UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

| Investment Company Act file number: | | 811-04304 |

| | | |

| Exact name of registrant as specified in charter: | | Delaware Group® Government Fund |

| | | |

| Address of principal executive offices: | | 610 Market Street |

| | Philadelphia, PA 19106 |

| | | |

| Name and address of agent for service: | | David F. Connor, Esq. |

| | 610 Market Street |

| | Philadelphia, PA 19106 |

| | | |

| Registrant’s telephone number, including area code: | | (800) 523-1918 |

| | | |

| Date of fiscal year end: | | July 31 |

| | | |

| Date of reporting period: | | July 31, 2020 |

Item 1. Reports to Stockholders

Annual report

Fixed income mutual fund

Delaware Emerging Markets Debt Corporate Fund

(formerly, Delaware Emerging Markets Debt Fund)

July 31, 2020

Beginning on or about June 1, 2021, as permitted by regulations adopted by the Securities and Exchange Commission, paper copies of your Fund’s shareholder reports will no longer be sent to you by mail, unless you specifically request them from the Fund or from your financial intermediary, such as a broker/dealer, bank, or insurance company. Instead, you will be notified by mail each time a report is posted on the website and provided with a link to access the report.

If you already elected to receive shareholder reports electronically, you will not be affected by this change and you do not need to take any action. You may elect to receive shareholder reports and other communications from the Fund electronically by signing up at delawarefunds.com/edelivery. If you own these shares through a financial intermediary, you may contact your financial intermediary.

You may elect to receive paper copies of all future shareholder reports free of charge. You can inform the Fund that you wish to continue receiving paper copies of your shareholder reports by contacting us at 800 523-1918. If you own these shares through a financial intermediary, you may contact your financial intermediary to elect to continue to receive paper copies of your shareholder reports. Your election to receive reports in paper will apply to all funds held with the Delaware Funds® by Macquarie or your financial intermediary.

Carefully consider the Fund’s investment objectives, risk factors, charges, and expenses before investing. This and other information can be found in the Fund’s prospectus and its summary prospectus, which may be obtained by visiting delawarefunds.com/literature or calling 800 523-1918. Investors should read the prospectus and the summary prospectus carefully before investing.

You can obtain shareholder reports and prospectuses online instead of in the mail.

Visit delawarefunds.com/edelivery.

Experience Delaware Funds® by Macquarie

Macquarie Investment Management (MIM) is a global asset manager with offices in the United States, Europe, Asia, and Australia. As active managers, we prioritize autonomy and accountability at the investment team level in pursuit of opportunities that matter for clients. Delaware Funds is one of the longest-standing mutual fund families, with more than 80 years in existence.

If you are interested in learning more about creating an investment plan, contact your financial advisor.

You can learn more about Delaware Funds or obtain a prospectus for Delaware Emerging Markets Debt Corporate Fund at delawarefunds.com/literature.

Manage your account online

| · | | Check your account balance and transactions |

| · | | View statements and tax forms |

| · | | Make purchases and redemptions |

Visit delawarefunds.com/account-access.

Macquarie Asset Management (MAM) offers a diverse range of products including securities investment management, infrastructure and real asset management, and fund and equity-based structured products. MIM is the marketing name for certain companies comprising the asset management division of Macquarie Group. This includes the following investment advisers: Macquarie Investment Management Business Trust (MIMBT), Macquarie Funds Management Hong Kong Limited, Macquarie Investment Management Austria Kapitalanlage AG, Macquarie Investment Management Global Limited, Macquarie Investment Management Europe Limited, and Macquarie Investment Management Europe S.A.

The Fund is distributed by Delaware Distributors, L.P. (DDLP), an affiliate of MIMBT and Macquarie Group Limited.

Other than Macquarie Bank Limited (MBL), none of the entities noted are authorized deposit-taking institutions for the purposes of the Banking Act 1959 (Commonwealth of Australia). The obligations of these entities do not represent deposits or other liabilities of MBL. MBL does not guarantee or otherwise provide assurance in respect of the obligations of these entities, unless noted otherwise.

The Fund is governed by US laws and regulations.

Table of contents

Unless otherwise noted, views expressed herein are current as of July 31, 2020, and subject to change for events occurring after such date.

The Fund is not FDIC insured and is not guaranteed. It is possible to lose the principal amount invested.

Advisory services provided by Delaware Management Company, a series of MIMBT, a US registered investment advisor.

All third-party marks cited are the property of their respective owners.

© 2020 Macquarie Management Holdings, Inc.

Portfolio management review

| | |

| Delaware Emerging Markets Debt Corporate Fund | | August 11, 2020 (Unaudited) |

| | | | | | |

Performance preview (for the year ended July 31, 2020) | |

Delaware Emerging Markets Debt Corporate Fund

(Institutional Class shares) | | 1-year return | | | +1.88% | |

Delaware Emerging Markets Debt Corporate Fund

(Class A shares) | | 1-year return | | | +1.73% | |

J.P. Morgan Corporate Emerging Markets Bond Index (CEMBI) Broad

Diversified (benchmark) | | 1-year return | | | +5.21% | |

Past performance does not guarantee future results.

For complete, annualized performance for Delaware Emerging Markets Debt Corporate Fund, please see the table on page 6.

Institutional Class shares are not subject to a sales charge and are offered for sale exclusively to certain eligible investors. In addition, Institutional Class shares pay no distribution and service fee.

The performance of Class A shares excludes the applicable sales charge. Both Institutional Class shares and Class A shares reflect the reinvestment of all distributions.

Please see page 9 for a description of the index. Index performance returns do not reflect any management fees, transaction costs, or expenses. Indices are unmanaged and one cannot invest directly in an index.

Investment objective

The Fund seeks current income and, secondarily, capital appreciation.

| | | | |

Market review Tepid global growth coupled with the US Federal Reserve’s looser, more accommodating monetary policy would have been the major story line for the Fund’s fiscal year ended July 31, 2020 had it not been for the coronavirus pandemic, which injected a jolt of extreme volatility that began in late February and persisted into early April. The fiscal period began much as the prior fiscal year left off, with emerging markets debt posting mixed returns that largely reflected external factors, most notably the sharp drop in US Treasury yields and expectations for continued monetary easing on the part of the European Central Bank (ECB) and the Fed. In the final quarter of 2019, emerging markets debt posted stronger returns. Compared with corporate credits in developed markets, emerging markets corporate debt with similar credit quality provided a relatively stable yield pickup of approximately 100 basis points for BB-rated debt and 50 basis | | | | • Emerging markets debt sold off sharply on coronavirus concerns. • Central bank and government stimulus led to a strong rebound. • Travel restrictions placed severe pressure on airlines. • In this crisis, emerging markets demonstrated notable maturity. |

1

Portfolio managment review

Delaware Emerging Markets Debt Corporate Fund

points for BBB-rated debt. (One basis point equals one hundredth of a percentage point.)

Emerging market currencies were also performing well at the end of 2019. A drag on performance for much of the year, emerging market currencies responded positively when a Phase 1 trade agreement between the United States and China appeared imminent. An apparent bottoming out of global economic activity also propelled emerging market currencies.

Overall, from August 2019 through January 2020, the combined backdrop of a stable rate and a stable dollar was broadly supportive of emerging markets risk assets. Given that hard currency assets in emerging markets were no exception, emerging markets debt enjoyed relatively strong performance during this time.

As the new year began, however, concern about the coronavirus, first identified in December 2019, began to swell. Little more than background chatter, particularly in the US, in January and early February, coronavirus fears suddenly became widespread and global markets sold off precipitously later in February.

As was the case with risk assets worldwide, by the end of the Fund’s fiscal year, many emerging markets debt markets had largely bounced back. The J.P. Morgan Government Bond Index–Emerging Markets (GBI-EM) Global Diversified dropped 15.21% in dollar terms in the first quarter of 2020 but gained 9.82% in the second quarter. Similarly, the J.P. Morgan Emerging Markets Bond Index (EMBI) Global Diversified (sovereigns), declined 13.38% in the first quarter but gained 12.26% in the second quarter. Finally, the J.P. Morgan Corporate Emerging Markets Bond Index (CEMBI) Broad Diversified (corporates), fell 10.17% in the first quarter but gained 11.15% in the second quarter.

Although emerging markets debt, like virtually all asset classes, succumbed to the coronavirus-induced selloff, it is important to note that emerging markets debt weathered this crisis much better than it did previous disruptions. In the past, emerging

markets have suffered disproportionately because of a mismatch of asset liabilities in the underlying economy. A country would borrow dollars and spend locally. If the local currency subsequently softened, debt balances were destroyed, wreaking havoc on the economy. Though this still happens, it has happened far less frequently, following several notable crises including the Mexican peso crisis or Tequila Crisis of 1994, the Russian debt crisis of 1998, and the so-called taper tantrum of 2013. In the aftermath of these and other notable economic disruptions, central bankers have improved policy making by rebalancing asset liabilities and reducing fundamental mismatches with emerging market economies.

In the crises mentioned above, emerging markets suffered more significantly than their developed counterparts. During the selloff in February and March, three countries – Argentina, Ecuador, and Lebanon – struggled due to poor fiscal and monetary policies. And all three are paying the price via defaults or restructuring. However, overall, the emerging markets asset class demonstrated maturity throughout the crisis. The problems in Argentina, Ecuador, and Lebanon were limited to those countries and did not spread. In our view, this is a sign of relative maturity in the emerging markets debt market.

Better management, at both the corporate and sovereign levels, is another sign of maturity that enabled emerging markets to come through the coronavirus selloff. We saw many companies maintain adequate liquidity and access to external financing. Despite battling the macroeconomic environment and headwinds, most companies, with a few exceptions noted further on, came through the crisis in reasonable shape.

