Neuberger Berman

Equity Funds

Investor Class Shares

Trust Class Shares

Advisor Class Shares

Institutional Class Shares

All Cap Core Fund

(Formerly Select Equities Fund)

Emerging Markets Equity Fund

Equity Income Fund

Focus Fund

Genesis Fund

Global Equity Fund

Global Thematic Opportunities Fund

Greater China Equity Fund

Guardian Fund

International Equity Fund

International Select Fund

(Formerly International Large Cap Fund)

Class A Shares

Class C Shares

Class R3 Shares

Class R6 Shares

Intrinsic Value Fund

Large Cap Disciplined Growth Fund

Large Cap Value Fund

Mid Cap Growth Fund

Mid Cap Intrinsic Value Fund

Multi-Cap Opportunities Fund

Real Estate Fund

Small Cap Growth Fund

Socially Responsive Fund

Value Fund

Annual Report

August 31, 2014

Contents

THE FUNDS

President's Letter | 1 | ||||||

PORTFOLIO COMMENTARY | |||||||

All Cap Core Fund (Formerly Select Equities Fund) | 2 | ||||||

Emerging Markets Equity Fund | 5 | ||||||

Equity Income Fund | 8 | ||||||

Focus Fund | 11 | ||||||

Genesis Fund | 14 | ||||||

Global Equity Fund | 17 | ||||||

Global Thematic Opportunities Fund | 20 | ||||||

Greater China Equity Fund | 23 | ||||||

Guardian Fund | 26 | ||||||

International Equity Fund | 29 | ||||||

International Select Fund (Formerly International Large Cap Fund) | 32 | ||||||

Intrinsic Value Fund | 35 | ||||||

Large Cap Disciplined Growth Fund | 38 | ||||||

Large Cap Value Fund | 41 | ||||||

Mid Cap Growth Fund | 44 | ||||||

Mid Cap Intrinsic Value Fund | 47 | ||||||

Multi-Cap Opportunities Fund | 50 | ||||||

Real Estate Fund | 53 | ||||||

Small Cap Growth Fund | 56 | ||||||

Socially Responsive Fund | 59 | ||||||

Value Fund | 62 | ||||||

FUND EXPENSE INFORMATION | 71 | ||||||

SCHEDULE OF INVESTMENTS/TOP TEN EQUITY HOLDINGS | |||||||

All Cap Core Fund (Formerly Select Equities Fund) | 75 | ||||||

Emerging Markets Equity Fund | 76 | ||||||

Equity Income Fund | 79 | ||||||

Focus Fund | 81 | ||||||

Genesis Fund | 82 | ||||||

Global Equity Fund | 85 | ||||||

Global Thematic Opportunities Fund | 88 | ||||||

Greater China Equity Fund | 91 | ||||||

Guardian Fund | 95 | ||||||

International Equity Fund | 96 | ||||||

International Select Fund (Formerly International Large Cap Fund) | 99 | ||||||

Intrinsic Value Fund | 102 | ||||||

Large Cap Disciplined Growth Fund | 104 | ||||||

Large Cap Value Fund | 106 | ||||||

Mid Cap Growth Fund | 108 | ||||||

Mid Cap Intrinsic Value Fund | 110 | ||||||

Multi-Cap Opportunities Fund | 112 | ||||||

Real Estate Fund | 113 | ||||||

Small Cap Growth Fund | 114 | ||||||

Socially Responsive Fund | 116 | ||||||

Value Fund | 117 | ||||||

FINANCIAL STATEMENTS | 129 | ||||||

FINANCIAL HIGHLIGHTS (ALL CLASSES)/PER SHARE DATA | |||||||

All Cap Core Fund (Formerly Select Equities Fund) | 193 | ||||||

Emerging Markets Equity Fund | 193 | ||||||

Equity Income Fund | 195 | ||||||

Focus Fund | 197 | ||||||

Genesis Fund | 199 | ||||||

Global Equity Fund | 201 | ||||||

Global Thematic Opportunities Fund | 203 | ||||||

Greater China Equity Fund | 203 | ||||||

Guardian Fund | 205 | ||||||

International Equity Fund | 207 | ||||||

International Select Fund (Formerly International Large Cap Fund) | 209 | ||||||

Intrinsic Value Fund | 211 | ||||||

Large Cap Disciplined Growth Fund | 213 | ||||||

Large Cap Value Fund | 215 | ||||||

Mid Cap Growth Fund | 217 | ||||||

Mid Cap Intrinsic Value Fund | 221 | ||||||

Multi-Cap Opportunities Fund | 223 | ||||||

Real Estate Fund | 225 | ||||||

Small Cap Growth Fund | 227 | ||||||

Socially Responsive Fund | 229 | ||||||

Value Fund | 233 | ||||||

Reports of Independent Registered Public Accounting Firms | 238 | ||||||

Directory | 241 | ||||||

Trustees and Officers | 242 | ||||||

Proxy Voting Policies and Procedures | 250 | ||||||

Quarterly Portfolio Schedule | 250 | ||||||

Notice to Shareholders | 251 | ||||||

The "Neuberger Berman" name and logo are registered service marks of Neuberger Berman Group LLC. "Neuberger Berman Management LLC" and the individual Fund names in this piece are either service marks or registered service marks of Neuberger Berman Management LLC. ©2014 Neuberger Berman Management LLC. All rights reserved.

President's Letter

Dear Shareholder,

This has been another positive year for the equity markets, with the S&P 500® Index advancing over 25% over the past 12 months and breaking 2000 for the first time in August 2014. Emerging markets rebounded, up 20% for the period, and while developed international equities trailed U.S. and emerging markets, they were still positive. Key drivers of returns this fiscal year have been two-fold—signs of growing economic momentum and constructive business activity.

On the economic side, after a positive 2013, data softened somewhat in the first quarter of 2014. By mid-year, however, improved statistics confirmed that the slippage had been temporary—caused by an unusually harsh winter. Stable growth in China and green shoots in the eurozone combined with generally positive trends in the U.S., where supports for improved consumer spending, by far the largest driver of U.S. GDP, remained apparent.

By August, unemployment declined to 6.1%, a post-crisis low. Wage inflation was beginning to appear, along with signs of a tightening skilled labor market. Auto sales in August peaked at pre-crisis rates, and the housing sector appeared healthy as well. Even with geopolitical tensions making headlines nightly, investor sentiment remained above long-term levels, and the Chicago Board Options Exchange Volatility Index (VIX) declined, touching 2007-era lows in July.

From a business management perspective, after years of caution and cash accumulation, we've seen companies deploying assets for future growth and to the benefit of shareholders, through capital investment, increased M&A activity, dividend increases and share buybacks. We believe the North American energy renaissance continues to have positive effects as well, and even as the U.S. Federal Reserve continues tapering, interest rates have fallen.

After marking a six-year rally in which the S&P 500 has gained more than 200% from its closing low in 2009, some would argue that valuations have climbed ahead of fundamentals, especially given subpar global economic growth and potential economic complications from Russian/Ukrainian tensions and conflict in the Middle East. As this bull market ages, we believe it's unlikely that we will continue to see outsized equity returns year over year. However, barring an unforeseen shock, we anticipate that markets will remain positive. From an investor's point of view, we've noted a falling correlation between stocks, suggesting individual fundamentals are again becoming paramount. We also see signs that the spread between top and bottom performers—fairly tight this year—may be widening.

As we move toward what we believe will be a more typical equity market—with more typical equity returns—we anticipate experienced active managers will have a clear opportunity to demonstrate their worth. We believe a fundamentally focused, differentiated market is a stock picker's market; one in which deep fundamental research and investment skill can add real value by uncovering opportunities outside the indices.

We thank you for your confidence in Neuberger Berman and look forward to continuing to serve your investment needs.

Sincerely,

ROBERT CONTI

PRESIDENT AND CEO

NEUBERGER BERMAN MUTUAL FUNDS

1

All Cap Core Fund Commentary* (Unaudited)

Neuberger Berman All Cap Core Fund (formerly Neuberger Berman Select Equities Fund) Institutional Class generated a 22.55% total return for the fiscal year ended August 31, 2014, but underperformed its benchmark, the S&P 500® Index, which generated a return of 25.25% for the period. (Performance for all share classes is provided in the table immediately following this letter.)

This past fiscal year, we decided to make a change to the management of the Fund in order to give ourselves more flexibility in overseeing your investment. Our team asked the Fund's Board of Trustees to allow us to invest in companies across the market capitalization spectrum rather than limiting our investments to companies over $7.5 billion in market cap. This modification was approved in June and implemented in September. We believe this change provides us with the added flexibility necessary to enhance our capabilities as we seek to provide our investors with attractive returns.

