UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: Parnassus Funds (811-04044) and Parnassus Income Funds (811-06673)

Parnassus Funds

Parnassus Income Funds

(Exact name of registrant as specified in charter)

1 Market Street, Suite 1600, San Francisco, California 94105

(Address of principal executive offices) (Zip code)

Marc C. Mahon

Parnassus Funds

Parnassus Income Funds

1 Market Street, Suite 1600, San Francisco, California 94105

(Name and address of agent for service)

Registrant’s telephone number, including area code: (415) 778-0200

Date of fiscal year end: December 31

Date of reporting period: December 31, 2016

Item 1: Report to Shareholders

PARNASSUS FUNDS®

ANNUAL REPORT ◾ DECEMBER 31, 2016

PARNASSUS FUNDS

| | |

| |

| Parnassus FundSM | | |

Investor Shares | | PARNX |

Institutional Shares | | PFPRX |

| |

| Parnassus Core Equity FundSM | | |

Investor Shares | | PRBLX |

Institutional Shares | | PRILX |

| |

| Parnassus Endeavor FundSM | | |

Investor Shares | | PARWX |

Institutional Shares | | PFPWX |

| |

| Parnassus Mid Cap FundSM | | |

Investor Shares | | PARMX |

Institutional Shares | | PFPMX |

| |

| Parnassus Asia FundSM | | |

Investor Shares | | PAFSX |

Institutional Shares | | PFPSX |

| |

| Parnassus Fixed Income FundSM | | |

Investor Shares | | PRFIX |

Institutional Shares | | PFPLX |

Table of Contents

| | | | |

| | |

| PARNASSUS FUNDS | | | | Annual Report • 2016 |

February 6, 2017

Dear Shareholder:

I’d like to give you an update on Wells Fargo and its unauthorized opening of accounts. While some of our shareholders have urged us to sell our shares, we believe that Wells Fargo is a far better bank than what is portrayed in the media, and that this is the most important time for an ESG investor to be involved. We met with CEO Tim Sloan in December and had a productive conversation about the bank’s remedies for its customers and employees, discriminatory banking practices towards minority and low-income customers, as well as its financing of the Dakota Access Pipeline. We would not have been able to have this dialogue had we sold our position. While we don’t disclose the results of our engagements, rest assured, we continue to engage with the highest levels of management on these issues.

Turning now to our investment performance, things didn’t look too good early last year, when the market started moving sharply lower in January. The S&P 500 dropped 10.3% from the first of the year until February 11, before shooting up 13.5% to close the first quarter in positive territory. The market swooned again as a result of the Brexit vote, then made another comeback. By the end of the year, the S&P 500 was up a respectable 11.9%.

It was also a very good year for the Parnassus Funds with four of our six funds beating their benchmarks – sometimes by a very significant margin. The Parnassus Endeavor Fund was up an amazing 21.42% for the year, while the Parnassus Asia Fund was up 13.98%, compared to 5.21% for the MSCI AC Asia Pacific Index, with Billy Hwan having an excellent year. Matt Gershuny and Lori Keith continue to do a great job managing the Parnassus Mid Cap Fund, which was up 16.07% compared to 13.80% for the Russell Midcap Index. The Parnassus Fund also beat the S&P 500, climbing 13.46% with Ian Sexsmith and Robert Klaber making a strong contribution. Samantha Palm turned in a solid year, managing the Parnassus Fixed Income Fund.

Finally, Todd Ahlsten and Ben Allen, managers of our largest fund, the Parnassus Core Equity Fund, did not beat the S&P 500 this year, but they came close, with the Parnassus Core Equity Fund – Investor Shares returning 10.41% for the year. More importantly, their long-term track record continues to be spectacular. For example, over the last ten years, the Parnassus Core Equity Fund – Investor Shares has gained an average of 9.47% per year, compared to an average return of 6.93% for the S&P 500. This performance makes the Parnassus Core Equity Fund – Investor Shares the best-performing of all 215 equity income funds followed by Lipper average over the past ten years.*

Speaking of Ben Allen, I have some interesting news to report. As of January 1, 2017, Ben is the new president of Parnassus Investments, the management company that runs the Parnassus Funds. I am now chairman of Parnassus Investments and will continue as chief executive officer. I expect Ben to succeed me as chief executive sometime in the middle of 2018. Although I will be stepping down as chief executive then, I will continue as portfolio manager of the Parnassus Endeavor Fund. I have no plans to stop managing the Parnassus Endeavor Fund, since I am in good health, and I enjoy managing the Fund. I plan to continue managing the Parnassus Endeavor Fund indefinitely, and there are no plans to retire from that job. If you’re wondering about a precedent, I would like to point out that Warren Buffett is still managing Berkshire Hathaway and he’s 86 years old. I’m only 73, so I have a long way to go.

Ben will be 41 years old in 2018, which is exactly the age I was when I became chief executive of Parnassus Investments. I will have served as chief executive for 34 years in 2018, so we can expect Ben to serve another 34 years until 2052 when he’s ready to retire at age 75. We like long-range planning at Parnassus, so our people stay here a long time.

I am delighted that Ben has agreed to serve as chief executive, and I know he’ll do a great job. Ben is one of the two portfolio managers of the Parnassus Core Equity Fund, and he will continue in that position as well, so don’t worry about your investment in the Parnassus Core Equity Fund. All of us at Parnassus do more than one

job, and it has worked well for us. Right now, I am the lead manager of the Parnassus Fund and the Parnassus Asia Fund, and I’m the sole manager of the Parnassus Endeavor Fund, and you’ll notice that all those funds are doing fine.

4

| | | | |

| | |

| Annual Report • 2016 | | | | PARNASSUS FUNDS |

Ben joined Parnassus as a research intern in 2004, when he was still in business school at Berkeley. In 2005, he joined us full-time as a Senior Research Analyst. In 2008, he became Director of Research, and in 2012, he became a portfolio manager of our largest fund, the Parnassus Core Equity Fund. Prior to joining Parnassus, he worked at Morgan Stanley in New York, first as an investment banking analyst, and later, in the firm’s venture capital group. Raised in Massachusetts, he is an alumnus of the Boston Latin School. Ben graduated Phi Beta Kappa and magna cum laude from Georgetown University with a bachelor’s degree in government, and completed the general course in philosophy at the London School of Economics. He received his master’s degree in business administration from the University of California at Berkeley. We are all proud that we have someone of Ben’s caliber to lead Parnassus into its next chapter.

Below, you will see a photo of the Trustees of the Parnassus Funds. From left to right are Jeanie Joe, Donald Boteler, Alecia DeCoudreaux and Jerome Dodson. These are the people who govern the Funds.

Yours truly,

Jerome L. Dodson

Chairman

| * | The Parnassus Core Equity Fund – Investor Shares placed 410 of 519 funds, 106 of 318 funds and 19 of 318 funds for the one-, three- and five-year periods, respectively. |

| | Performance data quoted represent past performance and are no guarantee of future returns. Current performance may be lower or higher than the performance data quoted. |

| | Please see the following pages for more detailed information regarding each fund’s performance and the risks associated with investing in the funds. |

5

| | | | |

| | |

| PARNASSUS FUNDS | | | | Annual Report • 2016 |

PARNASSUS FUND

Ticker: Investor Shares - PARNX

Ticker: Institutional Shares - PFPRX

As of December 31, 2016, the net asset value per share (“NAV”) of the Parnassus Fund – Investor Shares was $44.97, so after taking dividends into account, the total return for the year was 13.46%. This compares to a gain of 11.94% for the S&P 500 Index (“S&P 500”) and a gain of 10.25% for the Lipper Multi-Cap Core Average, which represents the average return of the multi-cap core funds followed by Lipper (“Lipper average”). In a volatile year for the stock market, the Parnassus Fund –Investor Shares performed very well, beating the S&P 500 by 1.52% and outpacing the Lipper average by more than three percentage points. We trailed the S&P 500 for most of the year, but we didn’t panic because we believed that sooner or later the market would recognize the value we saw in our securities. We’re pleased that our patience and conviction paid off.

