| OMB APPROVAL |

OMB Number: 3235-0570 Expires: March 31, 2017 Estimated average burden hours per response: 20.6 |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

| Investment Company Act file number | 811-07148 | |

| Schwartz Investment Trust |

| (Exact name of registrant as specified in charter) |

| 801 W. Ann Arbor Trail, Suite 244 Plymouth, Michigan | 48170 |

| (Address of principal executive offices) | (Zip code) |

George P. Schwartz

| Schwartz Investment Counsel, Inc. 801 W. Ann Arbor Trail, Plymouth, MI 48170 |

| (Name and address of agent for service) |

| Registrant's telephone number, including area code: | (248) 644-8500 | |

| Date of fiscal year end: | December 31 | |

| | | |

| Date of reporting period: | December 31, 2016 | |

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget ("OMB") control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to the Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

| Item 1. | Reports to Stockholders. |

Schwartz Value Focused Fund

Shareholder Services c/o Ultimus Fund Solutions, LLC P.O. Box 46707 Cincinnati, OH 45246 (888) 726-0753 | | Investment Adviser Schwartz Investment Counsel, Inc.

801 W. Ann Arbor Trail Suite 244 Plymouth, MI 48170 |

Dear Fellow Shareowner:

2016 was a good year for the Schwartz Value Focused Fund (the “Fund”) with a total return of 18.13%, compared to 13.03% for the S&P 1500 Index and 12.05% for the Russell 1000 Index. The Fund’s outperformance can be attributed mainly to 12 portfolio holdings which each appreciated more than 35% during the year. These issues were from a variety of industry sectors including mining, energy, industrial, financial, retail, and technology. The Fund’s best performing stocks were commodity and industrial related. Pan American Silver Corporation (+133%) and Barrick Gold Corporation (+118%) posted strong gains as their share prices rebounded from 2015’s depressed levels, owing to gold and silver prices that rose sharply in the first half of the year. Energy stocks bottomed early in the year and rebounded concomitantly with the rise in oil prices. At year end, the price of WTI crude oil breached $50/barrel, up 45% for the year and up nearly 100% from the February low. Holdings in the energy sector that produced substantial gains included Texas Pacific Land Trust (+85%), Devon Energy Corporation (+45%), and Apache Corporation (+45%). Industrial stocks benefitted from improving economic growth in the second half and to a lesser extent from rising oil and natural gas prices. Notable outperformers in the industrial sector included Colfax Corporation (+71%), MSC Industrial Direct Company, Inc. (+67%), Donaldson Company, Inc. (+39%), and Eaton Corporation plc (+35%). The Fund’s five best performing stocks in 2016 were:

Company | Industry | 2016 Performance |

Pan American Silver Corporation | Metals & Mining | +132.96% |

Barrick Gold Corp. | Metals & Mining | +118.07% |

Texas Pacific Land Trust | Oil & Gas Royalties/Real Estate | +84.98% |

Colfax Corporation | Industrial Machinery | +71.21% |

MSC Industrial Direct Co., Inc. | Industrial Equipment | +66.84% |

On the negative side, the Fund’s worst performing stock during 2016 was Liberty Interactive Corporation, which owns and operates QVC Group, a multinational corporation that sells consumer goods through its television network and online. The share price fell after the company experienced a U.S. sales decline due to weakness in its fashion business and hair care division. Due to QVC’s loyal customer base and strong viewership, we view this slowdown as temporary. The Fund’s five worst performing stocks in 2016 were:

Company | Industry | 2016 Performance |

Liberty Interactive Corporation | Consumer - Retail | -26.49% |

ServiceMaster Global Holdings | Business Services | -6.41% |

Moody’s Corporation | Business & Financial Services | -6.20% |

Liberty Global | Cable TV & Broadband | -4.07% |

ANSYS, Inc. | Software | -0.01% |

1

During the second half of 2016, six stocks were sold from the portfolio, having reached our estimate of intrinsic value: Citigroup, Inc. (financial services), Cubic Corporation (transportation & defense), Emerson Electric Co. (industrial electrical equipment), Exxon Mobil Corporation (integrated oil & gas), HP, Inc. (technology), and United Technologies Corporation (industrial products). New positions were established in four companies that meet our value investing criteria: AMERCO, AMETEK, Inc., Cognizant Technology Solutions Corp., and Moody’s Corporation. AMERCO owns the U-Haul self-moving and storage franchise. With a dominant market position, the company has an impressive track record of increasing earnings, and has ample growth opportunities. AMETEK manufactures and sells electronic instruments and electromechanical devices worldwide. The company generates high profit margins, strong free cash flow, and a high return on invested capital (ROIC). Cognizant Technology Solutions provides information technology consulting services worldwide. The business is highly profitable and generates strong free cash flow with a high ROIC. Moody’s provides credit ratings, research, and analysis of debt instruments and other securities. As such, the company enjoys a strong business franchise that produces high profit margins and loads of cash, which is used primarily for dividends and share repurchases.

2017 could be another good year for stock investors. We are confident that the new Trump Administration will be more hospitable to corporate America than the Obama Administration. President Trump’s pro-growth agenda of lower tax rates – corporate and personal, a less punishing regulatory environment, and a generally less intrusive government should lead to greater business and consumer confidence, more economic activity, and ultimately higher corporate profits.

As always, we’ll be working tirelessly to invest in well-managed, high-quality companies that are selling at a discount to our estimate of intrinsic value.

No realized capital gains or income distributions were paid at year end. The net asset value of the Fund ended the year at $25.02 per share.

Thank you for being a shareholder in the Schwartz Value Focused Fund.

|

|

Timothy S. Schwartz, CFA | George P. Schwartz, CFA |

Lead Portfolio Manager | Co-Portfolio Manager |

2

SCHWARTZ VALUE FOCUSED FUND

PERFORMANCE

(Unaudited)

Comparison of the Change in Value of a $10,000 Investment

in Schwartz Value Focused Fund, the S&P 1500 Index**

and the Russell 1000 Index

(a) | The returns shown do not reflect the deduction of taxes a shareholder would pay on Fund distributions or the redemption of Fund shares. |

Net Expense ratio as of 12-31-15 (as disclosed in May 1, 2016 prospectus) | 1.25%* |

Net Expense ratio for the year ended 12-31-16 | 1.25% |

* | Includes Acquired Fund Fees and Expenses. |

| | |

** | Effective January 1, 2017, the S&P 1500 Index will be the Fund’s primary benchmark instead of the Russell 1000 Index. |

This report is for the information of shareholders, but it may also be used as sales literature when preceded or accompanied by a current prospectus, which gives details about charges, expenses, investment objectives and operating policies of the Fund. The Fund is distributed by Ultimus Fund Distributors, LLC.

3

SCHWARTZ VALUE FOCUSED FUND

ANNUAL TOTAL RATES OF RETURN

COMPARISON WITH MAJOR INDICES (Unaudited)

| SCHWARTZ

VALUE

FOCUSED

FUND(a) | S&P 1500

INDEX(b) | RUSSELL

1000

INDEX | NASDAQ

COMPOSITE(c) | VALUE

LINE

COMPOSITE(d) | S&P 500

INDEX |

1984 | 11.1% | N/A | 4.8% | -11.2% | -8.4% | 6.1% |

1985 | 21.7% | N/A | 32.3% | 31.4% | 20.7% | 31.6% |

1986 | 16.4% | N/A | 17.9% | 7.4% | 5.0% | 18.7% |

1987 | -0.6% | N/A | 2.9% | -5.3% | -10.6% | 5.3% |

1988 | 23.1% | N/A | 17.3% | 15.4% | 15.4% | 16.8% |

1989 | 8.3% | N/A | 30.4% | 19.3% | 11.2% | 31.6% |

1990 | -5.3% | N/A | -4.2% | -17.8% | -24.3% | -3.2% |

1991 | 32.0% | N/A | 33.0% | 56.8% | 27.2% | 30.4% |

1992 | 22.7% | N/A | 8.9% | 15.5% | 7.0% | 7.6% |

1993 | 20.5% | N/A | 10.2% | 14.7% | 10.7% | 10.1% |

1994 | -6.8% | N/A | 0.4% | -3.2% | -6.0% | 1.3% |

1995 | 16.9% | 36.5% | 37.8% | 39.9% | 19.3% | 37.5% |

1996 | 18.3% | 22.4% | 22.5% | 22.7% | 13.4% | 22.9% |

1997 | 28.0% | 32.9% | 32.9% | 21.6% | 21.1% | 33.4% |

1998 | -10.4% | 26.4% | 27.0% | 39.6% | -3.8% | 28.6% |

1999 | -2.5% | 20.3% | 20.9% | 85.6% | -1.4% | 21.0% |

2000 | 9.3% | -7.0% | -7.8% | -39.3% | -8.7% | -9.1% |

2001 | 28.1% | -10.6% | -12.5% | -21.0% | -6.1% | -11.9% |

2002 | -14.9% | -21.3% | -21.7% | -31.5% | -28.6% | -22.1% |

2003 | 39.3% | 29.6% | 29.9% | 50.0% | 37.4% | 28.7% |

2004 | 22.6% | 11.8% | 11.4% | 8.6% | 11.5% | 10.9% |

2005 | 3.8% | 5.7% | 6.3% | 1.4% | 2.0% | 4.9% |

2006 | 14.3% | 15.3% | 15.5% | 9.5% | 11.0% | 15.8% |

2007 | -11.1% | 5.5% | 5.8% | 10.6% | -3.8% | 5.5% |

2008 | -35.9% | -36.7% | -37.6% | -40.0% | -48.7% | -37.0% |

2009 | 34.8% | 27.2% | 28.4% | 45.3% | 36.8% | 26.5% |

2010 | 12.0% | 16.4% | 16.1% | 18.0% | 20.5% | 15.1% |

2011 | 5.6% | 1.7% | 1.5% | -0.8% | -11.4% | 2.1% |

2012 | 5.4% | 16.2% | 16.4% | 17.5% | 9.5% | 16.0% |

2013 | 24.7% | 32.8% | 33.1% | 40.1% | 35.5% | 32.4% |

2014 | -4.7% | 13.1% | 13.2% | 14.8% | 2.7% | 13.7% |

2015 | -15.5% | 1.0% | 0.9% | 7.0% | -11.2% | 1.4% |

2016 | 18.1% | 13.0% | 12.1% | 8.9% | 13.5% | 12.0% |

(a) | Schwartz Value Focused Fund’s performance combines the performance of the Fund since its commencement of operations as a registered investment company on July 20, 1993, and the performance of RCM Partners Limited Partnership for periods prior thereto. |

