UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number | 811-01829 | |||||||

| ||||||||

Columbia Acorn Trust | ||||||||

(Exact name of registrant as specified in charter) | ||||||||

| ||||||||

227 W. Monroe Street Suite 3000 Chicago, IL |

| 60606 | ||||||

(Address of principal executive offices) |

| (Zip code) | ||||||

| ||||||||

Mary C. Moynihan Perkins Coie LLP 700 13th Street, NW Suite 600 Washington, DC 20005 | ||||||||

(Name and address of agent for service) | ||||||||

| ||||||||

Registrant’s telephone number, including area code: | 312-634-9200 |

| ||||||

| ||||||||

Date of fiscal year end: | December 31 |

| ||||||

| ||||||||

Date of reporting period: | June 30, 2013 |

| ||||||

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

Item 1. Reports to Stockholders.

Q2 2013

Columbia Acorn Family of Funds

Class A, B, C, I, R, R4, R5, Y and Z Shares

Managed by Columbia Wanger Asset Management, LLC

Semiannual Report

June 30, 2013

n Columbia

Acorn® Fund

n Columbia

Acorn International®

n Columbia

Acorn USA®

n Columbia

Acorn International SelectSM

n Columbia

Acorn SelectSM

n Columbia

Thermostat FundSM

n Columbia

Acorn Emerging Markets FundSM

n Columbia

Acorn European FundSM

Not FDIC insured • No bank guarantee • May lose value

Columbia Acorn Family of Funds

Descriptions of Indexes Included in this Report

• 50/50 Blended Benchmark, established by the Fund's investment manager, is an equally weighted custom composite of Columbia Thermostat Fund's primary equity and primary debt benchmarks, the S&P 500 Index and the Barclays U.S. Aggregate Bond Index, respectively. The percentage of the Fund's assets allocated to underlying stock and bond portfolio funds will vary, and accordingly the composition of the Fund's portfolio will not always reflect the composition of the 50/50 Blended Benchmark.

• Barclays U.S. Aggregate Bond Index is a market value-weighted index that tracks the daily price, coupon, pay-downs and total return performance of fixed-rate, publicly placed, dollar-denominated and non-convertible investment grade debt issues with at least $250 million par amount outstanding and with at least one year to final maturity.

• HSBC Smaller European Companies (inc UK) Index is a weighted combination of two indexes: the HSBC Smaller Europe (ex UK) Index and the HSBC Smaller UK Index. The index is rebalanced on a quarterly basis.

• Lipper Indexes include the largest funds tracked by Lipper, Inc. in the named category. Lipper Mid-Cap Growth Funds Index, 30 largest mid-cap growth funds, including Columbia Acorn Fund; Lipper International Small/Mid Growth Funds Index, 10 largest non-U.S. small/mid growth funds, including Columbia Acorn International; Lipper Small-Cap Growth Funds Index, 30 largest small-cap growth funds, including Columbia Acorn USA; Lipper Mid-Cap Core Funds Index, 30 largest mid-cap core funds; Lipper Flexible Portfolio Funds Index, an equal-weighted index of the 30 largest mutual funds within the Flexible Portfolio fund classification, as defined by Lipper. Lipper Emerging Markets Index, 30 largest emerging markets funds; Lipper European Region Index, 10 largest European funds.

• MSCI Europe, Australasia, Far East (EAFE) Index (Net) is a capitalization-weighted index that tracks the total return of common stocks in 22 developed-market countries within Europe, Australasia and the Far East. The returns of the MSCI EAFE Index (Net) are presented net of the withholding tax rate applicable to foreign non-resident institutional investors in the foreign companies included in the index who do not benefit from double taxation treaties.

• MSCI Emerging Markets Small Cap Index, a widely recognized international benchmark, is a free float-adjusted market capitalization index that is designed to measure small-cap emerging market equity performance. The MSCI Emerging Markets Small Cap Index currently consists of the following 21 emerging market country indexes: Brazil, Chile, China, Colombia, Czech Republic, Egypt, Hungary, India, Indonesia, Korea, Malaysia, Mexico, Morocco, Peru, Philippines, Poland, Russia, South Africa, Taiwan, Thailand and Turkey.

• Russell 2000 Index measures the performance of the 2,000 smallest companies in the Russell 3000 Index, which represents approximately 10% of the total market capitalization of the Russell 3000 Index.

• Russell 2500 Index measures the performance of the 2,500 smallest companies in the Russell 3000 Index, which represents approximately 17% of the total market capitalization of the Russell 3000 Index.

• Standard & Poor's (S&P) 500 Index tracks the performance of 500 widely held, large-capitalization U.S. stocks.

• Standard & Poor's (S&P) MidCap 400 Index is a market value-weighted index that tracks the performance of 400 mid-cap U.S. companies.

• S&P Developed Ex-U.S. Between $2B and $10B Index is a subset of the broad market selected by the index sponsor representing the mid-cap developed market, excluding the United States.

• S&P Emerging Markets Between $500M and $5B Index represents the institutionally investable capital of emerging market countries with market caps ranging between $500 million to $5 billion, as selected by S&P. The index currently consists of the following 21 emerging market country indexes: Brazil, Chile, China, Colombia, Czech Republic, Egypt, Hungary, India, Indonesia, Korea, Malaysia, Mexico, Morocco, Peru, Philippines, Poland, Russia, South Africa, Taiwan, Thailand and Turkey.

• S&P Europe Between $500M and $5B Index represents the institutionally investable capital of European countries with market caps ranging between $500 million to $5 billion, as selected by S&P. The index currently consists of the following 17 developed market country indexes: Austria, Belgium, Denmark, Finland, France, Germany, Greece, Ireland, Italy, Luxembourg, the Netherlands, Norway, Portugal, Spain, Sweden, Switzerland and the United Kingdom.

• S&P Global Ex-U.S. SmallCap Index consists of the bottom 20% of institutionally investable capital of developed and emerging countries, excluding the United States.

• S&P Global Ex-U.S. Between $500M and $5B Index is a subset of the broad market selected by the index sponsor representing the mid- and small-cap developed and emerging markets, excluding the United States.

Unlike mutual funds, indexes are not managed and do not incur fees or expenses. It is not possible to invest directly in an index.

You are invited to the 2013 Columbia Acorn Funds Shareholder Information Meeting

Join us to hear presentations by Columbia Acorn Fund's lead portfolio manager Chuck McQuaid and other members of the Columbia Wanger Asset Management investment team.

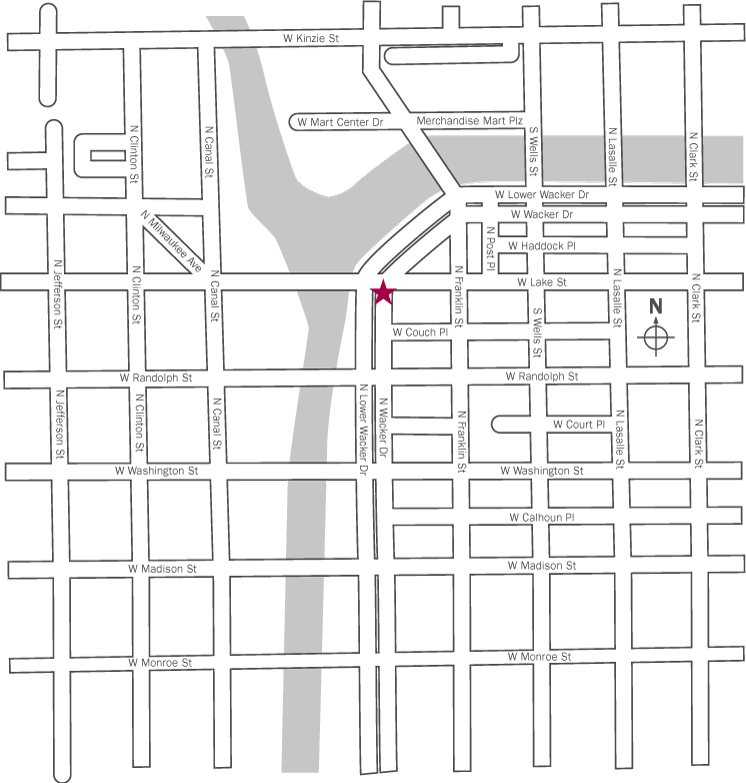

Where: Drinker Biddle & Reath LLP

191 North Wacker Drive, Suite 3700

Chicago, IL

When: Wednesday, September 18, 2013

12 p.m. CDT

A buffet lunch will be served beginning at 11:30.

RSVP: By calling 800.922.6769 or online at columbiamanagement.com. Please respond by September 13, 2013.

Webcast Replay: Available at columbiamanagement.com in October.

Public Transportation

Public Transportation

For directions using public transportation, call 312.836.7000 or visit the Chicago Transit Authority website at transitchicago.com. Metra information is also available by calling this number or can be found at metrarail.com.

Parking Information

Parking Information

Two parking options are located on Lake Street in the same block as the meeting location, which is between N. Wacker Drive and N. Franklin Street. Lake Street runs one way east after crossing N. Wacker Drive. Hourly parking rates apply at both locations. The first, with signage stating "Public Parking," provides direct access to the building in which the meeting will be held. The second option is a "Self Park" garage located next to the first but without direct access to the building.

Driving Directions

Driving Directions

From the south:

Take 1-57 to the Dan Ryan Expressway. Follow the signs for the Kennedy Expressway West. Travel on the Kennedy and exit using the Washington Blvd. exit (Exit 51C). Turn right onto W. Washington. Turn left onto N. Upper Wacker Drive. Destination will be on the right.

From the north:

Take the Kennedy Expressway (I-90/94) south to Chicago. Travel on the Kennedy and exit using the Washington Blvd. exit (Exit 51C). Turn left onto W. Washington. Turn left onto N. Upper Wacker Drive. Destination will be on the right.

From the west:

Take the Eisenhower Expressway (I-290) from the west. Follow the signs for the Kennedy Expressway West. Travel on the Kennedy and exit using the Washington Blvd. exit (Exit 51C). Turn right onto W. Washington. Turn left onto N. Upper Wacker Drive. Destination will be on the right.

From the southwest:

Take the Stevenson Expressway (I-55). Exit to the Kennedy Expressway (North-Wisconsin). Travel on the Kennedy and exit using the Washington Blvd. exit (Exit 51C). Turn right onto W. Washington. Turn left onto N. Upper Wacker Drive. Destination will be on the right.