Below is a table comparing the Parnassus Fund with the S&P 500 and the Lipper average over the past one-, three-, five- and ten-year periods. You will notice that we’re ahead of both benchmarks for all time periods. Most striking is the ten-year number, where we have gained an average of 9.66% per year, which is 2.73% per year ahead of the S&P 500 and 3.72% per year ahead of the Lipper average.

| | | | | | | | | | | | | | | | | | | | | | | | |

| Parnassus Fund | |

Average Annual Total

Returns (%) | | One

Year | | | Three

Years | | | Five

Years | | | Ten

Years | | | Gross

Expense

Ratio | | | Net

Expense

Ratio | |

for period ended

December 31, 2016 | | | | | | |

| | | | | | | |

Parnassus Fund

Investor Shares | | | 13.46 | | | | 9.26 | | | | 17.15 | | | | 9.66 | | | | 0.84 | | | | 0.84 | |

| | | | | | | |

| Parnassus Fund Institutional Shares | | | 13.59 | | | | 9.35 | | | | 17.21 | | | | 9.68 | | | | 0.70 | | | | 0.70 | |

| | | | | | | |

| S&P 500 Index | | | 11.94 | | | | 8.85 | | | | 14.63 | | | | 6.93 | | | | NA | | | | NA | |

| | | | | | | |

| Lipper Multi-Cap Core Average | | | 10.25 | | | | 6.08 | | | | 13.06 | | | | 5.94 | | | | NA | | | | NA | |

The average annual total return for the Parnassus Fund-Institutional Shares from commencement (April 30, 2015) was 6.40%. Performance shown prior to the inception of the Institutional Shares reflects the performance of the Parnassus Fund-Investor Shares and includes expenses that are not applicable to and are higher than those of the Institutional Shares. The performance of Institutional Shares differs from that shown for the Investor Shares to the extent that the classes do not have the same expenses. Performance data quoted represent past performance and are no guarantee of future returns. Current performance may be lower or higher than the performance data quoted. Current performance information to the most recent month-end is available on the Parnassus website (www.parnassus.com). Investment return and principal value will fluctuate, so an investor’s shares, when redeemed, may be worth more or less than their original principal cost. Returns shown in the table do not reflect the deduction of taxes a shareholder may pay on fund distributions or redemption of shares. The S&P 500 is an unmanaged index of common stocks, and it is not possible to invest directly in an index. Index figures do not take any expenses, fees or taxes into account, but mutual fund returns do.

Before investing, an investor should carefully consider the investment objectives, risks, charges and expenses of the Fund and should carefully read the prospectus or summary prospectus, which contain this and other information. The prospectus or summary prospectus can be obtained on the Parnassus website or by calling (800) 999-3505. As described in the Fund’s current prospectus dated May 1, 2016, Parnassus Investments has contractually agreed to limit total operating expenses to 0.99% of net assets for the Parnassus Fund-Investor Shares and to 0.94% of net assets for the Parnassus Fund-Institutional Shares. This agreement will not be terminated prior to May 1, 2017, and may be continued indefinitely by the Adviser on a year-to-year basis.

Company Analysis

Seven companies each contributed 100 basis points (a basis point is 1/100th of one percent) or more to the Parnassus Fund’s return this year, while only two subtracted 80 basis points or more from the return. The Fund’s weakest performer was Perrigo, the leading producer of store-brand generic drugs, as its stock plummeted 42.5% from $144.70 to $83.23, cutting 103 basis points from the Fund’s return. The shares sank in April after longtime CEO Joe Papa resigned to become the CEO of Valeant Pharmaceuticals. The stock continued to move lower throughout the year, as the company cut its earnings guidance three times, from nearly $10 per share to just $7. The business underperformed due to declining prescription generic drug prices and soft growth from Omega, Perrigo’s European business. We sold our position during the year due to our concerns that the prescription generic pricing environment would get worse, and that it would take longer than expected to fix Omega.

Our other laggard was Gilead, a biotechnology firm that makes therapies for HIV and hepatitis C. Gilead sliced 98 basis points off the Fund’s return, as its stock declined 29.2% from $101.19 to $71.61. The stock dropped due to weakness in the hepatitis C business, as pricing came under pressure due to increased competition, and the patient population fell because Gilead’s drugs cure patients of this damaging disease. The stock is on the bargain table, and the company has a strong balance sheet and a proven track record of innovation, so we increased our position throughout the year.

6

| | | | |

| | |

| Annual Report • 2016 | | | | PARNASSUS FUNDS |

The Fund’s best performer was Applied Materials, the semiconductor-equipment manufacturer. The stock soared 72.8% during the year from $18.67 to $32.27, increasing the Fund’s return by an astounding 216 basis points. Demand accelerated

for the company’s equipment, spurred by the transition in NAND-flash memory architecture from planar to 3D and the adoption of organic light-emitting diode (OLED) screens in smartphones. Investors celebrated, as new orders and product backlog both hit all-time highs, and the company forecasted more growth at its analyst meeting in September.

Micron Technology was right on Applied Materials’ heels, adding an amazing 215 basis points to the Fund’s return, as the stock raced higher by 54.8% from $14.16 to $21.92. It was a roller-coaster year for Micron, as prices of its main product, dynamic random access memory semiconductor chips (also known as DRAMS), were falling sharply to begin the year. DRAM chips are commodities, and their pricing is volatile, going up sharply when demand exceeds supply and dropping suddenly when the balance tilts in the other direction. We invested because production capacity growth had slowed below demand, so we were confident DRAM prices would eventually rise. Sure enough, in the second half of the year DRAM prices rose sharply, and we’re enjoying the upside.

International Business Machines (IBM), one of the world’s largest providers of information technology solutions and services, rose 20.6% from $137.62 to $165.99, contributing 119 basis points to the Fund’s return. The stock moved higher as investors became more optimistic about the company’s transformation from a stodgy, old provider of mainframes to an exciting trendsetter in data analytics, cloud software and cognitive solutions.

Trimble makes GPS positioning and precision-measurement products that increase the efficiency of construction workers, farmers and truck drivers. The stock soared 40.6% from $21.45 to $30.15, increasing the Fund’s return by 107 basis points, as Trimble returned to earnings growth despite a downturn in all three of its end markets. A number of new products and the increasing adoption of the company’s software programs boosted revenue, while a renewed focus on cost management expanded margins.

Cummins, the diesel-engine manufacturer, boosted the Fund’s return by 104 basis points, as its stock gained 55.3% from $88.01 to $136.67. We sold our position in the spring, as the stock shifted into high gear after Cummins’ 2016 earnings guidance, as management’s execution on its cost-cutting initiatives offset a cyclical downturn in truck sales.

John Deere, world-renowned for its big, green tractors, added 102 basis points to the Fund’s return, as the stock climbed 35.1% from $76.27 to $103.04. The stock ploughed ahead as Deere’s 2017 financial guidance exceeded expectations, giving investors hope that earnings have bottomed after three years of declines. Farmers coping with low crop prices have put off investing in equipment, but eventually they’ll need to buy new tractors. When they do, Deere’s earnings should move higher, so we’re holding onto our shares.

Charles Schwab, the San Francisco-based bank and brokerage firm, rose 19.9% from $32.93 to $39.47, contributing 101 basis points to the

|

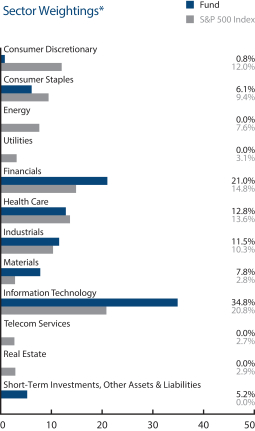

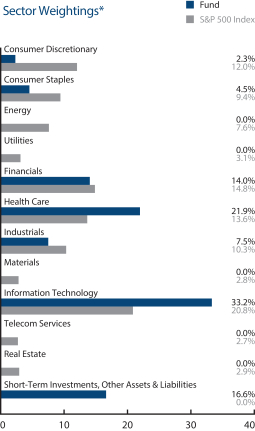

Parnassus Fund as of December 31, 2016 (percentage of net assets) |

* For purposes of categorizing securities for diversification requirements under the Investment Company Act, the Fund uses industry classifications that are more specific than those used for the chart.

Top 10 Holdings

(percentage of net assets)

| | | | |

| |

| Micron Technology Inc. | | | 5.1% | |

| |

| IBM Corp. | | | 4.6% | |

| |

| Allergan plc | | | 4.2% | |

| |

| Charles Schwab Corp. | | | 4.2% | |

| |

| Gilead Sciences Inc. | | | 4.1% | |

| |

| Motorola Solutions Inc. | | | 3.9% | |

| |

| Progressive Corp. | | | 3.3% | |

| |

| Pentair plc | | | 3.0% | |

| |

| Potash Corp. | | | 3.0% | |

| |

| Wells Fargo & Co. | | | 2.9% | |

Portfolio characteristics and holdings are subject to change periodically.

7

| | | | |

| | |

| PARNASSUS FUNDS | | | | Annual Report • 2016 |

Fund’s return. Schwab’s earnings on its bank assets and money market funds move up and down with interest rates. The stock spent most of the year underwater, as interest rates fell and central bankers in Japan and Europe pushed their rates into negative territory. The tide started to turn in July, however, as the U.S. economy improved and interest rates rose. Schwab’s stock jumped as rates surged even higher after the U.S. election, because many of President-elect Trump’s policies are inflationary.

