As filed with the Securities and Exchange Commission on November 1, 2013

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF

REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-00582

NEUBERGER BERMAN EQUITY FUNDS

(Exact Name of the Registrant as Specified in Charter)

c/o Neuberger Berman Management LLC

605 Third Avenue, 2nd Floor

New York, New York 10158-0180

(Address of Principal Executive Offices – Zip Code)

Registrant's telephone number, including area code: (212) 476-8800

Robert Conti

Chief Executive Officer and President

Neuberger Berman Equity Funds

c/o Neuberger Berman Management LLC

605 Third Avenue, 2nd Floor

New York, New York 10158-0180

Arthur C. Delibert, Esq.

K&L Gates LLP

1601 K Street, N.W.

Washington, D.C. 20006-1600

(Names and Addresses of agents for service)

Date of fiscal year end: August 31, 2013

Date of reporting period: August 31, 2013

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to the Secretary, Securities and Exchange Commission, 100 F Street, NE, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507. Item 1. Report to Shareholders.

Neuberger Berman

Equity Funds

Investor Class Shares

Trust Class Shares

Advisor Class Shares

Institutional Class Shares

Emerging Markets Equity Fund

Equity Income Fund

Focus Fund

Genesis Fund

Global Equity Fund

Global Thematic Opportunities Fund

Greater China Equity Fund

Guardian Fund

International Equity Fund

(Formerly International Institutional Fund)

International Large Cap Fund

Class A Shares

Class C Shares

Class R3 Shares

Class R6 Shares

Intrinsic Value Fund

Large Cap Disciplined Growth Fund

Large Cap Value Fund

Mid Cap Growth Fund

Mid Cap Intrinsic Value Fund

Multi-Cap Opportunities Fund

Real Estate Fund

Select Equities Fund

Small Cap Growth Fund

Socially Responsive Fund

Value Fund

Annual Report

August 31, 2013

Contents

THE FUNDS

President's Letter | | | 1 | | |

PORTFOLIO COMMENTARY | |

Emerging Markets Equity Fund | | | 2 | | |

Equity Income Fund | | | 6 | | |

Focus Fund | | | 10 | | |

Genesis Fund | | | 14 | | |

Global Equity Fund | | | 18 | | |

Global Thematic Opportunities Fund | | | 22 | | |

Greater China Equity Fund | | | 26 | | |

Guardian Fund | | | 30 | | |

International Equity Fund (Formerly International Institutional Fund) | | | 34 | | |

International Large Cap Fund | | | 38 | | |

Intrinsic Value Fund | | | 42 | | |

Large Cap Disciplined Growth Fund | | | 46 | | |

Large Cap Value Fund | | | 50 | | |

Mid Cap Growth Fund | | | 54 | | |

Mid Cap Intrinsic Value Fund | | | 58 | | |

Multi-Cap Opportunities Fund | | | 62 | | |

Real Estate Fund | | | 66 | | |

Select Equities Fund | | | 70 | | |

Small Cap Growth Fund | | | 74 | | |

Socially Responsive Fund | | | 78 | | |

Value Fund | | | 82 | | |

FUND EXPENSE INFORMATION | | | 92 | | |

SCHEDULE OF INVESTMENTS/TOP TEN EQUITY HOLDINGS | |

Emerging Markets Equity Fund | | | 96 | | |

Equity Income Fund | | | 99 | | |

Focus Fund | | | 101 | | |

Genesis Fund | | | 102 | | |

Global Equity Fund | | | 105 | | |

Global Thematic Opportunities Fund | | | 108 | | |

Greater China Equity Fund | | | 110 | | |

Guardian Fund | | | 112 | | |

International Equity Fund (Formerly International Institutional Fund) | | | 113 | | |

International Large Cap Fund | | | 116 | | |

Intrinsic Value Fund | | | 119 | | |

Large Cap Disciplined Growth Fund | | | 121 | | |

Large Cap Value Fund | | | 123 | | |

Mid Cap Growth Fund | | | 125 | | |

Mid Cap Intrinsic Value Fund | | | 127 | | |

Multi-Cap Opportunities Fund | | | 129 | | |

Real Estate Fund | | | 130 | | |

Select Equities Fund | | | 131 | | |

Small Cap Growth Fund | | | 132 | | |

Socially Responsive Fund | | | 134 | | |

Value Fund | | | 135 | | |

FINANCIAL STATEMENTS | | | 147 | | |

FINANCIAL HIGHLIGHTS (ALL CLASSES) PER SHARE DATA | |

Emerging Markets Equity Fund | | | 209 | | |

Equity Income Fund | | | 211 | | |

Focus Fund | | | 213 | | |

Genesis Fund | | | 215 | | |

Global Equity Fund | | | 217 | | |

Global Thematic Opportunities Fund | | | 217 | | |

Greater China Equity Fund | | | 219 | | |

Guardian Fund | | | 219 | | |

International Equity Fund (Formerly International Institutional Fund) | | | 223 | | |

International Large Cap Fund | | | 223 | | |

Intrinsic Value Fund | | | 225 | | |

Large Cap Disciplined Growth Fund | | | 227 | | |

Large Cap Value Fund | | | 229 | | |

Mid Cap Growth Fund | | | 231 | | |

Mid Cap Intrinsic Value Fund | | | 235 | | |

Multi-Cap Opportunities Fund | | | 237 | | |

Real Estate Fund | | | 237 | | |

Select Equities Fund | | | 239 | | |

Small Cap Growth Fund | | | 241 | | |

Socially Responsive Fund | | | 243 | | |

Value Fund | | | 247 | | |

Reports of Independent Registered Public Accounting Firms | | | 252 | | |

Directory | | | 254 | | |

Trustees and Officers | | | 255 | | |

Proxy Voting Policies and Procedures | | | 263 | | |

Quarterly Portfolio Schedule | | | 263 | | |

Board Consideration of the Management and

Sub-Advisory Agreements | | | 264 | | |

Notice to Shareholders | | | 266 | | |

The "Neuberger Berman" name and logo are registered service marks of Neuberger Berman Group LLC. "Neuberger Berman Management LLC" and the individual Fund names in this piece are either service marks or registered service marks of Neuberger Berman Management LLC. ©2013 Neuberger Berman Management LLC. All rights reserved.

Dear Shareholder,

Equity markets advanced sharply this fiscal year, with the S&P 500 up over 18% for the period. International developed markets reported similarly strong gains—with the MSCI EAFE® Index advancing over 19%. Emerging markets, while positive, lagged.

Five years after the global financial crisis, the world's developed economies seemed to have turned a corner, improving investor and business confidence and fueling this reporting period's rally. With a more solid macroeconomic foundation, market activity has been less volatile. The VIX Index (a forward-looking, short-term measure of S&P 500 Index option-implied volatility), which was near 80 in late 2008, generally remained under 20 this period, but in December, spiked above 22 during the fiscal cliff crisis. Perhaps more importantly, correlations among stocks—unusually high in recent years as the market struggled with shifting macroeconomic news—dropped significantly. The Chicago Board Options Exchange Implied Correlation Index, which tracks price movement within the S&P 500, had declined nearly 50% from its 2008 highs. While lower volatility suggests a more confident, less reactive market, lower correlations are an indication that investors are weighing the fundamentals of individual companies rather than betting on direction at the market or sector level. We believe this indicates a more typical—and healthier—equity market, and one that favors active management.

While markets continued to benefit from accommodative central bank policy this past fiscal year, better-than-expected GDP growth in the U.S., which closed the period at 2.5%, was the positive surprise. The resolution of some of 2012's "manufactured" crises—particularly the fiscal cliff, and its tax and policy unknowns—finally freed businesses and investors from fear-based inertia. At the same time, housing and unemployment improved steadily. By August 2013, U.S. existing home sales had risen over 13% year-over-year, to an annual rate of almost 5.5 million units, with the median price increasing more than $27,000 over the last 12 months. August's unemployment number was the lowest since December 2008. Consumer confidence increased as well, with the Consumer Confidence Index up 20 points year-over-year in August. We believe this combination should continue to support consumer spending, the most critical component of U.S. economic growth.

Elsewhere, within the eurozone, where an untenable debt situation has been the source of market consternation time and again, 2013 economic data thus far suggested the recession had ended and that a period of slow growth had begun. An expanding economy drove equities up and bond yields among the weaker economies down. Emerging markets struggled, however, due to real and perceived pressures from slower growth in China and increased risk aversion after the U.S. Federal Reserve's tapering announcement in May. While some economies are directly tied to China, most are not. During the reporting period, however, investors largely failed to differentiate.

