united states

securities and exchange commission

washington, d.c. 20549

form n-csr

certified shareholder report of registered management

investment companies

| Investment Company Act file number | 811-22208 | |

| Valued Advisers Trust |

| (Exact name of registrant as specified in charter) |

| Ultimus Fund Solutions, LLC 225 Pictoria Drive, Suite 450 Cincinnati, OH | 45246 |

| (Address of principal executive offices) | (Zip code) |

Ultimus Fund Solutions, LLC

Attn: Gregory Knoth

225 Pictoria Drive, Suite 450

Cincinnati, OH 45246

(Name and address of agent for service)

| Registrant's telephone number, including area code: | 513-587-3400 | |

| Date of fiscal year end: | 10/31 | |

| | | |

| Date of reporting period: | 10/31/2019 | |

Item 1. Reports to Stockholders.

Dana

Foundry

Green Owl

SMI

DANA LARGE CAP EQUITY FUND

DANA SMALL CAP EQUITY FUND

DANA EPIPHANY ESG EQUITY FUND

Annual Report

October 31, 2019

Beginning on January 1, 2021, as permitted by regulations adopted by the Securities and Exchange Commission, paper copies of the Funds’ shareholder reports like this one will no longer be sent by mail, unless you specifically request paper copies of the reports from the Funds or from your financial intermediary such as a broker-dealer or bank. Instead, the reports will be made available on a website, and you will be notified by mail each time a report is posted and provided with a website link to access the report.

If you already elected to receive shareholder reports electronically, you will not be affected by this change and you need not take any action. You may elect to receive shareholder reports and other communications from the Funds electronically by contacting the Funds at (855) 280-9648 or, if you own these shares through a financial intermediary, you may contact your financial intermediary.

You may elect to receive all future reports in paper free of charge. You can inform the Funds that you wish to continue receiving paper copies of your shareholder reports by contacting the Funds at (855) 280-9648. If you own shares through a financial intermediary, you may contact your financial intermediary or follow instructions included with this document to elect to continue to receive paper copies of your shareholder reports. Your election to receive reports in paper will apply to all funds held with the fund complex or at your financial intermediary.

Dana Investment Advisors, Inc.

20700 Swenson Drive, Suite 400

Waukesha, WI 53186

(855) 280-9648

www.danafunds.com

Dear Fellow Shareholders,

We are thankful to be able to offer you this annual report for the Dana Funds for the 12-month period ended October 31, 2019. Our Fund family grew by one in the 12-month period as we reorganized an existing mutual fund into the Dana Epiphany ESG Equity Fund in December 2018. We are extremely excited to offer this opportunity to investors, and with our history of 19 years managing ESG strategies for institutional clients, believe it is a great fit. It seems you can’t read a financial publication these days without some mention of ESG Investing, and at Dana we’ve been wondering when the rest of the Investment Universe would catch on. All the Funds had positive performance for the period with the Dana Large Cap Equity Fund (the “Large Cap Fund”) leading the way at +15.55% (Institutional Class), the Dana Epiphany ESG Equity Fund (the “Epiphany ESG Fund”) following at +12.76% (Institutional Class) and the Dana Small Cap Equity Fund (the “Small Cap Fund”) generating +0.83% (Institutional Class).

As we look forward to the next 12 months, we know there will be pressures on the markets from the upcoming election cycle, Fed policy, valuations and daily rhetoric from market pundits predicting the next economic slowdown, all likely to result in volatility. Although dealing with this shorter-term volatility can be frustrating for us, a longer-term fundamental investor, we are not changing our discipline, which is designed to seek out companies that are trading at a discount to peers and exhibit sustainable growth projections, competitive business operations and quality management teams. Our belief is that these events provide opportunities for our team to find the types of companies we desire to own in our Funds for the long-term. We know you have many investment options to choose from, and we thank you for your continued trust and support of the Dana Funds.

Economic and Market Recap

With the exception of Q4 calendar year 2018 and brief pockets in Q3 calendar year 2019, momentum has continued to be the driving force behind much of the equity market’s performance. During the last 12-month period, the market has digested uncertainty surrounding a trade deal with China and tempered earnings growth expectations, a tumultuous political environment and an inverted yield curve. Nevertheless, the S&P 500® Index, similar to the Energizer Bunny, keeps going and going, posting a strong return of +14.33% while the Russell 2000® Index posted a +4.90% return during the last 12 months.

The first two months of the fiscal year were in the midst of a broad-based market sell-off as the S&P 500® Index was down -12.98% and the Russell 2000® Index was down -15.96% from October 31st through December 25th. Much of this was predicated on fears of a recession or a significant slowdown in the U.S. economy following a series of rate hikes. However, fortunes changed drastically the day after Christmas with the S&P 500® Index generating its largest one-day gain since March of 2009, and with that, the V-shape recovery was on! From December 26th through the first quarter of calendar year 2019, both indices were up in excess of +20%. The primary catalyst, aside from easing of recessionary fears, was the Federal Reserve’s ‘pause’ from raising short-term interest rates. Later in the year, we saw a direct pivot from the Fed to cut short-term rates, which provided another catalyst to the equity markets in the second half of 2019. Trade wars continued to dampen the economic growth outlook, but equity markets were resilient in moving forward, providing the best calendar year first half since 1997.

The Fed played a big role in the trailing 12-month returns by aiding in the recovery and continuation of the rally from 2 rate cuts, one in July and one in September 2019, taking short-term rates back to 2.0%. These efforts were well received by the markets, but returns slowed in the second half with

1

trade war fears weighing heavily on the investing landscape. Overall, there were signs that the market breadth was continuing to improve and that investors were paying attention to valuation. If those trends continue, it should be beneficial to active management.

Large Cap Fund Discussion

This was an excellent year with good absolute and relative performance for the Large Cap Fund (Institutional Class) with a return of +15.55% versus the S&P 500® Index return of +14.33%. Despite growth style indices outperforming value style indices, often a headwind for Dana’s relative value approach, the Large Cap Fund’s favorable stock selection across many sectors drove returns upwards and ahead of the benchmark. The Large Cap Fund was able to take advantage of the market’s pullback in late 2018, positioning itself in attractively valued securities that were driven down with the overall market swoon. This proved advantageous to performance when the market bounced back early in 2019. Relative performance strengthened during the summer and fall months of 2019.

For the full fiscal year, the performance of the Large Cap Fund’s holdings in Real Estate (REITs) and Consumer Staples delivered the strongest absolute returns. Holdings in the Materials sector delivered the only negative return and that was slight. For the S&P 500® Index, Energy was the weakest sector, down over -10%, yet favorable stock selection for the Large Cap Fund in the Energy sector contributed to positive relative return. Top performing contributors to the Large Cap Fund for the year included several Information Technology holdings such as Zebra Technologies Corp. (ZBRA), a marking, tracking and computer printing company, CDW Corp. (CDW), which provides hardware and software IT solutions including security, data center and cloud services, and stalwart, Microsoft Corp. (MSFT). Consumer Discretionary holdings, Lululemon Athletica, Inc. (LULU) and homebuilder, D.R. Horton, Inc. (DHI), rounded out the top 5 contributors to performance. Holdings that detracted most from performance included NetApp, Inc. (NTAP), a storage and data management company that revised earnings estimates downward on slowing global growth, DXC Technology Co. (DXC), a B2B services company, and Broadridge Financial Solutions, Inc. (BR). Target Corp. (TGT) and KeyCorp (KEY) also lagged the market.

Our analysis shows that the Dana Large Cap Equity Fund is trading at attractive relative valuations versus its benchmark and is performing well in terms of actual earnings and cash flow generation. We remain committed to our investment discipline as investors sort out expectations for the coming year.

Small Cap Fund Discussion

The Small Cap Fund (Institutional Class) returned +0.83% for the fiscal year versus the Russell 2000® Index return of +4.90%. Underlying market currents over the year are not reflected in the Small Cap Fund’s or benchmark index’s absolute returns. Beginning on October 31, 2018, the fiscal year started out with a strong market sell-off, and through December 25th the Russell 2000® Index dropped nearly -16%. Investors’ angst regarding Fed action and possible recession led to weakness inside some of the most cyclical sectors. The Small Cap Fund’s holdings within the Consumer Discretionary, Financials, and Industrials sectors were not immune. Relative value did not provide downside protection against benchmark holdings in these sectors as investors assumed that earnings estimates were too high and likely to fall. The following months included a strong market rebound, and by February 2019, Russell 2000® Index returns were back into positive territory for the fiscal year. The dramatic volatility and V-shaped nature of market returns during this period was a challenge for our Small Cap Fund that focuses on relative value and quality. The remainder of the fiscal year, spanning March through October, exhibited a range of returns from +5% to -5% for the Russell 2000® Index as investors digested headlines surrounding tariffs, Brexit, Middle East tensions, and threats of impeachment.

2

During the fiscal year, the Small Cap Fund realized strong returns from the Information Technology, Utilities and Real Estate sectors, while Communications Services, Energy, and Consumer Discretionary detracted from relative performance. Two of the Small Cap Fund’s top contributing holdings were Cabot Microelectronics Corp. (CCMP) and Boot Barn Holdings, Inc. (BOOT). CCMP is a market leader selling chemical polishing solutions used in microchip and wafer production. This market is important and growing as microchips become more complex. The company’s recent acquisition of KMG Chemicals adds to CCMP’s lineup of consumable products while synergies and cost reductions have led to improving profitability. We anticipate a two to three-year window of significant growth opportunities as this industry shifts to 3D NAND memory chip production. BOOT continues to execute well, and the company boasts industry-leading growth with a dominant competitive position. Exclusive brands are increasing as a percentage of BOOT’s total sales, helping to boost margins. Two of the larger detractors for the fiscal year were Weight Watchers International, Inc. (WW) and Matador Resources Co. (MTDR). WW experienced pressure in membership trends as the brand went through a marketing and digital transformation. Management credibility eroded over the Fund’s holding period and guidance appeared aggressive. For these reasons, along with a balance sheet that appeared highly levered, the Fund was led to sell its WW position. The Energy sector has been plagued by low oil prices and was the worst performing Russell 2000® Index sector for the fiscal year. Small Cap Fund holding MTDR has attractive oil and natural gas assets within the Permian Basin in West Texas; however, investors were disappointed with management’s cash flow outspend and acquisitions.

