UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT

OF

REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-4526

Name of Registrant: Vanguard Quantitative Funds

Address of Registrant:

P.O. Box 2600

Valley Forge, PA 19482

Name and address of agent for service:

Heidi Stam, Esquire

P.O. Box 876

Valley Forge, PA 19482

Registrant’s telephone number, including area code: (610) 669-1000

Date of fiscal year end: September 30

Date of reporting period: October 1, 2011 – March 31, 2012

Item 1: Reports to Shareholders

|

|

| Semiannual Report | March 31, 2012 |

| |

| Vanguard Growth and Income Fund |

> For the six months ended March 31, Vanguard Growth and Income Fund returned nearly 27%.

> For the period, the fund outpaced its benchmark, the S&P 500 Index, as well as its large-cap core fund peers.

> Strong stock selection within the information technology and consumer sectors boosted returns relative to the benchmark.

| |

| Contents | |

| Your Fund’s Total Returns. | 1 |

| Chairman’s Letter. | 2 |

| Advisors’ Report. | 6 |

| Fund Profile. | 10 |

| Performance Summary. | 11 |

| Financial Statements. | 12 |

| About Your Fund’s Expenses. | 31 |

| Glossary. | 33 |

Please note: The opinions expressed in this report are just that—informed opinions. They should not be considered promises or advice. Also, please keep in mind that the information and opinions cover the period through the date on the front of this report. Of course, the risks of investing in your fund are spelled out in the prospectus.

See the Glossary for definitions of investment terms used in this report.

About the cover: Vanguard was named for the HMS Vanguard, flagship of British Admiral Horatio Nelson. A ship—whose performance and safety depend on the work of all hands—has served as a fitting metaphor for the Vanguard crew as we strive to help clients reach their financial goals.

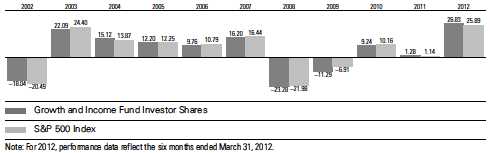

Your Fund’s Total Returns

| |

| Six Months Ended March 31, 2012 | |

| | Total |

| | Returns |

| Vanguard Growth and Income Fund | |

| Investor Shares | 26.83% |

| Admiral™ Shares | 26.91 |

| S&P 500 Index | 25.89 |

| Large-Cap Core Funds Average | 24.87 |

| Large-Cap Core Funds Average: Derived from data provided by Lipper Inc. |

| Admiral Shares carry lower expenses and are available to investors who meet certain account-balance requirements. |

| | | | |

| Your Fund’s Performance at a Glance | | | | |

| September 30, 2011, Through March 31, 2012 | | | | |

| | | | Distributions Per Share |

| | Starting | Ending | Income | Capital |

| | Share Price | Share Price | Dividends | Gains |

| Vanguard Growth and Income Fund | | | | |

| Investor Shares | $23.86 | $29.97 | $0.259 | $0.000 |

| Admiral Shares | 38.97 | 48.95 | 0.450 | 0.000 |

1

Chairman’s Letter

Dear Shareholder,

The first half of your fund’s fiscal year was, like last year’s, characterized by bullish sentiment in nearly all corners of the stock market. Benefiting from this upbeat environment, Vanguard Growth and Income Fund returned nearly 27% for the six months ended March 31, 2012, besting the return of its benchmark, the S&P 500 Index, and the average return of peer-group funds.

As I noted in our last report, Vanguard Growth and Income Fund adopted a multimanager approach on September 30, 2011. The fund’s new advisors, each of which manages approximately one-third of the fund’s assets, are D. E. Shaw Investment Management, L.L.C., Los Angeles Capital, and Vanguard’s Equity Investment Group.

The objective and investment strategy of the fund have not changed. The advisors have continued to follow a quantitative approach, using computer models to select a broadly diversified group of stocks that, as a whole, have investment characteristics similar to those of the S&P 500 Index but are hoped to provide a higher total return than that of the benchmark.

The advisors’ stock selections gained 10% or more in all ten market sectors for the period. Those selections outperformed in most market sectors, with particular success in the technology and consumer sectors.

2

A surge of optimism fueled a powerful global rally in stocks

During the past six months, optimism displaced the apprehension that had restrained stock prices through summer 2011. The broad U.S. stock market returned more than 26%. Markets abroad returned 15.37%. Investors’ good spirits reflected confidence that the slow, grinding economic expansion in the United States was at last gathering momentum, and that Europe’s debt crisis could be wrestled under control.

By the end of the period, however, that confidence had begun to evaporate in the face of ambiguous economic reports and renewed concern about Europe. The abrupt mood swing was consistent with the financial markets’ volatility since the 2008–2009 financial crisis.

For most bonds except munis, six-month returns were subdued

The broad taxable bond market produced a modest six-month return of 1.43%. In general, interest rates remained more or less steady at very low levels. In some segments of the bond market, however, yields crept lower still, boosting bond prices. The broad municipal bond market, for example, produced a solid six-month return of 3.91% as investors bid up muni prices.

As it has since December 2008, the Federal Reserve Board kept its target for the shortest-term interest rates between 0% and 0.25%. That policy has kept a tight lid on the returns available from money market funds and savings accounts.

| | | |

| Market Barometer | | | |

| |

| | | | Total Returns |

| | | Periods Ended March 31, 2012 |

| | Six | One | Five Years |

| | Months | Year | (Annualized) |

| Stocks | | | |

| Russell 1000 Index (Large-caps) | 26.27% | 7.86% | 2.19% |

| Russell 2000 Index (Small-caps) | 29.83 | -0.18 | 2.13 |

| Dow Jones U.S. Total Stock Market Index | 26.60 | 7.16 | 2.47 |

| MSCI All Country World Index ex USA (International) | 15.37 | -7.18 | -1.56 |

| |

| Bonds | | | |

| Barclays Capital U.S. Aggregate Bond Index (Broad | | | |

| taxable market) | 1.43% | 7.71% | 6.25% |

| Barclays Capital Municipal Bond Index (Broad | | | |

| tax-exempt market) | 3.91 | 12.07 | 5.42 |

| Citigroup Three-Month U.S. Treasury Bill Index | 0.00 | 0.05 | 1.11 |

| |

| CPI | | | |

| Consumer Price Index | 1.10% | 2.65% | 2.24% |

3

Technology and consumer stocks provided notable outperformance

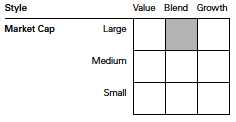

Vanguard Growth and Income Fund seeks to outperform the Standard & Poor’s 500 Index by investing in large-and mid-capitalization U.S. companies that reflect the index’s composition but which the fund’s advisors believe are poised to outperform.

This strategy was rewarded during the period as the fund’s return outpaced that of its benchmark and bested the average return of its peer funds by about 2 percentage points.

Information technology stocks, which made up about one-fifth of fund assets and represented the largest sector in the fund, provided the biggest margin of outperformance and about one-fourth of the fund’s return. Rising demand for computer hardware and IT services prompted investors to bid up the fund’s holdings by more than 34%, a return that was several percentage points higher than the return for the market overall.

The advisors’ selections in the consumer discretionary and consumer staples sectors also lifted relative performance. The fund’s internet and traditional retailers did well, as did several big-name food providers, as consumers gained confidence about the economy and increased their spending.

The fund’s holdings in financials offset some of its outperformance in other areas. While the fund’s portfolio of financial stocks outdistanced the overall market,

| | | |

| Expense Ratios | | | |

| Your Fund Compared With Its Peer Group | | | |

| | Investor | Admiral | Peer Group |

| | Shares | Shares | Average |

| Growth and Income Fund | 0.34% | 0.23% | 1.19% |

The fund expense ratios shown are from the prospectus dated January 26, 2012, and represent estimated costs for the current fiscal year. For the six months ended March 31, 2012, the fund’s annualized expense ratios were 0.36% for Investor Shares and 0.25% for Admiral Shares. The peer-group expense ratio is derived from data provided by Lipper Inc. and captures information through year-end 2011.

Peer group: Large-Cap Core Funds.

4

it trailed its counterpart in the index by several percentage points, providing the only notable drag on the fund’s relative showing.

More information about the advisors’ management of the fund can be found in the Advisors’ Report that follows this letter.

Stay focused on what you can control

As we tend to do after any period of strong performance, we caution shareholders that rising markets can’t be expected to continue indefinitely. Nor is it prudent to think that the lower volatility witnessed in much of the six-month period is a sign that the stress fractures in the global financial system have completely healed.

I note these concerns not to discourage you but as a way of helping you to maintain realistic expectations. We’re sure to experience stock downturns in the future, and when they occur, it will be essential to maintain a long-term perspective.

In addition to keeping a long-term view, it’s constructive to focus on two key elements of an investment plan: how much you’re investing and how long you’re investing for. This point was underscored in a recent Vanguard research paper, Penny Saved, Penny Earned, available at vanguard.com/research. The study found that retirement investors have a greater likelihood of reaching their goals by increasing their savings rate and savings time horizon. Those two factors, independently or together, can generally provide a higher chance of success than simply counting on the possibility of higher portfolio returns, the study’s authors concluded.

As always, Vanguard encourages you to create a long-term investment plan that includes a mix of stocks, bonds, and short-term investments that are appropriate for your goals and risk tolerance. A well-balanced portfolio can help cushion some of the market’s volatility while allowing you to participate in its long-term potential for growth. The Growth and Income Fund, which provides diversified, low-cost exposure to hundreds of large- and mid-cap U.S. stocks, can be a useful component in such a portfolio.

Thank you for your confidence in Vanguard.

Sincerely,

F. William McNabb III

Chairman and Chief Executive Officer

April 16, 2012

5

Advisors’ Report

Vanguard Growth and Income Fund’s Investor Shares returned 26.83% for the six months ended March 31. The Admiral Shares returned 26.91%. The S&P 500 Index returned 25.89%, while the average return of large-cap core funds was 24.87%.

Your fund is managed by three independent advisors, a strategy that enhances the fund’s diversification by providing exposure to distinct, yet complementary, investment approaches. It is not uncommon for different advisors to have different views about individual securities or the broader investment environment.

