UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF

REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-06520

MANAGERS TRUST I

|

| (Exact name of registrant as specified in charter) |

| | |

| 800 Connecticut Avenue, Norwalk, Connecticut 06854 |

| (Address of principal executive offices) (Zip code) |

Managers Investment Group LLC

800 Connecticut Avenue, Norwalk, Connecticut 06854

|

| (Name and address of agent for service) |

Registrant’s telephone number, including area code: (203) 299-3500

Date of fiscal year end: OCTOBER 31

Date of reporting period: NOVEMBER 1, 2006 – OCTOBER 31, 2007

(Annual Shareholder Report)

| Item 1. | Reports to Shareholders |

ANNUAL REPORT

Managers AMG

October 31, 2007

FQ Tax-Managed U.S. Equity Fund

FQ U.S. Equity Fund

FQ Global Alternatives Fund

Managers AMG FQ Funds

FQ Tax-Managed U.S. Equity, FQ U.S. Equity, FQ Global Alternatives

Annual Report—October 31, 2007

TABLE OF CONTENTS

| | |

| | | Page |

| |

LETTER TO SHAREHOLDERS | | 1 |

| |

ABOUT YOUR FUND’S EXPENSES | | 3 |

| |

INVESTMENT MANAGER’S COMMENTS, FUND SNAPSHOTS, | | |

AND SCHEDULES OF PORTFOLIO INVESTMENTS | | |

| |

FQ Tax-Managed U.S. Equity Fund | | 4 |

| |

FQ U.S. Equity Fund | | 9 |

| |

FQ Global Alternatives Fund | | 14 |

| |

FINANCIAL STATEMENTS: | | |

| |

Statements of Assets and Liabilities | | 16 |

| |

FQ Tax-Managed U.S. Equity and FQ U.S. Equity | | |

Fund balance sheets, net asset value (NAV) per share computation and cumulative undistributed amounts | | |

| |

Statement of Net Assets | | 17 |

| |

FQ Global Alternatives | | |

Portfolio of Investments, Fund balance sheet, net asset value (NAV) per share computation and cumulative undistributed amounts | | |

| |

Statements of Operations | | 18 |

Detail of sources of income, Fund expenses, and realized and unrealized gains (losses) during the fiscal year | | |

| |

Statements of Changes in Net Assets | | 19 |

Detail of changes in Fund assets for the past two fiscal years | | |

| |

FINANCIAL HIGHLIGHTS | | 20 |

Historical net asset values per share, distributions, total returns, expense ratios, turnover ratios and net assets | | |

| |

NOTES TO FINANCIAL STATEMENTS | | 25 |

Accounting and distribution policies, details of agreements and transactions with Fund management and affiliates, and descriptions of certain investment risks | | |

| |

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM | | 33 |

| |

TRUSTEES AND OFFICERS | | 34 |

| |

ANNUAL RENEWAL OF INVESTMENT ADVISORY AGREEMENTS | | 35 |

Nothing contained herein is to be considered an offer, sale or solicitation of an offer to buy shares of The Managers Funds or Managers AMG Funds. Such offering is made only by Prospectus, which includes details as to offering price and other material information.

Letter to Shareholders

Dear Fellow Shareholder:

Financial markets have been increasingly unsettled this past year, particularly during the summer months and currently as we write this report. While the economy has continued to grow, a liquidity crisis initiated by spreading weakness in subprime mortgage loans increased uncertainty about its sustainability. Bonds of all credit quality became unusually volatile, and credit spreads, having been extremely slim, widened dramatically, raising the cost of capital for many borrowers. Naturally the equity markets followed suit and became more volatile as the rising cost of capital pressured corporate profitability, penalized leverage, and hindered merger and acquisition activity.

As has been well documented in the financial press, the continued weakness in residential housing prices, combined with gradually rising interest rates, has put severe stress on low credit-quality (subprime) borrowers. Rising defaults pushed several mortgage lenders and leveraged subprime mortgage investors toward bankruptcy and catalyzed a swift and broad flight from various forms of investment risk over the past few months. These revelations began creating serious liquidity problems in the credit markets late in the second quarter and have been the root of uncertainty and market volatility ever since.

A rapid and at times indiscriminate flight from risk created unusual patterns of volatility within the bond market. Credit spreads widened significantly throughout July, as Moody’s and S&P downgraded hundreds of securities, and price moves forced leveraged investors to raise cash any way they could. Since much of the leverage had been funded with short-term debt, the short end of the yield curve bore the brunt of the liquidity crisis. The typically docile commercial paper market seized as demand dried up, and short-term Treasury yields vacillated between 2.9% and 4.9% as investors raced to safety, causing a dislocation in prices. Since then, prices for credits have generally recovered, as the Federal Reserve pumped liquidity into the system and investors have had time to evaluate underlying fundamentals and adjust their portfolios in a more rational manner.

After rallying strongly off of a February trough, the stock market followed the lead of the credit markets by trading sharply down during the liquidity crisis in July, then recovering from late August through October. Here, too, there were interesting anomalies in the indiscriminate flight from risk. Not surprisingly, small-and mid-cap stocks reacted more during the price declines, and underperformed large-cap stocks during the period. Interestingly, however, growth indices, which would normally react poorly to a rise in interest rates or a liquidity squeeze, significantly outperformed value indices during the period. We believe there were two primary reasons for this. One, since value indices had outperformed growth indices for an extended period of time, a typical “reversion to the mean” took place. Two, the quick reduction of leverage from the markets in general forced many quantitatively based hedge fund managers to reverse their trades in a very quick fashion. As it turned out, many of these investors used similar value-biased models to guide their purchase and sale decisions. The result was that the same stocks were being sold off not for investment reasons, but because of liquidity needs. Stocks recovered in late August and throughout October, as a result of an infusion of liquidity by the Federal Reserve, increasing visibility about where the risks were residing, and a much anticipated reduction of the Fed Funds Rate in mid-September.

Within this environment, all three of the Funds represented in this report provided positive returns for the 12-months ended October 31, 2007 (the Funds’ fiscal year end). The Managers AMG FQ U.S. Equity Fund and the Managers AMG FQ Tax-Managed U.S. Equity Fund provided strong gains, exceeded the return of their primary benchmarks, and performed well relative to their peer groups. A detailed review of the performance and positioning of each of the Funds is included within this report.

Lingering credit problems and further revelations of losses from large financial institutions are hindering not only the financial markets, but the economy as well. In our opinion, it appears this will continue for some time, pushing the economy closer to the tipping point of recession. Uncertainty about whether it will tip has driven volatility higher, as the financial markets have traded sharply higher or lower depending upon the news each day. The Federal Reserve has been accommodating, and although we think the risk of recession has increased, we still believe that portions of the U.S. and global economies remain healthy. In sum, we continue to believe that investors should maintain their portfolios with allocations near their long-run targets, rebalance if necessary and take full advantage of opportunities to participate in the growth of the global economy.

One of our foremost goals at Managers Investment Group is to structure and manage mutual funds that will help our shareholders and clients become more successful in reaching their investment goals and objectives. Each of our Funds is geared to provide you with exposure to a specific asset class, combination of

1

Letter to Shareholders (continued)

asset classes, or segment of the market. Investors tend to use our Funds as part of their overall asset allocation in order to structure a well-diversified portfolio intended to meet individual needs. Most of our Funds, like the First Quadrant Funds detailed in this report, are therefore designed to be building blocks.

The following report covers the one-year period ending October 31, 2007. Should you have any questions about this report, or if you’d like to receive a Prospectus and additional information, including fees and expenses, for this or any of the other Funds in our family, please feel free to contact us at 1-800-835-3879, or visit our website at www.managersinvest.com. As always, please read the Prospectus carefully before you invest or send money.

If you are curious about how you can better diversify your investment program, visit the Knowledge Center on our Web site and view our articles in the investment strategies section. You can rest assured that under all market conditions our team is focused on delivering excellent investment management services for your benefit.

We thank you for your continued confidence and investment in the Managers AMG Funds.

Sincerely,

| | | | |

| | | |  |

| John H. Streur | | | | Thomas G. Hoffman, CFA |

| Senior Managing Partner | | | | Executive Vice President |

| Managers Investment Group LLC | | | | Chief Investment Officer |

| | | | Managers Investment Group LLC |

2

About Your Fund’s Expenses

As a shareholder of a Fund, you may incur two types of costs: (1) transaction costs, which may include sales charges (loads) on purchase payments; redemption fees; and exchange fees; and (2) ongoing costs, including management fees; distribution (12b-1) fees; and other Fund expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds. The example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period as indicated below.

Actual Expenses

The first line of the table to the right provides information about the actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The second line of the table to the right provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed annual rate of return of 5% before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds by comparing this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads), redemption fees, or exchange fees. Therefore, the second line of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds.

| | | | | | | | | | | | |

Six Months Ended October 31, 2007 | | Expense

Ratio

for the

Period | | | Beginning

Account

Value

5/1/2007 | | Ending

Account

Value

10/31/2007 | | Expenses

Paid During

the Period* |

FQ Tax-Managed U.S. Equity Fund | | | | | | | | | | | | |

Class A Shares | | | | | | | | | | | | |

Based on Actual Fund Return | | 1.24 | % | | $ | 1,000 | | $ | 1,040 | | $ | 6.38 |

Hypothetical (5% return before expenses) | | 1.24 | % | | $ | 1,000 | | $ | 1,019 | | $ | 6.31 |

Class C Shares | | | | | | | | | | | | |

Based on Actual Fund Return | | 1.99 | % | | $ | 1,000 | | $ | 1,035 | | $ | 10.21 |

Hypothetical (5% return before expenses) | | 1.99 | % | | $ | 1,000 | | $ | 1,015 | | $ | 10.11 |

Institutional Class Shares | | | | | | | | | | | | |

Based on Actual Fund Return | | 0.99 | % | | $ | 1,000 | | $ | 1,040 | | $ | 5.09 |

Hypothetical (5% return before expenses) | | 0.99 | % | | $ | 1,000 | | $ | 1,020 | | $ | 5.04 |