We are pleased with the performance of the Fund during the 12-month period, especially given our lower-than-market risk profile and a cash position that averaged roughly 7% throughout the period. Stock selection drove our significant outperformance within the Financials and Industrials sectors. Our lack of exposure to the weaker Consumer Staples and Telecommunication Services sectors was also a relative benefit. We underperformed on a relative basis versus the index in the Information Technology, Health Care and Energy sectors, and our cash position was a disadvantage against a rising market.

We continue to believe that the growth of the U.S. economy will continue to follow a Nike swoosh-like trajectory. We feel that this path will carry on for quite some time and it is our responsibility to identify trends or themes within the U.S. or global economies that we believe may have the wherewithal to grow at rates faster than the broader economic environment. We also think that the direction of interest rates over the next few years will be higher and, as such, have moved the portfolio in the direction of more cyclically oriented securities in an attempt to take advantage of that growth, and we have reduced our exposure to securities more closely correlated to interest rates.

We hope tensions in the Middle East and Ukraine will decline; barring any major shocks, however, we believe that stocks generally are positioned better than other investable asset classes. We are increasingly optimistic about the value of stock picking within the current environment and we are finding companies we believe are in strong financial health, and we anticipate profit growth could continue. We also believe companies will continue to allocate capital for the benefit of shareholders.

Over the past number of years, we've seen a rising tide that lifted all boats in a highly correlated market. In our view, much of that was due to the external stimulus of quantitative easing. Now that quantitative easing is coming to an end, we think the market will be driven more by the fundamentals of underlying securities. We believe owning a concentrated portfolio that has flexibility in terms of market capitalization as well as sector allocation, without a value or growth bias, gives us the opportunity to succeed in generating attractive risk-adjusted returns.

Sincerely,

MICHAEL KAMINSKY, RICHARD WERMAN, JAMES GARTLAND AND MINDY SCHWARTZAPFEL

PORTFOLIO CO-MANAGERS

* Effective September 2, 2014, Neuberger Berman Select Equities Fund changed its name to Neuberger Berman All Cap Core Fund.

Information about principal risks of investing in the Fund is set forth in the prospectus and statement of additional information.

The portfolio composition, industries and holdings of the Fund are subject to change.

The opinions expressed are those of the Fund's portfolio managers. The opinions are as of the date of this report and are subject to change without notice.

References to any third-party logos or service marks do not imply any endorsement by the Firm. The Nike name and logo are trademarks of Nike, Inc. All rights reserved.

2

All Cap Core Fund (Unaudited)

TICKER SYMBOLS

Institutional Class | NBEIX | ||||||

Class A | NBEAX | ||||||

Class C | NBECX | ||||||

SECTOR ALLOCATION

(as a % of Total Investments) | |||||

Consumer Discretionary | 17.5 | % | |||

Energy | 13.4 | ||||

Financials | 16.3 | ||||

Health Care | 4.2 | ||||

Industrials | 21.4 | ||||

Information Technology | 11.6 | ||||

Utilities | 5.3 | ||||

Short-Term Investments | 10.3 | ||||

Total | 100.0 | % | |||

PERFORMANCE HIGHLIGHTS27

| Average Annual Total Return Ended 08/31/2014 | |||||||||||||||||||

| Inception Date | 1 Year | 5 Year | Life of Fund | ||||||||||||||||

At NAV | |||||||||||||||||||

Institutional Class | 12/20/2007 | 22.55 | % | 14.09 | % | 6.90 | % | ||||||||||||

Class A | 12/20/2007 | 21.95 | % | 13.55 | % | 6.51 | % | ||||||||||||

Class C | 12/20/2007 | 21.13 | % | 12.73 | % | 5.71 | % | ||||||||||||

With Sales Charge | |||||||||||||||||||

Class A | 14.99 | % | 12.22 | % | 5.57 | % | |||||||||||||

Class C | 20.13 | % | 12.73 | % | 5.71 | % | |||||||||||||

Index | |||||||||||||||||||

| S&P 500® Index1,16 | 25.25 | % | 16.88 | % | 7.24 | % | |||||||||||||

The performance data quoted represent past performance and do not indicate future results. Current performance may be lower or higher than the performance data quoted. For more current performance data, please visit www.nb.com/performance.

The results shown in the table reflect the reinvestment of income dividends and other distributions, if any. The results do not reflect the effect of taxes a shareholder would pay on Fund distributions or on the redemption of Fund shares.

The investment return and principal value of an investment will fluctuate and shares, when redeemed, may be worth more or less than their original cost.

Returns would have been lower if Neuberger Berman Management LLC (Management) had not reimbursed certain expenses and/or waived a portion of the investment management fees during certain of the periods shown. Repayment by a class (of expenses previously reimbursed and/or fees previously waived by Management) will decrease the class's returns. Please see Note B in the Notes to Financial Statements for specific information regarding expense reimbursement and/or fee waiver arrangements.

As stated in the Fund's most recent prospectus, the total annual operating expense ratios for fiscal year 2013 were 1.11%, 1.49% and 2.24% for Institutional Class, Class A and Class C shares, respectively (before expense reimbursements and/or fee waivers, if any). The expense ratios were 0.76%, 1.21% and 1.96% for Institutional Class, Class A and Class C shares, respectively, after expense reimbursements and/or fee waivers.

Returns shown with a sales charge reflect the deduction of the current maximum initial sales charge of 5.75% for Class A shares and the contingent deferred sales charge (CDSC) for Class C shares. The CDSC for Class C shares is 1%, which is reduced to 0% after 1 year. The performance of the Fund's share classes will differ primarily due to different sales charge structures and class expenses. Please see the prospectus for more information about sales charge structures, if any, and class expenses for your share class.

3

All Cap Core Fund (Unaudited)

COMPARISON OF A $1,000,000 INVESTMENT

(000's Omitted)

This graph shows the change in value of a hypothetical $1,000,000 investment in the Fund over the past 10 fiscal years, or since the Fund's inception if it has not operated for 10 years. The graph is based on the Institutional Class shares only; the performance of the Fund's share classes will differ primarily due to different sales charge structures and class expenses (see Performance Highlights chart on previous page). The result is compared with benchmarks, which include a broad-based market index and may include a more narrowly based index. Market indices have not been reduced to reflect any of the fees and costs of investing. The results shown in the graph reflect the reinvestment of income dividends and other distributions, if any. The results do not reflect the effect of taxes a shareholder would pay on Fund distributions or on the redemption of Fund shares. Results represent past performance and do not indicate future results.

4

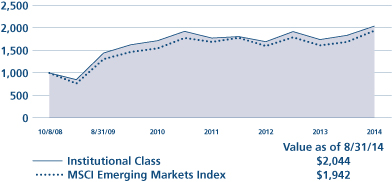

Emerging Markets Equity Fund Commentary (Unaudited)

Neuberger Berman Emerging Markets Equity Fund Institutional Class generated a 17.24% total return for the fiscal year ended August 31, 2014, but underperformed its benchmark, the MSCI Emerging Markets (EM) Index, which generated a 20.40% return during the period. (Performance for all share classes is provided in the table immediately following this letter.)

After weakness on relatively slow economic growth early in the reporting period, emerging markets have rebounded since early February. Markets were buoyed by a relative calming of the geopolitical tensions in Ukraine, on reform-minded Narendra Modi's landslide election victory in India, and on stabilizing economic data from China, along with generally improved sentiment.

All index sectors were positive this period, with Health Care, Information Technology and Utilities being the strongest performers. By country, Egypt, India and Brazil led the Index, while Hungary, United Arab Emirates and Qatar saw the worst negative returns.

Within the portfolio, excellent stock selection within the Consumer Discretionary sector—with consumer electronics/appliance names including China's Haier Electronics and Korea's Coway being among the top contributors—as well as stock selection and an overweight in Health Care had the most significant positive effects on relative performance from a sector perspective. By country, it was Indian and Chinese holdings, including India's Yes Bank, Chinese social networking company Tencent Holdings, and waste-to-energy plant builder China Everbright that had the most positive effect.

Stock selection within Energy, Financials and Materials was a relative detriment this period, and by country, holdings in Brazil and Korea underperformed. In Brazil, hopes for political change rather than fundamentals drove the market higher, while in Korea a large government stimulus package boosted the local stock market. We remain skeptical that this stimulus will be productive, and are not convinced these markets can continue their rallies without structural reforms. Individual detractors included China Child Care Corp., Brasil Insurance, China Vanke, as well as Lock & Lock (Korea), and Alamos Gold (Canada). Alamos Gold was sold during the reporting period and Lock & Lock was sold shortly afterward.

Our largest country overweights are currently India, China and the Philippines. Our greatest sector overweight is currently Industrials—where we own local infrastructure names, followed by Health Care and Consumer Staples. Considering slower global growth, we are currently underweighted in export markets, including Taiwan and Korea. We are also underweighted in Telecommunication Services stocks, Energy stocks, and Financials stocks.

