UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

| | |

| Investment Company Act file number: | | 811-07064 |

| |

| Exact name of registrant as specified in charter: | | The Target Portfolio Trust |

| |

| Address of principal executive offices: | | Gateway Center 3, |

| | 100 Mulberry Street, |

| | Newark, New Jersey 07102 |

| |

| Name and address of agent for service: | | Deborah A. Docs |

| | Gateway Center 3, |

| | 100 Mulberry Street, |

| | Newark, New Jersey 07102 |

| |

| Registrant’s telephone number, including area code: | | 800-225-1852 |

| |

| Date of fiscal year end: | | 10/31/2012 |

| |

| Date of reporting period: | | 10/31/2012 |

Item 1 – Reports to Stockholders

PRUDENTIAL INVESTMENTS»MUTUAL FUNDS

THE TARGET PORTFOLIO TRUST®

ANNUAL REPORT · OCTOBER 31, 2012

This report is not authorized for distribution to prospective investors unless preceded or accompanied by a current prospectus.

The views expressed in this report and information about the Trust portfolios’ securities are for the period covered by this report and are subject to change thereafter.

TARGET FUNDS and TARGET Portfolio Trust are distributed by Prudential Investment Management Services LLC, Newark, NJ, a Prudential Financial company and member of SIPC. Prudential Investments, Prudential, the Prudential logo, the Rock symbol, and Bring Your Challenges are service marks of Prudential Financial, Inc., and its related entities, registered in many jurisdictions worldwide.

December 14, 2012

Dear TARGET Shareholder:

We hope you find the annual report for TARGET informative and useful. The report covers performance for the 12-month period that ended October 31, 2012.

We recognize that ongoing market volatility may make it a difficult time to be an investor. We continue to believe a prudent response to uncertainty is to maintain a diversified portfolio of funds consistent with your tolerance for risk, time horizon, and financial goals. Whether you are looking for capital growth, current income, or a combination of both, the TARGET portfolios feature a wide range of strategies to suit a variety of investment needs.

TARGET is founded upon the belief that investment management talent is dispersed across a variety of firms and can be systematically identified through research. The managers for each portfolio are carefully chosen from among the leading institutional money managers and are monitored by our team of experienced investment management analysts. Of course, the future performance of the TARGET portfolios cannot be guaranteed.

Your selections among the TARGET portfolios can evolve as your needs change. Your financial professional can help you stay informed of important developments and assist you in determining whether you need to modify your investments.

Thank you for your continued confidence.

Sincerely,

Stuart S. Parker, President

The TARGET Portfolio Trust

| | | | |

| THE TARGET PORTFOLIO TRUST | | | 1 | |

Equity Portfolios’ Performance

Performance data quoted represent past performance. Past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate, so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the past performance data quoted. An investor may obtain performance data as of the most recent month-end by visiting our website at www.prudentialfunds.com or by calling (800) 225-1852.

Large Capitalization Growth Portfolio:

Gross operating expenses: Class R, 1.57%; Class T, 0.82%. Net operating expenses: Class R, 1.32%; Class T, 0.82%, after contractual reduction through 2/28/2014.

Large Capitalization Value Portfolio:

Gross operating expenses: Class R, 1.56%; Class T, 0.81%. Net operating expenses: Class R, 1.31%; Class T, 0.81%, after contractual reduction through 2/28/2014.

Small Capitalization Growth Portfolio:

Gross operating expenses: Class R, 1.67%; Class T, 0.92%. Net operating expenses: Class R, 1.42%; Class T, 0.92%, after contractual reduction through 2/28/2014.

Small Capitalization Value Portfolio:

Gross operating expenses: Class R, 1.43%; Class T, 0.68%. Net operating expenses: Class R, 1.18%; Class T, 0.68%, after contractual reduction through 2/28/2014.

International Equity Portfolio:

Gross operating expenses: Class Q, 0.84%; Class R, 1.70%; Class T, 0.95%. Net operating expenses: Class Q, 0.84%; Class R, 1.45%; Class T, 0.95%, after contractual reduction through 2/28/2014.

| | | | | | | | | | | | | | | | |

| | | Cumulative Total Returns

as of 10/31/12 | |

| | | One Year | | | Five Years | | | Ten Years | | | Since Inception | |

Large Capitalization Growth Portfolio (Class R) | | | 8.41 | % | | | –9.58 | % | | | N/A | | | | 13.64% (8/22/06) | |

Large Capitalization Growth Portfolio (Class T) | | | 8.92 | | | | –7.29 | | | | 77.77 | % | | | — | |

Russell 1000® Growth Index | | | 13.02 | | | | 10.11 | | | | 99.40 | | | | — | |

S&P 500 Index | | | 15.19 | | | | 1.81 | | | | 94.92 | | | | — | |

Lipper Large-Cap Growth Funds Avg. | | | 10.12 | | | | –0.24 | | | | 82.76 | | | | — | |

| | |

| 2 | | THE TARGET PORTFOLIO TRUST |

| | | | | | | | | | | | | | | | |

| | | Average Annual Total Returns

as of 9/30/12 | |

| | | One Year | | | Five Years | | | Ten Years | | | Since Inception | |

Large Capitalization Growth Portfolio (Class R) | | | 26.49 | % | | | –0.42 | % | | | N/A | | | | 2.76% (8/22/06) | |

Large Capitalization Growth Portfolio (Class T) | | | 27.08 | | | | 0.07 | | | | 7.38 | % | | | — | |

Russell 1000 Growth Index | | | 29.19 | | | | 3.24 | | | | 8.41 | | | | — | |

S&P 500 Index | | | 30.17 | | | | 1.05 | | | | 8.01 | | | | — | |

Lipper Large-Cap Growth Funds Avg. | | | 27.19 | | | | 1.40 | | | | 7.34 | | | | — | |

| |

| | | Average Annual Total Returns

as of 10/31/12 | |

| | | One Year | | | Five Years | | | Ten Years | | | Since Inception | |

Large Capitalization Growth Portfolio (Class R) | | | 8.41 | % | | | –1.99 | % | | | N/A | | | | 2.09% (8/22/06) | |

Large Capitalization Growth Portfolio (Class T) | | | 8.92 | | | | –1.50 | | | | 5.92 | % | | | — | |

| |

| | | Cumulative Total Returns

as of 10/31/12 | |

| | | One Year | | | Five Years | | | Ten Years | | | Since Inception | |

Large Capitalization Value Portfolio (Class R) | | | 13.23 | % | | | –19.15 | % | | | N/A | | | | –6.02% (8/22/06) | |

Large Capitalization Value Portfolio (Class T) | | | 13.86 | | | | –17.08 | | | | 86.40 | % | | | — | |

Russell 1000 Value Index | | | 16.89 | | | | –4.91 | | | | 103.14 | | | | — | |

S&P 500 Index | | | 15.19 | | | | 1.81 | | | | 94.92 | | | | — | |

Lipper Large-Cap Value Funds Avg. | | | 14.08 | | | | –7.03 | | | | 87.30 | | | | — | |

| |

| | | Average Annual Total Returns

as of 9/30/12 | |

| | | One Year | | | Five Years | | | Ten Years | | | Since Inception | |

Large Capitalization Value Portfolio (Class R) | | | 26.19 | % | | | –4.01 | % | | | N/A | | | | –0.92% (8/22/06) | |

Large Capitalization Value Portfolio (Class T) | | | 26.84 | | | | –3.53 | | | | 7.08 | % | | | — | |

Russell 1000 Value Index | | | 30.92 | | | | –0.90 | | | | 8.17 | | | | — | |

S&P 500 Index | | | 30.17 | | | | 1.05 | | | | 8.01 | | | | — | |

Lipper Large-Cap Value Funds Avg. | | | 27.74 | | | | –1.30 | | | | 7.09 | | | | — | |

| |

| | | Average Annual Total Returns

as of 10/31/12 | |

| | | One Year | | | Five Years | | | Ten Years | | | Since Inception | |

Large Capitalization Value Portfolio (Class R) | | | 13.23 | % | | | –4.16 | % | | | N/A | | | | –1.00% (8/22/06) | |

Large Capitalization Value Portfolio (Class T) | | | 13.86 | | | | –3.68 | | | | 6.43 | % | | | — | |

| | | | |

| THE TARGET PORTFOLIO TRUST | | | 3 | |

Equity Portfolios’ Performance (continued)

| | | | | | | | | | | | | | | | |

| | | Cumulative Total Returns

as of 10/31/12 | |

| | | One Year | | | Five Years | | | Ten Years | | | Since Inception | |

Small Capitalization Growth Portfolio (Class R) | | | 5.38 | % | | | –15.80 | % | | | N/A | | | | 4.71% (8/22/06) | |

Small Capitalization Growth Portfolio (Class T) | | | 5.87 | | | | –13.74 | | | | 64.44 | % | | | — | |

