united states

securities and exchange commission

washington, d.c. 20549

form n-csr

certified shareholder report of registered management

investment companies

Investment Company Act file number 811-22153

Dunham Funds

(Exact name of registrant as specified in charter)

10251 Vista Sorrento Pkwy, Ste. 200, San Diego, CA 92121

(Address of principal executive offices) (Zip code)

Richard Malinowski

Gemini Fund Services, LLC., 80Arkay Drive Hauppauge, NY 11788

(Name and address of agent for service)

Registrant's telephone number, including area code: 631-470-2619

Date of fiscal year end: 10/31

Date of reporting period: 10/31/18

Item 1. Reports to Stockholders.

BEGINNING ON JANUARY 1, 2021, AS PERMITTED BY REGULATIONS ADOPTED BY THE SECURITIES AND EXCHANGE COMMISSION, PAPER COPIES OF THE DUNHAM FUNDS’ SHAREHOLDER REPORTS LIKE THIS ONE WILL NO LONGER BE SENT BY MAIL, UNLESS YOU SPECIFICALLY REQUEST PAPER COPIES OF THE REPORTS FROM THE DUNHAM FUNDS OR FROM YOUR FINANCIAL INTERMEDIARY, SUCH AS A BROKER-DEALER OR BANK. INSTEAD, THE REPORTS WILL BE MADE AVAILABLE ON A WEBSITE, AND YOU WILL BE NOTIFIED BY MAIL EACH TIME A REPORT IS POSTED AND PROVIDED WITH A WEBSITE LINK TO ACCESS THE REPORT.

IF YOU ALREADY ELECTED TO RECEIVE SHAREHOLDER REPORTS ELECTRONICALLY, YOU WILL NOT BE AFFECTED BY THIS CHANGE AND YOU NEED NOT TAKE ANY ACTION. YOU MAY ELECT TO RECEIVE SHAREHOLDER REPORTS AND OTHER COMMUNICATIONS FROM THE DUNHAM FUNDS ELECTRONICALLY BY CALLING (888)-3DUNHAM (338-6426) OR CONTACTING YOUR FINANCIAL INTERMEDIARY.

YOU MAY ELECT TO RECEIVE ALL FUTURE REPORTS IN PAPER FREE OF CHARGE. YOU CAN INFORM THE DUNHAM FUNDS OR YOUR FINANCIAL INTERMEDIARY THAT YOU WISH TO CONTINUE RECEIVING PAPER COPIES OF YOUR SHAREHOLDER REPORTS BY CALLING (888)-3DUNHAM (338-6426) OR CONTACTING YOUR FINANCIAL INTERMEDIARY. YOUR ELECTION TO RECEIVE REPORTS IN PAPER WILL APPLY TO ALL DUNHAM FUNDS HELD BY YOU OR THROUGH YOUR FINANCIAL INTERMEDIARY.

THIS ANNUAL REPORT CONTAINS “FORWARD-LOOKING STATEMENTS” WITHIN THE MEANING OF THE PRIVATE SECURITIES LITIGATION REFORM ACT OF 1995. FORWARD-LOOKING STATEMENTS ALSO INCLUDE THOSE PRECEDED BY, FOLLOWED BY OR THAT INCLUDE THE WORDS “BELIEVES”, “EXPECTS”, “ANTICIPATES” OR SIMILAR EXPRESSIONS. SUCH STATEMENTS SHOULD BE VIEWED WITH CAUTION. ACTUAL RESULTS OR EXPERIENCE COULD DIFFER MATERIALLY FROM THE FORWARD-LOOKING STATEMENTS AS A RESULT OF MANY FACTORS. EACH FUND MAKES NO COMMITMENTS TO DISCLOSE ANY REVISIONS TO FORWARD-LOOKING STATEMENTS, OR ANY FACTS, EVENTS OR CIRCUMSTANCES AFTER THE DATE HERE OF THAT MAY BEAR UPON FORWARD-LOOKING STATEMENTS. IN ADDITION, PROSPECTIVE PURCHASERS OF THE FUNDS SHOULD CONSIDER CAREFULLY THE INFORMATION SET FORTH HERIN AND THE APPLICABLE FUND’S PROSPECTUS. OTHER FACTORS AND ASSUMPTIONS NOT IDENTIFIED ABOVE MAY ALSO HAVE BEEN INVOLVED IN THE DERIVATION OF THESE FORWARD-LOOKING STATEMENTS, AND THE FAILURE OF THESE OTHER ASSUMPTIONS TO BE REALIZED MAY ALSO CAUSE ACTUAL RESULTS TO DIFFER MATERIALLY FROM THOSE PROJECTED.

Dear Fellow Shareholders,

When a 30-year bull market for bonds likely finds itself in its twilight hours before its next bear market, it is not surprising that some spikes in volatility arise across the fixed income and equity markets. Similar to Paul Revere, many economists and institutional managers have been alerting and alarming that interest rates will rise from their historical lows and this will be to the detriment of the most interest rate sensitive bonds. The reason that the markets have responded as if in surprise is likely because these warnings that rates are rising have been prevalent for years, as global uncertainty resulted in higher demand for U.S. Treasury bonds – placing downward pressure on interest rates.

This prolonged compression in interest rates has contributed to the economic growth in the United States, which in turn increased the pressure on the Federal Reserve to raise the Fed Funds rate. As the rhetoric provided by the Federal Reserve was followed by corresponding actions, the Fed Funds rate was ratcheted up four times over the fiscal year, leading intermediate-term and long-term Treasuries into negative return territory for the 12-month period. Although equity markets broadly finished with positive returns at the end of the first six months of the fiscal year, foreign markets slid deeply negative in the latter half of the fiscal year, leaving only a few bastions of positive-performing asset classes. One of those strongholds was the United States, which at first may appear counterintuitive given that the vast majority of negative headlines during the latest six-month period surrounded the sustainability of the U.S.’s more recent increases in GDP growth rates. After peeling back the curtain to unveil what drove the positive performance, it clarified that the increase was primarily attributable to just a few sizeable sectors, notably technology and health care.

When the peril of the United States’ growth rate was not front-and-center, China’s relationship with the U.S. was generally the broadcast du jour. As fears of a trade war with China were exacerbated during the late summer months, it reached a crescendo at the same time as some mega-cap earnings reports missed expectations while the Federal Reserve reiterated its determination to continue its rate increases. These events coalesced into a broad sell-off to complete the fiscal year. Very few asset classes were spared in the last month’s carnage. Traditional bonds, U.S. equities, and foreign equities were all caught in the turmoil. Some of the Dunham Funds mitigated most of those losses, particularly the funds that implement strategies meant to behave differently from traditional investments. As we are vigilant to provide investment solutions that may benefit in our evolving marketplace, the Dunham Appreciation & Income Fund’s principal investment strategy was changed to a long / short credit strategy at the beginning of July. This strategy prevailed during October’s sell-off, finishing the month nearly flat amidst the sea of sizeable losses.

While we continue to navigate through this turbulence, we are optimistic that the Dunham Funds are positioned to capitalize on the opportunities that are generally uncovered in market environments like the one we are currently in. Sifting through the noise for the pertinent facts is crucial and we believe this diligence will reward our investors.

We thank you for your continued trust and the confidence you have placed in us. We take that trust very seriously and look forward to servicing your investment needs for years to come.

Sincerely,

| Jeffrey A. Dunham |

| President |

| Dunham & Associates |

| October 31, 2018 |

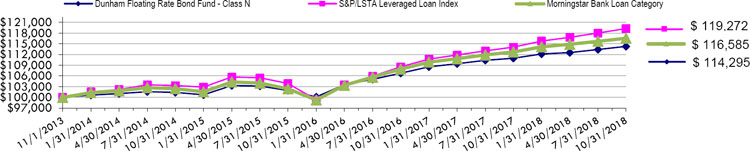

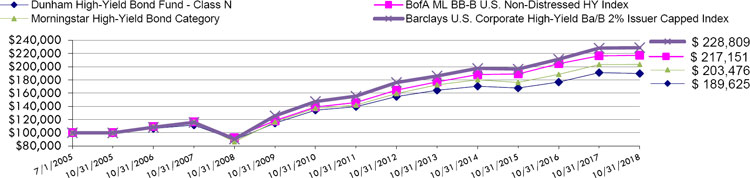

Dunham Floating Rate Bond Fund (Unaudited)

Message from the Sub-Adviser (Newfleet Asset Management, LLC)

The bank loan market reached a milestone this fiscal year by totaling over $1 trillion in market size and constituting over 1,000 distinct borrowers. The bank loan market has doubled since 2010 and is now similar in size to the $1.1 trillion high-yield market. Secondary market trading activity and liquidity have steadily improved, driven by the increased number of market participants seeking yield, deeper and broader secondary markets, and technological advancements. The loan market fared well through the relatively larger bouts of volatility over the fiscal year experienced in February and October.

Over the fiscal year ended October 31, 2018, U.S. stocks, as measured by the S&P 500, increased 7.3 percent. Over the fiscal year, interest rates on the 10-year U.S. Treasury fluctuated within a 76 basis point range, hitting a low of 2.32 percent a few times in late November, then marching higher to 3.23 percent in late October, before settling at 3.14 percent to end the fiscal year. Over the same time period, the Federal Reserve raised the Fed Funds Rate four times over the fiscal year, to 2.25 percent. Bond prices generally fall when interest rates rise. U.S. investment-grade bonds, as measured by the Bloomberg Barclays U.S. Aggregate Bond Index, fell 2.1 percent over the fiscal year ended October 31, 2018. The movement in rates aided the performance of bank loans, as measured by the S&P/ LSTA Leveraged Loan Index, which gained 4.5 percent over the three-month period. The London Interbank Offered Rate (“LIBOR”) continued its upward trend during the fiscal period. Three-month LIBOR began the fiscal year at 1.38 percent, its lowest point of the period, before beginning a steady climb to its high of 2.56 percent at the end of the fiscal period.

The Sub-Adviser looks for potential total return and income by investing in higher quality, non-investment grade bank loans. The Sub-Adviser uses extensive credit and company analysis and monitoring. The Sub-Adviser looks for securities with strong income potential while maintaining an emphasis on managing risk. The Sub-Adviser remains optimistic about the asset class’ potential as interest rates rise and investors continue to focus on income producing assets.

The yields on bank loans, as measured by the S&P / LSTA Leveraged Loan 100 Index, trended upward over the fiscal year, but trailed the pace of rise in Treasury yields. Bank loans, in general, as measured by the S&P / LSTA Leveraged Loan 100 Index, ended the most recent period with a yield-to-maturity of 5.5 percent. The changes in yield increased the spread to 1.4 percent when compared to their high-yield bond counterparts, as measured by the BofA Merrill Lynch High-Yield Bond Cash Pay Index, which ended the period with a 6.9 percent yield to maturity.

A strong contributor for the most recent fiscal quarter as well as the fiscal year was Neiman Marcus Group Ltd LLC (BL1250440) (holding weight*: 0.59 percent), a luxury retailer conducting integrated store and online operations. Neiman Marcus’ bank loan had a price increase from $79.81 at the beginning of the fiscal year to $91.38 at the end of the period, for a price return of 14.5 percent. This holding benefited from strong quarterly earnings that reflected a continued stabilization in the retail business. Another top performer was Seadrill Operating LP (BL1232042) (holding weight*: 0.55 percent), a company that owns and operates drilling rigs. The company came out of a bankruptcy restructuring and the Fund benefited from price appreciation of the bank loan. Seadrill’s bank loan had a price increase from $75.81 at the beginning of the fiscal year to $93.77 at the end of the period, for a price return of 23.7 percent. A position that contributed to performance over the most recent fiscal quarter ended October 31, 2018 but detracted from performance over the full fiscal year was CPI Card Group (BL1785619) (holding weight*: 0.52 percent), a company that engages in design, production, data personalization, packaging, and fulfillment of financial payment cards. The company has been troubled with a longer renewable cycle of credit cards at four years instead of three years. In addition, the company has faced challenges of larger banks and credit unions competing over market share. Despite these concerns, the loan traded higher in the final fiscal quarter following the release of strong earnings. Additionally, card volumes in the quarter improved both sequentially and year over year.

