Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-05371

| Russell Investment Funds |

(Exact name of registrant as specified in charter)

| 1301 2nd Avenue 18th Floor, Seattle Washington 98101 |

(Address of principal executive offices) (Zip code)

Mary Beth Rhoden, Secretary and Chief Legal Officer Russell Investment Funds 1301 2nd Avenue 18th Floor Seattle, Washington 98101 206-505-4846 |

(Name and address of agent for service)

Registrant’s telephone number, including area code: 206-505-7877

Date of fiscal year end: December 31

Date of reporting period: January 1, 2010 to December 31, 2010

Table of Contents

Item 1. Reports to Stockholders

Table of Contents

2010 ANNUAL REPORT

Russell Investment Funds

DECEMBER 31, 2010

FUND

Multi-Style Equity Fund

Aggressive Equity Fund

Non-U.S. Fund

Core Bond Fund

Real Estate Securities Fund

Table of Contents

Russell Investment Funds

Russell Investment Funds is a series investment company with nine different investment portfolios referred to as Funds. These financial statements report on five of these Funds.

Table of Contents

Russell Investment Funds

Annual Report

December 31, 2010

Table of Contents

Russell Investment Funds

Copyright © Russell Investments 2011. All rights reserved.

Russell Investments is a Washington, USA corporation, which operates through subsidiaries worldwide and is a subsidiary of The Northwestern Mutual Life Insurance Company.

Fund objectives, risks, charges and expenses should be carefully considered before investing. A prospectus containing this and other important information must precede or accompany this material. Please read the prospectus carefully before investing.

Securities products and services offered through Russell Financial Services, Inc., a member of FINRA and part of Russell Investments.

Indices and benchmarks are unmanaged and cannot be invested in directly. Returns represent past performance, are not a guarantee of future performance, and are not indicative of any specific investment. Index return information is provided by vendors and although deemed reliable, is not guaranteed by Russell Investments or its affiliates.

Russell Investments is the owner of the trademarks, service marks, and copyrights related to its respective indexes.

Performance quoted represents past performance and does not guarantee future results. The investment return and principal value of an investment will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted.

Table of Contents

I am pleased to share with you the results from the Russell Investment Funds’ 2010 Annual Report. It provides portfolio management discussions and fund-specific insights regarding fund performance for the fiscal year ending December 31, 2010.

Russell Investments’ mission is plain and simple — to improve financial security for people. We work to achieve this goal by delivering disciplined investment strategies, objective research and industry-leading service. Despite the difficult economic times and volatile investment markets, we will never lose sight of this primary mission.

Looking back at 2010, it has been a year of progress and challenges. Investors are still wrestling with the aftershocks of market disruptions. The broad equity market, represented by the Russell Global Index, is up more than 9% year-to-date at the writing of this letter in December. But employment numbers in the U.S. are still a cause for concern, as are the debt challenges of several European countries. We believe the experiences of 2010 continue to demonstrate the value of diversification and proactive investment management.

Now more than ever, we believe investors are best served by remaining focused on long-term investing using well-diversified, asset allocated portfolios. We believe it is equally important for investors to continue to talk with their financial advisors to ensure their portfolios remain aligned with their goals. Working with a trusted advisor is the best way to maintain this focus.

The Russell Investments team has decades of experience managing people’s investments through all kinds of market cycles. We believe monitoring investment managers continuously, and maintaining a disciplined approach to portfolio management and implementation is the best way to achieve long-term goals.

On behalf of the Russell Investments team, thank you for your continued support.

Best regards,

Sandra Cavanaugh

CEO, Americas Private Client Services

Russell Investment Management Company

| To Our Shareholders | 3 |

Table of Contents

Russell Investment Funds

Market Summary as of December 31, 2010 (Unaudited)

U.S. Equity Markets

For the fiscal year ended December 31, 2010, the U.S. equity market experienced high levels of volatility, but less than in the one year period ended December 31, 2009. While the markets experienced numerous reversals during the period, investors became increasingly, though cautiously, optimistic regarding the sustainability of the global economic recovery. Strong corporate earnings growth translated into strong positive returns for the major market indexes. The broad market Russell 3000® Index rose 16.93% over the period as global growth recovered and the U.S. economy appeared to be stabilizing.

The economy continued to grow over the fiscal year, but at a slow pace. Relative to past recoveries from deep recessions, economic growth as measured by gross domestic product (GDP) failed to rebound as quickly or with the strength necessary to increase employment and provide assurances that the recessionary period was truly over. Unemployment remained high, averaging approximately 9.5% over the period while wage growth remained stagnant. The national savings rate increased from a modestly negative percentage to a more substantial 6%. While this is a longer-term positive factor for the U.S. economy as it improves the financial health of consumers, the short-term result has been to lower consumer spending. Given the key role that consumer spending continues to play in driving U.S. GDP, expectations for a strong economic recovery moderated as the fiscal year progressed and investors began to expect a more slowly paced increase in economic activity going forward. Expectations were further moderated by a persistently weak housing market, where sales declined following the expiration of the first time home buyers tax credit in the spring.

In response to the slow pace of the economic recovery, and its jobless nature, the U.S. government stepped up its efforts to stimulate economic growth. Unemployment benefits were extended to support consumer demand, while stimulus spending injected capital into the economy. Toward the latter part of the fiscal year, the Federal Reserve announced its intention to expand its quantitative easing efforts beyond the purchase of mortgage backed securities and into direct purchases of U.S. government debt. The market rose as a result due to expectations that this direct injection of money into the economy would cause interest rates to decline in the intermediate-term, and inflationary expectations to rise in the longer-term. Investors took comfort in the Federal Reserve taking such actions to help provide support for the economy and guide it towards a sustainable recovery.

Over the course of the period, global economic growth rebounded on the strength of emerging markets demand and growth. This has been a key to improving investor sentiment and has driven the relative outperformance of some of the more export-oriented sectors including producer durables, materials and processing, and technology. The consumer discretionary sector, which was the best performing sector over the one year period, benefited from both international demand and a modest domestic recovery. Increased global wealth has driven up demand for aspirational goods and services, with leisure travel, lodging and gaming all benefiting.

Domestically, retailers with strong market share and the ability to increase profit margins performed well. The utilities sector outperformed as well. Demand for companies with a lower degree of perceived downside risk increased, as did the desire for steady sources of income. On the other end of the return spectrum, the financial services sector underperformed relative to the benchmark. Increasing financial regulations and an uncertain business landscape made investors wary of investing in banks, brokerage companies and other financial institutions. Concerns over additional losses related to the housing market and uncertainty over the health of loan portfolios also concerned investors. Health care stocks lagged as well, due largely to the uncertainty associated with the passage of new health care legislation and its impact on corporate profitability. Energy stocks underperformed due to concerns over weaker demand growth for gas and oil in a sluggish economic recovery. Potential fallout from the Gulf Coast oil spill also created uncertainty around deep water exploration and drilling firms. Lastly, the consumer staples sector lagged despite strong demand from overseas markets, as investors gravitated away from these companies’ higher relative valuations and the potential margin pressure they could face if commodity prices rise.

Overall, the period was marked by a high degree of correlation among stock price movements across large segments of the benchmark. As such, benchmark and market returns were driven by the performance of the higher and lower ends of

| 4 | Market Summary |

Table of Contents

Russell Investment Company

the risk spectrum where there was more stock price return differentiation. This was largely a result of significant oscillations in investor sentiment driven by macro-economic news and events. This resulted in a “risk on/risk off” phenomenon. Positive economic and company specific news resulted in a “risk on” scenario where companies with more economic sensitivity outperformed the benchmark when “risk” was in favor. In contrast, negative news on the economy, employment, housing, and the European sovereign debt situation resulted in a highly risk-averse (“risk off”) environment in which investors sought safe haven or more defensively oriented investments. Throughout the fiscal year it was a struggle between these two forces, as investors were heavily swayed more by macro-economic news than by company-specific data.

The high degree of uncertainty in the market regarding regulatory, fiscal and monetary policy resulted in a challenging active management environment in U.S. equities. Value-oriented managers had a particularly difficult time due to their almost perennial underweight to the strongly performing utilities sector, while growth-oriented managers fared better. The relative outperformance of consumer staples and parts of the health care sector in the more defensive periods decreased returns for value managers. Additionally, commodity-oriented stocks performed relatively well as investors bet on a sustainable global economic recovery. In contrast, value managers were overweight in technology and consumer discretionary sector companies that they believed had relatively higher and more sustainable growth characteristics. The more cyclical consumer and technology companies as well as those focusing on lower-end domestic consumer spending and targeting international growth performed relatively well.

Growth managers fared relatively well as investors favored growth companies, pushing up the price of stocks associated with international and emerging markets. This applied to technology and consumer product companies as well as agricultural, commodities, and industrial companies producing goods and basic resources needed to satiate emerging market demand. The stocks of the fastest growing companies outperformed the stocks of companies whose earnings grew at a slower rate. This is based on return data categorizing stocks according to each company’s 5-year historical EPS Growth, 1-Year Sales Growth, and IBES Long-Term Forecasted Growth.

Driven by expectations for a moderate global economic recovery, stock prices in the U.S. rose strongly across the investment style as well as the market capitalization spectra.

For the period, the Russell 1000® Growth Index returned 16.7% and the Russell 1000® Value Index returned 15.51%, while the Russell 2000® Growth Index returned 29.1% and the Russell 2000® Value Index returned 24.5%. Small capitalization stocks outperformed large capitalization stocks for the one year period as the Russell 2000® Index returned 26.9% and the Russell 1000® Index returned 16.1% for the period. Mid capitalization stocks once again performed well over the period, while micro capitalization stocks performed best as the Russell Midcap® Index returned 25.47% and the Russell Microcap® Index returned 28.9% for the fiscal year.