As we look ahead, we acknowledge pockets of geopolitical risks, but several factors suggest the current rally may continue, in our opinion. First, current account deficits appear to us to have been tamed in certain countries. This has helped a subset of EM currencies to stabilize, if not rebound. Second, developed market economies have rebounded, but only to muted levels, creating a benign interest rate environment. Third, we believe EM equities offer attractive relative valuations versus developed markets. Fourth, reported earnings have generally stabilized after several years of downgrades; and finally, we see positive prospects for structural reforms in several countries, including India. Especially based on the last two drivers, we believe select EM markets could offer attractive growth going forward.

In both rallies and retrenchments, we believe stock picking skills, deep knowledge of local economies and companies, and a tested process can be important differentiators in EM equity investing. We believe we are well positioned for the future.

Sincerely,

CONRAD SALDANHA

PORTFOLIO MANAGER

Information about principal risks of investing in the Fund is set forth in the prospectus and statement of additional information.

The portfolio composition, industries and holdings of the Fund are subject to change.

The opinions expressed are those of the Fund's portfolio manager. The opinions are as of the date of this report and are subject to change without notice.

5

Emerging Markets Equity Fund (Unaudited)

TICKER SYMBOLS

Institutional Class | NEMIX | ||||||

Class A | NEMAX | ||||||

Class C | NEMCX | ||||||

Class R3 | NEMRX | ||||||

Class R6 | NREMX | ||||||

SECTOR ALLOCATION

(as a % of Total Investments) | |||||

Consumer Discretionary | 11.3 | % | |||

Consumer Staples | 12.3 | ||||

Energy | 5.2 | ||||

Financials | 22.7 | ||||

Health Care | 6.1 | ||||

Industrials | 13.6 | ||||

Information Technology | 18.8 | ||||

Materials | 4.1 | ||||

Telecommunication Services | 2.4 | ||||

Utilities | 1.0 | ||||

Short-Term Investments | 2.5 | ||||

Total | 100.0 | % | |||

PERFORMANCE HIGHLIGHTS9

| Average Annual Total Return Ended 08/31/2014 | |||||||||||||||||||

| Inception Date | 1 Year | 5 Years | Life of Fund | ||||||||||||||||

At NAV | |||||||||||||||||||

Institutional Class | 10/08/2008 | 17.24 | % | 7.19 | % | 12.88 | % | ||||||||||||

Class A | 10/08/2008 | 16.99 | % | 6.94 | % | 12.62 | % | ||||||||||||

Class C | 10/08/2008 | 16.07 | % | 6.13 | % | 11.77 | % | ||||||||||||

| Class R310 | 06/21/2010 | 16.42 | % | 6.58 | % | 12.33 | % | ||||||||||||

| Class R623 | 03/15/2013 | 17.35 | % | 7.22 | % | 12.91 | % | ||||||||||||

With Sales Charge | |||||||||||||||||||

Class A | 10.28 | % | 5.68 | % | 11.49 | % | |||||||||||||

Class C | 15.07 | % | 6.13 | % | 11.77 | % | |||||||||||||

Index | |||||||||||||||||||

| MSCI Emerging Markets Index1,16 | 20.40 | % | 8.24 | % | 11.90 | % | |||||||||||||

The performance data quoted represent past performance and do not indicate future results. Current performance may be lower or higher than the performance data quoted. For more current performance data, please visit www.nb.com/performance.

The results shown in the table reflect the reinvestment of income dividends and other distributions, if any. The results do not reflect the effect of taxes a shareholder would pay on Fund distributions or on the redemption of Fund shares.

The investment return and principal value of an investment will fluctuate and shares, when redeemed, may be worth more or less than their original cost.

Returns would have been lower if Neuberger Berman Management LLC (Management) had not reimbursed certain expenses and/or waived a portion of the investment management fees during certain of the periods shown. Repayment by a class (of expenses previously reimbursed and/or fees previously waived by Management) will decrease the class's returns. Please see Note B in the Notes to Financial Statements for specific information regarding expense reimbursement and/or fee waiver arrangements.

As stated in the Fund's most recent prospectus, the total annual operating expense ratios for fiscal year 2013 were 1.60%, 2.01%, 2.74%, 2.32% and 1.57% for Institutional Class, Class A, Class C, Class R3 and Class R6 shares, respectively (before expense reimbursements and/or fee waivers, if any). The expense ratios were 1.25%, 1.50%, 2.25%, 1.91% and 1.18% for Institutional Class, Class A, Class C, Class R3 and Class R6 shares, respectively, after expense reimbursements and/or fee waivers.

Returns shown with a sales charge reflect the deduction of the current maximum initial sales charge of 5.75% for Class A shares and the contingent deferred sales charge (CDSC) for Class C shares. The CDSC for Class C shares is 1%, which is reduced to 0% after 1 year. The performance of the Fund's share classes will differ primarily due to different sales charge structures and class expenses. Please see the prospectus for more information about sales charge structures, if any, and class expenses for your share class.

6

Emerging Markets Equity Fund (Unaudited)

COMPARISON OF A $1,000,000 INVESTMENT

(000's Omitted)

This graph shows the change in value of a hypothetical $1,000,000 investment in the Fund over the past 10 fiscal years, or since the Fund's inception if it has not operated for 10 years. The graph is based on the Institutional Class shares only; the performance of the Fund's share classes will differ primarily due to different sales charge structures and class expenses (see Performance Highlights chart on previous page). The result is compared with benchmarks, which include a broad-based market index and may include a more narrowly based index. Market indices have not been reduced to reflect any of the fees and costs of investing. The results shown in the graph reflect the reinvestment of income dividends and other distributions, if any. The results do not reflect the effect of taxes a shareholder would pay on Fund distributions or on the redemption of Fund shares. Results represent past performance and do not indicate future results.

7

Equity Income Fund Commentary (Unaudited)

Neuberger Berman Equity Income Fund Institutional Class generated a 20.11% total return for the fiscal year ended August 31, 2014, but underperformed its benchmark, the S&P 500® Index, which returned 25.25%. (Performance for all share classes is provided in the table immediately following this letter.)

The Fund's investment goal remains to provide total return from both dividend yield and capital appreciation. Given its defensive characteristics and its focus on both yield and growth, the Fund tends to lag somewhat during strong equity rallies while endeavoring to protect principal in more volatile markets. During this period, the top performing sectors of the S&P 500 were those that are synonymous with volatility and that provide little to no dividend income, namely the Information Technology (IT) sector and Health Care's Biotechnology industry, with both returning in excess of 30% and 50%, respectively.

The Fund has limited access to those sectors due to our income criteria—with the exception of some large IT names, including Microsoft, which was among our top contributors for the period, and Cisco Systems, which detracted. However, areas that we tend to overweight were fruitful, such as the Utilities sector, with top performing holdings including NextEra and Dominion Resources.

The portfolio also tends to be overweighted to Real Estate Investment Trusts (REITs). It was a tale of two cities as REITs shifted from dismal performance early on in the period (pulling back sharply on early signs of higher interest rates) to being among the top performers in the second half of the period. Over longer periods, REITs tend to be more closely tied to supply and demand for various types of real estate and less to interest rate movements or levels. Successful REITs are generally run by proven, experienced managers with histories of prudent capital allocation, and, in our experience, they tend to prevail during times of economic strength. This period, top contributors with these characteristics included Equity Residential and Extra Space Storage. Seeing economic improvement, we anticipate continuing to maintain our overweight in both U.S. and non-U.S. names, and would view any volatility as an opportunity to increase our allocations.

In addition to being underweighted in IT on lack of yield potential, the portfolio maintained an underweight to U.S. consumer stocks. Stock selection in this area was challenging with Lagardere, a media name, and General Motors, which encountered significant litigation coupled with weak sales in Europe and was sold, being among the detractors.

Early this period, we made several investments into names we anticipated could perform well during a rising rate environment, such as banks. Theoretically, as rates rise, we believed the net interest margin of certain banks would expand, thus improving earnings. Overall, this strategy benefited the portfolio, as did several of the private equity asset managers that we incrementally added over the period. We believe these asset managers are well positioned to see increased fee revenues from investments made since the global financial crisis.

The portfolio currently holds a selection of companies that, we believe, could outperform as the global economy accelerates, but could also offer some risk mitigation in the event of a slow-down, disappointment or shock. At this point, we think it makes sense to maintain some balance between offense and defense, given the uncertainty across the U.S. and global economies.

Sincerely,

RICHARD LEVINE, TONY GLEASON AND SANDY POMEROY

PORTFOLIO CO-MANAGERS

Information about principal risks of investing in the Fund is set forth in the prospectus and statement of additional information.

