UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-07739

Harding, Loevner Funds, Inc.

(Exact name of registrant as specified in charter)

400 Crossing Boulevard

Fourth Floor

Bridgewater, NJ 08807

(Address of principal executive offices) (Zip code)

Owen T. Meacham

The Northern Trust Company

50 South LaSalle Street

Chicago, IL 60603

With a copy to:

Stephen H. Bier, Esq.

Dechert LLP

1095 Avenue of the Americas

New York, NY 10036

(Name and address of agent for service)

Registrant’s telephone number, including area code: (877) 435-8105

Date of fiscal year end: 10/31

Date of reporting period: 10/31/2015

Item 1. Reports to Stockholders.

¢ HARDING LOEVNER FUNDS

Global equity investing for institutions is Harding Loevner’s exclusive focus. Through Harding Loevner Funds it offers five distinct global strategies based on its quality-and-growth investment philosophy. It seeks to purchase shares of growing, financially strong, well-managed companies at favorable prices. Harding Loevner manages each of the Funds’ Portfolios according to a disciplined, research-based investment process. It identifies companies with sustainable competitive advantages and assesses the durability of their earnings growth by conducting in-depth fundamental research into global industries. In constructing portfolios, Harding Loevner diversifies carefully to limit risk.

¢ RECEIVE INVESTOR MATERIALS ELECTRONICALLY

Shareholders may sign up for electronic delivery of investor materials. By doing so, you will receive the information faster and help us reduce the impact on the environment of providing these materials. To enroll in electronic delivery,

| | 1. | Go to http://www.icsdelivery.com |

| | 2. | Select the first letter of your brokerage firm’s name. |

| | 3. | From the list that follows, select your brokerage firm. If your brokerage firm is not listed, electronic delivery may not be available. Please contact your brokerage firm. |

| | 4. | Complete the information requested, including the e-mail address where you would like to receive notifications for electronic documents. |

Your information will be kept confidential and will not be used for any purpose other than electronic delivery. If you change your mind, you can cancel electronic delivery at any time and revert to physical delivery of your materials. Just go to http://www.icsdelivery.com, perform the first three steps above, and follow the instructions for cancelling electronic delivery. If you have any questions, please contact your brokerage firm.

¢ TABLE OF CONTENTS

2 | Global Equity Portfolio

6 | International Equity Portfolio

10 | International Small Companies Portfolio

14 | Emerging Markets

18 | Frontier Emerging Markets Portfolio

¢ CONTACT

Harding, Loevner Funds, Inc.

c/o Northern Trust

Attn: Funds Center C5S

801 South Canal Street

Chicago, IL 60607

| | |

Phone: 877.435.8105 | | |

Fax: 312.267.3657 | | Must be preceded or accompanied by a current Prospectus. |

www.hardingloevnerfunds.com | | Quasar Distributors, LLC, Distributor |

PORTFOLIO MANAGEMENT TEAM

| | |

PETER BAUGHAN, CFA | | CHRISTOPHER MACK, CFA |

CO-LEAD PORTFOLIO MANAGER | | PORTFOLIO MANAGER |

| |

FERRILL ROLL, CFA | | RICHARD SCHMIDT, CFA |

CO-LEAD PORTFOLIO MANAGER | | PORTFOLIO MANAGER |

| |

| | ALEXANDER WALSH, CFA |

| | PORTFOLIO MANAGER |

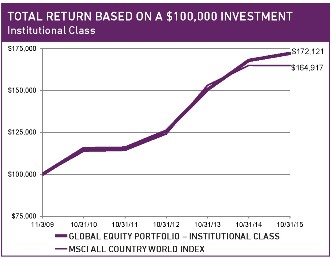

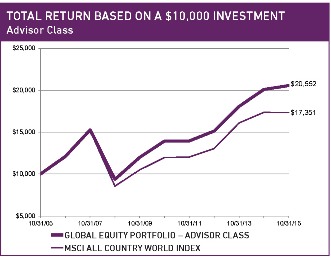

¢ PERFORMANCE SUMMARY

The Global Equity Portfolio – Institutional Class rose 2.51% and the Advisor Class gained 2.28% (net of fees and expenses) in the fiscal year ended October 31, 2015. The Portfolio’s benchmark, the MSCI All Country World Index, lost 0.03% (net of source taxes) in this period.

¢ MARKET REVIEW

Global stock markets achieved flat returns for the fiscal year. Positive returns from early 2015 were reversed by significant declines in the summer, when concerns about growth reversals in China and other Emerging Markets (EMs) weighed heavily on the energy- and commodity-related sectors globally, which had already been under pressure from the collapse in energy prices from the end of 2014.

China’s stock market peaked in June and then accelerated its decline in a messy bursting of its bubble—including a clumsy series of market interventions by government authorities. Developed stock markets weathered the decline of China’s stock market well at first, except for energy- and commodity-related stocks, along with capital goods, which had already begun to underperform in the summer on worsening economic data from China. However, in early August, on the heels of alarming data on contracting Chinese trade with Europe and other developed economies, the People’s Bank of China announced it would change its method of managing the value of the yuan. Investors leapt to the conclusion that the foreign exchange (FX) move signaled that conditions in the Chinese economy were so dire that the government was initiating a policy of sustained currency depreciation aimed at recharging the competitiveness of its export sector. The prospect of China entering the arena of “competitive devaluation” turned ripples of worry over slowing global growth into full-fledged fear of global deflation.

The US market marched to its own drummer for much of the year, until the China devaluation panic began. The Federal Reserve

| | | | |

FUND FACTS at October 31, 2015 |

TOTAL NET ASSETS | | | | $870.0 million |

SALES CHARGE | | | | NONE |

TOTAL # OF HOLDINGS | | | | 72 |

TURNOVER (5 YR. AVG.) | | | | 32% |

REDEMPTION FEE | | | | 2% FIRST 90 DAYS |

DIVIDEND POLICY | | | | ANNUAL |

| | INSTITUTIONAL CLASS | | ADVISOR CLASS |

TICKER | | HLMVX | | HLMGX |

CUSIP | | 412295602 | | 412295206 |

INCEPTION DATE | | 11/3/2009 | | 12/1/1996 |

MINIMUM INVESTMENT1 | | $100,000 | | $5,000 |

EXPENSE RATIO | | 0.92% | | 1.15% |

| 1Lower | minimums available through certain brokerage firms. |

was preparing the market to expect an interest rate increase at its September meeting, thanks to steady employment growth data in the summer. The resilient US economy has drawn in capital from other regions, boosting the dollar against most currencies. Online-and software-driven businesses continue to post strong results, led by Amazon.com. Merger activity recovered its stride, with deep-pocketed buyers picking up bargains in the muddy waters of the energy and capital goods industries. But things looked different by the time mid-September arrived, and with EM currencies and stock markets falling and US multinationals increasingly warning of weaker earnings abroad, the Fed deferred once again that first rate hike. Meanwhile, campaign rhetoric and political scrutiny of escalating prices for high-priced drugs triggered a sell-off in bio-tech stocks, which had previously been leading the market.

European markets began the third calendar quarter bracing for the aftermath of the Greek referendum’s “NO” vote to further bailout and austerity; the eurozone’s potential leap into the unknown (of either default or “Grexit”) was averted as the vote was set aside by the very politicians who devised it! Instead of disintegrating, the European economy actually gathered a bit of steam. Investors took encouragement from Spain and Ireland, formerly lumped amongst the so-called PIIGS economies, but now resuming growth, as well as from the UK and Scandinavian economies enjoying the positive spillover wealth effects of very strong property markets. Meanwhile the German economy has plowed ahead with equanimity in spite of dented exports of capital goods and luxury autos to China, bolstered by having its own fiscal house in order, and by its diversified range of trading partners. Nevertheless, many companies are contending with falling orders for large investment projects and related capital equipment, where European companies have a significant global presence.

Markets with a heavy resource orientation, including Australia, Norway, Canada, Brazil, and Indonesia, fared poorly. Markets with additional country-specific woes, such as Greece’s default,

TOTAL RETURNS (%)

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | for periods ending September 30, 2015 | | | | for periods ending October 31, 2015 | |

| | | | | | | | | | |

| |

| 1

YEAR |

| |

| 3

YEARS |

| |

| 5

YEARS |

| |

| 10

YEARS |

| |

| SINCE

INCEPTION* |

| |

| 1

YEAR |

| |

| 3

YEARS |

| |

| 5

YEARS |

| |

| 10

YEARS |

| |

| SINCE

INCEPTION* |

|

GLOBAL EQUITY PORTFOLIO - INSTITUTIONAL CLASS | | | -3.79 | | | | 6.95 | | | | 7.43 | | | | – | | | | 8.05 | | | | – | | | | 2.51 | | | | 11.02 | | | | 8.33 | | | | – | | | | 9.49 | | | | – | |

MSCI ALL COUNTRY WORLD INDEX | | | -6.65 | | | | 6.96 | | | | 6.83 | | | | 4,58 | | | | 7.45 | | | | – | | | | -0.03 | | | | 9.94 | | | | 7.69 | | | | 5.67 | | | | 8.71 | | | | – | |

GLOBAL EQUITY PORTFOLIO - ADVISOR CLASS | | | -4.02 | | | | 6.67 | | | | 7.16 | | | | 6.30 | | | | – | | | | 6.12 | | | | 2.28 | | | | 10.73 | | | | 8.08 | | | | 7.47 | | | | – | | | | 6.57 | |

Returns are annualized for periods greater than 1 year. *Inception of the Institutional Class, 11/3/09. Inception of the Advisor Class, 12/1/96. Index performance prior to 1/1/01 cannot be shown since it relies on back-filled data.

