Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSRS

CERTIFIED SHAREHOLDER REPORT OF

REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: Parnassus Funds (811-04044) and Parnassus Income Funds (811-06673)

Parnassus Funds

Parnassus Income Funds

(Exact name of registrant as specified in charter)

1 Market Street, Suite 1600, San Francisco, California 94105

(Address of principal executive offices) (Zip code)

Marc C. Mahon

Parnassus Funds

Parnassus Income Funds

1 Market Street, Suite 1600, San Francisco, California 94105

(Name and address of agent for service)

Registrant’s telephone number, including area code: (415) 778-0200

Date of fiscal year end: December 31

Date of reporting period: June 30, 2020

Table of Contents

Item 1: Report to Shareholders

Table of Contents

Parnassus Funds Semiannual Report

June 30, 2020

Parnassus Core Equity FundSM

Investor Shares: PRBLX | Institutional Shares: PRILX

Parnassus Mid Cap FundSM

Investor Shares: PARMX | Institutional Shares: PFPMX

Parnassus Endeavor FundSM

Investor Shares: PARWX | Institutional Shares: PFPWX

Parnassus Mid Cap Growth FundSM

Investor Shares: PARNX | Institutional Shares: PFPRX

Parnassus Fixed Income FundSM

Investor Shares: PRFIX | Institutional Shares: PFPLX

Table of Contents

Beginning on January 1, 2021, as permitted by regulations adopted by the SEC, paper copies of the Funds’ shareholder reports will no longer be sent by mail, unless you specifically request paper copies of the reports from the Funds or from your financial intermediary, such as a broker-dealer or bank. Instead, the reports will be made available on the Funds’ website (www.parnassus.com), and you will be notified by mail each time a report is posted and provided with a website link to access the report.

If you already elected to receive shareholder reports electronically, you will not be affected by this change and you need not take any action. You may elect to receive shareholder reports and other communications from the Funds by contacting your financial intermediary (such as a broker-dealer or bank) or, if you are a direct investor, by calling 800-999-3505 or by sending an email request to shareholder@parnassus.com.

You may elect to receive all future reports in paper copies free of charge. If you invest through a financial intermediary, you can contact your financial intermediary to request that you continue to receive paper copies of your shareholder reports. If you invest directly with the Funds, you can call 800-999-3505 or send an email request to shareholder@parnassus.com to let the Funds know you wish to continue receiving paper copies of your shareholder reports. Your election to receive paper copies of reports will apply to all funds held in your account if you invest through your financial intermediary.

This report must be preceded or accompanied by a current fund prospectus.

Mutual fund investing involves risk, including the potential for loss of principal.

There are no assurances the Fund’s investments objectives and ESG strategies will be successful.

Table of Contents

| Letter from Parnassus Investments | 4 | |

| Fund Performance and Commentary | ||

| Parnassus Core Equity Fund | 7 | |

| 11 | ||

| Parnassus Endeavor Fund | 15 | |

| 19 | ||

| Parnassus Fixed Income Fund | 23 | |

| Responsible Investing Notes | 26 | |

| Fund Expenses | 28 | |

| Portfolios of Investments | ||

| Parnassus Core Equity Fund | 29 | |

| Parnassus Mid Cap Fund | 31 | |

| Parnassus Endeavor Fund | 33 | |

| 35 | ||

| Parnassus Fixed Income Fund | 37 | |

| Financial Statements | 42 | |

| Notes to Financial Statements | 48 | |

| Financial Highlights | 58 | |

| Additional Information | 62 | |

3

Table of Contents

| Semiannual Report • 2020 | |||

August 7, 2020

The first half of 2020 has come to a close, and it’s almost incomprehensible how many unlikely and impactful events have occurred in just six months. The year began with two major political events, either one of which seemed at the time like it could be the story of the first half. The impeachment of Donald Trump dominated the national conversation until his acquittal on February 5. At the same time, we all watched the final stages of an unusually high-stakes Democratic primary battle. By the first week of March, Joe Biden’s decisive wins on Super Tuesday made him the odds-on favorite to win the nomination. But of course, by this time, the last thing on many people’s minds was politics.

In the second week of March, the World Health Organization declared COVID-19 a pandemic. The economic fallout that would inevitably result from the disease had already been anticipated by the stock market. Having made an all-time high in mid-February, the S&P 500 Index eventually gave up a third of its value in just over a month. This was the fastest 30% drop ever for American stocks, even worse than the previous top three declines, all of which happened during the Great Depression. The tragic loss of life caused by the virus, the devastating economic insecurity caused by unprecedented job losses and the evaporation of financial wealth were a staggering combination of blows to our national and individual psyches. As the curtain closed on the first quarter, it seemed impossible for anything else to take center stage.

The enormous and rapid support given to the economy and financial markets by Congress and the Federal Reserve made for a happy plot twist as we began the second quarter. Miraculously, the S&P 500 clawed its way back to positive territory for the year-to-date period on June 8. Like the first quarter decline, this rebound was also record-setting. Meanwhile, the real economy was still reeling and the pandemic raged on. But at least for stock market investors, there was positive momentum.

The murder of George Floyd by a Minneapolis police officer on May 25 changed all of this. By the first week of June, Mr. Floyd’s death had triggered massive and widespread protests across the nation and even overseas. The pain and outrage caused by more than 400 years of brutal and systemic racism in America took hold of our country as never before. For millions of Americans, and certainly for me personally, Mr. Floyd’s death and the movement it sparked brought a new awareness of the horror and profound unfairness caused by systemic racism.

Through all of this — impeachment, primaries, the pandemic, record-setting volatility and economic contraction, protests against racial injustice — we at Parnassus have done our best to focus on what we can control. First and foremost, this means managing your money as well as possible and continuing to provide high-quality service. I’m happy to report that our two largest funds, the Parnassus Core Equity Fund and the Parnassus Mid Cap Fund, outperformed their benchmarks for the first half of the year. Also noteworthy is the Parnassus Fixed Income Fund, which put up our best absolute return and also outpaced its benchmark for the first half. Lead portfolio manager, Samantha Palm, and recently added co-portfolio manager, Minh Bui, are doing a great job managing this fund. Meanwhile, our shareholder services team is ready to take your calls and receive your mail, just as it has been since the shelter-in-place began.

4

Table of Contents

| Semiannual Report • 2020 | | |||

As important as financial returns and service are, they are just part of what we offer. As responsible investors since our founding in 1984, we are keenly focused on the environmental, social and governance (ESG) impacts of our portfolio companies. As I write this letter, our director of ESG research, Iyassu Essayas, is leading a team effort to strengthen our anti-racism activities. We will report more about this in the months to come. You should also know that our team has done a tremendous job engaging with our portfolio companies on their responses to the pandemic, especially as they pertain to worker safety and job security. I think it’s more important than ever to demand environmental and social responsibility from one’s investment managers, and I’m very proud of the work that Iyassu, Rachel Nishimoto and Marissa LaFave have done so far this year leading our ESG efforts.

Interns

We have had interns for over 30 years at Parnassus, but there’s never been a summer like this one. Our research interns are all working remotely, and we’re doing our best to support and get to know them. So far, things are going much better than any of us expected. This is a tribute to our five interns, and our investment team members who are mentoring them.

Michael Beck is our only graduate student intern this year. He is an MBA candidate at the Haas School of Business at the University of California, Berkeley. Previously, Michael worked as a portfolio manager, analyst and trader for Opes Advisors, a Bay Area investment firm. Michael holds the Chartered Financial Analyst (CFA) designation and graduated with a mechanical engineering degree from the University of California, Los Angeles. Michael grew up in Southern California and enjoys basketball, skiing and visiting the beach.

Arda Erbil is also studying business at the Haas School, but as an undergraduate. Previously, Arda interned at TD Ameritrade as an analyst at the Office of the Chairman and was a venture capital intern at Redwood Consumer Group. In his free time, Arda enjoys sailing and volunteering on the Berkeley campus.

Andrew Green is pursuing a business major at the University of Michigan. Andrew is a portfolio manager for the TAMID Group student investment fund and consults for seed stage international startups. Previously, Andrew worked as a summer analyst for Ernst & Young’s mergers and acquisitions (M&A) Advisory group in Tel Aviv, Israel. Andrew grew up in South Florida and enjoys golfing, hiking, grilling and listening to classic rock music.

We have two interns from the University of Southern California (USC). Lena Shapiro is pursuing a degree in real estate development, and is a vice president of AIESEC, which is a global student-led nonprofit that creates cross-cultural volunteer experiences. She previously interned at a commercial and industrial real estate firm, Majestic Realty. When not working, Lena enjoys exploring the outdoors, playing volleyball and knitting.