The Lipper® Small Cap Value Funds Average outperformed the Russell 2000® Value Index by 1.25%, the Lipper® Small Cap Core Funds Average underperformed the Russell 2000® Index by 1.12% and the Lipper® Small Cap Growth Funds Average underperformed the Russell 2000® Growth Index by 2.05%. The Lipper® Large Cap Growth Funds Average underperformed the Russell 1000® Growth Index by 1.58%, the Lipper® Large Cap Core Funds Average underperformed the Russell 1000® Index by 3.94%, and the Lipper® Large Cap Value Funds Average underperformed the Russell 1000® Value Index by 1.81%.

Non-U.S. Developed Equity Markets

2010 was a rollercoaster year for investors. The Non-U.S. developed equity markets, as measured by the MSCI EAFE Index, rose 7.75% during the year, with most of the Index’s gains coming in the second half of the year. Fears of the European sovereign debt crisis igniting another global economic downturn subsided as a gradual recovery became more likely. Markets fell sharply at the end of April and remained extremely volatile until September, when riskier stocks began to improve as investors gained optimism. On a month-by-month basis, market leadership was inconsistent, but trends became more apparent when the whole of 2010 was taken into account.

The risk factor that was most rewarded was high beta, followed by high price-volatility and high price-momentum. All three factors are a reflection of the market environment that benefited riskier stocks. The prices of high beta stocks tend to rise faster than the broad market in positive return environments, but also fall faster when markets are negative. The price volatility factor represents stocks whose prices tend to change more than the average stock, meaning performance gains and losses are amplified. This is similar to market beta, except that there isn’t necessarily a relationship between the performance of the market and its underlying stocks. Stocks with high-price momentum performed better than the market during the 12 months prior. Their outperformance signals the fact that stocks that did well in 2009 continued to

| Market Summary | 5 |

Table of Contents

Russell Investment Company

outperform in 2010. Momentum made a comeback in 2010, as many of the stocks that rose in 2009 continued to lead the market. Stocks that are typically considered higher-quality, those with high profitability or return on equity, underperformed. However, financial leverage was the worst performing market factor. Financial leverage is a characteristic that investors can use to determine balance sheet quality. Financial leverage is the degree to which a company is utilizing borrowed money (debt) to finance its operations. Financial leverage can boost profits in certain periods, but when debt repayment is a concern, as it was in 2010, companies with a high-level of financial leverage, can perform poorly. Growth stocks significantly outperformed value stocks, with the MSCI EAFE Growth Index returning 12.25% and outperforming the MSCI EAFE Value Index by 9.0%.

Small cap stocks outperformed large cap stocks by a wide margin, as measured by the MSCI EAFE Small Cap Index and the MSCI EAFE Index. U.S. stocks, as measured by the Russell 1000® Index, outperformed developed non-U.S. stocks, as measured by the MSCI EAFE Index, by more than 8.35%, indicating that signs of economic recovery were more evident in the U.S. Extremely negative performance outcomes by the PIIGS countries (Portugal, Ireland, Italy, Greece and Spain), catalyzed by fears surrounding sovereign debt, weighed heavily on international markets. Greece and Spain were penalized most, with returns of -44.87% and -21.95%, respectively, as measured by the MSCI Greece Index and MSCI Spain Index. Both countries’ performance suffered due to uncertainty regarding their ability to service sovereign debt, but experienced some recovery toward the end of the year. Although markets tended to reward risk, stocks with severe debt issues lagged the market. Investors’ dislike for financial leverage impacted country-level returns as well. The weak performance from Greece and Spain confirm this sentiment. Japan as measured by MSCI Japan, out-performed the MSCI EAFE Index returning 15.44% for the year. Emerging markets companies continued to outpace developed markets with the strong return of 18.88%, as measured by the MSCI Emerging Markets Index. Argentina, Thailand, and Peru were the best performing emerging markets countries, all returning over 50% for the year, as measured by the MSCI Argentina Index, MSCI Thailand Index and MSCI Peru Index. China severely underperformed the broader MSCI Emerging Markets Index and the MSCI EAFE Index with a positive return of only 4.63%, as measured by the MSCI China Index , due to inflationary pressures and fears of economic overheating.

The industrials sector was the best performing of the ten sectors in the MSCI EAFE Index, with a return of 20.39%. The companies that make up the sector tend to be economically sensitive and thus performed well given the improving economic environment. Consumer discretionary stocks benefited from the upswing in consumer spending and the sector ended the year up 19.73%. The materials, technology and consumer staples sectors also out-performed the MSCI EAFE Index. Utilities and financials were the only two sectors with negative performance during the year, with returns of -4.88% and -1.62%, respectively, as measured by the MSCI EAFE Utilities and MSCI EAFE Financials Sector Indices . Consumer stocks were led by automobiles and retail. There remains a great deal of skepticism surrounding the health of commercial banks.

Emerging Markets

The MSCI Emerging Markets Index (“the Index”) was up 18.88% over the fiscal year ended December 31, 2010. In spite of persistent volatility, Emerging Markets finished ahead of Developed Markets, which gained 11.76% over the year, as measured by the MSCI Daily TR Net Developed Markets Index in U.S. dollar terms.

Emerging market gains during 2010 were largely driven by a strong recovery in the second half of the fiscal year as the global economic backdrop turned positive. The Index had a modest return of 2.40% during the first calendar quarter, driven by concerns over the sustainability of economic recovery resulting from moves to withdraw stimulus funding in the U.S. and China and by concerns about a growing debt crisis in Europe.

This was followed by a negative and challenging second quarter in which emerging market stocks, commodities and currencies fell sharply, as investor appetite for risk diminished in favor of safer assets, including gold — which reached a record high — and the U.S. dollar. The Index gave up 8.37%, led by heavy losses in May, when the Index endured its worst month since October 2008. The intensifying debt crisis in Europe, evidence of a slowdown in the U.S. and Chinese economies, a massive overhaul of the U.S. banking system and a crisis on the Korean peninsula all had a negative impact.

Emerging market stocks went on to rally sharply over the third quarter, notably in July and September, when the Index enjoyed its best monthly gain since July 2009. The Index gained 18.03% over the period, helped by the secular growth stories that prevailed in certain markets. Investors were also buoyed by news in July that the IMF had raised its global growth forecast and by second-quarter earnings releases from a number of the world’s biggest companies that were well in excess of expectations. Gains were reinforced by more upbeat news from Europe, where the results of the stress tests on banks were largely welcomed.

| 6 | Market Summary |

Table of Contents

Russell Investment Company

The positive trend continued in the fourth quarter, driven by further signs of a burgeoning recovery in the U.S., strong growth in China and by speculation that the second round of quantitative easing (i.e., a policy by which the Federal Reserve purchases U.S. treasuries with newly created central bank money) would help global growth accelerate. A very positive third quarter earnings season and central bank intervention in Europe also helped offset the negative impact of monetary tightening in China and renewed concerns over the debt crisis in Western Europe.

Throughout, there was notable dispersion across country returns over the calendar year, with the smaller emerging market countries performing best. Thailand gained 55.71%, as measured by the MSCI Daily TR Net Emerging Markets Thailand Index. In Latin America, key beneficiaries of the demand for raw materials and the increased risk appetite were strongest, including Peruvian stocks, which gained 53.32%, as measured by the MSCI Daily TR Net Emerging Markets Peru Index, Chilean stocks, which increased 44.16%, as measured by the MSCI daily TR Net Emerging Markets Chile Index in U.S. dollar terms, and Colombian stocks, which gained 43.41%, as measured by the MSCI Daily TR Net Emerging Markets Colombia Index in U.S. dollar terms.

From a regional standpoint, returns in Europe were generally weaker, reflected by the negative returns from Hungary, which declined 9.58%, as measured by the MSCI Daily TR Net Emerging Markets Hungary Index in U.S. dollar terms, and the Czech Republic, which fell 2.53%, as measured by MSCI Daily TR Net Emerging Markets Czech Republic Index in U.S. dollar terms. The larger emerging market countries China and Brazil also stood out in that both had modest returns over the calendar year relative to others, gaining just 4.63% and 6.54%, respectively, as per the MSCI daily TR Net Emerging Markets China Index in U.S. dollar terms and MSCI Daily TR Net Emerging Markets Brazil Index in U.S. dollar terms. At the sector level, the consumer theme dominated returns, with consumer staples stocks gaining 30.35%, as measured by the MSCI Daily TR Net Emerging Markets Consumer Staples Index in U.S. dollar terms, and consumer discretionary stocks gaining 31.40%, as measured by the MSCI Daily TR Net Emerging Markets Consumer Discretionary Index in U.S. dollar terms. This was well ahead of the more defensive utilities sector, which gained 8.10%, as measured by the MSCI Daily TR Net Emerging Markets Utilities Index in U.S. dollar terms, and energy, which gained 9.91%, as measured by the MSCI Daily TR Net Emerging Markets Energy Index in U.S. dollar terms over the calendar year.

Small capitalization stocks, as measured by the MSCI Daily TR Net Emerging Markets Small Cap Index in U.S. dollar terms, gained 27.17%, beating larger-capitalization counterparts, which rose 18.34%, as measured by the MSCI Daily TR Net Emerging Markets Large Cap Index in U.S. dollar terms.

