UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT

OF REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-3462

The Flex-funds Trust

6125 Memorial Drive

Dublin, OH 43017

Bruce McKibben

c/o The Flex-funds Trust

6125 Memorial Drive

Dublin, OH 43017

Registrant’s telephone number, including area code: 800-325-3539

Date of fiscal year end: December 31, 2006

Date of reporting period: June 30, 2006

| Item 1. | Report to Stockholders. |

The Flex-funds

2006 Semiannual Report

June 30, 2006

| | | | |

| | | | The Flex-funds |

| | |

| | | | Managed by Meeder Asset Management, Inc. |

| | | | 6125 Memorial Drive, Dublin Ohio, 43017 |

| | | | Call Toll Free 800-325-3539 | 760-2159 |

| | | | Fax: 614-766-6669 | www.flexfunds.com |

| | | | Email: flexfunds@meederfinancial.com |

Performance Review

Period & Average Annual Total Returns as of June 30, 2006

| | | | | | | | | | | | | | | | | | |

| | | Year

to-date | | | 1 year | | | 3

years | | | 5

years | | | 10

years | | | Since

inception | |

EQUITY FUNDS | | | | | | | | | | | | | | | | | | |

The Total Return Utilities Fund | | 5.47 | % | | 10.90 | % | | 16.03 | % | | 1.17 | % | | 8.05 | % | | 9.14 | %1 |

The Quantex Fund™* | | 2.93 | % | | 7.72 | % | | 10.57 | % | | 1.15 | % | | 5.91 | % | | 7.31 | %2 |

| | | | | | |

FUNDS OF FUNDS | | | | | | | | | | | | | | | | | | |

The Aggressive Growth Fund | | 2.50 | % | | 9.22 | % | | 10.98 | % | | 0.73 | % | | — | | | -4.62 | %3 |

The Dynamic Growth Fund | | 4.59 | % | | 10.74 | % | | 11.36 | % | | 2.02 | % | | — | | | -1.90 | %4 |

The Focused Growth Fund | | — | | | — | | | — | | | — | | | — | | | -2.50 | %5 |

The Muirfield Fund® | | 2.91 | % | | 8.06 | % | | 9.72 | % | | 3.82 | % | | 5.20 | % | | 8.43 | %6 |

The Defensive Growth Fund | | — | | | — | | | — | �� | | — | | | — | | | -3.30 | %7 |

| | | | | | |

FIXED INCOME FUND | | | | | | | | | | | | | | | | | | |

The U.S. Government Bond Fund | | 0.30 | % | | -0.50 | % | | -0.46 | % | | 1.50 | % | | 3.50 | % | | 5.54 | %8 |

| | | | | | |

MONEY MARKET FUNDS | | | | | | | | | | | | | | | | | | |

The Money Market Fund - Retail Class** | | 2.15 | % | | 3.87 | % | | 2.16 | % | | 2.02 | % | | 3.70 | % | | 5.03 | %9 |

Current & Effective Yields | | 7-day simple: 4.76% | | | 7-day compound: 4.87% | |

The Money Market Fund - Institutional Class ** | | 2.23 | % | | 4.01 | % | | — | | | — | | | — | | | 3.49 | %10 |

Current & Effective Yields | | 7-day simple: 4.90% | | | 7-day compound: 5.01% | |

| | | | | | |

BENCHMARK INDICES | | | | | | | | | | | | | | | | | | |

Dow Jones Industrial Average | | 5.22 | % | | 11.09 | % | | 9.86 | % | | 3.43 | % | | 9.13 | % | | | |

S&P 500 Index | | 2.71 | % | | 8.63 | % | | 11.20 | % | | 2.49 | % | | 8.31 | % | | | |

NASDAQ Composite Index | | -1.08 | % | | 6.48 | % | | 10.91 | % | | 0.66 | % | | 6.70 | % | | | |

S&P Mid-Cap 400 Index | | 4.24 | % | | 12.99 | % | | 18.11 | % | | 9.28 | % | | 13.80 | % | | | |

Russell 2000 Small-Cap Index | | 8.27 | % | | 14.67 | % | | 18.75 | % | | 8.58 | % | | 9.11 | % | | | |

S&P 500 Utilities Index | | 4.47 | % | | 5.92 | % | | 17.61 | % | | 1.23 | % | | 6.92 | % | | | |

Lehman Bros. Intermediate-Term Government/Credit Index | | -0.18 | % | | -0.19 | % | | 1.49 | % | | 4.61 | % | | 5.80 | % | | | |

To obtain a prospectus containing more complete information about The Flex-funds, including fees and other expenses that apply to a continued investment in the Funds, you may call The Flex-funds at Toll Free (800)325-3539, visit us online at www.flexfunds.com, or write P.O. Box 7177, Dublin OH 43017. Please read the prospectus carefully before investing.

Past performance does not guarantee future results. All performance figures represent total returns and average annual total returns for the periods ended June 30, 2006, and assumes reinvestment of all dividend and capital gain distributions. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Management fees were waived and/or expenses reimbursed in order to reduce the operating expenses of the Funds during all periods shown above. Source for index data: Bloomberg.

| * | Average annual total returns for The Quantex Fund™ for the periods prior to April 1, 2005 reflect a combination of the Fund’s current quantitative investment strategy and the Fund’s previous investment strategy. |

| ** | An investment in The Money Market Fund is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other governmental agency. Although The Money Market Fund seeks to preserve the value of your investment at $1.00 per share, it is possible to lose money by investing in the Fund. Yield quotations more closely reflect the current earnings of The Money Market Fund than do total return quotations. |

| 1 | Inception Date: 6/21/95. |

| 3 | Inception Date: 2/29/00. |

| 4 | Inception Date: 2/29/00. |

| 5 | Inception Date: 1/31/06. |

| 6 | Inception Date: 8/10/88. |

| 7 | Inception Date: 1/31/06. |

| 9 | Inception Date: 3/27/85. |

| 10 | Inception Date: 12/28/04. |

| | |

| The Flex-funds | | 2006 Semiannual Report | June 30, 2006 |

Letter to Shareholders

In our previous semiannual report to the shareholders of The Flex-funds, dated June 30, 2005, I discussed a company-wide initiative our firm had undertaken to improve our investment processes, our management team, and our operational procedures. The goal of this initiative was to enhance the overall performance of The Flex-funds for our shareholders.

I am pleased to report that with these improvements in place, a majority of our funds outperformed their benchmarks over the last six-month and one-year periods.

For example, The Dynamic Growth Fund outperformed its benchmark, the S&P 500 Index, for the six-month and one-year periods ended of June 30, 2006. The Fund returned 4.59% for the semiannual period, compared with the 2.71% six-month return of the S&P 500 Index. Over the last year, the Fund gained 10.74%, significantly outpacing the 8.63% 12-month return of the S&P 500 Index.

The Aggressive Growth Fund also outperformed its benchmark index, the NASDAQ Composite Index, over the last six-month and one-year periods ended June 30, 2006. The Fund returned 2.50% for the semiannual period, compared with the -1.08% six-month return for the NASDAQ Composite Index. Over the last year, the Fund returned 9.22%, significantly outpacing the 6.48% 12-month return of the NASDAQ Composite Index.

I am also pleased to report that both The Dynamic Growth Fund and The Aggressive Growth Fund have either performed better than or in line with their respective benchmark indices over the 3-year and 5-year periods ended June 30, 2006. The Performance Review table at right includes the longer-term returns of these funds along with the returns of their benchmark indicies for the same periods.

The Total Return Utilities Fund bested its benchmark index, the S&P 500 Utilities Index, for the six-month and one-year periods ended June 30, 2006. For the semiannual period, the Fund returned 5.47%, compared with the 4.47% return of its benchmark. For the one year period, the Fund returned 10.90%, significantly outpacing its benchmark’s 5.92% return for the same period.

The Muirfield Fund performed in line with its benchmark index, the S&P 500 Index, over the last six-month and one-year periods ended June 30, 2006. The Fund returned 2.91% for the semiannual period, compared with the 2.71% six-month return of the S&P 500 Index. Because the Fund sometimes is either partially or fully invested in cash equivalents, we believe a more appropriate comparison of performance is a blended index consisting of 60% of the S&P 500 Index and 40% of the 90-day U.S. Treasury Bill. For the first six months of this year, The Muirfield Fund outperformed this blended index, which returned 2.61% for the six-month period.

The Muirfield Fund continues to perform well relative to its benchmarks over longer-term periods as well. For the 5-year period ended June 30, 2006, the Fund returned 3.82% on an annualized basis, compared with the 2.49% annualized return of the S&P 500 Index and the 2.76% annualized return of the blended index over the same period.

Finally, The Flex-funds Money Market Fund has extended its track record as one of the leading general-purpose money market funds in its peer group. The Fund continued to rank among the top 10% of all general-purpose money market funds monitored by iMoneyNet, Inc. for total return for all 12-month periods since the Fund’s inception. That is a 21-year track record of success. For the six-month period, the Fund has outperformed its peer group with a 2.15% total return, compared with the 1.89% total return for the average general purpose money market fund, according to Lipper, Inc.

A performance review for each of The Flex-funds, along with a commentary on the decisions we made with your investments in our portfolios, is included on the following pages of this Semiannual Report. In addition, we have included a financial market review to provide some background on the investing conditions that we and other investment managers faced during the first half of 2006.

Semiannual Financial Market Review

“Most [Federal Reserve Board] members thought that the end of the tightening process was likely to be near, and some expressed concerns about the dangers of tightening too much, given the lags in the effects of the policy.”

