UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-04367

Columbia Funds Series Trust I

(Exact name of registrant as specified in charter)

One Financial Center, Boston, Massachusetts 02111

(Address of principal executive offices) (Zip code)

Scott R. Plummer

5228 Ameriprise Financial Center

Minneapolis, MN 55474

(Name and address of agent for service)

Registrant’s telephone number, including area code: 1-612-671-1947

Date of fiscal year end: June 30

Date of reporting period: June 30, 2010

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

| Item 1. | Reports to Stockholders. |

Columbia Small Cap Value Fund I

Annual Report for the Period Ended June 30, 2010

Table of Contents

The views expressed in this report reflect the current views of the respective parties. These views are not guarantees of future performance and involve certain risks, uncertainties and assumptions that are difficult to predict, so actual outcomes and results may differ significantly from the views expressed. These views are subject to change at any time based upon economic, market or other conditions and the respective parties disclaim any responsibility to update such views. These views may not be relied on as investment advice and, because investment decisions for a Columbia Fund are based on numerous factors, may not be relied on as an indication of trading intent on behalf of any particular Columbia Fund. References to specific securities should not be construed as a recommendation or investment advice.

President’s Message

Dear Shareholder:

On May 3, 2010, Ameriprise Financial, Inc. announced that it had completed the acquisition of the long-term asset management business of Columbia Management Group, LLC from Bank of America. This includes the business of managing its equity and fixed-income mutual funds. Ameriprise Financial has combined its current U.S. asset management business, RiverSource Investments, LLC, with Columbia Management. This transaction puts together two leading asset management firms to create one entity that ranks as one of the largest managers of long-term mutual fund assets in the United States. This combined business will operate under the well-regarded Columbia Management brand, where we will build on the strengths of our combined investment capabilities and talent, our broad and diversified product lineup and exceptional service.

Our combined business has a new breadth and depth of investment choices. William “Ted” Truscott, CEO, U.S. asset management and president of annuities for Ameriprise Financial, leads the combined U.S. asset management business. Michael Jones serves as president, U.S. asset management.1 Colin Moore continues to serve as chief investment officer.1 I am also continuing in my role as head of mutual funds, responsible for the delivery of mutual fund products and services to investors. The Columbia funds’ advisers, distributor and transfer agent are now subsidiaries of our parent company, Ameriprise Financial, but operate under the Columbia Management name. You will begin to see these names used in communications and statements going forward.

| | |

| | | Service provider name |

| Advisers | | Columbia Management Investment Advisers, LLC Columbia Wanger Asset Management, LLC |

| Distributor | | Columbia Management Investment Distributors, Inc. |

| Transfer Agent | | Columbia Management Investment Services Corp. |

As a valued investor in Columbia funds, please know that our goal is to ensure a smooth transition and provide the highest quality products and services. Transition teams across the organization continue their efforts to build on best practices from both legacy organizations with integration efforts including rebranding, vendor and system consolidations and client communications. Additionally, we want to assure you that the funds’ portfolio managers also continue to focus on providing uninterrupted service to all fund shareholders.

Although we have a lot of work ahead of us in 2010, Columbia Management and Ameriprise Financial are excited about the opportunities for our combined organization. I share this optimism and believe it positions us as a best-in-class asset management business with the ability to deliver more for our clients than ever before.

Sincerely,

J. Kevin Connaughton

President, Columbia Funds

| 1 | Associate joined Columbia Management Investment Advisers, LLC as part of its 2010 acquisition of the long-term asset management business of Columbia Management Group, LLC from Bank of America. |

Investors should consider the investment objectives, risks, charges and expenses of a mutual fund carefully before investing. For a free prospectus, which contains this and other important information about the funds, visit www.columbiamanagement.com. Read the prospectus carefully before investing.

Securities products offered through Columbia Management Investment Distributors, Inc. (formerly known as RiverSource Fund Distributors, Inc.), member FINRA. Advisory services provided by Columbia Management Investment Advisers, LLC (formerly known as RiverSource Investments, LLC).

© 2010 Columbia Management Investment Advisers, LLC. All rights reserved.

Fund Profile – Columbia Small Cap Value Fund I

Summary

| n | | For the 12-month period that ended June 30, 2010, the fund’s Class A shares returned 22.99% without sales charge. |

| n | | The fund’s performance lagged its benchmark, the Russell 2000 Value Index1. It also lagged the average return of funds in its peer group, the Lipper Small-Cap Value Funds Classification.2 |

| n | | We believe the fund’s focus on higher-quality small-cap companies and lack of exposure to mid-cap stocks hampered results relative to the peer group, as lower-quality and mid-cap stocks led a market rally. |

Portfolio Management

Stephen D. Barbaro has managed or co-managed the fund since June 2002 and has been associated with the advisor since May 2010. Prior to joining the advisor, Mr. Barbaro was associated with the fund’s previous advisor or its predecessors since 1976.

Jeremy Javidi has co-managed the fund since August 2005 and has been associated with the advisor since May 2010. Prior to joining the advisor, Mr. Javidi was associated with the fund’s previous advisor or its predecessors since 2000.

Effective May 1, 2010, RiverSource Investment, LLC, a subsidiary of Ameriprise Financial, Inc., became the investment advisor to the fund and changed its names to Columbia Management Investment Advisers, LLC. Please see the fund’s prospectuses, as supplemented, for more information regarding the change in investment advisor and certain other changes.

| 1 | The Russell 2000 Value Index tracks the performance of those Russell 2000 Index companies with lower price-to-book ratios and lower forecasted growth values. Indices are not available for investment, are not professionally managed and do not reflect sales charges, fees, brokerage commissions, taxes or other expenses of investing. Securities in the fund may not match those in an index. |

| 2 | Lipper Inc., a widely respected data provider in the industry, calculates an average total return (assuming reinvestment of distributions) for mutual funds with investment objectives similar to those of the fund. Lipper makes no adjustment for the effect of sales loads. |

Performance data quoted represents past performance and current performance may be lower or higher. Past performance is no guarantee of future results. The investment return and principal value will fluctuate so that shares, when redeemed, may be worth more or less than the original cost. Please visit www.columbiafunds.com for daily and most recent month-end performance updates.

Summary

1-year return as of 06/30/10

| | |

| |

| | +22.99% Class A shares (without sales charge) |

| |

| | +25.07% Russell 2000 Value Index |

|

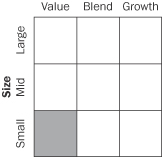

Morningstar Style Box™ |

|

Equity Style |

|

The Morningstar Style Box™ reveals a fund’s investment strategy. For equity funds, the vertical axis shows the market capitalization of the stocks owned, and the horizontal axis shows investment style (value, blend or growth). Information shown is based on the most recent data provided by Morningstar.

1

Economic Update – Columbia Small Cap Value Fund I

Summary

For the 12-month period that ended June 30, 2010

| | n | | Solid economic growth and relatively low interest rates boosted bond market returns. The Barclays Capital Aggregate Bond Index delivered solid results. High-yield bonds outperformed stocks, as measured by the BofA Merrill Lynch U.S. High Yield Cash Pay Index and the S&P 500 Index. | |

| | |

Barclays Aggregate Index | | BofA

Merrill Lynch Index |

| |

| |

|

9.50% | | 27.01% |

| | n | | The U.S. stock market, as measured by the S&P 500 Index, delivered solid returns, despite a correction in the last months of the period. Emerging market stocks, as measured by the MSCI Emerging Markets Index (Net), outperformed U.S. stocks as well as stock markets in developed foreign markets. | |

| | |

| S&P Index | | MSCI Index |

| |

| |

|

14.43% | | 23.15% |

Although it has been a year since U.S. economic growth turned positive, the economy continues to send mixed signals about the sustainability of this recovery. Economic growth, as measured by gross domestic product (GDP), was a solid 5.6% in the last quarter of 2009. However, it was 2.7% in the first quarter of 2010 and expectations are for lackluster growth through the end of the year, as government incentive programs have ended and stimulus spending winds down.

Consumer spending on cars, clothing and other goods was solid throughout most of the year, but in May, spending on these items fell 1.2%. And consumer confidence, which gained ground earlier in the period, fell sharply in June as consumers surveyed indicated they were concerned about business conditions and job prospects. The housing market — another bellwether for the consumer sector — showed some signs of stabilizing. However, a full recovery remained out of reach. Both new and existing home sales fell in June as a federal tax credit for new and repeat homebuyers was set to expire. Distressed properties continued to pressure prices and a huge backlog of foreclosed homes is likely to continue to keep a lid on prices for some time. The inventory of unsold homes rose to a level that would take eight and a half months to deplete at the current sales pace — the long-term average is on the order of six months.

News on the job front was mostly positive, but the number of new jobs added to the economy fell short of expectations. A good portion of the jobs added in March, April and May were temporary, government-sponsored census positions, which began to unwind in June. Private sector job growth was disappointing given the stage of economic recovery.

Reports from the business side of the economy were generally positive. A key measure of the nation’s manufacturing situation — the Institute for Supply Management’s Index — generally rose throughout the period, although there were slight downticks in February and May. Industrial production moved higher, as did the amount of manufacturing capacity utilized — a key measure of the health of the manufacturing sector. Perhaps the best news was about corporate profits. Of the S&P 500 companies announcing first-quarter results, 77% exceeded Wall Street earnings forecasts. Now, the focus has shifted to second-quarter earnings, which will be announced later in the summer.

