UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number | 811-8268 |

|

Firsthand Funds |

(Exact name of registrant as specified in charter) |

|

125 South Market, Suite 1200

San Jose, CA | | 95113 |

(Address of principal executive offices) | | (Zip code) |

|

Firsthand Capital Management, Inc.

125 South Market, Suite 1200

San Jose, CA 95113 |

(Name and address of agent for service) |

|

Registrant’s telephone number, including area code: | (408) 294-2200 | |

|

Date of fiscal year end: | December 31, 2006 | |

|

Date of reporting period: | December 31, 2006 | |

| | | | | | | |

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB’’) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

Item 1. Reports to Stockholders.

Include a copy of the report transmitted to stockholders pursuant to Rule 30e-1 under the Act (17 CFR 270.30e-1).

Firsthand Funds

Annual Report to Shareholders

Firsthand Technology Value Fund ®

Firsthand Technology Leaders Fund

Firsthand Technology Innovators Fund

Firsthand e-Commerce Fund

Firsthand Global Technology Fund

Firsthand Health Sciences Fund

December 31, 2006

This report is provided for the general information of the shareholders of Firsthand Funds. This report is not intended for distribution to prospective investors in the Funds, unless preceded or accompanied by an effective prospectus. For more complete information about Firsthand Funds, please call toll free 1.888.884.2675, option 2, or visit www.firsthandfunds.com for a prospectus, which contains more information, including risks, fees, and expenses. Read the prospectus carefully before investing or sending money.

Firsthand Funds are distributed by ALPS Distributors, Inc.

CONTENTS

Performance Summary | | 4 |

President’s Letter | | 6 |

Shareholder Fee Example | | 8 |

Performance and Portfolio Discussions | | 10 |

Report of Independent Registered Public | | |

Accounting Firm | | 22 |

Financial Statements | | |

Portfolio of Investments | | |

Firsthand Technology Value Fund | | 23 |

Firsthand Technology Leaders Fund | | 27 |

Firsthand Technology Innovators Fund | | 29 |

Firsthand e-Commerce Fund | | 32 |

Firsthand Global Technology Fund | | 34 |

Firsthand Health Sciences Fund | | 36 |

Statements of Assets and Liabilities | | 40 |

Statements of Operations | | 42 |

Statements of Changes in Net Assets | | 44 |

Financial Highlights | | |

Firsthand Technology Value Fund | | 50 |

Firsthand Technology Leaders Fund | | 51 |

Firsthand Technology Innovators Fund | | 52 |

Firsthand e-Commerce Fund | | 53 |

Firsthand Global Technology Fund | | 54 |

Firsthand Health Sciences Fund | | 55 |

Notes to Financial Statements | | 56 |

Additional Information | | 70 |

PERFORMANCE SUMMARY

Period Returns (average annual total returns as of 12/31/06)

| | | | | | | | | | Since | |

Fund | | 1-Year | | 3-Year | | 5-Year | | 10-Year | | Inception | |

| | | | | | | | | | | |

Firsthand Technology Value Fund® | | 8.97 | % | 4.56 | % | -2.64 | % | 5.37 | % | 14.42 | % |

Firsthand Technology Leaders Fund | | 6.75 | % | 5.50 | % | 1.41 | % | · | | 8.26 | % |

Firsthand Technology Innovators Fund | | 13.06 | % | -4.59 | % | -9.35 | % | · | | 3.52 | % |

Firsthand e-Commerce Fund | | 19.12 | % | 9.79 | % | 3.99 | % | · | | -11.63 | % |

Firsthand Global Technology Fund | | 14.83 | % | -0.88 | % | -2.67 | % | · | | -11.96 | % |

Firsthand Health Sciences Fund | | 9.90 | % | · | | · | | · | | 9.84 | % |

| | | | | | | | | | | |

NASDAQ | | 10.39 | % | 7.16 | % | 4.99 | % | 6.95 | % | · | |

S&P 500 | | 15.79 | % | 10.44 | % | 6.19 | % | 8.42 | % | · | |

Returns assume reinvestment of all dividends and distributions but do not reflect the impact of taxes. The performance data quoted represent past performance. Past performance cannot guarantee future results, and current performance may be lower or higher than the performance quoted. Both the return from and the principal value of an investment in the Funds will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. To obtain performance as of the most recent month-end, please contact Firsthand Funds by calling 1.888.884.2675 or go to www.firsthandfunds.com.

Each Fund may invest in small-capitalization companies and Initial Public Offerings (“IPOs”). These investments may be more volatile than investments in large-capitalization companies and loss of principal could be greater. The Funds may invest in foreign securities, which may be subject to greater risks than investing in domestic securities. Because the Funds are not diversified, they can take larger positions in fewer companies, increasing their risk profile. The Funds invest in several industries within the technology sector and the relative weightings of these industries in a Fund’s portfolio may change at any time.

The Nasdaq Composite Index (NASDAQ) is a capitalization-weighted index of all common stocks listed with NASDAQ. The Standard & Poor’s 500 Index (S&P 500) is a market-weighted index of 500 stocks of well-established companies. Each index represents an unmanaged, broad-based basket of stocks. These indices are typically used as benchmarks for overall market performance. The Lipper Science and Technology Fund Index includes the 30 largest mutual funds in the group, which, by prospectus or portfolio practice, invest at least 80% of their equity portfolios in science and technology stocks. The Lipper Health/Biotech Index is an equal-weight index that includes the 30 largest mutual funds in the Lipper Health/Biotech Fund category. The Goldman Sachs Health Care Index is a market capitalization-weighted index of stocks designed to measure the performance of companies in the health care sector. Investments cannot be made directly in an index.

This page intentionally left blank

PRESIDENT’S LETTER

Fellow Shareholders,

2006 was a good year for investors. U.S. companies achieved double-digit profit growth for the fourth consecutive year, and the major market indices, the Nasdaq Composite, the S&P 500, and the Dow, registered healthy gains of 10.39%, 15.79% and 19.04%, respectively.

While technology stocks did gain ground, they failed to keep pace with the broader market. Most technology indices finished in the high single digits, but I am pleased to report that several Firsthand Funds fared substantially better than that. Firsthand e-Commerce Fund, Firsthand Global Technology Fund, and Firsthand Technology Innovators Fund posted gains of 19.12%, 14.83%, 13.06%, respectively. The fund discussions on the pages that follow detail each fund’s relative performance versus its benchmarks for the 6- and 12-month periods ended December 31, 2006.

The technology sector’s relative under-performance can largely be explained by the year’s most unpleasant surprise: the options backdating scandal, which hit the tech sector harder than others. Over 100 companies have been investigated for backdating employee stock option grants. The fallout from these investigations has varied widely, but some companies have lost entire management teams as a result. Many others were forced to re-state earnings. For nearly every company involved it has become a significant distraction and the stocks have suffered accordingly.

Although some abusers of the practice probably knew they were cheating, others probably believed they were simply following standard industry practice. In viewing stock options as a free lunch, and in stretching the available rationale, many management teams were guilty of simply trying to be too clever for their own good. It cost some of them their jobs. Interestingly, the Silicon Valley audit and law firms that blessed the practice seem to have escaped relatively unscathed. Still, 2006 was a good year for the industry. Many companies were much more successful than their stock charts might lead you to believe. This means we are entering 2007 with a healthy business climate and attractive valuations. Add to that a growing interest in technology among asset allocators, and we believe you have a very promising outlook.

Some of the specific trends we are following in our technology investments include:

Globalization

By now the mega-trend of globalization is apparent to us all. The key insights come not just from observing that China and India have become fast-growing powerhouses, but from following the implications of that growth. The sustained surge in energy demand is a good example. It’s no coincidence that crude oil prices have skyrocketed as many millions of people around the world have joined the ranks of the consumer class.

Higher energy prices may hurt us as consumers, but they also open up new alternative energy investment opportunities. Some of our best performing and most promising investments today are in the solar power area. We expect many other alternative and “clean” technology opportunities to present themselves in the coming years.

Globalization has clearly re-ignited growth in the consumer electronics industry as well. Remember when total cellphone shipments “peaked” at 400 million units in 2000? It now appears 2006 was the first year with over 1 billion cellphones sold. Yes, that’s approximately one new cellphone for every six people on the planet. Now that’s a big number.

But technology investors prefer tech companies that can still grow. It’s going to be difficult for Motorola or Nokia to offer a compelling rate of growth in an increasingly saturated and brutally competitive market. An approach that has worked well for us is to focus on the new features that are likely to move from niche to mainstream status. A few years ago this meant investing in CMOS sensor suppliers as camera phones became popular. This year and next, we’re looking at location-based technologies and services.

Basic process technologies: SOI & perpendicular recording

As exciting as it is to watch new technologies open up new markets, it’s also important to pay attention to the breakthroughs that enable established industries to keep advancing. For instance, several leading edge semiconductor manufacturers have begun to adopt silicon-on-insulator (SOI) technology as a way to better isolate neighboring circuits from one another. SOI-based devices are expected to have fewer problems with power consumption and electrical noise.

The disk drive industry faces similar challenges. Every year competitive pressures force companies’ price per megabyte to decline anywhere from 35% to 45%. This year drive manufacturers will begin wide-scale deployment of a technology called perpendicular recording. It will enable these manufacturers to increase both their “tracks per inch” and their “bits per inch” to record much more data per given area. If they can control the cost side of the equation, perpendicular recording could be the answer for the next several years.

Health sciences

Health care stocks generally kept pace with the broad market for the first three quarters, but lagged substantially in the fourth quarter. We believe that one significant factor at play was the change in control to a Democratic U.S. congress. Equity markets tend to price in the possibility of congressional action towards health care price controls whenever the Democrats manage the agenda. (Whether that is rational is another discussion.)

Against this backdrop, I am pleased to report that Firsthand Health Sciences Fund had a stellar year in 2006, returning 9.90%. The Fund’s overweight position in biotech served it well, particularly in the fourth quarter, when some high-profile acquisitions boosted valuations across the industry.

The pendulum of investor sentiment seems to be swinging back toward technology stocks, particularly among institutional investors. While this is certainly welcome, it doesn’t affect how and what we do here at Firsthand. Our focus is on finding solid companies that are well positioned to take advantage of the most powerful technology trends and to value them appropriately.