The U.S. is going through another contentious political season, with budget and debt ceiling negotiations. Although the U.S. deficit has dropped significantly over the past five years, the same players in Washington failed to resolve the 2011 debt ceiling negotiations without a U.S. debt downgrade. We can hope for better this time around, but may again see negative economic and market impacts from weak leadership. Bad news from the world's largest economy could certainly have contagion effects considering the relative weakness of much of the developed world. Geopolitical events also have the potential to jar the markets. Developments in Syria, Iran and elsewhere bear watching.

In our view, however, long-term positives may outweigh current risks. We believe equity valuations remain reasonable and interest rates, while rising, are low. In our opinion, corporate balance sheets are healthy, and with the benefit of reduced policy uncertainty, management teams have deployed cash in positive ways—including mergers and acquisitions, increased dividends and share buybacks, and focused capital expenditures. If the market has turned, as we believe it has, to a more fundamentals-focused "weighing machine," skilled active management could have real impact on returns. In a proactive market, we would anticipate that the opportunities our teams and strategies uncover would be rewarded.

We thank you for your confidence in Neuberger Berman and look forward to continuing to serve your investment needs.

Sincerely,

ROBERT CONTI

PRESIDENT AND CEO

NEUBERGER BERMAN MUTUAL FUNDS

1

Emerging Markets Equity Fund Commentary (Unaudited)

Neuberger Berman Emerging Markets Equity Fund Institutional Class generated a 2.77% total return for the fiscal year ended August 31, 2013 and outperformed its benchmark, the MSCI Emerging Markets (EM) Index, which reported a return of 0.87%. (Performance for all share classes is provided in the table immediately following this letter.)

The MSCI EM Index posted solid gains during the first half of the reporting period. After that, however, the index gave back nearly everything, closing the fiscal year only slightly positive. In early 2013, the index declined as investors took profits and reallocated on signs of growth in the U.S. and Japan. After May, the EM Index dropped further, primarily driven by the U.S. Federal Reserve's announcement of plans to begin unwinding its quantitative easing program. At the same time, concerns arose about the stability of the Chinese banking system.

The MSCI EM Index sharply underperformed both the MSCI EAFE Index and the S&P 500 Index for the past fiscal year, though results were mixed. From a sector perspective, Information Technology led the MSCI EM Index, up 16%, followed by Health Care and Consumer Discretionary. Meanwhile, Materials and Utilities declined roughly 10%, with Energy, Telecommunication Services and Industrials also posting negative results. By country, Korea, the Philippines and Poland outperformed—as did China—while Peru, the Czech Republic and Chile posted significant losses.

Both stock selection and sector allocation were positive for the portfolio versus the benchmark this period, with relative performance benefiting the most from stock selection within Industrials, Consumer Staples and Consumer Discretionary. By contrast, Financials and Materials were areas of relative weakness versus the benchmark. Holdings within China, Russia and Mexico drove our outperformance, while investments in India and Taiwan, and an opportunistic allocation to Canada, detracted.

Top performers during the 12-month period included China Everbright International, Coway and Kimberly-Clark de Mexico. China Everbright reported strong earnings and good momentum in its order book. Coway, the Korean door-to-door marketer of home environment appliances, increased its service fees, which we believe could boost earnings going forward. Kimberly-Clark de Mexico, a paper-based consumer products company, continued to improve margins.

Detractors during the period included DLF Limited, an Indian property manager we sold due to slower growth and tightening liquidity conditions in India. SQM in Chile, an agriculture company, was also sold having come under pressure due to South American market weakness and declining potash prices. BR Malls Participoes, a Brazilian mall operator, fell on market concerns that rising Brazilian interest rates could bring down valuations on the company's properties. As longer-term investors, we continue to see value in the company.

In May 2013, the U.S. Federal Reserve's tapering comments quickly drove U.S. yields higher, causing liquidity to exit emerging markets, and posed a particular problem for markets such as Turkey, whose current account deficits have been funded by foreign investors. This situation resulted in sharp declines in the impacted emerging equity markets and their respective currencies. Further, while the People's Bank of China eventually stepped in, June's severe leap in China's interbank lending rates raised concerns about the stability of the Chinese banking system. Many investors read this as a sign that the government wanted to rein in the rapid credit expansion, in particular off-balance lending activity.

When we step back and look at 2013 so far, we observe two internal factors: earnings and policy issues. Earnings are generally down year-to-date and there have been roughly 15% cuts in earnings estimates for full year 2013 and 2014. This appears to be driven by the more cyclical sectors like Energy and Materials, which made up over 22% of the index weight, thereby making it difficult for the EM asset class to outperform. In regards to policy, we're seeing adjustments in China, noise in Brazil and reforms in India that have started but are moving slowly. While policy adjustments may take time to implement, we believe they could ultimately benefit these economies.

We continue to favor the small- to mid-cap domestically driven companies that have aided relative returns, believing these firms will benefit further from secular local growth. By sector, our greatest overweight is Industrials—in companies we anticipate will benefit from local infrastructure spending. We have added to Consumer Staples holdings, now our

2

second largest overweight, finding smaller-cap names at what we consider good valuations. Health Care is another significant overweight, with holdings focused around consumer-driven care providers and over-the-counter brands. We are still underweighted in Financials, Energy and Materials, and reduced our exposure to commodity materials names even further in recent months, as earnings have disappointed and we believe prospects remain poor.

From a country perspective, we exited several Korean holdings for company-specific reasons. We've also trimmed some Mexican Consumer Staples names as they approached their target prices, adding to newer domestically driven names that we believe offer greater potential upside. We remain biased towards Consumer Staples names in China, while avoiding the large Energy and Materials names that we believe could be negatively impacted by current reforms.

Overall, we continue to find what we believe are excellent bottom-up opportunities across markets. As we think the past year has shown, managers with strong stock picking skills and the capability and flexibility to look beyond the index could continue to have a real opportunity to add value.

Sincerely,

CONRAD SALDANHA

PORTFOLIO MANAGER

Information about the principal risks of investing in the Fund is set forth in the prospectus and statement of additional information.

The portfolio composition, industries and holdings of the Fund are subject to change.

The opinions expressed are those of the Fund's portfolio manager. The opinions are as of the date of this report and are subject to change without notice.

3

Emerging Markets Equity Fund (Unaudited)

TICKER SYMBOLS

Institutional Class | | NEMIX | |

Class A | | NEMAX | |

Class C | | NEMCX | |

Class R3 | | NEMRX | |

Class R6 | | NREMX | |

SECTOR ALLOCATION

(as a % of Total Investments) | |

Consumer Discretionary | | | 7.8 | % | |

Consumer Staples | | | 13.3 | | |

Energy | | | 9.8 | | |

Financials | | | 17.9 | | |

Health Care | | | 6.5 | | |

Industrials | | | 12.2 | | |

Information Technology | | | 15.9 | | |

Materials | | | 6.8 | | |

Telecommunication Services | | | 3.7 | | |

Short-Term Investments | | | 6.1 | | |

Total | | | 100.0 | % | |

PERFORMANCE HIGHLIGHTS9

| | | | | Average Annual Total

Return Ended 08/31/2013 | |

| | | Inception

Date | | 1 Year | | Life of

Fund | |

At NAV | |

Institutional Class | | 10/08/2008 | | | 2.77 | % | | | 12.01 | % | |

Class A | | 10/08/2008 | | | 2.54 | % | | | 11.74 | % | |

Class C | | 10/08/2008 | | | 1.78 | % | | | 10.92 | % | |

| Class R310 | | 06/21/2010 | | | 2.11 | % | | | 11.52 | % | |

| Class R624 | | 03/15/2013 | | | 2.83 | % | | | 12.02 | % | |

With Sales Charge | | | | | | | |

Class A | | | | | –3.36 | % | | | 10.40 | % | |

Class C | | | | | 0.78 | % | | | 10.92 | % | |

Index | | | | | | | |

| MSCI Emerging Markets Index1,16 | | | | | 0.87 | % | | | 10.24 | % | |

The performance data quoted represent past performance and do not indicate future results. Current performance may be lower or higher than the performance data quoted. For more current performance data, please visit www.nb.com/performance.

The results shown in the table reflect the reinvestment of income dividends and other distributions, if any. The results do not reflect the effect of taxes a shareholder would pay on Fund distributions or on the redemption of Fund shares.

The investment return and principal value of an investment will fluctuate and shares, when redeemed, may be worth more or less than their original cost.

