UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-07739

Harding, Loevner Funds, Inc.

(Exact name of registrant as specified in charter)

400 Crossing Boulevard

Fourth Floor

Bridgewater, NJ 08807

(Address of principal executive offices) (Zip code)

Owen T. Meacham

The Northern Trust Company

50 South LaSalle Street

Chicago, IL 60603

With a copy to:

Stephen H. Bier, Esq.

Dechert LLP

1095 Avenue of the Americas

New York, NY 10036

(Name and address of agent for service)

Registrant’s telephone number, including area code: (877) 435-8105

Date of fiscal year end: 10/31

Date of reporting period: 10/31/2013

Item 1. Reports to Stockholders.

About the Adviser

Harding Loevner Funds

Global equity investing for institutions is Harding Loevner’s exclusive focus. Through Harding Loevner Funds it offers five distinct global strategies based on its quality-and-growth investment philosophy. It seeks to purchase shares of growing, financially strong, well-managed companies at favorable prices. Harding Loevner manages each of the Funds’ Portfolios according to a disciplined, research-based investment process. It identifies companies with sustainable competitive advantages and assesses the durability of their earnings growth by conducting in-depth fundamental research into global industries. In constructing portfolios, Harding Loevner diversifies carefully to limit risk.

Receive Investor Materials Electronically

Shareholders may sign up for electronic delivery of investor materials. By doing so, you will receive the information faster and help us reduce the impact on the environment of providing these materials. To enroll in electronic delivery,

| | 1. | Go to http://www.icsdelivery.com |

| | 2. | Select the first letter of your brokerage firm’s name. |

| | 3. | From the list that follows, select your brokerage firm. If your brokerage firm is not listed, electronic delivery may not be available. Please contact your brokerage firm. |

| | 4. | Complete the information requested, including the e-mail address where you would like to receive notifications for electronic documents. |

Your information will be kept confidential and will not be used for any purpose other than electronic delivery. If you change your mind, you can cancel electronic delivery at any time and revert to physical delivery of your materials. Just go to http://www. icsdelivery.com, perform the first three steps above, and follow the instructions for cancelling electronic delivery. If you have any questions, please contact your brokerage firm.

Table of Contents

| | |

Harding, Loevner Funds, Inc. c/o Northern Trust Attn: Funds Center C5S 801 South Canal Street Chicago, IL 60607 | | |

Phone: (877) 435-8105 Fax: (312) 267-3657 www.HardingLoevnerFunds.com | | Must be preceded or accompanied by a current Prospectus. Quasar Distributors, LLC, Distributor |

Letter to Our Shareholders

| | |

| | from left: David R. Loevner, CFA Chairman of Harding, Loevner Funds, Inc. and CEO of the Adviser Simon Hallett, CFA CIO of the Adviser |

Each semester as we prepare to write to you, our shareholders, we consider how best to introduce the detailed discussions of our investment views, activities, and results that follow. This time we decided to invite our colleague Andrew West to use this space to share his observations on the place of our investment approach in the context of contemporary financial theory.

As Harding Loevner’s Manager of Investment Research, Andrew works closely with Simon on issues of portfolio construction and risk management, in addition to supporting the analysts at each stage of the investment process. Andrew joined Harding Loevner in 2006 as an analyst covering the automotive, transportation, and steel industries globally—duties that he still performs today.

We remain genuinely grateful to you for taking the time to read this report and, more importantly, for trusting us to invest on your behalf.

Sincerely,

| | |

| |  |

| |

| David R. Loevner, CFA | | Simon Hallett, CFA |

Opinions expressed are those of Harding Loevner and are not intended to be forecasts of future events, a guarantee of future results, nor investment advice. Please read the separate disclosure page for important information, including the risks of investing in the Portfolios.

Past performance is not a guarantee of future results.

1

Risk, Return, and the Overthrow of the Capital Asset Pricing Model

Andrew West, CFA

Manager, Investment Research

| | |

| | Harding Loevner invests based on common-sense principles drawn from our founders’ experience: we stick to high-quality, growing companies that we can identify through fundamental research. This general philosophy flows naturally from our nature as cautious, patient people. It has been a constant throughout our firm’s existence since it was |

founded in 1989. In contrast to the boring continuity of thought in our little community, the prevailing wisdom in the larger world of academic investment theory has turned about completely over this same quarter century. Theories regarding market behavior and investment outcomes that were proclaimed as essential verities and celebrated with Nobel Prizes at the beginning of this period were subsequently overturned at the end. That academic battle is an engrossing tale that we have followed with interest. But, when it comes to our own story, we continue to invest in accordance with our beliefs that the steady-growth, high-quality segment of the global equity universe provides the best returns and risk experience over time.

In 1990 the Nobel Prizes for Economics were awarded to William Sharpe, Henry Markowitz, and Merton Miller, theorists who had been influential in the investment world for some time. Their work suggested an investment approach quite different from our own. In fact, it implied that if we thought we could achieve better returns through fundamental research—especially on less-risky, high-quality companies—we were destined to fail! The essence of the emergent consensus at the time Harding Loevner was founded was that the only future predictor of stock returns was “beta,” a measure of risk calculated by taking the slope of the regression of a stock’s past returns against the market. However, over the following two decades it became clear that the award-winning theories of 1990 failed to describe market behavior and, like the emperor who was seen to have no clothes, their authority declined. New Nobel Prize-winning theories validate the common-sense approach to which we have consistently adhered; namely, using fundamental research to identify growth opportunities, and seeking to reduce risk through quality and diversification.

To explain the overthrow of the old “1990 Consensus” and its replacement with a new set of investment prescriptions, it is helpful first to explain in more detail our investment process and its divergence from this consensus.

Harding Loevner’s primary assessment of risk and return is driven by judgments about unique and concrete company and industry fundamentals rather than calculations of historical stock return volatilities and co-movements. We marry both qualitative and quantitative analysis to identify strong and sustainable corporate business models. To assure that there is rigor in the qualitative aspects of our analysis, we require that every company in which we consider investing possess each of these

four criteria: Competitive Advantage, Sustainable Growth, Financial Strength, and Quality Management. These four criteria form the backbone of our investment process and imply that there are distinctions amongst equities that are identifiable and that may predict differences in future returns.

Competitive Advantage within a favorable industry structure is a prerequisite for durable profitability in a company. A company in an industry with unfavorable dynamics has a much steeper challenge than one well-positioned with few rivals. But, we also require that our companies possess competitive advantages that we think will allow them to sustain superior levels of return over time. Our analysts are primarily organized by industry rather than by geography as we believe that the understanding of industry structure and peer groups is key to identifying such investment opportunities.

Sustainable Growth allows cash flow and earnings to compound as a consequence of predictable long-term forces, like demographic trends, rising product penetration rates, and consumer substitution of higher-quality goods as incomes rise. Over time, these forces will mitigate the short-term impacts of unpredictable economic cycles. Sustainability also means that our companies are growing within the limits of their strategic and financial resources and are adding to the sum of human wealth.

When it comes to our own story, we continue to invest in accordance with our beliefs that the steady-growth, high-quality segment of the global equity universe provides the best returns and risk experience over time.

Financial Strength can help insulate equity investors from the risks of illiquidity or dilution. Not only can it can provide a buffer during difficult economic environments, it may protect our interests at other times as well, since, when a company’s debt becomes too large relative to its business or cash flows, management tends to sacrifice the long-term interests of equity investors to the immediate demands of creditors. Firms with strong balance sheets and sharp management teams can also act opportunistically to snap up attractive assets when weaker competitors cannot.

Quality Management is the least quantifiable of our four criteria, but aims to shield us from failures of strategy, execution, and intent. We have often seen companies with competitive advantages and growth potential fail to deliver due to incompetent

2

Letter to Our Shareholders

management. Strong corporate governance is another prerequisite in this category to assure that the resources of the firm are directed to shareholder wealth creation rather than management enrichment.

After determining that a potential investment meets our fundamental criteria, our analysts and portfolio managers convert their understanding of company and industry fundamentals into growth forecasts and estimates of fair value. We recognize that valuation is a difficult and imprecise art, but are committed to investing at valuations that appear reasonable based on past history and future prospects.

We recognize that valuation is a difficult and imprecise art, but are committed to investing at valuations that appear reasonable based on past history and future prospects.

So, that is what we do, and we have been steadfast in our adherence to this process throughout our history.

Let’s now review the theories honored by the 1990 Nobel Prizes and the bases for their conclusions that none of our four investment criteria (or any other fundamental research) could help investors predict risk or return.

