UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-06520

MANAGERS TRUST I

(Exact name of registrant as specified in charter)

800 Connecticut Avenue, Norwalk, Connecticut 06854

(Address of principal executive offices) (Zip code)

Managers Investment Group LLC

800 Connecticut Avenue, Norwalk, Connecticut 06854

(Name and address of agent for service)

Registrant’s telephone number, including area code: (203) 299-3500

| | |

| Date of fiscal year end: | | OCTOBER 31 |

| |

| Date of reporting period: | | NOVEMBER 1, 2008 – OCTOBER 31, 2009 |

| | (Annual Shareholder Report) |

| Item 1. | Reports to Shareholders |

ANNUAL REPORT

Managers Funds

October 31, 2009

Managers Small Cap Fund

Managers Fremont Micro-Cap Fund

Managers Fremont Institutional Micro-Cap Fund

Managers Real Estate Securities Fund

Managers California Intermediate Tax-Free Fund

AR022-1009

Managers Funds

Annual Report – October 31, 2009

TABLE OF CONTENTS

| | |

| | | Page |

| |

LETTER TO SHAREHOLDERS | | 1 |

| |

ABOUT YOUR FUND’S EXPENSES | | 4 |

| |

INVESTMENT MANAGERS’ COMMENTS, FUND SNAPSHOTS, AND SCHEDULES OF PORTFOLIO INVESTMENTS | | |

| |

Managers Small Cap Fund | | 5 |

| |

Managers Fremont Micro-Cap Fund | | 11 |

| |

Managers Fremont Institutional Micro-Cap Fund | | 20 |

| |

Managers Real Estate Securities Fund | | 29 |

| |

Managers California Intermediate Tax-Free Fund | | 33 |

| |

NOTES TO SCHEDULES OF PORTFOLIO INVESTMENTS | | 45 |

| |

FINANCIAL STATEMENTS: | | |

| |

Statements of Assets and Liabilities | | 46 |

Funds’ balance sheets, net asset value (NAV) per share computations and cumulative undistributed amounts | | |

| |

Statements of Operations | | 47 |

Detail of sources of income, Fund expenses, and realized and unrealized gains (losses) during the fiscal year | | |

| |

Statements of Changes in Net Assets | | 48 |

Detail of changes in Fund assets for the past two fiscal years | | |

| |

FINANCIAL HIGHLIGHTS | | 50 |

Historical net asset values per share, distributions, total returns, expense ratios, turnover ratios and net assets | | |

| |

NOTES TO FINANCIAL STATEMENTS | | 54 |

Accounting and distribution policies, details of agreements and transactions with Fund management and affiliates, and descriptions of certain investment risks | | |

| |

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM | | 61 |

| |

TRUSTEES AND OFFICERS | | 62 |

| |

ANNUAL RENEWAL OF INVESTMENT ADVISORY AGREEMENTS | | 63 |

Nothing contained herein is to be considered an offer, sale or solicitation of an offer to buy shares of any series of the Managers Family of Funds. Such offering is made only by Prospectus, which includes details as to offering price and other material information.

Letter to Shareholders

Dear Shareholder:

The past twelve months will go down in the history books as one of the wildest rides in the history of Wall Street. Early in the period, securities markets were under severe pressure as the credit crisis which began in the summer of 2007, accelerated in the fourth quarter of last year amid ongoing concerns about deteriorating economic conditions and the health of some of the most prominent financial institutions. Banks of all sizes remained under pressure, which led to continued consolidation within the industry. Wachovia agreed to sell itself to Wells Fargo & Co. while PNC agreed to acquire the troubled National City. Meanwhile, the U.S. Government attempted to stabilize the system by formally bailing out companies like Citigroup and by providing injections of capital into hundreds of other financial institutions. Like a sprawling fire, the crises extended to other industries with the automakers finding themselves on the verge of collapse. Once again, the U.S. Government stepped in and in late December President Bush approved an emergency bailout of the U.S. auto industry, offering $17.4 billion in rescue loans to Chrysler and General Motors with the expectation that the companies would move quickly to develop acceptable plans for long-term viability.

Consumer and investor confidence continued to sink in the early part of 2009 despite the U.S. Government’s aggressive efforts to restore the economy and stabilize the financial markets. During January, February and early March, stocks plunged, sending broad indexes to levels not seen since the mid to late 1990s. From peak (October 10, 2007) to trough (March 9, 2009), stocks, as measured by the S&P 500 Index, lost 55.5%, the Index’s steepest decline since the Great Depression. Then, on March 10, a very sharp recovery began amid preliminary signs that the Government’s efforts might be starting to bear fruit. More specifically, Citigroup, which had been under extreme pressure and was essentially bailed out by the Government, reported that it returned to profitability in the months of January and February. Citigroup’s surprising news seemed to ignite the markets, contributing to a more than 6% gain for the S&P 500 Index and set the stage for a sharp recovery in equities and extended the rally in credit sensitive fixed income securities.

For the entire one-year period, large-cap stocks outperformed their smaller-cap brethren with the Russell 1000® (large cap), Russell 2000® (small cap), Russell 3000® (all cap), and the Russell Microcap® Indexes returning 11.2%, 6.5%, 10.8% and 5.1%, respectively. International stocks outperformed their domestic counterparts by a wide margin as the MSCI EAFE Index returned 27.7%, thanks partly to weakness in the U.S. Dollar during this period. Over the same time period, REITs underperformed domestic U.S. equities as the Dow Jones U.S. Select REIT Index returned -0.3%. Fixed-income securities in the U.S. and abroad moved substantially higher during the period as investors capitalized on opportunities in various fixed-income segments, with the broad high-quality indexes such as the Barclays Capital U.S. Aggregate Bond and the Barclays Capital Global Aggregate ex US Indexes, returning 13.8% and 21.3%, respectively. Within the fixed-income markets, lower-quality securities posted the best results as investors took advantage of extraordinarily wide credit spreads. This is best exemplified by the 48.1% and 6.3% returns generated by the Barclays Capital US Corporate High Yield Index and the Barclays Capital U.S. Government –Treasury Index, respectively.

Against this backdrop, the, Managers Small Cap Fund, Managers Fremont Micro-Cap Fund, Managers Fremont Institutional Micro-Cap Fund, Managers Real Estate Securities Fund, and the Managers California Intermediate Tax-Free Fund (each a “Fund” and collectively the “Funds”), generally posted solid absolute and relative returns in this volatile environment, as detailed below.

1

Letter to Shareholders (continued)

| | | | | | | | | | | | | | | | | |

Periods Ended 10/31/09 | | 6 Months | | | 1 Year | | | 3 Years | | | 5 Years | | | 10 Years | | | Inception

Date |

| | | | | | |

Managers Small Cap Fund | | 17.31 | % | | 14.80 | % | | (4.63 | )% | | 3.87 | % | | 0.22 | % | | 9/24/1997 |

| | | | | | |

Russell 2000® Growth Index | | 15.70 | % | | 11.34 | % | | (6.88 | )% | | 0.95 | % | | 0.12 | % | | |

| | | | | | |

Managers Fremont Micro-Cap Fund | | 15.25 | % | | 11.34 | % | | (6.37 | )% | | 0.31 | % | | 2.74 | % | | 6/30/1994 |

| | | | | | |

Russell Microcap® Index | | 18.17 | % | | 5.06 | % | | (12.50 | )% | | (2.57 | )% | | — | | | |

| | | | | | |

Managers Fremont Institutional Micro-Cap Fund | | 14.86 | % | | 11.44 | % | | (7.19 | )% | | (0.18 | )% | | 3.80 | % | | 12/31/1986 |

| | | | | | |

Russell Microcap® Index | | 18.17 | % | | 5.06 | % | | (12.50 | )% | | (2.57 | )% | | — | | | |

| | | | | | |

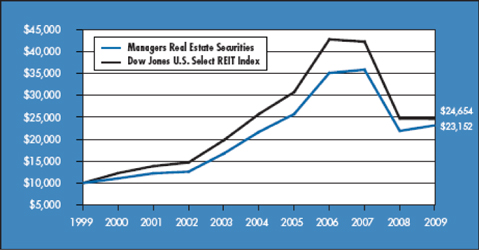

Managers Real Estate Securities Fund | | 29.40 | % | | 5.77 | % | | (12.96 | )% | | 1.34 | % | | 8.76 | % | | 12/31/1997 |

| | | | | | |

Dow Jones U.S. Select REIT Index | | 27.98 | % | | (0.26 | )% | | (16.77 | )% | | (0.87 | )% | | 9.44 | % | | |

| | | | | | |

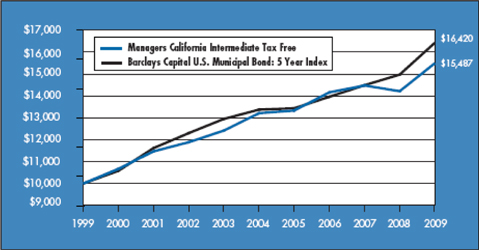

Managers California Intermediate Tax-Free Fund | | 2.42 | % | | 8.97 | % | | 3.03 | % | | 3.23 | % | | 4.47 | % | | 11/16/1990 |

| | | | | | |

Barclays Capital U.S. Municipal Bond: 5 Year Index | | 2.22 | % | | 9.70 | % | | 5.57 | % | | 4.19 | % | | 5.08 | % | | |

For the fiscal year that ended October 31, 2009, the Managers Small Cap Fund returned 14.80%, outperforming the Russell 2000® Growth Index, which returned 11.34%. As detailed in the above table, the Fund’s returns also exceed those of the benchmark on a three-, five- and ten-year basis as well as since inception. The primary driver of the Fund’s outperformance for the past year was strong relative stock performance in the health care, energy and financial services sectors of the market. In health care, Mentor Corp. a manufacturer, developer, and marketer of products for the aesthetic medicine market, was a top contributor. In December, Johnson & Johnson announced plans to acquire Mentor in all cash deal valued at $31 per share, which represented a substantial premium to its share price. In energy, the Fund’s top contributor was Natco Group Inc. which benefitted from the June announcement that the company would be acquired by Cameron International Corporation. On an organizational note, in September, Frontier Capital Management replaced TimesSquare Capital Management as the subadvisor for the Fund. Frontier will serve as the Fund’s interim subadvisor, pending shareholder approval of a new subadvisory agreement.