Vivian Zhu is pursuing a dual degree in business administration and economics at USC. She is one of the student managers for the Undergraduate Investment Fund. Vivian previously worked at Zana Capital, a private equity firm in Singapore. In her free time, she enjoys volunteering and snowboarding.

5

Table of Contents

| Semiannual Report • 2020 | |||

Thank you all for investing with the Parnassus Funds.

Sincerely,

Benjamin E. Allen

President and CEO

6

Table of Contents

| Semiannual Report • 2020 | | |||

Ticker: Investor Shares - PRBLX

Ticker: Institutional Shares - PRILX

As of June��30, 2020, the net asset value (“NAV”) of the Parnassus Core Equity Fund – Investor Shares was $45.87. After taking dividends into account, the total return for the second quarter was a gain of 17.86%. This compares to a total return of 20.54% for the S&P 500 Index (“S&P 500”) and a gain of 15.43% for the Lipper Equity Income Funds Average, which represents the average return of the equity income funds followed by Lipper (“Lipper average”). Year-to-date, the Parnassus Core Equity Fund – Investor Shares posted a loss of 2.06% versus a decline of 3.08% for the S&P 500 and a loss of 12.87% for the Lipper average.

Below is a table that summarizes the performances of the Parnassus Core Equity Fund, the S&P 500 and the Lipper average. The returns are for the one-, three-, five- and ten-year periods. We are pleased to report the Fund outperformed the Lipper average for all periods.

Parnassus Core Equity Fund

| Average Annual Total Returns (%) | ||||||||||||||||||||||||

| for period ended June 30, 2020 | ||||||||||||||||||||||||

| One Year | Three Years | Five Years | Ten Years | Gross Expense Ratio | Net Expense Ratio | |||||||||||||||||||

| Parnassus Core Equity Fund – Investor Shares | 6.48 | 11.69 | 10.60 | 13.41 | 0.86 | 0.86 | ||||||||||||||||||

| Parnassus Core Equity Fund – Institutional Shares | 6.75 | 11.93 | 10.84 | 13.63 | 0.63 | 0.63 | ||||||||||||||||||

| S&P 500 Index | 7.51 | 10.73 | 10.73 | 13.99 | NA | NA | ||||||||||||||||||

| Lipper Equity Income Funds Average | -5.32 | 3.41 | 5.50 | 9.97 | NA | NA | ||||||||||||||||||

The average annual total return for the Parnassus Core Equity Fund – Institutional Shares from commencement (April 28, 2006) was 10.40%. Performance shown prior to the inception of the Institutional Shares reflects the performance of the Parnassus Core Equity Fund –Investor Shares and includes expenses that are not applicable to and are higher than those of the Institutional Shares. The performance of the Institutional Shares differs from that shown for the Investor Shares to the extent that the classes do not have the same expenses. Performance data quoted represent past performance and are no guarantee of future returns. Current performance may be lower or higher than the performance data quoted, and current performance information to the most recent month end is available on the Parnassus website (www.parnassus.com). Investment return and principal value will fluctuate, so an investor’s shares, when redeemed, may be worth more or less than their original principal cost. Returns shown in the table do not reflect the deduction of taxes a shareholder may pay on fund distributions or redemption of shares. The S&P 500 is an unmanaged index of common stocks, and it is not possible to invest directly in an index. Index figures do not take any expenses, fees or taxes into account, but mutual fund returns do. The estimated impact of individual stocks on the Fund’s performance is provided by FactSet.

Before investing, an investor should carefully consider the investment objectives, risks, charges and expenses of the Fund and should carefully read the prospectus or summary prospectus, which contain this and other information. The prospectus or summary prospectus can be obtained on the Parnassus website or by calling (800) 999-3505. As described in the Fund’s current prospectus dated May 1, 2020, Parnassus Investments has contractually agreed to limit total operating expenses to 0.86% of net assets for the Parnassus Core Equity Fund – Investor Shares and to 0.63% of net assets for the Parnassus Core Equity Fund – Institutional Shares. This agreement will not be terminated prior to May 1, 2021, and may be continued indefinitely by the Adviser on a year-to-year basis.

Second Quarter Review

We started the second quarter deeply troubled by the catastrophic human and economic toll caused by the COVID-19 pandemic. Then, as the quarter unfolded, long-standing societal racism against Black Americans was brutally brought to light with the tragic killing of George Floyd. There have been far too many tragedies like this. We deeply lament these injustices, and we don’t pretend to have all the answers. We do, though, as members of our communities, as employees at Parnassus, and as investors, recognize our responsibility to play our part in making this world a better place.

We are living through a disorienting time. While emotions were running high in the midst of the pandemic and widespread calls for racial justice, the stock market soared during the second quarter. In fact, the S&P 500 recorded its best 50-day period in history during the second quarter. Governments around the world, including the United States, provided trillions of dollars to fill the gap of lost wages caused by the pandemic lockdowns. This liquidity boost, coupled with the perception of a government backstop on the economy, fueled bullishness about the prospects of a “V-shaped” recovery.

While the Parnassus Core Equity Fund – Investor Shares had a strong gain of 17.86% for the quarter, it underperformed the 20.54% rise by the S&P 500. Our upside capture was below our expectations. That said, the Fund fell less than the benchmark during the first quarter, so we’re pleased that we’re still ahead of our benchmarks for the first half of the year. Overall, stock selection subtracted about 190 basis points from our

7

Table of Contents

| Semiannual Report • 2020 | |||

relative performance in the second quarter, while sector allocation was modestly negative. The Fund’s weakest stock selection was in the industrials, financials and communication services sectors.

The Fund had only one stock that trimmed the NAV by more than 15 basis points during the quarter. American Express, the iconic financial services firm, reduced the Fund’s return by 28 basis points. (One basis point is 1/100th of one percent.) The stock’s total return was negative 13.6%* to our average selling price in April. We sold the stock because American Express will endure elevated credit card loan losses due to the high unemployment rate, while we believe its payment volumes will be slower to rebound than other card networks, due to American Express’s outsized exposure to travel and entertainment.

The Fund had six stocks that added more than 100 basis points to the NAV this quarter. The biggest positive contributor to the Fund’s performance was Microsoft, which added 189 basis points to the Fund’s return, as the stock gained 29.4%. The company reported strong results and high near-term visibility into future earnings despite the impact of COVID-19. Microsoft is an increasingly important strategic partner to their corporate customers, and we believe they will continue to be one of the primary beneficiaries of the growth in cloud computing.

Amazon contributed 159 basis points to the Fund’s performance with a total return of 41.5%. The current environment has accelerated the shift to e-commerce, and demand has been so overwhelming that Amazon has increased headcount by over 100,000 so far this year. Amazon Web Services (AWS) continues to have spectacular results, as cloud computing demand grows unabated.

NVIDIA added 120 basis points to the Fund’s performance with a total return of 44.2% this quarter. The company announced a new datacenter product that promises significantly improved performance. This strong product execution, coupled with the closing of their Mellanox acquisition and excellent quarterly results, drove the shares higher.

Cadence and Synopsys both provide software for designing semiconductors, and each reported impressive earnings during the quarter. Cadence added 118 basis points to the Fund’s performance with a total return of 45.3%, while Synopsys contributed 111 basis points, as its stock returned 51.4%. Both companies are continuing to benefit from the secular trends of increasing semiconductor complexity and an expanding customer base.

Danaher is a leading manufacturer of testing and diagnostic equipment. Its stock returned 27.9%, contributing 109 basis points to the Fund’s performance. Investors appreciated Danaher’s solid quarterly earnings and its involvement with many of the COVID-19 vaccine and therapy trials, which could boost revenue if any of these are successful.

* For this report, we quote total return to the portfolio, which includes price change and dividends.

8

Table of Contents

| Semiannual Report • 2020 | | |||

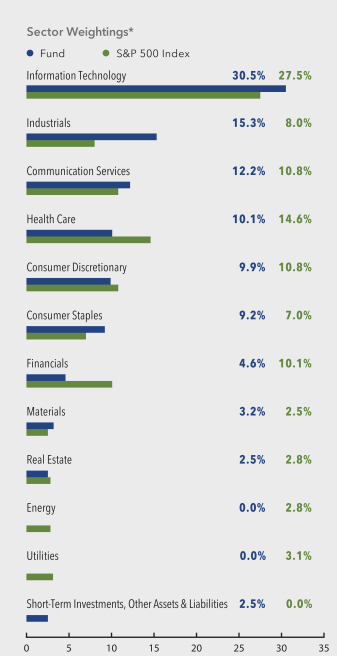

Parnassus Core Equity Fund

as of June 30, 2020

(percentage of net assets)

* For purposes of categorizing securities for diversification requirements under the Investment Company Act, the Fund uses industry classifications that are more specific than those used for the chart.

