UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT

OF

REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-03916

Name of Registrant: Vanguard Specialized Funds

Address of Registrant:

P.O. Box 2600

Valley Forge, PA 19482

Name and address of agent for service:

Heidi Stam, Esquire

P.O. Box 876

Valley Forge, PA 19482

Registrant’s telephone number, including area code: (610) 669-1000

Date of fiscal year end: January 31

Date of reporting period: February 1, 2013 – July 31, 2013

Item 1: Reports to Shareholders

|

|

| Semiannual Report | July 31, 2013 |

|

| Vanguard Energy Fund |

|

|

> For the six months ended July 31, 2013, the energy sector advanced at a slower pace than the broad U.S. stock market, which saw double-digit gains.

> Vanguard Energy Fund returned almost 3%; the returns of its comparative standards were negative.

> Holdings in U.S.-based oil and gas exploration and production companies helped boost the fund’s return compared with that of its benchmark index.

| |

| Contents | |

| Your Fund’s Total Returns. | 1 |

| Chairman’s Letter. | 2 |

| Advisors’ Report. | 7 |

| Fund Profile. | 11 |

| Performance Summary. | 13 |

| Financial Statements. | 14 |

| About Your Fund’s Expenses. | 27 |

| Trustees Approve Advisory Arrangements. | 29 |

| Glossary. | 31 |

Please note: The opinions expressed in this report are just that—informed opinions. They should not be considered promises or advice.

Also, please keep in mind that the information and opinions cover the period through the date on the front of this report. Of course, the risks of investing in your fund are spelled out in the prospectus.

See the Glossary for definitions of investment terms used in this report.

About the cover: Our cover photograph shows rigging on the HMSSurprise, a replica of an 18th-century Royal Navy frigate. It was featured in the 2003 movie Master and Commander: The Far Side of the World, which was based on Patrick O’Brian’s sea novels, set amid the Napoleonic Wars. Vanguard was named for another ship of that era, the HMSVanguard, which was the flagship of British Admiral Horatio Nelson at the Battle of the Nile.

Your Fund’s Total Returns

Six Months Ended July 31, 2013

| |

| | Total |

| | Returns |

| Vanguard Energy Fund | |

| Investor Shares | 2.83% |

| Admiral™ Shares | 2.85 |

| MSCI ACWI Energy Index | -0.40 |

| Global Natural Resources Funds Average | -2.42 |

Global Natural Resources Funds Average: Derived from data provided by Lipper, a Thomson Reuters Company.

Admiral Shares carry lower expenses and are available to investors who meet certain account-balance requirements.

Your Fund’s Performance at a Glance

January 31, 2013, Through July 31, 2013

| | | | |

| | | | Distributions Per Share |

| | Starting | Ending | Income | Capital |

| | Share Price | Share Price | Dividends | Gains |

| Vanguard Energy Fund | | | | |

| Investor Shares | $62.66 | $64.28 | $0.149 | $0.000 |

| Admiral Shares | 117.63 | 120.68 | 0.289 | 0.000 |

1

Chairman’s Letter

Dear Shareholder,

Vanguard Energy Fund returned 2.83% for Investor Shares for the six months ended July 31, 2013. The advisors’ decision to overweight some U.S.-based oil and gas exploration companies helped the fund outpace the –0.40% return of its benchmark index.

The fund’s performance was even stronger compared with the –2.42% average return of global natural resources funds. Many of these peer funds have significant allocations to nonenergy sectors such as materials, industrials, and utilities. Materials, in particular, suffered as declining demand pulled down prices for metals and many other natural resources.

In contrast, crude oil prices climbed during the period, in part because of lower production and some supply disruptions among OPEC members. U.S. natural gas prices also rose.

Even so, the energy sector as a whole lagged the broad U.S. stock market, as it has for the last two fiscal years. To a degree, this lag may reflect investors’ assessment of the possible effects of slower growth in energy demand on the profitability of the sector.

2

U.S. stocks set a brisk pace; international markets struggled

U.S. stocks returned about 14% for the half year, posting positive returns for five of the six months. The exception was June, when stocks slid after Federal Reserve Chairman Ben Bernanke said the central bank could begin unwinding its stimulative bond-buying program later this year. July saw domestic stocks rebound sharply, helped by favorable economic news and reassuring words from Fed officials.

Despite rising in July, international stocks finished the period with a return of less than 1%. Much of the weakness came from emerging markets, where the slowing rate of growth, especially in China and Brazil, has been a concern. Developed markets in the Pacific region and Europe posted modest gains.

Bonds encountered obstacles as market uncertainty increased

Bonds, which also suffered in June amid concerns that the Fed could start tapering its bond buying, posted negative six-month returns. Although July brought a little relief, the broad U.S. taxable bond market returned –1.62%. The yield of the 10-year Treasury note finished the period at 2.60%, up from 1.67% at the end of April. (Bond yields and prices move in opposite directions.)

| | | |

| Market Barometer | | | |

| |

| | | | Total Returns |

| | | Periods Ended July 31, 2013 |

| | Six | One | Five Years |

| | Months | Year | (Annualized) |

| Stocks | | | |

| Russell 1000 Index (Large-caps) | 13.83% | 26.23% | 8.49% |

| Russell 2000 Index (Small-caps) | 16.66 | 34.76 | 9.45 |

| Russell 3000 Index (Broad U.S. market) | 14.05 | 26.86 | 8.57 |

| MSCI All Country World Index ex USA (International) | 0.26 | 16.96 | 0.79 |

| |

| Bonds | | | |

| Barclays U.S. Aggregate Bond Index (Broad taxable market) | -1.62% | -1.91% | 5.23% |

| Barclays Municipal Bond Index (Broad tax-exempt market) | -3.94 | -2.19 | 5.07 |

| Citigroup Three-Month U.S. Treasury Bill Index | 0.03 | 0.08 | 0.20 |

| |

| CPI | | | |

| Consumer Price Index | 1.44% | 1.96% | 1.21% |

3

Municipal bonds fared worse, returning –3.94%. Although the municipal market was roiled in July by Detroit’s bankruptcy filing, it bears remembering that Detroit debt represents a tiny fraction—just 0.05%—of the entire muni bond market. We continue to believe that municipal bonds may make sense as part of a diversified portfolio for investors in higher tax brackets. As Sarah Hammer, a senior investment analyst with Vanguard Investment Strategy Group, put it, “State and local governments have the ability and willingness to continue to make their debt service payments.”

The Fed’s target for short-term rates remained between 0% and 0.25%, capping the returns from money market funds and savings accounts.

Exploration and production firms sprinted ahead of integrated giants

There are many lenses through which to view the energy sector and to help make sense of the often divergent performance of its various segments. Perhaps the most commonly used lens is price, where there was a noteworthy development during the period. The price of West Texas Intermediate (WTI) crude oil—the U.S. oil price benchmark—reconnected to that of the global market, represented by Brent crude from the North Sea.

Historically, WTI and Brent prices have traded within a few dollars of each other. They became disconnected in 2010, when a boom in Canadian oil production and oil shale drilling strained the U.S. transport

Expense Ratios

Your Fund Compared With Its Peer Group

| | | |

| | Investor | Admiral | Peer Group |

| | Shares | Shares | Average |

| Energy Fund | 0.31% | 0.26% | 1.32% |

The fund expense ratios shown are from the prospectus dated May 28, 2013, and represent estimated costs for the current fiscal year. For the six months ended July 31, 2013, the fund’s annualized expense ratios were 0.37% for Investor Shares and 0.31% for Admiral Shares. This increase from the estimated expense ratio reflects a performance-based investment advisory fee adjustment. When the performance adjustment is positive, the fund’s expenses increase; when it is negative, expenses decrease. The peer-group expense ratio is derived from data provided by Lipper, a Thomson Reuters Company, and captures information through year-end 2012.

Peer group: Global Natural Resources Funds.

4

and refining network. The resulting oversupply of oil in the midsection of the country that could not reach Gulf Coast refineries pulled down WTI prices. This summer, more pipeline and refining capacity became available and onshore production in Canada and the United States dropped. Accordingly, WTI prices rose, coming close to parity with Brent in July for the first time in nearly three years.

Because higher prices tend to benefit producers and pinch the profit margins of refiners, they can be a mixed blessing for integrated companies that do both. These effects played out, to varying degrees, among the Energy Fund’s holdings.

The standouts were U.S. exploration and production companies. Natural gas producers in Pennsylvania did best—including one of the fund’s top ten holdings (as of July 31), which returned more than 43% for the half year. In contrast, refining and marketing companies overall lost ground as their raw material costs increased.

Performance was mixed among the integrated behemoths whose operations span the globe. These companies represented more than 45% of fund assets on average during the period. Two of the fund’s largest holdings, both headquartered in the United States, advanced, but some overseas holdings declined.

Compared with the benchmark index, rewarding selections outnumbered disappointments. As noted, the advisors added the most value with their choices of U.S. exploration and production companies. Some integrated giants detracted from results.

The Advisors’ Report that follows this letter provides additional details about the management of the fund during the fiscal half year.