On the opposite end of the return spectrum, Fort Dearborn Holding Co (BL2249904) (holding weight*:0.20 percent) detracted from Fund performance over the most recent fiscal quarter and year. Fort Dearborn has managed to keep the top line relatively stable amid operational issues however, leverage continued to creep up. Increased costs, lower overall output, a fire at one of their facilities, and peak working capital causing them to draw on the revolver, all contributed to the negative performance. The Sub-Adviser believes that the credit is currently over-levered and lenders have started to lose patience with management. Also detracting from Fund performance over the fiscal quarter and year was Univision Communications, Inc. (BL2380501) (holding weight*: 1.46 percent), an American media company primarily serving Hispanic and Latino Americans. The bank loan had a price decrease from $99.63 at the beginning of the period to $97.06 at the end of the period, for a price loss of 2.7 percent. Klöckner Pentaplast Group (BL2450726) (holding weight*: 0.44 percent), a company that is among the world’s largest suppliers of films for pharmaceutical, medical devices, food, electronics, and general packaging, also had a difficult fiscal quarter and year. The bank loan had a price decrease from $100.98 at the beginning of the period to $97.06 at the end of the period, for a price loss of 4.0 percent.

The Sub-Adviser continues to find the loan market a compelling investment, especially in light of the impact that this year’s interest rate volatility has had on fixed-rate asset classes. The Sub-Adviser expects the coupon “carry” to continue for the remainder of the year, all else equal, and prove to be attractive on a risk-adjusted relative basis to fixed income alternatives. The Sub-Adviser also believes the constructive backdrop for credit spread assets is being met with continued spread tightening across the credit quality curve and transactions are becoming increasingly more aggressive on many levels. The Sub-Adviser feels that the fundamental backdrop for loans seems to be in good shape with low default rates, strong technicals, and strong investor demand. The Sub-Adviser is beginning to reassess risk positions from a credit quality and industry perspective with an eye towards slightly decreasing the overall risk in the Fund after having added risk since the summer of 2016 at broadly better valuations. The Sub-Adviser feels that the loan market is exhibiting late-cycle behavior, with the rise of single B-rated issuance, loosening loan terms and conditions, and a number of credit metrics exceeding pre-crisis levels. However, demand from retail and institutional investors remained at an above-average pace as rising rates and corresponding higher current yields relative to most other fixed income options has increased broad investor interest. With all of these factors, the Sub-Adviser does not currently view this current credit cycle as coming to end in the short-term, and the Sub-Adviser is contemplating how it might upgrade the credit quality of the Fund’s holdings, especially at current valuations.

* Holdings percentage(s) of total investments, excluding collateral for securities loaned, as of 10/31/2018.

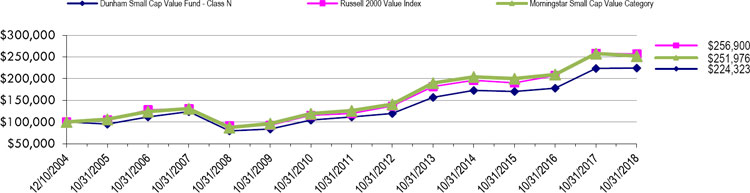

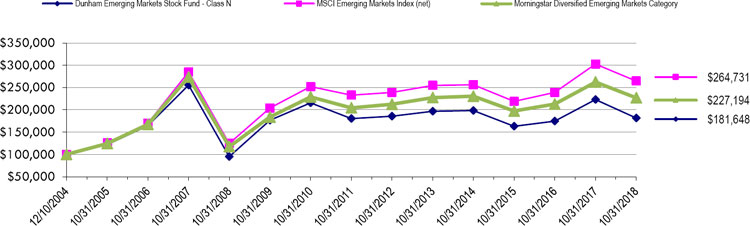

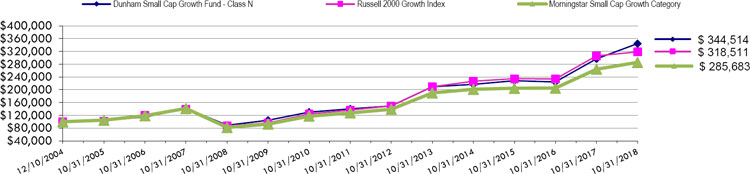

Growth of $100,000 Investment

| Total Returns as of October 31, 2018 |

| |

| | | Annualized |

| | One | Since Inception |

| | Year | (11/1/13) |

| Class N | 3.02% | 2.71% |

| Class C | 2.26% | 1.94% |

| Class A with load of 4.50% | (1.87)% | 1.51% |

| Class A without load | 2.77% | 2.44% |

| S&P/LSTA Leveraged Loan 100 Index | 4.54% | 3.59% |

| Morningstar Bank Loan Category | 3.42% | 3.12% |

| | | |

The S&P/LSTA Leveraged Loan 100 Index is designed to reflect the performance of the largest facilities in the leveraged loan market. Investors cannot invest directly in an index or benchmark.

The Morningstar Bank Loan Category is generally representative of mutual funds that primarily invest in floating- rate bank loans instead of bonds. These bank loans generally offer interest payments that typically float above a common short-term benchmark such as the London interbank offered rate, or LIBOR.

As disclosed in the Trust’s latest registration statement, the Fund’s total annual operating expenses, including cost of underlying funds, are 1.05% for Class N, 1.80% for Class C and 1.30% for Class A. Class A shares are subject to a sales load of 4.50% and a deferred sales charge of up to 0.75%. The performance data quoted here represents past performance, which is not indicative of future results. Current performance may be lower or higher than the performance data quoted. The investment return and NAV will fluctuate, so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Total returns are calculated assuming reinvestment of all dividends and capital gains distributions, if any. The returns do not reflect the deductions of taxes a shareholder would pay on the redemption of Fund shares or Fund distributions. For performance information current to the most recent month- end, please call 1-800- 442- 4358 or visit our website www.dunham.com

| SCHEDULE OF INVESTMENTS |

| Dunham Floating Rate Bond Fund |

| October 31, 2018 |

| | | Variable | | Principal | | | Interest | | Maturity | | | |

| Security | | Rate | | Amount | | | Rate % | | Date | | Value | |

| BANK LOANS - 91.6% | | | | | | | | | | | | | | |

| BASIC MATERIALS - 3.1% | | | | | | | | | | | | | | |

| Alpha 3 BV, Initial Term B-1 Loan + | | LIBOR + 3.000% | | $ | 219,880 | | | 5.398 | | 2/1/2024 | | $ | 220,258 | |

| Covia Holdings Corp., Initial Term Loan + | | LIBOR + 3.750% | | | 568,575 | | | 6.270 | | 5/31/2025 | | | 479,203 | |

| Graftech International Ltd., Initial Term Loan + | | LIBOR + 3.500% | | | 799,875 | | | 6.058 | | 2/12/2025 | | | 801,875 | |

| HB Fuller Co., Commitment Loan + | | LIBOR + 2.000% | | | 725,320 | | | 4.487 | | 10/20/2024 | | | 723,655 | |

| Ineos US Finance LLC, New 2024 Dollar Term Loan + | | LIBOR + 2.000% | | | 1,905,600 | | | 4.558 | | 3/31/2024 | | | 1,905,305 | |

| Kraton Polymers LLC, Dollar Replacement Term Loan (2018) + | | LIBOR + 2.500% | | | 281,710 | | | 5.058 | | 3/8/2025 | | | 281,621 | |

| Macdermind, Inc., Tranche B-7 Term Loan + | | LIBOR + 2.500% | | | 418,073 | | | 5.058 | | 6/8/2020 | | | 418,932 | |

| New Arclin Us Holding Corp., Replacement Term Loan (First Lien) + | | LIBOR + 3.500% | | | 267,438 | | | 5.898 | | 2/14/2024 | | | 267,103 | |

| Omnova Solutions, Inc., Term B-2 Loan + | | LIBOR + 3.250% | | | 501,249 | | | 5.808 | | 8/24/2023 | | | 502,502 | |

| Venator Finance Sarl, Initial Term Loan + | | LIBOR + 3.000% | | | 509,850 | | | 5.558 | | 8/8/2024 | | | 509,213 | |

| | | | | | | | | | | | | | 6,109,667 | |

| COMMUNICATIONS - 15.5% | | | | | | | | | | | | | | |

| Advantage Sales & Marketing LLC, Initial Term Loan (First Lien) + | | LIBOR + 3.250% | | | 390,319 | | | 5.808 | | 7/24/2021 | | | 356,654 | |

| Advantage Sales & Marketing LLC, Term B-2 Loan (First Lien) + | | LIBOR + 3.250% | | | 316,174 | | | 5.808 | | 7/24/2021 | | | 288,246 | |

| Altice France SA, USD TLB-13 Term Loan + | | LIBOR + 4.000% | | | 235,000 | | | 6.449 | | 8/14/2026 | | | 230,790 | |

| Altice US Financing Corp, March 2017 Refinancing Term Loan + | | LIBOR + 2.250% | | | 330,625 | | | 4.808 | | 7/28/2025 | | | 330,523 | |

| Centurylink, Inc., Initial Term B Loan + | | LIBOR + 2.750% | | | 1,366,058 | | | 5.308 | | 2/1/2025 | | | 1,353,251 | |

| Charter Communications Operating LLC, Term B Loan + | | LIBOR + 2.000% | | | 2,267,863 | | | 4.558 | | 4/30/2025 | | | 2,270,561 | |

| Csc Holdings, LLC, March 2017 Refinancing Term Loan + | | LIBOR + 2.250% | | | 1,765,260 | | | 4.699 | | 7/16/2025 | | | 1,763,689 | |

| Csc Holdings, LLC, October 2018 Incremental Term Loan + | | LIBOR + 2.250% | | | 380,000 | | | 4.670 | | 1/16/2026 | | | 379,823 | |

| Csc Holdings, LLC, January 2018 Incremental Term Loan + | | LIBOR + 2.500% | | | 129,350 | | | 4.949 | | 1/24/2026 | | | 129,451 | |

| Digicel International Finance Ltd., Initial Term B Loan (First Lien) + | | LIBOR + 3.250% | | | 212,850 | | | 5.571 | | 5/28/2024 | | | 204,602 | |

| Frontier Communications Corporation, Term B-1 Loan + | | LIBOR + 3.750% | | | 1,146,066 | | | 6.308 | | 6/16/2024 | | | 1,112,830 | |

| Global Tel*link Corp., Term Loan (First Lien) + | | LIBOR + 4.000% | | | 596,106 | | | 6.398 | | 5/24/2020 | | | 597,596 | |

| Go Daddy Operating Co. LLC, Tranche B-1 Term Loan + | | LIBOR + 2.250% | | | 380,516 | | | 4.808 | | 2/16/2024 | | | 381,374 | |

| Hoya Midco, LLC., Initial Term Loan (First Lien) + | | LIBOR + 3.500% | | | 596,091 | | | 6.058 | | 6/30/2024 | | | 594,350 | |

| Iheart Communications, Inc., Tranche D Term Loan + | | LIBOR + 6.750% | | | 1,510,000 | | | 9.148 | | 1/30/2019 | | | 1,096,011 | |

| Level 3 Financing, Inc., Tranche B 2024 Term Loan + | | LIBOR + 2.250% | | | 1,825,000 | | | 4.737 | | 2/22/2024 | | | 1,828,568 | |

| Mcc Iowa LLC, Tranche M Term Loan + | | LIBOR + 2.000% | | | 787,163 | | | 4.520 | | 1/16/2025 | | | 787,655 | |

| Mcgraw-Hill Global Education Holdings LLC, Term B Loan (First Lien) + | | LIBOR + 4.000% | | | 974,597 | | | 6.558 | | 5/4/2022 | | | 937,445 | |

| Mediacom LLC, Tranche N Term Loan + | | LIBOR + 1.750% | | | 650,020 | | | 4.270 | | 2/16/2024 | | | 649,617 | |

| Meredith Corporation, Tranche B-1 Term Loan + | | LIBOR + 3.000% | | | 797,750 | | | 5.308 | | 2/1/2025 | | | 797,626 | |

| Numericable U.S LLC, USD TLB-11 Term Loan + | | LIBOR + 2.750% | | | 640,250 | | | 5.308 | | 8/1/2025 | | | 619,392 | |

| Numericable U.S LLC, USD TLB-12 Term Loan + | | LIBOR + 3.688% | | | 324,859 | | | 6.136 | | 2/1/2026 | | | 317,889 | |

| Radiate Holdco LLC, Closing Date Term Loan + | | LIBOR + 3.000% | | | 858,964 | | | 5.558 | | 1/31/2024 | | | 853,596 | |

| Red Ventures LLC, Term Loan (First Lien) + | | LIBOR + 3.750% | | | 441,450 | | | 6.558 | | 11/8/2024 | | | 444,209 | |

