UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

Certified Shareholder Report of

Registered Management Investment Companies

Investment Company Act File Number: 811-05888

SMALLCAP World Fund, Inc.

(Exact Name of Registrant as Specified in Charter)

333 South Hope Street

Los Angeles, California 90071

(Address of Principal Executive Offices)

Registrant's telephone number, including area code: (213) 486-9200

Date of fiscal year end: September 30

Date of reporting period: September 30, 2013

Patrick F. Quan

SMALLCAP World Fund, Inc.

333 South Hope Street

Los Angeles, California 90071

(Name and Address of Agent for Service)

Copies to:

Mark D. Perlow

K&L Gates LLP

Four Embarcadero Center, Suite 1200

San Francisco, California 94111

(Counsel for the Registrant)

ITEM 1 – Reports to Stockholders

Developed economies are

fueling global growth.

Special feature page 4

| SMALLCAP World Fund® Annual report

for the year ended

September 30, 2013 |

SMALLCAP World Fund seeks long-term growth of capital through investments in smaller companies in the United States and around the world.

This fund is one of more than 40 offered by one of the nation’s largest mutual fund families, American Funds, from Capital Group. For more than 80 years, Capital has invested with a long-term focus based on thorough research and attention to risk.

Fund results shown in this report, unless otherwise indicated, are for Class A shares at net asset value. If a sales charge (maximum 5.75%) had been deducted, the results would have been lower. Results are for past periods and are not predictive of results for future periods. Current and future results may be lower or higher than those shown. Share prices and returns will vary, so investors may lose money. Investing for short periods makes losses more likely. Investments are not FDIC-insured, nor are they deposits of or guaranteed by a bank or any other entity, so they may lose value. For current information and month-end results, visit americanfunds.com.

See page 3 for Class A share results with relevant sales charges deducted. For other share class results, visit americanfunds.com and americanfundsretirement.com.

Investment results assume all distributions are reinvested and reflect applicable fees and expenses. When applicable, investment results reflect fee waivers, without which results would have been lower. Visit americanfunds.com for more information.

Investing outside the United States may be subject to risks, such as currency fluctuations and political instability. These risks may be heightened in connection with investments in developing countries. Investing in small-capitalization stocks can involve greater risk than is customarily associated with investing in stocks of larger, more established companies. Refer to the fund prospectus and the Risk Factors section of this report for more information on these and other risks associated with investing in the fund.

Special feature

Contents

Fellow investors:

Economic activity improved across the globe during SMALLCAP World Fund’s most recent fiscal year, prompting equity rallies in several major markets. In that environment, the fund produced a total return of 26.3% for the 12-month period ended September 30, 2013. This figure assumes the reinvestment of dividends, which totaled 54 cents a share for the fiscal year.

By way of comparison, the MSCI All Country World Small Cap Index, an unmanaged measure of global small-capitalization stocks, saw a total return of 25.0% for the same period. The index does not include management fees or other expenses. The Lipper Global Small-/Mid-Cap Funds Average, the fund’s peer group, returned 24.1%. The fund also surpassed the Lipper peer group measure over five- and 10-year periods, as well as through the lifetime of the fund.

The fund has changed its peer group category from the Lipper Global Small-Cap Funds Average to the Lipper Global Small-/Mid-Cap Funds Average; we feel that the latter category includes funds with investment objectives and strategies more similar to that of SMALLCAP World Fund.

The year in review

The strong equity rallies in markets around the world were spurred on by quantitative easing (QE), a monetary policy deployed by a number of the largest central banks in order to keep interest rates low and, ideally, restore confidence and economic growth. Concerns persist that a variety of economic problems — from a slowdown in developing nations’ growth to a spike in energy prices — could potentially derail the continued economic recovery from the 2008 financial crisis.

The United States has seen a strong equity rally over the past year, though economic growth has remained muted. In the spring, the Federal Reserve began to discuss tapering off QE by cutting back on bond repurchasing, though has backtracked somewhat since. The Fed’s benchmark rate remains steady, and it’s likely that stronger, more consistent economic improvement, particularly with regard to unemployment, will be needed before the Fed changes policy.

Europe continued to work through its fiscal and monetary issues, and with fewer headline crises than in past years, though economic growth in many nations remains poor. Peripheral European nations

Results at a glance

For periods ended September 30, 2013, with all distributions reinvested

| | | Cumulative

total returns | | Average annual total returns |

| | | 1 year | | 5 years | | 10 years | | Lifetime

(since 4/30/90) |

| | | | | | | | | | | | | | | | | |

| SMALLCAP World Fund (Class A shares) | | | 26.3 | % | | | 12.3 | % | | | 11.0 | % | | | 9.9 | % |

| MSCI All Country World Small Cap Index* | | | 25.0 | | | | 12.5 | | | | 11.1 | | | | n/a | |

| Lipper Global Small-/Mid-Cap Funds Average | | | 24.1 | | | | 10.9 | | | | 9.7 | | | | 9.7 | |

| * | The market index is unmanaged and, therefore, has no expenses. It is a free float-adjusted market capitalization weighted index that is designed to measure equity market results of smaller capitalization companies in both developed and emerging markets. Results reflect dividends net of withholding taxes. This index was not in existence as of the date the fund began investment operations; therefore, lifetime results are not available. |

endured deflationary and fiscal pressures, brought on by broader euro-zone policies, which will take time to work through. Equities in emerging markets began to sell off somewhat during the year, as the potential for rising rates in the U.S. prompted concerns that the flow of new credit in developing nations would be stemmed. For more on the interplay between developed and emerging markets, we suggest you turn to our special feature, beginning on page 4.

How the fund responded

The equities held by SMALLCAP World Fund originate from 40 different nations around the world. Just over 45% of the fund’s holdings were in U.S. equities, and these provided some of the strongest returns for the fund. The fund’s Japanese holdings, while just 3.9% of the portfolio, were among the strongest contributors as well. The weakest returns — while still positive overall — came from emerging markets.

The fund continues to be broadly diversified across sectors as well as geography. Consumer discretionary stocks, which represented 21% of the portfolio, provided the largest returns, while health care stocks, at 13% of the portfolio, were also strong contributors. The fund’s holdings in the energy sector, representing 5% of the portfolio, detracted from overall returns.

Among individual equities, each of the fund’s top 10 holdings produced positive returns. A number of the top holdings were up substantially including Netflix, which gained 468.0% in market value for the period; top holding ENN Energy Holdings returned 32.0%. Among detractors, Ophir Energy lost 45.0%.

The road ahead

The current market environment reflects a maturing bull market. Investors remain ambivalent about the prospects for stronger economic growth — and perhaps rightly so. This has kept many investors from delving into small-cap stocks more fully. There is, we believe, room for the current bull market to continue.

Of course, short-term projections of economic growth and stock market returns are notoriously difficult to make with a great deal of certainty. Our overwhelming focus remains on building a portfolio of small-cap investments that we believe can deliver robust absolute returns over the medium to long term. While this can be a challenging task in a fast-changing world, we remain convinced that continued change will allow for the creation of small companies that, in our view, could grow into rewarding investments for our shareholders.

It’s worth noting that prices of small-capitalization stocks historically have been more volatile than those of their large-cap counterparts, and this may be the case going forward. That said, and despite the difficult market environments over the past decade, the fund’s returns surpass those of certain large-cap measures, such as the MSCI EAFE (Europe, Australasia, Far East) Index. The fund’s returns have beaten those of the MSCI EAFE over one-, three-, five- and 10-year periods, and over the lifetime of the fund. The fund’s average annual total return has been 11.0% over the past decade, materially ahead of the official rate of inflation.

In closing, we thank you for the confidence you have placed in us; it is an honor and responsibility we take very seriously.

Sincerely,

Jonathan Knowles

Vice Chairman of the Board

Gregory W. Wendt

President

November 8, 2013

For current information about the fund, visit americanfunds.com.

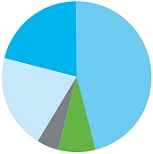

Where are SMALLCAP’s holdings located?

| As of September 30, 2013 | Percent of net assets |

| ▀ | United States | | | 46.3 | % |

| ▀ | Asia & Pacific Basin | | | 20.6 | |

| ▀ | Europe | | | 20.3 | |

| ▀ | Other (including Canada & Latin America) | | | 4.9 | |

| ▀ | Short-term securities & other assets less liabilities | | | 7.9 | |

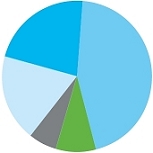

| | As of September 30, 2012 | Percent of

net assets |

| ▀ | United States | | | 44.9 | % |

| ▀ | Asia & Pacific Basin | | | 21.7 | |

| ▀ | Europe | | | 18.6 | |

| ▀ | Other (including Canada & Latin America) | | | 6.3 | |

| ▀ | Short-term securities & other assets less liabilities | | | 8.5 | |

Largest equity holdings

| | Percent of

net assets |

| Netflix | | | 1.5 | % |

| Regeneron Pharmaceuticals | | | 1.4 | |

| Lions Gate Entertainment | | | 1.1 | |

| ENN Energy Holdings | | | 1.0 | |

| AAC Technologies Holdings | | | .9 | |

| Domino’s Pizza | | | .8 | |

| Tesla | | | .8 | |

| DSW | | | .8 | |

| ASOS | | | .7 | |

| Incyte | | | .7 | |

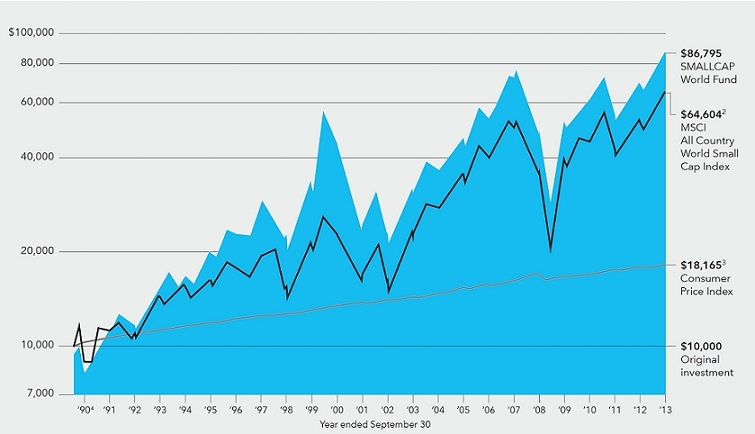

The value of a long-term perspective

This chart shows how a $10,000 investment in SMALLCAP World Fund’s Class A shares grew from April 30, 1990 — the fund’s inception — through September 30, 2013, the end of the fund’s latest fiscal year. As you can see, the $10,000 would have grown to $86,795 even after deducting the maximum 5.75% sales charge.

