UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-03651

Touchstone Strategic Trust

(Exact name of registrant as specified in charter)

303 Broadway, Suite 1100

Cincinnati, Ohio 45202-4203

(Address of principal executive offices) (Zip code)

Jill T. McGruder

303 Broadway, Suite 1100

Cincinnati, Ohio 45202-4203

(Name and address of agent for service)

Registrant's telephone number, including area code: 800-638-8194

Date of fiscal year end: March 31

Date of reporting period: March 31, 2018

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget ("OMB") control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

Item 1. Reports to Stockholders.

The Report to Shareholders is attached herewith.

March 31, 2018

Annual Report

Touchstone Strategic Trust

Touchstone Flexible Income Fund

Touchstone Focused Fund

Touchstone Growth Opportunities Fund

Touchstone International Growth Fund

Touchstone International Value Fund

Touchstone Mid Cap Growth Fund

Touchstone Sands Capital Emerging Markets Growth Fund

Touchstone Small Cap Growth Fund

Touchstone Sustainability and Impact Equity Fund

Table of Contents

This report identifies the Funds' investments on March 31, 2018. These holdings are subject to change. Not all investments in each Fund performed the same, nor is there any guarantee that these investments will perform as well in the future. Market forecasts provided in this report may not occur.

Letter from the President

Dear Shareholder:

We are pleased to provide this Annual Report for the Touchstone Strategic Trust. Inside you will find key financial information, as well as fund manager commentaries, for the 12 months ended March 31, 2018.

The worldwide economic recovery gained momentum during 2017 as economies participated in what could be characterized as a “synchronized global expansion.” The United States, Japan, the European Union and China all reported solid economic growth. Despite the solid economic fundamentals through much of the last 12 months, early 2018 saw an increase in market volatility as tariffs and trade tensions raised the specter of an escalating global trade war. Monetary policies across the major central banks remained divergent throughout the period as the Bank of Japan and the European Central Bank maintained accommodative stances, while the U.S. Federal Reserve Board (Fed) continued moving toward its goal of monetary policy normalization by raising rates three times in the fiscal year. Additionally, the Fed announced and began executing on plans to reduce the size of its balance sheet by selling securities it had acquired during its quantitative easing programs; this is expected to take place over a number of years.

Global equities posted strong returns with most broad indices generating double-digit returns. Non-U.S. markets led the way, with emerging market equities producing particularly strong performance. Within the U.S. equity markets, growth-oriented stocks outpaced their value-oriented counterparts, while large capitalization stocks outperformed small- and mid-capitalization stocks.

The Fed’s three rate hikes during the year pushed short-term rates higher and, after spending most of the year range bound, longer-term rates rose late in the fiscal year. While rising rates limited gains, investment grade bonds were still able to produce positive returns for the year. Amid stronger economic growth and a low default environment, non-investment grade bonds enjoyed tightening credit spreads and led the fixed income market.

After nearly a decade of strong gains, many investors may be wondering whether the volatility of early 2018 marks a turning point for the capital markets. We would offer the same counsel as always: maintain a long-term approach. Rather than reacting to last month’s returns, work with your financial advisor to establish an investment plan that will help you achieve your long-term financial objectives.

We greatly appreciate your continued support. Thank you for including Touchstone as part of your investment plan.

| Sincerely, | |

| | |

| |

| Jill T. McGruder | |

| President | |

| Touchstone Strategic Trust | |

Management's Discussion of Fund Performance (Unaudited)

Touchstone Flexible Income Fund

Sub-Advised by ClearArc Capital, Inc.

Investment Philosophy

The Touchstone Flexible Income Fund seeks a high level of income consistent with reasonable risk and seeks capital appreciation as a secondary goal. The Fund primarily invests in income-producing securities such as debt securities, common stocks and preferred stocks. The Fund’s sub-advisor seeks to provide value by investing in asset classes that appear to be attractive based on their risks and in companies with attractive price-to-cash flow ratios. The Fund seeks returns by investing across a broader array of investments than traditional investment-grade fixed-income funds, and ClearArc believes that a low correlation between various asset classes leads to stability of expected returns.

Fund Performance

The Touchstone Flexible Income Fund (Class A Shares) outperformed its benchmark, the Bloomberg Barclays U.S. Aggregate Bond Index, for the 12-month period ended March 31, 2018. The Fund’s total return was 3.46 percent (calculated excluding the maximum sales charge), while the total return of the benchmark was 1.20 percent.

Market Environment

Volatility was low for much of the 12-month period that ended on March 31, 2018, which saw a transition to a new U.S. Federal Reserve Board (Fed) Chairman, and continued slow interest rate hikes. This favorable environment for risky assets continued a trend we have seen for some time; however, market conditions changed near the end of the period. The first calendar quarter of 2018 saw an inflection in which equity volatility picked up. The Chicago Board Options Exchange Volatility Index (VIX), which measures expected volatility in the S&P 500® Index, spiked. This was driven by higher interest rates, rising inflation expectations and climbing economic growth expectations due to recently passed tax legislation in the U.S.

Over the 12 months, the U.S. dollar depreciated, confounding investors who were convinced that rising interest rates would cause the opposite. The U.S. dollar’s status as the global reserve currency appears to be starting to slowly erode due to the emergence of China and diminishing American influence in certain areas of the world. The weak U.S. dollar has generally kept financial conditions easy. However, as interest rates climbed in the first quarter of 2018 there was a sense that financial conditions may finally be getting tighter. For example, the three-month London Interbank Offer Rate (LIBOR) rose, as short-term borrowers demanded more return for the risks they were taking.

Over the full period, the yield curve in the U.S. flattened, with 2-year yields rising and 30-year yields falling. Inflation expectations moved down at the start of the year, but then started a climb that continued until the end of the period. The breakeven inflation rate, which is the yield difference between Treasury Inflation Protected Securities (TIPS) and a nominal fixed-rate Treasury of similar maturity, indicated the market expects higher future inflation.

Equity markets delivered the best return for the period, with the S&P 500® Index up despite the pick-up in interest rate volatility toward the end of the period. Bonds generated positive low returns but corporate credit performed well among major bond sectors despite rising interest rates. Preferreds had a strong year relative to credit, driven by shorter duration securities and European issuers, although these too lost momentum in the last quarter. Emerging markets generally saw strong returns too, but again, momentum faded as we moved into 2018. In contrast, the Real Estate Investment Trusts (REIT) market had a difficult year after a long run of outperformance. REITs experienced mid-single-digit negative total returns as investors fretted about interest

Management's Discussion of Fund Performance (Unaudited) (Continued)

rate pressures, REITs being net losers in the recent tax cuts, and accelerating REIT supply. Rounding out the major asset classes, commodities, including gold and oil, had a strong year.

Portfolio Review

The Fund’s shorter duration relative to the benchmark helped performance as interest rates rose. For much of the year, the market embraced risk as equities delivered strong performance. In addition, the credit environment was a positive during the period, especially for preferreds. On a relative basis, the preferred allocation represented the largest contributor to the Fund’s relative returns.

Turning to performance within asset classes, the bond portion of the Fund outperformed the benchmark. Top contributors included Commercial Mortgage-Backed Securities (CMBS) and residential Mortgage-Backed Securities (MBS). CMBS and MBS holdings both benefited from favorable security selection. Detracting from performance within the bond allocation was weak security selection within corporate bonds.

Preferred equities provided the biggest boost to the Fund’s relative returns, primarily due to strong security selection. Top contributors within the allocation were floating rate securities, shorter duration hybrids and European holdings. We started adding floating rate and shorter duration hybrid preferreds during the second half of 2016 and continued into 2017. Towards the end of the 12-month period, U.S. hybrid preferreds became rich after a rally, leading us to take profits and reduce the Fund’s exposure. Top performers among floating rate preferreds included Catlin Insurance Co., Ltd., NextEra Energy, Inc., and Reinsurance Group of America, Inc. Large contributors among the Fund’s European preferreds included Credit Agricole SA, Societe Generale SA, and BNP Paribas SA.