U.S./Global Fixed Income Markets

Over most of the fiscal year ended December 31, 2010, fixed income markets largely continued the global credit rally that started in the early part of 2009, which began with the announcement of government stimulus programs and the release of generally positive U.S. bank stress test results. Despite bouts of volatility brought on by concerns around European sovereign debt, the uncertainty of U.S. economic recovery, the Gulf Coast oil spill, and Federal Reserve market intervention, U.S. interest rates declined and broad bond market indices did well: The 2-year Treasury yield decreased 54 bps to 0.60% and the 10-year yield decreased 54 bps to 3.30%; the Barclays Capital U.S. Aggregate (investment grade) Bond Index, U.S. High Yield Bond Index and Emerging Market Bond Index returned 6.54%, 15.12% and 12.84%, respectively.

There was little market turmoil at the beginning of 2010. Investors anticipated that the U.S. economic recovery would soon stabilize and transition off of government stimulus support. As an example of this, at the end of March 2010, the U.S. Federal Reserve Bank (the Fed) completed its $1.25 trillion agency mortgage-backed security buying program without credit markets being materially disturbed.

By late April and early May, investors saw the return of volatility: The Greek and peripheral European sovereign debt crisis made investors anxious that credit events originating in one region could again spread to other parts of the world. At the same time, the Gulf Coast oil spill reminded investors that unexpected and seemingly random negative events could still pop up and roil financial markets. The U.S. Treasury yield curve reflected this anxiety, with the two-year Treasury yield dropping from 0.58% to 0.60%, and the ten-year Treasury yield dropping from 1.06% to 2.93%i, as investors ran to (and bid up the prices on) low-risk debt backstopped by the U.S. government. Simultaneously, the Fed again became concerned with the U.S. economy, and began to signal that it would hold the overnight target rate at its historically low range of 0.00% to 0.25% for an extended period (which it did through the end of the year). This effectively signaled to investors who had been expecting a rate increase by the end of 2010 to not look for one until well into 2011. Included in this message was that the Fed believed deflation was a greater near-term risk than inflation.

| Market Summary | 7 |

Table of Contents

Russell Investment Company

The housing market, which precipitated the financial crisis in the summer of 2007, continued to have an impact on the overall market throughout the year. Investors were concerned about the effectiveness of U.S. government programs to help borrowers refinance or modify their mortgages in an attempt to stem the rising tide of foreclosures. This problem was exacerbated in the latter part of the year with news that several large residential mortgage servicers were halting foreclosures due to inaccurate or incomplete paperwork, and lawsuits were filed that contended banks did not legally have the right to proceed with certain foreclosures. Despite these issues (which remained unresolved at year end), over the period both residential and commercial mortgage-backed securities performed well, both in terms of total return and relative returns, as compared to equivalent-duration U.S. Treasuries.

Despite the aforementioned bouts of volatility, it was the Fed’s announcement of more support in the form of another round of quantitative easing dubbed “QE2” (i.e., purchasing U.S. Treasuries with newly created central bank money) that caused the fixed income market to fluctuate and turn negative in the last two months of the year. The Fed had previously indicated the possibility of another round of monetary easing and the general expectation had been that QE2 would keep Treasury rates low and thus bode well for credit markets. However, investors focused on the inflationary and U.S. dollar-depressing effects of QE2, with many openly criticizing the $600 billion program. This caused Treasury yields to reverse course and start heading back up. During the first ten months of the year, the 2-year Treasury yield decreased 80 bps to 0.34% and the 10-year yield decreased 124 bps to 2.60%. Following the announcement of QE2, over November and December, 2-year and 10-year Treasury yields increased 26 bps and 69 bps, respectively. Thus it was the Fed’s effort to bolster the economy that caused Treasuries to return -2.6% in the fourth quarter of 2010, which in turn moved the U.S. Aggregate Bond Index to post its first negative quarterly total return in two years.

| i | April-June 2010 peak-to-trough changes |

| 8 | Market Summary |

Table of Contents

[This page intentionally left blank]

Table of Contents

Russell Investment Funds

Portfolio Management Discussion — December 31, 2010 (Unaudited)

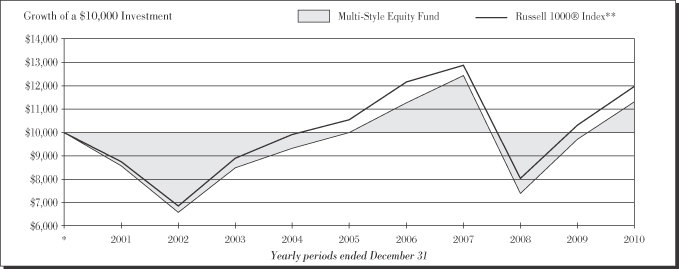

Multi-Style Equity Fund | ||||

| Total Return | ||||

1 Year | 16.46 | % | ||

5 Years | 2.51 | %§ | ||

10 Years | 1.25 | %§ | ||

| Russell 1000® Index ** | ||||

| Total Return | ||||

1 Year | 16.10 | % | ||

5 Years | 2.59 | %§ | ||

10 Years | 1.83 | %§ | ||

| 10 | Multi-Style Equity Fund |

Table of Contents

Russell Investment Funds

Multi-Style Equity Fund

Portfolio Management Discussion — December 31, 2010 (Unaudited)

The Multi-Style Equity Fund (the “Fund”) allocates most of its assets among multiple money managers. Russell Investment Management Company (“RIMCo”), as the Fund’s advisor, may change the allocation of the Fund’s assets among money managers at any time. An exemptive order from the Securities and Exchange Commission (“SEC”) permits RIMCo to engage or terminate a money manager at any time, subject to approval by the Fund’s Board without a shareholder vote. Pursuant to the terms of the exemptive order, the Fund is required to notify its shareholders within 60 days of when a money manager begins providing services. The Fund currently has eight money managers.

What is the Fund’s investment objective?

The Fund seeks to provide long-term capital growth.

How did the Fund perform relative to its benchmark for the fiscal year ended December 31, 2010?

For the fiscal year ended December 31, 2010, the Multi-Style Equity Fund gained 16.46%. This compared to the Russell 1000® Index, which gained 16.10% during the same period. The Fund’s performance includes operating expenses, whereas Index returns are unmanaged and do not include expenses of any kind.

For the fiscal year ended December 31, 2010, the Lipper® Large-Cap Core Funds (VIP) Average gained 13.50%. This average return serves as a peer comparison and is expressed net of operating expenses.

RIMCo may assign a money manager a specific style or capitalization benchmark other than the Fund’s index. However, the Fund’s primary index remains the benchmark for the Fund and is representative of the aggregate of each money manager’s benchmark index.

How did the market conditions described in the Market Summary report affect the Fund’s performance?

The fiscal year ended December 31, 2010 was marked by two almost separate periods — pre and post quantitative easing announced by the U.S. Federal Reserve. Quantitative easing involves purchasing U.S. Treasuries with newly created central bank money. During the first quarter, equity markets maintained some of the positive momentum generated during 2009, but gave back all gains and were posting negative year to date returns as late as August. Concerns over sovereign debt issues in Europe and negative housing data dragged down equity markets during the second and early third quarters. Near the end of the third quarter the U.S. Federal Reserve announced an additional amount of monetary stimulus and equity markets responded strongly by rallying for the duration of the year.

Growth stocks outperformed value stocks by more than 1.2% for the fiscal year ended December 31, 2010, as measured by the Russell 1000® Growth Index against the Russell 1000® Value Index. Stocks with high forecasted growth outperformed those with low forecasted growth and stocks with high historical growth outperformed those with low historical growth, Small cap stocks outperformed large cap stocks by more than 10% for the

year ended December 31, 2010, as measured by the Russell 2000® Index against the Russell 1000® Index. The relative performance of small capitalization stocks reflects the market’s preference for risk over the fiscal year. Stocks with greater volatility outperformed those with lower volatility, reinforcing the market’s increasing appetite for risk. Stocks with high long-term debt-to-capital outperformed those with low long-term debt-to-capital, as financials and other previously poor performing stocks rallied toward the end of the year.

The market also rewarded pro-cyclical sectors during the year. The consumer discretionary sector was the best performer as investors reacted to positive spending data and better-than- expected holiday sales. Utilities and consumer staples, both considered defensive sectors, posted negative returns for the year as investors looked for riskier stocks. The Fund benefited from the pro-cyclical trend through its overweight to consumer discretionary and underweight to consumer staples and utilities. The Fund also benefited from an underweight to health care, the worst performing sector in the Russell 1000® Index.

During the second half of the year, a focus on the performance of individual stocks began to outweigh some of the focus on general macro-economic conditions that had prevailed earlier in the year. The increased appetite for risk among investors, along with declining correlations among stocks in particular, provided a favorable backdrop for active money management in general and for the Fund. General views of the overall equity market began to improve at the end of the third quarter, led by a subsiding fear of European debt contagion and improved confidence in the sustainability of the global recovery. This trend was illustrated by a rotation into the financial services industry by the Fund, particularly into the diversified banks sector.

How did the investment strategies and techniques employed by the Fund and its money managers affect its performance?

Over the fiscal year, the Fund’s managers emphasized companies with high forecasted growth. They looked to companies with overseas exposure, particularly to emerging markets and companies with limited risk of sovereign debt contagion. This contributed positively to returns as the market rewarded risk over the year and emerging market economies, particularly China, exhibited incredible gross domestic product growth. From a strategic standpoint, the Fund aims to be positioned neutrally between growth and value. However, as managers rotated and markets rallied, the Fund experienced some tilt toward increased growth and momentum exposure, both of which contributed positively to returns during the year.

