UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-03752

THE MANAGERS FUNDS

(Exact name of registrant as specified in charter)

800 Connecticut Avenue, Norwalk, Connecticut 06854

(Address of principal executive offices) (Zip code)

Managers Investment Group LLC

800 Connecticut Avenue, Norwalk, Connecticut 06854

(Name and address of agent for service)

Registrant’s telephone number, including area code: (203) 299-3500

Date of fiscal year end: DECEMBER 31

Date of reporting period: JANUARY 1, 2009 – December 31, 2009

(Annual Shareholder Report)

| Item 1. | Reports to Shareholders |

ANNUAL REPORT

Managers Funds

December 31, 2009

Managers AMG Essex Large Cap Growth Fund

Managers International Equity Fund

Managers Emerging Markets Equity Fund

Managers Global Bond Fund

Managers Money Market Fund

AR001-1209

The Managers Funds

Annual Report — December 31, 2009

TABLE OF CONTENTS

| | |

| | | Page |

LETTER TO SHAREHOLDERS | | 1 |

| |

ABOUT YOUR FUND’S EXPENSES | | 3 |

| |

INVESTMENT MANAGER’S COMMENTS, FUND SNAPSHOTS, AND SCHEDULES OF PORTFOLIO INVESTMENTS | | |

| |

Managers AMG Essex Large Cap Growth Fund | | 4 |

| |

Managers International Equity Fund | | 9 |

| |

Managers Emerging Markets Equity Fund | | 18 |

| |

Managers Global Bond Fund | | 25 |

| |

NOTES TO SCHEDULES OF PORTFOLIO INVESTMENTS | | 32 |

| |

FINANCIAL STATEMENTS: | | |

| |

Statements of Assets and Liabilities | | 33 |

Funds’ balance sheets, net asset value (NAV) per share computations and cumulative undistributed amounts | | |

| |

Statements of Operations | | 34 |

Detail of sources of income, Fund expenses, and realized and unrealized gains (losses) during the year | | |

| |

Statements of Changes in Net Assets | | 35 |

Detail of changes in Fund assets for the past two years | | |

| |

| MANAGERS MONEY MARKET FINANCIAL STATEMENTS: | | |

| |

Statement of Assets and Liabilities | | 37 |

Fund balance sheet, net asset value (NAV) per share computation and cumulative undistributed amount | | |

| |

Statement of Operations | | 37 |

Detail of sources of income, Fund expenses, and realized and unrealized gains (losses) during the year | | |

| |

Statement of Changes in Net Assets | | 38 |

Detail of changes in Fund assets for the past two years | | |

| |

| FINANCIAL HIGHLIGHTS | | 38 |

Historical net asset values per share, distributions, total returns, expense ratios, turnover ratios and net assets | | |

| |

| NOTES TO FINANCIAL STATEMENTS | | 41 |

Accounting and distribution policies, details of agreements and transactions with Fund management and affiliates, and descriptions of certain investment risks | | |

| |

| REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM | | 51 |

| |

| TRUSTEES AND OFFICERS | | 52 |

Nothing contained herein is to be considered an offer, sale or solicitation of an offer to buy shares of any series of the Managers Family of Funds. Such offering is made only by Prospectus, which includes details as to offering price and other material information.

Letter to Shareholders

Dear Shareholder:

Our foremost goal at Managers Investment Group (“MIG”) is to structure and manage mutual funds that will help our shareholders and clients successfully reach their investment goals and objectives.

Each of our Funds is geared to provide you with exposure to a specific asset class or style of investing. Investors tend to use our Funds as part of their broader portfolio in order to tailor their asset allocation to meet their individual needs. Most of our Funds, like those detailed in this report, are therefore designed to be building blocks.

At MIG, we have overall responsibility for the investment management and administration of the Funds. As a “manager of managers,” we work with external investment managers that make the day-to-day investment decisions in the Funds (the “Portfolio Managers”). We devote considerable resources to our disciplined process of identifying and selecting unaffiliated Portfolio Managers for the Funds. As a manager of managers, MIG performs many activities to monitor the ongoing investment, compliance, and administrative aspects of all of the Funds, which gives our shareholders added confidence in their investments.

Our parent company, Affiliated Managers Group (“AMG”) is a global asset management company with ownership interests in a diverse group of boutique investment management firms (its “Affiliates”). MIG has the unique opportunity to access the investment skills and acumen of some of AMG’s Affiliates. The set of our Funds managed by these proprietary firms also benefit from our activities to monitor the investment, compliance, and administrative aspects of the Funds.

Below is a brief overview of the securities markets and the performance results for the Funds. Following this letter, we also provide the Portfolio Managers’ discussion of their investment management approach, performance results, and market outlook.

The year 2009 will go down in the history books as one in which securities markets sank to unimaginable levels and some investors briefly questioned the viability of capitalism. As it turned out, capitalism did not cease to exist and equities, as well as credit-sensitive fixed income securities, managed to regroup and record one of the most impressive rebounds in the history of the capital markets. The government’s unprecedented efforts with respect to healing the economy and stabilizing the securities markets via programs such as the Troubled Asset Relief Program (“TARP”), the Public-Private Investment Program (“PPIP”) and the Term Asset-Backed Securities Loan Facility (“TALF”) seem to have achieved their desired short-term effects, although some would argue that the programs played a minor role in the stabilization of the markets and that free market forces simply corrected oversold conditions, just as they have on numerous occasions in the past.

Against this backdrop, the Managers AMG Essex Large Cap Growth Fund, Managers International Equity Fund, Managers Emerging Markets Equity Fund, and the Managers Global Bond Fund, (each a “Fund” and collectively the “Funds”), generated strong absolute returns in this historic environment, as detailed below. (Note that unless otherwise stated, all performance cited in these commentaries is in U.S. Dollars.)

| | | | | | | | | | | | | | | | | |

Periods Ended 12/31/09 | | 6 Months | | | 1 Year | | | 3 Years | | | 5 Years | | | 10 Years | | | Inception Date |

| | | | | | |

Managers AMG Essex Large Cap Growth Fund | | 16.78 | % | | 32.39 | % | | (4.08 | )% | | (0.77 | )% | | (7.31 | )% | | 6/1/1984 |

| | | | | | |

Russell 1000® Growth Index | | 23.03 | % | | 37.21 | % | | (1.89 | )% | | 1.63 | % | | (3.99 | )% | | |

| | | | | | |

Managers International Equity Fund | | 19.04 | % | | 31.68 | % | | (8.24 | )% | | 2.60 | % | | 0.19 | % | | 12/31/1985 |

| | | | | | |

MSCI EAFE Index | | 22.07 | % | | 31.78 | % | | (6.04 | )% | | 3.54 | % | | 1.17 | % | | |

| | | | | | |

Managers Emerging Markets Equity Fund | | 29.60 | % | | 67.94 | % | | (0.67 | )% | | 11.80 | % | | 8.61 | % | | 2/9/1998 |

| | | | | | |

MSCI EM Index (Net) | | 31.24 | % | | 78.51 | % | | 5.11 | % | | 15.51 | % | | 9.78 | % | | |

| | | | | | |

MSCI EM Index (Gross) | | 31.42 | % | | 79.02 | % | | 5.42 | % | | 15.88 | % | | 10.11 | % | | |

| | | | | | |

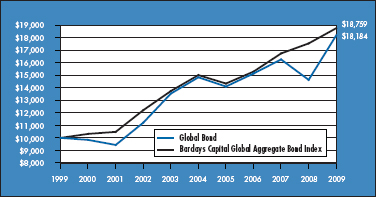

Managers Global Bond Fund | | 12.50 | % | | 24.26 | % | | 6.30 | % | | 4.15 | % | | 6.16 | % | | 3/25/1994 |

| | | | | | |

Barclays Capital Global Aggregate Bond Index | | 5.33 | % | | 6.93 | % | | 7.05 | % | | 4.56 | % | | 6.49 | % | | |

| | | | | | |

Money Market Fund | | 0.00 | % | | 0.27 | % | | 2.64 | % | | 3.05 | % | | 2.80 | % | | 6/1/1984 |

| | | | | | |

Merrill 3 Month T-Bill | | 0.11 | % | | 0.21 | % | | 2.41 | % | | 3.02 | % | | 2.99 | % | | |

1

Letter to Shareholders (continued)

As noted above, for the year ended December 31, 2009, the Managers AMG Essex Large Cap Growth Fund returned 32.39%, underperforming the Russell 1000® Growth Index, which returned 37.21%. In 2009, large-cap growth stocks performed very well on an absolute basis and also fared well versus other major domestic investment categories For example, large-cap growth stocks outperformed small-cap value stocks by almost 17% for the year thanks partly to strength in the technology sector. The primary driver of the Fund’s underperformance for the year relative to the benchmark was weak relative stock selection in the healthcare and industrial segments. In industrials, the key detractor was the Fund’s exposure to airlines while in health care, biotechnology exposure weighed heavily on results.

As noted above, for the year ended December 31, 2009, the Managers International Equity Fund returned 31.68%, trailing the return of 31.78% for its benchmark, the MSCI EAFE Index. Solid results for the Fund were primarily driven by non-benchmark exposure to the emerging markets and solid stock selection within the financials sector. This solid stock selection was somewhat mitigated, however, by weakness within the industrials sector and by holdings within Japan which failed to keep up with the broader global equity rally.

As noted in the table above, for the year ended December 31, 2009, the Managers Emerging Markets Fund returned 67.94%, trailing the return of 78.51% for its benchmark, the MSCI Emerging Markets Index. Much of the underperformance was concentrated during the first quarter of the year, prior to the markets’ recovery. The Fund was early in positioning for the eventual recovery, which weighed on first quarter performance. For the full year, stock selection within India and South Africa were the largest detractors from relative performance. On the other hand, the Fund benefited from an overweight position in Russia, an underweight to Mexico, and strong stock selection within Brazil.