For the 12 months that ended October 31, 2009, the Managers Fremont Micro-Cap Fund returned 11.34% and the Managers Fremont Institutional Micro-Cap Fund returned 11.44%, compared with 5.06% for its benchmark, the Russell Microcap® Index. Performance remains strong relative to both the Index and peers since the Fund was converted to a multi-manager, multi-style approach in early 2008. Solid outperformance over the last year has been driven by positive stock selection in several sectors including financials and information technology. In addition, the Fund has benefited from relative sector weightings versus the benchmark including a large underweight to the struggling financials sector and an overweight to the recovering consumer discretionary sector. The Fund’s growth subadvisors, in particular, performed well during this period as growth micro-cap stocks outperformed their value counterparts significantly.

For the 12 months that ended October 31, 2009, the Managers Real Estate Securities Fund returned 5.77%, compared with -0.26% for its benchmark, the Dow Jones U.S. Select REIT Index. This solid relative performance has helped to contribute to solid longer-term results

2

Letter to Shareholders (continued)

including performance over the last five years that places the Fund in the top decile amongst peers. The strong relative performance over the past fiscal year has been primarily driven by good stock selection in several areas of the REIT market. Early on, the primary contributors were within the office, shopping center, and healthcare sectors. In the latter half of the fiscal year, the Fund was able to keep pace with the benchmark as the REIT market rallied. The rally was led by low-quality issues while the Fund tends to focus on their high-quality counterparts. However, the solid stock selection exhibited earlier in the year helped after the market turned and enabled the Fund to overcome the headwinds of the lower-quality rally.

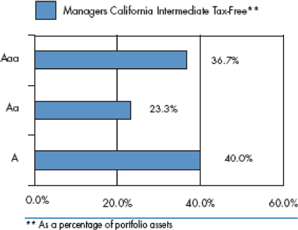

For the 12 months that ended October 31, 2009, the Managers California Intermediate Tax-Free Fund returned 8.97%, compared with 9.70% for its benchmark, the Barclays Capital 5-Year Municipal Bond Index. The Fund’s relative underperformance for the fiscal year can be mostly attributed to three key factors. First, the Fund focuses exclusively on California municipal bonds, while its benchmark is a national index that includes bonds from all states. Since California had the largest budget deficit and its general obligation debt was downgraded, the focus on California debt hurt relative performance. Second, the Fund had a shorter duration than its index and investors favored the long-end of the curve in search of higher yield. Third, A- and BBB-rated bonds led the way and the Fund generally has an average credit rating of AA. These biases all contributed to the Fund’s modest underperformance. Nevertheless, the Fund did generate strong absolute returns and still compares well to peers over longer time periods.

Looking forward, we expect that the economy will continue to recover but at a relatively slow pace. While there are certainly indications that economic conditions are improving on a number of fronts, the key metric, the unemployment rate, continues to deteriorate. While the pace of job losses has slowed considerably over the past few months, jobs are still being lost, and as a result, consumers remain concerned about the environment. Historically, consumer spending, which has accounted for up to 70% of all economic activity, has been a key driver of growth. If a high percentage of consumers remain unemployed or are concerned about job security, then spending and, therefore, economic growth may be subdued.

The following report covers the one year period that ended October 31, 2009. Should you have any questions about this report, or if you’d like to receive a prospectus and additional information, including fees and expenses for these or any of the other Funds in our family, please feel free to contact us at 1-800-835-3879, or visit our Web site at www.managersinvest.com. As always, please read the prospectus carefully before you invest or send money.

If you are curious about how you can better diversify your investment program, visit the Knowledge Center on our Web site and view our articles in the investment strategies section. You can rest assured that under all market conditions our team is focused on delivering excellent investment management services for your benefit.

We thank you for your continued confidence and investment in The Managers Funds.

|

Respectfully, |

|

|

John H. Streur |

Senior Managing Partner |

Managers Investment Group LLC |

3

About Your Fund’s Expenses

As a shareholder of a Fund, you may incur two types of costs: (1) transaction costs, which may include sales charges (loads) on purchase payments; redemption fees; and exchange fees; and (2) ongoing costs, including management fees; distribution (12b-1) fees; and other Fund expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds. The example is based on $1,000 invested at the beginning of the period and held for the entire period as indicated below.

Actual Expenses

The first line of the following table provides information about the actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The second line of the following table provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed annual rate of return of 5% before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds by comparing this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads), redemption fees, or exchange fees. Therefore, the second line of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds.

| | | | | | | | | | | | |

Six Months Ended October 31, 2009 | | Expense

Ratio for

the Period | | | Beginning

Account Value

05/01/2009 | | Ending

Account Value

10/31/2009 | | Expenses Paid

During the

Period* |

| | | | |

Managers Small Cap Fund | | | | | | | | | | | | |

| | | | |

Based on Actual Fund Return | | 1.44 | % | | $ | 1,000 | | $ | 1,173 | | $ | 7.89 |

| | | | |

Based on Hypothetical 5% Annual Return | | 1.44 | % | | $ | 1,000 | | $ | 1,018 | | $ | 7.32 |

| | | | |

Managers Fremont Micro-Cap Fund | | | | | | | | | | | | |

| | | | |

Based on Actual Fund Return | | 1.56 | % | | $ | 1,000 | | $ | 1,153 | | $ | 8.46 |

| | | | |

Based on Hypothetical 5% Annual Return | | 1.56 | % | | $ | 1,000 | | $ | 1,017 | | $ | 7.93 |

| | | | |

Managers Fremont Institutional Micro-Cap Fund | | | | | | | | | | | | |

| | | | |

Based on Actual Fund Return | | 1.35 | % | | $ | 1,000 | | $ | 1,149 | | $ | 7.31 |

| | | | |

Based on Hypothetical 5% Annual Return | | 1.35 | % | | $ | 1,000 | | $ | 1,018 | | $ | 6.87 |

| | | | |

Managers Real Estate Securities Fund | | | | | | | | | | | | |

| | | | |

Based on Actual Fund Return | | 1.50 | % | | $ | 1,000 | | $ | 1,294 | | $ | 8.67 |

| | | | |

Based on Hypothetical 5% Annual Return | | 1.50 | % | | $ | 1,000 | | $ | 1,018 | | $ | 7.63 |

| | | | |

Managers California Intermediate Tax-Free Fund | | | | | | | | | | | | |

| | | | |

Based on Actual Fund Return | | 0.55 | % | | $ | 1,000 | | $ | 1,024 | | $ | 2.81 |

| | | | |

Based on Hypothetical 5% Annual Return | | 0.55 | % | | $ | 1,000 | | $ | 1,022 | | $ | 2.80 |

| * | Expenses are equal to the Fund’s annualized expense ratio multiplied by the average account value over the period, multiplied by the number of days in the most recent fiscal half-year (184), then divided by 365. |

4

Managers Small Cap Fund

Portfolio Manager’s Comments

The Managers Small Cap Fund seeks to achieve long-term capital appreciation by investing primarily in the stocks of small-capitalization companies.

In September 2009, Frontier Capital Management Co., LLC (“Frontier”) replaced TimesSquare Capital Management, LLC (“TimesSquare”) as the subadvisor for the Managers Small Cap Fund. Frontier will serve as the Fund’s interim subadvisor, pending shareholder approval of a new subadvisory agreement. In addition, the Fund, which had been closed to new investors since June of 2006, has been reopened. Separately, Managers Investment Group filed with the SEC at the end of October 2009, to change the name of the Fund from Managers Small Cap Fund to Managers Frontier Small Cap Growth Fund which we anticipate launching in January 2010 assuming shareholder approval of the new subadvisory agreement with Frontier.

The Portfolio Manager

Frontier manages client assets in small-, small/mid-, mid- and large-cap U.S. equity strategies. The Managers Small Cap Fund follows a small-cap growth discipline as Frontier implements its “GARP” investment approach to select attractive small-cap stocks.

Frontier believes:

| | • | | Fundamental research is the cornerstone to adding value |

| | • | | Stock prices ultimately are linked to sales and earnings growth |

| | • | | Growth must be purchased at a reasonable price |

| | • | | Research is a continuous process |

Frontier utilizes and draws support from its entire team of 16 investment professionals to identify opportunities and conduct fundamental research. Through fundamental bottom-up research, Frontier seeks long-term capital appreciation by investing in small-capitalization companies that it believes have above-average earnings growth potential and are available at reasonable valuations.

Frontier looks for companies it believes can generate long-term, sustainable earnings, managed by qualified professionals capable of executing a well-conceived strategic plan. Frontier seeks businesses that can generate superior rates of return on capital in excess of their cost of capital over a business cycle due to above average secular growth prospects or a competitive advantage.

The Year in Review

For the fiscal year ending October 31, 2009, the Managers Small Cap Fund (the “Fund”) returned 14.8%, outperforming the Russell 2000® Growth Index, which returned 11.3%.

During the fiscal year ending October 31, 2009, it was determined by the National Bureau of Economic Research that the U.S. had been in a recession since December 2007. The fiscal year also saw rising unemployment levels and the increased usage of new financial acronyms from TARP (Troubled Asset Relief Program) to TALF (Term Asset-Backed Securities Loan Facility) to PPIP (Public-Private Investment Program). President Obama was sworn into office and new Secretary of the Treasury Geithner found himself immersed in economic turmoil and increased public backlash over government aid to troubled financial institutions such as AIG. After the U.S. equity markets fell to a twelve year low in March, the subsequent market rally, albeit driven mostly by higher beta and lower quality stocks, helped the period end with the Dow Jones Industrial Average crossing the 10,000 level for the first time since October 2008. Mixed signals of economic recovery gave the public the optimistic “green shoots” observations from Federal Reserve Chairman Bernanke, who was reappointed to his post. The $3 billion “cash for clunkers” program concluded well before the anticipated end date of November 1. The allocated federal proceeds to fund the program were quickly exhausted with car owners rushing to trade in their less fuel efficient vehicles, consequently boosting both new car sales and manufacturing activity expansion for the first time since January 2008. Access to credit appears to have stabilized, and the U.S. economy grew at a 3.5% annual rate for the third quarter of 2009, likely calling an end to the recession. Employment prospects, however, continued to remain weak and may impact the psyche of consumers leading into the holiday season, as disappointing consumer confidence data marked the end of the period.

