UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT

OF

REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-03916

Name of Registrant: Vanguard Specialized Funds

Address of Registrant:

P.O. Box 2600

Valley Forge, PA 19482

Name and address of agent for service:

Heidi Stam, Esquire

P.O. Box 876

Valley Forge, PA 19482

Registrant’s telephone number, including area code: (610) 669-1000

Date of fiscal year end: January 31

Date of reporting period: February 1, 2014 – July 31, 2014

Item 1: Reports to Shareholders

Semiannual Report | July 31, 2014

Vanguard Energy Fund

Vanguard’s Principles for Investing Success

We want to give you the best chance of investment success. These principles, grounded in Vanguard’s research and experience, can put you on the right path.

Goals. Create clear, appropriate investment goals.

Balance. Develop a suitable asset allocation using broadly diversified funds.

Cost. Minimize cost.

Discipline. Maintain perspective and long-term discipline.

A single theme unites these principles: Focus on the things you can control. We believe there is no wiser course for any investor.

| |

| Contents | |

| Your Fund’s Total Returns. | 1 |

| Chairman’s Letter. | 2 |

| Advisors’ Report. | 7 |

| Fund Profile. | 12 |

| Performance Summary. | 14 |

| Financial Statements. | 15 |

| About Your Fund’s Expenses. | 28 |

| Trustees Approve Advisory Arrangements. | 30 |

| Glossary. | 32 |

Please note: The opinions expressed in this report are just that—informed opinions. They should not be considered promises or advice.

Also, please keep in mind that the information and opinions cover the period through the date on the front of this report. Of course, the

risks of investing in your fund are spelled out in the prospectus.

See the Glossary for definitions of investment terms used in this report.

About the cover: The ship’s wheel represents leadership and guidance, essential qualities in navigating difficult seas.

This one is a replica based on an 18th-century British vessel. The HMS Vanguard, another ship of that era, served as the

flagship for British Admiral Horatio Nelson when he defeated a French fleet at the Battle of the Nile.

Your Fund’s Total Returns

| |

| Six Months Ended July 31, 2014 | |

| | Total |

| | Returns |

| Vanguard Energy Fund | |

| Investor Shares | 14.68% |

| Admiral™ Shares | 14.71 |

| MSCI ACWI Energy Index | 16.11 |

| Global Natural Resources Funds Average | 12.22 |

Global Natural Resources Funds Average: Derived from data provided by Lipper, a Thomson Reuters Company.Admiral Shares carry lower expenses and are available to investors who meet certain account-balance requirements.Your Fund’s Performance at a Glance

January 31, 2014, Through July 31, 2014

| | | | |

| | | | Distributions Per Share |

| | Starting | Ending | Income | Capital |

| | Share Price | Share Price | Dividends | Gains |

| Vanguard Energy Fund | | | | |

| Investor Shares | $63.85 | $72.99 | $0.000 | $0.217 |

| Admiral Shares | 119.83 | 137.02 | 0.000 | 0.407 |

1

Chairman’s Letter

Dear Shareholder,

After lagging the broad U.S. stock market for three consecutive fiscal years, the energy sector leaped ahead. For the six months ended July 31, 2014, the MSCI ACWI Energy Index returned 16.11%, almost double the return of the Russell 3000 Index and well ahead of the approximately 9% return of the broad global market. Higher oil prices stemming from strife in Iraq and elsewhere helped make energy the U.S. broad market’s best-performing sector.

Even with a robust return of 14.68% for Investor Shares (and a bit more for Admiral Shares), Vanguard Energy Fund lagged its benchmark index. Rewarding choices among integrated energy giants were more than offset by outsized stakes in some U.S.-based oil and gas exploration and production companies that sustained double-digit declines. However, the fund was more than 2 percentage points ahead of the average return of its global natural resource peers, many of which have significant allocations to sectors other than energy.

Stocks posted strong returns despite finishing with a thud

For the six months ended July 31, the broad U.S. stock market returned about 8% despite ending on a negative note. On the cusp of eking out a sixth straight monthly advance, returns tumbled on the period’s final day.

2

Overall, generally strong corporate earnings, investors’ willingness to embrace risk, and the Federal Reserve’s resolve to sustain historically low interest rates for an extended time were supportive. The market withstood conflict in the Middle East and Ukraine, economic concerns in China and Europe, and the Fed’s gradual reduction of its stimulative bond-buying program.

International stocks returned almost 10%. Emerging markets, which slumped notably in 2013, led the charge. The developed markets of the Pacific region managed double-digit returns as well. European stocks, despite retreating in July, also finished on positive ground.

Bonds’ recent rebound showed signs of fatigue

The broad U.S. taxable bond market returned 2.16%. Although bonds have rebounded after posting negative returns for 2013, they gradually lost momentum in June and July. The yield of the benchmark 10-year U.S. Treasury note ended the period at 2.56%, down from 2.70% on January 31 but up from 2.47% at the end of May. (Bond prices and yields move in opposite directions.)

Municipal bonds, lifted by the broad bond market’s rally and less restrained by the later decline in Treasury prices, returned 4.15%. Investor demand for tax-exempt income and a limited supply of new issues also helped.

| | | |

| Market Barometer | | | |

| |

| | | | Total Returns |

| | Periods Ended July 31, 2014 |

| | Six | One | Five Years |

| | Months | Year | (Annualized) |

| Stocks | | | |

| Russell 1000 Index (Large-caps) | 9.02% | 17.06% | 17.13% |

| Russell 2000 Index (Small-caps) | -0.30 | 8.56 | 16.56 |

| Russell 3000 Index (Broad U.S. market) | 8.25 | 16.37 | 17.08 |

| FTSE All-World ex US Index (International) | 9.73 | 15.78 | 9.13 |

| |

| Bonds | | | |

| Barclays U.S. Aggregate Bond Index (Broad taxable market) | 2.16% | 3.97% | 4.47% |

| Barclays Municipal Bond Index (Broad tax-exempt market) | 4.15 | 7.27 | 5.50 |

| Citigroup Three-Month U.S. Treasury Bill Index | 0.00 | 0.04 | 0.07 |

| |

| CPI | | | |

| Consumer Price Index | 1.85% | 1.99% | 2.04% |

3

Results for money market funds and savings accounts remained tempered by the Fed’s target of 0%–0.25% for short-term interest rates.

International bond markets (as measured by the Barclays Global Aggregate Index ex USD) returned 3.35%.

The fund gained in all subsectors; equipment and services stood out

Amid a rising chorus of headlines proclaiming that the United States is becoming energy self-sufficient, one might expect that our energy costs would become more insulated from geopolitical tensions involving oil-producing nations. Although there is some truth to that, renewed hostilities—such as those that flared up in June in Iraq—did lead to higher oil prices everywhere. This effect eased by the end of the period, but many energy company stocks benefited from the run-up.

Booming production from shale deposits in North Dakota and elsewhere helped lift many equipment and services providers, including some of your fund’s largest holdings. This subsector of the fund, about 10% of total assets on average for the period, was the best performer, with a six-month return of more than 20%. Integrated multinational oil and gas giants and companies focused on exploration and production, representing about three-quarters of total assets, weren’t far behind.

Expense Ratios

Your Fund Compared With Its Peer Group

| | | |

| | Investor | Admiral | Peer Group |

| | Shares | Shares | Average |

| Energy Fund | 0.38% | 0.32% | 1.34% |

The fund expense ratios shown are from the prospectus dated May 27, 2014, and represent estimated costs for the current fiscal year. For thesix months ended July 31, 2014, the fund’s annualized expense ratios were 0.37% for Investor Shares and 0.31% for Admiral Shares. Thepeer-group expense ratio is derived from data provided by Lipper, a Thomson Reuters Company, and captures information through year-end2013.Peer group: Global Natural Resources Funds.4

As I’ve noted in past reports, higher oil prices can pinch the profit margins of refiners who process crude oil into other products such as gasoline. As a group, oil and gas refiners and marketers—a small slice of the fund—had some of the lowest returns.

In a turnabout from last year, the Energy Fund’s advisors added the most value relative to the benchmark with their choices among integrated multinationals. Selections among equipment and service providers were also rewarding. However, results were held back by above-benchmark stakes in some U.S.-based oil and gas explorers and producers that declined.

The Advisors’ Report that follows this letter provides additional details about the management of the fund during the six months. I would also like to acknowledge the Energy Fund’s 30th anniversary in May and thank Wellington Management Company, llp, for three decades of dedicated and continuing service as the fund’s lead advisor.

Don’t let complacency set your portfolio adrift

At Vanguard, we often warn against letting emotions become entangled with investments. When the financial markets are in turmoil, for example, we’ll caution investors not to let fear lead to rash decisions. But complacency—that mild-mannered counterpoint to fear—can also stand in the way of achieving your financial goals. And lately, conditions have been ripe for complacency.

In the more than five years since its March 2009 bottom, the broad U.S. stock market, as measured by the Russell 3000 Index, has produced average annual returns of nearly 25%. That’s more than double the historical average annual return. And in recent weeks, several indexes touched all-time highs.

