Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-07739

Harding, Loevner Funds, Inc.

(Exact name of registrant as specified in charter)

400 Crossing Boulevard

Fourth Floor

Bridgewater, NJ 08807

(Address of principal executive offices) (Zip code)

Owen T. Meacham

The Northern Trust Company

50 South LaSalle Street

Chicago, IL 60603

With a copy to:

Stephen H. Bier, Esq.

Dechert LLP

1095 Avenue of the Americas

New York, NY 10036

(Name and address of agent for service)

Registrant’s telephone number, including area code: (877) 435-8105

Date of fiscal year end: 10/31

Date of reporting period: 10/31/2017

Table of Contents

Item 1. Reports to Stockholders.

Table of Contents

HARDING, LOEVNER FUNDS, INC. Annual Commentary Global Equity Portfolio International Equity Portfolio International Small Companies Portfolio Institutional Emerging Markets Portfolio Emerging Markets Portfolio Frontier Emerging Markets Portfolio Global Equity Research Portfolio International Equity Research Portfolio Emerging Markets Research Portfolio October 31, 2017 Fundamental. Thinking. Worldwide.

Table of Contents

HARDING LOEVNER FUNDS

HARDING LOEVNER FUNDS

Global equity investing for institutions is Harding Loevner’s exclusive focus. Through Harding Loevner Funds it offers distinct global strategies based on its quality-and-growth investment philosophy. It seeks to purchase shares of growing, financially strong, well-managed companies at favorable prices. Harding Loevner manages each of the Funds’ Portfolios according to a disciplined, research-based investment process. It identifies companies with sustainable competitive advantages and assesses the durability of their earnings growth by conducting in-depth fundamental research into global industries. In constructing portfolios, Harding Loevner diversifies carefully to limit risk.

RECEIVE INVESTOR MATERIALS ELECTRONICALLY

Shareholders may sign up for electronic delivery of investor materials. By doing so, you will receive the information faster and help us reduce the impact on the environment of providing these materials. To enroll in electronic delivery,

| 1. | Go to http://www.icsdelivery.com |

| 2. | Select the first letter of your brokerage firm’s name. |

| 3. | From the list that follows, select your brokerage firm. If your brokerage firm is not listed, electronic delivery may not be available. Please contact your brokerage firm. |

| 4. | Complete the information requested, including the e-mail address where you would like to receive notifications for electronic documents. |

Your information will be kept confidential and will not be used for any purpose other than electronic delivery. If you change your mind, you can cancel electronic delivery at any time and revert to physical delivery of your materials. Just go to http://www.icsdelivery.com, perform the first three steps above, and follow the instructions for cancelling electronic delivery. If you have any questions, please contact your brokerage firm.

Table of Contents

4 | Letter to Our Shareholders

10 | International Equity Portfolio

14 | International Small Companies Portfolio

18 | Emerging Markets

22 | Frontier Emerging Markets Portfolio

26 | Global Equity Research Portfolio

30 | International Equity Research Portfolio

34 | Emerging Markets Research Portfolio

CONTACT

Harding, Loevner Funds, Inc. c/o Northern Trust Attn: Funds Center C5S 801 South Canal Street Chicago, IL 60607

Phone: (877) 435-8105 Fax: (312) 267-3657 www.hardingloevnerfunds.com | Must be preceded or accompanied by a current Prospectus. Quasar Distributors, LLC, Distributor |

3

| ||||

Table of Contents

| DAVID LOEVNER, CFA, CIC CHAIRMAN OF THE FUNDS AND CEO OF THE ADVISER

SIMON HALLETT, CFA CO-CIO OF THE ADVISER

FERRILL ROLL, CFA CO-CIO OF THE ADVISER |

Don’t Count Out Active Management

In 1974, the American Express Asset Management Company proposed a novel investment product that would hold shares of every company in the S&P 500 Index. The “Index Fund of America” promised to avoid the decisions and some of the costs associated with researching and selecting individual securities.1 While this fund never got off the ground, the passive approach to investing eventually proved wildly popular as investors flocked to inexpensive funds that tracked rising markets. Today thousands of passive funds follow a bewildering variety of indexes—of which there are now over a million!2 Cheerleading for the passive approach has been led by investment theorists who characterize the stock market as a zero-sum game in which every active investor’s gain is offset by another’s loss.3 After active managers’ fees are taken into account, the theorists argue, active managers on the whole are predestined to fail to beat their benchmarks. Investors are increasingly buying this argument: over the last decade, equity mutual fund investors in the US have poured an estimated US$750 billion into passive funds even as they pulled about US$1 trillion from actively managed funds.4

Investors are in a difficult place. In choosing passive management, they minimize costs and the risk of underperformance while giving up any chance of outperformance. If they opt for active management, they have the opportunity to beat a benchmark index but also face a strong likelihood of underperformance, especially after fees. Investment theory offers little help. The zero-sum game arithmetic cited by supporters of the passive approach, for example, applies only to active managers as a group. Though the argument speaks volumes to the likelihood of a randomly selected manager beating its benchmark, it says little about the ability of a carefully selected manager to do so. In fact, while many managers do not outperform, some do. Our view is that active management can work for the benefit of investors. Making it work is our mission. The challenge for investors who seek to benefit from active management is to identify markets where stock picking is potentially effective, to select managers who show signs of skill, and then to stick with their approach long term.

Stacking the Odds in Your Favor

The pursuit of skilled managers begins by understanding where active managers have demonstrated the most and the least success. In practice, not all indexes are equally difficult to outperform. Most studies favoring passive investing have been based on

analysis of large-cap US stock funds due to the US market’s long unbroken history and the availability of stock, fund, and index return data. They have shown that the available quantity of information and the human energy devoted to researching US large-cap companies make the market in their stocks relatively efficient, so that few active managers are able to beat the S&P 500.

In contrast, active managers have experienced more success when not confined to large-cap US stocks. Investment universes that stretch across borders and include less prominent companies provide greater opportunities to take advantage of market inefficiencies. A recent study of global equity portfolios from 2002–2012 found that active managers on average outperformed their benchmarks by 1.2–1.4% a year before fees.5 Other research found that the majority of institutional portfolios of non-US equities generated excess return, net of fees, versus their indexes for the 15-year period ending March 31, 2017.6

Identifying Skill Not Luck

Even in markets where the average active manager adds value over an index after fees, choosing a manager who produces average results would hardly count as a big success. An investor must identify those who will outperform in the future and by a significant margin.

A manager’s success at picking investments is always a combination of luck and skill. Luck waxes and wanes, but skill can lead to long-term outperformance. The challenge is distinguishing between the two. It becomes harder as unskilled managers are squeezed out of the industry, shrinking the variations of skill among the remaining managers, and leading luck, paradoxically, to play a greater role in their relative results. Countless studies have proved what the advertisements warn: past performance is no guarantee of future results. In fact it’s worse—past performance alone has little to no predictive power. Rather than trying to divine differences in skill from results, an investor’s time is better spent studying the differences in a manager’s approach to discern the existence and sources of competitive edge.

The most obvious requirement for outperformance is high active share, which measures a manager’s willingness to invest differently than the benchmark index.7 Also important is the discipline to stick with decisions even in the face of short-term setbacks. Martijn Cremers of the University of Notre Dame explored these characteristics in his recent article, “Active Share and the Three Pillars of Active Management: Skill, Conviction, and Opportunity.” His analysis of US long-only retail mutual funds from 1990 to 2015 found that, on average, funds with high active share and long holding duration outperformed their benchmarks. The average fund in the top quintile of both active share and holding duration beat its benchmark by 188 basis points annually and beat its counterpart in the corresponding bottom quintiles by 311 basis points.8 High active share and patience are apparently among the ingredients required to outperform, but they are by no means sufficient.

4

|

Table of Contents

To reap excess returns a manager must have a competitive edge at developing insights and converting them into profitable investments.9 At Harding Loevner, our edge is based on an investment process that reflects our understanding of human decision-making. We look for and try to overcome biases that might hinder our investment decisions. One example is confirmation bias, which behavioral psychologists define as the tendency to look only for information that reinforces what one already knows or believes. Because this bias is often compounded in groups, we have created a process where every investment choice is made by a single individual who is held accountable for the decision and its consequences. We also strive to retain the benefits of group collaboration by encouraging our research team to question and challenge ideas. Our culture—which we call collaboration without consensus—is at the heart of our edge. It leads us to build portfolios significantly different from their respective indexes, while conviction in our process gives us the courage to maintain our long-term perspective when our approach inevitably will be out of favor.

After investors have identified a skilled manager, they must stay the course to realize the benefits. But it’s not easy. The difference between a portfolio and its benchmark index not only provides the opportunity to outperform, but also opens the door to underperformance.

Successful managers, regardless of their skill, will underperform their benchmarks for significant periods. In an analysis of the top quartile of active international equity managers for the decade ended September 30, 2017, every manager spent at least one three-year period below the benchmark.10 Many investors cannot stomach a year’s underperformance, much less three years. In fact, there is evidence that underperformance may lead investors to abandon skilled managers at inopportune times. As a result, they miss out on positive returns they would have received had they stayed put.11

We Believe in Active Management

Investors can benefit from both passive and active management: passive funds provide access to markets at low cost, and some active managers can identify mispriced securities to generate excess returns. At Harding Loevner, we invest actively across global, developed, and emerging markets, where there has been ample scope for successful active investing. We are relentless in trying to improve our competitive edge, which has delivered superior long-term results to our clients.

