UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-04642

Virtus Variable Insurance Trust

(Exact name of registrant as specified in charter)

100 Pearl Street

Hartford, CT 06103-4506

(Address of principal executive offices) (Zip code)

Jennifer S. Fromm, Esq.

Vice President, Chief Legal Officer, Counsel and Secretary for Registrant

100 Pearl Street

Hartford, CT 06103-4506

(Name and address of agent for service)

Registrant’s telephone number, including area code: (800) 367-5877

Date of fiscal year end: December 31

Date of reporting period: December 31, 2017

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

| Item 1. | Reports to Stockholders. |

The Report to Shareholders is attached herewith.

| | | | |

| ANNUAL REPORT | | |  | |

| VIRTUS VARIABLE INSURANCE TRUST | |

December 31, 2017

|

Virtus Duff & Phelps International Series |

Virtus Duff & Phelps Real Estate Securities Series |

Virtus KAR Capital Growth Series |

Virtus KAR Small-Cap Growth Series |

Virtus KAR Small-Cap Value Series |

Virtus Newfleet Multi-Sector Intermediate Bond Series |

Virtus Rampart Enhanced Core Equity Series |

Virtus Rampart Equity Trend Series |

Virtus Strategic Allocation Series |

|

The Annual Report describes one or more Series available for underlying investment through your variable contract. For information about your variable contract, including information about insurance-related expenses, see the prospectus for your variable contract. |

Not FDIC Insured

No Bank Guarantee

May Lose Value

Table of Contents

Proxy Voting Procedures and Voting Record (Form N-PX)

The adviser and subadvisers vote proxies relating to portfolio securities in accordance with procedures that have been approved by the Board of Trustees of the Trust (“Trustees,” or the “Board”). You may obtain a description of these procedures, along with information regarding how the Series voted proxies during the most recent 12-month period ended June 30, free of charge, by calling toll-free 1-800-367-5877. This information is also available through the Securities and Exchange Commission’s (the “SEC”) website at http://www.sec.gov.

Form N-Q Information

The Trust files a complete schedule of portfolio holdings for each Series with the SEC for the first and third quarters of each fiscal year on Form N-Q. Form N-Q is available on the SEC’s website at http://www.sec.gov. Form N-Q may be reviewed and copied at the SEC’s Public Reference Room. Information on the operation of the SEC’s Public Reference Room can be obtained by calling toll-free 1-800-SEC-0330.

MESSAGE TO SHAREHOLDERS

To Virtus Variable Insurance Trust Investors:

| | |

| | I am pleased to present this annual report that reviews the performance of your Series for the 12-month period ended December 31, 2017. Economic growth and strong corporate earnings were driving forces in the U.S. in 2017, capped off by the sweeping tax overhaul signed into law at year-end, which fueled optimism further. The Federal Reserve, buoyed by a steadily strengthening economy, raised interest rates three times over the course of the year, and began the process of unwinding its balance sheet debt accumulated since the Financial Crisis of 2008 – a clear signal that it believes the U.S. has resumed a growth path. Outside the U.S., global growth also strengthened, with other major central banks preparing to taper their own stimulus policies. |

The favorable investment backdrop lifted major U.S. equity markets to new all-time highs with near-record low volatility. Large-cap stocks, as measured by the S&P 500® Index, returned 21.83% for the year, outpacing small-cap stocks, which returned 14.65%, as measured by the Russell 2000® Index. Within international equities, emerging markets led their developed peers, with the MSCI Emerging Markets Index (net) up 37.28%, compared with the MSCI EAFE® Index (net), which returned 25.03%. Demand for U.S. Treasuries remained strong, driven by foreign investors who favored their yield advantage and credit quality over many foreign government bonds. On December 31, 2017, the benchmark 10-year U.S. Treasury yielded 2.40%, compared with 2.45% one year earlier. The broader U.S. fixed income market, as represented by the Bloomberg Barclays U.S. Aggregate Bond Index, which tracks Treasuries and other investment-grade debt securities, increased 3.54% for the 12 months, while non-investment grade bonds gained 7.50%, as measured by the Bloomberg Barclays U.S. Corporate High Yield Bond Index. Market uncertainty is an ever-present reminder of the importance of portfolio diversification, including exposure to traditional and alternative asset classes. While diversification cannot guarantee a profit or prevent a loss, owning a variety of asset classes may cushion your portfolio against inevitable market fluctuations. Your financial advisor can help you ensure that your variable investment portfolio is adequately diversified across asset classes and investment strategies. On behalf of our investment affiliates, thank you for entrusting assets to the Virtus Variable Insurance Trust. Should you have questions about your account or require assistance, please visit Virtus.com, or call our customer service team at

1-800-367-5877. We appreciate your business and remain committed to your long-term financial success. |

Sincerely,

George R. Aylward

President, Virtus Variable Insurance Trust

February 2018

Performance data quoted represents past results. Past performance is no guarantee of future results, and current performance may be higher or lower than the performance shown above.

1

KEY INVESTMENT TERMS

American Depositary Receipt (“ADR”)

Represents shares of foreign companies traded in U.S. dollars on U.S. exchanges that are held by a U.S. bank or a trust. Foreign companies use ADRs in order to make it easier for Americans to buy their shares.

Bloomberg Barclays U.S. Aggregate Bond Index

The Bloomberg Barclays U.S. Aggregate Bond Index measures the U.S. investment-grade fixed-rate bond market. The index is calculated on a total return basis. The index is unmanaged, its returns do not reflect any fees, expenses, or sales charges, and it is not available for direct investment.

Bloomberg Barclays U.S. Corporate High Yield Bond Index

The Bloomberg Barclays U.S. Corporate High Yield Bond Index measures the U.S. dollar-denominated, high yield, fixed-rate corporate bond market. The index is calculated on a total return basis. The index is unmanaged, its returns do not reflect any fees, expenses, or sales charges, and it is not available for direct investment.

Chicago Board Options Exchange Volatility Index® (“CBOE VIX®”)

The CBOE VIX® shows the market’s expectation of 30-day volatility. It is constructed using the implied volatilities of a wide range of S&P 500® Index options. This volatility is meant to be forward looking and is calculated from both calls and puts. The CBOE VIX® is a widely used measure of market risk and is often referred to as the “investor fear gauge.” The index is unmanaged, its returns do not reflect any fees, expenses, or sales charges, and it is not available for direct investment.

Composite Index for Strategic Allocation Series

The Composite Index for Strategic Allocation Series consists of 45% Russell 1000® Growth Index (a market capitalization-weighted index of growth-oriented stocks of the 1,000 largest companies in the Russell Universe, which comprises the 3,000 largest U.S. companies, calculated on a total return basis with dividends reinvested), 15% MSCI EAFE® Index (net) (a free floatadjusted market capitalization-weighted index that measures developed foreign market equity performance, excluding the U.S. and Canada, calculated on a total return basis with net dividends reinvested) and 40% Bloomberg Barclays U.S. Aggregate Bond Index (an index that measures the U.S. investment grade fixed rate bond market, calculated on a total return basis). The index is unmanaged, its returns do not reflect any fees, expenses, or sales charges, and is not available for direct investment. Performance of the Composite Index for Strategic Allocation Series prior to 9/7/2016 represents an allocation consisting of 60% S&P 500® Index and 40% Bloomberg Barclays U.S. Aggregate Bond Index.

European Central Bank (“ECB”)

The European Central Bank (ECB) is responsible for conducting monetary policy for the Euro area. The ECB was established as the core of the Eurosystem and the European System of Central Banks (ESCB). The ESCB comprises the ECB and the National Central Banks (NCBs) of all 17 EU Member States whether they have adopted the Euro or not.

European Union (“EU”)

The European Union (EU) is a unique economic and political union of 28 European countries. The EU was created in the aftermath of the Second World War that has become a single market for goods and services and it created the single currency the Euro.

Exchange-Traded Fund (“ETF”)

An open-end fund that is traded on a stock exchange. Most ETFs have a portfolio of stocks or bonds that track a specific market index.

Federal Funds Rate

The interest rate at which a depository institution lends funds maintained at the Federal Reserve to another depository institution overnight. The Federal Funds rate is generally only applicable to the most creditworthy institutions when they borrow and lend overnight funds to each other. The Federal Funds rate is one of the most influential interest rates in the U.S. economy, since it affects monetary and financial conditions, which in turn have a bearing on key aspects of the broad economy including employment, growth and inflation.

Federal Reserve (the “Fed”)

The Central Bank of the U.S., responsible for controlling the money supply, interest rates, and credit with the goal of keeping the U.S. economy and currency stable. Governed by a seven-member board, the system includes 12 regional Federal Reserve Banks, 25 branches, and all national and state banks that are part of the system.