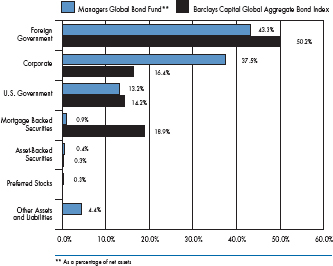

As noted in the table above, for the year ended December 31, 2009, the Managers Global Bond Fund returned 24.26%, widely outpacing the return of 6.93% for the Barclay’s Capital Global Aggregate Bond Index. The Fund’s greater-than-benchmark allocation to U.S. investment-grade corporate bonds and an underweight to U.S. Treasuries were the primary drivers of excess performance during the period. The Fund’s overweight Norwegian Krone, South Korean Won, and Canadian Dollar positions enhanced returns as these currencies appreciated on increasing global growth prospects and increasing risk appetites.

The following report covers the one-year period ended December 31, 2009. Should you have any questions about this report, or if you’d like to receive a prospectus and additional information, including fees and expenses for these or any of the other Funds in our family, please feel free to contact us at 1-800-835-3879, or visit our Web site at www.managersinvest.com. As always, please read the prospectus carefully before you invest or send money.

If you are curious about how you can better diversify your investment program, visit the Knowledge Center on our Web site and view our articles in the investment strategies section. You can rest assured that under all market conditions our team is focused on delivering excellent investment management services for your benefit.

We thank you for your continued confidence and investment in The Managers Funds.

Respectfully,

|

|

| John H. Streur |

| Senior Managing Partner |

| Managers Investment Group LLC |

2

About Your Fund’s Expenses

As a shareholder of a Fund, you may incur two types of costs: (1) transaction costs, which may include sales charges (loads) on purchase payments; redemption fees; and exchange fees; and (2) ongoing costs, including management fees; distribution (12b-1) fees; and other Fund expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds. The example is based on $1,000 invested at the beginning of the period and held for the entire period as indicated below.

Actual Expenses

The first line of the following table provides information about the actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The second line of the following table provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed annual rate of return of 5% before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds by comparing this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads), redemption fees, or exchange fees. Therefore, the second line of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds.

| | | | | | | | | | | | |

Six Months Ended December 31, 2009 | | Expense Ratio

for the Period | | | Beginning

Account Value

7/1/2009 | | Ending

Account Value

12/31/2009 | | Expenses Paid

During the

Period* |

| | | | |

Managers AMG Essex Large Cap Growth Fund | | | | | | | | | | | | |

| | | | |

Based on Actual Fund Return | | 1.61 | % | | $ | 1,000 | | $ | 1,168 | | $ | 8.80 |

| | | | |

Based on Hypothetical 5% Annual Return | | 1.61 | % | | $ | 1,000 | | $ | 1,017 | | $ | 8.19 |

| | | | |

Managers International Equity Fund | | | | | | | | | | | | |

| | | | |

Based on Actual Fund Return | | 1.48 | % | | $ | 1,000 | | $ | 1,190 | | $ | 8.17 |

| | | | |

Based on Hypothetical 5% Annual Return | | 1.48 | % | | $ | 1,000 | | $ | 1,018 | | $ | 7.53 |

| | | | |

Managers Emerging Markets Equity Fund | | | | | | | | | | | | |

| | | | |

Based on Actual Fund Return | | 1.77 | % | | $ | 1,000 | | $ | 1,296 | | $ | 10.24 |

| | | | |

Based on Hypothetical 5% Annual Return | | 1.77 | % | | $ | 1,000 | | $ | 1,016 | | $ | 9.00 |

| | | | |

Managers Global Bond Fund | | | | | | | | | | | | |

| | | | |

Based on Actual Fund Return | | 1.10 | % | | $ | 1,000 | | $ | 1,125 | | $ | 5.89 |

| | | | |

Based on Hypothetical 5% Annual Return | | 1.10 | % | | $ | 1,000 | | $ | 1,020 | | $ | 5.60 |

| | | | |

Managers Money Market Fund | | | | | | | | | | | | |

| | | | |

Based on Actual Fund Return | | 0.45 | %1 | | $ | 1,000 | | $ | 1,000 | | $ | 2.27 |

| | | | |

Based on Hypothetical 5% Annual Return | | 0.45 | %1 | | $ | 1,000 | | $ | 1,023 | | $ | 2.29 |

| * | Expenses are equal to the Fund’s annualized expense ratio multiplied by the average account value over the period, multiplied by the number of days in the most recent fiscal half-year (184), then divided by 365. |

| 1 | The ratio reflects the combined expenses of the Fund and the Capital Shares of the JPMorgan Liquid Assets Money Market Fund, the portfolio in which the Fund invests all of its assets. |

3

Managers AMG Essex Large Cap Growth Fund

Investment Manager’s Comments

For the year ended December 31, 2009, the Managers AMG Essex Large Cap Growth Fund (the “Fund”) returned 32.39%, under-performing the Russell 1000® Growth Index (the “Index), which returned 37.21%.

THE YEAR IN REVIEW:

Stabilizing home prices, improving global trade, and narrowing credit spreads boosted investor confidence that world economies are responding to the unprecedented policy actions implemented earlier in 2009. After several quarters of deteriorating U.S. economic conditions and falling economies overseas, rising expectations of global economic recovery benefited industrial, energy, and technology sectors. After bottoming out at half its value in 2008, financials staged an impressive rebound in March on the heels of the public/private bank plan. Investors then gravitated toward the sector, with banks and brokerage stocks leading in the second quarter of 2009, but finishing the calendar year lower as trading slowed as a result of corporate intentions to hang onto gains for the year. Consumer discretionary stocks also stepped to the front, outperforming most sectors for the year. Health care stocks remained in the penalty box as the debate on reform winds its way through Congress. Along the market capitalization and style spectrums, smaller-cap companies led the advance ceding to larger-sized companies in the fourth quarter, with growth stocks of all sizes outpacing the market averages.

Following a drumbeat of negative economic news early in the period, industrials rebounded based on expectations of an economic recovery but trailed the return of the Index. The Fund’s exposure in this segment weighed on relative performance. Specifically, returns were hampered by the Fund’s emphasis on engineering and contracting companies, which continued to be dragged down by the delayed impact of stimulus spending. The Fund’s holdings in AECOM Technology Corp., Quanta Services Inc., and URS Corp. were notable detractors. In addition, the Fund’s results were also negatively impacted by its exposure to air transport, which retreated following news that the industry issued downward short-term guidance.

The Fund benefited from its exposure to the materials segment with Freeport-McMoRan Copper & Gold Inc. and United States Steel Corp. leading the way. International pricing firmed during the period given an increase in coal and iron ore pricing. Both companies benefitted from these trends. Freeport-McMoRan Copper & Gold Inc. surpassed expectations, driven by commodity price increases for copper and gold. Following a turbulent year, fertilizer fundamentals bottomed during the fourth quarter, setting the stage for meaningful reacceleration in the near term. With fertilizer usage ultimately relying on firm crop pricing, strong phosphate trends show a tightened market with returning demand and thus upward pressure on pricing. This environment should have a positive impact on Potash Corp. of Saskatchewan Inc., which was a key contributor during the year.

In energy, a detrimental overweight allocation was more than offset by favorable stock selection. Offshore drilling company Transocean Ltd. benefitted from firm pricing as oil prices strengthened. Shares of Walter Energy, Inc. benefitted from an upsurge in metallurgical coal demand, with increased buying in China driving spot rates higher and generating positive sentiment for 2010 contract negotiations. Walter also began delivering more carry-over tonnage previously contracted at all-time record prices.

The 12-month period was volatile for consumer stocks. The group initially traded off on concerns about consumer spending in light of weakening employment and housing trends, but performance later rebounded as consumer sentiment was lifted. The Fund’s underweight position in the consumer staples sector had a positive impact but was partially offset by weak stock selection. The Fund’s results in the consumer discretionary sector were mixed. In retail, TJX Cos. and Kohl’s Corp. were both contributors for the period. Essex believes Kohl’s has a sustainable cost structure, thus implying that earnings flow will be even greater during a recovery. In contrast, the less cyclical education sector was a relative underperformer as investors worried about possible negative regulatory changes. The Fund’s holdings in the education sector included a position in Apollo Group Inc.

Financials experienced a robust turnaround in the middle of the period, led by banks and brokerage stocks. The Fund’s stock selection, however, led to underperformance relative to the benchmark. Financial services firms, Goldman Sachs Group Inc. and JPMorgan Chase & Co. accelerated in the first half of the period, driven by record capital markets revenues, a more favorable trading environment and stronger equity markets. Shares of JPMorgan pulled back later in the year, reflecting seasonal trends as the private equity market became more focused on protecting gains. Similarly, Intercontinental Exchange Inc. gave back gains, as its growth opportunities were dampened by regulatory risks limiting commodity speculation. Insurance companies, PartnerRe Ltd. and ACE Ltd., were detractors due to investor rotation out of more conservative financial stocks.

