Dear Fellow Shareholders,

Small cap stocks enjoyed strong gains in 2016 and dramatically outperformed their large cap brethren. The first quarter of 2017 witnessed precisely the opposite. Similarly, value and core strategies strongly outperformed growth in 2016 and reversed course in the first quarter. The Fund’s small core strategy performed in line with the above trends. Mean reversion is very much in play here and is not at all surprising.

“Trump bump” beneficiaries, such as financials and industrials, are in the process of trimming the significant post-election gains. We elected to monetize some of our winners in those two groups that we deemed to be ahead of fundamentals and that hit our price targets. Having said that, we do feel the fundamentals in these two industries are positive and believe we will have nice opportunities to reinvest subsequent to the ongoing correction. Our cash position should afford us some dry powder to deploy as this process unfolds.

As we write this, the three legs to the Trump economic policy – health reform, tax reform, and infrastructure build – are unsurprisingly bogged down in Congress. The sausage-making political process is never pretty to watch and always takes longer than originally hoped. We will monitor these important issues closely. Without them, we may not get the extended cycle we initially theorized immediately following the election. We have a long list of investment candidates for the portfolio pending lower prices and/or successful economic legislation. Stay tuned—this may get very interesting!

Reset Button for MGIC – Rick Lane, CFA

MGIC Investment Corporation (MTG) is our largest holding. The Milwaukee-based company provides mortgage insurance to lenders against default loss from low-down-payment borrowers (typically under 20%). Mortgage originations are tied to the strength of the economy and drive the company’s revenue. Credit losses are MGIC’s main expense and are typically hypersensitive to the state of the business cycle. The housing market has enjoyed a reasonably robust run over the past few years while credit losses have been extremely low (a point to which we will return shortly).

Given that backdrop, MGIC’s strong stock price performance over the past several years should hardly be a surprise. However, many investors, ourselves included, feared that political meddling could derail MGIC’s favorable operating environment. The election in November might have resulted in tighter financial regulation, higher taxes, and a general disposition to favor government programs over private market solutions. Indeed, in a post-election “Hail Mary,” the outgoing head of the Department of Housing and Urban Development, or HUD, lowered the insurance premium on Federal Housing Administration (FHA) insured low-down-payment home loans—its tenuous financial condition notwithstanding. The FHA is the government-backed insurer of low-down-payment mortgage loans, hence the principal competitor to MGIC and its private enterprise cohorts.

Donald Trump’s surprise win changed everything. His campaign promised regulatory reform/roll-back, tax reform, and an overall pro-business stance. The “Trump Era” likely extends the current economic cycle and should be positive for most industries and businesses. With respect to MGIC, very few industries are more levered to this dramatic change in events than the mortgage insurance industry. In his first official act, newly appointed HUD Secretary Dr. Ben Carson rescinded the FHA premium reduction, setting the stage for private mortgage insurers (PMIs) to claw back some market share. Having given the 20,000-foot view of the PMI investment case, the balance of the MGIC discussion delves into the investment case details.

The notion of an extended economic cycle is key to the MGIC investment case. This yields more time for the strong underlying fundamentals to play out. Based on this, there are three key drivers to our investment thesis.

The first is the new administration’s commitment to private market solutions. Since the start of this cycle (2008-2009 timeframe), the FHA has grown its book of insurance from roughly $500 billion to some $1.2 trillion. For perspective, the PMI industry collectively insures about $840 billion. The FHA was originally set up to insure low FICO, low down payment loans to homebuyers unable to qualify for conventional home financing. Prospective first time homebuyers qualifying for conventional financing were expected to avail themselves of private mortgage insurance.

In fact, encouraged by various government entities, the FHA encroached on PMI turf and wrestled away market share. Some 20% of the FHA’s book is now higher FICO score loans than could have been insured through the PMI industry. This FHA strategy has historically resulted in underpricing and severe losses. The Trump administration all but eliminates the FHA price reduction possibility. This is likely to further curb the FHA’s growth to the direct benefit of PMIs.