Columbia Acorn Family of Funds

Table of Contents

2013 Mid-year Distributions | 1 | ||||||

Net Asset Value Per Share | 2 | ||||||

Understanding Your Expenses | 3 | ||||||

Share Class Performance | 6 | ||||||

Fund Performance vs. Benchmarks | 7 | ||||||

Squirrel Chatter II: Health Care in the United States | 8 | ||||||

Columbia Acorn Fund | |||||||

In a Nutshell | 12 | ||||||

At a Glance | 13 | ||||||

Major Portfolio Changes | 28 | ||||||

Statement of Investments | 30 | ||||||

Columbia Acorn International | |||||||

In a Nutshell | 14 | ||||||

At a Glance | 15 | ||||||

Major Portfolio Changes | 43 | ||||||

Statement of Investments | 46 | ||||||

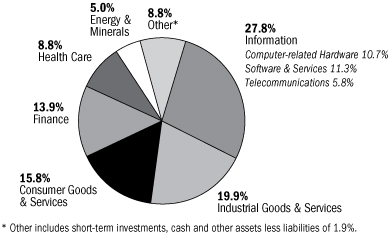

Portfolio Diversification | 55 | ||||||

Columbia Acorn USA | |||||||

In a Nutshell | 16 | ||||||

At a Glance | 17 | ||||||

Major Portfolio Changes | 56 | ||||||

Statement of Investments | 57 | ||||||

Columbia Acorn International Select | |||||||

In a Nutshell | 18 | ||||||

At a Glance | 19 | ||||||

Major Portfolio Changes | 64 | ||||||

Statement of Investments | 65 | ||||||

Portfolio Diversification | 69 | ||||||

Columbia Acorn Select | |||||||

In a Nutshell | 20 | ||||||

At a Glance | 21 | ||||||

Major Portfolio Changes | 70 | ||||||

Statement of Investments | 71 | ||||||

Columbia Thermostat Fund | |||||||

In a Nutshell | 22 | ||||||

At a Glance | 23 | ||||||

Statement of Investments | 76 | ||||||

Columbia Acorn Emerging Markets Fund | |||||||

In a Nutshell | 24 | ||||||

At a Glance | 25 | ||||||

Major Portfolio Changes | 78 | ||||||

Statement of Investments | 80 | ||||||

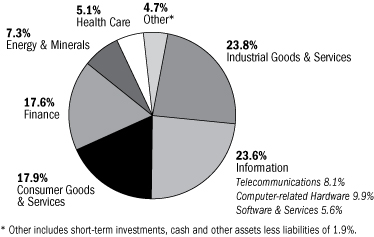

Portfolio Diversification | 84 | ||||||

Columbia Acorn European Fund | |||||||

In a Nutshell | 26 | ||||||

At a Glance | 27 | ||||||

Major Portfolio Changes | 85 | ||||||

Statement of Investments | 87 | ||||||

Portfolio Diversification | 91 | ||||||

Columbia Acorn Family of Funds | |||||||

Statements of Assets and Liabilities | 92 | ||||||

Statements of Operations | 94 | ||||||

Statements of Changes in Net Assets | 96 | ||||||

Financial Highlights | 102 | ||||||

Notes to Financial Statements | 118 | ||||||

Board Approval of the Advisory Agreement | 128 | ||||||

Expense Information | 133 | ||||||

The views expressed in the "Squirrel Chatter II" and "In a Nutshell" commentaries reflect the current views of the respective authors. These views are not guarantees of future performance and involve certain risks, uncertainties and assumptions that are difficult to predict so actual outcomes and results may differ significantly from the views expressed. These views are subject to change at any time based upon economic, market or other conditions and the respective authors disclaim any responsibility to update such views. These views may not be relied upon as investment advice and, because investment decisions for a Columbia Acorn Fund are based on numerous factors, may not be relied upon as an indication of trading intent on behalf of any particular Columbia Acorn Fund. References to specific company's securities should not be construed as a recommendation or investment advice and there can be no assurance that as of the date of publication of this report, the securities mentioned in each Fund's portfolio are still held or that the securities sold have not been repurchased.

Acorn®, Acorn USA® and Acorn International® are service marks owned and registered by Columbia Acorn Trust.

Columbia Acorn Family of Funds

2013 Mid-year Distributions

The following table lists the mid-year distributions for the Columbia Acorn Funds. The record date was June 4, 2013, and the ex-dividend date and the payable date was June 5, 2013. Columbia Acorn Emerging Markets Fund and Columbia Acorn European Fund did not have any distributions at mid-year.

Fund | Short-term Capital Gain | Long-term Capital Gain | Ordinary Income | Reinvestment Price | |||||||||||||||

Columbia Acorn Fund | |||||||||||||||||||

Class A | None | $ | 0.38297 | $ | 0.04178 | $ | 31.93 | ||||||||||||

Class B | None | $ | 0.38297 | None | $ | 29.06 | |||||||||||||

Class C | None | $ | 0.38297 | None | $ | 28.55 | |||||||||||||

Class I | None | $ | 0.38297 | $ | 0.04182 | $ | 33.20 | ||||||||||||

Class R4 | None | $ | 0.38297 | $ | 0.05083 | $ | 33.65 | ||||||||||||

Class R5 | None | $ | 0.38297 | $ | 0.04181 | $ | 33.65 | ||||||||||||

Class Y | None | $ | 0.38297 | $ | 0.04482 | $ | 33.67 | ||||||||||||

Class Z | None | $ | 0.38297 | $ | 0.03881 | $ | 33.17 | ||||||||||||

Columbia Acorn International | |||||||||||||||||||

Class A | None | None | $ | 0.47714 | $ | 43.39 | |||||||||||||

Class B | None | None | $ | 0.47714 | $ | 42.06 | |||||||||||||

Class C | None | None | $ | 0.47714 | $ | 41.87 | |||||||||||||

Class I | None | None | $ | 0.47714 | $ | 43.53 | |||||||||||||

Class R | None | None | $ | 0.47714 | $ | 43.32 | |||||||||||||

Class R4 | None | None | $ | 0.47714 | $ | 43.75 | |||||||||||||

Class R5 | None | None | $ | 0.47714 | $ | 43.48 | |||||||||||||

Class Y | None | None | $ | 0.47714 | $ | 43.77 | |||||||||||||

Class Z | None | None | $ | 0.47714 | $ | 43.50 | |||||||||||||

Columbia Acorn USA | |||||||||||||||||||

Class A | None | $ | 0.04426 | None | $ | 31.10 | |||||||||||||

Class B | None | $ | 0.04426 | None | $ | 28.36 | |||||||||||||

Class C | None | $ | 0.04426 | None | $ | 28.02 | |||||||||||||

Class I | None | $ | 0.04426 | None | $ | 32.56 | |||||||||||||

Class R4 | None | $ | 0.04426 | None | $ | 33.04 | |||||||||||||

Class R5 | None | $ | 0.04426 | None | $ | 33.02 | |||||||||||||

Class Y | None | $ | 0.04426 | None | $ | 33.07 | |||||||||||||

Class Z | None | $ | 0.04426 | None | $ | 32.51 | |||||||||||||

Columbia Acorn International Select | |||||||||||||||||||

Class A | None | $ | 0.52948 | None | $ | 25.76 | |||||||||||||

Class B | None | $ | 0.52948 | None | $ | 24.45 | |||||||||||||

Class C | None | $ | 0.52948 | None | $ | 24.31 | |||||||||||||

Class I | None | $ | 0.52948 | None | $ | 26.04 | |||||||||||||

Class R4 | None | $ | 0.52948 | None | $ | 26.18 | |||||||||||||

Class R5 | None | $ | 0.52948 | None | $ | 26.18 | |||||||||||||

Class Y | None | $ | 0.52948 | None | $ | 26.18 | |||||||||||||

Class Z | None | $ | 0.52948 | None | $ | 26.04 | |||||||||||||

1

Columbia Acorn Family of Funds

2013 Mid-year Distributions, continued

Fund | Short-term Capital Gain | Long-term Capital Gain | Ordinary Income | Reinvestment Price | |||||||||||||||

Columbia Acorn Select | |||||||||||||||||||

Class A | None | $ | 1.35142 | $ | 0.07036 | $ | 26.25 | ||||||||||||

Class B | None | $ | 1.35142 | None | $ | 24.05 | |||||||||||||

Class C | None | $ | 1.35142 | None | $ | 23.74 | |||||||||||||

Class I | None | $ | 1.35142 | $ | 0.16264 | $ | 27.22 | ||||||||||||

Class R4 | None | $ | 1.35142 | $ | 0.13444 | $ | 27.57 | ||||||||||||

Class R5 | None | $ | 1.35142 | $ | 0.15239 | $ | 27.56 | ||||||||||||

Class Y | None | $ | 1.35142 | $ | 0.17033 | $ | 27.61 | ||||||||||||

Class Z | None | $ | 1.35142 | $ | 0.14213 | $ | 27.17 | ||||||||||||

Columbia Thermostat Fund | |||||||||||||||||||

Class A | None | None | $ | 0.00911 | $ | 14.99 | |||||||||||||

Class B | None | None | $ | 0.00911 | $ | 15.06 | |||||||||||||

Class C | None | None | $ | 0.00911 | $ | 15.04 | |||||||||||||

Class R4 | None | None | $ | 0.00911 | $ | 14.89 | |||||||||||||

Class R5 | None | None | $ | 0.00911 | $ | 14.90 | |||||||||||||

Class Y | None | None | $ | 0.00911 | $ | 14.90 | |||||||||||||

Class Z | None | None | $ | 0.00911 | $ | 14.83 | |||||||||||||

Net Asset Value Per Share as of 6/30/13

| Columbia Acorn Fund | Columbia Acorn International | Columbia Acorn USA | Columbia Acorn International Select | Columbia Acorn Select | Columbia Thermostat Fund | Columbia Acorn Emerging Markets Fund | Columbia Acorn European Fund | ||||||||||||||||||||||||||||

Class A | $ | 31.98 | $ | 42.65 | $ | 31.36 | $ | 25.53 | $ | 26.26 | $ | 14.86 | $ | 11.99 | $ | 12.63 | |||||||||||||||||||

Class B | $ | 29.09 | $ | 41.31 | $ | 28.57 | $ | 24.21 | $ | 24.05 | $ | 14.93 | NA | NA | |||||||||||||||||||||

Class C | $ | 28.58 | $ | 41.13 | $ | 28.23 | $ | 24.08 | $ | 23.74 | $ | 14.91 | $ | 11.92 | $ | 12.55 | |||||||||||||||||||

Class I | $ | 33.26 | $ | 42.79 | $ | 32.83 | $ | 25.81 | $ | 27.25 | NA | $ | 12.04 | $ | 12.64 | ||||||||||||||||||||

Class R | NA | $ | 42.57 | NA | NA | NA | NA | NA | NA | ||||||||||||||||||||||||||

Class R4 | $ | 33.71 | $ | 43.01 | $ | 33.31 | $ | 25.95 | $ | 27.59 | $ | 14.77 | $ | 12.11 | NA | ||||||||||||||||||||

Class R5 | $ | 33.71 | $ | 42.74 | $ | 33.30 | $ | 25.94 | $ | 27.58 | $ | 14.78 | $ | 12.10 | $ | 12.75 | |||||||||||||||||||

Class Y | $ | 33.74 | $ | 43.03 | $ | 33.34 | $ | 25.94 | $ | 27.63 | $ | 14.78 | $ | 12.00 | NA | ||||||||||||||||||||

Class Z | $ | 33.23 | $ | 42.76 | $ | 32.78 | $ | 25.81 | $ | 27.19 | $ | 14.71 | $ | 12.02 | $ | 12.64 | |||||||||||||||||||

Class B shares of the Columbia Acorn Funds are closed to new investors. Class R, Class R4, Class R5, Class Y and Class Z shares of the Columbia Acorn Funds are available only to certain eligible investors described in the Funds' prospectuses. Class I shares of the Columbia Acorn Funds are only available to other Columbia Funds and are not available to individual investors.