| | |

(b) | Inception date of the S&P 1500 Index is December 30, 1994. |

| | |

(c) | Excluding dividends for the years ended 1984-2006. Effective 2007, the returns include dividends. |

| | |

(d) | Excluding dividends. |

4

SCHWARTZ VALUE FOCUSED FUND

AVERAGE ANNUAL TOTAL RETURNS

As of December 31, 2016 (Unaudited)

| SCHWARTZ

VALUE

FOCUSED

FUND(a) | S&P 1500

INDEX(b) | RUSSELL

1000

INDEX | NASDAQ

COMPOSITE(c) | VALUE

LINE

COMPOSITE(d) | S&P 500

INDEX |

3 Years | -1.7% | 8.9% | 8.6% | 10.1% | 1.2% | 8.9% |

5 Years | 4.6% | 14.8% | 14.7% | 17.1% | 9.0% | 14.7% |

10 Years | 1.3% | 7.2% | 7.1% | 8.3% | 1.0% | 7.0% |

15 Years | 4.6% | 7.1% | 7.0% | 7.0% | 2.1% | 6.7% |

33 Years | 8.6% | N/A | 10.9% | 9.4% | 2.9% | 10.9% |

(a) | Schwartz Value Focused Fund’s performance combines the performance of the Fund since its commencement of operations as a registered investment company on July 20, 1993, and the performance of RCM Partners Limited Partnership for periods prior thereto. |

| | |

(b) | Inception date of the S&P 1500 Index is December 30, 1994. |

| | |

(c) | Excluding dividends for the years ended 1984-2006. Effective 2007, the returns include dividends. |

| | |

(d) | Excluding dividends. |

5

SCHWARTZ VALUE FOCUSED FUND

TEN LARGEST EQUITY HOLDINGS

December 31, 2016 (Unaudited)

Shares | | Security Description | | Market

Value | | | % of

Net Assets | |

| | 180,000 | | Unico American Corporation | | $ | 1,935,000 | | | | 9.2 | % |

| | 50,000 | | ARRIS International plc | | | 1,506,500 | | | | 7.2 | % |

| | 3,500 | | Texas Pacific Land Trust | | | 1,038,695 | | | | 4.9 | % |

| | 4 | | Berkshire Hathaway, Inc. - Class A | | | 976,484 | | | | 4.7 | % |

| | 25,000 | | Colfax Corporation | | | 898,250 | | | | 4.3 | % |

| | 40,000 | | Liberty Interactive Corporation QVC Group - Series A | | | 799,200 | | | | 3.8 | % |

| | 50,000 | | Goldcorp, Inc. | | | 680,000 | | | | 3.2 | % |

| | 1,300 | | Graham Holdings Company - Class B | | | 665,535 | | | | 3.2 | % |

| | 9,000 | | Baker Hughes Incorporated | | | 584,730 | | | | 2.8 | % |

| | 12,000 | | AMETEK, Inc. | | | 583,200 | | | | 2.8 | % |

ASSET ALLOCATION (Unaudited)

Sector | % of

Net Assets |

Consumer Discretionary | 17.7% |

Energy | 10.3% |

Financials | 23.0% |

Industrials | 16.8% |

Information Technology | 14.0% |

Materials | 8.2% |

Warrants | 1.4% |

Open-End Funds | 0.1% |

Money Market Funds, Liabilities in Excess of Other Assets | 8.5% |

| | 100.0% |

6

SCHWARTZ VALUE FOCUSED FUND

SCHEDULE OF INVESTMENTS

December 31, 2016

COMMON STOCKS — 90.0% | | Shares | | | Market Value | |

Consumer Discretionary — 17.7% | | | | | | |

Diversified Consumer Services — 4.1% | | | | | | |

Graham Holdings Company - Class B | | | 1,300 | | | $ | 665,535 | |

ServiceMaster Global Holdings, Inc. * | | | 5,000 | | | | 188,350 | |

| | | | | | | | 853,885 | |

Household Durables — 1.6% | | | | | | | | |

Garmin Ltd. | | | 7,000 | | | | 339,430 | |

| | | | | | | | | |

Internet & Direct Marketing Retail — 3.8% | | | | | | | | |

Liberty Interactive Corporation QVC Group - Series A * | | | 40,000 | | | | 799,200 | |

| | | | | | | | | |

Media — 4.8% | | | | | | | | |

Discovery Communications, Inc. - Series A * | | | 20,000 | | | | 548,200 | |

Liberty Global plc - Series C * | | | 15,000 | | | | 445,500 | |

| | | | | | | | 993,700 | |

Multi-Line Retail — 0.9% | | | | | | | | |

Nordstrom, Inc. | | | 4,000 | | | | 191,720 | |

| | | | | | | | | |

Specialty Retail — 2.5% | | | | | | | | |

TJX Companies, Inc. (The) | | | 7,000 | | | | 525,910 | |

| | | | | | | | | |

Energy — 10.3% | | | | | | | | |

Energy Equipment & Services — 4.8% | | | | | | | | |

Baker Hughes Incorporated | | | 9,000 | | | | 584,730 | |

Schlumberger Limited | | | 5,000 | | | | 419,750 | |

| | | | | | | | 1,004,480 | |

Oil, Gas & Consumable Fuels — 5.5% | | | | | | | | |

Apache Corporation | | | 6,000 | | | | 380,820 | |

Devon Energy Corporation | | | 7,000 | | | | 319,690 | |

Noble Energy, Inc. | | | 12,000 | | | | 456,720 | |

| | | | | | | | 1,157,230 | |

Financials — 23.0% | | | | | | | | |

Capital Markets — 2.2% | | | | | | | | |

Moody's Corporation | | | 5,000 | | | | 471,350 | |

| | | | | | | | | |

Diversified Financial Services — 6.9% | | | | | | | | |

MasterCard, Inc. - Class A | | | 4,000 | | | | 413,000 | |

Texas Pacific Land Trust | | | 3,500 | | | | 1,038,695 | |

| | | | | | | | 1,451,695 | |

Insurance — 13.9% | | | | | | | | |

Berkshire Hathaway, Inc. - Class A * | | | 4 | | | | 976,484 | |

Unico American Corporation * | | | 180,000 | | | | 1,935,000 | |

| | | | | | | | 2,911,484 | |

7

SCHWARTZ VALUE FOCUSED FUND

SCHEDULE OF INVESTMENTS

(Continued)

COMMON STOCKS — 90.0% (Continued) | | Shares | | | Market Value | |

Industrials — 16.8% | | | | | | |

Electrical Equipment — 4.4% | | | | | | |

AMETEK, Inc. | | | 12,000 | | | $ | 583,200 | |

Eaton Corporation plc | | | 5,000 | | | | 335,450 | |

| | | | | | | | 918,650 | |

Machinery — 6.3% | | | | | | | | |

Colfax Corporation * | | | 25,000 | | | | 898,250 | |

Donaldson Company, Inc. | | | 10,000 | | | | 420,800 | |

| | | | | | | | 1,319,050 | |

Road & Rail — 2.6% | | | | | | | | |

AMERCO | | | 1,500 | | | | 554,385 | |

| | | | | | | | | |

Trading Companies & Distributors — 3.5% | | | | | | | | |

MSC Industrial Direct Company, Inc. - Class A | | | 3,000 | | | | 277,170 | |

W.W. Grainger, Inc. | | | 2,000 | | | | 464,500 | |

| | | | | | | | 741,670 | |

Information Technology — 14.0% | | | | | | | | |

Communications Equipment — 7.2% | | | | | | | | |

ARRIS International plc * | | | 50,000 | | | | 1,506,500 | |

| | | | | | | | | |

Electronic Equipment, Instruments & Components — 4.6% | | | | | | | | |

Arrow Electronics, Inc. * | | | 7,000 | | | | 499,100 | |

Avnet, Inc. | | | 10,000 | | | | 476,100 | |

| | | | | | | | 975,200 | |

IT Services — 1.3% | | | | | | | | |

Cognizant Technology Solutions Corporation - Class A * | | | 5,000 | | | | 280,150 | |

| | | | | | | | | |

Software — 0.9% | | | | | | | | |

ANSYS, Inc. * | | | 2,000 | | | | 184,980 | |

| | | | | | | | | |

Materials — 8.2% | | | | | | | | |

Chemicals — 0.9% | | | | | | | | |

Praxair, Inc. | | | 1,700 | | | | 199,223 | |

| | | | | | | | | |

Metals & Mining — 7.3% | | | | | | | | |

Barrick Gold Corporation | | | 20,000 | | | | 319,600 | |

Goldcorp, Inc. | | | 50,000 | | | | 680,000 | |

Pan American Silver Corporation | | | 35,000 | | | | 527,450 | |

| | | | | | | | 1,527,050 | |

| | | | | | | | | |

Total Common Stocks (Cost $14,713,910) | | | | | | $ | 18,906,942 | |

8

SCHWARTZ VALUE FOCUSED FUND

SCHEDULE OF INVESTMENTS

(Continued)