The role of central bank and government intervention in enabling emerging markets, indeed

2

global markets, to recover quickly cannot be overstated. Most notable were the Fed’s injection of trillions of dollars of liquidity into financial markets and the US government’s fiscal programs, including enhanced unemployment benefits and a payroll protection program. In conjunction with other global stimulative actions, governments acted quickly to curtail volatility, enabling asset prices to rebound sharply in the final months of the Fund’s fiscal year.

Source: Bloomberg.

Within the Fund

For the fiscal year ended July 31, 2020,

Delaware Emerging Markets Debt Corporate Fund underperformed its benchmark, the J.P. Morgan CEMBI Broad Diversified. The Fund’s Institutional Class shares gained 1.88%. The Fund’s Class A shares advanced 1.73% at net asset value and declined 2.85% at maximum offer price. These figures reflect all distributions reinvested. For the same period, the Fund’s benchmark gained 5.21%. For complete, annualized performance for Delaware Emerging Markets Debt Corporate Fund, please see the table on page 6.

The Fund was broadly diversified across regions, with fairly stable country allocations. Over the course of the fiscal year, the Fund was overweight Latin America, underweight Asia, and neutral to slightly underweight Central and Eastern Europe, the Middle East, and Africa (CEEMEA). We have a bias toward what we deem more attractive relative value and higher yielding regions. Consequently, we have positioned the Fund to be overweight high yield securities and underweight low-beta (low volatility) investment grade securities consistently throughout the fiscal year.

Within Latin America, Brazil and Panama made notable contributions to the Fund’s performance while Mexico, Chile, and Ecuador detracted from performance. Brazil represented the

Fund’s largest country overweight throughout the 12-month period. Brazil offers a large, liquid credit market that, in our opinion, provides a significant opportunity for credit selection. And despite being fairly acrimonious in its politics, its fiscal framework has been relatively conservative under the direction of Economy Minister Paulo Guedes and the Bolsonaro administration more broadly. The Fund also held a relative overweight in Panama, which offered the mid-quality investment grade credits that benefited from global demand for decently yielding investment grade assets.

In Brazil, the Fund’s two largest outperforming holdings were Cia Siderurgica Nacional S.A. (CSN) and JBS Investments II GmbH CSN is an iron-ore producer and is integrated into steel production. The company benefited from a benign demand environment prior to the February 2020 selloff and high iron ore prices, along with the successful completion of several liability-management transactions post the selloff. JBS S.A. (domiciled in Brazil) is the world’s largest meat-processing company; it profited from strong operating performance and continued improvement of its credit profile.

In addition to a favorable overweight in Panama, the Fund gained from positions in Banco General S.A. and C&W Senior Financing DAC.C&W Senior Financing (domiciled in Ireland) is a high yield credit that benefited from relatively stable operating trends as well as developed-market crossover investor sponsorship.

Latin America was also responsible for several of the Fund’s leading detractors from performance. As was the case in other regions, the coronavirus pandemic created significant distress for several of the Fund’s positions. Travel restrictions that were imposed to curb the spread of the virus were particularly detrimental, driving several airlines into default. Among them was Mexican flagship carrier Aerovias de Mexico S.A. de CV The imposition of travel restrictions combined with a leveraged balance sheet pushed the airline’s bonds into

3

Portfolio management review

Delaware Emerging Markets Debt Corporate Fund

default in mid-July. The month before, the airline had initiated Chapter 11 bankruptcy proceedings. The Fund continued to hold the position at the end of the fiscal year because we believed that the potential participation in the debtor-in-possession (DIP) financing process and subsequent restructuring could offer a better recovery value than what the bond prices reflected at that time.

The Fund’s second-largest underperformer, LATAM Finance Ltd., was from another airline that defaulted. In Chile, LATAM Airlines Group S.A. filed for bankruptcy in late May, seeking a coronavirus-related emergency reorganization. At the time of its filing, LATAM was the world’s largest airline to seek protection due to the coronavirus. Unlike some other carriers that had been experiencing management turmoil and losses for some time, LATAM had a solid financial footing prior to the pandemic, even approving a dividend payment earlier in the fiscal year. We exited the LATAM position before the end of the fiscal year and entered into a position in Azul, a Brazilian airline whose bonds performed well as of the time of this report and, in our opinion, has better prospects than LATAM due to its focus on domestic travel.

Ecuador was another problematic region for the Fund. Prior to the pandemic, we had sold an infrastructure company to invest in the sovereign bonds, which subsequently underwent significant distress, largely due to the pandemic. Ecuador sovereign, an off-benchmark position, is currently restructuring its debt.

YPF Luz, a generation company in Argentina, also detracted from the Fund’s performance. The negative election outcome in Argentina in August 2019 drove a significant selloff in Argentina corporate credit, and we decided to exit the electricity generation sector as the change in political landscape had negative consequences for all corporates, but even more for that sector in particular.

Within CEEMEA, the Fund benefited from its positions in Ukraine and Kazakhstan but was hurt by a position in Lithuania. In Ukraine, the election of Volodymyr Zelensky as president in May 2019 was a positive outcome, normalizing monetary policy that underpinned strength and credit. The Fund held several positive-performing credits, with security selection and sizing the most significant drivers. We complemented the Fund’s corporate holdings with Ukrainian sovereign bonds, an off-benchmark position that was the Fund’s overall strongest performer during the 12-month period. Within the benchmark, the Fund’s strongest performer was MHP S.A., a major grain and poultry producer in which the Fund was overweight. As was the case with JBS, MHP’s operating performance was relatively stable.

Like Panama, Kazakhstan benefited from global demand for investment grade assets with an attractive yield. Kaztransgas AO, the state-owned gas transportation company, was the leading contributor, and the Fund benefited from an overweight position.

The pandemic also took a toll on the Fund’s ASG Finance DAC holding from Avia Solutions Group PLC, a Lithuanian-based global aerospace company. Among Avia Solutions Group’s lines of business, Avia Support Services – which provides maintenance, repair, overhaul, and ground handling for airlines – suffered a significant downturn in business due to the effects of the virus on commercial aviation. We continued to hold Avia Solutions Group at the end of the fiscal year because we believe that even though operational performance will likely deteriorate, the company has a comfortable liquidity position to support the business until operations recover.

Our position in Tullow Oil, a Ghana-based exploration and production (E&P) company, also

4

detracted from performance. The bonds underperformed initially in late 2019 after a significant downward revision of production guidance. The pandemic accelerated the poor performance due to the sharp drop in oil prices, which coupled with low production levels, drove the company to burn cash and remain highly levered. The company presented an asset disposal program in late 2019 that is being executed.

In Asia, the Fund benefited from favorable security selection in Indonesia, although it suffered a significant coronavirus-related loss in India. While the Fund had an underweight position in Indonesia compared to the benchmark, Indonesian corporate credit is skewed down in quality. The Fund’s holdings, however, were generally up in quality, helping it to withstand a selloff. The Fund’s strongest performer was Listrindo Capital BV, a private electric utility (domiciled in Netherlands) that held up well in a highly volatile market.

In India, a coronavirus-related downturn in retailing led to severe distress for Future Retail Ltd., a diversified retailer owned by Future Group. In addition to a sharp drop in business for Future Retail itself, the sudden drop of Future Retail stock

drove to insufficient collateralization of debt at Future Group holding, which triggered a liquidity problem for the group. We continued to hold the position as of the end of fiscal year. Despite short-term liquidity problems, we believe the business is attractive. Additionally, Future Group is in conversations to sell a part of its business, injecting the cash that the company needs to keep performing on the bonds.

Throughout the Fund’s fiscal year, the portfolio composition remained consistent, with no dramatic changes to the Fund’s regional or quality biases. On a quality basis, at the end of the fiscal year, the Fund was overweight BB-rated and A-rated credits, much as it was throughout the

12-month period.

A note about derivatives

During the fiscal year, Delaware Emerging Markets Debt Corporate Fund invested in forward foreign currency exchange contracts, options, credit default swaps, and futures. These positions detracted 0.16 percentage points from performance for the fiscal year. The Fund had exposure to derivatives at the end of the fiscal year.

5

Performance summary

| | |

| Delaware Emerging Markets Debt Corporate Fund | | July 31, 2020 (Unaudited) |

The performance quoted represents past performance and does not guarantee future results. Investment return and principal value of an investment will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by calling 800 523-1918 or visiting delawarefunds.com/performance.

| | | | | | | | | | | | | | | | |

| Fund and benchmark performance1,2,3 | | Average annual total returns through July 31, 2020 | |

| | | | 1 year | | | | 3 year | | | | 5 year | | | | Lifetime | |

| | | | |

Class A (Est. September 30, 2013) | | | | | | | | | | | | | | | | |

Excluding sales charge | | | +1.73% | | | | +3.85% | | | | +5.42% | | | | +5.76% | |

Including sales charge | | | -2.85% | | | | +2.27% | | | | +4.46% | | | | +5.27% | |

Class C (Est. September 30, 2013) | | | | | | | | | | | | | | | | |

Excluding sales charge | | | +0.99% | | | | +3.05% | | | | +4.85% | | | | +5.18% | |

Including sales charge | | | +0.01% | | | | +3.05% | | | | +4.85% | | | | +5.18% | |

Class R (Est. September 30, 2013) | | | | | | | | | | | | | | | | |

Excluding sales charge | | | +2.00% | | | | +4.10% | | | | +5.57% | | | | +5.75% | |

Including sales charge | | | +2.00% | | | | +4.10% | | | | +5.57% | | | | +5.75% | |

Institutional Class (Est. September 30, 2013) | | | | | | | | | | | | | | | | |

Excluding sales charge | | | +1.88% | | | | +4.05% | | | | +5.56% | | | | +5.95% | |

Including sales charge | | | +1.88% | | | | +4.05% | | | | +5.56% | | | | +5.95% | |

J.P. Morgan Corporate Emerging Markets | | | | | | | | | | | | | | | | |

Bond Index (CEMBI) Broad Diversified | | | +5.21% | | | | +5.04% | | | | +5.62% | | | | +5.33%* | |

*The benchmark lifetime return is for Class A share comparison only and is calculated using the month end prior to the Fund’s Class A inception date (November 3, 2010).