2

Understanding Your Expenses

As a shareholder, you incur two types of costs. There are transaction costs, which generally include sales charges on purchases and may include redemption fees. There are also ongoing costs, which generally include management fees, distribution and service (Rule 12b-1) fees, and other Fund expenses. The following information is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to help you compare these costs with the ongoing costs of investing in other mutual funds.

Analyzing Your Fund's Expenses

To illustrate these ongoing costs, we have provided examples and calculated the expenses paid by investors in Class A, B, C, I, R, R4, R5, Y and Z shares of the Funds during the period. The actual and hypothetical information in the tables is based on an initial investment of $1,000 at the beginning of the period indicated and held for the entire period. Expense information is calculated two ways and each method provides you with different information. The amount listed in the "Actual" column is calculated using the Funds' actual operating expenses and total return for the period. You may use the Actual information, together with the amount invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the results by the expenses paid during the period under the Actual column. The amount listed in the "Hypothetical" column assumes a 5% annual rate of return before expenses (which is not the Funds' actual return) and then applies the Funds' actual expense ratio for the period to the hypothetical return. You should not use the hypothetical account values and expenses to estimate either your actual account balance at the end of the period or the expenses you paid during the period. See "Compare With Other Funds" below for details on how to use the hypothetical data.

In addition to the ongoing expenses which the Funds bear directly, Columbia Thermostat Fund's shareholders indirectly bear the Fund's allocable share of the costs and expenses of each underlying fund in which the Fund invests. You can also estimate the effective expenses paid during the period, which includes the indirect fees associated with investing in the underlying funds, by using the amounts listed in the effective expenses paid during the period column in the "Fund of Funds" table.

Compare With Other Funds

Since all mutual funds are required to include the same hypothetical calculations about expenses in shareholder reports, you can use this information to compare the ongoing cost of investing in the Funds with other funds. To do so, compare the hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of other funds. As you compare hypothetical examples of other funds, it is important to note that hypothetical examples are meant to highlight the ongoing costs of investing in a fund only and do not reflect any transaction costs, such as sales charges, or redemption or exchange fees. Therefore, the hypothetical calculations are useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. If transaction costs were included in these calculations, your costs would be higher.

January 1, 2013 — June 30, 2013

| Account value at the beginning of the period ($) | Account value at the end of the period ($) | Expenses paid during the period ($) | Fund's annualized expense ratio (%) | ||||||||||||||||||||||||||||

Actual | Hypothetical | Actual | Hypothetical | Actual | Hypothetical | Actual | |||||||||||||||||||||||||

Columbia Acorn Fund | |||||||||||||||||||||||||||||||

Class A | 1,000.00 | 1,000.00 | 1,103.70 | 1,019.27 | 5.52 | 5.30 | 1.07 | ||||||||||||||||||||||||

Class B | 1,000.00 | 1,000.00 | 1,099.80 | 1,016.13 | 8.80 | 8.45 | 1.71 | ||||||||||||||||||||||||

Class C | 1,000.00 | 1,000.00 | 1,099.60 | 1,015.74 | 9.22 | 8.85 | 1.79 | ||||||||||||||||||||||||

Class I | 1,000.00 | 1,000.00 | 1,105.50 | 1,021.04 | 3.67 | 3.52 | 0.71 | ||||||||||||||||||||||||

Class R4 | 1,000.00 | 1,000.00 | 1,105.00 | 1,020.74 | 3.97 | 3.82 | 0.77 | ||||||||||||||||||||||||

Class R5 | 1,000.00 | 1,000.00 | 1,105.40 | 1,020.94 | 3.77 | 3.62 | 0.73 | ||||||||||||||||||||||||

Class Y | 1,000.00 | 1,000.00 | 1,105.80 | 1,020.99 | 3.72 | 3.57 | 0.72 | ||||||||||||||||||||||||

Class Z | 1,000.00 | 1,000.00 | 1,105.20 | 1,020.70 | 4.03 | 3.86 | 0.78 | ||||||||||||||||||||||||

3

Understanding Your Expenses, continued

| Account value at the beginning of the period ($) | Account value at the end of the period ($) | Expenses paid during the period ($) | Fund's annualized expense ratio (%) | ||||||||||||||||||||||||||||

Actual | Hypothetical | Actual | Hypothetical | Actual | Hypothetical | Actual | |||||||||||||||||||||||||

Columbia Acorn International | |||||||||||||||||||||||||||||||

Class A | 1,000.00 | 1,000.00 | 1,057.10 | 1,018.54 | 6.15 | 6.04 | 1.22 | ||||||||||||||||||||||||

Class B | 1,000.00 | 1,000.00 | 1,053.20 | 1,014.96 | 9.82 | 9.63 | 1.95 | ||||||||||||||||||||||||

Class C | 1,000.00 | 1,000.00 | 1,053.10 | 1,014.76 | 10.02 | 9.83 | 1.99 | ||||||||||||||||||||||||

Class I | 1,000.00 | 1,000.00 | 1,058.70 | 1,020.30 | 4.34 | 4.26 | 0.86 | ||||||||||||||||||||||||

Class R | 1,000.00 | 1,000.00 | 1,055.10 | 1,016.87 | 7.86 | 7.71 | 1.56 | ||||||||||||||||||||||||

Class R4 | 1,000.00 | 1,000.00 | 1,058.40 | 1,020.01 | 4.64 | 4.56 | 0.92 | ||||||||||||||||||||||||

Class R5 | 1,000.00 | 1,000.00 | 1,058.80 | 1,020.11 | 4.54 | 4.46 | 0.90 | ||||||||||||||||||||||||

Class Y | 1,000.00 | 1,000.00 | 1,058.90 | 1,020.30 | 4.34 | 4.26 | 0.86 | ||||||||||||||||||||||||

Class Z | 1,000.00 | 1,000.00 | 1,058.50 | 1,020.01 | 4.64 | 4.56 | 0.92 | ||||||||||||||||||||||||

Columbia Acorn USA | |||||||||||||||||||||||||||||||

Class A | 1,000.00 | 1,000.00 | 1,113.20 | 1,018.00 | 6.89 | 6.58 | 1.33 | ||||||||||||||||||||||||

Class B | 1,000.00 | 1,000.00 | 1,108.70 | 1,014.12 | 10.96 | 10.47 | 2.12 | ||||||||||||||||||||||||

Class C | 1,000.00 | 1,000.00 | 1,109.20 | 1,014.61 | 10.45 | 9.98 | 2.02 | ||||||||||||||||||||||||

Class I | 1,000.00 | 1,000.00 | 1,115.50 | 1,020.06 | 4.72 | 4.51 | 0.91 | ||||||||||||||||||||||||

Class R4 | 1,000.00 | 1,000.00 | 1,114.80 | 1,019.57 | 5.24 | 5.00 | 1.01 | ||||||||||||||||||||||||

Class R5 | 1,000.00 | 1,000.00 | 1,115.20 | 1,019.62 | 5.19 | 4.95 | 1.00 | ||||||||||||||||||||||||

Class Y | 1,000.00 | 1,000.00 | 1,115.40 | 1,019.76 | 5.03 | 4.80 | 0.97 | ||||||||||||||||||||||||

Class Z | 1,000.00 | 1,000.00 | 1,114.60 | 1,019.27 | 5.55 | 5.30 | 1.07 | ||||||||||||||||||||||||

Columbia Acorn International Select | |||||||||||||||||||||||||||||||

Class A | 1,000.00 | 1,000.00 | 1,017.40 | 1,017.26 | 7.32 | 7.32 | 1.48 | ||||||||||||||||||||||||

Class B | 1,000.00 | 1,000.00 | 1,014.10 | 1,014.03 | 10.57 | 10.57 | 2.14 | ||||||||||||||||||||||||

Class C | 1,000.00 | 1,000.00 | 1,013.40 | 1,013.39 | 11.21 | 11.21 | 2.27 | ||||||||||||||||||||||||

Class I | 1,000.00 | 1,000.00 | 1,019.10 | 1,018.83 | 5.74 | 5.74 | 1.16 | ||||||||||||||||||||||||

Class R4 | 1,000.00 | 1,000.00 | 1,018.70 | 1,018.34 | 6.24 | 6.24 | 1.26 | ||||||||||||||||||||||||

Class R5 | 1,000.00 | 1,000.00 | 1,018.70 | 1,018.34 | 6.24 | 6.24 | 1.26 | ||||||||||||||||||||||||

Class Y | 1,000.00 | 1,000.00 | 1,018.70 | 1,018.83 | 5.74 | 5.74 | 1.16 | ||||||||||||||||||||||||

Class Z | 1,000.00 | 1,000.00 | 1,018.40 | 1,018.59 | 5.99 | 5.99 | 1.21 | ||||||||||||||||||||||||

Columbia Acorn Select | |||||||||||||||||||||||||||||||

Class A | 1,000.00 | 1,000.00 | 1,119.80 | 1,018.05 | 6.86 | 6.53 | 1.32 | ||||||||||||||||||||||||

Class B | 1,000.00 | 1,000.00 | 1,116.50 | 1,014.71 | 10.38 | 9.88 | 2.00 | ||||||||||||||||||||||||

Class C | 1,000.00 | 1,000.00 | 1,116.20 | 1,014.37 | 10.74 | 10.22 | 2.07 | ||||||||||||||||||||||||

Class I | 1,000.00 | 1,000.00 | 1,122.30 | 1,019.81 | 5.00 | 4.75 | 0.96 | ||||||||||||||||||||||||

Class R4 | 1,000.00 | 1,000.00 | 1,121.80 | 1,019.22 | 5.62 | 5.35 | 1.08 | ||||||||||||||||||||||||

Class R5 | 1,000.00 | 1,000.00 | 1,121.70 | 1,019.62 | 5.20 | 4.95 | 1.00 | ||||||||||||||||||||||||

Class Y | 1,000.00 | 1,000.00 | 1,122.10 | 1,019.18 | 5.67 | 5.40 | 1.09 | ||||||||||||||||||||||||