Returns would have been lower if Neuberger Berman Management LLC ("Management") had not reimbursed certain expenses and/or waived a portion of the investment management fees during certain of the periods shown. Repayment by a class (of expenses previously reimbursed and/or fees previously waived by Management) will decrease the class's returns. Please see Note B in the Notes to Financial Statements for specific information regarding expense reimbursement and/or fee waiver arrangements.

As stated in the Fund's most recent prospectus, the total annual operating expense ratios for fiscal year 2012 (estimated for 2013 for Class R6) were 1.77%, 2.23%, 2.94%, 2.50% and 1.49% for Institutional Class, Class A, Class C, Class R3 and Class R6 shares, respectively (before expense reimbursements and/or fee waivers, if any). These expense ratios were 1.26%, 1.51%, 2.26%, 1.92% and 1.19% for Institutional Class, Class A, Class C, Class R3 and Class R6 shares, respectively, after expense reimbursements and/or fee waivers.

Returns shown with a sales charge reflect the deduction of the current maximum initial sales charge of 5.75% for Class A shares and the applicable contingent deferred sales charges (CDSC) for Class C shares. The maximum CDSC for Class C shares is 1%, which is reduced to 0% after 1 year. The performance of the Fund's share classes will differ primarily due to different sales charge structures and class expenses. Please see the prospectus for more information about sales charge structures, if any, and class expenses for your share class.

4

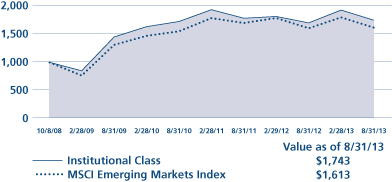

Emerging Markets Equity Fund (Unaudited)

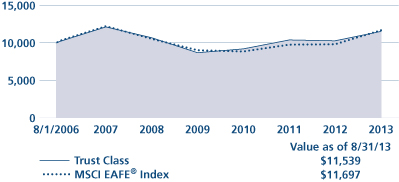

COMPARISON OF A $1,000,000 INVESTMENT

(000's Omitted)

This graph shows the change in value of a hypothetical $1,000,000 investment in the Fund over the past 10 fiscal years, or since the Fund's inception if it has not operated for 10 years. The graph is based on the Institutional Class shares only; the performance of the Fund's share classes will differ primarily due to different sales charge structures and class expenses (see Performance Highlights chart on previous page). The result is compared with benchmarks, which include a broad-based market index and may include a more narrowly based index. Market indices have not been reduced to reflect any of the fees and costs of investing. The results shown in the graph reflect the reinvestment of income dividends and other distributions, if any. The results do not reflect the effect of taxes a shareholder would pay on Fund distributions or on the redemption of Fund shares. Results represent past performance and do not indicate future results.

5

Equity Income Fund Commentary (Unaudited)

Neuberger Berman Equity Income Fund Institutional Class generated a 4.79% total return for the fiscal year ended August 31, 2013 but trailed its benchmark, the S&P 500 Index, which provided an 18.70% return. (Performance for all share classes is provided in the table immediately following this letter.)

The strong U.S. equity market rally experienced during the reporting period was attributable, in our view, to improving economic data that pointed to a recovery in housing and employment. Additionally, corporate America had benefited from its ability to refinance debt at lower interest rates, which helped improve fundamentals.

While these factors were positive, not all sectors benefited equally. In particular, real estate investment trusts (REITs) and utility stocks lagged the broader U.S. market. Utilities sold off in late 2012 due to fears that the dividend tax rate could double, which it did not—thereafter utilities saw a sharp rebound, making them the best performing sector through April 2013. However, REITs and utilities fell sharply following the U.S. Federal Reserve's tapering announcement in May, which hinted at a possible slowdown of its $85 billion monthly bond purchases. Interest rates on 10-Year U.S. Treasury bonds soared, triggering losses and hurting interest-rate sensitive stocks. From early May through August, the FTSE NAREIT All Equity REITs Index lost 13.3% while the S&P 500 returned 3.0%. Historically, better economic news has generally boded well for areas such as REITs, as we have seen in the past six economic cycles where rates rose dramatically in a short period of time. Once the initial shock has hit and the dust settled, this asset class has provided handsome returns thereafter.

The Fund's significant overweight to utility stocks (representing about 19% of Fund assets at the end of the reporting period) was a negative even though our holdings outperformed the broader Utilities sector and have committed to dividend increases over the upcoming cycle. Overall, the Fund's focus is on companies with exposure to energy infrastructure in the U.S. Top contributors included names such as NV Energy (which is being acquired), Sempra Energy and NiSource, which own storage facilities and pipeline assets. We believe dividend growth and attractive businesses can help mitigate some of the negative sentiment associated with interest rate-sensitive stocks in the short run while also potentially positioning them for longer-term outperformance.

REITs (roughly 21% of Fund assets at the end of the reporting period) suffered from the perception that higher interest rates mean higher borrowing costs, which posed a drag on profitability. However, we believe that in an improving economy, higher rates indicate increasing property values and higher lease rate renewals. In the U.S., American Campus Communities and Simon Property Group were the largest detractors from performance. Though representing only a small percentage of the Fund, non-U.S. REITs were hurt by weaker currencies relative to the U.S. dollar. A Mexican REIT, Fibra Uno Administracion was a detractor. Certain emerging markets have interesting business and strong dividend growth prospects, which are now trading at historic discounts. We anticipate we will continue investing accordingly—while being mindful of the risk/reward dynamics.

One final note about Utilities and REITs: while they detracted this past fiscal year, history shows they can revert quickly to their mean and even surpass the broader equity markets soon thereafter.

The Fund had an overweight to the gold industry through names like Royal Gold and Freeport McMoRan, as well as several mining companies that include Newcrest, Newmont and Market Vectors ETF. These names detracted from returns as the U.S. dollar continued to gain strength and investors' demand for gold began to wane. We built the position as a hedge against the inflation potential of unprecedented central bank intervention, but inflation remained subdued. Elsewhere within Materials, Potash declined as its commodity price came under pressure from oversupply driven by Eastern European competitors and was sold in July, while our gold-related positions were eliminated during spring 2013.

Given the S&P 500's sector performance, several big drivers of positive attribution included Health Care holdings Roche, Novartis and Johnson & Johnson, asset manager BlackRock within Financials, and Meredith, a Consumer Discretionary name that was subsequently sold for a profit when it reached our target price. The S&P 500 has a large allocation to

6

Health Care, Financials and Consumer Discretionary stocks. As of period's end, we are significantly underweighted in each of these areas, which together represent nearly 40% of the market, and whose returns approached 30% this period.

Historically, the stock market has generated an average annual total return in the 10% to 12% range. The bond market has generated an average total return ranging between 4% to 6%. Our strategy seeks a 7%–9% return, with half derived from income and the other half from appreciation. Historically, the strategy has tended to perform well in challenging times but may not keep up in strong markets. We anticipate potential disruptions from near-term geopolitical tensions and upcoming U.S. political events. In our view, the recent underperformance of sectors like REITs and Utilities creates buying opportunities for certain companies that we believe are poised to profit from an uptick in economic growth. We remain dedicated to uncovering attractive investment opportunities, with a focus on valuations, free cash flow and dividend growth—which we feel will be rewarded over time.

Sincerely,

RICHARD S. LEVINE, TONY GLEASON AND SANDY POMEROY

PORTFOLIO CO-MANAGERS

Information about the principal risks of investing in the Fund is set forth in the prospectus and statement of additional information.

The portfolio composition, industries and holdings of the Fund are subject to change.

The opinions expressed are those of the Fund's portfolio managers. The opinions are as of the date of this report and are subject to change without notice.