1 A privately offered fund managed by the Fund’s portfolio manager was reorganized into the Fund and the Fund commenced operations on September 30, 2013. This privately offered fund commenced operations on November 3, 2010 and had an investment objective and strategies that were, in all material respects, the same as those of the Fund, and was managed in a manner that, in all material respects, complied with the investment guidelines and restrictions of the Fund. However, the privately offered fund was not registered as an investment under the Investment Company Act of 1940 (1940 Act). As a result, the privately offered fund was not subject to certain investment limitations, diversification requirements, liquidity requirements, and other restrictions imposed by

the 1940 Act and the Internal Revenue Code of 1986, as amended, which, if applicable, may have adversely affected its performance.

The Fund’s performance for the periods prior to its commencement of operations on September 30, 2013 is that of the privately offered fund. Because the privately offered fund was a master fund that did not charge any management or other asset-based fees, the privately offered fund’s performance shown above has been restated, on a one-time basis, to reflect the fees, expenses, and waivers and reimbursements for each class of the Fund at the commencement of the Fund’s operations. If the performance of the privately offered fund had not been restated, the performance for such classes may have been

6

higher than the performance shown in the average annual total returns table on page 6.

2 Returns reflect the reinvestment of all distributions and are presented both with and without the applicable sales charges described below. Returns do not reflect the deduction of taxes the shareholder would pay on Fund distributions or redemptions of Fund shares.

Expense limitations were in effect for certain classes during some or all of the periods shown in the “Fund and benchmark performance” table. Expenses for each class are listed on the “Fund expense ratios” table on page 8. Performance would have been lower had expense limitations not been in effect.

Institutional Class shares are not subject to a sales charge and are offered for sale exclusively to certain eligible investors. In addition, Institutional Class shares pay no distribution and service (12b-1) fee.

Class A shares are sold with a maximum front-end sales charge of 4.50%, and have an annual 12b-1 fee of 0.25% of average daily net assets. Performance for Class A shares, excluding sales charges, assumes that no front-end sales charge applied.

Class C shares are sold with a contingent deferred sales charge of 1.00% if redeemed during the first 12 months. They are also subject to an annual 12b-1 fee of 1.00% of average daily net assets. Performance for Class C shares, excluding sales charges, assumes either that contingent deferred sales charges did not apply or that the investment was not redeemed.

Class R shares are available only for certain retirement plan products. They are sold without a sales charge and have an annual 12b-1 fee of 0.50% of average daily net assets.

Fixed income securities and bond funds can lose value, and investors can lose principal, as interest rates rise. They also may be affected by economic conditions that hinder an issuer’s ability

to make interest and principal payments on its debt. The Fund may also be subject to prepayment risk, the risk that the principal of a bond that is held by a portfolio will be prepaid prior to maturity, at the time when interest rates are lower than what the bond was paying. A portfolio may then have to reinvest that money at a lower interest rate.

High yielding, non-investment-grade bonds (junk bonds) involve higher risk than investment grade bonds. The high yield secondary market is particularly susceptible to liquidity problems when institutional investors, such as mutual funds and certain other financial institutions, temporarily stop buying bonds for regulatory, financial, or other reasons. In addition, a less liquid secondary market makes it more difficult for the Fund to obtain precise valuations of the high yield securities in its portfolio.

The Fund may invest in derivatives, which may involve additional expenses and are subject to risk, including the risk that an underlying security or securities index moves in the opposite direction from what the portfolio manager anticipated. A derivatives transaction depends upon the counterparties’ ability to fulfill their contractual obligations.

If and when the Fund invests in forward foreign currency contracts or uses other investments to hedge against currency risks, the Fund will be subject to special risks, including counterparty risk.

Diversification may not protect against market risk.

International investments entail risks including fluctuation in currency values, differences in accounting principles, or economic or political instability. Investing in emerging markets can be riskier than investing in established foreign markets due to increased volatility, lower trading volume, and higher risk of market closures. In many emerging markets, there is substantially less publicly available information and the available

7

Performance summary

Delaware Emerging Markets Debt Corporate Fund

information may be incomplete or misleading. Legal claims are generally more difficult to pursue.

The Fund may experience portfolio turnover in excess of 100%, which could result in higher transaction costs and tax liability.

Leverage risk is the risk associated with securities or practices (for example, borrowing and the use of certain derivatives) and investment in certain types of derivatives that multiply small index or market movements into larger changes in value. Use of derivative instruments may involve leverage. Leverage magnifies the potential for gain and the risk of loss. As a result, a relatively small decline in the value of the underlying investments could result in a relatively large loss. Although the Fund will seek to manage the Fund’s risk from the leverage associated with derivative investments by closely monitoring the volatility of such investments, the Fund may not be successful in this respect.

IBOR risk is the risk that changes related to the use of the London interbank offered rate (LIBOR) or similar rates (such as EONIA) could have adverse impacts on financial instruments that reference these rates. The potential abandonment of these rates and transition to alternative rates could affect the value and liquidity of instruments that reference them and could affect investment strategy performance.

The disruptions caused by natural disasters, pandemics, or similar events could prevent the Fund from executing advantageous investment decisions in a timely manner and could negatively impact the Fund’s ability to achieve its investment objective and the value of the Fund’s investments.

3 The Fund’s expense ratios, as described in the most recent prospectus, are disclosed in the following “Fund expense ratios” table. Delaware Management Company has agreed to reimburse certain expenses and/or waive certain fees in order to prevent total annual fund operating expenses (excluding any 12b-1 fees, acquired fund fees and expenses, taxes, interest, short sale dividend and interest expenses, brokerage fees, certain insurance costs, and nonroutine expenses or costs, including, but not limited to, those relating to reorganizations, litigation, conducting shareholder meetings, and liquidations (collectively, nonroutine expenses)) from exceeding 0.79% of the Fund’s average daily net assets from August 1, 2019 to July 31, 2020.* Please see the most recent prospectus and any applicable supplement(s) for additional information on these fee waivers and/or reimbursements. Please see the “Financial highlights” section in this report for the most recent expense ratios.

| | | | | | | | |

| Fund expense ratios | | Class A | | Class C | | Class R | | Institutional Class |

Total annual operating expenses | | | | | | | | |

(without fee waivers) | | 1.90% | | 2.65% | | 2.15% | | 1.65% |

Net expenses | | | | | | | | |

(including fee waivers, if any) | | 1.04% | | 1.79% | | 1.29% | | 0.79% |

Type of waiver | | Contractual | | Contractual | | Contractual | | Contractual |

*The aggregate contractual waiver period covering this report is from November 28, 2018 through November 29, 2020.

8

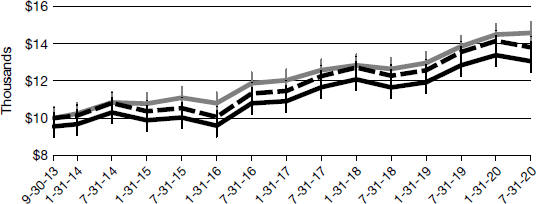

Performance of a $10,000 investment1

Average annual total returns from September 30, 2013 (Fund’s inception) through July 31, 2020

| | | | | | |

| | | |

| For period beginning September 30, 2013 through July 31, 2020 | | Starting value | | Ending value |

| | | |

| | J.P. Morgan Corporate Emerging Markets Bond Index (CEMBI) Broad Diversified | | $10,000 | | $14,581 |

| | Delaware Emerging Markets Debt Corporate Fund – Institutional Class shares | | $10,000 | | $13,808 |

| | Delaware Emerging Markets Debt Corporate Fund – Class A shares | | $9,550 | | $13,060 |

1 The “Performance of a $10,000 investment” graph assumes $10,000 invested in Institutional Class and Class A shares of the Fund on September 30, 2013, and includes the effect of a 4.50% front-end sales charge (for Class A shares) and the reinvestment of all distributions. The graph does not reflect the deduction of taxes the shareholders would pay on Fund distributions or redemptions of Fund shares. Expense limitations were in effect for some or all of the periods shown. Performance would have been lower had expense limitations not been in effect. Expenses are listed in the “Fund expense ratios” table on page 8. Please note additional details on pages 6 through 10.

The graph also assumes $10,000 invested in the J.P. Morgan Corporate Emerging Markets Bond Index (CEMBI) Broad Diversified as of September 30, 2013. The J.P. Morgan Corporate Emerging Markets Bond Index (CEMBI) Broad Diversified tracks

US dollar–denominated emerging market corporate bonds, limiting the weights of countries with larger corporate debt stocks by including only a specified portion of those countries’ eligible current face amounts of debt outstanding.

The J.P. Morgan Government Bond Index–Emerging Markets (GBI-EM) Global Diversified, mentioned on page 2, tracks local currency government bonds issued by emerging markets, limiting the weights of the index countries by only including a specified portion of those countries’ eligible current face amounts of debt outstanding.