Sincerely,

Kevin Landis

President, Firsthand Funds

SHAREHOLDER FEE EXAMPLE

Example—In general, mutual fund shareholders may incur two types of costs: (1) transaction costs, including sales charges (loads), redemption fees, and exchange fees; and (2) ongoing costs, including management fees, 12b-1 distribution and service fees, non-12b-1 service fees, and other Fund expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in a Fund and to compare these costs with the ongoing costs of investing in other mutual funds. Note that Firsthand Funds (“Trust”) does not charge transaction fees or 12b-1 distribution and service fees, though you may incur transaction fees if you purchase shares through a broker.

The example below is based on an investment of $1,000 made at the beginning of the period and held for the entire period from July 1, 2006, to December 31, 2006.

Actual Expenses—The section of the table at right entitled “Actual” provides information about actual account values and actual expenses. You may use this information, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), and multiply the result by the number in the section entitled “Actual” under the heading “Expenses Paid During Period” to estimate the expenses you paid on your account during this period. If your account is an IRA or other tax-qualified savings plan, your expenses may also have included a $10 annual fee. In either case, the amount of any fee paid through your account would increase the estimate of expenses you paid during the period and decrease your ending account value.

Hypothetical Example for Comparison Purposes—The section of the table at right entitled “Hypothetical” provides information about hypothetical account values and hypothetical expenses based on a Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate your actual ending account balance or the expenses you paid for the period. However, you may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds. As in the case of the actual expense example, if your account is subject to an IRA fee, the amount of the fee paid through your account would increase the hypothetical expenses you would have paid during the period and decrease the hypothetical ending account value.

Please note that the expenses shown in the table at right are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads), redemption fees, or exchange fees. Therefore, the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. If these transactional costs were included, your costs would have been higher. The examples also assume all dividends and distributions have been reinvested.

Firsthand Technology Value Fund

| | Beginning | | Ending | | Expenses Paid | | | |

| | Account Value | | Account Value | | During Period* | | Annualized | |

| | 7/1/06 | | 12/31/06 | | 7/1/06-12/31/06 | | Expense Ratio | |

Actual | | $ | 1,000 | | $ | 1,042.16 | | $ | 9.60 | | 1.92 | % |

Hypothetical** | | $ | 1,000 | | $ | 1,015.08 | | $ | 9.75 | | 1.92 | % |

Firsthand Technology Leaders Fund

| | Beginning | | Ending | | Expenses Paid | | | |

| | Account Value | | Account Value | | During Period* | | Annualized | |

| | 7/1/06 | | 12/31/06 | | 7/1/06-12/31/06 | | Expense Ratio | |

Actual | | $ | 1,000 | | $ | 1,082.98 | | $ | 10.04 | | 1.95 | % |

Hypothetical** | | $ | 1,000 | | $ | 1,014.93 | | $ | 9.90 | | 1.95 | % |

Firsthand Technology Innovators Fund

| | Beginning | | Ending | | Expenses Paid | | | |

| | Account Value | | Account Value | | During Period* | | Annualized | |

| | 7/1/06 | | 12/31/06 | | 7/1/06-12/31/06 | | Expense Ratio | |

Actual | | $ | 1,000 | | $ | 1,039.34 | | $ | 9.66 | | 1.95 | % |

Hypothetical** | | $ | 1,000 | | $ | 1,014.93 | | $ | 9.90 | | 1.95 | % |

Firsthand e-Commerce Fund

| | Beginning | | Ending | | Expenses Paid | | | |

| | Account Value | | Account Value | | During Period* | | Annualized | |

| | 7/1/06 | | 12/31/06 | | 7/1/06-12/31/06 | | Expense Ratio | |

Actual | | $ | 1,000 | | $ | 1,147.31 | | $ | 10.17 | | 1.95 | % |

Hypothetical** | | $ | 1,000 | | $ | 1,014.93 | | $ | 9.90 | | 1.95 | % |

Firsthand Global Technology Fund

| | Beginning | | Ending | | Expenses Paid | | | |

| | Account Value | | Account Value | | During Period* | | Annualized | |

| | 7/1/06 | | 12/31/06 | | 7/1/06-12/31/06 | | Expense Ratio | |

Actual | | $ | 1,000 | | $ | 1,154.24 | | $ | 10.29 | | 1.95 | % |

Hypothetical** | | $ | 1,000 | | $ | 1,014.93 | | $ | 9.90 | | 1.95 | % |

Firsthand Health Sciences Fund

| | Beginning | | Ending | | Expenses Paid | | | |

| | Account Value | | Account Value | | During Period* | | Annualized | |

| | 7/1/06 | | 12/31/06 | | 7/1/06-12/31/06 | | Expense Ratio | |

Actual | | $ | 1,000 | | $ | 1,107.86 | | $ | 10.36 | | 1.95 | % |

Hypothetical** | | $ | 1,000 | | $ | 1,014.93 | | $ | 9.90 | | 1.95 | % |

* Expenses are calculated by multiplying the Fund’s annualized expense ratio listed above by the average account value over the period and multiplying that number by 184/365 (to reflect the one-half year period).

** 5% return per year before expenses.

The expenses shown in the table do not reflect any fees that may be charged to you by brokers, financial intermediaries, or other financial institutions.

FIRSTHAND TECHNOLOGY VALUE FUND

Performance and Portfolio Discussion

How did the Fund perform in 2006?

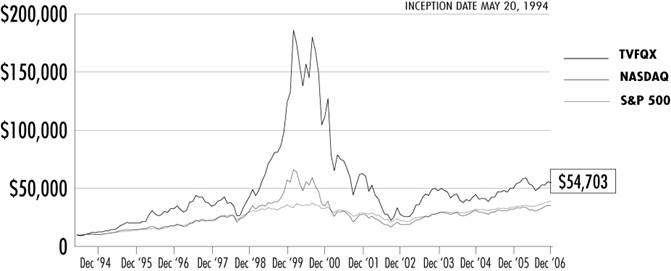

In 2006, Firsthand Technology Value Fund (TVFQX) posted an 8.97% gain, versus a 10.39% increase for the NASDAQ Composite Index and a 6.73% gain for the Lipper Science and Technology Fund Index. For the six months ending December 31, 2006, Firsthand Technology Value Fund rose 4.22% as compared to 11.60% and 9.93% gains for the NASDAQ and the Lipper peer group benchmarks, respectively.

Which industries had the greatest impact on the Fund’s performance?

For the period ending December 31, 2006, semiconductor and Internet stocks represented the portfolio’s largest weightings, followed by semiconductor equipment and communications equipment holdings. Despite strong results from the latter, as well as good returns from some of our networking stocks, Firsthand Technology Value Fund slightly underperformed its benchmarks in 2006 due to several disappointments in the software industry.

Which individual holdings were the largest contributors to the Fund’s performance?

The Fund’s largest contributor in 2006 was Web content delivery firm Akamai Technologies (AKAM). Akamai survived the dot-com collapse by building a vast global network of servers to bring Web content and applications physically closer to users, thus enabling online data to be delivered faster and more efficiently. Akamai finished 2006 with an impressive gain of 167%, as demand grew for more robust multimedia online content, such as video, music, and software downloads.

Disk drive manufacturing equipment maker Intevac (IVAC) saw its shares nearly double during 2006. The company provides equipment used to deposit specialized materials onto hard disks, and it profited from growing consumer demand for data storage devices and an industry-wide shift to a new recording technology (known as perpendicular recording). Disk drive manufacturer Seagate Technology (STX) also benefited from increasing storage demand, which sent its shares higher during 2006.

After languishing for the past few years, shares of networking giant Cisco Systems (CSCO) rallied more than 59%, due in part to its acquisition of Scientific Atlanta early in the year. The purchase of the set-top box maker enables Cisco to broaden its customer base by selling its networking products directly to consumers.

Shares of Soitec (no U.S. symbol) jumped shortly after we established a position in the French company in the fourth quarter. Soitec has experienced strong demand for its 300mm silicon-on-insulator (SOI) wafers, used in making high-performance semiconductors.

Which holdings were the greatest detractors from the Fund’s performance?

The Fund’s largest detractor during the period was Openwave Systems (OPWV), a provider of applications for wireline and wireless devices, including Internet browsers for cellphones. Although large growth was projected for Web-enabled phones, that growth has not yet materialized, and Openwave has suffered as a result. We closed our position in the software developer shortly after the company unexpectedly cut its revenue forecast for its fiscal fourth-quarter.

Shares of Wind River Systems (WIND) dropped after the software company fell short of Wall Street expectations and lowered its full-year outlook during the first quarter of 2006. After several years of lackluster performance with Wind River, we chose to close our position at a significant loss. Verisign (VRSN) was another notable laggard among our software holdings, which we sold for a loss in the third quarter of 2006.

We liquidated our position in Netflix (NFLX) during the year, realizing sizeable gains since acquiring the stock in 2004. While we managed to sell a good portion of the Fund’s position in the first half of the year, the stock’s subsequent decline hurt the Fund prior to our closing out the position in the fourth quarter.

Fund Performance and Holdings Information (as of 12/31/06)

Firsthand Technology Value Fund vs. Market Indices

| | TVFQX | | NASDAQ | | S&P 500 | |

Since Inception (5/20/04) | | 14.42 | % | 10.45 | % | 11.36 | % |

10-Year | | 5.37 | % | 6.95 | % | 8.42 | % |

5-Year | | -2.64 | % | 4.99 | % | 6.19 | % |

3-Year | | 4.56 | % | 7.16 | % | 10.44 | % |

1-Year | | 8.97 | % | 10.39 | % | 15.79 | % |

Growth of a Hypothetical $10,000 Investment

Returns assume reinvestment of all dividends and distributions but do not reflect the impact of taxes. The performance data quoted represent past performance. Past performance cannot guarantee future results, and current performance may be lower or higher than the performance quoted. Both the return from and the principal value of an investment in the Funds will fluctuate so that an investor’s shares, when redeemed, may be worrth more or less than their original cost. To obtain performance as of the most recent month-end, please contact Firsthand Funds by calling 1.888.884.2675 or go to www.firsthandfunds.com.

