UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-03651

Touchstone Strategic Trust

(Exact name of registrant as specified in charter)

303 Broadway, Suite 1100

Cincinnati, Ohio 45202-4203

(Address of principal executive offices) (Zip code)

Jill T. McGruder

303 Broadway, Suite 1100

Cincinnati, Ohio 45202-4203

(Name and address of agent for service)

Registrant's telephone number, including area code: 800-638-8194

Date of fiscal year end: March 31

Date of reporting period: March 31, 2017

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget ("OMB") control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

Item 1. Reports to Stockholders.

The Report to Shareholders is attached herewith.

March 31, 2017

Annual Report

Touchstone Strategic Trust

Touchstone Flexible Income Fund

Touchstone Focused Fund

Touchstone Growth Opportunities Fund

Touchstone International Growth Fund

Touchstone International Value Fund

Touchstone Mid Cap Growth Fund

Touchstone Sands Capital Emerging Markets Growth Fund

Touchstone Small Cap Growth Fund

Touchstone Sustainability and Impact Equity Fund

Table of Contents

This report identifies the Funds' investments on March 31, 2017. These holdings are subject to change. Not all investments in each Fund performed the same, nor is there any guarantee that these investments will perform as well in the future. Market forecasts provided in this report may not occur.

Letter from the President

Dear Shareholder:

We are pleased to provide you with the Touchstone Strategic Trust Annual Report. Inside you will find key financial information, as well as manager commentaries for the Funds, for the 12 months ended March 31, 2017.

The global economy endured two major surprises over the period, Britain’s vote in June to exit the European Union (i.e., “Brexit”), and the election of Donald Trump as U.S. President in November. In spite of the policy uncertainty created by these events, capital markets performed well during the period, led by U.S. small-capitalization stocks. Investor concerns about a slowing global economy and declining commodity prices dissipated in early 2016 when central bank leaders reiterated their willingness to maintain accommodative monetary policies. As a result, global capital markets entered the fiscal year rallying, led by a rebound in equities and commodity prices. U.S. economic data continued to show steady improvement in employment and Gross Domestic Product (GDP) growth throughout the 12-month period while inflation remained constrained. With this stable economic backdrop, the U.S. Federal Reserve Board (Fed) increased short-term rates twice, increasing the Federal Funds Rate by a total of half a percent.

Global equity markets finished the period in strong fashion with most major U.S. and non-U.S. indexes generating double-digit returns. U.S. small-cap stocks were the top performers, followed by U.S. mid-cap, large-cap and emerging market equities. China-led economic concerns abated early in the period and commodity exporting countries (e.g., South Africa, Brazil and Russia) and commodity-consuming emerging market countries (e.g., China and India) saw their equity markets rebound strongly. Developed stock markets posted strong absolute returns as well, led by the British and Japanese equity markets. Within the U.S. equity markets, value stocks outperformed their growth counterparts as the post-Financial Crisis bull market continued to mature.

While the Fed raised rates during the period, other developed market central banks in the European Union, United Kingdom and Japan continued their accommodative monetary policies. Stable U.S. economic growth and short-term rate hikes caused the U.S. Treasury yield curve to rise modestly as the bellwether 10-year Treasury yield increased by approximately half a percentage point during the period. The upward move in Treasury yields led to flat-to-negative returns for U.S. Treasury and Agency debt securities. Similarly non-U.S. government debt securities produced mostly negative returns for the period. Conversely, improvements in the U.S. economy gave investors the confidence to buy bank loans and corporate bonds across the credit quality spectrum. Credit spreads narrowed and these fixed income sectors all posted solid returns for the period.

After a year of strong returns across many asset classes, we believe that now is a good time to evaluate your financial situation. The counsel of a financial advisor can he1p determine an appropriate risk/return profile, prudent portfolio allocation, and the right path to addressing your long-term investment goals.

We greatly appreciate your continued support. Thank you for including Touchstone as part of your investment plan.

Sincerely,

Jill T. McGruder

President

Touchstone Strategic Trust

Management's Discussion of Fund Performance (Unaudited)

Touchstone Flexible Income Fund

Sub-Advised by ClearArc Capital, Inc.

Investment Philosophy

The Touchstone Flexible Income Fund seeks a high level of income consistent with reasonable risk and seeks capital appreciation as a secondary goal. The Fund primarily invests in income-producing securities such as debt securities, common stocks and preferred stocks. The Fund’s sub-advisor seeks to provide value by investing in asset classes that appear to be attractive based on their risks and in companies with attractive price-to-cash flow ratios. The Fund seeks returns by investing across a broader array of investments than traditional investment-grade fixed-income funds, and ClearArc believes that a low correlation between various asset classes leads to stability of expected returns.

Fund Performance

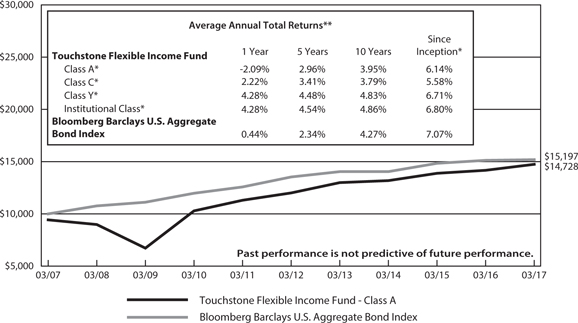

The Touchstone Flexible Income Fund (Class A Shares) outperformed its benchmark, the Bloomberg Barclays U.S. Aggregate Bond Index, for the 12-month period ended March 31, 2017. The Fund’s total return was 3.93 percent (calculated excluding the maximum sales charge), while the total return of the benchmark was 0.44 percent.

Market Environment

Two major unexpected events occurred during the 12-month period ended March 31, 2017: Britain’s June 2016 decision to exit the European Union, known as the “Brexit,” and the November 2016 election of Donald Trump as U.S. President; however, volatility was unusually low for most of the period. The U.S. Federal Reserve Board (Fed) raised interest rates twice with no ill effects and signaled it may step up the pace of rate hikes. During the majority of the period, inflation expectations rose from low levels on anticipated stimulus from Trump’s pro-growth agenda. The increase in inflation expectations started to fade as the 12-month period ended. The Trump Administration realized that Washington works at a slower pace than it had initially envisioned.

During the 12-month period, the S&P 500® Index, developed market non-U.S. equities and high yield corporate bond indexes all posted strong returns. Emerging market equities posted returns in line with U.S. equities. Foreign sovereign bonds performed poorly relative to credit markets as the European Union, Japanese and U.K. central banks maintained highly accommodative monetary policies.

Portfolio Review

There were a number of drivers of the Fund’s outperformance such as asset-backed bonds, preferred equities and dividend-paying common equities. Detractors to the Fund’s performance were in derivative positions in the Chicago Board Options Exchange Volatility Index (VIX), which measures volatility in the S&P 500® Index, and short forward contracts on emerging market currencies.

Outlook

The Fund continues to be defensively positioned. While we do see an improvement in economic growth, it is not clear how much of this is sustainable. We believe the current recovery is still fragile and can be derailed by any number of events. It is certainly possible that the rally in risky assets could last longer. However, we believe failure of the Trump Administration to pass pro-growth policies would mean a reversion to a deflationary environment at the margin. In contrast, we believe strong pro-growth policy progress by the Trump Administration would be more inflationary. Since we expect the overall long-term inflation trend to be upward and at times uneven, we will maintain a higher quality bias. We are emphasizing liquid positions and continue to look for relative value trades. Relative value focuses on price discrepancies among securities with similar economic or financial

Management's Discussion of Fund Performance (Unaudited) (Continued)

characteristics. Absent a major shift in the outlook, we expect the Fund’s duration to remain shorter than the benchmark’s. However, if we see progress on pro-growth Trump Administration policies and we see an increase in inflation expectations, we would likely reduce further the Fund’s duration.

Dividend-paying investments may not experience the same price appreciation as non-dividend paying instruments, dividend-issuing companies may choose not to pay a dividend, or the dividend may be less than what is anticipated.