Security selection within the Fund’s common equity allocation contributed to relative outperformance. Top equity performers included The Boeing Co. (Industrials sector), AbbVie Inc. (Health Care sector), The Estée Lauder Companies Inc. (Consumer Staples sector), Illinois Tool Works Inc. (Industrials sector), Valero Energy Corp. (Energy sector), Visa Inc. (Financials sector), and Raytheon Co. (Industrials sector). The Fund’s exchange traded fund (ETF) exposure saw Japanese and European equity ETFs deliver strong returns while a Chinese equity ETF and gold miner ETF represented the largest detractors. The Fund’s REIT holdings Crown Castle International Corp. and Prologis, Inc. contributed to Fund performance. We sold underperforming REITs such as Kimco Realty Corp., Boston Properties, Inc. and Ventas, Inc.

The Fund’s derivatives, namely the VIX volatility hedges had an overall drag on performance during the period. This was due to an expectation that volatility would increase when in fact, the market experienced an extraordinarily low level of volatility for most of the year. However, as volatility spiked up during the first calendar quarter of 2018, this hedge had a positive impact on returns.

Outlook

It appears the investment environment is becoming binary and extreme. After a robust return environment over the last few years, the recent increase in volatility should force risk managers to adjust to a more conservative stance. Moreover, now that U.S. tax cuts have been priced in it is not clear if there will be another catalyst to drive markets higher. Global debt levels remain elevated. This high leverage may exacerbate any moves in inflation, up or down. In addition, there is little tolerance for tighter money or higher interest rates. We are monitoring U.S. dollar movements and Fed actions to assess the tightness of financial conditions. The tone from Washington D.C. remains protectionist on global trade and the new Fed chairman appears determined to normalize interest rates by raising them to match inflation.

Our base case scenario continues to call for a reflationary environment, though we are not expecting significant inflation in 2018. There is no change in our belief that inflation risks persist, or that in the remainder of this year, these risks are rising. Over the near- to medium-term, we continue to view inflation as likely to surprise

Management's Discussion of Fund Performance (Unaudited) (Continued)

to the upside. Global labor markets continue to tighten, the U.S. dollar remains weak and an uptrend in oil and other commodity prices prevail. Tax stimulus in the U.S. also contributes to a more inflationary environment, which could make economic growth less sustainable. Finally, implementation of Chinese reforms may actually stifle growth but, for the moment, it appears any slowdown will be mild. We are keeping a close eye on China, which is now the world’s second largest economy.

The Fund continues to be defensively positioned, as we believe the market environment will be more volatile going forward driven by its less than certain view on central bank policy, as well as the prospect of an end to the strong move higher in global economic growth. Therefore, we think remaining focused on high-quality securities and patiently waiting for opportunity is paramount.

Dividend-paying investments may not experience the same price appreciation as non-dividend paying instruments, dividend-issuing companies may choose not to pay a dividend, or the dividend may be less than what is anticipated.

Management's Discussion of Fund Performance (Unaudited) (Continued)

Comparison of the Change in Value of a $10,000 Investment in the

Touchstone Flexible Income Fund - Class A* and the Bloomberg Barclays U.S. Aggregate Bond Index

| * | The chart above represents performance of Class A shares only, which will vary from the performance of Class C shares, Class Y shares and Institutional Class shares based on the differences in sales loads and fees paid by shareholders in the different classes. The inception date of Class A shares, Class C shares, Class Y shares and Institutional Class shares was April 1, 2004, October 29, 2001, September 1, 1998 and September 10, 2012, respectively. Class A shares, Class C shares and Class Y shares performance information was calculated using the historical performance of the Fifth Third/Maxus Income Fund Investor shares, with an inception date of March 10, 1985, for periods prior to April 1, 2004, October 29, 2001 and September 1, 1998, respectively. Institutional Class shares performance information was calculated using the historical performance of Class Y shares for the periods prior to September 10, 2012. The returns have been restated for sales loads and fees applicable to Class A, Class C, Class Y and Institutional Class shares. The returns of the index listed above are based on the inception date of the Fund. |

| ** | The average annual total returns shown above are adjusted for maximum sales loads and fees, if applicable. The maximum offering price per share of Class A shares is equal to the net asset value (“NAV”) per share plus a sales load equal to 6.10% of the NAV (or 5.75% of the offering price). Class C shares are subject to a contingent deferred sales charge (“CDSC”) of 1.00%. The CDSC will be assessed on an amount equal to the lesser of (1) the NAV at the time of purchase of the shares being redeemed or (2) the NAV of such shares being redeemed, if redeemed within a one-year period from the date of purchase. Class Y shares and Institutional Class shares are not subject to sales charges. |

The performance of the above Fund does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Note to Chart

Bloomberg Barclays U.S. Aggregate Bond Index is an unmanaged index comprised of U.S. investment grade, fixed rate bond market securities, including government, government agency, corporate and mortgage-backed securities between one and ten years.

Management's Discussion of Fund Performance (Unaudited)

Touchstone Focused Fund

Sub-Advised by Fort Washington Investment Advisors, Inc.

Investment Philosophy

The Fund may invest in companies of any market capitalization. The Fund seeks to invest in companies that are trading below what is believed to be the estimate of their intrinsic value and have a sustainable competitive advantage or a high barrier to entry in place. The barrier(s) to entry can be created through a cost advantage, economies of scale, high customer loyalty or a government barrier (e.g. license or subsidy). Fort Washington believes that the strongest barrier to entry is the combination of economies of scale and high customer loyalty.

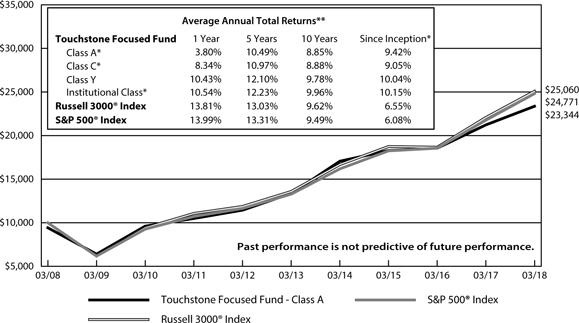

Fund Performance

The Touchstone Focused Fund (Class A Shares) underperformed its primary benchmark, the Russell 3000® Index (the “Index” or “benchmark”), and its secondary benchmark, the S&P 500® Index, for the 12-month period ended March 31, 2018. The Fund’s total return was 10.13 percent (calculated excluding the maximum sales charge), while the total return of the Russell 3000® Index was 13.81 percent and the total return of the S&P 500® Index was 13.99 percent.

Market Environment

In the last three quarters of 2017, U.S. equities continued the bull market that began in 2009 as the market experienced low volatility and ended the year near all-time highs. Solid financial conditions and strong profit growth were the key drivers. Markets benefited from an added boost in the later stages of 2017 as the White House and Congressional Republican leaders coalesced around a plan for tax reform. In the first quarter of 2018, the major theme in the U.S. equity market was the return of volatility. The primary drivers were concerns over higher interest rates and uncertainty about trade relations. The U.S. equity market experienced the first correction in more than a year and ended the quarter down slightly. Sectors that led the market higher included Information Technology, Financials, Industrials, and Consumer Discretionary. Telecommunication Services, Real Estate, Consumer Staples, Energy, and Utilities underperformed the Index during the period. The Health Care sector performed in line with the Index.