FQ U.S. Equity Fund | | | | | | | | | | | | |

Class A Shares | | | | | | | | | | | | |

Based on Actual Fund Return | | 1.04 | % | | $ | 1,000 | | $ | 1,029 | | $ | 5.32 |

Hypothetical (5% return before expenses) | | 1.04 | % | | $ | 1,000 | | $ | 1,020 | | $ | 5.30 |

Class C Shares | | | | | | | | | | | | |

Based on Actual Fund Return | | 1.79 | % | | $ | 1,000 | | $ | 1,025 | | $ | 9.14 |

Hypothetical (5% return before expenses) | | 1.79 | % | | $ | 1,000 | | $ | 1,016 | | $ | 9.10 |

Institutional Class Shares | | | | | | | | | | | | |

Based on Actual Fund Return | | 0.79 | % | | $ | 1,000 | | $ | 1,030 | | $ | 4.04 |

Hypothetical (5% return before expenses) | | 0.79 | % | | $ | 1,000 | | $ | 1,021 | | $ | 4.02 |

FQ Global Alternatives Fund | | | | | | | | | | | | |

Class A Shares | | | | | | | | | | | | |

Based on Actual Fund Return | | 2.50 | % | | $ | 1,000 | | $ | 975 | | $ | 12.45 |

Hypothetical (5% return before expenses) | | 2.50 | % | | $ | 1,000 | | $ | 1,013 | | $ | 12.68 |

Class C Shares | | | | | | | | | | | | |

Based on Actual Fund Return | | 3.25 | % | | $ | 1,000 | | $ | 970 | | $ | 16.14 |

Hypothetical (5% return before expenses) | | 3.25 | % | | $ | 1,000 | | $ | 1,009 | | $ | 16.46 |

| * | Expenses are equal to the Fund’s annualized expense ratio multiplied by the average account value over the period, multiplied by the number of days in the most recent fiscal half-year (184), then divided by 365. |

3

FQ Tax-Managed U.S. Equity Fund

Portfolio Manager’s Comments

The fiscal year ending October 31, 2007 was another very solid year. The Fund returned 20.68% on a pre-tax basis, while the benchmark Russell 3000® Index returned 14.53%. Please refer to the table on page 5 for returns for various classes of shares and for after-tax returns. It was another good twelve months for the market, with a significant portion of the gains occurring in the early half of 2007.

The past year continued to feature a market environment characterized by relatively strong corporate profit growth despite the overhang of the subprime mess in the mortgage markets and the subsequent credit crunch. From a style perspective, the tide finally began to turn over the past year with growth stocks handily beating their value counterparts after a long period of underperformance. Meanwhile, larger capitalization securities began to outperform their smaller capitalization counterparts, especially later in the fiscal year, as investors perceived more value in these holdings amidst the recent economic turmoil.

The Fund handily outperformed the market over this time period. The most significant driver of performance was very strong stock selection across a number of different sectors while portfolio positioning yielded relatively neutral results. From a stock selection perspective, strong performance was achieved in the consumer (both discretionary and staples), energy, materials, and utilities sectors during the past year. The top contributors to Fund performance exhibit the breadth of strong stock selection with significant results from holdings such as Tesoro (Energy, 91%), Apple (Information Technology, 58%), Kinetic Concepts Inc. (Health Care, 53%), Mirant (Utilities, 43%), and Phelps Dodge Corporation (Materials, 30%).

On a positioning basis, the move towards large capitalization stocks in the Fund was beneficial through the course of the year as was the shift away from value stocks to those stocks with more of a growth orientation. The solid performance generated by that positioning was tempered by weak relative sector positioning versus the index which included an underweight to the outperforming energy sector and an overweight to the underperforming consumer discretionary sector.

On the tax management side we continue to operate with a tax loss carry forward, and, once again, will not be delivering a capital gain distribution to our fellow shareholders for 2007. In fact we have never delivered a capital gain distribution over the entire history of the Fund, while significantly outperforming the market.

We remain worried about several things in the market. One is that the recent interest rate cuts run the risk of igniting inflationary pressure in the economy as a whole. The second is that the euphoria of the market reaction to the cuts poses its own risk. We recognize that rate cuts, particularly those that are larger than expected, have generally been a positive signal for the stock market, but rate cuts are also not a panacea. The rate cuts themselves do not solve the problems of the housing crisis, subprime crisis, and slowing economic growth. Those remain real problems facing the economy and the stock market. Given that, we continue to move toward larger capitalization stocks, in recognition of both the risks to the economy and recognizing that the larger capitalization stocks will benefit the most from the falling dollar, given their export focus. We are adding positions, and keeping positions, that serve as potential inflation hedges – commodity producers and suppliers in particular. We continue to worry about the subprime and housing crisis and continue to avoid the homebuilding and banking stocks. Although we have grown more cautious and more cognizant of the risks in the market, we remain optimistic that the market will continue to generate a solid return for investors going forward.

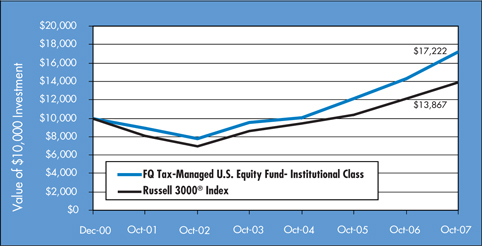

Cumulative Total Return Performance

Managers AMG FQ Tax-Managed U.S. Equity Fund’s cumulative total return is based on the daily change in net asset value (NAV), and assumes that all distributions were reinvested. The Russell 3000® Index is composed of the 3000 largest U.S. companies as measured by market capitalization, and represents about 98% of the U.S. stock market. Unlike the Fund, the Russell 3000® Index is unmanaged, is not available for investment, and does not incur expenses. The chart illustrates the performance of a hypothetical $10,000 investment made in the Institutional Class Shares of the Fund on December 18, 2000 (commencement of operations) to a $10,000 investment made in the Russell 3000® Index for the same time periods. Performance for periods longer than one year is annualized. Figures include reinvestment of capital gains and dividends. The listed returns for the Fund are net of expenses and the returns for the indices exclude expenses. Total returns for the Fund would have been lower had certain expenses not been reduced.

4

FQ Tax-Managed U.S. Equity Fund

Portfolio Manager’s Comments (continued)

Cumulative Total Return Performance

The table below shows the average annualized total returns for the Managers AMG FQ Tax- Managed U.S. Equity Fund and the Russell 3000® Index since inception through October 31, 2007.

| | | | | | | | | | | |

Average Annual Total Returns | | One Year | | | Five Years | | | Since

Inception | | | Inception

Date |

Managers AMG FQ Tax- Managed U.S. Equity Fund 1 | | | | | | | | | | | |

No Load Before Tax: | | | | | | | | | | | |

Institutional Class | | 20.68 | % | | 17.35 | % | | 8.24 | % | | 12/18/00 |

Class A* | | 20.42 | % | | | | | 16.35 | % | | 03/01/06 |

Class C* | | 19.45 | % | | | | | 15.39 | % | | 03/01/06 |

Russell 3000® Index | | 14.53 | % | | 14.83 | % | | | | | |

No Load After Tax on Distributions2 | | | | | | | | | | | |

Institutional Class | | 20.65 | % | | 17.14 | % | | 8.10 | % | | 12/18/00 |

Class A* | | 20.42 | % | | | | | 16.35 | % | | 03/01/06 |

Class C* | | 19.45 | % | | | | | 15.39 | % | | 03/01/06 |

No Load After Tax on Distributions & sale of shares2 | | | | | | | | | | | |

Institutional Class | | 13.44 | % | | 15.18 | % | | 7.11 | % | | 12/18/00 |

Class A* | | 13.27 | % | | | | | 14.00 | % | | 03/01/06 |

Class C* | | 12.64 | % | | | | | 13.17 | % | | 03/01/06 |

With Load Before Tax: | | | | | | | | | | | |

Class A* | | 13.48 | % | | | | | 12.31 | % | | 03/01/06 |

Class C* | | 18.45 | % | | | | | 15.39 | % | | 03/01/06 |

With Load After Tax on Distributions2 | | | | | | | | | | | |

Class A* | | 13.48 | % | | | | | 12.31 | % | | 03/01/06 |

Class C* | | 18.45 | % | | | | | 15.39 | % | | 03/01/06 |

With Load After Tax on Distributions & sale of shares2 | | | | | | | | | | | |

Class A* | | 8.76 | % | | | | | 10.52 | % | | 03/01/06 |

Class C* | | 11.99 | % | | | | | 13.17 | % | | 03/01/06 |

| * | Class A and Class C shares commenced operations on March 1, 2006. |

1 | Performance based on published NAV as of October 31, 2007. |

2 | After-tax returns are calculated using the historical highest individual federal marginal income tax rates and do not reflect the impact of state and local taxes. Actual after-tax returns depend on an investor’s tax situation and may differ from those shown, and after-tax returns are not relevant to investors who hold their Fund shares through tax-deferred arrangements, such as 401(k) plans or individual retirement accounts. |

The performance data shown represents past performance, which is not a guarantee of future results. Current performance may be lower or higher than the performance data quoted. The investment return and principal value of an investment in the Funds will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost.

For performance information through the most recent month end please call (800) 835-3879 or visit our website at www.managersinvest.com.

In choosing a Fund, investors should carefully consider the amount they plan to invest, their investment objectives, the Fund’s investment objectives, risks, charges and expenses before investing. For this and other information, please call 800.835.3879 or visit www.managersinvest.com for a free prospectus. Read it carefully before investing or sending money. Distributed by Managers Distributors, Inc., member FINRA.

The Russell 3000® Index is a trademark of the Frank Russell Company. Russell® is a trademark of the Frank Russell Company. An investment cannot be made directly into an Index.