The portfolio composition, industries and holdings of the Fund are subject to change.

The opinions expressed are those of the Fund's portfolio managers. The opinions are as of the date of this report and are subject to change without notice.

8

Equity Income Fund (Unaudited)

TICKER SYMBOLS

Institutional Class | NBHIX | ||||||

Class A | NBHAX | ||||||

Class C | NBHCX | ||||||

Class R3 | NBHRX | ||||||

SECTOR ALLOCATION

(as a % of Total Investments) | |||||

Consumer Discretionary | 4.4 | % | |||

Consumer Staples | 1.9 | ||||

Energy | 12.7 | ||||

Financials | 36.3 | ||||

Health Care | 10.1 | ||||

Industrials | 6.5 | ||||

Information Technology | 2.2 | ||||

Materials | 3.3 | ||||

Telecommunication Services | 2.3 | ||||

Utilities | 16.6 | ||||

Other | 2.4 | ||||

Short-Term Investments | 1.3 | ||||

Total | 100.0 | % | |||

PERFORMANCE HIGHLIGHTS9

| Average Annual Total Return Ended 08/31/2014 | |||||||||||||||||||

| Inception Date* | 1 Year | 5 Years | Life of Fund | ||||||||||||||||

At NAV | |||||||||||||||||||

| Institutional Class14 | 06/09/2008 | 20.11 | % | 13.81 | % | 8.24 | % | ||||||||||||

| Class A14 | 06/09/2008 | 19.72 | % | 13.38 | % | 7.90 | % | ||||||||||||

| Class C14 | 06/09/2008 | 18.77 | % | 12.56 | % | 7.28 | % | ||||||||||||

| Class R314 | 06/21/2010 | 19.42 | % | 13.16 | % | 7.84 | % | ||||||||||||

With Sales Charge | |||||||||||||||||||

| Class A14 | 12.87 | % | 12.05 | % | 7.08 | % | |||||||||||||

| Class C14 | 17.77 | % | 12.56 | % | 7.28 | % | |||||||||||||

Index | |||||||||||||||||||

| S&P 500® Index1,16 | 25.25 | % | 16.88 | % | 7.28 | % | |||||||||||||

*The performance data for each class includes the performance of the Fund's oldest share class, Trust Class, from November 2, 2006 through June 9, 2008. The performance data for Class R3 also includes the performance of the Fund's Institutional Class from June 9, 2008 through June 21, 2010. See endnote 14 for information about the effects of the different fees paid by each class.

The performance data quoted represent past performance and do not indicate future results. Current performance may be lower or higher than the performance data quoted. For more current performance data, please visit www.nb.com/performance.

The results shown in the table reflect the reinvestment of income dividends and other distributions, if any. The results do not reflect the effect of taxes a shareholder would pay on Fund distributions or on the redemption of Fund shares.

The investment return and principal value of an investment will fluctuate and shares, when redeemed, may be worth more or less than their original cost.

Returns would have been lower if Neuberger Berman Management LLC (Management) had not reimbursed certain expenses and/or waived a portion of the investment management fees during certain of the periods shown. Repayment by a class (of expenses previously reimbursed and/or fees previously waived by Management) will decrease the class's returns. Please see Note B in the Notes to Financial Statements for specific information regarding expense reimbursement and/or fee waiver arrangements.

As stated in the Fund's most recent prospectus, the total annual operating expense ratios for fiscal year 2013 were 0.69%, 1.06%, 1.81%, and 1.42% for Institutional Class, Class A, Class C, and Class R3 shares, respectively (before expense reimbursements and/or fee waivers, if any). The total annual operating expense ratio for Class R3 includes the class's repayment of expenses previously reimbursed and/or fees previously waived by Management.

Returns shown with a sales charge reflect the deduction of the current maximum initial sales charge of 5.75% for Class A shares and the contingent deferred sales charge (CDSC) for Class C shares. The CDSC for Class C shares is 1%, which is reduced to 0% after 1 year. The performance of the Fund's share classes will differ primarily due to different sales charge structures and class expenses. Please see the prospectus for more information about sales charge structures, if any, and class expenses for your share class.

9

Equity Income Fund (Unaudited)

COMPARISON OF A $1,000,000 INVESTMENT14

(000's Omitted)

This graph shows the change in value of a hypothetical $1,000,000 investment in the Fund over the past 10 fiscal years, or since the Fund's inception if it has not operated for 10 years. The graph is based on the Institutional Class shares only; the performance of the Fund's share classes will differ primarily due to different sales charge structures and class expenses (see Performance Highlights chart on previous page). The result is compared with benchmarks, which include a broad-based market index and may include a more narrowly based index. Market indices have not been reduced to reflect any of the fees and costs of investing. The results shown in the graph reflect the reinvestment of income dividends and other distributions, if any. The results do not reflect the effect of taxes a shareholder would pay on Fund distributions or on the redemption of Fund shares. Results represent past performance and do not indicate future results.

10

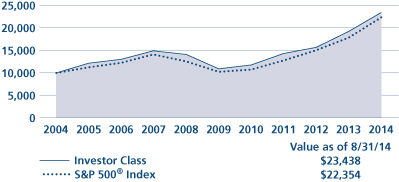

Focus Fund Commentary (Unaudited)

Neuberger Berman Focus Fund Investor Class produced a 22.65% total return for the fiscal year ended August 31, 2014, but underperformed its benchmark, the S&P 500® Index, which posted a 25.25% total return. (Performance for all share classes is provided in the table immediately following this letter.) While the Fund's Investor Class underperformed during the one-year period, it outperformed for the three-year period with the Investor Class delivering a 21.09% return and the S&P 500 delivering a 20.61% return.1

The ongoing U.S. economic recovery and high levels of monetary liquidity produced another strong year for the U.S. stock market. The S&P 500 experienced a brief dip in January but generally the year was marked by new highs. Investors kept a watchful eye on the U.S. Federal Reserve (Fed), but the response to the Fed's tapering of its bond buying program was muted since the move was well communicated and has been implemented gradually and without unnecessary surprises. The market continued to be supported by low interest rates.

While every sector in the S&P 500 delivered strong, double-digit returns in this positive environment, Information Technology and Health Care led performance. Telecommunication Services and Consumer Staples trailed the index but still delivered solid returns. The improving economic picture as well as high levels of liquidity provided a constructive backdrop for the entire market.

Neuberger Berman Focus Fund is a high conviction portfolio, driven by individual stock selection rather than sector calls. SanDisk and WhiteWave Foods were the Fund's strongest individual stock performers on a relative basis. SanDisk moved higher as technology companies in general rallied, but SanDisk also benefited from good supply/demand dynamics, strong management, and a high-quality product that is in demand by consumers willing to pay a premium. We held a relatively heavy weighting in the company during the reporting period. WhiteWave Foods is a food product manufacturer that has benefited from consumers' focus on natural foods and organics. It was spun out as a stand-alone company over one year ago and has executed well, producing positive results for shareholders. We have sold the stock.

ARIAD Pharmaceuticals, Inc. and CIT Group Inc. had the greatest negative impacts on the Fund's relative return overall. ARIAD is a speculative pharmaceutical company that presented specific risks as well as some potential rewards. However, during the past year, the company had an issue with the FDA that caused its stock price to decline. CIT Group, a financial company, lagged as it lowered guidance earlier in the year on projected lower margins. We have sold both ARIAD and CIT.

While the steep run-up in the market over the past 12 months makes us cautious, we continue to find what we believe to be good value in individual stocks. While Fed moves, geo-political events, and profit taking may result in some additional market volatility over the coming year, we focus on choosing individual stocks that we believe provide solid fundamentals and attractive valuations with the potential to generate good returns over the long run. We continue to diversify the portfolio across all areas of the economy to drive our results from stock selection.

Sincerely,

TIMOTHY CREEDON AND DAVID LEVINE

PORTFOLIO CO-MANAGERS

1 The performance data quoted represent past performance and do not indicate future results. Current performance may be lower or higher than the performance data quoted. For more current performance data, please visit www.nb.com/performance.

Information about principal risks of investing in the Fund is set forth in the prospectus and statement of additional information.

The portfolio composition, industries and holdings of the Fund are subject to change.

The opinions expressed are those of the Fund's portfolio managers. The opinions are as of the date of this report and are subject to change without notice.

