UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act file number 811-08004

Aston Funds

(Exact name of registrant as specified in charter)

120 North LaSalle Street, 25th Floor

Chicago, IL 60602

(Address of principal executive offices) (Zip code)

Jeffrey T. Cerutti, President

Aston Funds

120 North LaSalle Street, 25th Floor

Chicago, IL 60602

(Name and address of agent for service)

Registrant’s telephone number, including area code: (312) 268-1400

Date of fiscal year end: October 31

Date of reporting period: October 31, 2015

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 100 F Street, NE, Washington, DC 20549. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

Item 1. Reports to Stockholders.

The Report to Shareholders is attached herewith.

Annual Report 2015

October 31, 2015

Class N, I & R Shares

Equity

Fixed Income

Alternative

International

Sector

Balanced

Aston Funds

Dear Fellow Shareholder:

Overall, U.S. equity investors were rewarded with positive, albeit modest, returns despite increasing market volatility for the fiscal year ended October 31, 2015. The S&P 500® Index, a widely followed barometer of the U.S. equity market, returned 5.2% during the past twelve months. However, the U.S. equity market did experience its first correction in four years in August as investors worried about slowing China growth and the potential impact of a U.S. Federal Reserve (the “Fed”) rate hike on the slow recovery in the U.S. During the year, there was significant dispersion in performance across sectors with Consumer Discretionary stocks returning more than 21% while companies within the Energy sector fell 19%, driven in large part by the precipitous fall in oil prices. Meanwhile, international stocks fell during the prior year, returning -4.7%, as measured by the MSCI ACWI ex USA (in U.S. Dollar terms). International investment returns in U.S. Dollar terms were negatively impacted by continued strengthening in the U.S. Dollar. Despite the more recent difficult performance for equities, it’s worth noting that the first quarter of 2015 marked the six-year anniversary of the equity bull market.

The Barclays U.S. Aggregate Bond Index, a broad U.S. bond market benchmark, returned 2.0% for the fiscal year ended October 31, 2015. Interest rates fell throughout much of 2014 and for periods throughout the past fiscal year, lending positive support to bond prices. Investors, however, enter the new fiscal year with a close watch on the strength of the underlying U.S. economy and its potential impact on the Fed’s zero-interest-rate policy (and its subsequent impact on bond prices).

Our foremost goal at Aston Funds is to provide investment solutions that help our shareholders successfully reach their long-term investment goals. By partnering with our well-established investment managers, Aston Funds provides access to a distinctive array of actively-managed, return-oriented investment strategies. We thank you for your continued confidence and investment in Aston Funds. You can rest assured that under all market conditions our team is focused on delivering excellent investment management services for your benefit.

Respectfully,

Jeffrey Cerutti

Chief Executive Officer and President

Aston Funds

|

| The views expressed in this report reflect those of the portfolio managers only, through the end of the period covered and do not necessarily represent the views of Aston Funds or Aston Asset Management, LLC. Any such views are subject to change at any time based upon market or other conditions and Aston Funds and Aston Asset Management, LLC disclaim any responsibility to update such views. These views may not be relied on as investment advice and, because investment decisions for an Aston Fund are based on numerous factors, may not be relied on as an indication of trading intent on behalf of any Aston Fund. |

Aston Funds

Large Cap Funds

ASTON/Cornerstone Large Cap Value Fund

ASTON/Fairpointe Focused Equity Fund

ASTON/Herndon Large Cap Value Fund

ASTON/Montag & Caldwell Growth Fund

Equity Income Funds

ASTON/River Road Dividend All Cap Value Fund

ASTON/River Road Dividend All Cap Value Fund II

Mid Cap Funds

ASTON/Fairpointe Mid Cap Fund

ASTON/Montag & Caldwell Mid Cap Growth Fund

Table of Contents

Small Cap Funds

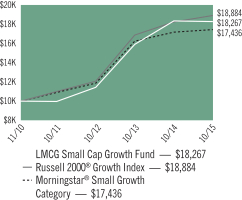

ASTON/LMCG Small Cap Growth Fund

ASTON/River Road Independent Value Fund

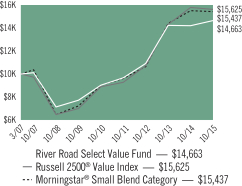

ASTON/River Road Select Value Fund

ASTON/River Road Small Cap Value Fund

ASTON/Silvercrest Small Cap Fund

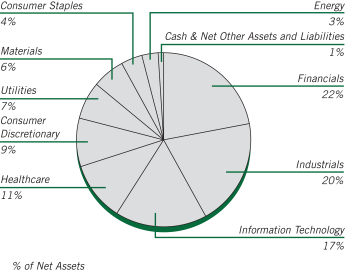

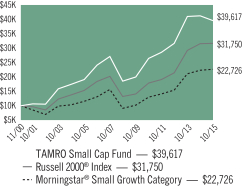

ASTON/TAMRO Small Cap Fund

Fixed Income Funds

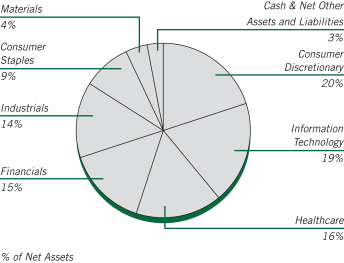

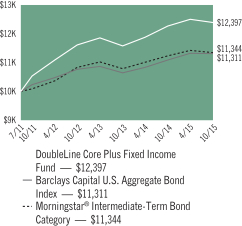

ASTON/DoubleLine Core Plus Fixed Income Fund ASTON/TCH Fixed Income Fund

Alternative Funds

ASTON/Anchor Capital Enhanced Equity Fund

ASTON/Lake Partners LASSO Alternatives Fund

ASTON/River Road Long-Short Fund

International Funds

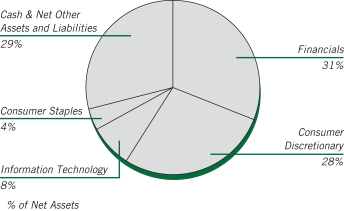

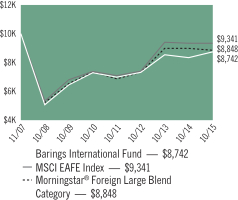

ASTON/Barings International Fund

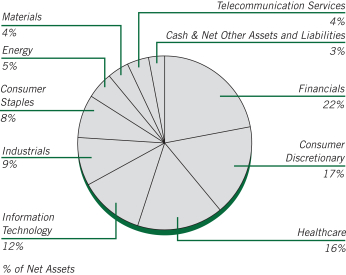

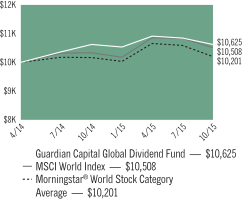

ASTON/Guardian Capital Global Dividend Fund

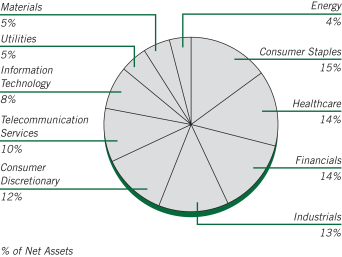

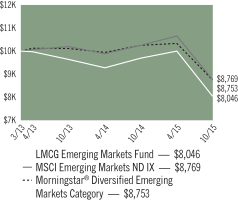

ASTON/LMCG Emerging Markets Fund

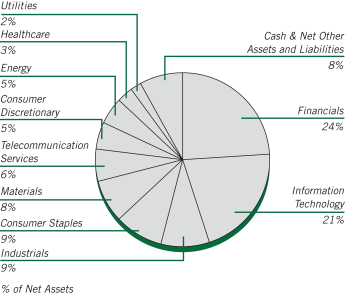

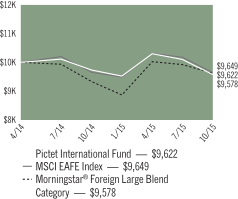

ASTON/Pictet International Fund

ASTON/TAMRO International Small Cap Fund

Sector Fund

ASTON/Harrison Street Real Estate Fund

Balanced Fund

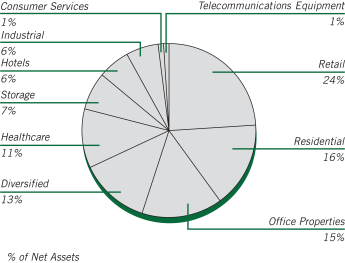

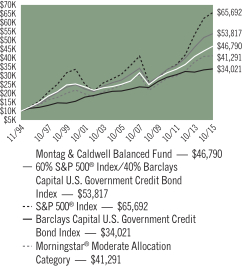

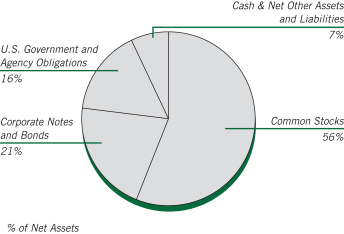

ASTON/Montag & Caldwell Balanced Fund

This report is submitted for general information to the shareholders of the funds. It is not authorized for distribution to prospective investors in the funds unless preceded or accompanied by an effective prospectus which includes details regarding the funds’ objectives, policies, expenses and other information.

