UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

| Investment Company Act file number: | 811-06324 | |

| Exact name of registrant as specified in charter: | Delaware Group® Global & International Funds | |

| Address of principal executive offices: | 2005 Market Street | |

| Philadelphia, PA 19103 | ||

| Name and address of agent for service: | David F. Connor, Esq. | |

| 2005 Market Street | ||

| Philadelphia, PA 19103 | ||

| Registrant’s telephone number, including area code: | (800) 523-1918 | |

| Date of fiscal year end: | November 30 | |

| Date of reporting period: | November 30, 2014 |

Item 1. Reports to Stockholders

Table of Contents

Annual report

Global / international equity funds

Delaware Emerging Markets Fund

Delaware Global Value Fund

Delaware International Value Equity Fund

November 30, 2014

Carefully consider the Funds’ investment objectives, risk factors, charges, and expenses before investing. This and other information can be found in the Funds’ prospectuses and their summary prospectuses, which may be obtained by visiting delawareinvestments.com or calling 800 523-1918. Investors should read the prospectus and the summary prospectus carefully before investing.

You can obtain shareholder reports and prospectuses online instead of in the mail.

Visit delawareinvestments.com/edelivery.

Table of Contents

Experience Delaware Investments

Delaware Investments is committed to the pursuit of consistently superior asset management and unparalleled client service. We believe in our investment processes, which seek to deliver consistent results, and in convenient services that help add value for our clients.

If you are interested in learning more about creating an investment plan, contact your financial advisor.

You can learn more about Delaware Investments or obtain a prospectus for Delaware Emerging Markets Fund, Delaware Global Value Fund, and Delaware International Value Equity Fund at delawareinvestments.com.

Manage your investments online

| • | 24-hour access to your account information |

| • | Obtain share prices |

| • | Check your account balance and recent transactions |

| • | Request statements or literature |

| • | Make purchases and redemptions |

Delaware Management Holdings, Inc. and its subsidiaries (collectively known by the marketing name of Delaware Investments) are wholly owned subsidiaries of Macquarie Group Limited, a global provider of banking, financial, advisory, investment and funds management services.

Investments in Delaware Emerging Markets Fund, Delaware Global Value Fund, and Delaware International Value Equity Fund are not and will not be deposits with or liabilities of Macquarie Bank Limited ABN 46 008 583 542 and its holding companies, including their subsidiaries or related companies (Macquarie Group), and are subject to investment risk, including possible delays in repayment and loss of income and capital invested. No Macquarie Group company guarantees or will guarantee the performance of the Funds, the repayment of capital from the Funds, or any particular rate of return.

| 1 | ||||

| 10 | ||||

| 22 | ||||

| 25 | ||||

| 31 | ||||

| 46 | ||||

| 50 | ||||

| 52 | ||||

| 58 | ||||

| 80 | ||||

| 99 | ||||

| 100 | ||||

| 106 | ||||

| 114 |

Unless otherwise noted, views expressed herein are current as of Nov. 30, 2014, and subject to change for events occurring after such date.

Funds are not FDIC insured and are not guaranteed. It is possible to lose the principal amount invested. Mutual fund advisory services provided by Delaware Management Company, a series of Delaware Management Business Trust, which is a registered investment advisor. Delaware Investments, a member of Macquarie Group, refers to Delaware Management Holdings, Inc. and its subsidiaries, including the Fund’s distributor, Delaware Distributors, L.P. Macquarie Group refers to Macquarie Group Limited and its subsidiaries and affiliates worldwide.

© 2015 Delaware Management Holdings, Inc.

All third-party marks cited are the property of their respective owners.

Table of Contents

| Portfolio management review | ||

| Delaware Emerging Markets Fund | December 9, 2014 | |

Performance preview (for the year ended November 30, 2014)

Delaware Emerging Markets Fund (Class A shares) | 1-year return | -0.20% | ||||||

MSCI Emerging Markets Index (Gross) | 1-year return | +1.40% | ||||||

MSCI Emerging Markets Index (Net) | 1-year return | +1.06% |

Past performance does not guarantee future results.

For complete, annualized performance for Delaware Emerging Markets Fund, please see the table on page 10.

The performance of Class A shares excludes the applicable sales charge and reflects the reinvestment of all distributions. For a description of the index, please see page 12.

Index performance returns do not reflect any management fees, transaction costs, or expenses. Indices are unmanaged and one cannot invest directly in an index

Emerging market equities rose slightly during the fiscal year ended Nov. 30, 2014, although performance across countries varied significantly. Economic conditions in most emerging markets were soft. China, in particular, experienced a pronounced slowdown in growth, which weighed on Chinese equities and also on global commodity prices, such as iron ore and petrochemicals.

Elections drove market performance in India and Brazil. Indian equities rallied, as a better-than-expected showing from the Bharatiya Janata Party during the general election fueled optimism for growth-oriented reforms. Brazilian equities, meanwhile, were volatile, and declined sharply in recent months on news of the re-election of incumbent president Dilma Rousseff, disappointing investors who had hoped for a change in leadership and policies.

In Russia, equities declined as tensions with Ukraine led to economic sanctions from the United States and the European Union (EU), fund outflows, and currency depreciation.

Fund performance

For the fiscal year ended Nov. 30, 2014, Delaware Emerging Markets Fund (Class A shares) returned -0.20% at net asset value and -5.93% at maximum offer price (both figures reflect all distributions reinvested). For the same period, the Fund’s benchmark, the MSCI Emerging Markets Index (net), returned +1.06%. For complete,

annualized performance for Delaware Emerging Markets Fund, please see the table on page 10.

Among countries, South Korea, Israel, and the U.S. contributed to performance. In South Korea, the Fund’s overweight positions in wireless telecommunications operator SK Telecom and paints and building materials manufacturer KCC helped bolster performance. Shares of SK Telecom rose as subscribers upgraded to higher-value 4G LTE services and as new regulations raised expectations for less intense competition in the sector. Shares of KCC rose as its core building materials business benefited from a recovery in the domestic housing market. The Fund’s underweight position in Hyundai Motor was also favorable after investors reacted negatively to the company’s purchase of high-priced land.

In Israel, the Fund’s overweight position in global generic drug manufacturer Teva Pharmaceutical Industries contributed to performance. Shares rose in response to positive news about U.S. approval of a higher-dosage version of its drug Copaxone. Additionally, Teva’s relatively defensive business provided stability amid volatility in broader emerging markets.

Finally, within the U.S., shares of renewable energy solution provider SunEdison rose as the company increased its targets for solar project completions. Yahoo! outperformed on rising

1

Table of Contents

| Portfolio management review | ||

| Delaware Emerging Markets Fund | ||

valuation expectations for Alibaba Group, in which Yahoo! holds a significant stake.

In China, the Fund’s large overweight position in internet search provider Baidu contributed positively to performance. The company has maintained its dominance in the search market and demonstrated strong growth in its mobile search business. However, the Fund’s positions in online media company SINA and internet company Sohu.com detracted from performance, offsetting Baidu’s contribution. SINA has faced regulatory challenges regarding content on its video site, while Sohu.com’s gaming business slowed as key games reached maturity.

In Russia, the Fund’s overweight position detracted from overall relative performance. Economic sanctions from the U.S. and EU not only affected the share prices of companies specifically named, including Russia’s largest bank Sberbank and integrated oil company Rosneft, but also contributed broadly to fund outflows from the country in general. As a result, the Fund’s investments in Yandex, Russia’s largest local language search-engine provider, and X5 Retail Group, the nation’s leading food retailer, also underperformed despite what we view as each company’s strong fundamental business performance.

In India, sector positioning somewhat hindered overall relative performance, particularly with regard to the Fund’s underweight positions in the industrials, financials, and healthcare sectors.

Among sectors, healthcare contributed the most to the Fund’s performance, primarily due to a position in Teva Pharmaceutical. The industrials sector was also positive due to the Fund’s holdings in KCC in South Korea and airport operator Airports of Thailand. Shares of Airports of Thailand rose as Thai tourism benefited from a more stable political environment following the country’s military coup.

The technology sector detracted from performance, mainly due to the Fund’s positions in SINA and Sohu.com. The Fund’s underweight position in the financials sector also dragged on performance, particularly in China.

We remain positive about emerging market economies. We believe urbanization, technology, and policy reforms represent the critical drivers for income and consumption growth, and we believe potential economic growth in emerging markets may exceed growth in developed markets. Furthermore, we believe that valuations for emerging market equities may prove inexpensive if we are correct about these economies’ long-term growth potential.

Over the short term, we believe that equity markets may remain volatile. Key factors to monitor include the following:

• Policy reforms in China, India, and Brazil that may stimulate or hinder growth.

• Economic conditions in China, including the health of the property and banking sectors.

• Geopolitical tensions in the Middle East, Russia, and China.

• Movements in U.S. interest rates, which have the potential to affect fund flows and currencies.