The advisors, the percentage of fund assets each manages, and brief descriptions of their investment strategies are presented in the table below. The advisors have also prepared a discussion of the investment environment that existed during the fiscal half-year and of how the portfolio’s positioning reflects this assessment. These comments were prepared on April 20, 2012.

| | | |

| Vanguard Growth and Income Fund Investment Advisors |

| |

| | Fund Assets Managed | |

| Investment Advisor | % | $ Million | Investment Strategy |

| D. E. Shaw Investment | 33 | 1,434 | Employs quantitative models that seek to capture |

| Management, L.L.C. | | | predominantly “bottom up” stock-specific return |

| | | | opportunities while aiming to keep the portfolio’s |

| | | �� | sector weights, size, and style characteristics similar to |

| | | | the benchmark. |

| Vanguard Equity Investment | 33 | 1,413 | Employs a quantitative, fundamental management |

| Group | | | approach, using models that assess valuation, growth |

| | | | prospects, management decisions, market sentiment, |

| | | | and earnings quality of companies versus their peers. |

| Los Angeles Capital | 32 | 1,400 | Employs a quantitative model that emphasizes stocks |

| | | | with characteristics investors are currently seeking and |

| | | | underweights stocks with characteristics investors are |

| | | | currently avoiding. As such, the portfolio’s sector |

| | | | weights, size, and style characteristics may differ |

| | | | modestly from the benchmark in a risk-controlled |

| | | | manner. |

| Cash Investments | 2 | 94 | These short-term reserves are invested by Vanguard in |

| | | | equity index products to simulate investments in |

| | | | stocks. Each advisor also may maintain a modest cash |

| | | | position. |

6

D. E. Shaw Investment Management, L.L.C.

Portfolio Manager:

Anthony Foley, Managing Director and Chief Investment Officer

Europe’s sovereign-debt crisis dominated perceptions about equity valuations in the early part of the fourth quarter of 2011. Europe’s banking sector seemed to be bolstered by the coordinated action of several central banks to boost liquidity. Over time, a steady drip of positive economic news suggesting that the U.S. economy was recovering—albeit slowly—began to outweigh negative news from Europe. This improving economic sentiment appeared to help drive equity markets higher in the second half of December, and that trend continued through the end of the first quarter of 2012 amid signs that the U.S. economy was gaining strength.

We evaluate our portfolio’s relative performance over the reporting period in light of three major factors: bottom-up stock selection; common risk factors such as value, growth, and capitalization; and industry groups.

In stock selection, Apple Inc., Priceline.com Inc., and JPMorgan Chase were among the best relative performers. An overweight position in International Flavors & Fragrances and underweight positions in Citigroup and Walgreen detracted the most from relative performance.

In our management of common risk factors, we received positive contributions, mostly in the first quarter of 2012, from a modest tilt toward low-dividend-yield stocks. The largest detractor was a tilt toward higher-volatility stocks. Overall, most of our portfolio’s performance was the product of many small, positive risk-factor exposures and relatively few negative ones.

Industry exposures subtracted slightly from the portfolio’s performance.

We believe equity markets are currently characterized by markedly lower levels of correlations among individual stocks than in recent years. Other things being equal, a reduction in correlations increases the potential for diversified, bottom-up stock selection strategies to outperform. At the same time, short-term stock market volatility is low by the standards of the last few years, even though many individual names have experienced substantial cumulative price movements in the past six months.

Substantial disappointment about the prospects for economic growth in the United States and a resurgence of concerns about the European debt crisis constitute clear risks in this environment. More generally, any macroeconomic shock that could significantly increase uncertainty or risk aversion among market participants could well have the same effect.

7

Los Angeles Capital

Portfolio Managers:

Thomas D. Stevens, CFA, Chairman and Principal

Hal W. Reynolds, CFA,

Chief Investment Officer and Principal

Over the six-month period, the market was led by significant gains in two risky sectors, technology and diversified financials. Apple’s shares rose 57% as its profits doubled from a year earlier, while large banks such as JPMorgan Chase and Bank of America, which were the primary beneficiaries of the Federal Reserve’s policy of maintaining low interest rates over the past four years, generated returns of 55% and 57%, respectively.

While much has been made of Apple’s quarterly profits soaring to $13.1 billion for the period that ended December 31, profit growth for the remainder of the market appears to have come to a standstill, with little to no growth over the past year. Despite slight improvements in the macroeconomic environment from small but steady employment gains, first-quarter equity returns were driven almost exclusively by a falling equity risk premium; market risk fell by one-third from year-end levels, and high-yield spreads, a measure of default risk, fell by more than 1 percentage point. Not surprisingly, risky stocks with weaker balance sheets were among the best performers during the quarter. With the significant rise in bank stocks, combined with low interest rates and contracting high-yield spreads, default risks appeared to be on the decline.

Over the six months, we maintained a bias toward higher-quality companies with strong balance sheets, above-average earnings growth, higher dividend yields, and positive earnings surprises. Overweight positions in technology names such as Apple, Microsoft, and Novellus contributed to performance. Conversely, our portfolio’s overweighting in higher-quality names with higher dividend yields, as well as underweight positions in Bank of America, JPMorgan Chase, and Citigroup, detracted from our relative results.

In an environment characterized by lower growth rates, we have maintained our bias toward larger-capitalization securities with higher earnings quality and higher dividend yields. As default risks have eased, we have increased our weighting in financials but remain underweighted in economically sensitive sectors such as materials and consumer cyclicals. The portfolio’s price/ earnings ratio and beta remain below those of the benchmark, while its earnings-per-share growth and dividend yield remain higher.

Vanguard Equity Investment Group

Portfolio Managers:

James D. Troyer, CFA, Principal

James P. Stetler, Principal

Michael R. Roach, CFA

Returns for the period for large-capitalization stocks were led by financial, information technology, and consumer discretionary companies. Telecommunications and utilities were the laggards. While all ten

8

sector groups provided positive returns, more economically sensitive sectors generally outperformed defensive ones.

Since the equity market started its current rally last fall, investors’ concerns regarding a double-dip recession, slowing growth in China, and Europe’s troubles appear to have eased. As a result of deep cost-cutting and conservatism, larger U.S. companies are coming out of the recession in the best fiscal health in recent years. They are more productive and more profitable, and have more cash and less leverage.

Although overall portfolio performance is affected by the macroeconomic factors described above, our approach to investing focuses on specific stock fundamentals. Specifically, we evaluate these five components:

1. Valuation, which measures the price we pay for earnings and cash flows.

2. Growth, which considers the growth of earnings.

3. Management decisions, an assessment of the actions taken by company management that signal its informed opinions of a firm’s future.

4. Market sentiment, which captures how investors reflect their opinions of a company through their activity in the market.

5. Quality, which measures balance-sheet strength and the sustainability of earnings.

For the fiscal half-year, our stock selection models produced mixed results. Our management-decisions, growth, and quality models were effective in distinguishing the outperformers from the underperformers. However, our market-sentiment and valuation indicators were not effective, and in fact detracted from our results.

Our selections within materials, energy, and health care added the most to our relative returns. In materials, CF Industries, Eastman Chemical, and International Paper were the largest contributors to our results.

In energy, Marathon Petroleum, National Oilwell, and Marathon Oil added the most to our relative returns. In health care, Aetna, Pfizer, and United Health were the largest contributors to our returns. Our selections were disappointing in financials; most of our underperformance in this sector resulted from underweight positions in Bank of America, Goldman Sachs, and MetLife.

9

Growth and Income Fund

Fund Profile

As of March 31, 2012

| | |

| Share-Class Characteristics | |

| | Investor | Admiral |

| | Shares | Shares |

| Ticker Symbol | VQNPX | VGIAX |

| Expense Ratio1 | 0.34% | 0.23% |

| 30-Day SEC Yield | 1.79% | 1.90% |

| | | |

| Portfolio Characteristics | | |

| | | | DJ |

| | | | U.S. Total |

| | | S&P 500 | Market |

| | Fund | Index | Index |

| Number of Stocks | 817 | 500 | 3,716 |

| Median Market Cap | $57.6B | $57.6B | $35.6B |

| Price/Earnings Ratio | 15.2x | 16.2x | 17.1x |

| Price/Book Ratio | 2.3x | 2.3x | 2.3x |

| Return on Equity | 19.4% | 19.6% | 18.1% |

| Earnings Growth Rate | 10.4% | 8.8% | 8.5% |

| Dividend Yield | 2.2% | 2.1% | 1.9% |

| Foreign Holdings | 0.1% | 0.0% | 0.0% |

| Turnover Rate | | | |

| (Annualized) | 100% | — | — |

| Short-Term Reserves | 0.6% | — | — |

| | | |

| Sector Diversification (% of equity exposure) |

| | | | DJ |

| | | | U.S. Total |

| | | S&P 500 | Market |

| | Fund | Index | Index |

| Consumer | | | |

| Discretionary | 11.6% | 10.9% | 12.0% |

| Consumer Staples | 10.5 | 10.8 | 9.4 |

| Energy | 10.8 | 11.2 | 10.5 |

| Financials | 16.2 | 14.9 | 15.9 |

| Health Care | 11.1 | 11.4 | 11.5 |

| Industrials | 10.2 | 10.6 | 11.0 |

| Information | | | |

| Technology | 21.6 | 20.5 | 19.8 |

| Materials | 2.8 | 3.5 | 4.0 |

| Telecommunication | | | |

| Services | 2.6 | 2.8 | 2.5 |

| Utilities | 2.6 | 3.4 | 3.4 |

| | |

| Volatility Measures | | |

| | | DJ |

| | | U.S. Total |

| | S&P 500 | Market |

| | Index | Index |

| R-Squared | 0.99 | 0.99 |

| Beta | 1.00 | 0.95 |

These measures show the degree and timing of the fund’s fluctuations compared with the indexes over 36 months.

| | |

| Ten Largest Holdings (% of total net assets) |

| Apple Inc. | Computer | |

| | Hardware | 5.0% |

| Exxon Mobil Corp. | Integrated Oil & | |

| | Gas | 2.7 |

| Microsoft Corp. | Systems Software | 2.3 |

| International Business | IT Consulting & | |

| Machines Corp. | Other Services | 2.1 |

| Pfizer Inc. | Pharmaceuticals | 2.1 |

| Philip Morris | | |

| International Inc. | Tobacco | 1.8 |

| JPMorgan Chase & Co. | Diversified Financial | |

| | Services | 1.8 |

| Chevron Corp. | Integrated Oil & | |

| | Gas | 1.7 |

| Procter & Gamble Co. | Household | |

| | Products | 1.6 |

| General Electric Co. | Industrial | |

| | Conglomerates | 1.6 |

| Top Ten | | 22.7% |

The holdings listed exclude any temporary cash investments and equity index products.

Investment Focus

1 The expense ratios shown are from the prospectus dated January 26, 2012, and represent estimated costs for the current fiscal year. For the six months ended March 31, 2012, the annualized expense ratios were 0.36% for Investor Shares and 0.25% for Admiral Shares.

10

Growth and Income Fund

Performance Summary

All of the returns in this report represent past performance, which is not a guarantee of future results that may be achieved by the fund. (Current performance may be lower or higher than the performance data cited. For performance data current to the most recent month-end, visit our website at vanguard.com/performance.) Note, too, that both investment returns and principal value can fluctuate widely, so an investor’s shares, when sold, could be worth more or less than their original cost. The returns shown do not reflect taxes that a shareholder would pay on fund distributions or on the sale of fund shares.

Fiscal-Year Total Returns (%): September 30, 2001, Through March 31, 2012

| | | | |

| Average Annual Total Returns: Periods Ended March 31, 2012 | | | |

| |

| | Inception | One | Five | Ten |

| | Date | Year | Years | Years |

| Investor Shares | 12/10/1986 | 9.16% | 0.38% | 3.55% |

| Admiral Shares | 5/14/2001 | 9.27 | 0.50 | 3.70 |

See Financial Highlights for dividend and capital gains information.

