Exact name of registrant as specified in charter) |

|

400 Skokie Blvd. Suite 500 Northbrook, Illinois | | 60062 |

(Address of principal executive offices) | | (Zip code) |

|

William D. Forsyth III 400 Skokie Blvd., Suite 500 Northbrook, Illinois 60062 |

(Name and address of agent for service) |

|

Registrant’s telephone number, including area code: | (847) 509-9860 | |

|

Date of fiscal year end: | June 30 | |

|

Date of reporting period: | June 30, 2013 | |

| | | | | | | | |

Item 1. Reports to Stockholders.

ANNUAL REPORT

Frontegra RobecoSAM Global Equity Fund

Frontegra MFG Global Equity Fund

Frontegra MFG Core Infrastructure Fund

Frontegra HEXAM Emerging Markets Fund

Frontegra Timpani Small Cap Growth Fund

Frontegra Netols Small Cap Value Fund

Frontegra Phocas Small Cap Value Fund

Lockwell Small Cap Value Fund

Frontegra Asset Management, Inc.

June 30, 2013

TABLE OF CONTENTS

Shareholder Letter | | | 1 | | |

Frontegra RobecoSAM Global Equity Fund | |

Report from RobecoSAM USA, Inc. | | | 4 | | |

Investment Highlights | | | 6 | | |

Frontegra MFG Global Equity Fund | |

Report from MFG Asset Management | | | 8 | | |

Investment Highlights | | | 11 | | |

Frontegra MFG Core Infrastructure Fund | |

Report from MFG Asset Management | | | 14 | | |

Investment Highlights | | | 16 | | |

Frontegra HEXAM Emerging Markets Fund | |

Report from HEXAM Capital Partners, LLP | | | 18 | | |

Investment Highlights | | | 20 | | |

Frontegra Timpani Small Cap Growth Fund | |

Report from Timpani Capital Management LLC | | | 22 | | |

Investment Highlights | | | 24 | | |

Frontegra Netols Small Cap Value Fund | |

Report from Netols Asset Management, Inc. | | | 26 | | |

Investment Highlights | | | 27 | | |

Frontegra Phocas Small Cap Value Fund | |

Report from Phocas Financial Corporation | | | 30 | | |

Investment Highlights | | | 32 | | |

Lockwell Small Cap Value Fund | |

Report from Lockwell Investments, LLC | | | 34 | | |

Investment Highlights | | | 35 | | |

Expense Example | | | 36 | | |

Schedules of Investments | |

Frontegra RobecoSAM Global Equity Fund | | | 38 | | |

Frontegra MFG Global Equity Fund | | | 40 | | |

Frontegra MFG Core Infrastructure Fund | | | 41 | | |

Frontegra HEXAM Emerging Markets Fund | | | 44 | | |

Frontegra Timpani Small Cap Growth Fund | | | 46 | | |

Frontegra Netols Small Cap Value Fund | | | 48 | | |

Frontegra Phocas Small Cap Value Fund | | | 50 | | |

Lockwell Small Cap Value Fund | | | 53 | | |

Statements of Assets and Liabilities | | | 54 | | |

Statements of Operations | | | 56 | | |

Statements of Changes in Net Assets | | | 58 | | |

Financial Highlights | | | 62 | | |

Notes to Financial Statements | | | 71 | | |

Report of Independent Registered Public Accounting Firm | | | 81 | | |

Board of Directors' Approval of Advisory and Subadvisory Agreements | | | 82 | | |

Additional Information | |

Directors and Officers | | | 92 | | |

Foreign Tax Credit | | | 97 | | |

Qualified Dividend Income/Dividends Received Deduction | | | 98 | | |

Additional Information Applicable to Foreign Shareholders Only | | | 98 | | |

This report is submitted for the general information of the shareholders of the Funds. It is not authorized for distribution to prospective investors unless accompanied or preceded by an effective Prospectus for the applicable Fund. The Prospectus may be obtained by calling 1-888-825-2100. Each Prospectus includes more complete information about management fees and expenses, investment objectives, risks and operating policies of the applicable Fund. Please read the Prospectus carefully.

Frontegra Funds, Inc. are distributed by Frontegra Strategies, LLC, 400 Skokie Blvd., Suite 500, Northbrook, IL 60062. Frontegra Strategies, LLC, member of FINRA and SIPC, is an affiliate of Frontegra Asset Management, Inc., the Funds' investment adviser.

DEAR FELLOW SHAREHOLDERS:

We are pleased to report on the progress of the Frontegra Funds over the past twelve months ending June 30, 2013. The S&P 500 Index was up 20.60%, and small capitalization stocks were up, with the Russell 2000® Index returning 24.21%. International stocks, as measured by the MSCI EAFE Index, returned 18.62% over the twelve-month period.

Fund Results

For the twelve month period ending June 30, 2013, the Frontegra RobecoSAM Global Equity Fund, managed by RobecoSAM USA, returned 19.78% (net) versus the MSCI World Index (Net) return of 18.58%.

The Frontegra MFG Global Equity Fund, managed by MFG Asset Management, returned 26.68% (net) versus the MSCI World Index (Net) return of 18.58% for the twelve month period ending June 30, 2013.

The Frontegra MFG Core Infrastructure Fund, also managed by MFG Asset Management, returned 12.73% (net) versus the UBS Developed Infrastructure & Utilities Index (Net) return of 9.04% and the MSCI World Index (Net) return of 18.58% for the twelve month period ending June 30, 2013.

For the twelve month period ending June 30, 2013, the Frontegra HEXAM Emerging Markets Fund, managed by HEXAM Capital Partners, returned -6.67% (net) versus the MSCI Emerging Markets Index (Net) return of 2.87%.

The Frontegra Timpani Small Cap Growth Fund, managed by Timpani Capital Management, returned 28.35% (net) versus the Russell 2000® Growth Index return of 23.67% for the twelve month period ending June 30, 2013.

For the twelve month period ending June 30, 2013, the Frontegra Netols Small Cap Value Fund — Institutional Class, managed by Netols Asset Management, returned 25.61% (net) versus the Russell 2000® Value Index return of 24.76%. The Class Y shares returned 25.15% (net) over the same time period.

The Frontegra Phocas Small Cap Value Fund, managed by Phocas Financial, returned 24.29% (net) versus the Russell 2000 Value Index return of 24.76% for the twelve month period ending June 30, 2013.

For the twelve month period ending June 30, 2013, the Lockwell Small Cap Value Fund, managed by Lockwell Investments, returned 27.66% (net) versus the Russell 2000 Value Index return of 24.76%.

Outlook

As we sit here in mid-2013, investment markets present a mixed picture. Despite a modestly improving unemployment picture, U.S. equity markets have performed very well over the past twelve months, while U.S. bond markets have struggled. The Japanese equity market has performed exceptionally well of late, but the Chinese stock market has languished. European equities have experienced fits and starts, occasionally showing signs of progress with their austerity measures while at other times backtracking due to the fragile state of affairs in countries like Greece and Turkey. As we enter a new fiscal year, we will work as diligently as ever to manage your assets with the skill and agility necessary in these uncertain times.

We will continue to oversee the investment management of the Frontegra Funds with the care and diligence that have served our shareholders well in the past. As always, we appreciate your investment and continued confidence in the Frontegra Funds.

Best regards,

William D. Forsyth, CFA

President

Frontegra Funds, Inc.

page 1

This page intentionally left blank.

FRONTEGRA

ROBECOSAM GLOBAL EQUITY FUND

REPORT FROM ROBECOSAM USA, INC.

Dear Shareholders:

The Frontegra RobecoSAM Global Equity Fund strives to achieve capital appreciation by investing in a diversified portfolio of equity and equity-related securities issued by U.S. and non-U.S. companies that combine their market and financial strategy with a high level of environmental awareness and a clearly defined social policy. The objective is measured against the MSCI World Index (Net).

Performance Review

The Frontegra RobecoSAM Global Equity Fund returned 19.78%, net of fees, for the year ended June 30, 2013. The Fund outperformed the 18.58% return of its benchmark, the MSCI World Index (Net).

Portfolio outperformance relative to the benchmark was primarily attributed to the positive contribution of stock selection across most sectors and was particularly strong within Financials, Health Care and Materials stocks. Stock selection had a negative contribution to performance within the Industrials and Utilities sectors.

The largest positive contributions at the stock level included positions in Hartford Financial, Life Technologies and SanDisk. Life Technologies' share price rose 64.5% (in USD terms) after Thermo Fisher announced a binding offer which valued the company at almost $13 billion. Hartford Financial's outperformance was mainly due to improving business fundamentals and strengthening capital position. Outperformance of U.S. semiconductor manufacturer SanDisk was attributed to a positive outlook for the flash memory market where the company enjoys a leading position.

Portfolio sector allocation was positioned with an overweight in Consumer Staples and Telecoms combined with underweight positions in Financials, Industrials and Materials. In terms of performance contribution, sector allocation had a negative impact. In particular, negative contribution came from underweighting Consumer Discretionary and Financials, as both sectors were among the best performing.