Bond returns ranged from solid to strong

As the economy strengthened, bonds delivered solid returns. The Barclays Capital Aggregate Bond Index1 returned 9.50%. Municipal bonds gained almost as much as taxable investment-grade bonds, even without factoring in potential tax advantages to investors in higher income-tax brackets. The Barclays Capital Municipal Bond Index2 returned 9.61%. The high-yield bond market outpaced stocks during the period by a margin of almost two to one. For the 12 months covered by this report, the BofA Merrill

| 1 | The Barclays Capital Aggregate Bond Index is a market value-weighted index that tracks the daily price, coupon, pay-downs and total return performance of fixed-rate, publicly placed, dollar-denominated and non-convertible investment grade debt issues with at least $250 million par amount outstanding and with at least one year to final maturity. |

| 2 | The Barclays Capital Municipal Bond Index is considered representative of the broad market for investment grade, tax-exempt bonds with a maturity of at least one year. |

2

Economic Update (continued) – Columbia Small Cap Value Fund I

Lynch U.S. High Yield Cash Pay Index3 returned 27.01%. Even the Treasury market was positive as the yield on the 10-year U.S. Treasury, a common bellwether for the bond market, fell just below 3.0% at the end of the 12-month period. Despite the pickup in economic activity, the Federal Reserve Board (the Fed) kept a key short-term interest rate — the federal funds rate — close to zero.

Stocks staged a solid comeback

Against a strengthening economic backdrop, a stock market rally that began in mid-March 2009 continued into the spring of 2010, when a debt crisis brewing in Europe spilled over and reclaimed some of the stock market’s earlier gains. The S&P 500 Index4 returned 14.43% for the 12-month period. Outside the United States, stock market returns were not as strong. The MSCI EAFE Index (Net),5 a broad gauge of stock market performance in foreign developed markets, returned 5.92% (net of dividends, in U.S. dollars) for the period, as concerns about the impact of a bailout for weak eurozone economies weighed on the markets. Emerging stock markets were more resilient. The MSCI Emerging Markets Index (Net)6 returned 23.15% (net of dividends, in U.S. dollars) for the 12-month period.

Past performance is no guarantee of future results.

| 3 | The BofA Merrill Lynch U.S. High Yield Cash Pay Index tracks the performance of non-investment-grade corporate bonds. |

| 4 | The Standard & Poor’s (S&P) 500 Index tracks the performance of 500 widely held, large-capitalization U.S. stocks. |

| 5 | The Morgan Stanley Capital International Europe, Australasia, Far East (MSCI EAFE) Index (Net) is a capitalization-weighted index that tracks the total return of common stocks in 22 developed-market countries within Europe, Australasia and the Far East. |

| 6 | The Morgan Stanley Capital International (MSCI) Emerging Markets Index (Net) is a free float-adjusted market capitalization index that is designed to measure equity market performance of emerging markets. As of May 2010, the MSCI Emerging Markets Index consisted of the following 21 emerging market country indices: Brazil, Chile, China, Colombia, Czech Republic, Egypt, Hungary, India, Indonesia, Korea, Malaysia, Mexico, Morocco, Peru, Philippines, Poland, Russia, South Africa, Taiwan, Thailand and Turkey. |

Indices are not available for investment, are not professionally managed and do not reflect sales charges, fees, brokerage commissions, taxes or other expenses of investing. Securities in the fund may not match those in an index.

3

Performance Information – Columbia Small Cap Value Fund I

Performance data quoted represents past performance and current performance may be lower or higher. Past performance is no guarantee of future results. The investment return and principal value will fluctuate so that shares, when redeemed, may be worth more or less than the original cost. Please visit www.columbiafunds.com for daily and most recent month-end performance updates.

| | |

| Annual operating expense ratio (%)* |

| |

Class A | | 1.33 |

Class B | | 2.08 |

Class C | | 2.08 |

Class Y | | 0.90 |

Class Z | | 1.08 |

| * | The annual operating expense ratio is as stated in the fund’s prospectus that is current as of the date of this report. Differences in expense ratios disclosed elsewhere in this report may result from the inclusion of fee waivers and expense reimbursements as well as different time periods used in calculating the ratios. |

|

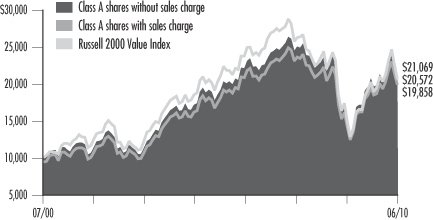

| Performance of a $10,000 investment 07/01/00 – 06/30/10 |

The chart above shows the change in value of a hypothetical $10,000 investment in Class A shares of Columbia Small Cap Value Fund I during the stated time period, and does not reflect the deduction of taxes that a shareholder may pay on fund distributions or on the redemption of fund shares.

| | | | |

| Performance of a $10,000 investment 07/01/00 – 06/30/10 ($) |

| | |

| Sales charge | | without | | with |

Class A | | 21,069 | | 19,858 |

Class B | | 19,520 | | 19,520 |

Class C | | 19,520 | | 19,520 |

Class Y | | 21,655 | | n/a |

Class Z | | 21,621 | | n/a |

| | | | | | | | | | | | | | | | |

| Average annual total return as of 06/30/10 (%) | | |

| | | | | |

| Share class | | A | | B | | C | | Y | | Z |

| Inception | | 07/25/86 | | 11/09/92 | | 01/15/96 | | 07/15/09 | | 07/31/95 |

| Sales charge | | without | | with | | without | | with | | without | | with | | without | | without |

1-year | | 22.99 | | 15.91 | | 22.02 | | 17.02 | | 22.04 | | 21.04 | | 23.47 | | 23.28 |

5-year | | 1.88 | | 0.68 | | 1.11 | | 0.81 | | 1.11 | | 1.11 | | 2.16 | | 2.13 |

10-year | | 7.74 | | 7.10 | | 6.92 | | 6.92 | | 6.92 | | 6.92 | | 8.03 | | 8.02 |

The “with sales charge” returns include the maximum initial sales charge of 5.75% for Class A shares and the applicable contingent deferred sales charge of 5.00% in the first year, declining to 1.00% in the sixth year and eliminated thereafter for Class B shares and 1.00% for Class C shares for the first year only. The “without sales charge” returns do not include the effect of sales charges. If they had, returns would be lower.

Performance results reflect any fee waivers or reimbursements of fund expenses by the investment advisor and/or any of its affiliates. Absent these fee waivers or expense reimbursement arrangements, performance results would have been lower.

All results shown assume reinvestment of distributions. Class Y and Class Z shares are sold at net asset value with no distribution and service (Rule 12b-1) fees. Class Y and Class Z shares have limited eligibility and the investment minimum requirements may vary. Please see the fund’s prospectus for details. Performance for different share classes will vary based on differences in sales charges and fees associated with each class.

The tables do not reflect the deduction of taxes that a shareholder may pay on fund distributions or on the redemption of fund shares.

The returns for Class Y shares include the returns for Class Z shares for the periods prior to July 15, 2009. The returns shown have not been adjusted to reflect any differences in expenses between Class Y shares and Class Z shares. Class Y shares were initially offered on July 15, 2009.

4

Understanding Your Expenses – Columbia Small Cap Value Fund I

Estimating your actual expenses

To estimate the expenses that you paid over the period, first you will need your account balance at the end of the period:

| | n | | For shareholders who receive their account statements from Columbia Management Investment Services Corp., your account balance is available online at www.columbiafunds.com or by calling Shareholder Services at 800.345.6611. | |

| | n | | For shareholders who receive their account statements from their financial intermediary, contact your financial intermediary to obtain your account balance. | |

| | 1. | Divide your ending account balance by $1,000. For example, if an account balance was $8,600 at the end of the period, the result would be 8.6. | |

| | 2. | In the section of the table below titled “Expenses paid during the period,” locate the amount for your share class. You will find this number in the column labeled “Actual.” Multiply this number by the result from step 1. Your answer is an estimate of the expenses you paid on your account during the period. | |

If the value of your account falls below the minimum initial investment requirement applicable to you, your account may be subject to a $20 annual fee. This fee is not included in the accompanying table. If you are subject to the fee, keep it in mind when you are estimating the ongoing expenses of investing in the fund and when comparing the expenses of this fund with other funds.

As a fund shareholder, you incur two types of costs. There are transaction costs, which generally include sales charges on purchases and may include redemption fees or exchange fees. There are also ongoing costs, which generally include investment advisory fees, distribution and service (Rule 12b-1) fees and other fund expenses. The information on this page is intended to help you understand the ongoing costs of investing in the fund and to compare these costs with the ongoing costs of investing in other mutual funds.

Analyzing your fund’s expenses by share class

To illustrate these ongoing costs, we have provided an example and calculated the expenses paid by investors in each share class during the period. The information in the following table is based on an initial investment of $1,000, which is invested at the beginning of the period and held for the entire period. Expense information is calculated two ways and each method provides you with different information. The amount listed in the “Actual” column is calculated using the fund’s actual operating expenses and total return for the period. The amount listed in the “Hypothetical” column for each share class assumes that the return each year is 5% before expenses and is calculated based on the fund’s actual operating expenses. You should not use the hypothetical account values and expenses to estimate either your actual account balance at the end of the period or the expenses you paid during this period.

Compare with other funds

Since all mutual funds are required to include the same hypothetical calculations about expenses in shareholder reports, you can use this information to compare the ongoing costs of investing in the fund with other funds. To do so, compare the 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of other funds. As you compare hypothetical examples of other funds, it is important to note that hypothetical examples are meant to highlight the ongoing costs of investing in a fund and do not reflect any transaction costs, such as sales charges, redemption fees or exchange fees.

| | | | | | | | | | | | | | |

| 01/01/10 – 06/30/10 |

| | | | |

| | | Account value at the

beginning of the period ($) | | Account value at the

end of the period ($) | | Expenses paid

during the period ($) | | Fund’s annualized

expense ratio (%) |

| | | Actual | | Hypothetical | | Actual | | Hypothetical | | Actual | | Hypothetical | | Actual |

Class A | | 1,000.00 | | 1,000.00 | | 993.10 | | 1,018.60 | | 6.18 | | 6.26 | | 1.25 |

Class B | | 1,000.00 | | 1,000.00 | | 989.10 | | 1,014.88 | | 9.86 | | 9.99 | | 2.00 |

Class C | | 1,000.00 | | 1,000.00 | | 989.40 | | 1,014.88 | | 9.87 | | 9.99 | | 2.00 |

Class Y | | 1,000.00 | | 1,000.00 | | 995.00 | | 1,020.63 | | 4.16 | | 4.21 | | 0.84 |

Class Z | | 1,000.00 | | 1,000.00 | | 994.40 | | 1,019.84 | | 4.95 | | 5.01 | | 1.00 |

Expenses paid during the period are equal to the annualized expense ratio for the share class, multiplied by the average account value over the period, then multiplied by the number of days in the fund’s most recent fiscal half-year and divided by 365.