Certainly, the most influential and widely promulgated theory to be recognized by a Nobel Prize was William Sharpe’s Capital Asset Pricing Model—CAPM—which stated that beta (the co-movement of stocks versus the index) is the only factor explaining expected stock and portfolio returns, and that the greater the beta (i.e., the higher the risk) the higher the expected returns. Sharpe’s CAPM was based on several important assumptions—namely that investors are perfectly rational; that they are perfectly informed about all security fundamentals; and that they all share the same view about the relationship between risk and return. In addition, the CAPM assumed that all investors create “optimal” portfolios through diversification, a tool for portfolio construction developed by Henry Markowitz and also awarded a Nobel Prize in 1990. Merton Miller’s theory that, in a perfect market, a company’s choice between debt and equity financing will not impact its value won the Nobel Prize in 1990 as well. In summary, the 1990 consensus proclaimed that business fundamentals don’t matter because markets are so efficient that all investors understand and price stocks perfectly and hold them in fully optimized portfolios. The only important factor was beta—with higher beta being the sole predictor of superior returns.

We beg to differ.

After twenty four years, have our efforts been a pointless waste of time, as would be indicated if returns are, indeed, determined by beta alone? The short answer is no. Years of data support different

conclusions: that within equity universes risk and return have not been positively correlated; that fundamental company characteristics matter (e.g. profitability, leverage, and valuation); and that investors and markets may not be as informed and rational as previously thought. Evidence has shown that, counter to the central CAPM tenet, low-beta equities have outperformed the market over decades and across geography.

Noting that the past twenty years of data were not supportive of the 1990 consensus, the academicians got to work to formulate theories with better explanatory power. This year the Nobel Committee awarded the supreme accolade to economists whose recent research validates the importance of company characteristics and valuation in determining equity returns. Eugene Fama was awarded the Prize based on his work on the Fama-French three-factor model, which adds size and value as additional factors in determining returns, noting the inadequacy of using beta alone. In November 2013, Fama published a new working paper that suggests company quality and investment behavior are also important and adds to the model profitability and investment measurements as the fourth and fifth factors, which “for applied purposes provide an acceptable description of average returns.”1 Robert Shiller, another Nobel recipient, was honored in part for his research into the long-run predictability of asset returns. This work suggests the importance of valuation, illustrating that stocks that are highly

We prefer our real-time experience and observations over academic studies of finance for many reasons.

priced relative to their dividends tend to generate lower long-run returns than higher-yielding equities.

Other recent research validates our long-held preference for companies with consistently higher profitability and lower indebtedness than the averages in their sectors by showing that such companies do, indeed, outperform their lower-quality peers.2 The issuance last year of new “Quality Indices” by MSCI is a further endorsement of the relevance of company quality. In backtests, MSCI found its World Quality Index, which represents developed markets, outperformed its standard World Index by 2.7% annually from November 1981 through November 2012. The Emerging Markets Quality Index outperformed the standard Emerging Markets Index by 2.8% annually from November 1998 through November 2012.

1 Eugene Fama and Kenneth French, “A Five-Factor Asset Pricing Model,” Draft Manuscript, Fama-Miller Working Paper Series, University of Chicago Booth School of Business, November 2013.

2 See, for example, Max Kozlov and Antti Petajisto, “Global Return Premiums on Earnings Quality, Value, and Size,” Blackrock, Inc., January 2013.

While we’re pleased to see theory moving in our direction, our track record over the last two decades is more compelling evidence to us than recent academic studies. We prefer our real-time experience and observations over academic studies of finance for many reasons. One major limitation of such studies is they can only rely upon what can be quantified, while our fundamental analysis incorporates more qualitative analysis of business models and industry characteristics whose uniqueness and specific applicability to the particular company and sector under examination make them less amenable to generalization or standardization. These characteristics are essential in informing analysts’ judgments, even though they are difficult to quantify and compare.

We don’t deny that qualitative investment research has its own weaknesses, including behavioral biases, subjectivity, and the difficulty of forecasting. Our process, favoring companies with high and steady profitability and growth, and strong balance sheets, was designed to help us overcome some common investor emotional biases, and reduce our dependence on forecasting unpredictable forces such as economic cycles (which we, like nearly all other investors and economists, do poorly). Over the years we have attempted to increase the objectivity of our company research, and created decision-making structures that reduce the impact of bias. We have also discovered that the higher confidence engendered by the quality and track records of our companies have made us less vulnerable to emotional, knee-jerk reactions.

We will continue to take an active interest in academic debates and disputes but, having no Nobel Prize winners among us, we are ill equipped to solve them! Rather, we have been gratified by the experience of actually applying our common-sense approach to the meaningful benefit of our clients. Our process of focusing on the long-term fundamentals of high-quality, value-creating companies around the world, and owning their stocks at prices we believe to be supportive of future positive returns, is a rational way to invest, and one that has the potential to produce above-average returns, while exposing our clients to below-average levels of risk.

We invite you to review the following commentaries to learn more about our investment process, our products, and results.

Global Equity Portfolio

Portfolio Managers

| | |

| | from left: |

| | Peter Baughan, CFA |

| | Co-Lead Portfolio Manager |

| | Ferrill Roll, CFA |

| | Co-Lead Portfolio Manager |

| | Alexander Walsh, CFA |

| | Portfolio Manager |

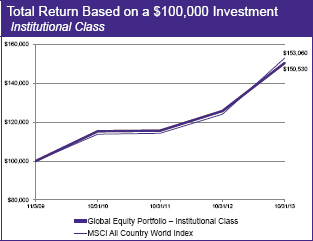

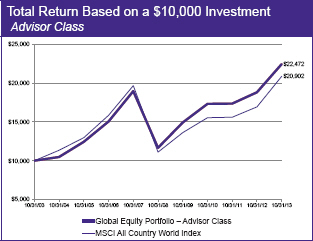

Performance Summary

The Global Equity Portfolio – Institutional Class rose 19.66% and the Advisor Class gained 19.33% (net of fees and expenses) in the fiscal year ended October 31, 2013. The Portfolio’s benchmark, the MSCI All Country World Index (the Index), rose 23.32% (net of source taxes) in this period.

Market Review

Equity markets turned in surprisingly good results considering the challenges markets faced at the outset of this fiscal year: political dysfunction and fiscal cliff worries in the US; slowing growth, political change, and capital outflows in emerging markets (EMs); competitive devaluation in Japan; and fiscal retrenchment in Europe, where the European Central Bank (ECB) was resistant to adopting the US Federal Reserve brand of quantitative monetary stimulus.

But Japan’s grand experiment in reflating its economy and the ECB’s creative finesse of sovereign and banking system fault lines allowed stock markets in the two regions to lead the Index in overall returns, with Japanese and euro-zone stocks both rising by more than a third in the year. EMs lagged a long way behind, still plagued by falling exports, political fragility, and capital outflows—a situation that worsened considerably when the US Fed hinted in the spring that it might begin to “taper” its massive purchases of US Treasury debt.

Sector-wise, there was confusion between leaders and laggards from a cyclical point of view. Consumer Discretionary stocks performed the best, with cyclical groups such as automobiles & components and media leading the way. Industrials—particularly capital goods—did well too, but the sector was edged out by the usually non-cyclical Health Care. Adding to the disorder, Materials and Energy, often cyclically correlated, fell to the bottom of the heap along with Utilities.

Quality factors played a role in overall returns, with low quality companies racing ahead of the Index in the US, Japan, and euro zone.