Performance data quoted represents past performance; past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the Portfolio may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by calling (877) 435-8105 or visiting www.hardingloevnerfunds.com. Performance data shown does not reflect the 2.00% redemption fee imposed on shares held 90 days or less; otherwise, total returns would be reduced.

The charts below illustrate the hypothetical return of an investment made in the corresponding share classes. Investment return reflects voluntary fee waivers in effect. Absent such waivers, total return would be reduced. The performance provided in the table above and charts below do not reflect the deduction of taxes that a shareholder would pay on Portfolio distributions or the redemption of Portfolio shares.

Brazil’s corruption scandal, or Turkey’s increasing entanglement in the civil war next door in Syria and renewed conflict with its own Kurdish minority, performed even worse than the average EM.

The strongest sector was Consumer Discretionary, possibly because consumers are beneficiaries of falling energy prices in terms of disposable income. Information Technology (IT) was also strong, sharing in the optimism about US economic recovery and thus about stronger capital spending. Utilities were weak, possibly due to a small rebound in the oil price that drove Energy shares higher. Financials performed worse than the Index, as investors added potential credit losses on loans to energy or commodity companies to their existing worries about weak interest income in a world of very low interest rates. On that latter front, banks got no help from the Fed.

The Fed’s postponement of a signaled mid-September rate hike was received poorly by stock markets and corporate bonds, and precipitated greater investor attention on weakening US economic indicators—including a September jobs report. The Fed’s decision (or lack of one) put a halt on the US dollar rally against most currencies. But the earlier damage to confidence was not reversed: in the twelve months ending October 2015, EM currencies in particular suffered badly from investor disenchantment with EM economies.

Against the US dollar, the Brazilian real lost 36%, while the South African rand lost 20% and the Turkish lira lost 24%. Much was made of China’s gambit for the yuan, but for all the headlines, the yuan depreciated just 3% against the US dollar. The British pound lost 4%, while the euro lost 12%, and the yen lost 8%.

¢ PERFORMANCE ATTRIBUTION

The Portfolio outperformed the benchmark, due to good stock selection in every region except EMs. Strongest amongst the US holdings were consumer-oriented businesses Amazon, Nike, and newly named Alphabet, formerly known as Google, the latter classified as IT but earning its revenues primarily from advertising. In Europe, we benefited from software provider Dassault Systèmes, and Essilor International, the spectacle lens maker. In Japan, strong performance from MonotaRO, M3, Makita, and Kakaku.com added value. Conversely, our EM holdings detracted from performance, hurt by poor performance from internet search engines in China (Baidu) and Russia (Yandex), from banks (Garanti Bank, ICICI), and from telecom service providers in South Africa (MTN Bank), and Mexico (América Móvil).

Viewed by sector, our significant underweight to Energy benefited the Portfolio. Our overweight to IT and good stocks there were

also helpful. Strong stock selection in Consumer Discretionary and Industrials contributed the most to the Portfolio by sector, while bad stocks from Consumer Staples and Telecom Services hurt most. Within Consumer Discretionary, Amazon and Nike each outperformed after reporting surprisingly strong operating results, the latter of which benefited from strong sales growth in Europe and China along with a mix shift towards its higher-margin direct-to-consumer business. Ctrip soared after announcing a merger with its largest competitor in online travel. Within Industrials, online industrial supplier MonotaRO, a holding with a strong “virtual” slant to its business model, outperformed. In Materials, our light holdings and our focus on less-cyclical industrial gas company Air Liquide cushioned the Portfolio against the sector’s sharp decline associated with falling commodity prices. Holdings from Consumer Staples (Magnit), Telecom Services (MTN Group and Sasol), and Health Care (Elekta), on the other hand, detracted from performance.

¢ PERSPECTIVES AND OUTLOOK

A salient aspect of the market reversal over the summer was the pair of missteps by central banks in signaling: a minor one by the US Federal Reserve, and a major one by the People’s Bank of China. By indicating that it would allow market forces a greater role in setting of daily FX movements, the Chinese central bank let loose a firestorm of portfolio adjustments that it did not anticipate and for which it was not adequately prepared, ultimately costing it billions in foreign currency reserves expended to stabilize the yuan exchange rate.

Meanwhile, deftness was neither in evidence at the Fed in late September when, having long prepared the markets for an interest rate hike, the governors voted to defer it. Markets took their inaction as a sign that the US and—since Fed’s Chair Janet Yellen specifically referenced it—China were in even worse shape than the markets had yet appreciated. Stocks tanked; bonds rallied. It was one of the first times since the financial crisis that stocks did not rise on the prospect of additional or extended monetary stimulus, and we note this for future reference, with trepidation. Could we be observing the edge of the capacity of monetary policy to

GEOGRAPHIC WEIGHTINGS (%) at October 31, 2015

| | | | | | | | |

COUNTRY/REGION | | | PORTFOLIO | | | | BENCHMARK | 1 |

CANADA | | | 0.0 | | | | 2.9 | |

EMERGING MARKETS | | | 12.4 | | | | 9.6 | |

EUROPE EMU | | | 8.7 | | | | 10.7 | |

EUROPE EX-EMU | | | 11.8 | | | | 12.0 | |

JAPAN | | | 8.7 | | | | 7.9 | |

MIDDLE EAST | | | 0.0 | | | | 0.2 | |

PACIFIC EX-JAPAN | | | 2.2 | | | | 3.7 | |

UNITED STATES | | | 55.7 | | | | 53.0 | |

FRONTIER MARKETS2 | | | 0.0 | | | | – | |

CASH | | | 0.5 | | | | – | |

1MSCI All Country World Index; 2Includes countries with less-developed markets outside the Index.

SECTOR WEIGHTINGS (%) at October 31, 2015

| | | | | | | | |

SECTOR | | | PORTFOLIO | | | | BENCHMARK | 1 |

CONSUMER DISCRETIONARY | | | 13.4 | | | | 13.1 | |

CONSUMER STAPLES | | | 5.9 | | | | 10.1 | |

ENERGY | | | 6.8 | | | | 6.8 | |

FINANCIALS | | | 15.3 | | | | 21.3 | |

HEALTH CARE | | | 17.1 | | | | 12.1 | |

INDUSTRIALS | | | 11.2 | | | | 10.4 | |

INFORMATION TECHNOLOGY | | | 24.9 | | | | 14.5 | |

MATERIALS | | | 3.1 | | | | 4.8 | |

TELECOM SERVICES | | | 1.8 | | | | 3.7 | |

UTILITIES | | | 0.0 | | | | 3.2 | |

CASH | | | 0.5 | | | | – | |

| 1MSCI | All Country World Index. |

stimulate the stock market and, by extension, the economy? It was ironic that assurances by Fed governors that a rate rise was still in the works brought about a bounce in stock prices some days later.

Still, with so much of the markets’ focus on China and other EMs, there are certain fundamental realities that are evident beyond just the latest “signals” coming from the government authorities. Investors have been correct to worry about the build-up of debt in EMs—even as private sector debt ratios have slowly been managed lower in most of the developed markets since the financial crisis. Debt growth across non-Japan Asia has increased by 50 percentage points relative to the region’s aggregate GDP since 2008. Despite ultra-low interest rates that reflect highly expansive monetary policies among developed country central banks, interest payments on debt by September consumed more than 20% of GDP in China, Hong Kong, and Singapore. This debt build-up reinforces, or even extends, our worldview since the global financial crisis: that the global economy faces a long, hard slog to return to its potential growth rate because so much focus of individuals, companies and policy makers is directed at reducing the burdens and constraints of debt.

We remind ourselves that China’s economy is now very large and increasingly complex, with the consumer sector also contributing increasingly to economic activity. This sector has been growing much faster than the capital investment side of the economy for a number of years—albeit from a low base—as the growth in employment and wages has translated into greater spending. So long as jobs don’t disappear and wages remain resilient, consumer spending appears resilient, especially given the high level of savings that has been the norm for Chinese households.

Exploring the linkage of turmoil in China to the rest of the global economy and to other stock markets around the world requires a degree of nuance. The export sector accounts for more than a fifth of China’s economy, and is a net contributor to China’s economic activity, with China’s trading surplus of goods and services amounting to 3.7% of its total GDP in the twelve months ending September 2015. That implies that China’s imports loom almost as large as its exports; this is the key link to other economies that

will affect global companies’ growth prospects. Chinese demand has represented as much as a quarter of global spending on capital goods, and, even more worrying, roughly half of all consumption of steel, aluminum, and copper. These are precisely the inputs into heavy industry and infrastructure or construction projects, which are slowing so precipitously. In contrast, China represents barely 10% of oil consumption, and only about 8% of global consumer spending. Even a significant slowing of growth (rather than a decline) in Chinese spending on oil or on consumer goods will have merely marginal, rather than dramatic, effects on those broad sectors in other economies.