It is important to note that the expense amounts shown in the table are meant to highlight only ongoing costs of investing in the fund and do not reflect any transaction costs, such as sales charges, redemption fees or exchange fees. Therefore, the hypothetical examples provided may not help you determine the relative total costs of owning shares of different funds. If these transaction costs were included, your costs would have been higher.

5

Portfolio Managers’ Report – Columbia Small Cap Value Fund I

Performance data quoted represents past performance and current performance may be lower or higher. Past performance is no guarantee of future results. The investment return and principal value will fluctuate so that shares, when redeemed, may be worth more or less than the original cost. Please visit www.columbiafunds.com for daily and most recent month-end performance updates.

| | |

| Net asset value per share |

| |

as of 06/30/10 ($) | | |

Class A | | 35.84 |

Class B | | 29.17 |

Class C | | 30.87 |

Class Y | | 37.63 |

Class Z | | 37.60 |

| | |

| Distributions declared per share |

| |

07/01/09 – 06/30/10 ($) | | |

Class A | | 0.18 |

Class B | | 0.07 |

Class C | | 0.07 |

Class Y | | 0.24 |

Class Z | | 0.22 |

For the 12-month period that ended June 30, 2010, the fund’s Class A shares returned 22.99% without sales charge. By comparison, the fund’s benchmark, the Russell 2000 Value Index, returned 25.07%. The average return of competing funds was 25.39%, as measured by the Lipper Small-Cap Value Funds Classification. Our focus was on high-quality small-cap companies with strong balance sheets and good cash flows whose stocks were selling at a discount to their peers. We believe that the fund’s lack of exposure to lower-quality and mid-cap stocks — both of which led the recent market rally — accounted for its modest shortfall versus the Lipper peer group.

A shifting market environment

The period began on an up note in the summer of 2009. Stocks were buoyed by an improving economic outlook that lifted investor confidence. Economically-sensitive sectors, such as consumer discretionary and materials, led the market’s climb. However, in the second half of the period, stocks gave back some of their gains, amid growing concerns over an unfolding European sovereign debt crisis, a potential slowdown in China and a lackluster recovery in the United States. As volatility increased, investors moved away from heavily indebted companies and economically-sensitive sectors into higher-quality, lower-risk companies and more defensive sectors. Our decision to avoid companies whose earnings growth depended on the strength of the economic recovery helped protect the fund during the downturn.

Strong stock selection in energy, utilities, technology

Going into 2010, we expected the best investment opportunities would come from companies that could gain market share, increase their dividend payments or yield to stronger industry players through mergers and acquisitions. This theme played out, as several holdings were acquired at handsome premiums and stock selection in the energy, utilities and technology sectors was rewarded. In this regard, Mariner Energy, Inc., an offshore driller in the Gulf of Mexico; Maine & Maritimes Corp., an electric utility company serving customers in northern Maine; and CPI International, Inc., a semiconductor company all did well. Another standout was semiconductor communications equipment company OmniVision Technologies, Inc. (0.4% of net assets), whose components go into the popular iPads and iPhones. The company gained market share during the period.

Disappointments in financials, health care and consumer discretionary

The fund lost ground versus the index in the financials sectors, primarily because it did not have exposure to heavily leveraged banks and real estate investment trusts (REITs), both of which made very strong comebacks during the period. In health care, facilities-based companies, including Res-Care, Inc. and MedCath Corp. (0.3% and 0.3% of net assets, respectively), hampered results, as concerns about changes in Medicare reimbursement policies pressured the stocks. In consumer discretionary, we avoided auto-related companies, many of which have weak balance sheets and are saddled with huge pension liabilities. However, auto stocks were strong performers early in the 12-month period as the government’s “Cash-for-Clunkers” program bolstered sales growth.

6

Portfolio Managers’ Report (continued) – Columbia Small Cap Value Fund I

Opportunities in technology and industrials

Going forward, we expect stock performance to be driven more by company-specific factors rather than economic growth. However, we expect certain sectors to benefit broadly as business investment slowly improves, which is why we raised the fund’s exposure relative to the index to technology and industrials stocks. Within these sectors, we are finding opportunities to buy reasonably priced stocks issued by strong companies that have the potential to pick up market share from weaker competitors in an environment of slow growth. The fund ended the period with underweights versus the index in financials, consumer discretionary and consumer staples — sectors where we have not found as many stocks that meet our investment criteria. Within financials, which represents nearly one-third of assets, the fund had underweights in REITs, which we think are overvalued, and in commercial banks, many of which could be hurt by their decision not to recognize losses from non-performing loans in the current period. Instead, we favored insurance stocks that were selling at extreme discounts relative to their asset values, as well as thrifts and mortgage finance companies with strong balance sheets, which are positioned to benefit as the federal government unwinds its involvement in the industry.

Portfolio characteristics and holdings are subject to change periodically and may not be representative of current characteristics and holdings. The outlook for the fund may differ from that presented for other Columbia Funds.

Equity securities are subject to stock market fluctuations that occur in response to economic and business developments.

Investments in small-cap stocks may be subject to greater volatility and price fluctuations because they may be thinly traded and less liquid than investments in larger companies.

Value stocks are stocks of companies that may have experienced adverse business or industry developments or may be subject to special risks that have caused the stocks to be out of favor. If the manager’s assessment of a company’s prospects is wrong, the price of its stock may not approach the value the manager has placed on it.