Outlook and Strategy

The S&P 500 was up nearly 11.94% in 2016, marking the fourth year out of the past five that the market has earned a double-digit return. But 2016 was a tumultuous year for investors, beginning with the worst 10-day start ever for the S&P 500. The market clawed its way back, only to fall again after the Brexit vote in June. However, the U.S. economy kept chugging along, and the S&P 500

|

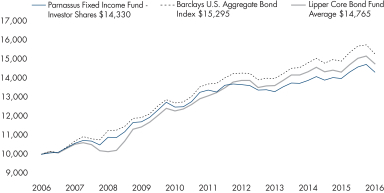

|

| Value on December 31, 2016 of $10,000 invested on December 31, 2006 |

The chart shows the growth in value of a hypothetical $10,000 investment over the last ten years and does not reflect the deduction of taxes a shareholder would pay on fund distributions or the redemption of fund shares.

quickly regained the lost ground. In November, the market plunged in after-hours trading the night of the U.S. election. But the next morning, investors assessed Mr. Trump’s proposed policies and became euphoric. The new administration’s plans to lower taxes, improve our aging infrastructure and bring jobs back to the U.S. propelled the S&P 500 to an all-time high.

Heading into 2017, the U.S. economy looks robust. An average of 180,000 jobs per month are being created, resulting in an unemployment rate of only 4.6% – the lowest level since August 2007. Interest rates remain low, and the housing market has recovered from the aftermath of the housing bubble. Abroad, growth in Europe has been stronger than analysts expected following Brexit, and China’s economy continues to grow at nearly a 7% clip.

The market is forward-looking, though, and has already priced in much of the positive news. At year-end, the S&P 500 traded at 20.3 times earnings for the last twelve months compared to a historic range of 15-16 times. The bull market has lasted more than seven years now, rising more than 259% from its trough in 2009.

After such a great run, some of you may instinctively want to sell everything and wait for a better time to reenter. We don’t try to time the market, and we don’t recommend that strategy. While the market is fully-valued, that doesn’t mean it will go down. It can stay fully-valued for a long time without dropping significantly lower. The robust economy, combined with Mr. Trump’s proposed policies, could cause an acceleration in corporate earnings, which could push the market even higher.

We’re excited by how the Parnassus Fund is positioned as we turn the page to 2017. Two of our largest overweight sectors, relative to the S&P 500, are financials and information technology. We expect rising interest rates and fewer regulations to boost bank earnings and push their stocks higher. Within the information technology sector, we own a collection of competitively advantaged businesses with strong growth profiles that trade at compelling valuations.

As always, you can count on us to do what we know best – search for great businesses to invest in at bargain prices. We have a long list of stocks that we monitor, and any weakness in the market should make some of these stocks go down, which should provide us with some exciting opportunities.

Yours truly,

| | | | |

| |

| |

|

Jerome L. Dodson Lead Portfolio Manager | | Robert J. Klaber Portfolio Manager | | Ian Sexsmith Portfolio Manager |

8

| | | | |

| | |

| Annual Report • 2016 | | | | PARNASSUS FUNDS |

PARNASSUS CORE EQUITY FUND

Ticker: Investor Shares - PRBLX

Ticker: Institutional Shares - PRILX

As of December 31, 2016, the net asset value (NAV) of the Parnassus Core Equity Fund – Investor Shares was $39.29. After taking dividends into account, the total return for the fourth quarter was 2.20%. This compares to increases of 3.82% for the S&P 500 Index (“S&P 500”) and 4.41% for the Lipper Equity Income Fund Average, which represents the average equity income funds followed by Lipper (“Lipper average”). For the year, the Fund gained 10.41%, which falls short of the 11.94% and 13.86% returns for the S&P 500 and Lipper average, respectively.

Below is a table that summarizes the performances of the Parnassus Core Equity Fund, the S&P 500 and the Lipper average. The returns are for the one-, three-, five- and ten-year periods.

| | | | | | | | | | | | | | | | | | | | | | | | |

| Parnassus Core Equity Fund | |

Average Annual Total

Returns (%) | | One

Year | | | Three

Years | | | Five

Years | | | Ten

Years | | | Gross

Expense

Ratio | | | Net

Expense

Ratio | |

for period ended

December 31, 2016 | | | | | | |

| | | | | | | |

| Parnassus Core Equity Fund Investor Shares | | | 10.41 | | | | 7.92 | | | | 14.22 | | | | 9.47 | | | | 0.88 | | | | 0.87 | |

| | | | | | | |

| Parnassus Core Equity Fund Institutional Shares | | | 10.61 | | | | 8.14 | | | | 14.42 | | | | 9.69 | | | | 0.67 | | | | 0.67 | |

| | | | | | | |

| S&P 500 Index | | | 11.94 | | | | 8.85 | | | | 14.63 | | | | 6.93 | | | | NA | | | | NA | |

| | | | | | | |

| Lipper Equity Income Fund Average | | | 13.86 | | | | 6.39 | | | | 11.52 | | | | 5.94 | | | | NA | | | | NA | |

The average annual total return for the Parnassus Core Equity Fund-Institutional Shares from commencement (April 28, 2006) was 9.79%. Performance shown prior to the inception of the Institutional Shares reflects the performance of the Parnassus Core Equity Fund-Investor Shares and includes expenses that are not applicable to and are higher than those of the Institutional Shares. The performance of the Institutional Shares differs from that shown for the Investor Shares to the extent that the classes do not have the same expenses. Performance data quoted represent past performance and are no guarantee of future returns. Current performance may be lower or higher than the performance data quoted, and current performance information to the most recent month-end is available on the Parnassus website (www.parnassus.com). Investment return and principal value will fluctuate, so an investor’s shares, when redeemed, may be worth more or less than their original principal cost. Returns shown in the table do not reflect the deduction of taxes a shareholder may pay on fund distributions or redemption of shares. The S&P 500 is an unmanaged index of common stocks, and it is not possible to invest directly in an index. Index figures do not take any expenses, fees or taxes into account, but mutual fund returns do.

Before investing, an investor should carefully consider the investment objectives, risks, charges and expenses of the Fund and should carefully read the prospectus or summary prospectus, which contain this and other information. The prospectus or summary prospectus can be obtained on the Parnassus website or by calling (800) 999-3505. As described in the Fund’s current prospectus dated May 1, 2016, Parnassus Investments has contractually agreed to limit total operating expenses to 0.87% of net assets for the Parnassus Core Equity Fund-Investor Shares and to 0.78% of net assets for the Parnassus Core Equity Fund-Institutional Shares. This agreement will not be terminated prior to May 1, 2017, and may be continued indefinitely by the Adviser on a year-to-year basis.

Year in Review

The Parnassus Core Equity Fund – Investor Shares returned 10.41% for the year and trailed the S&P 500 by 1.53%. Sector allocations had a slightly negative effect on our relative performance. Our underweight position in energy stocks cost us the most, as this group gained 27% on average during the year, far outpacing the index. We had a slight overweight vs. the S&P 500 in health care, which was the year’s worst performing sector. But far more damaging was that our health care stocks were down 19% in aggregate, much worse than the overall sector, which dropped 2%. This resulted in a headwind of more than 300 basis points for the Fund’s return. While our non-health care stocks outperformed the index, it simply wasn’t enough to overcome our losses in health care.

Not surprisingly, our three biggest losers this year were health care stocks. Our worst performer was Perrigo, the leading producer of store-brand generic drugs, which plummeted 36.0% from $144.70 to our average selling price of $92.68, cutting 131 basis points (a basis point is 1/100th of one percent) from the Fund’s return. Shares sank in April after longtime CEO Joe Papa resigned to become CEO of Valeant Pharmaceuticals. The stock continued to move lower throughout the year because the company cut its earnings guidance three times. Whereas management initially expected nearly $10 per share in 2016 earnings, by the end of the year, the company expected to earn just $7. The business underperformed due to declining generic drug prices and soft growth from Omega, Perrigo’s European business.

Gilead Sciences fell 29.2% in 2016 from $101.19 to $71.61 and trimmed 124 basis points off the Fund’s return. While Gilead is best-known for its

9

| | | | |

| | |

| PARNASSUS FUNDS | | | | Annual Report • 2016 |

life-saving HIV drugs, the spectacular rise of its hepatitis C cure has driven recent earnings growth. After the fastest drug sales launch in history (measured by sales), Gilead’s hepatitis C business declined in 2016 due to several headwinds, including an

unfavorable payer mix, fewer patients and increased competition.

Trading at just seven times earnings, Gilead’s stock appears to be an absolute bargain. Investors seem to be undervaluing Gilead’s innovative and growing HIV franchise. In addition, while Gilead’s hepatitis C drug sales will decline over time, a large population of untreated patients remains, so the drug should generate significant cash flows into the next decade. We also think that Gilead has a promising drug pipeline, for which investors are attributing very little value. For these reasons, Gilead was our second largest holding at year-end.

Allergan, a pharmaceutical company best known for developing Botox, reduced our fund’s return by 102 basis points as the stock dropped 32.8% from $312.50 to $210.01. Shares sank in April, when Pfizer terminated its plans to acquire Allergan after new rules from the U.S. Treasury made it almost certain that the combined entity would not receive favorable tax treatment. The stock fell again later in the year, after management reduced guidance due to weaker than expected sales.