The Small Cap Fund continues to seek opportunities to add value through a relative value discipline that focuses on fundamentally driven stock selection and we believe the strategy will reward investors over the long-term.

Epiphany ESG Fund Discussion

As mentioned early on, we took on the Epiphany ESG Fund in December 2018, and the first order of business was to reduce the overall expenses to the shareholder. We saw this as a positive for our current shareholders and believe it will help in the future as we look to remain competitive with other active managers offering ESG mutual funds. The Epiphany ESG Fund (Institutional Class) returned a healthy +12.76% for the most recent fiscal year. Despite lagging the S&P 500® Index return of +14.33%, we are pleased with the solid performance given the repositioning necessary to transition from legacy fund holdings. Investor preference for growth style securities compared to value was also a headwind to Dana’s relative value approach. Throughout the year, the Epiphany ESG Fund adhered to its strong Environmental, Social and Governance (ESG) pillars that are integrated with our disciplined relative value approach. Relative performance improved as the year progressed, with the most recent four months outperforming the benchmark.

For the full fiscal year, the performance of the Epiphany ESG Fund’s holdings in Utilities and Real Estate (REITs) delivered the strongest absolute returns, while Energy and Industrials had the lowest returns. The Energy sector was the only negative returning sector for the year. Top performing contributors included Microsoft Corp. (MSFT), NextEra Energy, Inc. (NEE), Mastercard, Inc. (MA), and Stryker Corp. (SYK). NextEra is the world’s largest producer of wind and solar energy, providing much needed renewable energy at the expense of fossil fuels. Stryker continues to make advancements in medical technology products and services within orthopedics, neurotechnology and spine segments. The Fund’s Health Care sector was up double-digits, yet a few health-related holdings declined. These included Cigna Holding Co. (CI), Insperity, Inc. (NSP), Celgene Corp. (CNC), and Gilead Sciences, Inc. (GILD). Human resource and professional services company Insperity experienced health insurance costs from its clients that were higher than expected and the stock declined. We remain concerned about this trend and sold the position.

3

The Dana Epiphany ESG Equity Fund continues to invest in companies that meet our ESG criteria and provide growth at attractive valuations relative to peers.

Respectfully submitted,

Mark R. Mirsberger, CPA

Chief Executive Officer – Dana Investment Advisors, Inc.

Duane Roberts, CFA

Portfolio Manager and Director of Equities – Dana Investment Advisors, Inc.

4

Investment Results (Unaudited) | |

Average Annual Total Returns(a) as of October 31, 2019

| One

Year | Three

Year | Five

Year | Since

Inception

(3/1/10) | Since

Inception

(10/29/13) |

Dana Large Cap Equity Fund | | | | | |

Institutional Class | 15.55% | 15.79% | 9.67% | N/A | 10.84% |

Investor Class | 15.29% | 15.50% | 9.38% | 13.13% | N/A |

S&P 500® Index(b) | 14.33% | 14.91% | 10.78% | 13.24% | 11.66% |

| | Expense Ratios(c) |

| Institutional

Class | Investor

Class |

Gross | 0.83% | 1.08% |

With Applicable Waivers | 0.73% | 0.98% |

The performance quoted represents past performance, which does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. The returns shown do not reflect deduction of taxes that a shareholder would pay on Dana Large Cap Equity Fund (the “Large Cap Fund”) distributions or the redemption of Large Cap Fund shares. Current performance of the Large Cap Fund may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by calling 1-855-280-9648.

(a) | Average annual total returns reflect any change in price per share and assume the reinvestment of all distributions. The Large Cap Fund’s returns reflect any fee reductions during the applicable period. If such reductions had not occurred, the quoted performance would have been lower. |

(b) | The S&P 500® Index (“S&P Index”) is a widely recognized unmanaged index of equity securities and is representative of a broader domestic equity market and range of securities than is found in the Large Cap Fund’s portfolio. Individuals cannot invest directly in the S&P Index; however, an individual can invest in exchange-traded funds (“ETFs”) or other investment vehicles that attempt to track the performance of a benchmark index. |

(c) | The expense ratios are from the Large Cap Fund’s prospectus dated February 28, 2019. Expense ratios with applicable waivers reflect that Dana Investment Advisors, Inc. (the “Adviser”) has contractually agreed to waive or limit its fees and to assume other expenses of the Large Cap Fund until February 29, 2020, so that total annual fund operating expenses do not exceed 0.73% of the Large Cap Fund’s average daily net assets. This operating expense limitation does not apply to brokerage fees and commissions, borrowing costs (such as interest and dividend expenses on securities sold short), taxes, extraordinary expenses, fees and expenses paid under a distribution plan adopted pursuant to Rule 12b-1, fees and expenses paid under a shareholder services plan, and indirect expenses (such as “Acquired Funds Fees and Expenses”). Each waiver or reimbursement of an expense by the Adviser is subject to repayment by the Fund within three years following the date of such waiver or reimbursement, provided that the Large Cap Fund is able to make the repayment without exceeding the expense limitation in place at the time of waiver or reimbursement and the expense limitation in place at the time of the repayment. This agreement may only be terminated by mutual consent of the Adviser and the Board of Trustees. Additional information pertaining to the Large Cap Fund’s expense ratios as of October 31, 2019 can be found in the financial highlights. |

The Large Cap Fund’s investment objectives, strategies, risks, charges and expenses must be considered carefully before investing. The prospectus contains this and other important information about the Large Cap Fund and may be obtained by calling the same number as above. Please read it carefully before investing.

The Large Cap Fund is distributed by Unified Financial Securities, LLC, member FINRA/SIPC.

5

Investment Results (Unaudited) | |

Average Annual Total Returns(a) as of October 31, 2019

| One

Year | Three

Year | Since

Inception

(11/3/15) |

Dana Small Cap Equity Fund | | | |

Institutional Class | 0.83% | 6.40% | 2.92% |

Investor Class | 0.55% | 6.12% | 2.64% |

Russell 2000® Index(b) | 4.90% | 10.96% | 8.53% |

| | Expense Ratios(c) |

| Institutional

Class | Investor

Class |

Gross | 1.72% | 1.97% |

With Applicable Waivers | 0.95% | 1.20% |

The performance quoted represents past performance, which does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. The returns shown do not reflect deduction of taxes that a shareholder would pay on Dana Small Cap Equity Fund (the “Small Cap Fund”) distributions or the redemption of Small Cap Fund shares. Current performance of the Small Cap Fund may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by calling 1-855-280-9648.

(a) | Average annual returns reflect any change in price per share and assume the reinvestment of all distributions. The Small Cap Fund’s returns reflect any fee reductions during the applicable period. If such reductions had not occurred, the quoted performance would have been lower. |

(b) | The Russell 2000® Index (“Russell Index”) is a widely recognized unmanaged index of equity securities and is representative of a broader domestic equity market and range of securities than are found in the Small Cap Fund’s portfolio. Individuals can not invest directly in the Russell Index; however, an individual can invest in ETFs or other investment vehicles that attempt to track the performance of a benchmark index. |

(c) | The expense ratios are from the Small Cap Fund’s prospectus dated February 28, 2019. Expense ratios with applicable waivers reflect that the Adviser has contractually agreed to waive or limit its fees and to assume other expenses of the Small Cap Fund until February 29, 2020, so that total annual fund operating expenses do not exceed 0.95% of the Small Cap Fund’s average daily net assets. This operating expense limitation does not apply to brokerage fees and commissions, borrowing costs (such as interest and dividend expenses on securities sold short), taxes, extraordinary expenses, fees and expenses paid under a distribution plan adopted pursuant to Rule 12b-1, fees and expenses paid under a shareholder services plan, and indirect expenses (such as “Acquired Funds Fees and Expenses”). Each waiver or reimbursement of an expense by the Adviser is subject to repayment by the Small Cap Fund within three years following the date of such waiver or reimbursement, provided that the Small Cap Fund is able to make the repayment without exceeding the expense limitation in place at the time of waiver or reimbursement and the expense limitation in place at the time of the repayment. This agreement may only be terminated by mutual consent of the Adviser and the Board of Trustees. Additional information pertaining to the Small Cap Fund’s expense ratios as of October 31, 2019 can be found in the financial highlights. |

The Small Cap Fund’s investment objectives, strategies, risks, charges and expenses must be considered carefully before investing. The prospectus contains this and other important information about the Small Cap Fund and may be obtained by calling the same number as above. Please read it carefully before investing.

The Small Cap Fund is distributed by Unified Financial Securities, LLC, member FINRA/SIPC.

6

Investment Results (Unaudited) | |

Average Annual Total Returns(a) as of October 31, 2019

| One

Year | Three

Year | Five

Year | Ten

Year |

Dana Epiphany ESG Equity Fund | | | | |

Institutional Class | 12.76% | 13.66% | 7.44% | 10.56% |

Investor Class | 12.45% | 13.57% | 7.83% | 11.21% |

S&P 500® Index(b) | 14.33% | 14.91% | 10.78% | 13.70% |

| | Expense Ratios(c) |

| Institutional

Class | Investor

Class |

Gross | 1.87% | 2.12% |

With Applicable Waivers | 0.85% | 1.10% |

The performance quoted represents past performance, which does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. The returns shown do not reflect deduction of taxes that a shareholder would pay on Dana Epiphany ESG Equity Fund (the “Epiphany ESG Fund”) distributions or the redemption of Epiphany ESG Fund shares. Current performance of the Epiphany ESG Fund may be lower or higher than the performance quoted. The Epiphany ESG Fund’s investment objectives, risks, charges and expenses must be considered carefully before investing. Performance data current to the most recent month end may be obtained by calling 1-855-280-9648.