7

Equity Income Fund (Unaudited)

TICKER SYMBOLS

Institutional Class | | NBHIX | |

Class A | | NBHAX | |

Class C | | NBHCX | |

Class R3 | | NBHRX | |

SECTOR ALLOCATION

(as a % of Total Investments) | |

Consumer Discretionary | | | 1.2 | % | |

Consumer Staples | | | 6.0 | | |

Energy | | | 13.4 | | |

Financials | | | 29.3 | | |

Health Care | | | 9.0 | | |

Industrials | | | 9.9 | | |

Information Technology | | | 4.3 | | |

Materials | | | 1.0 | | |

Telecommunication Services | | | 3.2 | | |

Utilities | | | 19.3 | | |

Other | | | 2.9 | | |

Short-Term Investments | | | 0.5 | | |

Total | | | 100.0 | % | |

PERFORMANCE HIGHLIGHTS9

| | | | | Average Annual Total

Return Ended 08/31/2013 | |

| | | Inception

Date* | | 1 Year | | 5 Years | | Life of

Fund | |

At NAV | |

| Institutional Class14 | | 06/09/2008 | | | 4.79 | % | | | 6.07 | % | | | 6.60 | % | |

| Class A14 | | 06/09/2008 | | | 4.32 | % | | | 5.62 | % | | | 6.27 | % | |

| Class C14 | | 06/09/2008 | | | 3.58 | % | | | 4.88 | % | | | 5.70 | % | |

| Class R314 | | 06/21/2010 | | | 3.94 | % | | | 5.59 | % | | | 6.24 | % | |

With Sales Charge | |

| Class A14 | | | | | –1.65 | % | | | 4.39 | % | | | 5.35 | % | |

| Class C14 | | | | | 2.58 | % | | | 4.88 | % | | | 5.70 | % | |

Index | |

| S&P 500 Index1,16 | | | | | 18.70 | % | | | 7.32 | % | | | 4.88 | % | |

*The performance data for each class includes the performance of the Fund's oldest share class, Trust Class, from November 2, 2006 through June 9, 2008. The performance data for Class R3 also includes the performance of the Fund's Institutional Class from June 9, 2008 through June 21, 2010. See endnote 14 for information about the effects of the different fees paid by each class.

The performance data quoted represent past performance and do not indicate future results. Current performance may be lower or higher than the performance data quoted. For more current performance data, please visit www.nb.com/performance.

The results shown in the table reflect the reinvestment of income dividends and other distributions, if any. The results do not reflect the effect of taxes a shareholder would pay on Fund distributions or on the redemption of Fund shares.

The investment return and principal value of an investment will fluctuate and shares, when redeemed, may be worth more or less than their original cost. Returns would have been lower if Neuberger Berman Management LLC ("Management") had not reimbursed certain expenses and/or waived a portion of the investment management fees during certain of the periods shown. Repayment by a class (of expenses previously reimbursed and/or fees previously waived by Management) will decrease the class's returns. Please see Note B in the Notes to Financial Statements for specific information regarding expense reimbursement and/or fee waiver arrangements.

As stated in the Fund's most recent prospectus, the total annual operating expense ratios for fiscal year 2012 were 0.71%, 1.13%, 1.84%, and 1.41% for Institutional Class, Class A, Class C, and Class R3 shares, respectively (before expense reimbursements and/or fee waivers, if any). The total annual operating expense ratio for each of Institutional Class, Class A, Class C and Class R3 includes the class's repayment of expenses previously reimbursed and/or fees previously waived by Management.

Returns shown with a sales charge reflect the deduction of the current maximum initial sales charge of 5.75% for Class A shares and the applicable contingent deferred sales charges (CDSC) for Class C shares. The maximum CDSC for Class C shares is 1%, which is reduced to 0% after 1 year. The performance of the Fund's share classes will differ primarily due to different sales charge structures and class expenses. Please see the prospectus for more information about sales charge structures, if any, and class expenses for your share class.

8

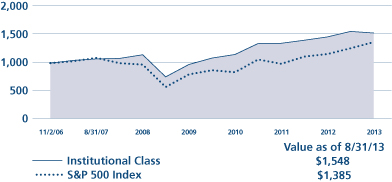

Equity Income Fund (Unaudited)

COMPARISON OF A $1,000,000 INVESTMENT14

(000's Omitted)

This graph shows the change in value of a hypothetical $1,000,000 investment in the Fund over the past 10 fiscal years, or since the Fund's inception if it has not operated for 10 years. The graph is based on the Institutional Class shares only; the performance of the Fund's share classes will differ primarily due to different sales charge structures and class expenses (see Performance Highlights chart on previous page). The result is compared with benchmarks, which include a broad-based market index and may include a more narrowly based index. Market indices have not been reduced to reflect any of the fees and costs of investing. The results shown in the graph reflect the reinvestment of income dividends and other distributions, if any. The results do not reflect the effect of taxes a shareholder would pay on Fund distributions or on the redemption of Fund shares. Results represent past performance and do not indicate future results.

9

Focus Fund Commentary (Unaudited)

Neuberger Berman Focus Fund Investor Class produced a 24.69% total return for the fiscal year ended August 31, 2013 and outperformed its benchmark, the S&P 500 Index, which posted an 18.70% return. (Performance for all share classes is provided in the table immediately following this letter.)

The stock market rose to record highs over the past 12 months with just a few bumps along the way, as continued sustenance from the U.S. Federal Reserve (the Fed) along with an improving domestic economy fueled momentum in equities, in our view, despite some overhanging macro issues. The first few months of the reporting period were somewhat challenging for stocks as the U.S. presidential election and ensuing policy decisions related to the fiscal cliff and other budgetary matters created uncertainty for investors. Yet the market's decline during this time marked a bottom for stocks as they quickly recovered alongside rising job growth and an improving U.S. housing market. The market received further support from a strong earnings season in January and February. Continued accommodative monetary policy on behalf of the Fed and European Central Bank perpetuated the market's steady rise over the next few months despite global woes that included weakening economic data from the eurozone and signs of a slowdown in China. The market then experienced a setback in late May/early June when investors fretted over continued sluggish U.S. manufacturing data while at the same time worried that the strengthening employment and housing markets would prompt the Fed to curb its accommodative monetary stance sooner than anticipated. However, the Fed stepped in with some reassuring language, which we believe alleviated immediate fears and cleared a path for stocks to ascend further despite mixed economic data and a rather tepid earnings season. The equity market attained new highs in July before retreating a bit in August as the focus began to turn towards the September meeting of the Fed's Federal Open Market Committee, in which it was anticipated the Fed might announce its intent to begin reducing its quantitative easing program in the near future. Escalating geopolitical tensions in the Middle East put added pressure on the market and caused a spike in oil and gas prices. Still, healthy corporate earnings projections for 2014, combined with strengthening macro data and accommodative monetary policy both at home and abroad, kept stocks in solidly positive territory for the past fiscal year.

Performance for the broad market (as measured by the S&P 500 Index) was led by the Financials and Health Care sectors, while the weakest areas were the Telecommunication Services and Information Technology (IT) sectors. Similar to the semi-annual period, Financials stocks rose over the fiscal year driven by, we believe, a stabilizing monetary system in Europe, improving credit conditions in the U.S. and a rising capital markets environment, which boosted profits for many diversified banks and brokers. The U.S. macro recovery also served the Consumer Discretionary sector as greater consumer spending lifted specialty retail stocks and a robust advertising industry drove earnings for several media companies. On the downside, the Telecommunication Services and IT sectors each suffered from the decline of a large industry bellwether, and IT had the added pressure of general sector rotation out of defensive areas and into more cyclical investments in light of the improving economy.

The Fund's return relative to the S&P 500 Index was largely attributable to strong stock selection in the Energy and IT sectors. Within the Energy sector, Cabot Oil & Gas had a total return of almost 90% over the past 12 months. Cabot is a leading low-cost gas producer in the U.S. with, in our view, the most desirable geological acreage in the Marcellus basin. Cabot's ascent was due in part to rising natural gas prices, but the stock also outperformed its gas-related peers owing to strong quarterly production results and solid forward-looking production guidance, as well as the company turning free cash flow positive during this time. Relative returns in the IT segment were lifted in part by a 30%+ rise in SanDisk during the year. SanDisk, which produces NAND flash memory, gained the most ground from January to March after industry manufacturers reported solid earnings results, which alleviated overhanging concerns about possible weak supply/demand dynamics for NAND. The company also reported a positive earnings surprise for every quarter during the past twelve months, which further boosted the stock. We continue to believe that SanDisk is well-positioned to benefit from industry tightening as companies reduce production capacity while demand for NAND rises as the technology is increasingly installed in PC's, notebooks, ultrabooks and other devices.

10

Although every sector of the Fund produced a positive overall return for the year, our investments in the Health Care and Materials segments detracted from performance on a relative basis. The primary source of loss within Health Care was Express Scripts, one of the largest pharmacy benefit managers in the U.S. The stock experienced a sharp decline in early November after management made some rather grim comments about expectations for 2013 that included "significant in-group member attrition, continued low utilization rates and increased client demands and expectations." Express Scripts traded within a limited range in the months that followed, and although we believe that management's tone was overly conservative and that Express Scripts could recover over time, we exited out of the position in late February to pursue other investment opportunities. In the Materials sector, the shortfall was largely due to gold producer Barrick Gold. We held a small position in the company during the period but the stock's decline caused a drag on absolute and relative performance. The decline in Barrick Gold was largely attributable to falling gold prices. The metal's price dropped as central banks around the world indicated a more imminent end to accommodative monetary policy, which reduced inflation expectations and caused interest rates to rise—two factors that typically have a negative impact on gold prices. Company-specific issues also weighed on the stock as Barrick Gold experienced complications that have delayed the development of its Pascua-Lama mine in Chile. In addition, concerns that the company may cut its dividend due to cash flow constraints also weighed on the stock and may continue to do so in the near term. We believe the long-term prospects for gold prices remain attractive, however; we sold out of Barrick Gold in late July to gain this exposure via other investments.