Portfolio Outlook and Strategy

Over the period, sentiment on the global equity market improved. The positive momentum was driven by central banks in the U.S. and Europe announcing aggressive monetary policy actions. The U.S. Federal Reserve announced plans to buy $40 billion of mortgage-backed securities each month until improvement is seen in the labour market. The Federal Reserve also extended the zero-interest rate policy into 2015. In Europe, the European Central Bank's (ECB) plan to buy euro-area government bonds was well received by investors. The so-called OMT plan (Outright Monetary Transactions) will have no ex ante limits on the size of the purchases, subject to conditions. European governments that want the ECB to buy their bonds must agree to a program of reforms and oversight by the bailout funds. Also, the Bank of Japan has announced the beginning of quantitative easing. Japanese Prime Minister Shinzo Abe's goal is to put the domestic economy back on self-sustaining growth using a combination of monetary and fiscal stimulus. Over the period, rising expectation of aggressive monetary stimulus fuelled a strong rally in Japanese equities.

Economic data released over the period continued to show growth tilted towards the downside. The euro-area sovereign crisis has hurt business confidence, making companies cautious to invest in new capacities. These problems have been compounded by weakening demand in key export markets such as China and by worries over tax and spending negotiations in the U.S. As a result, the euro-area economy remained in a recession over the period. Also, recent data on Chinese manufacturing activity shows a prolonged slowdown. This trend underlines a sustained slowdown in the country's economy and increases the likelihood of China missing its annual growth target.

In the coming quarters, the stock market will continue to be heavily influenced by further decisions of the U.S., European and Japanese central banks. Even though it can be expected that central banks will continue with a very accommodative monetary policy for the time being, the discussions about tapering bond purchases have just started and might weigh on the markets going forward. Our investment strategy remains focused on investing in sustainable companies with attractive valuations and stable earnings outlooks. We also continue

page 4

to underweight sectors where earnings visibility is lower, namely Financials. Our outlook for the Financial sector remains cautious as a result of the tightening regulation and the ongoing de-leveraging process. Our approach in this space remains very selective with focus on companies with solid cash generation, strong balance sheets and acceptable leverage.

Sincerely,

RobecoSAM USA, Inc.

page 5

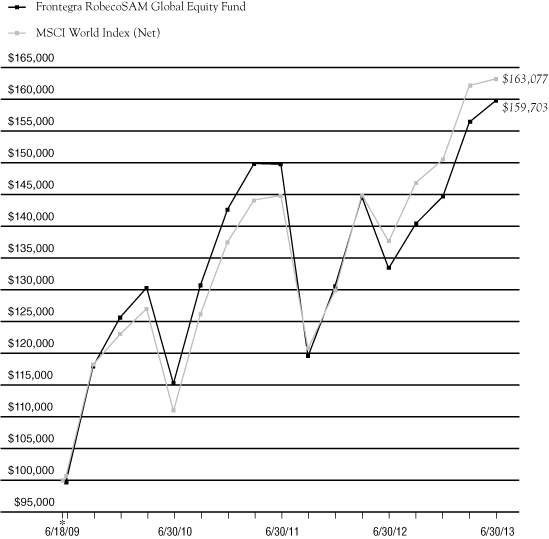

INVESTMENT HIGHLIGHTS

Growth of a $100,000 Investment (Unaudited)

* 6/18/09 commencement of operations.

This chart assumes an initial gross investment of $100,000 made on 6/18/09 (commencement of operations). Returns shown include the reinvestment of all distributions. Past performance is not predictive of future results. Investment return and principal value will fluctuate so that shares, when redeemed, may be worth more or less than the original cost. In the absence of existing fee waivers, total return would be reduced. Effective June 10, 2011, RobecoSAM USA, Inc. ("RobecoSAM") became subadviser to the Fund and Frontegra Asset Management, Inc. became adviser to the Fund. Prior to June 10, 2011, RobecoSAM served as adviser to the Fund. Effective February 20, 2013, the Fund changed its name from Frontegra SAM Global Equity Fund to Frontegra RobecoSAM Global Equity Fund. To receive current to the most recent month-end performance, please call 1-888-825-2100.

The MSCI World Index measures the overall performance of stock markets in 24 developed market countries in North America, Europe, and the Asia/Pacific Region. The Index does not reflect investment management fees, brokerage commissions and other expenses associated with investing in equity securities. A direct investment in the index is not possible.

Frontegra Asset Management, Inc. has contractually agreed through October 31, 2014 to waive its management fee and/or reimburse the Fund's operating expenses to the extent necessary to ensure that the Fund's total operating expenses (excluding taxes, interest, brokerage commissions, acquired fund fees and expenses and extraordinary expenses) do not exceed 1.20% of the Fund's average daily net assets. The expense ratios presented are based on the annualized expense ratios as reported in the Fund's current prospectus, which may differ from the expense ratios presented in the Fund's financial highlights.

** The returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Portfolio Total Return**

FOR PERIODS

ENDED 6/30/13 | | FUND | | INDEX | |

SIX MONTHS | | | 10.45 | % | | | 8.43 | % | |

ONE YEAR | | | 19.78 | % | | | 18.58 | % | |

AVERAGE ANNUAL

SINCE INCEPTION | | | 12.31 | % | | | 12.89 | % | |

Fund Expenses | |

GROSS EXPENSE RATIO | | | 1.62 | % | |

NET EXPENSE RATIO | | | 1.20 | % | |

page 6

FRONTEGRA

MFG GLOBAL EQUITY FUND

REPORT FROM MFG ASSET MANAGEMENT

Dear Fellow Shareholders:

The investment objective of the Frontegra MFG Global Equity Fund is capital appreciation. The objective is measured against the MSCI World Index (Net).

Performance Review

The Frontegra MFG Global Equity Fund returned 26.68%, net of fees, for the year ended June 30, 2013. The Fund's return outperformed the 18.58% return of its benchmark, the MSCI World Index (Net).

We do not manage the Fund against short-term performance metrics and it is inevitable that it will underperform equity markets at some point in the future. We aim (not guarantee) to produce absolute returns through the business cycle whilst minimizing the risk of a permanent capital loss. We will continue to focus on these objectives and will not chase short-term performance.

Fund Outlook and Strategy

Over the twelve months ending June 30, 2013, the MSCI World Index (Net) made strong gains, rising 18.58% in U.S. dollar terms, with global financial markets experiencing a number of interesting developments. In July 2012, comments from the ECB President, Mario Draghi, that Europe's central bank would do "whatever it takes" to preserve the euro caused markets to rally strongly.

As the twelve month period approached its end, investors became increasingly focused on the implications of the U.S. Federal Reserve ("the Fed") ending its quantitative easing programme. Over one month, U.S. 10 year Treasury yields rose from 2.2% to 2.5%, a 3% fall in value. It is also of note that gold fell around 23% over the past 12 months, notwithstanding common perceptions that it is a defensive store of value; in these markets it appears nothing could be further from the truth.

In our view, the major current investment risk is what will happen when the Fed ends its quantitative easing programme ("QE"). The endgame for QE presents a risk for equity and other asset markets (particularly currency and bond/credit markets) due to the potential redistribution of global money flows and possibility of rising bond yields.

United States

Fundamentally speaking, nothing has changed in our view of the U.S. economy over the past twelve months. There continue to be encouraging signs that the U.S. is undergoing a modest economic recovery. Importantly, house prices are rising and housing starts have increased substantially. However, we believe that there is unlikely to be a significant reduction in the unemployment rate until housing construction reverts to more normalised levels. When this occurs, the U.S. economy should recover significantly.

Europe

Since June 2012, the ECB has taken substantive action with Mario Draghi's "whatever it takes" statement in July and the announcement of the Outright Monetary Transactions (OMT) programme in September. These actions have significantly reduced the probability of a European sovereign-related financial system meltdown. The approaching German election could have important bearings on financial markets and the ongoing stability of Europe, though it appears that Angela Merkel is in a strong political position at the present time. Despite this, it is unlikely that significant progress, such as a move towards a comprehensive European Banking Union, will be made until after the election.

We continue to believe that many European countries face a prolonged period of sub-par (and potentially negative) economic growth due to the effects of fiscal austerity and deleveraging. The major near-term risk for Europe would be a dramatic uplift in European sovereign bond yields which could be triggered by a disorderly unwinding of QE in the U.S. This scenario would stoutly test the resolve of the ECB and test the veracity of its OMT programme.

page 8

China

It is becoming apparent that China's new leadership are intent on mitigating the risks associated with the country's banking and shadow banking systems, while addressing the overcapacity in certain parts of its economy. It is almost beyond comprehension that total credit outstanding in China has increased around 2.5 fold since the beginning of 2009. The ratio of credit to GDP has risen to around 200% over this period. This is probably the largest rapid increase in credit of any large economy in modern times. However, we think it is unlikely China will suffer a financial crisis in the next few years, given its government's substantial resources.

Over the past month, the People's Bank of China has tightened short-term liquidity to curtail lending in its unregulated shadow banking system. We believe there will also be an increased focus on reducing investment in additional production capacity. We regard both of these measures as necessary to preserve the longer-term stability of the country, though they will inevitably slow its economy. The main impact of any slowdown will be felt by Chinese savers, who have bought shadow banking products, and by commodity producers, through lower commodity prices. Indeed, if the Chinese leadership follows through with these policies commodity prices may fall far further. We don't think that the end of U.S. QE has large implications for China as the country's closed capital account means that large flows of capital out of the country are unlikely. We also believe the government will accept a slower rate of economic growth and is unlikely to embark on another large stimulus programme.