11

Focus Fund (Unaudited)

TICKER SYMBOLS

Investor Class | NBSSX | ||||||

Trust Class | NBFCX | ||||||

Advisor Class | NBFAX | ||||||

Institutional Class | NFALX | ||||||

Class A | NFAAX | ||||||

Class C | NFACX | ||||||

SECTOR ALLOCATION

(as a % of Total Investments) | |||||

Consumer Discretionary | 19.4 | % | |||

Consumer Staples | 6.8 | ||||

Energy | 9.9 | ||||

Financials | 15.0 | ||||

Health Care | 10.1 | ||||

Industrials | 9.2 | ||||

Information Technology | 19.2 | ||||

Materials | 4.0 | ||||

Utilities | 3.3 | ||||

Short-Term Investments | 3.1 | ||||

Total | 100.0 | % | |||

PERFORMANCE HIGHLIGHTS8

| Average Annual Total Return Ended 08/31/2014 | |||||||||||||||||||||||

| Inception Date | 1 Year | 5 Years | 10 Years | Life of Fund | |||||||||||||||||||

At NAV | |||||||||||||||||||||||

Investor Class | 10/19/1955 | 22.65 | % | 15.31 | % | 7.52 | % | 10.63 | % | ||||||||||||||

| Trust Class3 | 08/30/1993 | 22.40 | % | 15.07 | % | 7.30 | % | 10.62 | % | ||||||||||||||

| Advisor Class4 | 09/03/1996 | 22.21 | % | 14.87 | % | 7.09 | % | 10.56 | % | ||||||||||||||

| Institutional Class5 | 06/21/2010 | 22.86 | % | 15.50 | % | 7.62 | % | 10.64 | % | ||||||||||||||

| Class A20 | 06/21/2010 | 22.40 | % | 15.16 | % | 7.45 | % | 10.62 | % | ||||||||||||||

| Class C20 | 06/21/2010 | 21.52 | % | 14.45 | % | 7.12 | % | 10.56 | % | ||||||||||||||

With Sales Charge | |||||||||||||||||||||||

| Class A20 | 15.37 | % | 13.80 | % | 6.82 | % | 10.51 | % | |||||||||||||||

| Class C20 | 20.54 | % | 14.45 | % | 7.12 | % | 10.56 | % | |||||||||||||||

Index | |||||||||||||||||||||||

| S&P 500® Index1,16 | 25.25 | % | 16.88 | % | 8.38 | % | 10.21 | % | |||||||||||||||

The performance data quoted represent past performance and do not indicate future results. Current performance may be lower or higher than the performance data quoted. For more current performance data, please visit www.nb.com/performance.

The results shown in the table reflect the reinvestment of income dividends and other distributions, if any. The results do not reflect the effect of taxes a shareholder would pay on Fund distributions or on the redemption of Fund shares.

The investment return and principal value of an investment will fluctuate and shares, when redeemed, may be worth more or less than their original cost.

Returns would have been lower if Neuberger Berman Management LLC (Management) had not reimbursed certain expenses and/or waived a portion of the investment management fees during certain of the periods shown. Repayment by a class (of expenses previously reimbursed and/or fees previously waived by Management) will decrease the class's returns. Please see Note B in the Notes to Financial Statements for specific information regarding expense reimbursement and/or fee waiver arrangements.

As stated in the Fund's most recent prospectus, the total annual operating expense ratios for fiscal year 2013 were 0.94%, 1.14%, 1.29%, 0.78%, 1.20%, and 1.94% for Investor Class, Trust Class, Advisor Class, Institutional Class, Class A and Class C shares, respectively (before expense reimbursements and/or fee waivers, if any). The expense ratios were 0.75%, 1.11%, and 1.86% for Institutional Class, Class A and Class C shares, respectively, after expense reimbursements and/or fee waivers.

Returns shown with a sales charge reflect the deduction of the current maximum initial sales charge of 5.75% for Class A shares and the contingent deferred sales charge (CDSC) for Class C shares. The CDSC for Class C shares is 1%, which is reduced to 0% after 1 year. The performance of the Fund's share classes will differ primarily due to different sales charge structures and class expenses. Please see the prospectus for more information about sales charge structures, if any, and class expenses for your share class.

12

Focus Fund (Unaudited)

COMPARISON OF A $10,000 INVESTMENT

This graph shows the change in value of a hypothetical $10,000 investment in the Fund over the past 10 fiscal years, or since the Fund's inception if it has not operated for 10 years. The graph is based on the Investor Class shares only; the performance of the Fund's share classes will differ primarily due to different sales charge structures and class expenses (see Performance Highlights chart on previous page). The result is compared with benchmarks, which include a broad-based market index and may include a more narrowly based index. Market indices have not been reduced to reflect any of the fees and costs of investing. The results shown in the graph reflect the reinvestment of income dividends and other distributions, if any. The results do not reflect the effect of taxes a shareholder would pay on Fund distributions or on the redemption of Fund shares. Results represent past performance and do not indicate future results.

13

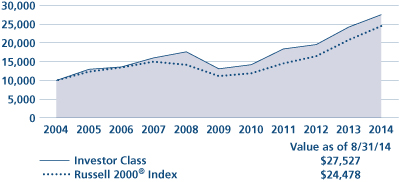

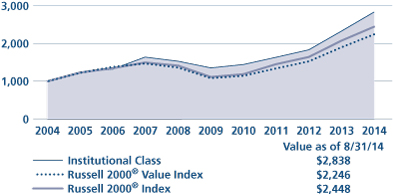

Genesis Fund Commentary (Unaudited)

Neuberger Berman Genesis Fund Investor Class posted a 13.65% total return for the fiscal year ended August 31, 2014, but underperformed its benchmark, the Russell 2000® Index, which provided a 17.68% return for the period. (Performance for all share classes is provided in the table immediately following this letter.)

The U.S. stock market rallied sharply during the reporting period. While the market experienced several periods of weakness, these proved to be only temporary setbacks as the S&P 500® Index repeatedly reached all-time highs during the period. Supporting the market were overall solid corporate profits and generally strong investor demand. While small-cap stocks posted strong results, they lagged the overall stock market as the S&P 500 Index gained 25.25% versus the 17.68% gain of the small-cap Russell 2000 Index during the 12-month period. Within the small-cap universe, value stocks outperformed their growth counterparts, as the Russell 2000 Value and Growth Indexes returned 18.10% and 17.30%, respectively.

While it produced a strong absolute return, the Fund's underperformance versus the benchmark was largely due to stock selection. This was partially driven by the outperformance of companies with a high degree of financial leverage as they benefited from the low interest rate environment. This was a headwind for the Fund as we emphasize less-leveraged, high-quality, profitable businesses. The sectors that detracted the most from performance were Financials and Health Care. Within Financials, mortgage servicing-related companies, including Ocwen Financial, were negative for performance. Following a period of significant growth, Ocwen Financial was impacted by the New York Department of Financial Services' request to halt its purchase of mortgage servicing rights from Wells Fargo. Within Health Care, a lack of exposure to outperforming pharmaceutical and biotechnology companies, many of which are more speculative in nature and have no earnings, detracted from results.

Contributing the most to performance was stock selection in the Information Technology sector, led by the Fund's position in Zebra Technologies Corp. The company manufactures and distributes thermal bar code printers, plastic card printers and products for use in data collection and automatic identification systems. It benefited the Fund's performance after announcing its intention to acquire Motorola Solutions' enterprise business. Other strong individual contributors to the Fund's results were Industrials company Westinghouse Air Brake Technologies Corp. and Consumer Discretionary firm Polaris Industries.

Sector positioning, overall, was a small drag on performance. In particular, while the portfolio's cash balance was modest and in line with historical levels, it detracted from results given the market's sharp rally and the low yields available from cash instruments. A lack of exposure to real estate investment trusts (REITs) was also negative for relative performance. On the upside, the Fund's overweights in the Materials and Energy sectors were beneficial for results.

Looking ahead, we believe the economy could continue to expand following the weather-induced slowdown earlier in the year. Turning to the small-cap market, in our view it appears to be fairly valued overall. That being said, we continue to find what we believe are pockets of opportunity. We also believe that investor demand may remain fairly strong if investors move out on the risk curve given the low interest rate environment and concerns for the negative impact rising rates can have on the bond market.

Sincerely,

JUDITH M. VALE AND ROBERT D'ALELIO

PORTFOLIO CO-MANAGERS

Information about principal risks of investing in the Fund is set forth in the prospectus and statement of additional information.

The portfolio composition, industries and holdings of the Fund are subject to change.

The opinions expressed are those of the Fund's portfolio managers. The opinions are as of the date of this report and are subject to change without notice.