11

Growth and Income Fund

Financial Statements (unaudited)

Statement of Net Assets

As of March 31, 2012

The fund reports a complete list of its holdings in regulatory filings four times in each fiscal year, at the quarter-ends. For the second and fourth fiscal quarters, the lists appear in the fund’s semiannual and annual reports to shareholders. For the first and third fiscal quarters, the fund files the lists with the Securities and Exchange Commission on Form N-Q. Shareholders can look up the fund’s Forms N-Q on the SEC’s website at sec.gov. Forms N-Q may also be reviewed and copied at the SEC’s Public Reference Room (see the back cover of this report for further information).

| | | |

| | | | Market |

| | | | Value |

| | | Shares | ($000) |

| Common Stocks (97.5%)1 | | |

| Consumer Discretionary (11.3%) | |

| | Home Depot Inc. | 769,132 | 38,695 |

| * | priceline.com Inc. | 51,343 | 36,839 |

| | McDonald’s Corp. | 347,109 | 34,051 |

| | Time Warner Inc. | 660,136 | 24,920 |

| | Time Warner Cable Inc. | 279,600 | 22,787 |

| | Wyndham Worldwide | | |

| | Corp. | 449,134 | 20,889 |

| | Viacom Inc. Class B | 407,750 | 19,352 |

| * | DIRECTV Class A | 358,057 | 17,667 |

| | Macy’s Inc. | 415,200 | 16,496 |

| | Coach Inc. | 206,200 | 15,935 |

| | Wynn Resorts Ltd. | 125,005 | 15,611 |

| * | O’Reilly Automotive Inc. | 162,900 | 14,881 |

| | News Corp. Class A | 719,456 | 14,166 |

| * | AutoZone Inc. | 37,747 | 14,034 |

| | CBS Corp. Class B | 385,900 | 13,086 |

| | TJX Cos. Inc. | 320,600 | 12,731 |

| | Target Corp. | 214,900 | 12,522 |

| * | Bed Bath & Beyond Inc. | 151,800 | 9,984 |

| | Gap Inc. | 361,316 | 9,445 |

| | Harley-Davidson Inc. | 174,000 | 8,540 |

| | Limited Brands Inc. | 172,100 | 8,261 |

| * | Big Lots Inc. | 185,158 | 7,965 |

| | McGraw-Hill Cos. Inc. | 163,077 | 7,904 |

| | Ford Motor Co. | 559,700 | 6,991 |

| | Ralph Lauren Corp. Class A | 39,100 | 6,816 |

| | Walt Disney Co. | 149,077 | 6,527 |

| | Starbucks Corp. | 110,317 | 6,166 |

| | Washington Post Co. | | |

| | Class B | 16,174 | 6,042 |

| | Expedia Inc. | 170,500 | 5,702 |

| | Genuine Parts Co. | 86,566 | 5,432 |

| * | Amazon.com Inc. | 26,400 | 5,346 |

| | Gannett Co. Inc. | 312,754 | 4,795 |

| | Lowe’s Cos. Inc. | 133,600 | 4,192 |

| | | |

| | | | Market |

| | | | Value |

| | | Shares | ($000) |

| * | Goodyear Tire & Rubber | | |

| | Co. | 247,900 | 2,781 |

| | Nordstrom Inc. | 49,800 | 2,775 |

| | Staples Inc. | 163,200 | 2,641 |

| | Cablevision Systems Corp. | | |

| | Class A | 178,863 | 2,626 |

| | Harman International | | |

| | Industries Inc. | 53,730 | 2,515 |

| | Comcast Corp. Class A | 78,800 | 2,365 |

| * | Discovery Communications | | |

| | Inc. | 47,121 | 2,209 |

| * | Apollo Group Inc. Class A | 47,042 | 1,818 |

| | Kohl’s Corp. | 28,400 | 1,421 |

| * | Netflix Inc. | 12,200 | 1,403 |

| * | Sears Holdings Corp. | 19,500 | 1,292 |

| | DeVry Inc. | 30,900 | 1,047 |

| | Whirlpool Corp. | 12,700 | 976 |

| | Six Flags Entertainment | | |

| | Corp. | 18,100 | 847 |

| | Hasbro Inc. | 22,807 | 837 |

| | Family Dollar Stores Inc. | 10,571 | 669 |

| * | Coinstar Inc. | 10,400 | 661 |

| | Omnicom Group Inc. | 12,800 | 648 |

| * | Orbitz Worldwide Inc. | 181,014 | 552 |

| | CTC Media Inc. | 44,541 | 518 |

| | Interpublic Group of Cos. | | |

| | Inc. | 44,165 | 504 |

| | Best Buy Co. Inc. | 16,400 | 388 |

| * | Delphi Automotive plc | 12,100 | 382 |

| | Blyth Inc. | 5,100 | 382 |

| | Marriott International Inc. | | |

| | Class A | 9,800 | 371 |

| | Domino’s Pizza Inc. | 7,700 | 279 |

| | Weight Watchers | | |

| | International Inc. | 3,499 | 270 |

| *,^ | LodgeNet Interactive Corp. | 75,900 | 266 |

| | H&R Block Inc. | 13,900 | 229 |

| | Newell Rubbermaid Inc. | 12,300 | 219 |

12

Growth and Income Fund

| | | |

| | | | Market |

| | | | Value |

| | | Shares | ($000) |

| * | NVR Inc. | 300 | 218 |

| | Ameristar Casinos Inc. | 11,509 | 214 |

| * | Aeropostale Inc. | 9,200 | 199 |

| * | Beazer Homes USA Inc. | 60,400 | 196 |

| * | Boyd Gaming Corp. | 24,843 | 195 |

| * | Liz Claiborne Inc. | 13,100 | 175 |

| * | Perry Ellis International Inc. | 8,029 | 150 |

| | Oxford Industries Inc. | 2,501 | 127 |

| | Scripps Networks Interactive | | |

| | Inc. Class A | 2,602 | 127 |

| * | Carmike Cinemas Inc. | 8,900 | 124 |

| | Abercrombie & Fitch Co. | 2,500 | 124 |

| * | Cumulus Media Inc. Class A | 30,952 | 108 |

| | Fred’s Inc. Class A | 7,000 | 102 |

| * | Charter Communications Inc. | | |

| | Class A | 1,600 | 102 |

| | Lear Corp. | 2,100 | 98 |

| * | Scientific Games Corp. | | |

| | Class A | 7,034 | 82 |

| * | Capella Education Co. | 2,200 | 79 |

| * | G-III Apparel Group Ltd. | 2,299 | 65 |

| | HOT Topic Inc. | 6,400 | 65 |

| * | VOXX International Corp. | | |

| | Class A | 4,600 | 62 |

| | Standard Motor Products Inc. | 3,433 | 61 |

| | Movado Group Inc. | 2,000 | 49 |

| * | Pinnacle Entertainment Inc. | 4,247 | 49 |

| | Universal Technical Institute | | |

| | Inc. | 3,561 | 47 |

| * | TripAdvisor Inc. | 1,300 | 46 |

| | American Greetings Corp. | | |

| | Class A | 3,000 | 46 |

| | PEP Boys-Manny Moe | | |

| | & Jack | 3,051 | 46 |

| * | Kenneth Cole Productions | | |

| | Inc. Class A | 2,800 | 45 |

| * | Lions Gate Entertainment | | |

| | Corp. | 3,100 | 43 |

| * | Charming Shoppes Inc. | 7,100 | 42 |

| | Yum! Brands Inc. | 559 | 40 |

| * | Barnes & Noble Inc. | 2,900 | 38 |

| * | Smith & Wesson Holding | | |

| | Corp. | 4,650 | 36 |

| * | Pier 1 Imports Inc. | 1,700 | 31 |

| * | Career Education Corp. | 3,619 | 29 |

| * | Isle of Capri Casinos Inc. | 3,462 | 24 |

| * | Wet Seal Inc. Class A | 6,841 | 24 |

| * | Liberty Global Inc. Class A | 400 | 20 |

| * | Coldwater Creek Inc. | 15,600 | 18 |

| * | Education Management | | |

| | Corp. | 1,300 | 18 |

| | Cinemark Holdings Inc. | 800 | 18 |

| | Churchill Downs Inc. | 300 | 17 |

| * | Overstock.com Inc. | 3,109 | 16 |

| | | |

| | | | Market |

| | | | Value |

| | | Shares | ($000) |

| * | Talbots Inc. | 4,768 | 14 |

| * | Penn National Gaming Inc. | 323 | 14 |

| * | American Apparel Inc. | 14,397 | 12 |

| | Cato Corp. Class A | 400 | 11 |

| * | Knology Inc. | 566 | 10 |

| * | Furniture Brands | | |

| | International Inc. | 6,000 | 10 |

| | Strayer Education Inc. | 100 | 9 |

| | Sonic Automotive Inc. | | |

| | Class A | 500 | 9 |

| | Advance Auto Parts Inc. | 100 | 9 |

| * | Valuevision Media Inc. | | |

| | Class A | 4,200 | 9 |

| | NIKE Inc. Class B | 80 | 9 |

| | Stage Stores Inc. | 500 | 8 |

| | Service Corp. International | 700 | 8 |

| | Chico’s FAS Inc. | 500 | 8 |

| * | Conn’s Inc. | 436 | 7 |

| * | New York & Co. Inc. | 1,700 | 6 |

| * | School Specialty Inc. | 1,500 | 5 |

| | International Game | | |

| | Technology | 274 | 5 |

| | DR Horton Inc. | 300 | 5 |

| * | PulteGroup Inc. | 500 | 4 |

| | International Speedway | | |

| | Corp. Class A | 124 | 3 |

| * | Multimedia Games Holding | | |

| | Co. Inc. | 280 | 3 |

| * | Dex One Corp. | 1,800 | 3 |

| * | Red Robin Gourmet Burgers | |

| | Inc. | 67 | 2 |

| | Lithia Motors Inc. Class A | 93 | 2 |

| * | Midas Inc. | 200 | 2 |

| * | O’Charleys Inc. | 212 | 2 |

| | Arcos Dorados Holdings Inc. | |

| | Class A | 100 | 2 |

| | | | 492,267 |

| Consumer Staples (10.2%) | | |

| | Philip Morris International | | |

| | Inc. | 899,089 | 79,668 |

| | Procter & Gamble Co. | 1,046,530 | 70,337 |

| | Coca-Cola Co. | 581,717 | 43,053 |

| | Wal-Mart Stores Inc. | 632,379 | 38,702 |

| | Altria Group Inc. | 1,068,168 | 32,974 |

| | Walgreen Co. | 741,497 | 24,833 |

| | Lorillard Inc. | 161,021 | 20,849 |

| | Dr Pepper Snapple | | |

| | Group Inc. | 342,801 | 13,784 |

| | PepsiCo Inc. | 198,595 | 13,177 |

| | Kroger Co. | 490,900 | 11,895 |

| | Estee Lauder Cos. Inc. | | |

| | Class A | 150,700 | 9,334 |