Despite these issues, we still own the stock. We believe Allergan has a terrific product portfolio, with several fast-growing cash pay businesses, and a rich pipeline. It’s also positive that Allergan sold its generic drug unit to Teva for $40 billion, a deal that strengthened the company’s balance sheet.

Our biggest winner was Applied Materials, the maker of equipment used in semiconductor manufacturing. The stock contributed 172 basis points to the Fund’s return, as it surged 72.8% from $18.67 to $32.27. During 2016, orders, revenues and earnings all grew to the highest levels in the company’s history. Additional market expansion and share gain opportunities, particularly around new transistor architectures and advanced display technologies, contributed to the record performance. We sold some of our position given the dramatic price appreciation, but continue to own some shares.

Xylem is a global industrial company that provides a complete set of products for the water industry, including pumps and filters. The company contributed 109 basis points to the Fund’s return, as its stock increased 35.7% from $36.50 to $49.52. Global public utility markets remained strong, as municipalities continued to invest in aging water infrastructure. During the year, the company completed the acquisition of Sensus, a leading provider of smart water meters, and Visenti, a water leak detection and pressure management business. These acquisitions meaningfully broaden Xylem’s advanced technology product suite and solidify its position as a market leader in intelligent water solutions.

Long-time portfolio holding Sysco Foodservices, the largest food distributor in the U.S., had a fantastic year as the stock rose 35.0% from $41.00 to $55.37 and boosted our fund’s return by 109 basis points. The company reported strong earnings growth in 2016 due to gross margin improvement, case volume growth and cost reductions. Sysco also grew its international business significantly with the acquisition of U.K.-based Brakes Group for $3.1 billion.

|

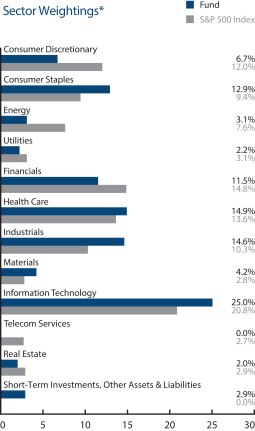

Parnassus Core Equity Fund as of December 31, 2016 (percentage of net assets) |

* For purposes of categorizing securities for diversification requirements under the Investment Company Act, the Fund uses industry classifications that are more specific than those used for the chart.

Top 10 Holdings

(percentage of net assets)

| | | | |

| |

| Wells Fargo & Co. | | | 4.9% | |

| |

| Gilead Sciences Inc. | | | 4.5% | |

| |

| Charles Schwab Corp. | | | 4.0% | |

| |

| Apple Inc. | | | 3.9% | |

| |

| The Walt Disney Co. | | | 3.8% | |

| |

| Danaher Corp. | | | 3.7% | |

| |

| Intel Corp. | | | 3.5% | |

| |

| United Parcel Service Inc., Class B | | | 3.3% | |

| |

| Allergan plc | | | 3.2% | |

| |

| Sysco Corp. | | | 3.2% | |

Portfolio characteristics and holdings are subject to change periodically.

10

| | | | |

| | |

| Annual Report • 2016 | | | | PARNASSUS FUNDS |

Outlook and Strategy

We are very focused on what impact Donald Trump will make on the business landscape as President. So far, he seems intent on reducing taxes and regulations, altering international trade deals, overhauling Obama’s Affordable Care Act and boosting infrastructure spending. In some of these areas, there is overlap with traditional Republican positions. In others, especially large scale deficit spending, Trump appears to be at odds with his party’s leadership in the legislative branch. As a result, there’s high uncertainty as to the specifics of Trump’s business-related policy changes. Whatever the details, there’s no doubt that the federal government’s policies and overall stance toward business will change dramatically, and there will be winners and losers among publicly traded companies.

The health care industry is especially sensitive to government policy, and we expect our portfolio

| | |

|

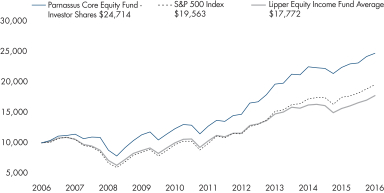

| Value on December 31, 2016 of $10,000 invested on December 31, 2006 |

The chart shows the growth in value of a hypothetical $10,000 investment over the last ten years and does not reflect the deduction of taxes a shareholder would pay on fund distributions or the redemption of fund shares.

companies in this area to face uncertainty in 2017. Our overall strategy in health care is to invest in companies that offer either novel science or cost-reducing products and services. Even though 2016 was very disappointing for our health care investments, we still think this formula will work over the long-term. An aging population that will demand high-quality medicine at affordable prices is a very powerful secular trend. This tailwind will persist and will hopefully support our health care stocks, regardless of what changes Trump and Congress make to existing health care laws.

We’re also intently watching the Federal Reserve. Its leader, Janet Yellen, has just over a year left in office, and it seems likely that she’ll finish her term with more interest rate hikes. We made two allocation decisions last year that should help returns if rates rise in 2017. First, the Fund is far more invested in financial stocks, which generally benefit from a higher interest rate environment. We added Wells Fargo to the portfolio in May, and we increased our position in Charles Schwab. As a result, we now have an allocation of 11.5% in financials, up from 5.1% a year ago. The second move was reducing our exposure to utilities stocks. If interest rates go up, we would expect the dividend yields for utilities to go up too, and this would mean the stocks would go down. At year end, the Fund was just 2.2% invested in utilities, down from 5.3% a year ago.

The Fund’s largest sector underweights relative to the S&P 500 are in consumer discretionary and energy stocks. These sectors tend to be highly cyclical, so our lack of exposure in these areas should bolster our downside protection in a market correction. Offsetting this are overweights in industrials and technology stocks, which also tend to be highly cyclical. Overall, we think the Fund is positioned to perform well in a wide range of potential outcomes in 2017. If stocks continue to move up, we have plenty of stocks that can outpace the index in a bull market. If stocks go down, we think our portfolio companies should hold up well, because of their relatively attractive valuations, robust balance sheets and attractive long-term business prospects.

We thank you for your investment in the Parnassus Core Equity Fund.

| | |

| |

|

Todd C. Ahlsten Lead Portfolio Manager | | Benjamin E. Allen Portfolio Manager |

11

| | | | |

| | |

| PARNASSUS FUNDS | | | | Annual Report • 2016 |

PARNASSUS ENDEAVOR FUND

Ticker: Investor Shares - PARWX

Ticker: Institutional Shares - PFPWX

As of December 31, 2016, the NAV of the Parnassus Endeavor Fund – Investor Shares was $32.99, so after taking dividends into account, the total return for the year was 21.42%. This compares to a return of 11.94% for the S&P 500 Index (“S&P 500”) and 10.25% for the Lipper Multi-Cap Core Average, which represents the average return of the multi-cap core funds followed by Lipper (“Lipper average”). It was a great year for the Parnassus Endeavor Fund, and I’m happy that we were able to give our shareholders such an attractive return. We beat the S&P 500 by more than nine percentage points, and we beat the Lipper average by more than 11 percentage points. This is even more remarkable, when we consider that the average mutual fund does not even beat the S&P 500.

Below is a table comparing the Parnassus Endeavor Fund with the S&P 500 and the Lipper average over the past one-, three-, five- and ten-year periods. As you can see, the Parnassus Endeavor Fund outperformed both benchmarks for all time periods.

| | | | | | | | | | | | | | | | | | | | | | | | |

| Parnassus Endeavor Fund | | | | | | | |

Average Annual Total

Returns (%) | | One

Year | | | Three

Years | | | Five

Years | | | Ten

Years | | | Gross

Expense

Ratio | | | Net

Expense

Ratio | |

for period ended

December 31, 2016 | | | | | | |

| | | | | | | |

Parnassus Endeavor Fund

Investor Shares | | | 21.42 | | | | 14.11 | | | | 18.91 | | | | 12.23 | | | | 0.98 | | | | 0.95 | |

| | | | | | | |

Parnassus Endeavor Fund

Institutional Shares | | | 21.68 | | | | 14.24 | | | | 18.99 | | | | 12.27 | | | | 0.75 | | | | 0.75 | |

| | | | | | | |

| S&P 500 Index | | | 11.94 | | | | 8.85 | | | | 14.63 | | | | 6.93 | | | | NA | | | | NA | |

| | | | | | | |

| Lipper Multi-Cap Core Average | | | 10.25 | | | | 6.08 | | | | 13.06 | | | | 5.94 | | | | NA | | | | NA | |

The average annual total return for the Parnassus Endeavor Fund-Institutional Shares from commencement (April 30, 2015) was 12.35%. Performance shown prior to the inception of the Institutional Shares reflects the performance of the Parnassus Endeavor Fund-Investor Shares and includes expenses that are not applicable to and are higher than those of the Institutional Shares. The performance of the Institutional Shares differs from that shown for the Investor Shares to the extent that the classes do not have the same expenses. Performance data quoted represent past performance and are no guarantee of future returns. Current performance may be lower or higher than the performance data quoted. Current performance information to the most recent month-end is available on the Parnassus website (www.parnassus.com). Investment return and principal value will fluctuate, so an investor’s shares, when redeemed, may be worth more or less than their original principal cost. Returns shown in the table do not reflect the deduction of taxes a shareholder may pay on fund distributions or redemption of shares. The S&P 500 is an unmanaged index of common stocks, and it is not possible to invest directly in an index. Index figures do not take any expenses, fees or taxes into account, but mutual fund returns do.