7

Investment Portfolio – Columbia Small Cap Value Fund I

June 30, 2010

Common Stocks – 97.4%

| | | | |

| | | Shares | | Value ($) |

| Consumer Discretionary – 8.5% | | | | |

| Diversified Consumer Services – 0.4% | | |

Regis Corp. | | 385,906 | | 6,008,556 |

| | | | |

Diversified Consumer Services Total | | | | 6,008,556 |

| |

| Hotels, Restaurants & Leisure – 1.6% | | |

Benihana, Inc., Class A (a) | | 698,267 | | 4,133,741 |

Bob Evans Farms, Inc. | | 254,571 | | 6,267,538 |

CEC Entertainment, Inc. (a) | | 142,841 | | 5,036,574 |

Jack in the Box, Inc. (a) | | 213,470 | | 4,151,991 |

Red Robin Gourmet Burgers, Inc. (a) | | 237,671 | | 4,078,434 |

| | | | |

Hotels, Restaurants & Leisure Total | | | | 23,668,278 |

| |

| Household Durables – 1.0% | | |

American Greetings Corp., Class A | | 235,130 | | 4,411,039 |

Cavco Industries, Inc. (a) | | 146,927 | | 5,168,892 |

CSS Industries, Inc. | | 276,352 | | 4,559,808 |

| | | | |

Household Durables Total | | | | 14,139,739 |

| |

| Leisure Equipment & Products – 0.4% | | |

JAKKS Pacific, Inc. (a) | | 376,350 | | 5,411,913 |

| | | | |

Leisure Equipment & Products Total | | | | 5,411,913 |

| |

| Media – 0.3% | | |

Scholastic Corp. | | 219,330 | | 5,290,240 |

| | | | |

Media Total | | | | 5,290,240 |

| |

| Specialty Retail – 4.2% | | |

America’s Car-Mart, Inc. (a) | | 215,260 | | 4,871,334 |

Christopher & Banks Corp. | | 695,020 | | 4,302,174 |

Finish Line, Inc., Class A | | 400,030 | | 5,572,418 |

Foot Locker, Inc. | | 483,475 | | 6,101,455 |

GameStop Corp., Class A (a) | | 275,790 | | 5,182,094 |

Men’s Wearhouse, Inc. | | 299,525 | | 5,499,279 |

OfficeMax, Inc. (a) | | 454,990 | | 5,942,169 |

Pacific Sunwear of California, Inc. (a) | | 2,391,786 | | 7,653,715 |

Rent-A-Center, Inc. (a) | | 464,084 | | 9,402,342 |

Shoe Carnival, Inc. (a) | | 271,649 | | 5,571,521 |

| | | | |

Specialty Retail Total | | | | 60,098,501 |

| |

| Textiles, Apparel & Luxury Goods – 0.6% | | |

Movado Group, Inc. (a) | | 420,819 | | 4,494,347 |

Wolverine World Wide, Inc. | | 150,680 | | 3,800,149 |

| | | | |

Textiles, Apparel & Luxury Goods Total | | | | 8,294,496 |

| | | | |

Consumer Discretionary Total | | | | 122,911,723 |

| | | | |

| | | Shares | | Value ($) |

| Consumer Staples – 1.5% | | | | |

| Food & Staples Retailing – 0.8% | | |

Ruddick Corp. | | 224,179 | | 6,947,307 |

Spartan Stores, Inc. | | 334,624 | | 4,591,041 |

| | | | |

Food & Staples Retailing Total | | | | 11,538,348 |

| |

| Food Products – 0.7% | | |

Fresh Del Monte Produce, Inc. (a) | | 478,995 | | 9,694,859 |

| | | | |

Food Products Total | | | | 9,694,859 |

| | | | |

Consumer Staples Total | | | | 21,233,207 |

| | | | |

| Energy – 5.5% | | | | |

| Energy Equipment & Services – 2.6% | | |

Dawson Geophysical Co. (a) | | 174,020 | | 3,701,405 |

Gulf Island Fabrication, Inc. | | 314,450 | | 4,880,264 |

Lufkin Industries, Inc. | | 52,463 | | 2,045,532 |

Matrix Service Co. (a) | | 410,370 | | 3,820,545 |

Patterson-UTI Energy, Inc. | | 436,140 | | 5,613,122 |

T-3 Energy Services, Inc. (a) | | 214,730 | | 5,990,967 |

TGC Industries, Inc. (a) | | 647,765 | | 1,962,728 |

Tidewater, Inc. | | 138,110 | | 5,347,619 |

Union Drilling, Inc. (a) | | 837,146 | | 4,612,675 |

| | | | |

Energy Equipment & Services Total | | | | 37,974,857 |

| |

| Oil, Gas & Consumable Fuels – 2.9% | | |

Berry Petroleum Co., Class A | | 177,410 | | 4,562,985 |

Bill Barrett Corp. (a) | | 203,560 | | 6,263,541 |

Forest Oil Corp. (a) | | 174,800 | | 4,782,528 |

Holly Corp. | | 177,109 | | 4,707,557 |

International Coal Group, Inc. (a) | | 873,440 | | 3,362,744 |

Stone Energy Corp. (a) | | 387,430 | | 4,323,719 |

Swift Energy Co. (a) | | 286,869 | | 7,719,645 |

World Fuel Services Corp. | | 199,900 | | 5,185,406 |

| | | | |

Oil, Gas & Consumable Fuels Total | | | | 40,908,125 |

| | | | |

Energy Total | | | | 78,882,982 |

| | | | |

| Financials – 31.3% | | | | |

| Capital Markets – 3.1% | | |

Federated Investors, Inc., Class B | | 164,549 | | 3,407,810 |

GFI Group, Inc. | | 762,162 | | 4,252,864 |

International Assets Holding Corp. (a) | | 277,170 | | 4,434,720 |

Investment Technology Group, Inc. (a) | | 491,068 | | 7,886,552 |

Knight Capital Group, Inc., Class A (a) | | 673,150 | | 9,282,739 |

Mass Financial Corp., Class A (a) | | 389,170 | | 3,580,364 |

See Accompanying Notes to Financial Statements.

8

Columbia Small Cap Value Fund I

June 30, 2010

Common Stocks (continued)

| | | | |

| | | Shares | | Value ($) |

| Financials (continued) | | | | |

optionsXpress Holdings, Inc. (a) | | 372,100 | | 5,856,854 |

Piper Jaffray Companies, Inc. (a) | | 196,002 | | 6,315,184 |

| | | | |

Capital Markets Total | | | | 45,017,087 |

| |

Commercial Banks – 7.1% | | |

Ameris Bancorp (a) | | 215,310 | | 2,079,895 |

BancFirst Corp. | | 167,433 | | 6,109,630 |

BancTrust Financial Group, Inc. (a) | | 474,228 | | 1,754,644 |

Bryn Mawr Bank Corp. | | 363,884 | | 6,105,974 |

Chemical Financial Corp. | | 432,303 | | 9,415,559 |

Columbia Banking System, Inc. | | 377,947 | | 6,901,312 |

Community Trust Bancorp, Inc. | | 267,460 | | 6,713,246 |

First Citizens BancShares, Inc., Class A | | 61,006 | | 11,733,284 |

First Commonwealth Financial Corp. | | 1,526,334 | | 8,013,253 |

First Financial Corp. Indiana | | 320,828 | | 8,280,571 |

First National Bank of Alaska | | 2,371 | | 4,379,237 |

Investors Bancorp, Inc. (a) | | 454,057 | | 5,957,228 |

Merchants Bancshares, Inc. | | 279,256 | | 6,205,068 |

Northfield Bancorp, Inc. | | 431,114 | | 5,595,860 |

Northrim BanCorp, Inc. (b) | | 343,766 | | 5,321,498 |

West Coast Bancorp | | 1,643,986 | | 4,192,164 |

Whitney Holding Corp. | | 336,462 | | 3,112,273 |

| | | | |

Commercial Banks Total | | | | 101,870,696 |

| |

Consumer Finance – 0.7% | | |

Cash America International, Inc. | | 283,839 | | 9,727,163 |

| | | | |

Consumer Finance Total | | | | 9,727,163 |

| |

| Diversified Financial Services – 0.5% | | |

Medallion Financial Corp. | | 480,975 | | 3,174,435 |

Pico Holdings, Inc. (a) | | 121,661 | | 3,646,180 |

| | | | |

Diversified Financial Services Total | | | | 6,820,615 |

| |

| Insurance – 9.2% | | |

Allied World Assurance Holdings Ltd. | | 118,010 | | 5,355,294 |

American Safety Insurance Holdings Ltd. (a) | | 405,810 | | 6,379,333 |

Argo Group International Holdings Ltd. | | 261,620 | | 8,002,956 |

Baldwin & Lyons, Inc., Class B (b) | | 271,632 | | 5,706,988 |

CNA Surety Corp. (a) | | 496,739 | | 7,982,596 |

eHealth, Inc. (a) | | 538,377 | | 6,121,347 |

EMC Insurance Group, Inc. | | 312,899 | | 6,861,875 |

| | | | |

| | | Shares | | Value ($) |

FBL Financial Group, Inc., Class A | | 317,783 | | 6,673,443 |

First Mercury Financial Corp. | | 531,575 | | 5,624,064 |

Hanover Insurance Group, Inc. | | 106,020 | | 4,611,870 |

Harleysville Group, Inc. | | 163,935 | | 5,086,903 |

Horace Mann Educators Corp. | | 619,542 | | 9,478,993 |

National Western Life Insurance Co., Class A | | 29,829 | | 4,556,678 |

Navigators Group, Inc. (a) | | 228,961 | | 9,417,166 |

RLI Corp. | | 98,790 | | 5,187,463 |

Safety Insurance Group, Inc. | | 272,721 | | 10,096,131 |

Stewart Information Services Corp. | | 394,820 | | 3,561,276 |

United America Indemnity Ltd., Class A (a) | | 1,692,453 | | 12,456,454 |

United Fire & Casualty Co. | | 494,388 | | 9,798,770 |

| | | | |

Insurance Total | | | | 132,959,600 |

|

| Real Estate Investment Trusts (REITs) – 5.3% |

DCT Industrial Trust, Inc. | | 1,593,129 | | 7,200,943 |

DiamondRock Hospitality Co. (a) | | 971,595 | | 7,986,511 |

Franklin Street Properties Corp. | | 518,290 | | 6,121,005 |

Getty Realty Corp. | | 232,146 | | 5,202,392 |

National Health Investors, Inc. | | 215,519 | | 8,310,412 |

Potlatch Corp. | | 272,922 | | 9,751,503 |

Starwood Property Trust, Inc. | | 485,580 | | 8,230,581 |

Sunstone Hotel Investors, Inc. (a) | | 568,526 | | 5,645,463 |

Terreno Realty Corp. (a) | | 282,310 | | 4,999,710 |

Universal Health Realty Income Trust | | 213,813 | | 6,869,812 |

Urstadt Biddle Properties, Inc., Class A | | 398,492 | | 6,427,676 |

| | | | |

Real Estate Investment Trusts (REITs) Total | | | | 76,746,008 |

|

| Real Estate Management & Development – 0.4% |

Avatar Holdings, Inc. (a) | | 298,751 | | 5,730,044 |

Maui Land & Pineapple Co., Inc. (a) | | 171,340 | | 639,098 |

| | | | |

Real Estate Management & Development Total | | | | 6,369,142 |

|

| Thrifts & Mortgage Finance – 5.0% |

Bank Mutual Corp. | | 1,286,326 | | 7,306,332 |

BankFinancial Corp. | | 810,825 | | 6,737,956 |

Beneficial Mutual Bancorp, Inc. (a) | | 831,029 | | 8,210,566 |

Brookline Bancorp, Inc. | | 854,209 | | 7,585,376 |

Clifton Savings Bancorp, Inc. | | 514,875 | | 4,453,669 |

ESSA Bancorp, Inc. | | 403,680 | | 4,969,301 |

Home Federal Bancorp, Inc. | | 655,028 | | 8,273,004 |

See Accompanying Notes to Financial Statements.

9

Columbia Small Cap Value Fund I

June 30, 2010

Common Stocks (continued)