Russell 2000 Growth Index | | | 9.70 | | | | 7.25 | | | | 151.39 | | | | — | |

Russell 2000 Index | | | 12.08 | | | | 6.11 | | | | 149.75 | | | | — | |

Lipper Small-Cap Growth Funds Avg. | | | 9.08 | | | | 3.09 | | | | 133.75 | | | | — | |

| |

| | | Average Annual Total Returns

as of 9/30/12 | |

| | | One Year | | | Five Years | | | Ten Years | | | Since Inception | |

Small Capitalization Growth Portfolio (Class R) | | | 24.32 | % | | | –2.12 | % | | | N/A | | | | 1.32% (8/22/06) | |

Small Capitalization Growth Portfolio (Class T) | | | 24.97 | | | | –1.62 | | | | 5.74 | % | | | — | |

Russell 2000 Growth Index | | | 31.18 | | | | 2.96 | | | | 10.55 | | | | — | |

Russell 2000 Index | | | 31.91 | | | | 2.21 | | | | 10.17 | | | | — | |

Lipper Small-Cap Growth Funds Avg. | | | 29.05 | | | | 1.87 | | | | 9.57 | | | | — | |

| |

| | | Average Annual Total Returns

as of 10/31/12 | |

| | | One Year | | | Five Years | | | Ten Years | | | Since Inception | |

Small Capitalization Growth Portfolio (Class R) | | | 5.38 | % | | | –3.38 | % | | | N/A | | | | 0.75% (8/22/06) | |

Small Capitalization Growth Portfolio (Class T) | | | 5.87 | | | | –2.91 | | | | 5.10 | % | | | — | |

| |

| | | Cumulative Total Returns

as of 10/31/12 | |

| | | One Year | | | Five Years | | | Ten Years | | | Since Inception | |

Small Capitalization Value Portfolio (Class R) | | | 9.51 | % | | | 12.08 | % | | | N/A | | | | 31.93% (8/22/06) | |

Small Capitalization Value Portfolio (Class T) | | | 10.11 | | | | 14.94 | | | | 202.48 | % | | | — | |

Russell 2000 Value Index | | | 14.47 | | | | 4.45 | | | | 145.10 | | | | — | |

Russell 2000 Index | | | 12.08 | | | | 6.11 | | | | 149.75 | | | | — | |

Lipper Small-Cap Core Funds Avg. | | | 10.44 | | | | 5.41 | | | | 144.96 | | | | — | |

Lipper Small-Cap Value Funds Avg. | | | 11.69 | | | | 8.52 | | | | 156.96 | | | | — | |

| |

| | | Average Annual Total Returns

as of 9/30/12 | |

| | | One Year | | | Five Years | | | Ten Years | | | Since Inception | |

Small Capitalization Value Portfolio (Class R) | | | 25.45 | % | | | 2.96 | % | | | N/A | | | | 4.77% (8/22/06) | |

Small Capitalization Value Portfolio (Class T) | | | 26.08 | | | | 3.48 | | | | 12.11 | % | | | — | |

Russell 2000 Value Index | | | 32.63 | | | | 1.35 | | | | 9.68 | | | | — | |

Russell 2000 Index | | | 31.91 | | | | 2.21 | | | | 10.17 | | | | — | |

Lipper Small-Cap Core Funds Avg. | | | 28.97 | | | | 1.65 | | | | 9.69 | | | | — | |

Lipper Small-Cap Value Funds Avg. | | | 28.90 | | | | 1.95 | | | | 10.14 | | | | — | |

| | |

| 4 | | THE TARGET PORTFOLIO TRUST |

| | | | | | | | | | | | | | |

| | | Average Annual Total Returns

as of 10/31/12 |

| | | One Year | | | Five Years | | | Ten Years | | | Since Inception |

Small Capitalization Value Portfolio (Class R) | | | 9.51 | % | | | 2.31 | % | | | N/A | | | 4.57% (8/22/06) |

Small Capitalization Value Portfolio (Class T) | | | 10.11 | | | | 2.82 | | | | 11.70 | % | | — |

| |

| | | Cumulative Total Returns

as of 10/31/12 |

| | | One Year | | | Five Years | | | Ten Years | | | Since Inception |

International Equity Portfolio (Class Q) | | | 5.60 | % | | | N/A | | | | N/A | | | –6.68% (3/1/11) |

International Equity Portfolio (Class R) | | | 5.10 | | | | –28.39 | % | | | N/A | | | –0.09 (8/22/06) |

International Equity Portfolio (Class T) | | | 5.62 | | | | –26.58 | | | | 102.16 | % | | — |

MSCI EAFE ND Index | | | 4.61 | | | | –25.88 | | | | 110.49 | | | — |

Lipper International Multi-Cap Core Funds Avg. | | | 5.75 | | | | –25.70 | | | | 104.80 | | | — |

Lipper Customized Blend Funds Avg. | | | 5.79 | | | | –25.41 | | | | 105.24 | | | — |

| |

| | | Average Annual Total Returns

as of 9/30/12 |

| | | One Year | | | Five Years | | | Ten Years | | | Since Inception |

International Equity Portfolio (Class Q) | | | 14.52 | % | | | N/A | | | | N/A | | | –5.00% (3/1/11) |

International Equity Portfolio (Class R) | | | 13.94 | | | | –5.82 | % | | | N/A | | | –0.20 (8/22/06) |

International Equity Portfolio (Class T) | | | 14.55 | | | | –5.34 | | | | 7.86 | % | | — |

MSCI EAFE ND Index | | | 13.75 | | | | –5.24 | | | | 8.20 | | | — |

Lipper International Multi-Cap Core Funds Avg. | | | 14.60 | | | | –5.24 | | | | 7.59 | | | — |

Lipper Customized Blend Funds Avg. | | | 14.90 | | | | –5.12 | | | | 7.69 | | | — |

| |

| | | Average Annual Total Returns

as of 10/31/12 |

| | | One Year | | | Five Years | | | Ten Years | | | Since Inception |

International Equity Portfolio (Class Q) | | | 5.60 | % | | | N/A | | | | N/A | | | –4.05% (3/1/11) |

International Equity Portfolio (Class R) | | | 5.10 | | | | –6.46 | % | | | N/A | | | –0.01 (8/22/06) |

International Equity Portfolio (Class T) | | | 5.62 | | | | –5.99 | | | | 7.29 | % | | — |

| | | | |

| THE TARGET PORTFOLIO TRUST | | | 5 | |

Equity Portfolios’ Performance (continued)

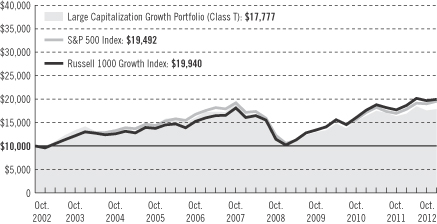

Growth of a $10,000 Investment

Large Capitalization Growth Portfolio

The graph compares a $10,000 investment in the TARGET Large Capitalization Growth Portfolio (Class T) with a similar investment in the S&P 500 Index and the Russell 1000 Growth Index by portraying the initial account values at the beginning of the 10-year period (October 31, 2002) and the account values at the end of the current fiscal year (October 31, 2012), as measured on a quarterly basis.

Total returns and the ending account values in the graph include changes in share price and reinvestment of dividends and capital gains distributions in a hypothetical investment for the periods shown. The Portfolio’s total returns do not reflect the deduction of income taxes on an individual’s investment. Taxes may reduce your actual investment returns on income or gains paid by the Portfolio or any gains you may realize if you sell your shares.

| | |

| 6 | | THE TARGET PORTFOLIO TRUST |

Large Capitalization Value Portfolio

The graph compares a $10,000 investment in the TARGET Large Capitalization Value Portfolio (Class T) with a similar investment in the S&P 500 Index and the Russell 1000 Value Index by portraying the initial account values at the beginning of the 10-year period (October 31, 2002) and the account values at the end of the current fiscal year (October 31, 2012), as measured on a quarterly basis.

Total returns and the ending account values in the graph include changes in share price and reinvestment of dividends and capital gains distributions in a hypothetical investment for the periods shown. The Portfolio’s total returns do not reflect the deduction of income taxes on an individual’s investment. Taxes may reduce your actual investment returns on income or gains paid by the Portfolio or any gains you may realize if you sell your shares.

| | | | |

| THE TARGET PORTFOLIO TRUST | | | 7 | |

Equity Portfolios’ Performance (continued)

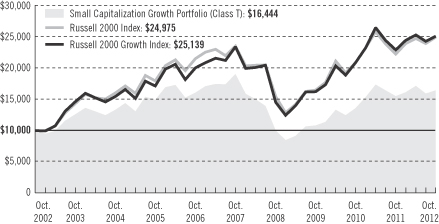

Small Capitalization Growth Portfolio

The graph compares a $10,000 investment in the TARGET Small Capitalization Growth Portfolio (Class T) with a similar investment in the Russell 2000 Index and the Russell 2000 Growth Index by portraying the initial account values at the beginning of the 10-year period (October 31, 2002) and the account values at the end of the current fiscal year (October 31, 2012), as measured on a quarterly basis.