Performance Attribution

The Portfolio lagged the Index in the fiscal year, with negative stock selection in seven of the nine sectors in which we were invested. Stocks in the Information Technology sector—where the Portfolio holds its largest overweight relative to the Index—detracted most from relative performance, primarily due to a handful of under-performing US companies, including Apple, Citrix Systems, and Teradata. Of course, had we owned less in this sector, the impact would have been lessened. Financials also detracted from performance, mainly because of our emphasis on EM-oriented banks,

| | | | |

Fund Facts at October 31, 2013 |

Total Net Assets | | | | $630.2 million |

Sales Charge | | | | None |

Number of Holdings | | | | 67 |

Turnover (5 Yr. Average) | | | | 30% |

Redemption Fee | | | | 2% first 90 days |

Dividend Policy | | | | Annual |

| | | Institutional Class | | Advisor Class |

Ticker | | HLMVX | | HLMGX |

CUSIP | | 412295602 | | 412295206 |

Inception Date | | 11/3/2009 | | 12/1/1996 |

Minimum Investment* | | $100,000 | | $5,000 |

Net Expense Ratio | | 0.95%† | | 1.24% |

Gross Expense Ratio | | 1.02% | | 1.25% |

*Lower minimums available through certain brokerage firms.†Harding Loevner has contractually agreed to Waive fees and/or reimburse expenses through February 28, 2014. The Net Expense Ratio is as of October 31, 2013. The Gross Expense Ratio is as of the Prospectus, February 28, 2013.

including India’s HDFC Bank and ICICI Bank, Turkey’s Garanti Bank, and Indonesia’s Bank Central Asia, as well as the UK’s Standard Chartered, which suffered inordinately in the EM carnage. Industrial stocks also fared badly, especially Fanuc, which saw demand for its robots fall afoul of Apple’s oversupply problems. Only our stocks within Energy and Materials served to add to relative performance, thanks to Schlumberger, and to our avoidance of mining and commodity-oriented businesses.

By region, our emphasis on holdings in the outperforming US market and our lack of holdings in resource-related markets, such as Canada and Brazil, helped performance but could not overcome poor stock selection within most regions. In addition to the clutch of US-based IT companies, we also suffered from Coach, the luxury handbag and accessory producer, which ceded US market share to competitors for the first time in many years, casting doubt on the continuance of its international expansion, which has been a key driver of its growth. Our EM holdings—again, focused on banks and Telecoms in a weak currency environment—lagged the poor performance of the regional index, more than offsetting the benefit of our below-benchmark allocation to the region. Our Japanese holdings lagged the Index, hurt by Fanuc and Unicharm. Strong performance in Europe ex-EMU partially cushioned the Portfolio’s overall underperformance because of outperformance from several UK holdings, including advertiser WPP, drug maker Shire Pharmaceutical, and semiconductor designer ARM Holdings.

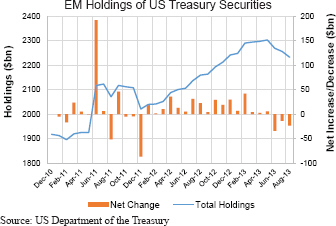

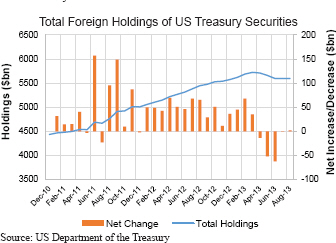

Perspectives

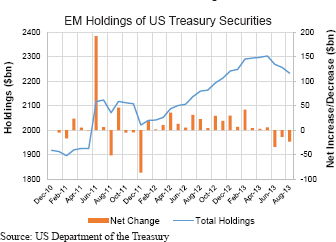

Market participants have focused on the volatility created by both the Fed’s notice of withdrawal of its extraordinary monetary stimulus (the tapering announcement in May) and then its subsequent about-face on ending Quantitative Easing while economic data remains anemic. But what has been much less appreciated, at least in the media and investment punditry that crosses our desks, is the fact that certain key long-term buyers of US Treasury securities have already been tapering their purchases for many months. That group is the collection of foreign central banks in developing countries that for years have been coping with sustained and large investment flows into their economies (both via public markets and by corporate direct investments) by standing in the middle of

Institutional Class HLMVX

Advisor Class HLMGX

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Performance | |

Average Annualized Total Returns (%) | |

at September 30, 2013 | | | | | | | | | | | | | | | | | | | | | | | | | | | at October 31, 2013 | |

| | | | | | | | | | | | |

| | |

| Inception

Date |

| | | 1 year | | | | 3 years | | | | 5 years | | | | 10 years | | |

| Since

Inception |

* | | | 1 year | | | | 3 years | | | | 5 years | | | | 10 years | | |

| Since

Inception |

* |

Global Equity Portfolio – Inst. Class | | | 11/3/09 | | | | 13.37 | | | | 9.86 | | | | – | | | | – | | | | 10.26 | | | | 19.66 | | | | 9.27 | | | | – | | | | – | | | | 10.79 | |

| | | | | | | | | | | | |

Global Equity Portfolio – Advisor Class | | | 12/1/96 | | | | 13.06 | | | | 9.58 | | | | 8.80 | | | | 8.70 | | | | 6.42 | | | | 19.33 | | | | 9.03 | | | | 14.01 | | | | 8.43 | | | | 6.56 | |

| | | | | | | | | | | | |

MSCI All Country World Index | | | | | | | 17.76 | | | | 10.22 | | | | 7.72 | | | | 7.86 | | | | 5.71 | | | | 23.32 | | | | 10.36 | | | | 13.47 | | | | 7.65 | | | | 5.93 | |

*The inception returns of the Institutional Class are since 11/3/09; those of the Advisor Class and Index are since 12/1/96.

Performance data quoted represent past performance; past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the Portfolio may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by calling (877) 435-8105 or visiting www.hardingloevnerfunds.com. The Portfolio imposes a 2% redemption fee on shares held 90 days or less. Performance data does not reflect the redemption fee. If reflected, total returns would be reduced. The Gross Expense Ratios for the Institutional Class and Advisor Class are 1.02% and 1.25%, respectively.

The charts below illustrate the hypothetical return of an investment made in the corresponding share classes. Investment return reflects voluntary fee waivers in effect. Absent such waivers, total return would be reduced. The performance provided in the table above and charts below do not reflect the deduction of taxes that a shareholder would pay on Portfolio distributions or the redemption of Portfolio shares.

those transactions, building reserves of US dollars and other foreign currencies, and injecting the money flows into their economies without allowing their exchange rates to adjust fully to reflect the sustained demand for the currency. Those reserves were mostly invested in US Treasury notes. As those flows have waned, so have the central banks’ desire to hold such large reserves, and indeed, some of them are trying to smooth the downward pressure on their exchange rates by using those reserves to satisfy the demands for

capital repatriation rather than allowing the currency to bear the full brunt of the “rush for the exits” by developed world investors. The result, as the accompanying chart shows, is that EM holdings of US Treasuries have switched from substantial increases every quarter (net purchases) to modest decreases (net sales, as well as valuation declines). The amount is significant, and has exceeded the modest tapering amount (whether temporarily or inevitably) threatened by Mr. Bernanke.

Global Equity Portfolio continued

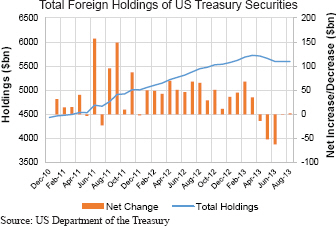

It is not just EM central banks that have reduced their purchases of US Treasuries. Japan is another country with large foreign currency reserves, including large holdings of US Treasuries; as the country’s very large annual current account surplus has shrunk dramatically in recent quarters, so, as a result, has its monthly net purchases of additional Treasury securities. Other developed market holdings of Treasuries have also declined, which may be related to the declining fears of a European sovereign default and a break-up of the euro. The flip side of the recovery of the European bank sector from the brink of insolvency is that the flight of capital to US Treasuries—once considered the ultimate safe haven—may decline. So, it is less surprising than might otherwise be recognized that the bear market in the long end of the US Treasury bond market is already one of the worst on record. Nor should we puzzle that the Fed’s backward step from tapering of Quantitative Easing has itself allowed bond markets to recover their poise. The cumulative effect of these central bank reserve shifts is the evaporation of tens of billions of dollars’ worth of new investments in US government securities monthly. Large providers of capital to the gigantic flow of US borrowing needs have begun to find other uses of their capital—at home. Absent further curtailing of those borrowing needs—smaller budget deficits still, or greater domestic savings—the cost of capital for US borrowers is not likely to remain near zero, after inflation, for much longer.

We have viewed the meltdown in some of the EMs with mixed feelings. On the one hand, we were happy to have leaned against the earlier prevailing winds of enthusiasm for EMs by constraining ourselves to a significantly smaller emphasis on EM-domiciled companies than the Index, and have found more attractively priced EM businesses within the multinational companies listed in less favored developed stock markets. On the other hand, we were chagrined to have held steadfastly onto several financial companies based in rapidly growing economies such as India, Brazil, and Turkey—countries amongst the worst-hit of the various EMs because of the deterioration of their currencies as stock and bond investors withdrew their capital.