Fund results shown reflect deduction of the maximum sales charge of 5.75% on the $10,000 investment.1 Thus, the net amount invested was $9,425.

Past results are not predictive of results for future periods. The results shown are before taxes on fund distributions and sale of fund shares.

| 1 | As outlined in the prospectus, the sales charge is reduced for accounts (and aggregated investments) of $25,000 or more and is eliminated for purchases of $1 million or more. There is no sales charge on dividends or capital gain distributions that are reinvested in additional shares. |

| 2 | The MSCI All Country World Small Cap Index is unmanaged and, therefore, has no expenses. Results reflect dividends net of withholding taxes. Because the index was not in existence at the time of the fund’s inception, cumulative returns through May 1994 reflect the returns of the S&P Developed <$1.2 Billion Index. |

| 3 | Computed from data supplied by the U.S. Department of Labor, Bureau of Labor Statistics. |

| 4 | For the period April 30, 1990 (when the fund began operations) through September 30, 1990. |

Average annual total returns based on a $1,000 investment (for periods ended September 30, 2013)*

| | | 1 year | | 5 years | | 10 years |

| | | | | | | |

| Class A shares | | 19.01% | | 10.93% | | 10.32% |

*Assumes reinvestment of all distributions and payment of the maximum 5.75% sales charge.

The total annual fund operating expense ratio is 1.13% for Class A shares as of the prospectus dated December 1, 2013 (unaudited).

Investment results assume all distributions are reinvested and reflect applicable fees and expenses. When applicable, investment results reflect fee waivers, without which results would have been lower. Visit americanfunds.com for more information.

Developed economies are fueling global growth.

Developed economies are showing better growth compared to emerging markets. But regardless of economic cycles, developed economies played host to some of the most influential, innovative companies in the world.

For more than a decade, investors in small-capitalization stocks have looked to emerging markets for new, high-growth companies — and with great success. Such companies have been, and will continue to be, a staple of SMALLCAP World Fund. Yet with economic growth slowing in many developing nations, it’s the companies from the developed world — the U.S. and Japan in particular — that have thrived.

“The benefits of going global are clear, and you can see it in the long-term results of this fund,” says portfolio manager Greg Wendt, “but right now, equities from developed markets have done particularly well, and we’ve been able to take advantage of that because we continued to do our research.”

“To be clear, economic growth doesn’t always correlate well to stock market returns, but what we’re seeing in the developed world is encouraging,” says portfolio manager Jonathan Knowles. “Really, those areas of the world always have been home to those really great, really ‘disruptive’ companies that not only can grow, but can change the world by creating new markets and, in essence, changing the way people do things.”

A Japanese renaissance?

Second acts have become almost commonplace in American politics, but remain very rare in Japan. Yet Shinzo Abe, Japan’s prime minster, returned to power last year in a convincing vote, one that gave him a mandate to try to lift Japan out of two decades of economic malaise. And he’s taking major, sometimes controversial, steps to do it.

“For years, you had companies dealing with little-to-no growth and a strong currency that harmed exports. Out of that, you ended up with some highly efficient companies,” says portfolio manager Blair Frank. “If you spur the economy and weaken the currency, those companies could see huge amounts of growth without really having to do a lot.”

The success of Abe’s “three-arrow” policy — monetary stimulus, more government spending and regulatory reform to encourage investment —remains to be seen, but already there’s been a sense of confidence in Japan not seen in years. “Up until a few weeks ago, I had my doubts, but I went to Japan and talked with a lot of companies there,” says portfolio manager Brady Enright, who notes the fund has maintained a

consistent presence in Japan for many years. “And time and again, they’re reporting the first signs of improvements, whether it’s an increase in sales or loan volume. It’s different.”

The government’s moves could benefit small companies like fund holding MonotaRO, an online and mail-order distributor of industrial parts. The company exploited a niche in parts distribution — commonly done via catalogs and wholesalers in Japan —by making online ordering easy and promising same- or next-day delivery on large portions of their inventory.

“MonotaRO is a great example of why we need to be doing research all around the world, not just in places that are doing well,” says investment analyst Roz Hongsaranagon. “We actually heard about them from another company, and we found nobody else had done any research on them. We don’t have to rely on a strong Japanese economy with this company, but if the economy does get better, growth could accelerate.”

Disruptive companies at home

Equities from the United States have been a staple of SMALLCAP World Fund for a number of reasons. The U.S. boasts a business-friendly regulatory environment and a highly educated workforce. It also has a history of incubating disruptive companies.

“One of the things I’ve always tried to do is find those acorns that can turn into oaks,” Jonathan says. “Perhaps more than anywhere else, they tend to be in the United States.”

With emerging-market economic growth slowing, the U.S. is on its way to becoming an engine of global growth once more. SMALLCAP’s portfolio managers and investment analysts have identified areas in which the U.S. has excelled recently: cloud computing, “big data,” health-care innovation and energy development.

“You see emerging markets come to the fore now and then, but it’s in the developed world where you see those companies pushing the envelope,” says investment analyst Andraz Razen. “There’s been a network of innovation here for more than 200 years.”

Tesla, for example, was founded by a South African who chose to set up shop in Silicon Valley because of the network of software programmers and innovators there. Andraz believes the big difference

between the electric vehicle maker and its competitors is that it leverages the software know-how in the region to create a more efficient vehicle.

“You see the same story in biotech, where a wave of innovation is occurring. Every month we hear from companies that are developing promising new approaches to treating diseases that historically have been very debilitating or lethal,” Brady adds. “Or in energy, where innovation around shale and fracking are altering the world’s supply-and-demand balance for fossil fuels. The rest of the world remains three to five years behind the United States. These are the disruptors, the ones who can start with a clean sheet of paper and do something different without a legacy business to worry about.”

Europe in recovery

Economic growth in Europe remains stymied as the euro zone recovers from not only the global economic recession but also the banking crises there. Yet as with Japan, the fund’s research efforts have spanned many economic cycles. And there are glimmers of optimism.

“Certainly, the economies in Europe have been through a lot, but many of them have also done the right things to come out of it,” Jonathan says. “Take a look at Ireland. They’ve bottomed out and done the right things, cut their imports, cut their pay. And now they have a current-account surplus, they’re saving again and they’ve rebalanced their economy.

Even in Spain, with such high unemployment, they’re recapitalizing the banks and starting to turn a corner.”

And even in the midst of tough times, there are small-capitalization companies that have made their mark. In the United Kingdom, online fashion retailer ASOS has gathered numerous brands alongside its own house label and paired it with free shipping. The company, whose initials stand for “As Seen On Screen,” specializes in finding or duplicating trends depicted in the media. The company has expanded from the U.K. to the U.S., Australia and elsewhere.

“I first met with ASOS in the summer of 2008. There weren’t many successful companies around to compare ASOS with, unfortunately. On the contrary,

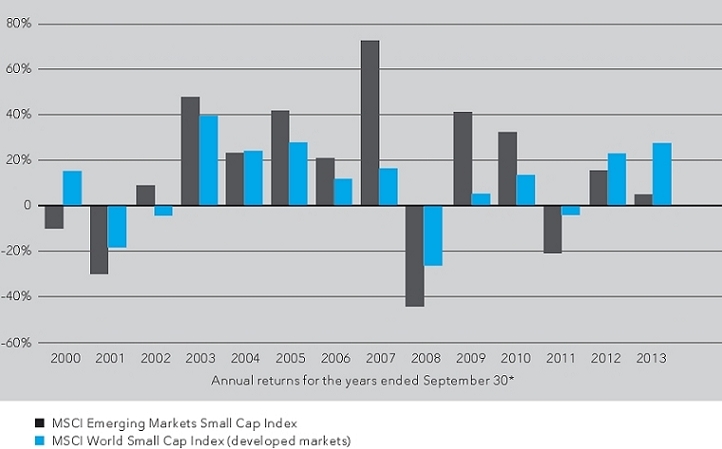

Finding favor: developed versus emerging market equities

Individual equities, certain industries, even entire geographic regions can come into — or fall out of — favor among equity investors. This chart illustrates the give-and-take between developed economy stocks, as represented by the MSCI World Small Cap Index, and emerging markets equities, as represented by the MSCI Emerging Markets Small Cap Index. While these trends are noteworthy, SMALLCAP World Fund continues to research potential investments throughout the world, in part so that there are portions of the portfolio poised to potentially make gains during different market environments.

| | Source: MSCI |

| | |

| | The market indexes are unmanaged and, therefore, have no expenses. Results for MSCI indexes reflect dividends net of withholding taxes. |

| | |

| * | Based on periods that align with SMALLCAP World Fund’s fiscal year (October 1–September 30). |

I found a lot of unsuccessful ones — but ASOS felt very different. I was struck by the strength and professionalism of its management team, who built the company on solid foundations — sophisticated supply chain and IT systems, for example —and with several years of experience at running successful fashion bricks and mortar companies,” says investment analyst Lara Pellini. “They have a very strong proprietary brand which accounts for 55% of group sales, and also a very broad product offering. They offer free shipping to 241 countries from their distribution center in the U.K. They have eight local language websites, with 65% of their sales now coming outside of the U.K.”

A global focus

Regardless of the current market environment, the fund continues to look across the globe — in developed and emerging markets alike — for potential equity investments. Indeed, as Roz pointed out, it’s because of the fund’s global research that many of today’s top holdings were uncovered in the first place.

Thus, the fund continues to look at companies in emerging markets, and will do so in the future. Many developing countries enjoyed prosperity while the U.S. kept its interest rates low; those rates are essentially global lending benchmarks, and much of the cheap capital that resulted ended up in emerging markets.