2

KEY INVESTMENT TERMS (Continued)

Financial Crisis of 2008

The Financial Crisis of 2008, also known as the Global Financial Crisis or Financial Crisis of 2007-2008, is considered by many economists to have been the worst financial and economic crisis since the Great Depression that lasted from 1929 to 1941. The Crisis began in 2007 with a crisis in the subprime mortgage market in the U.S., and it developed into an international banking crisis with the collapse of the investment bank Lehman Brothers in September of 2008. Although bail-outs of financial institutions as well as monetary and fiscal policies were put into place throughout the world to mitigate its impact, the Crisis led to the global economic downturn commonly referred to as the Great Recession. During the Crisis and through the Great Recession that followed, housing prices fell drastically and unemployment rose, leading to legislation designed to promote financial stability such as the Dodd-Frank Act in the U.S. and efforts by various central banks to stimulate their countries’ economies.

FTSE NAREIT Equity REITs Index

The FTSE NAREIT Equity REITs Index is a free-float market capitalization-weighted index measuring equity tax-qualified real estate investment trusts, which meet minimum size and liquidity criteria, that are listed on the New York Stock Exchange, the American Stock Exchange and the NASDAQ National Market System. The index is calculated on a total return basis with dividends reinvested. The index is unmanaged, its returns do not reflect any fees, expenses, or sales charges, and it is not available for direct investment.

Gross Domestic Product (“GDP”)

The GDP represents the market value of all goods and services produced by the economy during the period measured, including personal consumption, government purchases, private inventories, paid-in construction costs, and the foreign trade balance.

MSCI EAFE® Index (net)

The MSCI EAFE® (Europe, Australasia, Far East) Index (net) is a free float-adjusted market capitalization-weighted index that measures developed foreign market equity performance, excluding the U.S. and Canada. The index is calculated on a total return basis with net dividends reinvested. The index is unmanaged, its returns do not reflect any fees, expenses, or sales charges, and it is not available for direct investment.

MSCI Emerging Markets Index (net)

The MSCI Emerging Markets Index (net) is a free float-adjusted market capitalization-weighted index designed to measure equity market performance in the global emerging markets. The index is calculated on a total return basis with net dividends reinvested. The index is unmanaged, its returns do not reflect any fees, expenses, or sales charges, and it is not available for direct investment.

Payment-in-Kind Security (“PIK”)

A bond which pays interest in the form of additional bonds, or preferred stock which pays dividends in the form of additional preferred stock.

Real Estate Investment Trust (“REIT”)

A publicly traded company that owns, develops, and operates income-producing real estate such as apartments, office buildings, hotels, shopping centers, and other commercial properties.

Russell 1000® Growth Index

The Russell 1000® Growth Index is a market capitalization-weighted index of growth-oriented stocks of the 1,000 largest companies in the Russell Universe, which comprises the 3,000 largest U.S. companies. The index is calculated on a total return basis with dividends reinvested. The index is unmanaged, its returns do not reflect any fees, expenses, or sales charges, and it is not available for direct investment.

Russell 2000® Growth Index

The Russell 2000® Growth Index is a market capitalization-weighted index of growth-oriented stocks of the smallest 2,000 companies in the Russell Universe, which comprises the 3,000 largest U.S. companies. The index is calculated on a total return basis with dividends reinvested. The index is unmanaged, its returns do not reflect any fees, expenses, or sales charges, and it is not available for direct investment.

3

KEY INVESTMENT TERMS (Continued)

Russell 2000® Index

The Russell 2000® Index is a market capitalization-weighted index of the 2,000 smallest companies in the Russell Universe, which comprises the 3,000 largest U.S. companies. The index is calculated on a total return basis with dividends reinvested. The index is unmanaged, its returns do not reflect any fees, expenses, or sales charges, and it is not available for direct investment.

Russell 2000® Value Index

The Russell 2000® Value Index is a market capitalization-weighted index of value-oriented stocks of the smallest 2,000 companies in the Russell Universe, which comprises the 3,000 largest U.S. companies. The index is calculated on a total return basis with dividends reinvested. The index is unmanaged, its returns do not reflect any fees, expenses, or sales charges, and it is not available for direct investment.

S&P 500® Index

The S&P 500® Index is a free-float market capitalization-weighted index of 500 of the largest U.S. companies. The index is calculated on a total return basis with dividends reinvested. The index is unmanaged, its returns do not reflect any fees, expenses, or sales charges, and it is not available for direct investment.

Sponsored ADR (American Depositary Receipt)

An ADR which is issued with the cooperation of the company whose stock will underlie the ADR. Sponsored ADRs generally carry the same rights normally given to stockholders, such as voting rights. ADRs must be sponsored to be able to trade on a major U.S. exchange such as the New York Stock Exchange (“NYSE”).

Tax Cuts and Jobs Act (TCJA)

The Tax Cuts and Jobs Act, which became law in December 2017, provides the first major overhaul of the U.S. federal tax code since 1986. The TCJA modifies tax rates, policies, credits, and deductions for individuals and businesses.

Treasury Yield

The return on investment, expressed as a percentage, on the U.S. government’s debt obligations (bonds, notes and bills). The Treasury yield is considered a bellwether of the U.S. economy; the higher the yields on 10-, 20- and 30-year Treasuries, the better the economic outlook.

U.S. Dollar Index®

The U.S. Dollar Index® is a geometrically-averaged calculation of the following six currencies weighted against the U.S. dollar: the euro, Japanese yen, British pound, Canadian dollar, Swedish krona and Swiss franc. The index is compiled by ICE Futures U.S., Inc. The index is unmanaged, its returns do not reflect any fees, expenses, or sales charges, and it is not available for direct investment.

Yankee bonds

Yankee bonds are dollar-denominated instruments issued in the U.S. market by foreign branches of U.S. banks and U.S. branches of foreign banks.

4

VIRTUS VARIABLE INSURANCE TRUST

Disclosure of Series Expenses (Unaudited)

For the six-month period of July 1, 2017 to December 31, 2017

We believe it is important for you to understand the impact of costs on your investment. All mutual funds have operating expenses. As a shareholder of a Series (each a “Series”) of Virtus Variable Insurance Trust (the “Trust”), you incur ongoing costs including investment advisory fees and other expenses. These examples are intended to help you understand your ongoing costs (in dollars) of investing in a Series and to compare these costs with the ongoing costs of investing in other mutual funds. These examples are based on an investment of $1,000 invested at the beginning of the period and held for the entire six-month period.

Actual Expenses

The following Expense Table illustrates a Series’ information about actual account values and actual expenses. You may use the information in this section, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first table under the heading “Expenses Paid During Period” to estimate the expenses you paid on your account during this period. The Annualized Expense Ratios may be different from the expense ratios in the Financial Highlights which is for the fiscal year ended December 31, 2017. The expense estimate does not include the fees or expenses associated with the separate insurance accounts, and if such charges were included, your costs would have been higher.

| | | | | | | | | | | | | | | | | | |

| | | | | Beginning

Account Value

July 1,

2017 | | | Ending

Account Value

December 31,

2017 | | | Annualized

Expense

Ratio | | | Expenses

Paid

During

Period* | |

Duff & Phelps International Series | | Class A | | $ | 1,000.00 | | | $ | 1,088.00 | | | | 1.18 | % | | $ | 6.21 | |

| | Class I | | | 1,000.00 | | | | 1,089.60 | | | | 0.93 | | | | 4.90 | |

Duff & Phelps Real Estate Securities Series | | Class A | | | 1,000.00 | | | | 1,043.20 | | | | 1.16 | | | | 5.97 | |

| | Class I | | | 1,000.00 | | | | 1,044.60 | | | | 0.91 | | | | 4.69 | |

KAR Capital Growth Series | | Class A | | | 1,000.00 | | | | 1,126.40 | | | | 1.03 | | | | 5.52 | |

KAR Small-Cap Growth Series | | Class A | | | 1,000.00 | | | | 1,194.80 | | | | 1.19 | | | | 6.58 | |

| | Class I | | | 1,000.00 | | | | 1,196.20 | | | | 0.94 | | | | 5.20 | |

KAR Small-Cap Value Series | | Class A | | | 1,000.00 | | | | 1,123.70 | | | | 1.20 | | | | 6.42 | |

Newfleet Multi-Sector Intermediate Bond Series | | Class A | | | 1,000.00 | | | | 1,024.70 | | | | 0.93 | | | | 4.75 | |

| | Class I | | | 1,000.00 | | | | 1,026.00 | | | | 0.68 | | | | 3.47 | |

Rampart Enhanced Core Equity Series | | Class A | | | 1,000.00 | | | | 1,126.70 | | | | 0.98 | | | | 5.25 | |

Rampart Equity Trend Series | | Class A | | | 1,000.00 | | | | 1,108.00 | | | | 1.70 | | | | 9.03 | |

| | Class I | | | 1,000.00 | | | | 1,109.60 | | | | 1.45 | | | | 7.71 | |

Strategic Allocation Series | | Class A | | | 1,000.00 | | | | 1,077.00 | | | | 0.98 | | | | 5.13 | |

| * | Expenses are equal to the relevant Series’ annualized expense ratio, which is net of waived fees and reimbursed expenses, if applicable, multiplied by the average account value over the period, multiplied by the number of days (184) expenses were accrued in the most recent fiscal half-year, then divided by 365 to reflect the one-half year period. Exceptions noted below. |

A Series may invest in other funds, and the annualized expense ratios noted above do not reflect fees and expenses associated with the underlying funds. If such fees and expenses had been included, the expenses would have been higher.