| Red Ventures LLC, Term B-1 Loan (First Lien) + | | LIBOR + 3.000% | | | 380,000 | | | 5.449 | | 11/8/2024 | | | 382,375 | |

| Rodan & Fields, LLC, Closing Date Term Loan + | | LIBOR + 4.000% | | | 643,388 | | | 6.449 | | 6/16/2025 | | | 647,811 | |

| Sba Senior Finance II LLC, Initial Term Loan + | | LIBOR + 2.000% | | | 1,156,636 | | | 4.558 | | 4/12/2025 | | | 1,155,653 | |

| Securus Technologies Holdings, Inc., Initial Term Loan (First Lien) + | | LIBOR + 4.500% | | | 373,205 | | | 7.058 | | 10/31/2024 | | | 374,761 | |

| Securus Technologies Holdings, Inc., Delayed Term Loan + | | LIBOR + 4.500% | | | 168,000 | | | 6.812 | | 10/31/2024 | | | 168,420 | |

| Securus Technologies Holdings, Inc., Initial Loan (Second Lien) + | | LIBOR + 8.250% | | | 255,000 | | | 10.809 | | 10/31/2025 | | | 255,849 | |

| Sinclair Television Group, Inc., Tranche B Term Loan + | | LIBOR + 2.250% | | | 362,911 | | | 4.808 | | 1/4/2024 | | | 364,158 | |

| Sorenson Communications, Inc., Initial Term Loan (First Lien) + | | LIBOR + 5.750% | | | 385,880 | | | 8.148 | | 4/30/2020 | | | 387,568 | |

| Sprint Communications, Inc., Initial Term Loan + | | LIBOR + 2.500% | | | 1,048,566 | | | 5.058 | | 2/2/2024 | | | 1,049,384 | |

| Telenet Financing USD LLC., Term Loan AN Facility + | | LIBOR + 2.250% | | | 680,000 | | | 4.904 | | 8/16/2026 | | | 678,647 | |

| Tribune Media Co., Term B Loan + | | LIBOR + 3.000% | | | 22,405 | | | 5.558 | | 12/28/2020 | | | 22,493 | |

| Tribune Media Co., Term C Loan + | | LIBOR + 3.000% | | | 279,252 | | | 5.558 | | 1/26/2024 | | | 280,344 | |

| Univision Communications, Inc., 2017 Replacement Repriced First-Lien Term Loan + | | LIBOR + 2.750% | | | 2,917,851 | | | 5.308 | | 3/16/2024 | | | 2,807,061 | |

| Upc Financing Partnership, Facility AR + | | LIBOR + 2.500% | | | 624,684 | | | 5.154 | | 1/16/2026 | | | 623,159 | |

| Virgin Media Bristol LLC, K Facility + | | LIBOR + 2.500% | | | 690,000 | | | 4.949 | | 1/16/2026 | | | 690,214 | |

| West Corporation, Initial Term B Loan + | | LIBOR + 4.000% | | | 447,409 | | | 6.558 | | 10/10/2024 | | | 445,888 | |

| West Corporation, Incremental Term B-1 Loan + | | LIBOR + 3.500% | | | 249,375 | | | 6.058 | | 10/10/2024 | | | 246,934 | |

| Ziggo Secured Finance Partnership, Term Loan E Facility + | | LIBOR + 2.500% | | | 890,000 | | | 4.949 | | 4/16/2025 | | | 873,918 | |

| | | | | | | | | | | | | | 29,780,385 | |

See accompanying notes to financial statements.

| SCHEDULE OF INVESTMENTS |

| Dunham Floating Rate Bond Fund (Continued) |

| October 31, 2018 |

| | | Variable | | Principal | | | Interest | | Maturity | | | |

| Security | | Rate | | Amount | | | Rate % | | Date | | Value | |

| BANK LOANS - 91.6% (Continued) | | | | | | | | | | | | | | |

| CONSUMER, CYCLICAL - 19.0% | | | | | | | | | | | | | | |

| 84 Lumber Co., Term B-1 Loan + | | LIBOR + 5.250% | | $ | 440,625 | | | 7.759 | | 10/24/2023 | | $ | 444,298 | |

| Accuride Corporation, 2017 Refinancing Term Loan + | | LIBOR + 5.250% | | | 453,168 | | | 7.648 | | 11/16/2023 | | | 454,584 | |

| Affinity Gaming LLC, Initial Term Loan + | | LIBOR + 3.250% | | | 360,246 | | | 5.808 | | 6/30/2023 | | | 359,345 | |

| American Airlines, Inc., 2017 Class B Term Loan + | | LIBOR + 2.000% | | | 494,555 | | | 4.449 | | 12/14/2023 | | | 491,978 | |

| American Airlines, Inc., 2017 Class B Term Loans + | | LIBOR + 2.000% | | | 87,220 | | | 4.527 | | 4/28/2023 | | | 86,751 | |

| American Airlines, Inc., 2018 Replacement Term Loan + | | LIBOR + 1.750% | | | 426,723 | | | 4.277 | | 6/28/2025 | | | 418,521 | |

| American Axle & Manufacturing, Inc., Tranche B Term Loan + | | LIBOR + 2.250% | | | 277,875 | | | 4.759 | | 4/6/2024 | | | 277,051 | |

| American Builders & Contractors Supply Co., Inc., Term B-2 Loan + | | LIBOR + 2.000% | | | 580,471 | | | 4.558 | | 11/1/2023 | | | 575,755 | |

| American Greetings Corporation, Initial Term Loan + | | LIBOR + 4.500% | | | 344,138 | | | 7.020 | | 4/6/2024 | | | 345,213 | |

| Aramark Intermediate HoldCo Corp., U.S. Term B-2 Loan + | | LIBOR + 1.750% | | | 312,312 | | | 4.308 | | 3/28/2024 | | | 312,573 | |

| Aramark Intermediate HoldCo Corp., U.S. Term B-3 Loan + | | LIBOR + 1.750% | | | 1,357,024 | | | 4.308 | | 3/12/2025 | | | 1,358,937 | |

| Aristocrat International Pty, Ltd., Term B-3 Loan + | | LIBOR + 1.750% | | | 1,553,214 | | | 4.237 | | 10/20/2024 | | | 1,549,417 | |

| Bass Pro Group LLC, Initial Term Loan + | | LIBOR + 5.000% | | | 763,000 | | | 7.558 | | 9/24/2024 | | | 764,022 | |

| Beacon Roofing Supply, Inc., Initial Term Loan + | | LIBOR + 2.250% | | | 736,300 | | | 4.675 | | 1/2/2025 | | | 730,686 | |

| Boyd Gaming Corporation, Refinancing Term B Loan + | | LIBOR + 2.250% | | | 799,142 | | | 4.759 | | 9/16/2023 | | | 801,144 | |

| Caesars Resort Collection LLC, Term B Loan + | | LIBOR + 2.750% | | | 1,960,188 | | | 5.308 | | 12/24/2024 | | | 1,963,049 | |

| Carlisle Companies Incorporated, Delayed Draw Term Loan (First Lien) + | | LIBOR + 3.000% | | | 103,067 | | | 5.248 | | 3/20/2025 | | | 102,037 | |

| Carlisle Companies Incorporated, Initial Term Loan (First Lien) + | | LIBOR + 3.000% | | | 454,648 | | | 5.508 | | 3/20/2025 | | | 450,101 | |

| CBAC Borrower, LLC, Term B Loan + | | LIBOR + 4.000% | | | 232,650 | | | 6.558 | | 7/8/2024 | | | 233,871 | |

| CDS US Intermediate Holdings, Inc., Term B Loan (First Lien) + | | LIBOR + 3.750% | | | 625,503 | | | 6.148 | | 7/8/2022 | | | 619,248 | |

| CEOC LLC., Term B Loan + | | LIBOR + 2.000% | | | 1,404,388 | | | 4.558 | | 10/8/2024 | | | 1,399,121 | |

| CityCenter Holdings LLC., Term B Loan + | | LIBOR + 2.250% | | | 1,179,789 | | | 4.808 | | 4/18/2024 | | | 1,178,868 | |

| Crown Finance US, Inc., Initial Dollar Tranche Term Loan + | | LIBOR + 2.500% | | | 601,975 | | | 5.058 | | 2/28/2025 | | | 600,250 | |

| CSC SW Holdco, Inc., Term B-1 Loan (First Lien) + | | LIBOR + 3.250% | | | 977,382 | | | 5.695 | | 11/14/2022 | | | 979,518 | |

| Deck Chassis Acquisition, Inc., Initial Term Loan (Second Lien) + | | LIBOR + 6.000% | | | 110,000 | | | 8.559 | | 6/16/2023 | | | 111,238 | |

| Dexko Global, Inc., Replacement U.S. Dollar Term B Loan (First Lien) + | | LIBOR + 3.500% | | | 516,107 | | | 6.058 | | 7/24/2024 | | | 518,287 | |

| Eldorado Resorts, Inc., Term Loan + | | LIBOR + 2.250% | | | 789,246 | | | 4.666 | | 4/16/2024 | | | 790,975 | |

| Formula One Management, Ltd., Facility B3 (USD) + | | LIBOR + 2.500% | | | 615,202 | | | 5.300 | | 1/31/2024 | | | 609,563 | |

| Gateway Casinos & Entertainment Ltd., Initial Term Loan + | | LIBOR + 3.000% | | | 503,738 | | | 5.398 | | 11/30/2023 | | | 505,783 | |

| Global Appliance, Inc., Tranche B Term Loan + | | LIBOR + 4.000% | | | 600,950 | | | 6.558 | | 9/28/2024 | | | 597,570 | |

| Golden Nugget, Inc., Initial B Term Loan + | | LIBOR + 2.750% | | | 468,172 | | | 5.261 | | 10/4/2023 | | | 469,307 | |

| Gvc Holdings PLC, Facility B2 (USD) + | | LIBOR + 2.500% | | | 572,125 | | | 5.058 | | 3/28/2024 | | | 574,628 | |

| Hd Supply, Inc., Term B-5 Loan + | | LIBOR + 1.750% | | | 849,494 | | | 4.237 | | 10/16/2023 | | | 850,293 | |

| Hilton Worldwide Finance LLC, Series B-2 Term Loan + | | LIBOR + 1.750% | | | 1,324,558 | | | 4.259 | | 10/24/2023 | | | 1,327,459 | |

| Isagenix International LLC, Senior Lien Term Loan + | | LIBOR + 5.750% | | | 582,625 | | | 8.148 | | 6/14/2025 | | | 582,989 | |

| Leslie’s Poolmark, Inc., Tranche B-2 Term Loan + | | LIBOR + 3.500% | | | 308,011 | | | 6.058 | | 8/16/2023 | | | 307,682 | |

| Libbey Glass, Inc., Initial Loan + | | LIBOR + 3.000% | | | 558,464 | | | 5.420 | | 4/8/2021 | | | 557,766 | |

| Michaels Stores, Inc., 2018 New Replacement Term B Loan + | | LIBOR + 2.500% | | | 517,706 | | | 5.016 | | 1/30/2023 | | | 515,192 | |

| Navistar Financial Corp., New TLB Loan + | | LIBOR + 3.750% | | | 710,000 | | | 6.277 | | 7/30/2025 | | | 713,550 | |

| Navistar, Inc., Tranche B Term Loan + | | LIBOR + 3.500% | | | 932,950 | | | 5.925 | | 11/6/2024 | | | 936,075 | |

| Neiman Marcus Group Ltd. LLC, Other Term Loan + | | LIBOR + 3.250% | | | 1,249,334 | | | 5.670 | | 10/24/2020 | | | 1,140,879 | |

| Patriot Container Corp., Closing Date Term Loan (First Lien) + | | LIBOR + 3.500% | | | 636,800 | | | 6.008 | | 3/20/2025 | | | 640,780 | |

| Petsmart, Inc., Tranche B-2 Loan + | | LIBOR + 3.000% | | | 724,332 | | | 5.408 | | 3/12/2022 | | | 615,862 | |

| Playa Resorts Holding BV, Initial Term Loan + | | LIBOR + 2.750% | | | 1,044,355 | | | 5.308 | | 4/28/2024 | | | 1,031,301 | |

| Scientific Games International, Inc., Initial Term B-5 Loan + | | LIBOR + 2.750% | | | 803,972 | | | 5.179 | | 8/14/2024 | | | 797,296 | |

| Serta Simmons Bedding LLC, Initial Term Loan (First Lien) + | | LIBOR + 3.500% | | | 300,645 | | | 5.913 | | 11/8/2023 | | | 271,923 | |

| Siteone Landscape Supply Holding LLC, Tranche E Term Loan + | | LIBOR + 2.750% | | | 695,999 | | | 5.199 | | 10/28/2024 | | | 699,479 | |

| SRAM LLC, New Term Loan (2018) (First Lien) + | | LIBOR + 2.750% | | | 568,066 | | | 5.259 | | 3/16/2024 | | | 570,562 | |

| Stars Group Holdings BV, USD Term Loan + | | LIBOR + 3.500% | | | 214,463 | | | 5.898 | | 7/10/2025 | | | 215,654 | |

| Station Casinos LLC, Term B Facility Loan + | | LIBOR + 2.500% | | | 873,402 | | | 5.058 | | 6/8/2023 | | | 873,987 | |

| Tenneco, Inc., Tranche B Term Loan + | | LIBOR + 2.750% | | | 795,000 | | | 5.308 | | 9/30/2025 | | | 794,006 | |

| Ti Group Automotive Systems LLC., Initial US Term Loan + | | LIBOR + 2.500% | | | 380,738 | | | 5.058 | | 6/30/2022 | | | 379,944 | |

| Univar Usa, Inc., Term B-3 Loan + | | LIBOR + 2.250% | | | 873,217 | | | 4.808 | | 6/30/2024 | | | 874,147 | |

| Wyndham Hotels & Resorts, Inc., Term Loan B + | | LIBOR + 1.750% | | | 1,135,000 | | | 4.308 | | 5/30/2025 | | | 1,135,948 | |

| | | | | | | | | | | | | | 36,506,463 | |

See accompanying notes to financial statements.