Class Z | 1,000.00 | 1,000.00 | 1,121.80 | 1,019.37 | 5.46 | 5.20 | 1.05 | ||||||||||||||||||||||||

4

| Account value at the beginning of the period ($) | Account value at the end of the period ($) | Expenses paid during the period ($) | Fund's annualized expense ratio (%) | ||||||||||||||||||||||||||||

Actual | Hypothetical | Actual | Hypothetical | Actual | Hypothetical | Actual | |||||||||||||||||||||||||

Columbia Acorn Emerging Markets Fund | |||||||||||||||||||||||||||||||

Class A | 1,000.00 | 1,000.00 | 995.80 | 1,015.60 | 8.91 | 9.00 | 1.82 | ||||||||||||||||||||||||

Class C | 1,000.00 | 1,000.00 | 992.50 | 1,011.82 | 12.65 | 12.78 | 2.59 | ||||||||||||||||||||||||

Class I | 1,000.00 | 1,000.00 | 996.70 | 1,017.41 | 7.10 | 7.17 | 1.45 | ||||||||||||||||||||||||

Class R4 | 1,000.00 | 1,000.00 | 997.50 | 1,016.97 | 7.54 | 7.62 | 1.54 | ||||||||||||||||||||||||

Class R5 | 1,000.00 | 1,000.00 | 996.70 | 1,016.87 | 7.64 | 7.71 | 1.56 | ||||||||||||||||||||||||

Class Y | 1,000.00 | 1,000.00 | 982.00 | * | 1,016.97 | 0.59 | * | 7.62 | 1.54 | * | |||||||||||||||||||||

Class Z | 1,000.00 | 1,000.00 | 995.90 | 1,016.92 | 7.59 | 7.67 | 1.55 | ||||||||||||||||||||||||

Columbia Acorn European Fund | |||||||||||||||||||||||||||||||

Class A | 1,000.00 | 1,000.00 | 1,074.00 | 1,016.13 | 8.70 | 8.45 | 1.71 | ||||||||||||||||||||||||

Class C | 1,000.00 | 1,000.00 | 1,069.90 | 1,012.26 | 12.69 | 12.34 | 2.50 | ||||||||||||||||||||||||

Class I | 1,000.00 | 1,000.00 | 1,075.70 | 1,017.85 | 6.92 | 6.73 | 1.36 | ||||||||||||||||||||||||

Class R5 | 1,000.00 | 1,000.00 | 1,075.00 | 1,017.31 | 7.48 | 7.27 | 1.47 | ||||||||||||||||||||||||

Class Z | 1,000.00 | 1,000.00 | 1,074.80 | 1,017.65 | 7.12 | 6.93 | 1.40 | ||||||||||||||||||||||||

Fund of Funds—Columbia Thermostat Fund

January 1, 2013 – June 30, 2013

| Account value at the beginning of the period ($) | Account value at the end of the period ($) | Expenses paid during the period ($) | Fund's annualized expense ratio (%) | Effective expenses paid during the period ($) | Fund's effective annualized expense ratio (%) | ||||||||||||||||||||||||||||||||||||||

Actual | Hypothetical | Actual | Hypothetical | Actual | Hypothetical | Actual | Actual | Hypothetical | Actual | ||||||||||||||||||||||||||||||||||

Columbia Thermostat Fund | |||||||||||||||||||||||||||||||||||||||||||

Class A | 1,000.00 | 1,000.00 | 1,040.50 | 1,022.07 | 2.50 | 2.48 | 0.50 | 5.35 | 5.31 | 1.07 | |||||||||||||||||||||||||||||||||

Class B | 1,000.00 | 1,000.00 | 1,038.20 | 1,019.62 | 5.00 | 4.95 | 1.00 | 7.85 | 7.77 | 1.57 | |||||||||||||||||||||||||||||||||

Class C | 1,000.00 | 1,000.00 | 1,036.80 | 1,018.39 | 6.24 | 6.19 | 1.25 | 9.09 | 9.01 | 1.82 | |||||||||||||||||||||||||||||||||

Class R4 | 1,000.00 | 1,000.00 | 1,041.50 | 1,023.44 | 1.10 | 1.09 | 0.22 | 3.95 | 3.92 | 0.79 | |||||||||||||||||||||||||||||||||

Class R5 | 1,000.00 | 1,000.00 | 1,042.20 | 1,023.39 | 1.15 | 1.14 | 0.23 | 4.01 | 3.97 | 0.80 | |||||||||||||||||||||||||||||||||

Class Y | 1,000.00 | 1,000.00 | 1,043.00 | 1,023.83 | 0.70 | 0.69 | 0.14 | 3.56 | 3.52 | 0.71 | |||||||||||||||||||||||||||||||||

Class Z | 1,000.00 | 1,000.00 | 1,041.70 | 1,023.29 | 1.25 | 1.24 | 0.25 | 4.11 | 4.07 | 0.82 | |||||||||||||||||||||||||||||||||

Expenses paid during the period are equal to the annualized expense ratio, multiplied by the average account value over the period and then multiplied by the number of days in the Fund's most recent fiscal half year and divided by 365.

Except with respect to Columbia Thermostat Fund, expenses do not include any fees and expenses incurred indirectly by a Fund from the underlying funds in which the Fund may invest (also referred to as "acquired funds"), including affiliated and non-affiliated pooled investments vehicles (including mutual funds and exchange traded funds).

In the case of Columbia Thermostat Fund, effective expenses paid during the period and the Fund's effective annualized expense ratio include expenses borne directly by the class plus the Fund's pro rata portion of the ongoing expenses charged by the underlying funds using the expense ratio of each class of the underlying funds as of the underlying fund's most recent shareholder report.

Had the investment manager and/or certain of its affiliates not waived/reimbursed certain fees and expenses for Columbia Acorn International, Columbia Acorn International Select, Columbia Acorn Select, Columbia Thermostat Fund, Columbia Acorn Emerging Markets Fund and Columbia Acorn European Fund, account value at the end of the period would have been reduced.

* For the period from June 13, 2013 (commencement of operations) through June 30, 2013.

5

Columbia Acorn Family of Funds

Share Class Performance Average Annual Total Returns through 6/30/13

Class A | Class B | Class C | Class I | Class R | Class R4 | Class R5 | Class Y | Class Z | |||||||||||||||||||||||||||||||||||||||||||

| Without Sales Charge | With Sales Charge | Without Sales Charge | With Sales Charge | Without Sales Charge | With Sales Charge | ||||||||||||||||||||||||||||||||||||||||||||||

Columbia Acorn Fund | |||||||||||||||||||||||||||||||||||||||||||||||||||

Year to date* | 10.37 | % | 4.03 | % | 9.98 | % | 4.98 | % | 9.96 | % | 8.96 | % | 10.55 | % | NA | 10.50 | % | 10.54 | % | 10.58 | % | 10.52 | % | ||||||||||||||||||||||||||||

| 1 year | 18.98 | % | 12.14 | % | 18.27 | % | 13.27 | % | 18.12 | % | 17.12 | % | 19.41 | % | NA | 19.29 | % | 19.36 | % | 19.41 | % | 19.32 | % | ||||||||||||||||||||||||||||

| 5 years | 7.82 | % | 6.54 | % | 7.18 | % | 6.88 | % | 6.99 | % | 6.99 | % | 8.17 | % | NA | 8.13 | % | 8.14 | % | 8.15 | % | 8.13 | % | ||||||||||||||||||||||||||||

| 10 years | 10.66 | % | 10.00 | % | 9.97 | % | 9.97 | % | 9.81 | % | 9.81 | % | 11.02 | % | NA | 11.00 | % | 11.00 | % | 11.01 | % | 11.00 | % | ||||||||||||||||||||||||||||

Columbia Acorn International | |||||||||||||||||||||||||||||||||||||||||||||||||||

Year to date* | 5.71 | % | -0.37 | % | 5.32 | % | 0.32 | % | 5.31 | % | 4.31 | % | 5.87 | % | 5.51 | % | 5.84 | % | 5.88 | % | 5.89 | % | 5.85 | % | |||||||||||||||||||||||||||

| 1 year | 18.03 | % | 11.24 | % | 17.16 | % | 12.16 | % | 17.12 | % | 16.12 | % | 18.43 | % | 17.63 | % | 18.35 | % | 18.38 | % | 18.42 | % | 18.39 | % | |||||||||||||||||||||||||||

| 5 years | 3.62 | % | 2.40 | % | 2.93 | % | 2.57 | % | 2.82 | % | 2.82 | % | 4.03 | % | 3.33 | % | 3.98 | % | 3.99 | % | 3.99 | % | 3.99 | % | |||||||||||||||||||||||||||

| 10 years | 13.22 | % | 12.55 | % | 12.47 | % | 12.47 | % | 12.36 | % | 12.36 | % | 13.64 | % | 12.91 | % | 13.62 | % | 13.62 | % | 13.63 | % | 13.62 | % | |||||||||||||||||||||||||||

Columbia Acorn USA | |||||||||||||||||||||||||||||||||||||||||||||||||||

Year to date* | 11.32 | % | 4.93 | % | 10.87 | % | 5.87 | % | 10.92 | % | 9.92 | % | 11.55 | % | NA | 11.48 | % | 11.52 | % | 11.54 | % | 11.46 | % | ||||||||||||||||||||||||||||

| 1 year | 19.94 | % | 13.04 | % | 19.05 | % | 14.05 | % | 19.03 | % | 18.03 | % | 20.36 | % | NA | 20.19 | % | 20.23 | % | 20.26 | % | 20.18 | % | ||||||||||||||||||||||||||||

| 5 years | 7.55 | % | 6.28 | % | 6.85 | % | 6.54 | % | 6.73 | % | 6.73 | % | 7.90 | % | NA | 7.84 | % | 7.85 | % | 7.86 | % | 7.84 | % | ||||||||||||||||||||||||||||

| 10 years | 9.25 | % | 8.60 | % | 8.54 | % | 8.54 | % | 8.43 | % | 8.43 | % | 9.62 | % | NA | 9.59 | % | 9.59 | % | 9.59 | % | 9.59 | % | ||||||||||||||||||||||||||||

Columbia Acorn International Select | |||||||||||||||||||||||||||||||||||||||||||||||||||