Portfolio Review

Within the Fund, the Real Estate, Consumer Discretionary, Financials, and Consumer Staples sectors outperformed relative to the benchmark. Sectors that lagged relative to the benchmark included Industrials, Energy, Information Technology, Materials, and Telecommunication Services. Stock selection detracted from Fund performance for the 12-month period. Sector allocation contributed primarily due to the underweights to Consumer Staples and Utilities and the overweight to Information Technology stocks. Cash holdings had a negative impact to performance given the positive move in the market.

The Fund’s top contributing stocks relative to the benchmark were Amazon.com Inc., Yum China Holdings Inc. (both Consumer Discretionary sector) and Jones Lang Lasalle Inc. (Real Estate sector). Amazon.com rose due to acceleration of growth in Prime and Amazon Web Services. Yum China rose primarily due to higher margins and strength in its KFC brand in the Chinese market. Jones Lang Lasalle rose on higher fee revenue from leasing and property management.

Stocks that detracted the most include General Electric Co., Stericycle Inc. (both Industrials sector) and Simon Property Group Inc. (Real Estate sector). General Electric declined due to weakness in oil, gas, and power end markets combined with the guidance and dividend reset among other concerns. Stericycle fell on pricing pressure among small quantity medical waste customers and weakness in its communication services unit. Simon Property Group declined primarily due to investor concerns about an over-supplied retail sector in the U.S.

Management's Discussion of Fund Performance (Unaudited) (Continued)

From a market cap perspective, the Fund maintained an underweight to smaller-cap stocks (companies with a market cap below $2 billion). The Index weight to this segment is 4.0 percent compared to 0.0 percent for the Fund. The Fund remained underweight to mid-cap businesses, which now comprise 10.5 percent of assets, compared to an Index weight of 13.4 percent. Lastly, the Fund continued to maintain an overweight to larger-cap businesses (companies with a market cap above $10 billion). The Fund’s weight to that segment is currently 87.1 percent versus the Index weight of 82.6 percent.

During the period, the Fund bought Starbucks Corp. (Consumer Discretionary sector), Signature Bank, Bank of the Ozarks Inc. (both Financials sector), and Facebook Inc. (Information Technology sector). The Fund sold Vista Outdoor Inc. (Industrials sector), Abbott Laboratories (Health Care sector),The Bank of New York Mellon Corp. (Financials sector), World Fuel Services Corp. (Energy sector), and CVS Health Corp. (Consumer Staples sector).

As of the end of the 12-month period, the Fund had an overweight to the Consumer Discretionary, Information Technology, Financials, and Real Estate sectors and an underweight to the Consumer Staples, Energy, Materials, and Industrials sectors. The weights in the Health Care and Telecommunication Services sectors were generally equal to the Index. No positions were held in Utilities at the end of the quarter.

Outlook

While we do not see signs of what typically causes a severe pullback, Fund positioning reflects our belief that we are in the later stages of the market cycle. As we continue to look for businesses that we believe are mispriced by the market, we have been gradually improving the quality of the Fund’s portfolio with stocks of companies that tend to have higher returns on capital, less debt on their balance sheets, strong cash flow generation and high barriers to entry.

Management's Discussion of Fund Performance (Unaudited) (Continued)

Comparison of the Change in Value of a $10,000 Investment in the

Touchstone Focused Fund - Class A*, the Russell 3000® Index and the S&P 500® Index

| * | The chart above represents performance of Class A shares only, which will vary from the performance of Class C shares, Class Y shares and Institutional Class shares based on the differences in sales loads and fees paid by shareholders in the different classes. The inception date of Class A shares, Class C shares, Class Y shares and Institutional Class shares was September 30, 2003, April 12, 2012, February 12, 1999 and December 20, 2006, respectively. Class A shares, Class C shares and Institutional Class shares performance information was calculated using the historical performance of Class Y shares for the periods prior to September 30, 2003, April 12, 2012 and December 20, 2006, respectively. The returns have been restated for sales loads and fees applicable to Class A, Class C and Institutional Class shares. The returns of the indexes listed above are based on the inception date of the Fund. |

| ** | The average annual total returns shown above are adjusted for maximum sales loads and fees, if applicable. The maximum offering price per share of Class A shares is equal to the net asset value (“NAV”) per share plus a sales load equal to 6.10% of the NAV (or 5.75% of the offering price). Class C shares are subject to a contingent deferred sales charge (“CDSC”) of 1.00%. The CDSC will be assessed on an amount equal to the lesser of (1) the NAV at the time of purchase of the shares being redeemed or (2) the NAV of such shares being redeemed, if redeemed within a one-year period from the date of purchase. Class Y shares and Institutional Class shares are not subject to sales charges. |

The performance of the above Fund does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Notes to Chart

Russell 3000® Index measures the performance of the 3,000 largest U.S. companies based on total market capitalization, which represents approximately 98% of the investable U.S. equity market.

S&P 500® Index is a group of 500 widely held stocks and is commonly regarded to be representative of the large capitalization stock universe.

The Frank Russell Company (FRC) is the source and owner of the Russell 3000® Index data contained or reflected in this material and all trademarks and copyrights related thereto. The material may contain confidential information and unauthorized use, disclosure, copying, dissemination or redistribution is strictly prohibited. This is a Touchstone Investments presentation of the data, and FRC is not responsible for the formatting or configuration of this material or for any inaccuracy in the presentation thereof.

Management's Discussion of Fund Performance (Unaudited)

Touchstone Growth Opportunities Fund

Sub-Advised by Westfield Capital Management Company, L.P.

Investment Philosophy

The Touchstone Growth Opportunities Fund seeks long-term growth of capital by primarily investing in stocks of U.S. companies with large, medium and small market capitalizations. The Fund’s portfolio managers place focus on companies they believe to have demonstrated records of achievement with excellent prospects for earnings growth over a 1- to 3-year period. Westfield looks for companies that it believes are reasonably priced with high forecasted earnings potential.

Fund Performance

The Touchstone Growth Opportunities Fund (Class A Shares) underperformed its benchmark, the Russell 3000® Growth Index, for the 12-month period ended March 31, 2018. The Fund’s total return was 19.51 percent (calculated excluding the maximum sales charge), while the total return of the benchmark was 21.06 percent.

Market Environment

U.S. equity markets started the quarter much like they ended 2017 with strong returns and limited volatility. These gains were supported by continued strength in the underlying economy, robust earnings growth in corporate America, and further propelled by the stimulus of tax reform. However, as the quarter unfolded, volatility returned to the markets as investors grew concerned about the impact of rising inflation and the potential that the U.S. Federal Reserve Board may alter the course of expected future rate hikes. The political backdrop contributed to the market gyrations as escalating trade tensions between the U.S. and China called into question the continuation of synchronized global growth, which had been present over the preceding year.

Portfolio Review

Relative weakness in the Health Care and Industrials sectors outweighed relative strength in the Consumer Staples and Information Technology sectors.

The Health Care sector was the Fund’s largest source of weakness. Celgene Corp., a global biopharmaceutical company focused on discovering therapies for the treatment of cancer and immune-inflammatory diseases, was the Fund’s largest detractor in the sector. This long-term holding sold off in October after missing third quarter consensus estimates for psoriasis drug Otezla and lowering 2020 guidance. While the overall cut to long-term guidance was modest, the resultant revenue share increase from the business’s core franchise Revlimid raised concerns among investors as to the company’s ability to diversify away from its marquee drug over time. Despite disappointment with the quarterly report and the subsequent stock decline, we maintained the Fund’s investment. We believe the breadth of the late-stage pipeline, as well as deployment of the cash flow associated with the Revlimid franchise into additional assets should allow the company to successfully diversify its revenue concentration away from the drug over time. Medicines Co., which is developing an exciting cholesterol-lowering agent, was also a detractor from relative returns for the period. Investors had been anticipating a mergers and acquisitions (M&A) deal, but punished the stock when a deal failed to materialize. Our thesis on Medicines, however, is more long term in nature and focuses on the company’s Phase 3 product candidate for cholesterol management. Clinical data published for the product thus far has been encouraging and we believe the drug could become a key driver of revenue generation in the future for the company.