To see how our active approach translates to investment insights and actions, we invite you to read the commentaries that follow.

We thank you for your support and your trust.

Sincerely,

David R. Loevner, CFA, CIC |

Simon Hallett, CFA |

Ferrill D. Roll, CFA |

1“Marketplace: Fund to Invest in S. & P. 500,” The New York Times, February 23, 1974. In this year, a few other firms were also working to develop index funds. However, the first did not launch until 1976, when Vanguard introduced the First Index Investment Trust based on the S&P 500.

2“Financial-Market Index-Makers are Growing in Power,” Economist, August 24, 2017.

3The zero-sum game assumes that active and passive investors are working in the same closed system of securities. In reality, markets and the indexes that track them are not static. New listings, bankruptcies, and mergers regularly are sources of change. Index designers also make changes of their own volition. In addition, most active managers are under no obligation to invest in solely index-constituent stocks.

4Morningstar. Estimated net asset flows of US mutual funds for 10 years through September 30, 2017.

5David Gallagher et al., “Global Equity Fund Performance: an Attribution Approach,” Financial Analysts Journal 73, no. 1 (2017): 56–71.

6Ruchir Sharma, “What They Don’t Tell You About Passive Investing,” Morgan Stanley Investment Insight (2017).

7Active share is equal to the proportion of portfolio assets that is invested differently from the benchmark.

8Martijn Cremers, “Active Share and the Three Pillars of Active Management: Skill, Conviction, and Opportunity,” Financial Analysts Journal 73, no. 2 (2017): 61–79.

9Different skilled managers may have different competitive advantages, but they ultimately boil down to four key sources of edge: informational, analytical, behavioral, and organizational. For further discussion of how these sources of edge pertain to our investment process, please see our October 2016 letter available on Harding Loevner’s website.

10 eVestment. Based on net of fees performance for managers in eVestment’s ACWI ex-US Large Cap universe relative to the MSCI ACWI ex-US Index for 10 years through September 30, 2017.

11Russel Kinnel, “Mind the Gap: Global Investor Returns Show the Costs of Bad Timing Around the World,” Morningstar Manager Research, May 30, 2017.

Opinions expressed are those of Harding Loevner and are not intended to be forecasts of future events, a guarantee of future results, nor investment advice. Please read the separate disclosure page for important information, including the risks of investing in the Portfolios. Past performance is not a guarantee of future results.

5

|

Table of Contents

PORTFOLIO MANAGEMENT TEAM

| ||

PETER BAUGHAN, CFA CO-LEAD PORTFOLIO MANAGER

FERRILL ROLL, CFA CO-LEAD PORTFOLIO MANAGER | CHRISTOPHER MACK, CFA PORTFOLIO MANAGER

RICHARD SCHMIDT, CFA PORTFOLIO MANAGER | |

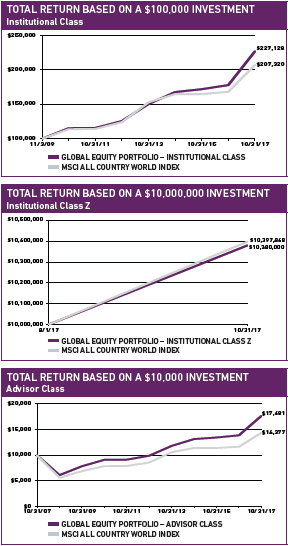

PERFORMANCE SUMMARY

PERFORMANCE SUMMARY

The Global Equity Portfolio – Institutional Class gained 27.58% and the Advisor Class gained 27.28% (net of fees and expenses) in the fiscal year ended October 31, 2017. The Portfolio’s benchmark, the MSCI All Country World Index, rose 23.19% (net of source taxes) in this period.

MARKET REVIEW

Markets had modest gains in the last two months of 2016, in US dollar terms, as investors reacted to the astonishing outcome of the US presidential election, but accelerated in 2017 as investor optimism returned amid improving economic data in most regions. The Index ended the fiscal year with a robust increase. Through October, the Index posted 12 consecutive positive monthly returns, the longest such stretch for the Index since the bear market recovery of 2003–04. Although the gains came 7 years since the last recession, investors cheered positive economic data as it suggested synchronized growth across all major regions, while inflation remained muted. Meanwhile, investors largely rationalized the threat to stability from the US Federal Reserve’s staggered exit from extremely loose monetary policy as being about normalization rather than inflation taming. Markets also mostly ignored escalating tensions between North Korea and the US, illustrated by the half-percent rise in the Japanese stock market on the day the latest intercontinental ballistic missile (ICBM) flew through its airspace in late August.

Information Technology (IT) stocks returned almost double the return of the Index in the trailing year. IT companies reported strong sales and earnings growth, with the biggest positive surprises coming from a handful of big Chinese internet companies.

The eurozone and Emerging Markets (EMs) led regional returns. Better economic growth data across Europe, along with relief over the defeat in the French general elections of the anti-EU far-right, allowed investors to view the future more optimistically. They favored stocks of more-cyclical businesses, especially energy, autos, and banks. The euro gained 6% against the US dollar, bolstering

FUND FACTS at October 31, 2017 | ||||||||||||

TOTAL NET ASSETS | $911.8M | |||||||||||

SALES CHARGE | NONE | |||||||||||

NUMBER OF HOLDINGS | 74 | |||||||||||

TURNOVER (5 YR. AVG.) | 30% | |||||||||||

REDEMPTION FEE | 2% FIRST 90 DAYS | |||||||||||

DIVIDEND POLICY | ANNUAL | |||||||||||

INSTITUTIONAL INVESTORS | INDIVIDUAL INVESTORS | |||||||||||

| INSTL CLASS | INSTL CLASS Z | ADVISOR CLASS | ||||||||||

TICKER | HLMVX | HLGZX | HLMGX | |||||||||

CUSIP | 412295602 | 412295727 | 412295206 | |||||||||

INCEPTION DATE | 11/3/2009 | 8/1/2017 | 12/1/1996 | |||||||||

MINIMUM INVESTMENT1 | $100,000 | $10,000,000 | $5,000 | |||||||||

NET EXPENSE RATIO | 0.92% | 0.90%2 | 1.19% | |||||||||

GROSS EXPENSE RATIO | 0.92% | 1.53% | 1.19% | |||||||||

1Lower minimums available through certain brokerage firms; 2Shown net of Harding Loevner’s contractual agreement through February 28, 2018.

European Monetary Union (EMU) stock returns to US investors. The strong performance of IT stocks, especially Chinese internet stocks, was important to EM gains.

The US stock market trailed the overall Index slightly, as accelerating economic growth and good earnings in IT and other cyclical sectors were offset by growth concerns in Consumer Staples and Health Care, and where optimism about government infrastructure spending or tax reform faded after other aims of the administration foundered in Congress in spite of the Republican majorities.

In addition to the US election, the end of 2016 was marked by a persistent value rally in which the least-expensive quintile of stocks outperformed the most-expensive quintile in every major region and in nearly every sector. And, because there is a high degree of overlap between low-quality or slow-growing businesses and companies with lowly priced stocks, the shares of the lowest-quality and slowest-growth businesses also performed better on average than shares of those with superior quality and growth records. This rally was reversed in the first six months of 2017, as style trends in the market favored stocks whose businesses demonstrated strong growth characteristics, while there was little differentiation in returns according to valuation. But then, from July to October, only the most-expensive quintile of stocks showed significant outperformance. Quality showed no pattern of effect on returns. Within developed markets, the growth preference waned late in September as US bond yields rose from the lowest levels of the year after Congress revealed plans for a large tax cut, and the Fed reiterated its intention to continue tightening monetary policy. Growth in EMs was strong throughout 2017.

6

|

Table of Contents

PERFORMANCE (% TOTAL RETURN)

| for periods ended September 30, 2017 | for periods ended October 31, 2017 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 1 YEAR | 3 YEARS | 5 YEARS | 10 YEARS | SINCE INCEPTION* | 1 YEAR | 3 YEARS | 5 YEARS | 10 YEARS | SINCE INCEPTION* | |||||||||||||||||||||||||||||||||||||||||||||||||

GLOBAL EQUITY PORTFOLIO - INSTL CLASS | 21.63 | 10.42 | 11.35 | – | – | 10.56 | – | 27.58 | 10.59 | 12.54 | – | – | 10.81 | – | ||||||||||||||||||||||||||||||||||||||||||||

GLOBAL EQUITY PORTFOLIO - INSTL CLASS Z | – | – | – | – | 1.10 | – | – | – | – | 3.80 | ||||||||||||||||||||||||||||||||||||||||||||||||

MSCI ALL COUNTRY WORLD INDEX | 18.63 | 7.43 | 10.20 | 3.88 | 1.86 | 9.37 | – | 23.19 | 7.92 | 10.81 | 3.70 | 3.98 | 9.55 | – | ||||||||||||||||||||||||||||||||||||||||||||

GLOBAL EQUITY PORTFOLIO - ADVISOR CLASS | 21.30 | 10.13 | 11.06 | 5.81 | – | – | 7.20 | 27.28 | 10.31 | 12.25 | 5.86 | – | – | 7.31 | ||||||||||||||||||||||||||||||||||||||||||||

Returns are annualized for periods greater than 1 year. *Inception of the Institutional Class, 11/3/09. Inception of the Institutional Class Z, 8/1/17. Inception of the Advisor Class, 12/1/96. Index performance prior to 1/1/01 cannot be shown since it relies on back-filled data.