Aston Funds are distributed by Foreside Funds Distributors LLC, 400 Berwyn Park, 899 Cassatt Road, Berwyn, PA 19312

Shareholder Services 800-992-8151 • www.astonfunds.com

NOT FDIC INSURED • NO BANK GUARANTEE • MAY LOSE VALUE

ASTON/Cornerstone Large Cap Value Fund

| | |

| |

| Portfolio Manager Commentary (unaudited) | | October 31, 2015 |

| John Campbell, CFA; Rick van Nostrand, CFA; Cameron Clement, CFA; & Dean Morris, CFA |

| Q. | What were the most significant market factors affecting Fund performance and returns relative to the benchmark during the past 12 months? |

| A. | The Russell 1000® Value Index posted a return of roughly 0.5% over the past year, but exhibited substantial volatility along the way. Our investment process focuses on valuation, as measured by Cornerstone Investment Partners’ proprietary valuation tool, paired with rigorous fundamental analysis. Occasionally, short-term, non-fundamental factors such as price momentum and earnings estimate revisions may drive market performance. We have experienced such a period not only for the last 12 months, but for most of the past two years. During these periods, it is not uncommon for expensive stocks to outperform their more attractively valued peers. However, it is our experience that these periods typically end without warning, and exhibit dramatic reversals in market leadership. As disciplined investors, our response to such periods is to stick to our investment philosophy, which is simple, sensible, and has proven its worth over the long term. |

| Q. | What were the best performing holdings for the Fund during the period? |

| A. | Cisco Systems (+21.5%) was the top performer over the trailing twelve-month period. The market has rewarded Cisco for consistently delivering quarterly results in excess of Wall Street consensus expectations. The company offers a deeply embedded position across a broad customer base, and its valuation is compelling. Microsoft (+15.1%) also performed well. The company has delivered strong results under CEO Satya Nadella, and appears to be embracing the opportunity presented by cloud computing. Boeing (+17.4%) has outperformed as it has become clear that the company’s 787 airplane program will likely become highly cash generative in the future. The company continues to operate in an effective duopoly and appears meaningfully undervalued. |

| Q. | What were the weakest performing holdings? |

| A. | Ensco (-57.1%) was the weakest performer. The stock has been pressured by the decline in the price of crude oil, which has raised concerns regarding demand for offshore rigs. Ensco operates with a sizable backlog, strong balance sheet, and a high caliber rig fleet. We believe the company is well positioned to survive the downturn in oil prices, and emerge stronger. Additionally, the company is trading well below our estimate of its fair value. Cummins (-27.5%) performed poorly, trading lower due to concerns regarding demand in emerging market economies such as China and Brazil. The company continues to operate with a reputation for technological leadership, as well as a very strong balance sheet. Gap (-26.4%) has traded downward after delivering results below expectations, particularly in its Gap and Banana Republic brands. The company has generated strong results in its Old Navy brand, margins well above many peers, and growth in the Athleta brand. The stock appears significantly undervalued, with low expectations from investors. |

| Q. | How was the Fund positioned as of October 31, 2015? |

| A. | Our actively constructed 800 stock universe is trading at 89% of fair value based on our proprietary Fair Value Model. Within the universe, approximately 416 stocks remain undervalued, with the median stock price near our fair value estimate. While the six-and-a-half-year bull market has placed the overall market close to fair value, we believe that we are able to find attractive value in those companies that have demonstrated long-term profitability. Despite the market’s current valuation level, our work suggests attractive valuations in the Consumer Discretionary, Industrial, and Technology sectors, and we are overweight these sectors as a result. We continue to believe that divergences between price and value create compelling opportunities for long-term performance, and that we are positioned to capitalize on these opportunities in 2016 and beyond. |

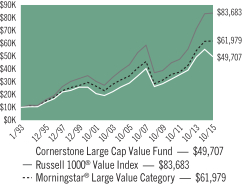

Growth of a Hypothetical

$10,000 Investment—Class N

All dividends and capital gains are reinvested. Indexes are unmanaged and do not take into account fees, expenses or other costs.

Returns shown in the chart and table do not reflect taxes that a shareholder would pay on Fund distributions or on the sale of the Fund shares.

Value investing involves the risk that a Fund’s investments in companies believed to be undervalued will not appreciate as anticipated.

RETURNSFOR PERIOD ENDED 10/31/15

Average Annual Total Returns - Class N

| | | | |

One Year | | | -10.17 | % |

Five Year | | | 9.09 | % |

Ten Year | | | 5.52 | % |

Since Inception | | | 7.28 | % |

Inception Date 01/04/93

Average Annual Total Returns - Class I

| | | | |

One Year | | | -9.88 | % |

Five Year | | | 9.40 | % |

Ten Year | | | 5.79 | % |

Since Inception | | | 5.55 | % |

Inception Date 09/20/05

The performance data quoted represents past performance. Past performance does not guarantee future results. Investment return and principal value will fluctuate so that an investor’s shares, upon redemption, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For performance data current to the most recent month-end, please visit our website at www.astonfunds.com.

The total expense ratios for Class N and Class I shares are 1.31% and 1.06%, respectively, as disclosed in the prospectus dated February 28, 2015. Please refer to the Financial Highlights section in this report for more information.

| | |

| |

| ASTON/Cornerstone Large Cap Value Fund | | October 31, 2015 |

| |

| Schedule of Investments | | |

| | | | | | | | |

Shares | | | | | Market

Value | |

| |

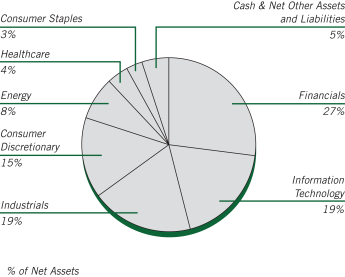

| | COMMON STOCKS – 95.59% | | | | |

| | |

| | | | Consumer Discretionary – 15.17% | | | | |

| | 101,200 | | | BorgWarner | | $ | 4,333,384 | |

| | 43,350 | | | Dollar General | | | 2,937,829 | |

| | 137,575 | | | Gap | | | 3,744,791 | |

| | 88,300 | | | Magna International (Canada) | | | 4,656,059 | |

| | 60,050 | | | VF | | | 4,054,576 | |

| | | | | | | | |

| | | | | | | 19,726,639 | |

| | | | | | | | |

| | |

| | | | Consumer Staples – 3.26% | | | | |

| | 95,525 | | | Tyson Foods, Class A | | | 4,237,489 | |

| | | | | | | | |

| | |

| | | | Energy – 7.54% | | | | |

| | 50,500 | | | Chevron | | | 4,589,440 | |

| | 134,800 | | | Ensco, Class A (United Kingdom) | | | 2,241,724 | |

| | 56,775 | | | Royal Dutch Shell, Class A SP ADR | | | 2,978,417 | |

| | | | | | | | |

| | | | | | | 9,809,581 | |

| | | | | | | | |

| | |

| | | | Financials – 26.98% | | | | |

| | 34,950 | | | ACE (Switzerland) | | | 3,968,223 | |

| | 71,050 | | | Capital One Financial | | | 5,605,845 | |

| | 101,850 | | | Citigroup | | | 5,415,364 | |

| | 98,700 | | | JPMorgan Chase | | | 6,341,475 | |

| | 73,150 | | | Lincoln National | | | 3,914,256 | |

| | 42,175 | | | PNC Financial Services Group | | | 3,806,716 | |

| | 42,400 | | | State Street | | | 2,925,600 | |

| | 73,700 | | | US Bancorp | | | 3,108,666 | |

| | | | | | | | |

| | | | | | | 35,086,145 | |

| | | | | | | | |

| | |

| | | | Healthcare – 4.43% | | | | |

| | 57,075 | | | Johnson & Johnson | | | 5,766,287 | |

| | | | | | | | |

| | |

| | | | Industrials – 18.78% | | | | |

| | 26,925 | | | Boeing | | | 3,986,785 | |

| | 41,025 | | | Cummins | | | 4,246,498 | |

| | | | | | | | |

Shares | | | | | Market

Value | |

| | |

| | | | Industrials (continued) | | | | |

| | 46,725 | | | Honeywell International | | $ | 4,825,758 | |

| | 40,250 | | | Norfolk Southern | | | 3,221,208 | |

| | 49,400 | | | Parker-Hannifin | | | 5,172,180 | |

| | 14,130 | | | WW Grainger | | | 2,967,300 | |

| | | | | | | | |

| | | | | | | 24,419,729 | |

| | | | | | | | |

| | |

| | | | Information Technology – 19.43% | | | | |

| | 3,875 | | | Alphabet, Class A * | | | 2,857,386 | |

| | 203,100 | | | Cisco Systems | | | 5,859,435 | |

| | 99,750 | | | EMC | | | 2,615,445 | |

| | 118,800 | | | Microsoft | | | 6,253,632 | |

| | 142,825 | | | Oracle | | | 5,547,323 | |

| | 31,900 | | | Western Digital | | | 2,131,558 | |

| | | | | | | | |

| | | | | | | 25,264,779 | |

| | | | | | | | |

| | |

| | | | Total Common Stocks

(Cost $133,553,841) | | | 124,310,649 | |

| | | | | | | | |

| |

| | INVESTMENT COMPANY – 3.70% | | | | |

| | |

| | 4,808,638 | | | BlackRock Liquidity Funds TempFund Portfolio | | | 4,808,638 | |

| | | | | | | | |

| | |

| | | | Total Investment Company

(Cost $4,808,638) | | | 4,808,638 | |

| | | | | | | | |

| Total Investments – 99.29%

(Cost $138,362,479)** | | | 129,119,287 | |

| | | | | | | | |

| Net Other Assets and Liabilities – 0.71% | | | 925,315 | |

| | | | | | | | |

| Net Assets – 100.00% | | $ | 130,044,602 | |

| | | | | | | | |

| * | | Non-income producing security. |

| ** | | Aggregate cost for Federal income tax purposes is $140,374,896. |

| | | | |

Gross unrealized appreciation | | $ | 4,523,285 | |

Gross unrealized depreciation | | | (15,778,894 | ) |

| | | | |

Net unrealized depreciation | | $ | (11,255,609 | ) |

| | | | |

| SP ADR | | Sponsored American Depositary Receipt |

See accompanying Notes to Financial Statements.