5

FQ Tax-Managed U.S. Equity Fund

Fund Snapshots

October 31, 2007

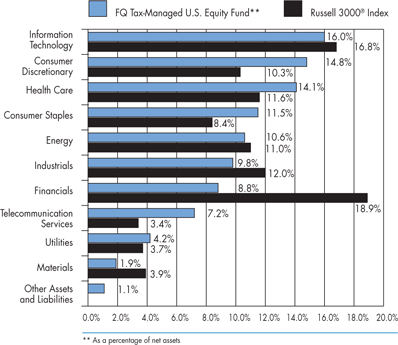

Portfolio Breakdown

| | | | | | |

Industry | | FQ Tax-Managed

U.S. Equity

Fund** | | | Russell 3000®

Index | |

Information | | | | | | |

Technology | | 16.0 | % | | 16.8 | % |

Consumer | | | | | | |

Discretionary | | 14.8 | % | | 10.3 | % |

Health Care | | 14.1 | % | | 11.6 | % |

Consumer Staples | | 11.5 | % | | 8.4 | % |

Energy | | 10.6 | % | | 11.0 | % |

Industrials | | 9.8 | % | | 12.0 | % |

Financials | | 8.8 | % | | 18.9 | % |

Telecommunication | | | | | | |

Services | | 7.2 | % | | 3.4 | % |

Utilities | | 4.2 | % | | 3.7 | % |

Materials | | 1.9 | % | | 3.9 | % |

Other Assets and | | | | | | |

Liabilities | | 1.1 | % | | 0.0 | % |

Top Ten Holdings

| | | |

Security Name | | Percentage

of Net Assets | |

Cisco Systems, Inc. | | 4.2 | % |

Humana, Inc. | | 3.4 | |

Tesoro Corp.* | | 3.4 | |

Goldman Sachs Group, Inc.* | | 3.3 | |

General Electric Co. | | 3.3 | |

Frontline, Ltd. | | 3.1 | |

Apple, Inc. | | 2.9 | |

Microsoft Corp. | | 2.9 | |

Aetna, Inc. | | 2.9 | |

Loews Corp. | | 2.7 | |

| | | |

Top Ten as a Group | | 32.1 | % |

| | | |

| * | Top Ten Holding at April 30, 2007 |

Any sectors, industries, or securities discussed should not be perceived as investment recommendations. Mention of a specific security should not be considered a recommendation to buy or solicitation to sell that security.

6

FQ Tax-Managed U.S. Equity Fund

Schedule of Portfolio Investments

October 31, 2007

| | | | | | |

| | | Shares | | | Value |

Common Stocks - 98.9% | | | | | | |

Consumer Discretionary - 14.8% | | | | | | |

1-800-FLOWERS.COM, Inc.* | | 76,300 | | | $ | 914,837 |

AutoZone, Inc.* | | 7,600 | | | | 945,516 |

EchoStar Communications Corp.* | | 68,000 | | | | 3,329,280 |

Expedia, Inc.* | | 75,600 | 2 | | | 2,469,096 |

J.C. Penney Co., Inc. | | 38,600 | | | | 2,170,864 |

Las Vegas Sands Corp.* | | 15,200 | 2 | | | 2,022,816 |

Playboy Enterprises, Inc. | | 27,400 | | | | 306,880 |

Service Corp. International | | 63,000 | | | | 911,610 |

Shaw Communications, Inc. | | 58,880 | | | | 1,643,930 |

Target Corp. | | 47,200 | | | | 2,896,192 |

Walt Disney Co., The | | 34,000 | | | | 1,177,420 |

Wynn Resorts Ltd.* | | 1,600 | 2 | | | 258,288 |

Total Consumer Discretionary | | | | | | 19,046,729 |

Consumer Staples - 11.5% | | | | | | |

Archer-Daniels-Midland Co. | | 85,000 | | | | 3,041,300 |

Energizer Holdings, Inc.* | | 21,000 | 2 | | | 2,190,300 |

Hormel Foods Corp. | | 5,000 | 2 | | | 182,400 |

Kellogg Co. | | 18,400 | 2 | | | 971,336 |

Kroger Co. | | 112,800 | | | | 3,315,192 |

Loews Corp. - Carolina Group | | 40,200 | | | | 3,448,356 |

Pantry, Inc., The* | | 3,400 | | | | 95,268 |

PepsiAmericas, Inc. | | 6,000 | 2 | | | 214,320 |

Seaboard Corp. | | 300 | | | | 489,600 |

Smithfield Foods, Inc.* | | 29,000 | | | | 831,430 |

Total Consumer Staples | | | | | | 14,779,502 |

Energy - 10.6% | | | | | | |

Callon Petroleum Co. | | 21,400 | | | | 312,012 |

ConocoPhillips | | 29,200 | | | | 2,480,832 |

Exxon Mobil Corp. | | 20,600 | | | | 1,894,994 |

Frontline, Ltd. | | 89,000 | 2 | | | 4,040,600 |

Pioneer Drilling Co.* | | 6,000 | | | | 73,080 |

Seacor Holdings, Inc.* | | 1,000 | 2 | | | 91,650 |

Tesoro Corp. | | 72,200 | 2 | | | 4,370,266 |

Valero Energy Corp. | | 6,200 | | | | 436,666 |

Total Energy | | | | | | 13,700,100 |

Financials - 8.8% | | | | | | |

Bank of America Corp. | | 5,000 | | | | 241,400 |

Center Financial Corp. | | 5,600 | | | | 71,624 |

Chubb Corp., The | | 11,200 | | | | 597,520 |

CIT Group, Inc. | | 4,000 | 2 | | | 140,960 |

Community Bancorp | | 3,200 | 2 | | | 64,864 |

Fannie Mae Co. | | 48,200 | | | | 2,749,328 |

Goldman Sachs Group, Inc. | | 17,400 | 2 | | | 4,313,808 |

JPMorgan Chase & Co. | | 2,400 | | | | 112,800 |

Lehman Brothers Holdings, Inc. | | 5,800 | 2 | | | 367,372 |

Loews Corp. | | 4,000 | | | | 196,360 |

National City Corp. | | 14,074 | | | | 341,294 |

PFF Bancorp, Inc. | | 3,800 | 2 | | | 40,470 |

PNC Financial Services Group, Inc., The | | 5,400 | | | | 389,664 |

Safeco Corp. | | 18,000 | | | | 1,042,200 |

Security Bank Corp. | | 9,000 | | | | 93,780 |

Southwest Bancorp, Inc. | | 7,000 | | | | 132,510 |

Transatlantic Holdings, Inc. | | 1,200 | | | | 89,436 |

Wachovia Corp. | | 7,894 | | | | 360,993 |

Total Financials | | | | | | 11,346,383 |

Health Care - 14.1% | | | | | | |

Aetna, Inc. | | 65,600 | | | | 3,684,752 |

Allergan, Inc. | | 4,600 | | | | 310,868 |

AmerisourceBergen Corp. | | 57,200 | | | | 2,694,692 |

Amgen, Inc.* | | 25,200 | | | | 1,464,372 |

CIGNA Corp. | | 8,400 | | | | 440,916 |

Cubist Pharmaceuticals, Inc.* | | 4,400 | | | | 102,960 |

Forest Laboratories, Inc.* | | 14,800 | | | | 578,236 |

Gilead Sciences, Inc.* | | 2,400 | | | | 110,856 |

Henry Schein, Inc. | | 7,600 | | | | 455,240 |

Humana, Inc.* | | 58,400 | | | | 4,377,080 |

Kinetic Concepts, Inc.* | | 36,000 | | | | 2,163,600 |

PharMerica Corp.* | | 4,769 | | | | 76,066 |

Sepracor, Inc.* | | 36,000 | | | | 991,440 |

Thermo Fisher Scientific, Inc.* | | 3,200 | | | | 188,192 |

WellPoint, Inc.* | | 7,000 | | | | 554,610 |

Total Health Care | | | | | | 18,193,880 |

Industrials - 9.8% | | | | | | |

Cummins, Inc. | | 3,400 | | | | 407,864 |

Delta Air Lines, Inc. | | 61,400 | 2 | | | 1,277,120 |

Dun & Bradstreet Corp., The | | 31,800 | | | | 3,079,830 |

FedEx Corp. | | 4,700 | 2 | | | 485,698 |

General Electric Co. | | 103,600 | | | | 4,264,176 |

Lockheed Martin Corp. | | 8,000 | | | | 880,320 |

Parker Hannifin Corp. | | 27,000 | | | | 2,169,990 |

Total Industrials | | | | | | 12,564,998 |

Information Technology - 16.0% | | | | | | |

Apple, Inc.* | | 19,800 | | | | 3,761,010 |

Cisco Systems, Inc.* | | 164,100 | | | | 5,425,145 |

Dell, Inc.* | | 16,000 | | | | 489,600 |

Google, Inc.* | | 2,000 | | | | 1,414,000 |

Hewlett-Packard Co. | | 19,200 | 2 | | | 992,256 |

iMergent, Inc. | | 38,200 | | | | 921,384 |

The accompanying notes are an integral part of these financial statements.