| | ConAgra Foods Inc. | 352,183 | 9,248 |

| | Whole Foods Market Inc. | 109,000 | 9,069 |

13

Growth and Income Fund

| | | |

| | | | Market |

| | | | Value |

| | | Shares | ($000) |

| | Colgate-Palmolive Co. | 81,712 | 7,990 |

| * | Constellation Brands Inc. | | |

| | Class A | 317,100 | 7,480 |

| | Kraft Foods Inc. | 185,300 | 7,043 |

| | Reynolds American Inc. | 165,142 | 6,844 |

| | Kimberly-Clark Corp. | 91,561 | 6,765 |

| | CVS Caremark Corp. | 129,300 | 5,793 |

| | Beam Inc. | 77,100 | 4,516 |

| | Avon Products Inc. | 170,000 | 3,291 |

| | Sysco Corp. | 102,599 | 3,064 |

| | Safeway Inc. | 139,104 | 2,811 |

| | Costco Wholesale Corp. | 30,393 | 2,760 |

| | Mead Johnson Nutrition | | |

| | Co. | 26,800 | 2,210 |

| ^ | SUPERVALU Inc. | 211,000 | 1,205 |

| | Archer-Daniels-Midland | | |

| | Co. | 32,125 | 1,017 |

| | Coca-Cola Enterprises Inc. | 22,300 | 638 |

| | Sara Lee Corp. | 24,100 | 519 |

| * | Fresh Market Inc. | 10,300 | 494 |

| | Tyson Foods Inc. Class A | 20,981 | 402 |

| | Brown-Forman Corp. | | |

| | Class B | 4,000 | 334 |

| | Molson Coors Brewing Co. | | |

| | Class B | 6,400 | 290 |

| | Hershey Co. | 3,384 | 208 |

| * | Dean Foods Co. | 14,400 | 174 |

| * | Spectrum Brands Holdings | | |

| | Inc. | 4,378 | 153 |

| * | Post Holdings Inc. | 3,280 | 108 |

| | JM Smucker Co. | 1,070 | 87 |

| * | Susser Holdings Corp. | 2,900 | 74 |

| * | Cott Corp. | 9,600 | 63 |

| * | Smart Balance Inc. | 9,363 | 62 |

| * | Rite Aid Corp. | 30,000 | 52 |

| | Fresh Del Monte Produce | | |

| | Inc. | 1,885 | 43 |

| *,^ | Star Scientific Inc. | 12,600 | 41 |

| | Hormel Foods Corp. | 1,400 | 41 |

| * | Central European | | |

| | Distribution Corp. | 5,100 | 26 |

| | Clorox Co. | 144 | 10 |

| * | Pantry Inc. | 600 | 8 |

| | Kellogg Co. | 61 | 3 |

| | Cosan Ltd. | 64 | 1 |

| | | | 443,543 |

| Energy (10.5%) | | |

| | Exxon Mobil Corp. | 1,374,516 | 119,212 |

| | Chevron Corp. | 699,250 | 74,988 |

| | ConocoPhillips | 891,284 | 67,746 |

| | Occidental Petroleum | | |

| | Corp. | 337,695 | 32,159 |

| | Anadarko Petroleum Corp. | 229,396 | 17,971 |

| | Devon Energy Corp. | 224,291 | 15,952 |

| | Schlumberger Ltd. | 212,719 | 14,875 |

| | | |

| | | | Market |

| | | | Value |

| | | Shares | ($000) |

| | National Oilwell Varco Inc. | 170,624 | 13,559 |

| | Marathon Petroleum Corp. | 281,000 | 12,184 |

| | Apache Corp. | 120,450 | 12,098 |

| | Marathon Oil Corp. | 369,334 | 11,708 |

| | Spectra Energy Corp. | 318,800 | 10,058 |

| | Valero Energy Corp. | 336,600 | 8,674 |

| * | Tesoro Corp. | 255,950 | 6,870 |

| | Diamond Offshore | | |

| | Drilling Inc. | 86,000 | 5,740 |

| | Helmerich & Payne Inc. | 94,700 | 5,109 |

| | Hess Corp. | 53,100 | 3,130 |

| | Noble Energy Inc. | 28,800 | 2,816 |

| | Halliburton Co. | 77,593 | 2,575 |

| | Williams Cos. Inc. | 70,100 | 2,160 |

| | Pioneer Natural Resources | | |

| | Co. | 19,196 | 2,142 |

| | Peabody Energy Corp. | 71,000 | 2,056 |

| * | WPX Energy Inc. | 112,899 | 2,033 |

| * | Denbury Resources Inc. | 101,400 | 1,848 |

| | Chesapeake Energy Corp. | 52,700 | 1,221 |

| | Baker Hughes Inc. | 19,781 | 830 |

| | El Paso Corp. | 27,100 | 801 |

| | Sunoco Inc. | 20,400 | 778 |

| * | Hercules Offshore Inc. | 109,000 | 516 |

| * | Comstock Resources Inc. | 27,200 | 431 |

| *,^ | ATP Oil & Gas Corp. | 53,700 | 395 |

| | Suncor Energy Inc. | 9,500 | 311 |

| * | Ocean Rig UDW Inc. | 14,951 | 253 |

| * | Laredo Petroleum Holdings | | |

| | Inc. | 10,400 | 244 |

| | Talisman Energy Inc. | 17,983 | 227 |

| | Teekay Tankers Ltd. | | |

| | Class A | 33,100 | 201 |

| * | Rentech Inc. | 85,997 | 179 |

| * | Cheniere Energy Inc. | 11,821 | 177 |

| | Crosstex Energy Inc. | 10,600 | 150 |

| * | Lone Pine Resources Inc. | 21,200 | 138 |

| * | Exterran Holdings Inc. | 10,309 | 136 |

| | W&T Offshore Inc. | 6,300 | 133 |

| | Range Resources Corp. | 2,100 | 122 |

| * | Harvest Natural Resources | | |

| | Inc. | 14,100 | 100 |

| | Cameco Corp. | 4,000 | 86 |

| * | Endeavour International | | |

| | Corp. | 5,700 | 67 |

| * | SEACOR Holdings Inc. | 700 | 67 |

| * | SemGroup Corp. Class A | 2,200 | 64 |

| * | Energy Partners Ltd. | 3,700 | 61 |

| * | Cloud Peak Energy Inc. | 3,778 | 60 |

| * | ZaZa Energy Corp. | 9,300 | 43 |

| * | Plains Exploration & | | |

| | Production Co. | 900 | 38 |

| * | FMC Technologies Inc. | 612 | 31 |

| | Targa Resources Corp. | 600 | 27 |

| | Alon USA Energy Inc. | 2,969 | 27 |

14

Growth and Income Fund

| | | |

| | | | Market |

| | | | Value |

| | | Shares | ($000) |

| * | Matador Resources Co. | 2,294 | 25 |

| * | Amyris Inc. | 4,800 | 25 |

| | DHT Holdings Inc. | 15,783 | 15 |

| * | USEC Inc. | 13,277 | 14 |

| * | Contango Oil & Gas Co. | 200 | 12 |

| * | Callon Petroleum Co. | 1,700 | 11 |

| * | Nabors Industries Ltd. | 400 | 7 |

| * | Newfield Exploration Co. | 200 | 7 |

| | Consol Energy Inc. | 200 | 7 |

| * | DHT Holdings Inc. Rights | | |

| | Exp. 04/27/2012 | 63 | 7 |

| | Murphy Oil Corp. | 100 | 6 |

| | Cabot Oil & Gas Corp. | 100 | 3 |

| | Delek US Holdings Inc. | 200 | 3 |

| | | | 455,719 |

| Exchange-Traded Fund (0.2%) | |

| | SPDR S&P 500 ETF Trust | 62,800 | 8,837 |

| |

| Financials (15.8%) | | |

| | JPMorgan Chase & Co. | 1,727,001 | 79,407 |

| | Wells Fargo & Co. | 1,936,600 | 66,115 |

| * | Berkshire Hathaway Inc. | | |

| | Class B | 326,055 | 26,459 |

| | Simon Property Group | | |

| | Inc. | 171,838 | 25,033 |

| | Bank of America Corp. | 2,555,000 | 24,451 |

| | US Bancorp | 746,041 | 23,635 |

| | American Express Co. | 401,237 | 23,216 |

| | Citigroup Inc. | 610,900 | 22,328 |

| | Franklin Resources Inc. | 166,050 | 20,595 |

| | CME Group Inc. | 69,511 | 20,112 |

| | Goldman Sachs Group | | |

| | Inc. | 142,900 | 17,772 |

| | Marsh & McLennan Cos. | | |

| | Inc. | 508,625 | 16,678 |

| | Public Storage | 116,989 | 16,164 |

| | ACE Ltd. | 215,924 | 15,806 |

| | Torchmark Corp. | 316,200 | 15,763 |

| | Discover Financial | | |

| | Services | 452,500 | 15,086 |

| * | NASDAQ OMX Group Inc. | 564,922 | 14,631 |

| | Fifth Third Bancorp | 856,200 | 12,030 |

| | T. Rowe Price Group Inc. | 183,766 | 12,000 |

| * | American Tower | | |

| | Corporation | 189,015 | 11,912 |

| | Aflac Inc. | 251,252 | 11,555 |

| | MetLife Inc. | 294,950 | 11,016 |

| | Invesco Ltd. | 403,855 | 10,771 |

| | Prudential Financial Inc. | 141,866 | 8,993 |

| | HCP Inc. | 223,145 | 8,805 |

| * | American International | | |

| | Group Inc. | 278,900 | 8,598 |

| | Assurant Inc. | 189,533 | 7,676 |

| | Legg Mason Inc. | 259,092 | 7,236 |

| | Hudson City Bancorp Inc. | 985,400 | 7,203 |

| | | |

| | | | Market |

| | | | Value |

| | | Shares | ($000) |

| | Equity Residential | 114,939 | 7,197 |

| | ProLogis Inc. | 188,000 | 6,772 |

| ^ | Federated Investors Inc. | | |

| | Class B | 287,762 | 6,449 |

| | Kimco Realty Corp. | 305,020 | 5,875 |

| | Chubb Corp. | 79,784 | 5,514 |

| | BlackRock Inc. | 24,900 | 5,102 |

| | M&T Bank Corp. | 58,102 | 5,048 |

| | Ameriprise Financial Inc. | 87,884 | 5,021 |

| | Health Care REIT Inc. | 71,700 | 3,941 |

| | Moody’s Corp. | 91,150 | 3,837 |

| | Regions Financial Corp. | 569,100 | 3,750 |

| | BB&T Corp. | 116,900 | 3,669 |

| | Loews Corp. | 87,100 | 3,473 |

| | Plum Creek Timber Co. Inc. | 78,386 | 3,258 |

| | State Street Corp. | 60,700 | 2,762 |

| | PNC Financial Services | | |

| | Group Inc. | 41,542 | 2,679 |

| | Unum Group | 109,254 | 2,675 |

| | Charles Schwab Corp. | 185,317 | 2,663 |

| | Leucadia National Corp. | 101,287 | 2,644 |

| | SunTrust Banks Inc. | 105,900 | 2,560 |

| | Travelers Cos. Inc. | 42,216 | 2,499 |

| | KeyCorp | 279,999 | 2,380 |

| | People’s United Financial | | |

| | Inc. | 179,684 | 2,379 |

| | Vornado Realty Trust | 25,500 | 2,147 |

| | MI Developments Inc. | 61,000 | 2,110 |