In our view, markets have more than priced-in what damage to consumer-facing profits will come from China in the near term. Longer term, the global companies who are investing in their brands and their distribution networks are likely to reap the rewards that historically have redounded to such investments in other economies: sustained growth rising alongside per capita spending, with attractive profits. Likewise, the Energy sector does not face collapse due to China’s wobbles. But energy company profits and stock prices have been battered due to current oversupply, which has induced very low spot prices. As a result, valuation spreads among energy companies are at record (100-year) wide levels. This is usually a fruitful environment for contrarian thinking in any market sector. On the other hand, the sector faces secular headwinds, as doubts arise that fossil fuels will be tolerated by society for long enough to make complete use of the existing stock of proven energy reserves.

Of course, the majority of the Portfolio has its focus elsewhere than on EMs. We have, over the past few years, gradually increased our emphasis of what we’d term “online-driven” businesses in a number of disparate industries, even as we have maintained the very large holdings within IT itself. The evidence continues to mount that customers, starting with consumers but now incorporating corporate customers, prefer to interact directly and immediately with businesses they deal with, and are comfortable trading off face-to-face interactions in exchange for speed, convenience, and tailored offerings. As a result, the leaders in establishing online platforms are enjoying more robust growth, and online distribution channels are disrupting the traditional channels at an increasingly material scale. The companies at the forefront of providing these online platforms typically have originated in the US, but the change is occurring very rapidly elsewhere, with China in particular producing a number of large, successful companies making their mark across broad sectors of e-commerce. Whatever their origin, these companies primarily operate online, but are producing huge revenues and good profits, therefore although their stocks command very high multiples of earnings, it is a very different ballgame than the 1999 “tech bubble”, when a company had merely to publish a business plan in order to garner a fancy IPO valuation. Our quest has been to identify the businesses whose competitive position we believe will allow their growth to continue, and should lead to sustained profitability in the future as well as the present.

1 International Monetary Fund, World Economic Outlook (October 2015).

TEN LARGEST HOLDINGS at October 31, 2015

| | | | | | |

COMPANY | | SECTOR | | COUNTRY | | % |

NIKE | | CONS DISCRETIONARY | | UNITED STATES | | 4.0 |

SCHLUMBERGER | | ENERGY | | UNITED STATES | | 3.2 |

ALPHABET | | INFO TECHNOLOGY | | UNITED STATES | | 2.9 |

ROPER | | INDUSTRIALS | | UNITED STATES | | 2.8 |

PRICELINE | | CONS DISCRETIONARY | | UNITED STATES | | 2.6 |

AIA GROUP | | FINANCIALS | | HONG KONG | | 2.2 |

FIRST REPUBLIC BANK | | FINANCIALS | | UNITED STATES | | 2.2 |

VERISK | | INDUSTRIALS | | UNITED STATES | | 2.1 |

MASTERCARD | | INFO TECHNOLOGY | | UNITED STATES | | 2.0 |

SVB FINANCIAL | | FINANCIALS | | UNITED STATES | | 2.0 |

¢ PORTFOLIO STRUCTURE

We estimate that roughly a fifth of the Portfolio is comprised of companies whose business is centered on an online relationship with its customers. Amazon, of course, is the poster child for such businesses. We have now bought, then sold, then bought again, as our view of Amazon’s competitive edge—and its share price—has changed. Its retail business continues to gain share in the most profitable segments, and to gain stickiness through the membership channel of Amazon Prime. But the company has broader visions for getting value out of its investments in data infrastructure and analytics. We have long believed that Amazon Web Services would be a disrupter for many other data services companies, but we were pleasantly surprised by just how profitable the division already is. But the rapid development of data analytics as a critical means of providing value in a timely fashion to customers goes far beyond retailing and hosted services. MonotaRO is an example of a company pioneering the online distribution channel for commercial customers. By creating an online catalog of maintenance, repair, and operational (MRO) products, and focusing on integrated inventory management and delivery speeds while keeping a very large array of items available, this Japanese company, partly owned by Grainger in the US, has achieved rapid (20%+) volume and pricing growth in its two large markets (Japan and the US) which has eluded its competitors saddled with traditional distribution methods. PayPal, split out from eBay this summer, is now a standalone payments business, with a long history of secure online payments, a very large existing user base, and thus a profitable running start in the burgeoning battle to move more payments from cash, checks, and card systems to mobile online payments.

Regarding our many holdings with substantial EM-oriented businesses, we are, for the most part, quite sanguine. For one thing, while their growth prospects have dimmed, EM economies are still growing roughly twice as fast as developed economies, according to recent International Monetary Fund forecasts.1 Additionally, our companies have very little exposure to the heavy industry segments that are most under pressure in China, and to the related industries supplying them from abroad.

Please read the separate disclosures page for important information, including the risks of investing in the Portfolio.

PORTFOLIO MANAGEMENT TEAM

| | |

FERRILL ROLL, CFA | | PETER BAUGHAN, CFA |

CO-LEAD PORTFOLIO MANAGER | | PORTFOLIO MANAGER |

| |

ALEXANDER WALSH, CFA | | BRYAN LLOYD, CFA |

CO-LEAD PORTFOLIO MANAGER | | PORTFOLIO MANAGER |

| |

| | ANDREW WEST, CFA |

| | PORTFOLIO MANAGER |

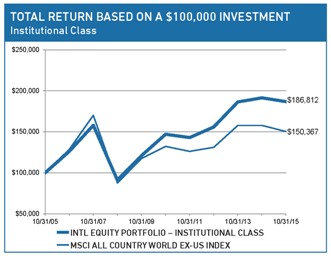

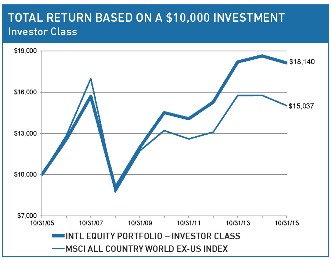

¢ PERFORMANCE SUMMARY

The International Equity Portfolio – Institutional Class declined 2.40% and the Investor Class lost 2.76% (net of fees and expenses) in the fiscal year ended October 31, 2015. The Portfolio’s benchmark, the MSCI All Country World ex-US Index, declined 4.70% (net of source taxes) in this period.

¢ MARKET REVIEW

Stock markets declined in the fiscal year. Positive returns from early 2015 were reversed by significant declines in the summer, when concerns about growth reversals in China and other Emerging Markets (EMs) weighed heavily on the energy- and commodity-related sectors globally, which had already been under pressure from the collapse in energy prices from the end of 2014.

European markets began the third calendar quarter bracing for the aftermath of the Greek referendum’s “NO” vote to further bailout and austerity; the eurozone’s potential leap into the unknown (of either default or “Grexit”) was averted as the vote was set aside by the very politicians who devised it! Instead of disintegrating, the European economy actually gathered a bit of steam. But hints of inventory build-ups in the supply chain for mobile phones and computers (which runs both into and out of Asia) sent ripples of worry through the global semiconductor industry and related parts of the Information Technology (IT) sector. This coincided with falling orders for large investment projects and related capital equipment, where European companies have a significant global presence.

China’s stock market peaked in June and then accelerated its decline in a messy bursting of its bubble—including a clumsy series of market interventions by government authorities. In early August, on the heels of alarming data on contracting Chinese trade with Europe and other developed economies, the People’s Bank of China announced it would change its method of managing the value of the yuan. Investors leapt to the conclusion that the

| | | | |

FUND FACTS at October 31, 2015 |

TOTAL NET ASSETS | | | | $4,996.9M |

SALES CHARGE | | | | NONE |

TOTAL # OF HOLDINGS | | | | 50 |

TURNOVER (5 YR. AVG.) | | | | 14% |

REDEMPTION FEE | | | | 2% FIRST 90 DAYS |

DIVIDEND POLICY | | | | ANNUAL |

| | INSTITUTIONAL CLASS | | INVESTOR CLASS |

TICKER | | HLMIX | | HLMNX |

CUSIP | | 412295107 | | 412295503 |

INCEPTION DATE | | 5/11/1994 | | 9/30/2005 |

MINIMUM INVESTMENT1 | | $100,000 | | $5,000 |

EXPENSE RATIO | | 0.86% | | 1.16% |

| 1Lower | minimums available through certain brokerage firms. |

foreign exchange (FX) move signaled that conditions in the Chinese economy were so dire that the government was initiating a policy of sustained currency depreciation aimed at recharging the competitiveness of its export sector. The prospect of China entering the arena of “competitive devaluation” turned ripples of worry over slowing global growth into full-fledged fear of global deflation.

Developed stock markets, especially in the US and Europe, fared better than EMs, with large and stable internal (domestic) economic sectors modestly growing and adding to employment. European markets took encouragement that Spain and Ireland, formerly lumped amongst the so-called PIIGS economies, had stabilized and actually resumed growth; the UK and Scandinavian economies have enjoyed the positive spillover wealth effects on their economies of very strong property markets. Meanwhile the German economy plowed ahead in spite of dented exports of capital goods and luxury autos to China, bolstered by having its own fiscal house in order, and by its diversified range of trading partners. The US economy, seemingly strong enough not only to eschew quantitative easing, but to prompt the Federal Reserve to warn markets of a rise in interest rates, has drawn in capital from other regions, boosting the dollar against most currencies. Markets with a heavy resource orientation, including Australia, Norway, Canada, Brazil, and Indonesia, fared poorly. Markets with additional country-specific woes, such as Greece’s default, Brazil’s corruption scandal, or Turkey’s increasing entanglement in the civil war next door in Syria and renewed conflict with its own Kurdish minority, performed even worse than the average EM.

