Exhibit (c)(2)

Private and Confidential Project Raptor Goldman, Sachs & Co. May 20, 2016 Goldman Sachs does not provide accounting, tax, or legal advice. Notwithstanding anything in this document to the contrary, you (and each of your employees, representatives, and other agents) may disclose to any and all persons the US federal income and state tax treatment and tax structure of the transaction and all materials of any kind (including tax opinions and other tax analyses) that are provided to you relating to such tax treatment and tax structure, without Goldman Sachs imposing any limitation of any kind.

Private and Confidential Disclaimer These materials have been prepared and are provided by Goldman Sachs on a confidential basis solely for the information and assistance of the Board of Directors (the “Board”) and senior management of Riverstone Holdings LLC (the “Company”) in connection with their consideration of the matters referred to herein. These materials and Goldman Sachs’ presentation relating to these materials (the “Confidential Information”) may not be disclosed to any third party or circulated or referred to publicly or used for or relied upon for any other purpose without the prior written consent of Goldman Sachs. The Confidential Information was not prepared with a view to public disclosure or to conform to any disclosure standards under any state, federal or international securities laws or other laws, rules or regulations, and Goldman Sachs does not take any responsibility for the use of the Confidential Information by persons other than those set forth above. Notwithstanding anything in this Confidential Information to the contrary, the Company may disclose to any person the US federal income and state income tax treatment and tax structure of any transaction described herein and all materials of any kind (including tax opinions and other tax analyses) that are provided to the Company relating to such tax treatment and tax structure, without Goldman Sachs imposing any limitation of any kind. The Confidential Information has been prepared by the Investment Banking Division of Goldman Sachs and is not a product of its research department. Goldman Sachs and its affiliates are engaged in advisory, underwriting and financing, principal investing, sales and trading, research, investment management and other financial and non-financial activities and services for various persons and entities. Goldman Sachs and its affiliates and employees, and funds or other entities they manage or in which they invest or have other economic interests or with which they co-invest, may at any time purchase, sell, hold or vote long or short positions and investments in securities, derivatives, loans, commodities, currencies, credit default swaps and other financial instruments of the Company, any other party to any transaction and any of their respective affiliates or any currency or commodity that may be involved in any transaction. Goldman Sachs’ investment banking division maintains regular, ordinary course client service dialogues with clients and potential clients to review events, opportunities, and conditions in particular sectors and industries and, in that connection, Goldman Sachs may make reference to the Company, but Goldman Sachs will not disclose any confidential information received from the Company. The Confidential Information has been prepared based on historical financial information, forecasts and other information obtained by Goldman Sachs from publicly available sources, the management of the Company or other sources (approved for our use by the Company in the case of information from management and non-public information). In preparing the Confidential Information, Goldman Sachs has relied upon and assumed, without assuming any responsibility for independent verification, the accuracy and completeness of all of the financial, legal, regulatory, tax, accounting and other information provided to, discussed with or reviewed by us, and Goldman Sachs does not assume any liability for any such information. Goldman Sachs does not provide accounting, tax, legal or regulatory advice. Goldman Sachs has not made an independent evaluation or appraisal of the assets and liabilities (including any contingent, derivative or other off-balance sheet assets and liabilities) of the Company or any other party to any transaction or any of their respective affiliates and has no obligation to evaluate the solvency of the Company or any other party to any transaction under any state or federal laws relating to bankruptcy, insolvency or similar matters. The analyses contained in the Confidential Information do not purport to be appraisals nor do they necessarily reflect the prices at which businesses or securities actually may be sold or purchased. Goldman Sachs’ role in any due diligence review is limited solely to performing such a review as it shall deem necessary to support its own advice and analysis and shall not be on behalf of the Company. Analyses based upon forecasts of future results are not necessarily indicative of actual future results, which may be significantly more or less favorable than suggested by these analyses, and Goldman Sachs does not assume responsibility if future results are materially different from those forecast. The Confidential Information does not address the underlying business decision of the Company to engage in any transaction, or the relative merits of any transaction or strategic alternative referred to herein as compared to any other transaction or alternative that may be available to the Company. The Confidential Information is necessarily based on economic, monetary, market and other conditions as in effect on, and the information made available to Goldman Sachs as of, the date of such Confidential Information and Goldman Sachs assumes no responsibility for updating or revising the Confidential Information based on circumstances, developments or events occurring after such date. The Confidential Information does not constitute any opinion, nor does the Confidential Information constitute a recommendation to the Board, any security holder of the Company or any other person as to how to vote or act with respect to any transaction or any other matter. The Confidential Information, including this disclaimer, is subject to, is governed by, any written agreement between the Company, the Board and/or any committee thereof, on the one hand, and Goldman Sachs, on the other hand. 2