Performance data quoted represents past performance; past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the Portfolio may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by calling (877) 435-8105 or visiting www.hardingloevnerfunds.com. Performance data shown does not reflect the 2.00% redemption fee imposed on shares held 90 days or less; otherwise, total returns would be reduced.

PERFORMANCE ATTRIBUTION

The Portfolio outperformed in five of the eight sectors in which we have holdings and benefited from holding no Telecom Services, Real Estate, or Utilities stocks. Our large holding of IT stocks contributed the most to performance over the year, driven in part by Chinese internet businesses Weibo and Tencent, each of which reported accelerating earnings growth as internet users consumed more advertisements, games, and other services than the market had anticipated. Additionally, PayPal reported robust sales and earnings growth, as mobile-payment transactions processed through its platform surpassed the market, while Cognex captured investors’ imaginations with broader applications for its machine-vision software and optical sensors.

We had good stocks in Financials as well, led by US-based commercial bank SVB Financial Group. Energy, especially Schlum-berger, was a detractor, as was our modest allocation to cash in a strong period for equity returns.

Stocks in Consumer Discretionary also detracted from relative performance. Nike reported disappointing earnings, negatively impacted by retail-store closings as distribution shifts toward internet-based sales. UK-based advertising agency WPP reported weak earnings, and management lowered its full-year guidance due to weaker ad spending by its customers.

Viewed geographically, our outperformance stemmed largely from good stock selection in the US, including SVB Financial Group, PayPal, Cognex, and IPG Photonics. Stocks in EMs were beneficial to relative returns as well, led by internet businesses in China as well as Yandex in Russia. Eurozone holdings trailed the Index, the worst being well-pipe supplier Tenaris.

PERSPECTIVE AND OUTLOOK

The investment environment has become increasingly challenging for investors concerned with the quality, growth, and price tripod that forms the foundation of Harding Loevner’s investment philosophy. Quality as a standalone factor has become expensive in stock-price terms, in spite of the surge in value stocks at the end of 2016. We have noted the investment industry’s

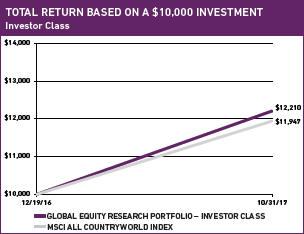

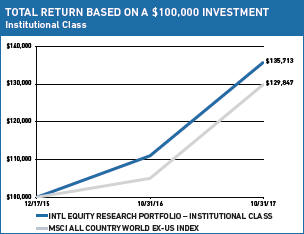

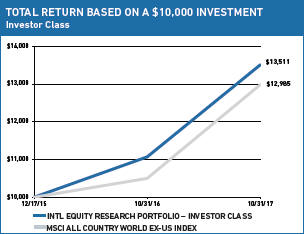

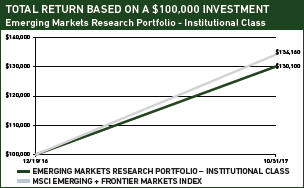

The charts above illustrate the hypothetical return of an investment made in the corresponding share classes. Investment return reflects voluntary fee waivers in effect. Absent such waivers, total return would be reduced. The performance provided in the table and charts above do not reflect the deduction of taxes that a shareholder would pay on Portfolio distributions or the redemption of Portfolio shares.

7

|

Table of Contents

efforts to reverse-engineer the successful performance that high-quality portfolios have enjoyed over the past decade by constructing “smart beta” portfolios that use quantitative tools to identify companies with similar high-quality attributes. These approaches implicitly promise future outperformance similar to that observed in the past. Smart beta approaches overlap with other managers employing optimization software to create “low volatility” portfolios that appeal to investors fearful of the inherent ups and downs of stock market investing, overlapping simply because the stocks of high-quality companies have traded with much more restrained gyrations than the average stock in past market tempests. The broader emphasis on quality, enshrined in the documenting by academics of a quality factor effect, and commercialized through the creation of “quality indexes” as benchmarks for passive money, has meant increasingly persistent and decreasingly price-sensitive demand for the stocks of high-quality companies.

Our Portfolio response has been to redouble our attention to the other two legs of our philosophical stool: growth and price. If quality is fashionable, based on either a blind embrace of its prior success or a backward-looking fear of another financial crisis, then the fruitful way forward must be one that remains discerning yet is courageously forward-looking. In the past 12 months, this route has involved an emphasis on price, encompassing the strong value rally capped by the “Trump bump,” but it has also, in recent months, coalesced around companies achieving faster growth. This latter focus on growth is the topic of this piece.

We have had a longstanding focus on growth companies in the IT sector, where the Portfolio has held an overweight position for over a decade. Our holdings have emphasized the emerging winners and beneficiaries of the promise now being realized by “Internet 2.0” and “Big Data.” Fifteen years after the tech bubble (wrongly) priced the first advent of internet-based business (“Internet 1.0”), we are witnessing the emergence in a number of industry segments of dominant or even winner-take-all internet-based businesses skillfully exploiting the “network effect” to secure their supremacy. While investors are clearly paying high prices for these businesses, their surge in the current year can

GEOGRAPHIC EXPOSURE (%) at October 31, 2017

| COUNTRY/REGION | PORTFOLIO | BENCHMARK1 | ||||||

CANADA | 0.0 | 3.1 | ||||||

EMERGING MARKETS | 14.0 | 11.7 | ||||||

EUROPE EMU | 14.0 | 10.9 | ||||||

EUROPE EX-EMU | 12.5 | 10.3 | ||||||

JAPAN | 9.8 | 7.9 | ||||||

MIDDLE EAST | 1.1 | 0.1 | ||||||

PACIFIC EX-JAPAN | 2.4 | 3.9 | ||||||

UNITED STATES | 43.7 | 52.1 | ||||||

FRONTIER MARKETS2 | 0.0 | – | ||||||

CASH | 2.5 | – | ||||||

1MSCI All Country World Index; 2Includes countries with less-developed markets outside the Index.

SECTOR EXPOSURE (%) at October 31, 2017

| SECTOR | PORTFOLIO | BENCHMARK1 | ||||||

CONSUMER DISCRETIONARY | 11.7 | 11.9 | ||||||

CONSUMER STAPLES | 5.6 | 8.6 | ||||||

ENERGY | 3.7 | 6.3 | ||||||

FINANCIALS | 13.8 | 18.6 | ||||||

HEALTH CARE | 16.6 | 10.8 | ||||||

INDUSTRIALS | 14.7 | 10.8 | ||||||

INFORMATION TECHNOLOGY | 22.4 | 18.4 | ||||||

MATERIALS | 9.0 | 5.4 | ||||||

REAL ESTATE | 0.0 | 3.1 | ||||||

TELECOM SERVICES | 0.0 | 3.0 | ||||||

UTILITIES | 0.0 | 3.1 | ||||||

CASH | 2.5 | – | ||||||

1MSCI All Country World Index.

mostly be explained by stronger-than-expected reported earnings rather than a re-estimation of their future growth rate.

We have been fortunate to own a number of internet businesses that have continued to generate strong results. We are aware of the great promise—and considerable hype—around emergent technologies such as artificial intelligence (AI), machine learning, and Big Data analytics of all types. For example, Facebook’s intimate personal profiles on hundreds of millions of consumers across the Western world (echoed in Tencent’s data on consumer behavior across China) have vast monetization potential. It is possible, however, that current valuations reflect peak optimism for the monetization of consumer data. Certainly, there is insufficient appreciation by investors of the rising risk that the collection and sale of consumer-behavior and other personal data will face more stringent regulation. At some point, Facebook’s ability to deliver yet another highly customized mobile advertisement or Amazon. com’s disruption of yet another consumer category will face diminishing marginal returns, but the share prices of these companies don’t discount that happening for many years.

The technologies that have catalyzed a global boom across online media, enterprise software, and e-commerce have applications in other industries that perhaps are less than fully discounted in stock prices. Our research efforts extend to companies in health care and life sciences that can use similar technology toolkits as Facebook or Amazon but whose products and penetration of end markets have yet to be fully realized. For example, there is now an extensive amount of human genetic data that is ripe for analysis by Health Care companies capable of exploiting advances in AI. By combining gene-sequencing data with other large data sets such as anonymized patient health records and diagnostic test results, Big Data can help make drug development faster and more precise. Portfolio holding Regeneron, a leading biotechnology company, is using Big Data today at its Regeneron Genetics Center to identify genomic biomarkers for new drug therapies and other applications at the intersection of pharmacology and genomics (“pharmacogenomics”). Regeneron is also an early investor in rapidly emerging gene-editing technologies, which have the potential to transform drug-discovery productivity and economics.

8

|

Table of Contents

Advancements in gene sequencing could also present opportunities for industrial application. Novozymes, the global leader in industrial enzymes, uses Big Data analytics to alter microbe DNA to create new enzymes that can replace polluting chemicals in consumer products such as detergents, as well as in agricultural fertilizers, an application it is currently pursuing through an alliance with Monsanto. Chr. Hansen, the global leader in bacterial cultures for food, is similarly using Big Data analytics to develop bacteria strains for promising new markets in bio-protection, animal health, and human health.

