Item 1. Reports to Stockholders

Annual report

Fixed income mutual funds

Delaware Corporate Bond Fund

Delaware Extended Duration Bond Fund

July 31, 2016

Carefully consider the Funds’ investment objectives, risk factors, charges, and expenses before investing. This and other information can be found in the Funds’ prospectus and their summary prospectuses, which may be obtained by visiting delawareinvestments.com/literature or calling 800 523-1918. Investors should read the prospectus and the summary prospectus carefully before investing.

You can obtain shareholder reports and prospectuses online instead of in the mail.

Visit delawareinvestments.com/edelivery.

Experience Delaware Investments

Delaware Investments is committed to the pursuit of consistently superior asset management and unparalleled client service. We believe in our investment processes, which seek to deliver consistent results, and in convenient services that help add value for our clients.

If you are interested in learning more about creating an investment plan, contact your financial advisor.

You can learn more about Delaware Investments or obtain a prospectus for Delaware Corporate Bond Fund and Delaware Extended Duration Bond Fund at delawareinvestments.com/literature.

Manage your investments online

| ● | | 24-hour access to your account information |

| ● | | Check your account balance and recent transactions |

| ● | | Request statements or literature |

| ● | | Make purchases and redemptions |

Delaware Management Holdings, Inc. and its subsidiaries (collectively known by the marketing name of Delaware Investments) are wholly owned subsidiaries of Macquarie Group Limited, a global provider of banking, financial, advisory, investment and funds management services.

Neither Delaware Investments nor its affiliates referred to in this document are authorized deposit-taking institutions for the purposes of the Banking Act 1959 (Commonwealth of Australia). The obligations of these entities do not represent deposits or other liabilities of Macquarie Bank Limited (MBL), a subsidiary of Macquarie Group Limited and an affiliate of Delaware Investments. MBL does not guarantee or otherwise provide assurance in respect of the obligations of these entities, unless noted otherwise. The Funds are governed by U.S. laws and regulations.

Table of contents

Unless otherwise noted, views expressed herein are current as of July 31, 2016, and subject to change for events occurring after such date.

The Funds are not FDIC insured and are not guaranteed. It is possible to lose the principal amount invested.

Mutual fund advisory services provided by Delaware Management Company, a series of Delaware Management Business Trust, which is a registered investment advisor. Delaware Investments, a member of Macquarie Group, refers to Delaware Management Holdings, Inc. and its subsidiaries, including the Funds’ distributor, Delaware Distributors, L.P. Macquarie Group refers to Macquarie Group Limited and its subsidiaries and affiliates worldwide.

© 2016 Delaware Management Holdings, Inc.

All third-party marks cited are the property of their respective owners.

| | |

| Portfolio management review | | |

| | | | |

| Delaware Corporate Bond Fund and Delaware Extended Duration Bond Fund | | | August 9, 2016 | |

| | | | |

| Performance preview (for the year ended July 31, 2016) | | | | |

Delaware Corporate Bond Fund (Institutional Class shares) | | 1-year return | | +6.18% |

Delaware Corporate Bond Fund (Class A shares) | | 1-year return | | +5.91% |

Bloomberg Barclays U.S. Corporate Investment Grade Index1 (benchmark) | | 1-year return | | +8.78% |

Past performance does not guarantee future results.

For complete, annualized performance for Delaware Corporate Bond Fund, please see the table on page 5. Institutional Class shares are available without sales or asset-based distribution charges only to certain eligible accounts. The performance of Class A shares excludes the applicable sales charge and reflects the reinvestment of all distributions. Please see page 7 for a description of the index.

Index performance returns do not reflect any management fees, transaction costs, or expenses. Indices are unmanaged and one cannot invest directly in an index.

| | | | |

Delaware Extended Duration Bond Fund (Institutional Class shares) | | 1-year return | | +12.26% |

Delaware Extended Duration Bond Fund (Class A shares) | | 1-year return | | +12.14% |

Bloomberg Barclays Long U.S. Corporate Index2 (benchmark) | | 1-year return | | +15.70% |

Past performance does not guarantee future results.

For complete, annualized performance for Delaware Extended Duration Bond Fund, please see the table on page 9. Institutional Class shares are available without sales or asset-based distribution charges only to certain eligible accounts. The performance of Class A shares excludes the applicable sales charge and reflects the reinvestment of all distributions. Please see page 12 for a description of the index.

Index performance returns do not reflect any management fees, transaction costs, or expenses. Indices are unmanaged and one cannot invest directly in an index.

1 Formerly known as the Barclays U.S. Corporate Investment Grade Index.

2 Formerly known as the Barclays Long U.S. Corporate Index.

To borrow a phrase from Charles Dickens, the Funds experienced a tale of two market environments during the fiscal year ended July 31, 2016.

For the first seven months of the Funds’ fiscal year – August 2015 through February 2016 – investment grade and high yield corporates lagged Treasury securities, by 2.96 percentage points and 9.68 percentage points, respectively (source: Barclays). The volatility in commodity prices that continued from the previous fiscal year appeared to be a contributing factor. China’s currency devaluation in August 2015, coming amid further signs of a slowdown in the country’s economy, further exacerbated corporate bond performance. New-issue supply was substantial across the board due to debt-financed mergers and

acquisitions. Typical of issuer behavior late in the credit cycle, share buybacks also increased. The combination of oversupply and global growth concerns put pressure on virtually every sector of the corporate bond market.

At the beginning of March 2016, however, the corporate market experienced a shift that lasted through the end of the fiscal year. During the final five months of the Funds’ fiscal year, investment grade corporate credits and high yield outperformed Treasurys by 4.72 percentage points and 11.48 percentage points, respectively (source: Barclays).

The proximate cause for this reversal was the European Central Bank’s (ECB’s) announcement of a quantitative-easing program that increased its

1

Portfolio management review

Delaware Corporate Bond Fund and Delaware Extended Duration Bond Fund

monthly bond purchases by 20 billion euros, equally divided between corporate credit and sovereign paper. This stimulus provided tsunami-like technical support for corporate credit prices, which in turn triggered a worldwide grab for yield. Government bonds in major markets such as Japan and Germany experienced negative yields, while France’s bellwether 10-year bond yield was barely in positive territory at the end of the fiscal year.

Another important reversal occurred in the energy sector, which had performed poorly in the first half of the fiscal year. Thanks to improved market technicals and a rebound in oil prices during the first quarter of 2016, energy companies were able to access the capital market, which had positive fundamental implications (source: Bloomberg).

Fund performance

For the fiscal year ended July 31, 2016, Delaware Corporate Bond Fund underperformed its benchmark, the Bloomberg Barclays U.S. Corporate Investment Grade Index. The Fund’s Institutional Class shares returned +6.18%. The Fund’s Class A shares returned +5.91% at net asset value and +1.21% at maximum offer price. These figures reflect all distributions reinvested. During the same period, the Fund’s benchmark returned +8.78%. For complete annualized performance of Delaware Corporate Bond Fund, please see the table on page 5.

During the same period, Delaware Extended Duration Bond Fund underperformed its benchmark, the Bloomberg Barclays Long U.S. Corporate Index. The Fund’s Institutional Class shares returned +12.26%. The Fund’s Class A shares returned +12.14% at net asset value and +7.03% at maximum offer price. These figures reflect all distributions reinvested. During the same period, the Fund’s benchmark returned +15.70%. For complete annualized performance of

Delaware Extended Duration Bond Fund, please see the table on page 9.

Delaware Corporate Bond Fund

Careful analysis of the fundamentals specific to each credit, evaluating both risk and opportunity, guides our security selection process for the Fund.

Most of the Fund’s underperformance occurred during the first half of the fiscal year. Our reading of the fundamentals – including rising interest rates and firming oil prices – gave us confidence that the credit cycle would support more risk. Believing high yield bonds would be an attractive allocation, we had increased the Fund’s holdings to 16% of the portfolio by the beginning of the fiscal year. (The Fund’s investment policy allows a 20% maximum high yield exposure.) We also had modestly increased the Fund’s energy sector exposure to 12%.

Unfortunately, the global economic backdrop deteriorated significantly in August 2015, with the unexpected devaluation of China’s currency and news of oversupply in the oil markets. Default expectations for high yield increased, and that placed tremendous technical selling pressure on the entire asset class, given its exposure to commodity-driven sectors. We cut the Fund’s high yield exposure from 16% to 9%, and its energy exposure from 12% to 5%, based on our concern with the potential for further declines in valuations.

At the same time, we increased the Fund’s allocation to cash and Treasurys to prepare for potential opportunities late in the first quarter or early in the second quarter of 2016. Thanks to the ECB’s surprise move, the market snapped back more quickly than we had anticipated. Although we did not catch the entire upward move, we were poised to reinvest and the Fund had strong absolute performance in the second half of the fiscal year.

The Fund’s weakest-performing sector was energy, where it detracted 0.95% from the Fund’s

2

overall performance due to poor security selection. The Fund owned Chesapeake Energy based on our view of the quality of its assets that could be used for deleveraging. However, late in 2015, Chesapeake proposed a debt exchange offer to certain of its creditors; we viewed this move as detrimental to our investment thesis, and we accordingly exited the position.

The Fund also underperformed in the communications sector, which contained some of the Fund’s problematic high yield credits. iHeartCommunications, Intelsat, and Abengoa all had plans in place to clean up their balance sheets; however, these plans did not materialize. We exited all three positions during the fiscal year.

Also in the communications sector, Charter Communications was one of the Fund’s strongest performers. We took positions in Charter Communications’ secured bonds when the company announced its plan to acquire Bright House Networks – and thereafter Time Warner Cable – to become the second-largest cable company in the United States.

Anheuser-Busch InBev also performed well following its proposed acquisition of SABMiller. We consider this a textbook example of a company taking on leverage to finance a deal that we view as having the potential to produce sufficient free cash flow over the next few years to return it to low, pre-merger leverage levels.

Lastly, long-dated Verizon Communications bonds were a meaningful contributor to the Fund’s performance. Verizon, in our view, remains committed to improving its balance sheet as evidenced by its modest deleveraging, disciplined approach to acquisitions, and transparency to investors.

The Fund’s use of derivatives was relatively modest during the fiscal period. We used Treasury futures to hedge duration. This strategy averaged 0.25% on a notional basis throughout the fiscal year, and we closed the position before the end of

the period. (Notional value is the face amount of a security that is used to calculate the payout on a derivative contract of that underlying security at settlement.) The Fund also held a single name 5-year credit default swap (CDS) instrument to hedge the risk of further declines in oil prices. This position averaged 0.30% on a notional basis during the fiscal year, and we held it at the end of the fiscal year. Altogether, the use of derivatives cost the Fund 0.05% in relative performance.

