| OMB APPROVAL |

OMB Number: 3235-0570 Expires: August 31, 2020 Estimated average burden hours per response: 20.6 |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

| Investment Company Act file number | 811-05685 | |

| Williamsburg Investment Trust |

| (Exact name of registrant as specified in charter) |

| 225 Pictoria Drive, Suite 450 Cincinnati, Ohio | 45246 |

| (Address of principal executive offices) | (Zip code) |

John H. Chilton, Esq.

| Sullivan & Worcester LLP 1666 K Street NW Washington, D.C. 20006 |

| (Name and address of agent for service) |

| Registrant's telephone number, including area code: | (513) 587-3400 | |

| Date of fiscal year end: | March 31 | |

| | | |

| Date of reporting period: | March 31, 2019 | |

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget ("OMB") control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to the Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

Item 1. Reports to Stockholders.

ANNUAL REPORT

March 31, 2019

Beginning on January 1, 2021, as permitted by regulations adopted by the U.S. Securities and Exchange Commission, paper copies of the Funds’ shareholder reports like this one will no longer be sent by mail, unless you specifically request paper copies of the reports from the Funds or from your financial intermediary, such as a broker-dealer or bank. Instead, the reports will be made available on a website, and you will be notified by mail each time a report is posted and provided with a website link to access the report.

If you already elected to receive shareholder reports electronically, you will not be affected by this change and you need not take any action. You may elect to receive shareholder reports and other communications from the Funds electronically by contacting the Funds at 1-800-281-3217 or, if you own these shares through a financial intermediary, by contacting your financial intermediary.

You may elect to receive all future reports in paper free of charge. You can inform the Funds that you wish to continue receiving paper copies of your shareholder reports by contacting the Funds at 1-800-281-3217. If you own shares through a financial intermediary, you may contact your financial intermediary or follow instructions included with this document to elect to continue to receive paper copies of your shareholder reports. Your election to receive reports in paper will apply to all Funds held with the Fund complex or at your financial intermediary.

THE DAVENPORT FUNDS

LETTER TO SHAREHOLDERS | May 1, 2019 |

Dear Shareholders,

Stocks surged higher to close out fiscal 2019. For the 3 months ended March 31, 2019, the S&P 500 Index gained 13.65% while the Russell 2000 Index was up 14.58%. Of note, this was the best quarter for the S&P 500 since 2009 and the best calendar first quarter since 1998. Clearly, this advance represented a dramatic turn of events from calendar Q4 2018, when stocks declined dramatically and the S&P 500 experienced its worst December since 1931. For the fiscal year ended March 31, 2019, the S&P 500 and Russell 2000 gained 9.50% and 2.05%, respectively.

What sparked this turn? For one, by late calendar 2018 it seemed investors had generally accepted signs of moderating economic growth. Shares of many companies, especially more economically sensitive concerns, even seemed to be discounting a full blow recession. With market expectations reset, it only took decent fourth quarter earnings reports from corporate America for stocks to rally. Also, fears of a trade war with China showed signs of diminishing as the Trump Administration appeared to make progress with Chinese leadership.

Perhaps most notable, the Federal Reserve (“Fed”) backed off its tightening agenda. The Fed had been raising interest rates and seemed intent on continuing to do so in response to low unemployment, economic growth (prompted in part by fiscal stimulus/tax cuts) and the threat of inflation. As signs of slowing growth became apparent, many feared the Fed’s agenda was misguided and Fed Chairman Jerome Powell gained some vocal critics. Ultimately, Powell acknowledged the case for raising rates had weakened and noted rate hikes were less likely. Investors promptly cheered a continuation of the “cheap money” environment that has buoyed stock valuations for much of the last decade. Many investors are going so far as to predict the Fed’s next move may actually be an interest rate cut.

Going forward, we continue to expect more moderate equity returns when compared to the heady returns of 2013-2017. However, as shown by the wild swings of fiscal Q3 and Q4 of this year, this clearly won’t happen in a smooth fashion. Our outlook is based on a fairly balanced risk/reward profile for the market. Although we think odds of a recession are low, we remain mindful of slowing earnings growth (partly a function of lapping corporate tax reductions) and “peakish” conditions for gauges such as unemployment and consumer credit. On the other hand, it appears the Fed still “has the market’s back” and valuations aren’t unreasonable. The S&P 500’s current P/E of 17x on 2019 earnings is only slightly above the average of the last 25 years.

In terms of the Davenport Funds, we were pleased with both absolute and relative performance in the first quarter. We continue to find new ideas, although the market’s impressive bounce has made it a little more difficult to find value. We are currently carrying some cash in the Funds and look to take advantage of any market pullbacks. Thank you for your trust and read on for a discussion of individual Fund themes and ideas.

1

Davenport Core Fund

The following chart represents Davenport Core Fund’s (DAVPX) performance and the performance of the S&P 500 Index*, the Core Fund’s primary benchmark, for the periods ended March 31, 2019.

| Fiscal

Q4

2018 | 1 Year | 3 Years** | 5 Years** | 10 Years** | Since

Inception

1/15/98** | Fiscal

Year 2019

Expense

Ratio |

Core Fund | 14.31% | 8.21% | 12.00% | 9.04% | 14.43% | 6.87% | 0.89% |

S&P 500 Index* | 13.65% | 9.50% | 13.51% | 10.91% | 15.92% | 7.29% | |

30-Day SEC Yield: 0.25%; Expense Ratio in current prospectus: 0.90%

Past performance is no guarantee of future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. Performance data, current to the most recent month end, may be obtained by calling 1-800-281-3217.

* | The S&P 500 Index is comprised of 500 U.S. stocks and is an indicator of the performance of the overall U.S. stock market. An investor cannot invest in an index and its returns are not indicative of the performance of any specific investment. |

** | Returns greater than one year are annualized. |

The Core Fund put up a strong showing in the final quarter of the fiscal year, returning 14.31%, ahead of the S&P 500’s 13.65% increase. For the full fiscal year, the Fund returned 8.21% compared to the benchmark’s 9.50% increase. We were pleased to see such a sharp snapback after fiscal Q3’s declines. Top performers in the quarter include Danaher (DHR), American Tower (AMT), Monster Beverage (MNST), Brookfield Asset Management (BAM) and Southwest Airlines (LUV), which were all up >20%. Detractors include insurers Markel (MKL) and Berkshire Hathaway (BRK.B), who continue to suffer from lackluster underwriting results, CME Group (CME), which suffered from the lack of volatility vs 1Q18, and CVS Health (CVS), which has experienced increasing headwinds in its pharmacy and pharmacy benefit manager businesses. For the full year, our top contributors included American Tower (AMT), Visa (V), and Danaher (DHR), while FedEx (FDX), CVS Health (CVS), and Markel (MKL) were our biggest detractors.

Amidst all the volatility, we were more active transacting in the Fund during the end of the fiscal year. Early in the quarter, we sold Starbucks (SBUX) after the stock had a massive move higher in 2H18 due to a modest increase in same-store sales. Midway through the quarter we had a timely sale of Southwest Airlines (LUV) as the stock had bounced off of its December lows and we wanted to reposition into a higher quality business, Air Products & Chemicals (APD – more below). Another timely sale was Monster Beverage (MNST), which we sold after an earnings spike. Competitive threats and valuation caused us to take profits. Towards the end of the quarter, we sold our position in Facebook (FB). FB has become a controversial name due to its disregard for properly managing customer data. While we continue to appreciate the excellent financial characteristics of the business, after a large move up in the share price during the quarter, we elected to take profits given the increased regulatory risk.

2

As former owners of Praxair, we have long been impressed with the global industry dynamics of industrial gas, characterized by limited competition and high customer switching costs. While we sold Praxair a couple years ago due to a complex merger with a European peer, we have continued to monitor the industry and in fiscal Q4 bought a position in Air Products (APD). APD historically has been an industry laggard, but in 2014 a management change led to a dramatic change in operations that resulted in a ten percentage point increase in margins. In late 2017, APD announced a large $15B capital investment program, which is centered around “gasification,” a new (but related) business line that converts low quality feedstocks such as coal or refinery residue into synthetic gas, which can be used to create chemicals or diesel. Gasification is already a well-established technology and reminds us of the gas processors’ step out into helium in the 1980s, which created substantial shareholder value. Early results have been encouraging. Should the investment work out as expected, earnings should grow by 50% over the next five years. The stock was also trading at a discount to its peer group despite industry leading margins, returns on capital and expected growth rate.

We also bought a stake in Walt Disney (DIS). DIS is known throughout the world for its creative and (often) family-friendly entertainment content. We have owned DIS in the Core Fund in the past but sold it over a year ago as the company was entering an investment cycle. While the company continues to invest in new initiatives, numerous uncertainties have cleared up since our sale, such as the terms for the Twenty-First Century Fox (FOX) acquisition as well as the initial outline for DIS’s direct streaming offering, Disney+. We have long viewed DIS as a core holding and have been particularly impressed with Michael Eisner’s stewardship and the execution of outstanding deals including Pixar, Marvel and Lucas Films. Now that some of the risk regarding new investments has declined, we decided to reinstate DIS into the Fund.

In addition to APD and DIS, we added to numerous Fund holdings that appeared particularly attractive during the quarter, such as Home Depot (HD), Anheuser-Busch InBev (BUD), CVS Health (CVS), Becton Dickinson (BDX), CarMax (KMX), and EOG Resources (EOG). Despite these additions, we still have an above-average level of cash, which we hope to deploy should attractive opportunities present themselves going forward.

The following are transactions performed in the Core Fund for the quarter ended March 31, 2019.

Recent Purchases

Air Products & Chemicals, Inc. (APD) The global industrial gas industry is currently a global oligopoly with three main players (Air Liquide, Linde, Air Products) and many local players, depending on end market and geography. We initiated a position in APD, the #3 player in the global industrial gas industry.

Anheuser-Busch InBev S.A./N.V. (BUD) BUD struggled last year, and we took the opportunity to add to our position. We note the stock is trading at a sharp discount to historical norms even after a nice rally this year.

Becton, Dickinson and Company (BDX)We added to our position as we continue to believe BDX is a high-quality company that has been an excellent value creator over time within the health care space.