| | Equity Lifestyle Properties | | |

| | Inc. | 28,500 | 1,988 |

| | Erie Indemnity Co. | | |

| | Class A | 25,106 | 1,957 |

| * | IntercontinentalExchange | | |

| | Inc. | 12,900 | 1,773 |

| | Capital One Financial Corp. | 27,334 | 1,524 |

| | SLM Corp. | 95,381 | 1,503 |

| * | E*Trade Financial Corp. | 130,641 | 1,430 |

| | Northern Trust Corp. | 27,900 | 1,324 |

| | Bank of New York Mellon | | |

| | Corp. | 53,883 | 1,300 |

| | NYSE Euronext | 42,548 | 1,277 |

| | Apartment Investment & | | |

| | Management Co. | 40,756 | 1,076 |

| | AvalonBay Communities | | |

| | Inc. | 7,611 | 1,076 |

| * | CNO Financial Group Inc. | 128,300 | 998 |

| * | Genworth Financial Inc. | | |

| | Class A | 87,500 | 728 |

| | Two Harbors Investment | | |

| | Corp. | 60,300 | 611 |

| | First Horizon National Corp. | 54,400 | 565 |

| | Credicorp Ltd. | 3,990 | 526 |

| | Symetra Financial Corp. | 44,059 | 508 |

| | Boston Properties Inc. | 4,500 | 472 |

| | Ventas Inc. | 8,200 | 468 |

15

Growth and Income Fund

| | | |

| | | | Market |

| | | | Value |

| | | Shares | ($000) |

| * | First Industrial Realty Trust | | |

| | Inc. | 37,000 | 457 |

| | XL Group plc Class A | 19,400 | 421 |

| | RLJ Lodging Trust | 18,500 | 345 |

| * | NewStar Financial Inc. | 24,100 | 268 |

| | Willis Group Holdings plc | 7,200 | 252 |

| | DuPont Fabros Technology | | |

| | Inc. | 9,500 | 232 |

| * | eHealth Inc. | 12,946 | 211 |

| | Alleghany Corp. | 613 | 202 |

| | Aon Corp. | 4,100 | 201 |

| | Horace Mann Educators | | |

| | Corp. | 11,000 | 194 |

| * | Strategic Hotels & Resorts | | |

| | Inc. | 29,352 | 193 |

| | Zions Bancorporation | 8,319 | 179 |

| | Extra Space Storage Inc. | 5,584 | 161 |

| | Huntington Bancshares Inc. | 24,100 | 155 |

| * | Sunstone Hotel Investors | | |

| | Inc. | 15,600 | 152 |

| | Dynex Capital Inc. | 15,820 | 151 |

| | MarketAxess Holdings Inc. | 3,600 | 134 |

| * | CBRE Group Inc. Class A | 6,623 | 132 |

| | Starwood Property Trust Inc. | 6,200 | 130 |

| | Comerica Inc. | 4,000 | 129 |

| | Principal Financial Group Inc. | 4,382 | 129 |

| | FBL Financial Group Inc. | | |

| | Class A | 3,799 | 128 |

| | Invesco Mortgage Capital | | |

| | Inc. | 6,900 | 122 |

| | RLI Corp. | 1,508 | 108 |

| * | Central Pacific Financial | | |

| | Corp. | 7,421 | 96 |

| | Weyerhaeuser Co. | 4,300 | 94 |

| | Newcastle Investment Corp. | 13,786 | 87 |

| | Potlatch Corp. | 2,300 | 72 |

| | Healthcare Realty Trust Inc. | 3,208 | 71 |

| | Hartford Financial Services | | |

| | Group Inc. | 3,300 | 70 |

| * | Sterling Financial Corp. | 3,103 | 65 |

| * | Citizens Republic Bancorp | | |

| | Inc. | 4,101 | 64 |

| | PrivateBancorp Inc. Class A | 3,983 | 60 |

| | Lincoln National Corp. | 1,652 | 44 |

| | Saul Centers Inc. | 1,000 | 40 |

| | PS Business Parks Inc. | 600 | 39 |

| * | United Community Banks | | |

| | Inc. | 3,974 | 39 |

| * | MBIA Inc. | 3,500 | 34 |

| | STAG Industrial Inc. | 2,277 | 32 |

| | Ashford Hospitality Trust Inc. | 3,331 | 30 |

| | Taubman Centers Inc. | 400 | 29 |

| * | iStar Financial Inc. | 3,900 | 28 |

| | Employers Holdings Inc. | 1,400 | 25 |

| | | |

| | | | Market |

| | | | Value |

| | | Shares | ($000) |

| | First Financial Bankshares | | |

| | Inc. | 700 | 25 |

| | Cash America International | | |

| | Inc. | 500 | 24 |

| * | Popular Inc. | 11,500 | 24 |

| | Terreno Realty Corp. | 1,581 | 23 |

| | CapitalSource Inc. | 3,200 | 21 |

| * | Southwest Bancorp Inc. | 2,039 | 19 |

| | Apollo Residential | | |

| | Mortgage Inc. | 1,000 | 18 |

| | CVB Financial Corp. | 1,500 | 18 |

| * | First Cash Financial | | |

| | Services Inc. | 325 | 14 |

| | Ramco-Gershenson | | |

| | Properties Trust | 1,100 | 13 |

| | Monmouth Real Estate | | |

| | Investment Corp. Class A | 1,100 | 11 |

| * | Virtus Investment Partners | | |

| | Inc. | 100 | 9 |

| | Winthrop Realty Trust | 700 | 8 |

| | Cogdell Spencer Inc. | 1,600 | 7 |

| * | PHH Corp. | 437 | 7 |

| * | Tejon Ranch Co. | 200 | 6 |

| | Platinum Underwriters | | |

| | Holdings Ltd. | 100 | 4 |

| | First Financial Bancorp | 200 | 3 |

| | CNA Financial Corp. | 100 | 3 |

| * | Phoenix Cos. Inc. | 1,180 | 3 |

| * | ICG Group Inc. | 256 | 2 |

| * | Altisource Portfolio | | |

| | Solutions SA | 27 | 2 |

| * | Netspend Holdings Inc. | 100 | 1 |

| | BGC Partners Inc. Class A | 70 | 1 |

| | Sovran Self Storage Inc. | 7 | — |

| | UDR Inc. | 7 | — |

| | | | 684,625 |

| Health Care (10.8%) | | |

| | Pfizer Inc. | 3,982,988 | 90,254 |

| | Abbott Laboratories | 713,123 | 43,707 |

| | Merck & Co. Inc. | 1,123,996 | 43,161 |

| | Johnson & Johnson | 606,142 | 39,981 |

| | Bristol-Myers Squibb Co. | 1,042,886 | 35,197 |

| | WellPoint Inc. | 409,562 | 30,226 |

| | UnitedHealth Group Inc. | 409,198 | 24,118 |

| | Eli Lilly & Co. | 544,775 | 21,938 |

| | Covidien plc | 285,995 | 15,638 |

| | Baxter International Inc. | 259,668 | 15,523 |

| | Humana Inc. | 142,516 | 13,180 |

| | Aetna Inc. | 258,320 | 12,957 |

| | Amgen Inc. | 145,700 | 9,906 |

| | Medtronic Inc. | 167,054 | 6,547 |

| * | Biogen Idec Inc. | 48,489 | 6,108 |

| | Stryker Corp. | 110,041 | 6,105 |

| * | Forest Laboratories Inc. | 172,411 | 5,981 |

16

Growth and Income Fund

| | | |

| | | | Market |

| | | | Value |

| | | Shares | ($000) |

| | McKesson Corp. | 61,963 | 5,438 |

| | St. Jude Medical Inc. | 104,800 | 4,644 |

| | PerkinElmer Inc. | 163,980 | 4,536 |

| | Becton Dickinson and Co. | 54,002 | 4,193 |

| | Thermo Fisher Scientific | | |

| | Inc. | 74,200 | 4,183 |

| * | Tenet Healthcare Corp. | 764,185 | 4,058 |

| | Zimmer Holdings Inc. | 35,800 | 2,301 |

| * | Mylan Inc. | 70,400 | 1,651 |

| * | Watson Pharmaceuticals | | |

| | Inc. | 21,300 | 1,428 |

| | Allergan Inc. | 14,900 | 1,422 |

| * | DaVita Inc. | 15,500 | 1,398 |

| * | Medco Health Solutions | | |

| | Inc. | 18,500 | 1,301 |

| | Cardinal Health Inc. | 25,600 | 1,104 |

| * | Celgene Corp. | 14,200 | 1,101 |

| * | Intuitive Surgical Inc. | 1,822 | 987 |

| * | Express Scripts Inc. | 12,700 | 688 |

| * | Idenix Pharmaceuticals Inc. | 65,100 | 637 |

| * | XenoPort Inc. | 127,355 | 573 |

| * | Theravance Inc. | 27,200 | 530 |

| | Agilent Technologies Inc. | 10,600 | 472 |

| * | MedAssets Inc. | 33,141 | 436 |

| * | Arthrocare Corp. | 11,120 | 299 |

| * | Furiex Pharmaceuticals Inc. | 12,000 | 284 |

| * | Orexigen Therapeutics Inc. | 61,300 | 251 |

| * | Life Technologies Corp. | 5,100 | 249 |

| * | Neurocrine Biosciences Inc. | 27,322 | 218 |

| * | Emergent Biosolutions Inc. | 13,030 | 208 |

| * | Pharmacyclics Inc. | 7,400 | 205 |

| * | Pain Therapeutics Inc. | 41,100 | 148 |

| * | AngioDynamics Inc. | 11,100 | 136 |

| * | Allos Therapeutics Inc. | 91,600 | 136 |

| * | LCA-Vision Inc. | 20,697 | 130 |

| * | Transcend Services Inc. | 3,500 | 103 |

| | Omnicare Inc. | 2,800 | 100 |

| * | NuVasive Inc. | 5,819 | 98 |

| * | Enzon Pharmaceuticals Inc. | 12,400 | 85 |

| * | GTx Inc. | 20,600 | 79 |

| * | Warner Chilcott plc Class A | 4,500 | 76 |

| * | Array Biopharma Inc. | 21,300 | 73 |

| * | Halozyme Therapeutics Inc. | 5,500 | 70 |

| | Hill-Rom Holdings Inc. | 2,100 | 70 |

| | Medicis Pharmaceutical | | |

| | Corp. Class A | 1,800 | 68 |

| | AmerisourceBergen Corp. | | |

| | Class A | 1,700 | 67 |

| * | Alnylam Pharmaceuticals | | |

| | Inc. | 5,700 | 63 |

| * | Pozen Inc. | 10,020 | 60 |

| * | NPS Pharmaceuticals Inc. | 7,400 | 51 |

| * | Amicus Therapeutics Inc. | 8,179 | 43 |

| * | TranS1 Inc. | 10,180 | 37 |

| | | |

| | | | Market |

| | | | Value |

| | | Shares | ($000) |

| * | Valeant Pharmaceuticals | | |

| | International Inc. | 666 | 36 |

| * | KV Pharmaceutical Co. | | |

| | Class A | 25,700 | 34 |

| * | PharMerica Corp. | 2,700 | 34 |

| * | Cambrex Corp. | 4,600 | 32 |

| *,^ | Biosante Pharmaceuticals | | |