With the U.S. looking to tighten its monetary policy in the months ahead, capital is now flowing back to the developed world.

“These things can go back and forth,” Greg says. “That’s why we have people all over the world covering markets through thick and thin. Right now, somebody’s out there in an emerging market meeting with a great company. And we’re going to take a look at it no matter where it is.” n

Summary investment portfolio September 30, 2013

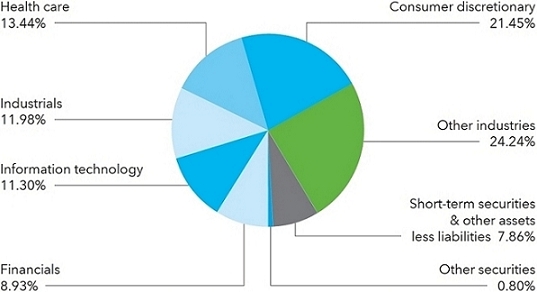

| Industry sector diversification | Percent of net assets |

| Country diversification | | Percent of

net assets |

| United States | | | 46.3 | % |

| United Kingdom | | | 8.9 | |

| Euro zone* | | | 7.5 | |

| Japan | | | 3.9 | |

| Hong Kong | | | 3.6 | |

| China | | | 3.3 | |

| Canada | | | 2.5 | |

| India | | | 2.1 | |

| Philippines | | | 2.1 | |

| Switzerland | | | 1.5 | |

| Australia | | | 1.4 | |

| Other countries | | | 9.0 | |

| Short-term securities & other assets less liabilities | | | 7.9 | |

| * | Countries using the euro as a common currency; those represented in the fund’s portfolio are Austria, Belgium, Finland, France, Germany, Greece, Ireland, Italy, the Netherlands, Portugal, Slovenia and Spain. |

| Common stocks 91.34% | | Shares | | | Value

(000) | | | Percent

of net

assets | |

| Consumer discretionary 21.45% | | | | | | | | | | | | |

| Netflix, Inc.1 | | | 1,143,723 | | | $ | 353,651 | | | | 1.45 | % |

| Internet subscription service for watching TV shows and movies. | | | | | | | | | | | | |

| Lions Gate Entertainment Corp.1,2 | | | 7,381,000 | | | | 258,704 | | | | 1.06 | |

| Independent motion picture and television producer and distributor. | | | | | | | | | | | | |

| Domino’s Pizza, Inc.2 | | | 2,940,000 | | | | 199,773 | | | | .82 | |

| Major global pizza delivery chain. | | | | | | | | | | | | |

| Tesla Motors, Inc.1 | | | 1,006,663 | | | | 194,709 | | | | .80 | |

| Manufacturer of electric cars and components. | | | | | | | | | | | | |

| DSW Inc., Class A | | | 2,246,500 | | | | 191,671 | | | | .78 | |

| U.S.-based retailer of footwear and accessories. | | | | | | | | | | | | |

| ASOS PLC1 | | | 2,174,955 | | | | 181,016 | | | | .74 | |

| Global online fashion and beauty retailer. | | | | | | | | | | | | |

| Paddy Power PLC | | | 1,967,177 | | | | 157,682 | | | | .64 | |

| Betting and gaming company operating primarily in the U.K., Ireland and Australia. | | | | | | | | | | | | |

| Melco International Development Ltd. | | | 58,168,000 | | | | 155,997 | | | | .64 | |

| Engaged in the leisure and entertainment business in Hong Kong, Macau, China and the Philippines. | | | | | | | | | | | | |

| TOD’S SpA | | | 744,000 | | | | 139,504 | | | | .57 | |

| Italian manufacturer of shoes, leather goods and accessories, and apparel. | | | | | | | | | | | | |

| Mr Price Group Ltd. | | | 8,228,383 | | | | 113,957 | | | | .47 | |

| Retail distribution chain based in South Africa. | | | | | | | | | | | | |

| Five Below, Inc.1 | | | 2,584,833 | | | | 113,086 | | | | .46 | |

| Operates as a specialty value retailer throughout the U.S. | | | | | | | | | | | | |

| Melco Crown Entertainment Ltd. (ADR)1 | | | 3,350,000 | | | | 106,631 | | | | .44 | |

| Casino gaming and resort operator based in Macau. | | | | | | | | | | | | |

| Dollarama Inc. | | | 1,155,000 | | | | 93,864 | | | | .38 | |

| Dollar store operator in Canada. | | | | | | | | | | | | |

| Ted Baker PLC2 | | | 2,882,993 | | | | 89,472 | | | | .36 | |

| British clothing retailer. | | | | | | | | | | | | |

| | | Shares | | | Value

(000) | | | Percent

of net

assets | |

| Chow Sang Sang Holdings International Ltd. | | | 28,609,000 | | | $ | 82,995 | | | | .34 | % |

| Jewelry store operator in China, with additional stores in Hong Kong, Macau and Taiwan. | | | | | | | | | | | | |

| John Wiley & Sons, Inc., Class A | | | 1,681,683 | | | | 80,199 | | | | .33 | |

| Global publisher specializing in academic publishing. | | | | | | | | | | | | |

| Rightmove PLC | | | 2,054,206 | | | | 78,782 | | | | .32 | |

| Operates a residential property website in the U.K. | | | | | | | | | | | | |

| Other securities | | | | | | | 2,651,711 | | | | 10.85 | |

| | | | | | | | 5,243,404 | | | | 21.45 | |

| | | | | | | | | | | | | |

| Health care 13.44% | | | | | | | | | | | | |

| Regeneron Pharmaceuticals, Inc.1 | | | 1,064,020 | | | | 332,900 | | | | 1.36 | |

| Biotechnology company focused on the treatment of serious medical conditions. | | | | | | | | | | | | |

| Incyte Corp.1 | | | 4,445,600 | | | | 169,600 | | | | .69 | |

| Biotechnology company focused on developing small molecule drugs for oncology and inflammation. | | | | | | | | | | | | |

| Synageva BioPharma Corp.1,2 | | | 2,230,074 | | | | 141,186 | | | | .58 | |

| Clinical stage biopharmaceutical company focused on life-threatening rare diseases and unmet medical needs. | | | | | | | | | | | | |

| Pharmacyclics, Inc.1 | | | 894,556 | | | | 123,824 | | | | .51 | |

| Biopharmaceutical company focused on the treatment of cancer and immune-mediated diseases. | | | | | | | | | | | | |

| Molina Healthcare, Inc.1,2 | | | 3,417,000 | | | | 121,645 | | | | .50 | |

| Managed care organization focused on Medicaid-related solutions for low-income families and individuals. | | | | | | | | | | | | |

| athenahealth, Inc.1 | | | 950,221 | | | | 103,156 | | | | .42 | |

| Provider of health care business and clinical services for physician practices. | | | | | | | | | | | | |

| BioMarin Pharmaceutical Inc.1 | | | 1,422,500 | | | | 102,733 | | | | .42 | |

| Biotechnology company engaged in the treatment of serious diseases and medical conditions. | | | | | | | | | | | | |

| Hikma Pharmaceuticals PLC | | | 5,814,153 | | | | 97,890 | | | | .40 | |

| Multinational pharmaceutical company based in the U.K. | | | | | | | | | | | | |

| Sysmex Corp. | | | 1,470,000 | | | | 93,618 | | | | .38 | |

| Japan-based manufacturer of medical laboratory testing equipment. | | | | | | | | | | | | |

| ArthroCare Corp.1,2 | | | 2,232,950 | | | | 79,448 | | | | .33 | |

| Maker of disposable medical devices for minimally invasive surgical procedures. | | | | | | | | | | | | |

| Endo Health Solutions Inc.1 | | | 1,745,100 | | | | 79,297 | | | | .33 | |

| Specialty health care solutions company focused on pain management. | | | | | | | | | | | | |

| Other securities | | | | | | | 1,838,648 | | | | 7.52 | |

| | | | | | | | 3,283,945 | | | | 13.44 | |

| | | | | | | | | | | | | |

| Industrials 11.98% | | | | | | | | | | | | |

| Moog Inc., Class A1,2 | | | 2,282,800 | | | | 133,932 | | | | .55 | |

| Manufacturer of precision motion control components and systems. | | | | | | | | | | | | |

| ITT Corp. | | | 3,581,621 | | | | 128,759 | | | | .52 | |

| Manufacturer of critical components and customized technology solutions for a variety of industries. | | | | | | | | | | | | |

| Intertek Group PLC | | | 2,225,000 | | | | 119,048 | | | | .49 | |

| Provider of business research, consulting and training to the financial services industry. | | | | | | | | | | | | |

| MonotaRO Co., Ltd.2 | | | 3,348,300 | | | | 97,797 | | | | .40 | |

| Retailer of indirect factory materials to domestic manufacturing companies through mail order. | | | | | | | | | | | | |

| Chart Industries, Inc.1 | | | 768,400 | | | | 94,544 | | | | .39 | |

| Global manufacturer of engineered equipment for cryogenic and heat transfer applications. | | | | | | | | | | | | |

| Common stocks (continued) | | Shares | | | Value

(000) | | | Percent

of net

assets | |

| Industrials (continued) | | | | | | | | | | | | |

| US Airways Group, Inc.1 | | | 4,627,000 | | | $ | 87,728 | | | | .36 | % |

| Air carrier serving the U.S., Canada, Mexico, Europe, the Middle East, the Caribbean, and Central and South America. | | | | | | | | | | | | |

| Other securities | | | | | | | 2,266,912 | | | | 9.27 | |

| | | | | | | | 2,928,720 | | | | 11.98 | |

| | | | | | | | | | | | | |

| Information technology 11.30% | | | | | | | | | | | | |

| AAC Technologies Holdings Inc. | | | 45,727,000 | | | | 207,826 | | | | .85 | |

| China-based manufacturer of miniature acoustic components. | | | | | | | | | | | | |

| Vistaprint NV1,2 | | | 1,860,000 | | | | 105,127 | | | | .43 | |

| Online provider of marketing products and services to micro businesses worldwide. | | | | | | | | | | | | |