Management's Discussion of Fund Performance (Unaudited) (Continued)

Comparison of the Change in Value of a $10,000 Investment in the

Touchstone Flexible Income Fund-Class A*and the Bloomberg Barclays U.S. Aggregate Bond Index

| * | The chart above represents performance of Class A shares only, which will vary from the performance of Class C shares, Class Y shares and Institutional Class shares based on the differences in sales loads and fees paid by shareholders in the different classes. The inception date of Class A shares, Class C shares, Class Y shares and Institutional Class shares was April 1, 2004, October 29, 2001, September 1, 1998 and September 10, 2012, respectively. Class A shares, Class C shares and Class Y shares performance information was calculated using the historical performance of the Fifth Third/Maxus Income Fund Investor shares, with an inception date of March 10, 1985, for periods prior to April 1, 2004, October 29, 2001 and September 1, 1998, respectively. Institutional Class shares performance information was calculated using the historical performance of Class Y shares for the periods prior to September 10, 2012. The returns have been restated for sales loads and fees applicable to Class A, Class C, Class Y and Institutional Class shares. The returns of the index listed above are based on the inception date of the Fund. |

| ** | The average annual total returns shown above are adjusted for maximum sales loads and fees, if applicable. The maximum offering price per share of Class A shares is equal to the net asset value (“NAV”) per share plus a sales load equal to 6.10% of the NAV (or 5.75% of the offering price). Class C shares are subject to a contingent deferred sales charge (“CDSC”) of 1.00%. The CDSC will be assessed on an amount equal to the lesser of (1) the NAV at the time of purchase of the shares being redeemed or (2) the NAV of such shares being redeemed, if redeemed within a one-year period from the date of purchase. Class Y shares and Institutional Class shares are not subject to sales charges. |

The performance of the above Fund does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Note to Chart

Bloomberg Barclays U.S. Aggregate Bond Index is an unmanaged index comprised of U.S. investment grade, fixed rate bond market securities, including government, government agency, corporate and mortgage-backed securities between one and ten years.

Management's Discussion of Fund Performance (Unaudited)

Touchstone Focused Fund

Sub-Advised by Fort Washington Investment Advisors, Inc.

Investment Philosophy

The Fund seeks to invest in companies of all capitalizations that are trading below what is believed to be the estimate of their intrinsic value and have a sustainable competitive advantage or a high barrier to entry in place. The barrier(s) to entry can be created through a cost advantage, economies of scale, high customer loyalty or a government barrier (e.g. license or subsidy). Fort Washington believes that the strongest barrier to entry is the combination of economies of scale and high customer loyalty.

Fund Performance

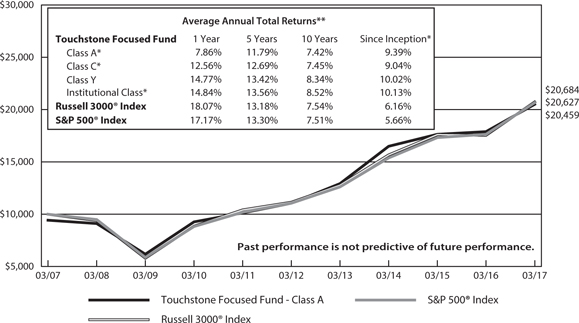

The Touchstone Focused Fund (Class A Shares) underperformed its benchmark, the Russell 3000® Index, for the 12-month period ended March 31, 2017. The Fund’s total return was 14.45 percent (calculated excluding the maximum sales charge) while total return of the benchmark was 18.07 percent.

Market Environment

The bull market in U.S. equities that began in 2009 ended the first quarter of 2017 at all-time highs. Investors shrugged off the sting of a positive vote in the U.K. to exit the European Union last June and enjoyed accommodative monetary policies by developed central banks throughout 2016. The market continued to gain momentum at the end of 2016 as investors cheered president-elect Donald Trump’s pro-growth agenda. The top performing sectors within the Russell 3000® Index for the 12-month period were Financials, Information Technology and Materials, while the worst performing sectors during the period were Real Estate, Consumer Staples and Telecommunication Services.

Portfolio Review

The Fund’s top contributing sectors relative to the benchmark were Consumer Discretionary, Consumer Staples, and Telecommunication Services. Sectors which detracted from the Fund’s relative performance were Industrials, Energy, and Financials. Investments made in international companies as well as domestic businesses underperformed the benchmark.

LinkedIn Corp. (Information Technology sector), Amazon.com Inc. (Consumer Discretionary sector) and Bio-Rad Laboratories Inc. (Health Care sector) were among the top Fund contributors during the past twelve months. LinkedIn was acquired by Microsoft Corp. (Information Technology sector) at a significant premium. Amazon.com continued its positive momentum as business fundamentals continued to improve for its core operations. In the past twelve months, Bio-Rad benefited from a stabilization of macro headwinds as well as improving investor confidence as the path to excess economic returns became more transparent.

Companies that detracted from Fund performance included Vista Outdoor Inc. (Industrials sector), World Fuel Services Corp. (Energy sector) and Owens & Minor (Health Care sector). Vista disappointed investors as it announced continued weakness in its core business and a sizable write off of previous acquisitions. World Fuel declined in value after reporting a weak fourth quarter and lowered forward guidance based on weakness in its marine transportation segment. Owens & Minor underperformed when it announced it would be losing a sizable customer to its main competitor.

During the past twelve months, the Fund increased its exposure to the Real Estate, Consumer Discretionary, and Industrials sectors. The Fund’s cash position decreased from a year ago to the end of the period.

From a market cap perspective, the Fund maintained an underweight to smaller-cap companies with a market cap below $2 billion. The benchmark weight for this segment is 4.6 percent compared to 1 percent for the

Management's Discussion of Fund Performance (Unaudited) (Continued)

Fund. The Fund remained underweight to mid-cap businesses which comprised 9.3 percent of assets, compared to a benchmark weight of 14.8 percent. Lastly, the Fund continued to maintain an overweight to larger-cap businesses with a market cap above $10 billion. The weight in that segment is currently 85.2 percent which is higher than the benchmark weight of 80.6 percent. This allocation decision had a positive impact on performance during the past year due to the underperformance of small-cap stocks.

Over the past twelve months, we believe the quality of the overall Fund portfolio remained high. We continued to focus on buying what we believe are high quality businesses with stable returns on capital, solid balance sheets and sustainable barriers to entry.

Outlook

Businesses and consumers are currently optimistic about the U.S. economy’s prospects, but so-called soft data, such as sentiment, has not yet translated into accelerated growth as reflected in hard, quantifiable data. With solid jobs growth and core inflation near 2 percent, the U.S. Federal Reserve Board (Fed) is likely to continue gradually raising interest rates. Looking ahead, we believe the markets will be fixated on pending tax legislation for businesses and households. Although House Republican leaders favor tax reform that is deficit neutral, President Trump campaigned on implementing a big tax cut for the middle class. It is too early to gauge the outcome, but we believe tax cuts are normally easier to pass than cuts in deductions. Amid this uncertainty, we expect market volatility to increase from unusually low levels. We will continue to add what we believe are high quality businesses to the Fund’s portfolio.

Management's Discussion of Fund Performance (Unaudited) (Continued)

Comparison of the Change in Value of a $10,000 Investment in the Touchstone Focused Fund - Class A*, the Russell 3000® Index and the S&P 500® Index

| * | The chart above represents performance of Class A shares only, which will vary from the performance of Class C shares, Class Y shares and Institutional Class shares based on the differences in sales loads and fees paid by shareholders in the different classes. The inception date of Class A shares, Class C shares, Class Y shares and Institutional Class shares was September 30, 2003, April 12, 2012, February 12, 1999 and December 20, 2006, respectively. Class A shares, Class C shares and Institutional Class shares performance information was calculated using the historical performance of Class Y shares for the periods prior to September 30, 2003, April 12, 2012 and December 20, 2006, respectively. The returns have been restated for sales loads and fees applicable to Class A, Class C and Institutional Class shares. The returns of the indexes listed above are based on the inception date of the Fund. |

| ** | The average annual total returns shown above are adjusted for maximum sales loads and fees, if applicable. The maximum offering price per share of Class A shares is equal to the net asset value (“NAV”) per share plus a sales load equal to 6.10% of the NAV (or 5.75% of the offering price). Class C shares are subject to a contingent deferred sales charge (“CDSC”) of 1.00%. The CDSC will be assessed on an amount equal to the lesser of (1) the NAV at the time of purchase of the shares being redeemed or (2) the NAV of such shares being redeemed, if redeemed within a one-year period from the date of purchase. Class Y shares and Institutional Class shares are not subject to sales charges. |

The performance of the above Fund does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Notes to Chart

Russell 3000® Index measures the performance of the 3,000 largest U.S. companies based on total market capitalization, which represents approximately 98% of the investable U.S. equity market.