WARRANTS — 1.4% | | Shares | | | Market Value | |

Financials — 1.4% | | | | | | |

Banks — 1.4% | | | | | | |

PNC Financial Services Group, Inc. (The), expires 12/31/18 * (Cost $109,308) | | | 6,000 | | | $ | 297,000 | |

OPEN-END FUNDS — 0.1% | | Shares | | | Market Value | |

Sequoia Fund, Inc. * (Cost $11,397) | | | 81 | | | $ | 13,008 | |

MONEY MARKET FUNDS — 8.6% | | Shares | | | Market Value | |

Federated Government Obligations Tax-Managed Fund - Institutional Shares, 0.35% (a) | | | 980,340 | | | $ | 980,340 | |

Federated Treasury Obligations Fund - Institutional Shares, 0.36% (a) | | | 837,830 | | | | 837,830 | |

Total Money Market Funds (Cost $1,818,170) | | | | | | $ | 1,818,170 | |

| | | | | | | | | |

Total Investments at Market Value — 100.1% (Cost $16,652,785) | | | | | | $ | 21,035,120 | |

| | | | | | | | | |

Liabilities in Excess of Other Assets — (0.1%) | | | | | | | (23,266 | ) |

| | | | | | | | | |

Net Assets — 100.0% | | | | | | $ | 21,011,854 | |

* | Non-income producing security. |

| | |

(a) | The rate shown is the 7-day effective yield as of December 31, 2016. |

| | |

See accompanying notes to financial statements. |

9

SCHWARTZ VALUE FOCUSED FUND

STATEMENT OF ASSETS AND LIABILITIES

December 31, 2016

ASSETS | | | |

Investments, at market value (cost of $16,652,785) (Note 1) | | $ | 21,035,120 | |

Cash | | | 3,570 | |

Dividends receivable | | | 2,928 | |

Other assets | | | 6,134 | |

TOTAL ASSETS | | | 21,047,752 | |

| | | | | |

LIABILITIES | | | | |

Payable to Adviser (Note 2) | | | 21,564 | |

Payable to administrator (Note 2) | | | 3,000 | |

Other accrued expenses | | | 11,334 | |

TOTAL LIABILITIES | | | 35,898 | |

| | | | | |

NET ASSETS | | $ | 21,011,854 | |

| | | | | |

NET ASSETS CONSIST OF: | | | | |

Paid-in capital | | $ | 17,138,776 | |

Accumulated net realized losses from security transactions | | | (509,257 | ) |

Net unrealized appreciation on investments | | | 4,382,335 | |

NET ASSETS | | $ | 21,011,854 | |

| | | | | |

Shares of beneficial interest outstanding (unlimited number of shares authorized, no par value) | | | 839,765 | |

| | | | | |

Net asset value, offering price and redemption price per share (Note 1) | | $ | 25.02 | |

See notes to financial statements. |

10

SCHWARTZ VALUE FOCUSED FUND

STATEMENT OF OPERATIONS

For the Year Ended December 31, 2016

INVESTMENT INCOME | | | |

Dividends (Net of foreign tax of $2,074) | | $ | 173,694 | |

| | | | | |

EXPENSES | | | | |

Investment advisory fees (Note 2) | | | 183,507 | |

Trustees’ fees and expenses (Note 2) | | | 49,892 | |

Administration, accounting and transfer agent fees (Note 2) | | | 36,000 | |

Legal and audit fees | | | 34,941 | |

Registration and filing fees | | | 14,337 | |

Postage and supplies | | | 8,783 | |

Custodian and bank service fees | | | 6,391 | |

Printing of shareholder reports | | | 3,399 | |

Insurance expense | | | 1,187 | |

Compliance service fees and expenses (Note 2) | | | 672 | |

Other expenses | | | 9,216 | |

TOTAL EXPENSES | | | 348,325 | |

Less fee reductions by the Adviser (Note 2) | | | (106,868 | ) |

NET EXPENSES | | | 241,457 | |

| | | | | |

NET INVESTMENT LOSS | | | (67,763 | ) |

| | | | | |

REALIZED AND UNREALIZED GAINS ON INVESTMENTS | | | | |

Net realized gains from security transactions | | | 29,217 | |

Net change in unrealized appreciation (depreciation) on investments | | | 3,288,843 | |

NET REALIZED AND UNREALIZED GAINS ON INVESTMENTS | | | 3,318,060 | |

| | | | | |

NET INCREASE IN NET ASSETS RESULTING FROM OPERATIONS | | $ | 3,250,297 | |

See notes to financial statements. |

11

SCHWARTZ VALUE FOCUSED FUND

STATEMENTS OF CHANGES IN NET ASSETS

| | Year Ended December 31, 2016 | | | Year Ended December 31, 2015 | |

FROM OPERATIONS | | | | | | |

Net investment loss | | $ | (67,763 | ) | | $ | (94,159 | ) |

Net realized gains (losses) from security transactions | | | 29,217 | | | | (538,474 | ) |

Net change in unrealized appreciation (depreciation) on investments | | | 3,288,843 | | | | (2,972,967 | ) |

Net increase (decrease) in net assets resulting from operations | | | 3,250,297 | | | | (3,605,600 | ) |

| | | | | | | | | |

FROM CAPITAL SHARE TRANSACTIONS | | | | | | | | |

Proceeds from shares sold | | | 1,533,951 | | | | 1,244,396 | |

Payments for shares redeemed | | | (2,544,502 | ) | | | (6,995,249 | ) |

Net decrease in net assets from capital share transactions | | | (1,010,551 | ) | | | (5,750,853 | ) |

| | | | | | | | | |

TOTAL INCREASE (DECREASE) IN NET ASSETS | | | 2,239,746 | | | | (9,356,453 | ) |

| | | | | | | | | |

NET ASSETS | | | | | | | | |

Beginning of year | | | 18,772,108 | | | | 28,128,561 | |

End of year | | $ | 21,011,854 | | | $ | 18,772,108 | |

| | | | | | | | | |

ACCUMULATED NET INVESTMENT LOSS | | $ | — | | | $ | — | |

| | | | | | | | | |

SUMMARY OF CAPITAL SHARE ACTIVITY | | | | | | | | |

Shares sold | | | 65,097 | | | | 51,114 | |

Shares redeemed | | | (111,549 | ) | | | (287,195 | ) |

Net decrease in shares outstanding | | | (46,452 | ) | | | (236,081 | ) |

Shares outstanding, beginning of year | | | 886,217 | | | | 1,122,298 | |

Shares outstanding, end of year | | | 839,765 | | | | 886,217 | |

See notes to financial statements. |

12

SCHWARTZ VALUE FOCUSED FUND

FINANCIAL HIGHLIGHTS

Per Share Data for a Share Outstanding Throughout Each Year

| | Year Ended Dec. 31, 2016 | | | Year Ended Dec. 31, 2015 | | | Year Ended Dec. 31, 2014 | | | Year Ended Dec. 31, 2013 | | | Year Ended Dec. 31, 2012 | |

Net asset value at beginning of year | | $ | 21.18 | | | $ | 25.06 | | | $ | 28.54 | | | $ | 23.31 | | | $ | 22.33 | |

| | | | | | | | | | | | | | | | | | | | | |

Income (loss) from investment operations: | | | | | | | | | | | | | | | | | | | | |

Net investment income (loss) | | | (0.08 | ) | | | (0.11 | ) | | | (0.08 | ) | | | (0.04 | ) | | | 0.23 | |

Net realized and unrealized gains (losses) on investments | | | 3.92 | | | | (3.77 | ) | | | (1.26 | ) | | | 5.80 | | | | 0.98 | |

Total from investment operations | | | 3.84 | | | | (3.88 | ) | | | (1.34 | ) | | | 5.76 | | | | 1.21 | |

| | | | | | | | | | | | | | | | | | | | | |

Less distributions: | | | | | | | | | | | | | | | | | | | | |

From net investment income | | | — | | | | — | | | | — | | | | — | | | | (0.23 | ) |

From net realized gains on investments | | | — | | | | — | | | | (2.14 | ) | | | (0.53 | ) | | | — | |

Total distributions | | | — | | | | — | | | | (2.14 | ) | | | (0.53 | ) | | | (0.23 | ) |

| | | | | | | | | | | | | | | | | | | | | |

Net asset value at end of year | | $ | 25.02 | | | $ | 21.18 | | | $ | 25.06 | | | $ | 28.54 | | | $ | 23.31 | |

| | | | | | | | | | | | | | | | | | | | | |

Total return (a) | | | 18.1 | % | | | (15.5 | %) | | | (4.7 | %) | | | 24.7 | % | | | 5.4 | % |

| | | | | | | | | | | | | | | | | | | | | |

Ratios/Supplementary Data: | | | | | | | | | | | | | | | | | | | | |

Net assets at end of year (000’s) | | $ | 21,012 | | | $ | 18,772 | | | $ | 28,129 | | | $ | 32,030 | | | $ | 30,573 | |

| | | | | | | | | | | | | | | | | | | | | |

Ratio of total expenses to average net assets | | | 1.80 | % | | | 1.59 | % | | | 1.46 | % | | | 1.45 | % | | | 1.41 | % |

| | | | | | | | | | | | | | | | | | | | | |

Ratio of net expenses to average net assets | | | 1.25 | %(b) | | | 1.35 | %(b) | | | 1.46 | % | | | 1.45 | % | | | 1.41 | % |

| | | | | | | | | | | | | | | | | | | | | |

Ratio of net investment income (loss) to average net assets | | | (0.35 | %)(b) | | | (0.40 | %)(b) | | | (0.28 | %) | | | (0.13 | %) | | | 0.90 | % |

| | | | | | | | | | | | | | | | | | | | | |

Portfolio turnover rate | | | 48 | % | | | 104 | % | | | 72 | % | | | 57 | % | | | 62 | % |

(a) | Total return is a measure of the change in value of an investment in the Fund over the period covered, which assumes any dividends or capital gains distributions are reinvested in shares of the Fund. Returns shown do not reflect the deduction of taxes a shareholder would pay on Fund distributions or the redemption of Fund shares. |

| | |

(b) | Ratio was determined after advisory fee reductions (Note 2). |

| | |

See notes to financial statements. |

13

SCHWARTZ VALUE FOCUSED FUND

NOTES TO FINANCIAL STATEMENTS

December 31, 2016

1. Significant Accounting Policies

Schwartz Value Focused Fund (the “Fund”), formerly Schwartz Value Fund, is a series of Schwartz Investment Trust (the “Trust”), an open-end management investment company established as an Ohio business trust under a Declaration of Trust dated August 31, 1992. Other series of the Trust are not incorporated in this report. The Fund is registered under the Investment Company Act of 1940 and commenced operations on July 20, 1993. At a meeting held on June 29, 2016, the shareholders of the Fund voted to change the classification of the Fund from a diversified fund to a non-diversified fund.