U.S. equities, as measured by the Russell indices, finished the twelve months ending October 31 in positive territory across the size spectrum. Mid-caps outperformed their large- and small-cap counterparts as the Russell Midcap® Index rose 18.8%, followed by

11.2% and 6.5% returns for the Russell 1000® Index and Russell 2000® Index, respectively. From a style perspective, the Russell 2000® Growth Index and its 11.3% return handily outperformed the 2.0% return of the Russell 2000® Value Index.

5

Managers Small Cap Fund

Portfolio Manager’s Comments (continued)

In this volatile but generally positive environment for stocks, the Fund outperformed its benchmark on a relative basis. The primary driver of the outperformance was strong relative stock selection in the health care, energy and financial services sectors. The Fund also benefited from an overweight to the surging technology sector and an underweight to the lagging health care sector. Partially offsetting the aforementioned contributors was weak results in the consumer discretionary space.

Among the Fund’s financially focused stocks, Wright Express Corporation, a provider of payment processing and information management services to the U.S. commercial and government vehicle fleet industry, was a top contributor. Wright Express shares soared 124%, with much of the rise coming after management reported a better than expected fourth quarter. Evercore Partners Inc., a leading advisory and merchant banking boutique, benefited from emerging signs of merger & acquisition activity as well as a shakeout among large investment banks. Evercore rose 117% during the period, which prompted TimesSquare to sell the stock on this strength. TimesSquare exited Webster Financial Corporation, a bank holding company focused on providing financial services to customers in southern New England and eastern New York, at a loss upon learning that loan losses and investment portfolio write-downs were much worse than anticipated; their shares fell 84%.

In the energy sector, NATCO Group Inc. appreciated by 114% during the period. This was driven by the June announcement that the company would be acquired by Cameron International Corporation. NATCO is a leading provider of equipment, systems, and services used in the production of oil and natural gas, and they possess a proprietary technology to separate oil, gas, and water while removing contaminants.

In the technology-oriented space, SBA Communications Corporation, an independent owner and operator of wireless communications towers, was a top contributor with its 117% return. This was a result of management continuing to reduce outstanding debt levels, and the company continuing to be aided by a stable environment for wireless communication tower companies. Atheros Communications, Inc., a designer of radio frequency chips for wired and wireless network equipment, was also a key contributor. Atheros rose 91%, capped by a strong quarterly report during the third quarter with better than expected revenues and strong forward guidance.

The industrials sector was home to the Fund’s most significant detractor during the period, Huron Consulting Group Inc. This consulting firm, for accounting and other professional services, announced that accounting irregularities on the earn-out payments for prior acquisitions would force it to restate several years of results. As a result, the CEO and CFO resigned. TimesSquare sold the position but after a 75% decline.

Within the consumer discretionary sector, the for-profit education industry was under pressure on concerns about debt loads for all schools (not solely regarding the for-profits), and some degree of investor rotation within the sector towards higher beta names. American Public Education Inc., a provider of online post-secondary education for the military and public service communities, depreciated 22% during the period despite increasing forward guidance and reporting solid quarterly results during the second quarter due in part to growth in civilian student enrollments.

Looking Forward

Looking forward, the Fund’s new subadvisor Frontier continues to believe the economic recovery will be muted by the dampening effects of increased personal savings, deleveraging of the banking system, and the likelihood of higher taxes. Imbalances that caused the global recession took years to develop and will take time to mend. On a positive note, corporate earnings have improved dramatically over the last three quarters on strong cost management and stabilizing revenues, and largely exceeded consensus expectations. Frontier believes that companies that show sustained earnings growth in a slow growth environment will be awarded premium valuations. As a result, its focus remains on identifying high quality, secular growth businesses.

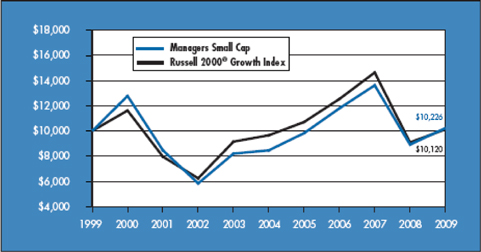

Cumulative Total Return Performance

Managers Small Cap’s cumulative total return is based on the daily change in net asset value (NAV), and assumes that all distributions were reinvested. The Russell 2000® Growth Index measures the performance of those Russell 2000® companies with higher price-to-book ratios and higher forecasted growth values. Unlike the Fund, the above stated index is unmanaged, is not available for investment, and does not incur expenses. This chart compares a hypothetical $10,000 investment made in the Managers Small Cap Fund on October 31, 1999 to a $10,000 investment made in the

6

Managers Small Cap Fund

Portfolio Manager’s Comments (continued)

Cumulative Total Return Performance

Russell 2000® Growth Index for the same time period. Performance for periods longer than one year is annualized. The graph and table do not reflect the deduction of taxes that a shareholder would pay on a Fund distribution or redemption of shares. The listed returns for the Fund are net of expenses and the returns for the index exclude expenses. Total returns for the Fund would have been lower had certain expenses not been reduced.

The table below shows the average annual total returns for the Managers Small Cap Fund and the Russell 2000® Growth Index for the one-year, five-year and ten-year periods ended October 31, 2009.

| | | | | | | | | |

Average Annualized Total Returns 1 | | One Year | | | Five Years | | | Ten Years | |

Managers Small Cap2,3 | | 14.80 | % | | 3.87 | % | | 0.22 | % |

Russell 2000® Growth Index | | 11.34 | % | | 0.95 | % | | 0.12 | % |

The performance data shown represents past performance. Past performance is not a guarantee of future results. Current performance may be lower or higher than the performance data quoted. The investment return and principal value of an investment in the Fund will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. For performance information through the most recent month end, please call (800) 835-3879 or visit our Web site at www.managersinvest.com.

In choosing a Fund, investors should carefully consider the amount they plan to invest, their investment objectives, the Fund’s investment objectives, risks, charges and expenses before investing. For this and other information, please call (800) 835-3879 or visit www.managersinvest.com for a free prospectus. Read it carefully before investing or sending money. Distributed by Managers Distributors, Inc., member FINRA.

| 1 | Total return equals income yield plus share price change and assumes reinvestment of all dividends and capital gain distributions. Returns are net of fees and may reflect offsets of Fund expenses as described in the Prospectus. No adjustment has been made for taxes payable by shareholders on their reinvested dividends and capital gain distributions. Returns for periods greater than one year are annualized. The listed returns on the Fund are net of expenses and based on the published NAV as of October 31, 2009. All returns are in U.S. dollars($). |

| 2 | Fund for which, from time to time, the advisor has waived its fees and/or absorbed Fund expenses, which has resulted in higher returns. |

| 3 | The Fund is subject to risks associated with investments in small-capitalization companies, such as erratic earnings patterns, competitive conditions, limited earnings history, and a reliance on one or a limited number of products. |

The Russell 2000® Growth Index is a trademark of Russell Investments. Russell® is a trademark of Russell Investments. An investment cannot be made directly into an index.

Not FDIC insured, nor bank guaranteed. May lose value.

7

Managers Small Cap Fund

Funds Snapshots

October 31, 2009

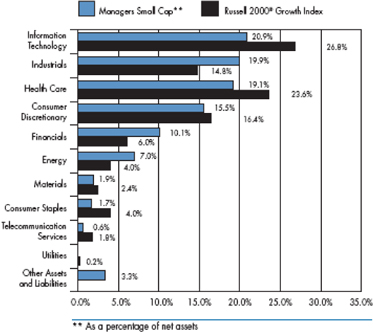

Portfolio Breakdown

| | | | | | |

Industry | | Managers

Small Cap** | | | Russell 2000®

Growth Index | |

Information Technology | | 20.9 | % | | 26.8 | % |

Industrials | | 19.9 | % | | 14.8 | % |

Health Care | | 19.1 | % | | 23.6 | % |

Consumer Discretionary | | 15.5 | % | | 16.4 | % |

Financials | | 10.1 | % | | 6.0 | % |

Energy | | 7.0 | % | | 4.0 | % |

Materials | | 1.9 | % | | 2.4 | % |

Consumer Staples | | 1.7 | % | | 4.0 | % |

Telecommunication Services | | 0.6 | % | | 1.8 | % |

Utilities | | 0.0 | % | | 0.2 | % |

Other Assets and Liabilities | | 3.3 | % | | 0.0 | % |

Top Ten Holdings

| | | |

Security Name | | Percentage

of Net Assets | |

Raymond James Financial, Inc. | | 2.9 | % |

Millipore Corp. | | 2.7 | |

Chico’s FAS, Inc. | | 2.5 | |

Mednax, Inc. | | 2.3 | |

Waddell & Reed Financial, Inc. | | 2.1 | |

Skyworks Solutions, Inc. | | 2.1 | |

Factset Research Systems, Inc. | | 2.0 | |

Watsco, Inc. | | 2.0 | |

Pall Corp. | | 2.0 | |

Tractor Supply Co. | | 1.8 | |

| | | |

Top Ten as a Group | | 22.4 | % |

| | | |

Any sectors, industries, or securities discussed should not be perceived as investment recommendations. Mention of a specific security should not be considered a recommendation to buy or solicitation to sell that security. Specific securities mentioned in this report may have been sold from the Fund’s portfolio of investments by the time you receive this report.