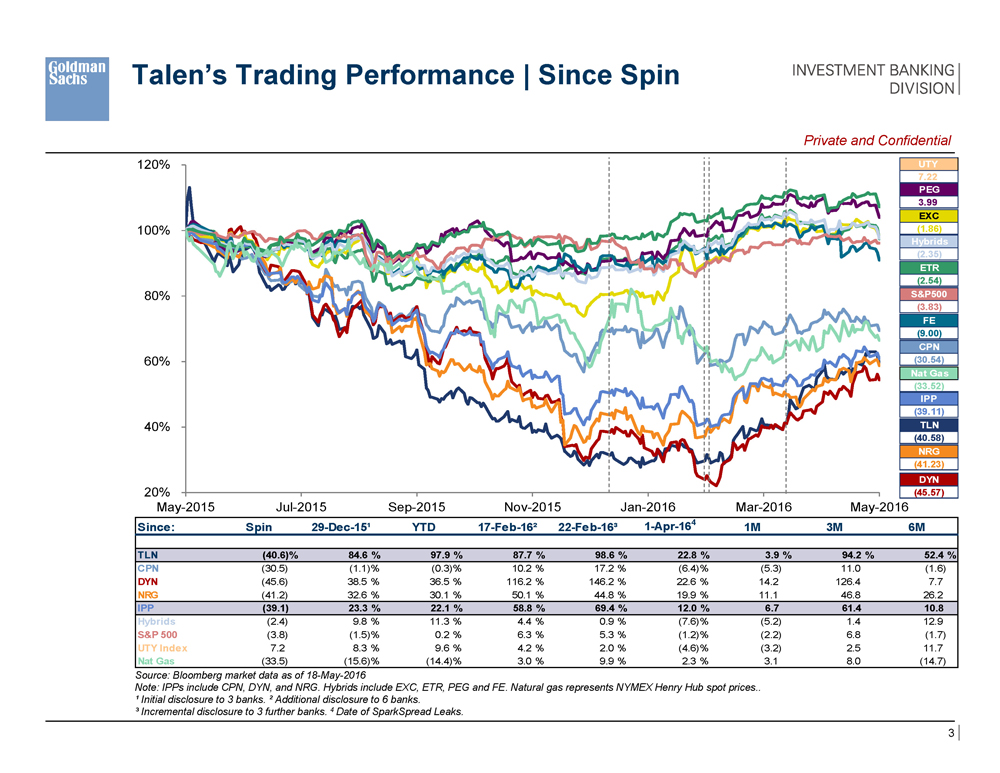

Talen’s Trading Performance | Since Spin Private and Confidential 20% 40% 60% 80% 100% 120% May-2015 Jul-2015 Sep-2015 Nov-2015 Jan-2016 Mar-2016 May-2016 UTY 7.22 3.99 EXC (1.86) Hybrids (2.35) ETR (2.54) S&P500 (3.83) FE (9.00) CPN (30.54) Nat Gas (33.52) IPP (39.11) TLN (40.58) NRG (41.23) DYN (45.57) Since: Spin 29-Dec-15¹ YTD 17-Feb-16² 22-Feb-16³ 1-Apr-164 1M 3M 6M TLN (40.6)% 84.6 % 97.9 % 87.7 % 98.6 % 22.8 % 3.9 % 94.2 % 52.4 % CPN (30.5) (1.1)% (0.3)% 10.2 % 17.2 % (6.4)% (5.3) 11.0 (1.6) DYN (45.6) 38.5 % 36.5 % 116.2 % 146.2 % 22.6 % 14.2 126.4 7.7 NRG (41.2) 32.6 % 30.1 % 50.1 % 44.8 % 19.9 % 11.1 46.8 26.2 IPP (39.1) 23.3 % 22.1 % 58.8 % 69.4 % 12.0 % 6.7 61.4 10.8 Hybrids (2.4) 9.8 % 11.3 % 4.4 % 0.9 % (7.6)% (5.2) 1.4 12.9 S&P 500 (3.8) (1.5)% 0.2 % 6.3 % 5.3 % (1.2)% (2.2) 6.8 (1.7) UTY Index 7.2 8.3 % 9.6 % 4.2 % 2.0 % (4.6)% (3.2) 2.5 11.7 Nat Gas (33.5) (15.6)% (14.4)% 3.0 % 9.9 % 2.3 % 3.1 8.0 (14.7)Source: Bloomberg market data as of 18-May-2016 Note: IPPs include CPN, DYN, and NRG. Hybrids include EXC, ETR, PEG and FE. Natural gas represents NYMEX Henry Hub spot prices.. ¹ Initial disclosure to 3 banks. ² Additional disclosure to 6 banks. ³ Incremental disclosure to 3 further banks. 4 Date of SparkSpread Leaks. 3