The investment objective of the Fund is to seek long-term capital appreciation. See the Prospectus for information regarding the principal investment strategies of the Fund.

Shares of the Fund are sold at net asset value (“NAV”). To calculate the NAV, the Fund’s assets are valued and totaled, liabilities are subtracted, and the balance is divided by the number of shares outstanding. The offering price and redemption price per share are equal to the NAV per share.

The following is a summary of significant accounting policies followed by the Fund. The policies are in conformity with accounting principles generally accepted in the United States of America (“GAAP”). As an investment company, as defined in Financial Accounting Standards Board (“FASB”) Accounting Standards Update 2013-08, the Fund follows accounting and reporting guidance under FASB Accounting Standards Codification Topic 946, “Financial Services – Investment Companies.”

In October 2016, the Securities and Exchange Commission (the “SEC”) released its final rule on Investment Company Reporting Modernization (the “Rule”). The Rule, which introduces two new regulatory reporting forms for investment companies – Form N-PORT and Form N-CEN, also contains amendments to Regulation S-X which impact financial statement presentation, particularly the presentation of derivative investments. Although still evaluating the impact of the Rule, management believes that many of the Regulation S-X amendments are consistent with the Fund’s current financial statement presentation and expects that the Fund will be able to comply with the Rule’s Regulation S-X amendments by the August 1, 2017 compliance date.

(a) Valuation of investments — Securities which are traded on stock exchanges, other than NASDAQ, are valued at the closing sales price as of the close of the regular session of trading on the New York Stock Exchange on the day the securities are being valued, or, if not traded on a particular day, at the closing bid price. Securities which are quoted by NASDAQ are valued at the NASDAQ Official Closing Price or, if an official close price is not available, at the most recently quoted bid price. Securities traded in the over-the-counter market are valued at the last reported sales price or, if there is no reported sale on the valuation date, at the most recently quoted bid price. Securities which are traded both in the over-the-counter market and on a stock exchange are valued according to the broadest and most representative market. Investments representing shares of other open-end investment companies are valued at their NAV as reported by such companies. Securities (and other assets) for which market quotations are not readily available are valued at their fair value as determined in good faith in accordance with consistently applied procedures established by and under the general supervision of the Board of

14

SCHWARTZ VALUE FOCUSED FUND

NOTES TO FINANCIAL STATEMENTS

(Continued)

Trustees, and will be classified as Level 2 or 3 within the fair value hierarchy (see below), depending on the inputs used. Fair value pricing may be used, for example, in situations where (i) a portfolio security is so thinly traded that there have been no transactions for that stock over an extended period of time; (ii) the exchange on which the portfolio security is principally traded closes early; or (iii) trading of the portfolio security is halted during the day and does not resume prior to the Fund’s NAV calculation. A portfolio security’s “fair value” price may differ from the price next available for that portfolio security using the Fund’s normal pricing procedures.

GAAP establishes a single authoritative definition of fair value, sets out a framework for measuring fair value and requires additional disclosures about fair value measurements.

Various inputs are used in determining the value of the Fund’s investments. These inputs are summarized in the three broad levels listed below:

| | ● | Level 1 – quoted prices in active markets for identical securities |

| | ● | Level 2 – other significant observable inputs |

| | ● | Level 3 – significant unobservable inputs |

The inputs or methodology used for valuing securities are not necessarily an indication of the risks associated with investing in those securities. The inputs used to measure fair value may fall into different levels of the fair value hierarchy. In such cases, for disclosure purposes, the level in the fair value hierarchy within which the fair value measurement falls in its entirety is determined based on the lowest level input that is significant to the fair value measurement.

The following is a summary of the inputs used to value the Fund’s investments, by security type, as of December 31, 2016:

| | Level 1 | | | Level 2 | | | Level 3 | | | Total | |

Common Stocks | | $ | 18,906,942 | | | $ | — | | | $ | — | | | $ | 18,906,942 | |

Warrants | | | 297,000 | | | | — | | | | — | | | | 297,000 | |

Open-End Funds | | | 13,008 | | | | — | | | | — | | | | 13,008 | |

Money Market Funds | | | 1,818,170 | | | | — | | | | — | | | | 1,818,170 | |

Total | | $ | 21,035,120 | | | $ | — | | | $ | — | | | $ | 21,035,120 | |

Refer to the Fund’s Schedule of Investments for a listing of the securities by industry type. As of December 31, 2016, the Fund did not have any transfers into and out of any Level. There were no Level 2 or 3 securities or derivative instruments held by the Fund as of December 31, 2016. It is the Fund’s policy to recognize transfers into and out of any Level at the end of the reporting period.

(b) Income taxes — The Fund has qualified and intends to continue to qualify as a regulated investment company under the Internal Revenue Code of 1986 (the “Code”). Qualification generally will relieve the Fund of liability for federal income taxes to the extent 100% of its net investment income and net realized capital gains are distributed in accordance with the Code.

15

SCHWARTZ VALUE FOCUSED FUND

NOTES TO FINANCIAL STATEMENTS

(Continued)

In order to avoid imposition of the excise tax applicable to regulated investment companies, it is also the Fund’s intention to declare as dividends in each calendar year at least 98% of its net investment income and 98.2% of its net realized capital gains plus undistributed amounts from prior years.

The following information is computed on a tax basis for each item as of December 31, 2016:

Federal income tax cost | | $ | 16,652,785 | |

Gross unrealized appreciation | | $ | 4,567,673 | |

Gross unrealized depreciation | | | (185,338 | ) |

Net unrealized appreciation | | | 4,382,335 | |

Accumulated capital and other losses | | | (509,257 | ) |

Accumulated earnings | | $ | 3,873,078 | |

As of December 31, 2016, the Fund had a short-term capital loss carryforward of $509,257 for federal income tax purposes. This capital loss carryforward, which does not expire, may be utilized in future years to offset net realized capital gains, if any, prior to distributing such gains to shareholders.

During the year ended December 31, 2016, the Fund reclassified $67,763 of net investment loss against paid-in capital on the Statement of Assets and Liabilities. Such reclassification, the result of permanent differences between the financial statement and income tax reporting requirements, has no effect on the Fund’s net assets or NAV per share.

The Fund recognizes the tax benefits or expenses of uncertain tax positions only when the position is “more-likely-than-not” to be sustained assuming examination by tax authorities. Management has reviewed the tax positions taken on federal income tax returns for all open tax years (tax years ended December 31, 2013 through December 31, 2016) and has concluded that no provision for unrecognized tax benefits or expenses is required in these financial statements.

(c) Security transactions and investment income — Security transactions are accounted for on the trade date. Dividend income is recorded on the ex-dividend date. Interest income is recognized on the accrual basis. Realized capital gains and losses on security transactions are determined on the identified cost basis. Withholding taxes on foreign dividends have been recorded in accordance with the Fund’s understanding of the appropriate country’s rules and tax rates.

(d) Dividends and distributions — Dividends from net investment income and distributions of net realized capital gains, if any, are declared and paid annually in December. Dividends and distributions to shareholders are recorded on the ex-dividend date. There were no distributions paid to shareholders during the years ended December 31, 2016 and 2015.

(e) Estimates — The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities

16

SCHWARTZ VALUE FOCUSED FUND

NOTES TO FINANCIAL STATEMENTS

(Continued)

as of the date of the financial statements and the reported amounts of revenues and expenses during the reporting period. Actual results could differ from those estimates.

(f) Common expenses — Common expenses of the Trust are allocated among the Fund and the other series of the Trust based on relative net assets of each series or the nature of the services performed and the relative applicability to each series.

2. Investment Advisory Agreement and Transactions with Related Parties

The Chairman and President of the Trust is also the Chairman and Chief Executive Officer of Schwartz Investment Counsel, Inc. (the “Adviser”). Certain other officers of the Trust are officers of the Adviser, or of Ultimus Fund Solutions, LLC (“Ultimus”), the administrative, accounting and transfer agent for the Fund, or of Ultimus Fund Distributors, LLC (the “Distributor”), the Fund’s principal underwriter.

Pursuant to an Investment Advisory Agreement between the Trust and the Adviser, the Adviser is responsible for the management of the Fund and provides investment advice along with the necessary personnel, facilities, equipment and certain other services necessary to the operations of the Fund. The Adviser receives from the Fund a quarterly fee at the annual rate of 0.95% per annum of the Fund’s average daily net assets.

The Adviser has contractually agreed to reduce its advisory fees or reimburse a portion of the Fund’s expenses until at least May 1, 2018 so that the ordinary operating expenses of the Fund do not exceed 1.25% per annum of average daily net assets. Accordingly, during the year ended December 31, 2016, the Adviser reduced its investment advisory fees by $106,868.

