UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act File Number 811-09025

New Covenant Funds

(Exact name of registrant as specified in charter)

SEI Investments

One Freedom Valley Drive

Oaks, PA 19456

(Address of principal executive offices) (Zip code)

Timothy D. Barto, Esq.

SEI Investments

One Freedom Valley Drive

Oaks, PA 19456

(Name and address of agent for service)

Registrant’s telephone number, including area code: 1-610-676-1000

Date of fiscal year end: June 30, 2021

Date of reporting period: June 30, 2021

| Item 1. | Reports to Stockholders. |

NEW COVENANT FUNDS® June 30, 2021 ANNUAL REPORT New Covenant Funds New Covenant Growth Fund New Covenant Income Fund New Covenant Balanced Growth Fund New Covenant Balanced Income Fund Paper copies of the Funds’ shareholder reports are no longer sent by mail, unless you specifically request them from the Funds or from your financial intermediary, such as a broker-dealer or bank. Shareholder reports are available online and you will be notified by mail each time a report is posted on the Funds’ website and provided with a link to access the report online. You may elect to receive all future reports in paper free of charge. If you invest through a nancial intermediary, you can contact your nancial intermediary to inform it that you wish to continue receiving paper copies of your shareholder reports. If you invest directly with the Funds, you can inform the Funds that you wish to continue receiving paper copies of your shareholder reports by calling 1-877-835-4531. Your election to receive reports in paper will apply to all funds held with the SEI Funds or your nancial intermediary. newcovenantfunds.com

TABLE OF CONTENTS

The Trust files its complete schedule of portfolio holdings with the Securities and Exchange Commission for the first and third quarters of each fiscal year as an exhibit to its reports on Form N-PORT. The Trust’s Form N-PORT reports are available on the Commission’s website at http://www.sec.gov.

A description of the policies and procedures that the Trust uses to determine how to vote proxies relating to portfolio securities, as well as information relating to how a Fund voted proxies relating to portfolio securities during the most recent 12-month period ended June 30, is available (i) without charge, upon request, by calling 1-877-835-4531; and (ii) on the Commission’s website at http://www.sec.gov.

NEW COVENANT FUNDS — JUNE 30, 2021 (Unaudited)

To Our Shareholders:

The fiscal year ending June 30, 2021, began with markets continuing their remarkable rally from the March 2020 lows. The “risk-on” sentiment came amid a push by local governments to slowly reverse lockdowns of non-essential economic activity; the promising news of progress made in the race to develop COVID-19 vaccines; and the sustained extraordinary support of central banks. U.S. equity markets eclipsed their pre-pandemic peaks by August and finished the fiscal year near all-time highs.

Central banks aggressively pursued accommodative monetary policy, asset purchase programs and record fiscal stimulus measures during the reporting period. In September, the millionth victim of the COVID-19 outbreak was claimed globally, a figure that would climb to nearly 4 million by the end of June. Cases had seemed to abate for a time during late-summer 2020, but then once again began to rise in the fall as variant strains were identified and met with another round of lockdowns in Europe and more sporadically in the U.S. Fears of yet another wave of outbreaks kept markets in a more cautious stance.

Markets advanced once it became clearer that former Vice President Joe Biden would become the next U.S. president in what would likely be a split government. Expectations of further, but less expansive, fiscal stimulus from Congress and a less likely reversal of the corporate tax cuts under the Trump administration fueled this appreciation. Investor exuberance kicked off in earnest in November after a series of positive vaccine clinical trial results; the enthusiasm was sustained by subsequent emergency use authorizations by the FDA.

Financial markets anticipated increased volatility around the U.S. presidential election, but with Joe Biden winning a close election for U.S. president and the announcement of effective vaccines thereafter, markets advanced higher and volatility declined. Despite no sign of the Federal Reserve tightening in the near term, the U.S. Treasury yield curve steepened over the course of the fiscal year, especially as future expectations for a rebound in economic growth increased along with rising inflation expectations; long-term yields rose more than shorter-term yields.

Government-bond yields (which had been rising slowly since the fall) began to spike further in February. The specter of a sharp increase in borrowing costs sent chills through markets during the second half of February, leading to selloffs of varying intensity before markets resumed their climb again in March.

The Federal Reserve’s (Fed) federal-funds rate target continued to range between 0.0% and 0.25%, and the Federal Open Market Committee (“FOMC”)—the Fed’s monetary policymakers—remained committed to purchasing Treasurys and agency mortgage-backed securities (“MBS”). Fed Chair Jerome Powell pledged to continue supporting the economy via monetary policy during his semi-annual congressional testimony on February 24, 2021.

The year was also characterized by a polarized equity market. Over the first half of the period, high-flying technology companies shared the spotlight with businesses that benefited from the pandemic. A narrow band of extraordinarily high-priced stocks led the market higher as reasonably priced, fundamentally sound businesses languished. However, a reflationary theme dominated the second half of the period as markets anticipated economic reopening and additional rounds of massive U.S. fiscal easing. Equities continued to roll along, although work-from-home and mega-cap stocks gave up ground to cyclical and “go-out” names before a slight reversal over the final few weeks of the period. Market observers attributed this to the FOMC deciding to increase its projection for the federal-funds rate in 2023. Meanwhile, for the first time since April this year, the seven-day moving average of new COVID-19 cases reported in the U.S. stopped falling in mid-June after an impressive period of declines that brought cases to their lowest levels since March 2020.

Geopolitical Events

In the U.S. general election in November, Joe Biden was declared the winner of the presidential race in early November. Most candidates from the Republican Party performed better in their races for state- and national-level offices compared to President Trump’s quest for a second term; in January, a violent security breach of the U.S. Capitol by a mob of protesters delayed—but did not stop—the counting of electoral votes in the U.S. Congress. Trump was impeached by the House of Representatives for inciting an insurrection—the first president in U.S. history to be impeached twice. Two weeks later, Joe Biden was inaugurated as president under heavy security provided by 25,000 National Guard troops.

| | | | |

New Covenant Funds / Annual Report / June 30, 2021 | | | 1 | |

NEW COVENANT FUNDS — JUNE 30, 2021 (Unaudited) (Continued)

President Joe Biden’s administration proposed a $6 trillion budget for the 2022 fiscal year that would serve as a starting point from which Congress can decide how to appropriate the country’s economic funding. The president incorporated his two major economic initiatives into the budget—infrastructure (estimated $2.3 trillion) and families programs (estimated $1.8 trillion)—along with $1.5 trillion for defense. Negotiations during May produced an offer from the White House to lower its infrastructure price tag to $1.7 trillion and a counter bid from Senate Republicans for a $928 billion package.

The prospect of a bipartisan U.S. infrastructure deal appeared to brighten in mid-June as a group of Senate Republicans and Democrats agreed to a White House compromise that would direct $1.2 trillion toward improving the country’s structures and facilities over an eight-year period. The plan would provide about $580 billion in new spending and sidestep tax increases. However, the possibility of a party-line vote on a larger package by President Biden’s Democrats remained on the table as Republicans took issue with plans by the Democrats to enact other parts of their spending agenda once the infrastructure deal had concluded.

The United States-Mexico-Canada trade agreement was ratified by all three countries and officially replaced the North American Free Trade Agreement at the start of the reporting period on July 1. The Trump administration announced in September that it would not pursue a 10% tariff on U.S. imports of Canadian aluminum previously announced in August, as trade is now expected to normalize following high import levels earlier in 2020. President Trump and France’s President Emmanuel Macron successfully walked back threats of tariffs that originated with French plans for a digital tax that would have targeted U.S.-based multi-national technology companies.

In a push to re-establish tourism ahead of the traditionally busy summer season, the EU approved a proposal made by the European Commission in May to ease travel restrictions within the bloc for vaccinated foreigners. Tensions between the EU and China—which have flared over the last six months as the EU condemned China’s record on human rights and China imposed retaliatory economic sanctions—remained unsettled. In May, the European Parliament suspended ratification of the Comprehensive Agreement on Investment that EU and Chinese leaders had finalized in December 2020. As for U.S.-EU trade relations, friction smoothed as the European Commission delayed an increase to tariffs on the U.S. that had been planned in response to the Trump administration’s tariffs on European metals; existing tariffs will remain as the two sides negotiate a long-term solution.

Economic Performance

U.S. gross domestic product (“GDP”) saw a record 33.4% rebound in the third quarter of 2020, fueled by over $3 trillion in pandemic relief. A 4.0% gain in the fourth quarter resulted in a decline of 3.5% for the full year, the worst figure since at least the end of World War II. The U.S. economy expanded at a robust annualized rate of 6.4% in the first quarter of 2021; consumer spending (which accounts for nearly 70% of U.S. economic activity) spiked by 11.3% as Americans put their stimulus payments to work, providing a much-needed boost to restaurants, hotels and airlines. GDPNow, a running estimate of real GDP growth based on available economic data for the current measured quarter, projected a 7.6% gain for the second quarter of 2021, as service-oriented businesses anticipated continued gains from the rise in vaccinations and reopenings.

After touching a 50-year low of 3.5% and then jumping as high as 14.8% prior to the start of the fiscal year, the U.S. unemployment rate remained over 7.0% through September, with the final figure settling at 5.9% in June 2021, down from 11.1% a year earlier. The labor-force participation rate ended at 61.6%, up from 61.4% a year earlier. Average hourly earnings gained 3.6% over the fiscal year, as the leisure and hospitality industry continued to reopen and looked to boost pay in order to fill vacant positions.