Total returns and the ending account values in the graph include changes in share price and reinvestment of dividends and capital gains distributions in a hypothetical investment for the periods shown. The Portfolio’s total returns do not reflect the deduction of income taxes on an individual’s investment. Taxes may reduce your actual investment returns on income or gains paid by the Portfolio or any gains you may realize if you sell your shares.

| | |

| 8 | | THE TARGET PORTFOLIO TRUST |

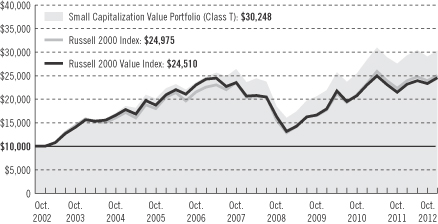

Small Capitalization Value Portfolio

The graph compares a $10,000 investment in the TARGET Small Capitalization Value Portfolio (Class T) with a similar investment in the Russell 2000 Index and the Russell 2000 Value Index by portraying the initial account values at the beginning of the 10-year period (October 31, 2002) and the account values at the end of the current fiscal year (October 31, 2012), as measured on a quarterly basis.

Total returns and the ending account values in the graph include changes in share price and reinvestment of dividends and capital gains distributions in a hypothetical investment for the periods shown. The Portfolio’s total returns do not reflect the deduction of income taxes on an individual’s investment. Taxes may reduce your actual investment returns on income or gains paid by the Portfolio or any gains you may realize if you sell your shares.

| | | | |

| THE TARGET PORTFOLIO TRUST | | | 9 | |

Equity Portfolios’ Performance (continued)

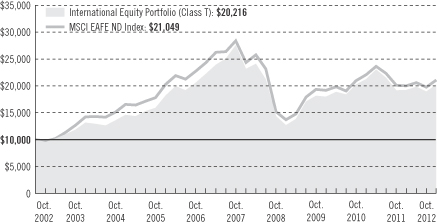

International Equity Portfolio

The graph compares a $10,000 investment in the TARGET International Equity Portfolio (Class T) with a similar investment in the Morgan Stanley Capital International Europe, Australasia, Far East Net Dividend Index (MSCI EAFE ND Index) by portraying the initial account values at the beginning of the 10-year period (October 31, 2002) and the account values at the end of the current fiscal year (October 31, 2012), as measured on a quarterly basis.

Total returns and the ending account values in the graph include changes in share price and reinvestment of dividends and capital gains distributions in a hypothetical investment for the periods shown. The Portfolio’s total returns do not reflect the deduction of income taxes on an individual’s investment. Taxes may reduce your actual investment returns on income or gains paid by the Portfolio or any gains you may realize if you sell your shares.

Source: Prudential Investments LLC and Lipper Inc.

Performance figures may reflect fee waivers and/or expense reimbursements. In the absence of such fee waivers and/or expense reimbursements, total returns would be lower.

Total returns assume the reinvestment of all dividends and distributions, and take into account all charges and expenses applicable to an investment in each Portfolio. Class R shares are subject to an annual distribution and service (12b-1) fee of 0.75%. Returns in the tables and graphs do not reflect the deduction of taxes that a shareholder would pay on Portfolio distributions or following the redemption of Portfolio shares.

Inception returns are provided for any share class with less than 10 calendar years of returns.

| | |

| 10 | | THE TARGET PORTFOLIO TRUST |

Benchmark Definitions

Lipper International Multi-Cap Core Funds Average

Lipper International Multi-Cap Core funds invest in a variety of market capitalization ranges without concentrating 75% of their equity assets in any one market capitalization range over an extended period of time. International multi-cap core funds typically have an average price-to-cash flow ratio, price-to-book ratio, and three-year sales-per- share growth value compared to the S&P/Citigroup World ex-U.S. BMI.

Lipper Customized Blend Funds Average

The Lipper Customized Blend Funds Average is a 50/50 blend of the Lipper International Multi-Cap Core Funds and Lipper International Large-Cap Core Funds Averages. The Lipper Customized Blend Funds Avg is utilized because PI believes that a blend of the two averages provides a more appropriate basis for Portfolio performance comparisons, although Lipper classifies the Portfolio in the Lipper International Multi-Cap Core Funds Universe.

Lipper Large-Cap Growth Funds Average

Lipper Large-Cap Growth funds invest at least 75% of their equity assets in companies with market capitalizations (on a three-year weighted basis) above Lipper’s U.S. Diversified Equity (USDE) large-cap floor. Large-cap growth funds typically have an above-average price-to-earnings ratio, price-to-book ratio, and three-year sales-per-share growth value compared with the S&P 500 Index.

Lipper Large-Cap Value Funds Average

Lipper Large-Cap Value funds invest at least 75% of their equity assets in companies with market capitalizations (on a three-year weighted basis) above Lipper’s U.S. Diversified Equity (USDE) large-cap floor. Large-cap value funds typically have a below-average price-to-earnings ratio and three-year sales-per-share growth value compared with the S&P 500 Index.

Lipper Small-Cap Growth Funds Average

Lipper Small-Cap Growth funds invest at least 75% of their equity assets in companies with market capitalizations (on a three-year weighted basis) less than 250% of the dollar-weighted median of the smallest 500 of the middle 1,000 securities of the S&P SuperComposite 1500 Index. Small-cap growth funds typically have an above-average price-to-earnings ratio, price-to-book ratio, and three-year sales-per-share-growth value compared with the S&P SmallCap 600 Index.

Lipper Small-Cap Core Funds Average

Lipper Small-Cap Core funds invest at least 75% of their equity assets in companies with market capitalizations (on a three-year weighted basis) below Lipper’s U.S. Diversified Equity (USDE) small-cap ceiling. Small-cap core funds typically have an average price-to-earnings ratio, price-to-book ratio, and three-year sales-per-share-growth value, compared to the S&P SmallCap 600 Index.

Lipper Small-Cap Value Funds Average

Lipper Small-Cap Value funds invest at least 75% of their equity assets in companies with market capitalizations (on a three-year weighted basis) below Lipper’s USDE small-cap ceiling. Small-cap value funds typically have a below-average price-to-earnings ratio, piece-to-book ratio, and a three-year sales-per-share growth value, compared to the S&P SmallCap 600 Index.

| | | | |

| THE TARGET PORTFOLIO TRUST | | | 11 | |

Equity Portfolios’ Performance (continued)

Morgan Stanley Capital International Europe, Australasia, and Far East Net Dividend Index

The Morgan Stanley Capital International Europe, Australasia, and Far East Net Dividend Index (MSCI EAFE ND Index) is an unmanaged, weighted index that reflects stock price movements in Europe, Australasia, and the Far East. It gives an indication of how foreign stocks have performed.

Russell 1000 Growth Index

The Russell 1000 Growth Index is an unmanaged index which contains those securities in the Russell 1000 Index with an above-average growth orientation. Companies in this index tend to exhibit higher price-to-book and price-to-earnings ratios, lower dividend yields, and higher forecasted growth rates.

Russell 1000 Value Index

The Russell 1000 Value Index is an unmanaged index which contains those securities in the Russell 1000 Index with a below-average growth orientation. Companies in this index generally have low price-to-book and price-to-earnings ratios, higher dividend yields, and lower forecasted growth values.

Russell 2000 Index

The Russell 2000 Index is an unmanaged index of the stocks of the 2,000 smallest U.S. companies included in the Russell 3000 Index. It gives an indication of how the stock prices of smaller companies have performed.

Russell 2000 Growth Index

The Russell 2000 Growth Index is an unmanaged index which contains those securities in the Russell 2000 Index with an above-average growth orientation. Companies in this index generally have higher price-to-book and price-to-earnings ratios.

Russell 2000 Value Index

The Russell 2000 Value Index is an unmanaged index which contains those securities in the Russell 2000 Index with a below-average growth orientation. Companies in this index generally have low price-to-earnings ratios, higher dividend yields, and lower forecasted growth values.

S&P 500 Index

The Standard & Poor’s 500 Composite Stock Price Index (S&P 500 Index) is an unmanaged index of 500 stocks of large U.S. companies. It gives a broad look at how stock prices have performed.

Benchmark Inception Returns

Large Capitalization Growth Portfolio—Russell 1000 Growth Index Closest Month-End to Inception cumulative total return as of 10/31/12 is 39.63% for Class R. Russell 1000 Growth Index Closest Month-End to Inception average annual total return as of 9/30/12 is 6.16% for Class R. S&P 500 Index Closest Month-End to Inception cumulative total return as of 10/31/12 is 23.53% for Class R. S&P 500 Index Closest Month-End to Inception average annual total return as of 9/30/12 is 3.85% for Class R. Lipper Average Closest Month-End to Inception cumulative total return as of 10/31/12 is 28.67% for Class R. Lipper Average Closest Month-End to Inception average annual total return as of 9/30/12 is 4.77% for Class R.

Large Capitalization Value Portfolio—Russell 1000 Value Index Closest Month-End to Inception cumulative total return as of 10/31/12 is 11.01% for Class R. Russell 1000 Value Index Closest Month-End to Inception average annual total return as of 9/30/12 is 1.81% for Class R. S&P 500 Index Closest Month-End to Inception

| | |

| 12 | | THE TARGET PORTFOLIO TRUST |

cumulative total return as of 10/31/12 is 23.53% for Class R. S&P 500 Index Closest Month-End to Inception average annual total return as of 9/30/12 is 3.85% for Class R. Lipper Average Closest Month-End to Inception cumulative total return as of 10/31/12 is 9.18% for Class R. Lipper Average Closest Month-End to Inception average annual total return as of 9/30/12 is 1.46% for Class R.