ASTON/Fairpointe Focused Equity Fund

| | |

| |

| Portfolio Manager Commentary (unaudited) | | October 31, 2015 |

| Robert S. Burnstine & Thyra E. Zerhusen |

| Q. | What were the most significant market factors affecting Fund performance and returns relative to the benchmark during the past 10 months? |

| A. | Macroeconomic concerns increased during 2015, primarily attributable to China’s devaluation of the yuan in August highlighting the slowing pace of China’s economic growth, the strong dollar weakening corporate earnings due to foreign currency exchange issues, and investor worries regarding the timing of interest rate increases by the Federal Reserve. In this macro-driven investment environment, stock price movements over the short term have been driven by momentum (both positive and negative) without regard to valuation. Over the longer term, however, valuation matters. Year to date, the Russell 1000® Growth benchmark has outperformed the Russell 1000® Value benchmark by over 900 basis points. As value investors, we focus on identifying companies that trade at significant discounts to our estimates of intrinsic value. Many of our holdings remain cyclically depressed and trade at the low end of their respective historical trading ranges on several financial metrics. And while the timing for change in investor sentiment is difficult to call, sentiment can change rather quickly. We anticipate our patience to be rewarded over time. |

| Q. | What were the best performing holdings for the Fund during the period? |

| A. | Our best performer, Hospira, agreed to be acquired by Pfizer for $90 per share in cash. Hologic, our second best performer, posted strong organic revenue growth across its diagnostic, breast health, surgical and skeletal health business segments. Management has led a broad turnaround focusing on better resource and capital allocation as well as excellent execution. Boston Scientific has benefited from solid organic revenue growth from its product pipeline and increasing margins due to better mix and productivity improvements. |

| Q. | What were the weakest performing holdings? |

| A. | Avon Products, our worst performer, was sold during the third quarter at a significant loss. Avon appeared inexpensive on several financial metrics, its own historical trading range, and competitor comparisons. While Avon’s balance sheet seemed secure several months ago, the magnitude of foreign currency issues created uncertainty regarding the ability of Avon to service its debt over time. Hewlett-Packard, our second worst performer, provided lower cash flow guidance due to currency headwinds and costs related to the separation into Hewlett-Packard Enterprises and HP Inc. We view the separation positively allowing each company to become more focused and enhance capital allocation efficiency. We believe its stock remains attractively valued. Teradata reported disappointing revenue and margins. Teradata is investing in its big data analytics applications as it seeks to expand its customer base to generate higher revenue growth. Teradata currently trades at the lower end of its historical trading range, yet continues to generate solid free cash flow and to repurchase a significant amount of its shares outstanding. |

| Q. | How was the Fund positioned as of October 31, 2015? |

| A. | While global equity markets have seen increased volatility, we have capitalized on opportunities that have emerged due to near-term disruptions. We continue to find undervalued stocks that, in our view, will perform well over a several year period. As our holding period is generally three to five years, we seek to be patient to allow the discount between current prices and our estimates of fair value to narrow. The Fund is overweight Consumer and Energy sectors relative to their respective benchmarks in our continued pursuit to hold stocks that we view as significantly undervalued. Conversely, we have reduced our exposure to Healthcare as the gap between price and our estimate of fair value narrowed for many of our Healthcare holdings. |

Note: A basis point (bp) is a unit of measure. 1 bp = .01%.

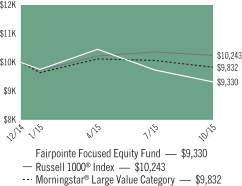

Growth of a Hypothetical

$10,000 Investment—Class N

All dividends and capital gains are reinvested. Indexes are unmanaged and do not take into account fees, expenses or other costs.

Returns shown in the chart and table do not reflect taxes that a shareholder would pay on Fund distributions or on the sale of the Fund shares.

Value investing involves the risk that a Fund’s investments in companies believed to be undervalued will not appreciate as anticipated.

RETURNSFOR PERIOD ENDED 10/31/15

Total Return - Class N

| | | | |

Cumulative Since Inception | | | -6.70 | % |

Inception Date 12/24/14

Total Return - Class I

| | | | |

Cumulative Since Inception | | | -6.50 | % |

Inception Date 12/24/14

The performance data quoted represents past performance. Past performance does not guarantee future results. Investment return and principal value will fluctuate so that an investor’s shares, upon redemption, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For performance data current to the most recent month-end, please visit our website at www.astonfunds.com.

The performance quoted would have been lower if fee waivers and/or expense reimbursements had not been in effect.

| | |

| |

| ASTON/Fairpointe Focused Equity Fund | | October 31, 2015 |

| |

| Schedule of Investments | | |

| | | | | | | | |

Shares | | | | | Market

Value | |

| |

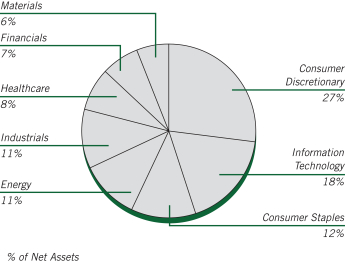

| | COMMON STOCKS – 99.64% | | | | |

| | |

| | | | Consumer Discretionary – 27.11% | | | | |

| | 11,100 | | | 21st Century Fox, Class A | | $ | 340,659 | |

| | 4,500 | | | Carnival | | | 243,360 | |

| | 11,600 | | | Discovery Communications, Class C * | | | 319,232 | |

| | 5,400 | | | Interpublic Group | | | 123,822 | |

| | 4,700 | | | Liberty Interactive, Class A * | | | 128,639 | |

| | 18,900 | | | News, Class A | | | 291,060 | |

| | 4,600 | | | Scholastic | | | 188,002 | |

| | 8,900 | | | Staples | | | 115,611 | |

| | | | | | | | |

| | | | | | | 1,750,385 | |

| | | | | | | | |

| | |

| | | | Consumer Staples – 12.04% | | | | |

| | 3,200 | | | PepsiCo | | | 327,008 | |

| | 5,500 | | | Unilever, SP ADR (Great Britain) | | | 244,475 | |

| | 3,600 | | | Wal-Mart Stores | | | 206,064 | |

| | | | | | | | |

| | | | | | | 777,547 | |

| | | | | | | | |

| | |

| | | | Energy – 10.78% | | | | |

| | 4,450 | | | Apache | | | 209,728 | |

| | 7,500 | | | BP, SP ADR | | | 267,750 | |

| | 13,800 | | | Transocean Ltd. (Switzerland) | | | 218,454 | |

| | | | | | | | |

| | | | | | | 695,932 | |

| | | | | | | | |

| | |

| | | | Financials – 6.90% | | | | |

| | 5,400 | | | Legg Mason | | | 241,650 | |

| | 2,900 | | | Northern Trust | | | 204,131 | |

| | | | | | | | |

| | | | | | | 445,781 | |

| | | | | | | | |

| | |

| | | | Healthcare – 8.43% | | | | |

| | 9,600 | | | Boston Scientific * | | | 175,488 | |

| | 3,000 | | | Hologic * | | | 116,580 | |

| | 700 | | | Quest Diagnostics | | | 47,565 | |

| | 2,400 | | | Varian Medical Systems * | | | 188,472 | |

| | 300 | | | VCA * | | | 16,431 | |

| | | | | | | | |

| | | | | | | 544,536 | |

| | | | | | | | |

| | | | | | | | |

Shares | | | | | Market

Value | |

| | |

| | | | Industrials – 11.19% | | | | |

| | 4,600 | | | AGCO | | $ | 222,594 | |

| | 5,100 | | | Fluor | | | 243,831 | |

| | 9,100 | | | Kennametal | | | 255,892 | |

| | | | | | | | |

| | | | | | | 722,317 | |

| | | | | | | | |

| | |

| | | | Information Technology – 17.69% | | | | |

| | 7,900 | | | Cisco Systems | | | 227,915 | |

| | 10,400 | | | Cree * | | | 261,976 | |

| | 12,300 | | | Hewlett-Packard * | | | 331,608 | |

| | 2,300 | | | Itron * | | | 84,479 | |

| | 8,400 | | | Teradata * | | | 236,124 | |

| | | | | | | | |

| | | | | | | 1,142,102 | |

| | | | | | | | |

| | |

| | | | Materials – 5.50% | | | | |

| | 4,300 | | | FMC | | | 175,053 | |

| | 5,500 | | | Greif, Class A | | | 180,290 | |

| | | | | | | | |

| | | | | | | 355,343 | |

| | | | | | | | |

| | |

| | | | Total Common Stocks

(Cost $6,754,384) | | | 6,433,943 | |

| | | | | | | | |

| |

| | INVESTMENT COMPANY – 0.71% | | | | |

| | |

| | 45,705 | | | BlackRock Liquidity Funds

TempFund Portfolio | | | 45,705 | |

| | | | | | | | |

| | |

| | | | Total Investment Company

(Cost $45,705) | | | 45,705 | |

| | | | | | | | |

| Total Investments – 100.35%

(Cost $6,800,089)** | | | 6,479,648 | |

| | | | | | | | |

| Net Other Assets and Liabilities – (0.35)% | | | (22,856 | ) |

| | | | | | | | |

| Net Assets – 100.00% | | $ | 6,456,792 | |

| | | | | | | | |

| * | | Non-income producing security. |

| ** | | Aggregate cost for Federal income tax purposes is $6,802,160. |

| | | | |

Gross unrealized appreciation | | $ | 261,688 | |

Gross unrealized depreciation | | | (584,200 | ) |

| | | | |

Net unrealized depreciation | | $ | (322,512 | ) |

| | | | |

| SP ADR | | Sponsored American Depositary Receipt |

See accompanying Notes to Financial Statements.

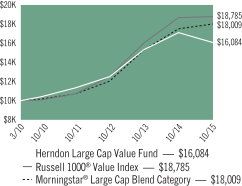

ASTON/Herndon Large Cap Value Fund

| | |

| |

| Portfolio Manager Commentary (unaudited) | | October 31, 2015 |

| | Randell A. Cain, Jr., CFA |

| Q. | What were the most significant market factors affecting Fund performance and returns relative to the benchmark during the past 12 months? |

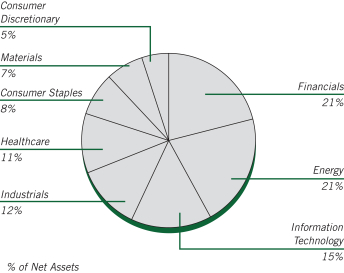

| A. | Over the past 1-year period ended October 31, 2015, the Russell 1000® Value Index increased less than 1%. The Fund underperformed the Russell 1000® Value Index by more than 500 basis points during the period. Both stock selection and sector allocation were negative; however, sector allocation was the main driver of relative performance. In terms of allocation, the portfolio’s overweight position in the underperforming Energy sector, along with the underweight position in Healthcare were the largest detractors from relative performance. |

The three sectors with the highest relative contribution for the period were Consumer Staples, Consumer Discretionary and Materials. The Consumer Staples sector garnered positive double-digit returns led by Altria Group, a domestic manufacturer and seller of cigarettes and other tobacco products. Consumer Discretionary benefited from the increased spending in US off-brand retail establishments such as TJX Companies and Ross Stores that appealed to investors over the period. Stock selection of chemical companies, Newmarket and Lyondellbassell, drove the relative outperformance in the Materials sector.