Two off-cycle moves before the start of the fiscal year brought the federal-funds rate to near zero and were designed to bolster the economy in response to the economic threat posed by the coronavirus outbreak; the emergency actions were the first since the global financial crisis. Additionally, the Fed committed to purchasing unlimited amounts of Treasurys and established or renewed multiple facilities designed to support the economy. The FOMC held the federal-funds rate near zero throughout the second quarter and continued its asset purchases apace ($80 billion in Treasurys and $40 billion in agency mortgage-backed securities per month). Its latest Summary of Economic Projections (SEP), released in mid-June, featured a projected increase in the federal-funds rate to 0.6% in 2023 (up from 0.1% in its March projection). The SEP also depicted significantly higher real gross domestic product (“GDP”) and inflation projections for 2021, although out-year projections were only modestly higher.

| | |

| 2 | | New Covenant Funds / Annual Report / June 30, 2021 |

Market Developments

The S&P 500 Index returned 40.79% during the fiscal year. Large-cap value stocks (as measured by the Russell 1000 Value Index) edged out large-cap growth stocks (as measured by the Russell 1000 Growth Index). At the sector level, financials, industrials and capital goods stocks led, while utilities, healthcare, consumer staples and real estate lagged. Overall, U.S. equities outpaced major developed markets during the fiscal year.

Small-cap stocks, which tend to be value-oriented and sensitive to the success or decline in a local economy, outperformed large caps overall. U.S. large-cap stocks (Russell 1000 Index) finished the reporting period up 43.07%, while small-cap stocks (Russell 2000 Index) finished the period ahead 62.03%.

The MSCI Emerging Markets Index (Net) finished the reporting period up 40.90% in U.S. dollar terms. Emerging-market equities were on a tear since bottoming early in the pandemic. Emerging-market stocks edged out developed markets, as measured by the MSCI World Index (Net), which finished up 39.04% for the year. The best-performing region was EM Latin America, which was lifted by strong performance from Brazil and Mexico, both of which benefitted from the shift in market appetite for cyclical sectors like materials. China was a relative benchmark laggard as government regulations weighed on social media and ecommerce equity prices.

The MSCI Europe Index (Net) advanced 35.09% in U.S. dollar terms. The MSCI ACWI Index (Net), a proxy for global equities in both developed and emerging markets, rose 39.26% in U.S. dollar terms. The FTSE UK Series All-Share Index recorded a 35.79% gain in U.S. dollar terms over the full reporting period.

The U.S. high-yield market, as measured by the ICE BofA US High Yield Constrained Index, was up 15.60% during the reporting period, while U.S. investment-grade corporate debt, as represented by the Bloomberg Barclays US Corporate Investment Grade Index, returned 3.30%. Within the high-yield market, the energy sector outperformed the broader market during the period, returning in excess of 28%. Lower-quality issues also outperformed, as CCC rated securities led, followed by B and BB rated. U.S. asset-backed securities managed gains during the fiscal year, benefiting from improving supply-and-demand dynamics; mortgage-backed securities were down slightly, as elevated supply and fast prepayment speeds offset the Fed adding around $40 billion of MBS to its balance sheet each month.

Global fixed income, as measured by the Bloomberg Barclays Global Aggregate Index, climbed 2.63%. Emerging-market debt (“EMD”) delivered positive performance due to an improving growth outlook in the region relative to developed markets. The J.P. Morgan Global Bond Index-Emerging Markets (“GBI-EM”) Global Diversified Index, which tracks local-currency-denominated EM bonds, gained 6.57% in U.S. dollar terms. The J.P. Morgan Emerging Markets Bond Index (“EMBI”) Global Diversified Index, which tracks EMD denominated in external currencies (such as the U.S. dollar), was up 7.53%.

After the U.S. dollar initially rebounded from its January low (relative to a trade-weighted basket of foreign currencies), it resumed an overall downward trend and neared its earlier low again in May before recovering some as the fiscal year closed. After hitting an all-time low before the start of the reporting period, the West Texas Intermediate crude-oil price reached a 40-month high near the end of the fiscal year due to optimistic forecasts for global economic growth and increased demand for crude.

Our view

Equity markets have long anticipated the economic improvement we now are watching unfold. There is increasing concern, however, that equity prices have risen so much that there is little appreciation potential left, even if the global economy continues to forge ahead into 2022.

The last several weeks have witnessed a partial unwinding of the rotation trade that began last autumn. So far, this appears to us as a temporary pause in a longer-term upswing. The global recovery and expansion have a long way to go, especially since many countries are still imposing lockdown measures to varying degrees.

We can’t rule out a choppier and more lackluster performance for U.S. equities in the months ahead, given elevated stock-market valuations relative to much of the rest of the world and the strong outperformance of the U.S. since March 2009. Investors shouldn’t get overly concerned if stock-market volatility increases. 5%-to-10% corrections can occur without any fundamental reason.

| | | | |

New Covenant Funds / Annual Report / June 30, 2021 | | | 3 | |

NEW COVENANT FUNDS — JUNE 30, 2021 (Unaudited) (Continued)

In today’s environment, with economies opening up and interest rates still at extraordinarily low levels, the dominant trend favors further price gains over the next year or two. Still, investors must take into account that the U.S. economy appears to have reached “peak growth.”

Growth slowdowns, not just recessions, can lead to equity underperformance versus bonds. The relative performance of equites versus bonds was phenomenal over the past 15 months; a major narrowing of the performance gap is inevitable. Yet, with interest rates still at exceptionally low levels, it is hard to see equities losing ground to fixed-income securities while economic growth remains so robust. Not only should consumer demand remain strong as the economy opens up, but businesses too are in a spending mood, desperately seeking materials and workers.

In the meantime, companies will enjoy a great deal of pricing power and will almost certainly pass along at least a portion of their increased costs to customers. Unfortunately, one person’s pricing power is another person’s inflation. The big question is whether the price pressures seen this year are transitory, as central bankers around the world say they are.

Investors in the bond market seem to agree with the central bankers. Although U.S. bond yields rose sharply in the first quarter, they have fallen over the past three months. There’s no telling how long bond investors will maintain such a calm perspective if prices keep rising at a pace that has not been seen in almost 30 years.

In his latest testimony, Fed Chairman Powell reiterated that the labor market still has a long way to go before it reaches full employment. Job openings in the U.S. are now soaring. If the rise in the Employment Cost Index accelerates as we expect, inflation could become a greater concern for investors than appears to be the case at the moment.

Markets reacted negatively to a surprising extent when the central bank revealed the FOMC’s updated “dot plot” of federal funds rate projections on June 16. The median FOMC projection now calls for two rate hikes in 2023, which was exactly what futures traders had already priced in. Those same traders have now priced in three rate hikes by the end of 2023, but a lot can happen between now and then.

The recent stumble in the rotation theme was exacerbated by this shift in the Fed’s expectations. It is clear, however, that the U.S. central bank will be cautiously moving away from its current policy stance. The first move will likely be the tapering of its bond-buying program, which might be announced in late August at the annual Jackson Hole conference, with actual tapering beginning in the first quarter of 2022 (at the earliest).

The path of U.S. fiscal policy is harder to decipher, given strained bipartisanship and the narrowness of the Democratic majority in the Congress. A traditional infrastructure bill is a good bet, but the push for non-traditional forms of infrastructure—and the taxes to pay for all the added spending—will depend on whether the Democrats in the Senate can come to terms with each other.

The combination of (1) above-average economic growth, (2) significantly higher inflation than seen in the past decade (3) a fiscal policy that expands the size of federal government spending and (4) extreme monetary ease aimed at suppressing interest rates is the perfect backdrop for risk assets—and for the creation of speculative bubbles.

The relative success of the vaccination effort in the U.S. and the country’s state-by-state response have resulted in a significantly stronger economy this year than in other major developed countries. Fortunately, vaccinations are accelerating in Europe and Japan. We anticipate that other advanced economies should record strong results in the second half of the year and into 2022, exceeding the pace in the U.S.

Although economists correctly point out that the United States has employed direct fiscal measures (emergency spending, income support and tax breaks) more aggressively than any other nation, other countries have used different tactics that far exceed the U.S. effort.

Several European nations and Japan have relied on equity injections, loans and guarantees. Italy (35% of GDP), Japan and Germany (both at 28%) are the most notable according to the International Monetary Fund1. In the eurozone, some of these loan commitments have only just begun to flow. Italy and Spain are big beneficiaries of the eurozone’s €750 billion in loans and grants as part of the so-called NextGenerationEU program.

| | |

| 4 | | New Covenant Funds / Annual Report / June 30, 2021 |

The ECB also seems dedicated to maintaining its pandemic-related monetary support at least through March 2022. As a percentage of GDP, the ECB’s balance sheet has risen more than 25% since the beginning of the COVID-19 crisis, more than any other major central bank besides the BOJ (30%). The ECB’s actions have succeeded in keeping peripheral Europe’s sovereign bond yields well behaved through the crisis period.

While the U.S., the U.K. and Canada seem to be enduring a much sharper price rise than Japan or the eurozone, the latter two are probably relieved to have a respite from the deflationary pressures that have been afflicting their economies for many years. There seems little reason for the ECB or the BOJ to join the Fed when it comes to discussing a near-term reduction in their asset purchases, much less raising their policy rates ahead of the U.S.

The trade-weighted dollar jumped to its highest level in three months against other major currencies in the days following the Fed’s latest announcement, although the currency remains some 10% below its March 19, 2020 high. Since any serious policy move by the Fed is still rather far in the future, we continue to expect the dollar to weaken over time as the rest of the world gains economic strength.

