UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT

OF

REGISTERED MANAGEMENT INVESTMENT COMPANIES

| | |

| Investment Company Act file number: | 811-22114 |

Name of Registrant: | Vanguard Montgomery Funds |

Address of Registrant: | P.O. Box 2600 |

| | Valley Forge, PA 19482 |

Name and address of agent for service: | Heidi Stam, Esquire |

| | P.O. Box 876 |

| | Valley Forge, PA 19482 |

Registrant’s telephone number, including area code: (610) 669-1000 |

Date of fiscal year end: December 31 | |

Date of reporting period: January 1, 2014 – December 31, 2014 |

Item 1: Reports to Shareholders | |

Annual Report | December 31, 2014

Vanguard Market Neutral Fund

The mission continues

On May 1, 1975, Vanguard began operations, a fledgling company based on the simple but revolutionary idea that a mutual fund company should be managed solely in the interest of its investors.

Four decades later, that revolutionary spirit continues to animate the enterprise. Vanguard remains on a mission to give investors the best chance of investment success.

As we mark our 40th anniversary, we thank you for entrusting your assets to Vanguard and giving us the opportunity to help you reach your financial goals in the decades to come.

| |

| Contents | |

| Your Fund’s Total Returns. | 1 |

| Chairman’s Letter. | 2 |

| Advisor’s Report. | 8 |

| Fund Profile. | 10 |

| Performance Summary. | 12 |

| Financial Statements. | 14 |

| Your Fund’s After-Tax Returns. | 29 |

| About Your Fund’s Expenses. | 30 |

| Glossary. | 32 |

Please note: The opinions expressed in this report are just that—informed opinions. They should not be considered promises or advice.

Also, please keep in mind that the information and opinions cover the period through the date on the front of this report. Of course, the

risks of investing in your fund are spelled out in the prospectus.

See the Glossary for definitions of investment terms used in this report.

About the cover: Since our founding, Vanguard has drawn inspiration from the enterprise and valor demonstrated by British

naval hero Horatio Nelson and his command at the Battle of the Nile in 1798. The photograph displays a replica of a merchant

ship from the same era as Nelson’s flagship, the HMS Vanguard.

Your Fund’s Total Returns

| |

| Fiscal Year Ended December 31, 2014 | |

| |

| | Total |

| | Returns |

| Vanguard Market Neutral Fund | |

| Investor Shares | 4.26% |

| Institutional Shares | 4.38 |

| Citigroup Three-Month U.S. Treasury Bill Index | 0.03 |

| Alternative Equity Market Neutral Funds Average | 0.43 |

| Alternative Equity Market Neutral Funds Average: Derived from data provided by Lipper, a Thomson Reuters Company. |

| Institutional Shares are available to certain institutional investors who meet specific administrative, service, and account-size criteria. |

Your Fund’s Performance at a Glance

December 31, 2013, Through December 31, 2014

| | | | | |

| | | | Distributions Per Share | |

| | Starting | Ending | | | |

| | Share | Share | Income | Capital | Return of |

| | Price | Price | Dividends | Gains | Capital |

| Vanguard Market Neutral Fund | | | | | |

| Investor Shares | $11.03 | $11.50 | $0.000 | $0.000 | $0.000 |

| Institutional Shares | 10.97 | 11.45 | 0.000 | 0.000 | 0.000 |

1

Chairman’s Letter

Dear Shareholder,

Vanguard Market Neutral Fund easily outpaced its peers and its benchmark index in 2014 as the broad stock market delivered another year of strong returns.

The fund returned 4.26% for Investor Shares and 4.38% for the lower-cost Institutional Shares. That compares with 0.03% for the benchmark Citigroup Three-Month U.S. Treasury Bill Index and 0.43% for peer funds, on average.

Of course, the fund’s advance pales next to the U.S. equity market’s double-digit return, but that disparity is to be expected. The fund is designed not to follow the returns of the broad stock market but to deliver performance that’s neutral to market conditions.

Not surprisingly, the stock market experienced volatility in 2014. At the beginning of the year and again in the summer, U.S. stocks suffered a steep monthly drop followed by a sharp rebound in the next month. Through these ups and downs, however, the Market Neutral Fund’s returns stayed relatively stable.

Please note that effective December 3, Vanguard eliminated the investment minimum for institutional and financial advisor clients in the fund’s Investor share class.

2

U.S. stocks finished higher for the sixth straight year

U.S. stocks returned nearly 13% for the 12 months ended December 31, 2014, posting gains for the sixth consecutive calendar year. Rising corporate earnings, the growing U.S. economy, and generally accommodative global monetary policies lifted domestic markets. Elsewhere, Europe and China faced economic challenges, tensions flared in the Middle East and Ukraine, and concerns arose over high stock valuations.

Although the Federal Reserve ended its bond-buying program in October, investors seemed to be reassured by its stance that it would be “patient” in deciding when to increase short-term interest rates. Other central banks—including the Bank of Japan, the European Central Bank, and the People’s Bank of China—announced significant stimulus measures.

International stocks didn’t fare as well as their U.S. counterparts, returning about –3% in dollar terms. Their performance was hurt as many foreign currencies weakened against the U.S. dollar. Emerging-market stocks rose slightly, but stocks from the developed markets of Europe and the Pacific region retreated.

Defying analysts’ expectations, bond prices rose during the period

Bond prices received a boost from many of the world’s central banks along with global economic, market, and geopolitical challenges that drew investors to perceived safe havens. In an unexpected rebound

| | | |

| Market Barometer | | | |

| |

| | Average Annual Total Returns |

| | Periods Ended December 31, 2014 |

| | One | Three | Five |

| | Year | Years | Years |

| Stocks | | | |

| Russell 1000 Index (Large-caps) | 13.24% | 20.62% | 15.64% |

| Russell 2000 Index (Small-caps) | 4.89 | 19.21 | 15.55 |

| Russell 3000 Index (Broad U.S. market) | 12.56 | 20.51 | 15.63 |

| FTSE All-World ex US Index (International) | -3.31 | 9.41 | 4.75 |

| |

| Bonds | | | |

| Barclays U.S. Aggregate Bond Index (Broad taxable market) | 5.97% | 2.66% | 4.45% |

| Barclays Municipal Bond Index (Broad tax-exempt market) | 9.05 | 4.30 | 5.16 |

| Citigroup Three-Month U.S. Treasury Bill Index | 0.03 | 0.04 | 0.06 |

| |

| CPI | | | |

| Consumer Price Index | 0.76% | 1.33% | 1.69% |

3

from the previous year, the broad U.S. bond market returned 5.97% for the period.

Even as the Fed pared back its bond purchases, prices climbed and yields fell. (Bond prices and yields move in opposite directions.) The yield of the 10-year Treasury note ended December at 2.19%, down from 2.97% at the close of December 2013.

Municipal bonds returned 9.05%, benefiting from increased demand and generally limited supply.

International bond markets (as measured by the Barclays Global Aggregate Index ex USD) returned –3.08%.

The fund’s long-short approach led to successful 12-month performance

In a sense, Vanguard Market Neutral Fund is actually two portfolios. From its “short” portfolio, it sells borrowed shares in the hope that the stocks’ price will fall. It can then profit by replacing the shares at the lower price. In its “long” portfolio, the fund invests with a traditional approach, in which stocks are selected based on the advisor’s belief that they’ll outperform.

The two portfolios are mirror images. They typically have about the same number of stocks and the same weightings—or allocation levels—to industry sectors. Success hinges on the selection of stocks by the fund’s advisor, Vanguard Equity

| |

| Total Returns | |

| Ten Years Ended December 31, 2014 | |

| | Average |

| | Annual Return |

| Market Neutral Fund Investor Shares | 2.46% |

| Citigroup Three-Month U.S. Treasury Bill Index | 1.46 |

| Alternative Equity Market Neutral Funds Average | 1.36 |

| Alternative Equity Market Neutral Funds Average: Derived from data provided by Lipper, a Thomson Reuters Company. |

The figures shown represent past performance, which is not a guarantee of future results. (Current performance may be lower or higher than the performance data cited. For performance data current to the most recent month-end, visit our website at vanguard.com/performance.) Note, too, that both investment returns and principal value can fluctuate widely, so an investor’s shares, when sold, could be worth more or less than their original cost.

4

Investment Group, through its Quantitative Equity Group. The advisor has developed—and continually refines—computer models to identify the most and least attractive stocks in each sector.

These models, on the whole, worked well for the fiscal year. On the long side, the fund scored big returns with its investments in airlines. These companies benefited from the steep slide in fuel prices as well as industry consolidation that has allowed carriers to raise fares. The fund also had success with short investments in a range of businesses from cosmetics to shipping.

Energy was a weak spot: Shares of oil and gas companies plunged in the second half of the year along with the price of oil. Although the fund had some success with short investments in the sector, it wasn’t enough to offset the big drop in its long positions.

The fund’s combination of short and long investments is intended to enhance diversification by providing returns that aren’t closely correlated with moves of the broad stock market. However, the technique doesn’t work in every sector in every period, as we saw with energy

|

| Vanguard’s outlook for investors: Expect less and stay balanced |

| |

| In Vanguard’s recently published market outlook, global chief economist Joe Davis and his |

| team discuss expected returns for various asset classes over the coming years. Although not |

| bearish, our outlook on global stocks and bonds is the most guarded since 2006. The report |

| cautions that, over the next decade, returns for a balanced portfolio are likely to be moderately |

| below long-run historical averages. |

| |

| Our simulations indicate that the average annualized returns of a 60% equity/40% bond |

| portfolio for the decade ending 2024 are most likely to be centered in the 3%–5% range |

| after inflation, below the actual average after-inflation return of 5.6% for the same portfolio |

| since 1926. |

| |

| Even so, Vanguard firmly believes that the principles for investing success—focusing on clear |

| goals, a suitable asset allocation, low costs, and long-term discipline—remain unchanged. |

| |

| For more information about our expectations and the probability of various outcomes, |

| see Vanguard’s Economic and Investment Outlook, available at vanguard.com/research. |

| |

| |

| |

| IMPORTANT: The projections and other information generated by the Vanguard Capital Markets Model (VCMM) |

| regarding the likelihood of various investment outcomes are hypothetical in nature, do not reflect actual invest- |

| ment results, and are not guarantees of future results. Distribution of return outcomes from VCMM, derived |

| from 10,000 simulations for U.S. equity returns and fixed income returns. Simulations as of September 30, 2014. |

| Results from the model may vary with each use and over time. For more information, please see page 6. |

5

stocks in 2014. The hope is that, in aggregate, the short and long positions will lead to a net positive result. Because of the Market Neutral Fund’s distinctive characteristics, investors should carefully evaluate its appropriateness for their specific situations. The fund can play a role as a portion of an already well-diversified portfolio.