PORTFOLIO HIGHLIGHTS

We have aimed to curb any increase in the forecast volatility of the Portfolio relative to the Index as we have made transactions over the last fiscal year. With few exceptions, our new purchases have been of stocks exhibiting lower volatility, including Chr. Hansen, Symrise, Check Point Software Technologies, Reckitt Benckiser, and HDFC Bank, while the reductions and sales we have made have been of holdings exhibiting higher-than-average volatility.

Within IT, we are concerned that investors have become too focused on the rewards Facebook and Google derive from their growing dominance of digital advertising in the West, and not enough on the risks that dominance creates. Their business models are inherently attractive: consumers willingly give large amounts of personal data to Google and Facebook, who analyze it for clues to buying preferences and sell their conclusions to the highest bidder, to be used in targeted advertising. Consumers thus see ads or news tailored to them, while advertisers don’t waste money marketing to disinterested targets. In practice, however, there is clear potential for abuse, including disregard of privacy rights and in the dissemination of false or misleading information. Critics assert that the power of the big social media companies has become too large. That is, can these companies’ demonstrated ability to influence behavior be allowed to roll on unrestrained, or at least without a political backlash?

For the moment, we have taken a different view of the two companies’ potential challenges, avoiding a rush to undifferentiated judgment. The abuse of Facebook’s platform and algorithms does not immediately indict the company, in our view, but the abusers. Facebook has seen its targeting tools used in ways it never imagined (e.g., targeting racist messages to organize and incite violence). The company has responded with a public expression of horror and has made changes to its filtering technologies. That said, the company’s response to the purchase of ads by Russian front companies has been considerably slower in coming. While retaining our Facebook holding, we are wary, wondering if we’ve seen peak margins, as structural costs of doing business rise in a more censorious environment—be it self-imposed or regulated by government agents. If so, we may also be witnessing peak valuation.

TEN LARGEST HOLDINGS at October 31, 2017

| COMPANY | SECTOR | COUNTRY | % | |||||||||

PAYPAL | INFO TECHNOLOGY | UNITED STATES | 3.3 | |||||||||

NIKE | CONS DISCRETIONARY | UNITED STATES | 3.1 | |||||||||

ROPER INDUSTRIES | INDUSTRIALS | UNITED STATES | 2.9 | |||||||||

PRICELINE GROUP | CONS DISCRETIONARY | UNITED STATES | 2.6 | |||||||||

SVB FINANCIAL GROUP | FINANCIALS | UNITED STATES | 2.4 | |||||||||

SYSMEX | HEALTH CARE | JAPAN | 2.4 | |||||||||

SYMRISE | MATERIALS | GERMANY | 2.4 | |||||||||

AIA GROUP | FINANCIALS | HONG KONG | 2.3 | |||||||||

SCHLUMBERGER | ENERGY | UNITED STATES | 2.0 | |||||||||

KUBOTA | INDUSTRIALS | JAPAN | 1.9 | |||||||||

On the other hand, Alphabet’s troubles with the European Commission are of a different character. There, the charge is not inadvertent abuse of the company’s powerful platform by malicious actors, but rather a violation of antitrust regulation through management’s conscious decision to favor its own products in its search rankings. We sold our large, longstanding holding in Alphabet in August 2017. We will revisit the company after the impact of still-to-come EU remedies can be assessed, or if its share price becomes meaningfully more attractive. We would also like to see less opacity and cash burn across Alphabet’s many “moon shot” ventures.

We redeployed Alphabet proceeds into two new holdings in Apple and Cognizant. We see Apple as being attractively priced in a world of very high valuations and believe the company probably to be least at risk among US large-cap techs from data-privacy concerns. Indeed, Apple has been vocal about its concerns of potential abuse of consumer data by the search and social media companies. We are also mightily impressed by Apple’s ability to deliver unprecedented performance—with design elegance—in its latest hardware products and suspect that the growth potential of its evolving software and services business is being underestimated. We also bought Cognizant, the IT consulting firm whose shares have underperformed the IT sector over the past two years, and whose management is focusing more on free cash flow generation than on growing at breakneck rates.

Please read the separate disclosures page for important information, including the risks of investing in the Portfolio.

9

|

Table of Contents

PORTFOLIO MANAGEMENT TEAM

FERRILL ROLL, CFA CO-LEAD PORTFOLIO MANAGER

ALEXANDER WALSH, CFA CO-LEAD PORTFOLIO MANAGER

| BRYAN LLOYD, CFA PORTFOLIO MANAGER

PATRICK TODD, CFA PORTFOLIO MANAGER

ANDREW WEST, CFA PORTFOLIO MANAGER |

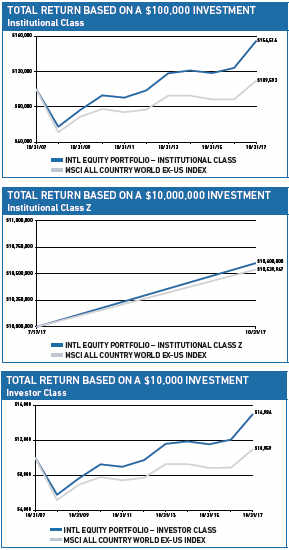

PERFORMANCE SUMMARY

PERFORMANCE SUMMARY

The International Equity Portfolio – Institutional Class gained 24.47% and the Investor Class gained 24.04% (net of fees and expenses) in the fiscal year ended October 31, 2017. The Portfolio’s benchmark, the MSCI All Country World ex-US Index (the Index), rose 23.65% (net of source taxes) in this period.

MARKET REVIEW

Non-US markets faced declines in the last two months of 2016 as investors reacted to the astonishing outcome of the US presidential election, but reversed course in 2017 as investor optimism returned amid improving economic data in most regions. The Index ended the fiscal year with a robust increase. Through October, the Index posted 11 consecutive positive monthly returns, the longest such stretch for the Index in the past 10 years. Although the gains came 7 years on since the last recession, investors cheered positive economic data as it suggested synchronized growth across all major regions, while inflation remained muted. Meanwhile, investors largely rationalized the threat to stability from the US Federal Reserve’s staggered exit from extremely loose monetary policy as being about normalization rather than inflation taming. Markets also mostly ignored escalating tensions between North Korea and the US, illustrated by the half-percent rise in the Japanese stock market on the day the latest ICBM flew through its airspace in late August.

Information Technology (IT) stocks returned roughly double the return of the Index in the trailing year. IT companies reported strong sales and earnings growth, with the biggest positive surprises coming from a handful of big Chinese internet companies.

The eurozone and Emerging Markets (EMs) led regional returns. Better economic growth data across Europe, along with relief over the defeat in the French general elections of the anti-EU far-right, allowed investors to view the future more optimistically. They favored stocks of more-cyclical businesses, especially energy, autos,

FUND FACTS at October 31, 2017 | ||||||||||||

TOTAL NET ASSETS | $11,918.9M | |||||||||||

SALES CHARGE | NONE | |||||||||||

NUMBER OF HOLDINGS | 55 | |||||||||||

TURNOVER (5 YR. AVG.) | 15% | |||||||||||

REDEMPTION FEE | 2% FIRST 90 DAYS | |||||||||||

DIVIDEND POLICY | ANNUAL | |||||||||||

INSTITUTIONAL INVESTORS | INDIVIDUAL INVESTORS | |||||||||||

| INSTL CLASS | INSTL CLASS Z | INVESTOR CLASS | ||||||||||

TICKER | HLMIX | HLIZX | HLMNX | |||||||||

CUSIP | 412295107 | 412295719 | 412295503 | |||||||||

INCEPTION DATE | 5/11/1994 | 7/17/2017 | 9/30/2005 | |||||||||

MINIMUM INVESTMENT1 | $100,000 | $10,000,000 | $5,000 | |||||||||

NET EXPENSE RATIO | 0.83% | 0.80%2 | 1.14% | |||||||||

GROSS EXPENSE RATIO | 0.83% | 1.43% | 1.14% | |||||||||

1Lower minimums available through certain brokerage firms; 2Shown net of Harding Loevner’s contractual agreement through February 28, 2018.

and banks. The euro gained 6% against the US dollar, bolstering European Monetary Union (EMU) stock returns to US investors. The strong performance of IT stocks, especially Chinese internet stocks, was important to EM gains.

In addition to the US election, the end of 2016 was marked by a sharp value rally in which the least-expensive quintile of stocks outperformed the most-expensive quintile in every major region and in nearly every sector. And, because there is a high degree of overlap between low-quality or slow-growing businesses and companies with lowly priced stocks, the shares of the lowest-quality and slowest-growth businesses also performed better on average than shares of those with superior quality and growth records. This value rally was reversed in the first six months of 2017, as style trends in the market favored stocks whose businesses demonstrated strong growth characteristics, while there was little differentiation in returns according to valuation. But then, from July to October, only the most-expensive quintile of stocks showed significant outperformance, while quality showed no pattern of effect on returns. Within developed markets, the growth preference waned late in September as US bond yields rose from the lowest levels of the year after Congress revealed plans for a large tax cut, and the Fed reiterated its intention to continue tightening monetary policy. Growth in EMs was strong throughout 2017.