Predicting the future is tricky, but preparing for it is prudent

Now that much of 2013 is in the rearview mirror, it’s clear that few of us anticipated several big events—such as record highs in some stock market indexes, the powerful rally in long-slumbering Japan, and renewed upheaval in Egypt. Of course, such unpredictability underscores the challenge of forecasting.

Vanguard’s approach to forecasting differs from that of many other investment firms. Joe Davis, our chief economist, is fond of saying that we “treat the future with the deference it deserves.”

Each January, our economists publish Vanguard’s Economic and Investment Outlook (available at vanguard.com/ research). They update their perspectives periodically and address significant developments—such as Detroit’s bankruptcy filing—with thoughtful, timely analysis and commentary. But, in keeping with Joe’s comment, our economists don’t make the pinpoint projections that you’ll see elsewhere.

5

Instead, using sophisticated statistical models, we provide a range and probability of potential outcomes—for the inflation rate or the 10-year Treasury yield, for example. And we explain our rationale for such outcomes.

In short, our forecasts acknowledge that no one has a crystal ball or can envision every scenario. And that underlines one of our core investment principles: Develop a suitable asset allocation using broadly diversified funds. Having a balanced portfolio can help you get through unforeseen events and achieve your goals—even without a crystal ball.

As always, thank you for investing with Vanguard.

Sincerely,

F. William McNabb III

Chairman and Chief Executive Officer

August 14, 2013

6

Advisors’ Report

Vanguard Energy Fund returned 2.83% for Investor Shares and 2.85% for Admiral Shares in the six months ended July 31, 2013, outpacing both its benchmark index and the average return of global natural resources funds. Your fund is managed by two advisors, a strategy that enhances the fund’s diversification by providing exposure to distinct yet complementary investment approaches. It’s not uncommon for different advisors to have different views about individual securities or the broader investment environment.

The advisors, the amount and percentage of fund assets each manages, and brief descriptions of their investment strategies are presented in the table below. The advisors have also provided a discussion of the investment environment that existed during the year and of how their portfolio positioning reflects this assessment. These reports were prepared on August 14, 2013.

Wellington Management Company, LLP

Portfolio Manager:

Karl E. Bandtel, Senior Vice President

The investment environment

Global equities shook off June’s pullback and advanced in July for the eighth time in the last nine calendar months. The MSCI All Country World Index rose 6.23% (in U.S. dollar terms) for the six months ended July 31, 2013. Accommodative rhetoric from the European Central Bank and the U.S. Federal Reserve increased investors’ risk appetites for U.S. stocks and, to a lesser extent, those of a number of other

| | | |

| Vanguard Energy Fund Investment Advisors | |

| |

| | Fund Assets Managed | |

| Investment Advisor | % | $ Million | Investment Strategy |

| Wellington Management | 96 | 11,296 | Emphasizes long-term total-return opportunities from |

| Company, LLP | | | the various energy subsectors: international oils, |

| | | | foreign integrated oils and foreign producers, North |

| | | | American producers, oil services and equipment, |

| | | | transportation and distribution, and refining and |

| | | | marketing. |

| Vanguard Equity Investment | 3 | 382 | Employs a quantitative fundamental management |

| Group | | | approach, using models that assess valuation, market |

| | | | sentiment, earnings quality, and management |

| | | | decisions of companies relative to their peers. |

| Cash Investments | 1 | 148 | These short-term reserves are invested by Vanguard in |

| | | | equity index products to simulate investments in stock. |

| | | | Each advisor may also maintain a modest cash |

| | | | position. |

7

developed markets. Emerging markets equity was a notable exception; the MSCI Emerging Markets Index declined almost 10% (in U.S. dollar terms).

The price of crude oil rose late in the period along with mounting tensions in Egypt. Natural gas prices remained lackluster amidst cooler weather and expectations of lower demand. They began the fiscal year just above $3.30 per million BTUs (U.S. Henry Hub) and exceeded $4 in the spring before dropping to finish below $3.50.

Our successes

Stock selection within the oil and gas subsector helped the portfolio outperform for the period. Cabot Oil & Gas was again the top contributor. The fund also benefited from positions in a number of other U.S. stocks, including EQT, Pioneer Natural Resources, EOG Resources, Noble Energy, and Range Resources.

Cabot’s strong results were driven largely by robust production in Pennsylvania’s Marcellus Shale. The company is a low-cost producer with a strong balance sheet. We believe the stock should benefit from reduced natural gas production industry-wide and ultimately from higher natural gas prices, which have remained below the industry’s marginal cost for an extended period. We trimmed our exposure on the stock’s strength, but Cabot remains one of our largest positions in both absolute and benchmark-relative terms.

Our shortfalls

The portfolio’s international exposure weighed on returns. Nine of the top ten absolute detractors were in stocks of companies domiciled outside of the United States. This list included Petrobras (Brazil), Inpex (Japan), Gazprom and Rosneft (Russia), Eni (Italy), and PetroChina (China).

Integrated oil and gas company Petrobras lost one-quarter of its value during the period. Production delays related to deployment of drilling platforms coupled with a broader sell-off across emerging markets in general created downward pressure on the stock. We believe that production growth will improve in the second half of the year and accelerate into 2014. Downstream retail margins should also improve to more normal levels. The company is expanding its deep sea production, with a number of rigs expected to come online in the next two years.

Petrobras shares are attractively valued on investor concern about continued losses in downstream refined products. We believe this concern is fully reflected in the share price and that sentiment will begin to turn as production improves and downstream losses narrow. We took advantage of the stock’s weakness to increase our position.

The fund’s positioning

Our long-term outlook remains favorable for the energy sector. However, as we always do, we urge caution regarding the near-term direction of commodity prices and the inherent volatility that accompanies investing in stocks of energy companies.

8

The portfolio remains skewed in favor of low-cost producers with compelling valuations based on our assessment of their respective long-term resource bases. We believe many of these companies have the ability to create value for shareholders absent generally rising commodity prices.

We believe that the eventual substitution of natural gas for oil, not only in the United States but also in Europe and Asia, is a significant opportunity for patient investors. Combined with the impact of several projects under way to enable the export of U.S. natural gas, it should continue to narrow the current wide price disparity between global energy prices and North American natural gas.

A significant portion of the portfolio’s assets are invested in international stocks (including emerging markets) domiciled in several countries. We will likely seek opportunities to increase our exposure to foreign stocks as we pare back positions in North America and redeploy the proceeds into more attractively valued investments.

Our low-turnover investment process remains steady, as does our emphasis on finding mid- and large-cap integrated oil and exploration and production companies that are attractively valued. We will continue to focus on stocks of companies that have clean balance sheets, long-lived resources, and high-quality management teams.

Vanguard Equity Investment Group

Portfolio Managers:

James D. Troyer, CFA, Principal

James P. Stetler, Principal

Michael R. Roach, CFA

The fund’s benchmark returned –0.40% for the six months ended July 31, 2013, lagging the 6.23% return of global equities (as measured by the MSCI All Country World Index). After a strong start to 2013, the capital markets saw a return of volatility in the second quarter. Initially, strong corporate earnings and economic optimism ushered stock markets to fresh highs. Rising interest rates in May tempered investor enthusiasm, however, and June brought a Federal Reserve statement that many interpreted as the beginning of a more hawkish approach to monetary policy. Markets swung wildly in the wake of the Fed’s comments, and bond yields climbed to a level last seen in 2011. Energy stocks were not immune to these fluctuations, and as a whole they provided investors with nearly flat returns.

Our model-based investment approach produced results in line with expectations. Our process has similarities to that of traditional fundamental managers but features a strict quantitative method of comparing stocks to identify those with potential to outperform over the long run. Our in-house research efforts center

9

on a combination of valuation and other factors focused on fundamental growth, allowing us to take advantage of market inefficiencies caused by persistent investor biases. We then use the results of our model to construct our portfolio, with the goal of minimizing exposure to risks that our research indicates do not improve returns, such as variances from the benchmark in market capitalization and volatility. In our view, these risk exposures are not justified by the possible rewards.

For the period, our most successful holdings were spread throughout various regions across the globe: First Solar (+75%) and Ultra Petroleum (+19%) in the United States, SBM Offshore (+28%) in the Netherlands, and Repsol (+10%) in Spain. Equally as important to our performance was our ability to limit exposure to underperforming stocks such as Ecopetrol (–24%) in Brazil and Pacific Rubiales Energy (–16%) in Canada.

Our results were dampened by overweighted positions in Inpex (–24%) and Cairn India (–18%), two stocks that underperformed the benchmark as a whole. Underweight positions in stronger performers such as Pioneer Natural Resources (+32%) and EQT (+46%) also hurt relative returns.

Overall, the increased volatility in the markets was not surprising, considering how quickly stocks had been rising domestically and internationally. Markets will always be subject to short-term fluctuations brought on by new headline risks. Too often, investors focus on short-term market gyrations, the most recent economic headlines, and short-term performance—and not enough on the fundamental principles that give them the best chance of success.