In the meantime, we also do not see much sign that the Fed’s shift toward an earlier lift-off in rates is leading to a 2013-style “taper tantrum” among emerging economies. A strong dollar would certainly threaten the bull market in commodity prices.

We are still bullish on the outlook for commodities, but we are watching price trends carefully. Commodity prices of all types have enjoyed a spectacular run since March 2020 and were already in the process of consolidating or correcting in the weeks before the Fed revised its views.

We remain optimistic that the more cyclical and value-oriented areas within emerging markets will bounce back from their modest stumble in June. But there are near-term challenges besides the shift in perceptions about Fed policy and the future course of the dollar and commodity prices. Credit growth has decelerated significantly in China, similar to the slowdowns recorded in 2013 and 2018—years when the performance of emerging markets was less than stellar.

Another potential source of market volatility could stem from the increasingly fraught relationship between China and the U.S. and its allies. If there is any consensus in Washington nowadays, it is focused on countering China’s growing economic and military strength, although market participants have mostly managed to look past political tensions to date.

Fundamentally, emerging markets continue to look relatively cheap versus most other regions. The forward price-to-earnings multiple of the MSCI Emerging Markets Index is still selling at a 36.5% discount to that of the MSCI USA Index. Outside the March-April 2020 low point, this is as cheap a relative multiple against the U.S. as seen at any time in the past 16 years.

We are counting on the advanced economies to take up the slack while vaccines ramp up in developing countries. There is a tremendous amount of excess savings and pent-up demand in North America and Europe. That said, as the northern hemisphere enters the autumn and winter, the possibility of regional spikes in cases cannot be dismissed. If severe enough, markets could switch back to a decidedly risk-off position.

As vaccination rates slow in the developed world, more shots will be available for the rest of the world. We expect a rolling reopening of the global economy that will extend well into 2022. This wave of recovery could resemble an extended up-cycle that keeps the pressure on supply chains, leading to continued shortages of goods and labor. Investor faith in the “transitory inflation” narrative probably will be tested as we head into year-end and into 2022.

| 1 | International Monetary Fund (IMF), 2021, “Database of Fiscal Responses to COVID-19” (Washington), available at https://www.imf.org/en/Topics/imf-and-covid19/ Fiscal-Policies-Database-in-Response-to-COVID-19 |

Sincerely,

James Smigiel

Chief Investment Officer

| | | | |

New Covenant Funds / Annual Report / June 30, 2021 | | | 5 | |

NEW COVENANT FUNDS — JUNE 30, 2021 (Unaudited) (Concluded)

Index Definitions

Bloomberg Barclays Global Aggregate Index: is a broad-based benchmark that is considered representative of global investment-grade, fixed-income markets.

Bloomberg Barclays US Corporate Investment Grade Index: is a broad-based benchmark that measures the investment-grade, fixed-rate, taxable corporate bond market.

Bloomberg Barclays US Aggregate Bond Index: The Bloomberg Barclays U.S. Aggregate Bond Index is a benchmark index composed of U.S. securities in Treasury, government-related, corporate and securitized sectors. It includes securities that are of investment-grade quality or better, have at least one year to maturity and have an outstanding par value of at least $250 million.

Dow Jones Industrial Average: The Index measures the stock performance of 30 large companies listed on stock exchanges in the United States.

FTSE UK Series All-Share Index: is a capitalization-weighted index, comprising around 600 of more than 2,000 companies traded on the London Stock Exchange.

ICE BofA US High Yield Constrained Index: tracks the performance of below-investment-grade, U.S. dollar-denominated corporate bonds publicly issued in the U.S. domestic market; exposure to individual issuers is capped at 2%.

JP Morgan EMBI Global Diversified Index: tracks the performance of external debt instruments (including U.S.-dollar-denominated and other external-currency-denominated Brady bonds, loans, eurobonds and local-market instruments) in emerging markets.

JP Morgan GBI-EM Global Diversified Composite Index: tracks the performance of debt instruments issued in local currencies by emerging-market governments.

MSCI Europe Index: is a free float-adjusted market-capitalization-weighted index designed to measure the performance of large- and mid-capitalization stocks across developed-market countries in Europe.

MSCI Emerging Markets Index: is a free float-adjusted market-capitalization-weighted index designed to measure the performance of global emerging-market equities.

MSCI World Index: is a free float-adjusted market-capitalization-weighted index that is designed to measure the equity-market performance of developed markets. The Index consists of 24 developed-market country indexes.

Russell 1000® Index: includes 1,000 of the largest U.S. stocks based on market cap and current index membership; it is used to measure the activity of the U.S. large-cap equity market.

Russell 2000® Index: The Russell 2000® Index measures the performance of the 2,000 smallest companies in the Russell 3000® Index, which represents approximately 8% of the total market capitalization of the Russell 3000® Index.

S&P 500 Index: is an unmanaged, market-weighted index that consists of 500 of the largest publicly-traded U.S. companies and is considered representative of the broad U.S. stock market.

| | |

| 6 | | New Covenant Funds / Annual Report / June 30, 2021 |

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FUND PERFORMANCE

June 30, 2021 (Unaudited)

New Covenant Growth Fund

I. Objective

The New Covenant Growth Fund’s (the “Fund”) investment objective is long-term capital appreciation. A modest amount of dividend income may be provided by the Fund’s equity securities.

II. Investment Approach

The Fund uses a sub-adviser to manage the Fund under the supervision of SEI Investments Management Corporation (“SIMC”). The sole sub-adviser as of June 30, 2021, was Parametric Portfolio Associates LLC (Parametric). There were no sub-adviser changes during the fiscal period.

III. Return vs. Benchmark

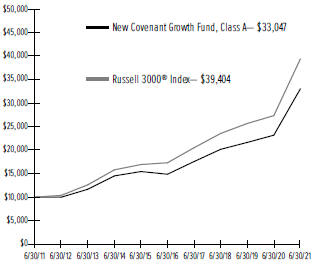

For the one-year period ending June 30, 2021, the Fund’s Class A shares returned 42.58%. The Fund’s primary benchmark, the Russell 3000® Index—which measures the performance of the 3000 largest U.S. companies and represents approximately 98% of the investable U.S. equity market—returned 44.16%.

IV. Fund Attribution

As noted in the shareholder letter, the U.S. equity market produced highly positive returns during the fiscal year as people generally became confident that the economy would rebound strongly from the pandemic-driven trough. With Democrats taking control of the U.S. congress and Joe Biden becoming President, U.S. government spending was expected to increase without the gridlock that may have existed if power had been evenly divided between the parties. Fiscal stimulus and vaccinations were key reasons for the improved economic outlook, while the potential for a significant increase in inflation remained on investors’ minds later in the period.

The financials sector was the best-performing sector during the reporting period as investors concluded that interest rates would be rising in the second half of the fiscal year. Additionally, banks’ loan-loss reserves were determined to be more than necessary for the situation. The energy and industrials sectors also outperformed as many of the companies represented were expected to benefit from an increase in economic activity coming out of the trough. Sectors traditionally considered to be non-cyclical—such as utilities, healthcare, and consumer staples—underperformed as company earnings in these areas were expected to gain little from the economic rebound; their lower-volatility characteristics were also out of favor as investor risk tolerance increased. Small-

cap stocks outperformed relative to larger-capitalization stocks. Despite a rotation toward value stocks that began part of the way through the fiscal year, some big growth stocks—namely Tesla, Alphabet and Apple—still outperformed and had a material impact on index returns.

In this environment, the Fund underperformed as the combination of its screens and environmental, social, and corporate governance tilt had a negative effect on performance. The sectors that were somewhat restricted due to the Fund’s guidelines, such as industrials and communications services, performed well during the fiscal year, and the resulting underweights of securities within those sectors hurt performance. Sectors that were more accepted by the Fund guidelines, such as healthcare and information technology, had returns that were either in line or below that of the market; the aggregate differences in weights relative to the index ended up hurting Fund performance during the fiscal year.

Investing is subject to risk, including the possible loss of principal. Past performance is no indication of future results.

| | | | | | | | | | | | | | | | | | | | |

|

| AVERAGE ANNUAL TOTAL RETURN 1 | |

| | | One Year

Return | | | Annualized

3 Year

Return | | | Annualized

5 Year

Return | | | Annualized

10 Year

Return | | | Annualized

Inception

to Date | |

| New Covenant Growth Fund, Class A | | | 42.58% | | | | 17.89% | | | | 17.30% | | | | 12.70% | | | | 6.34% | |

| Russell 3000® Index | | | 44.16% | | | | 18.73% | | | | 17.89% | | | | 14.70% | | | | 7.76% | |

| | | | |

New Covenant Funds / Annual Report / June 30, 2021 | | | 7 | |

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FUND PERFORMANCE

June 30, 2021 (Unaudited)

New Covenant Growth Fund (Concluded)

Comparison of Change in the Value of a $10,000 Investment in the New Covenant Growth Fund, Class A, versus the Russell 3000® Index.

| 1 | For the periods ended June 30, 2021. Past performance is not an indication of future performance. Fund Shares were offered beginning 7/1/99. Returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. The returns for certain periods reflect fee waivers and/or reimbursements in effect for that year; absent fee waivers and reimbursements, performance would have been lower. |

| | |

| 8 | | New Covenant Funds / Annual Report / June 30, 2021 |

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FUND PERFORMANCE

June 30, 2021 (Unaudited)

New Covenant Income Fund

I. Objective

The New Covenant Income Fund’s (the “Fund”) investment objective is a high level of current income with preservation of capital.