PERFORMANCE ATTRIBUTION

PERFORMANCE ATTRIBUTION

Our large holding of IT stocks added to performance over the year. We also benefited from good stock selection within Consumer Staples, especially soybean processor Bunge. We had good stocks in Financials as well, especially German insurer Allianz and

10

|

Table of Contents

PERFORMANCE (% TOTAL RETURN)

| for periods ended September 30, 2017 | for periods ended October 31, 2017 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||

1 YEAR | 3 YEARS | 5 YEARS | 10 YEARS | SINCE | 1 YEAR | 3 YEARS | 5 YEARS | 10 YEARS | SINCE | |||||||||||||||||||||||||||||||||||||||||||||||||

INTL EQUITY PORTFOLIO - INSTITUTIONAL CLASS | 18.66 | 8.28 | 9.02 | 4.83 | – | – | 6.48 | 24.47 | 8.42 | 9.38 | 4.45 | – | – | 6.55 | ||||||||||||||||||||||||||||||||||||||||||||

INTL EQUITY PORTFOLIO - INSTITUTIONAL CLASS Z | – | – | – | – | 3.80 | – | – | – | – | – | – | 6.00 | – | – | ||||||||||||||||||||||||||||||||||||||||||||

MSCI ALL COUNTRY WORLD EX-US INDEX | 19.62 | 4.70 | 6.98 | 1.28 | 3.45 | 4.86 | – | 23.65 | 5.71 | 7.29 | 0.92 | 5.40 | 4.99 | – | ||||||||||||||||||||||||||||||||||||||||||||

INTL EQUITY PORTFOLIO - INVESTOR CLASS | 18.23 | 7.94 | 8.67 | 4.51 | – | 6.79 | – | 24.04 | 8.07 | 9.03 | 4.13 | – | 6.92 | – | ||||||||||||||||||||||||||||||||||||||||||||

Returns are annualized for periods greater than 1 year. *Inception of the Institutional Class, 5/11/94. Inception of the Institutional Class Z, 7/17/17. Inception of the Investor Class, 9/30/05. Index performance prior to 1/1/01 cannot be shown since it relies on back-filled data.

Performance data quoted represents past performance; past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the Portfolio may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by calling (877) 435-8105 or visiting www.hardingloevnerfunds.com. Performance data shown does not reflect the 2.00% redemption fee imposed on shares held 90 days or less; otherwise, total returns would be reduced.

Singapore bank DBS Group. Our significant overweight to Health Care was a detractor from relative returns, as was our modest allocation to cash in a strong period for equity returns.

Viewed geographically, we benefited from good stock selection in EMs, Pacific Ex-Japan, the Middle East, the eurozone, and Canada. EM holdings bettered the Index due to Naspers and IT heavyweights Samsung Electronics and Taiwan Semiconductor. Our stock selection in Japan detracted from relative returns, due to declines in shares of M3, Park24, and Sysmex.

PERSPECTIVE AND OUTLOOK

The investment environment has become increasingly challenging for investors concerned with the quality, growth, and price tripod that forms the foundation of Harding Loevner’s investment philosophy. Quality as a standalone factor has become expensive in stock-price terms, in spite of the surge in value stocks at the end of 2016. We have noted the investment industry’s efforts to reverse-engineer the successful performance that high-quality portfolios have enjoyed over the past decade by constructing “smart beta” portfolios that use quantitative tools to identify companies with similar high-quality attributes. These approaches implicitly promise future outperformance similar to that observed in the past. Smart beta approaches overlap with other managers employing optimization software to create “low volatility” portfolios that appeal to investors fearful of the inherent ups and downs of stock market investing, overlapping simply because the stocks of high-quality companies have traded with much more restrained gyrations than the average stock in past market tempests. The broader emphasis on quality, enshrined in the documenting by academics of a quality factor effect, and commercialized through the creation of “quality indexes” as benchmarks for passive money, has meant increasingly persistent and decreasingly price-sensitive demand for the stocks of high-quality companies.

Our Portfolio response has been to redouble our attention to the other two legs of our philosophical stool: growth and price. If quality is fashionable, based on either a blind embrace of its prior success or a backward-looking fear of another financial crisis, then the fruitful way forward must be one that remains discerning

The charts above illustrate the hypothetical return of an investment made in the corresponding share classes. Investment return reflects voluntary fee waivers in effect. Absent such waivers, total return would be reduced. The performance provided in the table and charts above do not reflect the deduction of taxes that a shareholder would pay on Portfolio distributions or the redemption of Portfolio shares.

11

|

Table of Contents

yet is courageously forward-looking. In the past 12 months, this route has involved an emphasis on price, encompassing the strong value rally capped by the “Trump bump,” but it has also, in recent months, coalesced around companies achieving faster growth.

Faster economic growth has long been associated with rising labor productivity. Traditionally, labor productivity and wage growth were joined at the hip: as productivity grew, both companies and workers shared the benefits. However, the relationship between wage growth and productivity has steadily separated since the late 1970s, pressuring labor’s share of profits.

The fall of trade barriers over decades has dramatically increased consumer choices and lowered prices for those goods, while the outsourcing of manufacturing jobs from the developed world to the developing world enabled staggering gains in employment, and therefore per capita income, in developing countries. That weakened the bargaining position of less-skilled workers in the US and other developed economies. That labor arbitrage is essentially complete. Now, instead of low-skilled workers being replaced by cheaper labor abroad, their manufacturing jobs risk substitution by the application of industrial automation, robotics, and computing power. That substitution results in a similar dampening of wage growth. Furthermore, the service sector is no longer immune from the threat of technology. For example, in financial services the use of algorithmic trading and robo-advisors has begun eliminating high-paying jobs, while mobile phone apps have replaced human brokers.

Contrary to populist rhetoric, this is not solely an American or even a developed-world phenomenon. In their global company research travels, our analysts have seen the same application of industrial automation and robotics in Guangdong Province, China or Hwaseong, South Korea as they have in Peoria or Columbus. Wenting Shen, CFA, one of our China analysts, spent a month in the country this summer and noted as much: “Standing in the middle of China’s largest furniture factory last month, one can only hear the rhythms of machines, but hardly see any workers around… As frequently reported, China’s blue-collar wages have

GEOGRAPHIC EXPOSURE (%) at October 31, 2017

| COUNTRY/REGION | PORTFOLIO | BENCHMARK1 | ||||||

CANADA | 2.1 | 6.5 | ||||||

EMERGING MARKETS | 21.0 | 24.5 | ||||||

EUROPE EMU | 31.0 | 22.8 | ||||||

EUROPE EX-EMU | 19.2 | 21.4 | ||||||

JAPAN | 12.8 | 16.4 | ||||||

MIDDLE EAST | 2.2 | 0.3 | ||||||

PACIFIC EX-JAPAN | 6.4 | 8.1 | ||||||

FRONTIER MARKETS2 | 0.0 | – | ||||||

OTHER3 | 1.5 | – | ||||||

CASH | 3.8 | – | ||||||

1MSCI All Country World ex-US Index; 2Includes countries with less-developed markets outside the Index; 3Includes companies classified in countries outside the Index.

SECTOR EXPOSURE (%) at October 31, 2017

| SECTOR | PORTFOLIO | BENCHMARK1 | ||||||

CONSUMER DISCRETIONARY | 7.2 | 11.3 | ||||||

CONSUMER STAPLES | 7.5 | 9.5 | ||||||

ENERGY | 5.2 | 6.7 | ||||||

FINANCIALS | 18.8 | 23.0 | ||||||

HEALTH CARE | 16.5 | 7.6 | ||||||

INDUSTRIALS | 12.5 | 11.9 | ||||||

INFORMATION TECHNOLOGY | 21.0 | 11.7 | ||||||

MATERIALS | 6.8 | 7.9 | ||||||

REAL ESTATE | 0.7 | 3.2 | ||||||

TELECOM SERVICES | 0.0 | 4.1 | ||||||

UTILITIES | 0.0 | 3.1 | ||||||

CASH | 3.8 | – | ||||||

1MSCI All Country World ex-US Index.

been soaring, [while] automation equipment has become cheaper because of localized production of global brands as well as the improvement of substitute local brands.”

Companies that can facilitate faster, more efficient manufacturing (i.e., enable productivity gains) have enjoyed sustained and profitable growth, and many of them find a place in our Portfolio. Increasingly, their devices—such as Fanuc’s industrial robots, Keyence’s optical sensors, and Schlumberger’s downhole oil-well test tools—are integrated more fully with software and embedded with more semiconductor chips to gather information and precisely measure output, flows, temperatures, and tolerances. The prospect of machine learning has driven the capture of even more data, which will allow computers to use algorithms increasingly to make decisions independently.

PORTFOLIO HIGHLIGHTS

In our investment process, we first populate our stable of investment candidates with businesses that we believe meet our quality and growth criteria and then follow with valuation work to determine what we think a business is worth. Focusing first on the business and only later on the attractiveness of its shares means that if its shares are not attractively priced, we can monitor the progress and valuation of the business while waiting for a dislocation in the share price to provide an opening for a purchase. The market’s recent low volatility has been accompanied by high correlation among stock prices, so that there just have not been many relative price dislocations that afford us compelling opportunities to buy.