S&P 500® Index is a group of 500 widely held stocks and is commonly regarded to be representative of the large capitalization stock universe.

The Frank Russell Company (FRC) is the source and owner of the Russell 3000® Index data contained or reflected in this material and all trademarks and copyrights related thereto. The material may contain confidential information and unauthorized use, disclosure, copying, dissemination or redistribution is strictly prohibited. This is a Touchstone Investments presentation of the data, and FRC is not responsible for the formatting or configuration of this material or for any inaccuracy in the presentation thereof.

Management's Discussion of Fund Performance (Unaudited)

Touchstone Growth Opportunities Fund

Sub-Advised by Westfield Capital Management, L.P.

Investment Philosophy

The Touchstone Growth Opportunities Fund seeks long-term growth of capital by primarily investing in stocks of U.S. companies with large, medium and small market capitalizations. The Fund’s portfolio managers place focus on companies they believe to have demonstrated records of achievement with excellent prospects for earnings growth over a 1 to 3 year period. Westfield looks for companies that it believes are reasonably priced with high forecasted earnings potential.

Fund Performance

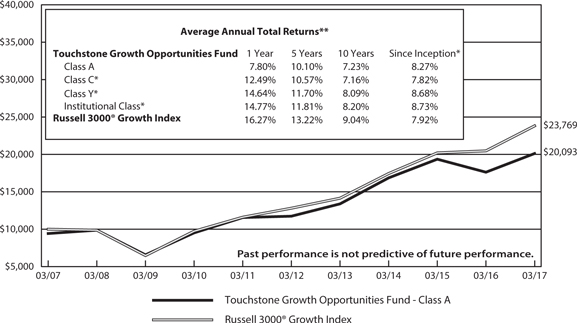

The Touchstone Growth Opportunities Fund (Class A Shares) underperformed its benchmark, the Russell 3000® Growth Index, for the 12-month period ended March 31, 2017. The Fund’s total return was 14.38 percent (calculated excluding the maximum sales charge), while the total return of the benchmark was 16.27 percent.

Market Environment

Domestic stocks generated solid returns during the 12-month period ended March 31, 2017, posting gains across all market sectors and capitalizations. Oil prices rose, consumer confidence hit a new five-year high, and unemployment claims continued to drop. In a step toward normalization of financial conditions after a prolonged period of zero-rate interest rates, the U.S. Federal Reserve Board raised short-term rates by 25 basis points twice and signaled a quicker pace of rate increases over the next two years. The past twelve months, however, have highlighted yet again a powerful dichotomy between two forces competing for equity market leadership: growth and safety. During periods of market duress, investors have sought refuge in the most defensive, bond-like segments, such as Utilities, Real Estate Investment Trusts (REITs), and Telecommunication Services sectors. Snapback rallies off the interim lows have been driven by economically-sensitive stocks.

U.S. equities surged following the Presidential election, lifting most stock indices to record highs. The rally began with a rotation into those stocks most exposed to domestic cyclical growth, with lower Price/Earnings, smaller capitalization companies leading the charge. Domestic stocks extended post-election gains into calendar year 2017, propelling most equity indices into new record territories. Their advance came against a stable economic backdrop in the U.S. and signs of improvements in the eurozone. The U.S. unemployment rate suggests that the domestic labor market remains in good shape, and business survey data has been strong, suggesting the potential for increased capital spending ahead. Despite mostly positive economic data and stronger consumer and business confidence, investors remain skeptical of the rally, as billions of dollars continue to pour into bond funds. The market’s advance tapered off by early spring, with cyclical and financial stocks pulling back as the “Trump trade” faded. The first quarter of 2017 witnessed a notable rotation into high-quality, large market capitalization, growth-oriented companies, primarily within the Information Technology and Health Care sectors.

Portfolio Review

Notable relative weakness within the Information Technology sector offset more modest relative strength in the Health Care and Consumer Discretionary sectors.

During the period, the Fund’s relative performance was weakest in the Information Technology sector. Palo Alto Networks, Inc., a provider of network security solutions, was the sector’s largest source of underperformance. Security fundamentals softened over the course of the period after several years of outsized growth. We recently exited the position following the company’s most recent quarterly results, which were weaker-than-expected.

Management's Discussion of Fund Performance (Unaudited) (Continued)

Palo Alto highlighted poor sales execution and lower pipeline conversion rates as reasons for the weakness. The soft results were at odds with both the positive channel feedback we had received and the better results exhibited from other security vendors. Also negatively impacting the sector’s relative performance was the Fund’s position in a manufacturer of computerized bar-code laser printers, Zebra Technologies Corp. We sold the stock after weaker than expected quarterly results indicated a disconnect between our investment case and the operational performance of the business. We had initially invested in the stock given our belief that industry consolidation would produce a stable competitive and pricing environment. Moreover, we anticipated that as retailers pushed into multiple sales channels, having the technology necessary to optimize inventory and logistics operations would become more important, requiring investment in data capture devices and specialty printers. However, a tighter spending environment in the enterprise mobility segment restrained the company’s earnings and revenue growth, leading Zebra to miss earnings expectations for the quarter and restate its full year 2016 earnings guidance. As a result, we exited the position.

The Health Care sector was the Fund’s top relative performing sector during the period and helped to offset a portion of the Fund’s weakness in the Information Technology sector. ARIAD Pharmaceuticals, Inc., an oncology-focused company with two commercial products and a drug candidate in clinical development, was the top relative performer in the sector. In early January, the company announced its agreement to be acquired by Takeda Pharmaceuticals for $24/share, approximately a 75 percent premium to the closing price on the prior day. Following the news, we sold the Fund’s position in the stock. Nektar Therapeutics, a clinical-stage biopharmaceutical company, was also a strong relative performer during the period. The stock price advanced sharply in March after the company’s drug NKTR-181—a “no-high” opioid that provides pain relief without a feeling of euphoria—met its primary and secondary endpoints on a phase 3 study of chronic pain. However, our main reason for investing in the company is its key product—NKTR-214—which is a cell-signaling protein that plays a central role in the immune system’s delicate balance of tolerance immunity. We believe that the upside for NKTR-214 could be significant and the drug could prove to be the backbone of immuno-oncology drugs. Mettler-Toledo International, Inc., a manufacturer of precision instruments for use in laboratory, industrial and food retailing applications, was also a top relative performer in the sector. The stock price responded positively to strong quarterly results posted in early February. We consider the company’s outlook for growth to be as strong as it has ever been, and view Mettler-Toledo as one of the best-managed businesses in the industry. The company is repurchasing a material percentage of its shares outstanding per year, resulting in a share count reduction of 40 percent over the last decade. We believe continued share buybacks along with margin improvement should drive strong earnings per share growth going forward.

Positioning in the Consumer Discretionary sector also provided relative outperformance versus the benchmark. Insulation installer Installed Building Products, Inc. was the sector’s top relative outperformer. The company posted strong quarterly results in late February, with best-in-class organic sales growth. We believe Installed Building Products continues to be a well-run company and is poised to benefit from the rebound in single–family housing starts and housing completions in the U.S. In addition, we believe the company’s acquisition activity should help drive further sales growth. Also positively impacting the sector’s relative gains was the Fund’s position in Charter Communications, Inc., a provider of broadband communications services. Charter is the fastest-growing pay-TV provider in the U.S. It has recently shown strong financial results and subscriber growth ahead of consensus expectations, as it transitions acquired Time Warner Cable markets to its pricing and promotional strategy. Overall, we continue to like Charter as a business that, in our opinion, has strong momentum and a modest risk profile.