Manager sector weighting decisions played a critical role in determining manager and Fund performance during the year with the consumer discretionary, producer durables and materials & processing sectors all outperforming the Russell 1000® Index. Managers with overweights to these sectors tended to perform better during the year. On the other hand, health care and utilities stocks underperformed the Fund’s benchmark.

| Multi-Style Equity Fund | 11 |

Table of Contents

Russell Investment Funds

Multi-Style Equity Fund

Portfolio Management Discussion — December 31, 2010 (Unaudited)

Stock selection in the health care sector was the largest detractor from returns during the fiscal year. The Fund was overweight to some of the worst performing stocks in the pharmaceuticals and biotechnology industries. Stock selection within the financial services sector was the second largest detractor from returns. Holdings within the financial data & systems and diversified financial services industries hurt performance. The Fund’s underweight to real estate investment trusts (REITs) also detracted from performance, as this industry outperformed the rest of the index during the year.

Stock selection within the producer durables, consumer discretionary and energy sectors contributed positively to the Fund’s performance during the fiscal year. Expectations that demand for oil would continue to increase due to the ongoing economic expansion in China and other emerging economies drove up select stock prices in the energy sector, especially in the second half of the year. Within the producer durables sector, returns were led by engines and construction & handling companies on the improved sentiment surrounding global, but specifically emerging market, economic growth. In the consumer discretionary sector, the casinos & gambling industry was the best performing industry, reflecting hopes of more discretionary spending by consumers.

First Eagle Investment Management, LLC (“First Eagle”), outperformed the Russell 1000® Index as a result of both sector allocation decisions and stock selection particularly within the consumer discretionary and materials & processing sectors. First Eagle also benefited from an overweight to the energy sector, specifically from a large overweight to the oil crude producers industry. In addition, they generated positive performance from the financial services sector, particularly in the diversified banks industry. Holdings within the consumer staples sector detracted from returns, mainly due to stock selection in the food industry.

BlackRock Capital Management, Inc. (“BlackRock”), outperformed the Russell 1000® Growth Index on the strength of their stock selection. The effect was strongest within the technology sector where positions in the computer services software & systems industry added to performance. BlackRock also benefited from stock selection within producer durables, where they benefited from holdings in engines and industrial machinery companies. Sector allocation detracted from returns due primarily to an overweight to technology and a neutral weighting to health care.

Given the pro-risk, cyclically driven environment particularly during the second half of the year, Montag & Caldwell, LLC’s (“Montag”) more defensively oriented consistent growth strategy underperformed the Russell 1000® Growth Index during the fiscal year due to both negative stock selection and sector allocation decisions. Stock selection in the financial services sector detracted most from returns, primarily through holdings in the financial data & systems and securities brokerage & services industries. An overweight to the health care sector also detracted from performance. Negative stock selection in the

consumer staples sector, particularly in the food industry, detracted from returns. In contrast, Montag benefited from positive stock selection in the energy sector.

RIMCo currently employs a “select holdings” strategy for a portion of the Fund’s assets that RIMCo determines not to allocate to the money managers. Pursuant to this strategy, RIMCo analyzes the holdings in the Fund segments assigned to money managers to identify particular stocks that have been selected and are held in overweight positions by multiple money managers. RIMCo uses a proprietary model to rank these stocks. Based on this ranking, RIMCo purchases additional shares of certain stocks for the Fund. RIMCo performs this analysis and ranking, and purchases or sells stocks based on this analysis and ranking, on a regular, periodic basis. The strategy is designed to increase the Fund’s exposure to stocks that are viewed as attractive by multiple money managers

The “select holdings” portions of the Fund’s portfolio underperformed the Russell 1000® Index during the year due to negative stock selection. The largest detractor from returns during the year was stock selection within the financial services industry. Poor stock selection in the health care and technology sectors also detracted meaningfully from returns. Large underweights to the consumer discretionary and materials & processing sectors hurt performance, as the two sectors performed well during the year. The portfolio’s large underweight to smaller cap companies further detracted from the Fund’s performance as small capitalization stocks substantially outperformed large capitalization stocks.

Describe any changes to the Fund’s structure or the money manager line-up.

During the year, there were no changes to the Fund’s structure or to the money manager line-up.

| Money Managers as of December 31, 2010 | Style | |

| BlackRock Capital Management, Inc. | Growth | |

| Columbus Circle Investors | Growth | |

| DePrince, Race & Zollo, Inc. | Value | |

| First Eagle Investment Management, LLC | Market Oriented | |

| Institutional Capital LLC | Value | |

| Jacobs Levy Equity Management, Inc. | Value | |

| Montag & Caldwell, LLC | Growth | |

| Suffolk Capital Management, Inc. | Market Oriented | |

The views expressed in this report reflect those of the portfolio managers only through the end of the period covered by the report. These views do not necessarily represent the views of RIMCo, or any other person in RIMCo or any other affiliated organization. These views are subject to change at any time based upon market conditions or other events, and RIMCo disclaims any responsibility to update the views contained herein. These views should not be relied on as investment advice and, because investment decisions for Russell Investment Funds (“RIF”) are based on numerous factors, should not be relied on as an indication of investment decisions of any RIF Fund.

| 12 | Multi-Style Equity Fund |

Table of Contents

Russell Investment Funds

Multi-Style Equity Fund

Portfolio Management Discussion — December 31, 2010 (Unaudited)

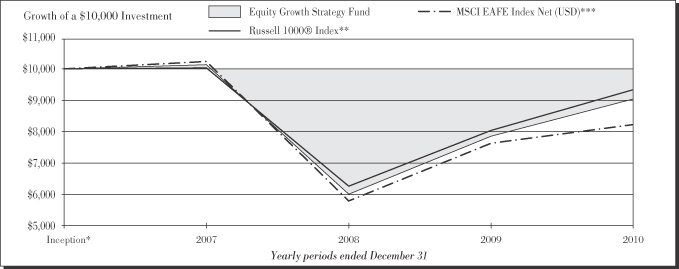

| * | Assumes initial investment on January 1, 2001. |

| ** | Russell 1000® Index includes the 1,000 largest companies in the Russell 3000® Index. The Russell 1000® Index represents the universe of stocks from which most active money managers typically select. The Russell 1000® Index return reflects adjustments from income dividends and capital gain distributions reinvested as of the ex-dividend dates. |

| § | Annualized. |

The performance shown in this section does not reflect any Insurance Company Separate Account or Policy Charges. Performance is historical and assumes reinvestment of all dividends and capital gains. Investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than when purchased. Past performance is not indicative of future results.

| Multi-Style Equity Fund | 13 |

Table of Contents

Russell Investment Funds

Multi-Style Equity Fund

Shareholder Expense Example — December 31, 2010 (Unaudited)

Fund Expenses

The following disclosure provides important information regarding each Fund’s Expense Example, which appears on each Fund’s individual page in this Annual Report. Please refer to this information when reviewing the Expense Example for a Fund.

Example

As a shareholder of the Fund, you incur two types of costs: (1) transaction costs, and (2) ongoing costs, including advisory fees and other Fund expenses. The Example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds. The Example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period indicated, which for this Fund is from July 1, 2010 to December 31, 2010.

Actual Expenses

The information in the table under the heading “Actual Performance” provides information about actual account values and actual expenses. You may use the information in this column, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first column in the row entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The information in the table under the heading “Hypothetical Performance (5% return before expenses)” provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs. Therefore, the information under the heading “Hypothetical Performance (5% return before expenses)” is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher. The fee and expenses shown in this section do not reflect any Insurance Company Separate Account or Policy Charges.

Core Class | Actual Performance | Hypothetical Performance (5% return before expenses) | ||||||

Beginning Account Value July 1, 2010 | $ | 1,000.00 | $ | 1,000.00 | ||||

Ending Account Value December 31, 2010 | $ | 1,244.50 | $ | 1,020.67 | ||||

Expenses Paid During Period* | $ | 5.09 | $ | 4.58 | ||||

| * | Expenses are equal to the Fund’s annualized expense ratio of 0.90% (representing the six month period annualized), multiplied by the average account value over the period, multiplied by 184/365 (to reflect the one-half year period). May reflect amounts waived, reimbursed and/or other credits. Without any waivers, reimbursements and/or other credits, expenses would have been higher. |

| 14 | Multi-Style Equity Fund |

Table of Contents

Russell Investment Funds

Multi-Style Equity Fund

Schedule of Investments — December 31, 2010

Amounts in thousands (except share amounts)