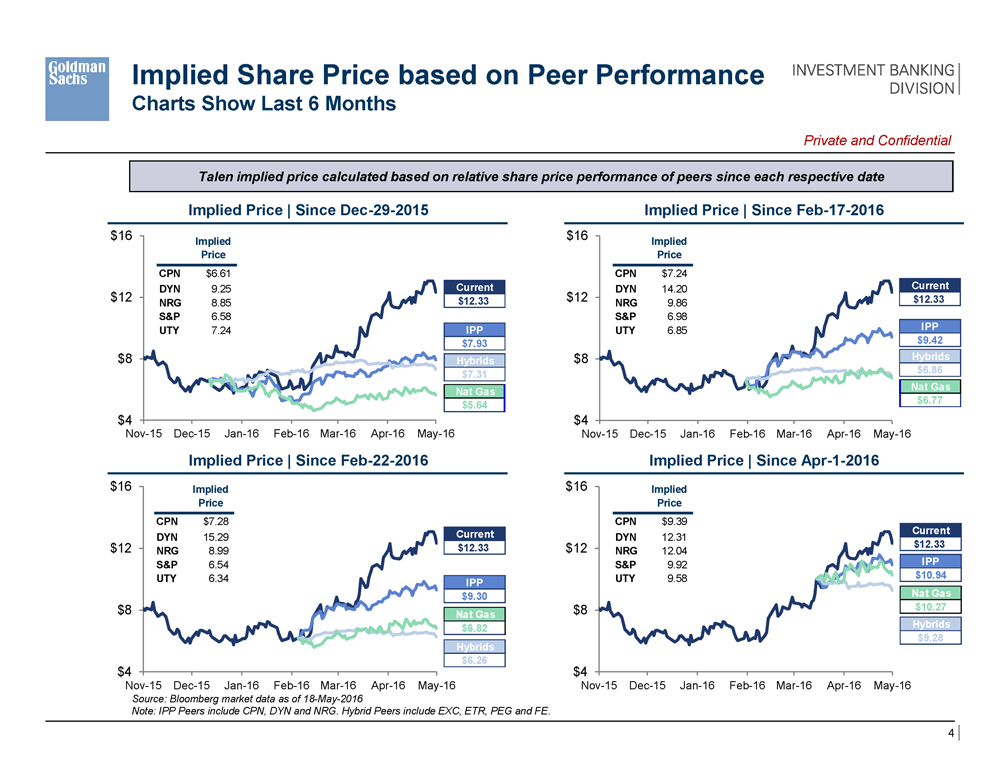

Implied Share Price based on Peer PerformanceC harts Show Last 6 Months Private and Confidential Talen implied price calculated based on relative share price performance of peers since each respective date Implied Price | Since Dec-29-2015 $4 $8 $12 $16 Nov-15 Dec-15 Jan-16 Feb-16 Mar-16 Apr-16 May-16 Implied Price CPN $6.61 DYN 9.25 NRG 8.85 S&P 6.58 UTY 7.24 Current $12.33 IPP $7.93 Hybrids $7.31 Nat Gas $5.64 Implied Price | Since Feb-17-2016 $4 $8 $12 $16 Nov-15 Dec-15 Jan-16 Feb-16 Mar-16 Apr-16 May-16 Implied Price CPN $7.24 DYN 14.20 NRG 9.86 S&P 6.98 UTY 6.85 Current $12.33 IPP $9.42 Hybrids $6.86 Nat Gas $6.77 Implied Price | Since Feb-22-2016 $4 $8 $12 $16 Nov-15 Dec-15 Jan-16 Feb-16 Mar-16 Apr-16 May-16 Current $12.33 IPP $9.30 Hybrids $6.26 Nat Gas $6.82 Implied Price | Since Apr-1-2016 $4 $8 $12 $16 Implied Price CPN $9.39 DYN 12.31 NRG 12.04 S&P 9.92 UTY 9.58 Current $12.33 IPP $10.94 Nat Gas $10.27 Hybrids $9.28 Nov-15 Dec-15 Jan-16 Feb-16 Mar-16 Apr-16 May-16 Source: Bloomberg market data as of 18-May-2016 Note: IPP Peers include CPN, DYN and NRG. Hybrid Peers include EXC, ETR, PEG and FE. 4