Portfolio characteristics and holdings are subject to change periodically.

| Top 10 Equity Holdings | ||||

| (percentage of net assets) | ||||

| Microsoft Corp. | 6.8% | |||

| Amazon.com Inc. | 5.4% | |||

| Danaher Corp. | 4.2% | |||

| Alphabet Inc., Class A | 4.0% | |||

| Comcast Corp., Class A | 4.0% | |||

| Mastercard Inc., Class A | 3.3% | |||

| Applied Materials Inc. | 3.3% | |||

| Costco Wholesale Corp. | 3.3% | |||

| Verizon Communications Inc. | 3.2% | |||

| Linde plc | 3.2% | |||

Portfolio characteristics and holdings are subject to change periodically.

Outlook and Strategy

Remarkably, the stock market has climbed back toward its previous peak. Clearly, the size and scope of the Federal Reserve’s actions, along with fiscal and monetary responses across the globe, have added liquidity and boosted equity markets. However, we’re concerned that investors are pricing in too much optimism about an economic recovery. As of June 30, the S&P 500 is trading at a valuation of 24.4 times 2021 earnings estimates, above its valuation of 20.8 times on February 19, the stock market’s all-time peak. The pandemic shows little signs of easing in the United States, and it’s unclear if the recent pick-up in economic activity reflects just an initial bounce due to pent-up demand or the beginning of a sustainable recovery to pre-pandemic levels.

Moving forward, the pandemic is likely to accelerate many structural changes already in progress. Recent events have emphasized technological disruption, global trade tensions, supply chains and calls for social change. As large cap core investors, we are intimately aware of the wide dispersion in performance between value and growth stocks. Certain internet and digital businesses exhibit winner-take-most dynamics, which creates a trend toward persistent winners and losers in certain sectors, and COVID-19 has only accelerated this trend. While some companies in the “value” category present opportunity thanks to their stable businesses and historically low valuations, many face earnings disruptions due to secular changes in the economy. Our focus is to build a portfolio that is anchored in the large cap core category, while identifying opportunities across the value and growth spectrum.

9

Table of Contents

| Semiannual Report • 2020 | |||

Given the wide range of economic outcomes ahead, we have chosen to own companies that sell essential product and have strong balance sheets and robust supply chains. In addition, we have spent considerable time discerning how our companies have responded to the pandemic on key issues, such as workplace safety, compensation, benefits and layoffs. We seek companies that are investing in their employees, retaining talent and building businesses that are positioned to emerge stronger over the long-term.

During the quarter, the Fund added to its technology holdings and is overweight the sector. We initiated a position in Micron, the memory semiconductor manufacturer. Long-term, we believe that growth in data, cloud computing and smart devices will fuel demand for Micron’s memory chips. We also bought shares of Intel, one of the few remaining owners of leading-edge semiconductor foundries. The digitization of the economy, along with advancements in artificial intelligence, should continue to drive strong growth in computer demand. We believe that Intel shares offer an opportunity to participate in this durable trend at an attractive valuation.

We reduced our underweight position in the consumer discretionary sector. The Fund bought shares of Booking Holdings, the online travel agency that owns and operates brands such as Booking.com, Priceline and KAYAK. The near-term prospects for the travel and hospitality sector have deteriorated meaningfully due to COVID-19. However, we believe that Booking’s shares are attractive as the company has ample liquidity, enjoys an increasingly advantaged competitive position and should benefit when travel inevitably returns.

The Fund remains overweight the industrials sector, and during the quarter added Kansas City Southern, a Class I railroad that links Mexico’s manufacturing regions to major markets in the U.S. and Canada. We believe that Kansas City Southern will be increasingly relevant as its strategically advantaged network enables it to participate in Mexico’s growing economy and to benefit from the reform of the Mexican energy

sector and the supply chain near-sourcing phenomenon.

We reduced our financials exposure during the quarter due to the sector’s exceptionally wide range of economic outcomes. Our main concern is that loan losses could wipe out a big portion of earnings and deplete capital for lenders if the economy doesn’t recover quickly. Meanwhile, lower interest rates will pressure earnings for lenders even in a strong economic recovery, as the Federal Reserve now projects that it won’t raise interest rates until 2023. Given this backdrop, we decided to sell our positions in Bank of America and American Express.

In the remaining sectors, the Fund had no material changes. We remain overweight the communications services sector with large positions in Comcast and Google’s parent company, Alphabet. We are also overweight the consumer staples sector, anchored by a large investment in Costco. We are underweight health care, with our most significant exposure in medical devices, life sciences and health care technology. We’re essentially equal weight materials and real estate. The Fund has zero exposure to the energy sector due to our fossil fuel free mandate. The Fund also has no holdings in the utility sector, as these stocks offer limited growth and trade at high valuations.

We deeply appreciate your trust and confidence in us, especially during these challenging times.

Sincerely,

Todd C. Ahlsten

Lead Portfolio Manager

Benjamin E. Allen

Portfolio Manager

10

Table of Contents

| Semiannual Report • 2020 | | |||

Ticker: Investor Shares - PARMX

Ticker: Institutional Shares - PFPMX

As of June 30, 2020, the net asset value (“NAV”) of the Parnassus Mid Cap Fund – Investor Shares was $32.65, so the total return for the quarter was a gain of 19.91%. This compares to a gain of 24.61% for the Russell Midcap Index (“Russell”) and a gain of 20.90% for the Lipper Mid-Cap Core Funds Average, which represents the average return of the mid-cap core fund followed by Lipper (“Lipper average”). For the first half of 2020, the Parnassus Mid Cap Fund – Investor Shares posted a loss of 8.36% compared to a loss of 9.13% for the Russell and a loss of 14.06% for the Lipper average.

Parnassus Mid Cap Fund

| Average Annual Total Returns (%) | ||||||||||||||||||||||||

| for period ended June 30, 2020 | ||||||||||||||||||||||||

| One Year | Three Years | Five Years | Ten Years | Gross Expense Ratio | Net Expense Ratio | |||||||||||||||||||

| Parnassus Mid Cap Fund – Investor Shares | -3.13 | 5.48 | 8.10 | 12.10 | 1.01 | 0.99 | ||||||||||||||||||

| Parnassus Mid Cap Fund – Institutional Shares | -2.86 | 5.72 | 8.34 | 12.24 | 0.75 | 0.75 | ||||||||||||||||||

| Russell Midcap Index | -2.24 | 5.79 | 6.76 | 12.35 | NA | NA | ||||||||||||||||||

| Lipper Mid-Cap Core Funds Average | -7.62 | 1.32 | 3.20 | 9.48 | NA | NA | ||||||||||||||||||

The average annual total return for the Parnassus Mid Cap Fund – Institutional Shares from commencement (April 30, 2015) was 7.83%. Performance shown prior to the inception of the Institutional Shares reflects the performance of the Parnassus Mid Cap Fund – Investor Shares and includes expenses that are not applicable to and are higher than those of the Institutional Shares. The performance of the Institutional Shares differs from that shown for the Investor Shares to the extent that the classes do not have the same expenses. Performance data quoted represent past performance and are no guarantee of future returns. Current performance may be lower or higher than the performance data quoted. Current performance information to the most recent month end is available on the Parnassus website (www.parnassus.com). Investment return and principal value will fluctuate, so an investor’s shares, when redeemed, may be worth more or less than their original principal cost. Returns shown in the table do not reflect the deduction of taxes a shareholder may pay on fund distributions or redemption of shares. The Russell Midcap Index is an unmanaged index of common stocks, and it is not possible to invest directly in an index. Index figures do not take any expenses, fees or taxes into account, but mutual fund returns do. Mid-cap companies can be more sensitive to changing economic conditions and have fewer financial resources than large-cap companies. The estimated impact of individual stocks on the Fund’s performance is provided by FactSet.

Before investing, an investor should carefully consider the investment objectives, risks, charges and expenses of the Fund and should carefully read the prospectus or summary prospectus, which contain this and other information. The prospectus or summary prospectus can be obtained on the Parnassus website or by calling (800) 999-3505. As described in the Fund’s current prospectus dated May 1, 2020, Parnassus Investments has contractually agreed to limit total operating expenses to 0.99% of net assets for the Parnassus Mid Cap Fund – Investor Shares and to 0.75% of net assets for the Parnassus Mid Cap Fund – Institutional Shares. This agreement will not be terminated prior to May 1, 2021, and may be continued indefinitely by the Adviser on a year-to-year basis.

To the left is a table comparing the Parnassus Mid Cap Fund with the Russell and the Lipper average for the one-, three-, five- and ten-year periods.