14

Genesis Fund (Unaudited)

TICKER SYMBOLS

Investor Class | NBGNX | ||||||

Trust Class | NBGEX | ||||||

Advisor Class | NBGAX | ||||||

Institutional Class | NBGIX | ||||||

Class R6 | NRGSX | ||||||

SECTOR ALLOCATION

(as a % of Total Investments) | |||||

Consumer Discretionary | 11.5 | % | |||

Consumer Staples | 5.5 | ||||

Energy | 7.2 | ||||

Financials | 12.5 | ||||

Health Care | 11.7 | ||||

Industrials | 20.3 | ||||

Information Technology | 16.6 | ||||

Materials | 10.4 | ||||

Utilities | 0.7 | ||||

Short-Term Investments | 3.6 | ||||

Total | 100.0 | % | |||

PERFORMANCE HIGHLIGHTS

| Average Annual Total Return Ended 08/31/2014 | |||||||||||||||||||||||

| Inception Date | 1 Year | 5 Years | 10 Years | Life of Fund | |||||||||||||||||||

Investor Class | 09/27/1988 | 13.65 | % | 16.04 | % | 10.66 | % | 12.63 | % | ||||||||||||||

| Trust Class3 | 08/26/1993 | 13.55 | % | 15.95 | % | 10.59 | % | 12.62 | % | ||||||||||||||

| Advisor Class4 | 04/02/1997 | 13.24 | % | 15.65 | % | 10.30 | % | 12.41 | % | ||||||||||||||

| Institutional Class5 | 07/01/1999 | 13.82 | % | 16.26 | % | 10.87 | % | 12.78 | % | ||||||||||||||

| Class R624 | 03/15/2013 | 13.92 | % | 16.12 | % | 10.70 | % | 12.65 | % | ||||||||||||||

Index | |||||||||||||||||||||||

| Russell 2000® Index1,16 | 17.68 | % | 17.03 | % | 9.36 | % | 9.92 | % | |||||||||||||||

The performance data quoted represent past performance and do not indicate future results. Current performance may be lower or higher than the performance data quoted. For more current performance data, please visit www.nb.com/performance.

The results shown in the table reflect the reinvestment of income dividends and other distributions, if any. The results do not reflect the effect of taxes a shareholder would pay on Fund distributions or on the redemption of Fund shares.

The investment return and principal value of an investment will fluctuate and shares, when redeemed, may be worth more or less than their original cost.

Returns would have been lower if Neuberger Berman Management LLC (Management) had not reimbursed certain expenses and/or waived a portion of the investment management fees during certain of the periods shown. Repayment by a class (of expenses previously reimbursed and/or fees previously waived by Management) will decrease the class's returns. Please see Note B in the Notes to Financial Statements for specific information regarding expense reimbursement and/or fee waiver arrangements.

As stated in the Fund's most recent prospectus, the total annual operating expense ratios for fiscal year 2013 were 1.02%, 1.11%, 1.38%, 0.86% and 0.80% for Investor Class, Trust Class, Advisor Class, Institutional Class and Class R6 shares, respectively (before expense reimbursements and/or fee waivers, if any). The expense ratios were 0.85% and 0.78% for Institutional Class and Class R6 shares, respectively, after expense reimbursements and/or fee waivers.

15

Genesis Fund (Unaudited)

COMPARISON OF A $10,000 INVESTMENT

This graph shows the change in value of a hypothetical $10,000 investment in the Fund over the past 10 fiscal years, or since the Fund's inception if it has not operated for 10 years. The graph is based on the Investor Class shares only; the performance of the Fund's share classes will differ primarily due to different class expenses (see Performance Highlights chart on previous page). The result is compared with benchmarks, which include a broad-based market index and may include a more narrowly based index. Market indices have not been reduced to reflect any of the fees and costs of investing. The results shown in the graph reflect the reinvestment of income dividends and other distributions, if any. The results do not reflect the effect of taxes a shareholder would pay on Fund distributions or on the redemption of Fund shares. Results represent past performance and do not indicate future results.

16

Global Equity Fund Commentary (Unaudited)

Neuberger Berman Global Equity Fund Institutional Class generated a 19.67% total return for the fiscal year ended August 31, 2014, but trailed its benchmark, the MSCI All Country World Index, which advanced 21.61% during the period. (Performance for all share classes is provided in the table immediately following this letter.)

The MSCI All Country World Index performed well this period, driven by relatively improving global economic data and buoyant investor sentiment. After a brief pause in first quarter of 2014, markets continued their upward trajectory from 2013 through the end of this fiscal period. U.S. equities outperformed emerging markets, which in turn outperformed international developed markets, though each asset class saw double-digit returns.

While the U.S. market performed well, the index was led by smaller markets including Egypt, India and Finland. Hungary, United Arab Emirates and Qatar posted the most significant losses for the period. Amongst major developed markets, European periphery countries bested the core, and Japan was positive but lagged the index. By sector, Information Technology (IT) and Health Care strongly outperformed. Consumer Staples and Materials were weakest, although they, too, posted double-digit positive results.

Within the portfolio, stock selection within Consumer Staples and Consumer Discretionary benefited relative performance. Stock selection in IT put the largest strain on relative results, while Industrials holdings also underperformed. By country, U.S., Canada and Israel were our strongest performers, while relative underperformers included France, Sweden and Korea.

Looking at individual stocks, three of our top five contributors were U.S.-based companies—SanDisk, Apple and Cardinal Health, each benefiting from strong business drivers that were being recognized by the markets. Detractors included Softbank (Japan), which had a strong year last year, Sberbank (Russia), which we sold, and St. James's Place (UK).

While markets have recently been marching upward, discounting mixed economic data and a variety of results from global corporations as they've done recently, our focus remains on the fundamentals of the stocks we own, and those of the opportunities we are researching. We have spent much of our time recently working on existing names to ensure we have the highest conviction possible in those ideas, and in a number of cases increasing our positions in higher conviction holdings.

We have also reexamined our positioning toward European banks and other Financials, slightly reducing the scale of our largest sector underweight. Elsewhere, we have no exposure to the Utilities sector, and are overweighted to both Industrials and IT.

We continue to anticipate a weak economic cycle in the eurozone and Japan, solid growth in U.S. and UK, and just slightly faster growth in emerging markets. By geography, the portfolio remains modestly overweighted in the U.S. at the expense of Japan and emerging market-domiciled companies.

As part of our global search for quality growth companies, another recent development has been co-portfolio manager Benjamin Segal's relocation to Singapore. His focus is on deepening the team's comprehension of local and global companies' strategies and operations in the Asian region—home to two of the world's largest economies.

With a proven strategy, a deep fundamental research capability, and "feet on the ground" across the globe, we believe the team is well positioned to add value going forward.

Sincerely,

BENJAMIN SEGAL AND SAURIN D. SHAH

PORTFOLIO CO-MANAGERS

Information about principal risks of investing in the Fund is set forth in the prospectus and statement of additional information.

The portfolio composition, industries and holdings of the Fund are subject to change.

The opinions expressed are those of the Fund's portfolio managers. The opinions are as of the date of this report and are subject to change without notice.

17

Global Equity Fund (Unaudited)

TICKER SYMBOLS

Institutional Class | NGQIX | ||||||

Class A | NGQAX | ||||||

Class C | NGQCX | ||||||

SECTOR ALLOCATION

(as a % of Total Investments) | |||||

Consumer Discretionary | 10.0 | % | |||

Consumer Staples | 7.8 | ||||

Energy | 8.0 | ||||

Financials | 16.8 | ||||

Health Care | 10.3 | ||||

Industrials | 14.2 | ||||

Information Technology | 16.1 | ||||

Materials | 7.8 | ||||

Telecommunication Services | 3.4 | ||||

Short-Term Investments | 5.6 | ||||

Total | 100.0 | % | |||

PERFORMANCE HIGHLIGHTS9

| Average Annual Total Return Ended 08/31/2014 | |||||||||||||||

| Inception Date | 1 Year | Life of Fund | |||||||||||||

At NAV | |||||||||||||||

Institutional Class | 06/30/2011 | 19.67 | % | 7.28 | % | ||||||||||

Class A | 06/30/2011 | 19.18 | % | 6.87 | % | ||||||||||

Class C | 06/30/2011 | 18.39 | % | 6.11 | % | ||||||||||

With Sales Charge | |||||||||||||||

Class A | 12.28 | % | 4.90 | % | |||||||||||

Class C | 17.39 | % | 6.11 | % | |||||||||||

Index | |||||||||||||||

| MSCI All Country World Index1,16 | 21.61 | % | 11.03 | % | |||||||||||

| MSCI World Index1,16,26 | 21.74 | % | 12.40 | % | |||||||||||

The performance data quoted represent past performance and do not indicate future results. Current performance may be lower or higher than the performance data quoted. For more current performance data, please visit www.nb.com/performance.

The results shown in the table reflect the reinvestment of income dividends and other distributions, if any. The results do not reflect the effect of taxes a shareholder would pay on Fund distributions or on the redemption of Fund shares.

The investment return and principal value of an investment will fluctuate and shares, when redeemed, may be worth more or less than their original cost.

Returns would have been lower if Neuberger Berman Management LLC (Management) had not reimbursed certain expenses and/or waived a portion of the investment management fees during certain of the periods shown. Repayment by a class (of expenses previously reimbursed and/or fees previously waived by Management) will decrease the class's returns. Please see Note B in the Notes to Financial Statements for specific information regarding expense reimbursement and/or fee waiver arrangements.