Any fee reductions or expense reimbursements by the Adviser are subject to repayment by the Fund for a period of three years after such fees and expenses were incurred, provided repayment to the Adviser does not cause the ordinary operating expenses of the Fund to exceed 1.25% per annum of average daily net assets. As of December 31, 2016, the Advisor may seek recoupment of investment advisory fee reductions totaling $163,484 no later than the dates stated below:

December 31, 2018 | December 31, 2019 |

$56,616 | $106,868 |

The Chief Compliance Officer of the Trust (the “CCO”) is an employee of the Adviser. The Trust pays the Adviser a fee for providing CCO services, of which the Fund pays its proportionate share along with the other series of the Trust. In addition, the Trust reimburses the Adviser for out-of-pocket expenses incurred, if any, for providing these services.

Pursuant to a Mutual Fund Services Agreement between the Trust and Ultimus, Ultimus supplies regulatory and compliance services, calculates the daily NAV per share, maintains the financial books and records of the Fund, maintains the records of each shareholder’s account, and processes purchases and redemptions of the Fund’s shares. For these services Ultimus receives fees computed as a percentage of the average daily net assets of the Fund, subject to a minimum monthly fee.

17

SCHWARTZ VALUE FOCUSED FUND

NOTES TO FINANCIAL STATEMENTS

(Continued)

Pursuant to a Distribution Agreement between the Trust and the Distributor, the Distributor serves as the Fund’s exclusive agent for the distribution of its shares. The Distributor is an affiliate of Ultimus.

Trustees and officers affiliated with the Adviser or Ultimus are not compensated by the Trust for their services. Each Trustee who is not an affiliated person of the Adviser or Ultimus (“Independent Trustee”) receives from the Trust an annual retainer of $35,000 (except that such fee is $45,000 for the Lead Independent Trustee and $39,000 for the Chairman of the Audit Committee), payable quarterly; a fee of $5,500 for attendance at each meeting of the Board of Trustees; plus reimbursement of travel and other expenses incurred in attending meetings. The Fund pays its proportionate share of Independent Trustees’ fees and expenses along with the other series of the Trust. Effective January 1, 2017, each Independent Trustee will receive from the Trust an annual retainer of $40,000 (except that such fee is $50,000 for the Lead Independent Trustee and $44,000 for the Chairman of the Audit Committee), payable quarterly; a fee of $6,000 for attendance at each meeting of the Board of Trustees; plus reimbursement of travel and other expenses incurred in attending meetings.

3. Investment Transactions

During the year ended December 31, 2016, cost of purchases and proceeds from sales and maturities of investment securities, excluding short-term investments and U.S. government securities, amounted to $8,490,036 and $9,734,367, respectively.

4. Contingencies and Commitments

The Fund indemnifies the Trust’s officers and Trustees for certain liabilities that might arise from their performance of their duties to the Fund. Additionally, in the normal course of business, the Fund enters into contracts that contain a variety of representations and warranties and which provide general indemnifications. The Fund’s maximum exposure under these arrangements is unknown, as this would involve future claims that may be made against the Fund that have not yet occurred. However, based on experience, the Fund expects the risk of loss to be remote.

5. Subsequent Events

The Fund is required to recognize in the financial statements the effects of all subsequent events that provide additional evidence about conditions that existed as of the date of the Statement of Assets and Liabilities. For non-recognized subsequent events that must be disclosed to keep the financial statements from being misleading, the Fund is required to disclose the nature of the event as well as an estimate of its financial effect, or a statement that such an estimate cannot be made. Management has evaluated subsequent events through the issuance of these financial statements and has noted no events.

18

SCHWARTZ VALUE FOCUSED FUND

REPORT OF INDEPENDENT REGISTERED

PUBLIC ACCOUNTING FIRM

Schwartz Value Focused Fund

We have audited the accompanying statement of assets and liabilities, including the schedule of investments, of Schwartz Value Focused Fund (formerly Schwartz Value Fund) (the “Fund”), a series of Schwartz Investment Trust, as of December 31, 2016, and the related statement of operations for the year then ended, the statements of changes in net assets for each of the two years in the period then ended, and the financial highlights for each of the five years in the period then ended. These financial statements and financial highlights are the responsibility of the Fund’s management. Our responsibility is to express an opinion on these financial statements and financial highlights based on our audits.

We conducted our audits in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audits to obtain reasonable assurance about whether the financial statements and financial highlights are free of material misstatement. The Fund is not required to have, nor were we engaged to perform, an audit of internal control over financial reporting. Our audits included consideration of internal control over financial reporting as a basis for designing audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Fund’s internal control over financial reporting. Accordingly, we express no such opinion. An audit also includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements, assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. Our procedures included confirmation of securities owned as of December 31, 2016, by correspondence with the custodian and brokers. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the financial statements and financial highlights referred to above present fairly, in all material respects, the financial position of Schwartz Value Focused Fund (formerly Schwartz Value Fund) as of December 31, 2016, the results of its operations for the year then ended, the changes in its net assets for each of the two years in the period then ended, and the financial highlights for each of the five years in the period then ended, in conformity with accounting principles generally accepted in the United States of America.

February 14, 2017

19

SCHWARTZ VALUE FOCUSED FUND

BOARD OF TRUSTEES AND EXECUTIVE OFFICERS

(Unaudited)

Overall responsibility for management of the Trust rests with the Board of Trustees. The Trustees serve during the lifetime of the Trust and until its termination, or until death, resignation, retirement or removal. The Trustees, in turn, elect the officers of the Trust to actively supervise its day-to-day operations. The officers have been elected for an annual term. The following are the Trustees and executive officers of the Trust:

Trustee/Officer | Address | Year of

Birth | Position Held

with the Trust | Length of

Time Served |

Interested Trustees: |

* | George P. Schwartz, CFA | 801 W. Ann Arbor Trail

Plymouth, MI | 1944 | Chairman of the Board/President/ Trustee | Since 1992 |

Independent Trustees: |

| | Louis C. Bosco, Jr. | 801 W. Ann Arbor Trail

Plymouth, MI | 1936 | Trustee | Since 2008 |

| | Donald J. Dawson, Jr. | 801 W. Ann Arbor Trail

Plymouth, MI | 1947 | Trustee | Since 1993 |

| | Joseph M. Grace | 801 W. Ann Arbor Trail

Plymouth, MI | 1936 | Trustee | Since 2007 |

| | John J. McHale, Jr. | 801 W. Ann Arbor Trail

Plymouth, MI | 1949 | Trustee | Since 2014 |

Executive Officers: |

* | Richard L. Platte, Jr., CFA | 801 W. Ann Arbor Trail

Plymouth, MI | 1951 | Vice President and Secretary | Since 1993 |

* | Robert C. Schwartz, CFP | 801 W. Ann Arbor Trail

Plymouth, MI | 1976 | Vice President | Since 2013 |

* | Timothy S. Schwartz, CFA | 5060 Annunciation Circle

Ave Maria, FL | 1971 | Treasurer | Since 2000 |

* | Cathy M. Stoner, CPA, IACCP | 801 W. Ann Arbor Trail

Plymouth, MI | 1970 | Chief Compliance Officer | Since 2010 |

* | George P. Schwartz, Richard L. Platte, Jr., Robert C. Schwartz, Timothy S. Schwartz and Cathy M. Stoner, as affiliated persons of Schwartz Investment Counsel, Inc., the Fund’s investment adviser, are “interested persons” of the Trust within the meaning of Section 2(a)(19) of the Investment Company Act of 1940. George P. Schwartz is the father of Robert C. Schwartz and Timothy S. Schwartz. |

20

SCHWARTZ VALUE FOCUSED FUND

BOARD OF TRUSTEES AND EXECUTIVE OFFICERS

(Unaudited) (Continued)

Each Trustee oversees six portfolios of the Trust: the Ave Maria Catholic Values Fund, the Ave Maria Growth Fund, the Ave Maria Rising Dividend Fund, the Ave Maria World Equity Fund, the Ave Maria Bond Fund and the Schwartz Value Focused Fund. The principal occupations of the Trustees and executive officers of the Trust during the past five years and public directorships held by the Trustees are set forth below:

George P. Schwartz, CFA is Chairman and Chief Executive Officer of Schwartz Investment Counsel, Inc. and is the co-portfolio manager of the Fund.

Louis C. Bosco, Jr. retired in April 2012. Prior to his retirement, he was a partner in Bosco Development Company (a real estate firm).

Donald J. Dawson, Jr. retired in March 2015. Prior to retirement, he was Chairman of Payroll 1, Inc. (a payroll processing company) from 1986 – 2015.

Joseph M. Grace is retired Senior Vice President of National Bank of Detroit (renamed JPMorgan Chase & Company).

John J. McHale, Jr. is Special Assistant to Commissioner of Major League Baseball since 2015. He was Executive Vice President of Major League Baseball from 2000 – 2015.

Richard L. Platte, Jr., CFA is President and Chief Investment Officer of Schwartz Investment Counsel, Inc.

Robert C. Schwartz, CFP is Vice President and Secretary of Schwartz Investment Counsel, Inc.

Timothy S. Schwartz, CFA is Executive Vice President and Chief Financial Officer of Schwartz Investment Counsel, Inc. and is the lead portfolio manager of the Fund.

Cathy M. Stoner, CPA, IACCP is Vice President and Chief Compliance Officer of Schwartz Investment Counsel, Inc.

Additional information about members of the Board of Trustees and executive officers is available in the Statement of Additional Information (“SAI”). To obtain a free copy of the SAI, please call (888) 726-0753.