3

CarMax, Inc. (KMX) We took the opportunity to increase the position in KMX, a business with plenty of room for internally funded store growth (and further market share gains), with a buyback program to boot.

EOG Resources, Inc. (EOG) We saw an attractive entry point due to recent weakness and added to our energy exposure in a company with low-risk assets.

CVS Health Corporation (CVS) We added to our position in CVS as we think there should be a resolution to the Aetna integration, and growth could improve significantly over the next several years, as CVS becomes an integrated health care company.

Home Depot, Inc. (The) (HD) We added to our position as HD remains a best-of-breed retailer with strong returns on capital, high free cash flow conversion, and scale/network advantages.

Walt Disney Company (The) (DIS)We initiated a position in DIS, a controversial stock given significant competition from the likes of Netflix and other over the top (OTT) content providers that have promoted additional cord cutting. In response, DIS is in the midst of a significant investment spend related to its own direct-to-consumer (DTC) offering, DIS+, which is set to launch late 2019 - early 2020. While we wait, Disney’s parks and resorts continue to grow nicely, and post the closing of the Fox deal, the company will control over 50% of the domestic box office.

Recent Sales

Ecolab, Inc. (ECL) The stock has performed very well and the valuation has expanded to record levels. As such, we elected to take some profits.

Electronic Arts, Inc. (EA)We continue to believe in the positive outlook for the video game industry but believe EA’s near-term headwinds may outweigh the longer-term positives. We elected to sell our position as shares rallied off their December lows.

Facebook, Inc. (FB) Despite having been a solid performer for us over our 2.5-year holding period, we sold our position in FB. While we continue to respect and admire the financial performance of this business model, regulatory risk to this profit stream is increasing, and ultimately we feel it is enough of a risk to take profits in the name.

iShares U.S. Home Construction ETF (ITB) While we continue to have a constructive outlook on the housing industry, we elected to sell our exposure given the recent run.

Monster Beverage Corporation (MNST) MNST has been a great stock for us since our purchase last May. While we remain positive on the outlook for MNST, we took the opportunity to take profits and reduce the risk of the portfolio.

Southwest Airlines Company (LUV) While we continue to like the prospects for LUV, we decided to sell one of our cyclical stocks to fund more appealing risk/reward opportunities.

Starbucks Corporation (SBUX)We sold the rest of our position, as the stock seemed fair-to-fully valued. Given the mixed performance at the operating level, we are more price sensitive than usual with this name and elected to take profits after a period of multiple expansion.

4

Davenport Value & Income Fund

The following chart represents Davenport Value & Income Fund (DVIPX) performance and the performance of the Russell 1000 Value Index*, the Value & Income Fund’s primary benchmark, the S&P 500 and the Lipper Equity Income Index for the periods ended March 31, 2019.

| Fiscal

Q4

2018 | 1 Year | 3 Years** | 5 Years** | Since

Inception

12/31/10** | Fiscal

Year 2019

Expense

Ratio |

Value & Income Fund | 11.05% | 2.96% | 8.98% | 7.60% | 11.16% | 0.88% |

Russell 1000 Value Index | 11.93% | 5.67% | 10.45% | 7.72% | 10.84% | |

S&P 500 Index* | 13.65% | 9.50% | 13.51% | 10.91% | 12.69% | |

Lipper Equity Income Index* | 11.50% | 6.94% | 10.60% | 7.85% | 10.25% | |

30-Day SEC Yield: 2.02%; Expense Ratio in current prospectus: 0.90%

Past performance is no guarantee of future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. Performance data, current to the most recent month end, may be obtained by calling 1-800-281-3217.

* | The S&P 500 Index is comprised of 500 U.S. stocks and is an indicator of the performance of the overall U.S. stock market. The S&P 500 Index is comprised of 500 U.S. stocks and is an indicator of the performance of the overall U.S. stock market. The Lipper Equity Income Index is an unmanaged index of the 30 largest Funds in the Lipper Equity Income Fund category. The Russell 1000® Value Index measures the performance of the Russell 1000 companies with lower price-to-book ratios and lower forecasted growth values. |

An investor cannot invest in an index and its returns are not indicative of the performance of any specific investment.

** | Returns greater than one year are annualized. |

The Value & Income Fund enjoyed a strong close to the fiscal year, increasing 11.05% in the quarter. This was slightly behind the Fund’s primary benchmark, the Russell 1000 Value Index, which increased 11.93%. The S&P 500 increased 13.65% in the final quarter. For the fiscal year, the Fund returned 2.96% compared to 5.67% and 9.50% for the Russell and S&P, respectively. We are encouraged to be in close proximity to the Russell given its strong run to close the year and our slightly higher than normal cash balance, which created some drag in a strong period.

Consumer Staples and Financials were the biggest contributors to performance in the final quarter. Staples stocks performed well as interest rates declined and their strong dividend yields became more attractive. Philip Morris International (PM), Anheuser-Busch InBev (BUD), and Mondelēz International (MDLZ) all increased more than 25% during the first quarter. Within Financials, Brookfield Asset Management (BAM) and Fidelity National Financial (FNF) performed well. BAM is one of our largest positions and seems to be firing on all cylinders. The company’s fundraising continues to exceed expectations and management is finding attractive new investments. Fidelity National has benefited from lower rates as mortgage applications have improved to start the year. For the year, Merck (MRK) and Microsoft (MSFT) were our biggest contributors to performance with each returning more than 30%.

Key detractors in the quarter were CVS Health (CVS) and Bristol-Myers Squibb (BMY). Shares of CVS have struggled as headwinds in the company’s core business have overshadowed the attractive opportunity from the Aetna acquisition. We continue to believe that CVS is building a

5

premier integrated health care company and that near-term issues are more than priced into the stock at the current valuation. BMY shares sold off on news it was acquiring Celgene (CELG) as investors worried about the debt necessary to complete the deal. We believe the massive cash flow from the combined company will allow for quick de-leveraging and that several drugs in CELG’s pipeline have significant potential. For the year, BMY was our biggest detractor to performance for the same reasons mentioned above.

We initiated a new position in Allstate (ALL) in the quarter. ALL is the second largest personal lines insurer in the U.S. and the 18th largest life insurer. The company has an excellent long-term record of underwriting at profitable levels and has rewarded shareholders through thoughtful capital allocation. Since 2012, the company has reduced shares outstanding by 35%, and the dividend has compounded at a 13% growth rate over the past five years. Additionally, we are attracted to the company’s strong brand and scale in a highly competitive industry. Lastly, we felt shares of ALL were attractively valued vs. peers and at a discount to its own trading history.

We had minimal Fund turnover in the final quarter as the only other trades included adding to our position in Marathon Petroleum (MPC), reducing our stake in W.P. Carey (WPC), and selling our position in Equity LifeStyle Properties (ELS). The latter two are REITS, which enjoyed very strong performance once the market realized that the Fed was unlikely to raise interest rates in 2019. We elected to take advantage of the strength as both names were close to our view of fair value.

In summary, we were pleased with the strong performance in the final quarter of the fiscal year. While we don’t expect 10% returns on a quarterly basis going forward, we do think the environment sets up well for value/income investing with moderate growth and low interest rates. Our cash balance remains modestly higher than normal, which we think puts us in an attractive position should the market’s recent run cool off. In the meantime, we continue to scour the investment universe for attractive opportunities to put capital to work.

Recent Purchases

Allstate Corp (ALL)ALL is the second largest personal lines insurer in the U.S. and the 18th largest life insurer. We believe the current valuation is attractive for a company with a strong brand and scale in a very competitive industry.

Comcast Corporation (CMCSA) Now that CMCSA has closed the acquisition of Sky and the Twenty-First Century Fox (FOX) deal is off the table, we believe that investors can again focus on CMCSA’s stable business fundamentals. We view the current valuation of the company as attractive and elected to increase our position.

Marathon Petroleum Corporation (MPC) A longtime favorite, we believe expectations could be far too low for MPC’s refining segment over the next few years. We added to our position.

Recent Sales

Equity Lifestyle Properties, Inc. (ELS) Though we view these assets as high quality and predictable, we feel the shares are fully valued and elected to take profits.

W.P. Carey, Inc. (WPC)WPC has made a nice move over the past year and we elected to reduce the position some as the valuation looks fairer at these levels. We remain attracted to WPC’s portfolio of “mission-critical” assets and its appealing dividend yield.

6

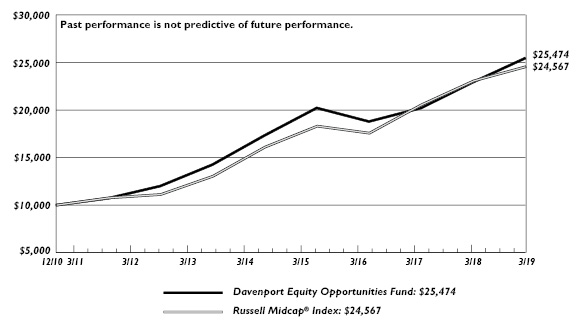

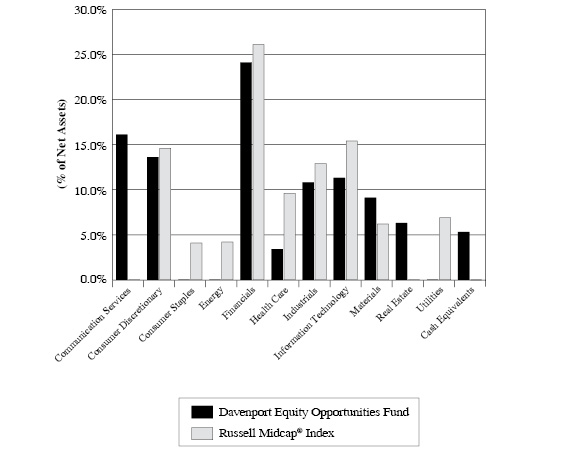

Davenport Equity Opportunities Fund

The following chart represents Davenport Equity Opportunities Fund (DEOPX) performance and the performance of the Russell Midcap Index*, the Fund’s primary benchmark, and the S&P 500 Index* for the periods ended March 31, 2019.

| Fiscal

Q4

2018 | 1 Year | 3 Years** | 5 Years** | Since

Inception

12/31/10** | Fiscal

Year 2019

Expense

Ratio |

Equity Opportunities Fund | 18.55% | 11.02% | 10.67% | 8.00% | 12.01% | 0.91% |

Russell Midcap Index | 16.54% | 6.47% | 11.82% | 8.81% | 11.52% | |

S&P 500 Index* | 13.65% | 9.50% | 13.51% | 10.91% | 12.69% | |

30-Day SEC Yield: -0.25%; Expense Ratio in current prospectus: 0.91%

Past performance is no guarantee of future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. Performance data, current to the most recent month end, may be obtained by calling 1-800-281-3217.