7

FQ Tax-Managed U.S. Equity Fund

Schedule of Portfolio Investments (continued)

| | | | | | | |

| | | Shares | | | Value | |

Information Technology - 16.0% (continued) | | | | | | | |

International Business Machines Corp. | | 10,200 | | | $ | 1,184,424 | |

Microsoft Corp. | | 100,400 | | | | 3,695,724 | |

NCR Corp.* | | 23,600 | | | | 651,124 | |

Oracle Corp.* | | 32,600 | | | | 722,742 | |

RF Micro Devices, Inc.* | | 112,200 | 2 | | | 697,884 | |

Teradata Corp. | | 23,600 | 2 | | | 673,308 | |

Total Information Technology | | | | | | 20,628,601 | |

Materials - 1.9% | | | | | | | |

Freeport-McMoRan Copper & Gold, Inc. | | 11,800 | | | | 1,388,624 | |

Reliance Steel & Aluminum Co. | | 18,600 | | | | 1,085,310 | |

Total Materials | | | | | | 2,473,934 | |

Telecommunication Services - 7.2% | | | | | | | |

AT&T, Inc. | | 65,800 | | | | 2,749,782 | |

Centennial Communications Corp.* | | 167,200 | | | | 1,712,128 | |

CenturyTel, Inc. | | 47,400 | 2 | | | 2,087,970 | |

Qwest Communications International, Inc.* | | 376,600 | 2 | | | 2,703,988 | |

Total Telecommunication Services | | | | | | 9,253,868 | |

Utilities - 4.2% | | | | | | | |

AES Corp., The* | | 25,800 | | | | 552,378 | |

Energen Corp. | | 25,600 | | | | 1,638,400 | |

Mirant Corp.* | | 42,300 | | | | 1,791,828 | |

NRG Energy, Inc.* | | 30,400 | 2 | | | 1,388,064 | |

Total Utilities | | | | | | 5,370,670 | |

Total Common Stocks

(cost $100,811,992) | | | | | | 127,358,665 | |

Other Investment Companies - 26.3%1 | | | | | | | |

Bank of New York Institutional Cash Reserves Fund, 5.09%3 | | 26,777,326 | | | | 26,777,326 | |

Dreyfus Cash Management Fund, Institutional Class Shares, 4.94% | | 7,118,085 | | | | 7,118,085 | |

Total Other Investment Companies

(cost $33,895,411) | | | | | | 33,895,411 | |

Total Investments - 125.2%

(cost $134,707,403) | | | | | | 161,254,076 | |

Other Assets, less Liabilities - (25.2)% | | | | | | (32,451,432 | ) |

Net Assets - 100.0% | | | | | $ | 128,802,644 | |

Note: Based on the cost of investments of $134,706,178 for Federal income tax purposes at October 31, 2007, the aggregate gross unrealized appreciation and depreciation were $27,123,289 and $575,391, respectively, resulting in net unrealized appreciation of investments of $26,547,898.

| * | Non-income-producing securities. |

1 | Yield shown for an investment company represents the October 31, 2007, seven-day average yield, which refers to the sum of the previous seven days’ dividends paid, expressed as an annual percentage. |

2 | Some or all of these shares, amounting to a market value of $26,487,281, or 20.6% of net assets, were out on loan to various brokers. |

3 | Collateral received from brokers for securities lending was invested in this short-term investment. |

The accompanying notes are an integral part of these financial statements.

8

FQ U.S. Equity Fund

Portfolio Manager’s Comments

The fiscal year ending October 31, 2007 was a good year. The Fund returned 16.54% while the benchmark Russell 3000® Index returned 14.53%. Please refer to the table on page 10 for returns for various classes of shares. It was another good twelve months for the market, with a significant portion of the gains occurring in the early half of 2007.

The past year continued to feature a market environment characterized by relatively strong corporate profit growth despite the overhang of the subprime mess in the mortgage markets and the subsequent credit crunch. From a style perspective, the tide finally began to turn over the past year with growth stocks handily beating their value counterparts after a long period of underperformance. Meanwhile, larger capitalization securities began to outperform their smaller capitalization counterparts, especially later in the fiscal year, as investors perceived more value in these holdings amidst the recent economic turmoil.

The Fund nicely outperformed the market over this time period. The most significant driver of performance was strong stock selection, a good portion of which was concentrated in the consumer discretionary and utilities sectors. The top performing stock in the Fund for the year was a new holding of Apple which continued its impressive multi-year performance by returning 77% during the last twelve months. Other big contributors, particularly towards the end of the fiscal year, include holdings of Vegas Sands and Wynn Resorts, two Las Vegas casino owners that have benefitted from recent forays into Asia via casinos in Macau. Vegas Sands and Wynn Resorts are also new portfolio holdings and each returned 71% during this period.

On a positioning basis, the move towards large capitalization stocks in the Fund was beneficial throughout the course of the year as was the shift away from value stocks to those stocks with more of a growth orientation. The solid performance generated by that positioning was also aided by strong sector positioning relative to the benchmark Russell 3000® Index. More specifically, overweights to the outperforming information technology and telecommunication sectors were the main drivers of this successful positioning.

We remain worried about several things in the market. One is that the recent interest rate cuts run the risk of igniting inflationary pressure in the economy as a whole. The second is that the euphoria of the market reaction to the cuts poses its own risk. We recognize that rate cuts, particularly those that are larger than expected, have generally been a positive signal for the stock market, but rate cuts are also not a panacea. The rate cuts themselves do not solve the problems of the housing crisis, subprime crisis, and slowing economic growth. Those remain real problems facing the economy and the stock market. Given that, we continue to move toward larger capitalization stocks, in recognition of both the risks to the economy and recognizing that the larger capitalization stocks will benefit the most from the falling dollar, given their export focus. We are adding positions, and keeping positions, that serve as potential inflation hedges – commodity producers and suppliers in particular. We continue to worry about the subprime and housing crisis and continue to avoid the homebuilding and banking stocks. Although we have grown more cautious and more cognizant of the risks in the market, we remain optimistic that the market will continue to generate a solid return for investors going forward.

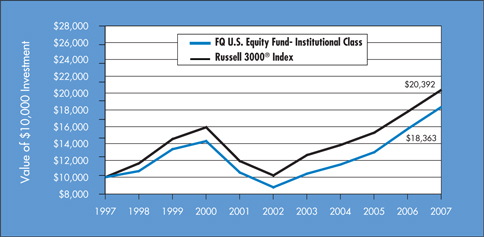

Cumulative Total Return Performance

Managers AMG FQ U.S. Equity Fund’s cumulative total return is based on the daily change in net asset value (NAV), and assumes that all distributions were reinvested. The Russell 3000® Index is composed of the 3000 largest U.S. companies as measured by market capitalization, and represents about 98% of the U.S. stock market. Unlike the Fund, the Russell 3000® Index is unmanaged, is not available for investment, and does not incur expenses. The chart illustrates the performance of a hypothetical $10,000 investment made in the Institutional Class Shares of the Fund on October 31, 1997 to a $10,000 investment made in the Russell 3000® Index for the same time periods. Performance for periods longer than one year is annualized. Figures include reinvestment of capital gains and dividends. The listed returns for the Fund are net of expenses and the returns for the indices exclude expenses. Total returns for the Fund would have been lower had certain expenses not been reduced.

9

FQ U.S. Equity Fund

Portfolio Manager’s Comments (continued)

Cumulative Total Return Performance

The table below shows the average annualized total returns for the Managers AMG FQ U.S. Equity Fund and the Russell 3000® Index since October 31, 1997 through October 31, 2007.

| | | | | | | | | | | | | | |

Average Annual Total Returns | | One Year | | | Five Years | | | Ten Years | | | Since

Inception | | | Inception

Date |

Managers AMG FQ U.S. Equity Fund | | | | | | | | | | | | | | |

No Load: | | | | | | | | | | | | | | |

Institutional Class | | 16.54 | % | | 15.84 | % | | 6.27 | % | | 10.14 | % | | 08/14/92 |

Class A* | | 16.28 | % | | | | | | | | 15.88 | % | | 03/01/06 |

Class C* | | 15.35 | % | | | | | | | | 15.18 | % | | 03/01/06 |

Russell 3000® Index | | 14.53 | % | | 14.83 | % | | 7.39 | % | | | | | |

With Load: | | | | | | | | | | | | | | |

Class A* | | 9.57 | % | | | | | | | | 11.82 | % | | 03/01/06 |

Class C* | | 14.35 | % | | | | | | | | 15.18 | % | | 03/01/06 |

| * | Class A and Class C shares commenced operations on March 1, 2006. |

The performance data shown represents past performance, which is not a guarantee of future results. Current performance may be lower or higher than the performance data quoted. The investment return and principal value of an investment in the Funds will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. For performance information through the most recent month end please call (800) 835-3879 or visit our website at www.managersinvest.com.

In choosing a Fund, investors should carefully consider the amount they plan to invest, their investment objectives, the Fund’s investment objectives, risks, charges and expenses before investing. For this and other information, please call 800.835.3879 or visit www.managersinvest.com for a free prospectus. Read it carefully before investing or sending money. Distributed by Managers Distributors, Inc., member FINRA.

The Russell 3000® Index is a trademark of the Frank Russell Company. Russell® is a trademark of the Frank Russell Company. An investment cannot be made directly into an Index.

10

FQ U.S. Equity Fund

Fund Snapshots

October 31, 2007

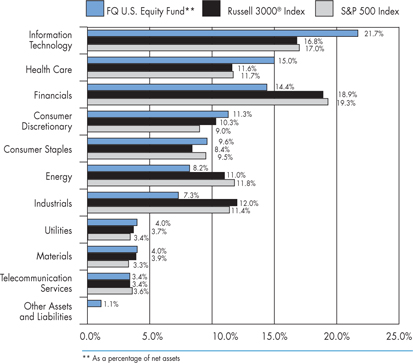

Portfolio Breakdown

| | | | | | | | | |

Industry | | FQ U.S.

Equity** | | | Russell 3000®

Index | | | S&P 500

Index | |

Information Technology | | 21.7 | % | | 16.8 | % | | 17.0 | % |

Health Care | | 15.0 | % | | 11.6 | % | | 11.7 | % |

Financials | | 14.4 | % | | 18.9 | % | | 19.3 | % |

Consumer Discretionary | | 11.3 | % | | 10.3 | % | | 9.0 | % |

Consumer Staples | | 9.6 | % | | 8.4 | % | | 9.5 | % |

Energy | | 8.2 | % | | 11.0 | % | | 11.8 | % |

Industrials | | 7.3 | % | | 12.0 | % | | 11.4 | % |

Utilities | | 4.0 | % | | 3.7 | % | | 3.4 | % |

Materials | | 4.0 | % | | 3.9 | % | | 3.3 | % |

Telecommunication Services | | 3.4 | % | | 3.4 | % | | 3.6 | % |

Other Assets and Liabilities | | 1.1 | % | | 0.0 | % | | 0.0 | % |

Top Ten Holdings

| | | |

Security Name | | Percentage of Net Assets | |

Microsoft Corp. | | 4.0 | % |

Apple, Inc. | | 3.8 | % |

Cisco Systems, Inc. | | 3.2 | % |

Kroger Co.* | | 3.2 | % |

Bank of America Corp.* | | 3.1 | % |

JPMorgan Chase & Co. | | 2.9 | % |

ConocoPhillips | | 2.8 | % |

Amgen, Inc.* | | 2.8 | % |

Northrop Grumman Corp. | | 2.7 | % |

Archer-Daniels-Midland Co. | | 2.1 | % |

| | | |

Top Ten as a Group | | 30.6 | % |

| | | |

| * | Top Ten Holding at April 30, 2007 |

Any sectors, industries, or securities discussed should not be perceived as investment recommendations. Mention of a specific security should not be considered a recommendation to buy or solicitation to sell that security.