Year to date* | 1.74 | % | -4.10 | % | 1.37 | % | -3.59 | % | 1.34 | % | 0.34 | % | 1.88 | % | NA | 1.87 | % | 1.87 | % | 1.87 | % | 1.84 | % | ||||||||||||||||||||||||||||

| 1 year | 12.64 | % | 6.18 | % | 11.88 | % | 7.12 | % | 11.76 | % | 10.81 | % | 12.99 | % | NA | 12.93 | % | 12.93 | % | 12.95 | % | 12.93 | % | ||||||||||||||||||||||||||||

| 5 years | 1.11 | % | -0.07 | % | 0.46 | % | 0.13 | % | 0.31 | % | 0.31 | % | 1.51 | % | NA | 1.47 | % | 1.47 | % | 1.48 | % | 1.47 | % | ||||||||||||||||||||||||||||

| 10 years | 12.01 | % | 11.35 | % | 11.29 | % | 11.29 | % | 11.14 | % | 11.14 | % | 12.39 | % | NA | 12.37 | % | 12.37 | % | 12.37 | % | 12.37 | % | ||||||||||||||||||||||||||||

Columbia Acorn Select | |||||||||||||||||||||||||||||||||||||||||||||||||||

Year to date* | 11.98 | % | 5.54 | % | 11.65 | % | 6.65 | % | 11.62 | % | 10.62 | % | 12.23 | % | NA | 12.18 | % | 12.17 | % | 12.21 | % | 12.18 | % | ||||||||||||||||||||||||||||

| 1 year | 21.59 | % | 14.62 | % | 20.82 | % | 15.82 | % | 20.68 | % | 19.68 | % | 22.09 | % | NA | 21.91 | % | 21.95 | % | 21.98 | % | 21.96 | % | ||||||||||||||||||||||||||||

| 5 years | 3.59 | % | 2.37 | % | 2.94 | % | 2.58 | % | 2.78 | % | 2.78 | % | 3.97 | % | NA | 3.89 | % | 3.90 | % | 3.90 | % | 3.90 | % | ||||||||||||||||||||||||||||

| 10 years | 7.88 | % | 7.24 | % | 7.17 | % | 7.17 | % | 7.03 | % | 7.03 | % | 8.24 | % | NA | 8.20 | % | 8.21 | % | 8.21 | % | 8.21 | % | ||||||||||||||||||||||||||||

Columbia Thermostat Fund | |||||||||||||||||||||||||||||||||||||||||||||||||||

Year to date* | 4.05 | % | -1.92 | % | 3.82 | % | -1.18 | % | 3.68 | % | 2.68 | % | NA | NA | 4.15 | % | 4.22 | % | 4.30 | % | 4.17 | % | |||||||||||||||||||||||||||||

| 1 year | 10.61 | % | 4.27 | % | 10.11 | % | 5.11 | % | 9.86 | % | 8.86 | % | NA | NA | 10.89 | % | 10.94 | % | 11.00 | % | 10.92 | % | |||||||||||||||||||||||||||||

| 5 years | 6.79 | % | 5.53 | % | 6.26 | % | 5.94 | % | 6.00 | % | 6.00 | % | NA | NA | 7.05 | % | 7.06 | % | 7.07 | % | 7.05 | % | |||||||||||||||||||||||||||||

| 10 years | 7.13 | % | 6.50 | % | 6.55 | % | 6.55 | % | 6.34 | % | 6.34 | % | NA | NA | 7.40 | % | 7.40 | % | 7.41 | % | 7.40 | % | |||||||||||||||||||||||||||||

Columbia Acorn Emerging Markets Fund | |||||||||||||||||||||||||||||||||||||||||||||||||||

Year to date* | -0.42 | % | -6.11 | % | NA | NA | -0.75 | % | -1.74 | % | -0.33 | % | NA | -0.25 | % | -0.33 | % | -0.34 | % | -0.41 | % | ||||||||||||||||||||||||||||||

| 1 year | 18.89 | % | 12.05 | % | NA | NA | 18.02 | % | 17.02 | % | 19.31 | % | NA | 19.24 | % | 19.22 | % | 19.17 | % | 19.07 | % | ||||||||||||||||||||||||||||||

Life of Fund | 10.58 | % | 7.13 | % | NA | NA | 9.86 | % | 9.86 | % | 11.06 | % | NA | 11.02 | % | 11.00 | % | 10.98 | % | 10.93 | % | ||||||||||||||||||||||||||||||

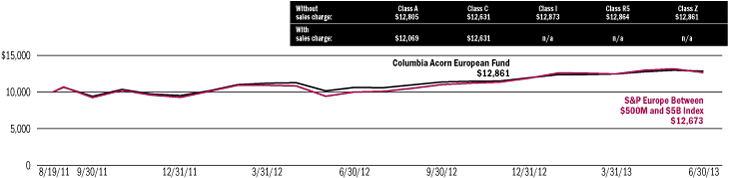

Columbia Acorn European Fund | |||||||||||||||||||||||||||||||||||||||||||||||||||

Year to date* | 7.40 | % | 1.20 | % | NA | NA | 6.99 | % | 5.99 | % | 7.57 | % | NA | NA | 7.50 | % | NA | 7.48 | % | ||||||||||||||||||||||||||||||||

| 1 year | 20.82 | % | 13.88 | % | NA | NA | 19.98 | % | 18.98 | % | 21.14 | % | NA | NA | 21.03 | % | NA | 21.00 | % | ||||||||||||||||||||||||||||||||

Life of Fund | 14.15 | % | 10.59 | % | NA | NA | 13.32 | % | 13.32 | % | 14.47 | % | NA | NA | 14.43 | % | NA | 14.41 | % | ||||||||||||||||||||||||||||||||

Returns for Class A shares are shown with and without the maximum initial sales charge of 5.75%. Returns for Class B shares are shown with and without the applicable contingent deferred sales charge (CDSC) of 5.00% in the first year, declining to 1.00% in the sixth year and eliminated thereafter. Returns for Class C shares are shown with and without the maximum CDSC of 1.00% for the first year after purchase. The Funds' other classes are not subject to sales charges and have limited eligibility. Please see the Funds' prospectuses for details. Performance for different share classes will vary based on differences in sales charges and certain fees associated with each class.

All results shown assume reinvestment of distributions during the period. Returns do not reflect the deduction of taxes that a shareholder may pay on Fund distributions or on the redemption of Fund shares. Performance results may reflect the effect of any fee waivers or reimbursements of Fund expenses by the investment manager and/or any of its affiliates. Absent these fee waivers and/or expense reimbursement arrangements, performance results would have been lower. Please see Page 133 of this report for information on contractual fee waiver and expense reimbursement agreements in place for Columbia Acorn International, Columbia Thermostat Fund, Columbia Acorn Emerging Markets Fund and Columbia Acorn European Fund and voluntary fee waiver and expense reimbursement arrangements in place for Columbia Acorn Select and Columbia Acorn International Select as of June 30, 2013.

The performance information shown represents past performance and is not a guarantee of future results. The investment return and principal value of your investment will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data shown. You may obtain performance information current to the most recent month-end by contacting your financial intermediary, visiting columbiamanagement.com or calling 800.922.6769.

The returns shown include the returns of each Fund's Class Z shares, each Fund's oldest share class, in cases where the inception date of the Fund is earlier than the inception date of the particular share class or where a period shown dates to before the inception date of the share class. These returns are adjusted to reflect any higher class-related operating expenses of the newer share classes, as applicable. Please visit columbiamanagement.com/mutual-funds/appended-performance for more information.

Continued on Page 7.

6

Fund Performance vs. Benchmarks Class Z Average Annual Total Returns through 6/30/13

Class Z Shares | 2nd quarter* | Year to date* | 1 year | 5 years | 10 years | Life of Fund | |||||||||||||||||||||

| Columbia Acorn Fund (ACRNX) (6/10/70) | 0.64 | % | 10.52 | % | 19.32 | % | 8.13 | % | 11.00 | % | 14.66 | % | |||||||||||||||

Russell 2500 Index | 2.27 | % | 15.42 | % | 25.61 | % | 9.21 | % | 10.34 | % | NA | ||||||||||||||||

S&P 500 Index** | 2.91 | % | 13.82 | % | 20.60 | % | 7.01 | % | 7.30 | % | 10.77 | % | |||||||||||||||

Russell 2000 Index | 3.08 | % | 15.86 | % | 24.21 | % | 8.77 | % | 9.53 | % | NA | ||||||||||||||||

Lipper Mid-Cap Growth Funds Index | 2.36 | % | 14.26 | % | 20.24 | % | 6.09 | % | 9.26 | % | NA | ||||||||||||||||

| Columbia Acorn International (ACINX) (9/23/92) | -1.10 | % | 5.85 | % | 18.39 | % | 3.99 | % | 13.62 | % | 11.17 | % | |||||||||||||||

S&P Global Ex-U.S. Between $500M and $5B Index | -3.46 | % | 1.95 | % | 15.91 | % | 2.88 | % | 12.36 | % | 8.32 | % | |||||||||||||||

S&P Global Ex-U.S. SmallCap Index | -3.72 | % | 2.13 | % | 17.11 | % | 2.02 | % | 11.60 | % | 7.64 | % | |||||||||||||||

MSCI EAFE Index (Net) | -0.98 | % | 4.10 | % | 18.62 | % | -0.63 | % | 7.67 | % | 5.83 | % | |||||||||||||||

Lipper International Small/Mid Growth Funds Index | -0.30 | % | 7.11 | % | 22.73 | % | 3.39 | % | 12.31 | % | NA | ||||||||||||||||

| Columbia Acorn USA (AUSAX) (9/4/96) | 0.91 | % | 11.46 | % | 20.18 | % | 7.84 | % | 9.59 | % | 10.45 | % | |||||||||||||||

Russell 2000 Index | 3.08 | % | 15.86 | % | 24.21 | % | 8.77 | % | 9.53 | % | 8.03 | % | |||||||||||||||

Lipper Small-Cap Growth Funds Index | 3.70 | % | 15.86 | % | 22.24 | % | 8.01 | % | 8.29 | % | 6.54 | % | |||||||||||||||

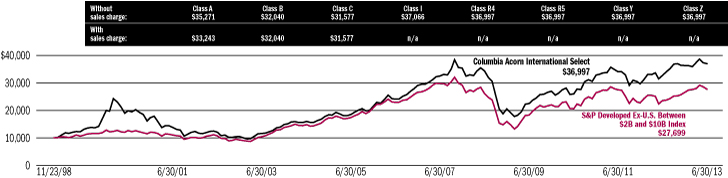

| Columbia Acorn Int'l Select (ACFFX) (11/23/98) | -1.26 | % | 1.84 | % | 12.93 | % | 1.47 | % | 12.37 | % | 9.37 | % | |||||||||||||||

S&P Developed Ex-U.S. Between $2B and $10B Index | -1.05 | % | 4.30 | % | 17.71 | % | 1.17 | % | 10.30 | % | 7.23 | % | |||||||||||||||

MSCI EAFE Index (Net) | -0.98 | % | 4.10 | % | 18.62 | % | -0.63 | % | 7.67 | % | 3.77 | % | |||||||||||||||

Lipper International Small/Mid Growth Funds Index | -0.30 | % | 7.11 | % | 22.73 | % | 3.39 | % | 12.31 | % | 10.23 | % | |||||||||||||||