So read the minutes of the March 27-28, 2006 Federal Open Market Committee (FOMC) meeting – the first under new Federal Reserve Chairman Ben Bernanke - during which the Fed raised its target rate for the 15th

Continued on Page 2.

| | |

| The Flex-funds 2006 Semiannual Report | June 30, 2006 | | Page 1 |

| | |

| The Flex-funds | | 2006 Semiannual Report | June 30, 2006 |

Letter to Shareholders Continued from Page 1.

consecutive time since June 2004 to 4.75%. The release of the meeting minutes on April 18th sparked a strong one-day rally in the stock market. Perhaps more importantly, this message from the country’s high priests of monetary policy gave credence to the belief among investors that the Fed’s current rate-tightening cycle may draw to a close after the next FOMC meeting. In fact, upon release of the March meeting minutes, the Fed funds futures market pegged the likelihood of a June rate hike to less than 30%.

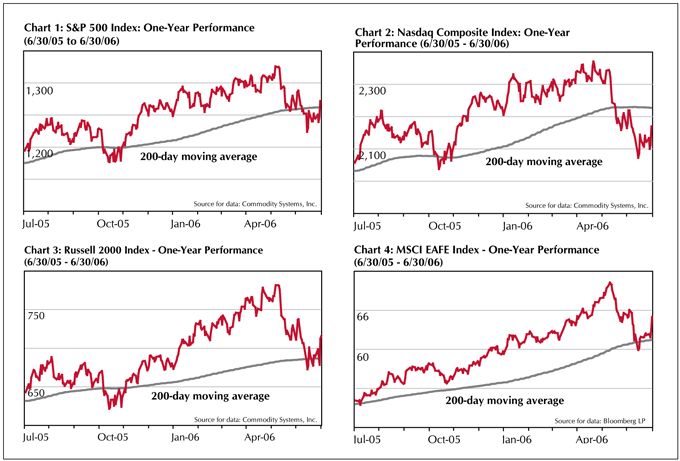

For much of the first six months of the year, speculation swirled about future Federal Reserve decisions on interest rates. As the apparent likelihood of a pause in the cycle grew, so did investors’ appetite for risk and, by extension, the on-going bull market for stocks. Building on the gains achieved in the first three months of 2006, the stock market surged to multi-year highs in April and early May. The venerable Dow Jones Industrial Average even closed in on its all-time record, climbing to within 80 points of its peak in 2000, a height last seen in the days of the tech-stock mania before the bursting of the dot-com bubble. The broader S&P 500 and Nasdaq Composite indices also performed strongly in the first half of the 2nd Quarter and eclipsed their respective four-year highs (see Charts 1 & 2 above.) although both market averages were still well below their bubble-era records.

Small-cap stocks continued to push the record bar higher and outpace their large-cap brethren in the early weeks of the 2nd Quarter. The Russell 2000 Index of small-cap stocks reached an all-time high of 781 on May 5th. Stocks on the international stage also performed well, with the MSCI EAFE Index rising 8.5% from the end of the 1st Quarter to its year-to-date peak on May 9. (See Charts 3 & 4 above.)

Investor demand for stocks was fed not only by the Federal Reserve but also by reports of robust economic growth, strong corporate profits, and relatively tame inflation. The U.S gross domestic product (GDP), a measure of economic growth, rose 5.6% in the 1st Quarter. This surge in growth reflected much of the economic activity of the post-Hurricane Katrina recovery efforts, but still was the strongest rate of growth since 2003. The 1st Quarter also saw an average 14% increase in profits for large U.S. corporations according to Thomson Financial, marking the 11th straight

| | |

| Page 2 | | The Flex-funds 2006 Semiannual Report | June 30, 2006 |

| | |

| The Flex-funds | | 2006 Semiannual Report | June 30, 2006 |

quarter of double-digit corporate profit increases. Even higher energy prices and geopolitical uncertainty did little to curb investors’ hunger for stocks.

But midway through the 2nd Quarter, the feast ended. Across the board, the major equity market indices fell, leaving stock investors with few places to hide. The S&P 500 Index tumbled nearly 4% from its peak through the end of the quarter, while the Nasdaq Composite Index slumped over 8%. The small-cap Russell 2000 Index outpaced its larger-cap siblings on the way down, falling more than 7% from its record high to the end of the quarter. The MSCI EAFE Index of international stocks lost over 7% from its year-to-date peak as well. By quarter-end, the decline erased a significant portion of the year-to-date gains achieved by the major stock indices and left many investors with the prospect of looking at their first quarterly losses since the 1st Quarter of 2005.

What happened? Naturally, there was a confluence of factors at work that impacted market performance in the 2nd Quarter. The shift in expectations about future Fed rate hikes clearly was one of them. Other factors included a surge in inflation, a mixed economic outlook, a slightly inverted yield curve, and an aging bull market.

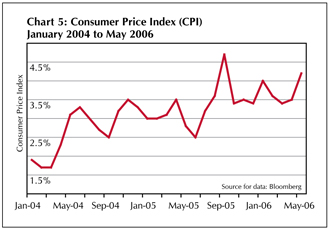

Inflation surges: With reports of strong economic growth, healthy corporate profits, and vigorous consumer spending – and not to forget higher energy prices – investors feared that a likely uptick in inflation was just around the corner. Was it wise, some wondered, for the Fed to consider a pause in interest rate hikes when inflationary pressures were threatening to boil over? These fears and doubts were manifested in June with the release of the May Consumer Price Index (CPI). This report revealed a jump in the annual pace of inflation to 4.2%, surpassing the market’s own dire expectation of a 3.9% increase. (See Chart 5 below.)

The rise in CPI took the guesswork out of the Fed’s decision to raise interest rates for the 17th consecutive time on June 29th. In fact, the strong jump in inflation also raised the probability of more rate hikes at future Federal Open Market Committee meetings in the coming months.

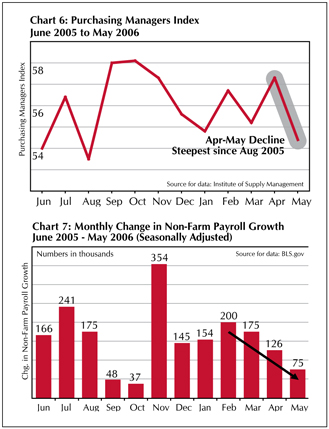

Mixed economic outlook: While corporate profits, consumer spending, and strong GDP figures stood out as bright spots, other indicators portrayed a different view for the U.S. economy. A host of market analysts – us included – have been keeping a careful watch for signs of decelerating growth in the economy, noting that the current expansion has become long in the tooth. This past quarter, several economic barometers pointed toward the possibility of a pending economic slowdown. Manufacturing activity, as measured by the Institute for Supply Management’s Purchasing Managers Index (PMI), slid dramatically from April to May. (See Chart 6 above.) Moreover, employment growth has been on a gradual decline since February and was significantly weak in May, with the number of new jobs created coming in well below market expectations. (See Chart 7 above.)

Continued on Page 4.

| | |

| The Flex-funds 2006 Semiannual Report | June 30, 2006 | | Page 3 |

| | |

| The Flex-funds | | 2006 Semiannual Report | June 30, 2006 |

Letter to Shareholders Continued from Page 3.

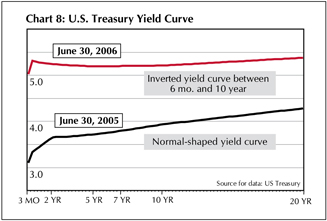

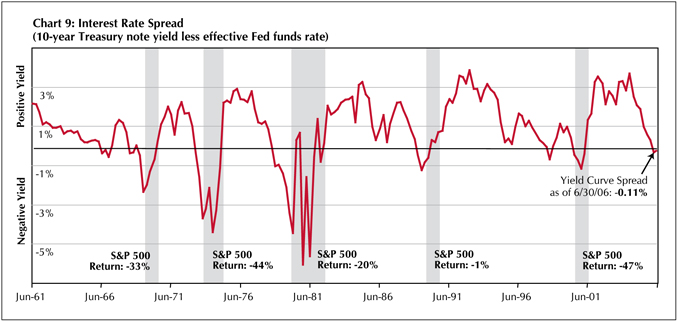

Inverted yield curve: The yield curve presents a picture of current interest rates for U.S. Treasury securities from a duration of 3-month bills to 30-year bonds. A normal yield curve will slope upward, with rates on short-term securities falling below rates on long-term securities. An inverted yield curve presents the opposite view; short-term rates higher than long-term rates, meaning that investors receive less reward for assuming the higher risks of longer-term bonds. Chart 8 above illustrates the difference between a more normal yield curve from June 30, 2005 and a slightly inverted yield curve from June 30, 2006.

What’s the significance of an inverted yield curve? Historically, inverted yield curves have often coincided with economic slowdowns, which typically result in a decline in the stock market. Chart 9 below illustrates the yield curve in a different way, marking the spread (or difference) between short-term and long-term rates over the last 45 years. The shaded areas identify periods during which economic recessions have occurred in the U.S. The percentage change figures for the S&P 500 Index represent the period from the close of the S&P 500 Index on the last day of the month that the yield curve became inverted (when the spread between the 10-year Treasury note yield and the Fed funds rate became negative) to the lowest close of the S&P 500 Index during the ensuing market correction.

The yield curve has inverted once already this year, for a week back in February. At the time, many market analysts crowed about the dire consequences for stocks, obviously to little effect. Less crowing has been heard about the current inversion. It is a significant development in the current market environment and contributed to our decision to reduce equity exposure in our defensively-managed portfolios. (For more information on this decision, please review the commentary for The Muirfield and Defensive Growth Funds on Page 6 of this Semiannual Report.)