For more about the advisor’s strategy and the fund’s positioning during the year, please see the Advisor’s Report that follows this letter.

The fund’s relative performance was solid over the past decade

For the ten years ended December 31, 2014, the Market Neutral Fund recorded an annualized return of 2.46% for Investor Shares. That exceeded the annual result of the benchmark index by one percentage point and the average annual return of peers by slightly more than that. As you may recall, the fund has been through significant changes in the last decade.

It became a Vanguard fund in 2007, and Vanguard Equity Investment Group became its sole advisor in 2010. We’re confident that the group will continue to successfully implement the fund’s long-short strategy.

To build for the long term, start with a solid foundation

As the leader of a major investment firm, I get asked a lot of questions on all kinds of topics, from the outlook for global markets to the best fund choices for an IRA. But a topic that almost never comes up—and one that I consider perhaps the most important—is setting investment goals.

IMPORTANT: The projections and other information generated by the Vanguard Capital Markets Model regarding the likelihood of various investment outcomes are hypothetical in nature, do not reflect actual investment results, and are not guarantees of future results. VCMM results will vary with each use and over time.

The VCMM projections are based on a statistical analysis of historical data. Future returns may behave differently from the historical patterns captured in the VCMM. More important, the VCMM may be underestimating extreme negative scenarios unobserved in the historical period on which the model estimation is based.

The Vanguard Capital Markets Model® is a proprietary financial simulation tool developed and maintained by Vanguard’s primary investment research and advice teams. The model forecasts distributions of future returns for a wide array of broad asset classes. Those asset classes include U.S. and international equity markets, several maturities of the U.S. Treasury and corporate fixed income markets, international fixed income markets, U.S. money markets, commodities, and certain alternative investment strategies. The theoretical and empirical foundation for the Vanguard Capital Markets Model is that the returns of various asset classes reflect the compensation investors require for bearing different types of systematic risk (beta). At the core of the model are estimates of the dynamic statistical relationship between risk factors and asset returns, obtained from statistical analysis based on available monthly financial and economic data from as early as 1960. Using a system of estimated equations, the model then applies a Monte Carlo simulation method to project the estimated interrelationships among risk factors and asset classes as well as uncertainty and randomness over time. The model generates a large set of simulated outcomes for each asset class over several time horizons. Forecasts are obtained by computing measures of central tendency in these simulations. Results produced by the tool will vary with each use and over time.

6

At Vanguard, we believe that following four timeless, straightforward principles can help put you on the right track toward investment success:

• Goals. Create clear, appropriate

investment goals.

• Balance. Develop a suitable asset

allocation using broadly diversified funds.

• Cost. Minimize cost.

• Discipline. Maintain perspective and

long-term discipline.

All four principles are essential, and the order in which they’re listed is intentional. Every good investment plan begins with a clearly defined goal, which sets the foundation for building your portfolio. (You can read more about our principles in Vanguard’s Principles for Investing Success, available at vanguard.com/ research.)

Setting an investment goal doesn’t have to be complicated. It can be as simple as saving for retirement or for a child’s college education. Being realistic about your goals—and how to meet them—can help you stick with your investment plan even when times get tough.

We’ve recently welcomed a new year, which for many means a new beginning. Now is a perfect time to revisit your investment plan and make any necessary adjustments to help you reach your long-term financial goals.

As always, thank you for investing with Vanguard.

Sincerely,

F. William McNabb III

Chairman and Chief Executive Officer

January 20, 2015

7

Advisor’s Report

U.S. equities delivered their sixth consecutive year of positive returns in 2014. The broad U.S. equity market rose nearly 13%, large-capitalization stocks bested smaller-caps by about 8 percentage points, and value-oriented companies modestly outpaced their growth counterparts. The U.S. equity market far surpassed international markets, both developed and emerging.

Performance in the U.S. market was broad-based: Nine of ten sectors generated positive returns. Results were best in utilities, health care, and information technology. Energy was the only sector to deliver negative returns as oil prices plummeted about 50%.

Vanguard Market Neutral Fund returned 4.26% for Investor Shares and 4.38% for Institutional Shares. The fund’s strategy is not to outperform the equity market but rather to be neutral to market conditions and produce results that exceed the returns of 3-month U.S. Treasury bills.

Conditions continued to improve for the U.S. economy in 2014. Third-quarter GDP growth came in at an annual rate of 5% and unemployment kept declining as the nation approached full employment. Hopefully, wage growth will soon begin to strengthen. As oil and gas prices decline, many consumers will have additional income to spend.

U.S. companies are raising their competitiveness, and that should bode well for profit growth in the near term. However, the economy is not without challenges. The housing market stalled for the year, and uncertainty remains about when and to what extent the Federal Reserve will begin to raise interest rates. Foreign economies are still struggling—some are near recession—and China’s growth rate is decelerating. These uncertainties could lead to volatility in our home markets.

Although it’s important to understand how overall portfolio performance is affected by the macro factors described above, our investment philosophy and process focus on specific stock fundamentals. We compare stocks in the same industry group against one another to identify those with characteristics that we believe will outperform and underperform over the long run. To do this, we use a strict quantitative process that concentrates on a combination of valuation and other factors focused on fundamental growth. We then construct our portfolio with the goal of maximizing expected return and minimizing exposure to risks that our research indicates do not improve returns.

Our analysis for the calendar year reveals that our stock selection model was effective in identifying the leaders

8

and laggards within sectors; all five of our stock selection signals produced positive performance. The growth and valuation models were the strongest contributors, followed by sentiment and quality.

Our stock selection was successful in six of the ten sectors in the benchmark, with the strongest results in industrials, consumer staples, and information technology. Choices in energy detracted most.

Long positions in Southwest Airlines and JetBlue Airways and short positions in Scorpio Bulkers and Chart Industries led our results in industrials. In consumer staples, long positions in Pilgrim’s Pride and Keurig Green Mountain and a short position in Elizabeth Arden drove returns. In information technology, long positions in Freescale Semiconductor and Booz Allen Hamilton contributed most to relative performance.

However, our results in energy were disappointing. Long positions in Basic Energy Services and Comstock Resources, as well as a short position in Cheniere Energy, did not perform as expected and were the largest detractors in this group.

We thank you for your investment and look forward to the new year.

James D. Troyer, CFA,

Principal, Portfolio Manager

James P. Stetler,

Principal, Portfolio Manager

Michael R. Roach, CFA,

Portfolio Manager

Vanguard Equity Investment Group

January 21, 2015

9

Market Neutral Fund

Fund Profile

As of December 31, 2014

| | |

| Share-Class Characteristics | | |

| | Investor | Institutional |

| | Shares | Shares |

| Ticker Symbol | VMNFX | VMNIX |

| Total Expense Ratio1 | 1.60% | 1.50% |

| Management Expenses | 0.19% | 0.09% |

| Dividend Expenses on | | |

| Securities Sold Short2 | 1.18% | 1.18% |

| Borrowing Expenses on | | |

| Securities Sold Short2 | 0.14% | 0.14% |

| Other Expenses | 0.09% | 0.09% |

| | |

| Portfolio Characteristics | | |

| | Long | Short |

| | Portfolio | Portfolio |

| Number of Stocks | 252 | 248 |

| Median Market Cap | $4.3B | $3.7B |

| Price/Earnings Ratio | 16.7x | 42.6x |

| Price/Book Ratio | 2.6x | 2.3x |

| Return on Equity | 13.5% | 12.2% |

| Earnings Growth | | |

| Rate | 18.6% | 13.2% |

| Foreign Holdings | 1.5% | 2.0% |

| |

| Fund Characteristics | |

| Turnover Rate | 73% |

| Short-Term Reserves | 2.3% |

| | |

| Volatility Measures | | |

| | Citigroup | DJ |

| | Three-Month | U.S. Total |

| | U.S. Treasury | Market |

| | Bill Index | FA Index |

| R-Squared | 0.02 | 0.13 |

| Beta | -28.00 | 0.13 |

| These measures show the degree and timing of the fund’s fluctuations compared with the index over 36 months. |

| | |

| Sector Diversification (% of equity exposure) |

| | Long | Short |

| | Portfolio | Portfolio |

| Consumer Discretionary | 17.8% | 18.2% |

| Consumer Staples | 4.8 | 4.0 |

| Energy | 3.7 | 3.9 |

| Financials | 17.3 | 17.4 |

| Health Care | 10.6 | 10.4 |

| Industrials | 14.9 | 15.0 |

| Information Technology | 18.2 | 18.8 |

| Materials | 6.2 | 6.2 |

| Telecommunication Services | 1.0 | 1.0 |

| Utilities | 5.5 | 5.1 |

1 The total expense ratios shown are from the prospectus dated April 25, 2014, and represent estimated costs for the current fiscal year. For the

fiscal year ended December 31, 2014, the annualized total expense ratios were 1.64% for Investor Shares and 1.54% for Institutional Shares.

2 In connection with a short sale, the fund may receive income or be charged a fee based on the market value of the borrowed stock. When a

cash dividend is declared on a stock the fund has sold short, the fund is required to pay an amount equal to that dividend to the party from which

the fund borrowed the stock and to record the payment of the dividend as an expense.