(a) | Average annual total returns reflect any change in price per share and assume the reinvestment of all distributions. The Epiphany ESG Fund’s returns reflect any fee reductions during the applicable period. If such reductions had not occurred, the quoted performance would have been lower. Investor Class returns shown for periods prior to December 19, 2018 are for Class A shares of the Epiphany FFV Fund, the Epiphany ESG Fund’s predecessor fund, and exclude the sales load. Institutional Class returns shown for periods prior to December 19, 2018 are for Class I shares of the Epiphany FFV Fund. |

(b) | The S&P 500® Index (“S&P Index”) is a widely recognized unmanaged index of equity securities and is representative of a broader domestic equity market and range of securities than is found in the Epiphany ESG Fund’s portfolio. Individuals cannot invest directly in the S&P Index; however, an individual can invest in ETFs or other investment vehicles that attempt to track the performance of a benchmark index. |

(c) | The expense ratios are from the Epiphany ESG Fund’s prospectus dated February 28, 2019. Expense ratios with applicable waivers reflect that the Adviser has contractually agreed to waive or limit its fees and to assume other expenses of the Epiphany ESG Fund until February 28, 2021, so that total annual fund operating expenses do not exceed 0.85% of the Epiphany ESG Fund’s average net assets. This operating expense limitation does not apply to brokerage fees and commissions, borrowing costs (such as interest and dividend expenses on securities sold short), taxes, extraordinary expenses, fees and expenses paid under a distribution plan adopted pursuant to Rule 12b-1, fees and expenses paid under a shareholder services plan, and indirect expenses (such as “Acquired Funds Fees and Expenses”). Each waiver or reimbursement of an expense by the Adviser is subject to repayment by the Epiphany ESG Fund within three years following the date of such waiver or reimbursement, provided that the Epiphany ESG Fund is able to make the repayment without exceeding the expense limitation in place at the time of waiver or reimbursement and the expense limitation in place at the time of the repayment. This agreement may only be terminated by mutual consent of the Adviser and the Board of Trustees. Additional information pertaining to the Epiphany ESG Fund’s expense ratios as of October 31, 2019 can be found in the financial highlights. |

The Epiphany ESG Fund’s investment objectives, strategies, risks, charges and expenses must be considered carefully before investing. The prospectus contains this and other important information about the Epiphany ESG Fund and may be obtained by calling the same number as above. Please read it carefully before investing.

The Epiphany ESG Fund is distributed by Unified Financial Securities, LLC, member FINRA/SIPC.

7

Comparison of Growth of $10,000 Investment in the

Dana Large Cap Equity Fund, Investor Class and

the S&P 500® Index (Unaudited)

The chart above assumes an initial investment of $10,000 made on March 1, 2010 (commencement of Investor Class operations) held through October 31, 2019. THE LARGE CAP FUND’S RETURN REPRESENTS PAST PERFORMANCE AND DOES NOT GUARANTEE FUTURE RESULTS. The returns shown do not reflect deduction of taxes that a shareholder would pay on Large Cap Fund distributions or the redemption of Large Cap Fund shares. Investment returns and principal values will fluctuate so that your shares, when redeemed, may be worth more or less than their original purchase price.

Current performance may be lower or higher than the performance data quoted. For more information on the Large Cap Fund, and to obtain performance data current to the most recent month end or to request a prospectus, please call 1-855-280-9648. You should carefully consider the investment objectives, potential risks, management fees, and charges and expenses of the Large Cap Fund before investing. The Large Cap Fund’s prospectus contains this and other information about the Large Cap Fund, and should be read carefully before investing.

The Large Cap Fund is distributed by Unified Financial Securities, LLC, member FINRA/SIPC.

8

Comparison of Growth of $10,000 Investment in the

Dana Small Cap Equity Fund, Investor Class and

the Russell 2000® Index (Unaudited)

The chart above assumes an initial investment of $10,000 made on November 3, 2015 (commencement of Investor Class operations) held through October 31, 2019. THE SMALL CAP FUND’S RETURN REPRESENTS PAST PERFORMANCE AND DOES NOT GUARANTEE FUTURE RESULTS. The returns shown do not reflect deduction of taxes that a shareholder would pay on Small Cap Fund distributions or the redemption of Small Cap Fund shares. Investment returns and principal values will fluctuate so that your shares, when redeemed, may be worth more or less than their original purchase price.

Current performance may be lower or higher than the performance data quoted. For more information on the Small Cap Fund, and to obtain performance data current to the most recent month end or to request a prospectus, please call 1-855-280-9648. You should carefully consider the investment objectives, potential risks, management fees, and charges and expenses of the Small Cap Fund before investing. The Small Cap Fund’s prospectus contains this and other information about the Small Cap Fund, and should be read carefully before investing.

The Small Cap Fund is distributed by Unified Financial Securities, LLC, member FINRA/SIPC.

9

Comparison of Growth of $10,000 Investment in the

Dana Epiphany ESG Equity Fund, Investor Class and

the S&P 500® Index (Unaudited)

The chart above assumes an initial investment of $10,000 made on October 31, 2009 held through October 31, 2019. THE EPIPHANY ESG FUND’S RETURN REPRESENTS PAST PERFORMANCE AND DOES NOT GUARANTEE FUTURE RESULTS. The returns shown do not reflect deduction of taxes that a shareholder would pay on Epiphany ESG Fund distributions or the redemption of Epiphany ESG Fund shares. Investment returns and principal values will fluctuate so that your shares, when redeemed, may be worth more or less than their original purchase price.

Current performance may be lower or higher than the performance data quoted. For more information on the Epiphany ESG Fund, and to obtain performance data current to the most recent month end or to request a prospectus, please call 1-855-280-9648. You should carefully consider the investment objectives, potential risks, management fees, and charges and expenses of the Epiphany ESG Fund before investing. The Epiphany ESG Fund’s prospectus contains this and other information about the Epiphany ESG Fund, and should be read carefully before investing.

The Epiphany ESG Fund is distributed by Unified Financial Securities, LLC, member FINRA/SIPC.

10

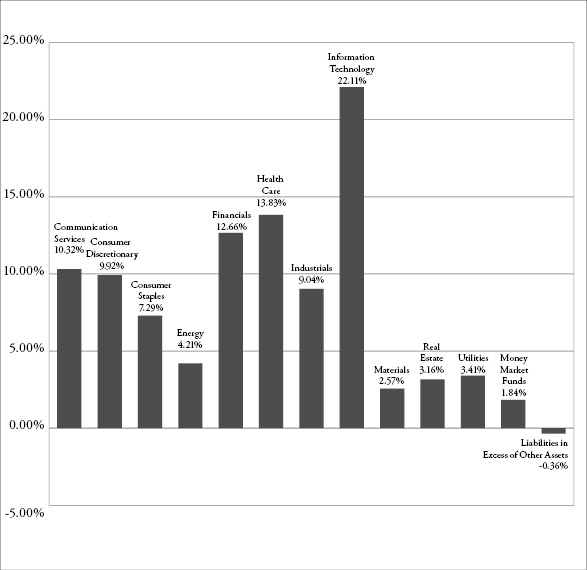

Portfolio Illustration (Unaudited)

October 31, 2019

The following chart gives a visual breakdown of the Large Cap Fund by sector weighting as a percentage of net assets as of October 31, 2019.

11

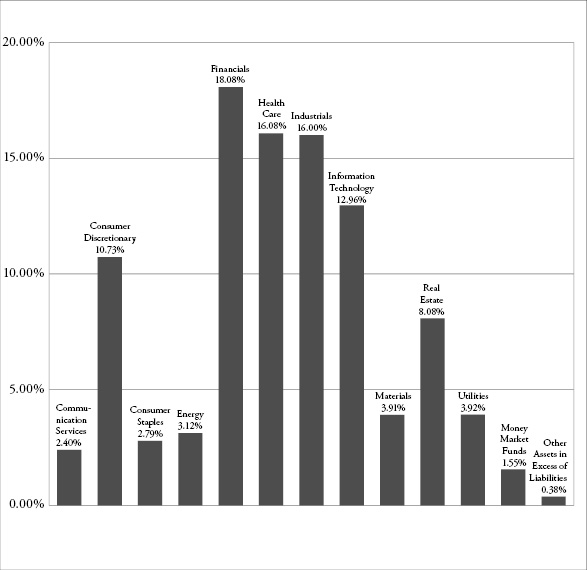

Portfolio Illustration (Unaudited)

October 31, 2019

The following chart gives a visual breakdown of the Small Cap Fund by sector weighting as a percentage of net assets as of October 31, 2019.

12

Portfolio Illustration (Unaudited)

October 31, 2019

The following chart gives a visual breakdown of the Epiphany ESG Fund by sector weighting as a percentage of net assets as of October 31, 2019.

Availability of Portfolio Schedules (Unaudited)

The Large Cap Fund, the Small Cap Fund, and the Epiphany ESG Fund (each a “Fund” and collectively the “Funds”) file their complete schedule of portfolio holdings with the Securities and Exchange Commission (“SEC”) for the first and third quarters of each fiscal year within sixty days after the end of the period. The Funds’ portfolio holdings are available at the SEC’s website at www.sec.gov.

13

Dana Large Cap Equity Fund

Schedule of Investments

October 31, 2019

| | Shares | | | Fair Value | |

COMMON STOCKS — 98.52% | | | | | | | | |

Communication Services — 10.32% | | | | | | | | |

Alphabet, Inc., Class A(a) | | | 2,300 | | | $ | 2,895,240 | |

AT&T, Inc. | | | 34,400 | | | | 1,324,056 | |

Comcast Corporation, Class A | | | 58,000 | | | | 2,599,560 | |

Facebook, Inc., Class A(a) | | | 13,500 | | | | 2,587,275 | |

T-Mobile US, Inc.(a) | | | 32,000 | | | | 2,645,120 | |

Walt Disney Company (The) | | | 12,400 | | | | 1,611,008 | |

| | | | | | | | 13,662,259 | |

Consumer Discretionary — 9.92% | | | | | | | | |

Amazon.com, Inc.(a) | | | 500 | | | | 888,330 | |

AutoZone, Inc.(a) | | | 2,000 | | | | 2,288,760 | |

Best Buy Company, Inc. | | | 35,600 | | | | 2,557,148 | |

D.R. Horton, Inc. | | | 52,000 | | | | 2,723,240 | |

Home Depot, Inc. (The) | | | 10,000 | | | | 2,345,800 | |

Royal Caribbean Cruises Ltd. | | | 21,400 | | | | 2,328,962 | |

| | | | | | | | 13,132,240 | |

Consumer Staples — 7.29% | | | | | | | | |

Ingredion, Inc. | | | 300 | | | | 23,700 | |

Kimberly-Clark Corporation | | | 17,800 | | | | 2,365,264 | |

Mondelez International, Inc., Class A | | | 45,200 | | | | 2,370,740 | |

Sysco Corporation | | | 30,400 | | | | 2,428,048 | |

Walmart, Inc. | | | 21,000 | | | | 2,462,460 | |

| | | | | | | | 9,650,212 | |

Energy — 4.21% | | | | | | | | |

Chevron Corporation | | | 15,000 | | | | 1,742,100 | |

Exxon Mobil Corporation | | | 25,000 | | | | 1,689,250 | |

Marathon Petroleum Corporation | | | 28,000 | | | | 1,790,600 | |

ONEOK, Inc. | | | 5,000 | | | | 349,150 | |

| | | | | | | | 5,571,100 | |

Financials — 12.66% | | | | | | | | |

American Express Company | | | 20,200 | | | | 2,369,056 | |

Bank of America Corporation | | | 75,000 | | | | 2,345,250 | |

Citizens Financial Group, Inc. | | | 68,000 | | | | 2,390,880 | |

JPMorgan Chase & Company | | | 19,400 | | | | 2,423,448 | |

MetLife, Inc. | | | 52,000 | | | | 2,433,080 | |

Morgan Stanley | | | 51,000 | | | | 2,348,550 | |

Starwood Property Trust, Inc. | | | 100,000 | | | | 2,460,000 | |

| | | | | | | | 16,770,264 | |

14 | See accompanying notes which are an integral part of these financial statements. | |