21

SCHWARTZ VALUE FOCUSED FUND

ABOUT YOUR FUND’S EXPENSES

(Unaudited)

We believe it is important for you to understand the impact of costs on your investment. As a shareholder of the Fund, you incur ongoing costs, including management fees and other Fund expenses. The following examples are intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

A mutual fund’s ongoing costs are expressed as a percentage of its average net assets. This figure is known as the expense ratio. The ongoing costs reflected in the table below are based on an investment of $1,000 made at the beginning of the most recent semi-annual period (July 1, 2016) and held until the end of the period (December 31, 2016).

The table below illustrates the Fund’s ongoing costs in two ways:

Actual fund return – This section helps you to estimate the actual expenses that you paid over the period. The “Ending Account Value” shown is derived from the Fund’s actual return, and the third column shows the dollar amount of operating expenses that would have been paid by an investor who started with $1,000 in the Fund. You may use the information here, together with the amount you invested, to estimate the expenses that you paid over the period.

To do so, simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number given for the Fund under the heading “Expenses Paid During Period.”

Hypothetical 5% return – This section is intended to help you compare the Fund’s ongoing costs with those of other mutual funds. It assumes that the Fund had an annual return of 5% before expenses during the period shown, but that the expense ratio is unchanged. In this case, because the return used is not the Fund’s actual return, the result does not apply to your investment. The example is useful in making comparisons because the SEC requires all mutual funds to calculate expenses based on a 5% return. You can assess the Fund’s ongoing costs by comparing this hypothetical example with the hypothetical examples that appear in shareholder reports of other funds.

Note that expenses shown in the table are meant to highlight and help you compare ongoing costs only. The Fund does not charge sales loads or redemption fees.

The calculations assume no shares were bought or sold during the period. Your actual costs may have been higher or lower, depending on the amount of your investment and the timing of any purchases or redemptions.

More information about the Fund’s expenses, including historical annual expense ratios, can be found in this report. For additional information on operating expenses and other shareholder costs, please refer to the Fund’s Prospectus.

| Beginning

Account Value

July 1, 2016 | Ending

Account Value

December 31, 2016 | Expenses Paid

During Period* |

Based on Actual Fund Return | $1,000.00 | $1,095.00 | $6.58 |

Based on Hypothetical 5% Return (before expenses) | $1,000.00 | $1,018.85 | $6.34 |

* | Expenses are equal to the Fund’s annualized net expense ratio of 1.25% for the period, multiplied by the average account value over the period, multiplied by 184/366 (to reflect the one-half year period). |

22

SCHWARTZ VALUE FOCUSED FUND

OTHER INFORMATION

(Unaudited)

A description of the policies and procedures the Fund uses to determine how to vote proxies relating to portfolio securities is available without charge upon request by calling toll-free (888) 726-0753, or on the SEC’s website at http://www.sec.gov. Information regarding how the Fund voted proxies relating to portfolio securities during the most recent 12-month period ended June 30 is also available without charge upon request by calling toll-free (888) 726-0753, or on the SEC’s website at http://www.sec.gov.

The Trust files a complete listing of portfolio holdings for the Fund with the SEC as of the end of the first and third quarters of each fiscal year on Form N-Q. The filings are available free of charge, upon request, by calling (888) 726-0753. Furthermore, you may obtain a copy of the filings on the SEC’s website at http://www.sec.gov. The Trust’s Forms N-Q may also be reviewed and copied at the SEC’s Public Reference Room in Washington, DC, and information on the operation of the Public Reference Room may be obtained by calling (800) SEC-0330.

23

This page intentionally left blank.

Shareholder Services c/o Ultimus Fund Solutions, LLC P.O. Box 46707 Cincinnati, OH 45246 (888) 726-9331 |

| Corporate Offices 801 W. Ann Arbor Trail Suite 244 Plymouth, MI 48170 (734) 455-7777 Fax (734) 455-7720 |

Dear Fellow Shareholders of:

Ave Maria Catholic Values Fund (AVEMX)

Ave Maria Growth Fund (AVEGX)

Ave Maria Rising Dividend Fund (AVEDX)

Ave Maria World Equity Fund (AVEWX)

Ave Maria Bond Fund (AVEFX)

Ave Maria Money Market Account

2016 saw wild swings in the global capital markets and investor sentiment. Throughout the year of many surprises with economic consequences, the words of Catholic Advisory Board member, Larry Kudlow, echoed through our organization “corporate profits are the mother’s milk of economic prosperity”. Despite a great deal of investor angst, U.S. corporate profits advanced modestly in 2016, and may increase another 10% - 15% in 2017, as the new administration is expected to usher in pro-growth policies. And importantly, pro-life policies.

There is a lot of work to be done and regulations to be undone. The Obama administration vastly expanded the government’s intrusion into the private economy, and imposed prosperity-stifling policies on corporations large and small, sapping confidence from business decision-makers, consumers and investors. Thankfully, the reverse seems to be taking place. In the same manner that the implementation of these stifling regulatory measures had negative consequences for economic growth, their removal could release the natural energy of our economy.

As you know, the portfolio managers and analysts of the Ave Maria Mutual Funds screen out companies based on the guidelines established by our Catholic Advisory Board. This eliminates from consideration, companies that support abortion, pornography and those that engage in embryonic stem cell research. That still leaves thousands of fine companies to choose from for the portfolios of the Funds. In 2016, our stock and bond selections were quite good, as each of

the Ave Maria Mutual Funds beat their respective benchmarks for investment performance. Our investment research process with emphasis on fundamentals and a long-term focus, seems to be working.

Thanks for being a shareholder.

Sincerely,

George P. Schwartz, CFA

Chairman & CEO

January 31, 2017

Past performance is not predictive of future performance. Investment results and principal value will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance data quoted. Performance data, current to the most recent month end, is available at the Ave Maria Mutual Funds website at www.avemariafunds.com or by calling 1-888-726-9331.

The Letter to Shareholders and the Portfolio Manager Commentaries that follow seek to describe some of the Adviser’s current opinions and views of the financial markets. Although the Adviser believes it has a reasonable basis for any opinions or views expressed, actual results may differ, sometimes significantly so, from those expected or expressed. Keep in mind that the information and opinions cover the period through the date of this report.

AVE MARIA MUTUAL FUNDS

TABLE OF CONTENTS

Ave Maria Catholic Values Fund: | |

Portfolio Manager Commentary | 2 |

Performance | 5 |

Annual Total Rates of Return Comparison with Major Indices | 6 |

Ten Largest Equity Holdings | 7 |

Asset Allocation | 7 |

Schedule of Investments | 8 |

| | |

Ave Maria Growth Fund: | |

Portfolio Manager Commentary | 12 |

Performance | 13 |

Annual Total Rates of Return Comparison with Major Indices | 14 |

Ten Largest Equity Holdings | 15 |

Asset Allocation | 15 |

Schedule of Investments | 16 |

| | |

Ave Maria Rising Dividend Fund: | |

Portfolio Manager Commentary | 19 |

Performance | 21 |

Annual Total Rates of Return Comparison with Major Indices | 22 |

Ten Largest Equity Holdings | 23 |

Asset Allocation | 23 |

Schedule of Investments | 24 |

| | |

Ave Maria World Equity Fund: | |

Portfolio Manager Commentary | 27 |

Performance | 29 |

Annual Total Rates of Return Comparison with Major Indices | 30 |

Ten Largest Equity Holdings | 31 |

Asset Allocation | 31 |

Schedule of Investments | 32 |

Summary of Common Stocks by Country | 35 |

| | |

Ave Maria Bond Fund: | |

Portfolio Manager Commentary | 36 |

Performance | 38 |

Annual Total Rates of Return Comparison with Major Indices | 39 |

Ten Largest Holdings | 40 |

Asset Allocation | 40 |

Schedule of Investments | 41 |

AVE MARIA MUTUAL FUNDS

TABLE OF CONTENTS

(Continued)

Statements of Assets and Liabilities | 46 |

| | |

Statements of Operations | 48 |

| | |

Statements of Changes in Net Assets: | |

Ave Maria Catholic Values Fund | 50 |

Ave Maria Growth Fund | 51 |

Ave Maria Rising Dividend Fund | 52 |

Ave Maria World Equity Fund | 53 |

Ave Maria Bond Fund | 54 |

| | |

Financial Highlights: | |

Ave Maria Catholic Values Fund | 55 |

Ave Maria Growth Fund | 56 |

Ave Maria Rising Dividend Fund | 57 |

Ave Maria World Equity Fund | 58 |

Ave Maria Bond Fund | 59 |

| | |

Notes to Financial Statements | 60 |

| | |

Report of Independent Registered Public Accounting Firm | 72 |

| | |

Board of Trustees and Executive Officers | 73 |

| | |

Catholic Advisory Board | 75 |

| | |

About Your Funds’ Expenses | 76 |

| | |

Federal Tax Information | 78 |

| | |

Other Information | 79 |

This report is for the information of the shareholders of the Ave Maria Mutual Funds. To obtain a copy of the prospectus, please visit our website at www.avemariafunds.com or call 1-888-726-9331 and a copy will be sent to you free of charge. Please read the prospectus carefully before you invest. The Ave Maria Mutual Funds are distributed by Ultimus Fund Distributors, LLC.

Past performance is not predictive of future performance. Investment results and principal value will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance data quoted. Performance data, current to the most recent month end, is available at the Ave Maria Mutual Funds website at www.avemariafunds.com or by calling 1-888-726-9331.