Strategies such as ours shift the focus back to fundamentals by seeking to capture the spread between undervalued and overvalued stocks. We believe that our approach can provide worthwhile returns for long-term investors and play an important role in building a diversified investment plan.

10

Energy Fund

Fund Profile

As of July 31, 2013

| | |

| Share-Class Characteristics | |

| | Investor | Admiral |

| | Shares | Shares |

| Ticker Symbol | VGENX | VGELX |

| Expense Ratio1 | 0.31% | 0.26% |

| 30-Day SEC Yield | 1.78% | 1.84% |

| | | |

| Portfolio Characteristics | | |

| | | | DJ U.S. |

| | | | Total |

| | | MSCI | Market |

| | | ACWI | FA |

| | Fund | Energy | Index |

| Number of Stocks | 127 | 173 | 3,619 |

| Median Market Cap | $42.1B | $71.7B | $40.3B |

| Price/Earnings Ratio | 14.2x | 11.7x | 18.9x |

| Price/Book Ratio | 1.6x | 1.5x | 2.5x |

| Return on Equity | 14.3% | 16.6% | 16.5% |

| Earnings Growth | | | |

| Rate | -2.9% | 1.8% | 10.4% |

| Dividend Yield | 2.2% | 3.0% | 1.9% |

| Foreign Holdings | 36.8% | 49.7% | 0.0% |

| Turnover Rate | | | |

| (Annualized) | 22% | — | — |

| Short-Term Reserves | 3.5% | — | — |

| | |

| Subindustry Diversification (% of equity exposure) | |

| | |

| | | MSCI |

| | | ACWI |

| | Fund | Energy |

| Coal & Consumable Fuels | 3.0% | 1.4% |

| Integrated Oil & Gas | 45.9 | 54.2 |

| Oil & Gas Drilling | 1.6 | 2.5 |

| Oil & Gas Equipment & | | |

| Services | 9.7 | 10.0 |

| Oil & Gas Exploration & | | |

| Production | 32.4 | 20.8 |

| Oil & Gas Refining & | | |

| Marketing | 4.9 | 5.6 |

| Oil & Gas Storage & | | |

| Transportation | 1.8 | 5.5 |

| Other | 0.7 | 0.0 |

| | |

| Volatility Measures | | |

| |

| | MSCI | DJ U.S. |

| | ACWI | Total Market |

| | Energy | FA Index |

| R-Squared | 0.98 | 0.83 |

| Beta | 1.05 | 1.42 |

These measures show the degree and timing of the fund’s fluctuations compared with the indexes over 36 months.

| | |

| Ten Largest Holdings (% of total net assets) |

| Exxon Mobil Corp. | Integrated Oil & Gas | 8.8% |

| Royal Dutch Shell plc | Integrated Oil & Gas | 6.0 |

| Chevron Corp. | Integrated Oil & Gas | 5.5 |

| Schlumberger Ltd. | Oil & Gas Equipment | |

| | & Services | 3.7 |

| BP plc | Integrated Oil & Gas | 3.3 |

| Total SA | Integrated Oil & Gas | 3.0 |

| Cabot Oil & Gas Corp. | Oil & Gas Exploration | |

| | & Production | 2.9 |

| Pioneer Natural | Oil & Gas Exploration | |

| Resources Co. | & Production | 2.6 |

| Eni SPA | Integrated Oil & Gas | 2.3 |

| EOG Resources Inc. | Oil & Gas Exploration | |

| | & Production | 2.3 |

| Top Ten | | 40.4% |

The holdings listed exclude any temporary cash investments and equity index products.

1 The expense ratios shown are from the prospectus dated May 28, 2013, and represent estimated costs for the current fiscal year. For the six months ended July 31, 2013, the annualized expense ratios were 0.37% for Investor Shares and 0.31% for Admiral Shares.

11

Energy Fund

Market Diversification (% of equity exposure)

| |

| Europe | |

| United Kingdom | 11.9% |

| France | 3.7 |

| Italy | 2.4 |

| Other | 2.5 |

| Subtotal | 20.5% |

| Pacific | |

| Japan | 1.6% |

| Other | 0.3 |

| Subtotal | 1.9% |

| Emerging Markets | |

| China | 2.1% |

| Russia | 1.8 |

| Brazil | 1.3 |

| Other | 0.9 |

| Subtotal | 6.1% |

| North America | |

| United States | 62.1% |

| Canada | 9.4 |

| Subtotal | 71.5% |

12

Energy Fund

Performance Summary

All of the returns in this report represent past performance, which is not a guarantee of future results that may be achieved by the fund. (Current performance may be lower or higher than the performance data cited. For performance data current to the most recent month-end, visit our website at vanguard.com/performance.) Note, too, that both investment returns and principal value can fluctuate widely, so an investor’s shares, when sold, could be worth more or less than their original cost. The returns shown do not reflect taxes that a shareholder would pay on fund distributions or on the sale of fund shares.

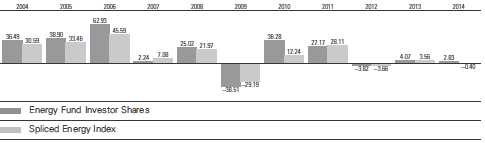

Fiscal-Year Total Returns (%): January 31, 2003, Through July 31, 2013

For a benchmark description, see the Glossary.

Note: For 2014, performance data reflect the six months ended July 31, 2013.

Average Annual Total Returns: Periods Ended June 30, 2013

This table presents returns through the latest calendar quarter—rather than through the end of the fiscal period.

Securities and Exchange Commission rules require that we provide this information.

| | | | |

| | Inception | One | Five | Ten |

| | Date | Year | Years | Years |

| Investor Shares | 5/23/1984 | 11.00% | -3.92% | 13.63% |

| Admiral Shares | 11/12/2001 | 11.06 | -3.86 | 13.70 |

See Financial Highlights for dividend and capital gains information.

13

Energy Fund

Financial Statements (unaudited)

Statement of Net Assets

As of July 31, 2013

The fund reports a complete list of its holdings in regulatory filings four times in each fiscal year, at the quarter-ends. For the second and fourth fiscal quarters, the lists appear in the fund’s semiannual and annual reports to shareholders. For the first and third fiscal quarters, the fund files the lists with the Securities and Exchange Commission on Form N-Q. Shareholders can look up the fund’s Forms N-Q on the SEC’s website at sec.gov. Forms N-Q may also be reviewed and copied at the SEC’s Public Reference Room (see the back cover of this report for further information).