II. Investment Approach

The Fund uses a multi-manager approach, relying on a number of sub-advisers with different investment approaches to manage portions of the Fund’s portfolio, under the general supervision of SEI Investments Management Corporation (“SIMC”). The Fund utilized the following sub-advisors as of June 30, 2021: Income Research & Management, Western Asset Management Company and Western Asset Management Company Limited. There were no sub-adviser changes during the fiscal period.

III. Return vs. Benchmark

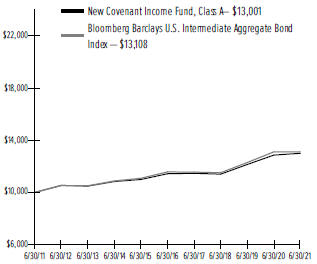

For the one-year period ending June 30, 2021, the Fund’s Class A shares returned 1.13%. The Fund’s primary benchmark, the Bloomberg Barclays U.S. Intermediate Aggregate Bond Index—a capitalization-weighted index that measures the performance of investment-grade bonds in the U.S. with maturities of less than 10 years—returned 0.05%.

IV. Fund Attribution

Risk assets outperformed comparable Treasurys over the course of the fiscal year as the Federal Reserve provided an unprecedented level of monetary support, sizable additional fiscal stimulus was passed following a Democrat sweep of congress, and the rollout of three vaccines in the United States led the economy toward a broad reopening. The Federal Reserve’s (“Fed”) support went beyond traditional monetary policy as the central bank purchased both individual corporate bonds and corporate bond exchange-traded funds through its Secondary Market Corporate Credit Facility, backstopped agency-backed securities as they re-instituted the Term Asset-Backed Securities Loan Facility (“TALF”), and continued to purchase agency mortgage-backed securities (“MBS”) and U.S. Treasurys at a pace of $120 billion per month during the period. Additional fiscal stimulus provided payments directly to Americans and extended unemployment benefits, serving to boost consumer spending as the economy moved toward a full reopening. As noted in the shareholder letter, a successful rollout of COVID-19 vaccines throughout the first six months of 2021 resulted in the lifting of health-related lockdowns, further propelling the economic rebound.

While these factors contributed to accelerated economic growth in the first quarter of 2021, investors became increasingly worried that inflation would run above expectations and that the Fed would raise rates sooner than expected. Due to increased inflation expectations, long-term yields were higher over the course of the fiscal year—including a sharp rise during the first three months of 2021—before retracing some of the move higher, with the 10-year U.S. Treasury rate ending the period at 1.47%. Risk assets rallied and excess returns relative to Treasurys were strong. Corporate credit spreads narrowed to near an all-time low on a combination of Fed support, low nominal yields, and improved economic growth prospects. The technical environment was favorable as U.S. investment-grade credit continued to out-yield much of the world’s debt. Securitized sectors also performed well as agency MBS benefited directly from the Fed’s purchases; spreads on high-quality asset-backed securities (“ABS”) continued to grind tighter as the income and employment situation of the U.S. consumer continued to improve throughout the year; while commercial mortgage-backed securities (“CMBS”) initially lagged the rally, performance rebounded during the second half of the period as it looked like worst-case scenarios for commercial property would be avoided.

Given the excess returns generated by risk assets, the Fund outperformed the Bloomberg Barclays U.S. Intermediate Aggregate Bond Index during the period. An overweight to corporate credit contributed to outperformance, while selection within the financials and insurance industries detracted. Security selection within ABS, particularly autos, added. An overweight to CMBS also added as the sector rallied later in the year. Selection within agency MBS added to performance as managers were able to implement a “follow the Fed” strategy.

Western Asset Management outperformed primarily due to its corporate overweight as spreads tightened past pre-pandemic levels. An overweight to securitized sectors such as ABS and CMBS contributed as well. Western’s overweight to the 30-year part of the curve and slightly longer duration subtracted as yields rose. The Fed backstopped the ABS market through the re-institution of TALF. Income Research & Management also outperformed and benefited from its overweight to and selection within corporate credit. Selection within ABS was beneficial as well.

The Fund used Treasury futures, eurodollar futures and to-be-announced (“TBA”) forward contracts to effectively manage duration (a measure of a bond’s price sensitivity to changes in interest rates), yield-curve and

| | | | |

New Covenant Funds / Annual Report / June 30, 2021 | | | 9 | |

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FUND PERFORMANCE

June 30, 2021 (Unaudited)

New Covenant Income Fund (Concluded)

market exposures. (TBA contracts confer the obligation to buy or sell future debt obligations of the three U.S. government-sponsored agencies that issue or guarantee MBS—Fannie Mae, Freddie Mac and Ginnie Mae.) None of these had a meaningful impact on the Fund’s performance.

Investing is subject to risk, including the possible loss of principal. Past performance is no indication of future results.

| | | | | | | | | | | | | | | | | | | | |

|

| AVERAGE ANNUAL TOTAL RETURN 1 | |

| | | | | | |

| | | One Year

Return | | | Annualized

3 Year

Return | | | Annualized

5 Year

Return | | | Annualized

10 Year

Return | | | Annualized

Inception

to Date | |

| New Covenant Income Fund, Class A | | | 1.13% | | | | 4.47% | | | | 2.61% | | | | 2.66% | | | | 3.52% | |

| Bloomberg Barclays U.S. Intermediate Aggregate Bond Index | | | 0.05% | | | | 4.41% | | | | 2.53% | | | | 2.74% | | | | 4.46% | |

Comparison of Change in the Value of a $10,000 Investment in the New Covenant Income Fund, Class A, versus the Bloomberg Barclays U.S. Intermediate Aggregate Bond Index.

| 1 | For the periods ended June 30, 2021. Past performance is not an indication of future performance. Fund Shares were offered beginning 7/1/99. Returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. The returns for certain periods reflect fee waivers and/or reimbursements in effect for that year; absent fee waivers and reimbursements, performance would have been lower. |

| | |

| 10 | | New Covenant Funds / Annual Report / June 30, 2021 |

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FUND PERFORMANCE

June 30, 2021 (Unaudited)

New Covenant Balanced Growth Fund

I. Objective

The Balanced Growth Fund’s (the “Fund”) investment objective is to produce capital appreciation with less risk than would be present in a portfolio of only common stocks.

II. Investment Approach

The Fund’s assets are managed under the direction of SEI Investments Management Corporation (“SIMC”), which manages the Fund’s assets in a way that it believes will achieve the Fund’s investment objective. In order to achieve its investment objective, SIMC allocates the Fund’s assets primarily in shares of the New Covenant Growth Fund (the Growth Fund) and the New Covenant Income Fund (the Income Fund), with a majority of its assets generally invested in shares of the Growth Fund. Between 45% and 75% of the Fund’s net assets (with a neutral position of approximately 60% of the Fund’s net assets) are invested in shares of the Growth Fund, with the balance of its assets invested in shares of the Income Fund. The Growth and Income Funds, in turn, invest directly in securities in accordance with their own varying investment objectives and policies.

III. Return vs. Benchmark

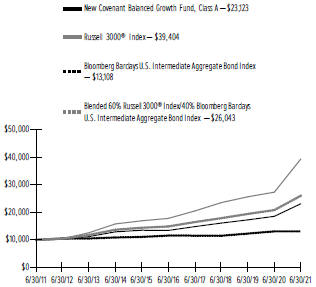

For the one-year period ending June 30, 2021, the Fund’s Class A shares returned 24.50%. The Fund’s primary benchmark, the Russell 3000® Index—which measures the performance of the 3000 largest U.S. companies and represents approximately 98% of the investable U.S. equity market—returned 44.16%.

IV. Fund Attribution

As noted in the shareholder letter, the U.S. equity market produced highly positive returns during the fiscal year as people generally became confident that the economy would rebound strongly from the pandemic-driven trough. Risk assets outperformed comparable Treasurys over the course of the fiscal year as the Federal Reserve (“Fed”) provided an unprecedented level of monetary support and the rollout of three vaccines in the United States led the economy toward a broad reopening.

The financials sector was the best-performing sector during the reporting period as investors concluded that interest rates would be rising in the second half of the fiscal year. Additionally, banks’ loan-loss reserves were determined to be more than necessary for the situation. The energy and industrials sectors also outperformed as many of the companies represented were expected

to benefit from an increase in economic activity coming out of the trough. Sectors traditionally considered to be non-cyclical—such as utilities, healthcare, and consumer staples—underperformed as company earnings in these areas were expected to gain little from the economic rebound; their lower-volatility characteristics were also out of favor as investor risk tolerance increased. Small-cap stocks outperformed relative to larger-capitalization stocks. Despite a rotation toward value stocks that began part of the way through the fiscal year, some big growth stocks—namely Tesla, Alphabet and Apple—still outperformed and had a material impact on index returns.

The Fed’s support went beyond traditional monetary policy as the central bank purchased both individual corporate bonds and corporate bond exchange-traded funds through its Secondary Market Corporate Credit Facility, backstopped agency-backed securities as they re-instituted the Term Asset-Backed Securities Loan Facility, and continued to purchase agency mortgage-backed securities (“MBS”) and U.S. Treasurys at a pace of $120 billion per month during the period. Additional fiscal stimulus provided payments directly to Americans and extended unemployment benefits, serving to boost consumer spending as the economy moved toward a full reopening. As also noted in the shareholder letter, a successful rollout of COVID-19 vaccines throughout the first six months of 2021 resulted in the lifting of health-related lockdowns, further propelling the economic rebound.