We recognize that emerging markets consist of many different countries at different stages of development, each with its own unique set of circumstances. Moreover, we believe that individual company fundamentals and valuations matter more than macroeconomics and politics in determining long-term investment performance. In this vein, our strategy is to construct a portfolio on a stock-by-stock basis, with the objective of investing in companies with what we view as sustainable franchises that trade at significant discounts to our estimate of their intrinsic value.

2

Table of Contents

| Delaware Global Value Fund | December 9, 2014 | |

Performance preview (for the year ended November 30, 2014)

Delaware Global Value Fund (Class A shares) | 1-year return | +4.57% | ||||||

MSCI World Index (Gross) | 1-year return | +9.50% | ||||||

MSCI World Index (Net) | 1-year return | +8.91% |

Past performance does not guarantee future results.

For complete, annualized performance for Delaware Global Value Fund, please see the table on page 13.

The performance of Class A shares excludes the applicable sales charge and reflects the reinvestment of all distributions. For a description of the index, please see page 15.

Index performance returns do not reflect any management fees, transaction costs, or expenses. Indices are unmanaged and one cannot invest directly in an index.

Global equity markets offered mixed results during the fiscal year ended Nov. 30, 2014 with the U.S. economy consistently improving throughout the period, particularly when compared to other international equity markets.

The U.S. Federal Reserve ended its quantitative easing program in October, and prepared investors for a likely rise in short-term interest rates in 2015. The finish of the Fed’s tapering of stimulatory bond purchases approached without a corresponding slowing of economic growth or an alarmingly abrupt increase in interest rates. Equity market performance in the United States demonstrated a greater level of resilience than other international markets with the S&P 500® Index returning 16.86% for the fiscal year.

Japan’s economy continued to struggle in 2014. Although Prime Minister Shinzo Abe’s economic stimulus package, dubbed “Abenomics,” was developed to battle two decades of deflation and stagnant growth, the program continued to face difficulties. These challenges included the effect of yen depreciation on energy and raw material import costs, aging demographics, a declining population, and the highest debt to gross domestic product ratio in the developed world. In October, the Bank of Japan increased the annual target for enlarging the monetary base by 80 trillion yen with the hope that the move could potentially increase exports and stimulate inflation. Although the Japanese recovery appears stagnant

in the short term, there has been strong performance in some areas.

Among euro-zone investors, confidence in the region’s nascent recovery to surpass stall-speed clearly waned as disappointing economic data emerged in the third quarter of 2014 from Italy, France, and Germany, among others. As eyes turned to the European Central Bank in anticipation of stimulatory intervention, currency markets produced the most pronounced depreciation of the euro since 2012 (source: Thomson Reuters). Equity market performance skewed away from cyclical segments such as industrial and consumer stocks, leaving healthcare as the region’s sole source of positive returns.

Within emerging markets, China’s 10-year growth trajectory appeared to be waning. Much of China’s growth has been driven by excess investment in real estate, infrastructure, and industrials funded by debt. Many investors now question how much growth potential remains within the nation. In addition to weakening in China, other developments within emerging markets include the continued appreciation of the U.S. dollar, ongoing conflict in Ukraine, the depreciation of the Russian ruble, and overt conflict in Iraq and Syria. Though their relative significance is subject to interpretation, their collective impact seemed to adversely affect sentiment associated with emerging market stocks as risky assets. This

3

Table of Contents

| Portfolio management review | ||

| Delaware Global Value Fund | ||

sentiment also correlated with the pronounced weakening of commodity prices and associated stocks, especially in the energy sector.

Fund performance

For the fiscal year ended Nov. 30, 2014, Delaware Global Value Fund (Class A shares) returned +4.57% at net asset value and -1.47% at maximum offer price (both figures reflect Class A shares with all distributions reinvested). For the same period, the Fund’s benchmark MSCI World Index (net) returned +8.91%. For complete, annualized performance for Delaware Global Value Fund, please see the table on page 13.

On a regional basis, positive stock selection in the U.S. and Japan was more than offset by adverse stock selection in Canada, Russia, and the United Kingdom. From a sector perspective, strong stock selection in consumer discretionary and industrials was more than offset by weak stock selection in energy, materials, telecommunications, and consumer staples.

During the fiscal year, the largest detractors from the Fund’s relative performance during the fiscal year included the following:

• Mobile Telesystems: Mounting tensions between Russia and Ukraine, coupled with U.S.-and European Union-imposed sanctions on Russia, led to a dramatic decline in the value of the Russian ruble. These factors had an adverse effect on the company’s stock price, despite what we view as its strong operational performance and a healthy competitive position.

• Standard Chartered: Asia had been the growth engine of the U.K.-listed bank for the past decade, but recently the region was responsible for the bank’s second profit warning of the year, sending shares to a five-year low. We continue to hold the company’s shares in the Fund, as valuations are at a decade low, the absolute level of nonperforming loans remains low, and the bank’s Asian international trade and wealth management

franchises remain intact – and therefore appear positioned to benefit from any recovery in the region. There is also considerable scope for cost-cutting and rationalization, and the bank is now actively spoken of as a possible takeover target.

• Yamana Gold: The Toronto-based mining company suffered largely due to dramatic fluctuations in the price of gold. Yamana has operations and development projects in South and Central America. The company has indicated it is focused on growing profitably through the careful management of costs. Through the development of several new mines, the expansion of key producing assets and the acquisitions, Yamana’s gold output appears poised to rise in 2015.

• Halliburton: The stock price of this U.S. oil field service company retreated dramatically in conjunction with falling oil prices and the proposed merger with Baker Hughes. However, we believe that the proposed merger may create a more valuable entity that has the potential to more effectively compete internationally.

• Saipem: The company faced worsening market conditions driven by lower oil prices and shrinking exploration and production budgets, with new order intake expected to slow down. On a positive note, lower margin legacy contracts are drawing down. From a longer-term perspective, as the company progresses towards margin improvement and it maintains its competitiveness, we will continue to carefully monitor the stock as weakened market conditions may alter the pace of the recovery.

During the fiscal year, the largest contributors to the Fund’s performance during the fiscal year included the following:

• American Airlines Group: The company recently emerged from bankruptcy and merged with U.S. Airways. We believe American Airlines has a solid route structure, which may provide strong earnings growth. We also think the company could potentially benefit from an

4

Table of Contents

improved operating mix, adjusted cost structure, and lower oil prices.

• Mylan: The U.S. domiciled global generic and specialty pharmaceutical company posted recent results which showed both generic and specialty sales performing well with every geographic region posting positive growth.

• Apple: The consumer electronics manufacturer realized particularly strong gains during the Fund’s fiscal year. Recent quarterly sales growth for Apple was also positive in every region, primarily driven by China.

• Teva Pharmaceuticals Industries: The Israeli generic drug manufacturer saw strong gains after the introduction of a new formulation of its multiple sclerosis treatment drug, Copaxone, which is patent protected through 2030. This should help insulate Teva from generic competition. The company has also benefited from a strong cost-cutting program and a new management structure.

• Time Warner: This consumer discretionary stock also contributed strongly to the Fund’s relative return. In terms of revenue, Time Warner is currently the third largest television network and film TV and entertainment company in the world. Time Warner owns, what we consider, high-quality content and has pricing power in its Networks business. Combined with cost cutting and share buybacks, this has led, in our view, to impressive earnings growth.

We believe that successful value investing requires both a sharp attention to developing valuation disparities across industries and regions and a clear-eyed view to the varying levels of secular growth and cyclical mean reversion that may justify those disparities. Through the course of the fiscal year, we considered there to be attractive valuations to be found in both Europe and Japan, but with the caveats that European cyclical recovery and Japanese structural

improvements would likely be needed to support the expansion of those valuation metrics. The U.S., by contrast, after enjoying a longer and stronger market up-cycle has the most richly valued of the world’s major markets (source: MSCI). While this general pattern remains intact, the market’s performance in the interim has been far from uniform and has been complicated significantly by shifts in currency exchange rates.

The euro-zone’s weak overall returns mask considerable variation across the region, and though returns in U.S. dollars in the two largest markets, France and Germany, were down, local investors saw a moderate gain and therefore valuations changed little. Japan’s returns in yen put that country at the top of major market rankings for local-currency performance, but the index-level gain was actually outpaced by improvements in underlying fundamentals, which brought valuation levels down slightly. This pattern was not replicated in the U.S., where rising valuations accompanied the strong market gains.

For U.S. optimists, though these valuations appear well above historic median levels, they are still well below prior peaks and may reflect the greater stability and secular growth prospects this country enjoys versus many other developed as well as emerging markets. As global stock pickers, what we find intriguing is this: In an interconnected global market, domicile does not limit opportunity. If a European multinational trades at a recessionary valuation multiple but has competitive positions in the world’s strongest growth markets, that company’s investors should, in the long term, enjoy the benefits of both valuation and strong fundamentals. As global equity managers taking a contrarian approach to bottom-up stock selection, we strive to use the uncertainty of macroeconomic and valuation cycles to bring to light potential opportunities at the company level, because we believe it is there that close analysis is most critical to performance.