| | |

| | | Market |

| | | Value |

| | Shares | ($000) |

| Common Stocks (96.0%)1 | | |

| United States (59.2%) | | |

| Energy Equipment & Services (10.2%) | | |

| Schlumberger Ltd. | 5,341,519 | 434,426 |

| Baker Hughes Inc. | 5,431,170 | 257,600 |

| Halliburton Co. | 3,844,097 | 173,715 |

| Ensco plc Class A | 2,955,824 | 169,487 |

| National Oilwell Varco Inc. | 1,238,296 | 86,891 |

| SEACOR Holdings Inc. | 875,753 | 76,681 |

| Transocean Ltd. | 79,394 | 3,744 |

| Patterson-UTI Energy Inc. | 108,100 | 2,137 |

| Diamond Offshore | | |

| Drilling Inc. | 30,300 | 2,044 |

| Nabors Industries Ltd. | 125,800 | 1,936 |

| | | 1,208,661 |

| Exchange-Traded Fund (0.7%) | |

| ^,2 Vanguard Energy ETF | 663,000 | 78,439 |

| |

| Oil, Gas & Consumable Fuels (48.3%) | |

| Coal & Consumable Fuels (2.2%) | |

| CONSOL Energy Inc. | 8,387,185 | 260,255 |

| |

| Integrated Oil & Gas (17.6%) | |

| Exxon Mobil Corp. | 11,127,444 | 1,043,198 |

| Chevron Corp. | 5,201,240 | 654,784 |

| Occidental Petroleum | | |

| Corp. | 2,854,773 | 254,218 |

| Hess Corp. | 941,839 | 70,129 |

| Murphy Oil Corp. | 791,700 | 53,614 |

| |

| Oil & Gas Exploration & Production (24.6%) |

| Cabot Oil & Gas Corp. | 4,447,807 | 337,233 |

| Pioneer Natural | | |

| Resources Co. | 1,969,495 | 304,799 |

| EOG Resources Inc. | 1,858,641 | 270,414 |

| Anadarko | | |

| Petroleum Corp. | 2,994,167 | 265,044 |

| | | |

| | | | Market |

| | | | Value |

| | | Shares | ($000) |

| | EQT Corp. | 2,775,770 | 240,104 |

| * | Southwestern | | |

| | Energy Co. | 4,944,185 | 191,785 |

| | Noble Energy Inc. | 3,026,078 | 189,100 |

| | Range Resources Corp. | 2,180,290 | 172,461 |

| * | Denbury Resources Inc. | 8,669,104 | 151,709 |

| | Devon Energy Corp. | 2,448,625 | 134,699 |

| | ConocoPhillips | 2,053,309 | 133,178 |

| * | Cobalt International | | |

| | Energy Inc. | 3,745,172 | 108,048 |

| | Apache Corp. | 982,650 | 78,858 |

| | Chesapeake | | |

| | Energy Corp. | 2,947,232 | 68,670 |

| | Marathon Oil Corp. | 1,857,046 | 67,522 |

| * | Whiting | | |

| | Petroleum Corp. | 1,085,355 | 55,863 |

| * | Newfield | | |

| | Exploration Co. | 1,855,658 | 45,649 |

| * | WPX Energy Inc. | 2,247,486 | 43,174 |

| | Energen Corp. | 718,861 | 43,052 |

| * | Ultra Petroleum Corp. | 107,200 | 2,321 |

| |

| | Oil & Gas Refining & Marketing (3.4%) |

| | Phillips 66 | 2,230,984 | 137,205 |

| | Marathon | | |

| | Petroleum Corp. | 1,824,650 | 133,802 |

| | Valero Energy Corp. | 3,540,884 | 126,657 |

| | HollyFrontier Corp. | 68,600 | 3,125 |

| |

| | Oil & Gas Storage & Transportation (0.5%) |

| | Kinder Morgan Inc. | 1,629,416 | 61,527 |

| | Williams Cos. Inc. | 27,900 | 953 |

| | | | 5,703,150 |

| Semiconductors & | | |

| Semiconductor Equipment (0.0%) | |

| * | First Solar Inc. | 47,850 | 2,356 |

| Total United States | | 6,992,606 |

14

| | | |

| Energy Fund | | |

| |

| |

| |

| | | | Market |

| | | | Value |

| | | Shares | ($000) |

| International (36.8%) | | |

| Australia (0.3%) | | |

| | Oil Search Ltd. | 3,907,545 | 28,428 |

| | Caltex Australia Ltd. | 127,094 | 2,137 |

| | Woodside Petroleum Ltd. | 20,294 | 685 |

| | | | 31,250 |

| Austria (0.0%) | | |

| | OMV AG | 59,944 | 2,652 |

| |

| Brazil (1.3%) | | |

| | Petroleo Brasileiro SA | | |

| | ADR | 10,894,275 | 148,598 |

| | Petroleo Brasileiro SA | | |

| | Prior Pfd. | 385,244 | 2,751 |

| | Petroleo Brasileiro SA | 249,132 | 1,679 |

| | | | 153,028 |

| Canada (9.1%) | | |

| | Suncor Energy Inc. | 7,576,682 | 239,650 |

| | Canadian Natural | | |

| | Resources Ltd. | 5,263,443 | 163,272 |

| | Cenovus Energy Inc. | 5,084,180 | 150,492 |

| | Encana Corp. | 6,938,890 | 121,569 |

| * | Tourmaline Oil Corp. | 2,412,470 | 92,990 |

| | TransCanada Corp. | 1,530,901 | 69,949 |

| | Canadian Oil Sands Ltd. | 3,462,710 | 67,201 |

| | Enbridge Inc. | 1,326,300 | 58,954 |

| | Cameco Corp. | 2,573,670 | 52,297 |

| | Pacific Rubiales Energy | | |

| | Corp. | 1,949,295 | 37,900 |

| ^ | Petrominerales Ltd. | 1,615,180 | 8,791 |

| | Suncor Energy Inc. | 249,434 | 7,883 |

| | Husky Energy Inc. | 104,200 | 3,003 |

| | Canadian Natural | | |

| | Resources Ltd. | 86,378 | 2,677 |

| | Enbridge Inc. | 52,350 | 2,323 |

| | Cenovus Energy Inc. | 26,539 | 786 |

| | Canadian Oil Sands Ltd. | 20,300 | 394 |

| | | | 1,080,131 |

| China (2.0%) | | |

| | PetroChina Co. Ltd. ADR | 1,240,895 | 144,664 |

| | Kunlun Energy Co. Ltd. | 32,151,555 | 47,305 |

| | China Shenhua | | |

| | Energy Co. Ltd. | 11,588,390 | 33,449 |

| | China Petroleum & | | |

| | Chemical Corp. | 5,749,600 | 4,270 |

| | China Oilfield | | |

| | Services Ltd. | 1,052,000 | 2,365 |

| | CNOOC Ltd. | 1,188,717 | 2,149 |

| | China Gas Holdings Ltd. | 1,828,000 | 2,065 |

| | China Longyuan | | |

| | Power Group Corp. | 1,676,000 | 1,763 |

| | PetroChina Co. Ltd. | 982,000 | 1,147 |

| | Xinjiang Goldwind Science | |

| | & Technology Co. Ltd. | 1,000,400 | 560 |

| | | | 239,737 |

| | |

| | | Market |

| | | Value |

| | Shares | ($000) |

| Finland (0.0%) | | |

| Neste Oil Oyj | 149,450 | 2,160 |

| |

| France (3.5%) | | |

| Total SA ADR | 6,512,720 | 345,500 |

| Technip SA | 522,614 | 57,665 |

| Total SA | 284,420 | 15,156 |

| | | 418,321 |

| Greece (0.0%) | | |

| Hellenic Petroleum SA | 64,940 | 638 |

| |

| Hungary (0.0%) | | |

| MOL Hungarian Oil | | |

| & Gas plc | 31,787 | 2,388 |

| |

| India (0.7%) | | |

| Reliance Industries Ltd. | 5,747,788 | 82,351 |

| Cairn India Ltd. | 430,743 | 2,092 |

| Oil India Ltd. | 136,255 | 1,158 |

| Hindustan Petroleum | | |

| Corp. Ltd. | 128,139 | 446 |

| Indian Oil Corp. Ltd. | 76,880 | 259 |

| | | 86,306 |

| Israel (0.0%) | | |

| Delek Group Ltd. | 3,000 | 842 |

| * Oil Refineries Ltd. | 809,908 | 348 |

| | | 1,190 |

| Italy (2.3%) | | |

| Eni SPA ADR | 5,952,505 | 262,803 |

| Eni SPA | 384,971 | 8,503 |

| | | 271,306 |

| Japan (1.6%) | | |

| Inpex Corp. | 27,276 | 119,259 |

| JX Holdings Inc. | 11,283,170 | 59,890 |

| Showa Shell Sekiyu KK | 253,900 | 2,339 |

| Idemitsu Kosan Co. Ltd. | 26,900 | 2,240 |

| | | 183,728 |

| Netherlands (0.0%) | | |

| * SBM Offshore NV | 131,514 | 2,545 |

| |

| Norway (0.8%) | | |

| Statoil ASA ADR | 4,090,890 | 88,322 |

| Statoil ASA | 200,381 | 4,350 |

| | | 92,672 |

| Poland (0.0%) | | |

| Polskie Gornictwo | | |

| Naftowe i Gazownictwo | | |

| SA | 1,225,230 | 2,375 |

| * Grupa Lotos SA | 147,504 | 1,521 |

| | | 3,896 |

| Portugal (0.9%) | | |

| Galp Energia SGPS SA | 6,436,169 | 102,806 |

15

| | | |

| Energy Fund | | |

| |

| |

| |

| | | | Market |

| | | | Value• |

| | | Shares | ($000) |

| Russia (1.8%) | | |

| | Gazprom OAO ADR | 13,040,733 | 100,773 |

| | Rosneft OAO GDR | 13,844,021 | 97,811 |

| | Lukoil OAO ADR | 103,280 | 6,077 |

| | AK Transneft OAO | | |

| | Prior Pfd. | 1,010 | 2,394 |

| | TMK OAO GDR | 128,997 | 1,741 |

| | Tatneft OAO ADR | 17,933 | 659 |

| | Surgutneftegas OAO | | |

| | ADR | 61,630 | 486 |

| | Gazprom OAO | 124,674 | 485 |

| | | | 210,426 |

| South Africa (0.1%) | | |

| | Sasol Ltd. | 111,032 | 5,101 |

| |

| South Korea (0.0%) | | |

| | SK Holdings Co. Ltd. | 15,884 | 2,495 |

| |

| Spain (0.8%) | | |

| | Repsol SA | 4,026,158 | 96,496 |

| |

| Thailand (0.1%) | | |

| | PTT PCL (Foreign) | 282,300 | 2,985 |

| * | PTT Global Chemical PCL | 1,061,200 | 2,239 |