Dana Large Cap Equity Fund

Schedule of Investments (continued)

October 31, 2019

| | Shares | | | Fair Value | |

COMMON STOCKS — 98.52% — (continued) |

Health Care — 13.83% | | | | | | | | |

AbbVie, Inc. | | | 400 | | | $ | 31,820 | |

Amgen, Inc. | | | 12,400 | | | | 2,644,300 | |

Bristol-Myers Squibb Company | | | 46,400 | | | | 2,661,968 | |

Hill-Rom Holdings, Inc. | | | 24,800 | | | | 2,596,312 | |

Merck & Company, Inc. | | | 30,400 | | | | 2,634,464 | |

Stryker Corporation | | | 12,000 | | | | 2,595,240 | |

Thermo Fisher Scientific, Inc. | | | 8,500 | | | | 2,566,830 | |

UnitedHealth Group, Inc. | | | 10,200 | | | | 2,577,540 | |

| | | | | | | | 18,308,474 | |

Industrials — 9.04% | | | | | | | | |

Boeing Company (The) | | | 200 | | | | 67,982 | |

Delta Air Lines, Inc. | | | 44,000 | | | | 2,423,520 | |

Eaton Corporation plc | | | 28,400 | | | | 2,473,924 | |

Norfolk Southern Corporation | | | 12,800 | | | | 2,329,600 | |

Raytheon Company | | | 12,000 | | | | 2,546,520 | |

Waste Management, Inc. | | | 19,000 | | | | 2,131,990 | |

| | | | | | | | 11,973,536 | |

Information Technology — 22.11% | | | | | | | | |

Accenture plc, Class A | | | 12,300 | | | | 2,280,666 | |

Adobe, Inc.(a) | | | 2,800 | | | | 778,204 | |

Apple, Inc. | | | 12,600 | | | | 3,134,376 | |

CDW Corporation | | | 21,000 | | | | 2,686,110 | |

Cisco Systems, Inc. | | | 45,000 | | | | 2,137,950 | |

Fidelity National Information Services, Inc. | | | 19,000 | | | | 2,503,440 | |

Intel Corporation | | | 48,000 | | | | 2,713,440 | |

Lam Research Corporation | | | 10,000 | | | | 2,710,400 | |

Mastercard, Inc., Class A | | | 8,700 | | | | 2,408,247 | |

Microsoft Corporation | | | 19,600 | | | | 2,810,052 | |

Visa, Inc., Class A | | | 14,000 | | | | 2,504,040 | |

Zebra Technologies Corporation, Class A(a) | | | 11,000 | | | | 2,616,570 | |

| | | | | | | | 29,283,495 | |

Materials — 2.57% | | | | | | | | |

Albemarle Corporation | | | 300 | | | | 18,222 | |

Avery Dennison Corporation | | | 13,000 | | | | 1,662,180 | |

Packaging Corporation of America | | | 15,800 | | | | 1,729,468 | |

| | | | | | | | 3,409,870 | |

| | See accompanying notes which are an integral part of these financial statements. | 15 |

Dana Large Cap Equity Fund

Schedule of Investments (continued)

October 31, 2019

| | Shares | | | Fair Value | |

COMMON STOCKS — 98.52% — (continued) |

Real Estate — 3.16% | | | | | | | | |

American Tower Corporation, Class A | | | 8,000 | | | $ | 1,744,640 | |

Prologis, Inc. | | | 20,000 | | | | 1,755,200 | |

STORE Capital Corporation | | | 17,000 | | | | 688,500 | |

| | | | | | | | 4,188,340 | |

Utilities — 3.41% | | | | | | | | |

CenterPoint Energy, Inc. | | | 75,000 | | | | 2,180,250 | |

NextEra Energy, Inc. | | | 9,800 | | | | 2,335,732 | |

| | | | | | | | 4,515,982 | |

Total Common Stocks (Cost $109,746,340) | | | | | | | 130,465,772 | |

| | | | | | | | | |

MONEY MARKET FUNDS — 1.84% | | | | | | | | |

| | | | | | | | | |

Federated Government Obligations Fund, Institutional Class, 1.71%(b) | | | 2,437,400 | | | | 2,437,400 | |

Total Money Market Funds (Cost $2,437,400) | | | | | | | 2,437,400 | |

| | | | | | | | | |

Total Investments — 100.36% (Cost $112,183,740) | | | | | | | 132,903,172 | |

| | | | | | | | | |

Liabilities in Excess of Other Assets — (0.36)% | | | | | | | (479,253 | ) |

| | | | | | | | | |

NET ASSETS — 100.00% | | | | | | $ | 132,423,919 | |

(a) | Non-income producing security. |

(b) | Rate disclosed is the seven day effective yield as of October 31, 2019. |

16 | See accompanying notes which are an integral part of these financial statements. | |

Dana Small Cap Equity Fund

Schedule of Investments

October 31, 2019

| | Shares | | | Fair Value | |

COMMON STOCKS — 98.07% | | | | | | | | |

Communication Services — 2.40% | | | | | | | | |

Marcus Corporation (The) | | | 5,236 | | | $ | 189,019 | |

QuinStreet, Inc.(a) | | | 12,631 | | | | 162,056 | |

| | | | | | | | 351,075 | |

Consumer Discretionary — 10.73% | | | | | | | | |

Boot Barn Holdings, Inc.(a) | | | 6,098 | | | | 213,735 | |

Boyd Gaming Corporation | | | 9,634 | | | | 262,527 | |

Chegg, Inc.(a) | | | 5,639 | | | | 172,892 | |

Fox Factory Holding Corporation(a) | | | 2,916 | | | | 177,701 | |

Marriott Vacations Worldwide Corporation | | | 2,510 | | | | 275,923 | |

Ruth’s Hospitality Group, Inc. | | | 10,375 | | | | 213,518 | |

YETI Holdings, Inc.(a) | | | 7,551 | | | | 251,524 | |

| | | | | | | | 1,567,820 | |

Consumer Staples — 2.79% | | | | | | | | |

Chefs’ Warehouse, Inc. (The)(a) | | | 5,462 | | | | 180,929 | |

Performance Food Group Company(a) | | | 5,326 | | | | 226,941 | |

| | | | | | | | 407,870 | |

Energy — 3.12% | | | | | | | | |

Delek US Holdings, Inc. | | | 4,161 | | | | 166,232 | |

Matador Resources Company(a) | | | 10,576 | | | | 147,112 | |

ProPetro Holding Corporation(a) | | | 18,372 | | | | 142,383 | |

| | | | | | | | 455,727 | |

Financials — 18.08% | | | | | | | | |

Argo Group International Holdings Ltd. | | | 3,730 | | | | 230,775 | |

Banner Corporation | | | 5,319 | | | | 287,120 | |

Blackstone Mortgage Trust, Inc., Class A | | | 7,927 | | | | 287,750 | |

CenterState Banks Corporation | | | 10,074 | | | | 255,477 | |

First Bancorp | | | 7,279 | | | | 274,782 | |

Independent Bank Corporation | | | 3,410 | | | | 279,893 | |

Primerica, Inc. | | | 2,306 | | | | 290,971 | |

United Community Banks, Inc. | | | 8,101 | | | | 244,731 | |

Western Alliance Bancorporation | | | 5,071 | | | | 250,152 | |

Wintrust Financial Corporation | | | 3,761 | | | | 240,027 | |

| | | | | | | | 2,641,678 | |

Health Care — 16.08% | | | | | | | | |

ANI Pharmaceuticals, Inc.(a) | | | 3,212 | | | | 250,889 | |

BioTelemetry, Inc.(a) | | | 5,278 | | | | 207,742 | |

Coherus BioSciences, Inc.(a) | | | 10,564 | | | | 183,497 | |

CONMED Corporation | | | 2,383 | | | | 262,178 | |

| | See accompanying notes which are an integral part of these financial statements. | 17 |

Dana Small Cap Equity Fund

Schedule of Investments (continued)