As stated in the Fund's most recent prospectus, the total annual operating expense ratios for fiscal year 2013 were 5.16%, 5.67% and 6.51% for Institutional Class, Class A and Class C shares, respectively (before expense reimbursements and/or fee waivers, if any). The expense ratios were 1.15%, 1.51% and 2.26% for Institutional Class, Class A and Class C shares, respectively, after expense reimbursements and/or fee waivers.

Returns shown with a sales charge reflect the deduction of the current maximum initial sales charge of 5.75% for Class A shares and the contingent deferred sales charge (CDSC) for Class C shares. The CDSC for Class C shares is 1%, which is reduced to 0% after 1 year. The performance of the Fund's share classes will differ primarily due to different sales charge structures and class expenses. Please see the prospectus for more information about sales charge structures, if any, and class expenses for your share class.

18

Global Equity Fund (Unaudited)

COMPARISON OF A $1,000,000 INVESTMENT

(000's Omitted)

This graph shows the change in value of a hypothetical $1,000,000 investment in the Fund over the past 10 fiscal years, or since the Fund's inception if it has not operated for 10 years. The graph is based on the Institutional Class shares only; the performance of the Fund's share classes will differ primarily due to different sales charge structures and class expenses (see Performance Highlights chart on previous page). The result is compared with benchmarks, which include a broad-based market index and may include a more narrowly based index. Market indices have not been reduced to reflect any of the fees and costs of investing. The results shown in the graph reflect the reinvestment of income dividends and other distributions, if any. The results do not reflect the effect of taxes a shareholder would pay on Fund distributions or on the redemption of Fund shares. Results represent past performance and do not indicate future results.

19

Global Thematic Opportunities Fund Commentary (Unaudited)

Neuberger Berman Global Thematic Opportunities Fund Institutional Class generated a 12.92% total return for the fiscal year ended August 31, 2014, but underperformed the MSCI All Country World Index, which returned 21.61% for the period. (Performance for all share classes is provided in the table immediately following this letter).

Global markets broadly advanced as economic prospects were lifted by improving fundamentals in the U.S., Europe and, in some cases, developing markets. From a regional perspective, holdings within the U.S. provided the greatest source of index returns, while those in China and Japan were were relative laggards.

During the reporting period, the U.S. equity markets advanced to record highs, in part driven by a flurry of merger and acquisition activity coupled with strong buybacks and earnings growth. Improving employment figures and continued momentum in energy production were tailwinds for consumer confidence in the U.S. Despite increasing geopolitical tensions, the Chicago Board Options Exchange VIX Index, a widely followed barometer of volatility, neared its record low, reflecting relative stability in the markets. Outside the U.S., developed Europe posted healthy returns, while macro factors including the continued economic slowdown in China and currency weakness in the Japanese yen caused underperformance in those markets.

Thematically, our "Man vs. Machine" theme was supported by two strong contributors, SanDisk and Google. Reasonable valuations, coupled with improved revenues, stronger earnings and continued share buybacks attracted investors to the Information Technology sector, which rose over 30% during the period. Within our "Money in Motion" theme, KKR, American International Group and BlackRock were among our top contributors. While our Consumer Discretionary names underperformed overall, among the portfolio's largest positive contributors was hotel giant Wynn Resorts, where gaming revenues from Macau operations boosted profitability, prompting us to "cash out" for opportunities elsewhere.

Our "Emerging Market Consumer" theme was the largest hindrance to results, particularly names tied to China, such as Sa Sa International, New Oriental Education & Technology Group and Genting Hong Kong. These proved to be our biggest detractors, triggering a reevaluation of our initial investment theses, and ultimately resulting in the sale of these securities.

Within our "Self Help" theme, TRI Pointe Homes and General Motors lagged the broader Consumer Discretionary sector and were subsequently sold. By contrast, within Consumer Staples, Australia's Treasury Wine Estates surged over 40% following a takeout bid from private equity investors (we sold the position).

Looking ahead, we believe valuations within the equity markets will continue to appear reasonable. We have reduced our emerging market exposure and deployed proceeds among several companies in Europe, where we continue to find what we believe are opportunities in companies that should grow if the region continues its slow recovery from recession. We will continue to seek companies with resiliency in the face of geopolitical risk, but believe any corrections could create opportunities to add to certain names.

As always, we remain dedicated to finding opportunities in what we believe are excellent companies across a broad spectrum of countries and sectors with the goal of identifying persistent, structural and investable trends before they are recognized by the broader investment community. We believe that this opportunistic, disciplined and patient approach could be rewarded with attractive returns over time.

Sincerely,

TONY GLEASON, SANDY POMEROY, WILLIAM HUNTER AND RICHARD LEVINE

PORTFOLIO CO-MANAGERS

Information about principal risks of investing in the Fund is set forth in the prospectus and statement of additional information.

The portfolio composition, industries and holdings of the Fund are subject to change.

The opinions expressed are those of the Fund's portfolio managers. The opinions are as of the date of this report and are subject to change without notice.

20

Global Thematic Opportunities Fund (Unaudited)

TICKER SYMBOLS

Institutional Class | NGHIX | ||||||

Class A | NGHAX | ||||||

Class C | NGHCX | ||||||

SECTOR ALLOCATION

(as a % of Total Investments) | |||||

Consumer Discretionary | 16.1 | % | |||

Consumer Staples | 1.3 | ||||

Energy | 6.9 | ||||

Financials | 26.2 | ||||

Health Care | 9.0 | ||||

Industrials | 11.7 | ||||

Information Technology | 16.2 | ||||

Materials | 2.4 | ||||

Other | 2.2 | ||||

Short-Term Investments | 8.0 | ||||

Total | 100.0 | % | |||

PERFORMANCE HIGHLIGHTS

| Average Annual Total Return Ended 08/31/2014 | |||||||||||||||

| Inception Date | 1 Year | Life of Fund | |||||||||||||

At NAV | |||||||||||||||

Institutional Class | 06/30/2011 | 12.92 | % | 2.55 | % | ||||||||||

Class A | 06/30/2011 | 12.40 | % | 2.14 | % | ||||||||||

Class C | 06/30/2011 | 11.66 | % | 1.41 | % | ||||||||||

With Sales Charge | |||||||||||||||

Class A | 5.91 | % | 0.26 | % | |||||||||||

Class C | 10.66 | % | 1.41 | % | |||||||||||

Index | |||||||||||||||

| MSCI All Country World Index1,16 | 21.61 | % | 11.03 | % | |||||||||||

The performance data quoted represent past performance and do not indicate future results. Current performance may be lower or higher than the performance data quoted. For more current performance data, please visit www.nb.com/performance.

The results shown in the table reflect the reinvestment of income dividends and other distributions, if any. The results do not reflect the effect of taxes a shareholder would pay on Fund distributions or on the redemption of Fund shares.

The investment return and principal value of an investment will fluctuate and shares, when redeemed, may be worth more or less than their original cost.

Returns would have been lower if Neuberger Berman Management LLC (Management) had not reimbursed certain expenses and/or waived a portion of the investment management fees during certain of the periods shown. Repayment by a class (of expenses previously reimbursed and/or fees previously waived by Management) will decrease the class's returns. Please see Note B in the Notes to Financial Statements for specific information regarding expense reimbursement and/or fee waiver arrangements.

As stated in the Fund's most recent prospectus, the total annual operating expense ratios for fiscal year 2013 were 1.62%, 2.02% and 2.87% for Institutional Class, Class A and Class C shares, respectively (before expense reimbursements and/or fee waivers, if any). The expense ratios were 1.28%, 1.64% and 2.39% for Institutional Class, Class A and Class C shares, respectively, after expense reimbursements and/or fee waivers.

Returns shown with a sales charge reflect the deduction of the current maximum initial sales charge of 5.75% for Class A shares and the contingent deferred sales charge (CDSC) for Class C shares. The CDSC for Class C shares is 1%, which is reduced to 0% after 1 year. The performance of the Fund's share classes will differ primarily due to different sales charge structures and class expenses. Please see the prospectus for more information about sales charge structures, if any, and class expenses for your share class.

21

Global Thematic Opportunities Fund (Unaudited)

COMPARISON OF A $1,000,000 INVESTMENT

(000's Omitted)

This graph shows the change in value of a hypothetical $1,000,000 investment in the Fund over the past 10 fiscal years, or since the Fund's inception if it has not operated for 10 years. The graph is based on the Institutional Class shares only; the performance of the Fund's share classes will differ primarily due to different sales charge structures and class expenses (see Performance Highlights chart on previous page). The result is compared with benchmarks, which include a broad-based market index and may include a more narrowly based index. Market indices have not been reduced to reflect any of the fees and costs of investing. The results shown in the graph reflect the reinvestment of income dividends and other distributions, if any. The results do not reflect the effect of taxes a shareholder would pay on Fund distributions or on the redemption of Fund shares. Results represent past performance and do not indicate future results.