The tapering warning from the Fed—which was to have amounted to a reduction in its purchases by less than ten billion dollars per month—has merely been the catalyst that accelerated the rush for the exits from EM stock and bond markets by global investors. But when Quantitative Easing does end—and we believe it is in its

| | | | | | | | |

Geographical Weightings (%) at October 31, 2013 | |

Institutional and Advisor Classes | | | | | |

Country/Region | | | Portfolio | | | | Benchmark | 1 |

Canada | | | 0.0 | | | | 3.7 | |

Emerging Markets | | | 8.5 | | | | 11.2 | |

Europe EMU | | | 7.1 | | | | 11.3 | |

Europe ex-EMU | | | 14.5 | | | | 13.4 | |

Japan | | | 9.3 | | | | 7.8 | |

Middle East | | | 0.0 | | | | 0.2 | |

Pacific ex-Japan | | | 3.0 | | | | 4.8 | |

United States | | | 54.9 | | | | 47.6 | |

Frontier Markets2 | | | 0.0 | | | | – | |

Cash | | | 2.7 | | | | – | |

1MSCI All Country World Index; 2Includes countries with less-developed markets outside the Index.

| | | | | | | | |

Sector Weightings (%) at October 31, 2013 | |

Institutional and Advisor Classes | | | | | |

Sector | | | Portfolio | | | | Benchmark | 1 |

Consumer Discretionary | | | 14.2 | | | | 11.8 | |

Consumer Staples | | | 11.2 | | | | 10.0 | |

Energy | | | 6.1 | | | | 9.9 | |

Financials | | | 18.9 | | | | 21.7 | |

Health Care | | | 9.0 | | | | 10.1 | |

Industrials | | | 8.8 | | | | 10.7 | |

Information Technology | | | 21.4 | | | | 12.1 | |

Materials | | | 6.3 | | | | 6.2 | |

Telecom Services | | | 1.4 | | | | 4.2 | |

Utilities | | | 0.0 | | | | 3.3 | |

Cash | | | 2.7 | | | | – | |

1MSCI All Country World Index

twilight, not only for the Fed but for other Western central banks—there will follow a sustained adjustment period for many of these less-developed capital markets, and probably for the less-developed economies that they serve. Adjustment will come in the form of weakening currencies and rising capital costs for investment. It may also result in the demise of some investments made earlier that were dependent on low capital costs—and that may well mean loan losses for their lenders. The opacity of capital flows, and of mismatched funding of investments, means that we can have no strong sense of how dramatic this reckoning might be. If the adjustment is large and drawn out, then we cannot avoid seeing some of the banks’ pain spilling into the underlying economies and hurting as well the businesses of a number of our multinational companies that have been investing in these growth markets so assiduously for so many years.

Japan is marching to a different drummer than either the western developed economies or the emerging ones. Prime Minister Shinzo Abe has actually amplified its monetary and fiscal stimulus and has hopes of further spurring domestic demand through more fundamental reforms of its economy. But we expect resistance from within his own political party when Abe tries to push through some of his suggested changes, especially in light of the implementation of already scheduled consumption tax hikes. We also wonder how long it will be before the fruits of growth strategies, such as potential corporate tax cuts, are realized and how sustainable the growth will be. While we are skeptical of the future success of Abe’s reforms, we continue to not only look for disruptions and secular changes that Abenomics may create, but also continue to look for companies that can achieve sustainable growth regardless of what Abe may or may not do.

If uncertainty is the order of the day from our perspective in Japan and in EMs, one thing of which we are confident is a continued increase in the regulatory burden on banks in developed markets. Swedish banks, among the most resilient through the financial crisis in spite of their longstanding funding reliance on covered bonds (mortgage-backed securities), are bracing for changes to their overall leverage and liquid capital ratios. The two nationalized banks in the UK, Royal Bank of Scotland and Lloyds Bank, are hiving off parts of their branch networks to satisfy the UK competition authorities. Other banks, from the Netherlands to Germany

7

Institutional Class HLMVX

Advisor Class HLMGX

to Spain to Austria, are continuing to shrink their assets in order to meet the capital requirements laid out in Basel III. American banks are facing an energized panoply of regulators, illustrated by their joint victory over JPMorgan Chase, which agreed to the largest fine of a corporation in US history this November. At the same time that regulators are maintaining the pressure on management and on capital, bank customers are not lining up to do more business: demand for borrowing remains weak in all markets, as individuals and companies continue to seek ways to reduce their exposure to, or dependence on, financial leverage.

Portfolio Structure

Markets have seized on the incrementally positive economic data coming from European economies as a sign that the worst of the sovereign crisis that followed the 2008 financial crisis is over. Meanwhile, there has been increasingly apparent optimism, not least from Fed comments, that the US economy is gathering momentum. We have some sympathy for that point of view, but have not altered our portfolio stance nor increased our risk tolerance in cyclical companies significantly over the past twelve months. The reason for that is, of course, that we have held a balanced Portfolio of cyclical and non-cyclical companies for quite some time already, anticipating an eventual rebound in capital spending and consumer discretionary spending, the two segments of the developed economy that were worst hit by the crises.

In fact, our Portfolio turnover has been unusually low over the past several months, as our substantial holdings of IT companies—whose products and services form a large piece of capital investment spending—saw valuations compress through stock price underperformance even as earnings proved resilient according to consensus estimates. Rather than give up and rotate into other sectors, we hunkered down in the companies we already owned, convinced that their headwinds would be temporary, and that their virtues would ultimately be recognized by the market.

We have held onto leading providers of equipment and software that is enabling the massive shift of data storage and analysis to remote sites, including F5 Networks, Teradata, and EMC, along with the companies who are helping enterprises to build their internal infrastructure, linking the new technologies to their existing operations, such as Cognizant Technology and Informatica. We continue to hold companies leading the explosion of mobile computing, including ARM Holdings and Citrix Systems. And, we continue to identify attractive internet-based business models in non-IT industries, such as Amazon.com in retailing, eBay in auctions and online payments, and M3 in medical information. We also added two credit card servicers to the Portfolio in the fiscal year, American Express and MasterCard, attracted to their toll-taker positions in consumer expenditures in the US and increasingly in EMs.

Our exposure to capital goods and related companies outside of the IT sector remains strong, with a near-benchmark weight in Industrials, including several companies that should benefit from the upswing in US manufacturing that is following the surge of US domestic oil and gas production. Roper and Emerson Electric have a large US presence, as do our two industrial gas specialists (from the Materials sector), Praxair and Air Liquide, both of which expect large new opportunities from the spate of new US refinery projects announced recently.

| | | | | | |

Ten Largest Holdings at October 31, 2013 | |

Institutional and Advisor Classes | | | | |

Company | | Country | | | % | |

Wells Fargo | | United States | | | 3.8 | |

Google | | United States | | | 3.4 | |

Schlumberger | | United States | | | 2.9 | |

Nestlé | | Switzerland | | | 2.7 | |

eBay | | United States | | | 2.6 | |

Unicharm | | Japan | | | 2.5 | |

Nike | | United States | | | 2.3 | |

AIA Group | | Hong Kong | | | 2.2 | |

Sigma-Aldrich | | United States | | | 2.1 | |

Fanuc | | Japan | | | 2.1 | |

Our Financials holdings remain concentrated in two regions, the US and EMs. We have retained our holding in JPMorgan in the face of acrimonious criticism of its management and its governance, and despite the record-breaking settlement it reached with government agencies and regulators in November. In our view, the settlements are a final clearing of the debris of the financial crisis, and the scale of the payments themselves are more representative of regulatory shakedown and backward-looking revisionism than of egregious wrongdoing on the part of JPMorgan management and staff. The clearest evidence of this are the sums that relate to mortgage securitization actions of Bear Stearns and Washing-ton Mutual, companies that the very same government agencies begged JPMorgan to acquire without time for extensive due diligence during the worst moments of the 2008 crisis. But as one of the few entities to come out of the crisis stronger, JPMorgan stands a good chance to reap the rewards of a chastened, more concentrated global investment banking industry in an interconnected world that still requires the global money center expertise and services at which JPMorgan excels.

Within EM Financials, we have so far resisted the urge to respond to lower prices and cheaper currencies that beckon us to add to our holdings. We are not at all sure, as discussed earlier, whether we are near the end of a correction or the beginning of a major adjustment in many of the developing countries’ capital accounts and capital markets. We are watching and waiting, taking cold comfort from the history of capital adjustments and financial crises: they always last longer than you expect.

Please read the separate disclosure page for important information, including the risks of investing in the Portfolio.