October 31, 2019

| | Shares | | | Fair Value | |

COMMON STOCKS — 98.07% — (continued) |

Health Care — (continued) | | | | | | | | |

Emergent BioSolutions, Inc.(a) | | | 4,198 | | | $ | 239,958 | |

HMS Holdings Corporation(a) | | | 7,689 | | | | 251,354 | |

Horizon Therapeutics plc(a) | | | 8,127 | | | | 234,952 | |

Ligand Pharmaceuticals, Inc., Class B(a) | | | 2,283 | | | | 248,413 | |

Repligen Corporation(a) | | | 3,454 | | | | 274,557 | |

Tabula Rasa HealthCare, Inc.(a) | | | 3,864 | | | | 196,832 | |

| | | | | | | | 2,350,372 | |

Industrials — 16.00% | | | | | | | | |

Albany International Corporation, Class A | | | 3,100 | | | | 260,338 | |

ASGN, Inc.(a) | | | 3,655 | | | | 232,421 | |

Comfort Systems USA, Inc. | | | 4,467 | | | | 225,181 | |

Cubic Corporation | | | 3,419 | | | | 252,117 | |

Curtiss-Wright Corporation | | | 1,806 | | | | 244,262 | |

Harsco Corporation(a) | | | 12,521 | | | | 253,801 | |

MasTec, Inc.(a) | | | 3,601 | | | | 226,647 | |

Moog, Inc., Class A | | | 2,668 | | | | 223,338 | |

SkyWest, Inc. | | | 4,124 | | | | 245,584 | |

TriNet Group, Inc.(a) | | | 3,316 | | | | 175,715 | |

| | | | | | | | 2,339,404 | |

Information Technology — 12.96% | | | | | | | | |

Cabot Microelectronics Corporation | | | 1,670 | | | | 252,370 | |

Five9, Inc.(a) | | | 4,701 | | | | 260,953 | |

Onto Innovation, Inc.(a) | | | 6,870 | | | | 221,223 | |

Perficient, Inc.(a) | | | 6,853 | | | | 268,638 | |

Rapid7, Inc.(a) | | | 3,994 | | | | 200,059 | |

RealPage, Inc.(a) | | | 4,395 | | | | 266,118 | |

SYNNEX Corporation | | | 1,972 | | | | 232,183 | |

Upland Software, Inc.(a) | | | 5,161 | | | | 193,434 | |

| | | | | | | | 1,894,978 | |

Materials — 3.91% | | | | | | | | |

Ingevity Corporation(a) | | | 1,942 | | | | 163,536 | |

PolyOne Corporation | | | 6,504 | | | | 208,453 | |

W.R. Grace & Company | | | 3,004 | | | | 199,616 | |

| | | | | | | | 571,605 | |

Real Estate — 8.08% | | | | | | | | |

CoreSite Realty Corporation | | | 2,554 | | | | 300,095 | |

EastGroup Properties, Inc. | | | 2,192 | | | | 293,618 | |

OUTFRONT Media, Inc. | | | 10,463 | | | | 275,282 | |

18 | See accompanying notes which are an integral part of these financial statements. | |

Dana Small Cap Equity Fund

Schedule of Investments (continued)

October 31, 2019

| | Shares | | | Fair Value | |

COMMON STOCKS — 98.07% — (continued) |

Real Estate — (continued) | | | | | | | | |

STAG Industrial, Inc. | | | 10,048 | | | $ | 311,890 | |

| | | | | | | | 1,180,885 | |

Utilities — 3.92% | | | | | | | | |

Chesapeake Utilities Corporation | | | 2,990 | | | | 283,452 | |

Southwest Gas Holdings, Inc. | | | 3,325 | | | | 290,273 | |

| | | | | | | | 573,725 | |

Total Common Stocks (Cost $13,067,906) | | | | | | | 14,335,139 | |

| | | | | | | | | |

MONEY MARKET FUNDS — 1.55% | | | | | | | | |

| | | | | | | | | |

Federated Government Obligations Fund, Institutional Class, 1.71%(b) | | | 227,053 | | | | 227,053 | |

Total Money Market Funds (Cost $227,053) | | | | | | | 227,053 | |

| | | | | | | | | |

Total Investments — 99.62% (Cost $13,294,959) | | | | | | | 14,562,192 | |

| | | | | | | | | |

Other Assets in Excess of Liabilities — 0.38% | | | | | | | 55,551 | |

| | | | | | | | | |

NET ASSETS — 100.00% | | | | | | $ | 14,617,743 | |

(a) | Non-income producing security. |

(b) | Rate disclosed is the seven day effective yield as of October 31, 2019. |

| | See accompanying notes which are an integral part of these financial statements. | 19 |

Dana Epiphany ESG Equity Fund

Schedule of Investments

October 31, 2019

| | Shares | | | Fair Value | |

COMMON STOCKS — 99.01% | | | | | | | | |

Communication Services — 10.34% | | | | | | | | |

Alphabet, Inc., Class C(a) | | | 250 | | | $ | 315,028 | |

AT&T, Inc. | | | 3,800 | | | | 146,262 | |

Comcast Corporation, Class A | | | 5,500 | | | | 246,510 | |

Facebook, Inc., Class A(a) | | | 740 | | | | 141,821 | |

T-Mobile US, Inc.(a) | | | 1,200 | | | | 99,192 | |

Verizon Communications, Inc. | | | 2,160 | | | | 130,615 | |

Walt Disney Company (The) | | | 1,900 | | | | 246,848 | |

| | | | | | | | 1,326,276 | |

Consumer Discretionary — 9.97% | | | | | | | | |

Amazon.com, Inc.(a) | | | 180 | | | | 319,799 | |

Best Buy Company, Inc. | | | 3,300 | | | | 237,039 | |

D.R. Horton, Inc. | | | 4,500 | | | | 235,665 | |

Home Depot, Inc. (The) | | | 1,100 | | | | 258,037 | |

Royal Caribbean Cruises Ltd. | | | 350 | | | | 38,091 | |

Tractor Supply Company | | | 2,000 | | | | 190,040 | |

| | | | | | | | 1,278,671 | |

Consumer Staples — 7.33% | | | | | | | | |

General Mills, Inc. | | | 4,200 | | | | 213,612 | |

Kimberly-Clark Corporation | | | 1,600 | | | | 212,608 | |

PepsiCo, Inc. | | | 2,000 | | | | 274,340 | |

Sysco Corporation | | | 3,000 | | | | 239,610 | |

| | | | | | | | 940,170 | |

Energy — 4.22% | | | | | | | | |

ConocoPhillips | | | 3,300 | | | | 182,160 | |

Marathon Petroleum Corporation | | | 3,000 | | | | 191,850 | |

Schlumberger Ltd. | | | 5,100 | | | | 166,719 | |

| | | | | | | | 540,729 | |

Financials — 12.68% | | | | | | | | |

American Express Company | | | 2,100 | | | | 246,288 | |

Bank of America Corporation | | | 5,000 | | | | 156,350 | |

BB&T Corporation | | | 4,000 | | | | 212,200 | |

JPMorgan Chase & Company | | | 1,400 | | | | 174,888 | |

MetLife, Inc. | | | 4,800 | | | | 224,592 | |

Morgan Stanley | | | 5,000 | | | | 230,250 | |

Starwood Property Trust, Inc. | | | 9,000 | | | | 221,400 | |

Wintrust Financial Corporation | | | 2,500 | | | | 159,550 | |

| | | | | | | | 1,625,518 | |

20 | See accompanying notes which are an integral part of these financial statements. | |

Dana Epiphany ESG Equity Fund

Schedule of Investments (continued)

October 31, 2019

| | Shares | | | Fair Value | |

COMMON STOCKS — 99.01% — (continued) |

Health Care — 13.97% | | | | | | | | |

Becton, Dickinson and Company | | | 920 | | | $ | 235,520 | |

Bristol-Myers Squibb Company | | | 4,500 | | | | 258,165 | |

CVS Health Corporation | | | 2,000 | | | | 132,780 | |

Emergent BioSolutions, Inc.(a) | | | 3,500 | | | | 200,060 | |

Encompass Health Corporation | | | 3,200 | | | | 204,864 | |

Hill-Rom Holdings, Inc. | | | 2,100 | | | | 219,849 | |

Medtronic plc | | | 1,820 | | | | 198,198 | |

Stryker Corporation | | | 1,100 | | | | 237,897 | |

Zoetis, Inc. | | | 800 | | | | 102,336 | |

| | | | | | | | 1,789,669 | |

Industrials — 8.68% | | | | | | | | |

Allison Transmission Holdings, Inc. | | | 5,000 | | | | 218,050 | |

Delta Air Lines, Inc. | | | 4,200 | | | | 231,336 | |

Insperity, Inc. | | | 2,200 | | | | 232,386 | |

Norfolk Southern Corporation | | | 1,200 | | | | 218,400 | |

Waste Management, Inc. | | | 1,900 | | | | 213,199 | |

| | | | | | | | 1,113,371 | |

Information Technology — 22.29% | | | | | | | | |

Accenture plc, Class A | | | 1,300 | | | | 241,046 | |

ANSYS, Inc.(a) | | | 400 | | | | 88,060 | |

Apple, Inc. | | | 1,300 | | | | 323,388 | |

Automatic Data Processing, Inc. | | | 1,400 | | | | 227,122 | |

CDW Corporation | | | 1,800 | | | | 230,238 | |

Cisco Systems, Inc. | | | 5,000 | | | | 237,550 | |

Fidelity National Information Services, Inc. | | | 1,600 | | | | 210,816 | |

Intel Corporation | | | 4,500 | | | | 254,385 | |

Lam Research Corporation | | | 940 | | | | 254,778 | |

Mastercard, Inc., Class A | | | 860 | | | | 238,057 | |

Microsoft Corporation | | | 2,100 | | | | 301,077 | |

Visa, Inc., Class A | | | 1,400 | | | | 250,404 | |

| | | | | | | | 2,856,921 | |

Materials — 2.69% | | | | | | | | |

Air Products & Chemicals, Inc. | | | 780 | | | | 166,343 | |

Avery Dennison Corporation | | | 1,400 | | | | 179,004 | |

| | | | | | | | 345,347 | |

| | See accompanying notes which are an integral part of these financial statements. | 21 |

Dana Epiphany ESG Equity Fund

Schedule of Investments (continued)

October 31, 2019

| | Shares | | | Fair Value | |

COMMON STOCKS — 99.01% — (continued) |

Real Estate — 3.28% | | | | | | | | |

American Tower Corporation, Class A | | | 480 | | | $ | 104,678 | |

Hannon Armstrong Sustainable Infrastructure Capital, Inc. | | | 6,900 | | | | 206,034 | |

STORE Capital Corporation | | | 2,700 | | | | 109,350 | |

| | | | | | | | 420,062 | |

Utilities — 3.56% | | | | | | | | |

Entergy Corporation | | | 1,800 | | | | 218,664 | |

NextEra Energy, Inc. | | | 1,000 | | | | 238,340 | |

| | | | | | | | 457,004 | |

Total Common Stocks (Cost $10,565,546) | | | | | | | 12,693,738 | |

| | | | | | | | | |

MONEY MARKET FUNDS — 0.57% | | | | | | | | |

| | | | | | | | | |

Fidelity Investments Money Market Government Portfolio, Institutional Class, 1.76%(b) | | | 72,696 | | | | 72,696 | |

Total Money Market Funds (Cost $72,696) | | | | | | | 72,696 | |

| | | | | | | | | |

Total Investments — 99.58% (Cost $10,638,242) | | | | | | | 12,766,434 | |

| | | | | | | | | |

Other Assets in Excess of Liabilities — 0.42% | | | | | | | 54,198 | |

| | | | | | | | | |

NET ASSETS — 100.00% | | | | | | $ | 12,820,632 | |

(a) | Non-income producing security. |

(b) | Rate disclosed is the seven day effective yield as of October 31, 2019. |

The sectors shown on the schedules of investments are based on the Global Industry Classification Standard, or GICS® (“GICS”). The GICS was developed by and/or is the exclusive property of MSCI, Inc. and Standard & Poor’s Financial Services LLC (“S&P”). GICS is a service mark of MSCI, Inc. and S&P and has been licensed for use by Ultimus Fund Solutions, LLC.