| OpenTable, Inc.1,2 | | | 1,490,000 | | | | 104,270 | | | | .43 | |

| Provider of online restaurant reservation solutions. | | | | | | | | | | | | |

| Demandware, Inc.1,2 | | | 2,200,000 | | | | 101,926 | | | | .42 | |

| Provider of on-demand e-commerce solutions. | | | | | | | | | | | | |

| ASM International NV | | | 2,798,000 | | | | 97,281 | | | | .40 | |

| Makes machinery used in semiconductor assembly, packaging and testing. | | | | | | | | | | | | |

| Concur Technologies, Inc.1 | | | 858,869 | | | | 94,905 | | | | .39 | |

| Provider of integrated travel and expense management solutions. | | | | | | | | | | | | |

| National Instruments Corp. | | | 2,960,479 | | | | 91,568 | | | | .37 | |

| Develops and manufactures hardware and software for test and measurement instrumentation. | | | | | | | | | | | | |

| Other securities | | | | | | | 1,957,411 | | | | 8.01 | |

| | | | | | | | 2,760,314 | | | | 11.30 | |

| | | | | | | | | | | | | |

| Financials 8.93% | | | | | | | | | | | | |

| Financial Engines, Inc. | | | 2,335,000 | | | | 138,792 | | | | .57 | |

| Investment advisory firm focused on portfolio management, investment advice and retirement income services. | | | | | | | | | | | | |

| SVB Financial Group1 | | | 1,355,900 | | | | 117,109 | | | | .48 | |

| Financial services provider for companies in the technology, life science, venture capital, private equity and premium wine markets. | | | | | | | | | | | | |

| Ocwen Financial Corp.1 | | | 1,900,000 | | | | 105,963 | | | | .43 | |

| Engaged in the servicing and origination of residential and commercial mortgage loans. | | | | | | | | | | | | |

| GT Capital Holdings, Inc. | | | 5,852,200 | | | | 102,151 | | | | .42 | |

| Investment holding company engaged in banking, real estate development, power generation, and automotive and life insurance. | | | | | | | | | | | | |

| Onex Corp. | | | 1,855,700 | | | | 97,465 | | | | .40 | |

| Private equity investment company based in Canada. | | | | | | | | | | | | |

| Validus Holdings, Ltd. | | | 2,495,000 | | | | 92,265 | | | | .38 | |

| Provides insurance and reinsurance coverage in the property, marine and specialty lines markets. | | | | | | | | | | | | |

| Other securities | | | | | | | 1,528,402 | | | | 6.25 | |

| | | | | | | | 2,182,147 | | | | 8.93 | |

| | | | | | | | | | | | | |

| Consumer staples 5.43% | | | | | | | | | | | | |

| Super Group Ltd.2 | | | 44,597,000 | | | | 150,724 | | | | .62 | |

| Singapore-based manufacturer of food and beverage products. | | | | | | | | | | | | |

| Puregold Price Club, Inc.2 | | | 149,636,300 | | | | 143,313 | | | | .58 | |

| Operates wholesale and retail stores, including supermarkets. | | | | | | | | | | | | |

| PZ Cussons PLC | | | 14,102,300 | | | | 94,494 | | | | .39 | |

| Develops and manufactures personal health care products and consumer goods. | | | | | | | | | | | | |

| Other securities | | | | | | | 939,140 | | | | 3.84 | |

| | | | | | | | 1,327,671 | | | | 5.43 | |

| | | Shares | | | Value

(000) | | | Percent

of net

assets | |

| Energy 5.19% | | | | | | | | | | | | |

| Ophir Energy PLC1,2 | | | 30,708,378 | | | $ | 165,945 | | | | .68 | % |

| Oil and gas exploration company with assets in Africa. | | | | | | | | | | | | |

| InterOil Corp.1 | | | 2,129,500 | | | | 151,855 | | | | .62 | |

| Engaged in the exploration and development of oil and natural gas properties in Papua New Guinea. | | | | | | | | | | | | |

| Other securities | | | | | | | 949,570 | | | | 3.89 | |

| | | | | | | | 1,267,370 | | | | 5.19 | |

| | | | | | | | | | | | | |

| Materials 5.14% | | | | | | | | | | | | |

| Chr. Hansen Holding A/S | | | 3,426,000 | | | | 121,303 | | | | .50 | |

| Denmark-based manufacturer of food cultures and colorings, probiotics, phytonutrients and enzymes for the food, pharmaceutical, nutritional and agricultural industries. | | | | | | | | | | | | |

| AptarGroup, Inc. | | | 1,832,591 | | | | 110,194 | | | | .45 | |

| Manufacturer of dispensing systems for fragrances, pharmaceuticals and personal care products. | | | | | | | | | | | | |

| Schweitzer-Mauduit International, Inc.2 | | | 1,742,800 | | | | 105,492 | | | | .43 | |

| Manufacturer of reconstituted tobacco products and specialized paper products. | | | | | | | | | | | | |

| James Hardie Industries PLC (CDI) | | | 9,733,929 | | | | 96,983 | | | | .40 | |

| Makes building materials including fiber cement, which is used in siding, walls and roofing. | | | | | | | | | | | | |

| Other securities | | | | | | | 822,494 | | | | 3.36 | |

| | | | | | | | 1,256,466 | | | | 5.14 | |

| | | | | | | | | | | | | |

| Utilities 2.09% | | | | | | | | | | | | |

| ENN Energy Holdings Ltd. | | | 42,058,296 | | | | 233,720 | | | | .95 | |

| China-based operator of gas pipeline infrastructure and a distributor of piped and bottled gas. | | | | | | | | | | | | |

| Other securities | | | | | | | 278,154 | | | | 1.14 | |

| | | | | | | | 511,874 | | | | 2.09 | |

| | | | | | | | | | | | | |

| Telecommunication services 1.43% | | | | | | | | | | | | |

| Telephone and Data Systems, Inc. | | | 2,731,869 | | | | 80,727 | | | | .33 | |

| Provides wireless and local telephone services in the U.S. | | | | | | | | | | | | |

| Other securities | | | | | | | 269,883 | | | | 1.10 | |

| | | | | | | | 350,610 | | | | 1.43 | |

| | | | | | | | | | | | | |

| Miscellaneous 4.96% | | | | | | | | | | | | |

| Other common stocks in initial period of acquisition | | | | | | | 1,212,383 | | | | 4.96 | |

| | | | | | | | | | | | | |

| Total common stocks (cost: $15,135,101,000) | | | | | | | 22,324,904 | | | | 91.34 | |

| | | | | | | | | | | | | |

| Warrants 0.00% | | | | | | | | | | | | |

| Energy 0.00% | | | | | | | | | | | | |

| Other securities | | | | | | | — | | | | .00 | |

| | | | | | | | | | | | | |

| Total warrants (cost: $1,125,000) | | | | | | | — | | | | .00 | |

| | | | | | | | | | | | | |

| Convertible securities 0.50% | | | | | | | | | | | | |

| Other 0.50% | | | | | | | | | | | | |

| Other securities | | | | | | | 121,349 | | | | .50 | |

| | | | | | | | | | | | | |

| Total convertible securities (cost: $81,559,000) | | | | | | | 121,349 | | | | .50 | |

| Bonds, notes & other debt instruments 0.30% | | Principal

amount

(000) | | | Value

(000) | | | Percent

of net

assets | |

| U.S. Treasury bonds & notes 0.30% | | | | | | | | | | | | |

| Other securities | | | | | | $ | 72,574 | | | | .30 | % |

| | | | | | | | | | | | | |

| Total bonds, notes & other debt instruments (cost: $72,526,000) | | | | | | | 72,574 | | | | .30 | |

| | | | | | | | | | | | | |

| Short-term securities 8.21% | | | | | | | | | | | | |

Freddie Mac 0.08%–0.16%

due 10/22/2013–5/1/2014 | | $ | 573,800 | | | | 573,714 | | | | 2.35 | |

Fannie Mae 0.13%–0.16%

due 10/1–12/16/2013 | | | 160,200 | | | | 160,196 | | | | .65 | |

Bank of Nova Scotia 0.09%–0.18%

due 12/4/2013–1/24/2014 | | | 146,800 | | | | 146,724 | | | | .60 | |

Nordea Bank AB 0.15%–0.225%

due 11/18/2013–1/3/20143 | | | 125,500 | | | | 125,470 | | | | .51 | |

Federal Home Loan Bank 0.05%–0.13%

due 10/4/2013–3/21/2014 | | | 117,600 | | | | 117,591 | | | | .48 | |

Toronto-Dominion Holdings USA Inc. 0.12%–0.23%

due 10/24/2013–2/24/20143 | | | 101,700 | | | | 101,679 | | | | .42 | |

Sumitomo Mitsui Banking Corp. 0.15%–0.215%

due 10/23–12/5/20133 | | | 97,500 | | | | 97,485 | | | | .40 | |

| Other securities | | | | | | | 684,811 | | | | 2.80 | |

| | | | | | | | | | | | | |

| Total short-term securities (cost: $2,007,485,000) | | | | | | | 2,007,670 | | | | 8.21 | |

| Total investment securities (cost: $17,297,796,000) | | | | | | | 24,526,497 | | | | 100.35 | |

| Other assets less liabilities | | | | | | | (85,824 | ) | | | (.35 | ) |

| | | | | | | | | | | | | |

| Net assets | | | | | | $ | 24,440,673 | | | | 100.00 | % |

This summary investment portfolio is designed to streamline the report and help investors better focus on the fund’s principal holdings. See the inside back cover for details on how to obtain a complete schedule of portfolio holdings.

The descriptions of the companies shown in the summary investment portfolio, which were obtained from published reports and other sources believed to be reliable, are supplemental and are not covered by the Report of Independent Registered Public Accounting Firm.

As permitted by U.S. Securities and Exchange Commission regulations, “Miscellaneous” securities include holdings in their first year of acquisition that have not previously been publicly disclosed.

“Other securities” includes all issues that are not disclosed separately in the summary investment portfolio, including a portion of a security which was pledged as collateral for net losses on unsettled forward currency contracts. The total value of pledged collateral was $349,000, which represented less than .01% of the net assets of the fund.