The three sectors with the lowest level of relative contribution were Energy, Financials and Healthcare. Much of the maligned performance of Energy occurred in the fourth quarter of 2014 as the decline in oil prices wreaked havoc on this part of the portfolio. The two worst performing Energy stocks during the period were Oasis Petroleum and SM Energy, which were challenged by the severe volatility and price declines in crude oil. The majority of the underperformance in Financials can be attributed to Nationstar Mortgage and Waddell & Reed. Nationstar was negatively impacted by disappointing earnings and heightened regulatory scrutiny. Nationstar Mortgage was sold from the portfolio at the end of the second quarter of 2015 as a result of it being removed from our universe, the Russell 1000®

Index. Waddell & Reed is an asset manager that underperformed due to negative sentiment associated with turnover in the portfolio management ranks. Increased outflows and weaker fund performance have disproportionately punished the company. Our stock selection in the biotechnology industry led the relative underperformance in the Healthcare sector.

| Q. | What were the best performing holdings for the Fund during the period? |

| A. | The top three positive individual stock contributors were Altria (+30%) a tobacco company in the Consumer Staples sector, Mylan (+9%) a global pharmaceuticals company in the Healthcare sector and Valero Energy (+35%) an oil refining and marketing company in the Energy sector. |

| Q. | What were the weakest performing holdings? |

| A. | The bottom three individual stock contributors were Nationstar Mortgage (-52%) a mortgage company in the Financials sector, SM Energy (-41%) and Oasis Petroleum (-58%). Both SM Energy and Oasis Petroleum are exploration and production companies within the Energy sector. |

| Q. | How was the Fund positioned as of October 31, 2015? |

| A. | As of October 31, 2015, the Fund was overweight in the Energy, Materials and Technology sectors while underweight in Financials, Utilities, and Telecom. We believe the stimulus in the global economy will eventually begin to have a more positive impact. We believe the portfolio is advantageously exposed and highly correlated with the sectors that have the potential to perform well during such a period of market performance and significantly underweight those that should lag. |

Note: A basis point (bp) is a unit of measure. 1 bp = .01%.

Growth of a Hypothetical

$10,000 Investment—Class N

All dividends and capital gains are reinvested. Indexes are unmanaged and do not take into account fees, expenses or other costs.

Returns shown in the chart and table do not reflect taxes that a shareholder would pay on Fund distributions or on the sale of the Fund shares.

Value investing involves the risk that a Fund’s investments in companies believed to be undervalued will not appreciate as anticipated.

RETURNSFOR PERIOD ENDED 10/31/15

Average Annual Total Returns - Class N

| | | | |

1 Year | | | -6.10 | % |

Five Year | | | 9.13 | % |

Since Inception | | | 8.87 | % |

Inception Date 03/31/10

Average Annual Total Returns - Class I

| | | | |

1 Year | | | -5.88 | % |

Since Inception | | | 7.72 | % |

Inception Date 03/02/11

The performance data quoted represents past performance. Past performance does not guarantee future results. Investment return and principal value will fluctuate so that an investor’s shares, upon redemption, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For performance data current to the most recent month-end, please visit our website at www.astonfunds.com.

| | |

| |

| ASTON/Herndon Large Cap Value Fund | | October 31, 2015 |

| |

| Schedule of Investments | | |

| | | | | | | | |

Shares | | | | | Market

Value | |

|

| | COMMON STOCKS – 99.66% | |

| | | | Consumer Discretionary – 5.23% | | | | |

| | 15,849 | | | Ross Stores | | $ | 801,642 | |

| | 60,753 | | | TJX | | | 4,446,512 | |

| | 14,969 | | | Yum! Brands | | | 1,061,452 | |

| | | | | | | | |

| | | | | | | 6,309,606 | |

| | | | | | | | |

| | | | Consumer Staples – 8.50% | | | | |

| | 73,080 | | | Altria Group | | | 4,419,148 | |

| | 41,098 | | | Campbell Soup | | | 2,087,367 | |

| | 42,263 | | | Philip Morris International | | | 3,736,049 | |

| | | | | | | | |

| | | | | | | 10,242,564 | |

| | | | | | | | |

| | | | Energy – 21.12% | | | | |

| | 43,731 | | | Apache | | | 2,061,042 | |

| | 119,745 | | | Chesapeake Energy | | | 853,782 | |

| | 67,797 | | | Continental Resources * | | | 2,298,996 | |

| | 25,828 | | | Exxon Mobil | | | 2,137,009 | |

| | 85,700 | | | Halliburton | | | 3,289,166 | |

| | 79,243 | | | Marathon Petroleum | | | 4,104,787 | |

| | 174,627 | | | Noble (United Kingdom) | | | 2,352,226 | |

| | 62,514 | | | SM Energy | | | 2,084,842 | |

| | 26,121 | | | Tesoro | | | 2,793,119 | |

| | 52,829 | | | Valero Energy | | | 3,482,488 | |

| | | | | | | | |

| | | | | | | 25,457,457 | |

| | | | | | | | |

| | | | Financials – 20.72% | | | | |

| | 31,697 | | | American Express | | | 2,322,122 | |

| | 82,471 | | | Apartment Investment & Management, Class A, REIT | | | 3,232,038 | |

| | 65,742 | | | CBOE Holdings | | | 4,407,344 | |

| | 5,283 | | | Credit Acceptance * | | | 998,962 | |

| | 54,590 | | | Discover Financial Services | | | 3,069,050 | |

| | 75,427 | | | Eaton Vance | | | 2,723,669 | |

| | 32,871 | | | McGraw-Hill Financial | | | 3,045,169 | |

| | 29,056 | | | Moody’s | | | 2,794,025 | |

| | 64,568 | | | Waddell & Reed Financial, Class A | | | 2,385,142 | |

| | | | | | | | |

| | | | | | | 24,977,521 | |

| | | | | | | | |

| | | | | | | | |

Shares | | | | | Market

Value | |

| | | | Healthcare – 10.68% | | | | |

| | 58,699 | | | AbbVie | | $ | 3,495,525 | |

| | 24,360 | | | Gilead Sciences | | | 2,634,047 | |

| | 24,414 | | | Jazz Pharmaceuticals (Ireland) * | | | 3,351,556 | |

| | 76,901 | | | Mylan * | | | 3,390,565 | |

| | | | | | | | |

| | | | | | | 12,871,693 | |

| | | | | | | | |

| | | | Industrials – 11.69% | | | | |

| | 22,012 | | | Lockheed Martin | | | 4,838,898 | |

| | 29,643 | | | Rockwell Collins | | | 2,570,641 | |

| | 37,274 | | | United Parcel Service, Class B | | | 3,839,967 | |

| | 39,622 | | | Verisk Analytics * | | | 2,837,331 | |

| | | | | | | | |

| | | | | | | 14,086,837 | |

| | | | | | | | |

| | | | Information Technology – 15.12% | | | | |

| | 12,621 | | | Accenture, Class A (Ireland) | | | 1,352,971 | |

| | 4,109 | | | Alliance Data Systems * | | | 1,221,647 | |

| | 33,458 | | | Apple | | | 3,998,231 | |

| | 16,142 | | | Harris | | | 1,277,316 | |

| | 40,796 | | | Hewlett-Packard * | | | 1,099,860 | |

| | 25,828 | | | MasterCard, Class A | | | 2,556,714 | |

| | 22,046 | | | Microsoft | | | 1,160,501 | |

| | 37,861 | | | Western Digital | | | 2,529,872 | |

| | 157,605 | | | Western Union | | | 3,033,896 | |

| | | | | | | | |

| | | | | | | 18,231,008 | |

| | | | | | | | |

| | | | Materials – 6.60% | | | | |

| | 47,252 | | | CF Industries Holdings | | | 2,398,984 | |

| | 29,937 | | | LyondellBasell Industries, Class A (Netherlands) | | | 2,781,447 | |

| | 7,044 | | | NewMarket | | | 2,773,505 | |

| | | | | | | | |

| | | | | | | 7,953,936 | |

| | | | | | | | |

| | |

| | | | Total Common Stocks

(Cost $110,469,323) | | | 120,130,622 | |

| | | | | | | | |

|

| | INVESTMENT COMPANY – 0.44% | |

| | |

| | 524,577 | | | BlackRock Liquidity Funds TempFund Portfolio | | | 524,577 | |

| | | | | | | | |

| | |

| | | | Total Investment Company

(Cost $524,577) | | | 524,577 | |

| | | | | | | | |

| Total Investments – 100.10%

(Cost $110,993,900)** | | | 120,655,199 | |

| | | | | | | | |

| Net Other Assets and Liabilities – (0.10)% | | | (115,144 | ) |

| | | | | | | | |

| Net Assets – 100.00% | | $ | 120,540,055 | |

| | | | | | | | |

| * | | Non-income producing security. |

| ** | | Aggregate cost for Federal income tax purposes is $111,531,704. |

| | | | |

Gross unrealized appreciation | | $ | 17,822,154 | |

Gross unrealized depreciation | | | (8,698,659 | ) |

| | | | |

Net unrealized appreciation | | $ | 9,123,495 | |

| | | | |

| REIT | | Real Estate Investment Trust |

See accompanying Notes to Financial Statements.