The investment winds don’t always blow favorably, of course—a point underscored by the sharp drop for stocks on the last day of July. This unwelcome retreat served to remind us that the exceptionally smooth sailing in the preceding months created risks of its own.

When markets are unusually tranquil, it can be easy to lose sight of fundamentals, especially the importance of rebalancing. Without periodically adjusting your asset allocation so that it stays in line with your goals and risk tolerance, you can end up with a portfolio that’s very different from, and potentially riskier than, the one you intended to have.

5

Whether the market’s moving up, down, or sideways, we always encourage our clients to stay focused on our four principles for investment success: Create clear, appropriate investment goals; develop a suitable asset allocation using broadly diversified funds; minimize cost; and maintain perspective and long-term discipline. (You can read more in Vanguard’s Principles for Investment Success, available at vanguard.com/research.)

As always, thank you for investing with Vanguard.

Sincerely,

F. William McNabb III

Chairman and Chief Executive Officer

August 13, 2014

6

Advisors’ Report

Vanguard Energy Fund returned 14.68% for Investor Shares and 14.71% for Admiral Shares for the six months ended July 31. The fund’s result lagged the 16.11% return of its benchmark index but outperformed the average return of global natural resources peer funds. Your fund is managed by two advisors, a strategy that enhances the fund’s diversification by providing exposure to distinct yet complementary investment approaches. It’s not uncommon for different advisors to have different views about individual securities or the broader investment environment.

The advisors, the amount and percentage of fund assets each manages, and brief descriptions of their investment strategies are presented in the table below. The advisors have also provided a discussion of the investment environment that existed during the period and of how their portfolio positioning reflects this assessment. These reports were prepared on August 12, 2014.

| | | |

| Vanguard Energy Fund Investment Advisors | |

| |

| | Fund Assets Managed | |

| Investment Advisor | % | $ Million | Investment Strategy |

| Wellington Management | 94 | 12,581 | Emphasizes long-term total-return opportunities from |

| Company, LLP | | | the various energy subsectors: international oils, |

| | | | foreign integrated oils and foreign producers, North |

| | | | American producers, oil services and equipment, |

| | | | transportation and distribution, and refining and |

| | | | marketing. |

| Vanguard Equity Investment | 3 | 452 | Employs a quantitative fundamental management |

| Group | | | approach using models that assess valuation, |

| | | | management decisions, market sentiment, and |

| | | | earnings and balance-sheet quality of companies as |

| | | | compared with their peers. |

| Cash Investments | 3 | 390 | These short-term reserves are invested by Vanguard in |

| | | | equity index products to simulate investments in stock. |

| | | | Each advisor may also maintain a modest cash |

| | | | position. |

7

Wellington Management Company, LLP

Portfolio Manager:

Karl E. Bandtel, Senior Vice President

The investment environment

Global equities advanced during the six months ended July 31, 2014, but ended on a weaker note as the market pulled back in July. The global energy sector, benefiting from a supportive commodity backdrop, returned more than 16%, significantly outpacing the broad MSCI All Country World Index return of more than 9%.

Natural gas prices peaked in February as prolonged cold weather across the United States brought inventories there and in Canada to historically low levels. The Marcellus shale formation continued to drive supply growth, but production has declined in most other areas. Although much recent price activity, particularly during the winter, was centered on near-term U.S. contracts, longer-dated gas represents one of the lowest-priced hydrocarbons globally. Prices have appreciated from a year ago, but we think that higher prices are needed for natural gas supply to keep up with demand.

Our successes

Top individual contributors to relative returns included our positions in U.S.-based exploration and production companies Pioneer Natural Resources, EOG Resources, and Athlon Energy, all focused on oil shale assets in the Permian and Bakken basins. Our underweighting of Exxon Mobil also helped.

Pioneer Natural Resources has some of the best oil acreage in the Permian Basin, which we believe presents a solid opportunity for value capture and long-term value creation. We remain optimistic about the company’s growth prospects and we increased our position.

EOG Resources has a strong asset portfolio focused primarily in North America with what we believe to be significant upside to current resource estimates. The company has high-quality assets in the Bakken Basin and an experienced management team that is able to allocate capital efficiently. The shares remain attractively priced in our view; we trimmed our position on relative strength.

Our shortfalls

Stock selection within producers, especially among natural gas-focused exploration and production companies, was the main driver of our relative underperformance. A frictional cash position in a rising equity market also weighed on relative results.

Our most significant detractors, also U.S.-based, included Cabot Oil & Gas, Range Resources, and CONSOL Energy. Not owning benchmark constituent Williams Companies, which returned more than 40% during the period, hurt as well.

8

Cabot Oil & Gas develops and explores oil and gas properties in North America. Producers in the Marcellus Formation disappointed as a lack of pipeline infrastructure caused Marcellus gas to trade at a discount. We believe this is a short-term issue; additional pipelines are under construction. Based on Cabot’s high-quality, low-cost assets in the basin, we added to the position on weakness and continue to hold the stock.

U.S.-based independent natural gas exploration and production company Range Resources also underperformed because of the lack of pipeline infrastructure in the Marcellus Formation. We trimmed the holding but maintain a position; we expect that demand and pricing will boost margins, as Range remains well-positioned in the basin.

The fund’s positioning

Our investment strategy emphasizes long-term total-return opportunities from the various energy subsectors. These include international oils, foreign integrated oils, foreign producers, North American producers, oil services and equipment, transportation and distribution, and refining and marketing. The portfolio holds stocks domiciled in 15 different countries. More than 35% of its assets are invested in international stocks (including roughly 5% in emerging markets).

We are excited by several themes within energy, including North American shale first movers and natural gas. The ongoing retirement of coal plants and low gas prices will structurally support increased natural gas demand over a longer time horizon. Total supply levels are still higher than we anticipated, but their growth has slowed. Although rig counts are down, improving results in shale drilling have allowed production to remain at higher levels.

Demand for natural gas continues to grow, with the largest projects expected to come online in the next three to five years. We believe natural gas resource owners represent an attractive opportunity at current prices. We are also excited by select oil shale producers whose growth and value creation potential are under-appreciated by the market as technology advancements progress.

We continue to believe that returns in energy are driven by companies with a track record of capturing attractive reinvestment opportunities. As a result, we tend to favor producers over larger integrated oil companies. We also assess where we are in the capital cycle of each subsector. We currently have some contrarian exposure to several select exploration firms that are investing in areas that others are less excited about.

9

Our low-turnover investment process remains steady and focused on stocks of companies that have clean balance sheets, long-lived resources, and high-quality management teams.

Vanguard Equity Investment Group

Portfolio Managers:

James D. Troyer, CFA, Principal

James P. Stetler, Principal

Michael R. Roach, CFA

Following very strong 2013 results, global equities continued their march upward before pulling back a bit in July. Emerging markets stocks far outperformed those of developed markets.

Central bank policies remained accommodative, and volatility across financial markets stayed at historic lows. In mid-June, the Chicago Board Options Exchange Volatility Index (VIX) registered 10.6, its lowest level in the last five years. Real estate and labor markets persisted in their slow but consistent recovery.

In what now appears to be a short-term dip, first-quarter GDP results were hampered by a difficult winter. However, the economic growth trend then reversed back to 2013 levels, as indicated by strong second-quarter growth of 4%. Lastly, bond credit spreads have decreased to a level not seen since 2006, an indicator of risk-taking and optimism that can drive equity markets higher.

Energy stocks produced especially strong results relative to the rest of the market. Performance within the sector was broad-based, and most countries generated positive returns. Turkish and Brazilian companies had some of the highest returns; those domiciled in Greece and Hungary had the largest declines.

Although it’s important to understand how overall portfolio performance is affected by the macro factors described above, our approach to investing focuses on specific stock fundamentals. We do not take a stand on the overall market for energy stocks. Nor do we attempt to make predictions about different geographic regions.

Our process seeks to compare all stocks in our investment universe in order to identify those that have characteristics we believe will help them outperform over the long run. To do this, we use a strict quantitative process that focuses on a combination of valuation and other factors focused on fundamental growth. Using the results of our model, we then construct our portfolio, with the goal of maximizing expected return and minimizing exposure to risks that our research indicates do not improve returns, such as market capitalization and other risks relative to our benchmark.

10

Over this period, our most successful overweights included Newfield Exploration (+62.7%), Bharat Petroleum (+65.5%), and First Solar (+34.08%). An important part of our performance came from underweighting companies that did not do well, such as Cabot Oil & Gas (–17.5%) and Range Resources (–12.2%).

Results were dragged down by overweighted positions in MOL Hungarian Oil & Gas (–17.6%) and Aker Solutions (–13.55%). Not holding Concho Resources and Cheniere Energy also hurt, as both had exceptionally strong double-digit gains.

Although it is difficult to predict the direction of the overall market, let alone a specific subset, we are confident that our model should continue capturing the relative attractiveness of individual stocks. Solid fundamentals remain one of the main drivers of our strategy, which we believe the market will reward in the long run. We thank you for your investment and look forward to the second half of the fiscal year.