With Energy by far the weakest sector, the strongest were the Consumer sectors, possibly because consumers are beneficiaries of falling energy prices in terms of disposable income. Health Care also performed well. Materials were weak, as were Utilities, possibly due to a small rebound in the oil price that drove Energy shares higher. Financials performed worse than the Index, as in-

TOTAL RETURNS (%)

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | for periods ending September 30, 2015 | | | | for periods ending October 31, 2015 | |

| | | | | | | | | | |

| |

| 1

YEAR |

| |

| 3

YEARS |

| |

| 5

YEARS |

| |

| 10

YEARS |

| |

| SINCE

INCEPTION* |

| |

| 1

YEAR |

| |

| 3

YEARS |

| |

| 5

YEARS |

| |

| 10

YEARS |

| |

| SINCE

INCEPTION* |

|

INTL EQUITY PORTFOLIO - INSTITUTIONAL CLASS | | | -9.03 | | | | 3.34 | | | | 3.74 | | | | 5.00 | | | | – | | | | 5.45 | | | | -2.40 | | | | 6.23 | | | | 4.92 | | | | 6.45 | | | | – | | | | 5.86 | |

MSCI ALL COUNTRY WORLD EX-US INDEX | | | -12.17 | | | | 2.34 | | | | 1.82 | | | | 3.03 | | | | 3.07 | | | | – | | | | -4.70 | | | | 4.68 | | | | 2.60 | | | | 4.16 | | | | 3.78 | | | | – | |

INTL EQUITY PORTFOLIO - INVESTOR CLASS | | | -9.28 | | | | 3.01 | | | | 3.40 | | | | 4.71 | | | | 4.72 | | | | – | | | | -2.76 | | | | 5.88 | | | | 4.55 | | | | 6.14 | | | | 5.59 | | | | – | |

Returns are annualized for periods greater than 1 year. *Inception of the Institutional Class, 5/11/94. Index performance prior to 1/1/01 cannot be shown since it relies on back-filled data. Inception of the Investor Class, 9/30/05.

Performance data quoted represents past performance; past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the Portfolio may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by calling (877) 435-8105 or visiting www. hardingloevnerfunds.com. Performance data shown does not reflect the 2.00% redemption fee imposed on shares held 90 days or less; otherwise, total returns would be reduced.

The charts below illustrate the hypothetical return of an investment made in the corresponding share classes. Investment return reflects voluntary fee waivers in effect. Absent such waivers, total return would be reduced. The performance provided in the table above and charts below do not reflect the deduction of taxes that a shareholder would pay on Portfolio distributions or the redemption of Portfolio shares.

vestors added potential credit losses on loans to energy or commodity companies to their existing worries about weak interest income in a world of very low interest rates. On that latter front, banks got no help from the Fed.

The Fed’s postponement of a signaled mid-September rate hike was received poorly by stock markets and corporate bonds, and anticipated greater investor attention on weakening US economic indicators—including a September jobs report released subsequently. The Fed’s decision (or lack of one) put a halt on the US dollar rally against most currencies. But the earlier damage to confidence was not reversed: in the twelve months ending October 2015, EM currencies in particular suffered badly from investor disenchantment with EM economies. Against the US dollar, the Brazilian real lost 36%, while the South African rand lost 20% and the Turkish lira lost 24%. Much was made of China’s gambit for the yuan, but for all the headlines, the yuan depreciated just 3% against the US dollar. The British pound lost 4%, while the euro lost 12%, and the yen lost 8%.

¢ PERFORMANCE ATTRIBUTION

The Portfolio outperformed the Index in the fiscal year due to strong stock selection across regions and sectors.

Viewed by sector, good stocks in Materials and Information Technology contributed most to the Portfolio—the former by a wide margin, thanks to specialty lubricant manufacturer Fuchs Petrolub and food ingredient producer Symrise, both German companies exhibiting the resilience in their stocks that we value in their businesses, along with industrial gas producers Air Liquide and Linde. Good stocks and positive underweight in Health Care also contributed, along with positive stock selection in the worst-performing Energy sector. Our Telecom Services and Financials holdings hurt performance because EMs are overrepresented among our holdings in those sectors relative to the Index, including Brazil’s Itau Unibanco and Turkey’s Garanti Bank, along with MTN Group, the South African mobile phone operator. Stock selection in the Consumer sectors was also negative.

Viewed geographically, the Portfolio enjoyed good stocks within both the eurozone and the rest of Europe, as well as in the Pacific ex-Japan. Our holdings from EMs hurt the Portfolio the most, as our exposures (Itau Unibanco, Garanti, MTN Group) were more hurt by EM currency weakness than the average, or else were themselves heavily exposed to China worries (Baidu).

¢ PERSPECTIVES AND OUTLOOK

A salient aspect of the market reversals over the summer was the pair of missteps by central banks in signaling, a minor one by the US Federal Reserve, and a major one by the People’s Bank of China. By indicating that it would allow market forces a greater role in setting of daily FX movements, the Chinese central bank let loose a firestorm of portfolio adjustments that it did not anticipate and for which it was not adequately prepared, ultimately costing it billions in foreign currency reserves expended to stabilize the yuan exchange rate.

Meanwhile, deftness was neither in evidence at the Fed in late September when, having long prepared the markets for an interest rate hike, the governors voted to defer it. Markets took their inaction as a sign that the US and—since Fed Chair Janet Yellen specifically referenced it—China were in even worse shape than the markets had yet appreciated. Stocks tanked; bonds rallied. It was one of the first times since the financial crisis that stocks did not rise on the prospect of additional or extended monetary stimulus, and we note this for future reference, with trepidation. Could we be observing the edge of the capacity of monetary policy to stimulate the stock market and, by extension, the economy? It was ironic that assurances by Fed governors that a rate rise was still in the works brought about a bounce in stock prices some days later.

Still, with so much of the markets’ focus on China and other EMs, there are certain fundamental realities that are evident beyond just the latest “signals” coming from the government authorities. Investors have been correct to worry about the build-up of debt in EMs—even as private sector debt ratios have slowly been managed lower in most of the developed markets since the financial crisis. Debt growth across non-Japan Asia has increased by 50 percentage points relative to the region’s aggregate GDP since 2008. Despite ultra-low interest rates that reflect highly expansive monetary policies among developed country central banks, debt service payments by September consumed more than 20% of GDP in China, Hong Kong, and Singapore. This debt build-up reinforces, or even extends, our worldview since the global financial crisis:

GEOGRAPHIC WEIGHTINGS (%) at October 31, 2015

| | | | | | | | |

COUNTRY/REGION | | | PORTFOLIO | | | | BENCHMARK | 1 |

CANADA | | | 3.1 | | | | 6.2 | |

EMERGING MARKETS | | | 14.5 | | | | 20.4 | |

EUROPE EMU | | | 27.6 | | | | 22.7 | |

EUROPE EX-EMU | | | 23.1 | | | | 25.4 | |

JAPAN | | | 15.4 | | | | 16.9 | |

MIDDLE EAST | | | 0.0 | | | | 0.5 | |

PACIFIC EX-JAPAN | | | 7.8 | | | | 7.9 | |

FRONTIER MARKETS2 | | | 0.0 | | | | – | |

OTHER3 | | | 4.0 | | | | – | |

CASH | | | 4.5 | | | | – | |

1MSCI All Country World ex-US Index; 2Includes countries with less-developed markets outside the Index; 3Includes countries with developed markets outside the Index where some holdings are incorporated.

SECTOR WEIGHTINGS (%) at October 31, 2015

| | | | | | | | |

SECTOR | | | PORTFOLIO | | | | BENCHMARK | 1 |

CONSUMER DISCRETIONARY | | | 8.8 | | | | 12.1 | |

CONSUMER STAPLES | | | 14.4 | | | | 10.8 | |

ENERGY | | | 7.0 | | | | 6.5 | |

FINANCIALS | | | 14.3 | | | | 27.1 | |

HEALTH CARE | | | 14.9 | | | | 9.3 | |

INDUSTRIALS | | | 11.0 | | | | 11.2 | |

INFORMATION TECHNOLOGY | | | 17.6 | | | | 7.5 | |

MATERIALS | | | 6.5 | | | | 6.8 | |

TELECOM SERVICES | | | 1.0 | | | | 5.2 | |

UTILITIES | | | 0.0 | | | | 3.5 | |

CASH | | | 4.5 | | | | – | |

1MSCI All Country World ex-US Index.

that the global economy faces a long, hard slog to return to its potential growth rate because so much focus of individuals, companies and policy makers is directed at reducing the burdens and constraints of debt.