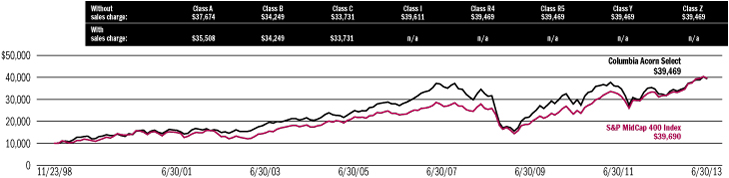

| Columbia Acorn Select (ACTWX) (11/23/98) | 1.40 | % | 12.18 | % | 21.96 | % | 3.90 | % | 8.21 | % | 9.86 | % | |||||||||||||||

S&P MidCap 400 Index | 1.00 | % | 14.59 | % | 25.18 | % | 8.91 | % | 10.74 | % | 9.90 | % | |||||||||||||||

S&P 500 Index** | 2.91 | % | 13.82 | % | 20.60 | % | 7.01 | % | 7.30 | % | 4.13 | % | |||||||||||||||

Lipper Mid-Cap Core Funds Index | 2.02 | % | 14.64 | % | 24.58 | % | 7.50 | % | 9.32 | % | 8.35 | % | |||||||||||||||

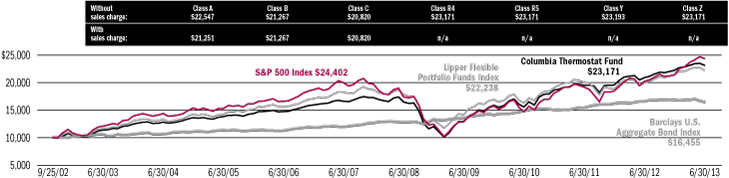

| Columbia Thermostat Fund (COTZX) (9/25/02) | 0.06 | % | 4.17 | % | 10.92 | % | 7.05 | % | 7.40 | % | 8.12 | % | |||||||||||||||

S&P 500 Index | 2.91 | % | 13.82 | % | 20.60 | % | 7.01 | % | 7.30 | % | 8.64 | % | |||||||||||||||

Barclays U.S. Aggregate Bond Index | -2.32 | % | -2.44 | % | -0.69 | % | 5.19 | % | 4.52 | % | 4.74 | % | |||||||||||||||

Lipper Flexible Portfolio Funds Index | -0.99 | % | 3.86 | % | 11.32 | % | 4.49 | % | 6.72 | % | 7.71 | % | |||||||||||||||

50/50 Blended Benchmark | 0.28 | % | 5.46 | % | 9.55 | % | 6.55 | % | 6.20 | % | 6.99 | % | |||||||||||||||

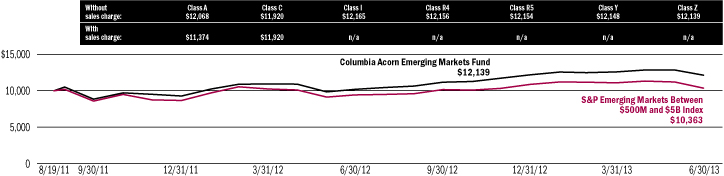

| Columbia Acorn Emerging Markets Fund (CEFZX) (8/19/11) | -3.69 | % | -0.41 | % | 19.07 | % | — | — | 10.93 | % | |||||||||||||||||

S&P Emerging Markets Between $500M and $5B Index | -6.55 | % | -4.74 | % | 9.98 | % | — | — | 1.93 | % | |||||||||||||||||

MSCI Emering Markets Small Cap Index | -7.47 | % | -3.58 | % | 9.86 | % | — | — | -0.95 | % | |||||||||||||||||

Lipper Emerging Markets Index | -7.48 | % | -8.01 | % | 4.66 | % | — | — | 1.57 | % | |||||||||||||||||

| Columbia Acorn European Fund (CAEZX) (8/19/11) | 3.10 | % | 7.48 | % | 21.00 | % | — | — | 14.41 | % | |||||||||||||||||

S&P Europe Between $500M and $5B Index | 1.50 | % | 6.46 | % | 26.83 | % | — | — | 13.52 | % | |||||||||||||||||

HSBC Smaller European Companies Index | 2.23 | % | 6.37 | % | 26.89 | % | — | — | 10.81 | % | |||||||||||||||||

Lipper European Region Index | 1.65 | % | 5.29 | % | 22.35 | % | — | — | 13.62 | % | |||||||||||||||||

The inception dates for Class A, B and C shares (if offered) are as follows: Columbia Acorn Fund, Columbia Acorn International, Columbia Acorn USA, Columbia Acorn International Select and Columbia Acorn Select, 10/16/00; Columbia Thermostat Fund, 3/3/03; Columbia Acorn Emerging Markets Fund and Columbia Acorn European Fund, 8/19/11. The inception dates for Class I shares are as follows: Columbia Acorn Fund, Columbia Acorn International, Columbia Acorn USA, Columbia Acorn International Select and Columbia Acorn Select, 9/27/10; Columbia Acorn Emerging Markets Fund and Columbia Acorn European Fund, 8/19/11. The inception date for Class R shares for Columbia Acorn International is 8/15/11. The inception date for Class R4, R5 and Y shares (if offered) is as follows: Columbia Acorn Fund, Columbia Acorn USA, Columbia Acorn International Select, Columbia Acorn Select, Columbia Thermostat Fund, Columbia Acorn Emerging Markets Fund and Columbia Acorn European Fund, 11/8/12, except that Class Y shares of Columbia Acorn Emerging Markets Fund commenced operations on June 13, 2013. The inception date for Class R5 shares of Columbia Acorn International is 8/15/11. The inception date for Class R4 and Y shares of Columbia Acorn International is 11/8/12. The inception date for Class Z shares is as follows: Columbia Acorn Fund, 6/10/70; Columbia Acorn International, 9/23/92; Columbia Acorn USA, 9/4/96; Columbia Acorn International Select and Columbia Acorn Select, 11/23/98; Columbia Thermostat Fund, 9/25/02; Columbia Acorn Emerging Markets Fund and Columbia Acorn European Fund, 8/19/11.

*Not annualized

**Although the Fund typically invests in small- and mid-sized companies, the comparison to the S&P 500 Index is presented to show performance against a widely recognized market index over the life of the Fund.

Please see inside front cover for a description of the indexes listed above.

7

Squirrel Chatter II: Health Care in the United States

Critics of the U.S. health care system note that the World Health Organization (WHO) ranked the United States thirtieth in the world in life expectancy1 despite the fact that the United States spends more money per capita on health care than any other country. They argue that health care in the United States is inferior to health care in many other developed countries.

Critics of the U.S. health care system note that the World Health Organization (WHO) ranked the United States thirtieth in the world in life expectancy1 despite the fact that the United States spends more money per capita on health care than any other country. They argue that health care in the United States is inferior to health care in many other developed countries.

Scott W. Atlas's book, In Excellent Health, Setting the Record Straight on America's Health Care,2 analyzes the consequences of poor lifestyle choices made by many Americans and how the U.S. health care system operates compared to health care systems elsewhere. His book cites numerous studies indicating the U.S. health care system does a great job addressing the health concerns of Americans and is likely the best system in the world.

Life Expectancy

The United States is much more violent and accident-prone than other developed countries. Homicide rates in the United States are ten times that of the United Kingdom and five times that of Canada.3 Death rates from transportation accidents in the United States are 250% that of the United Kingdom and 160% that of Canada.4 Murder and accidents account for the majority of deaths among young adults in the United States,5 and deaths at young ages substantially impact life expectancies.

Robert Ohsfeldt's and John Schneider's book, The Business of Health,6 attempts to quantify the impact of fatal injuries on life expectancy. Using linear regression, they calculate that after standardizing for fatal injuries alone, the United States would edge out Switzerland by 0.3 years and have the highest life expectancy of any country in the world.7

Other studies indicate that violence and accidents account for much, but not all, of the life expectancy shortfall in the United States. A National Academy of Sciences panel addressing cross-national health differences issued a paper that indicated 57% of the life expectancy gap for males under age 50 and 38% for females under 50 is

explained by higher violence and accidents in the United States.8

The United States has a much higher incidence of obesity than other developed countries. Atlas notes that in 2010 34% of people in the United States were obese compared to 15% in Canada, 17% in Western Europe and about 24% in the United Kingdom.9 The Organization for Economic Cooperation and Development (OECD) estimates that obesity reduces life spans by up to eight to ten years.10 Sadly, the worst is yet to come for the United States, as obesity rates have increased and there appears to be a 25-year time lag between becoming obese and suffering premature death.11

Cigarette use in the United States is down substantially; smoking rates are now lower than most other OECD countries.12 However, studies have found a time lag of roughly 25 to 30 years between smoking and lung cancer mortality.13 The United States had the highest rate of smoking in the developed world from the 1930s to the mid-1980s and, according to a 2007 study, 53% of Americans were current or former smokers, compared to 43% of Western Europeans.14 Clearly the United States' legacy of smoking continues to impact health. The Surgeon General estimates that cigarette smoking causes 443,000 deaths in the United States yearly, nearly one-fifth of all deaths.15

With respect to neonatal mortality, Atlas writes that the United States has stringent reporting requirements and definitions. Birth registrations in the United States are done by hospitals and health care professionals, while many other countries rely on reporting by families or surveys.16 In the United States, a live birth is tabulated should a newborn breathe, have a beating heart, move voluntary muscles or show any other evidence of life.17 According to WHO, countries representing only 13% of births worldwide had reliable data meeting this definition.18

Elsewhere, definitions for live births vary greatly. Some countries consider births as live only if 28 weeks gestation was achieved, if a baby is 30 centimeters long, or if a baby survives 24 hours.19 Otherwise, the baby is classified as stillborn and is not considered an infant mortality.

8

Atlas states, "... considering that roughly half of all U.S. infant mortality occurs in the first twenty-four hours, the single criterion of omitting deaths within the first twenty-four hours by many European nations generates their falsely superior infant mortality rates."20

Data from 2004 indicated that the United States had 12% of births classified as preterm (under 32 weeks gestation), a rate 50% to 100% higher than most European countries.21 These figures are impacted by the fact the United States has more multiple gestation pregnancies. Since the early 1980s, the incidence of triplets in the United States has more than tripled to over 140 births per 100,000.22 Atlas notes that in 2007, 17% of twins and 40% of triplets in the United States were associated with fertility treatments.

The U.S. health care system should be applauded for its efforts to save premature babies rather than write them off as stillborn, as many other countries do. Except for a very limited number of abusive cases, fertility treatment should be considered a virtue of the U.S. health care system. Yet, coupled with superior record keeping, these efforts depress the country's life expectancy ranking.