The Fund

As at 30 June 2013, the Fund consisted of 25 investments (compared with 24 investments at 30 June 2012). The top ten investments represented 51.6% of the portfolio (compared with 53.1% at 30 June 2012). Over the twelve months to 30 June 2013, the stocks with the strongest local currency returns were Google (+51.8%), Visa (+49.0%) and Lowe's (+46.7%) and the stocks with the weakest were Coca-Cola (+5.5%), Wal-Mart (+9.4%) and Yum! Brands (+9.8%).

We repositioned the defensive part of the Fund as some investments in this area performed strongly. We sold or reduced holdings in the most fully-valued companies, such as multi-national consumer staples names (e.g. Kraft, General Mills, Procter & Gamble and Mondelez), and increased our exposure to other defensive companies which should deliver more attractive returns (e.g. Yum! Brands and Target). We have recently made large investments in the out-of-favour, large-capitalisation technology companies, Microsoft and Oracle. Both these companies remain dominant in their markets but their valuations assume that this dominance (and subsequently earnings) will soon rapidly erode. While both companies have faced some near-term uncertainty, we believe they have strong futures.

The Fund continues to be exposed to the following major investment themes:

• Emerging market consumption growth via investments in multinational consumer franchises. The five largest investments in multinational consumer franchises at 30 June 2013 were Yum! Brands, Danone, McDonald's, Nestle and Colgate-Palmolive. These companies generate, on average, around 40% of their revenues in emerging markets.

• U.S. interest rates. We believe it is likely that U.S. short and long-term interest rates will "normalise" over the next three years as the U.S. economy recovers. This will be a result of the Federal Reserve lifting its base rate and ceasing its quantitative easing programme before taking steps to shrink (or sterilise) its balance sheet. We own four U.S. financial institutions which are likely to benefit from the change in U.S. interest rates; Wells Fargo, U.S. Bancorp, Bank of New York Mellon and State Street.

• A move to a cashless society. There continues to be a strong secular shift from spending via cash and cheque to cashless forms of payments such as credit cards, debit cards, electronic funds transfer and mobile payments. In our opinion, the explosion of smartphones will accelerate this shift on a global basis. We believe that there are only a limited number of companies that are well positioned to benefit from this structural shift. These companies are typically attractive and boast strong network effects, low capital intensity, high returns on capital and operate in industries that have high barriers to entry. Fund investments in this space include PayPal (via eBay), American Express, Visa and MasterCard.

page 9

• U.S. housing. A recovery in new housing construction should drive a strong cyclical recovery in companies exposed to the U.S. housing market, while providing a strong boost to the overall economy. Our major exposure to the U.S. housing market is via home improvement retailer, Lowe's, and the domestic U.S. banks, Wells Fargo and U.S. Bancorp.

• Technology/software. We believe that entrenched global software companies enjoy enormous competitive advantages and exhibit attractive investment characteristics. The Fund's technology/software investments include Microsoft and Oracle.

• Internet/e-commerce. There are a number of internet enabled businesses that also have very attractive investment characteristics with increasing competitive advantages. The Fund's investments in these areas include eBay and Google.

Sincerely,

Hamish Douglass

Portfolio Manager

MFG Asset Management

page 10

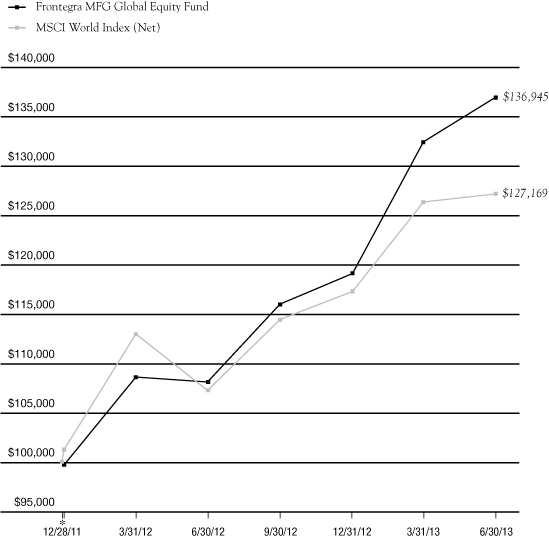

INVESTMENT HIGHLIGHTS

Growth of a $100,000 Investment (Unaudited)

* 12/28/11 commencement of operations.

This chart assumes an initial gross investment of $100,000 made on 12/28/11 (commencement of operations). Returns shown include the reinvestment of all distributions. Past performance is not predictive of future results. Investment return and principal value will fluctuate so that shares, when redeemed, may be worth more or less than the original cost. In the absence of existing fee waivers, total return would be reduced. To receive current to the most recent month-end performance, please call 1-888-825-2100.

The MSCI World Index measures the overall performance of stock markets in 24 developed market countries in North America, Europe, and the Asia/Pacific Region. The Index does not reflect investment management fees, brokerage commissions and other expenses associated with investing in equity securities. A direct investment in the index is not possible.

Frontegra Asset Management, Inc. has contractually agreed through October 31, 2014 to waive its management fee and/or reimburse the Fund's operating expenses to the extent necessary to ensure that the Fund's total operating expenses (excluding taxes, interest, brokerage commissions, acquired fund fees and expenses and extraordinary expenses) do not exceed 0.80% of the Fund's average daily net assets. The expense ratios presented are based on the annualized expense ratios as reported in the Fund's current prospectus, which may differ from the expense ratios presented in the Fund's financial highlights.

** The returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Portfolio Total Return**

FOR PERIODS ENDED 6/30/13 | | FUND | | INDEX | |

SIX MONTHS | | | 14.98 | % | | | 8.43 | % | |

ONE YEAR | | | 26.68 | % | | | 18.58 | % | |

AVERAGE ANNUAL

SINCE INCEPTION | | | 23.20 | % | | | 17.29 | % | |

Fund Expenses | |

GROSS EXPENSE RATIO | | | 1.14 | % | |

NET EXPENSE RATIO | | | 0.80 | % | |

page 11

This page intentionally left blank.

FRONTEGRA

MFG CORE INFRASTRUCTURE FUND

REPORT FROM MFG ASSET MANAGEMENT

Dear Fellow Shareholders:

The investment objective of the Frontegra MFG Core Infrastructure Fund is long-term capital appreciation. The objective is measured against the UBS Developed Infrastructure & Utilities Index (Net).

The types of infrastructure assets in which the Fund invests are natural monopolies that provide an essential service to the community. Infrastructure assets offer investors protection from the impacts of inflation because their earnings generally have some direct linkage to inflation. Over time the stable, reliable earnings of infrastructure assets are expected to lead to a combination of income and capital growth for investors.

The return from the infrastructure universe (as defined by MFG Asset Management ("MFGAM")) was more than 10% p.a. for the decade to the end of 2012. Just under half of that return was in the form of dividend income.

The universe of infrastructure assets that are held by the Fund is made up of two main sectors:

• Utilities, including both regulated energy utilities and regulated water utilities. Utilities comprise approximately 73% of the Fund. Utilities are typically subject to economic regulation. This requires the utility to efficiently provide an essential service to the community and, in return, permits the utility to earn a fair rate of return on the capital it has invested in its operations. As the utility provides a basic necessity, e.g. energy or water, there is minimal fluctuation in demanded volumes in response to the economic cycle and the price charged for the utility service can be adjusted with limited impact upon demanded volumes. As a result, the earnings of regulated utilities have been, and are expected to continue to be, stable irrespective of economic conditions; and

• Infrastructure, which includes airports, toll roads, ports and broadcast communications infrastructure. Regulation of infrastructure companies is generally done through contracts that regulate the prices the company can charge (rather than the earnings) and allows companies to accrue the benefits of volume growth (i.e. the returns of infrastructure companies are linked to growth in passengers, vehicles or containers). As economies develop, grow and become more inter-dependent, we expect the underlying level of aviation, shipping and vehicle traffic to increase. As a result, the revenues and earnings derived by infrastructure assets are expected to grow. In particular, airport stocks held by the Fund will benefit from the growing wealth of people in emerging markets and the resultant increase in tourism to European, Australian and New Zealand destinations.

Performance Review

The Frontegra MFG Core Infrastructure Fund returned 12.73%, net of fees, for the year ending June 30, 2013. The Fund's return outperformed the 9.04% return of its benchmark, the UBS Developed Infrastructure & Utilities Index (Net).

Most sectors held in the Core Infrastructure strategy performed well during the period with Airports up a weighted average 34%, Toll Roads up 30% and Gas Utilities up 16%. The Ports sector was the worst performing sector held by the Fund, and the only one not generating a positive return, down over 9% on average for the year.

Geographically, stocks held in the Fund and located in the Australia/New Zealand market were up a weighted average of 27%, while European stocks were up 20%. U.S. stocks were up almost 12%, but both U.K. and Canadian stocks underperformed the other sectors, both up approximately 8%.

