UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-4840

The Tocqueville Trust

(Exact name of registrant as specified in charter)

The Tocqueville Trust

40 West 57th Street, 19th Floor

New York, NY 10019

(Address of principal executive offices) (Zip code)

Robert W. Kleinschmidt

The Tocqueville Trust

40 West 57th Street, 19th Floor

New York, NY 10019

(Name and address of agent for service)

(212) 698-0800

Registrant’s telephone number, including area code

Date of fiscal year end: October 31

Date of reporting period: April 30, 2012

Item 1. Reports to Stockholders.

SEMI-ANNUAL REPORT

April 30, 2012

The Tocqueville Trust

Mutual Funds

The Tocqueville Fund

The Tocqueville Opportunity Fund

The Tocqueville International Value Fund

The Tocqueville Gold Fund

The Delafield Fund

The Tocqueville Select Fund

This report is not authorized for distribution to prospective investors unless preceded or accompanied by a currently effective prospectus of The Tocqueville Trust. Please call 1-800-697-FUND (3863) for a free prospectus. Read it carefully before you invest.

You are invited to visit our website @ www.tocqueville.com/mutual-funds

Dear Fellow Shareholder,

The stock market, as measured by the American S&P 500 index, has about doubled from the level to which it had fallen in the spring of 2009. Other market indices, in the United States and globally, have risen somewhat more or less, but most are up substantially from their Great Recession lows.

On the other hand, historians and serious students of the market, who tend to define “secular” bear markets in terms of valuation measures such as Price/Earnings ratios rather than simply prices, argue that we have been in such a long-term bear market since early 2000, the peak of the “tech” and Internet bubble.

Surely, the aftermath of the 2007-2010 financial crisis has been quite scary. Many countries are struggling with unsustainable levels of debt; elected governments are abdicating their fiscal responsibilities, leaving central banks to deal with both deflationary and inflationary threats; for corporations and governments alike, access to liquidity is uncertain; Europe is threatening to break down; the United States economy is facing a potentially disastrous fiscal cliff if all the “Bush” tax cuts are allowed to expire at once; and consumers are feeling the pain of de-leveraging almost everywhere.

On the other hand, twelve years of bear market is a long time. By now, courtesy of CNBC, Bloomberg TV and the likes, no one can ignore the world economies’ predicament. While it can’t quite be said yet that stock market investors have capitulated, they have been exiting equity mutual funds and individual shares steadily for months. So, from a purely contrarian perspective, things are becoming more alluring.

I am no market analyst but, in my recollection, major bear markets end either in a selling climax (like 1974) or in an extended attrition (like 1982). No one can say for sure how it will happen this time. But, already, some values are appearing.

In the United States some financially solid companies are selling at low price/earnings ratios and offering dividend yields that are very competitive with quality long-term bonds. In Europe, many companies are suffering of having their share prices labeled in Euros, whereas a majority of their revenues and profits comes from outside Europe. Similar comments could be made about other regions as well, with China’s Shanghai index, for example, still 50% below its peak high as economists debate whether the economy will grow at 6%, 7% or 8%.

We believe that opportunities might become more compelling in coming months.

Faithfully yours,

François Sicart

Chairman

The Tocqueville Fund

Dear Fellow Shareholder,

The investment world continues to be buffeted by the sovereign debt storm emanating from Europe. During periods of relative calm on that front, markets have rallied; only to plunge once again as the storm intensifies. These are dangerous times, and for more than just the mutual fund investor. We continue to be impressed with the magnitude of government fiscal and demographic problems, not only in Europe, but all over the developed world, even China. Being unsolvable by the political process, these problems are not about to go away, and we remain convinced that it is the bond market that will eventually play the role of the adult in bringing government borrowing and spending into line with what their respective economies can afford. That is not a pleasant thought and hardly an optimal solution, but the evidence is scant that governments or the general public they represent are willing to take their medicine and scale back the spending and the programs that have brought us to this precarious point. It is very hard to take away from people (voters no less) that which they feel entitled to receive. Nowhere has this been done on any kind of meaningful scale without social unrest and worse.

In an effort to avoid the inevitable, we expect central banks to continue to create money out of thin air, in order to pay for unaffordable government obligations with ever decreasing (in value) paper currencies. This isn’t a bad strategy, given the circumstances, and given the fact that the global deleveraging process has slowed what monetary economists call the velocity of money. Eventually, however, we expect the general public to get wise to the trick and to increase their inflationary expectations, leading to a rise in interest rates and the bond vigilantes’ pillaging of the debt markets. When all this is to happen is not within our power to predict with any degree of accuracy, but it is within our investment horizon, and thus we remain very cautious in our investment strategy.

Large, well-capitalized, dividend paying global companies with dominant market shares and high returns on capital strike me as the best place to weather the ongoing storms. All the more so, because many names in this category are not expensive by historical valuation yardsticks. Higher beta financial names, while quite possibly providing attractive trading opportunities from time to time, do not qualify for this designation, and we have generally avoided them. The large technology companies, other than Apple, consumer staple names and some pharmaceuticals remain our primary holdings along with a menu of well-run cyclical names, industrials as well as commodity producers, which would benefit from a stronger global economy than what markets are currently predicting. Why? Because we might be wrong.

The Fund’s results over the six month period ended April 30, 2012 were generally favorable as investors gained 8.53%. This was a bit disappointing relative to the S&P 500’s very strong 12.77% gain, but not surprising given our general underrepresentation in Financials and the absence of Apple in our portfolio. All but one sector of the fund, Energy, contributed to performance and several of our largest positions had the most significant impact on returns. The top five contributors to performance during the period all meet the criteria mentioned above of high quality dividend paying global companies and included Pfizer, MasterCard, Microsoft, General Electric and Home Depot. On the other side of the coin, with the exception of Newmont Mining which was the largest negative influence, the five names that were the biggest detractors from performance largely were victims of certain aspects of the fears facing the global economy. For instance, Chesapeake Energy and CARBO Ceramics succumbed to declining natural gas prices brought on by a glut of production in the face of a weak U.S. economy, Cliffs Natural Resources declined due to concerns that Chinese demand for iron ore was softening and Banco Santander was impacted by the European sovereign debt crisis. Newmont, however, declined somewhat ironically for the opposite reasons as perceptions of the economy had at the time improved sufficiently to slow the upward price momentum of gold as a safe haven. In some cases, such as Chesapeake, these lower prices presented further opportunity, and we added to our holdings, but in the case of CARBO Ceramics we judged the company was more susceptible to competition than we had previously anticipated and exited the position.

Trading activity was more concentrated on the sell side rather than the buy side as we monetized positions in response to demand for investor liquidity and in a few cases as a result of a change in investment thesis such as Vulcan Materials which received and then rebuffed a hostile takeover proposal. We initiated a number of new holdings including: Baker Hughes, which we believed to be attractively valued with significant opportunity for margin improvement despite

concerns about the impact of natural gas prices on drilling activity; Xerox, which is very cash generative with a high degree of recurring service revenue but suffers under the misperception that demand for copiers is likely to decline rapidly; and PepsiCo, which we believe will unlock value through the eventual split of its beverage and snack businesses. We also partially swapped Lowes for Home Depot as the former had underperformed and offered more upside than the latter which had approached our price target.

While we remain vigilant on the macroeconomic front in the face of the previously mentioned threats, we continue to look for equities that trade at a significant discount to their intrinsic value utilizing conservative assumptions that reflect our cautious outlook for the global economy.

Lastly, please let me extend our thanks for your continued interest in our Fund.

Sincerely,

Robert W. Kleinschmidt

Portfolio Manager

The Tocqueville Fund

(Unaudited)

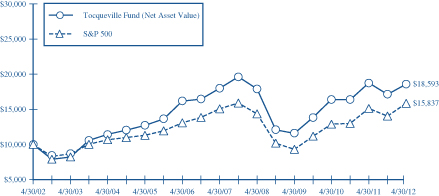

This chart assumes an initial gross investment of $10,000 made on 4/30/02. Returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Performance reflects fee waivers in effect. In the absence of fee waivers, total return would be reduced. Returns shown include the reinvestment of all dividends and other distributions. Past performance is not predictive of future performance. Investment return and principal value will fluctuate so that your shares, when redeemed, may be worth more or less than their original cost. The Fund imposes a 2% redemption fee on shares held for 90 days or less.

The Standard & Poor’s 500 Stock Index (S&P 500) is a capital-weighted index, representing the aggregate market value of the common equity of 500 stocks primarily traded on the New York Stock Exchange. Returns assume the reinvestment of all dividends.

AVERAGE ANNUAL RATE OF RETURN (%)

FOR PERIODS ENDED APRIL 30, 2012

| | | | | | | | | | | | | | | | |

| | | 1 Year | | | 3 Year | | | 5 Year | | | 10 Year | |

Tocqueville Fund | | | -0.88% | | | | 17.09% | | | | 0.68% | | | | 6.40% | |

Standard & Poor’s 500 Stock Index | | | 4.76% | | | | 19.46% | | | | 1.01% | | | | 4.71% | |

The Tocqueville Opportunity Fund

Dear Fellow Shareholder,

U.S. equity markets advanced smartly during the first half of the fiscal year ended April 30, 2012. The Tocqueville Opportunity Fund appreciated 13.30%, and outperformed its benchmark (Russell 2500 Growth Index) which gained 11.72%. During the six month period, the large capitalization Standard and Poor’s 500 Index rose 12.77% and outperformed the small capitalization Russell 2000 Index, which gained 11.02%. In the SMID capitalization asset class, value stocks lead the growth issues counterpart as the Russell 2500 Value Index gained 12.32%.