11

Energy Fund

Fund Profile

As of July 31, 2014

| | |

| Share-Class Characteristics | |

| | Investor | Admiral |

| | Shares | Shares |

| Ticker Symbol | VGENX | VGELX |

| Expense Ratio1 | 0.38% | 0.32% |

| 30-Day SEC Yield | 1.60% | 1.66% |

| | | |

| Portfolio Characteristics | | |

| | | | DJ |

| | | | U.S. |

| | | | Total |

| | | MSCI | Market |

| | | ACWI | FA |

| | Fund | Energy | Index |

| Number of Stocks | 137 | 167 | 3,718 |

| Median Market Cap | $54.0B | $69.7B | $48.5B |

| Price/Earnings Ratio | 16.9x | 16.1x | 20.2x |

| Price/Book Ratio | 1.9x | 1.7x | 2.6x |

| Return on Equity | 13.0% | 15.0% | 17.5% |

| Earnings Growth | | | |

| Rate | 2.8% | 4.9% | 14.8% |

| Dividend Yield | 2.0% | 2.9% | 1.9% |

| Foreign Holdings | 38.0% | 48.8% | 0.0% |

| Turnover Rate | | | |

| (Annualized) | 21% | — | — |

| Short-Term Reserves | 2.8% | — | — |

| | |

| Subindustry Diversification (% of equity | |

| exposure) | | |

| | | MSCI |

| | | ACWI |

| | Fund | Energy |

| Coal & Consumable Fuels | 2.6% | 1.2% |

| Industrials | 0.5 | 0.0 |

| Integrated Oil & Gas | 41.4 | 51.8 |

| Oil & Gas Drilling | 0.9 | 2.0 |

| Oil & Gas Equipment & | | |

| Services | 9.6 | 10.5 |

| Oil & Gas Exploration & | | |

| Production | 35.1 | 22.3 |

| Oil & Gas Refining & | | |

| Marketing | 4.9 | 5.5 |

| Oil & Gas Storage & | | |

| Transportation | 2.4 | 6.7 |

| Other | 2.6 | 0.0 |

| | |

| Volatility Measures | | |

| | | DJ |

| | MSCI | U.S. Total |

| | ACWI | Market |

| | Energy | FA Index |

| R-Squared | 0.98 | 0.80 |

| Beta | 1.05 | 1.43 |

| These measures show the degree and timing of the fund’s fluctuations compared with the indexes over 36 months. |

|

| | |

| Ten Largest Holdings (% of total net assets) |

| Exxon Mobil Corp. | Integrated Oil & Gas | 8.2% |

| Royal Dutch Shell plc | Integrated Oil & Gas | 5.1 |

| Chevron Corp. | Integrated Oil & Gas | 5.0 |

| Schlumberger Ltd. | Oil & Gas Equipment | |

| | & Services | 4.3 |

| Pioneer Natural | Oil & Gas Exploration | |

| Resources Co. | & Production | 3.7 |

| BP plc | Integrated Oil & Gas | 3.3 |

| EOG Resources Inc. | Oil & Gas Exploration | |

| | & Production | 3.2 |

| Total SA | Integrated Oil & Gas | 2.8 |

| Baker Hughes Inc. | Oil & Gas Equipment | |

| | & Services | 2.3 |

| Anadarko Petroleum | Oil & Gas Exploration | |

| Corp. | & Production | 2.3 |

| Top Ten | | 40.2% |

| The holdings listed exclude any temporary cash investments and equity index products. |

|

1 The expense ratios shown are from the prospectus dated May 27, 2014, and represent estimated costs for the current fiscal year. For the sixmonths ended July 31, 2014, the annualized expense ratios were 0.37% for Investor Shares and 0.31% for Admiral Shares.12

Energy Fund

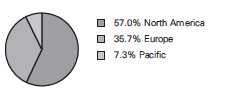

Market Diversification (% of equity exposure)

| |

| Europe | |

| United Kingdom | 10.5% |

| France | 2.9 |

| Italy | 1.8 |

| Other | 2.7 |

| Subtotal | 17.9% |

| Pacific | |

| Japan | 1.3% |

| Other | 0.7 |

| Subtotal | 2.0% |

| Emerging Markets | |

| Russia | 2.2% |

| China | 1.7 |

| Brazil | 1.2 |

| India | 1.0 |

| Subtotal | 6.1% |

| North America | |

| United States | 63.4% |

| Canada | 10.6 |

| Subtotal | 74.0% |

13

Energy Fund

Performance Summary

All of the returns in this report represent past performance, which is not a guarantee of future results that may be achieved by the fund. (Current performance may be lower or higher than the performance data cited. For performance data current to the most recent month-end, visit our website at vanguard.com/performance.) Note, too, that both investment returns and principal value can fluctuate widely, so an investor’s shares, when sold, could be worth more or less than their original cost. The returns shown do not reflect taxes that a shareholder would pay on fund distributions or on the sale of fund shares.

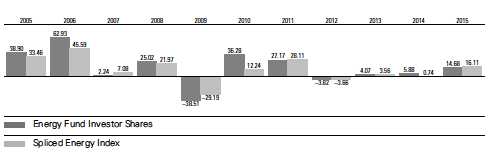

Fiscal-Year Total Returns (%): January 31, 2004, Through July 31, 2014

For a benchmark description, see the Glossary.

Note: For 2015, performance data reflect the six months ended July 31, 2014.

Average Annual Total Returns: Periods Ended June 30, 2014

This table presents returns through the latest calendar quarter—rather than through the end of the fiscal period.

Securities and Exchange Commission rules require that we provide this information.

| | | | |

| | Inception | One | Five | Ten |

| | Date | Year | Years | Years |

| Investor Shares | 5/23/1984 | 30.61% | 13.23% | 13.14% |

| Admiral Shares | 11/12/2001 | 30.70 | 13.30 | 13.21 |

See Financial Highlights for dividend and capital gains information.

14

Energy Fund

Financial Statements (unaudited)

Statement of Net Assets

As of July 31, 2014

The fund reports a complete list of its holdings in regulatory filings four times in each fiscal year, at the quarter-ends. For the second and fourth fiscal quarters, the lists appear in the fund’s semiannual and annual reports to shareholders. For the first and third fiscal quarters, the fund files the lists with the Securities and Exchange Commission on Form N-Q. Shareholders can look up the fund’s Forms N-Q on the SEC’s website at sec.gov. Forms N-Q may also be reviewed and copied at the SEC’s Public Reference Room (see the back cover of this report for further information).