Delaware Extended Duration Bond Fund

As with Delaware Corporate Bond Fund, careful analysis of the fundamentals specific to each credit, evaluating both risk and opportunity, guides our security selection process for the Fund. During periods in the markets when momentum-driven investing holds sway over fundamentals, conservative positioning within investment grade corporates tends to underperform the Fund’s benchmark.

This appeared to be the case for the fiscal year. Our conservative bias was pervasive across multiple industries, but was particularly pronounced in the Fund’s energy holdings. The commodity sector, which includes energy, makes up an important part of the overall longer-dated corporate market. Investors’ willingness to invest in lower-quality energy issues provided a significant boost to the benchmark’s returns. The Fund’s significant underweight in energy during the fiscal period seemed to play a meaningful role in its underperformance.

Within the Fund’s underweight allocation to energy holdings, we focused on midstream assets such as pipeline companies. Because they generally have more of a volume-driven business than a commodity-price-sensitive business, we viewed these companies as suitable Fund investments while adhering to our discipline. Nonetheless, this segment of the market moved lower. Pipeline companies Williams Partners, Energy Transfer Partners, and Enbridge Energy

3

Portfolio management review

Delaware Corporate Bond Fund and Delaware Extended Duration Bond Fund

Partners all detracted from Fund performance. We sold the Williams and Enbridge positions during the fiscal year.

Our conservative bias included underweight positions compared to the benchmark in what were the outperforming communications and basic industries sectors. Methanol producer Methanex, one of the Fund’s basic industries holdings, performed poorly in relative terms. The Fund’s lack of exposure to the metals and mining sector, which rebounded in conjunction with energy, also detracted from relative performance.

The Fund’s exposure to the electric utility sector was a strong contributor to Fund performance. Nearly 20% of the portfolio was held in electrics. This sector is somewhat more sensitive to changes in interest rates, and the Fund benefited when U.S. Treasurys rallied. Holdings in this space that performed well included Duke Energy and Appalachian Power.

The Fund also benefited from its allocation to broker–asset managers; Jefferies Group in

particular performed well. The Fund’s positions in noncorporate issues, including foreign local governments, also helped performance. U.S.-domiciled taxable municipal issues Long Island (N.Y.) Power Authority and Oregon Department of Transportation were among the Fund’s standout performers. The long maturity aspect and high-quality nature of these assets helped them outperform the broader market.

During the fiscal year, we used derivatives to manage the Fund’s underlying yield-curve risk and the overall duration of the portfolio. This was accomplished primarily through U.S. Treasury futures, and we maintained exposure to these futures at fiscal year end. Additionally, the Fund utilized credit default swaps to hedge volatility of the credit positions within the portfolio. Derivatives contributed to the Fund’s performance but accounted for less than 0.50% of performance at the portfolio level.

4

| | |

| Performance summaries | | |

| Delaware Corporate Bond Fund | | July 31, 2016 |

The performance data quoted represent past performance; past performance does not guarantee future results. Investment return and principal value will fluctuate so your shares, when redeemed, may be worth more or less than their original cost. Please obtain the performance data current for the most recent month end by calling 800 523-1918 or visiting our website at delawareinvestments.com/performance. Current performance may be lower or higher than the performance data quoted.

| | | | | | |

| Fund and benchmark performance1,2 | | Average annual total returns through July 31, 2016 |

| | | | | | | | | | | | |

| | | 1 year | | | 5 years | | | 10 years | |

Class A (Est. Sept. 15, 1998) | | | | | | | | | | | | |

Excluding sales charge | | | +5.91 | % | | | +5.44 | % | | | +7.11 | % |

Including sales charge | | | +1.21 | % | | | +4.46 | % | | | +6.61 | % |

Class C (Est. Sept. 15, 1998) | | | | | | | | | | | | |

Excluding sales charge | | | +5.12 | % | | | +4.66 | % | | | +6.31 | % |

Including sales charge | | | +4.12 | % | | | +4.66 | % | | | +6.31 | % |

Class R (Est. June 2, 2003) | | | | | | | | | | | | |

Excluding sales charge | | | +5.47 | % | | | +5.18 | % | | | +6.84 | % |

Including sales charge | | | +5.47 | % | | | +5.18 | % | | | +6.84 | % |

Institutional Class (Est. Sept. 15, 1998) | | | | | | | | | | | | |

Excluding sales charge | | | +6.18 | % | | | +5.70 | % | | | +7.39 | % |

Including sales charge | | | +6.18 | % | | | +5.70 | % | | | +7.39 | % |

Bloomberg Barclays U.S. Corporate

Investment Grade Index | | | +8.78 | % | | | +5.21 | % | | | +6.24 | % |

1Returns reflect the reinvestment of all distributions and are presented both with and without the applicable sales charges described below. Returns do not reflect the deduction of taxes the shareholder would pay on Fund distributions or redemptions of Fund shares.

Expense limitations were in effect for certain classes during some or all of the periods shown in the “Fund and benchmark performance” table. Expenses for each class are listed on the “Fund expense ratios” table on page 6. Performance would have been lower had expense limitations not been in effect.

Institutional Class shares are available without sales or asset-based distribution charges only to certain eligible accounts.

Class A shares are sold with a maximum front-end sales charge of 4.50%, and have an annual distribution and service fee of 0.25% of average daily net assets. Performance for Class A shares, excluding sales charges, assumes that no front-end sales charge applied.

Class C shares are sold with a contingent deferred sales charge of 1.00% if redeemed during the first 12 months. They are also subject to an annual distribution and service fee of 1.00% of average daily net assets. Performance for Class C shares, excluding sales charges, assumes either that contingent deferred sales charges did not apply or that the investment was not redeemed.

Class R shares are available only for certain retirement plan products. They are sold without a sales charge and have an annual distribution and service fee of 0.50% of average daily net assets.

5

Performance summaries

Delaware Corporate Bond Fund

Fixed income securities and bond funds can lose value, and investors can lose principal, as interest rates rise. They also may be affected by economic conditions that hinder an issuer’s ability to make interest and principal payments on its debt.

The Fund may also be subject to prepayment risk, the risk that the principal of a fixed income security that is held by the Fund may be prepaid prior to maturity, potentially forcing the Fund to reinvest that money at a lower interest rate.

International investments entail risks not ordinarily associated with U.S. investments including fluctuation in currency values, differences in accounting principles, or economic or political instability in other nations.

Investing in emerging markets can be riskier than investing in established foreign markets due to increased volatility and lower trading volume.

High yielding, non-investment-grade bonds (junk bonds) involve higher risk than investment grade bonds.

If and when the Fund invests in forward foreign currency contracts or uses other investments to hedge against currency risks, the Fund will be subject to special risks, including counterparty risk.

The Fund may experience portfolio turnover in excess of 100%, which could result in higher transaction costs and tax liability.

The Fund may invest in derivatives, which may involve additional expenses and are subject to risk, including the risk that an underlying security or securities index moves in the opposite direction from what the portfolio manager anticipated. A derivative transaction depends upon the counterparties’ ability to fulfill their contractual obligations.

2 The Fund’s expense ratios, as described in the most recent prospectus, are disclosed in the following “Fund expense ratios” table. Delaware Management Company has agreed to reimburse certain expenses and/or waive certain fees in order to prevent total annual fund operating expenses (excluding any 12b-1 fees, acquired fund fees and expenses, taxes, interest, short sale and dividend interest expenses, brokerage fees, certain insurance costs, and nonroutine expenses or costs, including, but not limited to, those relating to reorganizations, litigation, conducting shareholder meetings, and liquidations (collectively, nonroutine expenses)) from exceeding 0.69% of the Fund’s average daily net assets during the period from Aug. 1, 2015 through July 31, 2016.* Please see the most recent prospectus and any applicable supplement(s) for additional information on these fee waivers and/or reimbursements.

| | | | | | | | |

Fund expense ratios | | Class A | | Class C | | Class R | | Institutional Class |

Total annual operating expenses | | 0.95% | | 1.70% | | 1.20% | | 0.70% |

(without fee waivers) | | | | | | | | |

Net expenses | | 0.94% | | 1.69% | | 1.19% | | 0.69% |

(including fee waivers, if any) | | | | | | | | |

Type of waiver | | Contractual | | Contractual | | Contractual | | Contractual |

| | | | | | | | | |

*The aggregate contractual waiver period covering this report is from Nov. 28, 2014, through Nov. 28, 2016.

6

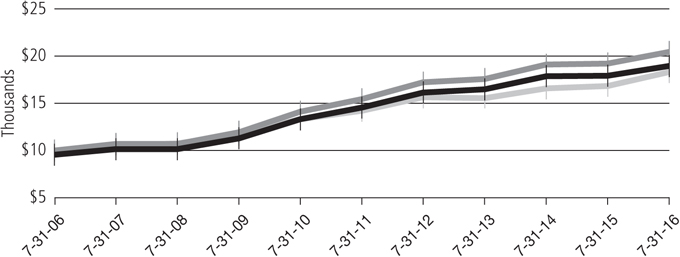

Performance of a $10,000 investment1

Average annual total returns from July 31, 2006, through July 31, 2016

| | | | | | | | | | |

For period beginning July 31, 2006, through July 31, 2016 | | Starting value | | | Ending value | |

Delaware Corporate Bond Fund — Institutional Class shares Delaware Corporate Bond Fund — Institutional Class shares

| | | $10,000 | | | | $20,405 | |

Delaware Corporate Bond Fund — Class A shares Delaware Corporate Bond Fund — Class A shares

| | | $9,550 | | | | $18,968 | |

Bloomberg Barclays U.S. Corporate Investment Grade Index Bloomberg Barclays U.S. Corporate Investment Grade Index

| | | $10,000 | | | | $18,310 | |

1 The “Performance of a $10,000 investment” graph assumes $10,000 invested in Institutional Class and Class A shares of the Fund on July 31, 2006, and includes the effect of a 4.50% front-end sales charge (for Class A shares) and the reinvestment of all distributions. The graph does not reflect the deduction of taxes the shareholders would pay on Fund distributions or redemptions of Fund shares. Expense limitations were in effect for some or all of the periods shown. Performance would have been lower had expense limitations not been in effect. Expenses are listed in the “Fund expense ratios” table on page 6. Please note additional details on pages 5 through 8.