The Industrials sector was another area of weakness for the period. Industrial distributor HD Supply Holdings Inc. was the sector’s largest relative detractor. The company’s price declined sharply in early June, following its quarterly earnings report. Although the earnings reported were in line with management’s initial guidance,

Management's Discussion of Fund Performance (Unaudited) (Continued)

they were slightly below consensus expectations and resulted in negative price action. Following an extensive internal review, the investment was sold out of the Fund as we lost faith in the company’s ability to meet its profitability goals. Manufacturer of air and ventilation systems Ingersoll-Rand PLC was also a relative detractor for the period. We purchased the stock back in April 2017 on the premise that the company would benefit from organic growth in the commercial construction markets given its HVAC (or heating, ventilation, and air conditioning) exposure. However, earnings reported during the last two quarters of 2017 showed somewhat disappointing results. Margins in the company’s Climate business segment were compressed by higher than expected raw material costs as well as heavy investment in a Chinese sales force for this segment, the latter of which management thought would position the company for long-term growth. Going forward, Ingersoll-Rand thinks it can offset these margin headwinds through pricing power. Despite the stock’s weakness, the Fund remains invested in the stock believing these margin headwinds to be temporary.

Consumer Staples was the Fund’s top-performing sector, contributing to relative returns primarily through an underweight positioning to the sector. The Fund remained underexposed to the sector as many of the constituents of the group lacked the growth and valuation profiles we seek in investments. However, the Fund maintains select investments with a bias to own above-average growers such as those involved in the sale of imported beer and reduced-risk cigarettes. For example, Constellation Brands Inc. is a producer and distributor of alcoholic beverages, and was the sector’s top relative performer. Improvement in the company’s beer business segment has been key to our investment thesis, and the company has been delivering on this front. Constellation generates ample free cash flow and we think they should execute on share repurchases down the road. Additionally, it has been encouraging to see the price recover and move higher from the declines experienced in the wake of the U.S. election and the corresponding Mexican/American trade policy uncertainty. We continue to believe that the company has painted a credible picture of how it will navigate various trade scenarios and with more clarity on the policy front, we believe the stock should maintain its momentum.

The Information Technology sector contributed to relative returns through positive stock selection. The Fund’s position in Red Hat Inc., a provider of open-source software solutions to various enterprises worldwide, was the sector’s top relative performer. Recent comments from the company’s Chief Executive Officer indicated that the company is facing pent-up demand in terms of technology spending from corporate decision makers. The company has also seen a recent resurgence in its core business which is taking share from UNIX and Windows. ServiceNow Inc., the leading provider of SaaS/cloud IT service management software, also enhanced the sector’s relative returns. The stock accelerated into the company’s latest round of quarterly results which came in ahead of Wall Street expectations and saw the company raise forward guidance. ServiceNow has compelling top-line growth and is generating meaningful cash flow, which we believe sets them apart from most other high-growth technology companies.

Outlook

As a fundamental, bottom-up manager, macro-economic forecasts do not drive our stock selection process, but do help to shape our investment themes. With that said, we look forward to markets normalizing and fundamentals once again driving stock prices. We believe the current environment is becoming more favorable to active security selection as intra-stock correlations have receded and idiosyncratic drivers, such as earnings, are helping to determine asset valuations. We further think these developments should favor bottom-up GARP (“growth-at-a-reasonable-price”) managers such as Westfield. At present, the Fund is focused on stocks that can benefit from such factors as tax reform, fiscal stimulus, repatriation of money from overseas, and reduced regulation out of Washington D.C under Republican leadership. These measures, if implemented successfully, could help accelerate economic growth and drive further market gains.

We believe Energy represents one of the most compelling sectors of the market with good growth and attractive valuations. Oil prices have recovered off of 2016 lows, yet the Energy sector has been the worst performing

Management's Discussion of Fund Performance (Unaudited) (Continued)

segment of the market over the last year. Looking forward, we feel there is now a significant disconnect between floundering stock prices and fundamentals, which have now recovered. We are also entering a seasonally strong period for the sector as well. With that said, we continue to be selective within Energy, focusing our attention on low cost producers with the best geology within exploration and production companies, and refining assets that benefit from the tailwinds of increased demand and production growth in the U.S.

As we exit the first quarter, risks appear balanced and we have structured the Fund accordingly. With increased volatility comes increased opportunity to identify and take advantage of favorable pricing in both directions and we believe this market environment plays into our strengths. While trade concerns make splashy headlines, we continue to believe the true driver of equity returns remains earnings and the domestic earnings growth story should remain intact for the time being. We are also keeping a keen eye on inflation developments and the pace of progress with regard to interest rates, as both have the potential to impact equity markets and optimal Fund positioning.

Management's Discussion of Fund Performance (Unaudited) (Continued)

Comparison of the Change in Value of a $10,000 Investment in the

Touchstone Growth Opportunities Fund - Class A* and the Russell 3000® Growth Index

| * | The chart above represents performance of Class A shares only, which will vary from the performance of Class C shares, Class Y shares and Institutional Class shares based on the differences in sales loads and fees paid by shareholders in the different classes. The inception date of Class A shares, Class C shares, Class Y shares and Institutional Class shares was September 29, 1995, August 2, 1999, February 2, 2009 and February 2, 2009, respectively. Class C shares, Class Y shares and Institutional Class shares performance information was calculated using the historical performance of Class A shares for periods prior to August 2, 1999, February 2, 2009 and February 2, 2009, respectively. The returns have been restated for sales loads and fees applicable to Class C, Class Y and Institutional Class shares. The returns of the index listed above are based on the inception date of the Fund. |

| ** | The average annual total returns shown above are adjusted for maximum sales loads and fees, if applicable. The maximum offering price per share of Class A shares is equal to the net asset value (“NAV”) per share plus a sales load equal to 6.10% of the NAV (or 5.75% of the offering price). Class C shares are subject to a contingent deferred sales charge (“CDSC”) of 1.00%. The CDSC will be assessed on an amount equal to the lesser of (1) the NAV at the time of purchase of the shares being redeemed or (2) the NAV of such shares being redeemed, if redeemed within a one-year period from the date of purchase. Class Y shares and Institutional Class shares are not subject to sales charges. |

The performance of the above Fund does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Notes to Chart

Russell 3000® Growth Index measures the performance of those Russell 3000® companies with higher price-to-book ratios and higher forecasted growth values.

The Frank Russell Company (FRC) is the source and owner of the Index data contained or reflected in this material and all trademarks and copyrights related thereto. The material may contain confidential information and unauthorized use, disclosure, copying, dissemination or redistribution is strictly prohibited. This is a Touchstone Investments presentation of the data, and FRC is not responsible for the formatting or configuration of this material or for any inaccuracy in the presentation thereof.

Management's Discussion of Fund Performance (Unaudited)

Touchstone International Growth Fund

Sub-Advised by Fiera Capital Inc.