Second Quarter Review

Domestic equity markets surged in the second quarter, with major stock markets posting their best quarterly performance in more than twenty years. This quarter’s stellar performance was a welcome contrast to the first quarter of 2020, when equity markets plunged given the sharp economic contraction resulting from the COVID-19 outbreak and corresponding economic shut-down. Stocks rose despite the reinvigorated pandemic, nationwide protests for racial equality and severe economic contraction. Investors set their hopes on a sharp and swift economic recovery, taking solace in the fact that employment, real estate and consumer confidence metrics came in slightly better than pundits’ dire predictions. Congress’s commitments, delivered through the CARES Act and the Federal Reserve’s unfettering support, also helped instill a base note of confidence.

During the quarter, it was challenging for our lower beta portfolio to keep up with its surging benchmarks. The Parnassus Mid Cap Fund – Investor Shares returned 19.91% during the second quarter, which captured 81% of the Russell’s 24.61% return. We’re pleased with the Fund’s absolute quarterly return but are disappointed that we fell behind the rocketing Russell. The Fund trailed its Lipper peers by a narrow margin, capturing 95% of the Lipper’s 20.90% return. On a more positive note for the year-to-date period, the Fund is ahead of the Russell by 77 basis points and its Lipper peers by a whopping 570 basis points. (One basis point is 1/100th of one percent.)

11

Table of Contents

| Semiannual Report • 2020 | |||

From an allocation perspective, the Fund was hurt because of its underweight position in the consumer discretionary sector, the best performing sector in the Russell. On the flip side, the Fund benefitted from having underweight positions in the financials and utilities sectors, because these sectors performed relatively poorly. The Fund’s overweight position in the information technology sector also helped performance, because this was the second-best performing Russell sector.

The Fund’s performance during the quarter was overwhelmingly the result of stock selection rather than sector allocation. The worst performer was Portland General Electric, a vertically integrated electric utility serving customers in Oregon. The company subtracted 22 basis points from the Fund’s return, as its total return was negative 12.0%.* The shares dropped after management lowered the company’s annual earnings guidance, citing a steep decline in commercial demand and higher expenses due to the shut-down restrictions related to COVID-19. On top of this, the company cut its 2020-2021 capital investments, resulting in slower near-term growth. Despite the near-term challenges, we believe Portland is positioned to deliver its long-term earnings guidance of 4-6%, as it benefits from a growing customer base, robust backlog of renewable energy capital projects, a healthy balance sheet and regulatory support.

Western Digital, a leading manufacturer of NAND data storage and disk drives, subtracted 6 basis points from the Fund’s return, as its total return was negative 7.7%. The company posted disappointing earnings due to higher costs associated with COVID-19 and weaker than expected sales of its hard disk drive products. Investor sentiment soured after the company paused its dividend in order to reinvest in the business and pay down debt. We think the stock offers an asymmetric risk-reward and believe the company will benefit from improved pricing in the NAND flash market and secular tailwinds as the explosion of data consumption drives greater demand for data storage technology.

ACI Worldwide, a provider of electronic payments software, reduced the Fund’s total return by 5 basis points, as the stock’s total return was negative 2.9%. The stock dropped after management suspended its annual earnings guidance, as the company saw delayed orders for its payment software and lower

payment transaction volumes. Due to our concerns with the company’s slowing growth and elevated debt, we exited our remaining modest position in the stock.

On the positive side, the largest contributor was Hologic, a leading medical device manufacturer of mammography, surgical and diagnostics equipment, that contributed 186 basis points to the Fund’s return, as its total return was 62.4%. Despite the weakness in its surgical business as elective procedures were put on hold during the shelter-in-place restrictions, the company announced better than expected revenues, driven largely by robust demand for its COVID-19 tests using its Panther Fusion diagnostics equipment. We see further upside in the stock as demand for increased diagnostic testing drives additional Panther placements and the breast health and surgical segments gain further international market penetration.

Nuance Communications, a leading voice and analytics software applications provider, added 136 basis points to the Fund’s return, as its total return was 50.8%. The shares jumped after the company delivered higher than expected earnings, driven by increasing demand for its voice products that are used in contact centers. Investor sentiment rose after the company reiterated its long-term fiscal year 2023 targets, which call for 3-6% revenue growth and margin expansion. We believe Nuance is well-positioned to benefit from the adoption of its cloud-based technology solutions, especially in health care, and the company’s continued shift toward a recurring revenue-based subscription model.

Our third big winner was Synopsys, a leading provider of design software, semiconductor intellectual property and security software used by semiconductor companies and corporate enterprises. The stock contributed 124 basis points to the Fund’s return, as the total return of its shares was 51.4%. Robust order demand for its design software, along with improved margins in its Software Integrity segment, drove better than expected earnings. We remain bullish on the company’s long-term growth prospects, as its mission-critical design software is increasingly used by its customers to develop advanced chip designs and new technologies, including artificial intelligence, 5G and cloud-end markets.

12

* For this report, we quote total return to the portfolio, which includes price change and dividends.

Table of Contents

| Semiannual Report • 2020 | | |||

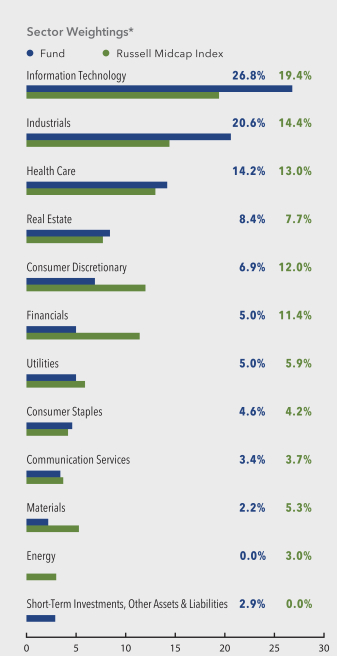

Parnassus Mid Cap Fund

as of June 30, 2020

(percentage of net assets)

* For purposes of categorizing securities for diversification requirements under the Investment Company Act, the Fund uses industry classifications that are more specific than those used for the chart.

Portfolio characteristics and holdings are subject to change periodically.

| Top 10 Equity Holdings | ||||

| (percentage of net assets) | ||||

| Hologic Inc. | 4.1% | |||

| Republic Services Inc. | 3.8% | |||

| Nuance Communications Inc. | 3.6% | |||

| Teleflex Inc. | 3.4% | |||

| Cerner Corp. | 3.4% | |||

| Synopsys Inc. | 3.1% | |||

| Cadence Design Systems Inc. | 3.0% | |||

| Verisk Analytics Inc. | 3.0% | |||

| Jack Henry & Associates Inc. | 3.0% | |||

| Xylem Inc. | 2.8% | |||

Portfolio characteristics and holdings are subject to change periodically.

Strategy and Outlook

The path forward for the economy is uncertain, so we are proceeding cautiously and considering a wide range of outcomes. We are optimistic that a COVID-19 vaccine will eventually emerge, but we have an especially low degree of confidence in predicting how the pandemic will manifest and limited visibility into how consumer and corporate spending will trend.

Our long-term, fundamental, quality-focused approach seems especially prudent at this difficult-to-assess time. This process has offered strong upside participation over the long-term, but it is our focus on downside risks and avoiding permanent capital loss that is key to our strategy. We remain acutely aware that potential negatives abound, which at this point relate to the uncertainty surrounding COVID-19. The CARES Act has helped avert the most severe negative economic outcome, but without additional action, government payments are set to expire and furloughed consumer debt obligations will soon resume, which will hamper the economy. We also recognize that corporate earnings are depressed due to the impacts of the pandemic but are cautious given the Russell’s expensive valuation of almost 24 times forward earnings estimates, which is a 20-year high. On top of these issues, we continue to be concerned about the unresolved trade wars, slowing growth in China and Europe, and heightened geopolitical risks around the globe. Longer term, potential issues resulting from the rapidly rising U.S. debt will also factor into our range of outcomes.

13

Table of Contents

| Semiannual Report • 2020 | |||

Given the recent run-up in stocks, we continue to position the Fund to outperform in the event of a downturn. As a reflection of our bottom-up research process, the Fund is significantly underweight in the more cyclical consumer discretionary and financial sectors. In contrast, we are significantly overweight in the information technology sector, focusing on discrete opportunities with asymmetric risk-reward.

In the technology sector, we added shares of Western Digital Corporation, a leading player of data storage solutions including NAND flash, memory and hard disk drives. The company operates in a highly cyclical market but is poised to benefit from multi-year secular tailwinds. These include the exponential growth of data consumption and storage and further market share gains for its lower latency NAND storage solutions relative to hard disk drive solutions. With the stock trading at a depressed valuation, we think the risk-reward for the stock is compelling and feel that investors are underappreciating the earnings power of the business as its higher-margin NAND business becomes a larger portion of the overall business and margins expand.

We are also overweight the industrial sector, though as discussed in previous reports, we have a bias toward less cyclical industrial businesses, specifically those with secular growth opportunities, competitive advantages, predictable revenue streams, well-capitalized balance sheets and attractive valuations. Within industrials, we have a fundamental bet on the domestic logistics space, because we believe the domestic economy will recover with more velocity than the trade-dependent global economy. Our positions here include FedEx, CH Robinson and a new position, Kansas City Southern a leading operator of rail networks in the United States and Mexico.