Aging bull market: Based on an analysis of historical market data by InvesTech Research, the length of the average bull market over the last 75 years has been 3.7 years. From the start of the current bull market in October 2002, the average point was passed sometime this past May. That in itself does not mean the end of the rally is at hand. In fact, there have been several bull markets that have lasted longer than 3.7 years, and this one may resume its charge in the quarters to come. But when taken into consideration with the factors

| | |

| Page 4 | | The Flex-funds 2006 Semiannual Report | June 30, 2006 |

| | |

| The Flex-funds | | 2006 Semiannual Report | June 30, 2006 |

mentioned above and our quantitative equity asset allocation model (which as of this writing indicates a deteriorating risk/reward relationship in the stock market), it could present a precarious environment for investors in the months to come.

Looking Ahead

While hopes for an end to the Federal Reserve’s rate hiking cycle may have been spoiled, they certainly were not without merit. What can investors expect when the Fed finally decides to stop raising rates?

If history repeats itself, investors should be prepared for changes in the market environment when the Fed finally does decide that enough rate hikes are enough. The Federal Reserve historically has gone too far in their “tightening” mode, which ultimately results in an economic slowdown. The stock market, which typically anticipates future economic conditions, often recognizes this pattern, resulting in generally weak market conditions in the months following the end of the interest rate cycle. Of course, no one can predict when the final interest rate hike of this cycle will take place or where stocks will go from that point. Our discipline is not predictive. Instead, we adhere to the quantitative disciplines in our investment process and analyze interest rate and monetary policy and other market statistics to evaluate the risk/reward relationship of the stock and bond markets.

For its part, the Fed seems to have altered its tune somewhat under new chairman Ben Bernanke. After more than 20 years of the Alan Greenspan “trust me” era, we now have a Federal Reserve Board that appears more data-dependent than its predecessor. In the words of Bernanke himself, taken from his testimony on the economy before Congress on April 27, 2006: “Future policy actions will be increasingly dependent on the evolution of the economic outlook, as reflected in the incoming data.”

That means, instead of trying to decipher the Alan Greenspan’s cryptic comments for clues on the direction of interest rates, investors can now scrutinize every report about inflation, employment, productivity, housing, and any other economic indicator that can be fathomed for signals on the Federal Reserve’s next interest rate move. More tinder to fuel the fire of emotional investors, to be sure. All the more reason to employ our highly quantitative investment disciplines for your investments.

As always, our Shareholder Services team is available for you to contact with questions about a specific investment strategy or your individual account. On behalf of all of the associates at Meeder Asset Management, Inc. and The Flex-funds, I thank you for your trust and confidence in our investment management services.

|

| Sincerely, |

|

|

Robert S. Meeder, Jr. President Meeder Asset Management, Inc. & The Flex-funds August 3, 2006 |

| | |

| The Flex-funds 2006 Semiannual Report | June 30, 2006 | | Page 5 |

| | |

| The Flex-funds | | 2006 Semiannual Report | June 30, 2006 |

The Muirfield Fund®

The Defensive Growth Fund

Performance Perspective

| | | | | | | | | | | | | | | | | | |

Period & Average Annual Total Returns as of June 30, 2006 | | Year

to date | | | One

Year | | | Three

Years | | | Five

Years | | | Ten

Years | | | Since

Inception | |

The Muirfield Fund | | 2.91 | % | | 8.06 | % | | 9.72 | % | | 3.82 | % | | 5.20 | % | | 8.43 | %1 |

Blended Index4 | | 2.61 | % | | 6.92 | % | | 7.77 | % | | 2.76 | % | | 6.85 | % | | 8.95 | %2 |

S&P 500 Index5 | | 2.71 | % | | 8.63 | % | | 11.20 | % | | 2.49 | % | | 8.31 | % | | 11.44 | %2 |

The Defensive Growth Fund | | — | | | — | | | — | | | — | | | — | | | -3.30 | %3 |

| 1 | Inception Date: 8/10/88. |

| 2 | Average annual total return from 8/1/88 to 6/30/06. |

| 3 | Inception Date: 1/31/06 Source for index data: Morningstar, Inc. |

Past performance does not guarantee future results. All performance figures represent average annual total returns for the periods ended June 30, 2006 and assume reinvestment of all dividend and capital gain distributions. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Management fees were waived and/or expenses were reimbursed in order to reduce the operating expenses of the Funds during the periods shown above.

| 4 | The blended index consists of 60% of the S&P 500 Index and 40% of the average 90-day U.S. Treasury bill. |

| 5 | The S&P 500 Index is a widely recognized unmanaged index of common stock prices. The S&P 500 Index does not take into account the deduction of expenses associated with a mutual fund, such as investment management and accounting fees. One cannot invest directly in an index. |

Semiannual Market Perspective

For the first half of 2006, The Muirfield Fund performed in line with its benchmark with a total return of 2.91% for the period. In comparison, the S&P 500 Index returned 2.71% for the semiannual period.

Given that, as conditions warrant, both The Muirfield Fund and The Defensive Growth Fund are sometimes partially or fully invested “defensively” in cash equivalent securities, therefore we believe the most appropriate comparison of performance is a blended index consisting of 60% of the S&P 500 Index and 40% of the 90-day U.S. Treasury Bill. With that said, we are pleased to report that The Muirfield Fund has outperformed this custom benchmark for the 6-month, 1-year, 3-year, and 5-years periods ended June 30, 2006.

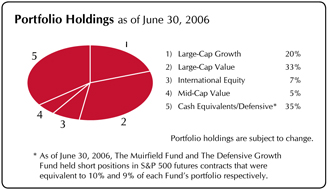

Stocks rallied strongly from the beginning of 2006 through early May, with many market indices reaching multiyear highs. During this time, our tactical asset allocation model indicated that the risk/reward relationship of the stock market remained on balance positive. Therefore, we maintained a fully-invested equity position for this period. Early in the year, the Funds were primarily invested in mid- and small-cap funds with some exposure to the international equity markets. Our international positions contributed positively to fund performance during the semiannual period.

Also during this six-month period, several economic indicators began to point toward a possible slowdown. Based on this analysis and our evaluation of relative strength in the equity market, we decided in March to rotate our portfolio emphasis toward large-cap value funds, which tend to come into favor during periods of slower economic growth. This shift toward large-cap value funds continued in the 2nd Quarter, as we limited our mid-cap and international exposure and eliminated our small-cap positions. By mid-June, the Portfolio was overweighted in large-cap stock funds, with smaller allocations to mid-cap value and international equity funds.

Also in June, the risk/reward relationship in the equity market began to change. As a result of a variety of factors in our model, including the continuing trend of Federal Reserve rate hikes, the extremely flat yield curve with periodic inversions, and the lack of price support in several of our trend indicators, we concluded the risk/reward relationship of the stock market had changed to the extent that we no longer believed that 100% equity exposure to the stock market was warranted. As a result, in mid-June we established a 35% “defensive” position in both funds. Further adjustments to this position may be made in the coming months as our model warrants.

| | |

| Page 6 | | The Flex-funds 2006 Semiannual Report | June 30, 2006 |

| | |

| The Flex-funds | | 2006 Semiannual Report | June 30, 2006 |

The Dynamic Growth Fund

The Focused Growth Fund

Performance Perspective

| | | | | | | | | | | | | | | |

Period & Average Annual Total Returns as of June 30, 2006 | | Year

to date | | | One

Year | | | Three

Years | | | Five

Years | | | Since

Inception | |

The Dynamic Growth Fund | | 4.59 | % | | 10.74 | % | | 11.36 | % | | 2.02 | % | | -1.90 | %1 |

S&P 500 Index4 | | 2.71 | % | | 8.63 | % | | 11.20 | % | | 2.49 | % | | 0.46 | %2 |

The Focused Growth Fund | | — | | | — | | | — | | | — | | | 2.50 | %3 |

| 1 | Inception Date: 2/29/2000. |

| 2 | Average annual total return from 2/29/2000 to 6/30/06. |

| 3 | Inception Date: 1/31/06. |

Source for index data: Bloomberg LP

Past performance does not guarantee future results. All performance figures represent average annual total returns for the periods ended June 30, 2006 and assume reinvestment of all dividend and capital gain distributions. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Management fees were waived and/or expenses were reimbursed in order to reduce the operating expenses of the Funds during the periods shown above.

| 4 | The S&P 500 Index is a widely recognized unmanaged index of common stock prices. The S&P 500 Index does not take into account the deduction of expenses associated with a mutual fund, such as investment management and accounting fees. One cannot invest directly in an index. |

Semiannual Market Perspective

For the first six months of 2006, The Dynamic Growth Fund outperformed the benchmark S&P 500 Index with a total return of 4.59%. In comparison, the S&P 500 Index returned 2.71% for the same period. More importantly, over the past 1-, 3-, and 5-year periods The Dynamic Growth Fund has also either exceeded or performed in line with the S&P 500 Index.

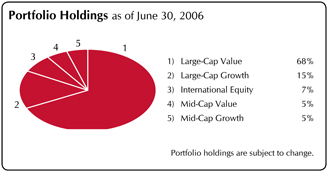

At the start of the year, the Funds were allocated primarily to large- and mid-cap funds with some exposure to small-cap and international equity funds. Our international holdings contributed positively to fund performance during the semiannual period, as global stock markets performed well along with U.S. stock markets. After reaching multi-year highs in early May, most major equity indices declined sharply through the latter half of the 2nd Quarter. The market’s revolving fixation on inflation concerns, the overall health of the economy, and the Federal Reserve’s next rate decision all weighed heavily on investors’ risk appetite. By June 30, 2006, many major equity market indices were close to both price and moving average support levels.

Our analysis continued to indicate that the U.S. economy is in the later stages of the current economic cycle and that domestic growth might slow in the months ahead. Typically at this point in the economic cycle, as growth begins to slow down, large-cap companies tend to come into favor while performance for small-cap companies wanes. Moreover, our measure of investor sentiment recently reached its highest level of volatility since March 2004, indicating increased fear among equity investors. This was also a key factor in the flight to quality witnessed in June.