International Equity Portfolio

Portfolio Managers

| | |

| | from left: Ferrill Roll, CFA Co-Lead Portfolio Manager Alexander Walsh, CFA Co-Lead Portfolio Manager Peter Baughan, CFA Portfolio Manager |

| | |

| | Institutional Class Best Fund in its Category for

5-Year Risk-Adjusted Performance for the period ended November 30, 2012. |

Performance Summary

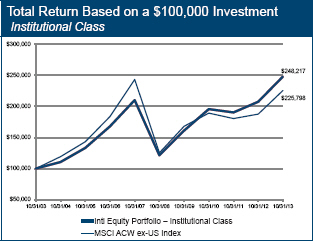

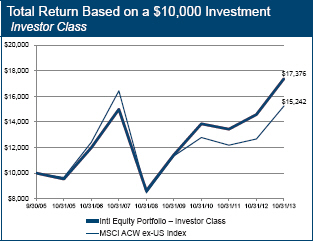

The International Equity Portfolio – Institutional Class rose 19.58% and the Investor Class gained 19.19% (net of fees and expenses) in the fiscal year ended October 31, 2013. The Portfolio’s benchmark, the MSCI All Country World ex-US Index (the Index), rose 20.31% (net of source taxes) in this period.

Market Review

Equity markets turned in surprisingly good results considering the challenges markets faced at the outset of this fiscal year: political dysfunction and fiscal cliff worries in the US; slowing growth, political change, and capital outflows in emerging markets (EMs); competitive devaluation in Japan; and fiscal retrenchment in Europe, where the European Central Bank (ECB) was resistant to adopting the US Federal Reserve brand of quantitative monetary stimulus.

But Japan’s grand experiment in reflating its economy and the ECB’s creative finesse of sovereign and banking system fault lines allowed stock markets in the two regions to lead the Index in overall returns, with Japanese and euro-zone stocks both rising by more than a third in the year. EMs were one of the worst performing regions in the Index, still plagued by falling exports, political fragility, and capital outflows—a situation that worsened considerably when the US Fed hinted in the spring that it might begin to “taper” its massive purchases of US Treasury debt.

Sector-wise, there was confusion between leaders and laggards from a cyclical point of view. Consumer Discretionary stocks performed the best, with cyclical groups such as automobiles & components and media leading the way. Industrials did well too, but the sector was edged out by the usually non-cyclical Health Care. Adding to the disorder, Energy and Materials, often cyclically correlated, fell to the bottom of the heap, with the latter being the only sector to experience negative returns in the fiscal year.

Quality factors did not play a clear-cut role in overall returns but were a significant factor on a regional basis, with low quality companies racing ahead of the Index in Japan and the European Monetary Union (EMU).

Performance Attribution

The Portfolio performed in-line with the Index in the fiscal year, with good sector allocations offset by poor stocks within several sectors. A heavy emphasis on Information Technology and Health Care companies proved beneficial, as did the Portfolio’s light

| | | | | | | | |

Fund Facts at October 31, 2013 | |

Total Net Assets | | | | | | | $3,877.5 million | |

Sales Charge | | | | | | | None | |

Number of Holdings | | | | | | | 53 | |

Turnover (5 Yr. Average) | | | | 20% | |

Redemption Fee | | | | | | | 2% first 90 days | |

Dividend Policy | | | | | | | Annual | |

| | | | Institutional Class | | | | Investor Class | |

Ticker | | | HLMIX | | | | HLMNX | |

CUSIP | | | 412295107 | | | | 412295503 | |

Inception Date | | | 5/11/1994 | | | | 9/30/2005 | |

Minimum Investment* | | | $100,000 | | | | $5,000 | |

Net Expense Ratio | | | 0.87% | | | | 1.20% | |

Gross Expense Ratio | | | 0.87% | | | | 1.24% | |

*Lower minimums available through certain brokerage firms. The Net Expense Ratio is as of October 31, 2013. The Gross Expense Ratio is as of the Prospectus, February 28, 2013.

allocation to Materials. However, our underweight to the strongly performing Financials sector diminished performance, and our focus on EM-oriented banks compounded the impact of our less-than-benchmark allocation. Garanti Bank was hit hard by political unrest in Turkey and suffered double-digit price declines. This came alongside poor performances from India’s ICICI Bank, Britain’s Standard Chartered, and, to a lesser extent, Brazil’s Itau Unibanco. We also suffered from poor stock selection within Industrials, where two Japanese companies, Fanuc and JGC Corp, under-performed. Fanuc saw demand for its robots fall afoul of Apple’s oversupply problems, while JGC suffered a highly publicized terrorist attack on one of its liquefied natural gas (LNG) projects in Algeria. While JGC’s share price mostly recovered in the months following the attack, Fanuc remained a significant laggard in the year. Notably, Schlumberger and Sasol drove good returns within Energy, but not enough to overcome the negative stock selection from other sectors.

Viewed regionally, the Portfolio experienced particularly strong performance in Europe ex-EMU, driven by our overweight to, and strongly performing holdings in, Switzerland (Roche Holding, Lonza Group, and Swatch Group), as well as good stocks within the UK (ARM Holdings and WPP). Our light holdings within EMs also helped performance, and, despite the emphasis on Financials, our EM stocks bettered the MSCI Emerging Markets Index—thanks in part to the very strong returns from Chinese internet search engine Baidu, a new holding this year. Stock selection in the euro zone detracted most from performance, primarily because of poor German holdings, including enterprise software giant SAP, and dialysis maker Fresenius Medical Care. The latter company’s shares reacted negatively to Medicare reimbursement rebasing proposals.

Perspectives

Market participants have focused on the volatility created by both the Fed’s notice of withdrawal of its extraordinary monetary stimulus (the tapering announcement in May) and then its subsequent about-face on ending Quantitative Easing while economic data remains anemic. But what has been much less appreciated, at least in the media and investment punditry that crosses our desks, is the fact that certain key long-term buyers of US Treasury securities have already been tapering their purchases for many months.

Institutional Class HLMIX

Investor Class HLMNX

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Performance | |

Average Annualized Total Returns (%) | | | | | |

at September 30, 2013 | | | | | | | | | | | | | | | | | | | | | | | | | | | at October 31, 2013 | | | | | |

| | | | | | | | | | | | |

| | |

| Inception

Date |

| | | 1 year | | | | 3 years | | | | 5 years | | | | 10 years | | |

| Since

Inception* |

| | | 1 year | | | | 3 years | | | | 5 years | | | | 10 years | | |

| Since

Inception* |

|

Intl Equity Portfolio – Institutional Class | | | 5/11/94 | | | | 16.27 | | | | 8.17 | | | | 8.76 | | | | 9.67 | | | | 6.32 | | | | 19.58 | | | | 8.24 | | | | 15.39 | | | | 9.52 | | | | 6.47 | |

| | | | | | | | | | | | |

Intl Equity Portfolio – Investor Class | | | 9/30/05 | | | | 15.80 | | | | 7.78 | | | | 8.41 | | | | – | | | | 6.70 | | | | 19.19 | | | | 7.85 | | | | 15.03 | | | | – | | | | 7.07 | |

| | | | | | | | | | | | |

MSCI ACW ex-US Index | | | | | | | 16.50 | | | | 5.96 | | | | 6.27 | | | | 8.78 | | | | 5.59 | | | | 20.31 | | | | 6.05 | | | | 12.50 | | | | 8.49 | | | | 5.76 | |

*The inception returns of the Institutional Class and Index are since 5/11/94; those of the Investor Class are since 9/30/05.

Performance data quoted represent past performance; past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the Portfolio may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by calling (877) 435-8105 or visiting www.hardingloevnerfunds.com. The Portfolio imposes a 2% redemption fee on shares held 90 days or less. Performance data does not reflect the redemption fee. If reflected, total returns would be reduced. The Gross Expense Ratios for the Institutional Class and Investor Class are 0.87% and 1.24%, respectively.

The charts below illustrate the hypothetical return of an investment made in the corresponding share classes. Investment return reflects voluntary fee waivers in effect. Absent such waivers, total return would be reduced. The performance provided in the table above and charts below do not reflect the deduction of taxes that a shareholder would pay on Portfolio distributions or the redemption of Portfolio shares.