Kansas City Southern has carved out a wide moat, supported by steep barriers to entry and significant scale with its 3,300 route miles in the United States. The company is uniquely positioned, with exclusive concession agreement in Mexico that enables it to

operate 3,200 miles of rail in Mexico. We believe the company is very well-positioned to deliver industry leading growth, as it benefits from cross-border intermodal volume growth, the near-shoring of supply chains to Mexico and North America and the implementation of its Precision Scheduled Railroad initiatives, which will drive significant cost savings over time.

We exited our position in Expeditors International this past quarter to further focus on the theme of domestic economic recovery. While we admire Expeditor’s asset-light logistics model focused on cross-border trade and high returns on capital, we are concerned about the company’s slowing growth due to weak trade volumes and relatively high valuation.

We own a relatively concentrated portfolio of companies that we believe have increasing relevancy, sustainable competitive advantages, prudent management teams, solid ESG records, compelling long-term risk-reward profiles and limited potential for permanent impairment. We continue to diligently use our process to identify new portfolio holdings and adjust or exit existing portfolio positions. We are confident that this strategy will lead to outperformance relative to our benchmarks over the long-term.

Thank you for your investment in the Parnassus Mid Cap Fund.

Yours truly,

Matthew D. Gershuny

Lead Portfolio Manager

Lori A. Keith

Portfolio Manager

14

Table of Contents

| Semiannual Report • 2020 | | |||

Ticker: Investor Shares - PARWX

Ticker: Institutional Shares - PFPWX

As of June 30, 2020, the net asset value (“NAV”) of the Parnassus Endeavor Fund – Investor Shares was $35.23, so the total return for the quarter was 23.10%. This compares to a gain of 20.54% for the S&P 500 Index (“S&P 500”) and a gain of 21.12% for the Lipper Multi-Cap Core Funds Average, which represents the average return of the multi-cap core funds followed by Lipper (“Lipper average”).

Although we’re ahead of both benchmarks for the quarter, we’re still behind them for the year-to-date, because we underperformed in the first quarter. The Parnassus Endeavor Fund – Investor Shares is still down 7.73% for the year-to-date, compared to a loss of 3.08% for the S&P 500 and a loss of 5.78% for the Lipper average.

Parnassus Endeavor Fund

| Average Annual Total Returns (%) | ||||||||||||||||||||||||

| for period ended June 30, 2020 | ||||||||||||||||||||||||

| One Year | Three Years | Five Years | Ten Years | Gross Expense Ratio | Net Expense Ratio | |||||||||||||||||||

| Parnassus Endeavor Fund – Investor Shares | 3.94 | 5.03 | 8.85 | 14.04 | 0.97 | 0.95 | ||||||||||||||||||

| Parnassus Endeavor Fund – Institutional Shares | 4.20 | 5.28 | 9.09 | 14.17 | 0.71 | 0.71 | ||||||||||||||||||

| S&P 500 Index | 7.51 | 10.73 | 10.73 | 13.99 | NA | NA | ||||||||||||||||||

| Lipper Multi-Cap Core Funds Average | 2.89 | 7.17 | 7.28 | 11.56 | NA | NA | ||||||||||||||||||

The average annual total return for the Parnassus Endeavor Fund – Institutional Shares from commencement (April 30, 2015) was 8.99%. Performance shown prior to the inception of the Institutional Shares reflects the performance of the Parnassus Endeavor Fund – Investor Shares and includes expenses that are not applicable to and are higher than those of the Institutional Shares. The performance of the Institutional Shares differs from that shown for the Investor Shares to the extent that the classes do not have the same expenses. Performance data quoted represent past performance and are no guarantee of future returns. Current performance may be lower or higher than the performance data quoted. Current performance information to the most recent month end is available on the Parnassus website (www.parnassus.com). Investment return and principal value will fluctuate, so an investor’s shares, when redeemed, may be worth more or less than their original principal cost. Returns shown in the table do not reflect the deduction of taxes a shareholder may pay on fund distributions or redemption of shares. The S&P 500 is an unmanaged index of common stocks, and it is not possible to invest directly in an index. Index figures do not take any expenses, fees or taxes into account, but mutual fund returns do. The estimated impact of individual stocks on the Fund’s performance is provided by FactSet.

Before investing, an investor should carefully consider the investment objectives, risks, charges and expenses of the Fund and should carefully read the prospectus or summary prospectus, which contain this and other information. The prospectus or summary prospectus can be obtained on the Parnassus website or by calling (800) 999-3505. As described in the Fund’s current prospectus dated May 1, 2020, Parnassus Investments has contractually agreed to limit total operating expenses to 0.95% of net assets for the Parnassus Endeavor Fund – Investor Shares and to 0.71% of net assets for the Parnassus Endeavor Fund – Institutional Shares. This agreement will not be terminated prior to May 1, 2021, and may be continued indefinitely by the Adviser on a year-to-year basis.

To the left is a table, showing the returns for the Parnassus Endeavor Fund for the one-, three-, five- and ten-year periods. We’re ahead of the Lipper average for the one-year period, but behind the S&P 500. For the three-year period, we’re behind both the S&P 500 and the Lipper average, because of our difficult first quarter. However, for the five-year period, we’re ahead of the Lipper average and we’re ahead of both indices for the ten-year period, so we still have a good long-term track record.

Company Analysis

Technology stocks contributed the most to our strong gains for the quarter, with five of our seven best-performing companies coming from that sector. Interestingly enough, the other two winners came from the low-tech apparel industry.

The best-performing issue was Applied Materials, which added 318 basis points to the NAV, as its share price increased 31.9%* from $45.82 to $60.45. (One basis point is 1/100th of one percent.) The stock’s performance mirrored what happened to the market as a whole. In the first quarter, it dropped 24.9% from $61.04 to $45.82, then in the second quarter, Applied gained back virtually everything it lost in the first quarter. In the March quarterly report, we wrote that Applied was seeing strong growth, because of increased manufacturing complexity and the demand for more chips – a demand that should keep growing for years because of increased manufacturing complexity. We indicated that the stock price sank due to concerns around possible disruptions in the supply chain and lower customer spending, but we saw this weakness as temporary, and we were confident of

* For this report, we quote total return to the portfolio, which includes price change and dividends.

15

Table of Contents

| Semiannual Report • 2020 | |||

Applied’s future growth. That’s pretty much what happened. The company is one of only two major suppliers of the equipment used in manufacturing semiconductors, so it has a very strong position in the marketplace.

The same thing happened with Micron Technology, which added 247 basis points to the value of each share, as its stock price rose from $42.06 to $51.52 for a total return of 22.5%. In the March quarter, Micron’s stock fell 21.8% from $53.78 to $42.06, so the stock basically did a round-trip, much like Applied Materials. The company had fairly good results in the first quarter, but the stock dropped because of concerns about consumer demand and possible disruption of the supply chain. In the last quarterly report, we wrote that, “The disruption will be temporary and Micron should survive the global pandemic because of its strong balance sheet and brisk demand for the quality memory chips that it supplies.” This is exactly what happened, and the share price is almost back to where it began the year, at $53.78.

Specialty retailer The Gap boosted the Fund’s return by 243 basis points, as its stock soared from $7.04 to $12.62 for a total return of 79.3%. Gap sells clothes and accessories under the Old Navy, Banana Republic, Athleta and other brands. Even as mandatory store closures depressed Americans demand for apparel, the company reported an acceleration in its e-commerce business, which now accounts for over one-quarter of total sales. Gap stores across the country also reopened with new safety protocols, and investors bid up the stock anticipating a return to full capacity. Finally, on June 26, Gap struck a 10-year partnership with popular rapper and artist Kanye West to bring West’s YEEZY brand into Gap stores and online in 2021.

Lam Research, the second member of the duopoly (with Applied Materials) that controls the semiconductor equipment market, followed a pattern very similar to Applied Materials and Micron Technology. The stock started the year at $297.40 a share, then dropped to $240.00 on March 31, before rising to $323.46 on June 30 for a gain of 35%. Unlike Applied and Micron, which ended the second quarter essentially where they started the year, Lam actually had a nice gain of almost 9% for the quarter. Lam faced headwinds from COVID-19 supply-chain disruptions and U.S. and China trade tensions just liked Applied

and Micron, but finished the quarter with strong demand and a backlog of orders. Lam will continue to play a critical role in semiconductors for years, with strong demand and new technologies requiring complex manufacturing processes.