Our equity asset allocation was adjusted halfway through the 2nd Quarter to emphasize stock funds with significant weightings in large-cap companies and to limit our mid-cap exposure. With small-cap stocks declining more than large-cap stocks, we believed that large-cap stocks presented more attractive prospects for growth than small-cap stocks. Therefore, we eliminated our remaining small-cap positions during the 2nd Quarter. We also reduced our exposure to international stocks in both funds. The European Central Bank’s bias of a tighter monetary policy contributed to our decision to trim our international exposure.

As of June 30, 2006, our target allocation for both funds was 83% in large-cap stock funds, 10% in mid-cap stock funds, and 7% in international stock funds.

| | |

| The Flex-funds 2006 Semiannual Report | June 30, 2006 | | Page 7 |

| | |

| The Flex-funds | | 2006 Semiannual Report | June 30, 2006 |

The Aggressive Growth Fund

Performance Perspective

| | | | | | | | | | | | | | | |

Period & Average Annual Total Returns as of June 30, 2006 | | Year

to date | | | One

Year | | | Three

Years | | | Five

Years | | | Since

Inception | |

The Aggressive Growth Fund | | 2.50 | % | | 9.22 | % | | 10.98 | % | | 0.73 | % | | -4.62 | %1 |

NASDAQ Composite Index3 | | -1.08 | % | | 6.48 | % | | 10.91 | % | | 0.66 | % | | -11.02 | %2 |

| 1 | Inception Date: 2/29/2000. |

| 2 | Average annual total return from 2/29/2000 to 6/30/06. |

Source for index data: Bloomberg LP.

Past performance does not guarantee future results. All performance figures represent average annual total returns for the periods ended June 30, 2006 and assume reinvestment of all dividend and capital gain distributions. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Management fees were waived and/or expenses were reimbursed in order to reduce the operating expenses of The Aggressive Growth Fund during the periods shown above.

| 3 | The NASDAQ Composite Index is a broad-based capitalization-weighted index of all NASDAQ National Market and Small Cap stocks. The NASDAQ Composite Index does not take into account the deduction of expenses associated with a mutual fund, such as investment management and accounting fees. One cannot invest directly in an index. |

Semiannual Market Perspective

The Aggressive Growth Fund outperformed its benchmark index for the six month period ending June 30, 2006. The Fund returned 2.50% for the period, while the NASDAQ Composite Index declined 1.08%. We are most pleased that the returns of the Fund over the past 1-, 3-, and 5-year periods as well as since inception have also outperformed their benchmark.

Performance for the Fund was aided by our allocation to international equity markets, specifically emerging market funds. Both U.S. and global equity markets performed well in the rally that lasted for much of the six-month period. But after reaching multi-year highs in early May, most major equity indices declined sharply through the latter half of the 2nd Quarter. The market’s revolving fixation on inflation concerns, the overall health of the economy, and the Federal Reserve’s next rate decision all weighed heavily on investors’ risk appetite. By June 30, 2006, many major equity market indices were close to both price and moving average support levels.

Our analysis continued to indicate that the U.S. economy is in the later stages of the current economic cycle and that domestic growth might slow in the months ahead. The supportive valuation and earnings growth environment may become vulnerable to the pressures of higher inflation and potential slower growth. Our equity asset allocation was adjusted halfway through the 2nd Quarter to emphasize stocks with significant weightings in large-cap companies and limit our mid-cap exposure. As we are entering a historically unfavorable time of the year, we also eliminated our more volatile positions such as small-cap stock funds. While some near-term strength remains a possibility given the bearish sentiment and oversold technical conditions, overall our indicators do not support the likelihood of a sustainable small-cap rally.

We also reduced our exposure to international stocks during the period. With many central banks around the world adopting a rate-tightening stance, we feel the reduction of liquidity by various central banks (European, China, and potentially Japan) poses as a headwind to global equity markets. We took the bounce from recent lows as an opportunity to reduce our international stock exposure. As we saw speculative inflows into the emerging markets countries continue to increase, we trimmed our emerging markets position, and eventually exited in Mid June.

As of June 30, 2006, our target allocation in The Aggressive Growth Fund was 83% in large-cap stock funds, 10% in mid-cap stock funds, and 7% in international stock funds.

| | |

| Page 8 | | The Flex-funds 2006 Semiannual Report | June 30, 2006 |

| | |

| The Flex-funds | | 2006 Semiannual Report | June 30, 2006 |

The Quantex Fund™

Performance Perspective

| | | | | | | | | | | | | | | | | | |

Period & Average Annual Total Returns as of June 30, 2006 | | Year

to date | | | One

Year | | | Three

Years | | | Five

Years | | | Ten

Years | | | Since

Inception | |

The Quantex Fund™ | | 2.93 | % | | 7.72 | % | | 10.57 | % | | 1.15 | % | | 5.91 | % | | 7.31 | %1 |

S&P Mid-Cap 400 Index3 | | 4.24 | % | | 12.99 | % | | 18.11 | % | | 9.28 | % | | 13.80 | % | | 13.15 | %2 |

Russell 2000 Small-Cap Index4 | | 8.27 | % | | 14.67 | % | | 18.75 | % | | 8.58 | % | | 9.11 | % | | 9.04 | %2 |

| 1 | Inception Date: 3/20/85. |

| 2 | Average annual total return from 3/31/85 to 6/30/06. |

Source for index data: Bloomberg LP.

Past performance does not guarantee future results. All performance figures represent average annual total returns for the periods ended June 30, 2006 and assume reinvestment of all dividend and capital gain distributions. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Management fees were waived and/or expenses were reimbursed in order to reduce the operating expenses of The Quantex Fund during the periods shown above.

| 3 | The S&P Mid-Cap 400 Index is a widely recognized unmanaged index of common stock prices of mid-sized companies. The S&P Mid-Cap 400 Index does not take into account the deduction of expenses associated with a mutual fund, such as investment management and accounting fees. One cannot invest directly in an index. |

| 4 | The Russell 2000 Index is a widely recognized unmanaged index of common stock prices of small-sized companies. The Russell 2000 Index does not take into account the deduction of expenses associated with a mutual fund, such as investment management and accounting fees. One cannot invest directly in an index. |

Semiannual Market Perspective

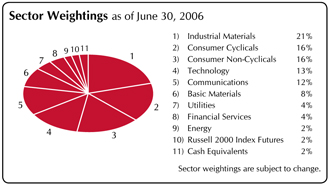

For the six-month period ended June 30, 2006, The Quantex Fund returned 2.93%. In comparison, the S&P Mid-Cap 400 Index returned 4.24% and the small-cap Russell 2000 Index returned 8.27%.

The Quantex Fund typically consists of approximately 100 equally-weighted securities selected using a quantitative screening process that has been consistently used since 1989. The Fund is rebalanced annually during the month of January.

Typically, a few of the companies whose stock is owned by the Fund are acquired every year. When this occurs, new stocks are added to the Fund to maintain a diverse selection of equity securities. The first half of 2006 has been no exception. During the 2nd Quarter alone, four companies in the Fund’s portfolio were acquired, including May-tag, Chiron, Engelhard and Knight Ridder. These securities were replaced with the appropriate securities selected in a manner consistent with how our investment strategy has dealt with acquisitions for over 15 years.

During the first half of 2006, an underweighted position in energy and financial services hurt fund performance relative to its benchmarks. These sectors have been among the equity market’s strongest performers over the last six months and contributed to the outperformance of the Fund’s benchmark indices for the semiannual period. The best performing holdings of the Fund included Allegheny Technologies (ATI, up over 92%), OfficeMax (OMX, up over 62%) and Ciena Corp.(CIEN, up over 61%). The two largest individual drags on performance were well-known names Radio Shack (RSH, down 33%) and Goodyear Tire & Rubber (GT, down 36%).

While the current investment environment has been challenging for investors, we believe that the quantitative strategy used by the Fund will continue to add value for investors over the long-term.

| | |

| The Flex-funds 2006 Semiannual Report | June 30, 2006 | | Page 9 |

| | |

| The Flex-funds | | 2006 Semiannual Report | June 30, 2006 |

The Total Return Utilities Fund

Performance Perspective

| | | | | | | | | | | | | | | | | | |

Period & Average Annual Total Returns as of June 30, 2006 | | Year

to date | | | One

Year | | | Three

Years | | | Five

Years | | | Ten

Years | | | Since Inception | |

The Total Return Utilities Fund | | 5.47 | % | | 10.90 | % | | 16.03 | % | | 1.17 | % | | 8.05 | % | | 9.14 | %1 |

S&P 500 Utilities Index3 | | 4.47 | % | | 5.92 | % | | 17.61 | % | | 1.23 | % | | 6.92 | % | | 7.90 | %2 |

| 1 | Inception Date: 6/21/1995. |

| 2 | Average annual total return from 6/30/95 to 6/30/06. |

Source for index data: Bloomberg LP.

Past performance does not guarantee future results. All performance figures represent average annual total returns for the periods ended June 30, 2006 and assume reinvestment of all dividend and capital gain distributions. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Management fees were waived and/or expenses were reimbursed in order to reduce the operating expenses of The Total Return Utilities Fund during the periods shown above. Because The Total Return Utilities Fund concentrates its investments in public utility companies, the value of the Fund’s shares may fluctuate more than if invested in a greater number of industries. Changes in interest rates may also affect the value of utility stocks, and rising interest rates can be expected to reduce the Fund’s net asset value.

| 3 | The S&P 500 Utilities Index is an unmanaged index of 33 utility sector stocks. This index does not take into account the deduction of expenses associated with a mutual fund, such as investment management and accounting fees. One cannot invest directly in an index. |

Semiannual Market Perspective

The Total Return Utilities Fund outperformed its benchmark index for the first half of 2006 with a total return of 5.47%. In comparison, the S&P 500 Utilities Index returned 4.47% over the same six-month period.