Forward currency contracts

The fund has entered into forward currency contracts to sell currencies as shown in the following table. The average notional amount of open forward currency contracts was $165,919,000 over the prior 12-month period.

| | | | | | | | | | | Unrealized | |

| | | | | | | | | | | appreciation | |

| | | | | | | Contract amount | | (depreciation) | |

| | | | | | | Receive | | Deliver | | at 9/30/2013 | |

| | | Settlement date | | Counterparty | | (000) | | (000) | | (000) | |

| Sales: | | | | | | | | | | | | |

| Australian dollars | | 10/21/2013 | | Barclays Bank PLC | | $9,148 | | A$9,800 | | | $ 19 | |

| Australian dollars | | 10/24/2013 | | UBS AG | | $3,756 | | A$4,000 | | | 31 | |

| British pounds | | 11/1/2013 | | UBS AG | | $185,541 | | £115,100 | | | (743 | ) |

| Euros | | 10/25/2013 | | HSBC Bank | | $9,253 | | €6,950 | | | (150 | ) |

| Japanese yen | | 10/10/2013 | | Bank of New York Mellon | | $35,644 | | ¥3,550,000 | | | (474 | ) |

| Japanese yen | | 10/11/2013 | | Barclays Bank PLC | | $32,554 | | ¥3,242,712 | | | (438 | ) |

| Japanese yen | | 10/21/2013 | | Bank of New York Mellon | | $8,842 | | ¥875,000 | | | (61 | ) |

| Japanese yen | | 10/24/2013 | | Bank of New York Mellon | | $20,026 | | ¥1,990,000 | | | (222 | ) |

| | | | | | | | | | | | | |

| | | | | | | | | | | | $(2,038 | ) |

Investments in affiliates

A company is considered to be an affiliate of the fund under the Investment Company Act of 1940 if the fund’s holdings in that company represent 5% or more of the outstanding voting shares. The value of the fund’s holdings in affiliated companies is included in “Other securities” under the respective industry sectors in the summary investment portfolio. Further details on these holdings and related transactions during the year ended September 30, 2013, appear below.

| | | Beginning

shares or

principal

amount | | | Additions | | | Reductions | | | Ending

shares or

principal

amount | | | Dividend

or interest

income

(000) | | | Value of

affiliates at

9/30/2013

(000) | |

| Lions Gate Entertainment Corp.1 | | | 8,000,000 | | | | 106,121 | | | | 725,121 | | | | 7,381,000 | | | $ | — | | | $ | 258,704 | |

| Domino’s Pizza, Inc. | | | 850,000 | | | | 2,090,000 | | | | — | | | | 2,940,000 | | | | 1,399 | | | | 199,773 | |

| Ophir Energy PLC1 | | | 16,717,585 | | | | 18,443,083 | | | | 4,452,290 | | | | 30,708,378 | | | | — | | | | 165,945 | |

| Super Group Ltd. | | | 44,597,000 | | | | — | | | | — | | | | 44,597,000 | | | | 2,549 | | | | 150,724 | |

| Puregold Price Club, Inc. | | | 87,206,000 | | | | 72,127,500 | | | | 9,697,200 | | | | 149,636,300 | | | | 316 | | | | 143,313 | |

| Synageva BioPharma Corp.1 | | | 1,570,000 | | | | 690,074 | | | | 30,000 | | | | 2,230,074 | | | | — | | | | 141,186 | |

| Moog Inc., Class A1 | | | 1,192,800 | | | | 1,090,000 | | | | — | | | | 2,282,800 | | | | — | | | | 133,932 | |

| Molina Healthcare, Inc.1 | | | 1,850,000 | | | | 1,567,000 | | | | — | | | | 3,417,000 | | | | — | | | | 121,645 | |

| Schweitzer-Mauduit International, Inc. | | | 2,370,000 | | | | 112,800 | | | | 740,000 | | | | 1,742,800 | | | | 2,415 | | | | 105,492 | |

| Vistaprint NV1 | | | 2,050,000 | | | | — | | | | 190,000 | | | | 1,860,000 | | | | — | | | | 105,127 | |

| OpenTable, Inc.1 | | | 1,290,000 | | | | 200,000 | | | | — | | | | 1,490,000 | | | | — | | | | 104,270 | |

| Demandware, Inc.1,4 | | | 507,171 | | | | 1,692,829 | | | | — | | | | 2,200,000 | | | | — | | | | 101,926 | |

| MonotaRO Co., Ltd. | | | 1,006,500 | | | | 2,341,800 | | | | — | | | | 3,348,300 | | | | 282 | | | | 97,797 | |

| Ted Baker PLC | | | — | | | | 2,882,993 | | | | — | | | | 2,882,993 | | | | 360 | | | | 89,472 | |

| ArthroCare Corp.1 | | | 1,809,802 | | | | 423,148 | | | | — | | | | 2,232,950 | | | | — | | | | 79,448 | |

| Coupons.com Inc., Series B, convertible preferred1,5,6 | | | 8,191,724 | | | | — | | | | — | | | | 8,191,724 | | | | — | | | | 77,657 | |

| Northgate PLC | | | 10,626,805 | | | | — | | | | — | | | | 10,626,805 | | | | 1,208 | | | | 73,976 | |

| Manila Water Co., Inc. | | | 81,300,900 | | | | 22,900,000 | | | | — | | | | 104,200,900 | | | | 1,081 | | | | 67,608 | |

| OM Group, Inc.1 | | | — | | | | 1,820,000 | | | | — | | | | 1,820,000 | | | | — | | | | 61,480 | |

| Domino’s Pizza Enterprises Ltd. | | | 3,602,300 | | | | 1,550,065 | | | | 400,000 | | | | 4,752,365 | | | | 1,268 | | | | 60,473 | |

| Exelixis, Inc.1 | | | 5,962,000 | | | | 3,254,800 | | | | — | | | | 9,216,800 | | | | — | | | | 53,642 | |

| Emeritus Corp.1 | | | 2,730,000 | | | | — | | | | 300 | | | | 2,729,700 | | | | — | | | | 50,581 | |

| Galapagos NV1 | | | 1,554,436 | | | | 1,574,492 | | | | 750,000 | | | | 2,378,928 | | | | — | | | | 50,206 | |

| Responsys, Inc.1 | | | — | | | | 2,815,000 | | | | — | | | | 2,815,000 | | | | — | | | | 46,447 | |

| Autoneum Holding AG | | | 373,780 | | | | — | | | | — | | | | 373,780 | | | | 261 | | | | 44,886 | |

| LSL Property Services PLC | | | — | | | | 5,956,350 | | | | — | | | | 5,956,350 | | | | — | | | | 44,670 | |

| bluebird bio, Inc.1,5,6 | | | — | | | | 1,179,648 | | | | — | | | | 1,179,648 | | | | — | | | | 28,623 | |

| bluebird bio, Inc.1 | | | — | | | | 516,000 | | | | — | | | | 516,000 | | | | — | | | | 13,911 | |

| bluebird bio, Inc., Series D, convertible preferred7 | | | 22,374,386 | | | | — | | | | 22,374,386 | | | | — | | | | — | | | | — | |

| Goodpack Ltd. | | | 30,060,000 | | | | 5,272,000 | | | | 4,555,000 | | | | 30,777,000 | | | | 1,227 | | | | 42,441 | |

| Goodpack Ltd., warrants, expire 20127 | | | 5,272,000 | | | | — | | | | 5,272,000 | | | | — | | | | — | | | | — | |

| Comfort Systems USA, Inc. | | | 2,476,000 | | | | — | | | | — | | | | 2,476,000 | | | | 508 | | | | 41,621 | |

| Orexigen Therapeutics, Inc.1,4 | | | 894,900 | | | | 5,640,100 | | | | — | | | | 6,535,000 | | | | — | | | | 40,125 | |

| Kingdee International Software Group Co. Ltd.1 | | | 123,194,000 | | | | 11,674,000 | | | | — | | | | 134,868,000 | | | | — | | | | 38,778 | |

| Iridium Communications Inc.1 | | | 4,206,609 | | | | 1,003,391 | | | | 488,188 | | | | 4,721,812 | | | | — | | | | 32,486 | |

| Iridium Communications Inc., Series A, convertible preferred3 | | | 60,000 | | | | — | | | | — | | | | 60,000 | | | | 400 | | | | 5,979 | |

| KEYW Holding Corp.1,4 | | | 1,613,500 | | | | 1,222,900 | | | | — | | | | 2,836,400 | | | | — | | | | 38,150 | |

| Cadence Pharmaceuticals, Inc.1 | | | 6,130,469 | | | | — | | | | 190,500 | | | | 5,939,969 | | | | — | | | | 37,481 | |

| | | Beginning

shares or

principal

amount | | | Additions | | | Reductions | | | Ending

shares or

principal

amount | | | Dividend

or interest

income

(000) | | | Value of

affiliates at

9/30/2013

(000) | |

| Mistras Group, Inc.1 | | | — | | | | 2,052,000 | | | | — | | | | 2,052,000 | | | $ | — | | | $ | 34,884 | |

| Bizim Toptan Satis Magazalari AS, non-registered shares | | | 1,720,474 | | | | 1,581,500 | | | | 835,974 | | | | 2,466,000 | | | | 298 | | | | 31,862 | |

| Tsukui Corp. | | | — | | | | 2,595,000 | | | | — | | | | 2,595,000 | | | | 150 | | | | 31,575 | |

| Boer Power Holdings Ltd. | | | 31,753,000 | | | | 7,449,000 | | | | — | | | | 39,202,000 | | | | 491 | | | | 29,063 | |

| Mothercare PLC1 | | | 4,480,000 | | | | — | | | | — | | | | 4,480,000 | | | | — | | | | 27,343 | |

| AIA Engineering Ltd. | | | 2,915,050 | | | | 1,925,000 | | | | — | | | | 4,840,050 | | | | 318 | | | | 24,299 | |

| Orthofix International NV1 | | | 1,110,100 | | | | 50,000 | | | | 43,274 | | | | 1,116,826 | | | | — | | | | 23,297 | |

| Houston Wire & Cable Co. | | | 1,678,900 | | | | — | | | | — | | | | 1,678,900 | | | | 672 | | | | 22,615 | |