The graph also assumes $10,000 invested in the Bloomberg Barclays U.S. Corporate Investment Grade Index as of July 31, 2006. The Bloomberg Barclays U.S. Corporate Investment Grade Index (formerly known as the Barclays U.S. Corporate Investment Grade Index) is composed of U.S. dollar-denominated, investment grade, SEC-registered corporate bonds issued by industrial, utility, and financial companies. All bonds in the index have at least one year to maturity.

Index performance returns do not reflect any management fees, transaction costs, or expenses. Indices are unmanaged and one cannot invest directly in an index. Past performance is not a guarantee of future results.

Performance of other Fund classes will vary due to different charges and expenses.

7

Performance summaries

Delaware Corporate Bond Fund

| | | | | | |

| | | Nasdaq symbols | | CUSIPs | | |

Class A | | DGCAX | | 245908785 | | |

Class C | | DGCCX | | 245908769 | | |

Class R | | DGCRX | | 245908744 | | |

Institutional Class | | DGCIX | | 245908751 | | |

8

| | | | |

| Performance summaries | | | | |

| Delaware Extended Duration Bond Fund | | | July 31, 2016 | |

The performance data quoted represent past performance; past performance does not guarantee future results. Investment return and principal value will fluctuate so your shares, when redeemed, may be worth more or less than their original cost. Please obtain the performance data current for the most recent month end by calling 800 523-1918 or visiting our website at delawareinvestments.com/performance. Current performance may be lower or higher than the performance data quoted.

| | | | | | | | | | | | | | | | |

| Fund and benchmark performance1,2 | | Average annual total returns through July 31, 2016 | |

| | | 1 year | | | 5 years | | | 10 years | | | Lifetime | |

Class A (Est. Sept. 15, 1998) | | | | | | | | | | | | | | | | |

Excluding sales charge | | | +12.14 | % | | | +8.85 | % | | | +9.76 | % | | | +8.52 | % |

Including sales charge | | | +7.03 | % | | | +7.85 | % | | | +9.26 | % | | | +8.24 | % |

Class C (Est. Sept. 15, 1998) | | | | | | | | | | | | | | | | |

Excluding sales charge | | | +11.14 | % | | | +8.01 | % | | | +8.92 | % | | | +7.72 | % |

Including sales charge | | | +10.14 | % | | | +8.01 | % | | | +8.92 | % | | | +7.72 | % |

Class R (Est. Oct. 3, 2005) | | | | | | | | | | | | | | | | |

Excluding sales charge | | | +11.84 | % | | | +8.57 | % | | | +9.50 | % | | | +8.47 | % |

Including sales charge | | | +11.84 | % | | | +8.57 | % | | | +9.50 | % | | | +8.47 | % |

Institutional Class (Est. Sept. 15, 1998) | | | | | | | | | | | | | | | | |

Excluding sales charge | | | +12.26 | % | | | +9.09 | % | | | +10.01 | % | | | +8.78 | % |

Including sales charge | | | +12.26 | % | | | +9.09 | % | | | +10.01 | % | | | +8.78 | % |

Class R6 (Est. May 2, 2016) | | | | | | | | | | | | | | | | |

Excluding sales charge | | | n/a | | | | n/a | | | | n/a | | | | +7.20 | % |

Including sales charge | | | n/a | | | | n/a | | | | n/a | | | | +7.20 | % |

Bloomberg Barclays Long U.S. Corporate Index* | | | +15.70 | % | | | +8.15 | % | | | +8.21 | % | | | +7.16 | % |

*The benchmark lifetime return is for Class A share comparison only and is calculated using the last business day in the month of the Fund’s Class A inception date.

1Returns reflect the reinvestment of all distributions and are presented both with and without the applicable sales charges described below. Returns do not reflect the deduction of taxes the shareholder would pay on Fund distributions or redemptions of Fund shares.

Expense limitations were in effect for certain classes during some or all of the periods shown in the “Fund and benchmark performance” table. Expenses for each class are listed on the “Fund expense ratios” table on page 11. Performance would have been lower had expense limitations not been in effect.

Institutional Class shares are available without sales or asset-based distribution charges only to certain eligible accounts.

Class A shares are sold with a maximum front-end sales charge of 4.50%, and have an annual distribution and service fee of 0.25% of average daily net assets. Performance for Class A shares, excluding sales charges, assumes that no front-end sales charge applied.

Class C shares are sold with a contingent deferred sales charge of 1.00% if redeemed during the first 12 months. They are also subject to an annual

9

Performance summaries

Delaware Extended Duration Bond Fund

distribution and service fee of 1.00% of average daily net assets. Performance for Class C shares, excluding sales charges, assumes either that contingent deferred sales charges did not apply or that the investment was not redeemed.

Class R shares are available only for certain retirement plan products. They are sold without a sales charge and have an annual distribution and service fee of 0.50% of average daily net assets.

Class R6 shares are available only to certain investors.

Fixed income securities and bond funds can lose value, and investors can lose principal, as interest rates rise. They also may be affected by economic conditions that hinder an issuer’s ability to make interest and principal payments on its debt.

The Fund may also be subject to prepayment risk, the risk that the principal of a fixed income security that is held by the Fund may be prepaid prior to maturity, potentially forcing the Fund to reinvest that money at a lower interest rate.

International investments entail risks not ordinarily associated with U.S. investments including fluctuation in currency values, differences in

accounting principles, or economic or political instability in other nations.

Investing in emerging markets can be riskier than investing in established foreign markets due to increased volatility and lower trading volume.

High yielding, non-investment-grade bonds (junk bonds) involve higher risk than investment grade bonds.

If and when the Fund invests in forward foreign currency contracts or uses other investments to hedge against currency risks, the Fund will be subject to special risks, including counterparty risk.

The Fund may experience portfolio turnover in excess of 100%, which could result in higher transaction costs and tax liability.

The Fund may invest in derivatives, which may involve additional expenses and are subject to risk, including the risk that an underlying security or securities index moves in the opposite direction from what the portfolio manager anticipated. A derivative transaction depends upon the counterparties’ ability to fulfill their contractual obligations.

10

2 The Fund’s expense ratios, as described in the most recent prospectus, are disclosed in the following “Fund expense ratios” table. Delaware Management Company has agreed to reimburse certain expenses and/or waive certain fees in order to prevent total annual fund operating expenses (excluding any 12b-1 fees, acquired fund fees and expenses, taxes, interest, short sale and dividend interest expenses, brokerage fees, certain insurance costs, and nonroutine expenses or costs, including, but not limited to, those relating to reorganizations, litigation, conducting shareholder meetings, and liquidations (collectively, nonroutine expenses)) from exceeding 0.71% of the Fund’s average daily net assets for all share classes other than Class R6 from Aug. 1, 2015 through July 31, 2016,* and 0.63% of the Fund’s Class R6 shares’ average daily net assets from April 30, 2016 (Class R6 inception date) through July 31, 2016.* Please see the most recent prospectus and any applicable supplement(s) for additional information on these fee waivers and/or reimbursements.

| | | | | | | | | | |

Fund expense ratios | | Class A | | Class C | | Class R | | Institutional Class | | Class R6 |

Total annual operating expenses | | 1.00% | | 1.75% | | 1.25% | | 0.75% | | 0.67% |

(without fee waivers) | | | | | | | | | | |

Net expenses | | 0.96% | | 1.71% | | 1.21% | | 0.71% | | 0.63% |

(including fee waivers, if any) | | | | | | | | | | |

Type of waiver | | Contractual | | Contractual | | Contractual | | Contractual | | Contractual |

|

*The aggregate contractual waiver period covering this report is from Nov. 28, 2014, through April 30, 2017.

11

Performance summaries

Delaware Extended Duration Bond Fund

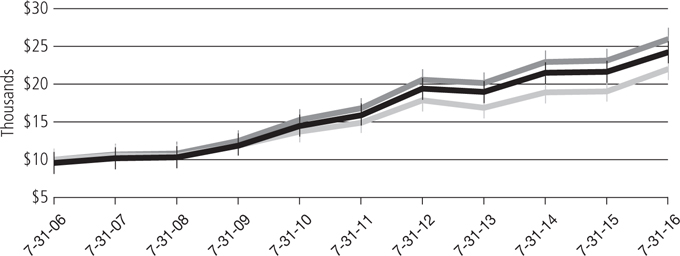

Performance of a $10,000 investment1

Average annual total returns from July 31, 2006, through July 31, 2016

| | | | | | | | | | |

For period beginning July 31, 2006, through July 31, 2016 | | Starting value | | | Ending value | |

Delaware Extended Duration Bond Fund — Institutional Class shares | | | $10,000 | | | | $25,949 | |

Delaware Extended Duration Bond Fund — Class A shares | | | $9,550 | | | | $24,249 | |

Bloomberg Barclays Long U.S. Corporate Index | | | $10,000 | | | | $22,023 | |

1The “Performance of a $10,000 investment” graph assumes $10,000 invested in Institutional Class and Class A shares of the Fund on July 31, 2006, and includes the effect of a 4.50% front-end sales charge (for Class A shares) and the reinvestment of all distributions. The graph does not reflect the deduction of taxes the shareholders would pay on Fund distributions or redemptions of Fund shares. Expense limitations were in effect for some or all of the periods shown. Performance would have been lower had expense limitations not been in effect. Expenses are listed in the “Fund expense ratios” table on page 11. Please note additional details on pages 9 through 13.

The graph also assumes $10,000 invested in the Bloomberg Barclays Long U.S. Corporate Index as of July 31, 2006. The Bloomberg Barclays Long U.S. Corporate Index (formerly known as the Barclays Long U.S. Corporate Index) is composed of U.S. dollar-denominated, investment grade, SEC-registered corporate bonds issued by industrial, utility, and financial companies. All bonds in the index have at least 10 years to maturity.

Index performance returns do not reflect any management fees, transaction costs, or expenses. Indices are unmanaged and one cannot invest directly in an index. Past performance is not a guarantee of future results.

Performance of other Fund classes will vary due to different charges and expenses.