We are also pleased to report that for the 1-, 5- and 10- year periods as well as since inception, the performance of the Fund has either exceeded or been in line with its benchmark.

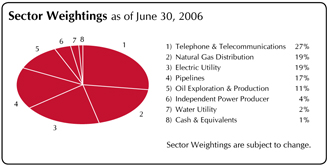

Performance for the stocks in our portfolio was quite volatile over the six month period, although our returns for the period were still positive. We have emphasized foreign telecommunications companies and natural gas producers in our portfolio, along with an allocation to the more conventional distribution and integrated utilities.

Natural gas and the growth of foreign economies seem to be two of the most fundamentally solid investable trends in the world at present. Though gas storage is nearly at full capacity as a consequence of a record warm winter, we believe that the weather may normalize and that the supply and demand for gas may favor firm or higher prices in the future. A number of major buyout deals for gas companies indicates that the valuations investors have placed in these firms is substantially lower than the estimations of those who are actually in the business, giving us a margin of safety in maintaining our positions.

As for the foreign telecoms, some traditional European companies are selling at lower valuations than their American counterparts. But the more interesting stories are coming from developing areas. We consider these emerging market telecoms to be a proxy for economic growth worldwide. It is true that there are technological challenges for these companies just as our domestics are faced with problems. But regulation is far more congenial to these enterprises, which are often the sole meaningful supplier of phone services in countries whose growth potential dwarfs our own right now.

We considered making changes to our portfolio in the 2nd Quarter, but found ourselves content with the stocks that we currently hold. A few of our supporting positions in utility service companies might change shape over the next quarter, but as of this writing we are basically confident in the stocks that we own. Investor interest in large electric companies should help support our traditional utilities, and the recent revival of our more aggressive holdings should add value to shareholders’ return as well.

| | |

| Page 10 | | The Flex-funds 2006 Semiannual Report | June 30, 2006 |

| | |

| The Flex-funds | | 2006 Semiannual Report | June 30, 2006 |

The U.S. Government Bond Fund

Performance Perspective

| | | | | | | | | | | | | | | | | | |

Period & Average Annual Total Returns as of June 30, 2006 | | Year

to date | | | One

Year | | | Three

Years | | | Five

Years | | | Ten

Years | | | Since

Inception | |

The U.S. Government Bond Fund | | 0.30 | % | | -0.50 | % | | -0.46 | % | | 1.50 | % | | 3.50 | % | | 5.54 | %1 |

Lehman Bros. Intermediate-Term Government/Credit Index2 | | -0.18 | % | | -0.19 | % | | 1.49 | % | | 4.61 | % | | 5.80 | % | | 7.50 | %2 |

| 2 | Average annual total return from 4/30/85 to 6/30/06. |

Source for index data: Morningstar, Inc.

Past performance does not guarantee future results. All performance figures represent average annual total returns for the periods ended June 30, 2006 and assume reinvestment of all dividend and capital gain distributions. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Management fees were waived and/or expenses were reimbursed in order to reduce the operating expenses of The U.S. Government Bond Fund during the periods shown above.

| 2 | The Lehman Brothers Intermediate-Term Government/Credit Index is an unmanaged index of fixed-rate bonds issued by the U.S. Government and its agencies that are rated investment grade or higher, have one to ten years remaining until maturity, and at least $100 million outstanding. The Lehman Brothers Intermediate-Term Government/Credit Index does not take into account the deduction of expenses associated with a mutual fund, such as investment management and accounting fees. One cannot invest directly in an index. |

Semiannual Market Perspective

The Flex-funds U.S. Government Bond Fund outperformed its benchmark for the six-month period ended June 30, 2006. Year to date, the Fund returned 0.30% while its benchmark index, the Lehman Brothers Intermediate-Term Government/Credit Index, returned -0.18% for the same period.

The Federal Reserve raised the Fed funds target rate four times during the first half of 2006. These rate hikes extended the Fed’s current rate-hiking streak to 17 consecutive increases, which has added 4.25% to the Fed funds target rate since the start of its tightening campaign in 2004 when the rate was only 1 percent. Recent Consumer Price Index readings at 4.2% suggest that inflation may still be a persistent concern and support the likelihood of further Fed rate increases in the months to come.

Interest rates rose across the spectrum of fixed income securities during the semiannual period. Our overall assessment of a rising rate environment for intermediate-term bonds aided performance, as we maintained a lower average maturity for the Fund. In this rising rate environment, we continued to seek alternative sources of additional yield through U.S. Government Agency bonds.

As of June 30th, our fixed income investment model continues to indicate that rates will likely be on the rise in the coming months. All interest rate trend components increased during the last quarter. These indicators, coupled with our fundamental factors of consumption, inflation, and unemployment, suggest that intermediate-term rates may still have room to increase in the near future. The balance of our trend and fundamental indicators suggest that a shorter maturity structure is appropriate at this time.

However, we are seeing a signal of what would imply the beginning of a more stable interest rate environment. Should our model indicate that intermediate-term interest rates may stabilize, we will begin to extend the average maturity of the Fund.

| | |

| The Flex-funds 2006 Semiannual Report | June 30, 2006 | | Page 11 |

| | |

| The Flex-funds | | 2006 Semiannual Report | June 30, 2006 |

The Money Market Fund

Performance Perspective

| | | | | | | | | | | | | | | | | | |

Period & Average Annual Total Returns as of June 30, 2006 | | Year

to date | | | One

Year | | | Three

Years | | | Five

Years | | | Ten

Years | | | Since

Inception | |

The Money Market Fund - Retail Class | | 2.15 | % | | 3.87 | % | | 2.16 | % | | 2.02 | % | | 3.70 | % | | 5.03 | %1 |

Current & Effective Yields5 | | 7-day Simple: 4.76% | | | 7-day Compound: 4.87% | |

Lipper’s Average General Purpose Money Market Fund6 | | 1.89 | % | | 3.35 | % | | 1.68 | % | | 1.51 | % | | 3.26 | % | | 4.64 | %2 |

The Money Market Fund - Institutional Class | | 2.23 | % | | 4.01 | % | | — | | | — | | | — | | | -3.49 | %3 |

Current & Effective Yields5 | | 7-day Simple: 4.90% | | | 7-day Compound: 5.01% | |

iMoneyNet, Inc. Average First-Tier Institutional Money Market Fund6 | | 2.17 | % | | 3.88 | % | | — | | | — | | | — | | | -3.42 | %4 |

| 1 | Inception Date: 3/27/85. |

| 2 | Average annual total return from 3/31/85 to 6/30/06. |

| 3 | Inception date: 12/28/04. |

| 4 | Average annual total return from 12/31/04 to 6/30/06. Source for average general purpose money market fund data: Lipper, Inc. Source for average first-tier institutional money market fund data: iMoneyNet, Inc. |

| 5 | For the period ended 6/30/06, yield quotations more closely reflect the current earnings of The Money Market Fund than do total return quotations. |

Past performance does not guarantee future results. Except for the current and effective yields, all performance figures represent average annual total returns for the periods ended June 30, 2006, and assume reinvestment of all dividend and capital gain distributions. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Management fees were waived and/or expenses were reimbursed in order to reduce the operating expenses of The Money Market Fund during the periods shown above. Investments in The Money Market Fund are neither insured nor guaranteed by the Federal Deposit Insurance Corporation or any other governmental agency. Although the Funds seek to preserve the value of your investment at $1.00 per share, it is possible to lose money by investing in The Money Market Fund.

| 6 | An index of funds such as Lipper’s Average General Purpose Money Market Fund Index and iMoneyNet, Inc.’s Average First Tier Institutional Money Market Fund Index includes a number of mutual funds grouped by investment objective. |

Semiannual Market Perspective

The retail class of The Money Market Fund continued to rank among the top general-purpose money market funds monitored by iMoneyNet, Inc. for the 12-month period ended June 30, 2006. More impressively, the retail class of The Money Market Fund has ranked in the top 10% of all general-purpose money market funds monitored by iMoneyNet, Inc. for every 12-month period since the Fund’s inception in 1985.

The Money Market Fund continued to maintain a high exposure to floating-rate instruments, as well as to corporate securities. This strategy enabled the Fund to earn a higher yield than what would have been realized had the Fund instead targeted a larger exposure to commercial paper. Corporate securities have consistently paid higher yields than commercial paper since the Federal Reserve began raising short-term interest rates on June 30, 2004.

During the past several months, we intentionally allowed the Fund’s weighted average maturity (WAM) to shorten so that we could more quickly invest the proceeds from maturing securities into higher-yielding instruments. At the end of the 1st Quarter, the Fund’s WAM was just under 30 days. By the end of the 2nd Quarter, we allowed the WAM to decline further to 25 days. This has worked to the Fund’s advantage, as the money market yield curve shifted higher by 30-40 basis points during the 2nd Quarter.

Our analysis of both money market rates and the Fed fund futures suggests that yields on maturities beyond the 60- 90 day range do not currently offer the proper additional yield to extend at this time. Our primary strategic focus revolves around Federal Reserve activities. Until the Fed indicates that it plans to stop raising short-term interest rates, we will continue to invest available cash in securities that have relatively short maturities.

| | |

| Page 12 | | The Flex-funds 2006 Semiannual Report | June 30, 2006 |

| | |

| The Flex-funds | | 2006 Semiannual Report | June 30, 2006 |

Shareholder Expense Analysis (Unaudited)

Shareholders of mutual funds pay ongoing expenses, such as advisory fees, distribution and service fees (12b-1 fees) and other fund expenses. The following examples are intended to help you understand your ongoing costs (in dollars) of investing in the Funds and to compare these costs with the ongoing costs of investing in other mutual funds.