| | | |

| | | | Market |

| | | | Value |

| | | Shares | ($000) |

| Common Stocks (94.9%)1 | | |

| United States (58.7%) | | |

| Construction & Engineering (0.3%) | |

| | KBR Inc. | 1,953,200 | 40,353 |

| |

| Energy Equipment & Services (10.0%) | |

| | Schlumberger Ltd. | 5,349,319 | 579,813 |

| | Baker Hughes Inc. | 4,442,170 | 305,488 |

| | Halliburton Co. | 3,854,872 | 265,948 |

| | Ensco plc Class A | 2,110,124 | 106,878 |

| * | SEACOR Holdings Inc. | 960,253 | 72,941 |

| | Helmerich & Payne Inc. | 33,300 | 3,538 |

| | Nabors Industries Ltd. | 121,600 | 3,303 |

| | Patterson-UTI Energy Inc. | 85,700 | 2,944 |

| * | Seventy Seven Energy Inc. | 94,900 | 2,128 |

| | National Oilwell Varco Inc. | 24,476 | 1,983 |

| | | | 1,344,964 |

| Oil, Gas & Consumable Fuels (48.0%) | |

| | Coal & Consumable Fuels (2.0%) | |

| | CONSOL Energy Inc. | 7,038,985 | 273,253 |

| |

| | Integrated Oil & Gas (15.5%) | |

| | Exxon Mobil Corp. | 11,124,594 | 1,100,667 |

| | Chevron Corp. | 5,172,040 | 668,434 |

| | Occidental | | |

| | Petroleum Corp. | 2,284,923 | 223,260 |

| | Hess Corp. | 938,339 | 92,877 |

| |

| | Oil & Gas Exploration & Production (27.0%) |

| | Pioneer Natural | | |

| | Resources Co. | 2,231,765 | 494,247 |

| | EOG Resources Inc. | 3,878,782 | 424,494 |

| | Anadarko Petroleum Corp. 2,831,400 | 302,535 |

| | Cabot Oil & Gas Corp. | 8,087,914 | 266,497 |

| | Range Resources Corp. | 2,981,190 | 225,348 |

| | Noble Energy Inc. | 3,015,678 | 200,512 |

| | ConocoPhillips | 2,259,309 | 186,393 |

| | EQT Corp. | 1,835,470 | 172,204 |

| * | Southwestern Energy Co. | 4,192,585 | 170,135 |

| * | Antero Resources Corp. | 2,769,605 | 159,972 |

| | | |

| | | | Market |

| | | | Value |

| | | Shares | ($000) |

| | Energen Corp. | 1,812,517 | 147,956 |

| | Denbury Resources Inc. | 8,530,204 | 144,587 |

| | Devon Energy Corp. | 1,422,725 | 107,416 |

| * | Athlon Energy Inc. | 2,099,476 | 100,061 |

| * | Whiting Petroleum Corp. | 1,072,555 | 94,910 |

| | Apache Corp. | 866,350 | 88,940 |

| * | Cobalt International | | |

| | Energy Inc. | 4,071,172 | 65,220 |

| * | Diamondback Energy Inc. | 701,425 | 57,678 |

| | Energy XXI Bermuda Ltd. | 2,855,600 | 56,998 |

| | QEP Resources Inc. | 1,652,573 | 54,618 |

| | Murphy Oil Corp. | 645,300 | 40,092 |

| * | Gulfport Energy Corp. | 591,400 | 31,587 |

| * | Memorial Resource | | |

| | Development Corp. | 411,800 | 9,463 |

| | Marathon Oil Corp. | 148,320 | 5,747 |

| | Chesapeake Energy Corp. | 167,200 | 4,409 |

| * | Newfield Exploration Co. | 77,000 | 3,103 |

| * | Ultra Petroleum Corp. | 100,900 | 2,313 |

| |

| | Oil & Gas Refining & Marketing (3.5%) |

| | Phillips 66 | 2,038,984 | 165,382 |

| | Marathon Petroleum Corp. 1,674,350 | 139,775 |

| | Valero Energy Corp. | 2,506,884 | 127,350 |

| | HollyFrontier Corp. | 727,100 | 34,181 |

| |

| | Oil & Gas Storage & Transportation (0.0%) |

| | Williams Cos. Inc. | 49,400 | 2,797 |

| | Kinder Morgan Inc. | 15,973 | 575 |

| | | | 6,445,986 |

| Other (0.4%) | | |

| ^,2 | Vanguard Energy ETF | 363,000 | 50,305 |

| |

| Semiconductors & | | |

| Semiconductor Equipment (0.0%) | |

| * | First Solar Inc. | 3,700 | 233 |

| |

| Trading Companies & Distributors (0.0%) | |

| * | NOW Inc. | 73,900 | 2,379 |

| Total United States | | 7,884,220 |

15

Energy Fund

| | | |

| | | | Market |

| | | | Value |

| | | Shares | ($000) |

| International (36.2%) | | |

| Australia (0.7%) | | |

| | Oil Search Ltd. | 10,115,898 | 88,478 |

| | Woodside Petroleum Ltd. | 44,269 | 1,738 |

| | | | 90,216 |

| Austria (0.0%) | | |

| | OMV AG | 65,295 | 2,626 |

| |

| Brazil (1.2%) | | |

| | Petroleo Brasileiro | | |

| | SA ADR | 9,828,525 | 156,667 |

| | Petroleo Brasileiro SA | | |

| | Preference Shares | 368,044 | 3,098 |

| | Petroleo Brasileiro SA | 249,132 | 1,975 |

| | Petroleo Brasileiro SA | | |

| | ADR Type A | 12,400 | 209 |

| | | | 161,949 |

| Canada (10.4%) | | |

| | Suncor Energy Inc. XNYS | 6,858,682 | 281,686 |

| | Canadian Natural | | |

| | Resources Ltd. XNYS | 4,813,443 | 209,866 |

| | Cenovus Energy Inc. | | |

| | XNYS | 5,064,180 | 155,470 |

| | Enbridge Inc. XTSE | 3,077,800 | 150,751 |

| | Encana Corp. XNYS | 4,668,790 | 100,612 |

| * | Tourmaline Oil Corp. | 2,090,870 | 98,431 |

| | TransCanada Corp. XNYS | 1,607,100 | 80,628 |

| | Pacific Rubiales | | |

| | Energy Corp. | 3,931,795 | 75,185 |

| | Cameco Corp. | 3,418,370 | 68,914 |

| * | Paramount Resources | | |

| | Ltd. Class A | 1,110,200 | 56,795 |

| | Imperial Oil Ltd. | 761,200 | 39,080 |

| ^ | Keyera Corp. | 377,400 | 28,251 |

| ^ | Trilogy Energy Corp. | 702,500 | 17,879 |

| | Suncor Energy Inc. XTSE | 246,534 | 10,123 |

| | Canadian Natural | | |

| | Resources Ltd. XTSE | 194,278 | 8,469 |

| | Encana Corp. XTSE | 198,600 | 4,277 |

| | Husky Energy Inc. | 103,700 | 3,155 |

| | Enbridge Inc. XNYS | 54,150 | 2,655 |

| | TransCanada Corp. XTSE | 36,796 | 1,846 |

| | Cenovus Energy Inc. XTSE | 21,739 | 668 |

| | | | 1,394,741 |

| China (1.7%) | | |

| ^ | PetroChina Co. Ltd. ADR | 1,132,485 | 146,170 |

| | Kunlun Energy Co. Ltd. | 37,747,555 | 64,111 |

| | PetroChina Co. Ltd. | 4,562,000 | 5,913 |

| | China Petroleum & | | |

| | Chemical Corp. | 5,725,600 | 5,605 |

| * | GCL-Poly Energy | | |

| | Holdings Ltd. | 8,615,000 | 2,781 |

| | CNOOC Ltd. | 697,717 | 1,234 |

| | China Oilfield Services Ltd. | 140,000 | 349 |

| | | | 226,163 |

| | | |

| | | | Market |

| | | | Value |

| | | Shares | ($000) |

| Denmark (0.0%) | | |

| * | Vestas Wind Systems A/S | 75,881 | 3,421 |

| |

| Finland (0.0%) | | |

| | Neste Oil Oyj | 138,698 | 2,563 |

| |

| France (2.9%) | | |

| | Total SA ADR | 5,638,520 | 363,685 |

| | Total SA | 289,354 | 18,662 |

| | | | 382,347 |

| Hong Kong (0.0%) | | |

| * | Brightoil Petroleum | | |

| | Holdings Ltd. | 2,679,000 | 815 |

| |

| Hungary (0.0%) | | |

| | MOL Hungarian Oil & | | |

| | Gas plc | 50,194 | 2,428 |

| |

| India (1.0%) | | |

| | Reliance Industries Ltd. | 7,258,700 | 119,899 |

| | Oil & Natural | | |

| | Gas Corp. Ltd. | 568,970 | 3,696 |

| * | Essar Oil Ltd. | 1,334,155 | 2,526 |

| | Bharat Petroleum | | |

| | Corp. Ltd. | 263,535 | 2,510 |

| | Indian Oil Corp. Ltd. | 450,622 | 2,457 |

| | Hindustan Petroleum | | |

| | Corp. Ltd. | 354,534 | 2,326 |

| * | Mangalore Refinery & | | |

| | Petrochemicals Ltd. | 1,071,676 | 1,146 |

| | GAIL India Ltd. | 45,395 | 326 |

| | Cairn India Ltd. | 55,189 | 287 |

| | | | 135,173 |

| Israel (0.0%) | | |

| | Paz Oil Co. Ltd. | 15,542 | 2,496 |

| |

| Italy (1.7%) | | |

| ^ | Eni SPA ADR | 4,482,005 | 227,686 |

| | Eni SPA | 240,352 | 6,116 |

| | | | 233,802 |

| Japan (1.3%) | | |

| | Inpex Corp. | 10,910,400 | 161,699 |

| | Showa Shell Sekiyu KK | 244,300 | 2,755 |

| | Cosmo Oil Co. Ltd. | 1,248,000 | 2,502 |

| | | | 166,956 |

| Netherlands (0.6%) | | |

| | Koninklijke Vopak NV | 1,433,327 | 66,349 |

| | Fugro NV | 285,967 | 11,012 |

| | | | 77,361 |

| Norway (0.7%) | | |

| ^ | Statoil ASA ADR | 2,476,590 | 70,434 |

| * | DNO ASA | 5,277,707 | 17,677 |

| | Statoil ASA | 197,859 | 5,654 |

| | Aker Solutions ASA | 160,224 | 2,365 |

| | | | 96,130 |

16

Energy Fund

| | |

| | | Market |

| | | Value |

| | Shares | ($000) |

| Poland (0.0%) | | |

| * Polskie Gornictwo | | |

| Naftowe i | | |

| Gazownictwo SA | 1,680,339 | 2,601 |

| |

| Portugal (0.7%) | | |

| Galp Energia SGPS SA | 5,442,953 | 96,609 |

| |

| Russia (2.2%) | | |

| Rosneft OAO GDR | 21,926,239 | 135,290 |

| Gazprom OAO ADR | 13,083,293 | 95,465 |

| Lukoil OAO ADR | 950,406 | 52,986 |

| Tatneft OAO ADR | 93,030 | 3,307 |

| Gazprom OAO | 124,674 | 457 |

| Surgutneftegas OAO ADR | 30,690 | 212 |

| | | 287,717 |

| Singapore (0.0%) | | |

| Sembcorp Industries Ltd. | 646,000 | 2,829 |

| |

| South Africa (0.1%) | | |

| Sasol Ltd. | 110,232 | 6,359 |

| |

| South Korea (0.0%) | | |

| SK Holdings Co. Ltd. | 16,388 | 2,776 |

| |

| Spain (0.7%) | | |

| Repsol SA | 3,678,522 | 91,734 |

| |

| Thailand (0.0%) | | |

| PTT Exploration & | | |

| Production PCL (Foreign) | 645,100 | 3,240 |