| Frigoglass SAIC1 | | | 3,052,380 | | | | — | | | | — | | | | 3,052,380 | | | | — | | | | 22,588 | |

| XenoPort, Inc.1 | | | 2,792,000 | | | | 828,000 | | | | — | | | | 3,620,000 | | | | — | | | | 20,562 | |

| Greenko Group PLC1 | | | 9,144,000 | | | | 604,155 | | | | — | | | | 9,748,155 | | | | — | | | | 19,490 | |

| Suprema Inc.1 | | | — | | | | 868,200 | | | | — | | | | 868,200 | | | | — | | | | 19,268 | |

| Gem Diamonds Ltd.1 | | | 7,350,000 | | | | 400,000 | | | | — | | | | 7,750,000 | | | | — | | | | 18,945 | |

| Home Federal Bancorp, Inc. | | | 1,384,249 | | | | — | | | | — | | | | 1,384,249 | | | | 498 | | | | 17,414 | |

| ChemoCentryx, Inc.1 | | | 668,596 | | | | 2,463,204 | | | | — | | | | 3,131,800 | | | | — | | | | 17,413 | |

| Cox and Kings (India) Ltd. | | | 10,592,000 | | | | — | | | | — | | | | 10,592,000 | | | | 160 | | | | 14,990 | |

| Cox and Kings (India) Ltd. (GDR)5 | | | 330,000 | | | | — | | | | — | | | | 330,000 | | | | 5 | | | | 467 | |

| Agilysys, Inc.1 | | | 520,313 | | | | 760,278 | | | | — | | | | 1,280,591 | | | | — | | | | 15,265 | |

| Mytrah Energy Ltd.1 | | | 7,918,000 | | | | 2,500,000 | | | | — | | | | 10,418,000 | | | | — | | | | 15,095 | |

| ValueVision Media, Inc., Class A1 | | | 3,875,293 | | | | — | | | | 434,532 | | | | 3,440,761 | | | | — | | | | 14,967 | |

| Vocus, Inc.1 | | | — | | | | 1,513,538 | | | | — | | | | 1,513,538 | | | | — | | | | 14,091 | |

| Mahindra Lifespace Developers Ltd. | | | 2,157,380 | | | | — | | | | — | | | | 2,157,380 | | | | 216 | | | | 13,980 | |

| BNK Petroleum Inc.1 | | | 5,763,380 | | | | 5,780,000 | | | | — | | | | 11,543,380 | | | | — | | | | 13,672 | |

| Manappuram Finance Ltd. | | | 50,330,986 | | | | 4,600,000 | | | | — | | | | 54,930,986 | | | | 1,902 | | | | 12,723 | |

| ARC Document Solutions, Inc.1 | | | — | | | | 2,765,764 | | | | — | | | | 2,765,764 | | | | — | | | | 12,695 | |

| Ultragenyx Pharmaceutical Inc., Series B, convertible preferred5,6 | | | — | | | | 2,789,614 | | | | — | | | | 2,789,614 | | | | — | | | | 12,490 | |

| TravelCenters of America LLC1 | | | — | | | | 1,581,250 | | | | — | | | | 1,581,250 | | | | — | | | | 12,413 | |

| First Southern Bancorp, Inc.1,5,6 | | | 1,344,915 | | | | — | | | | — | | | | 1,344,915 | | | | — | | | | 7,155 | |

| First Southern Bancorp, Inc., Series C, convertible preferred1,5,6 | | | 2,299 | | | | — | | | | — | | | | 2,299 | | | | — | | | | 4,759 | |

| Falkland Oil and Gas Ltd.1 | | | 24,225,000 | | | | — | | | | — | | | | 24,225,000 | | | | — | | | | 11,079 | |

| Lekoil Ltd. (CDI)1,3 | | | — | | | | 14,070,000 | | | | — | | | | 14,070,000 | | | | — | | | | 9,709 | |

| Duluth Metals Ltd.1 | | | 4,208,800 | | | | 3,490,900 | | | | — | | | | 7,699,700 | | | | — | | | | 8,821 | |

| Mvelaserve Ltd.1 | | | 9,194,800 | | | | — | | | | — | | | | 9,194,800 | | | | — | | | | 8,224 | |

| Tilaknager Industries Ltd. | | | 8,890,000 | | | | — | | | | — | | | | 8,890,000 | | | | 108 | | | | 8,073 | |

| Tribhovandas Bhimji Zaveri Ltd. | | | — | | | | 3,439,332 | | | | — | | | | 3,439,332 | | | | 127 | | | | 6,859 | |

| Mood Media Corp.1,3 | | | 6,375,000 | | | | — | | | | — | | | | 6,375,000 | | | | — | | | | 4,147 | |

| Mood Media Corp. (CDI)1,3 | | | 3,710,000 | | | | — | | | | — | | | | 3,710,000 | | | | — | | | | 2,413 | |

| Cape Lambert Resources Ltd.1 | | | 32,790,132 | | | | 14,540,693 | | | | — | | | | 47,330,825 | | | | — | | | | 5,740 | |

| Powerland AG, non-registered shares1 | | | 1,200,000 | | | | — | | | | — | | | | 1,200,000 | | | | — | | | | 4,886 | |

| China High Precision Automation Group Ltd.5 | | | 67,422,000 | | | | — | | | | — | | | | 67,422,000 | | | | 174 | | | | 3,477 | |

| Talwalkars Better Value Fitness Ltd. | | | 1,446,000 | | | | 248,000 | | | | — | | | | 1,694,000 | | | | 42 | | | | 3,340 | |

| Petrodorado Energy Ltd.1 | | | 38,400,000 | | | | — | | | | — | | | | 38,400,000 | | | | — | | | | 1,491 | |

| Gran Colombia Gold SA1 | | | 30,175,000 | | | | — | | | | 29,268,300 | | | | 906,700 | | | | — | | | | 1,118 | |

| Gran Colombia Gold SA, warrants, expire 2015 | | | 1,086,500 | | | | — | | | | 1,086,500 | | | | — | | | | — | | | | — | |

| | | Beginning

shares or

principal

amount | | | Additions | | | Reductions | | | Ending

shares or principal

amount | | | Dividend

or interest

income

(000) | | | Value of

affiliates at

9/30/2013

(000) | |

| CEC Unet PLC1,5 | | | 35,100,775 | | | | — | | | | — | | | | 35,100,775 | | | $ | — | | | $ | — | |

| Achillion Pharmaceuticals, Inc.1,7 | | | 3,750,000 | | | | 1,245,000 | | | | 865,000 | | | | 4,130,000 | | | | — | | | | — | |

| Afferro Mining Inc.7 | | | 6,460,000 | | | | — | | | | 6,460,000 | | | | — | | | | — | | | | — | |

| African Petroleum Corp. Ltd.1,7 | | | 93,646,868 | | | | 1,838,153 | | | | 31,250,294 | | | | 64,234,727 | | | | — | | | | — | |

| AVEO Pharmaceuticals, Inc.7 | | | 3,387,200 | | | | 759,800 | | | | 4,147,000 | | | | — | | | | — | | | | — | |

| BG Medicine, Inc.7 | | | 1,418,968 | | | | — | | | | 1,418,968 | | | | — | | | | — | | | | — | |

| Bloomsbury Publishing PLC7 | | | 21,695,000 | | | | — | | | | 21,695,000 | | | | — | | | | 82 | | | | — | |

| BrisConnections Unit Trusts7 | | | 27,290,000 | | | | — | | | | 27,290,000 | | | | — | | | | — | | | | — | |

| CJ CGV Co., Ltd.7 | | | 1,235,000 | | | | — | | | | 1,235,000 | | | | — | | | | 112 | | | | — | |

| Coal of Africa Ltd.1,7 | | | 55,734,459 | | | | 14,100,000 | | | | 18,375,774 | | | | 51,458,685 | | | | — | | | | — | |

| Comstock Resources, Inc.7 | | | 3,078,111 | | | | — | | | | 1,280,000 | | | | 1,798,111 | | | | 450 | | | | — | |

| Cymer, Inc.7 | | | 1,670,000 | | | | 25,000 | | | | 1,695,000 | | | | — | | | | — | | | | — | |

| Delticom AG7 | | | 761,501 | | | | — | | | | 761,501 | | | | — | | | | — | | | | — | |

| Douglas Dynamics, Inc.7 | | | 1,175,000 | | | | — | | | | 1,175,000 | | | | — | | | | 233 | | | | — | |

| EACOM Timber Corp.7 | | | 26,200,000 | | | | — | | | | 26,200,000 | | | | — | | | | — | | | | — | |

| Eastern Platinum Ltd.1,7 | | | 27,281,450 | | | | 37,125,000 | | | | 27,281,450 | | | | 37,125,000 | | | | — | | | | — | |

| Ebix, Inc.7 | | | 1,465,000 | | | | 745,000 | | | | 2,210,000 | | | | — | | | | 211 | | | | — | |

| ENN Energy Holdings Ltd.7 | | | 55,644,296 | | | | — | | | | 13,586,000 | | | | 42,058,296 | | | | 2,404 | | | | — | |

| Ennis, Inc.7 | | | 1,472,589 | | | | — | | | | 422,589 | | | | 1,050,000 | | | | 873 | | | | — | |

| Exponent, Inc.7 | | | 936,400 | | | | — | | | | 320,000 | | | | 616,400 | | | | 277 | | | | — | |

| Greatview Aseptic Packaging Co. Ltd.7 | | | 50,033,000 | | | | 17,900,000 | | | | 22,700,000 | | | | 45,233,000 | | | | 875 | | | | — | |

| Green Packet Bhd7 | | | 34,933,616 | | | | — | | | | 34,933,616 | | | | — | | | | — | | | | — | |

| Hittite Microwave Corp.1,7 | | | 1,794,950 | | | | — | | | | 1,034,000 | | | | 760,950 | | | | — | | | | — | |

| Home Loan Servicing Solutions, Ltd.7 | | | 1,546,400 | | | | 965,000 | | | | 212,400 | | | | 2,299,000 | | | | 3,776 | | | | — | |