Holdings by Industry*

| | % Net Assets | |

Semiconductors | | 31.5 | % |

Internet | | 8.6 | % |

Semiconductor Equipment | | 8.2 | % |

Communications Equipment | | 7.6 | % |

Photonics | | 6.5 | % |

Peripherals | | 5.6 | % |

Other Electronics | | 5.5 | % |

Alternative Energy | | 4.5 | % |

Networking | | 3.8 | % |

Software | | 3.7 | % |

Electronic Entertainment | | 3.6 | % |

Intellectual Property | | 3.2 | % |

Communications | | 1.6 | % |

Computer | | 1.6 | % |

Services | | 1.5 | % |

Other | | 2.2 | % |

Net Cash | | 0.8 | % |

Top 10 Holdings**

| | % Net Assets | |

Cypress Semiconductor Corp. | | 8.1 | % |

Seagate Technology, Inc. | | 5.6 | % |

Corning, Inc. | | 5.2 | % |

MEMC Electronic Materials, Inc. | | 4.5 | % |

Intevac, Inc. | | 4.3 | % |

Akamai Technologies, Inc. | | 4.1 | % |

Applied Materials, Inc. | | 4.0 | % |

Nintendo Co. Ltd. - ADR | | 3.6 | % |

Cisco Systems, Inc. | | 3.5 | % |

ASML Holding N.V. | | 3.3 | % |

* Based on percentage of net assets as of 12/31/06.

** Top 10 stock holdings total 46.2% of net assets. These holdings are current as of 12/31/06, and may not be representative of current or future investments. Firsthand includes only public companies in top 10 holdings.

FIRSTHAND TECHNOLOGY LEADERS FUND

Performance and Portfolio Discussion

How did the Fund perform in 2006?

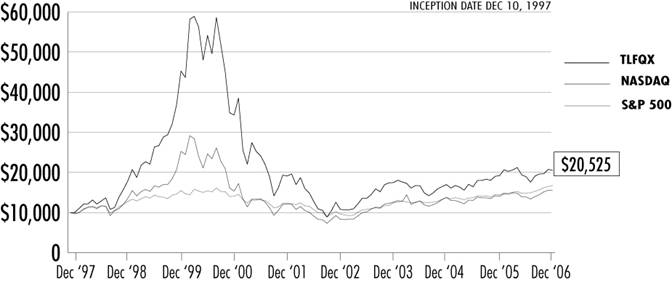

In 2006, Firsthand Technology Leaders Fund (TLFQX) posted a 6.75% gain, versus a 10.39% increase for the NASDAQ Composite Index and a 6.73% gain for the Lipper Science and Technology Fund Index. For the six months ended December 31, 2006, Firsthand Technology Leaders Fund rose 8.30% as compared to 11.60% and 9.93% gains for the NASDAQ and the Lipper peer group benchmarks, respectively.

Which industries had the greatest impact on the Fund’s performance?

For the year ended December 31, 2006, semiconductor and software stocks represented the portfolio’s largest weightings, followed by semiconductor equipment and communications equipment. Despite having a number of winners in the semiconductor sector, Firsthand Technology Leaders Fund underperformed its benchmarks in 2006 due to stock selection in the software and Internet industries.

Which individual holdings were the largest contributors to the Fund’s performance?

For the period, the Fund’s top contributor was networking giant Cisco Systems (CSCO). After languishing for the past few years, shares of Cisco rallied more than 59%, due in part to its acquisition of Scientific Atlanta early in the year. The purchase of the set-top box maker enabled Cisco to broaden its customer base by selling its networking products to the consumer market.

One of the bright spots among our software holdings was Amdocs (DOX), which provides billing and customer relationship management software. The company benefited from the telecom and cable industries move toward bundling high-speed Internet access with cable, wireless, and wireline services.

The rapid growth in both the number of cellphone subscribers and the average revenue per user helped boost shares of China Mobile (CHL) during the period. The telecom giant is China’s leading wireless carrier and has yet to tap into China’s rural areas where cellphone adoption remains low.

Shares of Dutch semiconductor equipment maker ASML Holding N.V. (ASML) rose 23% in 2006 after the company raised its outlook, citing strong customer demand for its lithography equipment.

Which holdings were the greatest detractors from the Fund’s performance?

VeriSign (VRSN) represented the Fund’s largest detractor during the period. Disappointing guidance and an ongoing stock options investigation pushed shares of the Internet infrastructure provider lower and led us to close our position during the third quarter of 2006.

Sales of videogames remained in a slump as consumers continued to put off purchasing new games until the next generation of gaming consoles was released. This news affected the short-term financial results for Electronic Arts (ERTS), the world’s largest videogame publisher.

Also detracting from performance were the Fund’s Internet holdings. Shares of eBay (EBAY) declined by 30% in 2006 as the online auction giant struggled with decelerating growth in several of its key markets. The company decided to cut its losses in China by shutting down its website and replacing it with a joint venture run by a Chinese Internet company.

Shares of Intel (INTC) slipped as weaker-than-expected sales and increasing competition from Advanced Micro Devices (AMD) hurt Intel’s profit margins. This news, along with a less-than-robust near-term outlook, led us to liquidate our position in Intel at a loss during the first quarter of 2006.

Fund Performance and Holdings Information (as of 12/31/06)

Firsthand Technology Leaders Fund vs. Market Indices

| | TLFQX | | NASDAQ | | S&P 500 | |

Since Inception (12/10/97) | | 8.26 | % | 4.97 | % | 5.86 | % |

5-Year | | 1.41 | % | 4.99 | % | 6.19 | % |

3-Year | | 5.50 | % | 7.16 | % | 10.44 | % |

1-Year | | 6.75 | % | 10.39 | % | 15.79 | % |

Growth of a Hypothetical $10,000 Investment

Returns assume reinvestment of all dividends and distributions but do not reflect the impact of taxes. The performance data quoted represent past performance. Past performance cannot guarantee future results, and current performance may be lower or higher than the performance quoted. Both the return from and the principal value of an investment in the Funds will fluctuate so that an investor’s shares, when redeemed, may be worrth more or less than their original cost. To obtain performance as of the most recent month-end, please contact Firsthand Funds by calling 1.888.884.2675 or go to www.firsthandfunds.com.

Holdings by Industry*

| | % Net Assets | |

Semiconductors | | 23.3 | % |

Software | | 20.9 | % |

Semiconductor Equipment | | 10.2 | % |

Communications Equipment | | 8.9 | % |

Internet | | 8.7 | % |

Networking | | 5.5 | % |

Photonics | | 5.2 | % |

Other Electronics | | 4.7 | % |

Peripherals | | 4.3 | % |

Computer | | 3.6 | % |

Communications | | 2.5 | % |

Net Cash | | 2.2 | % |

Top 10 Holdings**

| | % Net Assets | |

QUALCOMM, Inc. | | 6.3 | % |

Microsoft Corp. | | 6.1 | % |

Adobe Systems, Inc. | | 6.0 | % |

Taiwan Semi. Mfg. Co. - ADR | | 5.9 | % |

Cisco Systems, Inc. | | 5.5 | % |

Texas Instruments, Inc. | | 5.3 | % |

Applied Materials, Inc. | | 5.3 | % |

Corning, Inc. | | 5.2 | % |

Amdocs Ltd. | | 5.0 | % |

ASML Holding N.V. | | 4.9 | % |

* Based on percentage of net assets as of 12/31/06.

** Top 10 stock holdings total 55.5% of net assets. These holdings are current as of 12/31/06, and may not be representative of current or future investments. Firsthand includes only public companies in top 10 holdings.

FIRSTHAND TECHNOLOGY INNOVATORS FUND

Performance and Portfolio Discussion

How did the Fund perform in 2006?

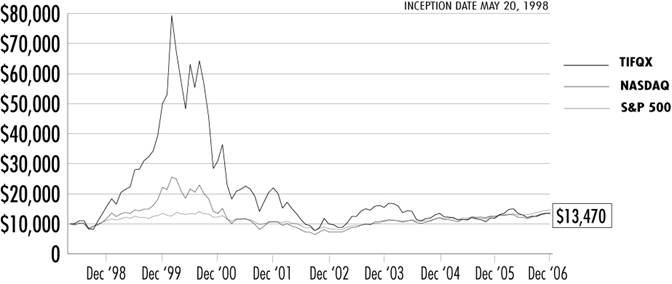

In 2006, Firsthand Technology Innovators Fund (TIFQX) posted a 13.06% gain, versus a 10.39% increase for the NASDAQ Composite Index and a 6.73% gain for the Lipper Science and Technology Fund Index. For the six months ended December 31, 2006, Firsthand Technology Innovators Fund rose 3.93% as compared to 11.60% and 9.93% gains for the NASDAQ and the Lipper peer group benchmarks, respectively.

Which industries had the greatest impact on the Fund’s performance?

For the year ended December 31, 2006, semiconductor stocks represented the portfolio’s largest weighting, followed by intellectual property and electronics. The Fund outperformed its benchmarks due to its holdings in electronics, communications equipment, and photonics companies.

Which individual holdings were the largest contributors to the Fund’s performance?

For the second straight year, the largest contributor to Fund performance was disk drive equipment supplier Intevac (IVAC), which saw its shares nearly double during 2006. The company provides equipment used to deposit specialized materials onto hard disks, and it profited from growing consumer demand for data storage devices and an industry-wide shift to a new recording technology (known as perpendicular recording).

After suffering through several lean years following the telecom collapse, optical equipment maker Finisar (FNSR) began to see its business turn around in 2006. Finisar returned to profitability as the company saw increased spending from phone companies upgrading their existing infrastructure, which included the push to rollout fiber optics to the home. Avici Systems (AVCI) also benefited from telecom spending growth after strong demand for its core networking router products resulted in the company’s highest quarterly revenue since mid-2001. Investors responded to the news by bidding up shares more than 84% on the day of the announcement and Avici finished the year up 98%.

Applied Films also helped Fund performance after the supplier of thin-film deposition equipment agreed to be acquired by Applied Materials (AMAT) for approximately $464 million during the second quarter of 2006. We also took profits and closed our position in Vyyo Inc. (VYYO) after the broadband access equipment maker saw its stock jump more than 60% in the first quarter of 2006.