4

Managers AMG Essex Large Cap Growth Fund

Investment Manager’s Comments (continued)

Health care performance moderated in 2009, lagging the overall market as investors dealt with the uncertainties of political reform. The Fund’s overweight position detracted from performance. Genentech was the top contributor in the Fund for the 12-month period. Roche purchased the remainder of Genentech during the first quarter, causing the share price to leap. Also in biotech, Human Genome Sciences Inc. continued to benefit from positive Phase III results for its Lupus drug, Benlysta. Physicians remain optimistic as Benlysta is the first promising drug for Lupus to emerge in fifty years. Shares of Vertex Pharmaceuticals Inc. responded positively to late-stage trial results for their current Hepatitis C drug, and rumors of a potential suitor for acquisition. However, this was not enough to offset losses from Celgene Corp. and Baxter International Inc., which failed to participate in the market’s rally. St. Jude Medical Inc. suffered from near-term concerns over lower patient volumes and softness in hospital purchasing patterns. This position was eliminated during the fourth quarter. Gilead Sciences Inc., another detractor, took a hit following the news that Darusentan had failed its Phase III trial. Investors reacted pessimistically to the news as they questioned two of the company’s recent acquisitions, Myogen and CV Therapeutics. Essex believes this news event had a modest financial impact on the company and should not prove to be damaging long term.

Despite pressure early in the period due to economic concerns, technology stocks rose dramatically over the 12-month period. Overly bearish estimates were exceeded, and expectations for a turn in cyclical demand continue to propel the sector. In computer technology, Google, Inc. and Apple, Inc. both continued their upward march. Google continues to dominate market share for online searching, and Essex believes the advertising arena will improve in the coming quarter. Shares of Apple remain resilient upon continued strong adoption of the iPhone, international expansion, further penetration of markets as carrier contracts roll off, solid Mac sales trends, and the widely anticipated release of a new product, a tablet PC, in the first quarter. EMC Corp. also contributed to returns. These gains were offset by losses from Palm Inc. and STEC Inc. STEC suffered from competitive concerns and near-term inventory overhang at EMC Corp. Sales of Palm’s products at Sprint failed to show material upside, and investors have concerns about the success of the company’s smartphones against competition from Android, iPhone, and Blackberry. In software, the Fund’s holdings in Salesforce.com Inc. contributed to performance. The company’s cloud computing products continue to gain market share and customer loyalty based on its proven business model consistency.

LOOKING FORWARD

A year ago investors feared the worst, with the U.S. economy on the edge of a debt-deflation led downturn. Bold fiscal and monetary intervention averted this scenario, asset prices recovered, and the economy returned to growth in the third quarter of 2009. As we enter a new year, forecasters are divided on the shape and durability of the rebound: will it be a “V,” “W,” or something else? While the pace of recovery is likely to remain uneven over the next few quarters, Essex believes the positives of inventory restocking, rising exports to developing countries, and unspent government stimulus funds outweigh the negative headwinds of deleveraging. Essex expects inflation to be subdued for some time, allowing the Federal Reserve to keep interest rate hikes on hold for most of 2010. This benign interest rate backdrop coupled with an abundance of cash looking for higher returns should continue to provide support to stock prices.

Following a nearly 65% rise from the market lows last March, equity investors face a number of crosscurrents in the year ahead. Unexpected economic setbacks, worries about the budget deficit, and the speed by which the U.S. monetary authorities retreat from their accommodative policies will likely test financial markets. More importantly, further advances in stocks will require increasing earnings, and the outlook remains encouraging. Essex believes corporate profits have the potential to surprise on the upside in 2010, as operating leverage in an expanding global economy could be significant. In an earnings driven market, sector and stock selection will become more important in achieving superior relative returns. Essex continues to focus its efforts on companies across a number of industries with accelerating revenues and strong financial management, which should result in sustained earnings growth over the next several years.

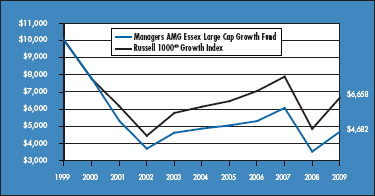

CUMULATIVE TOTAL RETURN PERFORMANCE

Managers AMG Essex Large Cap Growth Fund’s cumulative total return is based on the daily change in net asset value (NAV), and assumes that all dividends and distributions were reinvested. The Russell 1000® Growth Index is a market capitalization weighted index that measures the performance of those Russell 1000® companies with higher price-to-book ratio and higher forecasted growth values. Unlike the Fund, the Russell 1000® Growth Index is unmanaged, is not available for investment, and does not incur expenses. The Russell 1000® Growth Index is a trademark of Russell Investments. Russell® is a trademark of Russell Investments. The Index assumes reinvestment of dividends. This graph compares a hypothetical $10,000 investment made in Managers AMG

5

Managers AMG Essex Large Cap Growth Fund

Investment Manager’s Comments (continued)

CUMULATIVE TOTAL RETURN PERFORMANCE (continued)

Essex Large Cap Growth Fund on December 31, 1999, to a $10,000 investment made in the Russell 1000® Growth Index for the same time period. Performance for periods longer than one year is annualized. The graph and table do not reflect the deduction of taxes that a shareholder would pay on a Fund distribution or redemption of shares. The listed returns for the Fund are net of expenses and the returns for the index exclude expenses. Past performance is not indicative of future results. Total returns would have been lower had certain expenses not been reduced.

The table below shows the average annual total returns for Managers AMG Essex Large Cap Growth Fund and the Russell 1000® Growth Index from December 31, 1999 through December 31, 2009.

| | | | | | | | | |

Average Annual Total Returns1 | | One Year | | | Five Years | | | Ten Years | |

| | | |

Managers AMG Essex Large Cap Growth Fund2,3 | | 32.39 | % | | (0.77 | )% | | (7.31 | )% |

| | | |

Russell 1000® Growth Index | | 37.21 | % | | 1.63 | % | | (3.99 | )% |

The performance data shown represents past performance. Past performance is not a guarantee of future results. Current performance may be lower or higher than the performance data quoted. The investment return and principal value of an investment in the Fund will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. For performance information through the most recent month end, please call (800) 835-3879 or visit our Web site at www.managersinvest.com.

In choosing a Fund, investors should carefully consider the amount they plan to invest, their investment objectives, the Fund’s investment objectives, risks, charges and expenses before investing. For this and other information, please call (800) 835-3879 or visit www.managersinvest.com for a free prospectus. Read it carefully before investing or sending money. Distributed by Managers Distributors, Inc., member FINRA.

| 1 | Total return equals income yield plus share price change and assumes reinvestment of all dividends and capital gain distributions. Returns are net of fees and may reflect offsets of Fund expenses as described in the Prospectus. No adjustment has been made for taxes payable by shareholders on their reinvested dividends and capital gain distributions. Returns for periods greater than one year are annualized. The listed returns on the Fund are net of expenses and based on the published NAV as of December 31, 2009. All returns are in U.S. dollars($). |

| 2 | Fund for which, from time to time, the Fund’s advisor has waived its fees and/or absorbed Fund expenses, which has resulted in higher returns. |

| 3 | The Fund invests in large-capitalization companies that may underperform other stock funds (such as funds that focus on small- and medium-capitalization companies) when stocks of large-capitalization companies are out of favor. The Fund invests in growth stocks, which may be more sensitive to market movements because their prices tend to reflect future investor expectations rather than just current profits. Growth stocks may underperform value stocks during given periods. |

Not FDIC insured, nor bank guaranteed. May lose value.

6

Managers AMG Essex Large Cap Growth Fund

Fund Snapshots

December 31, 2009

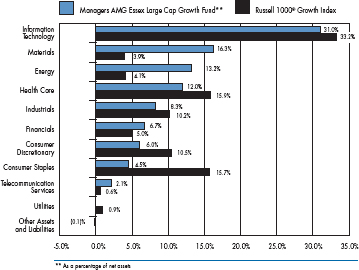

Portfolio Breakdown

| | | | | | |

Industry | | Managers AMG

Essex Large Cap

Growth Fund** | | | Russell 1000®

Growth Index | |

Information Technology | | 31.0 | % | | 33.2 | % |

Materials | | 16.3 | % | | 3.9 | % |

Energy | | 13.2 | % | | 4.1 | % |

Health Care | | 12.0 | % | | 15.9 | % |

Industrials | | 8.3 | % | | 10.2 | % |

Financials | | 6.7 | % | | 5.0 | % |

Consumer Discretionary | | 6.0 | % | | 10.5 | % |

Consumer Staples | | 4.5 | % | | 15.7 | % |

Telecommunication Services | | 2.1 | % | | 0.6 | % |

Utilities | | 0.0 | % | | 0.9 | % |

Other Assets and Liabilities | | (0.1 | )% | | 0.0 | % |

Top Ten Holdings

| | | |

Security Name | | Percentage of

Net Assets | |

Google, Inc.* | | 4.6 | % |

U.S. Steel Corp. | | 4.2 | |

Apple, Inc. | | 3.3 | |

Microsoft Corp.* | | 3.0 | |

Anadarko Petroleum Corp. | | 2.8 | |

FedEx Corp. | | 2.8 | |

Cisco Systems, Inc.* | | 2.7 | |

Goldman Sachs Group, Inc.* | | 2.4 | |

Celgene Corp. | | 2.2 | |

Walter Industries, Inc. | | 2.1 | |

| | | |

Top Ten as a Group | | 30.1 | % |

| | | |

| * | Top Ten Holding at June 30, 2009 |

Any sectors, industries, or securities discussed should not be perceived as investment recommendations. Mention of a specific security should not be considered a recommendation to buy or solicitation to sell that security. Specific securities mentioned in this report may have been sold from the Fund’s portfolio of investments by the time you receive this report.