10

Market Neutral Fund

| | |

| Ten Largest Holdings1 (% of total net assets) |

| Long Portfolio | | |

| Greenbrier Cos. Inc. | Construction | |

| | Machinery & Heavy | |

| | Trucks | 0.6% |

| Merrimack | | |

| Pharmaceuticals Inc. | Biotechnology | 0.5 |

| Murphy USA Inc. | Automotive Retail | 0.5 |

| ARRIS Group Inc. | Communications | |

| | Equipment | 0.5 |

| American States Water | | |

| Co. | Water Utilities | 0.5 |

| Nabors Industries Ltd. | Oil & Gas Drilling | 0.5 |

| Southwest Airlines Co. | Airlines | 0.5 |

| Century Aluminum Co. | Aluminum | 0.5 |

| JetBlue Airways Corp. | Airlines | 0.5 |

| Meritor Inc. | Auto Parts | 0.5 |

| Top Ten | | 5.1% |

| | |

| Ten Largest Holdings1 (% of total net assets) |

| Short Portfolio | | |

| |

| Knowles Corp. | Electronic | |

| | Components | 0.6% |

| DigitalGlobe Inc. | Aerospace & | |

| | Defense | 0.5 |

| WageWorks Inc. | Human Resource & | |

| | Employment | |

| | Services | 0.5 |

| Groupon Inc. | Internet Retail | 0.5 |

| Office Depot Inc. | Specialty Stores | 0.5 |

| Gulfport Energy Corp. | Oil & Gas | |

| | Exploration & | |

| | Production | 0.5 |

| Lumber Liquidators | Home | |

| Holdings Inc. | Improvement Retail | 0.5 |

| WellCare Health Plans | Managed Health | |

| Inc. | Care | 0.5 |

| FNF Group | Property & Casualty | |

| | Insurance | 0.5 |

| Aaron's Inc. | Homefurnishing | |

| | Retail | 0.5 |

| Top Ten | | 5.1% |

1 The holdings listed exclude any temporary cash investments and equity index products.

11

Market Neutral Fund

Performance Summary

All of the returns in this report represent past performance, which is not a guarantee of future results that may be achieved by the fund. (Current performance may be lower or higher than the performance data cited. For performance data current to the most recent month-end, visit our website at vanguard.com/performance.) Note, too, that both investment returns and principal value can fluctuate widely, so an investor’s shares, when sold, could be worth more or less than their original cost. The returns shown do not reflect taxes that a shareholder would pay on fund distributions or on the sale of fund shares.

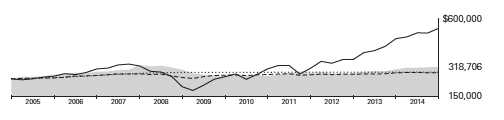

Cumulative Performance: December 31, 2004, Through December 31, 2014

Initial Investment of $250,000

| | | | | |

| | | Average Annual Total Returns | |

| | | Periods Ended December 31, 2014 | |

| |

| | | | | | Final Value |

| | | One | Five | Ten | of a $250,000 |

| | | Year | Years | Years | Investment |

| |

| | Market Neutral Fund*Investor Shares | 4.26% | 3.54% | 2.46% | $318,706 |

| | Citigroup Three-Month U.S. Treasury | | | | |

| •••••••• | Bill Index | 0.03 | 0.06 | 1.46 | 289,154 |

| |

| – – –– | Alternative Equity Market Neutral | | | | |

| | Funds Average | 0.43 | 1.08 | 1.36 | 286,232 |

| | Dow Jones U.S. Total Stock Market | | | | |

| | Float Adjusted Index | 12.47 | 15.72 | 8.09 | 544,466 |

| |

| Alternative Equity Market Neutral Funds Average: Derived from data provided by Lipper, a Thomson Reuters Company. |

| | | | |

| | | | | Final Value |

| | One | Five | Ten | of a $5,000,000 |

| | Year | Years | Years | Investment |

| |

| Market Neutral Fund Institutional Shares | 4.38% | 3.64% | 2.61% | $6,467,781 |

| Citigroup Three-Month U.S. Treasury Bill | | | | |

| Index | 0.03 | 0.06 | 1.46 | 5,783,080 |

| Dow Jones U.S. Total Stock Market Float | | | | |

| Adjusted Index | 12.47 | 15.72 | 8.09 | 10,889,319 |

See Financial Highlights for dividend and capital gains information.

12

Market Neutral Fund

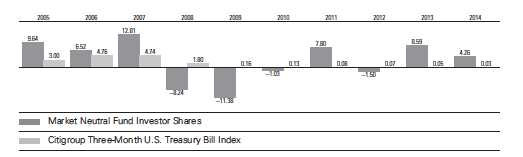

Fiscal-Year Total Returns (%): December 31, 2004, Through December 31, 2014

13

Market Neutral Fund

Financial Statements

Statement of Net Assets

As of December 31, 2014

The fund reports a complete list of its holdings in regulatory filings four times in each fiscal year, at the quarter-ends. For the second and fourth fiscal quarters, the lists appear in the fund’s semiannual and annual reports to shareholders. For the first and third fiscal quarters, the fund files the lists with the Securities and Exchange Commission on Form N-Q. Shareholders can look up the fund’s Forms N-Q on the SEC’s website at sec.gov. Forms N-Q may also be reviewed and copied at the SEC’s Public Reference Room (see the back cover of this report for further information).