Small Capitalization Growth Portfolio—Russell 2000 Growth Index Closest Month-End to Inception cumulative total return as of 10/31/12 is 34.21% for Class R. Russell 2000 Growth Index Closest Month-End to Inception average annual total return as of 9/30/12 is 5.50% for Class R. Russell 2000 Index Closest Month-End to Inception cumulative total return as of 10/31/12 is 23.64% for Class R. Russell 2000 Index Closest Month-End to Inception average annual total return as of 9/30/12 is 3.92% for Class R. Lipper Average Closest Month-End to Inception cumulative total return as of 10/31/12 is 31.86% for Class R. Lipper Average Closest Month-End to Inception average annual total return as of 9/30/12 is 5.02% for Class R.

Small Capitalization Value Portfolio—Russell 2000 Value Index Closest Month-End to Inception cumulative total return as of 10/31/12 is 13.11% for Class R. Russell 2000 Value Index Month-End to Inception average annual total return as of 9/30/12 is 2.26% for Class R. Russell 2000 Index Closest Month-End to Inception cumulative total return as of 10/31/12 is 23.64% for Class R. Russell 2000 Index Closest Month-End to Inception average annual total return as of 9/30/12 is 3.92% for Class R. Lipper Average Closest Month-End to Inception cumulative total return as of 10/31/12 is 23.76% for Class R. Lipper Average Closest Month-End to Inception average annual total return as of 9/30/12 is 3.69% for Class R. Lipper Small-Cap Value Funds Average Closest Month-End to Inception cumulative total return as of 10/31/12 is 22.28% for Class R. Lipper Small-Cap Value Funds Average Closest Month-End to Inception average annual total return as of 9/30/12 is 3.40% for Class R.

International Equity Portfolio—MSCI EAFE ND Index Closest Month-End to Inception cumulative total returns as of 10/31/12 are –7.77% for Class Q; –3.66% for Class R. MSCI EAFE ND Index Closest Month-End to Inception average annual total returns as of 9/30/12 are –8.53% for Class Q; –4.46% for Class R. Lipper Average Closest Month-End to Inception cumulative total returns as of 10/31/12 are –7.70% for Class Q; –3.25% for Class R. Lipper Average Closest Month-End to Inception average annual total returns as of 9/30/12 are –5.47% for Class Q; –0.82% for Class R. Lipper Customized Blend Funds Average Closest Month-End to Inception cumulative total returns as of 10/31/12 are –7.62% for Class Q and –2.54% for Class R. Lipper Customized Blend Funds Average Closest Month-End to Inception average annual total returns as of 9/30/12 are –5.38% for Class Q and –0.67% for Class R.

Investors cannot invest directly in an index or average. The returns for the benchmark indexes would be lower if they reflected deductions for portfolio operating expenses, sales charges, or taxes.

The Lipper averages represent returns based on an average of all funds in the respective Lipper categories for the periods noted. The returns for the Lipper averages would be lower if they reflected deductions for sales charges or taxes.

| | | | |

| THE TARGET PORTFOLIO TRUST | | | 13 | |

Fixed Income Portfolios’ Performance

Performance data quoted represent past performance. Past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate, so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the past performance data quoted. An investor may obtain performance data as of the most recent month-end by visiting our website at www.prudentialfunds.com or by calling (800) 225-1852.

Total Return Bond Portfolio:

Gross operating expenses: Class R, 1.38%; Class T, 0.63%. Net operating expenses: Class R, 1.13%; Class T, 0.63%, after contractual reduction through 2/28/2014.

Intermediate-Term Bond Portfolio:

Gross operating expenses: Class T, 0.66%. Net operating expenses: Class T, 0.66%.

Mortgage Backed Securities Portfolio:

Gross operating expenses: Class T, 0.93%. Net operating expenses: Class T, 0.93%.

| | | | | | | | | | | | | | | | |

| | | Cumulative Total Returns

as of 10/31/12 | |

| | | One Year | | | Five Years | | | Ten Years | | | Since Inception | |

Total Return Bond Portfolio (Class R) | | | 7.33 | % | | | 45.97 | % | | | N/A | | | | 56.14% (8/22/06) | |

Total Return Bond Portfolio (Class T) | | | 8.01 | | | | 49.94 | | | | 94.09 | % | | | — | |

Barclays U.S. Aggregate Bond Index | | | 5.25 | | | | 36.25 | | | | 69.10 | | | | — | |

Lipper Corporate Debt BBB-Rated Funds Avg. | | | 10.07 | | | | 43.59 | | | | 93.42 | | | | — | |

Lipper Intermediate Investment-Grade Debt Funds Avg. | | | 7.25 | | | | 35.15 | | | | 66.94 | | | | — | |

| |

| | | Average Annual Total Returns

as of 9/30/12 | |

| | | One Year | | | Five Years | | | Ten Years | | | Since Inception | |

Total Return Bond Portfolio (Class R) | | | 7.22 | % | | | 7.97 | % | | | N/A | | | | 7.54% (8/22/06) | |

Total Return Bond Portfolio (Class T) | | | 7.90 | | | | 8.55 | | | | 6.87 | % | | | — | |

Barclays U.S. Aggregate Bond Index | | | 5.16 | | | | 6.53 | | | | 5.32 | | | | — | |

Lipper Corporate Debt BBB-Rated Funds Avg. | | | 10.70 | | | | 7.41 | | | | 6.50 | | | | — | |

Lipper Intermediate Investment-Grade Debt Funds Avg. | | | 7.51 | | | | 6.20 | | | | 5.08 | | | | — | |

| |

| | | Average Annual Total Returns

as of 10/31/12 | |

| | | One Year | | | Five Years | | | Ten Years | | | Since Inception | |

Total Return Bond Portfolio (Class R) | | | 7.33 | % | | | 7.86 | % | | | N/A | | | | 7.46% (8/22/06) | |

Total Return Bond Portfolio (Class T) | | | 8.01 | | | | 8.44 | | | | 6.86 | % | | | — | |

| | |

| 14 | | THE TARGET PORTFOLIO TRUST |

| | | | | | | | | | | | |

| | | Cumulative Total Returns

as of 10/31/12 | |

| | | One Year | | | Five Years | | | Ten Years | |

Intermediate-Term Bond Portfolio (Class T) | | | 8.13 | % | | | 48.93 | % | | | 83.48 | % |

Barclays Intermediate Govt./Credit Bond Index | | | 4.24 | | | | 31.23 | | | | 60.04 | |

Lipper Intermediate Investment-Grade Debt Funds Avg. | | | 7.25 | | | | 35.15 | | | | 66.94 | |

| |

| | | Average Annual Total Returns

as of 9/30/12 | |

| | | One Year | | | Five Years | | | Ten Years | |

Intermediate-Term Bond Portfolio (Class T) | | | 8.28 | % | | | 8.28 | % | | | 6.23 | % |

Barclays Intermediate Govt./Credit Bond Index | | | 4.40 | | | | 5.71 | | | | 4.76 | |

Lipper Intermediate Investment-Grade Debt Funds Avg. | | | 7.51 | | | | 6.20 | | | | 5.08 | |

| |

| | | Average Annual Total Returns

as of 10/31/12 | |

| | | One Year | | | Five Years | | | Ten Years | |

Intermediate-Term Bond Portfolio (Class T) | | | 8.13 | % | | | 8.29 | % | | | 6.26 | % |

| |

| | | Cumulative Total Returns

as of 10/31/12 | |

| | | One Year | | | Five Years | | | Ten Years | |

Mortgage Backed Securities Portfolio (Class T) | | | 4.64 | % | | | 42.98 | % | | | 68.87 | % |

Barclays Mortgage-Backed Securities Index | | | 3.54 | | | | 34.46 | | | | 65.75 | |

Citigroup Mortgage-Backed Securities Index | | | 3.56 | | | | 34.92 | | | | 66.60 | |

Lipper U.S. Mortgage Funds Avg. | | | 4.86 | | | | 30.52 | | | | 53.58 | |

| |

| | | Average Annual Total Returns

as of 9/30/12 | |

| | | One Year | | | Five Years | | | Ten Years | |

Mortgage Backed Securities Portfolio (Class T) | | | 4.57 | % | | | 7.61 | % | | | 5.43 | % |

Barclays Mortgage-Backed Securities Index | | | 3.71 | | | | 6.35 | | | | 5.24 | |

Citigroup Mortgage-Backed Securities Index | | | 3.76 | | | | 6.42 | | | | 5.30 | |

Lipper U.S. Mortgage Funds Avg. | | | 4.97 | | | | 5.57 | | | | 4.35 | |

| |

| | | Average Annual Total Returns

as of 10/31/12 | |

| | | One Year | | | Five Years | | | Ten Years | |

Mortgage Backed Securities Portfolio (Class T) | | | 4.64 | % | | | 7.41 | % | | | 5.38 | % |

Source: Prudential Investments LLC and Lipper Inc.