7

Managers AMG Essex Large Cap Growth Fund

Schedule of Portfolio Investments

December 31, 2009

| | | | | | | |

| | | Shares | | | Value | |

Common Stocks - 100.1% | | | | | | | |

Consumer Discretionary - 6.0% | | | | | | | |

Harman International Industries, Inc. | | 4,669 | | | $ | 164,722 | |

Kohl’s Corp.* | | 5,466 | | | | 294,781 | |

Omnicom Group, Inc. | | 3,810 | | | | 149,162 | |

TJX Cos., Inc., The | | 7,271 | | | | 265,755 | |

Total Consumer Discretionary | | | | | | 874,420 | |

Consumer Staples - 4.5% | | | | | | | |

Costco Wholesale Corp. | | 3,704 | | | | 219,166 | |

PepsiCo, Inc. | | 4,901 | | | | 297,980 | |

Wal-Mart Stores, Inc. | | 2,646 | | | | 141,429 | |

Total Consumer Staples | | | | | | 658,575 | |

Energy - 13.2% | | | | | | | |

Anadarko Petroleum Corp. | | 6,612 | | | | 412,721 | |

Halliburton Co. | | 9,735 | | | | 292,926 | |

Occidental Petroleum Corp. | | 1,813 | | | | 147,488 | |

Petrohawk Energy Corp.* | | 7,817 | | | | 187,530 | |

Range Resources Corp. | | 2,952 | | | | 147,157 | |

Southwestern Energy Co.* | | 6,064 | | | | 292,285 | |

Tenaris, S.A. | | 7,011 | 2 | | | 299,019 | |

Weatherford International, Ltd.* | | 8,462 | | | | 151,554 | |

Total Energy | | | | | | 1,930,680 | |

Financials - 6.7% | | | | | | | |

Ameriprise Financial, Inc. | | 5,530 | | | | 214,675 | |

Goldman Sachs Group, Inc. | | 2,112 | | | | 356,590 | |

IntercontinentalExchange, Inc.* | | 721 | | | | 80,968 | |

Morgan Stanley Co. | | 5,830 | | | | 172,568 | |

State Street Corp. | | 3,394 | | | | 147,775 | |

Total Financials | | | | | | 972,576 | |

Health Care - 12.0% | | | | | | | |

Baxter International, Inc. | | 5,161 | | | | 302,847 | |

Celgene Corp.* | | 5,760 | | | | 320,717 | |

Genzyme Corp.* | | 3,518 | | | | 172,417 | |

Gilead Sciences, Inc.* | | 3,286 | | | | 142,218 | |

Human Genome Sciences, Inc.* | | 7,676 | | | | 234,886 | |

Medco Health Solutions, Inc.* | | 2,351 | | | | 150,252 | |

Teva Pharmaceutical Industries, Ltd., | | | | | | | |

Sponsored ADR | | 4,112 | | | | 231,012 | |

Vertex Pharmaceuticals, Inc.* | | 4,710 | | | | 201,824 | |

Total Health Care | | | | | | 1,756,173 | |

Industrials - 8.3% | | | | | | | |

Aecom Technology Corp.* | | 8,165 | | | | 224,538 | |

FedEx Corp. | | 4,826 | | | | 402,730 | |

Parker Hannifin Corp. | | 3,724 | | | | 200,649 | |

Quanta Services, Inc.* | | 7,881 | | | | 164,240 | |

United Technologies Corp. | | 3,179 | | | | 220,654 | |

Total Industrials | | | | | | 1,212,811 | |

Information Technology - 31.0% | | | | | | | |

Apple, Inc.* | | 2,296 | | | | 484,135 | |

ASML Holding, N.V. | | 5,489 | | | | 187,120 | |

Cisco Systems, Inc.* | | 16,613 | | | | 397,715 | |

CommScope, Inc.* | | 7,385 | | | | 195,924 | |

EMC Corp.* | | 17,681 | | | | 308,887 | |

Google, Inc.* | | 1,091 | | | | 676,398 | |

Marvell Technology Group, Ltd.* | | 14,741 | | | | 305,876 | |

MEMC Electronic Materials, Inc.* | | 12,732 | | | | 173,410 | |

Microsoft Corp. | | 14,465 | | | | 441,038 | |

Motorola, Inc. | | 36,556 | | | | 283,675 | |

ON Semiconductor Corp.* | | 27,045 | | | | 238,266 | |

Paychex, Inc. | | 6,631 | | | | 203,174 | |

QUALCOMM, Inc. | | 4,812 | | | | 222,603 | |

Salesforce.com, Inc.* | | 3,012 | | | | 222,195 | |

Yahoo!, Inc.* | | 11,240 | | | | 188,607 | |

Total Information Technology | | | | | | 4,529,023 | |

Materials - 16.3% | | | | | | | |

AK Steel Holding Corp. | | 13,673 | | | | 291,919 | |

Air Products & Chemicals, Inc. | | 1,749 | | | | 141,774 | |

Freeport McMoRan Copper & Gold, Inc., Class B* | | 2,567 | | | | 206,104 | |

Goldcorp, Inc. | | 7,684 | | | | 302,289 | |

Mosaic Co., The | | 3,843 | | | | 229,542 | |

Potash Corp. of Saskatchewan, Inc. | | 2,607 | | | | 282,860 | |

U.S. Steel Corp. | | 11,207 | | | | 617,729 | |

Walter Industries, Inc. | | 4,157 | | | | 313,064 | |

Total Materials | | | | | | 2,385,281 | |

Telecommunication Services - 2.1% | | | | | | | |

NII Holdings, Inc., Class B* | | 9,151 | | | | 307,291 | |

Total Common Stocks

(cost $12,042,850) | | | | | | 14,626,830 | |

Short-Term Investments - 2.2%1 | | | | | | | |

BNY Institutional Cash Reserves Fund, Series A, 0.05%3 | | 189,000 | | | | 189,000 | |

BNY Institutional Cash Reserves Fund, Series B*3,8 | | 119,397 | | | | 23,282 | |

Dreyfus Cash Management Fund, Institutional Class Shares, 0.08% | | 111,531 | | | | 111,531 | |

Total Short-Term Investments

(cost $419,928) | | | | | | 323,813 | |

Total Investments - 102.3%

(cost $12,462,778) | | | | | | 14,950,643 | |

Other Assets, less Liabilities - (2.3)% | | | | | | (338,325 | ) |

Net Assets - 100.0% | | | | | $ | 14,612,318 | |

The accompanying notes are an integral part of these financial statements.

8

Managers International Equity Fund

Investment Manager’s Comments

The Managers International Equity Fund’s (the “Fund”) investment objective is to achieve long-term capital appreciation. Income is the Fund’s secondary objective.

The Managers International Equity Fund ordinarily invests at least 80% of assets in equity securities, and at least 65% of assets in common and preferred stocks of companies domiciled outside the United States. The Fund intends to diversify investments among both countries and sectors. Investments may be made in companies in developed as well as developing countries. The Fund may also engage in currency-hedging strategies and may invest in companies of any size. The MSCI EAFE Index (the “Index”) is the benchmark for the Fund.

THE PORTFOLIO MANAGERS

The Fund employs multiple portfolio managers who specialize in distinct investment approaches. This “intelligence diversification” not only serves to manage risk, but also helps the Fund tap the market’s full potential by focusing different analytical insights on each potential investment. Fund management strives to achieve its performance goals and diversification while ensuring that the Fund operates within the framework of its investment objective and principal investment strategies.

AllianceBernstein L.P.’s Investment Research and Management (“AllianceBernstein”)

AllianceBernstein’s approach to investing is value-based and research-driven. The thesis of Bernstein’s investment philosophy is that human nature leads investors to buy and sell financial assets based on an overreaction to near-term events. They believe investors confuse temporary or cyclical characteristics with the creation of buying opportunities, as investors underestimate the potential for corrective strategies to restore long-term earnings power. The investment team, led by Kevin Simms, attempts to exploit this disconnect by using research to separate fact from emotion.

The primary driver of AllianceBernstein’s performance is research-driven security selection. AllianceBernstein screens their initial universe with a proprietary return model in order to identify the companies with the most attractive value attributes. The model derives an expected return for each company within the universe by assessing companies both from a global industry-based perspective and from a country-based standpoint, evaluating such factors as price-to-cash earnings, price-to-book, return on equity, and price momentum. The ideal company would exhibit strong fundamentals and have strong future business prospects.

Portfolio Construction

| • | | Initial investable universe is composed of all companies within the countries of the MSCI All Country World Index ex U.S. universe with a market capitalization greater than $750 million |

| • | | Investment team screens this universe using a proprietary-return model to identify the companies with the most attractive value attributes |

| | • | | The model derives an expected return for each company in the universe by assessing companies both from a global industry-based perspective and from a country-based standpoint |

| | • | | Factors include price-to-cash earnings, price-to-book, return on equity, and price momentum |

| • | | Analysts perform extensive research, focusing on the most attractively valued stocks |

| | • | | They then build detailed spreadsheets of historical and projected balance-sheet and income-statement information in order to estimate: |

| | • | | Normalized earnings power |

| | • | | Cash flow and asset values for each company for the next five years |

| | • | | Perform simulations to see the potential impact of changes in various financial-statement component |

| • | | Analysts present their estimates and ratings for each security to the Research Review Committee of the Investment Policy Group |

| | • | | The Committee challenges the analysts’ assumptions and conclusions to ensure they are sound |

The Portfolio

| • | | Typically holds 30-85 stocks |

| • | | Initial stock weightings are 0.5% - 3.5% |

Lazard Asset Management, LLC (“Lazard”)

Portfolio Manager William (Willy) Holzer believes that there is a single global economy and marketplace within which everything is connected. Within this single market it is important to distinguish between three types of companies: domestic companies are those that produce, sell, and raise capital all in their home country; international companies are those that produce at home, but sell their products and raise capital anywhere in the world; and global companies are those that produce, sell, and raise capital anywhere in the world. Holzer will invest in any of these types of companies

9

Managers International Equity Fund

Investment Manager’s Comments (continued)

in order to capitalize on a theme. However, he prefers global companies, which generally have the flexibility and resources to exploit global trends.