AVE MARIA CATHOLIC VALUES FUND

PORTFOLIO MANAGER COMMENTARY

(Unaudited)

Dear Fellow Shareowner:

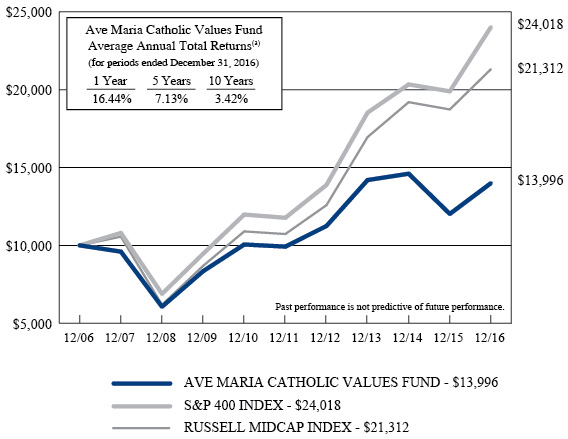

2016 was a good year for the Ave Maria Catholic Values Fund (the “Fund”), with a total return of 16.44%, compared to 20.74% for the S&P 400 Index and 13.8% for the Russell Midcap Index. The Fund’s performance can be attributed mainly to 13 portfolio holdings, which appreciated more than 40% during the year. These issues were from a variety of industry sectors including energy, industrial, financial, retail, and technology. The Fund’s best performing stocks were energy and industrial related. Energy stocks bottomed early in the year and rebounded concomitantly with the rise in oil prices. At year end, the price of WTI crude oil breached $50/barrel, up 45% for the year and up nearly 100% from the February low. Holdings in the energy sector that produced outsized gains included Texas Pacific Land Trust (+90%), Halliburton Company (+61%), and Pioneer Natural Resources Company (+46%). Our industrial stocks benefitted from improving economic growth in the second half, and to a lesser extent, from rising oil and natural gas prices. Notable outperformers in the industrial sector included Colfax Corporation (+68%), MSC Industrial Direct Co., Inc. (+68%), Donaldson Company, Inc. (+50%), and H.B. Fuller Company (+42%). The Fund’s five best performing stocks in 2016 were:

Company | Industry | 2016 Performance |

Texas Pacific Land Trust | Oil & Gas Royalties/Real Estate | +89.56% |

MSC Industrial Direct Co., Inc. | Industrial Equipment | +68.32% |

Colfax Corporation | Industrial Machinery | +67.93% |

Halliburton | Oil & Gas Equipment & Services | +61.48% |

Donaldson Company, Inc. | Industrial Machinery | +50.11% |

2

AVE MARIA CATHOLIC VALUES FUND

PORTFOLIO MANAGER COMMENTARY

(Unaudited) (Continued)

On the negative side, the Fund’s worst performing stock during 2016 was Liberty Interactive Corporation, which owns and operates QVC Group, a multinational corporation that sells consumer goods through its television network and online. The share price fell after the company experienced a U.S. sales decline due to weakness in its fashion business and hair care division. Due to QVC’s loyal customer base and strong viewership, we view this slowdown as temporary. Additionally, the international business appears unaffected by the current U.S. sales slowdown. The Fund’s five worst performing stocks in 2016 were:

Company | Industry | 2016 Performance |

Liberty Interactive Corporation | TV & Internet Retail | -17.41% |

Zimmer Biomet Holdings Inc. | Medical Equipment | -16.40% |

VF Corporation | Apparel | -15.80% |

Moody’s Corporation | Business & Financial Services | - 9.40% |

ANSYS, Inc. | Software | + 0.92% |

During the past six months, six stocks were liquidated from the portfolio, having reached our estimate of intrinsic value: Emerson Electric Co. (industrial electrical equipment), Flour Corporation (industrial goods), HP, Inc. (technology), Polaris Industries, Inc. (recreational vehicles), World Fuel Services Corporation (oil & gas refining), and St. Jude Medical, Inc. (medical equipment), which received a takeover offer from Abbot Laboratories. Finally, we exited Platform Specialty Products Corporation (specialty chemicals) due to heightened concerns regarding the company’s business model.

During the second half of the year, new positions were established in three companies that meet our value investing criteria: AMERCO, Cognizant Technology Solutions Corp., and Zimmer Biomet Holdings Inc. AMERCO owns the U-Haul self-moving and storage franchise. With a dominant market position, the company has an impressive track record of increasing earnings and we believe has ample opportunities for growth. Cognizant Technology Solutions provides information technology (IT) consulting services worldwide. The business is highly profitable and generates strong free cash flow with a high return on invested capital. Zimmer Biomet designs and markets orthopedic implants and fracture management devices and, in our opinion, is well-positioned for long-term growth.

3

AVE MARIA CATHOLIC VALUES FUND

PORTFOLIO MANAGER COMMENTARY

(Unaudited) (Continued)

2017 could be another good year for stocks generally. We are confident that the new Trump Administration will be more hospitable to corporate America than the Obama Administration. President Trump’s pro-growth agenda of lower tax rates – corporate and personal, a less-punishing regulatory environment, and a generally less intrusive government should lead to greater business and consumer confidence, more economy activity, and ultimately higher corporate profits. As always, we’ll be working tirelessly to invest in well-managed, high-quality companies selling at a discount to our estimate of intrinsic value.

No capital gains or income distributions were paid at year end. The net asset value of the Fund ended the year at $19.12 per share.

Thank you for being a shareholder in the Fund.

|

|

Timothy S. Schwartz, CFA | George P. Schwartz, CFA |

Lead Portfolio Manager | Co-Portfolio Manager |

| | |

| |

Joseph W. Skornicka, CFA | |

Co-Portfolio Manager | |

4

AVE MARIA CATHOLIC VALUES FUND

PERFORMANCE

(Unaudited) |

Comparison of the Change in Value of a $10,000 Investment

in the Ave Maria Catholic Values Fund, the S&P 400 Index**,

and the Russell Midcap Index

(a) | The returns shown do not reflect the deduction of taxes a shareholder would pay on Fund distributions or the redemption of Fund shares. |

Expense ratio as of 12-31-15 (as disclosed in May 1, 2016 prospectus) | 1.18%* |

Expense ratio for the year ended 12-31-16 | 1.20% |

* | Includes Acquired Fund Fees and Expenses. |

| | |

** | Effective January 1, 2017, the S&P 400 Index will be the Fund’s primary bench mark instead of the Russell Midcap Index. |

Past performance is not predictive of future performance. Investment results and principal value will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance data quoted. Performance data, current to the most recent month end, is available at the Ave Maria Mutual Funds website at www.avemariafunds.com or by calling 1-888-726-9331.

5

AVE MARIA CATHOLIC VALUES FUND

ANNUAL TOTAL RATES OF RETURN

COMPARISON WITH MAJOR INDICES (Unaudited) |

| AVE MARIA

CATHOLIC

VALUES FUND | S&P 400

INDEX | RUSSELL

MIDCAP

INDEX | S&P 500

INDEX |

2001(a) | 5.3% | -0.5% | -3.5% | -8.5% |

2002 | -9.8% | -14.5% | -16.2% | -22.1% |

2003 | 35.6% | 35.6% | 40.1% | 28.7% |

2004 | 20.1% | 16.5% | 20.2% | 10.9% |

2005 | 5.8% | 12.6% | 12.7% | 4.9% |

2006 | 14.2% | 10.3% | 15.3% | 15.8% |

2007 | -4.0% | 8.0% | 5.6% | 5.5% |

2008 | -36.8% | -36.2% | -41.5% | -37.0% |

2009 | 37.6% | 37.4% | 40.5% | 26.5% |

2010 | 20.5% | 26.7% | 25.5% | 15.1% |

2011 | -1.3% | -1.7% | -1.6% | 2.1% |

2012 | 13.3% | 17.9% | 17.3% | 16.0% |

2013 | 26.2% | 33.5% | 34.8% | 32.4% |

2014 | 2.9% | 9.8% | 13.2% | 13.7% |

2015 | -17.7% | -2.2% | -2.4% | 1.4% |

2016 | 16.4% | 20.7% | 13.8% | 12.0% |

AVERAGE ANNUAL TOTAL RETURNS

As of December 31, 2016 (Unaudited)

| AVE MARIA

CATHOLIC

VALUES FUND | S&P 400

INDEX | RUSSELL

MIDCAP

INDEX | S&P 500

INDEX |

3 Years | -0.5% | 9.0% | 7.9% | 8.9% |

5 Years | 7.1% | 15.3% | 14.7% | 14.7% |

10 Years | 3.4% | 9.2% | 7.9% | 7.0% |

Since Inception (b) | 6.3% | 9.3% | 8.8% | 5.8% |

(a) | Represents the period from the commencement of operations (May 1, 2001) through December 31, 2001. |

| | |

(b) | Represents the period from the commencement of operations (May 1, 2001) through December 31, 2016. |

6

AVE MARIA CATHOLIC VALUES FUND

TEN LARGEST EQUITY HOLDINGS

December 31, 2016 (Unaudited)

Shares | | Company | | Market Value | | | % of Net Assets | |

| | 100,000 | | MSC Industrial Direct Company, Inc. - Class A | | $ | 9,239,000 | | | | 4.1 | % |

| | 50,000 | | Pioneer Natural Resources Company | | | 9,003,500 | | | | 4.0 | % |

| | 65,000 | | Laboratory Corporation of America Holdings | | | 8,344,700 | | | | 3.7 | % |

| | 260,000 | | ARRIS International plc | | | 7,833,800 | | | | 3.5 | % |

| | 100,000 | | Discover Financial Services | | | 7,209,000 | | | | 3.2 | % |

| | 100,000 | | HEICO Corporation - Class A | | | 6,790,000 | | | | 3.0 | % |

| | 120,000 | | Halliburton Company | | | 6,490,800 | | | | 2.9 | % |

| | 10,536 | | Alleghany Corporation | | | 6,407,152 | | | | 2.9 | % |

| | 60,000 | | Zimmer Biomet Holdings, Inc. | | | 6,192,000 | | | | 2.8 | % |

| | 20,000 | | Texas Pacific Land Trust | | | 5,935,400 | | | | 2.6 | % |

ASSET ALLOCATION (Unaudited)