You can find more information about a Series’ expenses in the Financial Statements section that follows. For additional information on operating expenses and other shareholder costs, including contractual charges associated with the separate account, refer to the Series prospectus and the contract prospectus.

5

VIRTUS VARIABLE INSURANCE TRUST

Disclosure of Series Expenses (Unaudited) (Continued)

For the six-month period of July 1, 2017 to December 31, 2017

Hypothetical Example for Comparison Purposes

The accompanying table provides information about hypothetical account values and hypothetical expenses based on a Series’ actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not your Series’ actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in your Series and other funds. To do so, compare these 5% hypothetical examples with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the accompanying table are meant to highlight your ongoing costs only and do not reflect additional fees and expenses associated with the annuity or life insurance policy through which you invest. Therefore, the accompanying table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if the annuity or life insurance policy costs were included, your costs would have been higher. The calculations assume no shares were bought or sold during the period. Your actual costs may have been higher or lower, depending on the amount of your investment and the timing of any purchases or redemptions.

| | | | | | | | | | | | | | | | | | |

| | | | | Beginning

Account Value

July 1,

2017 | | | Ending

Account Value

December 31,

2017 | | | Annualized

Expense

Ratio | | | Expenses

Paid

During

Period* | |

Duff & Phelps International Series | | Class A | | $ | 1,000.00 | | | $ | 1,019.26 | | | | 1.18 | % | | $ | 6.01 | |

| | Class I | | | 1,000.00 | | | | 1,020.52 | | | | 0.93 | | | | 4.74 | |

Duff & Phelps Real Estate Securities Series | | Class A | | | 1,000.00 | | | | 1,019.36 | | | | 1.16 | | | | 5.90 | |

| | Class I | | | 1,000.00 | | | | 1,020.62 | | | | 0.91 | | | | 4.63 | |

KAR Capital Growth Series | | Class A | | | 1,000.00 | | | | 1,020.01 | | | | 1.03 | | | | 5.24 | |

KAR Small-Cap Growth Series | | Class A | | | 1,000.00 | | | | 1,019.21 | | | | 1.19 | | | | 6.06 | |

| | Class I | | | 1,000.00 | | | | 1,020.47 | | | | 0.94 | | | | 4.79 | |

KAR Small-Cap Value Series | | Class A | | | 1,000.00 | | | | 1,019.16 | | | | 1.20 | | | | 6.11 | |

Newfleet Multi-Sector Intermediate Bond Series | | Class A | | | 1,000.00 | | | | 1,020.52 | | | | 0.93 | | | | 4.74 | |

| | Class I | | | 1,000.00 | | | | 1,021.78 | | | | 0.68 | | | | 3.47 | |

Rampart Enhanced Core Equity Series | | Class A | | | 1,000.00 | | | | 1,020.27 | | | | 0.98 | | | | 4.99 | |

Rampart Equity Trend Series | | Class A | | | 1,000.00 | | | | 1,016.64 | | | | 1.70 | | | | 8.64 | |

| | Class I | | | 1,000.00 | | | | 1,017.90 | | | | 1.45 | | | | 7.37 | |

Strategic Allocation Series | | Class A | | | 1,000.00 | | | | 1,020.27 | | | | 0.98 | | | | 4.99 | |

| * | Expenses are equal to the relevant Series’ annualized expense ratio, which is net of waived fees and reimbursed expenses, if applicable, multiplied by the average account value over the period, multiplied by the number of days (184) expenses were accrued in the most recent fiscal half-year, then divided by 365 to reflect the one-half year period. Exceptions noted below. |

A Series may invest in other funds, and the annualized expense ratios noted above do not reflect fees and expenses associated with the underlying funds. If such fees and expenses had been included, the expenses would have been higher.

You can find more information about a Series’ expenses in the Financial Statements section that follows. For additional information on operating expenses and other shareholder costs, including contractual charges associated with the separate account, refer to the Series prospectus and the contract prospectus.

6

| | |

| Duff & Phelps International Series | | |

Series Summary (Unaudited)

Portfolio Manager Commentary by

Duff & Phelps Investment Management Co. (“Duff & Phelps”)

| ⬛ | | The Series is diversified and has an investment objective of high total return consistent with reasonable risk. There is no guarantee that the Series will meet its objective. |

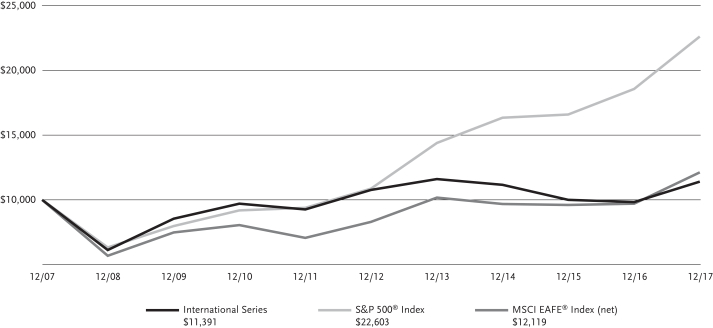

| ⬛ | | For the fiscal year ended December 31, 2017, the Series’ Class A shares at NAV returned 15.95% and Class I shares at NAV returned 16.17%. For the same period, the MSCI EAFE® Index (net), which serves as the Series’ broad-based and style-specific benchmark index appropriate for comparison, returned 25.03%. |

All performance figures assume reinvestment of distributions and exclude the effect of fees and expenses associated with the variable life insurance or annuity product through which you invest. Past performance is no guarantee of future results, and current performance may be higher or lower than the performance shown above. Investment return and principal value will fluctuate so your shares, when redeemed, may be worth more or less than their original cost. Please visit Virtus.com for performance data current to the most recent month-end.

How did the international equity markets perform during the fiscal year ended December 31, 2017?

| ⬛ | | International equity markets posted strong returns during each quarter of 2017, with the MSCI EAFE® Index (net) delivering a 25.03% return for the 12-month period. Equity markets worldwide displayed ongoing resilience on the back of continued global economic momentum. |

| ⬛ | | Geopolitical tensions, natural disasters, and political divisions within many countries were relegated to background noise in 2017 as economic momentum fueled persistent optimism across most major developed markets. |

What factors affected the Series’ performance during the fiscal year?

| ⬛ | | Both sector allocation and security selection detracted from the Series’ performance for the fiscal year ended December 31, 2017, with security selection having the greater impact. On a sector performance basis, all of the 11 market sectors posted positive returns, exemplifying the one-directional nature of international equity markets during the period. |

| ⬛ | | The Series’ consumer discretionary holdings had a challenging year, detracting 2.67% on a relative basis for the period primarily due to unfavorable security selection (particularly IMAX and Ctrip.com). The second largest detractor at the sector level was energy, due to both security selection (especially Technip) and the adverse effect of being overweight the sector as it lagged the index. The third largest detractor was consumer staples, due to security selection, although an underweight position in the sector was accretive as it and other defensive sectors lagged the market for the most part. |

| ⬛ | | On the positive side, the Series’ industrial sector investments contributed 1.02% to relative performance for the year, primarily due to favorable security selection (particularly Nidec and Airbus). The second largest contributor at the sector level was utilities, due to security selection (especially Veolia). The third largest contributor was information technology, due to being overweight the sector as it and other cyclical sectors led the market for the most part. |

| ⬛ | | While the Series’ positioning in the health care sector overall was not among the most impactful, it was notable in that the Series’ strongest relative contributor (ICON plc) and second biggest detractor (Allergan plc) were health care names. We reaped some benefit from being underweight the sector as a whole, as it underperformed, and the net overall detraction was fairly minimal compared to the impact of other sectors. |

| ⬛ | | Derivatives made a negative contribution to the Series’ performance. Specifically, a Japanese yen short forward currency contract detracted -0.83% from relative total return as the U.S. dollar weakened relative to the yen during the year. |

The preceding information is the opinion of portfolio management only through the end of the period of the report as stated on the cover. Any such opinions are subject to change at any time based upon market or other conditions and should not be relied upon as investment advice.