Another aspect to the private market focus of the new administration is the potential for government sponsored enterprise (GSE) reform. Recall that Fannie Mae (FNMA) and Freddie Mac (FMCC) purchase the majority of new mortgages from mortgage originators (banks and mortgage brokers). In turn, the GSEs securitize the newly created mortgages, essentially guaranteeing and pooling them into mortgage-backed securities sold to investors. Fannie Mae and Freddie Mac dictate “conventional” lending standards. Generally speaking, they require homebuyers to put at least 20% down or purchase mortgage insurance to cover the shortfall. Unique to the PMI industry, the lender is the beneficiary of the insurance even though the borrower pays the premium. In the event of a default, the PMIs are the first loss position, while the GSE absorbs any additional losses beyond the PMI coverage.

| Semi-Annual Report | March 31, 2017 | 1 |

| Broadview Opportunity Fund | Shareholder Letter |

March 31, 2017 (Unaudited)

Historically, investors and the PMIs themselves were justly paranoid that the GSEs would elbow out the PMIs by insuring 100% of the mortgage. This issue has ebbed and flowed over the years, a political tug-of-war. Given the magnitude of the 2008 mortgage debacle, the momentum has swung back in favor of the PMIs taking a larger role. The Trump administration would likely further that momentum, but given the volatile history of the GSEs, we are not holding our breath.

Several housing finance reform templates have been put forward, including the Royce bill and Johnson-Crapo bill. We believe Fannie Mae and Freddie Mac will eventually be recognized as an essential part of the mortgage origination industry. We believe they will be left in place with one important difference – the risk to tax payers will be reduced by private players who essentially take a greater piece of the risk. The increased risk sharing could take place up front by PMIs assuming a greater percent of the loan risk (known as deeper coverage), or on the back end through the securitization process/capital markets.

While the GSE reform opportunity represents significant upside to our base case, the odds are tough to call. Even without GSE reform, the absence of negative political risk is still significant. Historically, the risk to PMIs from government fiat put a ceiling on valuation no matter how strong the underlying business trends. We believe this risk is off the table for the next four years and should allow valuations to move up commensurate with the strong underlying fundamentals.

The second key driver to our investment case is our contention that the “old book” of business—mortgages guaranteed during the disastrous bubble years of 2004 through 2008—is over reserved. This “old book” has been in run-off mode for quite a while. Claims have stabilized and are starting to decline. Over the next several years, we believe MGIC could release up to several hundred million dollars in “excess reserves” in addition to reserves already released. Our analysis suggests the market is giving MGIC little-to-no credit on this front. Many investors will not even consider MGIC because of the perceived risk that the “old book” is in fact under reserved. The old book aspect sufficiently muddies and complicates the investment case, such that many investors just move on.

The third and final driver is the stunningly pristine and profitable “new book” of business – mortgages guaranteed after 2008. This new book is so conservatively underwritten that losses have been de minimis. As the old book burns off over the next few years, the new book “butterfly” should emerge and investors will have a much clearer understanding of just how outstanding the new book really is. As a check on MGIC’s combined new book and old book reserves, we reverse engineered competitor Essent Group Ltd.’s (ESNT) reserves. Essent went public after the 2008 mortgage bust, so it only has a “new book” of business. Its credit metrics are very similar to MGIC’s new book. We took Essent’s reserve metrics and applied those to MGIC’s new book, adjusted for MGIC’s larger book. We then assigned the balance of MGIC’s total reserves to MGIC’s old book of business. The result left a sufficiently large balance of reserves, which further assuaged our worry about insufficient reserves, bolstering our belief that substantial redundant reserves likely exist.

As an aside, Essent carries a large valuation premium to MGIC, which makes little sense. Again, investors have gravitated to the simplicity of the Essent story, uncomplicated by the old book. We believe the opposite is true – MGIC’s old book carries value in the form of excess reserves. Eventually, MGIC and Essent will approach each other in an asymptote fashion as MGIC’s old book of business runs off, with the excess old book reserves.

In summary, we believe MGIC is poised to deliver strong earnings growth for the next several years. The company’s excess capital, approximately $700 million vis a vis PMIERS (GSE capital requirements) and $1.7 billion at the State of Wisconsin level, only enhances the argument for higher valuation. Further, our research suggests that the tail risk long associated with the PMI industry will be mitigated by old book excess reserves and overly conservative underwriting of the new book.

With earnings power in the $1.25 to $1.35 range, assuming excess capital is deployed to shrink the outstanding shares, and return on equity is in the 13%-14% range longer term, we target a $15 price objective 18 months out. Upside could develop if investors embrace our higher valuation argument.

| Broadview Opportunity Fund | Shareholder Letter |

March 31, 2017 (Unaudited)

Hilltop Holdings Inc. (HTH) and Chemical Financial Corp. (CHFC) – Sam Koehler

In the first quarter, we took an opportunity to swap part of our Hilltop Holdings position for stock in Chemical Financial. Hilltop is a financial company in which we still have a long term positive outlook, so the position reduction is a reflection of the relative attractiveness in Chemical Financial. Hilltop’s stock appreciated materially since an early-2016 low caused by fears of energy credit losses. We were confident in the loan quality at Hilltop due to a long history of conservative credit culture and a low concentration in energy loans.