12

| | | | | | |

| | | Nasdaq symbols | | CUSIPs | | |

Class A | | DEEAX | | 245908835 | | |

Class C | | DEECX | | 245908819 | | |

Class R | | DEERX | | 245908728 | | |

Institutional Class | | DEEIX | | 245908793 | | |

Class R6 | | DEZRX | | 245908629 | | |

13

Disclosure of Fund expenses

For the six-month period from February 1, 2016 to July 31, 2016 (Unaudited)

As a shareholder of a Fund, you incur two types of costs: (1) transaction costs, including sales charges (loads) on purchase payments, reinvested dividends, or other distributions; redemption fees; and exchange fees; and (2) ongoing costs, including management fees; distribution and/or service (12b-1) fees; and other Fund expenses. These following examples are intended to help you understand your ongoing costs (in dollars) of investing in a Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The examples are based on an investment of $1,000 invested at the beginning of the period and held for the entire six-month period from Feb. 1, 2016 to July 31, 2016.

Actual expenses

The first section of the tables shown, “Actual Fund return,” provides information about actual account values and actual expenses. You may use the information in this section of the table, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first section under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical example for comparison purposes

The second section of the tables shown, “Hypothetical 5% return,” provides information about hypothetical account values and hypothetical expenses based on the Funds’ actual expense ratios and an assumed rate of return of 5% per year before expenses, which is not the Funds’ actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in each Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the tables are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads), redemption fees, or exchange fees. Therefore, the second section of each table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher. The Funds’ expenses shown in the tables reflect fee waivers in effect. The expenses shown in each table assume reinvestment of all dividends and distributions.

14

Delaware Corporate Bond Fund

Expense analysis of an investment of $1,000

| | | | | | | | | | | | | | | | |

| | | Beginning Account Value 2/1/16 | | | Ending Account Value 7/31/16 | | | Annualized Expense Ratio | | | Expenses Paid During Period 2/1/16 to 7/31/16* | |

Actual Fund return† | | | | | | | | | | | | | | | | |

Class A | | | $1,000.00 | | | | $1,078.20 | | | | 0.94% | | | | $4.86 | |

Class C | | | 1,000.00 | | | | 1,074.20 | | | | 1.69% | | | | 8.72 | |

Class R | | | 1,000.00 | | | | 1,076.80 | | | | 1.19% | | | | 6.14 | |

Institutional Class | | | 1,000.00 | | | | 1,079.50 | | | | 0.69% | | | | 3.57 | |

Hypothetical 5% return (5% return before expenses) | |

Class A | | | $1,000.00 | | | | $1,020.19 | | | | 0.94% | | | | $4.72 | |

Class C | | | 1,000.00 | | | | 1,016.46 | | | | 1.69% | | | | 8.47 | |

Class R | | | 1,000.00 | | | | 1,018.95 | | | | 1.19% | | | | 5.97 | |

Institutional Class | | | 1,000.00 | | | | 1,021.43 | | | | 0.69% | | | | 3.47 | |

15

Disclosure of Fund expenses

For the six-month period from February 1, 2016 to July 31, 2016 (Unaudited)

Delaware Extended Duration Bond Fund

Expense analysis of an investment of $1,000

| | | | | | | | | | | | | | | | |

| | | Beginning Account Value 2/1/16 | | | Ending Account Value 7/31/16 | | | Annualized Expense Ratio | | | Expenses Paid During Period 2/1/16 to 7/31/16* | |

Actual Fund return† | | | | | | | | | | | | | | | | |

Class A | | | $1,000.00 | | | | $1,128.20 | | | | 0.96% | | | | $5.08 | |

Class C | | | 1,000.00 | | | | 1,124.20 | | | | 1.71% | | | | 9.03 | |

Class R | | | 1,000.00 | | | | 1,126.60 | | | | 1.21% | | | | 6.40 | |

Institutional Class | | | 1,000.00 | | | | 1,128.10 | | | | 0.71% | | | | 3.76 | |

Class R6** | | | 1,000.00 | | | | 1,072.00 | | | | 0.63% | | | | 1.60 | |

Hypothetical 5% return (5% return before expenses) | |

Class A | | | $1,000.00 | | | | $1,020.09 | | | | 0.96% | | | | $4.82 | |

Class C | | | 1,000.00 | | | | 1,016.36 | | | | 1.71% | | | | 8.57 | |

Class R | | | 1,000.00 | | | | 1,018.85 | | | | 1.21% | | | | 6.07 | |

Institutional Class | | | 1,000.00 | | | | 1,021.33 | | | | 0.71% | | | | 3.57 | |

Class R6** | | | 1,000.00 | | | | 1,021.73 | | | | 0.63% | | | | 3.17 | |

| * | “Expenses Paid During Period” are equal to the relevant Fund’s annualized expense ratio, multiplied by the average account value over the period, multiplied by 182/366 (to reflect the one-half year period). |

| † | Because actual returns reflect only the most recent six-month period, the returns shown may differ significantly from fiscal year returns. |

| ** | The Class R6 shares commenced operations on May 2, 2016. The ending account value for “Actual” uses the performance since inception and is not annualized and the expenses paid during the period for “Actual” are equal to the Class R6 annualized expense ratio, multiplied by the average account value over the period, multiplied by 90/366 (to reflect the actual days since inception). |

16

| | | | |

| Security type / sector allocations | | | | |

| Delaware Corporate Bond Fund | | | As of July 31, 2016 (Unaudited) | |

Sector designations may be different than the sector designations presented in other Fund materials. The sector designations may represent the investment manager’s internal sector classifications, which may result in the sector designations for one fund being different than another fund’s sector designations.

| | | | |

Security type / sector | | Percentage of net assets | |

Convertible Bonds | | | 0.73% | |

Corporate Bonds | | | 93.89% | |

Banking | | | 18.14% | |

Basic Industry | | | 5.06% | |

Brokerage | | | 1.32% | |

Capital Goods | | | 1.90% | |

Communications | | | 13.50% | |

Consumer Cyclical | | | 4.62% | |

Consumer Non-Cyclical | | | 12.52% | |

Electric | | | 11.63% | |

Energy | | | 6.89% | |

Finance Companies | | | 2.92% | |

Insurance | | | 2.62% | |

Natural Gas | | | 0.81% | |

Real Estate Investment Trusts | | | 3.54% | |

Technology | | | 4.88% | |

Transportation | | | 3.54% | |

Municipal Bond | | | 0.74% | |

Senior Secured Loans | | | 1.21% | |

Sovereign Bond | | | 0.14% | |

U.S. Treasury Obligation | | | 0.21% | |

Preferred Stock | | | 2.20% | |

Short-Term Investments | | | 0.86% | |

Total Value of Securities | | | 99.98% | |

Receivables and Other Assets Net of Liabilities | | | 0.02% | |

Total Net Assets | | | 100.00% | |

17

| | | | |

| Security type / sector allocations | | | | |

| Delaware Extended Duration Bond Fund | | | As of July 31, 2016 (Unaudited) | |

Sector designations may be different than the sector designations presented in other Fund materials. The sector designations may represent the investment manager’s internal sector classifications, which may result in the sector designations for one fund being different than another fund’s sector designations.

| | | | |

Security type / sector | | Percentage of net assets | |

Corporate Bonds | | | 91.52% | |

Banking | | | 14.61% | |

Basic Industry | | | 4.99% | |

Brokerage | | | 1.79% | |

Capital Goods | | | 2.79% | |

Communications | | | 11.78% | |

Consumer Cyclical | | | 6.66% | |

Consumer Non-Cyclical | | | 15.32% | |

Electric | | | 16.85% | |

Energy | | | 5.09% | |

Finance Companies | | | 0.45% | |

Insurance | | | 4.76% | |

Natural Gas | | | 0.94% | |

Real Estate Investment Trusts | | | 0.27% | |

Technology | | | 3.51% | |

Transportation | | | 1.71% | |

Municipal Bonds | | | 4.06% | |

U.S. Treasury Obligations | | | 0.73% | |

Preferred Stock | | | 1.90% | |

Short-Term Investments | | | 1.68% | |

Total Value of Securities | | | 99.89% | |

Receivables and Other Assets Net of Liabilities | | | 0.11% | |

Total Net Assets | | | 100.00% | |

18

Schedules of investments

| | | | |

Delaware Corporate Bond Fund | | | July 31, 2016 | |

| | | | | | | | |

| | | Principal amount° | | | Value (U.S. $) | |

| |

Convertible Bonds – 0.73% | | | | | | | | |

| |

Clearwire Communications 144A 8.25% exercise price | | | | | | | | |

$19.90, expiration date 12/1/40 # | | | 5,502,000 | | | $ | 5,722,080 | |

Meritor 4.00% exercise price $26.73, expiration date | | | | | | | | |

2/15/27 f | | | 2,603,000 | | | | 2,533,044 | |

| | | | | | | | |

Total Convertible Bonds (cost $8,118,344) | | | | | | | 8,255,124 | |

| | | | | | | | |

|

| |

Corporate Bonds – 93.89% | | | | | | | | |

| |

Banking – 18.14% | | | | | | | | |

Ally Financial 8.00% 11/1/31 | | | 1,840,000 | | | | 2,249,400 | |

Bank of America 4.45% 3/3/26 | | | 10,770,000 | | | | 11,589,198 | |

Bank of New York Mellon 4.625% 12/29/49 ● | | | 3,430,000 | | | | 3,430,000 | |

Branch Banking & Trust 3.625% 9/16/25 | | | 10,125,000 | | | | 10,959,472 | |

Capital One Financial 3.75% 7/28/26 | | | 8,400,000 | | | | 8,473,861 | |

Citizens Financial Group 4.30% 12/3/25 | | | 6,955,000 | | | | 7,396,566 | |

Compass Bank 3.875% 4/10/25 | | | 7,970,000 | | | | 7,705,563 | |

Cooperatieve Rabobank 3.75% 7/21/26 | | | 5,490,000 | | | | 5,516,456 | |

Credit Suisse Group 144A 6.25% 12/29/49 #● | | | 3,865,000 | | | | 3,749,607 | |

Credit Suisse Group Funding Guernsey | | | | | | | | |

144A 3.80% 6/9/23 # | | | 1,745,000 | | | | 1,773,149 | |

144A 4.55% 4/17/26 # | | | 12,330,000 | | | | 13,039,086 | |

Fifth Third Bancorp 2.875% 7/27/20 | | | 4,065,000 | | | | 4,234,063 | |

Fifth Third Bank 3.85% 3/15/26 | | | 9,115,000 | | | | 9,741,766 | |

JPMorgan Chase | | | | | | | | |

2.95% 10/1/26 | | | 4,230,000 | | | | 4,276,517 | |

4.25% 10/1/27 | | | 10,300,000 | | | | 11,125,071 | |

6.75% 1/29/49 ● | | | 4,000,000 | | | | 4,509,600 | |

KeyBank | | | | | | | | |

3.18% 5/22/22 | | | 5,495,000 | | | | 5,684,001 | |

3.40% 5/20/26 | | | 12,610,000 | | | | 12,990,444 | |

Morgan Stanley | | | | | | | | |

3.125% 7/27/26 | | | 9,375,000 | | | | 9,461,925 | |

3.95% 4/23/27 | | | 10,355,000 | | | | 10,719,931 | |

PNC Bank | | | | | | | | |

2.45% 11/5/20 | | | 3,455,000 | | | | 3,571,986 | |

2.60% 7/21/20 | | | 2,500,000 | | | | 2,597,010 | |

Popular 7.00% 7/1/19 | | | 4,475,000 | | | | 4,575,688 | |

Royal Bank of Scotland Group 8.00% 12/29/49 ● | | | 1,100,000 | | | | 1,095,875 | |