Equity Securities: The market price of equity securities may be adversely affected by financial market, industry, or issuer-specific events. Focus on a particular style or on small or medium-sized companies may enhance that risk.

Foreign & Emerging Markets: Investing internationally, especially in emerging markets, involves additional risks such as currency, political, accounting, economic, and market risk.

Derivatives: Investments in derivatives such as futures, options, forwards, and swaps may increase volatility or cause a loss greater than the principal investment.

For information regarding the indexes and certain investment terms, see the Key Investment Terms starting on page 2.

7

| | |

| Duff & Phelps International Series (Continued) | | |

Prospectus: For additional information on risks, please see the Series’ prospectus.

| | | | |

| |

| Asset Allocation | |

| |

The following table presents asset allocations within certain sectors as a percentage of total investments as of December 31, 2017. | |

Financials | | | 29 | % |

Industrials | | | 16 | |

Materials | | | 13 | |

Information Technology | | | 9 | |

Consumer Discretionary | | | 8 | |

Energy | | | 7 | |

Consumer Staples | | | 5 | |

Other (includes short-term investments) | | | 13 | |

| | | | | |

Total | | | 100 | % |

| | | | | |

For information regarding the indexes and certain investment terms, see the Key Investment Terms starting on page 2.

8

| | |

| Duff & Phelps International Series (Continued) | | |

| | | | | | | | | | | | | | | | | | | | |

| Average Annual Total Returns1 for periods ended 12/31/17 | | | | | | | |

| | | | | |

| | | 1 year | | | 5 years | | | 10 years | | | Since

Inception | | | Inception

Date | |

| Class A shares at NAV2 | | | 15.95 | % | | | 1.13 | % | | | 1.31 | % | | | — | | | | — | |

| Class I shares at NAV2 | | | 16.17 | | | | — | | | | — | | | | 0.05 | % | | | 4/30/13 | |

| S&P 500® Index* | | | 21.83 | | | | 15.79 | | | | 8.50 | | | | 14.04 | 4 | | | — | |

| MSCI EAFE® Index (net)* | | | 25.03 | | | | 7.90 | | | | 1.94 | | | | 6.16 | 4 | | | — | |

| Series Expense Ratios3: Class A shares: Gross 1.26%, Net 1.19%; Class I shares: Gross 1.01%, Net 0.94%. | | | | | |

Returns represent past performance which is no guarantee of future results. The investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Total return does not reflect expenses associated with the separate account such as the administrative fees, account charges and surrender charges, which if reflected, would reduce total return. Performance figures may reflect fee waivers and/or expense reimbursements. In the absence of fee waivers and/or expense reimbursements, the total return would have been lower. Please visit Virtus.com for performance data current to the most recent month-end.

| 1 | Total returns are historical and include changes in share price and the reinvestment of both dividends and capital gains distributions. |

| 2 | “NAV” (Net Asset Value) total returns do not reflect any fees or expenses associated with the separate insurance accounts. |

| 3 | The expense ratios of the Series, both net and gross, are set forth according to the prospectus for the Series effective May 1, 2017, as supplemented and revised, and may differ from the expense ratios disclosed in the Financial Highlights tables in this report. See the Financial Highlights for more current information. Net Expenses: Expenses reduced by a contractual waiver in effect through April 30, 2018. Gross Expenses: Do not reflect the effect of the contractual waiver. Expense ratios include fees and expenses associated with underlying funds. |

| 4 | The since inception index returns are from the inception date of Class I shares. |

| * | The MSCI EAFE® Index (net) is an appropriate broad-based index. The Series is no longer using the S&P 500® Index. |

Growth of $10,000 For periods ended 12/31

This chart assumes an initial investment of $10,000 made on December 31, 2007 for Class A shares. Returns shown include the reinvestment of all distributions at net asset value, and the change in share price for the stated period.

The indexes are unmanaged and not available for direct investment; therefore, their performance does not reflect the expenses associated with active management of an actual portfolio.

For information regarding the indexes and certain investment terms, see the Key Investment Terms starting on page 2.

9

| | |

| Duff & Phelps Real Estate Securities Series | | |

Series Summary (Unaudited)

Portfolio Manager Commentary by

Duff & Phelps Investment Management Co.

| ⬛ | | The Series is diversified and has investment objectives of capital appreciation and income with approximately equal emphasis. There is no guarantee that the Series will meet its objectives. |

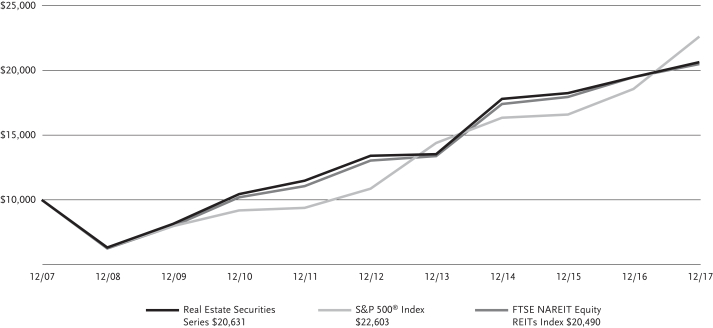

| ⬛ | | For the fiscal year ended December 31, 2017, the Series’ Class A shares at NAV returned 5.97% and Class I shares at NAV returned 6.25%. For the same period, the FTSE NAREIT Equity REITs Index, which serves as the Series’ broad-based and style-specific benchmark index appropriate for comparison, returned 5.23%. |

All performance figures assume reinvestment of distributions and exclude the effect of fees and expenses associated with the variable life insurance or annuity product through which you invest. Past performance is no guarantee of future results, and current performance may be higher or lower than the performance shown above. Investment return and principal value will fluctuate so your shares, when redeemed, may be worth more or less than their original cost. Please visit Virtus.com for performance data current to the most recent month-end.

How did the markets perform during the fiscal year ended December 31, 2017?

| ⬛ | | Equity markets, as measured by the S&P 500® Index, were quite strong during the Series’ fiscal year. |

| ⬛ | | U.S. REITs put up solid performance within real assets of 5.23%, as measured by the Series’ benchmark, the FTSE NAREIT Equity REITs Index. Cash flow and dividend growth were supportive, as were mergers and acquisitions (M&A) announcements within listed real estate, both in the U.S. and overseas, through the end of 2017. Private real estate funds had raised a significant amount of capital, which remained largely unspent, and were looking to purchase real estate from listed REITs, in part or in whole. Overall new supply remained contained, while there were some property sectors and markets in stronger positions on supply/demand dynamics than others. Certain sectors benefited from secular trends, such as industrial warehouses from e-commerce, as well as data centers, which provided an opportunity for security selection. |

| ⬛ | | Interest rate volatility picked up into the end of the fiscal year, and expectations grew of additional increases by the Federal Reserve (the Fed) in 2018 following three increases of 0.25% each in 2017 to normalize rates. |

| ⬛ | | At the end of the fiscal year, Congress was effective in passing tax reform, a material event and a notable fiscal stimulus. It is interesting to note that, following the global Financial Crisis of 2008, former Fed Chair Ben Bernanke called for a fiscal stimulus on top of a monetary one, but it was never implemented. The economic environment remained positive based on a number of macro factors, employment levels, and market returns. |

| ⬛ | | The S&P 500® Index had a good year. Corporate earnings lifted notably through the year and benefited from a weaker U.S. dollar, which declined roughly 10% as measured by the U.S. Dollar Index (DXY). The dollar’s weakness helped non-U.S. listed real estate outperform U.S. listed real estate in 2017. |

| ⬛ | | Central banks around the globe modified their quantitative easing programs during the fiscal year, and in some cases began to reduce the size of their balance sheets. The U.S. Fed is well ahead of the European Central Bank (ECB) in raising rates, tightening once in 2015, once in 2016, and three times in 2017. Equity REITs had positive returns in each of those years. M&A appeared to be picking up as the Fed hiked in 2017, just as it did from June ’04 to ’06, when the Fed hiked 17 times for 0.25% each. During that time period, equity REITs put up positive returns. |

What factors affected the Series’ performance during the fiscal year?

| ⬛ | | For the fiscal year ended December 31, 2017, the Series benefited from security selection and property sector allocation, outperforming its benchmark. |

| ⬛ | | Within the U.S., the data centers, manufactured homes, and industrial property sectors delivered the best total returns over the last 12 months. Retail, namely shopping centers and regional malls, as well as diversified property were the most significant laggards. |

| ⬛ | | The most significant individual positive contributor to relative performance during the Series’ fiscal year was an underweight allocation to and security selection within healthcare, which lagged. Other contributors included security selection within office, which performed in line; an overweight allocation and security selection within industrial, which outperformed; and an overweight allocation and security selection within data centers, which also outperformed. |

| ⬛ | | The most significant detractor from relative performance during the Series’ fiscal year was an overweight allocation to and security selection within apartments, which lagged. This was followed by an overweight allocation to shopping centers, which lagged and was partially offset by security selection; a zero-weight to specialty, which outperformed; and security selection within single family home rentals, which outperformed and was partially offset by an overweight allocation. |

The preceding information is the opinion of portfolio management only through the end of the period of the report as stated on the cover. Any such opinions are subject to change at any time based upon market or other conditions and should not be relied upon as investment advice.