5

Table of Contents

| Portfolio management review | ||

| Delaware International Value Equity Fund | December 9, 2014 | |

Performance preview (for the year ended November 30, 2014)

Delaware International Value Equity Fund (Class A shares) | 1-year return | -4.13% | ||||||

MSCI EAFE Index (Gross) | 1-year return | +0.41% | ||||||

MSCI EAFE Index (Net) | 1-year return | -0.02% |

Past performance does not guarantee future results.

For complete, annualized performance for Delaware International Value Equity Fund, please see the table on page 17.

The performance of Class A shares excludes the applicable sales charge and reflects the reinvestment of all distributions. For a description of the index, please see page 19.

Index performance returns do not reflect any management fees, transaction costs, or expenses. Indices are unmanaged and one cannot invest directly in an index.

Global equity markets offered mixed results during the fiscal year ended Nov. 30, 2014 with the U.S. economy consistently improving throughout the period, particularly when compared to other international equity markets.

The U.S. Federal Reserve ended its quantitative easing program in October, and prepared investors for a likely rise in short-term interest rates in 2015. The finish of the Fed’s tapering of stimulatory bond purchases approached without a corresponding slowing of economic growth or an alarmingly abrupt increase in interest rates. Equity market performance in the United States demonstrated a greater level of resilience than other international markets with the S&P 500 Index returning 16.86% for the fiscal year.

Japan’s economy continued to struggle in 2014. Although Prime Minister Shinzo Abe’s economic stimulus package, dubbed “Abenomics” was developed to battle two decades of deflation and stagnant growth, the program continued to face difficulties. These challenges included the effect of yen depreciation on energy and raw material import costs, aging demographics, a declining population, and the highest debt to gross domestic product ratio in the developed world. In October, the Bank of Japan increased the annual target for enlarging the monetary base by 80 trillion yen with the hope that the move could potentially increase exports and stimulate inflation.

Although the Japanese recovery appears stagnant in the short term, there has been strong performance in some areas.

Among euro-zone investors, confidence in the region’s nascent recovery to surpass stall-speed clearly waned as disappointing economic data emerged in the third quarter of 2014 from Italy, France, and Germany, among others. As eyes turned to the European Central Bank in anticipation of stimulatory intervention, currency markets produced the most pronounced depreciation of the euro since 2012 (source: Thomson Reuters). Equity market performance skewed away from cyclical segments such as industrial and consumer stocks, leaving health care as the region’s sole source of positive returns.

Within emerging markets, China’s 10-year growth trajectory appears to be waning. Much of China’s growth has been driven by excess investment in real estate, infrastructure, and industrials funded by debt. Many investors now question how much growth potential remains within the nation. In addition to weakening in China, other developments within emerging markets include the continued appreciation of the U.S. dollar, ongoing conflict in Ukraine, the depreciation of the Russian ruble, and overt conflict in Iraq and Syria. Though their relative significance is subject to

6

Table of Contents

interpretation, their collective impact seemed to adversely affect sentiment associated with emerging market stocks as risky assets. This sentiment also correlated with the pronounced weakening of commodity prices and associated stocks, especially in the energy sector.

Fund performance

For the fiscal year ended Nov. 30, 2014, Delaware International Value Equity Fund (Class A shares) returned -4.13% at net asset value and -9.64% at maximum offer price (both figures reflect Class A shares with all distributions reinvested). For the same period, the Fund’s benchmark MSCI EAFE Index (net) returned -0.02%. For complete, annualized performance for Delaware International Value Equity Fund, please see the table on page 17.

From a regional standpoint, positive contributions to relative return came primarily from stocks in Israel and Switzerland but were more than offset by adverse stock selection in stocks chiefly in the United Kingdom and Russia. From a sector perspective, detractors to return came primarily from stocks in energy, consumer staples and telecommunications, which more than offset contributions from stocks in the consumer discretionary and healthcare sectors.

During the fiscal year, the largest detractors from the Fund’s relative performance included the following:

• Standard Chartered: Asia had been the growth engine of the U.K.-listed bank for the past decade, but recently the region was responsible for the bank’s second profit warning of the year, sending shares to a five-year low. We continue to hold the company’s shares in the Fund, as valuations are at a decade low, the absolute level of non-performing loans remains low and the bank’s Asian international trade and wealth management franchises remain intact – and therefore appear positioned to benefit from any recovery in the region. There is also considerable scope for cost-

cutting and rationalization, and the bank is now actively spoken of as a possible takeover target.

• Tesco: The company’s share price worsened during the fiscal year, as its competitive industry position was undermined by aggressively low-cost competition. Although we believe the company may have the resources to recover eventually, we chose to exit the position due to its eroding competitive position.

• Mobile Telesystems: Mounting tensions between Russia and Ukraine, coupled with U.S.-and European Union-imposed sanctions on Russia led to a dramatic decline in the value of the Russian ruble. These factors had an adverse effect on the company’s stock price, despite what we view as its strong operational performance and a healthy competitive position.

• Saipem: The company faced worsening market conditions driven by lower oil prices and shrinking exploration and production budgets with new order intake expected to slow down. On a positive note, lower margin legacy contracts are drawing down. From a longer-term perspective, as the company progresses towards margin improvement and if it maintains its competitiveness, we will continue to carefully monitor the stock as weakened market conditions may alter the pace of the recovery.

• Subsea 7: This subsea engineering, construction, and services company serves the offshore energy industry. Although the company’s recent results were above consensus, the stock price did not react strongly largely due to uncertainty regarding the award time of large contracts and a falling book-bill ratio. Subsea 7 is planning to change the organizational structure of the business to better align it to the company’s strategic priorities. The oil services industry is entering a challenging time – we think thoughtful reorganizations to address a changing industry could potentially help address rising costs and execution risks.

7

Table of Contents

| Performance management review | ||

| Delaware International Value Equity Fund | ||

During the fiscal year, the largest contributors to the Fund’s relative performance included the following:

• Teva Pharmaceutical Industries: The Israeli generic drug manufacturer saw strong gains after the introduction of a new formulation of its multiple sclerosis treatment drug, Copaxone, which is patent protected through 2030. This should help insulate Teva from generic competition. The company has also benefited from a strong cost-cutting program and a new management structure.

• Aryzta: This Swiss-based company became the largest bakery in the world after acquiring more bakeries in Germany and North America in the first half of 2014. Recently reported third-quarter revenues rose year-on-year nearly 17%. Management successfully completed its three-year “Aryzta Transformation Initiative,” which helped boost operating margins to 11.8%. This was the sixth consecutive year of margin expansion.

• Novartis: The Swiss-based pharmaceuticals group is expected to complete its transformation to a more focused business mix in 2015, and its three core areas have performed well this year.

• Teleperformance: Based in France, this company is a global leader in customer service, technical support, and call-center services. The price of its shares were strengthened by its solid sales performance. Recent results included consolidated organic growth and what we believe was a sharp pick-up in organic growth for the Ibero-Latam region.

• Bank Rakyat Indonesia Persero: This is the largest bank by loans and second largest by assets and deposits in Indonesia. Micro loans, small commercial loans, and consumer loans make up the biggest portion of the company’s loan book. We like Bank Rakyat Indonesia Persero because of its entrenched microfinancing, business, and above average return on equity.

We believe that successful value investing requires both a sharp attention to developing valuation disparities across industries and regions and a clear-eyed view to the varying levels of secular growth and cyclical mean reversion that may justify those disparities. Through the course of the fiscal year, we considered there to be attractive valuations in both Europe and Japan, but with the caveats that European cyclical recovery and Japanese structural improvements would likely be needed to support the expansion of those valuation metrics. The U.S., by contrast, after enjoying a longer and stronger market up-cycle, has the most richly valued of the world’s major markets (source: MSCI). While this general pattern remains intact, the market’s performance in the interim has been far from uniform and has been complicated significantly by shifts in currency exchange rates.

The euro-zone’s weak overall returns mask considerable variation across the region, and though returns in U.S. dollars in the two largest markets, France and Germany, were down, local investors saw a moderate gain and therefore valuations changed little. Japan’s returns in yen put that country at the top of major market rankings for local-currency performance, but the index-level gain was actually outpaced by improvements in underlying fundamentals, which brought valuation levels down slightly. This pattern was not replicated in the U.S., where rising valuations accompanied the strong market gains.