11

FQ U.S. Equity Fund

Schedule of Portfolio Investments

October 31, 2007

| | | | | | |

| | | Shares | | | Value |

Common Stocks - 98.9% | | | | | | |

Consumer Discretionary - 11.3% | | | | | | |

1-800-FLOWERS.COM, Inc.* | | 25,000 | | | $ | 299,750 |

Amazon.com, Inc.* | | 800 | 2 | | | 71,320 |

American Eagles Outfitters, Inc. | | 3,400 | | | | 80,852 |

Big Lots, Inc.* | | 8,800 | | | | 211,024 |

Borders Group, Inc. | | 37,800 | 2 | | | 582,876 |

Coach, Inc.* | | 22,000 | | | | 804,320 |

Expedia, Inc.* | | 52,200 | 2 | | | 1,704,852 |

Great Wolf Resorts, Inc.* | | 17,800 | | | | 232,468 |

Guess?, Inc. | | 1,800 | 2 | | | 92,502 |

Harrah’s Entertainment, Inc. | | 2,000 | | | | 176,500 |

Idearc, Inc. | | 28,955 | | | | 781,206 |

J.C. Penney Co., Inc. | | 4,800 | | | | 269,952 |

Las Vegas Sands Corp.* | | 15,200 | 2 | | | 2,022,816 |

Liberty Global, Inc.* | | 26,000 | 2 | | | 1,020,500 |

Overstock.com, Inc.* | | 11,200 | | | | 438,256 |

Station Casinos, Inc. | | 2,100 | | | | 188,580 |

Washington Post Co., The | | 200 | | | | 169,800 |

Whirlpool Corp. | | 16,400 | 2 | | | 1,298,552 |

Wynn Resorts Ltd.* | | 5,200 | 2 | | | 839,436 |

XM Satellite Radio Holdings, Inc.* | | 60,000 | 2 | | | 796,800 |

Total Consumer Discretionary | | | | | | 12,082,362 |

Consumer Staples - 9.6% | | | | | | |

Altria Group, Inc. | | 14,600 | | | | 1,064,778 |

Anheuser-Busch Companies, Inc. | | 13,100 | | | | 671,768 |

Archer-Daniels-Midland Co. | | 63,600 | | | | 2,275,608 |

Del Monte Foods Co. | | 15,400 | | | | 159,236 |

Kroger Co. | | 115,200 | 2 | | | 3,385,728 |

Loews Corp. - Carolina Group | | 20,000 | | | | 1,715,600 |

Reynolds American, Inc. | | 1,200 | 2 | | | 77,316 |

Rite Aid Corp.* | | 231,000 | 2 | | | 903,210 |

Total Consumer Staples | | | | | | 10,253,244 |

Energy - 8.2% | | | | | | |

Bronco Drilling Co., Inc. | | 7,800 | | | | 106,080 |

Callon Petroleum Co. | | 9,000 | | | | 131,220 |

ConocoPhillips | | 35,800 | | | | 3,041,568 |

EL Paso Corp. | | 25,600 | | | | 452,096 |

Grey Wolf, Inc.* | | 95,400 | 2 | | | 537,102 |

Helmerich & Payne, Inc. | | 10,800 | 2 | | | 341,496 |

Marathon Oil Corp. | | 5,600 | | | | 331,128 |

Patterson-UTI Energy, Inc. | | 11,400 | 2 | | | 227,316 |

Pioneer Drilling Co.* | | 18,800 | | | | 228,984 |

Tesoro Corp. | | 30,800 | 2 | | | 1,864,324 |

Transocean, Inc. | | 4,200 | 2 | | | 501,354 |

VAALCO Energy, Inc.* | | 58,400 | 2 | | | 296,672 |

Valero Energy Corp. | | 9,600 | | | | 676,128 |

Total Energy | | | | | | 8,735,468 |

Financials - 14.4% | | | | | | |

Axis Capital Holdings Ltd. | | 25,600 | | | | 1,017,344 |

Bank of America Corp. | | 69,001 | | | | 3,331,368 |

Bear, Stearns & Co., Inc. | | 4,300 | 2 | | | 488,480 |

Capital One Financial Corp. | | 10,000 | 2 | | | 655,900 |

Central Pacific Financial Corp. | | 4,000 | | | | 89,720 |

Chubb Corp., The | | 17,400 | | | | 928,290 |

Corus Bankshares, Inc. | | 20,000 | | | | 220,400 |

Discover Financial Services | | 5,000 | | | | 96,500 |

Goldman Sachs Group, Inc. | | 5,800 | 2 | | | 1,437,936 |

JPMorgan Chase & Co. | | 65,800 | | | | 3,092,600 |

Merrill Lynch & Co., Inc. | | 3,000 | 2 | | | 198,060 |

Safeco Corp. | | 20,000 | 2 | | | 1,158,000 |

Travelers Companies, Inc., The | | 39,400 | | | | 2,057,074 |

Wachovia Corp. | | 4,400 | | | | 201,212 |

Washington Mutual, Inc. | | 5,800 | 2 | | | 161,704 |

XL Capital Ltd. | | 4,600 | | | | 330,970 |

Total Financials | | | | | | 15,465,558 |

Health Care - 15.0% | | | | | | |

Abbott Laboratories | | 8,400 | | | | 458,808 |

Aetna, Inc. | | 27,000 | | | | 1,516,590 |

Allergan, Inc. | | 14,400 | | | | 973,152 |

AmerisourceBergen Corp. | | 9,000 | | | | 423,990 |

Amgen, Inc.* | | 52,000 | | | | 3,021,720 |

AmSurg Corp.* | | 6,400 | | | | 169,280 |

Applera Corp. | | 3,600 | | | | 133,704 |

CIGNA Corp. | | 2,800 | | | | 146,972 |

Forest Laboratories, Inc.* | | 23,400 | | | | 914,238 |

Gilead Sciences, Inc.* | | 3,000 | 2 | | | 138,570 |

Humana, Inc.* | | 2,800 | | | | 209,860 |

Johnson & Johnson | | 21,600 | | | | 1,407,672 |

Kinetic Concepts, Inc.* | | 7,400 | | | | 444,740 |

Medtronic, Inc. | | 41,600 | | | | 1,973,504 |

Merck & Co., Inc. | | 29,800 | | | | 1,736,148 |

OSI Pharmaceuticals, Inc.* | | 15,800 | 2 | | | 656,806 |

RehabCare Group, Inc.* | | 5,600 | | | | 116,144 |

Sierra Health Services, Inc.* | | 16,200 | | | | 685,260 |

Tenet Healthcare Corp.* | | 50,000 | 2 | | | 175,500 |

Thermo Fisher Scientific, Inc.* | | 12,000 | | | | 705,720 |

WellCare Health Plans, Inc.* | | 2,000 | 2 | | | 48,380 |

Total Health Care | | | | | | 16,056,758 |

The accompanying notes are an integral part of these financial statements.

12

FQ U.S. Equity Fund

Schedule of Portfolio Investments (continued)