* | The Russell Midcap® Index measures the performance of the 800 smallest companies in the Russell 1000, which represent approximately 25% of the total market capitalization of the Russell 1000®. Frank Russell Company is the source and owner of the trademarks, service marks, and copyrights related to the Russell Indexes. Russell® is a trademark of Frank Russell Company. The S&P 500 Index is comprised of 500 U.S. stocks and is an indicator of the performance of the overall U.S. stock market. An investor cannot invest in an index and its returns are not indicative of the performance of any specific investment. |

** | Returns greater than one year are annualized. |

The Equity Opportunities Fund closed the fiscal year on a strong note. After proving resilient amid a significant market wide drawdown to end calendar 2018, we were pleased to see the Fund’s fiscal fourth quarter return of 18.55% come in nicely ahead of the 16.54% gain for the Russell Midcap Index. For the full fiscal year, the Fund returned 11.02% compared to the Russell’s 6.47%. Whereas our valuation discipline and avoidance of momentum have made it difficult to keep up during previous periods of intense market appreciation, the more broad-based nature of the fiscal fourth-quarter rally allowed our roster of companies to shine.

Latin American e-commerce leader, MercadoLibre (MELI), was a top performer during the last year, advancing nearly 75% in the fourth quarter. While the stock started the year with a nice bounce from oversold levels, the company’s late February earnings report sent the shares into overdrive as the market latched on to a meaningful acceleration in the company’s payments business (think PayPal of South America). Other key contributors included cyclical entities such as cabinet maker American Woodmark (AMWD) and trucking equipment manufacturer WABCO Holdings (WBC), which struggled during calendar 2018 but rewarded our patience with sharp rallies to start the year. AMWD advanced nearly 50% during Q4 in response to better housing sentiment and a solid earnings report. WBC announced it had agreed to be acquired by a competitor near quarter end, resulting in a 23% premium to the 90-day trading average prior to the deal speculation. While the deal will not close until early 2020, we elected to take profits due to the stock’s close proximity to the takeout value in addition to the low likelihood of another bidder emerging.

7

The Fund’s two largest positions, American Tower (AMT) and Brookfield Asset Management (BAM) were also top performers to close the year, each advancing north of 20%. AMT was our top contributor to performance for the full fiscal year, returning nearly 40%. While the stock remains a top position, we elected to trim our exposure. Elsewhere, we trimmed positions in high fliers such as Live Nation Entertainment (LYV) and Autodesk (ADSK), which have been significant contributors and grew to be above-average positions. LYV was our second leading contributor to performance during the full year, returning over 50%. These actions allowed us to continue to build positions in Fidelity National Financial (FNF) and Watsco (WSO), two high-quality names highlighted last quarter that failed to fully participate in the market’s recent rally. In addition, we added a new position in video game publisher and developer Take-Two Interactive (TTWO), a company we have followed for some time that we believe has become quite cheap amid industry volatility.

TTWO is a leading video game developer and publisher, best known for its wholly-owned labels Rockstar Games and 2K. The company is known for putting out the fewest annual releases with the least consistent release cadence, instead choosing to only produce high quality intellectual property and continuing to monetize games long after initial release. We believe TTWO’s strategy of “fewer, bigger, better” releases has led the company to release strong, immersive, and sticky franchises which is borne out in higher average review scores compared to peers. These blockbuster titles continue to provide a long revenue tail well after initial release thanks to online modes that include downloadable content such as bonus levels and “micro-transactions” such as purchasing cosmetic items to personalize characters. TTWO has a debt-free balance sheet and ample cash on hand to invest in the business and repurchase shares. The stock has weakened alongside the video game publishers of late and is significantly off its highs. When adjusting for the company’s ~$14 per share of cash on hand, the stock now trades at a multiple of free cash flow comparable to legacy media companies, who don’t enjoy the same structural industry tailwinds as TTWO. We believe this represents a meaningful misevaluation given the company’s leading franchises, rich pipeline, and a history of successful game launches. Lastly, we believe the company is the most attractive publisher for a takeout given its size and valuable intellectual property.

In sum, we are pleased with the end to the year and remain confident in the Fund’s positioning. As discussed above, we were quite active as the year ended with respect to reallocating funds from top performers/larger positions to better risk/reward opportunities. This process along with the takeout of a meaningful position (WBC) allowed the Fund to build a slightly above-average cash balance during the final quarter. While we never intend to make “market calls” with our cash balance, we like having a bit more dry powder around to take advantage of new opportunities should they present themselves.

The following are transactions performed in the Equity Opportunities Fund for the quarter ended March 31, 2019.

Recent Purchases

Fidelity National Financial, Inc. (FNF)The position size is slightly below average and recent weakness afforded us the opportunity to continue building our stake. FNF appears to offer significant value in a market where deals have recently been harder to come by.

8

Take-Two Interactive Software, Inc. (TTWO)We initiated a position in TTWO and added to the position during the quarter. The company is a leading video game developer and publisher, and we feel it may be a prime candidate for a takeout given its leading franchises, strong pipeline and history of successful game launches.

Watsco, Inc. (WSO)We added to WSO as it appears to offer significant value in a market where deals have been harder to come by. We also like the stock’s yield. We note that the company fits the “owner-operator” theme given material inside ownership.

Recent Sales

American Tower Corporation (AMT) We really like the long-term outlook here, but the valuation is full relative to history and the stock could take a breather. Therefore, we elected to take some profits.

Autodesk, Inc. (ADSK) With the stock hitting new all-time highs, we used the recent strength to peel back the position. We still love the Autodesk story and believe the on-going shift to a subscription model will continue to drive annual recurring revenue (ARR) and annual revenue per subscriber (ARPS) to new highs.

Dollar Tree, Inc. (DLTR)The stock had a recent lift from news of involvement by activist investor Starboard. We are holding on to the majority of our position as activist involvement should put a floor on the stock and modest improvement in results could drive the shares higher.

Genesee & Wyoming, Inc. (GWR)With the shares seemingly fairly valued, we chipped our position and may look to continue to wind the position down amid further appreciation.

Live Nation Entertainment, Inc. (LYV)LYV has been an excellent performer over the past couple years and has added to gains this year. We are maintaining a sizeable position because we think the company’s dominant position in live events may yield many years of growth for ticketing volume, ticket pricing, advertising/sponsorship and venue management.

O’Reilly Automotive, Inc. (ORLY) We chipped our position in ORLY after the stock posted a sharp move higher and seemed fully valued at estimates for next year. We love ORLY’s management and consistent growth, but upside has become more limited.

WABCO Holdings, Inc. (WBC) We sold our position following the announcement that the company had agreed to be acquired. WBC was a solid performer for the Fund, and while we preferred a better outcome, we are still pleased to receive liquidity at a meaningful premium to our average cost.

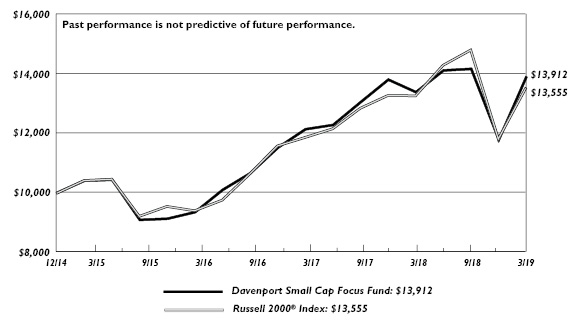

Davenport Small Cap Focus Fund

The following chart represents performance of the Davenport Small Cap Focus Fund (DSCPX) and the performance of the Fund’s primary benchmark, the Russell 2000 Index*, for the periods ended March 31, 2019.

| Fiscal

Q4

2018 | 1 Year | 3 Year | Since

Inception

12/31/14** | Fiscal

Year 2019

Expense

Ratio |

Small Cap Focus Fund | 17.99% | 3.90% | 14.17% | 8.08% | 0.97% |

Russell 2000 Index* | 14.58% | 2.05% | 12.92% | 7.43% | |

9

30-Day SEC Yield: 0.05%; Expense Ratio in current prospectus: 1.00%

Past performance is no guarantee of future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. Performance data, current to the most recent month end, may be obtained by calling 1-800-281-3217.

* | The Russell 1000 Value Index measures the performance of the Russell 1000 companies with lower price-to-book ratios and lower forecasted growth values. Frank Russell Company is the source and owner of the trademarks, service marks, and copyrights related to the Russell Indexes. Russell® is a trademark of Frank Russell Company. An investor cannot invest in an index and its returns are not indicative of the performance of any specific investment. |

** | Returns greater than one year are annualized. |

The Davenport Small Cap Focus Fund (DSCPX) enjoyed a strong fiscal fourth quarter. The Fund gained 17.99% relative to a 14.58% advance for the Russell 2000. Small caps rebounded impressively from their fiscal third-quarter swoon, and outsized gains from a few key positions allowed us to outperform the benchmark. We are pleased with how we fared during this upswing, especially when considering the Fund’s relative resilience during the previous quarter’s selloff. For the fiscal year, the Fund gained 3.90% compared to the Russell’s gain of 2.05%.

A rather eclectic mix of names supported our fourth quarter performance. A few of these names were holdings that struggled during the beginning of the year and bounced back very sharply. The most notable example is cabinetmaker American Woodmark (AMWD), which gained 48% alongside a recovery in deeply depressed housing-related stocks. We added to our position during the stock’s late year swoon and are pleased our resolve paid off. Another example is Eldorado Resorts (ERI). Shares of the casino operator dropped sharply to finish calendar 2018. Here again, we added to our stake at very attractive prices and have seen the shares stage an impressive recovery. In both of these cases (as well as a few others), we have used recent surges to slightly reduce our positions. Etsy (ETSY) was our biggest contributor to performance for the full fiscal year, following a successful transition period during which the company was able to unlock the value of its differentiated marketplace business model through cost reduction and use experience improvements.