For U.S. optimists, though these valuations appear well above historic median levels, they are still well below prior peaks and may reflect the greater stability and secular growth prospects this country enjoys versus many other developed as well as emerging markets. As global stock pickers, what we find intriguing is this: In an interconnected global market, domicile does not limit opportunity. If a European multinational trades at a recessionary valuation multiple but has competitive positions in the world’s strongest

8

Table of Contents

growth markets, that company’s investors should, in the long term, enjoy the benefits of both valuation and strong fundamentals. As global equity managers taking a contrarian approach to bottom-up stock selection, we strive to use the uncertainty of macroeconomic and valuation cycles to bring to light potential opportunities at the company level, because we believe it is there that close analysis is most critical to performance.

9

Table of Contents

Delaware Emerging Markets Fund | November 30, 2014 |

The performance data quoted represent past performance; past performance does not guarantee future results. Investment return and principal value will fluctuate so your shares, when redeemed, may be worth more or less than their original cost. Please obtain the performance data current for the most recent month end by calling 800 523-1918 or visiting our website at delawareinvestments.com/performance. Current performance may be lower or higher than the performance data quoted.

Fund and benchmark performance1,2 | Average annual total returns through November 30, 2014 | |||||||

| 1 year | 5 years | 10 years | Lifetime | |||||

Class A (Est. June 10, 1996) | ||||||||

Excluding sales charge | -0.20% | +5.42% | +9.93% | n/a | ||||

Including sales charge | -5.93% | +4.17% | +9.28% | n/a | ||||

Class C (Est. June 10, 1996) | ||||||||

Excluding sales charge | -0.97% | +4.63% | +9.11% | n/a | ||||

Including sales charge | -1.96% | +4.63% | +9.11% | n/a | ||||

Class R (Est. Aug. 31, 2009) | ||||||||

Excluding sales charge | -0.44% | +5.14% | n/a | +7.35% | ||||

Including sales charge | -0.44% | +5.14% | n/a | +7.35% | ||||

Institutional Class (Est. June 10, 1996) | ||||||||

Excluding sales charge | +0.04% | +5.69% | +10.20% | n/a | ||||

Including sales charge | +0.04% | +5.69% | +10.20% | n/a | ||||

MCSI Emerging Markets Index (Gross) | +1.40% | +3.88% | +9.81% | n/a | ||||

MCSI Emerging Markets Index (Net) | +1.06% | +3.54% | +9.45% | n/a | ||||

1 Returns reflect the reinvestment of all distributions and are presented both with and without the applicable sales charges described below. Returns do not reflect the deduction of taxes the shareholder would pay on Fund distributions or redemptions of Fund shares.

Expense limitations were in effect for certain classes during some or all of the periods shown in the “Fund and benchmark performance” table. Expenses for each class are listed on the “Fund expense ratios” table on page 11. Performance would have been lower had expense limitations not been in effect.

Class A shares are sold with a maximum front-end sales charge of 5.75%, and have an annual distribution and service fee of 0.25% of average

daily net assets. Performance for Class A shares, excluding sales charges, assumes that no front-end sales charge applied.

Class C shares are sold with a contingent deferred sales charge of 1.00% if redeemed during the first

12 months. They are also subject to an annual distribution and service fee of 1.00% of average daily net assets. Performance for C shares, excluding sales charges, assumes either that contingent deferred sales charges did not apply or that the investment was not redeemed.

Class R shares are available only for certain retirement plan products. They are sold without a sales charge and have an annual distribution and service fee of 0.50% of average daily net assets.

10

Table of Contents

Institutional Class shares are available without sales or asset-based distribution charges only to certain eligible institutional accounts.

The “Fund and benchmark performance” table does not reflect the deduction of taxes the shareholder would pay on Fund distributions or redemptions of Fund shares.

International investments entail risks not ordinarily associated with U.S. investments including

fluctuation in currency values, differences in accounting principles, or economic or political instability in other nations.

Investing in emerging markets can be riskier than investing in established foreign markets due to increased volatility and lower trading volume.

2The Fund’s expense ratios, as described in the most recent prospectus, are disclosed in the following “Fund expense ratios” table.

Fund expense ratios | Class A | Class C | Class R | Institutional Class | ||||

Total annual operating expenses (without fee waivers) | 1.71% | 2.46% | 1.96% | 1.46% | ||||

Net expenses (including fee waivers, if any) | 1.71% | 2.46% | 1.96% | 1.46% | ||||

Type of waiver | n/a | n/a | n/a | n/a |

11

Table of Contents

| Performance summaries | ||

| Delaware Emerging Markets Fund | ||

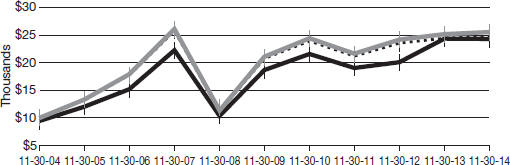

Performance of a $10,000 investment1

Average annual total returns from Nov. 30, 2004, through Nov. 30, 2014

| For the period beginning Nov. 30, 2004, through Nov. 30, 2014 | Starting value | Ending value | ||||||||

| MSCI Emerging Markets Index (gross) | $10,000 | $25,485 | |||||||

| MSCI Emerging Markets Index (net) | $10,000 | $24,676 | |||||||

| Delaware Emerging Markets Fund — Class A shares | $9,425 | $24,286 | |||||||

1 The “Performance of a $10,000 investment” graph assumes $10,000 invested in Class A shares of the Fund on Nov. 30, 2004, and includes the effect of a 5.75% front-end sales charge and the reinvestment of all distributions. The graph does not reflect the deduction of taxes the shareholders would pay on Fund distributions or redemptions of Fund shares. Expense limitations were in effect for some or all of the periods shown. Performance would have been lower had expense limitations not been in effect. Expenses are listed in the “Fund expense ratios” table on page 11. Please note additional details on pages 10 through 12.

The graph also assumes $10,000 invested in the MSCI Emerging Markets Index as of

Nov. 30, 2004. The MSCI Emerging Markets Index measures equity market performance across emerging market countries worldwide. Index “gross” return approximates the maximum possible dividend reinvestment. Index “net” return approximates the minimum possible dividend reinvestment, after deduction of withholding tax at the highest possible rate.

Index performance returns do not reflect any management fees, transaction costs, or expenses. Indices are unmanaged and one cannot invest directly in an index. Past performance is not a guarantee of future results.

Performance of other Fund classes will vary due to different charges and expenses.

| Nasdaq symbols | CUSIPs | |||||||

Class A | DEMAX | 245914841 | ||||||

Class C | DEMCX | 245914825 | ||||||

Class R | DEMRX | 245914569 | ||||||

Institutional Class | DEMIX | 245914817 | ||||||

12

Table of Contents

| Delaware Global Value Fund | November 30, 2014 |

The performance data quoted represent past performance; past performance does not guarantee future results. Investment return and principal value will fluctuate so your shares, when redeemed, may be worth more or less than their original cost. Please obtain the performance data current for the most recent month end by calling 800 523-1918 or visiting our website at delawareinvestments.com/performance. Current performance may be lower or higher than the performance data quoted.

Fund and benchmark performance1,2 | Average annual total returns through November 30, 2014 | |||||

| 1 year | 5 years | 10 years | ||||

Class A (Est. Dec. 19, 1997) | ||||||

Excluding sales charge | +4.57% | +8.79% | +5.97% | |||

Including sales charge | -1.47% | +7.51% | +5.34% | |||

Class C (Est. Sept. 28, 2001) | ||||||

Excluding sales charge | +3.80% | +7.98% | +5.18% | |||

Including sales charge | +2.80% | +7.98% | +5.18% | |||

Institutional Class (Est. Dec. 19, 1997) | ||||||

Excluding sales charge | +4.88% | +9.07% | +6.24% | |||

Including sales charge | +4.88% | +9.07% | +6.24% | |||

MCSI World Index (Gross) | +9.50% | +11.57% | +7.18% | |||

MCSI World Index (Net) | +8.91% | +10.96% | +6.60% | |||

1 Returns reflect the reinvestment of all distributions and are presented both with and without the applicable sales charges described below. Returns do not reflect the deduction of taxes the shareholder would pay on Fund distributions or redemptions of Fund shares.

Expense limitations were in effect for certain classes during some or all of the periods shown in the “Fund and benchmark performance” table. Expenses for each class are listed on the “Fund expense ratios” table on page 14. Performance would have been lower had expense limitations not been in effect.

Class A shares are sold with a maximum front-end sales charge of 5.75%, and have an annual distribution and service fee of 0.25% of average daily net assets. Performance for Class A shares, excluding sales charges, assumes that no front-end sales charge applied.

Class C shares are sold with a contingent deferred sales charge of 1.00% if redeemed during the first 12 months. They are also subject to an annual distribution and service fee of 1.00% of average daily net assets. Performance for Class C shares, excluding sales charges, assumes either that contingent deferred sales charges did not apply or that the investment was not redeemed.

Institutional Class shares are available without sales or asset-based distribution charges only to certain eligible institutional accounts.

The “Fund and benchmark performance” table does not reflect the deduction of taxes the shareholder would pay on Fund distributions or redemptions of Fund shares.