The J.P. Morgan Emerging Markets Bond Index (EMBI) Global Diversified, mentioned on page 2, tracks total returns for US dollar-denominated

9

Performance summary

Delaware Emerging Markets Debt Corporate Fund

debt instruments issued by emerging market sovereign and quasi-sovereign entities, including Brady bonds, loans, and Eurobonds, and limits the weights of the index countries by only including a specified portion of those countries’ eligible current face amounts of debt outstanding.

Index performance returns do not reflect any management fees, transaction costs, or expenses.

Indices are unmanaged and one cannot invest directly in an index. Past performance is not a guarantee of future results.

Performance of other Fund classes will vary due to different charges and expenses.

| | | | |

| | | Nasdaq symbols | | CUSIPs |

| Class A | | DEDAX | | 246094841 |

| Class C | | DEDCX | | 246094833 |

| Class R | | DEDRX | | 246094825 |

| Institutional Class | | DEDIX | | 246094817 |

10

Disclosure of Fund expenses

For the six-month period from February 1, 2020 to July 31, 2020 (Unaudited)

As a shareholder of the Fund, you incur two types of costs: (1) transaction costs, including sales charges (loads) on purchase payments, reinvested dividends, or other distributions; redemption fees; and exchange fees; and (2) ongoing costs, including management fees; distribution and service (12b-1) fees; and other Fund expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The example is based on an investment of $1,000 invested at the beginning of the period and held for the entire six-month period from February 1, 2020 to July 31, 2020.

Actual expenses

The first section of the table shown, “Actual Fund return,” provides information about actual account values and actual expenses. You may use the information in this section of the table, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first section under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical example for comparison purposes

The second section of the table shown, “Hypothetical 5% return,” provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads), redemption fees, or exchange fees. Therefore, the second section of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher. The Fund’s expenses shown in the table reflect fee waivers in effect and assume reinvestment of all dividends and distributions.

11

Disclosure of Fund expenses

For the six-month period from February 1, 2020 to July 31, 2020 (Unaudited)

Delaware Emerging Markets Debt Corporate Fund

Expense analysis of an investment of $1,000

| | | | | | | | | | | | | | |

| | | Beginning Account Value | | | Ending Account Value | | | Annualized | | | Expenses Paid During Period |

| | | 2/1/20 | | | 7/31/20 | | | Expense Ratio | | | 2/1/20 to 7/31/20* |

Actual Fund return† | | | | | | | | | | | | | | |

Class A | | | $1,000.00 | | | | $975.70 | | | | 1.04% | | | $5.11 |

Class C | | | 1,000.00 | | | | 972.00 | | | | 1.79% | | | 8.78 |

Class R | | | 1,000.00 | | | | 976.90 | | | | 0.79% | | | 3.88 |

Institutional Class | | | 1,000.00 | | | | 975.80 | | | | 0.79% | | | 3.88 |

|

Hypothetical 5% return (5% return before expenses) |

Class A | | | $1,000.00 | | | | $1,019.69 | | | | 1.04% | | | $5.22 |

Class C | | | 1,000.00 | | | | 1,015.96 | | | | 1.79% | | | 8.97 |

Class R | | | 1,000.00 | | | | 1,020.93 | | | | 0.79% | | | 3.97 |

Institutional Class | | | 1,000.00 | | | | 1,020.93 | | | | 0.79% | | | 3.97 |

*“Expenses Paid During Period” are equal to the Fund’s annualized expense ratio, multiplied by the average account value over the period, multiplied by 182/366 (to reflect the one-half year period).

†Because actual returns reflect only the most recent six-month period, the returns shown may differ significantly from fiscal year returns.

In addition to the Fund’s expenses reflected above, the Fund also indirectly bears its portion of the fees and expenses of the investment companies (Underlying Funds) in which it invests. The table above does not reflect the expenses of the Underlying Funds.

12

Security type / country and sector allocation

| | |

| Delaware Emerging Markets Debt Corporate Fund | | As of July 31, 2020 (Unaudited) |

Sector designations may be different than the sector designations presented in other Fund materials. The sector designations may represent the investment manager’s internal sector classifications.

| | |

| Security type / country | | Percentage of net assets |

| |

Corporate Bonds | | 94.67% |

Argentina | | 2.54% |

Brazil | | 11.08% |

Chile | | 3.77% |

China | | 5.52% |

Colombia | | 6.84% |

Congo (Democratic Republic) | | 0.97% |

Dominican Republic | | 0.65% |

Georgia | | 1.00% |

Ghana | | 0.51% |

Hong Kong | | 2.76% |

India | | 4.39% |

Indonesia | | 2.23% |

Israel | | 4.50% |

Jamaica | | 0.47% |

Kazakhstan | | 1.86% |

Kuwait | | 0.97% |

Lithuania | | 0.72% |

Macao | | 2.00% |

Mexico | | 7.58% |

Morocco | | 1.19% |

Nigeria | | 1.00% |

Panama | | 3.11% |

Paraguay | | 2.19% |

Peru | | 2.30% |

Qatar | | 2.20% |

Republic of Korea | | 2.81% |

Russia | | 3.80% |

Saudi Arabia | | 2.76% |

Singapore | | 1.01% |

South Africa | | 1.40% |

Thailand | | 1.59% |

Turkey | | 2.97% |

Ukraine | | 2.22% |

United Arab Emirates | | 1.39% |

United Kingdom | | 0.30% |

United States | | 0.42% |

Vietnam | | 1.04% |

Zambia | | 0.61% |

13

Security type / country and sector allocation

Delaware Emerging Markets Debt Corporate Fund

| | |

| Security type / country | | Percentage of net assets |

Sovereign Bonds | | 1.63% |

Argentina | | 0.60% |

Mongolia | | 1.03% |

Supranational Bank | | 0.80% |

Short-Term Investments | | 2.74% |

Total Value of Securities | | 99.84% |

Receivables and Other Assets Net of Liabilities | | 0.16% |

Total Net Assets | | 100.00% |

| |

| Corporate bonds by sector | | Percentage of net assets |

| |

Banking | | 17.25% |

Basic Industry | | 12.61% |

Capital Goods | | 0.73% |

Communications | | 11.62% |

Consumer Cyclical | | 6.07% |

Consumer Non-Cyclical | | 6.12% |

Electric | | 9.40% |

Energy | | 16.11% |

Industrials | | 9.68% |

Insurance | | 1.71% |

Real Estate | | 2.73% |

Utilities | | 0.64% |

Total | | 94.67% |

14

Schedule of investments

| | |

| Delaware Emerging Markets Debt Corporate Fund | | July 31, 2020 |

| | | | | | | | |

| | | Principal Amount° | | | Value (US $) | |

Corporate Bonds – 94.67%Ä | | | | | | | | |

Argentina – 2.54% | | | | | | | | |

Aeropuertos Argentina 2000 144A PIK 9.375% 2/1/27 #, * | | | 791,296 | | | $ | 583,581 | |

Tecpetrol 144A 4.875% 12/12/22 # | | | 235,000 | | | | 229,497 | |

Transportadora de Gas del Sur 144A 6.75% 5/2/25 # | | | 515,000 | | | | 451,431 | |

YPF 144A 8.50% 6/27/29 # | | | 637,000 | | | | 510,129 | |

| | | | | | | | |

| | | | | | | 1,774,638 | |

| | | | | | | | |

Brazil – 11.08% | | | | | | | | |

Aegea Finance 144A 5.75% 10/10/24 # | | | 435,000 | | | | 449,640 | |

Azul Investments 144A 5.875% 10/26/24 # | | | 650,000 | | | | 340,369 | |

Banco BTG Pactual 144A 4.50% 1/10/25 # | | | 470,000 | | | | 470,940 | |

Braskem Netherlands Finance 144A 8.50% 1/23/81 #, µ | | | 465,000 | | | | 470,840 | |

BRF 144A 4.875% 1/24/30 # | | | 380,000 | | | | 380,361 | |

Centrais Eletricas Brasileiras 144A 4.625% 2/4/30 # | | | 595,000 | | | | 602,066 | |

CSN Islands XI 144A 6.75% 1/28/28 # | | | 255,000 | | | | 237,150 | |

CSN Resources | | | 200,000 | | | | 202,750 | |

144A 7.625% 2/13/23 # | | | | | | | | |

144A 7.625% 4/17/26 # | | | 200,000 | | | | 198,140 | |

JBS Investments II | | | 490,000 | | | | 521,066 | |

144A 5.75% 1/15/28 # | | | | | | | | |

144A 7.00% 1/15/26 # | | | 295,000 | | | | 317,796 | |

Klabin Austria 144A 7.00% 4/3/49 # | | | 600,000 | | | | 660,750 | |

Petrobras Global Finance | | | 210,000 | | | | 220,684 | |

5.60% 1/3/31 | | | | | | | | |

6.75% 6/3/50 | | | 350,000 | | | | 381,407 | |

Rede D’or Finance 144A 4.50% 1/22/30 # | | | 520,000 | | | | 466,830 | |

Rumo Luxembourg 144A 5.25% 1/10/28 # | | | 650,000 | | | | 676,195 | |

Ultrapar International 144A 5.25% 6/6/29 # | | | 620,000 | | | | 625,447 | |

Vale Overseas 3.75% 7/8/30 | | | 495,000 | | | | 531,863 | |

| | | | | | | | |

| | | | | | | 7,754,294 | |

| | | | | | | | |

Chile – 3.77% | | | | | | | | |

AES Gener 144A 7.125% 3/26/79 #, µ | | | 605,000 | | | | 616,634 | |

Engie Energia Chile 144A 4.50% 1/29/25 # | | | 435,000 | | | | 478,907 | |

Inversiones CMPC 144A 3.85% 1/13/30 # | | | 410,000 | | | | 430,014 | |

Sable International Finance 144A 5.75% 9/7/27 # | | | 350,000 | | | | 367,728 | |