We remind ourselves that China’s economy is now very large and increasingly complex, with the consumer sector also contributing increasingly to economic activity. This sector has been growing much faster than the capital investment side of the economy for a number of years—albeit from a low base—as the growth in employment and wages has translated into greater spending. So long as jobs don’t disappear and wages remain resilient, consumer spending appears resilient, especially given the high level of savings that has been the norm for Chinese households.

Anecdotal evidence from announcements by companies we follow closely tends to support this two-speed picture of the Chinese economy. Companies involved in heavy construction are facing terrible conditions, illustrated by heavy equipment maker Komatsu’s disclosure in early September that its unit sales in China had fallen in half versus last year, an experience echoed in arch-rival Caterpillar’s profit warning this quarter. (Neither is owned by us currently.) In lighter manufacturing, the conditions are milder: Linde, the German industrial gas supplier to a broad range of process and manufacturing industries, reports that its sales in China are still growing 5%, albeit that is half the rate of last year. Misumi Group, the Japanese component maker for manufacturers, actually reported that its volumes in China are growing 14%. Meanwhile, at the branded consumer end of the spectrum, Nike reported “greater China” revenues to have risen 30%, and profits even more, while Apple sold 87% more iPhones, and enjoyed a doubling of its revenues in China. From Apple CEO Tim Cook’s vantage point, “The rise of the middle class there is continuing, and it is transforming China.”1 Indeed, Ctrip.com, China’s largest travel agency, indicated that bookings over National Day weekend at the beginning of October rose 20-30% over last year, suggesting

1Tim Bradshaw and Hannah Kuchler, “China concerns bring Apple down to earth,”Financial Times (August 3, 2015)

that the average consumer remains unfazed by the stock market turmoil. That would correspond with our prior expectation that the so-called “wealth effects” of a bursting bubble on the Shanghai Stock Exchange would only be felt by the very narrow (and elite?) band of buyers of stocks, rather than more broadly across the populace.

Exploring the linkage of turmoil in China to the rest of the global economy and to other stock markets around the world requires a degree of nuance. The export sector accounts for more than a fifth of China’s economy, and is a net contributor to China’s economic activity, with China’s trading surplus of goods and services amounting to 3.7% of its total GDP in the twelve months ending September 2015. That implies that China’s imports loom almost as large as its exports; this is the key link to other economies that will affect global companies’ growth prospects. Chinese demand has represented as much as a quarter of global spending on capital goods, and, even more worrying, roughly half of all consumption of steel, aluminum, and copper. These are precisely the inputs into heavy industry and infrastructure or construction projects, which are slowing so precipitously. In contrast, China represents barely 10% of oil consumption, and only about 8% of global consumer spending. Even a significant slowing of growth (rather than a decline) in Chinese spending on oil or on consumer goods will have merely marginal, rather than dramatic, effects on those broad sectors in other economies.

In our view, markets have more than priced-in what damage to consumer-facing profits will come from China in the near term. Longer term, the global companies who are investing in their brands and their distribution networks are likely to reap the rewards that historically have redounded to such investments in other economies: sustained growth rising alongside per capita spending, with attractive profits. Likewise, the Energy sector does not face collapse due to China’s wobbles. But energy company profits and stock prices have been battered due to current over-supply, which has induced very low spot prices. As a result, valuation spreads among energy companies are at record (100-year) wide levels. This is usually a fruitful environment for contrarian thinking in any market sector. On the other hand, the sector faces secular headwinds, as doubts arise that fossil fuels will be tolerated by society for long enough to make complete use of the existing stock of proven energy reserves.

¢ PORTFOLIO STRUCTURE

Regarding our many holdings with substantial EM-oriented businesses, we are, for the most part, quite sanguine. For one thing, while their growth prospects have dimmed, EM economies are still growing roughly twice as fast as developed economies, according to recent International Monetary Fund forecasts.2 Additionally, our companies have very little exposure to the heavy industry segments that are most under pressure in China, and to the related industries supplying it from abroad. Within Industrials, JGC Corp, a Japanese LNG engineering contractor, is one that

2International MonetaryFund, World Economic Outlook (October 2015).

TEN LARGEST HOLDINGS at October 31, 2015

| | | | | | |

| | | |

COMPANY | | SECTOR | | COUNTRY | | % |

DASSAULT SYSTÈMES | | INFO TECHNOLOGY | | FRANCE | | 4.1 |

NESTLÉ | | CONS STAPLES | | SWITZERLAND | | 4.0 |

AIA GROUP | | FINANCIALS | | HONG KONG | | 3.7 |

ROCHE HOLDING | | HEALTH CARE | | SWITZERLAND | | 3.4 |

WPP | | CONS DISCRETIONARY | | UNITED KINGDOM | | 3.4 |

ALLIANZ | | FINANCIALS | | GERMANY | | 3.0 |

AIR LIQUIDE | | MATERIALS | | FRANCE | | 3.0 |

BAIDU | | INFO TECHNOLOGY | | CHINA | | 2.8 |

SAMSUNG ELECTRONICS | | INFO TECHNOLOGY | | SOUTH KOREA | | 2.7 |

L’ORÉAL | | CONSUMER STAPLES | | FRANCE | | 2.6 |

has been hurt by order deferrals in the wake of slumping oil and gas prices. We believe that gas will be favored over coal, oil, and nuclear fuels enough that international trade in gas—not least via exports from the US and Canada—will grow substantially in the future and demand for JGC Corp’s services will return before long. In the meantime, it has a very strong balance sheet and a reasonable backlog of existing orders to tide it over. We met with Finnish elevator and escalator specialist Kone in Shanghai during September. The company reports that while very large projects have dried up, their high-volume, standardized products, used in residential and office buildings are still in demand. Meanwhile, providers of elevator maintenance services are increasingly coming under regulatory scrutiny, which favors integrated, full-service suppliers such as Kone over cut-rate independents.

In other sectors, our companies continue to build their businesses across a wide array of geographies, but with an emphasis on EMs. Symrise supplies ingredients to the food, cosmetic and pet food industries; we bought shares in the company especially because of its exposure to EMs, which provides nearly a fifth of its revenues. Multinational branded food and cosmetic producers continue to invest in EMs, where long-term trends in food distribution and consumption habits are towards historic Western patterns, and expenditures on daily consumption items has continued to grow faster than elsewhere. Unilever is one such company, and it may be comforting to note that its two largest businesses in EMs (which in aggregate provide nearly three-fifths of its revenues) are the two largest EM markets after China: India and Indonesia, where Unilever has invested in brand-building and distribution for more than a century. Unicharm expanded to developing Asian markets much later, but over the past twenty years has built very strong market shares, and we believe is well placed to benefit from trends toward using disposable diapers for the very young as well as for the rising tide of elderly. We expect its current (two-fifths) proportion of EM revenues to continue to rise over the next decade, as EM sales grow significantly faster than sales in its Japanese home market.

Please read the separate disclosures page for important information, including the risks of investing in the Portfolio.

PORTFOLIO MANAGEMENT

|

JAFAR RIZVI, CFA |

PORTFOLIO MANAGER |

¢ PERFORMANCE SUMMARY

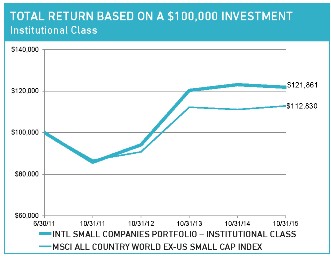

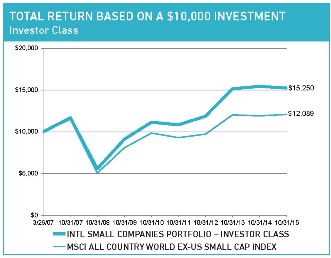

The International Small Companies Portfolio – Institutional Class fell 0.98% and the Investor Class fell 1.29% (net of fees and expenses in the fiscal year ended October 31, 2015. The Portfolio’s benchmark, the MSCI All Country World ex-US Small Cap Index (the Index), rose 1.54% (net of source taxes) in this period.

¢ MARKET REVIEW

The Index gained 8.3% in the first half of the year, but in the second half, fears of a global growth slowdown sparked selling across every region and sector, with news from China a particular focus of concern. In early August, on the heels of alarming data on contracting Chinese trade with Europe and other developed economies, the People’s Bank of China announced it would change its method of managing the value of the yuan to allow the market to have greater (albeit still limited) influence over the currency. Within a few days of the announcement, the value of the yuan fell 3% versus the dollar. Investors leapt to the conclusion that conditions in the Chinese economy were so dire that the government was initiating a policy of sustained currency depreciation to recharge the competitiveness of its export sector. The prospect of China entering the area of “competitive devaluation” turned ripples of worry over slowing global growth into full-fledged fears of global deflation.