8

Managers Small Cap Fund

Schedule of Portfolio Investments

October 31, 2009

| | | | | | |

| | | Shares | | | Value |

Common Stocks - 96.7% | | | | | | |

Consumer Discretionary - 15.5% | | | | | | |

1-800-FLOWERS.COM, Inc.* | | 24,700 | | | $ | 94,848 |

Bebe Stores, Inc. | | 12,500 | | | | 78,250 |

Cheesecake Factory, Inc., The* | | 21,500 | 2 | | | 390,870 |

Chico’s FAS, Inc.* | | 81,800 | | | | 977,510 |

Corinthian Colleges, Inc.* | | 18,800 | | | | 298,168 |

Dollar Tree, Inc.* | | 14,000 | | | | 631,820 |

Harman International Industries, Inc. | | 13,100 | | | | 492,691 |

hhgregg, Inc.* | | 12,800 | | | | 211,072 |

LKQ Corp.* | | 20,300 | | | | 350,581 |

P.F. Chang’s China Bistro, Inc.* | | 4,800 | 2 | | | 140,112 |

Panera Bread Co., Class A* | | 3,100 | | | | 185,938 |

Polaris Industries, Inc. | | 10,600 | | | | 445,942 |

Regis Corp. | | 13,100 | | | | 212,744 |

Tractor Supply Co.* | | 15,800 | | | | 706,260 |

WABCO Holdings, Inc. | | 20,800 | | | | 493,376 |

WMS Industries, Inc.* | | 10,400 | | | | 415,792 |

Total Consumer Discretionary | | | | | | 6,125,974 |

Consumer Staples - 1.7% | | | | | | |

Nu Skin Enterprises, Inc., Class A | | 28,800 | | | | 655,488 |

Energy - 7.0% | | | | | | |

Arena Resources, Inc.* | | 8,000 | | | | 298,080 |

Carrizo Oil & Gas, Inc.* | | 11,500 | 2 | | | 266,570 |

Core Laboratories, N.V. | | 4,000 | 2 | | | 417,200 |

Denbury Resources, Inc.* | | 42,300 | | | | 617,580 |

Rex Energy Corp.* | | 5,500 | | | | 44,495 |

St. Mary Land & Exploration Co. | | 15,800 | | | | 538,780 |

World Fuel Services Corp. | | 11,900 | | | | 605,115 |

Total Energy | | | | | | 2,787,820 |

Financials - 10.1% | | | | | | |

Argo Group International Holdings, Ltd.* | | 15,000 | | | | 509,400 |

Investment Technology Group, Inc.* | | 11,500 | | | | 248,055 |

Jefferies Group, Inc.* | | 24,600 | | | | 642,060 |

Penson Worldwide, Inc.* | | 16,500 | 2 | | | 160,875 |

Raymond James Financial, Inc. | | 48,500 | | | | 1,145,085 |

Thomas Weisel Partners Group, Inc.* | | 7,500 | | | | 33,975 |

W.R. Berkley Corp. | | 17,600 | | | | 435,072 |

Waddell & Reed Financial, Inc. | | 29,400 | | | | 824,964 |

Total Financials | | | | | | 3,999,486 |

Health Care - 19.1% | | | | | | |

American Medical Systems Holdings, Inc.* | | 31,900 | | | | 491,898 |

Beckman Coulter, Inc. | | 9,300 | | | | 598,269 |

Catalyst Health Solutions, Inc.* | | 20,400 | | | | 639,948 |

Charles River Laboratories International, Inc.* | | 16,900 | | | | 617,188 |

CONMED Corp.* | | 9,500 | | | | 201,305 |

Cumberland Pharmaceuticals, Inc.* | | 11,100 | | | | 132,090 |

Eclipsys Corp.* | | 20,700 | | | | 388,125 |

ev3, Inc.* | | 14,700 | | | | 173,166 |

Mednax, Inc.* | | 17,800 | | | | 924,176 |

Millipore Corp.* | | 15,900 | | | | 1,065,459 |

PAREXEL International Corp.* | | 18,400 | | | | 230,368 |

PSS World Medical, Inc.* | | 25,100 | | | | 507,522 |

Valeant Pharmaceuticals International* | | 4,900 | | | | 144,060 |

VCA Antech, Inc.* | | 24,900 | | | | 593,118 |

West Pharmaceutical Services, Inc. | | 14,200 | 2 | | | 560,474 |

Wright Medical Group, Inc.* | | 16,500 | | | | 268,125 |

Total Health Care | | | | | | 7,535,291 |

Industrials - 19.9% | | | | | | |

Advisory Board Co., The* | | 9,800 | | | | 241,472 |

Aecom Technology Corp.* | | 17,400 | | | | 439,176 |

A.O. Smith Corp. | | 14,500 | | | | 574,635 |

Brady Corp. | | 19,100 | | | | 517,228 |

CLARCOR, Inc. | | 12,400 | | | | 364,932 |

Comfort Systems USA, Inc. | | 9,800 | | | | 106,820 |

EnPro Industries, Inc.* | | 6,900 | | | | 155,802 |

Hub Group, Inc.* | | 17,400 | | | | 432,564 |

II-VI, Inc.* | | 9,000 | | | | 238,230 |

Kaydon Corp. | | 11,300 | | | | 395,387 |

Ladish Co., Inc.* | | 6,700 | | | | 86,832 |

Landstar System, Inc. | | 17,000 | | | | 599,080 |

MasTec, Inc.* | | 59,700 | 2 | | | 704,460 |

Navistar International Corp.* | | 6,900 | | | | 228,666 |

Pall Corp. | | 24,400 | | | | 774,456 |

Quanta Services, Inc.* | | 27,100 | | | | 574,520 |

Waste Connections, Inc.* | | 13,700 | | | | 430,591 |

Watsco, Inc. | | 15,400 | | | | 788,788 |

Wesco International, Inc.* | | 8,700 | | | | 222,372 |

Total Industrials | | | | | | 7,876,011 |

The accompanying notes are an integral part of these financial statements.

9

Managers Small Cap Fund

Schedule of Portfolio Investments (continued)

| | | | | | | |

| | | Shares | | | Value | |

Information Technology - 20.9% | | | | | | | |

Advanced Analogic Technologies, Inc.* | | 36,600 | | | $ | 115,290 | |

Ariba, Inc.* | | 32,600 | | | | 385,332 | |

ATMI, Inc.* | | 10,300 | | | | 156,045 | |

Blackboard, Inc.* | | 8,500 | | | | 301,495 | |

Cogent, Inc.* | | 12,100 | | | | 116,765 | |

Equinix, Inc.* | | 7,900 | 2 | | | 674,028 | |

Factset Research Systems, Inc. | | 12,400 | | | | 794,220 | |

iGATE Corp.* | | 32,800 | | | | 289,624 | |

Insight Enterprises, Inc.* | | 17,900 | | | | 188,308 | |

International Rectifier Corp.* | | 3,300 | | | | 60,324 | |

Jabil Circuit, Inc. | | 41,600 | | | | 556,608 | |

Loop Net, Inc.* | | 24,900 | | | | 217,377 | |

Monolithic Power Systems, Inc.* | | 14,800 | | | | 295,852 | |

Ness Technologies, Inc.* | | 18,500 | | | | 121,915 | |

QLogic Corp.* | | 22,700 | | | | 398,158 | |

Radisys Corp.* | | 15,500 | | | | 131,905 | |

RightNow Technologies, Inc.* | | 23,300 | | | | 355,558 | |

Rogers Corp.* | | 5,900 | | | | 153,105 | |

SAVVIS, Inc.* | | 24,800 | | | | 366,792 | |

Semtech Corp.* | | 19,700 | | | | 304,759 | |

Skyworks Solutions, Inc.* | | 77,800 | | | | 811,454 | |

Tech Data Corp.* | | 15,300 | | | | 587,979 | |

ValueClick, Inc.* | | 42,200 | | | | 415,248 | |

Verint Systems, Inc.* | | 12,400 | | | | 190,960 | |

Volterra Semiconductor Corp.* | | 20,200 | | | | 279,770 | |

Total Information Technology | | | | | | 8,268,871 | |

Materials - 1.9% | | | | | | | |

Albemarle Corp. | | 10,300 | | | | 325,274 | |

Brush Engineered Materials, Inc.* | | 7,500 | | | | 138,375 | |

Cabot Corp. | | 13,200 | | | | 289,476 | |

Total Materials | | | | | | 753,125 | |

Telecommunication Services - 0.6% | | | | | | | |

Premiere Global Services, Inc.* | | 33,100 | | | | 247,257 | |

Total Common Stocks

(cost $38,983,613) | | | | | | 38,249,323 | |

Short-Term Investments - 9.4% 1 | | | | | | | |

BNY Institutional Cash Reserves Fund,

Series A, 0.07% 3 | | 1,990,007 | | | | 1,990,007 | |

BNY Institutional Cash Reserves Fund,

Series B* 3,4 | | 118,432 | | | | 18,653 | |

Dreyfus Cash Management Fund, Institutional

Class Shares, 0.13% | | 1,696,817 | | | | 1,696,817 | |

Total Short-Term Investments

(cost $3,805,256) | | | | | | 3,705,477 | |

Total Investments - 106.1%

(cost $42,788,869) | | | | | | 41,954,800 | |

Other Assets, less Liabilities - (6.1)% | | | | | | (2,418,394 | ) |

Net Assets - 100.0% | | | | | $ | 39,536,406 | |

The accompanying notes are an integral part of these financial statements.

10

Managers Fremont Micro-Cap Fund

Portfolio Manager’s Comments

The Managers Fremont Micro-Cap Fund primarily invests in the stocks of U.S. micro-capitalization companies. These companies have market capitalizations that, at the time of initial purchase, place them among the smallest 5% of companies listed on U.S. stock markets. Normally the Fund will invest at least 80% of its assets in U.S. micro-cap stocks. The Fund employs multiple portfolio managers who specialize in distinct investment approaches. This “intelligence diversification” not only serves to manage risk, but also seeks to incorporate into the portfolio the breadth of the micro-cap market by focusing different analytical insights on micro-cap investing. The Fund’s team of subadvisors strive to achieve this performance and diversification while ensuring that the Fund operates within the framework of its investment objective and principal investment strategies. The Russell Microcap® Index is the benchmark for the Fund.

The Portfolio Managers

Lord, Abbett & Co., LLC (“Lord Abbett”)

The team focuses its stock selection effort by focusing on companies that have revenue growth of at least 15%, are experiencing year-to-year operating margin improvement and are experiencing earnings growth that is driven by top-line growth rather than being driven by one time events or simple cost-cutting measures. The focus is also on identifying companies with higher-quality balance sheets (often captured by finding companies with manageable debt-to-total-capital ratios) and that are already profitable. Once this process is completed, the focus for the team is on forecasting both revenue and earnings growth over the next several years. To achieve this goal, and to find companies that are expected to grow faster than their industry average, members of the team spend an extensive amount of time understanding the competitive advantages of a firm, the industry dynamics within which they operate, and the strength of management.