| | Inc. | 44,500 | 30 |

| * | Health Net Inc. | 700 | 28 |

| | Invacare Corp. | 1,663 | 28 |

| * | Arqule Inc. | 3,700 | 26 |

| * | Endocyte Inc. | 5,200 | 26 |

| * | Ardea Biosciences Inc. | 1,100 | 24 |

| * | Sciclone Pharmaceuticals | | |

| | Inc. | 3,700 | 23 |

| * | Agenus Inc. | 2,700 | 18 |

| * | Auxilium Pharmaceuticals | | |

| | Inc. | 900 | 17 |

| * | Zoll Medical Corp. | 180 | 17 |

| * | Rigel Pharmaceuticals Inc. | 1,900 | 15 |

| * | Sun Healthcare Group Inc. | 2,000 | 14 |

| * | Viropharma Inc. | 400 | 12 |

| * | BioDelivery Sciences | | |

| | International Inc. | 4,765 | 11 |

| * | Biolase Technology Inc. | 3,654 | 10 |

| * | Ligand Pharmaceuticals | | |

| | Inc. Class B | 600 | 10 |

| * | Ironwood Pharmaceuticals | | |

| | Inc. Class A | 700 | 9 |

| * | Targacept Inc. | 1,563 | 8 |

| * | Edwards Lifesciences Corp. | 100 | 7 |

| * | AMAG Pharmaceuticals Inc. | 433 | 7 |

| * | OncoGenex Pharmaceutical | | |

| | Inc. | 500 | 7 |

| * | Brookdale Senior Living Inc. | | |

| | Class A | 300 | 6 |

| * | Dynavax Technologies Corp. | 998 | 5 |

| | HCA Holdings Inc. | 200 | 5 |

| * | Myriad Genetics Inc. | 200 | 5 |

| * | Myrexis Inc. | 1,550 | 5 |

| * | Trius Therapeutics Inc. | 800 | 4 |

| * | Sunrise Senior Living Inc. | 400 | 2 |

| * | Boston Scientific Corp. | 146 | 1 |

| * | Vanda Pharmaceuticals Inc. | 100 | — |

| | | | 467,531 |

| Industrials (9.9%) | | |

| | General Electric Co. | 3,501,600 | 70,277 |

| | Tyco International Ltd. | 523,080 | 29,387 |

| | General Dynamics Corp. | 365,410 | 26,814 |

| | Northrop Grumman Corp. | 422,206 | 25,788 |

| | Lockheed Martin Corp. | 284,854 | 25,597 |

| | Union Pacific Corp. | 228,435 | 24,552 |

| | United Technologies Corp. | 291,900 | 24,210 |

| | Caterpillar Inc. | 209,821 | 22,350 |

17

Growth and Income Fund

| | | |

| | | | Market |

| | | | Value |

| | | Shares | ($000) |

| | Norfolk Southern Corp. | 308,802 | 20,328 |

| | Raytheon Co. | 368,831 | 19,467 |

| | Cummins Inc. | 121,567 | 14,593 |

| | Precision Castparts Corp. | 79,367 | 13,723 |

| | CSX Corp. | 566,389 | 12,189 |

| | L-3 Communications | | |

| | Holdings Inc. | 150,985 | 10,685 |

| | WW Grainger Inc. | 39,859 | 8,562 |

| | United Parcel Service Inc. | | |

| | Class B | 103,093 | 8,322 |

| | Equifax Inc. | 177,400 | 7,852 |

| | PACCAR Inc. | 137,600 | 6,444 |

| | Republic Services Inc. | | |

| | Class A | 210,300 | 6,427 |

| | Emerson Electric Co. | 117,329 | 6,122 |

| | Parker Hannifin Corp. | 71,822 | 6,073 |

| | Southwest Airlines Co. | 651,000 | 5,364 |

| | Snap-on Inc. | 52,422 | 3,196 |

| | Expeditors International of | | |

| | Washington Inc. | 63,965 | 2,975 |

| | Fluor Corp. | 49,000 | 2,942 |

| | Covanta Holding Corp. | 174,300 | 2,829 |

| | Cintas Corp. | 67,600 | 2,645 |

| * | Sensata Technologies | | |

| | Holding NV | 70,500 | 2,360 |

| | Illinois Tool Works Inc. | 36,650 | 2,093 |

| | Honeywell International Inc. | 33,700 | 2,057 |

| * | Verisk Analytics Inc. | | |

| | Class A | 32,600 | 1,531 |

| | Rockwell Automation Inc. | 18,937 | 1,509 |

| | Xylem Inc. | 46,900 | 1,302 |

| | Goodrich Corp. | 8,200 | 1,029 |

| * | Nielsen Holdings NV | 31,600 | 952 |

| | Masco Corp. | 67,937 | 908 |

| * | Esterline Technologies | | |

| | Corp. | 7,100 | 507 |

| * | WABCO Holdings Inc. | 8,320 | 503 |

| | Cooper Industries plc | 7,654 | 490 |

| | Dun & Bradstreet Corp. | 5,707 | 484 |

| | Flowserve Corp. | 3,495 | 404 |

| * | AerCap Holdings NV | 31,800 | 353 |

| * | Portfolio Recovery | | |

| | Associates Inc. | 4,682 | 336 |

| * | FuelCell Energy Inc. | 197,227 | 310 |

| | Albany International Corp. | 13,100 | 301 |

| * | Swift Transportation Co. | 25,600 | 295 |

| | Fastenal Co. | 5,100 | 276 |

| | Avery Dennison Corp. | 9,100 | 274 |

| * | Atlas Air Worldwide | | |

| | Holdings Inc. | 4,900 | 241 |

| | Ryder System Inc. | 4,400 | 232 |

| | 3M Co. | 2,300 | 205 |

| | Boeing Co. | 2,400 | 179 |

| * | EnerNOC Inc. | 22,200 | 160 |

| | | |

| | | | Market |

| | | | Value |

| | | Shares | ($000) |

| | John Bean Technologies | | |

| | Corp. | 8,753 | 142 |

| * | Federal Signal Corp. | 24,806 | 138 |

| * | Dycom Industries Inc. | 5,100 | 119 |

| * | EnPro Industries Inc. | 2,300 | 95 |

| | Timken Co. | 1,800 | 91 |

| | Aceto Corp. | 7,996 | 76 |

| * | Meritor Inc. | 8,100 | 65 |

| * | Interline Brands Inc. | 3,000 | 65 |

| | Quad/Graphics Inc. | 4,338 | 60 |

| * | GeoEye Inc. | 2,500 | 60 |

| * | Old Dominion Freight Line | | |

| | Inc. | 1,200 | 57 |

| | Corporate Executive Board | | |

| | Co. | 1,200 | 52 |

| * | United Rentals Inc. | 1,100 | 47 |

| * | Shaw Group Inc. | 1,400 | 44 |

| * | DigitalGlobe Inc. | 2,261 | 30 |

| * | GrafTech International Ltd. | 2,098 | 25 |

| * | Pendrell Corp. | 9,585 | 25 |

| * | ACCO Brands Corp. | 2,000 | 25 |

| * | Pacer International Inc. | 3,900 | 25 |

| | Arkansas Best Corp. | 1,300 | 24 |

| | Star Bulk Carriers Corp. | 27,146 | 24 |

| * | Navigant Consulting Inc. | 1,600 | 22 |

| * | Safe Bulkers Inc. | 3,300 | 22 |

| * | American Reprographics Co. | 3,710 | 20 |

| | Unifirst Corp. | 300 | 18 |

| | Kaman Corp. | 535 | 18 |

| * | Alaska Air Group Inc. | 500 | 18 |

| | LB Foster Co. Class A | 470 | 13 |

| * | Quality Distribution Inc. | 897 | 12 |

| * | Odyssey Marine Exploration | | |

| | Inc. | 3,523 | 11 |

| * | Accuride Corp. | 1,235 | 11 |

| * | NCI Building Systems Inc. | 900 | 10 |

| * | CRA International Inc. | 400 | 10 |

| * | KEYW Holding Corp. | 1,236 | 10 |

| | URS Corp. | 200 | 9 |

| * | Jacobs Engineering Group | | |

| | Inc. | 146 | 7 |

| | Iron Mountain Inc. | 223 | 6 |

| * | Beacon Roofing Supply Inc. | 200 | 5 |

| * | SYKES Enterprises Inc. | 321 | 5 |

| * | JetBlue Airways Corp. | 1,013 | 5 |

| * | Republic Airways Holdings | | |

| | Inc. | 904 | 5 |

| * | Navistar International Corp. | 100 | 4 |

| | Quanex Building Products | | |

| | Corp. | 200 | 4 |

| | Deere & Co. | 41 | 3 |

| | Comfort Systems USA Inc. | 72 | 1 |

| | | | 430,542 |

18

Growth and Income Fund

| | | |

| | | | Market |

| | | | Value |

| | | Shares | ($000) |

| Information Technology (21.1%) | |

| * | Apple Inc. | 364,423 | 218,461 |

| | Microsoft Corp. | 3,057,197 | 98,595 |

| | International Business | | |

| | Machines Corp. | 432,754 | 90,294 |

| | QUALCOMM Inc. | 862,906 | 58,695 |

| | Intel Corp. | 1,811,209 | 50,913 |

| | Cisco Systems Inc. | 2,074,789 | 43,882 |

| * | Google Inc. Class A | 68,009 | 43,610 |

| | Visa Inc. Class A | 311,530 | 36,760 |

| | Oracle Corp. | 885,525 | 25,822 |

| | Mastercard Inc. Class A | 55,939 | 23,525 |

| | Accenture plc Class A | 320,000 | 20,640 |

| | Motorola Solutions Inc. | 315,500 | 16,037 |

| * | Symantec Corp. | 649,600 | 12,147 |

| | Hewlett-Packard Co. | 505,700 | 12,051 |

| | KLA-Tencor Corp. | 216,505 | 11,782 |

| * | Dell Inc. | 677,026 | 11,239 |

| | Intuit Inc. | 153,500 | 9,230 |

| * | LSI Corp. | 1,054,800 | 9,156 |

| * | Western Digital Corp. | 220,200 | 9,114 |

| * | eBay Inc. | 216,066 | 7,971 |

| | Jabil Circuit Inc. | 315,100 | 7,915 |

| * | Novellus Systems Inc. | 135,350 | 6,755 |

| | Applied Materials Inc. | 542,625 | 6,750 |

| | VeriSign Inc. | 163,700 | 6,276 |

| * | Marvell Technology Group | | |

| | Ltd. | 395,336 | 6,219 |

| | CA Inc. | 193,000 | 5,319 |

| * | Cognizant Technology | | |

| | Solutions Corp. Class A | 63,218 | 4,865 |

| | Total System Services Inc. | 208,100 | 4,801 |

| * | Autodesk Inc. | 97,400 | 4,122 |

| * | Citrix Systems Inc. | 49,557 | 3,911 |

| | Texas Instruments Inc. | 112,102 | 3,768 |

| | Broadcom Corp. Class A | 94,355 | 3,708 |

| | Analog Devices Inc. | 76,684 | 3,098 |

| * | F5 Networks Inc. | 22,700 | 3,064 |

| * | Juniper Networks Inc. | 131,000 | 2,997 |

| * | Zebra Technologies Corp. | 72,734 | 2,995 |