Investment Philosophy

The Touchstone International Growth Fund seeks to achieve long-term capital growth by investing primarily in issuers located in developed markets utilizing an approach that combines “top-down” secular - and macro-economic trend analysis with “bottom-up” security selection. The “top-down” view seeks to provide a framework for “bottom-up” research by identifying sectors, industries and companies that may benefit from the sustainability of the observed trends. Fundamental “bottom-up” research is applied to identify individual companies that exhibit earnings growth potential and may benefit from observed secular- and macro-economic trends. The Fund typically invests in companies that are recognized as “established growth” companies which generally provide more stability and consistency in volatile markets. It also invests in companies that are in the earlier stages of their growth cycle that are known as “emerging growth” companies which typically exhibit more aggressive growth characteristics and may experience a significant positive transformation or a favorable catalyst impacting their long-term earnings potential.

Fund Performance

The Touchstone International Growth Fund (Class A Shares) outperformed its benchmark, the MSCI All Country World (ACWI) ex-U.S. Index, for the 12-month period ended March 31, 2018. The Fund’s total return was 19.35 percent (calculated excluding the maximum sales charge), while the total return of the benchmark was 16.53 percent.

Market Environment

International stocks outperformed U.S. Large-Cap stocks during the 12-month period ended March 31, 2018. This was in stark contrast to most of the post-financial crisis period in which international stocks trailed their U.S. counterparts. Emerging Markets performance over the past year told a similar story, where they outperformed U.S. large cap stocks and international stocks. In general, equity markets witnessed greater volatility during the first quarter of 2018 than in 2017. Since late January, markets around the world declined due to a variety of factors, including concerns over trade tariffs, valuation concerns and worries around the potential impact of a sharp rise in short-term interest rates.

During the 12-month period, all sectors within the Fund’s benchmark, the MSCI ACWI ex-U.S. Index produced positive gains. The Index was led by the Information Technology, Consumer Discretionary and Materials sectors. Fundamentals were strong for the Information Technology sector and valuation multiples expanded as expectations for future growth also increased. Commensurate with an increase in global economic growth, some of the cyclical sectors such as Consumer Discretionary and Materials, marginally outperformed the benchmark. The interest rate sensitive sectors (Real Estate, Telecommunication Services, Consumer Staples and Utilities) underperformed the Index, since a pickup in economic growth suggested that central banks around the developed world are more likely to increase short term interest rates and wind down their expansionary monetary policy operations. From a regional standpoint, most of the key emerging market regions produced strong gains. In Asia, a combination of a pickup in economic growth globally, a stabilization in domestic currencies relative to the dollar and an increase in corporate profitability across the region were the driving forces behind the strong performance. Eurozone, Japan and developed Asia also outperformed during the period, whereas the United Kingdom, Australia and Canada underperformed.

Portfolio Review

The Fund’s outperformance relative to its benchmark was due to a combination of sector allocation and stock selection. From a sector standpoint, overweights in the Information Technology and Consumer Discretionary

Management's Discussion of Fund Performance (Unaudited) (Continued)

sectors were key contributors to relative performance, while stock selection was strongest within the Financials and Consumer Staples sectors. In terms of specific stocks, Weibo Corp., Tencent Holdings Ltd., Alibaba Group Holding Ltd., Dassault Systemes SE and Sony Corp. were the largest contributors to performance, whereas Inditex SA, Grupo Aeroportuario del Sureste SAB CV, Luxoft Holding Inc., Subaru Corp., Hoya Corp. and Roche Holdings Ltd. were the largest detractors.

During the period, the Fund’s Emerging Markets allocation was increased, especially in Asia. Our optimism in this region stems from various factors that we believe are working in its favor. First, the global economy continued to gain momentum as indicated by the Purchasing Managers Index (PMI) numbers of various major regions. Second, currencies in the recent past that were major headwinds for many of the Emerging Markets countries due to deteriorating current account balances, are stabilizing and we believe might even become tailwinds going forward, as the current account balances showed improvement. We also either added to or initiated new Fund positions in many Emerging Markets companies that we believe will benefit from these trends but also because these companies were major beneficiaries of the secular themes that we find attractive. We also slightly increased the Fund’s exposure to Japan as we initiated new positions in companies that we believe are well positioned to benefit from the growth in industrial automation.

Outlook

Based on how the Fund is currently positioned, we believe the single biggest risk it faces is a sudden deterioration in the global macro situation. While we do not see signs of that happening anytime soon, we are paying attention to areas of the market that are currently weak, which may pose a risk to global recovery. Policy missteps such as trade wars could lead to a potential slowdown in economic activity. We believe a broader economic fallout of Brexit, political uncertainty in Europe or a reversal in Emerging Markets growth are risks that are worth monitoring. We are entering a new phase as central bankers across the developed markets are looking to exit their respective multi-year quantitative easing cycle as the global economic recovery strengthens. While we expect the tapering of the monetary easing to be gradual and measured, any substantial deviation from this or a sudden increase in interest rates could cause economic turmoil. While these issues are concerning and need to be monitored, we still believe there are reasons to be positive. Economic prospects across the globe look bright, and economic growth in the eurozone and Emerging Markets is strong.

We remain focused on individual companies with strong and sustainable organic growth backed by secular trends. Of particular interest are companies on the cutting edge of technology and those that benefit the most from the challenges of uncertainty. Examples include consumer mobility, big data and cloud computing, virtual reality, e-commerce and personalized medicine and genomics. We believe that these areas of long-term potential will be the key drivers in a more normalized market environment.

Management's Discussion of Fund Performance (Unaudited) (Continued)

Comparison of the Change in Value of a $10,000 Investment in the Touchstone International

Growth Fund - Class A* and the MSCI All Country World Ex-U.S. Index

| * | The chart above represents performance of Class A shares only, which will vary from the performance of Class C shares, Class Y shares and Institutional Class shares based on the differences in sales loads and fees paid by shareholders in the different classes. The inception date of Fund was March 31, 2016. The returns of the index listed above are based on the inception date of the Fund. |

| ** | The average annual total returns shown above are adjusted for maximum sales loads and fees, if applicable. The maximum offering price per share of Class A shares is equal to the net asset value (“NAV”) per share plus a sales load equal to 6.10% of the NAV (or 5.75% of the offering price). Class C shares are subject to a contingent deferred sales charge (“CDSC”) of 1.00%. The CDSC will be assessed on an amount equal to the lesser of (1) the NAV at the time of purchase of the shares being redeemed or (2) the NAV of such shares being redeemed, if redeemed within a one-year period from the date of purchase. Class Y shares and Institutional Class shares are not subject to sales charges. |

The performance of the above Fund does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Notes to Chart

MSCI All Country World Ex-U.S. Index measures the equity market performance of the non U.S. developed and emerging markets.

MSCI makes no express or implied warranties or representations and shall have no liability whatsoever with respect to any MSCI data contained herein. The MSCI data may not be further redistributed or used to create indices or financial products. This report is not approved or produced by MSCI.

Management's Discussion of Fund Performance (Unaudited)

Touchstone International Value Fund

Sub-Advised by Barrow, Hanley, Mewhinney & Strauss, LLC

Investment Philosophy

The Touchstone International Value Fund seeks long-term capital growth by primarily investing in equity securities of non-U.S. companies believed to be undervalued and seeks companies that have price-to-earnings and price-to-book ratios below the market, enterprise-value/free-cash-flow ratios at or below the market and dividend yields above the market.

Fund Performance

The Touchstone International Value Fund (Class A Shares) outperformed both of its benchmarks, the MSCI EAFE Value Index and the MSCI EAFE Index, for the 12-month period ended March 31, 2018. The Fund’s total return was 15.37 percent (calculated excluding the maximum sales charge), while the total return of the MSCI EAFE Value Index was 12.19 percent and the total return of the MSCI EAFE Index was 14.80 percent.