Diagnosis, Treatment and Outcomes

The Centers for Disease Control and Prevention (CDC) lists heart disease as the top killer in the United States, accounting for 25% of deaths, followed by cancer at 23%, and stroke a distant third at 6%.23 Rather than judge a health care system on reported life expectancy, Atlas assesses health care quality in the United States based on actual medical care, especially diagnosis and treatment of important diseases, using objective data.

Atlas notes the challenges facing the health care system due to the poor lifestyle choices of many Americans. The CDC estimates that 80% of diabetes, heart disease and stroke, and 40% of cancer, could be eliminated through reduction in obesity and smoking.24 The rate of diabetes in the United States is typically 33% to 100% higher than other developed countries.25 A 2007 study indicated that 12% of Americans over age 50 were diagnosed with cancer, compared to only 5% in a composite of 10 European countries.26

Atlas cites data showing more timely diagnosis and treatment in the United States as compared to other countries. He writes that, "... prolonged wait times are commonly found in health systems with government-controlled nationalized health insurance."27 Numerous countries with single payer systems had to create policies to address prolonged wait times, including Canada, England, Italy, Sweden and Spain.

The United States is among the world's leaders in per capita computerized tomography (CT) and magnetic resonance imaging (MRI) scanners,28 which are crucial to accurately diagnosing leading fatal diseases and guiding lower risk and more effective treatments. In the United States, referring doctors book CT and MRI appointments within days. In other countries, people wait. In 2010, the average wait time in Canada for a CT scan was four weeks and for an MRI, ten weeks.29 A 2011 study in the United Kingdom indicated thousands of people waited over six weeks for an MRI scan. With respect to breast cancer biopsies, another survey indicated that only 1% of U.S. patients waited three weeks or more while 44% of Canadian and 20% of U.K. patients waited that long.30

Treatment of diseases also tends to be very timely in the United States. One study indicated that no elective (non-emergency) cardiac bypass patients in the United States were known to have waited more than three months, while 47% in Canada and 89% in the United Kingdom waited at least that long.31

Furthermore, treatments in the United States tend to be aggressive. A 2009 paper written by University of Pennsylvania professor Samuel Preston and doctoral candidate Jessica Ho states that 88% of Americans with high cholesterol are being medicated versus 62% of Europeans. Likewise a higher percentage of Americans over age 50 with heart disease receive medication. Among those with hypertension in the United States, 66% were being successfully treated, versus 25% to 49% in other countries.32

With respect to cancer, Preston and Ho cite studies showing that the United States tends to have the highest percentage of screenings for breast, cervical, prostate and colon cancer.33 If cancer is detected, Americans tend to receive more surgery, chemotherapy and advanced cancer drugs. A 2008 study calculated five-year survival rates for

9

breast, colorectal and prostate cancers. Patients in the United States lead the world with a 74% survival rate. Second-best Canada came in at 71% and the United Kingdom was a laggard at 52%.

Atlas adds that new oncology drugs are most often approved and first used in the United States.34 Some 80% of worldwide medical innovation originates in the United States and, since the mid-1970s, U.S. scientists have won more than half of Nobel Prize awards in medicine and physiology.

The statistics are clear. Sick Americans are more likely to receive timely and aggressive health care than citizens of other countries. Atlas writes, "Availability of state-of-the-art medical technology, timely access to specialists, the most effective screening, the shortest wait times for life-changing surgeries, the newest, most effective drugs for more accurate, safer diagnosis and for the most advanced treatment are all superior in the United States."35

Many people appear to agree. In 2008, a McKinsey & Company study estimated that up to 85,000 patients sought in-patient treatment outside their home country. Of that number, 87% traveled to the United States for advanced medical technology, better quality care or quicker access to care. In contrast, critics of the U.S. health care system don't appear to be traveling to Cuba for treatment. Based on the facts, I agree with Atlas.

Health Care Economics and Investment Implications

Atlas states that the, "... only real crisis in America's health care today is the unsustainable and increasing burden of health care costs..."36 and recommends free market reforms. Health care costs are not the topic of this essay, but world-class health care clearly is expensive, and costs in the United States are exacerbated by detrimental lifestyle choices. I also believe that poor government policies result in few incentives for cost restraint.

Columbia Wanger Asset Management, the investment manager of the Columbia Acorn Funds, strives to provide Columbia Acorn Funds' shareholders with investments in health care companies that are pursuing breakthrough drugs and devices, with the potential to transform treatment of serious and poorly managed diseases. For example, in pivotal studies Seattle Genetics' drug

Adcetris delivered 80% response rates in advanced Hodgkin's lymphoma patients who had exhausted all other treatment options.37 In addition, we seek to invest in companies with products and services that we believe increase the cost effectiveness of health care delivery. We attempt to avoid investing in health care companies that may be more likely to be subject to cost cuts or price controls.

Charles P. McQuaid

President and Chief Investment Officer

Columbia Wanger Asset Management, LLC

The information and data provided in this analysis are derived from sources that we deem to be reliable and accurate. These views are not guarantees of future performance and involve certain risks, uncertainties and assumptions that are difficult to predict so actual outcomes and results may differ significantly from the views expressed. The views/opinions expressed here are those of the author and not of the Columbia Acorn Trust Board, are subject to change at any time based upon economic, market or other conditions, may differ from views expressed by other Columbia Management associates and the respective parties disclaim any responsibility to update such views. These views may not be relied on as investment advice and, because investment decisions for a Columbia Acorn Fund are based on numerous factors, may not be relied on as an indication of trading intent on behalf of any particular Columbia Acorn Fund.

1 Atlas, Scott W., In Excellent Health, Setting the Record Straight on American's Heath Care, (Stanford, California, Hoover Institution Press), p. 2.

2 Ibid.

3 Ohsfeldt, Robert L., and Schneider, John E., The Business of Health, The Role of Competition, Markets, and Regulation, (Washington, D.C., The AEI Press), p. 19.

4 Atlas, Scott W., op. cit., p. 28.

5 Ibid., p. 28.

6 Ohsfeldt, Robert L., and Schneider, John E., op. cit.

7 Ibid., p. 22.

8 Steven H. Woolf and Laudan Aron, Editors; Panel on Understanding Cross-National Health Differences Among High-Income Countries; Committee on Population; Division of Behavioral and Social Sciences and Education; National Research Council; Board on Population Health and Public Health Practice; Institute of Medicine, www.nap.edu.

9 Atlas, Scott W., op. cit., p. 105.

10 Ibid., p. 31.

11 Ibid., p. 107.

12 Ibid., p. 40.

13 Ibid., p. 41.

14 Ibid., p. 111.

15 Ibid., p. 108.

16 Ibid., p. 60.

17 Ibid., p. 67.

18 Ibid., p. 71.

19 Ibid., p. 68.

20 Ibid., p. 70.

10

21 Ibid., p. 73.

22 Ibid., p. 89.

23 Ibid., p. 119.

24 Ibid., p. 103.

25 Ibid., p. 113.

26 Preston, Samuel H., and Ho, Jessica Y., "Low Life Expectancy in the United States: Is the Health Care System at Fault?" University of Pennsylvania Scholarly Commons Working Paper Series, July 1, 2009, p. 4, http://repository.upenn.edu/psc_working_papers/13/. Accessed July 24, 2013.

27 Atlas, Scott W., op. cit., p. 159.

28 Ibid., p. 192-193.

29 Ibid., p. 194.

30 Ibid., p. 175.

31 Ibid., p. 187.

32 Preston, Samuel H., and Ho, Jessica Y., op. cit., p. 6.

33 Ibid., p. 3.

34 Atlas, Scott W., op. cit., p. 222.

35 Ibid., p. 233.

36 Ibid., p. 245.

37 Seattle Genetics is held in the following Columbia Acorn Funds: Columbia Acorn Fund, 1.0%; Columbia Acorn USA, 1.3%; Columbia Acorn Select, 1.4%. Please refer to Columbia Acorn Fund's and Columbia Acorn USA's "nutshell" commentaries for more on this stock's performance.

11

Columbia Acorn Fund

In a Nutshell

|

| ||||||

| Charles P. McQuaid Lead Portfolio Manager | Robert A. Mohn Co-Portfolio Manager | ||||||

Performance data shown represents past performance and is not a guarantee of future results. The investment return and principal value will fluctuate so that shares, when redeemed, may be worth more or less than the original cost. Current performance may be lower or higher than the performance data shown. Please visit columbiamanagement.com for most recent month-end performance updates.

Columbia Acorn Fund Class Z shares rose 0.64% in the second quarter and 10.52% in the first half of 2013. The Russell 2500 Index, the Fund's primary benchmark, rose 2.27% in the quarter and 15.42% in the half. As shown on Page 7, the Fund also underperformed its other benchmarks. We are pleased with the absolute return for the half, but disappointed that the gain fell short of the benchmarks.

Shutterfly, an Internet photo-centric retailer, jumped 26% in the second quarter and 87% in the half on strong market share gains, surging revenues and improving margins. It was the Fund's top dollar winner in the half.

Rental car companies Hertz and Avis Budget Group were also big winners; Hertz was up 11% in the second quarter and drove home a 52% gain in the half. Avis still needs to try a bit harder; it moved up 3% in the quarter and a fine 45% in the half. We've liked the car rental business for a while because the industry has been consolidating and companies in it can adjust capacity quickly. Also, rental car rates and car resale pricing have been bolstered by less aggressive discounting of new car prices by automakers.

Biotech stocks were generally nice winners in the first quarter, but several moderately corrected in the second quarter. Drug developers Seattle Genetics and BioMarin Pharmaceutical each fell about 10% in the second quarter, reducing Seattle Genetics' first-half gain to 36% and BioMarin's first-half gain to 13%. Equipment maker Cepheid fell 10% in the quarter, cutting its gain for the half to just 2%, on fears that demand may slow and competition could increase. Synageva Biopharma, a biotech company focused on orphan diseases, fell 23% in the second quarter and 9% in the half on rumors that a key drug study is progressing more slowly than expected. In contrast, NPS Pharmaceuticals jumped 48% in the quarter and 66% in the six-month period on optimism concerning the launch of a gastrointestinal drug.

Columbia Acorn Fund's international stocks were down 5.83% in the second quarter and 3.73% for the half year.* Netherlands-based Imtech, a technical installation and maintenance services provider, plunged 35% in the second quarter and 68% for the half year. Imtech had reported a fraud in its German and Polish operations in the first quarter, and in the second quarter disclosed that the fraud would be more costly than expected. Other international losers included Pacific Rubiales Energy, off 16% in the quarter and 24% in the six-month period on a slow environmental licensing process in Colombia, which in turn is delaying the company's oil exploration and production. Athabasca Oil Sands, another oil development company, fell 31% in the second quarter and 41% in the half on a regulatory ruling concerning an oil sands

property. Fertilizer company Sociedad Quimica y Minera de Chile dropped 27% in the quarter and 30% in the half. We've kept the Fund's international stock weighting toward the lower end of its 10-year range, and ended the quarter with a 7.8% weight.