Total returns assume the reinvestment of all dividends and distributions, and take into account all charges and expenses applicable to an investment in each Portfolio. Class R shares are subject to an annual distribution and service (12b-1) fee of 0.75%. Returns in the tables do not reflect the deduction of taxes that a shareholder would pay on Portfolio distributions or following the redemption of Portfolio shares.

| | | | |

| THE TARGET PORTFOLIO TRUST | | | 15 | |

Fixed Income Portfolios’ Performance (continued)

Inception returns are provided for any share class with less than 10 calendar years of returns.

Investors cannot invest directly in an index or average. The returns for the benchmark indexes would be lower if they reflected deductions for portfolio operating expenses, sales charges, or taxes.

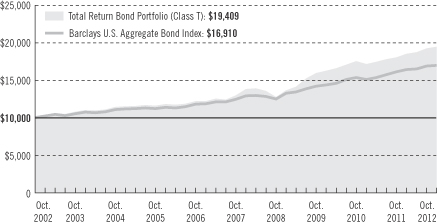

Growth of a $10,000 Investment

Total Return Bond Portfolio

The graph compares a $10,000 investment in the TARGET Total Return Bond Portfolio (Class T) with a similar investment in the Barclays U.S. Aggregate Bond Index by portraying the initial account values at the beginning of the 10-year period (October 31, 2002) and the account values at the end of the current fiscal year (October 31, 2012), as measured on a quarterly basis.

Total returns and the ending account values in the graph include changes in share price and reinvestment of dividends and capital gains distributions in a hypothetical investment for the periods shown. The Portfolio’s total returns do not reflect the deduction of income taxes on an individual’s investment. Taxes may reduce your actual investment returns on income or gains paid by the Portfolio or any gains you may realize if you sell your shares.

| | |

| 16 | | THE TARGET PORTFOLIO TRUST |

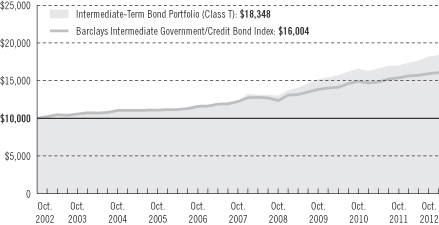

Intermediate-Term Bond Portfolio

The graph compares a $10,000 investment in the TARGET Intermediate-Term Bond Portfolio (Class T) with a similar investment in the Barclays Intermediate Government/Credit Bond Index by portraying the initial account values at the beginning of the 10-year period (October 31, 2002) and the account values at the end of the current fiscal year (October 31, 2012), as measured on a quarterly basis.

Total returns and the ending account values in the graph include changes in share price and reinvestment of dividends and capital gains distributions in a hypothetical investment for the periods shown. The Portfolio’s total returns do not reflect the deduction of income taxes on an individual’s investment. Taxes may reduce your actual investment returns on income or gains paid by the Portfolio or any gains you may realize if you sell your shares.

| | | | |

| THE TARGET PORTFOLIO TRUST | | | 17 | |

Fixed Income Portfolios’ Performance (continued)

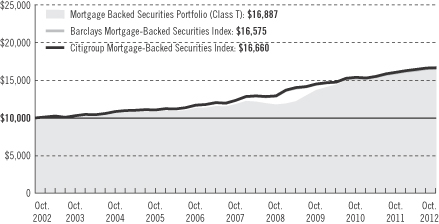

Mortgage Backed Securities Portfolio

The graph compares a $10,000 investment in the TARGET Mortgage Backed Securities Portfolio (Class T) with a similar investment in the Barclays Mortgage-Backed Securities Index and the Citigroup Mortgage-Backed Securities Index by portraying the initial account values at the beginning of the 10-year period (October 31, 2002) and the account values at the end of the current fiscal year (October 31, 2012), as measured on a quarterly basis.

Total returns and the ending account values in the graph include changes in share price and reinvestment of dividends and capital gains distributions in a hypothetical investment for the periods shown. The Portfolio’s total returns do not reflect the deduction of income taxes on an individual’s investment. Taxes may reduce your actual investment returns on income or gains paid by the Portfolio or any gains you may realize if you sell your shares.

Source: Prudential Investments LLC and Lipper Inc.

Total returns assume the reinvestment of all dividends and distributions, and take into account all charges and expenses applicable to an investment in each Portfolio. Class R shares are subject to an annual distribution and service (12b-1) fee of 0.75%. Returns in the tables and graphs do not reflect the deduction of taxes that a shareholder would pay on Portfolio distributions or following the redemption of Portfolio shares.

Inception returns are provided for any share class with less than 10 calendar years of returns.

Investors cannot invest directly in an index or average. The returns for the benchmark indexes would be lower if they reflected deductions for portfolio operating expenses, sales charges, or taxes.

| | |

| 18 | | THE TARGET PORTFOLIO TRUST |

Benchmark Definitions

Barclays Intermediate Government/Credit Bond Index

The Barclays Intermediate Government/Credit Bond Index is an unmanaged index of publicly traded U.S. government bonds and investment-grade corporate bonds with maturities of up to 10 years. It gives a broad indication of how intermediate-term bonds have performed.

Barclays Mortgage-Backed Securities Index

The Barclays Mortgage-Backed Securities Index is an unmanaged, market capitalization-weighted index of 15- and 30-year fixed-rate securities backed by GNMA, FNMA, and FHLMC mortgage pools, and balloon mortgages with fixed-rate coupons.

Barclays U.S. Aggregate Bond Index

The Barclays U.S. Aggregate Bond Index is an unmanaged index of investment-grade securities issued by the U.S. government and its agencies and by corporations with between one and 10 years remaining to maturity. It gives a broad indication of how bond prices of short- and intermediate-term bonds have performed.

Citigroup Mortgage-Backed Securities Index

The Citigroup Mortgage-Backed Securities Index is an unmanaged index of 15- and 30-year mortgage-related securities issued by U.S. government agencies. It gives a broad indication of how mortgage-backed securities have performed.

Lipper Corporate Debt BBB-Rated Funds Average

Lipper Corporate Debt BBB-Rated funds invest primarily in corporate and government debt issues rated in the top four grades.

Lipper Intermediate Investment-Grade Debt Funds Average

Lipper Intermediate Investment-Grade Debt funds invest primarily in investment-grade debt issues (rated in the top four grades) with dollar-weighted average maturities of five to 10 years.

Lipper U.S. Mortgage Funds Average

Lipper U.S. Mortgage funds invest primarily in mortgages/securities issued or guaranteed as to principal and interest by the U.S. government and certain federal agencies.

Benchmark Inception Returns

Total Return Bond Portfolio—Barclays U.S. Aggregate Bond Index Closest Month-End to Inception cumulative total return as of 10/31/12 is 45.80% for Class R. Barclays U.S. Aggregate Bond Index Closest Month-End to Inception average annual total return as of 9/30/12 is 6.36% for Class R. Lipper Average Closest Month-End to Inception cumulative total return as of 10/31/12 is 53.45% for Class R. Lipper Average Closest Month-End to Inception average annual total return as of 9/30/12 is 7.04% for Class R. Lipper Intermediate Investment-Grade Debt Funds Average Closest Month-End to Inception cumulative total return as of 10/31/12 is 43.21% for Class R. Lipper Intermediate Investment-Grade Debt Funds Average Closest Month-End to Inception average annual total return as of 9/30/12 is 5.95% for Class R.

The Lipper Averages represent returns based on an average of all funds in the respective Lipper categories for the periods noted. The returns for the Lipper averages would be lower if they reflected deductions for sales charges or taxes.

| | | | |

| THE TARGET PORTFOLIO TRUST | | | 19 | |

Strategy and Performance Overview

Large Capitalization Growth Portfolio

The Large Capitalization Growth Portfolio’s Class T shares returned 8.92% for the 12-month period ended October 31, 2012, which substantially trailed the 13.02% return of its benchmark, the Russell 1000 Growth Index (the Index) and fell below the 10.12% return of the Lipper Large Cap Growth Funds average.

The Large Capitalization Growth Portfolio uses a multi-manager approach, seeking to maximize returns by diversifying Portfolio performance across manager style and by combining complementary approaches. The Portfolio was managed during the fiscal year by Marsico Capital Management, LLC and MFS Investment Management. Marsico Capital Management, LLC (Marsico), a traditional large-cap growth manager, constructs a relatively concentrated portfolio using an active top-down, bottom-up approach to investing. MFS Investment Management (MFS) follows a more diversified strategy that takes a traditional approach to capture forward-looking earnings and rate of growth, that investors generally miss and/or underestimate. Effective November 2, 2012, Brown Advisory, LLC was added to the Portfolio as a co-manager.