Before investing, an investor should carefully consider the investment objectives, risks, charges and expenses of the Fund and should carefully read the prospectus or summary prospectus, which contain this and other information. The prospectus or summary prospectus can be obtained on the Parnassus website or by calling (800) 999-3505. As described in the Fund’s current prospectus dated May 1, 2016, Parnassus Investments has contractually agreed to limit total operating expenses to 0.95% of net assets for the Parnassus Endeavor Fund-Investor Shares and to 0.83% of net assets for the Parnassus Endeavor Fund-Institutional Shares. This agreement will not be terminated prior to May 1, 2017, and may be continued indefinitely by the Adviser on a year-to-year basis.

Most striking is the fact that the Parnassus Endeavor Fund – Investor Shares has beaten the S&P 500 by more than five percentage points per year over the past ten years, averaging 12.23% per year, compared to 6.93% per year for the S&P 500. This performance has made the Parnassus Endeavor Fund the best-performing of all 367 multi-cap core funds followed by Lipper over the past ten years.*

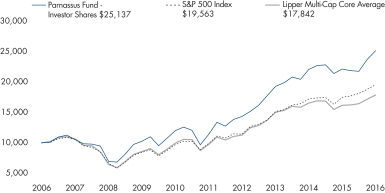

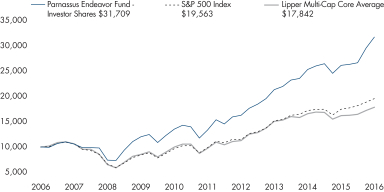

To put the Fund’s performance in dollar terms, look at the graph on page 14. It shows the growth of a hypothetical $10,000 investment in the Fund made ten years ago, compared to the growth of a $10,000 investment in the S&P 500 or the Lipper average. Had you been able to invest $10,000 in the S&P 500, you would have had $19,563 on December 31 of 2016, and if you would have invested $10,000 in the multi-cap core funds covered by Lipper average, you would have had $17,842. By comparison, you would have had $31,709 if you had invested in the Parnassus Endeavor Fund. In other words, you would have made $9,563 with the S&P and $7,842 with the Lipper average, but $21,709 with the Parnassus Endeavor Fund, or more than double over the ten-year period.

Quite often, people will ask me why the Parnassus Endeavor Fund has done so well. There are really two sets of answers. The first set revolves around environmental, social and governance factors (“ESG”) with workplace issues the most important. A company that treats its employees well has a much more motivated workforce, and it

(*For the one-, three- and five-year periods, the Fund was #14 of 746 funds, #1 of 645 funds and #6 out of 575 funds, respectively.)

12

| | | | |

| | |

| Annual Report • 2016 | | | | PARNASSUS FUNDS |

can attract better people. A firm that practices environmental responsibility is less likely to be sued or fined, and this type of firm is more likely to have enlightened and capable management.

The other set of issues involves valuation. At the Parnassus Endeavor Fund, we calculate the intrinsic value of a company, and we won’t invest in a company unless the stock price falls to one-third below its intrinsic value. This gives us an enormous margin of safety. Of course, there is always some negative event that causes the stock price to go down so much, so it’s emotionally difficult to invest in a stock after the company has suffered a big setback. That’s why most investors aren’t able to invest, when the stock drops by that much. I admit that it’s also difficult for me to do that, but I’m a pretty even-tempered person most of the time, so I have good control of my emotions. The three steps, then, are (1) knowing enough about finance to calculate the intrinsic value of a company, (2) determining if a company’s difficulties are temporary or permanent and (3) having the emotional wherewithal to invest when the stock is down.

Company Analysis

There were seven stocks that contributed the most to the Fund’s strong return in 2016, with each of them adding 149 basis points or more to the Fund’s return. (Each basis point is equal to 0.01% or one-hundredth of a percent, so a gain of 149 basis points is equal to 1.49%.) There were only two stocks that had a substantial negative impact on the Fund’s return, so I’ll discuss those first.

The stock that hurt us the most was Perrigo, the leading producer of store-branded generic drugs, which saw its stock drop 42.5% from $144.70 to $83.23, cutting 222 basis points or 2.2% off the value of the Fund’s return. Longtime CEO Joe Papa left the company in April to assume the same job at Valeant, the troubled pharmaceutical-maker. Also, the company bought Omega, a European pharmaceutical business, which turned out to have a lot of problems. Finally, Perrigo’s prescription generic drug business has faced more competition from Mylan and Teva Pharmaceuticals, which cut deeply into the company’s earnings. We added to our position in the stock as it moved lower, because the issue is very undervalued, and I think management can turn the company around. The store-brand generic business (non-prescription) continues to do very well and provides a stable base for a rebound.

Gilead, a biotechnology firm that makes therapies for HIV and hepatitis C, sliced 130 basis points off the Fund’s return, as the stock sank 29.2% from $101.19 to $71.61. Because the company’s hepatitis C therapy cured so many people, there is less demand for the drug, so earnings declined. The stock is now an absolute bargain, trading at only seven times earnings. We added to our position, since the company has a strong balance sheet, plenty of cash and has a proven track record of innovation.

Of the seven stocks that powered our performance for the year, four were semiconductor companies: Micron Technology, Applied Materials, Qualcomm and Lam Research. Strong demand for semiconductors in 2016 moved these stocks much higher. Micron Technology topped the charts, adding 448 basis points (4.48%) to the Fund’s return, as the

| | |

Parnassus Endeavor Fund as of December 31, 2016 (percentage of net assets) |

* For purposes of categorizing securities for diversification requirements under the Investment Company Act, the Fund uses industry classifications that are more specific than those used for the chart.

Top 10 Holdings

(percentage of net assets)

| | | | |

| |

| Micron Technology Inc. | | | 5.3% | |

| |

| Allergan plc | | | 5.1% | |

| |

| QUALCOMM Inc. | | | 4.7% | |

| |

| McKesson Corp. | | | 4.6% | |

| |

| American Express Co. | | | 4.6% | |

| |

| Perrigo Co. plc | | | 4.6% | |

| |

| Gilead Sciences Inc. | | | 4.6% | |

| |

| IBM Corp. | | | 4.6% | |

| |

| Whole Foods Market Inc. | | | 4.5% | |

| |

| Ciena Corp. | | | 3.9% | |

Portfolio characteristics and holdings are subject to change periodically.

13

| | | | |

| | |

| PARNASSUS FUNDS | | | | Annual Report • 2016 |

stock soared 103% from our cost of $10.80 where we bought it early in the year to $21.92 by the end of the year. Micron makes two kinds of memory chips, DRAMs (dynamic random access memory) and NAND flash memory chips. Micron’s shares are quite volatile, since both its main products are commodities, which are sensitive to supply-and-demand relationships. During 2016, demand grew more than supply, so prices firmed up and Micron’s earnings improved.

Applied Materials, the leading producer of equipment used in making semiconductors, soared 72.8% during the year from $18.67 to $32.27, adding 420 basis points to the Fund’s return. The stock rose early in the year, as demand accelerated for capital equipment by customers such as Intel and Samsung. The stock moved even higher in the second half of the year, after the company announced strong earnings and new orders that pushed backlog to an all-time high.

| | |

|

| Value on December 31, 2016 of $10,000 invested on December 31, 2006 |

The chart shows the growth in value of a hypothetical $10,000 investment over the last ten years and does not reflect the deduction of taxes a shareholder would pay on fund distributions or the redemption of fund shares.

Cummins Engine, a maker of diesel engines for trucks and other industrial applications, added 213 basis points to the Fund’s return, as its stock rose an amazing 55.3% from $88.01 to $136.67. I say amazing, because the diesel engine market has not been very strong, and revenue growth at Cummins has been relatively modest. However, Cummins was able to report good earnings, because of effective cost control. The stock hit a high of $150 in 2015, but had dropped to $88 by the end of that year. At this depressed price, any good news would move the stock higher, so this is what happened.

Qualcomm, the leading provider of software and semiconductors used in mobile devices, boosted the Fund’s return by 194 basis points. Investors cheered the company’s progress in China, as it signed licensing agreements with that country’s ten largest smartphone-makers. The stock moved even higher on reports that it would acquire NXP Semiconductors, a leading provider of chips to the automotive industry.