Which holdings were the greatest detractors from the Fund’s performance?

Airspan Networks (AIRN) was the largest detractor from Fund performance in 2006. The company revealed late in the second quarter that a contract to supply WiMAX wireless-networking equipment to one of its biggest customers would be delayed. WiMAX is a technology similar to Wi-Fi, but offering faster wireless data access over distances as great as 30 miles. Better relative investment opportunities led us to close our position in Airspan Networks at a loss.

We also exited our position in Neoware (NWRE) after the software services company failed to meet analysts’ revenue expectations in the second quarter of 2006. The company blamed lower-than-expected sales during the last two weeks of the quarter for the revenue shortfall. Investors reacted swiftly to the news, knocking shares of Neoware down more than 40%.

Chipmaker Monolithic Power Systems (MPWR) struggled throughout 2006 as fears over a negative outcome from ongoing patent litigation kept its shares from advancing. Additionally, Monolithic revised its revenue guidance below analysts’ estimates on more than one occasion, shaking investors’ confidence in the company.

Fund Performance and Holdings Information (as of 12/31/06)

Firsthand Technology Innovators Fund vs. Market Indices

| | TIFQX | | NASDAQ | | S&P 500 | |

Since Inception (5/20/98) | | 3.52 | % | 3.64 | % | 4.52 | % |

5-Year | | -9.35 | % | 4.99 | % | 6.19 | % |

3-Year | | -4.59 | % | 7.16 | % | 10.44 | % |

1-Year | | 13.06 | % | 10.39 | % | 15.79 | % |

Growth of a Hypothetical $10,000 Investment

Returns assume reinvestment of all dividends and distributions but do not reflect the impact of taxes. The performance data quoted represent past performance. Past performance cannot guarantee future results, and current performance may be lower or higher than the performance quoted. Both the return from and the principal value of an investment in the Funds will fluctuate so that an investor’s shares, when redeemed, may be worrth more or less than their original cost. To obtain performance as of the most recent month-end, please contact Firsthand Funds by calling 1.888.884.2675 or go to www.firsthandfunds.com.

Holdings by Industry*

| | % Net Assets | |

Semiconductors | | 26.1 | % |

Intellectual Property | | 16.9 | % |

Other Electronics | | 15.1 | % |

Services | | 8.9 | % |

Networking | | 6.1 | % |

Photonics | | 5.7 | % |

Software | | 4.9 | % |

Electronic Design Automation | | 4.2 | % |

Internet | | 4.0 | % |

Communications | | 3.3 | % |

Communications Equipment | | 1.5 | % |

Other | | 2.6 | % |

Net Cash | | 0.7 | % |

Top 10 Holdings**

| | % Net Assets | |

Intevac, Inc. | | 7.9 | % |

VASCO Data Security Int’l, Inc. | | 4.4 | % |

PDF Solutions, Inc. | | 4.2 | % |

iGATE Corp. | | 4.1 | % |

Echelon Corp. | | 4.0 | % |

Microtune, Inc. | | 4.0 | % |

Synaptics, Inc. | | 3.1 | % |

Verint Systems, Inc. | | 3.0 | % |

Avici Systems, Inc. | | 2.8 | % |

Netlogic Microsystems, Inc. | | 2.5 | % |

* Based on percentage of net assets as of 12/31/06.

** Top 10 stock holdings total 40.0% of net assets. These holdings are current as of 12/31/06, and may not be representative of current or future investments. Firsthand includes only public companies in top 10 holdings.

FIRSTHAND E-COMMERCE FUND

Performance and Portfolio Discussion

How did the Fund perform in 2006?

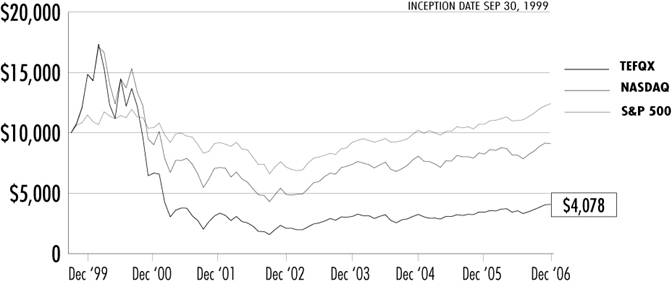

In 2006, Firsthand e-Commerce Fund (TEFQX) posted a 19.12% gain, versus a 10.39% increase for the NASDAQ Composite Index and a 6.73% gain for the Lipper Science and Technology Fund Index. For the six months ending December 31, 2006, Firsthand e-Commerce Fund rose 14.73% as compared to 11.60% and 9.93% gains for the NASDAQ and the Lipper peer group benchmarks, respectively.

Which industries had the greatest impact on the Fund’s performance?

For the period ending December 31, 2006, Internet stocks represented nearly half of the Fund’s portfolio, followed by holdings in the software industry. The Fund handily outperformed its benchmarks in 2006 due to its overweighting in these two categories.

Which individual holdings were the largest contributors to the Fund’s performance?

The Fund’s largest contributor in 2006 was Web content delivery firm Akamai Technologies (AKAM). Akamai survived the dot-com collapse by building a vast global network of servers to bring Web content and applications physically closer to users, thus enabling online data to be delivered faster and more efficiently. Akamai finished 2006 with an impressive gain of 167%, as demand grew for more robust multimedia online content, such as video, music, and software downloads.

2006 was a record year for merger and acquisition activity, and several of our portfolios benefited from acquisitions in the technology sector. We realized a nice gain in our position in RSA Security after the maker of identity management and encryption products agreed to be acquired by EMC (EMC) for approximately $2.1 billion in cash.

The diverse business model of Internet conglomerate IAC/InterActiveCorp (IACI) helped lift the company’s shares 31% during the period as strong results from Ticketmaster, Ask.com and Citysearch offset weakness in its real estate, lending, and retail websites. The stock also got a boost from its inclusion in the S&P 500 index in November 2006.

Shares of Adobe Systems (ADBE) helped lift Fund performance as investors welcomed the release of a new version of Adobe Acrobat, a program used to view and create PDF files, and the impending release of Creative Suite 3, a design software package that is expected to help drive sales in 2007.

Which holdings were the greatest detractors from the Fund’s performance?

Yahoo! (YHOO) was the largest detractor from Fund performance in 2006. The Internet portal stumbled amid increasing competition with Google in its online advertising business and was also affected by the delay of its new search platform, code-named “Panama,” which eventually was rolled out in the fourth quarter. These missteps weighed heavily on its forecast earnings and revenue and resulted in Yahoo! shares ending the period lower by 35%.

We liquidated our position in Netflix (NFLX) during the year, realizing sizeable gains since acquiring the stock in 2003. While we managed to sell a good portion of the Fund’s position in the first half of the year, the stock’s subsequent decline hurt the Fund prior to our closing out the position in the third quarter.

We also closed our position in CNET Networks (CNET) after the online media company, citing slowing online advertising sales, lowered its revenue guidance for two consecutive quarters in 2006.

Fund Performance and Holdings Information (as of 12/31/06)

Firsthand e-Commerce Fund vs. Market Indices

| | TEFQX | | NASDAQ | | S&P 500 | |

Since Inception (9/30/99) | | -11.63 | % | -1.28 | % | 3.04 | % |

5-Year | | 3.99 | % | 4.99 | % | 6.19 | % |

3-Year | | 9.79 | % | 7.16 | % | 10.44 | % |

1-Year | | 19.12 | % | 10.39 | % | 15.79 | % |

Growth of a Hypothetical $10,000 Investment

Returns assume reinvestment of all dividends and distributions but do not reflect the impact of taxes. The performance data quoted represent past performance. Past performance cannot guarantee future results, and current performance may be lower or higher than the performance quoted. Both the return from and the principal value of an investment in the Funds will fluctuate so that an investor’s shares, when redeemed, may be worrth more or less than their original cost. To obtain performance as of the most recent month-end, please contact Firsthand Funds by calling 1.888.884.2675 or go to www.firsthandfunds.com.

Holdings by Industry*

| | % Net Assets | |

Internet | | 48.9 | % |

Software | | 16.2 | % |

Communications | | 7.5 | % |

Other Electronics | | 6.3 | % |

Services | | 5.9 | % |

Computer | | 4.5 | % |

Networking | | 2.4 | % |

Other | | 1.2 | % |

Net Cash | | 7.1 | % |

Top 10 Holdings**

| | % Net Assets | |

Akamai Technologies, Inc. | | 6.0 | % |

Microsoft Corp. | | 5.9 | % |

eBay, Inc. | | 5.4 | % |

Yahoo! Inc. | | 4.6 | % |

IAC/InterActiveCorp | | 4.6 | % |

WebSideStory, Inc. | | 4.4 | % |

Adobe Systems, Inc. | | 4.2 | % |

Monster Worldwide, Inc. | | 4.0 | % |

NeuStar, Inc. | | 3.1 | % |

Dell, Inc. | | 3.1 | % |

* Based on percentage of net assets as of 12/31/06.

** Top 10 stock holdings total 45.3% of net assets. These holdings are current as of 12/31/06, and may not be representative of current or future investments. Firsthand includes only public companies in top 10 holdings.

FIRSTHAND GLOBAL TECHNOLOGY FUND

Performance and Portfolio Discussion

How did the Fund perform in 2006?

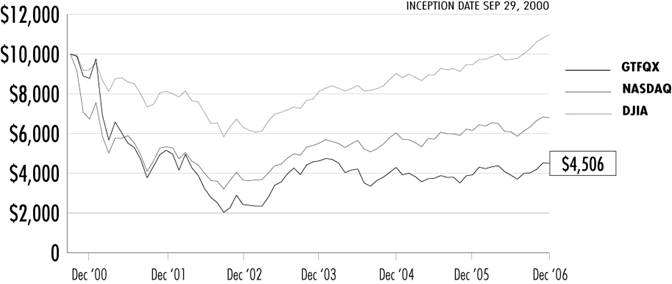

In 2006, Firsthand Global Technology Fund (GTFQX) posted a 14.83% gain, versus a 10.39% increase for the NASDAQ Composite Index and a 6.73% gain for the Lipper Science and Technology Fund Index. For the six months ended December 31, 2006, Firsthand Global Technology Fund rose 15.42% as compared to 11.60% and 9.93% gains for the NASDAQ and the Lipper peer group benchmarks, respectively.