The Consumer/Consumer Discretionary and Technology sectors have continued to hold the #1 and #2 positions with regard to investment weightings on an adjusted basis (from Unclassified), and collectively represent nearly half of the Fund’s investment allocations at 51.5%. Nevertheless, commitments to the top two sectors were reduced slightly over the past six months. We have continued to increase investment in the Health Care sector to approximately 16% of the Fund from under 12% on April 30, 2011. These three sectors represented nearly two-thirds of the Fund’s investments on April 30, 2012. During the period, investments in the Health Care and Consumer Discretionary sectors provided the top and second best performance on both an absolute basis and relative basis. Although sector allocations, other than the increases in Health Care, have remained relatively stable, we have continued to diversify the portfolio with new investment positions. The top 10 and top 25 holdings, as a percentage of the Fund total, have actually declined respectively since October 31, 2011 (16.7% versus 17.7%, and 30.6% versus 33.9%). During the period of increased macro-economic uncertainty and market volatility, the Fund’s diversification strategy has mitigated exposure to individual issue price risk. While the number of “home runs” may have been limited, we believe that containing “concentration” risk has been a critical and successful investment strategy for controlling overall portfolio risks. Measured against a benchmark with in excess of 2000 positions, the Fund’s 50% allocation to the top 50 names could be easily mistaken for being relatively concentrated.

During the six months ended April 30, 2012, four of the top five price leaders were Health Care issues: Pharmasset, Illumina, Alnylam Pharmaceuticals and Incyte. Pharmasset was taken over by Gilead Sciences and Roche made a hostile bid to buy Illumina in January. Equinix, Inc. provided the third best individual stock appreciation during the period with a gain of 71%; Equinix is an owner and provider of data center services and IT services for businesses. When accounting for the combination of weighting and price gain, the leading relative performance for the Fund included two Biotechnology holdings: Pharmasset and Alexion Pharmaceuticals. Apple, Facebook and Priceline.com also provided leading relative performance. The Fund also benefitted from merger/acquisition activity. Additional holdings which were taken over included: Success Factors (SAP), GeoResources (Halcon Resources), Gen-Probe (Hologic), Nalco (Ecolab), and Taleo (Oracle). Over the past twelve month period ended April 30, 2012, the Fund has benefitted from 17 takeovers/takeover attempts; the high level of activity has confirmed the considerable attractiveness of smaller capitalization issues as large capitalization companies seek to consolidate companies in order to sustain their own growth rates and competitive advantages as well as utilize their considerable balance sheets, which are cash laden.

While we were pleased with the overall performance during the period, there were several disappointing investments, which impacted the Fund. From a sector standpoint, the Fund’s largest drawdown was attributable to Financial Services; the Fund’s most underweight sector. This sector’s 14+% rally during the period exceeded the Fund’s collective Financial Services holdings’ performance and the Russell 2500 Growth Index as well. Allscripts Healthcare, Deckers Outdoor, and Accretive Health all declined over 50% during the period due to disappointing earnings, management turmoil, and/or legal actions. While the declines were significant, the overall impacts to the Fund were limited to less than 6/10ths of one percent on an absolute basis due to the Fund’s diversification strategy.

Investors will recall that the commencement date of the current fiscal period coincided with the ending of the waterfall correction from July 2011. That swift, severe market decline was driven by uncertainty with U.S. deficit financing and a rapid loss of confidence with the resolve of European decision makers to address the risks of the EU sovereign debt and any associated risks of financial contagion, devaluation or breakup of the EU currency bloc. As we moved into the Fund’s new fiscal year, the combination of extremely negative sentiment and attractive equity valuations

provided the impetus for substantial market gains. Furthermore, the European Central Bank provided a newly supportive, short-term financing and liquidity measure for the banking system—the Long Term Refinancing Operation. Although markets proved rewarding through the end of the first six month period, the European situation has continued to represent the single greatest macro risk confronting investors. Recent election results in Europe have indicated that there is considerable political turmoil and dissatisfaction with current economic reform. Moreover, there is increased concern with recessionary risks and weakness in the Spanish banking system. On the U.S. side, the economy had performed well enough through the end of April—the median price for existing homes in April was +10.1% from a year earlier. The April jobs report was weak and with the warm winter having shifted economic activity to the early months, investors had begun to shift to a less positive view on the sustainability of growth. Moreover, with the U.S. in an election year, investors have become increasingly concerned with the brinkmanship and gridlock over the expiration of tax cuts and the extension of fiscal stimulus which is being referred to as the “fiscal cliff”. We believe headway towards resolution of European and U.S. policy and economic risks will be critical for financial markets from the current price levels. Against these aforementioned headwinds, we will continue to maintain a diversified investment profile and a focus on those opportunities where solid execution is ongoing. As we have witnessed over the past six months, investors gravitate most quickly to invest in those companies with the steady or improved growth rates and leading market share positions. We expect that any near-term volatility will present continued opportunity to initiate or increase investments in such issues. We appreciate very much your ongoing confidence in our efforts on behalf of the Tocqueville Opportunity Fund.

Sincerely,

Thomas R. Vandeventer

Portfolio Manager

The Tocqueville Opportunity Fund

(Unaudited)

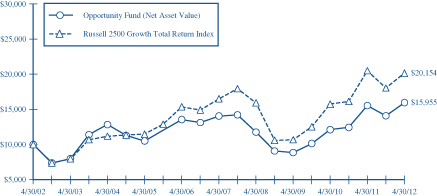

This chart assumes an initial gross investment of $10,000 made on 4/30/02. On July 1, 2010, a new portfolio management team assumed management of The Tocqueville Small Cap Fund and the Fund’s name and investment strategy changed as of October 12, 2010 (See Footnote 1 to the Financial Statements). Returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Returns shown include the reinvestment of all dividends and other distributions. Past performance is not predictive of future performance. Investment return and principal value will fluctuate so that your shares, when redeemed, may be worth more or less than their original cost. The Fund imposes a 2% redemption fee on shares held for 90 days or less.

The Russell 2500 Growth Total Return Index is an unmanaged index that measures the performance of the small to mid-cap growth segment of the U.S. equity universe. It includes those Russell 2500 companies with higher price-to-book ratios and higher forcasted growth values. Returns assume the reinvestment of all dividends.

AVERAGE ANNUAL RATE OF RETURN (%)

FOR PERIODS ENDED APRIL 30, 2012

| | | | | | | | | | | | | | | | |

| | | 1 Year | | | 3 Year | | | 5 Year | | | 10 Year | |

Tocqueville Opportunity Fund | | | 2.73% | | | | 21.72% | | | | 2.58% | | | | 4.78% | |

Russell 2500 Growth Total Return Index | | | -1.61% | | | | 23.64% | | | | 4.08% | | | | 7.26% | |

The Tocqueville International Value Fund

Dear Fellow Shareholder,

For the six months ended April 30, 2012, global equity markets produced modest gains. Equities advanced during much of the period as the European Central Bank’s LTRO helped to temporarily diffuse investor concerns about a financial meltdown in Europe, while improving macroeconomic data in Japan and the U.S. gave rise to the perception that a global recovery might gain traction. Then in April markets declined as a slowdown in LTRO activity and weak macroeconomic data in Europe caused investors once again to focus on risks, principal among them a possible slowdown in China, deterioration in Spain’s banking system, and a looming fiscal cliff in the U.S. The Tocqueville International Value Fund’s total U.S. dollar return for the period was a loss of 1.18%. In the same period, the Morgan Stanley EAFE Index, the benchmark against which we are most often compared, had a total U.S. dollar return of 2.71%.

During the six months, the European BE 500 index increased by 7.13% in local currency terms, the Japanese Nikkei 225 increased by 7.02% in local currency terms, and the MSCI Asia Pacific ex-Japan increased by 4.21%. The CRB Index of commodity prices declined by 4%, with industrial metals generally declining, gold declining, and agricultural commodities mixed, and oil increasing in value. Among developed equity markets, the U.S. fared well, while northern Europe and Japan made modest gains and southern Europe declined. Emerging markets were mixed, with Latin America and most of Asia up modestly and China down. In terms of sectors, beverages, consumer products and computer services led advances, while energy and telecom equipment declined. Most major currencies declined in value against the U.S. dollar as the market became more convinced about a recovery in the U.S. and fearful of a slowdown elsewhere.

Our holdings produced mixed results during the period, with our best performance coming from consumer related shares in the Asia Pacific region and our worst performance from gold mining shares. Standout positive contributors were Australian business services concern Spotless Group, subject of a takeover offer; Hong Kong broadcast television concern Television Broadcasts; Chinese outdoor advertising company Clear Media; Italian hydraulic equipment maker Interpump; German compact equipment maker Wacker Neuson; and, Japanese industrial conglomerate Hitachi. We had notable losses in Newmont Mining and Barrick Gold, as well as Spanish IT concern Indra Sistemas, Belgian wireless telecom services provider Mobistar and Italian auto parts maker Sogefi.

During the period, we exited positions in UK credit scoring concern Experian, Mexican beverage producer FEMSA, and UK business and construction services concern Interserve, which following strong performance approached our estimates of intrinsic value. We sold French integrated oil producer Total after a gas leak in the North Sea created an unquantifiable liability for the company. We sold Mobistar, where our investment thesis was undercut by a change in competitive conditions that had a negative impact on pricing and profit margins. And we sold Spanish IT services provider Indra Sistemas, where weakening payment terms from government customers undercut our thesis regarding free cash generation. We took new positions in Japanese company Disco, the global leader in chip dicing and wafer grinding equipment and related consumables which was depressed due to worries about the global IT cycle, in French television broadcaster M6, which generates a double digit free cash flow yield in a tepid economic environment, in Japanese footwear maker Asics, which is the global leader in performance running shoes and trades at a marked discount to intrinsic value, and in drug maker Novartis, which has a high free cash yield based on its existing pharma portfolio and where we were not paying much for an attractive pipeline of new products and the eye care franchise.