| SCHEDULE OF INVESTMENTS |

| Dunham Floating Rate Bond Fund (Continued) |

| October 31, 2018 |

| | | Variable | | Principal | | | Interest | | Maturity | | | |

| Security | | Rate | | Amount | | | Rate % | | Date | | Value | |

| BANK LOANS - 91.6% (Continued) | | | | | | | | | | | | | | |

| CONSUMER, NON-CYCLICAL - 20.4% | | | | | | | | | | | | | | |

| 21st Century Oncology Holdings, Inc., Tranche B Term Loan + | | LIBOR + 6.125% | | $ | 145,512 | | | 8.570 | | 1/16/2023 | | $ | 136,100 | |

| Accelerated Health Systems, LLC, Initial Term Loan + | | LIBOR + 3.500% | | | 465,000 | | | 6.020 | | 11/1/2025 | | | 467,325 | |

| Acuity Specialty Products, Inc., Initial Term Loan (First Lien) + | | LIBOR + 4.000% | | | 277,200 | | | 6.398 | | 8/12/2024 | | | 261,781 | |

| AHP Health Partners, Inc., Term Loan + | | LIBOR + 4.500% | | | 583,538 | | | 7.058 | | 6/30/2025 | | | 587,094 | |

| Albertson’s LLC, 2017-1 Term B-4 Loan + | | LIBOR + 2.750% | | | 1,147,885 | | | 5.308 | | 8/24/2021 | | | 1,147,626 | |

| Albertson’s LLC, 2017-1 Term B-5 Loan + | | LIBOR + 3.000% | | | 247,968 | | | 5.396 | | 12/20/2022 | | | 247,727 | |

| Albertson’s LLC, Term Loan B7 + | | LIBOR + 3.000% | | | 374,195 | | | 5.527 | | 10/28/2025 | | | 371,780 | |

| AlixPartners, LLP, 2017 Refinancing Term Loan + | | LIBOR + 2.750% | | | 950,070 | | | 5.308 | | 4/4/2024 | | | 952,150 | |

| Allied Universal Holdco LLC, Incremental Term Loan (First Lien) + | | LIBOR + 4.250% | | | 450,000 | | | 6.770 | | 7/28/2022 | | | 450,142 | |

| Amneal Pharmaceuticals LLC, Initial Term Loan + | | LIBOR + 3.500% | | | 608,334 | | | 6.058 | | 5/4/2025 | | | 612,973 | |

| Auris LuxCo, Term B (First Lien) + | | LIBOR + 3.750% | | | 95,000 | | | 6.258 | | 7/24/2025 | | | 95,812 | |

| Avantor, Inc., Initial Dollar Term Loan + | | LIBOR + 4.000% | | | 660,013 | | | 6.558 | | 11/20/2024 | | | 665,633 | |

| Bausch Health Companies, Inc., Initial Term Loan + | | LIBOR + 3.000% | | | 1,226,410 | | | 5.410 | | 6/2/2025 | | | 1,228,569 | |

| CCS-CMGC Holdings, Inc., Initial Term Loan (First Lien) + | | LIBOR + 5.500% | | | 400,000 | | | 8.059 | | 9/30/2025 | | | 398,500 | |

| Change Healthcare Holdings, Inc., Closing Date Term Loan + | | LIBOR + 2.750% | | | 970,125 | | | 5.308 | | 2/29/2024 | | | 970,188 | |

| CHG Healthcare Services, Inc., New Term Loan (2017) (First Lien) + | | LIBOR + 3.000% | | | 367,267 | | | 5.558 | | 6/8/2023 | | | 368,940 | |

| CHG PPC Parent LLC, Initial Term Loan (First Lien) + | | LIBOR + 2.750% | | | 588,525 | | | 5.308 | | 4/1/2025 | | | 587,789 | |

| Chobani LLC, New Term Loan (First Lien) + | | LIBOR + 3.500% | | | 652,242 | | | 6.058 | | 10/10/2023 | | | 638,588 | |

| Community Health Systems, Inc., Incremental 2021 Term H Loan + | | LIBOR + 3.250% | | | 733,185 | | | 5.571 | | 1/28/2021 | | | 719,272 | |

| Concordia International Corp., Initial Dollar Term Loan + | | LIBOR + 5.550% | | | 91,000 | | | 7.920 | | 9/6/2024 | | | 89,408 | |

| CPI Acquisition, Inc., Term Loan (First Lien) + | | LIBOR + 4.500% | | | 1,518,336 | | | 6.920 | | 8/16/2022 | | | 1,004,812 | |

| Cryolife, Inc., Initial Term Loan + | | LIBOR + 3.250% | | | 238,200 | | | 5.648 | | 12/2/2024 | | | 239,988 | |

| Diamond Bv, Initial USD Term Loan + | | LIBOR + 3.000% | | | 585,575 | | | 5.558 | | 9/6/2024 | | | 578,744 | |

| Dole Food Company, Inc., Tranche B Term Loan + | | LIBOR + 2.750% | | | 523,125 | | | 5.262 | | 4/6/2024 | | | 522,348 | |

| Endo Luxembourg Finance Company I Sarl, Initial Term Loan + | | LIBOR + 4.250% | | | 498,688 | | | 6.808 | | 4/28/2024 | | | 501,647 | |

| Envision Healthcare Corporation, Initial Term Loan + | | LIBOR + 3.750% | | | 1,994,578 | | | 6.308 | | 10/10/2025 | | | 1,956,711 | |

| Explorer Holdings, Inc., Initial Term Loan + | | LIBOR + 3.750% | | | 394,950 | | | 6.148 | | 5/2/2023 | | | 396,186 | |

| Financial & Risk US Holdings, Inc., Initial Dollar Term Loan + | | LIBOR + 3.750% | | | 940,000 | | | 6.308 | | 9/30/2025 | | | 931,775 | |

| Fort Dearborn Holding Company, Inc., Initial Term Loan (First Lien) + | | LIBOR + 4.000% | | | 394,610 | | | 6.410 | | 10/20/2023 | | | 375,866 | |

| Greatbatch Ltd., New Term B Loan (2017) + | | LIBOR + 3.000% | | | 64,373 | | | 5.425 | | 10/28/2022 | | | 64,735 | |

| Greenrock Finance, Inc., Initial USD Term B Loan (First Lien) + | | LIBOR + 3.500% | | | 253,088 | | | 6.058 | | 6/28/2024 | | | 254,353 | |

| GW Honos Security Corporation, Term B Loan + | | LIBOR + 3.500% | | | 227,777 | | | 5.823 | | 5/24/2024 | | | 228,970 | |

| Heartland Dental, LLC, Delayed Term Loan + | | LIBOR + 3.750% | | | 541,632 | | | 6.308 | | 4/30/2025 | | | 540,700 | |

| Heartland Dental, LLC, Initial Term Loan + | | LIBOR + 3.750% | | | 81,448 | | | 6.113 | | 4/30/2025 | | | 81,308 | |

| Herbalife Nutrition Ltd., Term Loan B + | | LIBOR + 3.250% | | | 245,000 | | | 5.648 | | 8/18/2025 | | | 246,430 | |

| H- Food Holdings, LLC, Initial Term Loan + | | LIBOR + 3.000% | | | 473,813 | | | 5.558 | | 5/24/2025 | | | 466,409 | |

| Hostess Brands, LLC, November 2017 Refinancing Term B Loan + | | LIBOR +2.250% | | | 925,426 | | | 4.808 | | 8/4/2022 | | | 922,390 | |

| Immucor, Inc., Term B-3 Loan + | | LIBOR + 5.000% | | | 39,500 | | | 7.398 | | 6/16/2021 | | | 40,204 | |

| Jaguar Holding Co., 2018 Term Loan + | | LIBOR + 2.500% | | | 939,599 | | | 5.058 | | 8/18/2022 | | | 937,954 | |

| JBS USA Lux S.A., Initial Term Loan + | | LIBOR + 2.500% | | | 943,079 | | | 4.847 | | 10/30/2022 | | | 944,494 | |

| Kronos Acquisition Intermediate, Inc., Initial Loan + | | LIBOR + 4.000% | | | 956,837 | | | 6.558 | | 5/16/2023 | | | 945,475 | |

| Laureate Education, Inc., Series 2024 Term Loan + | | LIBOR + 3.500% | | | 810,523 | | | 6.058 | | 4/26/2024 | | | 813,157 | |

| MedPlast Holdings, Inc., Initial Term Loan (First Lien) + | | LIBOR + 3.750% | | | 175,000 | | | 6.157 | | 7/2/2025 | | | 176,258 | |

| Milk Specialties Company, New Term Loan + | | LIBOR + 4.000% | | | 336,140 | | | 6.398 | | 8/16/2023 | | | 336,350 | |

| NAB Holdings, LLC, 2018 Refinancing Term Loan + | | LIBOR + 3.000% | | | 579,165 | | | 5.398 | | 6/30/2024 | | | 573,133 | |

| NVA Holdings, Inc., Term B-3 Loan (First Lien) + | | LIBOR + 2.750% | | | 776,100 | | | 5.308 | | 2/2/2025 | | | 770,279 | |

| One Call Corporation, Extended Term Loan (First Lien) + | | LIBOR + 5.250% | | | 614,970 | | | 7.699 | | 11/28/2022 | | | 580,489 | |

| Ortho-Clinical Diagnostics, Inc., Second Amendment New Term Loan + | | LIBOR + 3.250% | | | 641,115 | | | 5.770 | | 6/30/2025 | | | 641,996 | |

| Parexel International Corporation, Initial Term Loan + | | LIBOR + 2.750% | | | 618,750 | | | 5.308 | | 9/28/2024 | | | 611,115 | |

| Parfums Holding Co., Inc., Initial Term Loan (First Lien) + | | LIBOR + 4.250% | | | 464,186 | | | 6.616 | | 6/30/2024 | | | 464,766 | |

| Pearl Intermediate Parent LLC, Initial Term Loan (First Lien) + | | LIBOR + 2.750% | | | 465,163 | | | 5.237 | | 2/14/2025 | | | 459,348 | |

| Pearl Intermediate Parent LLC, Delayed Draw Term Loan (First Lien) + | | LIBOR + 2.750% | | | 137,405 | | | 4.622 | | 2/14/2025 | | | 135,687 | |

| Pharmerica Corporation, Initial Term Loan (First Lien) + | | LIBOR + 3.500% | | | 303,475 | | | 5.949 | | 12/6/2024 | | | 304,803 | |

| Pi UK Holdco II Ltd., Facility B1 + | | LIBOR + 3.500% | | | 1,467,625 | | | 6.058 | | 1/4/2025 | | | 1,465,336 | |

| Prime Security Services Borrower LLC, 2016-2 Refinancing Term B-1 Loan (First Lien) + | | LIBOR + 2.750% | | | 465,309 | | | 5.308 | | 5/2/2022 | | | 466,156 | |

| Prospect Medical Holdings, Inc., Term B-1 Loan + | | LIBOR + 5.500% | | | 253,725 | | | 7.910 | | 2/22/2024 | | | 255,945 | |

| Quorum Health Corp., Term Loan + | | LIBOR + 6.750% | | | 128,477 | | | 9.309 | | 4/28/2022 | | | 130,103 | |