In terms of the stocks included in the benchmark index but excluded from the Fund because they do not meet MFG's stringent definition of investment grade infrastructure, Japanese stocks were up over 60% on average reflecting increased appetite among international investors for exposure to the yen. These stocks had been very poor performers in previous years. In contrast, large, vertically integrated power companies in Europe with significant exposure to unregulated power generation continued to perform poorly.

page 14

Portfolio Outlook and Strategy

The Core Infrastructure strategy is designed to provide reliable returns in all but the most extreme market conditions. The Fund exceeded that expectation during the year, partly reflecting the continued recovery of stocks held by the Fund that had been over-sold in previous years. We now see the utilities market as broadly in equilibrium while infrastructure stocks, particularly those in Europe, remain cheap.

MFGAM believes that infrastructure and utility assets, with requisite earnings reliability and a linkage of earnings to inflation, offer an attractive, long-term investment proposition. Furthermore, given the predictable nature of earnings and the structural linkage of those earnings to inflation, the investment returns generated by infrastructure assets are different from standard asset classes and offer investors valuable diversification when included in an investment portfolio. In the current uncertain economic and investment climate, the reliable financial performance of infrastructure investments makes them particularly attractive and an investment in listed infrastructure can be expected to reward patient investors with a three to five year timeframe.

Sincerely,

Dennis Eagar | |

Portfolio Manager

MFG Asset Management | |

page 15

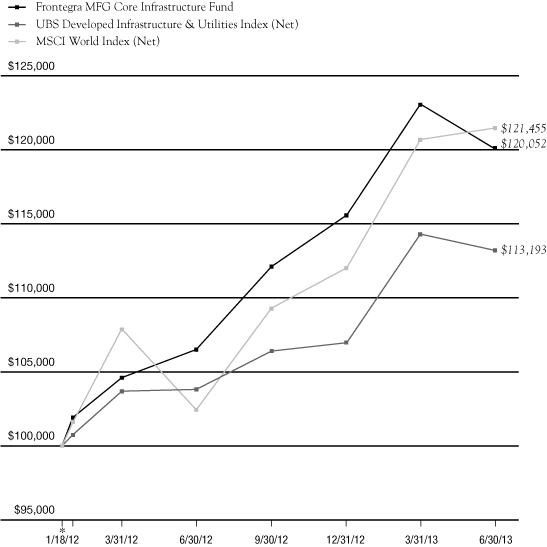

INVESTMENT HIGHLIGHTS

Growth of a $100,000 Investment (Unaudited)

* 1/18/12 commencement of operations.

This chart assumes an initial gross investment of $100,000 made on 1/18/12 (commencement of operations). Returns shown include the reinvestment of all distributions. Past performance is not predictive of future results. Investment return and principal value will fluctuate so that shares, when redeemed, may be worth more or less than the original cost. In the absence of existing fee waivers, total return would be reduced. To receive current to the most recent month-end performance, please call 1-888-825-2100.

The MSCI World Index measures the overall performance of stock markets in 24 developed market countries in North America, Europe, and the Asia/Pacific Region. The UBS Developed Infrastructure & Utilities Index is a global developed markets infrastructure and utilities benchmark. Neither index reflects investment management fees, brokerage commissions or other expenses associated with investing in equity securities. A direct investment in an index is not possible.

Frontegra Asset Management, Inc. has contractually agreed through October 31, 2014 to waive its management fee and/or reimburse the Fund's operating expenses to the extent necessary to ensure that the Fund's total operating expenses (excluding taxes, interest, brokerage commissions, acquired fund fees and expenses and extraordinary expenses) do not exceed 0.70% of the Fund's average daily net assets. The expense ratios presented are based on the annualized expense ratios as reported in the Fund's current prospectus, which may differ from the expense ratios presented in the Fund's financial highlights.

** The returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Portfolio Total Return**

FOR PERIODS

ENDED 6/30/13 | | FUND | | UBS

INDEX | | MSCI

INDEX | |

SIX MONTHS | | | 3.87 | % | | | 5.83 | % | | | 8.43 | % | |

ONE YEAR | | | 12.73 | % | | | 9.04 | % | | | 18.58 | % | |

AVERAGE ANNUAL

SINCE INCEPTION | | | 13.44 | % | | | 8.90 | % | | | 14.35 | % | |

Fund Expenses | |

GROSS EXPENSE RATIO | | | 6.55 | % | |

NET EXPENSE RATIO | | | 0.70 | % | |

page 16

FRONTEGRA

HEXAM EMERGING MARKETS FUND

REPORT FROM HEXAM CAPITAL PARTNERS, LLP

Dear Shareholders:

The Frontegra HEXAM Emerging Markets Fund aims to achieve long-term capital growth by investing at least 80% of its net assets in securities of emerging market companies. The Fund's benchmark is the MSCI Emerging Markets Index (Net).

Performance Review

The Frontegra HEXAM Emerging Markets Fund returned -6.67%, net of fees, for the year ended June 30, 2013. The Fund's return underperformed the 2.87% return of its benchmark, the MSCI Emerging Markets Index (Net).

Portfolio Review and Strategy

Investment sentiment remained negatively skewed over the past twelve months. On-going concerns about the euro zone, Chinese growth dynamics and leadership transition, and the U.S. fiscal cliff heightened risk-aversion further. In fact, these broader economic concerns are so elevated that the valuation gap between cyclical and defensive equities is at unprecedented levels. Interestingly, the performance of emerging markets relative to the S&P in recent years has resulted in a complete evaporation of relative return gains of the former since 1990. This is remarkable given the fundamental differences in the economies of emerging markets ("EM") versus developed markets ("DM") and the substantial earnings differentials over the period.

Over the reporting period, the Fund maintained its cyclical stance, and we have been increasing the number of non-commodity names in the portfolio that suffered most due to the negative sentiment towards cyclicals.

The biggest contribution to return at a country level came from an overweight position to China and underweight positions to South Africa, Chile and Peru. Overweight to Brazil was the biggest detraction at a country level, while underweights to Taiwan and ASEAN also detracted.

At a stock level, copper stocks (Kazakhstani Kazakhmys and Zambian First Quantum Minerals) detracted the most from the Fund's performance as sentiment towards commodities remained extremely negative. Brazilian Vale was one of the biggest laggards as well. The biggest contribution to return came from Kroton Educacional, an education company in Brazil, followed by Kingboard Chemicals, a Chinese laminate producer, and Qihoo 360, a leading Chinese Internet company.

Outlook

Although we have been witnessing historic high valuation gaps over the past three years and have experienced a few false bounces, some indicators are strongly suggesting that we have reached the bottom. A few points:

• U.S. corporate bonds are on course for their worst year (from a total return perspective) since 1973.

• June was the biggest month of global bond fund redemptions in over 20 years.

• The outperformance of defensive stocks versus cyclicals in emerging markets is now at its highest level since the 1998 Asia crisis.

• The Commitment of Traders speculative gold short positions on a contract basis are currently at their highest level ever.

Equities and the U.S. dollar are up 8-9% for the first six months of 2013, while bonds and commodities are down 4-6%. The biggest winners of 2013 are the U.S. and Japanese stock markets followed by Greek government bonds and Swiss equities. The two biggest debates we are witnessing among investors are those regarding EM versus DM and those over cyclical stocks versus defensive stocks. Investors withdrew $13.9 billion from equity mutual funds invested in BRIC countries this year or 27% of the inflows since 2005. The Defensives over Cyclicals gap is at extremes, while the DM over EM gap is approaching an inflection point (vs. 2009 trough). Anecdotal evidence from investment banks' trading flows also suggests that EM capitulation is near the end. We are in our third big period of EM defensives'

page 18

outperformance, the other two times being 1994-1998 and the financial crisis of 2008. The HEXAM strategy itself has never had valuations in the previous twelve years as low as current levels nor a dividend yield as high.

Thank you for your continued support.

Bryan Collings, CFA | | Grant Shotter, CFA | |

Managing Partner and Portfolio Manager

HEXAM Capital Partners, LLP | | Partner and Portfolio Manager

HEXAM Capital Partners, LLP | |

Stuart Richards | | Marina Akopian | |

Partner and Portfolio Manager

HEXAM Capital Partners, LLP | | Partner and Portfolio Manager

HEXAM Capital Partners, LLP | |

page 19

INVESTMENT HIGHLIGHTS

Growth of a $100,000 Investment (Unaudited)

* 12/20/10 commencement of operations.

This chart assumes an initial gross investment of $100,000 made on 12/20/10 (commencement of operations). Returns shown include the reinvestment of all distributions. Past performance is not predictive of future results. Investment return and principal value will fluctuate so that shares, when redeemed, may be worth more or less than the original cost. In the absence of existing fee waivers, total return would be reduced. To receive current to the most recent month-end performance, please call 1-888-825-2100.

The MSCI Emerging Markets Index is a free float-adjusted market capitalization index that is designed to measure equity market performance in the global emerging markets. The Index does not reflect investment management fees, brokerage commissions and other expenses associated with investing in equity securities. A direct investment in the index is not possible.