| | | | |

| | | Shares | | Value ($) |

| Financials (continued) | | | | |

TrustCo Bank Corp. NY | | 784,844 | | 4,395,126 |

United Financial Bancorp, Inc. | | 414,176 | | 5,653,502 |

Washington Federal, Inc. | | 410,201 | | 6,637,052 |

Westfield Financial, Inc. | | 895,876 | | 7,462,647 |

| | | | |

Thrifts & Mortgage Finance Total | | | | 71,684,531 |

| | | | |

Financials Total | | | | 451,194,842 |

| | | | |

| Health Care – 5.3% | | | | |

| Biotechnology – 0.2% | | | | |

Martek Biosciences Corp. (a) | | 137,130 | | 3,251,352 |

| | | | |

Biotechnology Total | | | | 3,251,352 |

| |

| Health Care Equipment & Supplies – 1.6% | | |

Analogic Corp. | | 99,729 | | 4,538,667 |

Cantel Medical Corp. | | 235,971 | | 3,940,716 |

ICU Medical, Inc. (a) | | 1,249 | | 40,180 |

Kensey Nash Corp. (a) | | 230,306 | | 5,460,555 |

Symmetry Medical, Inc. (a) | | 505,460 | | 5,327,548 |

Young Innovations, Inc. | | 143,180 | | 4,030,517 |

| | | | |

Health Care Equipment & Supplies Total | | | | 23,338,183 |

| |

| Health Care Providers & Services – 3.5% | | |

AmSurg Corp. (a) | | 272,817 | | 4,861,599 |

Healthspring, Inc. (a) | | 494,384 | | 7,667,896 |

Kindred Healthcare, Inc. (a) | | 443,901 | | 5,699,689 |

Magellan Health Services, Inc. (a) | | 149,060 | | 5,413,859 |

MedCath Corp. (a) | | 533,210 | | 4,191,030 |

NovaMed, Inc. (a) | | 321,986 | | 2,672,484 |

Owens & Minor, Inc. | | 160,965 | | 4,568,187 |

Res-Care, Inc. (a) | | 520,538 | | 5,028,397 |

Triple-S Management Corp., Class B (a) | | 276,300 | | 5,125,365 |

U.S. Physical Therapy, Inc. (a) | | 252,336 | | 4,259,432 |

| | | | |

Health Care Providers & Services Total | | | | 49,487,938 |

| | | | |

Health Care Total | | | | 76,077,473 |

| | | | |

| Industrials – 18.2% | | | | |

| Aerospace & Defense – 1.6% | | |

AAR Corp. (a) | | 237,975 | | 3,983,702 |

Ceradyne, Inc. (a) | | 295,366 | | 6,311,971 |

Esterline Technologies Corp. (a) | | 135,650 | | 6,436,592 |

Ladish Co., Inc. (a) | | 295,530 | | 6,714,442 |

| | | | |

Aerospace & Defense Total | | | | 23,446,707 |

| |

| Air Freight & Logistics – 0.4% | | |

Pacer International, Inc. (a) | | 776,893 | | 5,430,482 |

| | | | |

Air Freight & Logistics Total | | | | 5,430,482 |

| | | | |

| | | Shares | | Value ($) |

| Airlines – 0.3% | | |

Skywest, Inc. | | 397,171 | | 4,853,430 |

| | | | |

Airlines Total | | | | 4,853,430 |

| |

| Building Products – 1.6% | | |

A.O. Smith Corp. | | 151,820 | | 7,316,206 |

Ameron International Corp. | | 102,442 | | 6,180,326 |

Lennox International, Inc. | | 108,239 | | 4,499,495 |

NCI Building Systems, Inc. (a) | | 102,138 | | 854,895 |

Universal Forest Products, Inc. | | 155,541 | | 4,714,448 |

| | | | |

Building Products Total | | | | 23,565,370 |

| |

| Commercial Services & Supplies – 2.2% | | |

ABM Industries, Inc. | | 241,520 | | 5,059,844 |

ATC Technology Corp. (a) | | 284,580 | | 4,587,430 |

Consolidated Graphics, Inc. (a) | | 176,670 | | 7,639,211 |

Ennis, Inc. | | 317,047 | | 4,758,875 |

G&K Services, Inc., Class A | | 148,490 | | 3,066,318 |

United Stationers, Inc. (a) | | 128,800 | | 7,015,736 |

| | | | |

Commercial Services & Supplies Total | | | | 32,127,414 |

| |

| Construction & Engineering – 2.8% | | |

Comfort Systems USA, Inc. | | 464,281 | | 4,484,954 |

Dycom Industries, Inc. (a) | | 637,841 | | 5,453,541 |

EMCOR Group, Inc. (a) | | 356,240 | | 8,254,081 |

KBR, Inc. | | 307,689 | | 6,258,394 |

KHD Humboldt Wedag International AG | | 247,120 | | 1,297,346 |

Layne Christensen Co. (a) | | 215,920 | | 5,240,378 |

Pike Electric Corp. (a) | | 493,525 | | 4,649,005 |

Sterling Construction Co., Inc. (a) | | 313,972 | | 4,062,798 |

| | | | |

Construction & Engineering Total | | | | 39,700,497 |

| |

| Electrical Equipment – 1.6% | | |

Acuity Brands, Inc. | | 138,580 | | 5,041,540 |

Belden, Inc. | | 253,411 | | 5,575,042 |

Broadwind Energy, Inc. (a) | | 354,137 | | 991,584 |

GrafTech International Ltd. (a) | | 758,516 | | 11,089,504 |

| | | | |

Electrical Equipment Total | | | | 22,697,670 |

| |

| Machinery – 3.3% | | |

Astec Industries, Inc. (a) | | 194,787 | | 5,401,444 |

CIRCOR International, Inc. | | 180,480 | | 4,616,678 |

EnPro Industries, Inc. (a) | | 270,702 | | 7,620,261 |

FreightCar America, Inc. | | 204,711 | | 4,630,563 |

Harsco Corp. | | 172,767 | | 4,060,024 |

Kadant, Inc. (a) | | 346,690 | | 6,039,340 |

LB Foster Co., Class A (a) | | 161,751 | | 4,192,586 |

Mueller Industries, Inc. | | 284,010 | | 6,986,646 |

Robbins & Myers, Inc. | | 207,980 | | 4,521,485 |

| | | | |

Machinery Total | | | | 48,069,027 |

See Accompanying Notes to Financial Statements.

10

Columbia Small Cap Value Fund I

June 30, 2010

Common Stocks (continued)

| | | | |

| | | Shares | | Value ($) |

| Industrials (continued) | | | | |

| Professional Services – 1.8% | | |

CDI Corp. | | 331,076 | | 5,141,610 |

FTI Consulting, Inc. (a) | | 134,160 | | 5,848,034 |

Kforce, Inc. (a) | | 305,954 | | 3,900,913 |

Korn/Ferry International (a) | | 339,121 | | 4,713,782 |

LECG Corp. (a) | | 1,041,901 | | 2,708,943 |

Navigant Consulting, Inc. (a) | | 317,870 | | 3,299,491 |

| | | | |

Professional Services Total | | | | 25,612,773 |

| |

| Road & Rail – 1.8% | | |

Arkansas Best Corp. | | 177,970 | | 3,692,878 |

Heartland Express, Inc. | | 343,264 | | 4,984,193 |

Ryder System, Inc. | | 119,459 | | 4,805,836 |

Werner Enterprises, Inc. | | 566,689 | | 12,404,822 |

| | | | |

Road & Rail Total | | | | 25,887,729 |

| |

| Trading Companies & Distributors – 0.8% | | |

Applied Industrial Technologies, Inc. | | 217,300 | | 5,502,036 |

Kaman Corp. | | 257,799 | | 5,702,514 |

| | | | |

Trading Companies & Distributors Total | | | | 11,204,550 |

| | | | |

Industrials Total | | | | 262,595,649 |

| | | | |

| Information Technology – 13.8% | | | | |

| Communications Equipment – 2.7% | | |

ADC Telecommunications, Inc. (a) | | 750,869 | | 5,563,939 |

Anaren, Inc. (a) | | 336,050 | | 5,020,587 |

Bel Fuse, Inc., Class B (b) | | 137,017 | | 2,262,151 |

Black Box Corp. | | 212,369 | | 5,922,971 |

Plantronics, Inc. | | 187,040 | | 5,349,344 |

Symmetricom, Inc. (a) | | 825,920 | | 4,203,933 |

Tekelec (a) | | 433,010 | | 5,733,052 |

Tellabs, Inc. | | 626,950 | | 4,006,211 |

| | | | |

Communications Equipment Total | | | | 38,062,188 |

| |

| Computers & Peripherals – 0.2% | | |

Adaptec, Inc. (a) | | 1,110,973 | | 3,210,712 |

| | | | |

Computers & Peripherals Total | | | | 3,210,712 |

| |

| Electronic Equipment, Instruments & Components – 3.5% | | |

Anixter International, Inc. (a) | | 177,490 | | 7,561,074 |

Benchmark Electronics, Inc. (a) | | 506,030 | | 8,020,575 |

Brightpoint, Inc. (a) | | 829,382 | | 5,805,674 |

CTS Corp. | | 540,667 | | 4,995,763 |

Electro Scientific Industries, Inc. (a) | | 357,300 | | 4,773,528 |

| | | | |

| | | Shares | | Value ($) |

Littelfuse, Inc. (a) | | 159,211 | | 5,032,660 |

Methode Electronics, Inc. | | 510,544 | | 4,972,699 |

MTS Systems Corp. | | 203,714 | | 5,907,706 |

NAM TAI Electronics, Inc. (a) | | 949,350 | | 3,911,322 |

| | | | |

Electronic Equipment, Instruments & Components Total | | | | 50,981,001 |

| |

| Internet Software & Services – 0.5% | | |

InfoSpace, Inc. (a) | | 454,230 | | 3,415,810 |

United Online, Inc. | | 751,740 | | 4,330,022 |

| | | | |

Internet Software & Services Total | | | | 7,745,832 |

| |

| IT Services – 2.1% | | |

Acxiom Corp. (a) | | 332,810 | | 4,888,979 |

CACI International, Inc., Class A (a) | | 131,320 | | 5,578,474 |

CSG Systems International, Inc. (a) | | 285,429 | | 5,231,914 |

MAXIMUS, Inc. | | 94,089 | | 5,444,930 |

MoneyGram International, Inc. (a) | | 1,857,214 | | 4,550,174 |

TeleTech Holdings, Inc. (a) | | 339,700 | | 4,378,733 |

| | | | |

IT Services Total | | | | 30,073,204 |

| |

| Semiconductors & Semiconductor Equipment – 2.8% | | |

Amkor Technology, Inc. (a) | | 644,890 | | 3,553,344 |

ATMI, Inc. (a) | | 301,222 | | 4,409,890 |

Fairchild Semiconductor International, Inc. (a) | | 448,315 | | 3,770,329 |

Integrated Device Technology, Inc. (a) | | 658,280 | | 3,258,486 |

Kulicke & Soffa Industries, Inc. (a) | | 528,365 | | 3,709,122 |

MKS Instruments, Inc. (a) | | 241,702 | | 4,524,661 |

OmniVision Technologies, Inc. (a) | | 298,156 | | 6,392,465 |

Varian Semiconductor Equipment Associates, Inc. (a) | | 131,350 | | 3,764,491 |

Verigy Ltd. (a) | | 403,307 | | 3,504,738 |

Zoran Corp. (a) | | 414,956 | | 3,958,680 |

| | | | |

Semiconductors & Semiconductor Equipment Total | | | | 40,846,206 |

| |

| Software – 2.0% | | |

Compuware Corp. (a) | | 533,960 | | 4,261,001 |

Jack Henry & Associates, Inc. | | 157,360 | | 3,757,757 |

Mentor Graphics Corp. (a) | | 677,346 | | 5,994,512 |

Monotype Imaging Holdings, Inc. (a) | | 490,745 | | 4,421,613 |

Parametric Technology Corp. (a) | | 257,690 | | 4,038,002 |

See Accompanying Notes to Financial Statements.