| * PTT Global Chemical PCL | 211,600 | 431 |

| PTT PCL (Foreign) | 36,900 | 365 |

| | | 4,036 |

| Turkey (0.0%) | | |

| Tupras Turkiye Petrol | | |

| Rafinerileri AS | 114,306 | 2,794 |

| |

| United Kingdom (10.3%) | | |

| Royal Dutch Shell | | |

| plc ADR | 7,946,585 | 650,269 |

| BP plc ADR | 8,689,185 | 425,509 |

| BG Group plc | 9,989,115 | 196,979 |

| * Ophir Energy plc | 13,649,538 | 49,497 |

| BP plc | 2,583,954 | 21,043 |

| | | |

| | | | Market |

| | | | Value |

| | | Shares | ($000) |

| | Royal Dutch Shell plc | | |

| | Class A | 331,089 | 13,613 |

| | Royal Dutch Shell plc | | |

| | Class B | 281,866 | 12,138 |

| ^ | Royal Dutch Shell plc | | |

| | Class A | | |

| | (Amsterdam Shares) | 142,991 | 5,880 |

| * | Cairn Energy plc | 1 | — |

| | | | 1,374,928 |

| Total International | | 4,851,570 |

| Total Common Stocks | | |

| (Cost $7,097,293) | | 12,735,790 |

| Temporary Cash Investments (6.0%)1 | |

| Money Market Fund (3.1%) | | |

| 3,4 | Vanguard Market Liquidity | |

| | Fund, 0.118% | 415,373,064 | 415,373 |

| |

| | | Face | |

| | | Amount | |

| | | ($000) | |

| Repurchase Agreement (2.8%) | |

| | RBS Securities, Inc. | | |

| | 0.070%, 8/1/14 (Dated | | |

| | 7/31/14, Repurchase | | |

| | Value $369,901,000, | | |

| | collateralized by U.S | | |

| | Treasury Note/Bonds | | |

| | 0.250%–4.250%, | | |

| | 8/15/14–8/15/23, with a | | |

| | value of $377,300,000) | 369,900 | 369,900 |

| |

| U.S. Government and Agency Obligations (0.1%) |

| 5, | Federal Home Loan | | |

| | Bank Discount Notes, | | |

| | 0.053%–0.060%, | | |

| | 8/1/14 | 2,600 | 2,600 |

| 5,6 | Federal Home Loan | | |

| | Bank Discount Notes, | | |

| | 0.060%, 8/13/14 | 1,000 | 1,000 |

| 5 | Federal Home Loan | | |

| | Bank Discount Notes, | | |

| | 0.075%, 9/3/14 | 500 | 500 |

| 5,6 | Federal Home Loan | | |

| | Bank Discount Notes, | | |

| | 0.081%, 9/19/14 | 1,000 | 1,000 |

17

Energy Fund

| | | |

| | | Face | Market |

| | | Amount | Value |

| | | ($000) | ($000) |

| 5,6 | Federal Home Loan | | |

| | Bank Discount Notes, | | |

| | 0.080%–0.090%, | | |

| | 9/24/14 | 5,000 | 5,000 |

| 5,6 | Federal Home Loan | | |

| | Bank Discount Notes, | | |

| | 0.078%, 10/1/14 | 5,800 | 5,799 |

| 5,6 | Federal Home Loan | | |

| | Bank Discount Notes, | | |

| | 0.079%–0.080%, 10/8/14 | 4,000 | 4,000 |

| 5,6 | Federal Home Loan | | |

| | Bank Discount Notes, | | |

| | 0.095%, 10/15/14 | 100 | 100 |

| | | | 19,999 |

| Total Temporary Cash Investments | |

| (Cost $805,271) | | 805,272 |

| Total Investments (100.9%) | | |

| (Cost $7,902,564) | | 13,541,062 |

| Other Assets and Liabilities (-0.9%) | |

| Other Assets | | 107,253 |

| Liabilities3 | | (225,425) |

| | | | (118,172) |

| Net Assets (100%) | | 13,422,890 |

| |

| At July 31, 2014, net assets consisted of: |

| | Amount |

| | ($000) |

| Paid-in Capital | 7,357,927 |

| Undistributed Net Investment Income | 102,192 |

| Accumulated Net Realized Gains | 325,872 |

| Unrealized Appreciation (Depreciation) | |

| Investment Securities | 5,638,498 |

| Futures Contracts | (1,604) |

| Foreign Currencies | 5 |

| Net Assets | 13,422,890 |

| |

| |

| Investor Shares—Net Assets | |

| Applicable to 60,985,775 outstanding | |

| $.001 par value shares of beneficial | |

| interest (unlimited authorization) | 4,451,266 |

| Net Asset Value Per Share— | |

| Investor Shares | $72.99 |

| |

| |

| Admiral Shares—Net Assets | |

| Applicable to 65,475,006 outstanding | |

| $.001 par value shares of beneficial | |

| interest (unlimited authorization) | 8,971,624 |

| Net Asset Value Per Share— | |

| Admiral Shares | $137.02 |

• See Note A in Notes to Financial Statements.

*Non-income-producing security.

^ Includes partial security positions on loan to broker-dealers. The total value of securities on loan is $78,639,000.

1 The fund invests a portion of its cash reserves in equity markets through the use of index futures contracts. After giving effect to furtures investments, the funds's effective common stock and temporary cash investment positions represents 97.5% and 3.4%, respectively, of net assets.

2 Considered an affiliated company of the fund as the issuer is another member of The Vanguard Group.

3 Includes $83,138,000 of collateral received for securities on loan.

4 Affiliated money market fund available only to Vanguard funds and certain trusts and accounts managed by Vanguard. Rate shown is the 7-day yield.

5The issuer operates under a congressional charter; its securities are generally neither guaranteed by the U.S. Treasury no backed by the full faith and credit of the U.S. governement.

6 Securities with a value of $16,699,000 have been segregated as initial margin for open futures contracts.

ADR-- American Depositary Receipt.

GDR-- Global Depositary Receipt.

See accompanying Notes, which are an integral part of the Financial Statements.

18

Energy Fund

Statement of Operations

| |

| | Six Months Ended |

| | July 31, 2014 |

| | ($000) |

| Investment Income | |

| Income | |

| Dividends1,2 | 145,899 |

| Interest2 | 205 |

| Securities Lending | 3,783 |

| Total Income | 149,887 |

| Expenses | |

| Investment Advisory Fees—Note B | |

| Basic Fee | 9,255 |

| Performance Adjustment | 2,249 |

| The Vanguard Group—Note C | |

| Management and Administrative—Investor Shares | 3,858 |

| Management and Administrative—Admiral Shares | 4,928 |

| Marketing and Distribution—Investor Shares | 388 |

| Marketing and Distribution—Admiral Shares | 659 |

| Custodian Fees | 196 |

| Shareholders’ Reports—Investor Shares | 38 |

| Shareholders’ Reports—Admiral Shares | 14 |

| Trustees’ Fees and Expenses | 12 |

| Total Expenses | 21,597 |

| Expenses Paid Indirectly | (71) |

| Net Expenses | 21,526 |

| Net Investment Income | 128,361 |

| Realized Net Gain (Loss) | |

| Investment Securities Sold2 | 312,890 |

| Futures Contracts | 10,216 |

| Foreign Currencies | (61) |

| Realized Net Gain (Loss) | 323,045 |

| Change in Unrealized Appreciation (Depreciation) | |

| Investment Securities | 1,247,984 |

| Futures Contracts | 2,408 |

| Foreign Currencies | 63 |

| Change in Unrealized Appreciation (Depreciation) | 1,250,455 |

| Net Increase (Decrease) in Net Assets Resulting from Operations | 1,701,861 |

1 Dividends are net of foreign withholding taxes of $12,182,000. 2 Dividend income, interest income, and realized net gain (loss) from affiliated companies of the fund were $0,$126,000, and $0, respectively.See accompanying Notes, which are an integral part of the Financial Statements.

19

Energy Fund

Statement of Changes in Net Assets

| | |

| | Six Months Ended | Year Ended |

| | July 31, | January 31, |

| | 2014 | 2014 |

| | ($000) | ($000) |

| Increase (Decrease) in Net Assets | | |

| Operations | | |

| Net Investment Income | 128,361 | 241,331 |

| Realized Net Gain (Loss) | 323,045 | 322,801 |

| Change in Unrealized Appreciation (Depreciation) | 1,250,455 | 126,151 |

| Net Increase (Decrease) in Net Assets Resulting from Operations | 1,701,861 | 690,283 |

| Distributions | | |

| Net Investment Income | | |

| Investor Shares | — | (84,107) |

| Admiral Shares | — | (153,175) |

| Realized Capital Gain1 | | |

| Investor Shares | (13,933) | (78,608) |

| Admiral Shares | (25,435) | (143,323) |

| Total Distributions | (39,368) | (459,213) |

| Capital Share Transactions | | |

| Investor Shares | (275,666) | (1,350,467) |

| Admiral Shares | 358,237 | 678,643 |

| Net Increase (Decrease) from Capital Share Transactions | 82,571 | (671,824) |

| Total Increase (Decrease) | 1,745,064 | (440,754) |

| Net Assets | | |

| Beginning of Period | 11,677,826 | 12,118,580 |

| End of Period2 | 13,422,890 | 11,677,826 |

1 Includes fiscal 2015 and 2014 short-term gain distributions totaling $0 and $6,818,000. Short-term gain distributions are treated as ordinary income dividends for tax purposes.2 Net Assets-- End of Period includes undistributed (overdistributed) net investment income of $102192,000 and ($26,108,000).See accompanying Notes, which are an integral part of the Financial Statements.