| | | | | | | |

| | | Shares | | | Value | |

Industrials - 7.3% | | | | | | | |

Cummins, Inc. | | 800 | | | $ | 95,968 | |

Encore Wire Corp. | | 8,000 | | | | 168,000 | |

General Electric Co. | | 31,100 | | | | 1,280,076 | |

W.W. Grainger, Inc. | | 1,800 | | | | 161,856 | |

L-3 Communications Holdings, Inc. | | 1,200 | 2 | | | 131,568 | |

Lockheed Martin Corp. | | 17,800 | | | | 1,958,712 | |

Northrop Grumman Corp. | | 35,000 | | | | 2,926,700 | |

On Assignment, Inc.* | | 11,800 | | | | 98,412 | |

PACCAR, Inc. | | 13,350 | 2 | | | 741,726 | |

Parker Hannifin Corp. | | 1,500 | | | | 120,555 | |

Tredegar Corp. | | 6,400 | | | | 111,488 | |

Total Industrials | | | | | | 7,795,061 | |

Information Technology - 21.7% | | | | | | | |

Accenture Ltd. | | 53,600 | 2 | | | 2,093,080 | |

Adobe Systems, Inc.* | | 9,600 | | | | 459,840 | |

Advanced Micro Devices, Inc.* | | 27,800 | 2 | | | 363,624 | |

Apple, Inc.* | | 21,500 | | | | 4,083,925 | |

Applied Materials, Inc. | | 48,000 | | | | 932,160 | |

Automatic Data Processing, Inc. | | 4,800 | | | | 237,888 | |

Cisco Systems, Inc.* | | 105,200 | | | | 3,477,912 | |

Credence Systems Corp.* | | 26,400 | | | | 80,520 | |

Dell, Inc.* | | 4,800 | | | | 146,880 | |

eBay, Inc.* | | 2,600 | | | | 93,860 | |

EMC Corp.* | | 22,400 | | | | 568,736 | |

Google, Inc.* | | 2,600 | | | | 1,838,200 | |

International Business Machines Corp. | | 9,400 | | | | 1,091,528 | |

MasterCard, Inc. | | 1,800 | 2 | | | 341,190 | |

Microsoft Corp. | | 116,800 | | | | 4,299,408 | |

NCR Corp.* | | 5,000 | | | | 137,950 | |

Oracle Corp.* | | 34,600 | | | | 767,082 | |

Paychex, Inc. | | 10,800 | 2 | | | 451,224 | |

QUALCOMM, Inc. | | 4,000 | | | | 170,920 | |

RF Micro Devices, Inc.* | | 21,000 | | | | 130,620 | |

Safeguard Scientifics, Inc.* | | 53,800 | | | | 126,430 | |

Salesforce.com, Inc.* | | 5,200 | 2 | | | 293,124 | |

Teradata Corp. | | 5,000 | 2 | | | 142,650 | |

Teradyne, Inc.* | | 55,000 | | | | 678,700 | |

Xerox Corp.* | | 13,400 | | | | 233,696 | |

Total Information Technology | | | | | | 23,241,147 | |

Materials - 4.0% | | | | | | | |

Ecolab, Inc. | | 22,400 | 2 | | | 1,056,608 | |

Monsanto Co. | | 13,600 | 2 | | | 1,327,768 | |

Southern Copper Corp. | | 13,400 | 2 | | | 1,871,980 | |

Total Materials | | | | | | 4,256,356 | |

Telecommunication Services - 3.4% | | | | | | | |

AT&T, Inc. | | 24,800 | | | | 1,036,392 | |

CenturyTel, Inc. | | 22,400 | 2 | | | 986,720 | |

Qwest Communications International, Inc.* | | 227,800 | 2 | | | 1,635,604 | |

Total Telecommunication Services | | | | | | 3,658,716 | |

Utilities - 4.0% | | | | | | | |

AES Corp., The* | | 18,600 | | | | 398,226 | |

American Electric Power Co., Inc. | | 23,000 | 2 | | | 1,108,830 | |

CenterPoint Energy, Inc. | | 27,600 | 2 | | | 462,576 | |

CMS Energy Corp. | | 10,000 | 2 | | | 169,700 | |

Dynegy, Inc.* | | 49,242 | 2 | | | 453,519 | |

ONEOK, Inc. | | 4,000 | | | | 199,760 | |

Pepco Holdings, Inc. | | 22,800 | 2 | | | 649,572 | |

Sempra Energy | | 14,200 | 2 | | | 873,442 | |

Total Utilities | | | | | | 4,315,625 | |

Total Common Stocks

(cost $94,912,411) | | | | | | 105,860,295 | |

Other Investment Companies - 26.0%1 | | | | | | | |

Bank of New York Institutional Cash Reserves Fund, 5.09%3 | | 26,608,254 | | | | 26,608,254 | |

Dreyfus Cash Management Fund, Institutional Class Shares, 4.94% | | 1,170,163 | | | | 1,170,163 | |

Total Other Investment Companies

(cost $27,778,417) | | | | | | 27,778,417 | |

Total Investments - 124.9%

(cost $122,690,828) | | | | | | 133,638,712 | |

Other Assets, less Liabilities - (24.9)% | | | | | | (26,625,028 | ) |

Net Assets - 100.0% | | | | | $ | 107,013,684 | |

Note: Based on the cost of investments of $122,690,828 for Federal income tax purposes at October 31, 2007, the aggregate gross unrealized appreciation and depreciation were $13,971,073 and $3,023,189, respectively, resulting in net unrealized appreciation of investments of $10,947,884.

| * | Non-income-producing securities. |

1 | Yield shown for an investment company represents the October 31, 2007, seven-day average yield, which refers to the sum of the previous seven days’ dividends paid, expressed as an annual percentage. |

2 | Some or all of these shares, amounting to a market value of $26,229,500 or 24.5% of net assets, were out on loan to various brokers. |

3 | Collateral received from brokers for securities lending was invested in this short-term investment. |

The accompanying notes are an integral part of these financial statements.

13

FQ Global Alternatives Fund

Portfolio Manager’s Comments

The Managers AMG FQ Global Alternatives Fund delivered positive absolute returns for the past fiscal year but modestly under-performed its benchmark, the 30-Day T-Bill, during this time. The Fund returned 4.02% while the benchmark returned 4.80%. Please refer to the table on page 15 for returns for various classes of shares. It was another good twelve months for the global equity and global fixed income markets with global equities leading the surge amidst increased volatility, particularly towards the latter half of 2007.

The strong market performance over the last year was achieved despite increasing social and economic woes in the global economy ranging from war in the Middle East, a stagnant housing market in the U.S., the credit debacle caused by subprime lending, and alarming negative market movements in February and July/August. The resiliency of the global economy has been a little bit perplexing considering all of these issues. Risk has returned in force and, with it, opportunity, as shown by the increasing disparity of relative returns across both stock and bond markets.

The Fund modestly underperformed the benchmark during the past year but did add positive absolute performance. The most successful positioning during the fiscal year was within the asset class strategy, particularly during the third quarter of 2007 when a number of factors turned bearish for global equities and the Fund took a relatively large short position in global equities relative to global bonds. This had a very strong positive impact on performance during the early to mid stages of the third quarter and the strategy eased towards a neutral position by the end of that quarter as global equities rallied. Earlier in the fiscal year, the largest allocation of risk in the Fund was directed towards the currency strategy as relative valuation (purchasing power parity) indicated a number of currencies were significantly over or undervalued. This strategy in general, and the purchasing power parity specifically, were not particularly successful although we remain confident in the long term efficacy of this strategy and factor. The equity and bond country selection factors had mixed results throughout the course of the past year marginally contributing to the positive performance of the Fund.

Asset class positioning has essentially neutralized, especially from several months ago, as the stronger drivers of relative performance have unwound. For global stocks, the bearish cost of capital factor has disappeared, as falling interest rates tend to have a sustained impact. In addition, the relative return reversal strategy has similarly defused. For global bonds, a mildly bearish wealth effect strategy offsets a mildly bullish bond yield momentum indicator.

Currency positions have continued to feel an increasing impact from the fixed income flow strategies, due to the continued fluctuations in bond and cash yields. The Japanese yen remains the strongest long position, well ahead of the New Zealand dollar. The Australian and Canadian dollars are the strongest short positions, with Australia surpassing Canada as a result of reduced bearishness in the Canadian dollar with fixed income flow pressures diffusing and increased bearishness in the Australian dollar due to prospective bond flow and relative valuation pressures. Other notable changes include a bearish move away from neutral for the UK pound, a reduction of the short U.S. dollar position, and a bullish shift away from neutral for the New Zealand dollar.

The positioning in the stock country selection strategy remains well-diversified via a broad set of long and short positions. Stock country selection allocations include strong U.S., Japanese, and Swiss long positions, and strong short positions in Canada, Spain, and Australia. The factors that contribute to current positioning in the stock selection strategy are quite diverse.

The opportunity in the bond market selection strategy has expanded recently. Japan, Canada, and the U.S. comprise the long positions while the UK and the EMU are the major positions on the short side. While substantial opportunity has been created by recent interest rate movements, currency movements and macroeconomics have also played a notable role. A tightening in the money supply has contributed toward the decision to short bonds in Australia. Overall, the higher cross-sectional volatility experienced in the global capital markets gives the Fund increasing opportunities across the four major strategies used by the Fund.

Cumulative Total Return Performance

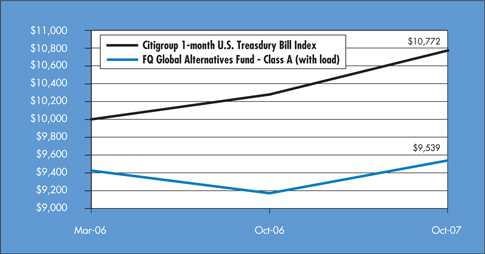

Managers AMG FQ Global Alternatives Fund’s cumulative total return is based on the daily change in net asset value (NAV), and assumes that all distributions were reinvested. The Citigroup 1-Month U.S. Treasury Bill Index (“1-Month Treasury Index”) measures returns of 1-month treasury bills. Unlike the Fund, the 1-Month Treasury Index is unmanaged, is not available for investment, and does not incur expenses. The chart illustrates the performance of a hypothetical $10,000 investment made in the Class A shares (with load) of the Fund on March 30, 2006 (commencement of operations), to a $10,000 investment made in the 1-Month Treasury Index for the same time period. Figures include reinvestment of capital gains and dividends. The listed returns for the Fund are net of expenses and the returns for the index exclude expenses. The graph and table do not reflect the deduction of taxes that a shareholder would pay on a Fund distribution or redemption of shares. Total returns for the Fund would have been lower had certain expenses not been reduced.

14

FQ Global Alternatives Fund

Portfolio Manager’s Comments (continued)

Cumulative Total Return Performance

The table below shows the average annualized total returns for the Managers AMG FQ Global Alternatives Fund and the Citigroup 1-Month U.S. Treasury Bill Index since inception through October 31, 2007.

| | | | | | | | |

Average Total Returns | | One Year | | | Since

Inception | | | Inception

Date |

Managers AMG FQ Global Alternatives Equity Fund* 1,2,3,4,5 | | | | | | | | |

No Load: | | | | | | | | |

Class A | | 4.02 | % | | 0.76 | % | | 3/30/06 |

Class C | | 3.20 | % | | 0.00 | % | | 3/30/06 |

Citigroup 1-Month U.S. Treasury Bill Index 1 | | 4.80 | % | | 4.80 | % | | 3/31/06 |

With Load: | | | | | | | | |

Class A | | (1.93 | )% | | (2.92 | )% | | 3/30/06 |

Class C | | 2.20 | % | | 0.00 | % | | 3/30/06 |

| * | Commencement of operations was March 30, 2006. |

The performance data shown represents past performance, which is not a guarantee of future results. Current performance may be lower or higher than the performance data quoted. The investment return and principal value of an investment in the Funds will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. For performance information through the most recent month end please call (800) 835-3879 or visit our website at www.managersinvest.com.

In choosing a Fund, investors should carefully consider the amount they plan to invest, their investment objectives, the Fund’s investment objectives, risks, charges and expenses before investing. For this and other information, please call 800.835.3879 or visit www.managersinvest.com for a free prospectus. Read it carefully before investing or sending money. Distributed by Managers Distributors, Inc., member FINRA

1 | Performance for the Citigroup 1-Month U.S. Treasury Bill Index reflects an inception date of March 31, 2006. |

2 | Performance based on published NAV as of October 31, 2007. |

3 | Fixed-income funds are subject to the risks associated with investments in debt securities, such as default risk, fluctuations in debtor’s perceived ability to pay its creditors, and changing interest rate risk. An increase in interest rates typically cause the value of bonds and other fixed-income securities to fall. |

4 | The Fund may use derivative instruments for hedging purposes or as part of its investment strategy. There is a risk that a derivative intended as a hedge may not perform as expected. The main risk with derivatives is that some types can amplify a gain or loss, potentially earning or losing substantially more money than the actual cost of the derivative or that the counterparty may fail to honor its contract terms, causing a loss for the Fund. Use of these instruments may also involve certain costs and risks such as liquidity risk, interest rate risk, market risk, credit risk, management risk, and the risk that a fund could not close out a position when it would be most advantageous to do so. |

5 | Investments in foreign securities and currency instruments are subject to additional risks such as erratic market conditions, economic and political instability, and currency exchange rate fluctuations. |

15

Managers AMG FQ Funds

Statements of Assets and Liabilities

October 31, 2007

| | | | | | | |

| | | FQ Tax-Managed

U.S. Equity | | | FQ U.S.