Overall, developed markets fared better than emerging markets (EMs). Among the Index regions, the European Monetary Union (EMU) performed the best (up nearly 14% in the trailing 12 months), while EMs fell 8%. Investors appeared worried about indications of cyclically high levels of US-dollar denominated debt among EM companies in a period of slowing growth. While the Federal Reserve elected in September to further delay a rate hike—it has been more than nine years since the Fed last raised the Federal Funds target rate—many believe a rate increase will happen in the near future, which would strengthen the dollar.1 Companies with interest payments in US dollars would as a result face higher interest payments in local currency terms; yet the slowing economic growth would make it incrementally more difficult for them to meet these payments. This concern has spurred a rise in capital outflows from EM countries. The Institute of International Finance (IIF) projects that there will be net outflows from

| | | | |

FUND FACTS at October 31, 2015 |

TOTAL NET ASSETS | | | | $97.4 M |

SALES CHARGE | | | | NONE |

TOTAL # OF HOLDINGS | | | | 83 |

TURNOVER (5 YR. AVG.) | | | | 39% |

REDEMPTION FEE | | | | 2% FIRST 90 DAYS |

DIVIDEND POLICY | | | | ANNUAL |

| | INSTITUTIONAL CLASS | | INVESTOR CLASS |

TICKER | | HLMRX | | HLMSX |

CUSIP | | 412295875 | | 412295883 |

INCEPTION DATE | | 6/30/2011 | | 3/26/2007 |

MINIMUM INVESTMENT1 | | $100,000 | | $5,000 |

NET EXPENSE RATIO2 | | 1.30% | | 1.55% |

GROSS EXPENSE RATIO | | 1.59% | | 1.88% |

1Lower minimums available through certain brokerage firms; 2Shown net of Harding Loevner’s contractual agreement, through February 29, 2016, to waive its management fee to the extent necessary to cap the fund’s total operating expenses.

EMs in 2015 for the first time since 1988. Moreover, the magnitude of flows is expected to be significant. In 2014, EMs enjoyed net capital inflows of US$32 billion; this year, the IIF projects the net outflows will be over US$500 billion.2

From a sector perspective, the less cyclical Health Care and Consumer Staples were the best performers in the Index; the more cyclical Energy sector performed the worst. This reflected the weakening demand for commodities, including oil—the price of which slid 42% this year.

Small-cap equities outperformed large caps (measured by the MSCI All Country World ex-US Index) by more than 600 basis points in the trailing twelve months. The majority of this outperformance came from Europe, reflecting the more domestic orientation of Europe’s small companies—and consequently their smaller revenue exposure to depreciating EM currencies—as compared with their larger European counterparts.

¢ PERFORMANCE ATTRIBUTION

The Portfolio lagged the Index this fiscal year primarily due to poor stock selection in the Industrials and Consumer Discretionary sectors. In Industrials, shares of Coastal Contracts—a Malaysian company that builds, charters, and maintains specialized marine vessels for the oil & gas and mining industries—suffered from poor operating results caused by a decline in vessel deliveries. The company’s total order book remains healthy at 3.4 billion ringgit

1 Federal Reserve Bank of New York, “Federal Funds Data Historical,” October 19, 2015.

2 Jonathan Wheatley and Sam Fleming, “Capital flight darkens economic prospects for emerging markets,”Financial Times (October 1, 2015).

TOTAL RETURNS (%)

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | for periods ending September 30, 2015 | | | | for periods ending October 31, 2015 | |

| | | | | | | | |

| |

| 1

YEAR |

| |

| 3

YEARS |

| |

| 5

YEARS |

| |

| SINCE

INCEPTION*

|

| |

| 1

YEAR |

| |

| 3

YEARS |

| |

| 5

YEARS |

| |

| SINCE

INCEPTION* |

|

INTL SMALL COMPANIES PORTFOLIO - INSTITUTIONAL CLASS | | | -5.97 | | | | 7.13 | | | | – | | | | 3.62 | | | | – | | | | -0.98 | | | | 9.00 | | | | – | | | | 4.66 | | | | – | |

MSCI ALL COUNTRY WORLD EX-US SMALL CAP INDEX | | | -6.41 | | | | 5.50 | | | | 3.84 | | | | 1.49 | | | | – | | | | 1.54 | | | | 7.53 | | | | 4.19 | | | | 2.82 | | | | – | |

INTL SMALL COMPANIES PORTFOLIO - INVESTOR CLASS | | | -6.27 | | | | 6.87 | | | | 6.51 | | | | – | | | | 4.51 | | | | -1.29 | | | | 8.71 | | | | 6.49 | | | | – | | | | 5.03 | |

Returns are annualized for periods greater than 1 year. *Inception of the Institutional Class, 6/30/11. Inception of the Investor Class, 3/26/07. Index performance prior to 6/1/07 cannot be shown since it relies on back-filled data.

Performance data quoted represents past performance; past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the Portfolio may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by calling (877) 435-8105 or visiting www.hardingloevnerfunds.com. Performance data shown does not reflect the 2.00% redemption fee imposed on shares held 90 days or less; otherwise, total returns would be reduced.

The charts below illustrate the hypothetical return of an investment made in the corresponding share classes. Investment return reflects voluntary fee waivers in effect. Absent such waivers, total return would be reduced. The performance provided in the table above and charts below do not reflect the deduction of taxes that a shareholder would pay on Portfolio distributions or the redemption of Portfolio shares.

(US$740 million), but we continue to monitor the end market as some of these orders could be at risk of cancellation if demand remains weak. In Consumer Discretionary, German women’s fashion wear designer and manufacturer Gerry Weber announced that it did not expect to meet revenue and earnings targets for 2015, citing a tough German market, lower profitability due to expansion-related costs, and trouble integrating the fashion retailer Hallhuber, which Gerry Weber acquired this past December. We sold our position in September due to these issues.

Returns relative to the Index were helped by strong stock selection in Information Technology (IT) and Health Care. The main contributors in each of these sectors were two German companies. Gerresheimer, a manufacturer of pharmaceutical packaging, agreed to acquire Rexam Healthcare’s Centor, the leading US manufacturer of prescription vials. The acquisition boosts profitability and gives Gerresheimer more meaningful scale and presence in the US. In IT, service provider Bechtle, reported strong second-quarter 2015 earnings after a weak start to 2015. The company’s IT System House and Managed Services segment (66% of total revenues) and IT e-commerce segment (34% of total revenues) saw strong operating profit growth; overall earnings were up 14% over the same quarter last year.

Viewed regionally, the Portfolio benefited most from our zero weight in the weak Canadian market and our overweight in the EMU region. These beneficial weightings were offset by poor stock selection in the EMU and EM regions.

¢ INVESTMENT PERSPECTIVES

Capital Expenditures and Returns in a Slow-Growth World

While many of the concerns and headlines impacting market returns in the second half of the fiscal year pertained to expectations about economic growth globally, our focus continues to be analyzing individual companies’ opportunities for growth. We seek companies that can achieve sustainable growth regardless of the macro environment and have the ability and financial wherewithal to skillfully invest in their businesses to deliver high returns.

In this section, we consider companies’ capital expenditure (capex) activity in a slow growth environment—the characteristics we seek regarding capex when analyzing businesses, how the weak growth outlook might be influencing capex among international small companies broadly, and how capital expenditure trends look for the model portfolio we use in managing the International Small Companies Portfolio.

Our expectations regarding capex decisions are simple: If a company can generate a return on an investment that is above its cost of capital, then it should invest. If a company cannot meet that cost-of-capital hurdle, then management should distribute that money back to shareholders, either through dividends or stock buybacks, rather than invest. In theory, this is an easy formula, though we acknowledge the challenges that company managers face completing forecasts of expected return that accurately reflect the actual return!

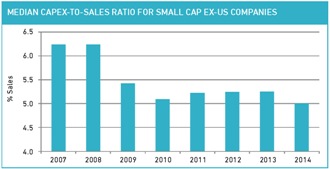

Since the global financial crisis (GFC) of 2008–2009, the willingness of international small companies to commit to capex has trended downward, as shown in the following chart. The chart shows the median ratio of capex to sales—which provides a view of “capex intensity” by measuring the percentage of revenues spent on investment—for the universe of non-US companies with market capitalizations between US$1–5 billion. This downward trend suggests managers are struggling to find projects that can generate returns above their cost of capital in the current low-growth environment, even during this period of low interest rates.

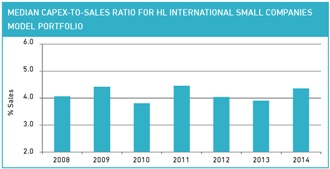

The next chart indicates that the median capex-to-sales ratio of the companies in our model portfolio has remained fairly steady since 2008, hovering in a narrow band around 4%. We believe a reason for this more stable trend of capex investment since the GFC is that our model portfolio companies have continued to find growth opportunities despite the sluggish economic environment.

GEOGRAPHIC WEIGHTINGS (%) at October 31, 2015

| | | | | | | | |

COUNTRY/REGION | | | PORTFOLIO | | | | BENCHMARK1 | |

CANADA | | | 0.0 | | | | 6.6 | |

EMERGING MARKETS | | | 28.5 | | | | 17.0 | |

EUROPE EMU | | | 22.1 | | | | 24.7 | |

EUROPE EX-EMU | | | 16.0 | | | | 21.6 | |

JAPAN | | | 5.0 | | | | 8.1 | |

MIDDLE EAST | | | 0.0 | | | | 0.8 | |

PACIFIC EX-JAPAN | | | 20.6 | | | | 21.2 | |

FRONTIER MARKETS2 | | | 5.3 | | | | – | |

OTHER3 | | | 0.6 | | | | – | |

CASH | | | 1.9 | | | | – | |

1MSCI All Country World ex-US Small Cap Index; 2Includes countries with less-developed markets outside the Index; 3Includes countries with developed markets outside the Index where some holdings are incorporated.