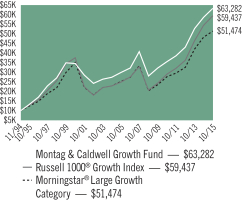

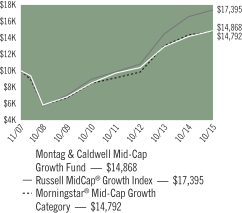

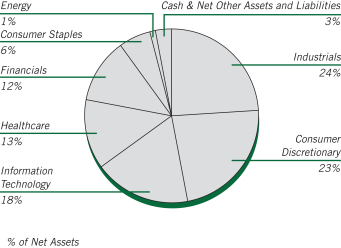

ASTON/Montag & Caldwell Growth Fund

| | |

| |

| Portfolio Manager Commentary (unaudited) | | October 31, 2015 |

Ronald E. Canakaris, CFA, CIC & Andrew W. Jung, CFA |

| Q. | What were the most significant market factors affecting Fund performance and returns relative to the benchmark during the past 12 months? |

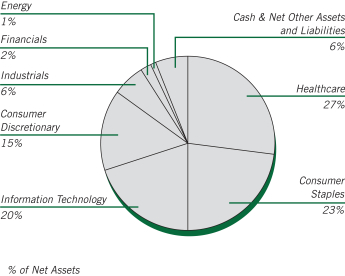

| A. | The Fund lagged its primary benchmark, the Russell 1000® Growth Index for the period. Performance benefited from an overweight allocation to Consumer Staples and underweight positions in Technology and Energy. We believe that the ending of Quantitative Easing (QE) in late 2014 allowed for normal market forces and company specific fundamentals to have a greater impact on share prices than was the case during the previous periods of significant liquidity being provided by the Fed. Against this backdrop we think active managers with strong, fundamentally-driven investment processes, like Montag & Caldwell, should benefit. |

| Q. | What were the best performing holdings for the Fund during the period? |

| A. | Our best performing stock was Starbucks (+67.9%) which benefited from strong same store sales and earnings growth as well as new initiatives such as mobile ordering which is anticipated to drive further sales/earnings strength. Nike rose 42.5%. Nike is a premier global athletic brand and sustained rapid growth across all key geographies during the period, propelling shares higher. Facebook rose 36% as the company demonstrated success monetizing its customers’ transition to mobile usage. IT consulting firm Accenture’s shares rose 35%. Fundamentals remained strong as Accenture assists its clients’ transition to mobile and digital applications. Walgreens Boots Alliance shares rose 34%. New management, resulting from the closing of the merger between Walgreens and European-based Alliance Boots, moved quickly to improve performance in US-based Walgreens stores and realize merger-related cost and revenue synergies. |

| Q. | What were the weakest performing holdings? |

| A. | Chipmaker Qualcomm shares fell 22% following losses to competitors and a patent dispute in China. We maintained only a modest position during the period, limiting its impact on relative performance. Union Pacific, one of our best performers the prior year, fell 22% as the slowdown in energy and industrial end markets resulted in slowing rail cargo volumes. Biogen shares fell 20% as sales for its key multiple sclerosis drug, Tecfidera, failed to meet expectations. Ralph Lauren lost 18% as ongoing heavy investments in stores, infrastructure and technology depressed earnings growth. Shares of online travel company Priceline fell 17%, as reported results suffered from the negative influence of the significant increase in the value of the dollar versus key currencies like the Euro. |

| Q. | How was the Fund positioned as of October 31, 2015? |

| A. | After several years of a zero interest rate policy and multiple rounds of QE, it appears that the Fed would like to begin raising interest rates off the zero-bound. Because economic growth is still very moderate, inflation is low and earnings growth continues to slow, the market is likely to be choppy as investors evaluate the Fed’s likely course of action. After the recent and overdue stock market correction in August, the market has recouped all of its losses even as the outlook for economic and earnings growth remains muted. With QE3 having ended a year ago, we think market forces will influence share prices more so than the Fed’s intervention in capital markets. As such, we expect stock market volatility to persist. We believe the high quality growth stocks in the Fund are well positioned for what could be a choppy and more volatile market environment. With the corporate earnings cycle maturing, these companies are particularly attractive as their earnings growth is more assured due to their strong business franchises both at home and abroad and their financial strength. |

Growth of a Hypothetical

$10,000 Investment—Class N

All dividends and capital gains are reinvested. Indexes are unmanaged and do not take into account fees, expenses or other costs.

Returns shown in the chart and table do not reflect taxes that a shareholder would pay on Fund distributions or on the sale of the Fund shares.

RETURNSFOR PERIOD ENDED 10/31/15

Average Annual Total Returns - Class N

| | | | |

One Year | | | 7.93 | % |

Five Year | | | 12.18 | % |

Ten Year | | | 7.79 | % |

Since Inception | | | 9.19 | % |

Inception Date 11/02/94

Average Annual Total Returns - Class I

| | | | |

One Year | | | 8.21 | % |

Five Year | | | 12.46 | % |

Ten Year | | | 8.07 | % |

Since Inception | | | 7.79 | % |

Inception Date 06/28/96

Average Annual Total Returns - Class R

| | | | |

One Year | | | 7.66 | % |

Five Year | | | 11.89 | % |

Ten Year | | | 7.54 | % |

Since Inception | | | 7.69 | % |

Inception Date 12/31/02

The performance data quoted represents past performance. Past performance does not guarantee future results. Investment return and principal value will fluctuate so that an investor’s shares, upon redemption, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For performance data current to the most recent month-end, please visit our website at www.astonfunds.com.

The total expense ratios for Class N, Class I and Class R shares are 1.04%, 0.79% and 1.29%, respectively, as disclosed in the prospectus dated February 28, 2015. Please refer to the Financial Highlights section in this report for more information.

| | |

| |

| ASTON/Montag & Caldwell Growth Fund | | October 31, 2015 |

| |

| Schedule of Investments | | |

| | | | | | | | |

Shares | | | | | Market Value | |

| |

| | COMMON STOCKS – 93.40% | | | | |

| | |

| | | | Consumer Discretionary – 14.84% | | | | |

| | 1,150,000 | | | Carnival | | $ | 62,192,000 | |

| | 570,000 | | | Dollar General | | | 38,628,900 | |

| | 987,080 | | | Dollar Tree * | | | 64,643,869 | |

| | 259,100 | | | NIKE, Class B | | | 33,949,873 | |

| | 955,000 | | | Starbucks | | | 59,754,350 | |

| | 890,000 | | | TJX | | | 65,139,100 | |

| | | | | | | | |

| | | | | | | 324,308,092 | |

| | | | | | | | |

| | |

| | | | Consumer Staples – 23.43% | | | | |

| | 880,000 | | | Colgate-Palmolive | | | 58,388,000 | |

| | 213,761 | | | Costco Wholesale | | | 33,799,889 | |

| | 665,000 | | | CVS Health | | | 65,688,700 | |

| | 737,400 | | | Estee Lauder, Class A | | | 59,331,204 | |

| | 2,200,000 | | | Mondelez International, Class A | | | 101,552,000 | |

| | 1,077,800 | | | PepsiCo | | | 110,140,382 | |

| | 984,256 | | | Walgreens Boots Alliance | | | 83,346,798 | |

| | | | | | | | |

| | | | | | | 512,246,973 | |

| | | | | | | | |

| | |

| | | | Energy – 0.41% | | | | |

| | 120,000 | | | Occidental Petroleum | | | 8,944,800 | |

| | | | | | | | |

| | |

| | | | Financials – 1.51% | | | | |

| | 610,100 | | | Wells Fargo | | | 33,030,814 | |

| | | | | | | | |

| | |

| | | | Healthcare – 26.71% | | | | |

| | 1,700,000 | | | Abbott Laboratories | | | 76,160,000 | |

| | 257,121 | | | Allergan PLC (Ireland) * | | | 79,314,115 | |

| | 425,000 | | | AmerisourceBergen | | | 41,016,750 | |

| | 405,923 | | | Amgen | | | 64,208,900 | |

| | 720,900 | | | Celgene * | | | 88,461,639 | |

| | 930,000 | | | Cerner * | | | 61,649,700 | |

| | 536,900 | | | Gilead Sciences | | | 58,054,997 | |

| | 245,000 | | | McKesson | | | 43,806,000 | |

| | 544,000 | | | Thermo Fisher Scientific | | | 71,144,320 | |

| | | | | | | | |

| | | | | | | 583,816,421 | |

| | | | | | | | |

| | | | | | | | |

Shares | | | | | Market Value | |

| | |

| | | | Industrials – 6.34% | | | | |

| | 650,000 | | | Honeywell International | | $ | 67,132,000 | |

| | 46,000 | | | Union Pacific | | | 4,110,100 | |

| | 655,000 | | | United Parcel Service, Class B | | | 67,478,100 | |

| | | | | | | | |

| | | | | | | 138,720,200 | |

| | | | | | | | |

| | |

| | | | Information Technology – 20.16% | | | | |

| | 570,000 | | | Accenture, Class A (Ireland) | | | 61,104,000 | |

| | 133,337 | | | Alphabet, Class A * | | | 98,321,371 | |

| | 791,591 | | | Cognizant Technology Solutions, Class A * | | | 53,915,263 | |

| | 537,000 | | | Facebook, Class A * | | | 54,757,890 | |

| | 415,000 | | | MasterCard, Class A | | | 41,080,850 | |

| | 485,300 | | | PayPal Holdings * | | | 17,475,653 | |

| | 125,000 | | | QUALCOMM | | | 7,427,500 | |

| | 1,373,000 | | | Visa, Class A | | | 106,517,340 | |

| | | | | | | | |

| | | | | | | 440,599,867 | |

| | | | | | | | |

| | |

| | | | Total Common Stocks

(Cost $1,757,868,622) | | | 2,041,667,167 | |

| | | | | | | | |

| |

| | INVESTMENT COMPANY – 5.45% | | | | |

| | |

| | 119,122,132 | | | BlackRock Liquidity Funds TempFund Portfolio | | | 119,122,132 | |

| | | | | | | | |

| | |

| | | | Total Investment Company

(Cost $119,122,132) | | | 119,122,132 | |

| | | | | | | | |

| Total Investments – 98.85%

(Cost $1,876,990,754)** | | | 2,160,789,299 | |

| | | | | | | | |

| Net Other Assets and Liabilities – 1.15% | | | 25,043,314 | |

| | | | | | | | |

| Net Assets – 100.00% | | $ | 2,185,832,613 | |

| | | | | | | | |

| * | | Non-income producing security. |

| ** | | Aggregate cost for Federal income tax purposes is $1,878,212,993. |

| | | | |

Gross unrealized appreciation | | $ | 310,150,622 | |

Gross unrealized depreciation | | | (27,574,316 | ) |

| | | | |

Net unrealized appreciation | | $ | 282,576,306 | |

| | | | |

See accompanying Notes to Financial Statements.