Activity in the Portfolio has been muted in recent months. Over the fiscal year, we have made thirty-two Portfolio transactions—including additions and reductions to existing positions as well as new purchases or dispositions. Nearly one-third of these transactions took place in November and December of 2016 alone, mainly reacting to large relative price changes that presented themselves in the more volatile and heterogeneous markets in the wake of the US election.

12

|

Table of Contents

One needs to look back over the past fiscal year to have a true sense of how incremental changes to the Portfolio have cumulated to substantial shifts in sectoral weights. We have reduced our holdings in Consumer Staples by about 370 basis points, largely on the sales of Bunge and Anheuser-Busch InBev (AB InBev). Owned in our Portfolio since 2012, AB InBev had been a successful investment. 3G Capital, the private equity group managing the business since its hostile takeover in late 2008, followed its cost-cutting template, wrenching down costs and boosting margins, but since AB InBev’s acquisition of another multinational beer giant, SABMiller, antitrust considerations likely rule out any further acquisitions of inefficient competitors to which to apply those methods next. Now, 3G faces the task of growing the business organically, despite slow growth in beer consumption globally and the constant challenge from the growing craft segment. Slower sales, coupled with fewer cost-cutting levers, meant to us that the company’s prospects were fully priced in its shares. Bunge, by comparison, had been a less profitable investment over our 12 years as owners. The weather-related vicissitudes of being an agriculture company, coupled with a significant exposure to recession-weary Brazilian consumers through its forward integration into cooking oils in that market, as well as long-term threats to government subsidies for its ethanol business were such that, after a bumper crop of three consecutive positive quarterly earnings surprises, we decided to exit, unconvinced that the inherently cyclical nature of the business had changed. To this point, the sale appears to have been well timed.

While our Consumer Staples holdings shrank, our Financials holdings grew. We made three new investments in EM banks in the fiscal year: India’s HDFC Bank and ICICI Bank and Mexico’s GF Banorte. All three investments were made after the Trump victory, when US dollar strength afforded the opportunity to buy EM securities more cheaply. This was especially the case with Banorte, whose share price was also depressed by Trump’s border-wall rhetoric and his threats to repeal NAFTA. We also bought a new holding in the UK-listed HSBC, believing that the regulatory environment for banks is poised to become easier, after seven years of capital, liquidity, and compliance directives following the global financial crisis. We added to our holding in BBVA, which has operations in both the US and in EMs. We believed that political consensus was building to stimulate US economic activity via government infrastructure spending, which would lead to higher interest rates and thus to higher net interest margins for the banks. Both those expectations have been dashed, with interest rates and spreads now back near pre-election levels. Nevertheless, given the outperformance of Financials against the overall market over the last year, the increased weight to Financials and our good stock selection have benefited the Portfolio by neutralizing an underweight stance that would have been costly. Today, Financials represents just under 20% of the Portfolio versus 23% for the Index.

TEN LARGEST HOLDINGS at October 31, 2017

| COMPANY | SECTOR | COUNTRY | % | |||||||||

SAMSUNG ELECTRONICS | INFO TECHNOLOGY | SOUTH KOREA | 3.7 | |||||||||

ALLIANZ | FINANCIALS | GERMANY | 3.6 | |||||||||

BAYER | HEALTH CARE | GERMANY | 3.5 | |||||||||

AIA GROUP | FINANCIALS | HONG KONG | 3.4 | |||||||||

DASSAULT SYSTÈMES | INFO TECHNOLOGY | FRANCE | 3.4 | |||||||||

NESTLE | CONS STAPLES | SWITZERLAND | 3.4 | |||||||||

FANUC | INDUSTRIALS | JAPAN | 3.2 | |||||||||

ROYAL DUTCH SHELL | ENERGY | UNITED KINGDOM | 3.1 | |||||||||

NASPERS | CONS DISCRETIONARY | SOUTH AFRICA | 3.0 | |||||||||

BAIDU | INFO TECHNOLOGY | CHINA | 2.8 | |||||||||

Please read the separate disclosures page for important information, including the risks of investing in the Portfolio.

13

|

Table of Contents

PORTFOLIO MANAGEMENT

JAFAR RIZVI, CFA PORTFOLIO MANAGER |

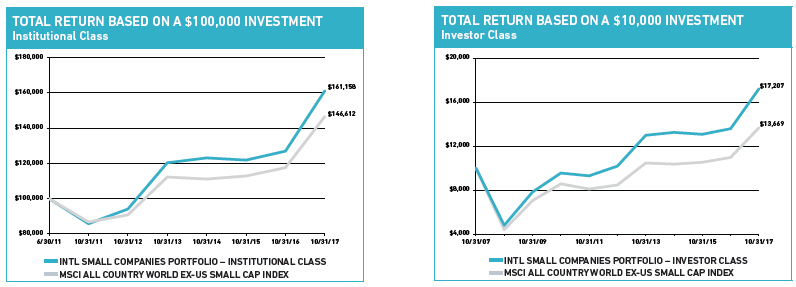

PERFORMANCE SUMMARY

PERFORMANCE SUMMARY

The International Small Companies Portfolio – Institutional Class gained 26.98% and the Investor Class gained 26.71% (net of fees and expenses) in the fiscal year ended October 31, 2017. The Portfolio’s benchmark, the MSCI All Country World ex-US Small Cap Index (the Index), rose 24.68% (net of source taxes) in this period.

MARKET REVIEW

The MSCI All Country World ex-US Small Cap Index rose 25% in the trailing 12 months, extending its string of monthly gains to eleven, the longest since 2012. Accelerating global economic growth has been an important factor underpinning investor optimism. The International Monetary Fund in July projected global economic growth of 3.5% for 2017, an improvement over 3.1% in 2016. Central banks in the US, Europe, and Japan have echoed this forecast. From our perspective deep within the company research trench, smaller companies continue to meet or exceed their growth expectations.

In contrast with the stock market’s sanguinity, political risks have been rising. Tensions between the US and North Korea heightened after North Korea launched several intercontinental ballistic missiles, two of which flew over Japanese territory. Although Angela Merkel won the election in Germany, the extreme right Alternative for Germany (AfD) party gained a foothold in the German parliament. The party draws those skeptical of the European Union; it has opposed German-backed bailouts of struggling members such as Greece and its manifesto calls for the dissolution of the euro.

The US dollar weakened as the Federal Reserve hesitated to raise rates and investors’ confidence in the administration’s ability to deliver on business-friendly tax policy changes waned. With the exception of the Swiss franc, all currencies in Europe—both inside and outside the eurozone—appreciated against the dollar, helping these two regions perform strongly in dollar terms.

Emerging Markets (EMs) also rose strongly, led by Peru. Many EM countries benefitted from rising commodity prices lifted by sustained global growth.

FUND FACTS at October 31, 2017 | ||||||||

TOTAL NET ASSETS | $194.5M | |||||||

SALES CHARGE | NONE | |||||||

NUMBER OF HOLDINGS | 87 | |||||||

TURNOVER (5 YR. AVG.) | 48% | |||||||

REDEMPTION FEE | 2% FIRST 90 DAYS | |||||||

DIVIDEND POLICY | ANNUAL | |||||||

INSTITUTIONAL INVESTORS | INDIVIDUAL INVESTORS | |||||||

| INSTITUTIONAL CLASS | INVESTOR CLASS | |||||||

TICKER | HLMRX | HLMSX | ||||||

CUSIP | 412295875 | 412295883 | ||||||

INCEPTION DATE | 6/30/2011 | 3/26/2007 | ||||||

MINIMUM INVESTMENT1 | $100,000 | $5,000 | ||||||

NET EXPENSE RATIO2 | 1.15% | 1.40% | ||||||

GROSS EXPENSE RATIO | 1.50% | 1.80% | ||||||

1Lower minimums available through certain brokerage firms; 2Shown net of Harding Loevner’s contractual agreement through February 28, 2018.

By sector, Information Technology (IT) rose the most, with companies in that sector reporting good earnings and providing strong guidance for the rest of 2017. Industrials and Financials also bettered the Index. In May, OPEC extended its crude oil production cuts by nine months, but the stubbornly slow declines in global crude oil inventories thus far this year—along with concerns about rising oil production in the US, Nigeria, and Libya as well as the lack of further OPEC actions to support oil prices—put pressure on oil prices in the period, impacting Energy sector performance.

PERFORMANCE ATTRIBUTION

Viewed by sector, our stock selection in Industrials and Financials contributed the most to relative returns. In Industrials, RPS Group, Bossard, Senior, and Arcadis had strong returns. BRAC Bank, GRUH Finance, and Rathbone Brothers led the way in Financials.

Our stock selection in IT, in particular Chinese PAX Global and Hong Kong-based Wasion Group Holdings, detracted significantly. PAX, a manufacturer of electronic payment terminals, reported a 15% fall in net income year-over-year for the first half of 2017 due to increased spending on sales, marketing, and technology. These investments are aimed at enhancing PAX’s distribution capabilities outside of China and at developing more software to enhance the company’s hardware products, pursuits that we believe will lead to future growth. However, our overweight to the IT sector in the period was a strong contributor.