With the S&P 500 multiple closer to its historical average, we believe stocks on the whole are no longer "cheap" and further appreciation will be increasingly dependent on company fundamentals. Meanwhile, consensus estimates seem to convey that earnings growth for U.S. companies could remain strong due in part to improving economic conditions abroad in key regions such as Europe and China. While we believe the market has the potential to rise further over the long term, we maintain a balanced view in the near term in light of various macroeconomic headwinds that could materialize. We believe the domestic economy continues on a slow path to recovery but remains vulnerable to rising interest rates and negative consumer sentiment if the Fed hardens its monetary stance earlier than anticipated. The debate over the Federal debt ceiling and budget cuts has been contentious and the geopolitical crisis in the Middle East remains highly erratic—two factors that have grabbed investor attention in the past and caused heightened volatility in the market. For these reasons, we always focus our efforts on choosing stocks with what we believe are solid fundamentals and attractive valuations in order to create a fund that can appreciate over the long run despite the myriad factors that can cause the broad market to fluctuate in the interim.

Sincerely,

TIM CREEDON AND DAVID LEVINE

PORTFOLIO CO-MANAGERS

Information about the principal risks of investing in the Fund is set forth in the prospectus and statement of additional information.

The portfolio composition, industries and holdings of the Fund are subject to change.

The opinions expressed are those of the Fund's portfolio managers. The opinions are as of the date of this report and are subject to change without notice.

11

TICKER SYMBOLS

Investor Class | | NBSSX | |

Trust Class | | NBFCX | |

Advisor Class | | NBFAX | |

Institutional Class | | NFALX | |

Class A | | NFAAX | |

Class C | | NFACX | |

SECTOR ALLOCATION

(as a % of Total Investments) | |

Consumer Discretionary | | | 16.4 | % | |

Consumer Staples | | | 10.0 | | |

Energy | | | 10.5 | | |

Financials | | | 15.7 | | |

Health Care | | | 9.4 | | |

Industrials | | | 9.0 | | |

Information Technology | | | 17.8 | | |

Materials | | | 3.7 | | |

Utilities | | | 3.1 | | |

Short-Term Investments | | | 4.4 | | |

Total | | | 100.0 | % | |

PERFORMANCE HIGHLIGHTS8

| | | | | Average Annual Total

Return Ended 08/31/2013 | |

| | | Inception

Date | | 1 Year | | 5 Years | | 10 Years | | Life of

Fund | |

At NAV | |

Investor Class | | 10/19/1955 | | | 24.69 | % | | | 5.59 | % | | | 5.26 | % | | | 10.43 | % | |

| Trust Class3 | | 08/30/1993 | | | 24.48 | % | | | 5.37 | % | | | 5.05 | % | | | 10.43 | % | |

| Advisor Class4 | | 09/03/1996 | | | 24.22 | % | | | 5.15 | % | | | 4.84 | % | | | 10.37 | % | |

| Institutional Class5 | | 06/21/2010 | | | 24.89 | % | | | 5.73 | % | | | 5.33 | % | | | 10.45 | % | |

| Class A20 | | 06/21/2010 | | | 24.47 | % | | | 5.49 | % | | | 5.22 | % | | | 10.42 | % | |

| Class C20 | | 06/21/2010 | | | 23.61 | % | | | 4.99 | % | | | 4.97 | % | | | 10.38 | % | |

With Sales Charge | |

| Class A20 | | | | | 17.30 | % | | | 4.25 | % | | | 4.59 | % | | | 10.31 | % | |

| Class C20 | | | | | 22.61 | % | | | 4.99 | % | | | 4.97 | % | | | 10.38 | % | |

Index | |

| S&P 500 Index1,16 | | | | | 18.70 | % | | | 7.32 | % | | | 7.12 | % | | | 9.96 | % | |

The performance data quoted represent past performance and do not indicate future results. Current performance may be lower or higher than the performance data quoted. For more current performance data, please visit www.nb.com/performance.

The results shown in the table reflect the reinvestment of income dividends and other distributions, if any. The results do not reflect the effect of taxes a shareholder would pay on Fund distributions or on the redemption of Fund shares.

The investment return and principal value of an investment will fluctuate and shares, when redeemed, may be worth more or less than their original cost.

Returns would have been lower if Neuberger Berman Management LLC ("Management") had not reimbursed certain expenses and/or waived a portion of the investment management fees during certain of the periods shown. Repayment by a class (of expenses previously reimbursed and/or fees previously waived by Management) will decrease the class's returns. Please see Note B in the Notes to Financial Statements for specific information regarding expense reimbursement and/or fee waiver arrangements.

As stated in the Fund's most recent prospectus, the total annual operating expense ratios for fiscal year 2012 were 0.98%, 1.17%, 1.32%, 0.81%, 1.22%, and 1.97% for Investor Class, Trust Class, Advisor Class, Institutional Class, Class A and Class C shares, respectively (before expense reimbursements and/or fee waivers, if any). These expense ratios were 0.75%, 1.11%, and 1.86% for Institutional Class, Class A and Class C shares, respectively, after expense reimbursements and/or fee waivers.

Returns shown with a sales charge reflect the deduction of the current maximum initial sales charge of 5.75% for Class A shares and the applicable contingent deferred sales charges (CDSC) for Class C shares. The maximum CDSC for Class C shares is 1%, which is reduced to 0% after 1 year. The performance of the Fund's share classes will differ primarily due to different sales charge structures and class expenses. Please see the prospectus for more information about sales charge structures, if any, and class expenses for your share class.

12

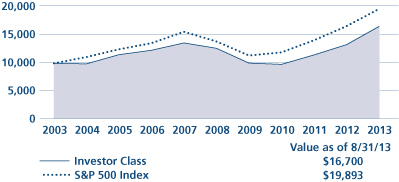

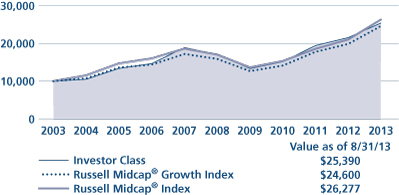

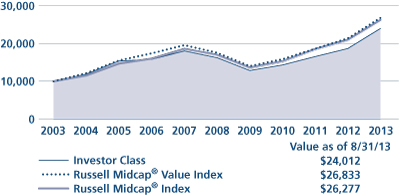

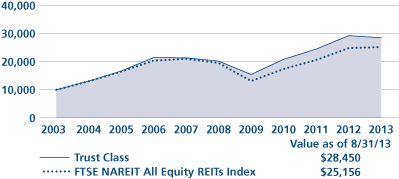

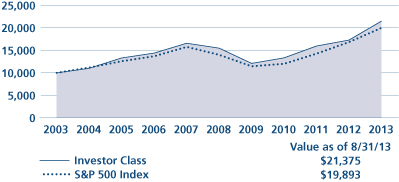

COMPARISON OF A $10,000 INVESTMENT

This graph shows the change in value of a hypothetical $10,000 investment in the Fund over the past 10 fiscal years, or since the Fund's inception if it has not operated for 10 years. The graph is based on the Investor Class shares only; the performance of the Fund's share classes will differ primarily due to different sales charge structures and class expenses (see Performance Highlights chart on previous page). The result is compared with benchmarks, which include a broad-based market index and may include a more narrowly based index. Market indices have not been reduced to reflect any of the fees and costs of investing. The results shown in the graph reflect the reinvestment of income dividends and other distributions, if any. The results do not reflect the effect of taxes a shareholder would pay on Fund distributions or on the redemption of Fund shares. Results represent past performance and do not indicate future results.

13

Genesis Fund Commentary (Unaudited)

Neuberger Berman Genesis Fund Investor Class posted a 23.91% total return for the fiscal year ended August 31, 2013 but underperformed its benchmark, the Russell 2000® Index, which provided a 26.27% return for the period. (Performance for all share classes is provided in the table immediately following this letter.)