| Principal Amount ($) or Shares | Market Value $ | |||||||

| Common Stocks - 97.3% | ||||||||

| Consumer Discretionary - 13.8% | ||||||||

Amazon.com, Inc. (Æ) | 16,882 | 3,038 | ||||||

Autoliv, Inc. (Ñ) | 600 | 47 | ||||||

Baidu, Inc. - ADR (Æ) | 3,800 | 367 | ||||||

Bed Bath & Beyond, Inc. (Æ) | 18,651 | 917 | ||||||

BJ’s Wholesale Club, Inc. (Æ) | 4,500 | 216 | ||||||

Carnival Corp. | 23,100 | 1,065 | ||||||

CBS Corp. Class B | 63,833 | 1,216 | ||||||

Coach, Inc. | 12,200 | 675 | ||||||

Comcast Corp. Class A | 55,376 | 1,217 | ||||||

Costco Wholesale Corp. (Ñ) | 26,000 | 1,877 | ||||||

DISH Network Corp. Class A (Æ) | 10,000 | 197 | ||||||

eBay, Inc. (Æ) | 16,800 | 468 | ||||||

Estee Lauder Cos., Inc. (The) Class A | 11,619 | 938 | ||||||

Ford Motor Co. (Æ)(Ñ) | 149,545 | 2,511 | ||||||

Gap, Inc. (The) (Ñ) | 41,400 | 917 | ||||||

General Motors Co. (Æ)(Ñ) | 24,964 | 921 | ||||||

Harman International Industries, Inc. (Æ) | 2,900 | 134 | ||||||

Home Depot, Inc. | 83,710 | 2,935 | ||||||

Hyatt Hotels Corp. (Æ) | 5,300 | 242 | ||||||

Johnson Controls, Inc. | 92,325 | 3,526 | ||||||

Kohl’s Corp. (Æ)(Ñ) | 13,300 | 723 | ||||||

Las Vegas Sands Corp. (Æ) | 39,915 | 1,834 | ||||||

Lear Corp. (Æ)(Ñ) | 4,334 | 428 | ||||||

Lowe’s Cos., Inc. | 82,150 | 2,059 | ||||||

McDonald’s Corp. | 25,200 | 1,934 | ||||||

NetFlix, Inc. (Æ)(Ñ) | 2,300 | 404 | ||||||

Nike, Inc. Class B | 31,100 | 2,657 | ||||||

priceline.com, Inc. (Æ)(Ñ) | 3,196 | 1,277 | ||||||

Royal Caribbean Cruises, Ltd. (Æ)(Ñ) | 15,400 | 724 | ||||||

Stanley Black & Decker, Inc. (Ñ) | 30,150 | 2,016 | ||||||

Starbucks Corp. | 45,760 | 1,470 | ||||||

Starwood Hotels & Resorts Worldwide, Inc. (Ñ)(ö) | 26,200 | 1,593 | ||||||

Target Corp. | 29,700 | 1,786 | ||||||

Tiffany & Co. (Ñ) | 6,800 | 423 | ||||||

Time Warner, Inc. | 18,000 | 579 | ||||||

TJX Cos., Inc. | 29,600 | 1,314 | ||||||

Tyco Electronics, Ltd. | 24,152 | 855 | ||||||

Urban Outfitters, Inc. (Æ)(Ñ) | 6,700 | 240 | ||||||

Viacom, Inc. Class A | 93,642 | 3,708 | ||||||

Wal-Mart Stores, Inc. | 28,800 | 1,554 | ||||||

Walt Disney Co. (The) | 94,940 | 3,561 | ||||||

Warnaco Group, Inc. (The) (Æ) | 9,800 | 540 | ||||||

Wendy’s/Arby’s Group, Inc. Class A | 26,700 | 123 | ||||||

| 55,226 | ||||||||

| Consumer Staples - 8.0% | ||||||||

Archer-Daniels-Midland Co. | 20,300 | 611 | ||||||

Clorox Co. | 4,300 | 272 | ||||||

Coca-Cola Co. (The) | 109,179 | 7,181 | ||||||

Colgate-Palmolive Co. | 6,200 | 498 | ||||||

ConAgra Foods, Inc. | 35,900 | 811 | ||||||

Corn Products International, Inc. | 8,000 | 368 | ||||||

CVS Caremark Corp. | 18,600 | 647 | ||||||

Energizer Holdings, Inc. (Æ) | 3,200 | 233 | ||||||

| Principal Amount ($) or Shares | Market Value $ | |||||||

JM Smucker Co. (The) | 16,200 | 1,064 | ||||||

Kimberly-Clark Corp. | 6,800 | 429 | ||||||

Kraft Foods, Inc. Class A (Ñ) | 49,800 | 1,569 | ||||||

Kroger Co. (The) | 20,000 | 447 | ||||||

Lorillard, Inc. | 4,800 | 394 | ||||||

Molson Coors Brewing Co. Class B | 16,450 | 826 | ||||||

PepsiCo, Inc. | 109,838 | 7,174 | ||||||

Procter & Gamble Co. (The) | 103,784 | 6,677 | ||||||

Safeway, Inc. (Ñ) | 25,300 | 569 | ||||||

Walgreen Co. (Ñ) | 18,800 | 732 | ||||||

Whole Foods Market, Inc. (Ñ) | 31,499 | 1,594 | ||||||

| 32,096 | ||||||||

| Energy - 11.9% | ||||||||

Anadarko Petroleum Corp. | 13,200 | 1,005 | ||||||

Apache Corp. | 42,006 | 5,009 | ||||||

Cameron International Corp. (Æ) | 27,200 | 1,380 | ||||||

Chevron Corp. | 70,707 | 6,452 | ||||||

ConocoPhillips | 75,797 | 5,162 | ||||||

Devon Energy Corp. | 13,633 | 1,070 | ||||||

Dresser-Rand Group, Inc. (Æ) | 3,400 | 145 | ||||||

EnCana Corp. | 15,600 | 454 | ||||||

Exxon Mobil Corp. | 12,100 | 885 | ||||||

Halliburton Co. | 44,500 | 1,817 | ||||||

Marathon Oil Corp. | 119,647 | 4,430 | ||||||

Massey Energy Co. | 16,600 | 891 | ||||||

Murphy Oil Corp. | 18,700 | 1,394 | ||||||

Nabors Industries, Ltd. (Æ) | 5,600 | 131 | ||||||

National Oilwell Varco, Inc. | 19,635 | 1,321 | ||||||

Occidental Petroleum Corp. | 74,330 | 7,291 | ||||||

Pioneer Natural Resources Co. (Ñ) | 23,235 | 2,017 | ||||||

Rowan Cos., Inc. (Æ)(Ñ) | 4,800 | 168 | ||||||

Royal Dutch Shell PLC - ADR | 10,400 | 695 | ||||||

Schlumberger, Ltd. | 37,300 | 3,114 | ||||||

SEACOR Holdings, Inc. (Ñ) | 740 | 75 | ||||||

Spectra Energy Corp. | 5,100 | 127 | ||||||

Statoil ASA - ADR (Ñ) | 30,400 | 723 | ||||||

SunPower Corp. Class B (Æ)(Ñ) | 62,000 | 769 | ||||||

Valero Energy Corp. (Ñ) | 21,700 | 502 | ||||||

Williams Cos., Inc. (The) | 27,700 | 685 | ||||||

| 47,712 | ||||||||

| Financial Services—16.0% | ||||||||

Aflac, Inc. | 31,650 | 1,786 | ||||||

Allied World Assurance Co. Holdings, Ltd. (Ñ) | 3,100 | 184 | ||||||

Allstate Corp. (The) (Ñ) | 37,700 | 1,202 | ||||||

American Express Co. | 47,570 | 2,041 | ||||||

American Financial Group, Inc. | 7,500 | 242 | ||||||

Ameriprise Financial, Inc. | 6,900 | 397 | ||||||

AON Corp. (Ñ) | 31,750 | 1,461 | ||||||

Ares Capital Corp. | 4,300 | 71 | ||||||

Assurant, Inc. | 7,900 | 304 | ||||||

Axis Capital Holdings, Ltd. (Ñ) | 5,700 | 205 | ||||||

Bank of America Corp. | 74,700 | 997 | ||||||

Bank of Hawaii Corp. (Ñ) | 1,900 | 90 | ||||||

Bank of New York Mellon Corp. (The) (Ñ) | 64,600 | 1,951 | ||||||

| Multi-Style Equity Fund | 15 |

Table of Contents

Russell Investment Funds

Multi-Style Equity Fund

Schedule of Investments, continued — December 31, 2010

Amounts in thousands (except share amounts)