| Immersion Corp.1,7 | | | 2,254,000 | | | | — | | | | 894,100 | | | | 1,359,900 | | | | — | | | | — | |

| InterOil Corp.1,7 | | | 2,461,200 | | | | — | | | | 331,700 | | | | 2,129,500 | | | | — | | | | — | |

| Liquidity Services, Inc.1,7 | | | 832,536 | | | | 1,263,667 | | | | 715,803 | | | | 1,380,400 | | | | — | | | | — | |

| MD Medical Group Investments PLC (GDR)5,7 | | | — | | | | 2,582,900 | | | | 84,200 | | | | 2,498,700 | | | | 489 | | | | — | |

| MD Medical Group Investments PLC (GDR)3,5,7 | | | — | | | | 1,179,100 | | | | — | | | | 1,179,100 | | | | — | | | | — | |

| National Financial Partners Corp. 4.00% convertible notes 20177 | | $ | 4,000,000 | | | | — | | | $ | 4,000,000 | | | | — | | | | 76 | | | | — | |

| National Financial Partners Corp.7 | | | 3,174,800 | | | | — | | | | 3,174,800 | | | | — | | | | — | | | | — | |

| NewSat Ltd.1,4,7 | | | 2,086,578 | | | | 12,313,985 | | | | — | | | | 14,400,563 | | | | — | | | | — | |

| NewSat Ltd.1,3,7 | | | — | | | | 12,155,000 | | | | — | | | | 12,155,000 | | | | — | | | | — | |

| NuVasive, Inc.1,7 | | | 2,492,536 | | | | — | | | | 985,100 | | | | 1,507,436 | | | | — | | | | — | |

| Pacific Coal Resources Ltd., warrants, expire 20161,5,7 | | | 8,500,000 | | | | — | | | | 7,285,715 | | | | 1,214,285 | | | | — | | | | — | |

| Pacific Coal Resources Ltd.7 | | | 18,280,000 | | | | — | | | | 18,280,000 | | | | — | | | | — | | | | — | |

| PT Sumber Alfaria Trijaya Tbk7 | | | 219,452,500 | | | | 805,617,000 | | | | 238,702,280 | | | | 786,367,220 | | | | 404 | | | | — | |

| Quantum Corp.7 | | | 13,699,097 | | | | — | | | | 13,699,097 | | | | — | | | | — | | | | — | |

| SPS Commerce, Inc.1,7 | | | 1,051,300 | | | | — | | | | 479,300 | | | | 572,000 | | | | — | | | | — | |

| Standard Parking Corp.7 | | | 1,048,600 | | | | — | | | | 1,048,600 | | | | — | | | | — | | | | — | |

| U.S. Auto Parts Network, Inc.7 | | | 1,980,000 | | | | — | | | | 1,980,000 | | | | — | | | | — | | | | — | |

| Yip’s Chemical Holdings Ltd.7 | | | 27,628,000 | | | | 2,350,000 | | | | 3,090,000 | | | | 26,888,000 | | | | 921 | | | | — | |

| Youku Inc., Class A (ADR)1,7 | | | 1,400,000 | | | | 810,000 | | | | 1,910,000 | | | | 300,000 | | | | — | | | | — | |

| | | | | | | | | | | | | | | | | | | $ | 29,618 | | | $ | 3,554,732 | |

The following footnotes apply to either the individual securities noted or one or more of the securities aggregated and listed as a single line item.

| 1 | Security did not produce income during the last 12 months. |

| 2 | Represents an affiliated company as defined under the Investment Company Act of 1940. |

| 3 | Acquired in a transaction exempt from registration under Rule 144A or section 4(2) of the Securities Act of 1933. May be resold in the U.S. in transactions exempt from registration, normally to qualified institutional buyers. The total value of all such securities, including those in “Other securities,” was $1,051,911,000, which represented 4.30% of the net assets of the fund. |

| 4 | This security was an unaffiliated issuer in its initial period of acquisition at 9/30/2012; it was not publicly disclosed. |

| 5 | Valued under fair value procedures adopted by authority of the board of directors. The total value of all such securities, including those in “Miscellaneous,” was $235,631,000, which represented .96% of the net assets of the fund. |

| 6 | Acquired through a private placement transaction exempt from registration under the Securities Act of 1933. May be subject to legal or contractual restrictions on resale. Further details on these holdings appear below. |

| | | Acquisition

date(s) | | Cost

(000) | | | Value

(000) | | | Percent of

net assets | |

| Coupons.com Inc., Series B, convertible preferred | | 6/1/2011 | | $ | 45,000 | | | $ | 77,657 | | | | .32 | % |

| bluebird bio, Inc. | | 7/20/2012 | | | 11,149 | | | | 28,623 | | | | .12 | |

| Ultragenyx Pharmaceutical Inc., Series B, convertible preferred | | 12/17/2012 | | | 7,726 | | | | 12,490 | | | | .05 | |

| First Southern Bancorp, Inc. | | 12/17/2009 | | | 22,070 | | | | 7,155 | | | | .03 | |

| First Southern Bancorp, Inc., Series C, convertible preferred | | 12/17/2009 | | | — | | | | 4,759 | | | | .02 | |

| Other restricted securities | | 10/5/2005-12/12/2012 | | | 104,275 | | | | 70,076 | | | | .29 | |

| Total restricted securities | | | | $ | 190,220 | | | $ | 200,760 | | | | .83 | % |

| 7 | Unaffiliated issuer at 9/30/2013. |

Key to abbreviations and symbols

ADR = American Depositary Receipts

CDI = CREST Depository Interest

GDR = Global Depositary Receipts

A$ = Australian dollars

€ = Euros

£ = British pounds

¥ = Japanese yen

See Notes to Financial Statements

Financial statements

| Statement of assets and liabilities | | |

| at September 30, 2013 | | (dollars in thousands) |

| | | |

| Assets: | | | | | | | | |

| Investment securities, at value: | | | | | | | | |

| Unaffiliated issuers (cost: $14,371,437) | | $ | 20,971,765 | | | | | |

| Affiliated issuers (cost: $2,926,359) | | | 3,554,732 | | | $ | 24,526,497 | |

| Cash denominated in currencies other than U.S. dollars (cost: $571) | | | | | | | 571 | |

| Cash | | | | | | | 433 | |

| Unrealized appreciation on open forward currency contracts | | | | | | | 50 | |

| Receivables for: | | | | | | | | |

| Sales of investments | | | 71,055 | | | | | |

| Sales of fund’s shares | | | 27,884 | | | | | |

| Dividends and interest | | | 19,898 | | | | 118,837 | |

| | | | | | | | 24,646,388 | |

| Liabilities: | | | | | | | | |

| Unrealized depreciation on open forward currency contracts | | | | | | | 2,088 | |

| Payables for: | | | | | | | | |

| Purchases of investments | | | 123,355 | | | | | |

| Repurchases of fund’s shares | | | 47,117 | | | | | |

| Closed forward currency contracts | | | 7,489 | | | | | |

| Investment advisory services | | | 12,448 | | | | | |

| Services provided by related parties | | | 9,952 | | | | | |

| Directors’ deferred compensation | | | 2,771 | | | | | |

| Other | | | 495 | | | | 203,627 | |

| Net assets at September 30, 2013 | | | | | | $ | 24,440,673 | |

| | | | | | | | | |

| Net assets consist of: | | | | | | | | |

| Capital paid in on shares of capital stock | | | | | | $ | 16,190,107 | |

| Distributions in excess of net investment income | | | | | | | (177,799 | ) |

| Undistributed net realized gain | | | | | | | 1,201,518 | |

| Net unrealized appreciation | | | | | | | 7,226,847 | |

| Net assets at September 30, 2013 | | | | | | $ | 24,440,673 | |

(dollars and shares in thousands, except per-share amounts)

Total authorized capital stock — 1,000,000 shares, $.01 par value

(503,032 total shares outstanding)

| | | Net assets | | | Shares

outstanding | | | Net asset

value per share | |

| Class A | | $ | 16,454,122 | | | | 336,383 | | | $ | 48.91 | |

| Class B | | | 185,139 | | | | 4,019 | | | | 46.06 | |

| Class C | | | 919,983 | | | | 20,202 | | | | 45.54 | |

| Class F-1 | | | 867,994 | | | | 17,892 | | | | 48.51 | |

| Class F-2 | | | 628,977 | | | | 12,827 | | | | 49.03 | |

| Class 529-A | | | 883,701 | | | | 18,186 | | | | 48.59 | |

| Class 529-B | | | 25,467 | | | | 548 | | | | 46.52 | |

| Class 529-C | | | 272,651 | | | | 5,892 | | | | 46.27 | |

| Class 529-E | | | 47,710 | | | | 997 | | | | 47.87 | |

| Class 529-F-1 | | | 73,408 | | | | 1,506 | | | | 48.73 | |

| Class R-1 | | | 41,678 | | | | 895 | | | | 46.56 | |

| Class R-2 | | | 736,561 | | | | 15,821 | | | | 46.56 | |

| Class R-3 | | | 835,737 | | | | 17,487 | | | | 47.79 | |

| Class R-4 | | | 712,107 | | | | 14,655 | | | | 48.59 | |

| Class R-5 | | | 549,736 | | | | 11,115 | | | | 49.46 | |

| Class R-6 | | | 1,205,702 | | | | 24,607 | | | | 49.00 | |

See Notes to Financial Statements

| Statement of operations | | | |

| for the year ended September 30, 2013 | | (dollars in thousands) | |

| | | | |

| Investment income: | | | | | | | | |

| Income: | | | | | | | | |

| Dividends (net of non-U.S. taxes of $13,296; also includes $29,542 from affiliates) | | $ | 271,605 | | | | | |

| Interest (includes $76 from affiliates) | | | 3,474 | | | $ | 275,079 | |

| Fees and expenses*: | | | | | | | | |

| Investment advisory services | | | 136,894 | | | | | |

| Distribution services | | | 62,007 | | | | | |

| Transfer agent services | | | 40,507 | | | | | |

| Administrative services | | | 4,810 | | | | | |

| Reports to shareholders | | | 1,452 | | | | | |

| Registration statement and prospectus | | | 424 | | | | | |

| Directors’ compensation | | | 818 | | | | | |

| Auditing and legal | | | 184 | | | | | |

| Custodian | | | 4,167 | | | | | |

| State and local taxes | | | 118 | | | | | |

| Other | | | 1,288 | | | | 252,669 | |

| Net investment income | | | | | | | 22,410 | |

| | | | | | | | | |

| Net realized gain and unrealized appreciation on investments, forward currency contracts and currency: | | | | | | | | |

| Net realized gain (loss) on: | | | | | | | | |

| Investments (net of non-U.S. taxes of $51; also includes $37,824 net loss from affiliates) | | | 1,826,413 | | | | | |

| Forward currency contracts | | | (8,633 | ) | | | | |

| Currency transactions | | | (6,051 | ) | | | 1,811,729 | |

| Net unrealized appreciation (depreciation) on: | | | | | | | | |

| Investments | | | 3,232,727 | | | | | |

| Forward currency contracts | | | (2,033 | ) | | | | |

| Currency translations | | | 205 | | | | 3,230,899 | |

| Net realized gain and unrealized appreciation on investments, forward currency contracts and currency | | | | | | | 5,042,628 | |

| | | | | | | | | |

| Net increase in net assets resulting from operations | | | | | | $ | 5,065,038 | |

*Additional information related to class-specific fees and expenses is included in the Notes to Financial Statements.