The sell discipline is enacted if there is a fundamental change in the business, a more attractive alternative is found, or if a holding reaches a 5% weight in the overall portfolio. The Lord Abbett portfolio typically holds between 75 and 100 stocks with no individual holding exceeding 5%. There is a risk constraint that prevents any individual industry from being greater than 25% of the total portfolio weight. The annual turnover of the portfolio is expected to be relatively high although there is no explicit target as part of either the stock selection or the portfolio-construction process.

Next Century Growth Investors, LLC (“Next Century”)

The team requires historical revenue growth of at least 15% for a company before conducting further research. Other key factors considered initially by the team are strong historical revenue growth, low debt and high ROE. Quantitative screening is done on a regular basis to see which stocks over the past year are experiencing significant growth. The next stage of this process involves intensive first-hand research to determine the growth prospects of a company with the team choosing a stock only when it has become convinced a company has an extraordinary opportunity to grow its business. The uniqueness of this process lies in the fact that the team seeks out these companies regardless of their short-term prospects and\ or current valuation. The team is looking for “home runs” and companies that will grow to the point that they will eventually reach a small market capitalization.

The sell discipline is enacted if there is a change in the original investment thesis or a fundamental change in business of the company. In addition, a holding will become a candidate for sale if it reaches an extreme valuation, becomes larger than 5% of the overall portfolio or as it approaches $1 billion in market capitalization. Typically companies are sold out of the micro-cap portfolio because they have approached $1 billion in market capitalization.

The Next Century portfolio is concentrated and typically has 40-60 holdings, which can create a high level of volatility. The only risk constraints are that sector weights can not exceed two times the Russell 2000® Growth sector weights, and no individual holding can be greater than 5% of the portfolio.

Managers Investment Group LLC (“MIG”)

Effective August 31, 2009, the subadvisory agreement with respect to the Fund between the Fund’s investment manager, Managers Investment Group LLC (“MIG”), and OFI Institutional Asset Management, Inc. (“OFII”) was terminated. The portion of the Fund previously managed by the OFII portfolio management team of Daniel Goldfarb, Christopher Crooks, and Steven Dray (collectively, the “OFII Team”), who were jointly and primarily responsible for the day-to-day management of the portion of the Fund managed by OFII since December 10, 2007, is currently managed by MIG in its capacity as the investment manager to the Fund. MIG is employing a transition manager to assist with the management of assets formerly managed by the OFII Team. Keitha L. Kinne is primarily responsible for overseeing the transition manager and is primarily responsible for day-to-day management of the portfolio managed directly by MIG. The OFI Team joined AlphaOne on September 1, 2009 and acts as a consultant to MIG with respect to the portion of the Fund previously managed by the AlphaOne team at OFII. AlphaOne retains no authority over the Fund, and Ms. Kinne, on behalf of MIG, retains full discretion over the purchase and sale of investments for the portion of the Fund managed directly by MIG.

WEDGE Capital Management L.L.P. (“WEDGE”)

The investment process is a combination of both quantitative and fundamental research insights. The quantitative portion of the investment process uses commonly found factors and characteristics that can be accessed via any number of commercial databases. The value-added portion of the process, therefore, uses a number of different factors across five major categories: valuation, earnings quality, operating efficiency, capital usage and momentum, whose efficacy has been verified via long-term regression analysis. This is the Fundamental Value model. The top results of this model are combined with the best resulting stocks from the Financial Quality model, which

11

Managers Fremont Micro-Cap Fund

Portfolio Manager’s Comments (continued)

measures stocks across categories such as multiple earnings growth, profitability, leverage and liquidity. The top stocks that appear in both models are eligible for fundamental research. The fundamental research portion of the investment process is exclusionary in nature and meant to eliminate stocks that are not strong in earnings forecasts, valuation metrics, sector\industry outlook or any factor that can not be easily captured quantitatively.

A stock is scrutinized for possible sale if it falls below the top four deciles in the Fundamental Value model. Stocks are sold when they become fairly valued, an upgrade opportunity develops or the original investment thesis materially deteriorates. The portfolio managed by WEDGE is confined to plus or minus 10% in any given sector although sector positions tend to be much closer to the index weight than this (it should be noted that these self-imposed sector weighting constraints are based on a proprietary liquidity analysis conducted on an ongoing basis by the micro-cap team and is NOT driven by the sector weightings of any micro-cap benchmark). The final portfolio is a well diversified micro-cap portfolio holding approximately 150 securities and consistently maintaining a value bias relative to the benchmark. The portfolio tends to hold securities within the $40 million to $400 million market capitalization range, although does not require a sale of a holding until it reaches $800 million in market capitalization.

The Year in Review

The past twelve months will go down in the history books as one of the wildest rides in the history of Wall Street. Early in the period, securities markets were under severe pressure as the credit crises which began in the summer of 2007, accelerated in the fourth quarter of last year amid ongoing concerns about deteriorating economic conditions and the health of some of our most prominent financial institutions. Banks of all sizes remained under pressure, which led to continued consolidation within the industry. Wachovia agreed to sell itself to Wells Fargo & Co. while PNC agreed to acquire the troubled National City. Meanwhile, the U.S. Government attempted to stabilize the system by formally bailing out companies like Citi-group and by providing injections of capital into hundreds of other financial institutions. Like a sprawling fire, the crises extended to other industries with the automakers finding themselves on the verge of collapse. Once again, the U.S. Government stepped in and in late December President Bush approved an emergency bailout of the U.S. auto industry, offering $17.4 billion in rescue loans to Chrysler and General Motors with the expectation that the companies would move quickly to develop acceptable plans for long-term viability. Consumer and investor confidence continued to sink in the early part of 2009 despite the U.S. Government’s aggressive efforts to restore the economy and stabilize the financial markets. During January, February, and early March, stocks plunged, sending broad indexes to levels not seen since the mid to late 1990s. From peak (October 10, 2007) to trough (March 9, 2009), stocks, as measured by the S&P 500 Index, lost 55.5%, marking this Index’s steepest decline since the Great Depression. Then, on March 10, a very sharp recovery began amid preliminary signs that the Government’s efforts might be starting to bear fruit. More specifically, Citigroup, which had been under extreme pressure and was essentially bailed out by the Government, reported that it returned to profitability in the months of January and February. Citigroup’s surprising news seemed to ignite the markets, contributing to a more than 6% gain for the S&P 500 Index and set the stage for a sharp recovery in equities and extended the rally in credit sensitive fixed income securities.

For the 12 months that ended October 31, 2009, the Managers Fremont Micro-Cap Fund returned 11.3%, compared with 5.1% for its benchmark, the Russell Microcap® Index. Performance remains strong relative to both the Index and peers since the Fund was converted to a multi-manager, multi-style approach in early 2008. Solid outperformance over the last year has been driven by positive stock selection in several sectors including financials and information technology. In addition, the Fund has benefited from relative sector weightings versus the benchmark including a large underweight to the struggling financials sector and an overweight to the recovering consumer discretionary sector. The Fund’s growth subadvisors, in particular, performed well during this period as growth micro-cap stocks outperformed their value counterparts significantly.

Looking Forward

The portfolio managers are cautiously optimistic about the prospects of a recovery and are seeking to take advantage of further consolidation within several sectors by tilting the Fund towards those companies the portfolio managers believe are best positioned to increase market share. Although the Fund’s subadvisors remain fairly active, relative sector positioning has remained fairly consistent throughout the course of the last fiscal year with the major exception being the information technology sector where strong performance resulted in the overweight position being reduced to a near neutral weight by the end of the period. Within the Fund, the largest overweight remains to the industrials sector and the largest underweight continues to remain to the financials sector.

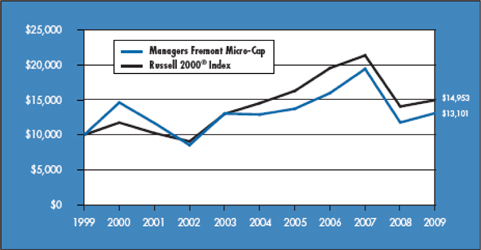

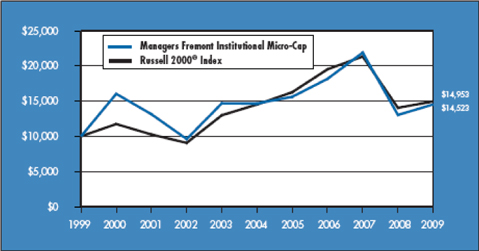

Cumulative Total Return Performance

Managers Fremont Micro-Cap Fund’s cumulative total return is based on the daily change in net asset value (NAV), and assumes that all distributions were reinvested. The Russell 2000 ® Index is composed of the 2,000 smallest stocks in the Russell 3000® Index and is widely regarded in the industry as the premier measure of small-cap stock performance. This chart compares a hypothetical $10,000 investment made in the Managers Fremont Micro-Cap Fund on October 31,

12

Managers Fremont Micro-Cap Fund

Portfolio Manager’s Comments (continued)

Cumulative Total Return Performance

1999, to a $10,000 investment made in the Russell 2000® Index for the same time period. Performance for periods longer than one year is annualized. The graph and table do not reflect the deduction of taxes that a shareholder would pay on a Fund distribution or redemption of shares. The listed returns for the Fund are net of expenses and the returns for the index exclude expenses. Total returns for the Fund would have been lower had certain expenses not been reduced.

The table below shows the average annualized total returns for the Managers Fremont Micro-Cap Fund, the Russell Microcap® Index and the Russell 2000® Index for the one-year, five-year and ten-year periods ended October 31, 2009.

| | | | | | | | | |

Average Annual Total Returns1,2 | | One Year | | | Five Years | | | Ten Years | |

Managers Fremont Micro-Cap4 | | 11.34 | % | | 0.31 | % | | 2.74 | % |

Russell Microcap® Index3 | | 5.06 | % | | (2.57 | )% | | — | 5 |

Russell 2000® Index6 | | 6.46 | % | | 0.59 | % | | 4.11 | % |

The performance data shown represents past performance. Past performance is not a guarantee of future results. Current performance may be lower or higher than the performance data quoted. The investment return and principal value of an investment in the Fund will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. For performance information through the most recent month end, please call (800) 835-3879 or visit our Web site at www.managersinvest.com.