| Principal Amount ($) or Shares | Market Value $ | |||||||

BB&T Corp. (Ñ) | 87,950 | 2,312 | ||||||

Berkshire Hathaway, Inc. Class B (Æ) | 1,700 | 136 | ||||||

BlackRock, Inc. Class A | 7,150 | 1,363 | ||||||

Charles Schwab Corp. (The) (Ñ) | 54,150 | 927 | ||||||

Chubb Corp. (Ñ) | 7,600 | 453 | ||||||

CIT Group, Inc. (Æ) | 8,100 | 382 | ||||||

Citigroup, Inc. (Æ) | 581,070 | 2,749 | ||||||

CNA Financial Corp. (Æ)(Ñ) | 3,500 | 95 | ||||||

Discover Financial Services (Ñ) | 24,400 | 452 | ||||||

Endurance Specialty Holdings, Ltd. (Ñ) | 7,000 | 322 | ||||||

Federated Investors, Inc. Class B (Ñ) | 18,800 | 492 | ||||||

Fifth Third Bancorp (Ñ) | 72,426 | 1,063 | ||||||

Fulton Financial Corp. (Ñ) | 17,500 | 181 | ||||||

Goldman Sachs Group, Inc. (The) | 21,178 | 3,561 | ||||||

Hartford Financial Services Group, Inc. (Ñ) | 36,100 | 956 | ||||||

HCC Insurance Holdings, Inc. | 8,800 | 255 | ||||||

Hersha Hospitality Trust Class A (ö) | 5,000 | 33 | ||||||

Hudson City Bancorp, Inc. (Ñ) | 50,900 | 648 | ||||||

Huntington Bancshares, Inc. | 171,100 | 1,175 | ||||||

Jefferies Group, Inc. (Ñ) | 12,800 | 341 | ||||||

JPMorgan Chase & Co. | 111,251 | 4,719 | ||||||

KeyCorp | 57,200 | 506 | ||||||

Liberty Property Trust (Ñ)(ö) | 5,100 | 163 | ||||||

Lincoln National Corp. | 40,300 | 1,121 | ||||||

Loews Corp. | 8,100 | 315 | ||||||

Marsh & McLennan Cos., Inc. | 26,400 | 722 | ||||||

Mastercard, Inc. Class A | 3,828 | 858 | ||||||

Mercury General Corp. (Ñ) | 11,200 | 482 | ||||||

MetLife, Inc. | 71,694 | 3,186 | ||||||

Morgan Stanley | 40,700 | 1,108 | ||||||

Netspend Holdings, Inc. (Æ)(Ñ) | 2,088 | 27 | ||||||

Northern Trust Corp. (Ñ) | 16,100 | 892 | ||||||

NYSE Euronext | 7,400 | 222 | ||||||

People’s United Financial, Inc. (Ñ) | 29,000 | 406 | ||||||

Piedmont Office Realty Trust, Inc. Class A (Ñ)(ö) | 1,200 | 24 | ||||||

Plum Creek Timber Co., Inc. (Ñ)(ö) | 15,000 | 562 | ||||||

PNC Financial Services Group, Inc. | 33,100 | 2,010 | ||||||

Progressive Corp. (The) | 13,600 | 270 | ||||||

Prudential Financial, Inc. | 27,300 | 1,603 | ||||||

Reinsurance Group of America, Inc. Class A (Ñ) | 3,100 | 167 | ||||||

Senior Housing Properties Trust (ö) | 8,800 | 193 | ||||||

State Street Corp. | 23,400 | 1,084 | ||||||

SunTrust Banks, Inc. (Ñ) | 28,000 | 826 | ||||||

Transatlantic Holdings, Inc. | 6,500 | 336 | ||||||

Travelers Cos., Inc. (The) (Ñ) | 8,500 | 474 | ||||||

Unum Group | 9,300 | 225 | ||||||

US Bancorp (Ñ) | 160,159 | 4,319 | ||||||

Valley National Bancorp (Ñ) | 32,239 | 461 | ||||||

Visa, Inc. Class A | 11,737 | 826 | ||||||

Washington Federal, Inc. (Ñ) | 2,900 | 49 | ||||||

Webster Financial Corp. (Ñ) | 4,700 | 93 | ||||||

Wells Fargo & Co. | 221,011 | 6,848 | ||||||

| 63,924 | ||||||||

| Principal Amount ($) or Shares | Market Value $ | |||||||

| Health Care - 11.3% | ||||||||

Abbott Laboratories | 61,026 | 2,924 | ||||||

Aetna, Inc. | 13,500 | 412 | ||||||

Alexion Pharmaceuticals, Inc. (Æ)(Ñ) | 4,500 | 362 | ||||||

Allergan, Inc. | 63,462 | 4,358 | ||||||

Amgen, Inc. (Æ) | 12,151 | 667 | ||||||

Baxter International, Inc. | 15,300 | 774 | ||||||

Boston Scientific Corp. (Æ)(Ñ) | 50,000 | 379 | ||||||

Bristol-Myers Squibb Co. | 19,004 | 503 | ||||||

Cardinal Health, Inc. | 3,800 | 146 | ||||||

Celgene Corp. (Æ) | 18,602 | 1,100 | ||||||

Cerner Corp. (Æ)(Ñ) | 5,400 | 512 | ||||||

Cigna Corp. | 9,000 | 330 | ||||||

Covance, Inc. (Æ)(Ñ) | 8,800 | 452 | ||||||

Coventry Health Care, Inc. (Æ) | 12,100 | 319 | ||||||

Covidien PLC | 33,850 | 1,546 | ||||||

Dendreon Corp. (Æ)(Ñ) | 10,100 | 353 | ||||||

Eli Lilly & Co. (Ñ) | 14,400 | 505 | ||||||

Express Scripts, Inc. Class A (Æ) | 13,200 | 713 | ||||||

Hologic, Inc. (Æ)(Ñ) | 8,900 | 167 | ||||||

Humana, Inc. (Æ) | 8,600 | 471 | ||||||

Illumina, Inc. (Æ)(Ñ) | 18,957 | 1,201 | ||||||

Johnson & Johnson | 34,600 | 2,140 | ||||||

Life Technologies Corp. (Æ) | 7,600 | 422 | ||||||

Lincare Holdings, Inc. (Ñ) | 16,400 | 440 | ||||||

Medicis Pharmaceutical Corp. Class A (Ñ) | 32,000 | 857 | ||||||

Medtronic, Inc. | 22,516 | 835 | ||||||

Merck & Co., Inc. | 169,450 | 6,107 | ||||||

Pfizer, Inc. | 372,184 | 6,518 | ||||||

Sanofi-Aventis SA - ADR | 72,050 | 2,322 | ||||||

St. Jude Medical, Inc. (Æ)(Ñ) | 25,416 | 1,087 | ||||||

Stryker Corp. (Ñ) | 36,000 | 1,933 | ||||||

Teleflex, Inc. (Ñ) | 7,000 | 377 | ||||||

Teva Pharmaceutical Industries, Ltd. - ADR | 11,900 | 620 | ||||||

Thermo Fisher Scientific, Inc. (Æ) | 16,517 | 914 | ||||||

UnitedHealth Group, Inc. | 23,600 | 852 | ||||||

Watson Pharmaceuticals, Inc. Class B (Æ) | 19,900 | 1,028 | ||||||

WellPoint, Inc. (Æ) | 8,500 | 483 | ||||||

| 45,129 | ||||||||

| Materials and Processing - 5.1% | ||||||||

Agnico-Eagle Mines, Ltd. (Þ) | 2,400 | 184 | ||||||

Air Products & Chemicals, Inc. (Ñ) | 10,400 | 946 | ||||||

Airgas, Inc. | 1,737 | 108 | ||||||

Alcoa, Inc. | 18,100 | 279 | ||||||

Celanese Corp. Class A | 12,100 | 498 | ||||||

CF Industries Holdings, Inc. (Ñ) | 4,466 | 604 | ||||||

Cytec Industries, Inc. | 4,700 | 249 | ||||||

Ecolab, Inc. | 5,900 | 297 | ||||||

EI du Pont de Nemours & Co. | 16,700 | 833 | ||||||

Freeport-McMoRan Copper & Gold, Inc. Class B | 13,100 | 1,574 | ||||||

Huntsman Corp. | 42,500 | 663 | ||||||

MeadWestvaco Corp. | 10,200 | 267 | ||||||

Monsanto Co. | 36,069 | 2,512 | ||||||

Newmont Mining Corp. | 41,317 | 2,537 | ||||||

| 16 | Multi-Style Equity Fund |

Table of Contents

Russell Investment Funds

Multi-Style Equity Fund

Schedule of Investments, continued — December 31, 2010

Amounts in thousands (except share amounts)