| | | |

| | | | Market |

| | | | Value |

| | | Shares | ($000) |

| Common Stocks—Long Positions (95.5%) | |

| Consumer Discretionary (17.0%) | | |

| * † | Murphy USA Inc. | 24,800 | 1,708 |

| † | Royal Caribbean Cruises Ltd. | 19,400 | 1,599 |

| † | Dana Holding Corp. | 73,380 | 1,595 |

| † | Best Buy Co. Inc. | 40,900 | 1,594 |

| * | Lands’ End Inc. | 29,300 | 1,581 |

| * | Madison Square Garden Co. | | |

| | Class A | 20,900 | 1,573 |

| * | American Axle | | |

| | & Manufacturing Holdings | | |

| | Inc. | 69,100 | 1,561 |

| * | Zumiez Inc. | 40,300 | 1,557 |

| * † | Barnes & Noble Inc. | 66,200 | 1,537 |

| * † | Outerwall Inc. | 20,350 | 1,531 |

| * † | NVR Inc. | 1,200 | 1,530 |

| † | Brown Shoe Co. Inc. | 47,600 | 1,530 |

| † | Marriott Vacations | | |

| | Worldwide Corp. | 20,500 | 1,528 |

| | Cato Corp. Class A | 36,200 | 1,527 |

| † | Cablevision Systems Corp. | | |

| | Class A | 73,600 | 1,519 |

| † | Jack in the Box Inc. | 18,900 | 1,511 |

| * † | O’Reilly Automotive Inc. | 7,800 | 1,502 |

| * † | Skechers U.S.A. Inc. Class A | 27,000 | 1,492 |

| † | Marriott International Inc. | | |

| | Class A | 19,000 | 1,483 |

| † | DeVry Education Group Inc. | 31,200 | 1,481 |

| | Big Lots Inc. | 37,000 | 1,481 |

| † | Expedia Inc. | 17,200 | 1,468 |

| † | Home Depot Inc. | 13,900 | 1,459 |

| * † | Vince Holding Corp. | 54,500 | 1,425 |

| † | Domino’s Pizza Inc. | 15,050 | 1,417 |

| † | Hanesbrands Inc. | 12,100 | 1,351 |

| | Whirlpool Corp. | 6,800 | 1,317 |

| * † | Visteon Corp. | 12,200 | 1,304 |

| † | Macy’s Inc. | 19,500 | 1,282 |

| † | Columbia Sportswear Co. | 28,200 | 1,256 |

| * | News Corp. Class A | 72,000 | 1,130 |

| * † | Starz | 34,700 | 1,031 |

| | | |

| * | BJ’s Restaurants Inc. | 18,600 | 934 |

| † | GameStop Corp. Class A | 27,200 | 919 |

| † | Buckle Inc. | 16,800 | 882 |

| † | Dillard’s Inc. Class A | 6,670 | 835 |

| † | Gap Inc. | 18,900 | 796 |

| † | TJX Cos. Inc. | 11,100 | 761 |

| * | Live Nation Entertainment | | |

| | Inc. | 20,800 | 543 |

| | Foot Locker Inc. | 5,200 | 292 |

| | AMC Entertainment | | |

| | Holdings Inc. | 9,800 | 257 |

| | | | 53,079 |

| Consumer Staples (4.6%) | | |

| | Archer-Daniels-Midland Co. | 29,600 | 1,539 |

| † | Bunge Ltd. | 16,200 | 1,473 |

| * † | Pilgrim’s Pride Corp. | 44,000 | 1,443 |

| † | Cal-Maine Foods Inc. | 36,700 | 1,432 |

| † | Sanderson Farms Inc. | 17,000 | 1,428 |

| † | Dr Pepper Snapple Group | | |

| | Inc. | 18,900 | 1,355 |

| † | Keurig Green Mountain Inc. | 9,500 | 1,258 |

| * † | Rite Aid Corp. | 145,900 | 1,097 |

| † | Andersons Inc. | 19,550 | 1,039 |

| | Kimberly-Clark Corp. | 7,800 | 901 |

| * | SUPERVALU Inc. | 64,200 | 623 |

| | Avon Products Inc. | 62,900 | 591 |

| | | | 14,179 |

| Energy (3.4%) | | |

| | Nabors Industries Ltd. | 125,200 | 1,625 |

| | Tesoro Corp. | 19,900 | 1,479 |

| * † | Kosmos Energy Ltd. | 151,200 | 1,269 |

| † | Valero Energy Corp. | 24,700 | 1,223 |

| † | Green Plains Inc. | 43,800 | 1,085 |

| * | Unit Corp. | 18,500 | 631 |

| † | Hess Corp. | 8,500 | 627 |

| * | Helix Energy Solutions Group | | |

| | Inc. | 28,700 | 623 |

| * † | Clayton Williams Energy Inc. | 9,600 | 612 |

| † | SM Energy Co. | 15,800 | 610 |

14

Market Neutral Fund

| | | |

| | | | Market |

| | | | Value |

| | | Shares | ($000) |

| * † | Basic Energy Services Inc. | 65,900 | 462 |

| * | Seventy Seven Energy Inc. | 37,357 | 202 |

| | | | 10,448 |

| Financials (16.5%) | | |

| † | Montpelier Re Holdings Ltd. | 44,500 | 1,594 |

| † | CIT Group Inc. | 33,000 | 1,578 |

| † | International Bancshares | | |

| | Corp. | 59,400 | 1,576 |

| † | Nelnet Inc. Class A | 34,000 | 1,575 |

| † | Reinsurance Group of | | |

| | America Inc. Class A | 17,700 | 1,551 |

| † | Navient Corp. | 71,500 | 1,545 |

| * | Springleaf Holdings Inc. | 42,700 | 1,544 |

| † | Voya Financial Inc. | 36,400 | 1,543 |

| | JPMorgan Chase & Co. | 24,600 | 1,539 |

| † | PrivateBancorp Inc. | 45,900 | 1,533 |

| | Associated Banc-Corp | 81,900 | 1,526 |

| † | Everest Re Group Ltd. | 8,900 | 1,516 |

| † | AmTrust Financial Services | | |

| | Inc. | 26,800 | 1,508 |

| | Assured Guaranty Ltd. | 57,500 | 1,494 |

| † | Santander Consumer USA | | |

| | Holdings Inc. | 75,400 | 1,479 |

| † | Radian Group Inc. | 88,100 | 1,473 |

| † | PartnerRe Ltd. | 12,700 | 1,449 |

| † | Aspen Insurance Holdings | | |

| | Ltd. | 33,100 | 1,449 |

| † | Capital One Financial Corp. | 17,500 | 1,445 |

| * † | Credit Acceptance Corp. | 10,260 | 1,400 |

| | Travelers Cos. Inc. | 12,500 | 1,323 |

| † | Goldman Sachs Group Inc. | 6,800 | 1,318 |

| | RenaissanceRe Holdings Ltd. | 13,400 | 1,303 |

| | Wells Fargo & Co. | 23,200 | 1,272 |

| | Axis Capital Holdings Ltd. | 24,700 | 1,262 |

| † | Talmer Bancorp Inc. Class A | 88,300 | 1,240 |

| † | Ameriprise Financial Inc. | 9,300 | 1,230 |

| * † | Western Alliance Bancorp | 43,800 | 1,218 |

| † | Allied World Assurance Co. | | |

| | Holdings AG | 32,000 | 1,213 |

| † | KeyCorp | 76,500 | 1,063 |

| | Lazard Ltd. Class A | 18,700 | 936 |

| † | Huntington Bancshares Inc. | 87,400 | 919 |

| † | Washington Federal Inc. | 40,600 | 899 |

| | Assurant Inc. | 13,000 | 890 |

| † | Regions Financial Corp. | 81,700 | 863 |

| * | World Acceptance Corp. | 10,650 | 846 |

| | Comerica Inc. | 17,500 | 820 |

| * | Beneficial Mutual Bancorp | | |

| | Inc. | 46,100 | 566 |

| * | MGIC Investment Corp. | 53,200 | 496 |

| | Cathay General Bancorp | 17,000 | 435 |

| | Symetra Financial Corp. | 16,200 | 373 |

| | FBL Financial Group Inc. | | |

| | Class A | 5,700 | 331 |

| | | |

| | Banco Latinoamericano de | | |

| | Comercio Exterior SA | 10,800 | 325 |

| | | | 51,458 |

| Health Care (10.1%) | | |

| * | Merrimack Pharmaceuticals | | |

| | Inc. | 151,600 | 1,713 |

| * † | Health Net Inc. | 29,900 | 1,601 |

| * † | Centene Corp. | 15,200 | 1,578 |

| * † | Quintiles Transnational | | |

| | Holdings Inc. | 26,000 | 1,531 |

| † | Omnicare Inc. | 20,900 | 1,524 |

| * † | Charles River Laboratories | | |

| | International Inc. | 23,400 | 1,489 |

| * † | Premier Inc. Class A | 43,600 | 1,462 |

| * † | Natus Medical Inc. | 40,500 | 1,460 |

| * † | Edwards Lifesciences Corp. | 11,400 | 1,452 |

| * † | Anthem Inc. | 11,000 | 1,382 |

| * † | Lannett Co. Inc. | 32,000 | 1,372 |

| * | Surgical Care Affiliates Inc. | 38,900 | 1,309 |

| † | AbbVie Inc. | 20,000 | 1,309 |

| * | Gilead Sciences Inc. | 13,600 | 1,282 |

| * † | PAREXEL International Corp. | 22,700 | 1,261 |

| * † | HCA Holdings Inc. | 15,355 | 1,127 |

| † | Eli Lilly & Co. | 15,400 | 1,062 |

| † | Select Medical Holdings | | |

| | Corp. | 71,200 | 1,025 |

| * | Globus Medical Inc. | 40,100 | 953 |

| * | Boston Scientific Corp. | 64,800 | 859 |

| * | Medivation Inc. | 8,600 | 857 |

| | Cardinal Health Inc. | 9,600 | 775 |

| * | VCA Inc. | 14,800 | 722 |

| * † | Bruker Corp. | 34,900 | 685 |

| * | MedAssets Inc. | 31,100 | 614 |

| † | Chemed Corp. | 4,600 | 486 |

| * | INC Research Holdings Inc. | | |

| | Class A | 18,200 | 468 |

| | CR Bard Inc. | 1,600 | 267 |

| | | | 31,625 |

| Industrials (14.2%) | | |

| | Greenbrier Cos. Inc. | 32,800 | 1,762 |

| † | Southwest Airlines Co. | 38,400 | 1,625 |

| * † | JetBlue Airways Corp. | 101,800 | 1,615 |

| * † | Meritor Inc. | 106,300 | 1,611 |

| * | Korn/Ferry International | 55,600 | 1,599 |

| * † | Spirit AeroSystems Holdings | | |

| | Inc. Class A | 36,900 | 1,588 |

| | Aircastle Ltd. | 73,900 | 1,579 |

| † | Pitney Bowes Inc. | 63,600 | 1,550 |

| * † | United Rentals Inc. | 14,800 | 1,510 |

| † | Textron Inc. | 35,800 | 1,508 |

| † | Illinois Tool Works Inc. | 15,800 | 1,496 |

| † | Huntington Ingalls Industries | | |

| | Inc. | 13,283 | 1,494 |

| | General Dynamics Corp. | 10,800 | 1,486 |

15

Market Neutral Fund

| | | |

| | | | Market |

| | | | Value |

| | | Shares | ($000) |

| † | Alaska Air Group Inc. | 24,820 | 1,483 |

| † | West Corp. | 44,900 | 1,482 |

| * † | TriNet Group Inc. | 46,800 | 1,464 |

| * | AECOM Technology Corp. | 47,000 | 1,427 |

| † | Cintas Corp. | 17,900 | 1,404 |

| † | Lockheed Martin Corp. | 6,700 | 1,290 |

| † | Deluxe Corp. | 20,200 | 1,258 |

| † | Masco Corp. | 49,000 | 1,235 |

| * | United Continental Holdings | | |

| | Inc. | 16,000 | 1,070 |

| | ArcBest Corp. | 22,800 | 1,057 |

| † | Trinity Industries Inc. | 37,740 | 1,057 |

| | SPX Corp. | 12,200 | 1,048 |

| † | ManpowerGroup Inc. | 14,300 | 975 |

| | Harsco Corp. | 51,500 | 973 |