Equity |

Assets: | | | | | | | |

Investments at value (including securities on loan valued at $26,487,281 and $26,229,500, respectively)* | | $ | 161,254,076 | | | $ | 133,638,712 |

Cash | | | 45,700 | | | | 26,622 |

Receivable for Fund shares sold | | | 243,601 | | | | 14,262 |

Dividends and other receivables | | | 96,056 | | | | 82,531 |

Receivable for variation margin on futures | | | — | | | | 14,175 |

Prepaid expenses | | | 19,584 | | | | 17,135 |

| | | | | | | |

Total assets | | | 161,659,017 | | | | 133,793,437 |

| | | | | | | |

Liabilities: | | | | | | | |

Payable upon return of securities loaned | | | 26,777,326 | | | | 26,608,254 |

Payable for Fund shares repurchased | | | 106,518 | | | | 48,058 |

Payable for investments purchased | | | 5,817,062 | | | | — |

Accrued expenses: | | | | | | | |

Investment advisory and management fees | | | 78,450 | | | | 31,571 |

Administrative fees | | | — | | | | 22,559 |

Distribution fees | | | 10,666 | | | | 6,572 |

Professional fees | | | 35,674 | | | | 37,037 |

Other | | | 30,677 | | | | 25,702 |

| | | | | | | |

Total liabilities | | | 32,856,373 | | | | 26,779,753 |

| | | | | | | |

Net Assets | | $ | 128,802,644 | | | $ | 107,013,684 |

| | | | | | | |

Net Assets Represent: | | | | | | | |

Paid-in capital | | $ | 148,617,941 | | | $ | 84,389,035 |

Undistributed net investment income | | | 349,337 | | | | 686,021 |

Accumulated net realized gain (loss) from investments and futures contracts | | | (46,711,307 | ) | | | 10,988,063 |

Net unrealized appreciation of investments and futures contracts | | | 26,546,673 | | | | 10,950,565 |

| | | | | | | |

Net Assets | | $ | 128,802,644 | | | $ | 107,013,684 |

| | | | | | | |

Class A Shares - Net Assets | | $ | 23,803,351 | | | $ | 21,773,357 |

Shares outstanding | | | 1,421,282 | | | | 1,411,129 |

| | | | | | | |

Net asset value, offering and redemption price per share | | $ | 16.75 | | | $ | 15.43 |

| | | | | | | |

Public offering price per share based on a maximum sales charge of 5.75% | | $ | 17.77 | | | $ | 16.37 |

Class C Shares - Net Assets | | $ | 9,489,699 | | | $ | 2,325,556 |

Shares outstanding | | | 574,253 | | | | 152,295 |

| | | | | | | |

Net asset value, offering and redemption price per share | | $ | 16.53 | | | $ | 15.27 |

| | | | | | | |

Institutional Class Shares - Net Assets | | $ | 95,509,594 | | | $ | 82,914,771 |

Shares outstanding | | | 5,684,248 | | | | 5,352,002 |

| | | | | | | |

Net asset value, offering and redemption price per share | | $ | 16.80 | | | $ | 15.49 |

| | | | | | | |

| | $ | 134,707,403 | | | $ | 122,690,828 |

The accompanying notes are an integral part of these financial statements.

16

Managers AMG FQ Global Alternatives Fund

Statement of Net Assets

October 31, 2007

| | | | | | | |

| | | Principal Amount | | Value | |

Assets: | | | | | | | |

Investments in Securities - 103.3% | | | | | | | |

U.S. Government Obligations- 13.2%1,2 | | | | | | | |

U.S. Treasury Bills, 3.510%, 11/01/07 | | $ | 703,000 | | $ | 703,000 | |

U.S. Treasury Bills, 3.680%, 11/08/07 | | | 1,038,000 | | | 1,037,128 | |

U.S. Treasury Bills, 3.820%, 12/27/07 | | | 750,000 | | | 745,456 | |

U.S. Treasury Bills, 3.930%, 12/06/07 | | | 3,504,000 | | | 3,490,720 | |

Total U.S. Government Obligations (cost $5,975,388) | | | | | | 5,976,304 | |

| | |

| | | Shares | | | |

Short-Term Investments - 90.1% | | | | | | | |

S&P 500 Depositary Receipts | | | 68,206 | | | 10,548,058 | |

Dreyfus Cash Management Fund, Institutional Class Shares, 4.94%3 | | | 30,158,668 | | | 30,158,668 | |

Total Short-Term Investments (cost $39,601,344) | | | | | | 40,706,726 | |

| | | | | | | |

Total Investments in securities (cost $45,576,732) | | | | | | 46,683,030 | |

| | | | | | | |

Cash | | | | | | 308,946 | |

Cash held as collateral4 | | | | | | 1,400,000 | |

Receivable for investments sold | | | | | | 18,838 | |

Receivable for Fund shares sold | | | | | | 190,983 | |

Interest and other receivables | | | | | | 161,076 | |

Receivable for variation margin on futures contracts | | | | | | 943,766 | |

Unrealized gains on forward foreign currency contracts | | | | | | 9,432,923 | |

Prepaid expenses | | | | | | 11,597 | |

| | | | | | | |

Total assets | | | | | | 59,151,159 | |

| | | | | | | |

Liabilities: | | | | | | | |

Payable for foreign currency contracts | | | | | | 106,971 | |

Payable for Fund shares repurchased | | | | | | 14,615 | |

Payable for investments purchased | | | | | | 18,822 | |

Unrealized losses on forward foreign currency contracts | | | | | | 12,500,834 | |

Payable for variation margin on futures contracts | | | | | | 1,152,251 | |

Accrued expenses: | | | | | | | |

Investment advisory and management fees | | | | | | 76,564 | |

Administrative fees | | | | | | 11,259 | |

Distribution fees | | | | | | 15,840 | |

Professional fees | | | | | | 42,305 | |

Other | | | | | | 31,795 | |

| | | | | | | |

Total liabilities | | | | | | 13,971,256 | |

| | | | | | | |

Net Assets | | | | | $ | 45,179,903 | |

| | | | | | | |

Net Assets Represent: | | | | | | | |

Paid-in capital | | | | | $ | 43,241,076 | |

Undistributed net investment income | | | | | | 3,073,916 | |

Accumulated net realized loss from investments and futures contracts | | | | | | 303,012 | |

Accumulated net realized gain from currency contracts | | | | | | 1,053,675 | |

Net unrealized depreciation of investments, futures and foreign currency contracts | | | | | | (2,491,776 | ) |

| | | | | | | |

Net Assets | | | | | $ | 45,179,903 | |

| | | | | | | |

Class A Shares - Net Assets | | | | | $ | 37,715,591 | |

Shares outstanding | | | | | | 3,794,098 | |

| | | | | | | |

Net asset value, offering and redemption price per share | | | | | $ | 9.94 | |

| | | | | | | |

Public offering price per share based on a maximum sales charge of 5.75% | | | | | $ | 10.55 | |

Class C Shares - Net Assets | | | | | $ | 7,464,312 | |

Shares outstanding | | | | | | 760,047 | |

| | | | | | | |

Net asset value, offering and redemption price per share | | | | | $ | 9.82 | |

| | | | | | | |

Note: Based on the cost of investments of $45,576,732 for Federal income tax purposes at October 31, 2007, the aggregate gross unrealized appreciation and depreciation were $1,106,461 and $163, respectively, resulting in net unrealized appreciation of investments of $1,106,298.

1 | Security held as collateral for futures contracts, amounting to a market value of $5,976,304, or 13%. |

2 | Represents yield to maturity at October 31, 2007. |

3 | Yield shown for an investment company represents the October 31, 2007, seven-day average yield, which refers to the sum of the previous seven days’ dividends paid, expressed as an annual percentage. |

4 | Cash held as collateral for forward contracts in a segregated account at The Bank of New York. |

The accompanying notes are an integral part of these financial statements.

17

Managers AMG FQ Funds

Statements of Operations

For the fiscal year ended October 31, 2007

| | | | | | | | | | | | |

| | | FQ Tax-Managed

U.S. Equity | | | FQ U.S. Equity | | | FQ Global

Alternatives | |

Investment Income: | | | | | | | | | | | | |

Dividend income | | $ | 1,403,631 | | | $ | 1,535,046 | | | $ | 101,475 | |

Interest income | | | — | | | | — | | | | 1,444,197 | |

Securities lending fees | | | 65,921 | | | | 29,603 | | | | — | |

Foreign withholding tax | | | (7,290 | ) | | | (25 | ) | | | — | |

| | | | | | | | | | | | |

Total investment income | | | 1,462,262 | | | | 1,564,624 | | | | 1,545,672 | |

| | | | | | | | | | | | |

Expenses: | | | | | | | | | | | | |

Investment advisory and management fees | | | 895,205 | | | | 315,787 | | | | 621,415 | |

Administrative fees | | | — | | | | 225,562 | | | | 91,385 | |

Distribution fees Class A | | | 20,173 | | | | 16,836 | | | | 85,214 | |

Distribution fees Class C | | | 44,700 | | | | 13,199 | | | | 24,682 | |

Transfer agent | | | 65,122 | | | | 50,138 | | | | 23,354 | |

Professional fees | | | 46,505 | | | | 44,992 | | | | 47,152 | |

Registration fees | | | 46,425 | | | | 42,120 | | | | 45,112 | |

Custodian | | | 33,073 | | | | 37,946 | | | | 11,029 | |

Reports to shareholders | | | 29,406 | | | | 18,108 | | | | 3,024 | |

Trustees fees and expenses | | | 4,300 | | | | 4,506 | | | | 1,010 | |

Miscellaneous | | | 5,982 | | | | 7,986 | | | | 1,749 | |

| | | | | | | | | | | | |

Total expenses before offsets | | | 1,190,891 | | | | 777,180 | | | | 955,126 | |

| | | | | | | | | | | | |

Less: Expense reimbursement | | | (82,277 | ) | | | (32,297 | ) | | | (18,181 | ) |