Which industries had the greatest impact on the Fund’s performance?

For the year ended December 31, 2006, semiconductor and semiconductor equipment stocks represented the portfolio’s largest weightings, followed by electronics and services. The Fund outperformed its benchmarks due to its holdings in electronics, Internet, and communications companies.

Which holdings were the largest contributors to the Fund’s performance?

For the second straight year, the largest contributor to Fund performance was disk drive equipment supplier Intevac (IVAC), which saw its shares nearly double during 2006. The company provides equipment used to deposit specialized materials onto hard disks, and it profited from growing consumer demand for data storage devices and an industry-wide shift to a new recording technology (known as perpendicular recording).

The rapid growth in both the number of cellphone subscribers and the average revenue per user helped boost shares of China Mobile (CHL) during the period. The telecom giant is China’s leading wireless carrier and has yet to tap into China’s rural areas where cellphone adoption remains low. After seeing its share price rapidly ascend during the second half of the year, we decided to take our profits and close our position.

Baidu.com (BIDU) was another China holding that performed well in 2006. We closed our position in Baidu.com at a significant gain during Q4 after shares of the Chinese online search company rose as a result of increasing market share, strengthening quarterly earnings, and an announcement that the company would enter the Japanese search market in 2007.

Other holdings that aided Fund performance during the period included Taiwanese electronics manufacturer Hon Hai Precision Industry (no U.S. symbol), software vendor Amdocs (DOX), and semiconductor manufacturer ASML Holding N.V. (ASML).

Which holdings were the greatest detractors from the Fund’s performance?

UTStarcom (UTSI) was the greatest detractor from Fund performance in 2006. The company provides telecommunications equipment for wireline and wireless networks in China and other emerging markets and has struggled with slowing growth in China. UTStarcom’s recent foray into the handset market has yet to pay off, as the better-established handset manufacturers continue to dominate the market. After several years of lackluster performance with UTStarcom, we decided to close our position at a loss in the first quarter.

Another telecom holding that hurt Fund performance was Israel-based Alvarion (ALVR). Alvarion is a provider of broadband wireless equipment and saw its stock lose about a quarter of its value in 2006 as the company continues its rollout of WiMAX. WiMAX is similar to Wi-Fi, but offers faster wireless data access over distances as great as 30 miles. Alvarion has made a big investment on the adoption of WiMAX, which to this point has not panned out.

WiMAX troubles also befell wireless equipment maker Airspan Networks (AIRN). Airspan slumped after the company revealed late in the second quarter that a contract to supply WiMAX products to one of its biggest customers would be delayed. Better relative investment opportunities led us to close our position in Airspan Networks at a loss.

Fund Performance and Holdings Information (as of 12/31/06)

Firsthand Global Technology Fund vs. Market Indices

| | GTFQX | | NASDAQ | | S&P 500 | |

Since Inception (9/29/00) | | -11.96 | % | -5.99 | % | 1.49 | % |

5-Year | | -2.67 | % | 4.99 | % | 6.19 | % |

3-Year | | -0.88 | % | 7.16 | % | 10.44 | % |

1-Year | | 14.83 | % | 10.39 | % | 15.79 | % |

Growth of a Hypothetical $10,000 Investment

Returns assume reinvestment of all dividends and distributions but do not reflect the impact of taxes. The performance data quoted represent past performance. Past performance cannot guarantee future results, and current performance may be lower or higher than the performance quoted. Both the return from and the principal value of an investment in the Funds will fluctuate so that an investor’s shares, when redeemed, may be worrth more or less than their original cost. To obtain performance as of the most recent month-end, please contact Firsthand Funds by calling 1.888.884.2675 or go to www.firsthandfunds.com.

Holdings by Industry*

| | % Net Assets | |

Semiconductors | | 20.8 | % |

Semiconductor Equipment | | 15.2 | % |

Other Electronics | | 13.7 | % |

Services | | 9.1 | % |

Electronics Manufacturing Services | | 8.9 | % |

Internet | | 7.7 | % |

Software | | 7.4 | % |

Communications Equipment | | 5.4 | % |

Computer | | 2.3 | % |

Communications | | 2.3 | % |

Alternative Energy | | 2.0 | % |

Net Cash | | 5.2 | % |

Top 10 Holdings**

| | % Net Assets | |

ASML Holding N.V. | | 6.8 | % |

Sharp Corp. | | 5.6 | % |

SiRF Technology Holdings, Inc. | | 4.7 | % |

Tokyo Electron Ltd. | | 4.4 | % |

Hon Hai Precision - GDR | | 4.3 | % |

Alvarion Ltd. | | 4.3 | % |

Intevac, Inc. | | 4.0 | % |

Applied Materials, Inc. | | 4.0 | % |

Ctrip.com International, Ltd. - ADR | | 3.7 | % |

Chartered Semi. Mnfg., Ltd. - ADR | | 3.5 | % |

* Based on percentage of net assets as of 12/31/06.

** Top 10 stock holdings total 45.3% of net assets. These holdings are current as of 12/31/06, and may not be representative of current or future investments. Firsthand includes only public companies in top 10 holdings.

FIRSTHAND HEALTH SCIENCES FUND

Performance and Portfolio Discussion

How did the Fund perform in 2006?

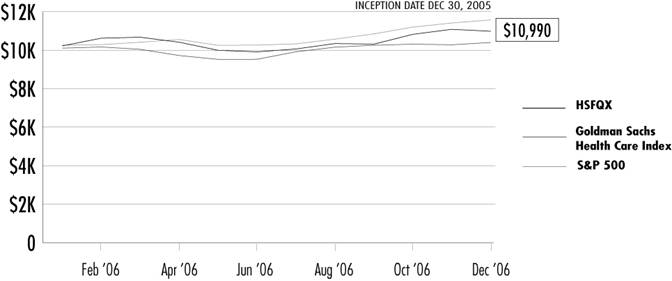

In 2006, Firsthand Health Sciences Fund (HSFQX) posted a 9.90% gain, versus a 4.07% increase for the Goldman Sachs Healthcare Index, a 4.80% gain for the Lipper Health and Biotech Fund Index, and a 15.79% gain for the S&P 500 Index. For the six months ended December 31, 2006, Firsthand Health Sciences Fund rose 10.79% as compared to 9.17% and 8.10% gains for the Goldman Sachs and Lipper peer group benchmarks, and a 12.74% gain for the S&P 500 Index.

Which industries had the greatest impact on the Fund’s performance?

For the year ended December 31, 2006, drug manufacturers represented the portfolio’s largest industry weighting followed by biotechnology and medical appliances holdings. The portfolio benefited from its diversification across market capitalizations, geographies and industry groups within the health care sector. Firsthand Health Sciences Fund outperformed its benchmarks primarily due to its overweight positions in the pharmaceutical and biotech industries.

Which individual holdings were the largest contributors to the Fund’s performance?

The Fund’s biggest contributor to performance in 2006 was Alexion Pharmaceuticals (ALXN). Shares of the biotech firm jumped after it announced promising results from a late-stage trial of one of its lead drug candidates for a rare type of anemia. Within the medical products industry, two foreign companies were performance stand-outs: Genmab A/S (no U.S. symbol), a Danish developer of human antibodies, and Ipsen (no U.S. symbol), a French pharmaceutical company. Wright Medical Group (WMGI) and Smith & Nephew (SNN), two relatively small orthopedics device companies, saw stock prices rebound after slumping in 2005.

The unprecedented wave of mergers and acquisitions of biotech firms by pharmaceutical companies confirmed the attractiveness of these innovative companies in terms of both products and valuation. The Fund held several stocks that were acquired at significant premiums during the year.

The more significant deals included Kos Pharmaceutical’s acquisition by Abbott Laboratories (ABT), Watson Pharmaceuticals’ (WPI) acquisition of Andrx, Myogen’s acquisition by Gilead Sciences (GILD), and the pending acquisitions of Tanox (TNOX) and ICOS (ICOS) by Genentech (DNA) and Eli Lilly (LLY) respectively.

Which holdings were the greatest detractors from the Fund’s performance?

Due to favorable market conditions in the health care sector, there were only a few portfolio holdings that significantly hurt Fund performance on an absolute basis in 2006. The largest detractor was biotech firm Onyx Pharmaceuticals (ONXX). Onyx hit a multi-year low after data showed that its kidney cancer drug Nexavar was ineffective in treating patients with advanced skin cancer.

Similar disappointing clinical trial results for Critical Therapeutics’ (CRTX) anti-inflammatory drug also sent shares of the small-cap biotech firm significantly lower in 2006.

Fund Performance and Holdings Information (as of 12/31/06)

Firsthand Health Sciences Fund vs. Market Indices

| | | | Goldman Sachs | | | |

| | | | Health Care | | | |

| | HSFQX | | Index | | S&P 500 | |

Since Inception (12/30/05) | | 9.84 | % | 4.04 | % | 15.70 | % |

1-Year | | 9.90 | % | 4.07 | % | 15.79 | % |

Growth of a Hypothetical $10,000 Investment

Returns assume reinvestment of all dividends and distributions but do not reflect the impact of taxes. The performance data quoted represent past performance. Past performance cannot guarantee future results, and current performance may be lower or higher than the performance quoted. Both the return from and the principal value of an investment in the Funds will fluctuate so that an investor’s shares, when redeemed, may be worrth more or less than their original cost. To obtain performance as of the most recent month-end, please contact Firsthand Funds by calling 1.888.884.2675 or go to www.firsthandfunds.com.

Holdings by Industry*

| | % Net Assets | |

Drug Manufacturers | | 48.9 | % |

Biotechnology | | 26.2 | % |

Medical Appliances & Equipment | | 5.0 | % |

Health Care Plans | | 2.3 | % |

Medical Instruments & Supplies | | 2.0 | % |

Drug Delivery | | 1.5 | % |

Other | | 6.6 | % |

Net Cash | | 7.5 | % |

Top 10 Holdings**

| | % Net Assets | |

Pfizer, Inc. | | 4.4 | % |

Glaxosmithkline PLC - ADR | | 3.8 | % |

Eli Lilly & Co. | | 3.7 | % |

Amgen, Inc. | | 3.4 | % |

Novartis AG - ADR | | 3.1 | % |

Schering-Plough Corp. | | 3.0 | % |

ICOS Corp. | | 2.5 | % |

Biogen Idec, Inc. | | 2.5 | % |

Gilead Sciences, Inc. | | 2.5 | % |

Alexion Pharmaceuticals, Inc. | | 2.5 | % |

* Based on percentage of net assets as of 12/31/06.