Sector | % of Net Assets |

Consumer Discretionary | 11.9% |

Energy | 11.7% |

Financials | 18.8% |

Health Care | 9.7% |

Industrials | 21.9% |

Information Technology | 15.0% |

Materials | 0.6% |

Warrants | 0.5% |

Money Market Funds, Liabilities in Excess of Other Assets | 9.9% |

| | 100.0% |

7

AVE MARIA CATHOLIC VALUES FUND

SCHEDULE OF INVESTMENTS

December 31, 2016

COMMON STOCKS — 89.6% | | Shares | | | Market Value | |

Consumer Discretionary — 11.9% | | | | | | |

Diversified Consumer Services — 2.3% | | | | | | |

Graham Holdings Company - Class B | | | 5,000 | | | $ | 2,559,750 | |

ServiceMaster Global Holdings, Inc. * | | | 70,000 | | | | 2,636,900 | |

| | | | | | | | 5,196,650 | |

Household Durables — 2.1% | | | | | | | | |

Garmin Ltd. | | | 60,000 | | | | 2,909,400 | |

PulteGroup, Inc. | | | 100,000 | | | | 1,838,000 | |

| | | | | | | | 4,747,400 | |

Internet & Direct Marketing Retail — 1.6% | | | | | | | | |

Liberty Interactive Corporation QVC Group - Series A * | | | 180,000 | | | | 3,596,400 | |

| | | | | | | | | |

Media — 2.4% | | | | | | | | |

Discovery Communications, Inc. - Series A * | | | 200,000 | | | | 5,482,000 | |

| | | | | | | | | |

Multi-Line Retail — 1.1% | | | | | | | | |

Nordstrom, Inc. | | | 50,000 | | | | 2,396,500 | |

| | | | | | | | | |

Textiles, Apparel & Luxury Goods — 2.4% | | | | | | | | |

VF Corporation | | | 100,000 | | | | 5,335,000 | |

| | | | | | | | | |

Energy — 11.7% | | | | | | | | |

Energy Equipment & Services — 5.2% | | | | | | | | |

Baker Hughes Incorporated | | | 40,000 | | | | 2,598,800 | |

FMC Technologies, Inc. * | | | 75,000 | | | | 2,664,750 | |

Halliburton Company | | | 120,000 | | | | 6,490,800 | |

| | | | | | | | 11,754,350 | |

Oil, Gas & Consumable Fuels — 6.5% | | | | | | | | |

Noble Energy, Inc. | | | 143,740 | | | | 5,470,744 | |

Pioneer Natural Resources Company | | | 50,000 | | | | 9,003,500 | |

| | | | | | | | 14,474,244 | |

Financials — 18.8% | | | | | | | | |

Banks — 1.5% | | | | | | | | |

Fifth Third Bancorp | | | 125,000 | | | | 3,371,250 | |

| | | | | | | | | |

Capital Markets — 3.6% | | | | | | | | |

Dundee Corporation - Class A * | | | 239,400 | | | | 1,060,542 | |

Federated Investors, Inc. - Class B | | | 50,000 | | | | 1,414,000 | |

Moody's Corporation | | | 60,000 | | | | 5,656,200 | |

| | | | | | | | 8,130,742 | |

Consumer Finance — 3.2% | | | | | | | | |

Discover Financial Services | | | 100,000 | | | | 7,209,000 | |

8

AVE MARIA CATHOLIC VALUES FUND

SCHEDULE OF INVESTMENTS

(Continued)

COMMON STOCKS — 89.6% (Continued) | | Shares | | | Market Value | |

Financials — 18.8% (Continued) | | | | | | |

Diversified Financial Services — 4.6% | | | | | | |

Texas Pacific Land Trust | | | 20,000 | | | $ | 5,935,400 | |

Western Union Company (The) | | | 200,000 | | | | 4,344,000 | |

| | | | | | | | 10,279,400 | |

Insurance — 5.9% | | | | | | | | |

Alleghany Corporation * | | | 10,536 | | | | 6,407,152 | |

Reinsurance Group of America, Inc. | | | 30,000 | | | | 3,774,900 | |

Unico American Corporation * # | | | 282,945 | | | | 3,041,659 | |

| | | | | | | | 13,223,711 | |

Health Care — 9.7% | | | | | | | | |

Health Care Equipment & Supplies — 4.8% | | | | | | | | |

Varian Medical Systems, Inc. * | | | 50,000 | | | | 4,489,000 | |

Zimmer Biomet Holdings, Inc. | | | 60,000 | | | | 6,192,000 | |

| | | | | | | | 10,681,000 | |

Health Care Providers & Services — 3.7% | | | | | | | | |

Laboratory Corporation of America Holdings * | | | 65,000 | | | | 8,344,700 | |

| | | | | | | | | |

Life Sciences Tools & Services — 1.2% | | | | | | | | |

Waters Corporation * | | | 20,000 | | | | 2,687,800 | |

| | | | | | | | | |

Industrials — 21.9% | | | | | | | | |

Aerospace & Defense — 3.0% | | | | | | | | |

HEICO Corporation - Class A | | | 100,000 | | | | 6,790,000 | |

| | | | | | | | | |

Electrical Equipment — 3.9% | | | | | | | | |

AMETEK, Inc. | | | 110,000 | | | | 5,346,000 | |

Eaton Corporation plc | | | 50,000 | | | | 3,354,500 | |

| | | | | | | | 8,700,500 | |

Machinery — 6.3% | | | | | | | | |

Colfax Corporation * | | | 150,000 | | | | 5,389,500 | |

Donaldson Company, Inc. | | | 90,000 | | | | 3,787,200 | |

Graco, Inc. | | | 60,000 | | | | 4,985,400 | |

| | | | | | | | 14,162,100 | |

Road & Rail — 2.5% | | | | | | | | |

AMERCO | | | 15,000 | | | | 5,543,850 | |

| | | | | | | | | |

Trading Companies & Distributors — 6.2% | | | | | | | | |

MSC Industrial Direct Company, Inc. - Class A | | | 100,000 | | | | 9,239,000 | |

W.W. Grainger, Inc. | | | 20,000 | | | | 4,645,000 | |

| | | | | | | | 13,884,000 | |

9

AVE MARIA CATHOLIC VALUES FUND

SCHEDULE OF INVESTMENTS

(Continued)

COMMON STOCKS — 89.6% (Continued) | | Shares | | | Market Value | |

Information Technology — 15.0% | | | | | | |

Communications Equipment — 3.5% | | | | | | |

ARRIS International plc * | | | 260,000 | | | $ | 7,833,800 | |

| | | | | | | | | |

Electronic Equipment, Instruments & Components — 3.9% | | | | | | | | |

Arrow Electronics, Inc. * | | | 75,000 | | | | 5,347,500 | |

Avnet, Inc. | | | 70,000 | | | | 3,332,700 | |

| | | | | | | | 8,680,200 | |

Internet Software & Services — 0.8% | | | | | | | | |

Equinix, Inc. | | | 4,948 | | | | 1,768,465 | |

| | | | | | | | | |

IT Services — 4.2% | | | | | | | | |

Cognizant Technology Solutions Corporation - Class A * | | | 75,000 | | | | 4,202,250 | |

InterXion Holding N.V. * | | | 150,000 | | | | 5,260,500 | |

| | | | | | | | 9,462,750 | |

Software — 1.6% | | | | | | | | |

ANSYS, Inc. * | | | 40,000 | | | | 3,699,600 | |

| | | | | | | | | |

Technology Hardware, Storage & Peripherals — 1.0% | | | | | | | | |

Hewlett Packard Enterprise Company | | | 100,000 | | | | 2,314,000 | |

| | | | | | | | | |

Materials — 0.6% | | | | | | | | |

Chemicals — 0.6% | | | | | | | | |

H.B. Fuller Company | | | 30,000 | | | | 1,449,300 | |

| | | | | | | | | |

Total Common Stocks (Cost $157,291,350) | | | | | | $ | 201,198,712 | |

WARRANTS — 0.5% | | Shares | | | Market Value | |

Financials — 0.5% | | | | | | |

Banks — 0.5% | | | | | | |

PNC Financial Services Group, Inc. (The), expires 12/31/18 * (Cost $472,385) | | | 25,000 | | | $ | 1,237,500 | |

10

AVE MARIA CATHOLIC VALUES FUND

SCHEDULE OF INVESTMENTS

(Continued)

MONEY MARKET FUNDS — 9.9% | | Shares | | | Market Value | |

Federated Government Obligations Tax-Managed Fund - Institutional Shares, 0.35% (a) | | | 10,814,344 | | | $ | 10,814,344 | |

Federated Treasury Obligations Fund - Institutional Shares, 0.36% (a) | | | 10,774,343 | | | | 10,774,343 | |

Federated U.S. Treasury Cash Reserves Fund - Institutional Shares, 0.30% (a) | | | 573,356 | | | | 573,356 | |

Total Money Market Funds (Cost $22,162,043) | | | | | | $ | 22,162,043 | |

| | | | | | | | | |

Total Investments at Market Value — 100.0% (Cost $179,925,778) | | | | | | $ | 224,598,255 | |

| | | | | | | | | |

Liabilities in Excess of Other Assets — (0.0%) (b) | | | | | | | (5,007 | ) |

| | | | | | | | | |

Net Assets — 100.0% | | | | | | $ | 224,593,248 | |

* | Non-income producing security. |

| | |

# | The Fund owned 5% or more of the company's outstanding voting shares thereby making the company an affiliated company as that term is defined in the Investment Company Act of 1940 (Note 5). |

| | |

(a) | The rate shown is the 7-day effective yield as of December 31, 2016. |

| | |

(b) | Percentage rounds to less than 0.1%. |

| | |

See notes to financial statements. |

11

AVE MARIA GROWTH FUND

PORTFOLIO MANAGER COMMENTARY

(Unaudited)

Dear Fellow Shareholders,