13

Table of Contents

| Performance summaries | ||

| Delaware Global Value Fund | ||

International investments entail risks not ordinarily associated with U.S. investments including fluctuation in currency values, differences in accounting principles, or economic or political instability in other nations.

Investing in emerging markets can be riskier than investing in established foreign markets due to increased volatility and lower trading volume.

Investments in small and/or medium-sized companies typically exhibit greater risk and higher volatility than larger, more established companies.

2The Fund’s expense ratios, as described in the most recent prospectus, are disclosed in the following “Fund expense ratios” table. Delaware Management Company has agreed to reimburse certain expenses and/or waive certain fees in order to prevent total fund operating expenses (excluding any 12b-1 fees, taxes, interest, short sale and dividend interest expenses, brokerage fees, certain insurance costs, acquired fund fees and expenses, and nonroutine expenses or costs, including, but not limited to, those relating to reorganizations, litigation, conducting shareholder meetings, and liquidations (collectively nonroutine expenses)) from exceeding 1.30% of the Fund’s average daily net assets during the period from Dec. 1. 2013 through Nov. 30, 2014.* Please see the most recent prospectus and any applicable supplement(s) for additional information on these fee waivers and/or reimbursements.

| Fund expense ratios | Class A | Class C | Institutional Class | |||

Total annual operating expenses (without fee waivers) | 1.78% | 2.53% | 1.53% | |||

Net expenses (including fee waivers, if any) | 1.55% | 2.30% | 1.30% | |||

Type of waiver | Contractual | Contractual | Contractual |

*The contractual waiver period is from March 29, 2013 through March 30, 2015.

14

Table of Contents

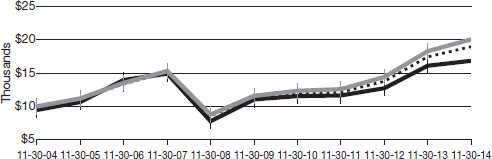

Performance of a $10,000 investment1

Average annual total returns from Nov. 30, 2004, through Nov. 30, 2014

| For the period beginning Nov. 30, 2004, through Nov. 30, 2014 | Starting value | Ending value | ||||||

| $10,000 | $20,010 | ||||||

| $10,000 | $18,947 | ||||||

| $9,425 | $16,823 | ||||||

1 The “Performance of a $10,000 investment” graph assumes $10,000 invested in Class A shares of the Fund on Nov. 30, 2004, and includes the effect of a 5.75% front-end sales charge and the reinvestment of all distributions. The graph does not reflect the deduction of taxes the shareholders would pay on Fund distributions or redemptions of Fund shares. Expense limitations were in effect for some or all of the periods shown. Performance would have been lower had expense limitations not been in effect. Expenses are listed in the “Fund expense ratios” table on page 14. Please note additional details on pages 13 through 16.

The graph also assumes $10,000 invested in the MSCI World Index as of Nov. 30, 2004. The MSCI World Index is a free float-adjusted market capitalization weighted index designed to measure equity market performance across developed markets worldwide. Index “gross” return approximates the maximum possible dividend reinvestment. Index “net” return approximates the minimum possible dividend reinvestment, after

deduction of withholding tax at the highest possible rate.

The S&P 500 Index, mentioned on page 3, measures the performance of 500 mostly large-cap stocks weighted by market value, and is often used to represent performance of the U.S. stock market.

Index performance returns do not reflect any management fees, transaction costs, or expenses. Indices are unmanaged and one cannot invest directly in an index. Past performance is not a guarantee of future results.

Performance of other Fund classes will vary due to different charges and expenses.

15

Table of Contents

| Performance summaries | ||

| Delaware Global Value Fund | ||

| Nasdaq symbols | CUSIPs | |||||||

Class A | DABAX | 245914718 | ||||||

Class C | DABCX | 245914684 | ||||||

Institutional Class | DABIX | 245914676 | ||||||

16

Table of Contents

| Performance summaries | ||

| Delaware International Value Equity Fund | November 30, 2014 | |

The performance data quoted represent past performance; past performance does not guarantee future results. Investment return and principal value will fluctuate so your shares, when redeemed, may be worth more or less than their original cost. Please obtain the performance data current for the most recent month end by calling 800 523-1918 or visiting our website at delawareinvestments.com/performance. Current performance may be lower or higher than the performance data quoted.

| Fund and benchmark performance1,2 | Average annual total returns through November 30, 2014 | |||||

| 1 year | 5 years | 10 years | ||||

Class A (Est. Oct. 31, 1991) | ||||||

Excluding sales charge | -4.13% | +4.97% | +3.95% | |||

Including sales charge | -9.64% | +3.72% | +3.33% | |||

Class C (Est. Nov. 29, 1995) | ||||||

Excluding sales charge | -4.80% | +4.20% | +3.21% | |||

Including sales charge | -5.75% | +4.20% | +3.21% | |||

Class R (Est. June 2, 2003) | ||||||

Excluding sales charge | -4.37% | +4.72% | +3.73% | |||

Including sales charge | -4.37% | +4.72% | +3.73% | |||

Institutional Class (Est. Nov. 9, 1992) | ||||||

Excluding sales charge | -3.88% | +5.26% | +4.24% | |||

Including sales charge | -3.88% | +5.26% | +4.24% | |||

MCSI EAFE Index (Gross) | +0.41% | +6.86% | +5.73% | |||

MCSI EAFE Index (Net) | -0.02% | +6.38% | +5.25% | |||

1 Returns reflect the reinvestment of all distributions and are presented both with and without the applicable sales charges described below. Returns do not reflect the deduction of taxes the shareholder would pay on Fund distributions or redemptions of Fund shares.

Expense limitations were in effect for certain classes during some or all of the periods shown in the “Fund and benchmark performance” table. Expenses for each class are listed on the “Fund expense ratios” table on page 18. Performance would have been lower had expense limitations not been in effect.

Class A shares are sold with a maximum front-end sales charge of 5.75%, and have an annual

distribution and service fee of 0.25% of average daily net assets. Performance for Class A shares, excluding sales charges, assumes that no front-end sales charge applied.

Class C shares are sold with a contingent deferred sales charge of 1.00% if redeemed during the first 12 months. They are also subject to an annual distribution and service fee of 1.00% of average daily net assets. Performance for Class C shares, excluding sales charges, assumes either that contingent deferred sales charges did not apply or that the investment was not redeemed.

Class R shares are available only for certain retirement plan products. They are sold without a

17

Table of Contents

| Performance summaries | ||

| Delaware International Value Equity Fund | ||

sales charge and have an annual distribution and service fee of 0.50% of average daily net assets.

Institutional Class shares are available without sales or asset-based distribution charges only to certain eligible institutional accounts.

The “Fund and benchmark performance” table does not reflect the deduction of taxes the shareholder would pay on Fund distributions or redemptions of Fund shares.

International investments entail risks not ordinarily associated with U.S. investments including fluctuation in currency values, differences in accounting principles, or economic or political instability in other nations.

Investing in emerging markets can be riskier than investing in established foreign markets due to increased volatility and lower trading volume.

2The Fund’s expense ratios, as described in the most recent prospectus, are disclosed in the following “Fund expense ratios” table. Delaware Management Company has agreed to reimburse certain expenses and/or waive certain fees in order to prevent total fund operating expenses (excluding any 12b-1 fees, taxes, interest, short sale and dividend interest expenses, brokerage fees, certain insurance costs, acquired fund fees and expenses, and nonroutine expenses or costs, including, but not limited to, those relating to reorganizations, litigation, conducting shareholder meetings, and liquidations (collectively nonroutine expenses)) from exceeding 1.21% of the Fund’s average daily net assets during the period from Dec. 1, 2013 through Nov. 30, 2014.* Please see the most recent prospectus and any applicable supplement(s) for additional information on these fee waivers and/or reimbursements.

| Fund expense ratios | Class A | Class C | Class R | Institutional Class | ||||

Total annual operating expenses (without fee waivers) | 1.47% | 2.22% | 1.72% | 1.22% | ||||

Net expenses (including fee waivers, if any) | 1.46% | 2.21% | 1.71% | 1.21% | ||||

Type of waiver | Contractual | Contractual | Contractual | Contractual |

*The contractual waiver period is from March 29, 2013 through March 30, 2015.