| * | Spirit Airlines Inc. | 12,800 | 967 |

| † | H&E Equipment Services | | |

| | Inc. | 31,700 | 891 |

| † | UniFirst Corp. | 6,800 | 826 |

| * † | Avis Budget Group Inc. | 11,200 | 743 |

| | Boeing Co. | 5,000 | 650 |

| † | Union Pacific Corp. | 4,300 | 512 |

| | Robert Half International Inc. | 8,300 | 485 |

| † | CIRCOR International Inc. | 8,000 | 482 |

| † | Steelcase Inc. Class A | 26,600 | 477 |

| † | Northrop Grumman Corp. | 2,730 | 402 |

| † | AMERCO | 1,000 | 284 |

| | | | 44,365 |

| Information Technology (17.4%) | | |

| * † | ARRIS Group Inc. | 54,800 | 1,654 |

| * † | RF Micro Devices Inc. | 96,100 | 1,594 |

| * † | Electronic Arts Inc. | 33,500 | 1,575 |

| * † | Freescale Semiconductor | | |

| | Ltd. | 62,410 | 1,575 |

| * † | Aspen Technology Inc. | 44,800 | 1,569 |

| * † | Take-Two Interactive | | |

| | Software Inc. | 55,900 | 1,567 |

| * | Super Micro Computer Inc. | 44,600 | 1,556 |

| * † | Blackhawk Network | | |

| | Holdings Inc. | 40,000 | 1,552 |

| † | CDW Corp. | 43,900 | 1,544 |

| * | VASCO Data Security | | |

| | International Inc. | 54,100 | 1,526 |

| * † | AVG Technologies NV | 77,300 | 1,526 |

| * † | Manhattan Associates Inc. | 36,600 | 1,490 |

| † | Booz Allen Hamilton Holding | | |

| | Corp. | 55,900 | 1,483 |

| † | Computer Sciences Corp. | 23,400 | 1,475 |

| † | Heartland Payment Systems | | |

| | Inc. | 27,000 | 1,457 |

| † | Western Digital Corp. | 13,150 | 1,456 |

| † | Science Applications | | |

| | International Corp. | 29,200 | 1,446 |

| * † | OmniVision Technologies | | |

| | Inc. | 55,200 | 1,435 |

| | | |

| * | Sanmina Corp. | 60,400 | 1,421 |

| * † | Sykes Enterprises Inc. | 60,300 | 1,415 |

| * | CommScope Holding Co. | | |

| | Inc. | 60,100 | 1,372 |

| * † | Gartner Inc. | 15,900 | 1,339 |

| † | SYNNEX Corp. | 16,006 | 1,251 |

| * | iGATE Corp. | 31,500 | 1,244 |

| † | Broadridge Financial | | |

| | Solutions Inc. | 26,800 | 1,238 |

| † | MAXIMUS Inc. | 22,500 | 1,234 |

| | Cypress Semiconductor | | |

| | Corp. | 85,300 | 1,218 |

| | DST Systems Inc. | 12,800 | 1,205 |

| * | TeleTech Holdings Inc. | 50,400 | 1,194 |

| * † | Tech Data Corp. | 16,600 | 1,050 |

| * † | Ciena Corp. | 53,700 | 1,042 |

| | Blackbaud Inc. | 23,800 | 1,030 |

| * | Benchmark Electronics Inc. | 40,400 | 1,028 |

| † | Brocade Communications | | |

| | Systems Inc. | 86,100 | 1,020 |

| | Lexmark International Inc. | | |

| | Class A | 24,500 | 1,011 |

| * † | Anixter International Inc. | 11,400 | 1,008 |

| * † | Advanced Micro Devices | | |

| | Inc. | 352,030 | 940 |

| * | Callidus Software Inc. | 54,800 | 895 |

| † | Avnet Inc. | 17,600 | 757 |

| * † | Rambus Inc. | 67,600 | 750 |

| † | Symantec Corp. | 21,100 | 541 |

| * † | PTC Inc. | 11,800 | 432 |

| * | Ingram Micro Inc. | 14,700 | 406 |

| | Skyworks Solutions Inc. | 5,000 | 364 |

| † | Accenture plc Class A | 2,500 | 223 |

| | Marvell Technology Group | | |

| | Ltd. | 15,200 | 220 |

| | | | 54,328 |

| Materials (6.0%) | | |

| * † | Century Aluminum Co. | 66,600 | 1,625 |

| † | LyondellBasell Industries NV | | |

| | Class A | 19,800 | 1,572 |

| | Alcoa Inc. | 99,400 | 1,569 |

| * † | Stillwater Mining Co. | 105,300 | 1,552 |

| † | Ball Corp. | 21,000 | 1,432 |

| † | United States Steel Corp. | 53,100 | 1,420 |

| * † | Berry Plastics Group Inc. | 43,800 | 1,382 |

| † | PPG Industries Inc. | 5,951 | 1,376 |

| † | CF Industries Holdings Inc. | 4,700 | 1,281 |

| * † | Graphic Packaging Holding | | |

| | Co. | 81,200 | 1,106 |

| | Scotts Miracle-Gro Co. | | |

| | Class A | 16,800 | 1,047 |

| | Avery Dennison Corp. | 17,600 | 913 |

| † | Westlake Chemical Corp. | 14,560 | 889 |

| | Sherwin-Williams Co. | 2,300 | 605 |

| | US Silica Holdings Inc. | 19,100 | 491 |

16

Market Neutral Fund

| | | |

| | | | Market |

| | | | Value |

| | | Shares | ($000) |

| | Cytec Industries Inc. | 6,700 | 309 |

| * | Ferro Corp. | 20,400 | 264 |

| | | | 18,833 |

| Telecommunication Services (1.0%) | | |

| * | Globalstar Inc. | 521,700 | 1,434 |

| * † | Level 3 Communications | | |

| | Inc. | 27,800 | 1,373 |

| | CenturyLink Inc. | 7,800 | 309 |

| | | | 3,116 |

| Utilities (5.3%) | | |

| | American States Water Co. | 43,800 | 1,650 |

| † | Vectren Corp. | 33,400 | 1,544 |

| | WGL Holdings Inc. | 28,100 | 1,535 |

| | Exelon Corp. | 41,200 | 1,528 |

| † | Portland General Electric Co. | 39,300 | 1,487 |

| * | Calpine Corp. | 66,200 | 1,465 |

| † | Entergy Corp. | 16,500 | 1,443 |

| † | Edison International | 21,400 | 1,401 |

| | New Jersey Resources | | |

| | Corp. | 21,400 | 1,310 |

| † | Pinnacle West Capital Corp. | 15,900 | 1,086 |

| † | UGI Corp. | 27,600 | 1,048 |

| | Empire District Electric Co. | 30,700 | 913 |

| | | | 16,410 |

| Total Common Stocks—Long Positions | |

| (Cost $248,775) | | 297,841 |

| Common Stocks Sold Short (-95.3%) | |

| Consumer Discretionary (-17.4%) | |

| * | Groupon Inc. Class A | (204,800) | (1,692) |

| * | Office Depot Inc. | (195,600) | (1,677) |

| * | Lumber Liquidators | | |

| | Holdings Inc. | (25,100) | (1,664) |

| | Aaron’s Inc. | (53,800) | (1,645) |

| * | Meritage Homes Corp. | (45,600) | (1,641) |

| | General Motors Co. | (46,800) | (1,634) |

| * | CarMax Inc. | (24,171) | (1,609) |

| * | DreamWorks Animation | | |

| | SKG Inc. Class A | (71,900) | (1,606) |

| | Men’s Wearhouse Inc. | (35,900) | (1,585) |

| | Brunswick Corp. | (30,900) | (1,584) |

| * | Tesla Motors Inc. | (7,100) | (1,579) |

| | Sotheby’s | (36,100) | (1,559) |

| | Signet Jewelers Ltd. | (11,800) | (1,553) |

| | DR Horton Inc. | (61,300) | (1,550) |

| | Rent-A-Center Inc. | (41,500) | (1,507) |

| * | AMC Networks Inc. | | |

| | Class A | (23,600) | (1,505) |

| * | Houghton Mifflin Harcourt | | |

| | Co. | (72,100) | (1,493) |

| | Ryland Group Inc. | (38,700) | (1,492) |

| * | Vitamin Shoppe Inc. | (30,700) | (1,492) |

| * | Amazon.com Inc. | (4,800) | (1,490) |

| * | Shutterfly Inc. | (35,500) | (1,480) |

| | | |

| * | Loral Space | | |

| | & Communications Inc. | (18,600) | (1,464) |

| * | Priceline Group Inc. | (1,250) | (1,425) |

| | Pier 1 Imports Inc. | (92,400) | (1,423) |

| | American Eagle Outfitters | | |

| | Inc. | (101,300) | (1,406) |

| | Coach Inc. | (37,300) | (1,401) |

| | Starbucks Corp. | (16,800) | (1,378) |

| * | LKQ Corp. | (40,400) | (1,136) |

| * | Toll Brothers Inc. | (29,100) | (997) |

| * | Drew Industries Inc. | (18,600) | (950) |

| * | Ascent Capital Group Inc. | | |

| | Class A | (17,600) | (932) |

| | Harley-Davidson Inc. | (13,600) | (896) |

| | Yum! Brands Inc. | (11,400) | (831) |

| | Churchill Downs Inc. | (8,200) | (781) |

| * | Liberty Broadband Corp. | | |

| | Class A | (15,100) | (756) |

| * | La Quinta Holdings Inc. | (33,500) | (739) |

| * | Liberty Broadband Corp. | (14,800) | (737) |

| | Lions Gate Entertainment | | |

| | Corp. | (22,900) | (733) |

| * | Cabela’s Inc. | (11,100) | (585) |

| * | Belmond Ltd. Class A | (44,400) | (549) |

| * | TRI Pointe Homes Inc. | (33,500) | (511) |

| * | Biglari Holdings Inc. | (1,000) | (400) |

| | Gannett Co. Inc. | (11,500) | (367) |

| * | Under Armour Inc. Class A | (4,400) | (299) |

| * | Pep Boys-Manny Moe | | |

| | & Jack | (30,000) | (295) |

| * | Liberty Media Corp. | (4,600) | (161) |

| | | | (54,189) |

| Consumer Staples (-3.8%) | | |

| * | Post Holdings Inc. | (37,200) | (1,558) |

| * | Darling Ingredients Inc. | (85,100) | (1,546) |

| * | TreeHouse Foods Inc. | (17,900) | (1,531) |

| * | United Natural Foods Inc. | (19,600) | (1,516) |

| | Flowers Foods Inc. | (77,955) | (1,496) |

| | B&G Foods Inc. | (47,200) | (1,411) |

| | Philip Morris International | | |

| | Inc. | (11,100) | (904) |

| | Universal Corp. | (18,400) | (809) |

| | Coca-Cola Co. | (9,500) | (401) |

| | Procter & Gamble Co. | (4,400) | (401) |

| | Whole Foods Market Inc. | (5,100) | (257) |

| | | | (11,830) |

| Energy (-3.7%) | | |

| * | Gulfport Energy Corp. | (39,900) | (1,665) |

| * | Cobalt International Energy | | |

| | Inc. | (178,800) | (1,590) |

| * | Antero Resources Corp. | (37,100) | (1,505) |

| * | Rice Energy Inc. | (61,800) | (1,296) |

| * | PDC Energy Inc. | (28,700) | (1,184) |

| | Williams Cos. Inc. | (22,500) | (1,011) |

17

Market Neutral Fund

| | | |

| | | | Market |

| | | | Value |

| | | Shares | ($000) |

| | CONSOL Energy Inc. | (26,400) | (893) |

| | Spectra Energy Corp. | (24,400) | (886) |

| * | Eclipse Resources Corp. | (101,800) | (716) |