20

Energy Fund

Financial Highlights

| | | | | | |

| Investor Shares | | | | | | |

| Six Months | | | | | |

| | Ended | | | | | |

| For a Share Outstanding | July 31, | Year Ended January 31, |

| Throughout Each Period | 2014 | 2014 | 2013 | 2012 | 2011 | 2010 |

| Net Asset Value, Beginning of Period | $63.85 | $62.66 | $62.60 | $69.20 | $57.17 | $42.62 |

| Investment Operations | | | | | | |

| Net Investment Income | .682 | 1.291 | 1.336 | 1.072 | 1.053 | .910 |

| Net Realized and Unrealized Gain (Loss) | | | | | | |

| on Investments | 8.675 | 2.413 | 1.098 | (3.949) | 14.103 | 14.591 |

| Total from Investment Operations | 9.357 | 3.704 | 2.434 | (2.877) | 15.156 | 15.501 |

| Distributions | | | | | | |

| Dividends from Net Investment Income | — | (1.277) | (1.340) | (1.102) | (.977) | (.951) |

| Distributions from Realized Capital Gains | (.217) | (1.237) | (1.034) | (2.621) | (2.149) | — |

| Total Distributions | (.217) | (2.514) | (2.374) | (3.723) | (3.126) | (.951) |

| Net Asset Value, End of Period | $72.99 | $63.85 | $62.66 | $62.60 | $69.20 | $57.17 |

| |

| Total Return1 | 14.68% | 5.88% | 4.07% | -3.82% | 27.17% | 36.28% |

| |

| Ratios/Supplemental Data | | | | | | |

| Net Assets, End of Period (Millions) | $4,451 | $4,138 | $5,340 | $5,945 | $6,731 | $6,536 |

| Ratio of Total Expenses to | | | | | | |

| Average Net Assets2 | 0.37% | 0.38% | 0.31% | 0.34% | 0.34% | 0.38% |

| Ratio of Net Investment Income to | | | | | | |

| Average Net Assets | 1.95% | 1.97% | 2.15% | 1.67% | 1.74% | 1.73% |

| Portfolio Turnover Rate | 21% | 17% | 18% | 24% | 31% | 27% |

The expense ratio, net income ratio, and turnover rate for the current period have been annualized.1 Total returns do not include transaction or account service fees that may have applied in the periods shown. Fund prospectuses provide information about any applicable transaction and account services fees. 2 Includes performance-based investment advisory fee increases (decreases) of 0.03%, 0.04%, (0.02%), 0.01%, 0.00%, and 0.03%.See accompanying Notes, which are an integral part of the Financial Statements.

21

Energy Fund

Financial Highlights

| | | | | | |

| Admiral Shares | | | | | | |

| Six Months | | | | | |

| | Ended | | | | | |

| For a Share Outstanding | July 31, | Year Ended January 31, |

| Throughout Each Period | 2014 | 2014 | 2013 | 2012 | 2011 | 2010 |

| Net Asset Value, Beginning of Period | $119.83 | $117.63 | $117.52 | $129.93 | $107.34 | $80.02 |

| Investment Operations | | | | | | |

| Net Investment Income | 1.326 | 2.530 | 2.586 | 2.101 | 2.045 | 1.780 |

| Net Realized and Unrealized Gain (Loss) | | | | | | |

| on Investments | 16.271 | 4.491 | 2.060 | (7.432) | 26.479 | 27.395 |

| Total from Investment Operations | 17.597 | 7.021 | 4.646 | (5.331) | 28.524 | 29.175 |

| Distributions | | | | | | |

| Dividends from Net Investment Income | — | (2.500) | (2.595) | (2.159) | (1.899) | (1.855) |

| Distributions from Realized Capital Gains | (.407) | (2.321) | (1.941) | (4.920) | (4.035) | — |

| Total Distributions | (.407) | (4.821) | (4.536) | (7.079) | (5.934) | (1.855) |

| Net Asset Value, End of Period | $137.02 | $119.83 | $117.63 | $117.52 | $129.93 | $107.34 |

| |

| Total Return1 | 14.71% | 5.94% | 4.14% | -3.76% | 27.24% | 36.37% |

| |

| Ratios/Supplemental Data | | | | | | |

| Net Assets, End of Period (Millions) | $8,972 | $7,540 | $6,778 | $6,756 | $6,871 | $4,439 |

| Ratio of Total Expenses to | | | | | | |

| Average Net Assets2 | 0.31% | 0.32% | 0.26% | 0.28% | 0.28% | 0.31% |

| Ratio of Net Investment Income to | | | | | | |

| Average Net Assets | 2.01% | 2.03% | 2.20% | 1.73% | 1.80% | 1.80% |

| Portfolio Turnover Rate | 21% | 17% | 18% | 24% | 31% | 27% |

The expense ratio, net income ratio, and turnover rate for the current period have been annualized.

1 Total returns do not include transaction or account service fees that may have applied in the periods shown. Fund prospectuses provide information about any applicable transaction and account services fees.

2 Includes performance-based investment advisory fee increases (decreases) of 0.03%, 0.04%, (0.02%), 0.01%, 0.00%, and 0.03%.

See accompanying Notes, which are an integral part of the Financial Statements.

22

Energy Fund

Notes to Financial Statements

Vanguard Energy Fund is registered under the Investment Company Act of 1940 as an open-end investment company, or mutual fund. The fund invests in securities of foreign issuers, which may subject it to investment risks not normally associated with investing in securities of U.S. corporations. The fund offers two classes of shares: Investor Shares and Admiral Shares. Investor Shares are available to any investor who meets the fund’s minimum purchase requirements. Admiral Shares are designed for investors who meet certain administrative, service, and account-size criteria.

A. The following significant accounting policies conform to generally accepted accounting principles for U.S. investment companies. The fund consistently follows such policies in preparing its financial statements.

1. Security Valuation: Securities are valued as of the close of trading on the New York Stock Exchange (generally 4 p.m., Eastern time) on the valuation date. Equity securities are valued at the latest quoted sales prices or official closing prices taken from the primary market in which each security trades; such securities not traded on the valuation date are valued at the mean of the latest quoted bid and asked prices. Securities for which market quotations are not readily available, or whose values have been affected by events occurring before the fund’s pricing time but after the close of the securities’ primary markets, are valued at their fair values calculated according to procedures adopted by the board of trustees. These procedures include obtaining quotations from an independent pricing service, monitoring news to identify significant market- or security-specific events, and evaluating changes in the values of foreign market proxies (for example, ADRs, futures contracts, or exchange-traded funds), between the time the foreign markets close and the fund’s pricing time. When fair-value pricing is employed, the prices of securities used by a fund to calculate its net asset value may differ from quoted or published prices for the same securities. Investments in Vanguard Market Liquidity Fund are valued at that fund’s net asset value. Temporary cash investments acquired over 60 days to maturity are valued using the latest bid prices or using valuations based on a matrix system (which considers such factors as security prices, yields, maturities, and ratings), both as furnished by independent pricing services. Other temporary cash investments are valued at amortized cost, which approximates market value.

2. Foreign Currency: Securities and other assets and liabilities denominated in foreign currencies are translated into U.S. dollars using exchange rates obtained from an independent third party as of the fund’s pricing time on the valuation date. Realized gains (losses) and unrealized appreciation (depreciation) on investment securities include the effects of changes in exchange rates since the securities were purchased, combined with the effects of changes in security prices. Fluctuations in the value of other assets and liabilities resulting from changes in exchange rates are recorded as unrealized foreign currency gains (losses) until the assets or liabilities are settled in cash, at which time they are recorded as realized foreign currency gains (losses).

3. Futures Contracts: The fund uses index futures contracts to a limited extent, with the objective of maintaining full exposure to the stock market while maintaining liquidity. The fund may purchase or sell futures contracts to achieve a desired level of investment, whether to accommodate portfolio turnover or cash flows from capital share transactions. The primary risks associated with the use of futures contracts are imperfect correlation between changes in market values of stocks held by the fund and the prices of futures contracts, and the possibility of an illiquid market. Counterparty risk involving futures is mitigated because a regulated clearinghouse is the counterparty instead of the clearing broker. To further mitigate counterparty risk, the fund trades futures contracts on an exchange, monitors the financial strength of its clearing brokers and clearinghouse, and has entered

23

Energy Fund

into clearing agreements with its clearing brokers. The clearinghouse imposes initial margin requirements to secure the fund’s performance and requires daily settlement of variation margin representing changes in the market value of each contract.