Despite several periods of weakness and heightened volatility, the U.S. stock market produced strong results during the 12-month period. The market's resiliency was impressive given a number of macro issues, including the U.S. fiscal cliff and sequestration, the European sovereign debt crisis, several geopolitical issues and, more recently, indications from the U.S. Federal Reserve (the Fed) that it may begin tapering its asset purchase program. Supporting the stock market were generally solid corporate earnings and overall robust demand as investors sought to generate incremental returns in the low interest rate environment.

As well as the U.S. stock market performed, small-cap stocks generated even better returns as the Russell 2000 Index outperformed the S&P 500 Index, which gained 18.70% during the period. During the first six months of the fiscal year, small-cap companies with a high degree of financial leverage and low levels of profitability generated the strongest results. However, this trend was less evident during the second half of the period. As always, we emphasized higher-quality/less-speculative issues (companies with higher-than-average profitability and less financial leverage, which are also less cyclical) during the reporting period. This approach generally performs the best when the economy is expanding at a normal pace and is highly defensive during market downturns. Conversely, the Fund typically lags the performance of higher-leveraged/lower-quality companies when the economy is sharply accelerating. The Fund's higher-quality approach has also been a headwind given the Fed's highly accommodative monetary stance, as low interest rates tend to favor companies with higher leverage. With interest rates close to zero, we believe the penalties associated with corporations that have sizable cash positions, as well as the benefits associated with highly leveraged companies, appear to have more or less run their course.

While it produced a strong absolute return, the Fund's underperformance versus the benchmark was largely due to stock selection. In addition, while the portfolio's cash balance was modest and in line with its historical levels, it detracted from results given the market's sharp rally and the low yields available from cash instruments. The sectors that detracted the most from the Fund's performance were Industrials and Materials. Within the Industrials sector, a number of our high-quality machinery companies produced solid results, but lagged the benchmark. We experienced the same trend in the Materials sector, as a number of our stocks in the chemicals and containers and packaging industries were relative underperformers versus the benchmark. In addition, our position in Alamos Gold was detrimental to results. The company is a low cost Canadian gold miner with major operations in Mexico and Turkey. Its shares declined along with other gold mining stocks as the price of gold declined sharply. Elsewhere, in the Information Technology (IT) sector, our positions in NETGEAR and MICROS Systems detracted from performance. NETGEAR provides networking products designed for small businesses and homes. The company encountered a number of headwinds, including supply chain issues that limited its ability to ship new products and weakness in its European markets. MICROS Systems designs, manufactures, markets and services information solutions for the restaurant, hotel and retail industries. The company was negatively impacted by a slowdown in its core markets, primarily in Europe. Additionally, there is growing concern around emerging competitors that could impact MICROS Systems' business.

Contributing the most to performance was stock selection in the Financials and Energy sectors. Within Financials, our decision to not own real estate investment trusts (REITs), emanating from their low barriers to entry and frequent external financing requirements, was beneficial for results. REITs produced very poor results during the last four months of the period given expectations for Fed tapering and rising interest rates. Our position in Ocwen Financial, which is engaged in the servicing and origination of mortgage loans, was a significant contributor to performance. Its shares almost doubled during the reporting period as the company has significantly grown its business as banks continue to reduce their exposure in this area. Within the Energy sector, Oceaneering International and Gulfport Energy were standout performers. Oceaneering International produces equipment for deep water oil production and exploration. The

14

company benefited as deep water well completions are accelerating, supported by higher oil prices. Gulfport Energy is an exploration and production company with major operations in Louisiana, Ohio and Canada. The company continues to develop its Utica Shale acreage, which has highly favorable economics in our opinion.

We were generally comfortable with the Fund's overall positioning from a sector perspective during the reporting period. However, we did make several adjustments. For example, we increased our allocations to the Financials, IT and Consumer Discretionary sectors, while paring our exposures to the Materials, Energy and Utilities sectors.

While there are a number of risks that could derail the strength in equities, we believe there are several positive factors supporting the U.S. economy and, subsequently, U.S.-centric equities. The energy renaissance in the U.S. has benefited the country by improving trade imbalances and mitigating the risks associated with the Middle East, as well as benefiting both corporations and consumers via lower natural gas prices. We believe the housing market has showed continued signs of improvement and the recapitalization of the U.S. financial sector has left U.S. banks in relatively good shape versus their global peers. Potential issues worth noting are uncertainties surrounding the eventual timing and magnitude of Fed tapering, questions regarding the raising of the U.S. debt ceiling and continued high levels of debt in both the U.S. and abroad. Even though the short-term outlook for the equity market is as uncertain as ever, we remain confident that the high-quality/free-cash flow generating businesses in the portfolio could serve investors well over the long run. This is especially true as Fed policy has favored lower-quality/higher-leveraged companies in recent reporting periods.

Sincerely,

JUDITH M. VALE AND ROBERT D'ALELIO

PORTFOLIO CO-MANAGERS

Information about the principal risks of investing in the Fund is set forth in the prospectus and statement of additional information.

The portfolio composition, industries and holdings of the Fund are subject to change.

The opinions expressed are those of the Fund's portfolio managers. The opinions are as of the date of this report and are subject to change without notice.

15

TICKER SYMBOLS

Investor Class | | NBGNX | |

Trust Class | | NBGEX | |

Advisor Class | | NBGAX | |

Institutional Class | | NBGIX | |

Class R6 | | NRGSX | |

SECTOR ALLOCATION

(as a % of Total Investments) | |

Consumer Discretionary | | | 11.1 | % | |

Consumer Staples | | | 6.9 | | |

Energy | | | 7.5 | | |

Financials | | | 13.2 | | |

Health Care | | | 10.9 | | |

Industrials | | | 19.9 | | |

Information Technology | | | 14.3 | | |

Materials | | | 10.0 | | |

Utilities | | | 1.9 | | |

Short-Term Investments | | | 4.3 | | |

Total | | | 100.0 | % | |

PERFORMANCE HIGHLIGHTS

| | | | | Average Annual Total

Return Ended 08/31/2013 | |

| | | Inception

Date | | 1 Year | | 5 Years | | 10 Years | | Life of

Fund | |

Investor Class | | 09/27/1988 | | | 23.91 | % | | | 6.58 | % | | | 10.82 | % | | | 12.59 | % | |

| Trust Class3 | | 08/26/1993 | | | 23.81 | % | | | 6.51 | % | | | 10.76 | % | | | 12.58 | % | |

| Advisor Class4 | | 04/02/1997 | | | 23.46 | % | | | 6.23 | % | | | 10.47 | % | | | 12.38 | % | |

| Institutional Class5 | | 07/01/1999 | | | 24.12 | % | | | 6.79 | % | | | 11.05 | % | | | 12.74 | % | |

| Class R625 | | 03/15/2013 | | | 24.06 | % | | | 6.61 | % | | | 10.84 | % | | | 12.60 | % | |

Index | |

| Russell 2000® Index1,16 | | | | | 26.27 | % | | | 7.98 | % | | | 8.76 | % | | | 9.62 | % | |

The performance data quoted represent past performance and do not indicate future results. Current performance may be lower or higher than the performance data quoted. For more current performance data, please visit www.nb.com/performance.

The results shown in the table reflect the reinvestment of income dividends and other distributions, if any. The results do not reflect the effect of taxes a shareholder would pay on Fund distributions or on the redemption of Fund shares.

The investment return and principal value of an investment will fluctuate and shares, when redeemed, may be worth more or less than their original cost.

Returns would have been lower if Neuberger Berman Management LLC ("Management") had not reimbursed certain expenses and/or waived a portion of the investment management fees during certain of the periods shown. Repayment by a class (of expenses previously reimbursed and/or fees previously waived by Management) will decrease the class's returns. Please see Note B in the Notes to Financial Statements for specific information regarding expense reimbursement and/or fee waiver arrangements.

As stated in the Fund's most recent prospectus, the total annual operating expense ratios for fiscal year 2012 (estimated for 2013 for Class R6) were 1.03%, 1.11%, 1.38%, 0.86%, and 0.78% for Investor Class, Trust Class, Advisor Class, Institutional Class, and Class R6 shares, respectively (before expense reimbursements and/or fee waivers, if any). The expense ratio was 0.85% for Institutional Class after expense reimbursements and/or fee waivers.