| | PTT Exploration & | | |

| | Production PCL (Foreign) | 189,100 | 939 |

| | | | 6,163 |

| United Kingdom (11.5%) | | |

| | Royal Dutch Shell plc | | |

| | ADR | 7,778,285 | 531,646 |

| | BP plc ADR | 8,889,185 | 368,368 |

| | BG Group plc | 9,972,896 | 179,834 |

| | Royal Dutch Shell plc | | |

| | Class B | 4,426,895 | 156,582 |

| * | Ophir Energy plc | 10,826,161 | 62,040 |

| * | Genel Energy plc | 1,705,482 | 24,896 |

| | BP plc | 2,573,179 | 17,778 |

| | Royal Dutch Shell plc | | |

| | Class A | 330,410 | 11,274 |

| | Royal Dutch | | |

| | Shell plc Class A | | |

| | (Amsterdam Shares) | 158,539 | 5,412 |

| * | Essar Energy plc | 417,156 | 843 |

| * | Cairn Energy plc | 1 | — |

| | | | 1,358,673 |

| Total International | | 4,354,108 |

| Total Common Stocks | | |

| (Cost $7,132,598) | | 11,346,714 |

| | | | |

| | | | | Market |

| | | | | Value• |

| | | | Shares | ($000) |

| Temporary Cash Investments (4.3%)1 | |

| Money Market Fund (0.8%) | | |

| 3,4 | Vanguard Market Liquidity | | |

| | Fund, 0.124% | 94,787,797 | 94,788 |

| |

| | | | Face | |

| | | | Amount | |

| | | | ($000) | |

| Repurchase Agreement (3.4%) | | |

| | RBS Securities, Inc. | | | |

| | 0.060%, 8/1/13 | | | |

| | (Dated 7/31/13, | | | |

| | Repurchase Value | | | |

| | $408,501,000, | | | |

| | collateralized by | | | |

| | U.S. Treasury Note/ | | |

| | Bonds 2.000%, | | | |

| | 7/31/20, with a value | | |

| | of $416,671,000) | | 408,500 | 408,500 |

| |

| U.S. Government and Agency Obligations (0.1%) |

| 5,6 | Fannie Mae Discount | | |

| | Notes, 0.110%, 8/21/13 | 5,000 | 5,000 |

| 5,6 | Fannie Mae Discount | | |

| | Notes, 0.100%, 11/13/13 | 500 | 500 |

| 5,6 | Freddie Mac Discount | | |

| | Notes, 0.130%, 9/16/13 | 3,000 | 2,999 |

| | | | | 8,499 |

| Total Temporary Cash Investments | |

| (Cost $511,787) | | | 511,787 |

| Total Investments (100.3%) | | |

| (Cost $7,644,385) | | | 11,858,501 |

| Other Assets and Liabilities (-0.3%) | |

| Other Assets | | | 36,296 |

| Liabilities4 | | | (68,723) |

| | | | | (32,427) |

| Net Assets (100%) | | | 11,826,074 |

16

Energy Fund

| |

| At July 31, 2013, net assets consisted of: |

| | Amount |

| | ($000) |

| Paid-in Capital | 7,316,326 |

| Undistributed Net Investment Income | 86,645 |

| Accumulated Net Realized Gains | 208,486 |

| Unrealized Appreciation (Depreciation) | |

| Investment Securities | 4,214,116 |

| Futures Contracts | 544 |

| Foreign Currencies | (43) |

| Net Assets | 11,826,074 |

| |

| |

| Investor Shares—Net Assets | |

| Applicable to 77,901,603 outstanding | |

| $.001 par value shares of beneficial | |

| interest (unlimited authorization) | 5,007,142 |

| Net Asset Value Per Share— | |

| Investor Shares | $64.28 |

| |

| |

| Admiral Shares—Net Assets | |

| Applicable to 56,502,758 outstanding | |

| $.001 par value shares of beneficial | |

| interest (unlimited authorization) | 6,818,932 |

| Net Asset Value Per Share— | |

| Admiral Shares | $120.68 |

See Note A in Notes to Financial Statements.

^ Part of security position is on loan to broker-dealers. The total value of securities on loan is $6,370,000.

* Non-income-producing security.

1 The fund invests a portion of its cash reserves in equity markets through the use of index futures contracts. After giving effect to futures investments, the fund’s effective common stock and temporary cash investment positions represent 96.7% and 3.6%, respectively, of net assets.

2 Considered an affiliated company of the fund as the issuer is another member of The Vanguard Group.

3 Affiliated money market fund available only to Vanguard funds and certain trusts and accounts managed by Vanguard. Rate shown is the 7-day yield.

4 Includes $6,609,000 of collateral received for securities on loan.

5 The issuer was placed under federal conservatorship in September 2008; since that time, its daily operations have been managed by the Federal Housing Finance Agency and it receives capital from the U.S. Treasury, as needed to maintain a positive net worth, in exchange for senior preferred stock.

6 Securities with a value of $4,300,000 have been segregated as initial margin for open futures contracts.

ADR—American Depositary Receipt.

GDR—Global Depositary Receipt.

See accompanying Notes, which are an integral part of the Financial Statements.

17

| |

| Energy Fund | |

| |

| |

| Statement of Operations | |

| |

| | Six Months Ended |

| | July 31, 2013 |

| | ($000) |

| Investment Income | |

| Income | |

| Dividends1,2 | 154,456 |

| Interest2 | 194 |

| Securities Lending | 3,737 |

| Total Income | 158,387 |

| Expenses | |

| Investment Advisory Fees—Note B | |

| Basic Fee | 8,487 |

| Performance Adjustment | 1,868 |

| The Vanguard Group—Note C | |

| Management and Administrative—Investor Shares | 4,326 |

| Management and Administrative—Admiral Shares | 3,832 |

| Marketing and Distribution—Investor Shares | 500 |

| Marketing and Distribution—Admiral Shares | 559 |

| Custodian Fees | 214 |

| Shareholders’ Reports—Investor Shares | 37 |

| Shareholders’ Reports—Admiral Shares | 10 |

| Trustees’ Fees and Expenses | 14 |

| Total Expenses | 19,847 |

| Net Investment Income | 138,540 |

| Realized Net Gain (Loss) | |

| Investment Securities Sold2 | 221,444 |

| Futures Contracts | 15,080 |

| Foreign Currencies | (462) |

| Realized Net Gain (Loss) | 236,062 |

| Change in Unrealized Appreciation (Depreciation) | |

| Investment Securities | (41,574) |

| Futures Contracts | (4,039) |

| Foreign Currencies | (63) |

| Change in Unrealized Appreciation (Depreciation) | (45,676) |

| Net Increase (Decrease) in Net Assets Resulting from Operations | 328,926 |

1 Dividends are net of foreign withholding taxes of $11,295,000.

2 Dividend income, interest income, and realized net gain (loss) from affiliated companies of the fund were $0, $51,000, and $0, respectively.

See accompanying Notes, which are an integral part of the Financial Statements.

18

| | |

| Energy Fund | | |

| |

| |

| Statement of Changes in Net Assets | | |

| |

| | Six Months Ended | Year Ended |

| | July 31, | January 31, |

| | 2013 | 2013 |

| | ($000) | ($000) |

| Increase (Decrease) in Net Assets | | |

| Operations | | |

| Net Investment Income | 138,540 | 262,512 |

| Realized Net Gain (Loss) | 236,062 | 25,428 |

| Change in Unrealized Appreciation (Depreciation) | (45,676) | 161,584 |

| Net Increase (Decrease) in Net Assets Resulting from Operations | 328,926 | 449,524 |

| Distributions | | |

| Net Investment Income | | |

| Investor Shares | (12,426) | (114,465) |

| Admiral Shares | (16,644) | (147,695) |

| Realized Capital Gain | | |

| Investor Shares | — | (98,885) |

| Admiral Shares | — | (111,067) |

| Total Distributions | (29,070) | (472,112) |

| Capital Share Transactions | | |

| Investor Shares | (460,177) | (570,595) |

| Admiral Shares | (132,185) | 10,358 |

| Net Increase (Decrease) from Capital Share Transactions | (592,362) | (560,237) |

| Total Increase (Decrease) | (292,506) | (582,825) |

| Net Assets | | |

| Beginning of Period | 12,118,580 | 12,701,405 |

| End of Period1 | 11,826,074 | 12,118,580 |

1 Net Assets—End of Period includes undistributed (overdistributed) net investment income of $86,645,000 and ($22,363,000).

See accompanying Notes, which are an integral part of the Financial Statements.