| | Scorpio Tankers Inc. | (62,700) | (545) |

| * | Rosetta Resources Inc. | (14,300) | (319) |

| | | | (11,610) |

| Financials (-16.6%) | | |

| | FNF Group | (47,800) | (1,647) |

| | NorthStar Asset | | |

| | Management Group Inc. | (71,600) | (1,616) |

| * | Genworth Financial Inc. | | |

| | Class A | (186,700) | (1,587) |

| | Loews Corp. | (37,500) | (1,576) |

| | American Equity Investment | | |

| | Life Holding Co. | (53,700) | (1,568) |

| | MB Financial Inc. | (47,600) | (1,564) |

| | Zions Bancorporation | (54,800) | (1,562) |

| | Home BancShares Inc. | (48,100) | (1,547) |

| | First Niagara Financial | | |

| | Group Inc. | (183,400) | (1,546) |

| | CNA Financial Corp. | (39,500) | (1,529) |

| * | PHH Corp. | (63,700) | (1,526) |

| * | Texas Capital Bancshares | | |

| | Inc. | (28,000) | (1,521) |

| | Leucadia National Corp. | (67,800) | (1,520) |

| | Old National Bancorp | (100,700) | (1,498) |

| | Cincinnati Financial Corp. | (28,800) | (1,493) |

| * | KCG Holdings Inc. Class A | (128,100) | (1,492) |

| | Investors Bancorp Inc. | (132,400) | (1,486) |

| | Arthur J Gallagher & Co. | (31,400) | (1,478) |

| * | Markel Corp. | (2,150) | (1,468) |

| | Umpqua Holdings Corp. | (85,100) | (1,448) |

| | Intercontinental Exchange | | |

| | Inc. | (6,600) | (1,447) |

| | PacWest Bancorp | (31,600) | (1,437) |

| | Union Bankshares Corp. | (56,700) | (1,365) |

| * | Hilltop Holdings Inc. | (67,100) | (1,339) |

| | White Mountains Insurance | | |

| | Group Ltd. | (2,100) | (1,323) |

| | Interactive Brokers Group | | |

| | Inc. | (45,200) | (1,318) |

| | CME Group Inc. | (14,500) | (1,286) |

| | Hartford Financial Services | | |

| | Group Inc. | (30,500) | (1,272) |

| | Old Republic International | | |

| | Corp. | (84,500) | (1,236) |

| | M&T Bank Corp. | (9,800) | (1,231) |

| | UMB Financial Corp. | (20,900) | (1,189) |

| | Charles Schwab Corp. | (34,800) | (1,051) |

| | Financial Engines Inc. | (27,800) | (1,016) |

| * | Ocwen Financial Corp. | (66,700) | (1,007) |

| | T. Rowe Price Group Inc. | (11,300) | (970) |

| | New York Community | | |

| | Bancorp Inc. | (44,600) | (714) |

| | | |

| * | Popular Inc. | (17,600) | (599) |

| | Synovus Financial Corp. | (20,442) | (554) |

| | Erie Indemnity Co. Class A | (3,500) | (318) |

| | City National Corp. | (3,900) | (315) |

| * | FNFV Group | (11,498) | (181) |

| | | | (51,840) |

| Health Care (-9.9%) | | |

| * | WellCare Health Plans Inc. | (20,100) | (1,649) |

| * | Alkermes plc | (27,000) | (1,581) |

| * | Medidata Solutions Inc. | (32,900) | (1,571) |

| | Perrigo Co. plc | (9,300) | (1,555) |

| * | Bluebird Bio Inc. | (16,900) | (1,550) |

| * | Neurocrine Biosciences Inc. | (68,900) | (1,539) |

| * | Thoratec Corp. | (46,800) | (1,519) |

| * | Spectranetics Corp. | (43,900) | (1,518) |

| | Owens & Minor Inc. | (43,100) | (1,513) |

| | Cooper Cos. Inc. | (9,300) | (1,507) |

| * | BioMarin Pharmaceutical | | |

| | Inc. | (16,400) | (1,483) |

| * | Masimo Corp. | (55,000) | (1,449) |

| * | Alnylam Pharmaceuticals | | |

| | Inc. | (14,700) | (1,426) |

| | Bio-Techne Corp. | (14,000) | (1,294) |

| * | Allscripts Healthcare | | |

| | Solutions Inc. | (90,200) | (1,152) |

| * | HMS Holdings Corp. | (53,600) | (1,133) |

| * | Puma Biotechnology Inc. | (5,900) | (1,117) |

| * | Tenet Healthcare Corp. | (21,600) | (1,094) |

| * | TESARO Inc. | (26,600) | (989) |

| * | Varian Medical Systems Inc. | (10,300) | (891) |

| * | Endologix Inc. | (56,700) | (867) |

| | Baxter International Inc. | (11,300) | (828) |

| * | Cepheid | (14,200) | (769) |

| * | Insulet Corp. | (8,700) | (401) |

| * | NxStage Medical Inc. | (20,100) | (360) |

| * | Auspex Pharmaceuticals | | |

| | Inc. | (3,825) | (201) |

| | | | (30,956) |

| Industrials (-14.3%) | | |

| * | DigitalGlobe Inc. | (55,300) | (1,713) |

| * | WageWorks Inc. | (26,400) | (1,705) |

| * | UTi Worldwide Inc. | (133,500) | (1,611) |

| * | Colfax Corp. | (31,200) | (1,609) |

| | Crane Co. | (27,300) | (1,602) |

| | Interface Inc. Class A | (97,000) | (1,598) |

| * | USG Corp. | (55,700) | (1,559) |

| * | Wesco Aircraft Holdings | | |

| | Inc. | (110,000) | (1,538) |

| | Babcock & Wilcox Co. | (50,300) | (1,524) |

| * | Armstrong World Industries | | |

| | Inc. | (29,800) | (1,523) |

| * | Nortek Inc. | (18,300) | (1,488) |

| | Heartland Express Inc. | (54,900) | (1,483) |

| * | Beacon Roofing Supply Inc. | (53,200) | (1,479) |

18

Market Neutral Fund

| | | |

| | | | Market |

| | | | Value |

| | | Shares | ($000) |

| | Healthcare Services Group | | |

| | Inc. | (47,600) | (1,472) |

| * | Clean Harbors Inc. | (30,500) | (1,466) |

| * | Advisory Board Co. | (28,000) | (1,371) |

| | Matthews International | | |

| | Corp. Class A | (27,200) | (1,324) |

| * | Jacobs Engineering Group | | |

| | Inc. | (28,500) | (1,274) |

| | JB Hunt Transport Services | | |

| | Inc. | (14,700) | (1,238) |

| * | Stericycle Inc. | (9,400) | (1,232) |

| | Kennametal Inc. | (34,300) | (1,228) |

| * | Copart Inc. | (33,600) | (1,226) |

| | Raven Industries Inc. | (48,600) | (1,215) |

| * | Roadrunner Transportation | | |

| | Systems Inc. | (50,800) | (1,186) |

| | Nielsen NV | (26,500) | (1,185) |

| | Forward Air Corp. | (22,800) | (1,148) |

| * | EnPro Industries Inc. | (17,800) | (1,117) |

| * | DXP Enterprises Inc. | (21,700) | (1,097) |

| * | MasTec Inc. | (47,000) | (1,063) |

| | Fastenal Co. | (21,700) | (1,032) |

| * | Chart Industries Inc. | (29,200) | (999) |

| | Precision Castparts Corp. | (3,900) | (939) |

| * | MRC Global Inc. | (39,000) | (591) |

| | MSA Safety Inc. | (7,642) | (406) |

| * | Scorpio Bulkers Inc. | (181,200) | (357) |

| | | | (44,598) |

| Information Technology (-17.9%) | |

| * | Knowles Corp. | (73,400) | (1,729) |

| * | CoStar Group Inc. | (8,800) | (1,616) |

| * | CommVault Systems Inc. | (30,900) | (1,597) |

| * | Splunk Inc. | (26,500) | (1,562) |

| * | Finisar Corp. | (80,300) | (1,559) |

| * | SunEdison Inc. | (79,700) | (1,555) |

| * | Cornerstone OnDemand Inc. | (43,900) | (1,545) |

| | FEI Co. | (17,100) | (1,545) |

| * | Palo Alto Networks Inc. | (12,600) | (1,544) |

| | Analog Devices Inc. | (27,400) | (1,521) |

| * | Pandora Media Inc. | (85,200) | (1,519) |

| | Altera Corp. | (40,500) | (1,496) |

| * | ServiceNow Inc. | (21,900) | (1,486) |

| * | Entegris Inc. | (111,500) | (1,473) |

| * | HomeAway Inc. | (49,000) | (1,459) |

| * | Trimble Navigation Ltd. | (54,400) | (1,444) |

| * | ViaSat Inc. | (22,600) | (1,424) |

| * | LinkedIn Corp. Class A | (6,200) | (1,424) |

| * | Fortinet Inc. | (46,400) | (1,423) |

| * | Zynga Inc. Class A | (534,100) | (1,421) |

| * | Twitter Inc. | (38,500) | (1,381) |

| | Equinix Inc. | (6,039) | (1,369) |

| * | Dealertrack Technologies | | |

| | Inc. | (29,300) | (1,298) |

| | EMC Corp. | (43,500) | (1,294) |

| | | |

| * | salesforce.com inc | (21,780) | (1,292) |

| | Corning Inc. | (56,100) | (1,286) |

| | Microchip Technology Inc. | (23,700) | (1,069) |

| | FLIR Systems Inc. | (31,400) | (1,015) |

| * | II-VI Inc. | (73,400) | (1,002) |

| * | Informatica Corp. | (25,500) | (972) |

| | Avago Technologies Ltd. | | |

| | Class A | (9,400) | (946) |

| | AVX Corp. | (66,700) | (934) |

| * | SolarWinds Inc. | (18,100) | (902) |

| * | Workday Inc. Class A | (10,700) | (873) |

| | Motorola Solutions Inc. | (13,000) | (872) |

| | KLA-Tencor Corp. | (12,300) | (865) |

| * | Nuance Communications | | |

| | Inc. | (58,900) | (841) |

| | Solera Holdings Inc. | (16,300) | (834) |

| * | Bottomline Technologies | | |

| | de Inc. | (32,100) | (811) |

| | Visa Inc. Class A | (2,900) | (760) |

| * | RealPage Inc. | (33,700) | (740) |

| * | FleetCor Technologies Inc. | (4,950) | (736) |

| * | Cognex Corp. | (17,600) | (727) |

| * | Rackspace Hosting Inc. | (15,300) | (716) |

| | Apple Inc. | (5,450) | (602) |

| * | Bankrate Inc. | (46,160) | (574) |

| | Maxim Integrated Products | | |

| | Inc. | (15,300) | (488) |

| | j2 Global Inc. | (5,400) | (335) |

| | | | (55,876) |

| Materials (-5.9%) | | |

| | HB Fuller Co. | (35,200) | (1,568) |

| | Balchem Corp. | (23,500) | (1,566) |

| | Carpenter Technology Corp. | (31,500) | (1,551) |

| | FMC Corp. | (26,900) | (1,534) |

| * | WR Grace & Co. | (16,000) | (1,526) |

| | Martin Marietta Materials | | |

| | Inc. | (13,800) | (1,523) |

| * | Louisiana-Pacific Corp. | (91,000) | (1,507) |