16

COMPARISON OF A $10,000 INVESTMENT

This graph shows the change in value of a hypothetical $10,000 investment in the Fund over the past 10 fiscal years, or since the Fund's inception if it has not operated for 10 years. The graph is based on the Investor Class shares only; the performance of the Fund's share classes will differ primarily due to different class expenses (see Performance Highlights chart on previous page). The result is compared with benchmarks, which include a broad-based market index and may include a more narrowly based index. Market indices have not been reduced to reflect any of the fees and costs of investing. The results shown in the graph reflect the reinvestment of income dividends and other distributions, if any. The results do not reflect the effect of taxes a shareholder would pay on Fund distributions or on the redemption of Fund shares. Results represent past performance and do not indicate future results.

17

Global Equity Fund Commentary (Unaudited)

Neuberger Berman Global Equity Fund Institutional Class generated an 11.65% total return for the fiscal year ended August 31, 2013 but trailed its benchmark, the MSCI World Index, which provided a return of 18.31%. (Performance for all share classes is provided in the table immediately following this letter.)

The MSCI World Index rose significantly this period, with positive returns across all sectors. Sentiment improved over the period, with supportive European Central Bank statements and resolution of the U.S. fiscal cliff followed by improving U.S. and eurozone growth data. This May, however, the U.S. Federal Reserve's (the Fed) tapering announcement startled investors with prospects of higher global interest rates. Volatility increased as investors worked to balance rate fears and heightened geopolitical concerns with generally better (ex-China) growth data. Consumer Discretionary, Financials and Health Care stocks outperformed, while Materials, Energy and Utilities underperformed—the first two on reduced Chinese demand, and the third on interest rates concerns.

Buoyed by improving growth and investor sentiment, large index components including the U.S., Japan and much of the eurozone outperformed. While all markets were positive, Greece, Finland and Ireland saw the strongest returns. Israel, along with Materials- and Energy-focused Canada, and Norway lagged the benchmark.

Within the portfolio, relative underperformance versus the benchmark primarily resulted from Financials, where we continue to underweight the large U.S. and Japanese banks that led the index this year. An overweight and stock selection within the weak Information Technology (IT) sector was another factor, as were certain Energy holdings. We saw relative benefits from stock selection within Materials and Health Care, and from a zero allocation to Utilities. By country, holdings in Israel, Germany and Switzerland were most beneficial, while UK, Canadian and Chinese holdings detracted.

In terms of individual holdings, many top contributors this year were U.S.-based, including packaging and food safety specialist Sealed Air and asset manager BlackRock. Sealed Air saw increased demand for their packaging and high performance material products as the U.S. economy continued its recovery. BlackRock outperformed as investors moved from fixed income into higher margin equity and alternative investments. Germany's Continental was another significant contributor. The tire and auto parts firm benefited from an uptick in global auto sales.

Underperformers included Apple, New Gold and ICICI Bank. Apple disappointed the market with lower gross margins. However, we believe recent software and services innovations will allow Apple to maintain margins going forward. Canadian gold producer New Gold suffered as the price of gold continued to retreat. Indian bank ICICI sold off with the rest of the Indian market following Mr. Bernanke's tapering comments in late May. The market grew concerned about the impact capital flight would have on India's ability to fund its current account deficit and on the value of the rupee.

Equity markets enjoyed strong performance through late May with investors initially discounting weak economic indicators. More recently, however, markets reversed their positive momentum, as policy uncertainty returned to the fore. The prospect of a Fed "taper" had raised concerns of higher global interest rates and dampened risk appetite, although exact timing remains unknown. Concurrently, lack of clarity on structural reform in Japan, worries about the Chinese banking system, and unrest in a number of nations have added to market concerns.

With policy uncertainty in the U.S., Japan and China, we remain focused on identifying what we believe are high-return companies delivering bottom-line earnings growth—typically companies with stable revenue streams, often as a result of operations spanning all regions. To this end, we are overweighted in IT, refined materials, and industrial names that meet these requirements, while underweighted in the more cyclically and/or China-dependent Financials and bulk Materials areas. We reiterate our doubts on Japan, as we believe the weaker yen will raise costs (e.g., imported energy) domestically rather than just improve wages. That being said, we do have exposure to quality Japanese exporters that we believe could benefit from a weaker yen. While our emerging markets holdings have fallen—as much on currency as stock price—we believe these names have strong franchises with consumer end-markets that could benefit as these markets mature.

18

In terms of sectors, our IT overweight is focused on market-leading equipment and services businesses. In Materials, we sold our industrial/bulk Materials exposure on concerns that further slowing in China would continue to pressure prices. Instead, our overweight centers around refined chemical names that we believe have pricing power and relatively stable end markets. Industrials is a third overweight, where our focus is differentiated innovators. Our Consumer Discretionary holdings are diversified across autos, as U.S. and China car sales have been showing continued growth, and North American retailers, based on consumer spending trends. We remain underweighted in Financials as developed market banks continue to be at the mercy of central bank policy and regulatory change.

In a market caught between policy and geopolitical uncertainties and clear signs of improving global growth, we anticipate that our fundamentals-focused Quality at a Reasonable Price discipline could continue to guide us to opportunities poised to deliver strong risk-adjusted returns over the longer term.

Sincerely,

BENJAMIN SEGAL AND SAURIN SHAH

PORTFOLIO CO-MANAGERS

Information about the principal risks of investing in the Fund is set forth in the prospectus and statement of additional information.

The portfolio composition, industries and holdings of the Fund are subject to change.

The opinions expressed are those of the Fund's portfolio managers. The opinions are as of the date of this report and are subject to change without notice.

19

Global Equity Fund (Unaudited)

TICKER SYMBOLS

Institutional Class | | NGQIX | |

Class A | | NGQAX | |

Class C | | NGQCX | |

SECTOR ALLOCATION

(as a % of Total Investments) | |

Consumer Discretionary | | | 11.5 | % | |

Consumer Staples | | | 8.6 | | |

Energy | | | 7.4 | | |

Financials | | | 15.3 | | |

Health Care | | | 12.8 | | |

Industrials | | | 13.2 | | |

Information Technology | | | 16.6 | | |

Materials | | | 10.1 | | |

Telecommunication Services | | | 2.6 | | |

Short-Term Investments | | | 1.9 | | |

Total | | | 100.0 | % | |

PERFORMANCE HIGHLIGHTS9

| | | | | Average Annual Total

Return Ended 08/31/2013 | |

| | | Inception

Date | | 1 Year | | Life of

Fund | |

At NAV | |

Institutional Class | | 06/30/2011 | | | 11.65 | % | | | 2.03 | % | |

Class A | | 06/30/2011 | | | 11.20 | % | | | 1.65 | % | |

Class C | | 06/30/2011 | | | 10.34 | % | | | 0.90 | % | |

With Sales Charge | |

Class A | | | | | 4.78 | % | | | –1.08 | % | |

Class C | | | | | 9.34 | % | | | 0.90 | % | |

Index | |

| MSCI World Index1,16 | | | | | 18.31 | % | | | 8.36 | % | |

The performance data quoted represent past performance and do not indicate future results. Current performance may be lower or higher than the performance data quoted. For more current performance data, please visit www.nb.com/performance.

The results shown in the table reflect the reinvestment of income dividends and other distributions, if any. The results do not reflect the effect of taxes a shareholder would pay on Fund distributions or on the redemption of Fund shares.

The investment return and principal value of an investment will fluctuate and shares, when redeemed, may be worth more or less than their original cost.

Returns would have been lower if Neuberger Berman Management LLC ("Management") had not reimbursed certain expenses and/or waived a portion of the investment management fees during certain of the periods shown. Repayment by a class (of expenses previously reimbursed and/or fees previously waived by Management) will decrease the class's returns. Please see Note B in the Notes to Financial Statements for specific information regarding expense reimbursement and/or fee waiver arrangements.

As stated in the Fund's most recent prospectus, the total annual operating expense ratios for fiscal year 2012 were 10.85%, 11.83%, and 12.88% for Institutional Class, Class A and Class C shares, respectively (before expense reimbursements and/or fee waivers, if any). These expense ratios were 1.15%, 1.51% and 2.26% for Institutional Class, Class A and Class C shares, respectively, after expense reimbursements and/or fee waivers.

Returns shown with a sales charge reflect the deduction of the current maximum initial sales charge of 5.75% for Class A shares and the applicable contingent deferred sales charges (CDSC) for Class C shares. The maximum CDSC for Class C shares is 1%, which is reduced to 0% after 1 year. The performance of the Fund's share classes will differ primarily due to different sales charge structures and class expenses. Please see the prospectus for more information about sales charge structures, if any, and class expenses for your share class.