See accompanying notes to financial statements.

| SCHEDULE OF INVESTMENTS |

| Dunham Floating Rate Bond Fund (Continued) |

| October 31, 2018 |

| | | Variable | | Principal | | | Interest | | Maturity | | | |

| Security | | Rate | | Amount | | | Rate % | | Date | | Value | |

| BANK LOANS - 91.6% (Continued) | | | | | | | | | | | | | | |

| CONSUMER, NON-CYCLICAL - 20.3% (Continued) | | | | | | | | | | | | | | |

| Revlon Consumer Products Corporation, Initial Term B Loan + | | LIBOR + 3.500% | | $ | 653,379 | | | 5.821 | | 9/8/2023 | | $ | 480,779 | |

| Select Medical Corp., Tranche B Term Loan + | | LIBOR + 2.500% | | | 295,500 | | | 5.020 | | 3/6/2025 | | | 296,363 | |

| Servicemaster Company, LLC, Tranche C Term Loan + | | LIBOR + 2.500% | | | 341,894 | | | 5.058 | | 11/8/2023 | | | 343,860 | |

| Sigma Holdco B.V, Facility B2 + | | LIBOR + 3.000% | | | 555,000 | | | 5.609 | | 7/2/2025 | | | 554,306 | |

| St. George’s University Scholastic Services LLC, Delayed Draw Term Loan + | | LIBOR + 3.500% | | | 215,932 | | | 5.842 | | 6/22/2025 | | | 218,631 | |

| St. George’s University Scholastic Services LLC, Term Loan + | | LIBOR + 3.500% | | | 694,068 | | | 6.058 | | 7/16/2025 | | | 702,743 | |

| Sterigenics- Nordion Holdings, LLC, Incremental Term Loan + | | LIBOR + 3.000% | | | 1,016,663 | | | 5.558 | | 5/16/2022 | | | 1,019,097 | |

| Surgery Center Holdings, Inc., Initial Term Loan + | | LIBOR + 3.250% | | | 757,350 | | | 5.571 | | 9/2/2024 | | | 756,971 | |

| Syneos Health, Inc., Replacement Term B Loan + | | LIBOR + 2.000% | | | 222,834 | | | 4.558 | | 7/31/2024 | | | 222,587 | |

| Team Health Holdings, Inc., Initial Term Loan + | | LIBOR + 2.750% | | | 293,344 | | | 5.308 | | 2/6/2024 | | | 278,311 | |

| Transunion LLC, 2017 Replacement Term B-3 Loan + | | LIBOR + 2.000% | | | 1,144,414 | | | 4.558 | | 4/10/2023 | | | 1,144,282 | |

| University Health Services, Inc., Incremental Tranche B Facility + | | LIBOR + 1.750% | | | 120,000 | | | 4.270 | | 11/1/2025 | | | 120,450 | |

| University Hospital Services, Delayed Draw Term Loan + | | LIBOR + 3.000% | | | 140,000 | | | 5.469 | | 10/18/2025 | | | 141,050 | |

| US Foods, Inc., Initial Term Loan + | | LIBOR + 2.000% | | | 458,448 | | | 4.558 | | 6/28/2023 | | | 458,305 | |

| U.S. Renal Care Inc., Initial Term Loan (First Lien) + | | LIBOR + 4.250% | | | 619,799 | | | 6.648 | | 12/30/2022 | | | 602,237 | |

| Wex Inc., Term B-2 Loan + | | LIBOR + 2.250% | | | 485,788 | | | 4.808 | | 6/30/2023 | | | 487,306 | |

| | | | | | | | | | | | | | 39,191,095 | |

| ENERGY - 3.7% | | | | | | | | | | | | | | |

| California Resources Corp., Initial Loan + | | LIBOR + 4.750% | | | 405,000 | | | 7.258 | | 1/1/2023 | | | 412,087 | |

| Contura Energy, Inc., Term Loan + | | LIBOR + 5.000% | | | 533,635 | | | 7.398 | | 3/18/2024 | | | 533,635 | |

| Fieldwood Energy LLC, Closing Date Loan (First Lien) + | | LIBOR + 5.250% | | | 180,554 | | | 7.808 | | 4/12/2022 | | | 182,022 | |

| Fieldwood Energy LLC, Closing Date Loan 2018 (Second Lien) + | | LIBOR + 7.250% | | | 81,748 | | | 9.809 | | 4/12/2023 | | | 79,091 | |

| Gavilan Resources LLC, Initial Term Loan (Second Lien) + | | LIBOR + 6.000% | | | 490,000 | | | 8.487 | | 2/29/2024 | | | 463,594 | |

| Mcdermott International, Inc., Term Loan + | | LIBOR + 5.000% | | | 711,425 | | | 7.558 | | 5/12/2025 | | | 704,133 | |

| Medallion Midland Acquisition LLC, Initial Term Loan + | | LIBOR + 3.250% | | | 570,688 | | | 5.808 | | 10/30/2024 | | | 568,191 | |

| Moda Ingleside Energy Center, LLC, Initial Term Loan + | | LIBOR + 3.250% | | | 95,000 | | | 5.777 | | 9/28/2025 | | | 95,871 | |

| MRC Global Inc., 2018 Refinancing Term Loan + | | LIBOR + 3.000% | | | 397,000 | | | 5.558 | | 9/20/2024 | | | 397,992 | |

| Ocean Rig UDW, Inc., Loan + | | LIBOR+ 8.000% | | | 28,380 | | | 8.000 | | 9/20/2024 | | | 29,869 | |

| Paragon Offshore Finance Co., Term Loan + | | LIBOR + 2.750% | | | 1,153 | | | 5.250 | | 7/16/2021 | | | — | |

| Seadrill Operating LP, Initial Term Loan + | | LIBOR + 6.000% | | | 1,142,417 | | | 8.398 | | 2/20/2021 | | | 1,063,082 | |

| Terraform Power Operating LLC, Specified Refinancing Term Loan + | | LIBOR + 2.000% | | | 605,425 | | | 4.558 | | 11/8/2022 | | | 607,129 | |

| Traverse Midstream Partners LLC, Advance + | | LIBOR + 4.000% | | | 655,000 | | | 6.398 | | 9/28/2024 | | | 660,220 | |

| Ultra Resources, Inc., Loan + | | LIBOR + 3.000% | | | 665,000 | | | 5.487 | | 4/12/2024 | | | 625,336 | |

| Weatherford International Ltd., Loan + | | LIBOR + 1.425% | | | 701,129 | | | 3.952 | | 7/12/2020 | | | 685,354 | |

| | | | | | | | | | | | | | 7,107,606 | |

| FINANCIAL - 5.7% | | | | | | | | | | | | | | |

| Asurion LLC, Amendment No. 14 Replacement B-4 Term Loan + | | LIBOR + 3.000% | | | 624,695 | | | 5.558 | | 8/4/2022 | | | 626,535 | |

| Asurion LLC, Replacement B-6 Term Loan + | | LIBOR + 3.000% | | | 325,614 | | | 5.558 | | 11/4/2023 | | | 326,361 | |

| Asurion LLC, New B-7 Term Loan + | | LIBOR + 3.000% | | | 389,025 | | | 5.558 | | 11/4/2024 | | | 390,033 | |

| Asurion LLC, Second Lien Replacement B-2 Term Loan + | | LIBOR + 6.500% | | | 787,456 | | | 9.059 | | 8/4/2025 | | | 809,603 | |

| BlackHawk Network Holdings, Inc., Term Loan (First Lien) + | | LIBOR + 3.000% | | | 573,563 | | | 5.398 | | 6/16/2025 | | | 575,447 | |

| Capital Automotive LP, Initial Tranche B-2 Term Loan (First Lien) + | | LIBOR + 2.500% | | | 627,174 | | | 5.058 | | 3/24/2024 | | | 628,115 | |

| Capital Automotive LP, Initial Tranche B Term Loan (Second Lien) + | | LIBOR + 6.000% | | | 367,573 | | | 8.559 | | 3/24/2025 | | | 374,464 | |

| Communications Sales & Leasing, Inc., Shortfall Term Loan + | | LIBOR + 3.000% | | | 578,011 | | | 5.558 | | 10/24/2022 | | | 548,099 | |

| Ditech Holding Corporation, Tranche B Term Loan + | | LIBOR + 6.000% | | | 1,133,876 | | | 8.559 | | 6/30/2022 | | | 1,057,339 | |

| Finco I LLC, 2018 Replacement Loan + | | LIBOR + 2.000% | | | 325,247 | | | 4.558 | | 12/28/2022 | | | 325,501 | |

| Franklin Square Holdings LP, Initial Term Loan + | | LIBOR + 2.500% | | | 195,000 | | | 4.908 | | 7/31/2025 | | | 195,975 | |

| Genworth Holdings, Inc., Initial Loan + | | LIBOR + 4.500% | | | 104,475 | | | 6.949 | | 3/8/2023 | | | 106,826 | |

| Istar Inc., Loan + | | LIBOR + 2.750% | | | 855,246 | | | 5.193 | | 6/28/2023 | | | 856,850 | |

| Lightstone Holdco LLC, Refinancing Term B Loan + | | LIBOR + 3.750% | | | 146,351 | | | 6.308 | | 1/30/2024 | | | 144,600 | |

| Lightstone Holdco LLC, Refinancing Term C Loan + | | LIBOR + 3.750% | | | 7,860 | | | 6.308 | | 1/30/2024 | | | 7,766 | |

| MGM Growth Properties Operating Partnership LP, Term B Loan + | | LIBOR + 2.000% | | | 367,575 | | | 4.558 | | 3/20/2025 | | | 366,919 | |

| Realogy Group LLC, Extended 2025 Term Loan + | | LIBOR + 2.250% | | | 446,479 | | | 4.699 | | 2/8/2025 | | | 445,852 | |

| Sedgwick Claims Management Services, Inc., Initial Term Loan (First Lien) + | | LIBOR + 2.750% | | | 1,283,310 | | | 5.308 | | 2/28/2021 | | | 1,284,619 | |

| Sedgwick Claims Management Services, Inc., Initial Loan (Second Lien) + | | LIBOR + 5.750% | | | 620,000 | | | 8.254 | | 2/28/2022 | | | 621,745 | |

| TKC Holdings, Inc., Initial Term Loan (First Lien) + | | LIBOR + 3.750% | | | 630,548 | | | 6.308 | | 1/31/2023 | | | 631,787 | |

| UFC Holdings LLC, Term Loan (First Lien) + | | LIBOR + 3.250% | | | 595,853 | | | 5.808 | | 8/18/2023 | | | 600,075 | |

| | | | | | | | | | | | | | 10,924,511 | |

See accompanying notes to financial statements.