Statements of changes in net assets

(dollars in thousands)

| | | Year ended September 30 | |

| | | 2013 | | | 2012 | |

| Operations: | | | | | | | | |

| Net investment income | | $ | 22,410 | | | $ | 31,013 | |

| Net realized gain on investments, forward currency contracts, and currency transactions | | | 1,811,729 | | | | 680,973 | |

| Net unrealized appreciation on investments, forward currency contracts, and currency translations | | | 3,230,899 | | | | 3,429,858 | |

| Net increase in net assets resulting from operations | | | 5,065,038 | | | | 4,141,844 | |

| | | | | | | | | |

| Dividends paid to shareholders from net investment income | | | (257,779 | ) | | | (53,307 | ) |

| | | | | | | | | |

| Net capital share transactions | | | (27,946 | ) | | | (1,481,164 | ) |

| | | | | | | | | |

| Total increase in net assets | | | 4,779,313 | | | | 2,607,373 | |

| | | | | | | | | |

| Net assets: | | | | | | | | |

| Beginning of year | | | 19,661,360 | | | | 17,053,987 | |

End of year (including distributions in excess of net investment income:

$(177,799) and $(72,885), respectively) | | $ | 24,440,673 | | | $ | 19,661,360 | |

See Notes to Financial Statements

Notes to financial statements

1. Organization

SMALLCAP World Fund, Inc. (the “fund”) is registered under the Investment Company Act of 1940 as an open-end, diversified management investment company. The fund seeks long-term growth of capital through investments in smaller companies in the U.S. and around the world. Shareholders approved a proposal to reorganize the fund from a Maryland corporation to a Delaware statutory trust. The reorganization may be completed in 2013 or 2014; however, the fund reserves the right to delay the implementation.

The fund has 16 share classes consisting of five retail share classes (Classes A, B and C, as well as two F share classes, F-1 and F-2), five 529 college savings plan share classes (Classes 529-A, 529-B, 529-C, 529-E and 529-F-1) and six retirement plan share classes (Classes R-1, R-2, R-3, R-4, R-5 and R-6). The 529 college savings plan share classes can be used to save for college education. The retirement plan share classes are generally offered only through eligible employer-sponsored retirement plans. The fund’s share classes are further described below:

| Share class | | Initial sales

charge | | Contingent deferred sales

charge upon redemption | | Conversion feature | |

| Classes A and 529-A | | Up to 5.75% | | None (except 1% for certain redemptions within one year of purchase without an initial sales charge) | | None | |

| Classes B and 529-B* | | None | | Declines from 5% to 0% for redemptions within six years of purchase | | Classes B and 529-B convert to Classes A and 529-A, respectively, after eight years | |

| Class C | | None | | 1% for redemptions within one year of purchase | | Class C converts to Class F-1 after 10 years | |

| Class 529-C | | None | | 1% for redemptions within one year of purchase | | None | |

| Class 529-E | | None | | None | | None | |

| Classes F-1, F-2 and 529-F-1 | | None | | None | | None | |

| Classes R-1, R-2, R-3, R-4, R-5 and R-6 | | None | | None | | None | |

* Class B and 529-B shares of the fund are not available for purchase.

Holders of all share classes have equal pro rata rights to assets, dividends and liquidation proceeds. Each share class has identical voting rights, except for the exclusive right to vote on matters affecting only its class. Share classes have different fees and expenses (“class-specific fees and expenses”), primarily due to different arrangements for distribution, administrative and shareholder services. Differences in class-specific fees and expenses will result in differences in net investment income and, therefore, the payment of different per-share dividends by each share class.

2. Significant accounting policies

The financial statements have been prepared to comply with accounting principles generally accepted in the United States of America. These principles require management to make estimates and assumptions that affect reported amounts and disclosures. Actual results could differ from those estimates. The fund follows the significant accounting policies described below, as well as the valuation policies described in the next section on valuation.

Security transactions and related investment income — Security transactions are recorded by the fund as of the date the trades are executed with brokers. Realized gains and losses from security transactions are determined based on the specific identified cost of the securities. In the event a security is purchased with a delayed payment date, the fund will segregate liquid assets sufficient to meet its payment obligations. Dividend income is recognized on the ex-dividend date and interest income is recognized on an accrual basis. Market discounts, premiums and original issue discounts on fixed-income securities are amortized daily over the expected life of the security.

Class allocations — Income, fees and expenses (other than class-specific fees and expenses) and realized and unrealized gains and losses are allocated daily among the various share classes based on their relative net assets. Class-specific fees and expenses, such as distribution, administrative and shareholder services, are charged directly to the respective share class.

Dividends and distributions to shareholders — Dividends and distributions to shareholders are recorded on the ex-dividend date.

Currency translation — Assets and liabilities, including investment securities, denominated in currencies other than U.S. dollars are translated into U.S. dollars at the exchange rates supplied by one or more pricing vendors on the valuation date. Purchases and sales of investment securities and income and expenses are translated into U.S. dollars at the exchange rates on the dates of such transactions. On the accompanying financial statements, the effects of changes in exchange rates on investment securities are included with the net realized gain or loss and net unrealized appreciation or depreciation on investments. The realized gain or loss and unrealized appreciation or depreciation resulting from all other transactions denominated in currencies other than U.S. dollars are disclosed separately.

3. Valuation

Capital Research and Management Company (“CRMC”), the fund’s investment adviser, values the fund’s investments at fair value as defined by accounting principles generally accepted in the United States of America. The net asset value of each share class of the fund is generally determined as of approximately 4:00 p.m. New York time each day the New York Stock Exchange is open.

Methods and inputs — The fund’s investment adviser uses the following methods and inputs to establish the fair value of the fund’s assets and liabilities. Use of particular methods and inputs may vary over time based on availability and relevance as market and economic conditions evolve.

Equity securities are generally valued at the official closing price of, or the last reported sale price on, the exchange or market on which such securities are traded, as of the close of business on the day the securities are being valued or, lacking any sales, at the last available bid price. Prices for each security are taken from the principal exchange or market on which the security trades.

Fixed-income securities, including short-term securities purchased with more than 60 days left to maturity, are generally valued at prices obtained from one or more pricing vendors. Vendors value such securities based on one or more of the inputs described in the following table. The table provides examples of inputs that are commonly relevant for valuing particular classes of fixed-income securities in which the fund is authorized to invest. However, these classifications are not exclusive, and any of the inputs may be used to value any other class of fixed-income security.

| Fixed-income class | Examples of standard inputs |

| All | Benchmark yields, transactions, bids, offers, quotations from dealers and trading systems, new issues, spreads and other relationships observed in the markets among comparable securities; and proprietary pricing models such as yield measures calculated using factors such as cash flows, financial or collateral performance and other reference data (collectively referred to as “standard inputs”) |

| Corporate bonds & notes; convertible securities | Standard inputs and underlying equity of the issuer |

| Bonds & notes of governments & government agencies | Standard inputs and interest rate volatilities |

When the fund’s investment adviser deems it appropriate to do so (such as when vendor prices are unavailable or not deemed to be representative), fixed-income securities will be valued in good faith at the mean quoted bid and ask prices that are reasonably and timely available (or bid prices, if ask prices are not available) or at prices for securities of comparable maturity, quality and type.

Securities with both fixed-income and equity characteristics, or equity securities traded principally among fixed-income dealers, are generally valued in the manner described above for either equity or fixed-income securities, depending on which method is deemed most appropriate by the fund’s investment adviser. Short-term securities purchased within 60 days to maturity are valued at amortized cost, which approximates fair value. The value of short-term securities originally purchased with maturities greater than 60 days is determined based on an amortized value to par when they reach 60 days. Forward currency contracts are valued at the mean of representative quoted bid and ask prices, generally based on prices supplied by one or more pricing vendors.

Securities and other assets for which representative market quotations are not readily available or are considered unreliable by the fund’s investment adviser are fair valued as determined in good faith under fair valuation guidelines adopted by authority of the fund’s board of directors as further described below. The investment adviser follows fair valuation guidelines, consistent with U.S. Securities and Exchange Commission rules and guidance, to consider relevant principles and factors when making fair value determinations. The investment adviser considers relevant indications of value that are reasonably and timely available to it in determining the fair value to be assigned to a particular security, such as the type and cost of the security; contractual or legal restrictions on resale of the security; relevant financial or business developments of the issuer; actively traded similar or related securities; conversion or exchange rights on the security; related corporate actions; significant events occurring after the close of

trading in the security; and changes in overall market conditions. In addition, the closing prices of equity securities that trade in markets outside U.S. time zones may be adjusted to reflect significant events that occur after the close of local trading but before the net asset value of each share class of the fund is determined. Fair valuations and valuations of investments that are not actively trading involve judgment and may differ materially from valuations that would have been used had greater market activity occurred.