Santander UK Group Holdings 3.125% 1/8/21 | | | 2,595,000 | | | | 2,640,553 | |

State Street 3.55% 8/18/25 | | | 2,310,000 | | | | 2,542,090 | |

SVB Financial Group 3.50% 1/29/25 | | | 655,000 | | | | 655,133 | |

UBS 7.625% 8/17/22 | | | 7,555,000 | | | | 8,801,575 | |

UBS Group Funding Jersey | | | | | | | | |

144A 3.00% 4/15/21 # | | | 200,000 | | | | 206,094 | |

19

Schedules of investments

Delaware Corporate Bond Fund

| | | | | | | | |

| | | Principal amount° | | | Value (U.S. $) | |

| |

Corporate Bonds (continued) | | | | | | | | |

| |

Banking (continued) | | | | | | | | |

UBS Group Funding Jersey | | | | | | | | |

144A 4.125% 4/15/26 # | | | 1,430,000 | | | $ | 1,514,985 | |

US Bancorp | | | | | | | | |

2.375% 7/22/26 | | | 5,175,000 | | | | 5,189,438 | |

3.60% 9/11/24 | | | 6,730,000 | | | | 7,324,770 | |

USB Capital IX 3.50% 10/29/49 @● | | | 3,207,000 | | | | 2,762,029 | |

Wells Fargo | | | | | | | | |

4.30% 7/22/27 | | | 1,450,000 | | | | 1,589,742 | |

4.40% 6/14/46 | | | 7,960,000 | | | | 8,460,676 | |

Zions Bancorporation 4.50% 6/13/23 | | | 4,100,000 | | | | 4,291,462 | |

| | | | | | | | |

| | | | | | | 206,444,782 | |

| | | | | | | | |

Basic Industry – 5.06% | | | | | | | | |

BHP Billiton Finance USA 144A 6.25% 10/19/75 #● | | | 2,705,000 | | | | 2,934,925 | |

Dow Chemical 8.55% 5/15/19 | | | 4,420,000 | | | | 5,266,770 | |

Eastman Chemical | | | | | | | | |

3.80% 3/15/25 | | | 695,000 | | | | 738,388 | |

4.65% 10/15/44 | | | 10,815,000 | | | | 11,398,848 | |

Georgia-Pacific 8.00% 1/15/24 | | | 8,345,000 | | | | 11,220,979 | |

International Paper 5.15% 5/15/46 | | | 4,350,000 | | | | 5,046,753 | |

INVISTA Finance 144A 4.25% 10/15/19 # | | | 4,580,000 | | | | 4,568,170 | |

Mexichem 144A 5.875% 9/17/44 # | | | 3,595,000 | | | | 3,562,465 | |

NOVA Chemicals 144A 5.00% 5/1/25 # | | | 3,860,000 | | | | 3,927,550 | |

Rio Tinto Finance USA 3.75% 6/15/25 | | | 5,900,000 | | | | 6,349,497 | |

Vale Overseas 5.875% 6/10/21 | | | 2,445,000 | | | | 2,536,688 | |

| | | | | | | | |

| | | | | | | 57,551,033 | |

| | | | | | | | |

Brokerage – 1.32% | | | | | | | | |

Affiliated Managers Group 3.50% 8/1/25 | | | 4,135,000 | | | | 4,166,170 | |

Jefferies Group | | | | | | | | |

5.125% 1/20/23 | | | 255,000 | | | | 271,185 | |

6.45% 6/8/27 | | | 5,627,000 | | | | 6,298,678 | |

6.50% 1/20/43 | | | 1,575,000 | | | | 1,636,970 | |

Lazard Group | | | | | | | | |

3.75% 2/13/25 | | | 1,075,000 | | | | 1,087,611 | |

6.85% 6/15/17 | | | 1,525,000 | | | | 1,593,148 | |

| | | | | | | | |

| | | | | | | 15,053,762 | |

| | | | | | | | |

Capital Goods – 1.90% | | | | | | | | |

Ardagh Packaging Finance 144A 4.625% 5/15/23 # | | | 2,900,000 | | | | 2,932,625 | |

Eagle Materials 4.50% 8/1/26 | | | 840,000 | | | | 854,175 | |

Fortive 144A 3.15% 6/15/26 # | | | 4,325,000 | | | | 4,585,214 | |

Fortune Brands Home & Security 3.00% 6/15/20 | | | 2,865,000 | | | | 2,955,038 | |

HD Supply 144A 5.75% 4/15/24 # | | | 1,310,000 | | | | 1,398,229 | |

Masco 3.50% 4/1/21 | | | 3,835,000 | | | | 4,002,896 | |

20

| | | | | | | | |

| | | Principal amount° | | | Value (U.S. $) | |

| |

Corporate Bonds (continued) | | | | | | | | |

| |

Capital Goods (continued) | | | | | | | | |

Reynolds Group Issuer 144A 5.125% 7/15/23 # | | | 2,815,000 | | | $ | 2,906,488 | |

Waste Management 2.40% 5/15/23 | | | 1,995,000 | | | | 2,034,581 | |

| | | | | | | | |

| | | | | | | 21,669,246 | |

| | | | | | | | |

Communications – 13.50% | | | | | | | | |

21st Century Fox America 4.95% 10/15/45 | | | 4,300,000 | | | | 5,121,003 | |

Altice Luxembourg 144A 7.75% 5/15/22 # | | | 2,270,000 | | | | 2,311,201 | |

American Tower | | | | | | | | |

2.80% 6/1/20 | | | 4,730,000 | | | | 4,881,261 | |

4.00% 6/1/25 | | | 9,130,000 | | | | 9,944,442 | |

AT&T | | | | | | | | |

3.60% 2/17/23 | | | 3,140,000 | | | | 3,339,939 | |

4.35% 6/15/45 | | | 2,800,000 | | | | 2,815,134 | |

5.65% 2/15/47 | | | 6,130,000 | | | | 7,334,324 | |

CCO Holdings | | | | | | | | |

144A 5.50% 5/1/26 # | | | 2,565,000 | | | | 2,683,631 | |

144A 5.875% 4/1/24 # | | | 335,000 | | | | 358,450 | |

Charter Communications Operating 144A | | | | | | | | |

4.908% 7/23/25 # | | | 9,555,000 | | | | 10,569,129 | |

Comcast 2.35% 1/15/27 | | | 9,245,000 | | | | 9,268,760 | |

Crown Castle International 5.25% 1/15/23 | | | 4,295,000 | | | | 4,932,421 | |

Crown Castle Towers 144A 3.663% 5/15/25 # | | | 7,035,000 | | | | 7,316,470 | |

Digicel 144A 6.00% 4/15/21 # | | | 2,100,000 | | | | 1,960,875 | |

Digicel Group 144A 8.25% 9/30/20 # | | | 2,785,000 | | | | 2,555,237 | |

DISH DBS 144A 7.75% 7/1/26 # | | | 2,720,000 | | | | 2,827,100 | |

Gray Television 144A 5.875% 7/15/26 # | | | 2,645,000 | | | | 2,725,673 | |

Grupo Televisa 5.00% 5/13/45 | | | 4,770,000 | | | | 4,856,680 | |

GTP Acquisition Partners I 144A 2.35% 6/15/20 # | | | 2,130,000 | | | | 2,122,609 | |

Historic TW 6.875% 6/15/18 | | | 5,285,000 | | | | 5,819,335 | |

Level 3 Financing 144A 5.25% 3/15/26 # | | | 3,505,000 | | | | 3,675,869 | |

Neptune Finco 144A 6.625% 10/15/25 # | | | 2,125,000 | | | | 2,295,000 | |

SBA Tower Trust | | | | | | | | |

144A 2.24% 4/16/18 # | | | 4,945,000 | | | | 4,954,881 | |

144A 2.898% 10/15/19 # | | | 3,005,000 | | | | 3,042,506 | |

SFR Group 144A 6.00% 5/15/22 # | | | 1,270,000 | | | | 1,243,013 | |

Sky 144A 3.75% 9/16/24 # | | | 7,675,000 | | | | 8,162,501 | |

Time Warner Cable 7.30% 7/1/38 | | | 7,785,000 | | | | 10,192,270 | |

T-Mobile USA | | | | | | | | |

6.00% 4/15/24 | | | 950,000 | | | | 1,016,206 | |

6.50% 1/15/26 | | | 1,885,000 | | | | 2,048,524 | |

UPCB Finance IV 144A 5.375% 1/15/25 # | | | 1,600,000 | | | | 1,620,128 | |

Verizon Communications | | | | | | | | |

1.75% 8/15/21 | | | 7,000,000 | | | | 7,007,000 | |

21

Schedules of investments

Delaware Corporate Bond Fund

| | | | | | | | |

| | | Principal amount° | | | Value (U.S. $) | |

| |

Corporate Bonds (continued) | | | | | | | | |

| |

Communications (continued) | | | | | | | | |

Verizon Communications | | | | | | | | |

4.522% 9/15/48 | | | 9,865,000 | | | $ | 10,573,603 | |

WPP Finance 2010 5.625% 11/15/43 | | | 3,446,000 | | | | 4,162,361 | |

| | | | | | | | |

| | | | | | | 153,737,536 | |

| | | | | | | | |

Consumer Cyclical – 4.62% | | | | | | | | |

BMW U.S. Capital 144A 2.00% 4/11/21 # | | | 2,500,000 | | | | 2,543,453 | |

Boyd Gaming 144A 6.375% 4/1/26 # | | | 2,100,000 | | | | 2,249,625 | |

Ford Motor Credit 3.336% 3/18/21 | | | 2,640,000 | | | | 2,756,625 | |

General Motors Financial | | | | | | | | |

3.45% 4/10/22 | | | 4,155,000 | | | | 4,243,950 | |

5.25% 3/1/26 | | | 5,445,000 | | | | 6,090,984 | |

GEO Group 6.00% 4/15/26 | | | 2,720,000 | | | | 2,798,200 | |

Hyundai Capital America 144A 3.00% 3/18/21 # | | | 5,860,000 | | | | 6,081,039 | |