11

Columbia Small Cap Value Fund I

June 30, 2010

Common Stocks (continued)

| | | | |

| | | Shares | | Value ($) |

| Information Technology (continued) | | |

Progress Software Corp. (a) | | 204,909 | | 6,153,417 |

| | | | |

Software Total | | | | 28,626,302 |

| | | | |

Information Technology Total | | | | 199,545,445 |

| | | | |

| Materials – 6.2% | | | | |

| Chemicals – 1.6% | | | | |

Cytec Industries, Inc. | | 134,834 | | 5,392,012 |

H.B. Fuller Co. | | 494,239 | | 9,385,598 |

OM Group, Inc. (a) | | 339,877 | | 8,109,465 |

| | | | |

Chemicals Total | | | | 22,887,075 |

| |

| Construction Materials – 0.3% | | |

Eagle Materials, Inc. | | 170,411 | | 4,418,757 |

| | | | |

Construction Materials Total | | | | 4,418,757 |

| |

| Containers & Packaging – 2.2% | | |

Greif, Inc., Class A | | 101,156 | | 5,618,205 |

Greif, Inc., Class B | | 268,877 | | 14,142,930 |

Packaging Corp. of America | | 244,400 | | 5,381,688 |

Silgan Holdings, Inc. | | 221,690 | | 6,291,562 |

| | | | |

Containers & Packaging Total | | | | 31,434,385 |

| |

| Metals & Mining – 2.1% | | |

Carpenter Technology Corp. | | 174,840 | | 5,739,997 |

Haynes International, Inc. | | 192,144 | | 5,923,800 |

Olympic Steel, Inc. | | 234,509 | | 5,386,672 |

RTI International Metals, Inc. (a) | | 283,521 | | 6,835,691 |

Terra Nova Royalty Corp. (a) | | 315,562 | | 2,628,632 |

Thompson Creek Metals Co., Inc. (a) | | 514,830 | | 4,468,724 |

| | | | |

Metals & Mining Total | | | | 30,983,516 |

| | | | |

Materials Total | | | | 89,723,733 |

| | | | |

| Telecommunication Services – 1.7% | | |

| Diversified Telecommunication Services – 0.3% |

Warwick Valley Telephone Co. (b) | | 342,773 | | 4,822,816 |

| | | | |

Diversified Telecommunication Services Total | | | | 4,822,816 |

|

| Wireless Telecommunication Services – 1.4% |

NTELOS Holdings Corp. | | 409,620 | | 7,045,464 |

Shenandoah Telecommunications Co. | | 279,269 | | 4,954,232 |

Syniverse Holdings, Inc. (a) | | 383,166 | | 7,835,745 |

| | | | |

Wireless Telecommunication Services Total | | | | 19,835,441 |

| | | | |

Telecommunication Services Total | | | | 24,658,257 |

| | | | |

| | | Shares | | Value ($) |

| Utilities – 5.4% | | |

| Electric Utilities – 2.0% |

ALLETE, Inc. | | 252,340 | | 8,640,122 |

El Paso Electric Co. (a) | | 385,642 | | 7,462,173 |

Great Plains Energy, Inc. | | 200 | | 3,404 |

Hawaiian Electric Industries, Inc. | | 163,451 | | 3,723,414 |

MGE Energy, Inc. | | 217,164 | | 7,826,590 |

UIL Holdings Corp. | | 9,617 | | 240,713 |

| | | | |

Electric Utilities Total | | | | 27,896,416 |

| |

| Gas Utilities – 1.2% | | |

Laclede Group, Inc. | | 239,040 | | 7,919,395 |

Nicor, Inc. | | 239,300 | | 9,691,650 |

| | | | |

Gas Utilities Total | | | | 17,611,045 |

| |

| Independent Power Producers & Energy Traders – 0.6% | | |

Black Hills Corp. | | 313,711 | | 8,931,352 |

| | | | |

Independent Power Producers & Energy Traders Total | | | | 8,931,352 |

| |

| Multi-Utilities – 1.6% | | |

Avista Corp. | | 441,790 | | 8,628,159 |

CH Energy Group, Inc. | | 159,414 | | 6,255,406 |

NorthWestern Corp. | | 325,011 | | 8,515,288 |

| | | | |

Multi-Utilities Total | | | | 23,398,853 |

| | | | |

Utilities Total | | | | 77,837,666 |

| | | | |

Total Common Stocks

(cost of $1,344,473,175) | | | | 1,404,660,977 |

See Accompanying Notes to Financial Statements.

12

Columbia Small Cap Value Fund I

June 30, 2010

Short-Term Obligation – 0.7%

| | | | |

| | | Par ($) | | Value ($) |

Repurchase agreement with Fixed Income Clearing Corp., dated 06/30/10, due 07/01/10 at 0.000%, collateralized by a U.S. Treasury obligation maturing 01/31/14, market value $9,681,125 (repurchase proceeds $9,490,000) | | 9,490,000 | | 9,490,000 |

| | | | |

Total Short-Term Obligation

(cost of $9,490,000) | | 9,490,000 |

| | | | |

Total Investments – 98.1%

(cost of $1,353,963,175) (c) | | 1,414,150,977 |

| | | | |

Other Assets & Liabilities, Net – 1.9% | | 27,422,729 |

| | | | |

Net Assets – 100.0% | | | | 1,441,573,706 |

Notes to Investment Portfolio:

| (a) | Non-income producing security. |

| (b) | An affiliate may include any company in which the fund owns five percent or more of its outstanding voting shares. Transactions with companies which are or were affiliated during the year ended June 30, 2010, are as follows: |

| | | | | | | | | | | | | | | |

Affiliate | | Value,

Beginning of

Period | | Purchases | | Sales

Proceeds | | Dividend

Income | | Value,

End of

Period |

Baldwin & Lyons, Inc., Class B | | $ | 4,112,217 | | $ | 1,484,593 | | $ | 34,132 | | $ | 308,980 | | $ | 5,706,988 |

Bel Fuse, Inc., Class B | | | 1,618,709 | | | 748,700 | | | 12,498 | | | 32,436 | | | 2,262,151 |

Northrim BanCorp, Inc. | | | 3,536,320 | | | 1,441,593 | | | — | | | 123,184 | | | 5,321,498 |

Warwick Valley Telephone Co. | | | 3,118,800 | | | 957,929 | | | 55,201 | | | 295,981 | | | 4,822,816 |

| | | | | | | | | | | | | | | |

| | $ | 12,386,046 | | $ | 4,632,815 | | $ | 101,831 | | $ | 760,581 | | $ | 18,113,453 |

| | | | | | | | | | | | | | | |

| (c) | Cost for federal income tax purposes is $1,364,259,641. |

The following table summarizes the inputs used, as of June 30, 2010, in valuing the Fund’s assets:

| | | | | | | | | | | | |

Description | | Quoted Prices

(Level 1) | | Other

Significant

Observable

Inputs

(Level 2) | | Significant

Unobser-

vable

Inputs

(Level 3) | | Total |

Common Stocks | | | | | | | | | | | | |

Consumer Discretionary | | $ | 122,911,723 | | $ | — | | $ | — | | $ | 122,911,723 |

Consumer Staples | | | 21,233,207 | | | — | | | — | | | 21,233,207 |

Energy | | | 78,882,982 | | | — | | | — | | | 78,882,982 |

Financials | | | 451,194,842 | | | — | | | — | | | 451,194,842 |

Health Care | | | 76,077,473 | | | — | | | — | | | 76,077,473 |

Industrials | | | 261,711,295 | | | 884,354 | | | — | | | 262,595,649 |

Information Technology | | | 199,545,445 | | | — | | | — | | | 199,545,445 |

Materials | | | 89,723,733 | | | — | | | — | | | 89,723,733 |

Telecommunication Services | | | 24,658,257 | | | — | | | — | | | 24,658,257 |

Utilities | | | 77,837,666 | | | — | | | — | | | 77,837,666 |

| | | | | | | | | | | | |

Total Common Stocks | | | 1,403,776,623 | | | 884,354 | | | — | | | 1,404,660,977 |

| | | | | | | | | | | | |

Total Short-Term Obligation | | | — | | | 9,490,000 | | | — | | | 9,490,000 |

| | | | | | | | | | | | |

Total Investments | | $ | 1,403,776,623 | | $ | 10,374,354 | | $ | — | | $ | 1,414,150,977 |

| | | | | | | | | | | | |

The Fund’s assets assigned to the Level 2 input category include certain foreign securities for which a third party statistical pricing service may be employed for purposes of fair market valuation.

For more information on valuation inputs, and their aggregation into the levels used in the table above, please refer to the Security Valuation section in the accompanying Notes to Financial Statements.

At June 30, 2010, the Fund held investments in the following sectors:

| | |

Sector (Unaudited) | | % of

Net Assets |

Financials | | 31.3 |

Industrials | | 18.2 |

Information Technology | | 13.8 |

Consumer Discretionary | | 8.5 |

Materials | | 6.2 |

Energy | | 5.5 |

Utilities | | 5.4 |

Health Care | | 5.3 |

Telecommunication Services | | 1.7 |

Consumer Staples | | 1.5 |

| | |

| | 97.4 |

Short-Term Obligation | | 0.7 |

Other Assets & Liabilities, Net | | 1.9 |

| | |

| | 100.0 |

| | |

See Accompanying Notes to Financial Statements.