In choosing a Fund, investors should carefully consider the amount they plan to invest, their investment objectives, the Fund’s investment objectives, risks, charges and expenses before investing. For this and other information, please call (800) 835-3879 or visit www.managersinvest.com for a free prospectus. Read it carefully before investing or sending money. Distributed by Managers Distributors, Inc., member FINRA.

| 1 | Total return equals income yield plus share price change and assumes reinvestment of all dividends and capital gain distributions. Returns are net of fees and may reflect offsets of Fund expenses as described in the Prospectus. No adjustment has been made for taxes payable by shareholders on their reinvested dividends and capital gain distributions. Returns for periods greater than one year are annualized. The listed returns on the Fund are net of expenses and based on the published NAV as of October 31, 2009. All returns are in U.S. dollars($). |

| 2 | The Funds are subject to the special risks associated with investments in micro-cap companies, such as relatively short earnings histories, competitive conditions, less publicly available corporate information, and reliance on a limited number of products. |

| 3 | The Russell Microcap® Index tracks the micro-cap segment of the U.S. equity market. It makes up less than 3% of the U.S. Equity market and is represented by the smallest 1,000 securities in the small-cap Russell 2000® Index plus the next 1,000 securities. The Index reflects no deduction of fees, expenses, or taxes. |

| 4 | Fund for which, from time to time, the advisor has waived its fees and/or absorbed Fund expenses, which has resulted in higher returns. |

| 5 | Since the Russell Microcap® Index’s inception date of June 30, 2000, the average annual total return for the Index was 2.45%. |

| 6 | The Russell 2000® Index is composed of the 2,000 smallest stocks in the Russell 3000® Index and is widely regarded in the industry as the premier measure of small-cap stock performance. The Index reflects no deduction of fees, expenses, or taxes. |

The Russell Microcap® Index and the Russell 2000® Index are registered trademarks of Russell Investments. Russell® is a trademark of Russell Investments.

Not FDIC insured, nor bank guaranteed. May lose value.

13

Managers Fremont Micro-Cap Fund

Fund Snapshots

October 31, 2009

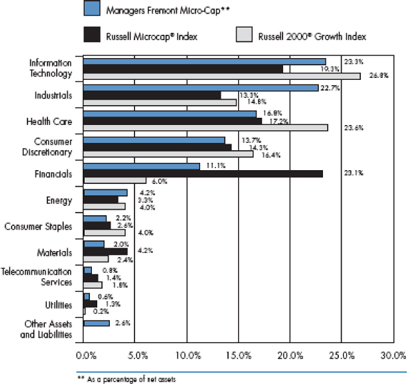

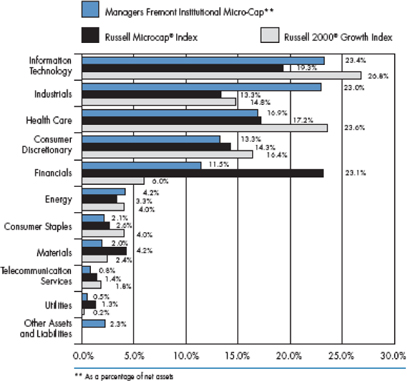

Portfolio Breakdown

| | | | | | | | | |

Industry | | Managers

Fremont

Micro Cap** | | | Russell

Microcap®

Index | | | Russell 2000®

Growth

Index | |

Information Technology | | 23.3 | % | | 19.3 | % | | 26.8 | % |

Industrials | | 22.7 | % | | 13.3 | % | | 14.8 | % |

Health Care | | 16.8 | % | | 17.2 | % | | 23.6 | % |

Consumer Discretionary | | 13.7 | % | | 14.3 | % | | 16.4 | % |

Financials | | 11.1 | % | | 23.1 | % | | 6.0 | % |

Energy | | 4.2 | % | | 3.3 | % | | 4.0 | % |

Consumer Staples | | 2.2 | % | | 2.6 | % | | 4.0 | % |

Materials | | 2.0 | % | | 4.2 | % | | 2.4 | % |

Telecommunication Services | | 0.8 | % | | 1.4 | % | | 1.8 | % |

Utilities | | 0.6 | % | | 1.3 | % | | 0.2 | % |

Other Assets and Liabilities | | 2.6 | % | | 0.0 | % | | 0.0 | % |

Top Ten Holdings

| | | |

Security Name | | Percentage of Net

Assets | |

LaBarge, Inc.* | | 1.2 | % |

Bio-Reference Laboratories, Inc.* | | 1.2 | |

U.S. Physical Therapy, Inc.* | | 1.0 | |

Forrester Research, Inc. | | 1.0 | |

Great Lakes Dredge & Dock Corp. | | 1.0 | |

HMS Holdings Corp.* | | 0.9 | |

Carrizo Oil & Gas, Inc. | | 0.9 | |

CyberSource Corp.* | | 0.9 | |

MWI Veterinary Supply, Inc.* | | 0.9 | |

Standard Parking Corp. | | 0.9 | |

| | | |

Top Ten as a Group | | 9.9 | % |

| | | |

| * | Top Ten Holding at April 30, 2009 |

Any sectors, industries, or securities discussed should not be perceived as investment recommendations. Mention of a specific security should not be considered a recommendation to buy or solicitation to sell that security. Specific securities mentioned in this report may have been sold from the Fund’s portfolio of investments by the time you receive this report.

14

Managers Fremont Micro-Cap Fund

Schedule of Portfolio Investments

October 31, 2009

| | | | | |

| | | Shares | | Value |

Common Stocks - 97.4% | | | | | |

Consumer Discretionary - 13.7% | | | | | |

Ambassadors Group, Inc. | | 61,513 | | $ | 781,830 |

America’s Car-Mart, Inc.* | | 20,700 | | | 429,111 |

Amerigon, Inc.* | | 29,200 | | | 187,756 |

BJ’s Restaurants, Inc.* | | 39,467 | | | 629,893 |

Bridgepoint Education, Inc.* | | 18,195 | | | 258,005 |

Buffalo Wild Wings, Inc.* | | 20,615 | | | 845,421 |

Cache, Inc.* | | 60,773 | | | 292,318 |

California Pizza Kitchen, Inc.* | | 29,500 | | | 383,205 |

Chinacast Education Corp.* | | 35,000 | | | 217,700 |

Citi Trends, Inc.* | | 14,688 | | | 386,735 |

CKE Restaurants, Inc. | | 15,600 | | | 136,500 |

Core-Mark Holding Co., Inc.* | | 5,600 | | | 153,272 |

CSS Industries, Inc. | | 12,400 | | | 251,720 |

FGX International Holdings, Ltd.* | | 32,671 | | | 430,931 |

Grand Canyon Education, Inc.* | | 12,895 | | | 209,157 |

Hawk Corp., Class A* | | 11,545 | | | 160,707 |

hhgregg, Inc.* | | 63,700 | | | 1,050,413 |

Hibbett Sports, Inc.* | | 21,561 | | | 404,053 |

Home Inns & Hotels Management, Inc., (ADR)* | | 9,002 | | | 239,273 |

Hooker Furniture Corp. | | 11,588 | | | 148,442 |

IMAX Corp.* | | 39,377 | | | 405,583 |

Jo-Ann Stores, Inc.* | | 6,500 | | | 173,030 |

K12, Inc.* | | 4,600 | | | 73,784 |

Kenneth Cole Productions, Inc. | | 26,107 | | | 248,278 |

Learning Tree International, Inc.* | | 13,600 | | | 147,968 |

Lincoln Educational Services Corp.* | | 7,300 | | | 144,686 |

Lumber Liquidators, Inc.* | | 45,460 | | | 966,025 |

Maidenform Brands, Inc.* | | 19,800 | | | 277,992 |

Marcus Corp., The | | 12,500 | | | 146,250 |

McCormick & Schmick’s Seafood Restaurants, Inc.* | | 58,979 | | | 355,054 |

Midas, Inc.* | | 17,500 | | | 141,050 |

Monro Muffler Brake, Inc. | | 23,900 | | | 740,661 |

Morton’s Restaurant Group, Inc.* | | 19,000 | | | 71,060 |

Movado Group, Inc. | | 34,796 | | | 364,662 |

New York & Company, Inc.* | | 48,000 | | | 211,200 |

Peet’s Coffee & Tea, Inc.* | | 13,100 | | | 445,400 |

Pinnacle Entertainment, Inc.* | | 59,033 | | | 498,829 |

RC2 Corp.* | | 5,125 | | | 66,932 |

Rentrak Corp.* | | 4,600 | | | 70,702 |

Shutterfly, Inc.* | | 45,850 | | | 646,485 |

Steiner Leisure, Ltd.* | | 16,020 | | | 592,099 |

Summer Infant, Inc.* | | 48,915 | | | 243,597 |

The Finish Line, Inc., Class A | | 18,500 | | | 187,590 |

True Religion Apparel, Inc.* | | 16,485 | | | 424,818 |

Universal Electronics, Inc.* | | 16,363 | | | 337,078 |

Vitacost.com, Inc.* | | 37,200 | | | 369,024 |

Volcom, Inc.* | | 32,000 | | | 531,520 |

Westport Innovations, Inc.* | | 43,500 | | | 425,430 |

Wonder Auto Technology, Inc.* | | 18,500 | | | 239,390 |

Zumiez, Inc.* | | 23,500 | | | 316,545 |

Total Consumer Discretionary | | | | | 17,459,164 |

Consumer Staples - 2.2% | | | | | |

Andersons, Inc., The | | 4,900 | | | 152,047 |

Boston Beer Co., Inc.* | | 4,800 | | | 182,400 |

China-Biotics, Inc.* | | 20,800 | | | 241,280 |

Diedrich Coffee, Inc.* | | 17,340 | | | 378,012 |

Elizabeth Arden, Inc.* | | 24,900 | | | 265,185 |

Inter Parfums, Inc. | | 8,708 | | | 106,934 |

J&J Snack Foods Corp. | | 5,500 | | | 215,435 |

Medifast, Inc.* | | 11,215 | | | 246,955 |

Nutraceutical International Corp.* | | 7,400 | | | 80,512 |

Pantry, Inc., The* | | 10,300 | | | 145,333 |

Rocky Mountain Chocolate Factory, Inc. | | 9,400 | | | 80,088 |

Smart Balance, Inc.* | | 93,132 | | | 491,737 |

Susser Holdings Corp.* | | 13,600 | | | 161,704 |

Total Consumer Staples | | | | | 2,747,622 |

Energy - 4.2% | | | | | |

Bolt Technology Corp.* | | 6,400 | | | 65,088 |

Carrizo Oil & Gas, Inc.* | | 48,945 | | | 1,134,545 |

Clean Energy Fuels Corp.* | | 48,100 | | | 557,960 |

Dawson Geophysical Co.* | | 6,400 | | | 154,560 |

Gulf Island Fabrication, Inc. | | 18,100 | | | 346,072 |

Natural Gas Services Group, Inc.* | | 18,600 | | | 313,782 |

Northern Oil & Gas, Inc.* | | 93,780 | | | 855,274 |

Panhandle Oil and Gas, Inc. | | 7,700 | | | 151,382 |

PetroQuest Energy, Inc.* | | 36,420 | | | 223,255 |

RPC, Inc. | | 86,609 | | | 809,794 |

Tetra Technologies, Inc.* | | 33,700 | | | 318,802 |

The accompanying notes are an integral part of these financial statements.