KFC Holding 144A 5.00% 6/1/24 # | | | 2,824,000 | | | | 2,958,140 | |

Marriott International 3.125% 6/15/26 | | | 7,310,000 | | | | 7,475,184 | |

MGM Growth Properties Operating Partnership 144A | | | | | | | | |

5.625% 5/1/24 # | | | 917,000 | | | | 984,399 | |

Starwood Hotels & Resorts Worldwide 3.75% 3/15/25 @ | | | 3,135,000 | | | | 3,326,188 | |

Walgreens Boots Alliance | | | | | | | | |

3.10% 6/1/23 | | | 9,520,000 | | | | 9,848,392 | |

4.80% 11/18/44 | | | 1,090,000 | | | | 1,238,451 | |

| | | | | | | | |

| | | | | | | 52,594,630 | |

| | | | | | | | |

Consumer Non-Cyclical – 12.52% | | | | | | | | |

AbbVie 3.20% 5/14/26 | | | 6,175,000 | | | | 6,346,375 | |

Anheuser-Busch InBev Finance 3.65% 2/1/26 | | | 12,865,000 | | | | 13,840,167 | |

AstraZeneca 3.375% 11/16/25 | | | 7,170,000 | | | | 7,699,153 | |

Biogen | | | | | | | | |

4.05% 9/15/25 | | | 1,200,000 | | | | 1,316,114 | |

5.20% 9/15/45 | | | 3,625,000 | | | | 4,361,875 | |

Celgene | | | | | | | | |

3.25% 8/15/22 | | | 2,315,000 | | | | 2,432,188 | |

3.875% 8/15/25 | | | 4,345,000 | | | | 4,722,724 | |

HCA 5.875% 2/15/26 | | | 2,660,000 | | | | 2,852,850 | |

HealthSouth 5.75% 11/1/24 | | | 2,405,000 | | | | 2,507,213 | |

JB y Cia 144A 3.75% 5/13/25 # | | | 8,965,000 | | | | 9,288,556 | |

Molson Coors Brewing | | | | | | | | |

2.10% 7/15/21 | | | 1,020,000 | | | | 1,034,739 | |

3.00% 7/15/26 | | | 2,865,000 | | | | 2,932,035 | |

4.20% 7/15/46 | | | 1,640,000 | | | | 1,735,527 | |

Mylan | | | | | | | | |

144A 3.15% 6/15/21 # | | | 1,930,000 | | | | 1,992,677 | |

144A 3.95% 6/15/26 # | | | 10,130,000 | | | | 10,570,027 | |

22

| | | | | | | | |

| | | Principal amount° | | | Value (U.S. $) | |

| |

Corporate Bonds (continued) | | | | | | | | |

| |

Consumer Non-Cyclical (continued) | | | | | | | | |

Pernod Ricard | | | | | | | | |

144A 3.25% 6/8/26 # | | | 7,100,000 | | | $ | 7,353,569 | |

144A 4.45% 1/15/22 # | | | 2,515,000 | | | | 2,783,552 | |

Perrigo Finance Unlimited 3.50% 12/15/21 | | | 2,710,000 | | | | 2,829,655 | |

Reynolds American | | | | | | | | |

4.00% 6/12/22 | | | 7,260,000 | | | | 7,973,026 | |

4.45% 6/12/25 | | | 6,720,000 | | | | 7,600,797 | |

Sigma Alimentos 144A 4.125% 5/2/26 # | | | 4,705,000 | | | | 4,893,200 | |

Sysco 3.30% 7/15/26 | | | 9,530,000 | | | | 10,091,574 | |

Tenet Healthcare 6.75% 6/15/23 | | | 2,700,000 | | | | 2,608,875 | |

Teva Pharmaceutical Finance Netherlands III | | | | | | | | |

2.20% 7/21/21 | | | 3,370,000 | | | | 3,390,938 | |

2.80% 7/21/23 | | | 3,530,000 | | | | 3,596,894 | |

3.15% 10/1/26 | | | 2,205,000 | | | | 2,258,229 | |

Thermo Fisher Scientific 3.00% 4/15/23 | | | 6,775,000 | | | | 7,000,506 | |

Universal Health Services 144A 4.75% 8/1/22 # | | | 2,170,000 | | | | 2,240,525 | |

Zimmer Biomet Holdings 4.45% 8/15/45 | | | 4,025,000 | | | | 4,320,254 | |

| | | | | | | | |

| | | | | | | 142,573,814 | |

| | | | | | | | |

Electric – 11.63% | | | | | | | | |

Ameren 3.65% 2/15/26 | | | 2,555,000 | | | | 2,778,673 | |

Ameren Illinois 9.75% 11/15/18 | | | 6,971,000 | | | | 8,248,770 | |

Appalachian Power | | | | | | | | |

3.40% 6/1/25 | | | 6,700,000 | | | | 7,202,306 | |

4.45% 6/1/45 | | | 2,850,000 | | | | 3,170,691 | |

Calpine 5.50% 2/1/24 | | | 3,155,000 | | | | 3,162,887 | |

Cleveland Electric Illuminating 5.50% 8/15/24 | | | 8,160,000 | | | | 9,809,634 | |

ComEd Financing III 6.35% 3/15/33 @ | | | 7,500,000 | | | | 7,963,387 | |

Commonwealth Edison 3.65% 6/15/46 | | | 5,075,000 | | | | 5,351,161 | |

Dominion Resources 3.90% 10/1/25 | | | 7,870,000 | | | | 8,572,917 | |

Duke Energy Ohio 3.70% 6/15/46 | | | 3,325,000 | | | | 3,538,166 | |

Electricite de France 144A 5.25% 12/29/49 #● | | | 4,860,000 | | | | 4,756,725 | |

Emera 6.75% 6/15/76 ● | | | 5,975,000 | | | | 6,471,003 | |

Emera US Finance 144A 4.75% 6/15/46 # | | | 1,870,000 | | | | 2,067,910 | |

Enel 144A 8.75% 9/24/73 #● | | | 4,125,000 | | | | 4,790,156 | |

Entergy 4.00% 7/15/22 | | | 1,620,000 | | | | 1,759,364 | |

Entergy Louisiana 3.78% 4/1/25 | | | 7,220,000 | | | | 7,844,479 | |

ITC Holdings 3.25% 6/30/26 | | | 4,355,000 | | | | 4,452,160 | |

Kansas City Power & Light 3.65% 8/15/25 | | | 10,115,000 | | | | 10,849,561 | |

National Rural Utilities Cooperative Finance | | | | | | | | |

5.25% 4/20/46 ● | | | 1,790,000 | | | | 1,893,641 | |

NV Energy 6.25% 11/15/20 | | | 4,475,000 | | | | 5,315,222 | |

Pennsylvania Electric 5.20% 4/1/20 | | | 8,131,000 | | | | 8,838,421 | |

23

Schedules of investments

Delaware Corporate Bond Fund

| | | | | | | | |

| | | Principal amount° | | | Value (U.S. $) | |

| |

Corporate Bonds (continued) | | | | | | | | |

| |

Electric (continued) | | | | | | | | |

Southern | | | | | | | | |

3.25% 7/1/26 | | | 8,340,000 | | | $ | 8,740,078 | |

4.40% 7/1/46 | | | 2,355,000 | | | | 2,620,211 | |

Trans-Allegheny Interstate Line 144A 3.85% 6/1/25 # | | | 2,000,000 | | | | 2,146,736 | |

| | | | | | | | |

| | | | | | | 132,344,259 | |

| | | | | | | | |

Energy – 6.89% | | | | | | | | |

Anadarko Petroleum 5.55% 3/15/26 | | | 2,325,000 | | | | 2,542,613 | |

ConocoPhillips | | | | | | | | |

4.95% 3/15/26 | | | 5,905,000 | | | | 6,579,445 | |

5.95% 3/15/46 | | | 2,400,000 | | | | 2,905,339 | |

Energy Transfer Partners | | | | | | | | |

4.75% 1/15/26 | | | 3,215,000 | | | | 3,291,585 | |

6.125% 12/15/45 | | | 770,000 | | | | 809,385 | |

EnLink Midstream Partners | | | | | | | | |

2.70% 4/1/19 | | | 5,895,000 | | | | 5,778,639 | |

4.85% 7/15/26 | | | 1,705,000 | | | | 1,660,510 | |

Enterprise Products Operating | | | | | | | | |

3.95% 2/15/27 | | | 3,485,000 | | | | 3,679,606 | |

5.10% 2/15/45 | | | 1,625,000 | | | | 1,769,073 | |

Noble Energy | | | | | | | | |

4.15% 12/15/21 | | | 3,440,000 | | | | 3,650,580 | |

5.05% 11/15/44 | | | 2,040,000 | | | | 2,030,934 | |

5.625% 5/1/21 | | | 1,520,000 | | | | 1,602,340 | |

Petroleos Mexicanos | | | | | | | | |

3.50% 7/23/20 | | | 925,000 | | | | 933,094 | |

5.50% 6/27/44 | | | 2,486,000 | | | | 2,261,987 | |

Regency Energy Partners 5.875% 3/1/22 | | | 3,991,000 | | | | 4,357,821 | |

Shell International Finance | | | | | | | | |

2.875% 5/10/26 | | | 8,155,000 | | | | 8,326,239 | |

4.00% 5/10/46 | | | 3,525,000 | | | | 3,635,428 | |

Sunoco Logistics Partners Operations 3.90% 7/15/26 | | | 3,185,000 | | | | 3,171,970 | |