The examples below are based on an investment of $1,000 invested at the beginning of the period and held for the six-month period from December 31, 2005 to June 30, 2006.

ACTUAL EXPENSES: The first table below provides information about actual account values and actual expenses. You may use the information in this table, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (e.g.: an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the line under the heading “Expenses Paid During the Period” to estimate the expenses you paid on your account during this period.

ACTUAL EXPENSES

| | | | | | | | | | | | |

| | | Beginning

Account Value

(12/31/2005) | | Ending

Account Value

(6/30/06) | | Expenses Paid

During Period1

(12/31/2005

- 6/30/06) | | Expense Ratio

(Annualized) | |

The Muirfield Fund | | $ | 1,000.00 | | $ | 1,029.10 | | $ | 7.30 | | 1.45 | % |

The Total Return Utilities Fund | | | 1,000.00 | | | 1,054.70 | | | 9.99 | | 1.96 | % |

The Quantex Fund | | | 1,000.00 | | | 1,029.30 | | | 7.90 | | 1.57 | % |

The Dynamic Growth Fund | | | 1,000.00 | | | 1,045.90 | | | 7.46 | | 1.47 | % |

The Aggressive Growth Fund | | | 1,000.00 | | | 1,025.00 | | | 8.69 | | 1.73 | % |

The Defensive Growth Fund2 | | | 1,000.00 | | | 967.00 | | | 8.73 | | 1.79 | % |

The Focused Growth Fund2 | | | 1,000.00 | | | 975.00 | | | 8.86 | | 1.81 | % |

The U.S. Government Bond Fund | | | 1,000.00 | | | 1,003.00 | | | 5.46 | | 1.10 | % |

The Money Market Fund - Retail Class | | | 1,000.00 | | | 1,021.50 | | | 2.41 | | 0.48 | % |

The Money Market Fund - Institutional Class | | | 1,000.00 | | | 1,022.30 | | | 1.70 | | 0.34 | % |

HYPOTHETICAL EXAMPLE FOR COMPARISON PURPOSES: The second table below provides information about hypothetical account values and hypothetical expenses based on the Funds’ actual expense ratios and assumed rates of return of 5% per year before expenses, which are not the Funds’ actual returns. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Funds to other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

HYPOTHETICAL EXAMPLE

(5% return before expenses)

| | | | | | | | | | | | |

| | | Beginning

Account Value

(12/31/2005) | | Ending

Account Value

(6/30/06) | | Expenses Paid

During Period1

(12/31/2005

- 6/30/06) | | Expense Ratio

(Annualized) | |

The Muirfield Fund | | $ | 1,000.00 | | $ | 1,017.60 | | $ | 7.25 | | 1.45 | % |

The Total Return Utilities Fund | | | 1,000.00 | | | 1,015.08 | | | 9.79 | | 1.96 | % |

The Quantex Fund | | | 1,000.00 | | | 1,017.01 | | | 7.85 | | 1.57 | % |

The Dynamic Growth Fund | | | 1,000.00 | | | 1,017.50 | | | 7.35 | | 1.47 | % |

The Aggressive Growth Fund | | | 1,000.00 | | | 1,016.22 | | | 8.65 | | 1.73 | % |

The Defensive Growth Fund2 | | | 1,000.00 | | | 1,015.92 | | | 8.95 | | 1.79 | % |

The Focused Growth Fund2 | | | 1,000.00 | | | 1,015.82 | | | 9.05 | | 1.81 | % |

The U.S. Government Bond Fund | | | 1,000.00 | | | 1,019.34 | | | 5.51 | | 1.10 | % |

The Money Market Fund - Retail Class | | | 1,000.00 | | | 1,022.41 | | | 2.41 | | 0.48 | % |

The Money Market Fund - Institutional Class | | | 1,000.00 | | | 1,023.11 | | | 1.71 | | 0.34 | % |

Please note that the expenses shown in the tables are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as redemption fees or exchange fees. Therefore, the second table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if any transactional costs were included, your costs would have been higher.

| 1 | Expenses are equal to the Funds’ annualized expense ratios, multiplied by the average account value over the period, multiplied by 181/365 (to reflect the total number of days in the six-month period). |

| 2 | The Defensive Growth and Focused Growth Funds commenced operations on January 31, 2006. |

| | |

| The Flex-funds 2006 Semiannual Report | June 30, 2006 | | Page 13 |

| | |

| The Flex-funds | | 2006 Semiannual Report | June 30, 2006 |

2006 Semiannual Report

Portfolio Holdings & Financial Statements

| | |

| Page 14 | | The Flex-funds 2006 Semiannual Report | June 30, 2006 |

Schedule of Investments

June 30, 2006 (unaudited)

The Muirfield Fund

| | | | | |

Security Description

| | Shares or

Principal

Amount ($)

| | Value ($)

| |

Registered Investment Companies — 76.0% | |

Allianz NACM International Fund — I | | 75,143 | | 1,653,887 | |

Allianz NFJ Dividend Value Fund — D | | 241,298 | | 3,711,163 | |

American Growth Fund of America — A | | 189,593 | | 6,010,107 | |

Artisan Mid Cap Value Fund | | 122,209 | | 2,361,075 | |

Goldman Sachs Structured Large Cap Value Fund — I | | 884,186 | | 11,963,043 | |

MFS Value Fund — A | | 285,627 | | 6,972,163 | |

SSgA International Stock Selection Fund | | 170,106 | | 2,100,805 | |

Transamerica Premier Equity Fund — I | | 93,073 | | 2,090,425 | |

| | | | |

|

|

Total Registered Investment Companies (Cost $36,537,716) | | | | 36,862,668 | |

| | | | |

|

|

U.S. Government Obligations — 1.0% | |

U.S. Treasury Bill,

4.854%, due 09/07/2006* | | 500,000 | | 495,371 | |

| | | | |

|

|

Total U.S. Government Obligations

(Cost $495,533) | | | | 495,371 | |

| | | | |

|

|

Repurchase Agreements — 23.1% | |

Morgan Stanley DW, Inc., 5.3725%, 07/03/2006, (Collateralized by $11,183,004 various Commercial Papers, Certificates of Deposit, Agency Strips, FNMAs, Treasury Notes, and SLMA, at 4.00% — 10.00%, due 07/05/2006 — 01/01/2036, value — $11,401,626) purchase date 06/30/2006 | | 11,178,000 | | 11,178,000 | |

| | | | |

|

|

Total Repurchase Agreements (Cost $11,178,000) | | | | 11,178,000 | |

| | | | |

|

|

Total Investments — 100.1%

(Cost $48,211,249)(a) | | | | 48,536,039 | |

| | | | |

|

|

Liabilities less Other Assets — (0.1%) | | | | (68,254 | ) |

| | | | |

|

|

Total Net Assets — 100.0% | | | | 48,467,785 | |

| | | | |

|

|

Trustee Deferred Compensation** | |

The Flex-funds Dynamic Growth Fund | | 2,390 | | 20,697 | |

The Flex-funds Quantex Fund | | 1,718 | | 30,220 | |

The Flex-funds Muirfield Fund | | 5,591 | | 29,632 | |

The Flex-funds Total Return Utilities Fund | | 435 | | 8,696 | |

| | | | |

|

|

Total Trustee Deferred Compensation (Cost $72,530) | | | | 89,245 | |

| | | | |

|

|

The Muirfield Fund

| | | | | | |

Security Description

| | Short

Contracts

| | | Unrealized

Appreciation

(Depreciation) ($)

| |

Futures Contracts | |

Standard & Poors 500 expiring September 2006, notional value $4,797,750 | | (15 | ) | | (109,585 | ) |

| | | | | |

|

|

Total Futures Contracts | | | | | (109,585 | ) |

| | | | | |

|

|

| (a) | Represents cost for financial reporting purposes and differs for federal income tax purposes by the amount of losses recognized in excess of federal income tax reporting of approximately $161,921. Cost for federal income tax purposes of $48,373,170 differs from value by net unrealized appreciation (depreciation) of securities as follows: |

| | | | |

Unrealized appreciation | | $ | 671,618 | |

Unrealized depreciation | | | (508,749 | ) |

| | |

|

|

|

Net unrealized appreciation (depreciation) | | $ | 162,869 | |

| | |

|

|

|

| # | Represents non-income producing securities. |

| * | Pledged as collateral on futures contracts. |

| ** | Assets of affiliates to The Muirfield Fund held for the benefit of the Fund’s Trustees in connection with the Trustee Deferred Compensation Plan. |

The accompanying notes are an integral part of these financial statements.