13

Statement of Assets and Liabilities – Columbia Small Cap Value Fund I

June 30, 2010

| | | | | |

| | | | | ($) | |

| Assets | | Unaffiliated investments, at cost | | 1,334,424,201 | |

| | Affiliated investments, at cost | | 19,538,974 | |

| | | | | |

| | Total investments, at cost | | 1,353,963,175 | |

| | |

| | Unaffiliated investments, at value | | 1,396,037,524 | |

| | Affiliated investments, at value | | 18,113,453 | |

| | | | | |

| | Total investments, at value | | 1,414,150,977 | |

| | Cash | | 8,771 | |

| | Receivable for: | | | |

| | Investments sold | | 15,886,367 | |

| | Fund shares sold | | 36,970,788 | |

| | Dividends | | 1,785,768 | |

| | Trustees’ deferred compensation plan | | 63,339 | |

| | Prepaid expenses | | 37,942 | |

| | | | | |

| | Total Assets | | 1,468,903,952 | |

| | |

| Liabilities | | Payable for: | | | |

| | Investments purchased | | 22,522,499 | |

| | Fund shares repurchased | | 2,870,715 | |

| | Investment advisory fee | | 907,069 | |

| | Pricing and bookkeeping fees | | 12,689 | |

| | Transfer agent fee | | 611,050 | |

| | Trustees’ fees | | 967 | |

| | Custody fee | | 52,618 | |

| | Distribution and service fees | | 191,244 | |

| | Chief compliance officer expenses | | 274 | |

| | Trustees’ deferred compensation plan | | 63,339 | |

| | Other liabilities | | 97,782 | |

| | | | | |

| | Total Liabilities | | 27,330,246 | |

| | |

| | | | | |

| | Net Assets | | 1,441,573,706 | |

| | |

| Net Assets Consist of | | Paid-in capital | | 1,398,361,371 | |

| | Undistributed net investment income | | 5,747,004 | |

| | Accumulated net realized loss | | (22,722,432 | ) |

| | Net unrealized appreciation (depreciation) on: | | | |

| | Investments | | 60,187,802 | |

| | Foreign currency translations | | (39 | ) |

| | | | | |

| | Net Assets | | 1,441,573,706 | |

See Accompanying Notes to Financial Statements.

14

Statement of Assets and Liabilities (continued) – Columbia Small Cap Value Fund I

June 30, 2010

| | | | | | |

| | | | | | |

| Class A | | Net assets | | $ | 593,209,149 | |

| | Shares outstanding | | | 16,553,689 | |

| | Net asset value per share | | $ | 35.84 | (a) |

| | Maximum sales charge | | | 5.75 | % |

| | Maximum offering price per share ($35.84/0.9425) | | $ | 38.03 | (b) |

| | |

| Class B | | Net assets | | $ | 22,775,432 | |

| | Shares outstanding | | | 780,724 | |

| | Net asset value and offering price per share | | $ | 29.17 | (a) |

| | |

| Class C | | Net assets | | $ | 49,887,864 | |

| | Shares outstanding | | | 1,616,212 | |

| | Net asset value and offering price per share | | $ | 30.87 | (a) |

| | |

| Class Y (c) | | Net assets | | $ | 1,110,772 | |

| | Shares outstanding | | | 29,518 | |

| | Net asset value, offering and redemption price per share | | $ | 37.63 | |

| | |

| Class Z | | Net assets | | $ | 774,590,489 | |

| | Shares outstanding | | | 20,602,843 | |

| | Net asset value, offering and redemption price per share | | $ | 37.60 | |

| (a) | Redemption price per share is equal to net asset value less any applicable contingent deferred sales charge. |

| (b) | On sales of $50,000 or more the offering price is reduced. |

| (c) | Class Y shares commenced operations on July 15, 2009. |

See Accompanying Notes to Financial Statements.

15

Statement of Operations – Columbia Small Cap Value Fund I

For the Year Ended June 30, 2010

| | | | | |

| | | | | ($) (a) | |

| Investment Income | | Dividends | | 20,966,107 | |

| | Dividends from affiliates | | 760,581 | |

| | Interest | | 6,780 | |

| | | | | |

| | Total Investment Income | | 21,733,468 | |

| | |

| Expenses | | Investment advisory fee | | 9,677,615 | |

| | Distribution fee: | | | |

| | Class B | | 221,359 | |

| | Class C | | 396,269 | |

| | Service fee: | | | |

| | Class A | | 1,442,237 | |

| | Class B | | 73,786 | |

| | Class C | | 132,091 | |

| | Pricing and bookkeeping fees | | 146,364 | |

| | Transfer agent fee – Class A, Class B, Class C and Class Z | | 2,295,916 | |

| | Transfer agent fee – Class Y | | 45 | |

| | Trustees’ fees | | 62,122 | |

| | Custody fee | | 328,221 | |

| | Chief compliance officer expenses | | 982 | |

| | Other expenses | | 536,995 | |

| | | | | |

| | Expenses before interest expense | | 15,314,002 | |

| | Interest expense | | 860 | |

| | | | | |

| | Total Expenses | | 15,314,862 | |

| | Expense reductions | | (27 | ) |

| | | | | |

| | Net Expenses | | 15,314,835 | |

| | |

| | | | | |

| | Net Investment Income | | 6,418,633 | |

| | |

| Net Realized and Unrealized Gain (Loss) on Investments and Foreign Currency | | Net realized gain on: | | | |

| | Unaffiliated investments | | 52,489,108 | |

| | Affiliated investments | | 864 | |

| | Foreign currency transactions | | 494 | |

| | | | | |

| | Net realized gain | | 52,490,466 | |

| | Net change in unrealized appreciation (depreciation) on: | | | |

| | Investments | | 146,219,335 | |

| | Foreign currency translations | | (39 | ) |

| | | | | |

| | Net change in unrealized appreciation (depreciation) | | 146,219,296 | |

| | | | | |

| | Net Gain | | 198,709,762 | |

| | |

| | | | | |

| | Net Increase Resulting from Operations | | 205,128,395 | |

| (a) | Class Y shares commenced operations on July 15, 2009. |

See Accompanying Notes to Financial Statements.

16

Statement of Changes in Net Assets – Columbia Small Cap Value Fund I

| | | | | | | | |

| | | | | Year Ended June 30, | |

| Increase (Decrease) in Net Assets | | | | 2010 ($) (a)(b) | | | 2009 ($) | |

| Operations | | Net investment income | | 6,418,633 | | | 5,865,359 | |

| | Net realized gain (loss) on investments and foreign currency transactions | | 52,490,466 | | | (67,787,043 | ) |

| | Net change in unrealized appreciation (depreciation) on investments and foreign currency translations | | 146,219,296 | | | (120,306,186 | ) |

| | | | | | | | |

| | Net increase (decrease) resulting from operations | | 205,128,395 | | | (182,227,870 | ) |

| | | |

| Distributions to Shareholders | | From net investment income: | | | | | | |

| | Class A | | (2,853,169 | ) | | (96,427 | ) |

| | Class B | | (69,066 | ) | | — | |

| | Class C | | (111,769 | ) | | — | |

| | Class Y | | (7,732 | ) | | — | |

| | Class Z | | (3,363,591 | ) | | (409,448 | ) |

| | From net realized gains: | | | | | | |

| | Class A | | — | | | (26,043,809 | ) |

| | Class B | | — | | | (2,603,676 | ) |

| | Class C | | — | | | (3,321,986 | ) |

| | Class Z | | — | | | (13,590,135 | ) |

| | | | | | | | |

| | Total distributions to shareholders | | (6,405,327 | ) | | (46,065,481 | ) |

| | | |

| | Net Capital Stock Transactions | | 362,267,219 | | | 247,711,791 | |

| | | |

| | Increase from Regulatory Settlements | | 4,978 | | | 20,959 | |

| | Total increase in net assets | | 560,995,265 | | | 19,439,399 | |

| | | |

| Net Assets | | Beginning of period | | 880,578,441 | | | 861,139,042 | |

| | End of period | | 1,441,573,706 | | | 880,578,441 | |

| | Undistributed net investment income at end of period | | 5,747,004 | | | 5,670,837 | |

| (a) | Class Y shares commenced operations on July 15, 2009. |

| (b) | Class Y shares reflects activity for the period July 15, 2009 through June 30, 2010. |

See Accompanying Notes to Financial Statements.

17

Statement of Changes in Net Assets (continued) – Columbia Small Cap Value Fund I

| | | | | | | | | | | | |

| | | Capital Stock Activity | |

| | | Year Ended

June 30, 2010 (a) | | | Year Ended

June 30, 2009 | |

| | | Shares | | | Dollars ($) | | | Shares | | | Dollars ($) | |

Class A | | | | | | | | | | | | |

Subscriptions | | 6,146,642 | | | 221,981,390 | | | 6,328,169 | | | 197,710,536 | |

Distributions reinvested | | 75,419 | | | 2,640,419 | | | 847,952 | | | 23,835,899 | |

Redemptions | | (4,797,429 | ) | | (173,704,231 | ) | | (5,050,685 | ) | | (152,493,634 | ) |

| | | | | | | | | | | | |

Net increase | | 1,424,632 | | | 50,917,578 | | | 2,125,436 | | | 69,052,801 | |

| | | | |

Class B | | | | | | | | | | | | |

Subscriptions | | 19,122 | | | 550,695 | | | 120,146 | | | 3,182,019 | |

Distributions reinvested | | 2,192 | | | 62,564 | | | 103,495 | | | 2,389,643 | |

Redemptions | | (450,056 | ) | | (13,437,067 | ) | | (553,019 | ) | | (14,125,365 | ) |

| | | | | | | | | | | | |

Net decrease | | (428,742 | ) | | (12,823,808 | ) | | (329,378 | ) | | (8,553,703 | ) |

| | | | |

Class C | | | | | | | | | | | | |

Subscriptions | | 304,578 | | | 9,288,017 | | | 450,221 | | | 12,286,660 | |

Distributions reinvested | | 2,808 | | | 85,020 | | | 104,710 | | | 2,558,051 | |

Redemptions | | (441,992 | ) | | (13,769,158 | ) | | (560,320 | ) | | (14,796,916 | ) |

| | | | | | | | | | | | |

Net increase (decrease) | | (134,606 | ) | | (4,396,121 | ) | | (5,389 | ) | | 47,795 | |

| | | | |

Class Y (b) | | | | | | | | | | | | |

Subscriptions | | 61,757 | | | 2,010,000 | | | — | | | — | |

Distributions reinvested | | 211 | | | 7,732 | | | — | | | — | |

Redemptions | | (32,450 | ) | | (1,129,792 | ) | | — | | | — | |

| | | | | | | | | | | | |

Net increase | | 29,518 | | | 887,940 | | | — | | | — | |

| | | | |

Class Z | | | | | | | | | | | | |

Subscriptions | | 13,255,465 | | | 499,789,626 | | | 8,119,589 | | | 249,737,204 | |

Distributions reinvested | | 55,528 | | | 2,036,209 | | | 348,224 | | | 10,237,790 | |

Redemptions | | (4,575,482 | ) | | (174,144,205 | ) | | (2,317,324 | ) | | (72,810,096 | ) |

| | | | | | | | | | | | |

Net increase | | 8,735,511 | | | 327,681,630 | | | 6,150,489 | | | 187,164,898 | |

| (a) | Class Y shares reflects activity for the period July 15, 2009 through June 30, 2010. |

| (b) | Class Y shares commenced operations on July 15, 2009. |

See Accompanying Notes to Financial Statements.