Williams Partners 7.25% 2/1/17 | | | 8,087,000 | | | | 8,285,617 | |

Woodside Finance | | | | | | | | |

144A 3.65% 3/5/25 # | | | 2,055,000 | | | | 2,051,184 | |

144A 8.75% 3/1/19 # | | | 7,800,000 | | | | 9,070,534 | |

| | | | | | | | |

| | | | | | | 78,393,923 | |

| | | | | | | | |

Finance Companies – 2.92% | | | | | | | | |

AerCap Ireland Capital | | | | | | | | |

3.95% 2/1/22 | | | 4,575,000 | | | | 4,802,286 | |

4.625% 10/30/20 | | | 3,095,000 | | | | 3,319,387 | |

Aviation Capital Group | | | | | | | | |

144A 2.875% 9/17/18 # | | | 405,000 | | | | 411,581 | |

24

| | | | | | | | |

| | | Principal amount° | | | Value (U.S. $) | |

| |

Corporate Bonds (continued) | | | | | | | | |

| |

Finance Companies (continued) | | | | | | | | |

Aviation Capital Group | | | | | | | | |

144A 4.875% 10/1/25 # | | | 2,870,000 | | | $ | 2,998,145 | |

144A 6.75% 4/6/21 # | | | 3,005,000 | | | | 3,515,099 | |

Depository Trust & Clearing 144A 4.875% 12/29/49 #● | | | 6,000,000 | | | | 6,090,000 | |

Peachtree Corners Funding Trust 144A 3.976% 2/15/25 # | | | 9,115,000 | | | | 9,273,929 | |

SMBC Aviation Capital Finance 144A 2.65% 7/15/21 # | | | 2,800,000 | | | | 2,819,852 | |

| | | | | | | | |

| | | | | | | 33,230,279 | |

| | | | | | | | |

Insurance – 2.62% | | | | | | | | |

Highmark 144A 6.125% 5/15/41 #@ | | | 920,000 | | | | 925,174 | |

MetLife 5.25% 12/29/49 ● | | | 4,200,000 | | | | 4,213,860 | |

MetLife Capital Trust X 144A 9.25% 4/8/38 # | | | 2,160,000 | | | | 3,091,500 | |

Principal Life Global Funding II 144A 3.00% 4/18/26 # | | | 3,584,000 | | | | 3,722,081 | |

Prudential Financial 5.375% 5/15/45 ● | | | 3,370,000 | | | | 3,509,013 | |

TIAA Asset Management Finance 144A 4.125% 11/1/24 # | | | 9,450,000 | | | | 10,003,061 | |

XLIT | | | | | | | | |

4.45% 3/31/25 | | | 2,380,000 | | | | 2,418,280 | |

6.50% 10/29/49 ● | | | 2,822,000 | | | | 1,954,235 | |

| | | | | | | | |

| | | | | | | 29,837,204 | |

| | | | | | | | |

Natural Gas – 0.81% | | | | | | | | |

Korea Gas 144A 2.875% 7/29/18 # | | | 6,425,000 | | | | 6,598,032 | |

Southern Gas Capital 3.25% 6/15/26 | | | 2,555,000 | | | | 2,658,531 | |

| | | | | | | | |

| | | | | | | 9,256,563 | |

| | | | | | | | |

Real Estate Investment Trusts – 3.54% | | | | | | | | |

Alexandria Real Estate Equities 3.95% 1/15/27 | | | 1,260,000 | | | | 1,319,773 | |

Corporate Office Properties 5.25% 2/15/24 | | | 5,730,000 | | | | 6,222,098 | |

CubeSmart 4.00% 11/15/25 | | | 4,690,000 | | | | 5,003,029 | |

Education Realty Operating Partnership 4.60% 12/1/24 | | | 4,170,000 | | | | 4,382,270 | |

ESH Hospitality 144A 5.25% 5/1/25 # | | | 3,070,000 | | | | 3,070,000 | |

Host Hotels & Resorts | | | | | | | | |

3.75% 10/15/23 | | | 8,645,000 | | | | 8,835,389 | |

4.50% 2/1/26 | | | 2,250,000 | | | | 2,405,317 | |

Kimco Realty 3.40% 11/1/22 | | | 875,000 | | | | 922,208 | |

Sovran Acquisition 3.50% 7/1/26 | | | 2,745,000 | | | | 2,784,317 | |

Trust F/1401 144A 5.25% 1/30/26 # | | | 2,030,000 | | | | 2,144,188 | |

WP Carey 4.60% 4/1/24 | | | 3,120,000 | | | | 3,250,129 | |

| | | | | | | | |

| | | | | | | 40,338,718 | |

| | | | | | | | |

Technology – 4.88% | | | | | | | | |

Apple | | | | | | | | |

2.45% 8/4/26 | | | 2,250,000 | | | | 2,257,029 | |

3.85% 8/4/46 | | | 4,250,000 | | | | 4,276,924 | |

Diamond 1 Finance | | | | | | | | |

144A 6.02% 6/15/26 # | | | 3,715,000 | | | | 3,987,250 | |

25

Schedules of investments

Delaware Corporate Bond Fund

| | | | | | | | |

| | | Principal amount° | | | Value (U.S. $) | |

| |

Corporate Bonds (continued) | | | | | | | | |

| |

Technology (continued) | | | | | | | | |

Diamond 1 Finance | | | | | | | | |

144A 8.10% 7/15/36 # | | | 4,360,000 | | | $ | 4,980,864 | |

Fidelity National Information Services 5.00% 10/15/25 | | | 7,410,000 | | | | 8,591,050 | |

First Data 144A 7.00% 12/1/23 # | | | 3,160,000 | | | | 3,262,700 | |

Iron Mountain 144A 4.375% 6/1/21 # | | | 2,605,000 | | | | 2,702,687 | |

National Semiconductor 6.60% 6/15/17 | | | 6,644,000 | | | | 6,971,576 | |

NXP | | | | | | | | |

144A 4.125% 6/1/21 # | | | 1,000,000 | | | | 1,032,499 | |

144A 4.625% 6/1/23 # | | | 2,765,000 | | | | 2,870,428 | |

Oracle | | | | | | | | |

2.40% 9/15/23 | | | 8,520,000 | | | | 8,612,698 | |

4.00% 7/15/46 | | | 5,735,000 | | | | 5,955,459 | |

| | | | | | | | |

| | | | | | | 55,501,164 | |

| | | | | | | | |

Transportation – 3.54% | | | | | | | | |

Air Canada 2015-1 Class A Pass Through Trust 144A | | | | | | | | |

3.60% 3/15/27 #¿ | | | 2,544,592 | | | | 2,633,652 | |

American Airlines 2014-1 Class A Pass Through Trust | | | | | | | | |

3.70% 10/1/26 ¿ | | | 1,849,618 | | | | 1,946,723 | |

American Airlines 2015-1 Class A Pass Through Trust | | | | | | | | |

3.375% 5/1/27 ¿ | | | 3,116,467 | | | | 3,229,439 | |

American Airlines 2015-2 Class AA Pass Through Trust | | | | | | | | |

3.60% 9/22/27 ¿ | | | 1,415,000 | | | | 1,523,035 | |

American Airlines 2016-1 Class AA Pass Through Trust | | | | | | | | |

3.575% 1/15/28 ¿ | | | 643,420 | | | | 692,480 | |

Canadian National Railway 3.20% 8/2/46 | | | 2,335,000 | | | | 2,333,566 | |

ERAC USA Finance 144A 3.30% 12/1/26 # | | | 6,515,000 | | | | 6,737,507 | |

Hertz 6.75% 4/15/19 | | | 1,630,000 | | | | 1,662,600 | |

Penske Truck Leasing | | | | | | | | |

144A 3.30% 4/1/21 # | | | 4,400,000 | | | | 4,552,759 | |

144A 3.375% 2/1/22 # | | | 3,135,000 | | | | 3,202,587 | |

TTX 144A 4.20% 7/1/46 # | | | 5,365,000 | | | | 5,858,092 | |

United Airlines 2014-1 Class A Pass Through Trust | | | | | | | | |

4.00% 4/11/26 ¿ | | | 1,470,657 | | | | 1,583,714 | |

United Airlines 2014-2 Class A Pass Through Trust | | | | | | | | |

3.75% 9/3/26 ¿ | | | 3,771,959 | | | | 4,021,851 | |

United Airlines 2016-1 Class AA Pass Through Trust | | | | | | | | |

3.10% 7/7/28 ¿ | | | 275,000 | | | | 286,344 | |

| | | | | | | | |

| | | | | | | 40,264,349 | |

| | | | | | | | |

Total Corporate Bonds (cost $1,026,236,770) | | | | | | | 1,068,791,262 | |

| | | | | | | | |

26

| | | | | | | | |

| | | Principal amount° | | | Value (U.S. $) | |

Municipal Bond – 0.74% | | | | | | | | |

Los Angeles, California Department of Water & Power Revenue (Taxable Build America Bond) | | | | | | | | |

Series D 6.574% 7/1/45 | | | 5,365,000 | | | $ | 8,463,770 | |

| | | | | | | | |

Total Municipal Bond (cost $5,365,000) | | | | | | | 8,463,770 | |

| | | | | | | | |

| | |

| | | | | | | | | |

Senior Secured Loans – 1.21%« | | | | | | | | |

Gardner Denver 1st Lien 4.25% 7/30/20 | | | 2,093,625 | | | | 1,996,142 | |

KIK Custom Products 1st Lien 6.00% 8/26/22 @ | | | 2,976,256 | | | | 2,967,575 | |

Mohegan Tribal Gaming Authority Tranche B 1st Lien | | | | | | | | |

5.50% 6/15/18 | | | 2,959,382 | | | | 2,959,843 | |

Rite Aid 2nd Lien 5.75% 8/21/20 | | | 2,849,000 | | | | 2,863,838 | |

Solera Tranche B 1st Lien 5.75% 3/3/23 | | | 2,952,600 | | | | 2,980,543 | |

| | | | | | | | |

Total Senior Secured Loans (cost $13,617,260) | | | | | | | 13,767,941 | |

| | | | | | | | |

| | |

| | | | | | | | | |

Sovereign Bond – 0.14%D | | | | | | | | |

Qatar – 0.14% | | | | | | | | |

Qatar Government International Bond 144A | | | | | | | | |

3.25% 6/2/26 # | | | 1,585,000 | | | | 1,628,730 | |

| | | | | | | | |

Total Sovereign Bond (cost $1,568,564) | | | | | | | 1,628,730 | |

| | | | | | | | |

| | |

| | | | | | | | | |

U.S. Treasury Obligation – 0.21% | | | | | | | | |

U.S. Treasury Note | | | | | | | | |

1.625% 5/15/26 | | | 2,400,000 | | | | 2,436,000 | |

| | | | | | | | |

Total U.S. Treasury Obligation (cost $2,424,656) | | | | | | | 2,436,000 | |

| | | | | | | | |

| | |

| | | Number of shares | | | | |

Preferred Stock – 2.20% | | | | | | | | |

Bank of America 6.50% ● | | | 2,610,000 | | | | 2,853,057 | |

DTE Energy 5.25% | | | 105,000 | | | | 2,709,000 | |

General Electric 5.00% ● | | | 9,227,000 | | | | 9,953,626 | |

GMAC Capital Trust I 6.411% ● | | | 50,000 | | | | 1,271,000 | |

PNC Preferred Funding Trust II 144A 1.875% #● | | | 8,600,000 | | | | 7,881,040 | |