| | SunCoke Energy Inc. | (63,800) | (1,234) |

| | Air Products & Chemicals | | |

| | Inc. | (7,950) | (1,147) |

| | Southern Copper Corp. | (37,950) | (1,070) |

| | Royal Gold Inc. | (16,350) | (1,025) |

| | Allegheny Technologies Inc. | (28,800) | (1,001) |

| | Mosaic Co. | (19,100) | (872) |

| | Freeport-McMoRan Inc. | (31,200) | (729) |

| | Praxair Inc. | (4,300) | (557) |

| | | | (18,410) |

| Telecommunication Services (-0.9%) | |

| * | United States Cellular Corp. | (39,000) | (1,553) |

| * | SBA Communications Corp. | | |

| | Class A | (12,310) | (1,364) |

| | | | (2,917) |

19

Market Neutral Fund

| | | |

| | | | Market |

| | | | Value |

| | | Shares | ($000) |

| Utilities (-4.9%) | | | |

| NiSource Inc. | | (37,000) | (1,570) |

| Laclede Group Inc. | | (29,100) | (1,548) |

| South Jersey Industries Inc. | (26,100) | (1,538) |

| Dominion Resources Inc. | (20,000) | (1,538) |

| Pattern Energy Group Inc. | | |

| Class A | | (62,300) | (1,536) |

| CMS Energy Corp. | | (42,600) | (1,480) |

| NRG Energy Inc. | | (47,800) | (1,288) |

| ALLETE Inc. | | (23,300) | (1,285) |

| OGE Energy Corp. | | (31,800) | (1,128) |

| ITC Holdings Corp. | | (22,200) | (898) |

| NorthWestern Corp. | | (10,900) | (617) |

| TECO Energy Inc. | | (19,900) | (408) |

| American Water Works Co. | | |

| Inc. | | (6,500) | (346) |

| | | | (15,180) |

| Total Common Stocks Sold Short | |

| (Proceeds $277,034) | | | (297,406) |

| Temporary Cash Investment (2.3%) | |

| Money Market Fund (2.3%) | | |

| 1 Vanguard Market | | | |

| Liquidity Fund, 0.126% | | |

| (Cost $7,114) | 7,114,439 | 7,114 |

| †Other Assets and Liabilities— | | |

| Net (97.5%) | | | 304,394 |

| Net Assets (100%) | | | 311,943 |

| |

| | Amount |

| | ($000) |

| Statement of Assets and Liabilities | |

| Assets | |

| Investment in Securities, | |

| Long Positions, at Value | |

| Unaffiliated Issuers | 297,841 |

| Affiliated Vanguard Funds | 7,114 |

| Total Long Positions | 304,955 |

| Cash Segregated for Short Positions | 302,403 |

| Other Assets | 2,448 |

| Total Assets | 609,806 |

| Liabilities | |

| Securities Sold Short, at Value | 297,406 |

| Other Liabilities | 457 |

| Total Liabilities | 297,863 |

| Net Assets (100%) | 311,943 |

| |

| |

| At December 31, 2014, net assets consisted of: |

| | Amount |

| | ($000) |

| Paid-in Capital | 300,791 |

| Accumulated Net Investment Losses | (166) |

| Accumulated Net Realized Losses | (17,376) |

| Unrealized Appreciation (Depreciation) | |

| Investment Securities—Long Positions | 49,066 |

| Investment Securities Sold Short | (20,372) |

| Net Assets | 311,943 |

| |

| |

| Investor Shares—Net Assets | |

| Applicable to 22,336,082 outstanding | |

| $.001 par value shares of beneficial | |

| interest (unlimited authorization) | 256,908 |

| Net Asset Value Per Share— | |

| Investor Shares | $11.50 |

| |

| |

| Institutional Shares—Net Assets | |

| Applicable to 4,805,766 outstanding | |

| $.001 par value shares of beneficial | |

| interest (unlimited authorization) | 55,035 |

| Net Asset Value Per Share— | |

| Institutional Shares | $11.45 |

See Note A in Notes to Financial Statements.

* Non-income-producing security.

† Long security positions with a value of $180,745,000 and cash of $302,403,000 are held in a segregated account at the fund’s custodian

bank and pledged to a broker-dealer as collateral for the fund’s obligation to return borrowed securities. For so long as such obligations

continue, the fund’s access to these assets is subject to authorization from the broker-dealer.

1 Affiliated money market fund available only to Vanguard funds and certain trusts and accounts managed by Vanguard. Rate shown is the

7-day yield.

See accompanying Notes, which are an integral part of the Financial Statements.

20

Market Neutral Fund

Statement of Operations

| |

| | Year Ended |

| | December 31, 2014 |

| | ($000) |

| Investment Income | |

| Income | |

| Dividends | 3,085 |

| Interest1 | 5 |

| Total Income | 3,090 |

| Expenses | |

| The Vanguard Group—Note B | |

| Investment Advisory Services | 233 |

| Management and Administrative—Investor Shares | 199 |

| Management and Administrative—Institutional Shares | 1 |

| Marketing and Distribution—Investor Shares | 46 |

| Marketing and Distribution—Institutional Shares | 9 |

| Custodian Fees | 32 |

| Audit Fees | 50 |

| Shareholders’ Reports—Investor Shares | 3 |

| Shareholders’ Reports—Institutional Shares | — |

| Dividend Expense on Securities Sold Short | 2,967 |

| Borrowing Expense on Securities Sold Short | 439 |

| Total Expenses | 3,979 |

| Net Investment Income (Loss) | (889) |

| Realized Net Gain (Loss) | |

| Investment Securities—Long Positions | 34,786 |

| Investment Securities Sold Short | (24,651) |

| Realized Net Gain (Loss) | 10,135 |

| Change in Unrealized Appreciation (Depreciation) | |

| Investment Securities—Long Positions | (7,209) |

| Investment Securities Sold Short | 7,463 |

| Change in Unrealized Appreciation (Depreciation) | 254 |

| Net Increase (Decrease) in Net Assets Resulting from Operations | 9,500 |

| 1 Interest income from an affiliated company of the fund was $5,000. |

See accompanying Notes, which are an integral part of the Financial Statements.

21

Market Neutral Fund

Statement of Changes in Net Assets

| | |

| | Year Ended December 31, |

| | 2014 | 2013 |

| | ($000) | ($000) |

| Increase (Decrease) In Net Assets | | |

| Operations | | |

| Net Investment Income (Loss) | (889) | (88) |

| Realized Net Gain (Loss) | 10,135 | 8,423 |

| Change in Unrealized Appreciation (Depreciation) | 254 | 9,099 |

| Net Increase (Decrease) in Net Assets Resulting from Operations | 9,500 | 17,434 |

| Distributions | | |

| Net Investment Income | | |

| Investor Shares | — | (33) |

| Institutional Shares | — | (8) |

| Realized Capital Gain | | |

| Investor Shares | — | — |

| Institutional Shares | — | — |

| Return of Capital | | |

| Investor Shares | — | (16) |

| Institutional Shares | — | (4) |

| Total Distributions | — | (61) |

| Capital Share Transactions | | |

| Investor Shares | 75,328 | 7,869 |

| Institutional Shares | 18,313 | 1,333 |

| Net Increase (Decrease) from Capital Share Transactions | 93,641 | 9,202 |

| Total Increase (Decrease) | 103,141 | 26,575 |

| Net Assets | | |

| Beginning of Period | 208,802 | 182,227 |

| End of Period1 | 311,943 | 208,802 |

| 1 Net Assets—End of Period includes accumulated net investment losses and overdistributed net investment income of ($166,000) and ($105,000), respectively. |

See accompanying Notes, which are an integral part of the Financial Statements.

22

Market Neutral Fund

Financial Highlights

| | | | | |

| Investor Shares | | | | | |

| |

| For a Share Outstanding | Year Ended December 31, |

| Throughout Each Period | 2014 | 2013 | 2012 | 2011 | 2010 |

| Net Asset Value, Beginning of Period | $11.03 | $10.16 | $10.36 | $9.61 | $9.71 |

| Investment Operations | | | | | |

| Net Investment Income (Loss) | (.032) | (.007) | .045 | (.024) | (.038)1 |

| Net Realized and Unrealized Gain (Loss) | | | | | |

| on Investments | .502 | .880 | (.200) | .774 | (.062) |

| Total from Investment Operations | .470 | .873 | (.155) | .750 | (.100) |

| Distributions | | | | | |

| Dividends from Net Investment Income | — | (.002) | (.045) | — | — |

| Distributions from Realized Capital Gains | — | — | — | — | — |

| Return of Capital | — | (.001) | — | — | — |

| Total Distributions | — | (.003) | (.045) | — | — |

| Net Asset Value, End of Period | $11.50 | $11.03 | $10.16 | $10.36 | $9.61 |

| |

| Total Return2 | 4.26% | 8.59% | -1.50% | 7.80% | -1.03% |

| |

| Ratios/Supplemental Data | | | | | |

| Net Assets, End of Period (Millions) | $257 | $174 | $151 | $158 | $116 |

| Ratio of Expenses to Average Net Assets | | | | | |

| Based on Total Expenses3 | 1.64% | 1.57% | 1.88% | 1.69% | 1.84%4 |

| Net of Dividend and Borrowing Expense | | | | | |

| on Securities Sold Short | 0.25% | 0.25% | 0.25% | 0.25% | 0.30%4 |

| Ratio of Net Investment Income (Loss) | | | | | |

| to Average Net Assets | (0.38%) | (0.06%) | 0.44% | (0.22%) | (0.38%) |

| Portfolio Turnover Rate | 73% | 68% | 89% | 91% | 153% |

1 Calculated based on average shares outstanding.

2 Total returns do not include transaction or account service fees that may have applied in the periods shown. Fund prospectuses provide

information about any applicable transaction and account service fees.