15

Managers Fremont Micro-Cap Fund

Schedule of Portfolio Investments (continued)

| | | | | |

| | | Shares | | Value |

Energy - 4.2% (continued) | | | | | |

TGC Industries, Inc. | | 39,543 | | $ | 172,012 |

Union Drilling, Inc.* | | 34,730 | | | 265,337 |

Total Energy | | | | | 5,367,863 |

Financials - 11.1% | | | | | |

Alliance Financial Corp. | | 3,100 | | | 80,724 |

American Physicians Capital, Inc. | | 10,000 | | | 282,800 |

American Safety Insurance Holdings, Ltd.* | | 4,900 | | | 72,618 |

Amerisafe, Inc.* | | 22,206 | | | 411,699 |

Associated Estates Realty Corp. | | 18,500 | | | 168,720 |

Baldwin & Lyons, Inc. | | 3,700 | | | 84,397 |

Bancorp Rhode Island, Inc. | | 20,397 | | | 520,531 |

Bank of Marin Bancorp | | 8,200 | | | 270,682 |

Bar Harbor Bankshares | | 2,500 | | | 71,000 |

Broadpoint Gleacher Securities Group, Inc.* | | 54,312 | | | 345,968 |

Bryn Mawr Bank Corp. | | 22,652 | | | 362,432 |

Columbia Banking System, Inc. | | 31,034 | | | 456,200 |

Community Trust Bancorp, Inc. | | 11,000 | | | 270,820 |

Cowen Group, Inc.* | | 88,382 | | | 667,284 |

Danvers Bancorp, Inc. | | 58,609 | | | 804,702 |

Donegal Group, Inc. | | 33,160 | | | 484,136 |

Eastern Insurance Holdings, Inc. | | 16,136 | | | 113,920 |

ESB Financial Corp. | | 5,600 | | | 65,296 |

ESSA Bancorp, Inc. | | 6,500 | | | 77,805 |

Evercore Partners, Inc., Class A | | 9,600 | | | 313,344 |

Financial Institutions, Inc. | | 46,755 | | | 493,733 |

First Cash Financial Services, Inc.* | | 17,000 | | | 292,060 |

First Community Bancshares, Inc. | | 25,575 | | | 297,693 |

First Mercury Financial Corp. | | 12,000 | | | 152,400 |

First of Long Island Corp., The | | 6,300 | | | 152,271 |

Hallmark Financial Services, Inc.* | | 22,200 | | | 170,274 |

Iberia Bank Corp. | | 15,403 | | | 667,104 |

Independent Bank Corp. (MA) | | 11,200 | | | 238,224 |

JMP Group, Inc. | | 26,100 | | | 219,762 |

Legacy Bancorp, Inc. | | 54,193 | | | 518,085 |

Meadowbrook Insurance Group, Inc. | | 55,100 | | | 370,823 |

Mercer Insurance Group, Inc. | | 9,200 | | | 170,936 |

Mission West Properties, Inc. | | 11,700 | | | 77,805 |

National Bankshares, Inc. | | 9,900 | | | 268,389 |

National Interstate Corp. | | 4,700 | | | 85,117 |

OceanFirst Financial Corp., Inc. | | 63,192 | | | 600,324 |

Penson Worldwide, Inc.* | | 85,312 | | | 831,792 |

Ramco-Gershenson Properties Trust | | 7,900 | | | 69,836 |

S.Y. Bancorp, Inc. | | 13,300 | | | 297,255 |

SCBT Financial Corp. | | 5,866 | | | 151,753 |

Shore Bancshares, Inc. | | 4,400 | | | 71,764 |

Simmons First National Corp., Class A | | 8,300 | | | 242,858 |

Smithtown Bancorp, Inc. | | 14,446 | | | 149,516 |

Southside Bancshares, Inc. | | 13,283 | | | 276,154 |

Texas Capital Bancshares, Inc.* | | 20,900 | | | 304,513 |

Urstadt Biddle Properties, Inc., Class A | | 10,700 | | | 158,039 |

ViewPoint Financial Group | | 6,000 | | | 80,400 |

Washington Trust Bancorp, Inc. | | 8,400 | | | 126,168 |

Webster Financial Corp. | | 42,500 | | | 480,675 |

WSFS Financial Corp. | | 9,100 | | | 251,160 |

Total Financials | | | | | 14,191,961 |

Health Care - 16.8% | | | | | |

Addus HomeCare Corp.* | | 34,600 | | | 316,590 |

Allos Therapeutics, Inc.* | | 27,700 | | | 156,505 |

ATS Medical, Inc.* | | 57,800 | | | 155,482 |

Bio-Reference Laboratories, Inc.* | | 47,438 | | | 1,533,671 |

Cardiovascular Systems, Inc.* | | 38,000 | | | 185,820 |

Clarient, Inc.* | | 81,565 | | | 264,271 |

Conceptus, Inc.* | | 31,565 | | | 553,650 |

Cyberonics, Inc.* | | 20,100 | | | 290,646 |

Cypress Bioscience, Inc.* | | 30,700 | | | 188,498 |

DexCom, Inc.* | | 84,100 | | | 576,926 |

Endologix, Inc.* | | 224,035 | | | 1,066,407 |

Ensign Group, Inc.,The | | 10,700 | | | 158,146 |

eResearch Technology, Inc.* | | 37,000 | | | 273,800 |

Eurand N.V.* | | 33,903 | | | 448,198 |

Exactech, Inc.* | | 45,967 | | | 689,505 |

Genomic Health, Inc.* | | 12,800 | | | 237,696 |

Genoptix, Inc.* | | 10,520 | | | 365,991 |

Hanger Orthopedic Group, Inc.* | | 69,658 | | | 964,067 |

Harvard Bioscience, Inc.* | | 114,400 | | | 414,128 |

HMS Holdings Corp.* | | 27,750 | | | 1,191,308 |

Home Diagnostics, Inc.* | | 12,830 | | | 80,187 |

Insulet Corp.* | | 64,600 | | | 717,060 |

IPC The Hospitalist Co., Inc.* | | 14,300 | | | 433,290 |

Kensey Nash Corp.* | | 5,900 | | | 141,069 |

Landauer, Inc. | | 4,400 | | | 227,876 |

LHC Group, Inc.* | | 6,400 | | | 178,624 |

MAKO Surgical Corp.* | | 39,700 | | | 359,285 |

The accompanying notes are an integral part of these financial statements.

16

Managers Fremont Micro-Cap Fund

Schedule of Portfolio Investments (continued)