Willy Holzer can be described as a “top-down” thematic investor whose themes are based on bottom-up observations and company analysis. He views the world as a single global economic unit as opposed to a collection of separate country economies. Willy focuses his efforts by first analyzing the connections within the global economy and from this analysis develops global investment themes. These themes target the segments of the global economy that he believes are most likely to provide attractive long-term investment returns and that also represent an asymmetric investment opportunity in the investor’s favor.

Portfolio Construction

| • | | Portfolio Manager leverages stock ideas and research from top-down themes based on bottom-up observations and company analysis |

| • | | Portfolio is constructed around approximately ten investment themes to diversify opportunity sets and provide risk benefits |

| • | | Portfolio heavily weights large-capitalization, multi-national companies |

| | • | | Concentrated in the developed markets |

| | • | | May have operations or distribution in the emerging markets |

The Portfolio

| • | | Portfolio typically holds 90 to 110 stocks |

| • | | Initial stock weightings are 1.0% to 1.5% |

| • | | Relatively low turnover in the 30% to 40% annual range |

Martin Currie Inc. (“Martin Currie”)

Martin Currie, based in Edinburgh, Scotland, is a 128 year old firm. It specializes in developed market ex-U.S. mandates and currently manages $16.3 billion for a global client-base of pension funds, family offices, multi-managers, banks, public funds, foundations, sub-advisory clients and wrap programs. Willie Watt, the firm’s Chief Executive Officer, joined the firm in 2000 and was at the forefront of evolving Martin Currie from a firm that focused on adding value via a top-down investment process to its current process which uses bottom-up stock selection analysis as its primary portfolio management focus.

James Fairweather, Chief Investment Officer, heads the international equity investment team which has four members who have 71 years of total investment experience. The team is supported in their efforts by an experienced 14 person global sector analyst staff with no member having less than 8 years of total investment experience. In addition, regional teams also support the stock selection process by contributing insights and ideas on companies within their specific geographic coverage area. Finally, a separate risk management team helps support the portfolio construction.

Portfolio Construction

| • | | Focused on identifying companies at the earlier stages of change with the thought that the market usually underestimates the amount by which change will take place |

| • | | Team uses a fully integrated global approach to stock selection and use a high level of communication across regions to build a truly global portfolio |

| • | | Focus on speaking a common language when doing all stock level research with the emphasis on quality, value, growth, and change |

| • | | Risk is managed at every level of the investment process including when conducting stock selection and when constructing the portfolio |

The Portfolio

| • | | Portfolio typically holds 45 to 80 stocks |

| • | | Holdings tend to have low cross-stock correlations |

| • | | Holdings tend to have low sensitivity to macro factors |

| • | | Forecasted tracking error 4% to 6% relative to MSCI EAFE Index |

THE YEAR IN REVIEW

For the year 2009, the Fund returned 31.68% versus 31.78% for the Index. (Note that unless otherwise stated, all performance cited in this commentary is in U.S. Dollars).

Non-U.S. equity markets delivered strong returns in 2009, led by huge returns in emerging markets which returned 79%. After a tumultuous 2008, the coordinated fiscal and monetary efforts of global governments and central banks in 2009 resulted in increased liquidity throughout the year and served to thaw previously frozen credit markets. At the sector level, more cyclically oriented issues led the surge in performance as during the initial rebound investors’ favored higher beta, lower- quality stocks on speculation that the worst of the economic downturn was behind us. By the fourth quarter, however, the low-quality portion of the rally began to slow as investors became more selective and looked to companies with higher-quality balance sheets and sustainable business models.

10

Managers International Equity Fund

Investment Manager’s Comments (continued)

For the year 2009, positive results within the Fund were primarily driven by non-benchmark exposure in emerging markets. Each of the subadvisors within the Fund opportunistically invested in these developing markets and this paid off in 2009 as emerging markets appreciated more significantly than developed markets. Stock selection was mixed for the Fund throughout the year as solid performance within the Fund’s financial holdings was offset by weakness within the industrials sector. At the subadvisor level, AllianceBernstein was the Fund’s best performer driven by solid stock selection. AllianceBernstein’s strong stock selection was most evident in its financials holdings and within its technology and energy positions. AllianceBernstein diversified its risk within the financials sector in 2009 by adding to the number of holdings within this sector to minimize potential idiosyncratic stock risk and this strategy worked well as the sector enjoyed a large rebound. Lazard, the Fund’s best performer in 2008, modestly underperformed in 2009. Lazard largely maintained the same mix of themes they had identified at the start of 2008 and avoided any major portfolio changes. The best performing theme was related to opportunities in the emerging markets and, more specifically, related to opportunities in China and India where companies whose fortunes are tied to growth in infrastructure performed very well. On the downside, Lazard’s “Antimatter” theme which focuses on finding investment opportunities within Japan and taking advantage of positive political and economic change, detracted value as the Japanese equity market failed to keep pace with the broader global recovery in equities. Lazard remains committed to this theme and finds encouragement in the political changes that Japan experienced in 2009 as well as the valuations of its Japanese holdings. Finally, Martin Currie joined the Fund as a growth subadvisor in early 2009 and underperformed the benchmark for the portion of the year it was included in the Portfolio. Martin Currie’s underperformance was due, in part, to the weakness of growth investing in general for international equity managers in 2009 as well as due to its higher quality bias which left a good portion of Martin Currie’s holdings with solid positive performance that, nevertheless, trailed the broader international equity universe.

LOOKING FORWARD

As we enter into 2010, investors will be looking to find companies with sustainable earnings models now that the worst part of the recession appears behind us. Improved earnings are already being achieved by many international companies, although more often than not as a result of cost-cutting measures, not top-line growth. Regardless, the Fund’s subadvisors expect an improved macroeconomic environment going forward and suspect that the low-quality rally that dominated returns over the course of the last several quarters to come to an end. Our subadvisors anticipate increased stock selection opportunities as stock dispersion expands and the market sorts out who is better positioned as we enter a period of expected lower nominal GDP growth.

Overall, the Fund is positioned conservatively as our subadvisors remain cautious but optimistic about the opportunities that lie ahead. Developed equity markets look to face a headwind from continued deleveraging and tougher lending policies, fiscal tightening, and a potentially muted recovery in capital expenditures and jobs in 2010. If this scenario plays out, an above average premium will be paid for companies able to offer superior growth. Our subadvisors are finding opportunity in several areas of the market including exposure to emerging markets (either directly or through exposure to developed market companies with an emerging market client base). On a sector level, the Fund continues to maintain its largest weighting to the recovering financials sector and maintains an overweight to the information technology sector. Meanwhile, the Fund continues to maintain an underweight to the consumer areas of the market and will likely continue to do so, for the time being, as consumers take time to improve their personal balance sheets and pay down debt.

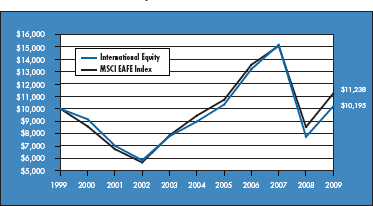

CUMULATIVE TOTAL RETURN PERFORMANCE

Managers International Equity Fund’s cumulative total return is based on the daily change in net asset value (NAV), and assumes that all distributions were reinvested. The Morgan Stanley Capital International Europe, Australasia, and Far East (MSCI EAFE) Index is composed of all the publicly traded stocks in developed non-U.S. Markets. The MSCI EAFE Index consisted of the following 21 developed market country indices: Australia, Austria, Belgium, Denmark, Finland, France, Germany, Greece, Hong Kong, Ireland, Italy, Japan, the Netherlands, New Zealand, Norway, Portugal, Singapore, Spain, Sweden, Switzerland and the United Kingdom. Unlike the Fund, the MSCI EAFE Index is unmanaged, is not available for investment, and does not incur expenses. The Index assumes reinvestment of dividends. This graph compares a hypothetical $10,000 investment made in Managers International Equity Fund on December 31, 1999, to a $10,000 investment made

11

Managers International Equity Fund

Investment Manager’s Comments (continued)

CUMULATIVE TOTAL RETURN PERFORMANCE (continued)

in the MSCI EAFE for the same time period. The table is not intended to imply any future performance of the Fund. Performance for periods longer than one year is annualized. The graph and table do not reflect the deduction of taxes that a shareholder would pay on a Fund distribution or redemption of shares. The listed returns for the Fund are net of expenses and the returns for the index exclude expenses. Past performance is not indicative of future results. Total returns would have been lower had certain expenses not been reduced.

The table below shows the average annual total returns for Managers International Equity Fund and the MSCI EAFE from December 31, 1999 through December 31, 2009.

| | | | | | | | | |

Average Annual Total Returns1 | | One Year | | | Five Years | | | Ten Years | |

| | | |

Managers International Equity Fund2,3,4 | | 31.68 | % | | 2.60 | % | | 0.19 | % |

| | | |

MSCI EAFE Index | | 31.78 | % | | 3.54 | % | | 1.17 | % |

The performance data shown represents past performance. Past performance is not a guarantee of future results. Current performance may be lower or higher than the performance data quoted. The investment return and principal value of an investment in the Fund will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. For performance information through the most recent month end, please call (800) 835-3879 or visit our Web site at www.managersinvest.com.