18

Table of Contents

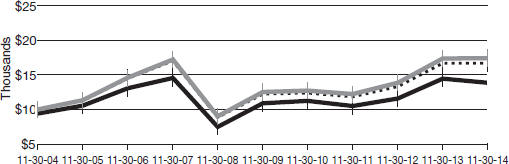

Performance of a $10,000 investment1

Average annual total returns from Nov. 30, 2004, through Nov. 30, 2014

For the period beginning Nov. 30, 2004, through Nov. 30, 2014 | Starting value | Ending value | ||||||||

| MSCI EAFE Index (gross) | $10,000 | $17,457 | |||||||

| MSCI EAFE Index (net) | $10,000 | $16,681 | |||||||

| Delaware International Value Equity Fund — Class A shares | $9,425 | $13,878 | |||||||

1 The “Performance of a $10,000 investment” graph assumes $10,000 invested in Class A shares of the Fund on Nov. 30, 2004, and includes the effect of a 5.75% front-end sales charge and the reinvestment of all distributions. The graph does not reflect the deduction of taxes the shareholders would pay on Fund distributions or redemptions of Fund shares. Expense limitations were in effect for some or all of the periods shown. Performance would have been lower had expense limitations not been in effect. Current expenses are listed in the “Fund expense ratios” table on page 18. Please note additional details on pages 17 through 20.

The graph also assumes $10,000 invested in the MSCI EAFE Index as of Nov. 30, 2004. The MSCI EAFE Index measures equity market performance across developed market countries in Europe, Australasia, and the Far East. Index “gross” return approximates the maximum possible dividend reinvestment. Index “net” return approximates the minimum possible dividend reinvestment, after

deduction of withholding tax at the highest possible rate.

The S&P 500 Index, mentioned on page 6, measures the performance of 500 mostly large-cap stocks weighted by market value, and is often used to represent performance of the U.S. stock market.

Index performance returns do not reflect any management fees, transaction costs, or expenses. Indices are unmanaged and one cannot invest directly in an index. Past performance is not a guarantee of future results.

Performance of other Fund classes will vary due to different charges and expenses.

19

Table of Contents

Performance summaries

Delaware International Value Equity Fund

| Nasdaq symbols | CUSIPs | |||||||

Class A | DEGIX | 245914106 | ||||||

Class C | DEGCX | 245914858 | ||||||

Class R | DIVRX | 245914577 | ||||||

Institutional Class | DEQIX | 245914403 |

20

Table of Contents

This page intentionally left blank.

Table of Contents

For the six-month period from June 1, 2014 to November 30, 2014 (Unaudited)

As a shareholder of a Fund, you incur two types of costs: (1) transaction costs, including sales charges (loads) on purchase payments, reinvested dividends, or other distributions; redemption fees; and exchange fees; and (2) ongoing costs, including management fees; distribution and/or service (12b-1) fees; and other Fund expenses. These following examples are intended to help you understand your ongoing costs (in dollars) of investing in a Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The examples are based on an investment of $1,000 invested at the beginning of the period and held for the entire six-month period from June 1, 2014 to Nov. 30, 2014.

Actual expenses

The first section of the tables shown, “Actual Fund return,” provides information about actual account values and actual expenses. You may use the information in this section of the table, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first section under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical example for comparison purposes

The second section of the tables shown, “Hypothetical 5% return,” provides information about hypothetical account values and hypothetical expenses based on the Funds’ actual expense ratios and an assumed rate of return of 5% per year before expenses, which is not the Funds’ actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the tables are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads), redemption fees, or exchange fees. Therefore, the second section of each table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher. The Funds’ expenses shown in the tables reflect fee waivers in effect. The expenses shown in each table assume reinvestment of all dividends and distributions.

22

Table of Contents

Delaware Emerging Markets Fund

Expense analysis of an investment of $1,000

| Beginning Account Value 6/1/14 | Ending Account Value 11/30/14 | Annualized Expense Ratio | Expenses Paid During Period 6/1/14 to 11/30/14* | |||||

Actual Fund return† | ||||||||

Class A | $1,000.00 | $971.60 | 1.70% | $8.40 | ||||

Class C | 1,000.00 | 968.00 | 2.45% | 12.09 | ||||

Class R | 1,000.00 | 970.60 | 1.95% | 9.63 | ||||

Institutional Class | 1,000.00 | 973.00 | 1.45% | 7.17 | ||||

Hypothetical 5% return (5% return before expenses) | ||||||||

Class A | $1,000.00 | $1,016.55 | 1.70% | $8.59 | ||||

Class C | 1,000.00 | 1,012.78 | 2.45% | 12.36 | ||||

Class R | 1,000.00 | 1,015.29 | 1.95% | 9.85 | ||||

Institutional Class | 1,000.00 | 1,017.80 | 1.45% | 7.33 | ||||

Delaware Global Value Fund Expense analysis of an investment of $1,000

| ||||||||

| Beginning Account Value 6/1/14 | Ending Account Value 11/30/14 | Annualized Expense Ratio | Expenses Paid During Period 6/1/14 to 11/30/14* | |||||

Actual Fund return† | ||||||||

Class A | $1,000.00 | $997.40 | 1.55% | $7.76 | ||||

Class C | 1,000.00 | 993.90 | 2.30% | 11.50 | ||||

Institutional Class | 1,000.00 | 999.20 | 1.30% | 6.52 | ||||

Hypothetical 5% return (5% return before expenses) | ||||||||

Class A | $1,000.00 | $1,017.30 | 1.55% | $7.84 | ||||

Class C | 1,000.00 | 1,013.54 | 2.30% | 11.61 | ||||

Institutional Class | 1,000.00 | 1,018.55 | 1.30% | 6.58 | ||||

23

Table of Contents

Disclosure of Fund expenses

For the six-month period from June 1, 2014 to November 30, 2014 (Unaudited)

Delaware International Value Equity Fund

Expense analysis of an investment of $1,000

| Beginning Account Value 6/1/14 | Ending Account Value 11/30/14 | Annualized Expense Ratio | Expenses Paid During Period 6/1/14 to 11/30/14* | |||||

Actual Fund return† | ||||||||

Class A | $1,000.00 | $922.30 | 1.43% | $6.89 | ||||

Class C | 1,000.00 | 919.00 | 2.18% | 10.49 | ||||

Class R | 1,000.00 | 920.70 | 1.68% | 8.09 | ||||

Institutional Class | 1,000.00 | 923.30 | 1.18% | 5.69 | ||||

Hypothetical 5% return (5% return before expenses) | ||||||||

Class A | $1,000.00 | $1,017.90 | 1.43% | $7.23 | ||||

Class C | 1,000.00 | 1,014.14 | 2.18% | 11.01 | ||||

Class R | 1,000.00 | 1,016.65 | 1.68% | 8.49 | ||||

Institutional Class | 1,000.00 | 1,019.15 | 1.18% | 5.97 | ||||

| * | “Expenses Paid During Period” are equal to the relevant Fund’s annualized expense ratio, multiplied by the average account value over the period, multiplied by 183/365 (to reflect the one-half year period). |

| † | Because actual returns reflect only the most recent six-month period, the returns shown may differ significantly from fiscal year returns. |

24

Table of Contents

| Security type / country and sector allocations | ||

Delaware Emerging Markets Fund | As of November 30, 2014 (Unaudited) | |

Sector designations may be different than the sector designations presented in other Fund materials. The sector designations may represent the investment manager’s internal sector classifications, which may result in the sector designations for one fund being different than another fund’s sector designations.

Security type / country | Percentage of net assets | |||||

Common Stock by Country | 94.65 | % | ||||

Argentina | 3.36 | % | ||||

Bahrain | 0.05 | % | ||||

Brazil | 15.21 | % | ||||

Canada | 0.02 | % | ||||

Chile | 0.85 | % | ||||

China/Hong Kong | 20.71 | % | ||||

Cyprus | 0.35 | % | ||||

France | 0.50 | % | ||||

India | 7.32 | % | ||||

Israel | 2.39 | % | ||||

Malaysia | 0.71 | % | ||||

Mexico | 6.39 | % | ||||

Peru | 0.42 | % | ||||

Poland | 0.73 | % | ||||

Republic of Korea | 19.73 | % | ||||

Russia | 6.00 | % | ||||

South Africa | 1.41 | % | ||||

Taiwan | 4.46 | % | ||||

Thailand | 1.55 | % | ||||

Turkey | 1.42 | % | ||||

United Kingdom | 0.06 | % | ||||

United States | 1.01 | % | ||||

Preferred Stock | 1.67 | % | ||||

Exchange-Traded Funds | 2.83 | % | ||||

Participation Notes | 0.00 | % | ||||

Short-Term Investments | 1.26 | % | ||||

Total Value of Securities | 100.41 | % | ||||

Liabilities Net of Receivables and Other Assets | (0.41 | %) | ||||

Total Net Assets | 100.00 | % | ||||

25

Table of Contents

| Security type / country and sector allocations | ||

| Delaware Emerging Markets Fund | ||

Common stock, participation notes and preferred stock by sector² | Percentage of net assets | |||||

Consumer Discretionary | 6.53 | % | ||||

Consumer Staples | 8.31 | % | ||||

Energy | 16.16 | % | ||||

Financials | 11.91 | % | ||||

Healthcare | 2.78 | % | ||||

Industrials | 5.78 | % | ||||

Information Technology* | 25.12 | % | ||||

Materials | 4.44 | % | ||||

Telecommunication Service | 14.97 | % | ||||

Utilities | 0.32 | % | ||||

Total | 96.32 | % | ||||

| ² | Narrow industries are utilized for compliance purposes for diversification whereas broad sectors are used for financial reporting. |

* To monitor compliance with the Fund’s concentration guidelines as described in the Fund’s Prospectus and Statement of Additional Information, the Information Technology sector (as disclosed herein for financial reporting purposes) is divided into various sub-categories or “industries,” in this case, electronics, internet, semiconductors, and software. As of Nov. 30, 2014, such amounts, as a percentage of total net assets, were 1.83%, 14.04%, 8.86%, and 0.39%, respectively. The percentage in any such single industry will comply with the Fund’s concentration policy even if the percentage in the “Information Technology sector” for financial reporting purposes may exceed 25%.