As our investors know, we have a concentrated approach (currently only 33 holdings) and love to find unique and underfollowed situations that appear to offer uncommon value. One recent example is OneSpaWorld (OSW), which has gotten off to a strong start for us and is currently our top position. OSW operates spas and fitness centers on cruise ships. The company has a 90%+ market share and exclusive contracts with all major cruise lines. We view the cruise industry as attractive with passenger counts growing consistently over the past 20 years and capacity projected to expand at a mid-single-digit rate over the new few years. OWS’s financials are enviable given low capital requirements (the cruise lines Fund the buildout of the spas) and a very low tax rate. This leads to significant free cash flow generation, which we think may ultimately lead to an attractive dividend stream. There are several initiatives underway that could drive double-digit EPS growth including price increases, targeted marketing and additional “medi-spa” services (Botox, CoolSculpting, etc.). When we began looking at the stock in late calendar 2018, it was a confusing situation (due to an acquisition) that was under the Street’s radar. Since then, we’ve been pleased to see the stock get some support.

10

Asset manager Diamond Hill Investment Group (DHIL) is another name we’ve been emphasizing. This relatively unknown (no analyst coverage) company appears to offer tremendous value following the stock’s recent weakness. DHIL manages roughly $21 billion for individuals and institutions across a suite of value-oriented mutual funds. While the company has an admirable long-term track record, recent results have been less impressive and DHIL has seen a modest decline in assets under management (AUM). The stock has traded down sharply and seems to have disconnected from company fundamentals. DHIL is generating $15/share of free cash flow (relative to a $138 stock price), has no debt and has roughly $60/share of cash & investments. Furthermore, it is actively returning capital to shareholders via a special dividend ($8/share last year) and a recently announced $50 million stock buyback (more than 10% of the total market cap). We also note employees own 20% of the company; hence, it squarely fits our owner-operator bias. We acknowledge that fund outflows may pressure near-term results, but a slight uptick in performance could produce solid upside and we are being paid nicely while we wait.

In sum, we are pleased with both the fiscal fourth quarter and full year gains, as well as our performance since inception. That said, we recognize the magnitude of Q4 gains is a bit unusual and not likely to be sustained. We anticipate returns will moderate and have raised cash alongside recent gains. We think this cash will come in handy if markets cool. We also aim to demonstrate less risk than our benchmark should turbulence resume. Our concentrated approach can yield substantial deviations from our benchmark, but our value bias and focus on profitable companies should dampen risk over time, as has been the case so far.

Davenport Balanced Income Fund

The following chart represents Davenport Balanced Income Fund (DBALX) performance, and performance of the Fund’s primary benchmark, the Russell 1000® Value Index, along with the Morningstar Allocation 50-70% Equity Index, and the blended 60% Russell 1000® Value Index / 40% Bloomberg Barclays Intermediate Government /Credit Bond Index for the period ended March 31, 2019.

| Fiscal

Q4

2018 | 1 Year | Since

Inception

12/31/15** | Fiscal

Year 2019

Expense

Ratio |

Balanced Income Fund | 7.96% | 3.35% | 6.06% | 0.96% |

Russell 1000® Value* | 11.93% | 5.67% | 10.16% | |

Morningstar Allocation 50-70% Equity* | 8.91% | 3.83% | 6.43% | |

60% Russell 1000® Value/40% BBIGC | 8.05% | 5.40% | 7.13% | |

30-Day SEC Yield: 2.06%; Expense Ratio in current prospectus: 0.97%

Past performance is no guarantee of future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. Performance data, current to the most recent month end, may be obtained by calling 1-800-281-3217.

* | TheRussell 1000® Value Index measures the performance of the Russell 1000 companies with lower price-to-book ratios and lower forecasted growth values. The Morningstar US OE Allocation 50-70% Equity Index is composed of Funds which seek to provide both income and capital appreciation by investing in multiple asset classes, including stocks, bonds, and cash. These portfolios are dominated by domestic holdings and have equity exposure between |

11

50% and 70%. The blended 60% Russell 1000 Value/40%Bloomberg Barclay’s Intermediate Government/Credit (BBIGC) Index is included as an additional comparative index because it is representative of a balanced portfolio consisting of 60% equity and 40% fixed income securities. The BBIGC measures the non-securitized component of the U.S. Aggregate Index. It includes investment grade, U.S. dollar-denominated, fixed-rate Treasuries, government-related and corporate rate securities. Intermediate maturity bonds include bonds with maturities of 1 to 9.999 years. An investor cannot invest in an index and its returns are not indicative of the performance of any specific investment.

** | Returns greater than one year are annualized. |

The Davenport Balanced Income Fund increased 7.96% during fiscal Q4, versus an 11.93% return for the Russell 1000® Value and 13.65% for the S&P 500 Index. The Fund just lagged the blended 60% Russell 1000® Value and 40% Bloomberg Barclays Intermediate Government/Credit Index return of 8.05% for the quarter. For the full fiscal year, the Fund returned 3.35%. The Russell 1000® Value, S&P 500 and blended benchmark returned 5.67%, 9.50%, and 5.40%, respectively.

After a volatile end to the third quarter, equities returned to favor and wiped out the losses seen in the previous quarter. Financials and Consumer Staples were the greatest contributors to the equity portion of the Fund during the quarter. Consumer Staples regained popularity as interest rates declined and their dividend yields became more compelling. Of our holdings within the sector, Philip Morris International (PM), Anheuser-Busch InBev (BUD), Mondelēz International (MDLZ) all posted returns greater than 25% during the period. Within our Financials exposure, Brookfield Asset Management (BAM) and Fidelity National Financial (FNF) were our top contributors to performance. BAM’s fundraising continues to thrive and find attractive investment opportunities. FNF is a provider of various services to the real estate and mortgage industry and has benefited from lower interest rates and an uptick in mortgage applications so far this year. For the year, Merck (MRK) and Universal Corp (UVV) were our top contributors to performance. Our two biggest detractors to Q4 performance fell within the Health Care sector. CVS Health (CVS) struggled as investors focused on the disappointing results from the core business that overshadowed the potential opportunities born from the Aetna acquisition. We believe these near-term issues have been fully priced into the stock. Bristol-Myers Squibb (BMY) was a key detractor during both the Q4 and full year periods, following the news it would be acquiring Celgene (CELG) as investors worried about the level of debt that would be needed to fund the purchase. We believe the combined entity will generate significant cash flow and allow for rapid de-leveraging.

During the fourth quarter, we initiated a position in Lazard Ltd. (LAZ), a leading financial advisory and asset management firm. Lazard’s advisory activities are relatively more stable than capital markets activity directed towards raising equity or fixed income capital. Additionally, the restructuring segment provides stability during tougher economic times. The company is managed by a top-notch team focused on long-term margin improvement and returns to shareholders through dividends and stock repurchases.

After a volatile ending to fiscal Q3, the bond market settled down, posting positive returns across the majority of U.S. bond indices for Q4. After a more dovish message from the Fed in March, U.S. Treasuries caught a bid ending the quarter with yields lower (prices higher) than where we began the year. The yield on the 2-yr Treasury fell 23bps, while the rates on the 10-yr Treasury and the 30-yr Treasury fell 28bps (2.41%) and 20bps (2.82%), respectively. The Bloomberg Barclays Intermediate Government/Credit Index returned 2.32% and the Bloomberg Barclays US FRN <5-yr Index recouped fiscal Q3 losses posting a 1.47% gain for Q4.

12

The bond allocation of the Balanced Fund consists of 29 high-quality bonds across eight sectors with the top allocations to U.S. Governments at 28.62%, Consumer Discretionary at 21.86%, Energy at 16.43%, and Financials at 15.68%. The credit quality of the Fund has improved to A+/A while having an effective maturity of 4.12 years and a duration of 3.15 years. During Q4, we took advantage of strong corporate credit demand to exit Becton Dickinson, Anheuser-Busch InBev, and Verizon locking in gains while we could. With the proceeds we initiated and added to our Treasury exposure in the two- six- and ten -year maturities and bought Citigroup 3.3% 2025. Our transactions during the end of the year are consistent with our theme of trading up in credit quality while remaining defensive, taking our U.S. Treasury exposure to 28.62% up from 18% at the end of Q3. Our floating-rate exposure decreased to 34% from 39% due to positions maturing. The income levels for the floating-rate notes change quarterly based on the level of 3-month LIBOR (London Inter-bank Offered Rate). This rate ended Q4 at 2.6% down from 2.8% in 2018 due to the decrease in Fed hike expectations. Going forward, we will gradually decrease our floating-rate exposure, but we are not outright sellers at the moment.

We were pleased with our performance to end the year and continue to see value in a balanced approach in a turbulent market with continuous headlines surrounding trade negotiations, interest rates, and Washington policy uncertainty. We believe our allocation to value-based equity and defensive positioning in fixed income may provide a volatility buffer in the near future, while focusing on current income and long-term capital appreciation.

In conclusion, we are pleased that the Davenport Funds are off to a good start thus far in 2019. We thank you for your trust and look forward to reporting back as we proceed through the year.