Market Environment

During the 12-month period ended March 31, 2018, investors reacted positively toward higher levels of global economic growth, driving stock markets to strong gains. The markets favored growth stocks over value stocks during this period, leading the MSCI EAFE Growth Index to outperform the MSCI EAFE Value Index by a meaningful margin. Stocks in the Information Technology sector, in particular, were strong drivers of outperformance, while the more defensive areas of the market, such as the Consumer Staples and Health Care sectors, fell out of favor with investors. Benefiting from a rally in crude oil and commodity prices, the Energy and Materials sectors enjoyed solid gains during the period.

Regionally, Emerging Markets stocks continued to outperform, far outpacing their developed market peers. During the 12-month period, Japan led the developed market rally, but still was unable to keep pace with its Emerging Markets counterparts. The U.K. was among the weakest performers, as investors’ concerns over Brexit (i.e., Britain’s exit from the European Union) continued to impact sentiment toward the region.

Portfolio Review

The Touchstone International Value Fund outpaced the MSCI EAFE Value Index for the 12-month period ended March 31, 2018. The Fund was aided by its strong security selection in the Financials and Consumer Discretionary sectors, which was partially offset by weaker stock picking in the Health Care and Consumer Staples market sectors. Fund positioning in the Industrials and Information Technology sectors also benefited relative returns.

Among the individual stocks that contributed to performance were Erste Group Bank AG, XL Group Ltd. (both from the Financials sector), Hitachi Ltd. (Information Technology sector), Fiat Chrysler Automobiles NV (Consumer Discretionary sector) and Ecopetrol SA (Energy sector). Erste Group is based in Austria and is one of the largest financial services providers in Central and Eastern Europe. The company benefited from a positive interest rate environment in the Czech Republic and Romania, along with favorable loan growth in its core market. XL Group is a global insurance company that generates the majority of its earnings from primary insurance and the remainder from reinsurance. XL contributed meaningfully after AXA, a French insurance conglomerate, announced its intent to acquire XL at a compelling premium. Hitachi is a highly diversified manufacturing corporation headquartered in Japan. The company outperformed during the period as it continued to execute well on its restructuring program which helped improve margins and increase profitability. Fiat Chrysler Automobiles is a global automotive original equipment manufacturer (OEM) that also outperformed during the period. Fiat reported strong profit growth as it continued to execute well on its strategic plan to reduce

Management's Discussion of Fund Performance (Unaudited) (Continued)

costs, improve margins and improve profitability. Columbia’s national oil company Ecopetrol added to relative results, benefiting from the tailwind of rising oil prices. Company specific drivers of the strong gains include its reduced debt load and an increase in its dividend.

Among the individual stocks that detracted from Fund performance were Imperial Brands PLC, Aryzta AG (both from the Consumer Staples sector) andTeva Pharmaceutical Industries Ltd. (Health Care sector). Imperial Brands is a U.K.-based cigarette, cigar and tobacco manufacturer that underperformed along with most other tobacco-related stocks during the year. The company faced added challenges due to its lack of a product in the heat-not-burn (or vapor) segment of the market. Imperial continued to trade at compelling valuations and we believe investor sentiment should change if the company can successfully bring its vapor product to market. Aryzta is a Switzerland-based food business with a primary focus on specialty baking, a niche segment of the overall bakery market. Aryzta fell short of its profit goals during the year as its North American operations were challenged by increasing labor and transportation costs. However, Aryzta has been in the process of selling assets, and a large divestiture remaining is food company Picard Surgelés SAS. The sale, combined with the stabilization of operating fundamentals, is expected to bolster the company’s balance sheet. Teva Pharmaceuticals, a multinational pharmaceutical company headquartered in Israel, continued to face challenges during the year due to falling generic drug prices and outside competition for its key drug COPAXONE®. The company was further impacted by challenges from a change in corporate management, a dividend cut and poor operating results during the year. As a result, we exited the Fund’s position.

Outlook

The turbulence in the markets during the most recent quarter marked a definitive turning point for investors who shrugged off many events last year. We believe many risks remain for equity and bond markets both here and around the globe, some of which began to unfold in the first quarter. An increased sensitivity to risk is occurring as markets around the globe are trading at above-average valuations. Notwithstanding the recent pull-back in stocks and even with the benefit of improving earnings growth, global equity markets are still trading well above their long-term averages. As we have discussed previously, these elevated valuations mean that market returns will likely be much more reliant on earnings growth and dividends than in the multiple expansion driven gains of recent years.

Previously, we have noted the risk of inflation across the globe as many central banks attempt to unwind nearly a decade of unprecedented easy monetary policies. With falling unemployment, high consumer confidence, higher energy costs and now added stimulus from the U.S. government, it would appear that prices are only set to move higher. As a result, we believe central banks may be forced to tighten monetary policies more quickly, causing economic growth to slow. We have begun to see this risk appear, as global economic indicators such as Purchasing Managers’ Indexes (PMIs) have pulled back from their recent highs. However, on the positive side, these indicators remain in expansion territory and, if they were to stabilize, we expect global economies to continue growing faster than during the last eight years. Investors’ sensitivity to risk is increasing as markets around the globe are trading at above-average valuations. Notwithstanding the recent pullback in stocks – even with the benefit of improved earnings growth – global equity markets have continued trading well above their long-term averages.

Looking forward, earnings expectations are forecast to grow rapidly, boosted by tax cuts and government spending. Given the extent to which this bull market has driven up valuations, it seems wise to focus on the contributions that earnings and dividends make to overall returns. As always, we seek stocks with meaningful valuation discounts to the overall market and those with the potential to return to normalized profitability that are underappreciated by investors. This is a sharp contrast to many of the highly-valued growth stocks with high embedded expectations for future profit growth. The Fund’s value process is built for the long-run and its long-term track record was based more closely on the long-term components of return than those of the current nine-year bull market.

Management's Discussion of Fund Performance (Unaudited) (Continued)

We believe that the next five years will not look like the past five years, with lower returns and increased volatility. This type of environment is when the Fund’s process has historically added the most value.

Dividend-paying investments may not experience the same price appreciation as non-dividend paying instruments, dividend-issuing companies may choose not to pay a dividend, or the dividend may be less than what is anticipated.

Management's Discussion of Fund Performance (Unaudited) (Continued)

Comparison of the Change in Value of a $10,000 Investment in the Touchstone International Value Fund - Class A*, the MSCI EAFE Value Index and the MSCI EAFE Index

| * | The chart above represents performance of Class A shares only, which will vary from the performance of Class C shares, Class Y shares and Institutional Class shares based on the differences in sales loads and fees paid by shareholders in the different classes. The inception date of Class A shares, Class C shares, Class Y shares and Institutional Class shares was August 18, 1994, April 25, 1996, October 9, 1998 and September 10, 2012, respectively. Class C shares, Class Y shares and Institutional Class shares performance information was calculated using the historical performance of Class A shares for periods prior to April 25, 1996, October 9, 1998 and September 10, 2012, respectively. The returns have been restated for sales loads and fees applicable to Class C, Class Y, and Institutional Class shares. The returns of the indexes listed above are based on the inception date of the Fund. |

| ** | The average annual total returns shown above are adjusted for maximum sales loads and fees, if applicable. The maximum offering price per share of Class A shares is equal to the net asset value (“NAV”) per share plus a sales load equal to 6.10% of the NAV (or 5.75% of the offering price). Class C shares are subject to a contingent deferred sales charge (“CDSC”) of 1.00%. The CDSC will be assessed on an amount equal to the lesser of (1) the NAV at the time of purchase of the shares being redeemed or (2) the NAV of such shares being redeemed, if redeemed within a one-year period from the date of purchase. Class Y shares and Institutional Class shares are not subject to sales charges. |

The performance of the above Fund does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Notes to Chart

MSCI EAFE Value Index captures large- and mid-cap securities exhibiting overall value style characteristics across developed markets countries around the world, excluding the U.S. and Canada.