18

Financial Highlights – Columbia Small Cap Value Fund I

Selected data for a share outstanding throughout each period is as follows:

| | | | | | | | | | | | | | | | | | | | |

| | | Year Ended June 30, | |

| Class A Shares | | 2010 | | | 2009 | | | 2008 | | | 2007 | | | 2006 | |

Net Asset Value, Beginning of Period | | $ | 29.29 | | | $ | 39.50 | | | $ | 52.16 | | | $ | 48.03 | | | $ | 43.12 | |

| | | | | |

Income from Investment Operations: | | | | | | | | | | | | | | | | | | | | |

Net investment income (a) | | | 0.15 | | | | 0.23 | (b) | | | 0.15 | | | | 0.12 | (c) | | | 0.06 | |

Net realized and unrealized gain (loss) on investments and foreign currency | | | 6.58 | | | | (8.50 | ) | | | (8.46 | ) | | | 7.61 | | | | 6.82 | |

| | | | | | | | | | | | | | | | | | | | |

Total from investment operations | | | 6.73 | | | | (8.27 | ) | | | (8.31 | ) | | | 7.73 | | | | 6.88 | |

| | | | | |

Less Distributions to Shareholders: | | | | | | | | | | | | | | | | | | | | |

From net investment income | | | (0.18 | ) | | | (0.01 | ) | | | (0.14 | ) | | | (0.01 | ) | | | — | |

From net realized gains | | | — | | | | (1.93 | ) | | | (4.21 | ) | | | (3.59 | ) | | | (1.97 | ) |

| | | | | | | | | | | | | | | | | | | | |

Total distributions to shareholders | | | (0.18 | ) | | | (1.94 | ) | | | (4.35 | ) | | | (3.60 | ) | | | (1.97 | ) |

| | | | | |

Increase from regulatory settlements | | | — | (d) | | | — | (d) | | | — | | | | — | | | | — | |

| | | | | |

Net Asset Value, End of Period | | $ | 35.84 | | | $ | 29.29 | | | $ | 39.50 | | | $ | 52.16 | | | $ | 48.03 | |

Total return (e) | | | 22.99 | % | | | (20.73 | )% | | | (16.96 | )% | | | 16.61 | % | | | 16.25 | %(f)(g) |

| | | | | |

Ratios to Average Net Assets/Supplemental Data: | | | | | | | | | | | | | | | | | | | | |

Net expenses before interest expense (h) | | | 1.27 | % | | | 1.38 | % | | | 1.26 | % | | | 1.29 | % | | | 1.28 | % |

Interest expense (i) | | | — | % | | | — | % | | | — | % | | | — | % | | | — | % |

Net expenses (h) | | | 1.27 | % | | | 1.38 | % | | | 1.26 | % | | | 1.29 | % | | | 1.28 | % |

Waiver/Reimbursement | | | — | | | | — | | | | — | | | | — | | | | 0.01 | % |

Net investment income (h) | | | 0.43 | % | | | 0.74 | % | | | 0.29 | % | | | 0.25 | % | | | 0.13 | % |

Portfolio turnover rate | | | 30 | % | | | 50 | % | | | 40 | % | | | 39 | % | | | 32 | % |

Net assets, end of period (000s) | | $ | 593,209 | | | $ | 443,154 | | | $ | 513,671 | | | $ | 663,160 | | | $ | 505,971 | |

| (a) | Per share data was calculated using the average shares outstanding during the period. |

| (b) | Net investment income per share reflects special dividends. The effect of these dividends amounted to $0.03 per share. |

| (c) | Net investment income per share reflects special dividends. The effect of these dividends amounted to $0.05 per share. |

| (d) | Rounds to less than $0.01 per share. |

| (e) | Total return at net asset value assuming all distributions reinvested and no initial sales charge or contingent deferred sales charge. |

| (f) | Total return includes a voluntary reimbursement by the investment advisor for a realized investment loss due to a trading error. This reimbursement increased total return and net asset value per share by less than 0.01% and less than $0.01, respectively. |

| (g) | Had the investment advisor and/or any of its affiliates not waived fees or reimbursed a portion of expenses, total return would have been reduced. |

| (h) | The benefits derived from expense reductions had an impact of less than 0.01%. |

| (i) | Rounds to less than 0.01%. |

See Accompanying Notes to Financial Statements.

19

Financial Highlights – Columbia Small Cap Value Fund I

Selected data for a share outstanding throughout each period is as follows:

| | | | | | | | | | | | | | | | | | | | |

| | | Year Ended June 30, | |

| Class B Shares | | 2010 | | | 2009 | | | 2008 | | | 2007 | | | 2006 | |

Net Asset Value, Beginning of Period | | $ | 23.96 | | | $ | 33.00 | | | $ | 44.51 | | | $ | 41.75 | | | $ | 38.00 | |

| | | | | |

Income from Investment Operations: | | | | | | | | | | | | | | | | | | | | |

Net investment loss (a) | | | (0.10 | ) | | | (0.01 | )(b) | | | (0.21 | ) | | | (0.24 | )(c) | | | (0.26 | ) |

Net realized and unrealized gain (loss) on investments and foreign currency | | | 5.38 | | | | (7.10 | ) | | | (7.09 | ) | | | 6.59 | | | | 5.98 | |

| | | | | | | | | | | | | | | | | | | | |

Total from investment operations | | | 5.28 | | | | (7.11 | ) | | | (7.30 | ) | | | 6.35 | | | | 5.72 | |

| | | | | |

Less Distributions to Shareholders: | | | | | | | | | | | | | | | | | | | | |

From net investment income | | | (0.07 | ) | | | — | | | | — | | | | — | | | | — | |

From net realized gains | | | — | | | | (1.93 | ) | | | (4.21 | ) | | | (3.59 | ) | | | (1.97 | ) |

| | | | | | | | | | | | | | | | | | | | |

Total distributions to shareholders | | | (0.07 | ) | | | (1.93 | ) | | | (4.21 | ) | | | (3.59 | ) | | | (1.97 | ) |

| | | | | |

Increase from regulatory settlements | | | — | (d) | | | — | (d) | | | — | | | | — | | | | — | |

| | | | | |

Net Asset Value, End of Period | | $ | 29.17 | | | $ | 23.96 | | | $ | 33.00 | | | $ | 44.51 | | | $ | 41.75 | |

Total return (e) | | | 22.02 | % | | | (21.31 | )% | | | (17.58 | )% | | | 15.74 | % | | | 15.36 | %(f)(g) |

| | | | | |

Ratios to Average Net Assets/Supplemental Data: | | | | | | | | | | | | | | | | | | | | |

Net expenses before interest expense (h) | | | 2.02 | % | | | 2.13 | % | | | 2.01 | % | | | 2.04 | % | | | 2.03 | % |

Interest expense (i) | | | — | % | | | — | % | | | — | % | | | — | % | | | — | % |

Net expenses (h) | | | 2.02 | % | | | 2.13 | % | | | 2.01 | % | | | 2.04 | % | | | 2.03 | % |

Waiver/Reimbursement | | | — | | | | — | | | | — | | | | — | | | | 0.01 | % |

Net investment loss (h) | | | (0.33 | )% | | | (0.02 | )% | | | (0.47 | )% | | | (0.55 | )% | | | (0.64 | )% |

Portfolio turnover rate | | | 30 | % | | | 50 | % | | | 40 | % | | | 39 | % | | | 32 | % |

Net assets, end of period (000s) | | $ | 22,775 | | | $ | 28,977 | | | $ | 50,784 | | | $ | 97,425 | | | $ | 135,721 | |

| (a) | Per share data was calculated using the average shares outstanding during the period. |

| (b) | Net investment income per share reflects special dividends. The effect of these dividends amounted to $0.03 per share. |

| (c) | Net investment income per share reflects special dividends. The effect of these dividends amounted to $0.05 per share. |

| (d) | Rounds to less than $0.01 per share. |

| (e) | Total return at net asset value assuming all distributions reinvested and no contingent deferred sales charge. |

| (f) | Total return includes a voluntary reimbursement by the investment advisor for a realized investment loss due to a trading error. This reimbursement increased total return and net asset value per share by less than 0.01% and less than $0.01, respectively. |

| (g) | Had the investment advisor and/or any of its affiliates not waived fees or reimbursed a portion of expenses, total return would have been reduced. |

| (h) | The benefits derived from expense reductions had an impact of less than 0.01%. |

| (i) | Rounds to less than 0.01%. |

See Accompanying Notes to Financial Statements.

20

Financial Highlights – Columbia Small Cap Value Fund I