SECTOR WEIGHTINGS (%) at October 31, 2015

| | | | | | | | |

SECTOR | | | PORTFOLIO | | | | BENCHMARK1 | |

CONSUMER DISCRETIONARY | | | 12.2 | | | | 17.3 | |

CONSUMER STAPLES | | | 11.6 | | | | 6.6 | |

ENERGY | | | 0.6 | | | | 3.0 | |

FINANCIALS | | | 12.7 | | | | 21.5 | |

HEALTH CARE | | | 11.6 | | | | 7.5 | |

INDUSTRIALS | | | 23.3 | | | | 20.5 | |

INFORMATION TECHNOLOGY | | | 20.0 | | | | 10.3 | |

MATERIALS | | | 2.5 | | | | 9.9 | |

TELECOM SERVICES | | | 1.1 | | | | 1.1 | |

UTILITIES | | | 2.5 | | | | 2.3 | |

CASH | | | 1.9 | | | | – | |

1MSCI All Country World ex-US Small Cap Index.

In fiscal 2014, the most recent period for which we have meaningful data, the median capex-to-sales neared an all-time high for the model portfolio.

Source: Bloomberg; Harding Loevner International Small Companies Model Portfolio.

Reviewing the current capex-to-sales ratio relative to history can give us a window into how optimistic company management teams are about growth opportunities. However, the absolute level of capex intensity is not a primary concern of our research process. In fact, as the charts indicate, the median capex-to-sales for the model portfolio has been, and continues to be, lower than that of the broader universe. Our goal is to identify companies that we believe can generate high returns by virtue of a combination of attributes. We find such companies partly by analyzing their past records of generating returns, as we believe that businesses with strong operational records are more likely than those without one to generate above-average returns on investment in the future. We also assess various qualitative characteristics of companies—including the quality and experience of their management teams, the attractiveness and competitive structures of their industries, and their competitive advantages relative to peers—to judge whether companies’ past strong returns could be sustainable.

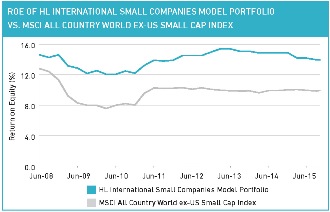

The final chart indicates the returns that our portfolio companies have achieved over time. Since 2008, the average return on equity (ROE) for the model portfolio has been steadily above that of the Index. We will continue seeking companies that we believe can uncover growth opportunities in their industries even in this lower-growth

environment, and possess the management skill and financial strength necessary to invest in these opportunities in an effort to generate solid returns for shareholders.

Source: Wilshire Atlas; Harding Loevner International Small Companies Model Portfolio; MSCI Barra.

¢ PORTFOLIO HIGHLIGHTS

Portfolio Management Team Update

Josephine Lewis, Co-Portfolio Manager of the International Small Companies Equity Strategy, resigned from Harding Loevner in October 2015. We value the contributions Josie made to Harding Loevner and the International Small Companies Equity Strategy and we wish her well in the next phase of her career.

Jafar Rizvi—a member of the strategy’s Portfolio Management team since 2011 and a Co-Portfolio Manager since 2013—now serves as Portfolio Manager. Jafar has sole responsibility for all stock-selection decisions for the portfolio.

The transition from a dual to single portfolio manager structure occasioned only modest adjustments to the portfolio. The number of holdings decreased from 88 to 83, for instance, and the portfolio’s sector and geographic weightings changed only slightly.

There has been no change to the Strategy’s fundamental investment approach. Jafar continues to adhere to the same high-quality, durable-growth philosophy and company-focused research process shared by all of Harding Loevner’s investment strategies.

Portfolio Activity

This year we made investments in companies across a variety of industries and sold some holdings whose businesses have not developed as strongly as we had thought they would.

Our purchases included two companies in Japan. Ariake is the largest producer of meat-extract-based natural seasonings in Japan, with a range of products that includes soups, sauces, bouillons, and consommé, as well as meat, seafood, and vegetable extracts. The company has a dominant market share position in Japan, where it generates nearly three-

quarters of its revenues. The growing demand from customers throughout Asia for ready-to-eat

TEN LARGEST HOLDINGS at October 31, 2015

| | | | | | | | |

COMPANY | | SECTOR | | COUNTRY | | | % | |

BECHTLE | | INFO TECHNOLOGY | | GERMANY | | | 3.0 | |

RUBIS | | UTILITIES | | FRANCE | | | 2.5 | |

INDUSTRIAL & FINANCIAL SYS. | | INFO TECHNOLOGY | | SWEDEN | | | 2.5 | |

SYNERGY HEALTH | | HEALTH CARE | | UNITED KINGDOM | | | 2.4 | |

MAX INDIA | | FINANCIALS | | INDIA | | | 2.3 | |

RPS GROUP | | INDUSTRIALS | | UNITED KINGDOM | | | 2.2 | |

HIDAY HIDAKA | | CONS DISCRETIONARY | | JAPAN | | | 2.2 | |

ALTEN | | INFO TECHNOLOGY | | FRANCE | | | 2.2 | |

WASION GROUP HOLDINGS | | INFO TECHNOLOGY | | CHINA | | | 1.9 | |

RATHBONE BROTHERS | | FINANCIALS | | UNITED KINGDOM | | | 1.9 | |

products, in addition to the traditional desire for natural-based ingredients, should support the company’s continued strong growth. We expect Ariake will also take advantage of growth opportunities in the US and Europe.

Park24 operates parking facilities throughout Japan; the business generates good cash flow and has solid growth prospects. The company’s newest opportunity for growth is the car-sharing business, an industry in its rapid-growth phase. As Japan’s largest parking-space provider and the largest car-share service provider, Park24 has an advantage over its rivals in becoming a major transportation infrastructure provider.

Our sales this period included SLC Agricola, a company that engages in the production and trade of agricultural products such as cotton, soybeans, and corn. We thought that because this is a well-managed producer with large scale, it could overcome the fact that it sells commodities to mainly three large buyers—Bunge, ADM, and Cargill. We underestimated the amount of pressure these buyers could put on SLC Agricola; even though the company generated yields per acre superior to those of its competitors, it was never able to reach the returns on capital that we had expected, and it thus failed to meet our criteria for above-average fundamental quality.

Lastly, we sold our position in the German payment service provider Wirecard. Wirecard has a dominant global position in the rapid-growth industry of online- and mobile-payment processing. Shareholders have enjoyed the benefit of these rapid growth rates as the company successfully took share throughout Europe. More recently, however, the company began pursuing anaggressive acquisition strategy in Asia, the costs of which started to weigh on the company’s free cash flows. We worried about Wirecard’s approach to allocating capital and decided that if the company did not reduce the amount it was spending on acquisitions in Asia, we would exit our position. Wirecard’s management showed no signs of altering its strategy, so we sold the position.

Please read the separate disclosures page for important information, including the risks of investing in the Portfolio.

PORTFOLIO MANAGEMENT TEAM

| | |

G. RUSTY JOHNSON, CFA | | PRADIPTA CHAKRABORTTY |

CO-LEAD PORTFOLIO MANAGER | | PORTFOLIO MANAGER |

| |

CRAIG SHAW, CFA | | SCOTT CRAWSHAW |

CO-LEAD PORTFOLIO MANAGER | | PORTFOLIO MANAGER |

| |

| | RICHARD SCHMIDT, CFA |

| | PORTFOLIO MANAGER |

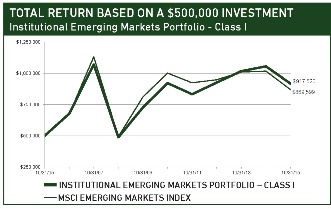

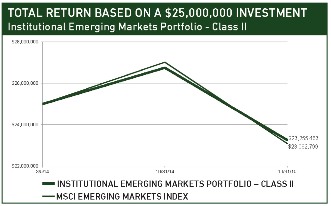

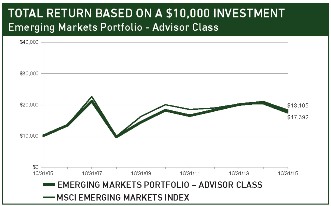

The Institutional Emerging Markets Portfolio – Class I and Class II – and the Emerging Markets Portfolio – Advisor Class (collectively, the “Portfolios”) are both managed in strict accordance with the Emerging Markets Equity Strategy model portfolio. The Portfolios, therefore, have highly similar holdings and characteristics. We have provided a single commentary to cover both Portfolios. The specific performance and characteristics of each are presented separately in the tables that follow.

¢ PERFORMANCE SUMMARY

The Institutional Emerging Markets Portfolio – Class I declined 13.14%, the Institutional Emerging Markets Portfolio – Class II fell 13.06%, and the Emerging Markets Portfolio – Advisor Class lost 13.17%, (net of fees and expenses) in the fiscal year ended October 31, 2015. The Portfolios’ benchmark, the MSCI Emerging Markets Index (the “Index”), declined 14.53% (net of source taxes) in this period.