Futures contracts are valued at their quoted daily settlement prices. The aggregate notional amounts of the contracts are not recorded in the Statement of Net Assets. Fluctuations in the value of the contracts are recorded in the Statement of Net Assets as an asset (liability) and in the Statement of Operations as unrealized appreciation (depreciation) until the contracts are closed, when they are recorded as realized futures gains (losses).

During the six months ended July 31, 2014, the fund’s average investments in long and short futures contracts represented 2% and 0% of net assets, respectively, based on the average of aggregate settlement values at each quarter-end during the period.

4. Repurchase Agreements: The fund enters into repurchase agreements with institutional counterparties. Securities pledged as collateral to the fund under repurchase agreements are held by a custodian bank until the agreements mature. Each agreement requires that the market value of the collateral be sufficient to cover payments of interest and principal. The fund further mitigates its counterparty risk by entering into repurchase agreements only with a diverse group of prequalified counterparties, monitoring their financial strength, and entering into master repurchase agreements with its counterparties. The master repurchase agreements provide that, in the event of a counterparty’s default (including bankruptcy), the fund may terminate any repurchase agreements with that counterparty, determine the net amount owed, and sell or retain the collateral up to the net amount owed to the fund. Such action may be subject to legal proceedings, which may delay or limit the disposition of collateral.

5. Federal Income Taxes: The fund intends to continue to qualify as a regulated investment company and distribute all of its taxable income. Management has analyzed the fund’s tax positions taken for all open federal income tax years (January 31, 2011–2014), and for the period ended July 31, 2014, and has concluded that no provision for federal income tax is required in the fund’s financial statements.

6. Distributions: Distributions to shareholders are recorded on the ex-dividend date.

7. Securities Lending: To earn additional income, the fund lends its securities to qualified institutional borrowers. Security loans are required to be secured at all times by collateral in an amount at least equal to the market value of securities loaned. Daily market fluctuations could cause the value of loaned securities to be more or less than the value of the collateral received. When this occurs, the collateral is adjusted and settled on the next business day. The fund further mitigates its counterparty risk by entering into securities lending transactions only with a diverse group of prequalified counter-parties, monitoring their financial strength, and entering into master securities lending agreements with its counterparties. The master securities lending agreements provide that, in the event of a counterparty’s default (including bankruptcy), the fund may terminate any loans with that borrower, determine the net amount owed, and sell or retain the collateral up to the net amount owed to the fund; however, such actions may be subject to legal proceedings. While collateral mitigates counterparty risk, in the absence of a default the fund may experience delays and costs in recovering the securities loaned. The fund invests cash collateral received in Vanguard Market Liquidity Fund, and records a liability in the Statement of Net Assets for the return of the collateral, during the period the securities are on loan. Securities lending income represents fees charged to borrowers plus income earned on invested cash collateral, less expenses associated with the loan.

24

Energy Fund

8. Credit Facility: The fund and certain other funds managed by The Vanguard Group participate in a $2.89 billion committed credit facility provided by a syndicate of lenders pursuant to a credit agreement that may be renewed annually; each fund is individually liable for its borrowings, if any, under the credit facility. Borrowings may be utilized for temporary and emergency purposes, and are subject to the fund’s regulatory and contractual borrowing restrictions. The participating funds are charged administrative fees and an annual commitment fee of 0.06% of the undrawn amount of the facility; these fees are allocated to the funds based on a method approved by the fund’s board of trustees and included in Management and Administrative expenses on the fund’s Statement of Operations. Any borrowings under this facility bear interest at a rate equal to the higher of the federal funds rate or LIBOR reference rate plus an agreed-upon spread.

The fund had no borrowings outstanding at July 31, 2014, or at any time during the period then ended.

9. Other: Dividend income is recorded on the ex-dividend date. Interest income includes income distributions received from Vanguard Market Liquidity Fund and is accrued daily. Premiums and discounts on debt securities purchased are amortized and accreted, respectively, to interest income over the lives of the respective securities. Security transactions are accounted for on the date securities are bought or sold. Costs used to determine realized gains (losses) on the sale of investment securities are those of the specific securities sold.

Each class of shares has equal rights as to assets and earnings, except that each class separately bears certain class-specific expenses related to maintenance of shareholder accounts (included in Management and Administrative expenses) and shareholder reporting. Marketing and distribution expenses are allocated to each class of shares based on a method approved by the board of trustees. Income, other non-class-specific expenses, and gains and losses on investments are allocated to each class of shares based on its relative net assets.

B. Wellington Management Company, LLP, provides investment advisory services to a portion of the fund for a fee calculated at an annual percentage rate of average net assets managed by the advisor. The basic fee is subject to quarterly adjustments based on performance for the preceding three years relative to the MSCI ACWI Energy Index.

The Vanguard Group provides investment advisory services to a portion of the fund on an at-cost basis; the fund paid Vanguard advisory fees of $287,000 for the six months ended July 31, 2014.

For the six months ended July 31, 2014, the aggregate investment advisory fee represented an effective annual basic rate of 0.14% of the fund’s average net assets, before an increase of $2,249,000 (0.03%) based on performance.

C. The Vanguard Group furnishes at cost corporate management, administrative, marketing, and distribution services. The costs of such services are allocated to the fund based on methods approved by the board of trustees. The fund has committed to provide up to 0.40% of its net assets in capital contributions to Vanguard. At July 31, 2014, the fund had contributed capital of $1,419,000 to Vanguard (included in Other Assets), representing 0.01% of the fund’s net assets and 0.57% of Vanguard’s capitalization. The fund’s trustees and officers are also directors and officers of Vanguard.

D. The fund has asked its investment advisors to direct certain security trades, subject to obtaining the best price and execution, to brokers who have agreed to rebate to the fund part of the commissions generated. Such rebates are used solely to reduce the fund’s management and administrative expenses. For the six months ended July 31, 2014, these arrangements reduced the fund’s expenses by $71,000 (an annual rate of 0.00% of average net assets).

25

Energy Fund

E. Various inputs may be used to determine the value of the fund’s investments. These inputs are summarized in three broad levels for financial statement purposes. The inputs or methodologies used to value securities are not necessarily an indication of the risk associated with investing in those securities.

Level 1—Quoted prices in active markets for identical securities.

Level 2—Other significant observable inputs (including quoted prices for similar securities, interest rates, prepayment speeds, credit risk, etc.).

Level 3—Significant unobservable inputs (including the fund’s own assumptions used to determine the fair value of investments).

The following table summarizes the market value of the fund’s investments as of July 31, 2014, based on the inputs used to value them:

| | | |

| | Level 1 | Level 2 | Level 3 |

| Investments | ($000) | ($000) | ($000) |

| Common Stocks—United States | 7,884,220 | — | — |

| Common Stocks—International | 3,440,443 | 1,411,127 | — |

| Temporary Cash Investments | 415,373 | 389,899 | — |

| Futures Contracts—Liabilities1 | (7,192) | — | — |

| Total | 11,732,844 | 1,801,026 | — |

| 1 Represents variation margin on the last day of the reporting period. |

F. At July 31, 2014, the aggregate settlement value of open futures contracts and the related unrealized appreciation (depreciation) were:

| | | | |

| | | | ($000) |

| | | | Aggregate | |

| | | Number of | Settlement | Unrealized |

| | | Long (Short) | Value | Appreciation |

| Futures Contracts | Expiration | Contracts | Long (Short) | (Depreciation) |

| S&P 500 Index | September 2014 | 545 | 262,254 | (412) |

| E-mini S&P 500 Index | September 2014 | 844 | 81,227 | (1,192) |

| | | | | (1,604) |

Unrealized appreciation (depreciation) on open futures contracts is required to be treated as realized gain (loss) for tax purposes.

G. Distributions are determined on a tax basis and may differ from net investment income and realized capital gains for financial reporting purposes. Differences may be permanent or temporary. Permanent differences are reclassified among capital accounts in the financial statements to reflect their tax character. Temporary differences arise when certain items of income, expense, gain, or loss are recognized in different periods for financial statement and tax purposes. These differences will reverse at some time in the future. Differences in classification may also result from the treatment of short-term gains as ordinary income for tax purposes. The fund’s tax-basis capital gains and losses are determined only at the end of each fiscal year.

During the six months ended July 31, 2014, the fund realized net foreign currency losses of $61,000, which decreased distributable net income for tax purposes; accordingly, such losses have been reclassified from accumulated net realized gains to undistributed net investment income.

26

Energy Fund

At July 31, 2014, the cost of investment securities for tax purposes was $7,905,314,000. Net unrealized appreciation of investment securities for tax purposes was $5,635,748,000, consisting of unrealized gains of $5,797,795,000 on securities that had risen in value since their purchase and $162,047,000 in unrealized losses on securities that had fallen in value since their purchase.

H. During the six months ended July 31, 2014, the fund purchased $1,268,785,000 of investment securities and sold $1,305,221,000 of investment securities, other than temporary cash investments.