As energy fears subsided, the stock strongly rebounded. Near-term acquisition opportunities may be harder to come by given a core competency is buying and fixing discounted banks. This extended bull market has not caused many bank credit issues or failures and therefore has reduced the potential pool of acquisitions for Hilltop. This is a name we still like over the long term and think highly of the future prospects. However, we believed that there was a strong relative opportunity in Chemical Financial.

Chemical Financial is the largest Michigan headquartered bank with a footprint extending into Indiana and Ohio. With a history as a strong community-oriented bank, the company was transformed by an early-2016 merger with Talmer Bancorp. We followed Talmer closely since the initial public offering in early-2014. We were impressed with the strong management team, success in buying troubled banks and the prospects for future growth. Talmer was led by an exceptionally strong management team including CEO David Provost, who has subsequently joined the Chemical board of directors, and CFO Dennis Klaeser, who serves in the same role at the combined organization.

The combined Chemical management team is impressive as well, with CEO David Ramaker leading the company since 2002. The merger between Chemical and Talmer created strong revenue growth and cost synergy opportunities and the organization is on track to meet targets, in our opinion. Chemical has been able to generate loan growth faster than the industry, while maintaining expense discipline and strong credit quality, which has resulted in above peer returns. Chemical faces its first stress test later this year because the combined assets will cross the $10 billion threshold. As the integration matures, we believe the company will be well positioned to consider more acquisitions to strengthen the franchise. Despite these attractive traits, Chemical trades at a discounted valuation compared to the regional bank index and moreover has a nice dividend yield.

K2M Group Holdings, Inc. (KTWO) – Aaron Garcia, CFA

Another recent addition to our portfolio is K2M, an orthopedic implant manufacturer specializing in complex spine technologies. We became aware of this company's product portfolio through our due diligence on LDR Spine USA, Inc., another orthopedic company we owned which was purchased by Zimmer Biomet Holdings, Inc. (ZBH) in 2016.

K2M has a differentiated product portfolio with a leading position in spinal deformity. This is a niche area of spinal implants which has limited innovation or competition from larger players. The company is also one of the leading innovators in 3D printed implants, which allow for easier manufacturing of structures that can promote bone growth and fusion.

We believe the lack of innovation by larger competitors provides K2M outsized revenue growth potential via market share gains and a large group of potential acquirers should the company seek a sale. We believe management is capable of continuing to grow the top line faster than the industry and the new product pipeline is robust. 2016 was a bit of a challenging year for the company due to international distributor issues and some delays in product registration, which caused revenue disappointment. In addition, private equity sponsors exited the stock, resulting in a surfeit of shares in a tough healthcare backdrop.

We think the company's financial performance is poised to bounce back in 2017 and the long-term growth opportunity is promising. We initiated the position in mid-2016, and have opportunistically added to the position in the first quarter of 2017.

Healthcare Reform – Brief Opinion – Aaron Garcia, CFA

We believe there is still a chance that the House Republicans will revive the American Health Care Act (AHCA). However, there remains a philosophical schism in the Republican Party as to the government's role in healthcare. We feel that any of the more austere solutions favored by the Freedom Caucus will face a tough road in the Senate.

Healthcare reform remains an incredibly difficult process. From an investment standpoint, we have avoided investing in hospitals, managed care, life sciences and pharmaceutical sectors. We think these areas offer the most reform risk and could be more volatile due to movement in Washington. We have focused our attention on low volatility distribution and supplier businesses, as well as small growth companies with significant product cycle opportunities. We think the likelihood of volatility from legislative headlines will provide further opportunities to buy strong franchises at cheap valuations.

| Semi-Annual Report | March 31, 2017 | 3 |

| Broadview Opportunity Fund | Shareholder Letter |

March 31, 2017 (Unaudited)

Best regards,

|  |  |  |

| Richard E. Lane, CFA | Faraz Farzam, CFA | Aaron J. Garcia, CFA | Richard J. Whiting |

The views and information discussed in this commentary are as of the date of publication, are subject to change, and may not reflect the writer’s current views. The views expressed represent an assessment of market conditions at a specific point in time, are opinions only and should not be relied upon as investment advice regarding a particular investment or markets in general. Such information does not constitute a recommendation to buy or sell specific securities or investment vehicles. It should not be assumed that any investment will be profitable or will equal the performance of the Fund or any securities or any sectors mentioned herein. The subject matter contained herein has been derived from several sources believed to be reliable and accurate at the time of compilation.