¢ MARKET REVIEW

Emerging market (EM) equities had a difficult trailing 12 months, with the steepest decline in the Index occurring in the second half of the fiscal year. Investors’ fears regarding EM equities since late April was stoked by a number of issues: growing concern over the true extent of China’s economic weakness, the fall in commodity prices (impacted by China’s slowing growth), the decline in oil prices, the continuing political dysfunction and Petrobras corruption scandal in Brazil, and currency weakness in many EM countries. Every country in the Index except Hungary registered a negative return with only six markets escaping a double-digit drop.

China’s slowing economy dominated the headlines throughout the summer, with anxiety about the country’s prospects reaching a fever pitch in August, when the People’s Bank of China (PBOC) made a surprise announcement that it was adjusting the pricing mechanism for the yuan. The yuan had been effectively pegged to the US dollar, and as a result had strengthened over the past year relative to global currencies. The new adjustment allowed

| | | | | | |

FUND FACTS at October 31, 2015 |

SALES CHARGE | | | | | | NONE |

TOTAL # OF HOLDINGS | | | | | | 76 |

REDEMPTION FEE | | | | | | 2% FIRST 90 DAYS |

DIVIDEND POLICY | | | | | | ANNUAL |

| | INSTITUTIONAL | | ADVISOR |

PORTFOLIO ASSETS | | $2,117.9M | | $2,381.7M |

TURNOVER (5 YR AVG) | | 32% | | 30% |

CLASS | | CLASS I | | CLASS II | | ADVISOR |

TICKER | | HLMEX | | HLEEX | | HLEMX |

CUSIP | | 412295701 | | 412295842 | | 412295305 |

INCEPTION DATE | | 10/17/2005 | | 3/5/2014 | | 11/9/1998 |

MINIMUM INVESTMENT1 | | $500,000 | | $25,000,000 | | $5,000 |

NET EXPENSE RATIO | | 1.30%2 | | 1.14%2 | | 1.45% |

GROSS EXPENSE RATIO | | 1.31% | | 1.30% | | 1.45% |

1Lower minimums available through certain brokerage firms; 2Shown net of Harding Loevner’s contractual agreement, through February 29, 2016, to waive its management fee to the extent necessary to cap the fund’s total operating expenses.

the market to have greater (albeit still limited) influence over the currency. Within a few days of the announcement, the value of the yuan fell 3% versus the dollar.

Investors quickly responded with alarm. They interpreted the PBOC’s move as a sign that China’s economy was slowing more rapidly than recent data suggested and that the government therefore felt compelled to spark export competitiveness to keep the growth train rolling. Yet the 3% depreciation was not remotely sufficient to close the gap between the yuan and other currencies—notably the euro—to provide a material boost to exports. Market participants feared there was much more depreciation to come and fled the probable losses ahead.

China ended up expending billions of dollars in foreign reserves to stabilize the yuan-to-dollar exchange rate, and the currency fell only a little more than 3% in the trailing 12 months through October 2015. But currency weakness elsewhere in the EM universe accounted for a large portion of the Index’s painful performance in the period.

The Russian ruble and the Brazilian real both continued to suffer from a heavy reliance on commodities and their governments’ dismal policies. In Colombia, the declining price of oil (the country’s primary export product) hurt the current account deficit and therefore pressured the peso. Turkey’s lira was pressured by the country’s high external debt levels, political turmoil, and proximity to the conflict in Syria. Countries in Asia also suffered currency depreciation (partly in response to the yuan news), reflecting a potential weakening in their competitiveness. Developed-market currencies did not escape entirely unscathed in the period, with

TOTAL RETURNS (%)

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | for periods ending September 30, 2015 | | | | for periods ending October 31, 2015 | | | | | |

| | | | | | | | | | |

| |

| 1

YEAR |

| |

| 3

YEARS |

| |

| 5

YEARS |

| |

| 10

YEARS |

| | | SINCE INCEPTION* | | |

| 1

YEAR |

| |

| 3

YEARS |

| |

| 5

YEARS |

| |

| 10

YEARS |

| | | SINCE INCEPTION* | |

INST. EMERGING MARKETS PORTFOLIO - CLASS I | | | -17.44 | | | | -2.19 | | | | -1.13 | | | | – | | | | – | | | | 5.47 | | | | – | | | | -13.14 | | | | -0.32 | | | | -0.09 | | | | 6.26 | | | | – | | | | 6.16 | | | | – | |

INST. EMERGING MARKETS PORTFOLIO - CLASS II | | | -17.31 | | | | – | | | | – | | | | – | | | | -8.65 | | | | – | | | | – | | | | -13.06 | | | | – | | | | – | | | | – | | | | -4.27 | | | | – | | | | – | |

MSCI EMERGING MARKETS INDEX | | | -19.28 | | | | -5.27 | | | | -3.58 | | | | 4.26 | | | | -9.00 | | | | 4.92 | | | | – | | | | -14.53 | | | | -2.88 | | | | -2.80 | | | | 5.69 | | | | -4.67 | | | | 5.60 | | | | – | |

EMERGING MARKETS PORTFOLIO - ADVISOR CLASS | | | -17.44 | | | | -2.19 | | | | -1.21 | | | | 4.60 | | | | – | | | | – | | | | 11.03 | | | | -13.17 | | | | -0.31 | | | | -0.17 | | | | 6.11 | | | | – | | | | – | | | | 11.43 | |

Returns are annualized for periods greater than 1 year. *Inception of Class I, 10/17/05. Inception of Class II, 3/5/14. Inception of the Advisor Class, 11/9/98. Index performance prior to 1/1/01 cannot be shown since it relies on back-filled data.

Performance data quoted represents past performance; past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the Portfolio may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by calling (877) 435-8105 or visiting www.hardingloevnerfunds.com. Performance data shown does not reflect the 2.00% redemption fee imposed on shares held 90 days or less; otherwise, total returns would be reduced.

the currencies of commodity-dependent Australia and Canada depreciating more than the majority of EM currencies.

Latin America (-35%) was the weakest region within the Index, largely due to Brazil (-46%), which was downgraded from investment grade to junk status by Standard & Poor’s (S&P) and endured a 36% depreciation in the real. Mexico was a relative outperformer (-18%) and has been one of the few EM economies that seems to be showing a cyclical upturn. The country’s policy stance has been more progressive, it is not heavily dependent on commodity exports, and it has a close link to the strong US economy.

EMs in Europe (-23%) underperformed, but there was marked resilience shown by Hungary (up 13%). Turkey (-22%) remained mired in political uncertainty and faced rising security concerns.

In Asia, there was a large dispersion in returns, with Malaysia (-30%) and Indonesia (-22%) falling the most. Indonesia’s market decline reflected the country’s heavy reliance on commodity exports and ultimately Chinese demand, although the hefty depreciation of the rupiah has helped reduce the current account deficit. China (-0.5%) had the best returns in the region, although its markets exhibited extreme volatility over the course of the year. Hong Kong-listed Chinese shares, which are represented in the Index and comprise the bulk of our Portfolios’ exposure to China, rallied almost 20% in April—spurred in part by a surreal boom in locally listed Chinese A-shares—but surrendered these gains and sharply declined over the next six months following the pop in the A-share bubble.

From a sector perspective, the best performers were Health Care (-3%) and Information Technology (-5%), while Energy (-28%) and Materials (-23%) lagged. Energy was the worst performer in the Index, suffering from a further sharp reversal in crude oil prices and a severe decline in Index heavyweight Petrobras, which continued to be roiled by the corruption scandal and faced the prospect of higher financing costs following S&P’s downgrade of Brazilian sovereign debt.

¢ PERFORMANCE ATTRIBUTION

The Portfolios outperformed the Index in the fiscal year through a combination of strong stock selection and favorable allocations

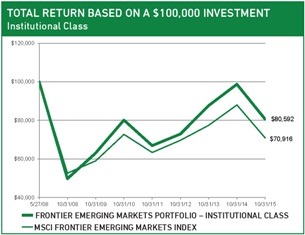

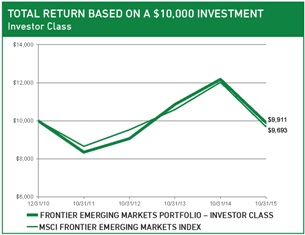

The charts above illustrate the hypothetical return of an investment made in the corresponding share classes. Investment return reflects voluntary fee waivers in effect. Absent such waivers, total return would be reduced. The performance provided in the table and charts above do not reflect the deduction of taxes that a shareholder would pay on Portfolio distributions or the redemption of Portfolio shares.

by sector and geography. The Portfolios’ overweight positions in Health Care and Consumer Discretionary as well as our underweight positions in Energy and Materials, together with positive stock selection in Industrials and Consumer Discretionary, helped offset our weak stocks in Consumer Staples, Financials, and Information Technology (IT). The Portfolios’ returns within Industrials benefited from CRRC Corporation and Mexican airport operator ASUR. CRRC Corporation was formed over the summer through a merger of CNR and Portfolio holding CSR Corporation, a Chinese manufacturer of high-speed electric locomotives and related equipment. CSR was a beneficiary of China’s targeted investment in transportation infrastructure as well as expectations of synergies following the merger. We sold CSR in May following a spike in its share price that took it well beyond our estimates of reasonable value.