Sociedad Quimica y Minera de Chile 144A 3.625% 4/3/23 # | | | 500,000 | | | | 522,073 | |

VTR Finance 144A 6.375% 7/15/28 # | | | 205,000 | | | | 219,200 | |

| | | | | | | | |

| | | | | | | 2,634,556 | |

| | | | | | | | |

15

Schedule of investments

Delaware Emerging Markets Debt Corporate Fund

| | | | | | | | |

| | | Principal Amount° | | | Value (US $) | |

Corporate BondsÄ (continued) | | | | | | | | |

China – 5.52% | | | | | | | | |

Baidu 3.875% 9/29/23 | | | 400,000 | | | $ | 430,062 | |

Bank of China 144A 5.00% 11/13/24 # | | | 420,000 | | | | 472,324 | |

China Overseas Finance Cayman V 3.95% 11/15/22 | | | 392,000 | | | | 413,773 | |

Kaisa Group Holdings 9.375% 6/30/24 | | | 545,000 | | | | 502,003 | |

Shimao Group Holdings 5.60% 7/15/26 | | | 615,000 | | | | 657,607 | |

Tencent Holdings 144A 3.28% 4/11/24 # | | | 640,000 | | | | 683,745 | |

Weibo 3.375% 7/8/30 | | | 670,000 | | | | 704,753 | |

| | | | | | | | |

| | | | | | | 3,864,267 | |

| | | | | | | | |

Colombia – 6.84% | | | | | | | | |

Bancolombia 3.00% 1/29/25 | | | 765,000 | | | | 761,894 | |

Colombia Telecomunicaciones 144A 4.95% 7/17/30 # | | | 460,000 | | | | 473,662 | |

Ecopetrol | | | 311,000 | | | | 344,627 | |

5.375% 6/26/26 | | | | | | | | |

6.875% 4/29/30 | | | 285,000 | | | | 343,885 | |

Geopark | | | 565,000 | | | | 495,788 | |

144A 5.50% 1/17/27 # | | | | | | | | |

144A 6.50% 9/21/24 # | | | 210,000 | | | | 198,450 | |

Gran Tierra Energy 144A 7.75% 5/23/27 # | | | 400,000 | | | | 192,250 | |

Grupo Energia Bogota 144A 4.875% 5/15/30 # | | | 610,000 | | | | 666,425 | |

Millicom International Cellular 144A 6.25% 3/25/29 # | | | 670,000 | | | | 739,054 | |

Oleoducto Central 144A 4.00% 7/14/27 # | | | 550,000 | | | | 569,387 | |

| | | | | | | | |

| | | | | | | 4,785,422 | |

| | | | | | | | |

Congo (Democratic Republic) – 0.97% | | | | | | | | |

HTA Group 144A 7.00% 12/18/25 # | | | 655,000 | | | | 679,058 | |

| | | | | | | | |

| | | | | | | 679,058 | |

| | | | | | | | |

Dominican Republic – 0.65% | | | | | | | | |

AES Andres 144A 7.95% 5/11/26 # | | | 440,000 | | | | 454,850 | |

| | | | | | | | |

| | | | | | | 454,850 | |

| | | | | | | | |

Georgia – 1.00% | | | | | | | | |

Bank of Georgia 144A 6.00% 7/26/23 # | | | 680,000 | | | | 697,136 | |

| | | | | | | | |

| | | | | | | 697,136 | |

| | | | | | | | |

Ghana – 0.51% | | | | | | | | |

Tullow Oil 144A 7.00% 3/1/25 # | | | 595,000 | | | | 355,878 | |

| | | | | | | | |

| | | | | | | 355,878 | |

| | | | | | | | |

Hong Kong – 2.76% | | | | | | | | |

AIA Group | | | | | | | | |

3.125% 3/13/23 | | | 715,000 | | | | 747,581 | |

144A 3.375% 4/7/30 # | | | 400,000 | | | | 448,820 | |

16

| | | | | | | | |

| | | Principal Amount° | | | Value (US $) | |

Corporate BondsÄ (continued) | | | | | | | | |

Hong Kong (continued) | | | | | | | | |

CLP Power Hong Kong Financing 2.875% 4/26/23 | | | 200,000 | | | $ | 208,075 | |

Goodman HK Finance 4.375% 6/19/24 | | | 485,000 | | | | 526,011 | |

| | | | | | | | |

| | | | | | | 1,930,487 | |

| | | | | | | | |

India – 4.39% | | | | | | | | |

Adani Electricity Mumbai 144A 3.949% 2/12/30 # | | | 610,000 | | | | 603,995 | |

Future Retail 144A 5.60% 1/22/25 # | | | 780,000 | | | | 509,124 | |

Greenko Solar Mauritius 144A 5.95% 7/29/26 # | | | 560,000 | | | | 570,507 | |

ICICI Bank 144A 4.00% 3/18/26 # | | | 450,000 | | | | 473,355 | |

ReNew Power 144A 5.875% 3/5/27 # | | | 590,000 | | | | 591,995 | |

Vedanta Resources Finance II 144A 9.25% 4/23/26 # | | | 455,000 | | | | 321,912 | |

| | | | | | | | |

| | | | | | | 3,070,888 | |

| | | | | | | | |

Indonesia – 2.23% | | | | | | | | |

Bayan Resources 144A 6.125% 1/24/23 # | | | 360,000 | | | | 346,412 | |

Hutama Karya Persero 144A 3.75% 5/11/30 # | | | 543,000 | | | | 591,940 | |

Listrindo Capital 144A 4.95% 9/14/26 # | | | 602,000 | | | | 624,575 | |

| | | | | | | | |

| | | | | | | 1,562,927 | |

| | | | | | | | |

Israel – 4.50% | | | | | | | | |

Altice Financing 144A 5.00% 1/15/28 # | | | 600,000 | | | | 616,719 | |

Bank Leumi Le-Israel 144A 3.275% 1/29/31 #, µ | | | 655,000 | | | | 649,662 | |

Israel Chemicals 6.375% 5/31/38 | | | 475,000 | | | | 582,238 | |

Israel Electric 144A 5.00% 11/12/24 # | | | 400,000 | | | | 451,258 | |

Teva Pharmaceutical Finance Netherlands III 6.75% 3/1/28 | | | 490,000 | | | | 544,794 | |

144A 7.125% 1/31/25 # | | | 275,000 | | | | 302,357 | |

| | | | | | | | |

| | | | | | | 3,147,028 | |

| | | | | | | | |

Jamaica – 0.47% | | | | | | | | |

Digicel Group 0.5 PIK 10.00% 4/1/24 * | | | 428,155 | | | | 325,398 | |

| | | | | | | | |

| | | | | | | 325,398 | |

| | | | | | | | |

Kazakhstan – 1.86% | | | | | | | | |

KazTransGas JSC 144A 4.375% 9/26/27 # | | | 575,000 | | | | 627,561 | |

Tengizchevroil Finance Co. International 144A 2.625% 8/15/25 # | | | 670,000 | | | | 676,765 | |