U.S. large-cap stock markets provided a strong return over the reporting period, but the Index both rose and fell more than its value counterpart and provided a somewhat lower 12-month return. During the first half of the period, actions of the U.S. Federal Reserve and the European Central Bank, coupled with healthier global economic conditions, moved stock markets upwards. However, in the latter part of the period, broadly weaker global economic indicators, as well as renewed concerns over the euro zone’s capacity and determination to address its ongoing crisis, brought weaker markets. Nonetheless, equity markets generally maintained their gains.

| | • | | The Portfolio’s stock selection was the primary detractor from its performance relative to the Index, particularly holdings in the information technology, consumer staples and healthcare sectors. On the positive side, positions in the consumer discretionary and financials sectors performed strongly. |

| | • | | Style factors slightly detracted from relative results. The Portfolio’s overexposure relative to the Index to stocks with above-average price volatility and underexposure to companies that had high debt ratios hurt its relative performance. However, the Portfolio benefited from its overexposure to firms whose share prices had recently been strong (momentum). |

The Portfolio of Investments following this report shows the size of the Portfolio’s positions at period-end.

| | |

| 20 | | THE TARGET PORTFOLIO TRUST |

Large Capitalization Value Portfolio

The Large Capitalization Value Portfolio’s Class T shares returned 13.86% for the 12-month reporting period ended October 31, 2012, trailing the 16.89% return of its benchmark, the Russell 1000® Value Index (the Index), and slightly underperforming the 14.08% return of the Lipper Large-Cap Value Funds Average.

The Portfolio was managed during the fiscal year by NFJ Investment Group LLC (NFJ), Hotchkis and Wiley Capital Management LLC (Hotchkis and Wiley), Eaton Vance Management (Eaton Vance), and Epoch Investment Partners, Inc. (Epoch). Effective July 19, 2012, Epoch replaced Eaton Vance as a co-manager to the Portfolio. NFJ follows a disciplined deep-value investment strategy, based on research that has shown that portfolios of low price-to-earnings (P/E) stocks have substantially outperformed market indexes throughout all capitalization levels over extended periods. The managers use an elaborate screening process to identify the lowest-valued stocks within an industry based on their P/E ratio. Hotchkis and Wiley uses a value-oriented investment style and a bottom-up approach to security selection, primarily investing in above-market yielding securities. Its investment team seeks to identify companies with strong cash flow, improving profit margins, sustainability of projected growth, and competitive/strategic positioning within their industries.

In contrast, Eaton Vance’s portion of the overall portfolio followed a relative value or “growthier” investment style. The Portfolio manager evaluated traditional measures of value, overall business health, and changes in business momentum to capture market inefficiencies in the universe of large capitalization companies. Eaton Vance focused on companies that exhibited strong business franchises with attractive earnings-per share (EPS) ratios and dividend growth potential. In July 2012, Epoch replaced Eaton Vance due both to its stand-alone strength and to the way its style complements that of the other two managers. Epoch’s flexible approach to investing is between core and relative value, with a risk profile generally similar to the Index and to Lipper Large Cap Value peers. It provides a good balance to the deep-value styles of NFJ and Hotchkis and Wiley.

U.S. large-cap stock markets provided a strong return over the reporting period, with the Index both rising and falling less, and providing a stronger 12-month return, than its growth counterpart. Financials, the Index’s largest sector with about a quarter of its market value, provided one of the Index’s higher returns, trailing only the very strong consumer discretionary and telecommunications services sectors. Overall sector

The Portfolio of Investments following this report shows the size of the Portfolio’s positions at period-end.

| | | | |

| THE TARGET PORTFOLIO TRUST | | | 21 | |

Strategy and Performance Overview (continued)

returns were varied, but strong, with the only negative total return by technology. The other large positive contributor to the Index total return was the healthcare sector.

| | • | | All four of the managers underperformed the Index, but NFJ had the largest negative impact, primarily during the first quarter of 2012. That quarter was characterized by a “risk-on” rally, when investors were optimistic and pushed up the prices of more volatile stocks. This hurt NFJ because it emphasizes stocks with higher dividend yields and lower volatility. |

| | • | | Sector selection was the primary driver of underperformance. All of the managers were overweight in the technology sector compared with the Index, and its negative return hurt their returns. |

| | • | | Stock selection by the managers also broadly hurt results, with the Portfolio trailing the Index in the technology, consumer discretionary, industrials, energy, and financials sectors. |

| | • | | Neither investment style factors nor the use of derivatives had a significant impact on returns. |

The Portfolio of Investments following this report shows the size of the Portfolio’s positions at period-end.

| | |

| 22 | | THE TARGET PORTFOLIO TRUST |

Small Capitalization Growth Portfolio

The Small Capitalization Growth Portfolio’s Class T shares rose 5.87% for the 12-month reporting period ended October 31, 2012, substantially trailing the 9.70% gain of the Russell 2000® Growth Index (the Index), and the 9.08% return of the Lipper Small-Cap Growth Funds Average.

The Portfolio was managed by Eagle Asset Management (Eagle) and Emerald Mutual Fund Advisers Trust (Emerald) during the reporting period. Effective January 18, 2012, Emerald was added to the Portfolio as a co-manager. The Portfolio employs a multi-manager approach combining complementary strategies to help manage risk and reduce volatility. Eagle describes its traditional growth investment process as “rapid growth at a reasonable price.” It seeks companies with accelerating and sustainable earnings growth, a positive catalyst, a high or expanding return on equity, and a credible and competent management team. Emerald’s philosophy looks to take advantage of market inefficiencies due to lack of coverage by street analysts. It has deep resources and an intense focus on small cap growth investing, and so can cover the full range of industries and sectors. Its risk profile tends to be in line with that of the Index, but can fluctuate from time to time while not compromising its overall risk-return attractiveness.

During the reporting period, the overall direction of small-cap growth stock performance was similar to that of small-cap value stocks, as the broad market was driven by significant economic and political influences, but the overall return was lower. The strong performance of its relatively large healthcare, consumer discretionary, and industrials sectors drove the Index return, while its largest sector, information technology, had a more modest positive return and its energy and utilities sectors declined in value.

| | • | | A few overweighted electrical components companies are in the industrials sectors. Electronic equipment and instruments companies are in the tech sector - they also detracted from electrical components and equipment firms that were poor performers in the technology sector and a consumer finance position in the financials sector were the primary detractors from the Portfolio’s performance compared with the Index. The slight overall underweight in more economically sensitive sectors such as industrials and financials also hurt relative performance as the Portfolio was underweight in some financial services industries that did well within the index during this period. The Portfolio had favored industries Eagle thought had better long-term prospects. |

The Portfolio of Investments following this report shows the size of the Portfolio’s positions at period-end.

| | | | |

| THE TARGET PORTFOLIO TRUST | | | 23 | |

Strategy and Performance Overview (continued)

| | • | | Certain healthcare technology and biotechnology holdings performed relatively poorly because of concerns about the impact of the election on health funding. |

| | • | | On the positive side, the Portfolio’s holdings in the energy sector posted meaningful positive results, despite the Index sector’s substantial decline. Positions in specialty retail, food and staples retailing, and semiconductor equipment also outperformed the Index positions. |

| | • | | Most of the underperformance can be attributed to Eagle, which was the sole manager through mid-January, 2012. It trailed the Index and peer median in the fourth quarter of 2011 and the second quarter of 2012. Although Emerald also underperformed in the second quarter of 2012, its overall contribution to the Portfolio’s performance was positive. |

The Portfolio of Investments following this report shows the size of the Portfolio’s positions at period-end.

| | |

| 24 | | THE TARGET PORTFOLIO TRUST |

Small Capitalization Value Portfolio

The Small Capitalization Value Portfolio’s Class T shares gained 10.11% for the 12-month reporting period ended October 31, 2012, which substantially trailed the 14.47% return of its benchmark, the Russell 2000® Value Index (the Index), and the 11.69% return of the Lipper Small-Cap Value Funds Average, but was essentially in line with the 10.44% return of the Lipper Small-Cap Core Funds Average.

Small companies may respond to economic trends differently from one another because, for example, some may occupy specific niches in which they are immune to economic cycles. Also, some inexpensive stocks may not be followed closely by analysts. Factors such as these mean that small-cap investment managers can benefit from informational inefficiencies in the market, and that research is critical. This is why the Portfolio selects several managers on the basis of their various experience and research capabilities. As managers reach their capacity limits, new asset managers may be added. EARNEST Partners, LLC; Lee Munder Capital Group LLC; J.P. Morgan Investment Management, Inc. (J.P. Morgan); NFJ Investment Group LLC (NFJ); and Vaughan Nelson Investment Management, LP co-managed the Portfolio during this reporting period.