Outlook

We are encouraged by the strength and resilience of the domestic economy and are optimistic about a nascent recovery overseas. Our expectation is that earnings growth will pick up this year, which, in combination with a moderate and well-telegraphed monetary policy, should drive equity markets higher. The financial markets

Management's Discussion of Fund Performance (Unaudited) (Continued)

have been remarkably placid for some time now, with measures of volatility remaining low. Additionally, average sector correlations in the S&P 500® Index have continued their decline and now sit at the lowest levels seen since the financial crisis of 2008. We believe lower asset correlations combined with lower market volatility should provide a favorable backdrop for active managers like Westfield, who rely on fundamental analysis and valuation discipline in their investment approach. We believe that our focus on identifying high growth companies that trade at attractive valuations should be rewarded in the current market environment.

Management's Discussion of Fund Performance (Unaudited) (Continued)

Comparison of the Change in Value of a $10,000 Investment in the

Touchstone Growth Opportunities Fund - Class A* and the Russell 3000® Growth Index

| * | The chart above represents performance of Class A shares only, which will vary from the performance of Class C shares, Class Y shares and Institutional Class shares based on the differences in sales loads and fees paid by shareholders in the different classes. The inception date of Class A shares, Class C shares, Class Y shares and Institutional Class shares was September 29, 1995, August 2, 1999, February 2, 2009 and February 2, 2009, respectively. Class C shares, Class Y shares and Institutional Class shares performance information was calculated using the historical performance of Class A shares for periods prior to August 2, 1999, February 2, 2009 and February 2, 2009, respectively. The returns have been restated for sales loads and fees applicable to Class C, Class Y and Institutional Class shares. The returns of the index listed above are based on the inception date of the Fund. |

| ** | The average annual total returns shown above are adjusted for maximum sales loads and fees, if applicable. The maximum offering price per share of Class A shares is equal to the net asset value (“NAV”) per share plus a sales load equal to 6.10% of the NAV (or 5.75% of the offering price). Class C shares are subject to a contingent deferred sales charge (“CDSC”) of 1.00%. The CDSC will be assessed on an amount equal to the lesser of (1) the NAV at the time of purchase of the shares being redeemed or (2) the NAV of such shares being redeemed, if redeemed within a one-year period from the date of purchase. Class Y shares and Institutional Class shares are not subject to sales charges. |

The performance of the above Fund does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Notes to Chart

Russell 3000® Growth Index measures the performance of those Russell 3000® companies with higher price-to-book ratios and higher forecasted growth values.

The Frank Russell Company (FRC) is the source and owner of the Index data contained or reflected in this material and all trademarks and copyrights related thereto. The material may contain confidential information and unauthorized use, disclosure, copying, dissemination or redistribution is strictly prohibited. This is a Touchstone Investments presentation of the data, and FRC is not responsible for the formatting or configuration of this material or for any inaccuracy in the presentation thereof.

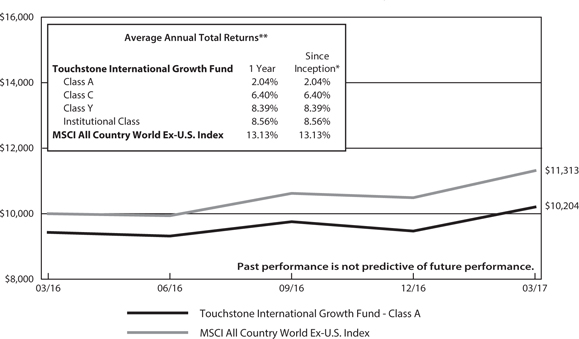

Management's Discussion of Fund Performance (Unaudited)

Touchstone International Growth Fund

Sub-Advised by Apex Capital Management1

Investment Philosophy

The Touchstone International Growth Fund seeks to achieve long-term capital growth by investing primarily in issuers located in developed markets utilizing an approach that combines “top-down” secular- and macro-economic trend analysis with “bottom-up” security selection. The “top-down” view seeks to provide a framework for “bottom-up” research by identifying sectors, industries and companies that may benefit from the sustainability of the observed trends. Fundamental “bottom-up” research is applied to identify individual companies that exhibit earnings growth potential and may benefit from the sustainability of observed secular- and macro-economic trends. The Fund typically invests in companies that are recognized as “established growth” companies which generally provide more stability and consistency in volatile markets as its core investments. It also invests in companies that are in the earlier stages of their growth cycle that are known as “emerging growth” companies which typically exhibit more aggressive growth characteristics and may experience a significant positive transformation or a favorable catalyst impacting their long-term earnings potential.

Fund Performance

The Touchstone International Growth Fund (Class A Shares) underperformed its benchmark, the MSCI All Country World ex-U.S. Index, for the 12-month period ended March 31, 2017. The Fund’s total return was 8.26 percent (calculated excluding the maximum sales charge), while the total return of the benchmark was 13.13 percent.

Market Environment

During the 12-month period ended March 31, 2017, U.S. equity markets outpaced their international counterparts; however, equities around the globe provided positive absolute returns, reflecting a rise in economic optimism. After trailing U.S. markets for the first nine months of the fiscal year, international stocks gained ground in the most recent quarter. Similarly, it was a period of shifting market leadership from a stylistic perspective. Growth stocks outperformed value stocks at the start and end of the 12-month period, but lower valuation securities outperformed during the middle of the period, driven in large part by returns following the U.S. Presidential election in November.

Portfolio Review

The Fund typically has a bias toward growth stocks. This proved to be a headwind during the period when international value stocks outperformed international growth stocks. From a sector perspective, the largest driver of Fund performance relative to its benchmark was positioning within the Health Care sector. Policy uncertainty stemming from campaign rhetoric in the U.S. caused significant volatility among Health Care stocks. For example, drug price turmoil in the diabetes space hurt the price of Novo Nordisk A/S and detracted from the Fund’s relative performance. Ono Pharmaceutical Co. Ltd. also declined meaningfully. Though its primary drug (Opdivo) was approved as hoped, some tests showed more efficacy from a competing Merck & Co. Inc. drug that also targets cancers. Given the deterioration in Ono Pharmaceuticals earnings outlook, the Fund exited the position.

Offsetting some of the weakness in the Health Care sector, the Fund benefited from strong performance by Sony Corp. (Information Technology sector), the Japanese consumer electronics conglomerate. The stock rose amid a resurgence in Japanese equities. Fund holding Broadcom Ltd. also experienced an increase in price after the announcement that it was being purchased by Avago Technologies Ltd. in one of the largest-ever deals in the Information Technology space.

Management's Discussion of Fund Performance (Unaudited) (Continued)

Outlook

Following the U.S. Presidential election, we were concerned about the potential that protectionist rhetoric would actually materialize in the form of trade wars, as we believe such an outcome would have a profound impact on the global economy. However, early signs from the new administration have reduced our concerns in this regard. Meanwhile, global growth continues and economic optimism appears to be on the rise around the world. Accordingly, we have increased Fund exposure to Industrials, a more economically sensitive sector. From a geographic perspective, the Fund has been notably underexposed to Emerging Markets for several quarters. While this has benefitted returns, we recently reduced that underweight by purchasing high quality stocks across the Emerging Market landscape. Again, this is a reflection of the improving outlook for global economic growth. We are optimistic that the more cyclical tilt in the Fund’s portfolio should benefit the Fund as the global economy continues to expand.

1 On June 1, 2016, Apex Capital Management (APEX) became part of Fiera Capital Inc., the U.S. division of Fiera Capital Corporation. Apex is a trade-name being used by Fiera Capital Inc. (the sub-advisor), a SEC-registered investment advisor.