Sincerely,

John P. Ackerly IV, CFA

President, The Davenport Funds

13

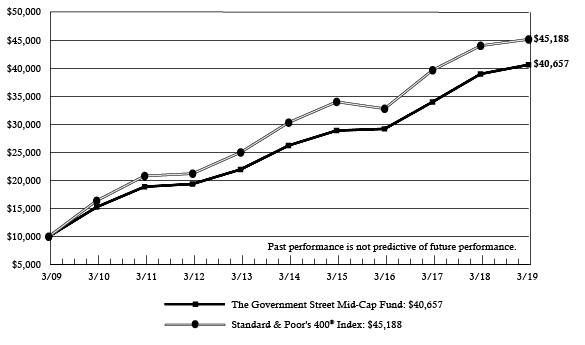

DAVENPORT CORE FUND

PERFORMANCE INFORMATION (Unaudited)

Comparison of the Change in Value of a $10,000 Investment in

Davenport Core Fund and the Standard & Poor’s 500® Index

| | Average Annual Total Returns

(for periods ended March 31, 2019) | |

| | 1 Year | 5 Years | 10 Years | |

Davenport Core Fund(a) | 8.21% | 9.04% | 14.43% | |

Standard & Poor’s 500® Index | 9.50% | 10.91% | 15.92% | |

(a) | The total returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. |

14

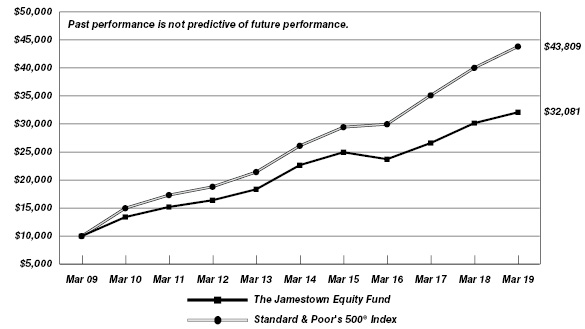

DAVENPORT VALUE & INCOME FUND

PERFORMANCE INFORMATION (Unaudited)

Comparison of the Change in Value of a $10,000 Investment in

Davenport Value & Income Fund, the Russell 1000® Value Index

and the Lipper Equity Income Index

| | Average Annual Total Returns

(for periods ended March 31, 2019) | |

| | 1 Year | 5 Years | Since

Inception(b) | |

Davenport Value & Income Fund(a) | 2.96% | 7.60% | 11.16% | |

Russell 1000® Value Index | 5.67% | 7.72% | 10.84% | |

Lipper Equity Income Index | 6.94% | 7.85% | 10.25% | |

(a) | The total returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. |

(b) | Commencement of operations was December 31, 2010. |

15

DAVENPORT EQUITY OPPORTUNITIES FUND

PERFORMANCE INFORMATION (Unaudited)

Comparison of the Change in Value of a $10,000 Investment in

Davenport Equity Opportunities Fund and the Russell Midcap® Index

| | Average Annual Total Returns

(for periods ended March 31, 2019) | |

| | 1 Year | 5 Years | Since

Inception(b) | |

Davenport Equity Opportunities Fund(a) | 11.02% | 8.00% | 12.01% | |

Russell Midcap® Index | 6.47% | 8.81% | 11.52% | |

(a) | The total returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. |

(b) | Commencement of operations was December 31, 2010. |

16

DAVENPORT SMALL CAP FOCUS FUND

PERFORMANCE INFORMATION (Unaudited)

Comparison of the Change in Value of a $10,000 Investment in

Davenport Small Cap Focus Fund and the Russell 2000® Index

| | Average Annual Total Returns

(for periods ended March 31, 2019) | |

| | 1 Year | 3 Years | Since

Inception(b) | |

Davenport Small Cap Focus Fund(a) | 3.90% | 14.17% | 8.08% | |

Russell 2000® Index | 2.05% | 12.92% | 7.43% | |

(a) | The total returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. |

(b) | Commencement of operations was December 31, 2014. |

17

DAVENPORT BALANCED INCOME FUND

PERFORMANCE INFORMATION (Unaudited)

Comparison of the Change in Value of a $10,000 Investment in Davenport Balanced

Income Fund, the Russell 1000® Value Index, a Blended 60% Russell 1000® Value

Index / 40% Bloomberg Barclays Intermediate Government/Credit Bond Index

and the Morningstar US OE Allocation — 50% to 70% Equity

| | Average Annual Total Returns

(for periods ended March 31, 2019) | |

| | 1 Year | 3 Years | Since

Inception(b) | |

Davenport Balanced Income Fund(a) | 3.35% | 5.56% | 6.06% | |

Russell 1000® Value Index | 5.67% | 10.45% | 10.16% | |

Blended 60% Russell 1000® ValueIndex / 40% Bloomberg Barclays Intermediate Government/Credit Bond Index | 5.40% | 7.02% | 7.13% | |

Morningstar US OE Allocation - 50% to 70% Equity | 3.79% | 7.29% | 7.01% | |

(a) | The total returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. |

(b) | Commencement of operations was December 31, 2015. |

18

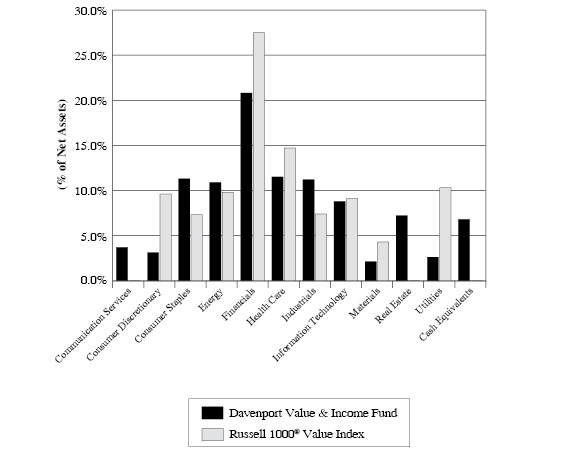

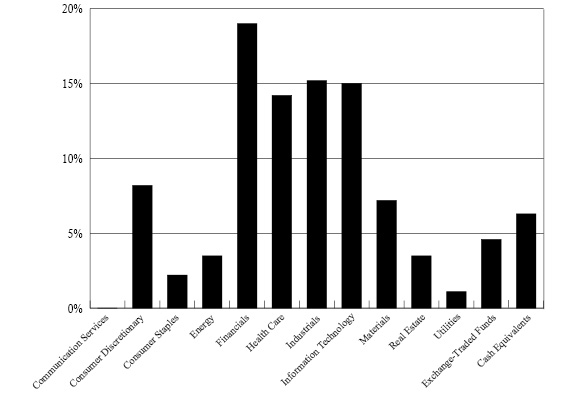

DAVENPORT CORE FUND

PORTFOLIO INFORMATION

March 31, 2019 (Unaudited)

Sector Allocation vs. the Standard & Poor’s 500® Index

Top Ten Equity Holdings

Security Description | % of Net Assets |

American Tower Corporation | 4.1% |

Visa, Inc. - Class A | 3.8% |

Danaher Corporation | 3.5% |

Brookfield Asset Management, Inc. - Class A | 3.4% |

Adobe, Inc. | 3.3% |

Berkshire Hathaway, Inc. - Class B | 3.2% |

Accenture plc - Class A | 3.2% |

Markel Corporation | 3.0% |

Johnson & Johnson | 2.7% |

Union Pacific Corporation | 2.7% |

19

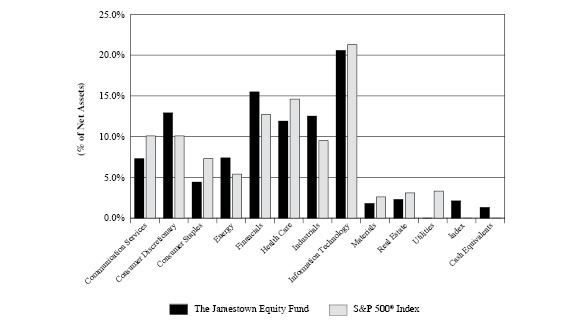

DAVENPORT VALUE & INCOME FUND

PORTFOLIO INFORMATION

March 31, 2019 (Unaudited)

Sector Allocation vs. the Russell 1000® Value Index

Top Ten Equity Holdings

Security Description | % of Net Assets |

Brookfield Asset Management, Inc. - Class A | 3.2% |

Johnson & Johnson | 3.1% |

Microsoft Corporation | 3.0% |

Royal Dutch Shell plc - Class B - ADR | 3.0% |

Cisco Systems, Inc. | 3.0% |

Fidelity National Financial, Inc. | 2.9% |

Merck & Company, Inc. | 2.8% |

JPMorgan Chase & Company | 2.8% |

Dominion Energy, Inc. | 2.6% |

Markel Corporation | 2.5% |

20

DAVENPORT EQUITY OPPORTUNITIES FUND

PORTFOLIO INFORMATION

March 31, 2019 (Unaudited)

Sector Allocation vs. the Russell Midcap® Index

Top Ten Equity Holdings

Security Description | % of Net Assets |

Brookfield Asset Management, Inc. - Class A | 6.6% |

American Tower Corporation | 6.3% |

Live Nation Entertainment, Inc. | 4.9% |

CarMax, Inc. | 4.6% |

Martin Marietta Materials, Inc. | 4.6% |

Sherwin-Williams Company (The) | 4.5% |

Markel Corporation | 4.5% |

Intuit, Inc. | 4.0% |

Autodesk, Inc. | 4.0% |

DISH Network Corporation - Class A | 3.9% |

21

DAVENPORT SMALL CAP FOCUS FUND

PORTFOLIO INFORMATION

March 31, 2019 (Unaudited)

Sector Allocation vs. the Russell 2000® Index

Top Ten Equity Holdings

Security Description | % of Net Assets |

OneSpaWorld Holdings Ltd. | 4.8% |

Diamond Hill Investment Group, Inc. | 4.1% |

American Woodmark Corporation | 4.0% |

Colfax Corporation | 3.7% |

Trupanion, Inc. | 3.7% |

Kinsale Capital Group, Inc. | 3.7% |

Black Knight, Inc. | 3.5% |

Evoqua Water Technologies Corporation | 3.3% |

Lamar Advertising Company - Class A | 3.3% |

Monarch Casino & Resort, Inc. | 3.3% |

22

DAVENPORT BALANCED INCOME FUND

PORTFOLIO INFORMATION

March 31, 2019 (Unaudited)

Asset Allocation (% of Net Assets) | | Ten Largest Equity Holdings | % of Net Assets |

| | Brookfield Asset Management, Inc. - Class A | 1.8% |

Johnson & Johnson | 1.7% |

Microsoft Corporation | 1.7% |

Royal Dutch Shell plc - Class B - ADR | 1.6% |

Cisco Systems, Inc. | 1.6% |

Fidelity National Financial, Inc. | 1.6% |

Merck & Company, Inc. | 1.5% |

JPMorgan Chase & Company | 1.5% |

Dominion Energy, Inc. | 1.4% |

Markel Corporation | 1.4% |

Equity Sector Concentration vs. the Russell 1000 Value Index (59.4% of Net Assets) |