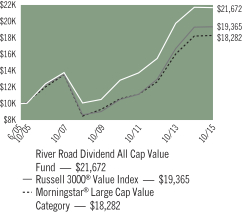

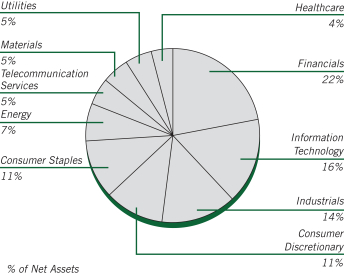

ASTON/River Road Dividend All Cap Value Fund

| | |

| |

| Portfolio Manager Commentary (unaudited) | | October 31, 2015 |

Henry W. Sanders, III, CFA; Thomas S. Forsha, CFA & James C. Shircliff, CFA

| Q. | What were the most significant market factors affecting Fund performance and returns relative to the benchmark during the past 12 months? |

| A. | Over the last 12 months, the most significant market factor affecting absolute return was increased volatility amidst the decline in commodity prices, weak corporate earnings, and uncertainty about the timing of monetary tightening by the Fed. Additionally, according to Ned Davis Research*, among S&P 500 companies, the companies with the lowest yields significantly outperformed those with the highest yields, creating a significant relative headwind for a dividend-oriented strategy. The Information Technology sector had the most significant positive impact on relative results in the period, primarily due to strong stock selection. The Financials sector had the most significant negative impact on relative results due to both weak stock selection and an underweight allocation. |

| Q. | What were the best performing holdings for the Fund during the period? |

| A. | The two holdings with the largest positive contribution to the Fund’s total return were Hasbro Inc., a worldwide leader in branded toys and games, and j2 Global Inc., a global provider of digital media and communications services. Hasbro shares surged following a dividend increase in the first quarter, followed by strong quarterly results in the second quarter, and excitement around the release of the new Jurassic Park film. The position was reduced multiple times and eventually eliminated at a substantial premium to our assessed valuation. j2 Global reported solid results from its Cloud Services and Digital Media divisions, driven by organic growth of the fax and voice customer base and improved monetization of media properties. We reduced the position twice during the year as it traded at a premium to its assessed valuation. |

| Q. | What were the weakest performing holdings? |

| A. | The two holdings with the lowest contribution to the Fund’s total return during the period were National Fuel Gas Co., an integrated natural gas utility, and Qualcomm Inc., which manufactures and sells integrated mobile communications technology. Shares of Natural Fuel Gas were down after the company introduced preliminary guidance for 2016 that included price-related production curtailments due to lower natural gas prices in the Marcellus Shale. We trimmed the position due to accumulated unrealized losses. Qualcomm faced two significant headwinds over the last year: (1) an anti-monopoly investigation by the Chinese government and (2) headwinds in its chip division due to increasing competition and Samsung’s decision to take its chip manufacturing in-house for its highest end smartphones. While Qualcomm settled favorably with the Chinese authorities, the Samsung decision resulted in a significant revenue headwind. We maintained the position during the period. |

| Q. | How was the Fund positioned as of October 31, 2015? |

| A. | The Fund remains significantly overweight in Consumer stocks (both Staples and Discretionary) and Information Technology, and is significantly underweight in Financials, Healthcare, and Energy. The underweight in Financials decreased meaningfully during the period versus the Russell 3000® Value Index benchmark, driven by a number of new positions that were added to the Fund. In Energy, the underweight increased rather dramatically versus the benchmark due to a number of holdings that were eliminated from this sector. Turnover remained elevated as we dealt with numerous overvalued positions and the average yield of Fund holdings increased marginally. We were pleased to see that the Fund largely behaved as expected over the duration of the brief pullback in recent months and were equally pleased with the participation in the sharp recovery. |

| * | | Ned Davis Research, Inc. examined S&P 500 Stock Constituents ranked by quartiles (Dividend Yield) for the twelve months ended October 31, 2015. |

Growth of a Hypothetical

$10,000 Investment—Class N

All dividends and capital gains are reinvested. Indexes are unmanaged and do not take into account fees, expenses or other costs.

Returns shown in the chart and table do not reflect taxes that a shareholder would pay on Fund distributions or on the sale of the Fund shares.

Value investing involves the risk that a Fund’s investments in companies believed to be undervalued will not appreciate as anticipated.

Small-cap and mid-cap stocks may be subject to a higher degree of market risk than the securities of more established companies because they tend to be more volatile and less liquid.

RETURNSFOR PERIOD ENDED 10/31/15

Average Annual Total Returns - Class N

| | | | |

One Year | | | -0.23 | % |

Five Year | | | 11.04 | % |

Ten Year | | | 8.01 | % |

Since Inception | | | 7.76 | % |

Inception Date 06/28/05

Average Annual Total Returns - Class I

| | | | |

One Year | | | 0.02 | % |

Five Year | | | 11.33 | % |

Since Inception | | | 5.65 | % |

Inception Date 06/28/07

The performance data quoted represents past performance. Past performance does not guarantee future results. Investment return and principal value will fluctuate so that an investor’s shares, upon redemption, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For performance data current to the most recent month-end, please visit our website at www.astonfunds.com.

The total expense ratios for Class N and Class I shares are 1.09% and 0.84%, respectively, as disclosed in the prospectus dated February 28, 2015. Please refer to the Financial Highlights section in this report for more information.

| | |

| |

| ASTON/River Road Dividend All Cap Value Fund | | October 31, 2015 |

| |

| Schedule of Investments | | |

| | | | | | | | |

Shares | | | | | Market

Value | |

|

| | COMMON STOCKS – 99.12% | |

| | |

| | | | Consumer Discretionary – 11.38% | | | | |

| | 243,952 | | �� | Cinemark Holdings | | $ | 8,645,659 | |

| | 573,097 | | | Ford Motor | | | 8,487,567 | |

| | 267,207 | | | Kohl’s | | | 12,323,587 | |

| | 135,813 | | | Macy’s | | | 6,923,747 | |

| | 464,584 | | | National CineMedia | | | 6,597,093 | |

| | 284,167 | | | Omnicom Group | | | 21,289,792 | |

| | 210,670 | | | Target | | | 16,259,511 | |

| | 394,152 | | | Thomson Reuters (Canada) | | | 16,168,115 | |

| | | | | | | | |

| | | | | | | 96,695,071 | |

| | | | | | | | |

| | |

| | | | Consumer Staples – 10.86% | | | | |

| | 150,574 | | | Kimberly-Clark | | | 18,025,214 | |

| | 190,014 | | | Molson Coors Brewing, Class B | | | 16,740,233 | |

| | 103,263 | | | PepsiCo | | | 10,552,446 | |

| | 454,868 | | | Sysco | | | 18,763,305 | |

| | 311,970 | | | Unilever, SP ADR (Great Britain) | | | 13,867,067 | |

| | 250,741 | | | Wal-Mart Stores | | | 14,352,415 | |

| | | | | | | | |

| | | | | | | 92,300,680 | |

| | | | | | | | |

| | |

| | | | Energy – 6.75% | | | | |

| | 104,056 | | | Chevron | | | 9,456,609 | |

| | 174,025 | | | Exxon Mobil | | | 14,398,829 | |

| | 256,218 | | | Martin Midstream Partners LP | | | 7,417,511 | |

| | 285,066 | | | Occidental Petroleum | | | 21,248,820 | |

| | 153,233 | | | TransMontaigne Partners LP | | | 4,857,486 | |

| | | | | | | | |

| | | | | | | 57,379,255 | |

| | | | | | | | |

| | |

| | | | Financials – 22.06% | | | | |

| | 138,865 | | | CME Group | | | 13,118,577 | |

| | 177,108 | | | CNA Financial | | | 6,475,068 | |

| | 179,114 | | | Communications Sales & Leasing, REIT | | | 3,598,400 | |

| | 281,794 | | | Compass Diversified Holdings | | | 4,635,511 | |

| | 326,398 | | | CyrusOne, REIT | | | 11,515,321 | |

| | | | | | | | |

Shares | | | | | Market

Value | |

| | |

| | | | Financials (continued) | | | | |

| | 470,711 | | | GEO Group, REIT | | $ | 15,189,844 | |

| | 776,653 | | | Iron Mountain, REIT | | | 23,796,636 | |

| | 290,443 | | | PNC Financial Services Group | | | 26,215,385 | |

| | 310,645 | | | Sabra Health Care, REIT | | | 7,045,429 | |

| | 140,147 | | | Stock Yards Bancorp | | | 5,280,739 | |

| | 487,563 | | | U.S. Bancorp | | | 20,565,407 | |

| | 255,629 | | | Ventas, REIT | | | 13,732,390 | |

| | 65,937 | | | Washington Trust Bancorp | | | 2,558,356 | |

| | 402,053 | | | Wells Fargo | | | 21,767,149 | |

| | 409,976 | | | Weyerhaeuser, REIT | | | 12,024,596 | |

| | | | | | | | |

| | | | | | | 187,518,808 | |

| | | | | | | | |

| | |

| | | | Healthcare – 3.69% | | | | |

| | 353,725 | | | Owens & Minor | | | 12,681,041 | |

| | 275,501 | | | Quest Diagnostics | | | 18,720,293 | |

| | | | | | | | |

| | | | | | | 31,401,334 | |

| | | | | | | | |

| | |

| | | | Industrials – 14.00% | | | | |

| | 657,948 | | | ADT | | | 21,738,602 | |

| | 586,070 | | | Aircastle (Bermuda) | | | 13,280,346 | |

| | 230,964 | | | Emerson Electric | | | 10,908,430 | |

| | 482,787 | | | Fastenal | | | 18,905,939 | |

| | 145,586 | | | MSC Industrial Direct, Class A | | | 9,138,433 | |

| | 136,824 | | | Parker-Hannifin | | | 14,325,473 | |

| | 285,842 | | | Republic Services | | | 12,502,729 | |

| | 176,201 | | | United Parcel Service, Class B | | | 18,152,227 | |

| | | | | | | | |

| | | | | | | 118,952,179 | |

| | | | | | | | |

| | |

| | | | Information Technology – 16.30% | | | | |

| | 489,065 | | | Corning | | | 9,096,609 | |

| | 185,862 | | | CSG Systems International | | | 6,230,094 | |

| | 687,481 | | | Intel | | | 23,278,107 | |

| | 136,011 | | | j2 Global | | | 10,547,653 | |

| | 646,420 | | | Microsoft | | | 34,027,549 | |

| | 309,953 | | | Motorola Solutions | | | 21,687,411 | |

| | 283,111 | | | QUALCOMM | | | 16,822,456 | |

| | 876,708 | | | Western Union | | | 16,876,629 | |

| | | | | | | | |

| | | | | | | 138,566,508 | |

| | | | | | | | |

| | |

| | | | Materials – 4.77% | | | | |

| | 172,986 | | | Bemis | | | 7,919,299 | |

| | 169,026 | | | Compass Minerals International | | | 13,731,672 | |

| | 113,025 | | | Innophos Holdings | | | 4,802,432 | |

| | 174,310 | | | Nucor | | | 7,373,313 | |

| | 60,226 | | | Praxair | | | 6,690,506 | |

| | | | | | | | |

| | | | | | | 40,517,222 | |

| | | | | | | | |

| | |

| | | | Telecommunication Services – 4.67% | | | | |

| | 92,158 | | | Atlantic Tele-Network | | | 7,042,714 | |

| | 245,463 | | | Rogers Communications, Class B (Canada) | | | 9,769,427 | |

| | 488,392 | | | Verizon Communications | | | 22,895,817 | |

| | | | | | | | |

| | | | | | | 39,707,958 | |

| | | | | | | | |

| | |

| | | | Utilities – 4.64% | | | | |

| | 244,788 | | | AmeriGas Partners LP | | | 10,437,760 | |

See accompanying Notes to Financial Statements.