| Principal Amount ($) or Shares | Market Value $ | |||||||

Nucor Corp. (Ñ) | 17,700 | 776 | ||||||

Owens-Illinois, Inc. (Æ) | 31,850 | 978 | ||||||

Packaging Corp. of America | 9,200 | 238 | ||||||

Potash Corp. of Saskatchewan, Inc. | 9,362 | 1,449 | ||||||

Reliance Steel & Aluminum Co. | 3,100 | 158 | ||||||

Rio Tinto PLC - ADR | 14,800 | 1,061 | ||||||

Sealed Air Corp. (Ñ) | 31,300 | 797 | ||||||

SPX Corp. | 12,400 | 887 | ||||||

Steel Dynamics, Inc. (Ñ) | 30,000 | 549 | ||||||

Textron, Inc. (Ñ) | 3,300 | 78 | ||||||

Vulcan Materials Co. (Ñ) | 18,100 | 803 | ||||||

Weyerhaeuser Co. (Ñ) | 54,266 | 1,027 | ||||||

| 20,352 | ||||||||

| Producer Durables - 10.3% | ||||||||

Accenture PLC Class A | 67,250 | 3,262 | ||||||

AGCO Corp. (Æ)(Ñ) | 2,300 | 117 | ||||||

Agilent Technologies, Inc. (Æ) | 18,382 | 762 | ||||||

AO Smith Corp. | 1,900 | 72 | ||||||

Atlas Air Worldwide Holdings, Inc. (Æ) | 600 | 33 | ||||||

Automatic Data Processing, Inc. (Ñ) | 15,600 | 722 | ||||||

Avery Dennison Corp. (Ñ) | 2,900 | 123 | ||||||

Boeing Co. (The) | 13,200 | 862 | ||||||

Carlisle Cos., Inc. | 9,900 | 393 | ||||||

Caterpillar, Inc. (Ñ) | 33,525 | 3,140 | ||||||

Chicago Bridge & Iron Co. NV (Æ) | 1,100 | 36 | ||||||

CNH Global NV (Æ) | 1,200 | 57 | ||||||

Crane Co. | 5,400 | 222 | ||||||

Danaher Corp. (Ñ) | 23,200 | 1,094 | ||||||

Deere & Co. | 13,802 | 1,146 | ||||||

Delta Air Lines, Inc. (Æ)(Ñ) | 62,200 | 784 | ||||||

Embraer SA (Æ) | 13,000 | 382 | ||||||

EMCOR Group, Inc. (Æ) | 1,200 | 35 | ||||||

Emerson Electric Co. | 23,000 | 1,315 | ||||||

FedEx Corp. (Ñ) | 12,378 | 1,151 | ||||||

Fluor Corp. (Ñ) | 35,600 | 2,360 | ||||||

General Dynamics Corp. | 18,000 | 1,277 | ||||||

General Electric Co. | 48,200 | 882 | ||||||

Harsco Corp. | 20,500 | 581 | ||||||

Honeywell International, Inc. | 87,798 | 4,668 | ||||||

Ingersoll-Rand PLC (Ñ) | 22,600 | 1,064 | ||||||

Jacobs Engineering Group, Inc. (Æ) | 2,800 | 128 | ||||||

Joy Global, Inc. | 5,100 | 442 | ||||||

KBR, Inc. | 7,200 | 219 | ||||||

L-3 Communications Holdings, Inc. | 4,600 | 324 | ||||||

Lexmark International, Inc. Class A (Æ) | 8,300 | 289 | ||||||

Lockheed Martin Corp. (Ñ) | 8,000 | 559 | ||||||

Manpower, Inc. (Ñ) | 15,300 | 960 | ||||||

McDermott International, Inc. (Æ) | 3,500 | 72 | ||||||

Moody’s Corp. (Ñ) | 20,000 | 531 | ||||||

Moog, Inc. Class A (Æ)(Ñ) | 2,100 | 84 | ||||||

Northrop Grumman Corp. (Ñ) | 7,400 | 479 | ||||||

PACCAR, Inc. | 15,000 | 861 | ||||||

Pitney Bowes, Inc. (Ñ) | 25,700 | 621 | ||||||

Robert Half International, Inc. (Ñ) | 14,700 | 450 | ||||||

Rockwell Automation, Inc. (Ñ) | 20,700 | 1,484 | ||||||

Ryder System, Inc. (Ñ) | 3,500 | 184 | ||||||

| Principal Amount ($) or Shares | Market Value $ | |||||||

Shaw Group, Inc. (The) (Æ) | 2,000 | 68 | ||||||

Terex Corp. (Æ)(Ñ) | 6,400 | 199 | ||||||

Tidewater, Inc. (Ñ) | 13,400 | 721 | ||||||

Union Pacific Corp. | 5,800 | 537 | ||||||

United Continental Holdings, Inc. (Æ) | 12,800 | 305 | ||||||

United Parcel Service, Inc. Class B | 53,262 | 3,866 | ||||||

URS Corp. (Æ) | 6,600 | 275 | ||||||

Verisk Analytics, Inc. Class A (Æ) | 322 | 11 | ||||||

Waste Management, Inc. (Ñ) | 12,200 | 450 | ||||||

Xerox Corp. (Ñ) | 40,000 | 461 | ||||||

| 41,120 | ||||||||

| Technology - 17.6% | ||||||||

Akamai Technologies, Inc. (Æ) | 7,000 | 329 | ||||||

Amdocs, Ltd. (Æ) | 13,100 | 360 | ||||||

Amphenol Corp. Class A (Ñ) | 37,733 | 1,992 | ||||||

Apple, Inc. (Æ) | 27,597 | 8,901 | ||||||

Applied Materials, Inc. (Ñ) | 94,400 | 1,326 | ||||||

BCE, Inc. (Ñ) | 51,900 | 1,840 | ||||||

Broadcom Corp. Class A | 109,444 | 4,766 | ||||||

Brocade Communications Systems, Inc. (Æ) | 16,500 | 87 | ||||||

CA, Inc. (Ñ) | 6,400 | 156 | ||||||

Check Point Software Technologies, Ltd. (Æ)(Ñ) | 17,100 | 791 | ||||||

Cisco Systems, Inc. (Æ) | 52,700 | 1,066 | ||||||

Citrix Systems, Inc. (Æ) | 9,400 | 643 | ||||||

Cognizant Technology Solutions Corp. Class A (Æ) | 22,671 | 1,661 | ||||||

Computer Sciences Corp. | 8,000 | 397 | ||||||

Cree, Inc. (Æ) | 9,000 | 593 | ||||||

Ctrip.com International, Ltd. - ADR (Æ) | 11,200 | 453 | ||||||

Diebold, Inc. (Ñ) | 10,500 | 337 | ||||||

Electronic Arts, Inc. (Æ)(Ñ) | 12,800 | 210 | ||||||

F5 Networks, Inc. (Æ)(Ñ) | 10,892 | 1,418 | ||||||

Google, Inc. Class A (Æ) | 11,815 | 7,018 | ||||||

Harris Corp. (Ñ) | 7,400 | 335 | ||||||

Hewlett-Packard Co. | 22,300 | 939 | ||||||

Ingram Micro, Inc. Class A (Æ) | 11,300 | 216 | ||||||

Intel Corp. | 33,000 | 694 | ||||||

International Business Machines Corp. | 11,145 | 1,636 | ||||||

Intuit, Inc. (Æ)(Ñ) | 9,180 | 453 | ||||||

Juniper Networks, Inc. (Æ) | 37,192 | 1,373 | ||||||

Lam Research Corp. (Æ) | 7,900 | 409 | ||||||

LSI Corp. (Æ) | 37,700 | 226 | ||||||

Maxim Integrated Products, Inc. (Ñ) | 43,600 | 1,030 | ||||||

Micron Technology, Inc. (Æ)(Ñ) | 45,400 | 364 | ||||||

Microsoft Corp. | 144,350 | 4,031 | ||||||

Molex, Inc. (Ñ) | 14,800 | 336 | ||||||

Motorola, Inc. (Æ) | 57,700 | 523 | ||||||

National Semiconductor Corp. (Ñ) | 58,400 | 804 | ||||||

NetApp, Inc. (Æ)(Ñ) | 28,581 | 1,571 | ||||||

Nokia OYJ - ADR (Ñ) | 32,100 | 331 | ||||||

Oracle Corp. | 131,440 | 4,115 | ||||||

QUALCOMM, Inc. | 157,653 | 7,802 | ||||||

Red Hat, Inc. (Æ) | 26,059 | 1,189 | ||||||

Salesforce.com, Inc. (Æ)(Ñ) | 9,400 | 1,241 | ||||||

SanDisk Corp. (Æ) | 12,782 | 637 | ||||||

| Multi-Style Equity Fund | 17 |

Table of Contents

Russell Investment Funds

Multi-Style Equity Fund

Schedule of Investments, continued — December 31, 2010

Amounts in thousands (except share amounts)

| Principal Amount ($) or Shares | Market Value $ | |||||||

Synopsys, Inc. (Æ) | 13,200 | 355 | ||||||

Tech Data Corp. (Æ) | 6,300 | 277 | ||||||

Texas Instruments, Inc. (Ñ) | 86,226 | 2,803 | ||||||

VMware, Inc. Class A (Æ)(Ñ) | 5,200 | 462 | ||||||

Vodafone Group PLC - ADR (Ñ) | 95,700 | 2,529 | ||||||

| 71,025 | ||||||||

| Utilities - 3.3% | ||||||||

AGL Resources, Inc. | 4,600 | 165 | ||||||

American Electric Power Co., Inc. | 19,400 | 699 | ||||||

American Water Works Co., Inc. | 21,000 | 531 | ||||||

AT&T, Inc. | 54,800 | 1,609 | ||||||

Calpine Corp. (Æ)(Ñ) | 59,368 | 792 | ||||||

CenterPoint Energy, Inc. (Ñ) | 25,800 | 406 | ||||||

Constellation Energy Group, Inc. | 11,800 | 361 | ||||||

Duke Energy Corp. | 25,900 | 461 | ||||||

Edison International (Ñ) | 11,600 | 448 | ||||||

Energen Corp. | 5,200 | 251 | ||||||

Entergy Corp. | 5,000 | 354 | ||||||

Exelon Corp. (Ñ) | 9,300 | 387 | ||||||

Frontier Communications Corp. (Ñ) | 23,900 | 233 | ||||||

Great Plains Energy, Inc. (Ñ) | 22,200 | 430 | ||||||

MDU Resources Group, Inc. | 21,800 | 442 | ||||||

NextEra Energy, Inc. | 22,300 | 1,160 | ||||||

NII Holdings, Inc. (Æ) | 8,100 | 362 | ||||||

NiSource, Inc. (Ñ) | 23,500 | 414 | ||||||

Northeast Utilities | 10,900 | 347 | ||||||

NV Energy, Inc. | 22,600 | 318 | ||||||

OGE Energy Corp. | 6,400 | 291 | ||||||

Pepco Holdings, Inc. (Ñ) | 20,400 | 372 | ||||||

PG&E Corp. | 8,100 | 388 | ||||||

PNM Resources, Inc. (Ñ) | 7,400 | 96 | ||||||

PPL Corp. (Ñ) | 11,100 | 292 | ||||||

Progress Energy, Inc. Class D | 7,700 | 335 | ||||||

Questar Corp. (Ñ) | 9,400 | 164 | ||||||

Southern Union Co. (Ñ) | 9,700 | 233 | ||||||

Veolia Environnement SA - ADR | 13,400 | 393 | ||||||

Verizon Communications, Inc. | 12,200 | 437 | ||||||

| 13,171 | ||||||||

| Total Common Stocks (cost $317,038) | 389,755 | |||||||

| Short-Term Investments - 2.2% | ||||||||

Russell U.S. Cash Management Fund | 8,880,639 | (¥) | 8,881 | |||||

| Total Short-Term Investments (cost $8,881) | 8,881 | |||||||

| Principal Amount ($) or Shares | Market Value $ | |||||||

| Other Securities - 17.0% | ||||||||

Russell Investment Funds Liquidating Trust (×) | 1,329,628 | (¥) | 1,330 | |||||

Russell U.S. Cash Collateral Fund (×) | 66,617,631 | (¥) | 66,617 | |||||

| Total Other Securities (cost $67,947) | 67,947 | |||||||

| Total Investments - 116.5% (identified cost $393,866) | 466,583 | |||||||

| Other Assets and Liabilities, Net - (16.5%) | (66,112 | ) | ||||||

| Net Assets - 100.0% | 400,471 | |||||||

See accompanying notes which are an integral part of the financial statements.

| 18 | Multi-Style Equity Fund |

Table of Contents

Russell Investment Funds

Multi-Style Equity Fund

Schedule of Investments, continued — December 31, 2010

Amounts in thousands

| Futures Contracts | Number of Contracts | Notional | Expiration Date | Unrealized Appreciation (Depreciation) $ | ||||||||||||||