A NOTE ON FORWARD LOOKING STATEMENTS

Except for historical information contained in this report for the Fund, the matters discussed in this report may constitute forward-looking statements made pursuant to the safe-harbor provisions of the Private Securities Litigation Reform Act of 1995. These include any adviser or portfolio manager predictions, assessments, analyses or outlooks for individual securities, industries, market sectors and/or markets. These statements involve risks and uncertainties. In addition to the general risks described for the Fund in the current Prospectus, other factors bearing on this report include the accuracy of the adviser’s or portfolio managers’ forecasts and predictions, and the appropriateness of the investment programs designed by the adviser or portfolio managers to implement their strategies efficiently and effectively. Any one or more of these factors, as well as other risks affecting the securities markets and investment instruments generally, could cause the actual results of the Fund to differ materially as compared to benchmarks associated with the Fund.

| Broadview Opportunity Fund | Manager Commentary |

March 31, 2017 (Unaudited)

MANAGEMENT’S DISCUSSION OF FUND PERFORMANCE

For the six months ended March 31, 2017, the Fund provided a return of 7.85%. This underperformed the Russell 2500 Index by 2.26% and the Russell 2000 Index by 3.67%. As the market rallied post-election, the Fund’s cash position was a significant drag on performance. Additional negative impact came from Consumer Discretionary and Energy sector holdings. On the other hand, holdings in the Financials and Health Care sectors positively affected performance. Bottom detractors to the Fund’s return included Hibbett Sports, Inc. (HIBB), MDC Partners Inc. (MDCA), and Range Resources Corp. (RRC). Top contributors to the Fund’s return included Veeco Instruments Inc. (VECO), Zions Bancorporation (ZION), and MGIC Investment Corp. (MTG).

GROWTH OF $10,000 INVESTMENT IN THE FUND

From its inception (12/16/96) to 3/31/17 as compared to the Russell 2500 Index(1) and the Russell 2000 Index(2)

| Semi-Annual Report | March 31, 2017 | 5 |

| Broadview Opportunity Fund | Manager Commentary |

March 31, 2017 (Unaudited)

PERFORMANCE (For Periods Ended 3/31/17)

| | Total Return* | | Annualized Total Return* |

| | 3 Months | | 1 Year | 5 Year | 10 Year | 15 Year | Since Inception** |

| Broadview Opportunity Fund | 1.56% | | 20.84% | 10.23% | 8.43% | 8.09% | 14.51% |

| Russell 2500 Index | 3.76% | | 21.53% | 12.60% | 7.71% | 9.17% | 9.70% |

| Russell 2000 Index | 2.47% | | 26.22% | 12.35% | 7.12% | 8.38% | 8.44% |

Performance data quoted represents past performance. Past performance does not guarantee future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when sold or redeemed, may be worth more or less than the original cost. Current performance data may be higher or lower than actual data quoted. For the most recent month-end performance please visit bvafunds.com or call 1-855-846-1463. As of the Fund’s Prospectus dated January 27, 2017, the Broadview Opportunity Fund’s annual operating expense ratio is 1.27%. One cannot invest directly in an index.

(1) | The Russell 2500 Index is a market cap weighted index that includes the smallest 2,500 companies covered in the Russell 3000 Index, which comprises the 3,000 largest U.S. companies based on total market capitalization. |

(2) | The Russell 2000 Index measures the performance of the 2,000 smallest companies in the Russell 3000 Index. |

| * | Total return includes changes in share prices and in each case includes reinvestments of any dividends, interest and capital gain distributions. The returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. |

| ** | Fund Inception Date: December 16, 1996. |

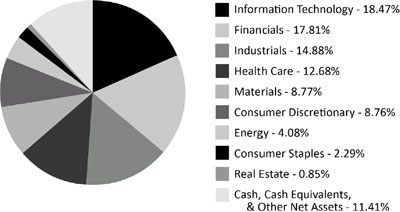

SECTOR ALLOCATION (as of March 31, 2017) (As a percentage of Net Assets)