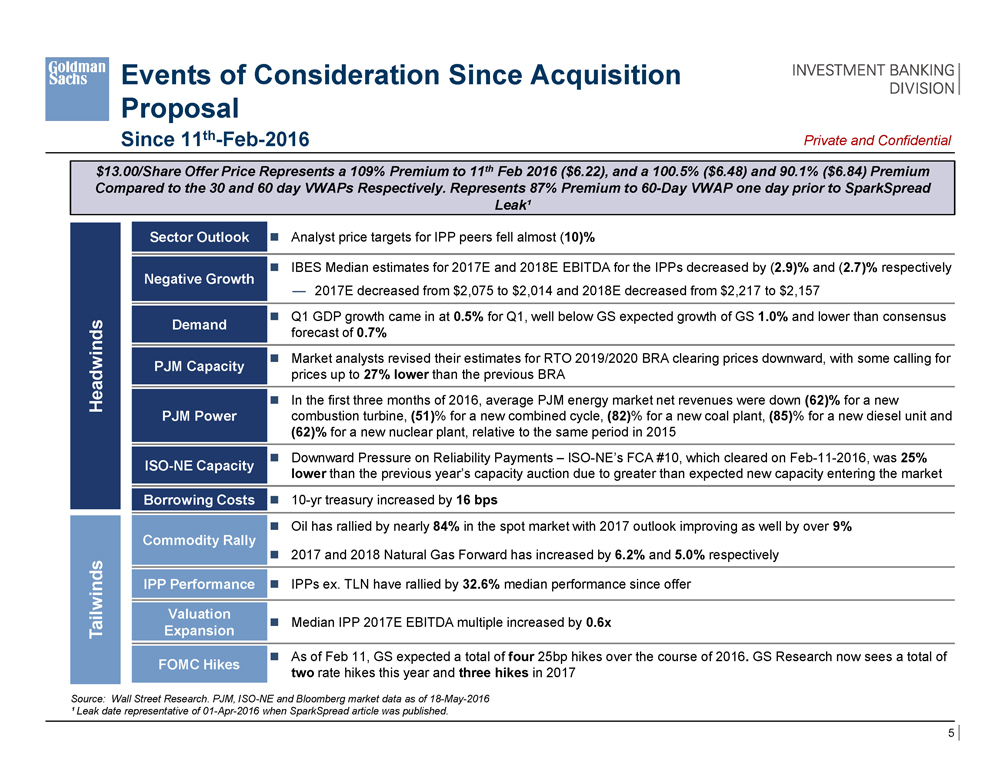

Events of Consideration Since Acquisition Proposal Since 11th-Feb-2016 Source: Wall Street Research. PJM, ISO-NE and Bloomberg market data as of 18-May-2016 ¹ Leak date representative of 01-Apr-2016 when SparkSpread article was published. $13.00/Share Offer Price Represents a 109% Premium to 11th Feb 2016 ($6.22), and a 100.5% ($6.48) and 90.1% ($6.84) Premium Compared to the 30 and 60 day VWAPs Respectively. Represents 87% Premium to 60-Day VWAP one day prior to SparkSpread Leak¹ Private and Confidential Headwinds Sector Outlook Analyst price targets for IPP peers fell almost (10)% Negative Growth IBES Median estimates for 2017E and 2018E EBITDA for the IPPs decreased by (2.9)% and (2.7)% respectively — 2017E decreased from $2,075 to $2,014 and 2018E decreased from $2,217 to $2,157 Demand Q1 GDP growth came in at 0.5% for Q1, well below GS expected growth of GS 1.0% and lower than consensus forecast of 0.7% PJM Capacity Market analysts revised their estimates for RTO 2019/2020 BRA clearing prices downward, with some calling for prices up to 27% lower than the previous BRA PJM Power In the first three months of 2016, average PJM energy market net revenues were down (62)% for a new combustion turbine, (51)% for a new combined cycle, (82)% for a new coal plant, (85)% for a new diesel unit and (62)% for a new nuclear plant, relative to the same period in 2015 ISO-NE Capacity Downward Pressure on Reliability Payments – ISO-NE’s FCA #10, which cleared on Feb-11-2016, was 25% lower than the previous year’s capacity auction due to greater than expected new capacity entering the market Borrowing Costs 10-yr treasury increased by 16 bps Tailwinds Commodity Rally Oil has rallied by nearly 84% in the spot market with 2017 outlook improving as well by over 9% 2017 and 2018 Natural Gas Forward has increased by 6.2% and 5.0% respectively IPP Performance IPPs ex. TLN have rallied by 32.6% median performance since offer Valuation Expansion Median IPP 2017E EBITDA multiple increased by 0.6x FOMC Hikes As of Feb 11, GS expected a total of four 25bp hikes over the course of 2016. GS Research now sees a total of two rate hikes this year and three hikes in 2017 Source: Wall Street Research. PJM, ISO-NE and Bloomberg market data as of 18-May-2016 ¹ Leak date representative of 01-Apr-2016 when SparkSpread article was published.