Developed market equity markets outside the U.S. are trading at very low valuations on a number of cash flow and book value metrics. Emerging markets valuations continue to deflate and are also reaching more attractive levels in absolute terms. There are indeed a number of potentially dangerous risks facing the global economy. Europe is slowing down and could slow further if the EU does not take action to recapitalize its banks, institute labor reforms and growth oriented economic policies, and provide for some form of jointly guaranteed debt issuance. And while the U.S. continues on a path of slow and uneven improvement, the so called fiscal cliff could knock the economy off track unless politicians take action to address spending cuts and tax increases scheduled to take effect in 2013. On the other hand, we think fears relating to China are overdone, and we are on balance sanguine about the skill with which the economy is being managed during a period of political transition as well as transition to a more consumer driven economic model. With sentiment

generally quite negative, interest rates low and valuations cheap, we think the balance of risks is in our favor. And there is no shortage of interesting stocks to investigate. But we will retain a portion of our cash position so that if a negative scenario develops we are in a position to capitalize on it.

We continue to employ our investment discipline, seeking to discover fundamentally attractive companies that are out of favor and undervalued, and to provide our shareholders with above average returns with below average risk over the course of an economic cycle.

Respectfully,

James Hunt

Portfolio Manager

The Tocqueville International Value Fund

(Unaudited)

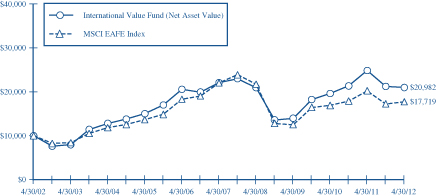

This chart assumes an initial gross investment of $10,000 made on 4/30/02. Returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Performance reflects fee waivers in effect. In the absence of fee waivers, total return would be reduced. Returns shown include the reinvestment of all dividends and other distributions. Past performance is not predictive of future performance. Investment return and principal value will fluctuate so that your shares, when redeemed, may be worth more or less than their original cost. The Fund imposes a 2% redemption fee on shares held 90 days or less.

The MSCI EAFE Index is an unmanaged market-capitalization-weighted index composed of companies representative of the market structure of 22 Developed Market Countries in Europe, Australia, Asia and the Far East.

AVERAGE ANNUAL RATE OF RETURN (%)

FOR PERIODS ENDED APRIL 30, 2012

| | | | | | | | | | | | | | | | |

| | | 1 Year | | | 3 Year | | | 5 Year | | | 10 Year | |

Tocqueville International Value Fund | | | -15.54% | | | | 14.50% | | | | -1.01% | | | | 7.69% | |

MSCI EAFE Index | | | -12.38% | | | | 12.30% | | | | -4.25% | | | | 5.89% | |

The Tocqueville Gold Fund

Dear Fellow Shareholder,

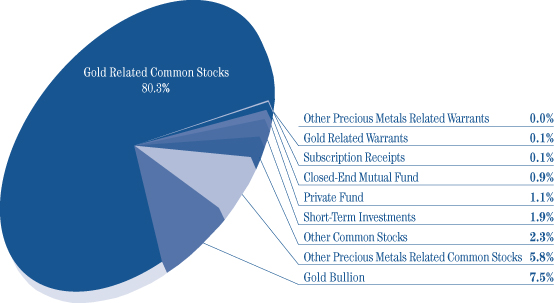

During the first six months of the 2012 fiscal year, the Tocqueville Gold Fund declined 15.91% vs. declines of 17.34% for the XAU (Philadelphia Stock Exchange Gold/Silver Index), and 2.92% for physical gold. In contrast, the S&P 500 gained 12.77% over this period. Currently, the Fund’s position in physical gold is 7.6% of its net assets and the balance is in shares of mining or processing companies whose principal business is the production of gold and other precious metals, and cash equivalents.

The first half of the fiscal year has been lively, to say the least. The gold market was whipsawed with liquidation selling in December, followed by news in January from the Federal Reserve that interest rates would be exceptionally low into 2014, and finally capped off in February by Fed Chairman Bernanke’s pronouncement that future quantitative easing was unlikely. Gold and precious metals shares meanwhile followed suit as investor sentiment ended the period at extreme lows.

Discouraged investors must be asking what it will take for precious metals shares to break out of their extended funk. We believe that the catalyst will be a move to new highs by gold during the remainder of the year. While this assertion may seem simplistic, the shares have underperformed the metal for an extended period, despite record earnings, cash flow, and dividends. From a contrarian point of view, we believe the stocks are table pounding buys unless the gold price plummets to levels substantially below that of December. We believe such a scenario is highly unlikely.

Against this backdrop, the Fund performed well relative to its benchmark during this period. The top contributors over this period included Gold Resource, European Goldfields, and Franco-Nevada which appreciated 22.1%, 17.6%, and 13.7% respectively. Notable among these was the performance by European Goldfields, which was the subject of an acquisition offer. This is another example of our strategy of investing in earlier stage companies that create value through exploration and development, and may eventually be acquired by a producing company. In contrast, our portfolio also had its share of disappointments during the period. The most notable were Ivanhoe Mines, Newmont, and IAMGOLD, which declined 42.9%, 27.8%, and 41.9% respectively. Despite the lackluster performance, we continue to believe that these companies will be able to deliver shareholder value over time.

Gold stocks are, in our view, demonstrably cheap and offer value comparable to the bottom in 2008. The ratio of the XAU to the price of gold is actually lower than at the historic low. Based on steadily rising inflation, negative real interest rates, the worsening sovereign debt crisis in Europe, and the prospect of further debt monetization by the Fed past the scheduled end of “Operation Twist” on June 30, or the likelihood of substantially higher interest rates which would stymie the feeble economic recovery, it would seem that the rationale for gold to surpass its highs of September 2011 is compelling.

Sincerely,

John C. Hathaway

Portfolio Manager

The Tocqueville Gold Fund

(Unaudited)

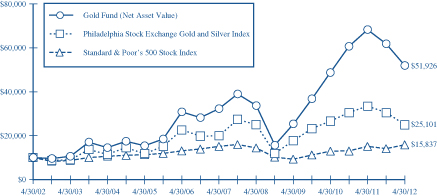

This chart assumes an initial gross investment of $10,000 made on 4/30/02. Returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Returns shown include the reinvestment of all dividends and other distributions. Past performance is not predictive of future performance. Investment return and principal value will fluctuate so that your shares, when redeemed, may be worth more or less than their original cost. The Fund imposes a 2% redemption fee on shares held 90 days or less.

In 2003, 2006, 2009, and 2010 the performance of The Tocqueville Gold Fund was achieved during a period of unusually favorable market conditions. Such performance may not be sustainable.

The Philadelphia Stock Exchange Gold and Silver Index is an unmanaged capitalization-weighted index which includes the leading companies involved in the mining of gold and silver. Returns include the reinvestment of all dividends.

The Standard & Poor’s 500 Stock Index (S&P 500) is a capital-weighted index, representing the aggregate market value of the common equity of 500 stocks primarily traded on the New York Stock Exchange. Returns include the reinvestment of all dividends.

AVERAGE ANNUAL RATE OF RETURN (%)

FOR PERIODS ENDED APRIL 30, 2012

| | | | | | | | | | | | | | | | |

| | | 1 Year | | | 3 Year | | | 5 Year | | | 10 Year | |

Tocqueville Gold Fund | | | -23.90% | | | | 27.04% | | | | 10.00% | | | | 17.91% | |

Philadelphia Stock Exchange Gold and Silver Index | | | -24.57% | | | | 12.43% | | | | 4.85% | | | | 9.64% | |

Standard & Poor’s 500 Stock Index | | | 4.76% | | | | 19.46% | | | | 1.01% | | | | 4.71% | |

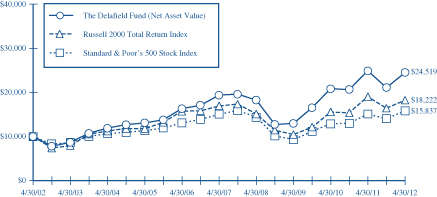

The Delafield Fund

Dear Fellow Shareholder,

For the six months ended April 30, 2012, the Fund’s net asset value increased 16.25% versus an increase of 11.02% for the Russell 2000 Index (“Russell 2000”) and 12.77% for the Standard & Poor’s 500 Index (“S&P 500”), each on a total return basis. The Fund’s net asset value as of April 30, 2012 was $31.21 per share. The net asset value amounted to $1,456,843,629, of which 82.7% was invested in equities, and the balance in treasury bills and cash reserves.

Equities experienced a strong recovery for almost the entire first half of the fiscal year. Investors responded enthusiastically to modest improvement in U.S. economic indicators and to solid corporate earnings. A pause in negative Eurozone related headlines during this period also seemed to calm investors’ nerves and helped drive the market’s upturn. Market volatility was prominent during the first three months of the period but was fairly benign for the last three months.

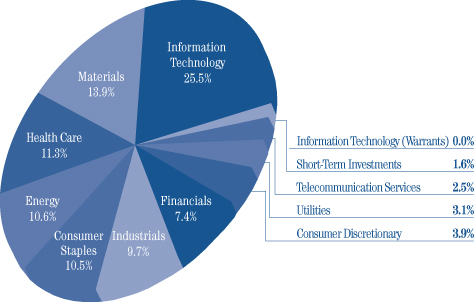

Industry weighting remains a coincidental result of our bottom-up investment approach. However, we had limited exposure to the energy sector, which benefited our performance relative to the Russell 2000, as it was among the weakest sectors for the period. We also had virtually no exposure to the financial sector, which negatively impacted our relative performance.

Our stock selection was generally positive to our return during the six month period, with our performance in five of the seven sectors in which we had exposure outperforming the corresponding index return. Investments in the industrials sector were most beneficial to performance relative to the Russell 2000, with holdings in materials also contributing favorably. Shares of Solutia Inc. advanced following the announcement of a takeover proposal in late January and the stock was the largest positive contributor to the portfolio’s performance. Ironically, our holdings in Eastman Chemical Company, Solutia’s would be suitor, were up nicely as well and it was the next largest positive contributor to performance. In contrast, Checkpoint Systems and Ferro Corporation were the largest detractors to our performance during the period.