** Top 10 stock holdings total 31.4% of net assets. These holdings are current as of 12/31/06, and may not be representative of current or future investments. Firsthand includes only public companies in top 10 holdings.

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

To the Shareholders and Board of Trustees

Firsthand Funds

San Jose, California

We have audited the accompanying statements of assets and liabilities of Firsthand Funds (the “Funds”) comprising, respectively, Firsthand Technology Value Fund, Firsthand Technology Leaders Fund, Firsthand Technology Innovators Fund, Firsthand e-Commerce Fund, Firsthand Global Technology Fund, and Firsthand Health Sciences Fund, including the portfolios of investments as of December 31, 2006, and the related statements of operations for the year then ended, statements of changes in net assets and the financial highlights for the periods indicated thereon. These financial statements and financial highlights are the responsibility of the Funds’ management. Our responsibility is to express an opinion on these financial statements and financial highlights based on our audits.

We conducted our audits in accordance with standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audits to obtain reasonable assurance about whether the financial statements and financial highlights are free of material misstatement. The Funds are not required to have, nor were we engaged to perform, an audit of the Funds’ internal control over financial reporting. Our audits included consideration of internal control over financial reporting as a basis for designing audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Funds’ internal control over financial reporting. Accordingly, we express no such opinion. An audit also includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. Our procedures included confirmation of securities owned as of December 31, 2006, by correspondence with the custodian, brokers, and by other auditing procedures as deemed necessary. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the financial statements and financial highlights referred to above present fairly, in all material respects, the financial position of Firsthand Funds as of December 31, 2006, the results of their operations, the changes in their net assets, and the financial highlights for the periods referred to above, in conformity with accounting principles generally accepted in the United States of America.

TAIT, WELLER & BAKER, LLP

Philadelphia, Pennsylvania

February 15, 2007

FIRSTHAND TECHNOLOGY VALUE FUND

Portfolio of Investments (as of 12/31/06)

| | SHARES | | MARKET VALUE | |

| | | | | |

COMMON STOCK - 98.5% | | | | | |

ADVANCED MATERIALS - 1.3% | | | | | |

UCT Coatings, Inc., Series B (2) * | | 500,000 | | $ | 5,000,000 | |

| | | | | |

ALTERNATIVE ENERGY - 4.1% | | | | | |

Evergreen Solar, Inc. * | | 500,000 | | 3,785,000 | |

Solaicx, Series B (1) (2) * | | 6,000,000 | | 7,247,400 | |

SoloPower, Series A (1) (2) * | | 2,721,088 | | 3,999,999 | |

| | | | 15,032,399 | |

COMMUNICATIONS - 1.6% | | | | | |

ViaSat, Inc. * | | 194,300 | | 5,792,083 | |

| | | | | |

COMMUNICATIONS EQUIPMENT - 7.6% | | | | | |

Harris Corp. | | 100,000 | | 4,586,000 | |

Stratex Networks, Inc. * | | 1,417,036 | | 6,844,284 | |

Tekelec, Inc. * | | 651,800 | | 9,666,194 | |

Tellabs, Inc. * | | 335,000 | | 3,437,100 | |

UTStarcom, Inc. * | | 403,300 | | 3,528,875 | |

| | | | 28,062,453 | |

COMPUTER - 1.6% | | | | | |

Sun Microsystems, Inc. * | | 1,100,000 | | 5,962,000 | |

| | | | | |

DEFENSE & AEROSPACE - 0.9% | | | | | |

FLIR Systems, Inc. * | | 103,456 | | 3,293,004 | |

| | | | | |

ELECTRONIC ENTERTAINMENT - 3.6% | | | | | |

Nintendo Co., Ltd. - ADR | | 413,407 | | 13,435,728 | |

| | | | | |

INTELLECTUAL PROPERTY - 3.0% | | | | | |

Silicon Genesis Corp., Common (1) (2) * | | 743,077 | | 41,612 | |

Silicon Genesis Corp., Series 1-D (1) (2) * | | 850,830 | | 4,363,141 | |

Silicon Genesis Corp., Series 1-E (1) (2) * | | 4,071,226 | | 6,701,239 | |

| | | | 11,105,992 | |

INTERNET - 8.6% | | | | | |

Akamai Technologies, Inc. * | | 285,800 | | 15,181,696 | |

Ctrip.com International Ltd. - ADR | | 79,400 | | 4,960,912 | |

Napster, Inc. (3) * | | 984,900 | | 3,575,187 | |

Yahoo! Inc. * | | 321,422 | | 8,209,118 | |

| | | | 31,926,913 | |

NETWORKING - 3.8% | | | | | |

Caspian Networks, Inc., Common (2) * | | 337 | | 0 | |

Cisco Systems, Inc. * | | 480,000 | | 13,118,400 | |

| | | | | | |

See accompanying notes to financial statements

| | SHARES | | MARKET VALUE | |

| | | | | |

IP Unity, Inc., Series C (2) * | | 1,104,265 | | $ | 753,970 | |

IP Unity, Inc., Series E (2) * | | 193,042 | | 118,844 | |

Polaris Networks, Inc., Series A (2) * | | 297,848 | | 0 | |

| | | | 13,991,214 | |

OTHER ELECTRONICS - 5.5% | | | | | |

Intevac, Inc. * | | 621,400 | | 16,125,330 | |

Zebra Technologies Corp., Class A * | | 124,500 | | 4,331,355 | |

| | | | 20,456,685 | |

PERIPHERALS - 5.6% | | | | | |

Seagate Technology, Inc. | | 789,700 | | 20,927,050 | |

| | | | | |

PHOTONICS - 6.5% | | | | | |

Celox Networks, Inc., Common (2) * | | 138,121 | | 0 | |

Celox Networks, Inc., Series A-1 (2) * | | 1,000,000 | | 0 | |

Corning, Inc. * | | 1,029,500 | | 19,261,945 | |

JDS Uniphase Corp. * | | 300,000 | | 4,998,000 | |

Luminous Networks, Inc., Common (2) * | | 28,513 | | 0 | |

Luminous Networks, Inc., Series A1 (2) * | | 129,664 | | 0 | |

Luminous Networks, Inc., Series B1 (2) * | | 259,236 | | 0 | |

| | | | 24,259,945 | |

SEMICONDUCTOR EQUIPMENT - 8.2% | | | | | |

Applied Materials, Inc. | | 800,000 | | 14,760,000 | |

ASML Holding N.V. * | | 500,000 | | 12,315,000 | |

FormFactor, Inc. * | | 94,594 | | 3,523,627 | |

| | | | 30,598,627 | |

SEMICONDUCTORS - 31.4% | | | | | |

Advanced Micro Devices, Inc. * | | 100,000 | | 2,035,000 | |

AuthenTec, Inc., Series C (2) * | | 1,472,495 | | 1,474,866 | |

AuthenTec, Inc., Series D (2) * | | 290,958 | | 290,958 | |

Chartered Semiconductor Manufacturing Ltd. - ADR * | | 926,100 | | 7,732,935 | |

Clarisay, Inc., Series B (1) (2) * | | 2,605,306 | | 0 | |

Clarisay, Inc., Series C (1) (2) * | | 7,194,244 | | 0 | |

Cypress Semiconductor Corp. * | | 1,785,100 | | 30,114,636 | |

Global Locate, Inc., Series A (1) (2) * | | 6,030,896 | | 2,052,917 | |

Global Locate, Inc., Series C (1) (2) * | | 1,111,111 | | 378,222 | |

Global Locate, Inc., Series D (1) (2) * | | 932,835 | | 749,999 | |

Ikanos Communications, Inc. * | | 100,000 | | 869,000 | |

Kopin Corp. * | | 299,100 | | 1,067,787 | |

MEMC Electronic Materials, Inc. * | | 428,300 | | 16,763,662 | |

PMC-Sierra, Inc. * | | 655,700 | | 4,399,747 | |

Semiconductor Manufacturing International Corp. * | | 1,000,000 | | 6,440,000 | |