Frontegra Asset Management, Inc. has contractually agreed through October 31, 2014 to waive its management fee and/or reimburse the Fund's operating expenses to the extent necessary to ensure that the Fund's total operating expenses (excluding taxes, interest, brokerage commissions, acquired fund fees and expenses and extraordinary expenses) do not exceed 1.30% of the Fund's average daily net assets. The expense ratios presented are based on the annualized expense ratios as reported in the Fund's current prospectus, which may differ from the expense ratios presented in the Fund's financial highlights.

** The returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Portfolio Total Return**

FOR PERIODS

ENDED 6/30/13 | | FUND | | INDEX | |

SIX MONTHS | | | (18.83 | )% | | | (9.57 | )% | |

ONE YEAR | | | (6.67 | )% | | | 2.87 | % | |

AVERAGE ANNUAL

SINCE INCEPTION | | | (16.98 | )% | | | (3.91 | )% | |

Fund Expenses | |

GROSS EXPENSE RATIO | | | 1.66 | % | |

NET EXPENSE RATIO | | | 1.31 | % | |

page 20

FRONTEGRA

TIMPANI SMALL CAP GROWTH FUND

REPORT FROM TIMPANI CAPITAL MANAGEMENT LLC

Dear Fellow Shareholders:

The Frontegra Timpani Small Cap Growth Fund strives to achieve capital appreciation by investing in a diversified portfolio of growth companies with small market capitalizations. Timpani seeks to:

• Invest in companies where growth is robust, sustainable and underestimated by the market.

• Conduct fundamental research that provides unique insights into the perception gap that exists between market expectations and a company's true growth rate.

• Manage risk by continuously evaluating the size of the perception gap relative to market expectations and monitoring market sentiment.

• Act on new relevant incremental data points, both positive and negative, in an effort to exploit investor biases.

Performance Review

We are pleased to report the Fund outperformed its benchmark, the Russell 2000® Growth Index, for the year ended June 30, 2013, returning 28.35% (net of fees) vs. 23.67% for the benchmark. The vast majority of outperformance occurred in 2013 as macro concerns abated and the market embraced company-specific fundamental drivers. We were relatively in line over the latter half of 2012 despite large stylistic headwinds caused by changes in U.S. tax law.

Strong stock selection drove the majority of the outperformance, and sector allocation was slightly accretive to performance. In particular, an overweight in Consumer Discretionary was a positive contributor to performance, while an overweight in Technology in the second half of 2012 was an almost equal detractor from performance. There were no other sector allocations that produced any meaningful performance, but in total, sector allocations were slightly positive. Stock selection was positive in every sector except for Technology. Health Care and Consumer Discretionary led the way with significant relative outperformance versus the benchmark.

As we expected, the individual stocks that outperformed during the period tended to be those with the largest perception gaps. The period was characterized by sustained improvement in macroeconomic fundamentals with a continued realization that systemic risk is declining. This led to declining volatility, falling stock correlations and valuation multiples expanding over the course of the period as investors were more comfortable taking on risk. As economic concerns have lessened, the Fund's absolute and relative performance has strengthened. Continued focus by the market on company-specific fundamentals should continue to be a positive for the Fund.

There were several companies with secular growth profiles that were rewarded with large positive absolute and relative performance as investors recognized the value in robust, sustainable growth and strong business models that were able to gain market share in a competitive environment. Consumer Discretionary companies led the outperformance in the portfolio with three of the top six best performers for the period. Companies levered to an improving consumer environment with strong business models and strong secular growth drivers such as Conn's, Lithia Motors and Multimedia Games contributed most to the outperformance. Capital Senior Living, TearLab and HCI Group were companies from other sectors that were rewarded by investors with strong relative and absolute performance because of their strong secular growth profiles.

Portfolio Outlook

The benchmark was up significantly during the period. Unusually high correlations among stocks started to ease in 2012 and have gone even lower in 2013. Investors have focused more of their attention on company fundamentals while still keeping an attentive eye on the potential changes in Federal Reserve interest rate policy. Stubbornly high unemployment, geopolitical risks, European debt and moderating growth in emerging markets continue to be issues that investors are fearful of despite mostly positive company fundamentals. During

page 22

2013, the relative performance of the portfolio versus the index has been more positive. This is a function of continued positive bottom-up stock selection within the portfolio. We are very aware of the macro risks that continue to exist and feel confident that the portfolio is well positioned with companies that are poised to grow and gain share in any type of economic environment.

On a micro level, companies maintained a constructive outlook on the economy although the number of companies able to exceed analyst expectations consistently has moderated. Corporate balance sheets are generally sound, and companies are generating ample cash flow which enables them to increase cash deployment in the form of dividends, share buybacks or accretive acquisitions. We believe that positive corporate fundamentals coupled with historically low borrowing rates will lead to the potential for increased M&A activity which could benefit the companies we own as both buyers and potential acquisition targets. This thesis came to fruition numerous times over the past year as many of our companies were bought out at significant premiums, including: Market Leader, Conceptus, National Financial Partners, Kenexa and Schiff Nutrition. Our analysis continues to confirm our optimism regarding the fundamental strength of the companies in our portfolio. In particular, meetings with company management teams and other fundamental data points indicate that many companies continue to achieve robust growth and that significant perception gaps still exist. More attention was finally given to company-specific fundamentals, which is a step in the right direction, but we remain vigilant in continuing to assess broader risks to the portfolio.

During the period, we continued to focus on finding robust and sustainable growers with company-specific perception gaps. The results from our disciplined bottom-up stock picking process resulted in some changes in portfolio sector allocation. Our weightings in Financial Services and Technology have declined, while our exposure to Consumer Discretionary and Energy has increased meaningfully. Current sector positioning has us overweight Consumer Discretionary and Energy and underweight Financial Services, Consumer Staples and Materials & Processing. We took advantage of the declining volatility during the past year by adding and initiating positions in companies where we believe there is secular growth and where the market has underestimated that growth. This is classic perception gap investing. Looking ahead, we are confident that our bottom-up process will continue to add value for shareholders.

Thank you for your continued support.

Sincerely,

Brandon Nelson, CFA | |

Chief Investment Officer

Timpani Capital Management LLC | |

page 23

INVESTMENT HIGHLIGHTS

Growth of a $100,000 Investment (Unaudited)

* 3/23/11 commencement of operations.

This chart assumes an initial gross investment of $100,000 made on 3/23/11. Returns shown include the reinvestment of all distributions. Past performance is not predictive of future results. Investment return and principal value will fluctuate so that shares, when redeemed, may be worth more or less than the original cost. In the absence of fee waivers, total return would be reduced. To receive current to the most recent month-end performance, please call 1-888-825-2100.

The Russell 2000® Growth Index measures the performance of the small-cap growth segment of the U.S. equity universe. The Index does not reflect investment management fees, brokerage commissions and other expenses associated with investing in equity securities. A direct investment in the index is not possible.

Timpani Capital Management LLC has contractually agreed through October 31, 2014 to waive its management fee and/or reimburse the Fund's operating expenses to the extent necessary to ensure that the Fund's total operating expenses (excluding taxes, interest, brokerage commissions, acquired fund fees and expenses and extraordinary expenses) do not exceed 1.10% of the Fund's average daily net assets. The expense ratios presented are based on the annualized expense ratios as reported in the Fund's current prospectus, which may differ from the expense ratios presented in the Fund's financial highlights.

** The returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Portfolio Total Return**

FOR PERIODS ENDED 6/30/13 | | FUND | | INDEX | |

SIX MONTHS | | | 23.21 | % | | | 17.44 | % | |

ONE YEAR | | | 28.35 | % | | | 23.67 | % | |

AVERAGE ANNUAL

SINCE INCEPTION | | | 13.08 | % | | | 10.42 | % | |

Fund Expenses | |

GROSS EXPENSE RATIO | | | 5.25 | % | |

NET EXPENSE RATIO | | | 1.10 | % | |

page 24

FRONTEGRA

NETOLS SMALL CAP VALUE FUND

REPORT FROM NETOLS ASSET MANAGEMENT, INC.

Dear Fellow Shareholders:

The Frontegra Netols Small Cap Value Fund strives to achieve capital appreciation by investing at least 80% of its assets in equity securities of small capitalization companies. The objective is relative to, and measured against, the Russell 2000® Value Index.

Performance Review

Since its inception on December 16, 2005, the Frontegra Netols Small Cap Value Fund (Institutional Class) has outperformed the benchmark after fees, returning 6.88% annualized, compared to 5.48% annualized for the Russell 2000 Value Index. For the year ended June 30, 2013, the Fund outperformed the benchmark, returning 25.61% net of fees, compared to 24.76% for the Index.

Portfolio Review

The dominant market factor over the past 12 months has been a slowly strengthening U.S. economy and the implications for Federal Reserve policy. An improving employment outlook and housing market were among the factors that increased consumer confidence. This drove the market higher as obstacles that included a drought, presidential election, fiscal cliff, and sequester deadline all passed without a significant disruption to the economy. During the past year, the portfolio was positioned for a stable to slightly improving economy. As the domestic outlook strengthened, more cyclical Consumer Discretionary and Industrial sectors outperformed. Conversely, Utilities and the more emerging market dependent Energy sector underperformed during the period.