In choosing a Fund, investors should carefully consider the amount they plan to invest, their investment objectives, the Fund’s investment objectives, risks, charges and expenses before investing. For this and other information, please call (800) 835-3879 or visit www.managersinvest.com for a free prospectus. Read it carefully before investing or sending money. Distributed by Managers Distributors, Inc., member FINRA.

| 1 | Total return equals income yield plus share price change and assumes reinvestment of all dividends and capital gain distributions. Returns are net of fees and may reflect offsets of Fund expenses as described in the Prospectus. No adjustment has been made for taxes payable by shareholders on their reinvested dividends and capital gain distributions. Returns for periods greater than one year are annualized. The listed returns on the Fund are net of expenses an based on the published NAV as of December 31, 2009. All returns are in U.S. dollars($). |

| 2 | Fund for which, from time to time, the Fund’s advisor has waived its fees and/ or absorbed Fund expenses, which has resulted in higher returns. |

| 3 | Investments in foreign securities are subject to additional risks such as changing market conditions, economic and political instability, and currency exchange rate fluctuations. |

| 4 | The Fund is subject to currency risk resulting from fluctuations in exchange rates that may affect the total loss or gain on a non-U.S. Dollar security when converted back to U.S. Dollars. |

All MSCI data is provided “as is.” The products described herein are not sponsored or endorsed and have not been reviewed or passed on by MSCI. In no event shall MSCI, its affiliates or any MSCI data provider have any liability of any kind in connection with the MSCI data or the products described herein. Copying or redistributing the MSCI data is strictly prohibited.

Not FDIC insured, nor bank guaranteed. May lose value.

12

Managers International Equity Fund

Fund Snapshots

December 31, 2009

Portfolio Breakdown

| | | | | | |

Industry | | Managers

International

Equity Fund** | | | MSCI EAFE

Index | |

Financials | | 27.7 | % | | 25.5 | % |

Industrials | | 10.9 | % | | 11.2 | % |

Materials | | 9.0 | % | | 10.4 | % |

Health Care | | 8.6 | % | | 8.4 | % |

Energy | | 8.4 | % | | 8.3 | % |

Information Technology | | 7.9 | % | | 4.7 | % |

Consumer Staples | | 7.2 | % | | 10.1 | % |

Consumer Discretionary | | 7.0 | % | | 9.7 | % |

Telecommunication Services | | 5.1 | % | | 5.8 | % |

Utilities | | 3.7 | % | | 5.9 | % |

Other Equities | | 0.7 | % | | 0.0 | % |

Other Assets and Liabilities | | 3.8 | % | | 0.0 | % |

Top Ten Holdings

| | | |

Security Name | | Percentage of

Net Assets | |

Sanofi-Aventis SA* | | 2.2 | % |

Banco Santander Central Hispano, S.A. | | 1.9 | |

Vodafone Group PLC* | | 1.7 | |

BP PLC* | | 1.7 | |

E.ON AG* | | 1.7 | |

GlaxoSmithKline PLC* | | 1.6 | |

Societe Generale* | | 1.6 | |

Roche Holding AG | | 1.4 | |

Mitsui Fudosan Co., Ltd. | | 1.4 | |

Royal Dutch Shell PLC, Class A | | 1.3 | |

| | | |

Top Ten as a Group | | 16.5 | % |

| | | |

| * | Top Ten Holding at June 30, 2009 |

Any sectors, industries, or securities discussed should not be perceived as investment recommendations. Mention of a specific security should not be considered a recommendation to buy or solicitation to sell that security. Specific securities mentioned in this report may have been sold from the Fund’s portfolio of investments by the time you receive this report.

13

Managers International Equity Fund

Fund Snapshots (continued)