26

Table of Contents

| Delaware Global Value Fund | As of November 30, 2014 (Unaudited) | |

Sector designations may be different than the sector designations presented in other Fund materials. The sector designations may represent the investment manager’s internal sector classifications, which may result in the sector designations for one fund being different than another fund’s sector designations.

Security type / country | Percentage of net assets | |||||

Common Stock by Country | 97.59 | % | ||||

Australia | 1.27 | % | ||||

Canada | 5.55 | % | ||||

France | 6.27 | % | ||||

Germany | 0.76 | % | ||||

Indonesia | 1.24 | % | ||||

Israel | 2.98 | % | ||||

Italy | 2.71 | % | ||||

Japan | 9.78 | % | ||||

Netherlands | 3.36 | % | ||||

Russia | 1.21 | % | ||||

Sweden | 2.13 | % | ||||

Switzerland | 2.64 | % | ||||

United Kingdom | 6.16 | % | ||||

United States | 51.53 | % | ||||

Short-Term Investments | 2.43 | % | ||||

Securities Lending Collateral | 0.46 | % | ||||

Total Value of Securities | 100.48 | % | ||||

Obligation to Return Securities Lending Collateral | (0.46 | %) | ||||

Liabilities Net of Receivables and Other Assets | (0.02 | %) | ||||

Total Net Assets | 100.00 | % | ||||

27

Table of Contents

| Security type / country and sector allocations | ||

| Delaware Global Value Fund | ||

Common stock by sector | Percentage of net assets | |||||

Consumer Discretionary | 15.42 | % | ||||

Consumer Staples | 3.91 | % | ||||

Energy | 6.24 | % | ||||

Financials | 23.01 | % | ||||

Healthcare | 12.04 | % | ||||

Industrials | 16.48 | % | ||||

Information Technology | 13.20 | % | ||||

Materials | 1.57 | % | ||||

Telecommunication Services | 5.04 | % | ||||

Utilities | 0.68 | % | ||||

Total | 97.59 | % | ||||

28

Table of Contents

| Delaware International Value Equity Fund | As of November 30, 2014 (Unaudited) |

Sector designations may be different than the sector designations presented in other Fund materials. The sector designations may represent the investment manager’s internal sector classifications, which may result in the sector designations for one fund being different than another fund’s sector designations.