In the Growth Fund, underperformance was driven by the combination of its screens and environmental, social and governance tilt. The sectors that were somewhat restricted due to the Fund’s guidelines, such as industrials and communications services, performed well during the fiscal year, and the resulting underweights of securities within those sectors hurt performance. Sectors that were more accepted by the Fund guidelines, such as healthcare and information technology, had returns that were either in line or below that of the market; the aggregate differences in weights relative to the index ended up hurting Fund performance during the fiscal year.

Given the excess returns generated by risk assets, the Income Fund outperformed the Bloomberg Barclays U.S. Intermediate Aggregate Bond Index during the period. An overweight to corporate credit contributed to outperformance, while selection within the financials and insurance industries detracted. Security selection within ABS, particularly autos, added. An overweight to commercial mortgage-backed securities also added

| | | | |

New Covenant Funds / Annual Report / June 30, 2021 | | | 11 | |

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FUND PERFORMANCE

June 30, 2021 (Unaudited)

New Covenant Balanced Growth Fund (Concluded)

as the sector rallied later in the year. Selection within agency MBS added to performance as managers were able to implement a “follow the Fed” strategy.

The Income Fund used Treasury futures, eurodollar futures and to-be-announced (“TBA”) forward contracts to effectively manage duration (a measure of a bond’s price sensitivity to changes in interest rates), yield-curve and market exposures. (TBA contracts confer the obligation to buy or sell future debt obligations of the three U.S. government-sponsored agencies that issue or guarantee MBS—Fannie Mae, Freddie Mac and Ginnie Mae.) None of these had a meaningful impact on the Fund’s performance.

Investing is subject to risk, including the possible loss of principal. Past performance is no indication of future results.

| | | | | | | | | | | | | | | | | | | | |

| AVERAGE ANNUAL TOTAL RETURN 1,2 | |

| | | | | |

| | | One Year

Return | | | Annualized

3 Year

Return | | | Annualized

5 Year

Return | | | Annualized

10 Year

Return | | | Annualized

Inception

to Date | |

| New Covenant Balanced Growth Fund, Class A | | | 24.50% | | | | 12.78% | | | | 11.47% | | | | 8.74% | | | | 5.45% | |

| Russell 3000® Index | | | 44.16% | | | | 18.73% | | | | 17.89% | | | | 14.70% | | | | 7.76% | |

| Bloomberg Barclays U.S. Intermediate Aggregate Bond Index | | | 0.05% | | | | 4.41% | | | | 2.53% | | | | 2.74% | | | | 4.46% | |

| Blended 60% Russell 3000® Index/40% Bloomberg Barclays U.S. Intermediate Aggregate Bond Index | | | 25.00% | | | | 13.32% | | | | 11.84% | | | | 10.04% | | | | 6.76% | |

Comparison of Change in the Value of a $10,000 Investment in the New Covenant Balanced Growth Fund, Class A, versus the Russell 3000® Index, Bloomberg Barclays U.S. Intermediate Aggregate Bond Index and Blended 60% Russell 3000® Index/40% Bloomberg Barclays U.S. Intermediate Aggregate Bond Index.

| 1 | For the periods ended June 30, 2021. Past performance is not an indication of future performance. Fund Shares were offered beginning 7/1/99. Returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. The returns for certain periods reflect fee waivers and/or reimbursements in effect for that year; absent fee waivers and reimbursements, performance would have been lower. |

| 2 | This table compares the Fund’s average annual total returns to those of a broad based index and the Fund’s 60/40 Blended Benchmark, which consists of the Russell 3000® Index and the Bloomberg Barclays U.S. Intermediate Aggregate Bond Index. The Fund’s Blended Benchmark is designed to provide a useful comparison to the Fund’s overall performance and more accurately reflects the Fund’s investment strategy than the broad-based index. |

| | |

| 12 | | New Covenant Funds / Annual Report / June 30, 2021 |

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FUND PERFORMANCE

June 30, 2021 (Unaudited)

New Covenant Balanced Income Fund

I. Objective

The Balanced Income Fund’s (the “Fund”) investment objective is to produce current income and long-term growth of capital.

II. Investment Approach

The Fund’s assets are managed under the direction of SEI Investments Management Corporation (“SIMC”), which manages the Fund’s assets in a way that it believes will achieve the Fund’s investment objective. In order to achieve its investment objective, SIMC allocates the Fund’s assets primarily in shares of the New Covenant Growth Fund (the Growth Fund) and the New Covenant Income Fund (the Income Fund), with a majority of its assets generally invested in shares of the Income Fund. Between fifty percent and seventy-five percent of the Fund’s net assets (with a neutral position of approximately 65%) are invested in shares of the Income Fund, with the balance of its net assets invested in shares of the Growth Fund. The Growth and Income Funds, in turn, invest directly in securities in accordance with their own varying investment objectives and policies.

III. Return vs. Benchmark

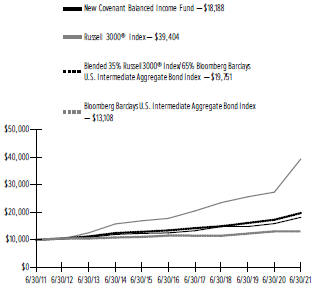

For the one-year period ending June 30, 2021, the Fund’s Class A shares returned 14.24%. The Fund’s primary benchmark, the Russell 3000® Index—which measures the performance of the 3000 largest U.S. companies and represents approximately 98% of the investable U.S. equity market—returned 44.16%.

IV. Fund Attribution

As noted in the shareholder letter, the U.S. equity market produced highly positive returns during the fiscal year as people generally became confident that the economy would rebound strongly from the pandemic-driven trough. Risk assets outperformed comparable Treasurys over the course of the fiscal year as the Federal Reserve (“Fed”) provided an unprecedented level of monetary support and the rollout of three vaccines in the United States led the economy toward a broad reopening.

The Fed’s support went beyond traditional monetary policy as the central bank purchased both individual corporate bonds and corporate bond exchange-traded funds through its Secondary Market Corporate Credit Facility, backstopped agency-backed securities as they re-instituted the Term Asset-Backed Securities Loan Facility, and continued to purchase agency mortgage-backed securities (“MBS”) and U.S. Treasurys at a pace

of $120 billion per month during the period. Additional fiscal stimulus provided payments directly to Americans and extended unemployment benefits, serving to boost consumer spending as the economy moved toward a full reopening. As also noted in the shareholder letter, a successful rollout of COVID-19 vaccines throughout the first six months of 2021 resulted in the lifting of health-related lockdowns, further propelling the economic rebound.

With Democrats taking control of the U.S. congress and Joe Biden becoming President, U.S. government spending was expected to increase without the gridlock that may have existed if power had been evenly divided between the parties. Fiscal stimulus and vaccinations were key reasons for the improved economic outlook, while the potential for a significant increase in inflation remained on investors’ minds later in the period.

The financials sector was the best-performing sector during the reporting period as investors concluded that interest rates would be rising in the second half of the fiscal year. Additionally, banks’ loan-loss reserves were determined to be more than necessary for the situation. The energy and industrials sectors also outperformed as many of the companies represented were expected to benefit from an increase in economic activity coming out of the trough. Sectors traditionally considered to be non-cyclical—such as utilities, healthcare, and consumer staples—underperformed as company earnings in these areas were expected to gain little from the economic rebound; their lower-volatility characteristics were also out of favor as investor risk tolerance increased. Small-cap stocks outperformed relative to larger-capitalization stocks. Despite a rotation toward value stocks that began part of the way through the fiscal year, some big growth stocks—namely Tesla, Alphabet and Apple—still outperformed and had a material impact on index returns.

In this environment, the Income Fund underperformed as the combination of its screens and environmental, social, and corporate governance tilt had a negative effect on performance. The sectors that were somewhat restricted due to the Fund’s guidelines, such as industrials and communications services, performed well during the fiscal year, and the resulting underweights of securities within those sectors hurt performance. Sectors that were more accepted by the Fund guidelines, such as health care and information technology, had returns that were either in line or below that of the market; the aggregate differences in weights relative to the index ended up hurting Fund performance during the fiscal year.

| | | | |

New Covenant Funds / Annual Report / June 30, 2021 | | | 13 | |

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FUND PERFORMANCE

June 30, 2021 (Unaudited)

New Covenant Balanced Income Fund (Concluded)

In the Growth Fund, underperformance was driven by the combination of its screens and environmental, social, and governance tilt. The sectors that were somewhat restricted due to the Fund’s guidelines, such as industrials and communications services, performed well during the fiscal year, and the resulting underweights of securities within those sectors hurt performance. Sectors that were more accepted by the Fund guidelines, such as healthcare and information technology, had returns that were either in line or below that of the market; the aggregate differences in weights relative to the index ended up hurting Fund performance during the fiscal year.

The Income Fund used Treasury futures, eurodollar futures and to-be-announced (“TBA”) forward contracts to effectively manage duration (a measure of a bond’s price sensitivity to changes in interest rates), yield-curve and market exposures. (TBA contracts confer the obligation to buy or sell future debt obligations of the three U.S. government-sponsored agencies that issue or guarantee MBS—Fannie Mae, Freddie Mac and Ginnie Mae.) None of these had a meaningful impact on the Fund’s performance.