Equity Securities: The market price of equity securities may be adversely affected by financial market, industry, or issuer-specific events. Focus on a particular style or on small or medium-sized companies may enhance that risk.

Industry/Sector Concentration: A fund that focuses its investments in a particular industry or sector will be more sensitive to conditions that affect that industry or sector than a non-concentrated fund.

Real Estate: The Series may be negatively affected by factors specific to the real estate market, including interest rates, leverage, property, and management.

For information regarding the indexes and certain investment terms, see the Key Investment Terms starting on page 2.

10

| | |

| Duff & Phelps Real Estate Securities Series (Continued) | | |

Prospectus: For additional information on risks, please see the Series’ prospectus.

| | | | |

| |

| Asset Allocation | |

| |

The following table presents asset allocations within certain sectors as a percentage of total investments as of December 31, 2017. | |

Apartments | | | 17 | % |

Office | | | 16 | |

Industrials | | | 14 | |

Data Centers | | | 13 | |

Shopping Centers | | | 8 | |

Regional Malls | | | 7 | |

Self Storage | | | 6 | |

Other (includes short-term investments) | | | 19 | |

| | | | | |

Total | | | 100 | % |

| | | | | |

For information regarding the indexes and certain investment terms, see the Key Investment Terms starting on page 2.

11

| | |

| Duff & Phelps Real Estate Securities Series (Continued) |

| | | | | | | | | | | | | | | | | | | | |

| Average Annual Total Returns1 for periods ended 12/31/17 | | | | | | | | | | |

| | | | | |

| | | 1 year | | | 5 years | | | 10 years | | | Since

Inception | | | Inception

Date | |

| Class A shares at NAV2 | | | 5.97 | % | | | 9.00 | % | | | 7.51 | % | | | — | | | | — | |

| Class I shares at NAV2 | | | 6.25 | | | | — | | | | — | | | | 7.14 | % | | | 4/30/13 | |

| S&P 500® Index* | | | 21.83 | | | | 15.79 | | | | 8.50 | | | | 14.04 | 4 | | | — | |

| FTSE NAREIT Equity REITs Index* | | | 5.23 | | | | 9.46 | | | | 7.44 | | | | 6.83 | 4 | | | — | |

| Series Expense Ratios3: Class A shares: Gross 1.24%, Net 1.16%; Class I shares: Gross 0.99%, Net 0.91%. | | | | | |

Returns represent past performance which is no guarantee of future results. The investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Total return does not reflect expenses associated with the separate account such as the administrative fees, account charges and surrender charges, which if reflected, would reduce total return. Performance figures may reflect fee waivers and/or expense reimbursements. In the absence of fee waivers and/or expense reimbursements, the total return would have been lower. Please visit Virtus.com for performance data current to the most recent month-end.

| 1 | Total returns are historical and include changes in share price and the reinvestment of both dividends and capital gains distributions. |

| 2 | “NAV” (Net Asset Value) total returns do not reflect any fees or expenses associated with the separate insurance products. |

| 3 | The expense ratios of the Series, both net and gross, are set forth according to the prospectus for the Series effective May 1, 2017, as supplemented and revised, and may differ from the expense ratios disclosed in the Financial Highlights tables in this report. See the Financial Highlights for more current information. Net Expenses: Expenses reduced by a contractual waiver in effect through April 30, 2018. Gross Expenses: Do not reflect the effect of the contractual waiver. Expense ratios include fees and expenses associated with underlying funds. |

| 4 | The since inception index returns are from the inception date of Class I shares. |

| * | The FTSE NAREIT Equity REITs Index is an appropriate broad-based index. The Series is no longer using the S&P 500® Index. |

Growth of $10,000 For periods ended 12/31

This chart assumes an initial investment of $10,000 made on December 31, 2007 for Class A shares. Returns shown include the reinvestment of all distributions at net asset value, and the change in share price for the stated period.

The indexes are unmanaged and not available for direct investment; therefore, their performance does not reflect the expenses associated with active management of an actual portfolio.

For information regarding the indexes and certain investment terms, see the Key Investment Terms starting on page 2.

12

| | |

| KAR Capital Growth Series | | |

Series Summary (Unaudited)

Portfolio Manager Commentary by

Kayne Anderson Rudnick Investment Management, LLC

| ⬛ | | The Series is diversified and has an investment objective of long-term growth of capital. There is no guarantee that the Series will meet its objective. |

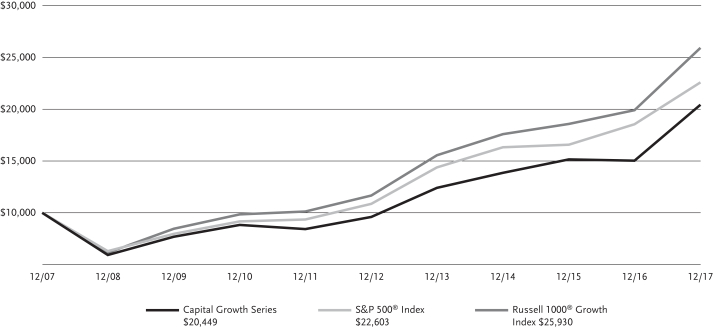

| ⬛ | | For the fiscal year ended December 31, 2017, the Series’ Class A shares at NAV returned 36.07%. For the same period, the Russell 1000® Growth Index, which serves as the Series’ broad-based and style-specific benchmark index appropriate for comparison, returned 30.21%. |

All performance figures assume reinvestment of distributions and exclude the effect of fees and expenses associated with the variable life insurance or annuity product through which you invest. Past performance is no guarantee of future results, and current performance may be higher or lower than the performance shown above. Investment return and principal value will fluctuate so your shares, when redeemed, may be worth more or less than their original cost. Please visit Virtus.com for performance data current to the most recent month-end.

How did the market perform during the fiscal year ended December 31, 2017?

| ⬛ | | The year 2017 was a banner one for global equities: The S&P 500® Index returned 21.83%; foreign markets, as measured by the MSCI EAFE® Index (net), gained 25.03%; and emerging markets stocks, as measured by the MSCI Emerging Markets Index (net), climbed 37.28%. Growth stocks across the market-cap spectrum outperformed value stocks for the year, the opposite of what occurred in 2016. |

| ⬛ | | The Russell 1000® Growth Index rose 30.21% in 2017. The utilities sector was by far the best performer, with a gain of 70.80%. Other contributing sectors included information technology (+41.55%), financials (+31.63%) and industrials (+31.42%). Energy was the only negative sector in the index for the year, down 6.70%. |

What factors affected the Series’ performance during the fiscal year?

| ⬛ | | The Series outperformed the Russell 1000® Growth Index for the year. The Series benefited from positive stock selection in the information technology and consumer staples sectors. Negative stock selection in health care and an overweight in energy detracted from performance. |

| ⬛ | | Stocks that contributed the most to the year’s gains were Facebook and Alibaba Group Holding. |

| ⬛ | | Facebook continued to grow advertising revenue and take share in the online digital marketing space. The company delivered an unprecedented global reach of about 30% of the earth’s population to advertisers in a measurable way. Facebook’s user growth remained stunning despite its scale, and Instagram’s Stories format had resounding success in fighting off competitors like Snapchat. |

| ⬛ | | Alibaba’s two marketplaces, Taobao and Tmall.com, combine to form the largest online commerce company in the world. Management has committed to a number of social initiatives to further improve mobile monetization over time. Alibaba’s marketplaces have huge network effects, and the company made efforts to foster the ecosystem with investments in payments and logistics partnerships. Taobao, in particular, has become a destination for consumers, merchants, and key opinion leaders to interact and engage in what Alibaba calls social commerce. E-commerce penetration, mobile usage, and growth in Chinese consumer spending power were all durable long-term tailwinds benefitting the company during the fiscal period. Alibaba has attempted to seize the opportunity by using data to improve targeting and increasingly consummating transactions through Alipay, its leading mobile payment offering. |

| ⬛ | | Positions that detracted the most from performance were Bristol-Myers Squibb and Schlumberger. |

| ⬛ | | Bristol-Myers dominated the initial immuno-oncology (I/O) market, securing a market share over 80%. The company is working on combination therapies with a broad set of checkpoint inhibitors to treat cancer. However, a failed trial in first-line lung cancer and positive results from competitors led analysts to adjust assumptions for Bristol’s ultimate market share and pricing power. When Bristol’s back-up plan also fell through and left the company potentially years behind competitors, we exited our position. |

| ⬛ | | Schlumberger has historically traded at a premium due to its technological prowess, scale, and efficiency. However, its shares underperformed peers during the fiscal year due to its exposure to late-cycle offshore and international customers rather than the faster-growing North American shale basins. Schlumberger’s business also became more capital intensive as it took ownership stakes in many of the fields alongside its operating customers. After trimming our position in April, we exited the name in July of 2017. |

The preceding information is the opinion of portfolio management only through the end of the period of the report as stated on the cover. Any such opinions are subject to change at any time based upon market or other conditions and should not be relied upon as investment advice.