Deere & Co., renowned for its big, green tractors, added 161 basis points to the Fund’s return, as the stock climbed 35.1% from $76.27 to $103.04. Late last year, Deere gave 2017 financial guidance that exceeded expectations, so investors hoped that earnings had bottomed after three years of declines. Farmers coping with low crop prices have put off investing in equipment, but eventually, they’ll need to buy new tractors. When they do, Deere’s earnings should move higher, so we’re holding on to the stock.

Like Applied Materials, Lam Research makes equipment used in manufacturing semiconductors, and its stock surged 33.1% during the year from $79.42 to $105.73, adding 151 basis points to the Fund’s return. The stock had a good start in 2016, as semiconductor-foundries and memory chip-makers ordered lots of equipment, which sent Lam’s earnings higher. The stock moved up again following an October presentation by the company that predicted further market growth and increased share for Lam.

Charles Schwab rose 19.9% from $32.93 to $39.47 for a contribution of 149 basis points to the Fund’s return. Although many people think of Schwab as a discount broker, interest earnings are its largest source of income. The stock moved higher as interest rates increased in 2016, and there were expectations of even higher interest rates in 2017.

Outlook and Strategy

In my opinion, the stock market is now fully-priced, so it’s vulnerable to a downward correction. The price/earnings ratio (“P/E ratio”) of the S&P 500 companies based on the last 12 months’ earnings is 20.3, which is pretty high considering that the historical range is around 15-16. That doesn’t mean that the market will necessarily go down, but it is one factor in the equation. The P/E ratio of the companies in the Parnassus Endeavor Fund is much lower at 14.5, but that doesn’t mean that we’re immune to a market correction. When the market drops, almost all stocks go down, and we will be caught in the downdraft if that happens.

14

| | | | |

| | |

| Annual Report • 2016 | | | | PARNASSUS FUNDS |

In my early years of managing the Parnassus Funds, I would try to time the market by increasing our cash position if I thought the market was overvalued, thinking that a big move down was imminent. I did this twice, and both times I lived to regret it, as the market kept going higher and we underperformed. Since then, I’ve realized my limitations and I don’t try to time the market. I don’t have any special talent for forecasts, but I do have some skill in analyzing individual companies. I can make a pretty good estimate of a stock’s intrinsic value, and when that stock drops to a third or more below that intrinsic value, we buy the stock. That’s what has worked for us in the past, and that’s what I’ll continue to do. Although I will not be making any forecasts, I do have some opinions on what might happen during the year. First of all, the economy looks pretty good right now with unemployment around 5%, and jobs increasing just under 200,000 every month. Interest rates are low, so that should help things.

The real wild card in the economic equation is Donald Trump. I was very surprised when the American people chose “The Donald” to be our next leader, but that’s what they did, so we’ll have to live with him for the next four years. His policy pronouncements keep contradicting each other, so it’s hard to know exactly what he will do. From what he says, there is some good news and some bad news.

The bad news is that he has threatened a trade war with other countries, focusing on China and Mexico. If he actually carries out those threats, it will be a disaster, and we’ll be plunged into a deep recession. The same thing applies to his threat to build a wall between the United States and Mexico. It would be an economic disaster for us. In California, we rely heavily on the labor of Mexican immigrants – both legal and undocumented. If even a portion of these people were forced to return to Mexico, California’s economy would fall into the doldrums. This phenomenon applies to many other parts of the country, but to a somewhat lesser degree. Trump’s policies do not take into account that immigration is great for the country and for all the people living here. What I’m hoping for is that all Trump’s words were just idle campaign rhetoric, and he has no intention of carrying them out. If we’re lucky, cooler heads in Trump’s cabinet will prevail, and none of these things will come to pass.

There are two elements in Trump’s program that I think are quite sensible: tax cuts and big investments in infrastructure. At 35%, our corporate tax rate is the highest in the developed world. We need to bring it down, so corporations won’t continue keeping cash overseas, but will bring it back and invest in the United States.

Trump is correct when he says we need big investments in infrastructure. Those of you who travel a lot realize that many of our roads are in poor condition, and they need lots of help. The same thing applies to airports – especially those in New York, Los Angeles and Newark. I could go on and on, but I think you get the general idea. Investment in infrastructure is a good idea, but I do worry about where the money will come from, and if we do borrow a lot more money, it might increase inflation to worrisome levels.

How does all this affect the stock market and our shares in the Parnassus Endeavor Fund? If The Donald can forget about building a wall next to Mexico and drop his ideas of starting a trade war with China and others, but focus on tax reform and infrastructure investment, it would be a winning strategy. The economy might start growing again at a rate of around 3% instead of 1.5%, and this would mean that corporate earnings would increase. Going back to the P/E ratio, this would mean that the “E” would increase, which would mean that the ratio would be lower, and that would mean that the stock market would no longer be as fully-valued as it is now. That’s what I’m hoping for, but who knows what will happen.

Yours truly,

Jerome L. Dodson

Portfolio Manager

15

| | | | |

| | |

| PARNASSUS FUNDS | | | | Annual Report • 2016 |

PARNASSUS MID CAP FUND

Ticker: Investor Shares - PARMX

Ticker: Institutional Shares - PFPMX

As of December 31, 2016, the NAV of the Parnassus Mid Cap Fund – Investor Shares was $28.87, so after taking dividends into account, the total return for 2016 was a gain of 16.07%. This compares favorably to a gain of 13.80% for the Russell Midcap Index (“Russell”) and a gain of 15.46% for the Lipper Mid-Cap Core Average, which represents the average mid-cap core funds followed by Lipper (“Lipper average”). For the quarter, the Parnassus Mid Cap Fund – Investor Shares was up 2.20%, behind the Russell’s 3.21% return and the Lipper average’s 5.83% gain.

Below is a table comparing the Parnassus Mid Cap Fund with the Russell and the Lipper average for the one-, three-, five- and ten-year periods. The Fund’s long-term track record remains very good, as it outperformed both benchmarks in nearly all of the listed periods.

| | | | | | | | | | | | | | | | | | | | | | | | |

| Parnassus Mid Cap Fund | | | | | | | |

Average Annual Total

Returns (%) | | One

Year | | | Three

Years | | | Five

Years | | | Ten

Years | | | Gross

Expense

Ratio | | | Net

Expense

Ratio | |

for period ended

December 31, 2016 | | | | | | |

| | | | | | | |

| Parnassus Mid Cap Fund Investor Shares | | | 16.07 | | | | 8.58 | | | | 14.25 | | | | 8.87 | | | | 1.07 | | | | 0.99 | |

| | | | | | | |

| Parnassus Mid Cap Fund Institutional Shares | | | 16.28 | | | | 8.72 | | | | 14.34 | | | | 8.91 | | | | 0.77 | | | | 0.77 | |

| | | | | | | |

| Russell Midcap Index | | | 13.80 | | | | 7.92 | | | | 14.72 | | | | 7.86 | | | | NA | | | | NA | |

| | | | | | | |

Lipper Mid-Cap

Core Average | | | 15.46 | | | | 6.38 | | | | 13.40 | | | | 6.98 | | | | NA | | | | NA | |

The average annual total return for the Parnassus Mid Cap Fund-Institutional Shares from commencement (April 30, 2015) was 8.62%. Performance shown prior to the inception of the Institutional Shares reflects the performance of the Parnassus Mid Cap Fund-Investor Shares and includes expenses that are not applicable to and are higher than those of the Institutional Shares. The performance of the Institutional Shares differs from that shown for the Investor Shares to the extent that the classes do not have the same expenses. Performance data quoted represent past performance and are no guarantee of future returns. Current performance may be lower or higher than the performance data quoted. Current performance information to the most recent month-end is available on the Parnassus website (www.parnassus.com). Investment return and principal value will fluctuate, so an investor’s shares, when redeemed, may be worth more or less than their original principal cost. Returns shown in the table do not reflect the deduction of taxes a shareholder may pay on fund distributions or redemption of shares. The Russell Midcap Index is an unmanaged index of common stocks, and it is not possible to invest directly in an index. Index figures do not take any expenses, fees or taxes into account, but mutual fund returns do. Mid-cap companies can be more sensitive to changing economic conditions and have fewer financial resources than large-cap companies.

Before investing, an investor should carefully consider the investment objectives, risks, charges and expenses of the Fund and should carefully read the prospectus or summary prospectus, which contain this and other information. The prospectus or summary prospectus can be obtained on the Parnassus website or by calling (800) 999-3505. As described in the Fund’s current prospectus dated May 1, 2016, Parnassus Investments has contractually agreed to limit total operating expenses to 0.99% of net assets for the Parnassus Mid Cap Fund-Investor Shares and to 0.85% of net assets for the Parnassus Mid Cap Fund-Institutional Shares. This agreement will not be terminated prior to May 1, 2017, and may be continued indefinitely by the Adviser on a year-to-year basis.

Year in Review

2016 was a good year for the Fund. We provided an excellent return for shareholders, outperformed both of our benchmarks, stayed true to our concentrated, quality-biased, low-turnover strategy and more than tripled assets under management.