That group is the collection of foreign central banks in developing countries that for years have been coping with sustained and large investment flows into their economies (both via public markets and by corporate direct investments) by standing in the middle of those transactions, building reserves of US dollars and other foreign currencies, and injecting the money flows into their economies without allowing their exchange rates to adjust fully to reflect the sustained demand for the currency. Those reserves were mostly invested in US Treasury notes. As those flows have waned, so have the central banks’ desire to hold such large reserves, and indeed,

some of them are trying to smooth the downward pressure on their exchange rates by using those reserves to satisfy the demands for capital repatriation rather than allowing the currency to bear the full brunt of the “rush for the exits” by developed world investors. The result, as the accompanying chart shows, is that EM holdings of US Treasuries have switched from substantial increases every quarter (net purchases) to modest decreases (net sales, as well as valuation declines). The amount is significant, and has exceeded the modest tapering amount (whether temporarily or inevitably) threatened by Mr. Bernanke.

International Equity Portfolio continued

It is not just EM central banks that have reduced their purchases of US Treasuries. Japan is another country with large foreign currency reserves, including large holdings of US Treasuries; as the country’s very large annual current account surplus has shrunk dramatically in recent quarters, so, as a result, has its monthly net purchases of additional Treasury securities. Other developed market holdings of Treasuries have also declined, which may be related to the declining fears of a European sovereign default and a break-up of the euro. The flip side of the recovery of the Eu-ropean bank sector from the brink of insolvency is that the flight of capital to US Treasuries—once considered the ultimate safe haven—may decline. So, it is less surprising than might otherwise be recognized that the bear market in the long end of the US Treasury bond market is already one of the worst on record. Nor should we puzzle that the Fed’s backward step from tapering of Quantitative Easing has itself allowed bond markets to recover their poise. The cumulative effect of these central bank reserve shifts is the evaporation of tens of billions of dollars’ worth of new investments in US government securities monthly. Large providers of capital to the gigantic flow of US borrowing needs have begun to find other uses of their capital—at home. Absent further curtailing of those borrowing needs—smaller budget deficits still, or greater domestic savings—the cost of capital for US borrowers is not likely to remain near zero, after inflation, for much longer.

We have viewed the meltdown in some of the EMs with mixed feelings. On the one hand, we were happy to have leaned against the earlier prevailing winds of enthusiasm for EMs by constraining ourselves to a significantly smaller emphasis on EM-domiciled companies than the Index, and have found more attractively priced EM businesses within the multinational companies listed in less-favored developed stock markets. On the other hand, we were chagrined to have held steadfastly onto several financial companies based in rapidly growing economies such as India, Brazil, and Turkey—countries amongst the worst-hit of the various EMs because of the deterioration of their currencies as stock and bond investors withdrew their capital.

The tapering warning from the Fed—which was to have amounted to a reduction in its purchases by less than ten billion dollars per month—has merely been the catalyst that accelerated the rush for the exits from EM stock and bond markets by global investors. But

| | | | | | | | |

Geographical Weightings (%) at October 31, 2013 Institutional and Investor Classes | |

Country/Region | | | Portfolio | | | | Benchmark | 1 |

| | | |

Canada | | | 3.2 | | | | 7.2 | |

| | | |

Emerging Markets | | | 16.8 | | | | 21.3 | |

| | | |

Europe EMU | | | 28.6 | | | | 21.5 | |

| | | |

Europe ex-EMU | | | 20.6 | | | | 25.6 | |

| | | |

Japan | | | 14.6 | | | | 15.0 | |

| | | |

Middle East | | | 0.0 | | | | 0.3 | |

| | | |

Pacific ex-Japan | | | 8.3 | | | | 9.1 | |

| | | |

Frontier Markets2 | | | 0.0 | | | | – | |

| | | |

Other3 | | | 4.4 | | | | – | |

| | | |

Cash | | | 3.5 | | | | – | |

1MSCI All Country World ex-US Index; 2Includes countries with less-developed markets outside the Index; 3Includes countries with developed markets outside the Index where some holdings are incorporated.

| | | | | | | | |

Sector Weightings (%) at October 31, 2013 Institutional and Investor Classes | |

Sector | | | Portfolio | | | | Benchmark | 1 |

| | | |

Consumer Discretionary | | | 10.4 | | | | 10.6 | |

| | | |

Consumer Staples | | | 14.8 | | | | 10.1 | |

| | | |

Energy | | | 8.0 | | | | 9.3 | |

| | | |

Financials | | | 19.1 | | | | 27.0 | |

| | | |

Health Care | | | 12.3 | | | | 7.7 | |

| | | |

Industrials | | | 12.1 | | | | 11.0 | |

| | | |

Information Technology | | | 15.9 | | | | 6.4 | |

| | | |

Materials | | | 3.0 | | | | 8.7 | |

| | | |

Telecom Services | | | 0.9 | | | | 5.8 | |

| | | |

Utilities | | | 0.0 | | | | 3.4 | |

| | | |

Cash | | | 3.5 | | | | – | |

1MSCI All Country World ex-US Index

when Quantitative Easing does end—and surely it is in its twilight, not only for the Fed but for other Western central banks—there will follow a sustained adjustment period for many of these less-developed capital markets, and probably for the less-developed economies that they serve. Adjustment will come in the form of weakening currencies and rising capital costs for investment. It may also result in the demise of some investments made earlier that were dependent on low capital costs—and that may well mean loan losses for their lenders. The opacity of capital flows, and of mismatched funding of investments, means that we can have no strong sense of how dramatic this reckoning might be. If the adjustment is large and drawn out, then we cannot avoid seeing some of the banks’ pain spilling into the underlying economies and hurting as well the businesses of a number of our multinational companies that have been investing in these growth markets so assiduously for so many years.

Japan is marching to a different drummer than either the western developed economies or the emerging ones. Prime Minister Shinzo Abe has actually amplified its monetary and fiscal stimulus and has hopes of further spurring domestic demand through more fundamental reforms of its economy. But we expect resistance from within his own political party when Abe tries to push through some of his suggested changes, especially in light of the implementation of already scheduled consumption tax hikes. We also wonder how long it will be before the fruits of growth strategies, such as potential corporate tax cuts, are realized and how sustainable the growth will be. While we are skeptical of the future success of Abe’s reforms, we continue to not only look for disruptions and secular changes that Abenomics may create, but also continue to look for companies that can achieve sustainable growth regardless of what Abe may or may not do.

If uncertainty is the order of the day from our perspective in Japan and in EMs, one thing of which we are confident is a continued increase in the regulatory burden on banks in developed markets. Swedish banks, among the most resilient through the financial crisis in spite of their longstanding funding reliance on covered bonds (mortgage-backed securities), are bracing for changes to their overall leverage and liquid capital ratios. The two nationalized banks in the UK, Royal Bank of Scotland and Lloyds Bank, are hiving off parts of their branch networks to satisfy the UK competition authorities. Other banks, from the Netherlands to Germany

Institutional Class HLMIX

Investor Class HLMNX

to Spain to Austria, are continuing to shrink their assets in order to meet the capital requirements laid out in Basel III. American banks are facing an energized panoply of regulators, illustrated by their joint victory over JPMorgan Chase, which agreed to the largest fine of a corporation in US history this November. At the same time that regulators are maintaining the pressure on management and on capital, bank customers are not lining up to do more business: demand for borrowing remains weak in all markets, as individuals and companies continue to seek ways to reduce their exposure to, or dependence on, financial leverage.

Portfolio Structure

Markets have seized on the incrementally positive economic data coming from European economies as a sign that the worst of the sovereign crisis that followed the 2008 financial crisis is over. We have some sympathy for that point of view, and have incrementally increased our risk tolerance in European companies over the past twelve months. We have held onto global cyclical companies, including compressor specialist Atlas Copco and low-voltage electrical equipment supplier Schneider Electric—which, together with our large holdings in enterprise software giant SAP, semiconductor design specialist ARM Holdings, and 3-D software specialist Dassault Systemes—are all exposed to an upturn in corporate capital spending. Sales of advertising giant WPP, luxury watchmaker Swatch Group, and winter tire manufacturer Nokian Renkaat are all correlated to any surge in consumer spending, as is luxury carmaker BMW, which we purchased earlier this year. We also bought a new holding in BBVA in the year, the Spanish commercial bank with operations in Latin America and a stake in Turkey’s Garanti Bank.