I. Capital share transactions for each class of shares were:

| | | | |

| | Six Months Ended | | Year Ended |

| | July 31, 2014 | January 31, 2014 |

| | Amount | Shares | Amount | Shares |

| | ($000) | (000) | ($000) | (000) |

| Investor Shares | | | | |

| Issued | 347,428 | 4,819 | 502,609 | 7,800 |

| Issued in Lieu of Cash Distributions | 13,226 | 197 | 153,964 | 2,391 |

| Redeemed | (636,320) | (8,846) | (2,007,040) | (30,600) |

| Net Increase (Decrease)—Investor Shares | (275,666) | (3,830) | (1,350,467) | (20,409) |

| Admiral Shares | | | | |

| Issued | 842,421 | 6,191 | 1,701,087 | 13,744 |

| Issued in Lieu of Cash Distributions | 23,090 | 183 | 266,568 | 2,204 |

| Redeemed | (507,274) | (3,819) | (1,289,012) | (10,651) |

| Net Increase (Decrease)—Admiral Shares | 358,237 | 2,555 | 678,643 | 5,297 |

J. Management has determined that no material events or transactions occurred subsequent to July 31, 2014, that would require recognition or disclosure in these financial statements.

27

About Your Fund’s Expenses

As a shareholder of the fund, you incur ongoing costs, which include costs for portfolio management, administrative services, and shareholder reports (like this one), among others. Operating expenses, which are deducted from a fund’s gross income, directly reduce the investment return of the fund.

A fund’s expenses are expressed as a percentage of its average net assets. This figure is known as the expense ratio. The following examples are intended to help you understand the ongoing costs (in dollars) of investing in your fund and to compare these costs with those of other mutual funds. The examples are based on an investment of $1,000 made at the beginning of the period shown and held for the entire period.

The accompanying table illustrates your fund’s costs in two ways:

• Based on actual fund return. This section helps you to estimate the actual expenses that you paid over the period. The ”Ending Account Value“ shown is derived from the fund‘s actual return, and the third column shows the dollar amount that would have been paid by an investor who started with $1,000 in the fund. You may use the information here, together with the amount you invested, to estimate the expenses that you paid over the period.

To do so, simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number given for your fund under the heading ”Expenses Paid During Period.“

• Based on hypothetical 5% yearly return. This section is intended to help you compare your fund‘s costs with those of other mutual funds. It assumes that the fund had a yearly return of 5% before expenses, but that the expense ratio is unchanged. In this case—because the return used is not the fund’s actual return—the results do not apply to your investment. The example is useful in making comparisons because the Securities and Exchange Commission requires all mutual funds to calculate expenses based on a 5% return. You can assess your fund’s costs by comparing this hypothetical example with the hypothetical examples that appear in shareholder reports of other funds.

Note that the expenses shown in the table are meant to highlight and help you compare ongoing costs only and do not reflect transaction costs incurred by the fund for buying and selling securities. Further, the expenses do not include any purchase, redemption, or account service fees described in the fund prospectus. If such fees were applied to your account, your costs would be higher. Your fund does not carry a “sales load.”

The calculations assume no shares were bought or sold during the period. Your actual costs may have been higher or lower, depending on the amount of your investment and the timing of any purchases or redemptions.

You can find more information about the fund’s expenses, including annual expense ratios, in the Financial Statements section of this report. For additional information on operating expenses and other shareholder costs, please refer to your fund’s current prospectus.

28

| | | |

| Six Months Ended July 31, 2014 | | | |

| | Beginning | Ending | Expenses |

| | Account Value | Account Value | Paid During |

| Energy Fund | 1/31/2014 | 7/31/2014 | Period |

| Based on Actual Fund Return | | | |

| Investor Shares | $1,000.00 | $1,146.84 | $1.97 |

| Admiral Shares | 1,000.00 | 1,147.14 | 1.65 |

| Based on Hypothetical 5% Yearly Return | | | |

| Investor Shares | $1,000.00 | $1,022.96 | $1.86 |

| Admiral Shares | 1,000.00 | 1,023.26 | 1.56 |

The calculations are based on expenses incurred in the most recent six-month period. The fund’s annualized six-month expense ratios for thatperiod are 0.37% for Investor Shares and 0.31% for Admiral Shares. The dollar amounts shown as “Expenses Paid” are equal to theannualized expense ratio multiplied by the average account value over the period, multiplied by the number of days in the most recentsix-month period, then divided by the number of days in the most recent 12-month period.29

Trustees Approve Advisory Arrangements

The board of trustees of Vanguard Energy Fund has renewed the fund’s investment advisory arrangements with The Vanguard Group, Inc. (Vanguard), through its Quantitative Equity Group, and Wellington Management Company, LLP (Wellington Management). The board determined that renewing the fund’s advisory arrangements was in the best interests of the fund and its shareholders.

The board based its decision upon an evaluation of each advisor’s investment staff, portfolio management process, and performance. The trustees considered the factors discussed below, among others. However, no single factor determined whether the board approved the arrangements. Rather, it was the totality of the circumstances that drove the board’s decision.

Nature, extent, and quality of services

The board considered the quality of the fund’s investment management services over both the short and long term, and took into account the organizational depth and stability of each advisor. The board noted the following:

Vanguard. Vanguard has been managing investments for more than three decades. The Quantitative Equity Group adheres to a sound, disciplined investment management process; the team has considerable experience, stability, and depth. Vanguard has managed a portion of the fund since 2005.

Wellington Management. Founded in 1928, Wellington Management is among the nation’s oldest and most respected institutional investment managers. The investment team uses a bottom-up approach in which stocks are selected based on the advisor’s estimates of fundamental investment value. The advisor’s investment process emphasizes company fundamentals, management track record, and security valuation. The firm has advised the fund since the fund’s inception in 1984.

The board concluded that each advisor’s experience, stability, depth, and performance, among other factors, warranted the continuation of the advisory arrangements.

Investment performance

The board considered the short- and long-term performance of the fund, including any periods of outperformance or underperformance relative to a benchmark index and peer group. The board concluded that the performance was such that the advisory arrangements should continue. Information about the fund’s most recent performance can be found in the Performance Summary section of this report.

Cost

The board concluded that the fund’s expense ratio was well below the average expense ratio charged by funds in its peer group and that the fund’s advisory fee rate was also well below its peer-group average. Information about the fund’s expenses appears in the About Your Fund’s Expenses section of this report as well as in the Financial Statements section, which also includes information about the fund’s advisory fee rate.

The board did not consider profitability of Wellington Management in determining whether to approve the advisory fee, because Wellington Management is independent of Vanguard, and the advisory fee is the result of arm’s-length negotiations. The board does not conduct a profitability analysis of Vanguard, because of Vanguard’s unique “at-cost” structure. Unlike most other mutual fund management companies, Vanguard is owned by the funds it oversees, and produces “profits” only in the form of reduced expenses for fund shareholders.

30

The benefit of economies of scale

The board concluded that the fund’s shareholders benefit from economies of scale because of breakpoints in the fund’s advisory fee schedule for Wellington Management. The breakpoints reduce the effective rate of the fee as the fund’s assets managed by Wellington Management increase. The board also concluded that the fund’s at-cost arrangement with Vanguard ensures that the fund will realize economies of scale as it grows, with the cost to shareholders declining as the fund’s assets managed by Vanguard increase.

The board will consider whether to renew the advisory arrangement again after a one-year period.

31

Glossary

30-Day SEC Yield. A fund’s 30-day SEC yield is derived using a formula specified by the U.S. Securities and Exchange Commission. Under the formula, data related to the fund’s security holdings in the previous 30 days are used to calculate the fund’s hypothetical net income for that period, which is then annualized and divided by the fund’s estimated average net assets over the calculation period. For the purposes of this calculation, a security’s income is based on its current market yield to maturity (for bonds), its actual income (for asset-backed securities), or its projected dividend yield (for stocks). Because the SEC yield represents hypothetical annualized income, it will differ—at times significantly—from the fund’s actual experience. As a result, the fund’s income distributions may be higher or lower than implied by the SEC yield.

Beta. A measure of the magnitude of a fund’s past share-price fluctuations in relation to the ups and downs of a given market index. The index is assigned a beta of 1.00. Compared with a given index, a fund with a beta of 1.20 typically would have seen its share price rise or fall by 12% when the index rose or fell by 10%. For this report, beta is based on returns over the past 36 months for both the fund and the index. Note that a fund’s beta should be reviewed in conjunction with its R-squared (see definition). The lower the R-squared, the less correlation there is between the fund and the index, and the less reliable beta is as an indicator of volatility.

Dividend Yield. Dividend income earned by stocks, expressed as a percentage of the aggregate market value (or of net asset value, for a fund). The yield is determined by dividing the amount of the annual dividends by the aggregate value (or net asset value) at the end of the period. For a fund, the dividend yield is based solely on stock holdings and does not include any income produced by other investments.

Earnings Growth Rate. The average annual rate of growth in earnings over the past five years for the stocks now in a fund.

Equity Exposure. A measure that reflects a fund’s investments in stocks and stock futures. Any holdings in short-term reserves are excluded.

Expense Ratio. A fund’s total annual operating expenses expressed as a percentage of the fund’s average net assets. The expense ratio includes management and administrative expenses, but does not include the transaction costs of buying and selling portfolio securities.

Foreign Holdings. The percentage of a fund represented by securities or depositary receipts of companies based outside the United States.