Hanesbrands, a leading manufacturer of undergarments and athletic apparel, added 143 basis points to the Fund’s return, as its stock price jumped from $7.87 to $11.29 for a total return of 45.8%. Management noted some improving consumer demand as retail stores began to gradually reopen. The company also saw online sales accelerating through April, reaching triple-digit growth rates across several retail partners websites. Finally, the board of directors appointed Stephen Bratspies as CEO effective August 3. He joins Hanesbrands with over 25 years of experience, including 15 at Walmart, where he most recently served as the chief merchandising officer. His considerable experience with consumer products and knowledge of the evolving retail landscape should help the company capitalize on growth opportunities.

Apple added 127 basis points to the Fund’s return, as its stock appreciated from $254.29 to $364.80 for a total return of 43.8%. The company reported results that were better than expected despite store closures and supply chain disruptions. The near-term shift to remote work environments benefitted hardware sales, while services continued to demonstrate strong growth. In response to the volatile environment, management also increased their buyback authorization. We believe Apple stock should continue to benefit as we approach the 5G smartphone upgrade cycle.

Cisco Systems added 113 basis points to the Fund’s return, as its stock appreciated from $39.31 to $46.64 for a total return of 19.7%. The company reported better than expected quarterly results despite significant headwinds from COVID-19. Many of Cisco’s customers have paused spending due to the uncertainty, but the company was still able to deliver healthy margins, while their software portfolio benefitted from the accelerated adoption of digital tools. We believe Cisco’s scale and incumbency along with their strong balance sheet will help them emerge stronger from this pandemic.

16

Table of Contents

| Semiannual Report • 2020 | | |||

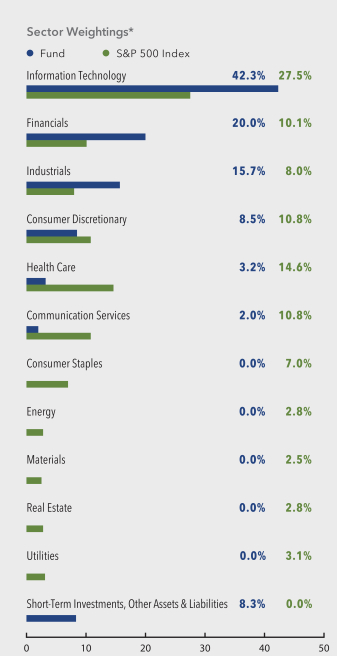

Parnassus Endeavor Fund

as of June 30, 2020

(percentage of net assets)

* For purposes of categorizing securities for diversification requirements under the Investment Company Act, the Fund uses industry classifications that are more specific than those used for the chart.

Portfolio characteristics and holdings are subject to change periodically.

| Top 10 Equity Holdings | ||||

| (percentage of net assets) | ||||

| Micron Technology Inc. | 11.8% | |||

| Applied Materials Inc. | 11.4% | |||

| Charles Schwab Corp. | 6.0% | |||

| Lam Research Corp. | 5.8% | |||

| The Gap Inc. | 4.7% | |||

| Capital One Financial Corp. | 4.5% | |||

| Cisco Systems Inc. | 4.2% | |||

| Apple Inc. | 3.9% | |||

| FedEx Corp. | 3.7% | |||

| W.W. Grainger Inc. | 3.7% | |||

Portfolio characteristics and holdings are subject to change periodically.

Outlook and Strategy

By Jerome L. Dodson

In the last quarterly report, I wrote that the stock market’s plunge was not a reasonable indicator of economic value, and that the disconnect between market price and intrinsic value was the most I had seen in 35 years. Well, the market has made a strong recovery, so I’m not surprised that we have gained back almost all that we lost, but I am surprised that it happened so quickly. The coronavirus is having a very negative effect on the economy, so I had expected the stock market to stay depressed for a while longer.

What seems to be happening is that investors are looking beyond the pandemic, expecting that science will find a cure very soon, and the economy will be back to normal. This has to be one of the fastest U-turn in history! The stock market started dropping in late February, hit bottom on March 23, then started climbing sharply to the point where now we’ve recovered virtually the entire loss. This experience shows why it’s important to stay invested at all times and not to try to time the market.

Although the market appears to be fully valued right now, it could still keep moving higher and go into an overvalued situation. For the most part, though, the stocks in the Parnassus Endeavor Fund are not overvalued, and I suspect that they will keep moving higher if the market stays strong.

17

Table of Contents

| Semiannual Report • 2020 | |||

Thank you for investing in the Parnassus Endeavor Fund.

Yours truly,

Jerome L. Dodson

Lead Portfolio Manager

Billy Hwan

Portfolio Manager

18

Table of Contents

| Semiannual Report • 2020 | | |||

Ticker: Investor Shares - PARNX

Ticker: Institutional Shares - PFPRX

As of June 30, 2020, the net asset value (“NAV”) of the Parnassus Mid Cap Growth Fund – Investor Shares was $50.99, resulting in a gain of 25.78% for the second quarter. During the quarter, we transitioned the Fund from a multi-cap strategy to a mid-cap growth strategy. To reflect the new strategy, our benchmark changed from the S&P 500 Index (“S&P 500”) to the Russell Midcap Growth Index (“Russell Midcap Growth”). We completed the transition mid-quarter, and the Fund’s 25.78% return for the second quarter was between the S&P 500’s return of 20.54% and the Russell Midcap Growth’s return of 30.26%. The Fund was substantially ahead of the 21.12% increase for the Lipper Multi-Cap Core Funds Average, which represents the average multi-cap core funds followed by Lipper (“Lipper average”). We anticipate that Lipper will eventually change the Fund’s peer group to reflect the new strategy.

Parnassus Mid Cap Growth Fund

| Average Annual Total Returns (%) | ||||||||||||||||||||||||

| for period ended June 30, 2020 | ||||||||||||||||||||||||

| One Year | Three Years | Five Years | Ten Years | Gross Expense Ratio | Net Expense Ratio | |||||||||||||||||||

| Parnassus Mid Cap Growth Fund – Investor Shares | 9.23 | 7.88 | 8.65 | 13.73 | 0.84 | 0.84 | ||||||||||||||||||

| Parnassus Mid Cap Growth Fund – Institutional Shares | 9.37 | 8.04 | 8.81 | 13.82 | 0.68 | 0.68 | ||||||||||||||||||

| Russell Midcap Growth Index | 11.91 | 14.76 | 11.60 | 15.09 | NA | NA | ||||||||||||||||||

| S&P 500 Index | 7.51 | 10.73 | 10.73 | 13.99 | NA | NA | ||||||||||||||||||

| Lipper Multi-Cap Core Funds Average | 2.89 | 7.17 | 7.28 | 11.56 | NA | NA | ||||||||||||||||||

The average annual total return for the Parnassus Mid Cap Growth Fund – Institutional Shares from commencement (April 30, 2015) was 8.61%. Performance shown prior to the inception of the Institutional Shares reflects the performance of the Parnassus Mid Cap Growth Fund – Investor Shares and includes expenses that are not applicable to and are higher than those of the Institutional Shares. The performance of Institutional Shares differs from that shown for the Investor Shares to the extent that the classes do not have the same expenses. Performance data quoted represent past performance and are no guarantee of future returns. Current performance may be lower or higher than the performance data quoted. Current performance information to the most recent month-end is available on the Parnassus website (www.parnassus.com). Investment return and principal value will fluctuate, so an investor’s shares, when redeemed, may be worth more or less than their original principal cost. Returns shown in the table do not reflect the deduction of taxes a shareholder may pay on fund distributions or redemption of shares. The Russell Midcap Growth and S&P 500 are unmanaged indexes of common stocks, and it is not possible to invest directly in an index. Index figures do not take any expenses, fees or taxes into account, but mutual fund returns do. The estimated impact of individual stocks on the Fund’s performance is provided by FactSet.

Before investing, an investor should carefully consider the investment objectives, risks, charges and expenses of the Fund and should carefully read the prospectus or summary prospectus, which contain this and other information. The prospectus or summary prospectus can be obtained on the Parnassus website or by calling (800) 999-3505. As described in the Fund’s current prospectus dated May 1, 2020, Parnassus Investments has contractually agreed to limit total operating expenses to 0.84% of net assets for the Parnassus Mid Cap Growth Fund – Investor Shares and to 0.68% of net assets for the Parnassus Mid Cap Growth Fund – Institutional Shares. This agreement will not be terminated prior to May 1, 2021, and may be continued indefinitely by the Adviser on a year-to-year basis. Prior to May 1, 2020, the benchmark for the Parnassus Mid Cap Growth Fund (formerly known as the Parnassus Fund) was the S&P 500 Index.

To the left is a table that summarizes the performance of the Parnassus Mid Cap Growth Fund, S&P 500, Russell Midcap Growth and Lipper average. The returns are for the one-, three-, five- and ten-year periods ended June 30, 2020.