Equity Securities: The market price of equity securities may be adversely affected by financial market, industry, or issuer-specific events. Focus on a particular style or on small or medium-sized companies may enhance that risk.

Limited Number of Investments: Because the Series has a limited number of securities, it may be more susceptible to factors adversely affecting its securities than a less concentrated fund.

For information regarding the indexes and certain investment terms, see the Key Investment Terms starting on page 2.

13

| | |

| KAR Capital Growth Series (Continued) | | |

Industry/Sector Concentration: A fund that focuses its investments in a particular industry or sector will be more sensitive to conditions that affect that industry or sector than a non-concentrated fund.

Prospectus: For additional information on risks, please see the Series’ prospectus.

| | | | |

| |

| Asset Allocation | |

| |

The following table presents asset allocations within certain sectors as a percentage of total investments as of December 31, 2017. | |

Information Technology | | | 42 | % |

Consumer Discretionary | | | 24 | |

Health Care | | | 8 | |

Industrials | | | 7 | |

Financials | | | 6 | |

Consumer Staples | | | 6 | |

Energy | | | 5 | |

Other (includes short-term investment) | | | 2 | |

| | | | | |

Total | | | 100 | % |

| | | | | |

For information regarding the indexes and certain investment terms, see the Key Investment Terms starting on page 2.

14

| | |

| KAR Capital Growth Series (Continued) | | |

| | | | | | | | | | | | |

| Average Annual Total Returns1 for periods ended 12/31/17 | |

| | | |

| | | 1 year | | | 5 years | | | 10 years | |

| Class A shares at NAV2 | | | 36.07 | % | | | 16.34 | % | | | 7.42 | % |

| S&P 500® Index* | | | 21.83 | | | | 15.79 | | | | 8.50 | |

| Russell 1000® Growth Index* | | | 30.21 | | | | 17.33 | | | | 10.00 | |

| Series Expense Ratios3: Class A shares: Gross 1.17%, Net 1.03%. | |

Returns represent past performance which is no guarantee of future results. The investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Total return does not reflect expenses associated with the separate account such as the administrative fees, account charges and surrender charges, which if reflected, would reduce total return. Performance figures may reflect fee waivers and/or expense reimbursements. In the absence of fee waivers and/or expense reimbursements, the total return would have been lower. Please visit Virtus.com for performance data current to the most recent month-end.

| 1 | Total returns are historical and include changes in share price and the reinvestment of both dividends and capital gains distributions. |

| 2 | “NAV” (Net Asset Value) total returns do not reflect any fees or expenses associated with the separate insurance accounts. |

| 3 | The expense ratios of the Series, both net and gross, are set forth according to the prospectus for the Series effective May 1, 2017, as supplemented and revised, and may differ from the expense ratios disclosed in the Financial Highlights tables in this report. See the Financial Highlights for more current information. Net Expenses: Expenses reduced by a contractual waiver in effect through April 30, 2018. Gross Expenses: Do not reflect the effect of the contractual waiver. Expense ratios include fees and expenses associated with underlying funds. |

| * | The Russell 1000® Growth Index is an appropriate broad-based index. The Series is no longer using the S&P 500® Index. |

Growth of $10,000 For periods ended 12/31

This chart assumes an initial investment of $10,000 made on December 31, 2007 for Class A shares. Returns shown include the reinvestment of all distributions at net asset value, and the change in share price for the stated period.

The indexes are unmanaged and not available for direct investment; therefore, their performance does not reflect the expenses associated with active management of an actual portfolio.

For information regarding the indexes and certain investment terms, see the Key Investment Terms starting on page 2.

15

| | |

| KAR Small-Cap Growth Series | | |

Series Summary (Unaudited)

Portfolio Manager Commentary by

Kayne Anderson Rudnick Investment Management, LLC

| ⬛ | | The Series is diversified and has an investment objective of long-term capital growth. There is no guarantee that the Series will meet its objective. |

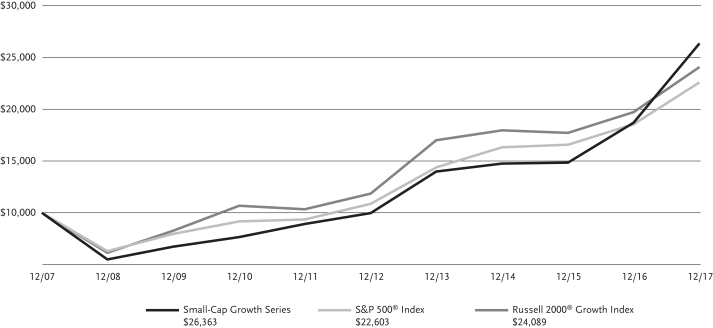

| ⬛ | | For the fiscal year ended December 31, 2017, the Series’ Class A shares at NAV returned 40.85% and Class I shares at NAV returned 41.16%. For the same period, the Russell 2000® Growth Index, which serves as the Series’ broad-based and style-specific benchmark index appropriate for comparison, returned 22.17%. |

All performance figures assume reinvestment of distributions and exclude the effect of fees and expenses associated with the variable life insurance or annuity product through which you invest. Past performance is no guarantee of future results, and current performance may be higher or lower than the performance shown above. Investment return and principal value will fluctuate so your shares, when redeemed, may be worth more or less than their original cost. Please visit Virtus.com for performance data current to the most recent month-end.

How did the market perform during the fiscal year ended December 31, 2017?

| ⬛ | | The year 2017 was a banner one for global equities: The S&P 500® Index returned 21.83%; foreign markets, as measured by the MSCI EAFE® Index (net), gained 25.03%; and emerging markets stocks, as measured by the MSCI Emerging Markets Index (net), climbed 37.28%. Growth stocks across the market-cap spectrum outperformed value stocks for the year, the opposite of what occurred in 2016. |

| ⬛ | | The Russell 2000® Growth Index rose 22.17% in 2017. Health care was the best performing sector, gaining 37.34% following a down year in 2016. Other sectors that posted solid performance in 2017 included technology (+21.87%), materials and processing (+19.92%), and consumer discretionary (+19.80%). Energy was the only negative sector in the index for the year, down 15.30%. |

What factors affected the Series’ performance during the fiscal year?

| ⬛ | | The Series outperformed the Russell 2000® Growth Index for the year. From a sector perspective, returns were largely driven by positive stock selection in the technology and consumer discretionary sectors. Performance was hurt by an underweight in health care. |

| ⬛ | | From an individual stock perspective, names that contributed the most to performance were Autohome and Ollie’s Bargain Outlet Holdings. |

| ⬛ | | Autohome’s share price increased meaningfully during 2017 as the company refined its strategy and exited a money-losing new car transaction business. This allowed the strong profitability of its core business to re-emerge, and translated into double-digit growth in revenue and earnings per share for the trailing 12 months. Autohome’s financial results also benefited from the ongoing secular shift of advertising budgets from traditional to online media. Given Autohome’s strong competitive positioning, improved capital allocation, and the expected long-term growth of the Chinese car market, the Fund remained invested in the business as of the end of the period. |

| ⬛ | | Throughout 2017, Ollie’s continued to defy the doom and gloom in retail and deliver healthy same-store sales growth and margins. The company focused on delivering best-in-class closeout deals, and as it grew, it continued to be the first choice for vendors looking to unload merchandise. The company slowly tilted inventory toward consumables, which helped to increase repeat purchases, as customers saw Ollie’s as more than just a once-a-year, deal-hunting adventure. |

| ⬛ | | Names that detracted the most from performance were Shutterstock and Abaxis. |

| ⬛ | | Shutterstock’s stock price had rebounded in the first half of 2016 as concerns regarding the competitive threat from Adobe’s new stock photo offering abated. However, a meaningful slowdown in revenue growth over the next two quarters sent the share price lower. Our original investment thesis was based on the network effects of Shutterstock’s core stock photo marketplace business. Even at lower growth rates, that marketplace business was profitable and valuable. Unfortunately, management sought growth by investing capital in other parts of the company where Shutterstock’s competitive advantage was less clear. Thus, we sold the Series’ position in early 2017. |

| ⬛ | | Abaxis saw its shares fall after experiencing a weak sales quarter as its veterinary business grew only slightly while the medical business declined due to distributor de-stocking. The company ramped up its research and development (R&D) efforts in an effort to drive the top line, but those efforts did not bear fruit in 2017. The company’s solid balance sheet and high consumables mix kept the Series as a shareholder through the end of the period. |

The preceding information is the opinion of portfolio management only through the end of the period of the report as stated on the cover. Any such opinions are subject to change at any time based upon market or other conditions and should not be relied upon as investment advice.