Viewed by region, the Portfolio had the greatest success in the European Monetary Union (EMU), due to both our large overweight compared to the Index and strong stock selection. Approximately 30% of our Portfolio is invested in Europe EMU, compared to just

14

|

Table of Contents

PERFORMANCE (% TOTAL RETURN)

| for periods ended September 30, 2017 | for periods ended October 31, 2017 | |||||||||||||||||||||||||||||||||||||||||||||||||

| 1 YEAR | 3 YEARS | 5 YEARS | 10 YEARS | SINCE INCEPTION* | 1 YEAR | 3 YEARS | 5 YEARS | 10 YEARS | SINCE INCEPTION* | |||||||||||||||||||||||||||||||||||||||||

INTL SMALL COMPANIES PORTFOLIO - INSTITUTIONAL CLASS | 23.31 | 8.91 | 11.06 | – | 7.79 | – | 26.98 | 9.40 | 11.36 | – | 7.82 | – | ||||||||||||||||||||||||||||||||||||||

MSCI ALL COUNTRY WORLD EX-US SMALL CAP INDEX | 19.17 | 8.14 | 9.67 | 3.57 | 6.00 | – | 24.68 | 9.68 | 10.07 | 3.17 | 6.22 | – | ||||||||||||||||||||||||||||||||||||||

INTL SMALL COMPANIES PORTFOLIO - INVESTOR CLASS | 23.03 | 8.62 | 10.78 | 5.81 | – | 6.77 | 26.71 | 9.13 | 11.09 | 5.58 | – | 6.80 | ||||||||||||||||||||||||||||||||||||||

Returns are annualized for periods greater than 1 year. *Inception of the Institutional Class, 6/30/11. Inception of the Investor Class, 3/26/07. Index performance prior to 6/1/07 cannot be shown in the table above since it relies on back-filled data.

Performance data quoted represents past performance; past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the Portfolio may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by calling (877) 435-8105 or visiting www.hardinglo-evnerfunds.com. Performance data shown does not reflect the 2.00% redemption fee imposed on shares held 90 days or less; otherwise, total returns would be reduced.

The charts below illustrate the hypothetical return of an investment made in the corresponding share classes. Investment return reflects voluntary fee waivers in effect. Absent such waivers, total return would be reduced. The performance provided in the table above and charts below do not reflect the deduction of taxes that a shareholder would pay on Portfolio distributions or the redemption of Portfolio shares.

18% of the Index. France, Germany, and the Netherlands are the main sources of the overweight. In terms of stock selection, Finland-based Vaisala was a top contributor. The company manufactures microscopic mechanical sensors primarily used in weather equipment. In April, the company disclosed that its first-quarter new-order growth increased by 26% year-over-year. Stock selection in France and Germany detracted, however.

Stock selection in Europe ex-EMU was strong thanks to UK-based industrials (RPS Group and Senior) and Switzerland-based Bossard, a supplier of specialized fasteners, which reported strong earnings. Bossard continued to exhibit robust growth in the US, where sales increased by 32%, largely due to revenue earned from Tesla.

Our modest cash position detracted from relative performance in a strong period for equity returns.

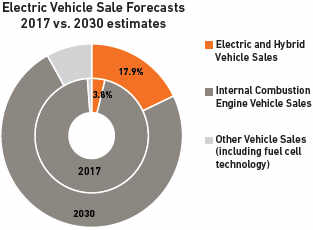

INVESTMENT PERSPECTIVES

The automotive trend toward electric and hybrid vehicles will provide a significant impetus to several of our holdings. Electric Vehicles (EVs) make up slightly less than 1% of all vehicles on the road

today. Hybrid vehicles1 constitute another 3%. Forecasts vary, but some middle-of-the-road forecasts suggest the proportion of EV’s and hybrids could rise to 11% by 2025, and 18% by 2030.

Source: Bank of America Merrill Lynch Global Research estimates, LMC Automotive, IHS Markit.

1Vehicles with an internal combustion engine and an electric motor.

15

|

Table of Contents

Investment in engineering and design for new EV and hybrid models means rising demand for Bertrandt, a provider of design and engineering services to German automakers. Special considerations pertaining to electrification include exterior and interior design, use of newer and lighter materials, noise reduction techniques, battery testing, and powertrain design.2 Given the extent of design and engineering services required, we estimate that at least a quarter of Bertrandt’s new business will relate to EVs and hybrids.

Companies that produce EV components will also benefit directly from the increased number of EVs and wider range of models. For example, LEM Holdings makes transducers that measure and control current and voltage. The company designs the chips that are used in its transducers, called application specific integrated circuits (ASICS), giving LEM a significant competitive advantage relative to competitors who rely on undifferentiated off-the-shelf chips. EVs use ten times as many transducers as internal combustion engine (ICE)-based cars. In the first quarter of 2017, the company increased sales of transducers for EVs and hybrids by 44%, and we estimate that they now represent 8% of its total sales. Bossard, the industrial fastener distributor, is also supplying the growing EV market. Tesla, one of Bossard’s largest clients, plans to produce 500,000 electric cars per year by 2018, five times its current rate. Bossard will be supplying parts for Tesla’s Model 3, which went into production in July, and its products will likely be chosen for new models that Tesla will introduce in the next few years. We estimate about 10% of Bossard’s total sales come from EVs currently. Other EV-oriented clients of Bossard include Proterra (electric buses), Gogoro (electric scooters), Alta Motors (electric motocross bikes), and Lucid Motors (electric cars). Sensata Technologies, which makes sensors for the automotive market, was recently added to the Portfolio and is discussed in the Portfolio Highlights section.

Though these companies may see sales related to traditional ICE cars decline, we expect their EV-related products to grow at a faster rate, offsetting the loss in sales to traditional business. Many automakers are setting targets that support these expectations. For instance, BMW aims for 15–25% of total sales to be from EVs by 2025.

GEOGRAPHIC EXPOSURE (%) at October 31, 2017

| COUNTRY/REGION | PORTFOLIO | BENCHMARK1 | ||||||

CANADA | 0.0 | 6.6 | ||||||

EMERGING MARKETS | 16.5 | 22.1 | ||||||

EUROPE EMU | 29.3 | 18.4 | ||||||

EUROPE EX-EMU | 23.6 | 22.5 | ||||||

JAPAN | 13.8 | 21.5 | ||||||

MIDDLE EAST | 0.6 | 1.1 | ||||||

PACIFIC EX-JAPAN | 4.0 | 7.8 | ||||||

FRONTIER MARKETS2 | 6.8 | – | ||||||

OTHER3 | 1.1 | – | ||||||

CASH | 4.3 | – | ||||||

1MSCI All Country World ex-US Small Cap Index; 2Includes countries with less- developed markets outside the Index; 3Includes companies classified in coun-tries outside the Index.

SECTOR EXPOSURE (%) at October 31, 2017

| SECTOR | PORTFOLIO | BENCHMARK1 | ||||||

CONSUMER DISCRETIONARY | 7.5 | 15.6 | ||||||

CONSUMER STAPLES | 11.5 | 6.4 | ||||||

ENERGY | 1.6 | 3.2 | ||||||

FINANCIALS | 12.5 | 10.5 | ||||||

HEALTH CARE | 13.2 | 6.7 | ||||||

INDUSTRIALS | 22.5 | 20.1 | ||||||

INFORMATION TECHNOLOGY | 22.4 | 12.8 | ||||||

MATERIALS | 2.9 | 11.0 | ||||||

REAL ESTATE | 0.0 | 9.8 | ||||||

TELECOM SERVICES | 0.6 | 1.1 | ||||||

UTILITIES | 1.0 | 2.8 | ||||||

CASH | 4.3 | – | ||||||

1MSCI All Country World ex-US Small Cap Index.

Other Portfolio companies don’t sell directly to the EV and hybrid car manufactures, but are still beneficiaries from the increasing demand in semiconductors for these cars. One of the main parts of a car, the powertrain, is expected to have 6 to 10 times more semiconductors by value for an EV than for a traditional ICE-based car. For example, analysts at UBS found US$580 worth of semiconductors in the powertrain of a Chevy Bolt, as opposed to US$60–90 in a traditional engine.3

In addition, EVs use advanced driver assistance systems, which include many safety features such as automatic braking, lane departure warning, and adaptive cruise control. These features require functionality provided by semiconductors including LiDAR (light detection and ranging), radar, sensors, and image processing.

Manufacturing of all of these semiconductors requires “clean rooms”—spaces that are cleansed of all particles by vacuum pumps. Pfeiffer Vacuum Technology is a German manufacturer of technologically-advanced pumps that can create near-perfect vacuums. Pfeiffer’s pumps are used in plants that operate at the nanometer scale and demand precision. About 38% of Pfeiffer’s sales are to manufacturers of semiconductors.

To pack more and more functionality onto the surface of a semiconductor, the integrated circuits must be made increasingly small. Deposition, which involves exposing silicon wafers to different chemicals to deposit thin films onto which the integrated circuits are etched, is the key process to create circuits on the molecular or even atomic scale. ASM International is the market leader in atomic layer deposition technology, and is benefitting from increased adoption of advanced semiconductors in EVs, which we estimate are the source of about 10–12% of ASM’s sales.

2The powertrain includes the main power-generating components of a vehicle: the engine, differentials, drive shafts, transfer case, and transmission.

3UBS Global Research, Q-Series: UBS Evidence Lab Electric Car Teardown. (May 18, 2017).