Second Quarter Review

The quarter began with the mounting human and economic toll of the COVID-19 pandemic. Then, the tragic killing of George Floyd spurred protests globally in support of racial justice. We were deeply saddened by his killing, and we hope that this is the beginning of the end for the systemic racism that permeates our society. Despite the tumultuous backdrop, the S&P 500 bounced back from its dramatic first quarter loss to record one of its best quarters in history.

The Parnassus Mid Cap Growth Fund – Investor Shares rose 25.78% for the quarter, far exceeding the S&P 500’s gain of 20.54%, but trailing the Russell Midcap Growth’s gain of 30.26%. This was an eventful quarter for the Fund, as we transitioned it to a mid-cap growth strategy. We started trading to the new portfolio on May 1 and completed the transition on May 15. We’re pleased to report that from May 15 to June 30, the Fund’s gain of 12.36% outperformed the Russell Midcap Growth’s gain of 10.73%.

During the quarter, six stocks contributed more than 100 basis points to the Fund’s return (One basis point is 1/100th of one percent.), while only one subtracted more than 20 basis points. That stock was VF Corporation, the global apparel company with key brands such as The North Face, Vans and Timberland. Its shares dropped 9.6% to our average selling cost, trimming 24 basis points from the Fund’s return, as investors worried about the impact of store closures on its revenue and earnings. We sold the stock to make

19

Table of Contents

| Semiannual Report • 2020 | |||

room for faster-growing retailers that are better positioned for the new post-pandemic world, like Lululemon and Grocery Outlet.

Our best-performing stock this quarter was Square, which added an incredible 224 basis points to the Fund’s return as its stock soared 100.3%.* The stock spiked higher as Cash App, Square’s peer-to-peer mobile payment network, merged as a leading digital bank. COVID-19 and the federal government’s associated stimulus payments have caused Cash App’s adoption to inflect higher, as consumers avoid brick-and-mortar bank branches and value the convenience of Cash App’s mobile direct deposit accounts.

Autodesk, a leading provider of design and construction software, added 147 basis points to the Fund’s return as the stock jumped 53.2%. The company reported results that were in-line with expectations and provided encouraging commentary around user engagement. Autodesk also held an investor day during the quarter that highlighted the secular tailwinds benefiting the business and the company’s widening moat.

Microsoft added 126 basis points to the Fund’s return as the stock rose 14.5% to our average selling price. The company reported strong results and high near-term visibility, as it becomes an increasingly important strategic partner to its customers. We sold Microsoft during the Fund transition in May, as its market cap is too large for the Fund’s new strategy.

Cadence Design Systems provides software for designing semiconductors. Its stock added 121 basis points to the Fund’s performance, as its total return was 45.3%. Cadence reported impressive earnings during the quarter, as it continues to benefit from the secular trends of increasing semiconductor complexity and an expanding customer base.

KLA Corporation’s 36.0% total return contributed 120 basis points to the Fund’s performance. KLA dominates the semiconductor process control equipment space, and the company reported a solid quarter as semiconductor manufacturers continue to invest in KLA’s mission-critical equipment.

Gene sequencing giant Illumina added 115 basis points to the Fund’s return, as the stock increased 35.6%. The stock moved higher with the anticipation that sequencing could play an important role in expanding COVID-19 testing. Given Illumina’s dominant position in gene sequencing, it could become a big opportunity for the company.

* For this report, we quote total return to the portfolio, which includes price change and dividends.

20

Table of Contents

| Semiannual Report • 2020 | | |||

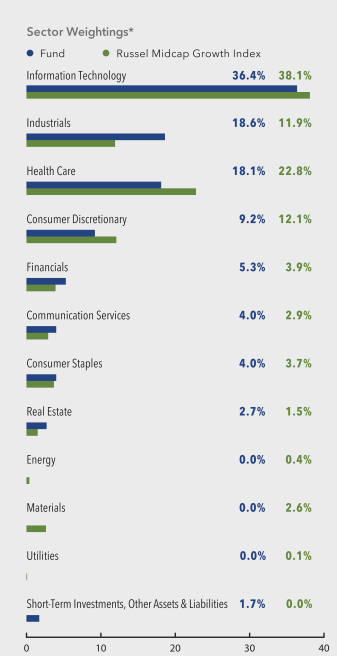

Parnassus Mid Cap Growth Fund

as of June 30, 2020 (percentage of net assets)

* For purposes of categorizing securities for diversification requirements under the Investment Company Act, the Fund uses industry classifications that are more specific than those used for the chart.

Portfolio characteristics and holdings are subject to change periodically.

| Top 10 Equity Holdings | ||||

| (percentage of net assets) | ||||

| Square Inc., Class A | 3.8% | |||

| Autodesk Inc. | 3.6% | |||

| Synopsys Inc. | 3.3% | |||

| Cerner Corp. | 3.2% | |||

| Cadence Design Systems Inc. | 3.2% | |||

| KLA Corporation | 3.1% | |||

| Agilent Technologies Inc. | 3.1% | |||

| Illumina Inc. | 3.0% | |||

| C.H. Robinson Worldwide Inc. | 3.0% | |||

| O’Reilly Automotive Inc. | 3.0% | |||

Portfolio characteristics and holdings are subject to change periodically.

Outlook and Strategy

Equity markets surged during the second quarter, with the Russell Midcap Growth Index up an astonishing 30.26% and the S&P 500 higher by 20.54%. Although the world continues to face a global pandemic and a weak economic environment, investors’ optimism was on full display, driven by a couple of factors. First, the Federal Reserve swiftly communicated that it will do whatever it takes to help bolster the economy. This includes buying securities and as keeping interest rates near 0% through 2022, which supports higher equity valuations and makes equities look attractive relative to other asset classes, such as bonds. In addition, due to the federal government’s fiscal stimulus programs, Goldman Sachs estimates that most unemployed workers have been making more money compared to when they were working. As a result, the market became confident that, as consumers spend their excess cash, the recovery would be quicker than originally expected.

In addition to the market’s strong rebound, the other exciting news during the quarter was that the Fund transitioned to become the Parnassus Mid Cap Growth Fund. We’re thrilled that the Fund consists of 44 high-quality and fast-growing companies that we believe will compound value year after year. These companies have positive ESG profiles, relatively low debt levels and represent what we believe are the winners of tomorrow. Since this is the first quarter for the new strategy, we wanted to provide more detail on our industry positioning and highlight some of our holdings.

Four sectors represent 82.3% of the Parnassus Mid Cap Growth Fund and 84.9% of the Russell Midcap Growth

21

Table of Contents

| Semiannual Report • 2020 | |||

Index as of June 30: Information technology, health care, consumer discretionary and industrials. The information technology sector represents 36.4% of the Fund and 38.1% of the Russell Midcap Growth Index, making it the largest sector in the benchmark. More than half of our exposure within information technology is to the software industry group, where we’re invested in companies that are winning in their markets through product design and innovation. Our software holdings include Autodesk, which focuses on the product design and construction end markets; Cadence and Synopsys, the dominant semiconductor design companies; Ansys, which provides engineering simulation; The Trade Desk, an online platform for digital ad buying; and Avalara, which automates tax compliance for businesses.

The industrials sector is 18.6% of our Fund compared to 11.9% for the benchmark, which makes it our largest overweight. Although the industrials sector is often associated with heavy equipment and machinery, this sector is more of a catch-all and our primary exposure is to best-in-class data providers. Our holdings include CoStar Group, a leading provider of commercial real estate data; Thomson Reuters, the premier provider of online research and data for legal, tax and accounting professionals; and Verisk Analytics, the dominant provider of risk assessment solutions for property and casualty insurers.

Health care represents 18.1% of our Fund and 22.8% of the benchmark. Within this sector, we’ve invested in companies with high recurring revenue and a long runway for growth. Importantly, we don’t have significant exposure to drug pricing risk or companies that depend on just one key drug. Examples of our holdings include Cerner and Veeva Systems, companies that are helping digitize the health care industry. We’re also invested in Illumina, the largest provider of gene sequencing instruments and consumables, as well as Agilent, a company whose products provide mission-critical testing across many end markets such as pharmaceuticals and food.

Consumer discretionary represents 9.2% of our Fund and 12.1% of the index. We’re underweight this cyclical sector due to our focus on resilient businesses with low financial leverage that can grow in most economic environments. We’re invested in category killers and consistent market share gainers, such as the athletic apparel retailer Lululemon and automotive aftermarket retailer O’Reilly Auto Parts. Another new addition, Pool Corporation, is the dominant distributor for pool related supplies.