In our opinion, our holdings in Japan remain of very high quality and are among the fastest-growing Japanese companies in the country. But as others have become attracted to their merits, their shares have become expensive, and indeed, our performance within Japan suffered relative to the Index over the first six months of Abe’s ascendancy. We are now casting our net slightly wider. If Abenomics succeeds in kindling some modest inflation as well as greater domestic investment demand, then we believe Tokyo office property will be in higher demand given the city’s central place in corporate Japan’s cultural hierarchy. With property values in Japan having suffered through a twenty-year bear market, and rents stable over the past decade, we believe that office rents in Japan have little downside, and potentially a lot of upside. We bought a new holding in Mitsubishi Estate, the quoted real-estate company with premier office property assets in prestigious Marunouchi, central Tokyo, which are partially financed by debt, a potent mixture for real profit creation if Mr. Abe succeeds.

Harding Loevner portfolios have long featured generous allocations to companies in the Consumer Staples and Health Care sectors, due to their consistent growth and persistent high quality—and we still hold more than a quarter of the Portfolio in those two sectors. Since purchasing a renewed holding in Novo Nor-disk in June, though, we sold our holding of Lonza Group, the Swiss-based bio-pharmaceutical and anti-microbial manufacturer, after shares rallied significantly on the installation of the new CEO and his embarkation on a substantial restructuring of the company’s various businesses. We also reduced our holding in Fresenius Medical Care, the global leader in kidney dialysis, because of the uncertainty over pricing for treatments in the US, which is under review by Medicare and Medicaid.

| | | | | | |

Ten Largest Holdings at October 31, 2013 | |

Institutional and Investor Classes | |

Company | | Country | | | % | |

| | | |

SAP | | Germany | | | 3.6 | |

| | | |

Nestlé | | Switzerland | | | 3.4 | |

| | | |

Dassault Systemes | | France | | | 3.4 | |

| | | |

WPP | | United Kingdom | | | 3.2 | |

| | | |

Roche Holding | | Switzerland | | | 3.0 | |

| | | |

Air Liquide | | France | | | 3.0 | |

| | | |

Allianz | | Germany | | | 3.0 | |

| | | |

Itau Unibanco | | Brazil | | | 2.9 | |

| | | |

AIA Group | | Hong Kong | | | 2.8 | |

| | | |

JGC Corp | | Japan | | | 2.5 | |

We have not gone whole hog in adding to companies domiciled in EMs. As mentioned, we bought a new holding in China’s largest internet search engine company, Baidu, which had underperformed along with most Chinese-related equities but appears to be grappling successfully with its biggest challenge: to adapt its revenue model from computer-based search to mobile search, where its business faces new competitors and new methods of information monetization. There are not yet many “internet-based” business models in non-US markets that meet our criteria for business quality and management consistency and also trade at remotely reasonable prices; in this case, we were able to exploit the market’s multiple fears over Baidu’s operations and home market to establish a position. We used the extended weakness in EM bank shares and currencies to add to holdings in India’s ICICI Bank and in Bra-zil’s Itau Unibanco. We also bought a new holding in Hong Kong Stock Exchange, which maintains our exposure to long-term trends in the financial integration of China to the world, but avoids significant credit risks. But we reduced our holding in Xinyi Glass, the Chinese producer of replacement glass for autos, after its share price recovered dramatically from China-related investor fears.

We also sold our holding in Potash, the Canadian producer of phosphates used in fertilizers, after the former Soviet bloc producers’ cartel broke ranks with each other and pricing discipline within the global potash industry fell apart.

The International Equity Portfolio, Institutional Class was ranked best out of 155 International Large-Cap Growth Funds for the 5-year period ended November 30, 2012. A Lipper Fund Award is awarded to one fund in each Lipper classification for achieving the strongest trend of consistent risk-adjusted performance against its classification peers over a three, five or ten-year period. Although Lipper makes reasonable efforts to ensure the accuracy and reliability of the data contained herein, the accuracy is not guaranteed by Lipper. Lipper Analytical Services, Inc. is an independent mutual fund research and rating service.© 2013, All Rights Reserved

Past performance does not guarantee future results.

Please read the separate disclosure page for important information, including the risks of investing in the Portfolio.

International Small Companies Portfolio

Portfolio Managers

| | |

| | from left: |

| | Josephine Lewis |

| | Co-Portfolio Manager |

| | Jafar Rizvi, CFA |

| | Co-Portfolio Manager |

Performance Summary

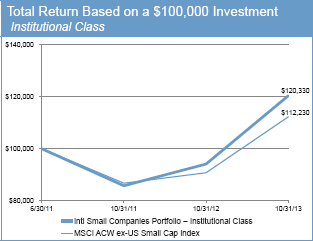

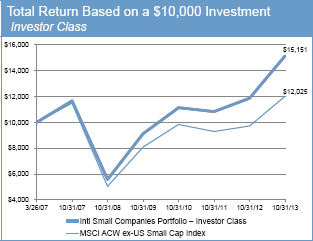

The International Small Companies Portfolio – Institutional Class rose 27.88% and the Investor Class gained 27.63% (net of fees and expenses) in the fiscal year ended October 31, 2013. The Portfolio’s benchmark, the MSCI All Country World ex-US Small Cap Index (the Index), rose 23.67% (net of source taxes) in this period.

Market Review

During the period, there were sharp divergences in performance for small company stocks among the Index’s different regions. From January to March 2013, euro-zone returns were dragged down by the news of a bank crisis and bailout in Cyprus, as government guarantees of bank deposits were cast aside as part of the European Monetary Union (EMU) bailout, giving depositors (and investors in EMU bank stocks) all over the continent reason to question the sanctity of their own nest eggs. However, incremental improvement of economic data toward the end of the fiscal year caused a slight positive change in growth prospects, which was enough to ignite investor optimism. Within the Index, small company stocks in Europe, both in the euro zone and outside of it, were up 47% and 37%, respectively, in the reporting period.

In contrast, shares of small companies in Emerging Markets (EMs) underperformed the Index by 14 percentage points. Currency depreciation among EM countries has been widespread, and markets of countries with especially large current account deficits, such as India and Indonesia, were especially punished. Concerns loom over how such countries will finance their deficits when the US Federal Reserve taps the brakes on its loose monetary policy of the last five years, by “tapering” its asset purchases. When implemented, this tightening will impact global liquidity and may cause further outflow of capital from EMs. However, the Fed’s retreat in September from plans to begin tapering helped EMs recover and post their largest two-month gain of the period.

Returns by sector did not show a clear pattern during the period, as the strongest returns in the Index came not only from cyclical sectors such as Information Technology and Consumer Discretionary, but also from the traditionally more defensive Telecom Services and Health Care sectors. The worst performing sectors in the Index were Energy and Materials, each underperforming the broader Index by more than 20 percentage points.

Small-cap stocks outperformed their large-cap counterparts (measured by the MSCI All Country World ex-US Index) by nearly four percentage points for the fiscal year ended October 31, 2013. This was partially due to the outperformance of small-

| | | | |

Fund Facts at October 31, 2013 |

Total Net Assets | | | | $79.1 million |

Sales Charge | | | | None |

Number of Holdings | | | | 105 |

Turnover (5 Yr. Average) | | | | 30% |

Redemption Fee | | | | 2% first 90 days |

Dividend Policy | | | | Annual |

| | | Institutional Class | | Investor Class |

Ticker | | HLMRX | | HLMSX |

CUSIP | | 412295875 | | 412295883 |

Inception Date | | 6/30/2011 | | 3/26/2007 |

Minimum Investment* | | $100,000 | | $5,000 |

Net Expense Ratio† | | 1.30% | | 1.55% |

Gross Expense Ratio | | 1.64% | | 2.02% |

*Lower minimums available through certain brokerage firms.†Harding Loevner has contractually agreed to waive fees and/or reimburse expenses through February 28, 2014. The Net Expense Ratio and the Gross Expense Ratio are as of the Prospectus, February 28, 2013.

cap European companies versus their large-cap counterparts. Returns by sector were similar to those of large-cap stocks, except in the case of Telecom Services and Information Technology, where small caps have trounced large caps in the period by approximately 12% in both sectors.

Performance Attribution

The Portfolio benefited from relative outperformance in seven of the ten economic sectors, led by stock selection in Consumer Staples. Pigeon, the Japanese provider of mother and baby care products, continues to expand into higher- margin, international markets such as China, which has helped operating results. The Portfolio’s longstanding underweights in Energy and Materials were a benefit this reporting period, as these were the weakest sectors in the Index. Conversely, our underweight to the strongly performing Consumer Discretionary sector detracted most from the Portfolio’s performance, though the companies we own fared modestly better than those in the Index. Stock selection in Industrials was weak, as Singapore-based crane maker Tat Hong Holdings underperformed due to weakness in Australian construction demand. We still believe in the company as it is a leading crane and heavy equipment operator in a fragmented industry, which allows it to benefit from its scale relative to small local operators. Further, the company derives nearly half of its revenues from South East Asia and should benefit from infrastructure development projects taking place there.