MSCI EAFE Index is a free float-adjusted market capitalization index that is designed to measure developed market equity performance excluding the U.S. and Canada.

MSCI makes no express or implied warranties or representations and shall have no liability whatsoever with respect to any MSCI data contained herein. The MSCI data may not be further redistributed or used to create indices or financial products. This report is not approved or produced by MSCI.

Management's Discussion of Fund Performance (Unaudited)

Touchstone Mid Cap Growth Fund

Sub-Advised by Westfield Capital Management Company, L.P.

Investment Philosophy

The Touchstone Mid Cap Growth Fund seeks to increase the value of Fund shares by primarily investing in stocks of mid-cap U.S. companies. The Fund’s portfolio managers place focus on companies that they believe to have a demonstrated record of achievement with excellent prospects for earnings growth over a 1-to-3-year period. Westfield looks for companies that it believes are reasonably priced with high forecasted earnings potential.

Fund Performance

The Touchstone Mid Cap Growth Fund (Class A Shares) underperformed its benchmark, the Russell Midcap® Growth Index, for the 12-month period ended March 31, 2018. The Fund’s total return was 19.28 percent (calculated excluding the maximum sales charge), while the total return of the benchmark was 19.74 percent.

Market Environment

By the end of 2017, U.S. equity markets pushed most major indices to new highs and closed out the best calendar year returns for stocks since 2013. Underpinning the market strength was continued strong economic data which consistently supported the view that growth was accelerating both in the U.S. and abroad. However, as the first quarter of 2018 unfolded, volatility returned to the markets as investors grew concerned about the impact of rising inflation and the potential that the U.S. Federal Reserve Board may alter the course of expected future rate hikes. In addition, the political backdrop contributed to the market gyrations as escalating trade tensions between the U.S. and China called into question the continuation of synchronized global growth, which had been present over the preceding year.

Portfolio Review

Relative strength in the Energy, Consumer Staples, and Materials sectors offset relative weakness in the Real Estate and Industrials sectors.

The Energy sector was the Fund’s top contributor to relative performance. Stock selection within the group was particularly important over the period as the dispersion of returns was significant. Oil and gas refiner Andeavor was the top relative contributor. Even after the positive recent results, we continue to be excited about the prospects for the company going forward. New regulations soon to be implemented put a sulfur cap on global maritime shipping operations which will require maritime traffic to use relatively cleaner and more expensive diesel fuel. We anticipate that this change should enhance Andeavor’s earnings power by increasing demand for these more-refined, and importantly higher margin, fuels.

The Consumer Staples sector was also a source of strength during the period. Constellation Brands Inc., a producer and distributor of alcoholic beverages, was the sector’s top relative performer. Improvement in the company’s beer business segment has been key to our investment thesis, and the company has been delivering on this front. Constellation generates ample free cash flow and we think it should execute on share repurchases down the road. Additionally, it has been encouraging to see the stock price recover and move higher from the declines experienced in the wake of the U.S. election and the corresponding Mexican/American trade policy uncertainty. We continue to believe that the company has painted a credible picture of how it will navigate various trade scenarios and with more clarity on the policy front, we believe the stock should maintain its momentum.

Management's Discussion of Fund Performance (Unaudited) (Continued)

The Materials sector contributed to relative returns through a combination of stock selection and the Fund’s underweight to this market trailing sector. Avery Dennison Corp., a manufacturer of self-adhesive materials, retail tags, and specialty tapes, among other products, was the top relative performer in the sector. We consider fundamentals to be healthy and expect the company to continue to generate solid organic sales growth. Avery is a high-quality business with what we believe are sustainable competitive advantages as the company benefits from strong pricing power driven by its robust market share and fragmented customer base. The company has also shown its ability to smartly develop capital, which we think should serve it well as it embarks on its announced acquisition strategy.

The Real Estate sector was the Fund’s biggest source of relative weakness. American Campus Communities Inc., an owner of on-campus housing properties, was the sector’s largest relative detractor. It declined in September after reporting its final leasing results for the 2018 academic year which showed occupancy rates below consensus expectations and rental rate growth only at the mid-point of the prior guidance. We exited the stock in light of these developments. As we continue to progress into the current rising interest rate environment, we are managing the Fund’s exposure to this sector with selectivity geared towards those real estate investment trusts (REIT) which we expect to experience growth next year despite the challenging backdrop.

Fund positioning in the Industrials sector detracted from relative returns. Macquarie Infrastructure Corp., which invests in infrastructure companies located in the U.S., was the Fund’s biggest source of relative weakness during the period. The stock declined sharply following the company’s most recent quarterly earnings release in which Macquarie reported earnings before interest, taxes, depreciation and amortization (EBITDA) and distributable cash flow per share numbers that fell short of investor expectations due to a drop in the utilization rates of its tank and storage businesses. The company is repurposing storage tanks to shift away from residual and heavy oil given changing storage needs for these products and the resultant guidance adjustment lower from this change in strategy weighed heavily on the stock price. As a result of this negative development, we determined that exiting the position was the most prudent course of action.

Outlook

As a fundamental, bottom-up manager, macro-economic forecasts do not drive the stock selection process, but do help to shape our investment themes. With that said, we look forward to markets normalizing and fundamentals once again driving stock prices. We believe the current environment is becoming more favorable to active security selection as intra-stock correlations have receded and idiosyncratic drivers, such as earnings, are helping to determine asset valuations. We further think these developments should favor bottom-up GARP (“growth-at-a-reasonable-price”) managers such as Westfield. At present, the Fund is focused on stocks that have the ability to benefit from such factors as tax reform, fiscal stimulus, repatriation of money from overseas, and reduced regulation out of Washington D.C. under Republican leadership. These measures, if implemented successfully, could help accelerate economic growth and drive further market gains.

We believe Energy represents one of the most compelling sectors of the market with good growth and attractive valuations. Oil prices have recovered off of 2016 lows, yet the Energy sector has been the worst performing segment of the market over the last year. Looking forward, we believe there is now a significant disconnect between floundering stock prices and fundamentals, which have now recovered. We are also entering a seasonally strong period for the sector as well. We continue to be very selective within Energy, focusing our attention on low cost producers with the best geology within exploration and production companies, and refining assets that benefit from the tailwinds of increased demand and production growth in the U.S.

At the end of the first quarter of 2018, risks appeared balanced and we have structured the Fund accordingly. With increased volatility comes increased opportunity to identify and take advantage of favorable pricing in both directions and we believe this market environment plays into our strengths. While trade concerns make splashy headlines, we continue to believe the true driver of equity returns remains earnings and the domestic

Management's Discussion of Fund Performance (Unaudited) (Continued)

earnings growth story should remain intact for the time being. We are also keeping a keen eye on inflation developments and the pace of progress with regard to interest rates, as both have the potential to impact equity markets and optimal Fund positioning.

Management's Discussion of Fund Performance (Unaudited) (Continued)

Comparison of the Change in Value of a $10,000 Investment in the Touchstone Mid Cap Growth Fund - Class A* and the Russell Midcap® Growth Index

| * | The chart above represents performance of Class A shares only, which will vary from the performance of Class C shares, Class Y shares and Institutional Class shares based on the differences in sales loads and fees paid by shareholders in the different classes. The inception date of Class A shares, Class C shares, Class Y shares and Institutional Class shares was October 3, 1994, October 3, 1994, February 2, 2009 and April 1, 2011. Class Y shares and Institutional Class shares performance information was calculated using the historical performance of Class A shares for periods prior to February 2, 2009 and April 1, 2011, respectively. The returns have been restated for fees applicable to Class Y and Institutional Class shares. The returns of the index listed above are based on the inception date of the Fund. |

| ** | The average annual total returns shown above are adjusted for maximum sales loads and fees, if applicable. The maximum offering price per share of Class A shares is equal to the net asset value (“NAV”) per share plus a sales load equal to 6.10% of the NAV (or 5.75% of the offering price). Class C shares are subject to a contingent deferred sales charge (“CDSC”) of 1.00%. The CDSC will be assessed on an amount equal to the lesser of (1) the NAV at the time of purchase of the shares being redeemed or (2) the NAV of such shares being redeemed, if redeemed within a one-year period from the date of purchase. Class Y shares and Institutional Class shares are not subject to sales charges. |

The performance of the above Fund does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Notes to Chart

Russell Midcap® Growth Index measures the performance of those Russell Midcap® companies with higher price-to-book ratios and higher forecasted growth values.