Bond Portfolio (35.0% of Net Assets) | | Credit Quality | Composite Quality |

Number of Fixed-Income Securities | 29 | | AAA | 29.2% |

Average Quality | A1 | | AA | 2.3% |

Effective Maturity | 4.1 yrs. | | A | 42.4% |

Average Effective Duration | 3.1 yrs. | | BBB | 26.1% |

| | | | Ba | 0.0% |

Sector Breakdown | % of Corporate

Bond Portfolio |

Communication Services | 1.9% |

Consumer Discretionary | 0.0% |

Consumer Staples | 14.5% |

Energy | 13.1% |

Financials | 23.1% |

Health Care | 7.7% |

Industrials | 3.6% |

Information Technology | 4.5% |

Materials | 2.5% |

Utilities | 0.0% |

U.S. Treasury | 29.1% |

23

DAVENPORT CORE FUND

SCHEDULE OF INVESTMENTS

March 31, 2019 |

COMMON STOCKS — 95.8% | | Shares | | | Value | |

Communication Services — 6.2% | | | | | | | | |

Alphabet, Inc. - Class A(a) | | | 7,961 | | | $ | 9,369,221 | |

Alphabet, Inc. - Class C(a) | | | 7,141 | | | | 8,378,607 | |

Liberty Broadband Corporation - Series C(a) | | | 103,475 | | | | 9,492,797 | |

Walt Disney Company (The) | | | 45,171 | | | | 5,015,336 | |

| | | | | | | | 32,255,961 | |

Consumer Discretionary — 9.8% | | | | | | | | |

Alibaba Group Holding Ltd. - ADR(a) | | | 40,475 | | | | 7,384,664 | |

Amazon.com, Inc.(a) | | | 6,395 | | | | 11,387,896 | |

CarMax, Inc.(a) | | | 184,187 | | | | 12,856,253 | |

Home Depot, Inc. (The) | | | 56,232 | | | | 10,790,358 | |

NIKE, Inc. - Class B | | | 94,083 | | | | 7,922,729 | |

| | | | | | | | 50,341,900 | |

Consumer Staples — 7.1% | | | | | | | | |

Anheuser-Busch InBev S.A./N.V. - ADR | | | 113,732 | | | | 9,550,076 | |

Mondelēz International, Inc. - Class A | | | 154,758 | | | | 7,725,519 | |

Nestlé S.A. - ADR | | | 123,854 | | | | 11,805,763 | |

PepsiCo, Inc. | | | 62,225 | | | | 7,625,674 | |

| | | | | | | | 36,707,032 | |

Energy — 5.1% | | | | | | | | |

Chevron Corporation | | | 69,694 | | | | 8,584,907 | |

EOG Resources, Inc. | | | 95,470 | | | | 9,086,835 | |

Marathon Petroleum Corporation | | | 148,825 | | | | 8,907,176 | |

| | | | | | | | 26,578,918 | |

Financials — 17.7% | | | | | | | | |

Berkshire Hathaway, Inc. - Class B(a) | | | 82,053 | | | | 16,483,627 | |

Brookfield Asset Management, Inc. - Class A | | | 373,978 | | | | 17,446,074 | |

Capital One Financial Corporation | | | 150,286 | | | | 12,276,863 | |

Citigroup, Inc. | | | 192,296 | | | | 11,964,657 | |

CME Group, Inc. | | | 52,565 | | | | 8,651,148 | |

JPMorgan Chase & Company | | | 93,517 | | | | 9,466,726 | |

Markel Corporation(a) | | | 15,355 | | | | 15,297,265 | |

| | | | | | | | 91,586,360 | |

Health Care — 11.7% | | | | | | | | |

Becton, Dickinson and Company | | | 43,084 | | | | 10,759,367 | |

CVS Health Corporation | | | 130,146 | | | | 7,018,774 | |

Danaher Corporation | | | 135,736 | | | | 17,919,867 | |

Johnson & Johnson | | | 100,240 | | | | 14,012,550 | |

Merck & Company, Inc. | | | 130,354 | | | | 10,841,542 | |

| | | | | | | | 60,552,100 | |

Industrials — 7.6% | | | | | | | | |

FedEx Corporation | | | 56,307 | | | | 10,214,653 | |

General Dynamics Corporation | | | 41,578 | | | | 7,038,324 | |

Honeywell International, Inc. | | | 49,524 | | | | 7,870,354 | |

24

DAVENPORT CORE FUND

SCHEDULE OF INVESTMENTS (Continued) |

COMMON STOCKS — 95.8% (Continued) | | Shares | | | Value | |

Industrials — 7.6% (Continued) | | | | | | | | |

Union Pacific Corporation | | | 83,365 | | | $ | 13,938,628 | |

| | | | | | | | 39,061,959 | |

Information Technology — 18.0% | | | | | | | | |

Accenture plc - Class A | | | 93,234 | | | | 16,411,049 | |

Adobe, Inc.(a) | | | 63,835 | | | | 17,011,389 | |

Apple, Inc. | | | 43,769 | | | | 8,313,921 | |

Broadcom, Inc. | | | 29,532 | | | | 8,880,568 | |

Mastercard, Inc. - Class A | | | 58,230 | | | | 13,710,253 | |

Microsoft Corporation | | | 75,568 | | | | 8,912,490 | |

Visa, Inc. - Class A | | | 125,494 | | | | 19,600,908 | |

| | | | | | | | 92,840,578 | |

Materials — 8.5% | | | | | | | | |

Air Products & Chemicals, Inc. | | | 45,394 | | | | 8,668,438 | |

Ecolab, Inc. | | | 50,016 | | | | 8,829,825 | |

Martin Marietta Materials, Inc. | | | 40,356 | | | | 8,118,820 | |

Sherwin-Williams Company (The) | | | 25,865 | | | | 11,140,314 | |

Vulcan Materials Company | | | 59,065 | | | | 6,993,296 | |

| | | | | | | | 43,750,693 | |

Real Estate — 4.1% | | | | | | | | |

American Tower Corporation | | | 106,472 | | | | 20,981,372 | |

| | | | | | | | | |

Total Common Stocks (Cost $315,391,620) | | | | | | $ | 494,656,873 | |

|

MONEY MARKET FUNDS — 1.4% | | Shares | | | Value | |

First American Treasury Obligations Fund - Class Z, 2.33%(b) (Cost $7,366,819) | | | 7,366,819 | | | $ | 7,366,819 | |

| | | | | | | | | |

Total Investments at Value — 97.2% (Cost $322,758,439) | | | | | | $ | 502,023,692 | |

| | | | | | | | | |

Other Assets in Excess of Liabilities — 2.8% | | | | | | | 14,204,148 | |

| | | | | | | | | |

Net Assets — 100.0% | | | | | | $ | 516,227,840 | |

ADR - American Depositary Receipt.

(a) | Non-income producing security. |

(b) | The rate shown is the 7-day effective yield as of March 31, 2019. |

See accompanying notes to financial statements.