| * | Fiserv Inc. | 36,700 | 2,547 |

| * | Compuware Corp. | 230,811 | 2,121 |

| | Seagate Technology plc | 78,500 | 2,116 |

| | Automatic Data Processing | | |

| | Inc. | 36,000 | 1,987 |

| * | BMC Software Inc. | 46,100 | 1,851 |

| * | Quest Software Inc. | 67,463 | 1,570 |

| | Altera Corp. | 34,700 | 1,382 |

| * | SanDisk Corp. | 27,800 | 1,379 |

| | Harris Corp. | 29,693 | 1,339 |

| | Paychex Inc. | 37,300 | 1,156 |

| * | Micron Technology Inc. | 127,400 | 1,032 |

| | Corning Inc. | 68,300 | 962 |

| | Linear Technology Corp. | 27,101 | 913 |

| | Xerox Corp. | 85,900 | 694 |

| | | |

| | | | Market |

| | | | Value |

| | | Shares | ($000) |

| | Microchip Technology Inc. | 17,252 | 642 |

| * | Acxiom Corp. | 42,800 | 628 |

| * | JDS Uniphase Corp. | 41,800 | 606 |

| * | Tessera Technologies Inc. | 34,400 | 593 |

| * | Polycom Inc. | 30,600 | 584 |

| | Avago Technologies Ltd. | 14,821 | 578 |

| * | AOL Inc. | 30,100 | 571 |

| * | Research In Motion Ltd. | 35,900 | 528 |

| | Computer Sciences Corp. | 15,826 | 474 |

| * | Electronic Arts Inc. | 22,823 | 376 |

| * | Agilysys Inc. | 30,416 | 273 |

| * | Mentor Graphics Corp. | 17,700 | 263 |

| * | NetApp Inc. | 5,400 | 242 |

| * | Red Hat Inc. | 3,200 | 192 |

| * | Comverse Technology Inc. | 26,900 | 185 |

| * | Salesforce.com Inc. | 1,187 | 183 |

| | Fidelity National Information | | |

| | Services Inc. | 5,500 | 182 |

| * | STEC Inc. | 18,437 | 174 |

| * | Vocus Inc. | 10,501 | 139 |

| * | SS&C Technologies | | |

| | Holdings Inc. | 5,500 | 128 |

| * | Dolby Laboratories Inc. | | |

| | Class A | 3,100 | 118 |

| * | ShoreTel Inc. | 20,200 | 115 |

| * | NXP Semiconductor NV | 4,100 | 109 |

| * | Unisys Corp. | 5,400 | 106 |

| * | Brocade Communications | | |

| | Systems Inc. | 17,800 | 102 |

| * | Dice Holdings Inc. | 10,200 | 95 |

| * | Digital River Inc. | 4,700 | 88 |

| * | Amkor Technology Inc. | 10,535 | 65 |

| * | Orbotech Ltd. | 5,300 | 61 |

| * | PMC - Sierra Inc. | 8,100 | 59 |

| * | Flextronics International Ltd. | 6,787 | 49 |

| * | DTS Inc. | 1,500 | 45 |

| * | THQ Inc. | 78,931 | 44 |

| * | InterXion Holding NV | 2,400 | 43 |

| * | Mattson Technology Inc. | 15,334 | 42 |

| * | Omnivision Technologies | | |

| | Inc. | 1,900 | 38 |

| * | VASCO Data Security | | |

| | International Inc. | 3,400 | 37 |

| * | WebMD Health Corp. | 1,400 | 36 |

| * | Global Cash Access | | |

| | Holdings Inc. | 4,383 | 34 |

| | TE Connectivity Ltd. | 905 | 33 |

| * | Ingram Micro Inc. | 1,700 | 32 |

| * | MoneyGram International | | |

| | Inc. | 1,700 | 31 |

| * | Web.com Group Inc. | 1,882 | 27 |

| * | IntraLinks Holdings Inc. | 5,100 | 27 |

| | Micrel Inc. | 2,500 | 26 |

| * | Allot Communications Ltd. | 1,079 | 25 |

| * | CoreLogic Inc. | 1,500 | 24 |

19

Growth and Income Fund

| | | |

| | | | Market |

| | | | Value• |

| | | Shares | ($000) |

| * | TIBCO Software Inc. | 800 | 24 |

| * | Demand Media Inc. | 3,200 | 23 |

| * | Checkpoint Systems Inc. | 2,011 | 23 |

| * | VMware Inc. Class A | 200 | 22 |

| * | Ancestry.com Inc. | 954 | 22 |

| *,^ | FriendFinder Networks Inc. | 14,515 | 20 |

| * | Applied Micro Circuits Corp. | 2,800 | 19 |

| * | LTX-Credence Corp. | 2,697 | 19 |

| * | TNS Inc. | 851 | 18 |

| * | UTStarcom Holdings Corp. | 11,400 | 16 |

| * | MIPS Technologies Inc. | | |

| | Class A | 3,000 | 16 |

| * | Entropic Communications | | |

| | Inc. | 2,600 | 15 |

| * | Powerwave Technologies | | |

| | Inc. | 6,500 | 13 |

| * | Imation Corp. | 1,800 | 11 |

| * | Integrated Device | | |

| | Technology Inc. | 1,500 | 11 |

| * | Aspen Technology Inc. | 516 | 11 |

| * | Silicon Image Inc. | 1,500 | 9 |

| * | Smith Micro Software Inc. | 3,500 | 8 |

| | Xilinx Inc. | 204 | 7 |

| * | Akamai Technologies Inc. | 200 | 7 |

| * | Entegris Inc. | 700 | 6 |

| * | Yandex NV Class A | 213 | 6 |

| * | Glu Mobile Inc. | 1,151 | 6 |

| * | Symmetricom Inc. | 893 | 5 |

| * | Amtech Systems Inc. | 500 | 4 |

| * | Comverge Inc. | 2,130 | 4 |

| * | EchoStar Corp. Class A | 100 | 3 |

| * | Convergys Corp. | 200 | 3 |

| * | Photronics Inc. | 393 | 3 |

| * | PLX Technology Inc. | 600 | 2 |

| * | Infinera Corp. | 271 | 2 |

| * | SunPower Corp. Class A | 300 | 2 |

| * | Monster Worldwide Inc. | 100 | 1 |

| * | Network Equipment | | |

| | Technologies Inc. | 600 | 1 |

| | | | 916,950 |

| Materials (2.7%) | | |

| | Freeport-McMoRan | | |

| | Copper & Gold Inc. | 661,373 | 25,159 |

| | Monsanto Co. | 278,300 | 22,197 |

| | CF Industries Holdings Inc. | 58,250 | 10,639 |

| | International Paper Co. | 265,200 | 9,309 |

| | EI du Pont de Nemours & | | |

| | Co. | 173,796 | 9,194 |

| | Eastman Chemical Co. | 155,045 | 8,014 |

| | PPG Industries Inc. | 64,000 | 6,131 |

| | Newmont Mining Corp. | 116,924 | 5,995 |

| | International Flavors & | | |

| | Fragrances Inc. | 67,758 | 3,971 |

| | Sealed Air Corp. | 161,210 | 3,113 |

| | Airgas Inc. | 30,200 | 2,687 |

| | | |

| | | | Market |

| | | | Value• |

| | | Shares | ($000) |

| | FMC Corp. | 23,674 | 2,506 |

| | Ball Corp. | 39,100 | 1,677 |

| | Nucor Corp. | 35,300 | 1,516 |

| * | Owens-Illinois Inc. | 43,346 | 1,012 |

| * | Georgia Gulf Corp. | 25,900 | 903 |

| | Cliffs Natural Resources | | |

| | Inc. | 12,640 | 875 |

| | Mosaic Co. | 11,300 | 625 |

| | Innophos Holdings Inc. | 10,900 | 546 |

| | MeadWestvaco Corp. | 17,066 | 539 |

| * | SunCoke Energy Inc. | 29,739 | 423 |

| * | Headwaters Inc. | 95,155 | 398 |

| * | Mercer International Inc. | 45,741 | 365 |

| | Titanium Metals Corp. | 20,300 | 275 |

| | Noranda Aluminum | | |

| | Holding Corp. | 17,400 | 173 |

| | Myers Industries Inc. | 8,100 | 119 |

| * | Clearwater Paper Corp. | 3,400 | 113 |

| | Boise Inc. | 13,200 | 108 |

| * | KapStone Paper and | | |

| | Packaging Corp. | 5,226 | 103 |

| * | Jaguar Mining Inc. | 18,200 | 85 |

| | Domtar Corp. | 800 | 76 |

| * | Agnico-Eagle Mines Ltd. | 2,100 | 70 |

| * | Silver Standard Resources | | |

| | Inc. | 4,600 | 69 |

| *,^ | Rare Element Resources | | |

| | Ltd. | 7,500 | 47 |

| * | AbitibiBowater Inc. | 2,886 | 41 |

| * | General Moly Inc. | 9,800 | 33 |

| | Packaging Corp. of | | |

| | America | 800 | 24 |

| | Valspar Corp. | 400 | 19 |

| * | Taseko Mines Ltd. | 4,800 | 17 |

| * | OM Group Inc. | 609 | 17 |

| * | Flotek Industries Inc. | 1,300 | 16 |

| | Commercial Metals Co. | 796 | 12 |

| | Ecolab Inc. | 170 | 11 |

| | Sherwin-Williams Co. | 100 | 11 |

| | Air Products & Chemicals | | |

| | Inc. | 100 | 9 |

| | Barrick Gold Corp. | 200 | 9 |

| * | Ferro Corp. | 1,400 | 8 |

| * | NovaGold Resources Inc. | 1,000 | 7 |

| | United States Steel Corp. | 200 | 6 |

| * | Louisiana-Pacific Corp. | 600 | 6 |

| | American Vanguard Corp. | 213 | 5 |

| * | Golden Star Resources Ltd. | 1,000 | 2 |

| * | Richmont Mines Inc. | 164 | 1 |

| * | Aurizon Mines Ltd. | 189 | 1 |

| | | | 119,287 |

| Telecommunication Services (2.5%) | |

| | AT&T Inc. | 1,820,264 | 56,847 |

| | Verizon Communications | | |

| | Inc. | 1,106,739 | 42,311 |

20

Growth and Income Fund

| | | |

| | | | Market |

| | | | Value |

| | | Shares | ($000) |

| | CenturyLink Inc. | 83,500 | 3,227 |

| * | Crown Castle International | | |

| | Corp. | 59,700 | 3,184 |

| * | Sprint Nextel Corp. | 447,800 | 1,276 |

| * | MetroPCS | | |

| | Communications Inc. | 43,100 | 389 |

| * | Level 3 Communications Inc. | 9,000 | 231 |

| * | Vonage Holdings Corp. | 61,600 | 136 |

| | Frontier Communications | | |

| | Corp. | 27,500 | 115 |

| | USA Mobility Inc. | 2,723 | 38 |

| * | Clearwire Corp. Class A | 16,300 | 37 |

| | Windstream Corp. | 400 | 5 |

| | | | 107,796 |

| Utilities (2.5%) | | |

| | Northeast Utilities | 346,900 | 12,877 |

| | FirstEnergy Corp. | 278,300 | 12,688 |

| | Public Service Enterprise | | |

| | Group Inc. | 374,665 | 11,468 |