19

| | | | | | |

| Energy Fund | | | | | | |

| |

| |

| Financial Highlights | | | | | | |

| |

| |

| Investor Shares | | | | | | |

| Six Months | | | | | |

| | Ended | | | | | |

| For a Share Outstanding | July 31, | | | Year Ended January 31, |

| Throughout Each Period | 2013 | 2013 | 2012 | 2011 | 2010 | 2009 |

| Net Asset Value, Beginning of Period | $62.66 | $62.60 | $69.20 | $57.17 | $42.62 | $73.93 |

| Investment Operations | | | | | | |

| Net Investment Income | .729 | 1.336 | 1.072 | 1.053 | . 910 | 1.2761 |

| Net Realized and Unrealized Gain (Loss) | | | | | | |

| on Investments | 1.040 | 1.098 | (3.949) | 14.103 | 14.591 | (28.853) |

| Total from Investment Operations | 1.769 | 2.434 | (2.877) | 15.156 | 15.501 | (27.577) |

| Distributions | | | | | | |

| Dividends from Net Investment Income | (.149) | (1.340) | (1.102) | (. 977) | (. 951) | (1.264) |

| Distributions from Realized Capital Gains | — | (1.034) | (2.621) | (2.149) | — | (2.469) |

| Total Distributions | (.149) | (2.374) | (3.723) | (3.126) | (. 951) | (3.733) |

| Net Asset Value, End of Period | $64.28 | $62.66 | $62.60 | $69.20 | $57.17 | $42.62 |

| |

| Total Return2 | 2.83% | 4.07% | -3.82% | 27.17% | 36.28% | -38.51% |

| |

| Ratios/Supplemental Data | | | | | | |

| Net Assets, End of Period (Millions) | $5,007 | $5,340 | $5,945 | $6,731 | $6,536 | $4,434 |

| Ratio of Total Expenses to | | | | | | |

| Average Net Assets3 | 0.37% | 0.31% | 0.34% | 0.34% | 0.38% | 0.28% |

| Ratio of Net Investment Income to | | | | | | |

| Average Net Assets | 2.33% | 2.15% | 1.67% | 1.74% | 1.73% | 1.84% |

| Portfolio Turnover Rate | 22% | 18% | 24% | 31% | 27% | 21% |

The expense ratio, net income ratio, and turnover rate for the current period have been annualized.

1 Calculated based on average shares outstanding.

2 Total returns do not include transaction or account service fees that may have applied in the periods shown. Fund prospectuses provide information about any applicable transaction and account service fees.

3 Includes performance-based investment advisory fee increases (decreases) of 0.03%, (0.02%), 0.01%, 0.00%, 0.03%, and 0.01%.

See accompanying Notes, which are an integral part of the Financial Statements.

20

| | | | | | |

| Energy Fund | | | | | | |

| |

| |

| Financial Highlights | | | | | | |

| |

| |

| |

| Admiral Shares | | | | | | |

| Six Months | | | | | |

| | Ended | | | | | |

| For a Share Outstanding | July 31, | | | Year Ended January 31, |

| Throughout Each Period | 2013 | 2013 | 2012 | 2011 | 2010 | 2009 |

| Net Asset Value, Beginning of Period | $117.63 | $117.52 | $129.93 | $107.34 | $80.02 | $138.86 |

| Investment Operations | | | | | | |

| Net Investment Income | 1.408 | 2.586 | 2.101 | 2.045 | 1.780 | 2.480 1 |

| Net Realized and Unrealized Gain (Loss) | | | | | | |

| on Investments | 1.931 | 2.060 | (7.432) | 26.479 | 27.395 | (54.203) |

| Total from Investment Operations | 3.339 | 4.646 | (5.331) | 28.524 | 29.175 | (51.723) |

| Distributions | | | | | | |

| Dividends from Net Investment Income | (. 289) | (2.595) | (2.159) | (1.899) | (1.855) | (2.480) |

| Distributions from Realized Capital Gains — | (1.941) | (4.920) | (4.035) | — | (4.637) |

| Total Distributions | (. 289) | (4.536) | (7.079) | (5.934) | (1.855) | (7.117) |

| Net Asset Value, End of Period | $120.68 | $117.63 | $117.52 | $129.93 | $107.34 | $80.02 |

| |

| Total Return2 | 2.85% | 4.14% | -3.76% | 27.24% | 36.37% | -38.46% |

| |

| Ratios/Supplemental Data | | | | | | |

| Net Assets, End of Period (Millions) | $6,819 | $6,778 | $6,756 | $6,871 | $4,439 | $2,889 |

| Ratio of Total Expenses to | | | | | | |

| Average Net Assets3 | 0.31% | 0.26% | 0.28% | 0.28% | 0.31% | 0.21% |

| Ratio of Net Investment Income to | | | | | | |

| Average Net Assets | 2.39% | 2.20% | 1.73% | 1.80% | 1.80% | 1.91% |

| Portfolio Turnover Rate | 22% | 18% | 24% | 31% | 27% | 21% |

The expense ratio, net income ratio, and turnover rate for the current period have been annualized.

1 Calculated based on average shares outstanding.

2 Total returns do not include transaction fees or account service fees that may have applied in the periods shown. Fund prospectuses provide information about any applicable transaction and account service fees.

3 Includes performance-based investment advisory fee increases (decreases) of 0.03%, (0.02%), 0.01%, 0.00%, 0.03%, and 0.01%.

See accompanying Notes, which are an integral part of the Financial Statements.

21

Energy Fund

Notes to Financial Statements

Vanguard Energy Fund is registered under the Investment Company Act of 1940 as an open-end investment company, or mutual fund. The fund invests in securities of foreign issuers, which may subject it to investment risks not normally associated with investing in securities of U.S. corporations. The fund offers two classes of shares: Investor Shares and Admiral Shares. Investor Shares are available to any investor who meets the fund’s minimum purchase requirements. Admiral Shares are designed for investors who meet certain administrative, service, and account-size criteria.

A. The following significant accounting policies conform to generally accepted accounting principles for U.S. mutual funds. The fund consistently follows such policies in preparing its financial statements.

1. Security Valuation: Securities are valued as of the close of trading on the New York Stock Exchange (generally 4 p.m., Eastern time) on the valuation date. Equity securities are valued at the latest quoted sales prices or official closing prices taken from the primary market in which each security trades; such securities not traded on the valuation date are valued at the mean of the latest quoted bid and asked prices. Securities for which market quotations are not readily available, or whose values have been affected by events occurring before the fund’s pricing time but after the close of the securities’ primary markets, are valued at their fair values calculated according to procedures adopted by the board of trustees. These procedures include obtaining quotations from an independent pricing service, monitoring news to identify significant market- or security-specific events, and evaluating changes in the values of foreign market proxies (for example, ADRs, futures contracts, or exchange-traded funds), between the time the foreign markets close and the fund’s pricing time. When fair-value pricing is employed, the prices of securities used by a fund to calculate its net asset value may differ from quoted or published prices for the same securities. Investments in Vanguard Market Liquidity Fund are valued at that fund’s net asset value. Temporary cash investments acquired over 60 days to maturity are valued using the latest bid prices or using valuations based on a matrix system (which considers such factors as security prices, yields, maturities, and ratings), both as furnished by independent pricing services. Other temporary cash investments are valued at amortized cost, which approximates market value.

2. Foreign Currency: Securities and other assets and liabilities denominated in foreign currencies are translated into U.S. dollars using exchange rates obtained from an independent third party as of the fund’s pricing time on the valuation date. Realized gains (losses) and unrealized appreciation (depreciation) on investment securities include the effects of changes in exchange rates since the securities were purchased, combined with the effects of changes in security prices. Fluctuations in the value of other assets and liabilities resulting from changes in exchange rates are recorded as unrealized foreign currency gains (losses) until the assets or liabilities are settled in cash, at which time they are recorded as realized foreign currency gains (losses).

3. Futures Contracts: The fund uses index futures contracts to a limited extent, with the objective of maintaining full exposure to the stock market while maintaining liquidity. The fund may purchase or sell futures contracts to achieve a desired level of investment, whether to accommodate portfolio turnover or cash flows from capital share transactions. The primary risks associated with the use of futures contracts are imperfect correlation between changes in market values of stocks held by the fund and the prices of futures contracts, and the possibility of an illiquid market.

Futures contracts are valued at their quoted daily settlement prices. The aggregate notional amounts of the contracts are not recorded in the Statement of Net Assets. Fluctuations in the value of the contracts are recorded in the Statement of Net Assets as an asset (liability) and in the Statement of Operations as unrealized appreciation (depreciation) until the contracts are closed, when they are recorded as realized futures gains (losses). Counterparty risk involving futures is mitigated because

22

Energy Fund

a regulated clearinghouse is the counterparty instead of the clearing broker. To further mitigate counterparty risk, the fund trades futures contracts on an exchange; monitors the financial strength of its clearing brokers and clearinghouse; and has entered into clearing agreements with its clearing brokers. The clearinghouse imposes initial margin requirements to secure the fund’s performance and requires daily settlement of variation margin representing changes in the market value of each contract.

During the six months ended July 31, 2013, the fund’s average investments in long and short futures contracts represented less than 1% and 0% of net assets, respectively, based on quarterly average aggregate settlement values.

4. Repurchase Agreements: The fund may enter into repurchase agreements with institutional counterparties. Securities pledged as collateral to the fund under repurchase agreements are held by a custodian bank until the agreements mature. Each agreement requires that the market value of the collateral be sufficient to cover payments of interest and principal. The fund further mitigates its counterparty risk by entering into repurchase agreements only with a diverse group of pre-qualified counterparties, monitoring their financial strength, and entering into master repurchase agreements with its counterparties. The master repurchase agreements provide that, in the event of a counterparty’s default (including bankruptcy), the fund may terminate any repurchase agreements with that counterparty, determine the net amount owed, and sell or retain the collateral up to the net amount owed to the fund.

5. Federal Income Taxes: The fund intends to continue to qualify as a regulated investment company and distribute all of its taxable income. Management has analyzed the fund’s tax positions taken for all open federal income tax years (January 31, 2010–2013), and for the period ended July 31, 2013, and has concluded that no provision for federal income tax is required in the fund’s financial statements.