We remain focused on identifying companies where our analytical insight suggests a largely unanticipated improvement in operations. Over the last six months we added a number of new names to the Fund that we believe represent good investment opportunities. For example, we established a position in Acco Brands Corporation, a company with $1.4 billion in sales, focused on products for the office supplies market (staplers, calendars, etc.). In November 2011, the company announced it would combine Acco with the office products business of MeadWestvaco Corporation. We believe that the transaction should be very positive as it is expected to sharply improve earnings to $1+ per share and provide greater clout with their suppliers and customers. Also, free cash flow should be nicely positive which should allow for debt reduction. Another new addition to the Fund during the period is Harsco Corporation, which announced the resignation of its CEO in late February. The company’s infrastructure and metals and mining operations have been underperforming for some time, and we believe that better execution under new management could lead to considerable improvements in both businesses. Looking out a couple of years, we believe that modest but achievable improvements in the operations could lead to a significant improvement in EBITDA.

Sincerely,

| | |

| |  |

| |

| J. Dennis Delafield | | Vincent Sellecchia |

| Portfolio Manager | | Portfolio Manager |

The Delafield Fund

(Unaudited)

This chart assumes an initial gross investment of $10,000 made on 4/30/02. Since the Delafield Fund did not commence operations until 9/28/09, returns prior to that date are those of the Predecessor Fund. The Delafield Fund assumed the net asset value and performance history of the Predecessor Fund (See Footnote 1 to the Financial Statements). Returns shown does not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Performance reflects fee wiaviers in effect. In the absence of fee waivers, total return would be reduced. Returns shown include the reinvestment of all dividends and other distributions. Past performance is not predictive of future performance. Investment return and principal value will fluctuate so that your shares, when redeemed, may be worth more or less than their original cost. The Fund imposes a 2% redemption fee on shares held 90 days or less.

The Russell 2000 Total Return Index is an unmanaged index that measures the performance of the 2,000 smallest companies in the Russell 3000 Index, which represent approximately 8% of the total market capitalization of the Russell 3000 Index. Returns include the reinvestment of all dividends.

The Standard & Poor’s 500 Stock Index (S&P 500) is a capital-weighted index, representing the aggregate market value of the common equity of 500 stocks primarily traded on the New York Stock Exchange. Returns include the reinvestment of all dividends.

AVERAGE ANNUAL RATE OF RETURN (%)

FOR PERIODS ENDED APRIL 30, 2012

| | | | | | | | | | | | | | | | |

| | | 1 Year | | | 3 Year | | | 5 Year | | | 10 Year | |

The Delafield Fund | | | -1.49% | | | | 23.59% | | | | 4.81% | | | | 9.38% | |

Russell 2000 Total Return Index | | | -4.25% | | | | 20.34% | | | | 1.45% | | | | 6.19% | |

Standard & Poor’s 500 Stock Index | | | 4.76% | | | | 19.46% | | | | 1.01% | | | | 4.71% | |

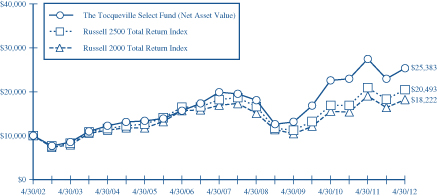

The Tocqueville Select Fund

Dear Fellow Shareholder,

For the six months ended April 30, 2012, the Fund’s net asset value increased 10.60% versus an increase of 12.03% for the Russell 2500 Index (“Russell 2500”) and 11.02% for the Russell 2000 Index (“Russell 2000”), each on a total return basis. The Fund’s net asset value as of April 30, 2012 was $12.11 per share. The net asset value amounted to $93,938,492, of which 82.1% was invested in equities with the balance held in treasury bills and cash reserves.

Equities experienced a strong recovery for almost the entire first half of the fiscal year. Investors responded enthusiastically to modest improvement in U.S. economic indicators and to solid corporate earnings. A pause in negative Eurozone related headlines during this period also seemed to calm investors’ nerves and helped drive the market’s upturn. Market volatility was prominent during the first three months of the period but was fairly benign for the last three months.

The Fund’s portfolio is built using a bottom-up approach. We focus intently on valuation and analyze cash flows and attempt to invest at prices that we believe undervalue the underlying franchise. We added several new stocks to the Fund since the start of the fiscal year. For example, we started a position in Avery Dennison Corporation, which designs and manufactures pressure sensitive and self-adhesive materials, retail branding and information tags and labels, and a variety of specialty materials. We believe that the long-term earnings power of the businesses is attractive and that the company should continue to generate ample free cash flow to further reduce debt, fund an annual common dividend and repurchase a substantial number of shares.

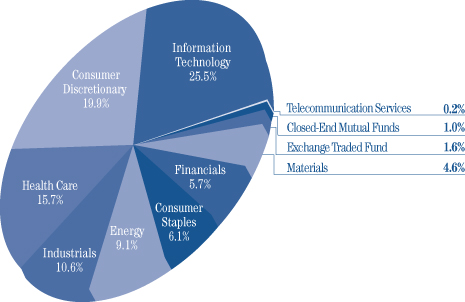

The Fund’s portfolio is not constructed with industry allocation targets. However, we were overweight in the industrials and materials sectors which benefited performance. We had no exposure to the energy and utilities sectors, which also helped our relative performance. Conversely, our avoidance of the financial sector negatively impacted our return relative to the Russell 2500.

Our stock selection was mixed during the six month period. Our investments in the industrials and materials sectors outperformed the corresponding index return, while consumer discretionary and information technology holdings underperformed. Solutia Inc. was the largest contributor to our performance, with the shares advancing on an announced takeover proposal from Eastman Chemical Company. In contrast, Summer Infant, Inc. and Checkpoint Systems were the largest detractors to our performance during the period.

| | | | |

| Sincerely, | | | | |

| | |

| | | |  |

| | |

| J. Dennis Delafield | | Vincent Sellecchia | | Donald Wang |

| Portfolio Manager | | Portfolio Manager | | Portfolio Manager |

The Tocqueville Select Fund

(Unaudited)

This chart assumes an initial gross investment of $10,000 made on 4/30/02. Since The Tocqueville Select Fund did not commence operations until 9/28/09, returns from the period from September 29, 2008 to September 27, 2009 are those of the Class Y Shares of the Predecessor Fund (See Footnote 1 to the Financial Statements). Prior to that period, returns shown are those of a limited partnership managed by the adviser. Returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Performance reflects fee waivers in effect. In the absence of fee waivers, total return would be reduced. Returns shown include the reinvestment of all dividends and other distributions. Past performance is not predictive of future performance. Investment return and principal value will fluctuate so that your shares, when redeemed, may be worth more or less than their original cost. The Fund imposes a 2% redemption fee on shares held 90 days or less.

The Russel 2500 Total Return Index is an unmanaged index that measures the performance of the 2,500 smallest companies in the Russell 3000 Index. Returns include the reinvestment of all dividends.

The Russell 2000 Total Return Index is an unmanaged index that measures the performance of the 2,000 smallest companies in the Russell 3000 Index, which represents approximately 8% of the total market capitalization of the Russell 3000 Index. Returns include the reinvestment of all dividends.

AVERAGE ANNUAL RATE OF RETURN (%)

FOR PERIODS ENDED APRIL 30, 2012

| | | | | | | | | | | | | | | | |

| | | 1 Year | | | 3 Year | | | 5 Year | | | 10 Year | |

The Tocqueville Select Fund | | | -7.68% | | | | 24.42% | | | | 5.01% | | | | 9.76% | |

Russell 2500 Total Return Index | | | -2.23% | | | | 22.13% | | | | 2.35% | | | | 7.44% | |

Russell 2000 Total Return Index | | | -4.25% | | | | 20.34% | | | | 1.45% | | | | 6.19% | |

Expense Example—April 30, 2012 (Unaudited)

As a shareholder of The Tocqueville Trust (the “Funds”), you incur ongoing costs, including management fees; distribution fees; and other Fund expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in the Funds and to compare costs with the ongoing costs of investing in other mutual funds.

The Example is based on an investment of $1,000 invested at the beginning of the period and held the entire period (November 1, 2011-April 30, 2012).

Actual Expenses

The first line of the table below provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The second line of the table below provides information about hypothetical account values and hypothetical expenses based on the Funds’ actual expense ratios and an assumed rate of return of 5% per year before expenses, which is not the Funds’ actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Funds and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads), redemption fees, or exchange fees. Therefore, the second line of the table is useful in comparing ongoing costs only, and will not help you determine the relative costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

Expense Example Tables (Unaudited)

| | | | | | | | | | | | |

The Tocqueville Fund | | Beginning

Account Value

November 1, 2011 | | | Ending

Account Value

April 30, 2012 | | | Expenses Paid

During Period*

November 1, 2011 -

April 30, 2012 | |

Actual | | $ | 1,000.00 | | | $ | 1,085.30 | | | $ | 6.53 | |

Hypothetical (5% return before expenses) | | | 1,000.00 | | | | 1,018.60 | | | | 6.32 | |

| | | |

| The Tocqueville Opportunity Fund | | | | | | | | | | | | |

Actual | | $ | 1,000.00 | | | $ | 1,133.00 | | | $ | 6.89 | |

Hypothetical (5% return before expenses) | | | 1,000.00 | | | | 1,018.40 | | | | 6.52 | |

| | | |

| The Tocqueville International Value Fund | | | | | | | | | | | | |

Actual | | $ | 1,000.00 | | | $ | 988.20 | | | $ | 7.66 | |

Hypothetical (5% return before expenses) | | | 1,000.00 | | | | 1,017.16 | | | | 7.77 | |

| | | |

| The Tocqueville Gold Fund | | | | | | | | | | | | |

Actual | | $ | 1,000.00 | | | $ | 840.90 | | | $ | 5.81 | |

Hypothetical (5% return before expenses) | | | 1,000.00 | | | | 1,018.55 | | | | 6.37 | |

| | | |

| The Delafield Fund | | | | | | | | | | | | |

Actual | | $ | 1,000.00 | | | $ | 1,162.50 | | | $ | 6.61 | |

Hypothetical (5% return before expenses) | | | 1,000.00 | | | | 1,018.75 | | | | 6.17 | |

| | | |

| The Tocqueville Select Fund | | | | | | | | | | | | |

Actual | | $ | 1,000.00 | | | $ | 1,106.00 | | | $ | 7.07 | |

Hypothetical (5% return before expenses) | | | 1,000.00 | | | | 1,018.15 | | | | 6.77 | |

| * | Expenses are equal to the Fund’s annualized six-month expense ratio (including extraordinary expenses) of 1.26%, 1.30%, 1.55%, 1.27%, 1.23% and 1.35% for The Tocqueville Fund, Opportunity Fund, International Value Fund, Gold Fund, Delafield Fund, and Select Fund, respectively, multiplied by the average account value over the period, multiplied by 182/366 to reflect the one-half year period. |