Equity Securities: The market price of equity securities may be adversely affected by financial market, industry, or issuer-specific events. Focus on a particular style or on small or medium-sized companies may enhance that risk.

Limited Number of Investments: Because the Series has a limited number of securities, it may be more susceptible to factors adversely affecting its securities than a less concentrated fund.

Industry/Sector Concentration: A fund that focuses its investments in a particular industry or sector will be more sensitive to conditions that affect that industry or sector than a non-concentrated fund.

For information regarding the indexes and certain investment terms, see the Key Investment Terms starting on page 2.

16

| | |

| KAR Small-Cap Growth Series (Continued) | | |

Prospectus: For additional information on risks, please see the Series’ prospectus.

| | | | |

| |

| Asset Allocation | |

| |

The following table presents asset allocations within certain sectors as a percentage of total investments as of December 31, 2017. | |

Information Technology | | | 28 | % |

Industrials | | | 19 | |

Consumer Discretionary | | | 18 | |

Financials | | | 17 | |

Health Care | | | 8 | |

Consumer Staples | | | 6 | |

Short-Term Investments | | | 4 | |

| | | | | |

Total | | | 100 | % |

| | | | | |

For information regarding the indexes and certain investment terms, see the Key Investment Terms starting on page 2.

17

| | |

| KAR Small-Cap Growth Series (Continued) | | |

| | | | | | | | | | | | | | | | | | | | |

| Average Annual Total Returns1 for periods ended 12/31/17 | | | | | | | | | | |

| | | | | |

| | | 1 year | | | 5 years | | | 10 years | | | Since

Inception | | | Inception

Date | |

| Class A shares at NAV2 | | | 40.85 | % | | | 21.45 | % | | | 10.18 | % | | | — | | | | — | |

| Class I shares at NAV2 | | | 41.16 | | | | — | | | | — | | | | 20.68 | % | | | 4/30/13 | |

| S&P 500® Index* | | | 21.83 | | | | 15.79 | | | | 8.50 | | | | 14.04 | 4 | | | — | |

| Russell 2000® Growth Index* | | | 22.17 | | | | 15.21 | | | | 9.19 | | | | 13.48 | 4 | | | — | |

| Series Expense Ratios3: Class A shares: Gross 1.36%, Net 1.19%; Class I shares: Gross 1.11%, Net 0.94%. | |

Returns represent past performance which is no guarantee of future results. The investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Total return does not reflect expenses associated with the separate account such as the administrative fees, account charges and surrender charges, which if reflected, would reduce total return. Performance figures may reflect fee waivers and/or expense reimbursements. In the absence of fee waivers and/or expense reimbursements, the total return would have been lower. Please visit Virtus.com for performance data current to the most recent month-end.

| 1 | Total returns are historical and include changes in share price and the reinvestment of both dividends and capital gains distributions. |

| 2 | “NAV” (Net Asset Value) total returns do not reflect any fees or expenses associated with the separate insurance products. |

| 3 | The expense ratios of the Series, both net and gross, are set forth according to the prospectus for the Series effective May 1, 2017, as supplemented and revised, and may differ from the expense ratios disclosed in the Financial Highlights tables in this report. See the Financial Highlights for more current information. Net Expenses: Expenses reduced by a contractual waiver in effect through April 30, 2018. Gross Expenses: Do not reflect the effect of the contractual waiver. Expense ratios include fees and expenses associated with underlying funds. |

| 4 | The since inception index returns are from the inception date of Class I shares. |

| * | The Russell 2000® Growth Index is an appropriate broad-based index. The Series is no longer using the S&P 500® Index. |

Growth of $10,000 For periods ended 12/31

This chart assumes an initial investment of $10,000 made on December 31, 2007 for Class A shares. Returns shown include the reinvestment of all distributions at net asset value, and the change in share price for the stated period.

The indexes are unmanaged and not available for direct investment; therefore, their performance does not reflect the expenses associated with active management of an actual portfolio.

For information regarding the indexes and certain investment terms, see the Key Investment Terms starting on page 2.

18

| | |

| KAR Small-Cap Value Series | | |

Series Summary (Unaudited)

Portfolio Manager Commentary by

Kayne Anderson Rudnick Investment Management, LLC

| ⬛ | | The Series is diversified and has an investment objective of long-term capital appreciation. There is no guarantee that the Series will meet its objective. |

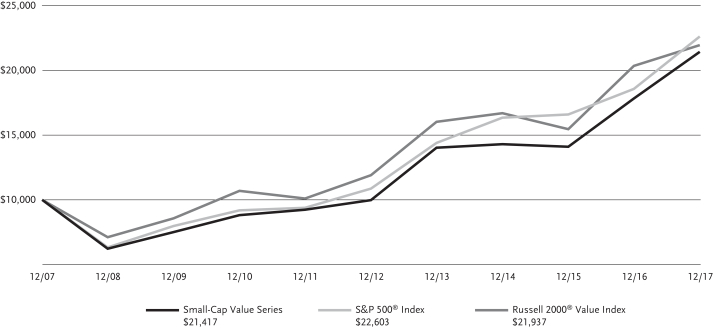

| ⬛ | | For the fiscal year ended December 31, 2017, the Series’ Class A shares at NAV returned 20.16%. For the same period, the Russell 2000® Value Index, which serves as the Series’ broad-based and style-specific benchmark index appropriate for comparison, returned 7.84%. |

All performance figures assume reinvestment of distributions and exclude the effect of fees and expenses associated with the variable life insurance or annuity product through which you invest. Past performance is no guarantee of future results, and current performance may be higher or lower than the performance shown above. Investment return and principal value will fluctuate so your shares, when redeemed, may be worth more or less than their original cost. Please visit Virtus.com for performance data current to the most recent month-end.

How did the market perform during the fiscal year ended December 31, 2017?

| ⬛ | | The year 2017 was a banner one for global equities: The S&P 500® Index returned 21.83%; foreign markets, as measured by the MSCI EAFE® Index (net), gained 25.03%; and emerging markets stocks, as measured by the MSCI Emerging Markets Index (net), climbed 37.28%. Growth stocks across the market-cap spectrum outperformed value stocks for the year, the opposite of what occurred in 2016. |

| ⬛ | | The Russell 2000® Value Index rose 7.84% in 2017. Health care and producer durables were the best performing sectors, returning 30.75% and 18.79%, respectively. Energy was the worst performing sector, down 17.46%, followed by consumer staples, which was down 5.33%. |

What factors affected the Series’ performance during the fiscal year?

| ⬛ | | The Series outperformed the Russell 2000® Value Index for the year. By sector, performance was driven by positive stock selection in the consumer staples, financial services, and producer durables sectors. Gains were offset by the effects of negative stock selection in health care. |

| ⬛ | | Companies that contributed the most to performance were SiteOne Landscape Supply and National Beverage Corp. |

| ⬛ | | SiteOne continued to consolidate the industry and saw accelerating organic daily sales growth. With the company’s increased scale and initiatives such as improving its supply chain, SiteOne was able to expand gross margins during the year. |

| ⬛ | | While National Beverage’s carbonated soft drink brands were weak like the rest of the industry, these declines were more than offset by growth in the company’s sparkling water portfolio, particularly the LaCroix brand. LaCroix’s sales grew at a rapid clip over the past several years as the brand gained additional points of distribution. As a result, National Beverage grew its consolidated revenue and profits by double digits over the past 12 months. The company recently launched a new Shasta-branded line of flavored sparkling water. |

| ⬛ | | Stocks that detracted the most from performance were Sally Beauty Holdings and Cass Information Systems, Inc. |

| ⬛ | | Throughout the year, Sally Beauty Supply, one of the two core segments of Sally Beauty Holdings, struggled to drive positive traffic into stores. The core business underwent a major transformation in terms of look, branding, service, and assortment. Sally also tinkered with its loyalty program, with plans to launch chain-wide in 2018. The company took price cuts on certain products in an effort to drive more traffic to its stores and maintain a more consistent value image. The professional segment had better results, with some execution missteps when it came to promotions. |

| ⬛ | | Although Cass’s shares lagged, driven by the persistently low interest rate environment, the company was a solid generator of free cash flow, returning excess cash to shareholders in the form of regular cash dividends (paid continuously since 1934), opportunistic stock dividends, and sizeable share repurchases. |

The preceding information is the opinion of portfolio management only through the end of the period of the report as stated on the cover. Any such opinions are subject to change at any time based upon market or other conditions and should not be relied upon as investment advice.