16

|

Table of Contents

The shift toward EVs will not be without negative impacts on some companies, however. Those with exposure to traditional fossil fuels, for instance, will face headwinds long term. Although we continue to hold a significant underweight in Energy relative to the Index, two companies in the Portfolio—Dialog Group Berhad and Nostrum Oil & Gas—are classified under the Energy sector. Dialog provides both upstream and downstream technical and engineering services including logistics, plant maintenance, fabrication, engineering, and construction. Nostrum Oil & Gas is a UK-listed oil and gas exploration and development company with fields in Kazakhstan.

We think the impact of EV penetration on oil and gas prices will be very gradual. Currently, the installed base of traditional ICE-based vehicles is so large that even a faster-than-expected adoption of hybrid and electric alternatives would not be an immediate threat to the future of these oil and gas companies. With over 1.2 billion traditional cars on the road, there is certainly a sizable market for oil and gas in the near term. That said, we do think sustained EV adoption poses a risk to energy suppliers, and we are closely monitoring the fundamentals of both businesses relative to their share prices.

PORTFOLIO HIGHLIGHTS

In the trailing 12 months, we continued to redeploy capital away from our most-expensive holdings in favor of relatively cheaper alternatives that nonetheless offer quality and growth characteristics.

For example, we sold Japan’s Sugi Holdings—as we considered it significantly overvalued—and Saudi Arabia’s Herfy Food Services—out of concern about intensifying competition from McDonald’s and Burger King. We also sold Coastal Contracts of Malaysia as its core business of building, selling, and chartering of offshore vehicles remains weak and could weaken further as low oil prices continue to impact demand for offshore exploration and production ships. In addition, the company is now venturing outside its main business to pursue offshore gas-treatment projects, detracting focus from its core business. Hong Kong-based electric-meter company Wasion Group Holdings was sold as we observed a significant slowdown in growth for Waison’s smart meters now that the penetration of these products in China has increased significantly. Competition has also increased, mainly from local companies.

We used the cash raised from these sales to establish positions in new high quality-growth companies whose stocks appeared more attractive on our financial models.

One new purchase was Emami Limited, an Indian company that manufactures personal care and medicinal products, such as skin cream, hair oils, pain-relief creams, and digestion aids. Emami’s products are mostly herbal based, which Indian consumers perceive as safer and more effective than chemical-based products.

TEN LARGEST HOLDINGS at October 31, 2017

| COMPANY | SECTOR | COUNTRY | % | |||||||||

VAISALA | INFO TECHNOLOGY | FINLAND | 3.1 | |||||||||

HIDAY HIDAKA | CONS DISCRETIONARY | JAPAN | 2.8 | |||||||||

ALTEN | INFO TECHNOLOGY | FRANCE | 2.7 | |||||||||

BECHTLE | INFO TECHNOLOGY | GERMANY | 2.7 | |||||||||

REPLY | INFO TECHNOLOGY | ITALY | 2.4 | |||||||||

LISI | INDUSTRIALS | FRANCE | 2.2 | |||||||||

BOSSARD | INDUSTRIALS | SWITZERLAND | 2.1 | |||||||||

ABCAM | HEALTH CARE | UNITED KINGDOM | 2.1 | |||||||||

BRAC BANK | FINANCIALS | BANGLADESH | 2.0 | |||||||||

CARL ZEISS MEDITEC | HEALTH CARE | GERMANY | 1.9 | |||||||||

Over its 43-year history, Emami has built up a distribution network of 4.6 million retail locations in India that sell its products. Through its 16 brands Emami controls approximately two-thirds of the Indian herbal-products market, a share we think it can maintain due to the nationwide reach of its distribution and customer loyalty to its brands. It would be very difficult and expensive for a competitor to build an equivalent network. Thanks to these competitive advantages, Emami grew its earnings 27% per annum over the last ten years and routinely generates a return on capital of over 20%. The negative impact of India’s 2016 currency demonetization on consumer spending is now largely behind the company. We expect it to resume growing its earnings rapidly, as consumers’ rising disposable income enables them to spend more on brand-name products.

We also purchased Sensata Technologies, which makes sensors and controls that measure physical phenomenon such as pressure, speed, and temperature. Its primary end markets are the industrial and automotive industries, both of which are increasingly adopting Sensata’s products—ranging from tire pressure monitoring systems to sensors that monitor the performance of energy-conserving industrial refrigerators—to enhance safety and efficiency. Sensata is a low-cost leader, with strong positions in both the sensor and control markets thanks to an ability to deliver high-quality, customized products. The company has consistently generated strong free cash flow and double-digit returns on invested capital and returns on equity.

Other high-quality companies added to the Portfolio in the past 12 months include five other Industrials companies, an Energy company, two Financials companies, two Health Care companies, and three IT companies.

Please read the separate disclosures page for important information, including the risks of investing in the Portfolio.

17

|

Table of Contents

| PORTFOLIO MANAGEMENT TEAM | ||

|

| G. RUSTY JOHNSON, CFA | PRADIPTA CHAKRABORTTY | |

CO-LEAD PORTFOLIO MANAGER

| PORTFOLIO MANAGER

| |

| CRAIG SHAW, CFA | SCOTT CRAWSHAW | |

| CO-LEAD PORTFOLIO MANAGER | PORTFOLIO MANAGER

| |

| RICHARD SCHMIDT, CFA | ||

PORTFOLIO MANAGER |

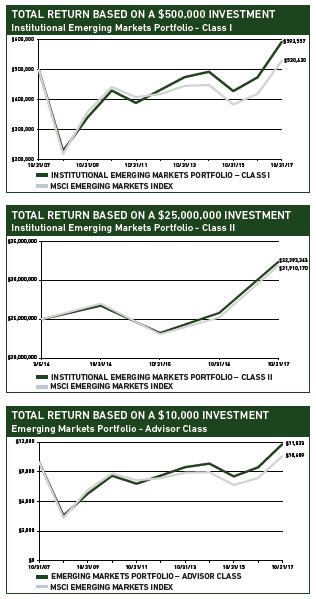

The Institutional Emerging Markets Portfolio and the Emerging Markets Portfolio are generally closed to new investors.

The Institutional Emerging Markets Portfolio – Class I and Class II – and the Emerging Markets Portfolio – Advisor Class (collectively, the “Portfolios”) are both managed in strict accordance with the Emerging Markets Equity strategy model portfolio. Therefore, the Portfolios have highly similar holdings and characteristics. We have provided a single commentary to cover both Portfolios. The specific performance and characteristics of each are presented separately in the tables that follow.

PERFORMANCE SUMMARY

PERFORMANCE SUMMARY

The Institutional Emerging Markets Portfolio – Class I rose 25.08%, the Institutional Emerging Markets Portfolio – Class II rose 25.43%, and the Emerging Markets Portfolio – Advisor Class rose 24.93% (all net of fees and expenses) in the fiscal year ended October 31, 2017. The Portfolios’ benchmark, the MSCI Emerging Markets Index rose 26.45% (net of source taxes) in this period.

MARKET REVIEW

The fiscal year ending October 31, 2017 began inauspiciously for Emerging Markets (EMs), which declined sharply in November as the surprise election of Donald Trump sparked concern among investors about the potential impact of his protectionist agenda on global trade and EM companies. Inflation expectations and bond yields also quickly rose, hurting the value of EM currencies versus the US dollar. But EMs recovered in January and enjoyed positive momentum for the rest of the fiscal year, propelled by a supportive combination of robust global economic growth, declining inflation expectations, and strong results in the Information Technology (IT) sector.

Investors were also heartened by China’s strong economic growth, the stabilization of its currency, and moderation of capital outflows. Rising corporate profits have eased fears about the corporate sector’s ability to service its high level of debt—which has been a key risk facing the Chinese economy. As corporate liabilities fell,

FUND FACTS at October 31, 2017 | ||||||||||||

SALES CHARGE | NONE | |||||||||||

NUMBER OF HOLDINGS | 78 | |||||||||||

REDEMPTION FEE | 2% FIRST 90 DAYS | |||||||||||

DIVIDEND POLICY | ANNUAL | |||||||||||

INSTITUTIONAL INVESTORS | INDIVIDUAL INVESTORS | |||||||||||

PORTFOLIO ASSETS | $4,844.8M | $4,015.0M | ||||||||||

TURNOVER (5 YR AVG) | 21% | 29% | ||||||||||

CLASS | CLASS I | CLASS II | ADVISOR | |||||||||

TICKER | HLMEX | HLEEX | HLEMX | |||||||||

CUSIP | 412295701 | 412295693 | 412295305 | |||||||||

INCEPTION DATE | 10/17/2005 | 3/5/2014 | 11/9/1998 | |||||||||

MINIMUM INVESTMENT1 | $500,000 | $25,000,000 | $5,000 | |||||||||

NET EXPENSE RATIO | 1.29% | 1.12%2 | 1.42% | |||||||||

GROSS EXPENSE RATIO | 1.29% | 1.24%3 | 1.42% | |||||||||

1Lower minimums available through certain brokerage firms;

2The Net Expense Ratio is as of October 31, 2017 as the Portfolio is operating below the contractual agreement, which is in effect until February 28, 2018;

3The Gross Expense Ratio is as of the Prospectus dated February 28, 2017.