| SCHEDULE OF INVESTMENTS |

| Dunham Floating Rate Bond Fund (Continued) |

| October 31, 2018 |

| | | Variable | | Principal | | | Interest | | Maturity | | | |

| Security | | Rate | | Amount | | | Rate % | | Date | | Value | |

| BANK LOANS - 91.6% (Continued) | | | | | | | | | | | | | | |

| INDUSTRIALS - 13.5% | | | | | | | | | | | | | | |

| Accudyne Industries Borrower, Initial Term Loan + | | LIBOR + 3.000% | | $ | 375,645 | | | 5.558 | | 8/18/2024 | | $ | 374,750 | |

| Accuride Corporation + | | LIBOR + 5.250% | | | 439,143 | | | 5.808 | | 2/1/2025 | | | 440,516 | |

| Anchor Glass Container Corp., July 2017 Additional Term Loan (First Lien) + | | LIBOR + 2.750% | | | 430,253 | | | 5.180 | | 12/8/2023 | | | 384,754 | |

| Anchor Glass Container Corp., Term Loan (Second Lien) + | | LIBOR + 7.750% | | | 244,000 | | | 10.200 | | 12/8/2024 | | | 164,496 | |

| Berlin Packaging LLC, Initial Term Loan (First Lien) + | | LIBOR + 3.000% | | | 593,513 | | | 5.420 | | 11/8/2025 | | | 593,634 | |

| Berry Global, Inc., Term S Loan + | | LIBOR + 1.750% | | | 226,743 | | | 4.175 | | 2/8/2020 | | | 226,695 | |

| Berry Global, Inc., Term T Loan + | | LIBOR + 1.750% | | | 417,785 | | | 4.175 | | 1/6/2021 | | | 417,446 | |

| Berry Global, Inc., Term Q Loan + | | LIBOR + 2.000% | | | 308,192 | | | 4.425 | | 9/30/2022 | | | 308,559 | |

| Berry Global, Inc., Term R Loan + | | LIBOR + 2.000% | | | 524,030 | | | 4.425 | | 1/20/2024 | | | 524,032 | |

| Brand Energy & Infrastructure Services, Inc., Initial Term Loan + | | LIBOR + 4.250% | | | 701,620 | | | 6.746 | | 6/20/2024 | | | 705,668 | |

| Brookfield WEC Holdings, Inc., Initial Term Loan (First Lien) + | | LIBOR + 3.750% | | | 700,000 | | | 6.308 | | 7/31/2025 | | | 705,299 | |

| Brookfield WEC Holdings, Inc., Initial Term Loan (Second Lien) + | | LIBOR + 6.750% | | | 280,000 | | | 9.309 | | 8/4/2026 | | | 285,110 | |

| Bway Holding Co., Inc., Initial Term Loan + | | LIBOR + 3.250% | | | 483,875 | | | 5.675 | | 4/4/2024 | | | 481,758 | |

| Ceva Logistics Finance BV, Facility B + | | LIBOR + 3.750% | | | 430,000 | | | 6.148 | | 8/4/2025 | | | 431,346 | |

| Circor International, Inc., Initial Term Loan + | | LIBOR + 3.500% | | | 689,788 | | | 5.936 | | 12/12/2024 | | | 690,360 | |

| CPG International LLC, New Term Loan + | | LIBOR + 3.750% | | | 1,274,636 | | | 6.148 | | 5/4/2024 | | | 1,279,951 | |

| Deliver Buyer, Inc., Term Loan + | | LIBOR + 5.000% | | | 646,725 | | | 7.321 | | 4/30/2024 | | | 649,959 | |

| Energizer Holdings, Inc., Term Loan B + | | LIBOR + 2.250% | | | 305,000 | | | 4.623 | | 6/20/2025 | | | 305,859 | |

| Filtration Group, Inc., Initial Dollar Term Loan + | | LIBOR + 3.000% | | | 860,675 | | | 5.558 | | 3/28/2025 | | | 865,361 | |

| Fluidra, S.A. + | | LIBOR + 2.250% | | | 548,625 | | | 4.808 | | 7/2/2025 | | | 549,741 | |

| Gardner Denver, Inc., Tranche B-1 Dollar Term Loan + | | LIBOR + 2.750% | | | 1,105,291 | | | 5.308 | | 7/30/2024 | | | 1,109,093 | |

| Gates Global LLC, Initial B-2 Dollar Term Loan + | | LIBOR + 2.750% | | | 626,445 | | | 5.308 | | 3/31/2024 | | | 628,152 | |

| GFL Environmental, Inc., Effective Date Incremental Term Loan + | | LIBOR + 2.750% | | | 615,000 | | | 5.148 | | 5/30/2025 | | | 606,544 | |

| Gopher Resource LLC, Initial Term Loan + | | LIBOR + 3.250% | | | 479,447 | | | 5.808 | | 3/6/2025 | | | 481,544 | |

| Hillman Group, Inc., Initial Term Loan + | | LIBOR + 4.000% | | | 708,225 | | | 6.558 | | 5/30/2025 | | | 696,893 | |

| Klockner Pentaplast Of America, Inc., Dollar Term Loan + | | LIBOR + 4.250% | | | 866,250 | | | 6.808 | | 6/30/2022 | | | 836,581 | |

| Nn, Inc., 2017 Incremental Term Loan + | | LIBOR + 3.250% | | | 178,600 | | | 5.808 | | 4/2/2021 | | | 178,488 | |

| Nn, Inc., Tranche B Term Loan + | | LIBOR + 3.750% | | | 214,577 | | | 6.308 | | 10/20/2022 | | | 215,247 | |

| Paladin Brands Holding, Inc., Loan + | | LIBOR + 5.500% | | | 253,418 | | | 7.898 | | 8/16/2022 | | | 254,368 | |

| Pro Mach Group, Inc., Initial Term Loan (First Lien) + | | LIBOR + 3.000% | | | 562,175 | | | 5.425 | | 3/8/2025 | | | 561,261 | |

| Quikrete Holdings, Inc., Initial Loan (First Lien) + | | LIBOR + 2.750% | | | 786,538 | | | 5.308 | | 11/16/2023 | | | 784,572 | |

| RBS Global, Inc., Refinancing Term Loan + | | LIBOR + 2.000% | | | 883,830 | | | 4.527 | | 8/20/2024 | | | 886,318 | |

| Reynolds Group Holdings, Inc, Incremental U.S. Term Loan + | | LIBOR + 2.750% | | | 826,733 | | | 5.308 | | 2/4/2023 | | | 828,324 | |

| Summit Materials, LLC, New Term Loan + | | LIBOR + 2.000% | | | 932,950 | | | 4.558 | | 11/20/2024 | | | 929,890 | |

| Thermon Holding Corp., Term B Loan + | | LIBOR + 3.750% | | | 158,490 | | | 6.148 | | 10/30/2024 | | | 159,679 | |

| Titan Acquisition, Ltd., Initial Term Loan + | | LIBOR + 3.000% | | | 1,014,900 | | | 5.558 | | 3/28/2025 | | | 959,441 | |

| Transdigm, Inc., New Tranche F Term Loan (2018) + | | LIBOR + 2.500% | | | 1,097,620 | | | 5.058 | | 6/8/2023 | | | 1,094,141 | |

| Transdigm, Inc., New Tranche G Term Loan + | | LIBOR + 2.500% | | | 741,643 | | | 5.058 | | 8/22/2024 | | | 739,407 | |

| Transdigm, Inc., New Tranche E Term Loan (2018) + | | LIBOR + 2.500% | | | 635,336 | | | 5.058 | | 5/30/2025 | | | 633,211 | |

| Tricorbraun Holdings, Inc., Closing Date Term Loan (First Lien) + | | LIBOR + 3.750% | | | 582,408 | | | 6.148 | | 11/30/2023 | | | 585,457 | |

| Tricorbraun Holdings, Inc., Delayed Draw Term Loan (First Lien) + | | LIBOR + 3.750% | | | 58,685 | | | 6.063 | | 11/30/2023 | | | 58,993 | |

| Trident TPI Holdings, Inc., Tranche B-1 Term Loan + | | LIBOR + 3.250% | | | 730,072 | | | 5.808 | | 10/16/2024 | | | 727,152 | |

| Tunnel Hill Partners, LP, Cov-Lite TLB + | | LIBOR + 3.500% | | | 405,000 | | | 5.898 | | 9/30/2025 | | | 407,025 | |

| Us Farathane LLC, Term B-4 Loan + | | LIBOR + 3.500% | | | 386,895 | | | 5.898 | | 12/24/2021 | | | 386,412 | |

| Wrangler Buyer Corp., Initial Term Loan + | | LIBOR + 2.750% | | | 804,037 | | | 5.308 | | 9/27/2024 | | | 805,975 | |

| | | | | | | | | | | | | | 25,939,462 | |

| TECHNOLOGY - 8.9% | | | | | | | | | | | | | | |

| Applied Systems, Inc., Initial Term Loan (First Lien) + | | LIBOR + 3.000% | | | 628,650 | | | 5.398 | | 9/20/2024 | | | 635,625 | |

| Applied Systems, Inc., Initial Term Loan (Second Lien) + | | LIBOR + 7.000% | | | 105,000 | | | 9.398 | | 9/20/2025 | | | 107,100 | |

| Blackboard Inc., Term B-4 Loan (First Lien) + | | LIBOR + 5.000% | | | 590,258 | | | 7.469 | | 6/30/2021 | | | 565,110 | |

| Boxer Parent Company, Inc., Initial Dollar Term Loan + | | LIBOR + 4.250% | | | 1,440,000 | | | 6.657 | | 10/2/2025 | | | 1,446,754 | |

| Dell International LLC, Refinancing Term B Loan + | | LIBOR + 2.000% | | | 1,460,628 | | | 4.558 | | 9/8/2023 | | | 1,460,760 | |

| Everi Payments, Inc., Term B Loan + | | LIBOR + 3.000% | | | 390,063 | | | 5.558 | | 5/8/2024 | | | 391,892 | |

| First Data Corporation, 2022D New Dollar Term Loan + | | LIBOR + 2.000% | | | 1,210,476 | | | 4.508 | | 7/8/2022 | | | 1,207,831 | |

| First Data Corporation, 2024A New Dollar Term Loan + | | LIBOR + 2.000% | | | 1,051,807 | | | 4.508 | | 4/26/2024 | | | 1,047,316 | |

| Infor, Inc., Tranche B-6 Term Loan + | | LIBOR + 2.750% | | | 746,484 | | | 5.148 | | 1/31/2022 | | | 744,711 | |

See accompanying notes to financial statements.

| SCHEDULE OF INVESTMENTS |

| Dunham Floating Rate Bond Fund (Continued) |

| October 31, 2018 |

| | | Variable | | Principal | | | Interest | | Maturity | | | |

| Security | | Rate | | Amount | | | Rate % | | Date | | Value | |

| BANK LOANS - 91.6% (Continued) | | | | | | | | | | | | | | |

| TECHNOLOGY - 8.9% (Continued) | | | | | | | | | | | | | | |

| Intralinks, Inc., Initial Term Loan (First Lien) + | | LIBOR + 4.000% | | $ | 496,954 | | | 6.558 | | 11/14/2024 | | $ | 498,551 | |

| Iqvia, Inc., Term B-1 Dollar Loan + | | LIBOR + 2.000% | | | 144,019 | | | 4.398 | | 3/8/2024 | | | 144,514 | |

| Iqvia, Inc., Incremental Term B-2 Dollar Loan + | | LIBOR + 2.000% | | | 74,250 | | | 4.398 | | 1/16/2025 | | | 74,412 | |

| Iqvia, Inc., Term B-3 Dollar Loan + | | LIBOR + 1.750% | | | 748,125 | | | 4.148 | | 6/12/2025 | | | 747,190 | |

| Kronos, Inc., Incremental Term Loan (First Lien) + | | LIBOR + 3.000% | | | 1,376,098 | | | 5.348 | | 10/31/2023 | | | 1,380,075 | |

| Kronos, Inc., Initial Term Loan (Second Lien) + | | LIBOR + 8.250% | | | 120,000 | | | 10.598 | | 10/31/2024 | | | 122,150 | |

| Neustar, Inc., TLB4 (First Lien) + | | LIBOR + 3.500% | | | 232,650 | | | 6.058 | | 8/8/2024 | | | 233,558 | |

| Neustar, Inc., TLB3 (First Lien) + | | LIBOR + 2.500% | | | 35,937 | | | 5.058 | | 1/8/2020 | | | 36,022 | |

| Presidio Holdings, Inc., Term B Loan + | | LIBOR + 2.750% | | | 563,075 | | | 5.150 | | 2/2/2024 | | | 564,015 | |

| Rackspace Hosting, Inc., Term B Loan (First Lien) + | | LIBOR + 3.000% | | | 672,488 | | | 5.343 | | 11/4/2023 | | | 654,135 | |

| Science Applications International Corporation, Trance B + | | LIBOR + 1.750% | | | 220,000 | | | 4.237 | | 11/1/2025 | | | 220,000 | |

| SS&C Technologies Holdings, Inc., Term B-3 Loan + | | LIBOR + 2.250% | | | 1,173,026 | | | 4.808 | | 4/16/2025 | | | 1,168,521 | |

| SS&C Technologies Holdings, Inc., Term B-4 Loan + | | LIBOR + 2.250% | | | 454,664 | | | 4.808 | | 4/16/2025 | | | 452,917 | |

| SS&C Technologies Holdings, Inc., Term B-5 Loan + | | LIBOR + 2.250% | | | 275,000 | | | 4.808 | | 4/16/2025 | | | 273,896 | |

| Tempo Acquisition LLC., Initial Term Loan + | | LIBOR + 3.000% | | | 553,000 | | | 5.558 | | 4/30/2024 | | | 554,106 | |