The Tocqueville Fund

Financial Highlights

| | | | | | | | | | | | | | | | | | | | | | | | |

Per share operating performance (For a share outstanding

throughout the period) | | Six Months

Ended

April 30,

2012 | | | Years Ended October 31, | |

| | | 2011 | | | 2010 | | | 2009 | | | 2008 | | | 2007 | |

| | | (unaudited) | | | | | | | | | | | | | | | | |

Net asset value, beginning of period | | $ | 22.23 | | | $ | 21.53 | | | $ | 18.47 | | | $ | 16.39 | | | $ | 28.93 | | | $ | 24.25 | |

| | | | | | | | | | | | | | | | | | | | | | | | |

Operations: | | | | | | | | | | | | | | | | | | | | | | | | |

Net investment income | | | 0.22 | | | | 0.23 | | | | 0.32 | | | | 0.28 | | | | 0.24 | | | | 0.18 | |

Net realized and unrealized gain (loss) | | | 1.65 | | | | 0.80 | | | | 2.97 | | | | 2.09 | | | | (10.56 | ) | | | 4.53 | |

| | | | | | | | | | | | | | | | | | | | | | | | |

Total from investment operations (1) | | | 1.87 | | | | 1.03 | | | | 3.29 | | | | 2.37 | | | | (10.32 | ) | | | 4.71 | |

| | | | | | | | | | | | | | | | | | | | | | | | |

Dividends and distributions to shareholders: | | | | | | | | | | | | | | | | | | | | | | | | |

Dividends from net investment income | | | (0.33 | ) | | | (0.33 | ) | | | (0.23 | ) | | | (0.29 | ) | | | (0.19 | ) | | | (0.03 | ) |

Distributions from net realized gains | | | — | | | | — | | | | — | | | | — | | | | (2.03 | ) | | | — | |

| | | | | | | | | | | | | | | | | | | | | | | | |

Total dividends and distributions | | | (0.33 | ) | | | (0.33 | ) | | | (0.23 | ) | | | (0.29 | ) | | | (2.22 | ) | | | (0.03 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | |

Change in net asset value for the period | | | 1.54 | | | | 0.70 | | | | 3.06 | | | | 2.08 | | | | (12.54 | ) | | | 4.68 | |

| | | | | | | | | | | | | | | | | | | | | | | | |

Net asset value, end of period | | $ | 23.77 | | | $ | 22.23 | | | $ | 21.53 | | | $ | 18.47 | | | $ | 16.39 | | | $ | 28.93 | |

| | | | | | | | | | | | | | | | | | | | | | | | |

Total return | | | 8.53 | %(3) | | | 4.77 | % | | | 17.95 | % | | | 14.80 | % | | | (38.47 | )% | | | 19.43 | % |

Ratios/supplemental data | | | | | | | | | | | | | | | | | | | | | | | | |

Net assets, end of period (000) | | $ | 396,536 | | | $ | 491,541 | | | $ | 489,670 | | | $ | 383,470 | | | $ | 328,609 | | | $ | 523,878 | |

Ratio to average net assets: | | | | | | | | | | | | | | | | | | | | | | | | |

Expenses (2) | | | 1.25 | %(4)(5) | | | 1.25 | % | | | 1.25 | % | | | 1.25 | % | | | 1.25 | % | | | 1.25 | % |

Net investment income (2) | | | 1.34 | %(4) | | | 0.98 | % | | | 1.66 | % | | | 1.68 | % | | | 0.94 | % | | | 0.69 | % |

Portfolio turnover rate | | | 7 | %(3) | | | 28 | % | | | 23 | % | | | 32 | % | | | 51 | % | | | 39 | % |

| (1) | Total from investment operations per share includes redemption fees of $0.001 for the six months ended April 30, 2012 and $0.002, $0.002, $0.004, $0.009 and $0.002 per share for the fiscal years ended October 31, 2011, 2010, 2009, 2008 and 2007, respectively. |

| (2) | Net of fees waived amounting to 0.03% for the six months ended April 30, 2012 and 0.01%, 0.01%, 0.08%, 0.04% and 0.01% of average net assets for the fiscal years ended October 31, 2011, 2010, 2009, 2008 and 2007, respectively. |

| (5) | Including interest expense increases the ratio by 0.01%. |

The Accompanying Notes are an Integral Part of these Financial Statements.

The Tocqueville Opportunity Fund

Financial Highlights

| | | | | | | | | | | | | | | | | | | | | | | | |

Per share operating performance (For a share outstanding throughout the

period) | | Six Months

Ended

April 30,

2012 | | | Years Ended October 31, | |

| | | 2011 | | | 2010 | | | 2009 | | | 2008 | | | 2007 | |

| | | (unaudited) | | | | | | | | | | | | | | | | |

Net asset value, beginning of period | | $ | 14.96 | | | $ | 13.20 | | | $ | 10.78 | | | $ | 9.77 | | | $ | 17.24 | | | $ | 18.04 | |

| | | | | | | | | | | | | | | | | | | | | | | | |

Operations: | | | | | | | | | | | | | | | | | | | | | | | | |

Net investment income (loss) | | | (0.06 | ) | | | (0.13 | ) | | | (0.12 | ) | | | (0.11 | ) | | | 0.02 | | | | 0.11 | |

Net realized and unrealized gain (loss) | | | 2.05 | | | | 1.89 | | | | 2.54 | | | | 1.23 | | | | (5.67 | ) | | | 1.26 | |

| | | | | | | | | | | | | | | | | | | | | | | | |

Total from investment operations (1) | | | 1.99 | | | | 1.76 | | | | 2.42 | | | | 1.12 | | | | (5.65 | ) | | | 1.37 | |

| | | | | | | | | | | | | | | | | | | | | | | | |

Dividends and distributions to shareholders: | | | | | | | | | | | | | | | | | | | | | | | | |

Dividends from net investment income | | | — | | | | — | | | | — | | | | (0.01 | ) | | | (0.12 | ) | | | — | |

Distributions from net realized gains | | | — | | | | — | | | | — | | | | (0.10 | ) | | | (1.70 | ) | | | (2.17 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | |

Total dividends and distributions | | | — | | | | — | | | | — | | | | (0.11 | ) | | | (1.82 | ) | | | (2.17 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | |

Change in net asset value for the period | | | 1.99 | | | | 1.76 | | | | 2.42 | | | | 1.01 | | | | (7.47 | ) | | | (0.80 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | |

Net asset value, end of period | | $ | 16.95 | | | $ | 14.96 | | | $ | 13.20 | | | $ | 10.78 | | | $ | 9.77 | | | $ | 17.24 | |

| | | | | | | | | | | | | | | | | | | | | | | | |

Total return | | | 13.30 | %(2) | | | 13.33 | % | | | 22.56 | % | | | 11.68 | % | | | (36.16 | )% | | | 8.42 | % |

Ratios/supplemental data | | | | | | | | | | | | | | | | | | | | | | | | |

Net assets, end of period (000) | | $ | 73,653 | | | $ | 46,963 | | | $ | 32,863 | | | $ | 30,498 | | | $ | 36,429 | | | $ | 49,543 | |

Ratio to average net assets: | | | | | | | | | | | | | | | | | | | | | | | | |

Expenses | | | 1.30 | %(3) | | | 1.36 | % | | | 1.41 | % | | | 1.41 | % | | | 1.35 | % | | | 1.32 | % |

Net investment income (loss) | | | (0.92 | )%(3) | | | (1.04 | )% | | | (1.08 | )% | | | (0.97 | )% | | | 0.12 | % | | | 0.63 | % |

Portfolio turnover rate | | | 29 | %(2) | | | 110 | % | | | 104 | % | | | 62 | % | | | 169 | % | | | 90 | % |

| (1) | Total from investment operations per share includes redemption fees of less than $0.001 for the six months ended April 30, 2012 and the fiscal years ended October 31, 2011 and 2010, $0.001, $0.005 and $0.001 for the fiscal years ended October 31, 2009, 2008 and 2007, respectively. |

The Accompanying Notes are an Integral Part of these Financial Statements.