USB Realty 144A 1.827% #@● | | | 400,000 | | | | 343,000 | |

| | | | | | | | |

Total Preferred Stock (cost $24,075,482) | | | | | | | 25,010,723 | |

| | | | | | | | |

27

Schedules of investments

Delaware Corporate Bond Fund

| | | | | | | | |

| | | Principal amount° | | | Value (U.S. $) | |

Short-Term Investments – 0.86% | | | | | | | | |

Repurchase Agreements – 0.86% | | | | | | | | |

Bank of America Merrill Lynch

0.29%, dated 7/29/16, to be repurchased on 8/1/16, repurchase price $2,771,378 (collateralized by U.S. government obligations 3.375% 5/15/44; market value $2,826,738) | | | 2,771,311 | | | $ | 2,771,311 | |

Bank of Montreal

0.26%, dated 7/29/16, to be repurchased on 8/1/16, repurchase price $4,618,951 (collateralized by U.S. government obligations 0.125%–3.125% 2/15/19–11/15/45; market value $4,711,229) | | | 4,618,851 | | | | 4,618,851 | |

BNP Paribas

0.33%, dated 7/29/16, to be repurchased on 8/1/16, repurchase price $2,378,903 (collateralized by U.S. government obligations 0.00%–4.250% 8/31/19–11/15/40; market value $2,426,415) | | | 2,378,838 | | | | 2,378,838 | |

| | | | | | | | |

| | | | | | | 9,769,000 | |

| | | | | | | | |

Total Short-Term Investments (cost $9,769,000) | | | | | | | 9,769,000 | |

| | | | | | | | |

| | |

Total Value of Securities – 99.98%

(cost $1,091,175,076) | | | | | | $ | 1,138,122,550 | |

| | | | | | | | |

| # | Security exempt from registration under Rule 144A of the Securities Act of 1933, as amended. At July 31, 2016, the aggregate value of Rule 144A securities was $298,403,386, which represents 26.21% of the Fund’s net assets. See Note 11 in “Notes to financial statements.” |

| @ | Illiquid security. At July 31, 2016, the aggregate value of illiquid securities was $18,287,353, which represents 1.61% of the Fund’s net assets. See Note 11 in “Notes to financial statements.” |

| ¿ | Pass Through Agreement. Security represents the contractual right to receive a proportionate amount of underlying payments due to the counterparty pursuant to various agreements related to the rescheduling of obligations and the exchange of certain notes. |

| ° | Principal amount shown is stated in U.S. dollars unless noted that the security is denominated in another currency. |

| ● | Variable rate security. The rate shown is the rate as of July 31, 2016. Interest rates reset periodically. |

| D | Securities have been classified by country of origin. |

| « | Senior secured loans generally pay interest at rates which are periodically redetermined by reference to a base lending rate plus a premium. These base lending rates are generally: (i) the prime rate offered by one or more U.S. banks, (ii) the lending rate offered by one or more European banks such as the London Interbank Offered Rate (LIBOR), and (iii) the certificate of deposit rate. Senior secured loans may be subject to restrictions on resale. Stated rate in effect at July 31, 2016. |

| f | Step coupon bond. Coupon increases or decreases periodically based on a predetermined schedule. Stated rate in effect at July 31, 2016. |

28

The following swap contract were outstanding at July 31, 2016:1

Swap Contract

CDS Contract2

| | | | | | | | | | | | | | | | | | | | | | |

Counterparty | | Swap

Referenced

Obligation | | Notional Value | | | Annual

Protection

Payments | | | Termination

Date | | | Upfront

Payment

Paid | | | Unrealized

Appreciation

(Depreciation)3 | |

| | Protection | | | | | | | | | | | | | | | | | | | | |

| | Purchased: | | | | | | | | | | | | | | | | | | | | |

| | Halliburton 5 yr | | | | | | | | | | | | | | | | | | | | |

MSC | | 8.75% 2/15/21 | | $ | 5,900,000 | | | | 1.00% | | | | 12/20/20 | | | $ | 119,905 | | | $ | (109,880 | ) |

The use of swap contracts involves elements of market risk and risks in excess of the amounts disclosed in the financial statements. The notional values presented above represents the Fund’s total exposure in such contracts, whereas only the net unrealized appreciation (depreciation) is reflected in the Fund’s net assets.

1See Note 8 in “Notes to financial statements.”

2 A CDS contract is a risk-transfer instrument through which one party (purchaser of protection) transfers to another party (seller of protection) the financial risk of a credit event (as defined in the CDS agreement), as it relates to a particular reference security or basket of securities (such as an index). Periodic payments (receipts) on such contracts are accrued daily and recorded as unrealized losses (gains) on swap contracts. Upon payment (receipt), such amounts are recorded as realized losses (gains) on swap contracts. Upfront payments made or received in connection with CDS contracts are amortized over the expected life of the CDS contracts as unrealized losses (gains) on swap contracts. The change in value of CDS contracts is recorded daily as unrealized appreciation or depreciation. A realized gain or loss is recorded upon a credit event (as defined in the CDS agreement) or the maturity or termination of the agreement.

3 Unrealized appreciation (depreciation) does not include periodic interest payments on swap contracts accrued daily in the amount of $(6,883).

Summary of abbreviations:

CDS – Credit Default Swap

MSC – Morgan Stanley Capital

yr – Year

See accompanying notes, which are an integral part of the financial statements.

29

| | | | |

| Schedules of investments | | | | |

| Delaware Extended Duration Bond Fund | | | July 31, 2016 | |

| | | | | | | | |

| | | Principal amount° | | | Value (U.S. $) | |

Corporate Bonds – 91.52% | | | | | | | | |

Banking – 14.61% | | | | | | | | |

Ally Financial 8.00% 11/1/31 | | | 595,000 | | | $ | 727,387 | |

Bank of America | | | | | | | | |

4.45% 3/3/26 | | | 4,690,000 | | | | 5,046,735 | |

5.00% 1/21/44 | | | 5,740,000 | | | | 6,838,699 | |

Bank of New York Mellon | | | | | | | | |

2.80% 5/4/26 | | | 1,405,000 | | | | 1,464,662 | |

4.625% 12/29/49 ● | | | 2,055,000 | | | | 2,055,000 | |

Citigroup 4.65% 7/30/45 | | | 2,950,000 | | | | 3,343,725 | |

Citizens Financial Group 4.30% 12/3/25 | | | 4,700,000 | | | | 4,998,398 | |

Credit Suisse Group 144A 6.25% 12/29/49 #● | | | 2,272,000 | | | | 2,204,167 | |

Credit Suisse Group Funding Guernsey 4.875% 5/15/45 | | | 6,825,000 | | | | 7,325,273 | |

Fifth Third Bank 3.85% 3/15/26 | | | 5,000,000 | | | | 5,343,810 | |

First Republic Bank 4.375% 8/1/46 | | | 3,195,000 | | | | 3,233,068 | |

Goldman Sachs Group 4.75% 10/21/45 | | | 5,240,000 | | | | 5,991,510 | |

JPMorgan Chase | | | | | | | | |

4.25% 10/1/27 | | | 5,255,000 | | | | 5,675,946 | |

4.85% 2/1/44 | | | 4,835,000 | | | | 5,907,011 | |

KeyBank 6.95% 2/1/28 | | | 2,467,000 | | | | 3,257,047 | |

Morgan Stanley | | | | | | | | |

3.125% 7/27/26 | | | 640,000 | | | | 645,934 | |

3.95% 4/23/27 | | | 5,180,000 | | | | 5,362,554 | |

4.30% 1/27/45 | | | 3,730,000 | | | | 4,051,433 | |

SVB Financial Group 3.50% 1/29/25 | | | 2,440,000 | | | | 2,440,495 | |

UBS 7.625% 8/17/22 | | | 4,020,000 | | | | 4,683,300 | |

US Bancorp | | | | | | | | |

2.375% 7/22/26 | | | 2,285,000 | | | | 2,291,375 | |

3.10% 4/27/26 | | | 2,830,000 | | | | 2,955,587 | |

5.125% 12/29/49 ● | | | 2,805,000 | | | | 2,952,291 | |

USB Capital IX 3.50% 10/29/49 @● | | | 810,000 | | | | 697,613 | |

Wells Fargo 4.40% 6/14/46 | | | 9,465,000 | | | | 10,060,339 | |

| | | | | | | | |

| | | | | | | 99,553,359 | |

| | | | | | | | |

Basic Industry – 4.99% | | | | | | | | |

CF Industries 5.375% 3/15/44 | | | 2,119,000 | | | | 2,098,927 | |

Eastman Chemical 4.65% 10/15/44 | | | 5,750,000 | | | | 6,060,414 | |

Georgia-Pacific 8.00% 1/15/24 | | | 3,280,000 | | | | 4,410,403 | |

International Paper 5.15% 5/15/46 | | | 6,889,000 | | | | 7,992,432 | |

LYB International Finance 4.875% 3/15/44 | | | 2,525,000 | | | | 2,785,416 | |

Methanex 5.65% 12/1/44 | | | 6,715,000 | | | | 5,946,670 | |

Mexichem 144A 5.875% 9/17/44 # | | | 1,775,000 | | | | 1,758,936 | |

Rio Tinto Finance USA 3.75% 6/15/25 | | | 2,755,000 | | | | 2,964,892 | |

| | | | | | | | |

| | | | | | | 34,018,090 | |

| | | | | | | | |

30

| | | | | | | | |

| | | Principal amount° | | | Value (U.S. $) | |

Corporate Bonds (continued) | | | | | | | | |

Brokerage – 1.79% | | | | | | | | |

Jefferies Group | | | | | | | | |

6.45% 6/8/27 | | | 2,640,000 | | | $ | 2,955,129 | |

6.50% 1/20/43 | | | 1,985,000 | | | | 2,063,102 | |