| Vertafore, inc., Initial Term Loan (First Lien) + | | LIBOR + 3.250% | | | 1,645,000 | | | 5.808 | | 7/2/2025 | | | 1,641,916 | |

| Western Digital Corporation, U.S. Term B-4 Loan + | | LIBOR + 1.750% | | | 746,222 | | | 4.270 | | 4/28/2023 | | | 742,957 | |

| | | | | | | | | | | | | | 17,116,034 | |

| UTILITIES - 1.9% | | | | | | | | | | | | | | |

| Aplp Holdings LP, Term Loan + | | LIBOR + 3.000% | | | 298,786 | | | 5.349 | | 4/12/2023 | | | 299,757 | |

| Calpine Construction Finance Co. LP, Term B Loan + | | LIBOR + 2.500% | | | 718,730 | | | 5.058 | | 1/16/2025 | | | 718,734 | |

| NRG Energy, Inc., Term Loan + | | LIBOR + 1.750% | | | 945,567 | | | 4.148 | | 6/30/2023 | | | 943,255 | |

| Talen Energy Supply LLC, Term B-1 Loan + | | LIBOR + 4.000% | | | 196,508 | | | 6.558 | | 7/16/2023 | | | 197,275 | |

| Talen Energy Supply LLC, Initial Term Loan + | | LIBOR + 4.000% | | | 328,635 | | | 6.558 | | 4/16/2024 | | | 329,918 | |

| Texas Competitive Electric Holdings Co. LLC Escrow Bonds | | | | | 635,000 | | | — | | 10/1/2020 | | | 444 | |

| Vistra Operations Co. LLC, Initial Term Loan + | | LIBOR + 2.000% | | | 228,582 | | | 4.558 | | 8/4/2023 | | | 228,343 | |

| Vistra Operations Co. LLC, 2018 Incremental Term Loan + | | LIBOR + 2.000% | | | 872,813 | | | 4.479 | | 1/1/2026 | | | 871,224 | |

| | | | | | | | | | | | | | 3,588,950 | |

| TOTAL BANK LOANS (Cost - $177,552,276) | | | | | | | | | | | | | 176,264,173 | |

| | | | | | | | | | | | | | | |

| BONDS & NOTES - 3.5% | | | | | | | | | | | | | | |

| CHEMICALS - 0.1% | | | | | | | | | | | | | | |

| Hexion, Inc. | | | | | 105,000 | | | 6.625 | | 4/15/2020 | | | 93,187 | |

| NOVA Chemicals Corp. - 144A | | | | | 65,000 | | | 4.875 | | 6/1/2024 | | | 59,962 | |

| NOVA Chemicals Corp. - 144A | | | | | 40,000 | | | 5.000 | | 5/1/2025 | | | 36,700 | |

| | | | | | | | | | | | | | 189,849 | |

| COMPUTERS - 0.3% | | | | | | | | | | | | | | |

| Exela Intermediate LLC - 144A | | | | | 520,000 | | | 10.000 | | | | | 543,244 | |

| | | | | | | | | | | | | | | |

| DIVERSIFIED FINANCIAL SERVICES - 0.1% | | | | | | | | | | | | | | |

| Springleaf Finance Corp. | | | | | 250,000 | | | 6.125 | | 5/15/2022 | | | 252,500 | |

| | | | | | | | | | | | | | | |

| FOOD - 0.1% | | | | | | | | | | | | | | |

| Dole Food Co., Inc. - 144A | | | | | 175,000 | | | 7.250 | | 6/15/2025 | | | 168,875 | |

| | | | | | | | | | | | | | | |

| HEALTHCARE-SERVICES - 0.4% | | | | | | | | | | | | | | |

| Eagle Holding Co II LLC - 144A | | | | | 175,000 | | | 7.625 | | 5/15/2022 | | | 176,312 | |

| Surgery Center Holdings, Inc. - 144A | | | | | 130,000 | | | 8.875 | | 4/15/2021 | | | 134,225 | |

| Tenet Healthcare Corp. ^ | | | | | 405,000 | | | 4.625 | | 7/15/2024 | | | 391,372 | |

| | | | | | | | | | | | | | 701,909 | |

| HOME BUILDERS - 0.3% | | | | | | | | | | | | | | |

| Lennar Corp. | | | | | 420,000 | | | 2.950 | | 11/29/2020 | | | 409,500 | |

| TRI Pointe Group, Inc. | | | | | 70,000 | | | 4.375 | | 6/15/2019 | | | 70,262 | |

| TRI Pointe Group, Inc. | | | | | 130,000 | | | 4.875 | | 7/1/2021 | | | 129,025 | |

| | | | | | | | | | | | | | 608,787 | |

See accompanying notes to financial statements.

| SCHEDULE OF INVESTMENTS |

| Dunham Floating Rate Bond Fund (Continued) |

| October 31, 2018 |

| | | Principal | | | Interest | | Maturity | | | |

| Security | | Amount | | | Rate % | | Date | | Value | |

| BONDS & NOTES - 3.5% (Continued) | | | | | | | | | | | | |

| LODGING - 0.1% | | | | | | | | | | | | |

| Hilton Domestic Operating Co., Inc. - 144A | | $ | 295,000 | | | 5.125 | | 5/1/2026 | | $ | 289,100 | |

| | | | | | | | | | | | | |

| MEDIA - 0.3% | | | | | | | | | | | | |

| CCO Holdings LLC - 144A | | | 180,000 | | | 4.000 | | 3/1/2023 | | | 171,900 | |

| Comcast Corp. | | | 108,000 | | | 2.848 | | 10/1/2021 | | | 108,085 | |

| Dish DBS Corp. ^ | | | 175,000 | | | 5.875 | | 7/15/2022 | | | 166,031 | |

| iHeartCommunications, Inc. | | | 95,000 | | | 9.000 | | 12/15/2019 | | | 68,875 | |

| | | | | | | | | | | | 514,891 | |

| OIL & GAS - 0.5% | | | | | | | | | | | | |

| Alta Mesa Holdings LP | | | 135,000 | | | 7.875 | | 12/15/2024 | | | 121,500 | |

| Carrizo Oil & Gas, Inc. | | | 140,000 | | | 6.250 | | 4/15/2023 | | | 138,250 | |

| Chesapeake Energy Corp. | | | 170,000 | | | 6.625 | | 8/15/2020 | | | 175,950 | |

| Denbury Resources, Inc. - 144A | | | 185,000 | | | 7.500 | | 2/15/2024 | | | 181,762 | |

| Denbury Resources, Inc. - 144A | | | 60,000 | | | 9.250 | | 3/31/2022 | | | 62,775 | |

| EP Energy LLC / Everest Acquisition Finance, Inc. - 144A | | | 160,000 | | | 8.000 | | 11/29/2024 | | | 155,200 | |

| Range Resources Corp. | | | 125,000 | | | 5.000 | | 3/15/2023 | | | 121,250 | |

| | | | | | | | | | | | 956,687 | |

| OIL & GAS SERVICES - 0.1% | | | | | | | | | | | | |

| Bristow Group, Inc. - 144A ^ | | | 200,000 | | | 8.750 | | 3/1/2023 | | | 189,000 | |

| | | | | | | | | | | | | |

| PACKAGING & CONTAINERS - 0.2% | | | | | | | | | | | | |

| Ardagh Packaging Finance PLC - 144A | | | 235,000 | | | 6.000 | | 2/15/2025 | | | 220,900 | |

| BWAY Holding Co. - 144A | | | 265,000 | | | 5.500 | | 4/15/2024 | | | 255,063 | |

| | | | | | | | | | | | 475,963 | |

| PHARMACEUTICALS - 0.2% | | | | | | | | | | | | |

| Bausch Health Cos, Inc. - 144A | | | 445,000 | | | 5.500 | | 11/1/2025 | | | 437,769 | |

| | | | | | | | | | | | | |

| PIPELINES - 0.1% | | | | | | | | | | | | |

| Energy Transfer Equity LP | | | 190,000 | | | 4.250 | | 3/15/2023 | | | 188,575 | |

| | | | | | | | | | | | | |

| PRIVATE EQUITY - 0.2% | | | | | | | | | | | | |

| Icahn Enterprises LP | | | 310,000 | | | 6.250 | | 2/1/2022 | | | 313,739 | |

| | | | | | | | | | | | | |

| REAL ESTATE INVESTMENT TRUSTS - 0.2% | | | | | | | | | | | | |

| IStar Financial, Inc. | | | 60,000 | | | 6.000 | | 4/1/2022 | | | 60,150 | |

| IStar Financial, Inc. | | | 335,000 | | | 5.250 | | 9/15/2022 | | | 324,950 | |

| | | | | | | | | | | | 385,100 | |

| RETAIL - 0.1% | | | | | | | | | | | | |

| Cumberland Farms, Inc. - 144A | | | 125,000 | | | 6.750 | | 5/1/2025 | | | 128,750 | |

| | | | | | | | | | | | | |

| SOFTWARE - 0.2% | | | | | | | | | | | | |

| First Data Corp. - 144A | | | 190,000 | | | 5.375 | | 8/15/2023 | | | 192,138 | |

| First Data Corp. - 144A | | | 90,000 | | | 5.000 | | 1/15/2024 | | | 89,213 | |

| First Data Corp. - 144A | | | 25,000 | | | 5.750 | | 1/15/2024 | | | 25,250 | |

| | | | | | | | | | | | 306,601 | |

| TELECOMMUNICATIONS - 0.0% | | | | | | | | | | | | |

| Frontier Communications Corp. | | | 90,000 | | | 8.500 | | 4/15/2020 | | | 90,675 | |

| | | | | | | | | | | | | |

| TOTAL BONDS & NOTES (Cost - $6,945,438) | | | | | | | | | | | 6,742,014 | |

See accompanying notes to financial statements.

| SCHEDULE OF INVESTMENTS |

| Dunham Floating Rate Bond Fund (Continued) |

| October 31, 2018 |

| Security | | Shares | | | | | | | Value | |

| RIGHTS - 0.0% | | | | | | | | | | | | |

| TRA Rights | | | 10,588 | | | | | | | $ | 8,555 | |

| TOTAL RIGHTS (Cost - $17,470) | | | | | | | | | | | | |

| | | | | | | | | | | | |

| | | Principal | | | Interest | | Maturity | | | | |

| | | Amount | | | Rate % | | Date | | | | |

| U.S. GOVERNMENT - 0.5% | | | | | | | | | | | | |

| Treasury Bill | | $ | 1,000,000 | | | 2.310 | + | 3/14/2019 | | | 991,479 | |

| TOTAL U.S. GOVERNMENT (Cost - $991,595) | | | | | | | | | | | | |

| | | | | | | | | | | | | |

| | | Shares | | | | | | | | | |

| SHORT-TERM INVESTMENT - 4.1% | | | | | | | | | | | |

| MONEY MARKET FUND - 4.1% | | | | | | | | | | | | |

| Fidelity Investments Money Market Fund - Class I | | | 7,927,289 | | | 1.580 | + | | | | 7,927,289 | |

| TOTAL SHORT-TERM INVESTMENT - (Cost - $7,927,289) | | | | | | | | | | | | |

| | | | | | | | | | | | | |

| COLLATERAL FOR SECURITIES LOANED - 1.5% | | | | | | | | | | | | |

| Mount Vernon Prime Portfolio # (Cost - $2,835,975) | | | 2,835,975 | | | 2.390 | + | | | | 2,835,975 | |

| | | | | | | | | | | | | |

| TOTAL INVESTMENTS - 101.2% (Cost - $196,270,043) | | | | | | | | | | | 194,769,485 | |

| LIABILITIES IN EXCESS OF OTHER ASSETS - (1.2)% | | | | | | | | | | | (2,392,377 | ) |

| NET ASSETS - 100.0% | | | | | | | | | | $ | 192,377,108 | |

LP - Limited Partnership.

LLC - Limited Liability Company.