25

DAVENPORT VALUE & INCOME FUND

SCHEDULE OF INVESTMENTS

March 31, 2019 |

COMMON STOCKS — 93.2% | | Shares | | | Value | |

Communication Services — 3.7% | | | | | | | | |

Comcast Corporation - Class A | | | 350,355 | | | $ | 14,007,193 | |

Verizon Communications, Inc. | | | 183,215 | | | | 10,833,503 | |

| | | | | | | | 24,840,696 | |

Consumer Discretionary — 3.1% | | | | | | | | |

Carnival Corporation | | | 205,680 | | | | 10,432,090 | |

Las Vegas Sands Corporation | | | 175,890 | | | | 10,722,254 | |

| | | | | | | | 21,154,344 | |

Consumer Staples — 11.3% | | | | | | | | |

Altria Group, Inc. | | | 178,636 | | | | 10,259,065 | |

Anheuser-Busch InBev S.A./N.V. - ADR | | | 157,460 | | | | 13,221,916 | |

Diageo plc - ADR | | | 90,780 | | | | 14,852,516 | |

Mondelēz International, Inc. - Class A | | | 246,890 | | | | 12,324,749 | |

PepsiCo, Inc. | | | 96,805 | | | | 11,863,453 | |

Philip Morris International, Inc. | | | 155,720 | | | | 13,764,091 | |

| | | | | | | | 76,285,790 | |

Energy — 10.9% | | | | | | | | |

Chevron Corporation | | | 68,366 | | | | 8,421,324 | |

Enbridge, Inc. | | | 301,622 | | | | 10,936,814 | |

Exxon Mobil Corporation | | | 85,975 | | | | 6,946,780 | |

Marathon Petroleum Corporation | | | 221,120 | | | | 13,234,032 | |

Occidental Petroleum Corporation | | | 204,105 | | | | 13,511,751 | |

Royal Dutch Shell plc - Class B - ADR | | | 313,175 | | | | 20,027,541 | |

| | | | | | | | 73,078,242 | |

Financials — 20.8% | | | | | | | | |

Allstate Corporation (The) | | | 110,620 | | | | 10,418,192 | |

Bank of America Corporation | | | 355,000 | | | | 9,794,450 | |

Brookfield Asset Management, Inc. - Class A | | | 467,865 | | | | 21,825,902 | |

Capital One Financial Corporation | | | 180,355 | | | | 14,733,200 | |

Citigroup, Inc. | | | 252,780 | | | | 15,727,972 | |

Fairfax Financial Holdings Ltd. | | | 26,755 | | | | 12,444,018 | |

Fidelity National Financial, Inc. | | | 532,110 | | | | 19,448,620 | |

JPMorgan Chase & Company | | | 186,385 | | | | 18,867,753 | |

Markel Corporation(a) | | | 16,890 | | | | 16,826,494 | |

| | | | | | | | 140,086,601 | |

Health Care — 11.5% | | | | | | | | |

Bristol-Myers Squibb Company | | | 288,780 | | | | 13,777,694 | |

CVS Health Corporation | | | 232,380 | | | | 12,532,253 | |

Johnson & Johnson | | | 151,165 | | | | 21,131,355 | |

Medtronic plc | | | 122,070 | | | | 11,118,136 | |

Merck & Company, Inc. | | | 227,735 | | | | 18,940,720 | |

| | | | | | | | 77,500,158 | |

26

DAVENPORT VALUE & INCOME FUND

SCHEDULE OF INVESTMENTS (Continued) |

COMMON STOCKS — 93.2% (Continued) | | Shares | | | Value | |

Industrials — 11.2% | | | | | | | | |

3M Company | | | 43,445 | | | $ | 9,027,002 | |

Boeing Company (The) | | | 36,075 | | | | 13,759,726 | |

Delta Air Lines, Inc. | | | 248,415 | | | | 12,830,635 | |

Eaton Corporation plc | | | 171,192 | | | | 13,791,228 | |

United Parcel Service, Inc. - Class B | | | 93,520 | | | | 10,449,925 | |

Watsco, Inc. | | | 109,050 | | | | 15,617,050 | |

| | | | | | | | 75,475,566 | |

Information Technology — 8.8% | | | | | | | | |

Cisco Systems, Inc. | | | 369,930 | | | | 19,972,521 | |

DXC Technology Company | | | 116,345 | | | | 7,482,147 | |

Microsoft Corporation | | | 172,493 | | | | 20,343,824 | |

TE Connectivity Ltd. | | | 145,775 | | | | 11,771,331 | |

| | | | | | | | 59,569,823 | |

Materials — 2.1% | | | | | | | | |

PPG Industries, Inc. | | | 122,945 | | | | 13,876,802 | |

| | | | | | | | | |

Real Estate — 7.2% | | | | | | | | |

Crown Castle International Corporation | | | 94,335 | | | | 12,074,880 | |

Gaming and Leisure Properties, Inc. | | | 269,164 | | | | 10,381,656 | |

Lamar Advertising Company - Class A | | | 189,120 | | | | 14,989,651 | |

W.P. Carey, Inc. | | | 139,374 | | | | 10,917,165 | |

| | | | | | | | 48,363,352 | |

Utilities — 2.6% | | | | | | | | |

Dominion Energy, Inc. | | | 225,465 | | | | 17,284,147 | |

| | | | | | | | | |

Total Common Stocks(Cost $515,813,618) | | | | | | $ | 627,515,521 | |

|

MONEY MARKET FUNDS — 6.7% | | Shares | | | Value | |

First American Treasury Obligations Fund - Class Z, 2.33%(b) (Cost $44,755,752) | | | 44,755,752 | | | $ | 44,755,752 | |

| | | | | | | | | |

Total Investments at Value — 99.9% (Cost $560,569,370) | | | | | | $ | 672,271,273 | |

| | | | | | | | | |

Other Assets in Excess of Liabilities — 0.1% | | | | | | | 683,077 | |

| | | | | | | | | |

Net Assets — 100.0% | | | | | | $ | 672,954,350 | |

ADR - American Depositary Receipt.

(a) | Non-income producing security. |

(b) | The rate shown is the 7-day effective yield as of March 31, 2019. |

See accompanying notes to financial statements.

27

DAVENPORT EQUITY OPPORTUNITIES FUND

SCHEDULE OF INVESTMENTS

March 31, 2019 |

COMMON STOCKS — 94.7% | | Shares | | | Value | |

Communication Services — 16.1% | | | | | | | | |

DISH Network Corporation - Class A(a) | | | 505,910 | | | $ | 16,032,288 | |

Liberty Broadband Corporation - Series C(a) | | | 171,035 | | | | 15,690,751 | |

Live Nation Entertainment, Inc.(a) | | | 317,209 | | | | 20,155,460 | |

Take-Two Interactive Software, Inc.(a) | | | 150,274 | | | | 14,181,357 | |

| | | | | | | | 66,059,856 | |

Consumer Discretionary — 13.6% | | | | | | | | |

CarMax, Inc.(a) | | | 270,745 | | | | 18,898,001 | |

Dollar Tree, Inc.(a) | | | 117,981 | | | | 12,392,724 | |

MercadoLibre, Inc.(a) | | | 30,241 | | | | 15,354,263 | |

O'Reilly Automotive, Inc.(a) | | | 22,880 | | | | 8,884,304 | |

| | | | | | | | 55,529,292 | |

Financials — 24.1% | | | | | | | | |

Brookfield Asset Management, Inc. - Class A | | | 581,227 | | | | 27,114,240 | |

Capital One Financial Corporation | | | 178,274 | | | | 14,563,203 | |

Cboe Global Markets, Inc. | | | 104,840 | | | | 10,005,930 | |

Fairfax Financial Holdings Ltd. | | | 27,203 | | | | 12,652,387 | |

Fidelity National Financial, Inc. | | | 430,940 | | | | 15,750,857 | |

Markel Corporation(a) | | | 18,427 | | | | 18,357,714 | |

| | | | | | | | 98,444,331 | |

Health Care — 3.4% | | | | | | | | |

Zoetis, Inc. | | | 138,935 | | | | 13,986,587 | |

| | | | | | | | | |

Industrials — 10.8% | | | | | | | | |

American Woodmark Corporation(a) | | | 170,450 | | | | 14,084,284 | |

Genesee & Wyoming, Inc. - Class A(a) | | | 81,510 | | | | 7,102,781 | |

Watsco, Inc. | | | 88,125 | | | | 12,620,381 | |

Xylem, Inc. | | | 131,400 | | | | 10,385,856 | |

| | | | | | | | 44,193,302 | |

Information Technology — 11.3% | | | | | | | | |

Autodesk, Inc.(a) | | | 104,575 | | | | 16,294,876 | |

Black Knight, Inc.(a) | | | 244,200 | | | | 13,308,900 | |

Intuit, Inc. | | | 62,899 | | | | 16,442,428 | |

| | | | | | | | 46,046,204 | |

Materials — 9.1% | | | | | | | | |

Martin Marietta Materials, Inc. | | | 92,382 | | | | 18,585,411 | |

Sherwin-Williams Company (The) | | | 42,950 | | | | 18,498,995 | |

| | | | | | | | 37,084,406 | |

Real Estate — 6.3% | | | | | | | | |

American Tower Corporation | | | 131,450 | | | | 25,903,537 | |

| | | | | | | | | |

Total Common Stocks (Cost $290,432,862) | | | | | | $ | 387,247,515 | |

28

DAVENPORT EQUITY OPPORTUNITIES FUND

SCHEDULE OF INVESTMENTS (Continued) |

MONEY MARKET FUNDS — 1.8% | | Shares | | | Value | |

First American Treasury Obligations Fund - Class Z, 2.33%(b) (Cost $7,498,616) | | | 7,498,616 | | | $ | 7,498,616 | |

| | | | | | | | | |

Total Investments at Value — 96.5%(Cost $297,931,478) | | | | | | $ | 394,746,131 | |

| | | | | | | | | |

Other Assets in Excess of Liabilities — 3.5% | | | | | | | 14,256,256 | |

| | | | | | | | | |

Net Assets — 100.0% | | | | | | $ | 409,002,387 | |

(a) | Non-income producing security. |

(b) | The rate shown is the 7-day effective yield as of March 31, 2019. |

See accompanying notes to financial statements.

29

DAVENPORT SMALL CAP FOCUS FUND

SCHEDULE OF INVESTMENTS

March 31, 2019 |

COMMON STOCKS — 89.2% | | Shares | | | Value | |

Communication Services — 6.3% | | | | | | | | |

Cable One, Inc. | | | 4,238 | | | $ | 4,159,089 | |

Meredith Corporation | | | 50,000 | | | | 2,763,000 | |

Shenandoah Telecommunications Company | | | 57,790 | | | | 2,563,564 | |

| | | | | | | | 9,485,653 | |

Consumer Discretionary — 13.3% | | | | | | | | |

Drive Shack, Inc.(a) | | | 516,437 | | | | 2,318,802 | |

Eldorado Resorts, Inc.(a) | | | 99,381 | | | | 4,640,099 | |

Etsy, Inc.(a) | | | 38,969 | | | | 2,619,496 | |

Monarch Casino & Resort, Inc.(a) | | | 113,893 | | | | 5,002,181 | |

Pool Corporation | | | 20,461 | | | | 3,375,451 | |

Red Rock Resorts, Inc. - Class A | | | 89,899 | | | | 2,323,889 | |

| | | | | | | | 20,279,918 | |

Consumer Staples — 2.7% | | | | | | | | |

Seaboard Corporation | | | 968 | | | | 4,147,590 | |

| | | | | | | | | |

Energy — 2.2% | | | | | | | | |

Alliance Resource Partners, L.P. | | | 57,309 | | | | 1,166,811 | |

CONSOL Coal Resources, L.P. | | | 125,800 | | | | 2,222,886 | |

| | | | | | | | 3,389,697 | |

Financials — 25.2% | | | | | | | | |

Cannae Holdings, Inc.(a) | | | 200,000 | | | | 4,852,000 | |

Cohen & Steers, Inc. | | | 108,350 | | | | 4,579,955 | |

Diamond Hill Investment Group, Inc. | | | 44,953 | | | | 6,293,420 | |

Kinsale Capital Group, Inc. | | | 81,151 | | | | 5,564,524 | |

OneSpaWorld Holdings Ltd.(a) | | | 531,932 | | | | 7,266,191 | |

TowneBank | | | 170,268 | | | | 4,214,133 | |

Trupanion, Inc.(a) | | | 170,562 | | | | 5,584,200 | |

| | | | | | | | 38,354,423 | |

Health Care — 3.0% | | | | | | | | |

Aratana Therapeutics, Inc.(a) | | | 599,956 | | | | 2,159,841 | |

Teladoc Health, Inc.(a) | | | 43,273 | | | | 2,405,979 | |

| | | | | | | | 4,565,820 | |

Industrials — 22.6% | | | | | | | | |

American Woodmark Corporation(a) | | | 73,641 | | | | 6,084,956 | |

Builders FirstSource, Inc.(a) | | | 210,886 | | | | 2,813,219 | |

Casella Waste Systems, Inc. - Class A(a) | | | 109,921 | | | | 3,908,791 | |

Colfax Corporation(a) | | | 190,000 | | | | 5,639,200 | |

Evoqua Water Technologies Corporation(a) | | | 401,576 | | | | 5,051,826 | |

Marten Transport Ltd. | | | 134,636 | | | | 2,400,560 | |

SiteOne Landscape Supply, Inc.(a) | | | 62,842 | | | | 3,591,420 | |

Watsco, Inc. | | | 33,593 | | | | 4,810,854 | |

| | | | | | | | 34,300,826 | |

30

DAVENPORT SMALL CAP FOCUS FUND

SCHEDULE OF INVESTMENTS (Continued) |

COMMON STOCKS — 89.2% (Continued) | | Shares | | | Value | |

Information Technology — 3.5% | | | | | | | | |

Black Knight, Inc.(a) | | | 98,267 | | | $ | 5,355,551 | |

| | | | | | | | | |

Materials — 5.5% | | | | | | | | |

MAG Silver Corporation(a) | | | 429,950 | | | | 4,583,267 | |

NewMarket Corporation | | | 8,641 | | | | 3,746,392 | |

| | | | | | | | 8,329,659 | |

Real Estate — 4.9% | | | | | | | | |

FRP Holdings, Inc.(a) | | | 50,556 | | | | 2,404,949 | |

Lamar Advertising Company - Class A | | | 63,300 | | | | 5,017,158 | |

| | | | | | | | 7,422,107 | |

| | | | | | | | | |

Total Common Stocks(Cost $120,384,224) | | | | | | $ | 135,631,244 | |

|

MONEY MARKET FUNDS — 8.5% | | Shares | | | Value | |

First American Treasury Obligations Fund - Class Z, 2.33%(b) (Cost $12,926,695) | | | 12,926,695 | | | $ | 12,926,695 | |