3 Includes 2014 dividend and borrowing expense on securities sold short of 1.21% and 0.18%, respectively. Includes 2013 dividend and

borrowing expense on securities sold short of 1.18% and 0.14%, respectively. Includes 2012 dividend and borrowing expense on securities

sold short of 1.52% and 0.11%, respectively. Includes 2011 dividend and borrowing expense on securities sold short of 1.30% and 0.14%,

respectively. Includes 2010 dividend and borrowing expense on securities sold short of 1.49% and 0.05%, respectively.

4 Includes performance-based advisory fee increases (decreases) of (0.07%). Performance-based investment advisory fees did not apply after

fiscal 2010.

See accompanying Notes, which are an integral part of the Financial Statements.

23

Market Neutral Fund

Financial Highlights

| | | | | |

| Institutional Shares | | | | | |

| |

| For a Share Outstanding | Year Ended December 31, |

| Throughout Each Period | 2014 | 2013 | 2012 | 2011 | 2010 |

| Net Asset Value, Beginning of Period | $10.97 | $10.10 | $10.33 | $9.57 | $9.66 |

| Investment Operations | | | | | |

| Net Investment Income (Loss) | (.023) | .006 | .071 | (.010) | (.015)1 |

| Net Realized and Unrealized Gain (Loss) | | | | | |

| on Investments | .503 | .868 | (.215) | .770 | (.075) |

| Total from Investment Operations | .480 | .874 | (.144) | .760 | (.090) |

| Distributions | | | | | |

| Dividends from Net Investment Income | — | (.003) | (.086) | — | — |

| Distributions from Realized Capital Gains | — | — | — | — | — |

| Return of Capital | — | (.001) | — | — | — |

| Total Distributions | — | (.004) | (.086) | — | — |

| Net Asset Value, End of Period | $11.45 | $10.97 | $10.10 | $10.33 | $9.57 |

| |

| Total Return2 | 4.38% | 8.66% | -1.39% | 7.94% | -0.93% |

| |

| Ratios/Supplemental Data | | | | | |

| Net Assets, End of Period (Millions) | $55 | $35 | $31 | $16 | $3 |

| Ratio of Expenses to Average Net Assets | | | | | |

| Based on Total Expenses3 | 1.54% | 1.47% | 1.78% | 1.59% | 1.74%4 |

| Net of Dividend and Borrowing Expense | | | | | |

| on Securities Sold Short | 0.15% | 0.15% | 0.15% | 0.15% | 0.20%4 |

| Ratio of Net Investment Income (Loss) | | | | | |

| to Average Net Assets | (0.28%) | 0.04% | 0.54% | (0.12%) | (0.28%) |

| Portfolio Turnover Rate | 73% | 68% | 89% | 91% | 153% |

1 Calculated based on average shares outstanding.

2 Total returns do not include transaction fees that may have applied in the periods shown. Fund prospectuses provide information about any applicable transaction fees.

3 Includes 2014 dividend and borrowing expense on securities sold short of 1.21% and 0.18%, respectively. Includes 2013 dividend and

borrowing expense on securities sold short of 1.18% and 0.14%, respectively. Includes 2012 dividend and borrowing expense on securities

sold short of 1.52% and 0.11%, respectively. Includes 2011 dividend and borrowing expense on securities sold short of 1.30% and 0.14%,

respectively. Includes 2010 dividend and borrowing expense on securities sold short of 1.49% and 0.05%, respectively.

4 Includes performance-based advisory fee increases (decreases) of (0.07%). Performance-based investment advisory fees did not apply after fiscal 2010.

See accompanying Notes, which are an integral part of the Financial Statements.

24

Market Neutral Fund

Notes to Financial Statements

Vanguard Market Neutral Fund is registered under the Investment Company Act of 1940 as an open-end investment company, or mutual fund. The fund offers two classes of shares, Investor Shares and Institutional Shares. Investor Shares are available to any investor who meets the fund’s minimum purchase requirements. Institutional Shares are designed for investors who meet certain administrative, service, and account-size criteria.

A. The following significant accounting policies conform to generally accepted accounting principles for U.S. investment companies. The fund consistently follows such policies in preparing its financial statements.

1. Security Valuation: Securities are valued as of the close of trading on the New York Stock Exchange (generally 4 p.m., Eastern time) on the valuation date. Equity securities are valued at the latest quoted sales prices or official closing prices taken from the primary market in which each security trades; such securities not traded on the valuation date are valued at the mean of the latest quoted bid and asked prices. Securities for which market quotations are not readily available, or whose values have been materially affected by events occurring before the fund’s pricing time but after the close of the securities’ primary markets, are valued by methods deemed by the board of trustees to represent fair value. Investments in Vanguard Market Liquidity Fund are valued at that fund’s net asset value.

2. Short Sales: Short sales are the sales of securities that the fund does not own. The fund sells a security it does not own in anticipation of a decline in the value of that security. In order to deliver the security to the purchaser, the fund borrows the security from a broker-dealer. The fund must segregate, as collateral for its obligation to return the borrowed security, an amount of cash and long security positions at least equal to the market value of the security sold short. This results in the fund holding a significant portion of its assets in cash. The fund later closes out the position by returning the security to the lender, typically by purchasing the security in the open market. A gain, limited to the price at which the fund sold the security short, or a loss, theoretically unlimited in size, is recognized upon the termination of the short sale. The fund may receive a portion of the income from the investment of collateral, or be charged a fee on borrowed securities, based on the market value of each borrowed security and a variable rate that is dependent upon the availability of such security. The net amounts of income or fees are recorded as interest income (for net income received) or borrowing expense on securities sold short (for net fees charged) on the Statement of Operations. Dividends on securities sold short are reported as an expense in the Statement of Operations.

Cash collateral segregated for securities sold short is recorded as an asset in the Statement of Assets and Liabilities. Long security positions segregated as collateral are shown in the Statement of Net Assets.

3. Federal Income Taxes: The fund intends to continue to qualify as a regulated investment company and distribute all of its taxable income. Management has analyzed the fund’s tax positions taken for all open federal income tax years (December 31, 2011–2014), and has concluded that no provision for federal income tax is required in the fund’s financial statements.

4. Distributions: Distributions to shareholders are recorded on the ex-dividend date.

5. Credit Facility: The fund and certain other funds managed by The Vanguard Group participate in a $2.89 billion committed credit facility provided by a syndicate of lenders pursuant to a credit agreement that may be renewed annually; each fund is individually liable for its borrowings, if any, under the credit facility. Borrowings may be utilized for temporary and emergency purposes, and are subject to the fund’s regulatory and contractual borrowing restrictions. The participating funds are charged administrative fees and an annual commitment fee of 0.06% of the undrawn amount

25

Market Neutral Fund

of the facility; these fees are allocated to the funds based on a method approved by the fund’s board of trustees and included in Management and Administrative expenses on the fund’s Statement of Operations. Any borrowings under this facility bear interest at a rate equal to the higher of the federal funds rate or LIBOR reference rate plus an agreed-upon spread.

The fund had no borrowings outstanding at December 31, 2014, or at any time during the period then ended.

6. Other: Dividend income (or dividend expense on short positions) is recorded on the ex-dividend date. Interest income includes income distributions received from Vanguard Market Liquidity Fund and is accrued daily. Security transactions are accounted for on the date securities are bought or sold. Costs used to determine realized gains (losses) on the sale of investment securities are those of the specific securities sold.

Each class of shares has equal rights as to assets and earnings, except that each class separately bears certain class-specific expenses related to maintenance of shareholder accounts (included in Management and Administrative expenses) and shareholder reporting. Marketing and distribution expenses are allocated to each class of shares based on a method approved by the board of trustees. Income, other non-class-specific expenses, and gains and losses on investments are allocated to each class of shares based on its relative net assets.

B. The Vanguard Group furnishes at cost investment advisory, corporate management, administrative, marketing, and distribution services. The costs of such services are allocated to the fund on methods approved by the board of trustees. The fund has committed to invest up to 0.40% of its net assets in Vanguard. At December 31, 2014, the fund had contributed capital of $27,000 to Vanguard (included in Other Assets), representing 0.01% of the fund’s net assets and 0.01% of Vanguard’s capitalization. The fund’s trustees and officers are also directors and officers of Vanguard.

C. Various inputs may be used to determine the value of the fund’s investments. These inputs are summarized in three broad levels for financial statement purposes. The inputs or methodologies used to value securities are not necessarily an indication of the risk associated with investing in those securities.

Level 1—Quoted prices in active markets for identical securities.

Level 2—Other significant observable inputs (including quoted prices for similar securities, interest rates, prepayment speeds, credit risk, etc.).

Level 3—Significant unobservable inputs (including the fund’s own assumptions used to determine the fair value of investments).

At December 31, 2014, 100% of the market value of the fund’s investments was based on Level 1 inputs.

D. Distributions are determined on a tax basis and may differ from net investment income and realized capital gains for financial reporting purposes. Differences may be permanent or temporary. Permanent differences are reclassified among capital accounts in the financial statements to reflect their tax character. Temporary differences arise when certain items of income, expense, gain, or loss are recognized in different periods for financial statement and tax purposes. These differences will reverse at some time in the future. Differences in classification may also result from the treatment of short-term gains as ordinary income for tax purposes.

26

Market Neutral Fund

For tax purposes, the fund had a net operating loss of $823,000 for the year ended December 31, 2014. This amount has been reclassified from accumulated net investment losses to paid-in capital. At December 31, 2014, the fund had no ordinary income for distribution. The fund used capital loss carryforwards of $10,238,000 to offset taxable capital gains realized during the year ended December 31, 2014. At December 31, 2014, the fund had available capital losses totaling $17,082,000 to offset future net capital gains. Of this amount, $13,688,000 is subject to expiration dates; $8,817,000 may be used to offset future net capital gains through December 31, 2017, and $4,871,000 through December 31, 2018. Capital losses of $3,394,000 realized beginning in fiscal 2011 may be carried forward indefinitely under the Regulated Investment Company Modernization Act of 2010, but must be used before any expiring loss carryforwards.