Investing is subject to risk, including the possible loss of principal. Past performance is no indication of future results.

| | | | | | | | | | | | | | | | | | | | |

| AVERAGE ANNUAL TOTAL RETURN 1,2 | |

| | | | | |

| | | One Year

Return | | | Annualized

3 Year

Return | | | Annualized

5 Year

Return | | | Annualized

10 Year

Return | | | Annualized Inception

to Date | |

| New Covenant Balanced Income Fund, Class A | | | 14.24% | | | | 9.33% | | | | 7.71% | | | | 6.16% | | | | 4.65% | |

| Russell 3000® Index | | | 44.16% | | | | 18.73% | | | | 17.89% | | | | 14.70% | | | | 7.76% | |

| Bloomberg Barclays U.S. Intermediate Aggregate Bond Index | | | 0.05% | | | | 4.41% | | | | 2.53% | | | | 2.74% | | | | 4.46% | |

| Blended 35% Russell 3000® Index/65% Bloomberg Barclays U.S. Intermediate Aggregate Bond Index | | | 14.08% | | | | 9.71% | | | | 7.99% | | | | 7.04% | | | | 5.91% | |

Comparison of Change in the Value of a $10,000 Investment in the New Covenant Balanced Income Fund, Class A, versus the Russell 3000® Index, Bloomberg Barclays U.S. Intermediate Aggregate Bond Index and Blended 35% Russell 3000® Index/65% Bloomberg Barclays U.S. Intermediate Aggregate Bond Index.

| 1 | For the periods ended June 30, 2021. Past performance is not an indication of future performance. Fund Shares were offered beginning 7/1/99. Returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. The returns for certain periods reflect fee waivers and/or reimbursements in effect for that year; absent fee waivers and reimbursements, performance would have been lower. |

| 2 | This table compares the Fund’s average annual total returns to those of a broad- based index and the Fund’s 35/65 Blended Benchmark, which consists of the Russell 3000® Index and the Bloomberg Barclays U.S. Intermediate Aggregate Bond Index. The Fund’s Blended Benchmark is designed to provide a useful comparison to the Fund’s overall performance and more accurately reflects the Fund’s investment strategy than the broad-based index. |

| | |

| 14 | | New Covenant Funds / Annual Report / June 30, 2021 |

SCHEDULE OF INVESTMENTS

June 30, 2021

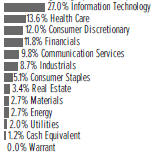

New Covenant Growth Fund

Sector Weightings (Unaudited)†:

†Percentages are based on total investments.

| | | | | | | | |

| | | |

| Description | | Shares | | | Market Value

($ Thousands) | |

| | |

COMMON STOCK — 96.1% | | | | | | | | |

United States — 96.1% | | | | | | | | |

Communication Services — 9.7% | | | | | | | | |

Activision Blizzard Inc | | | 8,807 | | | $ | 840 | |

Alphabet Inc, Cl A * | | | 4,202 | | | | 10,260 | |

Alphabet Inc, Cl C * | | | 3,995 | | | | 10,013 | |

AMC Entertainment Holdings, Cl A * | | | 2,754 | | | | 156 | |

AT&T Inc | | | 119,675 | | | | 3,444 | |

Bandwidth Inc, Cl A * | | | 74 | | | | 10 | |

Cable One Inc | | | 79 | | | | 151 | |

Cardlytics Inc * | | | 761 | | | | 97 | |

Cars.com Inc * | | | 4,178 | | | | 60 | |

Charter Communications Inc, Cl A * | | | 1,444 | | | | 1,042 | |

Cinemark Holdings Inc * | | | 4,289 | | | | 94 | |

Clear Channel Outdoor Holdings, Cl A * | | | 17,605 | | | | 46 | |

Cogent Communications Holdings Inc | | | 148 | | | | 11 | |

Comcast Corp, Cl A | | | 54,780 | | | | 3,124 | |

Discovery Inc, Cl C * | | | 354 | | | | 10 | |

Electronic Arts Inc | | | 2,676 | | | | 385 | |

Emerald Holding Inc * | | | 4,781 | | | | 26 | |

Eventbrite Inc, Cl A * | | | 2,537 | | | | 48 | |

EverQuote Inc, Cl A * | | | 1,468 | | | | 48 | |

EW Scripps Co/The, Cl A | | | 3,299 | | | | 67 | |

Facebook Inc, Cl A * | | | 30,770 | | | | 10,699 | |

Fox Corp, Cl A | | | 1,372 | | | | 51 | |

fuboTV * | | | 3,908 | | | | 125 | |

IAC * | | | 376 | | | | 58 | |

IMAX Corp * | | | 2,244 | | | | 48 | |

Interpublic Group of Cos Inc/The | | | 8,487 | | | | 276 | |

Iridium Communications Inc * | | | 366 | | | | 15 | |

John Wiley & Sons Inc, Cl A | | | 236 | | | | 14 | |

Liberty Broadband Corp, Cl A * | | | 81 | | | | 14 | |

Liberty Broadband Corp, Cl C * | | | 343 | | | | 60 | |

Liberty Media Corp-Liberty Formula One, Cl C * | | | 1,355 | | | | 65 | |

Liberty Media Corp-Liberty SiriusXM, Cl C * | | | 234 | | | | 11 | |

Live Nation Entertainment Inc * | | | 181 | | | | 16 | |

Lumen Technologies | | | 872 | | | | 12 | |

| | | | | | | | |

| | | |

| Description | | Shares | | | Market Value

($ Thousands) | |

| | |

COMMON STOCK (continued) | | | | | | | | |

Madison Square Garden Entertainment Corp * | | | 1,255 | | | $ | 105 | |

Madison Square Garden Sports Corp * | | | 39 | | | | 7 | |

Magnite Inc * | | | 2,551 | | | | 86 | |

Match Group Inc * | | | 1,841 | | | | 297 | |

Meredith Corp * | | | 1,401 | | | | 61 | |

MSG Networks Inc * | | | 2,988 | | | | 44 | |

Netflix Inc * | | | 5,139 | | | | 2,714 | |

New York Times Co/The, Cl A | | | 439 | | | | 19 | |

News Corp, Cl A | | | 829 | | | | 21 | |

Nexstar Media Group Inc, Cl A | | | 455 | | | | 67 | |

Omnicom Group Inc | | | 10,137 | | | | 811 | |

Pinterest, Cl A * | | | 3,339 | | | | 264 | |

Roku Inc, Cl A * | | | 818 | | | | 376 | |

Scholastic Corp | | | 1,266 | | | | 48 | |

Shenandoah Telecommunications Co | | | 222 | | | | 11 | |

Sirius XM Holdings Inc | | | 7,153 | | | | 47 | |

Skillz, Cl A * | | | 3,639 | | | | 79 | |

Spotify Technology SA * | | | 1,265 | | | | 349 | |

Take-Two Interactive Software Inc * | | | 830 | | | | 147 | |

TechTarget Inc * | | | 1,986 | | | | 154 | |

TEGNA Inc | | | 3,052 | | | | 57 | |

T-Mobile US Inc * | | | 5,933 | | | | 859 | |

TripAdvisor Inc * | | | 1,712 | | | | 69 | |

Twitter Inc * | | | 7,369 | | | | 507 | |

Verizon Communications Inc | | | 57,853 | | | | 3,242 | |

ViacomCBS Inc, Cl B | | | 7,304 | | | | 330 | |

Vimeo * | | | 610 | | | | 30 | |

Walt Disney Co/The * | | | 22,230 | | | | 3,907 | |

World Wrestling Entertainment Inc, Cl A | | | 780 | | | | 45 | |

Zillow Group Inc, Cl C * | | | 1,112 | | | | 136 | |

Zynga Inc, Cl A * | | | 14,448 | | | | 154 | |

| | | | | | | | |

| | | | | | | 56,439 | |

| | | | | | | | |

| | |

Consumer Discretionary — 11.8% | | | | | | | | |

1-800-Flowers.com Inc, Cl A * | | | 3,668 | | | | 117 | |

2U Inc * | | | 871 | | | | 36 | |

Aaron’s Co Inc | | | 416 | | | | 13 | |

Abercrombie & Fitch Co, Cl A * | | | 2,970 | | | | 138 | |

Adtalem Global Education Inc * | | | 1,460 | | | | 52 | |

Advance Auto Parts Inc | | | 317 | | | | 65 | |

Amazon.com Inc * | | | 5,544 | | | | 19,072 | |

American Eagle Outfitters Inc | | | 3,416 | | | | 128 | |

American Public Education Inc * | | | 1,831 | | | | 52 | |

Aramark | | | 260 | | | | 10 | |

Asbury Automotive Group Inc * | | | 425 | | | | 73 | |

At Home Group Inc * | | | 6,757 | | | | 249 | |

AutoNation Inc * | | | 970 | | | | 92 | |

AutoZone Inc * | | | 235 | | | | 351 | |

Bed Bath & Beyond Inc * | | | 517 | | | | 17 | |

Best Buy Co Inc | | | 14,318 | | | | 1,646 | |

Big Lots Inc | | | 1,758 | | | | 116 | |

Blink Charging * | | | 1,491 | | | | 61 | |

| | | | |

New Covenant Funds / Annual Report / June 30, 2021 | | | 15 | |

SCHEDULE OF INVESTMENTS

June 30, 2021

New Covenant Growth Fund (Continued)