Equity Securities: The market price of equity securities may be adversely affected by financial market, industry, or issuer-specific events. Focus on a particular style or on small or medium-sized companies may enhance that risk.

Limited Number of Investments: Because the Series has a limited number of securities, it may be more susceptible to factors adversely affecting its securities than a less concentrated fund.

Industry/Sector Concentration: A fund that focuses its investments in a particular industry or sector will be more sensitive to conditions that affect that industry or sector than a non-concentrated fund.

For information regarding the indexes and certain investment terms, see the Key Investment Terms starting on page 2.

19

| | |

| KAR Small-Cap Value Series (Continued) | | |

Prospectus: For additional information on risks, please see the Series’ prospectus.

| | | | |

| |

| Asset Allocation | |

| |

The following table presents asset allocations within certain sectors as a percentage of total investments as of December 31, 2017. | |

Industrials | | | 21 | % |

Financials | | | 16 | |

Information Technology | | | 16 | |

Consumer Discretionary | | | 15 | |

Real Estate | | | 11 | |

Consumer Staples | | | 6 | |

Health Care | | | 6 | |

Other (includes short-term investments) | | | 9 | |

| | | | | |

Total | | | 100 | % |

| | | | | |

For information regarding the indexes and certain investment terms, see the Key Investment Terms starting on page 2.

20

| | |

| KAR Small-Cap Value Series (Continued) | | |

| | | | | | | | | | | | |

| Average Annual Total Returns1 for periods ended 12/31/17 | |

| | | |

| | | 1 year | | | 5 years | | | 10 years | |

| Class A shares at NAV2 | | | 20.16 | % | | | 16.54 | % | | | 7.91 | % |

| S&P 500® Index* | | | 21.83 | | | | 15.79 | | | | 8.50 | |

| Russell 2000® Value Index* | | | 7.84 | | | | 13.01 | | | | 8.17 | |

| Series Expense Ratios3: Class A shares: Gross 1.39%, Net 1.20%. | |

Returns represent past performance which is no guarantee of future results. The investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Total return does not reflect expenses associated with the separate account such as the administrative fees, account charges and surrender charges, which if reflected, would reduce total return. Performance figures may reflect fee waivers and/or expense reimbursements. In the absence of fee waivers and/or expense reimbursements, the total return would have been lower. Please visit Virtus.com for performance data current to the most recent month-end.

| 1 | Total returns are historical and include changes in share price and the reinvestment of both dividends and capital gains distributions. |

| 2 | “NAV” (Net Asset Value) total returns do not reflect any fees or expenses associated with the separate insurance accounts. |

| 3 | The expense ratios of the Series, both net and gross, are set forth according to the prospectus for the Series effective May 1, 2017, as supplemented and revised, and may differ from the expense ratios disclosed in the Financial Highlights tables in this report. See the Financial Highlights for more current information. Net Expenses: Expenses reduced by a contractual waiver in effect through April 30, 2018. Gross Expenses: Do not reflect the effect of the contractual waiver. Expense ratios include fees and expenses associated with underlying funds. |

| * | The Russell 2000® Value Index is an appropriate broad-based index. The Series is no longer using the S&P 500® Index. |

Growth of $10,000 For periods ended 12/31

This chart assumes an initial investment of $10,000 made on December 31, 2007 for Class A shares. Returns shown include the reinvestment of all distributions at net asset value, and the change in share price for the stated period.

The indexes are unmanaged and not available for direct investment; therefore, their performance does not reflect the expenses associated with active management of an actual portfolio.

For information regarding the indexes and certain investment terms, see the Key Investment Terms starting on page 2.

21

|

| Newfleet Multi-Sector Intermediate Bond Series |

Series Summary (Unaudited)

Portfolio Manager Commentary by

Newfleet Asset Management, LLC

| ⬛ | | The Series is diversified and has an investment objective of long-term total return. There is no guarantee that the Series will meet its objective. |

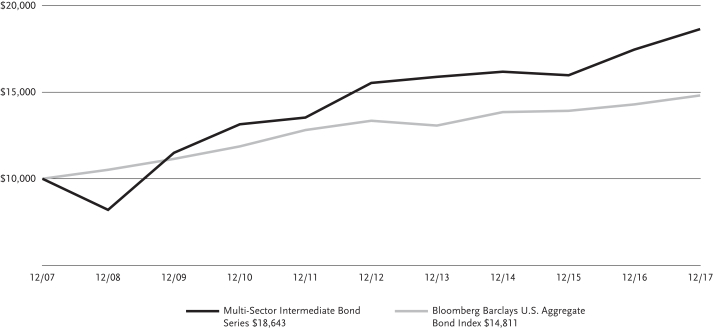

| ⬛ | | For the fiscal year ended December 31, 2017, the Series’ Class A shares at NAV returned 6.72% and Class I shares at NAV returned 7.00%. For the same period, the Bloomberg Barclays U.S. Aggregate Bond Index, which serves as the broad-based and style-specific benchmark index appropriate for comparison, returned 3.54%. |

All performance figures assume reinvestment of distributions and exclude the effect of fees and expenses associated with the variable life insurance or annuity product through which you invest. Past performance is no guarantee of future results, and current performance may be higher or lower than the performance shown above. Investment return and principal value will fluctuate so your shares, when redeemed, may be worth more or less than their original cost. Please visit Virtus.com for performance data current to the most recent month-end.

How did the markets perform during the fiscal year ended December 31, 2017?

Most spread sectors outperformed U.S. Treasuries during the fiscal year ended December 31, 2017. The global growth outlook remained favorable and the search for yield persisted through the end of the fiscal year. Within most fixed income sectors, longer duration and lower quality assets were key drivers of performance.

The positive tone of the market that continued after the surprise outcome of the U.S. presidential election faced numerous challenges over the fiscal year. Geopolitical tensions with North Korea, continued gridlock in Washington, moderate volatility in oil prices, and major weather events such as Hurricane Harvey caused periods of weakness within spread sectors. However, these periods were short-lived as investors bought into any meaningful dip in prices, quickly pushing prices higher.

As anticipated, the Federal Reserve (the Fed) raised its target rate 0.25% on three separate occasions during the last 12 months to a range of 1.25% to 1.50%. During its September 2017 meeting, the Fed announced the start of its balance sheet reduction plan.

Over the 12 months ended December 31, 2017, short-term interest rates increased while longer-term rates decreased. This was due to the Fed rate hikes and U.S. inflation data that was generally below expectations.

What factors affected the Fund’s performance during the fiscal year?

The underperformance of U.S. Treasuries relative to most fixed income spread sectors was the key driver of the Fund’s outperformance for the fiscal year ended December 31, 2017. Among fixed income sectors, the Fund’s allocations to corporate high yield, emerging markets high yield, and high quality Yankee bonds were the largest positive contributors to performance for the fiscal year.

During the fiscal year, the Fund’s allocation to high yield bank loans was the largest detractor from performance. Valuations in the sector remained attractive on a risk-adjusted relative basis, and warranted strategic allocation, especially given the short duration nature of the asset class in a rising rate environment.

The preceding information is the opinion of portfolio management only through the end of the period of the report as stated on the cover. Any such opinions are subject to change at any time based upon market or other conditions and should not be relied upon as investment advice.

Credit & Interest: Debt securities are subject to various risks, the most prominent of which are credit and interest rate risk. The issuer of a debt security may fail to make interest and/or principal payments. Values of debt securities may rise or fall in response to changes in interest rates, and this risk may be enhanced with longer-term maturities.

Foreign & Emerging Markets: Investing internationally, especially in emerging markets, involves additional risks such as currency, political, accounting, economic, and market risk.