Summary of Investments by Country

| | | | | | |

Country | | Managers International

Equity Fund* | | | MSCI EAFE Index | |

Australia | | 0.9 | % | | 8.4 | % |

Austria | | 0.4 | % | | 0.3 | % |

Belgium | | 0.0 | % | | 1.0 | % |

Bermuda | | 0.0 | % | | 0.4 | % |

Brazil | | 3.1 | % | | 0.0 | % |

Canada | | 3.7 | % | | 0.0 | % |

Cayman Islands | | 0.5 | % | | 0.1 | % |

China | | 2.4 | % | | 0.0 | % |

Denmark | | 0.9 | % | | 0.9 | % |

Finland | | 0.8 | % | | 1.1 | % |

France | | 11.1 | % | | 10.5 | % |

Germany | | 9.4 | % | | 8.0 | % |

Greece | | 0.0 | % | | 0.5 | % |

Hong Kong | | 4.3 | % | | 1.9 | % |

India | | 0.5 | % | | 0.0 | % |

Ireland | | 0.0 | % | | 0.3 | % |

Israel | | 0.6 | % | | 0.0 | % |

Italy | | 2.3 | % | | 3.4 | % |

Japan | | 12.7 | % | | 20.7 | % |

Jersey, Channel Islands | | 0.0 | % | | 0.4 | % |

Luxembourg | | 0.5 | % | | 0.6 | % |

Netherlands | | 5.3 | % | | 2.9 | % |

New Zealand | | 0.0 | % | | 0.1 | % |

Norway | | 1.1 | % | | 0.7 | % |

Portugal | | 0.6 | % | | 0.3 | % |

Russia | | 1.1 | % | | 0.0 | % |

Singapore | | 1.1 | % | | 1.4 | % |

South Africa | | 0.7 | % | | 0.0 | % |

South Korea | | 2.5 | % | | 0.0 | % |

Spain | | 2.4 | % | | 4.6 | % |

Supranational & Other | | 0.0 | % | | 0.1 | % |

Sweden | | 0.4 | % | | 2.5 | % |

Switzerland | | 7.3 | % | | 7.6 | % |

Taiwan | | 2.4 | % | | 0.0 | % |

Turkey | | 0.4 | % | | 0.0 | % |

United Kingdom | | 16.4 | % | | 21.2 | % |

United States | | 4.2 | % | | 0.1 | % |

| | | | | | |

| | 100.0 | % | | 100.0 | % |

| | | | | | |

| * | As a percentage of total market value on December 31, 2009. |

14

Managers International Equity Fund

Schedule of Portfolio Investments

December 31, 2009

| | | | | | |

| | | Shares | | | Value |

Common Stocks - 95.5% | | | | | | |

Consumer Discretionary - 7.0% | | | | | | |

Bayerische Motoren Werke AG (Germany) | | 14,400 | | | $ | 655,520 |

Bridgestone Corp. (Japan) | | 32,000 | | | | 564,474 |

Cyrela Brazil Realty, S.A. (Brazil) | | 37,800 | | | | 531,936 |

Esprit Holdings Limited (Hong Kong) | | 35,147 | | | | 233,191 |

Lagardere (France) | | 11,700 | | | | 473,681 |

Marks & Spencer Group PLC (United Kingdom) | | 52,800 | | | | 341,138 |

Matsushita Electric Industrial Co., Ltd. (Japan) | | 39,300 | | | | 565,779 |

New World Department Store China, Ltd. (China) | | 53,000 | | | | 48,376 |

Nikon Corp. (Japan) | | 36,000 | | | | 710,873 |

Nissan Motor Co., Ltd. (Japan)* | | 80,700 | | | | 709,185 |

Parkson Retail Group, Ltd. (China) | | 78,500 | | | | 138,137 |

Pearson PLC (United Kingdom) | | 63,815 | | | | 914,976 |

Persimmon PLC (United Kingdom)* | | 73,517 | | | | 555,914 |

Toyota Motor Corp. (Japan) | | 28,800 | | | | 1,214,235 |

Vivendi Universal SA (France) | | 33,820 | | | | 1,003,767 |

Wolters Kluwer, N.V. (Netherlands) | | 1,837 | | | | 40,175 |

WPP PLC (United Kingdom) | | 17,000 | | | | 166,265 |

Total Consumer Discretionary | | | | | | 8,867,622 |

Consumer Staples - 7.2% | | | | | | |

Associated British Foods PLC (United Kingdom) | | 14,100 | | | | 186,928 |

British American Tobacco PLC (United Kingdom) | | 13,671 | | | | 443,805 |

Cadbury PLC (United Kingdom) | | 17,179 | | | | 220,880 |

Carlsberg A/S, Class B (Denmark) | | 12,407 | | | | 913,337 |

Casino Guichard-Perrachon SA (France) | | 5,000 | | | | 445,475 |

Diageo PLC (United Kingdom) | | 29,766 | | | | 519,300 |

Groupe Danone SA (France) | | 4,452 | | | | 272,916 |

Heineken N.V. (Netherlands) | | 17,977 | | | | 853,431 |

Koninklijke Ahold, N.V. (Netherlands) | | 89,542 | | | | 1,186,315 |

Metro AG (Germany) | | 10,348 | | | | 631,981 |

Nestle SA, Registered (Switzerland) | | 5,333 | | | | 258,830 |

Seven & i Holdings Co., Ltd. (Japan) | | 20,600 | | | | 420,620 |

Uni-President Enterprises Corp. (Taiwan) | | 209,098 | | | | 257,802 |

Unilever PLC (United Kingdom) | | 18,700 | | | | 599,434 |

Unilever N.V. (Netherlands) | | 34,781 | | | | 1,132,009 |

William Morrison Supermarkets PLC (United Kingdom) | | 182,054 | | | | 812,257 |

Total Consumer Staples | | | | | | 9,155,320 |

Energy - 8.4% | | | | | | |

BP PLC (United Kingdom) | | 223,240 | | | | 2,155,641 |

Canadian Natural Resources, Ltd. (Canada) | | 8,700 | | | | 632,213 |

Cenovus Energy, Inc. (Canada) | | 11,468 | | | | 290,579 |

China Shenhua Energy Co., Ltd. (China) | | 179,500 | | | | 871,348 |

EnCana Corp. (Canada) | | 10,968 | | | | 357,717 |

INPEX Corp. (Japan) | | 78 | | | | 589,766 |

LUKOIL Holdings, ADR (Russia) | | 16,400 | 2 | | | 924,960 |

Nexen, Inc. (Canada) | | 21,246 | | | | 512,334 |

Petroleo Brasileiro, S.A., Sponsored ADR (Brazil) | | 10,300 | | | | 491,104 |

Petroplus Holdings AG (Switzerland)* | | 29,280 | | | | 535,675 |

Rosneft Oil, GDR (Russia) | | 53,550 | | | | 457,047 |

Royal Dutch Shell PLC, Class A (Netherlands) | | 53,900 | | | | 1,624,113 |

StatoilHydro ASA (Norway) | | 35,600 | | | | 887,851 |

Suncor Energy, Inc. (Canada) | | 9,684 | | | | 344,544 |

Total Energy | | | | | | 10,674,892 |

Financials - 27.7% | | | | | | |

Allianz SE (Germany) | | 8,700 | | | | 1,078,451 |

Aviva PLC (United Kingdom) | | 32,243 | | | | 205,102 |

Banco do Brasil, S.A. (Brazil) | | 45,800 | | | | 781,310 |

Banco Santander, S.A. (Brazil) | | 34,600 | | | | 474,980 |

Banco Santander Central Hispano, S.A. (Spain) | | 145,829 | | | | 2,409,774 |

Bank of China, Ltd., Class H (China) | | 1,489,000 | | | | 800,176 |

Bank of East Asia, Ltd. (Hong Kong) | | 57,390 | 2 | | | 225,460 |

Bank of Yokohama, Ltd., The (Japan) | | 114,000 | | | | 519,779 |

Barclays PLC (United Kingdom)* | | 255,809 | | | | 1,127,210 |

BNP Paribas SA (France) | | 14,410 | | | | 1,142,972 |

CapitaLand, Ltd. (Singapore) | | 198,500 | | | | 588,862 |

CapitaMalls Asia, Ltd. (Singapore)* | | 130,000 | | | | 235,043 |

Cathay Financial Holding Co., Ltd. (Taiwan)* | | 184,300 | | | | 343,123 |

China Life Insurance Co., Ltd. (China) | | 170,000 | | | | 831,857 |

China Minsheng Banking Corp., Ltd. (China)* | | 78,500 | | | | 88,286 |

China Overseas Land & Investment, Ltd. (Hong Kong) | | 537,360 | 2 | | | 1,125,923 |

Chinatrust Financial Holding Co., Ltd. (Taiwan) | | 378,917 | | | | 235,559 |

Credit Agricole SA (France) | | 43,569 | | | | 764,629 |

Credit Suisse Group AG (Switzerland) | | 14,524 | | | | 719,539 |

Daiwa House Industry Co., Ltd. (Japan) | | 32,000 | | | | 344,087 |

Daiwa Securities Group, Inc. (Japan) | | 36,000 | | | | 181,175 |

The accompanying notes are an integral part of these financial statements.

15

Managers International Equity Fund

Schedule of Portfolio Investments (continued)

| | | | | | |

| | | Shares | | | Value |

Financials - 27.7% (continued) | | | | | | |

Danske Bank A/S (United States)* | | 9,700 | | | $ | 217,759 |

DBS Group Holdings, Ltd. (Singapore) | | 54,500 | | | | 592,468 |

Deutsche Bank AG (Germany) | | 16,300 | | | | 1,152,572 |

Deutsche Boerse AG (Germany) | | 4,022 | | | | 333,060 |

Hang Lung Group, Ltd. (Hong Kong) | | 18,900 | | | | 93,470 |

Hang Lung Properties, Ltd. (Hong Kong) | | 41,000 | | | | 160,734 |

HDFC Bank, Ltd. (India) | | 13,795 | | | | 502,654 |

Henderson Land Development Co., Ltd. (Hong Kong) | | 67,000 | | | | 500,673 |

Hong Kong Exchanges and Clearing, Ltd. (Hong Kong) | | 56,400 | | | | 1,003,491 |

HSBC Holdings PLC (United Kingdom) | | 136,748 | | | | 1,560,065 |

Industrial and Commercial Bank of China, Ltd., Class H (China) | | 341,000 | 2 | | | 280,835 |

Itau Unibanco Banco Holding S.A. (Brazil) | | 21,964 | | | | 488,101 |

KB Financial Group, Inc. (South Korea)* | | 12,125 | | | | 617,408 |

Klepierre (France) | | 5,400 | | | | 218,782 |

Mitsubishi Estate Co., Ltd. (Japan) | | 23,000 | | | | 367,215 |

Mitsubishi Tokyo Financial Group, Inc. (Japan) | | 37,800 | | | | 186,195 |

Mitsui Fudosan Co., Ltd. (Japan) | | 103,000 | | | | 1,741,547 |

National Australia Bank, Ltd. (Australia) | | 18,400 | | | | 449,034 |

Nomura Holdings, Inc. (Japan) | | 123,100 | | | | 915,455 |

Old Mutual PLC (United Kingdom)* | | 291,700 | | | | 510,823 |

Prudential Corp. PLC (United Kingdom) | | 46,676 | | | | 477,787 |

Societe Generale (France) | | 28,475 | | | | 1,978,441 |

Standard Bank Group, Ltd. (South Africa) | | 11,600 | | | | 159,328 |

Standard Chartered PLC (United Kingdom) | | 21,998 | | | | 555,358 |

Storebrand ASA (Norway)* | | 64,996 | | | | 442,344 |

Sumitomo Mitsui Financial Group, Inc. (Japan) | | 9,200 | | | | 263,998 |

Sumitomo Realty & Development Co., Ltd. (Japan) | | 20,000 | | | | 377,550 |

Sun Hung Kai Properties, Ltd. (Hong Kong) | | 93,000 | | | | 1,382,828 |

T&D Holdings, Inc. (Japan) | | 10,500 | | | | 215,936 |

Turkiye Garanti Bankasi A.S. (Turkey) | | 103,200 | | | | 439,623 |

Unibail (France) | | 2,000 | | | | 439,359 |

UniCredito Italiano SpA (Italy)* | | 372,761 | | | | 1,246,422 |

Zurich Financial Services AG (Switzerland) | | 4,941 | | | | 1,080,220 |

Total Financials | | | | | | 35,174,832 |

Health Care - 8.6% | | | | | | |

Actelion, Ltd. (Switzerland)* | | 10,081 | | | | 538,430 |

AstraZeneca PLC (United Kingdom) | | 11,700 | | | | 549,867 |

Bayer AG (Germany) | | 16,400 | | | | 1,312,385 |

GlaxoSmithKline PLC (United Kingdom) | | 98,284 | | | | 2,084,196 |

Lonza Group AG (Switzerland) | | 3,122 | | | | 219,973 |

Novartis AG (Switzerland) | | 22,858 | | | | 1,248,258 |

Roche Holding AG (Switzerland) | | 10,611 | | | | 1,814,618 |

Sanofi-Aventis SA (France) | | 34,895 | | | | 2,744,240 |

Teva Pharmaceutical Industries, Ltd., Sponsored ADR (Israel) | | 7,100 | | | | 398,878 |

Total Health Care | | | | | | 10,910,845 |

Industrials - 10.9% | | | | | | |

ABB, Ltd. (Switzerland)* | | 49,291 | | | | 949,804 |

ABB, Ltd., ADR (Switzerland)* | | 39,030 | | | | 750,928 |

Adecco SA (Switzerland) | | 5,700 | | | | 314,440 |

Alstom SA (France) | | 8,013 | | | | 560,396 |

Babcock International Group PLC (United Kingdom) | | 50,247 | | | | 482,027 |

BAE Systems PLC (United Kingdom) | | 10,700 | | | | 61,928 |

Cie de Saint-Gobain (France) | | 22,842 | | | | 1,239,093 |

Deutsche Post AG (Germany) | | 52,050 | | | | 1,005,959 |

FANUC, Ltd. (Japan) | | 5,700 | | | | 531,252 |

Far Eastern Textile Co., Ltd. (Taiwan) | | 211,784 | | | | 264,811 |

HOCHTIEF AG (Germany) | | 5,400 | | | | 411,841 |

JGC Corp. (Japan) | | 36,000 | | | | 663,396 |

Kajima Corp. (Japan) | | 60,000 | | | | 121,401 |

MAN AG (Germany) | | 8,312 | | | | 644,946 |

Mitsubishi Corp. (Japan) | | 25,700 | | | | 640,151 |

Mitsubishi Heavy Inds., Ltd. (Japan) | | 107,000 | 2 | | | 377,385 |

Randstad Holding, N.V. (Netherlands)* | | 15,800 | | | | 786,165 |

Rolls-Royce Group PLC (United Kingdom) | | 64,300 | | | | 500,730 |

Rolls-Royce Group PLC, C Shares (United Kingdom) | | 3,858,000 | | | | 6,231 |

Shimizu Corp. (Japan) | | 44,000 | | | | 158,040 |

Siemens AG (Germany) | | 17,683 | | | | 1,622,783 |

Tostem Inax Holding Corp. (Japan) | | 15,000 | | | | 258,222 |

Vestas Wind Systems A/S (Denmark)* | | 4,070 | | | | 247,793 |

Wienerberger AG (Austria)* | | 26,470 | | | | 480,364 |

Wolseley PLC (United Kingdom)* | | 22,400 | | | | 448,377 |

Yamato Transport Co., Ltd. (Japan) | | 19,700 | | | | 274,225 |

Total Industrials | | | | | | 13,802,688 |

Information Technology - 7.9% | | | | | | |

ASML Holding, N.V. (Netherlands) | | 24,214 | | | | 826,709 |

AU Optronics Corp., Sponsored ADR (Taiwan) | | 46,453 | | | | 556,971 |

Autonomy Corporation PLC (United Kingdom)* | | 34,542 | | | | 838,831 |

Cia Brasileira de Meios de Pagamentos (Brazil) | | 19,100 | | | | 168,291 |

Ericsson (LM), Class B (Sweden) | | 54,370 | | | | 500,533 |

The accompanying notes are an integral part of these financial statements.