Schedule of Investments

June 30, 2006 (unaudited)

The Total Return Utilities Fund

| | | | |

Security Description

| | Shares or

Principal

Amount ($)

| | Value ($)

|

Common Stocks — 99.2% | | | | |

Electric Utility — 18.5% | | | | |

Energy East Corp. | | 33,830 | | 809,552 |

IDACORP, Inc. | | 17,495 | | 599,904 |

MDU Resources Group, Inc. | | 17,445 | | 638,662 |

Northeast Utilities | | 22,805 | | 471,379 |

Pepco Holdings, Inc. | | 16,140 | | 380,581 |

Sierra Pacific Resources | | 87,280 | | 1,221,852 |

| | | | |

|

(Cost 3,571,793) | | | | 4,121,930 |

| | | | |

|

Independent Power Producer — 3.9% | | | | |

Dynegy, Inc. | | 72,075 | | 394,250 |

NRG Energy, Inc. | | 10,010 | | 482,282 |

| | | | |

|

(Cost 774,843) | | | | 876,532 |

| | | | |

|

Natural Gas Distribution — 19.3% | | | | |

AGL Resources, Inc. | | 20,665 | | 787,750 |

ATMOS Energy Corp. | | 15,145 | | 422,697 |

NiSource, Inc. | | 37,065 | | 809,499 |

ONEOK, Inc. | | 21,460 | | 730,498 |

Peoples Energy Corp. | | 6,015 | | 215,999 |

Southern Union Co. | | 18,635 | | 504,263 |

Vectren Corp. | | 21,155 | | 576,474 |

WGL Holdings, Inc. | | 8,125 | | 235,219 |

| | | | |

|

(Cost 3,548,818) | | | | 4,282,399 |

| | | | |

|

Oil Exploration & Production — 11.4% | | | | |

Anadarko Petroleum Corp. | | 12,730 | | 607,094 |

Pioneer Natural Resources Co. | | 20,435 | | 948,388 |

Ultra Petroleum Corp.# | | 16,285 | | 965,212 |

| | | | |

|

(Cost 1,493,415) | | | | 2,520,694 |

| | | | |

|

Pipelines — 17.2% | | | | |

Enterprise Products Partners, L.P. | | 22,396 | | 557,660 |

Equitable Resources, Inc. | | 18,265 | | 611,878 |

Kinder Morgan Energy Partners, L.P. | | 18,918 | | 869,471 |

National Fuel Gas Co. | | 19,315 | | 678,729 |

Questar Corp. | | 14,185 | | 1,141,751 |

| | | | |

|

(Cost 2,680,473) | | | | 3,859,489 |

| | | | |

|

Telephone & Telecommunications — 27.4% | | |

AT&T, Inc. | | 23,995 | | 669,221 |

Brasil Telecom — ADR | | 11,855 | | 386,117 |

China Mobile Limited — ADR | | 21,505 | | 615,258 |

Cypress Semiconductor Corp.# | | 16,110 | | 234,240 |

Deutsche Telekom AG | | 26,535 | | 425,621 |

ESCO Technologies, Inc.# | | 9,115 | | 487,196 |

Nokia Corp. — ADR | | 26,455 | | 535,978 |

Powerwave Technologies, Inc. | | 21,430 | | 195,442 |

PT Telekomunikasi Indonesia — ADR | | 10,800 | | 346,680 |

Sprint Nextel Corp. | | 34,905 | | 697,751 |

Telefonos de Mexico SA de CV — ADR | | 10,285 | | 214,237 |

Telstra Corp., Ltd. — ADR | | 28,325 | | 388,053 |

Verizon Communications, Inc. | | 17,190 | | 575,693 |

Vimpel-Communications OAO — ADR# | | 7,410 | | 339,526 |

| | | | |

|

(Cost 5,684,699) | | | | 6,111,013 |

| | | | |

|

Water Utility — 1.5% | | | | |

United Utilities PLC — ADR | | 13,940 | | 330,517 |

| | | | |

|

(Cost 248,078) | | | | 330,517 |

| | | | |

|

Total Common Stocks

(Cost $18,002,119) | | | | 22,102,574 |

| | | | |

|

The Total Return Utilities Fund

| | | | | |

Security Description

| | Shares or

Principal

Amount ($)

| | Value ($)

| |

Repurchase Agreements — 0.9% | | | | | |

Morgan Stanley DW, Inc., 5.3725%, 07/03/2006, (Collateralized by $201,090 various Commercial Papers, Certificates of Deposit, Agency Strips, FNMAs, Treasury Notes, and SLMA, at 4.00% — 10.00%, due 07/05/2006 — 01/01/2036, value — $205,021) purchase date 06/30/2006 | | 201,000 | | 201,000 | |

| | | | |

|

|

Total Repurchase Agreements

(Cost $201,000) | | | | 201,000 | |

| | | | |

|

|

Total Investments — 100.1%

(Cost $18,203,119)(a) | | | | 22,303,574 | |

| | | | |

|

|

Liabilities less Other Assets — (0.1%) | | | | (32,823 | ) |

| | | | |

|

|

Total Net Assets — 100.0% | | | | 22,270,751 | |

| | | | |

|

|

Trustee Deferred Compensation* | | | | | |

The Flex-funds Dynamic Growth Fund | | 840 | | 7,274 | |

The Flex-funds Quantex Fund | | 599 | | 10,536 | |

The Flex-funds Muirfield Fund | | 1,966 | | 10,420 | |

The Flex-funds Total Return Utilities Fund | | 137 | | 2,739 | |

| | | | |

|

|

Total Trustee Deferred Compensation (Cost $25,014) | | | | 30,969 | |

| | | | |

|

|

| (a) | Cost for financial reporting purposes and federal income tax purposes are the same. Cost for federal income tax purposes differs from value by net unrealized appreciation (depreciation) of securities as follows: |

| | | | |

Unrealized appreciation | | $ | 4,560,971 | |

Unrealized depreciation | | | (460,516 | ) |

| | |

|

|

|

Net unrealized appreciation (depreciation) | | $ | 4,100,455 | |

| | |

|

|

|

ADR American Depositary Receipt

| # | Represents non-income producing securities. |

| * | Assets of affiliates to The Total Return Utilities Fund held for the benefit of the Fund’s Trustees in connection with the Trustees Deferred Compensation Plan. |

The accompanying notes are an integral part of these financial statements.

Schedule of Investments

June 30, 2006 (unaudited)

The Quantex Fund

| | | | |

Security Description

| | Shares or

Principal

Amount ($)

| | Value ($)

|

Common Stocks — 95.6% |

Basic Materials — 8.1% | | | | |

Allegheny Technologies, Inc. | | 4,000 | | 276,960 |

Ashland, Inc. | | 2,600 | | 173,420 |

Eastman Chemical Co. | | 3,000 | | 162,000 |

Hercules, Inc.# | | 13,900 | | 212,114 |

Int’l Flavors & Fragrances, Inc. | | 4,700 | | 165,628 |

Louisiana Pacific Corp. | | 5,700 | | 124,830 |

Sigma — Aldrich Corp. | | 2,400 | | 174,336 |

| | | | |

|

(Cost 1,032,473) | | | | 1,289,288 |

| | | | |

|

Communications — 12.0% | | | | |

ADC Telecommunications, Inc.# | | 6,814 | | 114,884 |

Andrew Corp.# | | 15,000 | | 132,900 |

Avaya, Inc.# | | 14,300 | | 163,306 |

CenturyTel, Inc. | | 4,700 | | 174,605 |

Ciena Corp.# | | 51,200 | | 246,272 |

Citizens Communications Co. | | 13,000 | | 169,650 |

Dow Jones & Co., Inc. | | 4,000 | | 140,040 |

EW Scripps Co. | | 3,100 | | 133,734 |

Interpublic Group of Cos., Inc. | | 15,800 | | 131,930 |

JDS Uniphase Corp.# | | 66,100 | | 167,233 |

Meredith Corp. | | 3,000 | | 148,620 |

New York Times Co. | | 5,700 | | 139,878 |

The McClatchy Co. | | 1,228 | | 49,280 |

| | | | |

|

(Cost 1,779,841) | | | | 1,912,332 |

| | | | |

|

Consumer Cyclical — 15.6% | | | | |

Autonation, Inc.# | | 7,000 | | 150,080 |

Big Lots, Inc.# | | 12,600 | | 215,208 |

Brunswick Corp. | | 3,800 | | 126,350 |

Circuit City Stores, Inc. | | 6,400 | | 174,208 |

Cooper Tire & Rubber Co. | | 10,200 | | 113,628 |

Dana Corp. | | 22,900 | | 62,288 |

Dillards, Inc. | | 6,100 | | 194,285 |

Family Dollar Stores, Inc. | | 6,100 | | 149,023 |

Hasbro, Inc. | | 7,600 | | 137,636 |

Jones Apparel Group, Inc. | | 5,200 | | 165,308 |

Liz Claiborne, Inc. | | 4,400 | | 163,064 |

Navistar International Corp.# | | 5,600 | | 137,816 |

OfficeMax, lnc. | | 6,400 | | 260,800 |

RadioShack Corp. | | 7,200 | | 100,800 |

Sabre Holdings Corp. | | 6,700 | | 147,400 |

The Goodyear Tire & Rubber Co.# | | 8,600 | | 95,460 |

Whirlpool Corp. | | 980 | | 80,997 |

| | | | |

|

(Cost 2,429,369) | | | | 2,474,351 |

| | | | |

|

Consumer Noncyclical — 15.3% | | | | |

Alberto — Culver Co. | | 3,400 | | 165,648 |

Bausch & Lomb, Inc. | | 2,300 | | 112,792 |

Convergys Corp.# | | 9,800 | | 191,100 |

Estee Lauder Cos. Inc. / The | | 4,100 | | 158,547 |

King Pharmaceuticals, Inc.# | | 8,800 | | 149,600 |

Manor Care, Inc. | | 3,900 | | 182,988 |

McCormick & Co., Inc. | | 4,900 | | 164,395 |

Millipore Corp.# | | 2,300 | | 144,877 |

Molson Coors Brewing Co. | | 2,300 | | 156,124 |

Mylan Laboratories, Inc. | | 7,700 | | 154,000 |

Patterson Cos., Inc.# | | 4,500 | | 157,185 |

Pepsi Bottling Group, Inc. | | 5,300 | | 170,395 |

The Quantex Fund

| | | | |

Security Description

| | Shares or

Principal

Amount ($)

| | Value ($)