| | | | | | | | |

| | | |

| Description | | Shares | | | Market Value

($ Thousands) | |

| |

COMMON STOCK (continued) | | | | |

Bloomin’ Brands Inc * | | | 2,259 | | | $ | 61 | |

Booking Holdings Inc * | | | 563 | | | | 1,232 | |

Boot Barn Holdings Inc * | | | 1,181 | | | | 99 | |

BorgWarner Inc | | | 321 | | | | 16 | |

Bright Horizons Family Solutions Inc * | | | 76 | | | | 11 | |

Brinker International Inc * | | | 1,180 | | | | 73 | |

Brunswick Corp/DE | | | 839 | | | | 84 | |

Buckle Inc/The | | | 1,885 | | | | 94 | |

Burlington Stores Inc * | | | 482 | | | | 155 | |

Callaway Golf Co | | | 2,383 | | | | 80 | |

Canoo * | | | 5,091 | | | | 51 | |

Capri Holdings Ltd * | | | 1,319 | | | | 75 | |

CarMax Inc * | | | 1,086 | | | | 140 | |

Carnival Corp * | | | 15,800 | | | | 416 | |

Carter’s Inc | | | 471 | | | | 49 | |

Carvana Co, Cl A * | | | 309 | | | | 93 | |

Cavco Industries Inc * | | | 255 | | | | 57 | |

Cheesecake Factory Inc/The * | | | 1,236 | | | | 67 | |

Chegg Inc * | | | 176 | | | | 15 | |

Children’s Place Inc/The * | | | 812 | | | | 76 | |

Chipotle Mexican Grill Inc, Cl A * | | | 232 | | | | 360 | |

Choice Hotels International Inc | | | 113 | | | | 13 | |

Columbia Sportswear Co | | | 891 | | | | 88 | |

Cracker Barrel Old Country Store Inc | | | 323 | | | | 48 | |

Dana Inc | | | 2,660 | | | | 63 | |

Darden Restaurants Inc | | | 705 | | | | 103 | |

Dave & Buster’s Entertainment Inc * | | | 1,283 | | | | 52 | |

Deckers Outdoor Corp * | | | 306 | | | | 117 | |

Denny’s Corp * | | | 2,500 | | | | 41 | |

Designer Brands Inc, Cl A * | | | 3,316 | | | | 55 | |

Dick’s Sporting Goods Inc | | | 1,054 | | | | 106 | |

Dillard’s Inc, Cl A | | | 726 | | | | 131 | |

Dollar General Corp | | | 2,608 | | | | 564 | |

Dollar Tree Inc * | | | 1,320 | | | | 131 | |

Domino’s Pizza Inc | | | 309 | | | | 144 | |

Dorman Products Inc * | | | 128 | | | | 13 | |

DR Horton Inc | | | 1,973 | | | | 178 | |

eBay Inc | | | 20,542 | | | | 1,442 | |

Etsy Inc * | | | 1,162 | | | | 239 | |

Expedia Group Inc * | | | 389 | | | | 64 | |

Fisker * | | | 2,626 | | | | 51 | |

Five Below Inc * | | | 410 | | | | 79 | |

Floor & Decor Holdings Inc, Cl A * | | | 232 | | | | 24 | |

Foot Locker Inc | | | 1,308 | | | | 81 | |

Ford Motor Co * | | | 32,028 | | | | 476 | |

Fox Factory Holding Corp * | | | 749 | | | | 117 | |

frontdoor Inc * | | | 251 | | | | 12 | |

Gap Inc/The | | | 11,382 | | | | 383 | |

General Motors Co * | | | 13,058 | | | | 773 | |

Gentex Corp | | | 440 | | | | 15 | |

Gentherm Inc * | | | 184 | | | | 13 | |

Genuine Parts Co | | | 109 | | | | 14 | |

| | | | | | | | |

| | | |

| Description | | Shares | | | Market Value

($ Thousands) | |

| | |

COMMON STOCK (continued) | | | | | | | | |

Goodyear Tire & Rubber Co/The * | | | 989 | | | $ | 17 | |

Graham Holdings Co, Cl B | | | 78 | | | | 49 | |

Grand Canyon Education Inc * | | | 121 | | | | 11 | |

Group 1 Automotive Inc | | | 86 | | | | 13 | |

GrowGeneration * | | | 2,599 | | | | 125 | |

Guess? Inc | | | 2,341 | | | | 62 | |

H&R Block Inc | | | 3,157 | | | | 74 | |

Hanesbrands Inc | | | 13,319 | | | | 249 | |

Harley-Davidson Inc | | | 306 | | | | 14 | |

Hasbro Inc | | | 2,632 | | | | 249 | |

Helen of Troy Ltd * | | | 57 | | | | 13 | |

Hilton Grand Vacations Inc * | | | 3,016 | | | | 125 | |

Hilton Worldwide Holdings Inc * | | | 3,186 | | | | 384 | |

Home Depot Inc/The | | | 13,012 | | | | 4,149 | |

Hyatt Hotels Corp, Cl A * | | | 135 | | | | 10 | |

Installed Building Products Inc | | | 694 | | | | 85 | |

iRobot Corp * | | | 1,013 | | | | 95 | |

Jack in the Box Inc | | | 658 | | | | 73 | |

Johnson Outdoors Inc, Cl A | | | 659 | | | | 80 | |

KB Home | | | 4,733 | | | | 193 | |

Kohl’s Corp | | | 1,859 | | | | 102 | |

Kontoor Brands Inc | | | 1,282 | | | | 72 | |

L Brands Inc | | | 638 | | | | 46 | |

La-Z-Boy Inc, Cl Z | | | 1,597 | | | | 59 | |

LCI Industries | | | 483 | | | | 63 | |

Lear Corp | | | 6,486 | | | | 1,137 | |

Leggett & Platt Inc | | | 222 | | | | 11 | |

Lennar Corp, Cl A | | | 651 | | | | 65 | |

Lennar Corp, Cl B | | | 728 | | | | 59 | |

LGI Homes Inc * | | | 127 | | | | 21 | |

LKQ Corp * | | | 317 | | | | 16 | |

Lowe’s Cos Inc | | | 15,716 | | | | 3,048 | |

M/I Homes Inc * | | | 198 | | | | 12 | |

Macy’s Inc * | | | 4,042 | | | | 77 | |

Malibu Boats Inc, Cl A * | | | 202 | | | | 15 | |

Marriott International Inc/MD, Cl A * | | | 3,599 | | | | 491 | |

Marriott Vacations Worldwide Corp * | | | 394 | | | | 63 | |

Mattel Inc * | | | 14,805 | | | | 298 | |

McDonald’s Corp | | | 11,361 | | | | 2,624 | |

Meritage Homes Corp * | | | 794 | | | | 75 | |

Mohawk Industries Inc * | | | 127 | | | | 24 | |

Monro Inc | | | 626 | | | | 40 | |

Murphy USA Inc | | | 422 | | | | 56 | |

National Vision Holdings Inc * | | | 447 | | | | 23 | |

Newell Brands Inc | | | 605 | | | | 17 | |

NIKE Inc, Cl B | | | 17,693 | | | | 2,733 | |

Nordstrom Inc * | | | 3,866 | | | | 141 | |

Norwegian Cruise Line Holdings Ltd * | | | 14,956 | | | | 440 | |

NVR Inc * | | | 13 | | | | 65 | |

Office Depot Inc * | | | 283 | | | | 14 | |

Ollie’s Bargain Outlet Holdings Inc * | | | 212 | | | | 18 | |

OneSpaWorld Holdings Ltd * | | | 3,063 | | | | 30 | |

| | |

| 16 | | New Covenant Funds / Annual Report / June 30, 2021 |

| | | | | | | | |

| | | |

| Description | | Shares | | | Market Value

($ Thousands) | |

| | |

COMMON STOCK (continued) | | | | | | | | |

O’Reilly Automotive Inc * | | | 677 | | | $ | 383 | |

Oxford Industries Inc | | | 665 | | | | 66 | |

Papa John’s International Inc | | | 806 | | | | 84 | |

Peloton Interactive Inc, Cl A * | | | 3,058 | | | | 379 | |

Penske Automotive Group Inc | | | 957 | | | | 72 | |

PetMed Express Inc | | | 366 | | | | 12 | |

Planet Fitness Inc, Cl A * | | | 3,228 | | | | 243 | |

Polaris Inc | | | 966 | | | | 132 | |

PulteGroup Inc | | | 5,125 | | | | 280 | |

PVH Corp * | | | 108 | | | | 12 | |

Qurate Retail Inc | | | 1,412 | | | | 18 | |

Ralph Lauren Corp, Cl A | | | 690 | | | | 81 | |

RealReal Inc/The * | | | 5,091 | | | | 101 | |

Rent-A-Center Inc/TX, Cl A | | | 1,764 | | | | 94 | |

RH * | | | 224 | | | | 152 | |

Ross Stores Inc | | | 3,209 | | | | 398 | |

Royal Caribbean Cruises Ltd * | | | 8,804 | | | | 751 | |

Sally Beauty Holdings Inc * | | | 2,794 | | | | 62 | |

SeaWorld Entertainment Inc * | | | 251 | | | | 12 | |

Service Corp International/US | | | 250 | | | | 13 | |

Shake Shack Inc, Cl A * | | | 157 | | | | 17 | |

Shutterstock Inc | | | 205 | | | | 20 | |

Signet Jewelers Ltd | | | 2,402 | | | | 194 | |

Six Flags Entertainment Corp * | | | 248 | | | | 11 | |

Sleep Number Corp * | | | 1,033 | | | | 114 | |

Stamps.com Inc * | | | 630 | | | | 126 | |

Standard Motor Products Inc | | | 943 | | | | 41 | |

Starbucks Corp | | | 16,902 | | | | 1,890 | |

Steven Madden Ltd | | | 1,178 | | | | 52 | |

Stitch Fix Inc, Cl A * | | | 1,021 | | | | 62 | |