Management's Discussion of Fund Performance (Unaudited) (Continued)

Comparison of the Change in Value of a $10,000 Investment in the Touchstone International Growth Fund - Class A* and the MSCI All Country World Ex-U.S. Index

| * | The chart above represents performance of Class A shares only, which will vary from the performance of Class C shares, Class Y shares and Institutional Class shares based on the differences in sales loads and fees paid by shareholders in the different classes. The inception date of Fund is March 31, 2016. The returns of the index listed above are based on the inception date of the Fund. |

| ** | The average annual total returns shown above are adjusted for maximum sales loads and fees, if applicable. The maximum offering price per share of Class A shares is equal to the net asset value (“NAV”) per share plus a sales load equal to 6.10% of the NAV (or 5.75% of the offering price). Class C shares are subject to a contingent deferred sales charge (“CDSC”) of 1.00%. The CDSC will be assessed on an amount equal to the lesser of (1) the NAV at the time of purchase of the shares being redeemed or (2) the NAV of such shares being redeemed, if redeemed within a one-year period from the date of purchase. Class Y shares and Institutional Class shares are not subject to sales charges. |

The performance of the above Fund does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Notes to Chart

MSCI All Country World Ex-U.S. Index measures the equity market performance of the non U.S. developed and emerging markets.

MSCI makes no express or implied warranties or representations and shall have no liability whatsoever with respect to any MSCI data contained herein. The MSCI data may not be further redistributed or used to create indices or financial products. This report is not approved or produced by MSCI.

Management's Discussion of Fund Performance (Unaudited)

Touchstone International Value Fund

Sub-Advised by Barrow, Hanley, Mewhinney & Strauss, LLC

Investment Philosophy

The Touchstone International Value Fund seeks long-term capital growth by primarily investing in equity securities of non-U.S. companies believed to be undervalued and seeks companies that have price-to-earnings and price-to-book ratios below the market, enterprise-value/free-cash-flow ratios at or below the market and dividend yields above the market.

Fund Performance

The Touchstone International Value Fund (Class A Shares) underperformed both its benchmarks, the MSCI EAFE Value Index and the MSCI EAFE Index, for the 12-month period ended March 31, 2017. The Fund’s total return was 10.80 percent (calculated excluding the maximum sales charge), while the total return of the MSCI EAFE Value Index was 15.98 percent and the total return of the MSCI EAFE Index was 11.67 percent. The MSCI EAFE Value Index was added as the Fund’s primary benchmark to better reflect the investment strategy currently used in the management of the Fund’s portfolio. The MSCI EAFE Value Index represents large and mid cap securities that exhibit overall value style characteristics across international developed market countries. These value style characteristics include lower price/book ratio, lower price/earnings ratio, and higher dividend yield. The MSCI EAFE Index will be maintained as the Fund’s secondary benchmark which will allow for performance comparisons against the non-US equity “market” as a whole, regardless of style.

Market Environment

During the 12-month period ended March 31, 2017, markets experienced robust returns across the majority of geographic regions. Emerging Market stocks led the way as investors’ concerns about increased interest rates in the U.S., a rising U.S. dollar and trade barriers proved unfounded. Global growth indicators such as Purchasing Managers’ Indexes (PMIs) continued to advance during the period, picking up momentum in the latter half of 2016 and continuing into 2017. Markets were also buoyed by expectations for fewer business regulations, stimulative infrastructure spending and tax cuts following the U.S. presidential election. If enacted, we believe these measures would not only boost the U.S. economy, but potentially benefit the global economy as well.

With economic fundamentals improving and market fears abating, value stocks meaningfully outperformed the broader markets during the period. The rally in value stocks was more concentrated in deeper value stocks such as metals and mining and the beleaguered Financials sector stocks. Conversely, sectors such as Consumer Staples, Telecommunication Services and Utilities – defensive areas that were bid up over the last several years as investors sought safety in an uncertain market environment – were shunned and meaningfully lagged the broader market.

Portfolio Review

For the period, the Fund’s stock selection within the Industrials and Consumer Discretionary sectors contributed the most to performance, while positioning in the Health Care and Materials sectors detracted. The Fund’s lower exposure to bond proxy sectors such as Telecommunication Services, Utilities and REITs (Real Estate sector) were key contributors to Fund performance as the market avoided these stocks in favor of deeper cyclicals.

Among the individual stocks that contributed to performance were Fuji Electric Co. Ltd., IHI Corp. (both from the Industrials sector) and Fiat Chrysler Automobiles NV (Consumer Discretionary sector). Fuji Electric, a Japan-based electrical equipment company, benefited from an improving global economy, a weak yen and improvement in China’s economy, an important end market for the company. IHI Corp. is a Japan-based

Management's Discussion of Fund Performance (Unaudited) (Continued)

heavy equipment manufacturer, which stabilized its business during the period after several missteps in its social infrastructure business. This allowed for positive economic improvements in the company’s auto and aerospace divisions, which benefited operating results and ultimately the stock’s price. Fiat Chrysler, a U.K.-based and Italian-controlled automobile manufacturer, posted strong performance resulting from improved operating profits as the company was able to reduce costs and improve margins.

Among the individual stocks that detracted from Fund performance were Teva Pharmaceutical Industries Ltd. (Health Care sector), Dairy Crest Group PLC, Imperial Brands PLC (both from the Consumer Staples sector) and DS Smith PLC (Materials sector). A multinational pharmaceutical company headquartered in Israel, Teva Pharmaceutical Industries declined along with other health care stocks, but was further impacted by untimely changes in corporate management. Further, its key drug COPAXONE® was under pressure from outside competition. We believe these issues are transitory in nature and believe the valuation is sufficiently compelling to warrant continued ownership. The Fund’s holdings in Dairy Crest (a U.K.-based consumer foods business), DS Smith (a U.K.-based packaging company) and Imperial Brands (a U.K.-based cigarette and tobacco manufacturer) were negatively impacted by the U.K.’s decision to exit the European Union (Brexit) and the resulting decline in the British pound. Dairy Crest and Imperial brands were also affected by the market’s shift away from defensive stocks. However, all three of these companies continue to exhibit improved operating fundamentals. We believe the selloff in these stocks was unwarranted and therefore the Fund continued to hold them at the end of the period.

The Fund was also negatively impacted by the stocks it did not own during the year. The metals and mining industry moved significantly higher over the year and represented a meaningful percent of the benchmark. Many of these companies did not meet the Fund’s investment criteria due to weak balance sheets and operating fundamentals that do not show signs of improvement. Additionally, banks based in France and the U.K rallied strongly after the Brexit vote but similarly lacked improved operating fundamentals.

Outlook

Valuations rose sharply during the last eight years and are now well above average. Considering that earnings growth has been flat or negative for several years, the market’s continued move upward was driven by valuation expansion and, more recently, by the expectation of new business-friendly policies from the Trump administration. We believe the selloff in late March was a sign that stocks had moved far ahead of the actual implementation of the potential policies. We believe that if markets cannot rely on new policy and tax initiatives or continued easy money policies as incentives to drive valuations higher, investors must once again look at earnings and fundamentals of underlying companies.

With the exception of the poorly performing Energy sector, operating margins remained at historical highs supported by low wage growth and low interest costs. Recent wage growth, however, has trended upward and, as interest rates increase, interest expense will also move higher thus creating downward earnings and margin pressure. Markets appear to be priced for robust earnings growth with the expectation that margins will remain high and pro-growth policies will be enacted. If markets stumble, as they did toward the end of the 12-month period, we believe the defensive characteristics of the Fund’s value-oriented investment process should benefit.

In light of these risks, and after an eight-year bull market driven not by fundamentals but by waves of easy money and a rising tide benefitting the most popular stocks, we believe that active stock selection is more important than ever. Although we recognize that markets will continue to provide positive returns over the longer term, we expect that markets may stumble in the near term. Accordingly, we believe that the Fund’s

Management's Discussion of Fund Performance (Unaudited) (Continued)

portfolio of stocks that are cheaper than the market with stable-to-improving operating fundamentals will provide protection through a tumultuous period. Further, dividends are a critical component of long-term overall returns, and are especially important if market returns are moderate or turn negative. We believe our philosophy of buying the stocks of companies paying dividends and committed to growing those dividends should provide for further protection of capital in tumultuous market environments.