Long Positions | ||||||||||||||||||

Russell 1000 Mini Index | 21 | USD | 1,458 | 03/11 | 30 | |||||||||||||

S&P 500 E-Mini Index (CME) | 96 | USD | 6,014 | 03/11 | 89 | |||||||||||||

S&P 500 Index (CME) | 7 | USD | 2,193 | 03/11 | 46 | |||||||||||||

S&P Midcap 400 E-Mini Index (CME) | 9 | USD | 815 | 03/11 | 9 | |||||||||||||

Total Unrealized Appreciation (Depreciation) on Open Futures Contracts | 174 | |||||||||||||||||

Presentation of Portfolio Holdings — December 31, 2010

Amounts in thousands

| Market Value | % of Net | |||||||||||||||||||

| Portfolio Summary | Level 1 | Level 2 | Level 3 | Total | ||||||||||||||||

Common Stocks | ||||||||||||||||||||

Consumer Discretionary | $ | 55,226 | $ | — | $ | — | $ | 55,226 | 13.8 | |||||||||||

Consumer Staples | 32,096 | — | — | 32,096 | 8.0 | |||||||||||||||

Energy | 47,712 | — | — | 47,712 | 11.9 | |||||||||||||||

Financial Services | 63,924 | — | — | 63,924 | 16.0 | |||||||||||||||

Health Care | 45,129 | — | — | 45,129 | 11.3 | |||||||||||||||

Materials and Processing | 20,352 | — | — | 20,352 | 5.1 | |||||||||||||||

Producer Durables | 41,120 | — | — | 41,120 | 10.3 | |||||||||||||||

Technology | 71,025 | — | — | 71,025 | 17.6 | |||||||||||||||

Utilities | 13,171 | — | — | 13,171 | 3.3 | |||||||||||||||

Short-Term Investments | — | 8,881 | — | 8,881 | 2.2 | |||||||||||||||

Other Securities | — | 67,947 | — | 67,947 | 17.0 | |||||||||||||||

Total Investments | 389,755 | 76,828 | — | 466,583 | 116.5 | |||||||||||||||

Other Assets and Liabilities, Net | (16.5 | ) | ||||||||||||||||||

| 100.0 | ||||||||||||||||||||

Other Financial Instruments | ||||||||||||||||||||

Futures Contracts | 174 | — | — | 174 | — | * | ||||||||||||||

Total Other Financial Instruments** | 174 | — | — | 174 | ||||||||||||||||

| * | Less than .05% of net assets. |

| ** | Other financial instruments reflected in the Schedule of Investments, such as futures, forwards, and swap contracts which are valued at the unrealized appreciation/depreciation on the instruments. |

For a description of the levels see note 2 in the Notes to Financial Statements.

See accompanying notes which are an integral part of the financial statements.

| Multi-Style Equity Fund | 19 |

Table of Contents

Russell Investment Funds

Multi-Style Equity Fund

Fair Value of Derivative Instruments — December 31, 2010

Amounts in thousands

| Derivatives not accounted for as hedging instruments | Equity Contracts | |||

Location: Statement of Assets and Liabilities - Assets | ||||

Daily variation margin on futures contracts* | $ | 174 | ||

| Derivatives not accounted for as hedging instruments | Equity Contracts | |||

Location: Statement of Operations - Net realized gain (loss) | ||||

Futures contracts | $ | 2,066 | ||

Location: Statement of Operations - Net change in unrealized appreciation (depreciation) | ||||

Futures contracts | $ | (189 | ) | |

| * | Includes cumulative appreciation/depreciation of futures contracts as reported in Schedule of Investments. Only current day’s variation margin is reported within the statement of assets and liabilities |

For further disclosure on derivatives see note 2 in Notes to Financial Statements.

See accompanying notes which are an integral part of the financial statements.

| 20 | Multi-Style Equity Fund |

Table of Contents

[This page intentionally left blank]

Table of Contents

Russell Investment Funds

Portfolio Management Discussion — December 31, 2010 (Unaudited)

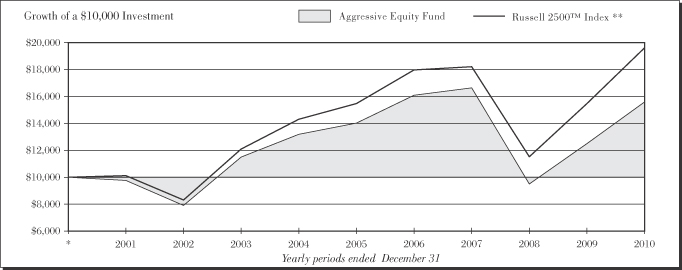

| Aggressive Equity Fund | ||||

| Total Return | ||||

1 Year | 24.88 | % | ||

5 Years | 2.14 | %§ | ||

10 Years | 4.56 | %§ | ||

| Russell 2500™ Index ** | ||||

| Total Return | ||||

1 Year | 26.71 | % | ||

5 Years | 4.86 | %§ | ||

10 Years | 6.98 | %§ | ||

| 22 | Aggressive Equity Fund |

Table of Contents

Russell Investment Funds

Aggressive Equity Fund

Portfolio Management Discussion — December 31, 2010 (Unaudited)

The Aggressive Equity Fund (the “Fund”) allocates most of its assets among multiple money managers. Russell Investment Management Company (“RIMCo”), as the Fund’s advisor, may change the allocation of the Fund’s assets among money managers at any time. An exemptive order from the Securities and Exchange Commission (“SEC”) permits RIMCo to engage or terminate a money manager at any time, subject to approval by the Fund’s Board without a shareholder vote. Pursuant to the terms of the exemptive order, the Fund is required to notify its shareholders within 60 days of when a money manager begins providing services. The Fund currently has six money managers.

What is the Fund’s investment objective?

The Fund seeks to provide long-term capital growth.

How did the Fund perform relative to its benchmark for the fiscal year ended December 31, 2010?

For the fiscal year ended December 31, 2010, the Aggressive Equity Fund gained 24.88%. This is compared to the Russell 2500™ Index, which gained 26.71% during the same period. The Fund’s performance includes operating expenses, whereas index returns are unmanaged and do not include expenses of any kind.

For the fiscal year ended December 31, 2010, the Lipper® Small-Cap Core Funds (VIP) Average gained 25.96%. This average return serves as a peer comparison and is expressed net of operating expenses.

RIMCo may assign a money manager a specific style or capitalization benchmark other than the Fund’s index. However, the Fund’s primary index remains the benchmark for the Fund and is representative of the aggregate of each money manager’s benchmark index.

How did the market conditions described in the Market Summary report affect the Fund’s performance?

A high degree of correlation among stock price movements resulted in a more difficult environment for active management. Price differentiation in the market was more prevalent at the higher and lower ends of the risk and growth spectrum and the returns of the Fund decreased when the “risk on” scenario was present. A “risk on” scenario exists where positive economic and company-specific news leads companies with more economic sensitivity to outperform the benchmark when “risk” is in favor. In this environment, companies with significant economic sensitivity and often poor fundamentals (in the form of high debt and low cash on the balance sheet) outperformed the market. This market environment was prevalent during the fiscal year and detracted from Fund performance as the Fund was clearly positioned in stocks with stronger fundamentals. The fiscal year could be characterized as driven more by macroeconomic forces than company specific data, which did not favor the multi-manager process of the Fund.

How did the investment strategies and techniques employed by the Fund and its money managers affect its performance?

The Fund employs six money managers: two growth-oriented, one market-oriented and three value-oriented. Three of the six managers and two of the three value managers outperformed their respective benchmarks. This was reflective of the conditions in the market with managers benefiting from a moderation in investors’ appetite for riskier companies (i.e., companies with significant levels of debt and negative earnings), but penalized by elevated stock correlations (i.e. similar as opposed to differentiated return patterns) caused investors’ focus on macro related events, such as European sovereign debt worries and ongoing weak U.S. housing and employment data, rather than on corporate earnings and company announcements. This made it a more difficult market for active management.

While the U.S. economic recovery was slower than many investors anticipated, which curtailed investors’ appetite for speculation, investors retained an overweight exposure to companies that were sensitive to these economic conditions. Consequently, managers across the style spectrum with exposure to cyclical stocks or sectors, specifically the technology sector, fared better than those managers without such exposure.

DePrince, Race & Zollo, Inc., (“DePrince”) a yield-focused value manager, underperformed its style benchmark, the Russell 2500™ Value Index, for the fiscal year. DePrince faced several headwinds during the fiscal year that meaningfully impeded their ability to outperform their benchmark. First, their focus on sustainable dividend yield was not rewarded, as investors alternated between high-yield stocks and zero yielding stocks. In addition, DePrince’s macro positioning created significant difficulties as DePrince reduced its risk exposure starting in late 2009 and into early 2010. This was in response to the duration and magnitude of the risk rally, which was predicated on the belief that the U.S. would rebound strongly from the recession. However, DePrince’s risk reduction efforts were premature, as a high tolerance for risk continued to be rewarded during the fiscal year. As a result of this environment, stock selection detracted from performance, with selection in financial services representing the largest detractor. DePrince’s overweight exposure to regional banks also detracted from performance relative to the style benchmark.

Tygh Capital Management, Inc. (“Tygh”), a quality-focused growth-oriented manager, underperformed its style benchmark, the Russell 2500™Growth Index, for the fiscal year. While investor preference for risk detracted from Tygh’s process, underperformance was driven mainly by weak stock selection. The largest detractors to performance relative to its style benchmark were in the consumer discretionary sector, specifically in Tygh’s specialty retail and restaurant holdings. This negative selection was a function of both the companies

| Aggressive Equity Fund | 23 |

Table of Contents

Russell Investment Funds

Aggressive Equity Fund

Portfolio Management Discussion — December 31, 2010 (Unaudited)

held in the sector and Tygh’s underweight or lack of exposure to several larger index constituents that performed well during the period.