|

Common Stocks — continued |

Supervalu, Inc. | | 4,900 | | 150,430 |

Tenet Healthcare Corp.# | | 19,900 | | 138,902 |

Tyson Foods, Inc. | | 8,900 | | 132,254 |

Watson Pharmaceuticals, lnc.# | | 4,600 | | 107,088 |

| | | | |

|

(Cost 2,243,377) | | | | 2,436,325 |

| | | | |

|

Energy — 1.9% | | | | |

Dynegy, Inc. | | 31,600 | | 172,852 |

Rowan Cos., Inc. | | 3,900 | | 138,801 |

| | | | |

|

(Cost 214,465) | | | | 311,653 |

| | | | |

|

Financial — 3.8% | | | | |

Apartment Investment & Management Co. | | 3,900 | | 169,455 |

Federated Investors, Inc. | | 4,200 | | 132,300 |

First Horizon National Corp. | | 3,900 | | 156,780 |

Janus Capital Group, Inc. | | 8,200 | | 146,780 |

Wachovia Corp. Pref. Dividend Equalization | | 1,700 | | — |

| | | | |

|

(Cost 523,918) | | | | 605,315 |

| | | | |

|

Industrial — 20.9% | | | | |

Allied Waste Industries, Inc. | | 17,500 | | 198,800 |

American Power Conversion Corp. | | 7,000 | | 136,430 |

Ball Corp. | | 3,800 | | 140,752 |

Bemis Co. | | 5,200 | | 159,224 |

Cummins, Inc. | | 1,800 | | 220,050 |

Leggett & Platt, Inc. | | 6,600 | | 164,868 |

Molex, Inc. | | 5,900 | | 198,063 |

Pactiv Corp.# | | 7,200 | | 178,200 |

Pall Corp. | | 5,800 | | 162,400 |

PerkinElmer, lnc. | | 6,800 | | 142,120 |

Ryder System, Inc. | | 3,800 | | 222,034 |

Sanmina — SCI Corp.# | | 37,400 | | 172,040 |

Sealed Air Corp. | | 2,700 | | 140,616 |

Snap — On, Inc. | | 4,300 | | 173,806 |

Solectron Corp.# | | 41,800 | | 142,956 |

Stanley Works / The | | 3,000 | | 141,660 |

Symbol Technologies, Inc. | | 12,400 | | 133,796 |

Tektronix, Inc. | | 5,000 | | 147,100 |

Thermo Electron Corp.# | | 5,000 | | 181,200 |

Waters Corp.# | | 4,000 | | 177,600 |

| | | | |

|

(Cost 2,876,067) | | | | 3,333,715 |

| | | | |

|

Technology — 12.5% | | | | |

Applied Micro Circuits Corp.# | | 59,900 | | 163,527 |

BMC Software, Inc.# | | 7,400 | | 176,860 |

Compuware Corp.# | | 15,900 | | 106,530 |

Gateway, Inc.# | | 58,600 | | 111,340 |

LSI Logic Corp.# | | 18,300 | | 163,785 |

Mercury Interactive Corp.# | | 5,800 | | 202,826 |

Novell, Inc. | | 17,100 | | 113,373 |

Novellus Systems, Inc.# | | 6,400 | | 158,080 |

Parametric Technology Corp.# | | 9,840 | | 125,066 |

PMC — Sierra, Inc.# | | 20,000 | | 188,000 |

QLogic Corp.# | | 9,600 | | 165,504 |

Teradyne, Inc.# | | 10,600 | | 147,658 |

Unisys Corp.# | | 28,100 | | 176,468 |

| | | | |

|

(Cost 1,865,904) | | | | 1,999,017 |

| | | | |

|

Schedule of Investments

June 30, 2006 (unaudited)

The Quantex Fund

| | | | |

Security Description

| | Shares or

Principal

Amount ($)

| | Value ($)

|

Common Stocks — continued |

Utilities — 5.5% | | | | |

Centrepoint Energy, Inc. | | 11,800 | | 147,500 |

CMS Energy Corp. | | 10,300 | | 133,282 |

Nicor, Inc. | | 3,900 | | 161,850 |

Peoples Energy Corp. | | 4,400 | | 158,004 |

Pinnacle West Capital Corp. | | 3,700 | | 147,667 |

TECO Energy, Inc. | | 8,800 | | 131,472 |

| | | | |

|

(Cost 895,262) | | | | 879,775 |

| | | | |

|

Total Common Stocks

(Cost $13,860,676) | | | | 15,241,771 |

| | | | |

|

U.S. Government Obligations — 1.9% |

U.S. Treasury Bill,

4.854%, due 09/07/2006* | | 300,000 | | 297,223 |

| | | | |

|

Total U.S. Government Obligations

(Cost $297,320) | | | | 297,223 |

| | | | |

|

Repurchase Agreements — 1.5% |

Morgan Stanley DW, Inc., 5.3725%, 07/03/2006, (Collateralized by $245,110 various Commercial Papers, Certificates of Deposit, Agency Strips, FNMAs, Treasury Notes, and SLMA, at 4.00% — 10.00%, due 07/05/2006 — 01/01/2036, value — $249,902) purchase date 06/30/2006 | | 245,000 | | 245,000 |

| | | | |

|

Total Repurchase Agreements

(Cost $245,000) | | | | 245,000 |

| | | | |

|

Total Investments — 99.0%

(Cost $14,402,996)(a) | | | | 15,783,994 |

| | | | |

|

Other Assets less Liabilities — 1.0% | | | | 167,144 |

| | | | |

|

Total Net Assets — 100.0% | | | | 15,951,138 |

| | | | |

|

Trustee Deferred Compensation** |

The Flex-funds Dynamic Growth Fund | | 1,235 | | 10,695 |

The Flex-funds Quantex Fund | | 802 | | 14,107 |

The Flex-funds Muirfield Fund | | 2,809 | | 14,888 |

The Flex-funds Total Return Utilities Fund | | 218 | | 4,358 |

| | | | |

|

Total Trustee Deferred Compensation (Cost $35,175) | | | | 44,048 |

| | | | |

|

The Quantex Fund

| | | | |

Security Description

| | Long

Contracts

| | Unrealized

Appreciation

(Depreciation) ($)

|

Futures Contracts |

Russell 2000 expiring September 2006, notional value $365,750 | | 1 | | 20,900 |

| | | | |

|

Total Futures Contracts | | | | 20,900 |

| | | | |

|

| (a) | Cost for financial reporting purposes and federal income tax purposes are the same. Cost for federal income tax purposes differs from value by net unrealized appreciation (depreciation) of securities as follows: |

| | | | |

Unrealized appreciation | | $ | 2,130,817 | |

Unrealized depreciation | | | (749,819 | ) |

| | |

|

|

|

Net unrealized appreciation (depreciation) | | $ | 1,380,998 | |

| | |

|

|

|

ADR American Depositary Receipt

| # | Represents non-income producing securities. |

| * | Pledged as collateral on Futures Contracts. |

| ** | Assets of affiliates to The Flex-funds Quantex Fund held for the benefit of the Fund’s Trustees in connection with the Trustee Deferred Compensation Plan. |

The accompanying notes are an integral part of these financial statements.

Schedule of Investments

June 30, 2006 (unaudited)

The Dynamic Growth Fund

| | | | | |

Security Description

| | Shares or

Principal

Amount ($)

| | Value ($)

| |

Registered Investment Companies — 92.7% | | | |

Allianz NACM International Fund — I | | 60,597 | | 1,333,734 | |

Allianz NFJ Dividend Value Fund — D | | 116,484 | | 1,791,517 | |

American Growth Fund of America — A | | 66,729 | | 2,115,297 | |

Goldman Sachs Structured Large Cap Value Fund — I | | 293,652 | | 3,973,114 | |

Goldman Sachs Mid Cap Value Fund | | 23,216 | | 849,022 | |

MFS Value Fund — A | | 83,344 | | 2,034,430 | |

Rydex Large Cap Value Fund — H | | 65,115 | | 1,929,354 | |

Rydex Mid Cap Value Fund — H | | 26,557 | | 847,432 | |

Transamerica Premier Equity Fund — I | | 38,631 | | 867,653 | |

| | | | |

|

|

Total Registered Investment Companies (Cost $15,634,263) | | | | 15,741,553 | |

| | | | |

|

|

U.S. Government Obligations — 2.3% | | | | | |

U.S. Treasury Bill,

4.854%, due 09/07/2006* | | 400,000 | | 396,297 | |

| | | | |

|

|

Total U.S. Government Obligations

(Cost $396,426) | | | | 396,297 | |

| | | | |

|

|

Repurchase Agreements — 5.2% | | | | | |

Morgan Stanley DW, Inc., 5.3725%, 07/03/2006, (Collateralized by $883,395 various Commercial Papers, Certificates of Deposit, Agency Strips, FNMAs, Treasury Notes, and SLMA, at 4.00% — 10.00%, due 07/05/2006 — 01/01/2036, value — $900,665) purchase date 06/30/2006 | | 883,000 | | 883,000 | |

| | | | |

|

|

Total Repurchase Agreements

(Cost $883,000) | | | | 883,000 | |

| | | | |

|

|

Total Investments — 100.2%

(Cost $16,913,689)(a) | | | | 17,020,850 | |

| | | | |

|

|

Liabilities less Other Assets — (0.2%) | | | | (26,084 | ) |

| | | | |

|

|

Total Net Assets — 100.0% | | | | 16,994,766 | |

| | | | |

|

|

Trustee Deferred Compensation** | | | | | |

The Flex-funds Dynamic Growth Fund | | 574 | | 4,971 | |

The Flex-funds Muirfield Fund | | 1,406 | | 7,452 | |

The Flex-funds Quantex Fund | | 460 | | 8,091 | |

The Flex-funds Total Return Utilities Fund | | 77 | | 1,539 | |

| | | | |

|

|

Total Trustee Deferred Compensation

(Cost $18,698) | | | | 22,053 | |

| | | | |

|

|

The Dynamic Growth Fund

| | | | |

Security Description

| | Long

Contracts

| | Unrealized

Appreciation

(Depreciation) ($)

|