Dividend-paying investments may not experience the same price appreciation as non-dividend paying instruments, dividend-issuing companies may choose not to pay a dividend, or the dividend may be less than what is anticipated

Management's Discussion of Fund Performance (Unaudited) (Continued)

Comparison of the Change in Value of a $10,000 Investment in the Touchstone International Value Fund - Class A*, the MSCI EAFE Value Index and the MSCI EAFE Index

| * | The chart above represents performance of Class A shares only, which will vary from the performance of Class C shares, Class Y shares and Institutional Class shares based on the differences in sales loads and fees paid by shareholders in the different classes. The inception date of Class A shares, Class C shares, Class Y shares and Institutional Class shares was August 18, 1994, April 25, 1996, October 9, 1998 and September 10, 2012, respectively. Class C shares, Class Y shares and Institutional Class shares performance information was calculated using the historical performance of Class A shares for periods prior to April 25, 1996, October 9, 1998 and September 10, 2012, respectively. The returns have been restated for sales loads and fees applicable to Class C, Class Y, and Institutional Class shares. The returns of the indexes listed above are based on the inception date of the Fund. |

| | | |

| ** | The average annual total returns shown above are adjusted for maximum sales loads and fees, if applicable. The maximum offering price per share of Class A shares is equal to the net asset value (“NAV”) per share plus a sales load equal to 6.10% of the NAV (or 5.75% of the offering price). Class C shares are subject to a contingent deferred sales charge (“CDSC”) of 1.00%. The CDSC will be assessed on an amount equal to the lesser of (1) the NAV at the time of purchase of the shares being redeemed or (2) the NAV of such shares being redeemed, if redeemed within a one-year period from the date of purchase. Class Y shares and Institutional Class shares are not subject to sales charges. |

The performance of the above Fund does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Notes to Chart

MSCI EAFE Value Index captures large- and mid-cap securities exhibiting overall value style characteristics across developed markets countries around the world, excluding the U.S. and Canada.

MSCI EAFE Index is a free float-adjusted market capitalization index that is designed to measure developed market equity performance excluding the U.S. and Canada.

MSCI makes no express or implied warranties or representations and shall have no liability whatsoever with respect to any MSCI data contained herein. The MSCI data may not be further redistributed or used to create indices or financial products. This report is not approved or produced by MSCI.

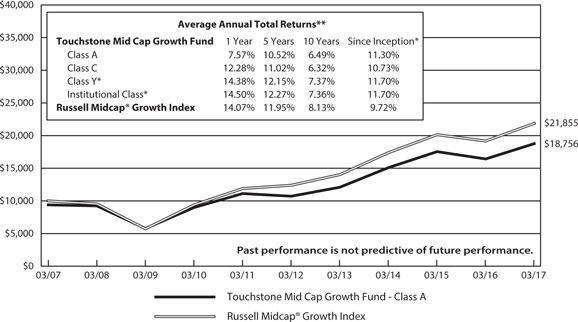

Management's Discussion of Fund Performance (Unaudited)

Touchstone Mid Cap Growth Fund

Sub-Advised by Westfield Capital Management, L.P.

Investment Philosophy

The Touchstone Mid Cap Growth Fund seeks to increase the value of Fund shares by primarily investing in stocks of mid-cap U.S. companies. The Fund’s portfolio managers place focus on companies that they believe to have a demonstrated record of achievement with excellent prospects for earnings growth over a 1-to-3-year period. Westfield looks for companies that it believes are reasonably priced with high forecasted earnings potential.

Fund Performance

The Touchstone Mid Cap Growth Fund (Class A Shares) outperformed its benchmark, the Russell Midcap® Growth Index, for the 12-month period ended March 31, 2017. The Fund’s total return was 14.13 percent (calculated excluding the maximum sales charge), while the total return of the benchmark was 14.07 percent.

Market Environment

Domestic stocks generated solid returns during the 12-month period ended March 31, 2017, posting gains across all market sectors and capitalizations. Oil prices rose, consumer confidence hit a new five-year high, and unemployment claims continued to drop. In a step toward normalization of financial conditions after a prolonged period of zero-rate interest rates, the U.S. Federal Reserve Board raised short-term rates by 25 bps twice and signaled a quicker pace of rate increases over the next two years. The past twelve months, however, have highlighted yet again a powerful dichotomy between two forces competing for equity market leadership: growth and safety. During periods of market duress, investors have sought refuge in the most defensive, bond-like segments, such as Utilities, Real Estate Investment Trusts (REITs), and Telecommunication Services sectors. Snapback rallies off the interim lows have been driven by economically-sensitive stocks.

U.S. equities surged following the Presidential election, lifting most stock indices to record highs. The rally began with a rotation into those stocks most exposed to domestic cyclical growth, with lower Price/Earnings, smaller capitalization companies leading the charge. Domestic stocks extended post-election gains into calendar year 2017, propelling most equity indices into new record territories. Their advance came against a stable economic backdrop in the U.S. and signs of improvements in the eurozone. The U.S. unemployment rate suggests that the domestic labor market remains in good shape, and business survey data has been strong, suggesting the potential for increased capital spending ahead. Despite mostly positive economic data and stronger consumer and business confidence, investors remain skeptical of the rally, as billions of dollars continue to pour into bond funds. The market’s advance tapered off by early spring, with cyclical and financial stocks pulling back as the “Trump trade” faded. The first quarter of 2017 witnessed a notable rotation into high-quality, large market capitalization, growth-oriented companies, primarily within the Information Technology and Health Care sectors.

Portfolio Review

The Fund’s relative outperformance was fairly broad-based, with seven sectors contributing to positive results. The Consumer Discretionary and Health Care sectors were the Fund’s greatest sources of relative strength, offsetting the relative performance shortfall within the Information Technology and Financials sectors.

The Fund maintained its underweight to the Consumer Discretionary sector, with investments concentrated primarily within less economically-sensitive areas, such as media, leisure, and restaurants. We are incrementally more constructive on the media industry, which has witnessed several important developments over the past few months. Cable broadband providers have merged and telecommunication companies have been acquiring

Management's Discussion of Fund Performance (Unaudited) (Continued)

video distribution and content assets. We think this trend could accelerate, and there are a number of business combinations that we believe would make strategic sense in the converging industry. Liberty Broadband Corp., an owner of communication companies, was the Fund’s top relative performer in the sector. Liberty Broadband was spun out of Liberty Media Corp. two years ago as a vehicle to implement a strategy to roll up cable assets in a tax-efficient manner. Worldwide operator and franchisor of hotels Marriott International, Inc. also contributed to relative performance within the sector. Lodging stocks reacted positively following the November election, with enthusiasm building for acceleration in corporate profit growth as a driver for lodging demand. We think Marriott stands out among its industry peers due to its asset light business model, characterized by high margins, low capital requirements, and consistent returns on invested capital. The company’s Starwood Hotels & Resorts Worldwide, LLC integration remains on track which we believe should deliver significant earnings upside through a combination of unit growth and the potential for increased credit card profits over time.

Investments in the Health Care sector contributed to relative returns, benefiting from positive stock selection across multiple sub-industries. Developer of innovative anti-cancer agents, Clovis Oncology, Inc., was the Fund’s top relative performer during the period as it advanced on improving sentiment for its therapies. The company develops PARP inhibitor therapies for subsets of cancers that do not respond to existing commercial drugs. Clovis had an important Phase III data announcement regarding ovarian cancer this year, owns global rights to its product candidates, and is fully financed. While we still have conviction in the thesis, given the recent price appreciation and risk profile, we trimmed the Fund’s position twice during the period. Veeva Systems Inc., a health care technology company focused on the life science niche, was also a top relative performer in the sector. Veeva’s products are core to the operations of life sciences companies. In addition to performing regular customer relationship management (CRM) functions, the company provides audit trails that ensure field representatives are not marketing drugs for off-label purposes. Following a strong advance, the stock was sold in June as it reached our price target.