In total, the remaining seven sectors account for 16.0% of the Fund and 15.1% of the benchmark. We’re overweight the financials sector, with our largest holdings being Morningstar, a provider of independent financial research and data, and MarketAxess, the largest electronic bond trading platform. None of our financials holdings take credit risk or have exposure to interest rates, as we focus on resilient businesses that can compound their earnings over time. We’re overweight the real estate sector, with our holdings in SBA Communications, an owner of wireless communication towers, and Americold Realty Trust, an owner of temperature-controlled food warehouses. We’re also overweight the communications services sector. We’re invested in the New York Times, the well-known publisher that is seeing robust online subscription growth, as well as Cable One, a provider of broadband services in rural communities.

Our exposure to the consumer staples sector is roughly in-line with the benchmark’s. We’re invested in spice manufacturer McCormick, as well as Grocery Outlet, an off-price grocery store. You’ll be amazed by the deals you find there!

We don’t own any materials companies because many of the stocks in the sector are highly levered and slow growers, so they’re not a good fit for the Fund. Finally, the Fund is fossil fuel free, so we don’t have exposure to the energy and utilities sectors.

The first half of the year has been a rollercoaster ride for the stock market. While we don’t know what the remainder of the year will bring, we have conviction that our portfolio of economically resilient and innovative growth compounders should perform well in any market environment.

Thank you for your investment in the Parnassus Mid Cap Growth Fund.

Your truly,

Robert J. Klaber

Portfolio Manager

Ian E. Sexsmith

Portfolio Manager

22

Table of Contents

| Semiannual Report • 2020 | | |||

Ticker: Investor Shares - PRFIX

Ticker: Institutional Shares - PFPLX

Effective May 1st, Minh Bui joined Lead Portfolio Manager Samantha Palm as Portfolio Manager of the Parnassus Fixed Income Fund. He has more than 15 years of experience at Parnassus in research and portfolio management roles. Mr. Bui served as portfolio manager for the Parnassus Fixed Income Fund from 2008 to 2013 before returning to an exclusive focus on research for several years, and he has been a member of the firm’s fixed income committee since its inception. While he will maintain his role as Senior Analyst covering equities, he will be a valuable resource to help Ms. Palm manage the Fund. As of June 30, 2020, the NAV of the Parnassus Fixed Income Fund was $18.03, producing a gain for the quarter of 3.20% (including dividends). This compares to a gain of 2.90% for the Barclays U.S. Aggregate Bond Index (“Barclays Aggregate Index”) and a gain of 4.95% for the Lipper Core Bond Fund Average, which represents the average return of the funds followed by Lipper that invest at least 85% of assets in domestic investment-grade bonds (“Lipper average”). For the first half of 2020, the Fund posted a gain of 6.65%, as compared to a gain of 6.14% for the Barclays Aggregate Index and a gain of 5.40% for the Lipper average.

Parnassus Fixed Income Fund

| Average Annual Total Returns (%) | ||||||||||||||||||||||||

| for period ended June 30, 2020 | ||||||||||||||||||||||||

| One Year | Three Years | Five Years | Ten Years | Gross Expense Ratio | Net Expense Ratio | |||||||||||||||||||

| Parnassus Fixed Income Fund – Investor Shares | 8.68 | 5.20 | 4.20 | 3.31 | 0.87 | 0.68 | ||||||||||||||||||

| Parnassus Fixed Income Fund – Institutional Shares | 8.99 | 5.46 | 4.42 | 3.42 | 0.49 | 0.45 | ||||||||||||||||||

| Bloomberg Barclays U.S. Aggregate Bond Index | 8.74 | 5.32 | 4.30 | 3.82 | NA | NA | ||||||||||||||||||

| Lipper Core Bond Funds Average | 7.82 | 4.81 | 3.97 | 3.81 | NA | NA | ||||||||||||||||||

The average annual total return for the Parnassus Fixed Income Fund – Institutional Shares from commencement (April 30, 2015) was 4.06%. Performance shown prior to the inception of the Institutional Shares reflects the performance of the Parnassus Fixed Income Fund – Investor Shares and includes expenses that are not applicable to and are higher than those of the Institutional Shares. The performance of the Institutional Shares differs from that shown for the Investor Shares to the extent that the classes do not have the same expenses. Performance data quoted represent past performance and are no guarantee of future returns. Current performance may be lower or higher than the performance data quoted. Current performance information to the most recent month end is available on the Parnassus website (www.parnassus.com). Investment return and principal value will fluctuate, so an investor’s shares, when redeemed, may be worth more or less than their original cost. Returns shown in the table do not reflect the deduction of taxes a shareholder would pay in fund distributions or redemption of shares. The Bloomberg Barclays U.S. Aggregate Bond Index (formerly known as the Barclays U.S. Aggregate Bond Index) is an unmanaged index of bonds, and it is not possible to invest directly in an index. Index figures do not take any expenses, fees or taxes into account, but mutual fund returns do. The estimated impact of individual stocks on the Fund’s performance is provided by FactSet.

Before investing, an investor should carefully consider the investment objectives, risks, charges and expenses of the Fund and should carefully read the prospectus or summary prospectus, which contain this and other information. The prospectus or summary prospectus can be obtained on the Parnassus website or by calling (800) 999 3505. As described in the Fund’s current prospectus dated May 1, 2020, Parnassus Investments has contractually agreed to limit total operating expenses to 0.68% of net assets for the Parnassus Fixed Income Fund – Investor Shares and to 0.45% of net assets for the Parnassus Fixed Income Fund – Institutional Shares. This agreement will not be terminated prior to May 1, 2021, and may be continued indefinitely by the Adviser on a year-to-year basis.

To the left is a table comparing the performance of the Fund with that of the Barclays Aggregate Index and the Lipper average. Average annual total returns are for the one-, three-, five- and ten-year periods. For June 30, the 30-day subsidized SEC yield was 0.35%, and the unsubsidized SEC yield was 0.30%.

Second Quarter in Review

The second quarter was another historic one, as the United States continued to grapple with the novel coronavirus. Despite a tragic escalation in deaths, the markets became jubilant at the prospect of a quick recovery. Investors seemed to overlook accelerating COVID-19 cases and, a nation rocked by social injustice and exceptionally high unemployment. In this historically turbulent quarter, the Parnassus Fixed Income Fund outperformed its index by 30 basis points. However, it trailed its Lipper peer group by 175 basis points, as its holdings were more conservatively positioned than the peer group. So far this year, the Fund is outperforming the Index and its Lipper group by 51 basis points and 125 basis points, respectively. (One basis point is 1/100th of one percent.)

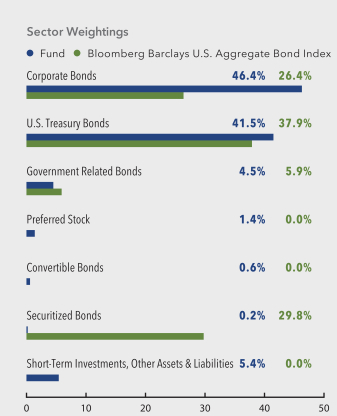

In the quarter, the Fund gained 135 basis points from its positive allocation across fixed income asset classes, as a very substantial overweight position in corporate bonds drove returns. Over the course of the quarter, the Fund held an average of 46.20% of its assets in corporate bonds versus the Index at 26.43%. The Parnassus Fixed Income Fund also benefited from not owning securitized bonds, a sector comprising nearly a third of the index but that only gained 0.96% in the quarter. By comparison, corporate bonds in the index gained 8.86%, and our corporate bond portfolio

23

Table of Contents

| Semiannual Report • 2020 | |||

gained 6.97%. Corporate bond returns for the Fund were dampened by its shorter duration than the Index, at 6.16 years versus 8.37 years.

Selection, or the individual bonds we chose, removed 75 basis points from the total return, principally due to our short-duration position in corporate bonds. This is similar to the Fund’s prior performance so far in 2020. Across the first half of the year, the Fund has accumulated 188 basis points of attribution from positive allocation across fixed income asset classes, while selection has detracted 70 basis points from the total return.

Our best performing assets in the quarter were all corporate bonds. Corporate bonds were penalized in the first quarter as lock downs dried up revenue and credit markets froze, but these bonds came roaring back in the second quarter on optimism and the Federal Reserve’s assistance. Bonds issued by FedEx, with a coupon of 4.75% maturing in November of 2045, recorded the largest gain for the Fund.

The bonds gained 16.09%* in the quarter and contributed 24 basis points to the total return. FedEx reported higher revenue than expected by investors and it continues to take advantage of gains in e-commerce spending. The company has also been instrumental in helping to restore supply chains that have been impacted by COVID-19 across the world.

Bonds issued by Masco, the parent company of popular home improvement brands like Behr Paint and Delta Faucets, were another top performer. The 4.45% coupon issue maturing April of 2025 gained 14.86%, adding 21 basis points to the total return. Masco’s brands remained resilient during the lock down as Americans spent more time in their homes and decided to refresh them. Since the last recession, Masco’s management team has transformed the company to make it more stable and consistent, and their efforts have paid off.