Positive Contributions to Relative Performance July 2012 through June 2013

• Stock Selection — Financials and Health Care

• Overweight — Consumer Discretionary and Industrials

• Best Performing Stocks — MGIC Investment Corp., Sunrise Senior Living, Domino's Pizza, TriMas, Cabela's

Negative Contributions to Relative Performance July 2012 through June 2013

• Stock Selection — Materials and Consumer Staples

• Underweight — Financials

• Worst Performing Stocks — Titan International, Merit Medical Systems, Ciber, Schnitzer Steel, Intrepid Potash

Overall, we believe the domestic economy should remain on a path of modest growth. Despite the residual impact of federal budget issues, the underpinnings of the economy appear to be strengthening. Continued improvement in the employment market should help drive the economy through improved consumer confidence. Additionally, with low wholesale inventories in the system, a restocking of the supply chain would be additive to an increase in general sales activity.

Thank you for your continued support.

Jeff Netols

President

Netols Asset Management, Inc.

page 26

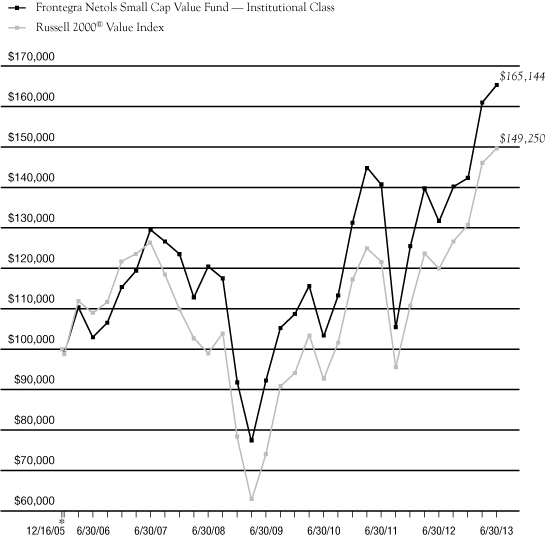

INVESTMENT HIGHLIGHTS

Growth of a $100,000 Investment (Unaudited)

* 12/16/05 commencement of operations.

This chart assumes an initial gross investment of $100,000 made on 12/16/05 (commencement of operations). Returns shown include the reinvestment of all distributions. Past performance is not predictive of future results. Investment return and principal value will fluctuate so that shares, when redeemed, may be worth more or less than the original cost. In the absence of existing fee waivers, total return would be reduced. To receive current to the most recent month-end performance, please call 1-888-825-2100.

The Russell 2000 Value Index measures the performance of those Russell 2000 companies with lower price-to-book ratios and lower forecasted growth values. The Index does not reflect investment management fees, brokerage commissions and other expenses associated with investing in equity securities. A direct investment in the index is not possible.

Frontegra Asset Management, Inc. has contractually agreed through October 31, 2014 to waive its management fee and/or reimburse the Fund's operating expenses to the extent necessary to ensure that the Fund's total operating expenses (excluding taxes, interest, brokerage commissions, acquired fund fees and expenses and extraordinary expenses) do not exceed 1.10% of the Fund's average daily net assets for the Institutional Class. The expense ratios presented are based on the annualized expense ratios as reported in the Fund's current prospectus, which may differ from the expense ratios presented in the Fund's financial highlights.

** The returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

The above graph relates to Institutional Class shares of the Fund. Performance for Class Y shares will vary from the performance of the Institutional Class shares shown above due to differences in expenses.

Portfolio Total Return**

FOR PERIODS

ENDED 6/30/13 | | FUND | | INDEX | |

SIX MONTHS | | | 16.11 | % | | | 14.39 | % | |

ONE YEAR | | | 25.61 | % | | | 24.76 | % | |

FIVE YEAR

AVERAGE ANNUAL | | | 6.53 | % | | | 8.59 | % | |

AVERAGE ANNUAL

SINCE INCEPTION | | | 6.88 | % | | | 5.48 | % | |

Fund Expenses | |

GROSS EXPENSE RATIO | | | 1.22 | % | |

NET EXPENSE RATIO | | | 1.10 | % | |

page 27

This page intentionally left blank.

FRONTEGRA

PHOCAS SMALL CAP VALUE FUND

REPORT FROM PHOCAS FINANCIAL CORPORATION

Dear Fellow Shareholders:

The Frontegra Phocas Small Cap Value Fund strives to achieve capital appreciation by investing in a diversified portfolio of equity securities of companies with small market capitalizations. The objective is relative to, and measured against, the Russell 2000® Value Index.

Performance Review

During the twelve month period ended June 30, 2013, the Frontegra Phocas Small Cap Value Fund returned 24.29%, net of fees, compared to the 24.76% return of the benchmark, the Russell 2000 Value Index (the "Benchmark").

The challenges for the year have been steady: economic headwinds continue in Europe, weakness in China, and continued uncertainty in the Middle East. In the U.S., healthcare implementation uncertainties and sluggish domestic expansion continue in the background. Despite all of these ongoing issues, the U.S. equities markets continued to climb up the wall of worry and deliver positive total returns for investors during the second quarter of 2013, just not as strongly as the first quarter of 2013.

For the year ended June 30, the Benchmark's sector performances were all up. The sector performance leader was Consumer Discretionary (+43.9%), that sector was followed by Industrials (+29.2%), Consumer Staples (+24.1%), Financials (+22.9%), Information Technology (+22.3%), Materials (+21.6%), Healthcare (+19.1%), Energy (+16.5%), Telecommunication Services (15.5%), and Utilities (+14.8%).

Despite a strong rebound in the second half of the year, the first half of the year saw the Fund's performance negatively impacted by several factors. The second half rebound was driven by stronger performance from the Energy, Industrials, Consumer Staples, Utilities, and Financials sectors in the third quarter, and for the fourth quarter by Materials, Healthcare, Energy, Financials, Consumer Staples and Utilities holdings. During the first quarter, the worst sectors were Materials, Consumer Staples, Industrials, and Financials. Consumer Discretionary was relatively flat versus the Benchmark. Though Materials represented only 5% of the Benchmark, many of the stocks within the index are mining/metals related companies as well as paper companies, neither of which the Fund owned at that time. Within Industrials, our largest positions had too much international revenue exposure, which greatly penalized them relative to pure domestic companies. As usual, earnings disappointments, no matter how small or insignificant, were met with share price compression inconsistent with the actual underlying financial performance — that may be because of factors including money flows affecting sector ETFs. High beta stocks and less liquid names continued to be excessively punished if on the wrong side of earnings estimates.

For the second quarter of the year, the Fund underperformed the Benchmark due to weaker performance from the Energy, Materials, and Healthcare sectors. Consumer Staples, though a small weight, continued to be a drag on the Fund's performance due to weakness in two of our three holdings. Within Consumer Discretionary, the Fund lost more ground, driven by lack of exposure to the homebuilding industry, which ran up significantly during the quarter as well as the year. No exposure to homebuilding stocks also cost the Fund during the quarter — that did not even include homebuilding related companies such as the furniture makers. We also lost ground in Financials, most of it coming from underperformance within the insurance subsector. Cash was also a drag, as it averaged about 3% of the total Fund value during the quarter, costing the Fund even more relative performance.

Portfolio Review and Strategy

At the end of June, Russell reconstituted their small cap equity index. Not only were individual names adjusted, but there were shifts in sector weights. The biggest changes were: (1) the Financials sector now represents almost 39% of the Benchmark, up from the prior level of 37%; (2) Consumer Discretionary declined from the 12% level to 11%; and (3) Technology went from 12% to under 11%.

page 30

To position for the rest of the year, we will be increasing our weight within Financials to align more closely with the Benchmark. We will remain underweighted within Utilities as the utility companies represent high valuations relative to their fundamentals. Because of the government's war on greenhouse gases and coal-fired power generators, utilities are confronting a rising yield curve as well as a tougher regulatory environment. Only those utilities that have a portion of their overall revenue mix from unregulated businesses will be able to provide a boost to EPS growth (i.e., Aqua America and Black Hills). We remain fans of the Technology company valuations and remain overweighted relative to the Benchmark.

Good news for the portfolio came with a couple of M&A deals that lifted the Fund's return in the most recent quarter. National Financial Partners, a financial services and insurance company, was acquired for $25.35/share by Madison Dearborn Partners, a private equity firm. Belo Corp., a media company that owns television stations and cable channels, was acquired for $13.75/share by Gannett. These deals usually add about 30+ bps. to the Fund's performance and, historically, we have benefitted from a number of these deals each year.

Because it is quite difficult, if not impossible, to time markets or sectors on a consistent basis, our core investment strategy remains to concentrate on identifying undervalued stocks in each sector. We believe that this will continue to be the best strategy, longer-term. We also feel that the best performing companies remain those that are finding new growth opportunities, are overhauling their operations to reduce costs significantly, or are investing their free cash flow and cash on their balance sheets to acquire promising businesses. In addition, we continue to search for companies with greatly discounted valuations based on concerns that we think can be repaired in a timely fashion. We remain fully invested with less than 5% cash or equivalents.

Thank you for your continued support.