SiRF Technology Holdings, Inc. * | | 457,500 | | 11,675,400 | |

| | | | | | |

See accompanying notes to financial statements

| | SHARES | | MARKET VALUE | |

| | | | | |

Skyworks Solutions, Inc. * | | 498,300 | | $ | 3,527,964 | |

Soitec S.A. * | | 72,740 | | 2,584,704 | |

Texas Instruments, Inc. | | 140,000 | | 4,032,000 | |

TranSwitch Corp. * | | 2,383,000 | | 3,336,200 | |

TriQuint Semiconductor, Inc. * | | 1,432,400 | | 6,445,800 | |

Zoran Corp. * | | 710,500 | | 10,359,090 | |

| | | | 116,330,887 | |

SERVICES - 1.5% | | | | | |

aQuantive, Inc. * | | 158,300 | | 3,903,678 | |

TeleCommunication Systems, Inc., Class A * | | 557,600 | | 1,728,560 | |

| | | | 5,632,238 | |

SOFTWARE - 3.7% | | | | | |

Citrix Systems, Inc. * | | 127,000 | | 3,435,350 | |

Comverse Technology, Inc. * | | 304,500 | | 6,427,995 | |

Witness Systems, Inc. * | | 215,003 | | 3,769,003 | |

| | | | 13,632,348 | |

Total COMMON STOCK | | | | 365,439,566 | |

| | | | | |

WARRANTS - 0.3% | | | | | |

ADVANCED MATERIALS - 0.0% | | | | | |

UCT Coatings, Inc., Common Warrant (2) * | | 600,000 | | 200 | |

| | | | | |

INTELLECTUAL PROPERTY - 0.2% | | | | | |

Silicon Genesis Corp., 1-E Warrant (1) (2) * | | 1,257,859 | | 1,070,439 | |

Silicon Genesis Corp., Common Warrant (1) (2) * | | 59,147 | | 59 | |

Silicon Genesis Corp., Common Warrant (1) (2) * | | 37,982 | | 38 | |

| | | | 1,070,536 | |

NETWORKING - 0.0% | | | | | |

IP Unity, Inc., E Warrant (2) * | | 69,496 | | 69 | |

Polaris Networks, Inc., Convertible Warrant (2) * | | 75,712 | | 0 | |

| | | | 69 | |

PHOTONICS - 0.0% | | | | | |

Celox Networks, Inc., A-1 Warrant (2) * | | 500,000 | | 0 | |

Luminous Networks, Inc., Common Warrant (2) * | | 3,822 | | 0 | |

| | | | 0 | |

SEMICONDUCTORS - 0.1% | | | | | |

AuthenTec, Inc., C Warrant (2) * | | 392,665 | | 196,497 | |

Clarisay, Inc., Warrants (1) (2) * | | 2,350,000 | | 0 | |

Global Locate, Inc., Board Warrants (1) (2) * | | 75,000 | | 375 | |

Global Locate, Inc., Board Warrants (1) (2) * | | 75,000 | | 375 | |

Global Locate, Inc., Board Warrants (1) (2) * | | 18,750 | | 94 | |

Global Locate, Inc., Board Warrants (1) (2) * | | 75,000 | | 375 | |

| | | | | | |

See accompanying notes to financial statements

| | SHARES/

PRINCIPAL | | MARKET VALUE | |

| | | | | |

Global Locate, Inc., C Warrant (1) (2) * | | 370,370 | | $ | 1,852 | |

Global Locate, Inc., D Warrant (1) (2) * | | 233,208 | | 2,332 | |

| | | | 201,900 | |

Total WARRANTS | | | | 1,272,705 | |

| | | | | |

CONVERTIBLE BONDS - 0.4% | | | | | |

ALTERNATIVE ENERGY - 0.4% | | | | | |

Solaicx, 10.25% (1) (2) | | 1,333,334 | | 1,333,334 | |

| | | | | |

NETWORKING - 0.0% | | | | | |

Polaris Networks, Inc., 10.00% (2) * | | 100,949 | | 0 | |

| | | | | |

SEMICONDUCTORS - 0.0% | | | | | |

Clarisay, Inc., 8.00% (1) (2) * | | 2,350,000 | | 0 | |

| | | | | |

Total CONVERTIBLE BONDS | | | | 1,333,334 | |

| | | | | |

CASH EQUIVALENTS - 0.1% | | | | | |

PNC Bank Money Market Portfolio | | 423,225 | | 423,225 | |

Total CASH EQUIVALENTS | | | | 423,225 | |

| | | | | |

Total Investments (Cost $462,543,743) - 99.3% | | | | 368,468,830 | |

Other assets in excess of liabilities - 0.7% | | | | 2,470,812 | |

NET ASSETS - 100.0% | | | | $ | 370,939,642 | |

*Non-income producing security

(1)Affiliated issuer

(2)Restricted security

(3)Napster, Inc. has the right to put a restriction of public sale on 600,000 shares of the Fund’s Napster, Inc. holding. As of December 31, 2006 there are no restrictions on the Fund’s shares of Napster, Inc.

ADR American Depositary Receipt

See accompanying notes to financial statements

FIRSTHAND TECHNOLOGY LEADERS FUND

Portfolio of Investments (as of 12/31/06)

| | SHARES | | MARKET VALUE | |

| | | | | |

COMMON STOCK - 97.8% | | | | | |

COMMUNICATIONS - 2.5% | | | | | |

China Mobile Hong Kong Ltd. - ADR | | 42,383 | | $ | 1,831,793 | |

| | | | | |

COMMUNICATIONS EQUIPMENT - 8.9% | | | | | |

Nokia Corp. - ADR | | 94,490 | | 1,920,037 | |

QUALCOMM, Inc. | | 123,235 | | 4,657,050 | |

| | | | 6,577,087 | |

COMPUTER - 3.6% | | | | | |

Apple Computer, Inc. * | | 31,484 | | 2,671,103 | |

| | | | | |

INTERNET - 8.7% | | | | | |

eBay, Inc. * | | 103,695 | | 3,118,109 | |

Google, Inc., Class A * | | 7,255 | | 3,340,782 | |

| | | | 6,458,891 | |

NETWORKING - 5.5% | | | | | |

Cisco Systems, Inc. * | | 149,770 | | 4,093,214 | |

| | | | | |

OTHER ELECTRONICS - 4.7% | | | | | |

Gemstar-TV Guide International, Inc. * | | 7,191 | | 28,836 | |

L-1 Identity Solutions, Inc. * | | 228,600 | | 3,458,718 | |

| | | | 3,487,554 | |

PERIPHERALS - 4.3% | | | | | |

Seagate Technology, Inc. | | 118,957 | | 3,152,361 | |

| | | | | |

PHOTONICS - 5.2% | | | | | |

Corning, Inc. * | | 207,527 | | 3,882,830 | |

| | | | | |

SEMICONDUCTOR EQUIPMENT - 10.2% | | | | | |

Applied Materials, Inc. | | 212,000 | | 3,911,400 | |

ASML Holding N.V. * | | 147,296 | | 3,627,900 | |

| | | | 7,539,300 | |

SEMICONDUCTORS - 23.3% | | | | | |

Altera Corp. * | | 146,987 | | 2,892,704 | |

Broadcom Corp., Class A * | | 111,825 | | 3,613,066 | |

Taiwan Semiconductor Manufacturing Co. - ADR | | 401,275 | | 4,385,936 | |

Texas Instruments, Inc. | | 136,611 | | 3,934,397 | |

Xilinx, Inc. | | 101,395 | | 2,414,215 | |

| | | | 17,240,318 | |

SOFTWARE - 20.9% | | | | | |

Adobe Systems, Inc. * | | 108,130 | | 4,446,306 | |

Amdocs Ltd. * | | 95,909 | | 3,716,474 | |

| | | | | | |

See accompanying notes to financial statements

| | | | SHARES | | MARKET VALUE | |

| | | | | | | |

Electronic Arts, Inc. * | | | | 54,200 | | $ | 2,729,512 | |

Microsoft Corp. | | | | 152,250 | | 4,546,184 | |

| | | | | | 15,438,476 | |

Total COMMON STOCK | | | | | | 72,372,927 | |

| | | | | | | |

CASH EQUIVALENTS - 1.8% | | | | | | | |

PNC Bank Money Market Portfolio | | | | 1,314,665 | | 1,314,665 | |

Total CASH EQUIVALENTS | | | | | | 1,314,665 | |

| | | | | | | |

Total Investments (Cost $59,377,588) - 99.6% | | | | | | 73,687,592 | |

Other assets in excess of liabilities - 0.4% | | | | | | 305,630 | |

NET ASSETS - 100.0% | | | | | | $ | 73,993,222 | |

*Non-income producing security

ADR American Depositary Receipt

See accompanying notes to financial statements

FIRSTHAND TECHNOLOGY INNOVATORS FUND

Portfolio of Investments (as of 12/31/06)