The Information Technology sector was the Fund’s greatest source of relative underperformance. A combination of stock specific weakness and a limited exposure to some of the benchmark’s high momentum/high valuation stocks led to the relative performance shortfall. Imperva, Inc., a provider of data security and web application firewall (WAF) software, delivered disappointing results. The company exceeded consensus expectations for earnings in the first quarter of 2016, but missed on license revenues, leading to a sell-off in the stock. While we believe the price weakness could be partially attributed to results falling short of lofty investor expectations, it also highlighted operational and competitive challenges in the company’s core WAF business. We viewed the deceleration in top-line growth as a red flag and sold the Fund’s position. Another relative underperformer that was sold from the Fund was Zebra Technologies Corp., a manufacturer of enterprise mobile computers and specialty printers for barcode labeling. We sold the stock after weaker than expected quarterly results indicated a disconnect between our investment case and the operational performance of the business. We had initially invested in the stock given our belief that industry consolidation would produce a stable competitive and pricing environment. Moreover, we anticipated that as retailers pushed into multiple sales channels, having the technology necessary to optimize inventory and logistics operations would become more important, requiring investment in data capture devices and specialty printers. However, a tighter spending environment in the enterprise mobility segment restrained the company’s earnings and revenue growth, leading Zebra to miss earnings expectations for the quarter and restate its full year 2016 earnings guidance. As a result, we exited the position. Another relative underperformer was NVIDIA Corp., a manufacturer of computer graphics processors and related multimedia software.We believed there was an outsized growth opportunity stemming from the company’s earnings momentum in the gaming and infotainment end markets and bought the stock in the second half of 2016. However, we sold the Fund’s position in December 2016, following a large advance in stock price and based on our channel checks, which indicated that there could be excess inventory in the graphics chip market, so we took advantage of the stock’s advance to lock in gains. The sale proved to be premature, as NVIDIA continued to advance following its exit from the Fund.

Management's Discussion of Fund Performance (Unaudited) (Continued)

The Fund’s holdings within the Financials sector also underperformed, detracting from the Fund’s relative performance. The Financials sector finished the twelve-month period as the benchmark’s third best performer, but most of its impressive gains came in November 2016 on the heels of the U.S. election. Heightened risk aversion in the equity markets in June 2016 following the U.K.’s decision to exit the European Union had a strong negative impact on price action within the sector. Bank United, Inc. traded sharply lower in June 2016, hurting relative performance. This well-capitalized regional bank has a strong footprint in its geographic markets, a robust credit culture, and virtually no exposure to European markets. However, after reviewing the bank’s quarterly operational results, we sold the Fund’s position. We thought the backdrop for banks was extremely challenging, with rock-bottom interest rates constraining lending margins, and Brexit uncertainty keeping investor appetite for banking stocks subdued. At the same time, we could see some potential growth catalysts for the group – a relatively strong domestic economy supported the demand for loans, while credit defaults remained at historically low levels. We think that banks that have a proven ability to grow loans/deposits faster than the market overall could see outsized Earnings per Share (EPS) growth, irrespective of the interest rate environment. In general, we try to maintain a barbell approach to the Financials sector, preferring to invest in idiosyncratic ideas that we believe can perform well regardless of the interest rate environment. We increased the Fund’s exposure to the sector in the past several months and are currently overweight the group versus the benchmark. The Fund’s sector position remains balanced, holding several rate-sensitive stocks while also having exposure to more defensive areas, such as financial exchanges and data analytics.

Outlook

We are encouraged by the strength and resilience of the domestic economy and are optimistic about a nascent recovery overseas. Our expectation is that earnings growth will pick up this year, which, in combination with a moderate and well-telegraphed monetary policy, should drive equity markets higher. The financial markets have been remarkably placid for some time now, with measures of volatility remaining low. Additionally, average sector correlations in the S&P 500 Index have continued their decline and now sit at the lowest levels seen since the financial crisis of 2008. We believe lower asset correlations combined with lower market volatility should provide a favorable backdrop for active managers like Westfield, who rely on fundamental analysis and valuation discipline in their investment approach. We believe that our focus on identifying high growth companies that trade at attractive valuations should be rewarded in the current market environment.

Dividend-paying investments may not experience the same price appreciation as non-dividend paying instruments, dividend-issuing companies may choose not to pay a dividend, or the dividend may be less than what is anticipated.

Management's Discussion of Fund Performance (Unaudited) (Continued)

Comparison of the Change in Value of a $10,000 Investment in the Touchstone Mid Cap Growth Fund - Class A* and the Russell Midcap® Growth Index

| * | The chart above represents performance of Class A shares only, which will vary from the performance of Class C shares, Class Y shares and Institutional Class shares based on the differences in sales loads and fees paid by shareholders in the different classes. The inception date of Class A shares, Class C shares, Class Y shares and Institutional Class shares was October 3, 1994, October 3, 1994, February 2, 2009 and April 1, 2011. Class Y shares and Institutional Class shares performance information was calculated using the historical performance of Class A shares for periods prior to February 2, 2009 and April 1, 2011, respectively. The returns have been restated for fees applicable to Class Y and Institutional Class shares. The returns of the index listed above are based on the inception date of the Fund. |

| ** | The average annual total returns shown above are adjusted for maximum sales loads and fees, if applicable. The maximum offering price per share of Class A shares is equal to the net asset value (“NAV”) per share plus a sales load equal to 6.10% of the NAV (or 5.75% of the offering price). Class C shares are subject to a contingent deferred sales charge (“CDSC”) of 1.00%. The CDSC will be assessed on an amount equal to the lesser of (1) the NAV at the time of purchase of the shares being redeemed or (2) the NAV of such shares being redeemed, if redeemed within a one-year period from the date of purchase. Class Y shares and Institutional Class shares are not subject to sales charges. |

The performance of the above Fund does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Notes to Chart

Russell Midcap® Growth Index measures the performance of those Russell Midcap® companies with higher price-to-book ratios and higher forecasted growth values.

The Frank Russell Company (FRC) is the source and owner of the Index data contained or reflected in this material and all trademarks and copyrights related thereto. The material may contain confidential information and unauthorized use, disclosure, copying, dissemination or redistribution is strictly prohibited. This is a Touchstone Investments presentation of the data, and FRC is not responsible for the formatting or configuration of this material or for any inaccuracy in the presentation thereof.

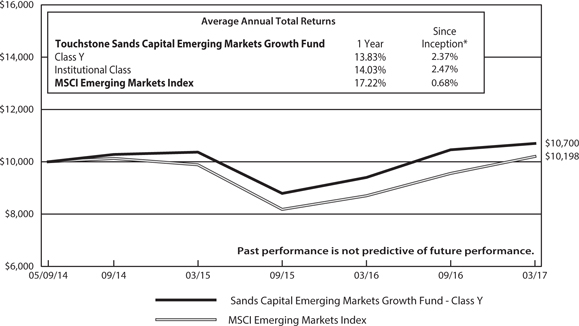

Management's Discussion of Fund Performance (Unaudited)

Touchstone Sands Capital Emerging Markets Growth Fund

Sub-Advised by Sands Capital Management, LLC

Investment Philosophy

The Touchstone Sands Capital Emerging Markets Growth Fund seeks long term capital appreciation. The Fund primarily invests in companies located in emerging market countries and opportunistically, in frontier market countries. Sands Capital generally seeks leading growth businesses with sustainable above average earnings growth and with capital appreciation potential. In addition, Sands Capital looks for companies that have a significant competitive advantage, a leadership position or proprietary niche, a clear mission in an understandable business, financial strength and are valued rationally in relation to comparable companies, the market and the business prospects for that particular company.

Fund Performance

The Touchstone Sands Capital Emerging Markets Growth Fund (Class Y Shares) underperformed its benchmark, the MSCI Emerging Markets Index, for the 12-month period ended March 31, 2017. The Fund’s total return was 13.83 percent, while the total return of the benchmark was 17.22 percent.

Market Environment

Oscillation defined the past twelve months in emerging market equities. We believe significant macro events drove share price returns in the second and fourth quarters of 2016, while the third quarter of 2016 and first quarter of 2017 were more sedated and fundamentally steered.