| | | | | |

| | | Shares | | Value |

Health Care - 16.8% (continued) | | | | | |

Medical Action Industries, Inc.* | | 19,800 | | $ | 216,612 |

MEDTOX Scientific, Inc.* | | 95,340 | | | 951,493 |

Merit Medical Systems, Inc.* | | 47,933 | | | 813,902 |

MWI Veterinary Supply, Inc.* | | 31,200 | | | 1,104,480 |

Neogen Corp.* | | 24,999 | | | 792,468 |

NxStage Medical, Inc.* | | 82,600 | | | 460,908 |

Obagi Medical Products, Inc.* | | 16,100 | | | 164,542 |

Odyssey HealthCare, Inc.* | | 6,100 | | | 85,034 |

Optimer Pharmaceuticals, Inc.* | | 26,500 | | | 306,340 |

Orthovita, Inc.* | | 54,100 | | | 189,350 |

Phase Forward, Inc.* | | 13,000 | | | 170,430 |

Psychemedics Corp. | | 44,047 | | | 238,294 |

Questcor Pharmaceuticals, Inc.* | | 31,100 | | | 141,194 |

Res-Care, Inc.* | | 21,600 | | | 259,848 |

Somanetics Corp.* | | 28,000 | | | 418,600 |

SXC Health Solutions Corp.* | | 12,465 | | | 569,401 |

U.S. Physical Therapy, Inc.* | | 91,785 | | | 1,288,661 |

Vanda Pharmaceuticals, Inc.* | | 27,922 | | | 284,804 |

Viropharma, Inc.* | | 30,100 | | | 226,954 |

Volcano Corp.* | | 2,946 | | | 42,275 |

Young Innovations, Inc. | | 5,985 | | | 141,545 |

Zoll Medical Corp.* | | 15,600 | | | 302,952 |

Total Health Care | | | | | 21,338,783 |

Industrials - 22.7% | | | | | |

51job, Inc., (ADR)* | | 32,200 | | | 479,780 |

AAON, Inc. | | 8,100 | | | 145,881 |

AeroVironment, Inc.* | | 7,752 | | | 206,668 |

Alamo Group, Inc. | | 10,600 | | | 145,220 |

Altra Holdings, Inc.* | | 61,092 | | | 535,777 |

American Ecology Corp. | | 39,700 | | | 659,814 |

Ameron International Corp. | | 4,700 | | | 277,206 |

Ampco-Pittsburgh Corp. | | 9,300 | | | 250,170 |

Apogee Enterprises, Inc. | | 11,000 | | | 145,640 |

Applied Signal Technology, Inc. | | 6,400 | | | 131,136 |

AZZ, Inc.* | | 11,995 | | | 410,949 |

Barrett Business Services, Inc. | | 22,637 | | | 262,589 |

Cascade Corp. | | 9,400 | | | 233,496 |

CBIZ, Inc.* | | 126,900 | | | 893,376 |

Celadon Group, Inc.* | | 24,400 | | | 238,144 |

Chart Industries, Inc.* | | 36,465 | | | 720,913 |

Colfax Corp.* | | 26,200 | | | 285,056 |

Columbus McKinnon Corp.* | | 18,300 | | | 302,865 |

Comfort Systems USA, Inc. | | 13,000 | | | 141,700 |

Courier Corp. | | 16,300 | | | 241,729 |

CRA International, Inc.* | | 21,200 | | | 524,700 |

Ducommun, Inc. | | 15,500 | | | 263,810 |

Duoyuan Global Water, Inc., (ADR)* | | 10,400 | | | 340,912 |

DXP Enterprises, Inc.* | | 62,626 | | | 718,947 |

Dynamex, Inc.* | | 13,600 | | | 252,008 |

Dynamic Materials Corp. | | 11,350 | | | 218,828 |

Energy Recovery, Inc.* | | 16,700 | | | 93,186 |

EnerNOC, Inc.* | | 23,471 | | | 674,322 |

Ennis, Inc. | | 11,400 | | | 172,710 |

EnPro Industries, Inc.* | | 11,400 | | | 257,412 |

Exponent, Inc.* | | 37,781 | | | 982,684 |

Furmanite Corp.* | | 53,800 | | | 192,604 |

GP Strategies Corp.* | | 108,533 | | | 764,072 |

Great Lakes Dredge & Dock Corp. | | 198,815 | | | 1,218,736 |

Harbin Electric, Inc.* | | 20,100 | | | 320,193 |

Hill International, Inc.* | | 105,963 | | | 712,071 |

ICF International, Inc.* | | 12,585 | | | 360,560 |

II-VI, Inc.* | | 30,604 | | | 810,088 |

Kforce, Inc.* | | 33,100 | | | 388,263 |

Kimball International, Inc., Class B | | 10,700 | | | 80,250 |

Knight Transportation, Inc. | | 31,350 | | | 502,854 |

Knoll, Inc. | | 32,600 | | | 319,480 |

LaBarge, Inc.* | | 138,932 | | | 1,542,145 |

LB Foster Co., Class A* | | 4,800 | | | 134,784 |

LMI Aerospace, Inc.* | | 42,494 | | | 457,660 |

LSI Industries, Inc. | | 42,597 | | | 297,753 |

Marten Transport, Ltd.* | | 45,817 | | | 803,630 |

Met-Pro Corp. | | 24,600 | | | 226,320 |

Michael Baker Corp.* | | 9,300 | | | 332,010 |

Multi-Color Corp. | | 67,329 | | | 893,456 |

MYR Group, Inc.* | | 20,800 | | | 357,344 |

Old Dominion Freight Line, Inc.* | | 11,950 | | | 310,580 |

On Assignment, Inc.* | | 54,200 | | | 327,368 |

Orion Marine Group, Inc.* | | 48,710 | | | 927,438 |

Raven Industries, Inc. | | 18,718 | | | 462,335 |

RBC Bearings, Inc.* | | 10,100 | | | 217,251 |

Saia, Inc.* | | 22,200 | | | 325,452 |

SmartHeat, Inc.* | | 38,700 | | | 345,978 |

Spherion Corp.* | | 12,800 | | | 63,360 |

The accompanying notes are an integral part of these financial statements.

17

Managers Fremont Micro-Cap Fund

Schedule of Portfolio Investments (continued)

| | | | | |

| | | Shares | | Value |

Industrials - 22.7% (continued) | | | | | |

Standard Parking Corp.* | | 62,581 | | $ | 1,101,426 |

Sterling Construction, Inc.* | | 39,290 | | | 633,748 |

Titan Machinery, Inc.* | | 45,046 | | | 483,344 |

TrueBlue, Inc. | | 26,800 | | | 324,280 |

Universal Truckload Services, Inc. | | 9,100 | | | 149,604 |

UQM Technologies, Inc.* | | 53,120 | | | 249,664 |

Vitran Corp., Inc., Class A* | | 102,763 | | | 879,651 |

Volt Information Sciences, Inc.* | | 15,800 | | | 128,138 |

Total Industrials | | | | | 28,851,518 |

Information Technology - 23.3% | | | | | |

3PAR, Inc.* | | 31,200 | | | 293,592 |

Actuate Corp.* | | 39,800 | | | 199,398 |

Anadigics, Inc.* | | 66,700 | | | 214,107 |

Anaren Microwave, Inc.* | | 18,100 | | | 264,622 |

Applied Micro Circuits Corp.* | | 40,900 | | | 319,838 |

Aruba Networks, Inc.* | | 44,830 | | | 350,571 |

Bel Fuse, Inc. | | 13,100 | | | 237,110 |

Cavium Networks, Inc.* | | 14,100 | | | 267,336 |

CommVault Systems, Inc.* | | 15,900 | | | 313,230 |

Compellent Technologies, Inc.* | | 56,515 | | | 1,036,485 |

Computer Task Group, Inc.* | | 12,000 | | | 83,640 |

Constant Contact, Inc.* | | 25,557 | | | 423,479 |

CTS Corp. | | 35,195 | | | 315,347 |

CyberSource Corp.* | | 68,233 | | | 1,117,656 |

DealerTrack Holdings, Inc.* | | 22,990 | | | 378,875 |

DemandTec, Inc.* | | 70,041 | | | 615,660 |

DG FastChannel, Inc.* | | 35,490 | | | 744,225 |

Digi International, Inc.* | | 31,428 | | | 249,853 |

Double-Take Software, Inc.* | | 24,300 | | | 225,261 |

DragonWave, Inc.* | | 16,800 | | | 133,896 |

DTS, Inc.* | | 16,890 | | | 477,142 |

Dynamics Research Corp.* | | 10,500 | | | 134,505 |

Ebix, Inc.* | | 7,335 | | | 451,836 |

EMS Technologies, Inc.* | | 60,520 | | | 1,054,864 |

Entegris, Inc.* | | 56,640 | | | 212,966 |

Forrester Research, Inc.* | | 50,264 | | | 1,273,187 |

Hackett Group, Inc., The* | | 30,500 | | | 95,160 |

iGATE Corp.* | | 52,320 | | | 461,986 |

Interactive Intelligence, Inc.* | | 23,800 | | | 399,126 |

IPG Photonics Corp.* | | 19,200 | | | 262,272 |

IXYS Corp.* | | 22,900 | | | 153,430 |

Knot, Inc., The* | | 48,000 | | | 512,160 |

Kulicke & Soffa Industries, Inc.* | | 66,600 | | | 309,690 |

LogMeIn, Inc.* | | 15,035 | | | 302,204 |

Maxwell Technologies, Inc.* | | 41,280 | | | 740,150 |

Mellanox Technologies, Ltd.* | | 48,613 | | | 848,297 |

Methode Electronics, Inc. | | 8,800 | | | 63,800 |

Mindspeed Technologies, Inc. | | 83,545 | | | 291,572 |

MIPS Technologies, Inc.* | | 60,375 | | | 238,481 |

Monolithic Power Systems, Inc.* | | 9,900 | | | 197,901 |

MTS Systems Corp. | | 14,000 | | | 371,000 |

Multi-Fineline Electronix, Inc.* | | 3,000 | | | 81,750 |

NCI, Inc., Class A* | | 27,714 | | | 745,784 |

Netezza Corp.* | | 45,600 | | | 421,344 |

NetLogic Microsystems, Inc.* | | 12,725 | | | 483,677 |

O2Micro International, Ltd.* | | 61,020 | | | 267,878 |

Online Resources Corp.* | | 93,740 | | | 492,135 |

OpenTable, Inc.* | | 17,000 | | | 419,220 |

OSI Systems, Inc.* | | 9,100 | | | 178,633 |

PC Connection, Inc.* | | 31,500 | | | 185,220 |

PDF Solutions, Inc.* | | 184,800 | | | 654,192 |

Perficient, Inc.* | | 37,200 | | | 302,808 |

Power Integrations, Inc. | | 6,645 | | | 207,324 |

PROS Holdings, Inc.* | | 63,900 | | | 574,461 |

Radiant Systems, Inc.* | | 71,800 | | | 706,512 |

Renaissance Learning, Inc. | | 8,300 | | | 75,364 |

Renesola, Ltd., (ADR)* | | 108,100 | | | 397,808 |

RightNow Technologies, Inc.* | | 18,100 | | | 276,206 |

S1 Corp.* | | 11,300 | | | 67,800 |

ShoreTel, Inc.* | | 51,200 | | | 336,384 |

SonicWALL, Inc.* | | 30,700 | | | 243,758 |

Sourcefire, Inc.* | | 15,285 | | | 310,286 |

Spectrum Control, Inc.* | | 28,100 | | | 237,445 |

Super Micro Computer, Inc.* | | 9,600 | | | 77,376 |

Supertex, Inc.* | | 29,550 | | | 716,588 |

Switch & Data Facilities Co., Inc.* | | 49,040 | | | 820,439 |

Symmetricom, Inc.* | | 27,292 | | | 130,729 |

Synchronoss Technologies, Inc.* | | 37,800 | | | 431,298 |

Taleo Corp.* | | 23,600 | | | 513,064 |

Terremark Worldwide, Inc.* | | 33,815 | | | 216,078 |

TESSCO Technologies, Inc. | | 5,000 | | | 84,750 |

The accompanying notes are an integral part of these financial statements.

18

Managers Fremont Micro-Cap Fund

Schedule of Portfolio Investments (continued)

| | | | | | |

| | | Shares | | Value | |

Information Technology - 23.3% (continued) | | | | | | |

Ultimate Software Group, Inc., The* | | 15,100 | | $ | 385,201 | |

VanceInfo Technologies, Inc., (ADR)* | | 20,800 | | | 314,080 | |

Veeco Instruments, Inc.* | | 16,100 | | | 392,035 | |

Virtusa Corp.* | | 71,910 | | | 645,752 | |

Volterra Semiconductor Corp.* | | 39,100 | | | 541,535 | |