| | SHARES | | MARKET VALUE | |

| | | | | |

COMMON STOCK - 96.7% | | | | | |

COMMUNICATIONS - 3.3% | | | | | |

NeuStar, Inc. * | | 18,752 | | $ | 608,315 | |

Symmetricom, Inc. * | | 30,000 | | 267,600 | |

| | | | 875,915 | |

COMMUNICATIONS EQUIPMENT - 1.5% | | | | | |

Finisar Corp. * | | 121,855 | | 393,592 | |

| | | | | |

COMPUTER - 1.1% | | | | | |

Rackable Systems, Inc. * | | 9,377 | | 290,406 | |

| | | | | |

ELECTRONIC DESIGN AUTOMATION - 4.2% | | | | | |

PDF Solutions, Inc. * | | 76,400 | | 1,103,980 | |

| | | | | |

INTELLECTUAL PROPERTY - 16.7% | | | | | |

Silicon Genesis Corp., Common (1) (2) * | | 108,815 | | 6,094 | |

Silicon Genesis Corp., Series 1-C (1) (2) * | | 82,914 | | 1,731,244 | |

Silicon Genesis Corp., Series 1-E (1) (2) * | | 1,633,254 | | 2,688,336 | |

| | | | 4,425,674 | |

INTERNET - 4.0% | | | | | |

LivePerson, Inc. * | | 102,400 | | 535,552 | |

WebSideStory, Inc. * | | 42,400 | | 536,784 | |

| | | | 1,072,336 | |

NETWORKING - 6.1% | | | | | |

Echelon Corp. * | | 131,198 | | 1,049,584 | |

IP Unity, Inc., Series C (2) * | | 827,957 | | 565,312 | |

| | | | 1,614,896 | |

OTHER ELECTRONICS - 15.1% | | | | | |

3D Systems Corp. * | | 11,900 | | 189,924 | |

Intevac, Inc. * | | 80,300 | | 2,083,785 | |

Microvision, Inc. * | | 180,300 | | 575,157 | |

VASCO Data Security International, Inc. * | | 98,100 | | 1,162,485 | |

| | | | 4,011,351 | |

PERIPHERALS - 1.1% | | | | | |

Universal Display Corp. * | | 20,000 | | 300,200 | |

| | | | | |

PHOTONICS - 5.7% | | | | | |

Avanex Corp. * | | 50,000 | | 94,500 | |

Avici Systems, Inc. * | | 95,000 | | 736,250 | |

EXFO Electro-Optical Engineering, Inc. * | | 50,100 | | 281,562 | |

Luminous Networks, Inc., Common (2) * | | 49,979 | | 0 | |

Luminous Networks, Inc., Series A1 (2) * | | 227,282 | | 0 | |

| | | | | | |

See accompanying notes to financial statements

| | SHARES | | MARKET VALUE | |

| | | | | |

Oplink Communications, Inc. * | | 20,000 | | $ | 411,200 | |

| | | | 1,523,512 | |

SEMICONDUCTOR EQUIPMENT - 0.4% | | | | | |

Therma-Wave, Inc. * | | 91,300 | | 108,647 | |

| | | | | |

SEMICONDUCTORS - 25.7% | | | | | |

AuthenTec, Inc., Series C (2) * | | 736,248 | | 737,433 | |

EMCORE Corp. * | | 84,353 | | 466,472 | |

Kopin Corp. * | | 68,700 | | 245,259 | |

Microtune, Inc. * | | 223,050 | | 1,048,335 | |

Monolithic Power Systems, Inc. * | | 39,800 | | 442,178 | |

Netlogic Microsystems, Inc. * | | 30,000 | | 650,700 | |

Nextest Systems Corp. * | | 25,200 | | 284,004 | |

PLX Technology, Inc. * | | 38,000 | | 495,520 | |

Ramtron International Corp. * | | 80,000 | | 297,600 | |

Silicon Optix, Inc., Series B (2) * | | 1,111,111 | | 700,000 | |

Synaptics, Inc. * | | 27,300 | | 810,537 | |

Trident Microsystems, Inc. * | | 20,000 | | 363,600 | |

Zygo Corp. * | | 15,000 | | 246,750 | |

| | | | 6,788,388 | |

SERVICES - 6.9% | | | | | |

iGATE Corp. * | | 157,720 | | 1,085,114 | |

Innovion Corp., Series C (1) (2) * | | 1,500,000 | | 744,675 | |

| | | | 1,829,789 | |

SOFTWARE - 4.9% | | | | | |

Verint Systems, Inc. * | | 23,200 | | 795,296 | |

Witness Systems, Inc. * | | 29,400 | | 515,382 | |

| | | | 1,310,678 | |

Total COMMON STOCK | | | | 25,649,364 | |

| | | | | |

WARRANTS - 0.6% | | | | | |

INTELLECTUAL PROPERTY - 0.2% | | | | | |

Silicon Genesis Corp., 1-E Warrant (1) (2) * | | 94,339 | | 55,283 | |

| | | | | |

PHOTONICS - 0.0% | | | | | |

Luminous Networks, Inc., Common Warrant (2) * | | 6,699 | | 0 | |

| | | | | |

SEMICONDUCTORS - 0.4% | | | | | |

AuthenTec, Inc., C Warrant (2) * | | 196,333 | | 98,248 | |

| | | | | | |

See accompanying notes to financial statements

| | SHARES/

PRINCIPAL | | MARKET VALUE | |

| | | | | |

SERVICES - 0.0% | | | | | |

Innovion Corp., Warrant (1) (2) * | | 30,129 | | $ | 30 | |

Innovion Corp., Warrant (1) (2) * | | 602,577 | | 603 | |

| | | | 633 | |

Total WARRANTS | | | | 154,164 | |

| | | | | |

CONVERTIBLE BONDS - 2.0% | | | | | |

SERVICES - 2.0% | | | | | |

Innovion Corp., 9.50% (1) (2) * | | 602,577 | | 542,319 | |

Total CONVERTIBLE BONDS | | | | 542,319 | |

| | | | | |

CASH EQUIVALENTS - 1.2% | | | | | |

PNC Bank Money Market Portfolio | | 325,001 | | 325,001 | |

Total CASH EQUIVALENTS | | | | 325,001 | |

| | | | | |

Total Investments (Cost $32,775,220) - 100.5% | | | | 26,670,848 | |

Liabilities in excess of other assets - (0.5)% | | | | (140,795 | ) |

NET ASSETS - 100.0% | | | | $ | 26,530,053 | |

*Non-income producing security

(1)Affiliated issuer

(2)Restricted security

See accompanying notes to financial statements

FIRSTHAND E-COMMERCE FUND

Portfolio of Investments (as of 12/31/06)

| | SHARES | | MARKET VALUE | |

| | | | | |

COMMON STOCK - 92.9% | | | | | |

COMMUNICATIONS - 7.5% | | | | | |

Comcast Corp., Special Class A * | | 15,000 | | $ | 628,200 | |

Equinix, Inc. * | | 15,000 | | 1,134,300 | |

NeuStar, Inc. * | | 38,400 | | 1,245,696 | |

| | | | 3,008,196 | |

COMPUTER - 4.5% | | | | | |

Apple Computer, Inc. * | | 7,000 | | 593,880 | |

Dell, Inc. * | | 49,200 | | 1,234,428 | |

| | | | 1,828,308 | |

INTERNET - 48.9% | | | | | |

51job, Inc. - ADR * | | 17,368 | | 296,472 | |

Akamai Technologies, Inc. * | | 45,500 | | 2,416,960 | |

Amazon.com, Inc. * | | 23,700 | | 935,202 | |

Baidu.com, Inc. - ADR * | | 4,873 | | 549,285 | |

Ctrip.com International Ltd. - ADR | | 14,499 | | 905,898 | |

CyberSource Corp. * | | 41,814 | | 460,790 | |

eBay, Inc. * | | 71,904 | | 2,162,153 | |

Google, Inc., Class A * | | 1,000 | | 460,480 | |

IAC/InterActiveCorp * | | 49,684 | | 1,846,257 | |

LivePerson, Inc. * | | 140,000 | | 732,200 | |

Monster Worldwide, Inc. * | | 34,900 | | 1,627,736 | |

Napster, Inc. * | | 104,500 | | 379,335 | |

RedEnvelope, Inc. * | | 42,700 | | 301,462 | |

The9 Ltd. - ADR * | | 30,000 | | 966,600 | |

ValueClick, Inc. * | | 46,300 | | 1,094,069 | |

VistaPrint Ltd. * | | 14,137 | | 468,076 | |

VitalStream Holdings, Inc. * | | 46,212 | | 463,968 | |

WebSideStory, Inc. * | | 138,967 | | 1,759,322 | |

Yahoo! Inc. * | | 72,534 | | 1,852,518 | |

| | | | 19,678,783 | |

MEDIA - 1.2% | | | | | |

News Corp., Class B | | 21,960 | | 488,830 | |

| | | | | |

NETWORKING - 2.4% | | | | | |

Cisco Systems, Inc. * | | 35,000 | | 956,550 | |

| | | | | |

OTHER ELECTRONICS - 6.3% | | | | | |

L-1 Identity Solutions, Inc. * | | 60,000 | | 907,800 | |

VASCO Data Security International, Inc. * | | 40,000 | | 474,000 | |

VeriFone Holdings, Inc. * | | 33,185 | | 1,174,749 | |

| | | | 2,556,549 | |

| | | | | | |

See accompanying notes to financial statements

| | SHARES | | MARKET VALUE | |

| | | | | |

SERVICES - 5.9% | | | | | |

aQuantive, Inc. * | | 42,713 | | $ | 1,053,303 | |

First Data Corp. | | 35,000 | | 893,200 | |

Western Union Co. | | 20,000 | | 448,400 | |

| | | | 2,394,903 | |

SOFTWARE - 16.2% | | | | | |

Adobe Systems, Inc. * | | 40,869 | | 1,680,533 | |

CheckFree Corp. * | | 21,277 | | 854,484 | |

Digital Insight Corp. * | | 25,095 | | 965,907 | |

Microsoft Corp. | | 80,000 | | 2,388,800 | |

RightNow Technologies, Inc. * | | 24,730 | | 425,851 | |

VeriSign, Inc. * | | 8,200 | | 197,210 | |

| | | | 6,512,785 | |

Total COMMON STOCK | | | | 37,424,904 | |

| | | | | |

CASH EQUIVALENTS - 7.5% | | | | | |

PNC Bank Money Market Portfolio | | 3,031,958 | | 3,031,958 | |

Total CASH EQUIVALENTS | | | | 3,031,958 | |

| | | | | |

Total Investments (Cost $32,417,399) - 100.4% | | | | 40,456,862 | |

Liabilities in excess of other assets - (0.4)% | | | | (152,051 | ) |

NET ASSETS - 100.0% | | | | $ | 40,304,811 | |

| | | | | | | |

*Non-income producing security

ADR American Depositary Receipt

See accompanying notes to financial statements

FIRSTHAND GLOBAL TECHNOLOGY FUND

Portfolio of Investments (as of 12/31/06)

| | SHARES | | MARKET VALUE | |

| | | | | |

COMMON STOCK - 94.8% | | | | | |

ALTERNATIVE ENERGY - 2.0% | | | | | |

Suntech Power Holdings Co., Ltd. - ADR * | | 8,000 | | $ | 272,080 | |

| | | | | |

COMMUNICATIONS - 2.3% | | | | | |

Singapore Telecommunications Ltd. - ADR | | 14,100 | | 301,427 | |

| | | | | |

COMMUNICATIONS EQUIPMENT - 5.4% | | | | | |

Alvarion Ltd. * | | 85,335 | | 573,451 | |

Nokia Corp. - ADR | | 7,200 | | 146,304 | |

| | | | 719,755 | |

COMPUTER - 2.3% | | | | | |

Lenovo Group Ltd. - ADR | | 38,000 | | 308,799 | |

| | | | | |

ELECTRONICS MANUFACTURING SERVICES - 8.9% | | | | | |

Flextronics International Ltd. * | | 29,800 | | 342,104 | |

Hon Hai Precision - GDR | | 40,270 | | 574,669 | |

Quanta Computer, Inc. - GDR | | 29,984 | | 271,913 | |

| | | | 1,188,686 | |

INTERNET - 7.7% | | | | | |

51job, Inc. - ADR * | | 8,880 | | 151,582 | |

Ctrip.com International Ltd. - ADR | | 7,855 | | 490,780 | |

The9 Ltd. - ADR * | | 12,000 | | 386,640 | |

| | | | 1,029,002 | |

OTHER ELECTRONICS - 13.7% | | | | | |

Intevac, Inc. * | | 20,400 | | 529,380 | |

LG.Philips LCD Co., Ltd. - ADR * | | 14,600 | | 220,022 | |

NIDEC Corp. | | 17,200 | | 333,336 | |

Sharp Corp. | | 43,288 | | 744,841 | |

| | | | 1,827,579 | |

SEMICONDUCTOR EQUIPMENT - 15.2% | | | | | |

Applied Materials, Inc. | | 28,672 | | 528,998 | |

ASML Holding N.V. * | | 36,758 | | 905,350 | |

Tokyo Electron Ltd. | | 7,500 | | 590,482 | |