We've spent some time analyzing Fund performance. It appears that the highest and lowest valued stocks in the Fund's benchmark tended to perform best in the second quarter and six months. Our style, growth-at-a-reasonable-price (GARP), results in Columbia Acorn Fund having a relatively low weighting of such stocks, which hurt performance somewhat during these periods. These market anomalies tend to be transitory, and we continue to believe that our GARP style should provide favorable long-term results. We also believe that our research process is sound and that we have an excellent core group of analysts. We've modestly downsized the domestic analyst team and increased coverage areas for some analysts. We think, but cannot guarantee, that this will result in more selectivity and improved relative performance.

*These returns are not comparable to mutual fund returns, as they are gross of fees and other expenses and do not portray the cash effects incurred by actual mutual funds. Columbia Acorn Fund's foreign stockholdings were not purchased as a balanced, stand-alone portfolio.

Stocks of small- and mid-cap companies pose special risks, including possible illiquidity and greater price volatility than stocks of larger, more established companies. International investing involves special risks, including foreign taxation, currency risks, risks associated with possible differences in financial standards, operational and settlement risks and other risks associated with future political and economic developments.

Portfolio holdings are subject to change periodically and may not be representative of current holdings.

Fund Positions in Mentioned Holdings

As a percentage of net assets, as of 6/30/13

Cepheid | 1.1 | % | |||||

Seattle Genetics | 1.0 | ||||||

Avis Budget Group | 0.7 | ||||||

BioMarin Pharmaceutical | 0.7 | ||||||

Shutterfly | 0.6 | ||||||

Hertz | 0.5 | ||||||

Synageva Biopharma | 0.4 | ||||||

NPS Pharmaceuticals | 0.3 | ||||||

Pacific Rubiales Energy | 0.3 | ||||||

Sociedad Quimica y Minera de Chile | 0.1 | ||||||

Athabasca Oil Sands | 0.1 | ||||||

Imtech | 0.1 | ||||||

12

Columbia Acorn Fund

At a Glance

Total Net Assets of the Fund:

$18.8 billion

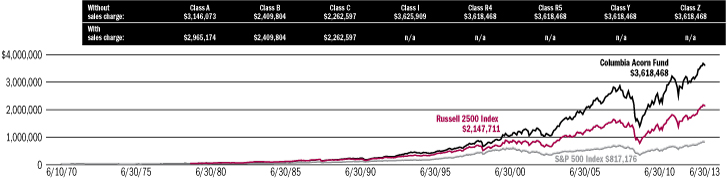

Performance data shown in the table and graph below represent past performance, do not guarantee future results, assume reinvestment of dividends and distributions and do not reflect the deduction of taxes that a shareholder may pay on Fund distributions or the redemption of Fund shares. The investment return and principal value of an investment will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data shown. Performance data reflect fee waivers or reimbursements of Fund expenses, if any; in their absence, performance results would have been lower. Indexes are unmanaged; their results do not reflect the effect of expenses or sales charges. Securities in the Fund may not match those in an index. Please visit columbiamanagement.com for performance data current to the most recent month-end.

The Growth of a $10,000 Investment in Columbia Acorn Fund Class Z Shares

June 10, 1970 (Fund inception) through June 30, 2013

This chart shows the change in value of a hypothetical $10,000 investment in Class Z shares of the Fund during the stated time period. A $10,000 investment in Columbia Acorn Fund at inception appreciated to $31,777 on December 31, 1978, the inception date of the Russell 2500 Index. For comparison with the Russell 2500 Index, we assigned the index the same value as the Fund at index inception. Although the Fund typically invests in small- and mid-sized companies, the comparison to the S&P 500 Index is presented to show performance against a widely recognized market index over the life of the Fund.

Average Annual Total Returns for period ended June 30, 2013

| 2nd quarter* | Year to date* | 1 year | 5 years | 10 years | Life of Fund | ||||||||||||||||||||||

| Class Z (6/10/70 inception) | 0.64 | % | 10.52 | % | 19.32 | % | 8.13 | % | 11.00 | % | 14.66 | % | |||||||||||||||

| Class A (10/16/00 inception) | |||||||||||||||||||||||||||

without sales charge | 0.54 | 10.37 | 18.98 | 7.82 | 10.66 | 14.29 | |||||||||||||||||||||

with sales charge | -5.25 | 4.03 | 12.14 | 6.54 | 10.00 | 14.13 | |||||||||||||||||||||

Russell 2500 Index** | 2.27 | 15.42 | 25.61 | 9.21 | 10.34 | N/A | |||||||||||||||||||||

Results for other share classes can be found on Page 6.

*Not annualized.

**The Fund's primary benchmark. Please see the inside front cover for index descriptions.

Returns for Class A shown with and without the maximum initial sales charge of 5.75%. As stated in the May 1, 2013, prospectus, the Fund's annual operating expense ratio is 0.82% for Class Z shares and 1.10% for Class A shares. The returns shown for periods prior to the inception of the Fund's Class A shares append the returns of the Fund's Class Z shares, the Fund's oldest share class. These returns are adjusted to reflect any higher class-related operating expenses of the newer share classes, as applicable. Please visit columbiamanagement.com/mutual-funds/

appended-performance for more information.

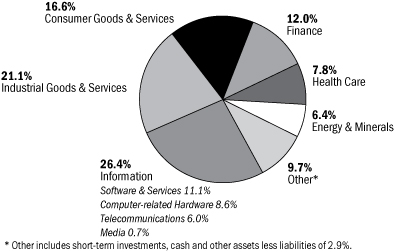

Portfolio Breakdown

as a percentage of net assets, as of 6/30/13

Top 10 Holdings

as a percentage of net assets, as of 6/30/13

| 1. | Ametek Aerospace/Industrial Instruments | 2.2 | % | ||||||||

| 2. | Mettler-Toledo International Laboratory Equipment | 1.7 | % | ||||||||

| 3. | Donaldson Industrial Air Filtration | 1.6 | % | ||||||||

| 4. | Crown Castle International Communications Towers | 1.5 | % | ||||||||

| 5. | tw telecom Fiber Optic Telephone/Data Services | 1.4 | % | ||||||||

| 6. | Amphenol Electronic Connectors | 1.4 | % | ||||||||

| 7. | FMC Technologies Oil & Gas Well Head Manufacturer | 1.4 | % | ||||||||

| 8. | SBA Communications Communications Towers | 1.3 | % | ||||||||

| 9. | Nordson Dispensing Systems for Adhesives & Coatings | 1.3 | % | ||||||||

| 10. | Cepheid Molecular Diagnostics | 1.1 | % | ||||||||

The Fund's top 10 holdings and portfolio diversification vary with changes in portfolio investments. See the Statement of Investments for a complete list of the Fund's holdings.

13

Columbia Acorn International

In a Nutshell

|

| ||||||

| P. Zachary Egan Co-Portfolio Manager | Louis J. Mendes III Co-Portfolio Manager | ||||||

Performance data shown represents past performance and is not a guarantee of future results. The investment return and principal value will fluctuate so that shares, when redeemed, may be worth more or less than the original cost. Current performance may be lower or higher than the performance data shown. Please visit columbiamanagement.com for most recent month-end performance updates.

Columbia Acorn International Class Z shares fell 1.10% in the second quarter of 2013, 2.36% better than the Fund's primary benchmark, the S&P Global Ex-U.S. Between $500M and $5B Index, which fell 3.46%. This comes on the heels of a solid first quarter, during which the Fund rose 7.03%. The Fund's return for the semiannual period was 5.85%, 3.90% ahead of its primary benchmark. For comparison, the large-cap, developed market MSCI EAFE Index (Net) rose 4.10% during the period.

In the second quarter, many bond markets experienced a sharp rise in mid-term interest rates following the mid-May remarks by U.S. Federal Reserve Bank Chairman Ben Bernanke that the Fed could "take a step down in our pace of purchase" of bonds, an unconventional practice that has supported low interest rates through the present financial crisis. How the Fed will manage this policy shift is of critical importance to investors globally, since many risk assets are priced off of U.S. government bonds. While Bernanke's remarks are grounded in signs of a normalizing U.S. economy—ostensibly good news—10-year bond rates rose on average 100 basis points in the ensuing weeks, which triggered a sell-off in international equities as investors discounted the impact more expensive money would have on economic activity and asset values in diverse markets. While the outlook for the U.S. economy may be brightening, things still appear grim in many parts of the world. In June, fears of stagflation in Brazil sent over one million people into the streets demanding more accountability from a government whose popularity has reached historic lows. Slowing economic growth in China upset already weak commodity markets and sent resources shares tumbling in the second quarter. Japanese stocks also took a breather in the quarter as the initial euphoria of "Abenomics" began to fade following two prior quarters of sharply rising markets. Despite the ebb and flow of market sentiment, many of the Fund's holdings have continued to post growth in earnings.

The Fund's top performer for the second quarter and the half year was Start Today, a Japanese online apparel retailer that has successfully managed costs to return the company to strong profitability after a rough 2012, during which its shares declined 60%. Start Today rose 54% in the second quarter and was up 114% for the six-month period. Siam Makro, a Thai-based cash and carry retailer of goods and produce, rose 41% in the quarter and 75% for the half year following a takeover bid from fellow Thai retailer CP-ALL. In recent years, Thailand has had a strong domestic economy as government policies and foreign investment have continued to increase the purchasing power of the rising middle class outside of urban Bangkok. Taiwan's St. Shine Optical, the world's leading manufacturer of daily disposable contact lenses,

rose 32% in the second quarter and ended the six-month period up 69%. Continued expansion of its overseas presence and increasing penetration of daily-wear contact lenses, which have become more affordable with rising regional incomes, drove gains.

Commodity-related holdings, namely in energy and basic materials, came under pressure as anxiety about the macroeconomic outlook spiked. Coal miner Mongolian Mining fell nearly 50% in the second quarter and was off 63% for the half year on disappointing volume throughput to China as logistic improvements continue to be delayed. Brazilian gold miner Beadell Resources and Australia's Regis Resources declined 51% and 39%, respectively, in the second quarter and were both off more than 50% for the half year as gold prices dropped over 25% in the first six months of 2013. Imtech, a Dutch technical installation and maintenance services provider, fell 35% in the second quarter as it became clear an earnings-dilutive rights issue was in the offing. This offering became necessary following news of fraud in Imtech's German and Polish operations. Year to date through June 30, Imtech's stock was down 68%. In Korea, Samsung Engineering fell 32% during the second quarter and was off 49% for the half year as the outlook for earnings declined amidst weakening overseas construction orders. We opted to sell the Fund's position in this stock.