22

Greater China Equity Fund Commentary (Unaudited)

Neuberger Berman Greater China Equity Fund Institutional Class generated a 21.37% total return for the fiscal year ended August 31, 2014 and outperformed its benchmark, the MSCI China Index, which generated a 17.91% return over the same period. (Performance for all share classes is provided in the table immediately following this letter.)

For the 12-month period, the Fund's overweight positions in the Health Care and Utilities sectors contributed to performance relative to benchmark. On the contrary, the Fund's underweights in Energy and Information Technology detracted from performance relative to benchmark. Stock selection in Energy, Telecommunication Services and Utilities positively impacted performance, while stock selection in Financials and Industrials had a negative impact to performance relative to the benchmark.

Reviewing the market environment over the past year, improving fundamentals, the Third Plenary Session of the 18th CPC Central Committee and the release of the Third Plenum reform document boosted investor sentiment. As a result, the China equity markets displayed solid performance in September, October and November of 2013. In December, despite the China Securities Regulatory Commission (CSRC)'s announcement to end a 14-month freeze on IPOs, concerns over liquidity led the offshore China equity markets to decline. Going into the New Year, investor sentiment further dampened after the release of worse-than-expected macroeconomic indicators in January, but rebounded after the Chinese New Year holidays ahead of expectations from the Communist Party Central Committee (CPCC) and National People's Congress (NPC) meetings in March.

In March, China's first-ever corporate bond default and disappointing February macro data negatively impacted the China equity markets. In April, the CSRC and the Hong Kong Securities and Futures Commission (SFC) announced a pilot trading program called the Shanghai-Hong Kong Stock Connect, which, if implemented, would allow two-way investment between the Shanghai Stock Exchange and the Stock Exchange of Hong Kong for the first time. Chinese equities rebounded after the State Council unveiled the new national nine rules in May, which are designed to accelerate the further opening up of China's capital markets. Positive momentum extended into June in response to improved macroeconomic data and the State Council's announcements to ease policies. The markets continued to rally in July due to easing rules on bank's loan-to-deposit ratios, better-than-expected second quarter GDP growth and implementation of additional policies, such as relaxing home purchase curbs, implementation of fiscal measures, and state-owned enterprise (SOE) and other reforms. China equity markets weakened in August amid tepid macroeconomic data published for July and liquidity concerns raised by the resumption of China A-shares IPOs, although August still ended in slightly positive territory.

The Fund continues to focus on companies that we believe have sustainable top and bottom line growth as evidenced by operating cash flow from recurring core businesses. As of August 31, 2014, the Fund's largest sector overweight relative to the benchmark was Utilities and the largest sector underweight was Energy. The Fund also held overweight positions in Consumer Discretionary and Health Care, and underweight positions in Consumer Staples and Financials. The Fund's top 10 positions comprised more than 47% of total portfolio assets at the end of August.

Sincerely,

LIHUI TANG AND FRANK YAO

PORTFOLIO CO-MANAGERS

Information about principal risks of investing in the Fund is set forth in the prospectus and statement of additional information.

The portfolio composition, industries and holdings of the Fund are subject to change.

The opinions expressed are those of the Fund's portfolio managers. The opinions are as of the date of this report and are subject to change without notice.

23

Greater China Equity Fund (Unaudited)

TICKER SYMBOLS

Institutional Class | NCEIX | ||||||

Class A | NCEAX | ||||||

Class C | NCECX | ||||||

SECTOR ALLOCATION

(as a % of Total Investments) | |||||

Consumer Discretionary | 14.3 | % | |||

Consumer Staples | 1.1 | ||||

Energy | 0.5 | ||||

Financials | 33.4 | ||||

Health Care | 6.6 | ||||

Industrials | 6.8 | ||||

Information Technology | 14.7 | ||||

Materials | 0.7 | ||||

Telecommunication Services | 7.6 | ||||

Utilities | 13.1 | ||||

Short-Term Investments | 1.2 | ||||

Total | 100.0 | % | |||

EXCHANGE ALLOCATION

(as a % of Long Term Investments) | |||||

Mainland China | 25.0 | % | |||

Hong Kong | 65.7 | ||||

United States | 9.3 | ||||

Total | 100.0 | % | |||

PERFORMANCE HIGHLIGHTS

| Average Annual Total Return Ended 08/31/2014 | |||||||||||||||

| Inception Date | 1 Year | Life of Fund | |||||||||||||

At NAV | |||||||||||||||

Institutional Class | 07/17/2013 | 21.37 | % | 20.45 | % | ||||||||||

Class A | 07/17/2013 | 21.07 | % | 20.19 | % | ||||||||||

Class C | 07/17/2013 | 20.09 | % | 19.22 | % | ||||||||||

With Sales Charge | |||||||||||||||

Class A | 14.10 | % | 14.03 | % | |||||||||||

Class C | 19.09 | % | 19.22 | % | |||||||||||

Index | |||||||||||||||

| MSCI China Index1,16 | 17.91 | % | 20.67 | % | |||||||||||

The performance data quoted represent past performance and do not indicate future results. Current performance may be lower or higher than the performance data quoted. For more current performance data, please visit www.nb.com/performance.

The results shown in the table reflect the reinvestment of income dividends and other distributions, if any. The results do not reflect the effect of taxes a shareholder would pay on Fund distributions or on the redemption of Fund shares.

The investment return and principal value of an investment will fluctuate and shares, when redeemed, may be worth more or less than their original cost.

Returns would have been lower if Neuberger Berman Management LLC (Management) had not reimbursed certain expenses and/or waived a portion of the investment management fees during certain of the periods shown. Repayment by a class (of expenses previously reimbursed and/or fees previously waived by Management) will decrease the class's returns. Please see Note B in the Notes to Financial Statements for specific information regarding expense reimbursement and/or fee waiver arrangements.

As stated in the Fund's most recent prospectus, the estimated total annual operating expense ratios for fiscal year 2013 were 1.91%, 2.27% and 3.02% for Institutional Class, Class A and Class C shares, respectively (before expense reimbursements and/or fee waivers, if any). The estimated expense ratios were 1.51%, 1.87% and 2.62% for Institutional Class, Class A and Class C shares, respectively, after expense reimbursements and/or fee waivers.

Returns shown with a sales charge reflect the deduction of the current maximum initial sales charge of 5.75% for Class A shares and the contingent deferred sales charge (CDSC) for Class C shares. The CDSC for Class C shares is 1%, which is reduced to 0% after 1 year. The performance of the Fund's share classes will differ primarily due to different sales charge structures and class expenses. Please see the prospectus for more information about sales charge structures, if any, and class expenses for your share class.

24

Greater China Equity Fund (Unaudited)

COMPARISON OF A $1,000,000 INVESTMENT

(000's Omitted)

This graph shows the change in value of a hypothetical $1,000,000 investment in the Fund over the past 10 fiscal years, or since the Fund's inception if it has not operated for 10 years. The graph is based on the Institutional Class shares only; the performance of the Fund's share classes will differ primarily due to different sales charge structures and class expenses (see Performance Highlights chart on previous page). The result is compared with benchmarks, which include a broad-based market index and may include a more narrowly based index. Market indices have not been reduced to reflect any of the fees and costs of investing. The results shown in the graph reflect the reinvestment of income dividends and other distributions, if any. The results do not reflect the effect of taxes a shareholder would pay on Fund distributions or on the redemption of Fund shares. Results represent past performance and do not indicate future results.

25

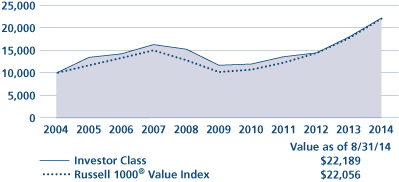

Guardian Fund Commentary (Unaudited)

Neuberger Berman Guardian Fund Investor Class generated a 21.87% total return for the fiscal year ended August 31, 2014 but trailed the 25.25% return of its benchmark, the S&P 500® Index. (Performance for all share classes is provided in the table immediately following this letter.)

The absolute performance of our portfolio companies was solid for this reporting period, but our holdings faced a relative headwind for much of the period. With economic momentum building and the U.S. Federal Reserve's (Fed) tapering program underway, consensus (and this team's) opinion was that interest rates would begin trending higher. Instead, they have fallen year to date. As a result, higher-yielding sectors such as Utilities, REITs, and pipelines have outperformed. So far into 2014, our underrepresentation in these industry groups has been a headwind to relative performance.