Despite the positive total return for the year, it was another bumpy ride for the stock market. The Russell plunged 12.63% in the first five weeks of the year ending February 11, 2016, but rallied 30.23% from its February low to finish up 13.80%. Investor sentiment was driven by an accommodative central bank policy, rising oil prices and the campaign promises of President-elect Donald Trump.

The Parnassus Mid Cap Fund – Investor Shares beat the Russell by 227 basis points (a basis point is 1/100th of one percent) and the Lipper average by 61 basis points. The Fund benefitted from having an underweight position relative to the Russell in consumer discretionary stocks, the second-worst performing sector in the benchmark. Our overweight position in the utilities sector also helped our performance, because this sector went up more than the market. Our overweight positions in the consumer staples and health care sectors were our poorest allocation decisions, because these sectors underperformed the Russell by a wide margin.

As usual, stock selection was the main driver of the Fund’s performance relative to the index. Our industrials and information technology holdings helped the Fund’s performance relative to the Russell by 250 and 242 basis points, respectively. Conversely, poor stock picks in the health care and materials sectors hurt our performance relative to the Russell by 206 and 167 basis points, respectively.

16

| | | | |

| | |

| Annual Report • 2016 | | | | PARNASSUS FUNDS |

The Fund’s weakest performer was Perrigo, the leading producer of store-brand generic drugs, as its stock plummeted 42.5% from $144.70 to $83.23, slicing 180 basis points from the Fund’s return. The stock sank in April after longtime CEO Joe Papa resigned to lead troubled Valeant Pharmaceuticals. The stock moved lower throughout the year, because the company cut its earnings guidance three times due to declining generic drug prices and soft growth in Europe. Whereas management initially expected nearly $10 in 2016 earnings-per-share, estimates are now at $7. We like the company’s core franchises and believe that management will turn around this attractively-valued business.

Drug-distributor Cardinal Health cut 56 basis points from the Fund’s return, as its stock fell 19.4% from $89.27 to $71.97. The stock dropped early in the year, after management lowered earnings guidance due to weak generic drug prices and the loss of its Safeway contract. Persistent pricing pressure for its generic and branded drugs prompted management to reduce earnings guidance again in the Fall. We expect pricing pressure to moderate over time, and the company should benefit from increasing demand for prescription drugs by an aging population. Share gains and cost efficiencies should also help earnings.

Hanesbrands, a leading manufacturer of undergarments and activewear, dropped 19.8% from $26.91, where we first bought shares, to $21.57, reducing the Fund’s return by 55 basis points. The stock slumped over the summer, after the company missed expectations due to weak demand and one-time charges related to its recent acquisitions of Champion Europe and Pacific Brands. Excessive inventories, U.S. retail bankruptcies and higher cotton prices caused the company to reduce guidance again in the Fall. In late 2016, investor concern over potential trade tariffs pushed the stock even lower. We believe the company is poised to deliver higher earnings by improving operational efficiency, buying back stock and increasing international sales.

For the second year in a row, our best performer was Insperity, a provider of human resource services to small- and mid-sized businesses. The shares surged 47.4% from $48.15 to $70.95, increasing the Fund’s return by 184 basis points. In 2015, activist investor Starboard Value took a large stake in the company and pressured management to reduce operating costs, repurchase stock and explore the sale of the company. The company has since performed well, increasing its client base and growing earnings at a double-digit rate. Management should continue improving sales and operations in the coming year, but we reduced our position in the company, because of the tremendous stock price rise.

Applied Materials, a maker of equipment used in semiconductor manufacturing, contributed 173 basis points to the Fund’s return, as its stock soared 72.8% during the year from $18.67 to $32.27. The stock rose early in the year, as demand accelerated for its capital equipment. The stock climbed even higher after the company delivered positive mid-year financial results and announced record-high orders. We are holding onto some of our shares, because the company should benefit from a healthy demand environment and further share gains.

MDU Resources, a diversified conglomerate with operations in electric and gas utilities, pipelines and construction materials and services, rose 57.0% from $18.32 to $28.77, increasing the Fund’s return by 160 basis points. A robust construction backlog, solid utility customer growth and contributions from its recently completed wind-power project drove better than expected earnings results early in the year. The stock climbed higher mid-year when management sold its unprofitable refinery to

| | |

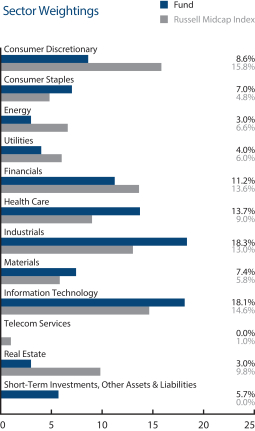

Parnassus Mid Cap Fund as of December 31, 2016 (percentage of net assets) |

Top 10 Holdings

(percentage of net assets)

| | | | |

| |

| Motorola Solutions Inc. | | | 4.1% | |

| |

| Fiserv Inc. | | | 3.4% | |

| |

| First Horizon National Corp. | | | 3.3% | |

| |

| Teleflex Inc. | | | 3.3% | |

| |

| KLA-Tencor Corp. | | | 3.2% | |

| |

| VF Corp. | | | 3.2% | |

| |

| SEI Investments Co. | | | 3.1% | |

| |

| Verisk Analytics Inc. | | | 3.1% | |

| |

| National Oilwell Varco Inc. | | | 3.0% | |

| |

| Iron Mountain Inc. | | | 3.0% | |

Portfolio characteristics and holdings are subject to change periodically.

17

| | | | |

| | |

| PARNASSUS FUNDS | | | | Annual Report • 2016 |

Tesoro. We see more upside in the stock given a healthy construction backlog and utility rate increases.

Outlook and Strategy

This year’s 14% surge in the Russell was a welcome change from last year’s 2% slump. After taking dividends into account, the Russell is up over 312% since the trough of 2009, which represents an annualized return of over 19%. At year end, the Russell traded at over 18 times forward earnings estimates, well above the ten-year average of 16 times. In short, stocks remain expensive. With this backdrop, along with the dynamic political environment, we remain focused on identifying stocks with asymmetric risk-reward opportunities.

In 2016, certain sectors went up much more or less than the Russell, creating opportunities for us to adjust our individual portfolio holdings. For

| | |

|

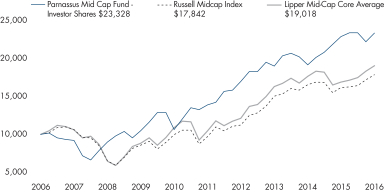

| Value on December 31, 2016 of $10,000 invested on December 31, 2006 |

The chart shows the growth in value of a hypothetical $10,000 investment over the last ten years and does not reflect the deduction of taxes a shareholder would pay on fund distributions or the redemption of fund shares.

example, the industrial and utilities sectors rose 19% and 18%, respectively. We reduced our exposure in these areas, because the range of outcomes for some stocks became less favorable. Conversely, the health care and consumer discretionary sectors were the worst performing sectors in 2016, falling 3% and rising only 4%, respectively. We took advantage of price drops in some quality businesses to buy more shares, resulting in an increase in our relative weightings in these sectors.

We added to our position in medical equipment provider Teleflex, after management reduced financial guidance due to pricing pressure and longer sales cycles for its new products. We believe the company has significant opportunities with its innovative products to accelerate sales growth. We also increased our position in dental distributor Patterson. The stock dropped after management provided disappointing guidance, driven by poor sales execution, pricing pressure in the branded pharmaceutical segment and the loss of an exclusive contract with Sirona. We believe that the company has levers to pull to deliver higher earnings.

We increased our position in VF Corp., a consumer discretionary company best known for top brands like The North Face, Timberland and Wrangler. The stock performed poorly, as demand from domestic department and sporting goods stores slumped, and the company was left holding too much inventory. Demand was also hurt by an unusually high rate of U.S. retailer bankruptcies in 2016. The valuation is attractive though, and we believe that management is taking the right steps to create shareholder value by optimizing the portfolio, realigning expenses to market conditions and focusing on returns on capital. Furthermore, the company should benefit from growth in Europe and Asia, the expansion of e-commerce and continued consumer interest in fitness and outdoor activities.

Thank you for your investment in the Parnassus Mid Cap Fund.

Yours truly,

| | |

| |  |

| Matthew D. Gershuny | | Lori A. Keith |

| Lead Portfolio Manager | | Portfolio Manager |

18

| | | | |

| | |

| Annual Report • 2016 | | | | PARNASSUS FUNDS |

PARNASSUS ASIA FUND

Ticker: Investor Shares - PAFSX

Ticker: Institutional Shares - PFPSX

As of December 31, 2016, the net asset value (“NAV”) of the Parnassus Asia Fund – Investor Shares was $16.80, so the total return for the year was 13.98%. This compares to a gain of 5.21% for the MSCI AC Asia Pacific Index (“MSCI Index”) and a gain of 4.28% for the Lipper Asia Pacific Region Average, which represents the average return of the Asia Pacific Region funds followed by Lipper (“Lipper average”). The Parnassus Asia Fund performed extremely well this year, both on an absolute basis and relative to its benchmarks. We surpassed the MSCI Index by nine percentage points, and we beat the Lipper average by 9.70%. In fact, this was the Fund’s best annual performance since its launch in 2013. We’re proud of the Fund’s achievements and our ability to reward our most loyal shareholders.