By geography, the largest contributor to the Portfolio’s outperformance was strong stock selection in Pacific ex-Japan, more than offsetting our overweight to the underperforming region. Australia’s TPG Telekom fared particularly well in an otherwise slowing Australian market as it leverages its low-cost provider status to syphon customers from more expensive competitors. Our positive stock selection in EMs, especially in China, also helped relative returns. Chinese company Haitian International, a producer of plastic injection molding machines, outperformed as the company launched a new product with capabilities superior to those of local Chinese competitors, and

Institutional Class HLMRX

Investor Class HLMSX

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Performance | |

Average Annualized Total Returns (%) | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

at September 30, 2013 | | | | | | | | | | | | | | | | | | | | | | | at October 31, 2013 | | | | | |

| | | Inception

Date | | | 1 year | | | 3 years | | | 5 years | | | Since

Inception* | | | 1 year | | | 3 years | | | 5 years | | | Since

Inception* | |

Intl Small Companies Portfolio – Institutional Class | | | 6/30/11 | | | | 23.69 | | | | – | | | | – | | | | 7.22 | | | | 27.88 | | | | – | | | | – | | | | 8.24 | |

| | | | | | | | | | |

Intl Small Companies Portfolio – Investor Class | | | 3/26/07 | | | | 23.45 | | | | 11.51 | | | | 15.02 | | | | 6.13 | | | | 27.63 | | | | 10.80 | | | | 22.10 | | | | 6.50 | |

| | | | | | | | | | |

MSCI ACW ex-US Small Cap Index | | | | | | | 20.01 | | | | 7.26 | | | | 11.37 | | | | 2.39 | | | | 23.67 | | | | 6.90 | | | | 18.94 | | | | 2.83 | |

*The inception returns of the Institutional Class are since 6/30/11; those of the Investor Class and Index are since 3/26/07.

Performance data quoted represent past performance; past performance does not predict future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the Portfolio may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by calling (877) 435-8105 or visiting www.hardingloevnerfunds.com. The Portfolio imposes a 2% redemption fee on shares held 90 days or less. Performance data does not reflect the redemption fee. If reflected, total returns would be reduced. The Gross Expense Ratio for the Institutional Class and Investor Class are 1.64% and 2.02%, respectively.

The charts below illustrate the hypothetical return of an investment made in the corresponding share classes. Investment return reflects voluntary fee waivers in effect. Absent such waivers, total return would be reduced. The performance provided in the table above and charts below do not reflect the deduction of taxes that a shareholder would pay on Portfolio distributions or the redemption of Portfolio shares.

comparable to machines produced by Japanese and German companies in its industry. The Portfolio’s underweight to the lagging, resource-heavy Canadian market also helped relative returns. However, our underweights in Europe ex-EMU and Japan hurt performance.

Investment Perspectives

A Quiet Year in M&A

We entered 2013 expecting it would be a good year for many of our companies to be acquired due to the continued pressure on larger companies to deliver revenue and earnings growth. The environment for M&A seemed particularly favorable given the combination of bleak economic prospects in many markets, easy-money monetary policies globally, and the strong competitive positioning of our Portfolio companies, which makes them attractive targets. Surprisingly, it has turned out to be a slow year for acquisitions with only one Portfolio company completely purchased year-to-date—a management buyout of Megane Top, a Japanese retailer of eyeglass lenses and frames. Management paid a price that was 40% below our estimate of fair value based on our forecasts for revenue and free cash flow growth. We were disappointed by the fact that the offer went through without granting shareholders an opportunity to dissent, particularly given the lack of any significant premium to the share price.

In August another Portfolio company, global provider of engineering and construction solutions Kentz, did receive acquisition offers from two rival companies, London-listed AMEC and German M+W Group. AMEC made the highest offer, which at Ł680 million represented a premium of about 20% over the previous day’s close. However, Kentz’s board unanimously rejected both bids on the grounds they undervalued the company. Based on our research, including interviews with the company, we concur that these offers did not reflect the fair value of the company. Kentz has an extensive addressable market and significant growth opportunities due to its wide range of capabilities across each segment of its end market: engineering, procurement, and construction. Taking these sources of future growth into account, our financial model confirms that AMEC’s higher offer still undervalued Kentz’s long-term free cash flows. While both buyout offers fell short, we were encouraged that two rival companies expressed interest in the business, confirming that Kentz’s competitive position is strong relative to its peers.

Two Portfolio companies initiated deals recently, demonstrating good discipline either in acquiring strategic assets or disposing non-

International Small Companies Portfolio continued

core businesses. Environmental, risk, and safety consultant RPS Group acquired three consultancy firms for a total cost of almost US$50 million. Ichron Limited, a UK-based geological and training services consultancy for the oil & gas sector, was acquired for US$20 million to further strengthen RPS’ position in Europe, Africa, and the Middle East. HMA Land Services, a Canadian consulting firm dedicated to infrastructure projects in North America, was also acquired for about US$20 million to help RPS enter the growing energy, pipeline, and utilities markets in North America. Finally, RPS acquired Asia-Pacific ASA Pty Ltd, an oceanographic consultancy whose specialties include coastal oil and gas exploration and marine emergency management, especially oil spills. The firm is based in Australia and was acquired for US$9 million. We liked these acquisitions for three reasons: they enhanced RPS’ core engineering consulting expertise in niche sectors and geographies; the amount paid was reasonable given the expertise acquired; and they provide RPS cross-sell opportunities to provide its consulting services to the clients of these three firms.

Although none of our Portfolio companies were acquired during the period, we think the deal environment remains favorable.

Meanwhile, Brazilian construction equipment rental company Mills decided to sell its industrial services business unit due to its relatively low profitability compared to the company’s other businesses. Mills had tried over the last few years to turn this business around, but return on invested capital (ROIC) remained only about 9% at the end of March 2013, while the company’s other business units had an average ROIC in the mid-to high-teens. In addition, the industrial services business had much higher volatility of ROIC, which increased risk and thus reduced the quality profile of the business. We think the sale was a good decision that not only enhanced Mills’ ROIC, but also improved the company’s risk profile. Although none of our Portfolio companies were acquired during

| | | | | | | | |

Geographical Weightings (%) at October 31, 2013 Institutional and Investor Classes | |

Country/Region | | | Portfolio | | | | Benchmark | 1 |

Canada | | | 1.0 | | | | 8.4 | |

Emerging Markets | | | 24.1 | | | | 20.7 | |

Europe EMU | | | 27.2 | | | | 17.3 | |

Europe ex-EMU | | | 21.4 | | | | 24.4 | |

Japan | | | 14.2 | | | | 19.1 | |

Middle East | | | 0.0 | | | | 0.8 | |

Pacific ex-Japan | | | 10.2 | | | | 9.3 | |

Frontier Markets2 | | | 0.0 | | | | – | |

Other3 | | | 0.6 | | | | – | |

Cash | | | 1.3 | | | | – | |

1MSCI All Country World ex-US Small Cap Index; 2Includes countries with less-developed markets outside the Index; 3Includes countries with developed markets outside the Index where some holdings are incorporated.

| | | | | | | | |

Sector Weightings (%) at October 31, 2013 Institutional and Investor Classes | |

Sector | | | Portfolio | | | | Benchmark | 1 |

Consumer Discretionary | | | 14.5 | | | | 18.4 | |

Consumer Staples | | | 13.0 | | | | 5.9 | |

Energy | | | 1.4 | | | | 5.5 | |

Financials | | | 8.9 | | | | 19.6 | |

Health Care | | | 12.0 | | | | 5.6 | |

Industrials | | | 28.3 | | | | 19.8 | |

Information Technology | | | 12.2 | | | | 10.4 | |

Materials | | | 4.1 | | | | 11.6 | |

Telecom Services | | | 3.2 | | | | 1.1 | |

Utilities | | | 1.1 | | | | 2.1 | |

Cash | | | 1.3 | | | | – | |

1MSCI All Country World ex-US Small Cap Index

the period, we think the deal environment remains favorable due to the reasons cited above. Nevertheless, our process doesn’t rely upon acquisitions to generate returns. We think the combination of strong competitive positions and sustainable growth prospects possessed by our companies will allow them to generate above-average risk-adjusted returns over the long term while continuing to operate independently.

Valuation Opportunities