The Tocqueville International Value Fund

Financial Highlights

| | | | | | | | | | | | | | | | | | | | | | | | |

Per share operating performance

(For a share outstanding throughout

the period) | | Six Months

Ended

April 30,

2012 | | | Years Ended October 31, | |

| | | 2011 | | | 2010 | | | 2009 | | | 2008 | | | 2007 | |

| | | (unaudited) | | | | | | | | | | | | | | | | |

Net asset value, beginning of period | | $ | 12.00 | | | $ | 12.12 | | | $ | 10.48 | | | $ | 8.49 | | | $ | 16.48 | | | $ | 16.72 | |

| | | | | | | | | | | | | | | | | | | | | | | | |

Operations: | | | | | | | | | | | | | | | | | | | | | | | | |

Net investment income | | | 0.07 | | | | 0.11 | | | | 0.11 | | | | 0.10 | | | | 0.13 | | | | 0.08 | |

Net realized and unrealized gain (loss) | | | (0.22 | ) | | | (0.16 | ) | | | 1.65 | | | | 2.59 | | | | (6.09 | ) | | | 2.25 | |

| | | | | | | | | | | | | | | | | | | | | | | | |

Total from investment operations (1) | | | (0.15 | ) | | | (0.05 | ) | | | 1.76 | | | | 2.69 | | | | (5.96 | ) | | | 2.33 | |

| | | | | | | | | | | | | | | | | | | | | | | | |

Dividends and distributions to shareholders: | | | | | | | | | | | | | | | | | | | | | | | | |

Dividends from net investment income | | | (0.12 | ) | | | (0.07 | ) | | | (0.12 | ) | | | (0.20 | ) | | | (0.10 | ) | | | (0.27 | ) |

Distributions from net realized gains | | | — | | | | — | | | | — | | | | (0.50 | ) | | | (1.93 | ) | | | (2.30 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | |

Total dividends and distributions | | | (0.12 | ) | | | (0.07 | ) | | | (0.12 | ) | | | (0.70 | ) | | | (2.03 | ) | | | (2.57 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | |

Change in net asset value for the period | | | (0.27 | ) | | | (0.12 | ) | | | 1.64 | | | | 1.99 | | | | (7.99 | ) | | | (0.24 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | |

Net asset value, end of period | | $ | 11.73 | | | $ | 12.00 | | | $ | 12.12 | | | $ | 10.48 | | | $ | 8.49 | | | $ | 16.48 | |

| | | | | | | | | | | | | | | | | | | | | | | | |

Total return | | | (1.18 | )%(2) | | | (0.47 | )% | | | 16.96 | % | | | 34.04 | % | | | (40.82 | )% | | | 15.29 | % |

Ratios/supplemental data | | | | | | | | | | | | | | | | | | | | | | | | |

Net assets, end of period (000) | | $ | 224,526 | | | $ | 199,848 | | | $ | 150,103 | | | $ | 131,613 | | | $ | 118,189 | | | $ | 219,220 | |

Ratio to average net assets: | | | | | | | | | | | | | | | | | | | | | | | | |

Expenses | | | 1.55 | %(3) | | | 1.56 | % | | | 1.56 | % | | | 1.62 | % | | | 1.56 | % | | | 1.59 | % |

Net investment income | | | 1.37 | %(3) | | | 0.99 | % | | | 1.03 | % | | | 0.96 | % | | | 1.07 | % | | | 0.49 | % |

Portfolio turnover rate | | | 20 | %(2) | | | 30 | % | | | 27 | % | | | 27 | % | | | 63 | % | | | 49 | % |

| (1) | Total from investment operations per share includes redemption fees of $0.001 for the six months ended April 30, 2012 and $0.010, $0.002, $0.001, $0.001 and $0.002 per share for the fiscal years ended October 31, 2011, 2010, 2009, 2008 and 2007, respectively. |

The Accompanying Notes are an Integral Part of these Financial Statements.

The Tocqueville Gold Fund

Financial Highlights

| | | | | | | | | | | | | | | | | | | | | | | | |

Per share operating performance

(For a share outstanding

throughout the period) | | Six Months

Ended

April 30,

2012 | | | Years Ended October 31, | |

| | | 2011 | | | 2010 | | | 2009 | | | 2008 | | | 2007 | |

| | | (unaudited) | | | | | | | | | | | | | | | | |

Net asset value, beginning of period | | $ | 81.97 | | | $ | 82.00 | | | $ | 49.71 | | | $ | 21.77 | | | $ | 64.36 | | | $ | 51.41 | |

| | | | | | | | | | | | | | | | | | | | | | | | |

Operations: | | | | | | | | | | | | | | | | | | | | | | | | |

Net investment loss | | | (0.23 | ) | | | (0.67 | ) | | | (0.58 | ) | | | (0.45 | ) | | | (0.57 | ) | | | (0.30 | ) |

Net realized and unrealized gain (loss) | | | (12.72 | ) | | | 2.25 | | | | 32.96 | | | | 29.28 | | | | (33.24 | ) | | | 18.52 | |

| | | | | | | | | | | | | | | | | | | | | | | | |

Total from investment operations (1) | | | (12.95 | ) | | | 1.58 | | | | 32.38 | | | | 28.83 | | | | (33.81 | ) | | | 18.22 | |

| | | | | | | | | | | | | | | | | | | | | | | | |

Dividends and distributions to shareholders: | | | | | | | | | | | | | | | | | | | | | | | | |

Dividends from net investment income | | | — | | | | — | | | | — | | | | — | | | | (0.46 | ) | | | (0.22 | ) |

Distributions from net realized gains | | | (1.33 | ) | | | (1.61 | ) | | | (0.09 | ) | | | (0.89 | ) | | | (8.32 | ) | | | (5.05 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | |

Total dividends and distributions | | | (1.33 | ) | | | (1.61 | ) | | | (0.09 | ) | | | (0.89 | ) | | | (8.78 | ) | | | (5.27 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | |

Change in net asset value for the period | | | (14.28 | ) | | | (0.03 | ) | | | 32.29 | | | | 27.94 | | | | (42.59 | ) | | | 12.95 | |

| | | | | | | | | | | | | | | | | | | | | | | | |

Net asset value, end of period | | $ | 67.69 | | | $ | 81.97 | | | $ | 82.00 | | | $ | 49.71 | | | $ | 21.77 | | | $ | 64.36 | |

| | | | | | | | | | | | | | | | | | | | | | | | |

Total return | | | (15.91 | )%(2) | | | 1.84 | % | | | 65.22 | % | | | 135.22 | % | | | (59.98 | )% | | | 38.35 | % |

Ratios/supplemental data | | | | | | | | | | | | | | | | | | | | | | | | |

Net assets, end of period (000) | | $ | 2,167,211 | | | $ | 2,647,078 | | | $ | 2,199,603 | | | $ | 937,492 | | | $ | 410,857 | | | $ | 1,231,475 | |

Ratios to average net assets: | | | | | | | | | | | | | | | | | | | | | | | | |

Expenses | | | 1.27 | %(3) | | | 1.25 | % | | | 1.34 | % | | | 1.50 | % | | | 1.43 | % | | | 1.42 | % |

Net investment income (loss) | | | (0.59 | )%(3) | | | (0.86 | )% | | | (1.11 | )% | | | (1.25 | )% | | | (1.07 | )% | | | (0.81 | )% |

Portfolio turnover rate | | | 4 | %(2) | | | 3 | % | | | 9 | % | | | 9 | % | | | 28 | % | | | 26 | % |

| (1) | Total from investment operations per share includes redemption fees of $0.015 for the six months ended April 30, 2012 and $0.102, $0.056, $0.025, $0.027 and $0.028 per share for the fiscal years ended October 31, 2011, 2010, 2009, 2008 and 2007, respectively. |

The Accompanying Notes are an Integral Part of these Financial Statements.

The Delafield Fund

Financial Highlights

| | | | | | | | | | | | | | | | | | | | | | | | |

Per share operating

performance (For a share

outstanding throughout the

period) | | Six Months

Ended

April 30,

2012 | | | Years Ended

October 31, | | | January 1,

2009

through

October 31, | | | Years Ended

December 31, | |

| | | 2011 | | | 2010 | | | 2009 | | | 2008 | | | 2007 | |

| | | (unaudited) | | | | | | | | | | | | | | | | |

Net asset value, beginning of period | | $ | 27.21 | | | $ | 26.65 | | | $ | 21.35 | | | $ | 15.10 | | | $ | 24.33 | | | $ | 25.64 | |

| | | | | | | | | | | | | | | | | | | | | | | | |

Operations: | | | | | | | | | | | | | | | | | | | | | | | | |

Net investment income (loss) | | | (0.02 | ) | | | (0.08 | ) | | | (0.00 | )(2) | | | 0.03 | | | | 0.07 | | | | 0.17 | |

Net realized and unrealized gain (loss) | | | 4.39 | | | | 0.64 | | | | 5.32 | | | | 6.25 | | | | (9.23 | ) | | | 1.10 | |

| | | | | | | | | | | | | | | | | | | | | | | | |

Total from investment operations (1) | | | 4.37 | | | | 0.56 | | | | 5.32 | | | | 6.28 | | | | (9.16 | ) | | | 1.27 | |

| | | | | | | | | | | | | | | | | | | | | | | | |

Dividends and distributions to shareholders: | | | | | | | | | | | | | | | | | | | | | | | | |

Dividends from net investment income | | | — | | | | — | | | | — | | | | (0.03 | ) | | | (0.07 | ) | | | (0.16 | ) |

Distributions from net realized gains | | | (0.37 | ) | | | — | | | | — | | | | — | | | | (0.00 | )(2) | | | (2.42 | ) |

Return of capital | | | — | | | | — | | | | (0.02 | ) | | | (0.00 | )(2) | | | (0.00 | )(2) | | | — | |

| | | | | | | | | | | | | | | | | | | | | | | | |

Total dividends and distributions | | | (0.37 | ) | | | — | | | | (0.02 | ) | | | (0.03 | ) | | | (0.07 | ) | | | (2.58 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | |

Change in net asset value for the period | | | 4.00 | | | | 0.56 | | | | 5.30 | | | | 6.25 | | | | (9.23 | ) | | | (1.31 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | |

Net asset value, end of period | | $ | 31.21 | | | $ | 27.21 | | | $ | 26.65 | | | $ | 21.35 | | | $ | 15.10 | | | $ | 24.33 | |

| | | | | | | | | | | | | | | | | | | | | | | | |

Total return | | | 16.25 | %(3) | | | 2.10 | % | | | 24.96 | % | | | 41.61 | %(3) | | | (37.62 | )% | | | 4.90 | % |

Ratios/supplemental data | | | | | | | | | | | | | | | | | | | | | | | | |

Net assets, end of period (000) | | $ | 1,456,844 | | | $ | 1,262,876 | | | $ | 933,674 | | | $ | 636,548 | | | $ | 404,860 | | | $ | 656,999 | |

Ratios to average net assets: | | | | | | | | | | | | | | | | | | | | | | | | |

Expenses | | | 1.23 | %(4) | | | 1.23 | % | | | 1.27 | % | | | 1.38 | %(4) | | | 1.34 | %(5) | | | 1.28 | %(5) |

Net investment income (loss) | | | (0.15 | )%(4) | | | (0.30 | )% | | | (0.02 | )% | | | 0.21 | %(4) | | | 0.35 | %(5) | | | 0.57 | %(5) |

Portfolio turnover rate | | | 26 | %(3) | | | 38 | % | | | 30 | % | | | 46 | %(3) | | | 81 | % | | | 61 | % |

| (1) | Total from investment operations per share includes redemption fees of $0.001 for the six months ended April 30, 2012 and $0.006 per share for the fiscal years ended October 31, 2011 and 2010, $0.008 per share for the period ended October 31, 2009, $0.01 for the fiscal year ended December 31, 2007 and less than $0.01 per share for the fiscal year ended December 31, 2008. |

| (2) | Represents less than $0.01. |

| (5) | Net of fees waived amounting to 0.06% and 0.05% for the fiscal years ended December 31, 2008 and 2007 respectively. |

The Accompanying Notes are an Integral Part of these Financial Statements.