| | | | | | | | |

| | | | | | | 1,304,326 | |

| | | | | | | | |

Kuwait – 0.97% | | | | | | | | |

Equate Petrochemical 144A 3.00% 3/3/22 # | | | 275,000 | | | | 279,969 | |

MEGlobal Canada 144A 5.875% 5/18/30 # | | | 335,000 | | | | 397,099 | |

| | | | | | | | |

| | | | | | | 677,068 | |

| | | | | | | | |

17

Schedule of investments

Delaware Emerging Markets Debt Corporate Fund

| | | | | | | | |

| | | Principal Amount° | | | Value (US $) | |

Corporate BondsD (continued) | | | | | | | | |

Lithuania – 0.72% | | | | | | | | |

ASG Finance Designated Activity 144A 7.875%

12/3/24 # | | | 734,000 | | | $ | 506,460 | |

| | | | | | | | |

| | | | | | | 506,460 | |

| | | | | | | | |

Macao – 2.00% | | | | | | | | |

MGM China Holdings 144A 5.25% 6/18/25 # | | | 495,000 | | | | 511,087 | |

Sands China

144A 3.80% 1/8/26 # | | | 380,000 | | | | 397,290 | |

144A 4.375% 6/18/30 # | | | 465,000 | | | | 490,180 | |

| | | | | | | | |

| | | | | | | 1,398,557 | |

Mexico – 7.58% | | | | | | | | |

Aerovias de Mexico 144A 7.00% 2/5/25 #, ‡ | | | 505,000 | | | | 114,888 | |

Banco Mercantil del Norte

144A 6.75% #, µ, y | | | 240,000 | | | | 228,983 | |

144A 8.375% #, µ, y | | | 410,000 | | | | 414,838 | |

Banco Santander Mexico Institucion de Banca | | | | | | | | |

Multiple Grupo Financiero | | | | | | | | |

144A 5.375% 4/17/25 # | | | 250,000 | | | | 277,606 | |

144A 5.95% 10/1/28 #, µ | | | 335,000 | | | | 347,499 | |

BBVA Bancomer 144A 5.125% 1/18/33 #, µ | | | 260,000 | | | | 245,053 | |

Cemex 144A 7.375% 6/5/27 # | | | 795,000 | | | | 849,545 | |

Grupo Cementos de Chihuahua 144A 5.25%

6/23/24 # | | | 500,000 | | | | 506,822 | |

Industrias Penoles 144A 4.75% 8/6/50 # | | | 670,000 | | | | 695,437 | |

Infraestructura Energetica Nova

144A 3.75% 1/14/28 # | | | 420,000 | | | | 423,070 | |

144A 4.875% 1/14/48 # | | | 300,000 | | | | 296,039 | |

Minera Mexico 144A 4.50% 1/26/50 # | | | 525,000 | | | | 573,604 | |

Petroleos Mexicanos 144A 5.95% 1/28/31 # | | | 385,000 | | | | 331,602 | |

| | | | | | | | |

| | | | | | | 5,304,986 | |

| | | | | | | | |

Morocco – 1.19% | | | | | | | | |

OCP | | | | | | | | |

144A 4.50% 10/22/25 # | | | 515,000 | | | | 539,483 | |

144A 6.875% 4/25/44 # | | | 235,000 | | | | 293,061 | |

| | | | | | | | |

| | | | | | | 832,544 | |

| | | | | | | | |

Nigeria – 1.00% | | | | | | | | |

IHS Netherlands Holdco 144A 7.125% 3/18/25 # | | | 685,000 | | | | 700,413 | |

| | | | | | | | |

| | | | | | | 700,413 | |

| | | | | | | | |

Panama – 3.11% | | | | | | | | |

Autoridad del Canal de Panama 144A 4.95%

7/29/35 # | | | 530,000 | | | | 619,064 | |

18

| | | | | | | | |

| | | Principal Amount° | | | Value (US $) | |

Corporate BondsD (continued) | | �� | | | | | | |

Panama (continued) | | | | | | | | |

Banco General 144A 4.125% 8/7/27 # | | | 400,000 | | | $ | 435,424 | |

Banistmo 144A 4.25% 7/31/27 # | | | 700,000 | | | | 696,150 | |

C&W Senior Financing 144A 7.50% 10/15/26 # | | | 400,000 | | | | 427,162 | |

| | | | | | | | |

| | | | | | | 2,177,800 | |

| | | | | | | | |

Paraguay – 2.19% | | | | | | | | |

Bioceanico Sovereign Certificate 144A 2.971%

6/5/34 #, ^ | | | 725,363 | | | | 524,982 | |

Rutas 2 and 7 Finance 144A 3.413% 9/30/36 #, ^ | | | 615,000 | | | | 426,656 | |

Telefonica Celular del Paraguay 144A 5.875%

4/15/27 # | | | 550,000 | | | | 584,078 | |

| | | | | | | | |

| | | | | | | 1,535,716 | |

| | | | | | | | |

Peru – 2.30% | | | | | | | | |

Banco de Credito del Peru 144A 2.70% 1/11/25 # | | | 505,000 | | | | 517,531 | |

Kallpa Generacion 144A 4.125% 8/16/27 # | | | 600,000 | | | | 617,700 | |

Lima Metro Line 2 Finance 144A 4.35% 4/5/36 # | | | 425,000 | | | | 470,760 | |

| | | | | | | | |

| | | | | | | 1,605,991 | |

| | | | | | | | |

Qatar – 2.20% | | | | | | | | |

Ooredoo International Finance 144A 5.00%

10/19/25 # | | | 510,000 | | | | 597,656 | |

QNB Finance 2.625%

5/12/25 | | | 355,000 | | | | 373,229 | |

3.50% 3/28/24 | | | 525,000 | | | | 565,364 | |

| | | | | | | | |

| | | | | | | 1,536,249 | |

| | | | | | | | |

Republic of Korea – 2.81% | | | | | | | | |

Kia Motors 144A 3.00% 4/25/23 # | | | 695,000 | | | | 721,999 | |

Shinhan Financial Group 144A 3.34% 2/5/30 #, µ | | | 555,000 | | | | 582,051 | |

Woori Bank 144A 4.75% 4/30/24 # | | | 600,000 | | | | 661,166 | |

| | | | | | | | |

| | | | | | | 1,965,216 | |

Russia – 3.80% | | | | | | | | |

Gazprom PJSC via Gaz Finance 144A 3.25%

2/25/30 # | | | 455,000 | | | | 459,265 | |

Lukoil Securities 144A 3.875% 5/6/30 # | | | 575,000 | | | | 610,382 | |

Novolipetsk Steel Via Steel Funding DAC 144A

4.00% 9/21/24 # | | | 600,000 | | | | 639,775 | |

Phosagro OAO Via Phosagro Bond Funding 144A

3.949% 4/24/23 # | | | 200,000 | | | | 208,674 | |

VEON Holdings 144A 4.00% 4/9/25 # | | | 708,000 | | | | 739,672 | |

| | | | | | | | |

| | | | | | | 2,657,768 | |

| | | | | | | | |

Saudi Arabia – 2.76% | | | | | | | | |

Arabian Centres Sukuk 144A 5.375% 11/26/24 # | | | 525,000 | | | | 472,762 | |

19

Schedule of investments

Delaware Emerging Markets Debt Corporate Fund

| | | | | | | | |

| | | Principal Amount° | | | Value (US $) | |

Corporate BondsD (continued) | | | | | | | | |

Saudi Arabia (continued) | | | | | | | | |

Saudi Arabian Oil 144A 2.875%

4/16/24 # | | | 485,000 | | | $ | 511,048 | |

144A 4.25% 4/16/39 # | | | 400,000 | | | | 482,112 | |

Saudi Electricity Global Sukuk 4 4.222% 1/27/24 | | | 430,000 | | | | 467,034 | |

| | | | | | | | |

| | | | | | | 1,932,956 | |

| | | | | | | | |

Singapore – 1.01% | | | | | | | | |

DBS Group Holdings 144A 4.52% 12/11/28 #, µ | | | 645,000 | | | | 703,112 | |

| | | | | | | | |

| | | | | | | 703,112 | |

| | | | | | | | |

South Africa – 1.40% | | | | | | | | |

Gold Fields Orogen Holdings BVI 144A 6.125% 5/15/29 # | | | 540,000 | | | | 634,500 | |

Sasol Financing USA 5.875% 3/27/24 | | | 370,000 | | | | 347,800 | |

| | | | | | | | |

| | | | | | | 982,300 | |

| | | | | | | | |

Thailand – 1.59% | | | | | | | | |

Bangkok Bank 144A 3.733% 9/25/34 #, µ | | | 625,000 | | | | 628,341 | |

PTTEP Treasury Center 144A 2.587% 6/10/27 # | | | 465,000 | | | | 483,543 | |

| | | | | | | | |

| | | | | | | 1,111,884 | |

| | | | | | | | |

Turkey – 2.97% | | | | | | | | |

Akbank T.A.S. 144A 6.80% 2/6/26 # | | | 530,000 | | | | 520,229 | |

Turk Telekomunikasyon 144A 6.875% 2/28/25 # | | | 600,000 | | | | 626,400 | |

Turkcell Iletisim Hizmetleri 144A 5.80% 4/11/28 # | | | 590,000 | | | | 579,079 | |

Turkiye Garanti Bankasi 144A 5.25% 9/13/22 # | | | 355,000 | | | | 351,177 | |

| | | | | | | | |

| | | | | | | 2,076,885 | |

| | | | | | | | |

Ukraine – 2.22% | | | | | | | | |

Kernel Holding 144A 6.50% 10/17/24 # | | | 645,000 | | | | 641,775 | |

Metinvest 144A 8.50% 4/23/26 # | | | 300,000 | | | | 295,677 | |

MHP

144A 6.95% 4/3/26 # | | | 400,000 | | | | 406,396 | |

144A 7.75% 5/10/24 # | | | 200,000 | | | | 210,868 | |

| | | | | | | | |

| | | | | | | 1,554,716 | |

| | | | | | | | |

United Arab Emirates – 1.39% | | | | | | | | |

DP World Crescent 144A 3.908% 5/31/23 # | | | 465,000 | | | | 487,692 | |

Emirates NBD Bank PJSC 2.625% 2/18/25 | | | 470,000 | | | | 482,721 | |

| | | | | | | | |

| | | | | | | 970,413 | |

| | | | | | | | |

United Kingdom – 0.30% | | | | | | | | |

CK Hutchison International 20 144A 2.50% 5/8/30 # | | | 200,000 | | | | 210,489 | |

| | | | | | | | |

| | | | | | | 210,489 | |

| | | | | | | | |

20

| | | | | | | | |

| | Principal Amount° | | | Value (US $) | |

Corporate BondsD (continued) | | | | | | | | |

United States – 0.42% | | | | | | | | |

Resorts World Las Vegas 144A 4.625% 4/16/29 # | | | 300,000 | | | $ | 296,738 | |

| | | | | | | | |

| | | | | | | 296,738 | |

| | | | | | | | |

Vietnam – 1.04% | | | | | | | | |

Mong Duong Finance Holdings 144A 5.125%

5/7/29 # | | | 720,000 | | | | 727,589 | |

| | | | | | | | |

| | | | | | | 727,589 | |

| | | | | | | | |

Zambia – 0.61% | | | | | | | | |

First Quantum Minerals 144A 7.50% 4/1/25 # | | | 425,000 | | | | 429,781 | |

| | | | | | | | |

| | | | | | | 429,781 | |

| | | | | | | | |

Total Corporate Bonds (cost $65,623,205) | | | | | | | 66,236,784 | |

| | | | | | | | |

| | | | | | | | |

Sovereign Bonds – 1.63%D | | | | | | | | |

Argentina – 0.60% | | | | | | | | |

Argentine Republic Government International Bond

5.625% 1/26/22 | | | 938,000 | | | | 417,424 | |

Mongolia – 1.03% | | | | | | | | |

Development Bank of Mongolia 144A 7.25%

10/23/23 # | | | 710,000 | | | | 720,673 | |

| | | | | | | | |

Total Sovereign Bonds (cost $1,257,013) | | | | | | | 1,138,097 | |

| | | | | | | | |

| | | | | | | | |

Supranational Bank – 0.80% | | | | | | | | |

Banque Ouest Africaine de Developpement

144A 4.70% 10/22/31 # | | | 548,000 | | | | 561,656 | |

| | | | | | | | |

Total Supranational Bank (cost $548,000) | | | | | | | 561,656 | |

| | | | | | | | |

| | |

| | | Number of shares | | | | |

Short-Term Investments – 2.74% | | | | | | | | |

Money Market Mutual Funds – 2.74% | | | | | | | | |

BlackRock FedFund – Institutional Shares | | | | | | | | |

(seven-day effective yield 0.060%) | | | 383,944 | | | | 383,944 | |

Fidelity Investments Money Market Government | | | | | | | | |

Portfolio – Class I (seven-day effective yield 0.050%) | | | 383,943 | | | | 383,943 | |