Strategic Education Inc | | | 331 | | | | 25 | |

Stride Inc * | | | 348 | | | | 11 | |

Tapestry Inc * | | | 2,803 | | | | 122 | |

Target Corp | | | 6,577 | | | | 1,590 | |

Taylor Morrison Home Corp, Cl A * | | | 12,743 | | | | 337 | |

Tempur Sealy International Inc | | | 2,272 | | | | 89 | |

Tenneco Inc, Cl A * | | | 3,599 | | | | 69 | |

Terminix Global Holdings Inc * | | | 303 | | | | 14 | |

Tesla Inc * | | | 9,636 | | | | 6,550 | |

Texas Roadhouse Inc, Cl A | | | 889 | | | | 85 | |

Thor Industries Inc | | | 106 | | | | 12 | |

TJX Cos Inc/The | | | 14,736 | | | | 993 | |

Toll Brothers Inc | | | 2,246 | | | | 130 | |

TopBuild Corp * | | | 476 | | | | 94 | |

Tractor Supply Co | | | 2,377 | | | | 442 | |

Travel + Leisure | | | 4,669 | | | | 278 | |

TRI Pointe Group Inc * | | | 3,236 | | | | 69 | |

Ulta Beauty Inc * | | | 279 | | | | 96 | |

Under Armour Inc, Cl C * | | | 556 | | | | 10 | |

Urban Outfitters Inc * | | | 417 | | | | 17 | |

Vail Resorts Inc | | | 46 | | | | 15 | |

VF Corp | | | 4,023 | | | | 330 | |

| | | | | | | | |

| | | |

| Description | | Shares | | | Market Value

($ Thousands) | |

| | |

COMMON STOCK (continued) | | | | | | | | |

Visteon Corp * | | | 551 | | | $ | 67 | |

Vroom * | | | 3,337 | | | | 140 | |

Wayfair Inc, Cl A * | | | 320 | | | | 101 | |

Wendy’s Co/The | | | 11,419 | | | | 267 | |

Whirlpool Corp | | | 638 | | | | 139 | |

Williams-Sonoma Inc | | | 160 | | | | 26 | |

Wingstop Inc | | | 582 | | | | 92 | |

Winnebago Industries Inc | | | 191 | | | | 13 | |

Wolverine World Wide Inc | | | 1,511 | | | | 51 | |

Workhorse Group Inc * | | | 4,879 | | | | 81 | |

WW International Inc * | | | 1,262 | | | | 46 | |

Wyndham Hotels & Resorts Inc | | | 189 | | | | 14 | |

Yum China Holdings Inc | | | 1,913 | | | | 127 | |

Yum! Brands Inc | | | 8,356 | | | | 961 | |

Zumiez Inc * | | | 1,593 | | | | 78 | |

| | | | | | | | |

| | | | | | | 68,700 | |

| | | | | | | | |

| | |

Consumer Staples — 5.0% | | | | | | | | |

Andersons Inc/The | | | 1,960 | | | | 60 | |

Archer-Daniels-Midland Co | | | 4,581 | | | | 278 | |

B&G Foods Inc | | | 862 | | | | 28 | |

Beyond Meat Inc * | | | 166 | | | | 26 | |

BJ’s Wholesale Club Holdings Inc * | | | 2,099 | | | | 100 | |

Bunge Ltd | | | 1,596 | | | | 125 | |

Calavo Growers Inc | | | 571 | | | | 36 | |

Campbell Soup Co | | | 10,354 | | | | 472 | |

Casey’s General Stores Inc | | | 65 | | | | 13 | |

Celsius Holdings * | | | 2,688 | | | | 204 | |

Chefs’ Warehouse Inc/The * | | | 1,366 | | | | 43 | |

Church & Dwight Co Inc | | | 1,025 | | | | 87 | |

Clorox Co/The | | | 2,716 | | | | 489 | |

Coca-Cola Co/The | | | 51,576 | | | | 2,791 | |

Colgate-Palmolive Co | | | 14,526 | | | | 1,182 | |

Conagra Brands Inc | | | 14,479 | | | | 527 | |

Costco Wholesale Corp | | | 5,088 | | | | 2,013 | |

Coty Inc, Cl A * | | | 1,026 | | | | 10 | |

Edgewell Personal Care Co | | | 310 | | | | 14 | |

Energizer Holdings Inc | | | 231 | | | | 10 | |

Estee Lauder Cos Inc/The, Cl A | | | 2,390 | | | | 760 | |

Flowers Foods Inc | | | 9,872 | | | | 239 | |

Fresh Del Monte Produce Inc | | | 1,442 | | | | 47 | |

General Mills Inc | | | 13,887 | | | | 846 | |

Grocery Outlet Holding Corp * | | | 263 | | | | 9 | |

Hain Celestial Group Inc/The * | | | 461 | | | | 18 | |

Hershey Co/The | | | 2,295 | | | | 400 | |

HF Foods Group Inc * | | | 2,213 | | | | 12 | |

Hormel Foods Corp | | | 4,797 | | | | 229 | |

Ingredion Inc | | | 1,110 | | | | 100 | |

J M Smucker Co/The | | | 6,494 | | | | 841 | |

Kellogg Co | | | 6,713 | | | | 432 | |

Keurig Dr Pepper Inc | | | 16,196 | | | | 571 | |

Kimberly-Clark Corp | | | 6,484 | | | | 867 | |

Kraft Heinz Co/The | | | 2,811 | | | | 115 | |

| | | | |

New Covenant Funds / Annual Report / June 30, 2021 | | | 17 | |

SCHEDULE OF INVESTMENTS

June 30, 2021

New Covenant Growth Fund (Continued)

| | | | | | | | |

| | | |

| Description | | Shares | | | Market Value

($ Thousands) | |

| | |

COMMON STOCK (continued) | | | | | | | | |

Kroger Co/The | | | 17,094 | | | $ | 655 | |

Lamb Weston Holdings Inc | | | 594 | | | | 48 | |

Lancaster Colony Corp | | | 319 | | | | 62 | |

McCormick & Co Inc/MD | | | 5,832 | | | | 515 | |

Medifast Inc | | | 71 | | | | 20 | |

Mondelez International Inc, Cl A | | | 17,402 | | | | 1,087 | |

Monster Beverage Corp * | | | 1,999 | | | | 183 | |

National Beverage Corp | | | 344 | | | | 16 | |

NewAge * | | | 16,448 | | | | 37 | |

PepsiCo Inc | | | 27,799 | | | | 4,119 | |

Performance Food Group Co * | | | 1,023 | | | | 50 | |

Pilgrim’s Pride Corp * | | | 355 | | | | 8 | |

Post Holdings Inc * | | | 108 | | | | 12 | |

PriceSmart Inc | | | 179 | | | | 16 | |

Procter & Gamble Co/The | | | 29,388 | | | | 3,965 | |

Sanderson Farms Inc | | | 297 | | | | 56 | |

SpartanNash Co | | | 1,252 | | | | 24 | |

Spectrum Brands Holdings Inc | | | 183 | | | | 15 | |

Sprouts Farmers Market Inc * | | | 623 | | | | 15 | |

Sysco Corp | | | 17,657 | | | | 1,373 | |

TreeHouse Foods Inc * | | | 237 | | | | 10 | |

Tyson Foods Inc, Cl A | | | 859 | | | | 63 | |

US Foods Holding Corp * | | | 2,211 | | | | 85 | |

Walgreens Boots Alliance Inc | | | 8,946 | | | | 471 | |

Walmart Inc | | | 16,737 | | | | 2,360 | |

| | | | | | | | |

| | | | | | | 29,259 | |

| | | | | | | | |

| | |

Energy — 2.6% | | | | | | | | |

Altus Midstream, Cl A | | | 815 | | | | 55 | |

Antero Midstream Corp | | | 7,912 | | | | 82 | |

APA | | | 7,933 | | | | 172 | |

Baker Hughes Co, Cl A | | | 4,496 | | | | 103 | |

Cabot Oil & Gas Corp | | | 3,306 | | | | 58 | |

Cactus Inc, Cl A | | | 1,525 | | | | 56 | |

Callon Petroleum * | | | 2,548 | | | | 147 | |

ChampionX Corp * | | | 383 | | | | 10 | |

Cheniere Energy Inc * | | | 1,265 | | | | 110 | |

Chevron Corp | | | 22,705 | | | | 2,378 | |

Cimarex Energy Co | | | 995 | | | | 72 | |

Clean Energy Fuels * | | | 4,579 | | | | 46 | |

CNX Resources Corp * | | | 6,091 | | | | 83 | |

ConocoPhillips | | | 28,962 | | | | 1,764 | |

Continental Resources Inc/OK | | | 337 | | | | 13 | |

Devon Energy Corp | | | 1,847 | | | | 54 | |

Diamond S Shipping Inc * | | | 3,276 | | | | 33 | |

Diamondback Energy Inc | | | 133 | | | | 12 | |

Dril-Quip Inc * | | | 1,072 | | | | 36 | |

EOG Resources Inc | | | 4,528 | | | | 378 | |

EQT Corp * | | | 2,732 | | | | 61 | |

Equitrans Midstream Corp | | | 2,185 | | | | 19 | |

Exxon Mobil Corp | | | 53,141 | | | | 3,352 | |

Frank’s International NV * | | | 9,174 | | | | 28 | |

Gevo * | | | 6,754 | | | | 49 | |

| | | | | | | | |

| | | |

| Description | | Shares | | | Market Value

($ Thousands) | |

| | |

COMMON STOCK (continued) | | | | | | | | |

Golar LNG Ltd * | | | 3,888 | | | $ | 51 | |

Halliburton Co | | | 4,450 | | | | 103 | |

Helmerich & Payne Inc | | | 1,494 | | | | 49 | |

Hess Corp | | | 4,195 | | | | 366 | |

HollyFrontier Corp | | | 3,119 | | | | 103 | |

International Seaways Inc | | | 1,773 | | | | 34 | |