The Frank Russell Company (FRC) is the source and owner of the Index data contained or reflected in this material and all trademarks and copyrights related thereto. The material may contain confidential information and unauthorized use, disclosure, copying, dissemination or redistribution is strictly prohibited. This is a Touchstone Investments presentation of the data, and FRC is not responsible for the formatting or configuration of this material or for any inaccuracy in the presentation thereof.

Management's Discussion of Fund Performance (Unaudited)

Touchstone Sands Capital Emerging Markets Growth Fund

Sub-Advised by Sands Capital Management, LLC

Investment Philosophy

The Touchstone Sands Capital Emerging Markets Growth Fund seeks long-term capital appreciation. The Fund invests in equity and equity-related securities issued by companies located in Emerging or Frontier Markets countries. The Fund’s sub-advisor, Sands Capital Management LLC, uses a “bottom-up” approach to investment selection, as opposed to sector or regional allocations that focuses on a company’s long-term business fundamentals. Sands Capital seeks companies that have: sustainable above-average earnings growth; a leadership position in a promising business space; significant competitive advantages such as profitability, superior quality or distribution relative to competitors or strong brand and consumer loyalty; a clear mission in an understandable business model; financial strength; and a rational valuation in relation to competitors, the market and business prospects.

Fund Performance

The Touchstone Sands Capital Emerging Markets Growth Fund (Class Y Shares) outperformed its benchmark, the MSCI Emerging Markets Index, for the 12-month period ended March 31, 2018. The Fund’s total return was 26.82 percent, while the total return of the benchmark was 24.93 percent.

Market Environment

Emerging Markets equities (as measured by the MSCI Emerging Markets Index) posted strong gains over the calendar year. The Information Technology sector was the strongest contributor to returns (with Chinese technology businesses accounting for a majority of the sector’s index contribution), and there were no detracting sectors, indicating market breadth. Only two countries—Qatar and Pakistan—modestly detracted from returns, while Chinese, South Korean, and Taiwanese businesses contributed the most.

Information Technology businesses posted strong results over the past year globally, as strong revenue and earnings growth translated into share price gains. Just three companies—Tencent Holdings Ltd., Alibaba Group Holding Ltd. and Taiwan Semiconductor Manufacturing Co. Ltd.—accounted for a majority of the sector’s overall contribution to the benchmark return. We believe these companies remain poised to benefit from the secular trends of increased internet connectivity, digital consumption and mobile access.

Solid corporate fundamentals were supported by broad economic strength. India posted the fastest year-over-year gross domestic product (GDP) growth among major economies, and Brazil finally returned to growth after two years of deep recession. In China, growth annually accelerated for the first time in seven years, and we believe President Xi Jinping’s consolidation of power could provide long-term stability, given his pro-growth policies. Additionally, a decline in the U.S. Dollar—coupled with an increase in oil prices—provided additional support.

As long-term investors, we attempt to look past external factors and stock price movements not explained by fundamentals. Market and macro environments change, and it is impossible to predict which sectors and countries will lead or lag on a short-term basis. Rather, we continue to believe that investing in leading franchises capable of generating above-average earnings growth across economic cycles is the most prudent way to add value over time.

Portfolio Review

During the 12-month period ended March 31, 2018, the largest five contributors to relative investment results were Alibaba Group Holding Ltd., MercadoLibre Inc., Jubilant Foodworks Ltd., Yandex NV and Medy-Tox Inc. MercadoLibre continued to take steps to widen its competitive moat and extend its market leadership,

Management's Discussion of Fund Performance (Unaudited) (Continued)

which drove strong topline results. In its most recently reported quarterly results, the company posted 63 percent gross merchandise volume (GMV) growth in U.S. dollar terms and 58 percent growth in units sold. The company saw strong contributions from Brazil and Mexico, where MercadoLibre recently introduced free shipping. This feature was launched recently in Argentina, which we believe should help sustain growth, because the country accounts for one-quarter of the company’s total revenue. E-commerce makes up less than five percent of total retail sales in Latin America, and MercadoLibre, domestic retailers and other internet businesses are all investing to accelerate retail’s shift from offline to online. While some work remains, we believe MercadoLibre’s existing market share leadership, strong brand recognition and third-party model will allow it to be one of the main beneficiaries of this shift and enjoy sustained above-average growth.

The top five detractors from relative investment results during the period were Hikma Pharmaceuticals PLC, Magnit PJSC, Siloam International Hospitals Tbk PT, Lupin Ltd. and Netshoes (Cayman) Ltd. We believe that the low liquidity of Siloam International Hospitals’ shares—along with relatively low current margins due to ongoing expansion—continued to overshadow the business’s underlying fundamentals. Siloam is the largest private healthcare group in Indonesia, and we believe it stands to benefit from the country’s hospital supply-demand imbalance. Gross revenue grew 16 percent year-over-year in the fourth quarter, in line with the longer-term growth trajectory we expect for the business. Earnings before interest, tax, depreciation and amortization (EBITDA) margins, excluding rental costs, showed meaningful improvement, increasing 230 basis points year-over-year to 18 percent, driven by increased profitability at established hospitals and narrowing losses at newer hospitals. Despite this, increased expansion efforts over the past year have depressed EBITDA margins and net margins—masking the underlying long-term earnings potential of the business. In 2017, the company opened eight new hospitals, increasing total bed count by 25 percent year-over-year. We expect this expansion to add value over time, as these hospitals mature and generate earnings, but patience may be required for the market to better appreciate this. While further expansion will continue to drag on margins, we believe this negative effect will be increasingly overwhelmed by Siloam’s growing base of more profitable, maturing hospitals. We expect annualized earnings growth in excess of 30 percent as the company continues to improve profitability over the next five years.

During the past 12 months, the following businesses were purchased: Avenue Supermarts Ltd., Bank Central Asia Tbk PT, Grupo Aeroportuario del Sureste SAB CV, Maruti Suzuki India Ltd., Netshoes (Cayman) Ltd., Sea Ltd. and Sunny Optical Technology (Group) Co. Ltd.

Avenue Supermarts (DMart) is the second-largest formal food retailer in India by revenue. Founded in 2001, Avenue Supermarts’s DMart chain now has a presence in over 30 cities with more than 100 stores, and is the industry leader in terms of sales per square foot, like-for-like sales growth, margins, operating costs and inventory turnover. DMart primarily caters to middle-class consumers across the food and grocery, fast-moving consumer goods and general merchandise and apparel categories. The majority of the company’s operations are in Gujarat and Majarashtra, which are two industrialized states with a combined population of nearly 200 million. Grocery remains a highly fragmented market in India, and we expect DMart to gain share as Indian consumers shift to modern store formats. In our view, government reform should further fuel this secular trend, which is likely to pressure margins for independent retailers. We believe that the combination of DMart’s operating model and the potential long-term structural tailwind supporting organized retail should allow Avenue Supermarts to sustain above-average annual revenue and earnings growth.