GS Financial Square Government Fund – | | | | | | | | |

Institutional Shares (seven-day effective yield 0.130%) | | | 383,943 | | | | 383,943 | |

21

Schedule of investments

Delaware Emerging Markets Debt Corporate Fund

| | | | | | | | |

| | | Number of shares | | | Value (US $) | |

Short-Term Investments (continued) | | | | | | | | |

Money Market Mutual Funds (continued) | | | | | | | | |

Morgan Stanley Government Portfolio – Institutional | | | | | | | | |

Share Class (seven-day effective yield 0.010%) | | | 383,944 | | | $ | 383,944 | |

State Street Institutional US Government Money | | | | | | | | |

Market Fund – Investor Class (seven-day effective yield 0.010%) | | | 383,943 | | | | 383,943 | |

| | | | | | | | |

Total Short-Term Investments (cost $1,919,717) | | | | | | | 1,919,717 | |

| | | | | | | | |

Total Value of Securities–99.84% | | | | | | | | |

(cost $69,347,935) | | | | | | $ | 69,856,254 | |

| | | | | | | | |

| D | Securities have been classified by country of origin. Aggregate classification by business sector has been presented on page 14 in “Security type / sector and country allocations.” |

| ○ | Principal amount shown is stated in USD unless noted that the security is denominated in another currency. |

| # | Security exempt from registration under Rule 144A of the Securities Act of 1933, as amended. At July 31, 2020, the aggregate value of Rule 144A securities was $57,056,310, which represents 81.38% of the Fund’s net assets. See Note 11 in “Notes to financial statements.” |

| * | PIK. 78% of the income received was in cash and 22% was in principal. |

| µ | Fixed to variable rate investment. The rate shown reflects the fixed rate in effect at July 31, 2020. Rate will reset at a future date. |

| ‡ | Non-income producing security. Security is currently in default. |

| y | No contractual maturity date. |

| ^ | Zero-coupon security. The rate shown is the effective yield at the time of purchase. |

The following futures and swap contracts were outstanding at July. 31, 2020:1

Futures Contracts

| | | | | | | | | | | | | | | | | | | | |

| | | Notional | | | Notional Cost | | | Expiration | | | Value/

Unrealized | | | Variation

Margin

Due from

(Due to) | |

Contracts to Buy (Sell) | | Amount | | | (Proceeds) | | | Date | | | Depreciation | | | Brokers | |

11 US Treasury 10 yr Ultra Notes | | $ | (1,751,750 | ) | | | $ (1,727,461) | | | | 9/21/20 | | | | $ (24,289) | | | $ | (859 | ) |

22

Swap Contracts

CDS Contracts2

| | | | | | | | | | | | | | | | | | | | | | | | |

Counterparty/ Reference Obligation/ Termination Date/ Payment Frequency | | Notional

Amount3 | | | Annual

Protection

Payments | | | Value | | | Upfront

Payments

Paid

(Received) | | | Unrealized

Depreciation4 | | | Variation

Margin

Due from

(Due to)

Brokers | |

Over-The-Counter: | | | | | | | | | | | | | | | | | | | | | | | | |

Protection Purchased | | | | | | | | | | | | | | | | | | | | | | | | |

Moody’s Ratings: | | | | | | | | | | | | | | | | | | | | | | | | |

JPMCB-Mexico

3.60% | | | | | | | | | | | | | | | | | | | | | | | | |

12/31/21 WR | | | | | | | | | | | | | | | | | | | | | | | | |

6/20/25-Quarterly | | | 3,709,000 | | | | 1.000 | % | | $ | 75,203 | | | $ | 259,306 | | | | $ (184,103) | | | $ | — | |

The use of futures and swap contracts involve elements of market risk and risks in excess of the amounts disclosed in these financial statements. The notional amounts presented above represent the Fund’s total exposure in such contracts, whereas only the variation margin is reflected in the Fund’s net assets.

| 1 | See Note 8 in “Notes to Financial statements”: |

| 2 | A CDS contract is a risk-transfer instrument through which one party (purchaser of protection) transfers to another party (seller of protection) the financial risk of a credit event (as defined in the CDS agreement), as it relates to a particular reference security or basket of securities (such as an index). Periodic payments (receipts) on such contracts are accrued daily and recorded as unrealized losses (gains) on swap contracts. Upon payment (receipt), such amounts are recorded as realized losses (gains) on swap contracts. Upfront payments made or received in connection with CDS contracts are amortized over the expected life of the CDS contracts as unrealized losses (gains) on swap contracts. The change in value of CDS contracts is recorded daily as unrealized appreciation or depreciation. A realized gain or loss is recorded upon a credit event (as defined in the CDS agreement) or the maturity or termination of the CDS agreement. |

| 3 | Notional amount shown is stated in USD unless noted that the swap is denominated in another currency. |

| 4 | Unrealized appreciation (depreciation) does not include periodic interest payments (receipt) on swap contracts accrued daily in the amount of $(4,121). |

Summary of abbreviations:

CDS – Credit Default Swap

DAC – Designated Activity Company

GS – Goldman Sachs

JPMCB – JPMorgan Chase Bank

JSC – Joint Stock Company

PIK – Payment-in-Kind

23

Schedule of investments

Delaware Emerging Markets Debt Corporate Fund

Summary of abbreviations: (continued)

PJSC – Private Joint Stock Company

yr – Year

See accompanying notes, which are an integral part of the financial statements.

24

Statement of assets and liabilities

| | |

Delaware Emerging Markets Debt Corporate Fund | | July 31, 2020 |

| | | | |

Assets: | | | | |

Investments, at value* | | $ | 69,856,254 | |

Cash | | | 92,499 | |

Cash collateral due from brokers | | | 27,500 | |

Foreign currencies, at valueD | | | 6 | |

Receivable for securities sold | | | 971,992 | |

Dividends and interest receivable | | | 701,151 | |

Receivable for fund shares sold | | | 103,060 | |

Upfront payments paid on over the counter credit default swap contracts | | | 259,306 | |

| | | | |

Total Assets | | | 72,011,768 | |

| | | | |

Liabilities: | | | | |

Payable for securities purchased | | | 1,603,525 | |

Unrealized depreciation on over the counter credit default swap contracts | | | 184,103 | |

Payable for fund shares redeemed | | | 105,112 | |

Cash collateral due to brokers | | | 80,000 | |

Other accrued expenses | | | 40,302 | |

Investment management fees payable to affiliates | | | 17,609 | |

Audit and tax fees payable | | | 6,500 | |

Swap payment payable | | | 4,121 | |

Variation margin due to broker on futures contracts | | | 859 | |

Dividend disbursing and transfer agent fees and expenses payable to affiliates | | | 544 | |

Accounting and administration expenses payable to affiliates | | | 537 | |

Trustees’ fees and expenses payable to affiliates | | | 235 | |

Legal fees payable to affiliates | | | 102 | |

Distribution fees payable to affiliates | | | 99 | |

Reports and statements to shareholders expenses payable to affiliates | | | 88 | |

| | | | |

Total Liabilities | | | 2,043,736 | |

| | | | |

Total Net Assets | | $ | 69,968,032 | |

| | | | |

| |

Net Assets Consist of: | | | | |

Paid-in capital | | $ | 71,089,042 | |

Total distributable earnings (loss) | | | (1,121,010 | ) |

| | | | |

Total Net Assets | | $ | 69,968,032 | |

| | | | |

25

Statement of assets and liabilities

Delaware Emerging Markets Debt Corporate Fund

| | | | |

Net Asset Value | | | | |

Class A: | | | | |

Net assets | | $ | 280,983 | |

Shares of beneficial interest outstanding, unlimited authorization, no par | | | 33,154 | |

Net asset value per share | | $ | 8.48 | |

Sales charge | | | 4.50 | % |

Offering price per share, equal to net asset value per share / (1 - sales charge) | | $ | 8.88 | |

Class C: | | | | |

Net assets | | $ | 83,901 | |

Shares of beneficial interest outstanding, unlimited authorization, no par | | | 9,909 | |

Net asset value per share | | $ | 8.47 | |

Class R: | | | | |

Net assets | | $ | 2,779 | |

Shares of beneficial interest outstanding, unlimited authorization, no par | | | 328 | |

Net asset value per share | | $ | 8.47 | |

Institutional Class: | | | | |

Net assets | | $ | 69,600,369 | |

Shares of beneficial interest outstanding, unlimited authorization, no par | | | 8,213,573 | |

Net asset value per share | | $ | 8.47 | |

| | | | |

*Investments, at cost | | $ | 69,347,935 | |

DForeign currencies, at cost | | | 6 | |

See accompanying notes, which are an integral part of the financial statements.