Expense reductions | | | (1,092 | ) | | | (4,790 | ) | | | (4,588 | ) |

| | | | | | | | | | | | |

Net expenses | | | 1,107,522 | | | | 740,093 | | | | 932,357 | |

| | | | | | | | | | | | |

Net investment income | | | 354,740 | | | | 824,531 | | | | 613,315 | |

| | | | | | | | | | | | |

Net Realized and Unrealized Gain (Loss): | | | | | | | | | | | | |

Net realized gain on investment transactions | | | 5,137,603 | | | | 10,927,818 | | | | 188 | |

Net realized gain on futures contracts | | | — | | | | 99,374 | | | | 439,499 | |

Net realized gain on foreign currency contracts | | | — | | | | — | | | | 1,032,691 | |

Net unrealized appreciation of investments | | | 13,324,156 | | | | 1,501,517 | | | | 874,635 | |

Net unrealized depreciation of futures contracts | | | — | | | | (25,929 | ) | | | (182,940 | ) |

Net unrealized depreciation of foreign currency contracts | | | — | | | | — | | | | (2,864,338 | ) |

| | | | | | | | | | | | |

Net realized and unrealized gain (loss) | | | 18,461,759 | | | | 12,502,780 | | | | (700,265 | ) |

| | | | | | | | | | | | |

Net Increase (Decrease) in Net Assets Resulting from Operations | | $ | 18,816,499 | | | $ | 13,327,311 | | | | ($86,950 | ) |

| | | | | | | | | | | | |

The accompanying notes are an integral part of these financial statements.

18

Managers AMG FQ Funds

Statements of Changes in Net Assets

For the fiscal year ended October 31,

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | FQ Tax-Managed U.S. Equity | | | FQ U.S. Equity | | | FQ Global Alternatives | |

| | | 2007 | | | 2006 | | | 2007 | | | 2006 | | | 2007 | | | 2006* | |

Increase (Decrease) in Net Assets From Operations: | | | | | | | | | | | | | | | | | | | | | | | | |

Net investment income | | $ | 354,740 | | | $ | 164,233 | | | $ | 824,531 | | | $ | 928,078 | | | $ | 613,315 | | | $ | 155,605 | |

Net realized gain (loss) on investments, futures and foreign currency transactions | | | 5,137,603 | | | | 6,163,511 | | | | 11,027,192 | | | | 7,928,499 | | | | 1,472,378 | | | | (401,267 | ) |

Net unrealized appreciation (depreciation) of investments, futures and foreign currency translations | | | 13,324,156 | | | | 4,777,717 | | | | 1,475,588 | | | | 5,821,972 | | | | (2,172,643 | ) | | | (319,133 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | |

Net increase (decrease) in net assets resulting from operations | | | 18,816,499 | | | | 11,105,461 | | | | 13,327,311 | | | | 14,678,549 | | | | (86,950 | ) | | | (564,795 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | |

Distributions to Shareholders: | | | | | | | | | | | | | | | | | | | | | | | | |

From net investment income | | | (63,118 | ) | | | (111,569 | ) | | | (826,430 | ) | | | (1,014,832 | ) | | | (428,312 | ) | | | — | |

From net realized gain on investments | | | — | | | | — | | | | (7,967,797 | ) | | | (2,823,880 | ) | | | — | | | | — | |

| | | | | | | | | | | | | | | | | | | | | | | | |

Total distributions to shareholders | | | (63,118 | ) | | | (111,569 | ) | | | (8,794,227 | ) | | | (3,838,712 | ) | | | (428,312 | ) | | | — | |

| | | | | | | | | | | | | | | | | | | | | | | | |

From Capital Share Transactions: | | | | | | | | | | | | | | | | | | | | | | | | |

Proceeds from the sale of shares | | | 51,835,490 | | | | 30,799,963 | | | | 33,962,254 | | | | 4,809,087 | | | | 46,376,569 | | | | 23,584,230 | |

Reinvestment of dividends and distributions | | | 58,882 | | | | 103,866 | | | | 8,561,477 | | | | 3,770,801 | | | | 425,858 | | | | — | |

Cost of shares repurchased | | | (26,335,187 | ) | | | (12,784,257 | ) | | | (18,579,846 | ) | | | (13,353,393 | ) | | | (22,463,071 | ) | | | (1,663,626 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | |

Net increase (decrease) from capital share transactions | | | 25,559,185 | | | | 18,119,572 | | | | 23,943,885 | | | | (4,773,505 | ) | | | 24,339,356 | | | | 21,920,604 | |

| | | | | | | | | | | | | | | | | | | | | | | | |

Total increase in net assets | | | 44,312,566 | | | | 29,113,464 | | | | 28,476,969 | | | | 6,066,332 | | | | 23,824,094 | | | | 21,355,809 | |

| | | | | | | | | | | | | | | | | | | | | | | | |

Net Assets: | | | | | | | | | | | | | | | | | | | | | | | | |

Beginning of year | | | 84,490,078 | | | | 55,376,614 | | | | 78,536,715 | | | | 72,470,383 | | | | 21,355,809 | | | | — | |

| | | | | | | | | | | | | | | | | | | | | | | | |

End of year | | $ | 128,802,644 | | | $ | 84,490,078 | | | $ | 107,013,684 | | | $ | 78,536,715 | | | $ | 45,179,903 | | | $ | 21,355,809 | |

| | | | | | | | | | | | | | | | | | | | | | | | |

End of year undistributed net investment income | | $ | 349,337 | | | $ | 61,925 | | | $ | 686,021 | | | $ | 687,920 | | | $ | 3,073,916 | | | $ | 348,385 | |

Share Transactions: | | | | | | | | | | | | | | | | | | | | | | | | |

Sale of shares | | | 3,273,716 | | | | 2,389,184 | | | | 2,282,565 | | | | 350,267 | | | | 4,509,114 | | | | 2,363,264 | |

Reinvestment of dividends and distributions | | | 3,711 | | | | 8,296 | | | | 619,547 | | | | 291,839 | | | | 43,154 | | | | — | |

Shares repurchased | | | (1,665,406 | ) | | | (986,692 | ) | | | (1,256,742 | ) | | | (976,209 | ) | | | (2,193,872 | ) | | | (167,515 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | |

Net increase (decrease) in shares | | | 1,612,021 | | | | 1,410,788 | | | | 1,645,370 | | | | (334,103 | ) | | | 2,358,396 | | | | 2,195,749 | |

| | | | | | | | | | | | | | | | | | | | | | | | |

| * | Commencement of operations was March 30, 2006. |

The accompanying notes are an integral part of these financial statements.

19

Managers AMG FQ Tax-Managed U.S. Equity Fund

Financial Highlights

For a share outstanding throughout each fiscal year

| | | | | | | | | | | | | | | | | | | | |

| | | For the fiscal year ended October 31, | |

Institutional Class Shares | | 2007 | | | 2006 | | | 2005 | | | 2004 | | | 2003 | |

Net Asset Value, Beginning of Year | | $ | 13.93 | | | $ | 11.89 | | | $ | 9.94 | | | $ | 9.39 | | | $ | 7.74 | |

| | | | | | | | | | | | | | | | | | | | |

Income from Investment Operations: | | | | | | | | | | | | | | | | | | | | |

Net investment income | | | 0.06 | | | | 0.03 | | | | 0.01 | | | | 0.11 | | | | 0.06 | |

Net realized and unrealized gain on investments | | | 2.82 | | | | 2.03 | | | | 2.04 | | | | 0.44 | | | | 1.69 | |

| | | | | | | | | | | | | | | | | | | | |

Total from investment operations | | | 2.88 | | | | 2.06 | | | | 2.05 | | | | 0.55 | | | | 1.75 | |

| | | | | | | | | | | | | | | | | | | | |

Less Distributions to Shareholders from: | | | | | | | | | | | | | | | | | | | | |

Net investment income | | | (0.01 | ) | | | (0.02 | ) | | | (0.10 | ) | | | — | | | | (0.10 | ) |

| | | | | | | | | | | | | | | | | | | | |

Net Asset Value, End of Year | | $ | 16.80 | | | $ | 13.93 | | | $ | 11.89 | | | $ | 9.94 | | | $ | 9.39 | |

| | | | | | | | | | | | | | | | | | | | |

Total Return1 | | | 20.68 | % | | | 17.37 | % | | | 20.75 | % | | | 5.86 | % | | | 22.90 | % |

| | | | | | | | | | | | | | | | | | | | |

Ratio of net expenses to average net assets | | | 0.99 | % | | | 0.99 | % | | | 0.99 | % | | | 0.99 | % | | | 0.99 | % |

Ratio of net investment income to average net assets1 | | | 0.37 | % | | | 0.23 | % | | | 0.04 | % | | | 0.99 | % | | | 0.68 | % |

Portfolio turnover | | | 65 | % | | | 98 | % | | | 105 | % | | | 131 | % | | | 143 | % |

Net assets at end of year (000’s omitted) | | $ | 95,510 | | | $ | 82,975 | | | $ | 55,377 | | | $ | 45,321 | | | $ | 53,538 | |

| | | | | | | | | | | | | | | | | | | | |

Expense Offsets:2 | | | | | | | | | | | | | | | | | | | | |

Ratio of total expenses to average net assets | | | 1.07 | % | | | 1.11 | % | | | 1.21 | % | | | 1.20 | % | | | 1.62 | % |

Ratio of net investment income (loss) to average net assets | | | 0.29 | % | | | 0.12 | % | | | (0.17 | )% | | | 0.79 | % | | | 0.06 | % |

| | | | | | | | | | | | | | | | | | | | |