22 | See accompanying notes which are an integral part of these financial statements. | |

Dana Funds

Statements of Assets and Liabilities

October 31, 2019

| | | Dana Large Cap

Equity Fund | | | Dana Small Cap

Equity Fund | | | Dana Epiphany

ESG Equity Fund | |

Assets | | | | | | | | |

Investments in securities at fair value (cost $112,183,740, $13,294,959 and $10,638,242) (Note 3) | | $ | 132,903,172 | | | $ | 14,562,192 | | | $ | 12,766,434 | |

Cash | | | 17,460 | | | | — | | | | 1,170 | |

Receivable for fund shares sold | | | 387,942 | | | | 48,000 | | | | 16 | |

Receivable for investments sold | | | 366,174 | | | | — | | | | 58,466 | |

Dividends receivable | | | 162,573 | | | | 1,313 | | | | 16,480 | |

Receivable from Adviser (Note 4) | | | — | | | | 8,636 | | | | 5,632 | |

Prepaid expenses | | | 31,121 | | | | 28,930 | | | | 18,561 | |

Total Assets | | | 133,868,442 | | | | 14,649,071 | | | | 12,866,759 | |

Liabilities | | | | | | | | |

Payable for fund shares redeemed | | | 175,899 | | | | — | | | | — | |

Payable for investments purchased | | | 1,186,638 | | | | — | | | | — | |

Payable to Adviser (Note 4) | | | 41,926 | | | | — | | | | — | |

Accrued Distribution (12b-1) fees (Note 4) | | | 5,279 | | | | 463 | | | | 1,623 | |

Payable to Administrator (Note 4) | | | 11,796 | | | | 8,866 | | | | 12,142 | |

Payable to trustees | | | 270 | | | | 315 | | | | 1,479 | |

Other accrued expenses | | | 22,715 | | | | 21,684 | | | | 30,883 | |

Total Liabilities | | | 1,444,523 | | | | 31,328 | | | | 46,127 | |

Net Assets | | $ | 132,423,919 | | | $ | 14,617,743 | | | $ | 12,820,632 | |

Net Assets consist of: | | | | | | | | | | | | |

Paid-in capital | | | 98,571,665 | | | | 13,495,943 | | | | 8,744,692 | |

Accumulated earnings | | | 33,852,254 | | | | 1,121,800 | | | | 4,075,940 | |

Net Assets | | $ | 132,423,919 | | | $ | 14,617,743 | | | $ | 12,820,632 | |

Institutional Class: | | | | | | | | | | | | |

Net Assets | | $ | 107,025,945 | | | $ | 12,421,202 | | | $ | 5,079,055 | |

Shares outstanding (unlimited number of shares authorized, no par value) | | | 4,716,222 | | | | 1,213,349 | | | | 438,722 | |

Net asset value, offering and redemption price per share (Note 2) | | $ | 22.69 | | | $ | 10.24 | | | $ | 11.58 | |

Investor Class: | | | | | | | | | | | | |

Net Assets | | $ | 25,397,974 | | | $ | 2,196,541 | | | $ | 7,741,577 | |

Shares outstanding (unlimited number of shares authorized, no par value) | | | 1,119,308 | | | | 216,719 | | | | 650,035 | |

Net asset value, offering and redemption price per share (Note 2) | | $ | 22.69 | | | $ | 10.14 | | | $ | 11.91 | |

| | See accompanying notes which are an integral part of these financial statements. | 23 |

Dana Funds

Statements of Operations

For the year ended October 31, 2019

| | | Dana Large Cap

Equity Fund | | | Dana Small Cap

Equity Fund | | | Dana Epiphany

ESG Equity Fund | |

Investment Income | | | | | | | | | | | | |

Dividend income | | $ | 3,533,851 | | | $ | 176,426 | | | $ | 272,111 | |

Total investment income | | | 3,533,851 | | | | 176,426 | | | | 272,111 | |

Expenses | | | | | | | | | | | | |

Investment Adviser fees (Note 4) | | | 953,872 | | | | 124,427 | | | | 85,603 | |

Administration fees (Note 4) | | | 76,228 | | | | 36,000 | | | | 28,295 | |

Distribution (12b-1) fees, Investor Class (Note 4) | | | 64,353 | | | | 6,721 | | | | 19,420 | |

Fund accounting fees (Note 4) | | | 42,749 | | | | 28,000 | | | | 20,774 | |

Registration expenses | | | 39,201 | | | | 34,561 | | | | 34,473 | |

Transfer agent fees (Note 4) | | | 20,392 | | | | 20,700 | | | | 21,824 | |

Custodian fees | | | 20,387 | | | | 4,047 | | | | 5,215 | |

Legal fees | | | 19,923 | | | | 20,351 | | | | 31,392 | |

Audit and tax preparation fees | | | 17,000 | | | | 17,000 | | | | 20,000 | |

Insurance expenses | | | 12,087 | | | | 2,834 | | | | 1,217 | |

Printing and postage expenses | | | 9,155 | | | | 3,233 | | | | 4,726 | |

Trustee fees | | | 6,549 | | | | 5,345 | | | | 8,751 | |

Interest | | | 62 | | | | 307 | | | | 4 | |

Miscellaneous expenses | | | 22,741 | | | | 14,534 | | | | 16,146 | |

Total expenses | | | 1,304,699 | | | | 318,060 | | | | 297,840 | |

Fees contractually waived and expenses reimbursed by Adviser (Note 4) | | | (169,051 | ) | | | (153,464 | ) | | | (159,882 | ) |

Net operating expenses | | | 1,135,648 | | | | 164,596 | | | | 137,958 | |

Net investment income | | | 2,398,203 | | | | 11,830 | | | | 134,153 | |

Net Realized and Change in Unrealized Gain (Loss) on Investments |

Net realized gain (loss) on investment securities transactions | | | 12,973,907 | | | | (111,430 | ) | | | 1,947,772 | |

Net change in unrealized appreciation (depreciation) on investment securities | | | 2,070,388 | | | | 73,430 | | | | (578,233 | ) |

Net realized and change in unrealized gain (loss) on investments | | | 15,044,295 | | | | (38,000 | ) | | | 1,369,539 | |

Net increase (decrease) in net assets resulting from operations | | $ | 17,442,498 | | | $ | (26,170 | ) | | $ | 1,503,692 | |

24 | See accompanying notes which are an integral part of these financial statements. | |

Dana Funds

Statements of Changes in Net Assets

| | | Dana Large Cap Equity Fund | | | Dana Small Cap Equity Fund | |

| | | For the

Year Ended

October 31, 2019 | | | For the

Year Ended

October 31, 2018 | | | For the

Year Ended

October 31, 2019 | | | For the

Year Ended

October 31, 2018 | |

Increase (Decrease) in Net Assets due to: | | | | | | | | | | | | |

Operations | | | | | | | | | | | | |

Net investment income (loss) | | $ | 2,398,203 | | | $ | 2,899,378 | | | $ | 11,830 | | | $ | (61,414 | ) |

Net realized gain (loss) on investment securities transactions | | | 12,973,907 | | | | 16,014,437 | | | | (111,430 | ) | | | 1,549,728 | |

Net change in unrealized appreciation (depreciation) of investment securities | | | 2,070,388 | | | | (13,223,401 | ) | | | 73,430 | | | | (2,109,601 | ) |

Net increase (decrease) in net assets resulting from operations | | | 17,442,498 | | | | 5,690,414 | | | | (26,170 | ) | | | (621,287 | ) |

Distributions to Shareholders from Earnings (Note 2) | | | | | | | | |

Institutional Class | | | (15,403,587 | ) | | | (7,459,066 | ) | | | (1,098,363 | ) | | | (4,138 | ) |

Investor Class | | | (3,132,699 | ) | | | (1,701,334 | ) | | | (245,803 | ) | | | — | |

Total distributions | | | (18,536,286 | ) | | | (9,160,400 | ) | | | (1,344,166 | ) | | | (4,138 | ) |

Capital Transactions – Institutional Class | | | | | | | | |

Proceeds from shares sold | | | 48,852,531 | | | | 111,001,907 | | | | 1,528,842 | | | | 5,280,124 | |

Reinvestment of distributions | | | 11,841,958 | | | | 5,913,368 | | | | 1,065,846 | | | | 3,493 | |

Amount paid for shares redeemed | | | (129,198,946 | ) | | | (70,457,043 | ) | | | (5,237,003 | ) | | | (2,548,354 | ) |

Total – Institutional Class | | | (68,504,457 | ) | | | 46,458,232 | | | | (2,642,315 | ) | | | 2,735,263 | |

Capital Transactions – Investor Class | | | | | | | | | | | | |

Proceeds from shares sold | | | 604,696 | | | | 1,935,954 | | | | 152,674 | | | | 320,769 | |

Reinvestment of distributions | | | 3,128,798 | | | | 1,700,677 | | | | 245,803 | | | | — | |

Amount paid for shares redeemed | | | (7,535,002 | ) | | | (16,049,342 | ) | | | (1,436,942 | ) | | | (3,548,803 | ) |

Total – Investor Class | | | (3,801,508 | ) | | | (12,412,711 | ) | | | (1,038,465 | ) | | | (3,228,034 | ) |

Net increase (decrease) in net assets resulting from capital transactions | | | (72,305,965 | ) | | | 34,045,521 | | | | (3,680,780 | ) | | | (492,771 | ) |