William Schaff, CFA | | Steve Block, CFA | |

Chief Executive Officer and Portfolio Manager

Phocas Financial Corporation | | Portfolio Manager

Phocas Financial Corporation | |

page 31

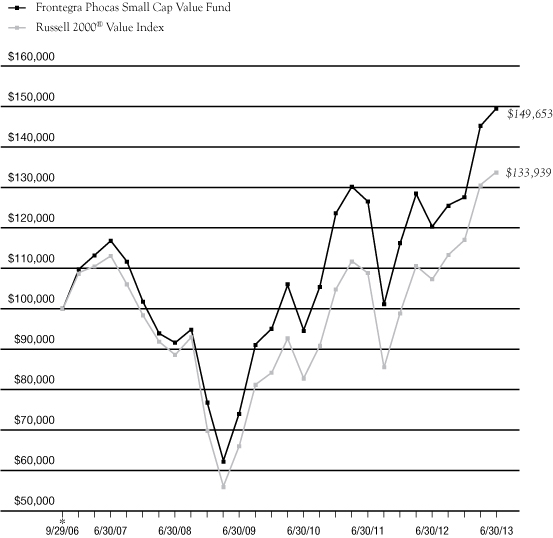

INVESTMENT HIGHLIGHTS

Growth of a $100,000 Investment (Unaudited)

* 9/29/06 commencement of operations.

This chart assumes an initial gross investment of $100,000 made on 9/29/06. Returns shown include the reinvestment of all distributions. Past performance is not predictive of future results. Investment return and principal value will fluctuate so that shares, when redeemed, may be worth more or less than the original cost. In the absence of fee waivers, total return would be reduced. Effective October 8, 2010, Phocas Financial Corp. ("Phocas") became subadviser to the Fund and Frontegra Asset Management, Inc. became adviser to the Fund. Prior to October 8, 2010, Phocas served as adviser to the Fund. To receive current to the most recent month-end performance, please call 1-888-825-2100.

The Russell 2000® Value Index measures the performance of those Russell 2000® companies with lower price-to-book ratios and lower forecasted growth values. The Index does not reflect investment management fees, brokerage commissions and other expenses associated with investing in equity securities. A direct investment in the index is not possible.

Frontegra Asset Management, Inc. has contractually agreed through October 31, 2014 to waive its management fee and/or reimburse the Fund's operating expenses to the extent necessary to ensure that the Fund's total operating expenses (excluding taxes, interest, brokerage commissions, acquired fund fees and expenses and extraordinary expenses) do not exceed 1.10% of the Fund's average daily net assets. The expense ratios presented are based on the annualized expense ratios as reported in the Fund's current prospectus, which may differ from the expense ratios presented in the Fund's financial highlights.

** The returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Portfolio Total Return**

FOR PERIODS ENDED 6/30/13 | | FUND | | INDEX | |

SIX MONTHS | | | 17.22 | % | | | 14.39 | % | |

ONE YEAR | | | 24.29 | % | | | 24.76 | % | |

FIVE YEAR

AVERAGE ANNUAL | | | 10.29 | % | | | 8.59 | % | |

AVERAGE ANNUAL

SINCE INCEPTION | | | 6.15 | % | | | 4.42 | % | |

Fund Expenses | |

GROSS EXPENSE RATIO | | | 2.57 | % | |

NET EXPENSE RATIO | | | 1.26 | % | |

page 32

LOCKWELL SMALL CAP VALUE FUND

REPORT FROM LOCKWELL INVESTMENTS, LLC

Dear Fellow Shareholders:

The Lockwell Small Cap Value Fund strives to take advantage of a number of investor biases which are particularly prevalent within the small cap equity universe. These biases result in an opportunity set of high-quality companies whose valuations, in our opinion, do not accurately reflect the attractiveness of their franchises or business prospects. The strategy attempts to exploit these biases by using an intensive, bottom-up, research-focused process; seeking high-quality companies with specific catalysts; and becoming involved with company managements when appropriate.

Performance Review

The Lockwell Small Cap Value Fund returned 27.66%, net of fees, for the twelve month period ending June 30, 2013. The Fund outperformed the 24.76% return of its benchmark, the Russell 2000® Value Index.

Outperformance was the result of both strong stock selection and sector allocation. The positive impact of stock selection came from many different sectors. The sector allocation aided performance largely through underweight positions in the REIT sector within Financials and the Utility sector. These bond proxies have long had stretched valuation multiples and so we have been underweight those areas for a number of years. When interest rates moved higher in the second quarter, our portfolio benefited.

Our overall sector positioning didn't significantly change during the first half of 2013. We continued to be overweight Industrials and Materials and underweight Financials. Additionally, we continued to maintain a frictional cash position of 3-5% in the Fund. Given the positive performance of the Fund during the first half of the year, the cash position slightly detracted from Fund performance.

Portfolio Outlook

The first half of 2013 had many similarities to the second half of 2012, with most markets continuing to be highly correlated and focused on macroeconomic issues although to a lesser extent than in 2012. Similar to 2012, investors were still concerned about the strength of the Euro bloc, the uncertainty of how the U.S. would handle fiscal and monetary issues and slowing economic growth across regions. However, markets in general reacted better in 2013 with greater clarity on central bank policy, the outcome of the elections and improving, albeit mildly improving, economic data in some parts of the world. Also similar to 2012, small cap companies continued to produce strong profits and cash flow. Many companies continued to buy back stock and/or pay dividends with their excess cash. We believe small cap valuations are close to fair value at this point and companies continue to be cautious with regard to their earnings forecasts for 2013. Our expectation for the second half of 2013 is that companies will deliver reasonable earnings, but without meaningful top line growth, they will likely not see much margin improvement as most cost cutting opportunities have already been realized. While merger and acquisition activity started to accelerate in the past year, we would not be surprised to see this to continue to grow as the year progresses given the strength of balance sheets and current valuations.

On June 20, 2013, the Board of Directors approved a plan to liquidate the Fund, which occurred on July 31, 2013.

Thank you for your investment in the Lockwell Small Cap Value Fund.

Richard Glass, CFA

Principal

Lockwell Investments, LLC

page 34

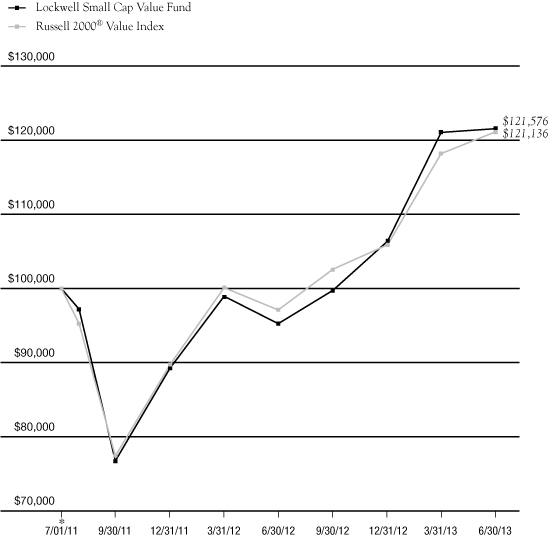

INVESTMENT HIGHLIGHTS

Growth of a $100,000 Investment (Unaudited)

* 7/01/11 commencement of operations.

This chart assumes an initial gross investment of $100,000 made on 7/01/11. Returns shown include the reinvestment of all distributions. Past performance is not predictive of future results. Investment return and principal value will fluctuate so that shares, when redeemed, may be worth more or less than the original cost. In the absence of fee waivers, total return would be reduced. To receive current to the most recent month-end performance, please call 1-888-825-2100.

The Russell 2000® Value Index measures the performance of those Russell 2000® companies with lower price-to-book ratios and lower forecasted growth values. The Index does not reflect investment management fees, brokerage commissions and other expenses associated with investing in equity securities. A direct investment in the index is not possible.

Lockwell Investments, LLC has contractually agreed through October 31, 2014 to waive its management fee and/or reimburse the Fund's operating expenses to the extent necessary to ensure that the Fund's total operating expenses (excluding taxes, interest, brokerage commissions, acquired fund fees and expenses and extraordinary expenses) do not exceed 1.10% of the Fund's average daily net assets. The expense ratios presented are based on the annualized expense ratios as reported in the Fund's current prospectus, which may differ from the expense ratios presented in the Fund's financial highlights.

** The returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Portfolio Total Return**

FOR PERIODS ENDED 6/30/13 | | FUND | | INDEX | |

SIX MONTHS | | | 14.27 | % | | | 14.39 | % | |

ONE YEAR | | | 27.66 | % | | | 24.76 | % | |

AVERAGE ANNUAL

SINCE INCEPTION | | | 10.26 | % | | | 10.06 | % | |

Fund Expenses | |

GROSS EXPENSE RATIO | | | 9.64 | % | |

NET EXPENSE RATIO | | | 1.11 | % | |

page 35

Frontegra Funds

EXPENSE EXAMPLE

June 30, 2013 (Unaudited)

As a shareholder of a mutual fund, you incur two types of costs: (1) transaction costs, including redemption fees, and (2) ongoing costs, including management fees, distribution and/or service (12b-1) fees and other fund expenses. Although the Funds charge no sales loads, you will be assessed fees for outgoing wire transfers, returned checks and stop payment orders at prevailing rates charged by U.S. Bancorp Fund Services, LLC, the Funds' transfer agent. If you request that a redemption be made by wire transfer, currently the Funds' transfer agent charges a $15.00 fee. A redemption fee of 2.00% of the then current value of the shares redeemed may be imposed on certain redemptions of shares made within 30 days of purchase for the Frontegra RobecoSAM Global Equity, Frontegra MFG Global Equity, Frontegra MFG Core Infrastructure, Frontegra HEXAM Emerging Markets and Lockwell Small Cap Value Funds.