| | American Electric Power | | |

| | Co. Inc. | 226,800 | 8,750 |

| | DTE Energy Co. | 143,000 | 7,869 |

| | Ameren Corp. | 239,100 | 7,790 |

| | Pinnacle West Capital | | |

| | Corp. | 157,100 | 7,525 |

| | PG&E Corp. | 172,676 | 7,496 |

| * | AES Corp. | 495,000 | 6,470 |

| | Exelon Corp. | 152,200 | 5,968 |

| | CenterPoint Energy Inc. | 232,537 | 4,586 |

| | Edison International | 78,553 | 3,339 |

| | CMS Energy Corp. | 123,300 | 2,713 |

| | Entergy Corp. | 33,600 | 2,258 |

| | Integrys Energy Group Inc. | 38,277 | 2,028 |

| | Dominion Resources Inc. | 28,194 | 1,444 |

| * | NRG Energy Inc. | 47,200 | 740 |

| | AGL Resources Inc. | 18,391 | 721 |

| | NorthWestern Corp. | 7,261 | 257 |

| | Consolidated Edison Inc. | 2,207 | 129 |

| | Westar Energy Inc. | 4,500 | 126 |

| | MGE Energy Inc. | 1,800 | 80 |

| | California Water Service | | |

| | Group | 4,300 | 78 |

| | IDACORP Inc. | 900 | 37 |

| * | Calpine Corp. | 1,800 | 31 |

| | Atmos Energy Corp. | 700 | 22 |

| | Sempra Energy | 128 | 8 |

| | Xcel Energy Inc. | 211 | 5 |

| | NV Energy Inc. | 200 | 3 |

| | | | 107,506 |

| Total Common Stocks | | |

| (Cost $3,549,295) | | 4,234,603 |

| | | |

| | | | Market |

| | | | Value |

| | | Shares | ($000) |

| Temporary Cash Investments (3.0%)1 | |

| Money Market Fund (2.7%) | | |

| 2,3 | Vanguard Market | | |

| | Liquidity Fund, | | |

| | 0.123% | 117,330,442 | 117,330 |

| |

| | | Face | |

| | | Amount | |

| | | ($000) | |

| U.S. Government and Agency Obligations (0.3%) |

| 4 | Federal Home Loan Bank | |

| | Discount Notes, | | |

| | 0.130%, 7/20/12 | 100 | 100 |

| 5,6 | Freddie Mac | | |

| | Discount Notes, | | |

| | 0.050%, 4/4/12 | 8,000 | 8,000 |

| 5,6 | Freddie Mac | | |

| | Discount Notes, | | |

| | 0.050%, 4/24/12 | 3,000 | 3,000 |

| 5,6 | Freddie Mac | | |

| | Discount Notes, | | |

| | 0.135%, 8/6/12 | 100 | 100 |

| 6 | United States Treasury | | |

| | Note/Bond, | | |

| | 1.000%, 4/30/12 | 100 | 100 |

| | | | 11,300 |

| Total Temporary Cash Investments | |

| (Cost $128,630) | | 128,630 |

| Total Investments (100.5%) | | |

| (Cost $3,677,925) | | 4,363,233 |

| Other Assets and Liabilities (-0.5%) | |

| Other Assets | | 36,133 |

| Liabilities3 | | (58,468) |

| | | | (22,335) |

| Net Assets (100%) | | 4,340,898 |

21

Growth and Income Fund

| |

| At March 31, 2012, net assets consisted of: |

| | Amount |

| | ($000) |

| Paid-in Capital | 4,790,079 |

| Undistributed Net Investment Income | 6,929 |

| Accumulated Net Realized Losses | (1,143,068) |

| Unrealized Appreciation (Depreciation) | |

| Investment Securities | 685,308 |

| Futures Contracts | 1,650 |

| Net Assets | 4,340,898 |

| |

| Investor Shares—Net Assets | |

| Applicable to 95,498,227 outstanding | |

| $.001 par value shares of beneficial | |

| interest (unlimited authorization) | 2,862,335 |

| Net Asset Value Per Share— | |

| Investor Shares | $29.97 |

| |

| Admiral Shares—Net Assets | |

| Applicable to 30,208,162 outstanding | |

| $.001 par value shares of beneficial | |

| interest (unlimited authorization) | 1,478,563 |

| Net Asset Value Per Share— | |

| Admiral Shares | $48.95 |

See Note A in Notes to Financial Statements.

* Non-income-producing security.

^ Part of security position is on loan to broker-dealers. The total value of securities on loan is $5,182,000.

1 The fund invests a portion of its cash reserves in equity markets through the use of index futures contracts. After giving effect to futures investments, the fund’s effective common stock and temporary cash investment positions represent 99.8% and 0.7%, respectively, of net assets.

2 Affiliated money market fund available only to Vanguard funds and certain trusts and accounts managed by Vanguard. Rate shown is the 7-day yield.

3 Includes $5,779,000 of collateral received for securities on loan.

4 The issuer operates under a congressional charter; its securities are generally neither guaranteed by the U.S. Treasury nor backed by the full faith and credit of the U.S. government.

5 The issuer was placed under federal conservatorship in September 2008; since that time, its daily operations have been managed by the Federal Housing Finance Agency and it receives capital from the U.S. Treasury in exchange for senior preferred stock.

6 Securities with a value of $11,200,000 have been segregated as initial margin for open futures contracts.

REIT—Real Estate Investment Trust.

See accompanying Notes, which are an integral part of the Financial Statements.

22

Growth and Income Fund

| |

| Statement of Operations | |

| |

| | Six Months Ended |

| | March 31, 2012 |

| | ($000) |

| Investment Income | |

| Income | |

| Dividends1 | 46,261 |

| Interest2 | 101 |

| Security Lending | 232 |

| Total Income | 46,594 |

| Expenses | |

| Investment Advisory Fees—Note B | |

| Basic Fee | 2,168 |

| Performance Adjustment | 94 |

| The Vanguard Group—Note C | |

| Management and Administrative—Investor Shares | 3,069 |

| Management and Administrative—Admiral Shares | 797 |

| Marketing and Distribution—Investor Shares | 275 |

| Marketing and Distribution—Admiral Shares | 117 |

| Custodian Fees | 97 |

| Shareholders’ Reports—Investor Shares | 31 |

| Shareholders’ Reports—Admiral Shares | 2 |

| Trustees’ Fees and Expenses | 5 |

| Total Expenses | 6,655 |

| Expenses Paid Indirectly | (31) |

| Net Expenses | 6,624 |

| Net Investment Income | 39,970 |

| Realized Net Gain (Loss) | |

| Investment Securities Sold | 235,016 |

| Futures Contracts | 21,616 |

| Realized Net Gain (Loss) | 256,632 |

| Change in Unrealized Appreciation (Depreciation) | |

| Investment Securities | 645,817 |

| Futures Contracts | 14,375 |

| Change in Unrealized Appreciation (Depreciation) | 660,192 |

| Net Increase (Decrease) in Net Assets Resulting from Operations | 956,794 |

| 1 Dividends are net of foreign withholding taxes of $5,000. |

| 2 Interest income from an affiliated company of the fund was $97,000. |

See accompanying Notes, which are an integral part of the Financial Statements.

23

Growth and Income Fund

| | |

| Statement of Changes in Net Assets | | |

| |

| | Six Months Ended | Year Ended |

| | March 31, | September 30, |

| | 2012 | 2011 |

| | ($000) | ($000) |

| Increase (Decrease) in Net Assets | | |

| Operations | | |

| Net Investment Income | 39,970 | 79,488 |

| Realized Net Gain (Loss) | 256,632 | 362,030 |

| Change in Unrealized Appreciation (Depreciation) | 660,192 | (312,354) |

| Net Increase (Decrease) in Net Assets Resulting from Operations | 956,794 | 129,164 |

| Distributions | | |

| Net Investment Income | | |

| Investor Shares | (26,232) | (53,125) |

| Admiral Shares | (13,689) | (26,147) |

| Realized Capital Gain | | |

| Investor Shares | — | — |

| Admiral Shares | — | — |

| Total Distributions | (39,921) | (79,272) |

| Capital Share Transactions | | |

| Investor Shares | (304,008) | (500,958) |

| Admiral Shares | 48,979 | (89,097) |

| Net Increase (Decrease) from Capital Share Transactions | (255,029) | (590,055) |

| Total Increase (Decrease) | 661,844 | (540,163) |

| Net Assets | | |

| Beginning of Period | 3,679,054 | 4,219,217 |

| End of Period1 | 4,340,898 | 3,679,054 |

| 1 Net Assets—End of Period includes undistributed net investment income of $6,929,000 and $6,880,000. |

See accompanying Notes, which are an integral part of the Financial Statements.

24

Growth and Income Fund

Financial Highlights

| | | | | | |

| Investor Shares | | | | | | |

| | Six Months | | | | | |

| | Ended | | | | | |

| For a Share Outstanding | March 31, | | | Year Ended September 30, |

| Throughout Each Period | 2012 | 2011 | 2010 | 2009 | 2008 | 2007 |

| Net Asset Value, Beginning of Period | $23.86 | $23.98 | $22.34 | $25.84 | $38.62 | $33.79 |

| Investment Operations | | | | | | |