Total Increase (Decrease) in Net Assets | | | (73,399,753 | ) | | | 30,575,535 | | | | (5,051,116 | ) | | | (1,118,196 | ) |

Net Assets | | | | | | | | | | | | | | | | |

Beginning of year | | | 205,823,672 | | | | 175,248,137 | | | | 19,668,859 | | | | 20,787,055 | |

End of year | | $ | 132,423,919 | | | $ | 205,823,672 | | | $ | 14,617,743 | | | $ | 19,668,859 | |

| | See accompanying notes which are an integral part of these financial statements. | 25 |

Dana Funds

Statements of Changes in Net Assets (continued)

| | | Dana Large Cap Equity Fund | | | Dana Small Cap Equity Fund | |

| | | For the

Year Ended

October 31, 2019 | | | For the

Year Ended

October 31, 2018 | | | For the

Year Ended

October 31, 2019 | | | For the

Year Ended

October 31, 2018 | |

Share Transactions – Institutional Class | | | | | | | | | | | | |

Shares sold | | | 2,457,771 | | | | 4,762,130 | | | | 155,114 | | | | 451,665 | |

Shares issued in reinvestment of distributions | | | 651,067 | | | | 256,328 | | | | 121,257 | | | | 298 | |

Shares redeemed | | | (6,308,605 | ) | | | (3,032,827 | ) | | | (523,215 | ) | | | (217,413 | ) |

Total – Institutional Class | | | (3,199,767 | ) | | | 1,985,631 | | | | (246,844 | ) | | | 234,550 | |

Share Transactions – Investor Class | | | | | | | | | | | | |

Shares sold | | | 28,606 | | | | 83,654 | | | | 15,249 | | | | 27,535 | |

Shares issued in reinvestment of distributions | | | 171,527 | | | | 73,934 | | | | 28,188 | | | | — | |

Shares redeemed | | | (372,375 | ) | | | (674,880 | ) | | | (141,956 | ) | | | (307,754 | ) |

Total – Investor Class | | | (172,242 | ) | | | (517,292 | ) | | | (98,519 | ) | | | (280,219 | ) |

26 | See accompanying notes which are an integral part of these financial statements. | |

Dana Funds

Statements of Changes in Net Assets (continued)

| | | Dana Epiphany ESG Equity Fund | |

| | | For the

Year Ended

October 31, 2019 | | | For the

Year Ended

October 31, 2018 | |

Increase (Decrease) in Net Assets due to: | | | | | | | | |

Operations | | | | | | | | |

Net investment income | | $ | 134,153 | | | $ | 88,672 | |

Net realized gain on investment securities transactions | | | 1,947,772 | | | | 1,642,707 | |

Net change in unrealized appreciation (depreciation) of investment securities | | | (578,233 | ) | | | (375,549 | ) |

Net increase in net assets resulting from operations | | | 1,503,692 | | | | 1,355,830 | |

Distributions to Shareholders from Earnings (Note 2) | | | | | | | | |

Institutional Class | | | (746,819 | ) | | | (1,192,255 | ) |

Investor Class | | | (1,014,147 | ) | | | (1,895,929 | ) |

Total distributions | | | (1,760,966 | ) | | | (3,088,184 | ) |

Capital Transactions – Institutional Class | | | | | | | | |

Proceeds from shares sold | | | 282,765 | | | | 790,410 | |

Reinvestment of distributions | | | 734,812 | | | | 1,191,071 | |

Amount paid for shares redeemed | | | (2,277,604 | ) | | | (2,245,859 | ) |

Total – Institutional Class | | | (1,260,027 | ) | | | (264,378 | ) |

Capital Transactions – Investor Class | | | | | | | | |

Proceeds from shares sold | | | 394,428 | | | | 594,407 | |

Reinvestment of distributions | | | 993,640 | | | | 1,843,847 | |

Amount paid for shares redeemed | | | (2,571,196 | ) | | | (5,958,253 | ) |

Total – Investor Class | | | (1,183,128 | ) | | | (3,519,999 | ) |

Net decrease in net assets resulting from capital transactions | | | (2,443,155 | ) | | | (3,784,377 | ) |

Total Decrease in Net Assets | | | (2,700,429 | ) | | | (5,516,731 | ) |

Net Assets | | | | | | | | |

Beginning of year | | | 15,521,061 | | | | 21,037,792 | |

End of year | | $ | 12,820,632 | | | $ | 15,521,061 | |

| | See accompanying notes which are an integral part of these financial statements. | 27 |

Dana Funds

Statements of Changes in Net Assets (continued)

| | | Dana Epiphany ESG Equity Fund | |

| | | For the

Year Ended

October 31, 2019 | | | For the

Year Ended

October 31, 2018 | |

Share Transactions – Institutional Class | | | | |

Shares sold | | | 25,958 | | | | 64,220 | |

Shares issued in reinvestment of distributions | | | 72,259 | | | | 100,783 | |

Shares redeemed | | | (208,847 | ) | | | (183,044 | ) |

Total – Institutional Class | | | (110,630 | ) | | | (18,041 | ) |

Share Transactions – Investor Class | | | | |

Shares sold | | | 34,862 | | | | 47,246 | |

Shares issued in reinvestment of distributions | | | 95,050 | | | | 152,260 | |

Shares redeemed | | | (226,525 | ) | | | (470,149 | ) |

Total – Investor Class | | | (96,613 | ) | | | (270,643 | ) |

28 | See accompanying notes which are an integral part of these financial statements. | |

Dana Large Cap Equity Fund – Institutional Class

Financial Highlights

(For a share outstanding during each year)

| | | Years Ended October 31, | |

| | | 2019 | | | 2018 | | | 2017 | | | 2016 | | | 2015 | |

Selected Per Share Data: | | | | | | | | | | | | | | | | | | | | |

Net asset value, beginning of year | | $ | 22.35 | | | $ | 22.64 | | | $ | 17.67 | | | $ | 18.22 | | | $ | 18.52 | |

| | | | | | | | | | | | | | | | | | | | | |

Investment operations: | | | | | | | | | | | | | | | | | | | | |

Net investment income | | | 0.38 | | | | 0.32 | | | | 0.32 | | | | 0.26 | (a) | | | 0.19 | |

Net realized and unrealized gain (loss) on investments | | | 2.46 | | | | 0.45 | | | | 4.96 | | | | (0.56 | ) | | | 0.52 | (b) |

Total from investment operations | | | 2.84 | | | | 0.77 | | | | 5.28 | | | | (0.30 | ) | | | 0.71 | |

| | | | | | | | | | | | | | | | | | | | | |

Less distributions to shareholders from: | | | | | | | | | | | | | | | | | | | | |

Net investment income | | | (0.36 | ) | | | (0.32 | ) | | | (0.31 | ) | | | (0.25 | ) | | | (0.19 | ) |

Net realized gains | | | (2.14 | ) | | | (0.74 | ) | | | — | | | | — | | | | (0.83 | ) |

Total distributions | | | (2.50 | ) | | | (1.06 | ) | | | (0.31 | ) | | | (0.25 | ) | | | (1.02 | ) |

| | | | | | | | | | | | | | | | | | | | | |

Redemption fees | | | — | | | | — | | | | — | (c) | | | — | (c) | | | 0.01 | |

| | | | | | | | | | | | | | | | | | | | | |

Net asset value, end of year | | $ | 22.69 | | | $ | 22.35 | | | $ | 22.64 | | | $ | 17.67 | | | $ | 18.22 | |

| | | | | | | | | | | | | | | | | | | | | |

Total Return(d) | | | 15.55 | % | | | 3.27 | % | | | 30.11 | % | | | (1.66 | )% | | | 3.89 | % |

| | | | | | | | | | | | | | | | | | | | | |

Ratios and Supplemental Data: | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

Net assets, end of year (000 omitted) | | $ | 107,026 | | | $ | 176,954 | | | $ | 134,291 | | | $ | 138,540 | | | $ | 117,663 | |

Before waiver | | | | | | | | | | | | | | | | | | | | |

Ratio of expenses to average net assets | | | 0.85 | % | | | 0.86 | % | | | 0.92 | % | | | 0.91 | % | | | 1.00 | % |

After waiver | | | | | | | | | | | | | | | | | | | | |

Ratio of expenses to average net assets | | | 0.73 | % | | | 0.73 | % | | | 0.74 | %(e) | | | 0.73 | % | | | 0.73 | % |

Ratio of net investment income to average net assets | | | 1.68 | % | | | 1.41 | % | | | 1.48 | % | | | 1.45 | % | | | 1.25 | % |

Portfolio turnover rate(f) | | | 50 | % | | | 58 | % | | | 50 | % | | | 69 | % | | | 45 | % |

| | | | | | | | | | | | | | | | | | | | | |

(a) | Per share net investment income has been determined on the basis of average shares outstanding during the year. |

(b) | The amount shown for a share outstanding throughout the period does not accord with the change in aggregate gains and losses in the portfolio of securities during the period because of the timing of sales and purchases of fund shares in relation to fluctuating market values during the period. |

(c) | Rounds to less than $0.005 per share. |

(d) | Total return in the above table represents the rate that the investor would have earned or lost on an investment in the Fund, assuming reinvestment of distributions. |

(e) | This ratio includes the impact of overdraft fees. If this cost had been excluded, the ratio of expenses to average net assets would have been 0.73% for the fiscal year ended October 31, 2017. |

(f) | Portfolio turnover is calculated on the basis of the Fund as a whole without distinguishing among the classes of shares. |

| | See accompanying notes which are an integral part of these financial statements. | 29 |

Dana Large Cap Equity Fund – Investor Class

Financial Highlights

(For a share outstanding during each year)

| | | Years Ended October 31, | |

| | | 2019 | | | 2018 | | | 2017 | | | 2016 | | | 2015 | |

Selected Per Share Data: | | | | | | | | | | | | | | | | | | | | |

Net asset value, beginning of year | | $ | 22.35 | | | $ | 22.64 | | | $ | 17.68 | | | $ | 18.23 | | | $ | 18.54 | |

| | | | | | | | | | | | | | | | | | | | | |

Investment operations: | | | | | | | | | | | | | | | | | | | | |

Net investment income | | | 0.30 | | | | 0.28 | | | | 0.24 | | | | 0.22 | (a) | | | 0.18 | |