144A- Security exempt from registration under Rule 144A of the Securities Act of 1933. These securities may be sold in transactions exempt from registration, normally to qualified institutional buyers. As of October 31, 2018 the total market value of 144A securities is $3,518,138 or 1.83% of net assets.

| * | Non-Income producing security. |

| ^ | All or a portion of these securities are on loan. Total loaned securities had a value of $2,757,563 at October 31, 2018. Securities loaned with a value of $2,001,870 have been sold and are pending settlement. |

| + | Variable rate security. Interest rate is as of October 31, 2018 |

| # | The Trust’s securities lending policies and procedures require that the borrower: (i) deliver cash or U.S. Government securities as collateral with respect to each new loan of U.S. securities, equal to at least 102% of the value of the portfolio securities loaned, and (ii) at all times thereafter mark-to-market the collateral on a daily basis so that the market value of such collateral is at least 100% of the value of securities loaned. From time to time the collateral may not be 102% due to end of day market movement. The next business day additional collateral is obtained/received from the borrower to replenish/reestablish 102%. |

| Portfolio Composition * - (Unaudited) |

| Bank Loans | | | 90.5 | % | | Oil & Gas | | | 0.5 | % |

| Short-Term Investment | | | 4.1 | % | | Healthcare-Services | | | 0.3 | % |

| Other ** | | | 2.1 | % | | Computers | | | 0.3 | % |

| Collateral for Securities Loaned | | | 1.4 | % | | Media | | | 0.3 | % |

| U.S. Government | | | 0.5 | % | | Total | | | 100.0 | % |

| * | Based on total value of investments as of October 31, 2018 |

| ** | Groupings less than 0.20% of holdings. |

Percentage may differ from Schedule of Investments which are based on Fund net assets.

See accompanying notes to financial statements.

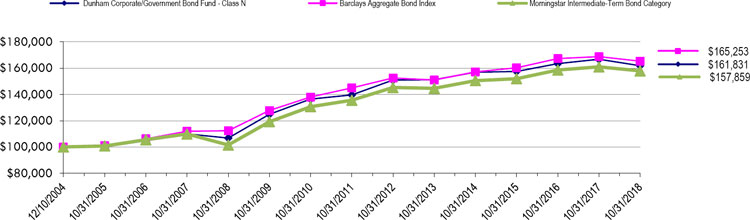

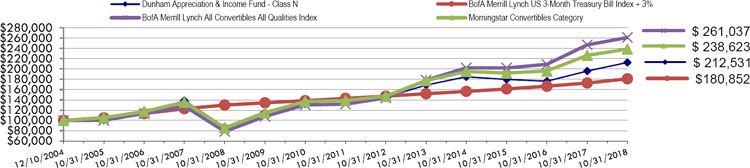

Dunham Corporate/Government Bond Fund (Unaudited)

Message from the Sub-Adviser (Newfleet Asset Management, LLC)

Investment-grade bonds, as measured by the Bloomberg Barclays Aggregate Bond Index, fell 2.1 percent in the fiscal year ended October 31, 2018, after increasing 0.9 percent over the previous fiscal year. Treasuries in the middle of the yield curve, as measured by the ICE BofA ML Treasuries 5-7 Years Index, fell 2.0 percent, while long-term Treasuries, as measured by the ICE BofA ML Treasuries 10+ Years Index, tumbled 6.2 percent over the same twelve months. Corporate bonds, as measured by the ICE BofA ML U.S. Corporate Bond Master Index, underperformed intermediate-term Treasury bonds, falling 2.8 percent over the fiscal year. High-yield bonds, as measured by the ICE BofA ML High-Yield Bond Cash Pay Index, also had a disappointing performance increasing just 0.8 percent.

The Fund continued to balance risk versus reward by choosing to emphasize lower duration bonds and overweighting lower credit quality securities, which benefitted the Fund for a fifth consecutive fiscal year. The average effective duration of the Fund was 5.29 years, while the benchmark index had an average duration of 5.99 years. While the lower duration exposure did not adversely affect performance during the most recent fiscal period, the overweight to lower credit quality securities versus the benchmark contributed to the Fund’s performance. Treasury yields fluctuated within a 76 basis point range over the fiscal period. The 10-year Treasury yield went from its lowest point of 2.31 percent early in the first fiscal quarter to its highest point of 3.23 late in the fiscal year, before settling at 3.14 percent. The overweight to securitized products contributed positively to Fund performance over the fiscal period. The Sub-Adviser’s overweight to the securitized products was slightly more than the previous fiscal year’s overweight, combining for over 20 percent of the Fund. The index had significantly less exposure to these products. The overweight to corporate investment-grade securities was increased slightly over the fiscal period, equaling roughly 34 percent of the Fund’s assets, and more than 8 percent greater than the index’s allocation to that sector.

Contributors over the fiscal year ended October 31, 2018, included the Safeway Inc. 7.25% 2/1/2031 (786514BA6) (holding weight*: 0.17 percent). Safeway bonds have benefited from positive underlying momentum in Albertson’s grocery business. Same store sales have been positive for three straight quarters and EBITDA growth has accelerated year-to-date. The failure of the proposed Rite Aid (RAD) (not held) Acquisition in August eliminated a significant amount of secured acquisition financing that would have further layered the unsecured Safeway bonds which lack guarantees from the other operating entities. After reporting a solid quarter in October and hinting at plans to pay down a substantial amount of debt, Albertsons announced the repayment of $1billion of secured term debt with cash on hand and a temporary revolver draw, which should be paid off as working capital releases through the holiday selling season. The debt pay down reinforced management’s commitment to delever ahead of another potential attempt at an IPO, which would be credit positive for the Safeway bonds. Another positive contributor to Fund performance was the Gateway Casinos & Entertainment Ltd. 8.25% 03/1/2024 (36760BAE9) (holding weight*: 0.10 percent). This holding reacted positively to a solid earnings report as well as a potential IPO.

Detractors over the fiscal year included two positions that came from emerging market countries. Turkey and Argentina drove a good amount of the overall emerging market sentiment over the past year. The weakening global macro backdrop (excluding the U.S.), caused most major equity markets to decline. Emerging market equities were down more. This in turn produced spread widening. In tandem, the U.S. dollar strengthened. Both tend to hurt emerging market countries as they raise the cost of servicing U.S. dollar denominated debt. The impact was most severe for emerging market countries with large global financing needs. This includes Argentina and Turkey. Turkiye Vakiflar Bankast 5.625% 05/30/2022 (90015WAF0) (holding weight**: 0.28 percent), a government owned Turkish bank traded down in tandem with Turkey. This position fell over 21 percent prior to being sold. The Argentine Republic Government International Bond 6.8975% 01/26/2027 (040114HL7) (holding weight**: 0.10 percent) also traded lower as Argentina reached a point where it had to seek IMF assistance. Over the fiscal year, the Argentine Republic Government International Bond 6.8975% 01/26/2027 declined 24.1 percent before being eliminated from the Fund in late August.

The Sub-Adviser is optimistic for the remainder of 2018 and 2019. It believes that fundamentals within corporate credit are still in good shape and are constructive on economic growth. The Sub-Adviser also believes that housing and consumer fundamentals are still in good shape and feels good about mortgage credit and the Fund’s exposure to asset-backed securities. It believes that the key risks moving forward are U.S. and China trade relations, inflation and consumer sentiment, and valuations as fiscal stimulus abates. They closely monitor economic data as it will drive the Fed’s interest rate decision. It is also important to stay diversified and granular, keeping small positions and maintaining liquidity. The Sub-Adviser believes that the prospect of continued volatility in the bond market will present opportunities and feels that the Fund is well positioned to take advantage of those opportunities as they arise.

| * | Holdings percentage(s) of total investments, excluding collateral for securities loaned, as of 10/31/2018. |

| ** | Holdings percentage(s) as of the date prior to the sale of the security. |

Growth of $100,000 Investment

Total Returns as of October 31, 2018

| | | Annualized | Annualized | Annualized Since Inception |

| | One Year | Five Years | Ten Years | (12/10/04) |

| Class N | (2.93)% | 1.37% | 4.25% | 3.53% |

| Class C | (3.67)% | 0.61% | 3.47% | 2.76% |

| Class A with load of 4.50% | (7.53)% | 0.20% | 3.50% | 2.88%* |

| Class A without load | (3.17)% | 1.12% | 3.98% | 3.29%* |

| Barclays Aggregate Bond Index | (2.05)% | 1.83% | 3.94% | 3.68% |

| Morningstar Intermediate-Term Bond Category | (1.91)% | 1.77% | 4.52% | 3.34% |

| * | Class A commenced operations on January 3, 2007. |

The Barclays Aggregate Bond Index is an unmanaged index which represents the U.S. investment-grade fixed- rate bond market (including government and corporate securities, mortgage pass-through securities and asset-backed securities). Investors cannot invest directly in an index or benchmark.

The Morningstar Intermediate-Term Bond Category is generally representative of intermediate-term bond mutual funds that primarily invest in corporate and other investment-grade U.S. fixed-income securities and typically have durations of 3.5 to 6.0 years.

As disclosed in the Trust’s latest registration statement, the Fund’s total annual operating expenses, including underlying funds, are 1.36% for Class N, 2.11% for Class C and 1.61% for Class A. Class A shares are subject to a sales load of 4.50% and a deferred sales charge of up to 0.75%. The performance data quoted here represents past performance, which is not indicative of future results. Current performance may be lower or higher than the performance data quoted. The investment return and NAV will fluctuate, so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Total returns are calculated assuming reinvestment of all dividends and capital gains distributions, if any. The returns do not reflect the deductions of taxes a shareholder would pay on the redemption of Fund shares or Fund distributions. For performance information current to the most recent month- end, please call 1-800-442-4358 or visit our website www.dunham.com.

| SCHEDULE OF INVESTMENTS |

| Dunham Corporate/Government Bond Fund |

| October 31, 2018 |

| | | Variable | | Principal | | | Interest | | Maturity | | | |

| Security | | Rate | | Amount | | | Rate % | | Date | | Value | |

| CORPORATE BONDS & NOTES - 63.3% | | | | | | | | | | | | | | | | |

| AEROSPACE / DEFENSE - 0.1% | | | | | | | | | | | | | | | | |

| TransDigm, Inc. | | | | $ | 50,000 | | | 6.375 | | | | 6/15/2026 | | $ | 49,125 | |

| | | | | | | | | | | | | | | | | |

| AGRICULTURE - 0.2% | | | | | | | | | | | | | | | | |

| Bunge Ltd Finance Corp. | | | | | 110,000 | | | 4.350 | | | | 3/15/2024 | | | 108,082 | |

| | | | | | | | | | | | | | | | | |

| AUTO PARTS & EQUIPMENT - 0.6% | | | | | | | | | | | | | | | | |

| Lear Corp. | | | | | 195,000 | | | 3.800 | | | | 9/15/2027 | | | 177,368 | |

| Tenneco, Inc. | | | | | 115,000 | | | 5.000 | | | | 7/15/2026 | | | 96,025 | |

| | | | | | | | | | | | | | | | 273,393 | |

| AUTOMOBILE ABS - 7.1% | | | | | | | | | | | | | | | | |

| American Credit Acceptance Receivables Trust 2017-2 - 144A | | | | | 135,000 | | | 2.860 | | | | 6/12/2023 | | | 134,485 | |

| American Credit Acceptance Receivables Trust 2018-3 - 144A | | | | | 165,000 | | | 3.750 | | | | 10/15/2024 | | | 164,707 | |

| Avid Automobile Receivables Trust 2018-1 - 144A | | | | | 167,757 | | | 2.840 | | | | 8/15/2023 | | | 166,365 | |

| Avis Budget Rental Car Funding AESOP LLC - 144A | | | | | 76,667 | | | 2.970 | | | | 2/20/2020 | | | 76,676 | |

| California Republic Auto Receivables Trust 2014-3 | | | | | 2,944 | | | 1.790 | | | | 3/16/2020 | | | 2,942 | |

| Capital Auto Receivables Asset Trust 2017-1 - 144A | | | | | 160,000 | | | 2.700 | | | | 9/20/2022 | | | 156,870 | |

| Carnow Auto Receivables Trust - 144A | | | | | 64,133 | | | 2.920 | | | | 9/15/2022 | | | 63,816 | |

| Centre Point Funding LLC - 144A | | | | | 91,776 | | | 2.610 | | | | 8/20/2020 | | | 90,737 | |

| CPS Auto Receivables Trust 2017-D - 144A | | | | | 100,000 | | | 2.430 | | | | 1/18/2022 | | | 98,988 | |

| Drive Auto Receivables Trust 2015-D - 144A | | | | | 37,643 | | | 3.380 | | | | 11/15/2021 | | | 37,679 | |

| Drive Auto Receivables Trust 2017-3 | | | | | 135,000 | | | 2.800 | | | | 7/15/2022 | | | 134,579 | |

| Drive Auto Receivables Trust 2017-A - 144A | | | | | 160,000 | | | 2.980 | | | | 1/18/2022 | | | 159,786 | |