Security type / country | Percentage of net assets | |||||

Common Stock by Country | 98.33 | % | ||||

Australia | 1.39 | % | ||||

Canada | 8.17 | % | ||||

China/Hong Kong | 5.46 | % | ||||

Denmark | 2.02 | % | ||||

France | 20.04 | % | ||||

Germany | 4.96 | % | ||||

Indonesia | 1.38 | % | ||||

Israel | 4.71 | % | ||||

Italy | 3.14 | % | ||||

Japan | 18.32 | % | ||||

Netherlands | 4.60 | % | ||||

Norway | 0.19 | % | ||||

Russia | 1.43 | % | ||||

Sweden | 5.58 | % | ||||

Switzerland | 7.29 | % | ||||

United Kingdom | 9.65 | % | ||||

Short-Term Investments | 1.43 | % | ||||

Securities Lending Collateral | 3.83 | % | ||||

Total Value of Securities | 103.59 | % | ||||

Obligation to Return Securities Lending Collateral | (3.83 | %) | ||||

Receivables and Other Assets Net of Liabilities | 0.24 | % | ||||

Total Net Assets | 100.00 | % | ||||

29

Table of Contents

| Security type / country and sector allocations | ||

| Delaware International Value Equity Fund | ||

Common stock by sector | Percentage of net assets | |||||

Consumer Discretionary | 15.44 | % | ||||

Consumer Staples | 6.40 | % | ||||

Energy | 6.20 | % | ||||

Financials | 18.69 | % | ||||

Healthcare | 13.76 | % | ||||

Industrials | 14.55 | % | ||||

Information Technology | 9.66 | % | ||||

Materials | 6.13 | % | ||||

Telecommunication Services | 6.21 | % | ||||

Utilities | 1.29 | % | ||||

Total | 98.33 | % | ||||

30

Table of Contents

| Schedules of investments | ||

| Delaware Emerging Markets Fund | November 30, 2014 | |

| Number of shares | Value (U.S. $) | |||||||

| ||||||||

Common Stock – 94.65%D | ||||||||

| ||||||||

Argentina – 3.36% | ||||||||

Arcos Dorados Holdings Class A @ | 3,864,818 | $ | 25,546,447 | |||||

Cresud ADR @ | 1,442,769 | 17,010,246 | ||||||

Grupo Clarin Class B GDR 144A #@= | 353,200 | 4,100,234 | ||||||

IRSA Inversiones y Representaciones ADR @ | 867,000 | 15,302,550 | ||||||

MercadoLibre | 198,000 | 27,906,120 | ||||||

Pampa Energia ADR † | 95,300 | 1,073,078 | ||||||

YPF ADR | 400,000 | 13,376,000 | ||||||

|

| |||||||

| 104,314,675 | ||||||||

|

| |||||||

Bahrain – 0.05% | ||||||||

Aluminum Bahrain ADR 144A #@ | 221,400 | 1,585,423 | ||||||

|

| |||||||

| 1,585,423 | ||||||||

|

| |||||||

Brazil – 15.21% | ||||||||

AES Tiete | 597,480 | 3,723,407 | ||||||

America Latina Logistica | 5,000,000 | 11,847,926 | ||||||

B2W Cia Digital @† | 5,402,365 | 59,964,283 | ||||||

Banco Santander Brasil ADR | 4,615,300 | 26,861,046 | ||||||

Brasil Foods ADR | 1,500,000 | 39,015,000 | ||||||

Braskem ADR | 321,033 | 4,812,285 | ||||||

Centrais Eletricas Brasileiras | 2,140,204 | 5,088,078 | ||||||

Cia Siderurgica Nacional ADR | 1,200,000 | 2,796,000 | ||||||

Fibria Celulose ADR † | 888,900 | 10,497,909 | ||||||

Gerdau @ | 2,764,900 | 9,741,293 | ||||||

Gol Linhas Aereas Inteligentes ADR | 4,800,000 | 27,600,000 | ||||||

Hypermarcas † | 5,200,000 | 35,263,168 | ||||||

Itau Unibanco Holding ADR | 4,100,000 | 61,746,000 | ||||||

Petroleo Brasileiro ADR | 8,900,000 | 86,508,000 | ||||||

Telefonica Brasil ADR | 1,470,363 | 30,230,663 | ||||||

Tim Participacoes ADR | 2,300,000 | 56,005,000 | ||||||

|

| |||||||

| 471,700,058 | ||||||||

|

| |||||||

Canada – 0.02% | ||||||||

Gran Tierra Energy † | 134,900 | 515,318 | ||||||

|

| |||||||

| 515,318 | ||||||||

|

| |||||||

Chile – 0.85% | ||||||||

Sociedad Quimica y Minera de Chile ADR | 1,049,534 | 26,448,257 | ||||||

|

| |||||||

| 26,448,257 | ||||||||

|

| |||||||

China/Hong Kong – 20.71% | ||||||||

Baidu ADR † | 600,000 | 147,066,000 | ||||||

China Mengniu Dairy | 4,060,000 | 16,465,332 | ||||||

China Mobile | 3,500,000 | 43,124,347 | ||||||

China Mobile ADR | 852,800 | 52,634,816 | ||||||

China Petroleum & Chemical | 38,000,000 | 31,115,811 | ||||||

31

Table of Contents

Schedules of investments |

Delaware Emerging Markets Fund |

| Number of shares | Value (U.S. $) | |||||||

| ||||||||

Common StockD (continued) | ||||||||

| ||||||||

China/Hong Kong (continued) | ||||||||

China Telecom | 15,044,000 | $ | 9,117,693 | |||||

CNOOC ADR | 100,000 | 14,393,000 | ||||||

Fosun International | 2,886,500 | 3,524,888 | ||||||

Guangshen Railway | 11,000,000 | 4,751,834 | ||||||

Hollysys Automation Technologies † | 550,000 | 14,030,500 | ||||||

Kunlun Energy | 12,000,000 | 12,982,759 | ||||||

PetroChina Class H | 36,000,000 | 39,041,122 | ||||||

Qunar Cayman Islands ADR † | 236,682 | 6,172,667 | ||||||

Shanda Games ADR @† | 1,768,490 | 11,583,609 | ||||||

SINA † | 1,600,000 | 60,720,000 | ||||||

Sinofert Holdings † | 7,324,000 | 1,274,987 | ||||||

Sinotrans | 15,326,332 | 11,561,599 | ||||||

Sohu.com @† | 1,550,000 | 78,445,500 | ||||||

Tianjin Development Holdings @ | 15,559,550 | 12,199,005 | ||||||

Tom Group † | 5,428,000 | 1,154,908 | ||||||

Travelsky Technology | 572,000 | 641,710 | ||||||

Uni-President China Holdings @ | 46,917,600 | 41,321,901 | ||||||

Weibo ADR † | 58,939 | 1,057,955 | ||||||

Youku Tudou ADR † | 1,500,000 | 27,750,000 | ||||||

|

| |||||||

| 642,131,943 | ||||||||

|

| |||||||

Cyprus – 0.35% | ||||||||

QIWI ADR | 385,284 | 10,726,307 | ||||||

|

| |||||||

| 10,726,307 | ||||||||

|

| |||||||

France – 0.50% | ||||||||

Sanofi ADR | 250,000 | 12,072,500 | ||||||

Vallourec | 99,235 | 3,293,205 | ||||||

|

| |||||||

| 15,365,705 | ||||||||

|

| |||||||

India – 7.32% | ||||||||

ICICI Bank | 1,100,000 | 31,021,379 | ||||||

Indiabulls Infrastructure and Power GDR † | 300,961 | 16,974 | ||||||

Indiabulls Real Estate GDR † | 102,021 | 134,362 | ||||||

Reliance Capital | 1,800,000 | 15,204,951 | ||||||

Reliance Communications † | 10,114,849 | 16,738,848 | ||||||

Reliance Industries | 6,400,000 | 102,013,181 | ||||||

Reliance Industries GDR 144A # | 1,451,526 | 46,231,103 | ||||||

Tata Chemicals | 2,198,589 | 15,451,264 | ||||||

|

| |||||||

| 226,812,062 | ||||||||

|

| |||||||

Israel – 2.39% | ||||||||

Teva Pharmaceutical Industries ADR | 1,300,000 | 74,074,000 | ||||||

|

| |||||||

| 74,074,000 | ||||||||

|

| |||||||

32

Table of Contents

| Number of shares | Value (U.S. $) | |||||||

| ||||||||

Common StockD (continued) |

| |||||||

Malaysia – 0.71% | ||||||||

Hong Leong Bank @ | 3,059,889 | $ | 12,936,116 | |||||

UEM Sunrise @ | 17,000,000 | 9,046,563 | ||||||

|

| |||||||

| 21,982,679 | ||||||||

|

| |||||||

Mexico – 6.39% | ||||||||

America Movil Series L ADR | 1,600,000 | 37,936,000 | ||||||

Cemex ADR † | 2,600,000 | 32,526,000 | ||||||

Empresas ICA † | 4,500,000 | 6,604,384 | ||||||

Fomento Economico Mexicano ADR | 146,122 | 14,179,679 | ||||||

Grupo Financiero Santander Mexico Class B ADR | 2,000,000 | 22,860,000 | ||||||

Grupo Lala | 2,724,000 | 5,647,482 | ||||||

Grupo Televisa ADR | 2,100,000 | 78,435,000 | ||||||

|

| |||||||

| 198,188,545 | ||||||||

|

| |||||||

Peru – 0.42% | ||||||||

Cia de Minas Buenaventura ADR | 1,400,000 | 12,950,000 | ||||||

|

| |||||||

| 12,950,000 | ||||||||

|

| |||||||

Poland – 0.73% | ||||||||

Jastrzebska Spolka Weglowa † | 254,155 | 1,579,260 | ||||||

Orange Polska | 7,500,000 | 21,160,993 | ||||||

|

| |||||||

| 22,740,253 | ||||||||

|

| |||||||

Republic of Korea – 19.73% | ||||||||

Daum Communications | 60,000 | 7,907,645 | ||||||

E-Mart | 90,000 | 17,788,159 | ||||||

Hite Jinro | 680,000 | 15,425,389 | ||||||

Hyundai Motor | 58,500 | 9,407,511 | ||||||

KB Financial Group ADR | 1,138,755 | 39,776,712 | ||||||

KCC @ | 118,000 | 58,411,643 | ||||||

KT ADR | 1,366,539 | 20,170,116 | ||||||

LG Display ADR † | 21,331 | 326,791 | ||||||

LG Electronics | 250,000 | 14,284,431 | ||||||

LG Uplus | 1,840,040 | 17,935,885 | ||||||

Lotte Chilsung Beverage @ | 21,718 | 31,998,491 | ||||||

Lotte Confectionery @ | 10,226 | 18,282,041 | ||||||

Samsung Electronics | 130,513 | 150,903,091 | ||||||

Samsung Life Insurance | 500,000 | 54,801,905 | ||||||

Shinhan Financial Group | 400,000 | 17,824,095 | ||||||

SK Innovation | 594,923 | 45,804,421 | ||||||

SK Telecom ADR | 3,204,700 | 90,789,151 | ||||||

|

| |||||||

| 611,837,477 | ||||||||

|

| |||||||

Russia – 6.00% | ||||||||

Chelyabinsk Zinc Plant GDR @† | 143,300 | 590,898 | ||||||

33

Table of Contents

Schedules of investments

Delaware Emerging Markets Fund

| Number of shares | Value (U.S. $) | |||||||

| ||||||||

Common StockD (continued) |

| |||||||

Russia (continued) | ||||||||

Enel OGK-5 GDR | 21,161 | $ | 18,135 | |||||

Etalon Group GDR 144A #@= | 1,616,300 | 4,590,292 | ||||||

Gazprom ADR | 4,000,000 | 23,380,000 | ||||||

LUKOIL ADR | 170,000 | 7,777,500 | ||||||

LUKOIL ADR (London International Exchange) | 99,144 | 4,614,162 | ||||||

MegaFon GDR | 450,000 | 9,292,500 | ||||||

Mobile Telesystems ADR | 1,100,000 | 13,442,000 | ||||||

Rosneft GDR | 7,730,000 | 36,601,550 | ||||||

Sberbank of Russia @= | 12,000,000 | 17,207,502 | ||||||

Sberbank of Russia ADR | 1,400,000 | 8,611,400 | ||||||

Surgutneftegas ADR | 500,000 | 2,942,500 | ||||||

TGK-5 =† | 35,084,000 | 895 | ||||||

X5 Retail Group GDR † | 526,952 | 9,274,355 | ||||||

Yandex Class A † | 1,915,000 | 47,721,800 | ||||||

|

| |||||||

| 186,065,489 | ||||||||

|

| |||||||

South Africa – 1.41% | ||||||||

Sasol | 400,000 | 16,676,143 | ||||||

Sun International | 290,543 | 3,215,757 | ||||||

Tongaat Hulett @ | 838,307 | 13,099,091 | ||||||

Vodacom Group | 900,000 | 10,800,325 | ||||||

|

| |||||||

| 43,791,316 | ||||||||

|

| |||||||

Taiwan – 4.46% | ||||||||

Hon Hai Precision Industry | 13,552,000 | 42,400,542 | ||||||

MediaTek | 3,000,000 | 44,995,646 | ||||||

Taiwan Semiconductor Manufacturing | 7,000,000 | 31,948,521 | ||||||

United Microelectronics | 43,000,000 | 19,070,735 | ||||||

|

| |||||||

| 138,415,444 | ||||||||

|

| |||||||

Thailand – 1.55% | ||||||||

Airports of Thailand-Foreign | 4,000,000 | 33,840,536 | ||||||

Bangkok Bank-Foreign | 2,300,000 | 14,138,770 | ||||||

|

| |||||||

| 47,979,306 | ||||||||

|

| |||||||

Turkey – 1.42% | ||||||||

Turk Telekomunikasyon | 951,192 | 3,042,649 | ||||||

Turkcell Iletisim Hizmetleri ADR † | 2,000,000 | 31,740,000 | ||||||

Turkiye Sise ve Cam Fabrikalari | 5,781,095 | 9,194,118 | ||||||

|

| |||||||

| 43,976,767 | ||||||||

|

| |||||||

United Kingdom – 0.06% | ||||||||

Griffin Mining @† | 3,056,187 | 1,708,915 | ||||||

|

| |||||||

| 1,708,915 | ||||||||

|

| |||||||

United States – 1.01% | ||||||||

SunEdison † | 251,600 | 5,447,140 | ||||||

34