20

Global Equity Fund (Unaudited)

COMPARISON OF A $1,000,000 INVESTMENT

(000's Omitted)

This graph shows the change in value of a hypothetical $1,000,000 investment in the Fund over the past 10 fiscal years, or since the Fund's inception if it has not operated for 10 years. The graph is based on the Institutional Class shares only; the performance of the Fund's share classes will differ primarily due to different sales charge structures and class expenses (see Performance Highlights chart on previous page). The result is compared with benchmarks, which include a broad-based market index and may include a more narrowly based index. Market indices have not been reduced to reflect any of the fees and costs of investing. The results shown in the graph reflect the reinvestment of income dividends and other distributions, if any. The results do not reflect the effect of taxes a shareholder would pay on Fund distributions or on the redemption of Fund shares. Results represent past performance and do not indicate future results.

21

Global Thematic Opportunities Fund Commentary (Unaudited)

Neuberger Berman Global Thematic Opportunities Fund Institutional Class generated a 9.53% total return for the fiscal year ended August 31, 2013 but underperformed its benchmark, the MSCI All Country World Index, which generated a return of 16.11%. (Performance for all share classes is provided in the table immediately following this letter.)

Investor sentiment improved as this reporting period progressed—from relief last fall that the European Central Bank would not let the eurozone fail, to offsetting a slower, more internally focused China with improving economic data from the U.S.

In the U.S., macro uncertainties faded with the resolution of last year's fiscal cliff and an improvement in housing and unemployment data, in addition to a natural gas renaissance which supported optimism. Markets paused following the U.S. Federal Reserve's tapering announcement in May, but shrugged it off against the better economic news. Meanwhile in Japan, "Abenomics" (economic policies advocated by Shinz? Abe, the current prime minister of Japan) continued to drive the market. Globally, the U.S. outperformed, followed by developed international markets, while emerging markets closed the year roughly flat.

The portfolio's "Emerging Consumer" theme, the largest by exposure as the year began, and currently the second largest, saw mixed results as emerging markets underperformed. The adage, "China sneezes and the emerging markets catch a cold" held true, regardless of whether a specific market was directly threatened by China's declining demand.

Performance in the "Emerging Consumer" theme benefited from Universal Robina, a Filipino snack foods conglomerate with ambitious plans for increasing market share across Southeast Asia. We have sold the position. Sa Sa International, a Hong Kong-based cosmetics business was also additive, enjoying exposure to both luxury and value-oriented consumers in a segment that seems fairly insulated.

Detractors included Indonesia's Global Mediacom, which we sold as its price pulled back. Indonesia was among the stronger markets for the past several years, but declined as capital left emerging markets, hurting its currency. Hong Kong-based Trinity Limited, a fashion retailer that declined with waning Chinese consumer spending, was also sold.

We made a conscious decision to reduce the portfolio's emerging markets exposure over this fiscal period—down from approximately 24% to 10% of total net assets—on the basis of the Chinese slowdown. Anticipating a trickle-down fall off in demand, we cut back on holdings with direct ties to China, especially in Thailand, Indonesia and the Philippines. This year's nearly 18% disparity between the MSCI Emerging Markets Index and the S&P 500 Index is something we generally only see about once a cycle.

Our "Money in Motion" theme contained two U.S.-based top contributors. Asset manager BlackRock benefited from increased ETF investing and on margin expansion as investors shifted from fixed income to equities. We believe insurance giant American International Group is in great shape following its bailout, an investment that ultimately earned the government $17 billion.

On the negative side, Hong Kong-based First Pacific was a detractor. China's work to reduce economic excesses put pressure on this company, which operates infrastructure, mining, investment management and other businesses. Japan's Mitsubishi UFJ Financial, a newer holding, saw a short-term pullback. We believe in the company's prospects and anticipate that Japanese banks will benefit from Shinz? Abe's bold monetary policies. We began building our Japanese exposure substantially in 2012, with banks, automakers and others that were benefiting from better (ex-China) export conditions.

Within our "Up, Up and Away" theme, we believe Boeing, which should continue to benefit from increases in air travel, was additive. Though volatile during its battery problems, it was purchased at a favorable price. Honeywell International, a supplier to both sides of the Boeing/Airbus duopoly, also outperformed.

22

"Agriculture," among the weaker themes this period, was reduced as an allocation by about 10 percentage points. Japanese tractor manufacturer Kubota was a top contributor, benefiting with Japanese exports, while Canada's Potash Corporation was our largest detractor. Potash declined as Eastern European rivals created supply gluts in the commodity, thus damaging its price. Chile's SQM also declined. Each of these holdings was sold.

With inflation seemingly benign, our "Inflation/Financial Repression" theme underperformed and was retired in the second quarter. Detractor Market Vectors Gold Trust ETF was part of this theme, designed to hedge against the inflationary pressures we expected after years of unprecedented global central bank easing.

Looking ahead, while there are unknowns on the horizon from the Middle East to potentially rising interest rates, we remain optimistic. We believe the global economy is in a state of slow recovery with GDP growth modestly improving in the U.S.—the world's largest market—and better prospects in Europe. Businesses and consumers are generally healthy in our opinion, both with improved balance sheets after the downturn.

With this optimistic perspective, we are working to take advantage of the compelling valuations we see—often as good as they've been since 2008, in our opinion. We think this could position the portfolio well if the spread between the U.S. rally and the rest of the world begins to compress. We remain dedicated to scouring the globe for the most attractive niche businesses that trade at appealing valuations. We believe that even when we are early to a theme, we have learned from decades of investing that being opportunistic, disciplined and patient with our investments can be rewarded through attractive returns over time.

Sincerely,

ANTHONY GLEASON, SANDY POMEROY, WILLIAM HUNTER AND RICHARD LEVINE

PORTFOLIO CO-MANAGERS

Information about the principal risks of investing in the Fund is set forth in the prospectus and statement of additional information.

The portfolio composition, industries and holdings of the Fund are subject to change.

The opinions expressed are those of the Fund's portfolio managers. The opinions are as of the date of this report and are subject to change without notice.

23

Global Thematic Opportunities Fund (Unaudited)

TICKER SYMBOLS

Institutional Class | | NGHIX | |

Class A | | NGHAX | |

Class C | | NGHCX | |

SECTOR ALLOCATION

(as a % of Total Investments) | |

Consumer Discretionary | | | 15.8 | % | |

Consumer Staples | | | 5.7 | | |

Energy | | | 4.5 | | |

Financials | | | 22.6 | | |

Health Care | | | 8.3 | | |

Industrials | | | 18.3 | | |

Information Technology | | | 14.5 | | |

Telecommunication Services | | | 2.9 | | |

Short-Term Investments | | | 7.4 | | |

Total | | | 100.0 | % | |

PERFORMANCE HIGHLIGHTS

| | | | | Average Annual Total

Return Ended 08/31/2013 | |

| | | Inception

Date | | 1 Year | | Life of

Fund | |

At NAV | |

Institutional Class | | 06/30/2011 | | | 9.53 | % | | | –1.89 | % | |

Class A | | 06/30/2011 | | | 9.20 | % | | | –2.25 | % | |

Class C | | 06/30/2011 | | | 8.34 | % | | | –2.98 | % | |

With Sales Charge | |

Class A | | | | | 2.93 | % | | | –4.88 | % | |

Class C | | | | | 7.34 | % | | | –2.98 | % | |

Index | |

| MSCI All Country World Index1,16 | | | | | 16.11 | % | | | 6.49 | % | |

The performance data quoted represent past performance and do not indicate future results. Current performance may be lower or higher than the performance data quoted. For more current performance data, please visit www.nb.com/performance.

The results shown in the table reflect the reinvestment of income dividends and other distributions, if any. The results do not reflect the effect of taxes a shareholder would pay on Fund distributions or on the redemption of Fund shares.

The investment return and principal value of an investment will fluctuate and shares, when redeemed, may be worth more or less than their original cost.

Returns would have been lower if Neuberger Berman Management LLC ("Management") had not reimbursed certain expenses and/or waived a portion of the investment management fees during certain of the periods shown. Repayment by a class (of expenses previously reimbursed and/or fees previously waived by Management) will decrease the class's returns. Please see Note B in the Notes to Financial Statements for specific information regarding expense reimbursement and/or fee waiver arrangements.

As stated in the Fund's most recent prospectus, the total annual operating expense ratios for fiscal year 2012 were 1.87%, 2.27% and 3.13%, for Institutional Class, Class A and Class C shares, respectively (before expense reimbursements and/or fee waivers, if any). These expense ratios were 1.27%, 1.63% and 2.38% for Institutional Class, Class A and Class C shares, respectively, after expense reimbursements and/or fee waivers.