The Tocqueville Select Fund

Financial Highlights

| | | | | | | | | | | | | | | | | | | | |

Per share operating performance

(For a share outstanding throughout the

period) | | Six Months

Ended

April 30,

2012 | | | Years Ended

October 31, | | | January 1, 2009

through

October 31, | | | Period from

September 29,

2008 (2)

through

December 31,

2008 | |

| | | 2011 | | | 2010 | | | 2009 | | |

| | | (unaudited) | | | | | | | | | | | | | |

Net asset value, beginning of period | | $ | 11.06 | | | $ | 11.54 | | | $ | 8.46 | | | $ | 5.77 | | | $ | 8.74 | |

| | | | | | | | | | | | | | | | | | | | |

Operations: | | | | | | | | | | | | | | | | | | | | |

Net investment income (loss) | | | (0.03 | ) | | | (0.07 | ) | | | (0.03 | ) | | | (0.00 | )(3) | | | 0.01 | |

Net realized and unrealized gain (loss) | | | 1.19 | | | | 0.12 | | | | 3.12 | | | | 2.70 | | | | (2.97 | ) |

| | | | | | | | | | | | | | | | | | | | |

Total from investment operations (1) | | | 1.16 | | | | 0.05 | | | | 3.09 | | | | 2.70 | | | | (2.96 | ) |

| | | | | | | | | | | | | | | | | | | | |

Dividends and distributions to shareholders: | | | | | | | | | | | | | | | | | | | | |

Dividends from net investment income | | | — | | | | — | | | | (0.01 | ) | | | (0.00 | )(3) | | | (0.01 | ) |

Distributions from net realized gains | | | (0.11 | ) | | | (0.53 | ) | | | — | | | | — | | | | — | |

Return of capital | | | — | | | | — | | | | — | | | | (0.01 | ) | | | — | |

| | | | | | | | | | | | | | | | | | | | |

Total dividends and distributions | | | (0.11 | ) | | | (0.53 | ) | | | (0.01 | ) | | | (0.01 | ) | | | (0.01 | ) |

| | | | | | | | | | | | | | | | | | | | |

Change in net asset value for the period | | | 1.05 | | | | (0.48 | ) | | | 3.08 | | | | 2.69 | | | | (2.97 | ) |

| | | | | | | | | | | | | | | | | | | | |

Net asset value, end of period | | $ | 12.11 | | | $ | 11.06 | | | $ | 11.54 | | | $ | 8.46 | | | $ | 5.77 | |

| | | | | | | | | | | | | | | | | | | | |

Total return | | | 10.60 | %(4) | | | (0.10 | )% | | | 36.55 | % | | | 46.73 | %(4) | | | (33.88 | )%(4) |

Ratios/supplemental data | | | | | | | | | | | | | | | | | | | | |

Net assets, end of period (000) | | $ | 93,938 | | | $ | 71,554 | | | $ | 41,788 | | | $ | 24,681 | | | $ | 9,226 | |

Ratios to average net assets: | | | | | | | | | | | | | | | | | | | | |

Expenses (6) | | | 1.35 | %(5) | | | 1.36 | % | | | 1.38 | % | | | 1.26 | %(5) | | | 1.15 | %(5) |

Net investment income (loss) (6) | | | (0.56 | )%(5) | | | (0.67 | )% | | | (0.43 | )% | | | (0.16 | )%(5) | | | 0.29 | %(5) |

Portfolio turnover rate | | | 14 | %(4) | | | 28 | % | | | 40 | % | | | 24 | %(4) | | | 29 | %(4) |

| (1) | Total from investment operations includes redemption fees of $0.001 for the six months ended April 30, 2012, $0.008 and $0.007 per share for the fiscal years ended October 31, 2011 and 2010 respectively. |

| (3) | Represents less than $0.01 per share. |

| (6) | Net of fees waived amounting to 0.77% and 2.32% for the periods ended October 31, 2009 and December 31, 2008, respectively. |

The Accompanying Notes are an Integral Part of these Financial Statements.

The Tocqueville Fund

Schedule of Investments as of April 30, 2012

(Unaudited)