The overall direction of small-cap value stock performance was similar to that of small-cap growth stocks over the twelve months ended October 31, 2012, as the broad market was driven by significant economic and political influences. However, the overall return for value investing in this market was higher. It was driven by the above-20% return of the financials sector, which makes up more than a third of the Index. The consumer discretionary, materials, healthcare, and industrials sectors also had strong returns. However, the negative returns of the energy and information technology sectors offset some of the gains.

| | • | | The Portfolio’s performance relative to the Index was hurt by lower exposure to value characteristics and to stocks of companies with high debt. In addition, the Portfolio’s holdings tended to have larger market capitalization (a greater value of total outstanding stock) than the Index, which was not favored in this market. On the positive side, the Portfolio benefited from having greater exposure to stocks with high price momentum. |

| | • | | An underweight in the financials sector compared with the Index hurt relative performance, although the impact was partially offset by the Portfolio’s overweight in the industrials sector. |

The Portfolio of Investments following this report shows the size of the Portfolio’s positions at period-end.

| | | | |

| THE TARGET PORTFOLIO TRUST | | | 25 | |

Strategy and Performance Overview (continued)

| | • | | The managers’ selection of individual positions apart from these factors also reduced the Portfolio’s relative performance, particularly in the financials and information technology sectors. The impact was mitigated by good selection within the healthcare sector. |

| | • | | J.P. Morgan was the only manager to outperform the Index. NFJ was the biggest detractor from relative performance. |

| | • | | The J.P. Morgan portion of the Portfolio took a small position in Russell 2000 futures (a form of derivative) to hedge its cash position, which helped manage cash flows and general market exposure. This had very little impact on Portfolio results during this reporting period. J.P. Morgan’s sole purpose for using these futures was to maintain full exposure to the overall market and not to increase leverage or take a short-term position on market movements. |

The Portfolio of Investments following this report shows the size of the Portfolio’s positions at period-end.

| | |

| 26 | | THE TARGET PORTFOLIO TRUST |

International Equity Portfolio

The International Equity Portfolio’s Class T shares returned 5.62% for the 12-month reporting period ended October 31, 2012, outperforming the Morgan Stanley Capital International Europe, Australasia, and Far East Net Dividend Index (MSCI EAFE ND Index) (the Index), which gained 4.61%. The Class T shares slightly underperformed the 5.75% gain of the Lipper International Multi-Cap Core Funds Average and the 5.79% return of the Lipper Customized Blend Funds Average.

LSV Asset Management (LSV) and Thornburg Investment Management, Inc. (Thornburg) are co-managers of the Portfolio, which combines the distinct approaches of LSV international value (deep value) and Thornburg international (core/relative value). LSV’s active quantitative strategy is based on research in value investing and behavioral finance. It believes that superior investment performance can be achieved by exploiting investor biases such as a tendency to extrapolate the past too far into the future, wrongly equating a good company with a good investment irrespective of price, ignoring statistical evidence, and developing a “mindset” about a firm. LSV’s approach is based purely on quantitative modeling of the markets, rather than traditional analysis of individual companies, to identify stocks with the potential for price increases in the near future. It does not use derivatives to manage its portion of the Portfolio.

Thornburg seeks companies trading at a discount to what it believes are their intrinsic value, even if the firms would be considered growth stocks by conventional analysis. It uses quantitative selection screens to identify stocks that are attractively valued relative to their peers on metrics such as price/earnings, price/ forward earnings, and price to cash/flow, or that are poised for improvement in business fundamentals such as earnings surprises or earnings revisions. Then, Thornburg intensively studies the business fundamentals of these firms, as well as those of many firms not first identified by the screen. Thornburg evaluates the need for currency hedging on a stock-by-stock basis, considering each company’s vulnerability. It uses forward contracts (a form of derivative) to hedge where it believes there is a significant risk of major adverse currency movement. Overall, foreign exchange hedging had a negligible effect on the Portfolio for the period.

Over this reporting period, international equity markets were concerned about economic slowdowns in both Europe and China, as well as the consequences of several countries’ euro-denominated debt. European markets fluctuated along with

The Portfolio of Investments following this report shows the size of the Portfolio’s positions at period-end.

| | | | |

| THE TARGET PORTFOLIO TRUST | | | 27 | |

Strategy and Performance Overview (continued)

investors’ views of the prospects of a solution to euro-zone imbalances and debt. Between mid-March and the end of May, there was a substantial decline, but the overall return for the period was moderately positive, even for the euro zone. Japan, on the other hand, finished the period slightly in the red, as it continued to suffer from the impact of the tsunami as well as from anemic economic growth. Overall, the healthcare and consumer staples sectors performed better than average, while technology and telecommunications services underperformed, and neither growth nor value investing styles performed significantly better than the other.

| | • | | The Portfolio outperformed the Index due to its greater or lesser exposure compared with the Index to particular countries, including positions in several not included in the Index at all, and to its sector weightings. It underweighted Japanese stocks and selected well among European markets, being overweight compared with the Index in Germany and Denmark and consistently underweight in Greece, Spain, and Portugal. Allocations to emerging markets countries also contributed, despite the mixed performance of the group. Positions in both China and Mexico were particularly beneficial. Favorable sector allocation decisions included underweights in the materials and utilities sectors and an overweight in healthcare. |

| | • | | Both LSV’s and Thornburg’s portions of the Portfolio outperformed the Index. LSV outperformed largely due to favorable stock selection in Japan and the United Kingdom. Its quantitative model led to positions in a significant number of outperforming stocks not represented within the Index, and away from many of its worst performing constituents, particularly several poor-performing Japanese technology and consumer discretionary stocks. The Thornburg portion outperformed on the strength of its country and sector allocations, particularly an average underweight in Japan of more than 10% compared with the Index weighting. It also benefited from allocations to China and Mexico and from an overweight in Germany. Its decision to underweight the materials, telecommunications, and utilities sectors proved profitable, while its overweight in the information technology sector was the largest detractor from its relative return. Thornburg’s selection of individual stocks, after accounting for its country and sector weightings, detracted broadly from its performance. |

The Portfolio of Investments following this report shows the size of the Portfolio’s positions at period-end.

| | |

| 28 | | THE TARGET PORTFOLIO TRUST |

Total Return Bond Portfolio

The Total Return Bond Portfolio’s Class T shares gained 8.01% for the 12-month reporting period ended October 31, 2012, outperforming the 5.25% gain of the Barclays U.S. Aggregate Bond Index (the Index) and the 7.25% gain of the Lipper Intermediate Investment-Grade Debt Funds Average. However, the Portfolio’s Class T shares lagged the 10.07% advance of the Lipper Corporate Debt BBB-Rated Funds Average. Pacific Investment Management Company LLC (PIMCO) manages the Portfolio.

Market volatility intensified during the one-year reporting period, exacerbated by a number of diverse and interrelated events. In response, investors oscillated between being either “risk on” or “risk off,” further amplifying overall market volatility.

| | • | | Several positive developments regarding the housing market in the U.S. and better-than-expected automobile and manufacturing outputs pointed to signs of modest improvement for the U.S. economy. |

| | • | | That said, concerns remained regarding the nation’s high level of unemployment and the looming fiscal cliff in January 2013, when several critical tax measures are set to expire and sequestration—or forced, across-the-board spending cuts—would take effect in the absence of a Congressional agreement to the contrary. |

| | • | | As anticipated by many investors, the Federal Reserve (the Fed) implemented a third round of quantitative easing (QE3) in September to offset weak employment data and below-target inflation. In this new bond-buying program, the Fed announced it would purchase an additional $40 billion of agency mortgage-backed securities per month. |

| | • | | The European sovereign debt crisis remained a major driver of investor sentiment during the period. Speculation around the risk of a Greek exit from the euro increased concerns over the potential for systemic contagion to the rest of the region, the global banking system, and the global economy. As a result, the European Central Bank initiated a number of efforts to stabilize the European banking system, including a long-term debt refinancing operation, lending over one trillion euros to European banks, and Outright Monetary Transactions (OMT), which entail unlimited, but conditional, purchases of euro zone government bonds. |

The Portfolio of Investments following this report shows the size of the Portfolio’s positions at period-end.

| | | | |

| THE TARGET PORTFOLIO TRUST | | | 29 | |

Strategy and Performance Overview (continued)

| | • | | These measures led to a decline in the yields of Italian and Spanish sovereign bonds. However, European countries continued to struggle with implementing the necessary austerity measures and continued to face weak growth. |

The following is a summary of the main factors that contributed to and detracted from the performance of the Portfolio relative to its benchmark for the fiscal year:

| | • | | Tactical duration positioning in the U.S. added to returns for most of the year. Duration measures a fund’s sensitivity to changes in the level of interest rates. |

| | • | | However, these benefits were more than offset by the Portfolio’s underweight to the long end of the yield curve, as the rates declined more on the long-end versus shorter maturities. |

| | • | | An overweight to agency mortgages during most of the year bolstered relative performance, as the mortgage sector outperformed like-duration Treasuries. Additionally, modest exposure to non-agency mortgages added to returns, as prices rose in this sector. |

| | • | | Within the credit sector, a focus on financials lifted returns, as the sector outperformed the broader corporate sector. |

| | • | | Modest duration exposure in non-U.S., developed countries, particularly Australia, bolstered performance, as yields fell in these countries. |

| | • | | Exposure to emerging markets through local rates in Brazil, implemented via interest rate swaps, aided results, as rates fell in that country. |

| | • | | An allocation to Build America Bonds (BABs) also benefited the Portfolio’s results, as investors continued to seek higher-yielding assets, which led these securities to outperform. |

| | • | | Modest currency exposure to emerging markets, particularly the Indian rupee, was slightly negative for performance, as most of these currencies depreciated versus the U.S. dollar. |

The Portfolio of Investments following this report shows the size of the Portfolio’s positions at period-end.

| | |

| 30 | | THE TARGET PORTFOLIO TRUST |

Intermediate-Term Bond Portfolio

The Intermediate-Term Bond Portfolio’s Class T shares gained 8.13% for the 12-month reporting period ended October 31, 2012, outperforming the 4.24% gain of the Barclays Intermediate Government/Credit Index (the Index). The Portfolio’s Class T shares also outperformed the 7.25% gain of the Lipper Intermediate Investment-Grade Debt Funds Average. Pacific Investment Management Company LLC (PIMCO) manages the Portfolio.