Net realized and unrealized gain (loss) on investments | | | 2.50 | | | | 0.43 | | | | 4.98 | | | | (0.57 | ) | | | 0.49 | (b) |

Total from investment operations | | | 2.80 | | | | 0.71 | | | | 5.22 | | | | (0.35 | ) | | | 0.67 | |

| | | | | | | | | | | | | | | | | | | | | |

Less distributions to shareholders from: | | | | | | | | | | | | | | | | | | | | |

Net investment income | | | (0.32 | ) | | | (0.26 | ) | | | (0.26 | ) | | | (0.20 | ) | | | (0.15 | ) |

Net realized gains | | | (2.14 | ) | | | (0.74 | ) | | | — | | | | — | | | | (0.83 | ) |

Total distributions | | | (2.46 | ) | | | (1.00 | ) | | | (0.26 | ) | | | (0.20 | ) | | | (0.98 | ) |

| | | | | | | | | | | | | | | | | | | | | |

Redemption fees | | | — | | | | — | | | | — | | | | — | (c) | | | — | (c) |

| | | | | | | | | | | | | | | | | | | | | |

Net asset value, end of year | | $ | 22.69 | | | $ | 22.35 | | | $ | 22.64 | | | $ | 17.68 | | | $ | 18.23 | |

| | | | | | | | | | | | | | | | | | | | | |

Total Return(d) | | | 15.29 | % | | | 3.01 | % | | | 29.72 | % | | | (1.91 | )% | | | 3.61 | % |

| | | | | | | | | | | | | | | | | | | | | |

Ratios and Supplemental Data: | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

Net assets, end of year (000 omitted) | | $ | 25,398 | | | $ | 28,870 | | | $ | 40,957 | | | $ | 32,514 | | | $ | 36,909 | |

Before waiver | | | | | | | | | | | | | | | | | | | | |

Ratio of expenses to average net assets | | | 1.10 | % | | | 1.11 | % | | | 1.17 | % | | | 1.16 | % | | | 1.25 | % |

After waiver | | | | | | | | | | | | | | | | | | | | |

Ratio of expenses to average net assets | | | 0.98 | % | | | 0.98 | % | | | 0.99 | %(e) | | | 0.98 | % | | | 0.98 | % |

Ratio of net investment income to average net assets | | | 1.40 | % | | | 1.17 | % | | | 1.20 | % | | | 1.22 | % | | | 1.00 | % |

Portfolio turnover rate(f) | | | 50 | % | | | 58 | % | | | 50 | % | | | 69 | % | | | 45 | % |

| | | | | | | | | | | | | | | | | | | | | |

(a) | Per share net investment income has been determined on the basis of average shares outstanding during the year. |

(b) | The amount shown for a share outstanding throughout the year does not accord with the change in aggregate gains and losses in the portfolio of securities during the year because of the timing of sales and purchases of fund shares in relation to fluctuating market values during the year. |

(c) | Rounds to less than $0.005 per share. |

(d) | Total return in the above table represents the rate that the investor would have earned or lost on an investment in the Fund, assuming reinvestment of distributions. |

(e) | This ratio includes the impact of overdraft fees. If this cost had been excluded, the ratio of expenses to average net assets would have been 0.98% for the fiscal year ended October 31, 2017. |

(f) | Portfolio turnover is calculated on the basis of the Fund as a whole without distinguishing among the classes of shares. |

30 | See accompanying notes which are an integral part of these financial statements. | |

Dana Small Cap Equity Fund – Institutional Class

Financial Highlights

(For a share outstanding during each period)

| | | Years Ended

October 31, | | | For the

Period

Ended

October 31, | |

| | | 2019 | | | 2018 | | | 2017 | | | 2016(a) | |

Selected Per Share Data: | | | | | | | | | | | | | | | | |

Net asset value, beginning of period | | $ | 11.09 | | | $ | 11.43 | | | $ | 9.30 | | | $ | 10.00 | |

| | | | | | | | | | | | | | | | | |

Investment operations: | | | | | | | | | | | | | | | | |

Net investment income (loss) | | | 0.01 | | | | (0.03 | ) | | | — | (b) | | | 0.01 | |

Net realized and unrealized gain (loss) on investments | | | (0.05 | ) | | | (0.31 | ) | | | 2.14 | | | | (0.70 | )(c) |

Total from investment operations | | | (0.04 | ) | | | (0.34 | ) | | | 2.14 | | | | (0.69 | ) |

| | | | | | | | | | | | | | | | | |

Less distributions to shareholders from: | | | | | | | | | | | | | | | | |

Net investment income | | | — | | | | — | (b) | | | (0.01 | ) | | | (0.01 | ) |

Net realized gains | | | (0.81 | ) | | | — | | | | — | | | | — | |

Total distributions | | | (0.81 | ) | | | — | (b) | | | (0.01 | ) | | | (0.01 | ) |

| | | | | | | | | | | | | | | | | |

Redemption fees | | | — | | | | — | | | | — | | | | — | (b) |

| | | | | | | | | | | | | | | | | |

Net asset value, end of period | | $ | 10.24 | | | $ | 11.09 | | | $ | 11.43 | | | $ | 9.30 | |

| | | | | | | | | | | | | | | | | |

Total Return(d) | | | 0.83 | % | | | (2.95 | )% | | | 23.08 | % | | | (6.87 | )%(e) |

| | | | | | | | | | | | | | | | | |

Ratios and Supplemental Data: | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

Net assets, end of period (000 omitted) | | $ | 12,421 | | | $ | 16,196 | | | $ | 14,011 | | | $ | 6,575 | |

Before waiver | | | | | | | | | | | | | | | | |

Ratio of expenses to average net assets | | | 1.88 | % | | | 1.75 | % | | | 2.02 | % | | | 4.11 | %(f) |

After waiver | | | | | | | | | | | | | | | | |

Ratio of expenses to average net assets | | | 0.95 | % | | | 0.95 | % | | | 0.95 | % | | | 0.95 | %(f) |

Ratio of net investment income (loss) to average net assets | | | 0.11 | % | | | (0.24 | )% | | | — | % | | | 0.12 | %(f) |

Portfolio turnover rate(g) | | | 50 | % | | | 78 | % | | | 58 | % | | | 54 | %(e) |

| | | | | | | | | | | | | | | | | |

(a) | For the period November 3, 2015 (commencement of operations) to October 31, 2016. |

(b) | Rounds to less than $0.005 per share. |

(c) | The amount shown for a share outstanding throughout the year does not accord with the change in aggregate gains and losses in the portfolio of securities during the year because of the timing of sales and purchases of fund shares in relation to fluctuating market values during the year. |

(d) | Total return in the above table represents the rate that the investor would have earned or lost on an investment in the Fund, assuming reinvestment of distributions. |

(g) | Portfolio turnover is calculated on the basis of the Fund as a whole without distinguishing among the classes of shares. |

| | See accompanying notes which are an integral part of these financial statements. | 31 |

Dana Small Cap Equity Fund – Investor Class

Financial Highlights

(For a share outstanding during each period)

| | | Years Ended

October 31, | | | For the

Period

Ended

October 31, | |

| | | 2019 | | | 2018 | | | 2017 | | | 2016(a) | |

Selected Per Share Data: | | | | | | | | | | | | | | | | |

Net asset value, beginning of period | | $ | 11.02 | | | $ | 11.38 | | | $ | 9.28 | | | $ | 10.00 | |

| | | | | | | | | | | | | | | | | |

Investment operations: | | | | | | | | | | | | | | | | |

Net investment loss | | | (0.03 | ) | | | (0.08 | ) | | | (0.02 | ) | | | — | (b) |

Net realized and unrealized gain (loss) on investments | | | (0.04 | ) | | | (0.28 | ) | | | 2.13 | | | | (0.71 | )(c) |

Total from investment operations | | | (0.07 | ) | | | (0.36 | ) | | | 2.11 | | | | (0.71 | ) |

| | | | | | | | | | | | | | | | | |

Less distributions to shareholders from: | | | | | | | | | | | | | | | | |

Net investment income | | | — | | | | — | | | | (0.01 | ) | | | (0.01 | ) |

Net realized gains | | | (0.81 | ) | | | — | | | | — | | | | — | |

Total distributions | | | (0.81 | ) | | | — | | | | (0.01 | ) | | | (0.01 | ) |

| | | | | | | | | | | | | | | | | |

Redemption fees | | | — | | | | — | | | | — | | | | — | (b) |

| | | | | | | | | | | | | | | | | |

Net asset value, end of period | | $ | 10.14 | | | $ | 11.02 | | | $ | 11.38 | | | $ | 9.28 | |

| | | | | | | | | | | | | | | | | |

Total Return(d) | | | 0.55 | % | | | (3.16 | )% | | | 22.73 | % | | | (7.13 | )%(e) |

| | | | | | | | | | | | | | | | | |

Ratios and Supplemental Data: | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

Net assets, end of period (000 omitted) | | $ | 2,197 | | | $ | 3,473 | | | $ | 6,776 | | | $ | 3,604 | |

Before waiver | | | | | | | | | | | | | | | | |

Ratio of expenses to average net assets | | | 2.13 | % | | | 2.00 | % | | | 2.27 | % | | | 4.53 | %(f) |

After waiver | | | | | | | | | | | | | | | | |

Ratio of expenses to average net assets | | | 1.20 | % | | | 1.20 | % | | | 1.20 | % | | | 1.20 | %(f) |

Ratio of net investment loss to average net assets | | | (0.13 | )% | | | (0.46 | )% | | | (0.25 | )% | | | (0.10 | )%(f) |

Portfolio turnover rate(g) | | | 50 | % | | | 78 | % | | | 58 | % | | | 54 | %(e) |

| | | | | | | | | | | | | | | | | |

(a) | For the period November 3, 2015 (commencement of operations) to October 31, 2016. |

(b) | Rounds to less than $0.005 per share. |

(c) | The amount shown for a share outstanding throughout the year does not accord with the change in aggregate gains and losses in the portfolio of securities during the year because of the timing of sales and purchases of fund shares in relation to fluctuating market values during the year. |

(d) | Total return in the above table represents the rate that the investor would have earned or lost on an investment in the Fund, assuming reinvestment of distributions. |

(g) | Portfolio turnover is calculated on the basis of the Fund as a whole without distinguishing among the classes of shares. |

32 | See accompanying notes which are an integral part of these financial statements. | |