Below is a table comparing the Parnassus Asia Fund with the MSCI Index and the Lipper average over the past one- and three-year periods, and since inception. The Fund is demonstrably ahead of both benchmarks for all time periods. As long-term

| | | | | | | | | | | | | | | | | | | | |

| Parnassus Asia Fund | |

Average Annual Total

Returns (%) | | One

Year | | | Three

Years | | | Since

Inception on

4/30/13 | | | Gross

Expense

Ratio | | | Net

Expense

Ratio | |

for period ended

December 31, 2016 | | | | | |

| | | | | | |

Parnassus Asia Fund

Investor Shares | | | 13.98 | | | | 2.71 | | | | 3.44 | | | | 2.50 | | | | 1.25 | |

| | | | | | |

Parnassus Asia Fund

Institutional Shares | | | 14.21 | | | | 2.88 | | | | NA | | | | 1.10 | | | | 0.94 | |

| | | | | | |

| MSCI AC Asia Pacific Index | | | 5.21 | | | | 1.23 | | | | 1.37 | | | | NA | | | | NA | |

| | | | | | |

| Lipper Asia Pacific Region Average | | | 4.28 | | | | 0.73 | | | | 0.26 | | | | NA | | | | NA | |

The average annual total return for the Parnassus Asia Fund-Institutional Shares from commencement (April 30, 2015) was -3.49%. Performance shown prior to the inception of the Institutional Shares reflects the performance of the Parnassus Asia Fund-Investor Shares and includes expenses that are not applicable to and are higher than those of the Institutional Shares. The performance of the Institutional Shares differs from that shown for the Investor Shares to the extent that the classes do not have the same expenses. Performance data quoted represent past performance and are no guarantee of future returns. Current performance may be lower or higher than the performance data quoted. Current performance information to the most recent month-end is available on the Parnassus website (www.parnassus.com). Investment return and principal value will fluctuate, so an investor’s shares, when redeemed, may be worth more or less than their original principal cost. Returns shown in the table do not reflect the deduction of taxes a shareholder may pay on fund distributions or redemption of shares. The MSCI AC Asia Pacific Index is an unmanaged index of Asian stock markets, and it is not possible to invest directly in an index. Index figures do not take any expenses, fees or taxes into account, but mutual fund returns do.

The Fund invests primarily in non-U.S. securities. Foreign markets can be more volatile than the U.S. market due to increased risks of adverse issuer, political, regulatory, market or economic developments and can perform differently from the U.S. market.

Before investing, an investor should carefully consider the investment objectives, risks, charges and expenses of the Fund and should carefully read the prospectus or summary prospectus, which contain this and other information. The prospectus or summary prospectus can be obtained on the Parnassus website or by calling (800) 999-3505. As described in the Fund’s current prospectus dated May 1, 2016, Parnassus Investments has contractually agreed to limit the total operating expenses to 1.25% of net assets for the Parnassus Asia Fund-Investor Shares and to 1.22% of net assets for the Parnassus Asia Fund-Institutional Shares. This agreement will not be terminated prior to May 1, 2017, and may be continued indefinitely by the Adviser on a year-to-year basis.

investors, we like to pay most attention to returns over an entire economic cycle, which typically lasts three to five years. Since inception then, we have gained an average of 3.44% per year, which is more than two percentage points per year ahead of the MSCI Index and more than three percentage points per year ahead of the Lipper average. This performance makes the Parnassus Asia Fund the third-best performing of all 49 Asia Pacific Region funds followed by Lipper. (For the one- and three-year periods, the Fund was #3 out of 61 funds, and #5 out of 49 funds, respectively.)

Company Analysis

The Asia Fund’s stellar performance was primarily attributable to our investments in select high-technology stocks, which rebounded strongly compared to the first quarter of the year. Six companies contributed 130 basis points or more to the Fund’s return in 2016, while only three stocks subtracted 70 basis points or more from the Fund’s return. (Each basis point is equal to 0.01% or one-hundredth of a percent, so a gain of 130 basis points is equal to 1.30%.)

The Fund’s worst performer was Lenovo, which decreased the Fund’s return by 163 basis points, as its stock price slipped 40.6% from $1.01 to $0.60. (We own the Hong Kong – listed shares, which are more liquid than the U.S.-listed ADR’s; one ADR is equal to 20 shares with a value of $12.00 at year-end.) The maker of personal computers and other technology products is the number-one brand in China and the largest PC manufacturer in the world. The stock fell because investors began to doubt whether Lenovo could build a successful enterprise business and turn around the mobile business simultaneously in the face of well-heeled rivals such as HP, Dell and Apple.

19

| | | | |

| | |

| PARNASSUS FUNDS | | | | Annual Report • 2016 |

Gilead, a biotechnology firm that makes therapies for HIV and hepatitis C, sliced 85 basis points off the Fund’s return, as its stock declined 11.6% from our average cost of $81.03 to $71.61. The stock dropped due to weakness in the hepatitis C business, as pricing came under pressure due to increased competition, and the patient population fell because Gilead’s drugs cure patients, thereby reducing demand for the therapy. The stock is on the bargain table, and the company has a strong balance sheet and a proven track record of innovation, so we increased our position throughout the year.

Our final laggard was Rakuten, whose stock price fell 14.9% from $11.52 to $9.80 and clipped the Fund’s return by 77 basis points. Based in Japan, Rakuten is an international online shopping mall with tens of thousands of merchants; it is also a major player in online financial services, including securities brokerage and credit cards. While Rakuten still dominates Japan’s e-commerce ecosystem, the competitive landscape has intensified. Amazon is using its Amazon Prime membership package of free shipping, same-day delivery and free online content to gain share, while Yahoo Shopping launched an offensive under the banner of e-commerce revolution. Consequently, profit growth slowed both in Rakuten’s domestic e-commerce and financial technology segments. Management’s ambitious turn-around plan resulted in cleaving off international operations and the company is redoubling efforts to grow in Japan.

Compared with our diverse set of losers, every one of our portfolio’s six top winners was a technology stock, as the semiconductor industry staged a strong cyclical recovery beginning in the second quarter. Thankfully, we scooped up shares in these quality names when prices were low, so we’re well-positioned for the upturn.

The Fund’s best performer was Applied Materials, a leading maker of equipment used in semiconductor manufacturing, which soared 72.8% during the year from $18.67 to $32.27, increasing the Fund’s return by a whopping 284 basis points. The stock rose early in the year, as demand accelerated for its capital equipment by semiconductor customers such as Intel and Samsung. The stock also climbed higher, after the company delivered positive mid-year earnings and then announced new orders and backlog reaching all-time highs.

Micron Technology added an impressive 238 basis points to the Fund’s return, as the stock marched higher by 54.8% from $14.16 to $21.92. It was a roller-coaster year for Micron, as prices of its two main products, dynamic random access memory chips (also known as DRAMs) and NANO flash memory chips, were falling sharply to begin the year. DRAMs and NANO flash memory chips are commodities, and their

|

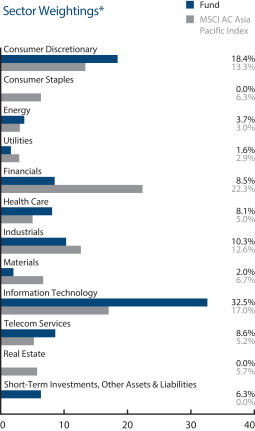

Parnassus Asia Fund as of December 31, 2016 (percentage of net assets) |

* For purposes of categorizing securities for diversification requirements under the Investment Company Act, the Fund uses industry classifications that are more specific than those used for the chart.

pricing is volatile, going up sharply when demand exceeds supply and dropping suddenly when the balance tilts in the other direction. During 2016, demand grew more than supply, so prices firmed up and Micron’s earnings improved.

Samsung Electronics contributed 183 basis points to the Fund’s return, as its stock surged 40.2% from $1,062.10 to $1,489.45. The South Korean consumer electronics giant ranks number one in sales of mobile phones and displays worldwide and number two behind Intel in semiconductors. In October, Samsung halted sales of its flagship Galaxy Note 7 smartphone, after reports that the devices could explode and catch fire. The company recovered quickly though, spending $5 billion on a complete, global recall that successfully restored customers’ faith in the brand. To branch out beyond smartphones, Samsung also purchased Harman, a U.S. automotive technology manufacturer. Investors applauded the move, which diversifies and expands Samsung’s end markets.

20

| | | | |

| | |

| Annual Report • 2016 | | | | PARNASSUS FUNDS |