26

Statement of operations

| | |

| Delaware Emerging Markets Debt Corporate Fund | | Year ended July 31, 2020 |

| | | | |

Investment Income: | | | | |

Interest | | $ | 3,256,046 | |

Dividends | | | 89,841 | |

| | | | |

| | | 3,345,887 | |

| | | | |

| |

Expenses: | | | | |

Management fees | | | 521,289 | |

Distribution expenses - Class A | | | 214 | |

Distribution expenses - Class C | | | 745 | |

Distribution expenses - Class R | | | 13 | |

Registration fees | | | 60,643 | |

Accounting and administration expenses | | | 54,906 | |

Dividend disbursing and transfer agent fees and expenses | | | 53,500 | |

Audit and tax fees | | | 49,716 | |

Reports and statements to shareholders expenses | | | 43,813 | |

Legal fees | | | 43,620 | |

Custodian fees | | | 4,843 | |

Trustees’ fees and expenses | | | 3,857 | |

Other | | | 23,248 | |

| | | | |

| | | 860,407 | |

Less expenses waived | | | (307,848 | ) |

Less waived distribution

expenses - Class R | | | (13 | ) |

Less expenses paid indirectly | | | (3,046 | ) |

| | | | |

Total operating expenses | | | 549,500 | |

| | | | |

Net Investment Income | | | 2,796,387 | |

| | | | |

27

Statement of operations

Delaware Emerging Markets Debt Corporate Fund

| | | | |

Net Realized and Unrealized Gain (Loss): | | | | |

Net realized gain (loss) on: | | | | |

Investments | | $ | (1,315,183 | ) |

Foreign currencies | | | (1,267 | ) |

Foreign currency exchange contracts | | | (21 | ) |

Futures contracts | | | 832 | |

Options purchased | | | (35,336 | ) |

Swap contracts | | | 157,078 | |

| | | | |

Net realized loss | | | (1,193,897 | ) |

| | | | |

| |

Net change in unrealized appreciation (depreciation) of: | | | | |

Investments | | | (284,482 | ) |

Foreign currencies | | | 635 | |

Futures contracts | | | (24,289 | ) |

Swap contracts | | | (188,224 | ) |

| | | | |

Net change in unrealized appreciation (depreciation) | | | (496,360 | ) |

| | | | |

Net Realized and Unrealized Loss | | | (1,690,257 | ) |

| | | | |

Net Increase in Net Assets Resulting from Operations | | $ | 1,106,130 | |

| | | | |

See accompanying notes, which are an integral part of the financial statements.

28

Statements of changes in net assets

Delaware Emerging Markets Debt Corporate Fund

| | | | | | | | |

| | | Year ended | |

| | |

| | | 7/31/20 | | | 7/31/19 | |

| | |

Increase (Decrease) in Net Assets from Operations: | | | | | | | | |

Net investment income | | $ | 2,796,387 | | | $ | 1,187,721 | |

Net realized loss | | | (1,193,897 | ) | | | (357,340 | ) |

Net change in unrealized appreciation (depreciation) | | | (496,360 | ) | | | 1,558,433 | |

| | | | | | | | |

Net increase in net assets resulting from operations | | | 1,106,130 | | | | 2,388,814 | |

| | | | | | | | |

| | |

Dividends and Distributions to Shareholders from: | | | | | | | | |

Distributable earnings: | | | | | | | | |

Class A | | | (3,482 | ) | | | (5,436 | ) |

Class C | | | (2,353 | ) | | | (2,388 | ) |

Class R | | | (110 | ) | | | (130 | ) |

Institutional Class | | | (2,848,204 | ) | | | (1,158,341 | ) |

| | |

Return of capital: | | | | | | | | |

Class A | | | (184 | ) | | | — | |

Class C | | | (55 | ) | | | — | |

Class R | | | (2 | ) | | | — | |

Institutional Class | | | (45,634 | ) | | | — | |

| | | | | | | | |

| | | (2,900,024 | ) | | | (1,166,295 | ) |

| | | | | | | | |

| | |

Capital Share Transactions: | | | | | | | | |

Proceeds from shares sold: | | | | | | | | |

Class A | | | 216,071 | | | | 111,456 | |

Class C | | | 24,880 | | | | 14,307 | |

Institutional Class | | | 43,794,371 | | | | 28,002,416 | |

| | |

Net asset value of shares issued upon reinvestment of

dividends and distributions: | | | | | | | | |

Class A | | | 3,136 | | | | 5,108 | |

Class C | | | 2,408 | | | | 2,387 | |

Class R | | | 112 | | | | 129 | |

Institutional Class | | | 2,887,015 | | | | 1,155,876 | |

| | | | | | | | |

| | | 46,927,993 | | | | 29,291,679 | |

| | | | | | | | |

29

Statements of changes in net assets

Delaware Emerging Markets Debt Corporate Fund

| | | | | | | | |

| | | Year ended | |

| | |

| | | 7/31/20 | | | 7/31/19 | |

| | |

Capital Share Transactions (continued): | | | | | | | | |

Cost of shares redeemed: | | | | | | | | |

Class A | | $ | (30,714 | ) | | $ | (86,125 | ) |

Class C | | | (2,119 | ) | | | (38,686 | ) |

Institutional Class | | | (27,074,534 | ) | | | (271,729 | ) |

| | | | | | | | |

| | | (27,107,367 | ) | | | (396,540 | ) |

| | | | | | | | |

Increase in net assets derived from capital share transactions | | | 19,820,626 | | | | 28,895,139 | |

| | | | | | | | |

Net Increase in Net Assets | | | 18,026,732 | | | | 30,117,658 | |

| | |

Net Assets: | | | | | | | | |

Beginning of year | | | 51,941,300 | | | | 21,823,642 | |

| | | | | | | | |

End of year | | $ | 69,968,032 | | | $ | 51,941,300 | |

| | | | | | | | |

See accompanying notes, which are an integral part of the financial statements.

30

This page intentionally left blank.

Financial highlights

Delaware Emerging Markets Debt Corporate Fund Class A

Selected data for each share of the Fund outstanding throughout each period were as follows:

| | | | | | | | | | | | | | | | | | | | |

| | | Year ended | |

| | | | |

| | | 7/31/20 | | | 7/31/19 | | | 7/31/18 | | | 7/31/17 | | | 7/31/16 | |

| |

Net asset value, beginning of period | | $ | 8.67 | | | $ | 8.26 | | | $ | 8.77 | | | $ | 8.48 | | | $ | 8.21 | |

| | | | | |

Income (loss) from investment operations: | | | | | | | | | | | | | | | | | | | | |

Net investment income1 | | | 0.32 | | | | 0.40 | | | | 0.39 | | | | 0.37 | | | | 0.36 | |

Net realized and unrealized gain (loss) | | | (0.18 | ) | | | 0.41 | | | | (0.39 | ) | | | 0.29 | | | | 0.24 | |

| | | | | | | | | | | | | | | | | | | | |

Total from investment operations | | | 0.14 | | | | 0.81 | | | | — | | | | 0.66 | | | | 0.60 | |

| | | | | | | | | | | | | | | | | | | | |

| | | | | |

Less dividends and distributions from: | | | | | | | | | | | | | | | | | | | | |

Net investment income | | | (0.32 | ) | | | (0.35 | ) | | | (0.38 | ) | | | (0.37 | ) | | | (0.33 | ) |

Net realized gain | | | — | | | | (0.05 | ) | | | (0.13 | ) | | | — | | | | — | |

Return of capital | | | (0.01 | ) | | | — | | | | — | | | | — | | | | — | |

| | | | | | | | | | | | | | | | | | | | |

Total dividends and distributions | | | (0.33 | ) | | | (0.40 | ) | | | (0.51 | ) | | | (0.37 | ) | | | (0.33 | ) |

| | | | | | | | | | | | | | | | | | | | |

| | | | | |

Net asset value, end of period | | $ | 8.48 | | | $ | 8.67 | | | $ | 8.26 | | | $ | 8.77 | | | $ | 8.48 | |

| | | | | | | | | | | | | | | | | | | | |

| | | | | |

Total return2 | | | 1.73% | | | | 10.21% | | | | (0.10%) | | | | 8.03% | | | | 7.62% | |

| | | | | |

Ratios and supplemental data: | | | | | | | | | | | | | | | | | | | | |

Net assets, end of period (000 omitted) | | $ | 281 | | | $ | 93 | | | $ | 57 | | | $ | 27 | | | $ | 3 | |

Ratio of expenses to average net assets3 | | | 1.04% | | | | 1.04% | | | | 1.16% | | | | 1.22% | | | | 1.03% | |

Ratio of expenses to average net assets prior to interest expenses reimbursed3 | | | 1.04% | | | | 1.04% | | | | 1.16% | | | | 1.22% | | | | 1.01% | |

Ratio of expenses to average net assets

prior to fees waived3 | | | 1.48% | | | | 1.90% | | | | 1.90% | | | | 1.91% | | | | 2.04% | |

Ratio of net investment income to average net assets | | | 3.77% | | | | 4.88% | | | | 4.57% | | | | 4.30% | | | | 4.42% | |

Ratio of net investment income to average net assets prior to interest expenses reimbursed | | | 3.77% | | | | 4.88% | | | | 4.57% | | | | 4.30% | | | | 4.44% | |

Ratio of net investment income to average net assets

prior to fees waived | | | 3.33% | | | | 4.02% | | | | 3.83% | | | | 3.61% | | | | 3.41% | |