In the second quarter, “Brexit,” or the United Kingdom’s referendum to leave the European Union (EU), ushered in a new wave of uncertainty and trading volatility. We believe the primary investor concern stemmed from speculation about Brexit’s second- and third-order effects on currencies and trade. In the fourth quarter, November 8 saw consequential events on both sides of the globe, with the election of Donald Trump in the U.S. and the announcement of demonetization in India. In the immediate aftermath, we believe investor concerns heightened due to President Trump’s anti-trade campaign rhetoric, as well as the implications for U.S. dollar strength. In India, the surprise announcement of demonetization rendered nearly 90 percent of the country’s currency notes immediately invalid, introducing a headwind to the largely cash-based economy.

While these events drove equity market returns in their respective quarters, investors seemed to take a digestive or “wait and see” approach in the quarters immediately following. If nothing else, the whipsawing nature of share price returns reminded investors of the inherently volatile nature of emerging market equities, and the seeming impossibility of timing the market.

Portfolio Review

During the 12-month period ended March 31, 2017, the top five contributors to relative investment results were MercadoLibre Inc., Alibaba Group Holding Ltd., Housing Development Finance Corp. Ltd., Adani Ports & Special Economic Zone Ltd. and Raia Drogasil SA. Housing Development Finance (HDFC) is a leading Indian mortgage finance company. A first mover with a 30-year history of strong execution, we believe HDFC benefits from the dual secular tailwind of favorable Indian demographics, and a shift away from the state-owned banks that historically controlled a large share of the corporate lending market. Historically, retail mortgage lending was HDFC’s core business; however we have been encouraged by the recent uptick in non-retail/corporate lending. In the most recent quarter, lending in this segment grew at 18 percent year-over-year, accelerating from low-teens growth earlier in the fiscal year. Longer term, we expect this elevated level of growth to persist in HDFC’s non-retail segment, driven by lease rental discounting, developer loans and corporate lending. We

Management's Discussion of Fund Performance (Unaudited) (Continued)

believe the company’s leading market position in an attractive business space, experienced management team and risk management track record should sustain high-teens revenue and earnings growth annually over the next five years.

The top five detractors from relative investment results were Baidu Inc., BIM Birlesik Magazalar AS, Amorepacific Corp., Universal Robina Corp. and Taiwan Semiconductor Manufacturing Co. Ltd. Baidu’s shares came under pressure over the past year, as executive turnover, a medical and scandal and continued investments in its online-to-offline commerce (“O2O”) segment obfuscated otherwise strong results from its core search business. We remain enthused by Baidu’s long-term prospects, which include leadership in mobile search, mobile user engagement and ongoing growth in core search revenues. The company remains a leader in mobile search with over 70 percent share, with 80 percent of all Chinese internet users engaging Baidu’s search on a monthly basis. As monthly user growth has matured, we believe new features like mobile newsfeed and the iQiyi video platform will drive engagement, increasing the amount of daily average users. Management expects a gradual recovery in search revenue during 2017, and we believe prioritization of artificial intelligence will increase targeting, monetization and user experience. We believe Baidu is on its path to recovery and will experience a reacceleration in revenue and earnings growth, ultimately generating earnings growth of more than thirty percent annually over the long term.

During the past 12 months, we purchased the following businesses: Anta Sports Products Ltd., HDFC Bank Ltd., IndusInd Bank Ltd., International Container Terminal Services Inc., MakeMyTrip Ltd., Siloam International Hospitals Tbk PT and Yandex NV.

Anta Sports Products is the leading mass-market sports apparel and footwear company in China, with nearly twice the market share of its next closest domestic brand competitor. The company’s products are primarily sold through wholesale channels to operators of stores located in smaller, less developed Chinese cities. In our view, this market opportunity is distinct from the high-end, top-tier cities that multinational brands tend to target. Following a period of industry overexpansion several years ago, we believe Anta emerged well positioned to continue to take share in these lower-tier cities, due in part to its experienced management team who implemented global best practices in branding, research and development and supply chain management. Overall, we expect the sportswear industry to grow high single-digits, as increasing incomes lead consumers toward more active lifestyles. We believe Anta has several initiatives that should help drive above-average growth, including partnering with provinces to push sports programs, category expansion beyond its core basketball and running franchises and a continued focus on best practices in inventory and financial management.

HFDC Bank is India’s largest private bank, with a customer base of approximately 40 million. Though the company offers both retail and corporate lending, retail is its most visible business, with a distribution network of nearly 5,000 branches. Spanning every Indian geography from major metro cities to rural areas, HDFC Bank’s retail footprint has contributed to its leading position in every major retail lending segment, including auto loans, credit cards and personal loans. Corporate lending accounts for approximately half of HDFC Bank’s loan book and most loans are made to high-quality blue chip and middle-market companies. Outside of lending activities, the bank is a major distributor and provider of other financial products and services, such as insurance, asset management and corporate finance. We believe HDFC Bank’s strong brand, extensive distribution network, business stability and experienced management team will drive continued success over the long term. Growth is further supported by what we believe is a secular shift underway in India; while state-owned banks have historically dominated the corporate lending market, they are becoming increasingly burdened by impaired assets. Over the next five years, we believe HDFC Bank should grow earnings in the high teens, annually.

IndusInd Bank is a leading Indian private bank, with over 1,000 branches and 1,800 ATMs spread across the country. Originally focused on vehicle financing, IndusInd today operates under a “universal” banking model, offering services across several segments of corporate and consumer banking. Despite its universal operating

Management's Discussion of Fund Performance (Unaudited) (Continued)

model, IndusInd seeks opportunities to maximize profits in select business segments where the company believes it has deep and sustainable competitive advantages, namely vehicle finance, gems and jewelry and micro lending. In areas such as mortgages, where IndusInd is less competitive, it has pursued an asset-light distribution model, which we believe adds to the company’s overall operating efficiency. We expect private banks to double their loan market share at the expense of public sector banks over the next decade. Our research indicates that state-owned banks are burdened by impaired assets, which constrains their ability to lend and compete with private banks. Furthermore, public banks generally cater more to corporate lending, which is growing more slowly than loans made to consumers. We believe IndusInd is positioned well to benefit from this shift, given its low loan losses, high capital ratios, experienced management team and innovative banking services.

International Container Terminal Services (ICT) is a global shipping terminal operator with an exclusive focus on containerized cargo. The company operates about 30 terminals in 20 countries across five continents, primarily in emerging and frontier regions. ICT’s strategy is to acquire and operate small to midsize port terminals in markets with what is considered to be superior growth potential. We believe the company should be able to grow organically through gross domestic product-driven (GDP) volume growth, as well as by increasing capacity utilization at its existing facilities. Additionally, ICT has a portfolio of projects under development that should increase its capacity by about 30 percent over the next three to five years. Beyond its current projects, the company has identified more than 400 terminals that fall within its operating sweet spot - too small for larger global competitors, a focus on origin and destination cargo (i.e., less risk of disintermediation or price competition), significant room for operating efficiency gains and attractive risk-adjusted return estimates. In many regions where ICT operates, the rate of containerization is still relatively low compared to the global average. As ICT is a pure container terminal operator, we expect the secular trend from bulk to containerized cargo will provide modest long-term volume growth.

MakeMyTrip is the leading Indian online travel service. Founded in 2000, the company originally only served consumers travelling between the U.S. and India, but has since expanded into domestic booking for flights, packaged tours, hotels, buses, railways and rental cars. Today MakeMyTrip is the leading channel for air and hotel bookings, and we expect a dramatic increase in its share of total travel spending due to a recently announced merger with Goibibo (online travel booking service). Combined, we estimate MakeMyTrip and Goibibo will have more than 50 percent share of Indian travel spending. We view online travel booking as one of the world’s most attractive internet services, and believe India is positioned to be the fastest-growing online travel market over the next decade. India’s travel market is equivalent to only approximately 20 percent of China’s market, and India’s GDP per capita is approaching the sweet spot where we expect travel spending to accelerate. The largest opportunity we see is in hotels, where online penetration is less than 15 percent. Mobile internet usage in India has begun to inflect, and we believe this should bolster hotel bookings, especially because of the last-minute booking habit in India. In our view, MakeMyTrip’s merger with Goibibo has created a leading business, which should greatly benefit from secular changes driving the growth of the Indian online travel market.