| | | | | | | | |

| Common Stocks—98.7% | | Shares | | | Value | |

Automobiles & Components—1.4% | |

Ford Motor Co. | | | 504,000 | | | $ | 5,685,120 | |

Banks—1.6% | | | | | | | | |

Banco Santander SA—ADR | | | 438,632 | | | | 2,776,541 | |

Mitsubishi UFJ Financial Group, Inc.—ADR | | | 750,000 | | | | 3,570,000 | |

| | | | | | | | 6,346,541 | |

Capital Goods—8.1% | | | | | | | | |

The Boeing Co. | | | 75,000 | | | | 5,760,000 | |

General Electric Co. | | | 750,000 | | | | 14,685,000 | |

Illinois Tool Works, Inc. | | | 125,000 | | | | 7,172,500 | |

Xylem, Inc. | | | 165,000 | | | | 4,600,200 | |

| | | | | | | | 32,217,700 | |

Commercial & Professional Services—1.6% | |

Steelcase, Inc. | | | 750,500 | | | | 6,484,320 | |

Diversified Financials—1.8% | |

The Bank of New York Mellon Corp. | | | 300,000 | | | | 7,095,000 | |

Energy—10.7% | | | | | | | | |

Baker Hughes, Inc. | | | 55,000 | | | | 2,426,050 | |

Cameco Corp.(a) | | | 171,400 | | | | 3,787,940 | |

Chesapeake Energy Corp. | | | 300,000 | | | | 5,532,000 | |

Exxon Mobil Corp. | | | 150,000 | | | | 12,951,000 | |

Murphy Oil Corp. | | | 150,000 | | | | 8,245,500 | |

Schlumberger Ltd.(a) | | | 125,000 | | | | 9,267,500 | |

| | | | | | | | 42,209,990 | |

Food & Staples Retailing—1.5% | | | | | | | | |

Wal-Mart Stores, Inc. | | | 100,000 | | | | 5,891,000 | |

Food, Beverage & Tobacco—5.2% | | | | | | | | |

Campbell Soup Co. | | | 200,000 | | | | 6,766,000 | |

The Coca-Cola Co. | | | 100,000 | | | | 7,632,000 | |

PepsiCo, Inc. | | | 50,000 | | | | 3,300,000 | |

Unilever NV—ADR | | | 85,600 | | | | 2,940,360 | |

| | | | | | | | 20,638,360 | |

Health Care Equipment & Services—1.0% | |

St. Jude Medical, Inc. | | | 100,000 | | | | 3,872,000 | |

Household & Personal Products—3.9% | |

Colgate-Palmolive Co. | | | 75,000 | | | | 7,420,500 | |

The Procter & Gamble Co. | | | 125,000 | | | | 7,955,000 | |

| | | | | | | | 15,375,500 | |

Insurance—3.0% | | | | | | | | |

Aflac, Inc. | | | 171,500 | | | | 7,724,360 | |

Fidelity National Financial, Inc. | | | 216,000 | | | | 4,162,320 | |

| | | | | | | | 11,886,680 | |

Materials—13.9% | | | | | | | | |

BHP Billiton Ltd.—ADR | | | 63,900 | | | | 4,747,770 | |

Cliffs Natural Resources, Inc. | | | 75,000 | | | | 4,669,500 | |

| Common Stocks (continued) | | Shares | | | Value | |

EI du Pont de Nemours & Co. | | | 250,000 | | | $ | 13,365,000 | |

Newmont Mining Corp. | | | 200,000 | | | | 9,530,000 | |

Owens-Illinois, Inc.(b) | | | 300,000 | | | | 6,975,000 | |

Sonoco Products Co. | | | 150,000 | | | | 4,969,500 | |

Vulcan Materials Co. | | | 100,000 | | | | 4,281,000 | |

Weyerhaeuser Co. | | | 325,000 | | | | 6,617,000 | |

| | | | | | | | 55,154,770 | |

Pharmaceuticals, Biotechnology & Life Sciences—10.4% | |

Alkermes PLC(a)(b) | | | 250,000 | | | | 4,325,000 | |

Johnson & Johnson | | | 150,000 | | | | 9,763,500 | |

Merck & Co., Inc. | | | 150,000 | | | | 5,886,000 | |

Myriad Genetics, Inc.(b) | | | 200,000 | | | | 5,202,000 | |

Pfizer, Inc. | | | 700,000 | | | | 16,051,000 | |

| | | | | | | | 41,227,500 | |

Real Estate—1.0% | | | | | | | | |

CBRE Group, Inc.(b) | | | 215,000 | | | | 4,044,150 | |

Retailing—2.5% | | | | | | | | |

The Home Depot, Inc. | | | 100,000 | | | | 5,179,000 | |

Lowe’s Companies, Inc. | | | 150,000 | | | | 4,720,500 | |

| | | | | | | | 9,899,500 | |

Semiconductors & Semiconductor Equipment—4.8% | |

Applied Materials, Inc. | | | 650,000 | | | | 7,793,500 | |

Intel Corp. | | | 400,000 | | | | 11,360,000 | |

| | | | | | | | 19,153,500 | |

Software & Services—13.4% | | | | | | | | |

Adobe Systems, Inc.(b) | | | 150,000 | | | | 5,034,000 | |

Akamai Technologies, Inc.(b) | | | 150,000 | | | | 4,890,000 | |

Automatic Data Processing, Inc. | | | 125,000 | | | | 6,952,500 | |

Google, Inc.(b) | | | 15,000 | | | | 9,078,450 | |

Mastercard, Inc. | | | 25,000 | | | | 11,306,750 | |

Microsoft Corp. | | | 500,000 | | | | 16,010,000 | |

| | | | | | | | 53,271,700 | |

Technology Hardware & Equipment—7.3% | |

Bio-key International, Inc.(b)(c)(d)(e) | | | 47,090 | | | | — | |

Canon, Inc.—ADR | | | 51,500 | | | | 2,336,040 | |

Cisco Systems, Inc. | | | 500,000 | | | | 10,075,000 | |

Hitachi Ltd.—ADR | | | 150,000 | | | | 9,495,000 | |

Plexus Corp.(b) | | | 125,000 | | | | 4,046,250 | |

Xerox Corp. | | | 400,000 | | | | 3,112,000 | |

| | | | | | | | 29,064,290 | |

Telecommunication Services—2.5% | | | | | | | | |

Verizon Communications, Inc. | | | 125,000 | | | | 5,047,500 | |

Vodafone Group PLC—ADR | | | 171,400 | | | | 4,770,062 | |

| | | | | | | | 9,817,562 | |

The Accompanying Footnotes are an Integral Part of these Financial Statements.

The Tocqueville Fund

Schedule of Investments as of April 30, 2012

(Unaudited)

| | | | | | | | |

| Common Stocks (continued) | | Shares | | | Value | |

Utilities—3.1% | | | | | | | | |

NextEra Energy, Inc. | | | 190,000 | | | $ | 12,226,500 | |

Total Common Stocks (Cost $338,113,351) | | | | | | | 391,561,683 | |

Warrants—0.0% | | | | | | | | |

Technology Hardware & Equipment—0.0% | |

EMCORE Corp. | | | | | | | | |

Expiration: 02/19/13, Exercise Price: $60.24(b)(c)(d)(e) | | | 9,844 | | | | 80 | |

Total Warrants

(Cost $0) | | | | | | | 80 | |

| Short-Term Investments—1.6% | |

| Principal

Amount |

| | | | |

Repurchase Agreement—1.6% | | | | | | | | |

Repurchase Agreement with U.S. Bank, N.A., 0.01% dated 4/30/2012, due 5/01/2012, collateralized by: Freddie Mac Giant 30 Year Fixed (Pool #G01543) valued at $2,013,512. Repurchase proceeds of $1,973,981. Fannie Mae Conventional Level Pay 15 Year Fixed (Pool #676656) valued at $4,417,344. Repurchase proceeds of $4,331,021. | | $ | 6,305,000 | | | | 6,305,000 | |

Total Short-Term Investments (Cost $6,305,000) | | | | | | | 6,305,000 | |

Total Investments

(Cost $344,418,351)—100.3% | | | | 397,866,763 | |

Liabilities in Excess of Other Assets—(0.3)% | | | | (1,330,979 | ) |

Total Net Assets—100.0% | | | | | | $ | 396,535,784 | |

| | | | | | | | |

Percentages are stated as a percent of net assets.

ADR—American Depository Receipt

| (a) | Foreign issued security. Foreign concentration (including ADRs) was as follows: Australia 1.2%; Britain 1.2%; Canada 1.0%; Curacao 2.3%; Ireland 1.1%; Japan 3.9%; Netherlands 0.7%; Spain 0.7%; |

| (b) | Non-income producing security. |

| (c) | Denotes a security is either fully or partially restricted to resale. The aggregate value of restricted securities at April 30, 2012 was $80 which represented 0.0% of net assets. |

| (d) | Fair valued security. The aggregate value of fair valued securities as of April 30, 2012 was $80 which represented 0.0% of net assets. |

| (e) | Security is considered illiquid and may be difficult to sell. |

The Global Industry Classification Standard (GICS®) was developed by and/or is the exclusive property of MSCI, Inc. and Standard & Poor Financial Services LLC (“S&P”). GICS is a service mark of MSCI and S&P and has been licensed for use by U.S. Bancorp Fund Services, LLC.

The Accompanying Footnotes are an Integral Part of these Financial Statements.

The Tocqueville Opportunity Fund

Schedule of Investments as of April 30, 2012

(Unaudited)

| | | | | | | | |

| Common Stocks—97.3% | | Shares | | | Value | |

Automobiles & Components—1.5% | | | | | | | | |

BorgWarner, Inc.(a) | | | 9,000 | | | $ | 711,360 | |

Gentex Corp. | | | 17,500 | | | | 384,475 | |

| | | | | | | | 1,095,835 | |

Banks—1.7% | | | | | | | | |

BankUnited, Inc. | | | 14,500 | | | | 356,700 | |

Pinnacle Financial Partners, Inc.(a) | | | 13,000 | | | | 237,900 | |

Signature Bank(a) | | | 10,500 | | | | 689,745 | |

| | | | | | | | 1,284,345 | |

Capital Goods—6.8% | | | | | | | | |

AO Smith Corp. | | | 10,500 | | | | 499,800 | |

Acuity Brands, Inc. | | | 4,200 | | | | 233,394 | |

AMETEK, Inc. | | | 8,700 | | | | 437,871 | |

BE Aerospace, Inc.(a) | | | 5,000 | | | | 235,150 | |

Dover Corp. | | | 3,500 | | | | 219,310 | |

Esterline Technologies Corp.(a) | | | 3,300 | | | | 226,017 | |

Gardner Denver, Inc. | | | 3,500 | | | | 227,990 | |

Hexcel Corp.(a) | | | 8,000 | | | | 219,040 | |

Joy Global, Inc. | | | 3,100 | | | | 219,387 | |

Polypore International, Inc.(a) | | | 6,000 | | | | 224,100 | |

RBC Bearings, Inc.(a) | | | 4,800 | | | | 225,024 | |

Robbins & Myers, Inc. | | | 2,400 | | | | 116,904 | |

SeaCube Container Leasing Ltd.(b) | | | 11,000 | | | | 204,050 | |

Spirit Aerosystems Holdings, Inc.(a) | | | 8,000 | | | | 200,000 | |

Timken Co. | | | 5,000 | | | | 282,550 | |

TransDigm Group, Inc.(a) | | | 3,900 | | | | 491,868 | |

Valmont Industries, Inc. | | | 2,500 | | | | 309,825 | |

WABCO Holdings, Inc.(a) | | | 7,200 | | | | 453,816 | |

| | | | | | | | 5,026,096 | |

Commercial & Professional Services—2.0% | | | | | |

Acacia Research Corp.(a) | | | 3,100 | | | | 127,100 | |

Clean Harbors, Inc.(a) | | | 6,500 | | | | 443,560 | |

Mistras Group, Inc.(a) | | | 11,100 | | | | 260,517 | |

Nielsen Holdings NV(a)(b) | | | 3,700 | | | | 108,114 | |

Portfolio Recovery Associates, Inc.(a) | | | 7,500 | | | | 516,150 | |

| | | | | | | | 1,455,441 | |

Consumer Durables & Apparel—6.2% | | | | | |

Deckers Outdoor Corp.(a) | | | 5,800 | | | | 295,858 | |

Fossil, Inc.(a) | | | 4,700 | | | | 614,149 | |

Hanesbrands, Inc.(a) | | | 7,500 | | | | 211,650 | |

Harman International Industries, Inc. | | | 2,000 | | | | 99,160 | |

Lululemon Athletica, Inc.(a) | | | 13,900 | | | | 1,030,546 | |

Polaris Industries, Inc. | | | 7,000 | | | | 556,080 | |

Prada SpA(b) | | | 38,000 | | | | 258,112 | |

Ralph Lauren Corp. | | | 3,500 | | | | 602,945 | |

Tempur-Pedic International, Inc.(a) | | | 7,000 | | | | 411,880 | |

Tupperware Brands Corp. | | | 7,500 | | | | 467,175 | |

| | | | | | | | 4,547,555 | |

Consumer Services—4.5% | | | | | | | | |

BJ’s Restaurants, Inc.(a) | | | 5,100 | | | $ | 220,269 | |

Buffalo Wild Wings, Inc.(a) | | | 2,400 | | | | 201,240 | |

Chipotle Mexican Grill, Inc.(a) | | | 2,000 | | | | 828,300 | |

Dunkin’ Brands Group, Inc. | | | 9,500 | | | | 307,515 | |

Hyatt Hotels Corp.(a) | | | 6,500 | | | | 279,695 | |

Panera Bread Co.(a) | | | 2,175 | | | | 343,476 | |

Sotheby’s | | | 9,100 | | | | 357,812 | |

Starwood Hotels & Resorts Worldwide, Inc. | | | 5,000 | | | | 296,000 | |

Wyndham Worldwide Corp. | | | 4,000 | | | | 201,360 | |

Wynn Resorts Ltd. | | | 2,000 | | | | 266,800 | |

| | | | | | | | 3,302,467 | |

Diversified Financials—3.7% | | | | | | | | |

Blackstone Group LP | | | 28,000 | | | | 379,680 | |

The Charles Schwab Corp. | | | 28,500 | | | | 407,550 | |

KKR & Co. LP | | | 28,000 | | | | 395,360 | |

Lazard Ltd.(b) | | | 6,000 | | | | 165,060 | |

MSCI, Inc.(a) | | | 15,500 | | | | 567,145 | |