Market volatility intensified during the one-year reporting period, exacerbated by a number of diverse and interrelated events. In response, investors oscillated between being either “risk on” or “risk off,” further amplifying overall market volatility.

| | • | | Several positive developments regarding the housing market in the U.S. and better-than-expected automobile and manufacturing outputs pointed to signs of modest improvement for the U.S. economy. |

| | • | | That said, concerns remained regarding the nation’s high level of unemployment and the looming fiscal cliff in January 2013, when several critical tax measures are set to expire and sequestration—or forced, across-the-board spending cuts—would take effect in the absence of a Congressional agreement to the contrary. |

| | • | | As anticipated by many investors, the Federal Reserve (the Fed) implemented a third round of quantitative easing (QE3) in September to offset weak employment data and below-target inflation. In this new bond-buying program, the Fed announced it would purchase an additional $40 billion of agency mortgage-backed securities per month. |

| | • | | The European sovereign debt crisis remained a major driver of investor sentiment during the period. Speculation around the risk of a Greek exit from the euro increased concerns over the potential for systemic contagion to the rest of the region, the global banking system, and the global economy. As a result, the European Central Bank initiated a number of efforts to stabilize the European banking system, including a long-term debt refinancing operation, lending over one trillion euros to European banks, and Outright Monetary Transactions (OMT), which entail unlimited, but conditional, purchases of euro zone government bonds. |

The Portfolio of Investments following this report shows the size of the Portfolio’s positions at period-end.

| | | | |

| THE TARGET PORTFOLIO TRUST | | | 31 | |

Strategy and Performance Overview (continued)

| | • | | These measures led to a decline in the yields of Italian and Spanish sovereign bonds. However, European countries continued to struggle with implementing the necessary austerity measures and continued to face weak growth. |

The following is a summary of the main factors that contributed to and detracted from the performance of the Portfolio relative to its benchmark for the fiscal year:

| | • | | Tactical duration positioning in the U.S. added to returns, as 10-year Treasury yields declined 42 basis points during the year. Duration measures a fund’s sensitivity to changes in the level of interest rates. |

| | • | | Modest exposure to agency mortgages during the year was positive for performance, as the mortgage sector outperformed like-duration Treasuries. Additionally, holdings of non-agency mortgages also added to returns, as prices rose in this sector. |

| | • | | Within the credit sector, a focus on financials lifted returns, as the sector outperformed the broader corporate sector. |

| | • | | Modest duration exposure in non-U.S., developed countries, particularly Australia, bolstered performance, as yields fell in these countries. |

| | • | | Exposure to emerging markets through local rates in Brazil, implemented via interest rate swaps, aided results, as rates fell in that country. |

| | • | | An allocation to Build America Bonds (BABs) added to returns, as investors continued to seek higher-yielding assets, which led these securities to outperform. |

| | • | | Modest currency exposure to emerging markets, particularly the Indian rupee, was negative for performance, as most of these currencies depreciated versus the U.S. dollar. |

The Portfolio of Investments following this report shows the size of the Portfolio’s positions at period-end.

| | |

| 32 | | THE TARGET PORTFOLIO TRUST |

Mortgage Backed Securities Portfolio

The Mortgage Backed Securities Portfolio’s Class T shares gained 4.64% for the 12-month reporting period ended October 31, 2012, outperforming the 3.54% gain of the Barclays U.S. Mortgage Backed Securities Index (the Index). The Portfolio modestly underperformed the 4.86% return of the Lipper U.S. Mortgage Funds Average. The Portfolio is managed by Wellington Management Company, LLP (Wellington Management).

Mortgage rates declined during the period and were flirting with all-time lows by the end of October 2012. Falling rates gave rise to concerns that a large volume of mortgage refinancings could trigger a wave of prepayments on mortgage-backed securities. However, although refinancing activity was healthy, particularly in the second half of the period, prepayments were slower than expected, as the availability of mortgage credit remained constrained and underwriting standards remained high, making it difficult for homeowners to refinance their loans.

An important driver of the Portfolio’s outperformance versus the Index was exposure to collateralized mortgage obligations (CMOs), which are created from pools of mortgage-backed securities of federal agencies and government-sponsored entities. Within this asset class, the managers particularly favored interest only (IO) and inverse IO bonds. CMOs are not included in the index.

| | • | | As their name implies, IO bonds do not receive principal payments from the underlying mortgages. Inverse IO securities have coupon payments that move inversely to a short-term floating rate. Reduced prepayments and low interest rate volatility continued to benefit inverse IOs, making them one of the primary contributors to performance versus the Index. |

| | • | | Strong security selection within mortgage pass-through securities also contributed to relative performance. In particular, the Portfolio benefited from its selection within the 30-year bonds of Ginnie Mae. A “barbell” coupon positioning, consisting of overweighting lower and higher coupons and underweighting the middle of the coupon stack, bolstered relative performance and maintained the Portfolio’s focus on securities that were least likely to prepay. |

| | • | | Exposure to non-agency residential mortgage-backed securities (RMBS) was another factor aiding relative results. The Portfolio was positioned in bonds |

The Portfolio of Investments following this report shows the size of the Portfolio’s positions at period-end.

| | | | |

| THE TARGET PORTFOLIO TRUST | | | 33 | |

Strategy and Performance Overview (continued)

| | where the Portfolio managers believed market prices did not reflect the fundamental value of the assets. Non-agency RMBS rallied during the period amid strong demand driven by improved credit conditions and negative net supply. Although the sector approached fair value, there were still attractive opportunities, in the Portfolio managers’ view. Long-term technical factors were also supportive, with approximately $125-$175 billion in annual net paydowns of the underlying mortgages. Based on current valuations and stable to improving fundamentals, the Portfolio managers believed non-agency RMBS remained well-positioned to benefit from even a modest housing recovery. |

| | • | | The Portfolio further benefited from an allocation to commercial mortgage-backed securities (CMBS). CMBS outperformed during the period, boosted by limited supply and strong investor demand. |

| | • | | While security selection within Ginnie Mae securities lifted the Portfolio’s performance versus the Index, an overweight allocation to this sector detracted. |

| | • | | The Portfolio’s tilt toward Ginnie Maes over conventional mortgage-backed securities was based on the Portfolio managers’ belief that these securities would outperform due to demand from overseas investors, and the fact that Ginnie Maes, unlike conventionals, are backed by the full faith and credit of the U.S. government. That said, while the Portfolio remained overweight Ginnie Maes at period end, the Portfolio managers reduced exposure here following this group’s strong performance in the last year. |

| | • | | Additionally, exposure to Fannie Mae multifamily issues detracted, and a stake in Fannie Mae Delegated Underwriting and Servicing (DUS) bonds had a slightly negative impact. |

| | • | | During the reporting period, the Portfolio used interest rate swaps and interest rate futures to tactically manage exposure to interest rate risk. These strategies contributed positively to the Portfolio’s performance versus the Index. |

The Portfolio of Investments following this report shows the size of the Portfolio’s positions at period-end.

| | |

| 34 | | THE TARGET PORTFOLIO TRUST |

Fees and Expenses (Unaudited)

As a shareholder of the Trust, you incur two types of costs: (1) transaction costs, including sales charges (loads) on purchase payments and redemptions, as applicable, and (2) ongoing costs, including management fees, and other Trust expenses, as applicable. This example is intended to help you understand your ongoing costs (in dollars) of investing in the Trust and to compare these costs with the ongoing costs of investing in other mutual funds.

The example is based on an investment of $1,000 invested on May 1, 2012, at the beginning of the period, and held through the six-month period ended October 31, 2012. The example is for illustrative purposes only; you should consult the Prospectus for information on initial and subsequent minimum investment requirements.

The Trust’s transfer agent may charge additional fees to holders of certain accounts that are not included in the expenses shown in the table on the following pages. These fees apply to individual retirement accounts (IRAs) and Section 403(b) accounts. As of the close of the six-month period covered by the table, IRA fees included an annual maintenance fee of $15 per account (subject to a maximum annual maintenance fee of $25 for all accounts held by the same shareholder). Section 403(b) accounts are charged an annual $25 fiduciary maintenance fee. Some of the fees may vary in amount, or may be waived, based on your total account balance or the number of Prudential Investments funds, including the Trust, that you own. You should consider the additional fees that were charged to your Trust account over the six-month period when you estimate the total ongoing expenses paid over the period and the impact of these fees on your ending account value, as these additional expenses are not reflected in the information provided in the expense table. Additional fees have the effect of reducing investment returns.

Actual Expenses

The first line for each share class in the table on the following pages provides information about actual account values and actual expenses. You may use the information on this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value ÷ $1,000 = 8.6), then multiply the result by the number on the first line under the heading “Expenses Paid During the Six-Month Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The second line for each share class in the table on the following pages provides information about hypothetical account values and hypothetical expenses based on the Trust’s actual expense ratio and an assumed rate of return of 5% per year before

| | | | |