This Example is intended to help you understand your ongoing costs (in dollars) of investing in the Funds and to compare these costs with the ongoing costs of investing in other mutual funds. The Example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period (1/1/13 – 6/30/13).

Actual Expenses

The first line of the table on the following page for each Fund provides information about actual account values and actual expenses. The Example includes management fees, registration fees, fee waivers/reimbursements and other expenses. However, the Example does not include portfolio trading commissions and related expenses and other extraordinary expenses as determined under generally accepted accounting principles. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled "Expenses Paid During the Period" to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The second line of the table for each Fund provides information about hypothetical account values and hypothetical expenses based on each of the Fund's actual expense ratios and an assumed rate of return of 5% per year before expenses, which is not the actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in each of the Funds and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as redemption fees. Therefore, the second line of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs could have been higher.

page 36

Frontegra Funds

EXPENSE EXAMPLE (continued)

June 30, 2013 (Unaudited)

| | Beginning Account

Value 1/1/2013 | | Ending Account

Value 6/30/2013 | | Annualized

Expense Ratio* | | Expenses Paid

During the Period* | |

RobecoSAM Global Equity Fund | |

Actual Fund Return | | $ | 1,000.00 | | | $ | 1,104.50 | | | | 1.20 | % | | $ | 6.26 | | |

Hypothetical 5% Return | | $ | 1,000.00 | | | $ | 1,018.84 | | | | 1.20 | % | | $ | 6.01 | | |

MFG Global Equity Fund | |

Actual Fund Return | | $ | 1,000.00 | | | $ | 1,149.80 | | | | 0.80 | % | | $ | 4.26 | | |

Hypothetical 5% Return | | $ | 1,000.00 | | | $ | 1,020.83 | | | | 0.80 | % | | $ | 4.01 | | |

MFG Core Infrastructure Fund | |

Actual Fund Return* | | $ | 1,000.00 | | | $ | 1,038.70 | | | | 0.70 | % | | $ | 3.54 | | |

Hypothetical 5% Return** | | $ | 1,000.00 | | | $ | 1,021.32 | | | | 0.70 | % | | $ | 3.51 | | |

HEXAM Emerging Markets Fund | |

Actual Fund Return | | $ | 1,000.00 | | | $ | 811.70 | | | | 1.30 | % | | $ | 5.84 | | |

Hypothetical 5% Return | | $ | 1,000.00 | | | $ | 1,018.35 | | | | 1.30 | % | | $ | 6.51 | | |

Timpani Small Cap Growth Fund | |

Actual Fund Return | | $ | 1,000.00 | | | $ | 1,232.10 | | | | 1.10 | % | | $ | 6.09 | | |

Hypothetical 5% Return | | $ | 1,000.00 | | | $ | 1,019.34 | | | | 1.10 | % | | $ | 5.51 | | |

Netols Small Cap Value

Fund – Institutional Class | |

Actual Fund Return | | $ | 1,000.00 | | | $ | 1,161.10 | | | | 1.10 | % | | $ | 5.89 | | |

Hypothetical 5% Return | | $ | 1,000.00 | | | $ | 1,019.34 | | | | 1.10 | % | | $ | 5.51 | | |

Netols Small Cap Value

Fund – Class Y | |

Actual Fund Return | | $ | 1,000.00 | | | $ | 1,157.90 | | | | 1.50 | % | | $ | 8.03 | | |

Hypothetical 5% Return | | $ | 1,000.00 | | | $ | 1,017.36 | | | | 1.50 | % | | $ | 7.50 | | |

Phocas Small Cap Value Fund | |

Actual Fund Return | | $ | 1,000.00 | | | $ | 1,172.20 | | | | 1.10 | % | | $ | 5.92 | | |

Hypothetical 5% Return | | $ | 1,000.00 | | | $ | 1,019.34 | | | | 1.10 | % | | $ | 5.51 | | |

Lockwell Small Cap Value Fund | |

Actual Fund Return | | $ | 1,000.00 | | | $ | 1,142.70 | | | | 1.10 | % | | $ | 5.84 | | |

Hypothetical 5% Return | | $ | 1,000.00 | | | $ | 1,019.34 | | | | 1.10 | % | | $ | 5.51 | | |

* Expenses are equal to each Fund's annualized expense ratio indicated above, multiplied by the average account value over the period, multiplied by 181/365 to reflect the one-half year period.

page 37

Frontegra RobecoSAM Global Equity Fund

SCHEDULE OF INVESTMENTS

June 30, 2013

Number of Shares | | | | Value | |

COMMON STOCKS 94.7% | | | |

| | | Australia 4.1% | |

| | 12,722 | | | AGL Energy Ltd. | | $ | 168,474 | | |

| | 7,528 | | | National Australia Bank Ltd. | | | 204,340 | | |

| | 5,252 | | | Westpac Banking Corp. | | | 138,717 | | |

| | 5,123 | | | Woodside Petroleum Ltd. | | | 164,031 | | |

| | | | 675,562 | | |

| | | Canada 3.0% | |

| | 2,227 | | | Canadian Imperial

Bank of Commerce | | | 158,052 | | |

| | 11,187 | | | TELUS Corp. | | | 326,558 | | |

| | | | 484,610 | | |

| | | France 3.6% | |

| | 11,945 | | | Total SA | | | 583,132 | | |

| | | Germany 3.2% | |

| | 1,972 | | | Adidas AG | | | 213,407 | | |

| | 2,472 | | | Fresenius SE & Co. KGaA | | | 304,745 | | |

| | | | 518,152 | | |

| | | Italy 3.1% | |

| | 14,313 | | | Eni SpA | | | 293,988 | | |

| | 48,191 | | | Snam SpA | | | 219,546 | | |

| | | | 513,534 | | |

| | | Japan 4.8% | |

| | 12,000 | | | Keihin Corp. | | | 183,182 | | |

| | 43,000 | | | Marubeni Corp. | | | 287,447 | | |

| | 15,800 | | | Stanley Electric Co. Ltd. | | | 307,780 | | |

| | | | 778,409 | | |

| | | Netherlands 2.4% | |

| | 5,195 | | | Koninklijke DSM NV | | | 338,508 | | |

| | 1,774 | | | Koninklijke Philips Electronics NV | | | 48,364 | | |

| | | | 386,872 | | |

| | | Norway 1.9% | |

| | 21,357 | | | DnB NOR ASA | | | 309,226 | | |

Number of Shares | | | | Value | |

| | | Sweden 0.8% | |

| | 3,200 | | | Svenska Handelsbanken AB -

Class A | | $ | 128,456 | | |

| | | Switzerland 10.7% | |

| | 2,420 | | | Roche Holding AG | | | 602,086 | | |

| | 4,984 | | | Swiss RE AG | | | 370,944 | | |

| | 910 | | | Swisscom AG | | | 398,471 | | |

| | 1,483 | | | Zurich Insurance Group AG | | | 384,665 | | |

| | | | 1,756,166 | | |

| | | United Kingdom 7.2% | |

| | 58,457 | | | Barclays PLC | | | 247,572 | | |

| | 74,165 | | | BT Group PLC | | | 348,783 | | |

| | 146,900 | | | Legal & General Group PLC | | | 382,957 | | |

| | 49,324 | | | WM Morrison Supermarkets PLC | | | 196,402 | | |

| | | | 1,175,714 | | |

| | | United States 49.9% | |

| | 1,413 | | | Caterpillar, Inc. | | | 116,558 | | |

| | 10,447 | | | Cisco Systems, Inc. | | | 253,967 | | |

| | 2,334 | | | Colgate-Palmolive Co. | | | 133,715 | | |

| | 6,423 | | | Dell, Inc. | | | 85,747 | | |

| | 4,093 | | | E.I. du Pont de Nemours & Co. | | | 214,883 | | |

| | 3,807 | | | Emerson Electric Co. | | | 207,634 | | |

| | 12,738 | | | Hartford Financial Services

Group, Inc. | | | 393,859 | | |

| | 3,413 | | | Illinois Tool Works, Inc. | | | 236,077 | | |

| | 2,539 | | | International Business

Machines Corp. | | | 485,228 | | |

| | 4,066 | | | Kimberly-Clark Corp. | | | 394,971 | | |

| | 4,400 | | | Life Technologies Corp. (a) | | | 325,644 | | |

| | 5,668 | | | Limited Brands, Inc. | | | 279,149 | | |

| | 349 | | | MasterCard, Inc. - Class A | | | 200,501 | | |

| | 2,908 | | | McDonald's Corp. | | | 287,892 | | |

| | 16,939 | | | Microsoft Corp. | | | 584,904 | | |

| | 2,156 | | | National Oilwell Varco, Inc. | | | 148,548 | | |

| | 3,090 | | | Noble Corp. | | | 116,122 | | |