16

Managers International Equity Fund

Schedule of Portfolio Investments (continued)

| | | | | | | |

| | | Shares | | | Value | |

Information Technology - 7.9% (continued) | | | | | | | |

Gemalto NV (France)* | | 14,784 | 2 | | $ | 643,167 | |

Hynix Semiconductor, Inc. (South Korea)* | | 43,500 | | | | 865,051 | |

Murata Manufacturing Co., Ltd. (Japan) | | 8,200 | | | | 409,239 | |

NetEase.com, Inc., ADR (Cayman Islands)* | | 16,500 | 2 | | | 620,565 | |

Nokia Oyj (Finland) | | 79,400 | | | | 1,026,640 | |

Redecard, S.A. (Brazil) | | 19,500 | | | | 324,813 | |

Samsung Electronics Co., Ltd. (South Korea) | | 1,370 | | | | 939,450 | |

Samsung Electronics Co., Ltd., GDR, (South | | | | | | | |

Korea) (a)* | | 2,251 | | | | 772,258 | |

Taiwan Semiconductor Manufacturing Co., | | | | | | | |

Ltd., Sponsored ADR (Taiwan) | | 88,220 | | | | 1,009,237 | |

Toshiba Corp. (Japan)* | | 92,000 | | | | 510,499 | |

Total Information Technology | | | | | | 10,012,254 | |

Materials - 9.0% | | | | | | | |

Air Liquide SA (France) | | 4,938 | | | | 587,265 | |

ArcelorMittal (Luxembourg) | | 13,548 | | | | 619,250 | |

Barrick Gold Corp. (Canada) | | 25,086 | | | | 994,469 | |

BASF SE (Germany) | | 7,300 | | | | 451,802 | |

Gold Fields, Ltd. (South Africa) | | 31,763 | | | | 417,107 | |

Goldcorp, Inc. (Canada) | | 19,600 | | | | 774,929 | |

Impala Platinum Holdings, Ltd. (South Africa) | | 9,400 | | | | 256,620 | |

Incitec Pivot, Ltd. (Australia) | | 229,237 | | | | 725,103 | |

Israel Chemicals, Ltd. (Israel) | | 29,500 | | | | 387,367 | |

Kinross Gold Corp. (Canada) | | 15,900 | 2 | | | 292,560 | |

Koninklijke DSM, N.V. (Netherlands) | | 5,400 | | | | 265,321 | |

Rio Tinto PLC (United Kingdom) | | 22,550 | | | | 1,217,626 | |

Shin-Etsu Chemical Co., Ltd. (Japan) | | 15,600 | | | | 880,750 | |

Svenska Cellulosa AB (SCA) (Sweden) | | 1,700 | | | | 22,666 | |

Syngenta AG (Switzerland) | | 2,871 | | | | 810,793 | |

Taiwan Fertilizer Co., Ltd. (Taiwan) | | 106,000 | | | | 377,434 | |

Toray Industries, Inc. (Japan) | | 84,700 | | | | 460,821 | |

Vale, S.A., Sponsored ADR (Brazil) | | 27,000 | | | | 670,140 | |

Xstrata PLC (United Kingdom)* | | 40,510 | | | | 722,538 | |

Yamana Gold, Inc. (Canada) | | 42,159 | | | | 483,729 | |

Total Materials | | | | | | 11,418,290 | |

Telecommunication Services - 5.1% | | | | | | | |

Bharti Tele-Ventures, Ltd. (India) | | 24,314 | | | | 171,797 | |

France Telecom SA (France) | | 39,779 | | | | 994,008 | |

Nippon Telegraph & Telephone Corp. (Japan) | | 24,700 | | | | 975,726 | |

Portugal Telecom SGPS SA (Portugal) | | 67,026 | | | | 817,857 | |

Telecom Italia S.p.A. (Italy) | | 506,800 | | | | 790,580 | |

Telecom Italia S.p.A. RSP (Italy) | | 464,100 | | | | 515,470 | |

Vodafone Group PLC (United Kingdom) | | 937,796 | | | | 2,171,662 | |

Total Telecommunication Services | | | | | | 6,437,100 | |

Utilities - 3.7% | | | | | | | |

E.ON AG (Germany) | | 50,795 | | | | 2,132,071 | |

Electricite de France SA (France) | | 9,800 | | | | 582,446 | |

Enel S.p.A. (Italy) | | 52,300 | | | | 302,785 | |

Hong Kong and China Gas Co., Ltd., The (Hong Kong) | | 307,670 | | | | 771,683 | |

Iberdrola Renovables SAU (Spain) | | 119,310 | | | | 568,153 | |

National Grid PLC (United Kingdom) | | 30,290 | | | | 330,612 | |

Total Utilities | | | | | | 4,687,750 | |

Total Common Stocks

(cost $106,442,031) | | | | | | 121,141,593 | |

Other Equities - 0.7% | | | | | | | |

Hirco PLC (South Africa)* | | 11,900 | | | | 28,659 | |

SPDR Gold Shares (United States)* | | 8,200 | | | | 879,942 | |

Total Other Equities

(cost $749,429) | | | | | | 908,601 | |

Short-Term Investments - 5.9%1 | | | | | | | |

BNY Institutional Cash Reserves Fund, | | | | | | | |

Series A, 0.05%3 | | 3,764,000 | | | | 3,764,000 | |

BNY Institutional Cash Reserves Fund, Series B*3,8 | | 104,356 | | | | 20,349 | |

Dreyfus Cash Management Fund, Institutional Class Shares, 0.08% | | 3,694,060 | | | | 3,694,060 | |

Total Short-Term Investments

(cost $7,562,416) | | | | | | 7,478,409 | |

Total Investments - 102.1%

(cost $114,753,876) | | | | | | 129,528,603 | |

Other Assets, less Liabilities - (2.1)% | | | | | | (2,733,294 | ) |

Net Assets - 100.0% | | | | | $ | 126,795,309 | |

The accompanying notes are an integral part of these financial statements.

17

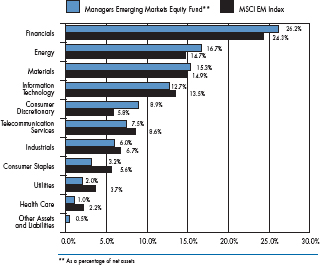

Managers Emerging Markets Equity Fund

Investment Manager’s Comments

The Managers Emerging Markets Equity Fund’s (the “Fund”) objective is to achieve long-term capital appreciation.

The Fund invests at least 80% of its assets in equity securities, i.e., common and preferred stocks of companies located in countries included in the MSCI Emerging Markets (“MSCI EM”) Index, mostly countries in Africa, Asia, Latin America, and the Middle East. The Fund may invest in companies of any size. The MSCI EM Index is the benchmark for the Fund.

THE PORTFOLIO MANAGERS

The Fund employs multiple subadvisors who specialize in distinct investment approaches. This “intelligence diversification” not only serves to manage risk, but also helps the Fund to tap the markets’ full potential by focusing different analytical insights on each prospective investment. Fund management strives to achieve its performance and diversification objectives while ensuring that the Fund operates within the framework of its investment objective and principal investment strategies.

Rexiter Capital Management Limited

The investment team at Rexiter Capital Management Limited (“Rexiter”) believes emerging markets are less efficient than developed markets, and an actively managed portfolio, with respect to both country weightings and stock selection, can add value over a market capitalization-weighted index without materially affecting risk. Rexiter’s approach is active in terms of both asset allocation and stock selection. Investment decisions are based on fundamental analysis of countries and stocks. Portfolio management is controlled by a disciplined process that seeks to add to returns through the exploitation of market inefficiency, while constraining risk.

Schroder Investment Management Limited

Schroder Investment Management Limited (“Schroders”) believes that emerging stock markets are inefficient and provide strong potential for adding value through active fund management. This value can be extracted through both country and stock selection. Schroders uses a time-tested quantitative model to aid in their country selection process, and seeks to add value equally over time from both country and stock selection. Schroders further believes that applying a systematic, disciplined approach along, with a strong team culture increases the ability to add value. Schroders believes that equal attention should be given to managing both return and risk.

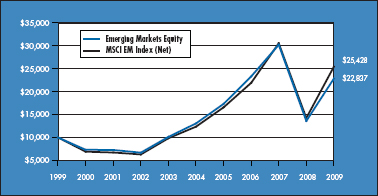

THE YEAR IN REVIEW

The Fund returned 67.94% in 2009, trailing the return of 78.51% for its benchmark, the MSCI EM Index. (Note that unless otherwise stated, all performance cited in this commentary is in U.S. Dollars.) Despite and the year’s slow start and continuing the decline of 2008, emerging markets rallied sharply after bottoming in March to finish 2009 significantly higher. Liquidity and increased appetite for risk were the key themes driving the markets. With the U.S. and other developed countries undertaking massive government stimulus programs and with global interest rates hovering around zero, capital flows sought out riskier, higher-yielding assets, and emerging markets were a clear beneficiary. After a record $49.5 billion flowed out of emerging market equities during 2008, nearly double that amount ($81 billion) 3 owed back into the asset class during 2009.