6. Distributions: Distributions to shareholders are recorded on the ex-dividend date.

7. Securities Lending: To earn additional income, the fund may lend its securities to qualified institutional borrowers. Security loans are required to be secured at all times by collateral in an amount at least equal to the market value of securities loaned. Daily market fluctuations could cause the value of loaned securities to be more or less than the value of the collateral received. When this occurs, the collateral is adjusted and settled on the next business day. The fund further mitigates its counterparty risk by entering into securities lending transactions only with a diverse group of pre-qualified counterparties, monitoring their financial strength, and entering into master securities lending agreements with its counterparties. The master securities lending agreements provide that, in the event of a counterparty’s default (including bankruptcy), the fund may terminate any loans with that borrower, determine the net amount owed, and sell or retain the collateral up to the net amount owed to the fund. The fund invests cash collateral received in Vanguard Market Liquidity Fund, and records a liability for the return of the collateral, during the period the securities are on loan. Securities lending income represents fees charged to borrowers plus income earned on invested cash collateral, less expenses associated with the loan.

8. Other: Dividend income is recorded on the ex-dividend date. Interest income is accrued daily. Premiums and discounts on debt securities purchased are amortized and accreted, respectively, to interest income over the lives of the respective securities. Security transactions are accounted for on the date securities are bought or sold. Costs used to determine realized gains (losses) on the sale of investment securities are those of the specific securities sold.

23

Energy Fund

Each class of shares has equal rights as to assets and earnings, except that each class separately bears certain class-specific expenses related to maintenance of shareholder accounts (included in Management and Administrative expenses) and shareholder reporting. Marketing and distribution expenses are allocated to each class of shares based on a method approved by the board of trustees. Income, other non-class-specific expenses, and gains and losses on investments are allocated to each class of shares based on its relative net assets.

B. Wellington Management Company, LLP, provides investment advisory services to a portion of the fund for a fee calculated at an annual percentage rate of average net assets managed by the advisor. The basic fee is subject to quarterly adjustments based on performance for the preceding three years relative to the MSCI ACWI Energy Index.

The Vanguard Group provides investment advisory services to a portion of the fund on an at-cost basis; the fund paid Vanguard advisory fees of $184,000 for the six months ended July 31, 2013.

For the six months ended July 31, 2013, the aggregate investment advisory fee represented an effective annual basic rate of 0.14% of the fund’s average net assets, before an increase of $1,868,000 (0.03%) based on performance.

C. The Vanguard Group furnishes at cost corporate management, administrative, marketing, and distribution services. The costs of such services are allocated to the fund under methods approved by the board of trustees. The fund has committed to provide up to 0.40% of its net assets in capital contributions to Vanguard. At July 31, 2013, the fund had contributed capital of $1,412,000 to Vanguard (included in Other Assets), representing 0.01% of the fund’s net assets and 0.56% of Vanguard’s capitalization. The fund’s trustees and officers are also directors and officers of Vanguard.

D. Various inputs may be used to determine the value of the fund’s investments. These inputs are summarized in three broad levels for financial statement purposes. The inputs or methodologies used to value securities are not necessarily an indication of the risk associated with investing in those securities.

Level 1—Quoted prices in active markets for identical securities.

Level 2—Other significant observable inputs (including quoted prices for similar securities, interest rates, prepayment speeds, credit risk, etc.).

Level 3—Significant unobservable inputs (including the fund’s own assumptions used to determine the fair value of investments).

The following table summarizes the market value of the fund’s investments as of July 31, 2013, based on the inputs used to value them:

| | | |

| | Level 1 | Level 2 | Level 3 |

| Investments | ($000) | ($000) | ($000) |

| Common Stocks—United States | 6,992,606 | — | — |

| Common Stocks—International | 2,974,462 | 1,379,646 | — |

| Temporary Cash Investments | 94,788 | 416,999 | — |

| Futures Contracts—Liabilities1 | (236) | — | — |

| Total | 10,061,620 | 1,796,645 | — |

| 1 Represents variation margin on the last day of the reporting period. |

24

Energy Fund

E. At July 31, 2013, the aggregate settlement value of open futures contracts and the related unrealized appreciation (depreciation) were:

| | | | |

| | | | | ($000) |

| | | | Aggregate | |

| | | Number of | Settlement | Unrealized |

| | | Long (Short) | Value | Appreciation |

| Futures Contracts | Expiration | Contracts | Long (Short) | (Depreciation) |

| E-mini S&P 500 Index | September 2013 | 940 | 78,984 | 245 |

| S&P 500 Index | September 2013 | 34 | 14,284 | 299 |

Unrealized appreciation (depreciation) on open futures contracts is required to be treated as realized gain (loss) for tax purposes.

F. Distributions are determined on a tax basis and may differ from net investment income and realized capital gains for financial reporting purposes. Differences may be permanent or temporary. Permanent differences are reclassified among capital accounts in the financial statements to reflect their tax character. Temporary differences arise when certain items of income, expense, gain, or loss are recognized in different periods for financial statement and tax purposes; these differences will reverse at some time in the future. Differences in classification may also result from the treatment of short-term gains as ordinary income for tax purposes.

During the six months ended July 31, 2013, the fund realized net foreign currency losses of $462,000, which decreased distributable net income for tax purposes; accordingly, such losses have been reclassified from accumulated net realized gains to undistributed net investment income. Certain of the fund’s investments are in securities considered to be “passive foreign investment companies,” for which any unrealized appreciation and/or realized gains are required to be included in distributable net income for tax purposes. Passive foreign investment companies held at July 31, 2013, had unrealized appreciation of $28,015,000, as of January 31, 2013, the most recent mark-to-market date for tax purposes. This amount has been distributed and is reflected in the balance of undistributed net investment income.

The fund’s tax-basis capital gains and losses are determined only at the end of each fiscal year. For tax purposes, at January 31, 2013, the fund had available capital losses totaling $15,701,000 that may be carried forward indefinitely to offset future net capital gains. The fund will use these capital losses to offset net taxable capital gains, if any, realized during the year ending January 31, 2014; should the fund realize net capital losses for the year, the losses will be added to the loss carryforward balance above.

At July 31, 2013, the cost of investment securities for tax purposes was $7,672,400,000. Net unrealized appreciation of investment securities for tax purposes was $4,186,101,000, consisting of unrealized gains of $4,414,448,000 on securities that had risen in value since their purchase and $228,347,000 in unrealized losses on securities that had fallen in value since their purchase.

G. During the six months ended July 31, 2013, the fund purchased $1,239,449,000 of investment securities and sold $1,577,970,000 of investment securities, other than temporary cash investments.

25

Energy Fund

H. Capital share transactions for each class of shares were:

| | | | |

| | Six Months Ended | | Year Ended |

| | | July 31, 2013 | January 31, 2013 |

| | Amount | Shares | Amount | Shares |

| | ($000) | (000) | ($000) | (000) |

| Investor Shares | | | | |

| Issued | 257,019 | 4,116 | 695,926 | 11,544 |

| Issued in Lieu of Cash Distributions | 11,879 | 191 | 204,348 | 3,375 |

| Redeemed1 | (729,075) | (11,630) | (1,470,869) | (24,672) |

| Net Increase (Decrease)—Investor Shares | (460,177) | (7,323) | (570,595) | (9,753) |

| Admiral Shares | | | | |

| Issued | 508,368 | 4,330 | 1,015,171 | 9,110 |

| Issued in Lieu of Cash Distributions | 14,941 | 128 | 233,904 | 2,064 |

| Redeemed1 | (655,494) | (5,578) | (1,238,717) | (11,038) |

| Net Increase (Decrease)—Admiral Shares | (132,185) | (1,120) | 10,358 | 136 |

1 Net of redemption fees for fiscal 2013 of $642,000 (fund total). Effective May 23, 2012, the redemption fee was eliminated.

I. Management has determined that no material events or transactions occurred subsequent to July 31, 2013, that would require recognition or disclosure in these financial statements.

26

About Your Fund’s Expenses

As a shareholder of the fund, you incur ongoing costs, which include costs for portfolio management, administrative services, and shareholder reports (like this one), among others. Operating expenses, which are deducted from a fund’s gross income, directly reduce the investment return of the fund.

A fund’s expenses are expressed as a percentage of its average net assets. This figure is known as the expense ratio. The following examples are intended to help you understand the ongoing costs (in dollars) of investing in your fund and to compare these costs with those of other mutual funds. The examples are based on an investment of $1,000 made at the beginning of the period shown and held for the entire period.

The accompanying table illustrates your fund’s costs in two ways:

• Based on actual fund return. This section helps you to estimate the actual expenses that you paid over the period. The ”Ending Account Value“ shown is derived from the fund‘s actual return, and the third column shows the dollar amount that would have been paid by an investor who started with $1,000 in the fund. You may use the information here, together with the amount you invested, to estimate the expenses that you paid over the period.