| | | | | | | | | |

Total Investments at Value — 97.7% (Cost $133,310,919) | | | | | | $ | 148,557,939 | |

| | | | | | | | | |

Other Assets in Excess of Liabilities — 2.3% | | | | | | | 3,504,950 | |

| | | | | | | | | |

Net Assets — 100.0% | | | | | | $ | 152,062,889 | |

(a) | Non-income producing security. |

(b) | The rate shown is the 7-day effective yield as of March 31, 2019. |

See accompanying notes to financial statements.

31

DAVENPORT BALANCED INCOME FUND

SCHEDULE OF INVESTMENTS

March 31, 2019 |

COMMON STOCKS — 59.4% | | Shares | | | Value | |

Communication Services — 2.1% | | | | | | | | |

Comcast Corporation - Class A | | | 41,880 | | | $ | 1,674,362 | |

Verizon Communications, Inc. | | | 21,190 | | | | 1,252,965 | |

| | | | | | | | 2,927,327 | |

Consumer Discretionary — 1.7% | | | | | | | | |

Carnival Corporation | | | 23,610 | | | | 1,197,499 | |

Las Vegas Sands Corporation | | | 20,380 | | | | 1,242,365 | |

| | | | | | | | 2,439,864 | |

Consumer Staples — 6.8% | | | | | | | | |

Altria Group, Inc. | | | 20,565 | | | | 1,181,048 | |

Anheuser-Busch InBev S.A./N.V. - ADR | | | 18,025 | | | | 1,513,559 | |

Diageo plc - ADR | | | 10,400 | | | | 1,701,544 | |

Mondelēz International, Inc. - Class A | | | 28,255 | | | | 1,410,490 | |

PepsiCo, Inc. | | | 11,200 | | | | 1,372,560 | |

Philip Morris International, Inc. | | | 18,275 | | | | 1,615,327 | |

Universal Corporation | | | 14,230 | | | | 820,075 | |

| | | | | | | | 9,614,603 | |

Energy — 6.7% | | | | | | | | |

Chevron Corporation | | | 7,910 | | | | 974,354 | |

Enbridge, Inc. | | | 34,808 | | | | 1,262,138 | |

Exxon Mobil Corporation | | | 9,960 | | | | 804,768 | |

Marathon Petroleum Corporation | | | 25,735 | | | | 1,540,240 | |

MPLX, L.P. | | | 30,425 | | | | 1,000,678 | |

Occidental Petroleum Corporation | | | 23,610 | | | | 1,562,982 | |

Royal Dutch Shell plc - Class B - ADR | | | 36,150 | | | | 2,311,792 | |

| | | | | | | | 9,456,952 | |

Financials — 14.9% | | | | | | | | |

Allstate Corporation (The) | | | 13,225 | | | | 1,245,530 | |

Bank of America Corporation | | | 41,400 | | | | 1,142,226 | |

Blackstone Group, L.P. (The) | | | 39,400 | | | | 1,377,818 | |

Brookfield Asset Management, Inc. - Class A | | | 53,770 | | | | 2,508,371 | |

Capital One Financial Corporation | | | 20,810 | | | | 1,699,969 | |

Citigroup, Inc. | | | 29,240 | | | | 1,819,313 | |

Cohen & Steers, Inc. | | | 28,405 | | | | 1,200,679 | |

Fairfax Financial Holdings Ltd. | | | 3,075 | | | | 1,430,213 | |

Fidelity National Financial, Inc. | | | 61,060 | | | | 2,231,743 | |

JPMorgan Chase & Company | | | 21,565 | | | | 2,183,025 | |

Lazard Ltd. - Class A | | | 34,100 | | | | 1,232,374 | |

Markel Corporation(a) | | | 1,967 | | | | 1,959,604 | |

MetLife, Inc. | | | 27,870 | | | | 1,186,426 | |

| | | | | | | | 21,217,291 | |

Health Care — 6.3% | | | | | | | | |

Bristol-Myers Squibb Company | | | 33,030 | | | | 1,575,862 | |

CVS Health Corporation | | | 26,585 | | | | 1,433,729 | |

32

DAVENPORT BALANCED INCOME FUND

SCHEDULE OF INVESTMENTS (Continued) |

COMMON STOCKS — 59.4% (Continued) | | Shares | | | Value | |

Health Care — 6.3% (Continued) | | | | | | | | |

Johnson & Johnson | | | 17,485 | | | $ | 2,444,228 | |

Medtronic plc | | | 14,125 | | | | 1,286,505 | |

Merck & Company, Inc. | | | 26,335 | | | | 2,190,282 | |

| | | | | | | | 8,930,606 | |

Industrials — 6.1% | | | | | | | | |

3M Company | | | 5,010 | | | | 1,040,978 | |

Boeing Company (The) | | | 4,165 | | | | 1,588,614 | |

Delta Air Lines, Inc. | | | 28,700 | | | | 1,482,355 | |

Eaton Corporation plc | | | 19,760 | | | | 1,591,866 | |

United Parcel Service, Inc. - Class B | | | 10,795 | | | | 1,206,233 | |

Watsco, Inc. | | | 12,605 | | | | 1,805,162 | |

| | | | | | | | 8,715,208 | |

Information Technology — 4.8% | | | | | | | | |

Cisco Systems, Inc. | | | 42,805 | | | | 2,311,042 | |

DXC Technology Company | | | 13,380 | | | | 860,468 | |

Microsoft Corporation | | | 19,970 | | | | 2,355,262 | |

TE Connectivity Ltd. | | | 16,710 | | | | 1,349,332 | |

| | | | | | | | 6,876,104 | |

Materials — 1.1% | | | | | | | | |

PPG Industries, Inc. | | | 14,225 | | | | 1,605,576 | |

| | | | | | | | | |

Real Estate — 5.7% | | | | | | | | |

Brookfield Property Partners, L.P. | | | 62,920 | | | | 1,294,265 | |

Crown Castle International Corporation | | | 10,795 | | | | 1,381,760 | |

Gaming and Leisure Properties, Inc. | | | 31,155 | | | | 1,201,648 | |

Lamar Advertising Company - Class A | | | 21,880 | | | | 1,734,209 | |

Tanger Factory Outlet Centers, Inc. | | | 56,140 | | | | 1,177,817 | |

W.P. Carey, Inc. | | | 16,275 | | | | 1,274,821 | |

| | | | | | | | 8,064,520 | |

Utilities — 3.2% | | | | | | | | |

Brookfield Infrastructure Partners, L.P. | | | 30,685 | | | | 1,284,781 | |

Brookfield Renewable Partners, L.P. | | | 37,660 | | | | 1,203,237 | |

Dominion Energy, Inc. | | | 26,770 | | | | 2,052,188 | |

| | | | | | | | 4,540,206 | |

| | | | | | | | | |

Total Common Stocks(Cost $77,949,773) | | | | | | $ | 84,388,257 | |

33

DAVENPORT BALANCED INCOME FUND

SCHEDULE OF INVESTMENTS (Continued) |

FIXED RATE CORPORATE BONDS — 14.5% | | Par Value | | | Value | |

Consumer Staples — 4.2% | | | | | | | | |

Altria Group, Inc., 4.75%, due 05/05/2021 | | $ | 1,500,000 | | | $ | 1,558,559 | |

J.M. Smucker Company (The), 3.50%, due 10/15/2021 | | | 1,500,000 | | | | 1,519,480 | |

PepsiCo, Inc., 2.75%, due 03/05/2022 | | | 1,200,000 | | | | 1,211,453 | |

Sysco Corporation, 2.60%, due 10/01/2020 | | | 1,700,000 | | | | 1,697,323 | |

| | | | | | | | 5,986,815 | |

Energy — 3.4% | | | | | | | | |

Boardwalk Pipelines, L.P., 4.45%, due 07/15/2027 | | | 1,250,000 | | | | 1,219,066 | |

MPLX, L.P., 4.125%, due 03/01/2027 | | | 1,750,000 | | | | 1,761,023 | |

Occidental Petroleum Corporation, 3.50%, due 06/15/2025 | | | 1,750,000 | | | | 1,797,961 | |

| | | | | | | | 4,778,050 | |

Financials — 3.7% | | | | | | | | |

BlackRock, Inc., 3.50%, due 03/18/2024 | | | 1,150,000 | | | | 1,195,469 | |

Citigroup, Inc., 3.30%, due 04/27/2025 | | | 2,250,000 | | | | 2,244,530 | |

General Motors Financial Company, 5.25%, due 03/01/2026 | | | 1,750,000 | | | | 1,806,052 | |

| | | | | | | | 5,246,051 | |

Health Care — 0.9% | | | | | | | | |

AbbVie, Inc., 2.50%, due 05/14/2020 | | | 1,300,000 | | | | 1,296,164 | |

| | | | | | | | | |