| | |

| |

| ASTON/River Road Dividend All Cap Value Fund | | October 31, 2015 |

| |

| Schedule of Investments – continued | | |

| | | | | | | | |

Shares | | | | | Market

Value | |

| | |

| | | | Utilities (continued) | | | | |

| | 290,877 | | | National Fuel Gas | | $ | 15,279,769 | |

| | 302,532 | | | Vectren | | | 13,756,130 | |

| | | | | | | | |

| | | | | | | 39,473,659 | |

| | | | | | | | |

| | |

| | | | Total Common Stocks

(Cost $704,654,279) | | | 842,512,674 | |

| | | | | | | | |

|

| | INVESTMENT COMPANY – 0.33% | |

| | |

| | 2,820,183 | | | BlackRock Liquidity Funds TempFund Portfolio | | | 2,820,183 | |

| | | | | | | | |

| | |

| | | | Total Investment Company

(Cost $2,820,183) | | | 2,820,183 | |

| | | | | | | | |

| Total Investments – 99.45%

(Cost $707,474,462)* | | | 845,332,857 | |

| | | | | | | | |

| Net Other Assets and Liabilities – 0.55% | | | 4,644,722 | |

| | | | | | | | |

| Net Assets – 100.00% | | $ | 849,977,579 | |

| | | | | | | | |

| * | | Aggregate cost for Federal income tax purposes is $705,527,430. |

| | | | |

Gross unrealized appreciation | | $ | 165,675,256 | |

Gross unrealized depreciation | | | (25,869,829 | ) |

| | | | |

Net unrealized appreciation | | $ | 139,805,427 | |

| | | | |

| REIT | | Real Estate Investment Trust |

| SP ADR | | Sponsored American Depositary Receipt |

See accompanying Notes to Financial Statements.

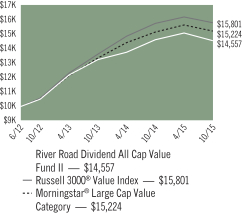

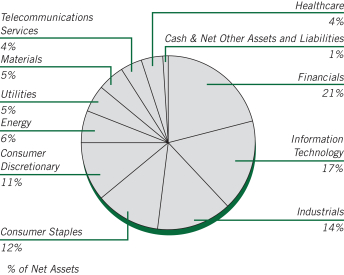

ASTON/River Road Dividend All Cap Value Fund II

| | |

| |

| Portfolio Manager Commentary (unaudited) | | October 31, 2015 |

Henry W. Sanders, III, CFA; Thomas S. Forsha, CFA & James C. Shircliff, CFA

| Q. | What were the most significant market factors affecting Fund performance and returns relative to the benchmark during the past 12 months? |

| A. | Over the last 12 months, the most significant market factor affecting absolute return was increased volatility amidst the decline in commodity prices, weak corporate earnings, and uncertainty about the timing of monetary tightening by the Federal Reserve. Additionally, according to Ned Davis Research*, among S&P 500 companies, the companies with the lowest yields significantly outperformed those with the highest yields, creating a significant relative headwind for a dividend-oriented strategy. The Information Technology sector had the most significant positive impact on relative results in the period, primarily due to strong stock selection. The Financials sector had the most significant negative impact on relative results due to both weak stock selection and an underweight allocation. |

| Q. | What were the best performing holdings for the Fund during the period? |

| A. | The two holdings with the largest positive contribution to the Fund’s total return were Hasbro Inc., a worldwide leader in branded toys and games, and Microsoft Corp., the company behind Windows and Office. Hasbro shares surged following a dividend increase in the first quarter, followed by strong quarterly results in the second quarter, and excitement around the release of the new Jurassic Park film. The position was reduced multiple times and eventually eliminated at a substantial premium to our assessed valuation. Microsoft reported strong fiscal third quarter results highlighted by significant growth in cloud revenue and constant currency revenue growth in its enterprise business. We maintained the position during the period. |

| Q. | What were the weakest performing holdings? |

| A. | The two holdings with the lowest contribution to the Fund’s total return during the period were National Fuel Gas Co., an integrated natural gas utility, and Qualcomm Inc., which manufactures and sells integrated mobile communications technology. Shares of National Fuel Gas were |

| | down after the company introduced preliminary guidance for 2016 that included price-related production curtailments due to lower natural gas prices in the Marcellus Shale. We trimmed the position due to accumulated unrealized losses. Qualcomm faced two significant headwinds over the last year: (1) an anti-monopoly investigation by the Chinese government and (2) headwinds in its chip division due to increasing competition and Samsung’s decision to take its chip manufacturing in-house for its highest end smartphones. While Qualcomm settled favorably with the Chinese authorities, the Samsung decision resulted in a significant revenue headwind. We maintained the position during the period. |

| Q. | How was the Fund positioned as of October 31, 2015? |

| A. | The Fund remains significantly overweight in Consumer stocks (Staples and Discretionary) and Information Technology, and is significantly underweight in Financials, Healthcare, and Energy. The underweight in Financials decreased meaningfully during the period versus the Russell 3000® Value Index benchmark, driven by a number of new positions that were added to the Fund. In Energy, the underweight increased rather dramatically versus the benchmark due to a number of holdings that were eliminated from this sector. Turnover remained elevated as we dealt with numerous overvalued positions and the average yield of Fund holdings increased marginally. We were pleased to see that the Fund largely behaved as expected over the duration of the brief pullback in recent months and were equally pleased with the participation in the sharp recovery. |

| * | | Ned Davis Research, Inc. examined S&P 500 Stock Constituents ranked by quartiles (Dividend Yield) for the twelve months ended October 31, 2015. |

Growth of a Hypothetical

$10,000 Investment—Class N

All dividends and capital gains are reinvested. Indexes are unmanaged and do not take into account fees, expenses or other costs.

Returns shown in the chart and table do not reflect taxes that a shareholder would pay on Fund distributions or on the sale of the Fund shares.

Value investing involves the risk that a Fund’s investments in companies believed to be undervalued will not appreciate as anticipated.

Small-cap and mid-cap stocks may be subject to a higher degree of market risk than the securities of more established companies because they tend to be more volatile and less liquid.

RETURNSFOR PERIOD ENDED 10/31/15

Average Annual Total Returns - Class N

| | | | |

One-Year | | | -0.47 | % |

Since Inception | | | 11.87 | % |

Inception Date 06/27/12

Average Annual Total Returns - Class I

| | | | |

One Year | | | -0.13 | % |

Since Inception | | | 12.17 | % |

Inception Date 06/27/12

The performance data quoted represents past performance. Past performance does not guarantee future results. Investment return and principal value will fluctuate so that an investor’s shares, upon redemption, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For performance data current to the most recent month-end, please visit our website at www.astonfunds.com.

The performance quoted would have been lower if fee waivers and/or expense reimbursements had not been in effect.