To do so, simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number given for your fund under the heading ”Expenses Paid During Period.“

• Based on hypothetical 5% yearly return. This section is intended to help you compare your fund‘s costs with those of other mutual funds. It assumes that the fund had a yearly return of 5% before expenses, but that the expense ratio is unchanged. In this case—because the return used is not the fund’s actual return—the results do not apply to your investment. The example is useful in making comparisons because the Securities and Exchange Commission requires all mutual funds to calculate expenses based on a 5% return. You can assess your fund’s costs by comparing this hypothetical example with the hypothetical examples that appear in shareholder reports of other funds.

Note that the expenses shown in the table are meant to highlight and help you compare ongoing costs only and do not reflect transaction costs incurred by the fund for buying and selling securities. Further, the expenses do not include any purchase, redemption, or account service fees described in the fund prospectus. If such fees were applied to your account, your costs would be higher. Your fund does not carry a “sales load.”

The calculations assume no shares were bought or sold during the period. Your actual costs may have been higher or lower, depending on the amount of your investment and the timing of any purchases or redemptions.

You can find more information about the fund’s expenses, including annual expense ratios, in the Financial Statements section of this report. For additional information on operating expenses and other shareholder costs, please refer to your fund’s current prospectus.

27

| | | |

| Six Months Ended July 31, 2013 | | | |

| | Beginning | Ending | Expenses |

| | Account Value | Account Value | Paid During |

| Energy Fund | 1/31/2013 | 7/31/2013 | Period |

| Based on Actual Fund Return | | | |

| Investor Shares | $1,000.00 | $1,028.31 | $1.86 |

| Admiral Shares | 1,000.00 | 1,028.46 | 1.56 |

| Based on Hypothetical 5% Yearly Return | | | |

| Investor Shares | $1,000.00 | $1,022.96 | $1.86 |

| Admiral Shares | 1,000.00 | 1,023.26 | 1.56 |

The calculations are based on expenses incurred in the most recent six-month period. The fund’s annualized six-month expense ratios for that period are 0.37% for Investor Shares and 0.31% for Admiral Shares. The dollar amounts shown as “Expenses Paid” are equal to the annualized expense ratio multiplied by the average account value over the period, multiplied by the number of days in the most recent six-month period, then divided by the number of days in the most recent 12-month period.

28

Trustees Approve Advisory Arrangements

The board of trustees of Vanguard Energy Fund has renewed the fund’s investment advisory arrangements with The Vanguard Group, Inc. (Vanguard), through its Equity Investment Group, and Wellington Management Company, LLP (Wellington Management). The board determined that renewing the fund’s advisory arrangement was in the best interests of the fund and its shareholders.

The board based its decision upon an evaluation of each advisor’s investment staff, portfolio management process, and performance. The trustees considered the factors discussed below, among others. However, no single factor determined whether the board approved the arrangements. Rather, it was the totality of the circumstances that drove the board’s decision.

Nature, extent, and quality of services

The board considered the quality of the fund’s investment management services over both the short and long term, and took into account the organizational depth and stability of each advisor. The board noted the following:

Vanguard. Vanguard has been managing investments for more than three decades. The Equity Investment Group adheres to a sound, disciplined investment management process; the team has considerable experience, stability, and depth. Vanguard has managed a portion of the fund since 2005.

Wellington Management. Founded in 1928, Wellington Management is among the nation’s oldest and most respected institutional investment managers. The investment team uses a bottom-up approach in which stocks are selected based on the advisor’s estimates of fundamental investment value. The advisor’s investment process emphasizes company fundamentals, management track record, and security valuation. The firm has advised the fund since the fund’s inception in 1984.

The board concluded that each advisor’s experience, stability, depth, and performance, among other factors, warranted the continuation of the advisory arrangements.

Investment performance

The board considered the short- and long-term performance of the fund, including any periods of outperformance or underperformance relative to a benchmark index and peer group. The board concluded that the performance was such that the advisory arrangement should continue. Information about the fund’s most recent performance can be found in the Performance Summary section of this report.

Cost

The board concluded that the fund’s expense ratio was well below the average expense ratio charged by funds in its peer group and that the fund’s advisory fee rate was also well below its peer-group average. Information about the fund’s expenses appears in the About Your Fund’s Expenses section of this report as well as in the Financial Statements section, which also includes information about the fund’s advisory fee rate.

The board did not consider profitability of Wellington Management in determining whether to approve the advisory fee, because Wellington Management is independent of Vanguard, and the advisory fee is the result of arm’s-length negotiations. The board does not conduct a profitability analysis of Vanguard, because of Vanguard’s unique “at-cost” structure. Unlike most other mutual fund management companies, Vanguard is owned by the funds it oversees, and produces “profits” only in the form of reduced expenses for fund shareholders.

29

The benefit of economies of scale

The board concluded that the fund’s shareholders benefit from economies of scale because of breakpoints in the fund’s advisory fee schedule for Wellington Management. The breakpoints reduce the effective rate of the fee as the fund’s assets managed by Wellington Management increase. The board also concluded that the fund’s at-cost arrangement with Vanguard ensures that the fund will realize economies of scale as it grows, with the cost to shareholders declining as the fund’s assets managed by Vanguard increase.

The board will consider whether to renew the advisory arrangement again after a one-year period.

30

Glossary

30-Day SEC Yield. A fund’s 30-day SEC yield is derived using a formula specified by the U.S. Securities and Exchange Commission. Under the formula, data related to the fund’s security holdings in the previous 30 days are used to calculate the fund’s hypothetical net income for that period, which is then annualized and divided by the fund’s estimated average net assets over the calculation period. For the purposes of this calculation, a security’s income is based on its current market yield to maturity (for bonds), its actual income (for asset-backed securities), or its projected dividend yield (for stocks). Because the SEC yield represents hypothetical annualized income, it will differ—at times significantly—from the fund’s actual experience. As a result, the fund’s income distributions may be higher or lower than implied by the SEC yield.

Beta. A measure of the magnitude of a fund’s past share-price fluctuations in relation to the ups and downs of a given market index. The index is assigned a beta of 1.00. Compared with a given index, a fund with a beta of 1.20 typically would have seen its share price rise or fall by 12% when the index rose or fell by 10%. For this report, beta is based on returns over the past 36 months for both the fund and the index. Note that a fund’s beta should be reviewed in conjunction with its R-squared (see definition). The lower the R-squared, the less correlation there is between the fund and the index, and the less reliable beta is as an indicator of volatility.

Dividend Yield. Dividend income earned by stocks, expressed as a percentage of the aggregate market value (or of net asset value, for a fund). The yield is determined by dividing the amount of the annual dividends by the aggregate value (or net asset value) at the end of the period. For a fund, the dividend yield is based solely on stock holdings and does not include any income produced by other investments.

Earnings Growth Rate. The average annual rate of growth in earnings over the past five years for the stocks now in a fund.

Equity Exposure. A measure that reflects a fund’s investments in stocks and stock futures. Any holdings in short-term reserves are excluded.

Expense Ratio. A fund’s total annual operating expenses expressed as a percentage of the fund’s average net assets. The expense ratio includes management and administrative expenses, but does not include the transaction costs of buying and selling portfolio securities.

Foreign Holdings. The percentage of a fund represented by securities or depositary receipts of companies based outside the United States.

Inception Date. The date on which the assets of a fund (or one of its share classes) are first invested in accordance with the fund’s investment objective. For funds with a subscription period, the inception date is the day after that period ends. Investment performance is measured from the inception date.

Median Market Cap. An indicator of the size of companies in which a fund invests; the midpoint of market capitalization (market price x shares outstanding) of a fund’s stocks, weighted by the proportion of the fund’s assets invested in each stock. Stocks representing half of the fund’s assets have market capitalizations above the median, and the rest are below it.

Price/Book Ratio. The share price of a stock divided by its net worth, or book value, per share. For a fund, the weighted average price/book ratio of the stocks it holds.

31

Price/Earnings Ratio. The ratio of a stock’s current price to its per-share earnings over the past year. For a fund, the weighted average P/E of the stocks it holds. P/E is an indicator of market expectations about corporate prospects; the higher the P/E, the greater the expectations for a company’s future growth.

R-Squared. A measure of how much of a fund’s past returns can be explained by the returns from the market in general, as measured by a given index. If a fund’s total returns were precisely synchronized with an index’s returns, its R-squared would be 1.00. If the fund’s returns bore no relationship to the index’s returns, its R-squared would be 0. For this report, R-squared is based on returns over the past 36 months for both the fund and the index.

Return on Equity. The annual average rate of return generated by a company during the past five years for each dollar of shareholder’s equity (net income divided by shareholder’s equity). For a fund, the weighted average return on equity for the companies whose stocks it holds.

Short-Term Reserves. The percentage of a fund invested in highly liquid, short-term securities that can be readily converted to cash.

Turnover Rate. An indication of the fund’s trading activity. Funds with high turnover rates incur higher transaction costs and may be more likely to distribute capital gains (which may be taxable to investors). The turnover rate excludes in-kind transactions, which have minimal impact on costs.

Benchmark Information