| | |

| |

| ASTON/River Road Dividend All Cap Value Fund II | | October 31, 2015 |

| |

| Schedule of Investments | | |

| | | | | | | | |

Shares | | | | | Market

Value | |

|

| | COMMON STOCKS – 98.52% | |

| | |

| | | | Consumer Discretionary – 11.25% | | | | |

| | 36,589 | | | Cinemark Holdings | | $ | 1,296,714 | |

| | 88,155 | | | Ford Motor | | | 1,305,576 | |

| | 42,143 | | | Kohl’s | | | 1,943,635 | |

| | 21,768 | | | Macy’s | | | 1,109,733 | |

| | 43,823 | | | Omnicom Group | | | 3,283,219 | |

| | 33,401 | | | Target | | | 2,577,889 | |

| | 60,228 | | | Thomson Reuters (Canada) | | | 2,470,553 | |

| | | | | | | | |

| | | | | | | 13,987,319 | |

| | | | | | | | |

| | |

| | | | Consumer Staples – 11.62% | | | | |

| | 22,751 | | | Kimberly-Clark | | | 2,723,522 | |

| | 30,020 | | | Molson Coors Brewing, Class B | | | 2,644,762 | |

| | 15,781 | | | PepsiCo | | | 1,612,660 | |

| | 72,160 | | | Sysco | | | 2,976,600 | |

| | 49,376 | | | Unilever, SP ADR (Great Britain) | | | 2,194,763 | |

| | 40,160 | | | Wal-Mart Stores | | | 2,298,758 | |

| | | | | | | | |

| | | | | | | 14,451,065 | |

| | | | | | | | |

| | |

| | | | Energy – 6.24% | | | | |

| | 16,345 | | | Chevron | | | 1,485,434 | |

| | 27,018 | | | Exxon Mobil | | | 2,235,469 | |

| | 23,709 | | | Martin Midstream Partners LP | | | 686,376 | |

| | 44,973 | | | Occidental Petroleum | | | 3,352,287 | |

| | | | | | | | |

| | | | | | | 7,759,566 | |

| | | | | | | | |

| | |

| | | | Financials – 20.64% | | | | |

| | 21,439 | | | CME Group | | | 2,025,342 | |

| | 16,274 | | | CNA Financial | | | 594,977 | |

| | 28,433 | | | Communications Sales & Leasing, REIT | | | 571,219 | |

| | 49,134 | | | CyrusOne, REIT | | | 1,733,448 | |

| | 68,237 | | | GEO Group, REIT | | | 2,202,008 | |

| | 122,758 | | | Iron Mountain, REIT | | | 3,761,307 | |

| | 45,780 | | | PNC Financial Services Group | | | 4,132,103 | |

| | | | | | | | |

Shares | | | | | Market

Value | |

| | |

| | | | Financials (continued) | | | | |

| | 75,776 | | | U.S. Bancorp | | $ | 3,196,232 | |

| | 40,475 | | | Ventas, REIT | | | 2,174,317 | |

| | 62,019 | | | Wells Fargo | | | 3,357,709 | |

| | 65,245 | | | Weyerhaeuser, REIT | | | 1,913,636 | |

| | | | | | | | |

| | | | | | | 25,662,298 | |

| | | | | | | | |

| | |

| | | | Healthcare – 3.86% | | | | |

| | 51,359 | | | Owens & Minor | | | 1,841,220 | |

| | 43,491 | | | Quest Diagnostics | | | 2,955,213 | |

| | | | | | | | |

| | | | | | | 4,796,433 | |

| | | | | | | | |

| | |

| | | | Industrials – 14.27% | | | | |

| | 101,728 | | | ADT | | | 3,361,093 | |

| | 59,306 | | | Aircastle (Bermuda) | | | 1,343,874 | |

| | 36,673 | | | Emerson Electric | | | 1,732,066 | |

| | 74,646 | | | Fastenal | | | 2,923,137 | |

| | 23,403 | | | MSC Industrial Direct, Class A | | | 1,469,006 | |

| | 21,107 | | | Parker-Hannifin | | | 2,209,903 | |

| | 45,205 | | | Republic Services | | | 1,977,267 | |

| | 26,492 | | | United Parcel Service, Class B | | | 2,729,206 | |

| | | | | | | | |

| | | | | | | 17,745,552 | |

| | | | | | | | |

| | |

| | | | Information Technology – 16.66% | | | | |

| | 77,480 | | | Corning | | | 1,441,128 | |

| | 108,522 | | | Intel | | | 3,674,555 | |

| | 21,603 | | | j2 Global | | | 1,675,313 | |

| | 102,277 | | | Microsoft | | | 5,383,861 | |

| | 47,713 | | | Motorola Solutions | | | 3,338,479 | |

| | 44,180 | | | QUALCOMM | | | 2,625,176 | |

| | 133,702 | | | Western Union | | | 2,573,764 | |

| | | | | | | | |

| | | | | | | 20,712,276 | |

| | | | | | | | |

| | |

| | | | Materials – 4.87% | | | | |

| | 27,006 | | | Bemis | | | 1,236,335 | |

| | 27,045 | | | Compass Minerals International | | | 2,197,136 | |

| | 10,825 | | | Innophos Holdings | | | 459,954 | |

| | 26,151 | | | Nucor | | | 1,106,187 | |

| | 9,549 | | | Praxair | | | 1,060,798 | |

| | | | | | | | |

| | | | | | | 6,060,410 | |

| | | | | | | | |

| | |

| | | | Telecommunication Services – 4.15% | | | | |

| | 38,921 | | | Rogers Communications, Class B (Canada) | | | 1,549,056 | |

| | 77,097 | | | Verizon Communications | | | 3,614,307 | |

| | | | | | | | |

| | | | | | | 5,163,363 | |

| | | | | | | | |

| | |

| | | | Utilities – 4.96% | | | | |

| | 37,631 | | | AmeriGas Partners LP | | | 1,604,586 | |

| | 45,683 | | | National Fuel Gas | | | 2,399,728 | |

| | 47,405 | | | Vectren | | | 2,155,505 | |

| | | | | | | | |

| | | | | | | 6,159,819 | |

| | | | | | | | |

| | |

| | | | Total Common Stocks

(Cost $114,067,613) | | | 122,498,101 | |

| | | | | | | | |

See accompanying Notes to Financial Statements.

| | |

| |

| ASTON/River Road Dividend All Cap Value Fund II | | October 31, 2015 |

| |

| Schedule of Investments – continued | | |

| | | | | | | | |

Shares | | | | | Market

Value | |

|

| | INVESTMENT COMPANY – 0.60% | |

| | |

| | 750,500 | | | BlackRock Liquidity Funds TempFund Portfolio | | $ | 750,500 | |

| | | | | | | | |

| | |

| | | | Total Investment Company

(Cost $750,500) | | | 750,500 | |

| | | | | | | | |

| Total Investments – 99.12%

(Cost $114,818,113)* | | | 123,248,601 | |

| | | | | | | | |

| Net Other Assets and Liabilities – 0.88% | | | 1,095,336 | |

| | | | | | | | |

| Net Assets – 100.00% | | $ | 124,343,937 | |

| | | | | | | | |

| * | | Aggregate cost for Federal income tax purposes is $114,625,396. |

| | | | |

Gross unrealized appreciation | | $ | 14,717,681 | |

Gross unrealized depreciation | | | (6,094,476 | ) |

| | | | |

Net unrealized appreciation | | $ | 8,623,205 | |

| | | | |

| REIT | | Real Estate Investment Trust |

| SP ADR | | Sponsored American Depositary Receipt |

See accompanying Notes to Financial Statements.

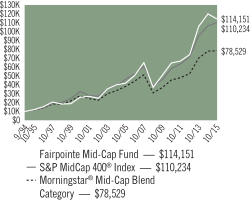

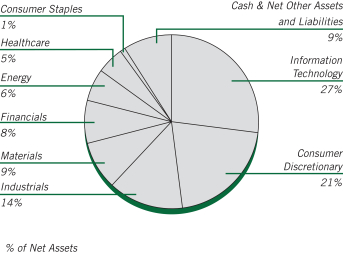

ASTON/Fairpointe Mid Cap Fund

| | |

| |

| Portfolio Manager Commentary (unaudited) | | October 31, 2015 |

Thyra E. Zerhusen; Marie L. Lorden & Mary L. Pierson

| Q. | What were the most significant market factors affecting Fund performance and returns relative to the benchmark during the past 12 months? |

| A. | In the past 12 months, the market has continued to value Healthcare, growth and momentum stocks at ever higher valuations while stocks related to Energy or with a value bias fell out of favor. Fears of slowing economic growth, principally in China, had a significant negative impact on both commodity prices and the currencies of countries exporting commodities. Our investment process led us to reduce the Fund’s exposure to relatively expensive Healthcare stocks and increase the exposure to more economically sensitive stocks, which we believe to be undervalued. |

| Q. | What were the best performing holdings for the Fund during the period? |

| A. | The Fund’s top three contributors to performance were Juniper Networks, Inc., Owens Corning, and Staples, Inc. Juniper is a leading provider of communication network equipment. The stock advanced as a turn-around plan, focusing on new product introductions and improved profitability, was implemented. Owens Corning, a global producer of building material products, benefited from a U.S. housing market recovery. Staples stock reacted to the announcement that Staples would acquire its rival Office Depot. We used the opportunity to exit most of the Fund’s position. |

| Q. | What were the weakest performing holdings? |

| A. | After being one of our best performing stocks in 2014, United States Steel Corp. was our worst performing stock in 2015. The stock declined due to a high level of subsidized steel imports from China as well as weak demand from the energy market. The company is in the midst of a restructuring plan that aims to increase manufacturing efficiency. U.S. Steel offers attractive upside potential as its restructuring plan may begin to improve profits in coming quarters. Copa Holdings, SA, provides passenger airline service to destinations in North, Central and |

| | South America from its strategically advantaged hub in Panama City, Panama. We expect Copa to be a long-term beneficiary of increasing airline traffic in Latin America by adding new destinations and flight frequencies to its network. The company’s stock decline was caused by the weak Brazilian economy and currency. Copa offers upside potential as the company is shifting capacity from weak to strong markets. Gerdau, SA, is the leading producer of long steel products used for construction markets in the Americas. The stock was hurt by the economic slowdown in Brazil. Gerdau operates efficient mini-mill assets and we believe the shares offer compelling upside when Brazil’s economy recovers. |

| Q. | How was the Fund positioned as of October 31, 2015? |

| A. | We maintain a long-term view and take advantage of both market and stock specific conditions to position the portfolio. Many of our holdings are trading near trough valuation multiples. The current price to revenue multiple is at a historical low for the Fund, at less than half of the S&P 500’s price to revenue multiple. In the coming year, we believe more companies may spur growth through mergers and acquisitions based on these valuations. Mid-cap companies experience more takeover activity than large caps, and historically, our portfolio has had a higher incidence of takeovers than the S&P MidCap 400® Index. Last year, three portfolio holdings received significant takeover offers including Polypore, Hospira and most recently, long-term portfolio holding Con-way, Inc. We continue to actively rebalance the portfolio on a stock by stock basis to keep the overall valuation attractive relative to the Fund’s S&P MidCap 400® benchmark and the broader market S&P 500® Index. |

Growth of a Hypothetical

$10,000 Investment—Class N

All dividends and capital gains are reinvested. Indexes are unmanaged and do not take into account fees, expenses or other costs.

Returns shown in the chart and table do not reflect taxes that a shareholder would pay on Fund distributions or on the sale of the Fund shares.

Small-cap and mid-cap stocks may be subject to a higher degree of market risk than the securities of more established companies because they tend to be more volatile and less liquid.

RETURNSFOR PERIOD ENDED 10/31/15

Average Annual Total Returns - Class N

| | | | |

One Year | | | -5.02 | % |

Five Year | | | 11.97 | % |

Ten Year | | | 10.48 | % |

Since Inception | | | 12.22 | % |

Inception Date 09/19/94

Average Annual Total Returns - Class I

| | | | |

One Year | | | -4.78 | % |

Five Year | | | 12.26 | % |

Ten Years | | | 10.77 | % |

Since Inception | | | 9.62 | % |

Inception Date 07/06/04

The performance data quoted represents past performance. Past performance does not guarantee future results. Investment return and principal value will fluctuate so that an investor’s shares, upon redemption, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For performance data current to the most recent month-end, please visit our website at www.astonfunds.com.

The total expense ratios for Class N and Class I shares are 1.11% and 0.86%, respectively, as disclosed in the prospectus dated February 28, 2015. Please refer to the Financial Highlights section in this report for more information.

| | |

| |

| ASTON/Fairpointe Mid Cap Fund | | October 31, 2015 |

| |

| Schedule of Investments | | |

| | | | | | | | |

Shares | | | | | Market

Value | |

|

| | COMMON STOCKS – 91.25% | |

| | |

| | | | Consumer Discretionary – 21.29% | | | | |

| | 1,238,600 | | | BorgWarner | | $ | 53,036,852 | |

| | 2,129,800 | | | Cooper Tire & Rubber | | | 89,004,342 | |

| | 3,886,100 | | | DeVry Education Group | | | 91,556,516 | |